Annual Report Anguilla Electricity Company Limited. Selected Financial Information. Developing Customer Satisfaction. Focusing on Employees

|

|

|

- Claribel Burke

- 5 years ago

- Views:

Transcription

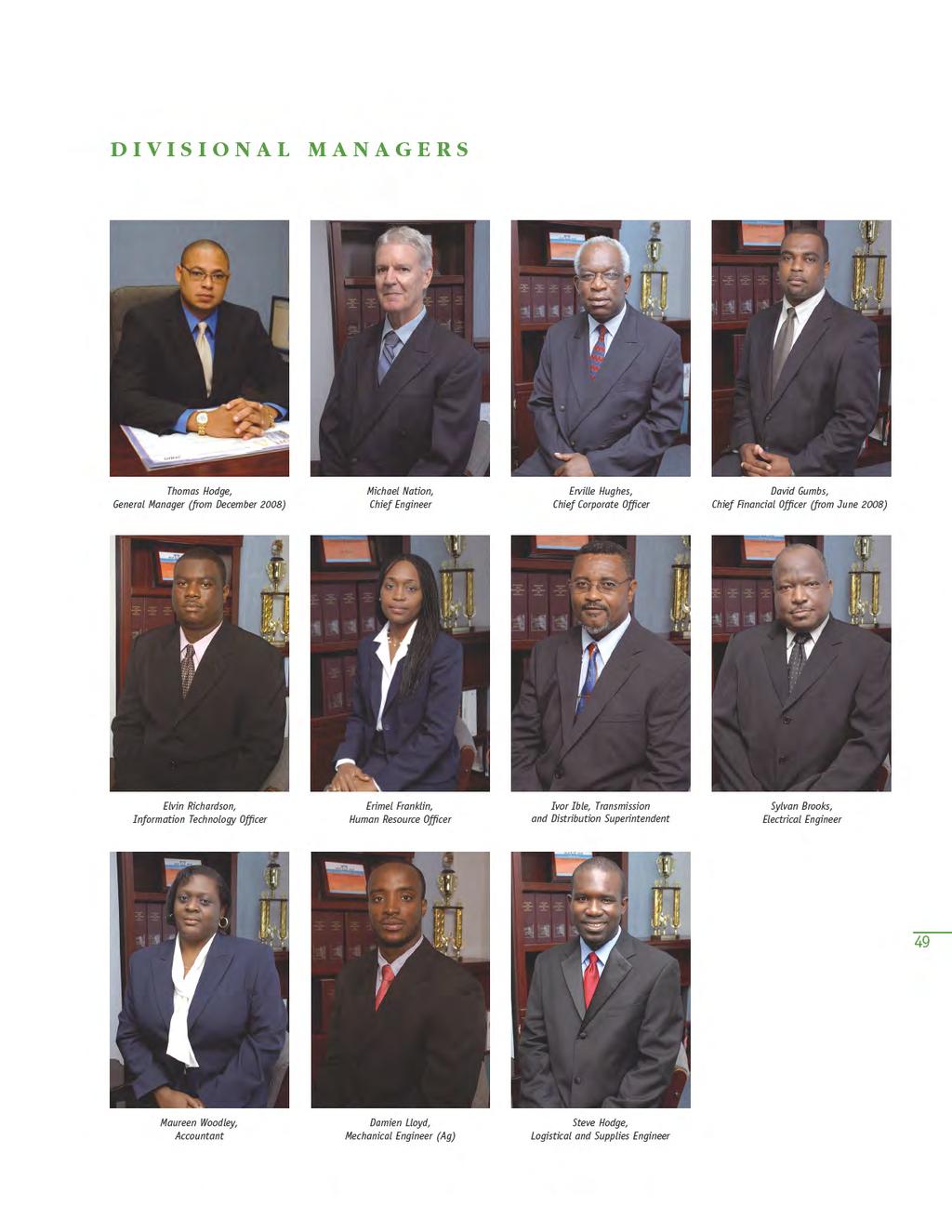

1 Annual Report 2008 Anguilla Electricity Company Limited Selected Financial Information Developing Customer Satisfaction Focusing on Employees Strategies for Success Corporate Information

2

3

4

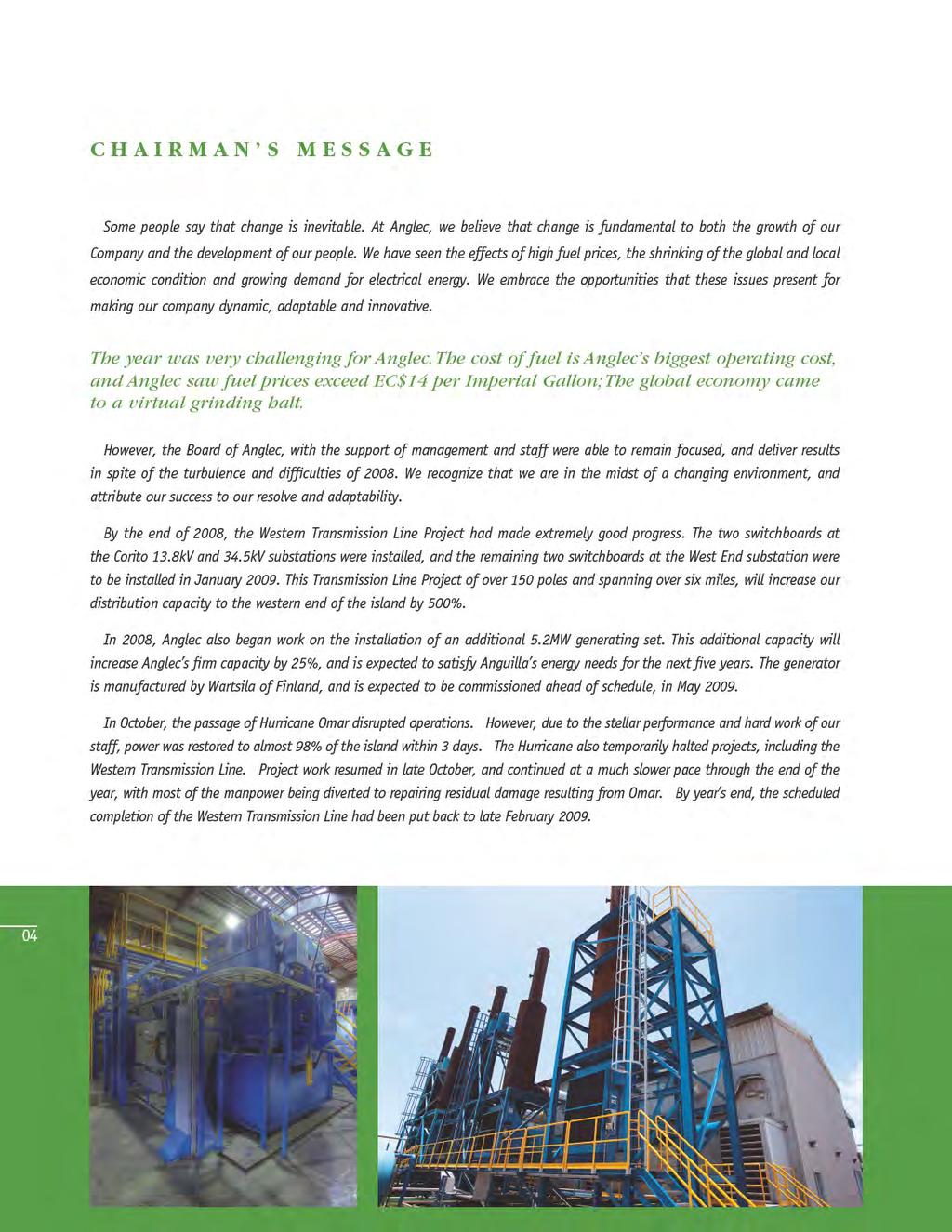

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

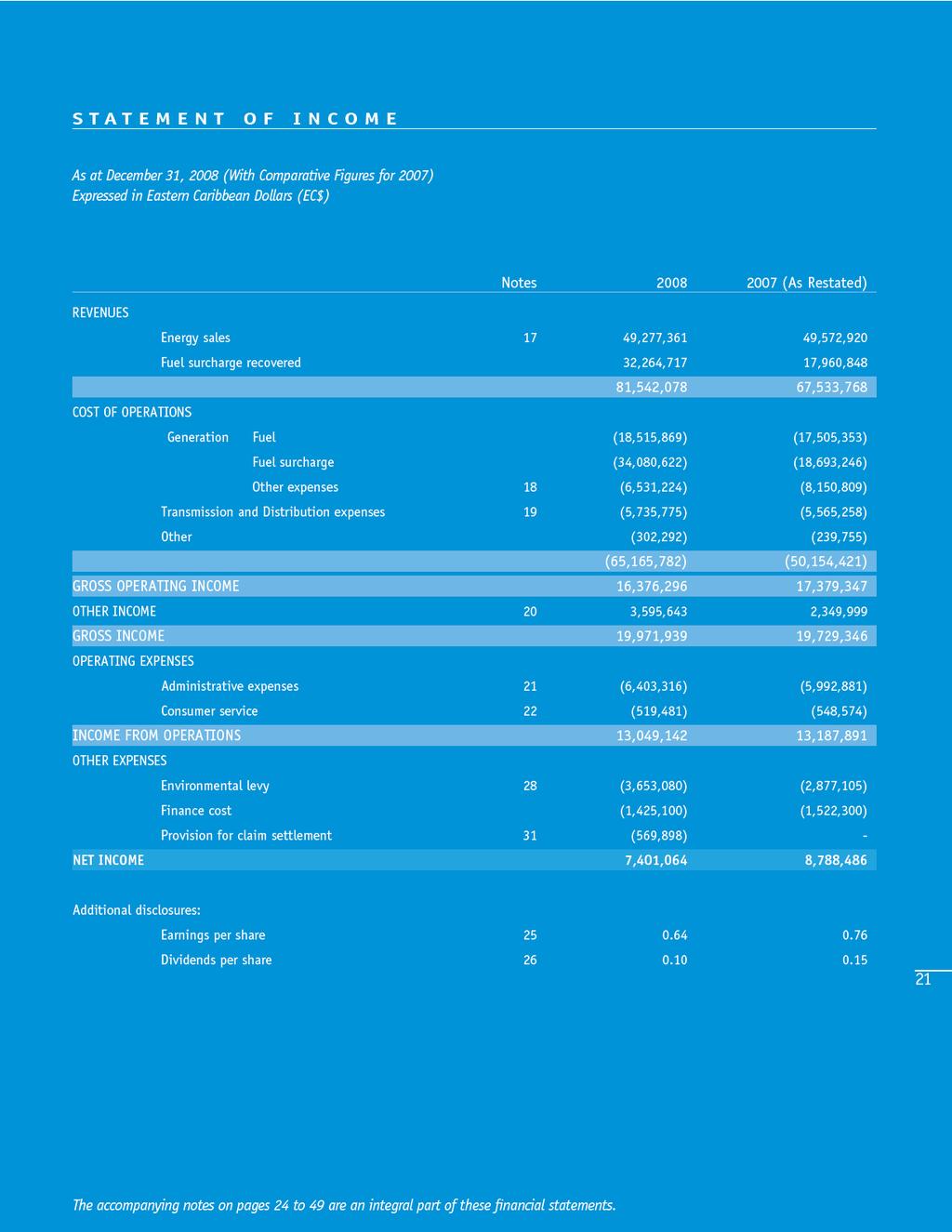

21

22

23

24 NOTES TO THE FINANCIAL STATEMENTS December 31, 2008 (With Comparative Figures for 2007) Expressed in Eastern Caribbean Dollars (EC$) 1. Reporting entity The Anguilla Electricity Company Limited (the Company) was incorporated in Anguilla on 11 January 1991 under the Companies Act and is governed by the Electricity Act, 1991, as amended, and operates in The Valley, Anguilla. The Company has an exclusive public supplier's license to generate, transmit and distribute electricity on the island of Anguilla for a period of fifty years from 1 April The Company's registered office address is Hannah Waiver House, The Valley, Anguilla, B.W.I. 2. Basis of preparation (a) Statement of compliance The financial statements of the Company have been prepared in accordance with International Financial Reporting Standards (IFRS) and interpretations issued by the International Accounting Standards Board (IASB). The financial statements were authorized for issue by the Board of Directors on July 20, 2009 (b) Basis of measurement The financial statements of the Company have been prepared on the historical cost basis. (c) Functional and presentation currency These financial statements are presented in Eastern Caribbean Dollars (EC Dollars), which is the Company's functional and presentation currency. Except as otherwise indicated, financial information presented in EC Dollars has been rounded to the nearest dollar. (d) Use of estimates and judgements The preparation of the financial statements in conformity with IFRS requires management to make judgments, estimates and assumptions that affect the application of accounting policies and the reported amounts of assets, liabilities, income and expenses. Actual results may differ from these estimates. Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the period in which the estimates are revised if the revision affects only that period or in the period of the revision and future periods if the revision affects both current and future periods. In particular, information about significant areas of estimation, uncertainty and critical judgments in applying accounting policies that have the most significant effect on the amount recognized in the financial statements is included in the following notes: Note 3 (b) Valuation of financial instruments Note 3 (d) Impairment of assets 24 Note 3 (f) Estimation of unbilled sales and fuel charges Note 3 (g) Measurement of defined benefit obligation Note 5 Determination of fair values 3. Summary of significant accounting policies The accounting policies set out below have been applied consistently by the Company to all periods presented in these financial statements, unless otherwise stated.

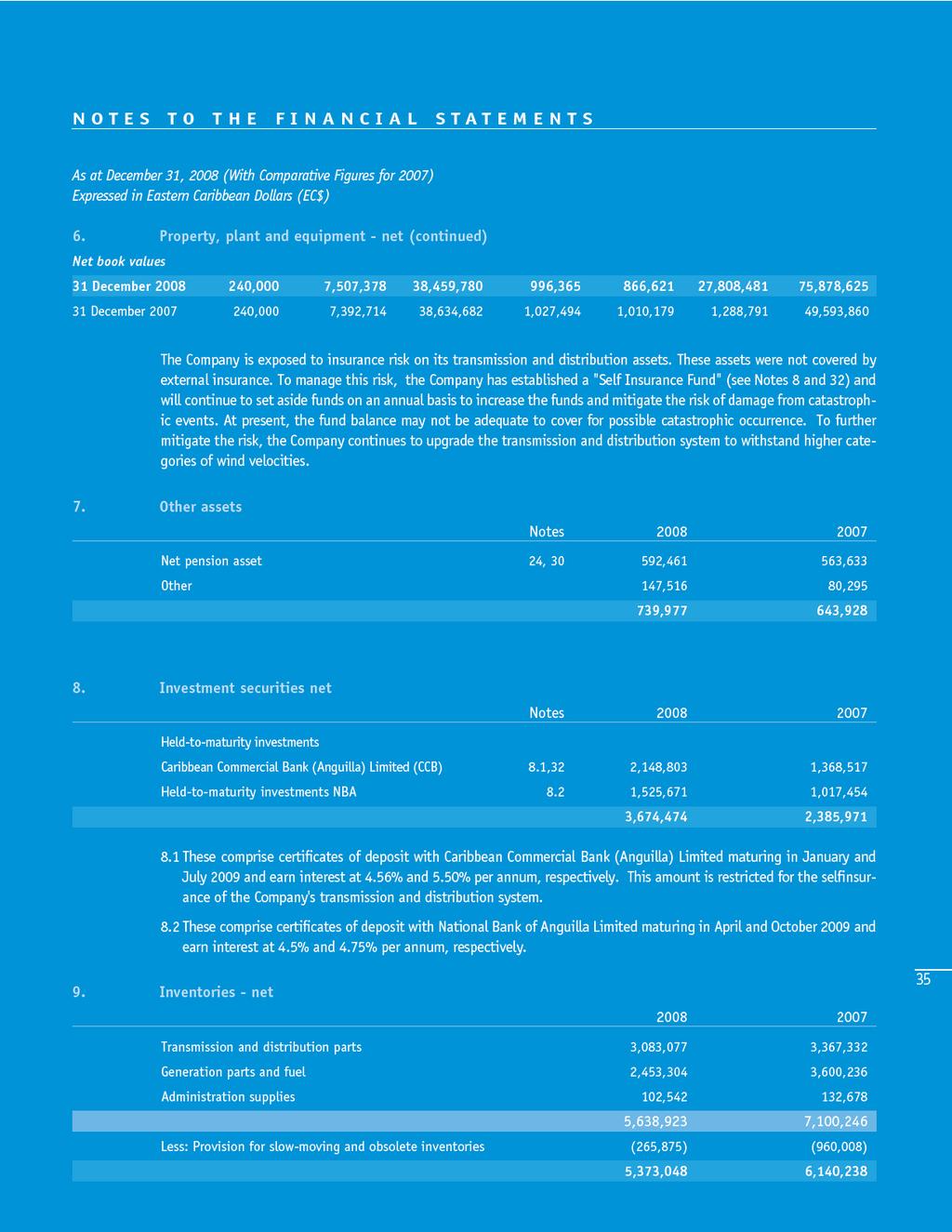

25 NOTES TO THE FINANCIAL STATEMENTS December 31, 2008 (With Comparative Figures for 2007) Expressed in Eastern Caribbean Dollars (EC$) 3. Summary of significant accounting policies (continued) (a) Property, plant and equipment i. Recognition and measurement Items of property, plant and equipment are measured at cost less accumulated depreciation and impairment losses, if any. Cost includes expenditures that are directly attributable to the acquisition of the asset. The cost of self-constructed assets includes the cost of materials and direct labor, any other costs directly attributable to bringing the asset to a working condition for its intended use, and the costs of dismantling and removing the items and restoring the site on which they are located. Purchased software that is integral to the functionality of the related equipment is capitalised as part of that equipment. When parts of an item of property, plant and equipment have different useful lives, they are accounted for as separate items (major components) of property, plant and equipment. Gains and losses on disposal of an item of property, plant and equipment are determined by comparing the proceeds from disposal with the carrying amount of property, plant and equipment and are recognized net within "Other income" in the statement of income. ii. Subsequent costs The cost of replacing part of an item of property, plant and equipment is recognized in the carrying amount of the item if it is probable that the future economic benefits embodied within the part will flow to the Company and its cost can be measured reliably. The costs of the day-to-day servicing of property, plant and equipment are recognized in the statement of income as incurred. iii. Depreciation Depreciation is recognized in the statement of income on a straight line basis over the estimated useful lives of each part of an item of property, plant and equipment. Land is not depreciated. The estimated useful lives for the current and comparative periods are as follows: Buildings Plant and machinery Furniture, fittings and equipment Motor vehicles 40 years years 5 years 3-5 years Depreciation methods, useful lives and residual values are reassessed at each balance sheet date. (b) Financial instruments i. Non-derivative financial instruments Non-derivative financial instruments comprise investment securities, trade and other receivables, cash and cash equivalents, borrowings, trade and other payables and bank overdraft. Non-derivative financial instruments are recognized initially at fair value plus, for instruments not at fair value through profit or loss, any directly attributable transaction costs. Subsequent to initial recognition, non-derivative financial instruments are measured as described below: Investments securities Held-to-maturity investments are nonderivative assets with fixed or determinable payments and fixed maturity that the Company has the positive intent and ability to hold to maturity, and which are not designated at fair value through profit or loss or available-for-sale. 25

26 NOTES TO THE FINANCIAL STATEMENTS December 31, 2008 (With Comparative Figures for 2007) Expressed in Eastern Caribbean Dollars (EC$) Summary of significant accounting policies (continued) (b) Financial instruments (continued) Held-to-maturity investments are carried at amortized cost using the effective interest method. Any sale or reclassification of a significant amount of held-to-maturity investments not close to their maturity would result in the reclassification of all held-to-maturity investments as available-for-sale, and prevent the Company from classifying securities as held-to-maturity for the current and the following two financial years. Trade and other receivables Trade and other receivables are initially measured at fair value plus incremental direct transaction costs, and subsequently measured at their amortized cost less provision for impairment. A provision for impairment of trade receivables is established when there is objective evidence that the Company will not be able to collect all amounts due according to the original terms of the receivable. The amount of provision is the difference between the asset's carrying amount and the present value of estimated future cash flows, discounted at the effective interest rate. The amount of provision is recognized in the statement of income. Trade receivables, being short-term, are not discounted. Cash and cash equivalents Cash and cash equivalents comprise cash balances on hand and short-term highly liquid investments with maturities of three months or less when purchased and that are subject to a significant risk of change in value. Bank overdrafts that are repayable on demand and form an integral part of the Company's cash management are included as a component of cash and cash equivalents for the purpose of the statement of cash flows. Borrowings Borrowings are recognized initially at cost, net of any transaction costs incurred. Subsequent to initial recognition, borrowings are stated at amortized cost. Trade and other payables Trade and other payables are stated at their cost, which is the fair value of the consideration to be paid in the future for goods and services received whether or not billed to the Company. Others Other non-derivative financial instruments are measured at cost less any impairment losses. ii. Share capital Ordinary shares Ordinary shares are classified as equity. Incremental costs directly attributable to the issue of ordinary shares and share options are recognized as a deduction from equity. Treasury shares When share capital recognized as equity is repurchased by the Company, the amount of the consideration paid, including directly attributable costs, is recognized as a deduction from equity. Repurchased shares are classified as treasury shares and presented as a deduction from total shareholders' equity. When treasury shares are sold or reissued subsequently, the amount received is recognized as an increase in equity, and the resulting surplus or deficit on the transaction is transferred to/from retained earnings. (c) Inventories Inventories are stated at the lower of cost and net realisable value. Cost is determined on a weighted average basis. Net realizable value is the estimated selling price in the ordinary course of business, less estimated costs of completion and selling expenses. An allowance is made for obsolete and slow moving items.

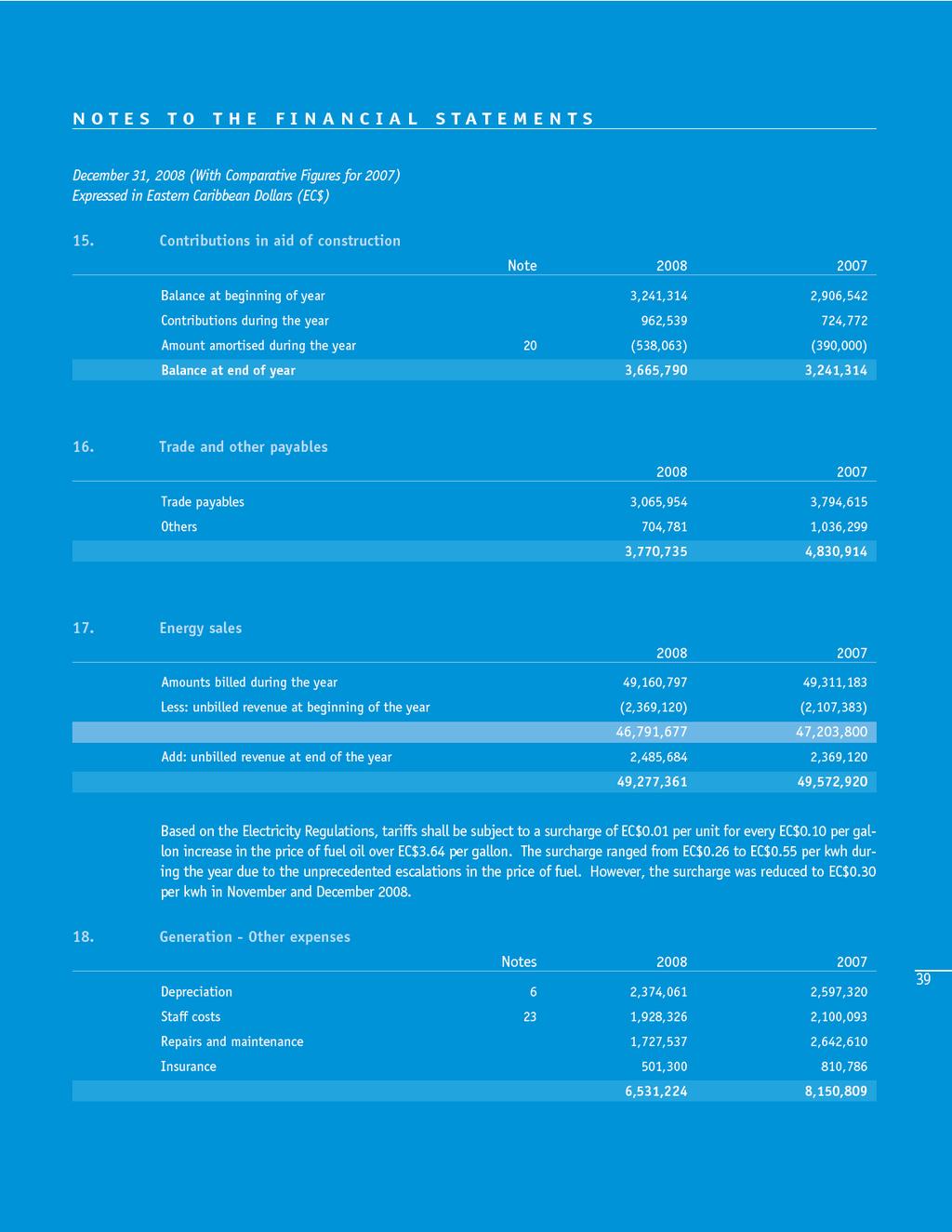

27 NOTES TO THE FINANCIAL STATEMENTS As at December 31, 2008 (With Comparative Figures for 2007) Expressed in Eastern Caribbean Dollars (EC$) 3. Summary of significant accounting policies (continued) (d) Impairment i. Financial assets A financial asset is assessed at each reporting date to determine whether there is any objective evidence that it is impaired. A financial asset is considered to be impaired if objective evidence indicates that one or more events have had a negative effect on the estimated future cash flows of that asset. An impairment loss in respect of a financial asset measured at amortized cost is calculated as the difference between its carrying amount, and the present value of the estimated future cash flows discounted at the original effective interest rate. Individually significant financial assets are tested for impairment on an individual basis. The remaining financial assets are assessed collectively in groups that share similar credit risk characteristics. All impairment losses are recognized in the statement of income. An impairment is reversed if the reversal can be related objectively to an event occuring after the impairment loss was recognized. For financial assets measured at amortized cost, the reversal is recognized in the statement of income. ii. Non-financial assets The carrying value of the Company's non-financial assets, other than inventories, are reviewed at each balance sheet date to determine whether there is any indication of impairment. If any such indication exists, the asset's recoverable amount is estimated. An impairment loss is recognized whenever the carrying amount of an asset exceeds its recoverable amount. Impairment losses are recognized in the statement of income. The recoverable amount of an asset or cash-generating unit is the greater of its value in use and its fair value less costs to sell. In assessing value in use, the estimated future cash flows are discounted to their present value using a pretax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset. For the purpose of impairment testing, assets are grouped together into the smallest group of assets that generates cash inflows from continuing use that are largely independent of the cash inflows of other assets or groups of assets ("the cash-generating unit"). An impairment loss is recognized whenever the carrying amount of an asset or its cash-generating unit exceeds its estimated recoverable amount. Impairment losses are recognized in the statement of income. Impairment loss recognized in prior periods are assessed at each reporting date for any indications that the loss has decreased or no longer exists. An impairment loss is reversed if there has been a change in the estimates used to determine the recoverable amount. An impairment loss is reversed only to the extent that the asset's carrying amount does not exceed the carrying amount that would have been determined, net of depreciation or amortization, if no impairment loss had been recognized. (e) Contributions in aid of construction Contributions in aid of construction are amounts received from customers towards the cost of providing services. These amounts are amortized over the estimated service lives of the related assets over the same period. Contributions received in respect of unfinished construction are amortized once the assets are placed in service. 27 (f) Revenue i. Sale of energy Revenue from the sale of electricity is recognized in the statement of income based on consumption recorded by monthly meter readings, with due adjustment made for unread consumption at year-end by apportioning the consumption of the following month.

28 A N G U I L L A E L E C T R I C I T Y C O M P A N Y L I M I T E D NOTES TO THE FINANCIAL STATEMENTS As at December 31, 2008 (With Comparative Figures for 2007) Expressed in Eastern Caribbean Dollars (EC$) 3. Summary of significant accounting policies (continued) In addition to the normal tariff rates charged for energy sales, a fuel surcharge is calculated which is based on the difference between the cost of fuel used to generate energy sales in the current month and the average fuel price for the succeeding year preceding January of the current year. The surcharge is recovered by applying the month's surcharge rate to units billed in the following month. ii. Interest income Interest income is recognized on a time-proportion basis using the effective interest method. (g) Employee benefits i. Defined contribution plan A defined benefit plan is a post-employment benefit plan other than a defined contribution plan. The Company operates a defined benefit pension for senior management. The plan is a multi-employer scheme with five contributing employers. The other participating companies are Montserrat Electricity Services Ltd., St. Lucia Mortgage Finance Company Ltd., St. Lucia Electricity Services Limited and St. Vincent Electricity Services Ltd. Multi-employers' schemes pool the assets contributed by the various enterprises that are not under common control, and use the assets to provide benefits to employees of more than one enterprise on the basis that contributed and benefit levels are determined without regard to the identity of the enterprise that employs the employees concerned. The Company's net obligation in respect of its defined benefit plan is calculated by estimating the amount of future benefit that employees have earned in return for their service in the current and prior periods; that benefit is discounted to determine its present value, and any unrecognized past service costs and the fair value of any plan assets are deducted. The calculation is performed by a qualified actuary using the projected unit credit method. When the benefits of a plan are improved, the portion of the increased benefit relating to past service by employees is recognized in the statement of income on a straight-line basis over the average period until the benefits become vested. To the extent that the benefits vest immediately, the expense is recognized immediately in the statement of income. In respect of actuarial gains and losses that arise in calculating the Company's obligation in respect of a plan, to the extent that any cumulative unrecognized actuarial gain or loss exceeds ten percent (10%) of the greater of the present value of the defined benefit obligation and the fair value of plan assets, that portion is recognized in the statement of income over the expected average remaining working lives of the employees participating in the plan. Otherwise, the actuarial gain or loss is not recognized. When the calculation results in a benefit to the Company, the recognized asset is limited to the net total of any unrecognized actuarial losses and past service costs and the present value of any future refunds from the plan or reductions in future contributions to the plan. 28 (h) Finance cost All interest and other costs incurred in connection with borrowings are expensed as incurred as part of finance costs. Borrowing costs that are directly attributable to the acquisition, construction or production of qualifying assets are capitalized as a part of the cost of the asset. (i) Earnings per share Earnings per share have been calculated by dividing the net profit for the year by the weighted average number of issued ordinary shares. (j) Dividends Dividends are recognized as a liability in the period in which they are sanctioned by the shareholders. Dividends per share have been calculated by dividing the dividend declared by the weighted average number of issued ordinary shares.

29 NOTES TO THE FINANCIAL STATEMENTS As at December 31, 2008 (With Comparative Figures for 2007) Expressed in Eastern Caribbean Dollars (EC$) 3. Summary of significant accounting policies (continued) (k) Foreign currency Transactions in foreign currencies are translated to EC Dollars at exchange rates at the dates of the transactions. Monetary assets and liabilities denominated in foreign currencies at the balance sheet date are retranslated to EC Dollars at the exchange rate at that date. The foreign currency gain or loss on monetary items is the difference between amortized cost in the functional currency at the beginning of the period, adjusted for effective interest and payments during the period, and the amortized cost in foreign currency translated at the exchange rate at the end of the period. Non-monetary assets and liabilities denominated in foreign currencies that are measured at fair value are re-translated to the functional currency at the exchange rate at the date that the fair value was determined. Foreign exchange differences arising on conversion and translation are recognized in the statement of income. Nonmonetary assets and liabilities denominated in foreign currencies that are stated at historical cost are translated to EC Dollars at the exchange rate at the date of the acquisition. (l) Income tax No provision is made for income tax since Anguilla does not have any form of income tax. (m) Provisions A provision is recognized if, as a result of a past event, the Company has a present legal or constructive obligation that can be estimated reliably, and it is probable that an outflow of economic benefits will be required to settle the obligation. Provisions are determined by discounting the expected future cash flows at a pretax rate that reflects current market assessments of the time value of money and the risks specific to the liability. (n) Amendments to standards and interpretations adopted in 2008 The Company adopted the following amendments to standards and interpretations: IAS 39, Financial Instruments: Recognition and Measurement and IFRS 7, Financial Instruments: Disclosures, Reclassification of Financial Assets (Amendments), permits an entity to reclassify non-derivative financial assets, other than those designated as at fair value through profit or loss upon initial recognition, out of the fair value through profit or loss (i.e., held for trading) category if they are no longer held for the purpose of being sold or repurchased in the near term, as follows: If the financial asset would have met the definition of loans and receivables, if the financial asset had not been required to be classified as held for trading at initial recognition, then it may be reclassified if the entity has the intention to hold the financial asset for the foreseeable future or until maturity; If the financial asset would not have met the definition of loans and receivables, then it may be reclassified out of the held for trading category only in "rare circumstances"; If the financial asset would have met the definition of loans and receivables, if the financial asset had not been designated as availableforsale, then it may be reclassified if the entity has the intention to hold the financial asset for the foreseeable future or until maturity. 29 The amendment to IFRS 7 introduces additional disclosure requirements if an entity has reclassified financial assets in accordance with the amendment to IAS 39. The amendments are effective retrospectively from 1 July The adoption of these amendments to standards did not affect the Company's reported net income or financial position during the year. IFRIC 12, Service Concession Arrangements, provides guidance on the accounting by operators of public-to-private service concession arrangements; and IFRIC 14, IAS 19 The Limited on a Defined Benefit Asset, Minimum Funding Requirements and their Interaction, addresses how to assess the limit, under IAS 19, Employee Benefits, on the amount of the surplus that can be recognized as an asset particularly when a minimum funding requirement exists.

30 A N G U I L L A E L E C T R I C I T Y C O M P A N Y L I M I T E D NOTES TO THE FINANCIAL STATEMENTS As at December 31, 2008 (With Comparative Figures for 2007) Expressed in Eastern Caribbean Dollars (EC$) 3. Summary of significant accounting policies (continued) The adoption of the above interpretations effective for periods beginning on or after 1 January 2008 did not affect the Company's reported net income or financial position during the year. (o) New standards, amendments to standards and interpretations not yet effective A number of new standards, amendments to standards and interpretations are not yet effective for the year ended 31 December 2008 and have not been early adopted by the Company or are not relevant to the Company's operations. These are as follows: Accounting standards Effective date IFRS 1 and IAS 27 IFRS 1 First-time Adoption of International Reporting Standards and IAS 27 1 January 2009 (Amendments) Consolidated and Separate Financial Statements Cost of an Investment in a Subsidiary, Jointly Controlled Entity or Associate IFRS 2 (Amendment) IFRS 2 Sharebased Payment Vesting Conditions and Cancellations 1 January 2009 IFRS 3 (Revised) IFRS 3 Business Combinations 1 July 2009 IFRS 8 Operating Segments 1 January 2009 IAS 1 (Revised) IAS 1 Presentation of Financial Statements 1 January 2009 IAS 23 (Revised) IAS 23 Borrowing Costs 1 January 2009 IAS 27 (Amendments) IAS 32 and IAS 1 (Amendments) IAS 27 Consolidated and Separate Financial Statements Cost of an Investment in a Subsidiary, Jointly Controlled Entity or Associate IAS 32 Financial Instruments: Presentation and IAS 1 Presentation of Financial Statements Puttable Financial Instruments and Obligations Arising on Liquidation 1 July January 2009 IAS 39 (Amendment) IAS 39 Financial Instruments: Recognition and Measurement Eligible Hedged Items 1 July 2009 IFRIC 13 Customer Loyalty Programmes 1 July 2008 IFRIC 15 Agreements for the Construction of Real Estate 1 January 2009 IFRIC 16 Hedges of a Net Investment in a Foreign Operation 1 October 2008 Various Improvements to IFRSs January Amendments to IFRS 1, First-time Adoption of International Reporting Standards and IAS 27, Consolidated and Separate Financial Statements Cost of an Investment in a Subsidiary, Jointly Controlled Entity or Associate, permits a first-time adopter of IFRSs, at the date of transition, to measure the cost of its investment in a subsidiary, jointly controlled entity or associate at a deemed cost in its separate financial statements rather than having to determine cost under IFRSs. Amendments to IFRS 1 and IAS 27, which will become mandatory for 2009 financial statements, are not expected to have any impact on the Company's financial statements. Amendment to IFRS 2, Sharebased Payment Vesting Conditions and Cancellations, clarifies the definition of vesting conditions, introduces the concept of non-vesting conditions, requires non-vesting conditions reflected in grant-date fair value and provides the accounting treatment for nonvesting conditions and cancellations. Amendment to IFRS 2, which will become mandatory for 2009 financial statements with retrospective application required, is not expected to have any impact on the Company's financial statements.

31 NOTES TO THE FINANCIAL STATEMENTS As at December 31, 2008 (With Comparative Figures for 2007) Expressed in Eastern Caribbean Dollars (EC$) 3. Summary of significant accounting policies (continued) Revised IFRS 3, Business Combinations, incorporates changes as to (a) the definition of business has been broadened; (b) contingent consideration will be measured at fair value, with subsequent changes in fair value recognized in the statements of income; (c) transaction costs, other than share and debt issue costs, will be expensed as incurred; (d) any pre-existing interest in an acquiree will be measured at fair value, with the related gain or loss recognized in the statements of income; (e) any non-controlling interest will be measured at either fair value, or at its proportionate interest in the identifiable assets and liabilities of an acquiree, on a transaction-by-transaction basis. Revised IFRS 3, which will become mandatory for 2010 financial statements, is not expected to have any impact on the Company's financial statements. IFRS 8, Operating Segments, requires segment disclosure based on the components of the Company that management monitors in making decisions about operating matters as well as qualitative disclosures on segments. Segments will be reportable based on threshold tests related to revenues, results and assets. IFRS 8, which will become mandatory for 2009 financial statements, is not expected to have any significant impact on the Company's financial statements. Revised IAS 1, Presentation of Financial Statements, introduces as a financial statement (formerly "primary" statement) the "statement of comprehensive income" (i.e., changes in equity during a period, other than those changes resulting from transactions with owners in their capacity as owners), which is presented either in : (a) one statement (i.e, a statement of comprehensive income); or (b) two statements (i.e., an income statement and a statement beginning with profit or loss and displaying components of other comprehensive income). The revised standard also prohibits presenting components of comprehensive income in the statements of changes in shareholders' equity. Other requirements in the revised standard that are not current IAS 1 requirement includes: (a) a statement of financial position (formerly "balance sheet") is required at the beginning of the earliest comparative period following a change in accounting policy, the correction of an error or the reclassification of items in the financial statements; (b) reclassification adjustments to profit or loss of amounts previously recognized in other comprehensive income (formerly "recycling") are disclosed for each component of other comprehensive income; (c) income tax is disclosed for each component of other comprehensive income; (d) dividends and related per-share amounts are disclosed either on the face of the statements of changes in shareholders' equity or in the notes. Revised IAS 1, which will become mandatory for 2009 financial statements, will require adjustments and additional disclosures in the Company's financial statements. Revised IAS 23, Borrowing Costs, removes the option of immediately recognising all borrowing costs as an expense, which was the benchmark treatment in the previous standard. The revised standard requires that an entity capitalise borrowing costs directly attributable to the acquisition, construction or production of a qualifying asset as part of the cost of that asset. Revised IAS 23, which will become mandatory for 2009 financial statements, is not expected to have any impact on the Company's financial statements. Amendments to IAS 27, Consolidated and Separate Financial Statements Cost of an Investment in a Subsidiary, Jointly Controlled Entity or Associate, requires accounting for changes in ownership interests in a subsidiary that occur without loss of control, to be recognized as an equity transaction. When the Company loses control of a subsidiary, any interest retained in the former subsidiary will be measured at fair value with the gain or loss recognized in the statements of income. Amendments to IAS 27, which will become mandatory for 2010 financial statements, are not expected to have any impact on the Company's financial statements. 31 Amendments to IAS 32, Financial Instruments: Presentation and IAS 1, Presentation of Financial Statements Puttable Financial Instruments and Obligations Arising on Liquidation, requires puttable instruments and instruments that impose on the entity an obligation to deliver to another party a pro rata share of the net assets of the entity only on liquidation to be classified as equity if certain conditions are met. The amendments, which will become mandatory for 2009 financial statements with retrospective application required, are not expected to have any impact on the Company's financial statements.

32 A N G U I L L A E L E C T R I C I T Y C O M P A N Y L I M I T E D NOTES TO THE FINANCIAL STATEMENTS As at December 31, 2008 (With Comparative Figures for 2007) Expressed in Eastern Caribbean Dollars (EC$) 3. Summary of significant accounting policies (continued) Amendment to IAS 39, Financial Instruments: Recognition and Measurement Eligible Hedged Items, clarifies the application of existing principles in a hedging relationship. The amendments, which will become mandatory for 2010 financial statements with retrospective application required, are not expected to have any impact on the Company's financial statements. IFRIC 13, Customer Loyalty Programmes, addresses the accounting by entities that operate or otherwise participate in customer loyalty programmes under which the customer can redeem credits for awards such as free or discounted goods or services. IFRIC 13, which will become mandatory for 2009 financial statements with retrospective application required, is not expected to have any impact on the Company's financial statements. IFRIC 15, Agreements for the Construction of Real Estate, determines whether an agreement for the construction of real estate is within the scope of IAS 11, Construction Contracts or IAS 18, Revenue. IFRIC 15, which will become mandatory for 2009 financial statements with retrospective application required, is not expected to have any impact on the Company's financial statements. IFRIC 16, Hedges of a Net Investment in a Foreign Operation, provides guidance in respect of hedges of foreign currency gains and losses on a net investment in a foreign operation. IFRIC 16, which will become mandatory for 2009 financial statements, is not expected to have any impact on the Company's financial statements. (p) Comparative information Comparative information has been reclassified where necessary to conform to the current year financial statements presentation. Such reclassifications do not affect previously reported net income or shareholders' equity Financial risk management Overview The Company has exposure to the following risks from its use of financial instruments: credit risk liquidity risk market risk capital management This note presents information about the Company's exposure to each of the above risks, the Company's objectives, policies and processes for measuring and managing risk, and the Company's management of capital. Further quantitative disclosures are included throughout these financial statements. The Board of Directors has overall responsibility for the establishment and oversight of the Company's risk management framework. The Company's risk management policies are established to identify and analyse the risks faced by the Company, to set appropriate risk limits and controls, and monitor risks and adherence to limits. Risk management policies and systems are reviewed regularly to reflect changes in market conditions and the Company's activities. The Company, through its training and management standards and procedures, aims to develop a disciplined and constructive control environment in which all employees understand their roles and obligations. The Board of Directors oversees how management monitors compliance with the Company's risk management policies and procedures and reviews the adequacy of the risk management framework in relation to the risks faced by the Company. Credit risk Credit risk is the risk of financial loss to the Company if a customer or counterparty to a financial instrument fails to meet its contractual obligations, and arises principally from the Company's receivables.

33 NOTES TO THE FINANCIAL STATEMENTS As at December 31, 2008 (With Comparative Figures for 2007) Expressed in Eastern Caribbean Dollars (EC$) 4. Financial risk management (continued) Trade and other receivables The Company's exposure to credit risk is influenced mainly by the individual characteristics of each customer. The demographics of the Company's customer base, including the default risk of the industry and country in which customers operate, has less influence on credit risk. Approximately 12 percent of the Company's revenue is attributable to sales transactions with a single customer. However, geographically there is no concentration of credit risk. The Company establishes an allowance for impairment that represents its estimate of incurred losses in respect of trade and other receivables and investment securities. The main components of this allowance are collective losses based on number of days in receivable. Liquidity risk Liquidity risk is the risk that the Company will not be able to meet its financial obligations as they fall due. The Company's approach to managing liquidity is to ensure, as far as possible, that it will always have sufficient liquidity to meet its liabilities when due, under both normal and stressed conditions, without incurring unacceptable losses or risking damage to the Company's reputation. Typically, the Company ensures that it has sufficient cash on demand to meet expected operational expenses for a period of 60 days, including the servicing of financial obligations; this excludes the potential impact of extreme circumstances that cannot reasonably be predicted, such as natural disasters. In addition, the Company maintains a line of credit with a limit of EC$3.2 million with the National Bank of Anguilla Limited with an interest rate of 9.2% per annum. Market risk Currency risk The Company's exposure to currency risk is minimal as the exchange rate of the Eastern Caribbean dollar (EC$) to the United States dollar (US$) has been formally pegged at EC$2.70 = US$1.00. Interest rate risk Differences in contractual repricing or maturity dates and changes in interest rates may expose the Company to interest rate risk. The Company's exposure and the interest rates on its financial liabilities are disclosed in Notes 14 and 27. Fair value The fair value of financial instruments that are not traded in an active market is determined by using valuation techniques. The Company uses a variety of methods and makes assumptions that are based on market conditions existing as at each balance sheet date. Quoted market prices or dealer quotes for similar instruments are used for intruments traded in the market. Other techniques, such as estimated discounted cash flows, are used to determine fair value for the remaining financial instruments. The nominal value less estimated credit adjustments of trade receivables and payables are assumed to approximate their fair values. The estimated fair value of cash and bank deposits with no stated maturity, which includes non-interest bearing deposits, is the amount repayable on demand. The estimated fair value of borrowings without quoted market price is based on discounted cash flows using interest rates for new debts with similar remaining maturity. Estimates and judgments are continually evaluated and are based on historical experience and other factors, including expectations of future events that are believed to be reasonable under the circumstances. Capital Management The Board's policy is to maintain a strong capital base so as to maintain investor, creditor and market confidence and to sustain future development of the business. The Board of Directors monitors both the demographic spread of shareholders, as well as the return on capital. 33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

- Photos by thierrydehove.com & Rebecca Haskins")

52 Main Office The Valley. Anguilla Power Station. Corito. Anguilla Mailing Address. P.O. Box 400 The Valley, Anguilla Telephone: (264) Facsimile: (264) Web site: Annual Report 2008 Anguilla Electricity Company Limited Design by T&T Publishing, LLC (Anguilla) - Photos by thierrydehove.com & Rebecca Haskins

EUROSTANDARD Banka AD Skopje. Consolidated Financial Statements for the year ended 31 December 2007

Consolidated Financial Statements for the year ended 31 December 2007 Contents Auditors' report Financial Statements Consolidated balance sheet 2 Consolidated income statement 3 Consolidated statement

Consolidated Financial Statements for the year ended 31 December 2007 Contents Auditors' report Financial Statements Consolidated balance sheet 2 Consolidated income statement 3 Consolidated statement

Universal Investment Bank AD Skopje. Financial Statements for the year ended 31 December 2007

for the year ended 31 December 2007 Contents Auditors' report Balance sheet 1 Income statement 2 Statement of changes in equity 3 Statement of cash flows 4 Notes to the financial statement 5 Income

for the year ended 31 December 2007 Contents Auditors' report Balance sheet 1 Income statement 2 Statement of changes in equity 3 Statement of cash flows 4 Notes to the financial statement 5 Income

Consolidated financial statements for the year ended December 31 st, In accordance with International Financial Reporting Standards («IFRS»)

") INFO-QUEST S.A. Consolidated financial statements for the year ended December 31 st, 2009 In accordance with International Financial Reporting Standards («IFRS») The attached financial statements have

INFO-QUEST S.A. Consolidated financial statements for the year ended December 31 st, 2009 In accordance with International Financial Reporting Standards («IFRS») The attached financial statements have

OAO Scientific Production Corporation Irkut

Consolidated Financial Statements for the year ended 31 December 2011 Consolidated Financial Statements for the year ended 31 December 2011 Contents Independent Auditors Report 3 Consolidated Income Statement

Consolidated Financial Statements for the year ended 31 December 2011 Consolidated Financial Statements for the year ended 31 December 2011 Contents Independent Auditors Report 3 Consolidated Income Statement

STATEMENT OF FINANCIAL POSITION as at 31 March 2009

STATEMENT OF FINANCIAL POSITION as at 31 March 2009 Restated Restated Restated Restated 31 March 31 March 1 April 31 March 31 March 1 April 2009 2008 2007 2009 2008 2007 Note R 000 R 000 R 000 R 000 R

STATEMENT OF FINANCIAL POSITION as at 31 March 2009 Restated Restated Restated Restated 31 March 31 March 1 April 31 March 31 March 1 April 2009 2008 2007 2009 2008 2007 Note R 000 R 000 R 000 R 000 R

Universal Investment Bank AD Skopje. Financial Statements for the year ended 31 December 2010

for the year ended 31 December 2010 Contents Independent Auditors' report Statement of financial position 1 Statement of comprehensive income 2 Statement of changes in equity 3 Statement of cash flows

for the year ended 31 December 2010 Contents Independent Auditors' report Statement of financial position 1 Statement of comprehensive income 2 Statement of changes in equity 3 Statement of cash flows

Alpha Bank AD Skopje. Financial Statements for the year ended 31 December 2007

for the year ended 31 December 2007 Contents Auditors' report Balance sheet 2 Income statement 3 Statement of changes in equity 4 Statement of cash flows 5 Notes to the financial statement 6 Balance sheet

for the year ended 31 December 2007 Contents Auditors' report Balance sheet 2 Income statement 3 Statement of changes in equity 4 Statement of cash flows 5 Notes to the financial statement 6 Balance sheet

Kuwait Telecommunications Company K.S.C.P. Financial Statements and Independent Auditors Report for the year ended 31 December 2014

Financial Statements and Independent Auditors Report 1 Contents Page Independent auditors report 1-2 Statement of financial position 3 Statement of profit or loss and comprehensive income 4 Statement of

Financial Statements and Independent Auditors Report 1 Contents Page Independent auditors report 1-2 Statement of financial position 3 Statement of profit or loss and comprehensive income 4 Statement of

RAIFFEISEN BANK SH.A.

. Consolidated financial statements for the year ended 31 December 2008 (with independent auditor s report thereon). Contents Page Independent auditors report i - ii Consolidated financial statements Consolidated

. Consolidated financial statements for the year ended 31 December 2008 (with independent auditor s report thereon). Contents Page Independent auditors report i - ii Consolidated financial statements Consolidated

Notes to consolidated financial statements (forming part of the financial statements)

") Notes to consolidated financial statements (forming part of the financial statements) 1 Reporting entity DP World Limited ( the Company ) was incorporated on 9 August 2006 as a Company Limited by Shares

Notes to consolidated financial statements (forming part of the financial statements) 1 Reporting entity DP World Limited ( the Company ) was incorporated on 9 August 2006 as a Company Limited by Shares

Accounting policies extracted from the 2016 annual consolidated financial statements

Steinhoff International Holdings N.V. (Steinhoff N.V.) is a Netherlands registered company with tax residency in South Africa. The consolidated annual financial statements of Steinhoff N.V. for the period

Steinhoff International Holdings N.V. (Steinhoff N.V.) is a Netherlands registered company with tax residency in South Africa. The consolidated annual financial statements of Steinhoff N.V. for the period

Home Credit a.s. Financial Statements for the period from 1 April 2007 to 31 December 2007

Financial Statements Translated from the Czech original Financial Statements Contents Independent Auditor s Report 3 Balance Sheet 5 Income Statement 6 Statement of Changes in Equity 7 Statement of Cash

Financial Statements Translated from the Czech original Financial Statements Contents Independent Auditor s Report 3 Balance Sheet 5 Income Statement 6 Statement of Changes in Equity 7 Statement of Cash

The notes on pages 7 to 59 are an integral part of these consolidated financial statements

CONSOLIDATED BALANCE SHEET As at 31 December Restated Restated Notes 2013 $'000 $'000 $'000 ASSETS Non-current Assets Investment properties 6 68,000 68,000 - Property, plant and equipment 7 302,970 268,342

CONSOLIDATED BALANCE SHEET As at 31 December Restated Restated Notes 2013 $'000 $'000 $'000 ASSETS Non-current Assets Investment properties 6 68,000 68,000 - Property, plant and equipment 7 302,970 268,342

CONSOLIDATED STATEMENT OF FINANCIAL POSITION

CONSOLIDATED STATEMENT OF FINANCIAL POSITION 31 March 2011 31 March 2010 31 March 2011 31 March 2010 Note R 000 R 000 R 000 R 000 ASSETS Non-current assets 27 357 913 26 587 912 26 135 050 25 368 290 Property,

CONSOLIDATED STATEMENT OF FINANCIAL POSITION 31 March 2011 31 March 2010 31 March 2011 31 March 2010 Note R 000 R 000 R 000 R 000 ASSETS Non-current assets 27 357 913 26 587 912 26 135 050 25 368 290 Property,

CARIBBEAN CREAM LIMITED 8 Statement of Profit or Loss and Other Comprehensive Income Restated* Notes Gross operating revenue 10 1,373,279,233 1,213,548,844 Cost of operating revenue 11 ( 952,953,996) (

CARIBBEAN CREAM LIMITED 8 Statement of Profit or Loss and Other Comprehensive Income Restated* Notes Gross operating revenue 10 1,373,279,233 1,213,548,844 Cost of operating revenue 11 ( 952,953,996) (

General notes to the consolidated financial statements

80 ARCADIS Financial Statements 2013 General notes to the consolidated financial statements General notes to the consolidated financial statements 1 General information ARCADIS NV is a public company organized

80 ARCADIS Financial Statements 2013 General notes to the consolidated financial statements General notes to the consolidated financial statements 1 General information ARCADIS NV is a public company organized

Auditors Report 2-3. Statement of Financial Position 4. Statement of Comprehensive Income 5. Statement of Changes in Shareholder's Equity 6

FINANCIAL STATEMENTS FOR THE YEAR ENDED DECEMBER 31, 2008 C O N T E N T S Pages Auditors Report 2-3 Statement of Financial Position 4 Statement of Comprehensive Income 5 Statement of Changes in Shareholder's

FINANCIAL STATEMENTS FOR THE YEAR ENDED DECEMBER 31, 2008 C O N T E N T S Pages Auditors Report 2-3 Statement of Financial Position 4 Statement of Comprehensive Income 5 Statement of Changes in Shareholder's

ST. KITTS-NEVIS-ANGUILLA NATIONAL BANK LIMITED

Consolidated balance sheet As of June 30, 2013 ASSETS Notes Cash and balances with Central Bank 6 355,574 254,466 Treasury bills 7 137,962 99,179 Deposits with other financial institutions 8 526,884 418,865

Consolidated balance sheet As of June 30, 2013 ASSETS Notes Cash and balances with Central Bank 6 355,574 254,466 Treasury bills 7 137,962 99,179 Deposits with other financial institutions 8 526,884 418,865

Consolidated Income Statement

59 Consolidated Income Statement For the year ended 31 December In millions of EUR Note 2016 2015 Revenue 5 20,792 20,511 income 8 46 411 Raw materials, consumables and services 9 (13,003) (12,931) Personnel

59 Consolidated Income Statement For the year ended 31 December In millions of EUR Note 2016 2015 Revenue 5 20,792 20,511 income 8 46 411 Raw materials, consumables and services 9 (13,003) (12,931) Personnel

Consolidated Financial Statements of ANGOSTURA HOLDINGS LIMITED. December 31, 2014 (Expressed in Trinidad and Tobago Dollars)

") Consolidated Financial Statements of (Expressed in Trinidad and Tobago Dollars) Consolidated Statement of Comprehensive Income Year ended (Expressed in Trinidad and Tobago Dollars) Restated Notes 2014

Consolidated Financial Statements of (Expressed in Trinidad and Tobago Dollars) Consolidated Statement of Comprehensive Income Year ended (Expressed in Trinidad and Tobago Dollars) Restated Notes 2014

Jamaica Broilers Group Limited Index 2 May 2009

Index Page Independent Auditors Report to the Members Statutory Financial Statements Group profit and loss account 1 Group balance sheet 2 Group statement of changes in stockholders equity 3 Group statement

Index Page Independent Auditors Report to the Members Statutory Financial Statements Group profit and loss account 1 Group balance sheet 2 Group statement of changes in stockholders equity 3 Group statement

Significant Accounting Policies

50 Low & Bonar Annual Report 2009 Significant Accounting Policies General information Low & Bonar PLC (the Company ) is a company domiciled in Scotland and incorporated in the United Kingdom under the

50 Low & Bonar Annual Report 2009 Significant Accounting Policies General information Low & Bonar PLC (the Company ) is a company domiciled in Scotland and incorporated in the United Kingdom under the

Profit/(Loss) before income tax 112, ,323. Income tax benefit/(expense) 11 (31,173) (37,501)

before income tax 112, ,323. Income tax benefit/(expense) 11 (31,173) (37,501)") Income statement For the year ended 31 July Note 2013 2012 Continuing operations Revenue 2,277,292 2,181,551 Cost of sales (1,653,991) (1,570,657) Gross profit 623,301 610,894 Other income 7 20,677 10,124

Income statement For the year ended 31 July Note 2013 2012 Continuing operations Revenue 2,277,292 2,181,551 Cost of sales (1,653,991) (1,570,657) Gross profit 623,301 610,894 Other income 7 20,677 10,124

NHN ENTERTAINMENT CORPORATION. Condensed Separate Interim Financial Statements

NHN ENTERTAINMENT CORPORATION Condensed Separate Interim Financial Statements (With Independent Auditors Review Report Thereon) Contents Page Independent Auditors Review Report 1 Condensed Separate Statement

NHN ENTERTAINMENT CORPORATION Condensed Separate Interim Financial Statements (With Independent Auditors Review Report Thereon) Contents Page Independent Auditors Review Report 1 Condensed Separate Statement

THE SRI LANKAN SCHOOL, MUSCAT

Financial statements 31 August 2015 Registered office and principal place of business: P.O. Box 2433, PC 112, Wadi Kabir, Sultanate of Oman Financial statements 31 August 2015 Contents Page Report of the

Financial statements 31 August 2015 Registered office and principal place of business: P.O. Box 2433, PC 112, Wadi Kabir, Sultanate of Oman Financial statements 31 August 2015 Contents Page Report of the

MOSENERGO GROUP IFRS CONSOLIDATED INTERIM FINANCIAL STATEMENTS (UNAUDITED)

") IFRS CONSOLIDATED INTERIM FINANCIAL STATEMENTS (UNAUDITED) 2017 Moscow 2017 1 Contents Consolidated interim balance sheet...... 3 Consolidated interim statement of comprehensive income...... 4 Consolidated

IFRS CONSOLIDATED INTERIM FINANCIAL STATEMENTS (UNAUDITED) 2017 Moscow 2017 1 Contents Consolidated interim balance sheet...... 3 Consolidated interim statement of comprehensive income...... 4 Consolidated

Consolidated financial statements for the year ended December 31 st, In accordance with International Financial Reporting Standards («IFRS»)

") INFO-QUEST S.A. Consolidated financial statements for the year ended December 31 st, 2008 In accordance with International Financial Reporting Standards («IFRS») The attached financial statements have

INFO-QUEST S.A. Consolidated financial statements for the year ended December 31 st, 2008 In accordance with International Financial Reporting Standards («IFRS») The attached financial statements have

It is time that brings results.

It is time that brings results. Financial statements The dimensions of growth are measured over time. Time defines how high we grow, how broadly our branches spread, and how far our ideas will grow. We

It is time that brings results. Financial statements The dimensions of growth are measured over time. Time defines how high we grow, how broadly our branches spread, and how far our ideas will grow. We

ACCOUNTING POLICIES. for the year ended 30 June MURRAY & ROBERTS ANNUAL FINANCIAL STATEMENTS 13

12 MURRAY & ROBERTS ANNUAL FINANCIAL STATEMENTS 13 ACCOUNTING POLICIES for the year ended 30 June 2013 1 PRESENTATION OF FINANCIAL STATEMENTS These accounting policies are consistent with the previous

12 MURRAY & ROBERTS ANNUAL FINANCIAL STATEMENTS 13 ACCOUNTING POLICIES for the year ended 30 June 2013 1 PRESENTATION OF FINANCIAL STATEMENTS These accounting policies are consistent with the previous

BUDAPEST STOCK EXCHANGE LTD. Financial Statements under IFRS as adopted by the EU and Independent Auditor s Report

BUDAPEST STOCK EXCHANGE LTD. Financial Statements under IFRS as adopted by the EU and Independent Auditor s Report Table of Contents Page Independent Auditor s Report 1 Financial Statements Statement of

BUDAPEST STOCK EXCHANGE LTD. Financial Statements under IFRS as adopted by the EU and Independent Auditor s Report Table of Contents Page Independent Auditor s Report 1 Financial Statements Statement of

TOTAL ASSETS 417,594, ,719,902

WABERER'S International NyRt. CONSOLIDATED STATEMENT OF FINANCIAL POSITION data in EUR Description Note FY 2014 FY 2015 restated NON-CURRENT ASSETS Property 8 15,972,261 17,995,891 Construction in progress

WABERER'S International NyRt. CONSOLIDATED STATEMENT OF FINANCIAL POSITION data in EUR Description Note FY 2014 FY 2015 restated NON-CURRENT ASSETS Property 8 15,972,261 17,995,891 Construction in progress

Financial review Refresco Financial review 2017

Financial review 2017 Financial review 2017 Financial review 2017 1 69 Consolidated income statement For the year ended December 31, 2017 (x 1 million euro) Note December 31, 2017 December 31, 2016 Revenue

Financial review 2017 Financial review 2017 Financial review 2017 1 69 Consolidated income statement For the year ended December 31, 2017 (x 1 million euro) Note December 31, 2017 December 31, 2016 Revenue

CONSOLIDATED STATEMENT OF FINANCIAL POSITION as at 31 March 2016

CONSOLIDATED STATEMENT OF FINANCIAL POSITION as at 31 March Notes (Restated) (Restated) 2014 ASSETS Non-current assets 5 604 3 654 3 368 Property, equipment and vehicles 5 3 199 2 985 2 817 Intangible

CONSOLIDATED STATEMENT OF FINANCIAL POSITION as at 31 March Notes (Restated) (Restated) 2014 ASSETS Non-current assets 5 604 3 654 3 368 Property, equipment and vehicles 5 3 199 2 985 2 817 Intangible

ACCOUNTING POLICIES 1 PRESENTATION OF FINANCIAL STATEMENTS. for the year ended 30 June BASIS OF PREPARATION 1.2 STATEMENT OF COMPLIANCE

14 MURRAY & ROBERTS ANNUAL FINANCIAL STATEMENTS 15 ACCOUNTING POLICIES for the year ended 30 June 2015 1 PRESENTATION OF FINANCIAL STATEMENTS 1.1 BASIS OF PREPARATION These consolidated and separate financial

14 MURRAY & ROBERTS ANNUAL FINANCIAL STATEMENTS 15 ACCOUNTING POLICIES for the year ended 30 June 2015 1 PRESENTATION OF FINANCIAL STATEMENTS 1.1 BASIS OF PREPARATION These consolidated and separate financial

Consolidated Financial Statements. Prince Rupert Port Authority. December 31, 2016

Consolidated Financial Statements Prince Rupert Port Authority December 31, 2016 Contents Page Independent Auditor s Report 1-2 Consolidated Statement of Financial Position 3 Consolidated Statement of

Consolidated Financial Statements Prince Rupert Port Authority December 31, 2016 Contents Page Independent Auditor s Report 1-2 Consolidated Statement of Financial Position 3 Consolidated Statement of

IBI Group 2014 Annual Financial Statements

IBI Group 2014 Annual Financial Statements TWELVE MONTHS ENDED DECEMBER 31, 2014 Consolidated Financial Statements of IBI GROUP INC. Years Ended December 31, 2014 and 2013 KPMG LLP Telephone (416) 777-8500

IBI Group 2014 Annual Financial Statements TWELVE MONTHS ENDED DECEMBER 31, 2014 Consolidated Financial Statements of IBI GROUP INC. Years Ended December 31, 2014 and 2013 KPMG LLP Telephone (416) 777-8500

Consolidated financial statements Joint Stock Company Russian Grids and its subsidiaries for the year ended 31 December 2014

Consolidated financial statements Joint Stock Company Russian Grids and its subsidiaries for the year ended 31 December 2014 with independent auditor s report Consolidated financial statements Joint Stock

Consolidated financial statements Joint Stock Company Russian Grids and its subsidiaries for the year ended 31 December 2014 with independent auditor s report Consolidated financial statements Joint Stock

Fast Retailing Co., Ltd. Consolidated Financial Statements for the year ended 31 August 2016

Fast Retailing Co., Ltd. Consolidated Financial Statements for the year ended CONSOLIDATED STATEMENT OF FINANCIAL POSITION FAST RETAILING CO., LTD. and consolidated subsidiaries and 2015 Millions of yen

Fast Retailing Co., Ltd. Consolidated Financial Statements for the year ended CONSOLIDATED STATEMENT OF FINANCIAL POSITION FAST RETAILING CO., LTD. and consolidated subsidiaries and 2015 Millions of yen

YIOULA GLASSWORKS S.A. AND SUBSIDIARIES NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS SEPTEMBER 30, 2012

1. CORPORATE INFORMATION: Yioula Glassworks S.A., a corporation formed under the laws of the Hellenic Republic (also known as Greece), οn August 5, 1959, by Messrs Kyriacos and Ioannis Voulgarakis is the

1. CORPORATE INFORMATION: Yioula Glassworks S.A., a corporation formed under the laws of the Hellenic Republic (also known as Greece), οn August 5, 1959, by Messrs Kyriacos and Ioannis Voulgarakis is the

QATARI GERMAN COMPANY FOR MEDICAL DEVICES Q.S.C. FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2013

FINANCIAL STATEMENTS FINANCIAL STATEMENTS CONTENTS Page(s) Independent auditors report 1-2 Financial statements Statement of financial position 3 Statement of comprehensive income 4 Statement of changes

FINANCIAL STATEMENTS FINANCIAL STATEMENTS CONTENTS Page(s) Independent auditors report 1-2 Financial statements Statement of financial position 3 Statement of comprehensive income 4 Statement of changes

Consolidated Financial Statements as at 31 December 2008 (with independent auditor s report thereon)

") (Previously known as American Bank of Albania Sh.a.) Consolidated Financial Statements as at 31 December (with independent auditor s report thereon) Contents Independent Auditors Report Page Consolidated

(Previously known as American Bank of Albania Sh.a.) Consolidated Financial Statements as at 31 December (with independent auditor s report thereon) Contents Independent Auditors Report Page Consolidated

Firm Transgarant LLC. Consolidated Financial Statements for the year ended 31 December 2012

Consolidated Financial Statements for the year ended 31 December 2012 Contents Auditors Report 3 Consolidated Statement of Financial Position 5 Consolidated Statement of Comprehensive Income 6 Consolidated

Consolidated Financial Statements for the year ended 31 December 2012 Contents Auditors Report 3 Consolidated Statement of Financial Position 5 Consolidated Statement of Comprehensive Income 6 Consolidated

PJSC Enel Russia Consolidated financial statements. For the year ended 31 December 2016 with independent auditor s report

Consolidated financial statements 31 December 2016 with independent auditor s report Consolidated financial statements 31 December 2016 Contents Independent auditor s report... 3 Consolidated statement

Consolidated financial statements 31 December 2016 with independent auditor s report Consolidated financial statements 31 December 2016 Contents Independent auditor s report... 3 Consolidated statement

GNC-ALFA CJSC. Financial Statements for the year ended 31 December 2010

Financial Statements for the year ended 31 December 2010 Contents Statement of Comprehensive Income 3 Statement of Financial Position 4 Statement of Changes in Equity 5 Statement of Cash Flows 6 Notes

Financial Statements for the year ended 31 December 2010 Contents Statement of Comprehensive Income 3 Statement of Financial Position 4 Statement of Changes in Equity 5 Statement of Cash Flows 6 Notes

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

1. Corporate information DP World PLC ( the Company ) formerly known as DP World Limited, was incorporated on 9 August 2006 as a Company Limited by Shares with the Registrar of Companies of the Dubai International

1. Corporate information DP World PLC ( the Company ) formerly known as DP World Limited, was incorporated on 9 August 2006 as a Company Limited by Shares with the Registrar of Companies of the Dubai International

PROCREDIT BANK AD - SKOPJE. Financial Statements prepared in accordance with International Financial Reporting Standards

PROCREDIT BANK AD - SKOPJE Financial Statements prepared in accordance with International Financial Reporting Standards For the year ended 31 December 2007 Financial statements for the year ended 31 December

PROCREDIT BANK AD - SKOPJE Financial Statements prepared in accordance with International Financial Reporting Standards For the year ended 31 December 2007 Financial statements for the year ended 31 December

NOTES TO THE GROUP ANNUAL FINANCIAL STATEMENTS FOR THE YEAR ENDED 30 SEPTEMBER 2014

14 NOTES TO THE GROUP ANNUAL FINANCIAL STATEMENTS 1. ACCOUNTING POLICIES The financial statements are presented in South African Rand, unless otherwise stated, rounded to the nearest million, which is

14 NOTES TO THE GROUP ANNUAL FINANCIAL STATEMENTS 1. ACCOUNTING POLICIES The financial statements are presented in South African Rand, unless otherwise stated, rounded to the nearest million, which is

Unaudited consolidated interim financial statements and independent auditor s review report BORETS INTERNATIONAL LIMITED 30 June 2015

Unaudited consolidated interim financial statements and independent auditor s review report BORETS INTERNATIONAL LIMITED 30 June 2015 Contents Independent Auditor s Review Report Unaudited Consolidated

Unaudited consolidated interim financial statements and independent auditor s review report BORETS INTERNATIONAL LIMITED 30 June 2015 Contents Independent Auditor s Review Report Unaudited Consolidated

(Continued) ~3~ March 31, 2017 December 31, 2016 March 31, 2016 Assets Notes AMOUNT % AMOUNT % AMOUNT % Current assets

~3~ March 31, 2017 December 31, 2016 March 31, 2016 Assets Notes AMOUNT % AMOUNT % AMOUNT % Current assets") Current assets DAVICOM SEMICONDUCTOR, INC. AND SUBSIDIARIES CONSOLIDATED BALANCE SHEETS (Expressed in thousands of New Taiwan dollars) (The consolidated balance sheets as of March 31,2017 and 2016 are

Current assets DAVICOM SEMICONDUCTOR, INC. AND SUBSIDIARIES CONSOLIDATED BALANCE SHEETS (Expressed in thousands of New Taiwan dollars) (The consolidated balance sheets as of March 31,2017 and 2016 are

Independent auditors report To the shareholders of St Kitts-Nevis-Anguilla National Bank Limited

Independent auditors report To the shareholders of St Kitts-Nevis-Anguilla National Bank Limited We have audited the accompanying financial statements of St Kitts-Nevis-Anguilla National Bank Limited and

Independent auditors report To the shareholders of St Kitts-Nevis-Anguilla National Bank Limited We have audited the accompanying financial statements of St Kitts-Nevis-Anguilla National Bank Limited and

NATIONAL MOBILE TELECOMMUNICATIONS COMPANY K.S.C.P. AND SUBSIDIARIES

NATIONAL MOBILE TELECOMMUNICATIONS COMPANY K.S.C.P. Consolidated Financial Statements and Independent Auditor s Report for the year ended 31 December 2017 Index Page Independent Auditor s Report 1 4 Consolidated

NATIONAL MOBILE TELECOMMUNICATIONS COMPANY K.S.C.P. Consolidated Financial Statements and Independent Auditor s Report for the year ended 31 December 2017 Index Page Independent Auditor s Report 1 4 Consolidated

Abu Dhabi Commercial Bank PJSC Consolidated financial statements For the year ended December 31, 2014

Consolidated financial statements For the year ended Consolidated financial statements are also available at: www.adcb.com Table of Contents Report of the independent auditor on the consolidated financial

Consolidated financial statements For the year ended Consolidated financial statements are also available at: www.adcb.com Table of Contents Report of the independent auditor on the consolidated financial

Financial Statements 2009

Financial Statements 2009 Financial Statements 2009 EADS FINANCIAL STATEMENTS 2009 1 2 EADS FINANCIAL STATEMENTS 2009 Financial Statements 2009 1 2 3 4 5 EADS N.V. Consolidated Financial Statements (IFRS)

Financial Statements 2009 Financial Statements 2009 EADS FINANCIAL STATEMENTS 2009 1 2 EADS FINANCIAL STATEMENTS 2009 Financial Statements 2009 1 2 3 4 5 EADS N.V. Consolidated Financial Statements (IFRS)

OJSC VOLGA TGC COMBINED AND CONSOLIDATED FINANCIAL STATEMENTS, PREPARED IN ACCORDANCE WITH INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRS) FOR THE

FOR THE") OJSC VOLGA TGC COMBINED AND CONSOLIDATED FINANCIAL STATEMENTS, PREPARED IN ACCORDANCE WITH INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRS) FOR THE YEARS ENDED 31 DECEMBER 2006 AND 2005 Independent Auditors

OJSC VOLGA TGC COMBINED AND CONSOLIDATED FINANCIAL STATEMENTS, PREPARED IN ACCORDANCE WITH INTERNATIONAL FINANCIAL REPORTING STANDARDS (IFRS) FOR THE YEARS ENDED 31 DECEMBER 2006 AND 2005 Independent Auditors

Tekstil Bankası Anonim Şirketi and Its Subsidiary

TABLE OF CONTENTS Independent Auditors Report Consolidated Statement of Financial Position 1 Consolidated Income Statement 2 Consolidated Statement of Comprehensive Income 3 Consolidated Statement of Changes

TABLE OF CONTENTS Independent Auditors Report Consolidated Statement of Financial Position 1 Consolidated Income Statement 2 Consolidated Statement of Comprehensive Income 3 Consolidated Statement of Changes

Consolidated Financial Statements (In thousands of Canadian dollars) CCL INDUSTRIES INC. Years ended December 31, 2013 and 2012

CCL INDUSTRIES INC. Years ended December 31, 2013 and 2012") Consolidated Financial Statements (In thousands of Canadian dollars) CCL INDUSTRIES INC. Years ended December 31, 2013 and 2012 To the Shareholders of CCL Industries Inc. KPMG LLP Telephone (416) 777-8500

Consolidated Financial Statements (In thousands of Canadian dollars) CCL INDUSTRIES INC. Years ended December 31, 2013 and 2012 To the Shareholders of CCL Industries Inc. KPMG LLP Telephone (416) 777-8500

PJSC PIK Group Consolidated Financial Statements for 2015 and Auditors Report

Consolidated Financial Statements for 2015 and Auditors Report Contents Consolidated Statement of Financial Position 3 Consolidated Statement of Profit or Loss and Other Comprehensive Income 4 Consolidated

Consolidated Financial Statements for 2015 and Auditors Report Contents Consolidated Statement of Financial Position 3 Consolidated Statement of Profit or Loss and Other Comprehensive Income 4 Consolidated

OJSC Enel OGK-5. Consolidated Financial Statements for the year ended 31 December 2010

Consolidated Financial Statements for the year ended 31 December 2010 Contents Independent Auditors Report 3 Consolidated Statement of Financial Position 5 Consolidated Statement of Comprehensive Income

Consolidated Financial Statements for the year ended 31 December 2010 Contents Independent Auditors Report 3 Consolidated Statement of Financial Position 5 Consolidated Statement of Comprehensive Income

QATAR ELECTRICITY & WATER COMPANY Q.S.C. CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS REPORT FOR THE YEAR ENDED 31 DECEMBER 2014

CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS REPORT FOR THE YEAR ENDED 31 DECEMBER 2014 CONSOLIDATED FINANCIAL STATEMENTS INDEX Page(s) Independent auditors report 1-2 Consolidated statement

CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS REPORT FOR THE YEAR ENDED 31 DECEMBER 2014 CONSOLIDATED FINANCIAL STATEMENTS INDEX Page(s) Independent auditors report 1-2 Consolidated statement

November Changes To The Financial Reporting Framework In Singapore

November 2009 Changes To The Financial Reporting Framework In Singapore The information in this booklet was prepared by the Technical Department of Deloitte & Touche LLP in Singapore ( Deloitte Singapore

November 2009 Changes To The Financial Reporting Framework In Singapore The information in this booklet was prepared by the Technical Department of Deloitte & Touche LLP in Singapore ( Deloitte Singapore

NOTES TO THE FINANCIAL STATEMENTS

NOTES TO THE FINANCIAL STATEMENTS 1. ACCOUNTING POLICIES 1.1 Nature of business Super Group Limited (Registration number 1943/016107/06), the holding Company (the Company) of the Group, is a Company listed

NOTES TO THE FINANCIAL STATEMENTS 1. ACCOUNTING POLICIES 1.1 Nature of business Super Group Limited (Registration number 1943/016107/06), the holding Company (the Company) of the Group, is a Company listed

C ONSOLIDATED FINANCIAL STATEMENTS. Algeco Scotsman Global S.à r.l. Years Ended December 31, 2012, 2011 and 2010 With Report of Independent Auditors

C ONSOLIDATED FINANCIAL STATEMENTS Algeco Scotsman Global S.à r.l. Years Ended December 31, 2012, 2011 and 2010 With Report of Independent Auditors Table of Contents Consolidated Statements of Comprehensive

C ONSOLIDATED FINANCIAL STATEMENTS Algeco Scotsman Global S.à r.l. Years Ended December 31, 2012, 2011 and 2010 With Report of Independent Auditors Table of Contents Consolidated Statements of Comprehensive

Interpretations effective in the year ended 28 February 2009 Standards and interpretations not yet effective

Accounting Policies Interpretations effective in the year ended 28 February 2009 IFRS 7 Financial instruments: disclosures. This amendment introduces new disclosures relating to financial instruments and

Accounting Policies Interpretations effective in the year ended 28 February 2009 IFRS 7 Financial instruments: disclosures. This amendment introduces new disclosures relating to financial instruments and

Fast Retailing Co., Ltd. Consolidated Financial Statements for the year ended 31 August 2017

Fast Retailing Co., Ltd. Consolidated Financial Statements for the year ended CONSOLIDATED STATEMENT OF FINANCIAL POSITION FAST RETAILING CO., LTD. and consolidated subsidiaries and 2016 Millions of yen

Fast Retailing Co., Ltd. Consolidated Financial Statements for the year ended CONSOLIDATED STATEMENT OF FINANCIAL POSITION FAST RETAILING CO., LTD. and consolidated subsidiaries and 2016 Millions of yen

Gulf Warehousing Company (Q.S.C.)

") FINANCIAL STATEMENTS 31 DECEMBER 2009 INDEPENDENT AUDITORS' REPORT TO THE SHAREHOLDERS OF GULF WAREHOUSING COMPANY (Q.S.C.) Report on the financial statements We have audited the accompanying financial

FINANCIAL STATEMENTS 31 DECEMBER 2009 INDEPENDENT AUDITORS' REPORT TO THE SHAREHOLDERS OF GULF WAREHOUSING COMPANY (Q.S.C.) Report on the financial statements We have audited the accompanying financial

HSBC BANK MIDDLE EAST LIMITED QATAR BRANCH FINANCIAL STATEMENTS AS AT AND FOR THE YEAR ENDED 31 DECEMBER 2008

HSBC BANK MIDDLE EAST LIMITED QATAR BRANCH FINANCIAL STATEMENTS AS AT AND FOR THE YEAR ENDED 31 DECEMBER 2008 FINANCIAL STATEMENTS As at and for the year ended 31 December 2008 Contents Page Independent

HSBC BANK MIDDLE EAST LIMITED QATAR BRANCH FINANCIAL STATEMENTS AS AT AND FOR THE YEAR ENDED 31 DECEMBER 2008 FINANCIAL STATEMENTS As at and for the year ended 31 December 2008 Contents Page Independent

Financial Statements and Independent Auditors' Report. Post and Telecommunication of Kosovo J.S.C. As of and for the year ended 31 December 2014

Financial Statements and Independent Auditors' Report Post and Telecommunication of Kosovo J.S.C As of and for the year ended 31 December Contents Independent Auditor s Report 1 Statement of financial

Financial Statements and Independent Auditors' Report Post and Telecommunication of Kosovo J.S.C As of and for the year ended 31 December Contents Independent Auditor s Report 1 Statement of financial

1 st National Bank St. Lucia Limited (formerly St. Lucia Co-operative Bank Limited)

") 1 st National Bank St. Lucia Limited (formerly St. Lucia Co-operative Bank Limited) Financial Statements March 29, 2005 Auditors Report To the Shareholders of We have audited the accompanying balance sheet

1 st National Bank St. Lucia Limited (formerly St. Lucia Co-operative Bank Limited) Financial Statements March 29, 2005 Auditors Report To the Shareholders of We have audited the accompanying balance sheet

GREEN CROSS CORPORATION. Separate Financial Statements. December 31, 2012 and (With Independent Auditors Report Thereon)

") Separate Financial Statements, 2012 and 2011 (With Independent Auditors Report Thereon) Contents Independent Auditors Report 1 Page Separate Financial Statements Separate Statements of Financial Position

Separate Financial Statements, 2012 and 2011 (With Independent Auditors Report Thereon) Contents Independent Auditors Report 1 Page Separate Financial Statements Separate Statements of Financial Position

ABC Company Limited Statement of profit or loss and other comprehensive income For the year ended 30 June 2017

Statement of profit or loss and other comprehensive income 2017 2016 $ $ Revenue 9,978,961 10,123,571 Cost of sales (9,042,681) (9,630,608) Gross profit 936,280 492,963 Other income 103,346 196,822 Selling

Statement of profit or loss and other comprehensive income 2017 2016 $ $ Revenue 9,978,961 10,123,571 Cost of sales (9,042,681) (9,630,608) Gross profit 936,280 492,963 Other income 103,346 196,822 Selling

11 Consolidated Statement of Profit or Loss and Other Comprehensive Income Year ended Notes 2017 2016 $ 000 $ 000 Revenue 19 16,513,084 15,780,756 Earnings before interest, depreciation, amortisation,

11 Consolidated Statement of Profit or Loss and Other Comprehensive Income Year ended Notes 2017 2016 $ 000 $ 000 Revenue 19 16,513,084 15,780,756 Earnings before interest, depreciation, amortisation,

Consolidated income statement For the year ended 31 March

Consolidated income statement For the year ended 31 March Continuing Operations Revenue 3,5 5,653.3 5,218.1 Operating costs (5,369.7) (4,971.8) Operating profit 5,6 283.6 246.3 Investment income 8 1.2

Consolidated income statement For the year ended 31 March Continuing Operations Revenue 3,5 5,653.3 5,218.1 Operating costs (5,369.7) (4,971.8) Operating profit 5,6 283.6 246.3 Investment income 8 1.2

Consolidated Financial Statements. Prince Rupert Port Authority. December 31, 2017

Consolidated Financial Statements Prince Rupert Port Authority December 31, 2017 Contents Page Independent Auditor s Report 1-2 Consolidated Statement of Financial Position 3 Consolidated Statement of

Consolidated Financial Statements Prince Rupert Port Authority December 31, 2017 Contents Page Independent Auditor s Report 1-2 Consolidated Statement of Financial Position 3 Consolidated Statement of

Notes to the Consolidated Financial Statements

251 Deutsche Bank Consolidated Statement of Income 245 Annual Report 2015 Consolidated Statement of Consolidated Financial Statements 251 Consolidated Statement of Consolidated Balance Sheet 289 Consolidated

251 Deutsche Bank Consolidated Statement of Income 245 Annual Report 2015 Consolidated Statement of Consolidated Financial Statements 251 Consolidated Statement of Consolidated Balance Sheet 289 Consolidated

The accompanying notes form an integral part of the financial statements.

4 CARIBBEAN PRODUCERS (JAMAICA) LIMITED Statement of Profit or Loss and Other Comprehensive Income Year ended Notes Group Company 2016 2015 2016 2015 Gross operating revenue 18 94,104,389 86,850,246 84,488,121

4 CARIBBEAN PRODUCERS (JAMAICA) LIMITED Statement of Profit or Loss and Other Comprehensive Income Year ended Notes Group Company 2016 2015 2016 2015 Gross operating revenue 18 94,104,389 86,850,246 84,488,121

SKNANB ANNUAL REPORT Audited Financial Statements

Audited Financial Statements 22 23 Consolidated Statement of Financial Position As of Assets Notes Cash and balances with Central Bank 5 239,699 293,229 Treasury bills 6 149,278 167,199 Deposits with other

Audited Financial Statements 22 23 Consolidated Statement of Financial Position As of Assets Notes Cash and balances with Central Bank 5 239,699 293,229 Treasury bills 6 149,278 167,199 Deposits with other

Financial Statements for the year ended December 31 st, 2006 in accordance with International Financial Reporting Standards («IFRS»)

") INFO-QUEST S.A. Financial Statements for the year ended December 31 st, 2006 in accordance with International Financial Reporting Standards («IFRS») The attached financial statements have been approved

INFO-QUEST S.A. Financial Statements for the year ended December 31 st, 2006 in accordance with International Financial Reporting Standards («IFRS») The attached financial statements have been approved

OAO Silvinit. Consolidated Financial Statements for the year ended 31 December 2010

Consolidated Financial Statements for the year ended 31 December 2010 Contents Independent Auditors Report 3 Consolidated Statement of Comprehensive Income 4 Consolidated Statement of Financial Position

Consolidated Financial Statements for the year ended 31 December 2010 Contents Independent Auditors Report 3 Consolidated Statement of Comprehensive Income 4 Consolidated Statement of Financial Position

BC LIQUOR DISTRIBUTION BRANCH

Financial Statements of BC LIQUOR DISTRIBUTION BRANCH For year ended March 31, 2017 This page left intentionally blank This page left intentionally blank INDEPENDENT AUDITOR'S REPORT To the Minister of

Financial Statements of BC LIQUOR DISTRIBUTION BRANCH For year ended March 31, 2017 This page left intentionally blank This page left intentionally blank INDEPENDENT AUDITOR'S REPORT To the Minister of

CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2017

CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2017 CONTENTS CONSOLIDATED FINANCIAL STATEMENTS Page(s) Independent auditor s report 1-5 Consolidated statement of financial position 6

CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2017 CONTENTS CONSOLIDATED FINANCIAL STATEMENTS Page(s) Independent auditor s report 1-5 Consolidated statement of financial position 6

November Changes to the financial reporting framework in Singapore.

November 2008 Changes to the financial reporting framework in Singapore. The information in this booklet was prepared by the Technical Department of Deloitte & Touche LLP in Singapore ( Deloitte Singapore

November 2008 Changes to the financial reporting framework in Singapore. The information in this booklet was prepared by the Technical Department of Deloitte & Touche LLP in Singapore ( Deloitte Singapore

MON REPOS EASTERN CO-OPERATIVE CREDIT UNION. Financial Statements. For the Year Ended December 31, (Expressed in Eastern Caribbean Dollars)

") AUDITOR S REPORT AND FINANCIALS MON REPOS EASTERN CO-OPERATIVE CREDIT UNION Financial Statements For the Year Ended December 31, 2017 (Expressed in Eastern Caribbean Dollars) Page 1 INDEX Audit Report

AUDITOR S REPORT AND FINANCIALS MON REPOS EASTERN CO-OPERATIVE CREDIT UNION Financial Statements For the Year Ended December 31, 2017 (Expressed in Eastern Caribbean Dollars) Page 1 INDEX Audit Report

OAO GAZ. Consolidated Financial Statements