Evaluation of the transmission of the monetary policy interest rate to the market interest rates considering agents expectations 1

|

|

|

- Agnes Leonard

- 5 years ago

- Views:

Transcription

1 Ninth IFC Conference on Are post-crisis statistical initiatives completed? Basel, August 2018 Evaluation of the transmission of the monetary policy interest rate to the market interest rates considering agents expectations 1 Deicy Cristiano-Botia, Eliana Gonzalez-Molano and Carlos Huertas-Campos, Bank of the Republic, Colombia 1 This paper was prepared for the meeting. The views expressed are those of the authors and do not necessarily reflect the views of the BIS, the IFC or the central banks and other institutions represented at the meeting.

2 Evaluation of the transmission of the monetary policy interest rate to the market interest rates considering agents expectations Deicy Cristiano-Botia, Eliana Gonzalez-Molano, Carlos Huertas-Campos 1 Abstract Alternative economic models are used to determine whether policy interest rate expectations and unanticipated changes in the reference interest rate affect saving and credit interest rates. We found empirical evidence that policy surprises have predict power to set passive and active interest rates. Similarly, results show that to fix their interest rate financial entities take into account their expectations about policy rate. On the other hand, we found evidence of changes in deposits rates in advance of the announcement of the monetary authority and no significant change on the day of the announcement and the day after the change. Keywords: Expectations, Monetary Policy, Interest Rates and Transmission Mechanism. JEL classification: D84, E43, E52, E58 1 dcristbo@banrep.gov.co, egonzamo@banrep.gov.co, chuertca@banrep.gov.co.

3 Contents Introduction... 2 Literature review... 3 Estimation of the impact of unanticipated shocks in the policy rate on market interest rates... 5 The effect of unanticipated monetary policy shocks on the market interest rates 6 Unanticipated monetary shocks estimated as the average of short-run expectations.. 9 Estimation of the effect of the changes in the policy rate through time.. 10 Conclusions References Introduction A way to evaluate the degree of transmission of changes in the monetary policy interest rate to market interest rates is to measure it after the decision of the Central Bank. I.e., calculating how much has changed a specific interest rate once the Board of Directos make a policy announcement. This methodology does not consider the effects of the expectations of agents on the transmission. For example, the market can anticipate and partially incorporate the changes in the policy rate to the rates of interest of the economy, and therefore, the transmission would be underestimated. This is important, since in theory, both not anticipated and anticipated changes in the policy rate by financial institutions have effects on the setting of market interest rates. In this context, this document analyzes the transmission of changes in the monetary policy interest rate on the 90-day deposit rate and the interest rates for credits for both ordinary and preferential loans, considering the expectations of agents on future monetary policy decisions. These expectations are based on the information available each period and the agents forecast ability. Empirical analysis comprises three exercises. Firstly, we evaluate the effect that has the unanticipated component of changes in the policy rate to market rates (Vargas et al (2012)). This component is defined as the forecasting error that agents make to project changes in the policy rate using all available information. Second, we present a model under the conditional expectations hypothesis, in which, a medium-term interest rate is defined as the average of the expected short term rates for all periods until maturity. Finally, an analysis of the behavior of short-term interest rates

4 is made considering daily data and taking into account the time intervals defined in Roley and Sellon (1995). To this end, we evaluate the prospective or anticipated effect and the immediate effect of the changes in the policy rate decomposing the estimation in three time periods: a day previous to the announcement, the day of the announcement and the day Post-announcement. This document consists of four sections and the first is this introduction. Section two contains a review of literature and section three explains the econometric models and present estimation results and the final section concludes. 2. Literature review According to Loayza and Schmidt-Hebbel (2002) monetary policy rules that use central banks evaluate its efficiency and optimality mainly through four channels of transmission of monetary policy: the interest rate channel, the channel of asset prices, the exchange rate channel and credit channel. These channels affect the macroeconomic variables in different speed and intensity. Alternatively, the literature identifies the expectations channel, which considers the intertemporal effects associated with the projections of the stance of the Monetary Authority and the present and future behavior of the main variables of the economy. In this way, the beliefs of agents on the shocks and the expected behavior of the main macroeconomic variables affect the effectiveness of the transmission. Similarly, effectiveness also depends on the credibility of the Central Bank and the agents reaction to future policy announcements. To the extent that the credibility of the Central Bank and other institutions is high, the expectations channel has a greater role given that the formation of expectations will be in line with the economic policy measures. In theory, long-term rates can be defined as the average of the expected interest rates of short term until the maturity plus a risk premium. Therefore, it is important to know the expectations of agents on future changes in the policty rate. Faced with this situation, Ellingsen & Söderström (2001) argue that monetary policy actions respond to new and private information, as well as changes in the preferences of the central bank in terms of the stabilization of the output and inflation. Thus, a forecast of the policy rate must include all these variables. One of the first analysis of the response of interest rates before the FED reference rate changes was made by Cook and Hahn (1989), who analyzed the daily relationship between the policy rate and the treasure bonds rates with maturities from 3 months up to 20 years. The authors analyzed for the 70's the movement of the interest rates of the Treasury bonds in the days close to the FED announcement (two days prior to each ad, the day of the announcement and the two days following the ads). They found that the market requires at least one day after the announcement of the FED to consider that the change is carried out. During this period the response of short-term rates was strong, moderate for the mid-term and weak for the long term (being significant for all maturities). Likewise, to analyze the relevance of the theory of expectations, the authors found a

5 strong influence of the expectations on the movements in the daily market rates at the different maturities. Roley and Sellon (1995) studied the response of the long-term rates taking into account the tendency of the market to anticipate monetary policy actions. They found that these forecasts influence the transmission of changes in the policy rates to long-term interest rates. As the authors says, financial institutions have incentives to match the profitability of its portfolio to different maturities. Therefore, they include and adjust their expectations on long-term interest rates, considering the expected future changes in the short-term rates. As an approach of future long-term interest rates, the authors build an average rate from rates of short-term futures. They warn that the response in the long term rates can be inverse to that described by the monetary traditional view, since it depends not only on the expectations of policy rate, but also in the expected persistence of this. In this regard, Roley and Sellon make one caveat to mention that the magnitude of the expected response may vary depending on the perception that agents have on the phase of the economic cycle in which the economy is currently. Thus, surprising policy announcements (which do not correspond to the perceived phase of the economic cycle) will generate a greater response in rates since agents should adjust their investments for short or long term depending on the expected persistence. Kuttner (2001) estimated for United States (between June 1989 and February 2000) a uniform and inferior interest rates response with respect to that found by Cook and Hahn, using the same methodology but with information from the federal funds futures market of the United States (as proposed by Roley and Sellon (1995)). The author suggests that the difference is in comparing changes in rates expected and unexpected in the period posterior to the monetary policy announcement. They found that the response of interest rates to anticiated policy action is low, while that of unanticipated changes is high and significant. The relationship between monetary policy and long-term interest rates is widely documented, however, responses differ across countries. Skinner and Zettelmeyer (1995) conducted an analysis for Germany, France, United Kingdom and United States on the response of long-term rates to policy actions using the unanticipated component of monetary policy. It was found that for the United States long term rates are adjusted in 41.2% of the unanticipated shock, for the United Kingdom this setting is 27.9%, while there is a lower setting for Germany and France (10.1% and 8.7%, respectively). On the other hand, authors like Thornton (2009) and Vargas et al (2012) analyzed the disconnection of the mechanism using market-based measures and structural factors such as fiscal policy. Thornton (2009) estimated again the response of interest rates reviewing Kuttner method, as it suggests that the changes in the federal funds rates respond to both monetary policy news, and others news of the market or the environment in general. To correct the problem of bias some authors suggest the use of high-frequency data, others suggest the structural identification through simultaneous equations using constraints in the matrix of variances and covariances 2. However, Thornton applied a model that conceptualizes more 2 See Gürkaynak, Sack, and Swanson (2007); and Craine and Martin (2008).

6 accurately changes in the market interest rate by including in the Kuttner method two parameters: one that considers the bias to shocks generated by news of the environment and another that estimates the bias to unexpected changes in the policy rate. Separately estimated the effect for all days of the sample, and not only for the days prior or subsequent to the policy announcement, including a dichotomous variable to identify the days when monetary events occur. Their results indicate that traditional specification overestimates the effect of monetary policy, and that there is no transmission at rates exceeding 3 years of maturity, with the exception of 20 years, which is significant but with negative effect. The literature also suggests that structural factors and the prevailing macroeconomic conditions may explain the transmission of the policy interest rate to market interest rates. Vargas et al (2012) analyzed the relationship between the credibility of the Central Bank and the transmission mechanism of monetary policy in Colombia for the period In particular they analyze whether under a regime of monetary policy credibility, a change in the policy interest rate has less chance of being understood as a transitional move and more likely to be incorporated in government long-term bonds and, in general, in the interest rate of the financial market as being considered as a persistent long term monetary policy signal. The authors apply the methodology of local projections proposed by Jorda (2005) in order to estimate the Impulse-response function (FIR) of the rate of interest on public bonds (TES) to an unexpected monetary shock. They later estimate a similar model to build the FIR of the market interest rate for loans and deposits given the shock in the monetary component as not anticipated by the agents. The results show, that after the reforms presented at the beginning of the decade of 2000, the response is more persistent for both the bonds and the market rates. They considered that structural improvements of policy that provide reliability to the economy, in particular the fiscal, has a positive effect on monetary policy, allowing to wide the maturity of bonds and as a result generate a deepening in that market. Therefore, they conclude that the strength of the monetary transmission mechanism is the result of structural factors as a sound fiscal policy and greater depth of fixed-rate public debt market. 3. Estimation of the impact of unanticipated shocks in the policy rate on market interest rates This section discusses three types of models that explain the behavior of interest rates (passive and active) in response to unanticipated shocks in the policy interest rate for the period between October 2008 and May 2018; Figure 1 shows the dynamics of the deposit, the commercial credit interest rates and the policy rate. The market rates move with the policiy rate, but not at the same pace and magnitude. In the first model we estimate the response of a monetary surprise on the market intrest rates. In the second, a passive interest rate to a horizon of p periods forward (where p is a short period for an interest rate) is expressed as the average of the expected short-term (policy rate) for each period until maturity p. In the latest model we analyze daily 90-day deposit rate to determine if the effect of monetary policy decisions is made before, the day of the announcement, or immediately after the announcement.

7 Figure 1. Policy rate and deposit and credit market interest rates Source: Financial Superintendency, Banco de la República. 3.1 The effect of unanticipated monetary policy shocks on the market interest rates The change in the market interest rate (Δ ) is explained by the unanticipated change in the policy rate (Ψ ). Δ = + Ψ + (Eq. 1) Where could be either the monthly 90-day deposit rate or the commercial loans rate for ordinary and preferential credits for the period from may,2002 to may,2018. (Ψ ) is defined using two alternatives. In the first one, a regression model for the policy rate is estimated as a function of a set of variables available for all economic agents when the Board of Directors make policy decisions. We follow the work of Vargas et al, (2012), in which, they asume monetary authority does not necessarily follows a standard Taylor rule, but appart from the output gap and inflation deviation from target may include expectations. Thus, we include other variables that may add some information and signals of future behaviour of the policy actions. So, with variables describe in equation 2, we obtained a onestep ahead forecast for the policy rate and we define the unanticipated monetary policy shock as the forecasting error obtained from this equation. =,,,,, +Ψ (Eq 2.) Ψ = Where Y : Output gap, : Inflation deviation from target, : USA Inflation, : Nominal devaluation, ICI: installed capacity index, CCI: consumer confidence index.

8 The second alternative (Equation 3), considers as a measure of the unanticipated monetary policy shocks the forecasting errors of the expectations of the policy rate made by the agents through the monthly expectations survey 3. Ψ = ( ) (Eq. 3) The estimation results for the 90-day deposit interest are shown in Table 1. Table 1. Estimation of effect of unanticipated monetary policy shock 90-day Deposit rate Coeficient 1 2 Shock (0.11) (0.17) constant (0.00) (0.00) Adjusted R * Significant at 10%, ** significant at 5%, *** significant at 1% 1: monetary shock estimated as the forecasting error from equation 2 2: monetary shock estimated as the forecasting error from expectation survey The coeficient associated to the monetary shock with both measures of the shock is positive, significant and close each other and may be interpreted as the change in the 90-day deposit rate due to an unanticipated change in the policy rate. The estimation results for the credit rates are shown in Table 2. Table 2. Estimation of the effect of unanticipated monetary policy shock on the commercial credit interest rates Commercial credit rates Ordinary loans Preferential loans Shock Shock (0.11) (0.22) (0.11) (0.22) constant constant (0.00) (0.00) (0.00) (0.00) Adjusted R Adjusted R * Significant at 10%, ** significant at 5%, *** significant at 1% 1: monetary shock estimated as the forecasting error from equation 2 2: monetary shock estimated as the forecasting error from expectation survey 3 The monthly expectations survey is applied to financial analysts and some institutions of economic research. It asks expectations about future inflation, Exchange rate, output and the policy rate for different horizons.

9 The results indicate that the monetary policy shock, obtained with both methodologies is significant in explaining the changes in both commercial credits rates. However, for preferential loans, the transmission is higher than for ordinary loans and there is a non negligible difference in the estimates of the two definitions of the shock. Using Equation 1 and the local proyections methodology proposed by Jordà (2005), we estimate the impulse-response function of a monetary shock on the market interest rates. The FIR for the 90- day deposit rate is shown in Figure 2 for both definitions of the shocks. The effect is larger and longer for the shock estimated from the model than from the survey of expectations. For expectations definition of the monetary shock, the effect is bigger one month after the shock (84%) and last up to 10 months. For the shock obtained from the model the peak of the effect of the monetary shock is also one month after the shock is observed, but the effect is smaller (55%) and last longer, up to 15 months. Figure 2. FIR of a monetary policy shock on the 90-deposit interest rate 120% 100% 80% 60% 40% 20% 0% -20% -40% 90-day deposit rate from model from expectations

10 Figure 3. FIR of a monetary policy shock on commercial credit interest rates 160% 140% 120% 100% 80% 60% 40% 20% 0% -20% -40% -60% 140% 120% 100% 80% 60% 40% 20% 0% -20% -40% -60% -80% Preferential loans interest rate Ordinary loans interest rate From model From expectations For credit rates, we observed that the effect is higher for the preferential than for the ordinary loans rate. The duration of the effect is shorter than the observed for the deposit rate, about 8 to 10 months. The reaction of credit rates is bigger for the shock defined from expectations than from the model. The preferential rate overreact to the unanticipated change in the policy rate with the former definition of the shock and the peak of the effect is two months after the shock occurs. For the ordinary rate the reaction is less than proportional to the shock but also the peak is two months after the shock occurs. With the later defintion of the shock, the effect last longer, like 12 to 13 months, and the magnitud of the responses are inferior to those of the shock measured with expectations. Again, the effect is bigger for the preferential rate than for the ordinary rate. 3.2 unanticipated monetary shocks estimated as the average of short-run expectations In theory, market interest rates can be defined as the average of the short run interest rates up to maturity. In this exercise, we use the policy rate as a proxy of the short-run interest rate and the 90- day deposit rate as the market rate. It is not possible to do this exercise for the commercial credit rates since the maturiry is at least a year and there is not expectations for the policy rate available for further horizons than eleven months ahead. Thus, the 90-day deposit rate in monrth t, is defined as

11 the average of the policty rate in month t, and the expectations for the next two months ( ), +1 y +2. = (Eq. 4) Thus, the change in the 90-day deposit rate is represented by: Δ = + + ( ) (Eq. 5) then, by adding an error term, the model may be rewritten as: Δ = (Eq. 6) Where we define the following terms: = = h h h = The last term is the total change of the monetary policy rate in the whole period up to maturity of the 90-day deposit rate, which is the average of the changes in the policy rate of each month. then, Δ +Δ +Δ (Eq. 7) Δ = h + + h h + In order to estimate the Equation 6 we use the expectations for the policy rate from the monthly expectation survey. Results are shown in Table 3. Table 3. Estimation of Equation 6 Coeficient Estimate std error Monetary policy surprise expectation revision expectation of total change in the polity rate * Significant at 10%, ** significaant at 5%, *** significant at 1% Both ( ) and ( ) coeficients are significant and thus, the monetary policy shocks and the expectations on the total change of the policy rate up to maturity are important to set martket 90- day deposit rate. On the other hand, it seems that the revisions of agents expectations ( ) has not effect on setting the market rate.

12 In general the estimated model validates the theorical model, since the hyphotesis of equal weights of the three components, equal to (1/3) is not rejected, although the parameter of the expectations revision is not significant. In summary, the changes in the 90-day deposit rate are mainly explained by the expectations of the agents about the changes in the policy rate as well as the monetary policy surprises, while the revisions of the expectations agents make about the policy rate on the different horizons up to maturity (90 days) seems not to be relevant to set this passive interest rate. 3.3 estimation of the effect of the changes in the policy rate through time. Another alternative to check the transmission of the changes in the monetary policy rate to the market rates that involve expectations of the agents about the policy rate is the methodology proposed by Roley y Sellon (1995). They propose to analyse the effect in different moments during a month. Thus, estimate the anticipated effect, the effect that ocurs the day of the policy announcement and the day after the announcement. So, if for example the Board of Directors made two announcements about changes in the policy rate at the end of month and at the end of month, then the three mentioned effects could be measure in the following way: 1. The anticipated effect = is the change in the market rate between the day after the later announcement ( +1) and the day before the actual announcement ( 1). Thus, this effect catches the revisions of the expectations of future actions of the monetary authority due to either a monetary policy surprise at time or for a change in the fundamentals, incorporating new information about the state of the economy, and then market interest rates are adjusted days before the actual announcement of the monetary authority. 2. The effect that ocurs the day of the announcement = is the change in the market rate between the day before the announcement ( 1) and the day of the announcement ( ). 3. The inmmediate effect = is the change in the market rate between the day of the announcement ( ) and the day after that ( +1). 4. Thus, the total effect = is the total change of the market rate between ( +1) y ( +1), which is the sum of the three former effects. Figure 4. Decomposition of the effect of a policy rate change in the market rate

13 With this definitions we can estimate the effect of a change in the policy rate on the market rate on the three periods of time and the aggregate response using the following model: Δ = + Δ + = 1,2,3,4 The results of this exercise for the 90-day deposit rate are shown in Table 4. Table 4. The effect of a change in the policy rate on the 90-day deposit rate Before MP decision Day of the MP decision Day after MP decision * Significant at 10%, ** significant at 5%, *** significant at 1% Total change *** -0, * 0.624*** (0,1476) (0,1472) (0,1363) (0,1090) *** *** -0,0001-0,0001 (0,0004) (0,0004) (0,0004) (0,0003) The estimation results suggest that the martket adjust interest rates with anticipation to the Board of Directors announcement and in second place, the day after the announcement. Changes that ocurr the day of the announcement are not significant in the setting of the market rates. As a result, summing up all the three effects, the complete response is around 62% of the change in the policy rate. In summary, the anticipated effect is the most important in setting the 90-day deposit rate by the financial institutions. 4. Conclusions In this document we evaluate three methodologies to estimate the effect of expectations about the monetary policy rate and the unanticipated changes in the policy rate on the market deposit and

14 credit interest rates. The results show that in first place, the monetary policy surprises have an important effect on setting the market rates for both deposits and credits finding a bigger effect on credit than in deposit rates. In the particular case of the 90-day deposit rate, the factor that seems to mainly explain the dynamic of the market rate are the expectations of the policy rate and in second place the presence of unanticipated changes in the policy rate. Finally, the third exercise, suggest that the 90-day deposit rate changes with anticipation to the changes in the policy rate as the agents expectations take into account that a change in the policy rate would take place in the future. On the other hand, changes after the announcement of monetary policy are not significant. These results validate the importance of expectations on the policy rate when setting market interest rates. 5. References Cook, T., and Hahn, T The effect of changes in the federal funds rate target on market interest rates in the 1970s. Journal of Monetary Economics, 24(3), Daniel L. Thornton, The identification of the response of interest rates to monetary policy actions using market-based measures of monetary policy shocks, Working Papers , Federal Reserve Bank of St. Louis. Ellingsen, Tore & Söderström, Ulf, Monetary Policy and Market Interest Rates, The American Economic Review Vol. 91, No. 5 (Dec., 2001), pp Vargas, H., González, A. and Lozano, I., Macroeconomic Effects of Structural Fiscal Policy Changes in Colombia, Borradores de economía 691, Banco de la República. Jordà, Ò Estimation and inference of impulse responses by local projections. American economic review, Kuttner, K. N Monetary policy surprises and interest rates: Evidence from the Fed funds futures market. Journal of monetary economics, 47(3),

15 Loayza, N. and Schmidt-Hebbel, K., Monetary Policy Functions and Transmission Mechanisms: An Overview, Central Banking, Analysis, and Economic Policies Book Series, Monetary Policy: Rules and Transmission Mechanisms, edition 1, volume 4, chapter 1, pages Central Bank of Chile. Skinner, T., and Zettelmeyer, J., Long rates and monetary policy: Is Europe different? in Zettelmeyer, Jeromin (ed.), Essays on monetary policy, Ph.D. dissertation, Massachusetts Institute of Technology, February Roley, V., and Sellon, G. H., Monetary policy actions and long-term interest rates, Economic Review, Federal Reserve Bank of Kansas City, issue Q IV, pages

16 Ninth IFC Conference on Are post-crisis statistical initiatives completed? Basel, August 2018 Evaluation of the transmission of the monetary policy interest rate to the market interest rates considering agents expectations 1 Deicy Cristiano-Botia, Eliana Gonzalez-Molano and Carlos Huertas-Campos, Bank of the Republic, Colombia 1 This presentation was prepared for the meeting. The views expressed are those of the authors and do not necessarily reflect the views of the BIS, the IFC or the central banks and other institutions represented at the meeting.

17 Transmission of the policy rate to market interest rates considering agentes expectations Eliana González, Deicy Cristiano and Carlos Huertas Banco de la República de Colombia August, 2018

18 MARKET INTEREST RATES AND MONETARY POLICY RATE

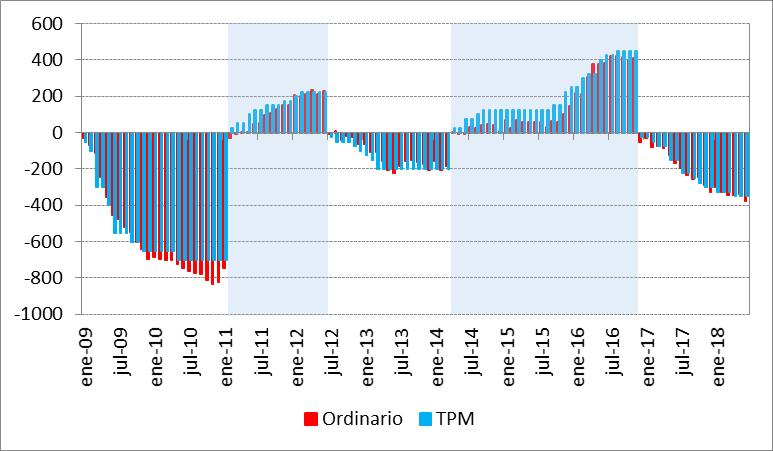

19 Cummulative change since the change in monetary policy stance(bp)

20 installed capacity The effect of unanticipated monetary policy shocks Δi t = α 0 + α 1 Ψ t + ε t 1. Estimación of monetary policy shocks as one-period forecasting errors from the model: i t p = f Y, തπ, π USA, s, ICI, CCI t p + Ψ t Ψ t = i p p t i tτt 1 Where Y : Output gap, തπ : Inflation gap from target, π USA : USA Inflation, s : Nominal devaluation, installed capacity index, consumer confidence index.

21 The effect of unanticipated monetary policy shocks 2. Estimation of monetary policy shocks as forecasting errors from the monetary policy rate expectations (survey of experts) Ψ t = i t p E t 1 (i t p ) Commercial credit rates Ordinary loans Preferential loans Shock Shock (0.11) (0.22) (0.11) (0.22) constant constant (0.00) (0.00) (0.00) (0.00) Adjusted R Adjusted R

22 120% 100% 80% 60% 40% 20% 0% -20% -40% 90-day deposit rate Impulse-response function of an unanticipated monetary policy shock 160% 140% 120% 100% 80% 60% 40% 20% 0% -20% -40% -60% Preferential loans interest rate % 120% 100% 80% 60% 40% 20% 0% -20% -40% -60% -80% Ordinary loans interest rate From model From expectations

23 unanticipated monetary shocks estimated as the average of shortrun expectations i 90 day t = 1 3 itmp + E t i mp t+1 mp + E t i t+2 Δi t 90 day = 1 3 i mp mp t E t 1 i t E t i mp t+1 E t 1 i t mp (E t i mp t+2 i mp t 1 ) Δi t 90 day = α 1 i t mp E t 1 i t mp + α 2 E t i mp t+1 mp E t 1 i t+1 + α 3 E t i mp t+2 i mp t 1 + ε t unanticipated monetary policy surprise = i mp mp t E t 1 i t expectations revision = E t i mp mp t+1 E t 1 i t+1 expectations of the change in MP rate in the whole period = E t i mp mp t+2 i t 1 = E t Δi mp t+2 + Δi mp mp t+1 + Δi t

24 Estimation results

25 How does the daily deposit interest rate change with The monetary policy decisions Δi T j = φ 0 + φ 1 ΔTI T + ν T with j = 1,2,3,4

26 How does the daily deposit interest rate change with The monetary policy decisions Before MP decision Day of the MP decision Day after MP decision Total change f *** -0, * 0.624*** (0,1476) (0,1472) (0,1363) (0,1090) f *** *** -0,0001-0,0001 (0,0004) (0,0004) (0,0004) (0,0003)

THE ROLE OF EXCHANGE RATES IN MONETARY POLICY RULE: THE CASE OF INFLATION TARGETING COUNTRIES

THE ROLE OF EXCHANGE RATES IN MONETARY POLICY RULE: THE CASE OF INFLATION TARGETING COUNTRIES Mahir Binici Central Bank of Turkey Istiklal Cad. No:10 Ulus, Ankara/Turkey E-mail: mahir.binici@tcmb.gov.tr

THE ROLE OF EXCHANGE RATES IN MONETARY POLICY RULE: THE CASE OF INFLATION TARGETING COUNTRIES Mahir Binici Central Bank of Turkey Istiklal Cad. No:10 Ulus, Ankara/Turkey E-mail: mahir.binici@tcmb.gov.tr

Inflation Regimes and Monetary Policy Surprises in the EU

Inflation Regimes and Monetary Policy Surprises in the EU Tatjana Dahlhaus Danilo Leiva-Leon November 7, VERY PRELIMINARY AND INCOMPLETE Abstract This paper assesses the effect of monetary policy during

Inflation Regimes and Monetary Policy Surprises in the EU Tatjana Dahlhaus Danilo Leiva-Leon November 7, VERY PRELIMINARY AND INCOMPLETE Abstract This paper assesses the effect of monetary policy during

Benjamin Miranda Tabak,1

Journal of Policy Modeling 26 (2004) 283 287 Short communication A note on the effects of monetary policy surprises on the Brazilian term structure of interest rates Benjamin Miranda Tabak,1 Banco Central

Journal of Policy Modeling 26 (2004) 283 287 Short communication A note on the effects of monetary policy surprises on the Brazilian term structure of interest rates Benjamin Miranda Tabak,1 Banco Central

Monetary Policy and Market Interest Rates in Brazil

Monetary Policy and Market Interest Rates in Brazil Ezequiel Cabezon November 14, 2014 Abstract This paper measures the effects of monetary policy on the term structure of the interest rate for Brazil

Monetary Policy and Market Interest Rates in Brazil Ezequiel Cabezon November 14, 2014 Abstract This paper measures the effects of monetary policy on the term structure of the interest rate for Brazil

Estimating the Impact of Changes in the Federal Funds Target Rate on Market Interest Rates from the 1980s to the Present Day

Estimating the Impact of Changes in the Federal Funds Target Rate on Market Interest Rates from the 1980s to the Present Day Donal O Cofaigh Senior Sophister In this paper, Donal O Cofaigh quantifies the

Estimating the Impact of Changes in the Federal Funds Target Rate on Market Interest Rates from the 1980s to the Present Day Donal O Cofaigh Senior Sophister In this paper, Donal O Cofaigh quantifies the

Using federal funds futures contracts for monetary policy analysis

Using federal funds futures contracts for monetary policy analysis Refet S. Gürkaynak rgurkaynak@frb.gov Division of Monetary Affairs Board of Governors of the Federal Reserve System Washington, DC 20551

Using federal funds futures contracts for monetary policy analysis Refet S. Gürkaynak rgurkaynak@frb.gov Division of Monetary Affairs Board of Governors of the Federal Reserve System Washington, DC 20551

Monetary policy and the yield curve

Monetary policy and the yield curve By Andrew Haldane of the Bank s International Finance Division and Vicky Read of the Bank s Foreign Exchange Division. This article examines and interprets movements

Monetary policy and the yield curve By Andrew Haldane of the Bank s International Finance Division and Vicky Read of the Bank s Foreign Exchange Division. This article examines and interprets movements

Credit Shocks and the U.S. Business Cycle. Is This Time Different? Raju Huidrom University of Virginia. Midwest Macro Conference

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

The identification of the response of interest rates to monetary policy actions using market-based measures of monetary policy shocks

Oxford Economic Papers Advance Access published February 13, 2013! Oxford University Press 2013 All rights reserved Oxford Economic Papers (2013), 1 of 21 doi:10.1093/oep/gps072 The identification of the

Oxford Economic Papers Advance Access published February 13, 2013! Oxford University Press 2013 All rights reserved Oxford Economic Papers (2013), 1 of 21 doi:10.1093/oep/gps072 The identification of the

MONEY SUPPLY ANNOUNCEMENTS AND STOCK PRICES: THE UK EVIDENCE

«ΣΠΟΥΔΑΙ», Τόμος 41, Τεύχος 4ο, Πανεπιστήμιο Πειραιώς / «SPOUDAI», Vol. 41, No 4, University of Piraeus MONEY SUPPLY ANNOUNCEMENTS AND STOCK PRICES: THE UK EVIDENCE By N. P. Tessaromatis P. E. Triantafillou

«ΣΠΟΥΔΑΙ», Τόμος 41, Τεύχος 4ο, Πανεπιστήμιο Πειραιώς / «SPOUDAI», Vol. 41, No 4, University of Piraeus MONEY SUPPLY ANNOUNCEMENTS AND STOCK PRICES: THE UK EVIDENCE By N. P. Tessaromatis P. E. Triantafillou

Cash holdings determinants in the Portuguese economy 1

17 Cash holdings determinants in the Portuguese economy 1 Luísa Farinha Pedro Prego 2 Abstract The analysis of liquidity management decisions by firms has recently been used as a tool to investigate the

17 Cash holdings determinants in the Portuguese economy 1 Luísa Farinha Pedro Prego 2 Abstract The analysis of liquidity management decisions by firms has recently been used as a tool to investigate the

S (17) DOI: Reference: ECOLET 7746

DOI: Reference: ECOLET 7746") Accepted Manuscript The time varying effect of monetary policy on stock returns Dennis W. Jansen, Anastasia Zervou PII: S0165-1765(17)30345-2 DOI: http://dx.doi.org/10.1016/j.econlet.2017.08.022 Reference:

Accepted Manuscript The time varying effect of monetary policy on stock returns Dennis W. Jansen, Anastasia Zervou PII: S0165-1765(17)30345-2 DOI: http://dx.doi.org/10.1016/j.econlet.2017.08.022 Reference:

Modelling Inflation Uncertainty Using EGARCH: An Application to Turkey

Modelling Inflation Uncertainty Using EGARCH: An Application to Turkey By Hakan Berument, Kivilcim Metin-Ozcan and Bilin Neyapti * Bilkent University, Department of Economics 06533 Bilkent Ankara, Turkey

Modelling Inflation Uncertainty Using EGARCH: An Application to Turkey By Hakan Berument, Kivilcim Metin-Ozcan and Bilin Neyapti * Bilkent University, Department of Economics 06533 Bilkent Ankara, Turkey

HIGH FREQUENCY IDENTIFICATION OF MONETARY NON-NEUTRALITY: THE INFORMATION EFFECT

HIGH FREQUENCY IDENTIFICATION OF MONETARY NON-NEUTRALITY: THE INFORMATION EFFECT Emi Nakamura and Jón Steinsson Columbia University January 2018 Nakamura and Steinsson (Columbia) Monetary Shocks January

HIGH FREQUENCY IDENTIFICATION OF MONETARY NON-NEUTRALITY: THE INFORMATION EFFECT Emi Nakamura and Jón Steinsson Columbia University January 2018 Nakamura and Steinsson (Columbia) Monetary Shocks January

THE CHANGING PROBABILITY OF A MONETARY POLICY RESPONSE TO INFLATION AND EMPLOYMENT ANNOUNCEMENTS

THE CHANGING PROBABILITY OF A MONETARY POLICY RESPONSE TO INFLATION AND EMPLOYMENT ANNOUNCEMENTS Adrienne A. Kearney University of Maine INTRODUCTION The response of Federal Reserve policymakers and financial

THE CHANGING PROBABILITY OF A MONETARY POLICY RESPONSE TO INFLATION AND EMPLOYMENT ANNOUNCEMENTS Adrienne A. Kearney University of Maine INTRODUCTION The response of Federal Reserve policymakers and financial

Has the Inflation Process Changed?

Has the Inflation Process Changed? by S. Cecchetti and G. Debelle Discussion by I. Angeloni (ECB) * Cecchetti and Debelle (CD) could hardly have chosen a more relevant and timely topic for their paper.

Has the Inflation Process Changed? by S. Cecchetti and G. Debelle Discussion by I. Angeloni (ECB) * Cecchetti and Debelle (CD) could hardly have chosen a more relevant and timely topic for their paper.

This is a repository copy of Asymmetries in Bank of England Monetary Policy.

This is a repository copy of Asymmetries in Bank of England Monetary Policy. White Rose Research Online URL for this paper: http://eprints.whiterose.ac.uk/9880/ Monograph: Gascoigne, J. and Turner, P.

This is a repository copy of Asymmetries in Bank of England Monetary Policy. White Rose Research Online URL for this paper: http://eprints.whiterose.ac.uk/9880/ Monograph: Gascoigne, J. and Turner, P.

Online Appendix (Not intended for Publication): Federal Reserve Credibility and the Term Structure of Interest Rates

: Federal Reserve Credibility and the Term Structure of Interest Rates") Online Appendix Not intended for Publication): Federal Reserve Credibility and the Term Structure of Interest Rates Aeimit Lakdawala Michigan State University Shu Wu University of Kansas August 2017 1

Online Appendix Not intended for Publication): Federal Reserve Credibility and the Term Structure of Interest Rates Aeimit Lakdawala Michigan State University Shu Wu University of Kansas August 2017 1

Monetary Policy Objectives During the Crisis: An Overview of Selected Southeast European Countries

Monetary Policy Objectives During the Crisis: An Overview of Selected Southeast European Countries 35 UDK: 338.23:336.74(4-12) DOI: 10.1515/jcbtp-2015-0003 Journal of Central Banking Theory and Practice,

Monetary Policy Objectives During the Crisis: An Overview of Selected Southeast European Countries 35 UDK: 338.23:336.74(4-12) DOI: 10.1515/jcbtp-2015-0003 Journal of Central Banking Theory and Practice,

The source of real and nominal exchange rate fluctuations in Thailand: Real shock or nominal shock

MPRA Munich Personal RePEc Archive The source of real and nominal exchange rate fluctuations in Thailand: Real shock or nominal shock Binh Le Thanh International University of Japan 15. August 2015 Online

MPRA Munich Personal RePEc Archive The source of real and nominal exchange rate fluctuations in Thailand: Real shock or nominal shock Binh Le Thanh International University of Japan 15. August 2015 Online

Monetary Policy and Long-term U.S. Interest Rates

September 2004 (Revised) Monetary Policy and Long-term U.S. Interest Rates Hakan Berument Bilkent University Ankara, Turkey Richard T. Froyen* University of North Carolina Chapel Hill, North Carolina *Corresponding

September 2004 (Revised) Monetary Policy and Long-term U.S. Interest Rates Hakan Berument Bilkent University Ankara, Turkey Richard T. Froyen* University of North Carolina Chapel Hill, North Carolina *Corresponding

Monetary Policy Surprises and Interest Rates:

RIETI Discussion Paper Series 08-E-031 Monetary Policy Surprises and Interest Rates: Choosing between the Inflation-Revelation and Excess Sensitivity Hypotheses THORBECKE, Willem RIETI Hanjiang ZHANG University

RIETI Discussion Paper Series 08-E-031 Monetary Policy Surprises and Interest Rates: Choosing between the Inflation-Revelation and Excess Sensitivity Hypotheses THORBECKE, Willem RIETI Hanjiang ZHANG University

José De Gregorio: Autonomy of the Central Bank of Chile, 20 years on

José De Gregorio: Autonomy of the Central Bank of Chile, 20 years on Presentation by Mr José De Gregorio, Governor of the Central Bank of Chile, at the commemoration of the 20 years of autonomy of the

José De Gregorio: Autonomy of the Central Bank of Chile, 20 years on Presentation by Mr José De Gregorio, Governor of the Central Bank of Chile, at the commemoration of the 20 years of autonomy of the

CONFIDENCE AND ECONOMIC ACTIVITY: THE CASE OF PORTUGAL*

CONFIDENCE AND ECONOMIC ACTIVITY: THE CASE OF PORTUGAL* Caterina Mendicino** Maria Teresa Punzi*** 39 Articles Abstract The idea that aggregate economic activity might be driven in part by confidence and

CONFIDENCE AND ECONOMIC ACTIVITY: THE CASE OF PORTUGAL* Caterina Mendicino** Maria Teresa Punzi*** 39 Articles Abstract The idea that aggregate economic activity might be driven in part by confidence and

WORKING PAPER SERIES MONETARY POLICY SURPRISES AND THE EXPECTATIONS HYPOTHESIS AT THE SHORT END OF THE YIELD CURVE. Selva Demiralp

TÜSİAD-KOÇ UNIVERSITY ECONOMIC RESEARCH FORUM WORKING PAPER SERIES MONETARY POLICY SURPRISES AND THE EXPECTATIONS HYPOTHESIS AT THE SHORT END OF THE YIELD CURVE Selva Demiralp Working Paper 080 February

TÜSİAD-KOÇ UNIVERSITY ECONOMIC RESEARCH FORUM WORKING PAPER SERIES MONETARY POLICY SURPRISES AND THE EXPECTATIONS HYPOTHESIS AT THE SHORT END OF THE YIELD CURVE Selva Demiralp Working Paper 080 February

Monetary Fiscal Policy Interactions under Implementable Monetary Policy Rules

WILLIAM A. BRANCH TROY DAVIG BRUCE MCGOUGH Monetary Fiscal Policy Interactions under Implementable Monetary Policy Rules This paper examines the implications of forward- and backward-looking monetary policy

WILLIAM A. BRANCH TROY DAVIG BRUCE MCGOUGH Monetary Fiscal Policy Interactions under Implementable Monetary Policy Rules This paper examines the implications of forward- and backward-looking monetary policy

Discussion. Benoît Carmichael

Discussion Benoît Carmichael The two studies presented in the first session of the conference take quite different approaches to the question of price indexes. On the one hand, Coulombe s study develops

Discussion Benoît Carmichael The two studies presented in the first session of the conference take quite different approaches to the question of price indexes. On the one hand, Coulombe s study develops

Volatility Clustering of Fine Wine Prices assuming Different Distributions

Volatility Clustering of Fine Wine Prices assuming Different Distributions Cynthia Royal Tori, PhD Valdosta State University Langdale College of Business 1500 N. Patterson Street, Valdosta, GA USA 31698

Volatility Clustering of Fine Wine Prices assuming Different Distributions Cynthia Royal Tori, PhD Valdosta State University Langdale College of Business 1500 N. Patterson Street, Valdosta, GA USA 31698

Investigating the Intertemporal Risk-Return Relation in International. Stock Markets with the Component GARCH Model

Investigating the Intertemporal Risk-Return Relation in International Stock Markets with the Component GARCH Model Hui Guo a, Christopher J. Neely b * a College of Business, University of Cincinnati, 48

Investigating the Intertemporal Risk-Return Relation in International Stock Markets with the Component GARCH Model Hui Guo a, Christopher J. Neely b * a College of Business, University of Cincinnati, 48

Blame the Discount Factor No Matter What the Fundamentals Are

Blame the Discount Factor No Matter What the Fundamentals Are Anna Naszodi 1 Engel and West (2005) argue that the discount factor, provided it is high enough, can be blamed for the failure of the empirical

Blame the Discount Factor No Matter What the Fundamentals Are Anna Naszodi 1 Engel and West (2005) argue that the discount factor, provided it is high enough, can be blamed for the failure of the empirical

Effect of Monetary Policy on Commercial Banks Across Different Business Conditions

1 Effect of Monetary Policy on Commercial Banks Across Different Business Conditions Syed M. Harun Texas A&M University-Kingsville, USA M. Kabir Hassan University of New Orleans, USA Tarek S. Zaher Indiana

1 Effect of Monetary Policy on Commercial Banks Across Different Business Conditions Syed M. Harun Texas A&M University-Kingsville, USA M. Kabir Hassan University of New Orleans, USA Tarek S. Zaher Indiana

Liquidity Matters: Money Non-Redundancy in the Euro Area Business Cycle

Liquidity Matters: Money Non-Redundancy in the Euro Area Business Cycle Antonio Conti January 21, 2010 Abstract While New Keynesian models label money redundant in shaping business cycle, monetary aggregates

Liquidity Matters: Money Non-Redundancy in the Euro Area Business Cycle Antonio Conti January 21, 2010 Abstract While New Keynesian models label money redundant in shaping business cycle, monetary aggregates

Evaluating the Impact of Macroprudential Policies in Colombia

Esteban Gómez - Angélica Lizarazo - Juan Carlos Mendoza - Andrés Murcia June 2016 Disclaimer: The opinions contained herein are the sole responsibility of the authors and do not reflect those of Banco

Esteban Gómez - Angélica Lizarazo - Juan Carlos Mendoza - Andrés Murcia June 2016 Disclaimer: The opinions contained herein are the sole responsibility of the authors and do not reflect those of Banco

Optimal Perception of Inflation Persistence at an Inflation-Targeting Central Bank

Optimal Perception of Inflation Persistence at an Inflation-Targeting Central Bank Kai Leitemo The Norwegian School of Management BI and Norges Bank March 2003 Abstract Delegating monetary policy to a

Optimal Perception of Inflation Persistence at an Inflation-Targeting Central Bank Kai Leitemo The Norwegian School of Management BI and Norges Bank March 2003 Abstract Delegating monetary policy to a

Economics Letters 108 (2010) Contents lists available at ScienceDirect. Economics Letters. journal homepage:

Contents lists available at ScienceDirect. Economics Letters. journal homepage:") Economics Letters 108 (2010) 167 171 Contents lists available at ScienceDirect Economics Letters journal homepage: www.elsevier.com/locate/ecolet Is there a financial accelerator in US banking? Evidence

Economics Letters 108 (2010) 167 171 Contents lists available at ScienceDirect Economics Letters journal homepage: www.elsevier.com/locate/ecolet Is there a financial accelerator in US banking? Evidence

Taper Tantrums: What is the Effect of Unconventional Monetary Policy on Emerging Market Capital Flows?

Taper Tantrums: What is the Effect of Unconventional Monetary Policy on Emerging Market Capital Flows? Anusha Chari Karlye Dilts Stedman Christian Lundblad December 10, 2015 Taper Tantrums 1-46 This crisis

Taper Tantrums: What is the Effect of Unconventional Monetary Policy on Emerging Market Capital Flows? Anusha Chari Karlye Dilts Stedman Christian Lundblad December 10, 2015 Taper Tantrums 1-46 This crisis

US real interest rates and default risk in emerging economies

US real interest rates and default risk in emerging economies Nathan Foley-Fisher Bernardo Guimaraes August 2009 Abstract We empirically analyse the appropriateness of indexing emerging market sovereign

US real interest rates and default risk in emerging economies Nathan Foley-Fisher Bernardo Guimaraes August 2009 Abstract We empirically analyse the appropriateness of indexing emerging market sovereign

News and Monetary Shocks at a High Frequency: A Simple Approach

WP/14/167 News and Monetary Shocks at a High Frequency: A Simple Approach Troy Matheson and Emil Stavrev 2014 International Monetary Fund WP/14/167 IMF Working Paper Research Department News and Monetary

WP/14/167 News and Monetary Shocks at a High Frequency: A Simple Approach Troy Matheson and Emil Stavrev 2014 International Monetary Fund WP/14/167 IMF Working Paper Research Department News and Monetary

António Afonso, Jorge Silva Debt crisis and 10-year sovereign yields in Ireland and in Portugal

Department of Economics António Afonso, Jorge Silva Debt crisis and 1-year sovereign yields in Ireland and in Portugal WP6/17/DE/UECE WORKING PAPERS ISSN 183-181 Debt crisis and 1-year sovereign yields

Department of Economics António Afonso, Jorge Silva Debt crisis and 1-year sovereign yields in Ireland and in Portugal WP6/17/DE/UECE WORKING PAPERS ISSN 183-181 Debt crisis and 1-year sovereign yields

STRESS TEST ON MARKET RISK: SENSITIVITY OF BANKS BALANCE SHEET STRUCTURE TO INTEREST RATE SHOCKS

STRESS TEST ON MARKET RISK: SENSITIVITY OF BANKS BALANCE SHEET STRUCTURE TO INTEREST RATE SHOCKS Juan F. Martínez S.* Daniel A. Oda Z.** I. INTRODUCTION Stress tests, applied to the banking system, have

STRESS TEST ON MARKET RISK: SENSITIVITY OF BANKS BALANCE SHEET STRUCTURE TO INTEREST RATE SHOCKS Juan F. Martínez S.* Daniel A. Oda Z.** I. INTRODUCTION Stress tests, applied to the banking system, have

Behavioral Theories of the Business Cycle

Behavioral Theories of the Business Cycle Nir Jaimovich and Sergio Rebelo September 2006 Abstract We explore the business cycle implications of expectation shocks and of two well-known psychological biases,

Behavioral Theories of the Business Cycle Nir Jaimovich and Sergio Rebelo September 2006 Abstract We explore the business cycle implications of expectation shocks and of two well-known psychological biases,

IS FINANCIAL REPRESSION REALLY BAD? Eun Young OH Durham Univeristy 17 Sidegate, Durham, United Kingdom

IS FINANCIAL REPRESSION REALLY BAD? Eun Young OH Durham Univeristy 17 Sidegate, Durham, United Kingdom E-mail: e.y.oh@durham.ac.uk Abstract This paper examines the relationship between reserve requirements,

IS FINANCIAL REPRESSION REALLY BAD? Eun Young OH Durham Univeristy 17 Sidegate, Durham, United Kingdom E-mail: e.y.oh@durham.ac.uk Abstract This paper examines the relationship between reserve requirements,

Interest Rate Smoothing and Calvo-Type Interest Rate Rules: A Comment on Levine, McAdam, and Pearlman (2007)

") Interest Rate Smoothing and Calvo-Type Interest Rate Rules: A Comment on Levine, McAdam, and Pearlman (2007) Ida Wolden Bache a, Øistein Røisland a, and Kjersti Næss Torstensen a,b a Norges Bank (Central

Interest Rate Smoothing and Calvo-Type Interest Rate Rules: A Comment on Levine, McAdam, and Pearlman (2007) Ida Wolden Bache a, Øistein Røisland a, and Kjersti Næss Torstensen a,b a Norges Bank (Central

INFORMATION EFFICIENCY HYPOTHESIS THE FINANCIAL VOLATILITY IN THE CZECH REPUBLIC CASE

INFORMATION EFFICIENCY HYPOTHESIS THE FINANCIAL VOLATILITY IN THE CZECH REPUBLIC CASE Abstract Petr Makovský If there is any market which is said to be effective, this is the the FOREX market. Here we

INFORMATION EFFICIENCY HYPOTHESIS THE FINANCIAL VOLATILITY IN THE CZECH REPUBLIC CASE Abstract Petr Makovský If there is any market which is said to be effective, this is the the FOREX market. Here we

This PDF is a selection from a published volume from the National Bureau of Economic Research

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: Europe and the Euro Volume Author/Editor: Alberto Alesina and Francesco Giavazzi, editors Volume

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: Europe and the Euro Volume Author/Editor: Alberto Alesina and Francesco Giavazzi, editors Volume

Empirical Analysis of the Impact of Inflation Targeting on the Risk Premium

Empirical Analysis of the Impact of Inflation Targeting on the Risk Premium 87 UDK: 336.748.12 DOI: 10.2478/jcbtp-2014-0016 Journal of Central Banking Theory and Practice, 2014, 3, pp. 87-99 Received:

Empirical Analysis of the Impact of Inflation Targeting on the Risk Premium 87 UDK: 336.748.12 DOI: 10.2478/jcbtp-2014-0016 Journal of Central Banking Theory and Practice, 2014, 3, pp. 87-99 Received:

ON THE LONG-TERM MACROECONOMIC EFFECTS OF SOCIAL SPENDING IN THE UNITED STATES (*) Alfredo Marvão Pereira The College of William and Mary

Alfredo Marvão Pereira The College of William and Mary") ON THE LONG-TERM MACROECONOMIC EFFECTS OF SOCIAL SPENDING IN THE UNITED STATES (*) Alfredo Marvão Pereira The College of William and Mary Jorge M. Andraz Faculdade de Economia, Universidade do Algarve,

ON THE LONG-TERM MACROECONOMIC EFFECTS OF SOCIAL SPENDING IN THE UNITED STATES (*) Alfredo Marvão Pereira The College of William and Mary Jorge M. Andraz Faculdade de Economia, Universidade do Algarve,

The Optimal Perception of Inflation Persistence is Zero

The Optimal Perception of Inflation Persistence is Zero Kai Leitemo The Norwegian School of Management (BI) and Bank of Finland March 2006 Abstract This paper shows that in an economy with inflation persistence,

The Optimal Perception of Inflation Persistence is Zero Kai Leitemo The Norwegian School of Management (BI) and Bank of Finland March 2006 Abstract This paper shows that in an economy with inflation persistence,

THE POLICY RULE MIX: A MACROECONOMIC POLICY EVALUATION. John B. Taylor Stanford University

THE POLICY RULE MIX: A MACROECONOMIC POLICY EVALUATION by John B. Taylor Stanford University October 1997 This draft was prepared for the Robert A. Mundell Festschrift Conference, organized by Guillermo

THE POLICY RULE MIX: A MACROECONOMIC POLICY EVALUATION by John B. Taylor Stanford University October 1997 This draft was prepared for the Robert A. Mundell Festschrift Conference, organized by Guillermo

Learning and Time-Varying Macroeconomic Volatility

Learning and Time-Varying Macroeconomic Volatility Fabio Milani University of California, Irvine International Research Forum, ECB - June 26, 28 Introduction Strong evidence of changes in macro volatility

Learning and Time-Varying Macroeconomic Volatility Fabio Milani University of California, Irvine International Research Forum, ECB - June 26, 28 Introduction Strong evidence of changes in macro volatility

THE EFFECTS OF FISCAL POLICY ON EMERGING ECONOMIES. A TVP-VAR APPROACH

South-Eastern Europe Journal of Economics 1 (2015) 75-84 THE EFFECTS OF FISCAL POLICY ON EMERGING ECONOMIES. A TVP-VAR APPROACH IOANA BOICIUC * Bucharest University of Economics, Romania Abstract This

South-Eastern Europe Journal of Economics 1 (2015) 75-84 THE EFFECTS OF FISCAL POLICY ON EMERGING ECONOMIES. A TVP-VAR APPROACH IOANA BOICIUC * Bucharest University of Economics, Romania Abstract This

MONETARY POLICY IN POLAND HOW THE FINANCIAL CRISIS CHANGED THE CENTRAL BANK S PREFERENCES

Financial Internet Quarterly e-finanse 2017, vol.13/ nr 1, s. 15-24 DOI: 10.1515/fiqf-2016-0015 MONETARY POLICY IN POLAND HOW THE FINANCIAL CRISIS CHANGED THE CENTRAL BANK S PREFERENCES Joanna Mackiewicz-Łyziak

Financial Internet Quarterly e-finanse 2017, vol.13/ nr 1, s. 15-24 DOI: 10.1515/fiqf-2016-0015 MONETARY POLICY IN POLAND HOW THE FINANCIAL CRISIS CHANGED THE CENTRAL BANK S PREFERENCES Joanna Mackiewicz-Łyziak

Structural Cointegration Analysis of Private and Public Investment

International Journal of Business and Economics, 2002, Vol. 1, No. 1, 59-67 Structural Cointegration Analysis of Private and Public Investment Rosemary Rossiter * Department of Economics, Ohio University,

International Journal of Business and Economics, 2002, Vol. 1, No. 1, 59-67 Structural Cointegration Analysis of Private and Public Investment Rosemary Rossiter * Department of Economics, Ohio University,

Applied Econometrics and International Development. AEID.Vol. 5-3 (2005)

") PURCHASING POWER PARITY BASED ON CAPITAL ACCOUNT, EXCHANGE RATE VOLATILITY AND COINTEGRATION: EVIDENCE FROM SOME DEVELOPING COUNTRIES AHMED, Mudabber * Abstract One of the most important and recurrent

PURCHASING POWER PARITY BASED ON CAPITAL ACCOUNT, EXCHANGE RATE VOLATILITY AND COINTEGRATION: EVIDENCE FROM SOME DEVELOPING COUNTRIES AHMED, Mudabber * Abstract One of the most important and recurrent

Inflation Targeting and Output Stabilization in Australia

6 Inflation Targeting and Output Stabilization in Australia Guy Debelle 1 Inflation targeting has been adopted as the framework for monetary policy in a number of countries, including Australia, over the

6 Inflation Targeting and Output Stabilization in Australia Guy Debelle 1 Inflation targeting has been adopted as the framework for monetary policy in a number of countries, including Australia, over the

IMPACT OF SOME OVERSEAS MONETARY VARIABLES ON INDONESIA: SVAR APPROACH

DE G DE GRUYTER OPEN IMPACT OF SOME OVERSEAS MONETARY VARIABLES ON INDONESIA: SVAR APPROACH Ahmad Subagyo STIE GICI BUSINESS SCHOOL, INDONESIA Armanto Witjaksono BINA NUSANTARA UNIVERSITY, INDONESIA date

DE G DE GRUYTER OPEN IMPACT OF SOME OVERSEAS MONETARY VARIABLES ON INDONESIA: SVAR APPROACH Ahmad Subagyo STIE GICI BUSINESS SCHOOL, INDONESIA Armanto Witjaksono BINA NUSANTARA UNIVERSITY, INDONESIA date

Household Heterogeneity in Macroeconomics

Household Heterogeneity in Macroeconomics Department of Economics HKUST August 7, 2018 Household Heterogeneity in Macroeconomics 1 / 48 Reference Krueger, Dirk, Kurt Mitman, and Fabrizio Perri. Macroeconomics

Household Heterogeneity in Macroeconomics Department of Economics HKUST August 7, 2018 Household Heterogeneity in Macroeconomics 1 / 48 Reference Krueger, Dirk, Kurt Mitman, and Fabrizio Perri. Macroeconomics

MARKET REACTION TO MONETARY POLICY NONANNOUNCEMENTS. V. Vance Roley. and. Gordon H. Sellon, Jr. First Version: March 6, 1998

MARKET REACTION TO MONETARY POLICY NONANNOUNCEMENTS V. Vance Roley and Gordon H. Sellon, Jr. First Version: March 6, 1998 This Version: August 21, 1998 V. Vance Roley is Hughes M. Blake Professor of Business

MARKET REACTION TO MONETARY POLICY NONANNOUNCEMENTS V. Vance Roley and Gordon H. Sellon, Jr. First Version: March 6, 1998 This Version: August 21, 1998 V. Vance Roley is Hughes M. Blake Professor of Business

MONETARY POLICY AND THE INVESTMENT COMPANIES

MONETARY POLICY AND THE INVESTMENT COMPANIES Syed M. Harun Department of Economics and Finance Texas A&M University Kingsville 700 University Boulevard, MSC 186, Kingsville, TX 78363. Tel: 361-593-3938

MONETARY POLICY AND THE INVESTMENT COMPANIES Syed M. Harun Department of Economics and Finance Texas A&M University Kingsville 700 University Boulevard, MSC 186, Kingsville, TX 78363. Tel: 361-593-3938

Can the Fed Predict the State of the Economy?

Can the Fed Predict the State of the Economy? Tara M. Sinclair Department of Economics George Washington University Washington DC 252 tsinc@gwu.edu Fred Joutz Department of Economics George Washington

Can the Fed Predict the State of the Economy? Tara M. Sinclair Department of Economics George Washington University Washington DC 252 tsinc@gwu.edu Fred Joutz Department of Economics George Washington

Is there a decoupling between soft and hard data? The relationship between GDP growth and the ESI

Fifth joint EU/OECD workshop on business and consumer surveys Brussels, 17 18 November 2011 Is there a decoupling between soft and hard data? The relationship between GDP growth and the ESI Olivier BIAU

Fifth joint EU/OECD workshop on business and consumer surveys Brussels, 17 18 November 2011 Is there a decoupling between soft and hard data? The relationship between GDP growth and the ESI Olivier BIAU

Quadratic Labor Adjustment Costs and the New-Keynesian Model. by Wolfgang Lechthaler and Dennis Snower

Quadratic Labor Adjustment Costs and the New-Keynesian Model by Wolfgang Lechthaler and Dennis Snower No. 1453 October 2008 Kiel Institute for the World Economy, Düsternbrooker Weg 120, 24105 Kiel, Germany

Quadratic Labor Adjustment Costs and the New-Keynesian Model by Wolfgang Lechthaler and Dennis Snower No. 1453 October 2008 Kiel Institute for the World Economy, Düsternbrooker Weg 120, 24105 Kiel, Germany

Risk-Adjusted Futures and Intermeeting Moves

issn 1936-5330 Risk-Adjusted Futures and Intermeeting Moves Brent Bundick Federal Reserve Bank of Kansas City First Version: October 2007 This Version: June 2008 RWP 07-08 Abstract Piazzesi and Swanson

issn 1936-5330 Risk-Adjusted Futures and Intermeeting Moves Brent Bundick Federal Reserve Bank of Kansas City First Version: October 2007 This Version: June 2008 RWP 07-08 Abstract Piazzesi and Swanson

Juan Carlos Castro-Fernández * Working Paper This version: 19 November 2017

BIG RECESSIONS AND SLOW RECOVERIES Juan Carlos Castro-Fernández * Working Paper This version: 19 November 17 ABSTRACT It has been frequently claimed that financial crises are more painful and lead to slower

BIG RECESSIONS AND SLOW RECOVERIES Juan Carlos Castro-Fernández * Working Paper This version: 19 November 17 ABSTRACT It has been frequently claimed that financial crises are more painful and lead to slower

Economic policy. Monetary policy (part 2)

") 1 Modern monetary policy Economic policy. Monetary policy (part 2) Ragnar Nymoen University of Oslo, Department of Economics As we have seen, increasing degree of capital mobility reduces the scope for

1 Modern monetary policy Economic policy. Monetary policy (part 2) Ragnar Nymoen University of Oslo, Department of Economics As we have seen, increasing degree of capital mobility reduces the scope for

The Implications for Fiscal Policy Considering Rule-of-Thumb Consumers in the New Keynesian Model for Romania

Vol. 3, No.3, July 2013, pp. 365 371 ISSN: 2225-8329 2013 HRMARS www.hrmars.com The Implications for Fiscal Policy Considering Rule-of-Thumb Consumers in the New Keynesian Model for Romania Ana-Maria SANDICA

Vol. 3, No.3, July 2013, pp. 365 371 ISSN: 2225-8329 2013 HRMARS www.hrmars.com The Implications for Fiscal Policy Considering Rule-of-Thumb Consumers in the New Keynesian Model for Romania Ana-Maria SANDICA

Economic Policy Uncertainty and Inflation Expectations

Economic Policy Uncertainty and Inflation Expectations Klodiana Istrefi and Anamaria Piloiu Banque de France DB Research SEM Conference 215 22-24 July, Paris 1 / 3 The views expressed herein are those

Economic Policy Uncertainty and Inflation Expectations Klodiana Istrefi and Anamaria Piloiu Banque de France DB Research SEM Conference 215 22-24 July, Paris 1 / 3 The views expressed herein are those

The Relationship among Stock Prices, Inflation and Money Supply in the United States

The Relationship among Stock Prices, Inflation and Money Supply in the United States Radim GOTTWALD Abstract Many researchers have investigated the relationship among stock prices, inflation and money

The Relationship among Stock Prices, Inflation and Money Supply in the United States Radim GOTTWALD Abstract Many researchers have investigated the relationship among stock prices, inflation and money

Asymmetric Information and the Impact on Interest Rates. Evidence from Forecast Data

Asymmetric Information and the Impact on Interest Rates Evidence from Forecast Data Asymmetric Information Hypothesis (AIH) Asserts that the federal reserve possesses private information about the current

Asymmetric Information and the Impact on Interest Rates Evidence from Forecast Data Asymmetric Information Hypothesis (AIH) Asserts that the federal reserve possesses private information about the current

Macroeconometrics - handout 5

Macroeconometrics - handout 5 Piotr Wojcik, Katarzyna Rosiak-Lada pwojcik@wne.uw.edu.pl, klada@wne.uw.edu.pl May 10th or 17th, 2007 This classes is based on: Clarida R., Gali J., Gertler M., [1998], Monetary

Macroeconometrics - handout 5 Piotr Wojcik, Katarzyna Rosiak-Lada pwojcik@wne.uw.edu.pl, klada@wne.uw.edu.pl May 10th or 17th, 2007 This classes is based on: Clarida R., Gali J., Gertler M., [1998], Monetary

Commentary: Housing is the Business Cycle

Commentary: Housing is the Business Cycle Frank Smets Prof. Leamer s paper is witty, provocative and very timely. It is also written with a certain passion. Now, passion and central banking do not necessarily

Commentary: Housing is the Business Cycle Frank Smets Prof. Leamer s paper is witty, provocative and very timely. It is also written with a certain passion. Now, passion and central banking do not necessarily

An analysis of momentum and contrarian strategies using an optimal orthogonal portfolio approach

An analysis of momentum and contrarian strategies using an optimal orthogonal portfolio approach Hossein Asgharian and Björn Hansson Department of Economics, Lund University Box 7082 S-22007 Lund, Sweden

An analysis of momentum and contrarian strategies using an optimal orthogonal portfolio approach Hossein Asgharian and Björn Hansson Department of Economics, Lund University Box 7082 S-22007 Lund, Sweden

Does Monetary Policy influence Stock Market in India? Or, are the claims exaggerated? Partha Ray

Does Monetary Policy influence Stock Market in India? Or, are the claims exaggerated? Partha Ray Monetary policy announcements tend to attract to attract huge media attention. Illustratively, the Economic

Does Monetary Policy influence Stock Market in India? Or, are the claims exaggerated? Partha Ray Monetary policy announcements tend to attract to attract huge media attention. Illustratively, the Economic

Return dynamics of index-linked bond portfolios

Return dynamics of index-linked bond portfolios Matti Koivu Teemu Pennanen June 19, 2013 Abstract Bond returns are known to exhibit mean reversion, autocorrelation and other dynamic properties that differentiate

Return dynamics of index-linked bond portfolios Matti Koivu Teemu Pennanen June 19, 2013 Abstract Bond returns are known to exhibit mean reversion, autocorrelation and other dynamic properties that differentiate

Monetary and Macroprudential Policy in Small Open Economies

Economic Studies Division FLAR X Meeting of Monetary Policy Managers, Asunción - Paraguay Monetary and Macroprudential Policy in Small Open Economies Febrero 08 de 2012 Bogotá D.C., Colombia Index Pg.

Economic Studies Division FLAR X Meeting of Monetary Policy Managers, Asunción - Paraguay Monetary and Macroprudential Policy in Small Open Economies Febrero 08 de 2012 Bogotá D.C., Colombia Index Pg.

Money Market Uncertainty and Retail Interest Rate Fluctuations: A Cross-Country Comparison

DEPARTMENT OF ECONOMICS JOHANNES KEPLER UNIVERSITY LINZ Money Market Uncertainty and Retail Interest Rate Fluctuations: A Cross-Country Comparison by Burkhard Raunig and Johann Scharler* Working Paper

DEPARTMENT OF ECONOMICS JOHANNES KEPLER UNIVERSITY LINZ Money Market Uncertainty and Retail Interest Rate Fluctuations: A Cross-Country Comparison by Burkhard Raunig and Johann Scharler* Working Paper

R-Star Wars: The Phantom Menace

R-Star Wars: The Phantom Menace James Bullard President and CEO 34th Annual National Association for Business Economics (NABE) Economic Policy Conference Feb. 26, 2018 Washington, D.C. Any opinions expressed

R-Star Wars: The Phantom Menace James Bullard President and CEO 34th Annual National Association for Business Economics (NABE) Economic Policy Conference Feb. 26, 2018 Washington, D.C. Any opinions expressed

Macro News and Exchange Rates in the BRICS. Guglielmo Maria Caporale, Fabio Spagnolo and Nicola Spagnolo. February 2016

Economics and Finance Working Paper Series Department of Economics and Finance Working Paper No. 16-04 Guglielmo Maria Caporale, Fabio Spagnolo and Nicola Spagnolo Macro News and Exchange Rates in the

Economics and Finance Working Paper Series Department of Economics and Finance Working Paper No. 16-04 Guglielmo Maria Caporale, Fabio Spagnolo and Nicola Spagnolo Macro News and Exchange Rates in the

The persistence of regional unemployment: evidence from China

Applied Economics, 200?,??, 1 5 The persistence of regional unemployment: evidence from China ZHONGMIN WU Canterbury Business School, University of Kent at Canterbury, Kent CT2 7PE UK E-mail: Z.Wu-3@ukc.ac.uk

Applied Economics, 200?,??, 1 5 The persistence of regional unemployment: evidence from China ZHONGMIN WU Canterbury Business School, University of Kent at Canterbury, Kent CT2 7PE UK E-mail: Z.Wu-3@ukc.ac.uk

Comment on The Central Bank Balance Sheet as a Commitment Device By Gauti Eggertsson and Kevin Proulx

Comment on The Central Bank Balance Sheet as a Commitment Device By Gauti Eggertsson and Kevin Proulx Luca Dedola (ECB and CEPR) Banco Central de Chile XIX Annual Conference, 19-20 November 2015 Disclaimer:

Comment on The Central Bank Balance Sheet as a Commitment Device By Gauti Eggertsson and Kevin Proulx Luca Dedola (ECB and CEPR) Banco Central de Chile XIX Annual Conference, 19-20 November 2015 Disclaimer:

Monetary and Fiscal Policy Switching with Time-Varying Volatilities

Monetary and Fiscal Policy Switching with Time-Varying Volatilities Libo Xu and Apostolos Serletis Department of Economics University of Calgary Calgary, Alberta T2N 1N4 Forthcoming in: Economics Letters

Monetary and Fiscal Policy Switching with Time-Varying Volatilities Libo Xu and Apostolos Serletis Department of Economics University of Calgary Calgary, Alberta T2N 1N4 Forthcoming in: Economics Letters

The Impact of Monetary Policy on Asset Prices 1

The Impact of Monetary Policy on Asset Prices 1 Roberto Rigobon Sloan School of Management, MIT and NBER Brian Sack Board of Governors of the Federal Reserve System January 7, 2004 1 The authors would

The Impact of Monetary Policy on Asset Prices 1 Roberto Rigobon Sloan School of Management, MIT and NBER Brian Sack Board of Governors of the Federal Reserve System January 7, 2004 1 The authors would

THE REACTION OF THE WIG STOCK MARKET INDEX TO CHANGES IN THE INTEREST RATES ON BANK DEPOSITS

OPERATIONS RESEARCH AND DECISIONS No. 1 1 Grzegorz PRZEKOTA*, Anna SZCZEPAŃSKA-PRZEKOTA** THE REACTION OF THE WIG STOCK MARKET INDEX TO CHANGES IN THE INTEREST RATES ON BANK DEPOSITS Determination of the

OPERATIONS RESEARCH AND DECISIONS No. 1 1 Grzegorz PRZEKOTA*, Anna SZCZEPAŃSKA-PRZEKOTA** THE REACTION OF THE WIG STOCK MARKET INDEX TO CHANGES IN THE INTEREST RATES ON BANK DEPOSITS Determination of the

Does Monetary Policy Affect Stock Prices and Treasury Yields? An Error Correction and Simultaneous Equation Approach

Does Monetary Policy Affect Stock Prices and Treasury Yields? An Error Correction and Simultaneous Equation Approach J. Benson Durham * Division of Monetary Affairs Board of Governors of the Federal Reserve

Does Monetary Policy Affect Stock Prices and Treasury Yields? An Error Correction and Simultaneous Equation Approach J. Benson Durham * Division of Monetary Affairs Board of Governors of the Federal Reserve

AMERICAN MONETARY POLICY NORMALIZATION AND ITS IMPACTS ON THE BRAZILIAN YIELD CURVE

AMERICAN MONETARY POLICY NORMALIZATION AND ITS IMPACTS ON THE BRAZILIAN YIELD CURVE Gian Barbosa da Silva 1 Guilherme Pinheiro de Deus Gustavo Miguel Nogueira Fleury Lucas Gurgel Leite Orlando Cesar de

AMERICAN MONETARY POLICY NORMALIZATION AND ITS IMPACTS ON THE BRAZILIAN YIELD CURVE Gian Barbosa da Silva 1 Guilherme Pinheiro de Deus Gustavo Miguel Nogueira Fleury Lucas Gurgel Leite Orlando Cesar de

Regional convergence in Spain:

ECONOMIC BULLETIN 3/2017 ANALYTICAL ARTIES Regional convergence in Spain: 1980 2015 Sergio Puente 19 September 2017 This article aims to analyse the process of per capita income convergence between the

ECONOMIC BULLETIN 3/2017 ANALYTICAL ARTIES Regional convergence in Spain: 1980 2015 Sergio Puente 19 September 2017 This article aims to analyse the process of per capita income convergence between the

THE CONVERGENCE OF THE BUSINESS CYCLES IN THE EURO AREA. Keywords: business cycles, European Monetary Union, Cobb-Douglas, Optimal Currency Areas

Romanian Economic and Business Review Vol. 7, No. 4 97 THE CONVERGENCE OF THE BUSINESS CYCLES IN THE EURO AREA Andrei Rădulescu 1 Abstract The Euro Area is confronted with the persistence of the sovereign

Romanian Economic and Business Review Vol. 7, No. 4 97 THE CONVERGENCE OF THE BUSINESS CYCLES IN THE EURO AREA Andrei Rădulescu 1 Abstract The Euro Area is confronted with the persistence of the sovereign

Monetary Policy rule in the presence of persistent excess liquidity: the case of Trinidad and Tobago

1 Monetary Policy rule in the presence of persistent excess liquidity: the case of Trinidad and Tobago Anthony Birchwood Presented at the 41 st conference, hosted by the Bank of Guyana in Georgetown, on

1 Monetary Policy rule in the presence of persistent excess liquidity: the case of Trinidad and Tobago Anthony Birchwood Presented at the 41 st conference, hosted by the Bank of Guyana in Georgetown, on

The Impact of Tax Policies on Economic Growth: Evidence from Asian Economies

The Impact of Tax Policies on Economic Growth: Evidence from Asian Economies Ihtsham ul Haq Padda and Naeem Akram Abstract Tax based fiscal policies have been regarded as less policy tool to overcome the

The Impact of Tax Policies on Economic Growth: Evidence from Asian Economies Ihtsham ul Haq Padda and Naeem Akram Abstract Tax based fiscal policies have been regarded as less policy tool to overcome the

Omitted Variables Bias in Regime-Switching Models with Slope-Constrained Estimators: Evidence from Monte Carlo Simulations

Journal of Statistical and Econometric Methods, vol. 2, no.3, 2013, 49-55 ISSN: 2051-5057 (print version), 2051-5065(online) Scienpress Ltd, 2013 Omitted Variables Bias in Regime-Switching Models with

Journal of Statistical and Econometric Methods, vol. 2, no.3, 2013, 49-55 ISSN: 2051-5057 (print version), 2051-5065(online) Scienpress Ltd, 2013 Omitted Variables Bias in Regime-Switching Models with

Identifying the exchange-rate balance sheet effect over firms

Identifying the exchange-rate balance sheet effect over firms CÉSAR CARRERA Banco Central de Reserva del Perú Abstract: This version: May 2014 I use firm-level data on investment and evaluate the balance

Identifying the exchange-rate balance sheet effect over firms CÉSAR CARRERA Banco Central de Reserva del Perú Abstract: This version: May 2014 I use firm-level data on investment and evaluate the balance

MAGNT Research Report (ISSN ) Vol.6(1). PP , 2019

Vol.6(1). PP , 2019") Does the Overconfidence Bias Explain the Return Volatility in the Saudi Arabia Stock Market? Majid Ibrahim AlSaggaf Department of Finance and Insurance, College of Business, University of Jeddah, Saudi

Does the Overconfidence Bias Explain the Return Volatility in the Saudi Arabia Stock Market? Majid Ibrahim AlSaggaf Department of Finance and Insurance, College of Business, University of Jeddah, Saudi

Inflation and Stock Market Returns in US: An Empirical Study

Inflation and Stock Market Returns in US: An Empirical Study CHETAN YADAV Assistant Professor, Department of Commerce, Delhi School of Economics, University of Delhi Delhi (India) Abstract: This paper

Inflation and Stock Market Returns in US: An Empirical Study CHETAN YADAV Assistant Professor, Department of Commerce, Delhi School of Economics, University of Delhi Delhi (India) Abstract: This paper

Sustainability of Current Account Deficits in Turkey: Markov Switching Approach

Sustainability of Current Account Deficits in Turkey: Markov Switching Approach Melike Elif Bildirici Department of Economics, Yıldız Technical University Barbaros Bulvarı 34349, İstanbul Turkey Tel: 90-212-383-2527

Sustainability of Current Account Deficits in Turkey: Markov Switching Approach Melike Elif Bildirici Department of Economics, Yıldız Technical University Barbaros Bulvarı 34349, İstanbul Turkey Tel: 90-212-383-2527

Asian Economic and Financial Review SOURCES OF EXCHANGE RATE FLUCTUATION IN VIETNAM: AN APPLICATION OF THE SVAR MODEL

Asian Economic and Financial Review ISSN(e): 2222-6737/ISSN(p): 2305-2147 journal homepage: http://www.aessweb.com/journals/5002 SOURCES OF EXCHANGE RATE FLUCTUATION IN VIETNAM: AN APPLICATION OF THE SVAR

Asian Economic and Financial Review ISSN(e): 2222-6737/ISSN(p): 2305-2147 journal homepage: http://www.aessweb.com/journals/5002 SOURCES OF EXCHANGE RATE FLUCTUATION IN VIETNAM: AN APPLICATION OF THE SVAR

Monetary Policy Surprises, Credit Costs and Economic Activity

Monetary Policy Surprises, Credit Costs and Economic Activity By Mark Gertler and Peter Karadi We provide evidence on the transmission of monetary policy shocks in a setting with both economic and financial

Monetary Policy Surprises, Credit Costs and Economic Activity By Mark Gertler and Peter Karadi We provide evidence on the transmission of monetary policy shocks in a setting with both economic and financial

Discussion of Trend Inflation in Advanced Economies

Discussion of Trend Inflation in Advanced Economies James Morley University of New South Wales 1. Introduction Garnier, Mertens, and Nelson (this issue, GMN hereafter) conduct model-based trend/cycle decomposition