Long term exchange rate and inflation

|

|

|

- Verity Wright

- 6 years ago

- Views:

Transcription

1 International Finance Master in International Economic Policy Long term exchange rate and inflation Lectures 5 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr

2 Motivation and roadmap What are the determinants of exchange rates in the long term? Is the Yuan undervalued? Why do poor countries have lower prices? Roadmap: The law of one price, purchasing power parity (PPP): theory and empirics The Balassa Samuelson effect: real exchange rates, growth and productivity

3 Lecture 5 Long term exchange rate and inflation 1. The law of one price, purchasing power parity (PPP): theory and empirics 2. The Balassa Samuelson effect: real exchange rates, growth and productivity

4 The law of one price (LOP) Long term perspective on exchange rates = when prices are flexible On competitive markets, in absence of transport costs and tariffs twoidenticalgoodsmustbesoldatthesameprice (expressed in the same currency) Law of one Price = long term arbitrage mechanism P i = E. P i $ IfP i >E.P i$ :buytheusproducedgood,sellitineurope; increase demand in US, increase supply in Europe: price converge

5 Purchasing power parity (PPP) P = E. P $ where P and P $ are price indices of US and euro zone E = P / P $ : Absolute version of PPP Idea developed by Ricardo ( ) then Cassel ( ) An increase in the general level of prices reduces purchasing power of domestic currency and leads to a depreciation The price levels of different countries are equalized when measured in the same currency: P = E x P $ PPP exchange rate: E PPP = P / P $

6 The PPP exchange rate: E PPP ( /$) = P / P $ P / P $ $ undervalued, overvalued $ overvalued, undervalued 45 Nominal Exchange rate ( /$)

7 Relative PPP The variation of the exchange rate is equal to the difference in the variation in prices, the difference in inflation rates (approximation) E t = P t / P $t (E t E t-1 )/E t-1 = π t -π $t π t and π $t : inflation in zone and US π t = (P t P t-1 )/ P t-1

8 Back to the monetary approach to exchange rates (long term, LT) PPP in LT: E = P / P $ Prices in LT: P = M S / L (r, Y ) ; P $ = M S $/ L (r $,Y $ ) where r, Y are LT values In LT, E is determined by relative supplies and demands of money in the two countries: E = P / P $ = (M S / M S $) x [L (r $, Y $ )/L (r, Y )] Hence under money neutrality in LT, E%Change = %Change in M S -%Change in M S $

9 The Fisher effect In LT, interest parity condition is also verified: r = r $ + (E e E)/ E In LT: relative PPP (E t E t-1 )/E t-1 = π t -π $t implies that expected depreciation equals expected inflation differential: (E e E)/ E = π e -π e $ Where π e = (P e P )/ P

10 The Fisher effect So: r -r $ = (E e E)/ E = π e -π e $ If inflation in euro zone is higher than in the US, the nominal interest rate r will also be higher In LT, a high nominal interest rate reflects expectations of high inflation: this explains the association of high interest rate and depreciation in LT Where does higher inflation come from? an in the rate of growth of money supply (not only its level). A change in the level of money supply changes the level of prices. A change in the growth rate of money supply changes the rate of growth of prices (inflation)

11

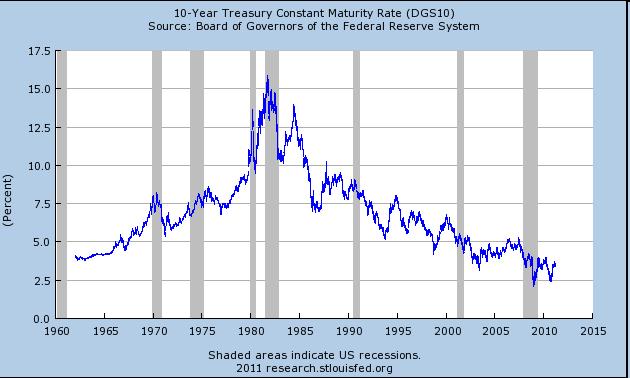

12 10 years interest rates: France and Germany: source ECB

13 Empirical validity of the LOP LOP fails in short run : not puzzling for non traded goods (haircuts); but also for traded goods Transport costs, trade barriers (tariffs and regulations): make arbitrage more difficult Imperfect competition: firms segment markets (to have high prices where price elasticity of demand is low) : pricing to market. Branding. Many goods considered to be highly traded contain nontraded components. Retail and wholesale costs (distribution costs) account for around 50% of final consumer price

14 Empirical validity of PPP Studies overwhelmingly reject PPP as a short-run relationship, better as long term The variance of floating nominal exchange rates is an order of magnitude greater than the variance of relative price indices The failure of short-run PPP can be attributed partly to the stickiness in nominal prices (short run) Works much better in the long term

15 The IKEA Law of One Price European Prices in USD Source: J Haskeland H Wolf, The Law of One Price: a case study, NBER WP 8112

16 Price differentials in Europe for identical car models (exc. taxes); 2009 France Germany UK Lowest VW Passat 115% 124% 82% UK Renault Clio 3 NISSAN Micra 130% 131% 98% Hungary 93% 113% 110% 77% Poland 71% FIAT Panda 116% 126% 94% Hungary 92% Source: EU commission

17 What is the exchange rate of country i consistent with LOP for the Big Mac? Required appreciation or depreciation to satisfy LOP? E Big Mac = P US /P i The Economist - Oct. 2010

18 Long term real exchange rate Real exchange rate (RER) defined as the relative price index of goods and services between two countries: q = E x P $ / P A real depreciation of visa visthe $ (q ) can come from nominal depreciation (E ), an increase in P $ or a fall in P Relative PPP RER is constant! PPP: (E t E t-1 )/E t-1 = π t -π $t (q t q t-1 )/q t-1 = (E t E t-1 )/E t-1 -π t + π $t = 0

19 Long Run PPP: $/ real exchange rate (in logs) 0.5 The mean reversion of real exchange rates overvalued relative to PPP undervalued relative to PPP Note: Higher values means a (real) dollar depreciation (or a appreciation)

20 Long Run PPP: $/ real exchange rate (in levels) 3 The mean reversion of real exchange rates 2,8 2,6 2,4 2,2 2 1,8 1,6 1,4 Mean RER value 1, Spot Exchange Rate $/ Real Exchange Rate (US/UK) (2000=Spot=1,5) Note: Higher values means a dollar depreciation (or a appreciation)

21 The Yen/$ exchange rate and the relative price ratio over the long term

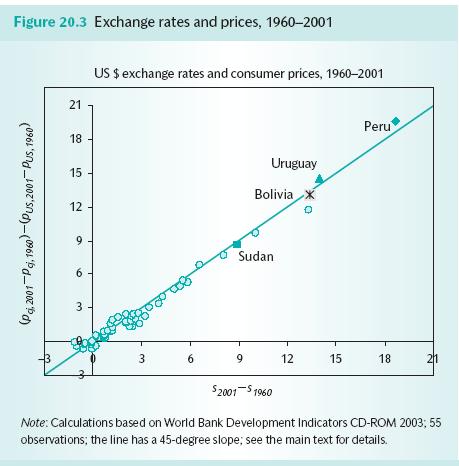

22 Empirical test of relative PPP in the long-run Looking across countries over a long time period [1960;2001], run the following regression where(i) is a country: i / us i us S 2001 P 2001 P 2001 log log log + / = α + β ε i us i us t + S 1960 P 1960 P RelativePPPassumption:βisexpecttobe=1(andα=zero). Can inflation differentials over 41 years explain exchange rate variations over the same period? YES! β is fairly close to one for this sample of countries (see graph) Convergence towards PPP: slow reversion towards PPP (from 3 to 5 yearstoeliminate halfofthegap)

23

24 Relative PPP prevails in the very long-run but fails in the short-run %Depreciation Year Window %Depreciation I n fl a ti o n d iffe r e n tia l %Depreciation Infla tion Diffe re ntia l Inflation Differential 20 Year Window Remember relative PPP: (E t E t-1 )/E t-1 = π t -π $t 5 Year Window

25 Lecture 5 Long term exchange rate and inflation 1. The law of one price, purchasing power parity (PPP): theory and empirics 2. The Balassa Samuelson effect: real exchange rates, growth and productivity

26 The Balassa-Samuelson effect Why are prices higher in rich countries? Same question as: why E x P rich > P poor? Why does the real exchange rate of countries that grow relative to rest of world appreciate? q = E x P world / P Examples: Japan, South Korea, Ireland, today China?

27

28 The Balassa-Samuelson model Key distinction: Tradable goods (manufactured goods) and non tradable (services) Around 75% of the consumption basket in industrialized countries is non tradable (health, education, most services ) even if definition of a tradable good/service becomes blurred (internet) Productivity differences between rich and poor countries is much larger for tradables than for non tradables: it is very large for example in manufacturing (of an order of 10), but much smaller in services (think of haircuts: technology is not hugely different across countries)

29 The Balassa-Samuelson model: a simple example Workers can be hairdressers (non-traded) or work in the textile industry (traded). Workers can produce haircuts or T-shirts. T-shirts sold 1$ in international markets. US worker produces 50 T-shirts/hour, Indian worker only 10. Both US and Indian hairdressers make 5 haircuts/ hour. Question: what is the price of an haircut in India and in the US?

30 The Balassa-Samuelson model 2 countries: Poor country, rich country (*) Price index depends on tradables (T) and nontradables (N) : P = (P T ) a x (P N ) 1-a ; P* = (P* T ) a x (P* N ) 1-a Share aand 1-a(around 25% and 75%) One factor of production: labor Mobile between sectors (in long term) but not between countries Two countries are identical except in productivity

31 Labor is mobile between sectors: Arbitrage w = w T = w N ; w*= w* T = w* N Profit max. by firms marginal cost of labor = marginal value of employing one more unit of labor (otherwise labor demand by firms does not max. profits): for example in T: w = P T A T A T : marginal productivity of labor (nb of units of goods produced with one more unit of labor) real wage = marginal productivity of labor : w/ P T = A T ; w/ P N = A N w*/ P* T = A* T ; w*/ P* N = A* N

32 PPP for tradable goods(not for non tradables) Choose numeraire so that E = 1 (normalization with no realconsequence):p T =P* T andp T =w/a T P* T =w*/a* T sow/w*=a T /A* T First result: wages in poorer countries are lower because labor productivity in tradables sector is lower (technology) Wages in non tradables are also lower in poorer countries because wages are equalized by arbitrage across sectors inside each country

33 Balassa Samuelson effect P N / P* N = (w/a N )/ (w*/a* N ) = (A T / A* T )/(A N / A *N ) as P N = w /A N, P* N = w/ A* N and w/w* = A T / A* T The relative price of non tradables depends on the relative productivities in the tradable and non tradable sectors. If rich country more productive in tradables (A T < A* T ), poor country has lower non-tradable prices like in the simple example

34 Relative Price index between countries (use PPP on tradables): (P T ) a x (P N ) 1-a (P N ) 1-a P/P* = = (P* T ) a x (P* N ) 1-a (P* N ) 1-a (Use PPP in T)

35 Balassa Samuelson effect Relative prices between countries depends on relative productivities between tradables and non tradables: (A T / A* T ) 1-a P/P* = < 1 if A T / A* T < A N / A *N (A N / A *N ) 1-a The productivity differential between poor and rich countries is much larger in T (A T << A* T ) than in N (A N < A *N ) No effect on relative prices P/P* if the gap in productivity is equal in both sectors

36 Balassa Samuelson effect Poorer countries have lower wages in tradables because of lower productivity; these translate in lower wagesinnontradablesandlowerpricesinthissector asproductivitygapisnotaslarge:pricesarelowerin poorer countries. Asacountrygetsricher, A T increases(morethana N ); itswagesinthetsector andthereforeinthen sector too. Its price index increases relative to other countries

37 The countries with the strongest productivity growth (in tradable relative to non-tradable) tend to show the strongest upward trend in the relative prices of non-tradable goods over the period

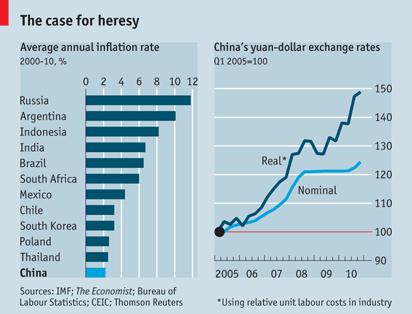

38 Is China real exchange rate undervalued? By Big mac index or PPP (on all goods) yardstick: around 40 to 50% Also, if calculate RER that eliminates the Chinese CA surplus But China is still a poor country (GDP/cap): relative to what Balassa Samuelson predicts, yuan is undervalued by 12% Could come through nominal appreciation or domestic inflation

39

40 Income convergence and exchange rate appreciation (here appreciation is up!) Source: Reisen, 2009

41 Brief Summary According to Purchasing Power Parity (PPP), exchange rates and prices should adjust such that goods in different countries have the same price when expressed in the same currency. In the (very) long run changes in nominal exchange rates reflect differences in inflation as predicted by relative PPP. Failures of PPP in the short-run are due to price rigidities, barriers to international trade, pricing-to-market Due to the Balassa Samuelson effect, poor countries have lower prices and face appreciating real exchange rates when catching-up in terms of productivity.

Open economy macroeconomics and exchange rates Part I

Understanding the World Economy Master in Economics and Business Open economy macroeconomics and exchange rates Part I Lecture 10 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 10 : Open

Understanding the World Economy Master in Economics and Business Open economy macroeconomics and exchange rates Part I Lecture 10 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 10 : Open

Open economy macroeconomics and exchange rates Part I

Understanding the World Economy Master in Economics and Business Open economy macroeconomics and exchange rates Part I Lecture 10 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 10 : Open

Understanding the World Economy Master in Economics and Business Open economy macroeconomics and exchange rates Part I Lecture 10 Nicolas Coeurdacier nicolas.coeurdacier@sciencespo.fr Lecture 10 : Open

LECTURE 10: Purchasing Power Parity

LECTURE 10: Purchasing Power Parity Primary Motivation: How realistic is the assumption P = P? Secondary motivation: How integrated are global goods markets? (1) Definition(s) of PPP (Absolute vs. Relative

LECTURE 10: Purchasing Power Parity Primary Motivation: How realistic is the assumption P = P? Secondary motivation: How integrated are global goods markets? (1) Definition(s) of PPP (Absolute vs. Relative

Final exam Non-detailed correction 3 hours

International Finance Master PEI Spring 2013 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours Documents not allowed. Basic calculator allowed. For the Multiple Choice Questions, use the answer

International Finance Master PEI Spring 2013 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours Documents not allowed. Basic calculator allowed. For the Multiple Choice Questions, use the answer

10/14/2011. EXCHANGE RATES I: PPP and THE MONETARY APPROACH IN THE LONG RUN. Introduction to Exchange Rates and Prices

EXCHANGE RATES I: PPP and THE MONETARY APPROACH IN THE LONG RUN 14 1 Exchange Rates and Prices in the Long Run 2 Money, Prices, and Exchange Rates in the Long Run 3 The Monetary Approach 4 Money, Interest,

EXCHANGE RATES I: PPP and THE MONETARY APPROACH IN THE LONG RUN 14 1 Exchange Rates and Prices in the Long Run 2 Money, Prices, and Exchange Rates in the Long Run 3 The Monetary Approach 4 Money, Interest,

Global Environment. The Real Exchange Rate. Francesco Franco. October 22, Nova SBE. Francesco Franco Global Environment 1/28

Global Environment The Real Exchange Rate Francesco Franco Nova SBE October 22, 2014 Francesco Franco Global Environment 1/28 Long Run What explains the long run behavior of exchange rates? Figure : Yen-Dollar

Global Environment The Real Exchange Rate Francesco Franco Nova SBE October 22, 2014 Francesco Franco Global Environment 1/28 Long Run What explains the long run behavior of exchange rates? Figure : Yen-Dollar

Chapter 16. Price Levels and the Exchange Rate in the Long Run

Chapter 16 Price Levels and the Exchange Rate in the Long Run Preview Law of one price Purchasing power parity Long-run model of exchange rates: monetary approach (based on absolute version of PPP) Relationship

Chapter 16 Price Levels and the Exchange Rate in the Long Run Preview Law of one price Purchasing power parity Long-run model of exchange rates: monetary approach (based on absolute version of PPP) Relationship

Associate reading: Krugman-Obstfeld chapter 15 p , p

3 Lecture 3: The determinants of the real exchange rate Associate reading: Krugman-Obstfeld chapter 15 p. 369-373, p. 379-393 Intertemporal theory of the current account: what determines international

3 Lecture 3: The determinants of the real exchange rate Associate reading: Krugman-Obstfeld chapter 15 p. 369-373, p. 379-393 Intertemporal theory of the current account: what determines international

HOMEWORK 8 (CHAPTER 16 PRICE LEVELS AND THE EXCHANGE RATE IN THE LONG RUN) ECO41 FALL 2015 UDAYAN ROY

ECO41 FALL 2015 UDAYAN ROY") HOMEWORK 8 (CHAPTER 16 PRICE LEVELS AND THE EXCHANGE RATE IN THE LONG RUN) ECO41 FALL 2015 UDAYAN ROY Each correct answer is worth 1 point. The maximum score is 20 points. This homework is due in class

HOMEWORK 8 (CHAPTER 16 PRICE LEVELS AND THE EXCHANGE RATE IN THE LONG RUN) ECO41 FALL 2015 UDAYAN ROY Each correct answer is worth 1 point. The maximum score is 20 points. This homework is due in class

in equilibrium, are supposed to hold across international markets. Covered Interest Rate Parity Purchasing Power Parity y( (also called the Law of

Week 4 The Parities The Parities There are three fundamental parity conditions that, in equilibrium, are supposed to hold across international markets. Covered Interest Rate Parity Purchasing Power Parity

Week 4 The Parities The Parities There are three fundamental parity conditions that, in equilibrium, are supposed to hold across international markets. Covered Interest Rate Parity Purchasing Power Parity

Chapter 6. International Parity Conditions. International Parity Conditions: Learning Objectives. Prices and Exchange Rates

Chapter 6 International arity Conditions International arity Conditions: Learning Objectives Examine how price levels and price level changes (inflation) in countries determine the exchange rate at which

Chapter 6 International arity Conditions International arity Conditions: Learning Objectives Examine how price levels and price level changes (inflation) in countries determine the exchange rate at which

dr Bartłomiej Rokicki Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw

Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw Purchasing Power Parity dr Bartłomiej Rokicki Purchasing power parity is derived from law of one

Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw Purchasing Power Parity dr Bartłomiej Rokicki Purchasing power parity is derived from law of one

Purchasing Power Parity: Reasons for Deviations of the Ruble from PPP

Purchasing Power Parity: Reasons for Deviations of the Ruble from PPP Anton A Cheremukhin Published in Russian: 17 January 2005, This Summary: 16 October 2005 Abstract This paper aims at testing of the

Purchasing Power Parity: Reasons for Deviations of the Ruble from PPP Anton A Cheremukhin Published in Russian: 17 January 2005, This Summary: 16 October 2005 Abstract This paper aims at testing of the

Lecture 5: Balassa-Samuelson Hypothesis

Lecture 5: Balassa-Samuelson Hypothesis Xu Hu School of Economics Fudan University September 29, 2013 Law of One Price Spatial Arbitrage: a highly trade-able and homogeneous good should have equal prices

Lecture 5: Balassa-Samuelson Hypothesis Xu Hu School of Economics Fudan University September 29, 2013 Law of One Price Spatial Arbitrage: a highly trade-able and homogeneous good should have equal prices

Part I: Multiple Choice (36%) circle the correct answer

circle the correct answer") Econ 434 Professor Ickes Fall 2009 Midterm Exam II: Answer Sheet Instructions: Read the entire exam over carefully before beginning. The value of each question is given. Allocate your time efficiently

Econ 434 Professor Ickes Fall 2009 Midterm Exam II: Answer Sheet Instructions: Read the entire exam over carefully before beginning. The value of each question is given. Allocate your time efficiently

Lecture 5: Intermediate macroeconomics, autumn 2014

Lecture 5: Intermediate macroeconomics, autumn 2014 Lars Calmfors Literature: Krugman Obstfeld Melitz, chapters 16 and 17. 1 1 Topics Absolute and relative purchasing power parity (PPP) The Balassa-Samuelson

Lecture 5: Intermediate macroeconomics, autumn 2014 Lars Calmfors Literature: Krugman Obstfeld Melitz, chapters 16 and 17. 1 1 Topics Absolute and relative purchasing power parity (PPP) The Balassa-Samuelson

Introduction to Exchange Rates and the Foreign Exchange Market

Introduction to Exchange Rates and the Foreign Exchange Market 2 1. Refer to the exchange rates given in the following table. Today One Year Ago June 25, 2010 June 25, 2009 Country Per $ Per Per Per $

Introduction to Exchange Rates and the Foreign Exchange Market 2 1. Refer to the exchange rates given in the following table. Today One Year Ago June 25, 2010 June 25, 2009 Country Per $ Per Per Per $

International Macroeconomics

Slides for Chapter 9: Determinants of the Real Exchange Rate International Macroeconomics Schmitt-Grohé Uribe Woodford Columbia University April 8, 2018 1 The LOOP LOOP stands for the Law of One Price.

Slides for Chapter 9: Determinants of the Real Exchange Rate International Macroeconomics Schmitt-Grohé Uribe Woodford Columbia University April 8, 2018 1 The LOOP LOOP stands for the Law of One Price.

Exchange rate: the price of one currency in terms of another. We will be using the notation E t = euro

Econ 330: Money and Banking Fall 2014, Handout 8 Chapter 17 : Foreign Exchange Market 1. Foreign Exchange Market Exchange rate: the price of one currency in terms of another. We will be using the notation

Econ 330: Money and Banking Fall 2014, Handout 8 Chapter 17 : Foreign Exchange Market 1. Foreign Exchange Market Exchange rate: the price of one currency in terms of another. We will be using the notation

Homework Assignment #2

Econ 434 Professor Ickes Homework Assignment #2 Fall 2009 This assignment is due on Thursday, October 15 at the beginning of class (or sooner). 1. Consider a small economy so the country is a price taker

Econ 434 Professor Ickes Homework Assignment #2 Fall 2009 This assignment is due on Thursday, October 15 at the beginning of class (or sooner). 1. Consider a small economy so the country is a price taker

Slides for International Finance Purchasing Power Parity

Purchasing Power Parity American University 2017-10-01 Preview Absolute vs. Relative Purchasing power parity Commodity price parity Absolute PPP vs. Relative PPP Classical model of price determination

Purchasing Power Parity American University 2017-10-01 Preview Absolute vs. Relative Purchasing power parity Commodity price parity Absolute PPP vs. Relative PPP Classical model of price determination

International Parity Conditions

International Parity Conditions Eiteman et al., Chapter 6 Winter 2004 Outline of the Chapter How are exchange rates determined? Can we predict them? Prices and Exchange Rates Prices Indices Inflation Rates

International Parity Conditions Eiteman et al., Chapter 6 Winter 2004 Outline of the Chapter How are exchange rates determined? Can we predict them? Prices and Exchange Rates Prices Indices Inflation Rates

Final exam Non-detailed correction 3 hours. This are indicative directions on how structure the essay questions and what was expected.

International Finance Master PEI Fall 2011 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours This are indicative directions on how structure the essay questions and what was expected. 1. Multiple

International Finance Master PEI Fall 2011 Nicolas Coeurdacier Final exam Non-detailed correction 3 hours This are indicative directions on how structure the essay questions and what was expected. 1. Multiple

Traded and non-traded goods

Traded and non-traded goods ECON4330 Spring 2013 Lecture 12A Asbjørn Rødseth University of Oslo April 22, 2013 Traded and non-traded goods April 22, 2013 1 / 16 Different market structures Mundell-Fleming

Traded and non-traded goods ECON4330 Spring 2013 Lecture 12A Asbjørn Rødseth University of Oslo April 22, 2013 Traded and non-traded goods April 22, 2013 1 / 16 Different market structures Mundell-Fleming

Relationships among Exchange Rates, Inflation, and Interest Rates

Relationships among Exchange Rates, Inflation, and Interest Rates Chapter Objectives To explain the purchasing power parity (PPP) and international Fisher effect (IFE) theories, and their implications

Relationships among Exchange Rates, Inflation, and Interest Rates Chapter Objectives To explain the purchasing power parity (PPP) and international Fisher effect (IFE) theories, and their implications

2. Discuss the implications of the interest rate parity for the exchange rate determination.

CHAPTER 5 INTERNATIONAL PARITY RELATIONSHIPS AND FORECASTING FOREIGN EXCHANGE RELATIONSHIPS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Give a full definition

CHAPTER 5 INTERNATIONAL PARITY RELATIONSHIPS AND FORECASTING FOREIGN EXCHANGE RELATIONSHIPS SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS QUESTIONS 1. Give a full definition

Rutgers University Spring Econ 336 International Balance of Payments Professor Roberto Chang. Problem Set 2. Deadline: March 1st.

Rutgers University Spring 2012 Econ 336 International Balance of Payments Professor Roberto Chang Problem Set 2. Deadline: March 1st Name: 1. The law of one price works under some assumptions. Which of

Rutgers University Spring 2012 Econ 336 International Balance of Payments Professor Roberto Chang Problem Set 2. Deadline: March 1st Name: 1. The law of one price works under some assumptions. Which of

Slides for International Finance Purchasing Power Parity

Purchasing Power Parity American University 2014-09-20 Preview Absolute vs. Relative Purchasing power parity Commodity price parity Absolute PPP vs. Relative PPP Classical model of price determination

Purchasing Power Parity American University 2014-09-20 Preview Absolute vs. Relative Purchasing power parity Commodity price parity Absolute PPP vs. Relative PPP Classical model of price determination

Lecture 12: SOURCES OF DEVIATIONS FROM PURCHASING POWER PARITY (PPP)

") Lecture 12: SOURCES OF DEVIATIONS FROM PURCHASING POWER PARITY (PPP) Barriers to International Integration Transportation costs Tariffs & non-tariff trade barriers Border frictions Currencies. Non-Traded

Lecture 12: SOURCES OF DEVIATIONS FROM PURCHASING POWER PARITY (PPP) Barriers to International Integration Transportation costs Tariffs & non-tariff trade barriers Border frictions Currencies. Non-Traded

The Misalignment of the Korean Won: Is It Overvalued? Taizo MOTONISHI Kansai University September 2006

The Misalignment of the Korean Won: Is It Overvalued? Taizo MOTONISHI Kansai University September 2006 Motivation There is much discussions on exchange rate misalignment Is Korean Won Overvalued? Is Japanese

The Misalignment of the Korean Won: Is It Overvalued? Taizo MOTONISHI Kansai University September 2006 Motivation There is much discussions on exchange rate misalignment Is Korean Won Overvalued? Is Japanese

Econ 340. Forms of Exchange Rates. Forms of Exchange Rates. Forms of Exchange Rates. Forms of Exchange Rates. Outline: Exchange Rates

Econ 34 Lecture 13 In What Forms Are Reported? What Determines? Theories of 2 Forms of Forms of What Is an Exchange Rate? The price of one currency in terms of another Examples Recent rates for the US

Econ 34 Lecture 13 In What Forms Are Reported? What Determines? Theories of 2 Forms of Forms of What Is an Exchange Rate? The price of one currency in terms of another Examples Recent rates for the US

Chapter 2 Foreign Exchange Parity Relations

Chapter 2 Foreign Exchange Parity Relations Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous editions. We adopted the convention that the first

Chapter 2 Foreign Exchange Parity Relations Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous editions. We adopted the convention that the first

Homework Assignment #2: Answer Sheet

Econ 434 Professor Ickes Fall 2008 Homework Assignment #2: Answer Sheet. Suppose that the price level in the home country is given by P = Pn α Pt α,wherep t is the price of traded goods, and α is the share

Econ 434 Professor Ickes Fall 2008 Homework Assignment #2: Answer Sheet. Suppose that the price level in the home country is given by P = Pn α Pt α,wherep t is the price of traded goods, and α is the share

Chapter 18 Exchange Rate Theories (modified version)

") Chapter 18 Exchange Rate Theories (modified version) Topics to be covered Exchange Rate Determination 1. The Elasticities Approach 2. The Asset Approach 2a. The Monetary Approach to the Exchange Rate 2b.

Chapter 18 Exchange Rate Theories (modified version) Topics to be covered Exchange Rate Determination 1. The Elasticities Approach 2. The Asset Approach 2a. The Monetary Approach to the Exchange Rate 2b.

Chapter 6. The Open Economy

Chapter 6 0 IN THIS CHAPTER, YOU WILL LEARN: accounting identities for the open economy the small open economy model what makes it small how the trade balance and exchange rate are determined how policies

Chapter 6 0 IN THIS CHAPTER, YOU WILL LEARN: accounting identities for the open economy the small open economy model what makes it small how the trade balance and exchange rate are determined how policies

OPEN-ECONOMY MACROECONOMICS: BASIC CONCEPTS

18 OPEN-ECONOMY MACROECONOMICS: BASIC CONCEPTS LEARNING OBJECTIVES: By the end of this chapter, students should understand: how net exports measure the international flow of goods and services. how net

18 OPEN-ECONOMY MACROECONOMICS: BASIC CONCEPTS LEARNING OBJECTIVES: By the end of this chapter, students should understand: how net exports measure the international flow of goods and services. how net

Exchange Rate Fluctuations Revised: January 7, 2012

The Global Economy Class Notes Exchange Rate Fluctuations Revised: January 7, 2012 Exchange rates (prices of foreign currency) are a central element of most international transactions. When Heineken sells

The Global Economy Class Notes Exchange Rate Fluctuations Revised: January 7, 2012 Exchange rates (prices of foreign currency) are a central element of most international transactions. When Heineken sells

Lessons V and VI: Overview

Lessons V and VI: Overview 1. FX parity conditions 2. Do the PPP and the IRPs (CIRP and UIRP) hold in practice? 1 FX parity conditions 2 FX parity conditions 1. The Law of One Price and the Purchasing

Lessons V and VI: Overview 1. FX parity conditions 2. Do the PPP and the IRPs (CIRP and UIRP) hold in practice? 1 FX parity conditions 2 FX parity conditions 1. The Law of One Price and the Purchasing

vox Research-based policy analysis and commentary from leading economists

vox Research-based policy analysis and commentary from leading economists On the renminbi and economic convergence Helmut Reisen 17 December 2009 Must China let its exchange rate appreciate to reduce global

vox Research-based policy analysis and commentary from leading economists On the renminbi and economic convergence Helmut Reisen 17 December 2009 Must China let its exchange rate appreciate to reduce global

The Open Economy. (c) Copyright 1998 by Douglas H. Joines 1

Copyright 1998 by Douglas H. Joines 1") The Open Economy (c) Copyright 1998 by Douglas H. Joines 1 Module Objectives Know the major items in the Balance of Payments Accounts Know the determinants of the trade balance Know the major determinants

The Open Economy (c) Copyright 1998 by Douglas H. Joines 1 Module Objectives Know the major items in the Balance of Payments Accounts Know the determinants of the trade balance Know the major determinants

Chapter 17. Exchange Rates and International Economic Policy

Chapter 17 Exchange Rates and International Economic Policy Preview To examine the financial market that determines exchange rates in the long and short runs To understand the role of exchange rates in

Chapter 17 Exchange Rates and International Economic Policy Preview To examine the financial market that determines exchange rates in the long and short runs To understand the role of exchange rates in

International Finance

Terminology International Finance Chris Edmond NYU Stern Spring 2008 Trade balance balance on merchandise trade ( goods ) balance on goods and services ( net exports ) Current account balance current account

Terminology International Finance Chris Edmond NYU Stern Spring 2008 Trade balance balance on merchandise trade ( goods ) balance on goods and services ( net exports ) Current account balance current account

Lessons V and VI: FX Parity Conditions

Lessons V and VI: FX March 27, 2017 Table of Contents Does the PPP Hold Parity s should be thought of as break-even values, where the decision-maker is indifferent between two available strategies. Parity

Lessons V and VI: FX March 27, 2017 Table of Contents Does the PPP Hold Parity s should be thought of as break-even values, where the decision-maker is indifferent between two available strategies. Parity

Aggregate real exchange rate persistence through the lens of sectoral data

Aggregate real exchange rate persistence through the lens of sectoral data Laura Mayoral and Lola Gadea Nashville, September 24 2010 Microeconomic Sources of Real Exchange Rate Behavior Motivation and

Aggregate real exchange rate persistence through the lens of sectoral data Laura Mayoral and Lola Gadea Nashville, September 24 2010 Microeconomic Sources of Real Exchange Rate Behavior Motivation and

The Open Economy. Inflation Worth Publishers, all rights reserved CHAPTER 5

6 The Open Economy Inflation CHAPTER 5 Modified by Ming Yi 2016 Worth Publishers, all rights reserved 5 IN THIS CHAPTER, YOU WILL LEARN: Accounting identities for the open economy The small open economy

6 The Open Economy Inflation CHAPTER 5 Modified by Ming Yi 2016 Worth Publishers, all rights reserved 5 IN THIS CHAPTER, YOU WILL LEARN: Accounting identities for the open economy The small open economy

Lectures 24 & 25: Determination of exchange rates

Lectures 24 & 25: Determination of exchange rates Building blocs - Interest rate parity - Money demand equation - Goods markets Flexible-price version: monetarist/lucas model - derivation - hyperinflation

Lectures 24 & 25: Determination of exchange rates Building blocs - Interest rate parity - Money demand equation - Goods markets Flexible-price version: monetarist/lucas model - derivation - hyperinflation

Assignment 4 Economics 222, Fall 2006 Due: Drop Box 2 nd floor Dunning Hall by noon Nov. 24th, 2006 Maximum Group Size: 4 people

Assignment 4 Economics 222, Fall 2006 Due: Drop Box 2 nd floor Dunning Hall by noon Nov. 24th, 2006 Maximum Group Size: 4 people A Long and Involved IS-LM-FE Numerical Example Our first task is to solve

Assignment 4 Economics 222, Fall 2006 Due: Drop Box 2 nd floor Dunning Hall by noon Nov. 24th, 2006 Maximum Group Size: 4 people A Long and Involved IS-LM-FE Numerical Example Our first task is to solve

Growth and Real Exchange Rate Appreciation in the CEECs: Some reflections on the catching up process

Growth and Real Exchange Rate Appreciation in the CEECs: Some reflections on the catching up process FIRST DRAFT Comments welcome Lars Nilsson a a Ministry for Foreign Affairs, Department for European

Growth and Real Exchange Rate Appreciation in the CEECs: Some reflections on the catching up process FIRST DRAFT Comments welcome Lars Nilsson a a Ministry for Foreign Affairs, Department for European

Chapter 8. Purchasing Power Parity and Real Exchange Rates Cambridge University Press 8-1

Chapter 8 Purchasing Power Parity and Real Exchange Rates 2018 Cambridge University Press 8-1 Purchasing Power Parity A model of the determination of exchange rates Baseline forecast for predicting exchange

Chapter 8 Purchasing Power Parity and Real Exchange Rates 2018 Cambridge University Press 8-1 Purchasing Power Parity A model of the determination of exchange rates Baseline forecast for predicting exchange

INTRODUCTION TO ECONOMIC GROWTH. Dongpeng Liu Department of Economics Nanjing University

INTRODUCTION TO ECONOMIC GROWTH Dongpeng Liu Department of Economics Nanjing University ROADMAP INCOME EXPENDITURE LIQUIDITY PREFERENCE IS CURVE LM CURVE SHORT-RUN IS-LM MODEL AGGREGATE DEMAND AGGREGATE

INTRODUCTION TO ECONOMIC GROWTH Dongpeng Liu Department of Economics Nanjing University ROADMAP INCOME EXPENDITURE LIQUIDITY PREFERENCE IS CURVE LM CURVE SHORT-RUN IS-LM MODEL AGGREGATE DEMAND AGGREGATE

Exchange Rate Regimes and Monetary Policy: Options for China and East Asia

Exchange Rate Regimes and Monetary Policy: Options for China and East Asia Takatoshi Ito, University of Tokyo and RIETI, and Eiji Ogawa, Hitotsubashi University, and RIETI 3/19/2005 RIETI-BIS Conference

Exchange Rate Regimes and Monetary Policy: Options for China and East Asia Takatoshi Ito, University of Tokyo and RIETI, and Eiji Ogawa, Hitotsubashi University, and RIETI 3/19/2005 RIETI-BIS Conference

Understanding the World Economy Final Exam Indicative answers

Nicolas Coeurdacier Master Economics & Business Spring 2017 Understanding the World Economy Final Exam Indicative answers I. Multiple choice [50 points = 2 per question] It is a multiple choice questionnaire.

Nicolas Coeurdacier Master Economics & Business Spring 2017 Understanding the World Economy Final Exam Indicative answers I. Multiple choice [50 points = 2 per question] It is a multiple choice questionnaire.

1 trillion units * ($1 per unit) = $500 billion * 2

= $500 billion * 2") Under the strict monetarist view, real interest rates and money supply are assumed to be independent. Under this assumption, inflation does not affect real rates. Nevertheless, nominal rates, R, are obviously

Under the strict monetarist view, real interest rates and money supply are assumed to be independent. Under this assumption, inflation does not affect real rates. Nevertheless, nominal rates, R, are obviously

Money, prices and exchange rates in the long run

Money, prices and exchange rates in the long run Outline Part I: Money and inflation 1. Definition of money 2. Money supply and money demand 3. The neutrality of money 4. The dichotomy principle and its

Money, prices and exchange rates in the long run Outline Part I: Money and inflation 1. Definition of money 2. Money supply and money demand 3. The neutrality of money 4. The dichotomy principle and its

Madura: International Financial Management Chapter 8

Madura: International Financial Management Chapter Chapter Relationships Between Inflation, Interest Rates, and Exchange Rates Chapter Objectives To explain the theories of purchasing power parity (PPP)

Madura: International Financial Management Chapter Chapter Relationships Between Inflation, Interest Rates, and Exchange Rates Chapter Objectives To explain the theories of purchasing power parity (PPP)

Public Affairs 856 Trade, Competition, and Governance in a Global Economy Guest Lecture: Currency Manipulation and Currency Misalignment 3/27/2017

Public Affairs 856 Trade, Competition, and Governance in a Global Economy Guest Lecture: Currency Manipulation and Currency Misalignment 3/27/2017 Instructor: Yi ZHANG UW Madison Spring 2017 Questions

Public Affairs 856 Trade, Competition, and Governance in a Global Economy Guest Lecture: Currency Manipulation and Currency Misalignment 3/27/2017 Instructor: Yi ZHANG UW Madison Spring 2017 Questions

Homework Assignment #3: Answer Key

Econ 434 Professor Ickes Fall 2006 Homework Assignment #3: Answer Key 1. Productivity growth has increased in Central and Eastern European countries relative to Western European countries. This has implications

Econ 434 Professor Ickes Fall 2006 Homework Assignment #3: Answer Key 1. Productivity growth has increased in Central and Eastern European countries relative to Western European countries. This has implications

19.2 Exchange Rates in the Long Run Introduction 1/24/2013. Exchange Rates and International Finance. The Nominal Exchange Rate

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

In this chapter, we study a theory of how exchange rates are determined "in the long run." The theory we will develop has two parts:

1. INTRODUCTION 1 Introduction In the last chapter, uncovered interest parity (UIP) provided us with a theory of how the spot exchange rate is determined, given knowledge of three variables: the expected

1. INTRODUCTION 1 Introduction In the last chapter, uncovered interest parity (UIP) provided us with a theory of how the spot exchange rate is determined, given knowledge of three variables: the expected

MCQ on International Finance

MCQ on International Finance 1. If portable disk players made in China are imported into the United States, the Chinese manufacturer is paid with a) international monetary credits. b) dollars. c) yuan,

MCQ on International Finance 1. If portable disk players made in China are imported into the United States, the Chinese manufacturer is paid with a) international monetary credits. b) dollars. c) yuan,

The Big Mac Index and the Valuation of the Chinese Currency

The Big Mac Index and the Valuation of the Chinese Currency Jiawen Yang * School of Business and Public Management The George Washington University November 2003 * Jiawen Yang is associate professor of

The Big Mac Index and the Valuation of the Chinese Currency Jiawen Yang * School of Business and Public Management The George Washington University November 2003 * Jiawen Yang is associate professor of

ECON 450 Development Economics

ECON 450 Development Economics Classic Theories of Economic Growth and Development The Empirics of the Solow Growth Model University of Illinois at Urbana-Champaign Summer 2017 Introduction This lecture

ECON 450 Development Economics Classic Theories of Economic Growth and Development The Empirics of the Solow Growth Model University of Illinois at Urbana-Champaign Summer 2017 Introduction This lecture

Exchange rates and price levels

Exchange rates and price levels Andrea Vaona University of Verona Fourth class of International Economic Policy A. Vaona (Uni. Verona) Exchange rates and price levels Fourth class 1 / 16 The law of one

Exchange rates and price levels Andrea Vaona University of Verona Fourth class of International Economic Policy A. Vaona (Uni. Verona) Exchange rates and price levels Fourth class 1 / 16 The law of one

QUEEN S UNIVERSITY FINAL EXAMINATION FACULTY OF ARTS AND SCIENCE DEPARTMENT OF ECONOMICS APRIL 2017

Page 1 of 5 QUEEN S UNIVERSITY FINAL EXAMINATION FACULTY OF ARTS AND SCIENCE DEPARTMENT OF ECONOMICS APRIL 2017 ECONOMICS 426 International Macroeconomics Gregor Smith Instructions: The exam is three hours

Page 1 of 5 QUEEN S UNIVERSITY FINAL EXAMINATION FACULTY OF ARTS AND SCIENCE DEPARTMENT OF ECONOMICS APRIL 2017 ECONOMICS 426 International Macroeconomics Gregor Smith Instructions: The exam is three hours

Chapter 19 MONEY SUPPLIES, PRICE LEVELS, AND THE BALANCE OF PAYMENTS

Chapter 19 MONEY SUPPLIES, PRICE LEVELS, AND THE BALANCE OF PAYMENTS In the Keynesian model, the international transmission of shocks took place via the trade balance, with changes in national income or

Chapter 19 MONEY SUPPLIES, PRICE LEVELS, AND THE BALANCE OF PAYMENTS In the Keynesian model, the international transmission of shocks took place via the trade balance, with changes in national income or

The Balassa-Samuelson Relationship and the Renminbi

December 13, 2006 The Balassa-Samuelson Relationship and the Renminbi Jeffrey Frankel Harpel Professor for Capital Formation and Growth Kennedy School of Government, Harvard University The author would

December 13, 2006 The Balassa-Samuelson Relationship and the Renminbi Jeffrey Frankel Harpel Professor for Capital Formation and Growth Kennedy School of Government, Harvard University The author would

Answers to Questions: Chapter 7

Answers to Questions in Textbook 1 Answers to Questions: Chapter 7 1. Any international transaction that creates a payment of money to a U.S. resident generates a credit. Any international transaction

Answers to Questions in Textbook 1 Answers to Questions: Chapter 7 1. Any international transaction that creates a payment of money to a U.S. resident generates a credit. Any international transaction

Is the real dollar rate highly volatile? Abstract

Is the real dollar rate highly volatile? Stefan Norrbin Florida State University Onsurang Pipatchaipoom Samford University Abstract This note updates the real exchange rate behavior observed by Lothian

Is the real dollar rate highly volatile? Stefan Norrbin Florida State University Onsurang Pipatchaipoom Samford University Abstract This note updates the real exchange rate behavior observed by Lothian

Period 3 MBA Program January February MACROECONOMICS IN THE GLOBAL ECONOMY Core Course. Professor Ilian Mihov

Period 3 MBA Program January February 2008 MACROECONOMICS IN THE GLOBAL ECONOMY Core Course Professor SOLUTIONS Final Exam February 25, 2008 Time: 09:00 12:00 Note: These are only suggested solutions.

Period 3 MBA Program January February 2008 MACROECONOMICS IN THE GLOBAL ECONOMY Core Course Professor SOLUTIONS Final Exam February 25, 2008 Time: 09:00 12:00 Note: These are only suggested solutions.

Name Student ID Summer Session II Midterm ECON160B There are 7 pages and 100 points. You have 100 minutes to complete the exam.

Name Student ID Summer Session II 2013 Midterm ECON160B There are 7 pages and 100 points. You have 100 minutes to complete the exam. Multiple Choice Choose the best answer. (2.5 points each, 30 points

Name Student ID Summer Session II 2013 Midterm ECON160B There are 7 pages and 100 points. You have 100 minutes to complete the exam. Multiple Choice Choose the best answer. (2.5 points each, 30 points

Chapter 3 Foreign Exchange Determination and Forecasting

Chapter 3 Foreign Exchange Determination and Forecasting Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous editions. We adopted the convention that

Chapter 3 Foreign Exchange Determination and Forecasting Note: In the sixth edition of Global Investments, the exchange rate quotation symbols differ from previous editions. We adopted the convention that

International Macroeconommics

International Macroeconommics Chapter 3: Exchange Rate, The Monetary Approach in the Long Run Department of Economics, UCDavis Outline Goods Market Equilibrium: PPP 1 Goods Market Equilibrium: PPP 2 3

International Macroeconommics Chapter 3: Exchange Rate, The Monetary Approach in the Long Run Department of Economics, UCDavis Outline Goods Market Equilibrium: PPP 1 Goods Market Equilibrium: PPP 2 3

8: Relationships among Inflation, Interest Rates, and Exchange Rates

8: Relationships among Inflation, Interest Rates, and Exchange Rates Infl ation rates and interest rates can have a significant impact on exchange rates (as explained in Chapter 4) and therefore can infl

8: Relationships among Inflation, Interest Rates, and Exchange Rates Infl ation rates and interest rates can have a significant impact on exchange rates (as explained in Chapter 4) and therefore can infl

Nominal exchange rate

Nominal exchange rate The nominal exchange rate between two currencies is the price of one currency in terms of the other. The nominal exchange rate (or, for short, exchange rate) will be denoted by the

Nominal exchange rate The nominal exchange rate between two currencies is the price of one currency in terms of the other. The nominal exchange rate (or, for short, exchange rate) will be denoted by the

Short Run vs Long Run Determinants of Exchange Rates

Fletcher School, Tufts University Short Run vs Long Run Determinants of Exchange Rates Prof. George Alogoskoufis Short Run Determinants of Exchange Rates We have seen that in the short run exchange rates

Fletcher School, Tufts University Short Run vs Long Run Determinants of Exchange Rates Prof. George Alogoskoufis Short Run Determinants of Exchange Rates We have seen that in the short run exchange rates

Midterm - Economics 160B, Spring 2012 Version A

Name Student ID Section (or TA) Midterm - Economics 160B, Spring 2012 Version A You will have 75 minutes to complete this exam. There are 6 pages and 111 points total. Good luck. Multiple choice: Mark

Name Student ID Section (or TA) Midterm - Economics 160B, Spring 2012 Version A You will have 75 minutes to complete this exam. There are 6 pages and 111 points total. Good luck. Multiple choice: Mark

David Youngberg ECON 201 Montgomery College LECTURE 08: TRADE I

David Youngberg ECON 201 Montgomery College LECTURE 08: TRADE I I. A trading game a. Trade increases aggregate utility. b. The Fundamental Theorem of Exchange voluntary trade with complete information

David Youngberg ECON 201 Montgomery College LECTURE 08: TRADE I I. A trading game a. Trade increases aggregate utility. b. The Fundamental Theorem of Exchange voluntary trade with complete information

Less Reliable International Parity Conditions

The International Parity Conditions The Law of One Price Interest Rate Parity Less Reliable International Parity Conditions The Real Exchange Rate 1 The International Parity Conditions Though this be madness,

The International Parity Conditions The Law of One Price Interest Rate Parity Less Reliable International Parity Conditions The Real Exchange Rate 1 The International Parity Conditions Though this be madness,

Exchange rates and trade

Exchange rates and trade Naoyuki Yoshino, Dean Pornpinun Chantapacdepong, Research Fellow Matthias Helble, Research Fellow Asian Development Bank Institute ADBI-JIIA International Symposium on current

Exchange rates and trade Naoyuki Yoshino, Dean Pornpinun Chantapacdepong, Research Fellow Matthias Helble, Research Fellow Asian Development Bank Institute ADBI-JIIA International Symposium on current

11. Short Run versus Medium Run Determinants of Exchange Rates

Fletcher School of Law and Diplomacy, Tufts University 11. Short Run versus Medium Run Determinants of Exchange Rates E212 Macroeconomics Prof. George Alogoskoufis Short Run versus Medium Run Determinants

Fletcher School of Law and Diplomacy, Tufts University 11. Short Run versus Medium Run Determinants of Exchange Rates E212 Macroeconomics Prof. George Alogoskoufis Short Run versus Medium Run Determinants

Bachelor Thesis Finance

Bachelor Thesis Finance What is the influence of the FED and ECB announcements in recent years on the eurodollar exchange rate and does the state of the economy affect this influence? Lieke van der Horst

Bachelor Thesis Finance What is the influence of the FED and ECB announcements in recent years on the eurodollar exchange rate and does the state of the economy affect this influence? Lieke van der Horst

2/10/2011 PREDICTING EXCHANGE RATES: THE LONG-RUN MONETARY APPROACH and the The SHORT-RUN ASSET APPROACH

PREDICTING EXCHANGE RATES: THE LONG-RUN MONETARY APPROACH and the The SHORT-RUN ASSET APPROACH Introduction to Exchange Rates and Prices Consider some hypothetical data on prices and exchange rates in

PREDICTING EXCHANGE RATES: THE LONG-RUN MONETARY APPROACH and the The SHORT-RUN ASSET APPROACH Introduction to Exchange Rates and Prices Consider some hypothetical data on prices and exchange rates in

Exchange rate in a long run

Exchange rate in a long run dr hab. Bart Rokicki Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw urchasing ower arity Bart Rokicki urchasing power

Exchange rate in a long run dr hab. Bart Rokicki Chair of Macroeconomics and International Trade Theory Faculty of Economic Sciences, University of Warsaw urchasing ower arity Bart Rokicki urchasing power

Chapter 9 Essential macroeconomic tools. Baldwin&Wyplosz 2009 The Economics of European Integration, 3 rd Edition

Chapter 9 Essential macroeconomic tools 2 Background theory A quick refresher on basic macroeconomic principles Application of these principles to the question of exchange rate regimes 3 Output and prices

Chapter 9 Essential macroeconomic tools 2 Background theory A quick refresher on basic macroeconomic principles Application of these principles to the question of exchange rate regimes 3 Output and prices

Introduction to Macroeconomics M Problem set 4

T1 T2 Introduction to Macroeconomics M5 2015-16 Problem set 4 dollar appreciate from T1 to T2? 1. Nominal rate. Consider tables T1 and T2, taken from http://www.x-rates.com/. In T1, for instance, 1 can

T1 T2 Introduction to Macroeconomics M5 2015-16 Problem set 4 dollar appreciate from T1 to T2? 1. Nominal rate. Consider tables T1 and T2, taken from http://www.x-rates.com/. In T1, for instance, 1 can

Midterm - Economics 160B, Fall 2011 Version A

Name Student ID Section (or TA) Midterm - Economics 160B, Fall 2011 Version A You will have 75 minutes to complete this exam. There are 5 pages and 108 points total. Good luck. Multiple choice: Mark best

Name Student ID Section (or TA) Midterm - Economics 160B, Fall 2011 Version A You will have 75 minutes to complete this exam. There are 5 pages and 108 points total. Good luck. Multiple choice: Mark best

In frictionless markets, freely tradable goods should have the same price anywhere: S = P P $

Prices and Exchange Rates In frictionless markets, freely tradable goods should have the same price anywhere: P $ S = P P $ price in US$ S Exchange rate in yen per dollar P Price in Japanese yen Purchasing

Prices and Exchange Rates In frictionless markets, freely tradable goods should have the same price anywhere: P $ S = P P $ price in US$ S Exchange rate in yen per dollar P Price in Japanese yen Purchasing

OPEN-ECONOMY MACROECONOMICS: BASIC CONCEPTS

17 OPEN-ECONOMY MACROECONOMICS: BASIC CONCEPTS LEARNING OBJECTIVES: By the end of this chapter, students should understand: how net exports measure the international flow of goods and services. how net

17 OPEN-ECONOMY MACROECONOMICS: BASIC CONCEPTS LEARNING OBJECTIVES: By the end of this chapter, students should understand: how net exports measure the international flow of goods and services. how net

Master Economics & Business Understanding the World Economy. Sample Multiple choice

Master Economics & Business Understanding the World Economy Sample Multiple choice It is a multiple choice questionnaire. You have to select at LEAST one answer from the four proposed answers. You have

Master Economics & Business Understanding the World Economy Sample Multiple choice It is a multiple choice questionnaire. You have to select at LEAST one answer from the four proposed answers. You have

1+R = (1+r)*(1+expected inflation) = r + expected inflation + r*expected inflation +1

*(1+expected inflation) = r + expected inflation + r*expected inflation +1") Expecting a 5% increase in prices, investors require greater nominal returns than real returns. If investors are insensitive to inflation risk, then the nominal return must compensate for expected inflation:

Expecting a 5% increase in prices, investors require greater nominal returns than real returns. If investors are insensitive to inflation risk, then the nominal return must compensate for expected inflation:

The Final Exam is Tuesday May 4 th at 1:00 in the normal Todd classroom

The Final Exam is Tuesday May 4 th at 1:00 in the normal Todd classroom The final exam is comprehensive. The best way to prepare is to review tests 1 and 2, the reviews for Test 1 and Test 2, and the Aplia

The Final Exam is Tuesday May 4 th at 1:00 in the normal Todd classroom The final exam is comprehensive. The best way to prepare is to review tests 1 and 2, the reviews for Test 1 and Test 2, and the Aplia

Applied Econometrics and International Development. AEID.Vol. 5-3 (2005)

") PURCHASING POWER PARITY BASED ON CAPITAL ACCOUNT, EXCHANGE RATE VOLATILITY AND COINTEGRATION: EVIDENCE FROM SOME DEVELOPING COUNTRIES AHMED, Mudabber * Abstract One of the most important and recurrent

PURCHASING POWER PARITY BASED ON CAPITAL ACCOUNT, EXCHANGE RATE VOLATILITY AND COINTEGRATION: EVIDENCE FROM SOME DEVELOPING COUNTRIES AHMED, Mudabber * Abstract One of the most important and recurrent

Chapter 11 An Introduction to International Finance Adapted by H. Dellas

Chapter 11 An Introduction to International Finance Adapted by H. Dellas Topics to be Covered Foreign accounts-balance of payments Exchange rates-exchange rate markets Prices and exchange rates Interest

Chapter 11 An Introduction to International Finance Adapted by H. Dellas Topics to be Covered Foreign accounts-balance of payments Exchange rates-exchange rate markets Prices and exchange rates Interest

Exchange Rates in the Long Run

Exchange Rates in the Long Run What determines exchange rates? Supply + Demand!» Flow models: Demand & supply of FX to purchase goods and services» Stock models, or asset models Demand & supply of available

Exchange Rates in the Long Run What determines exchange rates? Supply + Demand!» Flow models: Demand & supply of FX to purchase goods and services» Stock models, or asset models Demand & supply of available

Policy Discussion Assignment 1

Management 495 Spring 2016 Topics in Finance: International Macroeconomics Policy Discussion Assignment 1 April 6, 2016 Due: Instructor: E-mail: Wed, April 27, before 9:30am Marc-Andreas Muendler muendler@ucsd.edu

Management 495 Spring 2016 Topics in Finance: International Macroeconomics Policy Discussion Assignment 1 April 6, 2016 Due: Instructor: E-mail: Wed, April 27, before 9:30am Marc-Andreas Muendler muendler@ucsd.edu

Purchasing Power Parity (PPP) and Real Exchange Rates (RER)

and Real Exchange Rates (RER)") Purchasing Power Parity (PPP) and Real Exchange Rates (RER) Abstract: In this article, we introduce the Purchasing Power Parity, a theory that stipulates that in the long run, the exchange rate between

Purchasing Power Parity (PPP) and Real Exchange Rates (RER) Abstract: In this article, we introduce the Purchasing Power Parity, a theory that stipulates that in the long run, the exchange rate between

At the end of 1970, you could have bought 358 Japanese yen with a single

M15_KRUG3040_08_SE_C15.qxd 1/19/08 3:29 PM Page 382 Price Levels and the Exchange Rate in the Long Run 15 Chapter 382 At the end of 1970, you could have bought 358 Japanese yen with a single American dollar;

M15_KRUG3040_08_SE_C15.qxd 1/19/08 3:29 PM Page 382 Price Levels and the Exchange Rate in the Long Run 15 Chapter 382 At the end of 1970, you could have bought 358 Japanese yen with a single American dollar;

Lecture 7: Intermediate macroeconomics, autumn Lars Calmfors

Lecture 7: Intermediate macroeconomics, autumn 2008 Lars Calmfors 1 EMU Economic and Monetary Union An old idea in the European Union 1989: Delors report 1991: Maastricht treaty 1997: Stability pact Eleven

Lecture 7: Intermediate macroeconomics, autumn 2008 Lars Calmfors 1 EMU Economic and Monetary Union An old idea in the European Union 1989: Delors report 1991: Maastricht treaty 1997: Stability pact Eleven

Macroeconomic Theory and Policy

ECO 209Y Macroeconomic Theory and Policy Lecture 6: Introduction to the Open Economy Gustavo Indart Slide 1 The Balance of Payments On the one hand, the home country will export goods and services to other

ECO 209Y Macroeconomic Theory and Policy Lecture 6: Introduction to the Open Economy Gustavo Indart Slide 1 The Balance of Payments On the one hand, the home country will export goods and services to other

Chapter 15. The Foreign Exchange Market. Chapter Preview

Chapter 15 The Foreign Exchange Market Chapter Preview In the mid-1980s, American businesses became less competitive relative to their foreign counterparts. By the 2000s, though, competitiveness increased.

Chapter 15 The Foreign Exchange Market Chapter Preview In the mid-1980s, American businesses became less competitive relative to their foreign counterparts. By the 2000s, though, competitiveness increased.