Engineering Economics

|

|

|

- Maria Banks

- 6 years ago

- Views:

Transcription

1 Engineering Economics Lecture 7 Er. Sushant Raj Giri B.E. (Industrial Engineering), MBA Lecturer Department of Industrial Engineering Contemporary Engineering Economics 3 rd Edition Chan S Park 1

2 Chapter 9 Rate of Return Analysis Rate of Return Methods for Finding ROR Internal Rate of Return (IRR) Criterion Incremental Analysis Mutually Exclusive Alternatives 2

3 Rate of Return Definition: A relative percentage method which measures the yield as a percentage of investment over the life of a project Example: Vincent Gogh s painting Irises John Whitney Payson bought the art at $80,000. John sold the art at $53.9 million in 40 years. What is the rate of return on John s investment? 3

4 Rate of Return Given: P =$80,000, F = $53.9M, and N = 40 years Find: i Solution: $53. 9 M = $80, 000( 1+ i) i = % 40 0 $80,000 $53.9M 40 4

5 Meaning of Rate of Return In 1970, when Wal-Mart Stores, Inc. went public, an investment of 100 shares cost $1,650. That investment would have been worth $13,312,000 on January 31, What is the rate of return on that investment? 5

6 Solution: $13,312,000 0 $1, Given: P = $1,650 F = $13,312,000 N = 30 Find i: F = P( 1+ i) N $13,312,000 = $1,650 (1 + i ) 30 i = 34.97% Rate of Return 6

7 Suppose that you invested that amount ($1,650) in a savings account at 6% per year. Then, you could have only $9,477 on January, What is the meaning of this 6% interest here? This is your opportunity cost if putting money in savings account was the best you can do at that time! 7

8 So, in 1970, as long as you earn more than 6% interest in another investment, you will take that investment. Therefore, that 6% is viewed as a minimum attractive rate of return (or required rate of return). So, you can apply the following decision rule, to see if the proposed investment is a good one. ROR > MARR 8

9 Why ROR measure is so popular? This project will bring in a 15% rate of return on investment. This project will result in a net surplus of $10,000 in NPW. Which statement is easier to understand? 9

10 Return on Investment Definition 1: Rate of return (ROR) is defined as the interest rate earned on the unpaid balance of an installment loan. Example: A bank lends $10,000 and receives annual payment of $4,021 over 3 years. The bank is said to earn a return of 10% on its loan of $10,

11 Loan Balance Calculation: A = $10,000 (A/P, 10%, 3) = $4,021 Unpaid Return on Unpaid balance unpaid balance at beg. balance Payment at the end Year of year (10%) received of year $10,000 -$10,000 -$6,979 -$3,656 -$1,000 -$698 -$366 +$4,021 +$4,021 +$4,021 -$10,000 -$6,979 -$3,656 0 A return of 10% on the amount still outstanding at the beginning of each year 11

12 Rate of Return: Definition 2: Rate of return (ROR) is the break-even interest rate, i *, which equates the present worth of a project s cash outflows to the present worth of its cash inflows. Mathematical Relation: * * * PW( i ) = PW( i ) PW( i ) = 0 cash inflows cash outflows 12

13 Return on Invested Capital Definition 3: Return on invested capital is defined as the interest rate earned on the unrecovered project balance of an investment project. It is commonly known as internal rate of return (IRR). Example: A company invests $10,000 in a computer and results in equivalent annual labor savings of $4,021 over 3 years. The company is said to earn a return of 10% on its investment of $10,

14 Project Balance Calculation: Beginning project balance Return on invested capital Payment received Ending project balance $10,000 -$6,979 -$3,656 -$1,000 -$697 -$365 -$10,000 +$4,021 +$4,021 +$4,021 -$10,000 -$6,979 -$3,656 0 The firm earns a 10% rate of return on funds that remain internally invested in the project. Since the return is internal to the project, we call it internal rate of return. 14

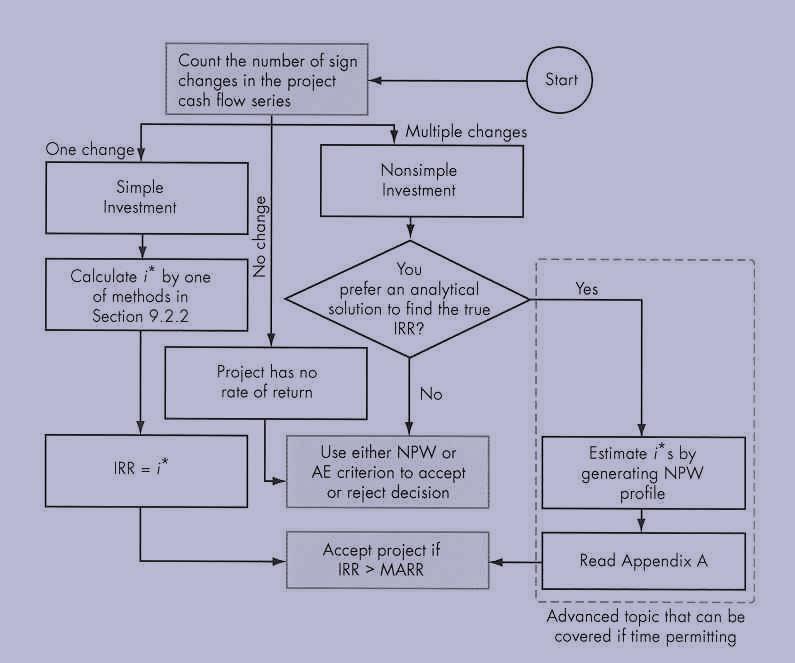

15 Methods for Finding Rate of Return Investment Classification Simple Investment Nonsimple Investment Computational Methods Direct Solution Method Trial-and-Error Method Computer Solution Method 15

16 Investment Classification Simple Investment Def: Initial cash flows are negative, and only one sign change occurs in the net cash flows series. Example: -$100, $250, $300 (-, +, +) ROR: A unique ROR Nonsimple Investment Def: Initial cash flows are negative, but more than one sign changes in the remaining cash flow series. Example: -$100, $300, -$120 (-, +, -) ROR: A possibility of multiple RORs 16

17 Period (N) Project A Project B Project C 0 -$1,000 -$1,000 +$1, , , ,500 2, ,000 Project A is a simple investment. Project B is a nonsimple investment. Project C is a simple borrowing. 17

18 Computational Methods Direct Solution Log Direct Solution Quadratic Trial & Error Method Computer Solution Method n Project A Project B Project C Project D 0 -$1,000 -$2,000 -$75,000 -$10, ,300 24,400 20, ,500 27,340 20, ,760 25, ,500 18

19 Direct Solution Methods Project A $1, 000 = $1, 500( P / F, i, 4) $1, 000 = $1, 500( 1+ i) = ( 1+ i) ln = ln( 1+ i) = ln( 1+ i) e i = 1+ i = e = 10.67% 1 4 Project B $1, 300 PW( i) = $2, ( 1+ i) 1 Let x =, then 1 + i PW( i) = 2, , 300x , x $1, 500 = 0 2 ( 1+ i) Solve for x: x = 0. 8 or Solving for i yields = i = 25%, = i = 160% 1 + i 1 + i * Since 100% < i <, the project's i = 25%. 2 19

20 Trial and Error Method Project C Step 1: Guess an interest rate, say, i = 15% Step 2: Compute PW(i) at the guessed i value. Step 4: If you bracket the solution, you use a linear interpolation to approximate the solution PW (15%) = $3,553 Step 3: If PW(i) > 0, then increase i. If PW(i) < 0, then decrease i. 3, % i 18% PW(18%) = -$749 i 3,553 = 15% + 3% 3, =17.45% 20

21 Graphical Solution Project D Step 1: Create a NPW plot using Excel. Step 2: Identify the point at which the curve crosses the horizontal axis closely approximates the i*. Note: This method is particularly useful for projects with multiple rates of return, as most financial softwares would fail to find all the multiple i*s. 21

22 Basic Decision Rule: If ROR > MARR, Accept This rule does not work for a situation where an investment has multiple rates of return 22

23 Multiple Rates of Return Problem $2,300 $1,000 $1,320 Find the rate(s) of return: PW( i) = $1, = 0 $2, 300 $1, i ( 1+ i) 23

24 1 Let x =. Then, 1 + i $2, 300 $1, 320 PW( i) = $1, ( 1+ i) ( 1+ i) = $1, $2, 300x $1, 320x = 0 Solving for x yields, x = 10 / 11 or x = 10 / 12 Solving for i yields i = 10% or 20% 2 24

25 NPW Plot for a Nonsimple Investment with Multiple Rates of Return 25

26 Project Balance Calculation i* =20% n = 0 n = 1 n = 2 Beg. Balance Interest Payment -$1,000 -$1,000 -$200 +$2,300 +$1,100 +$220 -$1,320 Ending Balance -$1,000 +$1,100 $0 Cash borrowed (released) from the project is assumed to earn the same interest rate through external investment as money that remains internally invested. 26

27 Critical Issue: Can the company be able to invest the money released from the project at 20% externally in Period 1? If your MARR is exactly 20%, the answer is yes, because it represents the rate at which the firm can always invest the money in its investment pool. Then, the 20% is also true IRR for the project.. Suppose your MARR is 15% instead of 20%. The assumption used in calculating i* is no longer valid. Therefore, neither 10% nor 20% is a true IRR. 27

28 How to Proceed: If you encounter multiple rates of return, abandon the IRR analysis and use the NPW criterion (or use the procedures outlined in Appendix A). If NPW criterion is used at MARR = 15% PW(15%) = -$1,000 + $2,300 (P/F, 15%, 1) - $1,320 (P/F, 15%, 2 ) = $1.89 > 0 Accept the investment 28

29 Decision Rules for Nonsimple Investment A possibility of multiple RORs. If PW (i) plot looks like this, then, IRR = ROR. If IRR > MARR, Accept i* i If PW(i) plot looks like this, Then, IRR ROR (i*). Find the true IRR by using the procedures in Appendix A or, Abandon the IRR method and use the PW method. PW (i) i* i* i 29

30 30

31 Comparing Mutually Exclusive Alternatives Based on IRR Issue: Can we rank the mutually exclusive projects by the magnitude of IRR? n A1 A2 0 -$1,000 -$5,000 1 IRR PW (10%) $2,000 $7, % > 40% $818 < $1,364 31

32 Incremental Investment n Project A1 Project A2 0 -$1,000 -$5,000 1 $2,000 $7,000 Incremental Investment (A2 A1) -$4,000 $5,000 ROR 100% 40% 25% PW(10%) $818 $1,364 $546 Assuming MARR of 10%, you can always earn that rate from other investment source, i.e., $4,400 at the end of one year for $4,000 investment. By investing the additional $4,000 in A2, you would make additional $5,000, which is equivalent to earning at the rate of 25%. Therefore, the incremental investment in A2 is justified. 32

33 Incremental Analysis (Procedure) Step 1: Step 2: Step 3: Compute the cash flows for the difference between the projects (A,B) by subtracting the cash flows for the lower investment cost project (A) from those of the higher investment cost project (B). Compute the IRR on this incremental investment (IRR B-A ). Accept the investment B if and only if IRR B-A > MARR 33

34 Example Incremental Rate of Return n B1 B2 B2 - B1 0 -$3,000 -$12,000 -$9, ,350 1,800 1,500 4,200 6,225 6,330 2,850 4,425 4,830 IRR 25% 17.43% 15% Given MARR = 10%, which project is a better choice? Since IRR B2-B1 =15% > 10%, and also IRR B2 > 10%, select B2. 34

35 35

36 IRR on Increment Investment: Three Alternatives n D1 D2 D3 0 -$2,000 -$1,000 -$3, , , , , ,000 IRR 34.37% 40.76% 24.81% Step 1: Examine the IRR for each project to eliminate any project that fails to meet the MARR. Step 2: Compare D1 and D2 in pairs. IRR D1-D2 =27.61% > 15%, so select D1. Step 3: Compare D1 and D3. IRR D3-D1 = 8.8% < 15%, so select D1. Here, we conclude that D1 is the best Alternative. 36

37 Incremental Borrowing Analysis Principle: If the difference in flow (B-A) represents an increment of investment, then (A-B) is an increment of borrowing. When considering an increment of borrowing, the rate i * A-B is the rate we paid to borrow money from the increment. Decision Rule: i * A B = BRR A B If BRR B-A < MARR, select B. If BRR B-A = MARR, select either one. If BRR B-A > MARR, select A. 37

38 Borrowing Rate of Return n B1 B2 B1-B2 0 -$3,000 -$12,000 +$9, ,350 4,200-2, ,800 6,225-4, ,500 6,330-4,830 38

39 Incremental Analysis for Cost-Only Projects Items CMS Option FMS Option Annual O&M costs: Annual labor cost $1,169,600 $707,200 Annual material cost 832, ,400 Annual overhead cost 3,150,000 1,950,000 Annual tooling cost 470, ,000 Annual inventory cost 141,000 31,500 Annual income taxes 1,650,000 1,917,000 Total annual costs $7,412,920 $5,504,100 Investment $4,500,000 $12,500,000 Net salvage value $500,000 $1,000,000 39

40 Incremental Cash Flow (FMS CMS) n CMS Option FMS Option Incremental (FMS-CMS) 0 -$4,500,000 -$12,500,000 -$8,000, ,412,920-5,504,100 1,908, ,412,920-5,504,100 1,908, ,412,920-5,504,100 1,908, ,412,920-5,504,100 1,908, ,412,920-5,504,100 1,908, ,412,920-5,504,100 Salvage + $500,000 + $1,000,000 $2,408,820 40

+ $2, 408, 820( P / F, i, 6) = 0 = 12.43% < 15%, select CMS.")

41 Solution: PW( i) = $8, 000, 000 IRR FMS CMS FMS CMS + $1,908, 820( P / A, i, 5) + $2, 408, 820( P / F, i, 6) = 0 = 12.43% < 15%, select CMS. 41

42 Ultimate Decision Rule: If IRR > MARR, Accept This rule works for any investment situations. In many situations, IRR = ROR but this relationship does not hold for an investment with multiple RORs. 42

43 Predicting Multiple RORs - 100% < i * < infinity Net Cash Flow Rule of Signs No. of real RORs (i*s) < No. of sign changes in the project cash flows 43

44 Example n Net Cash flow Sign Change $100 -$20 $50 0 $60 -$30 $100 No. of real i*s = 3 This implies that the project could have (0, 1, 2, or 3) i*s but NOT more than

45 Accumulated Cash Flow Sign Test Find the accounting sum of net cash flows at the end of each period over the life of the project Period Cash Flow Sum (n) (A n ) S n N A A A A N S0 = A0 S = S + A S = S + A S = S + A N N 1 N If the series S starts negatively and changes sign ONLY ONCE, there exists a unique positive i*. 45

46 Example n A n S n Sign change 0 -$100 -$ $20 -$120 2 $50 -$ $70 4 $60 -$10 5 -$30 -$40 6 $100 $60 1 No of sign change = 1, indicating a unique i*. i* = 10.46% 46

47 Example A.2 $3,900 $2, $1,000 $5,030 Is this a simple investment? How many RORs (i*s) can you expect from examining the cash flows? Can you tell if this investment has a unique rate of return? 47

48 Summary Rate of return (ROR) is the interest rate earned on unrecovered project balances such that an investment s cash receipts make the terminal project balance equal to zero. Rate of return is an intuitively familiar and understandable measure of project profitability that many managers prefer to NPW or other equivalence measures. Mathematically we can determine the rate of return for a given project cash flow series by locating an interest rate that equates the net present worth of its cash flows to zero. This break-even interest rate is denoted by the symbol i*. 48

49 Internal rate of return (IRR) is another term for ROR that stresses the fact that we are concerned with the interest earned on the portion of the project that is internally invested, not those portions that are released by (borrowed from) the project. To apply rate of return analysis correctly, we need to classify an investment into either a simple or a nonsimple investment. A simple investment is defined as one in which the initial cash flows are negative and only one sign change in the net cash flow occurs, whereas a nonsimple investment is one for which more than one sign change in the cash flow series occurs. Multiple i*s occur only in nonsimple investments. However, not all nonsimple investments will have multiple i*s, 49

50 For a simple investment, the solving rate of return (i*) is the rate of return internal to the project; so the decision rule is: If IRR > MARR, accept the project. If IRR = MARR, remain indifferent. If IRR < MARR, reject the project. IRR analysis yields results consistent with NPW and other equivalence methods. For a nonsimple investment, because of the possibility of having multiple rates of return, it is recommended the IRR analysis be abandoned and either the NPW or AE analysis be used to make an accept/reject decision. When properly selecting among alternative projects by IRR analysis, incremental investment must be used. 50

51 End of Lecture 7

Chapter 7 Rate of Return Analysis

Chapter 7 Rate of Return Analysis Rate of Return Methods for Finding ROR Internal Rate of Return (IRR) Criterion Incremental Analysis Mutually Exclusive Alternatives Why ROR measure is so popular? This

Chapter 7 Rate of Return Analysis Rate of Return Methods for Finding ROR Internal Rate of Return (IRR) Criterion Incremental Analysis Mutually Exclusive Alternatives Why ROR measure is so popular? This

Engineering Economy. Lecture 8 Evaluating a Single Project IRR continued Payback Period. NE 364 Engineering Economy

Engineering Economy Lecture 8 Evaluating a Single Project IRR continued Payback Period Internal Rate of Return (IRR) The internal rate of return (IRR) method is the most widely used rate of return method

Engineering Economy Lecture 8 Evaluating a Single Project IRR continued Payback Period Internal Rate of Return (IRR) The internal rate of return (IRR) method is the most widely used rate of return method

Engineering Economics

Engineering Economics Lecture 6 Er. Sushant Raj Giri B.E. (Industrial Engineering), MBA Lecturer Department of Industrial Engineering Contemporary Engineering Economics 3 rd Edition Chan S Park 1 Chapter

Engineering Economics Lecture 6 Er. Sushant Raj Giri B.E. (Industrial Engineering), MBA Lecturer Department of Industrial Engineering Contemporary Engineering Economics 3 rd Edition Chan S Park 1 Chapter

Chapter 7 Rate of Return Analysis

Chapter 7 Rate of Return Analysis 1 Recall the $5,000 debt example in chapter 3. Each of the four plans were used to repay the amount of $5000. At the end of 5 years, the principal and interest payments

Chapter 7 Rate of Return Analysis 1 Recall the $5,000 debt example in chapter 3. Each of the four plans were used to repay the amount of $5000. At the end of 5 years, the principal and interest payments

Lecture 5 Present-Worth Analysis

Seg2510 Management Principles for Engineering Managers Lecture 5 Present-Worth Analysis Department of Systems Engineering and Engineering Management The Chinese University of Hong Kong 1 Part I Review

Seg2510 Management Principles for Engineering Managers Lecture 5 Present-Worth Analysis Department of Systems Engineering and Engineering Management The Chinese University of Hong Kong 1 Part I Review

CHAPTER 7: ENGINEERING ECONOMICS

CHAPTER 7: ENGINEERING ECONOMICS The aim is to think about and understand the power of money on decision making BREAKEVEN ANALYSIS Breakeven point method deals with the effect of alternative rates of operation

CHAPTER 7: ENGINEERING ECONOMICS The aim is to think about and understand the power of money on decision making BREAKEVEN ANALYSIS Breakeven point method deals with the effect of alternative rates of operation

Discounted Cash Flow Analysis

Discounted Cash Flow Analysis Lecture No.16 Chapter 5 Contemporary Engineering Economics Copyright 2016 Net Present Worth Measure Principle: Compute the equivalent net surplus at n = 0 for a given interest

Discounted Cash Flow Analysis Lecture No.16 Chapter 5 Contemporary Engineering Economics Copyright 2016 Net Present Worth Measure Principle: Compute the equivalent net surplus at n = 0 for a given interest

IE463 Chapter 3. Objective: INVESTMENT APPRAISAL (Applications of Money-Time Relationships)

") IE463 Chapter 3 IVESTMET APPRAISAL (Applications of Money-Time Relationships) Objective: To evaluate the economic profitability and liquidity of a single proposed investment project. CHAPTER 4 2 1 Equivalent

IE463 Chapter 3 IVESTMET APPRAISAL (Applications of Money-Time Relationships) Objective: To evaluate the economic profitability and liquidity of a single proposed investment project. CHAPTER 4 2 1 Equivalent

INTERNAL RATE OF RETURN

INTERNAL RATE OF RETURN Introduction You put money in a bank account and expect to get a return 1 percent You can think of investment/business/project in the same way Every investment/business/project

INTERNAL RATE OF RETURN Introduction You put money in a bank account and expect to get a return 1 percent You can think of investment/business/project in the same way Every investment/business/project

Sixth Edition. Global Edition CONTEMPORARY ENGINEERING ECONOMICS. Chan S. Park Department of Industrial and Systems Engineering Auburn University

Sixth Edition Global Edition CONTEMPORARY ENGINEERING ECONOMICS Chan S. Park Department of Industrial and Systems Engineering Auburn University PEARSON Boston Columbus Indianapolis New York San Francisco

Sixth Edition Global Edition CONTEMPORARY ENGINEERING ECONOMICS Chan S. Park Department of Industrial and Systems Engineering Auburn University PEARSON Boston Columbus Indianapolis New York San Francisco

i* = IRR i*? IRR more sign changes Passes: unique i* = IRR

Decision Rules Single Alternative Based on Sign Changes of Cash Flow: Simple Investment i* = IRR Accept if i* > MARR Single Project start with zero, one sign change Non-Simple Investment i*? IRR Net Investment

Decision Rules Single Alternative Based on Sign Changes of Cash Flow: Simple Investment i* = IRR Accept if i* > MARR Single Project start with zero, one sign change Non-Simple Investment i*? IRR Net Investment

Overall ROR: 30,000(0.20) + 70,000(0.14) = 100,000(x) x = 15.8% Prepare a tabulation of cash flow for the alternatives shown below.

+ 70,000(0.14) = 100,000(x) x = 15.8% Prepare a tabulation of cash flow for the alternatives shown below.") Chapter 8, Problem 2. What is the overall rate of return on a $100,000 investment that returns 20% on the first $30,000 and 14% on the remaining $70,000? Chapter 8, Solution 2. Overall ROR: 30,000(0.20)

Chapter 8, Problem 2. What is the overall rate of return on a $100,000 investment that returns 20% on the first $30,000 and 14% on the remaining $70,000? Chapter 8, Solution 2. Overall ROR: 30,000(0.20)

Mutually Exclusive Choose at most one From the Set

1 Mutually Exclusive Choose at most one From the Set This lecture addresses an issue that is confusing to many users of the rate of return method. When choosing among mutually exclusive alternatives, never

1 Mutually Exclusive Choose at most one From the Set This lecture addresses an issue that is confusing to many users of the rate of return method. When choosing among mutually exclusive alternatives, never

Department of Humanities. Sub: Engineering Economics and Costing (BHU1302) (4-0-0) Syllabus

(4-0-0) Syllabus") Department of Humanities Sub: Engineering Economics and Costing (BHU1302) (4-0-0) Syllabus Module I (10 Hours) Time value of money : Simple and compound interest, Time value equivalence, Compound interest

Department of Humanities Sub: Engineering Economics and Costing (BHU1302) (4-0-0) Syllabus Module I (10 Hours) Time value of money : Simple and compound interest, Time value equivalence, Compound interest

Chapter 7. Net Present Value and Other Investment Rules

Chapter 7 Net Present Value and Other Investment Rules Be able to compute payback and discounted payback and understand their shortcomings Understand accounting rates of return and their shortcomings Be

Chapter 7 Net Present Value and Other Investment Rules Be able to compute payback and discounted payback and understand their shortcomings Understand accounting rates of return and their shortcomings Be

Chapter Organization. Net present value (NPV) is the difference between an investment s market value and its cost.

is the difference between an investment s market value and its cost.") Chapter 9 Net Present Value and Other Investment Criteria Chapter Organization 9.1. Net present value 9.2. The Payback Rule 9.3. The Discounted Payback 9.4. The Average Accounting Return 9.6. The Profitability

Chapter 9 Net Present Value and Other Investment Criteria Chapter Organization 9.1. Net present value 9.2. The Payback Rule 9.3. The Discounted Payback 9.4. The Average Accounting Return 9.6. The Profitability

Chapter 7 An Economic Appraisal II: NPV, AE, IRR Technique

Chapter 7 An Economic Appraisal II: NPV, AE, IRR Technique Powerpoint Templates Page 1 Net Present Value Technique NPV=The Sum of The Present Values of All Cash Inflows The Sum of The Present Value of

Chapter 7 An Economic Appraisal II: NPV, AE, IRR Technique Powerpoint Templates Page 1 Net Present Value Technique NPV=The Sum of The Present Values of All Cash Inflows The Sum of The Present Value of

Inflation Homework. 1. Life = 4 years

Inflation Homework 1. Life = 4 years 700 9001100 500 0 1 2 3 4-1500 You are to analyze the cash flow on the left with several assumptions regarding inflation. In all cases the general inflation rate is

Inflation Homework 1. Life = 4 years 700 9001100 500 0 1 2 3 4-1500 You are to analyze the cash flow on the left with several assumptions regarding inflation. In all cases the general inflation rate is

Engineering Economics

Economic Analysis Methods Engineering Economics Day 3: Rate of Return Analysis Three commonly used economic analysis methods are 1. Present Worth Analysis 2. Annual Worth Analysis 3. www.engr.sjsu.edu/bjfurman/courses/me195/presentations/engeconpatel3nov4.ppt

Economic Analysis Methods Engineering Economics Day 3: Rate of Return Analysis Three commonly used economic analysis methods are 1. Present Worth Analysis 2. Annual Worth Analysis 3. www.engr.sjsu.edu/bjfurman/courses/me195/presentations/engeconpatel3nov4.ppt

Economic Decision Making Using Fuzzy Numbers Shih-Ming Lee, Kuo-Lung Lin, Sushil Gupta. Florida International University Miami, Florida

Economic Decision Making Using Fuzzy Numbers Shih-Ming Lee, Kuo-Lung Lin, Sushil Gupta Florida International University Miami, Florida Abstract In engineering economic studies, single values are traditionally

Economic Decision Making Using Fuzzy Numbers Shih-Ming Lee, Kuo-Lung Lin, Sushil Gupta Florida International University Miami, Florida Abstract In engineering economic studies, single values are traditionally

IE 343 Midterm Exam 2

IE 343 Midterm Exam 2 April 6, 2012 Version A Closed book, closed notes. 50 minutes Write your printed name in the spaces provided above on every page. Show all of your work in the spaces provided. Interest

IE 343 Midterm Exam 2 April 6, 2012 Version A Closed book, closed notes. 50 minutes Write your printed name in the spaces provided above on every page. Show all of your work in the spaces provided. Interest

Comparing Mutually Exclusive Alternatives

Comparing Mutually Exclusive Alternatives Lecture No. 18 Chapter 5 Contemporary Engineering Economics Copyright 2016 Comparing Mutually Exclusive Projects: Basic Terminologies Mutually Exclusive Projects

Comparing Mutually Exclusive Alternatives Lecture No. 18 Chapter 5 Contemporary Engineering Economics Copyright 2016 Comparing Mutually Exclusive Projects: Basic Terminologies Mutually Exclusive Projects

Chapter 13 Breakeven and Payback Analysis

Chapter 13 Breakeven and Payback Analysis by Ir Mohd Shihabudin Ismail 13-1 LEARNING OUTCOMES 1. Breakeven point one parameter 2. Breakeven point two alternatives 3. Payback period analysis 13-2 Introduction

Chapter 13 Breakeven and Payback Analysis by Ir Mohd Shihabudin Ismail 13-1 LEARNING OUTCOMES 1. Breakeven point one parameter 2. Breakeven point two alternatives 3. Payback period analysis 13-2 Introduction

THE COST VOLUME PROFIT APPROACH TO DECISIONS

C H A P T E R 8 THE COST VOLUME PROFIT APPROACH TO DECISIONS I N T R O D U C T I O N This chapter introduces the cost volume profit (CVP) method, which can assist management in evaluating current and future

C H A P T E R 8 THE COST VOLUME PROFIT APPROACH TO DECISIONS I N T R O D U C T I O N This chapter introduces the cost volume profit (CVP) method, which can assist management in evaluating current and future

Chapter 7: Investment Decision Rules

Chapter 7: Investment Decision Rules -1 Chapter 7: Investment Decision Rules Note: Read the chapter then look at the following. Fundamental question: What criteria should firms use when deciding which

Chapter 7: Investment Decision Rules -1 Chapter 7: Investment Decision Rules Note: Read the chapter then look at the following. Fundamental question: What criteria should firms use when deciding which

Global Financial Management

Global Financial Management Valuation of Cash Flows Investment Decisions and Capital Budgeting Copyright 2004. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 2004

Global Financial Management Valuation of Cash Flows Investment Decisions and Capital Budgeting Copyright 2004. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 2004

Capital Budgeting and Business Valuation

Capital Budgeting and Business Valuation Capital budgeting and business valuation concern two subjects near and dear to financial peoples hearts: What should we do with the firm s money and how much is

Capital Budgeting and Business Valuation Capital budgeting and business valuation concern two subjects near and dear to financial peoples hearts: What should we do with the firm s money and how much is

Chapter 6 Rate of Return Analysis: Multiple Alternatives 6-1

Chapter 6 Rate of Return Analysis: Multiple Alternatives 6-1 LEARNING OBJECTIVES Work with mutually exclusive alternatives based upon ROR analysis 1. Why Incremental Analysis? 2. Incremental Cash Flows

Chapter 6 Rate of Return Analysis: Multiple Alternatives 6-1 LEARNING OBJECTIVES Work with mutually exclusive alternatives based upon ROR analysis 1. Why Incremental Analysis? 2. Incremental Cash Flows

ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA. Examiner's Report AA3 EXAMINATION - JULY 2015 (AA32) MANAGEMENT ACCOUNTING AND FINANCE

MANAGEMENT ACCOUNTING AND FINANCE") ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA Examiner's Report AA3 EXAMINATION - JULY 2015 (AA32) MANAGEMENT ACCOUNTING AND FINANCE OVERVIEW: This paper has three sections covering 100 marks, 1.

ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA Examiner's Report AA3 EXAMINATION - JULY 2015 (AA32) MANAGEMENT ACCOUNTING AND FINANCE OVERVIEW: This paper has three sections covering 100 marks, 1.

which considers any inflationary effects in the cash flows.

Note 1: Unless otherwise stated, all cash flows given in the problems represent aftertax cash flows in actual dollars. The MARR also represents a market interest rate, which considers any inflationary

Note 1: Unless otherwise stated, all cash flows given in the problems represent aftertax cash flows in actual dollars. The MARR also represents a market interest rate, which considers any inflationary

AFM 271. Midterm Examination #2. Friday June 17, K. Vetzal. Answer Key

AFM 21 Midterm Examination #2 Friday June 1, 2005 K. Vetzal Name: Answer Key Student Number: Section Number: Duration: 1 hour and 30 minutes Instructions: 1. Answer all questions in the space provided.

AFM 21 Midterm Examination #2 Friday June 1, 2005 K. Vetzal Name: Answer Key Student Number: Section Number: Duration: 1 hour and 30 minutes Instructions: 1. Answer all questions in the space provided.

Investment Decision Criteria. Principles Applied in This Chapter. Disney s Capital Budgeting Decision

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Investment Decision Criteria Chapter 11 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of

Carefully read all directions given in a problem. Please show all work for all problems, and clearly label all formulas.

Carefully read all directions given in a problem. Please show all work for all problems, and clearly label all formulas. 1. You have been asked to make a decision regarding two alternatives. To make your

Carefully read all directions given in a problem. Please show all work for all problems, and clearly label all formulas. 1. You have been asked to make a decision regarding two alternatives. To make your

ENG2000 Chapter 17 Evaluating and Comparing Projects: The IRR. ENG2000: R.I. Hornsey CM_2: 1

ENG2000 Chapter 17 Evaluating and Comparing Projects: The IRR ENG2000: R.I. Hornsey CM_2: 1 Introduction This chapter introduces a second method for comparing between projects While the result of the process

ENG2000 Chapter 17 Evaluating and Comparing Projects: The IRR ENG2000: R.I. Hornsey CM_2: 1 Introduction This chapter introduces a second method for comparing between projects While the result of the process

1 Week Recap Week 2

1 Week 3 1.1 Recap Week 2 pv, fv, timeline pmt - we don t have to keep it the same every period. Ex.: Suppose you are exactly 30 years old. You believe that you will be able to save for the next 20 years,

1 Week 3 1.1 Recap Week 2 pv, fv, timeline pmt - we don t have to keep it the same every period. Ex.: Suppose you are exactly 30 years old. You believe that you will be able to save for the next 20 years,

Benefit-Cost Ratio. Lecture No. 53 Chapter 16 Contemporary Engineering Economics Copyright Contemporary Engineering Economics, 6e, GE Park

Benefit-Cost Ratio Lecture No. 53 Chapter 16 Contemporary Engineering Economics Copyright 2016 Benefit-Cost Analysis Thebenefit-cost analysis is commonly used to evaluate public projects. Benefits of a

Benefit-Cost Ratio Lecture No. 53 Chapter 16 Contemporary Engineering Economics Copyright 2016 Benefit-Cost Analysis Thebenefit-cost analysis is commonly used to evaluate public projects. Benefits of a

Chapter 15 Inflation

Chapter 15 Inflation 15-1 The first sewage treatment plant for Athens, Georgia cost about $2 million in 1964. The utilized capacity of the plant was 5 million gallons/day (mgd). Using the commonly accepted

Chapter 15 Inflation 15-1 The first sewage treatment plant for Athens, Georgia cost about $2 million in 1964. The utilized capacity of the plant was 5 million gallons/day (mgd). Using the commonly accepted

IE 343 Midterm Exam 2

IE 343 Midterm Exam 2 Nov 16, 2011 Closed book, closed notes. 50 minutes Write your printed name in the spaces provided above on every page. Show all of your work in the spaces provided. Exam 2 has three

IE 343 Midterm Exam 2 Nov 16, 2011 Closed book, closed notes. 50 minutes Write your printed name in the spaces provided above on every page. Show all of your work in the spaces provided. Exam 2 has three

FAQ: Financial Statements

Question 1: What is the correct order in which financial reports must be created? Answer 1: The income statement is created first, then the owners' equity statement, and finally the balance sheet. This

Question 1: What is the correct order in which financial reports must be created? Answer 1: The income statement is created first, then the owners' equity statement, and finally the balance sheet. This

Chapter One. Definition and Basic terms and terminology of engineering economy

Chapter One Definition and Basic terms and terminology of engineering economy 1. Introduction: The need for engineering economy is primarily motivated by the work that engineers do in performing analysis,

Chapter One Definition and Basic terms and terminology of engineering economy 1. Introduction: The need for engineering economy is primarily motivated by the work that engineers do in performing analysis,

Present Worth Analysis

Present Worth Analysis Net Present Worth of initial and future cash flows can be used to select among alternative projects It is important to understand what Net Present Worth means, especially when the

Present Worth Analysis Net Present Worth of initial and future cash flows can be used to select among alternative projects It is important to understand what Net Present Worth means, especially when the

CAPITAL BUDGETING TECHNIQUES (CHAPTER 9)

") CAPITAL BUDGETING TECHNIQUES (CHAPTER 9) Capital budgeting refers to the process used to make decisions concerning investments in the long-term assets of the firm. The general idea is that a firm s capital,

CAPITAL BUDGETING TECHNIQUES (CHAPTER 9) Capital budgeting refers to the process used to make decisions concerning investments in the long-term assets of the firm. The general idea is that a firm s capital,

FE Review Economics and Cash Flow

4/4/16 Compound Interest Variables FE Review Economics and Cash Flow Andrew Pederson P = present single sum of money (single cash flow). F = future single sum of money (single cash flow). A = uniform series

4/4/16 Compound Interest Variables FE Review Economics and Cash Flow Andrew Pederson P = present single sum of money (single cash flow). F = future single sum of money (single cash flow). A = uniform series

TIME VALUE OF MONEY. Lecture Notes Week 4. Dr Wan Ahmad Wan Omar

TIME VALUE OF MONEY Lecture Notes Week 4 Dr Wan Ahmad Wan Omar Lecture Notes Week 4 4. The Time Value of Money The notion on time value of money is based on the idea that money available at the present

TIME VALUE OF MONEY Lecture Notes Week 4 Dr Wan Ahmad Wan Omar Lecture Notes Week 4 4. The Time Value of Money The notion on time value of money is based on the idea that money available at the present

QUADRATIC. Parent Graph: How to Tell it's a Quadratic: Helpful Hints for Calculator Usage: Domain of Parent Graph:, Range of Parent Graph: 0,

Parent Graph: How to Tell it's a Quadratic: If the equation's largest exponent is 2 If the graph is a parabola ("U"-Shaped) Opening up or down. QUADRATIC f x = x 2 Domain of Parent Graph:, Range of Parent

Parent Graph: How to Tell it's a Quadratic: If the equation's largest exponent is 2 If the graph is a parabola ("U"-Shaped) Opening up or down. QUADRATIC f x = x 2 Domain of Parent Graph:, Range of Parent

TAX ECONOMIC ANALYSIS 1 Haery Sihombing. Learning Objectives

Ir. /IP Pensyarah Pelawat Fakulti Kejuruteraan Pembuatan Universiti Teknologi Malaysia Melaka 1. Terminology and Rates 2. Before and After-Tax Analysis 6 3. Taxes and Depreciation 4. Depreciation Recapture

Ir. /IP Pensyarah Pelawat Fakulti Kejuruteraan Pembuatan Universiti Teknologi Malaysia Melaka 1. Terminology and Rates 2. Before and After-Tax Analysis 6 3. Taxes and Depreciation 4. Depreciation Recapture

INVESTMENT APPRAISAL TECHNIQUES FOR SMALL AND MEDIUM SCALE ENTERPRISES

SAMUEL ADEGBOYEGA UNIVERSITY COLLEGE OF MANAGEMENT AND SOCIAL SCIENCES DEPARTMENT OF BUSINESS ADMINISTRATION COURSE CODE: BUS 413 COURSE TITLE: SMALL AND MEDIUM SCALE ENTERPRISE MANAGEMENT SESSION: 2017/2018,

SAMUEL ADEGBOYEGA UNIVERSITY COLLEGE OF MANAGEMENT AND SOCIAL SCIENCES DEPARTMENT OF BUSINESS ADMINISTRATION COURSE CODE: BUS 413 COURSE TITLE: SMALL AND MEDIUM SCALE ENTERPRISE MANAGEMENT SESSION: 2017/2018,

Cash Flow and the Time Value of Money

Harvard Business School 9-177-012 Rev. October 1, 1976 Cash Flow and the Time Value of Money A promising new product is nationally introduced based on its future sales and subsequent profits. A piece of

Harvard Business School 9-177-012 Rev. October 1, 1976 Cash Flow and the Time Value of Money A promising new product is nationally introduced based on its future sales and subsequent profits. A piece of

Foundational Preliminaries: Answers to Within-Chapter-Exercises

C H A P T E R 0 Foundational Preliminaries: Answers to Within-Chapter-Exercises 0A Answers for Section A: Graphical Preliminaries Exercise 0A.1 Consider the set [0,1) which includes the point 0, all the

C H A P T E R 0 Foundational Preliminaries: Answers to Within-Chapter-Exercises 0A Answers for Section A: Graphical Preliminaries Exercise 0A.1 Consider the set [0,1) which includes the point 0, all the

UNIVERSITY OF TORONTO Joseph L. Rotman School of Management SOLUTIONS. C (1 + r 2. 1 (1 + r. PV = C r. we have that C = PV r = $40,000(0.10) = $4,000.

= $4,000.") UNIVERSITY OF TORONTO Joseph L. Rotman School of Management RSM332 PROBLEM SET #2 SOLUTIONS 1. (a) The present value of a single cash flow: PV = C (1 + r 2 $60,000 = = $25,474.86. )2T (1.055) 16 (b) The

UNIVERSITY OF TORONTO Joseph L. Rotman School of Management RSM332 PROBLEM SET #2 SOLUTIONS 1. (a) The present value of a single cash flow: PV = C (1 + r 2 $60,000 = = $25,474.86. )2T (1.055) 16 (b) The

ECLT 5930/SEEM 5740: Engineering Economics Second Term

ECLT 5930/SEEM 5740: Engineering Economics 2015 16 Second Term Master of Science in ECLT & SEEM Instructors: Dr. Anthony Man Cho So Department of Systems Engineering & Engineering Management The Chinese

ECLT 5930/SEEM 5740: Engineering Economics 2015 16 Second Term Master of Science in ECLT & SEEM Instructors: Dr. Anthony Man Cho So Department of Systems Engineering & Engineering Management The Chinese

IE463 Chapter 4. Objective: COMPARING INVESTMENT AND COST ALTERNATIVES

IE463 Chapter 4 COMPARING INVESTMENT AND COST ALTERNATIVES Objective: To learn how to properly apply the profitability measures described in Chapter 3 to select the best alternative out of a set of mutually

IE463 Chapter 4 COMPARING INVESTMENT AND COST ALTERNATIVES Objective: To learn how to properly apply the profitability measures described in Chapter 3 to select the best alternative out of a set of mutually

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture - 13 Multiple Cash Flow-1 and 2 Welcome to the lecture

Time value of money-concepts and Calculations Prof. Bikash Mohanty Department of Chemical Engineering Indian Institute of Technology, Roorkee Lecture - 13 Multiple Cash Flow-1 and 2 Welcome to the lecture

8: Economic Criteria

8.1 Economic Criteria Capital Budgeting 1 8: Economic Criteria The preceding chapters show how to discount and compound a variety of different types of cash flows. This chapter explains the use of those

8.1 Economic Criteria Capital Budgeting 1 8: Economic Criteria The preceding chapters show how to discount and compound a variety of different types of cash flows. This chapter explains the use of those

Capital Budgeting Decision Methods

Capital Budgeting Decision Methods Everything is worth what its purchaser will pay for it. Publilius Syrus In April of 2012, before Facebook s initial public offering (IPO), it announced it was acquiring

Capital Budgeting Decision Methods Everything is worth what its purchaser will pay for it. Publilius Syrus In April of 2012, before Facebook s initial public offering (IPO), it announced it was acquiring

Lecture Guide. Sample Pages Follow. for Timothy Gallagher s Financial Management 7e Principles and Practice

Lecture Guide for Timothy Gallagher s Financial Management 7e Principles and Practice 707 Slides Written by Tim Gallagher the textbook author Use as flash cards for terminology and concept review Also

Lecture Guide for Timothy Gallagher s Financial Management 7e Principles and Practice 707 Slides Written by Tim Gallagher the textbook author Use as flash cards for terminology and concept review Also

Chapter 8. Rate of Return Analysis. Principles of Engineering Economic Analysis, 5th edition

Chapter 8 Rate of Return Analysis Systematic Economic Analysis Technique 1. Identify the investment alternatives 2. Define the planning horizon 3. Specify the discount rate 4. Estimate the cash flows 5.

Chapter 8 Rate of Return Analysis Systematic Economic Analysis Technique 1. Identify the investment alternatives 2. Define the planning horizon 3. Specify the discount rate 4. Estimate the cash flows 5.

AFM 271 Practice Problem Set #2 Spring 2005 Suggested Solutions

AFM 271 Practice Problem Set #2 Spring 2005 Suggested Solutions 1. Text Problems: 6.2 (a) Consider the following table: time cash flow cumulative cash flow 0 -$1,000,000 -$1,000,000 1 $150,000 -$850,000

AFM 271 Practice Problem Set #2 Spring 2005 Suggested Solutions 1. Text Problems: 6.2 (a) Consider the following table: time cash flow cumulative cash flow 0 -$1,000,000 -$1,000,000 1 $150,000 -$850,000

Comparison and Selection among Alternatives Created By Eng.Maysa Gharaybeh

Comparison and Selection among Alternatives Created By Eng.Maysa Gharaybeh Quiz 1, 2, 7, 15,19, 20, 22, 26, 36, 40. The objective of chapter 6 is to evaluate correctly capital investment alternatives when

Comparison and Selection among Alternatives Created By Eng.Maysa Gharaybeh Quiz 1, 2, 7, 15,19, 20, 22, 26, 36, 40. The objective of chapter 6 is to evaluate correctly capital investment alternatives when

MFE8812 Bond Portfolio Management

MFE8812 Bond Portfolio Management William C. H. Leon Nanyang Business School January 16, 2018 1 / 63 William C. H. Leon MFE8812 Bond Portfolio Management 1 Overview Value of Cash Flows Value of a Bond

MFE8812 Bond Portfolio Management William C. H. Leon Nanyang Business School January 16, 2018 1 / 63 William C. H. Leon MFE8812 Bond Portfolio Management 1 Overview Value of Cash Flows Value of a Bond

Chapter 7: Investment Decision Rules

Chapter 7: Investment Decision Rules-1 Chapter 7: Investment Decision Rules I. Introduction and Review of NPV A. Introduction Q: How decide which long-term investment opportunities to undertake? Key =>

Chapter 7: Investment Decision Rules-1 Chapter 7: Investment Decision Rules I. Introduction and Review of NPV A. Introduction Q: How decide which long-term investment opportunities to undertake? Key =>

Capital Budgeting Process and Techniques 93. Chapter 7: Capital Budgeting Process and Techniques

Capital Budgeting Process and Techniques 93 Answers to questions Chapter 7: Capital Budgeting Process and Techniques 7-. a. Type I error means rejecting a good project. Payback could lead to Type errors

Capital Budgeting Process and Techniques 93 Answers to questions Chapter 7: Capital Budgeting Process and Techniques 7-. a. Type I error means rejecting a good project. Payback could lead to Type errors

Global Financial Management

Global Financial Management Bond Valuation Copyright 24. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 24. Bonds Bonds are securities that establish a creditor

Global Financial Management Bond Valuation Copyright 24. All Worldwide Rights Reserved. See Credits for permissions. Latest Revision: August 23, 24. Bonds Bonds are securities that establish a creditor

Many companies in the 80 s used this milking philosophy to extract money from the company and then sell it off to someone else.

Someone looking at a company and considering purchasing it is not going to be too impressed with the company paying out large dividends. Those dividends will go to the investors, the current owners. The

Someone looking at a company and considering purchasing it is not going to be too impressed with the company paying out large dividends. Those dividends will go to the investors, the current owners. The

Effects of Inflation on Project Cash Flows

Effects of Inflation on Project Cash Flows Lecture No. 37 Chapter 11 Contemporary Engineering Economics Copyright 2016 Effects of Inflation on Projects with Depreciable Assets Item Depreciation expense

Effects of Inflation on Project Cash Flows Lecture No. 37 Chapter 11 Contemporary Engineering Economics Copyright 2016 Effects of Inflation on Projects with Depreciable Assets Item Depreciation expense

1 Income statement and cash flows

The Chinese University of Hong Kong Department of Systems Engineering & Engineering Management SEG 2510 Course Notes 12 for review and discussion (2009/2010) 1 Income statement and cash flows We went through

The Chinese University of Hong Kong Department of Systems Engineering & Engineering Management SEG 2510 Course Notes 12 for review and discussion (2009/2010) 1 Income statement and cash flows We went through

ENGM 310 Engineering Economy Lecture Notes (MJ Zuo) Page 1 of 36. Introduction

Page 1 of 36. Introduction") ENGM 310 Engineering Economy Lecture Notes (MJ Zuo) Page 1 of 36 Introduction 1. Syllabus distributed: Dates of assignments, mid-terms, and final exams specified. (a) Let me know in writing about possible

ENGM 310 Engineering Economy Lecture Notes (MJ Zuo) Page 1 of 36 Introduction 1. Syllabus distributed: Dates of assignments, mid-terms, and final exams specified. (a) Let me know in writing about possible

Copyright Disclaimer under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news

Copyright Disclaimer under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news reporting, teaching, scholarship, and research. Fair use

Copyright Disclaimer under Section 107 of the Copyright Act 1976, allowance is made for "fair use" for purposes such as criticism, comment, news reporting, teaching, scholarship, and research. Fair use

SOLUTIONS TO SELECTED PROBLEMS. Student: You should work the problem completely before referring to the solution. CHAPTER 1

SOLUTIONS TO SELECTED PROBLEMS Student: You should work the problem completely before referring to the solution. CHAPTER 1 Solutions included for problems 1, 4, 7, 10, 13, 16, 19, 22, 25, 28, 31, 34, 37,

SOLUTIONS TO SELECTED PROBLEMS Student: You should work the problem completely before referring to the solution. CHAPTER 1 Solutions included for problems 1, 4, 7, 10, 13, 16, 19, 22, 25, 28, 31, 34, 37,

Measuring Interest Rates

Measuring Interest Rates Economics 301: Money and Banking 1 1.1 Goals Goals and Learning Outcomes Goals: Learn to compute present values, rates of return, rates of return. Learning Outcomes: LO3: Predict

Measuring Interest Rates Economics 301: Money and Banking 1 1.1 Goals Goals and Learning Outcomes Goals: Learn to compute present values, rates of return, rates of return. Learning Outcomes: LO3: Predict

Engineering Economics Financial Decision Making for Engineers Canadian 6th Edition Fraser TEST BANK Full download at:

Engineering Economics Financial Decision Making for Engineers Canadian 6th Edition Fraser TEST BANK Full download at: Engineering Economics Financial Decision Making for Engineers Canadian 6th Edition

Engineering Economics Financial Decision Making for Engineers Canadian 6th Edition Fraser TEST BANK Full download at: Engineering Economics Financial Decision Making for Engineers Canadian 6th Edition

Time Value of Money and Economic Equivalence

Time Value of Money and Economic Equivalence Lecture No.4 Chapter 3 Third Canadian Edition Copyright 2012 Chapter Opening Story Take a Lump Sum or Annual Installments q q q Millionaire Life is a lottery

Time Value of Money and Economic Equivalence Lecture No.4 Chapter 3 Third Canadian Edition Copyright 2012 Chapter Opening Story Take a Lump Sum or Annual Installments q q q Millionaire Life is a lottery

An Interesting News Item

ENGM 401 & 620 X1 Fundamentals of Engineering Finance Fall 2010 Lecture 26: Other Analysis Techniques If you work just for money, you'll never make it, but if you love what you're doing and you always

ENGM 401 & 620 X1 Fundamentals of Engineering Finance Fall 2010 Lecture 26: Other Analysis Techniques If you work just for money, you'll never make it, but if you love what you're doing and you always

Mathematical Economics dr Wioletta Nowak. Lecture 2

Mathematical Economics dr Wioletta Nowak Lecture 2 The Utility Function, Examples of Utility Functions: Normal Good, Perfect Substitutes, Perfect Complements, The Quasilinear and Homothetic Utility Functions,

Mathematical Economics dr Wioletta Nowak Lecture 2 The Utility Function, Examples of Utility Functions: Normal Good, Perfect Substitutes, Perfect Complements, The Quasilinear and Homothetic Utility Functions,

So far in the short-run analysis we have ignored the wage and price (we assume they are fixed).

.") Chapter 7: Labor Market So far in the short-run analysis we have ignored the wage and price (we assume they are fixed). Key idea: In the medium run, rising GD will lead to lower unemployment rate (more

Chapter 7: Labor Market So far in the short-run analysis we have ignored the wage and price (we assume they are fixed). Key idea: In the medium run, rising GD will lead to lower unemployment rate (more

Question: Insurance doesn t have much depreciation or inventory. What accounting methods affect return on book equity for insurance?

Corporate Finance, Module 4: Net Present Value vs Other Valuation Models (Brealey and Myers, Chapter 5) Practice Problems (The attached PDF file has better formatting.) Question 4.1: Accounting Returns

Corporate Finance, Module 4: Net Present Value vs Other Valuation Models (Brealey and Myers, Chapter 5) Practice Problems (The attached PDF file has better formatting.) Question 4.1: Accounting Returns

Lesson Exponential Models & Logarithms

SACWAY STUDENT HANDOUT SACWAY BRAINSTORMING ALGEBRA & STATISTICS STUDENT NAME DATE INTRODUCTION Compound Interest When you invest money in a fixed- rate interest earning account, you receive interest at

SACWAY STUDENT HANDOUT SACWAY BRAINSTORMING ALGEBRA & STATISTICS STUDENT NAME DATE INTRODUCTION Compound Interest When you invest money in a fixed- rate interest earning account, you receive interest at

a. Fill in the following table (you will need to expand it from the truncated form provided here). Round all your answers to the nearest hundredth.

. Round all your answers to the nearest hundredth.") Economics 102 Summer 2015 Answers to Homework #4 Due Monday, July 13, 2015 Directions: The homework will be collected in a box before the lecture. Please place your name on top of the homework (legibly).

Economics 102 Summer 2015 Answers to Homework #4 Due Monday, July 13, 2015 Directions: The homework will be collected in a box before the lecture. Please place your name on top of the homework (legibly).

In terms of covariance the Markowitz portfolio optimisation problem is:

Markowitz portfolio optimisation Solver To use Solver to solve the quadratic program associated with tracing out the efficient frontier (unconstrained efficient frontier UEF) in Markowitz portfolio optimisation

Markowitz portfolio optimisation Solver To use Solver to solve the quadratic program associated with tracing out the efficient frontier (unconstrained efficient frontier UEF) in Markowitz portfolio optimisation

Notes on a Basic Business Problem MATH 104 and MATH 184 Mark Mac Lean (with assistance from Patrick Chan) 2011W

2011W") Notes on a Basic Business Problem MATH 104 and MATH 184 Mark Mac Lean (with assistance from Patrick Chan) 2011W This simple problem will introduce you to the basic ideas of revenue, cost, profit, and demand.

Notes on a Basic Business Problem MATH 104 and MATH 184 Mark Mac Lean (with assistance from Patrick Chan) 2011W This simple problem will introduce you to the basic ideas of revenue, cost, profit, and demand.

Should there be a risk premium for foreign projects?

211 Should there be a risk premium for foreign projects? The exchange rate risk should be diversifiable risk (and hence should not command a premium) if the company has projects is a large number of countries

211 Should there be a risk premium for foreign projects? The exchange rate risk should be diversifiable risk (and hence should not command a premium) if the company has projects is a large number of countries

Other Analysis Techniques. Future Worth Analysis (FWA) Benefit-Cost Ratio Analysis (BCRA) Payback Period

Benefit-Cost Ratio Analysis (BCRA) Payback Period") Other Analysis Techniques Future Worth Analysis (FWA) Benefit-Cost Ratio Analysis (BCRA) Payback Period 1 Techniques for Cash Flow Analysis Present Worth Analysis Annual Cash Flow Analysis Rate of Return

Other Analysis Techniques Future Worth Analysis (FWA) Benefit-Cost Ratio Analysis (BCRA) Payback Period 1 Techniques for Cash Flow Analysis Present Worth Analysis Annual Cash Flow Analysis Rate of Return

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA Learning Objectives LO1 How to compute the net present value and why it is the best decision criterion. LO2 The payback rule and some of its shortcomings.

CHAPTER 9 NET PRESENT VALUE AND OTHER INVESTMENT CRITERIA Learning Objectives LO1 How to compute the net present value and why it is the best decision criterion. LO2 The payback rule and some of its shortcomings.

Chapter 6: Supply and Demand with Income in the Form of Endowments

Chapter 6: Supply and Demand with Income in the Form of Endowments 6.1: Introduction This chapter and the next contain almost identical analyses concerning the supply and demand implied by different kinds

Chapter 6: Supply and Demand with Income in the Form of Endowments 6.1: Introduction This chapter and the next contain almost identical analyses concerning the supply and demand implied by different kinds

CHAPTER 2 LITERATURE REVIEW

CHAPTER 2 LITERATURE REVIEW Capital budgeting is the process of analyzing investment opportunities and deciding which ones to accept. (Pearson Education, 2007, 178). 2.1. INTRODUCTION OF CAPITAL BUDGETING

CHAPTER 2 LITERATURE REVIEW Capital budgeting is the process of analyzing investment opportunities and deciding which ones to accept. (Pearson Education, 2007, 178). 2.1. INTRODUCTION OF CAPITAL BUDGETING

Mathematics of Financial Derivatives

Mathematics of Financial Derivatives Lecture 9 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Table of contents 1. Zero-coupon rates and bond pricing 2.

Mathematics of Financial Derivatives Lecture 9 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Table of contents 1. Zero-coupon rates and bond pricing 2.

Chapter 9 Net Present Value and Other Investment Criteria. Net Present Value (NPV) Net Present Value (NPV) Konan Chan. Financial Management, Fall 2018

Net Present Value (NPV) Konan Chan. Financial Management, Fall 2018") Chapter 9 Net Present Value and Other Investment Criteria Konan Chan Financial Management, Fall 2018 Topics Covered Investment Criteria Net Present Value (NPV) Payback Period Discounted Payback Average

Chapter 9 Net Present Value and Other Investment Criteria Konan Chan Financial Management, Fall 2018 Topics Covered Investment Criteria Net Present Value (NPV) Payback Period Discounted Payback Average

Mathematics of Financial Derivatives. Zero-coupon rates and bond pricing. Lecture 9. Zero-coupons. Notes. Notes

Mathematics of Financial Derivatives Lecture 9 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Zero-coupon rates and bond pricing Zero-coupons Definition:

Mathematics of Financial Derivatives Lecture 9 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Zero-coupon rates and bond pricing Zero-coupons Definition:

Corporate Finance, Module 4: Net Present Value vs Other Valuation Models

Corporate Finance, Module 4: Net Present Value vs Other Valuation Models (Brealey and Myers, Chapter 5) Practice Problems (The attached PDF file has better formatting.) Updated: December 13, 2006 Question

Corporate Finance, Module 4: Net Present Value vs Other Valuation Models (Brealey and Myers, Chapter 5) Practice Problems (The attached PDF file has better formatting.) Updated: December 13, 2006 Question

the display, exploration and transformation of the data are demonstrated and biases typically encountered are highlighted.

1 Insurance data Generalized linear modeling is a methodology for modeling relationships between variables. It generalizes the classical normal linear model, by relaxing some of its restrictive assumptions,

1 Insurance data Generalized linear modeling is a methodology for modeling relationships between variables. It generalizes the classical normal linear model, by relaxing some of its restrictive assumptions,

Chapter 9. Capital Budgeting Decision Models

Chapter 9 Capital Budgeting Decision Models Learning Objectives 1. Explain capital budgeting and differentiate between short-term and long-term budgeting decisions. 2. Explain the payback model and its

Chapter 9 Capital Budgeting Decision Models Learning Objectives 1. Explain capital budgeting and differentiate between short-term and long-term budgeting decisions. 2. Explain the payback model and its

Lecture 6 Capital Budgeting Decision

Lecture 6 Capital Budgeting Decision The term capital refers to long-term assets used in production, while a budget is a plan that details projected inflows and outflows during some future period. Thus,

Lecture 6 Capital Budgeting Decision The term capital refers to long-term assets used in production, while a budget is a plan that details projected inflows and outflows during some future period. Thus,

Glossary of Budgeting and Planning Terms

Budgeting Basics and Beyond, Third Edition By Jae K. Shim and Joel G. Siegel Copyright 2009 by John Wiley & Sons, Inc.. Glossary of Budgeting and Planning Terms Active Financial Planning Software Budgeting

Budgeting Basics and Beyond, Third Edition By Jae K. Shim and Joel G. Siegel Copyright 2009 by John Wiley & Sons, Inc.. Glossary of Budgeting and Planning Terms Active Financial Planning Software Budgeting

BFC2140: Corporate Finance 1

BFC2140: Corporate Finance 1 Table of Contents Topic 1: Introduction to Financial Mathematics... 2 Topic 2: Financial Mathematics II... 5 Topic 3: Valuation of Bonds & Equities... 9 Topic 4: Project Evaluation

BFC2140: Corporate Finance 1 Table of Contents Topic 1: Introduction to Financial Mathematics... 2 Topic 2: Financial Mathematics II... 5 Topic 3: Valuation of Bonds & Equities... 9 Topic 4: Project Evaluation

A Brief Guide to Engineering Management Financial Calculations in ENGM 401 Section B1 Winter 2009

A Brief Guide to Engineering Management Financial Calculations in ENGM 401 Section B1 Winter 2009 MG Lipsett 2008 last updated December 8, 2008 Introduction This document provides concise explanations

A Brief Guide to Engineering Management Financial Calculations in ENGM 401 Section B1 Winter 2009 MG Lipsett 2008 last updated December 8, 2008 Introduction This document provides concise explanations

IE 360 Engineering Economic Analysis Exam 2 Sample Test - Dr. Park

IE 360 Engineering Economic Analysis Exam 2 Sample Test - Dr. Park Name: Read the following instructions carefully Fill in your name on this exam sheet. Fill in your name, exam version number and the course

IE 360 Engineering Economic Analysis Exam 2 Sample Test - Dr. Park Name: Read the following instructions carefully Fill in your name on this exam sheet. Fill in your name, exam version number and the course

MANAGEMENT INFORMATION

CERTIFICATE LEVEL EXAMINATION SAMPLE PAPER 3 (90 MINUTES) MANAGEMENT INFORMATION This assessment consists of ONE scenario based question worth 20 marks and 32 short questions each worth 2.5 marks. At least

CERTIFICATE LEVEL EXAMINATION SAMPLE PAPER 3 (90 MINUTES) MANAGEMENT INFORMATION This assessment consists of ONE scenario based question worth 20 marks and 32 short questions each worth 2.5 marks. At least

MULTIPLE-CHOICE QUESTIONS Circle the correct answer on this test paper and record it on the computer answer sheet.

M I M E 3 1 0 E N G I N E E R I N G E C O N O M Y Class Test #2 Thursday, 23 March, 2006 90 minutes PRINT your family name / initial and record your student ID number in the spaces provided below. FAMILY

M I M E 3 1 0 E N G I N E E R I N G E C O N O M Y Class Test #2 Thursday, 23 March, 2006 90 minutes PRINT your family name / initial and record your student ID number in the spaces provided below. FAMILY

Analyzing Project Cash Flows. Chapter 12

Analyzing Project Cash Flows Chapter 12 1 Principles Applied in This Chapter Principle 3: Cash Flows Are the Source of Value. Principle 5: Individuals Respond to Incentives. 2 Learning Objectives 1. Identify

Analyzing Project Cash Flows Chapter 12 1 Principles Applied in This Chapter Principle 3: Cash Flows Are the Source of Value. Principle 5: Individuals Respond to Incentives. 2 Learning Objectives 1. Identify

Capital Budgeting (Including Leasing)

") Chapter 8 Capital Budgeting (Including Leasing) 8. CAPITAL BUDGETING DECISIONS DEFINED Capital budgeting is the process of making long-term planning decisions for investments. There are typically two types

Chapter 8 Capital Budgeting (Including Leasing) 8. CAPITAL BUDGETING DECISIONS DEFINED Capital budgeting is the process of making long-term planning decisions for investments. There are typically two types