Policy Values - additional topics

|

|

|

- Cynthia Kennedy

- 5 years ago

- Views:

Transcription

Policy Values - additional topics Spring 2015 - Valdez 1 /")

1 Policy Values - additional topics Lecture: Week 5 Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 1 / 38

2 Chapter summary additional topics Chapter summary - additional topics Other topics needed to be covered from this chapter: analysis of profit or loss and analysis by source (mortality, interest, expenses) asset shares Thiele s differential equation for reserve calculation policy alterations modified reserve systems Chapters 7 (Dickson, et al.): Sec 7.3.5, 7.5, 7.6, 7.9 Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 2 / 38

3

4 analysis of profit Profit defined Consider the period between years k and k + 1 and our block of policies at the beginning of this period has a total of N k (active) policies. Now denote by k V and k+1 V the gross premium reserves at the beginning and end of the period, on a per policy basis. Thus, on an expected basis, the ending (total) gross premium reserve for our block of policies is k+1v E = N k k+1 V Applying the recursion equation, we can express this total reserve as k+1v E = ( N k k V + N k G N k e k ) (1 + i) ( B k+1 V ) N k q x+k where clearly N k q x+k is the expected number of deaths for the period. If we denote the ending (total) actual gross premium reserve held for this block of policies by k+1 V A, then the insurer s profit for the period is the difference: Profit k = k+1 V A k+1 V E Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 3 / 38

5 analysis of profit sources of profit Sources of profit Clearly, the profit (or loss) earned during the period can be derived from essentially three sources: Interest there is a gain if we earn an interest higher than expected (and vice versa) Mortality there is a gain if we have fewer deaths than expected (and vice versa) Expenses there is a gain if we have lesser expenses than expected (and vice versa) Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 4 / 38

6 analysis of profit gain from interest Gain from interest Suppose that during the period, the insurer earned an interest rate of i instead of i. For simplicity (for now), suppose that the rest of the actual experience (i.e. mortality and expenses) are as expected. The (total) actual reserve at the end of the period is k+1v A = ( N k k V + N k G N k e k ) (1 + i ) ( B k+1 V ) N k q x+k The difference between the actual and expected reserves then can be written as gain from interest = ( N k k V + N k G N k e k ) (i i) Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 5 / 38

7 analysis of profit gain from expenses Gain from expenses Suppose that during the period, the insurer s actual expenses is e k on a per policy basis. Again for simplicity (for now), suppose that the rest of the actual experience (i.e. mortality and interest) are as expected. The (total) actual reserve at the end of the period is k+1v A = ( N k k V + N k G N k e k) (1 + i) ( B k+1 V ) N k q x+k The difference between the actual and expected reserves then can be written as gain from expenses = ( N k e k N k e k) (1 + i) = Nk ( ek e k) (1 + i) Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 6 / 38

8 analysis of profit gain from mortality Gain from mortality Suppose that during the period, the actual (total) number of deaths is D k. Note that the expected number of deaths from the N k lives is N k q x+k. Again for simplicity (for now), suppose that the rest of the actual experience (i.e. interest and expenses) are as expected. The (total) actual reserve at the end of the period is k+1v A = ( N k k V + N k G N k e k ) (1 + i) ( B k+1 V ) D k The difference between the actual and expected reserves then can be written as gain from mortality = ( B k+1 V )( N k q x+k D k ) Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 7 / 38

9 analysis of profit putting it together Putting all the sources together Suppose that during the period, the insurer earned an interest rate of i, the insurer s actual expenses is e k and the actual (total) number of deaths is D k. The (total) actual reserve at the end of the period is k+1v A = ( N k k V + N k G N k e k) (1 + i ) ( B k+1 V ) D k In this case, one should be able to have the relation: Profit k = gain from interest + gain from expenses + gain from mortality Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 8 / 38

(i i) gain from expenses = ( N k e k N k e k) (1 + i ( ) = N k ek e k) (1 + i ) gain from mortality = ( B k+1 V )( N k q x+k D k ) Lecture: Week 5")

10 analysis of profit interest expenses mortality interest expenses mortality Sources of profit with the following ordering: interest expenses mortality. gain from interest = ( N k k V + N k G N k e k ) (i i) gain from expenses = ( N k e k N k e k) (1 + i ( ) = N k ek e k) (1 + i ) gain from mortality = ( B k+1 V )( N k q x+k D k ) Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 9 / 38

(1 + i) = Nk ( ek e k) (1 + i) gain from interest = ( N k k V + N k G N k e k) (i i) gain from mortality = ( B k+1 V )( N k q x+k D k ) Lecture: Week 5 (STT")

11 analysis of profit expenses interest mortality expenses interest mortality Sources of profit with the following ordering: expenses interest mortality. gain from expenses = ( N k e k N k e k) (1 + i) = Nk ( ek e k) (1 + i) gain from interest = ( N k k V + N k G N k e k) (i i) gain from mortality = ( B k+1 V )( N k q x+k D k ) Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 10 / 38

12 analysis of profit remark Remark on gain from mortality Notice from the previous slides that the order where mortality is does not matter because its calculation neither involves interest nor expenses. However, there are instances where there may be death-related expenses, usually denoted by E k+1. In this case, it matters where you order the mortality. However, so long as you go with the following principle: when calculating gain of a source from the top, always use the expected experience of any sources unaccounted for, and once gain for a source is accounted for, use the actual experience. Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 11 / 38

13 analysis of profit illustration Illustrative example from book Consider Example 7.8 Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 12 / 38

14 analysis of profit illustrative example Illustrative example 1 For a fully discrete 20-year term life insurance of $10,000 on (40), you are given: The following actual and expected experience in year 4: Experience actual expected Gross annual premium $ 90 $ 90 Expenses as a percent of premium 2.5% 3.0% 1000 q Annual effective rate of interest Profits are calculated based on the following (per policy) gross premium reserves: 3V = 100 4V = 125 Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 13 / 38

15 analysis of profit illustrative example Illustrative example 1 - continued A company issued (such) 20-year term life insurance policies to 1,000 lives age 40 with independent future lifetimes. At the end of the 3rd year, 990 (of these) insurances remain in force. 1 Calculate the total gain in year 4. 2 Allocate this total gain from the following sources (in the given order): interest, expenses, and mortality. 3 Allocate this total gain from the following sources (in the given order): expenses, interest, and mortality. Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 14 / 38

16

17

18

19

20

21

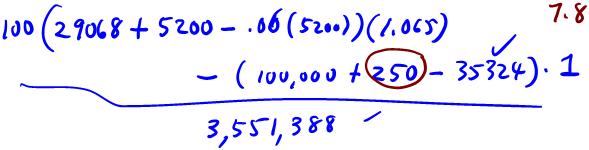

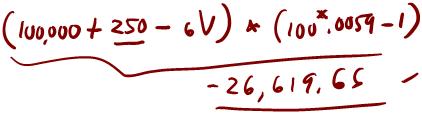

22 analysis of profit SOA question SOA question #17, Spring 2012 Your company issues fully discrete whole life policies to a group of lives age 40. For each policy, you are given: The death benefit is $ 50,000. Assumed mortality and interest are the Illustrative Life Table at 6%. Annual gross premium equals 125% of benefit premium. Assumed expenses are 5% of gross premium, payable at the beginning of each year, and $ 300 to process each death claim, payable at the end of the year of death. Profits are based on gross premium reserves. During year 11, actual experience is as follows: There are 1,000 lives in force at the beginning of the year. There are five deaths. Interest earned equals 6%. Expenses equal 6% of gross premium and $ 100 to process each death claim. Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 15 / 38

23 analysis of profit SOA question SOA question #17, Spring continued For year 11, you calculate the gain due to mortality and then the gain due to expenses. 1 Calculate the total gain in year Calculate the gain due to mortality during year Calculate the gain due to expenses during year 11. [only this question was asked in the exam] Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 16 / 38

24

25

26

27 Asset shares Asset shares An asset share, generally denoted by AS, is the share of the insurer s assets attributable to each policy in force at any given time. It is calculated using the (year by year) experience that actually emerge (over time). For our purposes, any symbol with a prime ( ) denotes actual experience. Thus the asset share for a single policy at the end of year k + 1 is equal to AS k+1 = ( ASk + G k e ) k (1 + i k ) ( B k+1 + E k+1 ) q x+k 1 q x+k. It is not difficult to see that if the actual experience is equal to expected experience in all years (which is highly unlikely), this is exactly equal to the gross premium reserve. Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 17 / 38

28

29 Asset shares illustration Illustrative example from book Consider Example 7.9 Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 18 / 38

30

31 Asset shares illustrative example Illustrative example 2 For a portfolio of fully discrete whole life insurances of $100 each on (x), you are given: The annual contract premium per policy is $0.98. Expenses incurred at the beginning of year 21 is $0.15. The annual effective interest rate earned in year 21 is 8%. Out of the remaining 950 policies at the beginning of year 21, there were a total of 6 deaths during the year. The asset share at the end of year 20 is $15. Calculate the asset share at the end of year 21. Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 19 / 38

32

33

34 Thiele s differential equation Thiele s differential equation for reserves The Thiele s differential equation is the continuous analogue of the recursive relation between policy years for reserves: Note: d dt t V = δ t t V + G t e t ( B t + E t t V ) µ [x]+t Proof can be found in Section of DHW book. Interpretation (which is quite similar to the discrete analogue) can be found on page 210. Notice some differences in symbols used: we have consistently used G for gross premiums and B for benefit amount. Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 20 / 38

35 Thiele s differential equation Euler s method Numerical solution to Thiele s The numerical approximation to the solution to Thiele s differential equation is based on what is often referred to as the Euler s method. According to this method, we approximate the derivative using the following (for some very small h): Note: d dt t V t+h V t V h h is sometimes referred to as a step size. The procedure is to solve backward equations using boundary conditions such as: term insurance: n V = 0 endowment insurance: n V = S where S denotes the benefit upon survival at maturity Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 21 / 38

36 Thiele s differential equation Euler s method - continued We then have the following approximate formula: t+hv t V = h [ δ t t V + G t e t ( B t + E t t V ) µ [x]+t ] Starting with the boundary condition for n V : nv n h V = h [ δ n h n h V +G n h e n h ( B n h +E n h n h V ) µ [x]+n h ] We solve for n h V from this approximate formula. Using this value, we then proceed to calculate for reserve at n 2h, and so forth. Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 22 / 38

37 Thiele s differential equation illustration Illustrative example from book Consider Example 7.12 Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 23 / 38

38 Thiele s differential equation illustrative example Illustrative example 3 For a 15-year term insurance policy issued to age 50, you are given: Death benefit of $10,000 is payable at the moment of death. Expense rate incurred continuously during each year is 10% of the annual premium rate; annual premium rate payable continuously throughout the year is equal to $ The force of mortality for age 50 is given by µ 50+t = A + B c 50+t, for t 0, where A = , B = and c = δ = 4.5% With step size of h = 0.05, estimate the reserve at the end of year 14 using the Euler s method. Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 24 / 38

39

40 Thiele s differential equation - continued Illustrative example 3 - continued Starting with 15 V = 0, use the equation (derived from the Euler s method): 1 tv = t+h V h ( 0.9G 10000µ 50+t ) 1 + hδ + hµ 50+t With steps of h = 0.05, one can verify the following calculations: t µ 50+t t V t µ 50+t t V corrected: Feb 22, 2012 Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 25 / 38

41

42

43 Surrender values Surrender values Many policies, especially those considered long term, contain non-forfeiture clauses which provide for cash surrender values. Minimum cash surrender values are generally imposed by regulation - called non-forfeiture laws. Terminal reserves are used to determine the appropriate policy values, hence cash surrender values are computed quite similar to reserves. However, the cash surrender value is generally smaller than the terminal reserve: CV t t V. The difference tv CV t is indeed called the surrender charge. Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 26 / 38

44 Surrender values computing surrender values Computing surrender values They may be computed quite similar to reserve calculations. For example on a prospective basis, we may have CV t = APV(Future Benefits) APV(Future Adjusted Premiums) Some possible differences may include: The calculation basis (mortality/interest assumptions) may be different from that used in reserve calculation - for conservatism. Premiums may also be adjusted to recoup expenses, especially the large first-year initial expense. Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 27 / 38

45 Surrender values surrender options Surrender options In lieu of receiving cash, some alternative options are generally available: (reduced) paid-up insurance extended term insurance Because these are generally initiated by the policyholder, these are sometimes called policy alterations. In a (reduced) paid-up insurance surrender option, the idea is to provide for a reduced amount of insurance which becomes paid-up. No further premium is required from surrender date onwards. In an extended term insurance, the idea is to provide for a term insurance protection, the length of which is determined depending on the cash surrender value. The amount of insurance is therefore maintained, but the duration of coverage is reduced. These will be illustrated in lectures. Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 28 / 38

46 Surrender values calculating altered contracts Calculating altered contracts Assume at time t the policyholder decides to alter the contract. At that time, he has the option to receive the cash surrender value, CV t, or use it to buy an altered contract. To determine the new benefits under an altered contract, one may use the following equation of value: CV t + APV(FP t ) = APV(FB t ), where FP t and FB t respectively denote future premiums and future benefits under the altered (new) contract. Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 29 / 38

47 Surrender values illustrative example Illustrative example 4 Consider a fully discrete whole life policy with B = 100, 000 issued to (45). You are given the following table of applicable cash values for various duration for this policy: k x A x 2 E x k V CV k k x A x 2 E x k V CV k Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 30 / 38

paid-up insurance. 2 The policyholder decides to lapse the policy after 20 years and wishes to purchase a paid-up insurance.")

48 Surrender values - continued Illustrative example 4 - continued Do the following: 1 The policyholder decides to lapse the policy after 10 years and wishes to purchase a paid-up insurance. Calculate the amount of (reduced) paid-up insurance. 2 The policyholder decides to lapse the policy after 20 years and wishes to purchase a paid-up insurance. Calculate the amount of (reduced) paid-up insurance. 3 The policyholder decides to lapse the policy after 10 years and wishes to purchase an extended term insurance. Estimate from the table the range of extended term while maintaining the same amount of insurance. Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 31 / 38

49

50

51 Deferred acquisition cost Deferred acquisition cost Recall that in most circumstances, there is usually an (extra) large expense item at point of sale. This expense item can either be: Immediately recognized as expenses in the year of sale: this will reduce income and therefore surplus. Amortize (or spread) this expense item over the life of the contract: this gives rise to the concept of deferred acquisition cost (DAC). Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 32 / 38

expense reserve and is referred to as the deferred acquisition cost.")

APV(future expense loadings) Lecture: Week 5 (STT 456) Policy Values - additional")

52 Deferred acquisition cost - continued Deferred acquisition cost - continued The difference between the gross premium reserve and the benefit premium reserve tv e = t V g t V n is called the (negative) expense reserve and is referred to as the deferred acquisition cost. Mathematically, if we define the difference between the gross premium and the benefit premium as the expense loading then it is not difficult to show that P e = P g P n, DAC = t V e = APV(future expenses) APV(future expense loadings) Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 33 / 38

53

54 Deferred acquisition cost illustration Illustrative example from study note Consider Example 7.17 Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 34 / 38

55

56

57 Deferred acquisition cost modified reserve systems Modified reserve systems In most jurisdictions, authorities specify the extent to which the level of expenses that can be amortized and reserved. There are clear explanations to this: If expenses are spread over the contract life, there is the possibility that the DAC may not be recovered especially when policy lapse. DAC may also lead to negative reserves in the first year. This gives rise to what are sometimes referred to as modified reserve systems. The most common of these methods is called the Full Preliminary Term or FPT. Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 35 / 38

58 Deferred acquisition cost FPT method The Full Preliminary Term (FPT) method The general idea with modified reserve method is to replace the level benefit premiums, P, with a first year premium of α and increased renewal premiums of β. For instance, in the case of a fully discrete whole life insurance of $1 on (x), we solve the equation of value: Therefore, we see that P ä x = α + βa x = βä x (β α) β = P + β α ä x. Then use α and β to calculate reserves. Because we know that to avoid negative reserves in the first year, the value of α must be at least the first year cost of insurance: vq x. Under FPT, set α = vq x. Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 36 / 38

59

60

61 Deferred acquisition cost illustrative example Illustrative example 5 Calculate 10 V FPT for each of the following cases: 1 A fully discrete whole life insurance of $100,000 issued to (40). 2 A fully discrete 25-pay whole life insurance of $100,000 issued to (40). Assume mortality follows the Illustrative Life Table with i = 6%. Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 37 / 38

62

63

reserve for this policy at the end of year 10.")

64 Deferred acquisition cost SOA question SOA question #8, Spring 2012 For a fully discrete whole life insurance of $ 1,000 on (80): i = 0.06 ä 80 = 5.89 ä 90 = 3.65 q 80 = Calculate the Full Preliminary Term (FPT) reserve for this policy at the end of year 10. Lecture: Week 5 (STT 456) Policy Values - additional topics Spring Valdez 38 / 38

65

66

Stat 476 Life Contingencies II. Policy values / Reserves

Stat 476 Life Contingencies II Policy values / Reserves Future loss random variables When we discussed the setting of premium levels, we often made use of future loss random variables. In that context,

Stat 476 Life Contingencies II Policy values / Reserves Future loss random variables When we discussed the setting of premium levels, we often made use of future loss random variables. In that context,

Policy Values. Lecture: Weeks 2-4. Lecture: Weeks 2-4 (STT 456) Policy Values Spring Valdez 1 / 33

Policy Values Spring Valdez 1 / 33") Policy Values Lecture: Weeks 2-4 Lecture: Weeks 2-4 (STT 456) Policy Values Spring 2015 - Valdez 1 / 33 Chapter summary Chapter summary Insurance reserves (policy values) what are they? how do we calculate

Policy Values Lecture: Weeks 2-4 Lecture: Weeks 2-4 (STT 456) Policy Values Spring 2015 - Valdez 1 / 33 Chapter summary Chapter summary Insurance reserves (policy values) what are they? how do we calculate

Multiple State Models

Multiple State Models Lecture: Weeks 6-7 Lecture: Weeks 6-7 (STT 456) Multiple State Models Spring 2015 - Valdez 1 / 42 Chapter summary Chapter summary Multiple state models (also called transition models)

Multiple State Models Lecture: Weeks 6-7 Lecture: Weeks 6-7 (STT 456) Multiple State Models Spring 2015 - Valdez 1 / 42 Chapter summary Chapter summary Multiple state models (also called transition models)

May 2012 Course MLC Examination, Problem No. 1 For a 2-year select and ultimate mortality model, you are given:

Solutions to the May 2012 Course MLC Examination by Krzysztof Ostaszewski, http://www.krzysio.net, krzysio@krzysio.net Copyright 2012 by Krzysztof Ostaszewski All rights reserved. No reproduction in any

Solutions to the May 2012 Course MLC Examination by Krzysztof Ostaszewski, http://www.krzysio.net, krzysio@krzysio.net Copyright 2012 by Krzysztof Ostaszewski All rights reserved. No reproduction in any

Premium Calculation. Lecture: Weeks Lecture: Weeks (Math 3630) Premium Caluclation Fall Valdez 1 / 35

Premium Caluclation Fall Valdez 1 / 35") Premium Calculation Lecture: Weeks 12-14 Lecture: Weeks 12-14 (Math 3630) Premium Caluclation Fall 2017 - Valdez 1 / 35 Preliminaries Preliminaries An insurance policy (life insurance or life annuity)

Premium Calculation Lecture: Weeks 12-14 Lecture: Weeks 12-14 (Math 3630) Premium Caluclation Fall 2017 - Valdez 1 / 35 Preliminaries Preliminaries An insurance policy (life insurance or life annuity)

Annuities. Lecture: Weeks 8-9. Lecture: Weeks 8-9 (Math 3630) Annuities Fall Valdez 1 / 41

Annuities Fall Valdez 1 / 41") Annuities Lecture: Weeks 8-9 Lecture: Weeks 8-9 (Math 3630) Annuities Fall 2017 - Valdez 1 / 41 What are annuities? What are annuities? An annuity is a series of payments that could vary according to:

Annuities Lecture: Weeks 8-9 Lecture: Weeks 8-9 (Math 3630) Annuities Fall 2017 - Valdez 1 / 41 What are annuities? What are annuities? An annuity is a series of payments that could vary according to:

Life Tables and Selection

Life Tables and Selection Lecture: Weeks 4-5 Lecture: Weeks 4-5 (Math 3630) Life Tables and Selection Fall 2017 - Valdez 1 / 29 Chapter summary Chapter summary What is a life table? also called a mortality

Life Tables and Selection Lecture: Weeks 4-5 Lecture: Weeks 4-5 (Math 3630) Life Tables and Selection Fall 2017 - Valdez 1 / 29 Chapter summary Chapter summary What is a life table? also called a mortality

Life Tables and Selection

Life Tables and Selection Lecture: Weeks 4-5 Lecture: Weeks 4-5 (Math 3630) Life Tables and Selection Fall 2018 - Valdez 1 / 29 Chapter summary Chapter summary What is a life table? also called a mortality

Life Tables and Selection Lecture: Weeks 4-5 Lecture: Weeks 4-5 (Math 3630) Life Tables and Selection Fall 2018 - Valdez 1 / 29 Chapter summary Chapter summary What is a life table? also called a mortality

Multiple Life Models. Lecture: Weeks Lecture: Weeks 9-10 (STT 456) Multiple Life Models Spring Valdez 1 / 38

Multiple Life Models Spring Valdez 1 / 38") Multiple Life Models Lecture: Weeks 9-1 Lecture: Weeks 9-1 (STT 456) Multiple Life Models Spring 215 - Valdez 1 / 38 Chapter summary Chapter summary Approaches to studying multiple life models: define

Multiple Life Models Lecture: Weeks 9-1 Lecture: Weeks 9-1 (STT 456) Multiple Life Models Spring 215 - Valdez 1 / 38 Chapter summary Chapter summary Approaches to studying multiple life models: define

2 hours UNIVERSITY OF MANCHESTER. 8 June :00-16:00. Answer ALL six questions The total number of marks in the paper is 100.

2 hours UNIVERSITY OF MANCHESTER CONTINGENCIES 1 8 June 2016 14:00-16:00 Answer ALL six questions The total number of marks in the paper is 100. University approved calculators may be used. 1 of 6 P.T.O.

2 hours UNIVERSITY OF MANCHESTER CONTINGENCIES 1 8 June 2016 14:00-16:00 Answer ALL six questions The total number of marks in the paper is 100. University approved calculators may be used. 1 of 6 P.T.O.

Annuities. Lecture: Weeks 8-9. Lecture: Weeks 8-9 (Math 3630) Annuities Fall Valdez 1 / 41

Annuities Fall Valdez 1 / 41") Annuities Lecture: Weeks 8-9 Lecture: Weeks 8-9 (Math 3630) Annuities Fall 2017 - Valdez 1 / 41 What are annuities? What are annuities? An annuity is a series of payments that could vary according to:

Annuities Lecture: Weeks 8-9 Lecture: Weeks 8-9 (Math 3630) Annuities Fall 2017 - Valdez 1 / 41 What are annuities? What are annuities? An annuity is a series of payments that could vary according to:

Michigan State University STT Actuarial Models II Class Test 1 Friday, 27 February 2015 Total Marks: 100 points

Michigan State University STT 456 - Actuarial Models II Class Test 1 Friday, 27 February 2015 Total Marks: 100 points Please write your name at the space provided: Name: There are ten (10) multiple choice

Michigan State University STT 456 - Actuarial Models II Class Test 1 Friday, 27 February 2015 Total Marks: 100 points Please write your name at the space provided: Name: There are ten (10) multiple choice

Annuities. Lecture: Weeks Lecture: Weeks 9-11 (Math 3630) Annuities Fall Valdez 1 / 44

Annuities Fall Valdez 1 / 44") Annuities Lecture: Weeks 9-11 Lecture: Weeks 9-11 (Math 3630) Annuities Fall 2017 - Valdez 1 / 44 What are annuities? What are annuities? An annuity is a series of payments that could vary according to:

Annuities Lecture: Weeks 9-11 Lecture: Weeks 9-11 (Math 3630) Annuities Fall 2017 - Valdez 1 / 44 What are annuities? What are annuities? An annuity is a series of payments that could vary according to:

A. 11 B. 15 C. 19 D. 23 E. 27. Solution. Let us write s for the policy year. Then the mortality rate during year s is q 30+s 1.

Solutions to the Spring 213 Course MLC Examination by Krzysztof Ostaszewski, http://wwwkrzysionet, krzysio@krzysionet Copyright 213 by Krzysztof Ostaszewski All rights reserved No reproduction in any form

Solutions to the Spring 213 Course MLC Examination by Krzysztof Ostaszewski, http://wwwkrzysionet, krzysio@krzysionet Copyright 213 by Krzysztof Ostaszewski All rights reserved No reproduction in any form

November 2012 Course MLC Examination, Problem No. 1 For two lives, (80) and (90), with independent future lifetimes, you are given: k p 80+k

and (90), with independent future lifetimes, you are given: k p 80+k") Solutions to the November 202 Course MLC Examination by Krzysztof Ostaszewski, http://www.krzysio.net, krzysio@krzysio.net Copyright 202 by Krzysztof Ostaszewski All rights reserved. No reproduction in

Solutions to the November 202 Course MLC Examination by Krzysztof Ostaszewski, http://www.krzysio.net, krzysio@krzysio.net Copyright 202 by Krzysztof Ostaszewski All rights reserved. No reproduction in

Gross Premium. gross premium gross premium policy value (using dirsct method and using the recursive formula)

") Gross Premium In this section we learn how to calculate: gross premium gross premium policy value (using dirsct method and using the recursive formula) From the ACTEX Manual: There are four types of expenses:

Gross Premium In this section we learn how to calculate: gross premium gross premium policy value (using dirsct method and using the recursive formula) From the ACTEX Manual: There are four types of expenses:

INSTRUCTIONS TO CANDIDATES

Society of Actuaries Canadian Institute of Actuaries Exam MLC Models for Life Contingencies Tuesday, April 29, 2014 8:30 a.m. 12:45 p.m. MLC General Instructions INSTRUCTIONS TO CANDIDATES 1. Write your

Society of Actuaries Canadian Institute of Actuaries Exam MLC Models for Life Contingencies Tuesday, April 29, 2014 8:30 a.m. 12:45 p.m. MLC General Instructions INSTRUCTIONS TO CANDIDATES 1. Write your

SOCIETY OF ACTUARIES. EXAM MLC Models for Life Contingencies EXAM MLC SAMPLE WRITTEN-ANSWER QUESTIONS AND SOLUTIONS

SOCIETY OF ACTUARIES EXAM MLC Models for Life Contingencies EXAM MLC SAMPLE WRITTEN-ANSWER QUESTIONS AND SOLUTIONS Questions September 17, 2016 Question 22 was added. February 12, 2015 In Questions 12,

SOCIETY OF ACTUARIES EXAM MLC Models for Life Contingencies EXAM MLC SAMPLE WRITTEN-ANSWER QUESTIONS AND SOLUTIONS Questions September 17, 2016 Question 22 was added. February 12, 2015 In Questions 12,

Errata for Actuarial Mathematics for Life Contingent Risks

Errata for Actuarial Mathematics for Life Contingent Risks David C M Dickson, Mary R Hardy, Howard R Waters Note: These errata refer to the first printing of Actuarial Mathematics for Life Contingent Risks.

Errata for Actuarial Mathematics for Life Contingent Risks David C M Dickson, Mary R Hardy, Howard R Waters Note: These errata refer to the first printing of Actuarial Mathematics for Life Contingent Risks.

Chapter 4 - Insurance Benefits

Chapter 4 - Insurance Benefits Section 4.4 - Valuation of Life Insurance Benefits (Subsection 4.4.1) Assume a life insurance policy pays $1 immediately upon the death of a policy holder who takes out the

Chapter 4 - Insurance Benefits Section 4.4 - Valuation of Life Insurance Benefits (Subsection 4.4.1) Assume a life insurance policy pays $1 immediately upon the death of a policy holder who takes out the

In this sample we provide a chapter from the manual, along with a page from the formula list.

Sample Study Guide Cover Letter The ACE manual was designed with the intent of clarifying complex text (and problems) with explanations in plain-english. This is accomplished via clear and concise summaries

Sample Study Guide Cover Letter The ACE manual was designed with the intent of clarifying complex text (and problems) with explanations in plain-english. This is accomplished via clear and concise summaries

Heriot-Watt University BSc in Actuarial Science Life Insurance Mathematics A (F70LA) Tutorial Problems

Tutorial Problems") Heriot-Watt University BSc in Actuarial Science Life Insurance Mathematics A (F70LA) Tutorial Problems 1. Show that, under the uniform distribution of deaths, for integer x and 0 < s < 1: Pr[T x s T x

Heriot-Watt University BSc in Actuarial Science Life Insurance Mathematics A (F70LA) Tutorial Problems 1. Show that, under the uniform distribution of deaths, for integer x and 0 < s < 1: Pr[T x s T x

INSTRUCTIONS TO CANDIDATES

Society of Actuaries Canadian Institute of Actuaries Exam MLC Models for Life Contingencies Friday, October 30, 2015 8:30 a.m. 12:45 p.m. MLC General Instructions 1. Write your candidate number here. Your

Society of Actuaries Canadian Institute of Actuaries Exam MLC Models for Life Contingencies Friday, October 30, 2015 8:30 a.m. 12:45 p.m. MLC General Instructions 1. Write your candidate number here. Your

Remember..Prospective Reserves

Remember..Prospective Reserves Notation: t V x Net Premium Prospective reserve at t for a whole life assurance convention: if we are working at an integer duration, the reserve is calculated just before

Remember..Prospective Reserves Notation: t V x Net Premium Prospective reserve at t for a whole life assurance convention: if we are working at an integer duration, the reserve is calculated just before

MLC Written Answer Model Solutions Spring 2014

MLC Written Answer Model Solutions Spring 214 1. Learning Outcomes: (2a) (3a) (3b) (3d) Sources: Textbook references: 4.4, 5.6, 5.11, 6.5, 9.4 (a) Show that the expected present value of the death benefit

MLC Written Answer Model Solutions Spring 214 1. Learning Outcomes: (2a) (3a) (3b) (3d) Sources: Textbook references: 4.4, 5.6, 5.11, 6.5, 9.4 (a) Show that the expected present value of the death benefit

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 28 th May 2013 Subject CT5 General Insurance, Life and Health Contingencies Time allowed: Three Hours (10.00 13.00 Hrs) Total Marks: 100 INSTRUCTIONS TO THE

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 28 th May 2013 Subject CT5 General Insurance, Life and Health Contingencies Time allowed: Three Hours (10.00 13.00 Hrs) Total Marks: 100 INSTRUCTIONS TO THE

MLC Spring Model Solutions Written Answer Questions

MLC Spring 2018 Model Solutions Written Answer Questions 1 Question 1 Model Solution Learning Outcomes: 1(a), 1(b), 1(d), 2(a) Chapter References: AMLCR Chapter 8, Sections 8.2 8.6 a) General comment:

MLC Spring 2018 Model Solutions Written Answer Questions 1 Question 1 Model Solution Learning Outcomes: 1(a), 1(b), 1(d), 2(a) Chapter References: AMLCR Chapter 8, Sections 8.2 8.6 a) General comment:

INSTITUTE AND FACULTY OF ACTUARIES. Curriculum 2019 SPECIMEN SOLUTIONS

INSTITUTE AND FACULTY OF ACTUARIES Curriculum 2019 SPECIMEN SOLUTIONS Subject CM1A Actuarial Mathematics Institute and Faculty of Actuaries 1 ( 91 ( 91 365 1 0.08 1 i = + 365 ( 91 365 0.980055 = 1+ i 1+

INSTITUTE AND FACULTY OF ACTUARIES Curriculum 2019 SPECIMEN SOLUTIONS Subject CM1A Actuarial Mathematics Institute and Faculty of Actuaries 1 ( 91 ( 91 365 1 0.08 1 i = + 365 ( 91 365 0.980055 = 1+ i 1+

STT 455-6: Actuarial Models

STT 455-6: Actuarial Models Albert Cohen Actuarial Sciences Program Department of Mathematics Department of Statistics and Probability A336 Wells Hall Michigan State University East Lansing MI 48823 albert@math.msu.edu

STT 455-6: Actuarial Models Albert Cohen Actuarial Sciences Program Department of Mathematics Department of Statistics and Probability A336 Wells Hall Michigan State University East Lansing MI 48823 albert@math.msu.edu

Pension Mathematics. Lecture: Weeks Lecture: Weeks (Math 3631) Pension Mathematics Spring Valdez 1 / 28

Pension Mathematics Spring Valdez 1 / 28") Pension Mathematics Lecture: Weeks 12-13 Lecture: Weeks 12-13 (Math 3631) Pension Mathematics Spring 2019 - Valdez 1 / 28 Chapter summary Chapter summary What are pension plans? Defined benefit vs defined

Pension Mathematics Lecture: Weeks 12-13 Lecture: Weeks 12-13 (Math 3631) Pension Mathematics Spring 2019 - Valdez 1 / 28 Chapter summary Chapter summary What are pension plans? Defined benefit vs defined

Institute of Actuaries of India

Institute of Actuaries of India CT5 General Insurance, Life and Health Contingencies Indicative Solution November 28 Introduction The indicative solution has been written by the Examiners with the aim

Institute of Actuaries of India CT5 General Insurance, Life and Health Contingencies Indicative Solution November 28 Introduction The indicative solution has been written by the Examiners with the aim

1 Cash-flows, discounting, interest rates and yields

Assignment 1 SB4a Actuarial Science Oxford MT 2016 1 1 Cash-flows, discounting, interest rates and yields Please hand in your answers to questions 3, 4, 5, 8, 11 and 12 for marking. The rest are for further

Assignment 1 SB4a Actuarial Science Oxford MT 2016 1 1 Cash-flows, discounting, interest rates and yields Please hand in your answers to questions 3, 4, 5, 8, 11 and 12 for marking. The rest are for further

INSTRUCTIONS TO CANDIDATES

Society of Actuaries Canadian Institute of Actuaries Exam MLC Models for Life Contingencies Tuesday, April 25, 2017 8:30 a.m. 12:45 p.m. MLC General Instructions 1. Write your candidate number here. Your

Society of Actuaries Canadian Institute of Actuaries Exam MLC Models for Life Contingencies Tuesday, April 25, 2017 8:30 a.m. 12:45 p.m. MLC General Instructions 1. Write your candidate number here. Your

Chapter 3: United-linked Policies

Chapter 3: United-linked Policies Tak Kuen (Ken) Siu Department of Actuarial Mathematics and Statistics School of Mathematical and Computer Sciences Heriot-Watt University Term III, 2006/07 Due to increasingly

Chapter 3: United-linked Policies Tak Kuen (Ken) Siu Department of Actuarial Mathematics and Statistics School of Mathematical and Computer Sciences Heriot-Watt University Term III, 2006/07 Due to increasingly

Society of Actuaries Exam MLC: Models for Life Contingencies Draft 2012 Learning Objectives Document Version: August 19, 2011

Learning Objective Proposed Weighting* (%) Understand how decrements are used in insurances, annuities and investments. Understand the models used to model decrements used in insurances, annuities and

Learning Objective Proposed Weighting* (%) Understand how decrements are used in insurances, annuities and investments. Understand the models used to model decrements used in insurances, annuities and

Stat 476 Life Contingencies II. Participating and Universal Life Insurance

Stat 476 Life Contingencies II Participating and Universal Life Insurance Purposes of Different Types of Insurance Term Insurance Solely indemnification No investment income or surrender benefits Whole

Stat 476 Life Contingencies II Participating and Universal Life Insurance Purposes of Different Types of Insurance Term Insurance Solely indemnification No investment income or surrender benefits Whole

MATH 3630 Actuarial Mathematics I Class Test 2 - Section 1/2 Wednesday, 14 November 2012, 8:30-9:30 PM Time Allowed: 1 hour Total Marks: 100 points

MATH 3630 Actuarial Mathematics I Class Test 2 - Section 1/2 Wednesday, 14 November 2012, 8:30-9:30 PM Time Allowed: 1 hour Total Marks: 100 points Please write your name and student number at the spaces

MATH 3630 Actuarial Mathematics I Class Test 2 - Section 1/2 Wednesday, 14 November 2012, 8:30-9:30 PM Time Allowed: 1 hour Total Marks: 100 points Please write your name and student number at the spaces

Chapter 5 - Annuities

5-1 Chapter 5 - Annuities Section 5.3 - Review of Annuities-Certain Annuity Immediate - It pays 1 at the end of every year for n years. The present value of these payments is: where ν = 1 1+i. 5-2 Annuity-Due

5-1 Chapter 5 - Annuities Section 5.3 - Review of Annuities-Certain Annuity Immediate - It pays 1 at the end of every year for n years. The present value of these payments is: where ν = 1 1+i. 5-2 Annuity-Due

Subject SP2 Life Insurance Specialist Principles Syllabus

Subject SP2 Life Insurance Specialist Principles Syllabus for the 2019 exams 1 June 2018 Life Insurance Principles Aim The aim of the Life Insurance Principles subject is to instil in successful candidates

Subject SP2 Life Insurance Specialist Principles Syllabus for the 2019 exams 1 June 2018 Life Insurance Principles Aim The aim of the Life Insurance Principles subject is to instil in successful candidates

INSTITUTE OF ACTUARIES OF INDIA

INSTITUTE OF ACTUARIES OF INIA EXAMINATIONS 21 st May 2009 Subject CT5 General Insurance, Life and Health Contingencies Time allowed: Three Hours (10.00 13.00 Hrs) Total Marks: 100 INSTRUCTIONS TO THE

INSTITUTE OF ACTUARIES OF INIA EXAMINATIONS 21 st May 2009 Subject CT5 General Insurance, Life and Health Contingencies Time allowed: Three Hours (10.00 13.00 Hrs) Total Marks: 100 INSTRUCTIONS TO THE

ACTEX ACADEMIC SERIES

ACTEX ACADEMIC SERIES Modekfor Quantifying Risk Sixth Edition Stephen J. Camilli, \S.\ Inn Dunciin, l\ \. I-I \. 1 VI \. M \.\ \ Richard L. London, f's.a ACTEX Publications, Inc. Winsted, CT TABLE OF CONTENTS

ACTEX ACADEMIC SERIES Modekfor Quantifying Risk Sixth Edition Stephen J. Camilli, \S.\ Inn Dunciin, l\ \. I-I \. 1 VI \. M \.\ \ Richard L. London, f's.a ACTEX Publications, Inc. Winsted, CT TABLE OF CONTENTS

Supplement Note for Candidates Using. Models for Quantifying Risk, Fourth Edition

Supplement Note for Candidates Using Models for Quantifying Risk, Fourth Edition Robin J. Cunningham, Ph.D. Thomas N. Herzog, Ph.D., ASA Richard L. London, FSA Copyright 2012 by ACTEX Publications, nc.

Supplement Note for Candidates Using Models for Quantifying Risk, Fourth Edition Robin J. Cunningham, Ph.D. Thomas N. Herzog, Ph.D., ASA Richard L. London, FSA Copyright 2012 by ACTEX Publications, nc.

FE610 Stochastic Calculus for Financial Engineers. Stevens Institute of Technology

FE610 Stochastic Calculus for Financial Engineers Lecture 13. The Black-Scholes PDE Steve Yang Stevens Institute of Technology 04/25/2013 Outline 1 The Black-Scholes PDE 2 PDEs in Asset Pricing 3 Exotic

FE610 Stochastic Calculus for Financial Engineers Lecture 13. The Black-Scholes PDE Steve Yang Stevens Institute of Technology 04/25/2013 Outline 1 The Black-Scholes PDE 2 PDEs in Asset Pricing 3 Exotic

SECOND EDITION. MARY R. HARDY University of Waterloo, Ontario. HOWARD R. WATERS Heriot-Watt University, Edinburgh

ACTUARIAL MATHEMATICS FOR LIFE CONTINGENT RISKS SECOND EDITION DAVID C. M. DICKSON University of Melbourne MARY R. HARDY University of Waterloo, Ontario HOWARD R. WATERS Heriot-Watt University, Edinburgh

ACTUARIAL MATHEMATICS FOR LIFE CONTINGENT RISKS SECOND EDITION DAVID C. M. DICKSON University of Melbourne MARY R. HARDY University of Waterloo, Ontario HOWARD R. WATERS Heriot-Watt University, Edinburgh

Stat 475 Winter 2018

Stat 475 Winter 208 Homework Assignment 4 Due Date: Tuesday March 6 General Notes: Please hand in Part I on paper in class on the due date. Also email Nate Duncan natefduncan@gmail.com the Excel spreadsheet

Stat 475 Winter 208 Homework Assignment 4 Due Date: Tuesday March 6 General Notes: Please hand in Part I on paper in class on the due date. Also email Nate Duncan natefduncan@gmail.com the Excel spreadsheet

Question Worth Score. Please provide details of your workings in the appropriate spaces provided; partial points will be granted.

MATH 3630 Actuarial Mathematics I Wednesday, 16 December 2015 Time Allowed: 2 hours (3:30-5:30 pm) Room: LH 305 Total Marks: 120 points Please write your name and student number at the spaces provided:

MATH 3630 Actuarial Mathematics I Wednesday, 16 December 2015 Time Allowed: 2 hours (3:30-5:30 pm) Room: LH 305 Total Marks: 120 points Please write your name and student number at the spaces provided:

1. For two independent lives now age 30 and 34, you are given:

Society of Actuaries Course 3 Exam Fall 2003 **BEGINNING OF EXAMINATION** 1. For two independent lives now age 30 and 34, you are given: x q x 30 0.1 31 0.2 32 0.3 33 0.4 34 0.5 35 0.6 36 0.7 37 0.8 Calculate

Society of Actuaries Course 3 Exam Fall 2003 **BEGINNING OF EXAMINATION** 1. For two independent lives now age 30 and 34, you are given: x q x 30 0.1 31 0.2 32 0.3 33 0.4 34 0.5 35 0.6 36 0.7 37 0.8 Calculate

Illinois State University, Mathematics 480, Spring 2014 Test No. 2, Thursday, April 17, 2014 SOLUTIONS

Illinois State University Mathematics 480 Spring 2014 Test No 2 Thursday April 17 2014 SOLUTIONS 1 Mr Rowan Bean starts working at Hard Knocks Life Insurance company at age 35 His starting salary is 100000

Illinois State University Mathematics 480 Spring 2014 Test No 2 Thursday April 17 2014 SOLUTIONS 1 Mr Rowan Bean starts working at Hard Knocks Life Insurance company at age 35 His starting salary is 100000

PSTAT 172A: ACTUARIAL STATISTICS FINAL EXAM

PSTAT 172A: ACTUARIAL STATISTICS FINAL EXAM March 17, 2009 This exam is closed to books and notes, but you may use a calculator. You have 3 hours. Your exam contains 7 questions and 11 pages. Please make

PSTAT 172A: ACTUARIAL STATISTICS FINAL EXAM March 17, 2009 This exam is closed to books and notes, but you may use a calculator. You have 3 hours. Your exam contains 7 questions and 11 pages. Please make

Subject ST2 Life Insurance Specialist Technical Syllabus

Subject ST2 Life Insurance Specialist Technical Syllabus for the 2018 exams 1 June 2017 Aim The aim of the Life Insurance Specialist Technical subject is to instil in successful candidates the main principles

Subject ST2 Life Insurance Specialist Technical Syllabus for the 2018 exams 1 June 2017 Aim The aim of the Life Insurance Specialist Technical subject is to instil in successful candidates the main principles

a b c d e Unanswered The time is 8:51

1 of 17 1/4/2008 11:54 AM 1. The following mortality table is for United Kindom Males based on data from 2002-2004. Click here to see the table in a different window Compute s(35). a. 0.976680 b. 0.976121

1 of 17 1/4/2008 11:54 AM 1. The following mortality table is for United Kindom Males based on data from 2002-2004. Click here to see the table in a different window Compute s(35). a. 0.976680 b. 0.976121

Stat 476 Life Contingencies II. Profit Testing

Stat 476 Life Contingencies II Profit Testing Profit Testing Profit testing is commonly done by actuaries in life insurance companies. It s useful for a number of reasons: Setting premium rates or testing

Stat 476 Life Contingencies II Profit Testing Profit Testing Profit testing is commonly done by actuaries in life insurance companies. It s useful for a number of reasons: Setting premium rates or testing

Handout 4: Deterministic Systems and the Shortest Path Problem

SEEM 3470: Dynamic Optimization and Applications 2013 14 Second Term Handout 4: Deterministic Systems and the Shortest Path Problem Instructor: Shiqian Ma January 27, 2014 Suggested Reading: Bertsekas

SEEM 3470: Dynamic Optimization and Applications 2013 14 Second Term Handout 4: Deterministic Systems and the Shortest Path Problem Instructor: Shiqian Ma January 27, 2014 Suggested Reading: Bertsekas

SOCIETY OF ACTUARIES. EXAM MLC Models for Life Contingencies EXAM MLC SAMPLE QUESTIONS. Copyright 2013 by the Society of Actuaries

SOCIETY OF ACTUARIES EXAM MLC Models for Life Contingencies EXAM MLC SAMPLE QUESTIONS Copyright 2013 by the Society of Actuaries The questions in this study note were previously presented in study note

SOCIETY OF ACTUARIES EXAM MLC Models for Life Contingencies EXAM MLC SAMPLE QUESTIONS Copyright 2013 by the Society of Actuaries The questions in this study note were previously presented in study note

INSTRUCTIONS TO CANDIDATES

Society of Actuaries Canadian Institute of Actuaries Exam MLC Models for Life Contingencies Friday, October 28, 2016 8:30 a.m. 12:45 p.m. MLC General Instructions 1. Write your candidate number here. Your

Society of Actuaries Canadian Institute of Actuaries Exam MLC Models for Life Contingencies Friday, October 28, 2016 8:30 a.m. 12:45 p.m. MLC General Instructions 1. Write your candidate number here. Your

Notation and Terminology used on Exam MLC Version: January 15, 2013

Notation and Terminology used on Eam MLC Changes from ugust, 202 version Wording has been changed regarding Profit, Epected Profit, Gain, Gain by Source, Profit Margin, and lapse of Universal Life policies.

Notation and Terminology used on Eam MLC Changes from ugust, 202 version Wording has been changed regarding Profit, Epected Profit, Gain, Gain by Source, Profit Margin, and lapse of Universal Life policies.

Exam MLC Models for Life Contingencies. Friday, October 27, :30 a.m. 12:45 p.m. INSTRUCTIONS TO CANDIDATES

Society of Actuaries Canadian Institute of Actuaries Exam MLC Models for Life Contingencies Friday, October 27, 2017 8:30 a.m. 12:45 p.m. MLC General Instructions 1. Write your candidate number here. Your

Society of Actuaries Canadian Institute of Actuaries Exam MLC Models for Life Contingencies Friday, October 27, 2017 8:30 a.m. 12:45 p.m. MLC General Instructions 1. Write your candidate number here. Your

Stat 476 Life Contingencies II. Pension Mathematics

Stat 476 Life Contingencies II Pension Mathematics Pension Plans Many companies sponsor pension plans for their employees. There are a variety of reasons why a company might choose to have a pension plan:

Stat 476 Life Contingencies II Pension Mathematics Pension Plans Many companies sponsor pension plans for their employees. There are a variety of reasons why a company might choose to have a pension plan:

ACTL5105 Life Insurance and Superannuation Models. Course Outline Semester 1, 2016

Business School School of Risk and Actuarial Studies ACTL5105 Life Insurance and Superannuation Models Course Outline Semester 1, 2016 Part A: Course-Specific Information Please consult Part B for key

Business School School of Risk and Actuarial Studies ACTL5105 Life Insurance and Superannuation Models Course Outline Semester 1, 2016 Part A: Course-Specific Information Please consult Part B for key

8.5 Numerical Evaluation of Probabilities

8.5 Numerical Evaluation of Probabilities 1 Density of event individual became disabled at time t is so probability is tp 7µ 1 7+t 16 tp 11 7+t 16.3e.4t e.16 t dt.3e.3 16 Density of event individual became

8.5 Numerical Evaluation of Probabilities 1 Density of event individual became disabled at time t is so probability is tp 7µ 1 7+t 16 tp 11 7+t 16.3e.4t e.16 t dt.3e.3 16 Density of event individual became

MATH/STAT 4720, Life Contingencies II Fall 2015 Toby Kenney

MATH/STAT 4720, Life Contingencies II Fall 2015 Toby Kenney In Class Examples () September 2, 2016 1 / 145 8 Multiple State Models Definition A Multiple State model has several different states into which

MATH/STAT 4720, Life Contingencies II Fall 2015 Toby Kenney In Class Examples () September 2, 2016 1 / 145 8 Multiple State Models Definition A Multiple State model has several different states into which

Master 2 Macro I. Lecture 3 : The Ramsey Growth Model

2012-2013 Master 2 Macro I Lecture 3 : The Ramsey Growth Model Franck Portier (based on Gilles Saint-Paul lecture notes) franck.portier@tse-fr.eu Toulouse School of Economics Version 1.1 07/10/2012 Changes

2012-2013 Master 2 Macro I Lecture 3 : The Ramsey Growth Model Franck Portier (based on Gilles Saint-Paul lecture notes) franck.portier@tse-fr.eu Toulouse School of Economics Version 1.1 07/10/2012 Changes

δ j 1 (S j S j 1 ) (2.3) j=1

(2.3) j=1") Chapter The Binomial Model Let S be some tradable asset with prices and let S k = St k ), k = 0, 1,,....1) H = HS 0, S 1,..., S N 1, S N ).) be some option payoff with start date t 0 and end date or maturity

Chapter The Binomial Model Let S be some tradable asset with prices and let S k = St k ), k = 0, 1,,....1) H = HS 0, S 1,..., S N 1, S N ).) be some option payoff with start date t 0 and end date or maturity

1. Suppose that µ x =, 0. a b c d e Unanswered The time is 9:27

1 of 17 1/4/2008 12:29 PM 1 1. Suppose that µ x =, 0 105 x x 105 and that the force of interest is δ = 0.04. An insurance pays 8 units at the time of death. Find the variance of the present value of the

1 of 17 1/4/2008 12:29 PM 1 1. Suppose that µ x =, 0 105 x x 105 and that the force of interest is δ = 0.04. An insurance pays 8 units at the time of death. Find the variance of the present value of the

1. For a special whole life insurance on (x), payable at the moment of death:

, payable at the moment of death:") **BEGINNING OF EXAMINATION** 1. For a special whole life insurance on (x), payable at the moment of death: µ () t = 0.05, t > 0 (ii) δ = 0.08 x (iii) (iv) The death benefit at time t is bt 0.06t = e, t

**BEGINNING OF EXAMINATION** 1. For a special whole life insurance on (x), payable at the moment of death: µ () t = 0.05, t > 0 (ii) δ = 0.08 x (iii) (iv) The death benefit at time t is bt 0.06t = e, t

A x 1 : 26 = 0.16, A x+26 = 0.2, and A x : 26

1 of 16 1/4/2008 12:23 PM 1 1. Suppose that µ x =, 0 104 x x 104 and that the force of interest is δ = 0.04 for an insurance policy issued to a person aged 45. The insurance policy pays b t = e 0.04 t

1 of 16 1/4/2008 12:23 PM 1 1. Suppose that µ x =, 0 104 x x 104 and that the force of interest is δ = 0.04 for an insurance policy issued to a person aged 45. The insurance policy pays b t = e 0.04 t

ACSC/STAT 3720, Life Contingencies I Winter 2018 Toby Kenney Homework Sheet 5 Model Solutions

Basic Questions ACSC/STAT 3720, Life Contingencies I Winter 2018 Toby Kenney Homework Sheet 5 Model Solutions 1. An insurance company offers a whole life insurance policy with benefit $500,000 payable

Basic Questions ACSC/STAT 3720, Life Contingencies I Winter 2018 Toby Kenney Homework Sheet 5 Model Solutions 1. An insurance company offers a whole life insurance policy with benefit $500,000 payable

Exam MLC Spring 2007 FINAL ANSWER KEY

Exam MLC Spring 2007 FINAL ANSWER KEY Question # Answer Question # Answer 1 E 16 B 2 B 17 D 3 D 18 C 4 E 19 D 5 C 20 C 6 A 21 B 7 E 22 C 8 E 23 B 9 E 24 A 10 C 25 B 11 A 26 A 12 D 27 A 13 C 28 C 14 * 29

Exam MLC Spring 2007 FINAL ANSWER KEY Question # Answer Question # Answer 1 E 16 B 2 B 17 D 3 D 18 C 4 E 19 D 5 C 20 C 6 A 21 B 7 E 22 C 8 E 23 B 9 E 24 A 10 C 25 B 11 A 26 A 12 D 27 A 13 C 28 C 14 * 29

1. The force of mortality at age x is given by 10 µ(x) = 103 x, 0 x < 103. Compute E(T(81) 2 ]. a. 7. b. 22. c. 23. d. 20

![1. The force of mortality at age x is given by 10 µ(x) = 103 x, 0 x < 103. Compute E(T(81) 2 ]. a. 7. b. 22. c. 23. d. 20](/thumbs/87/96643881.jpg "1. The force of mortality at age x is given by 10 µ(x) = 103 x, 0 x < 103. Compute E(T(81) 2 ]. a. 7. b. 22. c. 23. d. 20") 1 of 17 1/4/2008 12:01 PM 1. The force of mortality at age x is given by 10 µ(x) = 103 x, 0 x < 103. Compute E(T(81) 2 ]. a. 7 b. 22 3 c. 23 3 d. 20 3 e. 8 2. Suppose 1 for 0 x 1 s(x) = 1 ex 100 for 1

1 of 17 1/4/2008 12:01 PM 1. The force of mortality at age x is given by 10 µ(x) = 103 x, 0 x < 103. Compute E(T(81) 2 ]. a. 7 b. 22 3 c. 23 3 d. 20 3 e. 8 2. Suppose 1 for 0 x 1 s(x) = 1 ex 100 for 1

MASSACHUSETTS INSTITUTE OF TECHNOLOGY 6.265/15.070J Fall 2013 Lecture 19 11/20/2013. Applications of Ito calculus to finance

MASSACHUSETTS INSTITUTE OF TECHNOLOGY 6.265/15.7J Fall 213 Lecture 19 11/2/213 Applications of Ito calculus to finance Content. 1. Trading strategies 2. Black-Scholes option pricing formula 1 Security

MASSACHUSETTS INSTITUTE OF TECHNOLOGY 6.265/15.7J Fall 213 Lecture 19 11/2/213 Applications of Ito calculus to finance Content. 1. Trading strategies 2. Black-Scholes option pricing formula 1 Security

TRANSACTIONS OF SOCIETY OF ACTUARIES 1951 VOL. 3 NO. 7

TRANSACTIONS OF SOCIETY OF ACTUARIES 1951 VOL. 3 NO. 7 ACTUARIAL NOTE: THE EQUATION OF EQUILIBRIUM DONALD C. BAILLIE SEE PAGE 74 OF THIS VOLUME CECIL J. NESBITT: The Lidstone theory concerning the effect

TRANSACTIONS OF SOCIETY OF ACTUARIES 1951 VOL. 3 NO. 7 ACTUARIAL NOTE: THE EQUATION OF EQUILIBRIUM DONALD C. BAILLIE SEE PAGE 74 OF THIS VOLUME CECIL J. NESBITT: The Lidstone theory concerning the effect

Econ 424/CFRM 462 Portfolio Risk Budgeting

Econ 424/CFRM 462 Portfolio Risk Budgeting Eric Zivot August 14, 2014 Portfolio Risk Budgeting Idea: Additively decompose a measure of portfolio risk into contributions from the individual assets in the

Econ 424/CFRM 462 Portfolio Risk Budgeting Eric Zivot August 14, 2014 Portfolio Risk Budgeting Idea: Additively decompose a measure of portfolio risk into contributions from the individual assets in the

Exam M Fall 2005 PRELIMINARY ANSWER KEY

Exam M Fall 005 PRELIMINARY ANSWER KEY Question # Answer Question # Answer 1 C 1 E C B 3 C 3 E 4 D 4 E 5 C 5 C 6 B 6 E 7 A 7 E 8 D 8 D 9 B 9 A 10 A 30 D 11 A 31 A 1 A 3 A 13 D 33 B 14 C 34 C 15 A 35 A

Exam M Fall 005 PRELIMINARY ANSWER KEY Question # Answer Question # Answer 1 C 1 E C B 3 C 3 E 4 D 4 E 5 C 5 C 6 B 6 E 7 A 7 E 8 D 8 D 9 B 9 A 10 A 30 D 11 A 31 A 1 A 3 A 13 D 33 B 14 C 34 C 15 A 35 A

Two Equivalent Conditions

Two Equivalent Conditions The traditional theory of present value puts forward two equivalent conditions for asset-market equilibrium: Rate of Return The expected rate of return on an asset equals the

Two Equivalent Conditions The traditional theory of present value puts forward two equivalent conditions for asset-market equilibrium: Rate of Return The expected rate of return on an asset equals the

Notation and Terminology used on Exam MLC Version: November 1, 2013

Notation and Terminology used on Eam MLC Introduction This notation note completely replaces similar notes used on previous eaminations. In actuarial practice there is notation and terminology that varies

Notation and Terminology used on Eam MLC Introduction This notation note completely replaces similar notes used on previous eaminations. In actuarial practice there is notation and terminology that varies

Advanced Stochastic Processes.

Advanced Stochastic Processes. David Gamarnik LECTURE 16 Applications of Ito calculus to finance Lecture outline Trading strategies Black Scholes option pricing formula 16.1. Security price processes,

Advanced Stochastic Processes. David Gamarnik LECTURE 16 Applications of Ito calculus to finance Lecture outline Trading strategies Black Scholes option pricing formula 16.1. Security price processes,

fig 3.2 promissory note

Chapter 4. FIXED INCOME SECURITIES Objectives: To set the price of securities at the specified moment of time. To simulate mathematical and real content situations, where the values of securities need

Chapter 4. FIXED INCOME SECURITIES Objectives: To set the price of securities at the specified moment of time. To simulate mathematical and real content situations, where the values of securities need

Life annuities. Actuarial mathematics 3280 Department of Mathematics and Statistics York University. Edward Furman.

Edward Furman, Actuarial mathematics MATH3280 p. 1/53 Life annuities Actuarial mathematics 3280 Department of Mathematics and Statistics York University Edward Furman efurman@mathstat.yorku.ca Edward Furman,

Edward Furman, Actuarial mathematics MATH3280 p. 1/53 Life annuities Actuarial mathematics 3280 Department of Mathematics and Statistics York University Edward Furman efurman@mathstat.yorku.ca Edward Furman,

JARAMOGI OGINGA ODINGA UNIVERSITY OF SCIENCE AND TECHNOLOGY

OASIS OF KNOWLEDGE JARAMOGI OGINGA ODINGA UNIVERSITY OF SCIENCE AND TECHNOLOGY SCHOOL OF MATHEMATICS AND ACTUARIAL SCIENCE UNIVERSITY EXAMINATION FOR DEGREE OF BACHELOR OF SCIENCE ACTUARIAL 3 RD YEAR 1

OASIS OF KNOWLEDGE JARAMOGI OGINGA ODINGA UNIVERSITY OF SCIENCE AND TECHNOLOGY SCHOOL OF MATHEMATICS AND ACTUARIAL SCIENCE UNIVERSITY EXAMINATION FOR DEGREE OF BACHELOR OF SCIENCE ACTUARIAL 3 RD YEAR 1

Survival models. F x (t) = Pr[T x t].

![Survival models. F x (t) = Pr[T x t].](/thumbs/82/84951418.jpg "Survival models. F x (t) = Pr[T x t].") 2 Survival models 2.1 Summary In this chapter we represent the future lifetime of an individual as a random variable, and show how probabilities of death or survival can be calculated under this framework.

2 Survival models 2.1 Summary In this chapter we represent the future lifetime of an individual as a random variable, and show how probabilities of death or survival can be calculated under this framework.

Options. An Undergraduate Introduction to Financial Mathematics. J. Robert Buchanan. J. Robert Buchanan Options

Options An Undergraduate Introduction to Financial Mathematics J. Robert Buchanan 2014 Definitions and Terminology Definition An option is the right, but not the obligation, to buy or sell a security such

Options An Undergraduate Introduction to Financial Mathematics J. Robert Buchanan 2014 Definitions and Terminology Definition An option is the right, but not the obligation, to buy or sell a security such

TRANSACTIONS OF SOCIETY OF ACTUARIES 1988 VOk. 40 PT 2

TRANSACTIONS OF SOCIETY OF ACTUARIES 1988 VOk. 40 PT 2 SOURCE OF EARNINGS ANALYSIS FOR FLEXIBLE PREMIUM AND INTEREST-SENSITIVE LIFE AND ANNUITY PRODUCTS ROBERT W. STEIN AND JOSEPH H. TAN ABSTRACT Although

TRANSACTIONS OF SOCIETY OF ACTUARIES 1988 VOk. 40 PT 2 SOURCE OF EARNINGS ANALYSIS FOR FLEXIBLE PREMIUM AND INTEREST-SENSITIVE LIFE AND ANNUITY PRODUCTS ROBERT W. STEIN AND JOSEPH H. TAN ABSTRACT Although

Department of Mathematics. Mathematics of Financial Derivatives

Department of Mathematics MA408 Mathematics of Financial Derivatives Thursday 15th January, 2009 2pm 4pm Duration: 2 hours Attempt THREE questions MA408 Page 1 of 5 1. (a) Suppose 0 < E 1 < E 3 and E 2

Department of Mathematics MA408 Mathematics of Financial Derivatives Thursday 15th January, 2009 2pm 4pm Duration: 2 hours Attempt THREE questions MA408 Page 1 of 5 1. (a) Suppose 0 < E 1 < E 3 and E 2

Stat 475 Winter 2018

Stat 475 Winter 2018 Homework Assignment 4 Due Date: Tuesday March 6 General Notes: Please hand in Part I on paper in class on the due date Also email Nate Duncan (natefduncan@gmailcom) the Excel spreadsheet

Stat 475 Winter 2018 Homework Assignment 4 Due Date: Tuesday March 6 General Notes: Please hand in Part I on paper in class on the due date Also email Nate Duncan (natefduncan@gmailcom) the Excel spreadsheet

GAAP Ch. 4: Traditional Life

GAAP Ch. 4: Traditional Life GAAP Ch. 4: Traditional Life FAS 60 and FAS 97 LP Methodology Source Author: Thomas Herget (2006) Video By: J. Eddie Smith, IV, FSA GAAP Ch. 4: Traditional Life 1 / 76 Key

GAAP Ch. 4: Traditional Life GAAP Ch. 4: Traditional Life FAS 60 and FAS 97 LP Methodology Source Author: Thomas Herget (2006) Video By: J. Eddie Smith, IV, FSA GAAP Ch. 4: Traditional Life 1 / 76 Key

Manual for SOA Exam FM/CAS Exam 2.

Manual for SOA Exam FM/CAS Exam 2. Chapter 1. Basic Interest Theory. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics.

Manual for SOA Exam FM/CAS Exam 2. Chapter 1. Basic Interest Theory. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics.

A new Loan Stock Financial Instrument

A new Loan Stock Financial Instrument Alexander Morozovsky 1,2 Bridge, 57/58 Floors, 2 World Trade Center, New York, NY 10048 E-mail: alex@nyc.bridge.com Phone: (212) 390-6126 Fax: (212) 390-6498 Rajan

A new Loan Stock Financial Instrument Alexander Morozovsky 1,2 Bridge, 57/58 Floors, 2 World Trade Center, New York, NY 10048 E-mail: alex@nyc.bridge.com Phone: (212) 390-6126 Fax: (212) 390-6498 Rajan

Q2) Please analyse, if the following contracts qualify as insurance contracts according to IFRS 4. Please, give reasons for your answer.

Please analyse, if the following contracts qualify as insurance contracts according to IFRS 4. Please, give reasons for your answer.") Block 1: Insurance Contracts according to IFRS 4 Q1) A life insurance company wants to offer a deferred annuity that is equal to a financing contract during the deferral period. What is crucial for the

Block 1: Insurance Contracts according to IFRS 4 Q1) A life insurance company wants to offer a deferred annuity that is equal to a financing contract during the deferral period. What is crucial for the

Mathematics of Financial Derivatives

Mathematics of Financial Derivatives Lecture 9 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Table of contents 1. Zero-coupon rates and bond pricing 2.

Mathematics of Financial Derivatives Lecture 9 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Table of contents 1. Zero-coupon rates and bond pricing 2.

Default Guide. Variable Universal Life. Prepared and published by the Customer Value Center Ed. 10/2010 FOR INTERNAL USE ONLY

Default Guide Prepared and published by the Customer Value Center 0150633-00001-01 Ed. 10/2010 Table of Contents Overview.........................2 Premiums..........................2 Death Benefit Guarantees..............3

Default Guide Prepared and published by the Customer Value Center 0150633-00001-01 Ed. 10/2010 Table of Contents Overview.........................2 Premiums..........................2 Death Benefit Guarantees..............3

Lesson 3 Permanent Life Insurance

Lesson 3 Permanent Life Insurance Lesson 3 Introduction p1 (LHE) Permanent Life insurance products are designed to meet other needs in addition to the death benefit. Because these products accrue cash

Lesson 3 Permanent Life Insurance Lesson 3 Introduction p1 (LHE) Permanent Life insurance products are designed to meet other needs in addition to the death benefit. Because these products accrue cash

Commutation Functions. = v x l x. + D x+1. = D x. +, N x. M x+n. ω x. = M x M x+n + D x+n. (this annuity increases to n, then pays n for life),

,") Commutation Functions C = v +1 d = v l M = C + C +1 + C +2 + = + +1 + +2 + A = M 1 A :n = M M +n A 1 :n = +n R = M + M +1 + M +2 + S = + +1 + +2 + (this S notation is not salary-related) 1 C = v +t l +t

Commutation Functions C = v +1 d = v l M = C + C +1 + C +2 + = + +1 + +2 + A = M 1 A :n = M M +n A 1 :n = +n R = M + M +1 + M +2 + S = + +1 + +2 + (this S notation is not salary-related) 1 C = v +t l +t

Homework 3: Asset Pricing

Homework 3: Asset Pricing Mohammad Hossein Rahmati November 1, 2018 1. Consider an economy with a single representative consumer who maximize E β t u(c t ) 0 < β < 1, u(c t ) = ln(c t + α) t= The sole

Homework 3: Asset Pricing Mohammad Hossein Rahmati November 1, 2018 1. Consider an economy with a single representative consumer who maximize E β t u(c t ) 0 < β < 1, u(c t ) = ln(c t + α) t= The sole

MTH6154 Financial Mathematics I Interest Rates and Present Value Analysis

16 MTH6154 Financial Mathematics I Interest Rates and Present Value Analysis Contents 2 Interest Rates 16 2.1 Definitions.................................... 16 2.1.1 Rate of Return..............................

16 MTH6154 Financial Mathematics I Interest Rates and Present Value Analysis Contents 2 Interest Rates 16 2.1 Definitions.................................... 16 2.1.1 Rate of Return..............................

Errata and Updates for ASM Exam MLC (Fifteenth Edition Third Printing) Sorted by Date

Sorted by Date") Errata for ASM Exam MLC Study Manual (Fifteenth Edition Third Printing) Sorted by Date 1 Errata and Updates for ASM Exam MLC (Fifteenth Edition Third Printing) Sorted by Date [1/25/218] On page 258, two

Errata for ASM Exam MLC Study Manual (Fifteenth Edition Third Printing) Sorted by Date 1 Errata and Updates for ASM Exam MLC (Fifteenth Edition Third Printing) Sorted by Date [1/25/218] On page 258, two

Elements of Economic Analysis II Lecture II: Production Function and Profit Maximization

Elements of Economic Analysis II Lecture II: Production Function and Profit Maximization Kai Hao Yang 09/26/2017 1 Production Function Just as consumer theory uses utility function a function that assign

Elements of Economic Analysis II Lecture II: Production Function and Profit Maximization Kai Hao Yang 09/26/2017 1 Production Function Just as consumer theory uses utility function a function that assign

U.S. GAAP & IFRS: Today and Tomorrow Sept , New York. Reinsurance Under GAAP

U.S. GAAP & IFRS: Today and Tomorrow Sept. 13-14, 2010 New York Reinsurance Under GAAP David Rogers Reinsurance Accounting Society of Actuaries US GAAP & IFRS: Today and Tomorrow Session 3b David Y. Rogers,

U.S. GAAP & IFRS: Today and Tomorrow Sept. 13-14, 2010 New York Reinsurance Under GAAP David Rogers Reinsurance Accounting Society of Actuaries US GAAP & IFRS: Today and Tomorrow Session 3b David Y. Rogers,

Mortality profit and Multiple life insurance

Lecture 13 Mortality profit and Multiple life insurance Reading: Gerber Chapter 8, CT5 Core Reading Units 3 and 6 13.1 Reserves for life assurances mortality profit Letuslookmorespecificallyattheriskofaninsurerwhohasunderwrittenaportfolioofidentical

Lecture 13 Mortality profit and Multiple life insurance Reading: Gerber Chapter 8, CT5 Core Reading Units 3 and 6 13.1 Reserves for life assurances mortality profit Letuslookmorespecificallyattheriskofaninsurerwhohasunderwrittenaportfolioofidentical

Modelling Economic Variables

ucsc supplementary notes ams/econ 11a Modelling Economic Variables c 2010 Yonatan Katznelson 1. Mathematical models The two central topics of AMS/Econ 11A are differential calculus on the one hand, and

ucsc supplementary notes ams/econ 11a Modelling Economic Variables c 2010 Yonatan Katznelson 1. Mathematical models The two central topics of AMS/Econ 11A are differential calculus on the one hand, and

TEACHING NOTE 98-04: EXCHANGE OPTION PRICING

TEACHING NOTE 98-04: EXCHANGE OPTION PRICING Version date: June 3, 017 C:\CLASSES\TEACHING NOTES\TN98-04.WPD The exchange option, first developed by Margrabe (1978), has proven to be an extremely powerful

TEACHING NOTE 98-04: EXCHANGE OPTION PRICING Version date: June 3, 017 C:\CLASSES\TEACHING NOTES\TN98-04.WPD The exchange option, first developed by Margrabe (1978), has proven to be an extremely powerful