INVESTMENT OPPORTUNITIES AND THE VALUE-RELEVANCE OF EARNINGS, CASH FLOWS AND ACCRUALS

|

|

|

- Percival Lyons

- 6 years ago

- Views:

Transcription

1 INVESTMENT OPPORTUNITIES AND THE VALUE-RELEVANCE OF EARNINGS, CASH FLOWS AND ACCRUALS Gopal V. Krishnan Department of Accountancy City University of Hong Kong, Kowloon, Hong Kong and Krishna R. Kumar School of Business and Public Management The George Washington University, Washington, DC 20052, USA Address correspondence to: Krishna R. Kumar Department of Accountancy School of Business and Public Management The George Washington University Washington DC Phone: (202) June 2003 (Work still in progress, please do not quote) We gratefully acknowledge helpful comments and suggestions from Steve Christophe, Chris Jones, Sok-Hyon Kang, Fred Lindahl, James Livingstone, Jim Patton, Kumar Visvanathan, and especially Bill Baber. We also thank participants for comments at the accounting research workshop at The George Washington University, and at conferences of the Washington Area Finance Association, European Accounting Association and the American Accounting Association.

2 Investment Opportunities and the Value-Relevance of Earnings, Cash Flows and Accruals Abstract (Under construction) Data Availability: All data are publicly available. Keywords: Capital markets; Investment opportunities; Earnings; Cash flows from operations; Accruals; Value Relevance

3 Investment Opportunities and the Value-Relevance of Earnings, Cash Flows and Accruals I. Introduction Investment (growth) opportunities (IOS) are, for many firms, a substantial and valuable component of corporate assets. Frequently, they represent a greater part of a firm s potential for competitive advantage, abnormal profits and value creation than assets-in-place. 1 Thus, investors have a strong need for information about investment opportunities, the assessment of their value and the likelihood of their realization. Evidence is mixed on the usefulness of financial information for firms with investment opportunities. Using the ratio of market-to-book-value of equity (MB ratio) as a growth opportunities proxy, Collins and Kothari (1989) argue that earnings response coefficients (ERCs) increase with investment opportunities. On the other hand, Ahmed (1994) uses a proxy based on investment in research and development (R&D) expenditures to demonstrate that ERCs decline with growth opportunities. In the context of the wireless communications industry, Amir and Lev (1996) find that non-financial information (market potential and market penetration) dominates financial information [earnings and cash flows from operations (CFO)] in determining security prices for high-growth firms. On a stand-alone basis, they find financial information to be uninformative. Finally, Bodnar and Weintrop (BW) (1997) document higher ERCs for foreign earnings of US multinationals and make the case, using realized sales growth rates as the proxy for growth prospects, that ERCs are higher for foreign operations due to higher growth opportunities. In this paper, we reexamine relations between investment opportunities and the valuerelevance of earnings while addressing a variety of limitations in prior studies. A distinguishing feature of our study is a specification that allows ERCs to vary non-linearly with IOS. This 1

4 approach considers the possibility that the inconsistent findings across previous studies are due in part to the fitting of linear models to samples that represent different segments of the IOS spectrum. We also use a substantially larger sample, a more comprehensive and better-validated measure of investment opportunities and a measure of unexpected earnings that considers transitory earnings. Our results support a characterization wherein ERCs first increase and then decrease as IOS increases. As noted earlier, prior research offers opposing predictions for the behavior of ERCs as IOS increases. CK argue that if current earnings provide useful information to investors about the extent of abnormal profits in current and future investments, and if such abnormal profits increase with investment opportunities, then ERCs will increase with IOS. On the other hand, Ahmed (1994) and Amir and Lev (1996) argue that accounting conservatism, by proscribing the recognition of growth options on the balance sheet and requiring the immediate expensing of investments in R&D, advertising and other costs of intangible assets, compromises the informativeness of earnings as IOS increases and causes ERCs to decline. Yet other arguments, which we outline below, suggest that return responses to the CFO component of earnings may either increase or decrease as IOS increase. Our empirical results suggest that factors that cause ERCs to increase with IOS dominate for relatively low IOS values and then ERC-decreasing factors dominate for higher IOS values. Next, we extend the analysis by decomposing earnings into CFO and accruals to investigate how security returns respond to each of these earnings components as IOS increases. We are motivated by the fact that theoretical predictions for security return responses for each component as IOS increases differ from the other. On the one hand, increasing cost differentials between internal and external financing as IOS increases, attributable to information 2

5 asymmetries, agency costs and transaction costs, can cause CFO to be an increasingly important determinant of whether or not investment opportunities are realized. Consequently, security price responses to CFO denoted as the cash flow response coefficient (CRC) can increase with IOS. CRCs can also increase with IOS if, as suggested by CK, CFO as a component of earnings inform investors about abnormal earnings in current and future investments. On the other hand, the usefulness of CFO as a performance measure is potentially compromised by the deduction from CFO of investment outlays for R&D, and other intangible-asset-building expenditures dedicated to the development and realization of investment opportunities. Which of these effects dominates at various levels of IOS and how the net effect varies with IOS is an empirical question, which we address in this paper. Dechow (1994) argues that timing and matching problems in CFO increase with the volatility of working capital and cause working capital accruals to play an increasing role in the usefulness of earnings. She suggests that the informativeness of working capital accruals increases with the length of the operating cycle and the level of working capital. In the present context, her analysis suggests that the usefulness to investors of working capital accruals is likely to decline as IOS increases. This is because as IOS increases, operating assets, and more specifically working capital, are a decreasing proportion of total assets (including investment opportunities). Furthermore, the usefulness of non-current accruals is also likely to decline as IOS increases. This is because, many non-current assets, particularly intangibles, are not recorded on the balance sheet because of accounting conservatism. Others, such as goodwill and purchased intangibles, are often amortized at arbitrary rates (Ahmed 1994, Amir and Lev 1996). Thus, we expect security return responses to accruals denoted as the accrual response coefficient (ARC) to decline as IOS increases. 3

6 As a further test of our predictions, we examine whether CRC and ARC sensitivity to IOS varies with the nature of assets acquired tangibles such as inventory, receivables, land, building and equipment versus intangibles such as intellectual property, knowledge and brand power in order to realize investment opportunities. Following Smith and Watts (1992), we expect that information asymmetries and agency costs are lower for tangible assets. We also expect that the usefulness of both working capital and non-current accruals is greater when tangible assets are acquired. Thus, we expect that as IOS increases, the informativeness of CFO increases and that of accruals decreases at a faster rate for firms realizing investment opportunities through intangible rather than tangible investments. Using the ratio of R&D-plusadvertising expense to capital-expenditures as a proxy for the relative intensity of investment in intangible assets, we document that CRC sensitivity to IOS increases at a faster rate and ARC sensitivity to IOS declines at a faster rate when investment opportunities are realized to intangible investments rather than tangible investments. This study contributes in several ways to research on how investment opportunities influence security price responses to earnings and its components. First, it reconciles the conflicting results in prior research by using a more general model specification and addressing limitations, in order to provide a more complete understanding of how earnings informativeness varies with investment opportunities. Second, it extends current research by considering how the value-relevance of two important earnings components CFO and accruals varies with IOS. 2 This evidence is potentially of value to investors and analysts in determining which earnings component CFO or accruals to emphasize when they evaluate high-ios versus low-ios firms. Third, the paper contributes to research that looks beyond earnings in studying the valuation of high-growth firms. Whereas, Amir and Lev (1996) demonstrate the importance of 4

7 non-financial information, the present study shows how the usefulness of important elements of the financial information set varies as IOS increases. A standard-setting implication of our findings is that investors in large-ios firms may benefit from more detailed disclosures on operating cash flows. At the same time, new standards for large-ios firms, designed to generate more value-relevant accruals, may be called for. Finally, the paper considers a number of economic explanations for why the value-relevance of CFO increases and that of accruals decreases as IOS increases and provide evidence on them. 3 The next section of the paper discusses prior studies and how this paper addresses several of their limitations. It also presents potential explanations for how the informativeness of earnings, CFO, and accruals varies as IOS increases. Section three presents the research design and empirical methods. Sample selection, data sources and variable measurement are addressed in section four. Results are reported in section five. Conclusions are in section six. II. Prior research, theory and motivation Prior Research Studies investigating how security return responses to earnings vary with investment opportunities typically adopt model specifications of the following form. Inferences are based on coefficient a 2. CAR it = a var 0 + a1ueit + a2iosit UEit + an control _ iablesit + ε it (1) n where CAR it = the cumulative abnormal returns during the disclosure period in which performance-related information for firm i for period t is disclosed; UE it = the unexpected earnings relative to expectations for firm i at the beginning of the disclosure period; 5

8 IOS it = investment opportunities for firm i in period t; control_variables it = variables to control for potentially correlated omitted effects; a 0, a 1, a 2,, a n are parameter estimates; and γ is the error term. CK use earnings changes and the market-to-book-value-of-equity ratio to proxy for unexpected earnings and growth opportunities respectively. They limit their sample to NYSElisted firms with a minimum of three years of data. Their research design suffers from three limitations. First, the random walk specification for earnings expectations assumes that all earnings surprises are permanent. Ali and Zarowin (1992) show that estimated ERCs are biased if a random walk specification is used when earnings have transitory components and recommend inclusion of earnings levels as an additional proxy for unexpected earnings in such instances. If earnings persistence is correlated with growth opportunities, then the use of a random walk specification can result in a biased coefficient a 2 in expression (1). This is because measurement error in unexpected earnings, and the resulting bias in ERC, varies with IOS. A second limitation of CK is the use of the MB-ratio as a proxy for growth opportunities. Ahmed (1994) notes that the increase in ERC with IOS documented by CK may be driven by associations between MB ratios and expected returns. Third, CK s the selection criteria potentially bias the sample in favor of large, successful firms. Their exclusion of NASDAQlisted firms may imply that nascent, high-growth companies are underrepresented in the sample. Similar limitations characterize BW. First, they too use the random walk specification for unexpected earnings. Second, they limit their sample to firms with multinational operations for which a minimum of five years of stock returns are available. By excluding firms that have domestic operations only or have existed for less than five years, these criteria also likely cause 6

9 the sample to under-represent small firms with high-growth potential. Finally, they use historical sales growth rates to proxy for future growth expectations. Evidence in Baber, Janakiraman and Kang (1996) suggests that relative to several other measures identified by them, past revenue growth rate is a poor predictor of future growth rates. The Amir and Lev (1996) study, being limited to the wireless communications industry, focuses on a small, high-growth segment of the investment opportunities spectrum. Thus, their findings about the lack of usefulness of financial information may not be generalizable even to other high-growth industries and may be attributable to their small sample size. They do, however, address the problem of potential measurement error in earnings changes as proxies for unexpected earnings and CFO by including levels as additional explanatory variables in their specifications. Recognizing the possibility that the observed positive association between ERCs and the MB-ratio may be attributable to relations between the MB-ratio and expected returns, Ahmed (1994) uses a proxy comprised of non-market measures R&D expenditures and the replacement cost of plant, property and equipment. However, he provides no evidence to validate this measure as a proxy for future growth opportunities. Furthermore, Ahmed uses the seasonal random walk model to proxy for unexpected earnings. Thus, his results for the ERC- IOS relations can also biased because of measurement error in unexpected earnings. Finally, he limits his sample to manufacturing firms. If manufacturing firms enjoy substantially different levels of growth opportunities relative to service and other non-manufacturing industries, then Ahmed s findings may be biased, especially if the nature of ERC-IOS relations varies with the level of IOS. 7

10 How this study addresses limitations in prior studies Three features of this study are designed to address the limitations identified above. First, we require firms to have only two consecutive years data on Compustat and CRSP files in order to be included in our sample. We include all firms with sufficient data except firms in regulated industries utilities (SIC 49) and financial institutions (SIC 60). We exclude these industries in order to be consistent with Baber et al. (1996), whose measure we use to estimate investment opportunities. Thus, our sample selection process is less restrictive than prior studies and hence is more likely to include small, young firms. Second, our investment opportunities measure, originally developed by Baber, Janakiraman and Kang (1996), combines four commonly-used growth opportunities metrics the ratio of the market to book value of assets, firm growth rate, R&D intensity and investment intensity. Two key features of this measure are noteworthy. First, the four underlying metrics are similar to those used in previous studies investigating ERC-IOS relations. Specifically, the market to book value of assets is similar to the market to book value of equity ratio used in CK. The R&D and investment intensity measures are similar to the R&D stock measure used by Ahmed (1994) and the asset growth measure is similar to the revenue growth measure used in BW. Second, these growth measures are not selected arbitrarily, but rather, through a step-wise regression process that identifies them from a set of sixteen IOS metrics, based on their ability to predict the intensity of investment activity over the following five years. This validation process gives us greater confidence in our growth proxy than in those used in prior studies. We discuss this measure in greater detail in the following section. Finally, we use both earnings changes and levels as proxies for unexpected earnings. Several prior studies recommend the inclusion of earnings levels as an explanatory variable in 8

11 addition to earnings changes to mitigate bias in the estimated ERC when earnings are transitory (Ali and Zarowin, 1992; Brown et al., 1987; Easton and Harris, 1991). In subsequent analysis, we use changes and levels of CFO and accruals to proxy for unexpected CFO and accruals when we decompose unexpected earnings into these two components to examine the behavior of CRCs and ARCs as IOS increase. As noted earlier, measurement error in the unexpected earnings proxies can be correlated with IOS if persistence and IOS are correlated. If so, the use of changes and levels can reduce measurement error and mitigate bias in relations between response coefficients and IOS due to such error. Predictions about how ERCs vary with IOS A number of factors potentially affect how ERCs vary with IOS. First, CK argue that current period abnormal earnings can help investors assess the potential for abnormal earnings from future investments and hence the value of future investment opportunities. If the potential for above normal earnings is greater from investment opportunities than from assets already in place, then we expect ERCs to increase as investment opportunities increase relative to assets in place. Above normal earnings potential can be lower for assets-in-place if competition erodes their opportunities for such earnings more rapidly. Second, firms need cash in order to exploit investment opportunities. Such cash needs can be met from internal resources or through external financing. Under perfect and complete markets, such financing choices do not affect investment decisions and therefore are not relevant to firm value (Modigliani and Miller, 1958). However, market frictions such as information asymmetries, agency costs and transaction costs cause the cost of external capital to be higher than that from internal sources (Jensen and Meckling, 1976; Myers and Majluf 1984; Oliner and Rudebusch 1992). In the presence of such cost differentials, the availability of internal 9

12 resources to finance investment opportunities increases firm value. This happens for at least two reasons. First, investment projects that have positive net present values (NPVs) when financed externally have even higher NPVs when lower-cost internal resources are used instead. Second, some of the investment opportunities that are not viable (that is, have negative NPVs) if financed externally become viable positive NPV projects when financed with lower cost internal funds. We expect differences between the costs of internal and external financing to increase as investment opportunities increase. This is because, holding internal financing constant, the level of external financing increases as investment opportunities increase. External financing of investment opportunities is typically not collateralized; therefore, the marginal cost of such financing increases with the level of financing (Kaplan and Zingales 1997, p. 174; Hubbard 1998, p. 197). On the other hand, the opportunity cost of internal financing, being determined by external credit and equity market rates, is unrelated to investment opportunities. If cost differentials between internal and external financing increase with investment opportunities, then, the marginal benefits that is, the contribution to firm value of an additional dollar of internal financing increases with investment opportunities. CFO is an important internal cash resource. Therefore, it follows from the above discussion that unexpected changes in CFO can cause investors to reassess the extent that lower cost internal resources are available to realize marginal investment opportunities or to substitute for higher cost external capital, and hence, to revise stock prices. Such revisions will correlate positively with unexpected CFO. Moreover, holding unexpected CFO constant, such reassessments should be greater for large-ios firms than for small-ios firms. In other words, stock price responses to unexpected CFO are predicted to increase with IOS. 10

13 However, as noted in the introduction, deductions from CFO of investment outlays for R&D, advertising and other expenditures that potentially create intangible assets adds measurement error to reported CFO. Lack of detailed disclosures about such expenditures makes it difficult for investors to add back the deductions to CFO. As such outlays are likely to increase with investment opportunities, we expect them to increasingly compromise the informativeness of CFO as IOS increases. Together, these two arguments suggest that, to the extent that earnings consist of CFO, financing cost differentials cause ERCs to increase with IOS and mismeasurement of CFO causes ERCs to decrease as IOS increases. Accruals also potentially affect how ERCs vary with IOS. While there is strong empirical evidence indicating that accruals are highly value-relevant for the average firm (Bowen et al. 1987, Bernard and Stober, 1989), there is reason to believe that this property varies with IOS. Dechow (1994) observes that accruals enhance the value-relevance of earnings by addressing matching and timing problems in operating cash flows. This is achieved by accruing non-cash assets and liabilities on the balance sheet from the date of the cash flows to the date on which revenues or expenses are recognized. However, accruals appear to be most effective in addressing matching and timing problems for investments in tangibles such as working capital, and plant, property and equipment. This is because measurements involved in recording accruals for such assets appear to be subject to less error than for intangibles. Firms create investment opportunities through investment in specialized physical, knowledge, brand and human capital (Smith and Watts 1992). A significant portion of such investment such as on research and development, advertising, market development, and employee education and training is intangible in nature. Even tangible assets used in such 11

14 contexts, for example, laboratory equipment, are likely to be highly specialized with few alternative uses. Problems in identifying the amounts and timing of the returns on such investments imply that the accrual and allocation across time-periods of the costs of such investment can be quite arbitrary and subject to error and manipulation. Accounting standardsetters have responded conservatively to these problems by requiring the immediate expensing of such investments, particularly when they are intangible. Even in the instances when costs are capitalized, as with tangible assets or purchased intangibles, the depreciation or amortization of costs can be arbitrary. Both tangible assets and intangibles such as patents, copyrights or trademarks may be impaired by competition or obsolescence long before the end of their estimated useful lives. Alternatively, brand equity and market penetration achieved through such investments can last for many years after the assets have been fully depreciated or amortized on the balance sheet. Thus, estimates used in measuring accruals can be subject to considerable error for firms investing to create investment opportunities. Therefore, the value-relevance of accruals, and consequently ERCs, are likely to decline as investment opportunities increase relative to assets-in-place. We have identified several factors that potentially determine how ERCs vary with IOS. Some are expected to cause ERCs to increase and others to cause them to decrease as IOS increases. Prior studies have focused on one or a few of these factors and predicted monotonic trends in ERC as IOS increases. However, when several factors are present, such trends are likely only if one set of factors, either ERC-increasing or ERC-decreasing, dominate the other over the entire range of IOS. If the dominant effect(s) vary with IOS, non-monotonic patterns are likely to arise. Alternatively, if factors are uniformly offsetting across all IOS, no trend will 12

15 be detected. The inconsistent results of prior studies suggest that multiple factors influence how ERCs vary with IOS. Although we are unable to make unambiguous predictions about how ERCs vary with IOS, it is clear from our discussions that the trend in security return responses to CFO as IOS increases differs from that of return responses to accruals as IOS increases. The two factors that influence how CRCs vary with IOS the role of CFO as an internal resource and the measurement error in CFO due to the inclusion of R&D and other expenditures appear to have opposing effects, and the net trend in CRCs as IOS increases remains an empirical question. On the other hand, our discussion unambiguously predicts a decline in ARCs as IOS increases. III. Research design, empirical proxies and model specifications The primary ERC specification Our primary empirical specification to investigate how ERCs vary with IOS follows expression (1) in section II. Year and firm subscripts are suppressed. CAR = b 0 + b 1 E + b 2 E + b 3 IOS + b 4 E IOS + b 5 E IOS + b 6 E IOS 2 where + b 7 E IOS 2 + C b C control variable C + Y b Y D Y + I b I D I + b (2) CAR = the market-model-based cumulative residual stock return relative to the valueweighted NYSE, AMEX, NASD market index, aggregated over the one-year period beginning with the fourth month of the current fiscal year t; market model parameters are estimated over 250 trading days preceding the annual return window; E (Earnings change) = change in reported income before extraordinary items (Compustat annual data item #18) from the previous fiscal year t-1 to the current year t, scaled by the beginning of period market value of equity (Compustat annual data item #24 #25); E (Earnings level) = reported income before extraordinary items for the current year t, scaled by the beginning of period market value of equity; 13

16 IOS = a measure of investment opportunities estimated as in Baber, Janakiraman and Kang (1996) from a factor analysis of the variables listed in Exhibit 1; control variables C = BETA, PERSIST and INTRATE and their interactions with E and E; where BETA is a measure of systematic risk, estimated as the slope coefficient from a market-model regression of daily stock returns on the value-weighted NYSE, AMEX, NASD market index return over the one-year window beginning the fourth month of the fiscal year; PERSIST is a measure of earnings persistence, specified an indicator variable that takes the value of one when the earnings-to-price (E t-1 /P t-1 ) ratio at the beginning of fiscal year t is in the extreme four sample deciles and zero otherwise; INTRATE is the average 30-year treasury bond yield for year t; D Y = six year dummy variables for 1990 through 1995; D I = twelve industry dummy variables representing 2-digit SIC code numbers 13, 20, 28, 33, 34, 35, 36, 37, 38, 48, 50 and 73; b 0, b 1, b 2,, b I are parameter estimates; and b is the error term. Unexpected earnings proxies: Expression (2) includes current period earnings changes E and earnings levels E as empirical proxies for unexpected earnings UE in expression (1). Prior research, with the exception of Amir and Lev (1996), has typically assumed a random-walk annual earnings process and used earnings changes only as the unexpected earnings process. Following, Ali and Zarowin (1992), Brown et al. (1987) and others, we include earnings levels as an additional unexpected earnings proxy to address measurement error in earnings changes when earnings innovations are partly transitory. ERCs are estimated as the sum of the coefficients on the two proxies. Quadratic terms: We also include quadratic interaction terms E IOS 2 and E IOS 2 to allow the specification to reflect potential non-linear relations between ERCs and IOS. The discussion in the previous section indicates that ERCs may increase or decrease with IOS 14

17 depending on which of several factors dominate. The inclusion of a quadratic term allows for the possibility that the dominance of one or other factor may vary with the level of IOS. IOS measure: Earlier, we noted several limitations of investment opportunities measures used in prior studies. These included concerns that they may proxy for correlated omitted variables (as in the case of the MB ratio), that they are weakly related to future realized growth (as in the case of historical revenue growth rates) or that there is a lack of evidence to validate them as predictors of future growth [as in the case of Ahmed s (1994) R&D stock measure]. We address such concerns by using an investment opportunities measure developed by Baber et al. (1996). This measure is obtained by identifying through step-wise regression, a parsimonious set of four growth opportunities proxies from an initial list of sixteen commonly-used variables. These four measures are them aggregated into one using factor analysis and then validated by demonstrating strong associations with future realized growth measures. 4 This measure has several advantages. First, the process of aggregation through factor analysis should help reduce error in measuring the underlying investment opportunities construct relative to any individual proxy. Second, the measure uses a parsimonious set of variables and a short time-series of data, thus, minimizing loss of observations due to missing data Third, growth proxies included in the measure include growth measures commonly used in previous research. Finally, the validation of the measure by estimating correlations with realized future investment intensity and growth rates gives us confidence about the construct validity of the measure. The four measures that make up IOS are recent investment intensity (INVINT), recent asset growth rate (MVAGR), the ratio of market-to-book values of assets (MKTBKASS), and R&D intensity (R&D). Definitions of these variables are in Exhibit 1. [Insert Exhibit 1 about here] 15

18 Factor loadings used to combine the four components into a single score can vary over time and Baber et al. s loadings may not apply to our data. Hence, we re-estimate loadings. The estimation process yields an IOS mean (standard deviation) across all observations equal to zero (one) by construction. 5 Control variables: In addition to growth opportunities, prior research identifies risk, earnings persistence and interest rate as determinants of earnings response coefficients (Kormendi and Lipe 1987, Easton and Zmijewski 1989, Collins and Kothari 1989). If these variables are correlated with growth opportunities, any documented associations between ERCs and IOS may be spurious. We address such concerns by including BETA, PERSIST and INTRATE as proxies for risk, earnings persistence and interest rates. Note that the interactions of these variables with unexpected earnings measures )E and E must enter the specification in order to control for the possibility that observed ERC variations with IOS are driven by these other correlated determinants of ERCs. We follow CK in using systematic risk (Beta) as the measure of risk and long-term government bond-yields to proxy for risk-free interest rates. We adopt Ou and Penman s (1989) binary measure of persistence based on price-earnings ratios because, unlike alternative earnings time-series based measures, it uses only current data and does not require a long time-series of earnings. We include year and industry dummies in the specifications as controls for the mean effects of any remaining correlated omitted variables and to address residual cross-correlations in security returns that can bias test statistics (Bernard 1987). Specification to investigate return responses to CFO and accruals We examine the separate security return responses to CFO and accruals as IOS increases, by disaggregating earnings changes and levels in expression (2) into CFO and accrual changes 16

19 and levels in expression (3). Note that the control variables in expression (3) include interactions of BETA, PERSIST and INTRATE with changes and levels of CFO and accruals instead of changes and levels of earnings as in expression (2). CAR = c 0 + c 1 CFO + c 2 CFO + c 3 ACC + c 4 ACC + c 5 IOS + c 6 CFO IOS + c 7 CFO IOS + c 8 ACC IOS + c 9 ACC IOS + c 10 CFO IOS 2 + c 11 CFO IOS 2 + c 12 ACC IOS 2 + c 13 ACC IOS 2 + C' c C control variable C + Y c Y D Y + I c I D I + c (3) where CFO (CFO change) = change in cash flows from operations (Compustat annual data item # 308) from the previous fiscal year t-1 to the current year t, scaled by the beginning of period market value of equity; CFO (CFO level) = cash flows from operations for the current year t, scaled by the beginning of period market value of equity; ACC (Accruals change) = change in accruals from the previous fiscal year t-1 to the current year t, scaled by the beginning of period market value of equity; accruals are defined as net income before extraordinary items minus cash flows from operations; ACC (Accruals level) = accruals for the current year t, scaled by the beginning of period market value of equity; control variables C = BETA, PERSIST and INTRATE and their interactions with CFO, CFO, ACC and ACC; c 0, c 1, c 2,, c I are parameter estimates; c is the error term; and other variables are as defined in expression (2). In addition to being a natural extension of the use of earnings changes and levels as proxies for unexpected earnings, our use of CFO and accrual changes and levels as proxies for 17

20 unexpected CFO and accruals is motivated by two observations from prior studies. First, Dechow (1994) documents large negative first-order serial correlations for both CFO and accruals, thus indicating substantial mean reversion, and hence, the presence of transitory elements in these earnings components. Second, Pfeiffer and Elgers (1999) demonstrate that the inclusion of current and lagged levels a procedure that is equivalent to the inclusion of changes and levels reduces bias in the estimated response coefficients. IV. Sample selection and descriptive statistics For our sample firms, we require stock return data on the CRSP daily-returns file for at least one complete year beginning the fourth month of a fiscal year in 1990 through 1996, and for 250 trading days preceding each such year. We also require financial data to be available on Standard and Poor s Compustat. We begin with fiscal 1990 so that CFO is reported under SFAS 95 for all firms in our sample. 6 Following Baber et al. (1996) and Gaver and Gaver (1993), we exclude firms in regulated industries, in particular, utilities (SIC 49) and financial institutions (SIC 60). We also exclude firm-years with extreme values for IOS components, INVINT, MVAGR, MKTBKASS and R&D, defined as values greater than 100, 5, 30, and 1, respectively. The objective is to exclude observations for which IOS is likely to have large measurement error. Following Easton and Harris (1991) and Cheng et al. (1996), we exclude observations with values greater than 1.50 or less than for earnings and CFO changes and levels scaled by beginning of period market value of equity. After deleting outliers identified using Belsley, Kuh and Welsch (1980) diagnostics, 18,108 observations remain in our sample. Data are adjusted for stock dividends and splits. [Insert Tables 1 and 2 about here] 18

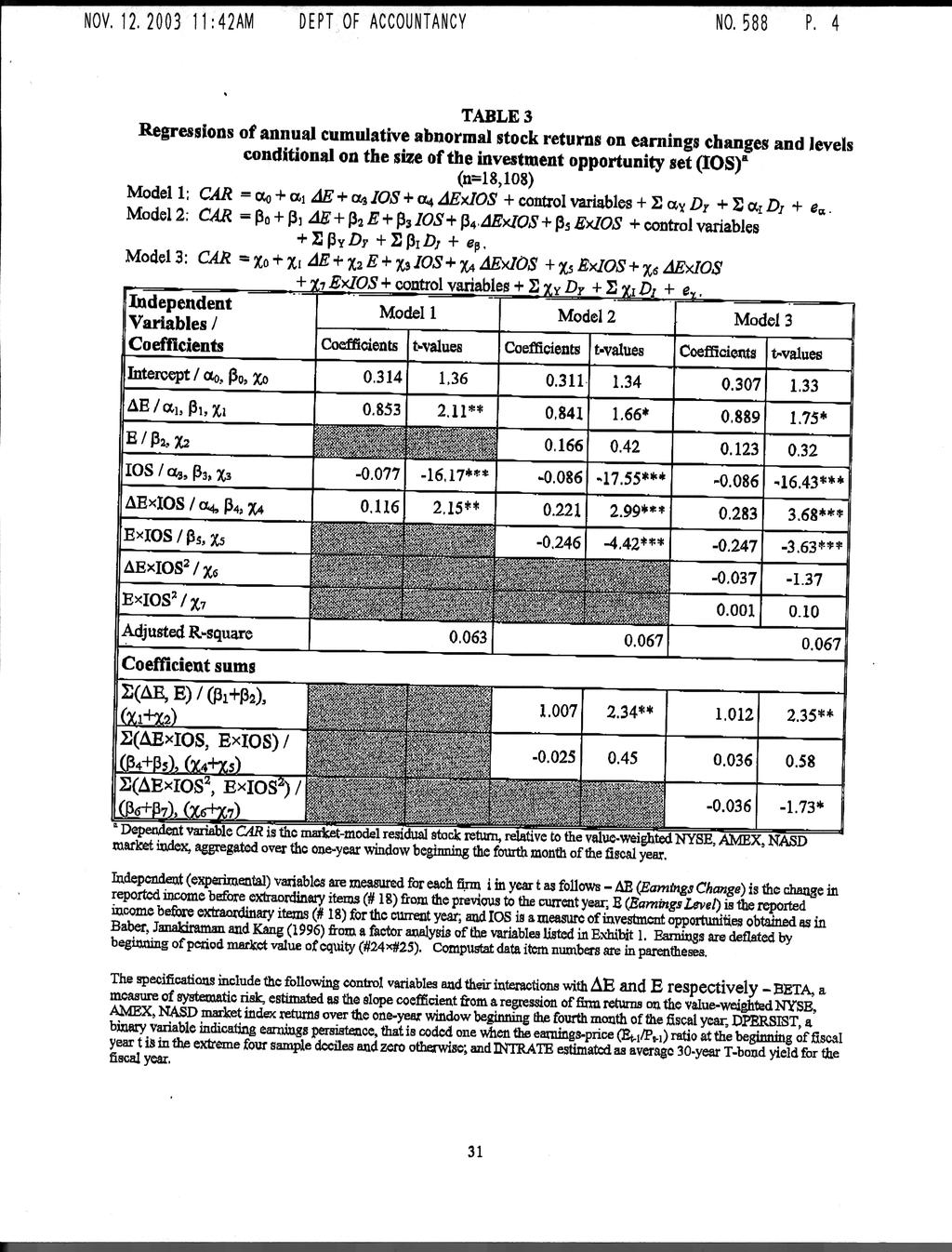

21 Descriptive statistics are in Panel A of Table 1. Pair-wise correlations are in Panel B. Comparisons of sample statistics with Dechow (1994) indicate somewhat lower earnings and CFO levels (lower means and medians) for our sample observations. 7 The 2-digit SIC Industry distribution for the sample is in Table 2. V. Results The primary ERC specification Table 3 presents results for two restricted versions of expression (2) [Models 1 and 2] and the full version [Model 3]. Model 1 includes earnings changes only ( E), as a main effect and in interactions with IOS and the control variables BETA, PERSIST and INTRATE. In addition to these variables, Model 2 includes earnings levels (E) and its interactions with IOS and the three control variables. Neither model includes E interactions with IOS 2. We present these specifications for comparison with CK and other prior studies, and to demonstrate the implications for observed ERC-IOS relations of using earnings changes as unexpected earnings proxies and specifying such relations as linear. All three models include year and industry dummy variables as in expression (2). In Model 1, the coefficient of E indicates the ERC for firms with zero values for IOS. Since zero is the mean value of IOS by construction, these are firms with average investment opportunities (see section III). Coefficient α 1 indicates that ERC is positive and significant (p 0.05) for the average firm, consistent with a large volume of prior evidence. Coefficient α 4 on the E IOS interaction suggests that ERCs increase with IOS, consistent with CK and BW. However, this result that ERCs increase with IOS is not replicated when earnings levels E and interactions are included in the specification in Model 2. In this specification, the 19

22 ERC of the average firm is indicated by the sum β 1 +β 2 of the coefficients of the main effects E and E. The coefficient sum is 1.007, positive and significant (p 0.05), and about 18% larger than the estimate from Model 1. The coefficient sum β 4 +β 5 of the interaction terms E IOS and E IOS is negative (-0.025) but not statistically significant. Thus, the effect of including earnings level E in the specification is to increase estimated ERCs by greater amounts for low-ios firms than for high-ios firms. This suggests that the ERC estimates from Model 1 are biased downwards to a greater extent for low-ios firms than for high-ios firms. This would be the case if earnings have a larger transitory component for low-ios firms; that is, if earnings persistence and IOS are positively correlated. Observed correlations between earnings persistence and IOS for our sample are indeed positive and significant (0.074, p 0.01), thus validating our concern that the use of random-walk earnings expectation models biases estimated relations between ERCs and IOS. Model 2 imposes linearity, and hence, monotonicity on the estimated ERC-IOS relation. However, our discussion in section III identifies some factors that potentially cause increases in ERCs with IOS and others that cause declines. Unless one or the other set of factors dominate over the entire range of IOS values, ERC-IOS relations are likely to be non-monotonic. In such circumstances, a non-linear model specification is preferable, because a linear specification picks up only the average trend across all observations and not the change in trend as the independent variable (IOS) changes. Moreover, when the underlying functional relationship is non-linear, the estimated slope from a linear model will vary across samples, to the extent that samples represent different parts of the population. Model 3, which follows expression (2), includes two interaction terms )EΗIOS 2 and EΗIOS 2, which allow the ERC-IOS relation, as represented by the sum of the coefficients of 20

23

24

25 return responses to accruals decline as IOS increases, consistent with the premise that accrual informativeness is increasingly impaired by conservatism and other accounting deficiencies as IOS increases. In Model 5, Ν 1 + Ν 2 indicates the CRC for the average (zero IOS) firm and has a value of 1.084, positive and significant (p 0.05), and comparable to the corresponding estimate in Model 4. Similarly, Ν 3 + Ν 4, which indicates the ARC for the average firm, is and is comparable to the estimate from Model 4. Coefficients sums Ν 6 + Ν 7 and Ν 8 + Ν 9, representing the rates of change of CRC and ARC with IOS, are positive and negative with values of and respectively. CRC increases with IOS while ARC decreases, as in Model 4. Coefficients sums Ν 10 + Ν 11 and Ν 12 + Ν 13 indicate the rate of change of the CRC-IOS and the ARC-IOS relations with IOS. The former is negative (-0.055) and significant (p 0.05), but the latter is not significantly different from zero. Thus, the rate of increase in the sensitivity of return reponses to CFO slows down as IOS increases but the rate of decline in return responses to accruals does not change materially. The partial derivative of the expression (Ν 1 + Ν 2 + Ν 6 IOS + Ν 7 IOS + Ν 10 IOS 2 + Ν 11 IOS 2 ) with respect to IOS indicates the rate at which the CRC- IOS relation changes with IOS. Setting it equal to zero, we find that, ceteris paribus, CRCs reach a maximum for IOS equal to about 5.3 and then decline. This value of IOS is in the top one percentile of the IOS distribution for our sample. Thus, CRC-IOS relations increase with IOS except for extremely high-ios firms. CFO and accrual informativeness and the nature of assets acquired Table 5 reports results for Model 6. This model modifies expression (3) in two ways. First, it includes a binary variable D as a main effect and in interaction with the unexpected CFO measures, the unexpected accrual measures, the IOS measure and their interactions. D is coded 23

26 one for firms that have high levels of expenditures on intangibles relative to tangibles defined as the ratio of R&D and advertising expenditures to capital expenditures and zero otherwise. We specify D by partitioning observations with non-zero R&D-plus-advertising-expenses-tocapital-expenditures ratio into three groups. D equals one for observations in the highest group and equals zero for observations in the lowest group. Observations in the middle group are excluded for this estimation. Finally, observations with zero R&D-plus-advertising-expenses-tocapital-expenditures ratio are assigned D equal to zero. Thus, observations with D coded as one have more intensive investments in intangibles than observations with D coded zero. The full specification of the model is in Table 5. We do not include interactions with IOS 2 in this specification in order to mitigate multicollinearity. The coefficient sum (3 rd column and 2 nd row from the bottom of the table) is positive and significant (0.243, p 0.10), indicating that CRCs increase at a faster rate with IOS for when investment is more intangible intensive. The coefficient sum (3 rd column and last row) is negative and significant ( , p 0.05), indicating that ARCs decline at a faster rate with IOS for when investment is more intangible intensive. Thus, the informativeness of CFO increases and that of accruals declines at a faster rate for firms with more intangible intensive investments as IOS increases. If information asymmetries and measurement error in accruals are greater for firms investing in intangibles, then these findings lend additional support for our explanations for CRC-IOS and ARC-IOS relations. Conclusions (Under construction) 24

27 References Ahmed, A Accounting earnings and future economic rents: An empirical analysis. Journal of Accounting and Economics 17: Ali, A The incremental information content of earnings, working capital from operations, and cash flows. Journal of Accounting Research 32: Ali. A., and P. Zarowin The role of earnings levels in annual earnings-returns studies. Journal of Accounting Research 30: Amir, E., and B. Lev Value-relevance of nonfinancial information: The wireless communications industry. Journal of Accounting and Economics 22: Baber, W. R., S. N. Janakiraman, and S-H. Kang Investment opportunities and the structure of executive compensation. Journal of Accounting and Economics 21: Belsley, D., E. Kuh, and R. Welsch Regression diagnostics: Identifying influential data and sources of collinearity. New York, NY: Wiley. Bernard, V. L Cross-sectional dependence and problems in inference in market-based accounting research. Journal of Accounting Research 25: Bernard, V. L., and T. L. Stober. 1989, The nature and amount of information in cash flows and accruals. The Accounting Review 64: Bodnar, G. M., and J. Weintrop The valuation of the foreign income of US multinational firms: A growth opportunities perspective. Journal of Accounting and Economics 24: Bowen, R. M., D. Burgstahler, and L. A. Daley The incremental information content of accruals versus cash flows. The Accounting Review 62: Brown, L. D., P. A. Griffin, R. L. Hagerman, and M. E. Zmijewski An evaluation of alternative proxies for the market's assessment of unexpected earnings. Journal of Accounting and Economics 9: Cheng, C. S. A., C-S. Liu, and T. F. Schaefer Earnings permanence and the incremental information content of cash flows from operations. Journal of Accounting Research 34: Collins, D. W., and S. P. Kothari An analysis of inter-temporal and cross-sectional determinants of earnings response coefficients. Journal of Accounting and Economics 11: Dechow, P Accounting earnings and cash flows as measures of firm performance: The role of accounting accruals. Journal of Accounting and Economics 18:

28 Easton, P. D., and T. S. Harris Earnings as an explanatory variable for returns. Journal of Accounting Research 29: Easton, P. D., and M. E. Zmijewski Cross-sectional variation in the stock market response to accounting earnings announcements. Journal of Accounting and Economics 11: Gaver, J. J. and K. M. Gaver Additional evidence on the association between the investment opportunity set and corporate financing, dividend, and compensation policies. Journal of Accounting and Economics 16: Hubbard, R. G Capital-market imperfections and investment. Journal of Economic Literature: Jensen, M. C., and W. H. Meckling Theory of the firm: Managerial behavior, agency costs and ownership structure. Journal of Financial Economics 3: Johnson, M. F. and D-W. Lee Financing constraints and the role of cash flow from operations in the prediction of future profitability. Journal of Accounting, Auditing and Finance 9: Kaplan, S. N. and L. Zingales Do investment-cash flow sensitivities provide useful measures of financing constraints? The Quarterly Journal of Economics 112: Kormendi, R. C. and R. Lipe Earnings innovations, earnings persistence, and stock prices. Journal of Business 60: Modigliani, F. and M. Miller The cost of capital, corporation finance and the theory of investment. American Economic Review 48: Myers, S. C., and N. S. Majluf Corporate financing and investment decisions when firms have information that investors do not have. Journal of Financial Economics 13: Oliner, S. D., and G. D. Rudebusch Sources of the financing heirarchy for business investment. The Review of Economics and Statistics 74: Oppong, A Information content of annual earnings announcements revisited. Journal of Accounting Research 18: Ou, J., and S. Penman Accounting measurement, price-earnings ratio, and the information content of security prices. Journal of Accounting Research 27: Pfeiffer, R. J., and P. T. Elgers Controlling for lagged stock price responses in pricing regression: An application to the pricing of cash flows and accruals. Journal of Accounting Research 37:

29 Smith, C., and R. Watts The investment opportunity set and corporate financing, dividend, and compensation policies. Journal of Financial Economics 32:

30

31 TABLE 1 Descriptive Statistics and Correlations (n=18,108) Panel A: Descriptive Statistics Variable Mean Standard Minimum 25% Median 75% Maximum Deviation CAR Ret E E CFO CFO ACC ACC IOS Panel B: Correlations a Variable CAR Ret E E CFO CFO ACC ACC IOS CAR Ret E E CFO CFO ACC ACC IOS a Pearson (Spearman) correlations are reported above (below) the diagonal. Neither correlation between the pairs, )CFO and IOS, and ACC and CAR, is statistically significant at conventional levels. Both correlations are significant at the 0.05 level or better for all other pairs. Ret is the raw return for the one-year window beginning the fourth month of the fiscal year. )E and )CFO are changes in earnings before extraordinary items (#18) and changes in cash flows from operations (#308) respectively for firm i in year t. E and CFO are the levels of earnings and cash flows from operations respectively for firm i in year t. )ACC (ACC) is computed as )E minus )CFO (E minus CFO). Changes and levels of earnings, operating cash flows, and accruals are deflated by the beginning of period market value of equity (#24 #25). Compustat data item numbers are in parentheses. IOS is a measure of the size of a firm s investment opportunity set and is estimated, as a common factor extracted from the four variables listed in exhibit 1, as in Baber et al. (1996). 29

32 TABLE 2 Industry distribution for sample firms 2-digit SIC codes Industry Number of firms Agricultural and Forestry Mining, including Oil and Gas Exploration Construction Food and Tobacco Products Textile and Apparel Lumber, Wood and Furniture Products Paper, Printing, and Publishing Chemicals and Allied Products Petroleum Refining Rubber, Plastic and Leather Products Stone, Clay, Glass and Concrete Products Primary Metal Industries Fabricated Metal Industries Industrial and Commercial Machinery including Computing Equipment Electrical Machinery and Equipment Transportation Equipment Instruments Miscellaneous Manufacturing Transportation Services Communication Services Durable Goods Wholesale Non-Durable Goods Wholesale Retail Various Brokerage and Credit Services Insurance Other Financial Services Hotels and Lodging Services Personal Services Business Services Automobile Repair and Services 8 76 Miscellaneous Repair Services Motion Pictures and Other Entertainment Services Health, Legal, Educational, and Consultancy Services Others 3 Total

33

Internal versus external equity funding sources and earnings response coefficients

Title Internal versus external equity funding sources and earnings response coefficients Author(s) Park, CW; Pincus, M Citation Review Of Quantitative Finance And Accounting, 2001, v. 16 n. 1, p. 33-52

Title Internal versus external equity funding sources and earnings response coefficients Author(s) Park, CW; Pincus, M Citation Review Of Quantitative Finance And Accounting, 2001, v. 16 n. 1, p. 33-52

The Unique Effect of Depreciation on Earnings Properties: Persistence and Value Relevance of Earnings

The Unique Effect of Depreciation on Earnings Properties: Persistence and Value Relevance of Earnings C.S. Agnes Cheng The Hong Kong PolyTechnic University Cathy Zishang Liu University of Houston Downtown

The Unique Effect of Depreciation on Earnings Properties: Persistence and Value Relevance of Earnings C.S. Agnes Cheng The Hong Kong PolyTechnic University Cathy Zishang Liu University of Houston Downtown

Management Science Letters

Management Science Letters 3 (2013) 2039 2048 Contents lists available at GrowingScience Management Science Letters homepage: www.growingscience.com/msl A study on relationship between investment opportunities

Management Science Letters 3 (2013) 2039 2048 Contents lists available at GrowingScience Management Science Letters homepage: www.growingscience.com/msl A study on relationship between investment opportunities

Core CFO and Future Performance. Abstract

Core CFO and Future Performance Rodrigo S. Verdi Sloan School of Management Massachusetts Institute of Technology 50 Memorial Drive E52-403A Cambridge, MA 02142 rverdi@mit.edu Abstract This paper investigates

Core CFO and Future Performance Rodrigo S. Verdi Sloan School of Management Massachusetts Institute of Technology 50 Memorial Drive E52-403A Cambridge, MA 02142 rverdi@mit.edu Abstract This paper investigates

The Reconciling Role of Earnings in Equity Valuation

The Reconciling Role of Earnings in Equity Valuation Bixia Xu Assistant Professor School of Business Wilfrid Laurier University Waterloo, Ontario, N2L 3C5 (519) 884-0710 ext. 2659; Fax: (519) 884.0201;

The Reconciling Role of Earnings in Equity Valuation Bixia Xu Assistant Professor School of Business Wilfrid Laurier University Waterloo, Ontario, N2L 3C5 (519) 884-0710 ext. 2659; Fax: (519) 884.0201;

A Synthesis of Accrual Quality and Abnormal Accrual Models: An Empirical Implementation

A Synthesis of Accrual Quality and Abnormal Accrual Models: An Empirical Implementation Jinhan Pae a* a Korea University Abstract Dechow and Dichev s (2002) accrual quality model suggests that the Jones

A Synthesis of Accrual Quality and Abnormal Accrual Models: An Empirical Implementation Jinhan Pae a* a Korea University Abstract Dechow and Dichev s (2002) accrual quality model suggests that the Jones

Pricing and Mispricing in the Cross Section

Pricing and Mispricing in the Cross Section D. Craig Nichols Whitman School of Management Syracuse University James M. Wahlen Kelley School of Business Indiana University Matthew M. Wieland J.M. Tull School

Pricing and Mispricing in the Cross Section D. Craig Nichols Whitman School of Management Syracuse University James M. Wahlen Kelley School of Business Indiana University Matthew M. Wieland J.M. Tull School

Accounting Conservatism and the Relation Between Returns and Accounting Data

Review of Accounting Studies, 9, 495 521, 2004 Ó 2004 Kluwer Academic Publishers. Manufactured in The Netherlands. Accounting Conservatism and the Relation Between Returns and Accounting Data PETER EASTON*

Review of Accounting Studies, 9, 495 521, 2004 Ó 2004 Kluwer Academic Publishers. Manufactured in The Netherlands. Accounting Conservatism and the Relation Between Returns and Accounting Data PETER EASTON*

J. Account. Public Policy

J. Account. Public Policy 28 (2009) 16 32 Contents lists available at ScienceDirect J. Account. Public Policy journal homepage: www.elsevier.com/locate/jaccpubpol The value relevance of R&D across profit

J. Account. Public Policy 28 (2009) 16 32 Contents lists available at ScienceDirect J. Account. Public Policy journal homepage: www.elsevier.com/locate/jaccpubpol The value relevance of R&D across profit

The Persistence of Cash Flow Components into Future Cash Flows

The Persistence of Cash Flow Components into Future Cash Flows C. S. Agnes Cheng * Securities Exchange Commission, Washington, DC University of Houston, Houston, Texas 77204-4852 CHENGA@SEC.GOV Dana Hollie

The Persistence of Cash Flow Components into Future Cash Flows C. S. Agnes Cheng * Securities Exchange Commission, Washington, DC University of Houston, Houston, Texas 77204-4852 CHENGA@SEC.GOV Dana Hollie

Valuation of tax expense

Valuation of tax expense Jacob Thomas Yale University School of Management (203) 432-5977 jake.thomas@yale.edu Frank Zhang Yale University School of Management (203) 432-7938 frank.zhang@yale.edu August

Valuation of tax expense Jacob Thomas Yale University School of Management (203) 432-5977 jake.thomas@yale.edu Frank Zhang Yale University School of Management (203) 432-7938 frank.zhang@yale.edu August

Personal Dividend and Capital Gains Taxes: Further Examination of the Signaling Bang for the Buck. May 2004

Personal Dividend and Capital Gains Taxes: Further Examination of the Signaling Bang for the Buck May 2004 Personal Dividend and Capital Gains Taxes: Further Examination of the Signaling Bang for the Buck

Personal Dividend and Capital Gains Taxes: Further Examination of the Signaling Bang for the Buck May 2004 Personal Dividend and Capital Gains Taxes: Further Examination of the Signaling Bang for the Buck

MIT Sloan School of Management

MIT Sloan School of Management Working Paper 4262-02 September 2002 Reporting Conservatism, Loss Reversals, and Earnings-based Valuation Peter R. Joos, George A. Plesko 2002 by Peter R. Joos, George A.

MIT Sloan School of Management Working Paper 4262-02 September 2002 Reporting Conservatism, Loss Reversals, and Earnings-based Valuation Peter R. Joos, George A. Plesko 2002 by Peter R. Joos, George A.

Discussion Reactions to Dividend Changes Conditional on Earnings Quality

Discussion Reactions to Dividend Changes Conditional on Earnings Quality DORON NISSIM* Corporate disclosures are an important source of information for investors. Many studies have documented strong price

Discussion Reactions to Dividend Changes Conditional on Earnings Quality DORON NISSIM* Corporate disclosures are an important source of information for investors. Many studies have documented strong price

Research Methods in Accounting

01130591 Research Methods in Accounting Capital Markets Research in Accounting Dr Polwat Lerskullawat: fbuspwl@ku.ac.th Dr Suthawan Prukumpai: fbusswp@ku.ac.th Assoc Prof Tipparat Laohavichien: fbustrl@ku.ac.th

01130591 Research Methods in Accounting Capital Markets Research in Accounting Dr Polwat Lerskullawat: fbuspwl@ku.ac.th Dr Suthawan Prukumpai: fbusswp@ku.ac.th Assoc Prof Tipparat Laohavichien: fbustrl@ku.ac.th

Yale ICF Working Paper No March 2003

Yale ICF Working Paper No. 03-07 March 2003 CONSERVATISM AND CROSS-SECTIONAL VARIATION IN THE POST-EARNINGS- ANNOUNCEMENT-DRAFT Ganapathi Narayanamoorthy Yale School of Management This paper can be downloaded

Yale ICF Working Paper No. 03-07 March 2003 CONSERVATISM AND CROSS-SECTIONAL VARIATION IN THE POST-EARNINGS- ANNOUNCEMENT-DRAFT Ganapathi Narayanamoorthy Yale School of Management This paper can be downloaded

Earnings Response Coefficients and Default Risk: Case of Korean Firms

Earnings Response Coefficients and Default Risk: Case of Korean Firms Yohan An Department of Finance and Accounting, Tongmyoung University, Busan, South Korea Correspondence: Dr. Yohan An, Assistant Professor,

Earnings Response Coefficients and Default Risk: Case of Korean Firms Yohan An Department of Finance and Accounting, Tongmyoung University, Busan, South Korea Correspondence: Dr. Yohan An, Assistant Professor,

How Does Earnings Management Affect Innovation Strategies of Firms?

How Does Earnings Management Affect Innovation Strategies of Firms? Abstract This paper examines how earnings quality affects innovation strategies and their economic consequences. Previous literatures

How Does Earnings Management Affect Innovation Strategies of Firms? Abstract This paper examines how earnings quality affects innovation strategies and their economic consequences. Previous literatures

Unexpected Earnings, Abnormal Accruals, and Changes in CEO Bonuses

The International Journal of Accounting Studies 2006 Special Issue pp. 25-50 Unexpected Earnings, Abnormal Accruals, and Changes in CEO Bonuses Chih-Ying Chen Hong Kong University of Science and Technology

The International Journal of Accounting Studies 2006 Special Issue pp. 25-50 Unexpected Earnings, Abnormal Accruals, and Changes in CEO Bonuses Chih-Ying Chen Hong Kong University of Science and Technology

Cash holdings determinants in the Portuguese economy 1

17 Cash holdings determinants in the Portuguese economy 1 Luísa Farinha Pedro Prego 2 Abstract The analysis of liquidity management decisions by firms has recently been used as a tool to investigate the

17 Cash holdings determinants in the Portuguese economy 1 Luísa Farinha Pedro Prego 2 Abstract The analysis of liquidity management decisions by firms has recently been used as a tool to investigate the

Dividend Changes and Future Profitability

THE JOURNAL OF FINANCE VOL. LVI, NO. 6 DEC. 2001 Dividend Changes and Future Profitability DORON NISSIM and AMIR ZIV* ABSTRACT We investigate the relation between dividend changes and future profitability,

THE JOURNAL OF FINANCE VOL. LVI, NO. 6 DEC. 2001 Dividend Changes and Future Profitability DORON NISSIM and AMIR ZIV* ABSTRACT We investigate the relation between dividend changes and future profitability,

The Journal of Applied Business Research March/April 2015 Volume 31, Number 2

Accounting Conservatism, Changes In Real Investment, And Analysts Earnings Forecasts Kyong Soo Choi, Keimyung University, South Korea Se Joong Lee, Ph.D student, The University of Hong Kong, Hong Kong

Accounting Conservatism, Changes In Real Investment, And Analysts Earnings Forecasts Kyong Soo Choi, Keimyung University, South Korea Se Joong Lee, Ph.D student, The University of Hong Kong, Hong Kong

Investment Opportunity Set Dependence of Dividend Yield and Price Earnings Ratio

Volume 27 Number 3 2001 65 Investment Opportunity Set Dependence of Dividend Yield and Price Earnings Ratio by Ahmed Riahi-Belkaoui and Ronald D. Picur, University of Illinois at Chicago Abstract This

Volume 27 Number 3 2001 65 Investment Opportunity Set Dependence of Dividend Yield and Price Earnings Ratio by Ahmed Riahi-Belkaoui and Ronald D. Picur, University of Illinois at Chicago Abstract This

Managerial compensation and the threat of takeover

Journal of Financial Economics 47 (1998) 219 239 Managerial compensation and the threat of takeover Anup Agrawal*, Charles R. Knoeber College of Management, North Carolina State University, Raleigh, NC

Journal of Financial Economics 47 (1998) 219 239 Managerial compensation and the threat of takeover Anup Agrawal*, Charles R. Knoeber College of Management, North Carolina State University, Raleigh, NC

Online Appendix to. The Value of Crowdsourced Earnings Forecasts

Online Appendix to The Value of Crowdsourced Earnings Forecasts This online appendix tabulates and discusses the results of robustness checks and supplementary analyses mentioned in the paper. A1. Estimating

Online Appendix to The Value of Crowdsourced Earnings Forecasts This online appendix tabulates and discusses the results of robustness checks and supplementary analyses mentioned in the paper. A1. Estimating

Do Auditors Use The Information Reflected In Book-Tax Differences? Discussion

Do Auditors Use The Information Reflected In Book-Tax Differences? Discussion David Weber and Michael Willenborg, University of Connecticut Hanlon and Krishnan (2006), hereinafter HK, address an interesting

Do Auditors Use The Information Reflected In Book-Tax Differences? Discussion David Weber and Michael Willenborg, University of Connecticut Hanlon and Krishnan (2006), hereinafter HK, address an interesting

Business Cycles and the Relation between Security Returns and Earnings

Review of Accounting Studies, 4, 93 117 (1999) c 1999 Kluwer Academic Publishers, Boston. Manufactured in The Netherlands. Business Cycles and the Relation between Security Returns and Earnings MARILYN

Review of Accounting Studies, 4, 93 117 (1999) c 1999 Kluwer Academic Publishers, Boston. Manufactured in The Netherlands. Business Cycles and the Relation between Security Returns and Earnings MARILYN

Sources of Financing in Different Forms of Corporate Liquidity and the Performance of M&As

Sources of Financing in Different Forms of Corporate Liquidity and the Performance of M&As Zhenxu Tong * University of Exeter Jian Liu ** University of Exeter This draft: August 2016 Abstract We examine

Sources of Financing in Different Forms of Corporate Liquidity and the Performance of M&As Zhenxu Tong * University of Exeter Jian Liu ** University of Exeter This draft: August 2016 Abstract We examine

Managerial Horizons, Accounting Choices and Informativeness of Earnings

Managerial Horizons, Accounting Choices and Informativeness of Earnings by Albert L. Nagy University of Tennessee (423) 974-2551 Kathleen Blackburn Norris University of Tennessee Richard A. Riley, Jr.

Managerial Horizons, Accounting Choices and Informativeness of Earnings by Albert L. Nagy University of Tennessee (423) 974-2551 Kathleen Blackburn Norris University of Tennessee Richard A. Riley, Jr.

The Effect of Financial Constraints, Investment Policy and Product Market Competition on the Value of Cash Holdings

The Effect of Financial Constraints, Investment Policy and Product Market Competition on the Value of Cash Holdings Abstract This paper empirically investigates the value shareholders place on excess cash

The Effect of Financial Constraints, Investment Policy and Product Market Competition on the Value of Cash Holdings Abstract This paper empirically investigates the value shareholders place on excess cash

Earnings quality and earnings management : the role of accounting accruals Bissessur, S.W.

UvA-DARE (Digital Academic Repository) Earnings quality and earnings management : the role of accounting accruals Bissessur, S.W. Link to publication Citation for published version (APA): Bissessur, S.

UvA-DARE (Digital Academic Repository) Earnings quality and earnings management : the role of accounting accruals Bissessur, S.W. Link to publication Citation for published version (APA): Bissessur, S.

A Matter of Principle: Accounting Reports Convey Both Cash-Flow News and Discount-Rate News. Stephen H. Penman*

A Matter of Principle: Accounting Reports Convey Both Cash-Flow News and Discount-Rate News Stephen H. Penman* Columbia Business School, Columbia University Nir Yehuda University of Texas at Dallas January

A Matter of Principle: Accounting Reports Convey Both Cash-Flow News and Discount-Rate News Stephen H. Penman* Columbia Business School, Columbia University Nir Yehuda University of Texas at Dallas January

The Free Cash Flow Effects of Capital Expenditure Announcements. Catherine Shenoy and Nikos Vafeas* Abstract

The Free Cash Flow Effects of Capital Expenditure Announcements Catherine Shenoy and Nikos Vafeas* Abstract In this paper we study the market reaction to capital expenditure announcements in the backdrop

The Free Cash Flow Effects of Capital Expenditure Announcements Catherine Shenoy and Nikos Vafeas* Abstract In this paper we study the market reaction to capital expenditure announcements in the backdrop

Deviations from Optimal Corporate Cash Holdings and the Valuation from a Shareholder s Perspective

Deviations from Optimal Corporate Cash Holdings and the Valuation from a Shareholder s Perspective Zhenxu Tong * University of Exeter Abstract The tradeoff theory of corporate cash holdings predicts that

Deviations from Optimal Corporate Cash Holdings and the Valuation from a Shareholder s Perspective Zhenxu Tong * University of Exeter Abstract The tradeoff theory of corporate cash holdings predicts that

Eli Amir ab, Eti Einhorn a & Itay Kama a a Recanati Graduate School of Business Administration,

This article was downloaded by: [Tel Aviv University] On: 18 December 2013, At: 02:20 Publisher: Routledge Informa Ltd Registered in England and Wales Registered Number: 1072954 Registered office: Mortimer

This article was downloaded by: [Tel Aviv University] On: 18 December 2013, At: 02:20 Publisher: Routledge Informa Ltd Registered in England and Wales Registered Number: 1072954 Registered office: Mortimer

Pricing and Mispricing in the Cross-Section

Pricing and Mispricing in the Cross-Section D. Craig Nichols Whitman School of Management Syracuse University James M. Wahlen Kelley School of Business Indiana University Matthew M. Wieland Kelley School

Pricing and Mispricing in the Cross-Section D. Craig Nichols Whitman School of Management Syracuse University James M. Wahlen Kelley School of Business Indiana University Matthew M. Wieland Kelley School

The Usefulness of Core and Non-Core Cash Flows in Predicting Future Cash Flows

The Usefulness of Core and Non-Core Cash Flows in Predicting Future Cash Flows by C. S. Agnes Cheng University of Houston Houston, Texas 77204-4852 Dana Hollie* University of Houston Houston, Texas 77204-4852

The Usefulness of Core and Non-Core Cash Flows in Predicting Future Cash Flows by C. S. Agnes Cheng University of Houston Houston, Texas 77204-4852 Dana Hollie* University of Houston Houston, Texas 77204-4852

The Effect of Matching on Firm Earnings Components

Scientific Annals of Economics and Business 64 (4), 2017, 513-524 DOI: 10.1515/saeb-2017-0033 The Effect of Matching on Firm Earnings Components Joong-Seok Cho *, Hyung Ju Park ** Abstract Using a sample

Scientific Annals of Economics and Business 64 (4), 2017, 513-524 DOI: 10.1515/saeb-2017-0033 The Effect of Matching on Firm Earnings Components Joong-Seok Cho *, Hyung Ju Park ** Abstract Using a sample

Further Test on Stock Liquidity Risk With a Relative Measure

International Journal of Education and Research Vol. 1 No. 3 March 2013 Further Test on Stock Liquidity Risk With a Relative Measure David Oima* David Sande** Benjamin Ombok*** Abstract Negative relationship

International Journal of Education and Research Vol. 1 No. 3 March 2013 Further Test on Stock Liquidity Risk With a Relative Measure David Oima* David Sande** Benjamin Ombok*** Abstract Negative relationship

The Separate Valuation Relevance of Earnings, Book Value and their Components in Profit and Loss Making Firms: UK Evidence

MPRA Munich Personal RePEc Archive The Separate Valuation Relevance of Earnings, Book Value and their Components in Profit and Loss Making Firms: UK Evidence S Akbar The University of Liverpool 2007 Online

MPRA Munich Personal RePEc Archive The Separate Valuation Relevance of Earnings, Book Value and their Components in Profit and Loss Making Firms: UK Evidence S Akbar The University of Liverpool 2007 Online

Appendix. In this Appendix, we present the construction of variables, data source, and some empirical procedures.

Appendix In this Appendix, we present the construction of variables, data source, and some empirical procedures. A.1. Variable Definition and Data Source Variable B/M CAPX/A Cash/A Cash flow volatility

Appendix In this Appendix, we present the construction of variables, data source, and some empirical procedures. A.1. Variable Definition and Data Source Variable B/M CAPX/A Cash/A Cash flow volatility

Pricing and Mispricing Effects of SFAS 131

Journal of Business Finance & Accounting, 35(3) & (4), 281 306, April/May 2008, 0306-686X doi: 10.1111/j.1468-5957.2007.02071.x Pricing and Mispricing Effects of SFAS 131 Ole-Kristian Hope, Tony Kang,

Journal of Business Finance & Accounting, 35(3) & (4), 281 306, April/May 2008, 0306-686X doi: 10.1111/j.1468-5957.2007.02071.x Pricing and Mispricing Effects of SFAS 131 Ole-Kristian Hope, Tony Kang,

Web Appendix: Do Arbitrageurs Amplify Economic Shocks?

Web Appendix: Do Arbitrageurs Amplify Economic Shocks? Harrison Hong Princeton University Jeffrey D. Kubik Syracuse University Tal Fishman Parkcentral Capital Management We have carried out a number of

Web Appendix: Do Arbitrageurs Amplify Economic Shocks? Harrison Hong Princeton University Jeffrey D. Kubik Syracuse University Tal Fishman Parkcentral Capital Management We have carried out a number of

The Role of Credit Ratings in the. Dynamic Tradeoff Model. Viktoriya Staneva*

The Role of Credit Ratings in the Dynamic Tradeoff Model Viktoriya Staneva* This study examines what costs and benefits of debt are most important to the determination of the optimal capital structure.

The Role of Credit Ratings in the Dynamic Tradeoff Model Viktoriya Staneva* This study examines what costs and benefits of debt are most important to the determination of the optimal capital structure.

Adjusting for earnings volatility in earnings forecast models

Uppsala University Department of Business Studies Spring 14 Bachelor thesis Supervisor: Joachim Landström Authors: Sandy Samour & Fabian Söderdahl Adjusting for earnings volatility in earnings forecast

Uppsala University Department of Business Studies Spring 14 Bachelor thesis Supervisor: Joachim Landström Authors: Sandy Samour & Fabian Söderdahl Adjusting for earnings volatility in earnings forecast

A Replication Study of Ball and Brown (1968): Comparative Analysis of China and the US *

: Comparative Analysis of China and the US *") DOI 10.7603/s40570-014-0007-1 66 2014 年 6 月第 16 卷第 2 期 中国会计与财务研究 C h i n a A c c o u n t i n g a n d F i n a n c e R e v i e w Volume 16, Number 2 June 2014 A Replication Study of Ball and Brown (1968):

DOI 10.7603/s40570-014-0007-1 66 2014 年 6 月第 16 卷第 2 期 中国会计与财务研究 C h i n a A c c o u n t i n g a n d F i n a n c e R e v i e w Volume 16, Number 2 June 2014 A Replication Study of Ball and Brown (1968):

Evaluating the accrual-fixation hypothesis as an explanation for the accrual anomaly

Evaluating the accrual-fixation hypothesis as an explanation for the accrual anomaly Tzachi Zach * Olin School of Business Washington University in St. Louis St. Louis, MO 63130 Tel: (314)-9354528 zach@olin.wustl.edu

Evaluating the accrual-fixation hypothesis as an explanation for the accrual anomaly Tzachi Zach * Olin School of Business Washington University in St. Louis St. Louis, MO 63130 Tel: (314)-9354528 zach@olin.wustl.edu

Investor Uncertainty and the Earnings-Return Relation

Investor Uncertainty and the Earnings-Return Relation Dissertation Proposal Defended: December 3, 2004 Kenneth J. Reichelt Ph.D. Candidate School of Accountancy University of Missouri Columbia Columbia,

Investor Uncertainty and the Earnings-Return Relation Dissertation Proposal Defended: December 3, 2004 Kenneth J. Reichelt Ph.D. Candidate School of Accountancy University of Missouri Columbia Columbia,

Audit Quality of Second-Tier Auditors: Are All Created Equally? R. Mithu Dey and Lucy S. Lim. Web Appendix

Audit Quality of Second-Tier Auditors: Are All Created Equally? R. Mithu Dey and Lucy S. Lim The BRC Academy Journal of Business 4, no. 1 (2014): 1-26. http://dx.doi.org/10.15239/j.brcacadjb.2014.04.01.ja01

Audit Quality of Second-Tier Auditors: Are All Created Equally? R. Mithu Dey and Lucy S. Lim The BRC Academy Journal of Business 4, no. 1 (2014): 1-26. http://dx.doi.org/10.15239/j.brcacadjb.2014.04.01.ja01

Accrued Earnings and Growth: Implications for Earnings Persistence and Market Mispricing

Accrued Earnings and Growth: Implications for Earnings Persistence and Market Mispricing by Patricia M. Fairfield a Scott Whisenant b Teri Lombardi Yohn a November 2001 Corresponding author Teri Lombardi

Accrued Earnings and Growth: Implications for Earnings Persistence and Market Mispricing by Patricia M. Fairfield a Scott Whisenant b Teri Lombardi Yohn a November 2001 Corresponding author Teri Lombardi

Real Estate Ownership by Non-Real Estate Firms: The Impact on Firm Returns

Real Estate Ownership by Non-Real Estate Firms: The Impact on Firm Returns Yongheng Deng and Joseph Gyourko 1 Zell/Lurie Real Estate Center at Wharton University of Pennsylvania Prepared for the Corporate

Real Estate Ownership by Non-Real Estate Firms: The Impact on Firm Returns Yongheng Deng and Joseph Gyourko 1 Zell/Lurie Real Estate Center at Wharton University of Pennsylvania Prepared for the Corporate

Earnings Announcements, Analyst Forecasts, and Trading Volume *

Seoul Journal of Business Volume 19, Number 2 (December 2013) Earnings Announcements, Analyst Forecasts, and Trading Volume * Minsup Song **1) Sogang Business School Sogang University Abstract Empirical

Seoul Journal of Business Volume 19, Number 2 (December 2013) Earnings Announcements, Analyst Forecasts, and Trading Volume * Minsup Song **1) Sogang Business School Sogang University Abstract Empirical

Earnings quality and earnings management : the role of accounting accruals Bissessur, S.W.

UvA-DARE (Digital Academic Repository) Earnings quality and earnings management : the role of accounting accruals Bissessur, S.W. Link to publication Citation for published version (APA): Bissessur, S.

UvA-DARE (Digital Academic Repository) Earnings quality and earnings management : the role of accounting accruals Bissessur, S.W. Link to publication Citation for published version (APA): Bissessur, S.

Evidence of conditional conservatism: fact or artifact? Panos N. Patatoukas Yale University

Evidence of conditional conservatism: fact or artifact? Panos N. Patatoukas Yale University panagiotis.patatoukas@yale.edu Jacob Thomas Yale University jake.thomas@yale.edu Current Version: October 5,

Evidence of conditional conservatism: fact or artifact? Panos N. Patatoukas Yale University panagiotis.patatoukas@yale.edu Jacob Thomas Yale University jake.thomas@yale.edu Current Version: October 5,

Do Investors Fully Understand the Implications of the Persistence of Revenue and Expense Surprises for Future Prices?

Do Investors Fully Understand the Implications of the Persistence of Revenue and Expense Surprises for Future Prices? Narasimhan Jegadeesh Dean s Distinguished Professor Goizueta Business School Emory

Do Investors Fully Understand the Implications of the Persistence of Revenue and Expense Surprises for Future Prices? Narasimhan Jegadeesh Dean s Distinguished Professor Goizueta Business School Emory

Journal of Applied Business Research Volume 20, Number 4

Management Compensation And Project Life Charles I. Harter, (E-mail: charles.harter@ndsu.nodak.edu), North Dakota State University T. Harikumar, New Mexico State University Abstract The goal of this paper

Management Compensation And Project Life Charles I. Harter, (E-mail: charles.harter@ndsu.nodak.edu), North Dakota State University T. Harikumar, New Mexico State University Abstract The goal of this paper

What Drives the Earnings Announcement Premium?

What Drives the Earnings Announcement Premium? Hae mi Choi Loyola University Chicago This study investigates what drives the earnings announcement premium. Prior studies have offered various explanations

What Drives the Earnings Announcement Premium? Hae mi Choi Loyola University Chicago This study investigates what drives the earnings announcement premium. Prior studies have offered various explanations

Internet Appendix to Broad-based Employee Stock Ownership: Motives and Outcomes *

Internet Appendix to Broad-based Employee Stock Ownership: Motives and Outcomes * E. Han Kim and Paige Ouimet This appendix contains 10 tables reporting estimation results mentioned in the paper but not

Internet Appendix to Broad-based Employee Stock Ownership: Motives and Outcomes * E. Han Kim and Paige Ouimet This appendix contains 10 tables reporting estimation results mentioned in the paper but not

Is Residual Income Really Uninformative About Stock Returns?

Preliminary and Incomplete Please do not cite Is Residual Income Really Uninformative About Stock Returns? by Sudhakar V. Balachandran* and Partha Mohanram* October 25, 2006 Abstract: Prior research found