Homework see handout

|

|

|

- Regina Moore

- 6 years ago

- Views:

Transcription

1 BUS512M Accounting for Investment Decisions: Property, Plant, & Equipment & Intangibles; Long-term Investments including Available for Sale, Equity, and Consolidations Module 8

2 Homework see handout

3 Investments

4 P8-1 Applying mark-to-market rule to equity securities O Leary Enterprises began investing in short-term equity securities in The following information was extracted from its 2014 internal financial records. Houser and Miller were classified as trading securities, while Letter and Nordic were classified as available-for-sale securities. a. Compute the effect on reported 2014 income from all investment transactions and price changes. b. Compute the effect on reported income if O Leary Enterprises exercised the fair market value option for all its investments.

5 P8-1 Applying mark-to-market rule to equity securities continued Security Purchases Sales Total Dividends Received Market Value per share Houser Company $40 $25 Miller, Inc. 85 $35 Letter Books 30 $46 Nordic Equipment 50 $90

6

7 E8-4 Short-term investment account across time periods On Wadsworth Company purchased 20 shares of ZZZ for $8 per share. Wadsworth held the investment for the remainder of 2014, and as of 12.31, the per share market value of ZZZ had risen to $10. During 2015, Wadsworth sold 10 shares of ZZZ for $9 each, and at the end of 2015, the per-share market price of the remaining 10 shares was $12. During 2016, the remaining shares of ZZZ were sold for $14 each. Assume that Wadsworth held no other equity investments during this time period. a. Complete the chart. The first column assumes that the investment was classified as trading securities; the second column assumes the investment was classified as available-for-sale securities. b. Comment on the differences.

8

9 E8-4 Short-term investment account across time periods continued Trading Available-for-Sale 2014 income balance sheet investment value 2015 income balance sheet investment value 2016 income Total income( )

10 Your Turn E8-3 Mark-to-Market Accounting a. Prepare journal entries for each transaction, excluding the June 30 AJE. Use the asset account Short-term Investments and assume that dividends were declared and paid on the same day. b. Prepare the June 30 AJE and describe the effect on reported income, assuming that: (1) Able and Baker shares are both considered trading securities; (2) Able is considered a trading security, and Baker is considered available-forsale security; (3) Able is considered an available-for-sale security, and Baker is considered a trading security; and (4) both Able and Baker are considered available-for-sale securities. c. What combination in (b) depicts management as most successful in the current period?

11 E8-3 Mark-to-Market Accounting The following information relates to the activity in the short-term investment account of Lido International which held no shortterm investments as of January Jan 28 Purchased 10 shares of Able Co. stock at $14/share. 2. Feb 18 Purchased 20 shares of Baker Co. stock at $26/share. 3. Mar 15 Received dividends from Able Co. of $1/share. 4. April 29 Sold 5 shares of Able Co. for $15/share. 5. May 18 Received dividends from Baker Co. of $2/share. 6. June 1 Sold 5 shares of Baker Co. for $22 per share. June 30 Market value Able Co. is $17/share. Market value of Baker Co. is $20/share. (1) Assume Able and Baker shares are both considered trading securities;

12 E8-3 Mark-to-Market Accounting The following information relates to the activity in the short-term investment account of Lido International which held no shortterm investments as of January Jan 28 Purchased 10 shares of Able Co. stock at $14/share. 2. Feb 18 Purchased 20 shares of Baker Co. stock at $26/share. 3. Mar 15 Received dividends from Able Co. of $1/share. 4. April 29 Sold 5 shares of Able Co. for $15/share. 5. May 18 Received dividends from Baker Co. of $2/share. 6. June 1 Sold 5 shares of Baker Co. for $22 per share. June 30 Market value Able Co. is $17/share. Market value of Baker Co. is $20/share. Assume (2) Able is considered a trading security, and Baker is considered available-for-sale security;

13 E8-3 Mark-to-Market Accounting The following information relates to the activity in the short-term investment account of Lido International which held no short-term investments as of January Jan 28 Purchased 10 shares of Able Co. stock at $14/share. 2. Feb 18 Purchased 20 shares of Baker Co. stock at $26/share. 3. Mar 15 Received dividends from Able Co. of $1/share. 4. April 29 Sold 5 shares of Able Co. for $15/share. 5. May 18 Received dividends from Baker Co. of $2/share. 6. June 1 Sold 5 shares of Baker Co. for $22 per share. June 30 Market value Able Co. is $17/share. Market value of Baker Co. is $20/share. Assume (3) Able is considered an available-for-sale security, and Baker is considered a trading security;

14 E8-3 Mark-to-Market Accounting The following information relates to the activity in the short-term investment account of Lido International which held no shortterm investments as of January Jan 28 Purchased 10 shares of Able Co. stock at $14/share. 2. Feb 18 Purchased 20 shares of Baker Co. stock at $26/share. 3. Mar 15 Received dividends from Able Co. of $1/share. 4. April 29 Sold 5 shares of Able Co. for $15/share. 5. May 18 Received dividends from Baker Co. of $2/share. 6. June 1 Sold 5 shares of Baker Co. for $22 per share. June 30 Market value Able Co. is $17/share. Market value of Baker Co. is $20/share. Assume (4) both Able and Baker are considered available-for-sale securities.

15 Long-term Equity Investments

16 Long-Term Equity Investments

17 Inter-corporate Equity Investments 3 Categories of Equity Investors: Passive Investors: Less than 20% of the outstanding voting stock. Use Mark-to-Market method if shares are readily marketable. Otherwise, use Cost method. Influential Investors: 20% to 50% of the outstanding voting stock. Use the Equity method. Controlling Investors: More than 50% of the outstanding voting stock. Use the Equity method, along with Consolidation.

18 Passive(<20%): Mark-to-Market Method & Cost Method Recap 1. Record initial investment at cost. 2. Dividends received are recognized as income on IS. If no dividends are received, then no income is recorded. 3. At the end of each period, the investment is adjusted to market value with the increase or decrease in market value reported as an: Unrealized gain or loss on the IS (and closed to RE) if investments are held in a trading account, i.e. Trading securities are a current asset). Unrealized gain or loss not on IS but in a special SHE account for Unrealized Holding Gains or Losses and reported as part of Comprehensive Income if investments held in an AFS portfolio. 4. If securities are not readily marketable, the Cost Method is used, which includes only Steps 1 &2 above. Under the cost method, investment only written down if there is an other than temporary loss in value, i.e., a permanent write down or the investment is sold.

19 Influential (20-50%): Equity Method Recap 1. Record investment at original cost. 2. At year-end, the Investor s proportionate share of Investee s net income or loss is recognized by Investor as investment income on IS and offset by an increase or decrease in the equity investment account. [i.e., single line consolidation] 3. Dividends received are recognized as a reduction in the investment account (not as dividend income on IS). 4. The investment is not marked to market; however, the market value is disclosed in the footnotes. 5. If there is goodwill implied by the purchase price, it is not amortized or evaluated for impairment separately from the investment. 6. If more than 20% equity does not result in significant influence, the investment should not be accounted for by the equity method, but by the mark-to-market method, if readily marketable.

20

21 The Cost Method- Market value hard to determine

22 E8-8 Cost Method Mystic Lakes Food Company began investing in equity securities for the first time in During 2014, the company engaged in the following transactions involving equity securities. Assume that the stock of Thayers International and Bayhe Enterprises is not considered marketable that ownership is less than 20 percent of the equity. Prepare journal entries to record these transactions.

23 E Purchased 10,000 shares of Thayers International for $26 per share. 2. Purchased 25,000 shares of Bayhe Enterprises for $35 per share. 3. Thayers International declared a $2-per-share dividend to be paid at a later date.

24 E Sold 4,500 shares of Bayhe Enterprises for $30 per share. 5. Sold 8,000 shares of Thayers International for $32 per share.

25 The Equity Method

26

27 E8-10 Equity Method On January 1, Nover Solar Systems purchased 10,000 shares of Reilly Inc for $190,000. The investment represented 25% of Reilly s outstanding common stock. Nover intended to hold the investment indefinitely. During the year, Reilly earned net income of $75,000, and during the next year Reilly suffered a net loss of $6,000. Reilly paid dividends both years of $1.50 per share. a. Prepare all relevant entries that Nover would have recorded during both years. b. Compute the book value of Nover s long-term equity investment account at the end of both years.

28 E8-12 Equity Method Inference from FS Mainmont Industries uses the equity method for its long-term equity investments from affiliates. The following information from the financial statements of Mainmont refers to an investment in the securities of Tumbleweed Construction, a company owned 30% by Mainmont Long-term investment in equity securities $29,000 $25,000 Income from equity securities 12,000 7,000 Mainmont neither purchased nor sold any equity securities during a. How much net income did Tumbleweed Construction earn during 2014? b. What was the dollar amount of the total dividend declared by Tumbleweed during 2014? c. Provide the journal entries recorded by Mainmont during 2014 with respect to its investment in Tumbleweed.

29 Consolidation Method Controlling investments of more than 50% are accounted for by the Equity method and then the parent and subsidiary financials are consolidated on a spreadsheet at the end of the accounting period. 1. The Investment account balance on the Investor s balance sheet is replaced with the Investor s share of the actual assets and liabilities of the Investee plus any goodwill implied by the Investor s purchase. 2. The assets and liabilities of the investee attributable to the non-controlling shareholders are added to the Investor s balance sheet along with the noncontrolling interest equity in those net assets, based on the fair market value of the non-controlling equity on the acquisition date. Any goodwill implied by such mark to fair value would also be recognized. [Minority Interest liability] 3. The income statement of the investee company is combined with the income statement of the investor. The equity income of the Investee recognized by the Investor is eliminated to avoid double counting this income. The total net income is apportioned between the net income attributable to the controlling shareholders and non-controlling shareholders. [Minority interest income] 4. Goodwill recognized in the consolidated financials is not amortized; however, if goodwill becomes impaired, it is written down. Goodwill must be evaluated each period of possible impairment.

30 Business Combinations Two Ways to Obtain Control: Asset acquisition-all the company s net assets are acquired directly from the company-the books of acquired company are closed and only one set of books remain. Stock acquisition-a controlling interest in another firm s voting common stock is acquired two sets of books remain and an Investment in Sub account is carried on the acquirer s books.

31 Stock Acquisition and Consolidated Financial Statements A business acquisition occurs when an investor company acquires a controlling interest (more than 50 percent of the voting stock) in another company. The companies continue as separate legal entities, the investor company is referred to as the parent company, and the investee company is called the subsidiary. A Corp + B Corp = Consolidated A and B A merger, or business combination, occurs when two or more companies combine to form a single legal entity.

32 Asset Acquisition-Purchase Method All identifiable net assets (assets less liabilities assumed) are recorded at their FMV, both tangible and intangible (assuming a controlling interest is acquired). Goodwill is created when the price paid exceeds the FMV of the net assets acquired. A gain is recorded when the price paid is less than the FMV of the net assets acquired. Direct acquisition costs (costs paid to consultants) and indirect acquisition costs (internal costs) are expensed. A single combined entity exists, no consolidation process is necessary.

33 Legal Forms of Business Combinations Statutory consolidation (100% ownership) A Corp + B Corp = C Corp (new company) Statutory merger (100% ownership) A Corp + B Corp = A Corp

Equity Securities Classified as Current Two criteria must be met for an investment in a security to be considered current and thus warrant inclusion

BUS210 Accounting for Investment Decisions: Short-term and Long-term Investments including Trading Securities, Available for Sale, Cost, Equity, and Consolidations Equity Securities Classified as Current

BUS210 Accounting for Investment Decisions: Short-term and Long-term Investments including Trading Securities, Available for Sale, Cost, Equity, and Consolidations Equity Securities Classified as Current

Before Class starts.(make sure your name is on all submissions)

") Before Class starts.(make sure your name is on all submissions) Fifth (DEAD) Homework due 3/20 before class. Help session was Sunday 3/16 1:30-3pm in GBS130 EXAM Thursday March 27 6pm-9pm Rooms TBA; covers

Before Class starts.(make sure your name is on all submissions) Fifth (DEAD) Homework due 3/20 before class. Help session was Sunday 3/16 1:30-3pm in GBS130 EXAM Thursday March 27 6pm-9pm Rooms TBA; covers

b. What is the largest category of property, plant, and equipment?

BUS512M Accounting for Investment Decisions: Property, Plant, & Equipment & Intangibles; Long-term Investments including Available for Sale, Equity, and Consolidations Module 8 ID9-13 Google 10-K Disclosures

BUS512M Accounting for Investment Decisions: Property, Plant, & Equipment & Intangibles; Long-term Investments including Available for Sale, Equity, and Consolidations Module 8 ID9-13 Google 10-K Disclosures

a. (1) Trading Securities (+A)... 50,000 Cash ( A)... 50,000 Invested in IBM.

Trading Securities (+A)... 50,000 Cash ( A)... 50,000 Invested in IBM.") Pratt Chapter 8 Solutions BE8 1 a. Comprehensive income includes all non-owner changes in shareholder equity that do not already appear on the income statement. For example, the change in value of assets

Pratt Chapter 8 Solutions BE8 1 a. Comprehensive income includes all non-owner changes in shareholder equity that do not already appear on the income statement. For example, the change in value of assets

Chapter 8: Investments in Equity Securities

1 Chapter 8: Investments in Equity Securities 2 Equity Securities Classified as Current Two criteria must be met for an investment in a security to be considered current and thus warrant inclusion as a

1 Chapter 8: Investments in Equity Securities 2 Equity Securities Classified as Current Two criteria must be met for an investment in a security to be considered current and thus warrant inclusion as a

FINANCIAL ACCOUNTING WEEK 7 INVESTMENTS IN EQUITY SECURITIES

FINANCIAL ACCOUNTING WEEK 7 INVESTMENTS IN EQUITY SECURITIES I. Learning Objectives A. Understand the criteria that must be met before a security can be listed in the current assets section of the balance

FINANCIAL ACCOUNTING WEEK 7 INVESTMENTS IN EQUITY SECURITIES I. Learning Objectives A. Understand the criteria that must be met before a security can be listed in the current assets section of the balance

Investments and Fair Value Accounting

C H A P T E R 15 Investments and Fair Value Accounting QUIZ AND TEST HINTS The following hints may be helpful to you in preparing for a quiz or a test over the material covered in Chapter 15. 1. This chapter

C H A P T E R 15 Investments and Fair Value Accounting QUIZ AND TEST HINTS The following hints may be helpful to you in preparing for a quiz or a test over the material covered in Chapter 15. 1. This chapter

Statement of Earnings

audited financial statements Statement of Earnings General Electric Company and consolidated affiliates For the years ended December 31 (In millions; per-share amounts in dollars) 2009 2008 2007 Revenues

audited financial statements Statement of Earnings General Electric Company and consolidated affiliates For the years ended December 31 (In millions; per-share amounts in dollars) 2009 2008 2007 Revenues

US GAAP Accounting Treatment Alternatives, Private Investments, Operating Affiliates

US GAAP Accounting Treatment Alternatives, Private Investments, Operating Affiliates This memorandum is intended to supplement the Investor Day presentation of May 24, 2007 in order to highlight the accounting

US GAAP Accounting Treatment Alternatives, Private Investments, Operating Affiliates This memorandum is intended to supplement the Investor Day presentation of May 24, 2007 in order to highlight the accounting

C521 CHAPTER 13 & REVIEW FOR MIDTERM FINANCIAL ACCOUNTING EXAM

1 C521 CHAPTER 13 & REVIEW FOR MIDTERM FINANCIAL ACCOUNTING EXAM What have we done in the course? On a chapter by chapter basis, we primarily have examined specific transactions and the effect on financial

1 C521 CHAPTER 13 & REVIEW FOR MIDTERM FINANCIAL ACCOUNTING EXAM What have we done in the course? On a chapter by chapter basis, we primarily have examined specific transactions and the effect on financial

Equity Investments -- Fair Value Method and Equity Method

Equity Investments -- Fair Value Method and Equity Method Prof. Hui Chen Advanced Financial Accounting, H. Chen 1 Intercorporate Equity Investments Why do companies invest in other companies? To earn a

Equity Investments -- Fair Value Method and Equity Method Prof. Hui Chen Advanced Financial Accounting, H. Chen 1 Intercorporate Equity Investments Why do companies invest in other companies? To earn a

Investments. 1. Discuss why corporations invest in debt and share securities.

12-1 Chapter 12 Investments Learning Objectives After studying this chapter, you should be able to: 1. Discuss why corporations invest in debt and share securities. 2. Explain the accounting for debt investments.

12-1 Chapter 12 Investments Learning Objectives After studying this chapter, you should be able to: 1. Discuss why corporations invest in debt and share securities. 2. Explain the accounting for debt investments.

Reconciliation of Non-GAAP Measures

Earnings Before Interest, Taxes, Depreciation, Amortization and Acquisition & Integration Expenses Net income applicable to TRC Companies, Inc.'s common shareholders $ 3,998 $ 3,937 Interest expense 841

Earnings Before Interest, Taxes, Depreciation, Amortization and Acquisition & Integration Expenses Net income applicable to TRC Companies, Inc.'s common shareholders $ 3,998 $ 3,937 Interest expense 841

Q1 (30 points): Choose the right answer.

: Choose the right answer.") Islamic university Gaza College of commerce Accounting department Final exam 2017-2018 Advanced Accounting Tuesday 09.01.2018 Mohammed Alashi Name: Q1 (30 points): Choose the right answer. Id:.. 1. Each

Islamic university Gaza College of commerce Accounting department Final exam 2017-2018 Advanced Accounting Tuesday 09.01.2018 Mohammed Alashi Name: Q1 (30 points): Choose the right answer. Id:.. 1. Each

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D. C FORM 6-K

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D. C. 20549 FORM 6-K Report of Foreign Private Issuer Pursuant to Rule 13a-16 or 15d-16 under the Securities Exchange Act of 1934 For the month

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D. C. 20549 FORM 6-K Report of Foreign Private Issuer Pursuant to Rule 13a-16 or 15d-16 under the Securities Exchange Act of 1934 For the month

BUS512M Session 9. Accounting for Financing Decisions: Long-Term Liabilities and Stockholders Equity

BUS512M Session 9 Accounting for Financing Decisions: Long-Term Liabilities and Stockholders Equity Liabilities Current or Short-term Liabilities Long-term Debt (borrowed funds) Lease Liabilities Deferred

BUS512M Session 9 Accounting for Financing Decisions: Long-Term Liabilities and Stockholders Equity Liabilities Current or Short-term Liabilities Long-term Debt (borrowed funds) Lease Liabilities Deferred

Chapter 2 : Reporting Intercorporate Investments and Consolidation of Wholly Owned Subsidiaries with No Differential

Types of Business expansion 1- Internal Expansion Through: establishment of New Subsidiary 2- External Expansion ( Business Combination ) Through: a. Statutory Merger P + S = P Note : S Company Dissolved

Types of Business expansion 1- Internal Expansion Through: establishment of New Subsidiary 2- External Expansion ( Business Combination ) Through: a. Statutory Merger P + S = P Note : S Company Dissolved

Reconciliation of Non-GAAP Measures

Earnings Before Interest, Taxes, Depreciation, Amortization and Goodwill & Intangible Asset Impairment Q4-2015 Q4-2016 Net income applicable to TRC Companies, Inc.'s common shareholders $6.8 $5.9 Interest

Earnings Before Interest, Taxes, Depreciation, Amortization and Goodwill & Intangible Asset Impairment Q4-2015 Q4-2016 Net income applicable to TRC Companies, Inc.'s common shareholders $6.8 $5.9 Interest

CAA South Central Ontario and Subsidiary Companies. Selected Financial Information of Consolidated Financial Statements December 31, 2012

and Subsidiary Companies Selected Financial Information of Consolidated Financial Statements December 31, 2012 Consolidated Balance Sheet As at December 31 Assets Cash and cash equivalents $ 123,791 $

and Subsidiary Companies Selected Financial Information of Consolidated Financial Statements December 31, 2012 Consolidated Balance Sheet As at December 31 Assets Cash and cash equivalents $ 123,791 $

Appendix D Investments Study Guide Solutions Fill-in-the-Blank Equations. Exercises. 1. Accrued interest 2. Dividends

Appendix D Investments Study Guide Solutions Fill-in-the-Blank Equations 1. Accrued interest 2. Dividends Exercises 1. A corporation has excess cash due to the introduction of a new product. The corporation

Appendix D Investments Study Guide Solutions Fill-in-the-Blank Equations 1. Accrued interest 2. Dividends Exercises 1. A corporation has excess cash due to the introduction of a new product. The corporation

CHAPTER 13 INVESTMENTS AND FAIR VALUE ACCOUNTING

INVESTMENTS AND FAIR VALUE ACCOUNTING DISCUSSION QUESTIONS 1. A company may temporarily have excess cash that is not needed for use in its current operations. Instead of letting excess cash remain idle

INVESTMENTS AND FAIR VALUE ACCOUNTING DISCUSSION QUESTIONS 1. A company may temporarily have excess cash that is not needed for use in its current operations. Instead of letting excess cash remain idle

Via Technologies, Inc. and Subsidiaries. Consolidated Financial Statements for the Three Months Ended March 31, 2018 and 2017

Via Technologies, Inc. and Subsidiaries Consolidated Financial Statements for the Three Months Ended March 31, 2018 and 2017 CONSOLIDATED BALANCE SHEETS March 31, 2018 (Reviewed) December 31, 2017 (Audited)

Via Technologies, Inc. and Subsidiaries Consolidated Financial Statements for the Three Months Ended March 31, 2018 and 2017 CONSOLIDATED BALANCE SHEETS March 31, 2018 (Reviewed) December 31, 2017 (Audited)

International Standards Convergence

International Standards Convergence I. INTERNATIONAL FINANCIAL REPORTING STANDARDS The International Accounting Standards Board (IASB) develops and issues International Financial Reporting Standards ().

International Standards Convergence I. INTERNATIONAL FINANCIAL REPORTING STANDARDS The International Accounting Standards Board (IASB) develops and issues International Financial Reporting Standards ().

Schedule 54: Consolidated Statement of Cash Flows

Schedule 54: Consolidated Statement of Cash Flows The consolidated statement of cash flows reflects the effects of a municipality s activities on its cash resources. The statement of cash flows shows how

Schedule 54: Consolidated Statement of Cash Flows The consolidated statement of cash flows reflects the effects of a municipality s activities on its cash resources. The statement of cash flows shows how

Fill-in-the-Blank Equations. Exercises

Chapter 15 Investments and Fair Value Accounting Study Guide Solutions 1. Accrued interest 2. Dividends Fill-in-the-Blank Equations 3. Market price per share of common stock Exercises 1. A corporation

Chapter 15 Investments and Fair Value Accounting Study Guide Solutions 1. Accrued interest 2. Dividends Fill-in-the-Blank Equations 3. Market price per share of common stock Exercises 1. A corporation

RAS AL KHAIMAH POULTRY & FEEDING CO. P.S.C. Financial statements and independent auditor s report for the year ended 31 December 2016

RAS AL KHAIMAH POULTRY & FEEDING CO. P.S.C. Financial statements and independent auditor s report for the year ended 31 December 2016 RAS AL KHAIMAH POULTRY & FEEDING CO. P.S.C. Contents Pages Independent

RAS AL KHAIMAH POULTRY & FEEDING CO. P.S.C. Financial statements and independent auditor s report for the year ended 31 December 2016 RAS AL KHAIMAH POULTRY & FEEDING CO. P.S.C. Contents Pages Independent

Guidance on Accounting Standard for Business Combinations and Accounting Standard for Business Divestitures

ASBJ Statement No. 7 Accounting Standard for Business Divestitures ASBJ Guidance No. 10 Guidance on Accounting Standard for Business Combinations and Accounting Standard for Business Divestitures December

ASBJ Statement No. 7 Accounting Standard for Business Divestitures ASBJ Guidance No. 10 Guidance on Accounting Standard for Business Combinations and Accounting Standard for Business Divestitures December

IAS 28- Investments in Associates

- Investments in Associates 1 1 - Broad outline Scope Significant influence Equity accounting Separate financial statements Presentation and Disclosure 2 Scope IAS 28 Applies to investments in associates

- Investments in Associates 1 1 - Broad outline Scope Significant influence Equity accounting Separate financial statements Presentation and Disclosure 2 Scope IAS 28 Applies to investments in associates

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D. C FORM 6-K

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D. C. 20549 FORM 6-K Report of Foreign Private Issuer Pursuant to Rule 13a-16 or 15d-16 under the Securities Exchange Act of 1934 For the month

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D. C. 20549 FORM 6-K Report of Foreign Private Issuer Pursuant to Rule 13a-16 or 15d-16 under the Securities Exchange Act of 1934 For the month

Financial Statement Balance Sheet

Financial Statement Balance Sheet Provided by: RUENTEX INDUSTRIES LIMITED Finacial year: Yearly Accounting Title 2016/12/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and

Financial Statement Balance Sheet Provided by: RUENTEX INDUSTRIES LIMITED Finacial year: Yearly Accounting Title 2016/12/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and

CH ENERGY GROUP, INC. & CENTRAL HUDSON GAS & ELECTRIC CORP. QUARTERLY FINANCIAL REPORT. for the period ended

CH ENERGY GROUP, INC. & CENTRAL HUDSON GAS & ELECTRIC CORP. QUARTERLY FINANCIAL REPORT for the period ended JUNE 30, 2015 FINANCIAL STATEMENTS QUARTER ENDED JUNE 30, 2015 TABLE OF CONTENTS CH Energy Group,

CH ENERGY GROUP, INC. & CENTRAL HUDSON GAS & ELECTRIC CORP. QUARTERLY FINANCIAL REPORT for the period ended JUNE 30, 2015 FINANCIAL STATEMENTS QUARTER ENDED JUNE 30, 2015 TABLE OF CONTENTS CH Energy Group,

MITSUI & CO. (U.S.A.), INC.

, INC.") 8OCT200409534112 ANNUAL REPORT 2007 April 1, 2006 - March 31, 2007 MITSUI & CO. (U.S.A.), INC. 8OCT200409534564 INDEPENDENT AUDITORS REPORT To the Board of Directors of Mitsui & Co. (U.S.A.), Inc.: We

8OCT200409534112 ANNUAL REPORT 2007 April 1, 2006 - March 31, 2007 MITSUI & CO. (U.S.A.), INC. 8OCT200409534564 INDEPENDENT AUDITORS REPORT To the Board of Directors of Mitsui & Co. (U.S.A.), Inc.: We

Purpose, content, and technicalities

Purpose, content, and technicalities 1 1. Understand the reasons why consolidated financial statements (CFSs) are prepared. 2. Understand the content of the consolidated financial statements. 3. Understand

Purpose, content, and technicalities 1 1. Understand the reasons why consolidated financial statements (CFSs) are prepared. 2. Understand the content of the consolidated financial statements. 3. Understand

KKR STATEMENTS OF OPERATIONS SUPPLEMENTAL PRIOR PERIOD SEGMENT INFORMATION QUARTER ENDED MARCH 31, 2014 (Amounts in thousands)

") QUARTER ENDED MARCH 31, 2014 Management Fees $ 123,039 $ 72,354 $ - $ 195,393 Monitoring Fees 36,363 - - 36,363 Transaction Fees 93,020 6,022 64,474 163,516 Fee Credits (80,338) (4,330) - (84,668) Total

QUARTER ENDED MARCH 31, 2014 Management Fees $ 123,039 $ 72,354 $ - $ 195,393 Monitoring Fees 36,363 - - 36,363 Transaction Fees 93,020 6,022 64,474 163,516 Fee Credits (80,338) (4,330) - (84,668) Total

FA4 Module 4 Consolidation Subsequent to Acquisition

FA4 Module 4 Consolidation Subsequent to Acquisition Goodwill Impairment According to the Handbook, if an intangible asset is deemed to have an indefinite useful life then the asset is subject to an annual

FA4 Module 4 Consolidation Subsequent to Acquisition Goodwill Impairment According to the Handbook, if an intangible asset is deemed to have an indefinite useful life then the asset is subject to an annual

CHAPTER 17. Investments. 1. Debt securities. 1, 2, 3, , 7 (a) Held-to-maturity. 4, 5, 7, 8, 1, 3 1, 2, 3, 5 1, 7 4

Held-to-maturity. 4, 5, 7, 8, 1, 3 1, 2, 3, 5 1, 7 4") CHAPTER 17 Investments ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Debt securities. 1, 2, 3, 13 1 4, 7 (a) Held-to-maturity.

CHAPTER 17 Investments ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Debt securities. 1, 2, 3, 13 1 4, 7 (a) Held-to-maturity.

IAS Investments in Associates. By:

IAS - 28 Investments in Associates International Accounting Standard No. 28 (IAS 28) Investments in associates Scope 1. This Standard applies to accounting for investments in associates. However, shall

IAS - 28 Investments in Associates International Accounting Standard No. 28 (IAS 28) Investments in associates Scope 1. This Standard applies to accounting for investments in associates. However, shall

Lesson 3 The Equity Method of Accounting for Investments. Università degli Studi di Trieste D.E.A.M.S. Paolo Altin

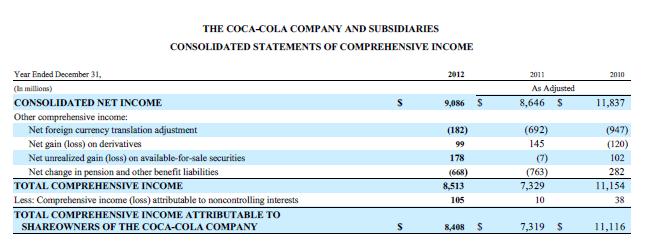

Lesson 3 The Equity Method of Accounting for Investments Università degli Studi di Trieste D.E.A.M.S. Paolo Altin 68 The Equity Method of Accounting for Investments In its annual report, The Coca-Cola

Lesson 3 The Equity Method of Accounting for Investments Università degli Studi di Trieste D.E.A.M.S. Paolo Altin 68 The Equity Method of Accounting for Investments In its annual report, The Coca-Cola

Chapter 2 STOCK INVESTMENTS INVESTOR ACCOUNTING AND REPORTING

Advanced Accounting 13th Edition Beams SOLUTIONS MANUAL Full clear download (no formatting errors) at: https://testbankreal.com/download/advanced-accounting-13th-edition-beamssolutions-manual-2/ Chapter

Advanced Accounting 13th Edition Beams SOLUTIONS MANUAL Full clear download (no formatting errors) at: https://testbankreal.com/download/advanced-accounting-13th-edition-beamssolutions-manual-2/ Chapter

F83. I168 other information. financial report

Dufry Annual Report 2010 financial report F83 F83 financial report 84 CONSOLIDATED FINANCIAL STATEMENTS AS OF DECEMber 31, 2010 84 Consolidated Income Statement 85 Consolidated Statement of Comprehensive

Dufry Annual Report 2010 financial report F83 F83 financial report 84 CONSOLIDATED FINANCIAL STATEMENTS AS OF DECEMber 31, 2010 84 Consolidated Income Statement 85 Consolidated Statement of Comprehensive

Annual Financial Report KONAMI CORPORATION and its subsidiaries Consolidated Financial Statements For the fiscal year ended March 31, 2015

Annual Financial Report KONAMI CORPORATION and its subsidiaries Consolidated Financial Statements For the fiscal year ended March 31, 2015 KONAMI CORPORATION TABLE OF CONTENTS 1. Consolidated Financial

Annual Financial Report KONAMI CORPORATION and its subsidiaries Consolidated Financial Statements For the fiscal year ended March 31, 2015 KONAMI CORPORATION TABLE OF CONTENTS 1. Consolidated Financial

ACCT 434: Advanced Financial Accounting Module 01 Activities

ACCT 434: Advanced Financial Accounting Module 01 Activities Question 1 Part 1: On January 1, 2014, Phantom Corp. acquires $300,000 of Spider Inc. 9% bonds. The interest is payable each June 30 and December

ACCT 434: Advanced Financial Accounting Module 01 Activities Question 1 Part 1: On January 1, 2014, Phantom Corp. acquires $300,000 of Spider Inc. 9% bonds. The interest is payable each June 30 and December

Apr-Jun Apr-Jun Jan-Jun Jan-Jun. Cash and cash equivalents 377, ,861 Depreciation 52,448 68,594

INTERIM CONSOLIDATED STATEMENT OF INCOME (Un audited) All Figures in SAR '000 Particulars Apr-Jun Apr-Jun Jan-Jun Jan-Jun Net Sales 1,078,268 1,325,210 2,005,355 2,291,927 Cost of Sales 835,550 1,044,173

INTERIM CONSOLIDATED STATEMENT OF INCOME (Un audited) All Figures in SAR '000 Particulars Apr-Jun Apr-Jun Jan-Jun Jan-Jun Net Sales 1,078,268 1,325,210 2,005,355 2,291,927 Cost of Sales 835,550 1,044,173

CISCO SYSTEMS, INC. (Exact name of registrant as specified in its charter)

") (Mark One) UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-Q x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly

(Mark One) UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-Q x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly

ACER INCORPORATED AND SUBSIDIARIES. Consolidated Balance Sheets

Consolidated Balance Sheets June 30, 2016, December 31, 2015 and June 30, 2015 (June 30, 2016 and 2015 are reviewed, not audited) Assets 2016.6.30 2015.12.31 2015.6.30 Current assets: Cash and cash equivalents

Consolidated Balance Sheets June 30, 2016, December 31, 2015 and June 30, 2015 (June 30, 2016 and 2015 are reviewed, not audited) Assets 2016.6.30 2015.12.31 2015.6.30 Current assets: Cash and cash equivalents

Group Financial Statements

IAS 27 & 28 IFRS 3 IFRS 10, 11 & 12 IFRS 13 Group Financial Statements 04 CONCEPT OF GROUP ACCOUNTS Many large companies actually consist of several companies controlled by one central or administrative

IAS 27 & 28 IFRS 3 IFRS 10, 11 & 12 IFRS 13 Group Financial Statements 04 CONCEPT OF GROUP ACCOUNTS Many large companies actually consist of several companies controlled by one central or administrative

Consolidated Financial Statements AT DECEMBER 31, 2016

AT DECEMBER 31, 2016 Index to Income Statement 136 Statement of Comprehensive Income/(Loss) 137 Statement of Financial Position 138 Statement of Cash Flows 139 Statement of Changes in Equity 140 Notes

AT DECEMBER 31, 2016 Index to Income Statement 136 Statement of Comprehensive Income/(Loss) 137 Statement of Financial Position 138 Statement of Cash Flows 139 Statement of Changes in Equity 140 Notes

Advantech Co., Ltd. and Subsidiaries

Advantech Co., Ltd. and Subsidiaries Consolidated Financial Statements for the Three Months Ended March 31, 2013 and and Independent Accountants Review Report INDEPENDENT ACCOUNTANTS REVIEW REPORT The

Advantech Co., Ltd. and Subsidiaries Consolidated Financial Statements for the Three Months Ended March 31, 2013 and and Independent Accountants Review Report INDEPENDENT ACCOUNTANTS REVIEW REPORT The

Financial Statement Analysis L5: Analyzing Investing Activities - Intercorporate Investments

5-1 Financial Statement Analysis L5: Analyzing Investing Activities - Intercorporate Investments 5-2 Investment Securities Composition Investment (marketable) securities: Debt Securities Government or

5-1 Financial Statement Analysis L5: Analyzing Investing Activities - Intercorporate Investments 5-2 Investment Securities Composition Investment (marketable) securities: Debt Securities Government or

May & Baker Nig Plc RC. UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS 31 MARCH 2017

` May & Baker Nig Plc RC. 558 UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS 31 MARCH 2017 UNAUDITED CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME Note Continuing operations Revenue

` May & Baker Nig Plc RC. 558 UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS 31 MARCH 2017 UNAUDITED CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME Note Continuing operations Revenue

Financial Results For the Fiscal Year 2016 ending January 31, 2016

Financial Results For the Fiscal Year 2016 ending January 31, 2016 March 16, 2016 Balance Sheets (Consolidated) Thousands of Yen 31 Jan., 2016 Assets Current assets: Cash & Cash equivalents 1,984,469 Accounts

Financial Results For the Fiscal Year 2016 ending January 31, 2016 March 16, 2016 Balance Sheets (Consolidated) Thousands of Yen 31 Jan., 2016 Assets Current assets: Cash & Cash equivalents 1,984,469 Accounts

FORM 6-K UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D. C KYOCERA CORPORATION

FORM 6-K UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D. C. 20549 Report of Foreign Private Issuer Pursuant to Rule 13a-16 or 15d-16 under the Securities Exchange Act of 1934 For the month

FORM 6-K UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D. C. 20549 Report of Foreign Private Issuer Pursuant to Rule 13a-16 or 15d-16 under the Securities Exchange Act of 1934 For the month

Statement of Earnings

audited financial statements Statement of Earnings General Electric Company and consolidated affiliates For the years ended December 31 (In millions; per-share amounts in dollars) 2012 2011 2010 REVENUES

audited financial statements Statement of Earnings General Electric Company and consolidated affiliates For the years ended December 31 (In millions; per-share amounts in dollars) 2012 2011 2010 REVENUES

ILLUSTRATION 12-1 TYPES OF INTANGIBLE ASSETS

ILLUSTRATION 12-1 TYPES OF INTANGIBLE ASSETS INTANGIBLE ASSETS Identifiable Intangible Assets (Rights Type) Externally Acquired Internally Developed Financial Statement Treatment Unidentifiable Intangible

ILLUSTRATION 12-1 TYPES OF INTANGIBLE ASSETS INTANGIBLE ASSETS Identifiable Intangible Assets (Rights Type) Externally Acquired Internally Developed Financial Statement Treatment Unidentifiable Intangible

Gun Ei Chemical Industry Co., Ltd.

Gun Ei Chemical Industry Co., Ltd. Consolidated Financial Statements Consolidated balance sheets As of 2015 and 2016 2015 2016 Assets Current assets Cash and deposits 7,524 10,648 Notes and accounts receivable-trade

Gun Ei Chemical Industry Co., Ltd. Consolidated Financial Statements Consolidated balance sheets As of 2015 and 2016 2015 2016 Assets Current assets Cash and deposits 7,524 10,648 Notes and accounts receivable-trade

Consolidated Balance Sheets Mitsui O.S.K. Lines, Ltd. March 31, 2007 and 2006

Consolidated Balance Sheets Mitsui O.S.K. Lines, Ltd. March 31, 2007 and 2006 ASSETS Current assets: Cash and cash equivalents......................................... 51,383 60,267 $ 435,265 Marketable

Consolidated Balance Sheets Mitsui O.S.K. Lines, Ltd. March 31, 2007 and 2006 ASSETS Current assets: Cash and cash equivalents......................................... 51,383 60,267 $ 435,265 Marketable

EITF ABSTRACTS. Dates Discussed: September 23 24, 1998; November 18 19, 1998; January 21, 1999

EITF ABSTRACTS Issue No. 98-13 Title: Accounting by an Equity Method Investor for Investee Losses When the Investor Has Loans to and Investments in Other Securities of the Investee Dates Discussed: September

EITF ABSTRACTS Issue No. 98-13 Title: Accounting by an Equity Method Investor for Investee Losses When the Investor Has Loans to and Investments in Other Securities of the Investee Dates Discussed: September

INVESTMENTS AND INTERNATIONAL OPERATIONS

15-1 Chapter 15 INVESTMENTS AND INTERNATIONAL OPERATIONS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D.,

15-1 Chapter 15 INVESTMENTS AND INTERNATIONAL OPERATIONS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D.,

Highlights of Consolidated Results for Fiscal Year ended March 31, 2016

May 9, 2016 Highlights of Consolidated Results for Fiscal Year ended March 31, 2016 (except for per share amounts) Year ended Year ended March 31, March 31, 2016 2015 Change Y 745,888 Y 707,237 5.5 Operating

May 9, 2016 Highlights of Consolidated Results for Fiscal Year ended March 31, 2016 (except for per share amounts) Year ended Year ended March 31, March 31, 2016 2015 Change Y 745,888 Y 707,237 5.5 Operating

FORM 6-K UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D. C KYOCERA CORPORATION

FORM 6-K UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D. C. 20549 Report of Foreign Private Issuer Pursuant to Rule 13a-16 or 15d-16 under the Securities Exchange Act of 1934 For the month

FORM 6-K UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D. C. 20549 Report of Foreign Private Issuer Pursuant to Rule 13a-16 or 15d-16 under the Securities Exchange Act of 1934 For the month

GREEN CROSS HOLDINGS CORPORATION AND ITS SUBSIDIARIES

GREEN CROSS HOLDINGS CORPORATION AND ITS SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED DECEMBER 31, 2015 AND 2014 ATTACHMENT : INDEPENDENT AUDITORS REPORT GREEN CROSS HOLDINGS

GREEN CROSS HOLDINGS CORPORATION AND ITS SUBSIDIARIES CONSOLIDATED FINANCIAL STATEMENTS AS OF AND FOR THE YEAR ENDED DECEMBER 31, 2015 AND 2014 ATTACHMENT : INDEPENDENT AUDITORS REPORT GREEN CROSS HOLDINGS

LG CORP. SEPARATE FINANCIAL STATEMENTS AS OF AND FOR THE YEARS ENDED DECEMBER 31, 2012 AND 2011, AND INDEPENDENT AUDITORS REPORT

LG CORP. SEPARATE FINANCIAL STATEMENTS AS OF AND FOR THE YEARS ENDED DECEMBER 31, 2012 AND 2011, AND INDEPENDENT AUDITORS REPORT Deloitte Anjin LLC 9F., One IFC, 23, Yoido-dong, Youngdeungpo-gu, Seoul

LG CORP. SEPARATE FINANCIAL STATEMENTS AS OF AND FOR THE YEARS ENDED DECEMBER 31, 2012 AND 2011, AND INDEPENDENT AUDITORS REPORT Deloitte Anjin LLC 9F., One IFC, 23, Yoido-dong, Youngdeungpo-gu, Seoul

Could Duke net $2.35B from international asset sale? Feb 12, 2016, 6:00am EST. Charlotte Business Journal

Note to Acct 6120 class from instructor. (UNC Charlotte) There are three reasons for this post. First, I want to let you know that I have posted (on my course webpage) updated files for the Chapter 5 supplementary

Note to Acct 6120 class from instructor. (UNC Charlotte) There are three reasons for this post. First, I want to let you know that I have posted (on my course webpage) updated files for the Chapter 5 supplementary

Reviewed Reviewed Not Reviewed Not Reviewed. Notes 2018

As of September 30, Statement of Financial Position (Balance Sheet) Reviewed Audited Notes September 30, December 31, ASSETS Current assets 968.088.116 967.988.419 Cash and cash equivalents 5 37.103.817

As of September 30, Statement of Financial Position (Balance Sheet) Reviewed Audited Notes September 30, December 31, ASSETS Current assets 968.088.116 967.988.419 Cash and cash equivalents 5 37.103.817

Accounting Title 2013/12/ /12/ /1/1 Balance Sheet

Financial Statement Balance Sheet Accounting Title 2013/12/31 2012/12/31 2012/1/1 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 471,574 507,692 394,913 Notes

Financial Statement Balance Sheet Accounting Title 2013/12/31 2012/12/31 2012/1/1 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 471,574 507,692 394,913 Notes

Management s Report on Internal Control Over Financial Reporting

Internal Control Over Financial Reporting Management s Report on Internal Control Over Financial Reporting Management of Brookfield Asset Management Inc. ( Brookfield ) is responsible for establishing

Internal Control Over Financial Reporting Management s Report on Internal Control Over Financial Reporting Management of Brookfield Asset Management Inc. ( Brookfield ) is responsible for establishing

Annual Financial Statements 2017

Annual Financial Statements 2017 For the year ended March 31, 2017 Contents 02 Consolidated Statement of Income 02 Consolidated Statement of Comprehensive Income 03 Consolidated Statement of Financial

Annual Financial Statements 2017 For the year ended March 31, 2017 Contents 02 Consolidated Statement of Income 02 Consolidated Statement of Comprehensive Income 03 Consolidated Statement of Financial

CONSOLIDATED BALANCE SHEET

CONSOLIDATED BALANCE SHEET December 31, 2017 A S S E T S CURRENT ASSETS: Cash and time deposits 31,380 Accounts receivable trade 98,188 Inventories 1,096 Short-term loans receivable 46,282 Deferred tax

CONSOLIDATED BALANCE SHEET December 31, 2017 A S S E T S CURRENT ASSETS: Cash and time deposits 31,380 Accounts receivable trade 98,188 Inventories 1,096 Short-term loans receivable 46,282 Deferred tax

Financial review Refresco Financial review 2017

Financial review 2017 Financial review 2017 Financial review 2017 1 69 Consolidated income statement For the year ended December 31, 2017 (x 1 million euro) Note December 31, 2017 December 31, 2016 Revenue

Financial review 2017 Financial review 2017 Financial review 2017 1 69 Consolidated income statement For the year ended December 31, 2017 (x 1 million euro) Note December 31, 2017 December 31, 2016 Revenue

Date: 19 April 2018 ESMA

Date: 19 April 2018 ESMA32-63-365 List of decisions published in the Extracts from the EECS s Database of Enforcement (updated October 2017) Number Package Number Decision referenfinancial year-end Name

Date: 19 April 2018 ESMA32-63-365 List of decisions published in the Extracts from the EECS s Database of Enforcement (updated October 2017) Number Package Number Decision referenfinancial year-end Name

Fast Retailing Co., Ltd. Consolidated Financial Statements for the year ended 31 August 2017

Fast Retailing Co., Ltd. Consolidated Financial Statements for the year ended CONSOLIDATED STATEMENT OF FINANCIAL POSITION FAST RETAILING CO., LTD. and consolidated subsidiaries and 2016 Millions of yen

Fast Retailing Co., Ltd. Consolidated Financial Statements for the year ended CONSOLIDATED STATEMENT OF FINANCIAL POSITION FAST RETAILING CO., LTD. and consolidated subsidiaries and 2016 Millions of yen

MAY & BAKER NIGERIA PLC CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2013

` MAY & BAKER NIGERIA PLC CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2013 REPORT OF THE INDEPENDENT AUDITORS TO THE MEMBERS OF MAY & BAKER NIGERIA PLC ` We have audited the accompanying consolidated

` MAY & BAKER NIGERIA PLC CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2013 REPORT OF THE INDEPENDENT AUDITORS TO THE MEMBERS OF MAY & BAKER NIGERIA PLC ` We have audited the accompanying consolidated

Consolidated Financial Statements (Workshop 1) 24 April 2012

24 April 2012") Consolidated Financial Statements (Workshop 1) 24 April 2012 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2005-12 Nelson Consulting Limited 1

Consolidated Financial Statements (Workshop 1) 24 April 2012 LAM Chi Yuen Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2005-12 Nelson Consulting Limited 1

UNITED STATES SECURITIES AND EXCHANGE COMMISSION. Washington, D.C FORM 10-Q

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

FASB Emerging Issues Task Force Draft Abstract EITF Issue Notice for Recipients of This Draft EITF Abstract

FASB Emerging Issues Task Force Draft Abstract EITF Issue 08-6 Notice for Recipients of This Draft EITF Abstract October 1, 2008 EITF Issue No. 08-6, "Equity Method Investment Accounting Considerations,"

FASB Emerging Issues Task Force Draft Abstract EITF Issue 08-6 Notice for Recipients of This Draft EITF Abstract October 1, 2008 EITF Issue No. 08-6, "Equity Method Investment Accounting Considerations,"

ZAMIL INDUSTRIAL INVESTMENT COMPANY AND ITS SUBSIDIARIES (SAUDI JOINT STOCK COMPANY)

") ZAMIL INDUSTRIAL INVESTMENT COMPANY AND ITS SUBSIDIARIES CONSOLIDATED INTERIM FINANCIAL STATEMENTS AND AUDITORS REPORT (LIMITED REVIEW) FOR THE THREE MONTHS AND YEAR ENDED DECEMBER 31, 2013 CONSOLIDATED

ZAMIL INDUSTRIAL INVESTMENT COMPANY AND ITS SUBSIDIARIES CONSOLIDATED INTERIM FINANCIAL STATEMENTS AND AUDITORS REPORT (LIMITED REVIEW) FOR THE THREE MONTHS AND YEAR ENDED DECEMBER 31, 2013 CONSOLIDATED

CIMA Managerial Level Paper F2 FINANCIAL MANAGEMENT (REVISION SUMMARIES)

") CIMA Managerial Level Paper F2 FINANCIAL MANAGEMENT (REVISION SUMMARIES) Chapter Title Page number 1 The regulatory framework 3 2 What is a group 9 3 Group accounts the statement of financial position

CIMA Managerial Level Paper F2 FINANCIAL MANAGEMENT (REVISION SUMMARIES) Chapter Title Page number 1 The regulatory framework 3 2 What is a group 9 3 Group accounts the statement of financial position

LG HOUSEHOLD & HEALTH CARE, LTD. AND SUBSIDIARIES. Consolidated Financial Statements

LG HOUSEHOLD & HEALTH CARE, LTD. AND SUBSIDIARIES Consolidated Financial Statements December 31, 2010 and 2009 (With Independent Auditors Report Thereon) Contents Page Independent Auditors Report 1 Consolidated

LG HOUSEHOLD & HEALTH CARE, LTD. AND SUBSIDIARIES Consolidated Financial Statements December 31, 2010 and 2009 (With Independent Auditors Report Thereon) Contents Page Independent Auditors Report 1 Consolidated

Copyright 2009 The Learning House, Inc. Income Taxes and Investments Page 1 of 17

Copyright 2009 The Learning House, Inc. Income Taxes and Investments Page 1 of 17 Introduction Taxes are a significant expense for most companies and must be considered when analyzing a company. Differences

Copyright 2009 The Learning House, Inc. Income Taxes and Investments Page 1 of 17 Introduction Taxes are a significant expense for most companies and must be considered when analyzing a company. Differences

Note of Transition to IFRS

- 11 - Note of Transition to Upon to, the Company s opening consolidated statement of financial position was prepared by 1 as of April 1, 2013, its date to, with required adjustments made to the consolidated

- 11 - Note of Transition to Upon to, the Company s opening consolidated statement of financial position was prepared by 1 as of April 1, 2013, its date to, with required adjustments made to the consolidated

Preparation of consolidated statements of comprehensive income, changes in equity and cash flows

CHAPTER 22 Preparation of consolidated statements of comprehensive income, changes in equity and cash flows 22.1 Introduction The main purpose of this chapter is to explain how to prepare a consolidated

CHAPTER 22 Preparation of consolidated statements of comprehensive income, changes in equity and cash flows 22.1 Introduction The main purpose of this chapter is to explain how to prepare a consolidated

Three Months Ended Twelve Months Ended 12/31/ /31/ /31/ /31/

Consolidated Statements of Operations (In thousands, except share and per share data) TABLE 1 Software licenses $11,336 $8,901 $37,859 $30,709 Support and maintenance 12,631 12,194 49,163 45,591 Professional

Consolidated Statements of Operations (In thousands, except share and per share data) TABLE 1 Software licenses $11,336 $8,901 $37,859 $30,709 Support and maintenance 12,631 12,194 49,163 45,591 Professional

Chapter 12 - Reporting and Analyzing Cash Flows. Chapter Outline

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

CORNING INCORPORATED AND SUBSIDIARY COMPANIES CONSOLIDATED STATEMENTS OF (LOSS) INCOME (Unaudited; in millions, except per share amounts)

INCOME (Unaudited; in millions, except per share amounts)") CONSOLIDATED STATEMENTS OF (LOSS) INCOME (Unaudited; in millions, except per share amounts) March 31, Net sales $ 2,500 $ 2,375 Cost of sales 1,545 1,424 Gross margin 955 951 Operating expenses:. Selling,

CONSOLIDATED STATEMENTS OF (LOSS) INCOME (Unaudited; in millions, except per share amounts) March 31, Net sales $ 2,500 $ 2,375 Cost of sales 1,545 1,424 Gross margin 955 951 Operating expenses:. Selling,

Issue No: 03-1 Title: The Meaning of Other-Than-Temporary Impairment and Its Application to Certain Investments

EITF Issue No. 03-1 The views in this report are not Generally Accepted Accounting Principles until a consensus is reached and it is FASB Emerging Issues Task Force Issue No: 03-1 Title: The Meaning of

EITF Issue No. 03-1 The views in this report are not Generally Accepted Accounting Principles until a consensus is reached and it is FASB Emerging Issues Task Force Issue No: 03-1 Title: The Meaning of

General notes to the consolidated financial statements

80 ARCADIS Financial Statements 2013 General notes to the consolidated financial statements General notes to the consolidated financial statements 1 General information ARCADIS NV is a public company organized

80 ARCADIS Financial Statements 2013 General notes to the consolidated financial statements General notes to the consolidated financial statements 1 General information ARCADIS NV is a public company organized

CONSOLIDATED BALANCE SHEET

CONSOLIDATED BALANCE SHEET December 31, 2018 A S S E T S CURRENT ASSETS: Cash and time deposits 51,215 Accounts receivable-trade 95,065 Inventories 5,405 Short-term loans receivable 43,021 Deferred tax

CONSOLIDATED BALANCE SHEET December 31, 2018 A S S E T S CURRENT ASSETS: Cash and time deposits 51,215 Accounts receivable-trade 95,065 Inventories 5,405 Short-term loans receivable 43,021 Deferred tax

CH ENERGY GROUP, INC. & CENTRAL HUDSON GAS & ELECTRIC CORP. QUARTERLY FINANCIAL REPORT. for the period ended

CH ENERGY GROUP, INC. & CENTRAL HUDSON GAS & ELECTRIC CORP. QUARTERLY FINANCIAL REPORT for the period ended JUNE 30, 2014 FINANCIAL STATEMENTS (Unaudited) QUARTER ENDED JUNE 30, 2014 TABLE OF CONTENTS

CH ENERGY GROUP, INC. & CENTRAL HUDSON GAS & ELECTRIC CORP. QUARTERLY FINANCIAL REPORT for the period ended JUNE 30, 2014 FINANCIAL STATEMENTS (Unaudited) QUARTER ENDED JUNE 30, 2014 TABLE OF CONTENTS

Advantech Co., Ltd. and Subsidiaries

Advantech Co., Ltd. and Subsidiaries Consolidated Financial Statements for the Nine Months Ended 2018 and and Independent Auditors Review Report INDEPENDENT AUDITORS REVIEW REPORT The Board of Directors

Advantech Co., Ltd. and Subsidiaries Consolidated Financial Statements for the Nine Months Ended 2018 and and Independent Auditors Review Report INDEPENDENT AUDITORS REVIEW REPORT The Board of Directors

Midlands Minerals Corporation. Consolidated Financial Statements. As at and for the years ended

Consolidated Financial Statements As at and for the years ended Schwartz Levitsky Feldman llp CHARTERED ACCOUNTANTS LICENSED PUBLIC ACCOUNTANTS TORONTO MONTREAL INDEPENDENT AUDITORS REPORT To the Shareholders

Consolidated Financial Statements As at and for the years ended Schwartz Levitsky Feldman llp CHARTERED ACCOUNTANTS LICENSED PUBLIC ACCOUNTANTS TORONTO MONTREAL INDEPENDENT AUDITORS REPORT To the Shareholders

INTERMEDIATE ACCOUNTING

Chapter 13 Investments and Long-Term Receivables INTERMEDIATE ACCOUNTING whole or in part. Objectives 1. Explain the classification and valuation of investments. 2. Account for investments in debt securities

Chapter 13 Investments and Long-Term Receivables INTERMEDIATE ACCOUNTING whole or in part. Objectives 1. Explain the classification and valuation of investments. 2. Account for investments in debt securities

SECURITIES & EXCHANGE COMMISSION WASHINGTON, D.C FORM 10-Q

SECURITIES & EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-Q (Mark One) [X] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended March

SECURITIES & EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-Q (Mark One) [X] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended March

OPERATING INCOME AND OPERATING MARGIN

OPERATING INCOME AND OPERATING MARGIN Reconciliation of U.S. GAAP to Non-GAAP (US$ Millions) 2013 2014 2015 2016 U.S. GAAP REVENUES Less transaction-based expenses $1,895 $2,067 $2,090 $2,277 U.S. GAAP

OPERATING INCOME AND OPERATING MARGIN Reconciliation of U.S. GAAP to Non-GAAP (US$ Millions) 2013 2014 2015 2016 U.S. GAAP REVENUES Less transaction-based expenses $1,895 $2,067 $2,090 $2,277 U.S. GAAP

Statement of Financial Accounting Standards No. 5. Statement of Financial Accounting Standards No.5. Long-Term Investments in Equity Securities

Statement of Financial Accounting Standards No. 5 Statement of Financial Accounting Standards No.5 Long-Term Investments in Equity Securities Revised on 18 June 1998 Translated by Chung-yueh Conrad Chang,

Statement of Financial Accounting Standards No. 5 Statement of Financial Accounting Standards No.5 Long-Term Investments in Equity Securities Revised on 18 June 1998 Translated by Chung-yueh Conrad Chang,

Financial Reporting Framework for Small- and Medium-Sized Entities FRF for SMEs Accounting Framework

Financial Reporting Framework for Small- and Medium-Sized Entities FRF for SMEs Accounting Framework December 11, 2013 Presented by: Jackie H. White, CPA www.pbmares.com An Introduction to the New Financial

Financial Reporting Framework for Small- and Medium-Sized Entities FRF for SMEs Accounting Framework December 11, 2013 Presented by: Jackie H. White, CPA www.pbmares.com An Introduction to the New Financial

Introduction to Ind-AS By Neeraj Sharma

Introduction to Ind-AS By Neeraj Sharma neerajsharma2002in@yahoo.com 1 Agenda Ind-AS An Overview Five Key Standards GAAP Differences Other GAAP Differences Questions & Answers 2 Ind-AS An Overview Set

Introduction to Ind-AS By Neeraj Sharma neerajsharma2002in@yahoo.com 1 Agenda Ind-AS An Overview Five Key Standards GAAP Differences Other GAAP Differences Questions & Answers 2 Ind-AS An Overview Set

HTC Corporation and Subsidiaries. Consolidated Financial Statements for the Six Months Ended June 30, 2010 and 2011 and Independent Auditors Report

HTC Corporation and Subsidiaries Consolidated Financial Statements for the Six Months Ended June 30, 2010 and 2011 and Independent Auditors Report INDEPENDENT AUDITORS REPORT The Board of Directors and

HTC Corporation and Subsidiaries Consolidated Financial Statements for the Six Months Ended June 30, 2010 and 2011 and Independent Auditors Report INDEPENDENT AUDITORS REPORT The Board of Directors and

IFRS illustrative consolidated financial statements

IFRS illustrative consolidated financial statements 2016 This publication has been prepared for illustrative purposes only and does not constitute accounting or other professional advice, nor is it a substitute

IFRS illustrative consolidated financial statements 2016 This publication has been prepared for illustrative purposes only and does not constitute accounting or other professional advice, nor is it a substitute

YAHOO INC FORM 10-Q. (Quarterly Report) Filed 05/08/14 for the Period Ending 03/31/14

Filed 05/08/14 for the Period Ending 03/31/14") YAHOO INC FORM 10-Q (Quarterly Report) Filed 05/08/14 for the Period Ending 03/31/14 Address YAHOO! INC. 701 FIRST AVENUE SUNNYVALE, CA 94089 Telephone 4083493300 CIK 0001011006 Symbol YHOO SIC Code 7373

YAHOO INC FORM 10-Q (Quarterly Report) Filed 05/08/14 for the Period Ending 03/31/14 Address YAHOO! INC. 701 FIRST AVENUE SUNNYVALE, CA 94089 Telephone 4083493300 CIK 0001011006 Symbol YHOO SIC Code 7373

ASUSTEK COMPUTER INC. Financial Statements and. Report of independent accountants. December 31, 2011 and 2010

ASUSTEK COMPUTER INC. Financial Statements and Report of independent accountants December 31, 2011 and 2010 --------------------------------------------------------------------------------------------------------------------------------

ASUSTEK COMPUTER INC. Financial Statements and Report of independent accountants December 31, 2011 and 2010 --------------------------------------------------------------------------------------------------------------------------------