Unit 2 Finance for Business

|

|

|

- Aleesha Montgomery

- 5 years ago

- Views:

Transcription

1 Pupil Name: Learner name: Teacher name: Unit 2 Finance for Business External Assessment Unit introduction All businesses have to spend money before they can make a profit, and when they spend money, they incur costs. In this unit, you will explore the types of costs that businesses incur, from the initial start-up costs involved in setting up a business to the on-going daily costs of running the business. You will then explore the ways in which the sale of products and services generates revenue, so that you can develop your understanding of profit. Next, you will examine how businesses plan for success and learn about the techniques used to assist the planning process. In particular, you will learn how to calculate the break-even point the point at which sales equal costs (fixed and variable). All sales over the break-even point produce profits, while any drop in sales below that point will produce losses. You will be introduced to the benefits of breakeven analysis to ensure that a business knows how and when to prevent losses. As well as profit, cash is an important factor in business success. It is vital for any business to ensure that it budgets correctly and that it knows what money is coming in to the business and what needs to be paid out, and when. In this unit, you will learn how to use budgets and cash flow forecasts to deal with these important issues. The final part of the unit explores the ways in which businesses measure success and identify areas for improvement. You will understand how gross profit and net profit are calculated and you will learn about the relationship between sales, cost of sales and gross profit. You will analyse key financial statements (e.g. profit and loss accounts, balance sheets) and review their importance in the successful financial management of a business. Learning aims in this unit you will be: A understand the costs involved in business and how businesses make a profit B understand how businesses plan for success C understand how businesses measure success and identify areas for improvement. This activity will test your understanding of the different types of costs there are in business and how they are related to each other. 1

2 Your tasks on Costs and Profit: What is a fixed cost? What is a variable cost? In the table are some costs from a furniture manufacturing business. Complete the table to show whether the cost is fixed or variable. Cost Fixed or variable cost? Power Wood used to make chairs Supervisor s wages Salesman s commission Business rates Insurance Hourly-paid operatives A bicycle manufacturer makes 100 bikes a week. It has the following costs: Rent 1,000 per week Admin 1,000 per week Interest 500 per week Materials 100 per bike Wages 50 per bike Power 10 per bike For each week, calculate the following: a Fixed costs b Variable costs Write here the formula for Total costs: + = 2

3 Most businesses have more than one source of revenue (money coming in). In pairs, identify four sources of revenue for each of the well-known organisations below. Use the Internet to find out more about them. Company Nike Sources of revenue 1 Running shoes 2 Jackets 3 Replica kits 4 Sports clothes Starbucks 1 McDonalds TM 1 Facebook 1 Manchester United FC To work out a business s total revenue, you need to add together everything they sell. Dave sells the following items in his pizzeria in a year. What is his total revenue? Items sold in a year Cost ( ) 7,000 pizzas at each 10,000 chip portions at 1.50 each 7,000 garlic bread portions at 4.00 each 5,000 soft drinks at 1.50 each Total revenue 3

4 In this activity, you will test your understanding of revenue, expenditure and profit, by advising the owner of a new business. Your tasks: Robert is setting up a sandwich shop on a local industrial estate. He hopes to sell the following quantities of sandwiches each month: 2,000 at 3.00 each 3,000 at 2.50 each 2,000 at 2.00 each. Robert expects to have the following expenses: rent 1,000 per month lighting and heating 200 per month advertising 200 per month part-time help 500 per month ingredients 2.00 for the 3.00 sandwich, 1.50 for the 2.00 sandwich and 1.00 for the 2.00 sandwich. To help Robert with his calculations, complete the table below. Robert s sandwich shop Revenue Variable costs Fixed costs Total costs Profit/loss Amount per month ( ) Amount per year ( ) Robert is worried that his predictions may be wrong and his costs could go up. However, he thinks his sandwiches will do well because they are special. The feedback from a survey he carries out on the industrial estate is excellent and people say the prices are reasonable. That makes Robert think he can charge more, giving him a greater margin of safety. He considers increasing the price of all his sandwiches by 0.50 and spending an extra 0.10 on making them look more attractive. He expects to sell the same quantities. What would his new revenue be per month? What would his new profit/loss be per month? 4

5 Do you think Robert is right to expect sales to stay the same given the price rise? Give a reason for your answer. After the first month Robert decides to sell crisps and soft drinks because people keep asking for them, and keep the original price for the sandwiches. A packet of crisps costs him 0.30 and he will sell them for 0.50; a soft drink costs 0.80 and he will sell them for He expects to sell 4,000 of each per month. What will his new profit per month be? This is what needs to be learnt, how are you after those activities? Task; work through the table and score yourself 1-3. Highlight any areas you need to revise. Learning aim A: Understand the costs involved in business and how businesses make a profit Topic A.1 Understand the costs involved in business Checklist of knowledge 1. Very good 2. Needs improvement 3. Need to learn understand and identify costs of a business, including: o start-up costs the costs incurred when setting up a business o operating (running) costs the costs incurred in the day-to-day running of a business understand, define and identify the differences between fixed and variable costs, direct and indirect costs, total costs calculate total costs (formula will not be given in the assessment) Fixed costs + Variable costs = Total costs Topic A.2 Understand how businesses make a profit understand and identify how businesses make money (generate revenue) from selling their products or services identify sources of revenue for a business calculate revenue (formula will not be given in the assessment) describe how businesses have to spend money (expenditure) in order to succeed 5

6 identify types of expenditure (including overheads) businesses may have understand that expenditure is anything a business pays out and overheads are the everyday running costs of a business understand that businesses must know how much money is coming in (revenue) and going out (expenditure), before they can work out whether the business has: o made a profit o made a loss define: o profit revenue is more than expenditure o loss expenditure is more than revenue calculate profit (formula will not be given in the assessment) profit = revenue expenditure The following activities will help you with Learning aim B: understand how businesses plan for success Complete the following: Define breakeven: What is a Break even chart? Define margin of safety: What is the break even formula? Capon Ltd, a fashion retail company, produces a break-even chart, shown below, for the sales of a new skirt they are considering buying from a supplier. The employee who is preparing the presentation for this product asks for your help to understand the chart. 6

7 Your tasks: 1 On the chart: a label the sales, total costs and fixed costs lines b mark clearly the break-even point c shade in and label the profit area d shade in and label the loss area e mark clearly the margin of safety in units. 2 Explain the term margin of safety and why it is important to know what it is. 3 On the grid below, produce a break-even chart for Capon Ltd for sales of slippers up to 10,000 units. The selling price is 10 per unit, variable costs are 5 per unit, and fixed costs are 20,000. Answer the questions below. 7

8 a What is the break-even point in units? b What is the maximum profit they can make in s? c What is the margin of safety in units? d What would the break-even point be in s if the selling price was increased to 12? Break even calculations Ben runs a sports equipment maufacturing business. His job is demanding and he needs a holiday. He asks you to help him work out whether he has enough money for a holiday. Your tasks: Ben wants to know whether he can make a profit by manufacturing a football which he would sell for 25. The costs involved are: Materials (per ball) 9 Labour (per ball) 8 Rent (annual) 15,000 Power 5,000 Insurance 4,000. 8

9 Complete the table. Output Fixed cost Variable cost Total cost Revenue Profit/loss ,000 1,500 2,000 2,500 3,000 3,500 4,000 4,500 5,000 Ben thinks it would be a good idea to start a new line football boots. At first, he thinks he can sell them for 40, but then realises that he may have to sell them for 35 to break into the market. The costs involved are: Materials 15 per pair Labour 5 per pair Rent 5,000 per year Power 6,000 per year Insurance 4,000 per year e f How many pairs does Ben need to sell at 40 to break even? How many pairs does Ben need to sell at 35 to break even? 9

10 Topic B.2 Understand the tools businesses use to plan for success Define Budget: What is the purpose of a budget? What is the difference between budgeting and budgetary control Define cash flow forecast: Give an example for Cash Inflow Give an example of Cash outlfow Cash Flow Activity: Martin is opening a small shop selling puzzles. He asks you to help him work out his cash flow as he needs to know whether he will have any cash at the end of his first four months. Martin currently has 15,000 in the bank. He expects the following cash totals to come into the business: July 17,000 August 18,000 September 20,500 October 21,

11 Martin has the following expenses: Business rates 15,000 per year (payable in equal monthly instalments) Purchases of stock July 9,000; August 10,500; September 11,000; October 12,000 Rent (paid monthly) 700 in July, then 800 from August Wages 10,000 per month Estimated gas usage for four months 500 (payable in October). Your tasks: 4 Complete the cash flow forecast for Martin. July August September October Opening balance Receipts Sales Total receipts Payments Purchases Rent Wages Rates Gas Total payments Closing balance g Is Martin s cash flow positive or negative? Explain why. h Suggest two steps Martin can take to improve his cash flow. 11

12 Learning aim B. understand how businesses plan for success Topic B.1 Understand the planning tools businesses use to predict when they will start making a profit define breakeven when a business has made enough money through product sales to cover the cost of making the product (no profit and no loss) Checklist of knowledge 1. Very good 2. Needs improvement 3. Need to learn be able to interpret from a break-even chart: o break-even point o profit o loss o variable costs o fixed costs o total revenue o total costs o margin of safety calculate the breakeven (formula will be given in the assessment) analyse and explain the value and importance of breakeven analysis to businesses when planning for success analyse and explain the associated risks to businesses of not completing a breakeven Analysis present given information graphically on a break-even chart analyse the effect on the break-even point if sales or (fixed and variable) costs change, and explain the impact of these changes on the business Topic B.2 Understand the tools businesses use to plan for success Budgeting the purpose of budgeting in setting expenditure and revenue budgets the difference between budgeting and budgetary control (checking performance against plan) Cash flow forecasting learners should: know the purpose of a cash flow forecast to identify the money that should be coming into a business (inflows) and the money going out of the business (outflows) over a period of time be able to identify inflows and outflows explain the purpose of a cash flow forecast, including that it identifies the flow of cash through a business over a period of time understand the sources of cash coming into the business (inflows) 12

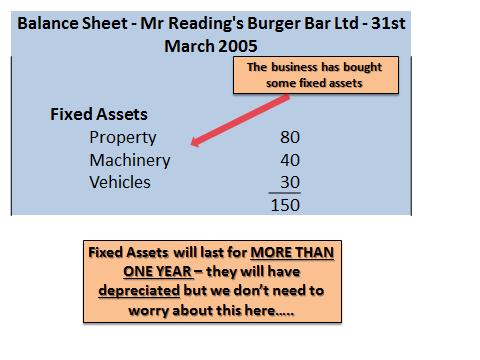

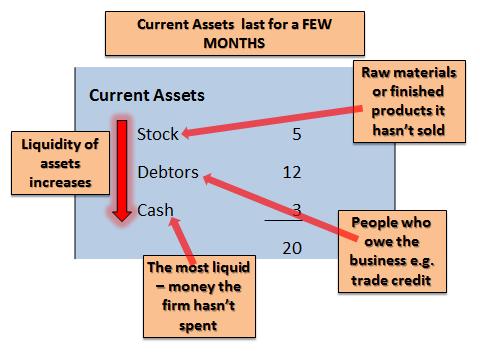

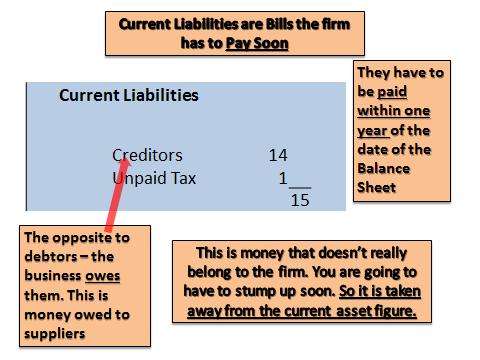

13 understand the sources and destination of cash leaving the business (outflows) identify the impact of timings of inflows and outflows What needs to be learnt understand the benefits of using a cash flow forecast to plan for success in a business (e.g. to produce new goods/services, invest in new resources, expand/reduce activities) and explain the associated risks to businesses of not completing a cash flow forecast complete a cash flow forecast from given information, showing individual and total inflows, individual and total outflows, net inflows and outflows, and opening and closing balances analyse a business finances based on cash flow information and identify possible issues for the business from any cash surplus or deficit The following activities will help you with Learning aim C: understand how businesses measure success and identify areas for improvement Much of the terminology used in business finance is associated with the statement of the financial position of a business. Define the following terms in the table below: Term Definition Creditors Current assets Share capital Retained profit Overdraft Stock Net assets Balance sheet Current Liabilities Loan 13

14 Working Capital Fixed assets Debtors Capital Long term liability Profit Identify the formula to calculate gross profit: Explain the impact of positive and negative gross profit on businesses: Define net profit: Identify the formula to calculate net profit: Your tasks: Match the terms in the box at the bottom of this page to the clues in the table. Clue Answer 1 Resources owned and used by a business over the long term, such as buildings and machinery. 2 People, businesses or other organisations to which a business owes money in the short term. 3 Debts owed to the business by other organisations they trade with. 4 A loan facility from the bank that may have to be repaid at any time. 14

15 Clue Answer 5 Creditors and overdraft are examples of these. 6 Current assets current liabilities = 7 A mortgage is an example of this. 8 The money required to set up, run and expand a business. 9 Where money is borrowed and repaid under agreed terms and conditions. 10 Shows the financial position (assets and liabilities) of a business at a specific moment in time. 11 Cash, debtors and stock are all examples of them. 12 Raw materials, work-in-progress and finished goods held for resale. 13 The difference between the total value of assets owned by a business and the total value of its liabilities. 14 Money invested in a company by the shareholders. 15 Profits earned by a business that are reinvested in the business rather than paid out as dividends. Creditors Retained profit Net assets Loan Debtors Current assets Overdraft Balance sheet Working capital Capital Share capital Stock Current liabilities Fixed assets Long-term liability What is the purpose of a balance sheet? Below is a balance sheet; 15

16 Below is a balance sheet broken down 16

17 Top Tips: Make sure you know what all the headings mean and what goes under it Remember there are 2 parts: what it has done with it s money and where the money came from colour to e business is how where it g key terms: stock, lities, Net Assets, d finally Net Assets = Capital employed It shows the current position of a business on one particular date it is a snap shot of what it owns and what it owes 17

18 Balance Sheet task 2: Here is the balance sheet for Rex Motors as at 31 September Fill in the shaded boxes. You may want to use the balance sheet guide above. Rex Motors at 31 September 2005 Fixed Assets Buildings 4,000 Motor Vehicles 2,000 Machinery 800 Current Assets Stocks Debtors Cash in bank Cash in firm 1,000 2,320 1, Current Liabilities Creditors 1,500 Working Capital Net Assets: Financed by: (Where the money has come from) Owners funds 7,000 Retained Profit 2070 Long Term Liabilities Bank loan Capital employed: 10,570 18

19 The amount of profit or loss a business has made over the previous financial year is shown in the Trading and Profit and Loss Account Task: Complete the definitions below Key word Sales Definition Cost of Sales Expenses Gross Profit Net Profit 19

20 Trading and Profit and Loss Accounts Dreamy Chocolate Bars Sales Revenue (Turnover) Cost of Sales GROSS PROFIT Expenses Rent and Rates Wages/Salaries Transport Electricity Insurance Advertising Depreciation Total Expenses NET PROFIT Tasks: Fill in the Trading Profit and Loss Account above using the following figures: Sales revenue: 30,000 Cost of sales: 15,000 Rent: 5,000 Wages: 4,500 Transport: 1000 Electricity: 850 Insurance: 550 Advertising: 620 Depreciation: 200 A: Fill in the company s total expenses B: Work out the company s gross profit show your workings out C: Work out the company s net profit show your workings out D: Circle or highlight the trading part of the account E: Circle or highlight the profit and loss part of the account 20

21 Answer the following True or False on Profit or Loss: 1 There is only one section in a Profit and Loss Account T/F 2 Net Profit is shown in the Trading account T/F 3 The amount of profit or loss a business has made is shown in the profit and loss account T/F 4 Cost of sales is shown in the trading account T/F 5 Gross profit is calculated by: Sales (Turnover) cost of sales T/F 6 Depreciation is the term used for the amount of money items such as equipment and machinery fall by in the year T/F Learning aim C. Understand how businesses measure success and identify areas for improvement Checklist of knowledge 1. Very good 2. Needs improvement 3. Need to learn Topic C.1 Understand how businesses measure success Making a profit learners should: define cost of sales the cost of producing a product define gross profit the money made from selling a product (revenue) after the cost of producing the product (cost of sales) has been deducted calculate gross profit (formula will not be given in the assessment) explain the impact of positive and negative gross profit on businesses define net profit the money made from selling a product after all costs (expenditure) have been deducted (formula will not be given in the assessment) calculate net profit explain the impact of positive and negative net profit on businesses Measuring success by looking at financial statements understand what financial statements are documents that record the financial activities of a business, sometimes required by law, including income statement (profit and loss account) and statement of financial position (balance sheet) 21

22 Income statement (profit and loss account) identify the purpose of an income statement (profit and loss account) to show how the business performed financially over a period of time (usually one year) complete an income statement (profit and loss account) from given figures, including: o trading account (top section of the income statement) includes figures for revenue (turnover) and cost of sales and calculates the amount of gross profit o expenses/overheads (bottom section of the income statement) o calculating net profit Statement of financial position (balance sheet) identify the purpose of a statement of financial position (balance sheet) to show the financial position of a business at a point in time understand the format of a statement of financial position (balance sheet) categorise total assets and liabilities using a statement of financial position (balance sheet) understand that a statement of financial position (balance sheet) shows at a point in time: o how a business is funded (capital) o how a business is using these funds (net assets) Understand ; o net assets what the business owns, or is owed (debtors/trade receivables), including fixed assets and short-term assets o liabilities what the business owes to others (creditors/trade payables), including current liabilities and long-term liabilities o capital how the business is funded (money invested in the business to generate revenue) from: internal sources money from shareholders (share capital) or retained profits external sources bank loans or other forms of finance that have to be repaid o working capital the amount of capital used to run day-to-day activities (current assets minus current liabilities): if this figure is negative, the business may have problems financing its day-to-day activities Topic C.2 Understand how businesses can be more successful Learners should: identify ways in which a business can increase profits analyse financial statements for a small business (such as a sole trader or partnership) and suggest appropriate actions the business can take to succeed 22

23 REMEMBER!!! This unit is externally assessed using an onscreen test. Answer the following questions to see how much you know. Complete the table by adding the formulas for the following: Total costs Formula Revenue Break-even point Gross profit Net profit Multiple choice 1. If current assets are 50,000 and current liabilities are 90,000, which of the following describes the business? a) Insolvent b) Solvent c) Making a loss 2. What is used to show the flow of money in and out of the business over a year? a) A trading account b) A cash flow statement c) A balance sheet 3. Using the following figures, select the correct break-even point: selling price 25; variable cost 5 per unit; fixed costs 38,900. a) 1628 b) 1945 c)

24 4. Which of the following would not be a way of improving cash flow? a) Upgrading equipment b) Chasing debtors c) Reducing stock 5. How is the net cash flow figure calculated on a cash flow forecast? a) cash outflows cash inflows b) cash inflows cash outflows c) opening balance + cash inflows 6. Which of the following is not a direct cost? a) Raw materials b) Production workers wages c) Production supervisor Further websites:

Globe Academy Home Learning Booklet

Globe Academy Home Learning Booklet Name: Term: Autumn 2 Class: Teacher: 1 Dear Parents and Carers, Important Message for Parents and Carers The teachers of Globe Academy believe that Home Learning is

Globe Academy Home Learning Booklet Name: Term: Autumn 2 Class: Teacher: 1 Dear Parents and Carers, Important Message for Parents and Carers The teachers of Globe Academy believe that Home Learning is

A.1 Answer Sheet 1: Understand the Costs Involved in Business Complete the revision sheet then use the answer sheet to self-assess your answers

Finance Revision Worksheet A.1 Answer Sheet 1: Understand the Costs Involved in Business Complete the revision sheet then use the answer sheet to self-assess your answers No Question Your answer Score

Finance Revision Worksheet A.1 Answer Sheet 1: Understand the Costs Involved in Business Complete the revision sheet then use the answer sheet to self-assess your answers No Question Your answer Score

Introduction to Small Business

Introduction to Small Business Revision Notes Topic 1.3 Putting a business idea into practice Objectives when starting up Financial objectives targets expressed in money terms, such as making a profit,

Introduction to Small Business Revision Notes Topic 1.3 Putting a business idea into practice Objectives when starting up Financial objectives targets expressed in money terms, such as making a profit,

Small Business Management MGMT5601 Topic 9: Financing the Small Firm (2) Cash & Profit

Cash & Profit") Small Business Management MGMT5601 Topic 9: Financing the Small Firm (2) Cash & Profit Professor Tim Mazzarol UWA Business School SBM MGMT5601 UWA Business School MBA Program tim.mazzarol@uwa.edu.au Learning

Small Business Management MGMT5601 Topic 9: Financing the Small Firm (2) Cash & Profit Professor Tim Mazzarol UWA Business School SBM MGMT5601 UWA Business School MBA Program tim.mazzarol@uwa.edu.au Learning

Cambridge IGCSE Accounting (0452)

") www.xtremepapers.com Cambridge IGCSE Accounting (0452) International Accounting Standards (IAS) Guidance for Teachers Contents Introduction... 2 Use of this document... 2 Users of financial statements...

www.xtremepapers.com Cambridge IGCSE Accounting (0452) International Accounting Standards (IAS) Guidance for Teachers Contents Introduction... 2 Use of this document... 2 Users of financial statements...

Economic and Management Sciences Grade 7 - Term 2. FINANCIAL LITERACY Topic 5: Accounting Concepts

1 Economic and Management Sciences Grade 7 - Term 2 FINANCIAL LITERACY Topic 5: Accounting Concepts There are certain basic accounting concepts that are used throughout the business world. It is important

1 Economic and Management Sciences Grade 7 - Term 2 FINANCIAL LITERACY Topic 5: Accounting Concepts There are certain basic accounting concepts that are used throughout the business world. It is important

Name of Document PURCHASE ORDER DELIVERY NOTE. Shows a list of transactions and the amount owed at the end of the month The Customer

Topic Area : Flow & Purpose of Financial Documents Purchase Order Delivery Note Name of Document PURCHASE ORDER DELIVERY NOTE GRN INVOICE Purpose of Document Used by the purchaser to order goods from a

Topic Area : Flow & Purpose of Financial Documents Purchase Order Delivery Note Name of Document PURCHASE ORDER DELIVERY NOTE GRN INVOICE Purpose of Document Used by the purchaser to order goods from a

1 ACCOUNTING PREPARATION GR 12

1 2 Bank reconciliations Analysis & interpretation of bank statements and bank reconciliation statements Debtors' and creditors' reconciliation Analysis & interpretation of control accounts Reconciliation

1 2 Bank reconciliations Analysis & interpretation of bank statements and bank reconciliation statements Debtors' and creditors' reconciliation Analysis & interpretation of control accounts Reconciliation

BUSINESS FINANCIAL BASICS

BUSINESS FINANCIAL BASICS HERE ARE THREE BASIC FINANCIAL STATEMENTS THAT ARE IMPORTANT FOR YOUR SMALL BUSINESS: BALANCE SHEET. P&L. CASHFLOW STATEMENT 1 BALANCE SHEET A financial statement captures a person

BUSINESS FINANCIAL BASICS HERE ARE THREE BASIC FINANCIAL STATEMENTS THAT ARE IMPORTANT FOR YOUR SMALL BUSINESS: BALANCE SHEET. P&L. CASHFLOW STATEMENT 1 BALANCE SHEET A financial statement captures a person

Marginal and. this chapter covers...

7 Marginal and absorption costing this chapter covers... This chapter focuses on the costing methods of marginal and absorption costing and compares the profit made by a business under each method. The

7 Marginal and absorption costing this chapter covers... This chapter focuses on the costing methods of marginal and absorption costing and compares the profit made by a business under each method. The

GRAAD 12 NATIONAL SENIOR CERTIFICATE GRADE 12

GRAAD 12 NATIONAL SENIOR CERTIFICATE GRADE 12 ACCOUNTING NOVEMBER 2011 MARKS: 300 TIME: 3 hours This question paper consists of 19 pages and an 18-page answer book. Accounting 2 DBE/November 2011 INSTRUCTIONS

GRAAD 12 NATIONAL SENIOR CERTIFICATE GRADE 12 ACCOUNTING NOVEMBER 2011 MARKS: 300 TIME: 3 hours This question paper consists of 19 pages and an 18-page answer book. Accounting 2 DBE/November 2011 INSTRUCTIONS

Cambridge International General Certificate of Secondary Education 0452 Accounting June 2014 Principal Examiner Report for Teachers

ACCOUNTING Cambridge International General Certificate of Secondary Education Paper 0452/11 Paper 11 Key Messages Question 1 consisted of ten multiple choice items covering topics across the whole syllabus.

ACCOUNTING Cambridge International General Certificate of Secondary Education Paper 0452/11 Paper 11 Key Messages Question 1 consisted of ten multiple choice items covering topics across the whole syllabus.

B292 Revision Part 4

B292 Revision Part 4 EX 1 The following represent four independent situations from which one amount is missing. Products Annual Quantity Carrying (Holding) Cost/Unit Ordering Cost/Order EOQ A 4,500 $1

B292 Revision Part 4 EX 1 The following represent four independent situations from which one amount is missing. Products Annual Quantity Carrying (Holding) Cost/Unit Ordering Cost/Order EOQ A 4,500 $1

State Examinations Commission. Coimisiún na Scrúduithe Stáit. Leaving Certificate Marking Scheme. Accounting. Ordinary Level

Coimisiún na Scrúduithe Stáit State Examinations Commission Leaving Certificate 2018 Marking Scheme Accounting Ordinary Level Note to teachers and students on the use of published marking schemes Marking

Coimisiún na Scrúduithe Stáit State Examinations Commission Leaving Certificate 2018 Marking Scheme Accounting Ordinary Level Note to teachers and students on the use of published marking schemes Marking

FACTFILE: GCSE BUSINESS STUDIES. UNIT 2: Break-even. Break-even (BE) Learning Outcomes

Learning Outcomes") FACTFILE: GCSE BUSINESS STUDIES UNIT 2: Break-even Break-even (BE) Learning Outcomes Students should be able to: calculate break-even both graphically and by formula; explain the significance of the break-even

FACTFILE: GCSE BUSINESS STUDIES UNIT 2: Break-even Break-even (BE) Learning Outcomes Students should be able to: calculate break-even both graphically and by formula; explain the significance of the break-even

ECONOMIC MANAGEMENT SCIENCES FINANCIAL LITERACY TERM 2

2018 ECONOMIC MANAGEMENT SCIENCES FINANCIAL LITERACY TERM 2 1 Contents Contents... 1 Capital, Assets and Liabilities... 5 Lesson 1... 5 Capital... 5 Fixed capital or physical capital... 5 Financial capital...

2018 ECONOMIC MANAGEMENT SCIENCES FINANCIAL LITERACY TERM 2 1 Contents Contents... 1 Capital, Assets and Liabilities... 5 Lesson 1... 5 Capital... 5 Fixed capital or physical capital... 5 Financial capital...

Contents. 1 - Finance Financial Statements 4. 3 Accounting Concept & Conventions 5. 4 Capital & Revenue Expenditure 8

Contents 1 - Finance 3 2 - Financial Statements 4 3 Accounting Concept & Conventions 5 4 Capital & Revenue Expenditure 8 5 - Financial Statements Analysis 15 6 - Management Accounting 21 7 - Working Capital

Contents 1 - Finance 3 2 - Financial Statements 4 3 Accounting Concept & Conventions 5 4 Capital & Revenue Expenditure 8 5 - Financial Statements Analysis 15 6 - Management Accounting 21 7 - Working Capital

WHITE PAPER UNDERSTANDING FINANCIAL STATEMENTS

WHITE PAPER UNDERSTANDING FINANCIAL STATEMENTS Contents 1.0 Understanding Financial Statements... 3 2.0 Types of Financial Statements... 3 3.0 Balance Sheets... 3 4.0 Profit & Loss Statement (also known

WHITE PAPER UNDERSTANDING FINANCIAL STATEMENTS Contents 1.0 Understanding Financial Statements... 3 2.0 Types of Financial Statements... 3 3.0 Balance Sheets... 3 4.0 Profit & Loss Statement (also known

Coimisiún na Scrúduithe Stáit State Examinations Commission

2014. M55 Coimisiún na Scrúduithe Stáit State Examinations Commission LEAVING CERTIFICATE EXAMINATION 2014 A C C O U N T I N G - H I G H E R L E V E L (400 marks) This paper is divided into 3 Sections:

2014. M55 Coimisiún na Scrúduithe Stáit State Examinations Commission LEAVING CERTIFICATE EXAMINATION 2014 A C C O U N T I N G - H I G H E R L E V E L (400 marks) This paper is divided into 3 Sections:

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS General Certificate of Education Advanced Subsidiary Level and Advanced Level

*2013075856* UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS General Certificate of Education Advanced Subsidiary Level and Advanced Level ACCOUNTING 9706/12 Paper 1 Multiple Choice October/November

*2013075856* UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS General Certificate of Education Advanced Subsidiary Level and Advanced Level ACCOUNTING 9706/12 Paper 1 Multiple Choice October/November

The figures in the left (debit) column are all either ASSETS or EXPENSES.

column are all either ASSETS or EXPENSES.") Correction of Errors & Suspense Accounts. 2008 Question 7. Correction of Errors & Suspense Accounts is pretty much the only topic in Leaving Cert Accounting that requires some knowledge of how T Accounts

Correction of Errors & Suspense Accounts. 2008 Question 7. Correction of Errors & Suspense Accounts is pretty much the only topic in Leaving Cert Accounting that requires some knowledge of how T Accounts

Cambridge International General Certificate of Secondary Education 0452 Accounting November 2012 Principal Examiner Report for Teachers

ACCOUNTING Cambridge International General Certificate of Secondary Education Paper 0452/11 Paper 1 Key Messages This question paper contained a mixture of multiple-choice, short-answer and structured

ACCOUNTING Cambridge International General Certificate of Secondary Education Paper 0452/11 Paper 1 Key Messages This question paper contained a mixture of multiple-choice, short-answer and structured

NATIONAL 5 Accounting

MADRAS COLLEGE FACULTY OF TECHNOLOGIES DEPARTMENT OF BUSINESS AND ENTERPRISE NATIONAL 5 Accounting Course Information Name: ACCOUNTING NATIONAL 5 COURSE AIMS AND STRUCTURE The course aims to enable learners

MADRAS COLLEGE FACULTY OF TECHNOLOGIES DEPARTMENT OF BUSINESS AND ENTERPRISE NATIONAL 5 Accounting Course Information Name: ACCOUNTING NATIONAL 5 COURSE AIMS AND STRUCTURE The course aims to enable learners

Coimisiún na Scrúduithe Stáit State Examinations Commission. Leaving Certificate Marking Scheme. Accounting. Ordinary Level

Coimisiún na Scrúduithe Stáit State Examinations Commission Leaving Certificate 2017 Marking Scheme Accounting Ordinary Level Note to teachers and students on the use of published marking schemes Marking

Coimisiún na Scrúduithe Stáit State Examinations Commission Leaving Certificate 2017 Marking Scheme Accounting Ordinary Level Note to teachers and students on the use of published marking schemes Marking

Cash Flow Statement and Analysis of Ratios

Topic 1: Cash Flow Statement and Analysis of Ratios QUESTION 1 Cash Flow Statement and Interpretation (Adapted from March 2010 Question 5) (70 marks; 45 minutes) You are provided with information relating

Topic 1: Cash Flow Statement and Analysis of Ratios QUESTION 1 Cash Flow Statement and Interpretation (Adapted from March 2010 Question 5) (70 marks; 45 minutes) You are provided with information relating

MARK SCHEME for the October/November 2011 question paper for the guidance of teachers 9706 ACCOUNTING

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS GCE Advanced Subsidiary Level and GCE Advanced Level MARK SCHEME for the October/November 2011 question paper for the guidance of teachers 9706 ACCOUNTING

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS GCE Advanced Subsidiary Level and GCE Advanced Level MARK SCHEME for the October/November 2011 question paper for the guidance of teachers 9706 ACCOUNTING

TRADING, PROFIT & LOSS ACCOUNT (INCOME STATEMENT) FOR THE YEAR ENDED 31 AUGUST 20*7

FOR THE YEAR ENDED 31 AUGUST 20*7") GCSE Revision- Unit 2 Finance 1. What are the advantages and disadvantages of a large business using the following sources of finance: (5 marks) Retained profits: these are profits that the owners put

GCSE Revision- Unit 2 Finance 1. What are the advantages and disadvantages of a large business using the following sources of finance: (5 marks) Retained profits: these are profits that the owners put

School of Business & Enterprise. Module Code: ACCT08009 ACCOUNTING & FINANCE. Date: 19 June 2017 Time:

School of Business & Enterprise Paisley Campus Session 2016-17 Resit Paper Module Code: ACCT08009 ACCOUNTING & FINANCE Date: 19 June 2017 Time: 0900-1100 EXAM PAPER HAS TWO SECTIONS: A AND B Answer Questions

School of Business & Enterprise Paisley Campus Session 2016-17 Resit Paper Module Code: ACCT08009 ACCOUNTING & FINANCE Date: 19 June 2017 Time: 0900-1100 EXAM PAPER HAS TWO SECTIONS: A AND B Answer Questions

Tiill now you have learnt about the financial

Cash Flow Statement 6 LEARNING OBJECTIVES After studying this chapter, you will be able to : state the purpose and preparation of statement of cash flow statement; distinguish between operating activities,

Cash Flow Statement 6 LEARNING OBJECTIVES After studying this chapter, you will be able to : state the purpose and preparation of statement of cash flow statement; distinguish between operating activities,

MANAGE FINANCES CAQNDIDATE RESOURCE & ASSESSMENT BSBFIM601A

MANAGE FINANCES CAQNDIDATE RESOURCE & ASSESSMENT BSBFIM601A Precision Group (Australia) Pty Ltd 9 Koppen Tce, Cairns, QLD, 4870 Email: info@precisiongroup.com.au Website: www.precisiongroup.com.au BSBFIM601A

MANAGE FINANCES CAQNDIDATE RESOURCE & ASSESSMENT BSBFIM601A Precision Group (Australia) Pty Ltd 9 Koppen Tce, Cairns, QLD, 4870 Email: info@precisiongroup.com.au Website: www.precisiongroup.com.au BSBFIM601A

MANAGEMENT INFORMATION

CERTIFICATE LEVEL EXAMINATION SAMPLE PAPER 3 (90 MINUTES) MANAGEMENT INFORMATION This assessment consists of ONE scenario based question worth 20 marks and 32 short questions each worth 2.5 marks. At least

CERTIFICATE LEVEL EXAMINATION SAMPLE PAPER 3 (90 MINUTES) MANAGEMENT INFORMATION This assessment consists of ONE scenario based question worth 20 marks and 32 short questions each worth 2.5 marks. At least

Management Accounting

Examiner s Report and Model Answers for Management Accounting THIRD LEVEL Series 4 (Code 3023) 2000 LCCI Examinations Board MH N T336 9 RNM >f2[ew2r@o2`0t1f3]e]2r2[1_# Management Accounting Third Level

Examiner s Report and Model Answers for Management Accounting THIRD LEVEL Series 4 (Code 3023) 2000 LCCI Examinations Board MH N T336 9 RNM >f2[ew2r@o2`0t1f3]e]2r2[1_# Management Accounting Third Level

Coimisiún na Scrúduithe Stáit State Examinations Commission. Leaving Certificate Marking Scheme. Accounting. Ordinary Level

Coimisiún na Scrúduithe Stáit State Examinations Commission Leaving Certificate 2012 Marking Scheme Accounting Ordinary Level LEAVING CERTIFICATE EXAMINATION, 2012 ACCOUNTING - ORDINARY LEVEL Solutions

Coimisiún na Scrúduithe Stáit State Examinations Commission Leaving Certificate 2012 Marking Scheme Accounting Ordinary Level LEAVING CERTIFICATE EXAMINATION, 2012 ACCOUNTING - ORDINARY LEVEL Solutions

Introduction to Finance. 1 March Examination Paper. Time: 3 hours

Introduction to Finance 1 March 2016 Examination Paper Answer any FOUR (4) questions. Clearly cross out surplus answers. Failure to do this will result in only the first FOUR (4) answers being marked.

Introduction to Finance 1 March 2016 Examination Paper Answer any FOUR (4) questions. Clearly cross out surplus answers. Failure to do this will result in only the first FOUR (4) answers being marked.

MGT402 - COST & MANAGEMENT ACCOUNTING

MGT402 - COST & MANAGEMENT ACCOUNTING Lesson No. TOPICS Page No. 1 Cost Classification and Cost Behavior 1 2 Important Terminologies 11 3 Financial Statements 15 4 Financial Statements (Continued)....

MGT402 - COST & MANAGEMENT ACCOUNTING Lesson No. TOPICS Page No. 1 Cost Classification and Cost Behavior 1 2 Important Terminologies 11 3 Financial Statements 15 4 Financial Statements (Continued)....

National Quali cations 2015

N5 National Quali cations 2015 X700/75/11 Accounting MONDAY, 18 MAY 9:00 AM 10:30 AM Total marks 100 Section 1 60 marks Attempt BOTH questions. Section 2 40 marks Attempt ALL questions. Write your answers

N5 National Quali cations 2015 X700/75/11 Accounting MONDAY, 18 MAY 9:00 AM 10:30 AM Total marks 100 Section 1 60 marks Attempt BOTH questions. Section 2 40 marks Attempt ALL questions. Write your answers

NATIONAL SENIOR CERTIFICATE GRADE 12

NATIONAL SENIOR CERTIFICATE GRADE 12 ACCOUNTING FEBRUARY/MARCH 2014 MARKS: 300 TIME: 3 hours This question paper consists of 24 pages and an 18-page answer book. Accounting 2 DBE/Feb. Mar. 2014 INSTRUCTIONS

NATIONAL SENIOR CERTIFICATE GRADE 12 ACCOUNTING FEBRUARY/MARCH 2014 MARKS: 300 TIME: 3 hours This question paper consists of 24 pages and an 18-page answer book. Accounting 2 DBE/Feb. Mar. 2014 INSTRUCTIONS

National Hunting & Shooting Association

National Hunting & Shooting Association FINANCIAL REPORT FOR THE YEAR ENDED FEBRUARY 2017 Content: 1. Statement of Financial Position 1.1. Breakdown of the assets 1.2. Breakdown of the equity and liabilities

National Hunting & Shooting Association FINANCIAL REPORT FOR THE YEAR ENDED FEBRUARY 2017 Content: 1. Statement of Financial Position 1.1. Breakdown of the assets 1.2. Breakdown of the equity and liabilities

NATIONAL SENIOR CERTIFICATE GRADE 12

NATIONAL SENIOR CERTIFICATE GRADE 12 ACCOUNTING FEBRUARY/MARCH 2009 MARKS: 300 TIME: 3 hours This question paper consists of 18 pages. Accounting 2 DoE/Feb. March 2009 INSTRUCTIONS AND INFORMATION Read

NATIONAL SENIOR CERTIFICATE GRADE 12 ACCOUNTING FEBRUARY/MARCH 2009 MARKS: 300 TIME: 3 hours This question paper consists of 18 pages. Accounting 2 DoE/Feb. March 2009 INSTRUCTIONS AND INFORMATION Read

MANAGEMENT INFORMATION

CERTIFICATE LEVEL EXAMINATION SAMPLE PAPER 1 (90 MINUTES) MANAGEMENT INFORMATION This assessment consists of ONE scenario based question worth 20 marks and 32 short questions each worth 2.5 marks. At least

CERTIFICATE LEVEL EXAMINATION SAMPLE PAPER 1 (90 MINUTES) MANAGEMENT INFORMATION This assessment consists of ONE scenario based question worth 20 marks and 32 short questions each worth 2.5 marks. At least

Management, Control and Accountability for Financial Resources 2 June Marking Scheme

Management, Control and Accountability for Financial Resources 2 June 215 Marking Scheme This marking scheme has been prepared as a guide only to markers. This is not a set of model answers, or the exclusive

Management, Control and Accountability for Financial Resources 2 June 215 Marking Scheme This marking scheme has been prepared as a guide only to markers. This is not a set of model answers, or the exclusive

NATIONAL SENIOR CERTIFICATE GRADE 11

NATIONAL SENIOR CERTIFICATE GRADE 11 REKENINGKUNDE EXEMPLAR 2007 This memorandum consists of 23 pages. Accounting 2 QUESTION MARKS FINAL MARKS 1 40 2 45 3 40 4 40 5 50 6 50 7 35 300 Accounting 3 QUESTION

NATIONAL SENIOR CERTIFICATE GRADE 11 REKENINGKUNDE EXEMPLAR 2007 This memorandum consists of 23 pages. Accounting 2 QUESTION MARKS FINAL MARKS 1 40 2 45 3 40 4 40 5 50 6 50 7 35 300 Accounting 3 QUESTION

BUSINESS AND MANAGEMENT ACCOUNTING AND FINANCE

BUSINESS AND MANAGEMENT ACCOUNTING AND FINANCE Unit 3.4 Budgeting (Higher Level) Content and Learning Outcomes Content! Types and purpose of budgets! Cash Flow Forecasts! Variance Analysis Learning Outcomes!

BUSINESS AND MANAGEMENT ACCOUNTING AND FINANCE Unit 3.4 Budgeting (Higher Level) Content and Learning Outcomes Content! Types and purpose of budgets! Cash Flow Forecasts! Variance Analysis Learning Outcomes!

LEAVING CERTIFICATE 2009 MARKING SCHEME ACCOUNTING ORDINARY LEVEL

Coimisiún na Scrúduithe Stáit State Examinations Commission LEAVING CERTIFICATE 2009 MARKING SCHEME ACCOUNTING ORDINARY LEVEL LEAVING CERTIFICATE ACCOUNTING - 2009 Ordinary Level Marking Scheme INTRODUCTION

Coimisiún na Scrúduithe Stáit State Examinations Commission LEAVING CERTIFICATE 2009 MARKING SCHEME ACCOUNTING ORDINARY LEVEL LEAVING CERTIFICATE ACCOUNTING - 2009 Ordinary Level Marking Scheme INTRODUCTION

BALRAM SANGAL & CO. (Advocates)

") BALRAM SANGAL & CO. (Advocates) Registration Delhi Value Added Tax & Central Sales Tax Registration as per DVAT Act, 2004 & CST Act, 1956. and Other States. Company Registration Under Company Act, 1956.

BALRAM SANGAL & CO. (Advocates) Registration Delhi Value Added Tax & Central Sales Tax Registration as per DVAT Act, 2004 & CST Act, 1956. and Other States. Company Registration Under Company Act, 1956.

ACCOUNTING GRADE 12 SEPTEMBER 2015

Metro East Education District ACCOUNTING GRADE 12 SEPTEMBER 2015 MARKS: 300 TIME: 3 hours This question paper consists of 20 pages and an answer book of 19 pages. Accounting 2 MEED September 2015 INSTRUCTIONS

Metro East Education District ACCOUNTING GRADE 12 SEPTEMBER 2015 MARKS: 300 TIME: 3 hours This question paper consists of 20 pages and an answer book of 19 pages. Accounting 2 MEED September 2015 INSTRUCTIONS

Accounting Question Booklet. Examination information. Questions 1 to 4 Answer all questions Write your answers in this question booklet

South Australian Certificate of Education Accounting 2017 Question Booklet Questions 1 to 4 Answer all questions Write your answers in this question booklet Examination information Materials Question Booklet

South Australian Certificate of Education Accounting 2017 Question Booklet Questions 1 to 4 Answer all questions Write your answers in this question booklet Examination information Materials Question Booklet

FINANCIAL ACCOUNTING II. Berjaya Engineering Sdn Bhd produces the following balances from its books at 31 December 20x1:

Question 1 Berjaya Engineering Sdn Bhd produces the following balances from its books at 31 December 20x1: Stocks at 1 January 20x1 Raw materials Work-in-progress (factory cost) Finished goods (transfer

Question 1 Berjaya Engineering Sdn Bhd produces the following balances from its books at 31 December 20x1: Stocks at 1 January 20x1 Raw materials Work-in-progress (factory cost) Finished goods (transfer

TRADITIONAL ABSORPTION V ACTIVITY BASED COSTING

TRADITIONAL ABSORPTION V ACTIVITY BASED COSTING A company manufactures two products: X and Y. Information is available as follows: (a) Product Total production Labour time per unit X 1,000 0.5 hours Y

TRADITIONAL ABSORPTION V ACTIVITY BASED COSTING A company manufactures two products: X and Y. Information is available as follows: (a) Product Total production Labour time per unit X 1,000 0.5 hours Y

Contents. Revision List Confidence Checklist Forms of Ownership... 7 Activity Activity End of topic review...

0 Contents Revision List... 3 Confidence Checklist... 4 Forms of Ownership... 7 Activity 1... 8 Activity 2... 9 End of topic review... 10 Sources of Finance... 11 Activity... 13 End of Topic Review...

0 Contents Revision List... 3 Confidence Checklist... 4 Forms of Ownership... 7 Activity 1... 8 Activity 2... 9 End of topic review... 10 Sources of Finance... 11 Activity... 13 End of Topic Review...

Financial and Management Accounting MB0041

Descriptive Question paper Financial and Management Accounting MB0041 Marks(140) Time (3 hrs) 1Mark *50= 50 Marks 1. The book in which the transactions are first recorded is called a. a. Ledger b. Balance

Descriptive Question paper Financial and Management Accounting MB0041 Marks(140) Time (3 hrs) 1Mark *50= 50 Marks 1. The book in which the transactions are first recorded is called a. a. Ledger b. Balance

CERTIFICATE IN MANAGEMENT ACCOUNTING

Series 2 Examination 2007 CERTIFICATE IN MANAGEMENT ACCOUNTING Level 3 Monday 2 April Subject Code: 3023 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal

Series 2 Examination 2007 CERTIFICATE IN MANAGEMENT ACCOUNTING Level 3 Monday 2 April Subject Code: 3023 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal

C O V E N A N T U N I V E RS I T Y P R O G R A M M E : A C C O U N T I N G A L P H A S E M E S T E R T U T O R I A L K I T L E V E L

C O V E N A N T U N I V E RS I T Y T U T O R I A L K I T P R O G R A M M E : A C C O U N T I N G A L P H A S E M E S T E R 2 0 0 L E V E L DISCLAIMER The contents of this document are intended for practice

C O V E N A N T U N I V E RS I T Y T U T O R I A L K I T P R O G R A M M E : A C C O U N T I N G A L P H A S E M E S T E R 2 0 0 L E V E L DISCLAIMER The contents of this document are intended for practice

E X A M I N A T I O N S C O U N C I L

C A R I B B E A N E X A M I N A T I O N S C O U N C I L CARIBBEAN SECONDARY EDUCATION CERTIFICATE EXAMINATION * Barcode Area * Front Page Bar Code FILL IN ALL THE INFORMATION REQUESTED CLEARLY IN CAPITAL

C A R I B B E A N E X A M I N A T I O N S C O U N C I L CARIBBEAN SECONDARY EDUCATION CERTIFICATE EXAMINATION * Barcode Area * Front Page Bar Code FILL IN ALL THE INFORMATION REQUESTED CLEARLY IN CAPITAL

Understanding Where You Stand

SMALL BUSINESS Access to Opportunity Understanding Where You Stand A Simple Guide to Your Company s Financial Statements Reading Your Statements Balance Sheets Income Statements Ratios Cash Flow Statements

SMALL BUSINESS Access to Opportunity Understanding Where You Stand A Simple Guide to Your Company s Financial Statements Reading Your Statements Balance Sheets Income Statements Ratios Cash Flow Statements

Distractor B: Candidate gets it wrong way round. Distractors C & D: Candidate only compares admin fee to cost without factor.

Answers ACCA Certified Accounting Technician Examination, Paper T10 Managing Finances June 2010 Answers Section A 1 D 2 A 365/ 23 100 1 173 % 100 1 = 365/ 23 1 1+ 1 173 99 = % Candidates should answer

Answers ACCA Certified Accounting Technician Examination, Paper T10 Managing Finances June 2010 Answers Section A 1 D 2 A 365/ 23 100 1 173 % 100 1 = 365/ 23 1 1+ 1 173 99 = % Candidates should answer

PLEASE READ THE FOLLOWING INSTRUCTIONS CAREFULLY

Time: 2 hours ACCOUNTING GRADE 12 Paper 1 200 marks PLEASE READ THE FOLLOWING INSTRUCTIONS CAREFULLY 1. This paper consists of 9 pages. Please check that your question paper is complete. 2. Read the questions

Time: 2 hours ACCOUNTING GRADE 12 Paper 1 200 marks PLEASE READ THE FOLLOWING INSTRUCTIONS CAREFULLY 1. This paper consists of 9 pages. Please check that your question paper is complete. 2. Read the questions

Unit 5 Finance Categorised Past Papers

Prepared by D. El-Hoss 1 Unit 5 Finance Categorised Past Papers Prepared by D. El-Hoss 2 8 4 Trucker is a public limited company that makes products such as tractors and construction vehicles. Table 1

Prepared by D. El-Hoss 1 Unit 5 Finance Categorised Past Papers Prepared by D. El-Hoss 2 8 4 Trucker is a public limited company that makes products such as tractors and construction vehicles. Table 1

A-level Business 7132/1

A-level Business 7132/1 Paper 1 Business 1 Specimen 2017 Morning 2 hours Materials For this paper you must have: a calculator. Instructions Use black ink or black ball-point pen. Fill in the boxes at the

A-level Business 7132/1 Paper 1 Business 1 Specimen 2017 Morning 2 hours Materials For this paper you must have: a calculator. Instructions Use black ink or black ball-point pen. Fill in the boxes at the

GRADE 11 NOVEMBER 2013 ACCOUNTING

NATIONAL SENIOR CERTIFICATE GRADE 11 NOVEMBER 2013 ACCOUNTING MARKS: 300 TIME: 3 hours This question paper consists of 18 pages. 2 ACCOUNTING (NOVEMBER 2013) INSTRUCTIONS AND INFORMATION 1. This question

NATIONAL SENIOR CERTIFICATE GRADE 11 NOVEMBER 2013 ACCOUNTING MARKS: 300 TIME: 3 hours This question paper consists of 18 pages. 2 ACCOUNTING (NOVEMBER 2013) INSTRUCTIONS AND INFORMATION 1. This question

Paper Reference(s) 6002/01 London Examinations GCE. Accounting (Modular Syllabus) Advanced Subsidiary/Advanced Level

6002/01 London Examinations GCE. Accounting (Modular Syllabus) Advanced Subsidiary/Advanced Level") Paper Reference(s) 6002/01 London Examinations GCE Accounting (Modular Syllabus) Advanced Subsidiary/Advanced Level Unit 2 Corporate and Management Accounting Thursday 16 June 2011 Morning Source booklet

Paper Reference(s) 6002/01 London Examinations GCE Accounting (Modular Syllabus) Advanced Subsidiary/Advanced Level Unit 2 Corporate and Management Accounting Thursday 16 June 2011 Morning Source booklet

BUSINESS FINANCE. Financial Statement Analysis. 1. Introduction to Financial Analysis. Copyright 2004 by Larry C. Holland

BUSINESS FINANCE Financial Statement Analysis 1. Introduction to Financial Analysis Slide 1 Welcome to the study of business finance. The major topic in this module is Financial Statement Analysis. And

BUSINESS FINANCE Financial Statement Analysis 1. Introduction to Financial Analysis Slide 1 Welcome to the study of business finance. The major topic in this module is Financial Statement Analysis. And

Engineering Economics and Financial Accounting

Engineering Economics and Financial Accounting Unit 5: Accounting Major Topics are: Balance Sheet - Profit & Loss Statement - Evaluation of Investment decisions Average Rate of Return - Payback Period

Engineering Economics and Financial Accounting Unit 5: Accounting Major Topics are: Balance Sheet - Profit & Loss Statement - Evaluation of Investment decisions Average Rate of Return - Payback Period

Analysing cost and revenues

Osborne Books Tutor Zone Analysing cost and revenues Chapter activities Osborne Books Limited, 2013 2 a n a l y s i n g c o s t s a n d r e v e n u e s t u t o r z o n e 1 An introduction to cost accounting

Osborne Books Tutor Zone Analysing cost and revenues Chapter activities Osborne Books Limited, 2013 2 a n a l y s i n g c o s t s a n d r e v e n u e s t u t o r z o n e 1 An introduction to cost accounting

A-level ACCOUNTING. Paper 2 Accounting for analysis and decision-making. Time allowed: 3 hours SPECIMEN MATERIAL

SPECIMEN MATERIAL Please write clearly, in block capitals. Centre number Candidate number Surname Forename(s) Candidate signature A-level ACCOUNTING Paper 2 Accounting for analysis and decision-making

SPECIMEN MATERIAL Please write clearly, in block capitals. Centre number Candidate number Surname Forename(s) Candidate signature A-level ACCOUNTING Paper 2 Accounting for analysis and decision-making

GRADE 11 NOVEMBER 2013 ACCOUNTING MARKING GUIDELINE (MEMORANDUM)

") NATIONAL SENIOR CERTIFICATE GRADE 11 NOVEMBER ACCOUNTING MARKING GUIDELINE (MEMORANDUM) MARKS: 300 GENERAL PRINCIPLES: 1. Where calculations are required, award full marks for the final answer. If the

NATIONAL SENIOR CERTIFICATE GRADE 11 NOVEMBER ACCOUNTING MARKING GUIDELINE (MEMORANDUM) MARKS: 300 GENERAL PRINCIPLES: 1. Where calculations are required, award full marks for the final answer. If the

Financial and Management Accounting Concepts

Financial and Management Accounting Concepts Editorial This month's newsletter focuses on the way in which you can interpret fully the information you present in the form of financial statements to either

Financial and Management Accounting Concepts Editorial This month's newsletter focuses on the way in which you can interpret fully the information you present in the form of financial statements to either

FNSACC503A: Assessment 2

FNSACC503A: Assessment 2 What you have to do This assessment will test your understanding of budgeting principles and the preparation of sales budgets, operational budgets and cash budgets for a Manufacturing

FNSACC503A: Assessment 2 What you have to do This assessment will test your understanding of budgeting principles and the preparation of sales budgets, operational budgets and cash budgets for a Manufacturing

THE ACCOUNTING EQUATION

Where are we headed? After completing this chapter, you should be able to: define identify explain calculate explain define identify prepare apply analyse CHAPTER 2 THE ACCOUNTING EQUATION KEY TERMS After

Where are we headed? After completing this chapter, you should be able to: define identify explain calculate explain define identify prepare apply analyse CHAPTER 2 THE ACCOUNTING EQUATION KEY TERMS After

Outline. 1. The Venture

Business Plan The business plan is a very basic document necessary to cover two communications. The first is to explain, for the benefit of the author (business person, entrepreneur), the vision for the

Business Plan The business plan is a very basic document necessary to cover two communications. The first is to explain, for the benefit of the author (business person, entrepreneur), the vision for the

BPC6C Cost and Management Accounting. Unit : I to V

BPC6C Cost and Management Accounting Unit : I to V UNIT -1 FUNDAMENTALS OF COST ACCOUNTING Nature and scope of Cost Accounting, Distinction between cost and financial accounting, Cost sheet, tenders Characteristics

BPC6C Cost and Management Accounting Unit : I to V UNIT -1 FUNDAMENTALS OF COST ACCOUNTING Nature and scope of Cost Accounting, Distinction between cost and financial accounting, Cost sheet, tenders Characteristics

ACCOUNTING PAPER I. 1. This paper consists of 9 pages. Please check that your question paper is complete.

GRADE 11 EXAMINATION NOVEMBER ACCOUNTING PAPER I Time: 2 hours 200 marks PLEASE READ THE FOLLOWING INSTRUCTIONS CAREFULLY 1. This paper consists of 9 pages. Please check that your question paper is complete.

GRADE 11 EXAMINATION NOVEMBER ACCOUNTING PAPER I Time: 2 hours 200 marks PLEASE READ THE FOLLOWING INSTRUCTIONS CAREFULLY 1. This paper consists of 9 pages. Please check that your question paper is complete.

BOOKKEEPERS IRELAND BOOKKEEPING STANDARDS IN IRELAND. In this issue WAGES VAT OFFICE ADMINISTRATION PAYE/PRSI INCOME LEVY FEEDBACK BOOKKEEPING PODCAST

BOOKKEEPERS IRELAND THE MAGAZINE DEDICATED TO BOOKKEEPING IN IRELAND JUNE 2010 BOOKKEEPING STANDARDS IN IRELAND OR RATHER THE LACK OF THEM Anyone can call themselves an accountant in Ireland, but only

BOOKKEEPERS IRELAND THE MAGAZINE DEDICATED TO BOOKKEEPING IN IRELAND JUNE 2010 BOOKKEEPING STANDARDS IN IRELAND OR RATHER THE LACK OF THEM Anyone can call themselves an accountant in Ireland, but only

BUSINESS STUDIES REVISION GUIDE

BUSINESS STUDIES REVISION GUIDE Answer booklet Name: 1 Contents This answer booklet is designed to help you mark your own work. Don t use it to cheat! That would be silly and ultimately pointless because

BUSINESS STUDIES REVISION GUIDE Answer booklet Name: 1 Contents This answer booklet is designed to help you mark your own work. Don t use it to cheat! That would be silly and ultimately pointless because

Cambridge International Advanced Subsidiary and Advanced Level 9706 Accounting June 2016 Principal Examiner Report for Teachers

ACCOUNTING Cambridge International Advanced Subsidiary and Advanced Level Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 D 16 C 2 A 17 A 3 C 18 B 4 D 19 B 5 B 20 A 6 C 21 C 7 C

ACCOUNTING Cambridge International Advanced Subsidiary and Advanced Level Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 D 16 C 2 A 17 A 3 C 18 B 4 D 19 B 5 B 20 A 6 C 21 C 7 C

Please spread the word about OpenTuition, so that all ACCA students can benefit.

ACCA COURSE NOTES June 2014 Examinations ACCA F2 FIA FMA Management Accounting Please spread the word about OpenTuition, so that all ACCA students can benefit. ONLY with your support can the site exist

ACCA COURSE NOTES June 2014 Examinations ACCA F2 FIA FMA Management Accounting Please spread the word about OpenTuition, so that all ACCA students can benefit. ONLY with your support can the site exist

Revision Guide for Finance Exam

Revision Guide for Finance Exam Financial Documents Financial Document Purchase Order (what is to be ordered) Delivery Notes (sent with goods - check you have received the correct goods) Goods received

Revision Guide for Finance Exam Financial Documents Financial Document Purchase Order (what is to be ordered) Delivery Notes (sent with goods - check you have received the correct goods) Goods received

SUGGESTED SOLUTIONS/ ANSWERS WINTER 2018 EXAMINATIONS 1 of 7 MANAGEMENT ACCOUNTING [M5] MANAGERIAL LEVEL-2 MARKS

![SUGGESTED SOLUTIONS/ ANSWERS WINTER 2018 EXAMINATIONS 1 of 7 MANAGEMENT ACCOUNTING [M5] MANAGERIAL LEVEL-2 MARKS](/thumbs/95/123099856.jpg "SUGGESTED SOLUTIONS/ ANSWERS WINTER 2018 EXAMINATIONS 1 of 7 MANAGEMENT ACCOUNTING [M5] MANAGERIAL LEVEL-2 MARKS") SUGGESTED SOLUTIONS/ ANSWERS WINTER 2018 EXAMINATIONS 1 of 7 Question No. 2 (a) (i) Daily Break-even Volume in Lunches and Dinners: Contribution Margin on Lunches and Dinners: Variable cost percentage

SUGGESTED SOLUTIONS/ ANSWERS WINTER 2018 EXAMINATIONS 1 of 7 Question No. 2 (a) (i) Daily Break-even Volume in Lunches and Dinners: Contribution Margin on Lunches and Dinners: Variable cost percentage

HIGHER SCHOOL CERTIFICATE EXAMINATION BUSINESS STUDIES 2/3 UNIT (COMMON) Time allowed Three hours (Plus 5 minutes reading time)

Time allowed Three hours (Plus 5 minutes reading time)") HIGHER SCHOOL CERTIFICATE EXAMINATION 1998 BUSINESS STUDIES /3 UNIT (COMMON) Time allowed Three hours (Plus 5 minutes reading time) DIRECTIONS TO CANDIDATES You may ask for extra Writing Booklets if you

HIGHER SCHOOL CERTIFICATE EXAMINATION 1998 BUSINESS STUDIES /3 UNIT (COMMON) Time allowed Three hours (Plus 5 minutes reading time) DIRECTIONS TO CANDIDATES You may ask for extra Writing Booklets if you

Balancing double entry accounts

Balancing Accounts and the Trial Balance Chapter 4 1 Balancing double entry accounts 2 Step 1: total both sides Bank a/c 1,500 17-May debit side = Credit side = 3 Page 1 of 6 Step 2: get the balancing

Balancing Accounts and the Trial Balance Chapter 4 1 Balancing double entry accounts 2 Step 1: total both sides Bank a/c 1,500 17-May debit side = Credit side = 3 Page 1 of 6 Step 2: get the balancing

Examinations for Academic Year Semester I / Academic Year 2015 Semester II. 1. This question paper consists of Section A and Section B.

PROGRAMME COHORT BSc (Hons) Human Resource Management BSc (Hons) Management BHRM/14B/FT BMAN/15A/FT B1, B2 Examinations for Academic Year 2015 2016 Semester I / Academic Year 2015 Semester II MODULE: COST

PROGRAMME COHORT BSc (Hons) Human Resource Management BSc (Hons) Management BHRM/14B/FT BMAN/15A/FT B1, B2 Examinations for Academic Year 2015 2016 Semester I / Academic Year 2015 Semester II MODULE: COST

NC 824. First Year B. C. A. Examination. April / May Financial Accounting & Management. Time : 3 Hours] [Total Marks : 50

![NC 824. First Year B. C. A. Examination. April / May Financial Accounting & Management. Time : 3 Hours] [Total Marks : 50](/thumbs/95/123010063.jpg "NC 824. First Year B. C. A. Examination. April / May Financial Accounting & Management. Time : 3 Hours] [Total Marks : 50") NC 824 First Year B. C. A. Examination April / May 2003 Financial Accounting & Management Seat No. Time : 3 Hours] [Total Marks : 50 Instructions : (1) Figures to the right indicate marks. (2) Show calculations

NC 824 First Year B. C. A. Examination April / May 2003 Financial Accounting & Management Seat No. Time : 3 Hours] [Total Marks : 50 Instructions : (1) Figures to the right indicate marks. (2) Show calculations

LCCI International Qualifications. Accounting (IAS) Level 3. Model Answers Series (3902)

Level 3. Model Answers Series (3902)") LCCI International Qualifications Accounting (IAS) Level 3 Model Answers Series 2 2011 (3902) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Accounting

LCCI International Qualifications Accounting (IAS) Level 3 Model Answers Series 2 2011 (3902) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Accounting

REVISION: COST ACCOUNTING & BUDGETS 18 SEPTEMBER 2014

REVISION: COST ACCOUNTING & BUDGETS 18 SEPTEMBER 2014 Lesson Description In this lesson we revise: Cost Accounting Budgeting Cost Accounting Question 1 Improve your Skills (Adapted from Nov 2012, DoE,

REVISION: COST ACCOUNTING & BUDGETS 18 SEPTEMBER 2014 Lesson Description In this lesson we revise: Cost Accounting Budgeting Cost Accounting Question 1 Improve your Skills (Adapted from Nov 2012, DoE,

Accounting 3.5. Management accounting. Unit 1 Budgets. Demonstrate understanding of management accounting to inform decision-making

Accounting 3.5 Demonstrate understanding of management accounting to inform decision-making Externally assessed 4 credits Copy correctly Up to 3% of a workbook Copying or scanning from ESA workbooks is

Accounting 3.5 Demonstrate understanding of management accounting to inform decision-making Externally assessed 4 credits Copy correctly Up to 3% of a workbook Copying or scanning from ESA workbooks is

MODULE 13 COST ACCOUNTING (MANUFACTURING)

") Note to the Teacher: MODULE 13 COST ACCOUNTING (MANUFACTURING) In Grade 10 learners were exposed to cost concepts and then in Grade 11 they drew up manufacturing ledger accounts, calculated costs of manufacturing

Note to the Teacher: MODULE 13 COST ACCOUNTING (MANUFACTURING) In Grade 10 learners were exposed to cost concepts and then in Grade 11 they drew up manufacturing ledger accounts, calculated costs of manufacturing

INTER CA MAY Test Code M32 Branch: MULTIPLE Date: (50 Marks) Note: All questions are compulsory.

Note: All questions are compulsory.") (5 Marks) Note: All questions are compulsory. INTER CA MAY 218 COSTING Topic: Contract Costing, Budgetary Control, Labour, Joint & By- Product, Absorption Costing, Overheads, Integral & Non Integral, Marginal

(5 Marks) Note: All questions are compulsory. INTER CA MAY 218 COSTING Topic: Contract Costing, Budgetary Control, Labour, Joint & By- Product, Absorption Costing, Overheads, Integral & Non Integral, Marginal

Management Accounting. Pilot Paper 3 Questions and Suggested Solutions

Management Accounting Pilot Paper 3 Questions and Suggested Solutions NOTES TO USERS ABOUT PILOT PAPERS Pilot papers are published by Accounting Technicians Ireland. They are intended to provide guidance

Management Accounting Pilot Paper 3 Questions and Suggested Solutions NOTES TO USERS ABOUT PILOT PAPERS Pilot papers are published by Accounting Technicians Ireland. They are intended to provide guidance

Detailed below is a table showing the prices of airline tickets and the number of passengers booked on each flight.

Topic 1.3 Putting a business idea into practice Q1. Detailed below is a table showing the prices of airline tickets and the number of passengers booked on each flight. Which flight generated the highest

Topic 1.3 Putting a business idea into practice Q1. Detailed below is a table showing the prices of airline tickets and the number of passengers booked on each flight. Which flight generated the highest

CERTIFICATE IN MANAGEMENT ACCOUNTING

Series 2 Examination 2007 CERTIFICATE IN MANAGEMENT ACCOUNTING Level 3 Tuesday 29 May Subject Code: 3623/M Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal

Series 2 Examination 2007 CERTIFICATE IN MANAGEMENT ACCOUNTING Level 3 Tuesday 29 May Subject Code: 3623/M Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS General Certificate of Education Advanced Subsidiary Level and Advanced Level

*1011372598* UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS General Certificate of Education Advanced Subsidiary Level and Advanced Level ACCOUNTING 9706/12 Paper 1 Multiple Choice October/November

*1011372598* UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS General Certificate of Education Advanced Subsidiary Level and Advanced Level ACCOUNTING 9706/12 Paper 1 Multiple Choice October/November

F2 FIA FMA. ACCA Qualification ACCA. Accounting. December 2012 Examinations. OpenTuition Course Notes can be downloaded FREE from

ACCA Qualification Course NOTES ACCA F2 FIA FMA Management Accounting December 2012 Examinations OpenTuition Course Notes can be downloaded FREE from www.opentuition.com Copyright belongs to OpenTuition.com

ACCA Qualification Course NOTES ACCA F2 FIA FMA Management Accounting December 2012 Examinations OpenTuition Course Notes can be downloaded FREE from www.opentuition.com Copyright belongs to OpenTuition.com

Use of receipts and payments forms

Receipts and Payments Accounts Introductory Notes Purpose of pro forma receipts and payments accounts In England and Wales many smaller non-company charities may choose to prepare receipts and payments

Receipts and Payments Accounts Introductory Notes Purpose of pro forma receipts and payments accounts In England and Wales many smaller non-company charities may choose to prepare receipts and payments

ACCOUNTING 9706/33 Paper 3 Structured Questions October/November 2016 MARK SCHEME Maximum Mark: 150. Published

Cambridge International Examinations Cambridge International Advanced Level ACCOUNTING 9706/33 Paper 3 Structured Questions October/November 2016 MARK SCHEME Maximum Mark: 150 Published This mark scheme

Cambridge International Examinations Cambridge International Advanced Level ACCOUNTING 9706/33 Paper 3 Structured Questions October/November 2016 MARK SCHEME Maximum Mark: 150 Published This mark scheme

AS/A-Level Business Studies Pack 2. 2 Classifying costs

2 Classifying costs Cost centres How the costs relate to each other: Cost centres are where a business divides up costs into certain centres such as production, marketing, distribution, personnel, administration

2 Classifying costs Cost centres How the costs relate to each other: Cost centres are where a business divides up costs into certain centres such as production, marketing, distribution, personnel, administration

MANAGEMENT ACCOUNTING

Series 3 Examination 2008 MANAGEMENT ACCOUNTING Level 3 Monday 9 June Subject Code: 3023 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

Series 3 Examination 2008 MANAGEMENT ACCOUNTING Level 3 Monday 9 June Subject Code: 3023 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

THE INCOME STATEMENT. Dr. J. Herbert Smith/ACOA Chair Technology Management and Entrepreneurship Faculty of Engineering University of New Brunswick

Home Page - The Income Statement THE INCOME STATEMENT by Dr. J. Herbert Smith/ACOA Chair Technology Management and Entrepreneurship Faculty of Engineering University of New Brunswick Copyright 2001 ALL

Home Page - The Income Statement THE INCOME STATEMENT by Dr. J. Herbert Smith/ACOA Chair Technology Management and Entrepreneurship Faculty of Engineering University of New Brunswick Copyright 2001 ALL

PLEASE READ THE FOLLOWING INSTRUCTIONS CAREFULLY

PLEASE READ THE FOLLOWING INSTRUCTIONS CAREFULLY 1. This paper consists of 8 pages. Please check that your question paper is complete. 2. Read the questions carefully. 3. Answer the questions in the Answer

PLEASE READ THE FOLLOWING INSTRUCTIONS CAREFULLY 1. This paper consists of 8 pages. Please check that your question paper is complete. 2. Read the questions carefully. 3. Answer the questions in the Answer

Cambridge International Advanced Subsidiary Level and Advanced Level 9706 Accounting June 2014 Principal Examiner Report for Teachers

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 C 16 B 2 B 17 D 3 C 18 C 4 C 19 A 5 B 20 A 6 C 21

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 C 16 B 2 B 17 D 3 C 18 C 4 C 19 A 5 B 20 A 6 C 21

CERTIFICATE IN ACCOUNTING

Series 2 Examination 2011 CERTIFICATE IN ACCOUNTING Level 3 Friday 8 April Subject Code: 3012 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer any 4 questions. There are no compulsory questions.

Series 2 Examination 2011 CERTIFICATE IN ACCOUNTING Level 3 Friday 8 April Subject Code: 3012 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer any 4 questions. There are no compulsory questions.