ISLAMIC BANKS: INTRODUCTION AND COMPARISON WITH THE CONVENTIONAL BANKS Corresponding Author: Houssam Mabrouk

|

|

|

- Derek Norton

- 5 years ago

- Views:

Transcription

1 International Journal of Humanities and Social Science Invention (IJHSSI) ISSN (Online): , ISSN (Print): Volume 7 Issue 05 Ver. II May PP ISLAMIC BANKS: INTRODUCTION AND COMPARISON WITH THE CONVENTIONAL BANKS Corresponding Author: Houssam Mabrouk The Banks represent the heart of the economy of any country. In countries with muslim beliefs, where the society doesn't accept interests, and are sceptic to deal with the conventional banks, because of their religion that forbids Riba/Intrests. Islamic banks have been created and introduced to these muslim population to meet their demand and to provide its services with no interest on any bank transaction. Since we are living in muslim countries, and that our religion is Islam. We follow the laws and principals of Islam. One of these principles treats the question of the interests in the financial transactions. In Islam the interests - or what s called Riba- is simply prohibited Date of Submission: Date of acceptance: As we mentioned before, the role of the banks in our actual world and society is undeniable, and since the religion forbids the transactions of these conventional banks, it was mandatory for these muslim countries to create banks that are in accordance with their islamic laws and principals. But now with the islamic banks, the aim is the development of the economy and at the same time get these muslim clients, who do not like to transact with the conventional banks. This article compares the main differences between an Islamic bank and a conventional bank. Let s start by understanding one of the biggest differences between an Islamic bank and a conventional bank through this small illustration. On the left we have the conventional Banking with the bank giving Money ( credit/loan) to the client, and the client giving it back with extra addition - which is called Riba. On the right we have the Islamic banking, with bank giving either goods or services. No money, to avoid Riba: If you need money to buy a good or services, the bank buys it for you, and sells it to you. The client gives back the agreed value/amount of the goods or services he received. Analysis: detailed comparison between Islamic banks and conventional banks 65 Page

2 66 Page

as fundamental basis. The conventional banks system is based on self-made principles and rules.")

3 Let s try to resume the most important differences between the conventional bank and the islamic one The biggest difference between the 2 banking systems is as follows. The Islamic banks system have the Islamic Law (Sharia) as fundamental basis. The conventional banks system is based on self-made principles and rules. The Sharia governs and rules all the laws and rules governing the Islamic population in all the aspects of life. Unlike the conventional banks, which make the customers pay interests even their businesses are making no profit ( suffer losses), the islamic banks runs on the basis of loss/profit sharing. If their customer makes profit, they also get profit. But if their customer suffer losses, the bank shares the loss as well. The loss shared with the bank depends on the mode of financing adopted. While the orthodox banks employ the money as a store of value, mode of exchange and commodity. The Islamic banks employ it only as store of value and mode of exchange. But never as Commodity. The explanation for this is that, unlike the Islamic banking, conventional banks trade money with huge prices and also rent it out. Concerning the profit-making, the Orthodox banks relays on time value to charge interests on Capital. While the source of profit charging of the Islamic banks is based on the profit of the exchange of goods and services. Unlike the orthodox banks, where they predetermine the income coming from loan. The Islamic banks concentrate their activities on debtor investment projects, assessments and valuations. This point is a result of the profit/loss sharing. While the conventional banks never share the losses of their customers. In the Islamic laws, the banks guarantee to repay the sums for the deposit accounts under one condition. the account has to be an Al-Wadiah based account. Otherwise, the losses will be shared by the depositor and the banks following the Mudharabah guidelines. As the Islamic banks system follow the Islamic laws (Sharia a), it s logical that the banks are excepted to care for the public interest FIRST. Also the banks should guarantee a lawful economic development and progress. The conventional banks have as main objective The Profit. Unlike the Islamic banks, the conventional banks s interest comes first. Compared to the orthodox banks, it s proven that Islamic banks have a better capitalisation, better asset, and a higher inter mediation ratio. Also fairness is one of the biggest difference between the two banking systems. Islamic banks represent fairness in all aspects by sharing the losses of their customers, while the conventional banks only think about the maximisation of their profits and the minimisation of their losses. Size and Location: reach of the banks in the world: Islamic vs conventional It s known that banks are implemented in almost every country in the world. it s the heart of the economies and the motor of any GDP development. In this part we would like to compare the extension of the islamic banks compared to the conventional banks. Unlike the conventional banks which are implemented in every country in the world the islamic banks have a limited number of countries compared to the conventional ones. With an annual growth rate of 17.6% between 2009 and 2013 and an estimated size of $2 trillion, the Islamic banking system have grown even faster than the conventional banks. But it still represents only 1%, and therefore, compared to the conventional banks, is much smaller. In 2010, They Islamic banks were present in a way or other in almost 105 countries. Analysis and statistics converge concerning the country with largest number of Islamic institutions. But according to World Islamic Banking Competitiveness Report the 6 top countries would probably be as follow: 67 Page

4 - Saudi Arabia - Malaysia - United Arab Emirates - Kuwait - Qatar - Turkey These 6 countries alone cover 87% of the international islamic assets. However, brahim Warde- a famous scholar in the field of international finance- with $345 billion in Islamic assets Iran should be on the top, then comes Saudi Arabia with $258 billion. Malaysia comes in the third place with $142 billion. Kuwait and UAE follow with respectively $118 and $112 billion. Another studies conducted by Reuters claims that Iranian Islamic banks represent a 1/3 of the Islamic finance assets in the whole world. Indeed, the economical sanctions applied against Iran by the west affected the Iranian conventional banking sector; as result the Islamic banks have known an immense development and progress in the country. as we mentioned before, there s islamic financing branches in almost 105 countries in the world. But if we talk about a real signifiant market part, there s only 9 countries where islamic banks are dominating. These following 9 countries - without surprise- are all Muslim countries. Percentage of world market shareof Islamic banking industryby country, 2016 Saudi Arabia 33 Malaysia 15.5 UAE 15.4 Kuwait 10.1 Qatar 8.1 Turkey 5.1 Indonesia 2.5 Bahrain 1.6 Pakistan 1.4 Rest of the world 7.3 Source: World Islamic Banking Competitiveness Report 2016 A selection of our prominent and very active Islamic bank clients in London include: Gatehouse Bank, ABC International Bank, QIB (UK) and Ahli United Bank. In the european side, the islamic banking system is available, but not everywhere. Britain is the largest market for the islamic banking system in Europe. Islamic baking system is becoming significant in the United Kingdom. More than any banking sector in Europe, we can count 6 real Islamic banks in the UK. To these 6 banks we add more than 20 lenders, who offer services and products in accordance with the Sharia a laws and values. Among these islamic banks or lenders with islamic services and products we can list: - Gatehouse Bank - ABC International Bank - QIB (UK) - Ali United Bank - United Bank - Al Rayan BANK What s the reason behind this fact? Well, the Britain legal jurisdiction fits with the Islamic baking laws. Also there s complementation between the English legal system and the Islamic Laws. Moreover, since 2003 in the framework of a series of Finance Acts the Britain government has decided the removal of tax barriers. As results, the Islamic banking Services were way less tax efficient compared to the orthodox counterparts. 68 Page

5 Clients: Islamic banks vs conventional banks As the conventional banks are implemented in every country, it s logical that they have much more clients than any islamic bank. There s no marge for comparison between the conventional market share and the islamic market share. In revenge what s interesting is the study of the islamic banks s clients. Indeed we notice that many Non-Muslims are trying the islamic financing and banking system. It s known that Islamic banks aren t only for Islamic population. This statement has 2 explanations. The first one is that even Non-Muslim individuals can open and use an account in an Islamic bank. The second one is that Islamic banking services could be provided to non-muslims. Because of the fixed lending rules and principals Islamic financing institutions are getting bigger and more success even with non-muslims in the whole world. Since the Sharia a is mixture of islamic principals and modern banking principles, its services and products are provided to Muslims and non-muslims Non Muslim investors have also been looking for less risky alternatives since the onset of the global credit crisis over a year ago cast doubt on many Western risk management practices. As we know, the market of the Islamic banking system has been created by and for Muslims. In order to avoid Riba, which is interests in the western banking system. With the years the interests-fee system of the Islamic banks became more popular and reached the non-muslim countries. This could be explained by the rich Arab investors from Saudi Arabia, Qatar and UAE, who through their wealth are constantly investing in Europe, and are demanding for ethical investments. Since the crush and crisis occurring in the worldwide economy there s more and more non-muslims investors who started to trust less and less the conventional system with their hunger for the profit. Therefore they step into the Islamic banking system. Balance Sheet: the Comparison Let s analyse the comparison of the balance sheets of the islamic banks and conventional banks. Balance Sheet: conventional banks Assets Liabilities Loans and advances to customers Cash and cash balances with other banks Investments in associates, subsidiaries and joint ventures Financial assets held for trading Cash and cash balances with the central bank Customers deposits Due to banks and other financial institutions Other liabilities Sundry creditors Equity and reserves Concerning the asset side of the conventional balance sheet, we can notice a much bigger diversification. This big variance can be explained by the marketable securities, trading accounts, or even corporations and consumers lending. Liabilities are immediately generated through the deposits without taking in consideration the purpose of use of the money on the asset side. Therefore there s a discrepancy that results between the assets and liabilities. Liquidity of the short-term liabilities cover the long-term assets, which increases the chances for a bank to encounter a maturity discrepancy and becomes skeptical regarding the long-term non liquid investments. By enlarging the amount of the funding/deposits, which aren t retail, the conventional bank could face a huge volatility in meeting its funding requirements, thus needing a liquidity risk management, which has to be developed and sophisticated. The Islamic financial institutions and the conventional financial institutions have not the same nature of financial intermediation. The contract of Mudarabah is the vital element of the financial negotiation and also of banking for the Islamic banks. The concept can be explained as follow; all the parties involved in the operation share the profit/losses.the financial intermediation is slightly a passage agreement, which is identical to the management of funds. But on the asset corner, there s several portfolios. Balance Sheet: Islamic Bank Application of funding Cash balances Financing assets (murabaha, salam, ijara, istisna) Investment assets (mudarabah, musharakah) Sources of funding Demand deposits (amanah) Investment accounts (mudarabah) Special investment accounts (mudarabah, musharakah) 69 Page

6 Fee-based services (ju ala, kafala, and so forth) Non-banking assets (property) Reserves Equity capital Here we can see a balance sheet of an Islamic bank showing various activities and financial instruments. It will serve us to understand the fundamental risks faced by the Islamic institutions. The Classification of the Functionalities and the use of different instruments is a normal proceeding in the islamic banks. On the asset side, we have Islamic financing and Investing accounts-which is the loans given to customers in a conventional bank. While we have investments accounts given by the customers and demand deposits on the liability side.the structure of this balance sheet displays the nature of banks and its role as intermediator. Also because of its low capital to liabilities, the leverage will not be accepted in any other business besides the financial services industry. Just the shares of different asset products and the changes operated on the shares with the time, should enable an analyst to evaluate profile risks of the bank. The prices and supply features of all the different kind of liabilities, as well as the business conducted by the bank and the market orientation define the variation of the composition of the liabilities in an Islamic bank s balance sheet. The level of risk, potential profit and the cost of the transactions of any bank is determined by its funding structure. Also the specific asset-liability and the policy of the risk management is determined by the structure of the liabilities of the bank. As we mentioned before, the balance sheet risk profile of an islamic bank is completely different from the one of an orthodox bank. The passage aspect of the nature of the balance sheet is the main characteristic of an islamic institution. Unlike the conventional banks, this aspect of the islamic balance sheet avoid the risk for its bank to get into an asset-liability discrepancy through the link between the depositors return and the assets return of the bank. This nature of the balance causes some problems in the operational field. Indeed the estimation and the increase of the returns ( ex-post) and also the intra-period withdrawal of deposits are considerably affect by these issues. Moreover the nature of assets of the conventional bank and the islamic bank isn t the same at all. The first one insists on keeping a fixed income and decreasing any credit risk on debt securities. Meanwhile the second one has a strong asset-based investments. But with a real asset backing the credit risk. These features of the islamic banking lead the institution s ability of lending to be restricted by the availability of the real assets, which also leads to the absence a (leveraged) credit creation. This feature is not a design issue but is a temporal phenomenon until a well-functioning securities market for Shari ah-compliant instruments is developed. In the Assets of an Islamic institution we can find different assets such as financial assets, which are characterised by the sell of goods and commodities to the customers. Such practice exposes the bank until certain level. The assets are financed through a credit given to the customer in a conventional bank. But in an Islamic bank, the asset itself and the financing of this asset are linked. In Addition to these exposures mentioned above, the bank could face other issues coming from the physical assets. Another difference between the conventional bank and the islamic bank is the unavailability of the liquid securities on the asset side of an Islamic bank s balance sheet. The hesitation towards the creation of leverage comes from the prohibition of Riba (Interests),which leads to an inability to distribute debts in order to finance the assets.the fact that there s little leverage makes the islamic banks more stable and less risky in a crisis period. Due to the increased leverage and the complex financial system, which lead to the development of several layers of intermediaries, the actual economy crisis has been accelerated. Through a detailed analysis of the risk profile of the various financial contracts in the balance sheet, we will try to understand the risk faced by the Islamic financial institutions. The methods used in this analysis are standard. Such as: - Trend analysis - Impact analysis - Bucketing - Duration and maturity mismatch These types of analysis would be used to analyse each financial contract and instruments. After the analysis finished and the results known. It should be integrated in the balance sheet to have a general view at an institutional level. 70 Page

7 The classic analyse of risk is the one that always concentrate on financial risks on the asset side. An effective analysis of an Islamic bank always take in consideration the non-financial risks on the liability side. Indeed non-financial aspects (for example withdrawal risk and restricted geographical diversification) have to be included in the analysis as well as the competition made by the the orthodox banks. increasing the share of financing on PlS basin and decreasing the share of financing on the basis of Mode of financing such as Murabah, these are the gradual steps that Islamic banks and financial institutions should conduct in order to gain more influence and market share. In case the Islamic banks are capable creating and spreading a socio-economic justice example, by increasing their PLS ( profit-loss-sharing) based transactions and getting more operational results, there will be a bigger cooperation between the european and western banks and the Islamic banks. Indeed many of these banks are already attracted by the PLS concept. Some of the western banks are already using and integrating Islamic services in their subsidiaries and affiliates. The Islamic banks will no longer be the banks of muslim population, but all of the individuals who would like to deal with a bank, which put them first, rather than profit. Also as we mentioned before there s more and more non-muslims who are changing from the conventional banks to Islamic banks, because of its fairness and interests-free operations. The era of a fair banking system can be imagined where the products and services of Islamic banking system would be provided to a large amount of people, resulting to an over-all social and economic prosperity. Houssam Mabrouk." ISLAMIC BANKS: INTRODUCTION AND COMPARISON WITH THE CONVENTIONAL BANKS." International Journal of Humanities and Social Science Invention (IJHSSI) 7.05 (2018): Page

Islamic Finance Achievements and Prospects

Islamic Finance Achievements and Prospects Emeritus Professor Rodney Wilson Toronto University lecture, 30 th October 2014 The Second Annual Conference of Islamic Economics & Islamic Finance Venue: Chestnut

Islamic Finance Achievements and Prospects Emeritus Professor Rodney Wilson Toronto University lecture, 30 th October 2014 The Second Annual Conference of Islamic Economics & Islamic Finance Venue: Chestnut

Keynote Speech on Islamic Banking

The Third Annual Conference of Islamic Economics & Islamic Finance Venue: Chestnut Conference Center, Toronto University, Toronto, Canada Date: October 29 th, 2016 Organized by: ECO-ENA, Inc., Canada Keynote

The Third Annual Conference of Islamic Economics & Islamic Finance Venue: Chestnut Conference Center, Toronto University, Toronto, Canada Date: October 29 th, 2016 Organized by: ECO-ENA, Inc., Canada Keynote

Building an Effective Islamic Financial System

Building an Effective Islamic Financial System Dr. Shamshad Akhtar Governor, State Bank of Pakistan Global Islamic Financial Forum Governor s: Financial Regulators Forum in Islamic Finance Kuala Lumpur,

Building an Effective Islamic Financial System Dr. Shamshad Akhtar Governor, State Bank of Pakistan Global Islamic Financial Forum Governor s: Financial Regulators Forum in Islamic Finance Kuala Lumpur,

ISLAMIC BANKING IN EUROPEAN UNION COUNTRIES: CHALLENGES AND OPPORTUNITIES

ISLAMIC BANKING IN EUROPEAN UNION COUNTRIES: CHALLENGES AND OPPORTUNITIES Diana Sadoveanu Alexandru Ioan Cuza University of Iași diana.sadoveanu@gmail.com Abstract: Islamic banking is a relative young

ISLAMIC BANKING IN EUROPEAN UNION COUNTRIES: CHALLENGES AND OPPORTUNITIES Diana Sadoveanu Alexandru Ioan Cuza University of Iași diana.sadoveanu@gmail.com Abstract: Islamic banking is a relative young

THE PROSPECT OF ISLAMIC FINANCE IN THE PHILIPPINES. MEHOL K. SADAIN Commissioner NCMF February 9, 2015

THE PROSPECT OF ISLAMIC FINANCE IN THE PHILIPPINES MEHOL K. SADAIN Commissioner NCMF February 9, 2015 Definition of Terms Finance is the science or study of management of funds; the system that includes

THE PROSPECT OF ISLAMIC FINANCE IN THE PHILIPPINES MEHOL K. SADAIN Commissioner NCMF February 9, 2015 Definition of Terms Finance is the science or study of management of funds; the system that includes

DISCUSSION PAPER FOR COMMENTS. Conceptual issues in Measuring Islamic Finance National Accounts Alick Mjuma Nyasulu 1

WORKSHOP ON ISLAMIC BANKING IN NATIONAL ACCOUNTS 24-26 October 2017, Beirut, Lebanon DISCUSSION PAPER FOR COMMENTS Conceptual issues in Measuring Islamic Finance National Accounts Alick Mjuma Nyasulu 1

WORKSHOP ON ISLAMIC BANKING IN NATIONAL ACCOUNTS 24-26 October 2017, Beirut, Lebanon DISCUSSION PAPER FOR COMMENTS Conceptual issues in Measuring Islamic Finance National Accounts Alick Mjuma Nyasulu 1

Attendance at the Singapore Due Diligence 2012 is strictly by invitation only. The content of this presentation is intended solely for invited guests

should not be reproduced or distributed to persons other than the invited guests. Overview of Islamic Finance Hanifah Hashim Head of Fixed Income (Malaysia) Franklin Templeton Investments September 26,

should not be reproduced or distributed to persons other than the invited guests. Overview of Islamic Finance Hanifah Hashim Head of Fixed Income (Malaysia) Franklin Templeton Investments September 26,

Wealth Creation and Wealth Management in an Islamic Economy

Wealth Creation and Wealth Management in an Islamic Economy Professor Rodney Wilson IRTI Distance Learning Programme Islamic Development Bank, April 2011 Outline Material wealth, spiritual fulfilment and

Wealth Creation and Wealth Management in an Islamic Economy Professor Rodney Wilson IRTI Distance Learning Programme Islamic Development Bank, April 2011 Outline Material wealth, spiritual fulfilment and

MANUAL MONETARY AND FINANCIAL STATISTICS MANUAL AND COMPILATION GUIDE

MANUAL MONETARY AND FINANCIAL STATISTICS MANUAL AND COMPILATION GUIDE 2015 2016 I N T E R N A T I O N A L M O N E T A R Y F U N D ANNEX 1 Islamic 4.3 Financial Institutions and Instruments 4.256 This annex

MANUAL MONETARY AND FINANCIAL STATISTICS MANUAL AND COMPILATION GUIDE 2015 2016 I N T E R N A T I O N A L M O N E T A R Y F U N D ANNEX 1 Islamic 4.3 Financial Institutions and Instruments 4.256 This annex

Zeti Akhtar Aziz: Potential role of Islamic finance in strengthening the New Silk Road

Zeti Akhtar Aziz: Potential role of Islamic finance in strengthening the New Silk Road Special address by Dr Zeti Akhtar Aziz, Governor of the Central Bank of Malaysia, at GIFF Investors & Issuers Forum:

Zeti Akhtar Aziz: Potential role of Islamic finance in strengthening the New Silk Road Special address by Dr Zeti Akhtar Aziz, Governor of the Central Bank of Malaysia, at GIFF Investors & Issuers Forum:

Takaful. Mohammad Khan Head of Islamic Finance in PwC. Mohammad Khan

Takaful Mohammad Khan Mohammad Khan Head of Islamic Finance in PwC Partner in PwC Actuarial Services Head of general insurance personal and commercial lines at PwC Member of PwC s Global Islamic Finance

Takaful Mohammad Khan Mohammad Khan Head of Islamic Finance in PwC Partner in PwC Actuarial Services Head of general insurance personal and commercial lines at PwC Member of PwC s Global Islamic Finance

Islamic Finance Seminar Wednesday 2 December

Islamic Finance Seminar Wednesday 2 December Islamic Finance Seminar Wednesday 2 December Chris Fletcher Greater Manchester Chamber Policy & Marketing Director Islamic Finance Seminar Wednesday 2 December

Islamic Finance Seminar Wednesday 2 December Islamic Finance Seminar Wednesday 2 December Chris Fletcher Greater Manchester Chamber Policy & Marketing Director Islamic Finance Seminar Wednesday 2 December

International Islamic Liquidity Management Corporation

International Islamic Liquidity Management Corporation An Overview of Liquidity Management Issues for Institutions Offering Islamic Financial Services March 9 th, 2016/ Jumada Al- Awwal 29, 1437 IRTI Eminent

International Islamic Liquidity Management Corporation An Overview of Liquidity Management Issues for Institutions Offering Islamic Financial Services March 9 th, 2016/ Jumada Al- Awwal 29, 1437 IRTI Eminent

Sharing of Risks in Islamic Finance

IBSU Scientific Journal, 5(2): 13-20, 2011 ISSN: 1512-3731 print / 2233-3002 online Sharing of Risks in Islamic Finance Ahmet SEKRETER Abstract For most of the people the prohibition on interest is the

IBSU Scientific Journal, 5(2): 13-20, 2011 ISSN: 1512-3731 print / 2233-3002 online Sharing of Risks in Islamic Finance Ahmet SEKRETER Abstract For most of the people the prohibition on interest is the

Islamic Banking Processes and Products

Islamic Banking Processes and Products Key Regional Variations O R A C L E W H I T E P A P E R S E P T E M B E R 2 0 1 7 Disclaimer The following is intended to outline our general product direction. It

Islamic Banking Processes and Products Key Regional Variations O R A C L E W H I T E P A P E R S E P T E M B E R 2 0 1 7 Disclaimer The following is intended to outline our general product direction. It

ISLAMIC FINANCE AND THE CONCEPT OF PROFIT AND RISK SHARING

Middle East Islamic Journal finance of Entrepreneurship, and the concept Leadership of profit and Sustainable risk sharing Development Vol. 1, No. 1 2017 89 ISLAMIC FINANCE AND THE CONCEPT OF PROFIT AND

Middle East Islamic Journal finance of Entrepreneurship, and the concept Leadership of profit and Sustainable risk sharing Development Vol. 1, No. 1 2017 89 ISLAMIC FINANCE AND THE CONCEPT OF PROFIT AND

Luxembourg A prime location for Sukuk issuance

Luxembourg A prime location for issuance Contents Islamic finance in Luxembourg listed in Luxembourg 5 Structuring transactions 6 al-ijara 8 Mixed-asset 9 al-musharaka 0 al-murabaha al-istisna al-salam

Luxembourg A prime location for issuance Contents Islamic finance in Luxembourg listed in Luxembourg 5 Structuring transactions 6 al-ijara 8 Mixed-asset 9 al-musharaka 0 al-murabaha al-istisna al-salam

Sharia Issues in Liquidity Risk Management

Sharia Issues in Liquidity Risk Management Summer School in Islamic Banking and Finance Durham University July 5 th - 9 th, 2010 Rifki Ismal Durham University Outline Liquidity Risk in Islamic Banking

Sharia Issues in Liquidity Risk Management Summer School in Islamic Banking and Finance Durham University July 5 th - 9 th, 2010 Rifki Ismal Durham University Outline Liquidity Risk in Islamic Banking

Introduction to Islamic Finance & Banking

Introduction to Islamic Finance & Banking World Bank BRSA - TKBB Joint Workshop on Innovative Product Development in Islamic Banks Istanbul, Turkey March 2, 2017 Zamir Iqbal, PhD. Lead Financial Sector

Introduction to Islamic Finance & Banking World Bank BRSA - TKBB Joint Workshop on Innovative Product Development in Islamic Banks Istanbul, Turkey March 2, 2017 Zamir Iqbal, PhD. Lead Financial Sector

COMCEC STRATEGY COMCEC FINANCIAL OUTLOOK. Cafer Biçer. 9 th Meeting of COMCEC Financial Cooperation Working Group

COMCEC FINANCIAL OUTLOOK Cafer Biçer 9 th Meeting of COMCEC Financial Cooperation Working Group October 26 th, 217 Ankara, Turkey OUTLINE Recent Global Economic and Financial Developments Financial Outlook

COMCEC FINANCIAL OUTLOOK Cafer Biçer 9 th Meeting of COMCEC Financial Cooperation Working Group October 26 th, 217 Ankara, Turkey OUTLINE Recent Global Economic and Financial Developments Financial Outlook

Islamic Risk Management. Instruments. First International Islamic Finance Conference Labuan - Malaysia. (6-7 July 2004)

") First International Islamic Finance Conference Labuan - Malaysia (6-7 July 2004) Islamic Risk Management Corporate and Investment Banking Instruments Table of contents SECTION 1 The FX & Debt/Deposit issues

First International Islamic Finance Conference Labuan - Malaysia (6-7 July 2004) Islamic Risk Management Corporate and Investment Banking Instruments Table of contents SECTION 1 The FX & Debt/Deposit issues

Islamic Banking Vs Conventional Banking in Malaysia

International Journal of Business and Management Invention (IJBMI) ISSN (Online): 2319 8028, ISSN (Print): 2319 801X Volume 8 Issue 01 Ver. IV January 2019 PP 34-40 Ashfaq Hameed 1, Tarun Koshy Varghese

International Journal of Business and Management Invention (IJBMI) ISSN (Online): 2319 8028, ISSN (Print): 2319 801X Volume 8 Issue 01 Ver. IV January 2019 PP 34-40 Ashfaq Hameed 1, Tarun Koshy Varghese

Issuing Sukuk and the Excessive Liquidity in the Islamic Financial Institutions in Jordan

Issuing Sukuk and the Excessive Liquidity in the Islamic Financial Institutions in Jordan Dr. Abeer F.A. Al ABBADI Economics, Finance, and Banking Department, the World Islamic Sciences & Education University

Issuing Sukuk and the Excessive Liquidity in the Islamic Financial Institutions in Jordan Dr. Abeer F.A. Al ABBADI Economics, Finance, and Banking Department, the World Islamic Sciences & Education University

American Journal of Humanities & Islamic Studies Vol: 1 (1), Al-Huda University 1902 Baker Rd, Houston, TX 77094

, Al-Huda University 1902 Baker Rd, Houston, TX 77094") Investment Practices for Islamic Mutual Funds within the Saudi Arabian Capital Market Salman Ghani Al-Huda University 1902 Baker Rd, Houston, TX 77094 1 Abstract The burgeoning Islamic asset management

Investment Practices for Islamic Mutual Funds within the Saudi Arabian Capital Market Salman Ghani Al-Huda University 1902 Baker Rd, Houston, TX 77094 1 Abstract The burgeoning Islamic asset management

Islamic Instruments for Asset Management

Islamic Instruments for Asset Management Professor Rodney Wilson IRTI 15th Distance Learning Programme Intermediate Level Course Tuesday, March 20, 2012 Contents Islamic asset management vehicles Advantages

Islamic Instruments for Asset Management Professor Rodney Wilson IRTI 15th Distance Learning Programme Intermediate Level Course Tuesday, March 20, 2012 Contents Islamic asset management vehicles Advantages

Managing credit risk in Islamic banking

Managing credit risk in Islamic banking Bilal Ahmed bilal.mbam1@yahoo.com HRMARS, Pakistan www.hrmars.com 1 Managing credit risk in Islamic banking: Islamic banking is a system based on the principle of

Managing credit risk in Islamic banking Bilal Ahmed bilal.mbam1@yahoo.com HRMARS, Pakistan www.hrmars.com 1 Managing credit risk in Islamic banking: Islamic banking is a system based on the principle of

J. P. M O R G A N I S L A M I C F I N A N C E

Islamic Finance Overview May 2014 S T R I C T L Y P R I V A T E A N D C O N F I D E N T I A L English_General 2013 JPMorgan Chase & Co. All rights reserved. These materials herein are provided for informational

Islamic Finance Overview May 2014 S T R I C T L Y P R I V A T E A N D C O N F I D E N T I A L English_General 2013 JPMorgan Chase & Co. All rights reserved. These materials herein are provided for informational

INTEREST FREE BANKING-COMPLEMENT FOR INDIAN ECONOMY

INTEREST FREE BANKING-COMPLEMENT FOR INDIAN ECONOMY Author Name: Sameera Afroze Affiliation: Assistant Professor, Aristotle PG College Paper Title: Interest Free banking, complement for Indian Economy

INTEREST FREE BANKING-COMPLEMENT FOR INDIAN ECONOMY Author Name: Sameera Afroze Affiliation: Assistant Professor, Aristotle PG College Paper Title: Interest Free banking, complement for Indian Economy

Islamic Finance Instruments, growth & Real Estate. Maisam Fazal Head of Commercial Finance. Banking you can believe in. alrayanbank.co.

Islamic Finance Instruments, growth & Real Estate Maisam Fazal Head of Commercial Finance Islamic Finance Islam prohibits Interest (Riba) Uncertainty (Gharar) Gambling (Mayser) Principles of Islamic Banking

Islamic Finance Instruments, growth & Real Estate Maisam Fazal Head of Commercial Finance Islamic Finance Islam prohibits Interest (Riba) Uncertainty (Gharar) Gambling (Mayser) Principles of Islamic Banking

EXPLORING GROWTH OF TAKAFUL MARKET IN PAKISTAN. Muhammad Kashif Siddiqee, ACA Joint Director - SECP

EXPLORING GROWTH OF TAKAFUL MARKET IN PAKISTAN Muhammad Kashif Siddiqee, ACA Joint Director - SECP 1 2 THE NEED FOR INSURANCE All humans and/or Organizations inevitably are exposed to various types of

EXPLORING GROWTH OF TAKAFUL MARKET IN PAKISTAN Muhammad Kashif Siddiqee, ACA Joint Director - SECP 1 2 THE NEED FOR INSURANCE All humans and/or Organizations inevitably are exposed to various types of

The Successful Development of a Dual Islamic Finance and Takaful System in Malaysia - Takaful Zainal Abidin Mohd. Kassim, FIA

The Successful Development of a Dual Islamic Finance and Takaful System in Malaysia - Takaful Zainal Abidin Mohd. Kassim, FIA 23rd Pacific Insurance Conference Kuala Lumpur October 2007 Introduction The

The Successful Development of a Dual Islamic Finance and Takaful System in Malaysia - Takaful Zainal Abidin Mohd. Kassim, FIA 23rd Pacific Insurance Conference Kuala Lumpur October 2007 Introduction The

The asset side of Takaful and implications on product design

building value together 13 November 2012 The asset side of Takaful and implications on product design Hassan Scott Odierno, FSA Istanbul www.actuarialpartners.com Conventional bonds Bonds are the backbone

building value together 13 November 2012 The asset side of Takaful and implications on product design Hassan Scott Odierno, FSA Istanbul www.actuarialpartners.com Conventional bonds Bonds are the backbone

Profitability Comparison of Islamic and Conventional Banks

Profitability Comparison of Islamic and Conventional Banks Tariq Alzoubi * The study examines 33 conventional banks and 10 Islamic banks from Saudi Arabia, Kuwait, United Arab Emirates (UAE), and Jordan,

Profitability Comparison of Islamic and Conventional Banks Tariq Alzoubi * The study examines 33 conventional banks and 10 Islamic banks from Saudi Arabia, Kuwait, United Arab Emirates (UAE), and Jordan,

Swiss Passport to Islamic Finance

Swiss Passport to Islamic Finance by The Swiss Asset Management Magazine www.banco.ch No. 2 Spring - Summer 2007 Islamic Finance Survey Michael Saleh Gassner Michael Gassner Consultancy Ltd. Market segments,

Swiss Passport to Islamic Finance by The Swiss Asset Management Magazine www.banco.ch No. 2 Spring - Summer 2007 Islamic Finance Survey Michael Saleh Gassner Michael Gassner Consultancy Ltd. Market segments,

Financial Inclusiveness in Islamic Banking: Comparison of Ideals and Practices Based on Maqasid-e-Shari ah

Financial Inclusiveness in Islamic Banking: Comparison of Ideals and Practices Based on Maqasid-e-Shari ah A B D U L G H A F A R I S M A I L M O H D A D I B I S M A I L S H A H I D A S H A H I M I S A

Financial Inclusiveness in Islamic Banking: Comparison of Ideals and Practices Based on Maqasid-e-Shari ah A B D U L G H A F A R I S M A I L M O H D A D I B I S M A I L S H A H I D A S H A H I M I S A

International Standards for Islamic Finance

International Standards for Islamic Finance AAOIFI Introduction AAOIFI & IFRS - Comparison on structural objectives AAOIFI & IFRS - Categories of accounting standards for Islamic financial institutions

International Standards for Islamic Finance AAOIFI Introduction AAOIFI & IFRS - Comparison on structural objectives AAOIFI & IFRS - Categories of accounting standards for Islamic financial institutions

FINANCE. Islamic Finance as Social Impact Investing. Issue Brief 2013/08. Dec Andrew Sheng

Dec 2013 Issue Brief 2013/08 FINANCE Andrew Sheng The principles of Islamic finance, as defined by the Shariah, prescribe that finance must serve society and prohibit unfair and speculative activities.

Dec 2013 Issue Brief 2013/08 FINANCE Andrew Sheng The principles of Islamic finance, as defined by the Shariah, prescribe that finance must serve society and prohibit unfair and speculative activities.

Takaful: Concepts and Practical Issues

Takaful: Concepts and Practical Issues Singapore Actuarial Society Inaugural General Insurance Conference 06-07 May 2009, Singapore Hussain Ahmad, FCAS Consulting Actuary Towers Perrin Agenda What is takaful

Takaful: Concepts and Practical Issues Singapore Actuarial Society Inaugural General Insurance Conference 06-07 May 2009, Singapore Hussain Ahmad, FCAS Consulting Actuary Towers Perrin Agenda What is takaful

IEF WORLD ISLAMIC ECO~O.\IIC forum FOUNDATION

IEF WORLD ISLAMIC ECO~O.\IIC forum FOUNDATION 54 Achieving Global Standards in Islamic Asset Management John A. Sandwick Independent Consultant Islamic Wealth & Asset Management, Switzerland The vibrant

IEF WORLD ISLAMIC ECO~O.\IIC forum FOUNDATION 54 Achieving Global Standards in Islamic Asset Management John A. Sandwick Independent Consultant Islamic Wealth & Asset Management, Switzerland The vibrant

An Islamic Perspective of Business Finance (A Comparative Study with Conventional and Capitalistic Financing)

") DOI : 10.18843/ijms/v5i1(4)/16 DOIURL :http://dx.doi.org/10.18843/ijms/v5i1(4)/16 An Islamic Perspective of Business Finance (A Comparative Study with Conventional and Capitalistic Financing) Syed Mahmood

DOI : 10.18843/ijms/v5i1(4)/16 DOIURL :http://dx.doi.org/10.18843/ijms/v5i1(4)/16 An Islamic Perspective of Business Finance (A Comparative Study with Conventional and Capitalistic Financing) Syed Mahmood

Islamic Banking Two steps forward and four steps backward?

Islamic Banking Two steps forward and four steps backward? Under Islamic Banking (IB) the sharia laws or Islamic laws of banking are followed. It is also referred to Sharia Banking or Interest Free Banking.

Islamic Banking Two steps forward and four steps backward? Under Islamic Banking (IB) the sharia laws or Islamic laws of banking are followed. It is also referred to Sharia Banking or Interest Free Banking.

SUKUK Islamic Bonds. by Mr. Hamad Rasool.

SUKUK Islamic Bonds by Mr. Hamad Rasool 1 2 Sukuk is the Arabic name for a financial certificate, Islamic alternative to conventional bonds, Sukuk is a Trust certificate in which investor returns are derived

SUKUK Islamic Bonds by Mr. Hamad Rasool 1 2 Sukuk is the Arabic name for a financial certificate, Islamic alternative to conventional bonds, Sukuk is a Trust certificate in which investor returns are derived

Islamic Finance More Than Window Dressing?

Islamic Finance More Than Window Dressing? This article considers the most common structures employed in Islamic finance and deals with some of the criticisms surrounding its practice. Introduction Islamic

Islamic Finance More Than Window Dressing? This article considers the most common structures employed in Islamic finance and deals with some of the criticisms surrounding its practice. Introduction Islamic

Euromoney Conference Kuwait April 2011 Financing Development Development Financing

Euromoney Conference Kuwait April 2011 Financing Development Development Financing Agenda 1- Benefits of Islamic Finance 2 - Precedents of Islamic Finance in Financing Development 3 - Aspects of Kuwait

Euromoney Conference Kuwait April 2011 Financing Development Development Financing Agenda 1- Benefits of Islamic Finance 2 - Precedents of Islamic Finance in Financing Development 3 - Aspects of Kuwait

Sharia Issues in Liquidity Risk Management

Sharia Issues in Liquidity Risk Management Paper Presented in Colloque International Banque et Finance Islamiques Universite Robert Schuman, Strasbourg (France) January, 11 th, 2008 Rifki Ismal Doctoral

Sharia Issues in Liquidity Risk Management Paper Presented in Colloque International Banque et Finance Islamiques Universite Robert Schuman, Strasbourg (France) January, 11 th, 2008 Rifki Ismal Doctoral

Specific Stability Risks in Islamic Banking

Specific Stability Risks in Islamic Banking Dawood Ashraf Ph.D., CFA Senior Researcher Islamic Finance Disclaimer: The views expressed in this presentation are those of the author and do not necessarily

Specific Stability Risks in Islamic Banking Dawood Ashraf Ph.D., CFA Senior Researcher Islamic Finance Disclaimer: The views expressed in this presentation are those of the author and do not necessarily

Green Finance and Islamic Finance

Green Finance and Islamic Finance Ahmet Sekreter 1 1 Faculty of Administrative Sciences and Economics, Ishik University, Erbil, Iraq Correspondence: Ahmet Sekreter, Ishik University, Erbil, Iraq. Email:

Green Finance and Islamic Finance Ahmet Sekreter 1 1 Faculty of Administrative Sciences and Economics, Ishik University, Erbil, Iraq Correspondence: Ahmet Sekreter, Ishik University, Erbil, Iraq. Email:

DEVELOPMENT OF LIQUIDITY MANAGEMENT INSTRUMENTS: CHALLENGES AND OPPORTUNITIES

DEVELOPMENT OF LIQUIDITY MANAGEMENT INSTRUMENTS: CHALLENGES AND OPPORTUNITIES By Abdul Rais Abdul Majid Chief Executive Officer International Islamic Financial Market (IIFM) International Conference on

DEVELOPMENT OF LIQUIDITY MANAGEMENT INSTRUMENTS: CHALLENGES AND OPPORTUNITIES By Abdul Rais Abdul Majid Chief Executive Officer International Islamic Financial Market (IIFM) International Conference on

Analysis of the Sukuk Market. Dubai, April 25, 2007

Analysis of the Sukuk Market Dubai, April 25, 2007 Overview Introduction What is a Sukuk? Types of Sukuk Composition of the Sukuk Market Breakdown of the Sukuk Market Expected Growth of the Sukuk Market

Analysis of the Sukuk Market Dubai, April 25, 2007 Overview Introduction What is a Sukuk? Types of Sukuk Composition of the Sukuk Market Breakdown of the Sukuk Market Expected Growth of the Sukuk Market

Volume of deals in the Middle East

MENA The economic prospects for the Middle East remain bright with the Gulf Co-operation Council (GCC) dominating the IMF rankings with an average of 4% GDP growth across the region. Many GCC markets continued

MENA The economic prospects for the Middle East remain bright with the Gulf Co-operation Council (GCC) dominating the IMF rankings with an average of 4% GDP growth across the region. Many GCC markets continued

Risk Management in Islamic Banking (lecture 3)

") Risk Management in Islamic Banking (lecture 3) Course Material in Master Degree Program in Finance Islamiques Universite Robert Schuman, Strasbourg (France) July, 4th, 2009 Rifki Ismal Durham University

Risk Management in Islamic Banking (lecture 3) Course Material in Master Degree Program in Finance Islamiques Universite Robert Schuman, Strasbourg (France) July, 4th, 2009 Rifki Ismal Durham University

Chapter 3. Islamic Finance and Investment- An Overview. outlining Shariah principles, features of the investment, key components of Shariah

Chapter 3 Islamic Finance and Investment- An Overview Introduction This chapter gives an overview about the concept of Shariah Finance by outlining Shariah principles, features of the investment, key components

Chapter 3 Islamic Finance and Investment- An Overview Introduction This chapter gives an overview about the concept of Shariah Finance by outlining Shariah principles, features of the investment, key components

The State of the Islamic Capital Market & Future Prospects

The State of the Islamic Capital Market & Future Prospects Ijlal Alvi CEO IIFM Contents Global Market Perspective The Islamic Capital Market OIC Equity Market Malaysian Capital Markets Way Forward Future

The State of the Islamic Capital Market & Future Prospects Ijlal Alvi CEO IIFM Contents Global Market Perspective The Islamic Capital Market OIC Equity Market Malaysian Capital Markets Way Forward Future

The Response of Islamic finance to the recession. 12 May 2009 Farmida Bi, Partner

The Response of Islamic finance to the recession 12 May 2009 Farmida Bi, Partner Islamic Finance: A different model September 2008 confidence Islamic banks had not invested in toxic assets, held actual

The Response of Islamic finance to the recession 12 May 2009 Farmida Bi, Partner Islamic Finance: A different model September 2008 confidence Islamic banks had not invested in toxic assets, held actual

Introduction to Islamic Banking. Salman Ahmed Shaikh

Introduction to Islamic Banking Salman Ahmed Shaikh islamiceconomicsproject@gmail.com www.islamiceconomicsproject.wordpress.com HISTORY OF ISLAMIC BANKING Islamic banking and the field of Islamic finance

Introduction to Islamic Banking Salman Ahmed Shaikh islamiceconomicsproject@gmail.com www.islamiceconomicsproject.wordpress.com HISTORY OF ISLAMIC BANKING Islamic banking and the field of Islamic finance

Innovation in Islamic Liquidity Management 2017

Innovation in Islamic Liquidity Management 2017 Transforming Islamic Finance Business Supported by: Powered by: EVERYONE'S FAVORITE PLACE TO SAVE AND INVEST Licensed and regulated by Central Bank of UAE

Innovation in Islamic Liquidity Management 2017 Transforming Islamic Finance Business Supported by: Powered by: EVERYONE'S FAVORITE PLACE TO SAVE AND INVEST Licensed and regulated by Central Bank of UAE

DISCLOSURES OF THE FINANCIAL STATEMENTS OF BANKS AND SIMILAR FINANCIAL INSTITUTIONS THE CASE OF: (TRANSPARENCY AND BANK FAILURES)

") DISCLOSURES OF THE FINANCIAL STATEMENTS OF BANKS AND SIMILAR FINANCIAL INSTITUTIONS THE CASE OF: (TRANSPARENCY AND BANK FAILURES) FATEMEH PANAHI INTERNATIONAL FINANCIAL REPORTING AND ANALYSIS Berndt Andersson

DISCLOSURES OF THE FINANCIAL STATEMENTS OF BANKS AND SIMILAR FINANCIAL INSTITUTIONS THE CASE OF: (TRANSPARENCY AND BANK FAILURES) FATEMEH PANAHI INTERNATIONAL FINANCIAL REPORTING AND ANALYSIS Berndt Andersson

Seminar on Islamic Finance. Challenges in Developing Islamic Financial Services in Europe. 11 November 2009, Rome, Italy.

Seminar on Islamic Finance Challenges in Developing Islamic Financial Services in Europe 11 November 2009, Rome, Italy Speech by Professor Rifaat Ahmed Abdel Karim Secretary-General Islamic Financial Services

Seminar on Islamic Finance Challenges in Developing Islamic Financial Services in Europe 11 November 2009, Rome, Italy Speech by Professor Rifaat Ahmed Abdel Karim Secretary-General Islamic Financial Services

Shari ah Standard No. (44) Obtaining and Deploying Liquidity

Obtaining and Deploying Liquidity") Shari ah Standard No. (44) Obtaining and Deploying Liquidity Contents Subject Page Preface... 1087 Statement of the Standard... 1088 1. Scope of the Standard... 1088... 1088 3. Need to Utilise Liquidity

Shari ah Standard No. (44) Obtaining and Deploying Liquidity Contents Subject Page Preface... 1087 Statement of the Standard... 1088 1. Scope of the Standard... 1088... 1088 3. Need to Utilise Liquidity

IIFM Master Agreement for Treasury Placement (MATP) and Managing Liquidity - challenges faced and overcome

and Managing Liquidity - challenges faced and overcome") Ijlal Ahmed Alvi IIFM Master Agreement for Treasury Placement (MATP) and Managing Liquidity - challenges faced and overcome Contents 1) Managing Liquidity in Islamic Finance 2) Commodity Murabaha as a

Ijlal Ahmed Alvi IIFM Master Agreement for Treasury Placement (MATP) and Managing Liquidity - challenges faced and overcome Contents 1) Managing Liquidity in Islamic Finance 2) Commodity Murabaha as a

I for Impact: Blending Islamic Finance and Impact Investing for the Global Goals

Islamic Economic Studies Vol. 25, No. 2, July, 2017 DOI: 10.12816/0038224 I for Impact: Blending Islamic Finance and Impact Investing for the Global Goals Description: This report launched in May 2017,

Islamic Economic Studies Vol. 25, No. 2, July, 2017 DOI: 10.12816/0038224 I for Impact: Blending Islamic Finance and Impact Investing for the Global Goals Description: This report launched in May 2017,

SNA/M1.18/6.a. 12 th Meeting of the Advisory Expert Group on National Accounts, November 2018, Luxembourg. Agenda item: 6.a.

SNA/M1.18/6.a 12 th Meeting of the Advisory Expert Group on National Accounts, 27-29 November 2018, Luxembourg Agenda item: 6.a. Islamic finance in the national accounts Introduction At its 11 th meeting

SNA/M1.18/6.a 12 th Meeting of the Advisory Expert Group on National Accounts, 27-29 November 2018, Luxembourg Agenda item: 6.a. Islamic finance in the national accounts Introduction At its 11 th meeting

COMCEC STRATEGY COMCEC FINANCIAL OUTLOOK. Cafer Biçer. 10 th Meeting of COMCEC Financial Cooperation Working Group

COMCEC FINANCIAL OUTLOOK Cafer Biçer 1 th Meeting of COMCEC Financial Cooperation Working Group March 29 th, 218 Ankara, Turkey OUTLINE Recent Global Economic and Financial Developments Financial Outlook

COMCEC FINANCIAL OUTLOOK Cafer Biçer 1 th Meeting of COMCEC Financial Cooperation Working Group March 29 th, 218 Ankara, Turkey OUTLINE Recent Global Economic and Financial Developments Financial Outlook

FINANCIAL COOPERATION

FINANCIAL COOPERATION OIC/COMCEC-FC/34-18/D(..) CCO BRIEF ON FINANCIAL COOPERATION COMCEC COORDINATION OFFICE April 2018 2017 0 CCO BRIEF ON FINANCIAL COOPERATION Financial Cooperation among the Member

FINANCIAL COOPERATION OIC/COMCEC-FC/34-18/D(..) CCO BRIEF ON FINANCIAL COOPERATION COMCEC COORDINATION OFFICE April 2018 2017 0 CCO BRIEF ON FINANCIAL COOPERATION Financial Cooperation among the Member

The Evolution of Islamic Finance

The Evolution of Islamic Finance Islamic finance lexicon/1 Ijara: leasing transaction where the purchase of the leased equipment at the end of the rental period is optional Mudaraba: form of financial

The Evolution of Islamic Finance Islamic finance lexicon/1 Ijara: leasing transaction where the purchase of the leased equipment at the end of the rental period is optional Mudaraba: form of financial

Sukuk: Definition, Structure and Accounting Issues

MPRA Munich Personal RePEc Archive Sukuk: Definition, Structure and Accounting Issues Khalil Ahmed USIM 2011 Online at http://mpra.ub.uni-muenchen.de/33675/ MPRA Paper No. 33675, posted 25. September 2011

MPRA Munich Personal RePEc Archive Sukuk: Definition, Structure and Accounting Issues Khalil Ahmed USIM 2011 Online at http://mpra.ub.uni-muenchen.de/33675/ MPRA Paper No. 33675, posted 25. September 2011

CURRENT ACCOUNT (WADI A/QARD) DEPOSIT

DEPOSIT") DEPOSIT PRODUCTS Mobilization of funds from depositors/savers to borrowers/investors is an important task of a financial intermediary in the economy. Financial intermediaries attempt to achieve this goal

DEPOSIT PRODUCTS Mobilization of funds from depositors/savers to borrowers/investors is an important task of a financial intermediary in the economy. Financial intermediaries attempt to achieve this goal

Economic and Social Council

United Nations E/C.18/2007/9 Economic and Social Council Distr.: General 21 August 2007 Original: English Committee of Experts on International Cooperation in Tax Matters Third session Geneva, 29 October-2

United Nations E/C.18/2007/9 Economic and Social Council Distr.: General 21 August 2007 Original: English Committee of Experts on International Cooperation in Tax Matters Third session Geneva, 29 October-2

ISLAMIC finance. We are the only law firm headquartered outside of London to be listed in the Legal 500 for Islamic finance.

ISLAMIC finance We are the only law firm headquartered outside of London to be listed in the Legal 500 for Islamic finance. Nine members of our Islamic Finance team hold the IFQ and the lead Partner of

ISLAMIC finance We are the only law firm headquartered outside of London to be listed in the Legal 500 for Islamic finance. Nine members of our Islamic Finance team hold the IFQ and the lead Partner of

The Potential of Islamic Finance in Achieving the SDGs

The Potential of Islamic Finance in Achieving the SDGs Dr. Rami Ahmad Special Envoy on SDGs Senior Advisor to the President Islamic Development Bank Group SUSTAINABLE DEVELOPMENT TRANSITION FORUM 2017

The Potential of Islamic Finance in Achieving the SDGs Dr. Rami Ahmad Special Envoy on SDGs Senior Advisor to the President Islamic Development Bank Group SUSTAINABLE DEVELOPMENT TRANSITION FORUM 2017

Takaful and Retakaful Challenges and Opportunities for Actuaries

Life Conference and Exhibition 2011 Safder Jaffer and Lindsay Unwin (Milliman) Takaful and Retakaful Challenges and Opportunities for Actuaries 22 November 2011 2010 The Actuarial Profession www.actuaries.org.uk

Life Conference and Exhibition 2011 Safder Jaffer and Lindsay Unwin (Milliman) Takaful and Retakaful Challenges and Opportunities for Actuaries 22 November 2011 2010 The Actuarial Profession www.actuaries.org.uk

Looking East: The Islamic Alternative? by Helen Sanders, Editor

Looking East: The Islamic Alternative? by Helen Sanders, Editor particularly in relation to corporate treasury, and how does it differ from conventional banking? We hear vague mentions about Islamic products

Looking East: The Islamic Alternative? by Helen Sanders, Editor particularly in relation to corporate treasury, and how does it differ from conventional banking? We hear vague mentions about Islamic products

EXCEPTIONAL SALES: SALAM AND ISTISNA'

EXCEPTIONAL SALES: SALAM AND ISTISNA' Murabaha and ijara constitute the core financing activities of Islamic banks. They are easily understood because of their proximity to conventional financing techniques,

EXCEPTIONAL SALES: SALAM AND ISTISNA' Murabaha and ijara constitute the core financing activities of Islamic banks. They are easily understood because of their proximity to conventional financing techniques,

Q: What types of Financial Institutions and transactions are involved in Islamic finance?

Q: What is Islamic Finance Islamic finance is an interest free finance system. There is therefore, no charge for its use. Islamic finance is asset based as opposed to being currency based. A deal is structured

Q: What is Islamic Finance Islamic finance is an interest free finance system. There is therefore, no charge for its use. Islamic finance is asset based as opposed to being currency based. A deal is structured

Islamic Finance as a Means of Shaping the Future of Sustainable Finance

Islamic Finance as a Means of Shaping the Future of Sustainable Finance Can Mehmet International University of Sarajevo Hrasnička Cesta 1, 71210 Ilidža/Sarajevo,Bosnia and Herzegovina mcan@ius.edu.ba Abstract

Islamic Finance as a Means of Shaping the Future of Sustainable Finance Can Mehmet International University of Sarajevo Hrasnička Cesta 1, 71210 Ilidža/Sarajevo,Bosnia and Herzegovina mcan@ius.edu.ba Abstract

Asset & Liability Management : challenges facing Islamic financial institutions! Majdi Chaabouni!

Asset & Liability Management : challenges facing Islamic financial institutions! Majdi Chaabouni! Presented at the Durham Islamic Finance Autumn School 21 jointly organised by Durham Centre for Islamic

Asset & Liability Management : challenges facing Islamic financial institutions! Majdi Chaabouni! Presented at the Durham Islamic Finance Autumn School 21 jointly organised by Durham Centre for Islamic

Comments on Corporate leverage in emerging Asia

Comments on Corporate leverage in emerging Asia Dragon Yongjun Tang 1 1. Findings and contributions of the paper This paper empirically examines the determinants of capital structure of Asian firms and

Comments on Corporate leverage in emerging Asia Dragon Yongjun Tang 1 1. Findings and contributions of the paper This paper empirically examines the determinants of capital structure of Asian firms and

Abu Dhabi Islamic Bank PJSC INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 JUNE 2012 (UNAUDITED)

") INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 JUNE 2012 (UNAUDITED) INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS Contents Page Report on review of interim condensed consolidated financial

INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 JUNE 2012 (UNAUDITED) INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS Contents Page Report on review of interim condensed consolidated financial

Revisiting the Fundamentals

Islamic Financial Services Group trends and future direction Noor Ur Rahman Abid International Islamic Financial Market Board Meeting 4 February 2008 Revisiting the Fundamentals Investment avenues in conventional

Islamic Financial Services Group trends and future direction Noor Ur Rahman Abid International Islamic Financial Market Board Meeting 4 February 2008 Revisiting the Fundamentals Investment avenues in conventional

9 ISLAMIC FINANCIAL SERVICES

9 ISLAMIC FINANCIAL SERVICES Initially conceived in response to a faith-based logic of conforming to the principles of Shariah in all spheres of life, 1 the astounding growth of the Islamic Financial industry

9 ISLAMIC FINANCIAL SERVICES Initially conceived in response to a faith-based logic of conforming to the principles of Shariah in all spheres of life, 1 the astounding growth of the Islamic Financial industry

Deloitte A Middle East Point of View - Fall 2016 Islamic Finance

16 Islamic megabank The redeemer? 17 Liquidity instruments available to Islamic Banks are few, with many lacking universal Sharia approval across jurisdictions. As a result, IFIs face greater difficulty

16 Islamic megabank The redeemer? 17 Liquidity instruments available to Islamic Banks are few, with many lacking universal Sharia approval across jurisdictions. As a result, IFIs face greater difficulty

Abu Dhabi Islamic Bank PJSC

INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 SEPTEMBER 2015 (UNAUDITED) INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 September 2015 (unaudited) Contents Page Review report of interim

INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 SEPTEMBER 2015 (UNAUDITED) INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 September 2015 (unaudited) Contents Page Review report of interim

Securitization and Structuring Sukuk

Securitization and Structuring Sukuk Workshop on Developing Sukuk Markets Arab Monetary Fund World Bank Group Abu Dhabi, UAE April 19, 2015 Zamir Iqbal, PhD. The World Bank Global Islamic Finance Development

Securitization and Structuring Sukuk Workshop on Developing Sukuk Markets Arab Monetary Fund World Bank Group Abu Dhabi, UAE April 19, 2015 Zamir Iqbal, PhD. The World Bank Global Islamic Finance Development

Capital Adequacy, Liquidity, and Risk: Is Islamic Banking Too Expensive? Camille Paldi 1

Journal of Finance and Bank Management June 2014, Vol. 2, No. 2, pp. 173-177 ISSN: 2333-6064 (Print) 2333-6072 (Online) Copyright The Author(s). 2014. All Rights Reserved. Published by American Research

Journal of Finance and Bank Management June 2014, Vol. 2, No. 2, pp. 173-177 ISSN: 2333-6064 (Print) 2333-6072 (Online) Copyright The Author(s). 2014. All Rights Reserved. Published by American Research

Tax Planning Retirement Planning Wills & Inheritance Tax Mortgage Advice Investments & Savings Zakat

PROVIDING SOUND FINANCIAL ADVICE FOR YOU AND YOUR FAMILIES FUTURE Tax Planning Retirement Planning Wills & Inheritance Tax Mortgage Advice Investments & Savings Zakat THE UK S PREMIER PROVIDER OF HALAL

PROVIDING SOUND FINANCIAL ADVICE FOR YOU AND YOUR FAMILIES FUTURE Tax Planning Retirement Planning Wills & Inheritance Tax Mortgage Advice Investments & Savings Zakat THE UK S PREMIER PROVIDER OF HALAL

ISLAMIC FINANCE INDUSTRY OUTPERFORMS IN 2013

The global Islamic finance industry has sustained impressive double-digit growth in 2013 despite challenging global economic conditions, such as the emerging markets funds outflows in the light of tapering

The global Islamic finance industry has sustained impressive double-digit growth in 2013 despite challenging global economic conditions, such as the emerging markets funds outflows in the light of tapering

Liquidity Risk Management in Islamic Banking. Prasanna Seshachellam July 2010

Liquidity Risk Management in Islamic Banking Prasanna Seshachellam July 2010 Islamic Banking (IB) Market - Global overview More than 300 IBs globally spread over 51 countries IB market Total assets of

Liquidity Risk Management in Islamic Banking Prasanna Seshachellam July 2010 Islamic Banking (IB) Market - Global overview More than 300 IBs globally spread over 51 countries IB market Total assets of

Diversity of Islamic financial instruments

ISWGNA Task Force on Islamic Banking Classification of property income associated with Islamic financial services Russell Krueger Economic and Social Commission for Western Asia (ESCWA) Beirut October

ISWGNA Task Force on Islamic Banking Classification of property income associated with Islamic financial services Russell Krueger Economic and Social Commission for Western Asia (ESCWA) Beirut October

Takaful. Azeem Pirani Head of Marketing & Alternate Distribution Pak-Qatar Family Takaful. July. 13 th, 2007 M.A.J.U. Karachi.

Takaful Azeem Pirani Head of Marketing & Alternate Distribution Pak-Qatar Family Takaful July. 13 th, 2007 M.A.J.U. Karachi 13th July 2007 1 Agenda Takaful A product and an ideology History of Takaful

Takaful Azeem Pirani Head of Marketing & Alternate Distribution Pak-Qatar Family Takaful July. 13 th, 2007 M.A.J.U. Karachi 13th July 2007 1 Agenda Takaful A product and an ideology History of Takaful

Content. n Why? n Objectives. n Shariah Standards issued by BNM. n AAOIFI Shariah Standards

Shariah Standards 1 Content n Why? n Objectives n Shariah Standards issued by BNM n AAOIFI Shariah Standards Why? n Differences in interpreting Shari ah has led to a diverse legal and regulatory landscape

Shariah Standards 1 Content n Why? n Objectives n Shariah Standards issued by BNM n AAOIFI Shariah Standards Why? n Differences in interpreting Shari ah has led to a diverse legal and regulatory landscape

International Trade under Islamic Banking

International Trade under Islamic Banking Muhammad Bilal University of Sargodha Sub-campus Mianwali, Pakistan Abstract The crucial area of this study is to identify the international trade under Islamic

International Trade under Islamic Banking Muhammad Bilal University of Sargodha Sub-campus Mianwali, Pakistan Abstract The crucial area of this study is to identify the international trade under Islamic

CHEVALIER & SCIALES LUXEMBOURG: A HUB FOR ISLAMIC FINANCE

CHEVALIER & SCIALES LUXEMBOURG: A HUB FOR ISLAMIC FINANCE client memorandum banking & finance summary Well established as a world leader in the investment funds industry (second only to the USA), Luxembourg

CHEVALIER & SCIALES LUXEMBOURG: A HUB FOR ISLAMIC FINANCE client memorandum banking & finance summary Well established as a world leader in the investment funds industry (second only to the USA), Luxembourg

An Overview of Sukuk and its Application In Global Fixed Income Markets

An Overview of Sukuk and its Application In Global Fixed Income Markets Sukuk, commonly known as Islamic bonds, are a recent entry to the world of finance. (Sukuk were used extensively in the Middle Ages,

An Overview of Sukuk and its Application In Global Fixed Income Markets Sukuk, commonly known as Islamic bonds, are a recent entry to the world of finance. (Sukuk were used extensively in the Middle Ages,

DOHA BANK (Q.S.C.) DOHA - QATAR CONSOLIDATED FINANCIAL STATEMENTS FOR YEAR ENDED DECEMBER 31, 2007 TOGETHER WITH INDEPENDENT AUDITOR S REPORT

DOHA - QATAR CONSOLIDATED FINANCIAL STATEMENTS FOR YEAR ENDED DECEMBER 31, 2007 TOGETHER WITH INDEPENDENT AUDITOR S REPORT") DOHA BANK (Q.S.C.) DOHA - QATAR CONSOLIDATED FINANCIAL STATEMENTS FOR YEAR ENDED DECEMBER 31, 2007 TOGETHER WITH INDEPENDENT AUDITOR S REPORT DOHA BANK (Q.S.C.) DOHA QATAR CONSOLIDATED FINANCIAL STATEMENTS

DOHA BANK (Q.S.C.) DOHA - QATAR CONSOLIDATED FINANCIAL STATEMENTS FOR YEAR ENDED DECEMBER 31, 2007 TOGETHER WITH INDEPENDENT AUDITOR S REPORT DOHA BANK (Q.S.C.) DOHA QATAR CONSOLIDATED FINANCIAL STATEMENTS

The Saudi Sukuk Market

The Saudi Sukuk Market For comments and queries please contact: Brad Bourland Chief Economist jadwaresearch@jadwa.com Paul Gamble Head of Research pgamble@jadwa.com or the author: Haitham al-fayez Senior

The Saudi Sukuk Market For comments and queries please contact: Brad Bourland Chief Economist jadwaresearch@jadwa.com Paul Gamble Head of Research pgamble@jadwa.com or the author: Haitham al-fayez Senior

Risk Management in Islamic Banks: A Case Study of the Faisal Islamic Bank of Egypt

Risk Management in Islamic Banks: A Case Study of the Faisal Islamic Bank of Egypt Mohamed Saad Ahmed Hussien Abstract This paper discusses the management in Islamic banks and aims to determine the difference

Risk Management in Islamic Banks: A Case Study of the Faisal Islamic Bank of Egypt Mohamed Saad Ahmed Hussien Abstract This paper discusses the management in Islamic banks and aims to determine the difference

AN INTRODUCTION TO ISLAMIC FINANCE AND THE MALAYSIAN EXPERIENCE

AN INTRODUCTION TO ISLAMIC FINANCE AND THE MALAYSIAN EXPERIENCE by Renuka Bhupalan, Director, TAXAND MALAYSIA 1. Introduction Islamic financing is a burgeoning area in the field of banking and finance.

AN INTRODUCTION TO ISLAMIC FINANCE AND THE MALAYSIAN EXPERIENCE by Renuka Bhupalan, Director, TAXAND MALAYSIA 1. Introduction Islamic financing is a burgeoning area in the field of banking and finance.

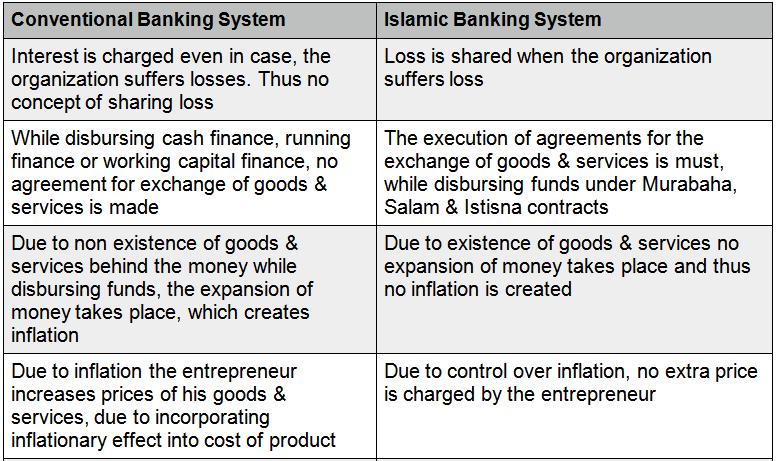

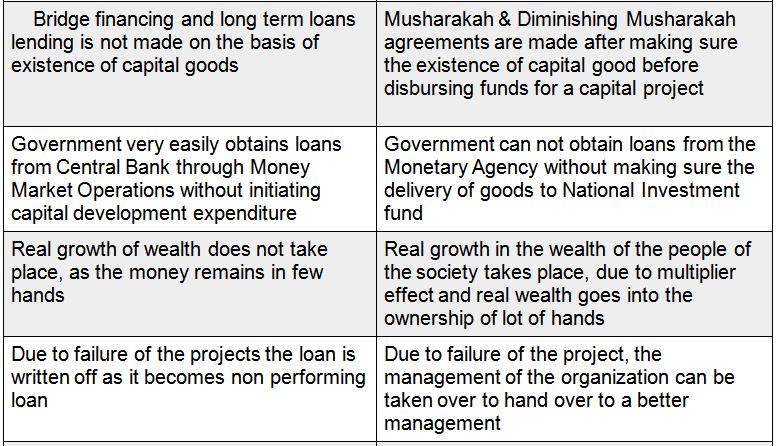

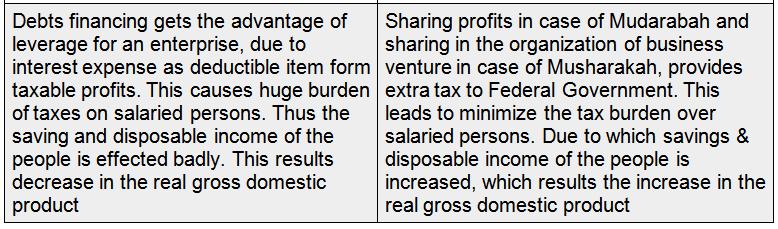

Islamic Financing Shift from Debt to Equity An analysis of Business Framework

Islamic Financing Shift from Debt to Equity An analysis of Business Framework Muhammad Hanif (FCMA) Assistant Professor NU-FAST Islamabad. i Electronic copy available at: http://ssrn.com/abstract=1690867

Islamic Financing Shift from Debt to Equity An analysis of Business Framework Muhammad Hanif (FCMA) Assistant Professor NU-FAST Islamabad. i Electronic copy available at: http://ssrn.com/abstract=1690867

Careplus paper.pdf. Universiti Utara Malaysia. From the SelectedWorks of Yong Shun Xiong. Yong Shun Xiong, Universiti Utara Malaysia

Universiti Utara Malaysia From the SelectedWorks of Yong Shun Xiong Spring April 16, 2017 Careplus paper.pdf Yong Shun Xiong, Universiti Utara Malaysia Available at: https://works.bepress.com/yong-shunxiong/1/

Universiti Utara Malaysia From the SelectedWorks of Yong Shun Xiong Spring April 16, 2017 Careplus paper.pdf Yong Shun Xiong, Universiti Utara Malaysia Available at: https://works.bepress.com/yong-shunxiong/1/

Shariah Guidelines for Sukuk. Mufti Ismail Ebrahim Shariah Advisor Malta, October 2014

Shariah Guidelines for Sukuk Mufti Ismail Ebrahim Shariah Advisor Malta, October 2014 0 Outline of Presentation Page Credentials Mufti Ismail Ebrahim [2] Islamic Financial Services Products Mufti Ismail

Shariah Guidelines for Sukuk Mufti Ismail Ebrahim Shariah Advisor Malta, October 2014 0 Outline of Presentation Page Credentials Mufti Ismail Ebrahim [2] Islamic Financial Services Products Mufti Ismail