Bank of Ayudhya PCL. September A member of MUFG, a global financial group

|

|

|

- Miles Jones

- 6 years ago

- Views:

Transcription

1 Bank of Ayudhya PCL September 2017 A member of MUFG, a global financial group

2 Who we are Key Financials & Development Highlights Mid Term Business Plan 2017 Business Strategy and Key Focus 2

Co.")

3 Krungsri Group Overview Officially established in 1945 Shareholding Structure (as of 8 Sep 2017) BTMU 76.88% Ratanarak Group & Others 23.12% 2007: BAY and GE become strategic partners 2008: Acquisition of GE Capital Auto Lease, subsequently renamed to Krungsri Auto 2009: Acquisition of AIG Retail Bank Pcl. and AIG Card (Thailand) Co., Ltd. 2009: Acquisition of Ngern Tid Lor Co., Ltd., a micro finance business from AIG 2009: Acquisition of GE Money Thailand, a consumer finance company 2012: Acquisition of HSBC Thailand s retail banking businesses Dec 2013: BTMU replaced GE as the strategic shareholder of Krungsri Jan 2015: Integration of BTMU Bangkok Branch into Krungsri Sep 2016: Acquisition of Hattha Kaksekar Limited (HKL) Mar 2017: Set up Krungsri Finnovate Company Limited 3

USD$0.7Bn THB 32.80 Bn Acquired GE Money(Thailand) USD$1.9Bn THB 53.")

4 Who we are: Our History of Growth Acquisitions & Organic Growth Total Asset Size (Dec 2007) THB Bn Feb 2008 Apr 2009 Nov 2009 Acquired GE Auto THB USD$2.6Bn Bn Acquired AIG Retail Bank and AIG Card (Thailand) USD$0.7Bn THB Bn Acquired GE Money(Thailand) USD$1.9Bn THB Bn Year 2010 One KRUNGSRI Integration Q Acquired HSBC (Retail Portfolio in Thailand) USD$440MM THB Bn Jan 2007 Sep 2009 Krungsri & GE JV Acquired Ngern Tid Lor USD$64.9MM THB 2.00 Bn Dec 2013 BTMU New strategic shareholder Jan 2015 Integration of BTMU Bangkok Branch Sep 2016 Acquired Hattha Kaksekar Limited THB 2.00 Bn Total Asset Size (Sep 2017) THB 2.0 Trillion BTMU 72.0% Ratanarak Group 25.0% Free Float 3.0% BTMU 76.88% Ratanarak Group & Others 23.12% 4

5 Fact about Krungsri: Thailand s 5th largest universal bank with leadership position in consumer finance & Japanese Corporate market Unique & Strong Krungsri 5 th largest universal bank in Thailand Strong leadership position in consumer finance Global product offering capabilities One of the world s largest comprehensive financial group Most extensive overseas network with over 2,000 offices in more than 50 countries The combination of Krungsri s new found global capabilities and network as part of the MUFG family, giving us unique strength and enhanced competitiveness. 5

6 Our Position: Fifth largest financial group in Thailand Japanese Corporate Personal Loan 3.7 million accounts 30% market share Credit Card 3.3 million CIFs 1/ 16% market share Global Ranking 1,259 Forbes The Global 2000 Sales, Profits, Assets and Market Capitalization SET Ranking 13 THB bn 2/ Market Capitalization Thai Banks Ranking Commercial 5 Banks by Assets, Deposits and Loans 1 Credit Ratings Highest rating (A ) among top banks in Thailand by Fitch Ratings 2 Auto (HP) # 1 in used car financing * 25% market share 1/ CIFs: Card in Force International Ratings 2/ Stock Exchange of Thailand (29 Sep 2017) Standard & Poor s Issuer Credit Rating Moody s Long Term Bank Deposit Fitch Ratings Issuer Default Rating Krungsri BBB+ Baa1 A Thailand BBB+ Baa1 BBB+ 6

7 Our Strong and Broad Franchise ATMs Domestic Branches Overseas Branches Exclusive Banking & Business Center 6, Branches + 1 Rep Office... First Choice Microfinance Krungsri Auto EDC Branches ,500 Dealers 37 Auto Business Branches Overseas 163 Branches 660 Banking Branches Domestic 574 Branches 10,200 Dealers 74,

8 Krungsri Group Companies Credit Card, Personal Loan & Sale Finance Krungsriayudhya Card Co., Ltd (KCC) 99.99% Ayudhya Capital Services Co., Ltd. (AYCAP) 99.99% Tesco Card Services Ltd. (TCS) 50.00% General Card Services Ltd. (GCS) 99.99% Auto Hire Purchase and Leasing Ayudhya Capital Auto Lease Plc. (AYCAL) 99.99% Krungsri Leasing Services Co., Ltd (KLS) 90.00% Investment Management Krungsri Asset Management Co., Ltd. (KSAM) 76.59% Factoring Krungsri Factoring Co., Ltd. (KSF) 99.99% Securities Krungsri Securities Plc. (KSS) 99.74% Collection Services Total Services Solutions Plc. (TSS) 99.99% Support Business Siam Realty and Services Co., Ltd. (SRS) 99.99% Microfinance Ngern Tid Lor Co., Ltd. (NTL) 99.99% Hattha Kaksekar Limited (HKL) % Life Insurance Krungsri Life Assurance Broker Ltd. (KLAB) % Tesco Life Assurance Broker Ltd. (TLAB) 50.00% Leasing Ayudhya Development Leasing Co., Ltd. (ADLC) 99.99% Non life Insurance Krungsri General Insurance Broker Ltd. (KGIB) % Tesco General Insurance Broker Ltd. (TGIB) 50.00% Asset Management Krungsri Ayudhya AMC Ltd. (KAMC) 99.99% Venture Capital Krungsri Finnovate Co., Ltd. (KFin) 99.99% Krungsri full fledged Universal Bank 8

9 Krungsri: Credit Ratings International Ratings Fitch Ratings Moody s Standard & Poor s Krungsri Foreign currency Foreign Long Term Issuer Credit Rating Outlook Outlook Outlook Long Term Deposit Long Term A Stable Baa1 Stable BBB+ Stable National Ratings Fitch Ratings (Thailand) Tris Rating Long Term Outlook Company Rating Outlook Krungsri AAA (tha) Stable AAA Stable Krungsri Auto /1 na na AA Stable Krungsri Card /2 na na AAA Stable Ngern Tid Lor na na A Stable /1 Ayudhya Capital Auto Lease Plc. (AYCAL) /2 Krungsriayudhya Card Co., Ltd. (KCC) 9

10 What guides us: Mission, Vision and Values Krungsri MISSION To be a leading regional financial institution with global reach, committed responsibly to meeting the needs of our customers and serving society through sustainable growth. Krungsri VISION Highly qualified team of professionals providing innovative products and services, dedicated to becoming our customers number one preferred financial group. Krungsri VALUES Customer Centricity Integrity Team Spirit Passion for Excellence Embracing Changes Global Awareness 10

11 Our Philosophy Our Corporate Governance: Adherence to best corporate governance practices Employees Supervisory Authority Shareholders Customers Board of Directors Management Staff Shareholders Investors Commercial banks or Other financial institutions Business partners/creditors Society and country Our People: The key driving force of Krungsri Our Products: Developing & delivering financial solutions that best match with the need of customers. 11

12 Who we are Key Financials & Development Highlights Mid Term Business Plan 2017 Business Strategy and Key Focus 12

13 3Q 2017 Key Financial Highlights Loan Growth +1.4% QoQ / +6.6% YoY Deposit Growth +2.9% QoQ / +10.3% YoY CASA Consolidated (Baht Billion) 1, , , ,197.3 NIM 2Q/17 3Q/17 2Q/17 3Q/17 Non interest Income Growth +10.6% QoQ / +2.9% YoY Cost to Income Ratio NPL % 46.1% Coverage 2Q/17 3Q/17 2Q/17 3Q/17 13

14 Loans by Segments A broad based expansion in Corporate, SME and Retail segment Consolidated (Baht Billion) Corporate Loan SME Loan Retail Loan -0.6% +1.5% +3.1% June 17 Sep 17 June 2017 Sep 2017 THB 1,475.5 bn. THB 1,496.2 bn. June 17 Sep 17 June 17 Sep 17 Thai Corporate 29% 11% 15% Retail 45% JPC/MNC SME JPC/MNC Thai Corporate 28% 11% 15% Retail 46% SME Retail Auto HP 21% Mortgage 14% Credit Card & 11% Personal Loans 14

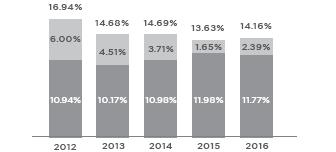

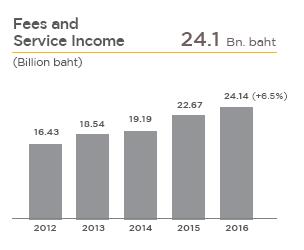

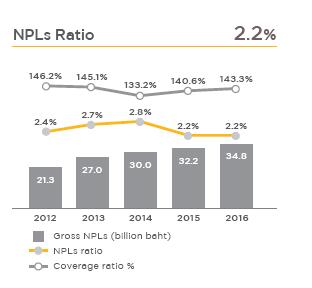

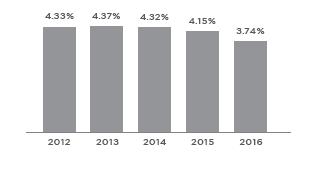

15 5 years Financial Highlights 15

16 Who we are Key Financials & Development Highlights Mid Term Business Plan 2017 Business Strategy and Key Focus 16

17 Mid Term Business Plan (MTBP) A strategic framework formulated as a guide for Krungsri s business operations over the next three years ( ), formulated in a forward looking approach. Domestic Regulatory External Operating Environment Rise of middle income Growth outside Bangkok Aging population AEC Political uncertainty Change in tax structure (Corporate/VAT) Credit Card Act Krungsri Strength & Weakness Auto loan, credit card and personal loan Business and financial support from MUFG Global product capabilities & network Strong franchise and customer base Retail deposit & mortgage Lower share in Thai corp & SME Our ASPIRATION: To be a Top Tier Financial Group in Thailand Key Strategic Themes Grow Asset Increase Noninterest Income Reduce Cost of Funds 17

18 MTBP Key Principles To achieve aspiration, Krungsri will implement 3 business strategies which is key strategic themes, and four management platform themes to strengthen governance in support of business endeavors. I. Key Strategic Themes II. Key Drivers Customer Centric Approach Products & Services Delivery Channels Marketing / Branding Increase Noninterest Income Grow Assets Reduce Cost of Funds Operate Productively & Efficiently Strengthen Internal Control Align Robust Process Talent Management & Working Environment III. Key Attitude Make Life Simple Products & Services Delivery Channels Marketing / Branding OneKrungsri 18

19 MTBP Key Principles (Cont d) Key Strategic Themes Grow Asset Keep Leading Position in Consumer and Auto Become a Tier 1 Mortgage Player Become a Core Bank to Commercial Customers Enhance Trade Finance & Transaction Banking Increase Noninterest Income Reduce Cost of Funds Increase CASA * Expand Customer Base Enhance Delivery Channels, Including Branches MUFG BTMU Synergy Retail & Commercial Collaboration * CASA: Current and Saving Accounts 19

20 Regional Expansion Key Strategies Alignment of coverage segment between Krungsri and BTMU Except for Laos, Krungsri focusses on expansion opportunities in auto, consumer and microfinance spaces and leverage BTMU network in corporate segments for Mekong strategies. Conduct feasibility study and seeking investment opportunities. Myanmar: BTMU: Yangon Branch Krungsri : Representative Office Laos Krungsri to lead the coverage of both bank and non bank segments Focus: Auto, consumer and microfinance Myanmar & Cambodia Use BTMU platform for corporate segment Retail and SME are open space for further assessment Focus: Auto/Consumer Finance and MFI Vietnam Collaborating with VietinBank Explore opportunity Focus: Auto, consumer and microfinance fields Cambodia: Acquired Hattha Kaksekar Co., Ltd. (HKL), a leading microfinance provider in Cambodia. 20

21 Krungsri s Future Maintain No.1 in Consumer Finance Stronger Commercial Banking Platform Larger Customer Base Strong corporate Governance & Internal Control Top Tier Financial Group in Thailand 21

22 Who we are Key Financials & Development Highlights Mid Term Business Plan 2017 Business Strategy and Key Focus 22

23 Thailand Economic Outlook Outlook: The Thai economy is likely to see a more balanced recovery with projected growth of 3.8% this year and 3.7% next year Key Economic Forecasts % YoY growth unless otherwise stated 2016A 2017F* 2018F* GDP Private Consumption Private Investment Exports ( In USD term) Headline Inflation Policy Interest Rate (%, end of period) Note: * forecast by Krungsri Research Key drivers are growing consumption, rebounding exports, recovering tourism sector, increasing public spending and economic stimulus measures After facing drought in the past several years, favorable weather this year boosts farm output and income. Government is speeding up infrastructure investment. However, new foreign labor law may create risks to domestic construction and investment. Policy interest rate is likely to be unchanged at least until mid 2018 given low inflation and still weak private investment Tailwinds Global economic recovery Infrastructure and EEC projects Stronger confidence with clearer timeframe of general election Lower first car debt burden, favorable farm income, measures to help low income earners Resilient tourism sector Sound economic fundamentals Headwinds Domestic political uncertainty US policy uncertainties and China s economic slowdown High global risks and volatile financial markets Labor shortage and potential impact of new foreign labor law High household debt Structural problems e.g. competitiveness problem Source: Krungsri Research 23

24 Recent Economic Development A recovery of economic activity continues and becomes broader based Consumer spending recovers moderately and private investment begins to show a positive growth rate Pro cyclical government spending continues to buoy economic recovery Exports surprisingly expand across the board in both key markets and products amid strengthening external demand Foreign tourist arrivals rebounded as negative impact of crackdown on illegal tours dissipated. % YoY GDP: continues to expand in 3Q17 3Q17F = 3.9% 1Q14 2Q 3Q 4Q 1Q15 2Q 3Q 4Q 1Q16 2Q 3Q 4Q 1Q17 2Q 3Q Domestic demand: consumption grows and investment picks up Exports: surprised growth amid rising global demand and higher prices Tourism: Chinese arrivals turn around Consumption (% YoY) Private consumption index Private investment index Investment (% YoY) 1Q14 2Q 3Q 4Q 1Q15 2Q 3Q 3Q 1Q16 2Q 3Q 4Q 1Q17 2Q Jul Aug % YoY Q14 2Q 3Q 4Q 1Q15 2Q 3Q 4Q 1Q16 2Q 3Q 4Q 1Q17 2Q Jul Aug Million Persons Foreign tourist arrivals % 10 % YoY Q14 2Q 3Q 4Q 1Q15 2Q 3Q 4Q 1Q16 2Q 3Q 4Q 1Q17 2Q Jul Aug Source: BOT, Department of Tourism, Krungsri Research 24

25 Emerging Changes to Banking Landscape Challenges to respond to change in need & expectation Customers needs FinTech Customer Centricity & Digital Banking Challenges for Topline New normal growth Competition from new rivals Regulatory changes Productivity and efficiency 25

26 Business Strategy and Key Focus: 2017 Continuation of MTBP and leveraging MUFG s global capabilities and networks to deliver superior financial solutions. MTBP Synergy Strategies Increase Noninterest Income Grow Assets Reduce Cost of Funds Europe & MEA 36 locations Thailand 697 locations Asia and Oceania 68 locations Japan 1,086 locations Americas 399 locations MUFG global network: over 2,000 offices in more than 50 countries Strengthen Internal Control CIB CLMV Align Robust Process Operate Productively & Efficiently Thai JP Collaboration Leveraging MUFG s global capabilities and networks Retail Talent Management Working Environment Transaction Banking Dealer / Vendor Finance 26

27 Continuation of MTBP Area of special focus in Keep Leading Position in Consumer and Auto Grow Assets 2 3 Become a Tier 1 Mortgage Player Become a Core Bank to Commercial Customers Increase Non Interest Income Reduce Cost of Funds Operate Productively & Efficiently Enhance Transaction Banking Strengthen FX Business Increase Low Cost CASA Expand Customer Base Enhance Delivery Channels, Including Branches MUFG/BTMU Synergy Retail & Commercial Collaboration 27

28 Segment focus to support growth in 2017 To be a Tier 1 Bank in Thai corporations Thai Corporate Explore and deepen relationship with existing customers, expand customer base (new customers/new industry) To enhance No. 1 position JPC/MNC Expand customer base Provide local services to JPC/MNC To become a main operating bank for SMEs SMEs Expand Krungsri s value chain solutions New product & new chain Continue growing trade finance assets Maintain & Assure Leadership Position Retail & Consumer Improving customer experience across retail and consumer banking Differentiated position in the market 28

29 Moving toward Digital Banking 29

30 3 elements of Fintech to be a leader in digital banking Venture Capital / Accelerator & Academic Collaboration/ Fintech Collaboration Venture Capital Krungsri Finnovate (Investment Fund: USD 30 million) Accelerator & Academic Collaboration Fintech Collaboration Investment Focus Payment system AI Continue the success of Krungsri RISE and Krungsri Uni Startup Working together with MUFG to further develop innovative financial technology to capture new business opportunities. 30

31 The Summary of Key Financial Performance Consolidated H/17 3Q/17 9M/ Targets Loan Growth (Net) bn +11.2% bn +1.8% bn +1.4% bn +3.3% 6 8% NPLs Ratio 2.21% 2.24% 2.16% 2.16% < 2.5% Deposit Mix: Savings and Current 53% 50% 48% 48% > 50% ~ Loan Mix : Retail 44% 45% 46% 46% ~ 40% L/Deposit+Debenture+B/E 117% 114% 115% 115% n.d. n.d. NIM 3.74% 3.82% 3.89% 3.82% ~ 3.7% Non interest income growth* (YoY) 11.7% 6.5% 2.9% 5.2% 5.0%+ Cost to Income Ratio 47.1% 48.0% 46.1% 47.4% < 50% Provisions 147 bps 146 bps 165 bps 151 bps ~ 140 bps ~ Loan Loss Coverage 143% 144% 149% 149% 140%+ CAR (Bank Only) 14.16% 15.96% 16.28% 16.28% n.d. n.d. * Net Fees Income + Non Interest and Non Fees Income 31

TRIS Rating AAA Credit Card 1 16% Auto (HP) 2 25% SME 5 5% Corporate 4 12% As of September 2017 Extensive Franchise: 33,492 Service Outlets Number")

32 Krungsri Group Profile International Ratings Fitch Ratings Standard & Poor s Moody s A BBB+ Baa1 Leadership Position Consumer As of August 2017 In consumer finance Market % Share Position Personal Loan 1 30% National Ratings Fitch Ratings AAA (tha) TRIS Rating AAA Credit Card 1 16% Auto (HP) 2 25% SME 5 5% Corporate 4 12% As of September 2017 Extensive Franchise: 33,492 Service Outlets Number As of September 2017 Number Domestic Branches 697 * Krungsri Business Centres 63 Overseas Branches 2 First Choice Branches 157 Branches + Dealers + 20,500 Dealers Representative Office 1 Krungsri Auto Dealers > + 10,200 Dealers ATMs 6,454 Microfinance Branches 574 Exchange Booths 97 Microfinance Overseas Branches (HKL) 163 Krungsri Exclusive 38 Thai Post Offices > + 1,000 * Krungsri Domestic Branches = 697 Branch, of which 660 are Banking Branches and 37 are Auto Business Branches 32

33 What guides us: Sustainability is a founding concept of our mission In our pursuit of being a responsible financial service provider, we established a guideline of action for achieving sustainability development in the following 3 dimensions: Economic Aligning business strategies with the economic outlook Maintaining a well balanced portfolio while serving as our customers trusted business partner and financial advisor. A true financial solution provider for customers. Social Improving financial access and enhancing financial literacy among Thai people Engaging Krungsri Staff in valued community development initiatives and CSR practices. A responsible corporate citizen. Environment Taking care to minimize the negative impact on our environment through implementation of green initiatives within our business and through our prudent support of customers growth initiatives. We place great emphasis on various green initiatives 33

34 This presentation has been prepared by Bank of Ayudhya Public Company Limited (the Bank ) solely for informational purposes. It does not constitute an offer or sale or a solicitation of an offer to purchase securities, nor does it constitute a prospectus within the meaning of the Securities and Exchange Act B.E of Thailand. Neither this presentation nor any part of it shall form the basis of, or be relied on in connection with, or act as an inducement to enter into, any contract or commitment whatsoever. No person should rely on the information contained in this presentation in making an investment decision in respect of any of the Bank s securities. Any decision to purchase or subscribe for any securities of the Bank must be made on the basis of a thorough review of publicly available information of the Bank, including information made publicly available by the Bank pursuant to the requirements of the Securities Exchange of Thailand and the Thai Securities Exchange Commission. The information contained herein is only accurate as of its date. Contact Public and Investor Relations Department : Telephone : (662) Fax : (662) E mail : irgroup@krungsri.com Krungsri Website : Join us!

Bank of Ayudhya PCL. March A member of MUFG, a global financial group

Bank of Ayudhya PCL March 2018 A member of MUFG, a global financial group Who we are Key Financials & Development Highlights Medium Term Business Plan 2018 2020 2 Krungsri Group Overview Officially established

Bank of Ayudhya PCL March 2018 A member of MUFG, a global financial group Who we are Key Financials & Development Highlights Medium Term Business Plan 2018 2020 2 Krungsri Group Overview Officially established

Bank of Ayudhya PCL Invest ASEAN 2 March Make Life Simple เร องเง น เร องง าย

Bank of Ayudhya PCL Invest ASEAN 2 March 2013 Make Life Simple เร องเง น เร องง าย Thailand Economic outlook 2012 2013 Key Economic Forecasts %Change 2011 2012 2013 Forecast* GDP 0.1 6.4 4.8 5.3 Private

Bank of Ayudhya PCL Invest ASEAN 2 March 2013 Make Life Simple เร องเง น เร องง าย Thailand Economic outlook 2012 2013 Key Economic Forecasts %Change 2011 2012 2013 Forecast* GDP 0.1 6.4 4.8 5.3 Private

Investor Presentation. For 2016

Investor Presentation For 216 Bangkok Bank 1. Operating Environment 2. Our Financial Results 216 3. Bangkok Bank s Position 4. Our Key Focus & Strategy 2 The Thai Economy: Steady Trend of Moderate Recovery

Investor Presentation For 216 Bangkok Bank 1. Operating Environment 2. Our Financial Results 216 3. Bangkok Bank s Position 4. Our Key Focus & Strategy 2 The Thai Economy: Steady Trend of Moderate Recovery

Investor Presentation. December 2013

Investor Presentation December 2013 24.02.2014 Table of Contents 1. Thai economy 2. Strengthening bank and client base 3. BBL s financial results Thai economy in 2014-2015 Thailand is facing short-term

Investor Presentation December 2013 24.02.2014 Table of Contents 1. Thai economy 2. Strengthening bank and client base 3. BBL s financial results Thai economy in 2014-2015 Thailand is facing short-term

Strategic Investment in Bank Danamon. December 26, 2017

Strategic Investment in Bank Danamon December 26, 2017 This document contains forward-looking statements in regard to forecasts, targets and plans of PT Bank Danamon Indonesia, Tbk. and its group companies

Strategic Investment in Bank Danamon December 26, 2017 This document contains forward-looking statements in regard to forecasts, targets and plans of PT Bank Danamon Indonesia, Tbk. and its group companies

Siam Commercial Bank PCL DB Access Asia Conference 2012

Siam Commercial Bank PCL DB Access Asia Conference 2012 May, 2012 Agenda Page 1. Review of Result 1Q12 3-17 2. Future Positioning 19-23 3. 2012 Targets 25 IMPORTANT DISCLAIMER: Information contained in

Siam Commercial Bank PCL DB Access Asia Conference 2012 May, 2012 Agenda Page 1. Review of Result 1Q12 3-17 2. Future Positioning 19-23 3. 2012 Targets 25 IMPORTANT DISCLAIMER: Information contained in

Siam Commercial Bank PCL

Siam Commercial Bank PCL CLSA Investors Forum 2011 September 2011 1. Agenda Review of Result 2Q11 Page 3-17 2. Going Forward 19-23 IMPORTANT DISCLAIMER: Information contained in this document has been

Siam Commercial Bank PCL CLSA Investors Forum 2011 September 2011 1. Agenda Review of Result 2Q11 Page 3-17 2. Going Forward 19-23 IMPORTANT DISCLAIMER: Information contained in this document has been

Economic outlook. Bangkok Bank position. Strategic priorities and targets

20110721 1 Topics 1 2 3 Economic outlook Bangkok Bank position Strategic priorities and targets 2 GDP growth outlook remains strong 6 Baht trn 4 +2.5% 2.3% +7.8% +4 5% +3.2% +2.6% 2 0 2008 2009 2010 2011f

20110721 1 Topics 1 2 3 Economic outlook Bangkok Bank position Strategic priorities and targets 2 GDP growth outlook remains strong 6 Baht trn 4 +2.5% 2.3% +7.8% +4 5% +3.2% +2.6% 2 0 2008 2009 2010 2011f

0 V1 25/02/59 16:05 น.

0 1 Management Discussion and Analysis Overview of the Economy and Banking Thai Economy in In, the Thai economy grew by 2.8 percent. Major growth factors were government sector investment which grew by

0 1 Management Discussion and Analysis Overview of the Economy and Banking Thai Economy in In, the Thai economy grew by 2.8 percent. Major growth factors were government sector investment which grew by

United Overseas Bank Investor Roadshow November 2006

United Overseas Bank Investor Roadshow November 2006 Disclaimer : This material that follows is a presentation of general background information about the Bank s activities current at the date of the presentation.

United Overseas Bank Investor Roadshow November 2006 Disclaimer : This material that follows is a presentation of general background information about the Bank s activities current at the date of the presentation.

KASIKORNBANK. Presentation for Analyst Meeting as of 4Q17. January 2018

KASIKORNBANK Presentation for Analyst Meeting as of 4Q17 January 218 For further information, please contact the Investor Relations Unit or visit our website at www.kasikornbank.com 1 KASIKORNBANK at a

KASIKORNBANK Presentation for Analyst Meeting as of 4Q17 January 218 For further information, please contact the Investor Relations Unit or visit our website at www.kasikornbank.com 1 KASIKORNBANK at a

Monthly Economic Insight

Monthly Economic Insight Prepared by : TMB Analytics Date: 22 February 2018 Executive Summary Synchronized global economic growth continued to brighten global economic outlook and global trade outlook.

Monthly Economic Insight Prepared by : TMB Analytics Date: 22 February 2018 Executive Summary Synchronized global economic growth continued to brighten global economic outlook and global trade outlook.

Investor Presentation. For 3Q18

Investor Presentation For 3Q18 Bangkok Bank 1. Operating Environment 2. Our Key Focus and Position 3. Our Financial Result 3Q18 2 For 2018, global economic expansion remains solid However, the outlook

Investor Presentation For 3Q18 Bangkok Bank 1. Operating Environment 2. Our Key Focus and Position 3. Our Financial Result 3Q18 2 For 2018, global economic expansion remains solid However, the outlook

SIAM COMMERCIAL BANK PCL.

SIAM COMMERCIAL BANK PCL. 1Q17 Financial Results Analyst Meeting Presentation April 21 st, 2017 IMPORTANT DISCLAIMER: Information contained in this document has been prepared from several sources and the

SIAM COMMERCIAL BANK PCL. 1Q17 Financial Results Analyst Meeting Presentation April 21 st, 2017 IMPORTANT DISCLAIMER: Information contained in this document has been prepared from several sources and the

AIRA Capital Public Company Limited AC Group Opportunity Day FY16

AIRA Capital Public Company Limited AC Group Opportunity Day FY16 27 March 2017 Group Structure AIRA Capital Public Company Limited ( AIRA Capital ) has incorporated as a holding company with investments

AIRA Capital Public Company Limited AC Group Opportunity Day FY16 27 March 2017 Group Structure AIRA Capital Public Company Limited ( AIRA Capital ) has incorporated as a holding company with investments

INVESTOR PRESENTATION

INVESTOR PRESENTATION J.P. MORGAN THAILAND CONFERENCE 2011 Deepak Sarup, CFO 17 th March 2011 AGENDA Pages I. Review of Results 2010 3-15 II. Future Positioning 17-27 III. 2011 Targets 29 IMPORTANT DISCLAIMER:

INVESTOR PRESENTATION J.P. MORGAN THAILAND CONFERENCE 2011 Deepak Sarup, CFO 17 th March 2011 AGENDA Pages I. Review of Results 2010 3-15 II. Future Positioning 17-27 III. 2011 Targets 29 IMPORTANT DISCLAIMER:

Economic outlook. Bangkok Bank position. Strategic priorities and targets

20110603 1 Topics 1 2 3 Economic outlook Bangkok Bank position Strategic priorities and targets 2 GDP growth outlook remains strong 6 Baht trn 4 +2.5% 2.3% +7.8% +4 5% +3.0% 2 0 2008 2009 2010 2011f 1Q11(A)

20110603 1 Topics 1 2 3 Economic outlook Bangkok Bank position Strategic priorities and targets 2 GDP growth outlook remains strong 6 Baht trn 4 +2.5% 2.3% +7.8% +4 5% +3.0% 2 0 2008 2009 2010 2011f 1Q11(A)

INVESTOR PRESENTATION

INVESTOR PRESENTATION CREDIT SUISSE ASIAN INVESTMENT CONFERENCE 2012 Kannikar Chalitaporn, President Deepak Sarup, CFO 19 th -20 th March 2012 Agenda Page 1. Review of Result 2011 3-17 2. Future Positioning

INVESTOR PRESENTATION CREDIT SUISSE ASIAN INVESTMENT CONFERENCE 2012 Kannikar Chalitaporn, President Deepak Sarup, CFO 19 th -20 th March 2012 Agenda Page 1. Review of Result 2011 3-17 2. Future Positioning

Investor Presentation. For 2017

Investor Presentation For 2017 Bangkok Bank 1. Operating Environment 2. Our Key Focus and Position 3. Our Financial Result 2017 2 For 2018, global economic expansion is synchronous with rising global investment

Investor Presentation For 2017 Bangkok Bank 1. Operating Environment 2. Our Key Focus and Position 3. Our Financial Result 2017 2 For 2018, global economic expansion is synchronous with rising global investment

Investor Presentation. For 2018

Investor Presentation For 2018 Bangkok Bank Operating Environment 2019 Focus Financial Performance 2 Global Economy in 2019 is set to slow against the backdrop of the US-China trade tension and quantitative

Investor Presentation For 2018 Bangkok Bank Operating Environment 2019 Focus Financial Performance 2 Global Economy in 2019 is set to slow against the backdrop of the US-China trade tension and quantitative

Summary of Operating Results for the Bank and its Subsidiaries Quarter and Nine Months Ended September 30, 2015

1 Summary of Operating Results for the Bank and its Subsidiaries Quarter and Nine Months Ended September 30, Bangkok Bank and its subsidiaries have reported a consolidated net profit of Baht 9.1 billion

1 Summary of Operating Results for the Bank and its Subsidiaries Quarter and Nine Months Ended September 30, Bangkok Bank and its subsidiaries have reported a consolidated net profit of Baht 9.1 billion

Management Discussion and Analysis

Management Discussion and Analysis For the second quarter and first half ended June 30, 2018 The Siam Commercial Bank Public Company Limited The Siam Commercial Bank Public Company Limited 9 Ratchadapisek

Management Discussion and Analysis For the second quarter and first half ended June 30, 2018 The Siam Commercial Bank Public Company Limited The Siam Commercial Bank Public Company Limited 9 Ratchadapisek

KBank Capital Markets Perspectives 29 February 2016

KBank Capital Markets Perspectives 29 February 2016 Thailand Economic Monitor and BoT Forecast : March 2016 Thailand s economy steadied in February, though domestic demand decelerated slightly from January

KBank Capital Markets Perspectives 29 February 2016 Thailand Economic Monitor and BoT Forecast : March 2016 Thailand s economy steadied in February, though domestic demand decelerated slightly from January

Key developments and outlook

1/22 Key developments and outlook Economic growth projection is revised up from a stronger recovery of exports. Meanwhile, government spending remains an important growth driver. Private spending gradually

1/22 Key developments and outlook Economic growth projection is revised up from a stronger recovery of exports. Meanwhile, government spending remains an important growth driver. Private spending gradually

United Overseas Bank Limited

United Overseas Bank Limited July 2007 This material that follows is a presentation of general background information about United Overseas Bank Limited s ( UOB or the Bank ) activities current at the

United Overseas Bank Limited July 2007 This material that follows is a presentation of general background information about United Overseas Bank Limited s ( UOB or the Bank ) activities current at the

0 V3 12/11/58 15:51 น.

0 1 Management Discussion and Analysis Overview of the Economy and Banking Thai Economy in the Third Quarter of Thailand s economy in the third quarter of recovered at a moderate pace. Domestic demand

0 1 Management Discussion and Analysis Overview of the Economy and Banking Thai Economy in the Third Quarter of Thailand s economy in the third quarter of recovered at a moderate pace. Domestic demand

China Economic Outlook 2013

China Economic Outlook 2 Key Developments in Brief - Mild recovery of GDP growth: +8 8.5% - Construction and consumption as main drivers - Inflationary pressure to increase: +3% - Tight labor market and

China Economic Outlook 2 Key Developments in Brief - Mild recovery of GDP growth: +8 8.5% - Construction and consumption as main drivers - Inflationary pressure to increase: +3% - Tight labor market and

Economic Outlook Economic Intelligence Center 27 th November 2015

Economic Outlook 2016 Economic Intelligence Center 27 th November 2015 Global outlook Domestic outlook 2 In 2016, recovery pace in most regions are expected to pick up except for China Eurozone 2.0 1.5

Economic Outlook 2016 Economic Intelligence Center 27 th November 2015 Global outlook Domestic outlook 2 In 2016, recovery pace in most regions are expected to pick up except for China Eurozone 2.0 1.5

Important economic directions

3Q 2012 Important economic directions 1. Higher investment both from government and private sectors 2. Higher investment both from foreign direct investment and Thai direct investment 2 Private investment

3Q 2012 Important economic directions 1. Higher investment both from government and private sectors 2. Higher investment both from foreign direct investment and Thai direct investment 2 Private investment

Capital and Business Alliance with Security Bank Corporation

The Bank of Tokyo-Mitsubishi UFJ, Ltd. Capital and Business Alliance with Security Bank Corporation Tokyo, January 1---The Bank of Tokyo-Mitsubishi UFJ, Ltd. (BTMU) (President: Nobuyuki Hirano) announced

The Bank of Tokyo-Mitsubishi UFJ, Ltd. Capital and Business Alliance with Security Bank Corporation Tokyo, January 1---The Bank of Tokyo-Mitsubishi UFJ, Ltd. (BTMU) (President: Nobuyuki Hirano) announced

Management Discussion and Analysis

Management Discussion and Analysis For the year ended December 31, 2018 (Audited) Page 0 This report discusses the principal changes in the audited consolidated financial statement for the year ended December

Management Discussion and Analysis For the year ended December 31, 2018 (Audited) Page 0 This report discusses the principal changes in the audited consolidated financial statement for the year ended December

KCB INVESTOR AND MEDIA PRESENTATION 2012 FULL YEAR GROUP AUDITED FINANCIAL RESULTS

KCB INVESTOR AND MEDIA PRESENTATION 2012 FULL YEAR GROUP AUDITED FINANCIAL RESULTS 1 Outline 1. East Africa Macroeconomic View 2. The Bank at a Glance 3. 2012 full year KCB group Financial Results 4. Future

KCB INVESTOR AND MEDIA PRESENTATION 2012 FULL YEAR GROUP AUDITED FINANCIAL RESULTS 1 Outline 1. East Africa Macroeconomic View 2. The Bank at a Glance 3. 2012 full year KCB group Financial Results 4. Future

1Q18 Financial Results

1Q18 Financial Results Analyst Meeting Presentation 23 April 2018 IMPORTANT DISCLAIMER: Information contained in this document has been prepared from several sources and the Bank does not confirm the accuracy

1Q18 Financial Results Analyst Meeting Presentation 23 April 2018 IMPORTANT DISCLAIMER: Information contained in this document has been prepared from several sources and the Bank does not confirm the accuracy

Key developments and outlook

1/17 Key developments and outlook Economic growths in 2016 and 2017 remain close to the previous assessment. Better-than-expected merchandise exports and private consumption compensate for weaker-than-expected

1/17 Key developments and outlook Economic growths in 2016 and 2017 remain close to the previous assessment. Better-than-expected merchandise exports and private consumption compensate for weaker-than-expected

26 October 2017 MEXICO. January September 2017

26 October 2017 MEXICO January September 2017 Disclaimer Banco Santander, S.A. ("Santander") cautions that this presentation contains statements that constitute forward-looking statements within the meaning

26 October 2017 MEXICO January September 2017 Disclaimer Banco Santander, S.A. ("Santander") cautions that this presentation contains statements that constitute forward-looking statements within the meaning

Investor Presentation. For 2017

Investor Presentation For 2017 Bangkok Bank 1. Operating Environment 2. Our Key Focus and Position 3. Our Financial Result 2017 2 For 2018, global economic expansion is synchronous with rising global investment

Investor Presentation For 2017 Bangkok Bank 1. Operating Environment 2. Our Key Focus and Position 3. Our Financial Result 2017 2 For 2018, global economic expansion is synchronous with rising global investment

TISCO Financial Group Public Co., Ltd.

TISCO Financial Group Public Co., Ltd. Analyst Presentation 4Q09 & FY09 Results 14 January 2010 Disclaimer: This presentation material may contain forward-looking statements. These forward-looking statements

TISCO Financial Group Public Co., Ltd. Analyst Presentation 4Q09 & FY09 Results 14 January 2010 Disclaimer: This presentation material may contain forward-looking statements. These forward-looking statements

0 V2 30/08/61 14:31 น.

0 1 Management Discussion and Analysis Overview of the Economy and Banking Industry Thai Economy in the Second Quarter of The Thai economy in the second quarter of continued to improve. Export performance

0 1 Management Discussion and Analysis Overview of the Economy and Banking Industry Thai Economy in the Second Quarter of The Thai economy in the second quarter of continued to improve. Export performance

Asia s strongest brand in banking, banking the world s strongest economies

Credit Suisse Investor Conference Peter Wong, Chief Executive, HSBC Asia-Pacific Asia s strongest brand in banking, banking the world s strongest economies 21 March 2011 www.hsbc.com Forward-looking statements

Credit Suisse Investor Conference Peter Wong, Chief Executive, HSBC Asia-Pacific Asia s strongest brand in banking, banking the world s strongest economies 21 March 2011 www.hsbc.com Forward-looking statements

26 th April 2017 MEXICO. January March 2017

26 th April 2017 MEXICO January March 2017 Disclaimer IMPORTANT INFORMATION Banco Santander, S.A. ( Santander ) Warns that this presentation contains forward-looking statements within the meaning of the

26 th April 2017 MEXICO January March 2017 Disclaimer IMPORTANT INFORMATION Banco Santander, S.A. ( Santander ) Warns that this presentation contains forward-looking statements within the meaning of the

INVESTOR PRESENTATION

INVESTOR PRESENTATION CLSA ASEAN CORPORATE ACCESS FORUM 2013 14 th March 2013 Agenda Page 1. Review of Result 2012 3-19 2. Future Positioning 21-23 IMPORTANT DISCLAIMER: Information contained in this document

INVESTOR PRESENTATION CLSA ASEAN CORPORATE ACCESS FORUM 2013 14 th March 2013 Agenda Page 1. Review of Result 2012 3-19 2. Future Positioning 21-23 IMPORTANT DISCLAIMER: Information contained in this document

Thailand. Respectable Growth in Monday, February 20, 2017

Thailand Respectable Growth in 2016 Treasury Advisory Corporate FX & Structured Products Tel: 6349-1888 / 1881 Interest Rate Derivatives Tel: 6349-1899 Investments & Structured Products Tel: 6349-1886

Thailand Respectable Growth in 2016 Treasury Advisory Corporate FX & Structured Products Tel: 6349-1888 / 1881 Interest Rate Derivatives Tel: 6349-1899 Investments & Structured Products Tel: 6349-1886

Westpac Banking Corporation

Westpac Banking Corporation David Morgan Chief Executive Officer March 2007 Westpac Banking Corporation at a glance Australia s first bank est. 1817 Top 50 bank globally 1 Consistent earnings growth Strong

Westpac Banking Corporation David Morgan Chief Executive Officer March 2007 Westpac Banking Corporation at a glance Australia s first bank est. 1817 Top 50 bank globally 1 Consistent earnings growth Strong

Value Creation Initiatives

Value Creation MUFG Net Operating Profits 1,26.8 billion* 1, * 2 363.5 billion Asset Management & Investor Service Business Group (AM/IS) 71.1 billion Global Commercial Banking Business Group (GCB) 192.6

Value Creation MUFG Net Operating Profits 1,26.8 billion* 1, * 2 363.5 billion Asset Management & Investor Service Business Group (AM/IS) 71.1 billion Global Commercial Banking Business Group (GCB) 192.6

B-GUIDE: Economic Outlook

Aug-12 Apr-13 Dec-13 Aug-14 Apr-15 Dec-15 Aug-16 Apr-17 Jul-15 Nov-15 Mar-16 Jul-16 Nov-16 Mar-17 Jul-17 Quarterly Economic Outlook: Quarter 4 2017 4 January 2018 B-GUIDE: Economic Outlook The economy

Aug-12 Apr-13 Dec-13 Aug-14 Apr-15 Dec-15 Aug-16 Apr-17 Jul-15 Nov-15 Mar-16 Jul-16 Nov-16 Mar-17 Jul-17 Quarterly Economic Outlook: Quarter 4 2017 4 January 2018 B-GUIDE: Economic Outlook The economy

Public Bank Group. Presentation to Investors J.P. Morgan Asia Financials Conference Hong Kong March 2011

Public Bank Group Presentation to Investors J.P. Morgan Asia Financials Conference Hong Kong 10-11 March 2011 Disclaimer The materials and information in the presentations and other documents are for informational

Public Bank Group Presentation to Investors J.P. Morgan Asia Financials Conference Hong Kong 10-11 March 2011 Disclaimer The materials and information in the presentations and other documents are for informational

Investor Presentation. For 1Q18

Investor Presentation For 1Q18 Bangkok Bank 1. Operating Environment 2. Our Key Focus and Position 3. Our Financial Result 1Q18 2 For 2018, global economic expansion is synchronous with rising global investment

Investor Presentation For 1Q18 Bangkok Bank 1. Operating Environment 2. Our Key Focus and Position 3. Our Financial Result 1Q18 2 For 2018, global economic expansion is synchronous with rising global investment

Public Bank Group. Unaudited Q1 Group Results 31 March 2010

Public Bank Group Unaudited Q1 Group Results 31 March 2010 Release Date: 15 April 2010 Quarter 1 2010 Results EXECUTIVE SUMMARY FINANCIAL PERFORMANCE GROWTH PERFORMANCE BUSINESS PERFORMANCE OTHER HIGHLIGHTS

Public Bank Group Unaudited Q1 Group Results 31 March 2010 Release Date: 15 April 2010 Quarter 1 2010 Results EXECUTIVE SUMMARY FINANCIAL PERFORMANCE GROWTH PERFORMANCE BUSINESS PERFORMANCE OTHER HIGHLIGHTS

0 V2 23/02/60 21:52 น.

0 1 Management Discussion and Analysis Overview of the Economy and Banking Industry Thai Economy in Thailand s economy continued to grow steadily in, despite external volatility. The major factors supporting

0 1 Management Discussion and Analysis Overview of the Economy and Banking Industry Thai Economy in Thailand s economy continued to grow steadily in, despite external volatility. The major factors supporting

27 July 2016 MEXICO. First half 2016

27 July 2016 MEXICO First half 2016 Disclaimer IMPORTANT INFORMATION Banco Santander, S.A. ( Santander ) Warns that this presentation contains forward-looking statements within the meaning of the U.S.

27 July 2016 MEXICO First half 2016 Disclaimer IMPORTANT INFORMATION Banco Santander, S.A. ( Santander ) Warns that this presentation contains forward-looking statements within the meaning of the U.S.

The Korean Economy: Resilience amid Turbulence

The Korean Economy: Resilience amid Turbulence Dr. Il SaKong Special Economic Advisor Adviser to the President Republic of Korea November 17, 17, 2008 November 17, 2008 1. Recent Macroeconomic Developments

The Korean Economy: Resilience amid Turbulence Dr. Il SaKong Special Economic Advisor Adviser to the President Republic of Korea November 17, 17, 2008 November 17, 2008 1. Recent Macroeconomic Developments

UOB Group Strength and resilience within a challenging market environment

UOB Group Strength and resilience within a challenging market environment Investor Roadshow March 2009 Disclaimer : This material that follows is a presentation of general background information about

UOB Group Strength and resilience within a challenging market environment Investor Roadshow March 2009 Disclaimer : This material that follows is a presentation of general background information about

Bank of Queensland. Half-Year Results 29 February FY08 Half-Year Results

Bank of Queensland Half-Year Results 29 February 2008 1 Agenda Result highlights Financial result in detail BOQ Portfolio Strategy and outlook David Liddy Managing Director & CEO Ram Kangatharan Group

Bank of Queensland Half-Year Results 29 February 2008 1 Agenda Result highlights Financial result in detail BOQ Portfolio Strategy and outlook David Liddy Managing Director & CEO Ram Kangatharan Group

Thailand Update. Yield Movements. Size and Composition. Thailand s government bond yield curve flattened between end-december 2010 and end-july

Asia Bond Monitor Thailand Update Yield Movements Thailand s government bond yield curve flattened between end-december 2010 and end-july (Figure 1). Yields at the short-end of the curve increased as much

Asia Bond Monitor Thailand Update Yield Movements Thailand s government bond yield curve flattened between end-december 2010 and end-july (Figure 1). Yields at the short-end of the curve increased as much

Recent Economic Developments

REPUBLIC OF INDONESIA Recent Economic Developments January, 2010 Published by Investors Relations Unit Republic of Indonesia Address Bank Indonesia International Directorate Investor Relations Unit Sjafruddin

REPUBLIC OF INDONESIA Recent Economic Developments January, 2010 Published by Investors Relations Unit Republic of Indonesia Address Bank Indonesia International Directorate Investor Relations Unit Sjafruddin

Investor Briefing & Q Performance. April 2016

Investor Briefing & Q1 2016 Performance April 2016 Presentation Outline 1. Macro-economic overview 2. Governance & leadership structure 3. Regional expansion and diversification 4. Digital bank 5. SME

Investor Briefing & Q1 2016 Performance April 2016 Presentation Outline 1. Macro-economic overview 2. Governance & leadership structure 3. Regional expansion and diversification 4. Digital bank 5. SME

Performance and Outlook. December 2015

Performance and Outlook December 2015 Agenda Macro Picture Performance Highlights Q&A 2 Agenda Macro Picture Performance Highlights Fundamentals (IIP) Output conditions Inflation Rates Credit and Deposit

Performance and Outlook December 2015 Agenda Macro Picture Performance Highlights Q&A 2 Agenda Macro Picture Performance Highlights Fundamentals (IIP) Output conditions Inflation Rates Credit and Deposit

24 April Mexico. Q1'18 Earnings Presentation

24 April 2018 Mexico Q1'18 Earnings Presentation Disclaimer Banco Santander, S.A. ("Santander") cautions that this presentation contains statements that constitute forward-looking statements within the

24 April 2018 Mexico Q1'18 Earnings Presentation Disclaimer Banco Santander, S.A. ("Santander") cautions that this presentation contains statements that constitute forward-looking statements within the

30 January Mexico Earnings Presentation

30 January 2019 Mexico 2018 Earnings Presentation Disclaimer Banco Santander, S.A. ("Santander") cautions that this presentation contains statements that constitute forward-looking statements within the

30 January 2019 Mexico 2018 Earnings Presentation Disclaimer Banco Santander, S.A. ("Santander") cautions that this presentation contains statements that constitute forward-looking statements within the

Quarterly Meeting # 2/2015

Quarterly Meeting # 2/2015 1Q15 Performance & Outlook 18 May 2015 The views expressed here contain some information derived from publicly available sources that have not been independently verified. No

Quarterly Meeting # 2/2015 1Q15 Performance & Outlook 18 May 2015 The views expressed here contain some information derived from publicly available sources that have not been independently verified. No

26 October 2016 MEXICO. January September 2016

26 October 2016 MEXICO January September 2016 Disclaimer IMPORTANT INFORMATION Banco Santander, S.A. ( Santander ) Warns that this presentation contains forward-looking statements within the meaning of

26 October 2016 MEXICO January September 2016 Disclaimer IMPORTANT INFORMATION Banco Santander, S.A. ( Santander ) Warns that this presentation contains forward-looking statements within the meaning of

Quarterly Economic Outlook: Quarter on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

Investor Presentation Macquarie ASEAN Conference Singapore August

Macquarie ASEAN Conference Singapore 27-29 August 2013 www.publicbank.com.my/corporate Disclaimer 2 The materials and information in the presentations and other documents are for informational purposes

Macquarie ASEAN Conference Singapore 27-29 August 2013 www.publicbank.com.my/corporate Disclaimer 2 The materials and information in the presentations and other documents are for informational purposes

Investor Presentation OSK-DMG ASEAN Corporate Day 2012 Kuala Lumpur 27 June

OSK-DMG ASEAN Corporate Day 2012 Kuala Lumpur 27 June 2012 www.publicbank.com.my Disclaimer 2 The materials and information in the presentations and other documents are for informational purposes only,

OSK-DMG ASEAN Corporate Day 2012 Kuala Lumpur 27 June 2012 www.publicbank.com.my Disclaimer 2 The materials and information in the presentations and other documents are for informational purposes only,

PT Bank Rakyat Indonesia (Persero) Tbk.

Tbk.") PT Bank Rakyat Indonesia (Persero) Tbk. Q2-2014 Financial Update Presentation Maintaining profitability in a challenging environment Jakarta, 22 July 2014 Outline Macro Economy Q2 2014 - a maintained performance

PT Bank Rakyat Indonesia (Persero) Tbk. Q2-2014 Financial Update Presentation Maintaining profitability in a challenging environment Jakarta, 22 July 2014 Outline Macro Economy Q2 2014 - a maintained performance

B-GUIDE: Market Outlook

Quarterly Market Outlook: Quarter 1 2018 on 5 th January 2018 Investment Outlook for 1 st Quarter 2018 Accelerating Global Economy Supports the Rising Earnings Equity Thailand US Europe Japan Asia Bond

Quarterly Market Outlook: Quarter 1 2018 on 5 th January 2018 Investment Outlook for 1 st Quarter 2018 Accelerating Global Economy Supports the Rising Earnings Equity Thailand US Europe Japan Asia Bond

Investor Presentation. June 2018

Investor Presentation June 2018 Contents Bank Muscat Introduction Operating environment Bank Muscat business - Overview Financial Performance Annexure Note: The financial information is updated as of 30

Investor Presentation June 2018 Contents Bank Muscat Introduction Operating environment Bank Muscat business - Overview Financial Performance Annexure Note: The financial information is updated as of 30

Thailand s economic resilience amid global uncertainties. March 2017

Thailand s economic resilience amid global uncertainties March 217 Thailand s economic resilience amid global uncertainties I. Thailand s economic resilience II. Thai corporates target for sustainable

Thailand s economic resilience amid global uncertainties March 217 Thailand s economic resilience amid global uncertainties I. Thailand s economic resilience II. Thai corporates target for sustainable

KASIKORNBANK. Investor Presentation. Monthly Economic Information By KASIKORN RESEARCH CENTER. June 2017

KASIKORNBANK Investor Presentation Monthly Economic Information By KASIKORN RESEARCH CENTER June 7 For further information, please contact Investor Relations Unit or visit our website at www.kasikornbankgroup.com

KASIKORNBANK Investor Presentation Monthly Economic Information By KASIKORN RESEARCH CENTER June 7 For further information, please contact Investor Relations Unit or visit our website at www.kasikornbankgroup.com

BUSINESS MODEL AND STRATEGIC DIRECTION

BUSINESS MODEL AND STRATEGIC DIRECTION HNB Group HNB Assurance PLC Life Insurance 60% owned listed subsidiary HNB General Insurance Ltd 100% owned General Insurance company HNB PLC Sithma Development Ltd

BUSINESS MODEL AND STRATEGIC DIRECTION HNB Group HNB Assurance PLC Life Insurance 60% owned listed subsidiary HNB General Insurance Ltd 100% owned General Insurance company HNB PLC Sithma Development Ltd

Performance of the Thai Banking System in the Second Quarter of 2017

Performance of the Thai Banking System in the Second Quarter of Overall Performance of the Thai Banking System in the Second Quarter of Loan growth increased to a level comparable to GDP growth. Loan growth

Performance of the Thai Banking System in the Second Quarter of Overall Performance of the Thai Banking System in the Second Quarter of Loan growth increased to a level comparable to GDP growth. Loan growth

0 V3 22/02/62 14:27 น.

0 1 Management Discussion and Analysis Overview of the Economy and Banking Industry Thai Economy in In the Thai economy grew by 4.1 percent, up from 4.0 percent in. Nominal GDP for the year totaled Baht

0 1 Management Discussion and Analysis Overview of the Economy and Banking Industry Thai Economy in In the Thai economy grew by 4.1 percent, up from 4.0 percent in. Nominal GDP for the year totaled Baht

TMB BANK. 3Q06 Preliminary Key Accomplishments Economic Outlook & Regulatory Change Appendix. Unaudited 3Q06 & 9M06 in Summary

24 October 26 TMB BANK 3 rd Quarter & 9 Months 26 Results CEO/CFO 1 Unaudited 3Q6 & 9M6 in Summary Unaudited 3Q6 & 9M6 in Summary Unit : THB mm Unit : THB mm Items 9M6 9M5 % 3Q6 2Q6 % Items Sep 6 Jun 6

24 October 26 TMB BANK 3 rd Quarter & 9 Months 26 Results CEO/CFO 1 Unaudited 3Q6 & 9M6 in Summary Unaudited 3Q6 & 9M6 in Summary Unit : THB mm Unit : THB mm Items 9M6 9M5 % 3Q6 2Q6 % Items Sep 6 Jun 6

ICICI Group: Strategy & Performance

ICICI Group: Strategy & Performance Agenda India: macroeconomic scenario Indian banking sector ICICI Group 2 Growth indicators Strong long term growth fundamentals Key drivers of growth Favourable demographics

ICICI Group: Strategy & Performance Agenda India: macroeconomic scenario Indian banking sector ICICI Group 2 Growth indicators Strong long term growth fundamentals Key drivers of growth Favourable demographics

TMB Bank Plc. Building the Best Transactional Bank. Make THE Difference. Day with Executive Management

TMB Bank Plc. Building the Best Transactional Bank Day with Executive Management November 1, 215 Make THE Difference AGENDA 3Q15 Financial Performance 9M15 Financial Performance Looking Forward [2] Executive

TMB Bank Plc. Building the Best Transactional Bank Day with Executive Management November 1, 215 Make THE Difference AGENDA 3Q15 Financial Performance 9M15 Financial Performance Looking Forward [2] Executive

Eurozone Economic Watch Higher growth forecasts for January 2018

Eurozone Economic Watch Higher growth forecasts for 2018-19 January 2018 Eurozone Economic Watch January 2018 Eurozone: Higher growth forecasts for 2018-19 Our MICA-BBVA model estimates a broadly stable

Eurozone Economic Watch Higher growth forecasts for 2018-19 January 2018 Eurozone Economic Watch January 2018 Eurozone: Higher growth forecasts for 2018-19 Our MICA-BBVA model estimates a broadly stable

Hector Grisi. Country Head Mexico. Helping people and businesses prosper

Hector Grisi Country Head Mexico Helping people and businesses prosper Banco Santander, S.A. ("Santander") cautions that this presentation contains statements that constitute forward-looking statements

Hector Grisi Country Head Mexico Helping people and businesses prosper Banco Santander, S.A. ("Santander") cautions that this presentation contains statements that constitute forward-looking statements

United Overseas Bank. Investor Roadshow. January 2008

United Overseas Bank Investor Roadshow January 2008 Disclaimer : This material that follows is a presentation of general background information about the Bank s activities current at the date of the presentation.

United Overseas Bank Investor Roadshow January 2008 Disclaimer : This material that follows is a presentation of general background information about the Bank s activities current at the date of the presentation.

Presentation to Tier 1 Investors April 2005

Presentation to Tier 1 Investors April 2005 Michael Oliver Director of Investor Relations John Gillbe Group Capital and BSM Director Overview of Lloyds TSB Group plc 3 businesses* UK Retail Banking: GBP

Presentation to Tier 1 Investors April 2005 Michael Oliver Director of Investor Relations John Gillbe Group Capital and BSM Director Overview of Lloyds TSB Group plc 3 businesses* UK Retail Banking: GBP

Summary of Operating Results for the Bank and its Subsidiaries Quarter and Year Ended December 31, 2018

1 Summary of Operating Results for the Bank and its Subsidiaries Quarter and Year Ended 31, Thailand s economic growth in is expected to be 4.1 percent, up from 3.9 percent in. While exports weakened in

1 Summary of Operating Results for the Bank and its Subsidiaries Quarter and Year Ended 31, Thailand s economic growth in is expected to be 4.1 percent, up from 3.9 percent in. While exports weakened in

Shin Corporation. Macquarie Thailand Corporate Day. Building a stronger portfolio. Mrs.Siripen Sitasuwan President & Group CFO

Shin Corporation Macquarie Thailand Corporate Day Mrs.Siripen Sitasuwan President & Group CFO November 30 December 2, 2005 Building a stronger portfolio SHIN Corporation Mkt cap of Bt 111.7bn* (US$2.7bn)

Shin Corporation Macquarie Thailand Corporate Day Mrs.Siripen Sitasuwan President & Group CFO November 30 December 2, 2005 Building a stronger portfolio SHIN Corporation Mkt cap of Bt 111.7bn* (US$2.7bn)

0 V2 13/11/61 17:55 น.

0 1 Management Discussion and Analysis Overview of the Economy and Banking Industry Thai Economy in the Third Quarter of The Thai economy in the third quarter of continued to grow year-on-year on the back

0 1 Management Discussion and Analysis Overview of the Economy and Banking Industry Thai Economy in the Third Quarter of The Thai economy in the third quarter of continued to grow year-on-year on the back

Eurozone Economic Watch. July 2018

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Investors Call Presentation

Investors Call Presentation Q3 2014 Results 11 NOVEMBER 2014 Forward looking statements This presentation contains or incorporates by reference forward-looking statements regarding the belief or current

Investors Call Presentation Q3 2014 Results 11 NOVEMBER 2014 Forward looking statements This presentation contains or incorporates by reference forward-looking statements regarding the belief or current

Year-end results. 18 May

Year-end results 18 May Highlights for the year Strong operational performance Good performance across all areas of activity Deepened our core franchise Sound levels of corporate client and private client

Year-end results 18 May Highlights for the year Strong operational performance Good performance across all areas of activity Deepened our core franchise Sound levels of corporate client and private client

Strategic Investment in Bank Danamon. Main Q&A

Strategic Investment in Bank Danamon Main Q&A Q :You ve said share purchase prices for Steps 2 and 3 have yet to be determined. Can you share with us the logic you re going to apply to determine pricing?

Strategic Investment in Bank Danamon Main Q&A Q :You ve said share purchase prices for Steps 2 and 3 have yet to be determined. Can you share with us the logic you re going to apply to determine pricing?

World Bank Thailand Economic Monitor November Press Launch November 4, 2009

World Bank Thailand Economic Monitor November 2009 Press Launch November 4, 2009 overview The Thai economy is rebounding from a rocky first half of 2009, but the medium-term outlook is uncertain. The Thai

World Bank Thailand Economic Monitor November 2009 Press Launch November 4, 2009 overview The Thai economy is rebounding from a rocky first half of 2009, but the medium-term outlook is uncertain. The Thai

Schroder Asian Income Monthly Fund Update

Schroder Asian Income Monthly Fund Update Fund Performance As at 30 September 2014, SGD 1 month Year to date Since launch* Schroder Asian Income Fund (Bid-Bid) (%) -1.7 8.4 35.2 Schroder Asian Income Fund

Schroder Asian Income Monthly Fund Update Fund Performance As at 30 September 2014, SGD 1 month Year to date Since launch* Schroder Asian Income Fund (Bid-Bid) (%) -1.7 8.4 35.2 Schroder Asian Income Fund

BAHT DENOMINATED BOND IN THAILAND BY PUBLIC DEBT MANAGEMENT OFFICE - MINISTRY OF FINANCE, KINGDOM OF THAILAND

BAHT DENOMINATED BOND IN THAILAND BY PUBLIC DEBT MANAGEMENT OFFICE - MINISTRY OF FINANCE, KINGDOM OF THAILAND Baht-denominated Bond in Thailand (Baht Bond) OBJECTIVES BENEFITS TRADE - OFF INVESTORS ISSUERS

BAHT DENOMINATED BOND IN THAILAND BY PUBLIC DEBT MANAGEMENT OFFICE - MINISTRY OF FINANCE, KINGDOM OF THAILAND Baht-denominated Bond in Thailand (Baht Bond) OBJECTIVES BENEFITS TRADE - OFF INVESTORS ISSUERS

CONTENTS. Introduction to HFG Fundamentals KEB Acquisition DISCLAIMER

Financial Group This information contained in this presentation material is not audited by a third party independent auditor and is subject to change. CONTENTS Introduction to HFG Fundamentals KEB Acquisition

Financial Group This information contained in this presentation material is not audited by a third party independent auditor and is subject to change. CONTENTS Introduction to HFG Fundamentals KEB Acquisition

Management Trainee 1

Management Trainee 1 Agenda Corporate Profile Project Management Trainee 2 ONEAM Corporate Profile 3 One Asset Management Limited ( ONEAM ) Mission : - Provide investment solutions for investors through

Management Trainee 1 Agenda Corporate Profile Project Management Trainee 2 ONEAM Corporate Profile 3 One Asset Management Limited ( ONEAM ) Mission : - Provide investment solutions for investors through

KASIKORNBANK. Investor Presentation as of 2Q17. August 2017

KASIKORNBANK Investor Presentation as of 2Q17 August 217 For further information, please contact the Investor Relations Unit or visit our website at www.kasikornbank.com 1 KASIKORNBANK at a Glance Established

KASIKORNBANK Investor Presentation as of 2Q17 August 217 For further information, please contact the Investor Relations Unit or visit our website at www.kasikornbank.com 1 KASIKORNBANK at a Glance Established

Monetary Policy Report, June 2017

No. 32/2017 Monetary Policy Report, June 2017 Mr. Jaturong Jantarangs, Assistant Governor of the Bank of Thailand (BOT) and Secretary of the Monetary Policy Committee (MPC), released the June 2017 issue

No. 32/2017 Monetary Policy Report, June 2017 Mr. Jaturong Jantarangs, Assistant Governor of the Bank of Thailand (BOT) and Secretary of the Monetary Policy Committee (MPC), released the June 2017 issue

Chile. 3Q09 Results. Boadilla, October 2009

3Q09 Results Boadilla, October 2009 Important Information 2 Banco Santander, S.A. ("Santander") cautions that this presentation contains forward-looking statements within the meaning of the US Private

3Q09 Results Boadilla, October 2009 Important Information 2 Banco Santander, S.A. ("Santander") cautions that this presentation contains forward-looking statements within the meaning of the US Private

Global Equites declined from Concern over Trade War

Quarterly Market Outlook: Quarter 2 2018 on 3 April 2018 Global Equites declined from Concern over Trade War Investment Outlook for 2 nd Quarter 2018 Equity Thailand U.S. Europe Japan Asia Bond Thailand

Quarterly Market Outlook: Quarter 2 2018 on 3 April 2018 Global Equites declined from Concern over Trade War Investment Outlook for 2 nd Quarter 2018 Equity Thailand U.S. Europe Japan Asia Bond Thailand

3Q16 Results. October, 27 th Carlos Torres Vila Chief Executive Officer

3Q16 Results October, 27 th 2016 Carlos Torres Vila Chief Executive Officer 2 Disclaimer This document is only provided for information purposes and does not constitute, nor should it be interpreted as,

3Q16 Results October, 27 th 2016 Carlos Torres Vila Chief Executive Officer 2 Disclaimer This document is only provided for information purposes and does not constitute, nor should it be interpreted as,

MANAGEMENT S DISCUSSION AND ANALYSIS

MANAGEMENT S DISCUSSION AND ANALYSIS For the three-month period ended 31 March 2018 (Reviewed Financial Statements) Thanachart Bank Public Company Limited Tel: 0 2217 8000, 0 2217 8444 Fax: 0 2217 8451

MANAGEMENT S DISCUSSION AND ANALYSIS For the three-month period ended 31 March 2018 (Reviewed Financial Statements) Thanachart Bank Public Company Limited Tel: 0 2217 8000, 0 2217 8444 Fax: 0 2217 8451

2.1 Supply. Bank of Thailand, January Nominal Farm Income. Manufacturing Production Index (MPI)

") Bank of Thailand, uary 2.1 Supply Farm income continually increased but concentrated in certain crops and regions. Service sector continued to expand, especially for tourism-related activities on the back

Bank of Thailand, uary 2.1 Supply Farm income continually increased but concentrated in certain crops and regions. Service sector continued to expand, especially for tourism-related activities on the back

Asia Key Economic and Financial Indicators 13-Jul-17

Asia Key Economic and Financial Indicators -Jul-7 ASEAN Brunei (BN) Cambodia (KH) Indonesia () Laos (LA) Malaysia () Myanmar (MM) Philippines () Singapore () Thailand () Vietnam () East Asia China (CN)

Asia Key Economic and Financial Indicators -Jul-7 ASEAN Brunei (BN) Cambodia (KH) Indonesia () Laos (LA) Malaysia () Myanmar (MM) Philippines () Singapore () Thailand () Vietnam () East Asia China (CN)

Monetary Policy Committee s Decision 8/2017

No. 66/2017 Monetary Policy Committee s Decision 8/2017 Mr. Jaturong Jantarangs, Secretary of the Monetary Policy Committee (MPC), announced the outcome of the meeting on 20 December 2017 as follows. The

No. 66/2017 Monetary Policy Committee s Decision 8/2017 Mr. Jaturong Jantarangs, Secretary of the Monetary Policy Committee (MPC), announced the outcome of the meeting on 20 December 2017 as follows. The