Submission. 10 March 2016

|

|

|

- Lester Patrick

- 5 years ago

- Views:

Transcription

1 Submission Best practices, challenges and lessons learned from insurance-related solutions that address the risk of loss and damage associated with the adverse effects of climate change 1 Munich Climate Insurance Initiative (MCII) With inputs from RESULTS UK Submitted to the Executive Committee of the Warsaw International Mechanism on Loss and Damage 10 March This submission from the Munich Climate Insurance Initiative (MCII) (with inputs from RESULTS UK) is part of its mission to develop insurance-related solutions to help manage the impacts of climate change. MCII was founded in response to the growing realization that insurance solutions can play a role in addressing some of the negative impacts of climatic stressors, as suggested in the Framework Convention and the Paris Agreement. With membership on the part of insurers, climate change and adaptation experts, NGOs and policy researchers, MCII provides a forum for insurance related expertise applied to climate change issues. 1

2 Table of contents 1. Introduction Practical solutions - the MCII Livelihood Protection Policy (LPP) and the Loan Portfolio Cover (LPC) in the Caribbean The Livelihood Protection Policy (LPP) The Loan Portfolio Cover (LPC) Development and implementation of climate risk insurance approaches - lessons learned from the LPP and LPC What sequence of key activities and measures are needed in designing comprehensive climate risk management approaches? What actors need to be involved in the design and implementation process? Challenges in implementing climate risk insurance approaches Success factors for climate risk insurance approaches References

3 1. Introduction Climate change and the associated pressures threaten society through changing rainfall regimes, intensified and more frequent storms, sea level rise, widespread desertification and the loss of geological water sources such as glaciers. This threatens to undermine resilience, especially for lower income countries and their citizens, by weakening their capacity to recover and absorb losses from extreme weather events. In order to support governments and households to reduce the immediate and long-term repercussions from these events, countries can apply comprehensive climate risk management approaches to support adaptation and build climate risk resilience. There are a range of tools that governments can combine in a comprehensive climate risk management strategy. These include risk prevention and reduction, risk transfer such as insurance, funds for flood protection, contingency planning and other forms of risk management instruments. Countries can decide on how to manage and finance these risks according to detailed methodologies of risk management, for instance through a risk layering analysis, which separates risk into different segments according to their potential frequency and severity. Climate-related risks which happen often (high frequency) but which are less serious (low severity) can be addressed most effectively by preventative and risk reduction activities. The risk posed by more severe and less frequent events can be transferred by using private and/or public insurance mechanisms. The loss and damage that remains once all feasible measures are taken (i.e., residual risk) requires several approaches, such as strengthening institutional arrangements and socio-economic policies or relocation of populations, flood control investments, fund for irrigation systems, etc. This submission to the Executive Committee of the Warsaw International Mechanism for Loss and Damage: Shares insights from the work of the Munich Climate Insurance Initiative (MCII) on designing and implementing climate risk insurance solutions as part of comprehensive risk management approaches; Introduces practical climate risk insurance solutions that MCII is currently implementing in the Caribbean - the Livelihood Protection Policy (LPP) which helps protect the livelihoods of vulnerable low-income individuals by providing swift non-bureaucratic cash payouts following extreme weather events and the Loan Portfolio Cover (LPC), a loan portfolio hedge that can help create a space of certainty for institutions with credit portfolios exposed to natural disaster risk. Outlines sequencing of key activities and involvement of relevant actors as well as challenges in the process of designing and implementing climate risk insurance solutions as part of comprehensive climate risk management approaches, based on the lessons learned in the Caribbean; Reflects on five success factors for direct and indirect climate risk insurance solutions based on insights gathered by MCII expert interviews with thought leaders and innovators from primary and reinsurance companies, pioneers using risk transfer to reshape humanitarian assistance, and practitioners at the vanguard of risk management and adaptation in Practical solutions - the MCII Livelihood Protection Policy (LPP) and the Loan Portfolio Cover (LPC) in the Caribbean Over the last 30 years in the Caribbean, flood and tropical storm damage affected 1.5 million persons directly and caused over USD 5 billion in damage. Climate change is a reality that can no longer be denied. As extreme weather events such as droughts, floods, hurricanes and storms 3

4 increase in frequency and intensity, they place significant stress on societies and natural systems. These events lead to loss of income and productive potential, forcing affected low-income individuals to resort to a variety of desperate coping strategies that include: reducing food consumption, taking children out of school, borrowing money and selling assets. These strategies diminish their ability to cope with current and future climate change impacts. As a result, there is a growing need to explore meaningful options for managing and transferring risks associated with climate change. One feasible measure to support adaptation to climate change is climate risk insurance. The Climate Risk Adaptation and Insurance in the Caribbean project seeks to address climate change, adaptation and vulnerability by promoting weather-index based insurance as a risk management instrument in the Caribbean. The project has developed two parametric weatherindex based risk insurance products aimed at low-income individuals and lending institutions exposed to climate stressors. The following explanations are based on MCII 2013a and MCII 2013b. 2.1 The Livelihood Protection Policy (LPP) The Livelihood Protection Policy (LPP) is targeted at individuals; this product helps protects the livelihoods of vulnerable low-income individuals by providing swift un-bureaucratic cash payouts following extreme weather events (i.e. high wind speed and heavy rainfall). This crucial support reduces poverty and vulnerability by enabling these groups to recover quickly following a disaster. CHALLENGE The Caribbean is prone to extreme weather events, making it a challenge for people to cope with the damaging effects of weather-related risks and the threats such risks pose to their lives and livelihoods. The expected increase in the frequency and intensity of extreme weather events brought on by climate change will further exacerbate the plight of vulnerable individuals in the Caribbean, many of whom are employed in climate vulnerable sectors such as agriculture and tourism. Continual exposure to weather-related risk reduces economic opportunity, exhausts financial resources and erodes the overall coping capacity of low-income individuals, leading to lost livelihoods and poverty in the long-term. Protecting the livelihoods of low-income, vulnerable individuals by improving their ability to cope with weather-related risks can make a positive contribution to socio-economic development in the Caribbean. SOLUTION Appropriately designed weather risk insurance solutions can help people respond better to weatherrelated threats. The LPP is a weather-index based insurance policy designed specifically to help vulnerable, low-income individuals recover from the damage caused by strong winds and/or heavy rainfall during hurricanes and tropical storms. Targeted at all individuals irrespective of income level, the LPP provides timely cash payouts soon after a weather event, enabling policy holders to start rebuilding their lives in the wake of a natural disaster. OUTCOME The LPP stabilizes the financial situation of vulnerable, low-income individuals after a disaster and allows them to avoid adopting coping strategies that could lead them deeper into poverty. The simplicity and flexibility of the LPP makes it easier for people to get the level of coverage they need. Having access to insurance coverage improves the credit worthiness of individuals in the long-term, giving them access to financial services that they previously may not have had access to. Access to credit can create a space of certainty for people to make investments, allowing them to safeguard their livelihoods. 4

5 HOW LPP MAKES A DIFFERENCE Antoine is a farmer whose family depends on his small plot of land for food and income. In hopes of providing a better life for his family, Antoine took out a loan and bought three greenhouses to grow vegetables. The following year, in 2007, Hurricane Dean struck. What Antoine experienced Before the hurricane Antoine did not know a hurricane was approaching and did not secure his greenhouses or other assets in time. Immediately after two out of three greenhouses were lost, along with his sugarcane crop and livestock. He and his family barely escaped with their lives. Medium-term Antoine spent all of his savings on food and medicine for his family. He could not pay back his loan for the greenhouses and must resort to selling other assets and asking relatives for money. Long-term Antoine and his family ended up deeply in debt. The lost greenhouses were not replaced, making the family more vulnerable to subsequent hurricanes. These are likely to destroy more of their assets and lead them deeper into poverty. How LPP could have helped Antoine Before the hurricane Antoine receives an SMS warning of an approaching hurricane. He secures his property and leads his family to a safe location. Immediately after as he was able to secure his property, only one greenhouse is lost. The hurricane exceeded the rainfall/wind speed threshold, so Antoine gets an SMS telling him he will receive a payout within 14 days. Medium-term with the payout deposited in his bank account Antoine can repay his loan and start rebuilding his livelihood without resorting to more desperate coping measures. Long-term Antoine is able to both repay his loan and rebuild the lost greenhouses with the payout he receives from his policy. This puts him and his family in a better position for when another hurricane inevitably strikes. Source: MCII 2013a. 2.2 The Loan Portfolio Cover (LPC) The Loan Portfolio Cover (LPC) is targeted at lending institutions; this product is a loan portfolio hedge that can help create a space of certainty for institutions with credit portfolios exposed to 5

6 natural disaster risk. As loan portfolios are insured against climate risk, investment can reach areas previously considered too risky for traditional lending. In the short run, this creates a win-win situation for the lender and the borrower, while also contributing to economic development in the region in the long run. CHALLANGE When extreme weather events affect many borrowers at the same time, financial institutions (e.g. credit unions, cooperatives, etc.) often experience the double blow of heavy withdrawals from savings accounts and the inability of borrowers to repay their loans. Climate shocks are thus one of the leading causes of high loan default rates experienced by financial institutions. These loan defaults can lead to portfolio-level problems that may erode their equity base and liquidity. In the Caribbean, the ability of financial institutions to provide credit is often impeded by recurring extreme weather events (e.g. hurricanes), which leaves them reluctant to lend to climate vulnerable individuals who need it most. The management of portfolio risk needs to be improved to allow financial service providers expand their funding base, and increase lending capacity to vulnerable, low-income individuals and micro, small and medium enterprises (MSMEs). This is critical for ensuring that these groups have access to credit to withstand environmental stressors and invest in their livelihoods. SOLUTION Unmanaged exposure to climate risk limits economic growth and increases the cost of providing financial services. The Loan Portfolio Cover (LPC) is an insurance instrument that transfers risks arising from natural catastrophes to international risk pooling markets. As a parametric insurance policy designed to protect loan portfolios from climate shocks and eventual loan default, the LPC helps financial institutions better manage their credit risk. The simple and flexible structure of the policy allows financial institutions to select the level of insurance cover to be applied to their overall exposed loan portfolio a payout is triggered when predetermined threshold values for wind speed and/or rainfall are exceeded, irrespective of any proven loan default the financial institution may have suffered. OUTCOME Transferring the risk of a financial institution s weather-related loan default means the financial position of these institutions continues to be stable after an extreme weather event, enabling them to avoid curbing their lending activity or instituting unfavourable terms of credit. The LPC can help overcome the reluctance to invest, improve access to lending and contribute to reducing the cost of providing financial services. HOW LPC MAKES A DIFFERENCE Financial institutions/financial cooperatives (FI) in the Caribbean cater to a wide cross-section of society, many of whom are vulnerable to natural disasters (e.g. small scale farmers). In addition to encouraging savings, they provide credit at favourable interest rates to enable clients to make investments in their livelihoods (e.g. buying greenhouses). However, a modest equity base means that these FIs are vulnerable to weather-related shocks, which compromise their financial position and leave them reluctant to grant loans to vulnerable individuals during times of stress. This was the case in 2007 after hurricane Dean. How the FIs were impacted Before the hurricane The FIs have no forewarning of the approaching hurricane. The number of withdrawals increases exponentially as clients need funds to rebuild their lives and livelihoods. Immediately after As the number of withdrawals increases exponentially the FIs do not have enough liquidity to honor withdrawals. 6

7 Medium-term Loan default rates increase as borrowers are unable to repay their loans on time. The FIs equity base is eroded, forcing them to curb lending activity. Long-term The FIs institute less favourable terms of credit, which reduces access to credit to those who need it most (e.g. hurricane survivors). Investments are postponed or cancelled, carrying direct consequences for long-term economic growth. Clients are unable to recover fully, leaving them more vulnerable to subsequent hurricanes and driving them deeper into poverty. How LPC could have helped Before the hurricane The FIs receive an SMS to alert them of an approaching hurricane. By being aware of the burden such a weather event would place on their clients, the FIs are in a better position to manage exposure to default risk. Immediately after The FIs equity base will not be significantly impacted, as the LPC is likely to ensure that they continue to have access to new credit. Medium-term The FIs equity base remains stable. There is no immediate need to curtail credit operations; therefore, clients can rebuild their livelihoods with their savings. Long-term The LPC strengthens the FIs so that they are able to provide access to credit to enable their clients to rebuild their lives following a disaster. In general, when local Fis manage their risk more effectively, they do not have to curtail lending operations and can lend at lower interest rates. The FIs are even able to write-off some defaulted loans and absorb these losses during critical times, leaving clients in a better position to recover. Source: MCII

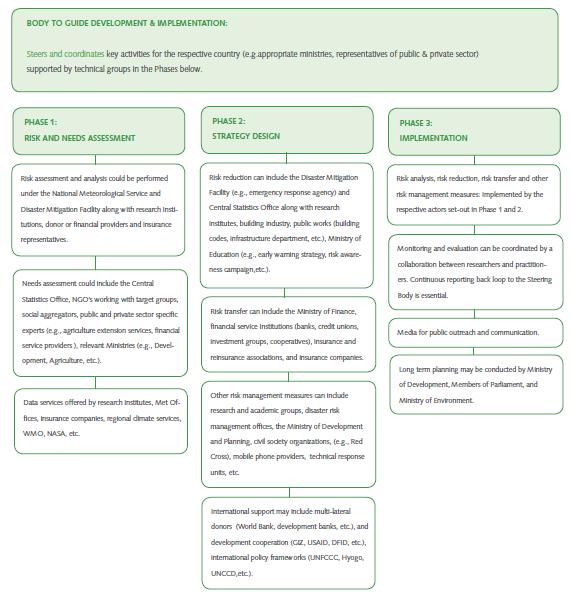

8 3. Development and implementation of climate risk insurance approaches - lessons learned from the LPP and LPC It must be emphasized that insurance is not a universal remedy for all types of loss and damage resulting from climate change. As the figure below shows, insurance options can support adaptation and resilience against the risks of extreme weather events, but are not appropriate for many, usually slower-onset, climate-induced impacts. As we see in the figure below, insurance is not appropriate or generally feasible for slowly developing and foreseeable events or processes that happen with high certainty under different climate change scenarios. The losses from long-term foreseeable risks, such as sea level rise, desertification and the loss of glaciers and other cryospheric water sources, are estimated to be substantial in the future. Even for weather-related events, insurance would be an ill-advised solution for disastrous events that occur with very high frequency, such as recurrent flooding. Resilience building and prevention of loss and damage in such instances may be cost-effective ways to address these risks Insurance is a feasible adaptation measure to address extreme weather events, including insurance for households (e.g., micro-insurance), farms (e.g., index based crop insurance) and also governments with sovereign insurance. As we will be discussing in this document, insurance arrangements at these scales might be usefully supported with regional and global risk management facilities. 3.1 What sequence of key activities and measures are needed in designing comprehensive climate risk management approaches? A comprehensive climate risk management approach combines ex ante risk assessment to gather information with a subsequent decision on how to manage and finance these risks. Sequencing of key activities starts with a risk and needs assessment, followed by strategy design, making improvements to the enabling environment and finally implementation and ongoing monitoring and adjustment as needed to fit changing conditions. The following graphic, based on MCII 2014, provides an overview of key activities and measures needed in the design process: 8

9 3.2 What actors need to be involved in the design and implementation process? The following graphic provides an overview of relevant actors that need to be involved in the key phases of design and implementation of climate risk insurance appraoches. It also lists important factors constituting the enabling environment in these phases. 9

10 Source: MCII

11 4. Challenges in implementing climate risk insurance approaches There are some limitations that countries might need to address when implementing a comprehensive climate risk management approach. The following table is based on MCII Country Level Community National Regional Limitation Policy holders often expect payouts every year. Low-income countries often lack resources and capacity for testing new products. Overcoming barriers to private sector insurance such as high startup costs and lack of infrastructure requirements for data collection. Difficult to provide funds in a post disaster situation under fraud and corruption as well as biases towards certain groups Institutional inertia: institutions do what they always do. In the case of small island states, sea level rise is expected to increase. Thus, governments need to decide between approaches to address slow-onset events versus extreme weather events. High turnover rate in the government and loss of knowledge. Governments want to invest into something more visible and short term as opposed to a long-term vision. Different operating parameters for the public and private sector Solutions Insurance products should be complemented by disaster risk reduction and additional services that offer value to their livelihoods. Ensure sufficient resources for example, technical skills, institutional capacity-building, policy and planning, and knowledge dissemination. > Insurance risk assessment can facilitate regional data analysis and help establish data standards, methods and repositories. > Open source initiatives for catastrophic risk models along with standardized hazard maps can reduce the cost of risk analysis. > New technologies such as satellite data and simulation models. > Weather stations can be used for multiple services to reduce infrastructure costs. > Governments have to establish post disaster contingency plans that specify how to disburse and distribute funds to avoid fraud and corruption. These plans should be developed transparently, in meaningful consultation with affected communities, and should set out how they will target and track the most vulnerable groups. > Organizational development and capacity building based on an overarching strategy with clear objectives, roles and mandates is required. > Sea level rise can be addressed, for example, through a fund invested at the international market (e.g., risk pooling) where profits can be used to fund adaptation measures in relation to sea level rise. > Identify champions on a technical level and ensure government officials have financial and actuarial education. > Knowledge management and transparency. > Elaboration of training modules, documentation of lessons learned and public communication. > Connect a comprehensive climate risk management approach with a long-term development strategy that is usually medium to long-term. > Need role models in both the public and private sector that showcase the benefits of insurance in a comprehensive approach. > Public sector capacity building to manage expectations and highlight the value added of integrating insurance into risk management planning. 11

12 Political unrest and currency risk. Sharing of sensitive data at regional level. > Third party country can host the insurance. For example, for the African Risk Capacity Insurance Company Ltd, the financial affiliate will temporarily be in Bermuda as a private, non-profit company. Draft agreements outlining how sensitive data may be used by the different parties. 5. Success factors for climate risk insurance approaches The following 9 success factors for direct and indirect climate risk insurance approaches are based on insights gathered by MCII expert interviews with thought leaders and innovators from primary and reinsurance companies, pioneers using risk transfer to reshape humanitarian assistance, and practitioners at the vanguard of risk management and adaptation in More details can be found in MCII 2015a and MCII 2015b. Focus insurance on needs of poor & vulnerable people, securing development goals Exposure to climate risks causes significant financial losses for the poor. These households also face high uncertainty about whether and when losses might happen. Insurance approaches for the poor should address the most pressing needs uncertainty to livelihoods, food security and development aspirations that get in the way of opportunities to reduce poverty. At the micro-level, insurance works when it brings added value to policyholders, and rarely as a standalone product. In an agricultural context this is partly because smallholders and pastoralists typically face multiple, interlocking risk factors and economic barriers. Pro-poor insurance schemes should be integrated with essential livelihood and poverty reduction services such as credit, savings, quality inputs, extension services and training, and weather alerts to deliver tangible value in both bad years (when a payout is made) and good (when it is not). To safeguard that existing risk management approaches are enhanced, locally driven and owned schemes will help ensure that local needs and capacities are taken into account. Partnerships that link traditional risk management approaches and social cohesion with new ways of providing financial risk transfer (cooperatives, microfinance, and bundling with cell phone services) can add value to locally driven and owned schemes. Women are a particularly vulnerable group whose needs must be adequately addressed by climate risk insurance and related instruments. Evidence shows that they are disproportionately affected by climate shocks and natural disasters, disproportionately lack access to financial services, and typically face larger barriers to improving productivity in agriculture and small-scale enterprise. Lessons from both the fields of financial inclusion and community climate adaptation suggest that unless insurance programmes (at micro, meso and macro levels) specifically integrate a gender analysis and framework into their design, implementation, monitoring and evaluation, women are vulnerable to being excluded or even further disadvantaged. Provide smart support for insurance related instruments for the poor Based on lessons learned from current experience and expert interviews MCII defines smart support as including: A): Providing targeted premium support: Experts assert that few if any insurance related approaches worldwide specifically targeted towards the poor have been started and sustained without public private cooperation, often in a way of premium support 2. Donor countries could: Directly cover the mark up part of the premium while the risk based part is covered by the beneficiary (see box), thereby incentivizing risk reducing behavior through the price signal. 2 See e.g. Mecheler, R. /Linnerooth-Bayer, J. 2006: Disaster Insurance for the Poor? A review of micro insurance for natural disaster risks in developing countries. 12

13 Directly cover premiums for the poorest of the poor: We documented cases where premiums for the poorest of the poor have been covered by third parties and designed in such a way that beneficiaries contribute to risk reduction in other ways. Examples of this include the R4 Initiative, and innovative insurance funds linked to income support programs and other safety nets currently being developed. Provide capital reserves or reinsurance-like capacity which drive down the costs of climate risk insurance products. ARC and CCRIF estimate that premiums for member countries are half that of commercially available insurance for weather-related extreme cover. B): Providing sustainable, credible delivery channels Insurance premiums usually comprise of two major cost factors: a risk based part and a mark-up part. While the risk based part reflects the actual costs of the risk of insuring a % of the exposure, the mark-up includes transaction, administration and capital/reinsurance costs. In developing countries, mark-ups are often particularly high because of a lack of important data, insufficient risk assessments and therefore the return periods of risks are more uncertain. To reach the target group, experts recommend using aggregators like regional rural banks, mutual, refinancing banks, microfinance institutions, social protection pools of governments. Awareness building, marketing, and claims assistance need face-to-face interaction (e.g. by civil society organizations). A national identification system through which people can be identified and reached and mobile phone networks in remote areas, can facilitate effective insurance enrollment. If regulators permit, premiums can also be collected through technology (e.g. mobile banking). Other important factors that should not be neglected include the following: Enhance capacity Reaching poor and vulnerable people with climate risk insurance requires significant capacity building measures, often involving actors not yet familiar with the tools or principles of insurance. For beneficiaries: Measures to improve financial literacy include knowledge of personal financial issues, skills to manage personal finances, and confidence to make sound financial decisions including building up savings, protecting themselves against risk, and investing prudently. Beneficiaries need specific understanding of index insurance, trust and transparency with insurance providers, and comprehensive knowledge of links between disaster risk reduction and insurance. For local primary insurers: Build capacity in catastrophe risk modeling to price risk-adequate premiums, train financial services experts with skills to access and market to new beneficiary groups and financial institutions that serve them (microfinance, credit unions, etc.), as well as capacity to manage claims and payments. For distribution channels: Build capacity of value chains, safety net programs, etc. to manage financial services such as hiring trained financial experts, building incentives to reduce risks, building capacity for marketing, enrollment, and claims management assistance. For governments: Building capacity in producing data that is required (socio-economic, losses, exposure, etc.), modeling weather risk, operational capacity and expertise, financial protection strategies, and systematically integrating contingency plans into policies (e.g. NAP, agricultural strategy plans, construction policies, etc.). Embed in regulatory frameworks and risk management policies An insurance supervisor maintains trust and ensures consumer protection by overseeing all insurance activities. Reputable insurers will not engage without regulatory frameworks and guidelines for insurance licensing and operations. Governments can incentivize industry sector participation through tax exemptions on products for poor people. Furthermore, policies and measures for risk reduction and adaptation reduce the exposure to risks and can indirectly reduce premiums. Governments can strengthen provision of relevant data including hazard, asset exposure, agricultural production, and market demand assessments. 13

14 Incentivize climate adaptation and disaster risk reduction Prevention and insurance should be closely linked with an ex ante climate risk management strategy that prioritizes reducing human and economic losses. Such activities include: Mapping risks and avoiding settlements in high-risk zones; Building hazard-resistant infrastructures and houses; Protecting and developing hazard buffers (forests, reefs, mangroves, etc.); Improving early warning and response systems; Mainstreaming risk reduction in National Adaptation Plans (NAPs). Foster financial inclusion Poor people need access to tools like savings, loans, remittances, and insurance that helps them smooth household consumption and break the cycle of poverty. Financial inclusion could be improved by identity cards, financial or bank accounts to make and receive insurance payments, and processes to establish a financial history. Insurance schemes need to be designed to receive premium payments in appropriate time intervals that are linked to the financial cycles of poor households. Similarly, schemes must make timely payouts after an insured event. Apply a participatory approach and foster public private partnership Successful insurance schemes are based on the effective involvement of all relevant actors, providing the basis for a meaningful long-term partnership. Facilitating stakeholder dialogue is a first step in this process. It is crucial to include beneficiaries in the co-design and implementation of insurance solutions to assure products truly match needs. Target group ownership is essential for effective use of insurance as a risk management tool. There should be effective and meaningful representation of the target groups in discussions about the design and delivery of insurance programmes (including through substantive consultation on government contingency planning). Civil society can help engage the target group, build capacity through training, builds trust with financial intermediaries, and monitor and evaluate scheme governance and implementation. Development cooperation partners can support risk and needs assessments, product design, and other forms of technical support. To harness the strength of all those partners, the most effective way to set up such insurance schemes is to strive for innovative and effective public private partnerships. The risk management expertise of the private sector must be utilized to assess risks, design viable insurance products, and reach beneficiaries through effective distribution channels. The involvement of governments is key to political buy-in, ownership and integration of the insurance approaches in national planning, policies, and regulations (such as consumer protection). Governments can set incentives that facilitate insurance provision across a range of programs, including social protection and risk management, education, and agriculture. Design for sustainability and viability To effectively chart climate resilient pathways, activities need to be sustainable and viable, both in economic and social terms. Planning with a view towards long-term engagements is crucial as most insurance interventions need time to mature and be fully incorporated into local risk management strategies. Applying risk adequate premiums is one of the central elements for ensuring the viability of approaches and incentivisation of risk reduction measures. 14

15 6. References MCII 2015a: Statement on Success Criteria for G7 InsuResilience by the Munich Climate Insurance Initiative (MCII). Available at: 21/ _MCII_Statement_on_Success_Factors_for_G7_InsuResilience.pdf. MCII (Warner, Koko/Schäfer, Laura) 2015b: Climate risk insurance for the poor. Success factors and enabling conditions for InsuResilience the Initiative on Climate Risk Insurance. Findings from MCII expert interviews. Available at: 21/G7_InsuResilience_MCII_Factsheet_SuccessFactors EnablingConditions.pdf. MCII (Yuzva, Kristina/ Zissener, Michael/ Warner, Koko) 2014: Countries addressing climate change using innovative insurance solutions. Countries addressing climate change using innovative insurance solutions. How to integrate climate risk insurance into a comprehensive climate risk management approach in different country contexts. Available at: AddressingClimateChangeUsingInsurance.pdf. MCII 2013a: For Individuals: The LPP. Factsheet. Available at: MCII 2013b: For Financial Institutions: The LPC. Available at: 15

Climate Risk. Insurance in the Caribbean. Making Weather Index Microinsurance Work for Vulnerable Individuals Latin American Workshop on

Climate Risk Adaptation and Insurance in the Caribbean Making Weather Index Microinsurance Work for Vulnerable Individuals Microinsurance Sobiah Becker September 29, 2013 Guadalajara Getting to Know Our

Climate Risk Adaptation and Insurance in the Caribbean Making Weather Index Microinsurance Work for Vulnerable Individuals Microinsurance Sobiah Becker September 29, 2013 Guadalajara Getting to Know Our

Climate Risk Adaptation and Insurance in the Caribbean

Climate Risk Adaptation and Insurance in the Caribbean Making Weather-Index Microinsurance Work for Vulnerable Individuals Sobiah Becker Background Munich Climate Insurance Initiative Initiated in 2005

Climate Risk Adaptation and Insurance in the Caribbean Making Weather-Index Microinsurance Work for Vulnerable Individuals Sobiah Becker Background Munich Climate Insurance Initiative Initiated in 2005

Weathering Climate Change through Climate Risk Transfer Solutions

The G20's role on climate risk insurance & pooling: Weathering Climate Change through Climate Risk Transfer Solutions With this document, the Munich Climate Insurance Initiative (MCII) provides suggestions

The G20's role on climate risk insurance & pooling: Weathering Climate Change through Climate Risk Transfer Solutions With this document, the Munich Climate Insurance Initiative (MCII) provides suggestions

THE CLIMATE RISK INSURANCE INITIATIVE

THE CLIMATE RISK INSURANCE INITIATIVE InsuResilience at a glance The InsuResilience Climate Risk Insurance Initiative was adopted by the G7 partner countries Germany, France, Italy, Japan, Canada, the

THE CLIMATE RISK INSURANCE INITIATIVE InsuResilience at a glance The InsuResilience Climate Risk Insurance Initiative was adopted by the G7 partner countries Germany, France, Italy, Japan, Canada, the

How insurance can support climate resilience

Accepted manuscript - 1 Embargoed till 24 March at 9am GMT (10:00 CET) How insurance can support climate resilience Swenja Surminski (Grantham Research Institute on Climate Change and the Environment at

Accepted manuscript - 1 Embargoed till 24 March at 9am GMT (10:00 CET) How insurance can support climate resilience Swenja Surminski (Grantham Research Institute on Climate Change and the Environment at

Ex Ante Financing for Disaster Risk Management and Adaptation

Ex Ante Financing for Disaster Risk Management and Adaptation A Public Policy Perspective Dr. Jerry Skees H.B. Price Professor, University of Kentucky, and President, GlobalAgRisk, Inc. Piura, Peru November

Ex Ante Financing for Disaster Risk Management and Adaptation A Public Policy Perspective Dr. Jerry Skees H.B. Price Professor, University of Kentucky, and President, GlobalAgRisk, Inc. Piura, Peru November

Developing a Disaster Insurance Framework for Pakistan

Developing a Disaster Insurance Framework for Pakistan Fund Design Options RECURRING NATURAL HAZARDS ERODE RESILIENCE A NATIONAL DISASTER INSURANCE FUND TO SUPPORT VULNERABLE LOW-INCOME PEOPLE The people

Developing a Disaster Insurance Framework for Pakistan Fund Design Options RECURRING NATURAL HAZARDS ERODE RESILIENCE A NATIONAL DISASTER INSURANCE FUND TO SUPPORT VULNERABLE LOW-INCOME PEOPLE The people

FINAL CONSULTATION DOCUMENT May CONCEPT NOTE Shaping the InsuResilience Global Partnership

FINAL CONSULTATION DOCUMENT May 2018 CONCEPT NOTE Shaping the InsuResilience Global Partnership 1 Contents Executive Summary... 3 1. The case for the InsuResilience Global Partnership... 5 2. Vision and

FINAL CONSULTATION DOCUMENT May 2018 CONCEPT NOTE Shaping the InsuResilience Global Partnership 1 Contents Executive Summary... 3 1. The case for the InsuResilience Global Partnership... 5 2. Vision and

International Agricultural and Natural Catastrophe Insurance Forum. Experience by GIZ Matthias Range

International Agricultural and Natural Catastrophe Insurance Forum Experience by GIZ Rüschlikon, Switzerland, October 2016 Seite 1 Agenda GIZ GIZ and Financial Systems Development GIZ and Agricultural

International Agricultural and Natural Catastrophe Insurance Forum Experience by GIZ Rüschlikon, Switzerland, October 2016 Seite 1 Agenda GIZ GIZ and Financial Systems Development GIZ and Agricultural

TERMINOLOGY. What is Climate risk insurance? What is Disaster risk insurance?

TERMINOLOGY What is Climate risk insurance? Climate risk insurance describes a suite of instruments for financial risk transfer that provides protection against risks arising from extreme weather events

TERMINOLOGY What is Climate risk insurance? Climate risk insurance describes a suite of instruments for financial risk transfer that provides protection against risks arising from extreme weather events

SECTOR ASSESSMENT (SUMMARY): FINANCE (DISASTER RISK MANAGEMENT) 1. Sector Performance, Problems, and Opportunities

: FINANCE (DISASTER RISK MANAGEMENT) 1. Sector Performance, Problems, and Opportunities") National Disaster Risk Management Fund (RRP PAK 50316) SECTOR ASSESSMENT (SUMMARY): FINANCE (DISASTER RISK MANAGEMENT) A. Sector Road Map 1. Sector Performance, Problems, and Opportunities a. Performance

National Disaster Risk Management Fund (RRP PAK 50316) SECTOR ASSESSMENT (SUMMARY): FINANCE (DISASTER RISK MANAGEMENT) A. Sector Road Map 1. Sector Performance, Problems, and Opportunities a. Performance

SCF Forum, 5+6 September 2016, Manila. The odds and beauties of risk transfer schemes

SCF Forum, 5+6 September 2016, Manila The odds and beauties of risk transfer schemes MCII: What Do We Do? 1. Support policy making processes: UNFCCC, Sendai Framework, SDGs, IPCC, etc. 2. Research efficient

SCF Forum, 5+6 September 2016, Manila The odds and beauties of risk transfer schemes MCII: What Do We Do? 1. Support policy making processes: UNFCCC, Sendai Framework, SDGs, IPCC, etc. 2. Research efficient

DEFINING THE PROTECTION GAP. 1: Decide who /what should be protected:

DEFINING THE PROTECTION GAP Introduction In recent years, we ve seen a considerable increase in disasters, both in their frequency and severity. Overall economic losses from such disasters currently average

DEFINING THE PROTECTION GAP Introduction In recent years, we ve seen a considerable increase in disasters, both in their frequency and severity. Overall economic losses from such disasters currently average

Sendai Cooperation Initiative for Disaster Risk Reduction

Sendai Cooperation Initiative for Disaster Risk Reduction March 14, 2015 Disasters are a threat to which human being has long been exposed. A disaster deprives people of their lives instantly and afflicts

Sendai Cooperation Initiative for Disaster Risk Reduction March 14, 2015 Disasters are a threat to which human being has long been exposed. A disaster deprives people of their lives instantly and afflicts

Norway 11. November 2013

Institutional arrangements under the UNFCCC for approaches to address loss and damage associated with climate change impacts in developing countries that are particularly vulnerable to the adverse effects

Institutional arrangements under the UNFCCC for approaches to address loss and damage associated with climate change impacts in developing countries that are particularly vulnerable to the adverse effects

shocks do not have long-lasting adverse development consequences (Food Security Information Network)

") Submission by the World Food Programme to the Executive Committee of the Warsaw International Mechanism for Loss and Damage on best practices, challenges and lessons learned from existing financial instruments

Submission by the World Food Programme to the Executive Committee of the Warsaw International Mechanism for Loss and Damage on best practices, challenges and lessons learned from existing financial instruments

Munich Climate Insurance Initiative (MCII)

") Bonn, 11.29.2017 Munich Climate Insurance Initiative (MCII) Webinar: Climate Risk Insurance and Relevance to RegionsAdapt Kehinde Balogun balogun@ehs.unu.edu OUTLINE Who we are? Team members General overview

Bonn, 11.29.2017 Munich Climate Insurance Initiative (MCII) Webinar: Climate Risk Insurance and Relevance to RegionsAdapt Kehinde Balogun balogun@ehs.unu.edu OUTLINE Who we are? Team members General overview

DISASTER RISK FINANCING ADB Operational Innovations in South Asia

DISASTER RISK FINANCING ADB Operational Innovations in South Asia Erik Kjaergaard, Disaster Risk Management Specialist South Asia Department with input from Mayumi Ozaki, Senior Portfolio Management Specialist

DISASTER RISK FINANCING ADB Operational Innovations in South Asia Erik Kjaergaard, Disaster Risk Management Specialist South Asia Department with input from Mayumi Ozaki, Senior Portfolio Management Specialist

RESILIENCE Provisional copy

RESILIENCE Promoting Disaster and Climate Risk Resilience Through Regional Programmatic and Risk Financing Mechanisms Action Statement and Action Plan Provisional copy Overview and Context Climate change

RESILIENCE Promoting Disaster and Climate Risk Resilience Through Regional Programmatic and Risk Financing Mechanisms Action Statement and Action Plan Provisional copy Overview and Context Climate change

Business for Resilience

Business for Resilience ARISE is the private sector initiative of the UN Office for Disaster Risk Reduction (UNISDR). Its main role is to mobilize business in support of the goals of the 2015 Sendai Framework.

Business for Resilience ARISE is the private sector initiative of the UN Office for Disaster Risk Reduction (UNISDR). Its main role is to mobilize business in support of the goals of the 2015 Sendai Framework.

RUTH VARGAS HILL MAY 2012 INTRODUCTION

COST BENEFIT ANALYSIS OF THE AFRICAN RISK CAPACITY FACILITY: ETHIOPIA COUNTRY CASE STUDY RUTH VARGAS HILL MAY 2012 INTRODUCTION The biggest source of risk to household welfare in rural areas of Ethiopia

COST BENEFIT ANALYSIS OF THE AFRICAN RISK CAPACITY FACILITY: ETHIOPIA COUNTRY CASE STUDY RUTH VARGAS HILL MAY 2012 INTRODUCTION The biggest source of risk to household welfare in rural areas of Ethiopia

Francesco Rispoli, IFAD, Italy

Scaling up insurance as a disaster resilience strategy for smallholder farmers in Latin America 11 th Consultative Forum on microinsurance regulation for insurance supervisory authorities, insurance practitioners

Scaling up insurance as a disaster resilience strategy for smallholder farmers in Latin America 11 th Consultative Forum on microinsurance regulation for insurance supervisory authorities, insurance practitioners

CDEMA Symposium to Commemorate the 10th Anniversary of Hurricane Ivan Exploring Response and Recovery, Embracing Resilience

CDEMA Symposium to Commemorate the 10th Anniversary of Hurricane Ivan Exploring Response and Recovery, Embracing Resilience Radisson Grenada Beach Resort, Grand Anse, Grenada 1st 3rd December, 2014 CCRIF

CDEMA Symposium to Commemorate the 10th Anniversary of Hurricane Ivan Exploring Response and Recovery, Embracing Resilience Radisson Grenada Beach Resort, Grand Anse, Grenada 1st 3rd December, 2014 CCRIF

RISK TRANSFER AND FINANCE EXPERIENCE IN THE CARIBBEAN. Orville Grey March 2016

RISK TRANSFER AND FINANCE EXPERIENCE IN THE CARIBBEAN Orville Grey March 2016 WHO WE ARE? WHER E WE ARE? WEATHER-RELATED LOSS & DAMAGE RISING Caribbean is vulnerable to weather related hazards e.g. drought,

RISK TRANSFER AND FINANCE EXPERIENCE IN THE CARIBBEAN Orville Grey March 2016 WHO WE ARE? WHER E WE ARE? WEATHER-RELATED LOSS & DAMAGE RISING Caribbean is vulnerable to weather related hazards e.g. drought,

REPUBLIC OF BULGARIA

REPUBLIC OF BULGARIA DISASTER RISK REDUCTION STRATEGY INTRUDUCTION Republic of Bulgaria often has been affected by natural or man-made disasters, whose social and economic consequences cause significant

REPUBLIC OF BULGARIA DISASTER RISK REDUCTION STRATEGY INTRUDUCTION Republic of Bulgaria often has been affected by natural or man-made disasters, whose social and economic consequences cause significant

Adaptation for developing countries in a post-2012 UN Climate Regime

November 2009 WWF Global Climate Policy Position Paper Sandeep Chamling Rai WWF International Adaptation Policy Coordinator Mobile : +65 9829 1890 scrai@wwf.sg Adaptation for developing countries in a

November 2009 WWF Global Climate Policy Position Paper Sandeep Chamling Rai WWF International Adaptation Policy Coordinator Mobile : +65 9829 1890 scrai@wwf.sg Adaptation for developing countries in a

Developing Catastrophe and Weather Risk Markets in Southeast Europe: From Concept to Reality

Developing Catastrophe and Weather Risk Markets in Southeast Europe: From Concept to Reality First Regional Europa Re Insurance Conference October 2011 Aleksandra Nakeva Ruzin, MPPM Executive Director

Developing Catastrophe and Weather Risk Markets in Southeast Europe: From Concept to Reality First Regional Europa Re Insurance Conference October 2011 Aleksandra Nakeva Ruzin, MPPM Executive Director

Weathering the Risks: Scalable Weather Index Insurance in East Africa

Weathering the Risks: Scalable Weather Index Insurance in East Africa Having enough food in East Africa depends largely on the productivity of smallholder farms, which in turn depends on farmers ability

Weathering the Risks: Scalable Weather Index Insurance in East Africa Having enough food in East Africa depends largely on the productivity of smallholder farms, which in turn depends on farmers ability

Policy Implementation for Enhancing Community. Resilience in Malawi

Volume 10 Issue 1 May 2014 Status of Policy Implementation for Enhancing Community Resilience in Malawi Policy Brief ECRP and DISCOVER Disclaimer This policy brief has been financed by United Kingdom (UK)

Volume 10 Issue 1 May 2014 Status of Policy Implementation for Enhancing Community Resilience in Malawi Policy Brief ECRP and DISCOVER Disclaimer This policy brief has been financed by United Kingdom (UK)

Overview of PADR process

SECTION 3 Overview of PADR process PADR is a methodology for use at community level. It involves active engagement, with the community, in a process to explore the risks they face and the factors contributing

SECTION 3 Overview of PADR process PADR is a methodology for use at community level. It involves active engagement, with the community, in a process to explore the risks they face and the factors contributing

Summary report on and recommendations of the 2016 forum of the Standing Committee on Finance

Annex III Summary report on and recommendations of the 2016 forum of the Standing Committee on Finance [English only] A. Summary report on the 2016 forum of the Standing Committee on Finance on financial

Annex III Summary report on and recommendations of the 2016 forum of the Standing Committee on Finance [English only] A. Summary report on the 2016 forum of the Standing Committee on Finance on financial

Submission by State of Palestine. Thursday, January 11, To: UNFCCC / WIMLD_CCI

Submission by State of Palestine Thursday, January 11, 2018 To: UNFCCC / WIMLD_CCI Type and Nature of Actions to address Loss & Damage for which finance is required Dead line for submission 15 February

Submission by State of Palestine Thursday, January 11, 2018 To: UNFCCC / WIMLD_CCI Type and Nature of Actions to address Loss & Damage for which finance is required Dead line for submission 15 February

An Operational Framework for Disaster Risk Financing and Insurance

Financial Protection Against Natural Disasters An Operational Framework for Disaster Risk Financing and Insurance This part seeks to tie together the experience and collected knowledge from partners in

Financial Protection Against Natural Disasters An Operational Framework for Disaster Risk Financing and Insurance This part seeks to tie together the experience and collected knowledge from partners in

Disaster Management The

Disaster Management The UKRAINIAN Agricultural AGRICULTURAL Dimension WEATHER Global Facility for RISK Disaster MANAGEMENT Recovery and Reduction Seminar Series February 20, 2007 WORLD BANK COMMODITY RISK

Disaster Management The UKRAINIAN Agricultural AGRICULTURAL Dimension WEATHER Global Facility for RISK Disaster MANAGEMENT Recovery and Reduction Seminar Series February 20, 2007 WORLD BANK COMMODITY RISK

TRAINING CATALOGUE ON IMPACT INSURANCE Building practitioner skills in providing valuable and viable insurance products

TRAINING CATALOGUE ON IMPACT INSURANCE Building practitioner skills in providing valuable and viable insurance products 2017 Contents of the training catalogue The ILO s Impact Insurance Facility... 3

TRAINING CATALOGUE ON IMPACT INSURANCE Building practitioner skills in providing valuable and viable insurance products 2017 Contents of the training catalogue The ILO s Impact Insurance Facility... 3

Insuring Climate Change-related Risks

Insuring Climate Change-related Risks 19 February 2016 Austrian Climate Change Workshop Day 2 Tobias Grimm Senior Project Manager Corporate Climate Centre Climate & Renewables Munich Re some facts About

Insuring Climate Change-related Risks 19 February 2016 Austrian Climate Change Workshop Day 2 Tobias Grimm Senior Project Manager Corporate Climate Centre Climate & Renewables Munich Re some facts About

From managing crises to managing risks: The African Risk Capacity (ARC)

") Page 1 of 7 Home > Topics > Risk Dialogue Magazine > Strengthening food security > From managing crises to managing risks: The African Risk Capacity (ARC) From managing crises to managing risks: The African

Page 1 of 7 Home > Topics > Risk Dialogue Magazine > Strengthening food security > From managing crises to managing risks: The African Risk Capacity (ARC) From managing crises to managing risks: The African

TOPICS FOR DEBATE. By Haresh Bhojwani, Molly Hellmuth, Daniel Osgood, Anne Moorehead, James Hansen

TOPICS FOR DEBATE By Haresh Bhojwani, Molly Hellmuth, Daniel Osgood, Anne Moorehead, James Hansen This paper is a policy distillation adapted from IRI Technical Report 07-03 Working Paper - Poverty Traps

TOPICS FOR DEBATE By Haresh Bhojwani, Molly Hellmuth, Daniel Osgood, Anne Moorehead, James Hansen This paper is a policy distillation adapted from IRI Technical Report 07-03 Working Paper - Poverty Traps

SOVEREIGN CATASTROPHE RISK POOLS A Brief for Policy Makers 1

SOVEREIGN CATASTROPHE RISK POOLS A Brief for Policy Makers 1 More than 1 billion people have lifted themselves out of poverty in the past 15 years, but climate and disaster risks threaten these achievements.

SOVEREIGN CATASTROPHE RISK POOLS A Brief for Policy Makers 1 More than 1 billion people have lifted themselves out of poverty in the past 15 years, but climate and disaster risks threaten these achievements.

Approaches to Address Loss and Damage for Climate Change Impacts: Lessons from Bangladesh. Photo Habib Torikul

Approaches to Address Loss and Damage for Climate Change Impacts: Lessons from Bangladesh Photo Habib Torikul Photo Habib Torikul Background Bangladesh is one of the most climate-vulnerable countries in

Approaches to Address Loss and Damage for Climate Change Impacts: Lessons from Bangladesh Photo Habib Torikul Photo Habib Torikul Background Bangladesh is one of the most climate-vulnerable countries in

Climate Insurance Fund (CIF) Luxembourg, June 2017

Luxembourg, June 2017") Climate Insurance Fund (CIF) Luxembourg, June 2017 KfW Development Bank s Role in Insurance Our Mandate As the German development bank, our objectives is help our partners to fight poverty, maintain peace,

Climate Insurance Fund (CIF) Luxembourg, June 2017 KfW Development Bank s Role in Insurance Our Mandate As the German development bank, our objectives is help our partners to fight poverty, maintain peace,

InsuResilience Solutions Fund (ISF) Transforming concepts into products

Transforming concepts into products") InsuResilience Solutions Fund (ISF) Transforming concepts into products The need for climate risk insurance solutions Increasing risks of natural disasters Increasing intensity and frequency of extreme

InsuResilience Solutions Fund (ISF) Transforming concepts into products The need for climate risk insurance solutions Increasing risks of natural disasters Increasing intensity and frequency of extreme

Insurance Instruments for Adapting to Climate Risks A proposal for the Bali Action Plan 1, Version 1.0

SUBMISSION BY THE MUNICH CLIMATE INSURANCE INITIATIVE (MCII) 18 August 2008 Insurance Instruments for Adapting to Climate Risks A proposal for the Bali Action Plan 1, Version 1.0 3rd session of the Ad

SUBMISSION BY THE MUNICH CLIMATE INSURANCE INITIATIVE (MCII) 18 August 2008 Insurance Instruments for Adapting to Climate Risks A proposal for the Bali Action Plan 1, Version 1.0 3rd session of the Ad

Southeast Asia Disaster Risk Insurance Facility

Southeast Asia Disaster Risk Insurance Facility PROTECT THE GREATEST HOME OF ALL: OUR COUNTRIES SEADRIF is a regional platform to provide ASEAN countries with financial solutions and technical advice to

Southeast Asia Disaster Risk Insurance Facility PROTECT THE GREATEST HOME OF ALL: OUR COUNTRIES SEADRIF is a regional platform to provide ASEAN countries with financial solutions and technical advice to

Managing Risk for Development

WDR 2014 Managing Risk for Development Norman Loayza Berlin Workshop December 2012 Context and Objective 2 The topic is timely! Why a WDR on Risk? Ongoing global food / fuel crisis Global financial crisis

WDR 2014 Managing Risk for Development Norman Loayza Berlin Workshop December 2012 Context and Objective 2 The topic is timely! Why a WDR on Risk? Ongoing global food / fuel crisis Global financial crisis

Addressing Loss and Damage with Microinsurance

Addressing Loss and Damage with Microinsurance Kees van der Geest, Michael Zissener & Koko Warner 2014 To be cited as: Van der Geest, K., Zissener, M. & Warner, K. (2014). Addressing Loss and Damage with

Addressing Loss and Damage with Microinsurance Kees van der Geest, Michael Zissener & Koko Warner 2014 To be cited as: Van der Geest, K., Zissener, M. & Warner, K. (2014). Addressing Loss and Damage with

PROGRAM INFORMATION DOCUMENT (PID) CONCEPT STAGE Report No.: Second Disaster Risk Management Development Policy Loan with a CAT-DDO Region

CONCEPT STAGE Report No.: Second Disaster Risk Management Development Policy Loan with a CAT-DDO Region") Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized PROGRAM INFORMATION DOCUMENT (PID) CONCEPT STAGE Report No.: Operation Name Second Disaster

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized PROGRAM INFORMATION DOCUMENT (PID) CONCEPT STAGE Report No.: Operation Name Second Disaster

Austrian Climate Change Workshop Summary Report The Way forward on Climate and Sustainable Finance

Austrian Climate Change Workshop 2018 - Summary Report The Way forward on Climate and Sustainable Finance In close cooperation with the Austrian Federal Ministry of Sustainability and Tourism, Kommunalkredit

Austrian Climate Change Workshop 2018 - Summary Report The Way forward on Climate and Sustainable Finance In close cooperation with the Austrian Federal Ministry of Sustainability and Tourism, Kommunalkredit

Catastrophe Risk Pooling Mechanism: CCRIF

Catastrophe Risk Pooling Mechanism: CCRIF Simon Young CEO, Caribbean Risk Managers Ltd Facility Supervisor, CCRIF Seminar on Disaster Risk Financing Mechanisms for the Mexican States Mexico City, 1 December

Catastrophe Risk Pooling Mechanism: CCRIF Simon Young CEO, Caribbean Risk Managers Ltd Facility Supervisor, CCRIF Seminar on Disaster Risk Financing Mechanisms for the Mexican States Mexico City, 1 December

Introduction to risk sharing and risk transfer with examples from Mongolia and Peru

Introduction to risk sharing and risk transfer with examples from Mongolia and Peru Dr. Jerry Skees H.B. Price Professor, University of Kentucky, and President, GlobalAgRisk, Inc. UNFCCC Workshop Lima,

Introduction to risk sharing and risk transfer with examples from Mongolia and Peru Dr. Jerry Skees H.B. Price Professor, University of Kentucky, and President, GlobalAgRisk, Inc. UNFCCC Workshop Lima,

Planning, Budgeting and Financing

English Version Planning, Budgeting and Financing Post-Disaster Recovery and Reconstruction Activities in Khammouane Province, Lao PDR Developed under the Khammouane Development Project (KDP), Implemented

English Version Planning, Budgeting and Financing Post-Disaster Recovery and Reconstruction Activities in Khammouane Province, Lao PDR Developed under the Khammouane Development Project (KDP), Implemented

CARIBBEAN DEVELOPMENT BANK SUPPORT FOR HAITI TO MEET COMMITMENT TO CARIBBEAN CATASTROPHE RISK INSURANCE FACILITY FOR THE HURRICANE SEASON

PUBLIC DISCLOSURE AUTHORISED CARIBBEAN DEVELOPMENT BANK SUPPORT FOR HAITI TO MEET COMMITMENT TO CARIBBEAN CATASTROPHE RISK INSURANCE FACILITY FOR THE 2017-2018 HURRICANE SEASON This Document is being made

PUBLIC DISCLOSURE AUTHORISED CARIBBEAN DEVELOPMENT BANK SUPPORT FOR HAITI TO MEET COMMITMENT TO CARIBBEAN CATASTROPHE RISK INSURANCE FACILITY FOR THE 2017-2018 HURRICANE SEASON This Document is being made

PROTECTED AGAINST CLIMATE DAMAGE?

Policy Brief PROTECTED AGAINST CLIMATE DAMAGE? 1 PROTECTED AGAINST CLIMATE DAMAGE? THE OPPORTUNITIES AND LIMITATIONS OF CLIMATE RISK INSUR- ANCE FOR THE PROTECTION OF VULNERABLE POPULATIONS In autumn 2015,

Policy Brief PROTECTED AGAINST CLIMATE DAMAGE? 1 PROTECTED AGAINST CLIMATE DAMAGE? THE OPPORTUNITIES AND LIMITATIONS OF CLIMATE RISK INSUR- ANCE FOR THE PROTECTION OF VULNERABLE POPULATIONS In autumn 2015,

Standing Committee on Finance

Standing Committee on Finance SCF/2016/14/4 3 5 October 2016 Fourteenth meeting of the Standing Committee on Finance Bonn, Germany, 3 5 October 2016 Background paper on the 2016 SCF forum Proposed actions

Standing Committee on Finance SCF/2016/14/4 3 5 October 2016 Fourteenth meeting of the Standing Committee on Finance Bonn, Germany, 3 5 October 2016 Background paper on the 2016 SCF forum Proposed actions

Linking Social Protection with Disaster Risk Management (DRM) & Climate Change Adaptation (CCA)

& Climate Change Adaptation (CCA)") Protecting Children from Poverty and Disasters in East Asia and the Pacific. A Symposium on Linkages between Social Protection and Disaster Risk. 22-23 May 2014 in Bangkok, Thailand Linking Social Protection

Protecting Children from Poverty and Disasters in East Asia and the Pacific. A Symposium on Linkages between Social Protection and Disaster Risk. 22-23 May 2014 in Bangkok, Thailand Linking Social Protection

African Risk Capacity. Sovereign Disaster Risk Solutions A Project of the African Union

African Risk Capacity Sovereign Disaster Risk Solutions A Project of the African Union The Way Disaster Assistance Works Now EVENT ASSESS APPEAL FUNDING RESPONSE CNN EFFECT time The Way Disaster Assistance

African Risk Capacity Sovereign Disaster Risk Solutions A Project of the African Union The Way Disaster Assistance Works Now EVENT ASSESS APPEAL FUNDING RESPONSE CNN EFFECT time The Way Disaster Assistance

Catastrophe Risk Financing Instruments. Abhas K. Jha Regional Coordinator, Disaster Risk Management East Asia and the Pacific

Catastrophe Risk Financing Instruments Abhas K. Jha Regional Coordinator, Disaster Risk Management East Asia and the Pacific Structure of Presentation Impact of Disasters in developing Countries The Need

Catastrophe Risk Financing Instruments Abhas K. Jha Regional Coordinator, Disaster Risk Management East Asia and the Pacific Structure of Presentation Impact of Disasters in developing Countries The Need

MCII CLIMATE INSURANCE INITIATIVE MUNICH PUBLICATION SERIES

MUNICH CLIMATE INSURANCE INITIATIVE UNU-EHS PUBLICATION SERIES MCII BY KOKO WARNER, SÖNKE KREFT, MICHAEL ZISSENER, PETER HÖPPE, CHRISTOPH BALS, THOMAS LOSTER, JOANNE LINNEROOTH-BAYER, SILVIO TSCHUDI, EUGENE

MUNICH CLIMATE INSURANCE INITIATIVE UNU-EHS PUBLICATION SERIES MCII BY KOKO WARNER, SÖNKE KREFT, MICHAEL ZISSENER, PETER HÖPPE, CHRISTOPH BALS, THOMAS LOSTER, JOANNE LINNEROOTH-BAYER, SILVIO TSCHUDI, EUGENE

Sri Lanka: Preliminary Damage and Needs Assessment Page 25 of 29

Sri Lanka: Preliminary Damage and Needs Assessment Page 25 of 29 F. IMMEDIATE AND MEDIUM TERM RECOVERY STRATEGY Implementation Approach 75. One of the main challenges of developing a comprehensive, as

Sri Lanka: Preliminary Damage and Needs Assessment Page 25 of 29 F. IMMEDIATE AND MEDIUM TERM RECOVERY STRATEGY Implementation Approach 75. One of the main challenges of developing a comprehensive, as

DISASTER RISK FINANCING AND INSURANCE PROGRAM

DISASTER RISK FINANCING AND INSURANCE PROGRAM Strengthening Financial Resilience to Disasters What We Do DRFIP helps developing countries manage the cost of disaster and climate shocks. The initiative

DISASTER RISK FINANCING AND INSURANCE PROGRAM Strengthening Financial Resilience to Disasters What We Do DRFIP helps developing countries manage the cost of disaster and climate shocks. The initiative

Disaster risk management for climate change adaptation: Experiences from German development cooperation

Disaster risk management for climate change adaptation: Experiences from German development cooperation Britta Heine 1, Jens Etter 2 1 Deutsche Gesellschaft für Technische Zusammenarbeit (GTZ) GmbH, Postfach

Disaster risk management for climate change adaptation: Experiences from German development cooperation Britta Heine 1, Jens Etter 2 1 Deutsche Gesellschaft für Technische Zusammenarbeit (GTZ) GmbH, Postfach

Decision 3/CP.17. Launching the Green Climate Fund

Decision 3/CP.17 Launching the Green Climate Fund The Conference of the Parties, Recalling decision 1/CP.16, 1. Welcomes the report of the Transitional Committee (FCCC/CP/2011/6 and Add.1), taking note

Decision 3/CP.17 Launching the Green Climate Fund The Conference of the Parties, Recalling decision 1/CP.16, 1. Welcomes the report of the Transitional Committee (FCCC/CP/2011/6 and Add.1), taking note

Introduction to Disaster Management

Introduction to Disaster Management Definitions Adopted By Few Important Agencies WHO; A disaster is an occurrence disrupting the normal conditions of existence and causing a level of suffering that exceeds

Introduction to Disaster Management Definitions Adopted By Few Important Agencies WHO; A disaster is an occurrence disrupting the normal conditions of existence and causing a level of suffering that exceeds

African Risk Capacity Strategic Framework December

African Risk Capacity Strategic Framework 2016-2020 December 2016 www.africanriskcapacity.org Contents Definitions... 3 Overview of the Strategic Framework... 5 The Strategic Framework in Context... 5

African Risk Capacity Strategic Framework 2016-2020 December 2016 www.africanriskcapacity.org Contents Definitions... 3 Overview of the Strategic Framework... 5 The Strategic Framework in Context... 5

UNEP FI Adaption How Insurance can serve the poor. Thomas Loster

UNEP FI Adaption How Insurance can serve the poor Thomas Loster November 2006 The Munich Re Foundation Focus humans at risk Water: Resource and risk factor Population development Environmental and climate

UNEP FI Adaption How Insurance can serve the poor Thomas Loster November 2006 The Munich Re Foundation Focus humans at risk Water: Resource and risk factor Population development Environmental and climate

Resilience and the Economics of Risk. NACo s Resilient Counties Advisory Board February 2016

Resilience and the Economics of Risk NACo s Resilient Counties Advisory Board February 2016 The growing burden of uninsured losses Natural catastrophe losses 1970 2014 (in 2014 USD) 450 400 350 300 Uninsured

Resilience and the Economics of Risk NACo s Resilient Counties Advisory Board February 2016 The growing burden of uninsured losses Natural catastrophe losses 1970 2014 (in 2014 USD) 450 400 350 300 Uninsured

Regional Conference on Risk Transfer and Micro-Insurance for Resilience Building in the IGAD region

Background Concept Note Regional Conference on Risk Transfer and Micro-Insurance for Resilience Building in the IGAD region Kampala, Uganda September 2-3, 2016 With the increasing number of disasters over

Background Concept Note Regional Conference on Risk Transfer and Micro-Insurance for Resilience Building in the IGAD region Kampala, Uganda September 2-3, 2016 With the increasing number of disasters over

ANNEX 9 Terms of reference for a Climate Risk Assessment

126 ANNEX 9 Terms of reference for a Climate Risk Assessment These model ToR need to be adapted according to the specific project and its context. To respond to a variety of circumstances, this model includes

126 ANNEX 9 Terms of reference for a Climate Risk Assessment These model ToR need to be adapted according to the specific project and its context. To respond to a variety of circumstances, this model includes

Bone Bolango, Indonesia

Bone Bolango, Indonesia Local progress report on the implementation of the 10 Essentials for Making Cities Resilient (2013-2014) Name of focal point: Yusniar Nurdin Organization: BNPB Title/Position: Technical

Bone Bolango, Indonesia Local progress report on the implementation of the 10 Essentials for Making Cities Resilient (2013-2014) Name of focal point: Yusniar Nurdin Organization: BNPB Title/Position: Technical

Agricultural Insurance and Regulatory Implications

Report of the 4th A2ii IAIS Consultation Call Agricultural Insurance and Regulatory Implications 26 June 2014 Governments are increasingly recognizing the relevance of insurance for farmers and rural dwellers

Report of the 4th A2ii IAIS Consultation Call Agricultural Insurance and Regulatory Implications 26 June 2014 Governments are increasingly recognizing the relevance of insurance for farmers and rural dwellers

Andrew Goodland RISK MANAGEMENT: THE CASE OF THE LIVESTOCK SECTOR IN MONGOLIA

Andrew Goodland RISK MANAGEMENT: THE CASE OF THE LIVESTOCK SECTOR IN MONGOLIA Outline 1. Brief context nature of risk in Mongolia 2. Conceptual framework for understanding and addressing risk in the agricultural

Andrew Goodland RISK MANAGEMENT: THE CASE OF THE LIVESTOCK SECTOR IN MONGOLIA Outline 1. Brief context nature of risk in Mongolia 2. Conceptual framework for understanding and addressing risk in the agricultural

CHAPTER 1 AGRICULTURAL RISKS AND RISK MANAGEMENT 1

CHAPTER 1 AGRICULTURAL RISKS AND RISK MANAGEMENT 1 Chapter 1: AGRICULTURAL RISKS AND RISK MANAGEMENT Risk and uncertainty are ubiquitous and varied within agriculture and agricultural supply chains. This

CHAPTER 1 AGRICULTURAL RISKS AND RISK MANAGEMENT 1 Chapter 1: AGRICULTURAL RISKS AND RISK MANAGEMENT Risk and uncertainty are ubiquitous and varied within agriculture and agricultural supply chains. This

UN-OHRLLS COUNTRY-LEVEL PREPARATIONS

UN-OHRLLS COMPREHENSIVE HIGH-LEVEL MIDTERM REVIEW OF THE IMPLEMENTATION OF THE ISTANBUL PROGRAMME OF ACTION FOR THE LDCS FOR THE DECADE 2011-2020 COUNTRY-LEVEL PREPARATIONS ANNOTATED OUTLINE FOR THE NATIONAL

UN-OHRLLS COMPREHENSIVE HIGH-LEVEL MIDTERM REVIEW OF THE IMPLEMENTATION OF THE ISTANBUL PROGRAMME OF ACTION FOR THE LDCS FOR THE DECADE 2011-2020 COUNTRY-LEVEL PREPARATIONS ANNOTATED OUTLINE FOR THE NATIONAL

Executive Board Annual Session Rome, May 2015 POLICY ISSUES ENTERPRISE RISK For approval MANAGEMENT POLICY WFP/EB.A/2015/5-B

Executive Board Annual Session Rome, 25 28 May 2015 POLICY ISSUES Agenda item 5 For approval ENTERPRISE RISK MANAGEMENT POLICY E Distribution: GENERAL WFP/EB.A/2015/5-B 10 April 2015 ORIGINAL: ENGLISH

Executive Board Annual Session Rome, 25 28 May 2015 POLICY ISSUES Agenda item 5 For approval ENTERPRISE RISK MANAGEMENT POLICY E Distribution: GENERAL WFP/EB.A/2015/5-B 10 April 2015 ORIGINAL: ENGLISH

Managing Natural Disasters

Managing Natural Disasters Lucy Conger With research assistant from Cory Siskind, Inter-American Dialogue Prepared for the Colombian Government for the Sixth Summit of the Americas August 2011 Managing

Managing Natural Disasters Lucy Conger With research assistant from Cory Siskind, Inter-American Dialogue Prepared for the Colombian Government for the Sixth Summit of the Americas August 2011 Managing

African Risk Capacity. Sovereign Disaster Risk Solutions A Project of the African Union

African Risk Capacity Sovereign Disaster Risk Solutions A Project of the African Union The Way Disaster Assistance Works Now EVENT ASSESS APPEAL FUNDING RESPONSE CNN EFFECT time The Way Disaster Assistance

African Risk Capacity Sovereign Disaster Risk Solutions A Project of the African Union The Way Disaster Assistance Works Now EVENT ASSESS APPEAL FUNDING RESPONSE CNN EFFECT time The Way Disaster Assistance

IS DISASTER-RELATED MICROINSURANCE A VIABLE DISASTER RISK REDUCTION STRATEGY?: LEARNING FROM CARIBBEAN SIDS

IS DISASTER-RELATED MICROINSURANCE A VIABLE DISASTER RISK REDUCTION STRATEGY?: LEARNING FROM CARIBBEAN SIDS By Denise D.P. Thompson, PhD John Jay College of Criminal Justice American Society for Public

IS DISASTER-RELATED MICROINSURANCE A VIABLE DISASTER RISK REDUCTION STRATEGY?: LEARNING FROM CARIBBEAN SIDS By Denise D.P. Thompson, PhD John Jay College of Criminal Justice American Society for Public

PUBLIC DISCLOSURE AUTHORISED

PUBLIC DISCLOSURE AUTHORISED CARIBBEAN DEVELOPMENT BANK SUPPORT FOR HAITI TO MEET COMMITMENT TO CARIBBEAN CATASTROPHE RISK INSURANCE FACILITY FOR THE 2013-2014 HURRICANE SEASON This Document is being made

PUBLIC DISCLOSURE AUTHORISED CARIBBEAN DEVELOPMENT BANK SUPPORT FOR HAITI TO MEET COMMITMENT TO CARIBBEAN CATASTROPHE RISK INSURANCE FACILITY FOR THE 2013-2014 HURRICANE SEASON This Document is being made

Drought Financing Facility

Drought Financing Facility AN PL 02 Start Network Drought Financing Facility Executive summary The vision for the Start Network Drought Financing Facility (DFF) is of an NGO-led network of interconnected

Drought Financing Facility AN PL 02 Start Network Drought Financing Facility Executive summary The vision for the Start Network Drought Financing Facility (DFF) is of an NGO-led network of interconnected

Loan Agreements and Human Rights: The Role of Human Rights Impact Assessments

Loan Agreements and Human Rights: The Role of Human Rights Impact Assessments By Noel G Villaroman Monash University Paper presented during the Regional Consultation on the Draft General Guidelines On

Loan Agreements and Human Rights: The Role of Human Rights Impact Assessments By Noel G Villaroman Monash University Paper presented during the Regional Consultation on the Draft General Guidelines On

Financial Products to Promote Climate Change Resilience in Bolivia

Financial Products to Promote Climate Change Resilience in Bolivia Country / Region: Bolivia Project Id: PPCRBO602A Fund Name: PPCR Comment Type Commenter Name Commenter Profile Comment Date Comment 1

Financial Products to Promote Climate Change Resilience in Bolivia Country / Region: Bolivia Project Id: PPCRBO602A Fund Name: PPCR Comment Type Commenter Name Commenter Profile Comment Date Comment 1

WFP Climate Change Policy One Year On an Update on Programmes, Knowledge and Partnerships

WFP Climate Change Policy One Year On an Update on Programmes, Knowledge and Partnerships 14:00-14:10: Welcome (Valerie Guarnieri, Assistant Executive Director) 14:10-14:30: Climate mainstreaming in WFP

WFP Climate Change Policy One Year On an Update on Programmes, Knowledge and Partnerships 14:00-14:10: Welcome (Valerie Guarnieri, Assistant Executive Director) 14:10-14:30: Climate mainstreaming in WFP

PROMOTING ACCESS TO AGRICULTURAL INSURANCE IN DEVELOPING COUNTRIES 1

PROMOTING ACCESS TO AGRICULTURAL INSURANCE IN DEVELOPING COUNTRIES 1 AGRICULTURAL INSURANCE DEVELOPMENT PROGRAM (AIDP) STRATEGY PAPER - 2013-2015 APRIL 15, 2013 INTRODUCTION 1. Many pilot agricultural

PROMOTING ACCESS TO AGRICULTURAL INSURANCE IN DEVELOPING COUNTRIES 1 AGRICULTURAL INSURANCE DEVELOPMENT PROGRAM (AIDP) STRATEGY PAPER - 2013-2015 APRIL 15, 2013 INTRODUCTION 1. Many pilot agricultural

Assets Channel: Adaptive Social Protection Work in Africa

Assets Channel: Adaptive Social Protection Work in Africa Carlo del Ninno Climate Change and Poverty Conference, World Bank February 10, 2015 Chronic Poverty and Vulnerability in Africa Despite Growth,

Assets Channel: Adaptive Social Protection Work in Africa Carlo del Ninno Climate Change and Poverty Conference, World Bank February 10, 2015 Chronic Poverty and Vulnerability in Africa Despite Growth,

FIRST WORKSHOP ON (LTF)

") FIRST WORKSHOP ON LONG TERM FINANCE (LTF) Session II: Understanding the long term finance needs of developing countries Maritim Hotel Godesberger Allee 53175 Bonn, Germany 1 Evolution of discussion on

FIRST WORKSHOP ON LONG TERM FINANCE (LTF) Session II: Understanding the long term finance needs of developing countries Maritim Hotel Godesberger Allee 53175 Bonn, Germany 1 Evolution of discussion on

Building. Resilience. Integrating Climate and Disaster Risk into Development The World Bank Group Experience. Public Disclosure Authorized

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Building Resilience Integrating Climate and Disaster Risk into Development The World

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Building Resilience Integrating Climate and Disaster Risk into Development The World

Hawala cash transfers for food assistance and livelihood protection

Afghanistan Hawala cash transfers for food assistance and livelihood protection EUROPEAN COMMISSION Humanitarian Aid and Civil Protection In response to repeated flooding, ACF implemented a cash-based

Afghanistan Hawala cash transfers for food assistance and livelihood protection EUROPEAN COMMISSION Humanitarian Aid and Civil Protection In response to repeated flooding, ACF implemented a cash-based

Regional NAP Expo Asia Seoul, Republic of Korea September 2017

Nepal s experience in integrating climate change adaptation in national budget Regional NAP Expo Asia Seoul, Republic of Korea 11-12 September 2017 Raju Babu Pudasani, Chief, Sustainable Development and

Nepal s experience in integrating climate change adaptation in national budget Regional NAP Expo Asia Seoul, Republic of Korea 11-12 September 2017 Raju Babu Pudasani, Chief, Sustainable Development and

INVESTING IN DISASTER RESILIENCE: RISK TRANSFER THROUGH FLOOD INSURANCE IN SOUTH ASIA

INVESTING IN DISASTER RESILIENCE: RISK TRANSFER THROUGH FLOOD INSURANCE IN SOUTH ASIA GIRIRAJ AMARNATH International Water Management Institute (IWMI) Photo: World Bank Workshop on Addressing Disaster

INVESTING IN DISASTER RESILIENCE: RISK TRANSFER THROUGH FLOOD INSURANCE IN SOUTH ASIA GIRIRAJ AMARNATH International Water Management Institute (IWMI) Photo: World Bank Workshop on Addressing Disaster

OVERVIEW. Linking disaster risk reduction and climate change adaptation. Disaster reduction - trends Trends in economic impact of disasters

Linking disaster risk reduction and climate change adaptation Inter-Agency Secretariat for the International Strategy for Disaster Reduction (UNISDR) A. Trends OVERVIEW B. Disaster reduction a tool for

Linking disaster risk reduction and climate change adaptation Inter-Agency Secretariat for the International Strategy for Disaster Reduction (UNISDR) A. Trends OVERVIEW B. Disaster reduction a tool for

Consultative report. Committee on Payment and Settlement Systems. Board of the International Organization of Securities Commissions

Committee on Payment and Settlement Systems Board of the International Organization of Securities Commissions Consultative report Recovery of financial market infrastructures August 2013 This publication