MPI 2015 General Rate Application

|

|

|

- Morgan Potter

- 5 years ago

- Views:

Transcription

of the Freedom of Information and Protection of Privacy")

1 MPI 2015 General Rate Application October 22, 2014 This report has been prepared as advice, opinions, proposals, recommendations, analyses or policy options developed by or for the public body or a minister, as per Section 23(1) of the Freedom of Information and Protection of Privacy Act.

2 2015 GRA A 2.4% rate increase An RSR Rebuilding Fee of 1.0% A minimum (lower) RSR target of $194 million in retained earnings based on the results of the 2014 DCAT report. A minimum (lower) RSR target of $213 million in total equity based on the results of the 2014 DCAT report. A range above the recommended minimum RSR target (based on the minimum DCAT amount) with the upper range based on a 100% MCT value ($325 million). 2

3 2015 Rate Change including 1% RSR Decreasing Increasing 62.1% Increasing 11.4% No Change 26.5% Decreasing

4 Rate and Rebate History Year Rebates Total ($millions) Per cent of premiums 2011 $336 M $63M $60 M $58 M $80M 16.6 Rate Changes Year Applied Order (includes 1% RSR)*

5 2013/14 RESULTS 5

6 2013/14 Results ($16M) 3% more collision and property damage claims ($24M) 10% physical damage severity increase ($26M) increase in injury claims reserves ($9M) increase in loss adjustment expense provision 6

7 2013/14 Results ($25M) premium deficiency liability ($22M) capital losses on marketable bonds ($10M) - all other unfavourable variances $57M higher than expected gains on sales of equities ($75M) - greater loss than forecast 7

8 2014/15 UPDATED FORECAST 8

9 2014/15 Forecast 2014 GRA -2014/15 forecast ($7.5M) 2015 GRA 2014/15 budget ($38.0M) Deterioration of ($30.5M) ($17M) increase in severity assumptions ($9M) increase in injury claims forecast ($4M) everything else 9

10 SECOND QUARTER RESULTS 10

11 YTD results six months ended August 31, 2014 in millions of $ Basic Budget Better/ (Worse) Earned Revenues (2.3) Net Claims Incurred (57.3) Claims Expenses (including Loss Prevention/Road Safety) Expenses - Operating, Commissions, Premium Taxes, Regulatory Investment/other income Net income

12 Interest Rate Impact Basic in millions of $ Actual Budget B / (W) Gains(losses) on Mktble Bonds 30.6 (31.9) 62.5 Basic Allocation 83.7% 83.9% Basic Share 25.6 (26.8) 52.4 (Increase)/Decrease to Claims due to Discount Rate Changes (26.6) 39.9 (66.5) Net Impact (1.0) 13.1 (14.1) 12

13 2015/16 INDICATED RATES 13

14 14

15 2015/16 Rating Period Forecast 2015 GRA versus 2014 GRA (M s) 2015GRA 2014GRA Difference Earned Revenues $888.7 $901.6 ($12.9) Claim Costs $832.6 $795.8 $36.7 Expenses $141.2 $136.1 $5.0 Investment Income $69.1 $41.7 $27.4 Net Income (Loss) ($15.9) $11.3 ($27.2) The 2015/16 indicated break even rate change deteriorated from a 1.7% rate decrease (2014 GRA) to a 2.4% rate increase (2015 GRA) over the past year. 15

16 Components of the 2015/16 Rate Indication 2014 GRA vs 2015 GRA 6.0% 5.0% 4.0% +0.83% +0.62% -2.14% 3.0% 2.0% +3.93% -1.62% +0.76% +2.40% 1.0% 0.0% -1.0% -2.0% -1.70% +1.12% +0.43% -3.0% 16

17 Impact of 2014 PUB Order on 2015/16 Rate Indication The Corporation s 2014/15 break-even rate indication was 1.8%. The PUB ordered a rate increase of 0.9%. Impact of 2014 PUB order on 2015/16 break-even net income = ($7.4M) Proportion of total 2.4% rate requirement = ($7.4M)/ ($15.9M) x 2.4% = 1.1% 17

18 Collision 12 Months Repair Total Loss Total Accident Year Severity % Change Severity % Change Severity % Change 2004/05 $1,580 $4,409 2, /06 $1, % $4, % 2, % 2006/07 $1, % $4, % 2, % 2007/08 $1, % $4, % 2, % 2008/09 $1, % $4, % 2, % 2009/10 $1, % $4, % 2, % 2010/11 $1, % $4, % 2, % 2011/12 $1, % $5, % 2, % 2012/13 $1, % $5, % 2, % 2013/14 $2, % $5, % 2, % Straight Average 3 year 1, % 5, % 2, % 5 year 1, % 5, % 2, % 10 year 1, % 4, % 2, % 18

19 Comparison of Average Blackbook Values versus Actual Average Total Loss Claim Settlements Average Total Loss Severity / Blackbook Value $8,000 $7,500 $7,000 $6,500 $6,000 $5,500 $5,000 $6,247 $5,687 $6,385 $5,809 $6,792 $6,360 $6,931 $6,716 $7, Fiscal Year $7, to 2013 Annual Growth Rate: - Blackbook: 6.04% / year - Actual TL Settlements: 4.34% / year Average Claim Settlement Value Average Blackbook Value 19

20 Collision Severity Growth vs Rate Changes 20

21 Impact of Revised Physical Damage Forecast on 2015/16 Rate Indication The physical damage incurred forecast increased by $26M in the 2015/16 rating period. The majority of the increase is attributable to the significant and unexpected 10% severity increase in 2013/14. The remaining portion is attributable to an increase in the Corporation s forecasted severity growth trend rate. Proportion of total 2.4% rate requirement = ($26.2M)/ ($15.9M) x 2.4% = 3.9% 21

22 PIPP Reserve Review 2012/13: Chief Actuary identifies changes in development patterns on injury claims. Paid losses and open claims counts trending higher; case reserves trending much lower. $30M+ in IBNR added to estimates. 2013/14: Injury Claims Management conducts full review of all open injury claims. More case reserves are added than expected in the forecast ($57M more than budget). 22

23 Impact of PIPP Forecast on 2015/16 Rate Indication The PIPP forecast was revised upward by approximately $5.5M / year, mainly as a result of the PIPP claims review. Proportion of total 2.4% rate requirement = ($5.5M)/ ($15.9M) x 2.4% = 0.8% 23

24 Equity Return Assumption Impact on 2015/16 Rate Indication The assumed total return on Canadian and U.S. equities was increased from 6.2% per year in the 2014 GRA to 7.3% per year in the 2015 GRA. This change was the main reason for the approximately $10.6M improvement in realized equity gains over the rating period compared to last year s forecast. Proportion of total 2.4% rate requirement = $10.6M/ ($15.9M) x 2.4% = (1.6)% (favourable) 24

25 Interest Rates This year s interest rate forecast has a greater net benefit to net income than last year s forecast. Interest Rate Impacts ($millions) 2015 GRA 2015/ /17 Claims Incurred ($51.2) ($39.7) Investment Income ($42.4) ($24.5) Net Income Impact $8.8 $ GRA 2015/ /17 Claims Incurred ($36.0) ($53.6) Investment Income ($39.3) ($55.2) Net Income Impact ($3.3) ($1.6) 2015/ /17 Change in Net Income $12.1 $

26 Interest Rate Forecast Impact on 2015/16 Rate Indication It is the change in interest rates during the rating period, not the absolute value of interest rates, that causes market value changes to assets and liabilities. During the 2015/16 rating period, interest rates increase by 98 basis points in the 2015 GRA versus 89 basis points in the 2014 GRA. Average improvement in net income over the rating period from the revised interest rate forecast = $14.5M Proportion of total 2.4% rate requirement = $14.5M/ ($15.9M) x 2.4% = (2.1)% (favourable) 26

27 EXPENSES 27

28 Expenses Total expenses 2015 rating period - $214.1M, 2014 rating period - $206.7M Difference $7.4M $4.0M of this increase is due to an increase in the overall expense allocation to Basic due to higher claims incurred in 2013/14 The balance is due to the mix of improvement initiatives 28

29 Normal operating EXPENSES Improvement Initiatives Implementation Expenses Improvement Initiatives Ongoing Expenses Amortization Depreciation Other 29

30 Normal Operating Expenses Basic Share ($millions) 2012/13 (restated) 2013/ / / /17 Compensation Data Processing Other Subtotal Amortization / Depreciation Total Normal Operating Expenses % Increase / (Decrease) % 2.19% 4.19% 1.31% 2.00% 30

31 EXPENSES Normal Operating Expenses are not the key driver in the rate increase request. The basic average normal operating expenses forecasted in the rating years (2015/16 and 2016/17) is $200.8 million. This represents an increase of 1.3% and 2.0% respectively These year over year increases are at or below forecasted CPI of 2.0%. 31

32 EXPENSES MPI is containing overall increases in normal operating expenses despite contractual commitments for salary increases of 4.5%. 32

33 Compensation Expenses Basic Share ($millions) 2012/13 (restated) 2013/ / / /17 Gross Salaries Vacancy Allowance Overtime Benefits H & E Tax Total Compensation Expenses Basic Allocation % 71.55% 73.48% 74.28% 74.84% 74.59% Total Compensation Expenses Basic Share % Increase / (Decrease) -0.86% 3.93% 2.46% 5.27% 3.66% 33

34 COMPENSATION Why does compensation expense fluctuate? Four Main Reasons: General Wage Increases negotiated Changes in the number of staff employed Changes due to movement on scale increased experience in current job Job classification changes change in mix of staff Change in benefits (both cost and type) 34

35 COMPENSATION General Wage Increase negotiated based on mandate provided by Compensation Committee of Cabinet, Province of Manitoba Last contract September 2012 September %, 0%, 2.75%, 2.75% Steps on scale - 3.5% (imbedded in Union contract) estimated at 50% or 1.75% 35

36 COMPENSATION In the last four years (2009/10 to 2013/14) cumulative increase due to: Four-Year Total $millions Average Annual $millions Compounded Annual % Increase GWI # of staff employed Movement on scale Benefits TOTAL

37 COMPENSATION The next three years 2014/15 to 2016/17 3 Years Total $ millions Annual Average $millions Compounded Annual % Increase GWI # of staff employed Movement on scale Benefits TOTAL

38 Other Expenses Non compensation expenses and excluding depreciation and amortization In the rating years are forecasted to increase 1.8% and 2.7% The only reason they are forecasted to increase by more than inflation in 16/17 is due to an equipment refresh which occurs every 3-4 years Represents 1.2% almost half of the overall increase in 16/17 38

39 Improvement Initiative Expenses There are two components of expense related to improvement initiatives: Implementation expense Ongoing expense (after implementation) Amortization of deferred expenses Depreciation of capital expenditures Other (maintenance) 39

40 Improvement Initiative Expenses Basic Share ($millions) $millions 2012/ / / / /17 Implementation Expenses Ongoing Expenses Total Improvement Initiative Expenses % Increase / (Decrease) 15.8% -24.0% 25.8% 57.6% 40

41 Capitalized Costs ($millions) $millions 2009/ / / / / / / /17 Deferred Expenses Capital Expenditures TOTAL Deferred Expenses are amortized over 5 years once the project is complete. Capital expenditures are depreciated over 3 years starting at a ½ year in the year acquired. When the Physical Damage Reengineering project is complete there will be a significant increase in Deferred Expense Amortization. 41

42 INVESTMENT INCOME 42

43 Basic Investment Income 08/09 09/10 10/11 11/12 12/13 13/14 14/15 15/16 16/17 TOTAL Real and forecasted volatility in investment income 2013/14 high investment income 2 main reasons: Forecasted sale of U.S. equities generated gain of $58.1 million. A required rebalancing of Canadian Equities netted $57.4 million. Forecasted negative impact of rising interest rates on investment income diminishes in subsequent years (from 2014/15 to 2016/17). 2016/17 Canadian equities rebalance resulting in approximately $13 million increase. 43

44 4.0% 2014 GRA Actual/Forecasted GoC 10 Year Bond Rate until 2015/16 (Rating Period) 3.5% 3.0% 2.5% 2.0% 1.5% Standard, March 2013 Low Growth (2014 GRA), March 2013 Actual Standard, September

45 4.5% 4.0% 3.5% 3.0% 2015 GRA Actual/Forecasted GoC 10 Year Bond Rate until 2016/17 (Rating Period) Rating Years Rating Year Increase 98 bps 118 bps 61 bps 89 bps 2.5% 2.0% 1.5% Standard (2015 GRA), March 2014 Low Growth, March 2014 Standard, September 2014 Low Growth, September 2014 Actual 45

46 INTEREST RATES Up until last year MPI did not forecast the impact of interest rate changes in its financial forecast In a rising interest rate environment if duration of assets is less than liabilities (negative duration gap), there will be a positive impact to net income Impact of interest rate changes is smaller this year compared to last year Decreased the forecasted duration gap from -1.8 years (2014 GRA) to -1.0 years (2015 GRA). 46

47 RATE STABILIZATION RESERVE (RSR) 47

48 RSR: Purpose The purpose of the RSR is to protect motorists from rate increases made necessary by unexpected events and losses arising from non-recurring events or factors. 48

49 DCAT What is it? A tool to examine the effects of adverse scenarios on an insurer s forecasted capital adequacy - Canadian Institute of Actuaries, Standard of Practice 49

50 Why use DCAT for determining the lower RSR target? Follows Actuarial Standards of Practice and Best Practices Risks reflect those of the Basic program Management and Regulatory Actions reflect Manitoba situation i.e. Made-in-Manitoba scenarios Flexibility e.g. Risk tolerance adjusted to meet both the desired target of the Regulator, while still complying with actuarial standards (currently using 1-in-40). Improved understanding of key risks for MPI and the Board Transparent (MPI DCAT) Collaborative (MPI DCAT) 50

51 Retained Earnings (RSR) Target or Total Equity Target? RSR is currently utilized as the basis for determining Basic capital requirements. There has been debate over whether Accumulated Other Comprehensive Income (AOCI) should be included in this measure. RSR + AOCI = Total Equity Appointed Actuary has recommended that AOCI be included to meet Actuarial Standards. Since the RSR is the current method, the Corporation provided recommended capital targets based on both RSR and Total Equity. The Corporation s preference is to use a Total Equity target. 51

52 Minimum Capital Test Developed by Office of the Superintendent of Financial Institutions Capital requirements determined by applying risk factors to balance sheet items (e.g. claim liabilities by coverage; different asset categories) Standardized approach. Allows fair comparisons between insurers. Capital Available / Capital Required = MCT Ratio 52

53 Why 100% MCT for upper RSR target? Objective measure that is independent of the assumptions used in the made-in-manitoba DCAT. Directly comparable to other insurers Used by other public insurers (SGI, ICBC) Proposed as an upper capital target only ( made-in- Manitoba DCAT is still the basis for the minimum capital target) Significantly lower than the 150% MCT private sector minimum supervisory target and the average 225% MCT of the industry. 53

54 DCAT Technical Conference Part 1: April 2013 Follow Actuarial Standards of Practice Include Balance Sheets Provide improved disclosure and reconciliation of assumptions/calculations Provide results at multiple risk tolerance levels (e.g. 1-in- 20, 1-in-40, 1-in-100) Provide results over multiple time periods (1 to 4 years) Calculate results including the impact of interest rates Provide results with and without management action 54

55 DCAT Technical Conference Part 2: April 2014 Standardized financial model output for each adverse scenario Improved understanding of financial model through Technical Conference discussions and offline discussions between MPI/PUB/CAC actuaries Include projected MCT ratios in the financial model Chief Actuary to evaluate the financial condition of Basic Autopac based on Total Equity rather than only on the RSR balance (i.e. include AOCI in the evaluation) 55

56 2014 DCAT: Four Key Risk Areas Declining or Sustained Low Interest Rates Declines in Equity Asset Values Claims Incurred over Budget Combined Adverse Interest Rate, Equity Returns, and Claims scenarios. Other scenarios tested that were not in the top 4 risk areas: Inflation Underestimation of claim liabilities (excluding impact of interest rates) Declines in other asset categories (e.g. real estate) IFRS impacts 56

57 Plausible Adverse Scenarios Credible The key risk models are all built on large samples of relevant historical data Stable Because the models rely on historical data, the results should not change significantly from year-to-year (assuming no significant change in the risk profile of Basic) Collaborative MPI has shown genuine interest to collaborate with stakeholders Scenarios have been improved based on feedback Management Action Reflects the Manitoba situation Transparent MPI has provided significant amounts of information in support of the financial and actuarial models 57

58 Claims Incurred Model 45.0% Simulated Cumulative Claims Incurred over 1 to 4 Year Periods $millions 40.0% % of Observations 35.0% 30.0% 25.0% 20.0% 15.0% 1 year 2 year 3 year 4 year 10.0% 5.0% 0.0% Simulated Cumulative Claims Incurred Difference From Budget ($millions) 58

59 Equity Return Model 25% TSX Cumulative Total Return Over 1 to 4 Year Periods Monthly Historical Data since January 1957 % of Observations since January % 15% 10% 5% 1 year 2 year 3 year 4 year 0% TSX Cumulative Total Return 59

60 Interest Rate Model 30% Change in Government of Canada 10 Year Bond Yield Over 1 to 4 Year Periods Monthly Historical Data since January % % of Observations since January % 15% 10% 1 year 2 year 3 year 4 year 5% 0% -4.5% -4.0% -3.5% -3.0% -2.5% -2.0% -1.5% -1.0% -0.5% 0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% 3.5% 4.0% 4.5% Change from the Current GOC 10 Year Bond Yield 60

61 Results without Management Action DCAT Adverse Scenarios before Management Action: RSR (in $millions) 1-in-40 Year Risk Level 2015/ / / /19 Combined Scenario ($17) ($83) ($153) ($221) Interest Rates ($15) ($85) ($126) ($179) Equity Decline $72 $72 $85 $72 High Loss Ratio $10 $0 $72 $29 DCAT Base Forecast $80 $91 $131 $153 61

62 Management and Regulatory Action: Assumptions Base Forecast: The 1% RSR rebuilding fee will remain in place for the entire forecast period No capital transfers from other lines of business Rate Increases: All forecasts are restated at the end of each year to determine the break-even rate requirement for the next GRA. The Corporation will apply for this rate increase and the PUB will approve it. RSR Rebuilding Fees: Our maximum combined rate increase and RSR rebuilding fee in any GRA is 5.0%. Capital Transfers: The risks for the Basic program do not change in the presence of possible capital transfers. If a capital transfer from competitive lines is considered, it will increase the speed at which MPI rebuilds Basic capital, but it will not change the Basic capital target. 62

63 Combined Scenario Results after Management Action Assumed Management and Regulatory Action: 4 year, 1-in-40 Combined Scenario GRA Additional RSR Rebuilding Fee Rate Change 2015/16 1.0% 2.4% 2016/17 5.0% 0.0% 2017/18 2.0% 2.0% 2018/19 2.0% 0.0% Impact of Assumed Management and Regulatory Action: 4 year, 1-in-40 Combined Scenario Ending RSR Balance Fiscal Year Before Management Action After Management Action Impact of Management Action 2015/16 ($17) ($17) $0 2016/17 ($83) ($53) $ /18 ($151) ($58) $ /19 ($219) ($38) $181 63

64 Combined Scenario Results after Management Action Impacts to Retained Earnings and Total Equity from the 4 year, 1-in-40 year Combined Scenario relative to the Base Forecast (in $millions) 2015/ / / /19 Base: Retained Earnings $80 $91 $131 $153 Base: Total Equity $158 $177 $212 $229 DCAT: Retained Earnings ($15) ($54) ($60) ($40) DCAT: Total Equity $50 $7 ($1) $17 Impact: Retained Earnings ($95) ($145) ($191) ($194) Impact: Total Equity ($108) ($169) ($213) ($212) 64

65 MCT Results As calculated by the MCT Test as of Feb 28, 2014: Capital Available = $135M Capital Required = $325M MCT Ratio = 42% Implied MCT Ratio for MPI s proposed lower RSR Total Equity target of $213M = 65% 65

2013 DCAT Report Approved by Board of Directors October 4, 2013

2013 DCAT Report Approved by Board of Directors October 4, 2013 2013 Dynamic Capital Adequacy Testing Report Basic Compulsory Automobile Insurance TABLE OF CONTENTS 1.0 Executive Summary... 1 SUMMARY OF

2013 DCAT Report Approved by Board of Directors October 4, 2013 2013 Dynamic Capital Adequacy Testing Report Basic Compulsory Automobile Insurance TABLE OF CONTENTS 1.0 Executive Summary... 1 SUMMARY OF

MANITOBA PUBLIC INSURANCE

MANITOBA PUBLIC INSURANCE Round 1 Information Requests 2015 GRA July 31, 2014 Public Utilities Board Automotive Recyclers Association Canadian Automobile Association Consumers Association of Canada (Manitoba)

MANITOBA PUBLIC INSURANCE Round 1 Information Requests 2015 GRA July 31, 2014 Public Utilities Board Automotive Recyclers Association Canadian Automobile Association Consumers Association of Canada (Manitoba)

MANITOBA PUBLIC INSURANCE

MANITOBA PUBLIC INSURANCE AI.11 RATE STABILIZATION RESERVE AI.11 Discussion of the Rate Stabilization Reserve (RSR) AI.11.A Background The purpose of the Rate Stabilization Reserve (RSR) is to protect

MANITOBA PUBLIC INSURANCE AI.11 RATE STABILIZATION RESERVE AI.11 Discussion of the Rate Stabilization Reserve (RSR) AI.11.A Background The purpose of the Rate Stabilization Reserve (RSR) is to protect

1) Role of the DCAT and 2) Interest Rate Forecasting in the 2019 GRA

Role of the DCAT and 2) Interest Rate Forecasting in the 2019 GRA") 1) Role of the DCAT and 2) Interest Rate Forecasting in the 2019 GRA Consumers' Association of Canada (Manitoba) Submitted by the Public Interest Law Centre Co-Authored by Dr. Wayne Simpson and Ms Andrea

1) Role of the DCAT and 2) Interest Rate Forecasting in the 2019 GRA Consumers' Association of Canada (Manitoba) Submitted by the Public Interest Law Centre Co-Authored by Dr. Wayne Simpson and Ms Andrea

MANITOBA PUBLIC INSURANCE

MANITOBA PUBLIC INSURANCE TESTIMONY OF LUKE JOHNSTON CHIEF ACTUARY & DIRECTOR OF PRICING & ECONOMICS Good morning, Mr. Chairman, members of the Board, ladies and gentlemen. My name is Luke Johnston. I

MANITOBA PUBLIC INSURANCE TESTIMONY OF LUKE JOHNSTON CHIEF ACTUARY & DIRECTOR OF PRICING & ECONOMICS Good morning, Mr. Chairman, members of the Board, ladies and gentlemen. My name is Luke Johnston. I

July 31, 2014 Information Requests Round 1

CMMG (MPI) CMMG (MPI) 1-1 Please update last years CMMG (MPI) 1-1 re: comparison of projected vs actual loss data for motorcycle major class. Refer to the attached table. CMMG (MPI) 1-1 CMMG (MPI) 1-1

CMMG (MPI) CMMG (MPI) 1-1 Please update last years CMMG (MPI) 1-1 re: comparison of projected vs actual loss data for motorcycle major class. Refer to the attached table. CMMG (MPI) 1-1 CMMG (MPI) 1-1

Interveners of Past Record (2016 General Rate Application) Manitoba Public Insurance 2017/18 General Rate Application

Manitoba Public Insurance 2017/18 General Rate Application") June 20, 2016 VIA EMAIL ATTENTION: Interveners of Past Record (2016 General Rate Application) Re: Manitoba Public Insurance 2017/18 General Rate Application Background The 2017/18 GRA of MPI was filed

June 20, 2016 VIA EMAIL ATTENTION: Interveners of Past Record (2016 General Rate Application) Re: Manitoba Public Insurance 2017/18 General Rate Application Background The 2017/18 GRA of MPI was filed

OPENING STATEMENT OF THE PUBLIC INTEREST LAW CENTRE ON BEHALF OF THE CONSUMERS ASSOCIATION OF CANADA (MANITOBA BRANCH) 2017/2018 MPI GRA

2017/2018 MPI GRA") OPENING STATEMENT OF THE PUBLIC INTEREST LAW CENTRE ON BEHALF OF THE CONSUMERS ASSOCIATION OF CANADA (MANITOBA BRANCH) 2017/2018 MPI GRA October 14, 2016 CAC Manitoba 2 Over two decades of rate hearings

OPENING STATEMENT OF THE PUBLIC INTEREST LAW CENTRE ON BEHALF OF THE CONSUMERS ASSOCIATION OF CANADA (MANITOBA BRANCH) 2017/2018 MPI GRA October 14, 2016 CAC Manitoba 2 Over two decades of rate hearings

Interest Rate Forecasting. Technical Conference Tuesday August 16, 2016

Interest Rate Forecasting Risk Factor Technical Conference Tuesday August 16, 2016 Technical Conference Agenda Welcome 1) 9:00 9:15 Welcome and introductions 2) 9:15 9:30 Review purpose of the meeting

Interest Rate Forecasting Risk Factor Technical Conference Tuesday August 16, 2016 Technical Conference Agenda Welcome 1) 9:00 9:15 Welcome and introductions 2) 9:15 9:30 Review purpose of the meeting

MANITOBA PUBLIC INSURANCE

MANITOBA PUBLIC INSURANCE TESTIMONY OF HEATHER REICHERT VICE-PRESIDENT, FINANCE AND CHIEF FINANCIAL OFFICER Good morning, Mr. Chairman, members of the Board, ladies and gentlemen. My name is Heather Reichert.

MANITOBA PUBLIC INSURANCE TESTIMONY OF HEATHER REICHERT VICE-PRESIDENT, FINANCE AND CHIEF FINANCIAL OFFICER Good morning, Mr. Chairman, members of the Board, ladies and gentlemen. My name is Heather Reichert.

Volume: 3, Actuarial Reports Page No.: 22, Oct report 4, Feb report

CAC (MPI) CAC (MPI) 1-1 CAC (MPI) 1-1 Volume: 3, Actuarial Reports Page No.: 22, Oct report 4, Feb report Topic: Sub Topic: Issue: Actuarial Reports Ensuring the reasonableness of the Actuarial Reports

CAC (MPI) CAC (MPI) 1-1 CAC (MPI) 1-1 Volume: 3, Actuarial Reports Page No.: 22, Oct report 4, Feb report Topic: Sub Topic: Issue: Actuarial Reports Ensuring the reasonableness of the Actuarial Reports

EXHIBIT LIST FOR MANITOBA PUBLIC INSURANCE 2018 INSURANCE RATES. March 7, 2018

THE PUBLIC UTILITIES BOARD'S (PUB) EXHIBITS EXHIBIT LIST FOR MANITOBA PUBLIC INSURANCE 2018 INSURANCE RATES March 7, 2018 PUB 1 PUB 2 Notice of Public Hearing and Pre Hearing Conference issued by the Board

THE PUBLIC UTILITIES BOARD'S (PUB) EXHIBITS EXHIBIT LIST FOR MANITOBA PUBLIC INSURANCE 2018 INSURANCE RATES March 7, 2018 PUB 1 PUB 2 Notice of Public Hearing and Pre Hearing Conference issued by the Board

Quarterly Financial Report. 3rd QUARTER

Quarterly Financial Report 3rd QUARTER Nine months ended November 30, 2017 Management Discussion and Analysis Management s discussion and analysis provides a review of the financial results and future

Quarterly Financial Report 3rd QUARTER Nine months ended November 30, 2017 Management Discussion and Analysis Management s discussion and analysis provides a review of the financial results and future

September 24, 2014 Information Requests Round 3. CAC (MPI) 1-3 and PUB (MPI) 1-75 Collaborative Estimating Initiative

1-3 and PUB (MPI) 1-75 Collaborative Estimating Initiative") CAC (MPI) CAC (MPI) 3-1 Reference: CAC (MPI) 1-3 and PUB (MPI) 1-75 Collaborative Estimating Initiative Preamble: With respect to the detailed Collaborative Estimating Initiative project costs, the response

CAC (MPI) CAC (MPI) 3-1 Reference: CAC (MPI) 1-3 and PUB (MPI) 1-75 Collaborative Estimating Initiative Preamble: With respect to the detailed Collaborative Estimating Initiative project costs, the response

Workplace Safety and Insurance Board

Sufficiency Plan Annual Update Workplace Safety and Insurance Board Commission de la sécurité professionnelle et de l assurance contre les accidents du travail Table of Contents Sections Page Description

Sufficiency Plan Annual Update Workplace Safety and Insurance Board Commission de la sécurité professionnelle et de l assurance contre les accidents du travail Table of Contents Sections Page Description

Workplace Safety and Insurance Board

Sufficiency Plan Annual Update June 18, 2015 Workplace Safety and Insurance Board Commission de la sécurité professionnelle et de l assurance contre les accidents du travail Table of Contents Sections

Sufficiency Plan Annual Update June 18, 2015 Workplace Safety and Insurance Board Commission de la sécurité professionnelle et de l assurance contre les accidents du travail Table of Contents Sections

RESPONSE: July 31, 2014 Information Requests Round 1. Please file the Corporation's quarterly report for the period ending May 31, 2014.

PUB (MPI) July 31, 2014 Information Requests Round 1 PUB (MPI) 1-1 Reference: Quarterly Report Please file the Corporation's quarterly report for the period ending May 31, 2014. RESPONSE: Please see attached.

PUB (MPI) July 31, 2014 Information Requests Round 1 PUB (MPI) 1-1 Reference: Quarterly Report Please file the Corporation's quarterly report for the period ending May 31, 2014. RESPONSE: Please see attached.

DURATION MATCHING DISCUSSION PAPER

0 RATE APPLICATION 0 0 0 DURATION MATCHING DISCUSSION PAPER In the most recent PUB Order / from December 0, it was ordered that: MPI shall submit a discussion paper of the duration matching of its claims

0 RATE APPLICATION 0 0 0 DURATION MATCHING DISCUSSION PAPER In the most recent PUB Order / from December 0, it was ordered that: MPI shall submit a discussion paper of the duration matching of its claims

September 9, 2015 Information Requests Round 2 CMMG (MPI) 2-1

2-1") CMMG (MPI) CMMG (MPI) 2-1 CMMG (MPI) 2-1 Please explain the Corporations forecast for a reduction in projected total premium for 2016 shown in the response to CMMG/PUB 1-1. Is this solely a function of

CMMG (MPI) CMMG (MPI) 2-1 CMMG (MPI) 2-1 Please explain the Corporations forecast for a reduction in projected total premium for 2016 shown in the response to CMMG/PUB 1-1. Is this solely a function of

A FINE BALANCE: PROTECTING CURRENT AND FUTURE CONSUMERS OPENING STATEMENTS OF THE CONSUMERS ASSOCIATION OF CANADA (MANITOBA BRANCH) 2016/2017 MPI GRA

2016/2017 MPI GRA") 1 A FINE BALANCE: PROTECTING CURRENT AND FUTURE CONSUMERS OPENING STATEMENTS OF THE CONSUMERS ASSOCIATION OF CANADA (MANITOBA BRANCH) 2016/2017 MPI GRA October 5, 2015 CAC Manitoba 2 Over two decades of

1 A FINE BALANCE: PROTECTING CURRENT AND FUTURE CONSUMERS OPENING STATEMENTS OF THE CONSUMERS ASSOCIATION OF CANADA (MANITOBA BRANCH) 2016/2017 MPI GRA October 5, 2015 CAC Manitoba 2 Over two decades of

Quarterly Financial Report. 1st QUARTER

Quarterly Financial Report 1st QUARTER Three months ended May 31, 2018 Management Discussion and Analysis Management s discussion and analysis provides a review of the financial results and future outlook

Quarterly Financial Report 1st QUARTER Three months ended May 31, 2018 Management Discussion and Analysis Management s discussion and analysis provides a review of the financial results and future outlook

Order No. 162/16. December 15, 2016

MANITOBA PUBLIC INSURANCE CORPORATION (MPI OR THE CORPORATION): COMPULSORY 2017/2018 DRIVER AND VEHICLE INSURANCE PREMIUMS AND OTHER MATTERS BEFORE: Robert Gabor, Q.C., Chair Karen Botting, B.A., B.Ed.,

MANITOBA PUBLIC INSURANCE CORPORATION (MPI OR THE CORPORATION): COMPULSORY 2017/2018 DRIVER AND VEHICLE INSURANCE PREMIUMS AND OTHER MATTERS BEFORE: Robert Gabor, Q.C., Chair Karen Botting, B.A., B.Ed.,

Insurance Corporation of British Columbia

Financial Report Discussion of Results Financial Resource Summary Table This report contains statements regarding the business of the Corporation. The table below provides an overview of ICBC s financial

Financial Report Discussion of Results Financial Resource Summary Table This report contains statements regarding the business of the Corporation. The table below provides an overview of ICBC s financial

The Role of the DCAT and Interest Rate Forecasting in the 2019 GRA. Manitoba Public Insurance 2019/20 GRA

The Role of the DCAT and Interest Rate Forecasting in the 2019 GRA Manitoba Public Insurance 2019/20 GRA Consumers' Association of Canada (Manitoba) Submitted by the Public Interest Law Centre Co-Authored

The Role of the DCAT and Interest Rate Forecasting in the 2019 GRA Manitoba Public Insurance 2019/20 GRA Consumers' Association of Canada (Manitoba) Submitted by the Public Interest Law Centre Co-Authored

A Note on Ratemaking in Accordance with Accepted Actuarial Practice in Canada and Impact of Investment (Discount) Rates

Rates") A Note on Ratemaking in Accordance with Accepted Actuarial Practice in Canada and Impact of Investment (Discount) Rates Manitoba Public Insurance 2017/18 GRA CAC Manitoba Submitted by the Public Interest

A Note on Ratemaking in Accordance with Accepted Actuarial Practice in Canada and Impact of Investment (Discount) Rates Manitoba Public Insurance 2017/18 GRA CAC Manitoba Submitted by the Public Interest

Régis Gosselin, B ès Arts, MBA, CGA, Chair The Hon. Anita Neville, P.C., BA Hons., Member Karen Botting, BA, B.Ed, M.Ed, Member

M A N I T O B A ) ) THE PUBLIC UTILITIES BOARD ACT ) Order 151/13 ) THE MANITOBA PUBLIC INSURANCE ACT ) ) December 16, 2013 THE CROWN CORPORATIONS PUBLIC ) REVIEW AND ACCOUNTABILITY ACT ) Before: Régis

M A N I T O B A ) ) THE PUBLIC UTILITIES BOARD ACT ) Order 151/13 ) THE MANITOBA PUBLIC INSURANCE ACT ) ) December 16, 2013 THE CROWN CORPORATIONS PUBLIC ) REVIEW AND ACCOUNTABILITY ACT ) Before: Régis

Workplace Safety and Insurance Board

Funding Sufficiency Plan June 30, 2013 Workplace Safety and Insurance Board Commission de la sécurité professionnelle et de l assurance contre les accidents du travail Table of Contents Page Description

Funding Sufficiency Plan June 30, 2013 Workplace Safety and Insurance Board Commission de la sécurité professionnelle et de l assurance contre les accidents du travail Table of Contents Page Description

MANITOBA PUBLIC INSURANCE ANNUAL BUSINESS PLAN

MANITOBA PUBLIC INSURANCE ANNUAL BUSINESS PLAN 2018-2019 February 2018 TABLE OF CONTENTS 1.0 Mandate & Strategic Direction... 4 1.1 Corporation's Mandate, Objects or Purposes as set out in The Manitoba

MANITOBA PUBLIC INSURANCE ANNUAL BUSINESS PLAN 2018-2019 February 2018 TABLE OF CONTENTS 1.0 Mandate & Strategic Direction... 4 1.1 Corporation's Mandate, Objects or Purposes as set out in The Manitoba

Quarterly Financial Report. 2nd QUARTER

Quarterly Financial Report 2nd QUARTER Six months ended August 31, 2017 Management Discussion and Analysis Management s discussion and analysis provides a review of the financial results and future outlook

Quarterly Financial Report 2nd QUARTER Six months ended August 31, 2017 Management Discussion and Analysis Management s discussion and analysis provides a review of the financial results and future outlook

Public Utilities Board (PUB) 2019 GRA Information Requests on Intervener Evidence October 10, 2018

2019 GRA Information Requests on Intervener Evidence October 10, 2018") Public Utilities Board (PUB) 2019 GRA Information Requests on Intervener Evidence October 10, 2018 Page 1 of 29 PUB (CAC) 1-1 Document: PUB Approved Issue No.: The Role of the DCAT and Interest Rate Forecasting

Public Utilities Board (PUB) 2019 GRA Information Requests on Intervener Evidence October 10, 2018 Page 1 of 29 PUB (CAC) 1-1 Document: PUB Approved Issue No.: The Role of the DCAT and Interest Rate Forecasting

A Note on an Interest Rate Forecast Risk Factor (IRFRF) and the RSR Target Established by the Dynamic Capital Asset Test (DCAT)

and the RSR Target Established by the Dynamic Capital Asset Test (DCAT)") A Note on an Interest Rate Forecast Risk Factor (IRFRF) and the RSR Target Established by the Dynamic Capital Asset Test (DCAT) Manitoba Public Insurance 2017/18 GRA CAC Manitoba Submitted by the Public

A Note on an Interest Rate Forecast Risk Factor (IRFRF) and the RSR Target Established by the Dynamic Capital Asset Test (DCAT) Manitoba Public Insurance 2017/18 GRA CAC Manitoba Submitted by the Public

MANITOBA PUBLIC INSURANCE

MANITOBA PUBLIC INSURANCE SM.5 MATTERS ARISING FROM PUB HEARINGS AND CORRESPONDENCE SM.5.1 IT Optimization In Order 162/11, the Public Utilities Board ordered that: For rate-setting purposes, the IT Optimization

MANITOBA PUBLIC INSURANCE SM.5 MATTERS ARISING FROM PUB HEARINGS AND CORRESPONDENCE SM.5.1 IT Optimization In Order 162/11, the Public Utilities Board ordered that: For rate-setting purposes, the IT Optimization

MANITOBA PUBLIC INSURANCE: COMPULSORY 2012/13 DRIVER AND VEHICLE INSURANCE PREMIUMS AND OTHER MATTERS

M A N I T O B A THE PUBLIC UTILITIES BOARD ACT THE MANITOBA PUBLIC INSURANCE ACT THE CROWN CORPORATIONS PUBLIC REVIEW AND ACCOUNTABILITY ACT December 2, 2011 Before: Susan Proven, P.H.Ec., Acting Chairperson

M A N I T O B A THE PUBLIC UTILITIES BOARD ACT THE MANITOBA PUBLIC INSURANCE ACT THE CROWN CORPORATIONS PUBLIC REVIEW AND ACCOUNTABILITY ACT December 2, 2011 Before: Susan Proven, P.H.Ec., Acting Chairperson

MANITOBA PUBLIC INSURANCE

MANITOBA PUBLIC INSURANCE Round 2 Information Requests 2016 GRA September 9, 2015 Public Utilities Board Bike Winnipeg Consumers Association of Canada (Manitoba) Coalition of Manitoba Motorcycles Groups

MANITOBA PUBLIC INSURANCE Round 2 Information Requests 2016 GRA September 9, 2015 Public Utilities Board Bike Winnipeg Consumers Association of Canada (Manitoba) Coalition of Manitoba Motorcycles Groups

Closing Submissions. MPI Exhibit 50 CLOSING SUBMISSIONS 2019 GENERAL RATE APPLICATION. October 30, 2018

CLOSING SUBMISSIONS Table of Contents 1 Introduction and Summary... 4 2 Setting the Direction... 9 3 Capital Adequacy... 13 4 Net Capital Maintenance Provision... 14 4.1 Capital Maintenance Provision is

CLOSING SUBMISSIONS Table of Contents 1 Introduction and Summary... 4 2 Setting the Direction... 9 3 Capital Adequacy... 13 4 Net Capital Maintenance Provision... 14 4.1 Capital Maintenance Provision is

Graham Lane, CA, Chairman Len Evans, LLD, Member MANITOBA PUBLIC INSURANCE: COMPULSORY 2011/12 DRIVER AND VEHICLE INSURANCE PREMIUMS AND OTHER MATTERS

M A N I T O B A THE PUBLIC UTILITIES BOARD ACT THE MANITOBA PUBLIC INSURANCE CORPORATION ACT THE CROWN CORPORATIONS PUBLIC REVIEW AND ACCOUNTABILITY ACT December 08, 2010 Before: Graham Lane, CA, Chairman

M A N I T O B A THE PUBLIC UTILITIES BOARD ACT THE MANITOBA PUBLIC INSURANCE CORPORATION ACT THE CROWN CORPORATIONS PUBLIC REVIEW AND ACCOUNTABILITY ACT December 08, 2010 Before: Graham Lane, CA, Chairman

Genworth MI Canada Inc. Management s Discussion and Analysis For the fourth quarter and year ended December 31, 2010

Management s Discussion and Analysis For the fourth quarter and year ended December 31, 2010 February 17, 2011 Formation of the Company ( Genworth Canada or the Company ) completed its initial public offering

Management s Discussion and Analysis For the fourth quarter and year ended December 31, 2010 February 17, 2011 Formation of the Company ( Genworth Canada or the Company ) completed its initial public offering

UNIVERSAL COMPULSORY AUTOMOBILE INSURANCE (BASIC INSURANCE) REVENUE FORECAST

REVENUE FORECAST") UNIVERSAL COMPULSORY AUTOMOBILE INSURANCE (BASIC INSURANCE) REVENUE FORECAST DATA BOOK 2011 Table of Contents SECTION 1: MANITOBA ECONOMIC OVERVIEW AND FORECAST... 1 1.1 MANITOBA S REAL GROSS DOMESTIC

UNIVERSAL COMPULSORY AUTOMOBILE INSURANCE (BASIC INSURANCE) REVENUE FORECAST DATA BOOK 2011 Table of Contents SECTION 1: MANITOBA ECONOMIC OVERVIEW AND FORECAST... 1 1.1 MANITOBA S REAL GROSS DOMESTIC

Workplace Safety and Insurance Board

Workplace Safety and Insurance Board 2015 Sufficiency Report to Stakeholders Workplace Safety and Insurance Board Commission de la sécurité professionnelle et de l assurance contre les accidents du travail

Workplace Safety and Insurance Board 2015 Sufficiency Report to Stakeholders Workplace Safety and Insurance Board Commission de la sécurité professionnelle et de l assurance contre les accidents du travail

Consolidated Statement of Financial Position

Consolidated Statement of Financial Position March 31 Assets Cash and cash equivalents $ 27,128 $ 45,815 Accrued interest 75,863 55,327 Assets held for sale (note 5) 25,712 - Financial investments (note

Consolidated Statement of Financial Position March 31 Assets Cash and cash equivalents $ 27,128 $ 45,815 Accrued interest 75,863 55,327 Assets held for sale (note 5) 25,712 - Financial investments (note

August 5, Rate Application Information Requests Round 1 PUB (MPI) 1-1

1-1") PUB (MPI) August 5, 2016 2017 Rate Application Information Requests Round 1 PUB (MPI) 1-1 PUB (MPI) 1-1 Volume: N/A Page No.: Topic: Sub Topic: Issue: Strategic Plan of the Public Utilities Board Public

PUB (MPI) August 5, 2016 2017 Rate Application Information Requests Round 1 PUB (MPI) 1-1 PUB (MPI) 1-1 Volume: N/A Page No.: Topic: Sub Topic: Issue: Strategic Plan of the Public Utilities Board Public

MANITOBA PUBLIC INSURANCE

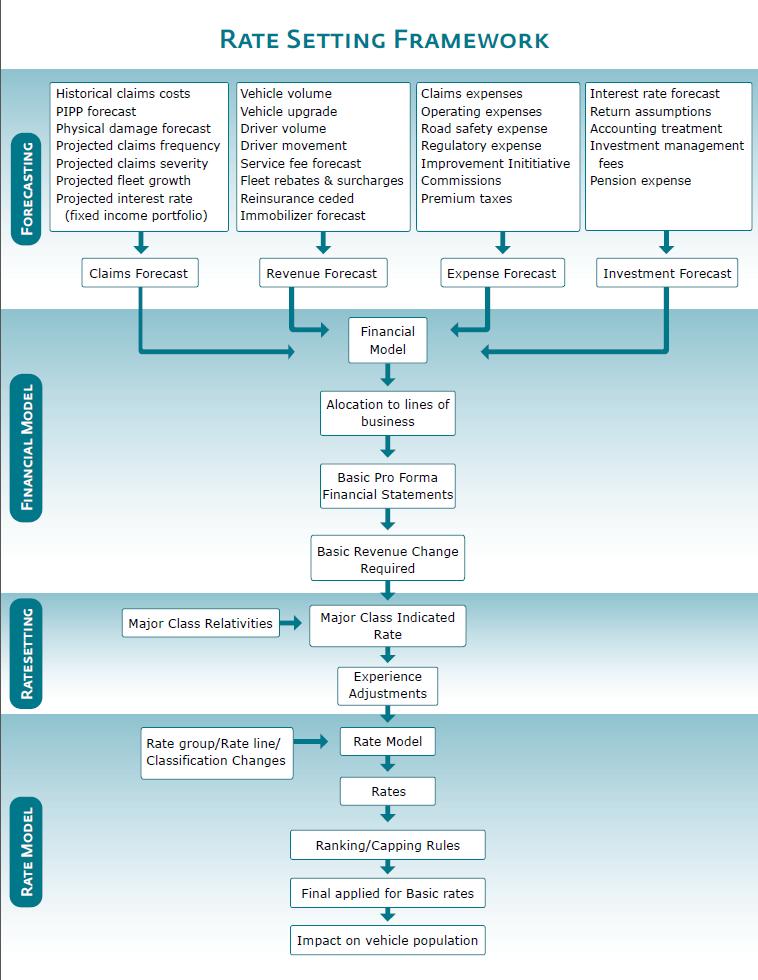

MANITOBA PUBLIC INSURANCE SM.1 THE BASIC INSURANCE RATE SETTING FRAMEWORK SM.1.1 Corporate Goals The Corporation s goals, as outlined in Manitoba Public Insurance s Corporate Strategic Plan, A1.7 Part

MANITOBA PUBLIC INSURANCE SM.1 THE BASIC INSURANCE RATE SETTING FRAMEWORK SM.1.1 Corporate Goals The Corporation s goals, as outlined in Manitoba Public Insurance s Corporate Strategic Plan, A1.7 Part

Genworth MI Canada Inc. Financial Supplement Third Quarter 2017

Genworth MI Canada Inc. Financial Supplement Third Quarter 2017 Table of Contents Page Non-IFRS Financial Measures 3 Selected Quarterly Financial Data 4 Selected Annual Financial Data 5 Insurance In-Force

Genworth MI Canada Inc. Financial Supplement Third Quarter 2017 Table of Contents Page Non-IFRS Financial Measures 3 Selected Quarterly Financial Data 4 Selected Annual Financial Data 5 Insurance In-Force

Direct Billing for Loss of Use. Rental Companies

Direct Billing for Loss of Use Rental Companies Version 1.5 February 23, 2017 Contents Introduction... 3 1. Rental Vehicle Rates... 4 2. Managing Loss of Use Costs... 4 2.1 Role of Rental Vehicle Company...

Direct Billing for Loss of Use Rental Companies Version 1.5 February 23, 2017 Contents Introduction... 3 1. Rental Vehicle Rates... 4 2. Managing Loss of Use Costs... 4 2.1 Role of Rental Vehicle Company...

Table of Contents Page

1 Table of Contents Page President and CEO s Message... 3 Management s Responsibility for Financial Reporting... 4 Sufficiency Discussion and Analysis... 5 Sufficiency Statement... 12 Notes to Sufficiency

1 Table of Contents Page President and CEO s Message... 3 Management s Responsibility for Financial Reporting... 4 Sufficiency Discussion and Analysis... 5 Sufficiency Statement... 12 Notes to Sufficiency

Insurance Corporation of British Columbia 2015/ /18 SERVICE PLAN

2015/16 2017/18 SERVICE PLAN For more information on the Insurance Corporation of British Columbia contact: In the Lower Mainland 604-661-2800 Elsewhere in B.C., Canada, or the U.S. 1-800-663-3051 Head

2015/16 2017/18 SERVICE PLAN For more information on the Insurance Corporation of British Columbia contact: In the Lower Mainland 604-661-2800 Elsewhere in B.C., Canada, or the U.S. 1-800-663-3051 Head

2 Page No. 3 List of Exhibits 5. 4 List of Undertakings Opening Remarks Opening Comments by CAC/MSOS Opening Comments by CMMG 214

1 2 3 MANITOBA PUBLIC UTILITIES BOARD 4 5 6 Re: MANITOBA PUBLIC INSURANCE COMPANY (MPI) 7 GENERAL RATE APPLICATION 8 FOR 2011/12 INSURANCE YEAR 9 10 11 12 13 Before Board Panel: 14 Graham Lane - Board

1 2 3 MANITOBA PUBLIC UTILITIES BOARD 4 5 6 Re: MANITOBA PUBLIC INSURANCE COMPANY (MPI) 7 GENERAL RATE APPLICATION 8 FOR 2011/12 INSURANCE YEAR 9 10 11 12 13 Before Board Panel: 14 Graham Lane - Board

MANITOBA PUBLIC INSURANCE

MANITOBA PUBLIC INSURANCE SM.5 PUB ORDERS, RECOMMENDATIONS & UNDERTAKINGS SM.5.1 Wildlife Loss Allocation In Order 122/10, the Public Utilities Board ordered that: The loss attribution rules provided in

MANITOBA PUBLIC INSURANCE SM.5 PUB ORDERS, RECOMMENDATIONS & UNDERTAKINGS SM.5.1 Wildlife Loss Allocation In Order 122/10, the Public Utilities Board ordered that: The loss attribution rules provided in

Financial Supplement Second Quarter 2018 July 31, 2018

Genworth MI Canada Inc. Financial Supplement Second Quarter 2018 July 31, 2018 Table of Contents Page Non-IFRS Financial Measures 3 Selected Quarterly Financial Data 4 Selected Annual Financial Data 5

Genworth MI Canada Inc. Financial Supplement Second Quarter 2018 July 31, 2018 Table of Contents Page Non-IFRS Financial Measures 3 Selected Quarterly Financial Data 4 Selected Annual Financial Data 5

Management s Discussion and Analysis

Management s Discussion and Analysis For the year ended December 31, 2013 As of December 31, 2013 The fourth quarter and full year results and prior-period comparative results for Genworth MI Canada Inc.

Management s Discussion and Analysis For the year ended December 31, 2013 As of December 31, 2013 The fourth quarter and full year results and prior-period comparative results for Genworth MI Canada Inc.

Genworth MI Canada Inc. Management s Discussion and Analysis For the first quarter ended March 31, 2011

Management s Discussion and Analysis For the first quarter ended March 31, 2011 May 2, 2011 ( Genworth Canada or the Company ) completed its initial public offering ( IPO ) on July 7, 2009. The full three-month

Management s Discussion and Analysis For the first quarter ended March 31, 2011 May 2, 2011 ( Genworth Canada or the Company ) completed its initial public offering ( IPO ) on July 7, 2009. The full three-month

November 30, 2018 Index MANITOBA HYDRO 2019/20 ELECTRIC RATE APPLICATION

MANITOBA HYDRO 0/0 ELECTRIC RATE APPLICATION November 0, 0 Index 0 0 0 INDEX.0 Overview and Reasons for the Requested Rate Increase....0 Manitoba Hydro s Financial Position and Outlook.... 0/ Actual Financial

MANITOBA HYDRO 0/0 ELECTRIC RATE APPLICATION November 0, 0 Index 0 0 0 INDEX.0 Overview and Reasons for the Requested Rate Increase....0 Manitoba Hydro s Financial Position and Outlook.... 0/ Actual Financial

CLOSING SUBMISSION VEHICLES FOR HIRE 2018 INTERIM APPLICATION JANUARY 5, 2018

CLOSING SUBMISSION VEHICLES FOR HIRE 2018 INTERIM APPLICATION JANUARY 5, 2018 Table of Contents Table of Contents... 1 1 Introduction... 2 2 Interim Application due to compressed implementation timeline...

CLOSING SUBMISSION VEHICLES FOR HIRE 2018 INTERIM APPLICATION JANUARY 5, 2018 Table of Contents Table of Contents... 1 1 Introduction... 2 2 Interim Application due to compressed implementation timeline...

Insurance Corporation of British Columbia 2014 ANNUAL SERVICE PLAN REPORT

2014 ANNUAL SERVICE PLAN REPORT For more information on the Insurance Corporation of British Columbia contact: In the Lower Mainland 604-661-2800 Elsewhere in B.C., Canada, or the U.S. 1-800-663-3051 Head

2014 ANNUAL SERVICE PLAN REPORT For more information on the Insurance Corporation of British Columbia contact: In the Lower Mainland 604-661-2800 Elsewhere in B.C., Canada, or the U.S. 1-800-663-3051 Head

THE INSURANCE COMPANY OF THE WEST INDIES LIMITED Bahamas Branch Financial Statements

Financial Statements Independent Auditors Report 1 2 Appointed Actuary Report to the Board of Directors 3 Statement of Financial Position 4 Statement of Comprehensive Income 5 Statement of Changes in Home

Financial Statements Independent Auditors Report 1 2 Appointed Actuary Report to the Board of Directors 3 Statement of Financial Position 4 Statement of Comprehensive Income 5 Statement of Changes in Home

EDUCATIONAL NOTE DYNAMIC CAPITAL ADEQUACY TESTING PROPERTY AND CASUALTY COMMITTEE ON SOLVENCY STANDARDS FOR FINANCIAL INSTITUTIONS

EDUCATIONAL NOTE Educational notes are not binding. They are provided to help actuaries perform actuarial work and may include eamples, eplanations and/or options. DYNAMIC CAPITAL ADEQUACY TESTING PROPERTY

EDUCATIONAL NOTE Educational notes are not binding. They are provided to help actuaries perform actuarial work and may include eamples, eplanations and/or options. DYNAMIC CAPITAL ADEQUACY TESTING PROPERTY

THE INSURANCE COMPANY OF THE WEST INDIES LIMITED Bahamas Branch Financial Statements

Financial Statements Independent Auditors Report 1 2 Appointed Actuary Report to the Board of Directors 3 Statement of Financial Position 4 Statement of Comprehensive Income 5 Statement of Changes in Home

Financial Statements Independent Auditors Report 1 2 Appointed Actuary Report to the Board of Directors 3 Statement of Financial Position 4 Statement of Comprehensive Income 5 Statement of Changes in Home

CENTRA GAS MANITOBA INC. 2013/14 GENERAL RATE APPLICATION VOLUME I INTEGRATED FINANCIAL FORECAST & ECONOMIC OUTLOOK. 4.0 Overview of Tab 4...

Tab Index January, 0 CENTRA GAS MANITOBA INC. 0/ GENERAL RATE APPLICATION VOLUME I INTEGRATED FINANCIAL FORECAST & ECONOMIC OUTLOOK INDEX.0 Overview of Tab.... Economic Outlook.... Integrated Financial

Tab Index January, 0 CENTRA GAS MANITOBA INC. 0/ GENERAL RATE APPLICATION VOLUME I INTEGRATED FINANCIAL FORECAST & ECONOMIC OUTLOOK INDEX.0 Overview of Tab.... Economic Outlook.... Integrated Financial

building trust. driving confidence.

~ building trust. driving confidence. January 29, British Columbia Utilities Commission Sixth Floor 900 Howe Street Vancouver, BC V6Z 2N3 Attention: Ms. Erica Hamilton, Commission Secretary and Director

~ building trust. driving confidence. January 29, British Columbia Utilities Commission Sixth Floor 900 Howe Street Vancouver, BC V6Z 2N3 Attention: Ms. Erica Hamilton, Commission Secretary and Director

Workplace Safety and Insurance Board

Workplace Safety and Insurance Board 2013 Sufficiency Report to Stakeholders Workplace Safety and Insurance Board Commission de la sécurité professionnelle et de l assurance contre les accidents du travail

Workplace Safety and Insurance Board 2013 Sufficiency Report to Stakeholders Workplace Safety and Insurance Board Commission de la sécurité professionnelle et de l assurance contre les accidents du travail

Report on Performance

Report on Performance As a Crown corporation, ICBC continually works to align with government goals and objectives. ICBC fulfilled the expectations outlined in the Mandate Letter (see Appendix C) to which

Report on Performance As a Crown corporation, ICBC continually works to align with government goals and objectives. ICBC fulfilled the expectations outlined in the Mandate Letter (see Appendix C) to which

CENTRA GAS MANITOBA INC. 2019/20 GENERAL RATE APPLICATION GAS OPERATIONS FINANCIAL FORECAST (CGM18) INDEX

INDEX") CENTRA GAS MANITOBA INC. 0/0 GENERAL RATE APPLICATION GAS OPERATIONS FINANCIAL FORECAST (CGM) Tab Index November 0, 0 0 0 0 INDEX.0 Overview of Tab.... Gas Operations Financial Forecast..... Key Economic

CENTRA GAS MANITOBA INC. 0/0 GENERAL RATE APPLICATION GAS OPERATIONS FINANCIAL FORECAST (CGM) Tab Index November 0, 0 0 0 0 INDEX.0 Overview of Tab.... Gas Operations Financial Forecast..... Key Economic

2018/ /21 SERVICE PLAN

2018/19 2020/21 SERVICE PLAN February 2018 For more information on the Insurance Corporation of British Columbia, contact: In the Lower Mainland 604-661-2800 Elsewhere in B.C., Canada, or the U.S. 1-800-663-3051

2018/19 2020/21 SERVICE PLAN February 2018 For more information on the Insurance Corporation of British Columbia, contact: In the Lower Mainland 604-661-2800 Elsewhere in B.C., Canada, or the U.S. 1-800-663-3051

YARMOUTH MUTUAL INSURANCE COMPANY Financial Statements For the year ended December 31, 2018

Financial Statements For the year ended Financial Statements For the year ended Table of Contents Page Independent Auditor's Report 2 Statement of Financial Position 4 Statement of Comprehensive Income

Financial Statements For the year ended Financial Statements For the year ended Table of Contents Page Independent Auditor's Report 2 Statement of Financial Position 4 Statement of Comprehensive Income

Order No. 130/17. December 4, 2017

MANITOBA PUBLIC INSURANCE CORPORATION (MPI OR THE CORPORATION): COMPULSORY 2018/2019 DRIVER AND VEHICLE INSURANCE PREMIUMS AND OTHER MATTERS BEFORE: Robert Gabor, Q.C., Chair Carol Hainsworth, Member Allan

MANITOBA PUBLIC INSURANCE CORPORATION (MPI OR THE CORPORATION): COMPULSORY 2018/2019 DRIVER AND VEHICLE INSURANCE PREMIUMS AND OTHER MATTERS BEFORE: Robert Gabor, Q.C., Chair Carol Hainsworth, Member Allan

Instruments-Classification. Measurement and Impairment. Credibility. Professionalism. AccountAbility

IFRS IFRS 139 Fair Financial Value Instruments-Classification Measurement and Impairment Credibility. Professionalism. AccountAbility Agenda Adoption permutations Scope of the standard Definitions Classification

IFRS IFRS 139 Fair Financial Value Instruments-Classification Measurement and Impairment Credibility. Professionalism. AccountAbility Agenda Adoption permutations Scope of the standard Definitions Classification

Erie Mutual Fire Insurance Company Consolidated Financial Statements For the year ended December 31, 2017

Consolidated Financial Statements For the year ended Consolidated Financial Statements For the year ended Table of Contents Page Independent Auditor's Report 2 Consolidated Statement of Financial Position

Consolidated Financial Statements For the year ended Consolidated Financial Statements For the year ended Table of Contents Page Independent Auditor's Report 2 Consolidated Statement of Financial Position

Own what you did - Regulatory Revisionism and the 2018/19 General Rate Application

Own what you did - Regulatory Revisionism and the 2018/19 General Rate Application CLOSING ARGUMENT OF THE PUBLIC INTEREST LAW CENTRE ON BEHALF OF THE CONSUMERS ASSOCIATION OF CANADA (MANITOBA BRANCH)

Own what you did - Regulatory Revisionism and the 2018/19 General Rate Application CLOSING ARGUMENT OF THE PUBLIC INTEREST LAW CENTRE ON BEHALF OF THE CONSUMERS ASSOCIATION OF CANADA (MANITOBA BRANCH)

MANITOBA PUBLIC INSURANCE 2017/18 ANNUAL FINANCIAL STATEMENTS MANITOBA PUBLIC INSURANCE

MANITOBA PUBLIC INSURANCE 2017/18 ANNUAL FINANCIAL STATEMENTS MANITOBA PUBLIC INSURANCE FOR THE FISCAL YEAR ENDED FEBRUARY 28, 2018 RESPONSIBILITY FOR FINANCIAL STATEMENTS The financial statements are

MANITOBA PUBLIC INSURANCE 2017/18 ANNUAL FINANCIAL STATEMENTS MANITOBA PUBLIC INSURANCE FOR THE FISCAL YEAR ENDED FEBRUARY 28, 2018 RESPONSIBILITY FOR FINANCIAL STATEMENTS The financial statements are

NOVA SCOTIA TEACHERS' PENSION PLAN

Financial Statements of NOVA SCOTIA TEACHERS' PENSION PLAN KPMG LLP Telephone (902) 492-6000 Chartered Accountants Fax (902) 429-1307 Purdy's Wharf Tower One Internet www.kpmg.ca 1959 Upper Water Street,

Financial Statements of NOVA SCOTIA TEACHERS' PENSION PLAN KPMG LLP Telephone (902) 492-6000 Chartered Accountants Fax (902) 429-1307 Purdy's Wharf Tower One Internet www.kpmg.ca 1959 Upper Water Street,

WORKERS COMPENSATION BOARD OF NOVA SCOTIA. Discussion Document. Funding Strategy 2013 FINANCIAL PROJECTIONS

WORKERS COMPENSATION BOARD OF NOVA SCOTIA Discussion Document Funding Strategy 2013 FINANCIAL PROJECTIONS 2014 2018 Prepared for consideration by the Finance and Investment Committee June 11, 2013 Date:

WORKERS COMPENSATION BOARD OF NOVA SCOTIA Discussion Document Funding Strategy 2013 FINANCIAL PROJECTIONS 2014 2018 Prepared for consideration by the Finance and Investment Committee June 11, 2013 Date:

Export Development Canada Quarterly Financial Report September 30, 2018 Unaudited TRADE UNLIMITED

Export Development Canada Quarterly Financial Report September 30, 2018 Unaudited TRADE UNLIMITED MANAGEMENT S DISCUSSION AND ANALYSIS TABLE OF CONTENTS MANAGEMENT S DISCUSSION AND ANALYSIS Overview...

Export Development Canada Quarterly Financial Report September 30, 2018 Unaudited TRADE UNLIMITED MANAGEMENT S DISCUSSION AND ANALYSIS TABLE OF CONTENTS MANAGEMENT S DISCUSSION AND ANALYSIS Overview...

YARMOUTH MUTUAL INSURANCE COMPANY Financial Statements For the year ended December 31, 2017

Financial Statements For the year ended Financial Statements For the year ended Table of Contents Page Independent Auditor's Report 2 Statement of Financial Position 3 Statement of Comprehensive Income

Financial Statements For the year ended Financial Statements For the year ended Table of Contents Page Independent Auditor's Report 2 Statement of Financial Position 3 Statement of Comprehensive Income

Financial Statements of. FACILITY ASSOCIATION RESIDUAL MARKET SEGMENT and UNINSURED AUTOMOBILE FUNDS

Financial Statements of FACILITY ASSOCIATION RESIDUAL MARKET SEGMENT and Table of Contents October 31, 2017 Independent Auditor s Report 1 Appointed Actuary s Report 3 Statement of Financial Position 4

Financial Statements of FACILITY ASSOCIATION RESIDUAL MARKET SEGMENT and Table of Contents October 31, 2017 Independent Auditor s Report 1 Appointed Actuary s Report 3 Statement of Financial Position 4

February 11, Review of Alberta Automobile Insurance Experience. as of June 30, 2004

February 11, 2005 Review of Alberta Automobile Insurance Experience as of June 30, 2004 Contents 1. Introduction and Executive Summary...1 Data and Reliances...2 Limitations...3 2. Summary of Findings...4

February 11, 2005 Review of Alberta Automobile Insurance Experience as of June 30, 2004 Contents 1. Introduction and Executive Summary...1 Data and Reliances...2 Limitations...3 2. Summary of Findings...4

Treasury Board Secretariat. Follow-Up on VFM Section 3.07, 2015 Annual Report RECOMMENDATION STATUS OVERVIEW

Chapter 1 Section 1.07 Treasury Board Secretariat Infrastructure Planning Follow-Up on VFM Section 3.07, 2015 Annual Report Chapter 1 Follow-Up Section 1.07 RECOMMENDATION STATUS OVERVIEW # of Status of

Chapter 1 Section 1.07 Treasury Board Secretariat Infrastructure Planning Follow-Up on VFM Section 3.07, 2015 Annual Report Chapter 1 Follow-Up Section 1.07 RECOMMENDATION STATUS OVERVIEW # of Status of

Regulatory Impact Analysis: Cost Recovery Impact Statement - Overview of Required Information 1

ACC Levies for 2019/20 and 2020/21 Cost Recovery Impact Statement Agency Disclosure Statement This Cost Recovery Impact Statement has been prepared by the Ministry of Business, Innovation and Employment.

ACC Levies for 2019/20 and 2020/21 Cost Recovery Impact Statement Agency Disclosure Statement This Cost Recovery Impact Statement has been prepared by the Ministry of Business, Innovation and Employment.

Manitoba Public Insurance Impact of IAS 19R

AI.8 IFRS - Impact of IAS 19R Manitoba Public Insurance Impact of IAS 19R May 15, 2012 AI.8 IFRS - Impact of IAS 19R Table of contents 1.0 Executive summary... 1 2.0 Analysis of significant differences

AI.8 IFRS - Impact of IAS 19R Manitoba Public Insurance Impact of IAS 19R May 15, 2012 AI.8 IFRS - Impact of IAS 19R Table of contents 1.0 Executive summary... 1 2.0 Analysis of significant differences

Financial Statements of. FACILITY ASSOCIATION RESIDUAL MARKET SEGMENT and UNINSURED AUTOMOBILE FUNDS

Financial Statements of FACILITY ASSOCIATION RESIDUAL MARKET SEGMENT and Table of Contents October 31, 2016 Independent Auditor s Report 1 Appointed Actuary s Report 3 Statement of Financial Position 4

Financial Statements of FACILITY ASSOCIATION RESIDUAL MARKET SEGMENT and Table of Contents October 31, 2016 Independent Auditor s Report 1 Appointed Actuary s Report 3 Statement of Financial Position 4

September 9, 2015 Information Requests Round 2 BW (MPI) 2-1

2-1") BW (MPI) BW (MPI) 2-1 BW (MPI) 2-1 Volume: Topic: Sub Topic: Issue: III, Loss Prevention and Implementation plan Priority Setting Page No.: Claims costs related fatalities and injuries A1.13 Appx 6 p 43

BW (MPI) BW (MPI) 2-1 BW (MPI) 2-1 Volume: Topic: Sub Topic: Issue: III, Loss Prevention and Implementation plan Priority Setting Page No.: Claims costs related fatalities and injuries A1.13 Appx 6 p 43

PUBLIC SERVICE SUPERANNUATION PLAN

Financial Statements of PUBLIC SERVICE SUPERANNUATION PLAN 2016-2017 Nova Scotia Public Service Superannuation Plan Annual Report 20 KPMG LLP Telephone (902) 492-6000 Suite 1500 Purdy s Wharf Tower 1 Fax

Financial Statements of PUBLIC SERVICE SUPERANNUATION PLAN 2016-2017 Nova Scotia Public Service Superannuation Plan Annual Report 20 KPMG LLP Telephone (902) 492-6000 Suite 1500 Purdy s Wharf Tower 1 Fax

Page 1 MANITOBA PUBLIC UTILITIES BOARD. Re: MANITOBA PUBLIC INSURANCE COMPANY GENERAL RATE APPLICATION FOR 2009/10 INSURANCE YEAR. Before Board Panel:

Page MANITOBA PUBLIC UTILITIES BOARD Re: MANITOBA PUBLIC INSURANCE COMPANY GENERAL RATE APPLICATION FOR 0/ INSURANCE YEAR Before Board Panel: Graham Lane Eric Jorgensen Alain Molgat HELD AT: - Board Chairman

Page MANITOBA PUBLIC UTILITIES BOARD Re: MANITOBA PUBLIC INSURANCE COMPANY GENERAL RATE APPLICATION FOR 0/ INSURANCE YEAR Before Board Panel: Graham Lane Eric Jorgensen Alain Molgat HELD AT: - Board Chairman

BRANDON UNIVERSITY RETIREMENT PLAN ANNUAL REPORT Incorporating the Annual Financial Statements

BRANDON UNIVERSITY RETIREMENT PLAN ANNUAL REPORT - 2016 Incorporating the Annual Financial Statements June 2017 Dear Member: Enclosed is a detailed report on the operation of the Brandon University Retirement

BRANDON UNIVERSITY RETIREMENT PLAN ANNUAL REPORT - 2016 Incorporating the Annual Financial Statements June 2017 Dear Member: Enclosed is a detailed report on the operation of the Brandon University Retirement

TESTIMONY. Manitoba Public Insurance 2017/18 GRA. Valter Viola President, Holland Park

TESTIMONY Manitoba Public Insurance 2017/18 GRA Valter Viola President, Holland Park vviola@hollandparkrisk.com 416 819 2307 1. OVERVIEW 2. REMEDIES SYMPTOMS VS PROBLEMS 3 TERMINOLOGY 4 TRUTHS AND CONSEQUENCES

TESTIMONY Manitoba Public Insurance 2017/18 GRA Valter Viola President, Holland Park vviola@hollandparkrisk.com 416 819 2307 1. OVERVIEW 2. REMEDIES SYMPTOMS VS PROBLEMS 3 TERMINOLOGY 4 TRUTHS AND CONSEQUENCES

Financial Statements of FACILITY ASSOCIATION ONTARIO RISK SHARING POOL

Financial Statements of FACILITY ASSOCIATION Table of Contents October 31, 2017 Independent Auditor s Report 1 Appointed Actuary s Report 3 Statement of Financial Position 4 Statement of Operations 5 Statement

Financial Statements of FACILITY ASSOCIATION Table of Contents October 31, 2017 Independent Auditor s Report 1 Appointed Actuary s Report 3 Statement of Financial Position 4 Statement of Operations 5 Statement

other information alberta teachers retirement fund board Alberta Teachers Retirement Fund Board financial statements Education Annual Report

Alberta Teachers Retirement Fund Board financial statements 287 Alberta Teachers Retirement Fund Board Teachers Pension Plan and Private School Teachers Pension Plan Financial Statements August 31, 2016

Alberta Teachers Retirement Fund Board financial statements 287 Alberta Teachers Retirement Fund Board Teachers Pension Plan and Private School Teachers Pension Plan Financial Statements August 31, 2016

Quarterly Financial Report

Quarterly Financial Report FIRST QUARTER March 3, 208 (Unaudited) Management s Discussion and Analysis TABLE OF CONTENTS MANAGEMENT S DISCUSSION AND ANALYSIS... 3 OVERVIEW... 3 THE OPERATING ENVIRONMENT

Quarterly Financial Report FIRST QUARTER March 3, 208 (Unaudited) Management s Discussion and Analysis TABLE OF CONTENTS MANAGEMENT S DISCUSSION AND ANALYSIS... 3 OVERVIEW... 3 THE OPERATING ENVIRONMENT

NORTH WATERLOO FARMERS MUTUAL INSURANCE COMPANY

Consolidated Financial Statements of NORTH WATERLOO FARMERS MUTUAL INSURANCE COMPANY (Subsequently amalgamated to form Heartland Farm Mutual Inc.) NORTH WATERLOO FARMERS MUTUAL INSURANCE COMPANY CONSOLIDATED

Consolidated Financial Statements of NORTH WATERLOO FARMERS MUTUAL INSURANCE COMPANY (Subsequently amalgamated to form Heartland Farm Mutual Inc.) NORTH WATERLOO FARMERS MUTUAL INSURANCE COMPANY CONSOLIDATED

ORGANIZATION AND STAFF DEVELOPMENT - AN AGENCY OF THE SPECIAL OPERATING AGENCIES FINANCING AUTHORITY

ORGANIZATION AND STAFF DEVELOPMENT - AN AGENCY OF THE SPECIAL OPERATING AGENCIES FINANCING AUTHORITY Financial Statements Financial Statements Contents Management's Responsibility for Financial Reporting

ORGANIZATION AND STAFF DEVELOPMENT - AN AGENCY OF THE SPECIAL OPERATING AGENCIES FINANCING AUTHORITY Financial Statements Financial Statements Contents Management's Responsibility for Financial Reporting

The Alberta Lawyers Insurance Exchange. Financial Statements December 31, 2017

The Alberta Lawyers Insurance Exchange Financial Statements December 31, 2017 Statement of financial position As at December 31, 2017 Assets 2017 2016 Cash and cash equivalents (note 2) 4,086,884 37,241

The Alberta Lawyers Insurance Exchange Financial Statements December 31, 2017 Statement of financial position As at December 31, 2017 Assets 2017 2016 Cash and cash equivalents (note 2) 4,086,884 37,241

Property & Casualty Dynamic Capital Adequacy Testing and Stress Testing The Canadian Framework

Property & Casualty Dynamic Capital Adequacy Testing and Stress Testing The Canadian Framework Caribbean Actuarial Conference December 5, 2009 Xavier Bénarosch, FCAS, FCIA, CFA, FRM Table of contents Concept

Property & Casualty Dynamic Capital Adequacy Testing and Stress Testing The Canadian Framework Caribbean Actuarial Conference December 5, 2009 Xavier Bénarosch, FCAS, FCIA, CFA, FRM Table of contents Concept

BRANDON UNIVERSITY RETIREMENT PLAN ANNUAL REPORT Incorporating the Annual Financial Statements

BRANDON UNIVERSITY RETIREMENT PLAN ANNUAL REPORT - 2017 Incorporating the Annual Financial Statements June 2018 Dear Member: Enclosed is a detailed report on the operation of the Brandon University Retirement

BRANDON UNIVERSITY RETIREMENT PLAN ANNUAL REPORT - 2017 Incorporating the Annual Financial Statements June 2018 Dear Member: Enclosed is a detailed report on the operation of the Brandon University Retirement

The WCB s Funding Policy:

Discussion Paper The WCB s Funding Policy The WCB s Funding Policy: Recommended Changes to the WCB s Funding Policy & Call for Feedback Page 1 A. Introduction/Abstract The purpose of this discussion paper

Discussion Paper The WCB s Funding Policy The WCB s Funding Policy: Recommended Changes to the WCB s Funding Policy & Call for Feedback Page 1 A. Introduction/Abstract The purpose of this discussion paper

Status of Women Canada Statement of Management Responsibility

Status of Women Canada Statement of Management Responsibility Responsibility for the compilation, content, and presentation of the accompanying future-oriented statement of operations for the years ending

Status of Women Canada Statement of Management Responsibility Responsibility for the compilation, content, and presentation of the accompanying future-oriented statement of operations for the years ending

Co-operators General Insurance Company. Management s Discussion and Analysis

Co-operators General Insurance Company Management s Discussion and Analysis For the third quarter ended September 30, Co-operators General Insurance Company Management s Discussion and Analysis For the

Co-operators General Insurance Company Management s Discussion and Analysis For the third quarter ended September 30, Co-operators General Insurance Company Management s Discussion and Analysis For the

Rental Vehicle Insurance

Rental Vehicle Insurance Save on rentals in Manitoba, Canada and the United States Get the most protection Control your risks When you rent or borrow a vehicle, think about the insurance protection you

Rental Vehicle Insurance Save on rentals in Manitoba, Canada and the United States Get the most protection Control your risks When you rent or borrow a vehicle, think about the insurance protection you

WORKPLACE SAFETY AND INSURANCE BOARD FUNDING POLICY

Policy The Workplace Safety and Insurance Act, 1997 (WSIA) requires the Workplace Safety and Insurance Board (WSIB) to maintain the insurance fund such that the amount in the fund is sufficient to meet

Policy The Workplace Safety and Insurance Act, 1997 (WSIA) requires the Workplace Safety and Insurance Board (WSIB) to maintain the insurance fund such that the amount in the fund is sufficient to meet

Report on Performance

The goal of these and many other ongoing efforts is to make insurance more affordable for British Columbians, by addressing rising claims costs and improving rate fairness. Report on Performance As a Crown

The goal of these and many other ongoing efforts is to make insurance more affordable for British Columbians, by addressing rising claims costs and improving rate fairness. Report on Performance As a Crown

Second Quarter Report FRESHWATER FISH MARKETING CORPORATION

Second Quarter Report FRESHWATER FISH MARKETING CORPORATION For the period ended Statement of Management Responsibility by Senior Officials Management is responsible for the preparation and fair presentation

Second Quarter Report FRESHWATER FISH MARKETING CORPORATION For the period ended Statement of Management Responsibility by Senior Officials Management is responsible for the preparation and fair presentation

Financialfacts Life participating life insurance PERFORMANCE STRENGTH ACCOUNTABILITY

2016 Great-West Financialfacts Life participating life insurance PERFORMANCE STRENGTH ACCOUNTABILITY This guide provides key financial facts about the performance, strength and management of the Great-West

2016 Great-West Financialfacts Life participating life insurance PERFORMANCE STRENGTH ACCOUNTABILITY This guide provides key financial facts about the performance, strength and management of the Great-West