Chapter 6 Earnings Management 6-1

|

|

|

- Arron Roberts

- 6 years ago

- Views:

Transcription

1 Chapter 6 Earnings Management 1. Identify the factors that motivate earnings management 2. List the common techniques used to manage earnings 3. Critically discuss whether a company should manage its earnings 4. Describe the common elements of earnings management meltdown 5. Explain how good accounting standards and ethical behavior by accountants lower the cost of obtaining capital 6-1

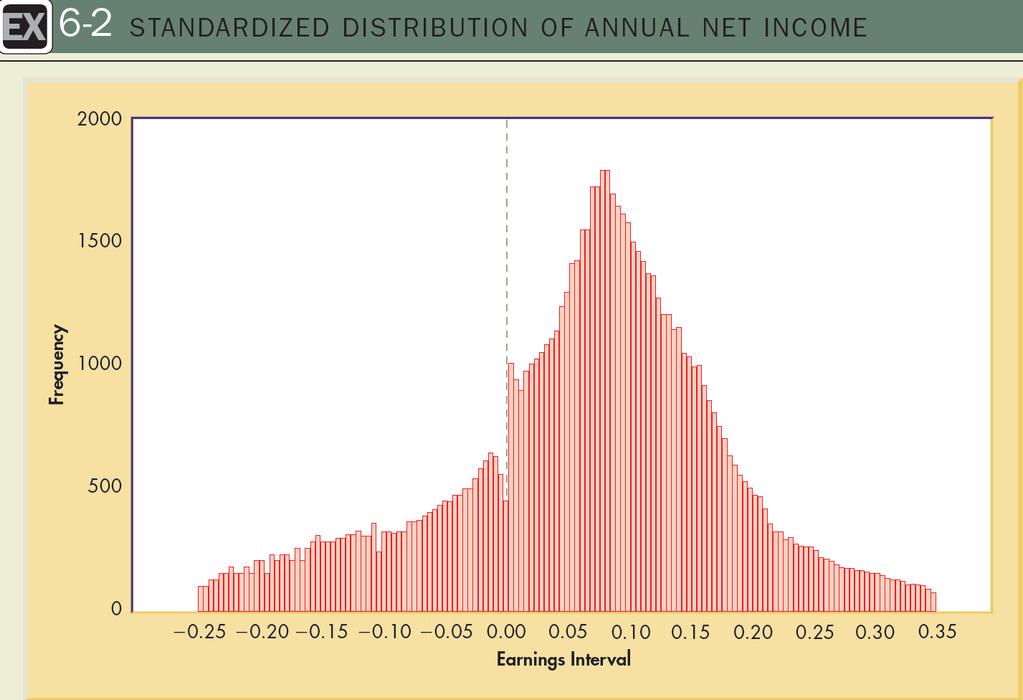

2 1. Identify the factors that motivate earnings management Government Budgetary Arena The following statement, though perhaps a bit overstated, still contains a grain of truth: Perception dictates policy, accounting determines perception, therefore, accounting rules the world. 6-2

3 Motivation for Managing Reported Earnings Forces that push managers to manipulate results: 1. Meet internal targets. 2. Meet external expectations. 3. Provide income smoothing. 4. Provide window dressing for an IPO or a loan. (continued) 6-3

4 Meet Internal Targets Internal earnings targets represent an important tool in motivating managers to increase sales efforts, control costs, and use resources more efficiently. As with any performance measurement tool, it is a fact of life that the person being evaluated will have a tendency to forget the economic factors underlying the measurement and instead focus on the measured number itself. (continued) 6-4

5 Meet External Expectations Employees and customers want a company to do well so that it can survive for the long run and make good on its long-term pension and warranty obligations. Suppliers want assurance that they will receive payment and, more importantly, that the purchasing company will be a reliable purchaser for many years into the future. (continued) 6-5

6 (continued) 6-6

7 Meet External Expectations Extensive research has shown that announcing net income less than the income forecast by analysts results in a drop in stock price. Companies have an incentive to manage earnings to make sure that the announced number is at least equal to the earnings expected by analysts. (continued) 6-7

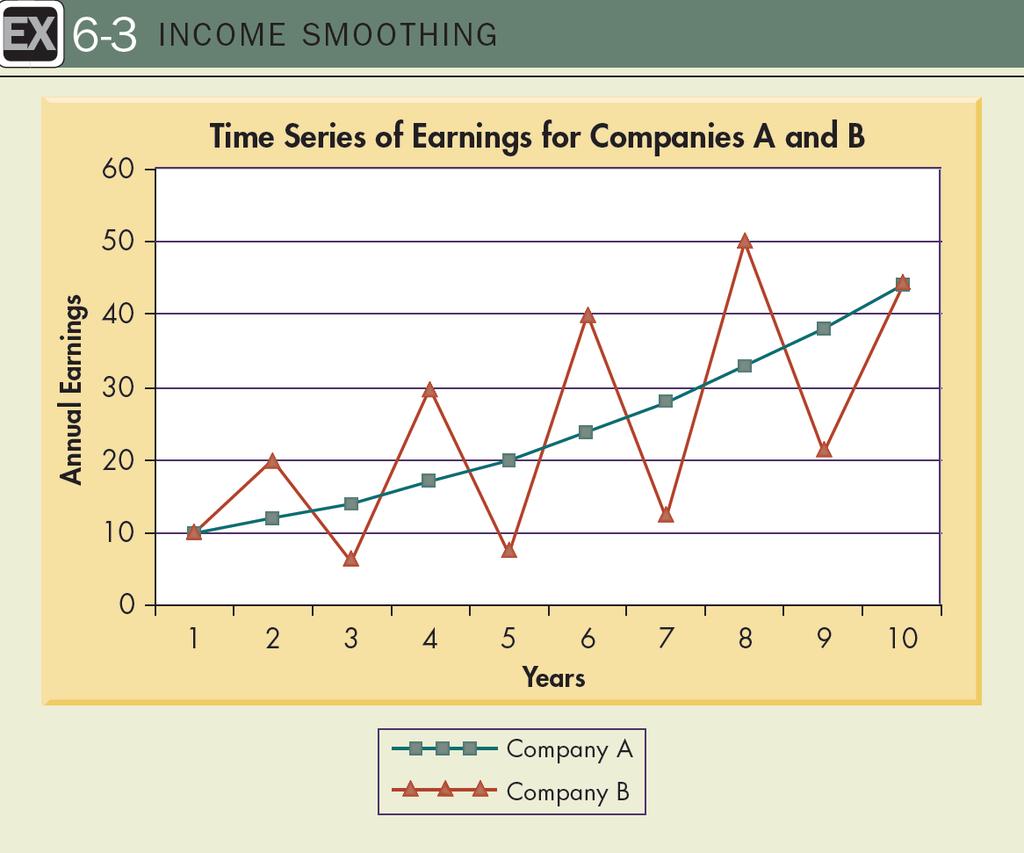

8 Provide Income Smoothing The practice of carefully timing the recognition of revenues and expenses to even out the amount of reported earnings from one year to the next is called income smoothing. (continued) 6-8

9 (continued) 6-9

10 Provide Window Dressing for an IPO or a Loan For companies entering a phase in which it is critical that reported earnings look good (especially before the IPO of stock), accounting assumptions can be stretched. This is known as window dressing. 6-10

11 2. List the common techniques used to manage earnings Earnings Management Continuum Earnings management can range from savvy timing of transactions to outright fraud. The display of the range of possibilities for earnings management is called the earnings management continuum. 6-11

12 Change in Methods or Estimates with Full Disclosure Companies frequently change accounting estimates respecting bad debts, return on pension funds, depreciation lives, and so forth. Although such changes are a routine part of adjusting accounting estimates to reflect the most current information available, they can be used to manage the amount of reported earnings. (continued) 6-12

13 Change in Methods or Estimates with Little or No Disclosure Making an accounting change in method or estimation is acceptable as long as there is full disclosure. One might debate whether the new estimated amount is more appropriate, but what is certain is that failing to disclose the impact of a change can mislead financial statement users. (continued) 6-13

14 Non-GAAP Accounting A more descriptive title for non-gaap accounting is fraudulent reporting. It can be the result of inadvertent errors. Some firms, like Enron, violated the spirit of the accounting standards. In some cases, Enron also violated the letter of the accounting standards. (continued) 6-14

15 Fictitious Transactions Creating fictitious transactions is outright fraud. A classic case of fictitious fraud is Barry Minkow and ZZZZ Best. Today, because he is considered a fraud expert, he speaks to college and business communities in an effort to prevent fraud. 6-15

16 Chairman Levitt s Top Five Accounting Hocus-Pocus Items 1. Big bath charges 2. Creative acquisition accounting 3. Cookie jar reserves 4. Materiality 5. Revenue recognition Arthur Levitt Former SEC Chairman (continued) 6-16

17 Big Bath Charges The concept behind a big bath is that if a company expects to have a series of hits to earnings in future years, it is better to try to recognize all the bad news in one year, leaving future years unencumbered by continuing losses. (continued) 6-17

18 Company D recognized its bad news in one year, and thus took a big bath. (continued) 6-18

19 Creative Acquisition Accounting Since 1998, new acquisition account rules have been adopted (FASB ASC Topic 805); these standards give more extensive guidelines on how the purchase price of business acquisitions should be allocated. The SEC staff informed companies they would be skeptical of large amounts being allocated to in-process R&D. (continued) 6-19

20 Cookie Jar Reserves Recognizing high estimated expenses when revenue is high so that less estimated expenses can be recognized when earnings are lower and deferring revenue for tougher times are examples of building a cookie jar reserve. The SEC has issued SABs 101 and 104, identifying more carefully the circumstances in which it is appropriate for a company to defer revenue. (continued) 6-20

21 Materiality Falling short of the market s expectation of earnings by one penny per share can cause a company to lose billions of dollars in market value. If a questionable practice helps a firm meet analysts expectations, the firm should be required to change the data or to convince the auditor that it complies with GAAP. The SEC released SAB 99 that outlines a more comprehensive definition of materiality. (continued) 6-21

22 Revenue Recognition Firms would like to report revenue when contracts are signed or partially complete rather than waiting until the promised product or service has been fully delivered. The SEC has released SAB 101, which reduced the flexibility companies have in the timing of revenue recognition. (continued) 6-22

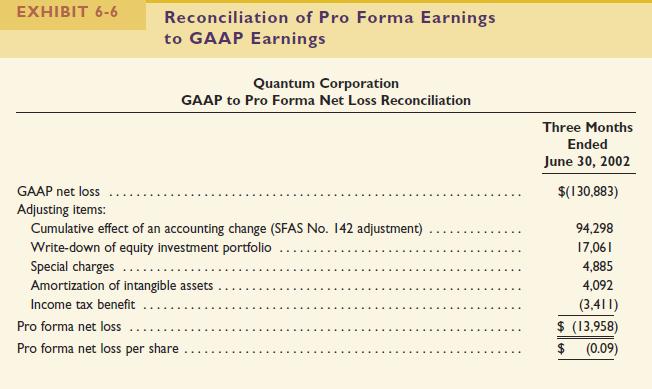

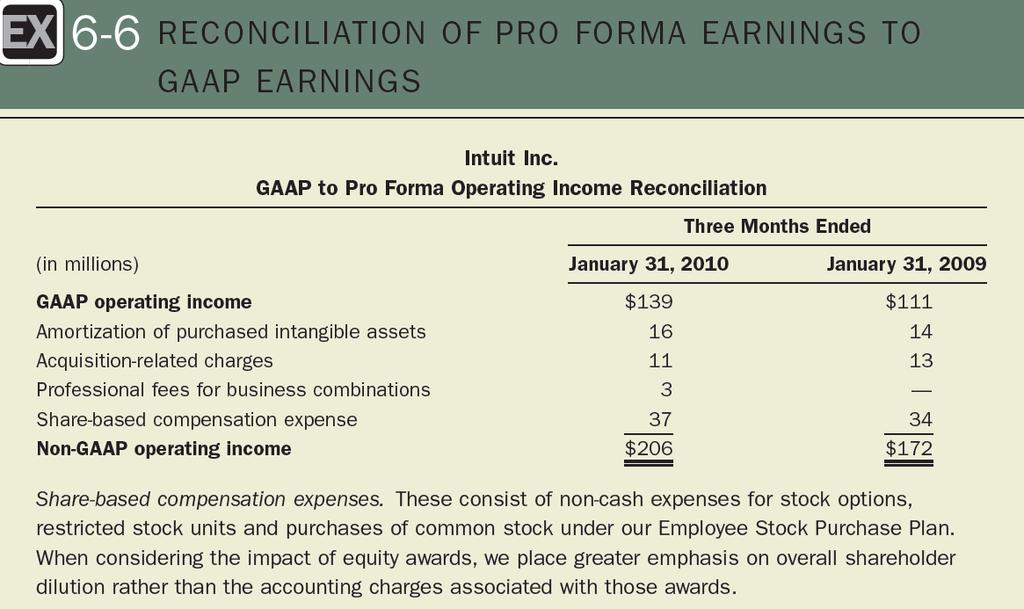

23 Pro Forma Earnings A pro forma earnings number is the regular GAAP earnings number with some revenues, expenses, gains, or losses excluded. The key question is whether the number helps financial statement users better understand a company or whether it is a blatant attempt to cover up poor performance. If a manager is trustworthy, the GAAP earnings are reliable, and the manager can reveal even better information about the underlying economics of the business through appropriate adjustments in computing pro forma earnings. 6-23

24 6-24

25 6-25

26 3. Critically discuss whether a company should manage its earnings Financial Reporting as a Part of Public Relations QUESTION. Does a manager have an ethical and fiduciary responsibility to carefully manage the resources of a publicly traded company in order to maximize the value to the stockholder? ANSWER. Yes. In fact, this is the very definition of the responsibility of a corporate manager. 6-26

27 Financial Reporting as a Part of Public Relations QUESTION. Does the public perception of a company impact the company s success in terms of finding customers, securing relationships with suppliers, attracting employees, etc.? ANSWER. Certainly. It is impossible to rally people to put their time and money behind a company unless they are convinced the company can be successful. (continued) 6-27

28 Financial Reporting as a Part of Public Relations QUESTION. Does the amount of reported earnings impact the public s perception of a company? ANSWER. Absolutely. Accounting net income is not the only piece of information relevant to assessing a company s viability, but it certainly is one influential data point. (continued) 6-28

29 Financial Reporting as a Part of Public Relations QUESTION. Does a manager have a responsibility to manage reported earnings, within the constraints of GAAP? ANSWER. It is difficult to answer no to this question. In light of the answers to the preceding questions, it would be an irresponsible manager indeed who did not do all possible, within the constraints of GAAP, to burnish the company s public image. (continued) 6-29

30 Everybody agrees that the creation of fictitious transactions is unethical. (continued) 6-30

6-31")

31 There is wide disagreement as to whether or not these categories are ethical or unethical. (continued) 6-31

32 Does the manager have the responsibility to try to report earnings numbers exactly in the middle of the possible range. 6-32

33 Personal Ethics In an effort to increase the personal cost to company executives of allowing a company to report earnings that violate GAAP, in 2002 the SEC began requiring CEOs and CFOs to submit sworn statements asserting that they had personally confirmed that their company s financial statements contained no materiallymisleading items. 6-33

")

34 4. Describe the common elements of an earnings management meltdown (continued) 6-34

35 Downturn in Business Excessive earnings management almost always begins with a downturn in business. When operating results are consistently good, the need for earnings management is not as great. (continued) 6-35

36 (continued) 6-36

37 (continued) 6-37

38 Pressure to Meet Expectations A powerful factor motivating managers to manage earnings is the desire to continue to meet expectations. The accounting manipulation carried out by Xerox is a good example of pressure to meet expectations. 6-38

39 Attempted Accounting Solution When the accountants, instead of the operations or marketing people, are asked to return a company to profitability through earnings management, the solution is a temporary one at best. At worst, the counterproductive mentality associated with papering over a company s problems through earnings management can ultimately lead to even larger business problems. (continued) 6-39

40 Auditor s Calculated Risk The financial statements represent a negotiated settlement between the management of the company and the company s auditor. An auditor is frequently required to decide whether to accept a debatable accounting treatment, engage in further discussion with management, or, as a final resort, withdraw from the audit. 6-40

41 (continued) 6-41

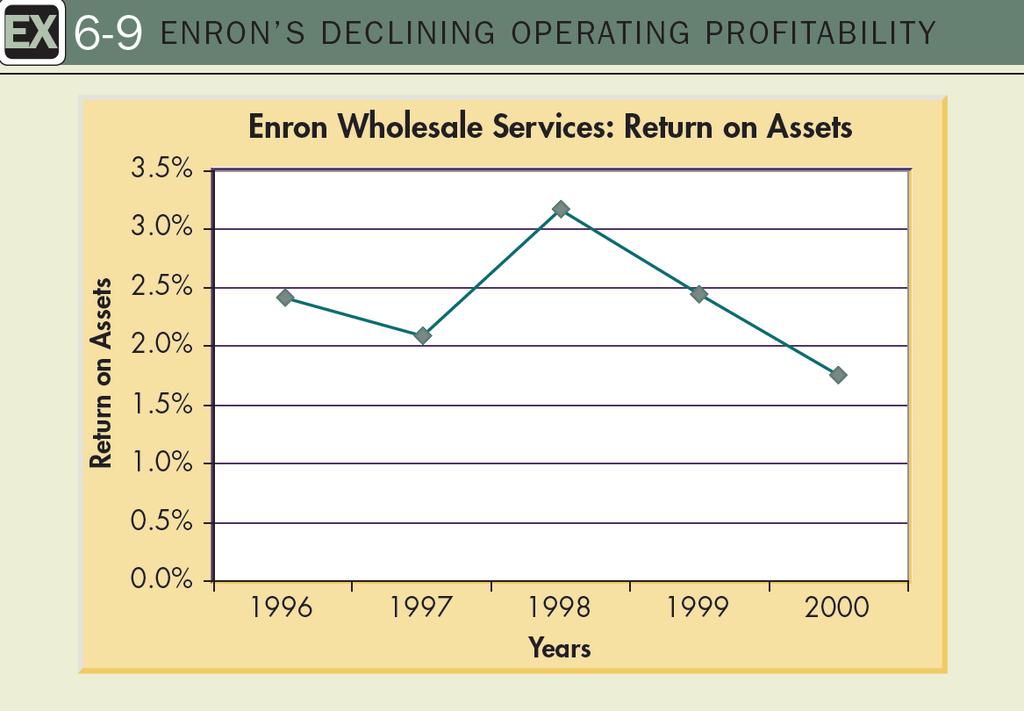

42 Insufficient User Skepticism In October 2001, just before Enron s earnings restatement led to the company s bankruptcy less than two months later, 11 of the 13 financial analysts following Enron recommended the company s stock as a buy or strong buy. Enron s published financial statements had indications in them that should have led a skeptical analyst and investment community to question the company s fundamental business model. (continued) 6-42

43 Insufficient User Skepticism Financial statement users have usually accepted companies financial statements at face value with the realization that there was some risk of deceptive reporting. Some analysts and members of the investment community have not exhibited enough financial statement skepticism because these parties often stand to benefit economically as companies obtain loans, issue stock, and engage in merger and acquisition activity. (continued) 6-43

44 Insufficient User Skepticism From 1997 through 2010, five major periods of decline in worldwide stock prices occurred. 1997: Concern about the reliability of banking and financial information in a number of Asian countries. 2000: A return to reality after initial euphoria about the business possibilities associated with Internet. 2001: The wake of political and economic uncertainty created by the 9/11 attack on the World Trade Center. (continued) 6-44

45 Insufficient User Skepticism 2002: The widespread uncertainty about the credibility of financial reports of U.S. corporations. 2008: The real estate greed that had inflated U.S. real estate prices coupled with investor uncertainty about what was really inside the mortgage-backed securities that had flooded the market. 6-45

46 Regulatory Investigation Investigations are often conducted when companies are suspected of passing outside the boundary of the GAAP oval in Exhibit 6-7 into the area of fraudulent financial reporting. In addition to regulatory investigations, fraudulent financial reporting can also lead to criminal charges. 6-46

47 Massive Loss of Reputation The final step in an earnings management meltdown is the huge loss of credibility experienced by the company that has been found to have manipulated the reported earnings. The loss of credibility harms all of the company s relationships and drastically impairs its economic value. 6-47

48 5. Explain how good accounting standards and ethical behavior by accountants lower the cost of obtaining capital Transparent Financial Reporting An important fact often forgotten by financial statement preparers and users is that the entire purpose of accounting, both financial and managerial, is to lower the cost of doing business. 6-48

49 What is the Cost of Capital? The cost of capital is the cost a company bears to obtain external financing. The cost of debt financing is simply the after-tax interest cost associated with borrowing the money. The cost of equity financing is the expected return necessary to induce investors to provide equity capital. (continued) 6-49

50 What is the Cost of Capital? A company often computes its weightedaverage cost of capital, which is the average of the cost of debt and equity financing weighted by the proportion of each type of financing. A company s cost of capital is critical because it determines which long-term projects are profitable to undertake. (continued) 6-50

51 What is the Cost of Capital? In a capital budgeting setting, the cost of capital can be thought of as the discount rate or hurdle rate used in evaluating longterm projects. A key factor in determining a company s cost of capital is the risk associated with the company. 6-51

52 Cockroach Theory When managers are willing to try to deceive lenders and investors through misleading financial reporting, those same lenders and investors naturally wonder what other types of deception the managers are attempting. This is called the cockroach theory. 6-52

53 The Role of Accounting Standards The FASB and the AICPA help lower the cost of capital by promulgating uniform recognition and disclosure standards for use by companies in the United States. The SEC has the primary mission of protecting investors and maintaining the integrity of the securities market. (continued) 6-53

54 The Role of Accounting Standards The IASB is playing an increasingly important role in enhancing the credibility of international financial reporting. Financial statement users are concerned that increased reliance on accounting judgment will make the reported numbers under IFRS more vulnerable to management manipulation, increasing information risk and thus increasing the cost of capital. 6-54

55 The Necessity of Ethical Behavior Managers have strong economic incentives to report favorable financial results, and these incentives can lead to deceptive or fraudulent reporting. Managers also have strong incentives to maintain a reputation for credibility for both the company and for themselves personally. 6-55

56 AICPA Code of Professional Conduct In discharging their professional responsibilities, members may encounter conflicting pressures... In resolving those conflicts, members should act with integrity, guided by the precept that when members fulfill their responsibility to the public, clients and employers interests are best served. 6-56

7 2010, 2011, 2012 & 2013 AICPA

The 7 Financial Shenanigans: How Companies Cook the Books Leah Donti Ldonti@AdvantageMontrealSeminars.com 2010, 2011, 2012 & 2013 AICPA Outstanding Discussion Leader Award Recipient Welcome! Agenda Games

The 7 Financial Shenanigans: How Companies Cook the Books Leah Donti Ldonti@AdvantageMontrealSeminars.com 2010, 2011, 2012 & 2013 AICPA Outstanding Discussion Leader Award Recipient Welcome! Agenda Games

Scenic Video Transcript End-of-Period Accounting and Business Decisions Topics. Accounting decisions: o Accrual systems.

Income Statements» What s Behind?» Income Statements» Scenic Video www.navigatingaccounting.com/video/scenic-end-period-accounting-and-business-decisions Scenic Video Transcript End-of-Period Accounting

Income Statements» What s Behind?» Income Statements» Scenic Video www.navigatingaccounting.com/video/scenic-end-period-accounting-and-business-decisions Scenic Video Transcript End-of-Period Accounting

CHAPTER 2. Financial Reporting: Its Conceptual Framework CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS

2-1 CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS NUMBER Q2-1 Conceptual Framework Q2-2 Conceptual Framework Q2-3 Conceptual Framework Q2-4 Conceptual Framework Q2-5 Objective of Financial Reporting Q2-6

2-1 CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS NUMBER Q2-1 Conceptual Framework Q2-2 Conceptual Framework Q2-3 Conceptual Framework Q2-4 Conceptual Framework Q2-5 Objective of Financial Reporting Q2-6

BBB2154 Business Ethics Prepared by Dr Khairul Anuar. L5 Ethics and Financial Reporting Compliance

BBB2154 Business Ethics Prepared by Dr Khairul Anuar L5 Ethics and Financial Reporting Compliance 1 When is a Doughnut Hole a Real Doughnut Hole? Krispy Kreme became a sensation whenever a new store was

BBB2154 Business Ethics Prepared by Dr Khairul Anuar L5 Ethics and Financial Reporting Compliance 1 When is a Doughnut Hole a Real Doughnut Hole? Krispy Kreme became a sensation whenever a new store was

Chapter 01 - Introducing Accounting in Business. Chapter Outline

I. Importance of Accounting Accounting is an information and measurement system that identifies, records and communicates relevant, reliable, and comparable information about an organization s business

I. Importance of Accounting Accounting is an information and measurement system that identifies, records and communicates relevant, reliable, and comparable information about an organization s business

Fried, Frank, Harris, Shriver & Jacobson August 26, 2003

August 26, 2003 Timeline Effective Dates for Implementing The Sarbanes-Oxley Act of 2002 ("SOX") and New and Proposed SEC, NYSE & Nasdaq Rules for Non-U.S. Issuers Disclosure 1. CEO/CFO certification A.

August 26, 2003 Timeline Effective Dates for Implementing The Sarbanes-Oxley Act of 2002 ("SOX") and New and Proposed SEC, NYSE & Nasdaq Rules for Non-U.S. Issuers Disclosure 1. CEO/CFO certification A.

INTERMEDIATE ACCOUNTING

INTERMEDIATE ACCOUNTING Earl K. Sfice, PhD Brigham Young University James D. Slice, PhD Brigham Young University K. Fred Skousen, PhD, CPA Brigham Young University / - SOUTH-WESTERN fie? CENGAGE Learning-

INTERMEDIATE ACCOUNTING Earl K. Sfice, PhD Brigham Young University James D. Slice, PhD Brigham Young University K. Fred Skousen, PhD, CPA Brigham Young University / - SOUTH-WESTERN fie? CENGAGE Learning-

CHAPTER 2. Financial Reporting: Its Conceptual Framework CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS

2-1 CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS CHAPTER 2 Financial Reporting: Its Conceptual Framework NUMBER TOPIC CONTENT LO ADAPTED DIFFICULTY 2-1 Conceptual Framework 2-2 Conceptual Framework 2-3

2-1 CONTENT ANALYSIS OF END-OF-CHAPTER ASSIGNMENTS CHAPTER 2 Financial Reporting: Its Conceptual Framework NUMBER TOPIC CONTENT LO ADAPTED DIFFICULTY 2-1 Conceptual Framework 2-2 Conceptual Framework 2-3

Accounting - the recording, measurement, and interpretation of financial information essential in making business decisions.

Introduction to Business Administration Lesson 8 8. Accounting Accounting is the language of business. Accounting - the recording, measurement, and interpretation of financial information essential in

Introduction to Business Administration Lesson 8 8. Accounting Accounting is the language of business. Accounting - the recording, measurement, and interpretation of financial information essential in

AN ANALYSIS OF SMALL COMPANY FRAUDS AND IMPLICATONS FOR AUDITORS IN DETECTING FRAUDS

AN ANALYSIS OF SMALL COMPANY FRAUDS AND IMPLICATONS FOR AUDITORS IN DETECTING FRAUDS Michael Ulinski Pace University mulinski@pace.edu ABSTACT: While much has been written about large company corporate

AN ANALYSIS OF SMALL COMPANY FRAUDS AND IMPLICATONS FOR AUDITORS IN DETECTING FRAUDS Michael Ulinski Pace University mulinski@pace.edu ABSTACT: While much has been written about large company corporate

Section 6 Earnings quality

Section 6 Earnings quality In the long run managements stressing accounting appearance over economic substance usually achieve little of either. --Warren Buffett 1 Learning objectives After studying this

Section 6 Earnings quality In the long run managements stressing accounting appearance over economic substance usually achieve little of either. --Warren Buffett 1 Learning objectives After studying this

Chapter 2 Professional Standards

True/False Questions 1. The generally accepted auditing standards of field work include a requirement that the auditors obtain sufficient competent evidential matter. Answer: True Difficulty: Easy 2. The

True/False Questions 1. The generally accepted auditing standards of field work include a requirement that the auditors obtain sufficient competent evidential matter. Answer: True Difficulty: Easy 2. The

Kush Bottles, Inc. A Nevada corporation (the Company )

") Kush Bottles, Inc. A Nevada corporation (the Company ) Audit Committee Charter The Audit Committee (the Committee ) is created by the Board of Directors of the Company (the Board ) to: assist the Board

Kush Bottles, Inc. A Nevada corporation (the Company ) Audit Committee Charter The Audit Committee (the Committee ) is created by the Board of Directors of the Company (the Board ) to: assist the Board

CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS OF TOPBUILD CORP. I. MISSION II. MEMBERSHIP

CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS OF TOPBUILD CORP. I. MISSION The Audit Committee (the Committee ) of the Board of Directors (the Board ) of TopBuild Corp., a Delaware corporation

CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS OF TOPBUILD CORP. I. MISSION The Audit Committee (the Committee ) of the Board of Directors (the Board ) of TopBuild Corp., a Delaware corporation

CHECKFREE CORPORATION CODE OF BUSINESS CONDUCT FOR DIRECTORS, OFFICERS AND ASSOCIATES

CHECKFREE CORPORATION CODE OF BUSINESS CONDUCT FOR DIRECTORS, OFFICERS AND ASSOCIATES INTRODUCTION CheckFree Corporation operates its business in accordance with the highest ethical standards and relevant

CHECKFREE CORPORATION CODE OF BUSINESS CONDUCT FOR DIRECTORS, OFFICERS AND ASSOCIATES INTRODUCTION CheckFree Corporation operates its business in accordance with the highest ethical standards and relevant

AVERY DENNISON CORPORATION AUDIT AND FINANCE COMMITTEE CHARTER *

AVERY DENNISON CORPORATION AUDIT AND FINANCE COMMITTEE CHARTER * Purpose The Audit & Finance Committee ( Committee ) is appointed by the Board to assist the Board with its oversight responsibilities in

AVERY DENNISON CORPORATION AUDIT AND FINANCE COMMITTEE CHARTER * Purpose The Audit & Finance Committee ( Committee ) is appointed by the Board to assist the Board with its oversight responsibilities in

ASA Fair Value Conference SEC Update

ASA Fair Value Conference SEC Update May 7, 2009 Evan Sussholz Professional Accounting Fellow - Valuation Specialist Office of the Chief Accountant 1 Disclaimer The Securities and Exchange Commission,

ASA Fair Value Conference SEC Update May 7, 2009 Evan Sussholz Professional Accounting Fellow - Valuation Specialist Office of the Chief Accountant 1 Disclaimer The Securities and Exchange Commission,

INTERMEDIATE ACCOUNTING

Chapter 2 Financial Reporting: Its Conceptual Framework INTERMEDIATE ACCOUNTING Objectives 1. Explain the FASB Conceptual Framework. 2. Explain the general and specific objectives of general purpose financial

Chapter 2 Financial Reporting: Its Conceptual Framework INTERMEDIATE ACCOUNTING Objectives 1. Explain the FASB Conceptual Framework. 2. Explain the general and specific objectives of general purpose financial

AUDIT COMMITTEE CHARTER. Purpose

AUDIT COMMITTEE CHARTER Purpose The Audit Committee (the Committee ) is appointed by the Board of Directors of Cabot Corporation (the Company ) to (a) appoint and oversee the performance of the independent

AUDIT COMMITTEE CHARTER Purpose The Audit Committee (the Committee ) is appointed by the Board of Directors of Cabot Corporation (the Company ) to (a) appoint and oversee the performance of the independent

Prof Albrecht s Notes Income Statement Intermediate Accounting 1

Prof Albrecht s Notes Intermediate Accounting 1 The income statement has been the most important of the required financial statements in the United States. This importance is revealed in several ways:

Prof Albrecht s Notes Intermediate Accounting 1 The income statement has been the most important of the required financial statements in the United States. This importance is revealed in several ways:

Auditing and Assurance Standards Council

Auditing and Assurance Standards Council Philippine Standard on Auditing 240 (Redrafted) THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS PHILIPPINE STANDARD ON AUDITING

Auditing and Assurance Standards Council Philippine Standard on Auditing 240 (Redrafted) THE AUDITOR S RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS PHILIPPINE STANDARD ON AUDITING

STAGE STORES, INC. AUDIT COMMITTEE CHARTER

A. Purpose STAGE STORES, INC. AUDIT COMMITTEE CHARTER The Audit Committee ( Committee ) is a standing committee of the Board of Directors ( Board ) of Stage Stores, Inc. ( Company ). The Committee s purpose

A. Purpose STAGE STORES, INC. AUDIT COMMITTEE CHARTER The Audit Committee ( Committee ) is a standing committee of the Board of Directors ( Board ) of Stage Stores, Inc. ( Company ). The Committee s purpose

Mark T. Williams Boston University Finance Department

Accounting Finance & Risk Management: Session 600 Mark T. Williams Boston University Finance Department Williams@bu.edu Goals Explain core concepts 1. Role of accounting and finance in business 2. Core

Accounting Finance & Risk Management: Session 600 Mark T. Williams Boston University Finance Department Williams@bu.edu Goals Explain core concepts 1. Role of accounting and finance in business 2. Core

Intro to Fundamental Analysis Tutorial

Intro to Fundamental Analysis Tutorial http://www.investopedia.com/university/fundamentalanalysis/ Thanks very much for downloading the printable version of this tutorial. As always, we welcome any feedback

Intro to Fundamental Analysis Tutorial http://www.investopedia.com/university/fundamentalanalysis/ Thanks very much for downloading the printable version of this tutorial. As always, we welcome any feedback

Lecture 12 Creditors and Auditors. Prof. Daniel Sungyeon Kim

Lecture 12 Creditors and Auditors Prof. Daniel Sungyeon Kim Debt as a disciplinary mechanism Institutional lenders as corporate monitors Credit rating agencies International perspective Financial Reporting

Lecture 12 Creditors and Auditors Prof. Daniel Sungyeon Kim Debt as a disciplinary mechanism Institutional lenders as corporate monitors Credit rating agencies International perspective Financial Reporting

International Standard on Auditing (UK) 240 (Revised June 2016)

240 (Revised June 2016)") Standard Audit and Assurance Financial Reporting Council July 2017 International Standard on Auditing (UK) 240 (Revised June 2016) The Auditor s Responsibilities Relating to Fraud in an Audit of Financial

Standard Audit and Assurance Financial Reporting Council July 2017 International Standard on Auditing (UK) 240 (Revised June 2016) The Auditor s Responsibilities Relating to Fraud in an Audit of Financial

Audit Committee Charter

Amended and Restated as of March 2017 Audit Committee Charter Purpose of Committee The purpose of the Audit Committee (the Committee ) of the Board of Directors (the Board ) of The Goldman Sachs Group,

Amended and Restated as of March 2017 Audit Committee Charter Purpose of Committee The purpose of the Audit Committee (the Committee ) of the Board of Directors (the Board ) of The Goldman Sachs Group,

Accounting Issues for Publicly Traded Gaining Co1npanies

Accounting Issues for Publicly Traded Gaining Co1npanies Karl M. Brunner Senior Audit Manager Deloite & Touche The expansion of gaming throughout the world has resulted in the emergence of large publicly

Accounting Issues for Publicly Traded Gaining Co1npanies Karl M. Brunner Senior Audit Manager Deloite & Touche The expansion of gaming throughout the world has resulted in the emergence of large publicly

I. Ensuring the Basis for an Effective Corporate Governance Framework

OECD Corporate Governance Committee 4 January 2015 Re: OECD Principles of Corporate Governance CFA Institute 1 appreciates the opportunity to comment on the review of the OECD Principles of Corporate Governance.

OECD Corporate Governance Committee 4 January 2015 Re: OECD Principles of Corporate Governance CFA Institute 1 appreciates the opportunity to comment on the review of the OECD Principles of Corporate Governance.

Financial reports give a snapshot of a company s value at the end of a

Chapter 1 Opening the Cornucopia of Reports In This Chapter Reviewing the importance of financial reports Exploring the different types of financial reporting Discovering the key financial statements Financial

Chapter 1 Opening the Cornucopia of Reports In This Chapter Reviewing the importance of financial reports Exploring the different types of financial reporting Discovering the key financial statements Financial

PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD. Public Meeting on the Auditor s Reporting Model. Washington, D.C. April 2, 2014

PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD Public Meeting on the Auditor s Reporting Model Washington, D.C. April 2, 2014 Lynn Turner 1 I want to thank Chairman Doty and his fellow board members for inviting

PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD Public Meeting on the Auditor s Reporting Model Washington, D.C. April 2, 2014 Lynn Turner 1 I want to thank Chairman Doty and his fellow board members for inviting

MACC Courses. MACC Accounting Foundations Tutorial (ACCT 562 for MACC students; not a graded course)

") Summer Foundations Courses MACC Courses January 2014 ACCT 560 Introduction to Financial Accounting In this course, we will study the three fundamental financial accounting issues, including (1) recognition,

Summer Foundations Courses MACC Courses January 2014 ACCT 560 Introduction to Financial Accounting In this course, we will study the three fundamental financial accounting issues, including (1) recognition,

Note that there is an overlap between the T/F and multiple-choice questions, as some of the T/F statements are used in multiple-choice questions.

Fundamentals of Financial Management 14th Edition Brigham Houston TEST BANK Complete download test bank for Fundamentals of Financial Management 14th Edition Brigham https://testbankarea.com/download/test-bank-fundamentals-financialmanagement-14th-edition-brigham-houston/

Fundamentals of Financial Management 14th Edition Brigham Houston TEST BANK Complete download test bank for Fundamentals of Financial Management 14th Edition Brigham https://testbankarea.com/download/test-bank-fundamentals-financialmanagement-14th-edition-brigham-houston/

EUROSTAT Conference "Towards Implementing European Public Sector Accounting Standards", Brussels, May 2013

EUROSTAT Conference "Towards Implementing European Public Sector Accounting Standards", Brussels, 29-30 May 2013 The need for fiscal transparency and harmonised public sector accounting standards Olivier

EUROSTAT Conference "Towards Implementing European Public Sector Accounting Standards", Brussels, 29-30 May 2013 The need for fiscal transparency and harmonised public sector accounting standards Olivier

INTERNATIONAL STANDARD ON AUDITING 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS CONTENTS

INTERNATIONAL STANDARD ON AUDITING 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph

INTERNATIONAL STANDARD ON AUDITING 240 THE AUDITOR S RESPONSIBILITY TO CONSIDER FRAUD (Effective for audits of financial statements for periods beginning on or after December 15, 2004) CONTENTS Paragraph

CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS OF APARTMENT INVESTMENT AND MANAGEMENT COMPANY (Reviewed & Modified October 24, 2017)

") CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS OF APARTMENT INVESTMENT AND MANAGEMENT COMPANY (Reviewed & Modified October 24, 2017) The Audit Committee (the Committee ) of the Board of Directors

CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS OF APARTMENT INVESTMENT AND MANAGEMENT COMPANY (Reviewed & Modified October 24, 2017) The Audit Committee (the Committee ) of the Board of Directors

JSC GAZPROM ENXHINALLBANI S A B I N A K A L DY B E KOVA

JSC GAZPROM ENXHI N A LLBANI SABINA K A LDYBEKOVA Overview of Russia In 1991 Soviet Union collapsed and it started a massive reorganization of Russia s political, social and economic infrastructure During

JSC GAZPROM ENXHI N A LLBANI SABINA K A LDYBEKOVA Overview of Russia In 1991 Soviet Union collapsed and it started a massive reorganization of Russia s political, social and economic infrastructure During

Chapters 1-4 (Part One)

") Profession of Accounting Chapters 1-4 (Part One) The accounting profession is varied. It includes private accounting, where accountants work for their clients (e.g., Controllers). It also includes public

Profession of Accounting Chapters 1-4 (Part One) The accounting profession is varied. It includes private accounting, where accountants work for their clients (e.g., Controllers). It also includes public

International Standard on Auditing (Ireland) 240

240") International Standard on Auditing (Ireland) 240 The Auditor s Responsibilities Relating to Fraud in an Audit of Financial Statements July 2017 MISSION To contribute to Ireland having a strong regulatory

International Standard on Auditing (Ireland) 240 The Auditor s Responsibilities Relating to Fraud in an Audit of Financial Statements July 2017 MISSION To contribute to Ireland having a strong regulatory

CFGINSIGHTS PERSPECTIVES REVENUE CONVERGENCE: A NEW RECOGNITION MODEL

WINTER 2014 CFGINSIGHTS INDUSTRY TRENDS AND DEVELOPMENTS FROM CFGI Welcome to the Winter 2014 edition of CFGInsights. Our goal is to provide you with a round-up of the most pressing accounting and reporting

WINTER 2014 CFGINSIGHTS INDUSTRY TRENDS AND DEVELOPMENTS FROM CFGI Welcome to the Winter 2014 edition of CFGInsights. Our goal is to provide you with a round-up of the most pressing accounting and reporting

AUDIT COMMITTEE CHARTER

AUDIT COMMITTEE CHARTER Purpose The Audit Committee is appointed by the Board of Directors (the Board ) to assist the Board in monitoring (1) the integrity of the financial statements of the Company, (2)

AUDIT COMMITTEE CHARTER Purpose The Audit Committee is appointed by the Board of Directors (the Board ) to assist the Board in monitoring (1) the integrity of the financial statements of the Company, (2)

Auditing and Assurance Services, 15e (Arens) Chapter 2 The CPA Profession. Learning Objective 2-1

Chapter 2 The CPA Profession. Learning Objective 2-1") Auditing and Assurance Services, 15e (Arens) Chapter 2 The CPA Profession Learning Objective 2-1 1) The legal right to perform audits is granted to a CPA firm by regulation of: A) each state. B) the Financial

Auditing and Assurance Services, 15e (Arens) Chapter 2 The CPA Profession Learning Objective 2-1 1) The legal right to perform audits is granted to a CPA firm by regulation of: A) each state. B) the Financial

IMPACT OF IFRS ON SMEs SECTOR

IMPACT OF IFRS ON SMEs SECTOR Shankar S. Sodha ABSTRACT Being an emerging country Small and medium sizes enterprises (SMEs) perform imperative part in economy of India. SMEs most backing in job angle,

IMPACT OF IFRS ON SMEs SECTOR Shankar S. Sodha ABSTRACT Being an emerging country Small and medium sizes enterprises (SMEs) perform imperative part in economy of India. SMEs most backing in job angle,

Audit Committee Charter

ESTERLINE TECHNOLOGIES CORPORATION Audit Committee Charter Purpose and Authority It is the policy of this Company to have an Audit Committee (the Committee ) of the Board of Directors to assist the Board

ESTERLINE TECHNOLOGIES CORPORATION Audit Committee Charter Purpose and Authority It is the policy of this Company to have an Audit Committee (the Committee ) of the Board of Directors to assist the Board

AUDIT COMMITTEE CHARTER

AUDIT COMMITTEE CHARTER PURPOSE AND AUTHORITY The purpose of the Audit Committee is to assist the Board of Directors in its oversight of: (1) the integrity of the Corporation s accounting and financial

AUDIT COMMITTEE CHARTER PURPOSE AND AUTHORITY The purpose of the Audit Committee is to assist the Board of Directors in its oversight of: (1) the integrity of the Corporation s accounting and financial

Financial and Managerial Accounting Information for Decisions 4th Edition by John Wild, Ken Shaw, Barbara Chiappetta Test Bank

Financial and Managerial Accounting Information for Decisions 4th Edition by John Wild, Ken Shaw, Barbara Chiappetta Test Bank Link download full: http://testbankcollection.com/download/financial-andmanagerialaccounting-information-for-decisions-4th-edition-by-wild-test-bank/

Financial and Managerial Accounting Information for Decisions 4th Edition by John Wild, Ken Shaw, Barbara Chiappetta Test Bank Link download full: http://testbankcollection.com/download/financial-andmanagerialaccounting-information-for-decisions-4th-edition-by-wild-test-bank/

CODE OF ETHICS CODE OF ETHICS BGC PARTNERS, INC. CODE OF BUSINESS CONDUCT AND ETHICS UPDATED: NOVEMBER 2017

BGC PARTNERS, INC. CODE OF BUSINESS CONDUCT AND ETHICS UPDATED: NOVEMBER 2017 The reputation and integrity of BGC Partners, Inc. and its subsidiaries (collectively, the Company ) are valuable assets that

BGC PARTNERS, INC. CODE OF BUSINESS CONDUCT AND ETHICS UPDATED: NOVEMBER 2017 The reputation and integrity of BGC Partners, Inc. and its subsidiaries (collectively, the Company ) are valuable assets that

Sarbanes-Oxley Simplified

Sarbanes-Oxley Simplified 2nd edition Michel Morley, CPA Nixon-Carre Ltd., Toronto, ON Contents Introduction pg xi Chapter 1 - The Birth of the Act...

Sarbanes-Oxley Simplified 2nd edition Michel Morley, CPA Nixon-Carre Ltd., Toronto, ON Contents Introduction pg xi Chapter 1 - The Birth of the Act...

Name Chapter 1--Financial Reporting Description Instructions

Name Chapter 1--Financial Reporting Description Instructions Modify Question 1 Multiple Choice 0 points Modify Remove Question The overall objective of financial reporting is to provide information Answer

Name Chapter 1--Financial Reporting Description Instructions Modify Question 1 Multiple Choice 0 points Modify Remove Question The overall objective of financial reporting is to provide information Answer

What Real Estate Lawyers Need to Know About the Sarbanes-Oxley Act of 2002

What Real Estate Lawyers Need to Know About the Sarbanes-Oxley Act of 2002 Ann M. Saegert Dennis R. Cassell Bart J. Biggers Peter D. Christofferson Haynes and Boone, LLP 2505 North Plano Road, Suite 4000

What Real Estate Lawyers Need to Know About the Sarbanes-Oxley Act of 2002 Ann M. Saegert Dennis R. Cassell Bart J. Biggers Peter D. Christofferson Haynes and Boone, LLP 2505 North Plano Road, Suite 4000

ANTI-FRAUD CODE CONTENTS INTRODUCTION GOAL CORPORATE REFERENCE FRAMEWORK CONCEPTUAL FRAMEWORK ACTION FRAMEWORK GOVERNANCE STRUCTURE

ANTI-FRAUD CODE CONTENTS INTRODUCTION GOAL CORPORATE REFERENCE FRAMEWORK CONCEPTUAL FRAMEWORK ACTION FRAMEWORK GOVERNANCE STRUCTURE PREVENTION, DETECTION, INVESTIGATION AND RESPONSE MECHANISMS APPLICATION

ANTI-FRAUD CODE CONTENTS INTRODUCTION GOAL CORPORATE REFERENCE FRAMEWORK CONCEPTUAL FRAMEWORK ACTION FRAMEWORK GOVERNANCE STRUCTURE PREVENTION, DETECTION, INVESTIGATION AND RESPONSE MECHANISMS APPLICATION

MATTEL, INC. AMENDED AND RESTATED AUDIT COMMITTEE CHARTER

Purpose MATTEL, INC. AMENDED AND RESTATED AUDIT COMMITTEE CHARTER The purpose of the Audit Committee (the Committee ) is to provide assistance to the Board of Directors (the Board ) of Mattel, Inc. (the

Purpose MATTEL, INC. AMENDED AND RESTATED AUDIT COMMITTEE CHARTER The purpose of the Audit Committee (the Committee ) is to provide assistance to the Board of Directors (the Board ) of Mattel, Inc. (the

CBOE GLOBAL MARKETS, INC. AND SUBSIDIARIES CODE OF BUSINESS CONDUCT AND ETHICS. Adopted October 27, 2017

CBOE GLOBAL MARKETS, INC. AND SUBSIDIARIES CODE OF BUSINESS CONDUCT AND ETHICS Adopted October 27, 2017 Purpose This Code of Business Conduct and Ethics (the Code ) has been adopted by the Board of Directors

CBOE GLOBAL MARKETS, INC. AND SUBSIDIARIES CODE OF BUSINESS CONDUCT AND ETHICS Adopted October 27, 2017 Purpose This Code of Business Conduct and Ethics (the Code ) has been adopted by the Board of Directors

Intergovernmental Working Group of Experts on International Standards of Accounting and Reporting (ISAR) Keynote address

Keynote address") Intergovernmental Working Group of Experts on International Standards of Accounting and Reporting (ISAR) 32nd SESSION 4-6 November 2015 Room XVIII, Palais des Nations, Geneva Wednesday, 4 November 2015

Intergovernmental Working Group of Experts on International Standards of Accounting and Reporting (ISAR) 32nd SESSION 4-6 November 2015 Room XVIII, Palais des Nations, Geneva Wednesday, 4 November 2015

The Auditor s Responsibilities. Audit of Financial Statements

HKSA 240 Issued July 2009; revised July 2010, May 2013, February 2015 Effective for audits of financial statements for periods beginning on or after 15 December 2009 Hong Kong Standard on Auditing 240

HKSA 240 Issued July 2009; revised July 2010, May 2013, February 2015 Effective for audits of financial statements for periods beginning on or after 15 December 2009 Hong Kong Standard on Auditing 240

Module Behind the scenes Case studies International spotlights

International and US comparative curriculum master user guide: behind the scenes, case studies and international spotlights The document provides an overview of the behind the scenes, case studies and

International and US comparative curriculum master user guide: behind the scenes, case studies and international spotlights The document provides an overview of the behind the scenes, case studies and

CHAPTER II THEORETICAL REVIEW AND HYPOTHESIS DEVELOPMENT

CHAPTER II THEORETICAL REVIEW AND HYPOTHESIS DEVELOPMENT 2.1. Theories 2.1.1. Agency Theory Definition of Agency Theory based on William R. Scott (2015) is a branch of game theory that studies the design

CHAPTER II THEORETICAL REVIEW AND HYPOTHESIS DEVELOPMENT 2.1. Theories 2.1.1. Agency Theory Definition of Agency Theory based on William R. Scott (2015) is a branch of game theory that studies the design

CHAPTER 2 ANSWERS TO QUESTIONS

CHAPTER 2 Note: The letter A indicated for a question, exercise, or problem means that the question, exercise, or problem relates to a chapter appendix. ANSWERS TO QUESTIONS 1. At the acquisition date,

CHAPTER 2 Note: The letter A indicated for a question, exercise, or problem means that the question, exercise, or problem relates to a chapter appendix. ANSWERS TO QUESTIONS 1. At the acquisition date,

Related Parties 547. Source: SAS No. 122; SAS No Effective for audits of financial statements for periods ending on or after December 15, 2012.

Related Parties 547 AU-C Section 550 Related Parties Source: SAS No. 122; SAS No. 128. Effective for audits of financial statements for periods ending on or after December 15, 2012. Introduction Scope

Related Parties 547 AU-C Section 550 Related Parties Source: SAS No. 122; SAS No. 128. Effective for audits of financial statements for periods ending on or after December 15, 2012. Introduction Scope

UNITEDHEALTH GROUP BOARD OF DIRECTORS AUDIT COMMITTEE CHARTER (November 8, 2016)

") UNITEDHEALTH GROUP BOARD OF DIRECTORS AUDIT COMMITTEE CHARTER (November 8, 2016) INTRODUCTION AND PURPOSE UnitedHealth Group Incorporated (the "Company") is a publicly-held company and operates in a complex,

UNITEDHEALTH GROUP BOARD OF DIRECTORS AUDIT COMMITTEE CHARTER (November 8, 2016) INTRODUCTION AND PURPOSE UnitedHealth Group Incorporated (the "Company") is a publicly-held company and operates in a complex,

Re: File Number S

April 9, 2009 Ms. Florence Harmon Acting Secretary U.S. Securities and Exchange Commission 100 F Street, NE Washington, D.C. 20549-1090 Dear Ms. Harmon: Re: File Number S7-27-08 The American Institute

April 9, 2009 Ms. Florence Harmon Acting Secretary U.S. Securities and Exchange Commission 100 F Street, NE Washington, D.C. 20549-1090 Dear Ms. Harmon: Re: File Number S7-27-08 The American Institute

Chapter 5. Multiple Choice

Chapter 5 Multiple Choice 1. One concept of income suggests that income be measured by determining the net change over time in the discounted present value of net cash flow expected to be received by the

Chapter 5 Multiple Choice 1. One concept of income suggests that income be measured by determining the net change over time in the discounted present value of net cash flow expected to be received by the

SCHNEIDER NATIONAL, INC. AUDIT COMMITTEE OF THE BOARD OF DIRECTORS CHARTER

SCHNEIDER NATIONAL, INC. AUDIT COMMITTEE OF THE BOARD OF DIRECTORS CHARTER Purpose The primary function of the Schneider National, Inc. Audit Committee (the Committee ) is to assist the Board of Directors

SCHNEIDER NATIONAL, INC. AUDIT COMMITTEE OF THE BOARD OF DIRECTORS CHARTER Purpose The primary function of the Schneider National, Inc. Audit Committee (the Committee ) is to assist the Board of Directors

Questions are emerging regarding the historic release of the new revenue recognition standard we re here to answer them.

MFA PERSPECTIVE New Revenue Recognition Standard: Frequently Asked Questions The new converged revenue recognition standard will provide seamless guidance between U.S. GAAP and International Financial

MFA PERSPECTIVE New Revenue Recognition Standard: Frequently Asked Questions The new converged revenue recognition standard will provide seamless guidance between U.S. GAAP and International Financial

Fair value accounting debate and the future of the profession

University of Northern Iowa UNI ScholarWorks Honors Program Theses University Honors Program 2011 Fair value accounting debate and the future of the profession Kristina Ann Bowers University of Northern

University of Northern Iowa UNI ScholarWorks Honors Program Theses University Honors Program 2011 Fair value accounting debate and the future of the profession Kristina Ann Bowers University of Northern

CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS OF MINERALS TECHNOLOGIES INC.

I. PURPOSE The primary purposes of the Audit Committee (the Committee ) are to: 1. Assist the Board of Directors (the Board ) in its oversight of (i) the integrity of the Company s financial statements,

I. PURPOSE The primary purposes of the Audit Committee (the Committee ) are to: 1. Assist the Board of Directors (the Board ) in its oversight of (i) the integrity of the Company s financial statements,

SEC INFLUENCE ON ACCOUNTING

A P P E N D I X A SEC INFLUENCE ON ACCOUNTING Accountants recognize the influence of the Securities and Exchange Commission (SEC) on the development of accounting and reporting principles. Congress gave

A P P E N D I X A SEC INFLUENCE ON ACCOUNTING Accountants recognize the influence of the Securities and Exchange Commission (SEC) on the development of accounting and reporting principles. Congress gave

Vycor Medical, Inc. Audit Committee Charter

Vycor Medical, Inc. Audit Committee Charter I. Purpose and authority The audit committee is established by and among the board of directors for the primary purpose of assisting the board in: Overseeing

Vycor Medical, Inc. Audit Committee Charter I. Purpose and authority The audit committee is established by and among the board of directors for the primary purpose of assisting the board in: Overseeing

NEW REVENUE RECOGNITION STANDARD: FREQUENTLY ASKED QUESTIONS

BDO FLASH REPORT FASB 1 JUNE 2014 www.bdo.com SUBJECT NEW REVENUE RECOGNITION STANDARD: FREQUENTLY ASKED QUESTIONS SUMMARY On May 28, 2014, the FASB issued ASU 2014-09, Revenue from Contracts with Customers.

BDO FLASH REPORT FASB 1 JUNE 2014 www.bdo.com SUBJECT NEW REVENUE RECOGNITION STANDARD: FREQUENTLY ASKED QUESTIONS SUMMARY On May 28, 2014, the FASB issued ASU 2014-09, Revenue from Contracts with Customers.

CHARTER OF AUDIT COMMITTEE MONEYGRAM INTERNATIONAL, INC. As amended February 5, 2018

CHARTER OF AUDIT COMMITTEE MONEYGRAM INTERNATIONAL, INC. Purpose As amended February 5, 2018 The Audit Committee is appointed by the Board of Directors (the Board ) of MoneyGram International, Inc. (the

CHARTER OF AUDIT COMMITTEE MONEYGRAM INTERNATIONAL, INC. Purpose As amended February 5, 2018 The Audit Committee is appointed by the Board of Directors (the Board ) of MoneyGram International, Inc. (the

THE GOING CONCERN THEORY AND PRACTICE IN THE FINANCIAL AUDIT

THE GOING CONCERN THEORY AND PRACTICE IN THE FINANCIAL AUDIT Tara Ioan Gheorghe University of Oradea, Economic Sciences Department Introduction The whole financial and economic world is really interested

THE GOING CONCERN THEORY AND PRACTICE IN THE FINANCIAL AUDIT Tara Ioan Gheorghe University of Oradea, Economic Sciences Department Introduction The whole financial and economic world is really interested

CHAPTER 8: Accounting

CHAPTER 8: Accounting DECISION MAKING BY THE NUMBERS 1 LOOKING AHEAD What is accounting? How is accounting information used? What are career opportunities in accounting? What are the goals of generally

CHAPTER 8: Accounting DECISION MAKING BY THE NUMBERS 1 LOOKING AHEAD What is accounting? How is accounting information used? What are career opportunities in accounting? What are the goals of generally

Susan S Bies: Lessons to be re-learned from recent breakdowns in corporate accounting

Susan S Bies: Lessons to be re-learned from recent breakdowns in corporate accounting Remarks by Ms Susan S Bies, Member of the Board of Governors of the US Federal Reserve System, before the Institute

Susan S Bies: Lessons to be re-learned from recent breakdowns in corporate accounting Remarks by Ms Susan S Bies, Member of the Board of Governors of the US Federal Reserve System, before the Institute

Accounting in Action

1 Accounting in Action Learning Objectives 1 2 3 4 5 Identify the activities and users associated with accounting. Explain the building blocks of accounting: ethics, principles, and assumptions. State

1 Accounting in Action Learning Objectives 1 2 3 4 5 Identify the activities and users associated with accounting. Explain the building blocks of accounting: ethics, principles, and assumptions. State

The Auditor s Responsibility to Consider Fraud in an Audit of Financial Statements

Issued December 2007 International Standard on Auditing The Auditor s Responsibility to Consider Fraud in an Audit of Financial Statements The Malaysian Institute of Certified Public Accountants (Institut

Issued December 2007 International Standard on Auditing The Auditor s Responsibility to Consider Fraud in an Audit of Financial Statements The Malaysian Institute of Certified Public Accountants (Institut

NASBA 103 rd Annual Meeting

NASBA 103 rd Annual Meeting James L. Kroeker Chief Accountant U.S. Securities and Exchange Commission October 2010 1 2 t What We ve Been Working On " IFRS Work Plan Overview and Update " Major Convergence

NASBA 103 rd Annual Meeting James L. Kroeker Chief Accountant U.S. Securities and Exchange Commission October 2010 1 2 t What We ve Been Working On " IFRS Work Plan Overview and Update " Major Convergence

How to Ensure You Are Protecting Your Directors and Officers in These Troubled Times

How to Ensure You Are Protecting Your Directors and Officers in These Troubled Times Risks, Realities, and a New Paradigm Patricia J. Villareal Head, Litigation Group Securities and Corporate Governance

How to Ensure You Are Protecting Your Directors and Officers in These Troubled Times Risks, Realities, and a New Paradigm Patricia J. Villareal Head, Litigation Group Securities and Corporate Governance

Financial Accounting Theory SeventhEdition William R. Scott. Chapter 11 Earnings Management

Financial Accounting Theory SeventhEdition William R. Scott Chapter 11 Earnings Management I Chapter 11 Earnings Management What Is Earnings Management? Earnings management is the choice by a manager of

Financial Accounting Theory SeventhEdition William R. Scott Chapter 11 Earnings Management I Chapter 11 Earnings Management What Is Earnings Management? Earnings management is the choice by a manager of

FREQUENTLY ASKED QUESTIONS ABOUT PERIODIC REPORTING REQUIREMENTS FOR U.S. ISSUERS PRINCIPAL EXCHANGE ACT REPORTS

FREQUENTLY ASKED QUESTIONS ABOUT PERIODIC REPORTING REQUIREMENTS FOR U.S. ISSUERS PRINCIPAL EXCHANGE ACT REPORTS These Frequently Asked Questions should be read together with our Frequently Asked Questions

FREQUENTLY ASKED QUESTIONS ABOUT PERIODIC REPORTING REQUIREMENTS FOR U.S. ISSUERS PRINCIPAL EXCHANGE ACT REPORTS These Frequently Asked Questions should be read together with our Frequently Asked Questions

ACC105. Managing Risk in Nonprofit Organizations - 20 hours. Objectives

ACC105 Managing Risk in Nonprofit Organizations - 20 hours Objectives Like all organizations in today s volatile marketplace, nonprofits are under tremendous pressure to be more accountable for their operations,

ACC105 Managing Risk in Nonprofit Organizations - 20 hours Objectives Like all organizations in today s volatile marketplace, nonprofits are under tremendous pressure to be more accountable for their operations,

Chapters 3 and 4 Accounting Analysis (HP)

") Chapters 3 and 4 (HP) Key Learning Outcomes: Develop an understanding of the institutional environment and framework under which financial reporting standards are set, monitored and enforced. This (potentially)

Chapters 3 and 4 (HP) Key Learning Outcomes: Develop an understanding of the institutional environment and framework under which financial reporting standards are set, monitored and enforced. This (potentially)

COMPANY POLICY CODE OF BUSINESS CONDUCT AND ETHICS

COMPANY POLICY Number: 1-96-206 Effective Date: 6/28/89 Revision: 05/13/13 Reviewed: 02/27/18 Approved: Board of Directors of Appvion, Inc. CODE OF BUSINESS CONDUCT AND ETHICS I. PURPOSE. The purpose of

COMPANY POLICY Number: 1-96-206 Effective Date: 6/28/89 Revision: 05/13/13 Reviewed: 02/27/18 Approved: Board of Directors of Appvion, Inc. CODE OF BUSINESS CONDUCT AND ETHICS I. PURPOSE. The purpose of

U.S. Securities Laws Presentation. November 29, 2010 Horace Nash

U.S. Securities Laws Presentation November 29, 2010 Horace Nash hnash@fenwick.com Securities Act of 1933 Laws and Regulations Regulates sales of securities Securities Exchange Act of 1934 Regulates public

U.S. Securities Laws Presentation November 29, 2010 Horace Nash hnash@fenwick.com Securities Act of 1933 Laws and Regulations Regulates sales of securities Securities Exchange Act of 1934 Regulates public

ABC Company Business Plan

ABC Company Business Plan Web Site: www.yourdomainhere.com Email: name@yourdomainhere.com Main Office: 123 North Somewhere Street Anywhere, Michigan 12345 USA Phone: 317-000-1111 Fax: 317-111-2222 53 Confidentiality

ABC Company Business Plan Web Site: www.yourdomainhere.com Email: name@yourdomainhere.com Main Office: 123 North Somewhere Street Anywhere, Michigan 12345 USA Phone: 317-000-1111 Fax: 317-111-2222 53 Confidentiality

VIRTU FINANCIAL, INC. DISCLOSURE CONTROLS AND PROCEDURES POLICY. (adopted by the Board of Directors on April 3, 2015)

") VIRTU FINANCIAL, INC. DISCLOSURE CONTROLS AND PROCEDURES POLICY (adopted by the Board of Directors on April 3, 2015) This document sets forth the policy of Virtu Financial, Inc. a Delaware corporation

VIRTU FINANCIAL, INC. DISCLOSURE CONTROLS AND PROCEDURES POLICY (adopted by the Board of Directors on April 3, 2015) This document sets forth the policy of Virtu Financial, Inc. a Delaware corporation

CHARTER OF THE AUDIT JOINT COMMITTEE OF THE BOARDS OF DIRECTORS OF FIFTH THIRD BANCORP AND FIFTH THIRD BANK

As Approved by the Boards of Directors of Fifth Third Bancorp on March 14, 2016 and of Fifth Third Bank on March 14, 2016 CHARTER OF THE AUDIT JOINT COMMITTEE OF THE BOARDS OF DIRECTORS OF FIFTH THIRD

As Approved by the Boards of Directors of Fifth Third Bancorp on March 14, 2016 and of Fifth Third Bank on March 14, 2016 CHARTER OF THE AUDIT JOINT COMMITTEE OF THE BOARDS OF DIRECTORS OF FIFTH THIRD

CHARTER of the AUDIT COMMITTEE of the BOARD of DIRECTORS of TYSON FOODS, INC.

I. PURPOSE CHARTER of the AUDIT COMMITTEE of the BOARD of DIRECTORS of TYSON FOODS, INC. The primary function of the Audit Committee (the "Committee") is to assist the Board of Directors of Tyson Foods,

I. PURPOSE CHARTER of the AUDIT COMMITTEE of the BOARD of DIRECTORS of TYSON FOODS, INC. The primary function of the Audit Committee (the "Committee") is to assist the Board of Directors of Tyson Foods,

CHAPTER 1. Financial Accounting and Accounting Standards ASSIGNMENT CLASSIFICATION TABLE

Intermediate Accounting 14 th edition Kieso, Weygandt, Warfield Solutions Manual Link download of Solution Manual for Intermediate Accounting 14th Edition by Kieso Weygandt and Warfield: https://digitalcontentmarket.org/download/solution-manual-forintermediate-accounting-14th-edition-by-kieso-weygandt-and-warfield/

Intermediate Accounting 14 th edition Kieso, Weygandt, Warfield Solutions Manual Link download of Solution Manual for Intermediate Accounting 14th Edition by Kieso Weygandt and Warfield: https://digitalcontentmarket.org/download/solution-manual-forintermediate-accounting-14th-edition-by-kieso-weygandt-and-warfield/

California Resources Corporation. Business Ethics

California Resources Corporation Business Ethics Statement of Integrity California Resources Corporation carries on a tradition of producing oil and gas in California that stretches back many decades.

California Resources Corporation Business Ethics Statement of Integrity California Resources Corporation carries on a tradition of producing oil and gas in California that stretches back many decades.

Sarbanes-Oxley Act. The U.S. Sarbanes-Oxley Act of 2002: 2004 Update for Non-U.S. Issuers.

Sarbanes-Oxley Act The U.S. Sarbanes-Oxley Act of 2002: 2004 Update for Non-U.S. Issuers www.lw.com Sarbanes-Oxley REPORT September 1, 2004 The U.S. Sarbanes-Oxley Act of 2002: 2004 Update for Non-U.S.

Sarbanes-Oxley Act The U.S. Sarbanes-Oxley Act of 2002: 2004 Update for Non-U.S. Issuers www.lw.com Sarbanes-Oxley REPORT September 1, 2004 The U.S. Sarbanes-Oxley Act of 2002: 2004 Update for Non-U.S.

CONVERGENCE IN THE REGULATION OF INTERNATIONAL FINANCIAL MARKETS WILTON PARK CONFERENCE NOVEMBER 2005

CONVERGENCE IN THE REGULATION OF INTERNATIONAL FINANCIAL MARKETS WILTON PARK CONFERENCE 11-12 NOVEMBER 2005 PANEL 2 - PRINCIPLES OF FINANCIAL REGULATION Philippe Richard, IOSCO Secretary General I am delighted

CONVERGENCE IN THE REGULATION OF INTERNATIONAL FINANCIAL MARKETS WILTON PARK CONFERENCE 11-12 NOVEMBER 2005 PANEL 2 - PRINCIPLES OF FINANCIAL REGULATION Philippe Richard, IOSCO Secretary General I am delighted

MONDELĒZ INTERNATIONAL, INC. AMENDED AND RESTATED AUDIT COMMITTEE CHARTER. Effective January 26, 2015

Purpose. MONDELĒZ INTERNATIONAL, INC. AMENDED AND RESTATED AUDIT COMMITTEE CHARTER Effective January 26, 2015 The Audit Committee (the Committee ) of the Board of Directors (the Board ) of Mondelēz International,

Purpose. MONDELĒZ INTERNATIONAL, INC. AMENDED AND RESTATED AUDIT COMMITTEE CHARTER Effective January 26, 2015 The Audit Committee (the Committee ) of the Board of Directors (the Board ) of Mondelēz International,

HARLEY-DAVIDSON, INC. Audit and Finance Committee Charter

I. Committee s Purpose HARLEY-DAVIDSON, INC. Audit and Finance Committee Charter The Audit and Finance Committee (the Committee ) is appointed by the Board of Directors (the Board ) of Harley-Davidson,

I. Committee s Purpose HARLEY-DAVIDSON, INC. Audit and Finance Committee Charter The Audit and Finance Committee (the Committee ) is appointed by the Board of Directors (the Board ) of Harley-Davidson,

not have participated in the preparation of the Company s or any of its subsidiaries financial statements at any time during the past three years;

SABRE CORPORATION AUDIT COMMITTEE CHARTER I. Statement of Purpose The Audit Committee (the Committee ) is a standing committee of the Board of Directors (the Board ). The purpose of the Committee is to

SABRE CORPORATION AUDIT COMMITTEE CHARTER I. Statement of Purpose The Audit Committee (the Committee ) is a standing committee of the Board of Directors (the Board ). The purpose of the Committee is to

FEI Accounting and SEC/PCAOB Update

FEI Accounting and SEC/PCAOB Update Billy W. Tilotta Assurance Partner Moss Adams Mark Zilberman Assurance Partner Moss Adams Agenda for Today Accounting/FASB update Big 3 Leases Financial Instruments

FEI Accounting and SEC/PCAOB Update Billy W. Tilotta Assurance Partner Moss Adams Mark Zilberman Assurance Partner Moss Adams Agenda for Today Accounting/FASB update Big 3 Leases Financial Instruments

Aligning Marketing and Finance with Generally Accepted Standards for Valuing Brands: Opportunities and Obstacles

Aligning Marketing and Finance with Generally Accepted Standards for Valuing Brands: Opportunities and Obstacles James Gregory Michael Moore September 2012 Aligning Marketing and Finance with Generally

Aligning Marketing and Finance with Generally Accepted Standards for Valuing Brands: Opportunities and Obstacles James Gregory Michael Moore September 2012 Aligning Marketing and Finance with Generally

NARUC: REVENUE RECOGNITION JULIE PETIT AUDIT SENIOR MANAGER BRIAN JONES AUDIT SENIOR MANAGER MONDAY, SEPTEMBER 11 TH, 2017

NARUC: REVENUE RECOGNITION JULIE PETIT AUDIT SENIOR MANAGER BRIAN JONES AUDIT SENIOR MANAGER MONDAY, SEPTEMBER 11 TH, 2017 Mazars USA LLP is an independent member firm of Mazars Group. Mazars USA LLP is

NARUC: REVENUE RECOGNITION JULIE PETIT AUDIT SENIOR MANAGER BRIAN JONES AUDIT SENIOR MANAGER MONDAY, SEPTEMBER 11 TH, 2017 Mazars USA LLP is an independent member firm of Mazars Group. Mazars USA LLP is

MODULE 1 FINANCIAL ENVIRONMENT

MODULE 1 FINANCIAL ENVIRONMENT OUTLINES Aims and objectives of profit-seeking and non-profit seeking organizations. The inter-relationship between financial management, management accounting and financial

MODULE 1 FINANCIAL ENVIRONMENT OUTLINES Aims and objectives of profit-seeking and non-profit seeking organizations. The inter-relationship between financial management, management accounting and financial

GENESCO INC. CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS

GENESCO INC. CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS PURPOSE The primary purpose of the Audit Committee (the Committee ) is to assist the Board of Directors (the Board ) in fulfilling

GENESCO INC. CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS PURPOSE The primary purpose of the Audit Committee (the Committee ) is to assist the Board of Directors (the Board ) in fulfilling

SAILPOINT TECHNOLOGIES HOLDINGS, INC. AUDIT COMMITTEE OF THE BOARD OF DIRECTORS CHARTER. As Approved and Adopted by the Board of Directors

SAILPOINT TECHNOLOGIES HOLDINGS, INC. AUDIT COMMITTEE OF THE BOARD OF DIRECTORS CHARTER As Approved and Adopted by the Board of Directors November 15, 2017 I. Purpose The Board of Directors (the Board

SAILPOINT TECHNOLOGIES HOLDINGS, INC. AUDIT COMMITTEE OF THE BOARD OF DIRECTORS CHARTER As Approved and Adopted by the Board of Directors November 15, 2017 I. Purpose The Board of Directors (the Board