Presented by : Ali Muhammad Lakdawala. GLOBOIL 2017, Mumbai

|

|

|

- Jane Fowler

- 6 years ago

- Views:

Transcription

Email : alimuhammad.lakdawala@itc.")

1 "Revisiting Asian Financial Crisis for Envisioning Commodity Market Outlook Presented by : Ali Muhammad Lakdawala ITC Ltd (Foods Division) alimuhammad.lakdawala@itc.in GLOBOIL 2017, Mumbai

2 Disclaimer Views shared in the paper are author s view and not to be considered as company s view or being endorsed by company which author represents.

3 Why Revisiting 1997 Crisis???

4 WORLD BANK REPORT 1993 EAST ASIA HAS A REMARKABLE RECORD OF HIGH AND SUSTAINED economic growth. From 1965 to 1990 economies of East Asia grew faster than all other regions. Compared with other developing economies, they have lower and declining levels of inequality. Rapid growth and improving equity are the defining characteristics of the East Asian miracle

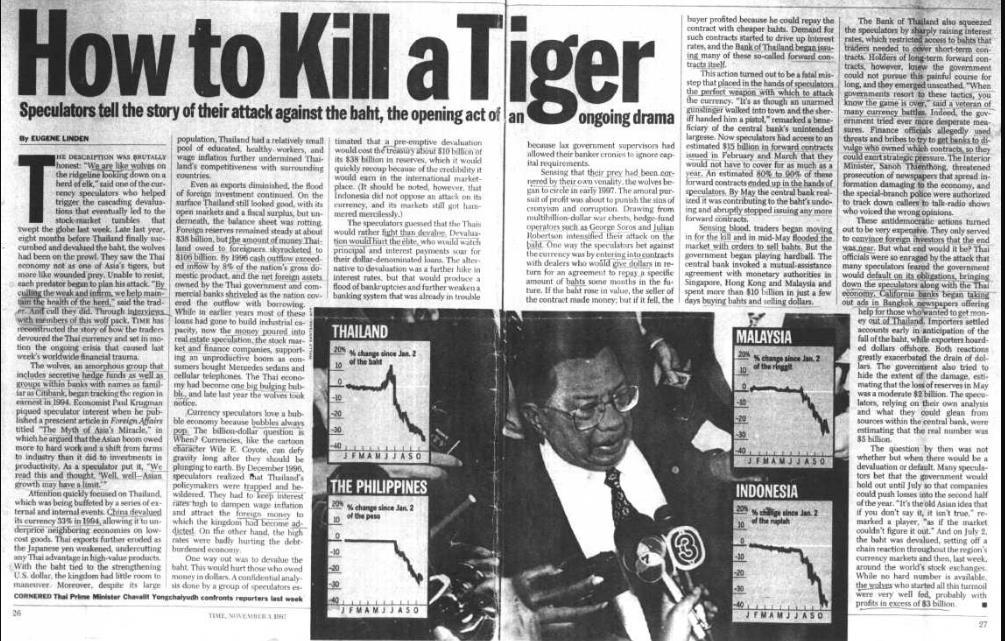

5 ECONOMIST COVER 1997 NOT so long ago, the Association of South-East Asian Nations (ASEAN) was on a roll. Most of its members were enjoying political stability and economic growth rates that were the envy of the world. Suddenly it looks less sure of itself. One member, Thailand, faces economic catastrophe

6 Abstract The crisis takes a much longer time coming than you think, and then it happens much faster than you would have thought." Rudiger Dornbusch The above quote by German Economist holds good while analysing 1997 Asian Financial Crisis, as region enjoyed decades of buoyant growth, suddenly what started out as a currency crisis (Thai Baht) with large devaluation of domestic currencies, quickly evolved into a financial crisis in which banks were unable to repay their foreign debts. In turn, this lead to an economic crisis as domestic firms were starved of credit and went bankrupt : illiquidity turned quickly into insolvency. Was Asian economy's growth model flawed or was it due to MULTIPLE EQUILIBRIA : both good and bad due to which an external event triggered a move from a good to a bad one or was it a Commodity /Resource Curse??? The purpose of this paper is to shed some light on this questions, post which it will analyse how it impacted Key Commodities. Followed by understanding the on-going tectonic shift in global growth as baton gets exchanged between developed & developing nations. Finally concluding with analysing the market structure for commodities and estimating the price forecasts for next year.

7 Presentation Flow Asia Growth Story Was it really Asia Financial Crisis??? Impact on Commodities Current Scenario What NEXT??? Commodity Market Structure

8 VUCA ASIA GROWTH STORY Rapid economic growth, Persistence of rapid economic growth an unprecedented long period of economic expansion, Moderate Inflation & Political stability

9 WMD Where are they???"

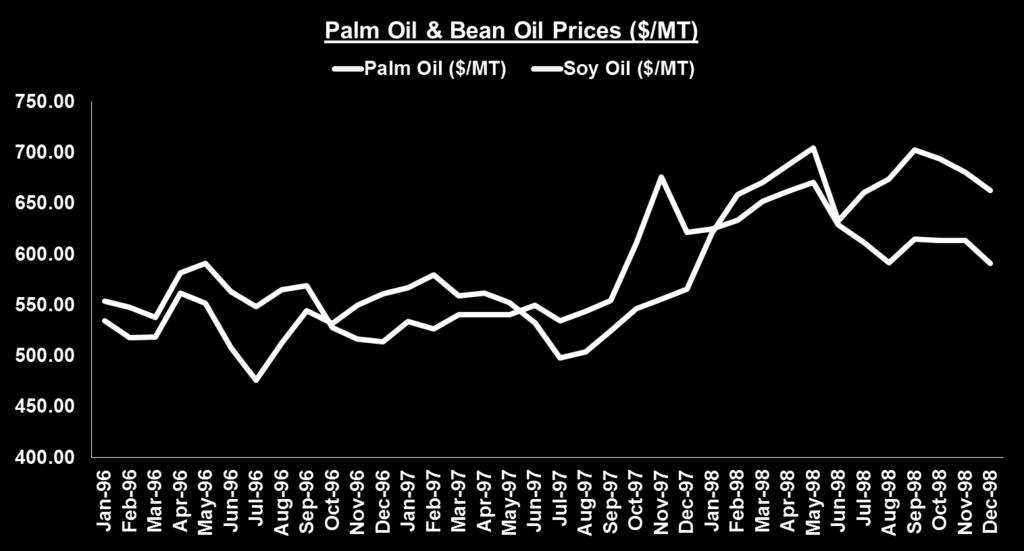

10 WMD Where are they???"

11 WMD Where are they???"

12 Was it really ASIA FINANCIAL CRISIS??? VUCA Capital inflows, especially when volatile, denominated in foreign currencies and not properly hedged against exchange rate risks, may pose macroeconomic and financial problems in the recipient economy

13

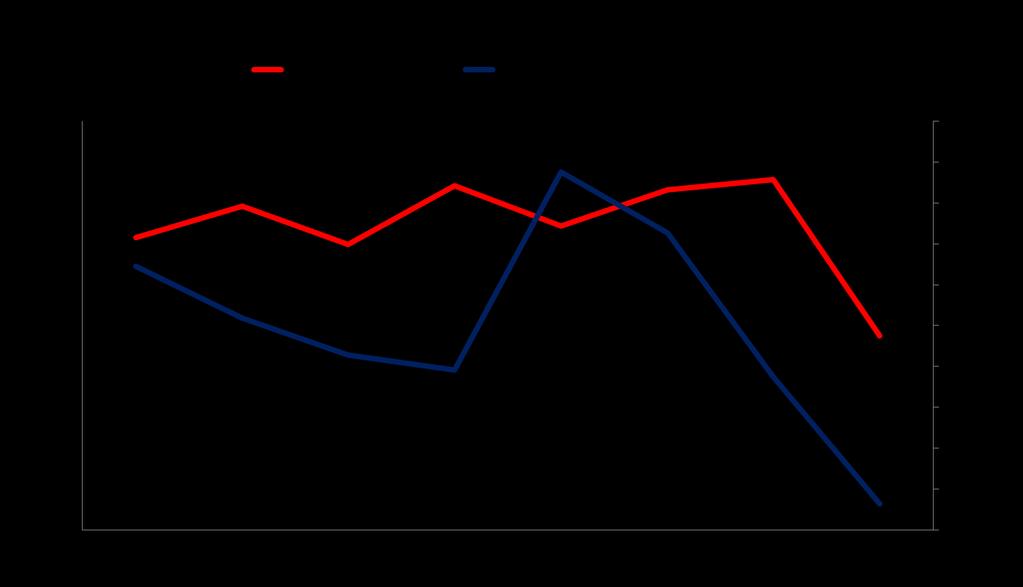

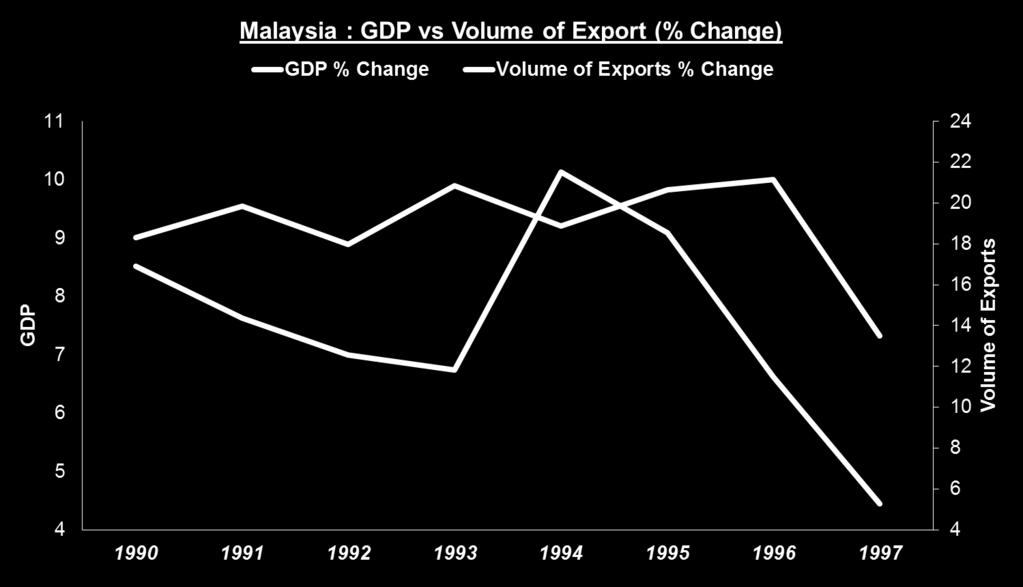

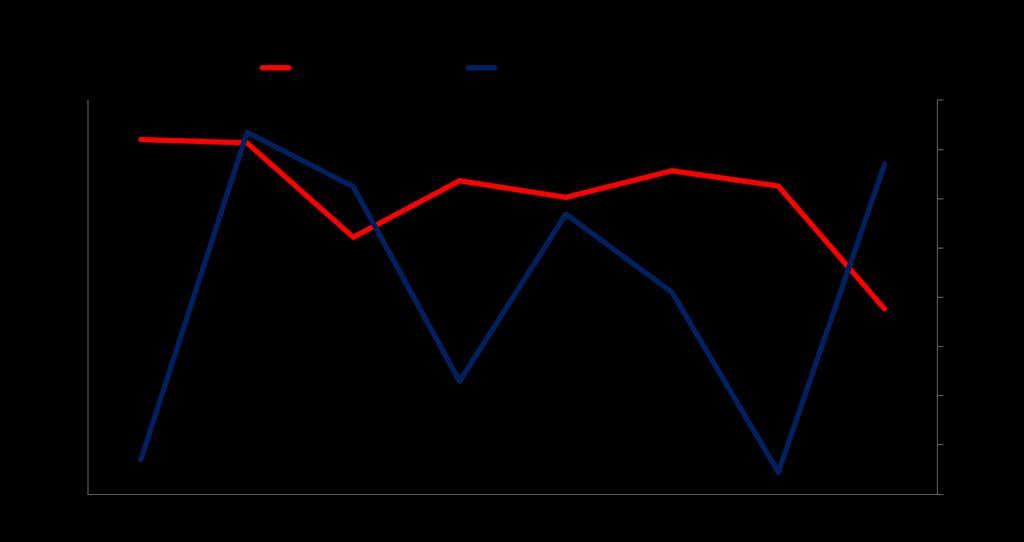

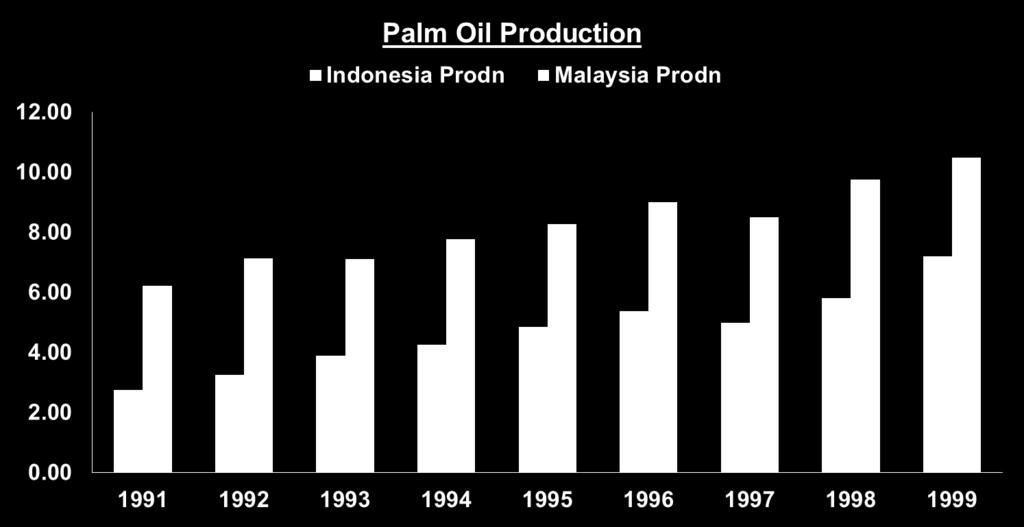

14 GDP Volume of Exports Thailand : GDP vs Volume of Export (% Change) GDP % Change Volume of Exports % Change

15

16

17 VUCA IMPACT ON COMMODITIES Most populous region of the world needs resources to feed & fuel its economy : hence key influencer in commodity market

18 Jan-96 Feb-96 Mar-96 Apr-96 May-96 Jun-96 Jul-96 Aug-96 Sep-96 Oct-96 Nov-96 Dec-96 Jan-97 Feb-97 Mar-97 Apr-97 May-97 Jun-97 Jul-97 Aug-97 Sep-97 Oct-97 Nov-97 Dec-97 Jan-98 Feb-98 Mar-98 Apr-98 May-98 Jun-98 Jul-98 Aug-98 Sep-98 Oct-98 Nov-98 Dec Brent Crude $/bbl

19 Jan-96 Feb-96 Mar-96 Apr-96 May-96 Jun-96 Jul-96 Aug-96 Sep-96 Oct-96 Nov-96 Dec-96 Jan-97 Feb-97 Mar-97 Apr-97 May-97 Jun-97 Jul-97 Aug-97 Sep-97 Oct-97 Nov-97 Dec-97 Jan-98 Feb-98 Mar-98 Apr-98 May-98 Jun-98 Jul-98 Aug-98 Sep-98 Oct-98 Nov-98 Dec Copper ($/MT)

20 Jan-96 Feb-96 Mar-96 Apr-96 May-96 Jun-96 Jul-96 Aug-96 Sep-96 Oct-96 Nov-96 Dec-96 Jan-97 Feb-97 Mar-97 Apr-97 May-97 Jun-97 Jul-97 Aug-97 Sep-97 Oct-97 Nov-97 Dec-97 Jan-98 Feb-98 Mar-98 Apr-98 May-98 Jun-98 Jul-98 Aug-98 Sep-98 Oct-98 Nov-98 Dec Dollar Index

21

22 Global Oils & Fats : production & consumption (Y-o-Y Change MMT) 7 Oils & Fats Production Oils & Fats Consumption

23

24 World Oils & Fats Export Share 1997 Rapeseed Oil, 5.93% Others, 23.00% Palm Oil, 40.40% Sun Oil, 9.77% Soy Oil, 20.90%

25 3.50 India Palm Oil Imports (MMT)

26 VUCA CURRENT SCENARIO Fast Forwarding from 1997 to 2017

27 Era of VUCA : Volatility, Uncertainty, Complexity, and Ambiguity reflecting an unstable and rapidly changing economic environment

28 Global Growth Engine Emerging Economies growth was dependent on Developed Economies Consumption Model. It has now reversed back to Developed countries with high amount of uncertaininty BRIC Volume of Exports of Goods & Services (%) World GDP (%) World GDP vs BRIC Volume of Exports of Goods & Services 35 Brazil Russia India China World GDP Tech Bubble Growth Driven by Excess Liquidity Subprime Slowdown Recovery??? Crisis

29 THE ONLY GAME IN TOWN (by) CENTRAL BANKERS : are we getting ready to live in an era of rising interest rates??? Within the year s time we have started to see significant change in interest rates movement across the globe & FED looks more aggressive compared to others Interest Rates % US Japan Sweden Denmark Switzerland

30 THE KISS OF DEBT (Made in China) We have seen the downturn in history has always been made in US of A but next downturn will be made in China. With its ever growing debt which has resulted in its current account balance detoriating in last 10years in comparison to developed nations like US & Japan. AT PRESNET CHINA IS IN CATCH 22 situation & can explode anytime Current Account Balance % of GDP Argentina Brazil China India Japan Russia United States

31 VUCA WHAT NEXT??? It s Gonna be 4D World

32 DEGLOBALISATION increasing PROTECTIONISM & TECHNOLOGICAL ADVANCEMENT will inflict pain in GLOBAL TRADE

33 DEPOPULATION Time bomb Aging population may explode for that reason countries need to be more accommodative towards refuges else economy wheel will get rusted & will not generate enough growth

34 DEMONITISATION a sudden shift towards demonetisation would slow down growth engine also it opens up major risk of Cyber Crime

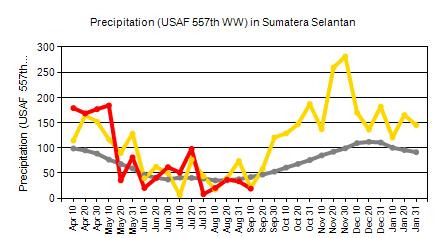

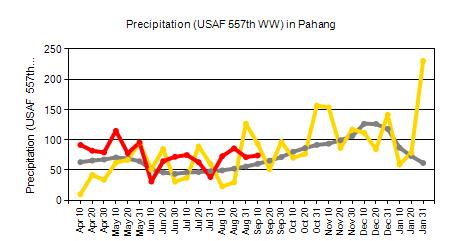

35 DEBT GLUT is rising across

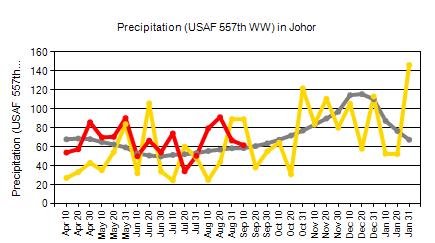

36 VUCACOMMODITY MARKET STRUCTURE

37 Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q Q China GDP Metal Index Chinese GDP vs Metal Index Chinese GDP expenditure method considered which totals consumption, investment, government spending and net exports. It is the most common way to estimate GDP, and it says everything that the private sector, including consumers and private firms, and government spend within the borders of a particular country must add up to the total value of all finished goods and services produced over a certain period of time

38 Jan-07 Jun-07 Nov-07 Apr-08 Sep-08 Feb-09 Jul-09 Dec-09 May-10 Oct-10 Mar-11 Aug-11 Jan-12 Jun-12 Nov-12 Apr-13 Sep-13 Feb-14 Jul-14 Dec-14 May-15 Oct-15 Mar-16 Aug-16 Jan-17 Jun-17 Yuan ComDex Decade Relationsip of Yuan & Commodity Index Yuan ComDex depreciation of 1% in Yuan leads to a decline of 0.6% in commodity prices (as per BoFA) (ie) A cheaper yuan will erode the purchasing power of the Chinese, pushing prices down

39 Fed Fund Rate US Liquidity Index US Fed Rate vs Liquidity Index (Jan 2007 Jul 2017) Fed Fund Rate % US Liquity Index

40 Jan-07 Jun-07 Nov-07 Apr-08 Sep-08 Feb-09 Jul-09 Dec-09 May-10 Oct-10 Mar-11 Aug-11 Jan-12 Jun-12 Nov-12 Apr-13 Sep-13 Feb-14 Jul-14 Dec-14 May-15 Oct-15 Mar-16 Aug-16 Jan-17 Jun-17 DXY ComDex Decade Relationsip of Dollar Index & Commodity Index DXY ComDex

41 Jan-07 Jun-07 Nov-07 Apr-08 Sep-08 Feb-09 Jul-09 Dec-09 May-10 Oct-10 Mar-11 Aug-11 Jan-12 Jun-12 Nov-12 Apr-13 Sep-13 Feb-14 Jul-14 Dec-14 May-15 Oct-15 Mar-16 Aug-16 Jan-17 Jun-17 Energy Index Edible Oil Index Energy Index vs Edible Oil Index (Jan 2007-Aug 2017) Energy Index Edible Oil Index

42 VUCA WHAT s IN STORE FOR OIL COMPLEX???

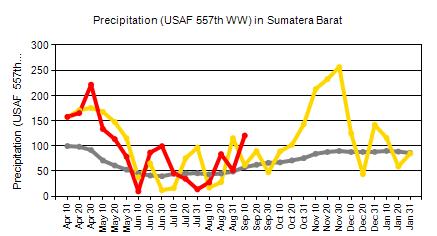

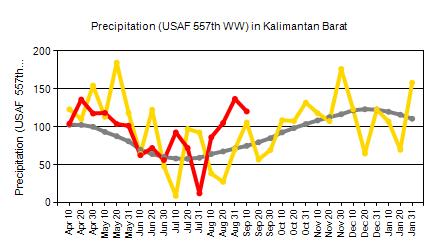

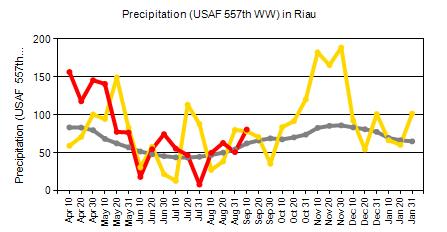

43 Indonesia Current Precipitation at Key Growing Areas (as on 10 th Sep 2017) SUMATRA KALIMANTAN RIAU

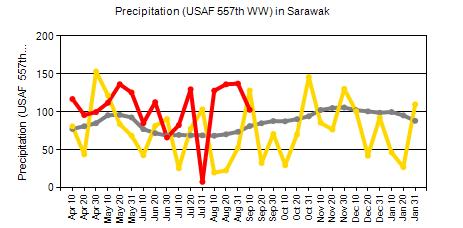

44 Malaysia Current Precipitation at Key Growing Areas (as on 10 th Sep 2017)

45 Overall oilseeds in 2H 2017 will be well supplied. Total production is expected to be at 578MMT versus 570MMT. However, US weather will be key factor in deciding the further trend for prices On palm front markets will be continue to take cues from external environment. However, fundamental would continue to provide much needed impetus for prices. On production front palm production has revived but the revival has been muted. However, tracking precipitation in both Indonesia & Malaysia looks like we are set to see bountiful recovery in 2H 2017 most likely from October onwards which would coincide with WWD (weak winter demand) However, BioD sector is getting the much needed attention with Brent Crude finding support from Hurricane we could see demand coming from BioD segment US Weather Tracker

46 KEY TAKEAWAYS World is all set to face the 4D effect & Global Growth has become too fragile & uncertain : 2017 was challenging year & 2018 will surpass the same in surprises Currency Volatility will continue & DXY will try to get its foothold as FED will be direction provider (rising debt will put FED on backfoot) Actual PAIN will be felt by Raw material exporting nations as global demand needs strong revival Health of Edible Oil & Oilseeds will be more driven by US Weather, Currency and Much Awaited Revival in Palm Oil Production

47 VUCA OUTLOOK THE Stone Age did not end for lack of stone, and the Oil Age will end long before the world runs out of oil. Sheikh Zaki Yamani

48 EL NINO front = FUGAZI in 2017 but will 2018 have La Nina??? BRENT Crude finally got much needed steam from HURRICANE-GEOPOLITICS-OPEC CUTS. Is it for to support listing??? Overall CRUDE with near term support could try $57-60$/bbl but will not sustain & loose it steam as market glut will pull down prices towards $48 initially followed by $45/bbl by Q DOLLAR under influence of FED rate decision will give much needed impetus to COMMODITIY PRICE CHINA BLACKBOX could be busted : will be bearish commodities price trend BioD market in dilema due to attack from US & EU on Arg & Indo BioD exports (just near term support but it will not hold good in long run) PALM market near term supported due to weak revival in Prodn, Slow stock build up & Festivity that will be until Mid OCT 17 could push prices towards 3000MYR/MT after which markets should correct in Q towards 2700 followed by 2400 MYR/MT until fraternity POC 2018

49 VUCA Thank You Disclaimer : Views shared in the paper are author s view and not to be considered as company s view or being endorsed by company which author represents.

Economic Outlook Economic Intelligence Center 27 th November 2015

Economic Outlook 2016 Economic Intelligence Center 27 th November 2015 Global outlook Domestic outlook 2 In 2016, recovery pace in most regions are expected to pick up except for China Eurozone 2.0 1.5

Economic Outlook 2016 Economic Intelligence Center 27 th November 2015 Global outlook Domestic outlook 2 In 2016, recovery pace in most regions are expected to pick up except for China Eurozone 2.0 1.5

Commercial Cards & Payments Leo Abruzzese October 2015 New York

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

US, China and emerging markets: What s next for the global economy? Commercial Cards & Payments Leo Abruzzese October 2015 New York Overview Key points for 2015-16 Global economy struggling to gain traction

Latin America: the shadow of China

Latin America: the shadow of China Juan Ruiz BBVA Research Chief Economist for South America Latin America Outlook Second Quarter Madrid, 13 May Latin America Outlook / May Key messages 1 2 3 4 5 The global

Latin America: the shadow of China Juan Ruiz BBVA Research Chief Economist for South America Latin America Outlook Second Quarter Madrid, 13 May Latin America Outlook / May Key messages 1 2 3 4 5 The global

B-GUIDE: Economic Outlook

Aug-12 Apr-13 Dec-13 Aug-14 Apr-15 Dec-15 Aug-16 Apr-17 Jul-15 Nov-15 Mar-16 Jul-16 Nov-16 Mar-17 Jul-17 Quarterly Economic Outlook: Quarter 4 2017 4 January 2018 B-GUIDE: Economic Outlook The economy

Aug-12 Apr-13 Dec-13 Aug-14 Apr-15 Dec-15 Aug-16 Apr-17 Jul-15 Nov-15 Mar-16 Jul-16 Nov-16 Mar-17 Jul-17 Quarterly Economic Outlook: Quarter 4 2017 4 January 2018 B-GUIDE: Economic Outlook The economy

Key developments and outlook

1/17 Key developments and outlook Economic growths in 2016 and 2017 remain close to the previous assessment. Better-than-expected merchandise exports and private consumption compensate for weaker-than-expected

1/17 Key developments and outlook Economic growths in 2016 and 2017 remain close to the previous assessment. Better-than-expected merchandise exports and private consumption compensate for weaker-than-expected

Global Economic Prospects and the Developing Countries William Shaw December 1999

Global Economic Prospects and the Developing Countries 2000 William Shaw December 1999 Prospects for Growth and Poverty Reduction in Developing Countries Recovery from financial crisis uneven International

Global Economic Prospects and the Developing Countries 2000 William Shaw December 1999 Prospects for Growth and Poverty Reduction in Developing Countries Recovery from financial crisis uneven International

Exports decline 4.7% during Rising rupee a concern for exporters

Exports decline 4.7% during 2009-10 Rising rupee a concern for exporters India s merchandise exports for the fiscal year 2009-10, declined by 4.7% from around US$ 184 billion at the end of 2008-09 to US$

Exports decline 4.7% during 2009-10 Rising rupee a concern for exporters India s merchandise exports for the fiscal year 2009-10, declined by 4.7% from around US$ 184 billion at the end of 2008-09 to US$

Monthly Update of the ASEAN+3 Regional Economic Outlook (AREO)

") Monthly Update of the ASEAN+3 Regional Economic Outlook (AREO) Special Edition ASEAN+3 Macroeconomic Research Office (AMRO) Singapore January 2018 This Monthly Update of the AREO was prepared by the Regional

Monthly Update of the ASEAN+3 Regional Economic Outlook (AREO) Special Edition ASEAN+3 Macroeconomic Research Office (AMRO) Singapore January 2018 This Monthly Update of the AREO was prepared by the Regional

SEPTEMBER Overview

Overview SEPTEMBER 214 Global growth. Global growth has been weaker than expected so far this year, as economic activity disappointed in a number of major countries in the first six months (Figure 1).

Overview SEPTEMBER 214 Global growth. Global growth has been weaker than expected so far this year, as economic activity disappointed in a number of major countries in the first six months (Figure 1).

GROWTH IN ASEAN SHOWS RESILIENCE UNDER GLOBAL LIQUIDITY INFUSION

May-1 Nov-1 May-1 Nov-1 THIS QUARTER IN ASIA Asian Business Cycle Indicators (ABCIs), Vol.11 April July 213 Source: OECD Development Centre GROWTH IN ASEAN SHOWS RESILIENCE UNDER GLOBAL LIQUIDITY INFUSION

May-1 Nov-1 May-1 Nov-1 THIS QUARTER IN ASIA Asian Business Cycle Indicators (ABCIs), Vol.11 April July 213 Source: OECD Development Centre GROWTH IN ASEAN SHOWS RESILIENCE UNDER GLOBAL LIQUIDITY INFUSION

Improved Macroeconomic Conditions Boost Consumer Sentiment to Its Highest Level in 3½-Year

ECONOMIC REPORT Business & Consumer Confidence 17 April 2018 Improved Macroeconomic Conditions Boost Consumer Sentiment to Its Highest Level in 3½-Year MIER s CSI rebounded to 3.5-year high. Underpin by

ECONOMIC REPORT Business & Consumer Confidence 17 April 2018 Improved Macroeconomic Conditions Boost Consumer Sentiment to Its Highest Level in 3½-Year MIER s CSI rebounded to 3.5-year high. Underpin by

Global Equites declined from Concern over Trade War

Quarterly Market Outlook: Quarter 2 2018 on 3 April 2018 Global Equites declined from Concern over Trade War Investment Outlook for 2 nd Quarter 2018 Equity Thailand U.S. Europe Japan Asia Bond Thailand

Quarterly Market Outlook: Quarter 2 2018 on 3 April 2018 Global Equites declined from Concern over Trade War Investment Outlook for 2 nd Quarter 2018 Equity Thailand U.S. Europe Japan Asia Bond Thailand

Global Economic Prospects: Navigating strong currents

Global Economic Prospects: Navigating strong currents Andrew Burns World Bank January 18, 2011 http://www.worldbank.org/globaloutlook Main messages Most developing countries have passed with flying colors

Global Economic Prospects: Navigating strong currents Andrew Burns World Bank January 18, 2011 http://www.worldbank.org/globaloutlook Main messages Most developing countries have passed with flying colors

Finally, A Global Tailwind for U.S. Manufacturing Growth

Finally, A Global Tailwind for U.S. Manufacturing Growth MAPI Foundation Webinar December 12, 217 Cliff Waldman Chief Economist cwaldman@mapi.net Key Takeaways The global economic recovery is both strengthening

Finally, A Global Tailwind for U.S. Manufacturing Growth MAPI Foundation Webinar December 12, 217 Cliff Waldman Chief Economist cwaldman@mapi.net Key Takeaways The global economic recovery is both strengthening

Quarterly Economic Outlook: Quarter on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

Foregin Direct Investment (Billion USD) China U.S. Asia World Quarterly Economic Outlook: Quarter 3 2018 on 25 September 2018 Strong Economic Expansions amidst Uncertainty of Trade War Thai Economy: Thai

PURSUING SHARED PROSPERITY IN AN ERA OF TURBULENCE AND HIGH COMMODITY PRICES

2012 Key messages Asia-Pacific growth to slow in 2012 amidst global turbulence: Spillovers of the euro zone turmoil Global oil price hikes Excess liquidity and volatile capital flows Key long-term challenge:

2012 Key messages Asia-Pacific growth to slow in 2012 amidst global turbulence: Spillovers of the euro zone turmoil Global oil price hikes Excess liquidity and volatile capital flows Key long-term challenge:

Advanced and Emerging Economies Two speed Recovery

Advanced and Emerging Economies Two speed Recovery 23 November 2 Bauhinia Foundation Research Centre Masaaki Shirakawa Governor of the Bank of Japan Slide 1 Japan s Silver Yen and Hong Kong s Silver Yuan

Advanced and Emerging Economies Two speed Recovery 23 November 2 Bauhinia Foundation Research Centre Masaaki Shirakawa Governor of the Bank of Japan Slide 1 Japan s Silver Yen and Hong Kong s Silver Yuan

GLOBAL MARKET OUTLOOK

GLOBAL MARKET OUTLOOK Max Darnell, Managing Partner, Chief Investment Officer All material has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. performance is no

GLOBAL MARKET OUTLOOK Max Darnell, Managing Partner, Chief Investment Officer All material has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. performance is no

Asian Insights Third quarter 2016 Asia s commitment in policies and reforms

Asian Insights Third quarter 2016 Asia s commitment in policies and reforms One of the commonalities between most Asian governments is the dedicated commitment they have in using policies and initiatives

Asian Insights Third quarter 2016 Asia s commitment in policies and reforms One of the commonalities between most Asian governments is the dedicated commitment they have in using policies and initiatives

Russia: Macro Outlook for 2019

October 2018 Russia: Macro Outlook for 2019 Natalia Orlova Head of Alfa Bank Macro Insights +7 495 795 36 77 norlova@alfabank.ru Egypt Saudi Arabia Brazil S. Africa UAE Iraq China Japan US Mexico UK Russia

October 2018 Russia: Macro Outlook for 2019 Natalia Orlova Head of Alfa Bank Macro Insights +7 495 795 36 77 norlova@alfabank.ru Egypt Saudi Arabia Brazil S. Africa UAE Iraq China Japan US Mexico UK Russia

Monthly Economic Insight

Monthly Economic Insight Prepared by : TMB Analytics Date: 22 February 2018 Executive Summary Synchronized global economic growth continued to brighten global economic outlook and global trade outlook.

Monthly Economic Insight Prepared by : TMB Analytics Date: 22 February 2018 Executive Summary Synchronized global economic growth continued to brighten global economic outlook and global trade outlook.

The real change in private inventories added 0.15 percentage points to the second quarter GDP growth, after subtracting 0.65% in the first quarter.

QIRGRETA Monthly Macroeconomic Commentary United States The U.S. economy rebounded in the second quarter of 2007, growing at an annual rate of 3.4% Q/Q (+1.8% Y/Y), according to the GDP advance estimates

QIRGRETA Monthly Macroeconomic Commentary United States The U.S. economy rebounded in the second quarter of 2007, growing at an annual rate of 3.4% Q/Q (+1.8% Y/Y), according to the GDP advance estimates

Trade Balance (LHS) Exports (RHS) Imports (RHS)

Exports (RHS) Imports (RHS)") 14,000 RM Million % change y-o-y 50.0 12,000 40.0 10,000 30.0 8,000 20.0 6,000 10.0 4,000 0.0 2,000 (10.0) 0 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16

14,000 RM Million % change y-o-y 50.0 12,000 40.0 10,000 30.0 8,000 20.0 6,000 10.0 4,000 0.0 2,000 (10.0) 0 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16

Themes in bond investing

For professional investors only Not for public distribution Themes in bond investing June Asia 2011 2009 outlook Introduction Asian markets enjoyed a Goldilocks economic scenario in 2010 that helped them

For professional investors only Not for public distribution Themes in bond investing June Asia 2011 2009 outlook Introduction Asian markets enjoyed a Goldilocks economic scenario in 2010 that helped them

World Economy Geopolitics Investment Strategy. The Impact of EU s Sovereign Risks on Turkish Economy. Presentation given by

World Economy Geopolitics Investment Strategy OUTLOOK FOR WORLD S MAJOR FINANCIAL MARKETS The Impact of EU s Sovereign Risks on Turkish Economy Presentation given by Dr. Michael Ivanovitch, President MSI

World Economy Geopolitics Investment Strategy OUTLOOK FOR WORLD S MAJOR FINANCIAL MARKETS The Impact of EU s Sovereign Risks on Turkish Economy Presentation given by Dr. Michael Ivanovitch, President MSI

ECONOMIC OUTLOOK FINALLY, SYNCHRONIZED GLOBAL GROWTH

ECONOMIC OUTLOOK FINALLY, SYNCHRONIZED GLOBAL GROWTH Augustine Faucher Chief Economist November 13, 2017 Senior Economic Advisor Chief Economist BETTER GROWTH THIS YEAR, AND AN UPGRADE TO 2018 World output,

ECONOMIC OUTLOOK FINALLY, SYNCHRONIZED GLOBAL GROWTH Augustine Faucher Chief Economist November 13, 2017 Senior Economic Advisor Chief Economist BETTER GROWTH THIS YEAR, AND AN UPGRADE TO 2018 World output,

Otaviano Canuto Vice President & Head of Network Poverty Reduction and Economic Management The World Bank

Otaviano Canuto Vice President & Head of Network Poverty Reduction and Economic Management The World Bank The 11th International Academic Conference on Economic and Social Development April 6-8, 2010 Moscow

Otaviano Canuto Vice President & Head of Network Poverty Reduction and Economic Management The World Bank The 11th International Academic Conference on Economic and Social Development April 6-8, 2010 Moscow

Bualuang Exclusive Investment Outlook. March 2017

Bualuang Exclusive Investment Outlook March 2017 1 Theme: Trump support global equities Positive Risk Many countries return to stimulate economies. Many government will increase spending and support economy.

Bualuang Exclusive Investment Outlook March 2017 1 Theme: Trump support global equities Positive Risk Many countries return to stimulate economies. Many government will increase spending and support economy.

B-GUIDE: Market Outlook

Quarterly Market Outlook: Quarter 1 2018 on 5 th January 2018 Investment Outlook for 1 st Quarter 2018 Accelerating Global Economy Supports the Rising Earnings Equity Thailand US Europe Japan Asia Bond

Quarterly Market Outlook: Quarter 1 2018 on 5 th January 2018 Investment Outlook for 1 st Quarter 2018 Accelerating Global Economy Supports the Rising Earnings Equity Thailand US Europe Japan Asia Bond

Key Economic Challenges in Japan and Asia. Changyong Rhee IMF Asia and Pacific Department February

Key Economic Challenges in Japan and Asia Changyong Rhee IMF Asia and Pacific Department February 2017 1 Global and Asia Outlook 2 Global activity strengthening, with rising dispersion and uncertainty

Key Economic Challenges in Japan and Asia Changyong Rhee IMF Asia and Pacific Department February 2017 1 Global and Asia Outlook 2 Global activity strengthening, with rising dispersion and uncertainty

LATIN AMERICA OUTLOOK 4Q2016 OUTLOOK LATIN AMERICA. 4th QUARTER 2016

LATIN AMERICA OUTLOOK 4Q OUTLOOK LATIN AMERICA 4th QUARTER LATIN AMERICA OUTLOOK 4Q Main messages The global economy is heading for a slow recovery. Global GDP growth will improve slightly from the second

LATIN AMERICA OUTLOOK 4Q OUTLOOK LATIN AMERICA 4th QUARTER LATIN AMERICA OUTLOOK 4Q Main messages The global economy is heading for a slow recovery. Global GDP growth will improve slightly from the second

Emerging Global Challenges and implications for Indonesia

Emerging Global Challenges and implications for Indonesia Muhammad Chatib Basri Harvard Kennedy School and University of Indonesia Short term problems: macroeconomic stability 2 The macroeconomic impact

Emerging Global Challenges and implications for Indonesia Muhammad Chatib Basri Harvard Kennedy School and University of Indonesia Short term problems: macroeconomic stability 2 The macroeconomic impact

THIS QUARTER IN ASIA ASEAN SHOWING RESILIENCE WHILE CHINA AND INDIA WEAKENING

Apr-9 Oct-9 Apr-1 Oct-1 Apr-9 Oct-9 Apr-1 Oct-1 THIS QUARTER IN ASIA Asian Business Cycle Indicators (ABCIs), Vol.8 April June 212 Source: OECD Development Centre ASEAN SHOWING RESILIENCE WHILE CHINA AND

Apr-9 Oct-9 Apr-1 Oct-1 Apr-9 Oct-9 Apr-1 Oct-1 THIS QUARTER IN ASIA Asian Business Cycle Indicators (ABCIs), Vol.8 April June 212 Source: OECD Development Centre ASEAN SHOWING RESILIENCE WHILE CHINA AND

Economic Outlook: Global and India. Ajit Ranade IEEMA T & D Conclave December 12, 2014

Economic Outlook: Global and India Ajit Ranade IEEMA T & D Conclave December 12, 2014 Global scenario US expected to drive global growth in 2015 Difference from % YoY Growth October Actual October Projections

Economic Outlook: Global and India Ajit Ranade IEEMA T & D Conclave December 12, 2014 Global scenario US expected to drive global growth in 2015 Difference from % YoY Growth October Actual October Projections

Malaysia s export growth at record high in 2017

Dr. Mohd Afzanizam Abdul Rashid Chief Economist 03-2088 8075 afzanizam@bankislam.com.my Malaysia s export growth at record high in 2017 Facts Total exports in 2017 grew by 18.9% (2016: 1.2%) to RM935.4

Dr. Mohd Afzanizam Abdul Rashid Chief Economist 03-2088 8075 afzanizam@bankislam.com.my Malaysia s export growth at record high in 2017 Facts Total exports in 2017 grew by 18.9% (2016: 1.2%) to RM935.4

2008 CRISIS : COLD OR CANCER?

2008 CRISIS : COLD OR CANCER? MARTIAL FOUCAULT Université de Montréal 28 juin 2010 1 Plan of the talk Crisis: what does it mean? The American financial crisis followed by a worldwide economic crisis Market

2008 CRISIS : COLD OR CANCER? MARTIAL FOUCAULT Université de Montréal 28 juin 2010 1 Plan of the talk Crisis: what does it mean? The American financial crisis followed by a worldwide economic crisis Market

Global Markets Group. Trade Performance: Depressed by the Eid holiday Author: Juniman Chief Economist. Economic Research. Trade Outlook Monthly Report

Global Markets Group Trade Outlook Monthly Report Economic Research August 2016 Trade Performance: Depressed by the Eid holiday Author: Juniman Chief Economist Trade Highlights Exports in June 2016 rose

Global Markets Group Trade Outlook Monthly Report Economic Research August 2016 Trade Performance: Depressed by the Eid holiday Author: Juniman Chief Economist Trade Highlights Exports in June 2016 rose

Indonesia Economic Quarterly: October 2012 Maintaining resilience

Indonesia Economic Quarterly: October 1 Maintaining resilience Ndiame Diop Lead Economist & Economic Advisor, Indonesia World Bank October 15, 1 Paramadina Public Policy Institute www.worldbank.org/id

Indonesia Economic Quarterly: October 1 Maintaining resilience Ndiame Diop Lead Economist & Economic Advisor, Indonesia World Bank October 15, 1 Paramadina Public Policy Institute www.worldbank.org/id

11 May Energy Coal

11 May 217 Energy Coal Energy coal: dislocation from fundamentals Size of the Asia Pacific market 2 Energy Coal Market Volumes by Basin (Million Tonnes) 1, 9 8 7 6 5 4 3 2 1 The Asia-Pacific market is

11 May 217 Energy Coal Energy coal: dislocation from fundamentals Size of the Asia Pacific market 2 Energy Coal Market Volumes by Basin (Million Tonnes) 1, 9 8 7 6 5 4 3 2 1 The Asia-Pacific market is

GLOBAL FIXED INCOME OVERVIEW

2016 Global Market Outlook Press Briefing GLOBAL FIXED INCOME OVERVIEW Edward A. Wiese, CFA, Head of Fixed Income November 18, 2015 Global Fixed Income Outlook: Summary Environment Developed market yields

2016 Global Market Outlook Press Briefing GLOBAL FIXED INCOME OVERVIEW Edward A. Wiese, CFA, Head of Fixed Income November 18, 2015 Global Fixed Income Outlook: Summary Environment Developed market yields

Summary. Economic Update 1 / 7 May Global Global GDP growth is forecast to accelerate to 2.9% in 2017 and maintain at 3.0% in 2018.

Economic Update Economic Update 1 / 7 Summary 2 Global Global GDP growth is forecast to accelerate to 2.9% in 2017 and maintain at 3.0% in 2018. 3 Eurozone The eurozone s recovery appears to strengthen

Economic Update Economic Update 1 / 7 Summary 2 Global Global GDP growth is forecast to accelerate to 2.9% in 2017 and maintain at 3.0% in 2018. 3 Eurozone The eurozone s recovery appears to strengthen

RECENT EVOLUTION AND OUTLOOK OF THE MEXICAN ECONOMY BANCO DE MÉXICO OCTOBER 2003

OCTOBER 23 RECENT EVOLUTION AND OUTLOOK OF THE MEXICAN ECONOMY BANCO DE MÉXICO 2 RECENT DEVELOPMENTS OUTLOOK MEDIUM-TERM CHALLENGES 3 RECENT DEVELOPMENTS In tandem with the global economic cycle, the Mexican

OCTOBER 23 RECENT EVOLUTION AND OUTLOOK OF THE MEXICAN ECONOMY BANCO DE MÉXICO 2 RECENT DEVELOPMENTS OUTLOOK MEDIUM-TERM CHALLENGES 3 RECENT DEVELOPMENTS In tandem with the global economic cycle, the Mexican

Chapter 1 International economy

Chapter International economy. Main points from the OECD's Economic Outlook A broad-based recovery has taken hold Asia, the US and the UK have taken the lead. Continental Europe will follow Investment

Chapter International economy. Main points from the OECD's Economic Outlook A broad-based recovery has taken hold Asia, the US and the UK have taken the lead. Continental Europe will follow Investment

BNM Maintains OPR at 3.25%, Hawkish About Economic Outlook

7 March 2018 ECONOMIC REVIEW March 2018 BNM MPC BNM Maintains OPR at 3.25%, Hawkish About Economic Outlook Overnight Policy Rate maintained at 3.25%. In line with our expectation, overnight policy rate,

7 March 2018 ECONOMIC REVIEW March 2018 BNM MPC BNM Maintains OPR at 3.25%, Hawkish About Economic Outlook Overnight Policy Rate maintained at 3.25%. In line with our expectation, overnight policy rate,

Indonesia Economic Quarterly, July 2014 Hard choices. Ndiamé Diop Lead Economist

Indonesia Economic Quarterly, July 214 Hard choices Ndiamé Diop Lead Economist The new administration will face major near-term challenges Fiscal pressures Economic growth Poverty and inequality reduction

Indonesia Economic Quarterly, July 214 Hard choices Ndiamé Diop Lead Economist The new administration will face major near-term challenges Fiscal pressures Economic growth Poverty and inequality reduction

KINDLY REFER TO THE LAST PAGE OF THIS PUBLICATION FOR IMPORTANT DISCLOSURES

1 June 2017 MONTHLY ECONOMIC REVIEW May 2017 Malaysia Economy Riding High in 1Q17 Leading index recorded the highest in two years. In March 2017, leading index grew by 1.8%yoy, the highest since March

1 June 2017 MONTHLY ECONOMIC REVIEW May 2017 Malaysia Economy Riding High in 1Q17 Leading index recorded the highest in two years. In March 2017, leading index grew by 1.8%yoy, the highest since March

Oct-Dec st Preliminary GDP Estimate

Japan's Economy 15 February 2016 (No. of pages: 5) Japanese report: 15 Feb 2016 Oct-Dec 2015 1 st Preliminary GDP Estimate GDP experiences negative growth for first time in two quarters hinting at risk

Japan's Economy 15 February 2016 (No. of pages: 5) Japanese report: 15 Feb 2016 Oct-Dec 2015 1 st Preliminary GDP Estimate GDP experiences negative growth for first time in two quarters hinting at risk

The real change in private inventories added 0.22 percentage points to the second quarter GDP growth, after subtracting 0.65% in the first quarter.

QIRGRETA Monthly Macroeconomic Commentary United States The U.S. economy bounced back in the second quarter of 2007, growing at the fastest pace in more than a year. According the final estimates released

QIRGRETA Monthly Macroeconomic Commentary United States The U.S. economy bounced back in the second quarter of 2007, growing at the fastest pace in more than a year. According the final estimates released

Macroeconomic Outlook: Implications for Agriculture. It has been 26 years since we have experienced a significant recession

Macroeconomic Outlook: Implications for Agriculture John B. Penson, Jr. Regents Professor and Stiles Professor of Agriculture Texas A&M University Our Recession History September 1902 August1904 23 May

Macroeconomic Outlook: Implications for Agriculture John B. Penson, Jr. Regents Professor and Stiles Professor of Agriculture Texas A&M University Our Recession History September 1902 August1904 23 May

Ferrochrome Market Overview 2017

Ferrochrome Market Overview 217 Presented by: Mark Beveridge Principal Consultant CRU Nickel, Chrome, Stainless Steel Group Key Themes Which factors define the chrome market? 1. Chinese demand and the

Ferrochrome Market Overview 217 Presented by: Mark Beveridge Principal Consultant CRU Nickel, Chrome, Stainless Steel Group Key Themes Which factors define the chrome market? 1. Chinese demand and the

Mexico: Dealing with international financial uncertainty. Manuel Sánchez

Manuel Sánchez United States Mexico Chamber of Commerce, Chicago, IL, August 6, 2015 Contents 1 Moderate economic growth 2 Waiting for the liftoff 3 Taming inflation 2 Since 2014, Mexico s economic recovery

Manuel Sánchez United States Mexico Chamber of Commerce, Chicago, IL, August 6, 2015 Contents 1 Moderate economic growth 2 Waiting for the liftoff 3 Taming inflation 2 Since 2014, Mexico s economic recovery

Power of Travel Promotion Evolution

Power of Travel Promotion Evolution Promotion More Important than Ever Power of Promotion $7 million Median state = marketing budget FY 2014-15 OR 45 seconds worth of Super Bowl ads $100 million = Presidential

Power of Travel Promotion Evolution Promotion More Important than Ever Power of Promotion $7 million Median state = marketing budget FY 2014-15 OR 45 seconds worth of Super Bowl ads $100 million = Presidential

All the BRICs dampening world trade in 2015

Aug Weekly Economic Briefing Emerging Markets All the BRICs dampening world trade in World trade in has been hit by an unexpectedly sharp drag from the very largest emerging economies. The weakness in

Aug Weekly Economic Briefing Emerging Markets All the BRICs dampening world trade in World trade in has been hit by an unexpectedly sharp drag from the very largest emerging economies. The weakness in

Jan-Mar nd Preliminary GDP Estimate

Japan's Economy 8 June 2016 (No. of pages: 5) Japanese report: 08 Jun 2016 Jan-Mar 2016 2 nd Preliminary GDP Estimate Real GDP growth rate revised upwards slightly from 1 st preliminary; results in accordance

Japan's Economy 8 June 2016 (No. of pages: 5) Japanese report: 08 Jun 2016 Jan-Mar 2016 2 nd Preliminary GDP Estimate Real GDP growth rate revised upwards slightly from 1 st preliminary; results in accordance

Emerging Markets Weekly Economic Briefing

Emerging Markets Weekly Economic Briefing The risks of renewed capital flight from emerging markets Recent episodes of capital flight from emerging markets have highlighted the vulnerability of a number

Emerging Markets Weekly Economic Briefing The risks of renewed capital flight from emerging markets Recent episodes of capital flight from emerging markets have highlighted the vulnerability of a number

FY2017, FY2018, FY2019 Economic Outlook - Firm outlook on both domestic and overseas economic growth remains unchanged -

REVISED to reflect the 2 nd QE for the Oct-Dec Qtr of 2017 FY2017, FY2018, FY2019 Economic Outlook - Firm outlook on both domestic and overseas economic growth remains unchanged - March 8, 2018 Copyright

REVISED to reflect the 2 nd QE for the Oct-Dec Qtr of 2017 FY2017, FY2018, FY2019 Economic Outlook - Firm outlook on both domestic and overseas economic growth remains unchanged - March 8, 2018 Copyright

Inflation Remains Tepid in November at 0.2% as Transport Cost Trending Downward

19 December 2018 ECONOMIC REVIEW November 2018 Consumer Price Index Inflation Remains Tepid in November at 0.2% as Transport Cost Trending Downward Headline inflation back to near 4-year low. Consumer

19 December 2018 ECONOMIC REVIEW November 2018 Consumer Price Index Inflation Remains Tepid in November at 0.2% as Transport Cost Trending Downward Headline inflation back to near 4-year low. Consumer

ASIAN ECONOMIES. Economics, interest rates and currencies chart pack

ASIAN ECONOMIES Economics, interest rates and currencies chart pack Amy Auster Senior Economist Melbourne 2 May 25 E-mail: austera@anz.com Internet: http://www.anz.com/go/economics 1 Major revisions to

ASIAN ECONOMIES Economics, interest rates and currencies chart pack Amy Auster Senior Economist Melbourne 2 May 25 E-mail: austera@anz.com Internet: http://www.anz.com/go/economics 1 Major revisions to

APPENDIX ECONOMIC INDICATORS DEVELOPED ECONOMIES

16 QUARTERLY INVESTMENT STRATEGY APPENDIX ECONOMIC INDICATORS DEVELOPED ECONOMIES Purchasing Managers Index EMERGING ECONOMIES Purchasing Managers Index US Eurozone Japan Brazil Russia India China Industrial

16 QUARTERLY INVESTMENT STRATEGY APPENDIX ECONOMIC INDICATORS DEVELOPED ECONOMIES Purchasing Managers Index EMERGING ECONOMIES Purchasing Managers Index US Eurozone Japan Brazil Russia India China Industrial

Snapshot of SA Economy

Snapshot of SA Economy Kgotso Radira 1 September 29 Economic Outlook Global share indices 2 Indices 18 16 14 12 1 8 6 4 25 26 27 28 29 S&P 5 FTSE 1 DAX Nikkei 3 Global interest rates 7 % 6 5 4 3 2 1 1999

Snapshot of SA Economy Kgotso Radira 1 September 29 Economic Outlook Global share indices 2 Indices 18 16 14 12 1 8 6 4 25 26 27 28 29 S&P 5 FTSE 1 DAX Nikkei 3 Global interest rates 7 % 6 5 4 3 2 1 1999

KBank Capital Markets Perspectives 29 February 2016

KBank Capital Markets Perspectives 29 February 2016 Thailand Economic Monitor and BoT Forecast : March 2016 Thailand s economy steadied in February, though domestic demand decelerated slightly from January

KBank Capital Markets Perspectives 29 February 2016 Thailand Economic Monitor and BoT Forecast : March 2016 Thailand s economy steadied in February, though domestic demand decelerated slightly from January

Review of Natural Rubber Market during the Year 2007 and the Outlook for the Short and Medium Terms

Review of Natural Rubber Market during the Year 2007 and the Outlook for the Short and Medium Terms This report is organized into three sections. Section 1 examines the trends in NR prices from January

Review of Natural Rubber Market during the Year 2007 and the Outlook for the Short and Medium Terms This report is organized into three sections. Section 1 examines the trends in NR prices from January

The Internationalisation of the Renminbi

Tel: (852)3550-7070; Fax: (852)2104-6938 Email: lawrence@lawrencejlau.hk; WebPages: www.igef.cuhk.edu.hk/ljl *All opinions expressed herein are the author s own and do not necessarily reflect the views

Tel: (852)3550-7070; Fax: (852)2104-6938 Email: lawrence@lawrencejlau.hk; WebPages: www.igef.cuhk.edu.hk/ljl *All opinions expressed herein are the author s own and do not necessarily reflect the views

North American Steel Industry Recent Market Developments, Future Prospects and Key Challenges

North American Steel Industry Recent Market Developments, Future Prospects and Key Challenges OECD Steel Committee December 1-11, 29 Paris, France * American Iron and Steel Institute (AISI) Steel Manufacturers

North American Steel Industry Recent Market Developments, Future Prospects and Key Challenges OECD Steel Committee December 1-11, 29 Paris, France * American Iron and Steel Institute (AISI) Steel Manufacturers

INVESTMENT MARKET UPDATE UBC FACULTY PENSION PLAN

INVESTMENT MARKET UPDATE UBC FACULTY PENSION PLAN MIKE LESLIE, FACULTY PENSION PLAN NEIL WATSON, LEITH WHEELER FEBRUARY 12, 2014 Presenters Mike Leslie Executive Director, Investments Faculty Pension Plan

INVESTMENT MARKET UPDATE UBC FACULTY PENSION PLAN MIKE LESLIE, FACULTY PENSION PLAN NEIL WATSON, LEITH WHEELER FEBRUARY 12, 2014 Presenters Mike Leslie Executive Director, Investments Faculty Pension Plan

Equity Market Outlook. May, 2016

Equity Market Outlook May, 2016 Global Economy Update Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 Global Central Bank Monetary Policies

Equity Market Outlook May, 2016 Global Economy Update Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16 Apr-16 Global Central Bank Monetary Policies

Global Economic Prospects

Global Economic Prospects Assuring growth over the medium term Andrew Burns DEC Prospects Group January 213 1 Despite better financial conditions, stronger growth remains elusive More than 4 years after

Global Economic Prospects Assuring growth over the medium term Andrew Burns DEC Prospects Group January 213 1 Despite better financial conditions, stronger growth remains elusive More than 4 years after

Turkey Macroeconomic Outlook

June 2011 The study analyzes the macroeconomic scenario in Turkey and its effect on the investment prospects. We believe domestic consumption will be strong and the core driver of growth in this new era.

June 2011 The study analyzes the macroeconomic scenario in Turkey and its effect on the investment prospects. We believe domestic consumption will be strong and the core driver of growth in this new era.

Peru Outlook Third quarter July 2017

Peru Outlook Third quarter 2017 July 2017 Summary 1 We project low growth this year with a rebound in 2018, driven by reconstruction and infrastructure spending 2 Fiscal policy: the institutional framework

Peru Outlook Third quarter 2017 July 2017 Summary 1 We project low growth this year with a rebound in 2018, driven by reconstruction and infrastructure spending 2 Fiscal policy: the institutional framework

Chikahisa Sumi Director, Regional Office for Asia and the Pacific International Monetary Fund

Chikahisa Sumi Director, Regional Office for Asia and the Pacific International Monetary Fund (percent YOY) 8 6 Real GDP Growth ASSUMPTIONS A more gradual monetary policy normalization 4 2 21 211 212

Chikahisa Sumi Director, Regional Office for Asia and the Pacific International Monetary Fund (percent YOY) 8 6 Real GDP Growth ASSUMPTIONS A more gradual monetary policy normalization 4 2 21 211 212

(0.7) (17.0) (11.0) (21.7) (20.0) (21.2) 5.5 (14.7) (17.3) (7.6) (14.5) (19.2) 1Y Rtn (12/31/10-12/30/11)

(17.0) (11.0) (21.7) (20.0) (21.2) 5.5 (14.7) (17.3) (7.6) (14.5) (19.2) 1Y Rtn (12/31/10-12/30/11)") Research Division Monthly Unit Trust Review AMB Dec 2011:The MUTI continues expansion albeit slumps in the stock markets TABLE 1: MAJOR & REGIONAL INDICES AS AT 30 DECEMBER 2011 Index Points % MOM % YOY

Research Division Monthly Unit Trust Review AMB Dec 2011:The MUTI continues expansion albeit slumps in the stock markets TABLE 1: MAJOR & REGIONAL INDICES AS AT 30 DECEMBER 2011 Index Points % MOM % YOY

Commodities Forecast Update Weakness awaits rest of 2014

Investment Research 15 October 2014 2014 Commodities Forecast Update Weakness awaits rest of 2014 Key themes Oil A markedly stronger dollar and concerns about the outlook have weighed on demand for commodities

Investment Research 15 October 2014 2014 Commodities Forecast Update Weakness awaits rest of 2014 Key themes Oil A markedly stronger dollar and concerns about the outlook have weighed on demand for commodities

World Bank Thailand Economic Monitor November Press Launch November 4, 2009

World Bank Thailand Economic Monitor November 2009 Press Launch November 4, 2009 overview The Thai economy is rebounding from a rocky first half of 2009, but the medium-term outlook is uncertain. The Thai

World Bank Thailand Economic Monitor November 2009 Press Launch November 4, 2009 overview The Thai economy is rebounding from a rocky first half of 2009, but the medium-term outlook is uncertain. The Thai

After the Rate Increase, What Then?

After the Rate Increase, What Then? Robert Eisenbeis, Ph.D. Vice Chairman & Chief Monetary Economist Bob.Eisenbeis@Cumber.com What the FOMC Did At Dec Meeting The Fed made the first step towards normalization

After the Rate Increase, What Then? Robert Eisenbeis, Ph.D. Vice Chairman & Chief Monetary Economist Bob.Eisenbeis@Cumber.com What the FOMC Did At Dec Meeting The Fed made the first step towards normalization

Japan s Economy: Monthly Review

Japan's Economy 18 July 214 (No. of pages: 8) Japanese report: 18 Jul 214 Japan s Economy: Monthly Review China s shadow banking problem requires continued monitoring Economic Intelligence Team Mitsumaru

Japan's Economy 18 July 214 (No. of pages: 8) Japanese report: 18 Jul 214 Japan s Economy: Monthly Review China s shadow banking problem requires continued monitoring Economic Intelligence Team Mitsumaru

Developing Asia s Short-Run Economic Outlook and Main Risks

Developing Asia s Short-Run Economic Outlook and Main Risks Dr. Donghyun Park, Asian Development Bank Workshop on Bond Market Development in Emerging East Asia Raffles Hotel Le Royal Phnom Penh, Cambodia,

Developing Asia s Short-Run Economic Outlook and Main Risks Dr. Donghyun Park, Asian Development Bank Workshop on Bond Market Development in Emerging East Asia Raffles Hotel Le Royal Phnom Penh, Cambodia,

Investor Presentation. December 2013

Investor Presentation December 2013 24.02.2014 Table of Contents 1. Thai economy 2. Strengthening bank and client base 3. BBL s financial results Thai economy in 2014-2015 Thailand is facing short-term

Investor Presentation December 2013 24.02.2014 Table of Contents 1. Thai economy 2. Strengthening bank and client base 3. BBL s financial results Thai economy in 2014-2015 Thailand is facing short-term

Global Economic Prospects

Global Economic Prospects Back from the Brink? Andrew Burns World Bank Prospects Group April 12, 212 1 Amid some signs of improvement, global recovery remains fragile First quarter of 212 has been generally

Global Economic Prospects Back from the Brink? Andrew Burns World Bank Prospects Group April 12, 212 1 Amid some signs of improvement, global recovery remains fragile First quarter of 212 has been generally

PART 1. recent trends and developments

PART 1 recent trends and developments 1 REGIONAL OVERVIEW OF MERCHANDISE TRADE A. A RETURN TO TRADE CONTRACTION The sluggish growth in developed economies and uncertainty linked to the European economic

PART 1 recent trends and developments 1 REGIONAL OVERVIEW OF MERCHANDISE TRADE A. A RETURN TO TRADE CONTRACTION The sluggish growth in developed economies and uncertainty linked to the European economic

Can Emerging Economies Decouple?

Can Emerging Economies Decouple? M. Ayhan Kose Research Department International Monetary Fund akose@imf.org April 2, 2008 This talk is primarily based on the following sources IMF World Economic Outlook

Can Emerging Economies Decouple? M. Ayhan Kose Research Department International Monetary Fund akose@imf.org April 2, 2008 This talk is primarily based on the following sources IMF World Economic Outlook

Global Economics Monthly Review

Global Economics Monthly Review January 8 th, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Please see important disclaimer on the last page of this report 1 Key Issues Global

Global Economics Monthly Review January 8 th, 2018 Arie Tal, Research Economist The Finance Division, Economics Department Please see important disclaimer on the last page of this report 1 Key Issues Global

HKU announces 2015 Q2 HK Macroeconomic Forecast

Press Release HKU announces 2015 Q2 HK Macroeconomic Forecast April 9, 2015 1 Overview The APEC Studies Programme of the Hong Kong Institute of Economics and Business Strategy at the University of Hong

Press Release HKU announces 2015 Q2 HK Macroeconomic Forecast April 9, 2015 1 Overview The APEC Studies Programme of the Hong Kong Institute of Economics and Business Strategy at the University of Hong

Managing Global Shocks: The Case of Indonesia

Managing Global Shocks: The Case of Indonesia Dr. Hartadi A. Sarwono Deputy Governor IIF Asian Regional Economic Forum Singapore, March 5, 2009 Outline 2 1. Crisis highlights 2. Macroconomic Condition

Managing Global Shocks: The Case of Indonesia Dr. Hartadi A. Sarwono Deputy Governor IIF Asian Regional Economic Forum Singapore, March 5, 2009 Outline 2 1. Crisis highlights 2. Macroconomic Condition

China Economic Outlook 2018 Feb 13, 2018

Feb 13, Key Developments in Brief Economic Development Drivers of Growth Risks Predicted GDP growth of 6.5% in In 2017 growth exceeded the official target Service and modern production grow faster than

Feb 13, Key Developments in Brief Economic Development Drivers of Growth Risks Predicted GDP growth of 6.5% in In 2017 growth exceeded the official target Service and modern production grow faster than

The World Economic & Financial System: Risks & Prospects

The World Economic & Financial System: Risks & Prospects Dr. Jacob A. Frenkel Chairman & CEO Group of Thirty (G30).Bank Indonesia 7th Annual International Seminar Global Financial Tsunami: What Can We

The World Economic & Financial System: Risks & Prospects Dr. Jacob A. Frenkel Chairman & CEO Group of Thirty (G30).Bank Indonesia 7th Annual International Seminar Global Financial Tsunami: What Can We

Mexican Q1 economic data: a reality shock, or there is still a brighter outlook?

Mexican Q1 economic data: a reality shock, or there is still a brighter outlook? Rafael Amiel, Director Latin America Economics IHS Global Insight Julio 2013 Mexico becomes fashionable again Mexico Makes

Mexican Q1 economic data: a reality shock, or there is still a brighter outlook? Rafael Amiel, Director Latin America Economics IHS Global Insight Julio 2013 Mexico becomes fashionable again Mexico Makes

World Sugar Market Outlook

World Sugar Market Outlook 28 th of September 216 Platts conference New Delhi Benoît Boisleux 1 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16

World Sugar Market Outlook 28 th of September 216 Platts conference New Delhi Benoît Boisleux 1 Jan-15 Feb-15 Mar-15 Apr-15 May-15 Jun-15 Jul-15 Aug-15 Sep-15 Oct-15 Nov-15 Dec-15 Jan-16 Feb-16 Mar-16

INFLATION REPORT. March Recent trends and macroeconomic forecasts

INFLATION REPORT March 2016 Recent trends and macroeconomic forecasts 2016-2017 INFLATION REPORT: Recent trends and macroeconomic forecasts 2016-2017 March 2016 International environment Public Monetary

INFLATION REPORT March 2016 Recent trends and macroeconomic forecasts 2016-2017 INFLATION REPORT: Recent trends and macroeconomic forecasts 2016-2017 March 2016 International environment Public Monetary

World Sugar in flux - Forecasting the Market Movements

World Sugar in flux - Forecasting the Market Movements Peter de Klerk Senior Economist 1 Source: https://theprogenygroup.com/blog/the-follies-of-making-market-predictions/ The trouble with forecasting

World Sugar in flux - Forecasting the Market Movements Peter de Klerk Senior Economist 1 Source: https://theprogenygroup.com/blog/the-follies-of-making-market-predictions/ The trouble with forecasting

Indonesia Economic Quarterly Launch Jakarta, March 18, Jim Brumby Sector Manager and Lead Economist

Indonesia Economic Quarterly Launch Jakarta, March 18, 214 Jim Brumby Sector Manager and Lead Economist MARCH 214 IEQ: INVESTMENT IN FLUX Fixed investment: subdued, and risks Risks to fiscal space needed

Indonesia Economic Quarterly Launch Jakarta, March 18, 214 Jim Brumby Sector Manager and Lead Economist MARCH 214 IEQ: INVESTMENT IN FLUX Fixed investment: subdued, and risks Risks to fiscal space needed

Juda Agung. Department of Economic Research and Monetary Policy BANK INDONESIA

Juda Agung Department of Economic Research and Monetary Policy BANK INDONESIA 1 Roadmap: Recent Capital Inflows Benefits and Challenges Policy Responses Final Remarks Recent Capital Inflows 2 Indonesia

Juda Agung Department of Economic Research and Monetary Policy BANK INDONESIA 1 Roadmap: Recent Capital Inflows Benefits and Challenges Policy Responses Final Remarks Recent Capital Inflows 2 Indonesia

Commodity Price Outlook & Risks

Commodity Outlook & Risks Research Department, Commodities Team March, 2 www.imf.org/commodities commodities@imf.org This monthly report presents a price outlook and risk assessment for selected commodities

Commodity Outlook & Risks Research Department, Commodities Team March, 2 www.imf.org/commodities commodities@imf.org This monthly report presents a price outlook and risk assessment for selected commodities

Global Markets Group. Trade Performance: Narrowing Surplus Author: Juniman Chief Economist. Economic Research. Trade Outlook Monthly Report

Global Markets Group Trade Outlook Monthly Report Economic Research November 2016 Trade Performance: Narrowing Surplus Author: Juniman Chief Economist Trade Highlights Exports in September 2016 fell to

Global Markets Group Trade Outlook Monthly Report Economic Research November 2016 Trade Performance: Narrowing Surplus Author: Juniman Chief Economist Trade Highlights Exports in September 2016 fell to

Indonesia Economic Outlook and Policy Challenges

Indonesia Economic Outlook and Policy Challenges Daniel A. Citrin Asia and Pacific Department, IMF April 3, 28 Global Financial Stability Map: risks have risen; conditions have deteriorated October 27

Indonesia Economic Outlook and Policy Challenges Daniel A. Citrin Asia and Pacific Department, IMF April 3, 28 Global Financial Stability Map: risks have risen; conditions have deteriorated October 27

Global Financial Crisis: Impact on India

Global Financial Crisis: Impact on India Mathew Joseph Pankaj Vashisht ICRIER-INVENT Workshop Current Developments in Indian Financial System New Delhi 20 March 2009 1 Roots of Global Crisis Global macroeconomic

Global Financial Crisis: Impact on India Mathew Joseph Pankaj Vashisht ICRIER-INVENT Workshop Current Developments in Indian Financial System New Delhi 20 March 2009 1 Roots of Global Crisis Global macroeconomic

RUSSIAN ECONOMIC OUTLOOK AND MONETARY POLICY. RUSSIA S ECONOMIC OUTLOOK AND MONETARY POLICY December 2018

4% RUSSIA S ECONOMIC OUTLOOK AND December 1 2 Consumer prices (1) At the end of 1, inflation is expected to be close to 4%, which corresponds to the Bank of Russia s target 2 Inflation indicators, % YoY

4% RUSSIA S ECONOMIC OUTLOOK AND December 1 2 Consumer prices (1) At the end of 1, inflation is expected to be close to 4%, which corresponds to the Bank of Russia s target 2 Inflation indicators, % YoY

Indonesia Economic Quarterly: December 2012 Policies in focus

Indonesia Economic Quarterly: December 212 Policies in focus Ndiame Diop Lead Economist & Economic Advisor, Indonesia World Bank December 18, 212 World Bank and The Habibie Center Joint Launch Event Intercontinental

Indonesia Economic Quarterly: December 212 Policies in focus Ndiame Diop Lead Economist & Economic Advisor, Indonesia World Bank December 18, 212 World Bank and The Habibie Center Joint Launch Event Intercontinental

Investment Strategy Note 24 Nov 2015

India: muddling through a difficult environment India remains a long term positive story based on its economic and demographic potential despite disappointments in the recent pace of recovery. The global

India: muddling through a difficult environment India remains a long term positive story based on its economic and demographic potential despite disappointments in the recent pace of recovery. The global

FY2018, FY2019 Economic Outlook - The Japanese economy is continuing to follow a recovery track -

REVISED to reflect the 2 nd QE for the Apr-Jun Qtr of 2018 FY2018, FY2019 Economic Outlook - The Japanese economy is continuing to follow a recovery track - September 10, 2018 Copyright Mizuho Research

REVISED to reflect the 2 nd QE for the Apr-Jun Qtr of 2018 FY2018, FY2019 Economic Outlook - The Japanese economy is continuing to follow a recovery track - September 10, 2018 Copyright Mizuho Research

Global Economic Prospects: Update Global Recovery in Transition

Global Economic Prospects: Update Global Recovery in Transition April 2015 M. Ayhan Kose 1 Global Prospects: Three Questions 1. How have global economic conditions changed since December? Broadly as expected;

Global Economic Prospects: Update Global Recovery in Transition April 2015 M. Ayhan Kose 1 Global Prospects: Three Questions 1. How have global economic conditions changed since December? Broadly as expected;