THE INDIAN COMMUNITY SCHOOL, KUWAIT

|

|

|

- Jerome O’Connor’

- 5 years ago

- Views:

Transcription

1 THE INDIAN COMMUNITY SCHOOL, KUWAIT SERIES : II MTE / FN/ CODE : N 055 TIME ALLOWED : 3 HOURS NAME OF STUDENT : MAX. MARKS : 80 ROLL NO. :.. CLASS/SEC :.. NO. OF PAGES : 8 ACCOUNTANCY ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~ 1. K, N and A are partners in a firm sharing P/L in the ratio 3:2:1. At the time of admission of a partner, the goodwill of a firm was valued at Rs4, 00,000. The accountant of the firm passed the entry in the books of accounts and therefore showed goodwill at Rs2, 00,000 as an asset in the Balance Sheet was correct in doing so? Why? (1) 2. What are the circumstances where there is a need for revaluation of assets and liabilities? (1) 3. State any two deductions that may have to be made from the amount payable to retiring partner. (1) 4. Pass necessary journal entry:-dissolution expense Rs. 800paid by firm. (1) 5. What are the circumstances where there is a need for revaluation of assets and liabilities? (1) 6. At what rate is interest payable on the amount remaining unpaid to the executor of deceased partner. (1) 7. Differentiate between profit and loss appropriation account and profit and loss suspense account. (1) 8. When is memorandum revaluation account prepared? (1) 9. Pass the necessary journal entries for the following transaction on dissolution of firm of P and Q after various assets (other than cash) and outside liabilities have been transferred to Realisation a/c. a. Bank Loan Rs1,200 was paid. b. Stock worth Rs1,600 was taken over by partner Q. c. Partner P paid a creditor Rs400 d. An asset not appearing in the books of accounts realised Rs1,20 e. Expenses on Realisation Rs200 were paid by partner Q f. Profit on realisation Rs3,600 was distributed between P and Q in 5:4 (3)

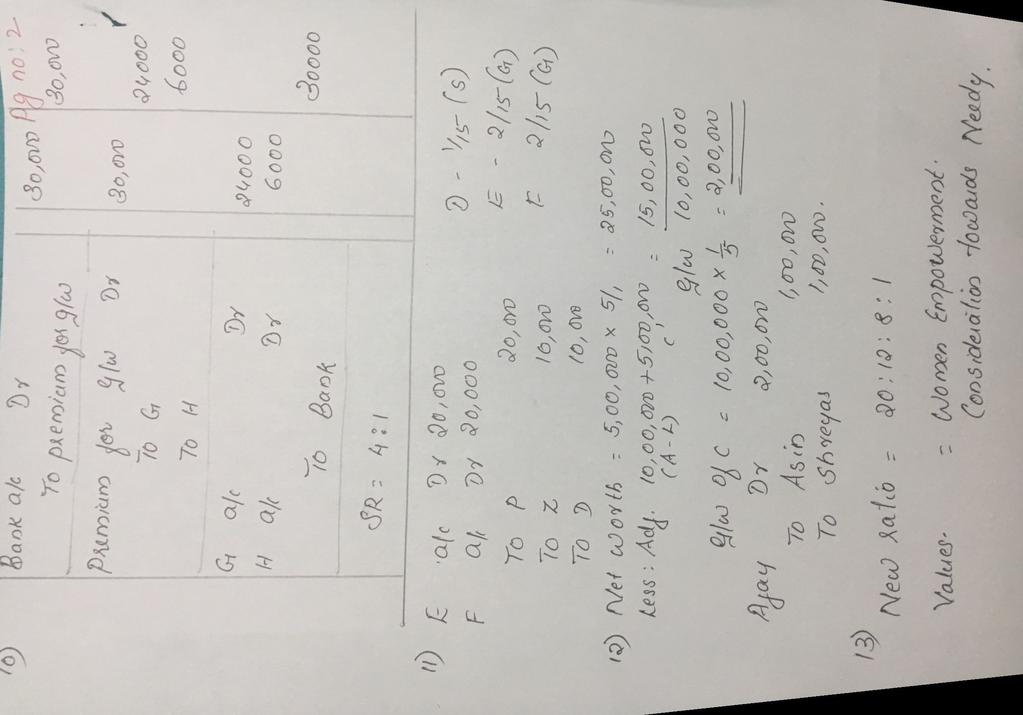

2 10. Gahlot and Harrison are partners in a firm sharing profits and losses in the ratio of 3:2. Thomas is admitted into partnership for 1/5 th share in profits. He brings in Rs 30,000 as his share of goodwill premium. The new profit sharing ratio among Ghalot, Harrison and Thomas is 11:9:5. No goodwill account appears in the books. Show how the amount of premium brought in by Thomas will be shared by Ghalot and Harrison and pass journal entries assuming that the amount of goodwill is withdrawn fully by the old partners. (3) 11. D, E, F, P, Z were partners in a firm sharing profits and losses in the ratio 5:4:3:2:1 respectively. Un fortunately, p and z met with a tragic car accident in which both of them died.the goodwill of the firm was valued at Rs. 1,50,000 and D,E AND F decided to share the future profits and losses in the ratio 4:6:5 respectively. Give the Journal entry to record the above. (3) 12. Asin and shreyas are partners in a firm.they admit Ajay as a new partner with 1/5 share in profits of the firm. Ajay brings Rs. 5, 00,000 as his share of capital. The value of total assets of the firm was Rs.15, 00,000 and outside liabilities were valued at Rs.5, 00,000 on that date. Give necessary journal entries to record the goodwill at the time of Ajay's admission. Also show the workings. (3) 13. Ram, Gurdeep and Seemaare partners dealing in manufacturing of electric power saver machine. They share profits and losses in the ratio of 5: 3: 2. They admitted Mathew for 2/10th share. Seema is a single parent of two small kids. On the admission of Mathew, Seema requested to Ram and Gurdeep that she does not want to change her profit share and wants to retain her original (old) share. (a) Find out the new profit sharing ratio of Ram, Gurdeep, Seema and Mathew. (b) What values you can identify in the above problem? (4) 14.. Pass necessary journal entries on retirement of a partner a. Depreciate furniture by 20% (Book value Rs. 1, 00,000) b. Half of investments were to be taken over by P and Q in their profit sharing ratio and remaining sold at Rs. 2,6000 (Book value Rs. 44, 000) c. Bank loan was settled at Rs. 14,000. (Book value Rs.16, 000) d. Stock was found overvalued by 20 % (Book value 50, 000) (4) 15. Give any four points of difference between Dissolution of partnership and Dissolution of a firm. (4)

3 16. A,B, C are sharing profits in the ratio of 2:2:1. B died on 30 June Accounts are closed on 31 March. Sales for the year ended 31 march 2015 amounted to Rs.3, 00,000.Sales of Rs. 1,00,000 amounted between the period from 1 April 2015 to 30 June 2015.The profits for the year ended 31 march 2015 amounted to Rs.30,000. Calculate deceased partners share in the profits of the firm. (4) 17. Record necessary entries in the following cases in case of dissolution of partnership firm : (i) Realisation expenses to be borne by A, a partner for which she was allowed commission of 2% of net cash realized from dissolution. The net cash realized from dissolution was 5,00,000 & actual expenses were 37,000. (ii) Sunil, a creditor to whom 32,000 were due to be paid, took over office equipment at 40,000. Balance was paid by him in cash. (iii) P, a partner, paid creditors 51,000 in full settlement of their claim 60,000. (iv) A debtor, Sam, whose debt of 18,600 was written off in the books, paid 15,000 in full settlement. (4) 18. (A)A & B are partners in a partnership firm which deals in mosquito repellents. They decided to supply their product in different slum areas in order to restrict water bond diseases. a) State three values that are being reflected in this case. b) B being an active partner claims salary of Rs. 20,000 per month. State whether his claim is valid or not. (B) Give reasons for the following: a) When an asset is taken over by a partner, his capital account is debited. b) When a liability is discharged by a partner, his capital account is credited. c) On the admission of a partner, assets and liabilities of the firm are revalued. d) Interest on capital is proportionately allowed to the extent of profits if there are insufficient profit in the firm. (6) 19.Anu Beena and Chander are partners in a firm, sharing profit in the ratio of 3 : 2 : 1. Their Balance Sheet as on March 31, 2006 was as follows: Liabilities Amount Assets Amount Sundry Creditors 3,200 Cash in hand 1,200 General Reserve 12,000 Cash at Bank 2,000

4 Capitals: Debtors 18,000 Anu 20,000 Stocks 14,000 Beena 20,000 Machinery 12,000 Chander 20,000 60,000 Building 28,000 75,200 75,200 On the date of Balance Sheet Chander retires from firm. It is agreed to adjust the value of assets as follows: (a) Provide a reserve of 5% on Sundry Debtors for Doubtful Debts. (b) Building to be revalued at Rs.30,200. (c) Depreciate stock by 5% and Machinery by 10%. Prepare Revaluation account, Partners Capital account.(6) 20. X, Y and Z were partners in a firm sharing profits and losses in the ratio of 5:3:2. On their Balance Sheet was as follows: Liabilities (Rs) Assets (Rs) CapitalAccounts: Building 50,000 X 75,000 Patents 15,000 Y 62,000 Machinery 75,000 Z 38,000 1,75,000 Stock 37,500 Creditors 42,500 Debtors 20,000 Cash at Bank 20,000 2,17,500 2,17,500 Z died on 31 st July It was agreed that: a) Goodwill be valued at 2 ½ year s purchase of the average profits of the last four years, which were as follows: Years Profits (Rs) , , , ,500 b) Machinery be valued at Rs 70,000; Patents at Rs 20,000 and Building Rs 62,500.

5 c) For the purpose of calculating Z s share of profits in the year of his death the profits in should be taken to have been accrued on the same scale as in d) A sum of Rs 17,500 was paid immediately to the executors of Z and the balance was paid in four half yearly instalments together with interest at 12% p.a starting from Give necessary journal entries to record the above transactions and Z executors account.(6) 21. Harsh, Kaushal and Vaman decided to dissolve their firm. The accountant of the firm prepared accounts and left some figures and entries incomplete. You are required to complete the missing figures in the following accounts:(6) Dr. Realisation Account Cr. Particulars (Rs) Particulars (Rs) To Land & Building A/c 23,500 By Accounts Payable 50,400 To Stock A/c 16,000 By Joint Life Policy Reserve A/c 10,000 To Accounts Receivable 20,100 By Harsh s Capital A/c (Stock) 18,000 (Debtors) To Investments A/c 62,600 By Kaushal s Capital A/c (building) 17,500 To Office EquipmentsA/c. By Vaman s Capital A/c (Debtors) 3,700 To Bank A/c (Realisation Expense) 450 By Bank A/c 82,000 To Bank A/c 50,900 To Capital A/c ( profit) Harsh 3/6.. Kaushal 2/6 Vaman 1/6.. 4,350. Dr. Partners Capital Accounts Cr. Particulars Harsh (Rs) Kaushal (Rs) Vaman (Rs) Particulars Harsh (Rs) Kaushal (Rs) Dr. Bank Account Cr. Particulars ( Rs) Particulars ( Rs) Vaman (Rs) To Realisation A/c. By Balance b/d 30,000 20,000 10,000 To Bank A/c 17,175 5,950 8,025 By General.... Reserve By Realisation..... A/c 35,175 23,450 11,725 35,175 23,450 11,725

6 To Balance b/d 500 By Realisation A/c To Realisation A/c ( Assets Realised) 82,000 By Realisation Ac 50,900 By Harsh s Capital A/c By Kausha s Capital A/c. By Vaman s Capital A/c Narang, Suri and Bajaj are partners in a firm sharing profits and losses in proportion of 1/2, 1/6 and 1/3 respectively. The Balance Sheet on 31 st March 2015 was as follows: Balance Sheet Liabilities (Rs) Assets (Rs) Capital Accounts: Freehold Premises 40,000 Narang 30,000 Machinery 30,000 Suri 30,000 Furniture 12,000 Bajaj 28,000 88,000 Stock 22,000 Bills Payable 12,000 Sundry Debtors 22,000 Reserves 12,000 Less: Provisions for Bad Debts 3,000 19,000 Sundry Creditors 18,000 Cash 7,000 Total 1,30,000 1,30,000 Bajaj retires from the business on the above date and the partners agree to the following : a) Freehold premises and stock are to be appreciated by 20% and 15 % respectively. b) Machinery and furniture are to be depreciated by 10% and 7 % respectively. c) Provision for bad debts is to be increased to Rs 1,500 d) Goodwill is valued at Rs 21,000 on Bajaj s retirement. e) The continuing partners have decided to adjust their capitals in their new profit-sharing ratio after retirement of Bajaj. Surplus/deficit, if any, in their accounts will be adjusted through their current accounts. Prepare necessary ledger accounts and draw the Balance Sheet of the reconstituted firm(8) Or Aand B are partners sharing profits in the ratio of A 3/6, B 2/6 and transfer to reserve 1/6. Their Balance sheet on 31st March, 2012 was as follows:

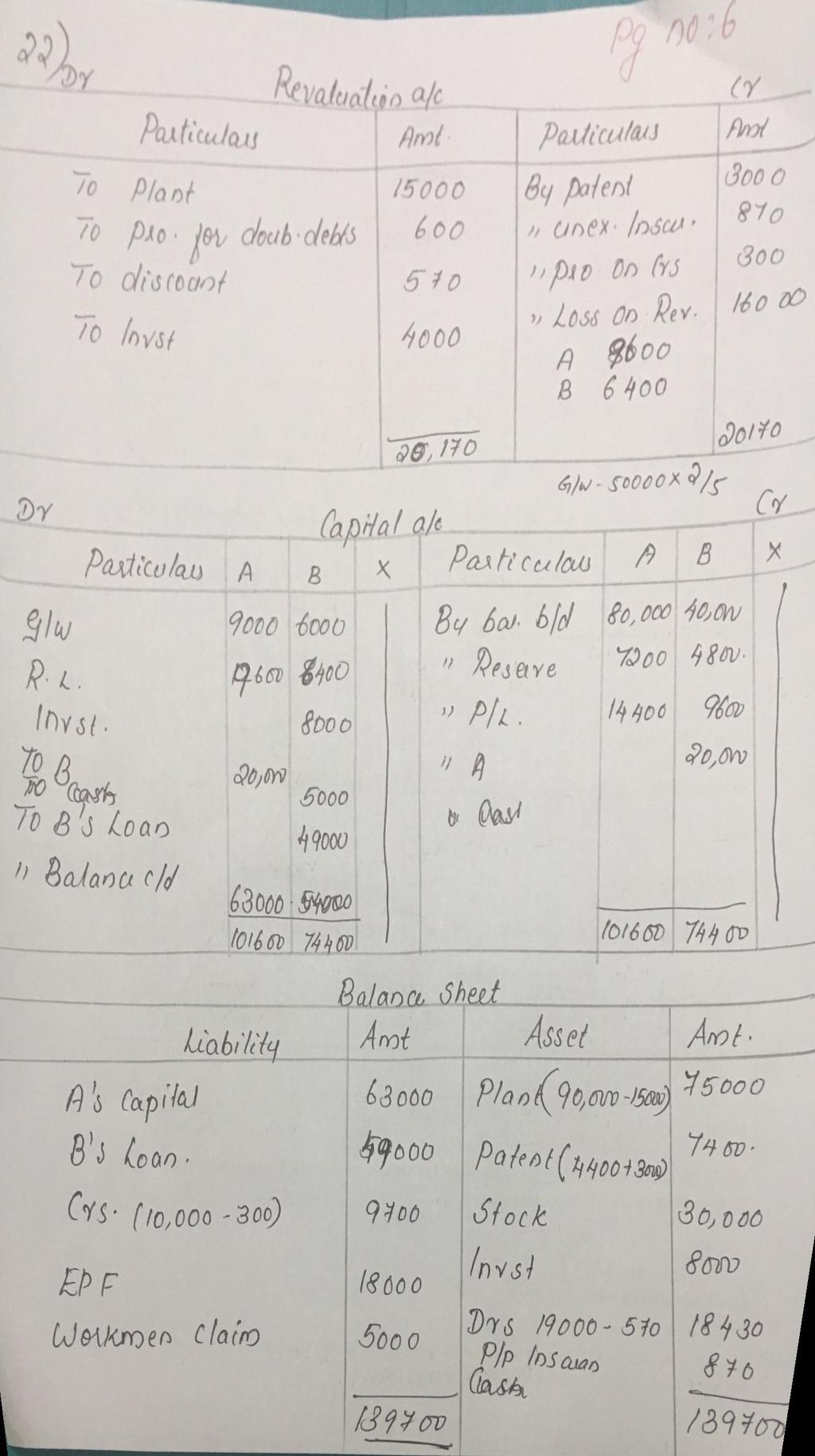

7 LIABILITY AMOUNT ASSET AMOUNT Employee provident goodwill fund Reserve plant Creditors patents 4400 Profit and loss a/c stock Capitals: investment A cash 5000 B Debtors Less: bad debts B retires on 1st April, The terms were: a) Goodwill is to be valued at Rs. 50,000 b) Value of patents is to be increased by Rs. 3,000 but Plant was found over valued by Rs. 15,000. c) Provision for doubtful debts should be 5% on debtors and provision for discount should also be made on debtors and creditors at 3%. d) Out of insurance which was entirely debited to profit & loss Account Rs.870 be carried forward as unexpired insurance. e) Investments were revalued at Rs. 16,000.Half of these investments were taken over by B. f) There is a claim for workmen's compensation to the extent of Rs. 5,000. g) B was paid off in full. Prepare Revaluation Account, Capital Accounts and the Balance sheet of A.(8) 23. Shikhar and Rohit were partners in a firm sharing profits in the ratio of 7 : 3. On 1st April, 2013 they admitted Kavi as a new partner for 1/4 share in profits of the firm. Kavi brought Rs. 4,30,000 as his capital and Rs.25,000 for his share of goodwill premium. The Balance Sheet of Shikhar and Rohit as on 1st April, 2013 was as follows : Balance Sheet of Shikhar and Rohit as on 1st April, LIABILITY AMOUNT ASSET AMOUNT Creditors Cash at Bank Workmen compensation machinery fund General reserve Stock Capital Accounts: Land and building A Debtors B Less: provision 20000

8 it was agreed that: (i) The value of Land and Building will be appreciated by 20%. (ii) The value of Machinery will be depreciated by 10%. (iii) The liabilities of Workmen s Compensation Fund was determined at Rs. 50,000. (iv) Capitals of Shikhar and Rohit will be adjusted on the basis of Kavi s capital and actual cash to be brought in or to be paid off as the case may be. Prepare Revaluation Account, Partners Capital Accounts and the Balance Sheet of the new firm.(8) Or T,N, S were partners in a firm two years ago when S died. Later on, T and N had decided to carry on the partnership among them sharing profits in the ratio of 2:1. However, in wake of deteriorating financial position of the family of S, both T & N agreed upon admitting the minor daughter of S named M into the firm. The mother of M consented to act as the legal guardian of the child until she attained the age of maturity. On 31 st December, 2015 the Balance Sheet of T and N stood as follows: Liabilities (Rs) Assets (Rs) T s Capital 30,000 Freehold Property 10,000 N s Capital 15,000 Furniture 3,000 General Reserve 12,000 Stock 6,000 Creditors 8,000 Debtors 40,000 Cash 6,000 65,000 65,000 T & N share profits and losses in the ratio of 2:1. They agree to admit M into the firm subject to the following terms and conditions: a) M will bring in Rs10, 500 of which Rs4, 500 will be treated as her share of goodwill to be retained in the business. b) M will be entitled to 1/4 th share of profits in the firm. c) A reserve for bad and doubtful debts is to be credited at 3% on the debtors. d) Furniture is to be depreciated by 5%. e) Stock is to be revaluated at Rs5,250 i) Mention the values displayed by T and N in admitting M into the partnership. ii) Mention the provision of the Partnership Act affected by the admission of M and the clauses governing this provision.

9 Prepare Revaluation Account, Partners Capital Accounts and Opening Balance Sheet of the new firm. (8)

10

11

12

13

14

15

16

17

18

19

ACCOUNTANCY MODEL TEST PAPER-1

ACCOUNTANCY MODEL TEST PAPER-1 Q1- Is it correct that interest on capital is payable whether there is profit or loss in the business? (1) Q2-*-K,L & M were partners sharing profits in the ratio of 3:2:1.

ACCOUNTANCY MODEL TEST PAPER-1 Q1- Is it correct that interest on capital is payable whether there is profit or loss in the business? (1) Q2-*-K,L & M were partners sharing profits in the ratio of 3:2:1.

Accountancy Class-XII Assignment

Chapter 1 Accounting For fundamentals Accountancy Class-XII Assignment 2017-18 Q1. Lata and Mamta are partners with capital of Rs. 3,00,000 and Rs. 2,00,000 respectively sharing profits as Lata 70% and

Chapter 1 Accounting For fundamentals Accountancy Class-XII Assignment 2017-18 Q1. Lata and Mamta are partners with capital of Rs. 3,00,000 and Rs. 2,00,000 respectively sharing profits as Lata 70% and

ACCOUNTANCY Class XII

Time allowed:3 hours General Instructions: S A M P L E P A P E R - 2 0 1 4 ACCOUNTANCY Class XII This question paper is divided into two parts A&B. All parts of the questions should be attempted at one

Time allowed:3 hours General Instructions: S A M P L E P A P E R - 2 0 1 4 ACCOUNTANCY Class XII This question paper is divided into two parts A&B. All parts of the questions should be attempted at one

SAMPLE PAPER - 5 ACCOUNTANCY CLASS-XII PART A ACCOUNTING FOR PARTNERSHIP FIRMS AND COMPANIES

SAMPLE PAPER - 5 ACCOUNTANCY CLASS-XII Time allowed: 3hrs Maximum Marks: 80 General Instructions: 1) This question paper contains two parts A and B. 2) Part A is compulsory for all. 3) Part B is Financial

SAMPLE PAPER - 5 ACCOUNTANCY CLASS-XII Time allowed: 3hrs Maximum Marks: 80 General Instructions: 1) This question paper contains two parts A and B. 2) Part A is compulsory for all. 3) Part B is Financial

Downloaded from

Downloaded from www.udieoday.com SAMPLE PAPER 2 SAMPLE QUESTION PAPER (055) CLASS-XII Time allowed : 3 hours Max Marks 80 General Inructions: 1) This queion paper contains two parts A and B. 2) Part A

Downloaded from www.udieoday.com SAMPLE PAPER 2 SAMPLE QUESTION PAPER (055) CLASS-XII Time allowed : 3 hours Max Marks 80 General Inructions: 1) This queion paper contains two parts A and B. 2) Part A

Sample Paper. 4. Differentiate between Capital Reserve and Reserve Capital. (1)

") Sample Paper Time allowed Three hours ACCOUNTANCY (055) CLASS-XII Max Marks 80 General Instructions: 2015 1) This question paper contains two parts A and B. 2) Part A is compulsory for all. 3) Part B has

Sample Paper Time allowed Three hours ACCOUNTANCY (055) CLASS-XII Max Marks 80 General Instructions: 2015 1) This question paper contains two parts A and B. 2) Part A is compulsory for all. 3) Part B has

ACCOUNTING FOR PARTNERSHIP FIRMS: BASIC CONCEPTS

ARMY PUBLIC SCHOOL JAMMU CANTT HOLIDAY HOMEWROK ( SESSION 2018 2019 ) SUBJECT : ACCOUNTANCY CLASS : XII ACCOUNTING FOR PARTNERSHIP FIRMS: BASIC CONCEPTS Q1: State the conditions under which capital balances

ARMY PUBLIC SCHOOL JAMMU CANTT HOLIDAY HOMEWROK ( SESSION 2018 2019 ) SUBJECT : ACCOUNTANCY CLASS : XII ACCOUNTING FOR PARTNERSHIP FIRMS: BASIC CONCEPTS Q1: State the conditions under which capital balances

Question Paper Design Accountancy (Code No. 055) Class XII ( ) March 2015 Examination

Class XII ( ) March 2015 Examination") Question Paper Design Accountancy (Code No. 055) Class XII (2014-15) March 2015 Examination One Paper Theory: 80 Marks Duration: 3 hrs. S. No Typology of Question Very Short Answer 1 Mark 1. Remembering-

Question Paper Design Accountancy (Code No. 055) Class XII (2014-15) March 2015 Examination One Paper Theory: 80 Marks Duration: 3 hrs. S. No Typology of Question Very Short Answer 1 Mark 1. Remembering-

PARTNERSHIP ACCOUNTS

CHAPTER-2 Q. 1. Thin, Short and Fat were in partnership sharing profits and losses in the ratio of 2 : 2 : 1. On 30th September, 2012 their Balance Sheet was as follows : Capital Accounts : Premises 50,000

CHAPTER-2 Q. 1. Thin, Short and Fat were in partnership sharing profits and losses in the ratio of 2 : 2 : 1. On 30th September, 2012 their Balance Sheet was as follows : Capital Accounts : Premises 50,000

CHAPTER - II Accounting for partnership firms - Fundamentals Q.1 What is the status of partnership from an accounting viewpoint? Q.2 List the items that may appear on the debit side and credit side of

CHAPTER - II Accounting for partnership firms - Fundamentals Q.1 What is the status of partnership from an accounting viewpoint? Q.2 List the items that may appear on the debit side and credit side of

PARTNERSHIP ACCOUNTS

PARTNERSHIP ACCOUNTS 1. Following is the Balance Sheet of A and B who share profits und losses equally : Liabilities Amount Assets Amount Capital Machinery 18,000 A 20,000 Plant 20,000 B 14,000 Debtors

PARTNERSHIP ACCOUNTS 1. Following is the Balance Sheet of A and B who share profits und losses equally : Liabilities Amount Assets Amount Capital Machinery 18,000 A 20,000 Plant 20,000 B 14,000 Debtors

CHAPTER 6 DISSOLUTION OF A PARTNERSHIP FIRM

CHAPTER 6 DISSOLUTION OF A PARTNERSHIP FIRM Dissolution of a firm: As per Indian Partnership Act, 1932: Dissolution of firm means termination of partnership among all the partners of the firm. When a firm

CHAPTER 6 DISSOLUTION OF A PARTNERSHIP FIRM Dissolution of a firm: As per Indian Partnership Act, 1932: Dissolution of firm means termination of partnership among all the partners of the firm. When a firm

Time allowed : 3 hours Maximum Marks : 80

Time allowed : 3 hours Maximum Marks : 80 General Instructions: (i) This question paper contains three parts A, B, and C. (ii) Part A is compulsory for all candidates. (iii) Candidates can attempt only

Time allowed : 3 hours Maximum Marks : 80 General Instructions: (i) This question paper contains three parts A, B, and C. (ii) Part A is compulsory for all candidates. (iii) Candidates can attempt only

ACCOUNTANCY CLASS XII DESIGN OF THE QUESTION PAPER. Times : 3Hours Maximum Marks 80 S. NO. OBJECTIVES MARKS % OF MARKS. 1.

78 ACCOUNTANCY CLASS XII DESIGN OF THE QUESTION PAPER Times : 3Hours Maximum Marks 80 1. Weightage of Objectives S. NO. OBJECTIVES MARKS % OF MARKS 1. Knowledge 16 20% 2. Understanding 56 70% 3. Application

78 ACCOUNTANCY CLASS XII DESIGN OF THE QUESTION PAPER Times : 3Hours Maximum Marks 80 1. Weightage of Objectives S. NO. OBJECTIVES MARKS % OF MARKS 1. Knowledge 16 20% 2. Understanding 56 70% 3. Application

Bharatiya Vidya Bhavan s V.M Public School Vadodara. Accountancy. Class XII Sample Paper-6

Bharatiya Vidya Bhavan s V.M Public School Vadodara Accountancy Class XII 2017-18 Sample Paper-6 Set-6 TIME: 3 HOURS MARKS: 80 GENERAL INSTRUCTIONS: 1. This question paper contains three parts A, B & C.

Bharatiya Vidya Bhavan s V.M Public School Vadodara Accountancy Class XII 2017-18 Sample Paper-6 Set-6 TIME: 3 HOURS MARKS: 80 GENERAL INSTRUCTIONS: 1. This question paper contains three parts A, B & C.

NCERT Solutions for Class 12 Accountancy. Partnership Accounts Chapter 3 Reconstitution of a Partnership Firm - Retirement/Death of a partner

NCERT Solutions for Class 12 Accountancy Partnership Accounts Chapter 3 Reconstitution of a Partnership Firm - Retirement/Death of a partner Short answers : Solutions of Questions on Page Number : 217

NCERT Solutions for Class 12 Accountancy Partnership Accounts Chapter 3 Reconstitution of a Partnership Firm - Retirement/Death of a partner Short answers : Solutions of Questions on Page Number : 217

KENDRIYA VIDYALAYA ERNAKULAM REGION MODEL PAPER ACCOUNTANCY Class XII Time 3.hrs M.Marks 80 PART A

KENDRIYA VIDYALAYA ERNAKULAM REGION MODEL PAPER ACCOUNTANCY Class XII Time 3.hrs M.Marks 80 PART A 1. What are the circumstances in which the capital balances of the partners fluctuate, when the capitals

KENDRIYA VIDYALAYA ERNAKULAM REGION MODEL PAPER ACCOUNTANCY Class XII Time 3.hrs M.Marks 80 PART A 1. What are the circumstances in which the capital balances of the partners fluctuate, when the capitals

X and Y are partners in a firm sharing profits in the ratio of 3:2. They admit Z into partnership for 20 Paise

Admission of a new Partner 1 State any two Financial rights acquired by a new partner. State any two adjustments required on admission of partner. Why does a new partner bring in goodwill into the firm?

Admission of a new Partner 1 State any two Financial rights acquired by a new partner. State any two adjustments required on admission of partner. Why does a new partner bring in goodwill into the firm?

QUESTION BANK ( ) Class XII Subject:- ACCOUNTANCY

Class XII Subject:- ACCOUNTANCY") QUESTION BANK (2017-2018) Class XII Subject:- ACCOUNTANCY 1. Give any one rule in absence of partnership deed. 1 2. Write two items of debit side of partner s current Accounts. 1 3. Mention two items that

QUESTION BANK (2017-2018) Class XII Subject:- ACCOUNTANCY 1. Give any one rule in absence of partnership deed. 1 2. Write two items of debit side of partner s current Accounts. 1 3. Mention two items that

THE TOUGHER YOU PLAY THE HIGHER YOU RISE! 10+2 (Accounts)Test 02 ( 2014) M.Marks : 80

Test 02 ( 2014) M.Marks : 80") PART-A Q.1 Would a charitable dispensary run by 8 members be deemed a partnership firm? Give reason in support of your answer. (1) Q.2 Can a partner be exempted from sharing the losses in a firm? If yes,

PART-A Q.1 Would a charitable dispensary run by 8 members be deemed a partnership firm? Give reason in support of your answer. (1) Q.2 Can a partner be exempted from sharing the losses in a firm? If yes,

DESIGN OF THE QUESTION PAPER

DESIGN OF THE QUESTION PAPER SUBJECT : ACCOUNTANCY MAX MARKS : 80 CLASS : XII TIME : 3 HRS. 1. Weightage to Objectives S.NO. OBJECTIVES MARKS % OF MARKS 1. Knowledge 16 20% 2. Understanding 56 70% 3. Application

DESIGN OF THE QUESTION PAPER SUBJECT : ACCOUNTANCY MAX MARKS : 80 CLASS : XII TIME : 3 HRS. 1. Weightage to Objectives S.NO. OBJECTIVES MARKS % OF MARKS 1. Knowledge 16 20% 2. Understanding 56 70% 3. Application

THE INDIAN COMMUNITY SCHOOL, KUWAIT

THE INDIAN COMMUNITY SCHOOL, KUWAIT SERIES : II MTE / FN/2017-2018 CODE : M 055 TIME ALLOWED : 2 HOURS NAME OF STUDENT : MAX. MARKS : 50 ROLL NO. :.. CLASS/SEC :.. NO. OF PAGES : 5 ACCOUNTANCY ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

THE INDIAN COMMUNITY SCHOOL, KUWAIT SERIES : II MTE / FN/2017-2018 CODE : M 055 TIME ALLOWED : 2 HOURS NAME OF STUDENT : MAX. MARKS : 50 ROLL NO. :.. CLASS/SEC :.. NO. OF PAGES : 5 ACCOUNTANCY ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Issues in Partnership Accounts

14 Issues in Partnership Accounts BASIC CONCEPTS Partnership is defined as the relationship between persons who have agreed to share the profit or loss of a business carried on by all or any of them acting

14 Issues in Partnership Accounts BASIC CONCEPTS Partnership is defined as the relationship between persons who have agreed to share the profit or loss of a business carried on by all or any of them acting

PART A - PARTNERSHIP FIRMS AND COMPANY ACCOUNTS

SUB : ACCOUNTANCY CLASS : XII General Instructions: i) All questions are compulsory. ii) Show your working notes clearly. iii) Avoid cut work and untidy presentation. Time : 3 Hrs. M.M : 80 PART A - PARTNERSHIP

SUB : ACCOUNTANCY CLASS : XII General Instructions: i) All questions are compulsory. ii) Show your working notes clearly. iii) Avoid cut work and untidy presentation. Time : 3 Hrs. M.M : 80 PART A - PARTNERSHIP

BOARD QUESTION PAPER : OCTOBER 2014

392 BOARD QUESTION PAPER : OCTOBER 2014 Time: 3 Hours Max. Marks: 80 Q. 1. Attempt any THREE of the following sub-questions: [15] (A) Answer the following in one sentence each: (5) (1) What is balance

392 BOARD QUESTION PAPER : OCTOBER 2014 Time: 3 Hours Max. Marks: 80 Q. 1. Attempt any THREE of the following sub-questions: [15] (A) Answer the following in one sentence each: (5) (1) What is balance

AHLCON PUBLIC SCHOOL ACCOUNTANCY CLASS XII ASSIGNMENT FUNDAMENTALS OF PARTNERSHIP

AHLCON PUBLIC SCHOOL ACCOUNTANCY CLASS XII ASSIGNMENT FUNDAMENTALS OF PARTNERSHIP One Mark Questions 1. Why Profit and Loss Appropriation Account is prepared? 2. Do all firms of business organizations

AHLCON PUBLIC SCHOOL ACCOUNTANCY CLASS XII ASSIGNMENT FUNDAMENTALS OF PARTNERSHIP One Mark Questions 1. Why Profit and Loss Appropriation Account is prepared? 2. Do all firms of business organizations

Unit 2: RECONSTITUTION OF PARTNERSHIP ADMISSION OF A PARTNER Q.1 On what occasions does the need for valuation of goodwill arise? Q.2 Why is it necessary to revalue assets and liabilities at the time of

Unit 2: RECONSTITUTION OF PARTNERSHIP ADMISSION OF A PARTNER Q.1 On what occasions does the need for valuation of goodwill arise? Q.2 Why is it necessary to revalue assets and liabilities at the time of

Pre-Board Exam 01. Accountancy. Class: XII. Q1. What do you mean by drawings against capital and how will you treat it in partnership accounts?

Max. Marks: 80 Instructions: Pre-Board Exam 01 Accountancy Class: XII 1. Question paper consists of 25 questions. 2. All questions are compulsory.. Attempt all parts of a question together.. State question

Max. Marks: 80 Instructions: Pre-Board Exam 01 Accountancy Class: XII 1. Question paper consists of 25 questions. 2. All questions are compulsory.. Attempt all parts of a question together.. State question

chapter - 8 PARTNERSHIP ACCOUNTS Unit 3 Admission of a New Partner The Institute of Chartered Accountants of India

chapter - 8 PARTNERSHIP ACCOUNTS Unit 3 Admission of a New Partner Learning Objectives : After studying this unit, you will be able to : Understand the reasons for which revaluation of assets and recomputation

chapter - 8 PARTNERSHIP ACCOUNTS Unit 3 Admission of a New Partner Learning Objectives : After studying this unit, you will be able to : Understand the reasons for which revaluation of assets and recomputation

UNIT 4 : RETIREMENT OF A PARTNER

8.81 UNIT 4 : RETIREMENT OF A PARTNER LEARNING OUTCOMES After studying this unit, you will be able to: Learn how to compute the gaining ratio and observe the use of such gaining ratio. Be familiar with

8.81 UNIT 4 : RETIREMENT OF A PARTNER LEARNING OUTCOMES After studying this unit, you will be able to: Learn how to compute the gaining ratio and observe the use of such gaining ratio. Be familiar with

ACCOUNTANCY (Principal and Practice of Financial Accounting) Time: 3 Hours] [Maximum Marks: 100 SECTION A

![ACCOUNTANCY (Principal and Practice of Financial Accounting) Time: 3 Hours] [Maximum Marks: 100 SECTION A](/thumbs/86/93694708.jpg "ACCOUNTANCY (Principal and Practice of Financial Accounting) Time: 3 Hours] [Maximum Marks: 100 SECTION A") ACCOUNTANCY (Principal and Practice of Financial Accounting) Time: 3 Hours] [Maximum Marks: 100 Note: (i) (ii) (iii) This Question Paper consists of two Sections, viz., A and B All questions from Section

ACCOUNTANCY (Principal and Practice of Financial Accounting) Time: 3 Hours] [Maximum Marks: 100 Note: (i) (ii) (iii) This Question Paper consists of two Sections, viz., A and B All questions from Section

ACCOUNTANCY. Part A. Q1. Name the financial statement prepared by a Not-For-Profit Organisation on accrual

ACCOUNTANCY [Time allowed: 3 hours] [Maximum marks:80] General Instructions: (i) This question paper contains three parts A, B and C. (ii) Part A is compulsory for all candidates. (iii) Candidates can

ACCOUNTANCY [Time allowed: 3 hours] [Maximum marks:80] General Instructions: (i) This question paper contains three parts A, B and C. (ii) Part A is compulsory for all candidates. (iii) Candidates can

Book Recommended : Ultimate Book of Accountancy 12 th CBSE. ACCOUNTANCY (055) CLASS XII Time allowed: 3Hours Sample Paper - 2 M.

CLASS XII Time allowed: 3Hours Sample Paper - 2 M.") Book Recommended : Ultimate Book of Accountancy 12 th CBSE ACCOUNTANCY (055) CLASS XII Time allowed: 3Hours Sample Paper - 2 M.M 80 General Instructions: 1. This question paper contains Two parts A& B.

Book Recommended : Ultimate Book of Accountancy 12 th CBSE ACCOUNTANCY (055) CLASS XII Time allowed: 3Hours Sample Paper - 2 M.M 80 General Instructions: 1. This question paper contains Two parts A& B.

ACCOUNTS. (Maximum Marks: 80) (Time allowed: Three hours)

(Time allowed: Three hours)") ACCOUNTS (Maximum Marks: 80) (Time allowed: Three hours) (Candidates are allowed additional 15 minutes for only reading the paper. They must NOT start writing during this time.) ----------------------------------------------------------------------------------------------------------------

ACCOUNTS (Maximum Marks: 80) (Time allowed: Three hours) (Candidates are allowed additional 15 minutes for only reading the paper. They must NOT start writing during this time.) ----------------------------------------------------------------------------------------------------------------

14 Issues in Partnership Accounts

14 Issues in Partnership Accounts Question 1 Ram, Rahim and Robert are partners, sharing Profits and Losses in the ratio of 5 : 3 : 2. It was decided that Robert would retire on 31.3.2005 and in his place

14 Issues in Partnership Accounts Question 1 Ram, Rahim and Robert are partners, sharing Profits and Losses in the ratio of 5 : 3 : 2. It was decided that Robert would retire on 31.3.2005 and in his place

CH- 1 ACCOUNTING FOR PARTNERSHIP FIRMS

CH 1 ACCOUNTING FOR PARTNERSHIP FIRMS FILL IN THE BLANKS (Reverse Questions) 1. X, Y and Z were partners in a firm. Their capitals on 01042011 were X Y, and Z The partnership deed provided for the following:

CH 1 ACCOUNTING FOR PARTNERSHIP FIRMS FILL IN THE BLANKS (Reverse Questions) 1. X, Y and Z were partners in a firm. Their capitals on 01042011 were X Y, and Z The partnership deed provided for the following:

Downloaded from

QUESTION PAPER (055) CLASS-XII Time allowed 3 hours Maximum Marks 80 General Instructions: 1) This question paper contains two parts A and B. 2) Part A is compulsory for all. 3) Part B has two options-financial

QUESTION PAPER (055) CLASS-XII Time allowed 3 hours Maximum Marks 80 General Instructions: 1) This question paper contains two parts A and B. 2) Part A is compulsory for all. 3) Part B has two options-financial

QUESTION BANK ( ) Class XII Subject:- ACCOUNTANCY

Class XII Subject:- ACCOUNTANCY") QUESTION BANK (2011-2012) Class XII Subject:- ACCOUNTANCY 1. State two characteristics of Not for profit organization. 1 2. Give any one point of difference between a Cash Book and receipts and Payments

QUESTION BANK (2011-2012) Class XII Subject:- ACCOUNTANCY 1. State two characteristics of Not for profit organization. 1 2. Give any one point of difference between a Cash Book and receipts and Payments

INDIAN SCHOOL AL WADI AL KABIR

INDIAN SCHOOL AL WADI AL KABIR SAMPLE PAPER- Class: XII Sub: ACCOUNTANCY (055) M.M: 80 General Instructions:. All questions are compulsory. 2. The question paper consists of 25 questions. There is no overall

INDIAN SCHOOL AL WADI AL KABIR SAMPLE PAPER- Class: XII Sub: ACCOUNTANCY (055) M.M: 80 General Instructions:. All questions are compulsory. 2. The question paper consists of 25 questions. There is no overall

SAMPLE QUESTION PAPER ACCOUNTANCY (055) CLASS XII C ( ) BLUE PRINT PART A - PARTNERSHIP & COMPANY ACCOUNTS. Answer 6,8

CLASS XII C ( ) BLUE PRINT PART A - PARTNERSHIP & COMPANY ACCOUNTS. Answer 6,8") SAMPLE QUESTION PAPER ACCOUNTANCY (055) CLASS XII C (2012-13) BLUE PRINT PART A - PARTNERSHIP & COMPANY ACCOUNTS Form of Questions/Units Long Short Very short Total Answer 6,8 Answer 3,4 Answer 1 1. Accounting

SAMPLE QUESTION PAPER ACCOUNTANCY (055) CLASS XII C (2012-13) BLUE PRINT PART A - PARTNERSHIP & COMPANY ACCOUNTS Form of Questions/Units Long Short Very short Total Answer 6,8 Answer 3,4 Answer 1 1. Accounting

Test Series No 4-60 Marks

Test Series No 4-60 Marks 1. In the absence of a partnership deed, the allowable rate of interest on partners loan account will be (a) 4% (b) 7% (c) 6% (d) 12% 2. In-------- method, depreciation is charged

Test Series No 4-60 Marks 1. In the absence of a partnership deed, the allowable rate of interest on partners loan account will be (a) 4% (b) 7% (c) 6% (d) 12% 2. In-------- method, depreciation is charged

Accountancy. Time Allowed: 3 hours Maximum : The question paper consists of Part A and Part B

Sample Paper (CBSE) Series SC/SP Accountancy Code No. SP-16 Time Allowed: 3 hours Maximum : 80 General Instructions: 1. All questions are compulsory. 2. The question paper consists of Part A and Part B

Sample Paper (CBSE) Series SC/SP Accountancy Code No. SP-16 Time Allowed: 3 hours Maximum : 80 General Instructions: 1. All questions are compulsory. 2. The question paper consists of Part A and Part B

TOPPER SAMPLE PAPER 4

TOPPER Sample Papers 237 TOPPER SAMPLE PAPER 4 ACCOUNTANCY XII Time Allowed - 3 Hrs. Max. Marks - 80 General Instructions:- 1. This question paper contains two parts A & B only. 2. All parts of questions

TOPPER Sample Papers 237 TOPPER SAMPLE PAPER 4 ACCOUNTANCY XII Time Allowed - 3 Hrs. Max. Marks - 80 General Instructions:- 1. This question paper contains two parts A & B only. 2. All parts of questions

SINGLE ENTRY SYSTEM:

SINGLE ENTRY SYSTEM: A) In the year of formation: 1. Bharath a trader, does not maintain complete set of books of accounts. He started the business on st 1 January 2010 with 2 and. The position of his

SINGLE ENTRY SYSTEM: A) In the year of formation: 1. Bharath a trader, does not maintain complete set of books of accounts. He started the business on st 1 January 2010 with 2 and. The position of his

TOPPER SAMPLE PAPER 2

TOPPER Sample Papers 209 TOPPER SAMPLE PAPER 2 ACCOUNTANCY XII Time Allowed - 3 Hrs. Max. Marks - 80 General Instructions:- 1. This question paper contains two parts A & B only. 2. All parts of questions

TOPPER Sample Papers 209 TOPPER SAMPLE PAPER 2 ACCOUNTANCY XII Time Allowed - 3 Hrs. Max. Marks - 80 General Instructions:- 1. This question paper contains two parts A & B only. 2. All parts of questions

DESIGN OF QUESTION PAPER ACCOUNTANCY Class - XII. Time Allowed - 3 Hrs. Max. Marks - 80

DESIGN OF QUESTION PAPER ACCOUNTANCY Class - XII Time Allowed - 3 Hrs. Max. Marks - 80 The weightage to marks over different dimensions of the question paper shall be as under : A. Weightage to Content/

DESIGN OF QUESTION PAPER ACCOUNTANCY Class - XII Time Allowed - 3 Hrs. Max. Marks - 80 The weightage to marks over different dimensions of the question paper shall be as under : A. Weightage to Content/

Partnership: Fundamentals Guarantee of profits An assurance is given to a partner that a minimum amount is given to him irrespective of profits The firm or the partner who has given the guarantee is DEBITED

Partnership: Fundamentals Guarantee of profits An assurance is given to a partner that a minimum amount is given to him irrespective of profits The firm or the partner who has given the guarantee is DEBITED

Book Recommended : Ultimate Book of Accountancy 12 th CBSE. ACCOUNTANCY (055) CLASS XII Time allowed: 3Hours Sample Paper - 1 M.

CLASS XII Time allowed: 3Hours Sample Paper - 1 M.") Book Recommended : Ultimate Book of Accountancy 12 th CBSE ACCOUNTANCY (055) CLASS XII Time allowed: 3Hours Sample Paper - 1 M.M 80 General Instructions: 1. This question paper contains Two parts A& B.

Book Recommended : Ultimate Book of Accountancy 12 th CBSE ACCOUNTANCY (055) CLASS XII Time allowed: 3Hours Sample Paper - 1 M.M 80 General Instructions: 1. This question paper contains Two parts A& B.

Part-I. Choose the correct answer: 20x1=20

Higher secondary second year Accountancy Model Question paper - II Time: 2.30 hrs Marks:90 Part-I Choose the correct answer: 20x1=20 1. Trial balance shows sundry debtors Rs.75,000/- as on 31.12.2005.

Higher secondary second year Accountancy Model Question paper - II Time: 2.30 hrs Marks:90 Part-I Choose the correct answer: 20x1=20 1. Trial balance shows sundry debtors Rs.75,000/- as on 31.12.2005.

MOCK TEST PAPER-3 CBSE-XII ACCOUNTANCY

MOCK TEST PAPER-3 CBSE-XII ACCOUNTANCY Mock Test Paper-3 11 Max. Marks : 80 Time Allowed : 3 hrs. General Instruction: As per Model Test Paper-I. Part A (Accounting for Not-for-Profit Organisations, Partnership

MOCK TEST PAPER-3 CBSE-XII ACCOUNTANCY Mock Test Paper-3 11 Max. Marks : 80 Time Allowed : 3 hrs. General Instruction: As per Model Test Paper-I. Part A (Accounting for Not-for-Profit Organisations, Partnership

3 Advanced Issues in Partnership Accounts

3 Advanced Issues in Partnership Accounts Unit 1: Dissolution of firms Question 1 X and Y carrying on business in partnership sharing Profit and Losses equally, wished to dissolve the firm and sell the

3 Advanced Issues in Partnership Accounts Unit 1: Dissolution of firms Question 1 X and Y carrying on business in partnership sharing Profit and Losses equally, wished to dissolve the firm and sell the

Sample Paper 2014 Class XII Subject Accountancy 1. Find the interest on drawings at 6 % per annum for partner Rajesh, who withdrew Rs 1,200 at the end of every month for six months ending on 31.3.2012.

Sample Paper 2014 Class XII Subject Accountancy 1. Find the interest on drawings at 6 % per annum for partner Rajesh, who withdrew Rs 1,200 at the end of every month for six months ending on 31.3.2012.

SAMPLE QUESTION PAPER 2 ACCOUNTANCY

SAMPLE QUESTION PAPER 2 ACCOUNTANCY Class XII Time allowed: 3hrs Maximum Marks: 80 General Instructions: (i) This question paper contains two parts A, B. (ii) All parts of a question should be attempted

SAMPLE QUESTION PAPER 2 ACCOUNTANCY Class XII Time allowed: 3hrs Maximum Marks: 80 General Instructions: (i) This question paper contains two parts A, B. (ii) All parts of a question should be attempted

KENDRIYA VIDYALAYA SANGATHAN, CHENNAI REGION COMMON PRE-BOARD EXAMINATION ACCOUNTANCY

KENDRIYA VIDYALAYA SANGATHAN, CHENNAI REGION COMMON PRE-BOARD EXAMINATION 2008-09 ACCOUNTANCY SET-III Time allowed : 3 hours Maximum marks: 80 General Instructions i. This paper contains two parts part

KENDRIYA VIDYALAYA SANGATHAN, CHENNAI REGION COMMON PRE-BOARD EXAMINATION 2008-09 ACCOUNTANCY SET-III Time allowed : 3 hours Maximum marks: 80 General Instructions i. This paper contains two parts part

RETIREMENT OF A PARTNER

CHAPER 05 REIREMEN OF A PARNER Question 5:1 he Balance Sheet of Amar, Akber and Anthoni who where sharing profit in the ratio of 4:3:2 stood as following on 31st December 2004. Balance Sheet as on 31st

CHAPER 05 REIREMEN OF A PARNER Question 5:1 he Balance Sheet of Amar, Akber and Anthoni who where sharing profit in the ratio of 4:3:2 stood as following on 31st December 2004. Balance Sheet as on 31st

DISSOLUTION OF PARTNERSHIP FIRM. After Studying this unit, the students will be able to understand:

DISSOLUTION OF PARTNERSHIP FIRM Learning Objectives After Studying this unit, the students will be able to understand: *Meaning of Dissolution * Distinction between Dissolution of Partnership and Dissolution

DISSOLUTION OF PARTNERSHIP FIRM Learning Objectives After Studying this unit, the students will be able to understand: *Meaning of Dissolution * Distinction between Dissolution of Partnership and Dissolution

Downloaded from

CHAPTER -3 ADMISSION OF A PARTNER ONE MARK QUESTIONS. 1. Why is it necessary to revalue assets and reassess liabilities of a firm in case of admission of a new partner? Ans. The assets are revalued and

CHAPTER -3 ADMISSION OF A PARTNER ONE MARK QUESTIONS. 1. Why is it necessary to revalue assets and reassess liabilities of a firm in case of admission of a new partner? Ans. The assets are revalued and

Brilliant Public School

Brilliant Public School Seepat Road Bahatarai, Bilaspur (C.G.) Pre Board - I, 2017-18 Class XII Subject Accountancy Time: 3:00 Hours M.M. 80 Date: 19.12.2017 Tuesday General Instructions: (i) This question

Brilliant Public School Seepat Road Bahatarai, Bilaspur (C.G.) Pre Board - I, 2017-18 Class XII Subject Accountancy Time: 3:00 Hours M.M. 80 Date: 19.12.2017 Tuesday General Instructions: (i) This question

This transactions during the year (i.e. from to ) were as follows: 8

were as follows: 8") This transactions during the year 2008-09 (i.e. from 1-4-2008 to 31-3-2009) were as follows: 8 Receipts Rs. Payments Rs. Sundry Debtors 15,000 Bank overdraft 10,000 Cash sales 80,000 Drawings 3,000 Expenses

This transactions during the year 2008-09 (i.e. from 1-4-2008 to 31-3-2009) were as follows: 8 Receipts Rs. Payments Rs. Sundry Debtors 15,000 Bank overdraft 10,000 Cash sales 80,000 Drawings 3,000 Expenses

ITL Public School Answer Key (Set A)

") ITL Public School Answer Key (Set A) Date of Exam: 23.09.206 Class: XII Time:3 hrs M. M:80 Subject: Accountancy General Instructions:. All questions are compulsory 2. Marks for each question are indicated

ITL Public School Answer Key (Set A) Date of Exam: 23.09.206 Class: XII Time:3 hrs M. M:80 Subject: Accountancy General Instructions:. All questions are compulsory 2. Marks for each question are indicated

Steps in Accounting for Dissolution of Partnership Firm 1) Scrap the Balance Sheet: For this purpose we open one special Account Realisation Account

Scrap the Balance Sheet: For this purpose we open one special Account Realisation Account") 14 Chapter Partnership Accounts Dissolution of Partnership A firm stands dissolved in the following cases: 1. The partners agree that the firm should be dissolved. 2. All partners except one become insolvent.

14 Chapter Partnership Accounts Dissolution of Partnership A firm stands dissolved in the following cases: 1. The partners agree that the firm should be dissolved. 2. All partners except one become insolvent.

12. PARTNERSHIP ACCOUNTS-1

(i) No.1 for CA/CWA & MEC/CEC SOLUTIONS TO ASSIGNMENT PROBLEMS PROBLEM NO.1 1. PARTNERSHIP ACCOUNTS1 Statement of Affairs of A,B & C As on 0 th June, 008 Liabilities Assets,8 0,000 Capital (Bal. Fig.)

(i) No.1 for CA/CWA & MEC/CEC SOLUTIONS TO ASSIGNMENT PROBLEMS PROBLEM NO.1 1. PARTNERSHIP ACCOUNTS1 Statement of Affairs of A,B & C As on 0 th June, 008 Liabilities Assets,8 0,000 Capital (Bal. Fig.)

SURANA IND. PU COLLEGE

SURANA IND. PU COLLEGE SOUTH END ROAD, BANGALORE II PUC ACCOUNTANCY MODEL QUESTION PAPER III Time 3Hrs 15Mins Max. Marks: 100 SECTION A I Answer any seven questions each carrying two marks: 7x2=I4 1. State

SURANA IND. PU COLLEGE SOUTH END ROAD, BANGALORE II PUC ACCOUNTANCY MODEL QUESTION PAPER III Time 3Hrs 15Mins Max. Marks: 100 SECTION A I Answer any seven questions each carrying two marks: 7x2=I4 1. State

2. The capital accounts of A and B stood at Rs.4,00,000/- and Rs.3,00,000/- respectively after

DEHRADUN PUBLIC SCHOOL I TERM ASSIGNMENT(201617) SUBJECT ACCOUNTANCY (055) CLASS XII Ch 1 FUNDAMANTAL OF PARTNERSHIP 1. Amit and Vijay started a partnership business on 1 st April, 2010. Their capital

DEHRADUN PUBLIC SCHOOL I TERM ASSIGNMENT(201617) SUBJECT ACCOUNTANCY (055) CLASS XII Ch 1 FUNDAMANTAL OF PARTNERSHIP 1. Amit and Vijay started a partnership business on 1 st April, 2010. Their capital

Downloaded from INTERNATIONAL INDIAN SCHOOL-RIYADH

INTERNATIONAL INDIAN SCHOOL-RIYADH ACCOUNTANCY 2014-2015 GRADE 12 WORKSHEET -3 1. A, B are partners sharing profits in the ratio of 5:3.Their balance sheet as on 31 st December 2013 was as follows Balance

INTERNATIONAL INDIAN SCHOOL-RIYADH ACCOUNTANCY 2014-2015 GRADE 12 WORKSHEET -3 1. A, B are partners sharing profits in the ratio of 5:3.Their balance sheet as on 31 st December 2013 was as follows Balance

NAVODAYA VIDYALAYA SAMITI. Class-XII ACCOUNTANCY

Practice Paper Set - V Code No. 055 NAVODAYA VIDYALAYA SAMITI Class-XII 2015-16 ACCOUNTANCY ROLL NO. STUDENT NAME Time Allowed: - 3 Hours General Instructions:- (i) This question paper contains two parts-a

Practice Paper Set - V Code No. 055 NAVODAYA VIDYALAYA SAMITI Class-XII 2015-16 ACCOUNTANCY ROLL NO. STUDENT NAME Time Allowed: - 3 Hours General Instructions:- (i) This question paper contains two parts-a

Liabilities Rs. Assets Rs.

MARKING SCHEME SAMPLE QUESTION PAPER -I ACCOUNTANCY Class - XII Set - I Part A Accounting for Not for Profit Organizations, Partnership Firms and Companies 1. Such organisations are formed for providing

MARKING SCHEME SAMPLE QUESTION PAPER -I ACCOUNTANCY Class - XII Set - I Part A Accounting for Not for Profit Organizations, Partnership Firms and Companies 1. Such organisations are formed for providing

INDIAN SCHOOL MUSCAT Senior Section Department of Commerce and Humanities

INDIAN SCHOOL MUSCAT Senior Section Department of Commerce and Humanities Class : 12 Date of issue --------------2018 Worksheet-6 : Dissolution of Partnership Firm Accountancy (055) Reference: Grewal T.S.

INDIAN SCHOOL MUSCAT Senior Section Department of Commerce and Humanities Class : 12 Date of issue --------------2018 Worksheet-6 : Dissolution of Partnership Firm Accountancy (055) Reference: Grewal T.S.

Professor Vipin Conversion of Partnership into Company. Meaning

Meaning Conversion of Partnership into Company For various reasons, an existing partnership may sell its entire business to an existing Joint Stock Company. It can also convert itself into a Joint Stock

Meaning Conversion of Partnership into Company For various reasons, an existing partnership may sell its entire business to an existing Joint Stock Company. It can also convert itself into a Joint Stock

TOPPER SAMPLE PAPER 1

196 Accounts XII TOPPER SAMPLE PAPER 1 ACCOUNTANCY XII Time Allowed - 3 Hrs. Max. Marks - 80 General Instructions:- 1. This question paper contains two parts A & B only. 2. All parts of questions should

196 Accounts XII TOPPER SAMPLE PAPER 1 ACCOUNTANCY XII Time Allowed - 3 Hrs. Max. Marks - 80 General Instructions:- 1. This question paper contains two parts A & B only. 2. All parts of questions should

ITL PUBLIC SCHOOL HOLIDAY HOME WORK CLASS XII- ACCOUNTANCY

ITL PUBLIC SCHOOL HOLIDAY HOME WORK CLASS XII- ACCOUNTANCY I. Prepare a comprehensive project on any sole proprietorship or partnership firm for its entire year s financial transactions. The following

ITL PUBLIC SCHOOL HOLIDAY HOME WORK CLASS XII- ACCOUNTANCY I. Prepare a comprehensive project on any sole proprietorship or partnership firm for its entire year s financial transactions. The following

ACCOUNTANCY CLASS-XII. Time Allowed: 3 Hours Maximum Marks : 80

ACCOUNTANCY CLASS-XII Time Allowed: 3 Hours Maximum Marks : 80 General Instructions: (i) This question paper contains two parts: A and B. (ii) Part A is compulsory for all candidates. (iii) Part B has

ACCOUNTANCY CLASS-XII Time Allowed: 3 Hours Maximum Marks : 80 General Instructions: (i) This question paper contains two parts: A and B. (ii) Part A is compulsory for all candidates. (iii) Part B has

INDIAN SCHOOL MUSCAT Senior Section Department of Commerce and Humanities

INDIAN SCHOOL MUSCAT Senior Section Department of Commerce and Humanities Class : 12 Worksheet-6 : Death of Partner Reference: Grewal T.S. Date of issue Accountancy (055) Date of submission --------------2017

INDIAN SCHOOL MUSCAT Senior Section Department of Commerce and Humanities Class : 12 Worksheet-6 : Death of Partner Reference: Grewal T.S. Date of issue Accountancy (055) Date of submission --------------2017

ACCOUNTANCY. Time allowed : 3 hours Maximum Marks : 80

ACCOUNTANCY Time allowed : 3 hours Maximum Marks : 80 General Instructions : (i) This question paper contains three parts A, B and C. (ii) Part-A is compulsory for all candidates. (iii) Candidates can

ACCOUNTANCY Time allowed : 3 hours Maximum Marks : 80 General Instructions : (i) This question paper contains three parts A, B and C. (ii) Part-A is compulsory for all candidates. (iii) Candidates can

Accountancy. Class XII: Sample Paper. Source: mycbseguide.com

Accountancy Class XII: Sample Paper Source: mycbseguide.com SAMPLE PAPER- 1 (solved) ACCOUNTANCY Class XII Time allowed: 3 hours Maximum Marks: 80 General Instructions: 1. This question paper contains

Accountancy Class XII: Sample Paper Source: mycbseguide.com SAMPLE PAPER- 1 (solved) ACCOUNTANCY Class XII Time allowed: 3 hours Maximum Marks: 80 General Instructions: 1. This question paper contains

ACCOUNTANCY Ch.4 Reconstitution of Partnership: Admission of a Partner Name: Date: Class: XII

ACCOUNTANCY Ch.4 Reconstitution of Partnership: Admission of a Partner Name: Date: Class: XII 1. A and B are partners sharing profit and loss in the ratio of 3:2.C is admitted for 1/5 th share. Afterwards

ACCOUNTANCY Ch.4 Reconstitution of Partnership: Admission of a Partner Name: Date: Class: XII 1. A and B are partners sharing profit and loss in the ratio of 3:2.C is admitted for 1/5 th share. Afterwards

CBSE-XII (2018) CBSE BOARD PAPER WITH SOLUTION ACCOUNTANCY. Candidate must write the Code on the titile page of the answer-book.

CBSE BOARD PAPER WITH SOLUTION ACCOUNTANCY. Candidate must write the Code on the titile page of the answer-book.") CBSE-XII (2018) CBSE BOARD PAPER WITH SOLUTION ACCOUNTANCY Code No. 67/1 Roll.No. Candidate must write the Code on the titile page of the answer-book. Time allowed : 3 hours Maximum Marks : 80 Code number

CBSE-XII (2018) CBSE BOARD PAPER WITH SOLUTION ACCOUNTANCY Code No. 67/1 Roll.No. Candidate must write the Code on the titile page of the answer-book. Time allowed : 3 hours Maximum Marks : 80 Code number

KENDRIYA VIDYALAYA SANGATHAN-KOLKATA REGION 2ND PRE-BOARD EXAMINATION: SUB: ACCOUNTANCY TIME ALLOWED: 3 HOURS M.M :80

KENDRIYA VIDYALAYA SANGATHAN-KOLKATA REGION 2ND PRE-BOARD EXAMINATION: 2014-15 SUB: ACCOUNTANCY TIME ALLOWED: 3 HOURS M.M :80 General Instructions: 1. This question paper contains two parts- A and B. 2.

KENDRIYA VIDYALAYA SANGATHAN-KOLKATA REGION 2ND PRE-BOARD EXAMINATION: 2014-15 SUB: ACCOUNTANCY TIME ALLOWED: 3 HOURS M.M :80 General Instructions: 1. This question paper contains two parts- A and B. 2.

MINIMUM LEARNING MATERIAL

MINIMUM LEARNING MATERIAL FUNDAMENTAL OF PARTNERSHIP (1 mark question) Q1 If date or drawings of the partner is not giving in the questions interest is charged for how much time? (a)1 month (b) 3 months

MINIMUM LEARNING MATERIAL FUNDAMENTAL OF PARTNERSHIP (1 mark question) Q1 If date or drawings of the partner is not giving in the questions interest is charged for how much time? (a)1 month (b) 3 months

CBSE Examination PAPER 2017

CBSE Examination PAPER 2017 Accountancy (All India) General Instructions 1. This question paper contains two parts A and B. 2. Part A is compulsory for all. 3. Part B has two options Analysis of Financial

CBSE Examination PAPER 2017 Accountancy (All India) General Instructions 1. This question paper contains two parts A and B. 2. Part A is compulsory for all. 3. Part B has two options Analysis of Financial

SAMPLE PAPER-III ACCOUNTANCY CLASS XII

SAMPLE PAPER-III ACCOUNTANCY CLASS XII PART-A : Accounting for Not for profit Organisation, Partnership and Company Q.1. How do you treat amount received from individual as per will in the final Accounts

SAMPLE PAPER-III ACCOUNTANCY CLASS XII PART-A : Accounting for Not for profit Organisation, Partnership and Company Q.1. How do you treat amount received from individual as per will in the final Accounts

Accountancy Set-2 Time allowed: 3 hours Maximum Marks: 90

Accountancy Set-2 Time allowed: 3 hours Maximum Marks: 90 General Instructions: 1) This question paper contains two parts A and B. 2) Part A is compulsory for all. 3) Part B has two options-option-i Analysis

Accountancy Set-2 Time allowed: 3 hours Maximum Marks: 90 General Instructions: 1) This question paper contains two parts A and B. 2) Part A is compulsory for all. 3) Part B has two options-option-i Analysis

STUDENT SUPPORT MATERIAL Table of Contents

INDIAN SCHOOL MUSCAT Senior Section Department of Commerce and Humanities Class : 12 Date of issue -------------- 2017 SOLVED SUPPORT MATERIAL ALL CHAPTERS ACCOUNTANCY (055) Reference: KVS Question Bank,

INDIAN SCHOOL MUSCAT Senior Section Department of Commerce and Humanities Class : 12 Date of issue -------------- 2017 SOLVED SUPPORT MATERIAL ALL CHAPTERS ACCOUNTANCY (055) Reference: KVS Question Bank,

Perfectio Sample Paper for CBSE. Class XII. Accountancy By Dr. Vikas Vijay (Accounts Guru )

") Perfectio - 2016 Sample Paper for CBSE Class XII Accountancy By Dr. Vikas Vijay (Accounts Guru ) M Com, B Ed, CWA(I), M Phil, Ph D, LLB + 91-9810278915 Author of Together with Accountancy and Business

Perfectio - 2016 Sample Paper for CBSE Class XII Accountancy By Dr. Vikas Vijay (Accounts Guru ) M Com, B Ed, CWA(I), M Phil, Ph D, LLB + 91-9810278915 Author of Together with Accountancy and Business

SAMPLE QUESTION PAPER IN ACCOUNTANCY

SAMPLE QUESTION PAPER IN ACCOUNTANCY Time : Three Hours Maximum Marks: 100 Note : The question paper is divided into two sections A and B. Attempt all questions of Section A and five questions of one part

SAMPLE QUESTION PAPER IN ACCOUNTANCY Time : Three Hours Maximum Marks: 100 Note : The question paper is divided into two sections A and B. Attempt all questions of Section A and five questions of one part

Admission of a Partner

Admission of a Partner Q.1 Dinesh, Yasmine and Faria are partners in a firm, sharing profits and losses in 11:7:2 respectively. The Balance Sheet of the firm as on 31st Dec 2001 was as follows: Sundry

Admission of a Partner Q.1 Dinesh, Yasmine and Faria are partners in a firm, sharing profits and losses in 11:7:2 respectively. The Balance Sheet of the firm as on 31st Dec 2001 was as follows: Sundry

ACCOUNTANCY. Std.: XII- Com. (As per new pattern) Time : 3 Hrs. 80. General Instructions:

Time : 3 Hrs. 80. General Instructions:") ACCOUNTANCY Time : 3 Hrs. 80 M.M.: Std.: XII- Com. (As per new pattern) General Instructions: 1. This question paper contains two parts A and B. 2. All parts of a question should be attempted at one place.

ACCOUNTANCY Time : 3 Hrs. 80 M.M.: Std.: XII- Com. (As per new pattern) General Instructions: 1. This question paper contains two parts A and B. 2. All parts of a question should be attempted at one place.

The Question Paper Design, Syllabus, Sample Question Paper. and. Marking Scheme. Accountancy (Code No.055) Class XII

Class XII") The Question Paper Design, Syllabus, Sample Question Paper and Marking Scheme In Accountancy (Code No.055) Class XII Effective for Board Examination 2015 CENTRAL BOARD OF SECONDARY EDUCATION 1 SYLLABUS

The Question Paper Design, Syllabus, Sample Question Paper and Marking Scheme In Accountancy (Code No.055) Class XII Effective for Board Examination 2015 CENTRAL BOARD OF SECONDARY EDUCATION 1 SYLLABUS

THE INDIAN COMMUNITY SCHOOL, KUWAIT

THE INDIAN COMMUNITY SCHOOL, KUWAIT SERIES : II TERM /FN/ 2018-2019 CODE :N 055 TIME ALLOWED :3 HOURS NAME OF STUDENT : MAX. MARKS :80 ROLL NO. :.. CLASS/SEC :.. NO. OF PAGES :7 ACCOUNTANCY ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

THE INDIAN COMMUNITY SCHOOL, KUWAIT SERIES : II TERM /FN/ 2018-2019 CODE :N 055 TIME ALLOWED :3 HOURS NAME OF STUDENT : MAX. MARKS :80 ROLL NO. :.. CLASS/SEC :.. NO. OF PAGES :7 ACCOUNTANCY ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Pre-Board Exam 02. Accountancy. Class : XII

Pre-Board Exam 02 Accountancy Class : XII Max. Marks: 80 Duration : hours Instructions:. Question paper consists of 25 questions. 2. All questions are compulsory.. Attempt all parts of a question together..

Pre-Board Exam 02 Accountancy Class : XII Max. Marks: 80 Duration : hours Instructions:. Question paper consists of 25 questions. 2. All questions are compulsory.. Attempt all parts of a question together..

SURANA IND. PU COLLEGE

SURANA IND. PU COLLEGE SOUTH END ROAD, BANGALORE II PUC ACCOUNTANCY MODEL QUESTION PAPER VI Time 3Hrs 15Mins Max. Marks: 100 SECTION A I. Answer any seven questions each carrying two marks: 7x2=I4 1. Bring

SURANA IND. PU COLLEGE SOUTH END ROAD, BANGALORE II PUC ACCOUNTANCY MODEL QUESTION PAPER VI Time 3Hrs 15Mins Max. Marks: 100 SECTION A I. Answer any seven questions each carrying two marks: 7x2=I4 1. Bring

UNIT - 1: DISSOLUTION OF PARTNERSHIP FIRMS. Go through the circumstances in which a partnership is dissolved.

CHAPTER 15 PARTNERSHIP ACCOUNTS UNIT - 1: DISSOLUTION OF PARTNERSHIP FIRMS LEARNING OUTCOMES After studying this chapter, you will be able to r r r r Go through the circumstances in which a partnership

CHAPTER 15 PARTNERSHIP ACCOUNTS UNIT - 1: DISSOLUTION OF PARTNERSHIP FIRMS LEARNING OUTCOMES After studying this chapter, you will be able to r r r r Go through the circumstances in which a partnership

, 1, --r-1 ---,--I --r--1 --,-----I I

Bir la Public School, Doha - Qatar First Mock Examination - December 2017 Roll No., 1, --r-1 ---,--I --r--1 --,-----I I Series SSR / 1 Code No. 055/ 1 / 3 Class: XII Please check that this question paper

Bir la Public School, Doha - Qatar First Mock Examination - December 2017 Roll No., 1, --r-1 ---,--I --r--1 --,-----I I Series SSR / 1 Code No. 055/ 1 / 3 Class: XII Please check that this question paper

KENDRIYA VIDYALAYA SANGATHAN, CHENNAI REGION COMMON PRE-BOARD EXAMINATION ACCOUNTANCY

KENDRIYA VIDYALAYA SANGATHAN, CHENNAI REGION COMMON PRE-BOARD EXAMINATION 2008-09 ACCOUNTANCY SET-V Time allowed : 3 hours Maximum marks: 80 General Instructions i. This paper contains two parts part A

KENDRIYA VIDYALAYA SANGATHAN, CHENNAI REGION COMMON PRE-BOARD EXAMINATION 2008-09 ACCOUNTANCY SET-V Time allowed : 3 hours Maximum marks: 80 General Instructions i. This paper contains two parts part A

INTERNATIONAL COMMERCE OLYMPIAD CLASS XII ACCOUNTANCY ASSIGNMENT. Non profit organisations

INTERNATIONAL COMMERCE OLYMPIAD -2018 CLASS XII ACCOUNTANCY ASSIGNMENT Non profit organisations 1. If there is match fund then, match expenses and match receipts are transferred to a]income and expenditure

INTERNATIONAL COMMERCE OLYMPIAD -2018 CLASS XII ACCOUNTANCY ASSIGNMENT Non profit organisations 1. If there is match fund then, match expenses and match receipts are transferred to a]income and expenditure

THE INDIAN COMMUNITY SCHOOL, KUWAIT

THE INDIAN COMMUNITY SCHOOL, KUWAIT SERIES : II TERM /FN/ 2018-2019 CODE : 055 TIME ALLOWED : 2 HOURS NAME OF STUDENT : MAX. MARKS : 50 ROLL NO. :.. CLASS/SEC :.. NO. OF PAGES :4 ACCOUNTANCY ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

THE INDIAN COMMUNITY SCHOOL, KUWAIT SERIES : II TERM /FN/ 2018-2019 CODE : 055 TIME ALLOWED : 2 HOURS NAME OF STUDENT : MAX. MARKS : 50 ROLL NO. :.. CLASS/SEC :.. NO. OF PAGES :4 ACCOUNTANCY ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

PC-07. Time : 3 Hours (Printed pages 7) Max. Marks: Attempt any THREE of the following:- 15. (A) Answer in one sentence only:- 5

Max. Marks: Attempt any THREE of the following:- 15. (A) Answer in one sentence only:- 5") ROLL NO. PC-07 Time : 3 Hours (Printed pages 7) Max. Marks: 80 1. Attempt any THREE of the following:- 15 (A) Answer in one sentence only:- 5 1. What is meant by Reconstitution of Partnership? 2. Why is

ROLL NO. PC-07 Time : 3 Hours (Printed pages 7) Max. Marks: 80 1. Attempt any THREE of the following:- 15 (A) Answer in one sentence only:- 5 1. What is meant by Reconstitution of Partnership? 2. Why is

CBSE SAMPLE PAPER- 01 (solved) for ACCOUNTANCY Class XII. Part A Partnership, Share Capital and Debentures

for ACCOUNTANCY Class XII. Part A Partnership, Share Capital and Debentures") CBSE SAMPLE PAPER- 01 (solved) for 2015-16 ACCOUNTANCY Class XII Time allowed: 3 hours Maximum Marks: 80 General Instructions: 1. This question paper contains Two parts A& B. 2. Both the parts are compulsory

CBSE SAMPLE PAPER- 01 (solved) for 2015-16 ACCOUNTANCY Class XII Time allowed: 3 hours Maximum Marks: 80 General Instructions: 1. This question paper contains Two parts A& B. 2. Both the parts are compulsory

Test Series: September, 2014

MOCK TEST PAPER 1 INTERMEDIATE (IPC) : GROUP I PAPER 1: ACCOUNTING Question No. 1 is compulsory. Answer any five questions from the remaining six questions. Test Series: September, 2014 Wherever necessary

MOCK TEST PAPER 1 INTERMEDIATE (IPC) : GROUP I PAPER 1: ACCOUNTING Question No. 1 is compulsory. Answer any five questions from the remaining six questions. Test Series: September, 2014 Wherever necessary

FINAL CA May 2018 Financial Reporting

FINAL CA May 2018 Financial Reporting Test Code F5 Branch: Andheri Date: 10.12.2017 (50 Marks) Note: All questions are compulsory. Question 1 (9 marks) Value Added Statement of Pradeep Ltd. for the period

FINAL CA May 2018 Financial Reporting Test Code F5 Branch: Andheri Date: 10.12.2017 (50 Marks) Note: All questions are compulsory. Question 1 (9 marks) Value Added Statement of Pradeep Ltd. for the period