APPENDIX 2 PRINCIPAL PROTECTED DOW JONES INDUSTRIAL AVERAGE LINKED FUND WITH TARGET AUTO REDEMPTION (USD) ( )

|

|

|

- Brook Jacobs

- 5 years ago

- Views:

Transcription

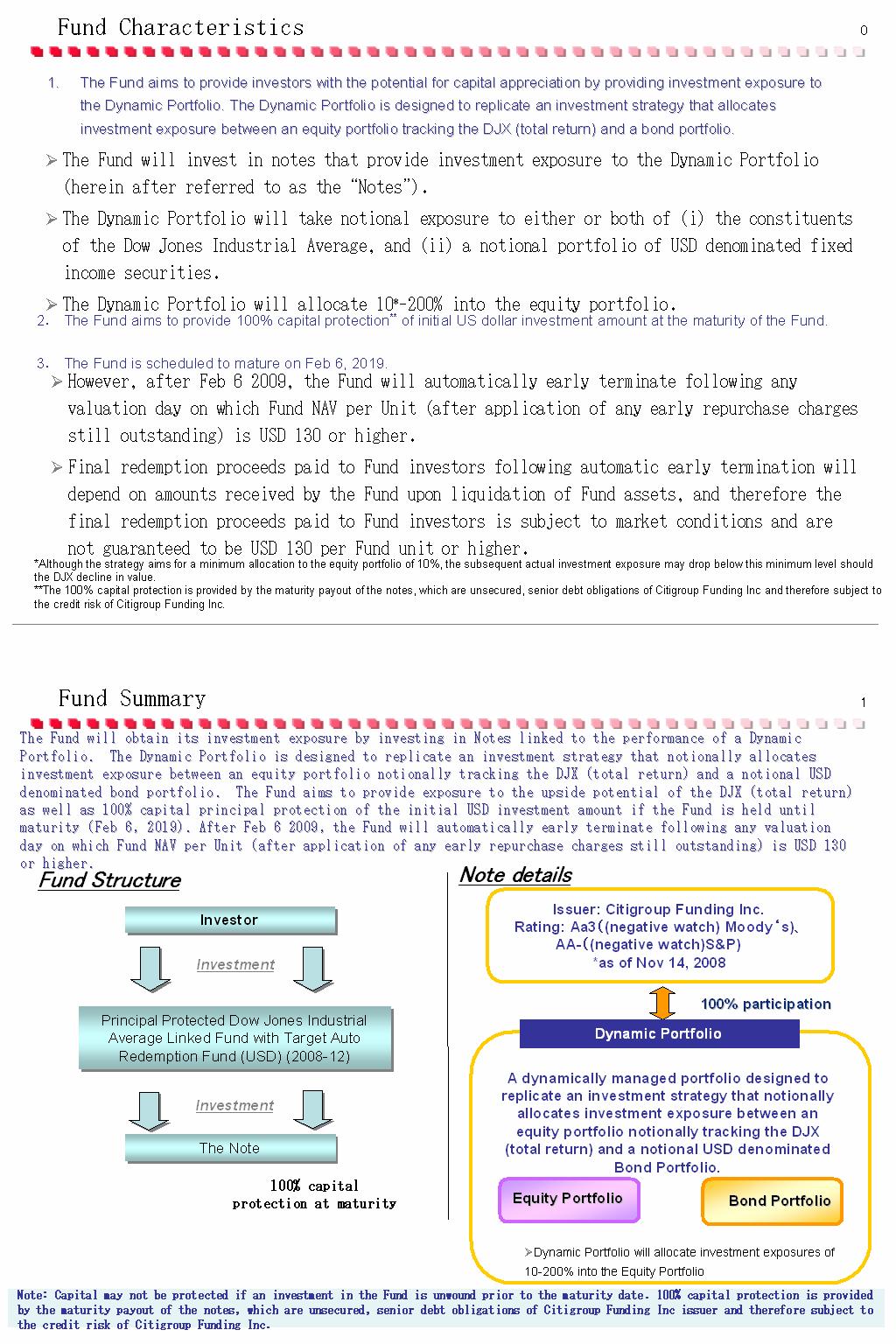

1 APPENDIX 2 PRINCIPAL PROTECTED DOW JONES INDUSTRIAL AVERAGE LINKED FUND WITH TARGET AUTO REDEMPTION (USD) ( ) Units will be offered in Japan pursuant to Article 2, Paragraph 3, Item 1 of the FIEL. DEFINITIONS Except where the context otherwise requires, in this Appendix 2, the following expressions have the following meanings: "Application Form" "Beneficiary" "Bond Floor" "Bond Units" "Business Day" "Calculation Agent" "Calculation Amount" means the form of application for Units available from the Manager or the Administrator; means, in respect of any Unit, the beneficial owner of that Unit; means the value as determined by the Calculation Agent in the manner described below in the section headed "Investment Objective and Policies The Series Trust The Dynamic Portfolio"; means the units described below in the section headed "Investment Objective and Policies The Series Trust The Dynamic Portfolio"; means any day (other than a Saturday, a Sunday or a public holiday) on which commercial banks are open for normal banking business in Hong Kong, London, Luxembourg, New York and Tokyo and/or such other day or days designated in writing by the Manager from time to time (in the Manager's absolute discretion); has the meaning given below in the section headed Investment Objective and Policies The Notes ; has the meaning given below in the section headed Investment Objective and Policies The Notes ; "Closing Date" means 19 December 2008; "DJX Index" means the Dow Jones Industrial Average SM Index, or any successor thereto; "DJX Index Portfolio" "DJX Index Portfolio Value" "DJX Index Reallocation Event" means the portfolio as described below in the section headed "Investment Objective and Policies The Series Trust The Dynamic Portfolio"; has the meaning given below in the section below headed "Investment Objective and Policies The Series Trust - The Dynamic Portfolio"; has the meaning given below in the section headed "Investment Objective and Policies The Series Trust - The Dynamic Portfolio"; SXP\642621\ v19

2 "DJX Total Return Index" "Dynamic Portfolio" "Dynamic Portfolio Adjustment Factor" "Dynamic Portfolio Value" Early Closure "Eligible Investor" Exchange Exchange Disruption means the Dow Jones Industrial Average SM Total Return Index, or any successor thereto; means a portfolio comprised of the Notional Participation Facility (if any) and a notional allocation of investments to the DJX Index Portfolio and the Notional Bond Portfolio"; means the amount determined in the manner described below in the section headed "Investment Objective and Policies The Series Trust The Dynamic Portfolio"; means the value determined by the Calculation Agent in the manner described below in the section headed "Investment Objective and Policies The Series Trust The Dynamic Portfolio"; means the closure on any Scheduled Trading Day of any Exchange(s) relating to securities/commodities that comprise 20 per cent. or more of the level of any Index or any Related Exchange(s) for such Index prior to its Scheduled Closing Time unless such earlier closing time is announced by such Exchange(s) or Related Exchange(s) at least one hour prior to the earlier of (i) the actual closing time for the regular trading session on such Exchange(s) or Related Exchange(s) on such Scheduled Trading Day and (ii) the submission deadline for orders to be entered into the relevant Exchange or Related Exchange system for execution at the relevant Valuation Time, on such Scheduled Trading Day; means any person, corporation or entity which is not (i) a resident of the US, a partnership organised or existing in the US, or any corporation, trust or other entity organised under the laws of or existing in the US; (ii) a person or entity resident or domiciled in the Cayman Islands (excluding any object of a charitable trust or power or an exempted or non-resident Cayman Islands company); (iii) unable to subscribe for or hold Units without violating applicable laws; or (iv) a custodian, nominee, or trustee for any person, corporation or entity described in (i) to (iii) above, or such other persons, corporations or entities as determined from time to time by the Manager and notified to the Trustee in respect of the Series Trust; means the principal stock exchange on which a component security/commodity of the relevant Index is principally traded, as determined by the Calculation Agent; means, any event (other than an Early Closure) that disrupts or impairs (as determined by the Calculation Agent) the ability of market participants in general (A) to effect transactions in, or obtain market values for, on any Exchange(s), securities/commodities that comprise 20 per cent. or more of the level of any Index, or (B) to effect transactions in, or obtain market values for, futures or options contracts relating to any Index on any relevant Related Exchange; SXP\642621\ v19 2

3 "Fixed Costs Provision" "Gap Ratio" "Hedging Disruption Event" "Index" "Index Sponsor" Initial Costs "Initial Offer Period" "Interest Distribution Adjustment Factor" "Issuer" "Market Disruption Event" has the meaning given in the section below headed Charges and Expenses Other Fees and Expenses ; means the ratio described below in the section headed "Investment Objective and Policies The Series Trust The Dynamic Portfolio"; has the meaning given below in the section headed "Investment Objective and Policies The Notes"; means each of the DJX Index and the DJX Total Return Index and, together, the "Indices"; means, in respect of an Index, the Dow Jones & Company, Inc., or any successor thereto; has the meaning given below in the section headed Charges and Expenses Other Fees and Expenses ; means the period as defined below in the section headed Issue and Repurchase of Units Subscription for Units Initial Offer ; means the amount calculated as set out in the section below headed Investment Objectives and Policies The Series Trust The Dynamic Portfolio Adjustment Factor ; has the meaning given below in the section headed "Investment Objective and Policies The Series Trust"; means the occurrence or existence of (i) a Trading Disruption, (ii) an Exchange Disruption, at any time during the one hour period that ends at the relevant Valuation Time, (iii) an Early Closure which, in each case, the Calculation Agent determines is material, or if any Exchange or any Related Exchange fails to open for trading during its regular trading session; provided that for the purposes of determining whether a Market Disruption Event exists if an event giving rise to a Market Disruption Event occurs in respect of a security included in an Index at that time, then the relevant percentage contribution of that security to the level of such Index shall be based on a comparison of (x) the portion of the level of that Index attributable to that security and (y) the overall level of that Index, in each case, immediately before the occurrence of such Market Disruption Event; provided further that if the Calculation Agent determines that it is not material that any day in respect of which the Calculation Agent is required to determine the level of an Index (a Relevant Day ) is: (i) not a Scheduled Trading Day in respect of an Index because one or more Related Exchanges relating to such Index is/are not scheduled to be open; or (ii) a day on which there is a Market Disruption Event for an Index solely because any Related Exchange relating to such Index fails to open, the Calculation Agent shall have the discretion to determine such day to be the Relevant Day (notwithstanding the fact that such day is not a Scheduled Trading Day in respect of an Index because one or more Related Exchanges is/are not scheduled to be open or there is a Market Disruption Event solely because any Related SXP\642621\ v19 3

4 Exchange fails to open), and in determining what is "material", the Calculation Agent shall have regard to such circumstances as it deems appropriate, which may include (but are not limited to) the Issuer's hedging arrangements in respect of the Notes. "Minimum Allocation Reallocation Event" "Net Asset Value" "Net Asset Value per Unit" "Note Maturity Date" "Notes" "Note Repurchase Day" "Note Valuation Date" "Notional Bond Portfolio" "Notional Participation Facility" "Observation Date" "Offering Memorandum" "Official Closing Level" "Reallocation Events" has the meaning given below in the section headed "Investment Objective and Policies The Series Trust The Dynamic Portfolio"; means the Net Asset Value of the Series Trust; means the Net Asset Value divided by the number of Units in issue at the time of calculation; has the meaning given in the section below headed "Investment Objective and Policies The Notes"; has the meaning given in the section below headed "Investment Objective and Policies The Series Trust"; means a day which is both an Observation Date and a day on which Citigroup Global Markets Inc. provides a bid price in respect of the Notes; means, subject as provided below in the sub-section headed "Investment Objective and Policies The Series Trust The Dynamic Portfolio Market Disruption Event", 20 December In the event that 20 December 2018 is not an Observation Date, the Note Valuation Date will be the immediately succeeding Observation Date; means the portfolio as described in the section below headed "Investment Objective and Policies The Series Trust The Dynamic Portfolio"; means the notional financing facility as described below in the section headed "Investment Objective and Policies The Series Trust The Dynamic Portfolio"; means a day which is both a Scheduled Trading Day for both the Indices and a day on which commercial banks are open for general business (including dealings in foreign exchange and foreign currency deposits) in New York City; means the offering memorandum relating to the Trust dated November 2008, as revised or supplemented from time to time thereafter; means, subject as provided below in the sub-section headed "Investment Objective and Policies The Series Trust" in respect of any Observation Date, the official closing level of the DJX Index or the DJX Total Return Index, as the case may be, as published by the Index Sponsor on such Observation Date as determined by the Calculation Agent; means the events described below in the section headed "Investment Objective and Policies The Series Trust The SXP\642621\ v19 4

5 Dynamic Portfolio"; "Reallocation Percentage" Related Exchange Relevant Day "Repurchase Application Day" "Repurchase Day" "Repurchase Notice" Scheduled Closing Time Scheduled Trading Day "Series Trust" "Specified Denomination" "Target Auto Redemption Condition" "Termination Date" means the proportion described below in the section headed "Investment Objective and Policies The Series Trust The Dynamic Portfolio"; means, in relation to an Index, each exchange or quotation system where trading has a material effect (as determined by the Calculation Agent) on the overall market for futures or options contracts relating to the Index; has the meaning given above in the definition Market Disruption Event ; means, in relation to any Repurchase Day, the third Business Day prior to that Repurchase Day; means, subject as provided in the section headed Issue and Repurchase of Units Repurchase of Units, (a) during the period from, and including, 6 February 2009 to, and including, 6 December 2018, the sixth day of each calendar month or if any such day is not a Business Day, the immediately following Business Day; (b) during the period from, and including, the Note Maturity Date to 6 February 2019, each Business Day; and (c) if the Target Auto Redemption Condition is satisfied, each Business Day following the day on which the Custodian receives the net proceeds from the sale of all the Notes up to the Termination Date; means the form of repurchase notice available from the Manager or the Administrator; means, in respect of an Index and an Exchange or Related Exchange and a Scheduled Trading Day for such Index, the scheduled weekday closing time of such Exchange or Related Exchange on such Scheduled Trading Day, without regard to after hours or any other trading outside of the regular trading session hours; means, in respect of either Index, any day on which the Exchange and each Related Exchange for such Index are scheduled to be open for trading for their respective regular trading sessions; means Principal Protected Dow Jones Industrial Average Linked Fund with Target Auto Redemption (USD) ( ), a series trust of the Trust created and established pursuant to the Trust Deed and a supplemental trust deed made on 19 November 2008 between the Trustee and the Manager; means US$100; means the condition described below in the section headed "Investment Objective and Policies The Series Trust"; means 6 February 2019 or such earlier date as the Manager may determine in the manner described below in the section headed SXP\642621\ v19 5

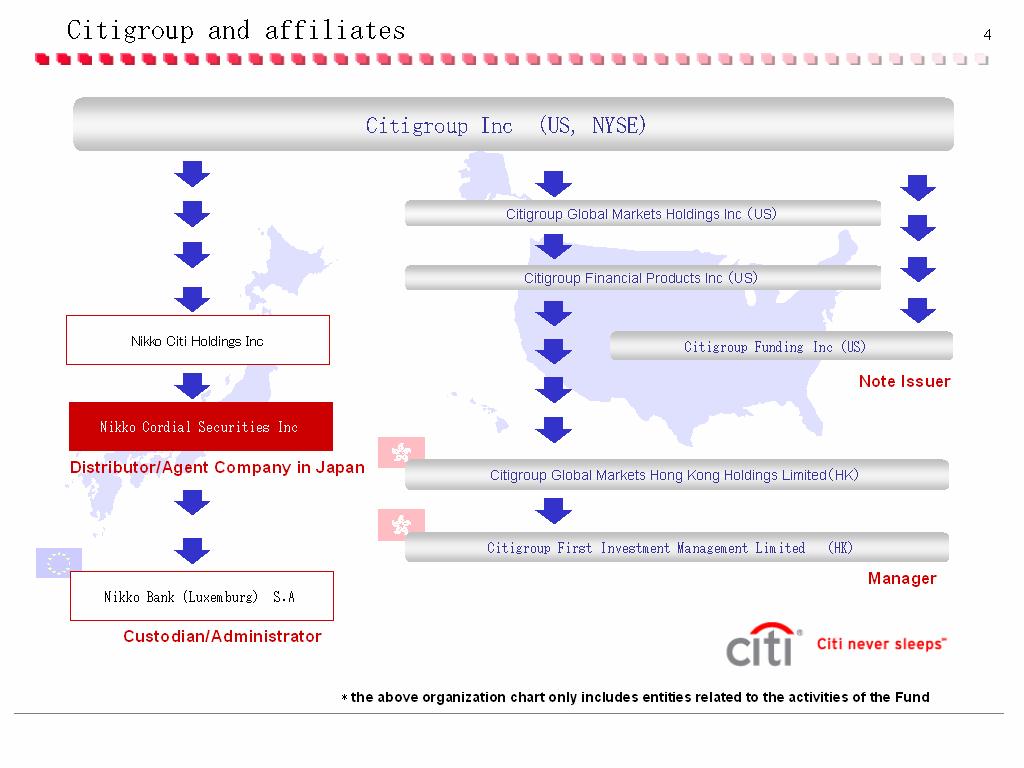

6 "Investment Objective and Policies The Series Trust"; Trading Disruption "Unit" "Unitholder" Unspent Provision "US" Valuation Day "Valuation Time" "Yen" and " " means any suspension of or limitation imposed on trading by any Exchange(s) or Related Exchange or otherwise and whether by reason of movements in price exceeding limits permitted by any Exchange or Related Exchange or otherwise either (a) relating to securities/commodities that comprise 20 per cent. or more of the level of any Index on the Exchange or (b) in futures or options contracts relating to such Index on any relevant Related Exchange; means a Unit of the Series Trust; means the registered holder for the time being of a Unit and includes all persons jointly registered as the holders of a Unit; has the meaning given in the section below headed Risk Factors Net Asset Value per Unit ; means the United States of America, its territories and possessions; means each Business Day, and/or any other day or days designated in writing by the Manager from time to time; means, in respect of an Index and as determined by the Calculation Agent, the time at which the level of the DJX Index or the DJX Total Return Index, as the case may be, is determined; and means the lawful currency of Japan. Unless the context otherwise requires, other expressions used in this Appendix 2 shall have the same meaning as in the Offering Memorandum. FUNCTIONAL CURRENCY The Functional Currency of the Series Trust is US dollars. The Series Trust INVESTMENT OBJECTIVE AND POLICIES The investment objective of the Series Trust is to provide Unitholders with the potential for capital growth and 100% capital protection if the Units are held until and including 6 February 2019, through investment of all, or substantially all, of the proceeds from the issue of the Units in certain notes which will be redeemed at an amount calculated by reference to the Dynamic Portfolio (the "Notes"). The Notes will form part of a series of unsecured senior debt securities issued by Citigroup Funding Inc. (the Issuer ), the payments on which are fully and unconditionally guaranteed by Citigroup Inc. The Notes will rank equally with all other unsecured and unsubordinated debt of the Issuer, and the guarantee of any payments due under the Notes will rank equally with all other unsecured and unsubordinated debt of Citigroup Inc. As of 14 November 2008, the rating of the Issuer is Aa3 (Negative Review) (by Moody's Investors Service) and AA- (Watch Negative) (by Standard & Poor's) based upon a guarantee from its parent company, Citigroup Inc. The SXP\642621\ v19 6

7 100% capital protection for the Units, which is provided by the maturity payout of the Notes, is therefore subject to the credit risk of the issuer and Citigroup Inc. If on any Valuation Day falling on or after the first Repurchase Day, the Target Auto Redemption Condition is satisfied, the Manager will inform Citigroup Global Markets Inc. at the open of business on the immediately following Note Repurchase Day that it wishes to sell the Series Trust's entire portfolio of Notes. Subject to liquidity, such sale will be executed on one or more Note Repurchase Days, starting on such Note Repurchase Day and ending no later than the Note Valuation Date. The number of Note Repurchase Days required to complete the sale of the Series Trust's entire portfolio of Notes will depend on the number of Notes held and the prevailing market liquidity conditions at or around the time the Target Auto Redemption Condition is satisfied. Following completion of the sale of the Series Trust's entire portfolio of Notes, the Manager will deposit all the sale proceeds in a US dollar deposit account, and will determine that the Termination Date will be the day falling one calendar month after the receipt by the Custodian of all the proceeds from the sale of the Notes. In the event that the Notes are redeemed before the Note Maturity Day, including in the circumstances described in the section headed Risk Factors Investment in the Notes The Notes may be redeemed early at an amount less than US$100 per Note, the Manager may determine to terminate the Series Trust on such Termination Date as it may determine. The Target Auto Redemption Condition will be satisfied if Net Asset Value per Unit less the Repurchase Fee per Unit calculated in the manner described below in the section headed "Repurchase of Units Repurchase Price" is equal to or greater than US$130. Investors should note, however, that the Manager can give no guarantee that the net proceeds payable per Unit following completion of the sale of the Series Trust s entire Notes will equal at least US$130. The Dynamic Portfolio The following description is the methodology for determining the Dynamic Portfolio as at the date of this Appendix 2. No assurance can be given that market, regulatory, juridical or fiscal circumstances or, without limitation, any other circumstances will not arise that would, in the view of the Calculation Agent, necessitate a modification of or change to such methodology. General description The Dynamic Portfolio is designed to replicate an investment strategy that allocates investment exposures between two types of assets, namely the DJX Index Portfolio and the Notional Bond Portfolio. The notional allocation of capital between the DJX Index Portfolio and the Notional Bond Portfolio changes during the Investment Period in response to the performance of the DJX Index Portfolio, aiming to increase the exposure to the DJX Index Portfolio to benefit from any rises in its value whilst protecting an investor's initial capital investment, as described below. Positive performance of the DJX Index Portfolio will tend to result in an increased allocation to the DJX Index Portfolio, and negative performance of the DJX Index Portfolio will tend to result in a decreased allocation. These allocations will be adjusted by the Calculation Agent according to the methodology described below at any time during regular trading session hours in the United States (as determined by the Calculation Agent) on any Observation Date. References herein to "any time" shall be deemed to be references to any time during such regular trading session hours. As further described below, any such allocation to the DJX Index Portfolio can never be (i) more than 200% of the value of the Dynamic Portfolio (the "Dynamic Portfolio Value") at the time of the reallocation pursuant to the provisions set out below in the sub-section headed "Reallocation of exposure", subject at all times to a leverage cap of US$100, or (ii) less than 10% of the Dynamic Portfolio Value at the time of the reallocation pursuant to such provisions SXP\642621\ v19 7

8 provided, however, that the exact allocation to the DJX Index Portfolio may vary thereafter based on changes in the Dynamic Portfolio Value. "Investment Period" means, in relation to the Dynamic Portfolio, the period from and including the Dynamic Portfolio Commencement Date to but excluding the Note Valuation Date. The Dynamic Portfolio Value is expressed in US dollars. Composition of the Dynamic Portfolio General At any time, the notional investments represented by the Dynamic Portfolio will be allocated between the DJX Index Portfolio and the Notional Bond Portfolio. The pre-determined allocation methodology is intended to maximize the Dynamic Portfolio's participation in any appreciation in the value of the DJX Index Portfolio while endeavouring to achieve a Final Portfolio Value of greater than US$100. DJX Index Portfolio The DJX Index Portfolio will comprise a notional investment in a number of DJX Index Portfolio Units. "DJX Index Portfolio Unit" means, in relation to the DJX Index Portfolio, a synthetic security representing a notional investment in the DJX Index which has a value on the Dynamic Portfolio Commencement Date of US$100 and has a value equal to the DJX Total Return Index Value thereafter. Notional investments in the DJX Index Portfolio will be increased or decreased through notional purchases (or sales) of DJX Index Portfolio Units. The value of the DJX Index Portfolio (the "DJX Index Portfolio Value") at any time after the Dynamic Portfolio Commencement Date (as defined in the sub-section below headed "Dynamic Portfolio Value and initial composition of the Dynamic Portfolio - Initial Composition of the Dynamic Portfolio"), is equal to the product of (i) the number of DJX Index Portfolio Units in the DJX Index Portfolio at that time and (ii) the DJX Total Return Index Value (as defined below in the sub-section headed The DJX Total Return Index Value ) at that time all as determined by the Calculation Agent. Notional Bond Portfolio The Notional Bond Portfolio will comprise a notional investment in a number of Bond Units. Notional investments in the Notional Bond Portfolio will be increased or decreased through notional purchases (or sales) of Bond Units. The value of the Notional Bond Portfolio (the "Notional Bond Portfolio Value") at any time after the Dynamic Portfolio Commencement Date is equal to the product of (i) the number of Bond Units in the Notional Bond Portfolio at that time and (ii) the Bond Unit Value (as described below) at that time, all as determined by the Calculation Agent. Any Bond Units are purely notional and are not capable of being traded and do not give any Noteholder rights in respect of any such Bond Units. Each Bond Unit will comprise one bond having the following characteristics: (a) (b) (c) it is denominated in US dollars; it matures on 20 December 2018; and has a redemption amount equal to US$1.00. SXP\642621\ v19 8

9 The Bond Unit Value will equal the value of one Bond Unit. The value of a Bond Unit at any time will be determined by the Calculation Agent by discounting the notional redemption amount of the Bond Unit from the date of redemption to the date of calculation using discount rates equal to the interpolated yields derived from the US dollar swap rate (or US dollar LIBOR rates for maturities of one year or shorter) interpolated to the maturity date of the Bond Unit, any such rate as provided by Bloomberg Financial Markets or another recognized source selected by the Calculation Agent at that time. The US dollar swap rate at any time is based upon the U.S. Treasury rate plus a credit spread commonly referred to as a swap spread, as provided by Bloomberg Financial Markets or another recognized source selected by the Calculation Agent at that time. As a result, the value of the Bond Unit will change from time to time (including intraday) in response to changes in interest rates and the swap spread. In the event that the Calculation Agent is not able to determine any such US dollar swap rate, US dollar LIBOR rate or swap spread as provided above for any reason (including by reason of a disruption in the relevant market), such US dollar swap rate, US dollar LIBOR rate or swap spread shall be determined by the Calculation Agent by reference to such sources as it deems appropriate. Notional Participation Facility Subject as provided in the sub-section below headed "Reallocation of exposure Limitations on reallocations", where the Calculation Agent effects additional purchases of DJX Index Portfolio Units following a reallocation, it may, in certain circumstances described below, fund such purchases by using the Notional Participation Facility. The Notional Participation Facility is a notional financing facility that permits the allocation to the DJX Index Portfolio to exceed 100% of the Dynamic Portfolio Value, subject to a maximum of 200% of the Dynamic Portfolio Value at the time of the occurrence of the Reallocation Event or the DJX Index Reallocation Event, as the case may be, and subject at all times to a leverage cap of US$100 as further described in the sub-section below headed "Reallocation of exposure Limitations on reallocations". The value of the Notional Participation Facility (the "Notional Participation Facility Amount") at any time (t) will equal the sum of the notional borrowed funds outstanding under the Notional Participation Facility at such time (t) plus any Notional Participation Facility Fees (as described below) outstanding at such time (t). The Notional Participation Facility Fee on any day will be calculated at close of business (as determined by the Calculation Agent) on such day and will be effective from such time of calculation and will equal the product of (i) (1/365); (ii) the Notional Participation Facility Amount at the end of that day after any reallocations effected on that day, including any outstanding Notional Participation Facility Fees; and (iii) Overnight US dollar LIBOR (as described below) for that day plus 1.00%. The Notional Participation Facility Fee will accrue daily and will be computed on the basis of a 365-day year. Overnight US dollar LIBOR on any day will be the overnight US dollar LIBOR rate as provided by Bloomberg Financial Markets or another recognized source selected by the Calculation Agent PROVIDED THAT in the event that the Calculation Agent is not able to determine such overnight rate as aforesaid for any reason (including by reason of a disruption in the relevant market), such overnight rate shall be determined by the Calculation Agent by reference to such sources as it deems appropriate. The Notional Participation Facility Fee will be calculated and subtracted from the DJX Index Portfolio and the Notional Bond Portfolio on a pro rata basis at the end of each day after effecting any reallocation(s) on that day, commencing on the first day after the Dynamic Portfolio Commencement Date. Subtraction of the Notional Participation Facility Fee will be effected by reducing the number of DJX Index Portfolio Units and Bond Units with an aggregate value as of SXP\642621\ v19 9

10 the close of business on that Observation Date equal to the pro rata portion of the Notional Participation Facility Fee relating to the DJX Index Portfolio or the Notional Bond Portfolio, as the case may be. Dynamic Portfolio Value and initial composition of the Dynamic Portfolio Dynamic Portfolio Value The Dynamic Portfolio Value at any time on any Observation Date shall be determined by the Calculation Agent in accordance with the following formula: Where: DPV t = DJXP t + NBPV t - NPFA t DPV t means the Dynamic Portfolio Value at such time; DJXP t means, in respect of any time on an Observation Date, the DJX Index Portfolio Value at such time on such Observation Date, net of the pro-rata portion of the Dynamic Portfolio Adjustment Factor allocated to the DJX Index Portfolio for such Observation Date; NBPV t means, in respect of any time on an Observation Date, the Notional Bond Portfolio Value at such time on such Observation Date, net of the pro-rata portion of the Dynamic Portfolio Adjustment Factor allocated to the Notional Bond Portfolio for such Observation Date; and NPFA t means, in respect of any time on an Observation Date, the Notional Participation Facility Amount (if any) at such time on such Observation Date. The Dynamic Portfolio Value on any day that is not an Observation Date will equal the Dynamic Portfolio Value on the previous day minus the Dynamic Portfolio Adjustment Factor and the Notional Participation Facility Fee for that day, and the DJX Index Portfolio and the Notional Bond Portfolio shall be reduced on such day to reflect such deduction, as provided herein. Initial composition of the Dynamic Portfolio The Dynamic Portfolio will be established on 19 December 2008 (the "Dynamic Portfolio Commencement Date"). As at the Dynamic Portfolio Commencement Date: (a) (b) (c) (d) the Dynamic Portfolio Value ("DPV 0 ") will be US$100, less the Initial Costs and Fixed Costs Provision in respect of each Unit, as determined on the Dynamic Portfolio Commencement Date; the DJX Index Portfolio Value ("DJXP 0 ") will be determined on the Dynamic Portfolio Commencement Date; the Notional Bond Portfolio Value ("NBPV 0 ") will be determined on the Dynamic Portfolio Commencement Date; and the Notional Participation Facility Amount ("NPFA 0 ") will be US$0.00. The Dynamic Portfolio Adjustment Factor The Dynamic Portfolio Adjustment Factor will accrue daily (including on any day which is not an Observation Date) on the basis of a 365-day year and on any day will equal the sum of: SXP\642621\ v19 10

11 (a) (b) (c) the product of (i) (1/365), (ii) the Relevant Rate (as described below) and (iii) the greater of US$100 and the Dynamic Portfolio Value at the end of the previous day, after effecting any required reallocation(s); a fixed coupon equal to the product of (i) (1/365), (ii) 0.9% and (iii) US$100; and the product of (i) (1/365), (ii) the Interest Distribution Adjustment Factor and (iii) US$100. Where Relevant Rate for any day means 1.2 per cent. per annum (or 0.7 per cent. per annum if the Minimum Allocation to the DJX Index Portfolio has been reached on that day and no subsequent reallocation has occurred on such day): Interest Distribution Adjustment Factor for any day means: (a) (b) (c) in respect of any day prior to (and including) the first anniversary of the Dynamic Portfolio Commencement Date, X % per annum, where "X" is an annual percentage rate to be determined by the Calculation Agent on the Dynamic Portfolio Commencement Date and which was indicatively 2% per annum as of 14 November 2008; in respect of any day after the first anniversary and prior to (and including) the fifth anniversary of the Dynamic Portfolio Commencement Date, 0.6% per annum; and thereafter, 0% per annum. The Dynamic Portfolio Adjustment Factor will be calculated and subtracted from the DJX Index Portfolio and the Notional Bond Portfolio on a pro rata basis at the end of each day after effecting any reallocation(s) on that day, commencing on the first day after the Dynamic Portfolio Commencement Date. Subtraction of the Dynamic Portfolio Adjustment Factor will be effected by reducing the number of DJX Index Portfolio Units and Bond Units with an aggregate value as of the close of business on the immediately preceding Observation Date equal to the pro rata portion of the Dynamic Portfolio Adjustment Factor relating to the DJX Index Portfolio or the Notional Bond Portfolio, as the case may be. Other than the fixed coupon specified above (see item 9 of the terms and conditions of the Notes), the notional value of the Dynamic Portfolio Adjustment Factor accrued and deducted will be retained by the Calculation Agent or one of its affiliates. Reallocation of exposure Reallocation Events Subject as provided in the sub-sections below headed "Limitations on reallocations" and Market Disruption Event, a reallocation of the notional investment represented by the Dynamic Portfolio to the DJX Index Portfolio and the Notional Bond Portfolio will be effected if the Calculation Agent determines that either of the following events (each a "Reallocation Event") has occurred at any time on any Observation Date: (a) (b) the Gap Ratio (as described below in the sub-section headed Gap Ratio ) is greater than 30% (the "Maximum Gap Ratio"); or the Gap Ratio is less than 20% (the "Minimum Gap Ratio"). If at any time on an Observation Date the Calculation Agent determines that a Reallocation Event has occurred at such time, the Calculation Agent, as soon as reasonably practicable (which may be intraday or at the close of business), will determine the Reallocation Percentage and will reallocate the Dynamic Portfolio so that the percentage of the Dynamic Portfolio notionally SXP\642621\ v19 11

12 invested in the DJX Index Portfolio is as close as is reasonably practicable to the Reallocation Percentage. In determining the Reallocation Percentage for the purposes hereof, the Dynamic Portfolio Value, the DJX Index Portfolio Value, the Notional Bond Portfolio Value and the Bond Floor will be their values at the time of the occurrence of the Reallocation Event. In effecting any necessary reallocation, the Dynamic Portfolio Value, the DJX Index Portfolio Value, the Notional Bond Portfolio Value and the Bond Floor will be their values at the time the reallocation is effected. Reallocation following a 10% decrease in the value of the DJX Index Subject as provided in the sub-sections below headed "Limitations on reallocations" and Market Disruption Event, if at any time on an Observation Date the level of the DJX Index declines from its Official Closing Level on the immediately preceding Observation Date by 10% or more, as determined by the Calculation Agent (a "DJX Index Reallocation Event"), the Calculation Agent, as soon as reasonably practicable (which may be intraday or at the close of business), will determine the Reallocation Percentage and will reallocate the Dynamic Portfolio so that the percentage of the Dynamic Portfolio notionally invested in the DJX Index Portfolio is as close as is reasonably practicable to the Reallocation Percentage. In determining the Reallocation Percentage for the purposes hereof, the Dynamic Portfolio Value, the DJX Index Portfolio Value, the Notional Bond Portfolio Value and the Bond Floor will be their values at the time of the occurrence of the DJX Index Reallocation Event. In effecting any necessary reallocation, the Dynamic Portfolio Value, the DJX Index Portfolio Value, the Notional Bond Portfolio Value and the Bond Floor will be their values at the time the reallocation is effected. Reallocation of the Dynamic Portfolio to the Minimum Allocation Subject as provided in the sub-sections below headed "Limitations on reallocations" and Market Disruption Event, if at any time on an Observation Date the Dynamic Portfolio Value is less than or equal to 103% of the Bond Floor at such time, as determined by the Calculation Agent (a "Minimum Allocation Reallocation Event"), the Calculation Agent, as soon as reasonably practicable (which may be intraday or at the close of business), will determine the Reallocation Percentage to be 10% (the "Minimum Allocation") and will reallocate the Dynamic Portfolio so that the percentage of the Dynamic Portfolio notionally invested in the DJX Index Portfolio is as close as is reasonably practicable to the Reallocation Percentage of 10%. In effecting any necessary reallocation, the Dynamic Portfolio Value, the DJX Index Portfolio Value, the Notional Bond Portfolio Value and the Bond Floor will be their values at the time the reallocation is effected. Such Minimum Allocation is only required upon the occurrence of a Minimum Allocation Reallocation Event and there is no guarantee that in the absence of a Minimum Allocation Reallocation Event that any particular percentage of the dynamic Portfolio will be notionally invested in the DJX Index Portfolio. Similarly, even where a Minimum Allocation Reallocation Event occurs, any future changes in the respective values of the DJX Index Portfolio and the Notional Bond Portfolio may result in an amount greater or less than the Minimum Allocation being allocated to the DJX Index Portfolio. General Reallocations will involve notional sales and purchases of DJX Index Portfolio Units and Bond Units or fractions of such DJX Index Portfolio Units and Bond Units, as the case may be. The number of DJX Index Portfolio Units and/or Bond Units or fractions thereof to be notionally sold or purchased will be determined by the Calculation Agent and the notional sales and purchases of DJX Index Portfolio Units and Bond Units or fractions thereof will be effected as soon as possible following the relevant reallocation. SXP\642621\ v19 12

13 If the reallocation results in an increased percentage of the proportion of the Dynamic Portfolio allocated to the DJX Index Portfolio, the reallocation will involve the notional sale of Bond Units and the notional purchase of DJX Index Portfolio Units with the notional proceeds of such sale. Subject as provided in the sub-section below headed "Limitations on reallocations", any purchase of DJX Index Portfolio Units that cannot be effected through the sale of Bond Units comprising the Notional Bond Portfolio (if any) will be effected using the Notional Participation Facility. The Notional Participation Facility Amount will be increased by the remaining amount necessary to purchase the DJX Index Portfolio Units, subject to the cap on the Notional Participation Facility Amount as described herein. If the reallocation results in a decreased percentage of the proportion of the Dynamic Portfolio allocated to the DJX Index Portfolio, the reallocation will involve the notional sale of DJX Index Portfolio Units. The notional proceeds of this sale will be used first to reduce the Notional Participation Facility Amount to zero and then to make notional purchases of Bond Units. Following any such reallocation, the number of DJX Index Portfolio Units and Bond Units in the DJX Index Portfolio and the Notional Bond Portfolio, respectively, will be adjusted to reflect the DJX Index Portfolio Units or the Bond Units notionally sold or purchased as a result of the reallocation and the Notional Participation Facility Amount will also be adjusted to reflect any increase or decrease (if any) following such reallocation. In general, an allocation to the DJX Index Portfolio may increase following increases in the value of the DJX Index Portfolio (which increases the difference between the value of the Dynamic Portfolio and the Bond Floor) and an allocation to the DJX Index Portfolio may decrease following decreases in the value of the DJX Index Portfolio. If more than one of a Reallocation Event or a DJX Index Reallocation Event occurs at the same time as a Minimum Allocation Reallocation Event, the Minimum Allocation Reallocation Event shall take precedence, subject as provided in the sub-section below headed "Limitations on reallocations". Limitations on reallocations If at the time of the occurrence of the Reallocation Event on any day, the reallocation to the DJX Index Portfolio pursuant to the sub-sections above headed "Reallocation Events", "Reallocation following a 10% decrease in the value of the DJX Index" and "Reallocation of the Dynamic Portfolio to the Minimum Allocation" would be greater than or equal to 200% of the Dynamic Portfolio Value at the time of the occurrence of the Reallocation Event, the allocation to the DJX Index Portfolio will only be increased to 200% of such Dynamic Portfolio Value and no further increase will be made in respect of that reallocation. In addition, if at any time on any day the Notional Participation Facility Amount would be greater than or equal to US$100 as a result of a reallocation pursuant to the sub-sections above headed "Reallocation Events", "Reallocation following a 10% decrease in the value of the DJX Index" and "Reallocation of the Dynamic Portfolio to the Minimum Allocation", the reallocation to the DJX Index Portfolio will only be increased to the extent that the Notional Participation Facility Amount would not be greater than or equal to US$100. However, no reallocation in which the allocation to the DJX Index Portfolio is decreased will occur solely because the DJX Index Portfolio Value is greater than or equal to 200% of the Dynamic Portfolio Value at the relevant time or because the Notional Participation Facility Amount equals or exceeds US$100. If, in relation to a reallocation, the allocation to the DJX Index Portfolio would be lower than the Minimum Allocation of the Dynamic Portfolio at the time of the occurrence of the Reallocation Event, the DJX Index Reallocation Event or the Minimum Allocation Reallocation Event, as the case may be, such reallocation will only be effected to the extent that the allocation to the DJX Index Portfolio is as close as is reasonably practicable to the Minimum Allocation of the Dynamic Portfolio and no further decrease in the allocation to the DJX Index Portfolio will be made in respect of that reallocation. For the avoidance of doubt, the exact percentage of the Dynamic SXP\642621\ v19 13

14 Portfolio allocated to the DJX Index Portfolio may vary thereafter based on changes in the value of the Dynamic Portfolio. Gap Ratio The Gap Ratio is the ratio of (i) the Dynamic Portfolio Value minus the Bond Floor and (ii) the amount of the Dynamic Portfolio allocated to the DJX Index Portfolio. The Gap Ratio at any time on any Observation Date will equal: Where: DPV BF DPV * DJP "DPV" is the Dynamic Portfolio Value at such time; "BF" is the Bond Floor (as described below) as determined by the Calculation Agent at such time; and "DJP" is the percentage of the Dynamic Portfolio allocated to the DJX Index Portfolio at such time, taking into account the Dynamic Portfolio Adjustment Factor allocated to the DJX Index Portfolio in respect of such day. The Gap Ratio will change in response to changes in the Dynamic Portfolio Value and to changes in interest rates (which affect the level of the Bond Floor and the value of the Notional Bond Portfolio). Reallocation Percentage The Reallocation Percentage is the proportion of the Dynamic Portfolio that the Calculation Agent shall target to allocate to the DJX Index Portfolio (subject as provided in the sub-section above headed "Limitations on reallocations") upon the occurrence of (i) a Reallocation Event or (ii) a DJX Index Reallocation Event or (iii) a Minimum Allocation Reallocation Event. The Reallocation Percentage in relation to (i) or (ii) above will be determined by the Calculation Agent by reference to the following formula: DPV BF 4.00 DPV In determining the Reallocation Percentage, the Dynamic Portfolio Value, the DJX Index Portfolio Value, the Notional Bond Portfolio Value and the Bond Floor will be their values at the time of the occurrence of the Reallocation Event, the DJX Index Reallocation Event or the Minimum Allocation Reallocation Event, as the case may be. In effecting any necessary reallocation, the Dynamic Portfolio Value, the DJX Index Portfolio Value, the Notional Bond Portfolio Value and the Bond Floor will be their values at the time the reallocation is effected. The Bond Floor The Bond Floor at any time on any day is the discounted present value, as determined by the Calculation Agent, of the sum of: (a) (b) US$100, discounted from 20 December 2018 to such day; and the Dynamic Portfolio Adjustment Factor (based upon the amount of the Dynamic Portfolio Adjustment Factor calculated as though the Minimum Allocation to the DJX SXP\642621\ v19 14

15 Index Portfolio has been reached for the purposes of this computation) for each day from the day on which the Bond Floor is being determined to and including the Note Valuation Date in relation to a Dynamic Portfolio with a value of US$100.00, discounted from the day that the relevant Dynamic Portfolio Adjustment Factor will be calculated and deducted to such day. The Calculation Agent will calculate the discount rate at any time: (a) (b) in respect of (a) above, using the interpolated yield derived from the US dollar swap rate plus Y % (or US dollar LIBOR rates plus Y % for maturities of one year or shorter) interpolated to 20 December 2018, any such rate as provided by Bloomberg Financial Markets or another recognized source selected by the Calculation Agent at that time. The US dollar swap rate at any time is based upon the US Treasury rate plus a credit spread commonly referred to as a swap spread, as provided by Bloomberg Financial Markets or another recognized source selected by the Calculation Agent at that time; and in respect of (b) above, using the interpolated yields derived from the US dollar swap rate plus Y % (or US dollar LIBOR rates plus Y % for maturities of one year or shorter) interpolated based upon the expected timing of the calculation of the Dynamic Portfolio Adjustment Factor, any such rate as provided by Bloomberg Financial Markets or another recognised source selected by the Calculation Agent at that time. "Y" will be determined by the Calculation Agent on the Dynamic Portfolio Commencement Date and which was indicatively 0.65 as of 1 December In the event that the Calculation Agent is not able to determine any such US dollar swap rate, US dollar LIBOR rate or swap spread as provided above for any reason (including by reason of a disruption in the relevant market), such US dollar swap rate, US dollar LIBOR rate or swap spread shall be determined by the Calculation Agent by reference to such sources as it deems appropriate. Accordingly, the Bond Floor will increase in response to decreases in interest rates and will decrease in response to increases in interest rates. Market Disruption Event If the level of the relevant Index cannot be determined at any time on any Observation Date due to the occurrence of a Market Disruption Event in respect of the relevant Index or otherwise, unless deferred by the Calculation Agent as described below, the Calculation Agent will determine the level of the relevant Index for such time on such Observation Date using commercially reasonable methods. If the level of the relevant Index cannot be determined at any time on any Observation Date due to the occurrence of a Market Disruption Event in respect of the relevant Index or otherwise, the determination of the level of the relevant Index or of a Reallocation Event by the Calculation Agent may, in the discretion of the Calculation Agent, be deferred by the Calculation Agent for up to five consecutive Observation Dates on which a Market Disruption Event in respect of the relevant Index is occurring or, if a Market Disruption Event in respect of an Index occurs on the Note Valuation Date, the relevant determination may be deferred by the Calculation Agent for up to two consecutive Observation Dates on which a Market Disruption Event in respect of the relevant Index is occurring. If, on such fifth or second Observation Date, as the case may be, the relevant determination still cannot be determined, the Calculation Agent will determine the level of the relevant Index for such time on such Observation Date using commercially reasonable methods. No reallocation or determination of the Dynamic Portfolio will occur on any day on which the determination of any of the above values is so deferred. SXP\642621\ v19 15

16 Index Adjustment Events If an Index is (i) not calculated and announced by or on behalf of the relevant Index Sponsor but is calculated and announced by or on behalf of a successor to the relevant Index Sponsor (the Successor Index Sponsor ) acceptable to the Calculation Agent, or (ii) replaced by a successor index using, in the determination of the Calculation Agent, the same or a substantially similar formula for and method of calculation as used in the calculation of that Index, then in each case that index (the Successor Index ) will be deemed to be the relevant Index. If (i) on or prior to any Relevant Day, the relevant Index Sponsor makes or announces that it will make a material change in the formula for or the method of calculating an Index or in any other way materially modifies that Index (other than a modification prescribed in that formula or method to maintain that Index in the event of changes in constituent stock and capitalisation, contracts or commodities and other routine events) (an Index Modification ), or permanently cancels an Index and no Successor Index exists (an Index Cancellation ), or (ii) on any Relevant Day, the relevant Index Sponsor or any person or entity on its behalf fails to calculate and announce an Index (an Index Disruption and, together with an Index Modification and an Index Cancellation, each an Index Adjustment Event ), then the Issuer may take the action described in (i) or (ii) below: (i) require the Calculation Agent to determine if such Index Adjustment Event has a material effect on the Notes and, if so, to either (A) in relation to any Relevant Day, determine the relevant level of the DJX Index and/or the DJX Total Return Index, as applicable, using commercially reasonable methods or (B) substitute the relevant Index with a replacement index using, in the determination of the Calculation Agent, the same or a substantially similar method of calculation as used in the calculation of such Index (the Substitute Index ) and the Calculation Agent shall determine the adjustments, if any, to be made to the conditions of the Notes to account for such substitution; or (ii) on giving notice to holders of Notes in accordance with the conditions of the Notes, the Issuer shall redeem all but not some only of the Notes, each Calculation Amount being redeemed by payment of an amount (which, for the avoidance of doubt, shall include amounts in respect of accrued interest (if applicable)) equal to the fair market value of such Calculation Amount, on a day selected by the Issuer, taking into account the Index Adjustment Event, less the cost to the Issuer and/or its affiliates of unwinding any underlying related hedging arrangements, all as determined by the Calculation Agent. Calculation Agent While the Calculation Agent currently employs the above described methodology to make determinations in relation to the Dynamic Portfolio, no assurance can be given that market, regulatory, juridical or fiscal circumstances or, without limitation, any other circumstances in the determination of the Calculation Agent will not arise that would, in the view of the Calculation Agent, necessitate a modification of or change to such methodology. In the event that the Calculation Agent makes any such modification or change, it shall notify the holders of the Notes. Records The Calculation Agent shall maintain detailed records (the "Records") with respect to the DJX Index Portfolio, the Notional Bond Portfolio and the Notional Participation Facility. The Records shall also include, in respect of each Observation Date, details of all the information required for its calculations in respect of such day for the Dynamic Portfolio Value, the DJX Index Portfolio Value, the Notional Bond Portfolio Value, the Bond Floor, the number of DJX Index Portfolio Units and the number of Bond Units. All information contained in the Records shall, in the absence of manifest error, be final and binding as to the matters to which they relate. SXP\642621\ v19 16

17 The DJX Total Return Index Value The DJX Total Return Index Value is US$100 on the Dynamic Portfolio Commencement Date. The DJX Total Return Index Value at any time on any Observation Date after the Dynamic Portfolio Commencement Date will be determined by the Calculation Agent in accordance with the following formula: DJIATR Level DJIATR Level t 0 *100 Where: DJIATR Level t means, subject as provided in the sub-section above headed "Market Disruption Event and Index Adjustment Events" and in respect of: (i) (ii) the time at which the Official Closing Level of the DJX Total Return Index is published by the Index Sponsor, the Official Closing Level of the DJX Total Return Index; and at any time on an Observation Date, other than the time at which the Official Closing Level of the DJX Total Return Index is published by the Index Sponsor, the level of the DJX Total Return Index for the immediately preceding Observation Date as adjusted to take into account the changes in the level of the DJX Index at such time on such day as compared to the Official Closing Level of the DJX Index on the immediately preceding Observation Date, all as determined by the Calculation Agent. DJIATR Level 0 means the Official Closing Level of the DJX Total Return Index on the Dynamic Portfolio Commencement Date. The Notes The following is a summary of the terms and conditions of the Notes: 1. (a) Issuer: Citigroup Funding Inc. (b) Guarantor: Citigroup Inc. 2. Specified Currency or Currencies: US dollars 3. (a) Specified Denomination: US$100 (b) Calculation Amount: US$ Issue Date: 6 January Note Maturity Date: 7 January Interest Basis: 0.9% fixed rate 7. Redemption/Payment Basis Formula Linked Redemption 8. (a) Status of the Notes: Senior (b) Status of the Deed of Guarantee: Senior SXP\642621\ v19 17

18 9. Fixed Rate Note Provisions Applicable (a) Interest Rate: 0.9% per annum payable monthly in arrear (b) Interest Payment Date(s): sixth day of each calendar month from (and including) 6 February 2009 to (and including) 6 December 2018 and the Note Maturity Date (c) Interest Amount: The Interest Amount per Calculation Amount will be determined in respect of any period by applying the Interest Rate to the Calculation Amount and multiplying such sum by the Day Count fraction and rounding the resultant figure to the nearest sub-unit of the Specified Currency, half of any such sub-unit being rounded upwards or otherwise in accordance with applicable market convention (d) Day Count Fraction: Actual/365 (e) Determination Dates: Not Applicable (f) Other terms relating to the method of calculating interest for Fixed Rate Notes The Interest Amount payable on each Interest Payment Date reflects the fixed coupon element of the Dynamic Portfolio Adjustment Factor 10. Redemption Amount of each Note The Formula Linked Redemption Amount specified below 11. Formula Linked Redemption Amount Unless the Notes have been previously redeemed or purchased and cancelled, the Formula Linked Redemption Amount in respect of each Calculation Amount will be determined by the Calculation Agent and will be an amount in US dollars equal to the sum of: (i) (ii) US$100; and the Dynamic Return Amount where: "Dynamic Return Amount" means the product of (i) US$100 and (ii) the Dynamic Portfolio Return Percentage. "Dynamic Portfolio Return Percentage" means an amount expressed as a percentage (which will not be less than 0%) calculated by the Calculation Agent on the basis of the following formula: Final Portfolio Value US$100 SXP\642621\ v19 18

19 US$100 "Final Portfolio Value" means the Dynamic Portfolio Value at the close of business on the Note Valuation Date, as determined by the Calculation Agent. 12. (a) Early Redemption Amount payable on redemption for taxation reasons or illegality or on event of default (pursuant to the terms and conditions of the Notes) and/or the method of calculating the same: (b) Early Redemption Amount includes amount in respect of accrued interest: An amount in respect of each principal amount of the Notes equal to the Calculation Amount calculated as an amount equal to an amount in the Specified Currency determined by the Calculation Agent which represents the fair market value of such Calculation Amount on a day selected by the Issuer (ignoring the relevant unlawfulness, illegality or prohibition) less the proportionate cost to the Issuer and/or its affiliates of unwinding any underlying and/or related hedging and funding arrangements in respect of the Notes (including without limitation, any equity options hedging the Issuer's obligations under the Notes). Yes: no additional amount in respect of accrued interest to be paid. (c) Early Redemption following a Hedging Disruption Event: If a Hedging Disruption Event occurs, the Issuer may, on giving notice to the holders of the Notes, redeem all but not some only of the Notes, each Calculation Amount being redeemed by payment of an amount equal to the fair market value of such Calculation Amount, on a day selected by the Issuer, taking into account the Hedging Disruption Event, less the cost to the Issuer and/or its affiliates of unwinding any underlying related hedging arrangements, all as determined by the Calculation Agent. Payments will be made in such manner and subject to such conditions as will be notified to the holders and upon such payment in respect of such Calculation Amount, the Issuer's obligations in respect thereof will be discharged. For the foregoing purposes, "Hedging Disruption Event" means that the Issuer and/or any of its affiliates is unable, after using commercially reasonable efforts, to (a) acquire, establish, re-establish, substitute, maintain, unwind or dispose of any transaction(s) or asset(s) it deems necessary to hedge the equity or other risk of the Issuer issuing and performing its obligations with respect to the Notes, or (b) realise, recover or remit the proceeds of any such transaction(s) SXP\642621\ v19 19

20 or asset(s). 13. Form of Notes: Registered Notes: Global Certificate registered in the name of a nominee for Euroclear and Clearstream, Luxembourg which is exchangeable for definitive Certificates in the limited circumstances described in the Global Certificate 14. Calculation Agent: Citigroup Global Markets Inc. at 390 Greenwich Street, New York, NY Citigroup Global Markets Inc. undertakes to use reasonable efforts to make a secondary market in the Notes by providing bid prices (purchase prices at which it would be prepared to purchase Notes, based on the market value of the Notes at the relevant time) on each Observation Date on which there is no Market Disruption Event, less a repurchase percentage of the Specified Denomination determined on the basis of the following: Repurchase during following period: Repurchase percentage of the Specified Denomination: From (and including) 19 December 2008 to (but excluding) 6 April 2009 From (and including) 6 April 2009 to (but excluding) 6 July 2009 From (and including) 6 July 2009 to (but excluding) 6 October 2009 From (and including) 6 October 2009 to (but excluding) 6 January 2010 From (and including) 6 January 2010 to (but excluding) 6 April 2010 From (and including) 6 April 2010 to (but excluding) 6 July 2010 From (and including) 6 July 2010 to (but excluding) 6 October 2010 From (and including) 6 October 2010 to (but excluding) 6 January 2011 From (and including) 6 January 2011 to (but excluding) 6 April 2011 From (and including) 6 April 2011 to (but excluding) 6 July 2011 From (and including) 6 July 2011 to (but excluding) 6 October % 3.55% 3.10% 2.60% 2.15% 2.00% 1.90% 1.75% 1.60% 1.45% 1.30% SXP\642621\ v19 20

21 From (and including) 6 October 2011 to (but excluding) 6 January 2012 From (and including) 6 January 2012 to (but excluding) 6 April 2012 From (and including) 6 April 2012 to (but excluding) 6 July 2012 From (and including) 6 July 2012 to (but excluding) 6 October 2012 From (and including) 6 October 2012 to (but excluding) 6 January 2013 From (and including) 6 January 2013 to (but excluding) 6 April 2013 From (and including) 6 April 2013 to (but excluding) 6 July 2013 From (and including) 6 July 2013 to (but excluding) 6 October 2013 From (and including) 6 October 2013 to (but excluding) 6 January 2014 From (and including) 6 January 2014 to (but excluding) the Note Valuation Date 1.20% 1.05% 0.90% 0.80% 0.65% 0.50% 0.40% 0.25% 0.15% 0% The DJX Index and the DJX Total Return Index The description of the DJX Index and the DJX Total Return Index set out below is of limited scope and consists only of extracts from, or summaries of, documents which are publicly available and assumed to be reliable. However, this information is provided to prospective investors for their convenience only and none of the Manager, the Issuer and Citigroup Global Markets Inc. or any of its or their affiliates accept any responsibility for the accuracy or completeness of the information concerning the DJX Index or the DJX Total Return Index or for the occurrence of any event which would affect the accuracy or completeness of such information. The Units are not sponsored, endorsed, sold or promoted by Dow Jones or any of its licensors. Neither Dow Jones nor any of its licensors makes any representation or warranty, express or implied, to Unitholders or any member of the public regarding the advisability of investing in securities generally or in the Units particularly. The only relationship of Dow Jones and its licensors to the Manager is the licensing of certain trademarks, trade names and service marks and of the Dow Jones Industrial Average SM Index and Dow Jones Industrial Average SM Total Return Index, which is determined, composed and calculated without regard to the Manager or the Units. Neither Dow Jones nor any of its licensors has any obligation to take the needs of the Manager or Unitholders into consideration in determining, composing or calculating the Dow Jones Industrial Average SM Index and Dow Jones Industrial Average SM Total Return Index. Neither Dow Jones nor any of its licensors is responsible for or has participated in the SXP\642621\ v19 21

22 determination of the timing of, prices at, or quantities of the Units to be issued or in the determination or calculation of the equation by which the Units are to be converted into cash. None of Dow Jones or any of its licensors has any obligation or liability in connection with the administration, marketing or trading of the Units. DOW JONES AND ITS LICENSORS DO NOT GUARANTEE THE ACCURACY AND/OR THE COMPLETENESS OF THE DOW JONES INDUSTRIAL AVERAGE SM INDEX AND DOW JONES INDUSTRIAL AVERAGE SM TOTAL RETURN INDEX OR ANY DATA RELATED THERETO AND NONE OF DOW JONES NOR ANY OF ITS LICENSORS SHALL HAVE ANY LIABILITY FOR ANY ERRORS, OMISSIONS, OR INTERRUPTIONS THEREIN. DOW JONES AND ITS LICENSORS MAKE NO WARRANTY, EXPRESS OR IMPLIED, AS TO RESULTS TO BE OBTAINED BY THE MANAGER, OWNERS OF THE UNITS, OR ANY OTHER PERSON OR ENTITY FROM THE USE OF THE DOW JONES INDUSTRIAL AVERAGE SM INDEX AND DOW JONES INDUSTRIAL AVERAGE SM TOTAL RETURN INDEX OR ANY DATA RELATED THERETO. NONE OF DOW JONES OR ITS LICENSORS MAKES ANY EXPRESS OR IMPLIED WARRANTIES, AND EACH EXPRESSLY DISCLAIMS ALL WARRANTIES, OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE WITH RESPECT TO THE DOW JONES INDUSTRIAL AVERAGE SM INDEX AND DOW JONES INDUSTRIAL AVERAGE SM TOTAL RETURN INDEX OR ANY DATA RELATED THERETO. WITHOUT LIMITING ANY OF THE FOREGOING, IN NO EVENT SHALL DOW JONES OR ANY OF ITS LICENSORS HAVE ANY LIABILITY FOR ANY LOST PROFITS OR INDIRECT, PUNITIVE, SPECIAL OR CONSEQUENTIAL DAMAGES OR LOSSES, EVEN IF NOTIFIED OF THE POSSIBILITY THEREOF. EXCEPT FOR THE LICENSORS, THERE ARE NO THIRD PARTY BENEFICIARIES OF ANY AGREEMENTS OR ARRANGEMENTS BETWEEN DOW JONES AND THE MANAGER. General The Dow Jones Industrial Average SM is a price-weighted index comprised of 30 common stocks selected at the discretion of the editors of The Wall Street Journal (the "WSJ"), which is published by Dow Jones & Company, Inc. ("Dow Jones"), as representative of the broad market of US industry. The DJX Index is reported by Bloomberg under the ticker symbol "INDU <Index>". There are no pre-determined criteria for selection of a component stock except that component companies represented by the DJX Index should be established US companies that are leaders in their industries. The DJX Index serves as a measure of the entire US market, including such sectors as financial services, technology, retail, entertainment and consumer goods, and is not limited to traditionally defined industrial stocks. Changes in the composition of the DJX Index are made entirely by the editors of the WSJ without consultation with the component companies represented in the DJX Index, any stock exchange, any official agency or the Issuer, the guarantor of the Issuer, the Calculation Agent or any of its or their affiliates. In order to maintain continuity, changes to the component stocks included in the DJX Index tend to be made infrequently and generally occur only after corporate acquisitions or other dramatic shifts in a component company's core business. When one component stock is replaced, the entire DJX Index is reviewed. As a result, multiple component changes are often implemented simultaneously. The component stocks of the DJX Index may be changed at any time for any reason. The DJX Index is price-weighted rather than market capitalisation-weighted. Therefore, the component stock weightings are affected only by changes in the stocks' prices, in contrast with the weightings of other indices that are affected by both price changes and changes in the number of shares outstanding. The value of the DJX Index is the sum of the primary exchange prices of each of the 30 common stocks included in the DJX Index, divided by a divisor. The divisor is changed in accordance with a mathematical formula to adjust for stock dividends, splits, SXP\642621\ v19 22

23 spin-offs and other corporate actions such as rights offerings and extraordinary dividends. Normal cash dividends are not taken into account in the calculation of the DJX Index. The current divisor of the DJX Index is published daily in the WSJ and other publications. While this methodology reflects current practice in calculating the DJX Index, no assurance can be given that Dow Jones will not modify or change this methodology in a manner that may affect the Notes. The current formula used to calculate divisor adjustments is as follows: the new divisor (i.e., the divisor on the next trading session) is equal to (1) the divisor on the current trading session, times; (2) the quotient of (a) the sum of the adjusted (for stock dividends, splits spin-offs and other applicable corporate actions) closing prices of the DJX Index components on the current trading session and (b) the sum of the unadjusted closing prices of the DJX Index components on the current trading session. Additional information on the DJX Index is available on the following website: http// The following is a list of companies included in the DJX Index as of 14 November 2008: Ticker Name % Weight in the Index Shares in the Index Last Price MMM UN Equity 3M Co AA UN Equity Alcoa Inc AXP UN Equity American Express Co T UN Equity AT&T Inc BAC UN Equity Bank of America Corp BA UN Equity Boeing Co CAT UN Equity Caterpillar Inc CVX UN Equity Chevron Corp C UN Equity Citigroup Inc KO UN Equity The Coca-Cola Co DD UN Equity EI Du Pont de Nemours & Co XOM UN Equity Exxon Mobil Corp GE UN Equity General Electric Co GM UN Equity General Motors Corp HPQ UN Equity Hewlett-Packard Co HD UN Equity Home Depot Inc INTC UW Equity Intel Corp IBM UN Equity International Business Machines Corp JNJ UN Equity Johnson & Johnson JPM UN Equity JPMorgan Chase & Co KFT UN Equity Kraft Foods Inc MCD UN Equity McDonald 's Corp MRK UN Equity NJ Merck & Co Inc MSFT UW Equity Microsoft Corp PFE UN Equity Pfizer Inc PG UN Equity Procter & Gamble Co UTX UN Equity United Technologies Corp VZ UN Equity Verizon Communications Inc WMT UN Equity Wal-Mart Stores Inc DIS UN Equity The Walt Disney Co SM DESCRIPTION OF THE DOW JONES INDUSTRIAL AVERAGE TOTAL RETURN INDEX SXP\642621\ v19 23

24 The Dow Jones Industrial Average Total Return Index is calculated by reinvesting dividends back into the Dow Jones Industrial Average on the ex-date of each component's declared dividend. The Dow Jones Industrial Average Total Return Index is reported by Bloomberg under the ticker symbol "DJITR <index>" at the close of each day. The component stocks are the same as those in the Dow Jones Industrial Average Index, as listed above. Historical Performance of the DJX Index and the DJX Total Return Index Historical data is not indicative of the future performance of the DJX Index or the DJX Total Return Index. Any historical upward or downward trend in the value of the DJX Index or the DJX Total Return Index during any period set forth below is not any indication that the DJX Index or the DJX Total Return Index is more or less likely to increase or decrease at any time during the term of the Notes. The high and low closing values (price-return) for the DJX Index and the DJX Total Return Index for the periods specified are set out below: Period DJX Index High DJX Index Low DJX Total Return Index High DJX Total Return Index Low , , , , , , , , , , , , , , , , January , , , , February , , , , March , , , , April , , , , May , , , , June , , , , July , , , , August , , , , September , , , , October , , , , Source: Index Sponsor's website; Bloomberg Disclaimer "Dow Jones", "Dow Jones Industrial Average SM ", "Dow Jones Industrial Average SM Total Return", "DJIA SM " are service marks of Dow Jones & Company, Inc. and have been licensed for use for certain purposes by the Issuer. The Notes based on the Dow Jones Industrial Average SM Total Return Index, are not sponsored, endorsed, sold or promoted by Dow Jones or any of its subsidiaries or affiliates, and neither Dow Jones nor any of their respective subsidiaries or affiliates, makes any representation regarding the advisability of investing in such product(s). NO ASSURANCE CAN BE GIVEN THAT THE INVESTMENT OBJECTIVE OF THE SERIES TRUST WILL BE ATTAINED. SXP\642621\ v19 24

25 Investment Restrictions The Manager will invest more than 50% of the latest available Net Asset Value in "securities" as defined in the FIEL (such as corporate or government debt securities, commercial paper, units of securities investment trusts and shares of mutual funds) other than those rights considered to be securities pursuant to the second sentence of Article 2, Paragraph 2 of the FIEL and in derivatives relating to such securities. The Manager will not on behalf of the Series Trust: (a) (b) (c) (d) (e) (f) enter into any transactions with itself or any of its directors as principal; enter into any transactions which are intended to benefit the Manager or any party other than the Unitholders; acquire any equity security or make any equity investment; sell any security short if, as a result of such short sale, the aggregate value of the securities sold short on behalf of the Series Trust would exceed the latest available Net Asset Value; invest in any (i) contractual type investment fund which invests in equity securities or makes equity investments or in any (ii) corporate investment fund; or acquire any Investment which is not listed on any exchange or which is not readily realisable if, as a result thereof, the total value of all such Investments held by the Series Trust would immediately following such acquisition exceed 15% of the latest available Net Asset Value. The Manager is not required to sell Investments immediately if any of the aforesaid restrictions are exceeded as a result of, inter alia, changes in the value of any of the Series Trust's Investments, reconstructions or amalgamations, payments out of the assets of the Series Trust or repurchases of Units. However, the Manager will take such steps as are reasonably practicable having regard to the interests of the Unitholders to comply with the aforesaid restrictions within a reasonable period of time after a breach is identified. Borrowings No borrowings will be effected in respect of the Series Trust. Distribution Policy The current policy in relation to the Series Trust is not to make distributions to Unitholders. RISK FACTORS Investors should be aware that the value of Units may fall as well as rise. Investment in the Series Trust involves significant risks. There is unlikely to be a secondary market in the Units. It is possible that an investor may lose a substantial portion or all of its investment in the Series Trust. As a result, each investor should carefully consider whether it can afford to bear the risks of investing in the Series Trust. The following description of risk factors does not purport to be a complete explanation of the risks involved in investing in the Series Trust. Absence of Secondary Market There is not expected to be any secondary market for Units. Consequently, Unitholders will be able to dispose of their Units only by means of repurchase in accordance with the procedures SXP\642621\ v19 25

26 and restrictions set out below in the section headed "Repurchase of Units". The risk of any decline in the Net Asset Value attributable to the Units held by a Unitholder requesting the repurchase of his Units during the period from the date of the relevant Repurchase Notice until the relevant Repurchase Day will be borne by the Unitholder requesting the repurchase. Investment Objective and Trading Risks There is no guarantee that in any time period, particularly in the short term, the Series Trust's investment portfolio will achieve appreciation in terms of capital growth. Investors should be aware that the value of Units may fall as well as rise. Investment in the Series Trust involves significant risks. Whilst it is the intention of the Manager to implement strategies which are designed to minimise potential losses, there can be no assurance that these strategies will be successful. Distributions The current policy in relation to the Series Trust is not to make distributions to Unitholders. Accordingly, an investment in the Series Trust may not be suitable for investors seeking current returns for financial or tax planning purposes. Net Asset Value per Unit The Initial Costs and the Fixed Costs Provision will be amortized over the period from the launch of the Series Trust to 6 February As a result of such amortization, Net Asset Value of the Series Trust will be reduced. Unitholders who elect to have Units repurchased prior to the Termination Date will bear a disproportionately larger percentage of the Fixed Costs Provision than had they had their Units repurchased at the date of termination of the Series Trust. When the Series Trust is terminated either on 6 February 2019, or before if the Target Auto Redemption Condition is satisfied, the Net Asset Value will be increased by an amount equal to that portion of the Fixed Costs Provision (if any) that remains in the Trust Fund at its termination after accounting for all known fixed costs incurred up to the termination ( Unspent Provision ). Such Unspent Provision will be shared among the Units outstanding at that point. Unitholders who have had their Units repurchased prior to that point would not receive a share of this Unspent Provision. Foreign Exchange Rate Fluctuation As the Functional Currency of the Series Trust is US dollars, those investors whose financial assets are measured in currencies other than the US dollars will be exposed to fluctuations in foreign exchange rates. Consequently, the value of a Unitholder's holding of Units when converted into the currency in which its financial assets are measured may fall even when the Net Asset Value per Unit in US dollars is increasing. Early Repurchase Unitholders will benefit from the Notes principal protection only if they hold their Units until 6 February The Net Asset Value per Unit could fall below US$100 and accordingly the repurchase price of Units which are repurchased before 6 February 2019 could be below US$100. Furthermore, any repurchase of Units effected prior to 6 January 2014 will be subject to an extraordinary charge and/or a repurchase fee as described below in the section headed "Issue and Repurchase of Units Repurchase of Units". Target Auto Redemption Condition SXP\642621\ v19 26

27 The amount of the proceeds of the sale of the Series Trust's entire portfolio of Notes following satisfaction of the Target Auto Redemption Condition will be equal to the purchase price provided by the Calculation Agent based on the market value of the Notes at the relevant time less the weighted average value of the Repurchase Fees that applied during the period of the sale of the relevant Notes, as further detailed in the section headed Investment Objectives and Policies The Series Trust The Notes. Such price will be dependent upon prevailing market conditions at the time of such sale and the number of Note Repurchase Days required to complete the sale. For the avoidance of doubt, the Manager can give no guarantee that the Net Asset Value per Unit following completion of the sale of the Series Trust's entire portfolio of Notes will equal at least US$130. Political and Regulatory Risks The value of the assets of the Series Trust may be affected by uncertainties such as political unrest, changes in government policies and taxation, restrictions on foreign investment and currency repatriation, and other developments in applicable laws and regulations. Credit Risk The Series Trust will be subject to the risk of the inability of the Issuer (and in the case of a default by the Issuer the risk of the inability of Citigroup Inc. as guarantor) to perform its obligations with respect to the Notes whether due to insolvency, bankruptcy or other causes. No Performance History of the Series Trust The Series Trust is about to commence its investment programme and has no operating history nor performance record. The past performance of investment funds managed by the Manager is not necessarily predictive of future results of the Series Trust. Investment in the Notes The Series Trust s investment in the Notes involves risks. The following description of investment risks does not purport to be an exhaustive description of all the risks associated with an investment in the Notes. The Notes may not be a suitable investment Investment in the Notes is only suitable for investors who: (a) (b) (c) have the requisite knowledge and experience in financial and business matters to evaluate the merits and risks of an investment in the Notes; are capable of bearing the economic risk of an investment in the Notes for a period of ten years; and are willing to accept the risk of an investment in the Notes in the context of their financial situation. On the Note Maturity Date, the Notes may not redeem above US$100 per Note If the Dynamic Portfolio Value on the Note Valuation Date is equal to or less than US$100 per Note, the amount payable on the Note Maturity Date will be limited to US$100, even if the Dynamic Portfolio Value is greater than US$100 at one or more times during the term of the Notes. SXP\642621\ v19 27