Knightian uncertainty and asset markets

|

|

|

- Rose Pearson

- 5 years ago

- Views:

Transcription

1 Knightian uncertainty and asset markets SUJOY MUKERJI PROFESSOR AND HEAD OF SCHOOL OF ECONOMICS AND FINANCE QUEEN MARY UNIVERSITY OF LONDON

2 Knightian uncertainty ( ambiguity/aversion, robustness/model uncertainty concerns) The recent global economic crisis stemmed, in part, from the realisation of financial institutions of their inability to effectively judge the riskiness of their investments. For this reason, the crisis cast new attention on an idea about risk from decades past: Knightian uncertainty. Frank Knight pioneered the idea of drawing a distinction between risk and uncertainty in his 1921 book, Risk, Uncertainty, and Profit. As Knight saw it, an ever-changing world brings new opportunities for businesses to make profits, but also means we have imperfect knowledge of future events. According to Knight, risk applies to situations where we do not know the outcome of a given situation, but can accurately measure the odds. Uncertainty, on the other hand, applies to situations where we cannot know all the information we need in order to set accurate odds in the first place.

3 Most analysts link the recent credit crisis to the sub-prime mortgage business, in which US banks give high-risk loans to people with poor credit histories. These and other loans, bonds or assets are bundled into portfolios - or Collateralised Debt Obligations (CDOs) - and sold on to investors globally.

4 Between 2004 and 2006 US interest rates rose from 1% to 5.35%, triggering a slowdown in the US housing market. Homeowners, many of whom could only barely afford their mortgage payments when interest rates were low, began to default on their mortgages. Default rates on sub-prime loans - high risk loans to clients with poor or no credit histories - rose to record levels (around 2007). The impact of these defaults were felt across the financial system as many of the mortgages had been bundled up and sold on to banks and investors.

5 Falling house prices and rising interest rates lead to high numbers of people who cannot repay their mortgages. Investors suffer losses, making them reluctant to take on more CDOs. Credit markets freeze as banks are reluctant to lend to each other, not knowing how many bad loans could be on their rivals' books.

6 The US Federal Bank and the European Central Bank tries to bolster the money markets by making funds available for banks to borrow on more favourable terms. Interest rates are also cut in an effort to encourage lending.

7 But the short-term help does not solve the liquidity crisis - or availability of cash for banks - as banks remain cautious about lending to each other. A lack of credit - to banks, companies and individuals - brings with it the threat of recession, job losses, bankruptcies, repossessions and a rise in living costs.

8 Seeking a long-term solution, the US government agrees a $700bn bail-out that will buy up Wall Street's bad debts in return for stake in the banks. The US government plans to borrow the money from world financial markets and hopes it can sell the distressed assets back once the housing market has stabilised.

9 Knightian uncertainty The recent global economic crisis stemmed, in part, from the realisation of financial institutions of their inability to effectively judge the riskiness of their investments. For this reason, the crisis cast new attention on an idea about risk from decades past: Knightian uncertainty. Frank Knight was an idiosyncratic economist who formalized a distinction between risk and uncertainty in his 1921 book, Risk, Uncertainty, and Profit. As Knight saw it, an ever-changing world brings new opportunities for businesses to make profits, but also means we have imperfect knowledge of future events. According to Knight, risk applies to situations where we do not know the outcome of a given situation, but can accurately measure the odds. Uncertainty, on the other hand, applies to situations where we cannot know all the information we need in order to set accurate odds in the first place.

10 Ellsberg Experiment about Knightian uncertainty Each urn contains a mixture of 100 red and blue balls. In urn I, the mixture is known to be 50:50. The subjects do not know the proportions of the two colours in urn II. A ball is drawn at random from each urn, generating events IR (i.e., a red ball is drawn from urn I), IB, IIR, IIB. DM is offered bets on these events. E.g. 10 if IR, 0 otherwise. It is usually found that preferences in any particular experiment are: IR IIR and IB IIB. Such preferences are not expected utility preferences. Suppose, we assume Pr(IR) = Pr(IB) = 0.5. Then the preferences imply, Pr(IIR) < 0.5 and Pr(IIB) < 0.5

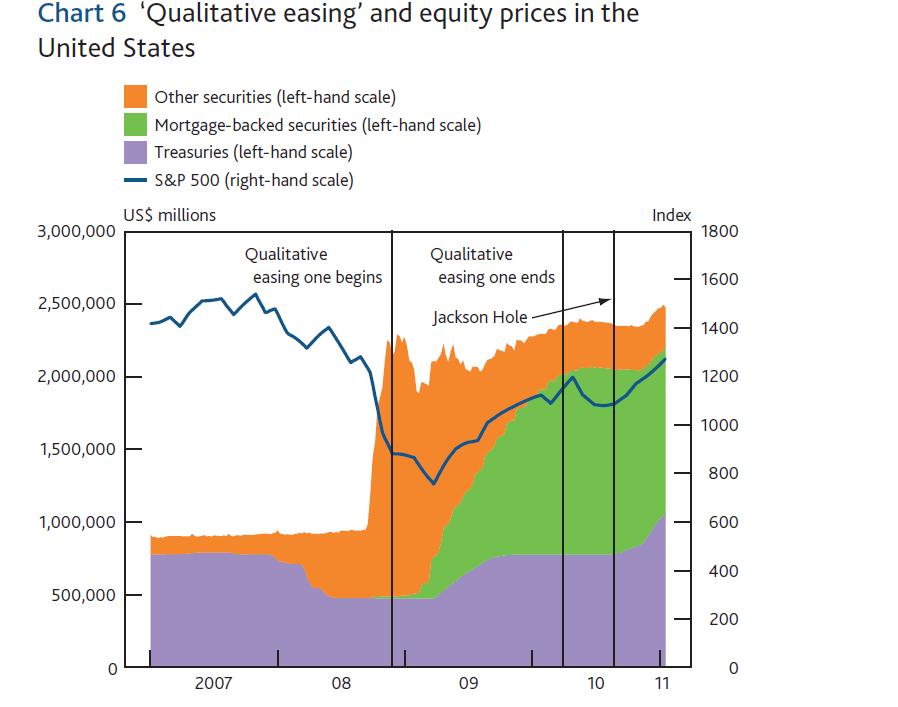

11 Knigtian uncertainty/ambiguity, or lack of good knowledge of probabilities affecting contingent outcomes of a chosen action, is pervasive in economic decision making. It is not particular to the ill informed and less sophisticated. Even a professional decision maker (DM) in a financial market knows it is often hard to distinguish (on the basis of historical data) between different models providing distinct (stochastic) forecasts of relevant financial variables. Such DMs may well think it is prudent to choose actions that are robust to the uncertainty about the correct model.

12 An example of such a robust decision rule is Maximin Expected Utility A basic version of the rule may be understood as follows.: Identify a set of probability distributions consistent with available data. Calculate the expected payoff of action for each possible probability An action is finally evaluated by the minimum of possible expected payoffs. The rule asks that you choose the action with the maximum evaluation.

13 Suppose a DM is offered a choice between a unit long and a unit short and a zero position on an asset which pays off contingent on the draw of a ball from Urn II, as in the Ellsberg example discussed earlier. The following table shows the contingent payoffs from each of the three choices. Colour of ball drawn from urn II Payoff from a long position Payoff from a short position Payoff from a zero position Red Blue

14 Suppose the DM believes that the probability that a red ball is drawn (from Urn II) lies in the interval [0.4, 0.6], with complementary beliefs about the event a blue ball is drawn. Applying the rule, it may be checked that the DM will evaluate the unit long position as = 4; similarly, he evaluates the short position as 0.6 (-)10 = -6. This implies that the DM will strictly prefer a zero position when market price lies in the interval [4, 6], thereby exhibiting a portfolio inertia. Colour of ball drawn from urn II Payoff from a long position Payoff from a short position Payoff from a zero position Red Blue

15 Increase ambiguity or uncertainty, indicated by an increase in the size of interval of beliefs, increases incidence of no trade in risky assets by increasing the price interval where portfolio inertia occurs. The volume of trade/lending bears an inverse relationship to the ambient uncertainty. The increased (Knightian) uncertainty is about the valuation of securitized assets banks hold which are used as collateral for inter-bank lending. The uncertainty is triggered by unusual events and untested financial innovations that lead agents to question their worldview of risks and risk models.

16 Knight s distinction about risk and uncertainty may still help us analyse the recent behavior of financial firms and other investors. Investment banks that regarded their own apparently precise risk assessments as trustworthy may have thought they were operating in conditions of risk. Once the banks recognized those assessments were inadequate, however, they understood that they were operating in conditions of Knightian uncertainty and held back from making trades or providing capital, further slowing the economy as a result.

17 The logic of portfolio inertia thus provides an explanation for the "seizure" of lending activity among banks based on Knightian uncertainty (aversion). The idea explains crisis regularities such as market-wide capital immobility, agents disengagement from risk, and liquidity hoarding. It also gives a great insight in the working of central bank policies, why a certain policy did not work and why another policy did.

18 Central banks throughout the world have recently engaged in two kinds of unconventional monetary policies: quantitative easing (QE), which is an increase in the size of the balance sheet of the central bank through an increase it is monetary liabilities, and qualitative easing (QuaE) which is a shift in the composition of the assets of the central bank towards less liquid and riskier assets, holding constant the size of the balance sheet.

19 The effectiveness of qualitative easing A government policy that is designed to mitigate risk through central bank purchases of privately held risky assets and their replacement by government debt, with a return that is guaranteed by the taxpayer. Policies of this kind have recently been carried out by national central banks, backed by implicit guarantees from national treasuries.

20

21 Aggregate uncertainty and equity returns The assumed source of the ambiguity in the agent's beliefs about macro uncertainty is the occurrence of periodic, temporary changes in the probability distribution governing next period's growth outcome due to the effect of the business cycle. These transient deviations are assumed to be governed by an auto-regressive (AR(1)) latent variable. The agent is, however, unsure about the value of the persistence parameter of the process since, even with a large sample of growth rates, it is difficult to distinguish the case where the latent growth state is highly volatile but moderately persistent, from the case were the state is less volatile but highly persistent.

22 Macro (Knightian) uncertainty Uncertainty about persistence, in turn makes it harder to estimate the evolving location of the latent variable precisely. Furthermore, depending on the observed history, the imprecision of the estimate of the location will vary over time, making the uncertainty about the probability distribution governing next period's growth vary over time.

23 Endogenous accentuation of uncertainty The ambiguity-averse agent's robustness concerns generate, endogenously, doubt and pessimism. The portfolio choice of the ambiguity-averse agent in the model may be understood as that of an expected utility agent with an ``as if'' (probabilistic) belief that is more uncertain and pessimistic than the one obtained by objective inference, in the standard fashion, from data.

24 Endogenous accentuation of uncertainty Moreover, the endogenous accentuation of doubt depends on the observed history and the level of ambiguity aversion, making the severity of the effect of uncertainty endogenously time-varying. For instance, after a negative shock that follows a series of ``normal'' ones, the agent behaves as if the uncertainty is more severe and more persistent than what is implied by pure Bayesian inference (and the opposite, if it were a positive shock that broke the normal sequence).

25 Equity premium predicted by Knightian uncertainty and macro-uncertainty indices The model generated conditional equity premium is a measure of conditional macroeconomic uncertainty as revealed by the behavior of the agent in the model. We show its time-series properties match those of the purely statistical index of macro-economic uncertainty, recently developed in Jurado Ludvigson Ng (2015) and Carriero Clarke Marcellino (2018).

26

27 We discussed the idea of Knightian uncertainty We argued that the idea is singularly useful in explaining and understanding the key facts of the credit crises. The understanding has significant policy implications about how such crises may be alleviated. Finally, we considered why episodic macro uncertainty can be understood as Knightian and how that understanding is revealed in the (excess) returns on aggregate equity. Thank you!

28 (very) brief bibliography S. Mukerji and JM Tallon (2004): An Overview of economic applications of David Schmeidler s models of decision making under uncertainty. R. Caballero (2009): Sudden Financial Arrest R. Farmer (2013): Qualitative Easing: a new tool for stabilisation of financial markets F. Collard, S. Mukerji, K. Sheppard, JM Tallon (2018): Ambiguity and the historical equity premium

Macro-Insurance. How can emerging markets be aided in responding to shocks as smoothly as Australia does?

markets began tightening. Despite very low levels of external debt, a current account deficit of more than 6 percent began to worry many observers. Resident (especially foreign) banks began pulling resources

markets began tightening. Despite very low levels of external debt, a current account deficit of more than 6 percent began to worry many observers. Resident (especially foreign) banks began pulling resources

Donald L Kohn: Asset-pricing puzzles, credit risk, and credit derivatives

Donald L Kohn: Asset-pricing puzzles, credit risk, and credit derivatives Remarks by Mr Donald L Kohn, Vice Chairman of the Board of Governors of the US Federal Reserve System, at the Conference on Credit

Donald L Kohn: Asset-pricing puzzles, credit risk, and credit derivatives Remarks by Mr Donald L Kohn, Vice Chairman of the Board of Governors of the US Federal Reserve System, at the Conference on Credit

Impairment of financial instruments under IFRS 9

Applying IFRS Impairment of financial instruments under IFRS 9 December 2014 Contents In this issue: 1. Introduction... 4 1.1 Brief history and background of the impairment project... 4 1.2 Overview of

Applying IFRS Impairment of financial instruments under IFRS 9 December 2014 Contents In this issue: 1. Introduction... 4 1.1 Brief history and background of the impairment project... 4 1.2 Overview of

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 52

The Financial System 1 / 52") The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 52 Financial System Definition The financial system consists of those institutions in the economy that matches saving with

The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 52 Financial System Definition The financial system consists of those institutions in the economy that matches saving with

Speculative Trade under Ambiguity

Speculative Trade under Ambiguity Jan Werner March 2014. Abstract: Ambiguous beliefs may lead to speculative trade and speculative bubbles. We demonstrate this by showing that the classical Harrison and

Speculative Trade under Ambiguity Jan Werner March 2014. Abstract: Ambiguous beliefs may lead to speculative trade and speculative bubbles. We demonstrate this by showing that the classical Harrison and

Ambiguity Aversion. Mark Dean. Lecture Notes for Spring 2015 Behavioral Economics - Brown University

Ambiguity Aversion Mark Dean Lecture Notes for Spring 2015 Behavioral Economics - Brown University 1 Subjective Expected Utility So far, we have been considering the roulette wheel world of objective probabilities:

Ambiguity Aversion Mark Dean Lecture Notes for Spring 2015 Behavioral Economics - Brown University 1 Subjective Expected Utility So far, we have been considering the roulette wheel world of objective probabilities:

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall Module I

Fall Module I") UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall 2018 Module I The consumers Decision making under certainty (PR 3.1-3.4) Decision making under uncertainty

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall 2018 Module I The consumers Decision making under certainty (PR 3.1-3.4) Decision making under uncertainty

Queen s Global Markets A PREMIER UNDERGRADUATE THINK-TANK

Negative Sovereign Bond Yields: Eurozone s New Conundrum June 2015 Introduction With headlines of deflation and reckless spending in the Eurozone ubiquitous since 2009, investors and policymakers alike

Negative Sovereign Bond Yields: Eurozone s New Conundrum June 2015 Introduction With headlines of deflation and reckless spending in the Eurozone ubiquitous since 2009, investors and policymakers alike

Response to submissions on the Consultation Paper: Serviceability Restrictions as a Potential Macroprudential Tool in New Zealand.

Response to submissions on the Consultation Paper: Serviceability Restrictions as a Potential Macroprudential Tool in New Zealand November 2017 2 1. The Reserve Bank undertook a public consultation process

Response to submissions on the Consultation Paper: Serviceability Restrictions as a Potential Macroprudential Tool in New Zealand November 2017 2 1. The Reserve Bank undertook a public consultation process

This short article examines the

WEIDONG TIAN is a professor of finance and distinguished professor in risk management and insurance the University of North Carolina at Charlotte in Charlotte, NC. wtian1@uncc.edu Contingent Capital as

WEIDONG TIAN is a professor of finance and distinguished professor in risk management and insurance the University of North Carolina at Charlotte in Charlotte, NC. wtian1@uncc.edu Contingent Capital as

A Steadier Course for Monetary Policy. John B. Taylor. Economics Working Paper 13107

A Steadier Course for Monetary Policy John B. Taylor Economics Working Paper 13107 HOOVER INSTITUTION 434 GALVEZ MALL STANFORD UNIVERSITY STANFORD, CA 94305-6010 April 18, 2013 This testimony before the

A Steadier Course for Monetary Policy John B. Taylor Economics Working Paper 13107 HOOVER INSTITUTION 434 GALVEZ MALL STANFORD UNIVERSITY STANFORD, CA 94305-6010 April 18, 2013 This testimony before the

Financial Regulation and the Economic Security of Low-Income Households

Financial Regulation and the Economic Security of Low-Income Households Karen Dynan Brookings Institution October 14, 2010 Note. This presentation was prepared for the Institute for Research on Poverty

Financial Regulation and the Economic Security of Low-Income Households Karen Dynan Brookings Institution October 14, 2010 Note. This presentation was prepared for the Institute for Research on Poverty

FRBSF ECONOMIC LETTER

FRBSF ECONOMIC LETTER 2010-31 October 18, 2010 Underwater Mortgages BY JOHN KRAINER AND STEPHEN LEROY House prices have fallen approximately 30% from their peak in 2006, accompanied by a level of defaults

FRBSF ECONOMIC LETTER 2010-31 October 18, 2010 Underwater Mortgages BY JOHN KRAINER AND STEPHEN LEROY House prices have fallen approximately 30% from their peak in 2006, accompanied by a level of defaults

Our Interview with Robert Shiller September 9, 2008

Our Interview with Robert Shiller September 9, 2008 Robert J. Shiller is the Arthur M. Okun Professor of Economics at Yale University, and Professor of Finance and Fellow at the International Center for

Our Interview with Robert Shiller September 9, 2008 Robert J. Shiller is the Arthur M. Okun Professor of Economics at Yale University, and Professor of Finance and Fellow at the International Center for

Workshop on the pricing and hedging of environmental and energy-related financial derivatives

Socially efficient discounting under ambiguity aversion Workshop on the pricing and hedging of environmental and energy-related financial derivatives National University of Singapore, December 7-9, 2009

Socially efficient discounting under ambiguity aversion Workshop on the pricing and hedging of environmental and energy-related financial derivatives National University of Singapore, December 7-9, 2009

Lecture 11: Critiques of Expected Utility

Lecture 11: Critiques of Expected Utility Alexander Wolitzky MIT 14.121 1 Expected Utility and Its Discontents Expected utility (EU) is the workhorse model of choice under uncertainty. From very early

Lecture 11: Critiques of Expected Utility Alexander Wolitzky MIT 14.121 1 Expected Utility and Its Discontents Expected utility (EU) is the workhorse model of choice under uncertainty. From very early

EconS Micro Theory I Recitation #8b - Uncertainty II

EconS 50 - Micro Theory I Recitation #8b - Uncertainty II. Exercise 6.E.: The purpose of this exercise is to show that preferences may not be transitive in the presence of regret. Let there be S states

EconS 50 - Micro Theory I Recitation #8b - Uncertainty II. Exercise 6.E.: The purpose of this exercise is to show that preferences may not be transitive in the presence of regret. Let there be S states

Opening Remarks. Alan Greenspan

Opening Remarks Alan Greenspan Uncertainty is not just an important feature of the monetary policy landscape; it is the defining characteristic of that landscape. As a consequence, the conduct of monetary

Opening Remarks Alan Greenspan Uncertainty is not just an important feature of the monetary policy landscape; it is the defining characteristic of that landscape. As a consequence, the conduct of monetary

FORECASTS William E. Cullison

FORECASTS 1980 A CONSENSUS FOR A RECESSION William E. Cullison The views and opinions set forth in this article are those of the various forecasters. No agreement or endorsement by this Bank is implied.

FORECASTS 1980 A CONSENSUS FOR A RECESSION William E. Cullison The views and opinions set forth in this article are those of the various forecasters. No agreement or endorsement by this Bank is implied.

QED. Queen s Economics Department Working Paper No Junfeng Qiu Central University of Finance and Economics

QED Queen s Economics Department Working Paper No. 1317 Central Bank Screening, Moral Hazard, and the Lender of Last Resort Policy Mei Li University of Guelph Frank Milne Queen s University Junfeng Qiu

QED Queen s Economics Department Working Paper No. 1317 Central Bank Screening, Moral Hazard, and the Lender of Last Resort Policy Mei Li University of Guelph Frank Milne Queen s University Junfeng Qiu

Global Financial Crisis. Econ 690 Spring 2019

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Global Financial Crisis Econ 690 Spring 2019 1 Timeline of Global Financial Crisis 2002-2007 US real estate prices rise mid-2007 Mortgage loan defaults rise, some financial institutions have trouble, recession

Introduction Background of country

Monetary Policy 1 2 Introduction Monetary policy is one of the most effective tools that have been used by policy makers around the world to stimulate economic growth of a country. Monetary policy has

Monetary Policy 1 2 Introduction Monetary policy is one of the most effective tools that have been used by policy makers around the world to stimulate economic growth of a country. Monetary policy has

Capital Adequacy and Liquidity in Banking Dynamics

Capital Adequacy and Liquidity in Banking Dynamics Jin Cao Lorán Chollete October 9, 2014 Abstract We present a framework for modelling optimum capital adequacy in a dynamic banking context. We combine

Capital Adequacy and Liquidity in Banking Dynamics Jin Cao Lorán Chollete October 9, 2014 Abstract We present a framework for modelling optimum capital adequacy in a dynamic banking context. We combine

Path dependence. Federico Frattini. Advanced Applied Economics

Path dependence Federico Frattini Advanced Applied Economics Scott E. Page (2006) Path dependence, Quarterly Journal of Political Science, 2006, 1, 87-115. Basic notion a small initial advantage or a few

Path dependence Federico Frattini Advanced Applied Economics Scott E. Page (2006) Path dependence, Quarterly Journal of Political Science, 2006, 1, 87-115. Basic notion a small initial advantage or a few

FRBSF ECONOMIC LETTER

FRBSF ECONOMIC LETTER 2010-38 December 20, 2010 Risky Mortgages and Mortgage Default Premiums BY JOHN KRAINER AND STEPHEN LEROY Mortgage lenders impose a default premium on the loans they originate to

FRBSF ECONOMIC LETTER 2010-38 December 20, 2010 Risky Mortgages and Mortgage Default Premiums BY JOHN KRAINER AND STEPHEN LEROY Mortgage lenders impose a default premium on the loans they originate to

UK Cost of Housing. The long-term view. More than two generations

UK Cost of Housing The long-term view More than two generations UK Cost of Housing (3/7/1) - 1 of Average "Real" House Prices (In 17 's) against Average Annual Real Earnings (In 17 's) 5,, Average "Real"

UK Cost of Housing The long-term view More than two generations UK Cost of Housing (3/7/1) - 1 of Average "Real" House Prices (In 17 's) against Average Annual Real Earnings (In 17 's) 5,, Average "Real"

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer NOTES ON THE MIDTERM

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer NOTES ON THE MIDTERM Preface: This is not an answer sheet! Rather, each of the GSIs has written up some

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer NOTES ON THE MIDTERM Preface: This is not an answer sheet! Rather, each of the GSIs has written up some

Maturity, Indebtedness and Default Risk 1

Maturity, Indebtedness and Default Risk 1 Satyajit Chatterjee Burcu Eyigungor Federal Reserve Bank of Philadelphia February 15, 2008 1 Corresponding Author: Satyajit Chatterjee, Research Dept., 10 Independence

Maturity, Indebtedness and Default Risk 1 Satyajit Chatterjee Burcu Eyigungor Federal Reserve Bank of Philadelphia February 15, 2008 1 Corresponding Author: Satyajit Chatterjee, Research Dept., 10 Independence

Housing Markets and the Macroeconomy During the 2000s. Erik Hurst July 2016

Housing Markets and the Macroeconomy During the 2s Erik Hurst July 216 Macro Effects of Housing Markets on US Economy During 2s Masked structural declines in labor market o Charles, Hurst, and Notowidigdo

Housing Markets and the Macroeconomy During the 2s Erik Hurst July 216 Macro Effects of Housing Markets on US Economy During 2s Masked structural declines in labor market o Charles, Hurst, and Notowidigdo

An Improved Framework for Assessing the Risks Arising from Elevated Household Debt

51 An Improved Framework for Assessing the Risks Arising from Elevated Household Debt Umar Faruqui, Xuezhi Liu and Tom Roberts Introduction Since 2008, the Bank of Canada has used a microsimulation model

51 An Improved Framework for Assessing the Risks Arising from Elevated Household Debt Umar Faruqui, Xuezhi Liu and Tom Roberts Introduction Since 2008, the Bank of Canada has used a microsimulation model

Bailouts, Bail-ins and Banking Crises

Bailouts, Bail-ins and Banking Crises Todd Keister Rutgers University Yuliyan Mitkov Rutgers University & University of Bonn 2017 HKUST Workshop on Macroeconomics June 15, 2017 The bank runs problem Intermediaries

Bailouts, Bail-ins and Banking Crises Todd Keister Rutgers University Yuliyan Mitkov Rutgers University & University of Bonn 2017 HKUST Workshop on Macroeconomics June 15, 2017 The bank runs problem Intermediaries

Box 1.3. How Does Uncertainty Affect Economic Performance?

Box 1.3. How Does Affect Economic Performance? Bouts of elevated uncertainty have been one of the defining features of the sluggish recovery from the global financial crisis. In recent quarters, high uncertainty

Box 1.3. How Does Affect Economic Performance? Bouts of elevated uncertainty have been one of the defining features of the sluggish recovery from the global financial crisis. In recent quarters, high uncertainty

Dynamic Change, Economic Fluctuations, and the AD-AS Model

Dynamic Change, Economic Fluctuations, and the AD-AS Model Full Length Text Part: Macro Only Text Part: 3 Chapter: 10 3 Chapter: 10 To Accompany Economics: Private and Public Choice 13th ed. James Gwartney,

Dynamic Change, Economic Fluctuations, and the AD-AS Model Full Length Text Part: Macro Only Text Part: 3 Chapter: 10 3 Chapter: 10 To Accompany Economics: Private and Public Choice 13th ed. James Gwartney,

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 55

The Financial System 1 / 55") The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 55 The financial system consists of those institutions in the economy that matches saving with investment. The financial system

The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 55 The financial system consists of those institutions in the economy that matches saving with investment. The financial system

Panel Discussion: " Will Financial Globalization Survive?" Luzerne, June Should financial globalization survive?

Some remarks by Jose Dario Uribe, Governor of the Banco de la República, Colombia, at the 11th BIS Annual Conference on "The Future of Financial Globalization." Panel Discussion: " Will Financial Globalization

Some remarks by Jose Dario Uribe, Governor of the Banco de la República, Colombia, at the 11th BIS Annual Conference on "The Future of Financial Globalization." Panel Discussion: " Will Financial Globalization

Structuring Mortgages for Macroeconomic Stability

Structuring Mortgages for Macroeconomic Stability John Y. Campbell, Nuno Clara, and Joao Cocco Harvard University and London Business School CEAR-RSI Household Finance Workshop Montréal November 16, 2018

Structuring Mortgages for Macroeconomic Stability John Y. Campbell, Nuno Clara, and Joao Cocco Harvard University and London Business School CEAR-RSI Household Finance Workshop Montréal November 16, 2018

International Money and Banking: 6. Problems with Monetarism

International Money and Banking: 6. Problems with Monetarism Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Money and Inflation Spring 2018 1 / 30 The Basic Elements of Monetarism Last

International Money and Banking: 6. Problems with Monetarism Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Money and Inflation Spring 2018 1 / 30 The Basic Elements of Monetarism Last

Predicting a US recession: has the yield curve lost its relevance?

Global Perspective Predicting a US recession: has the yield curve lost its relevance? For professional investor use only Asset Management August 2018 Executive summary It is becoming apparent the US economy

Global Perspective Predicting a US recession: has the yield curve lost its relevance? For professional investor use only Asset Management August 2018 Executive summary It is becoming apparent the US economy

Brian P Sack: Implementing the Federal Reserve s asset purchase program

Brian P Sack: Implementing the Federal Reserve s asset purchase program Remarks by Mr Brian P Sack, Executive Vice President of the Federal Reserve Bank of New York, at the Global Interdependence Center

Brian P Sack: Implementing the Federal Reserve s asset purchase program Remarks by Mr Brian P Sack, Executive Vice President of the Federal Reserve Bank of New York, at the Global Interdependence Center

CHAPTER 31 Money, Banking, and Financial Institutions

CHAPTER 31 Money, Banking, and Financial Institutions Answers to Short-Answer, Essays, and Problems 1. What is money? Explain in terms of the functions of money. Money is whatever performs the three basic

CHAPTER 31 Money, Banking, and Financial Institutions Answers to Short-Answer, Essays, and Problems 1. What is money? Explain in terms of the functions of money. Money is whatever performs the three basic

The Impact of Monetary Policy on Banks Risktaking: Evidence from the Post Crisis Data

The Hilltop Review Volume 9 Issue 2 Spring 2017 Article 9 June 2017 The Impact of Monetary Policy on Banks Risktaking: Evidence from the Post Crisis Data Nardos Moges Beyene Western Michigan University

The Hilltop Review Volume 9 Issue 2 Spring 2017 Article 9 June 2017 The Impact of Monetary Policy on Banks Risktaking: Evidence from the Post Crisis Data Nardos Moges Beyene Western Michigan University

Financial Crises, Stabilization, and Deficits

PART IV FURTHER MACROECONOMICS ISSUES Financial Crises, Stabilization, and Deficits 15 CHAPTER OUTLINE The Stock Market, the Housing Market, and Financial Crises Stocks and Bonds Determining the Price

PART IV FURTHER MACROECONOMICS ISSUES Financial Crises, Stabilization, and Deficits 15 CHAPTER OUTLINE The Stock Market, the Housing Market, and Financial Crises Stocks and Bonds Determining the Price

ECONOMIC FACTORS ASSOCIATED WITH DELINQUENCY RATES ON CONSUMER INSTALMENT DEBT A. Charlene Sullivan *

ECONOMIC FACTORS ASSOCIATED WITH DELINQUENCY RATES ON CONSUMER INSTALMENT DEBT A. Charlene Sullivan * Trends in loan delinquencies and losses over time and among credit types contain important information

ECONOMIC FACTORS ASSOCIATED WITH DELINQUENCY RATES ON CONSUMER INSTALMENT DEBT A. Charlene Sullivan * Trends in loan delinquencies and losses over time and among credit types contain important information

Expansions (periods of. positive economic growth)

") Practice Problems IV EC 102.03 Questions 1. Comparing GDP growth with its trend, what do the deviations from the trend reflect? How is recession informally defined? Periods of positive growth in GDP (above

Practice Problems IV EC 102.03 Questions 1. Comparing GDP growth with its trend, what do the deviations from the trend reflect? How is recession informally defined? Periods of positive growth in GDP (above

Estimating Key Economic Variables: The Policy Implications

EMBARGOED UNTIL 11:45 A.M. Eastern Time on Saturday, October 7, 2017 OR UPON DELIVERY Estimating Key Economic Variables: The Policy Implications Eric S. Rosengren President & Chief Executive Officer Federal

EMBARGOED UNTIL 11:45 A.M. Eastern Time on Saturday, October 7, 2017 OR UPON DELIVERY Estimating Key Economic Variables: The Policy Implications Eric S. Rosengren President & Chief Executive Officer Federal

Financial Crises and the Great Recession

Financial Crises and the Great Recession ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 40 Readings GLS Ch. 33 2 / 40 Financial Crises Financial crises

Financial Crises and the Great Recession ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 40 Readings GLS Ch. 33 2 / 40 Financial Crises Financial crises

A Primer on Inflation Targeting

A Primer on Inflation Targeting Publication No. 2011-111-E 9 November 2011 Brett Stuckey International Affairs, Trade and Finance Division Parliamentary Information and Research Service A Primer on Inflation

A Primer on Inflation Targeting Publication No. 2011-111-E 9 November 2011 Brett Stuckey International Affairs, Trade and Finance Division Parliamentary Information and Research Service A Primer on Inflation

Discussion of The initial impact of the crisis on emerging market countries Linda L. Tesar University of Michigan

Discussion of The initial impact of the crisis on emerging market countries Linda L. Tesar University of Michigan The US recession that began in late 2007 had significant spillover effects to the rest

Discussion of The initial impact of the crisis on emerging market countries Linda L. Tesar University of Michigan The US recession that began in late 2007 had significant spillover effects to the rest

Advanced Macroeconomics 5. Rational Expectations and Asset Prices

Advanced Macroeconomics 5. Rational Expectations and Asset Prices Karl Whelan School of Economics, UCD Spring 2015 Karl Whelan (UCD) Asset Prices Spring 2015 1 / 43 A New Topic We are now going to switch

Advanced Macroeconomics 5. Rational Expectations and Asset Prices Karl Whelan School of Economics, UCD Spring 2015 Karl Whelan (UCD) Asset Prices Spring 2015 1 / 43 A New Topic We are now going to switch

TCH Research Note: 2016 Federal Reserve s Stress Testing Scenarios

TCH Research Note: 2016 Federal Reserve s Stress Testing Scenarios March 2016 Francisco Covas +1.202.649.4605 francisco.covas@theclearinghouse.org I. Executive Summary On January 28, the Federal Reserve

TCH Research Note: 2016 Federal Reserve s Stress Testing Scenarios March 2016 Francisco Covas +1.202.649.4605 francisco.covas@theclearinghouse.org I. Executive Summary On January 28, the Federal Reserve

LECTURE 8 Monetary Policy at the Zero Lower Bound: Quantitative Easing. October 10, 2018

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 8 Monetary Policy at the Zero Lower Bound: Quantitative Easing October 10, 2018 Announcements Paper proposals due on Friday (October 12).

Economics 210c/236a Fall 2018 Christina Romer David Romer LECTURE 8 Monetary Policy at the Zero Lower Bound: Quantitative Easing October 10, 2018 Announcements Paper proposals due on Friday (October 12).

Group 14 Dallas Hall, Chuck Dobson, Guy Tahye, Tunde Olabiyi

In order to understand how we have gotten to the point where government intervention is needed to save our financial markets, it is necessary to look back and examine the many causes that lead to this

In order to understand how we have gotten to the point where government intervention is needed to save our financial markets, it is necessary to look back and examine the many causes that lead to this

FRBSF ECONOMIC LETTER

FRBSF ECONOMIC LETTER 211-15 May 16, 211 What Is the Value of Bank Output? BY TITAN ALON, JOHN FERNALD, ROBERT INKLAAR, AND J. CHRISTINA WANG Financial institutions often do not charge explicit fees for

FRBSF ECONOMIC LETTER 211-15 May 16, 211 What Is the Value of Bank Output? BY TITAN ALON, JOHN FERNALD, ROBERT INKLAAR, AND J. CHRISTINA WANG Financial institutions often do not charge explicit fees for

Perspectives on the U.S. Economy

Perspectives on the U.S. Economy Presentation for Irish Institute Seminar, April 14, 2008 Bob Murphy Department of Economics Boston College Three Perspectives 1. Historical Overview of U.S. Economic Performance

Perspectives on the U.S. Economy Presentation for Irish Institute Seminar, April 14, 2008 Bob Murphy Department of Economics Boston College Three Perspectives 1. Historical Overview of U.S. Economic Performance

Extract from a speech by Mervyn King, Governor of the Bank of England. Bank of Israel, Jerusalem 31 March 2008

1 Extract from a speech by Mervyn King, Governor of the Bank of England Bank of Israel, Jerusalem 31 March 2008 Acknowledgements if applicable. Double click here to edit/delete All speeches are available

1 Extract from a speech by Mervyn King, Governor of the Bank of England Bank of Israel, Jerusalem 31 March 2008 Acknowledgements if applicable. Double click here to edit/delete All speeches are available

ABSTRACT. Exchange Rates and Macroeconomic Policy with Income-sensitive Capital Flows. J.O.N. Perkins, University of Melbourne

1 ABSTRACT Exchange Rates and Macroeconomic Policy with Income-sensitive Capital Flows J.O.N. Perkins, University of Melbourne This paper considers some implications for macroeconomic policy in an open

1 ABSTRACT Exchange Rates and Macroeconomic Policy with Income-sensitive Capital Flows J.O.N. Perkins, University of Melbourne This paper considers some implications for macroeconomic policy in an open

Cost Forecasting: Where Do We Get It Wrong (and Why)? Matt Bassford Director, Defence & Security Programme

? Matt Bassford Director, Defence & Security Programme") Cost Forecasting: Where Do We Get It Wrong (and Why)? Matt Bassford Director, Defence & Security Programme This presentation draws on RAND s experience of defence analysis in the US, UK, and Europe A global

Cost Forecasting: Where Do We Get It Wrong (and Why)? Matt Bassford Director, Defence & Security Programme This presentation draws on RAND s experience of defence analysis in the US, UK, and Europe A global

How to Consider Risk Demystifying Monte Carlo Risk Analysis

How to Consider Risk Demystifying Monte Carlo Risk Analysis James W. Richardson Regents Professor Senior Faculty Fellow Co-Director, Agricultural and Food Policy Center Department of Agricultural Economics

How to Consider Risk Demystifying Monte Carlo Risk Analysis James W. Richardson Regents Professor Senior Faculty Fellow Co-Director, Agricultural and Food Policy Center Department of Agricultural Economics

The Financial Turmoil in 2007 and 2008 Events

The Financial Turmoil in 2007 and 2008 Events Gerald P. Dwyer, Jr. May 2008 Copyright Gerald P. Dwyer, Jr., 2008 Caveats I am speaking for myself, not the Federal Reserve Bank of Atlanta or the Federal

The Financial Turmoil in 2007 and 2008 Events Gerald P. Dwyer, Jr. May 2008 Copyright Gerald P. Dwyer, Jr., 2008 Caveats I am speaking for myself, not the Federal Reserve Bank of Atlanta or the Federal

Corporate Finance, Module 3: Common Stock Valuation. Illustrative Test Questions and Practice Problems. (The attached PDF file has better formatting.

Corporate Finance, Module 3: Common Stock Valuation Illustrative Test Questions and Practice Problems (The attached PDF file has better formatting.) These problems combine common stock valuation (module

Corporate Finance, Module 3: Common Stock Valuation Illustrative Test Questions and Practice Problems (The attached PDF file has better formatting.) These problems combine common stock valuation (module

Why are interest rates so low?

Why are interest rates so low? 18 November 214 Dieter Guffens Senior economist KBC Corporate Chief Economist Department Overview Low interest rates in a historical perspective Driving forces of interest

Why are interest rates so low? 18 November 214 Dieter Guffens Senior economist KBC Corporate Chief Economist Department Overview Low interest rates in a historical perspective Driving forces of interest

Measuring and managing market risk June 2003

Page 1 of 8 Measuring and managing market risk June 2003 Investment management is largely concerned with risk management. In the management of the Petroleum Fund, considerable emphasis is therefore placed

Page 1 of 8 Measuring and managing market risk June 2003 Investment management is largely concerned with risk management. In the management of the Petroleum Fund, considerable emphasis is therefore placed

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall Module I

Fall Module I") UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall 2016 Module I The consumers Decision making under certainty (PR 3.1-3.4) Decision making under uncertainty

UC Berkeley Haas School of Business Economic Analysis for Business Decisions (EWMBA 201A) Fall 2016 Module I The consumers Decision making under certainty (PR 3.1-3.4) Decision making under uncertainty

BUSM 411: Derivatives and Fixed Income

BUSM 411: Derivatives and Fixed Income 3. Uncertainty and Risk Uncertainty and risk lie at the core of everything we do in finance. In order to make intelligent investment and hedging decisions, we need

BUSM 411: Derivatives and Fixed Income 3. Uncertainty and Risk Uncertainty and risk lie at the core of everything we do in finance. In order to make intelligent investment and hedging decisions, we need

Bank of America 2018 Dodd-Frank Act Mid-Cycle Stress Test Results BHC Severely Adverse Scenario October 18, 2018

Bank of America 2018 Dodd-Frank Act Mid-Cycle Stress Test Results BHC Severely Adverse Scenario October 18, 2018 Important Presentation Information The 2018 Dodd-Frank Act Mid-Cycle Stress Test Results

Bank of America 2018 Dodd-Frank Act Mid-Cycle Stress Test Results BHC Severely Adverse Scenario October 18, 2018 Important Presentation Information The 2018 Dodd-Frank Act Mid-Cycle Stress Test Results

Analysing the IS-MP-PC Model

University College Dublin, Advanced Macroeconomics Notes, 2015 (Karl Whelan) Page 1 Analysing the IS-MP-PC Model In the previous set of notes, we introduced the IS-MP-PC model. We will move on now to examining

University College Dublin, Advanced Macroeconomics Notes, 2015 (Karl Whelan) Page 1 Analysing the IS-MP-PC Model In the previous set of notes, we introduced the IS-MP-PC model. We will move on now to examining

International Money and Banking: 15. The Phillips Curve: Evidence and Implications

International Money and Banking: 15. The Phillips Curve: Evidence and Implications Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) The Phillips Curve Spring 2018 1 / 26 Monetary Policy

International Money and Banking: 15. The Phillips Curve: Evidence and Implications Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) The Phillips Curve Spring 2018 1 / 26 Monetary Policy

Speculative Attacks and the Theory of Global Games

Speculative Attacks and the Theory of Global Games Frank Heinemann, Technische Universität Berlin Barcelona LeeX Experimental Economics Summer School in Macroeconomics Universitat Pompeu Fabra 1 Coordination

Speculative Attacks and the Theory of Global Games Frank Heinemann, Technische Universität Berlin Barcelona LeeX Experimental Economics Summer School in Macroeconomics Universitat Pompeu Fabra 1 Coordination

Economics 430 Handout on Rational Expectations: Part I. Review of Statistics: Notation and Definitions

Economics 430 Chris Georges Handout on Rational Expectations: Part I Review of Statistics: Notation and Definitions Consider two random variables X and Y defined over m distinct possible events. Event

Economics 430 Chris Georges Handout on Rational Expectations: Part I Review of Statistics: Notation and Definitions Consider two random variables X and Y defined over m distinct possible events. Event

Modelling the Sharpe ratio for investment strategies

Modelling the Sharpe ratio for investment strategies Group 6 Sako Arts 0776148 Rik Coenders 0777004 Stefan Luijten 0783116 Ivo van Heck 0775551 Rik Hagelaars 0789883 Stephan van Driel 0858182 Ellen Cardinaels

Modelling the Sharpe ratio for investment strategies Group 6 Sako Arts 0776148 Rik Coenders 0777004 Stefan Luijten 0783116 Ivo van Heck 0775551 Rik Hagelaars 0789883 Stephan van Driel 0858182 Ellen Cardinaels

Dodd-Frank Act Stress Test Results. October 20, 2017

Dodd-Frank Act Stress Test Results October 20, 2017 Overview Synovus Financial Corp. (Synovus or the Company) regularly evaluates financial and capital forecasts under various economic scenarios as part

Dodd-Frank Act Stress Test Results October 20, 2017 Overview Synovus Financial Corp. (Synovus or the Company) regularly evaluates financial and capital forecasts under various economic scenarios as part

Fiduciary Insights LEVERAGING PORTFOLIOS EFFICIENTLY

LEVERAGING PORTFOLIOS EFFICIENTLY WHETHER TO USE LEVERAGE AND HOW BEST TO USE IT TO IMPROVE THE EFFICIENCY AND RISK-ADJUSTED RETURNS OF PORTFOLIOS ARE AMONG THE MOST RELEVANT AND LEAST UNDERSTOOD QUESTIONS

LEVERAGING PORTFOLIOS EFFICIENTLY WHETHER TO USE LEVERAGE AND HOW BEST TO USE IT TO IMPROVE THE EFFICIENCY AND RISK-ADJUSTED RETURNS OF PORTFOLIOS ARE AMONG THE MOST RELEVANT AND LEAST UNDERSTOOD QUESTIONS

Business fluctuations in an evolving network economy

Business fluctuations in an evolving network economy Mauro Gallegati*, Domenico Delli Gatti, Bruce Greenwald,** Joseph Stiglitz** *. Introduction Asymmetric information theory deeply affected economic

Business fluctuations in an evolving network economy Mauro Gallegati*, Domenico Delli Gatti, Bruce Greenwald,** Joseph Stiglitz** *. Introduction Asymmetric information theory deeply affected economic

Exam Number. Section

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Core Course Professor Antonio Fatás Final Exam February 24, 2011 9:00-12:00 Instructions: (PLEASE READ) SUGGESTED ANSWERS Space to answer the questions

Exam Number Section MACROECONOMICS IN THE GLOBAL ECONOMY Core Course Professor Antonio Fatás Final Exam February 24, 2011 9:00-12:00 Instructions: (PLEASE READ) SUGGESTED ANSWERS Space to answer the questions

Committee on Payments and Market Infrastructures. Board of the International Organization of Securities Commissions

Committee on Payments and Market Infrastructures Board of the International Organization of Securities Commissions Recovery of financial market infrastructures October 2014 (Revised July 2017) This publication

Committee on Payments and Market Infrastructures Board of the International Organization of Securities Commissions Recovery of financial market infrastructures October 2014 (Revised July 2017) This publication

Turkey: Credit Shock & the Economy

Turkey: Credit Shock & the Economy The effects of Credit Guarantee Fund (KGF) on the Turkish economy Alvaro Ortiz October 10 th 2017 The Credit Guarantee Fund (KGF) was implemented in March 2017 as a countercyclical

Turkey: Credit Shock & the Economy The effects of Credit Guarantee Fund (KGF) on the Turkish economy Alvaro Ortiz October 10 th 2017 The Credit Guarantee Fund (KGF) was implemented in March 2017 as a countercyclical

Ambiguity Aversion in Standard and Extended Ellsberg Frameworks: α-maxmin versus Maxmin Preferences

Ambiguity Aversion in Standard and Extended Ellsberg Frameworks: α-maxmin versus Maxmin Preferences Claudia Ravanelli Center for Finance and Insurance Department of Banking and Finance, University of Zurich

Ambiguity Aversion in Standard and Extended Ellsberg Frameworks: α-maxmin versus Maxmin Preferences Claudia Ravanelli Center for Finance and Insurance Department of Banking and Finance, University of Zurich

Answers to Questions: Chapter 5

Answers to Questions: Chapter 5 1. Figure 5-1 on page 123 shows that the output gaps fell by about the same amounts in Japan and Europe as it did in the United States from 2007-09. This is evidence that

Answers to Questions: Chapter 5 1. Figure 5-1 on page 123 shows that the output gaps fell by about the same amounts in Japan and Europe as it did in the United States from 2007-09. This is evidence that

Chapter 9 The IS LM FE Model: A General Framework for Macroeconomic Analysis

Chapter 9 The IS LM FE Model: A General Framework for Macroeconomic Analysis The main goal of Chapter 8 was to describe business cycles by presenting the business cycle facts. This and the following three

Chapter 9 The IS LM FE Model: A General Framework for Macroeconomic Analysis The main goal of Chapter 8 was to describe business cycles by presenting the business cycle facts. This and the following three

The U.S. Economy and Monetary Policy. Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City

The U.S. Economy and Monetary Policy Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City Central Exchange Kansas City, Missouri January 10, 2013 The views expressed

The U.S. Economy and Monetary Policy Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City Central Exchange Kansas City, Missouri January 10, 2013 The views expressed

made available a few days after the next regularly scheduled and the Board's Annual Report. The summary descriptions of

FEDERAL RESERVE press release For Use at 4:00 p.m. October 20, 1978 The Board of Governors of the Federal Reserve System and the Federal Open Market Committee today released the attached record of policy

FEDERAL RESERVE press release For Use at 4:00 p.m. October 20, 1978 The Board of Governors of the Federal Reserve System and the Federal Open Market Committee today released the attached record of policy

The Economic Outlook and The Fed s Roles in Monetary Policy and Financial Stability

1 The Economic Outlook and The Fed s Roles in Monetary Policy and Financial Stability Main Line Chamber of Commerce Economic Forecast Breakfast Philadelphia Country Club, Gladwyne, PA January 8, 2008 Charles

1 The Economic Outlook and The Fed s Roles in Monetary Policy and Financial Stability Main Line Chamber of Commerce Economic Forecast Breakfast Philadelphia Country Club, Gladwyne, PA January 8, 2008 Charles

Liquidity and Asset Prices in Rational Expectations Equilibrium with Ambiguous Information

Liquidity and Asset Prices in Rational Expectations Equilibrium with Ambiguous Information Han Ozsoylev SBS, University of Oxford Jan Werner University of Minnesota September 006, revised March 007 Abstract:

Liquidity and Asset Prices in Rational Expectations Equilibrium with Ambiguous Information Han Ozsoylev SBS, University of Oxford Jan Werner University of Minnesota September 006, revised March 007 Abstract:

2013 Workplace Benefits Report

RETIREMENT & BENEFIT PLAN SERVICES WORKPLACE INSIGHTS TM 2013 Workplace Benefits Report Employees Views on Achieving Financial Wellness 2 2013 WORKPLACE BENEFITS REPORT Empowering Employees to Improve

RETIREMENT & BENEFIT PLAN SERVICES WORKPLACE INSIGHTS TM 2013 Workplace Benefits Report Employees Views on Achieving Financial Wellness 2 2013 WORKPLACE BENEFITS REPORT Empowering Employees to Improve

The Macro-economy and the Global Financial Crisis

The Macro-economy and the Global Financial Crisis Ian Sheldon Andersons Professor of International Trade sheldon.1@osu.edu Department of Agricultural, Environmental & Development Economics Global economic

The Macro-economy and the Global Financial Crisis Ian Sheldon Andersons Professor of International Trade sheldon.1@osu.edu Department of Agricultural, Environmental & Development Economics Global economic

Empirical research, considers 20 countries with fixed exchange rate, crawling peg or floating within a band.

Connection between Banking and Currency Crises Literature: Kaminsky & Reinhart (1999) Empirical research, considers 20 countries with fixed exchange rate, crawling peg or floating within a band. Monthly

Connection between Banking and Currency Crises Literature: Kaminsky & Reinhart (1999) Empirical research, considers 20 countries with fixed exchange rate, crawling peg or floating within a band. Monthly

Theory of the rate of return

Macroeconomics 2 Short Note 2 06.10.2011. Christian Groth Theory of the rate of return Thisshortnotegivesasummaryofdifferent circumstances that give rise to differences intherateofreturnondifferent assets.

Macroeconomics 2 Short Note 2 06.10.2011. Christian Groth Theory of the rate of return Thisshortnotegivesasummaryofdifferent circumstances that give rise to differences intherateofreturnondifferent assets.

Citation for published version (APA): Shehzad, C. T. (2009). Panel studies on bank risks and crises Groningen: University of Groningen

: Shehzad, C. T. (2009). Panel studies on bank risks and crises Groningen: University of Groningen") University of Groningen Panel studies on bank risks and crises Shehzad, Choudhry Tanveer IMPORTANT NOTE: You are advised to consult the publisher's version (publisher's PDF) if you wish to cite from it.

University of Groningen Panel studies on bank risks and crises Shehzad, Choudhry Tanveer IMPORTANT NOTE: You are advised to consult the publisher's version (publisher's PDF) if you wish to cite from it.

The economics of entrepreneurship 3: What makes a typical entrepreneur? (II) Finance

Finance") The economics of entrepreneurship 3: What makes a typical entrepreneur? (II) Finance Robert Cressy Professor of SME and Entrepreneurial Finance Cass Business School Learning objectives To understand the

The economics of entrepreneurship 3: What makes a typical entrepreneur? (II) Finance Robert Cressy Professor of SME and Entrepreneurial Finance Cass Business School Learning objectives To understand the

The Real Effects of Disrupted Credit Evidence from the Global Financial Crisis

The Real Effects of Disrupted Credit Evidence from the Global Financial Crisis Ben S. Bernanke Distinguished Fellow Brookings Institution Washington DC Brookings Papers on Economic Activity September 13

The Real Effects of Disrupted Credit Evidence from the Global Financial Crisis Ben S. Bernanke Distinguished Fellow Brookings Institution Washington DC Brookings Papers on Economic Activity September 13

Informational Easing: Improving Credit Conditions through the Release of Information

Matthew Pritsker Informational Easing: Improving Credit Conditions through the Release of Information T 1. Introduction o ensure repayment of borrowed funds, lenders require that borrowers undergo costly

Matthew Pritsker Informational Easing: Improving Credit Conditions through the Release of Information T 1. Introduction o ensure repayment of borrowed funds, lenders require that borrowers undergo costly

Black Scholes Equation Luc Ashwin and Calum Keeley

Black Scholes Equation Luc Ashwin and Calum Keeley In the world of finance, traders try to take as little risk as possible, to have a safe, but positive return. As George Box famously said, All models

Black Scholes Equation Luc Ashwin and Calum Keeley In the world of finance, traders try to take as little risk as possible, to have a safe, but positive return. As George Box famously said, All models

Impact of Imperfect Information on the Optimal Exercise Strategy for Warrants

Impact of Imperfect Information on the Optimal Exercise Strategy for Warrants April 2008 Abstract In this paper, we determine the optimal exercise strategy for corporate warrants if investors suffer from

Impact of Imperfect Information on the Optimal Exercise Strategy for Warrants April 2008 Abstract In this paper, we determine the optimal exercise strategy for corporate warrants if investors suffer from

C A Y M A N I S L A N D S MONETARY AUTHORITY

Statement of Guidance Credit Risk Classification, Provisioning and Management Policy and Development Division Page 1 of 22 Table of Contents 1 Statement of Objectives... 3 2 Scope... 3 3 Terminology...

Statement of Guidance Credit Risk Classification, Provisioning and Management Policy and Development Division Page 1 of 22 Table of Contents 1 Statement of Objectives... 3 2 Scope... 3 3 Terminology...

ECN 106 Macroeconomics 1. Lecture 10

ECN 106 Macroeconomics 1 Lecture 10 Giulio Fella c Giulio Fella, 2012 ECN 106 Macroeconomics 1 - Lecture 10 279/318 Roadmap for this lecture Shocks and the Great Recession of 2008- Liquidity trap and the

ECN 106 Macroeconomics 1 Lecture 10 Giulio Fella c Giulio Fella, 2012 ECN 106 Macroeconomics 1 - Lecture 10 279/318 Roadmap for this lecture Shocks and the Great Recession of 2008- Liquidity trap and the

The Lack of an Empirical Rationale for a Revival of Discretionary Fiscal Policy. John B. Taylor Stanford University

The Lack of an Empirical Rationale for a Revival of Discretionary Fiscal Policy John B. Taylor Stanford University Prepared for the Annual Meeting of the American Economic Association Session The Revival

The Lack of an Empirical Rationale for a Revival of Discretionary Fiscal Policy John B. Taylor Stanford University Prepared for the Annual Meeting of the American Economic Association Session The Revival

ECON Intermediate Macroeconomic Theory

ECON 3510 - Intermediate Macroeconomic Theory Fall 2015 Mankiw, Macroeconomics, 8th ed., Chapter 12 Chapter 12: Aggregate Demand 2: Applying the IS-LM Model Key points: Policy in the IS LM model: Monetary

ECON 3510 - Intermediate Macroeconomic Theory Fall 2015 Mankiw, Macroeconomics, 8th ed., Chapter 12 Chapter 12: Aggregate Demand 2: Applying the IS-LM Model Key points: Policy in the IS LM model: Monetary

Chapter 14 : Statistical Inference 1. Note : Here the 4-th and 5-th editions of the text have different chapters, but the material is the same.

Chapter 14 : Statistical Inference 1 Chapter 14 : Introduction to Statistical Inference Note : Here the 4-th and 5-th editions of the text have different chapters, but the material is the same. Data x

Chapter 14 : Statistical Inference 1 Chapter 14 : Introduction to Statistical Inference Note : Here the 4-th and 5-th editions of the text have different chapters, but the material is the same. Data x

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 74

The Financial System 1 / 74") The Sherif Khalifa Sherif Khalifa () The 1 / 74 The financial system consists of those institutions that match saving with investment. The financial system channels funds from those who save to those with

The Sherif Khalifa Sherif Khalifa () The 1 / 74 The financial system consists of those institutions that match saving with investment. The financial system channels funds from those who save to those with

Banking Crises and Real Activity: Identifying the Linkages

Banking Crises and Real Activity: Identifying the Linkages Mark Gertler New York University I interpret some key aspects of the recent crisis through the lens of macroeconomic modeling of financial factors.

Banking Crises and Real Activity: Identifying the Linkages Mark Gertler New York University I interpret some key aspects of the recent crisis through the lens of macroeconomic modeling of financial factors.