Financial Statement Analysis

|

|

|

- Bruno James

- 6 years ago

- Views:

Transcription

1 14-1

2 Chapter 14 Financial Statement Analysis 14-2 Learning Objectives After studying this chapter, you should be able to: 1. Discuss the need for comparative analysis. 2. Identify the tools of financial statement analysis. 3. Explain and apply horizontal analysis. 4. Describe and apply vertical analysis. 5. Identify and compute ratios used in analyzing a firm s liquidity, profitability, and solvency. 6. Understand the concept of earning power, and how discontinued operations are presented. 7. Understand the concept of quality of earnings.

3 Preview of Chapter Financial Accounting IFRS Second Edition Weygandt Kimmel Kieso

4 Basics of Financial Statement Analysis Need for Comparative Analysis Every item reported in a financial statement has significance. Various analytical techniques are used to evaluate the significance of financial statement data LO 1 Discuss the need for comparative analysis.

5 Basics of Financial Statement Analysis Analyzing financial statements involves: Characteristics Comparison Bases Tools of Analysis Liquidity Intracompany Horizontal Profitability Solvency Industry averages Intercompany Vertical Ratio 14-5 LO 1 LO 2 Discuss the need for comparative analysis. Identify the tools of financial statement analysis.

6 Horizontal Analysis Horizontal analysis, also called trend analysis, is a technique for evaluating a series of financial statement data over a period of time. Purpose is to determine the increase or decrease that has taken place. Commonly applied to the statement of financial position, income statement, and retained earnings statement LO 3 Explain and apply horizontal analysis.

7 Horizontal Analysis Illustration 14-5 Horizontal analysis of statements of financial position Changes suggest that the company expanded its asset base during 2014 and financed this expansion primarily by retaining income rather than assuming additional long-term debt LO 3 Explain and apply horizontal analysis.

8 Horizontal Analysis Illustration 14-6 Horizontal analysis of Income statements Overall, gross profit and net income were up substantially. Gross profit increased 17.1%, and net income, 26.5%. Quality s profit trend appears favorable LO 3 Explain and apply horizontal analysis.

9 Horizontal Analysis Illustration 14-7 Horizontal analysis of retained earnings statements In the horizontal analysis of the statement of financial position the ending retained earnings increased 38.6%. As indicated earlier, the company retained a significant portion of net income to finance additional plant facilities LO 3 Explain and apply horizontal analysis.

10 Vertical Analysis Vertical analysis, also called common-size analysis, is a technique that expresses each financial statement item as a percent of a base amount. On an income statement, we might say that selling expenses are 16% of net sales. On a statement of financial position, we might say that current assets are 22% of total assets. Vertical analysis is commonly applied to the statement of financial position and the income statement LO 4 Describe and apply vertical analysis.

11 Vertical Analysis Illustration 14-8 Vertical analysis of statements of financial position These results reinforce the earlier observations that Quality is choosing to finance its growth through retention of earnings rather than through issuing additional debt LO 4 Describe and apply vertical analysis.

12 Vertical Analysis Illustration 14-9 Vertical analysis of Income statements Quality appears to be a profitable enterprise that is becoming even more successful LO 4 Describe and apply vertical analysis.

13 Vertical Analysis Enables a comparison of companies of different sizes. Illustration Intercompany income statement comparison LO 4 Describe and apply vertical analysis.

14 Ratio Analysis Ratio analysis expresses the relationship among selected items of financial statement data. Financial Ratio Classifications Liquidity Profitability Solvency Measure short-term ability of the company to pay its maturing obligations and to meet unexpected needs for cash. Measure the income or operating success of a company for a given period of time. Measure the ability of the company to survive over a long period of time LO 5 Identify and compute ratios used in analyzing a firm s liquidity, profitability, and solvency.

15 14-15

16 Ratio Analysis Liquidity Ratios Measure the short-term ability of the company to pay its maturing obligations and to meet unexpected needs for cash. Short-term creditors such as bankers and suppliers are particularly interested in assessing liquidity. Ratios include the current ratio, the acid-test ratio, receivable turnover, and inventory turnover LO 5 Identify and compute ratios used in analyzing a firm s liquidity, profitability, and solvency.

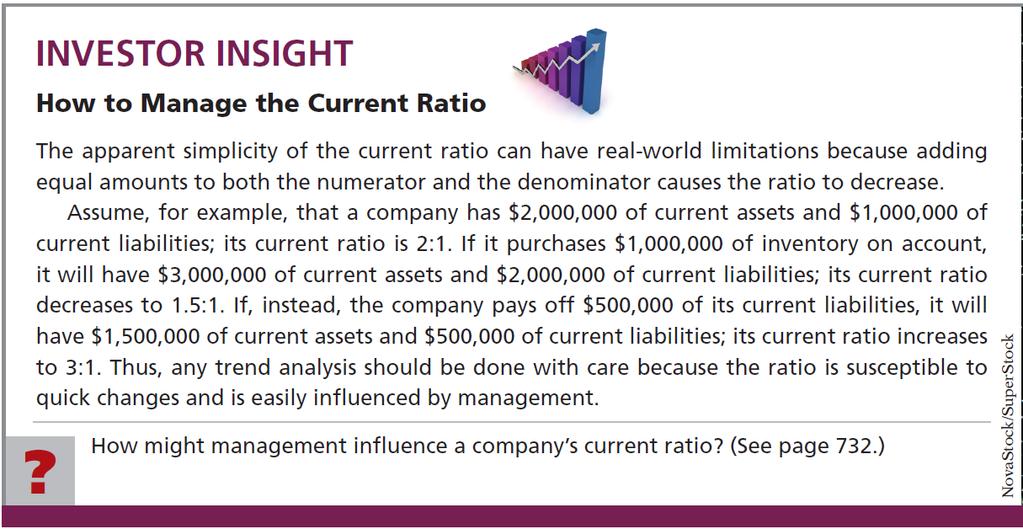

17 Ratio Analysis 1. Current Ratio Liquidity Ratios Illustration Ratio of 2.96:1 means that for every dollar of current liabilities, Quality has $2.96 of current assets LO 5 Identify and compute ratios used in analyzing a firm s liquidity, profitability, and solvency.

18 Ratio Analysis 2. Acid-Test Ratio Liquidity Ratios Illustration LO 5 Identify and compute ratios used in analyzing a firm s liquidity, profitability, and solvency.

19 Ratio Analysis Liquidity Ratios 2. Acid-Test Ratio Illustration Acid-test ratio measures immediate liquidity LO 5 Identify and compute ratios used in analyzing a firm s liquidity, profitability, and solvency.

20 14-20

21 Ratio Analysis Liquidity Ratios 3. Accounts Receivable Turnover Illustration Measures the number of times, on average, the company collects receivables during the period LO 5

22 Ratio Analysis Liquidity Ratios 2,097,000 ( 180, ,000) / 2 Receivable Turnover = 10.2 times A variant of the Accounts Receivable Turnover ratio is to convert it to an average collection period in terms of days. 365 days / 10.2 times = every days Receivables are collected on average every 36 days LO 5 Identify and compute ratios used in analyzing a firm s liquidity, profitability, and solvency.

23 Ratio Analysis Liquidity Ratios 4. Inventory Turnover Illustration Measures the number of times, on average, the inventory is sold during the period LO 5

24 Ratio Analysis Liquidity Ratios 1,281,000 Inventory Turnover = 2.3 times ( 500, ,000) / 2 A variant of inventory turnover is the days in inventory. 365 days / 2.3 times = every 159 days Inventory turnover ratios vary considerably among industries LO 5 Identify and compute ratios used in analyzing a firm s liquidity, profitability, and solvency.

25 Ratio Analysis Profitability Ratios Measure the income or operating success of a company for a given period of time. Income, or the lack of it, affects the company s ability to obtain debt and equity financing, liquidity position, and the ability to grow. Ratios include the profit margin, asset turnover, return on assets, return on ordinary shareholders equity, earnings per share, price-earnings, and payout ratio LO 5 Identify and compute ratios used in analyzing a firm s liquidity, profitability, and solvency.

26 Ratio Analysis Profitability Ratios 5. Profit Margin Illustration Measures the percentage of each dollar of sales that results in net income. LO 5 Identify and compute ratios used in analyzing a firm s liquidity, profitability, and solvency.

27 Ratio Analysis 6. Asset Turnover Profitability Ratios Illustration Measures how efficiently a company uses its assets to generate sales LO 5 Identify and compute ratios used in analyzing a firm s liquidity, profitability, and solvency.

28 Ratio Analysis 7. Return on Asset Profitability Ratios Illustration An overall measure of profitability LO 5 Identify and compute ratios used in analyzing a firm s liquidity, profitability, and solvency.

29 Ratio Analysis Profitability Ratios 8. Return on Ordinary Shareholders Equity Illustration Shows how many euros of net income the company earned for each euro invested by the owners LO 5

Profitability Ratios Illustration 14-21 A measure")

30 Ratio Analysis 9. Earnings Per Share (EPS) Profitability Ratios Illustration A measure of the net income earned on each ordinary share LO 5

31 Ratio Analysis 10. Price-Earnings Ratio Profitability Ratios Illustration Reflects investors assessments of a company s future earnings LO 5

32 Ratio Analysis 11. Payout Ratio Profitability Ratios Illustration Measures the percentage of earnings distributed in the form of cash dividends. LO 5

33 Ratio Analysis Solvency Ratios Solvency ratios measure the ability of a company to survive over a long period of time. Debt to Total Assets and Times Interest Earned are two ratios that provide information about debt-paying ability LO 5 Identify and compute ratios used in analyzing a firm s liquidity, profitability, and solvency.

34 Ratio Analysis 12. Debt to Total Assets Ratio Solvency Ratios Illustration Measures the percentage of the total assets that creditors provide LO 5

35 Ratio Analysis 13. Times Interest Earned Solvency Ratios Illustration Provides an indication of the company s ability to meet interest payments as they come due. LO 5

36 Ratio Analysis Summary of Ratios Illustration LO 5

37 Summary of Ratios Illustration LO 5

38 Summary of Ratios Illustration LO 5

39 Earning Power and Irregular Items Earning power means the normal level of income to be obtained in the future. Discontinued operations: 1. Irregular item separately identified on the income statement. 2. Reported net of income taxes LO 6 Understand the concept of earning power, and how discontinued operations are presented.

40 Earning Power and Irregular Items Discontinued Operations (a) (b) Disposal of a significant component of a business. Report the income (loss) from discontinued operations in two parts: 1. income (loss) from operations (net of tax) and 2. gain (loss) on disposal (net of tax) LO 6 Understand the concept of earning power, and how discontinued operations are presented.

41 Earning Power and Irregular Items Illustration: During 2014 Acro Energy Inc. has income before income taxes of $800,000. During 2014, Acro Energy discontinued and sold its unprofitable chemical division. The loss in 2014 from chemical operations (net of $60,000 taxes) was $140,000. The loss on disposal of the chemical division (net of $30,000 taxes) was $70,000. Assuming a 30% tax rate on income LO 6 Understand the concept of earning power, and how discontinued operations are presented.

42 Earning Power and Irregular Items Illustration LO 6

43 14-43

44 Earning Power and Irregular Items Change in Accounting Principle Occurs when the principle used in the current year is different from the one used in the preceding year. Accounting rules permit a change if justified. Most changes are reported retroactively. Example would include a change in inventory costing method (such as FIFO to average-cost) LO 6 Understand the concept of earning power, and how discontinued operations are presented.

45 Earning Power and Irregular Items Comprehensive Income Income Statement (in thousands) Sales 285,000 Cost of goods sold 149,000 Gross profit 136,000 Operating expenses: Advertising expense 10,000 Depreciation expense 43,000 Total operating expense 53,000 Income from operations 83,000 Other revenue: Interest revenue 17,000 Total other 17,000 Income before taxes 100,000 Income tax expense 24,000 Net income 76,000 + All changes in equity except those resulting from investments by shareholders and distributions to shareholders. Reported in Equity Unrealized gains and losses on non-trading securities. Plus other items LO 6

46 Earning Power and Irregular Items Comprehensive Income Why are gains and losses on non-trading securities excluded from net income? Because disclosing them separately 1) reduces the volatility of net income due to fluctuations in fair value, 2) yet informs the financial statement user of the gain or loss that would be incurred if the securities were sold at fair value LO 6 Understand the concept of earning power, and how discontinued operations are presented.

47 Quality of Earnings A company that has a high quality of earnings provides full and transparent information that will not confuse or mislead users of the financial statements. Alternate Accounting Methods Variations among companies in the application of IFRS may hamper comparability and reduce quality of earnings LO 7 Understand the concept of quality of earnings.

48 Quality of Earnings Pro Forma Income Pro forma income usually excludes items that the company thinks are unusual or nonrecurring. Some companies have abused the flexibility that pro forma numbers allow LO 7 Understand the concept of quality of earnings.

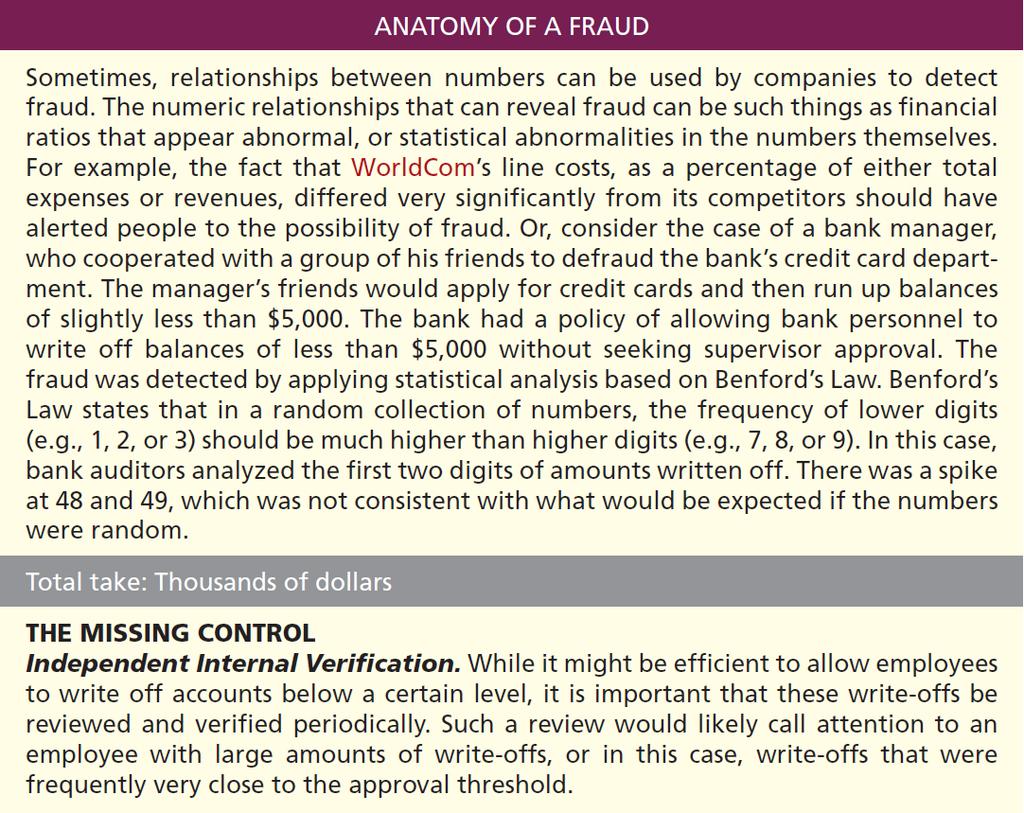

49 Quality of Earnings Improper Recognition Some managers have felt pressure to continually increase earnings and have manipulated the earnings numbers to meet these expectations. Abuses include: Improper recognition of revenue (channel stuffing). Improper capitalization of operating expenses (WorldCom - USA). Failure to report all liabilities (Enron - USA) LO 7 Understand the concept of quality of earnings.

50 Another Perspective Key Points The tools of financial statement analysis covered in this chapter are universal and therefore no significant differences exist in the analysis methods used. The basic objectives of the income statement are the same under both GAAP and IFRS. As indicated in the textbook, a very important objective is to ensure that users of the income statement can evaluate the earning power of the company. Earning power is the normal level of income to be obtained in the future. Thus, both the IASB and the FASB are interested in distinguishing normal levels of income from irregular items in order to better predict a company s future profitability

51 Another Perspective Key Points The basic accounting for discontinued operations is the same under GAAP and IFRS. Under GAAP, items that are considered to be both unusual in nature and infrequent in occurrence are reported as extraordinary items in a separate line item, net of tax. Under IFRS, there is no classification for extraordinary items. In other words, extraordinary item treatment is prohibited under IFRS. In recent years, the types of items that can receive extraordinary item treatment under GAAP have been reduced to the point where the classification is rarely used. The accounting for changes in accounting principles and changes in accounting estimates are the same for both GAAP and IFRS

52 Another Perspective Key Points Both IFRS and GAAP follow the same approach in reporting comprehensive income. The statement of comprehensive income can be prepared under the one-statement approach or the two statement approach. Under the one-statement approach, all components of revenue and expense are reported in the income statement. This combined statement of comprehensive income first computes net income or loss, which is then followed by components of other comprehensive income or loss items to arrive at comprehensive income

53 Another Perspective Key Points Under the two-statement approach, all the components of revenues and expenses are reported in a traditional income statement except for other comprehensive income or loss. In addition, a second statement (the statement of comprehensive income) is then prepared, starting with net income and followed by other comprehensive income or loss items to arrive at comprehensive income. The issues related to quality of earnings are the same under both GAAP and IFRS. It is hoped that by adopting a more principlesbased approach, as found in IFRS, many of the earnings quality issues will disappear

54 Another Perspective Looking to the Future The FASB and the IASB are working on a project that would rework the structure of financial statements. Recently, the IASB decided to require a statement of comprehensive income, similar to what was required under GAAP. In addition, another part of this project addresses the issue of how to classify various items in the income statement. A main goal of this new approach is to provide information that better represents how businesses are run. In addition, the approach draws attention away from one number net income

55 Copyright Copyright 2013 John Wiley & Sons, Inc. All rights reserved. Reproduction or translation of this work beyond that permitted in Section 117 of the 1976 United States Copyright Act without the express written permission of the copyright owner is unlawful. Request for further information should be addressed to the Permissions Department, John Wiley & Sons, Inc. The purchaser may make back-up copies for his/her own use only and not for distribution or resale. The Publisher assumes no responsibility for errors, omissions, or damages, caused by the use of these programs or from the use of the information contained herein

Investments. 1. Discuss why corporations invest in debt and share securities.

12-1 Chapter 12 Investments Learning Objectives After studying this chapter, you should be able to: 1. Discuss why corporations invest in debt and share securities. 2. Explain the accounting for debt investments.

12-1 Chapter 12 Investments Learning Objectives After studying this chapter, you should be able to: 1. Discuss why corporations invest in debt and share securities. 2. Explain the accounting for debt investments.

PREVIEW OF CHAPTER 5-2

5-1 PREVIEW OF CHAPTER 5 5-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 5 and Statement of Cash Flows Statement of Financial Position LEARNING OBJECTIVES After studying this

5-1 PREVIEW OF CHAPTER 5 5-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 5 and Statement of Cash Flows Statement of Financial Position LEARNING OBJECTIVES After studying this

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 5-1 5-2 PREVIEW OF CHAPTER 5 5-3

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 5-1 5-2 PREVIEW OF CHAPTER 5 5-3

PREVIEW OF CHAPTER Slide 4-2

4-1 PREVIEW OF CHAPTER 4 4-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 4 Related Information Income Statement and LEARNING OBJECTIVES After studying this chapter, you should

4-1 PREVIEW OF CHAPTER 4 4-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 4 Related Information Income Statement and LEARNING OBJECTIVES After studying this chapter, you should

Accounting Building Business Skills. Learning Objectives: Learning Objectives: Paul D. Kimmel. Chapter Eleven: Financial Statement Analysis

Accounting Building Business Skills Paul D. Kimmel Chapter Eleven: Financial Statement Analysis PowerPoint presentation by Kate Wynn-Williams University of Otago, Dunedin 2003 John Wiley & Sons Australia,

Accounting Building Business Skills Paul D. Kimmel Chapter Eleven: Financial Statement Analysis PowerPoint presentation by Kate Wynn-Williams University of Otago, Dunedin 2003 John Wiley & Sons Australia,

Accounting in Action. Chapter 1. Learning Objectives. After studying this chapter, you should be able to:

1-1 Chapter 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: 1. Explain what accounting is. 2. Identify the users and uses of accounting. 3. Understand why

1-1 Chapter 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: 1. Explain what accounting is. 2. Identify the users and uses of accounting. 3. Understand why

PREVIEW OF CHAPTER 24

24-1 PREVIEW OF CHAPTER 24 24-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield Presentation and 24 Disclosure in Financial Reporting LEARNING OBJECTIVES After studying this chapter,

24-1 PREVIEW OF CHAPTER 24 24-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield Presentation and 24 Disclosure in Financial Reporting LEARNING OBJECTIVES After studying this chapter,

Adjusting the Accounts

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

The Recording Process

2-1 Chapter 2 The Recording Process Learning Objectives After studying this chapter, you should be able to: [1] Explain what an account is and how it helps in the recording process. [2] Define debits and

2-1 Chapter 2 The Recording Process Learning Objectives After studying this chapter, you should be able to: [1] Explain what an account is and how it helps in the recording process. [2] Define debits and

PREVIEW OF CHAPTER 20-2

20-1 PREVIEW OF CHAPTER 20 20-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 20 Accounting for Pensions and Postretirement Benefits LEARNING OBJECTIVES After studying this chapter,

20-1 PREVIEW OF CHAPTER 20 20-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 20 Accounting for Pensions and Postretirement Benefits LEARNING OBJECTIVES After studying this chapter,

C H A P T E R 5 BALANCE SHEET AND STATEMENT OF CASH FLOWS. Balance Sheet and Statement of of Cash Flows. Usefulness of the Balance Sheet

C H A P T E R 5 BALANCE SHEET AND STATEMENT OF CASH FLOWS Intermediate Accounting 13th Edition Kieso, Weygandt, and Warfield 5-1 5-2 Balance Sheet and Statement of of Cash Flows Balance Sheet Balance Sheet

C H A P T E R 5 BALANCE SHEET AND STATEMENT OF CASH FLOWS Intermediate Accounting 13th Edition Kieso, Weygandt, and Warfield 5-1 5-2 Balance Sheet and Statement of of Cash Flows Balance Sheet Balance Sheet

2/2/2009. Financial statement EARNING POWER AND IRREGULAR ITEMS. EARNING POWER AND IRREGULAR ITEMS continued. Chapter 14

Chapter 14 Financial statement analysis PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd EARNING POWER AND IRREGULAR ITEMS Earning power refers to

Chapter 14 Financial statement analysis PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd EARNING POWER AND IRREGULAR ITEMS Earning power refers to

The Recording Process

Prepared by Coby Harmon University of California, Santa Barbara Westmont College 2-1 2 The Recording Process Learning Objectives After studying this chapter, you should be able to: [1] Explain what an

Prepared by Coby Harmon University of California, Santa Barbara Westmont College 2-1 2 The Recording Process Learning Objectives After studying this chapter, you should be able to: [1] Explain what an

PREVIEW OF CHAPTER 17-2

17-1 PREVIEW OF CHAPTER 17 17-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 17 Investments LEARNING OBJECTIVES After studying this chapter, you should be able to: 1. Describe

17-1 PREVIEW OF CHAPTER 17 17-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 17 Investments LEARNING OBJECTIVES After studying this chapter, you should be able to: 1. Describe

BAT 4M1 CPT Chapter 17 Notes

BAT 4M1 CPT Chapter 17 Notes Basics of Financial Statement Analysis Financial statement analysis involves evaluating a company s liquidity, solvency, and profitability Objective: to give capital providers

BAT 4M1 CPT Chapter 17 Notes Basics of Financial Statement Analysis Financial statement analysis involves evaluating a company s liquidity, solvency, and profitability Objective: to give capital providers

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 20-1 20-2 PREVIEW OF CHAPTER 20 20-3

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 20-1 20-2 PREVIEW OF CHAPTER 20 20-3

CHAPTER4. The Recording Process. PreviewofCHAPTER4. Using a Worksheet. Steps in Preparing a Worksheet

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

CHAPTER4 The Recording Process 4-1 4-2 PreviewofCHAPTER4 Using a Worksheet Steps in Preparing a Worksheet Multiple-column form used in preparing financial statements. Not a permanent accounting record.

1-1. Prepared by Coby Harmon University of California, Santa Barbara Westmont College

1-1 Prepared by Coby Harmon University of California, Santa Barbara Westmont College 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: [1] Explain what accounting

1-1 Prepared by Coby Harmon University of California, Santa Barbara Westmont College 1 Accounting in Action Learning Objectives After studying this chapter, you should be able to: [1] Explain what accounting

PREVIEW OF CHAPTER 2-2

2-1 PREVIEW OF CHAPTER 2 2-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 2 for Financial Reporting Conceptual Framework LEARNING OBJECTIVES After studying this chapter, you should

2-1 PREVIEW OF CHAPTER 2 2-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 2 for Financial Reporting Conceptual Framework LEARNING OBJECTIVES After studying this chapter, you should

Chapter 5: Using Financial Statement Information

1 Chapter 5: Using Financial Statement Information 2 Control and Prediction Financial accounting numbers are useful in two fundamental ways: They help investors and creditors influence and monitor the

1 Chapter 5: Using Financial Statement Information 2 Control and Prediction Financial accounting numbers are useful in two fundamental ways: They help investors and creditors influence and monitor the

Chapter 11. Corporations: Organization, Share Transactions, Dividends, and Retained Earnings. Learning Objectives

11-1 Chapter 11 Corporations: Organization, Share Transactions, Dividends, and Retained Earnings Learning Objectives After studying this chapter, you should be able to: 1. Identify the major characteristics

11-1 Chapter 11 Corporations: Organization, Share Transactions, Dividends, and Retained Earnings Learning Objectives After studying this chapter, you should be able to: 1. Identify the major characteristics

PREVIEW OF CHAPTER 14-2

14-1 PREVIEW OF CHAPTER 14 14-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 14 Non-Current Liabilities LEARNING OBJECTIVES After studying this chapter, you should be able to:

14-1 PREVIEW OF CHAPTER 14 14-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 14 Non-Current Liabilities LEARNING OBJECTIVES After studying this chapter, you should be able to:

Liabilities. Chapter 10. Learning Objectives. After studying this chapter, you should be able to:

10-1 Chapter 10 Liabilities 10-2 Learning Objectives After studying this chapter, you should be able to: 1. Explain a current liability, and identify the major types of current liabilities. 2. Describe

10-1 Chapter 10 Liabilities 10-2 Learning Objectives After studying this chapter, you should be able to: 1. Explain a current liability, and identify the major types of current liabilities. 2. Describe

C H A P T E R 16 DILUTIVE SECURITIES AND EARNINGS PER SHARE

16-1 C H A P T E R 16 DILUTIVE SECURITIES AND EARNINGS PER SHARE Intermediate Accounting 13th Edition Kieso, Weygandt, and Warfield 16-2 Dilutive Securities and Earnings Per Share Dilutive Securities and

16-1 C H A P T E R 16 DILUTIVE SECURITIES AND EARNINGS PER SHARE Intermediate Accounting 13th Edition Kieso, Weygandt, and Warfield 16-2 Dilutive Securities and Earnings Per Share Dilutive Securities and

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 22-1 22-2 PREVIEW OF CHAPTER 22 22-3

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 22-1 22-2 PREVIEW OF CHAPTER 22 22-3

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 15-1 15-2 PREVIEW OF CHAPTER 15 15-3

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 15-1 15-2 PREVIEW OF CHAPTER 15 15-3

CHAPTER 4. Income Statement and Related Information 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 32, 35 12, 13, 14, 23, 25 12, 14, 15, 16, 19, 20

CHAPTER 4 Income Statement and Related Information ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Income measurement concepts. 1,

CHAPTER 4 Income Statement and Related Information ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Income measurement concepts. 1,

Visit Free Slides and Ebooks : CHAPTER 23. Statement of Cash Flows

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement.

CHAPTER 23 Statement of Cash Flows ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Format, objectives purpose, and source of statement.

Statement of Cash Flows

13-1 13 Statement of Cash Flows Learning Objectives 1 2 Discuss the usefulness and format of the statement of cash flows. Prepare a statement of cash flows using the indirect method. 3 Analyze the statement

13-1 13 Statement of Cash Flows Learning Objectives 1 2 Discuss the usefulness and format of the statement of cash flows. Prepare a statement of cash flows using the indirect method. 3 Analyze the statement

Accounting in Action

1 Accounting in Action Learning Objectives 1 2 3 4 5 Identify the activities and users associated with accounting. Explain the building blocks of accounting: ethics, principles, and assumptions. State

1 Accounting in Action Learning Objectives 1 2 3 4 5 Identify the activities and users associated with accounting. Explain the building blocks of accounting: ethics, principles, and assumptions. State

Chapter 14. Statement of Cash Flows

1 Chapter 14 Statement of Cash Flows 2 Figure 14-1 3 Definition of Cash Cash consists of coin, currency, and available funds on deposit at the bank. Negotiable instruments such as money orders, certified

1 Chapter 14 Statement of Cash Flows 2 Figure 14-1 3 Definition of Cash Cash consists of coin, currency, and available funds on deposit at the bank. Negotiable instruments such as money orders, certified

International Standards Convergence

International Standards Convergence I. INTERNATIONAL FINANCIAL REPORTING STANDARDS The International Accounting Standards Board (IASB) develops and issues International Financial Reporting Standards ().

International Standards Convergence I. INTERNATIONAL FINANCIAL REPORTING STANDARDS The International Accounting Standards Board (IASB) develops and issues International Financial Reporting Standards ().

Chapter 4 Income Statement 4-1

Chapter 4 Income Statement 1. The concept of income 2. Why income measure is important 3. How income is measured 4. The format of an income statement 5. The components of an income statement 6. The comprehensive

Chapter 4 Income Statement 1. The concept of income 2. Why income measure is important 3. How income is measured 4. The format of an income statement 5. The components of an income statement 6. The comprehensive

Accounting for Receivables

8-1 Chapter 8 Accounting for Receivables 8-2 Learning Objectives After studying this chapter, you should be able to: 1. Identify the different types of receivables. 2. Explain how companies recognize accounts

8-1 Chapter 8 Accounting for Receivables 8-2 Learning Objectives After studying this chapter, you should be able to: 1. Identify the different types of receivables. 2. Explain how companies recognize accounts

Adjusting The Accounts

3 Adjusting The Accounts Learning Objectives 1 2 Explain the accrual basis of accounting and the reasons for adjusting entries. Prepare adjusting entries for deferrals. 3 Prepare adjusting entries for

3 Adjusting The Accounts Learning Objectives 1 2 Explain the accrual basis of accounting and the reasons for adjusting entries. Prepare adjusting entries for deferrals. 3 Prepare adjusting entries for

Accounting consists of three basic activities it

1-1 LEARNING OBJECTIVE 1 Identify the activities and users associated with accounting. Accounting consists of three basic activities it identifies, records, and communicates the economic events of an organization

1-1 LEARNING OBJECTIVE 1 Identify the activities and users associated with accounting. Accounting consists of three basic activities it identifies, records, and communicates the economic events of an organization

Accounting Principles

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 4 COMPLETION OF THE ACCOUNTING CYCLE WORK SHEET A work sheet is a multiple-column

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 4 COMPLETION OF THE ACCOUNTING CYCLE WORK SHEET A work sheet is a multiple-column

CHAPTER1. Accounting in Action. PreviewofCHAPTER1. What is Accounting?

CHAPTER1 Accounting in Action 1-1 1-2 PreviewofCHAPTER1 What is Accounting? Purpose of accounting is to: 1. identify, record, and communicate the economic events of an 2. organization to 3. interested

CHAPTER1 Accounting in Action 1-1 1-2 PreviewofCHAPTER1 What is Accounting? Purpose of accounting is to: 1. identify, record, and communicate the economic events of an 2. organization to 3. interested

Chapter 3: The Measurement Fundamentals of Financial Accounting

1 Chapter 3: The Measurement Fundamentals of Financial Accounting 2 Basic Assumptions Basic assumptions are foundations of financial accounting measurements The basic assumptions are Economic entity Fiscal

1 Chapter 3: The Measurement Fundamentals of Financial Accounting 2 Basic Assumptions Basic assumptions are foundations of financial accounting measurements The basic assumptions are Economic entity Fiscal

CHAPTER3 Adjusting the Accounts

CHAPTER3 Adjusting the Accounts 3-1 3-2 Timing Issues Accountants divide the economic life of a business into artificial time periods (Time Period Assumption)...... Jan. Feb. Mar. Apr. Dec. Generally a

CHAPTER3 Adjusting the Accounts 3-1 3-2 Timing Issues Accountants divide the economic life of a business into artificial time periods (Time Period Assumption)...... Jan. Feb. Mar. Apr. Dec. Generally a

Accounting Principles

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 2 THE RECORDING PROCESS THE ACCOUNT An account is an individual accounting

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 2 THE RECORDING PROCESS THE ACCOUNT An account is an individual accounting

Chapter 8: Investments in Equity Securities

1 Chapter 8: Investments in Equity Securities 2 Equity Securities Classified as Current Two criteria must be met for an investment in a security to be considered current and thus warrant inclusion as a

1 Chapter 8: Investments in Equity Securities 2 Equity Securities Classified as Current Two criteria must be met for an investment in a security to be considered current and thus warrant inclusion as a

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 11-1 11-2 PREVIEW OF CHAPTER 11 11-3

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 11-1 11-2 PREVIEW OF CHAPTER 11 11-3

Chapter 4 The Income Statement, Comprehensive Income, and the Statement of Cash Flows

Chapter 4 The Income Statement, Comprehensive Income, and the Statement of Cash Flows QUESTIONS FOR REVIEW OF KEY TOPICS Question 4 1 The income statement is a change statement that reports transactions

Chapter 4 The Income Statement, Comprehensive Income, and the Statement of Cash Flows QUESTIONS FOR REVIEW OF KEY TOPICS Question 4 1 The income statement is a change statement that reports transactions

Chapter. Chapter. Accounting and the Time Value of Money. Time Value of Money. Basic Time Value Concepts. Basic Time Value Concepts

Accounting and the Time Value Money 6 6-1 Prepared by Coby Harmon, University California, Santa Barbara Basic Time Value Concepts Time Value Money In accounting (and finance), the term indicates that a

Accounting and the Time Value Money 6 6-1 Prepared by Coby Harmon, University California, Santa Barbara Basic Time Value Concepts Time Value Money In accounting (and finance), the term indicates that a

PREVIEW OF CHAPTER 1-2

1-1 PREVIEW OF CHAPTER 1 1-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 1 Accounting Standards Financial Reporting and LEARNING OBJECTIVES After studying this chapter, you should

1-1 PREVIEW OF CHAPTER 1 1-2 Intermediate Accounting IFRS 2nd Edition Kieso, Weygandt, and Warfield 1 Accounting Standards Financial Reporting and LEARNING OBJECTIVES After studying this chapter, you should

Modul ke: Pengantar Akuntansi. Accounting in Action. 1Fakultas Ekonomi dan Bisnis. Yullia Yustikasari, SE, M.Sc. Program Studi Akuntansi

Modul ke: 1Fakultas Ekonomi dan Bisnis Pengantar Akuntansi Accounting in Action Yullia Yustikasari, SE, M.Sc. Program Studi Akuntansi CHAPTER1 Accounting in Action PreviewofCHAPTER1 What is Accounting?

Modul ke: 1Fakultas Ekonomi dan Bisnis Pengantar Akuntansi Accounting in Action Yullia Yustikasari, SE, M.Sc. Program Studi Akuntansi CHAPTER1 Accounting in Action PreviewofCHAPTER1 What is Accounting?

Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 7-2

7-1 C H A P T E R 7 CASH AND RECEIVABLES Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 7-2 Learning Objectives 1. Identify items considered cash. 2. Indicate how to report cash and

7-1 C H A P T E R 7 CASH AND RECEIVABLES Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 7-2 Learning Objectives 1. Identify items considered cash. 2. Indicate how to report cash and

KARACHI UNIVERSITY BUSINESS SCHOOL UNIVERSITY OF KARACHI BS (BBA) V

V") 60 P a g e B S ( B B A ) S y l l a b u s KARACHI UNIVERSITY BUSINESS SCHOOL UNIVERSITY OF KARACHI BS (BBA) V Course Title : FINANCIAL ACCOUNTING Course Number : BA(BS) 501 Credit Hours : 03 Course 1. Introduction

60 P a g e B S ( B B A ) S y l l a b u s KARACHI UNIVERSITY BUSINESS SCHOOL UNIVERSITY OF KARACHI BS (BBA) V Course Title : FINANCIAL ACCOUNTING Course Number : BA(BS) 501 Credit Hours : 03 Course 1. Introduction

CHAPTER 4. Income Statement and Related Information 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 18, 28, 31, 32, 33, 36 13, 14, 15, 16, 27, 29, 35, 37

CHAPTER 4 Income Statement and Related Information ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Income measurement concepts. 1,

CHAPTER 4 Income Statement and Related Information ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Income measurement concepts. 1,

CHAPTER 18. Financial Statement Analysis. Brief Exercises Exercises 4, 5, 6, 7 3, 4, 5 2, 3, , 9, 10, 11, 12, 13, 14, 15, 16

CHAPTER 18 Financial Statement Analysis ASSIGNMENT CLASSIFICATION TABLE Study Objectives 1. Explain and apply horizontal analysis. Questions 1, 2, 3, 4, 5 Brief Exercises Exercises Problems Set A Problems

CHAPTER 18 Financial Statement Analysis ASSIGNMENT CLASSIFICATION TABLE Study Objectives 1. Explain and apply horizontal analysis. Questions 1, 2, 3, 4, 5 Brief Exercises Exercises Problems Set A Problems

Chapter 16: Dilutive Securities and Earnings per Share

Intermediate Accounting, 11th ed. Kieso, Weygandt, and Warfield Chapter 16: Dilutive Securities and Earnings per Share Prepared by Jep Robertson and Renae Clark New Mexico State University Chapter 16:

Intermediate Accounting, 11th ed. Kieso, Weygandt, and Warfield Chapter 16: Dilutive Securities and Earnings per Share Prepared by Jep Robertson and Renae Clark New Mexico State University Chapter 16:

Revenue Recognition PREVIEW OF CHAPTER LEARNING OBJECTIVES. Intermediate Accounting 15th Edition Kieso Weygandt Warfield

Irsan Lubis - Dosen Perbanas Institute 18 Revenue Recognition LEARNING OBJECTIVES After studying this chapter, you should be able to: 1. Apply the revenue recognition principle. 2. Describe accounting

Irsan Lubis - Dosen Perbanas Institute 18 Revenue Recognition LEARNING OBJECTIVES After studying this chapter, you should be able to: 1. Apply the revenue recognition principle. 2. Describe accounting

Gleim CMA Review Updates to Part Edition, 1st Printing March 2015

Page 1 of 5 Gleim CMA Review Updates to Part 2 2015 Edition, 1st Printing March 2015 NOTE: Text that should be deleted is displayed with a line through it. New text is shown with a blue background. Study

Page 1 of 5 Gleim CMA Review Updates to Part 2 2015 Edition, 1st Printing March 2015 NOTE: Text that should be deleted is displayed with a line through it. New text is shown with a blue background. Study

Chapter 17. Page 1. Company Analysis. Learning Objectives. INVESTMENTS: Analysis and Management Second Canadian Edition

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 17 Company Analysis Learning Objectives Define fundamental analysis at the company level. Explain the

INVESTMENTS: Analysis and Management Second Canadian Edition W. Sean Cleary Charles P. Jones Chapter 17 Company Analysis Learning Objectives Define fundamental analysis at the company level. Explain the

Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield. Slide 3-2

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

Analysis and interpretation of financial statements

Chapter 19 Analysis and interpretation of financial statements PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd SOURCES OF FINANCIAL INFORMATION Financial

Chapter 19 Analysis and interpretation of financial statements PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd SOURCES OF FINANCIAL INFORMATION Financial

Chapter 10. Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies

1 Chapter 10 Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies 2 Liabilities What is a liability? Probable future sacrifice of economic benefits arising from present

1 Chapter 10 Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies 2 Liabilities What is a liability? Probable future sacrifice of economic benefits arising from present

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 7-1 7-2 PREVIEW OF CHAPTER 7 7-3

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 7-1 7-2 PREVIEW OF CHAPTER 7 7-3

THE ACCOUNTING INFORMATION SYSTEM

Study Objectives THE ACCOUNTING INFORMATION SYSTEM 1. Analyze the effect of business transactions on the basic accounting equation. 2. Explain what an account is and how it helps in the recording process.

Study Objectives THE ACCOUNTING INFORMATION SYSTEM 1. Analyze the effect of business transactions on the basic accounting equation. 2. Explain what an account is and how it helps in the recording process.

Chapter 10. Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies

1 Chapter 10 Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies 2 Liabilities What is a liability? FASB - Probable future sacrifice of economic benefits arising from

1 Chapter 10 Introduction to Liabilities: Economic Consequences, Current Liabilities and Contingencies 2 Liabilities What is a liability? FASB - Probable future sacrifice of economic benefits arising from

Budgetary Planning. Managerial Accounting, Fourth Edition. Chapter 9-2

9-1 CHAPTER 9 Budgetary Planning Managerial Accounting, Fourth Edition 9-2 Study Objectives 1. Indicate the benefits of budgeting. 2. State the essentials of effective budgeting. 3. Identify the budgets

9-1 CHAPTER 9 Budgetary Planning Managerial Accounting, Fourth Edition 9-2 Study Objectives 1. Indicate the benefits of budgeting. 2. State the essentials of effective budgeting. 3. Identify the budgets

Chap002 Accrual Accounting and Net income determination

Chap002 Accrual Accounting and Net income determination True/False 1. Accrual accounting decouples measured earnings from operating cash inflows and outflows. Answer: True Learning Objective: 02-01 Topic:

Chap002 Accrual Accounting and Net income determination True/False 1. Accrual accounting decouples measured earnings from operating cash inflows and outflows. Answer: True Learning Objective: 02-01 Topic:

Chapter 11. Notes, Bonds, and Leases

1 Chapter 11 Long- Term Liabilities Notes, Bonds, and Leases 2 Long- Term Liabilities Many companies finance their operations and growth opportunities through the use of long term debt instruments: Notes

1 Chapter 11 Long- Term Liabilities Notes, Bonds, and Leases 2 Long- Term Liabilities Many companies finance their operations and growth opportunities through the use of long term debt instruments: Notes

CHAPTER 2. A Further Look at Financial Statements. Learning Objectives. 1. Identify the sections of a classified balance sheet.

Accounting: Tools for Business Decision Making, 6th Edition SOLUTIONS MANUAL Kimmel Weygandt Kieso Full download at: https://testbankreal.com/download/accounting-tools-business-decision-making-6thedition-solutions-manual-kimmel-weygandt-kieso/

Accounting: Tools for Business Decision Making, 6th Edition SOLUTIONS MANUAL Kimmel Weygandt Kieso Full download at: https://testbankreal.com/download/accounting-tools-business-decision-making-6thedition-solutions-manual-kimmel-weygandt-kieso/

Basic Elements of Balance Sheet Assets Liabilities

FINANCIAL ANALYSIS COURSE OUT LINE Course Objectives: This course is an advance subject which uses the out put of accounting records/data. The outline of this course is basthink about the firm.ed on the

FINANCIAL ANALYSIS COURSE OUT LINE Course Objectives: This course is an advance subject which uses the out put of accounting records/data. The outline of this course is basthink about the firm.ed on the

Accounting Principles

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 9 ACCOUNTING FOR RECEIVABLES Hey Sabres Accountants of Tomorrow, look for

Accounting Principles Second Canadian Edition Weygandt Kieso Kimmel Trenholm Prepared by: Carole Bowman, Sheridan College CHAPTER 9 ACCOUNTING FOR RECEIVABLES Hey Sabres Accountants of Tomorrow, look for

Financial Statement Fraud

Financial Statement Fraud 91 Errors, Irregularities, and Fraud Error unintentional misstatements or omissions of amounts or disclosures on financial statements Fraud is intentional 92 How errors and manipulations

Financial Statement Fraud 91 Errors, Irregularities, and Fraud Error unintentional misstatements or omissions of amounts or disclosures on financial statements Fraud is intentional 92 How errors and manipulations

ANALYSIS OF THE INCOME STATEMENT

ANALYSIS OF THE INCOME STATEMENT 1. INTRODUCTION The income statement shows the calculation of a company s profit over a period, such as a quarter or a year. A company s profit (also known as net income

ANALYSIS OF THE INCOME STATEMENT 1. INTRODUCTION The income statement shows the calculation of a company s profit over a period, such as a quarter or a year. A company s profit (also known as net income

A Manager's Guide to Financial Analysis

A Manager's Guide to Financial Analysis A Manager's Guide to Financial Analysis Fifth Edition Steven D. Grossman Contents About This Course How to Take This Course Introduction ix xi xiii 1 Financial

A Manager's Guide to Financial Analysis A Manager's Guide to Financial Analysis Fifth Edition Steven D. Grossman Contents About This Course How to Take This Course Introduction ix xi xiii 1 Financial

Accounting for Receivables

9 Accounting for Receivables Learning Objectives 1 2 3 4 Explain how companies recognize accounts receivable. Describe how companies value accounts receivable and record their disposition. Explain how

9 Accounting for Receivables Learning Objectives 1 2 3 4 Explain how companies recognize accounts receivable. Describe how companies value accounts receivable and record their disposition. Explain how

Interim Financial Report

Interim Financial Report Preliminary note The interim consolidated financial report is in accordance with IAS 34 Interim Financial Reporting as at and for the six months period ended June 30, 2005. Consolidated

Interim Financial Report Preliminary note The interim consolidated financial report is in accordance with IAS 34 Interim Financial Reporting as at and for the six months period ended June 30, 2005. Consolidated

University of Palestine

Question 1: Multiple Choice: 1. A common measure of liquidity is a. Profit margin. b. Debt to equity. c. Return on assets. d. Accounts receivable turnover. 2. A high accounts receivable turnover ratio

Question 1: Multiple Choice: 1. A common measure of liquidity is a. Profit margin. b. Debt to equity. c. Return on assets. d. Accounts receivable turnover. 2. A high accounts receivable turnover ratio

Prof Albrecht s Notes Income Statement Intermediate Accounting 1

Prof Albrecht s Notes Intermediate Accounting 1 The income statement has been the most important of the required financial statements in the United States. This importance is revealed in several ways:

Prof Albrecht s Notes Intermediate Accounting 1 The income statement has been the most important of the required financial statements in the United States. This importance is revealed in several ways:

Session Number. Date Held. Session Duration. Assignments (to be completed prior to next class session) Content Covered

Content Covered") 1 [insert date] Course Introduction Introduction to CMA Credential and Wiley CMAexcel Learning System Section A: External Financial Reporting Decisions Topic 1: Financial Statements Topic 2: Recognition,

1 [insert date] Course Introduction Introduction to CMA Credential and Wiley CMAexcel Learning System Section A: External Financial Reporting Decisions Topic 1: Financial Statements Topic 2: Recognition,

WILEY. Paul D. Kimmel PhD, CPA University of Wisconsin Milwaukee Milwaukee, Wisconsin

O o o c TOOLS FOR BUSINESS DECISION MAKING 5e WILEY Paul D. Kimmel PhD, CPA University of Wisconsin Milwaukee Milwaukee, Wisconsin Jerry J. Weygandt PhD, CPA : University of Wisconsin Madison Madison,

O o o c TOOLS FOR BUSINESS DECISION MAKING 5e WILEY Paul D. Kimmel PhD, CPA University of Wisconsin Milwaukee Milwaukee, Wisconsin Jerry J. Weygandt PhD, CPA : University of Wisconsin Madison Madison,

UNDERSTANDING THE INCOME STATEMENTS

UNDERSTANDING THE INCOME STATEMENTS 1 IS = Income Statement R = Revenue E = Expenses FV = Fair Value SL = Straight-Line AFS = Available For Sale Securities I.S is sometimes referred to as statement of

UNDERSTANDING THE INCOME STATEMENTS 1 IS = Income Statement R = Revenue E = Expenses FV = Fair Value SL = Straight-Line AFS = Available For Sale Securities I.S is sometimes referred to as statement of

Introduction to CMA Part Section A External Financial Reporting Decisions... 2 A.1. Financial Statements... 2

CMA Part 1 Introduction to CMA Part 1... 1 Section A External Financial Reporting Decisions... 2 A.1. Financial Statements... 2 Users of Financial Information 2 The Financial Statements 3 Differences Between

CMA Part 1 Introduction to CMA Part 1... 1 Section A External Financial Reporting Decisions... 2 A.1. Financial Statements... 2 Users of Financial Information 2 The Financial Statements 3 Differences Between

Financial Statement Fraud

Financial Statement Fraud ^rateg/es for Detection and Investigation GERARD M. ZACK CFE, CPA, CIA, CCEP WILEY John Wiley & Sons, Inc. Contents Foreword Preface xvii xiii Acknowledgments xxi II PART I REVENUE-BASED

Financial Statement Fraud ^rateg/es for Detection and Investigation GERARD M. ZACK CFE, CPA, CIA, CCEP WILEY John Wiley & Sons, Inc. Contents Foreword Preface xvii xiii Acknowledgments xxi II PART I REVENUE-BASED

FINANCIAL STATEMENT PRESENTATION DISCUSSION PAPER SUMMARY

FINANCIAL STATEMENT PRESENTATION DISCUSSION PAPER SUMMARY INTRODUCTION S1. How an entity presents information in its financial statements is vitally important because financial statements are a central

FINANCIAL STATEMENT PRESENTATION DISCUSSION PAPER SUMMARY INTRODUCTION S1. How an entity presents information in its financial statements is vitally important because financial statements are a central

WEEK 10 Analysis of Financial Statements

WEEK 10 Analysis of Financial Statements Learning Objectives 1. Organize a systematic financial statements analysis using common-size financial statements and ratio analysis. 2. Recognize the potential

WEEK 10 Analysis of Financial Statements Learning Objectives 1. Organize a systematic financial statements analysis using common-size financial statements and ratio analysis. 2. Recognize the potential

Instant download and all chapters Solutions Manual Interpreting and Analyzing Financial Statements 6th Edition Karen P. Schoenebeck, Mark P.

Instant download and all chapters Solutions Manual Interpreting and Analyzing Financial Statements 6th Edition Karen P. Schoenebeck, Mark P. Holtzman https://testbankdata.com/download/solutions-manual-interpretinganalyzing-financial-statements-6th-edition-karen-p-schoenebeck-markp-holtzman/

Instant download and all chapters Solutions Manual Interpreting and Analyzing Financial Statements 6th Edition Karen P. Schoenebeck, Mark P. Holtzman https://testbankdata.com/download/solutions-manual-interpretinganalyzing-financial-statements-6th-edition-karen-p-schoenebeck-markp-holtzman/

Chapter 17 Notes - Part 1

Basics of Financial Statement Analysis Chapter 17 Notes - Part 1 Involves evaluating a company and its liquidity, solvency, and profitability All extremely important for investors and creditors Comparative

Basics of Financial Statement Analysis Chapter 17 Notes - Part 1 Involves evaluating a company and its liquidity, solvency, and profitability All extremely important for investors and creditors Comparative

Financial Statement Analysis

Financial Statement Analysis Introduction to Financial Reporting 1. Financial Accounting Standard Board (FASB) conceptual framework is applicable to general purpose financial statements. 2. Financial statements

Financial Statement Analysis Introduction to Financial Reporting 1. Financial Accounting Standard Board (FASB) conceptual framework is applicable to general purpose financial statements. 2. Financial statements

Income Statement. (Flashcards: Single-sided)

") Income Statement (Flashcards: Single-sided) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. This financial

Income Statement (Flashcards: Single-sided) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. This financial

Chapter 1 Introduction to Business Combinations and the Conceptual Framework

Chapter 1 Introduction to Business Combinations and the Conceptual Framework Multiple Choice 1. Stock given as consideration for a business combination is valued at a. fair market value b. par value c.

Chapter 1 Introduction to Business Combinations and the Conceptual Framework Multiple Choice 1. Stock given as consideration for a business combination is valued at a. fair market value b. par value c.

Understanding Financial Statements. Elizabeth Rankin

Understanding Financial Statements Elizabeth Rankin Overview Accounting Concepts Principles Financial Statements Evaluating Performance Horizontal Analysis Vertical Analysis Ratio Analysis Entity Concept

Understanding Financial Statements Elizabeth Rankin Overview Accounting Concepts Principles Financial Statements Evaluating Performance Horizontal Analysis Vertical Analysis Ratio Analysis Entity Concept

Introduction to Fund Accounting

Classification of of Nonbusiness Organizations Introduction to Accounting for nonbusiness organizations. Five Major Classifications 1. Governmental units. 2. Hospitals and other health care providers.

Classification of of Nonbusiness Organizations Introduction to Accounting for nonbusiness organizations. Five Major Classifications 1. Governmental units. 2. Hospitals and other health care providers.

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE LEARNING OBJECTIVES 1. PREPARE A WORKSHEET. 2. EXPLAIN THE PROCESS OF CLOSING THE BOOKS. 3. DESCRIBE THE CONTENT AND PURPOSE OF A POST-CLOSING TRIAL BALANCE. 4.

CHAPTER 4 COMPLETING THE ACCOUNTING CYCLE LEARNING OBJECTIVES 1. PREPARE A WORKSHEET. 2. EXPLAIN THE PROCESS OF CLOSING THE BOOKS. 3. DESCRIBE THE CONTENT AND PURPOSE OF A POST-CLOSING TRIAL BALANCE. 4.

Section 2 - Cash and Cash Equivalents & Balance Sheet

Section 2 - Cash and Cash Equivalents & Balance Sheet 12-1 Cash Currency and coins Balances in checking accounts Items for deposit such as checks and money orders from customers Cash equivalents are short-term

Section 2 - Cash and Cash Equivalents & Balance Sheet 12-1 Cash Currency and coins Balances in checking accounts Items for deposit such as checks and money orders from customers Cash equivalents are short-term

Financial Accounting and Reporting (FAR) Content Outline Effective January 2014

Content Outline Effective January 2014") Financial Accounting and Reporting (FAR) Content Outline Effective January 2014 The Financial Accounting and Reporting section tests knowledge and understanding of the financial reporting framework used

Financial Accounting and Reporting (FAR) Content Outline Effective January 2014 The Financial Accounting and Reporting section tests knowledge and understanding of the financial reporting framework used

Time Value of Money. Appendix E. Learning Objectives. After studying this chapter, you should be able to:

E- 1 Appendix E Time Value of Money E- 2 Learning Objectives After studying this chapter, you should be able to: 1. Distinguish between simple and compound interest. 2. Solve for future value of a single

E- 1 Appendix E Time Value of Money E- 2 Learning Objectives After studying this chapter, you should be able to: 1. Distinguish between simple and compound interest. 2. Solve for future value of a single

Analysis and Interpretation of Financial Statements

Chapter 23 Analysis and Interpretation of Financial Statements o Prepare comparative financial statements using horizontal analysis o Prepare comparative financial statements using vertical analysis o

Chapter 23 Analysis and Interpretation of Financial Statements o Prepare comparative financial statements using horizontal analysis o Prepare comparative financial statements using vertical analysis o

LIMITED EDITION. Conceptual Framework, Standards, Standard Setting, and Presentation of Financial Statements

LIMITED EDITION Conceptual Framework, Standards, Standard Setting, and Presentation of Financial Statements Contents Learning Outcomes 1 1.1 U.S. Securities and Exchange Commission 2 SEC Rulemaking Process

LIMITED EDITION Conceptual Framework, Standards, Standard Setting, and Presentation of Financial Statements Contents Learning Outcomes 1 1.1 U.S. Securities and Exchange Commission 2 SEC Rulemaking Process

The Allstate Corporation. Definitions of GAAP Operating Ratios and Definitions and Reconciliations of Non-GAAP Measures and Operating Measures

The Allstate Corporation Definitions of GAAP Operating Ratios and Definitions and Reconciliations of Non-GAAP Measures and Operating Measures First Quarter 200 This document sets forth definitions of operating

The Allstate Corporation Definitions of GAAP Operating Ratios and Definitions and Reconciliations of Non-GAAP Measures and Operating Measures First Quarter 200 This document sets forth definitions of operating

Section 2 - Cash and Cash Equivalents & Balance Sheet

Section 2 - Cash and Cash Equivalents & Balance Sheet 12-1 Cash Currency and coins Balances in checking accounts Items for deposit such as checks and money orders from customers Cash equivalents are short-term

Section 2 - Cash and Cash Equivalents & Balance Sheet 12-1 Cash Currency and coins Balances in checking accounts Items for deposit such as checks and money orders from customers Cash equivalents are short-term

Statement of Financial Accounting Standards No. 101

Statement of Financial Accounting Standards No. 101 FAS101 Status Page FAS101 Summary Regulated Enterprises Accounting for the Discontinuation of Application of FASB Statement No. 71 December 1988 Financial

Statement of Financial Accounting Standards No. 101 FAS101 Status Page FAS101 Summary Regulated Enterprises Accounting for the Discontinuation of Application of FASB Statement No. 71 December 1988 Financial

Copyright 2009 The Learning House, Inc. Income Taxes and Investments Page 1 of 17

Copyright 2009 The Learning House, Inc. Income Taxes and Investments Page 1 of 17 Introduction Taxes are a significant expense for most companies and must be considered when analyzing a company. Differences

Copyright 2009 The Learning House, Inc. Income Taxes and Investments Page 1 of 17 Introduction Taxes are a significant expense for most companies and must be considered when analyzing a company. Differences

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 13-1 13-2 PREVIEW OF CHAPTER 13 13-3

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 13-1 13-2 PREVIEW OF CHAPTER 13 13-3

Discontinued Operations and Extraordinary Items

Statutory Issue Paper No. 24 Discontinued Operations and Extraordinary Items STATUS Finalized March 16, 1998 Original SSAP and Current Authoritative Guidance: SSAP No. 24 Type of Issue: Common Area SUMMARY

Statutory Issue Paper No. 24 Discontinued Operations and Extraordinary Items STATUS Finalized March 16, 1998 Original SSAP and Current Authoritative Guidance: SSAP No. 24 Type of Issue: Common Area SUMMARY