AML- Risk assessment & RBA

|

|

|

- Madison Long

- 5 years ago

- Views:

Transcription

1 AML- Risk assessment & RBA EARLEEN MOULTON VP COMPLIANCE, BRIDGEFORCE FINANCIAL GROUP

2 Agenda What we ll cover and what we won t Background on RBA Working through it

3 What is Money Laundering? Any effort to disguise the source of money or assets derived from criminal activity. The act of transforming dirty money into clean money. Concealing or converting property or proceeds, knowing or believing the property was derived from committing an offense. Money laundering is a prolonged and complicated process. Insurance products get used near the end of the process, when cash has already entered the banking system, been converted and has been through a few wash cycles. CAILBA 2016

4 What rules apply to you? Mandatory Compliance Regime you must adopt a compliance program and ensure that your employees and those who act on your behalf comply with the Act. Advisors do not act on behalf of the MGA. Some insurers make compliance program templates available for you to use. See also Advocis and IFB. CAILBA 2016

5 Mandatory Compliance Regime 1. Appointment of Compliance Officer 2. Development, application and maintenance of up-to-date written policies and procedures. 3. Documented risk assessment 4. Ongoing training program for staff 5. Regular review of policies and procedures (at least every 2 years) self assessment CAILBA 2016

6 Mandatory Compliance Regime 1. Appointment of Compliance Officer 2. Development, application and maintenance of up-to-date written policies and procedures. 3. Documented risk assessment 4. Ongoing training program for staff 5. Regular review of policies and procedures (at least every 2 years) self assessment CAILBA 2016

7 Expectation FINTRAC expects a well-developed, documented and justifiable RBA process that appropriately identifies, rates, and mitigates the risks to a given entity.

8 This isn t new Customer risk assessment You must look at every piece of business to determine whether a customer poses a risk. When you are looking at an application or change form and determining whether it is in good order, also review product type and all relevant information about the customer. CAILBA 2016

9 Risk Assessment You are required to do a risk assessment at least every two years and client risk assessments for each new client. Risk assessments should take into account Product risk Channel risk Client risk Supplier risk Geographic risk Other risk

10

11

12 Explanations/definitions What is risk? -the likelihood of an event and its consequences. -can be seen as a combination of the chance that something may happen and the degree of damage or loss that may result from such an occurrence.

13 At the reporting entity level Risks = threats and vulnerabilities that put the reporting entity at risk of being used to facilitate ML/TF. Threats: could be a person (or group), object that could cause harm. In the ML/TF context, a threat could be criminals, facilitators, their funds or even terrorist groups. Vulnerabilities: elements of a business that could be exploited by the identified threat. In the ML/TF context, vulnerabilities could be weak controls within a reporting entity, offering high risk products or services, etc. Impact: refers to the seriousness of the damage that would occur if the ML/TF risk materializes (i.e. threats and vulnerabilities)

14 What is risk management? a process widely used in the public and private sector to assist in decision-making. When dealing with ML/TF, it s the process that includes: the recognition of ML/TF risks, the assessment of these risks, and the development of methods to manage and mitigate the risks identified.

15 What are inherent & residual risks? Inherent risk is the intrinsic risk of an event or circumstance that exists before the application of controls or mitigation measures. Residual risk is the level of risk that remains after the implementation of mitigation measures and controls. Important to note - the risk assessment exercise described in this document focuses on the inherent risks to your business, activities and clients.

16 What is a risk-based approach(rba)? The risk assessment of your business activities and clients using certain prescribed elements; Products, services and delivery channels; Geography; Clients and business relationships, and Other relevant factors. The mitigation of risk through the implementation of controls and measures tailored to the identified risks; Keeping client identification and, if required, beneficial ownership and business relationship information up to date relative to the assessed level of risk; and The ongoing monitoring of transactions and business relationships in accordance with the assessed level of risk.

17 This is not a static exercise Assessing and mitigating risk is a step by step process, and cyclical. Risks assessed may change/evolve over time. Your RBA must be re-evaluated and updated when the risk factors change

18 Risk-based approach cycle 1. Identification of your inherent risks (business-based risk assessment along with the relationship-based risk assessment) 2. Setting your risk tolerance 3. Creating risk-reduction measures and key controls 4. Evaluating your residual risks 5. Implementing your risk-based approach 6. Reviewing your risk-based approach.

19 Step 1 - Identify inherent risks Business-based risks: Products, services, delivery channels Geography Other relevant factors

20 Assess the risk in your business activities Take a business-wide perspective. This will allow you to consider where risks occur across business lines, clientele or particular products Look at your vulnerabilities to ML/TF Areas identified as high-risk will require documented mitigation strategies The actual number of risks in your inventory will vary based on the type of business activity you conduct and products and services you offer

21 Products If product sold is non-registered - UL/whole life - segregated fund - endowment or annuity or - any plan with a lump sum payment of $100,000 or more, Consider these higher risk. CAILBA 2016

22 Why are insurance products attractive? Lots of investment options Liquidity Portability and ease of transfer Can purchase in large amounts without triggering a regulatory inquiry Insurance changes the form of the funds Sometimes money launderers use dirty money to buy insurance because they need insurance like the rest of us CAILBA 2016

23 High risk business practices Do you conduct non face-to-face sales? Do you take cash and/or money orders? Do you deal with corporations, trusts, foundations/charities? Do you deal with lawyers, accountants POA or others acting for the client? Do you deal with third parties? Are your clients PEPs(foreign or domestic)?

24 Geography Border-crossings, especially with other countries Rural/urban setting Located in known high crime-rate areas Connection to high-risk countries Special Economic Measures Act (SEMA) Financial Action Task Force (FATF) list of High-Risk Countries and Non-Cooperative Jurisdictions Freezing Assets of Corrupt Foreign Officials Act Sanctions (FACFOA)

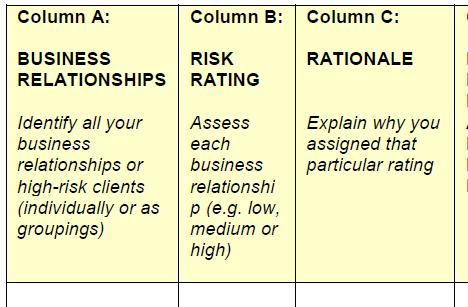

25 Other relevant factors Business model: Size of your business Number of locations/branches, number of employees and/or subagents Turnover of staff Use of service providers, especially where they may be checking client ID

26 Documenting your assessment A couple of options: Simple, bullet-form notation Enhance your existing risk assessment Consider the following

27

28

29 Scoring your assessment All inherent risks identified need to be given a risk level The scale should be tailored to the size and type of business, for example: Advisor (sole proprietor) engaged in traditional practice could use L and H risk Agency with staff, sub-agents, multiple locations - e.g. medium, medium-high, high

30 The law requires you: Every risk element identified as high-risk must be addressed with mitigation measures and be documented. You will have to be able to demonstrate to FINTRAC that controls/measures have been put in place to address these high-risk elements (e.g. in your policies and procedures, training program) and that they are effective (through your internal or independent review).

31

32 Step 1 (B) - Identify inherent risks Relationship-based risks - Advisors encounter specific and direct ML/TF risks because of the nature and type of business that your clientele has with you through: Products, services and delivery channels they utilize Their geography Characteristics and patterns of activity

33 Examples of high risk clients/transactions Behaviour or transactions that are unusual compared to other similar clients. A client s business is cash intensive or generates cash for transactions not normally cash intensive A client s business structure makes it difficult to identify its true owners or controllers An individual with a high-level position, influence and/or connections (Politically Exposed Foreign Persons) A client has ties to or conducts business in a high-risk country A client transactions are non-face-to-face

34 More examples Does owner s or payor s occupation generate a lot of cash, if known? (i.e. variety stores, pizzerias, money service businesses, etc). Cash businesses are higher risk than others. Does the customer have ties to any countries that: have weak AML-ATF laws or are not FATF members Appear in the Special Economic Measures Act Regulations ( Appear on the OSFI List of Designated names? You are required to pay attention to this and check these sites. If you believe you have a name match, do not continue with the transaction. Contact BFG or insurer.

35 Where do most clients fall? Most advisors will only have one or two client risk groupings. If you identify high-risk clients or groups what s the predominant reason for most to be classified as highrisk?

36 Scoring your assessment All inherent risks need to be given a risk level The scale should be tailored to the size and type of business, for example: Advisor (sole proprietor) engaged in traditional practice could use L and H risk Agency with staff, sub-agents, multiple locations - e.g. medium, medium-high, high

37 Documenting your assessment If you can, keep it simple, bullet-form notation For example: I ve identified no high-risk client relationships in my business. My relationship-based risk is low because transactions are low to medium in value, conducted face-toface and transactions are in line with the client s profile If you have multiple risk-groupings, your documentation should be tailored to your risk.

38

39 Step 2 Set your risk tolerance Set risk tolerance you are willing to accept. Risk categories to consider: Regulatory risk Reputation risk Legal risk Financial risk Must be taken into account before moving on to consider how risks can be addressed. Risk tolerance has direct impact on Step 3, policies and procedures, and your training plan.

40 Ask yourself: Are you willing to accept regulatory, reputational, legal or financial risks? What risks are you willing to accept only after implementing some mitigation measures? What risks are you not willing to accept?

41 Your obligation The PCMLTF Act and Regulations state that you/your organization has mandatory obligations in situations where high-risk business activities and high-risk business relationships are identified. This step does not allow reporting entities to avoid these obligations.

42 Step 3 Risk reduction measures and key controls As part of your compliance program, you must develop and document risk mitigation strategies This serves to limit the ML/TF risks you ve identified during the risk assessment Allows you/your business to stay within the risk tolerance you ve set.

43 Expectations For all situation and all clients: Internal controls to mitigate overall risks (training, servicing clients, keep your compliance program up to date) Conduct on-going monitoring, keep a record of what and how For high-risk business and client relationships: Document measures to mitigate risk Conduct more frequent monitoring of high-risk relationships Enhance measures to ascertain ID, keep client information up to date

44 Specifics? For detailed information on risk mitigation measures, consult sections 6.2, 6.3 and 6.4 of Guideline 4: Implementation of a Compliance Regime. Ensure you re keeping records on the information obtained on product applications.

45

46

47

48

49

50

51

52 Step 4 Evaluate your Residual Risks The remaining level of risk after taking into account the mitigation measures and controls Even with all measures and controls in place, there will be some residual exposure to manage. Tolerated risks: They re still risks, and may increase over time. Mitigated risks: Although lessened/reduced, they re still risks. Measures to mitigate could fail, not be followed, etc.

53 Step 5 Implement RBA Implement your risk mitigation measures and controls as part of your day to day activities. Apply or put into practice, the risk-reduction strategies and key control for high-risk (ML and TF) situations.

54 Step 6 Review your RBA Review or test your risk-based assessment for effectiveness. Minimum every 24 months, more often if there are material changes Make changes or adjust as necessary

55 Questions?

AML/CTF and Sanctions Policy

AML/CTF and Sanctions Policy May 2018 Purpose and Objective The purpose of this policy is to set the high-level principles and standards of management of financial crime risks, including money laundering,

AML/CTF and Sanctions Policy May 2018 Purpose and Objective The purpose of this policy is to set the high-level principles and standards of management of financial crime risks, including money laundering,

Anti Money Laundering /Anti Terrorist Financing & FINTRAC (Financial Transactions & Reports Analysis Center of Canada) Training Presentation

Training Presentation") Anti Money Laundering /Anti Terrorist Financing & FINTRAC (Financial Transactions & Reports Analysis Center of Canada) Training Presentation Presented by: Mary Mellin Compliance Officer June 2015 What

Anti Money Laundering /Anti Terrorist Financing & FINTRAC (Financial Transactions & Reports Analysis Center of Canada) Training Presentation Presented by: Mary Mellin Compliance Officer June 2015 What

Policy on Anti Money Laundering and Countering Terrorist Financing

Policy on Anti Money Laundering and Countering Terrorist Financing Adopted by Date of adoption Applies for Group Framework Owner Distribution Language version Information class Basis the Board 22 June

Policy on Anti Money Laundering and Countering Terrorist Financing Adopted by Date of adoption Applies for Group Framework Owner Distribution Language version Information class Basis the Board 22 June

GUIDELINES ON RISK-BASED APPROACH (RBA) FOR THE PURPOSE OF ANTI-MONEY LAUNDERING AND COUNTERING THE FINANCING OF TERRORISM (AML/CFT)

FOR THE PURPOSE OF ANTI-MONEY LAUNDERING AND COUNTERING THE FINANCING OF TERRORISM (AML/CFT)") GUIDELINES ON RISK-BASED APPROACH (RBA) FOR THE PURPOSE OF ANTI-MONEY LAUNDERING AND COUNTERING THE FINANCING OF TERRORISM (AML/CFT) Guidelines on Risk-Based Approach (RBA) for the purpose of Anti-Money

GUIDELINES ON RISK-BASED APPROACH (RBA) FOR THE PURPOSE OF ANTI-MONEY LAUNDERING AND COUNTERING THE FINANCING OF TERRORISM (AML/CFT) Guidelines on Risk-Based Approach (RBA) for the purpose of Anti-Money

Money Laundering and Terrorist Financing Risk Assessment and Management

Money Laundering and Terrorist Financing Risk Assessment and Management 1. 1 Introduction Overview of ML&TF Risk The success of AML&CFT program highly depends on efficient assessment of related threat/vulnerability/risk

Money Laundering and Terrorist Financing Risk Assessment and Management 1. 1 Introduction Overview of ML&TF Risk The success of AML&CFT program highly depends on efficient assessment of related threat/vulnerability/risk

Anti-Money Laundering & Terrorist Financing (AMLTF) Training Course. Module: Introduction

Training Course. Module: Introduction") Anti-Money Laundering & Terrorist Financing (AMLTF) Training Course Module: Introduction About this Anti-Money Laundering & Terrorist Financing Training Course (AMLTF): The AMLTF course is designed to

Anti-Money Laundering & Terrorist Financing (AMLTF) Training Course Module: Introduction About this Anti-Money Laundering & Terrorist Financing Training Course (AMLTF): The AMLTF course is designed to

A NATIONAL RISK ASSESSMENT REGARDING AML-CFT

A NATIONAL RISK ASSESSMENT REGARDING AML-CFT Symposium `Enhancing Integrity in the Dutch Caribbean` Aruba, November 15, 2010 Mrs. J.A. Kellermann De Nederlandsche Bank Executive Director Overview Introduction

A NATIONAL RISK ASSESSMENT REGARDING AML-CFT Symposium `Enhancing Integrity in the Dutch Caribbean` Aruba, November 15, 2010 Mrs. J.A. Kellermann De Nederlandsche Bank Executive Director Overview Introduction

UPDATE ON CANADA S 2008 ANTI-MONEY LAUNDERING REQUIREMENTS FOR CAs

UPDATE ON CANADA S 2008 ANTI-MONEY LAUNDERING REQUIREMENTS FOR CAs Chartered accountants and accounting firms are not on the front line in the war against money laundering and terrorist financing! But,

UPDATE ON CANADA S 2008 ANTI-MONEY LAUNDERING REQUIREMENTS FOR CAs Chartered accountants and accounting firms are not on the front line in the war against money laundering and terrorist financing! But,

Registry General September 2015

Registry General September 2015 1 Charities Compliance Officer Training Topics What is FATF? How FATF relates to charities Guidance Notes on the Charities (Anti-Money Laundering, Anti-Terrorist Financing

Registry General September 2015 1 Charities Compliance Officer Training Topics What is FATF? How FATF relates to charities Guidance Notes on the Charities (Anti-Money Laundering, Anti-Terrorist Financing

ABCsolutions Inc. CREA - Introduction

CREA - Introduction The AMLTF course is designed to assist CREA members to comply in part with the training component under Canada s Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA)

CREA - Introduction The AMLTF course is designed to assist CREA members to comply in part with the training component under Canada s Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA)

AML/CFT Phase II. Kate Reid NZLS CLE live stream 28 November /11/2017. Check it out by logging in at:

Check it out by logging in at: www.lawyerseducation.co.nz AML/CFT Phase II Kate Reid NZLS CLE live stream 28 November 2017 1 What this presentation is about Phase II what and why What you have to do What

Check it out by logging in at: www.lawyerseducation.co.nz AML/CFT Phase II Kate Reid NZLS CLE live stream 28 November 2017 1 What this presentation is about Phase II what and why What you have to do What

Webinar 01: AML/CFT Requirements Overview. 4 th July 2018

Webinar 01: AML/CFT Requirements Overview 4 th July 2018 About Your Presenter Neil has a unique background in financial crime risk management, spanning 25 years. This includes working within Law Enforcement

Webinar 01: AML/CFT Requirements Overview 4 th July 2018 About Your Presenter Neil has a unique background in financial crime risk management, spanning 25 years. This includes working within Law Enforcement

Anti Money Laundering Policy

Anti Money Laundering Policy I. Definition of Money Laundering Money laundering is the process by which large amounts of illegally obtained money (from drug trafficking, terrorist activity or other serious

Anti Money Laundering Policy I. Definition of Money Laundering Money laundering is the process by which large amounts of illegally obtained money (from drug trafficking, terrorist activity or other serious

PROCEEDS OF CRIME (MONEY LAUNDERING) & ANTI-TERRORIST FINANCING (AML/ATF)

& ANTI-TERRORIST FINANCING (AML/ATF)") PROCEEDS OF CRIME (MONEY LAUNDERING) & ANTI-TERRORIST FINANCING (AML/ATF) Overview For Advisor Use Only Revised April 2014 Registered trademark of The Empire Life Insurance Company. Policies are issued

PROCEEDS OF CRIME (MONEY LAUNDERING) & ANTI-TERRORIST FINANCING (AML/ATF) Overview For Advisor Use Only Revised April 2014 Registered trademark of The Empire Life Insurance Company. Policies are issued

BRIEFING NOTE ON THE BAILIWICK OF GUERNSEY S NATIONAL RISK ASSESSMENT 7 July 2016

BRIEFING NOTE ON THE BAILIWICK OF GUERNSEY S NATIONAL RISK ASSESSMENT 7 July 2016 Introduction The purpose of this briefing note is to provide financial services businesses, prescribed businesses and e-gambling

BRIEFING NOTE ON THE BAILIWICK OF GUERNSEY S NATIONAL RISK ASSESSMENT 7 July 2016 Introduction The purpose of this briefing note is to provide financial services businesses, prescribed businesses and e-gambling

financial intelligence centre REPUBLIC OF SOUTH AFRICA Financial Intelligence Centre FAIS Workshop Presented by The Financial Intelligence Centre

Financial Intelligence Centre FAIS Workshop Presented by The Financial Intelligence Centre 3 December 2013 Agenda The FIC Functions of the FIC Value Chain FIC - 2012/2013 in review Compliance framework

Financial Intelligence Centre FAIS Workshop Presented by The Financial Intelligence Centre 3 December 2013 Agenda The FIC Functions of the FIC Value Chain FIC - 2012/2013 in review Compliance framework

Risk-based approach and the risk management and compliance programme. Presented by Ashleigh Mooij 11 September 2018

Risk-based approach and the risk management and compliance programme Presented by Ashleigh Mooij 11 September 2018 SCOPE Risk-based approach What is risk What is required of an accountable institution

Risk-based approach and the risk management and compliance programme Presented by Ashleigh Mooij 11 September 2018 SCOPE Risk-based approach What is risk What is required of an accountable institution

AML PROCEDURE. c. Similar techniques are used for both purposes, typically involving three stages:

Page 1 of 8 1. Preamble a. On May 15 th 2015, Singapore introduced regulation for corporate service providers ( CSPs ) like Healy Consultants in line with Financial Action Task Force ( FATF ) standards;

Page 1 of 8 1. Preamble a. On May 15 th 2015, Singapore introduced regulation for corporate service providers ( CSPs ) like Healy Consultants in line with Financial Action Task Force ( FATF ) standards;

The Risk Factors Guidelines

JC 2017 37 04/01/2018 Final Guidelines Joint Guidelines under Articles 17 and 18(4) of Directive (EU) 2015/849 on simplified and enhanced customer due diligence and the factors credit and financial institutions

JC 2017 37 04/01/2018 Final Guidelines Joint Guidelines under Articles 17 and 18(4) of Directive (EU) 2015/849 on simplified and enhanced customer due diligence and the factors credit and financial institutions

Guidelines for Compliance with Canada s Anti-Money Laundering and Terrorist Financing Regime

Guidelines for Compliance with Canada s Anti-Money Laundering and Terrorist Financing Regime Updated January 2012 Contents An Introduction to FINTRAC... 3 Understanding FINTRAC Obligations... 4 Mandatory

Guidelines for Compliance with Canada s Anti-Money Laundering and Terrorist Financing Regime Updated January 2012 Contents An Introduction to FINTRAC... 3 Understanding FINTRAC Obligations... 4 Mandatory

TECHNICAL PAPER: A risk-based approach to AML/CFT inspections Prepared by Council of Europe Expert Ms Maud Bokkerink

Project against Money Laundering and Terrorist Financing in Serbia MOLI Serbia DGI(2013) 29 September 2013 TECHNICAL PAPER: A risk-based approach to AML/CFT inspections Prepared by Council of Europe Expert

Project against Money Laundering and Terrorist Financing in Serbia MOLI Serbia DGI(2013) 29 September 2013 TECHNICAL PAPER: A risk-based approach to AML/CFT inspections Prepared by Council of Europe Expert

EXECUTIVE SUMMARY. 4. Individuals and groups seeking to

CONCEALMENT OF BENEFICIAL OWNERSHIP 5 EXECUTIVE SUMMARY 1. Criminals employ a range of techniques and mechanisms to obscure their ownership and control of illicitly obtained assets. Identifying the true

CONCEALMENT OF BENEFICIAL OWNERSHIP 5 EXECUTIVE SUMMARY 1. Criminals employ a range of techniques and mechanisms to obscure their ownership and control of illicitly obtained assets. Identifying the true

July 2017 CONSULTATION DRAFT. Guidelines on. Anti-Money Laundering. and. Counter-Terrorist Financing for Professional Accountants

July 2017 CONSULTATION DRAFT Guidelines on Anti-Money Laundering and Counter-Terrorist Financing for Professional Accountants CONTENTS Page SUMMARY OF MAIN REQUIREMENTS... 4 Section 1: OVERVIEW AND APPLICATION...

July 2017 CONSULTATION DRAFT Guidelines on Anti-Money Laundering and Counter-Terrorist Financing for Professional Accountants CONTENTS Page SUMMARY OF MAIN REQUIREMENTS... 4 Section 1: OVERVIEW AND APPLICATION...

4th Anti-Money Laundering Directive and 2d Fund Transfers Regulation- General overview and impact on payments

4th Anti-Money Laundering Directive and 2d Fund Transfers Regulation- General overview and impact on payments Payment systems market expert group Brussels, 3 December 2015 European Commission DG Justice

4th Anti-Money Laundering Directive and 2d Fund Transfers Regulation- General overview and impact on payments Payment systems market expert group Brussels, 3 December 2015 European Commission DG Justice

PROCEEDS OF CRIME (MONEY LAUNDERING) & TERRORIST FINANCING (AML/ATF)

& TERRORIST FINANCING (AML/ATF)") PROCEEDS OF CRIME (MONEY LAUNDERING) & TERRORIST FINANCING (AML/ATF) Overview October 2016 Registered trademark of The Empire Life Insurance Company. Policies are issued by The Empire Life Insurance Company.

PROCEEDS OF CRIME (MONEY LAUNDERING) & TERRORIST FINANCING (AML/ATF) Overview October 2016 Registered trademark of The Empire Life Insurance Company. Policies are issued by The Empire Life Insurance Company.

Financial Crime Governance, Risk and Compliance Fund Managers & Fund Administrators. Thematic Review 2017

Financial Crime Governance, Risk and Compliance Fund Managers & Fund Administrators Thematic Review 2017 Foreword During late 2016 a thematic review of fund managers and fund administrators governance,

Financial Crime Governance, Risk and Compliance Fund Managers & Fund Administrators Thematic Review 2017 Foreword During late 2016 a thematic review of fund managers and fund administrators governance,

TECHNICAL PAPER: Guidance on the National Risk Assessment of Terrorist Financing in the Republic of Serbia

Project against Money Laundering and Terrorist Financing in Serbia MOLI Serbia DGI (2014) 28 February 2014 TECHNICAL PAPER: Guidance on the National Risk Assessment of Terrorist Financing in the Republic

Project against Money Laundering and Terrorist Financing in Serbia MOLI Serbia DGI (2014) 28 February 2014 TECHNICAL PAPER: Guidance on the National Risk Assessment of Terrorist Financing in the Republic

Supranational risk assessment on money laundering and terrorist financing (SNRA) DG Justice and Consumers B3 Financial crime Kallina SIMEONOFF

DG Justice and Consumers B3 Financial crime Kallina SIMEONOFF") Supranational risk assessment on money laundering and terrorist financing (SNRA) DG Justice and Consumers B3 Financial crime Kallina SIMEONOFF Disclaimer This presentation represents the views of the author

Supranational risk assessment on money laundering and terrorist financing (SNRA) DG Justice and Consumers B3 Financial crime Kallina SIMEONOFF Disclaimer This presentation represents the views of the author

BRIDGEFORCE FINANCIAL GROUP ADVISOR MARKET CONDUCT COMPLIANCE GUIDANCE (ABRIDGED VERSION OF CAILBA TOOLBOX UNIT)

") BRIDGEFORCE FINANCIAL GROUP ADVISOR MARKET CONDUCT COMPLIANCE GUIDANCE (ABRIDGED VERSION OF CAILBA TOOLBOX UNIT) REQUIRED READ BEFORE USE DISCLAIMER AND COPYRIGHT NOTICE The material provided herein, as

BRIDGEFORCE FINANCIAL GROUP ADVISOR MARKET CONDUCT COMPLIANCE GUIDANCE (ABRIDGED VERSION OF CAILBA TOOLBOX UNIT) REQUIRED READ BEFORE USE DISCLAIMER AND COPYRIGHT NOTICE The material provided herein, as

ANTI-MONEY LAUNDERING POLICY

ANTI-MONEY LAUNDERING POLICY This Policy represents the basic standards of Anti-Money Laundering and Combating Terrorism Financing (hereinafter collectively referred to as AML) procedures of RBFXPRO Limited,

ANTI-MONEY LAUNDERING POLICY This Policy represents the basic standards of Anti-Money Laundering and Combating Terrorism Financing (hereinafter collectively referred to as AML) procedures of RBFXPRO Limited,

Anti-Money Laundering in e-banking and Fintech. Roland Guennou OSACO Financial

Anti-Money Laundering in e-banking and Fintech Roland Guennou OSACO Financial About OSACO Financial Exclusive focus on I.R. Iran Advisory and capacity building for financial services firms Tehran branch

Anti-Money Laundering in e-banking and Fintech Roland Guennou OSACO Financial About OSACO Financial Exclusive focus on I.R. Iran Advisory and capacity building for financial services firms Tehran branch

Anti-money laundering and countering the financing of terrorism the Reserve Bank s responsibilities and approach

Anti-money laundering and countering the financing of terrorism the Reserve Bank s responsibilities and approach Hamish Armstrong Taking action to reduce money laundering and the financing of terrorism

Anti-money laundering and countering the financing of terrorism the Reserve Bank s responsibilities and approach Hamish Armstrong Taking action to reduce money laundering and the financing of terrorism

SUMMARY Seychelles National Risk Assessment Report for Money Laundering & Terrorist Financing 2017

SUMMARY Seychelles National Risk Assessment Report for Money Laundering & Terrorist Financing 2017 Introduction The National Risk Assessment (NRA) is a process of identifying and evaluating the Money Laundering

SUMMARY Seychelles National Risk Assessment Report for Money Laundering & Terrorist Financing 2017 Introduction The National Risk Assessment (NRA) is a process of identifying and evaluating the Money Laundering

AML/CFT TRAINING FOR ACCOUNTANTS AND AUDITORS

AML/CFT TRAINING FOR ACCOUNTANTS AND AUDITORS 1 16 MARCH 2016 BANK USE PROMOTION & SUPPRESSION OF MONEY LAUNDERING UNIT 2 3 What is Money Laundering? the process of concealing illicit gains from criminal

AML/CFT TRAINING FOR ACCOUNTANTS AND AUDITORS 1 16 MARCH 2016 BANK USE PROMOTION & SUPPRESSION OF MONEY LAUNDERING UNIT 2 3 What is Money Laundering? the process of concealing illicit gains from criminal

Update No (Issued 28 February 2018) Document Reference and Title Instructions Explanations

Document Reference and Title Instructions Explanations") Update No. 216 (Issued 28 February 2018) Document Reference and Title Instructions Explanations VOLUME I Contents of Volume I PROFESSIONAL ETHICS Code of Ethics for Professional Accountants (Revised) [Part

Update No. 216 (Issued 28 February 2018) Document Reference and Title Instructions Explanations VOLUME I Contents of Volume I PROFESSIONAL ETHICS Code of Ethics for Professional Accountants (Revised) [Part

Developed by the APG Implementation Issues Working Group (IIWG) and the World Bank

and the World Bank") Strategic Implementation Planning (SIP) Framework An implementation tool to prioritise your Mutual Evaluation Report/Detailed Assessment Report recommendations Developed by the APG Implementation Issues

Strategic Implementation Planning (SIP) Framework An implementation tool to prioritise your Mutual Evaluation Report/Detailed Assessment Report recommendations Developed by the APG Implementation Issues

ANTI-MONEY LAUNDERING IN

ANTI-MONEY LAUNDERING IN THE ACQUIRING INDUSTRY Presented by Laura H. Goldzung, CAMS, CCFE, CFCF, CCRP AML Audit Services, LLC March 8, 2016 AGENDA AML Regulatory Overview OFAC Regulatory Overview AML

ANTI-MONEY LAUNDERING IN THE ACQUIRING INDUSTRY Presented by Laura H. Goldzung, CAMS, CCFE, CFCF, CCRP AML Audit Services, LLC March 8, 2016 AGENDA AML Regulatory Overview OFAC Regulatory Overview AML

AUSTRAC Guidance Note. Risk management and AML/CTF programs

AUSTRAC Guidance Note Risk management and AML/CTF programs AUSTRAC Guidance Note Risk management and AML/CTF programs Anti-Money Laundering and Counter-Terrorism Financing Act 2006 Contents Page 1. Introduction

AUSTRAC Guidance Note Risk management and AML/CTF programs AUSTRAC Guidance Note Risk management and AML/CTF programs Anti-Money Laundering and Counter-Terrorism Financing Act 2006 Contents Page 1. Introduction

Politically Exposed Persons (PEPs) in relation to AML/CFT

in relation to AML/CFT") Middle East & North Africa Financial Action Task Force Politically Exposed Persons (PEPs) in relation to AML/CFT 11 November 2008 Document Language: English Original: Arabic 2008 MENAFATF. All rights reserved.

Middle East & North Africa Financial Action Task Force Politically Exposed Persons (PEPs) in relation to AML/CFT 11 November 2008 Document Language: English Original: Arabic 2008 MENAFATF. All rights reserved.

Date: Version: Reason for Change:

Applicant Name: Leo Tyndall Application Number: 89562543 Attachment Name: Number of Pages: 60 Date Prepared: 1/08/2014 Special Status (if any): Anti-Money Laundering and Counter-Terrorism Financing Policy

Applicant Name: Leo Tyndall Application Number: 89562543 Attachment Name: Number of Pages: 60 Date Prepared: 1/08/2014 Special Status (if any): Anti-Money Laundering and Counter-Terrorism Financing Policy

PCM Brokers DMCC. Anti-Money Laundering Policy

PCM Brokers DMCC Anti-Money Laundering Policy This Policy represents the basic standards of Anti-Money Laundering and Combating Terrorism Financing (hereinafter collectively referred to as AML) procedures

PCM Brokers DMCC Anti-Money Laundering Policy This Policy represents the basic standards of Anti-Money Laundering and Combating Terrorism Financing (hereinafter collectively referred to as AML) procedures

STEP CERTIFICATE IN ANTI-MONEY LAUNDERING. Syllabus

STEP CERTIFICATE IN ANTI-MONEY LAUNDERING Syllabus In collaboration with Delivered by INTRODUCTION This document contains the detailed syllabus for the. This syllabus should be read in conjunction with

STEP CERTIFICATE IN ANTI-MONEY LAUNDERING Syllabus In collaboration with Delivered by INTRODUCTION This document contains the detailed syllabus for the. This syllabus should be read in conjunction with

ANTI-MONEY LAUNDERING GUIDANCE FOR THE ACCOUNTANCY SECTOR

ANTI-MONEY LAUNDERING GUIDANCE FOR THE ACCOUNTANCY SECTOR March 2018 CCAB Ltd 2018, All rights reserved ICAEWICAE Introduction Accountants are key gatekeepers for the financial system, facilitating vital

ANTI-MONEY LAUNDERING GUIDANCE FOR THE ACCOUNTANCY SECTOR March 2018 CCAB Ltd 2018, All rights reserved ICAEWICAE Introduction Accountants are key gatekeepers for the financial system, facilitating vital

Anti-Money Laundering Awareness Training Insurance Industry-Hong Kong

Anti-Money Laundering Awareness Training Overview This program is intended to give individuals working in the Hong Kong Insurance Industry a basic knowledge of money laundering and terrorism financing,

Anti-Money Laundering Awareness Training Overview This program is intended to give individuals working in the Hong Kong Insurance Industry a basic knowledge of money laundering and terrorism financing,

Due Diligence Policy. 1. Money Laundering Risk

The continuing threat of money laundering is most effectively managed by understanding and addressing the potential money laundering risk associated with customers and their transactions. Based on Wolfsberg

The continuing threat of money laundering is most effectively managed by understanding and addressing the potential money laundering risk associated with customers and their transactions. Based on Wolfsberg

Reviewing Canada s Anti-Money Laundering and Anti-Terrorist Financing Regime Summary, Analysis and Discussion Points. Matt McGuire

Reviewing Canada s Anti-Money Laundering and Anti-Terrorist Financing Regime Summary, Analysis and Discussion Points Matt McGuire The Review 2 1. Reviewing Canada s Anti-Money Laundering and Anti-Terrorist

Reviewing Canada s Anti-Money Laundering and Anti-Terrorist Financing Regime Summary, Analysis and Discussion Points Matt McGuire The Review 2 1. Reviewing Canada s Anti-Money Laundering and Anti-Terrorist

The Practical Impact of the FATF Mutual Evaluation on the US AML Professional

The Practical Impact of the FATF Mutual Evaluation on the US AML Professional Monday, April 3 1:30 PM Moderator: Rick McDonell, Executive Director, ACAMS, and Former Executive Secretary, Financial Action

The Practical Impact of the FATF Mutual Evaluation on the US AML Professional Monday, April 3 1:30 PM Moderator: Rick McDonell, Executive Director, ACAMS, and Former Executive Secretary, Financial Action

Settlement Agreement between the Central Bank of Ireland and Intesa Sanpaolo Life dac

Settlement Agreement between the Central Bank of Ireland and Intesa Sanpaolo Life dac Intesa Sanpaolo Life dac fined 1,000,000 by the Central Bank of Ireland in respect of antimoney laundering and terrorist

Settlement Agreement between the Central Bank of Ireland and Intesa Sanpaolo Life dac Intesa Sanpaolo Life dac fined 1,000,000 by the Central Bank of Ireland in respect of antimoney laundering and terrorist

Money Laundering and Terrorist Financing Risks in the E-Money Sector

Money Laundering and Terrorist Financing Risks in the E-Money Sector Thematic Review TR18/3 October 2018 TR18/3 Contents 1 Introduction 3 2 Overview 5 3 Findings 7 Annex 1 Glossary 16 How to navigate this

Money Laundering and Terrorist Financing Risks in the E-Money Sector Thematic Review TR18/3 October 2018 TR18/3 Contents 1 Introduction 3 2 Overview 5 3 Findings 7 Annex 1 Glossary 16 How to navigate this

Anti-money laundering guidance for money service businesses

Anti-money laundering guidance for money service businesses MLR8 MSB Contents 1 Introduction 1 Purpose of this guidance 1 Status of the guidance 2 Contents of this guidance 2 Managing and mitigating the

Anti-money laundering guidance for money service businesses MLR8 MSB Contents 1 Introduction 1 Purpose of this guidance 1 Status of the guidance 2 Contents of this guidance 2 Managing and mitigating the

OPTIMUM FINANCIAL SERVICES GROUP (PTY) LTD FINANCIAL INTELLIGENCE CENTRE ACT ( FICA ) POLICY

LTD FINANCIAL INTELLIGENCE CENTRE ACT ( FICA ) POLICY") OPTIMUM FINANCIAL SERVICES GROUP (PTY) LTD FINANCIAL INTELLIGENCE CENTRE ACT ( ) POLICY POLICY STATEMENT Any reference to the organisation shall be interpreted to include the policy owner. Optimum s governing

OPTIMUM FINANCIAL SERVICES GROUP (PTY) LTD FINANCIAL INTELLIGENCE CENTRE ACT ( ) POLICY POLICY STATEMENT Any reference to the organisation shall be interpreted to include the policy owner. Optimum s governing

HANDBOOK ON ANTI-MONEY LAUNDERING AND COMBATING THE FINANCING OF TERRORISM. for Nonbank Financial Institutions ASIAN DEVELOPMENT BANK

HANDBOOK ON ANTI-MONEY LAUNDERING AND COMBATING THE FINANCING OF TERRORISM for Nonbank Financial Institutions ASIAN DEVELOPMENT BANK HANDBOOK ON ANTI-MONEY LAUNDERING AND COMBATING THE FINANCING OF TERRORISM

HANDBOOK ON ANTI-MONEY LAUNDERING AND COMBATING THE FINANCING OF TERRORISM for Nonbank Financial Institutions ASIAN DEVELOPMENT BANK HANDBOOK ON ANTI-MONEY LAUNDERING AND COMBATING THE FINANCING OF TERRORISM

Customer Identification Procedures for Brokers

Customer Identification Procedures for Brokers Procedures for identifying and verifying the identity of customers under the Anti-Money Laundering and Counter-Terrorism Financing Act and verifying the identity

Customer Identification Procedures for Brokers Procedures for identifying and verifying the identity of customers under the Anti-Money Laundering and Counter-Terrorism Financing Act and verifying the identity

Money Laundering in the Trinidad & Tobago Securities Sector

Money Laundering in the Trinidad & Tobago Securities Sector J A N U A R Y 7, 2 0 1 5 M A R K E T S E S S I O N - A M L - C F T - T H E M O N E Y, T H E L A W A N D Y O U T R I N I D A D H I L T O N H O

Money Laundering in the Trinidad & Tobago Securities Sector J A N U A R Y 7, 2 0 1 5 M A R K E T S E S S I O N - A M L - C F T - T H E M O N E Y, T H E L A W A N D Y O U T R I N I D A D H I L T O N H O

POLICIES FOR PROPER IMPLEMENTATION OF THE FOURTH ANTI MONEY LAUNDERING DIRECTIVE

POLICIES FOR PROPER IMPLEMENTATION OF THE FOURTH ANTI MONEY LAUNDERING DIRECTIVE I. OVERVIEW AND OBJECTIVES 1. The European Organization for Gaming Law (EOGL), representing the EU-wide licensed online

POLICIES FOR PROPER IMPLEMENTATION OF THE FOURTH ANTI MONEY LAUNDERING DIRECTIVE I. OVERVIEW AND OBJECTIVES 1. The European Organization for Gaming Law (EOGL), representing the EU-wide licensed online

TRUST COMPANY BUSINESS

TRUST COMPANY BUSINESS ON-SITE EXAMINATION PROGRAMME 2009 SUMMARY FINDINGS DOCUMENT OVERVIEW 1 Introduction... 1 2 Scope... 2 3 Process... 2 4 Overview... 2 5 Findings arising from AML corporate governance

TRUST COMPANY BUSINESS ON-SITE EXAMINATION PROGRAMME 2009 SUMMARY FINDINGS DOCUMENT OVERVIEW 1 Introduction... 1 2 Scope... 2 3 Process... 2 4 Overview... 2 5 Findings arising from AML corporate governance

BERMUDA INSURANCE (PRUDENTIAL STANDARDS) (INSURANCE MANAGERS ANNUAL RETURN) AMENDMENT RULES 2018 BR 4 / 2018

(INSURANCE MANAGERS ANNUAL RETURN) AMENDMENT RULES 2018 BR 4 / 2018") BERMUDA INSURANCE (PRUDENTIAL STANDARDS) (INSURANCE MANAGERS ANNUAL RETURN) AMENDMENT RULES 2018 BR 4 / 2018 TABLE OF CONTENTS 1 Citation 2 Interpretation 3 Annual return 4 Declaration SCHEDULES Matters

BERMUDA INSURANCE (PRUDENTIAL STANDARDS) (INSURANCE MANAGERS ANNUAL RETURN) AMENDMENT RULES 2018 BR 4 / 2018 TABLE OF CONTENTS 1 Citation 2 Interpretation 3 Annual return 4 Declaration SCHEDULES Matters

Attachment: References for formulating a list of countries/regions with higher risks of money

Appendix Guidance on Assessment of Money Laundering and Terrorism Financing Risks and Formulation of Related Control Programs by Futures Trust Enterprises and Managed Futures Enterprises 1. This Guidance

Appendix Guidance on Assessment of Money Laundering and Terrorism Financing Risks and Formulation of Related Control Programs by Futures Trust Enterprises and Managed Futures Enterprises 1. This Guidance

MEDIA STATEMENT MINISTER SIGNS FIC AMENDMENT ACT INTO OPERATION

MEDIA STATEMENT MINISTER SIGNS FIC AMENDMENT ACT INTO OPERATION The Minister of Finance, Malusi Gigaba, has signed and gazetted the coming into operation of various provisions of the Financial Intelligence

MEDIA STATEMENT MINISTER SIGNS FIC AMENDMENT ACT INTO OPERATION The Minister of Finance, Malusi Gigaba, has signed and gazetted the coming into operation of various provisions of the Financial Intelligence

Regulatory Update on AML/CFT

Regulatory Update on AML/CFT Putting Risk-Based in AML: The Road Ahead Mr Stewart McGlynn Division Head Anti-Money Laundering and Financial Crime Risk Hong Kong Monetary Authority 25 September 2015 Disclaimer

Regulatory Update on AML/CFT Putting Risk-Based in AML: The Road Ahead Mr Stewart McGlynn Division Head Anti-Money Laundering and Financial Crime Risk Hong Kong Monetary Authority 25 September 2015 Disclaimer

XPRESS MONEY SERVICES (CANADA) LTD. ANTI-MONEY LAUNDERING AND ANTI-TERRORIST FINANCING COMPLIANCE MANUAL

LTD. ANTI-MONEY LAUNDERING AND ANTI-TERRORIST FINANCING COMPLIANCE MANUAL") XPRESS MONEY SERVICES (CANADA) LTD. ANTI-MONEY LAUNDERING AND ANTI-TERRORIST FINANCING COMPLIANCE MANUAL ANTI-MONEY LAUNDERING AND ANTI-TERRORIST FINANCING COMPLIANCE MANUAL 2 TABLE OF CONTENTS OVERVIEW

XPRESS MONEY SERVICES (CANADA) LTD. ANTI-MONEY LAUNDERING AND ANTI-TERRORIST FINANCING COMPLIANCE MANUAL ANTI-MONEY LAUNDERING AND ANTI-TERRORIST FINANCING COMPLIANCE MANUAL 2 TABLE OF CONTENTS OVERVIEW

WIND OF CHANGE: Risk Assessment. Anti-Money Laundering, Countering Terrorism Financing, Application of International Sanctions

WIND OF CHANGE: Risk Assessment Anti-Money Laundering, Countering Terrorism Financing, Application of International Sanctions The 4th EU Anti-Money Laundering Directive encompasses significant changes

WIND OF CHANGE: Risk Assessment Anti-Money Laundering, Countering Terrorism Financing, Application of International Sanctions The 4th EU Anti-Money Laundering Directive encompasses significant changes

Assessment of international and domestic risks of money laundering and terrorist financing affecting Scottish solicitors (May 2017)

") 1 Law Society of Scotland Assessment of international and domestic risks of money laundering and terrorist financing affecting Scottish solicitors (May 2017) 2 Index Introduction 3 Overall Conclusion 4

1 Law Society of Scotland Assessment of international and domestic risks of money laundering and terrorist financing affecting Scottish solicitors (May 2017) 2 Index Introduction 3 Overall Conclusion 4

ANNEX III Sector-Specific Guidance Notes for Investment Business Providers, Investment Funds and Fund Administrators

ANNEX III Sector-Specific Guidance Notes for Investment Business Providers, Investment Funds and Fund Administrators These sector-specific guidance notes should be read in conjunction with the main guidance

ANNEX III Sector-Specific Guidance Notes for Investment Business Providers, Investment Funds and Fund Administrators These sector-specific guidance notes should be read in conjunction with the main guidance

JC /05/2017. Final Report

JC 2017 08 30/05/2017 Final Report On Joint draft regulatory technical standards on the criteria for determining the circumstances in which the appointment of a central contact point pursuant to Article

JC 2017 08 30/05/2017 Final Report On Joint draft regulatory technical standards on the criteria for determining the circumstances in which the appointment of a central contact point pursuant to Article

Guidance on Assessment of Money Laundering and Terrorism Financing Risks and Formulation of Related Control Programs by Futures Commission Merchants

Appendix Guidance on Assessment of Money Laundering and Terrorism Financing Risks and Formulation of Related Control Programs by Futures Commission Merchants 1. This Guidance is established in accordance

Appendix Guidance on Assessment of Money Laundering and Terrorism Financing Risks and Formulation of Related Control Programs by Futures Commission Merchants 1. This Guidance is established in accordance

Presentation Notes Derek Ramm, Officer FINTRAC. April 20, 2010

Presentation Notes Derek Ramm, Officer FINTRAC April 20, 2010 About FINTRAC FINTRAC is a regulator False. We are considered a Financial Intelligence Unit, with a primary mandate to assist in the detection

Presentation Notes Derek Ramm, Officer FINTRAC April 20, 2010 About FINTRAC FINTRAC is a regulator False. We are considered a Financial Intelligence Unit, with a primary mandate to assist in the detection

APPLICATION PAPER ON COMBATING MONEY LAUNDERING AND TERRORIST FINANCING

APPLICATION PAPER ON COMBATING MONEY LAUNDERING AND TERRORIST FINANCING OCTOBER 2013 About the IAIS The International Association of Insurance Supervisors (IAIS) is a voluntary membership organization

APPLICATION PAPER ON COMBATING MONEY LAUNDERING AND TERRORIST FINANCING OCTOBER 2013 About the IAIS The International Association of Insurance Supervisors (IAIS) is a voluntary membership organization

RBA Compliance. Pocket Handbook

RBA Compliance Pocket Handbook RBA Compliance Pocket Handbook Ana Maria de Alba, AMLCA and CPAML, has created the RBA Compliance Pocket Handbook to serve as a reference guide for risk and compliance officers.

RBA Compliance Pocket Handbook RBA Compliance Pocket Handbook Ana Maria de Alba, AMLCA and CPAML, has created the RBA Compliance Pocket Handbook to serve as a reference guide for risk and compliance officers.

Anti- Money Laundering & Combating Financing of Terrorism. Training for Insurance Agents By Joseph Owuor

Anti- Money Laundering & Combating Financing of Terrorism Training for Insurance Agents By Joseph Owuor Anti-Money Laundering & Combating Financing of Terrorism Agenda Agenda 1. Introduction to ML & TF

Anti- Money Laundering & Combating Financing of Terrorism Training for Insurance Agents By Joseph Owuor Anti-Money Laundering & Combating Financing of Terrorism Agenda Agenda 1. Introduction to ML & TF

COMMISSION STAFF WORKING DOCUMENT Accompanying the document. Report from the Commission to the European Parliament and the Council

EUROPEAN COMMISSION Brussels, 26.6.2017 SWD(2017) 241 final PART 1/2 COMMISSION STAFF WORKING DOCUMENT Accompanying the document Report from the Commission to the European Parliament and the Council on

EUROPEAN COMMISSION Brussels, 26.6.2017 SWD(2017) 241 final PART 1/2 COMMISSION STAFF WORKING DOCUMENT Accompanying the document Report from the Commission to the European Parliament and the Council on

United Republic of Tanzania Financial Intelligence Unit Anti Money Laundering and Counter Terrorist Financing Guidelines to Insurers

United Republic of Tanzania Financial Intelligence Unit Anti Money Laundering and Counter Terrorist Financing Guidelines to Insurers GUIDELINES NO: 4 i TABLE OF CONTENTS ACRONYMS... 1 1 INTRODUCTION...

United Republic of Tanzania Financial Intelligence Unit Anti Money Laundering and Counter Terrorist Financing Guidelines to Insurers GUIDELINES NO: 4 i TABLE OF CONTENTS ACRONYMS... 1 1 INTRODUCTION...

National Bank of Angola. Implementation guide for a money laundering and terrorism financing prevention program

National Bank of Angola Implementation guide for a money laundering and terrorism financing prevention program Document intended for financial institutions under the supervision of the National Bank of

National Bank of Angola Implementation guide for a money laundering and terrorism financing prevention program Document intended for financial institutions under the supervision of the National Bank of

Anti-money laundering Annual report 2017/18

Anti-money laundering Annual report 2017/18 Anti-money laundering Contents 1 Introduction 4 2 Policy developments 5 3 OPBAS 7 4 How our AML supervision is evolving 8 5 Findings and outcomes 9 6 Financial

Anti-money laundering Annual report 2017/18 Anti-money laundering Contents 1 Introduction 4 2 Policy developments 5 3 OPBAS 7 4 How our AML supervision is evolving 8 5 Findings and outcomes 9 6 Financial

The Handbook. Sator Regulatory Consulting Limited. Helen M Hatton, Managing Director

The Handbook Sator Regulatory Consulting Limited Helen M Hatton, Managing Director THE NEW AML REGIME CBA OVERSIGHT THE NEW HANDBOOK STANDARDS Law and Regulation The State Ordinance on the Prevention and

The Handbook Sator Regulatory Consulting Limited Helen M Hatton, Managing Director THE NEW AML REGIME CBA OVERSIGHT THE NEW HANDBOOK STANDARDS Law and Regulation The State Ordinance on the Prevention and

Criminal Justice (Money Laundering and Terrorist Financing) (Amendment) Act 2018

(Amendment) Act 2018") Criminal Justice (Money Laundering and Terrorist Financing) (Amendment) Act 2018 The long awaited Criminal Justice (Money Laundering and Terrorist Financing) (Amendment) Act 2018 (the Act) is now in force.

Criminal Justice (Money Laundering and Terrorist Financing) (Amendment) Act 2018 The long awaited Criminal Justice (Money Laundering and Terrorist Financing) (Amendment) Act 2018 (the Act) is now in force.

The Wolfsberg Correspondent Banking Due Diligence Questionnaire (CBDDQ) Completion Guidance 22 February 2018

Completion Guidance 22 February 2018") The Wolfsberg Correspondent Banking Due Diligence Questionnaire (CBDDQ) Completion Guidance 22 February 2018 1 Overview In response to both an increase in regulatory expectations as well as a call for

The Wolfsberg Correspondent Banking Due Diligence Questionnaire (CBDDQ) Completion Guidance 22 February 2018 1 Overview In response to both an increase in regulatory expectations as well as a call for

The Handbook is in final draft form as the legislation is awaiting approval by the States of Guernsey next month [December 2018].

![The Handbook is in final draft form as the legislation is awaiting approval by the States of Guernsey next month [December 2018].](/thumbs/92/110726346.jpg "The Handbook is in final draft form as the legislation is awaiting approval by the States of Guernsey next month [December 2018].") Key points made by Fiona Crocker, Director of the Financial Crime Division at presentations on 28 November 2018 on the draft revised Handbook on Countering Financial Crime and Terrorist Financing. These

Key points made by Fiona Crocker, Director of the Financial Crime Division at presentations on 28 November 2018 on the draft revised Handbook on Countering Financial Crime and Terrorist Financing. These

PART III BANKS AND OTHER DEPOSIT TAKING FINANCIAL INSTITUTIONS SECTOR SPECIFIC AML/CFT GUIDANCE

GUIDANCE NOTES ON THE PREVENTION AND DETECTION OF MONEY LAUNDERING AND TERRORIST FINANCING IN THE CAYMAN ISLANDS PART III BANKS AND OTHER DEPOSIT TAKING FINANCIAL INSTITUTIONS SECTOR SPECIFIC AML/CFT GUIDANCE

GUIDANCE NOTES ON THE PREVENTION AND DETECTION OF MONEY LAUNDERING AND TERRORIST FINANCING IN THE CAYMAN ISLANDS PART III BANKS AND OTHER DEPOSIT TAKING FINANCIAL INSTITUTIONS SECTOR SPECIFIC AML/CFT GUIDANCE

Knowing your customer

Knowing your customer IN A GLOBAL WORLD The basics of Australia s AML/CTF regime For accountants, conveyancers, lawyers, real estate agents and other business professionals. An increasing threat Anti-Money

Knowing your customer IN A GLOBAL WORLD The basics of Australia s AML/CTF regime For accountants, conveyancers, lawyers, real estate agents and other business professionals. An increasing threat Anti-Money

Money Laundering Detection Regimes

Money Laundering Detection Regimes Credit Unions in Canada Chris Randle, CAMS Contents Executive Summary... 4 Notice to Reader:... 5 Understanding the Requirements... 6 Understanding Suspicious Transactions:...

Money Laundering Detection Regimes Credit Unions in Canada Chris Randle, CAMS Contents Executive Summary... 4 Notice to Reader:... 5 Understanding the Requirements... 6 Understanding Suspicious Transactions:...

Anti-Money Laundering Policy

Anti-Money Laundering Policy SMFX is a trading name of Scope Markets Ltd, registration number 145,138 (registered address: 5 Cork street, Belize City, Belize). Scope Markets Ltd is regulated by the International

Anti-Money Laundering Policy SMFX is a trading name of Scope Markets Ltd, registration number 145,138 (registered address: 5 Cork street, Belize City, Belize). Scope Markets Ltd is regulated by the International

ANTI-MONEY LAUNDERING/ COUNTER FINANCING OF TERRORISM GUIDELINES FOR REGISTERED FILING AGENTS

ANTI-MONEY LAUNDERING/ COUNTER FINANCING OF TERRORISM GUIDELINES FOR REGISTERED FILING AGENTS Published 17 Oct 2017 TABLE OF CONTENTS 1 INTRODUCTION... 2 2 APPLICATION OF THESE GUIDELINES... 2 2.1 Definitions

ANTI-MONEY LAUNDERING/ COUNTER FINANCING OF TERRORISM GUIDELINES FOR REGISTERED FILING AGENTS Published 17 Oct 2017 TABLE OF CONTENTS 1 INTRODUCTION... 2 2 APPLICATION OF THESE GUIDELINES... 2 2.1 Definitions

So you think all your clients property is clean? 25 October 2017

So you think all your clients property is clean? 25 October 2017 Nigel Lubbock Director Tom Bailey Director Why this topic? Statistics Professions Increased legislation Softer options for prosecution ICAEW

So you think all your clients property is clean? 25 October 2017 Nigel Lubbock Director Tom Bailey Director Why this topic? Statistics Professions Increased legislation Softer options for prosecution ICAEW

Phase 2 AML/CFT Sector Risk Assessment. December 2017

Phase 2 AML/CFT Sector Risk Assessment December 2017 NOTE: This sector risk assessment is intended to provide a summary and general overview. It does not assess every risk relevant to the covered sectors.

Phase 2 AML/CFT Sector Risk Assessment December 2017 NOTE: This sector risk assessment is intended to provide a summary and general overview. It does not assess every risk relevant to the covered sectors.

FINANCIAL CRIME GUIDE (AMENDMENT NO 3) INSTRUMENT 2015

INSTRUMENT 2015") FINANCIAL CRIME GUIDE (AMENDMENT NO 3) INSTRUMENT 2015 Powers exercised A. The Financial Conduct Authority makes this instrument in the exercise of its powers under: (1) section 139A (Guidance) of the

FINANCIAL CRIME GUIDE (AMENDMENT NO 3) INSTRUMENT 2015 Powers exercised A. The Financial Conduct Authority makes this instrument in the exercise of its powers under: (1) section 139A (Guidance) of the

Introduction to AML/CFT in New Zealand

Introduction to AML/CFT in New Zealand What You Will Learn This will give you a very quick overview of what AML/CFT is, how it impacts Cryptopia, and introduces you to the concepts you ll be hearing a

Introduction to AML/CFT in New Zealand What You Will Learn This will give you a very quick overview of what AML/CFT is, how it impacts Cryptopia, and introduces you to the concepts you ll be hearing a

AML/ KYC Policy & Procedures AML/ KYC POLICY & PROCEDURES. For Prevention of Money Laundering HABIB BANK LIMITED

AML/ KYC POLICY & PROCEDURES For Prevention of Money Laundering HABIB BANK LIMITED Owner: GLOBAL COMPLIANCE GROUP ISSUE DATE: October, 2006 Global Compliance Group 1 Slogan for HBL Compliance is My Responsibility

AML/ KYC POLICY & PROCEDURES For Prevention of Money Laundering HABIB BANK LIMITED Owner: GLOBAL COMPLIANCE GROUP ISSUE DATE: October, 2006 Global Compliance Group 1 Slogan for HBL Compliance is My Responsibility

JC/GL/2017/ September Final Guidelines

JC/GL/2017/16 22 September 2017 Final Guidelines Joint Guidelines under Article 25 of Regulation (EU) 2015/847 on the measures payment service providers should take to detect missing or incomplete information

JC/GL/2017/16 22 September 2017 Final Guidelines Joint Guidelines under Article 25 of Regulation (EU) 2015/847 on the measures payment service providers should take to detect missing or incomplete information

FATF Mutual Evaluation of Ireland 2017

FATF Mutual Evaluation of Ireland 2017 Introduction Background The Financial Action Task Force ( FATF ) was established in 1989 with a high level objective that: Financial systems and the broader economy

FATF Mutual Evaluation of Ireland 2017 Introduction Background The Financial Action Task Force ( FATF ) was established in 1989 with a high level objective that: Financial systems and the broader economy

GAMLG s AML Risk Assessment for Licensed Betting Offices (LBOs) and Remote Gambling Industries

and Remote Gambling Industries") GAMLG s AML Risk Assessment for Licensed Betting Offices (LBOs) and Remote Gambling Industries TABLE OF CONTENTS From the Chairman...3 Introduction...4 Scope...5 Methodology...6 Licensed Betting Offices

GAMLG s AML Risk Assessment for Licensed Betting Offices (LBOs) and Remote Gambling Industries TABLE OF CONTENTS From the Chairman...3 Introduction...4 Scope...5 Methodology...6 Licensed Betting Offices

CUSTOMER DUE DILIGENCE (CDD) & ANTI-MONEY

& ANTI-MONEY") CUSTOMER DUE DILIGENCE (CDD) & ANTI-MONEY LAUNDERING (AML) / COMBATING FINANCING OF TERRORISM (CFT) POLICY MCB SRI LANKA OPERATIONS 2017 Version 2.0 For Internal Use Only Document Control Sheet Title Of

CUSTOMER DUE DILIGENCE (CDD) & ANTI-MONEY LAUNDERING (AML) / COMBATING FINANCING OF TERRORISM (CFT) POLICY MCB SRI LANKA OPERATIONS 2017 Version 2.0 For Internal Use Only Document Control Sheet Title Of

Preparing for the 4 th Round of Mutual Evaluations ANGUILLA, FRIDAY 8 TH OF MAY 2015

Preparing for the 4 th Round of Mutual Evaluations ANA FOLGAR L EGAL ADVISOR CFATF ANGUILLA, FRIDAY 8 TH OF MAY 2015 Content The FATF Mandate Role of the CFATF in relation to FATF Involvement of CFATF

Preparing for the 4 th Round of Mutual Evaluations ANA FOLGAR L EGAL ADVISOR CFATF ANGUILLA, FRIDAY 8 TH OF MAY 2015 Content The FATF Mandate Role of the CFATF in relation to FATF Involvement of CFATF

Anti-Money Laundering & Financial Crimes Conference April 18th 20th, 2018

Anti-Money Laundering & Financial Crimes Conference 2018 April 18th 20th, 2018 Know Your Customer's Customer (KYCC) The next level of due diligence obligations Introduction 1. FATF Standards, CDD and KYC

Anti-Money Laundering & Financial Crimes Conference 2018 April 18th 20th, 2018 Know Your Customer's Customer (KYCC) The next level of due diligence obligations Introduction 1. FATF Standards, CDD and KYC

PREVENTION OF MONEY LAUNDERING AND FINANCING OF TERROR, AND CUSTOMER IDENTIFICATION

Page 411-1 PREVENTION OF MONEY LAUNDERING AND FINANCING OF TERROR, AND CUSTOMER IDENTIFICATION Introduction 1. (a) Effective knowledge of banking corporations customers, including an understanding of the

Page 411-1 PREVENTION OF MONEY LAUNDERING AND FINANCING OF TERROR, AND CUSTOMER IDENTIFICATION Introduction 1. (a) Effective knowledge of banking corporations customers, including an understanding of the

AML & ATF Policy and Procedures for Deposit Agents of Peoples Trust Company

PROCEEDS OF CRIME (MONEY LAUNDERING) AND TERRORIST FINANCING ACT AND REGULATIONS In order to comply with the Office of the Superintendent of Financial Institutions (OFSI) and the Financial Transactions

PROCEEDS OF CRIME (MONEY LAUNDERING) AND TERRORIST FINANCING ACT AND REGULATIONS In order to comply with the Office of the Superintendent of Financial Institutions (OFSI) and the Financial Transactions

- Due diligence process is a continuous process customer service representatives (C/S Rep.) need to be aware of:

need to be aware of:") ANTI MONEY LAUNDERING The Fundamental Principles of The Policy Overview The internal policy of The UNBE is to prevent and combat money laundering. This includes financial monitoring, which is in conformity

ANTI MONEY LAUNDERING The Fundamental Principles of The Policy Overview The internal policy of The UNBE is to prevent and combat money laundering. This includes financial monitoring, which is in conformity

Risk management policy

Risk management policy November 2017 Risk management policy Page 0 of 8 Contents 1. Policy objectives and background 2 1.1 Policy background 2 1.2 Policy objective 2 1.3 Policy sponsor and maintenance

Risk management policy November 2017 Risk management policy Page 0 of 8 Contents 1. Policy objectives and background 2 1.1 Policy background 2 1.2 Policy objective 2 1.3 Policy sponsor and maintenance

ZIMBABWE NATIONAL ANTI-MONEY LAUNDERING AND COMBATING FINANCING OF TERRORISM STRATEGIC PLAN FOR THE PERIOD:

ZIMBABWE NATIONAL ANTI-MONEY LAUNDERING AND COMBATING FINANCING OF TERRORISM STRATEGIC PLAN FOR THE PERIOD: 2015-2018 JUNE 2015 1 P a g e Table of Contents INTRODUCTION... 3 VISION STATEMENT... 3 MISSION

ZIMBABWE NATIONAL ANTI-MONEY LAUNDERING AND COMBATING FINANCING OF TERRORISM STRATEGIC PLAN FOR THE PERIOD: 2015-2018 JUNE 2015 1 P a g e Table of Contents INTRODUCTION... 3 VISION STATEMENT... 3 MISSION

The National Anti-Money Laundering Committee and the Bermuda Monetary Authority

The National Anti-Money Laundering Committee and the Bermuda Monetary Authority CONSULTATION PAPER Proposed Legislative Amendments Anti-Money Laundering Legislation and Financial Institutions February

The National Anti-Money Laundering Committee and the Bermuda Monetary Authority CONSULTATION PAPER Proposed Legislative Amendments Anti-Money Laundering Legislation and Financial Institutions February