Initiation into IFRS Overview, Applicability, Issues on convergence, Roadmap of IFRS Implementation, Schedule of implementation, IFRS Framework

|

|

|

- Collin Hill

- 5 years ago

- Views:

Transcription

1 Initiation into IFRS Overview, Applicability, Issues on convergence, Roadmap of IFRS Implementation, Schedule of implementation, IFRS Framework 22 January 2011 WIRC Mumbai, Kohinoor Hotel Khushroo B. Panthaky Senior Partner Walker Chandiok & Co

2 Convergence with IFRS The Road Ahead Challenges in transition Impact on the enterprise The way ahead Convergence with IFRS The Road Ahead

3 Convergence with IFRS in India an introduction Need for convergence in India Global economy - need to speak in a language which is globally accepted. International Financial Reporting Standards ( IFRS ) has now evolved into being the most widely accepted and trusted financial reporting language Major economies US, Japan, BRIC moving/moved to IFRS Considering the emerging role of India in the global economy, it was imperative for India to harmonize with global financial reporting standards 3

4 Convergence with IFRS in India International scenario 4

5 Convergence with IFRS Current Landscape Progress to date MCA reiterates commitment to transition by 2011 MCA sets up core group to develop roadmap MCA's roadmap on transition released Oct 2007 May 2008 Feb 2009 July 2009 Nov 2009 Jan 2010 Mar / Apr 2010 ICAI released concept paper on convergence with IFRS ICAI releases update on convergence process SEBI approves move to permit voluntary early adoption of IFRS BFSI Roadmap issued by MCA Amendment to Listing agreement permits IFRS reporting Government remains strongly committed to achieving the 2011 deadline 5

6 Convergence with IFRS Current Landscape MCA Roadmap: Highlights Phased approach to convergence Companies (except banking & insurance) to 2014 Banking & Insurance Companies 2012 to 2014 Two separate sets of accounting standards to be maintained under Section 211(3C) Early adoption of IFRS converged standards permitted Clarifications on implementation matters issued by MCA Clarity still required on several practical aspects 6

7 Convergence with IFRS Current Landscape Roadmap: Phased Approach Classes of Companies Listed (only in India) Listed overseas (any securities) Unlisted Company in Nifty or Sensex Phase I Phase I NA Net worth > Rs 1,000 Cr Phase I Phase I Phase I Net worth > Rs 500 Cr upto Rs 1,000 Cr Phase II Phase I Phase II Net worth upto Rs 500 Cr Phase III Phase I Exempt Companies in Phase 2 and 3 can early adopt from years beginning April 1, 2011 onwards Companies not covered in the 3 phases (including Small and Medium Companies can voluntarily adopt converged standards 7

8 Convergence with IFRS Current Landscape Roadmap: Phased Approach MANDATORY REQUIREMENT OPTION FOR EARLY ADOPTION Phases Opening balance sheet date First year end (without IFRS comparatives) Opening balance sheet date First year end (with IFRS comparatives) Phase I 1 April March April March 2012 Phase II 1 April March April March 2012 Phase III 1 April March April March 2012 March 31, 2011 information to be given in an additional column (in addition to existing Indian GAAP comparatives) Phase II and III companies can early adopt from year starting April 1, 2011 onwards 8

9 Convergence with IFRS Current Landscape MCA roadmap - BFSI: A phased approach Companies Insurance Companies Opening balance sheet First financial statements April 1, 2012 March 31, 2013 April 1, 2013 March 31, 2014 Urban co-operative banks with net worth > Rs 200 cr but not exceeding Rs 300 cr April 1, 2014 March 31, 2015 NSE- Nifty 50 or BSE- Sensex 30 Index Listed & unlisted with net worth > Rs 1,000 cr April 1, 2013 March 31, 2014 All other listed NBFCs Unlisted NBFCs with net worth > Rs 500 cr (other than above) April 1, 2014 March 31, 2015 Criteria for phased implementation All insurance companiesall scheduled commercial banks Banking Companies Non Banking Financial Companies (NBFCs) 9 Urban co-operative banks net worth >Rs 300 cr Urban Co-operative Banks with net worth less than Rs 200 Crores, Unlisted NBFCs with net worth less than Rs 500 Crores and Regional Rural Banks are exempt, though they may voluntarily opt to do so

10 Convergence with IFRS Current Landscape MCA Roadmap: clarifications Net worth: reference date for companies (other than banking & insurance) is March 31, 2009 For banking, it is supposed to be as at 31 March 2011 Standalone net-worth to be considered Net worth = share capital + reserves revaluation reserves miscellaneous expenditure debit balance of P&L Early adoption permitted for those in Phase II & Phase III from April 1, 2011 onwards (opening balance sheet on 1 April 2010?) Once converged standards adopted, cannot revert to existing Indian GAAP Securities listed overseas to cover GDRs, ADRs, FCCBs, etc. 10

11 Convergence with IFRS Current Landscape MCA Roadmap: clarifications Group situations each entity to apply its own criteria. However, early adoption permitted Comparative information for first year no IFRS comparatives required but voluntary disclosures permitted IFRS or Indian GAAP Companies to follow converged standards and not IFRS First public reporting SEBI to clarify on quarterly reporting requirements (relevant for listed entities in the Group) Retrospective or prospective application of specific standards to be clarified through standards 11

12 Convergence with IFRS in India the way ahead Roadmap: Developments to track 12 Company law Draft Companies (Amendment) Bill NACAS to finalise amendments to Schedule VI Schedule XIV to also be amended shortly New Companies Bill under evaluation of Parliamentary Committees will also need revision before enactment Accounting Standards ICAI to finalise NACAS to recommend by mid year Taxation ICAI and CBDT set up joint study group to recommend changes MCA considering a tax neutral state for year 1 Direct Tax Code under evaluation of Parliamentary Committees will also need revision before enactment Potential impact Several of these changes will impact your IFRS transition strategies Key areas to watch out for include: New standards, primarily IFRS 1 equivalent as it would spell out the exact transitional provisions Tax laws the Group would like to minimize the tax impact due to the transition to IFRS key decisions and accounting choices would be impacted by these changes Schedule VI being amended may require additional disclosures and possibly functional classification

13 Convergence with IFRS in India the way ahead Exposure drafts of Converged AS issued by ICAI Accounting Standard (AS) 1 (Revised 20XX) (Corresponding to IAS 1), Presentation of Financial Statements Accounting Standard (AS) 2, Inventories Accounting Standard (AS) 3 (revised), Statement of Cash Flows Accounting Standard (AS) 4 (Revised 20XX) (Corresponding to IAS 10) Events after the Reporting Period Accounting Standard (AS) 12 (revised), Accounting for Government Grants and Disclosure of Government Assistance Accounting Standard (AS) 16 (revised) (Corresponding to IAS 23), Borrowing Costs Accounting Standard (AS) 25 (Revised 20XX) (Corresponding to IAS 34) Interim Financial Reporting Accounting Standard (AS) 17 (Revised 20XX) (Corresponding to IFRS 8) Operating Segments (Comments to be received by 31 May 2010) Accounting Standard (AS) 18 (Revised 20XX) (Corresponding to IAS 24) Related Party Disclosures (Comments to be received by 25 May 2010) Accounting Standard (AS) 20 (Revised 20XX) (Corresponding to IAS 33) Earnings per Share (Comments to be received by 25 May 2010) 13

14 Convergence with IFRS in India the way ahead Exposure drafts of Converged AS issued by ICAI Accounting Standard (AS) 29 (Revised 20XX) (Corresponding to IAS 37) Provisions, Contingent Liabilities and Contingent Assets (Comments to be received by 25 May 2010) Accounting Standard (AS) 23 (Revised 20XX) (Corresponding to IAS 28) Investments in Associates (Comments to be received by 10 May 2010) Accounting Standard (AS) 21 (Revised 20XX) (Corresponding to IAS 27) Consolidated and Separate Financial Statements (Comments to be received by 7 May 2010) Accounting Standard (AS) 37 (Issued 20XX) (Corresponding to IAS 40) Investment Property (Comments to be received by 7 May 2010) 14 Accounting Standard (AS) 7 (Revised 20XX) (Corresponding to IAS 11) Construction Contracts (Comments to be received by 30 April 2010) Accounting Standard (AS) 19 (Revised 20XX) (Corresponding to IAS 17) Leases (Comments to be received by 22 April 2010) Accounting Standard (AS) 10 (Revised 20XX) (Corresponding to IAS 16) Property, Plant and Equipment (Comments to be received by 19 April 2010) Accounting Standard (AS) 11 (Revised 20XX) (Corresponding to IAS 21) The Effects of Changes in Foreign Exchange Rates (Comments to be received by 19 April 2010)

15 Convergence with IFRS in India the way ahead Exposure drafts of Converged AS issued by ICAI Accounting Standard (AS) 5 (Revised 20XX) (Corresponding to IAS 8), Accounting Policies, Changes in Accounting Estimates and Errors (Comments to be received by 7 April 2010) Accounting Standard (AS) 34 (Issued 20XX) (Corresponding to IAS 29), Financial Reporting in Hyperinflationary Economies (Comments to be received by 7 April 2010) Accounting Standard (AS) 35 (Issued 20XX) (Corresponding to IFRS 6), Exploration for and Evaluation of Mineral Resources (Comments to be received by 7 April 2010) 15

16 Convergence with IFRS Current Landscape SEBI Amendment to Listing Agreement Insertion of clause 41(I) (g): Voluntary adoption of IFRS by listed entities having subsidiaries Provides an option to submit consolidated financial results in accordance with IFRS Where companies exercise this option and report results in compliance with IFRS for the current year the comparative numbers for the previous year may be as per notified Accounting Standards. In such cases, Companies shall provide reconciliation in respect of significant differences between figures as disclosed as per IFRS and the figures as they would have been if the notified Accounting standards were adopted. Standalone results will continue to be reported and submitted in accordance with IGAAP 16

17 Convergence with IFRS Current Landscape SEBI Amendment to Listing Agreement key issues Restricted to Companies presenting consolidated financial statements - may not significantly contribute to comparability among listed entities. It is our understanding that IFRS refers to IFRS as issued by International Accounting Standards Board ( IASB ). IFRS requires full comparatives hence would need Indian GAAP& IFRS comparatives The date of transition to IFRS (as issued by IASB) could be different from the transition date to the converged Indian Accounting Standards (i.e. April 1, 2011 onwards in a phased manner) Companies will need to carefully evaluate this option. Would need to maintain accounts in accordance with the existing Indian GAAP (for reporting standalone & taxation purposes); IFRS as issued by IASB; and reconciliation to Indian GAAP on a line-by-line basis for significant variances. 17

18 Convergence with IFRS the way ahead International scenario 18 IFRS continues to evolve IFRS 9 to replace IAS 39 (AS 30) in the process of development Part issued significant portions in progress. Expected completion date end 2010 Several significant projects in pipeline Apart from 3 exposure drafts (ED) relating to Financial Instruments, 10 other EDs expected in next 6 months Revenue recognition, leases, financial statement presentation, income taxes, etc Working to a moving target

19 Convergence with IFRS The Road Ahead Challenges in transition Impact on the enterprise The way ahead Challenges in transition

20 Convergence with IFRS Challenges in transition Key External Challenges Legal and Regulatory changes Multiple ministries and regulators MCA, SEBI, RBI, IRDA, etc Taxation changes - DTC Availability of skill sets IFRS industry and profession Valuation IFRS in academic curriculum IFRS in a moving target Significant changes between now and 2011 revenues, leases, financial instruments, etc Indian GAAP Capabilities Regulatory Education Considering the complexity and the practical difficulties, MCA is adopting a phased implementation of IFRS in India IFRS 20

21 Convergence with IFRS Challenges in transition Key Internal Challenges 21 Accounting impact People /Technical capabilities Internal capabilities accountants, specialists, functional, etc External capabilities valuers, specialists, auditors, etc Business processes Technological changes Extent of changes to systems IFRS in a moving target Significant changes on key standards - revenues, leases, financial instruments, etc Indian GAAP People Accounting Process & Technology IFRS Transition to IFRS is not an 'accounting' change; it impacts all aspects of the enterprise Systems and processes, both business and internal, would undergo change Key decision making metrics would undergo change

22 Convergence with IFRS The Road Ahead Challenges in transition Impact on the enterprise The way ahead Impact on the enterprise

23 Impact on the enterprise Key challenges for enterprise 23 Conversion to IFRS has strategic implications Reported earnings volatility Business plans, earnings estimate, debt covenants and management remunerations plans that have reported earnings as the basis will have to be revisited as these are expected to undergo some degree of impact due to this convergence. Requires harmonization of internal and external reporting. Expected to be the single largest accounting shift in India with significant challenges

24 Impact on the enterprise IFRS will have an Enterprise wide impact People Indian GAAP Accounting IFRS Process & Technology 24

25 Accounting related issues

26 Impact on the Enterprise Accounting issues Theme GAAP differences Policy selection Disclosure requirements Questions to consider What are the key differences between local GAAP and IFRS that will affect my results? Where IFRS offers accounting policy choices, which ones shall we apply? Which IFRS 1 exemptions from retrospective application will be taken up? In which areas will IFRS require us to collect and process data to meet disclosure requirements (eg related party disclosures, IFRS 7, impairment disclosures)? 26

27 Impact on the enterprise Accounting Issues - Overview Indian GAAP Financial Statements Company's Accounting policies and practices Indian accounting requirements Indian disclosure requirements Legal requirements Format of financial statement presentation IFRS Financial Statements Current IFRS requirements Proposed changes to IFRS Proposed changes to Indian GAAP Legal requirements Format of financial statement presentation Proposed changes in Accounting policie es and disclosures 27

28 Impact on the enterprise Accounting Issues - Overview Principles based framework similar to Indian GAAP Fills in the gaps in Indian GAAP several new standards Several areas with differences in application of guidance Detailed implementation guidance under IFRS to facilitate consistency in application Very detailed disclosure requirements under IFRS IFRS has specific standards on: Investment Properties Biological assets Insurance Contracts 28

29 Impact on the enterprise Overview of requirements under IFRS Area Accounting Framework Presentation of Financial statements. Requirements under IFRS Historical cost but also requires fair value estimation for accounting certain type of assets Consolidated Financial statements = general purpose financial statements Current and non current classification of assets & liabilities Statement of Comprehensive income (No concept of extraordinary income) Statement of changes in equity Additional disclosures on judgments, estimates, capital managements, new standards, etc Increased use of fair values results in increased income statement volatility Classification of assets and liabilities undergoes changes impacting key ratios Very detailed financial statements increased level of disclosures approx 3000 disclosures 29

30 Impact on the enterprise Overview of requirements under IFRS Area First time adoption of IFRS Requirements under IFRS Retrospective application of all IFRS. Optional exemption of certain standards available careful evaluation property plant and equipment business combinations financial instruments debt/equity classification foreign currency translation reserve employee benefits Reconciliation of equity and profit or loss for all periods presented and opening balance sheet date AN INDIAN EQUIVALENT BEING DEVELOPED FOR TRANSITION FROM EXISTING STANDARDS TO CONVERGED STANDARDS Retrospective application to impact retained and current earnings 30

31 Impact on the enterprise Overview of requirements under IFRS Area Revenue recognition Requirements under IFRS Conceptually similar to Indian GAAP; Several differences in detail Revenues recognised based on fair value of consideration cash & non-cash Multiple element arrangements will need to be addressed to identify separate components of the transaction and recognise revenue accordingly relative fair value method used residual method used in certain limited circumstances Deferred settlement terms to be normalized in recognition of revenues converse could be true in certain circumstances Contract accounting would require bundling and unbundling based on substance of these transactions New guidance expected in 2011/2012 Discussion paper current available 31

32 Impact on the enterprise Overview of requirements under IFRS Area Property, plant and equipment Requirements under IFRS More stringent guidance relating to various components of cost, which can be included within property, plant and equipment. Requires component accounting Major inspection and maintenance costs are recognized using the built in overhaul method. Yearly review of method of depreciation, residual values and useful life On first time adoption, may be possible to opt for revaluation of items of property, plant and equipment and treat as deemed cost. De-capitalization of part of cost of PPE Componentization to result in accelerated depreciation reflective of actual life Depreciation on economic useful life 32

33 Impact on the enterprise Overview of requirements under IFRS Area Business combinations Wider coverage of transactions Requirements under IFRS Only purchase method is allowed. Assets and liabilities are fair valued including those previously unrecognized Identification and valuation of Contingent liabilities & Contingent considerations Gain on bargain purchase recognized in profit or loss Goodwill tested for impairment and not amortized Increased coverage of transactions Consistent accounting irrespective of transaction structure Reflection of assets and liabilities at fair values possibly lower goodwill Impact on earnings generally lower earnings due to higher amortization, finance costs, etc 33

34 Impact on the enterprise Overview of requirements under IFRS Area Consolidated & Separate financial statements Requirements under IFRS Requires all parent companies to present CFS (limited exemptions) Wider coverage based on definition of control Existence of currently exercisable potential voting rights Financial reporting periods - 3 month difference All SPEs to be consolidated (eg. employee trusts, ) where control exists Unlisted entities to prepare consolidated financial statements Possibly larger number of entities consolidated under parent company Profitability impacted due to fair value adjustments 34

35 Impact on the enterprise Overview of requirements under IFRS Area Financial Instruments Requirements under IFRS AS 30, 31 & 32 issued in line with IFRS Equity & liability classification Splitting of compound financial instruments Concept of embedded derivatives Categorization of financial assets and liabilities Hedge accounting rules - Detailed evaluation and documentation required Comprehensive quantitative and qualitative disclosures on financial instruments and related risks CURRENTLY UNDERGOING CHANGE - IFRS 9 TO BE READY BY END 2010 Significant income statement volatility due to fair valuation Onerous hedge accounting requirements Potential increase in debt and related costs impacts net worth and ratios Very detailed disclosures 35

36 Impact on the enterprise Overview of requirements under IFRS Area IFRS 2 Share based payments Related Party transactions Requirements under IFRS Detailed guidance given on the standard. Expense is recognized based on fair value of the equity awarded or liability incurred Transactions with non-employees based on fair value of goods or services received Group ESOP plans accounted at subsidiary levels as well There is a specific exemption under IFRS for Government companies not to disclose transactions with other Government entities controlled/significantly influenced by the same government. However, some disclosures required of nature and quantum of transactions, etc for significant transactions. Significant earnings impact on expensing based on fair value of share based payments Earnings impacted on fair valuation of investment property 36

37 Process and System issues

38 Impact on the enterprise Process and Systems issues Proposed changes in Accounting policies and disclosures Impact on business, people and processes Internal controls Financial reporting requirements Business processes Business management requirements Education and training Impact on Information Systems and processes Operational System Data collection & coding Asset Management System Data collection & coding Middleware Transactions ERP Workflow, calculations, GL, reporting Consolidation and reporting systems Data Conversion, storage & security Information Systems Access and controls A key decision is whether to 'embed' IFRS or to adjust information produced by existing systems Collecting the necessary data is at least as challenging as applying the rules correctly to 'work out the numbers' 38

39 Impact on the enterprise Process Implications - Financial Reporting Changes to Financial Statement Presentation: Layout and items included on Balance Sheet and Income Statement Balance Sheet Presentation of Current vs. Non-Current Income Statement Classification of Expenses Extraordinary Items Significant Items Changes in Equity Disclosure of Performance Measures Comparative financial periods are REQUIRED 39 39

40 Impact on the enterprise Process Implications - Policies and Procedures Considerations: Current policies and procedures manuals will become obsolete and will require updating Staff will need to be trained to comply with new policies and procedures New principle-based hierarchy of guidance in the absence of a specific rule-based requirement Policies should be uniform for parent and all subsidiaries (no exemptions even if business is different in nature) 40 40

Changes in calculations Don t be next to underestimate the IFRS impact on IT systems! 41 41")

41 Impact on the enterprise Technology Implications - Conversion Considerations Considerations: Modification/Creation of systems System upgrades System access and authentication Changes to the chart of accounts Consolidating entities Costs and changes to reporting systems Dual reporting (transitional) Changes in calculations Don t be next to underestimate the IFRS impact on IT systems! 41 41

42 Impact on the enterprise Systems issues balancing flexibility and cost Option 1 Topside adjustments Option 2 Embedded workarounds Option 3 Fully embedded Systems impact Low Medium High Workarounds High Medium Low Flexibility Low Medium High Investment Low Medium High Operating costs High Medium Low 42

43 Organizational and people issues

44 Impact on the enterprise Organisational issues - people and skills Theme Training Performance management Specialist skills Questions to consider What are the training needs at different levels of the organisation (including Board level)? Insource or outsource technical training? How will existing incentive plans etc be affected by a change in KPIs? Should we align KPIs with IFRS measures or reconcile from IFRS to existing measures? Do we need to invest in additional specialist skills e.g. valuations, hedge effectiveness? 44

45 Wider enterprise level issues

46 Impact on the enterprise Wider enterprise level issues Key IFRS financial indicators Net Income EPS Net-worth Key Ratios Earnings Guidance Segment Performance Impact on the various aspects of the Enterprise Treasury Debt covenants, borrowing limits Dividend policies Free reserves, distributable profits Taxation Impact on current tax and cash flows Human Resources Profitability or stock based Compensation Investor Relations Communication strategy and education MIS Alignment of internal and external reporting The numbers and metrics under IFRS/converged standards have a much wider impact. Requires upfront consideration and planning from a medium to long term perspective 46

47 Impact on the Enterprise Financial issues - dividend policy 47 Theme Retained earnings Profit volatility Questions to consider Will IFRS result in additional 'hits' to retained earnings that will affect my ability to pay a dividend? E.g. share-based payment charges deferred tax pensions What mitigating actions are available/appropriate? Will IFRS result in more volatile earnings that will affect my ability to predict next year's dividends? E.g. derivatives being marked to market impairment

48 Impact on the Enterprise Financial issues - treasury planning Theme Loan covenants Borrowing limits Questions to consider Will IFRS affect compliance with existing loan covenants e.g. current and non current splitting of assets and liabilities changes to calculation of interest expense from an accruals basis to 'amortised cost using the effective interest method'? Will IFRS result in additional 'borrowings' that affect borrowing limits (e.g. in Articles)? e.g. separation of property leases into an operating lease of land and finance lease of buildings deferred tax liabilities 48

49 Impact on the enterprise Financial issues - tax impacts 49 Theme Tax and accounting profits Tax planning Questions to consider What is the interaction between accounting profit and taxable profit in my jurisdiction? How will IFRS affect my tax liabilities? E.g. tax treatment of unrealised fair value gains or losses on financial instruments and other assets MAT based on gross assets move from tax basis of depreciation to an economic basis Should I be taking any actions to mitigate tax affects? E.g. continue to use local GAAP for tax purposes and/or for company-only accounting

50 Convergence with IFRS The Road Ahead Challenges in transition Impact on the enterprise The way ahead The way ahead

51 The way ahead Common pitfalls The most common issues faced by companies converging to IFRS are: Lack of a convergence plan and under estimation of efforts involved Lack of senior management commitment Significant investment in IT Systems and training manpower Lack of communication with stakeholders and users of financial reports Difficulties in estimating fair values Complexities in the presentation of financial statements Non availability of skilled manpower 51

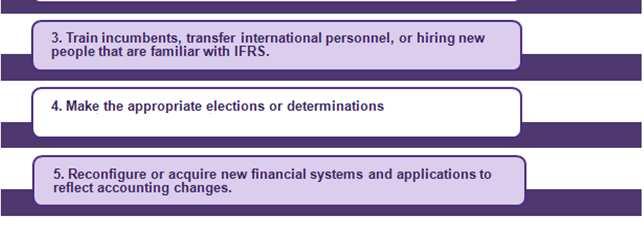

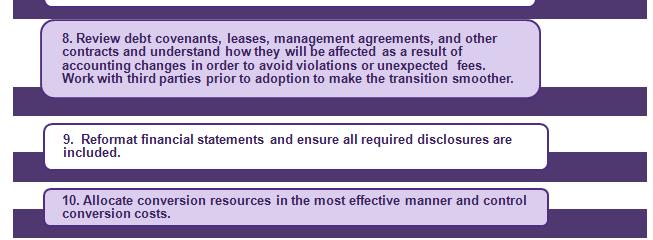

52 The way ahead Top 10 Considerations 52 52

53 The way ahead Top 10 Considerations 53 53

54 Questions

55 Thank you Khushroo B. Panthaky Head of Assurance and Western Region Practice Leader Walker, Chandiok & Co Or write to us at : ifrs@wcgt.in

Walker, Chandiok & Co

Initiation into IFRS Overview, Convergence, Roadmap, Framework and a Practical Perspective June 13, 2011 ICAI WIRC Mumbai, Juhu Princess Hotel CA Khushroo B. Panthaky Assurance Head & Western Region Practice

Initiation into IFRS Overview, Convergence, Roadmap, Framework and a Practical Perspective June 13, 2011 ICAI WIRC Mumbai, Juhu Princess Hotel CA Khushroo B. Panthaky Assurance Head & Western Region Practice

Ind-AS Implementation Issues. Himanshu Kishnadwala

Ind-AS Implementation Issues Himanshu Kishnadwala What is I-GAAP? Accounting Standards in India Till 2006, Standards issued by ASB of ICAI were to be followed Companies (Accounting Standards) Rules, notified

Ind-AS Implementation Issues Himanshu Kishnadwala What is I-GAAP? Accounting Standards in India Till 2006, Standards issued by ASB of ICAI were to be followed Companies (Accounting Standards) Rules, notified

Ind AS pocket guide 2015 Concepts and principles of Ind AS in a nutshell

Ind AS pocket guide 2015 Concepts and principles of Ind AS in a nutshell 2 PwC Introduction This pocket guide provides a brief summary of the recognition, measurement, presentation and disclosure requirements

Ind AS pocket guide 2015 Concepts and principles of Ind AS in a nutshell 2 PwC Introduction This pocket guide provides a brief summary of the recognition, measurement, presentation and disclosure requirements

Overview of Transition to IND-AS. CA Sanjeev Maheshwari

Overview of Transition to IND-AS CA Sanjeev Maheshwari sm@gmj.co.in 98211 19043 Need for one Common language of Accounting GMJ & Co. 2 GMJ & Co. 3 GMJ & Co. 4 GMJ & Co. 5 GMJ & Co. 6 GMJ & Co. 7 GMJ &

Overview of Transition to IND-AS CA Sanjeev Maheshwari sm@gmj.co.in 98211 19043 Need for one Common language of Accounting GMJ & Co. 2 GMJ & Co. 3 GMJ & Co. 4 GMJ & Co. 5 GMJ & Co. 6 GMJ & Co. 7 GMJ &

UNIT 1 INTERNATIONAL FINANCIAL REPORTING STANDARDS

1 UNIT 1 INTERNATIONAL FINANCIAL REPORTING STANDARDS Meaning The term International Financial Reporting Standards includes IFRS, IAS and interpretations originated by the IFRIC or the former Standing Interpretations

1 UNIT 1 INTERNATIONAL FINANCIAL REPORTING STANDARDS Meaning The term International Financial Reporting Standards includes IFRS, IAS and interpretations originated by the IFRIC or the former Standing Interpretations

PRESS RELEASE. PRESS RELEASE-4/2010 No.1/1/2009-IFRS Dated the 4 th May, 2010

PRESS RELEASE A meeting of the Core Group constituted by the Ministry of Corporate Affairs for convergence of Indian Accounting Standards with the International financial Reporting Standards (IFRSs) from

PRESS RELEASE A meeting of the Core Group constituted by the Ministry of Corporate Affairs for convergence of Indian Accounting Standards with the International financial Reporting Standards (IFRSs) from

Ind AS Overview, Impact and Anaysis

Ind AS Overview, Impact and Anaysis Organised by: Gurugram Branch of NIRC of ICAI Hotel Plazzio, June 9, 2018 IFRS Journey History and Background of IFRS 1. IASG : AICPA, CICA & ICAEW (1966-67) 2. Australia,

Ind AS Overview, Impact and Anaysis Organised by: Gurugram Branch of NIRC of ICAI Hotel Plazzio, June 9, 2018 IFRS Journey History and Background of IFRS 1. IASG : AICPA, CICA & ICAEW (1966-67) 2. Australia,

Guide to First-time Adoption of Ind AS

Guide to First-time Adoption of Ind AS 2 Guide to First-time Adoption of Ind AS Contents Overview of Ind AS roadmap 06 Key differences between Ind AS and Indian GAAP 10 First-time adoption of Ind AS 42

Guide to First-time Adoption of Ind AS 2 Guide to First-time Adoption of Ind AS Contents Overview of Ind AS roadmap 06 Key differences between Ind AS and Indian GAAP 10 First-time adoption of Ind AS 42

Introduction to Ind-AS By Neeraj Sharma

Introduction to Ind-AS By Neeraj Sharma neerajsharma2002in@yahoo.com 1 Agenda Ind-AS An Overview Five Key Standards GAAP Differences Other GAAP Differences Questions & Answers 2 Ind-AS An Overview Set

Introduction to Ind-AS By Neeraj Sharma neerajsharma2002in@yahoo.com 1 Agenda Ind-AS An Overview Five Key Standards GAAP Differences Other GAAP Differences Questions & Answers 2 Ind-AS An Overview Set

Overview of Indian Accounting Standards (Ind AS)

") Overview of Indian Accounting Standards (Ind AS) CA Rajkumar S Adukia B.Com (Hons), FCA, ACS, ACWA, LLB, DIPR, DLL &LP, IFRS(UK), MBA email id: rajkumarradukia@caaa.in Mob: 09820061049/09323061049 To receive

Overview of Indian Accounting Standards (Ind AS) CA Rajkumar S Adukia B.Com (Hons), FCA, ACS, ACWA, LLB, DIPR, DLL &LP, IFRS(UK), MBA email id: rajkumarradukia@caaa.in Mob: 09820061049/09323061049 To receive

Filling the GAAP India and IFRS

Filling the GAAP India and IFRS Global challenges to trade have been falling over the past decades and this has resulted in countries around the globe being linked by a thread of economic interdependence.

Filling the GAAP India and IFRS Global challenges to trade have been falling over the past decades and this has resulted in countries around the globe being linked by a thread of economic interdependence.

Convergence with IFRS Challenges and Strategies

Convergence with IFRS Challenges and Strategies By P.R. Ramesh Partner Deloitte Haskins and Sells Bombay Chartered Accountants Society November 19, 2008 AGENDA IFRS LANDSCAPE INDIAN GAAP AND CONVERGENCE

Convergence with IFRS Challenges and Strategies By P.R. Ramesh Partner Deloitte Haskins and Sells Bombay Chartered Accountants Society November 19, 2008 AGENDA IFRS LANDSCAPE INDIAN GAAP AND CONVERGENCE

I. VARIOUS OPTIONS FOR CONVERGENCE WITH IFRSs IN INDIA

P I. VARIOUS OPTIONS FOR CONVERGENCE WITH IFRSs IN INDIA 1. Background 1.1 International Financial Reporting Standards (IFRSs), issued by the International Accounting Standards Board (IASB), which are

P I. VARIOUS OPTIONS FOR CONVERGENCE WITH IFRSs IN INDIA 1. Background 1.1 International Financial Reporting Standards (IFRSs), issued by the International Accounting Standards Board (IASB), which are

An Insight into IFRS 1 First Time Adoption of IFRS Simardeep Singh

An Insight into IFRS 1 First Time Adoption of IFRS Simardeep Singh Mail your comments and feedback at simardeep88@hotmail.com An Insight into IFRS 1 First Time Adoption of IFRS Simardeep Singh The author

An Insight into IFRS 1 First Time Adoption of IFRS Simardeep Singh Mail your comments and feedback at simardeep88@hotmail.com An Insight into IFRS 1 First Time Adoption of IFRS Simardeep Singh The author

The Game Changers of financial reporting

A primer to Ind AS Issues and Strategies Presentation at the Metro Conference organised by SIRC of ICAI on 3 February 2015 Chinnsamy Ganesan FCA DISA(ICA) The Game Changers of financial reporting Companies

A primer to Ind AS Issues and Strategies Presentation at the Metro Conference organised by SIRC of ICAI on 3 February 2015 Chinnsamy Ganesan FCA DISA(ICA) The Game Changers of financial reporting Companies

Ind AS Transition Facilitation Group (ITFG) Clarification Bulletin 3

Clarification Bulletin 3") Ind AS Transition Facilitation Group (ITFG) Clarification Bulletin 3 Ind AS Transition Facilitation Group (ITFG) of Ind AS (IFRS) Implementation Committee has been constituted for providing clarifications

Ind AS Transition Facilitation Group (ITFG) Clarification Bulletin 3 Ind AS Transition Facilitation Group (ITFG) of Ind AS (IFRS) Implementation Committee has been constituted for providing clarifications

OVERVIEW OF IND AS INCLUDING CARVE OUTS. C.A. Sanjay Vasudeva S. C. Vasudeva & Co. Chartered Accountants

Seminar of North Ex CA Study Circle Hotel Oasis, New Delhi OVERVIEW OF IND AS INCLUDING CARVE OUTS C.A. Sanjay Vasudeva S. C. Vasudeva & Co. Chartered Accountants 16th December 2016 Overview Need for International

Seminar of North Ex CA Study Circle Hotel Oasis, New Delhi OVERVIEW OF IND AS INCLUDING CARVE OUTS C.A. Sanjay Vasudeva S. C. Vasudeva & Co. Chartered Accountants 16th December 2016 Overview Need for International

A New Era of Financial Reporting

A New Era of Financial Reporting The Agra Branch of CIRC of ICAI 30 th April 2016 FCA Aditya Singhal M.Com, DISA(ICAI), DipIFRS (ACCA) +91 8800334745 adityaagra@gmail.com Current Global Reporting Requirements

A New Era of Financial Reporting The Agra Branch of CIRC of ICAI 30 th April 2016 FCA Aditya Singhal M.Com, DISA(ICAI), DipIFRS (ACCA) +91 8800334745 adityaagra@gmail.com Current Global Reporting Requirements

Change in Employee Benefits Accounting

Change in Employee Benefits Accounting Planning the transition Move from AS 15 to Ind AS 19 2015 All rights reserved 1 Efforts toward convergence of I- GAAP and IFRS Transition timeline from AS 15 to Ind

Change in Employee Benefits Accounting Planning the transition Move from AS 15 to Ind AS 19 2015 All rights reserved 1 Efforts toward convergence of I- GAAP and IFRS Transition timeline from AS 15 to Ind

Introduction to Ind-AS. M/s Pranjal Joshi & Co Chartered Accountants

Introduction to Ind-AS M/s Pranjal Joshi & Co Chartered Accountants What is the importance of financial statements? Financial statements are very important as they are the basis for variety of decisions

Introduction to Ind-AS M/s Pranjal Joshi & Co Chartered Accountants What is the importance of financial statements? Financial statements are very important as they are the basis for variety of decisions

BRINGING EXPERT GLOBAL AND LOCAL KNOWLEDGE TO YOUR ENVIRONMENT THE NEW AXIS OF FINANCIAL REPORTING - IND AS AND ICDS THE POWER OF BEING UNDERSTOOD

BRINGING EXPERT GLOBAL AND LOCAL KNOWLEDGE TO YOUR ENVIRONMENT THE NEW AXIS OF FINANCIAL REPORTING - IND AS AND ICDS THE POWER OF BEING UNDERSTOOD in India Consistently ranked amongst India s top six accounting

BRINGING EXPERT GLOBAL AND LOCAL KNOWLEDGE TO YOUR ENVIRONMENT THE NEW AXIS OF FINANCIAL REPORTING - IND AS AND ICDS THE POWER OF BEING UNDERSTOOD in India Consistently ranked amongst India s top six accounting

Financial Reporting Matters

Financial Reporting Matters March 2009 Issue 26 AUDIT In this issue, we discuss some of the accounting issues to consider as entities prepare for their 31 March 2009 quarterly or year-end financial reporting.

Financial Reporting Matters March 2009 Issue 26 AUDIT In this issue, we discuss some of the accounting issues to consider as entities prepare for their 31 March 2009 quarterly or year-end financial reporting.

IMPORTANT TAKEAWAYS ON IFRS

IMPORTANT TAKEAWAYS ON IFRS 1. Four Major Pillars of IFRS : 1. Historical cost is not relevant : It is no more relevant for measurement of Assets and Liabilities. 2. Time Value of Money : Cash Flows to

IMPORTANT TAKEAWAYS ON IFRS 1. Four Major Pillars of IFRS : 1. Historical cost is not relevant : It is no more relevant for measurement of Assets and Liabilities. 2. Time Value of Money : Cash Flows to

Impact of Ind AS adoption on Industry Applying it in simple way

Impact of Ind AS adoption on Industry Applying it in simple way CA Rakesh Agarwal Alumni - Harvard Business School Vice President Finance, Compliance and Accounts Centers of Excellence (CoE) Reliance Industries

Impact of Ind AS adoption on Industry Applying it in simple way CA Rakesh Agarwal Alumni - Harvard Business School Vice President Finance, Compliance and Accounts Centers of Excellence (CoE) Reliance Industries

26 th Year of Publication. A monthly publication from South Indian Bank. To kindle interest in economic affairs... To empower the student community...

Experience Next Generation Banking A monthly publication from South Indian Bank To kindle interest in economic affairs... To empower the student community... www.southindianbank.com Student s corner ho2099@sib.co.in

Experience Next Generation Banking A monthly publication from South Indian Bank To kindle interest in economic affairs... To empower the student community... www.southindianbank.com Student s corner ho2099@sib.co.in

Archieves*of*Business*Research* *Vol.4,*No.1* Publication*Date: DOI

Archieves*of*Business*Research* *Vol.4,*No.1* Publication*Date:Feb.25,2015 DOI:10.14738/abr.41.1754. Abbasi,E.H.(2016).InternationalFinancialReportingStandards(IFRS)forInternationalAccountingandFinancial

Archieves*of*Business*Research* *Vol.4,*No.1* Publication*Date:Feb.25,2015 DOI:10.14738/abr.41.1754. Abbasi,E.H.(2016).InternationalFinancialReportingStandards(IFRS)forInternationalAccountingandFinancial

Opening balance sheet 1 April Opening balance sheet 1 April Unlisted companies whose net worth is >= INR 250 crores but < INR 500 crores

Step up to Ind AS Ind AS an overview India made a commitment towards the convergence of Indian accounting standards with IFRS at the G20 summit in 2009. In line with this, the Ministry of Corporate Affairs,

Step up to Ind AS Ind AS an overview India made a commitment towards the convergence of Indian accounting standards with IFRS at the G20 summit in 2009. In line with this, the Ministry of Corporate Affairs,

Implementation of Ind AS Experience so far

Implementation of Ind AS Experience so far Dolphy D Souza December 2017 Ind AS Implementation: A Giant Leap Step in the right direction Substantial improvement in accounting Financial instruments Business

Implementation of Ind AS Experience so far Dolphy D Souza December 2017 Ind AS Implementation: A Giant Leap Step in the right direction Substantial improvement in accounting Financial instruments Business

Voices on Reporting. Quarterly updates. October Contents. Updates relating to Ind AS. Updates relating to the Companies Act, 2013

Voices on Reporting Quarterly updates October 2017 Contents Updates relating to Ind AS Updates relating to the Companies Act, 2013 Updates relating to SEBI regulations Other regulatory updates 01 18 25

Voices on Reporting Quarterly updates October 2017 Contents Updates relating to Ind AS Updates relating to the Companies Act, 2013 Updates relating to SEBI regulations Other regulatory updates 01 18 25

IFRS Considerations for Audit Committees. February 2009

IFRS Considerations for Audit Committees. February 2009 Contents Introduction... 3 Using This Publication... 3 More Information... 3 Significant Accounting Topics... 4 Inventory... 4 Consolidation... 5

IFRS Considerations for Audit Committees. February 2009 Contents Introduction... 3 Using This Publication... 3 More Information... 3 Significant Accounting Topics... 4 Inventory... 4 Consolidation... 5

Voices on Reporting. 25 May KPMG.com/in

Voices on Reporting 25 May 2016 KPMG.com/in 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative

Voices on Reporting 25 May 2016 KPMG.com/in 2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative

Indian Accounting Standards (Ind AS) are issued by Accounting Standard Board to converge Indian GAAP with International Financial Accounting

are issued by Accounting Standard Board to converge Indian GAAP with International Financial Accounting") Indian Accounting Standards (Ind AS) are issued by Accounting Standard Board to converge Indian GAAP with International Financial Accounting Standards (IFRS). Their objective is to remove variations in

Indian Accounting Standards (Ind AS) are issued by Accounting Standard Board to converge Indian GAAP with International Financial Accounting Standards (IFRS). Their objective is to remove variations in

2009 International Financial Reporting Standards update

2009 International Financial Reporting Standards update Contents Introduction 3 Section 1: New and amended standards and interpretations applicable to December 2009 year-end 5 IFRS 1 First-time Adoption

2009 International Financial Reporting Standards update Contents Introduction 3 Section 1: New and amended standards and interpretations applicable to December 2009 year-end 5 IFRS 1 First-time Adoption

Voices on Reporting. 18 November KPMG.com/in

Voices on Reporting 18 November 2015 KPMG.com/in Welcome Series of knowledge sharing calls Covering current and emerging reporting issues Scheduled towards the end of each month Look out for our Accounting

Voices on Reporting 18 November 2015 KPMG.com/in Welcome Series of knowledge sharing calls Covering current and emerging reporting issues Scheduled towards the end of each month Look out for our Accounting

BCA - Workshop on NBFC St Regis Hotel Palladium, Mumbai 4 August 2016

NBFC - Statutory Audit aspects under Companies Act, 2013 BCA - Workshop on NBFC St Regis Hotel Palladium, Mumbai 4 August 2016 Agenda 1 Key aspects of audit of NBFCs 2 Laws / Regulatory Aspects 3 Accounting

NBFC - Statutory Audit aspects under Companies Act, 2013 BCA - Workshop on NBFC St Regis Hotel Palladium, Mumbai 4 August 2016 Agenda 1 Key aspects of audit of NBFCs 2 Laws / Regulatory Aspects 3 Accounting

Indian Accounting Standards

Indian Accounting Standards Employee benefits perspective Implementation of Ind AS 19 and Ind AS 102 October 2016 ACTUARIAL SERVICES ABOUT THIS DOCUMENT THIS IS A WHITE PAPER This document belongs to the

Indian Accounting Standards Employee benefits perspective Implementation of Ind AS 19 and Ind AS 102 October 2016 ACTUARIAL SERVICES ABOUT THIS DOCUMENT THIS IS A WHITE PAPER This document belongs to the

IFRS 1 - First-Time Adoption of IFRS

IFRS 1 - First-Time Adoption of IFRS P C First time adoption session outline Overview Exemptions and exceptions Disclosure IFRS 1 General principles Application Requires To the first IFRS financial statements

IFRS 1 - First-Time Adoption of IFRS P C First time adoption session outline Overview Exemptions and exceptions Disclosure IFRS 1 General principles Application Requires To the first IFRS financial statements

New Developments on Revenue Recognition. Uphold public interest

New Developments on Revenue Recognition Uphold public interest IFRS 15-Revenue From Contracts with Customers Background IFRS 15 was finalised in May 2014 with the initial effective date being 1 st January

New Developments on Revenue Recognition Uphold public interest IFRS 15-Revenue From Contracts with Customers Background IFRS 15 was finalised in May 2014 with the initial effective date being 1 st January

Ind AS 16 Property, Plant & Equipment CA Hemal D Shah

Ind AS 16 Property, Plant & Equipment CA Hemal D Shah Page 1 Contents 1. Property Plant & Equipment - Ind AS 16 2. Government Grant Ind AS 20 Page 2 Property Plant & Equipment Ind AS 16 Measurement Depreciation

Ind AS 16 Property, Plant & Equipment CA Hemal D Shah Page 1 Contents 1. Property Plant & Equipment - Ind AS 16 2. Government Grant Ind AS 20 Page 2 Property Plant & Equipment Ind AS 16 Measurement Depreciation

Amendments to IFRS for SMEs

A C C O U N T I N G U P D A T E ( I F R S f o r S M E s ) s to IFRS for SMEs Introduction The International Accounting Standards Board (IASB) has published amendments to its 'International Financial Reporting

A C C O U N T I N G U P D A T E ( I F R S f o r S M E s ) s to IFRS for SMEs Introduction The International Accounting Standards Board (IASB) has published amendments to its 'International Financial Reporting

Winds of Change in AS. M P Vijay Kumar FCA, ACMA, FCS

Winds of Change in AS M P Vijay Kumar FCA, ACMA, FCS INSURANCE!! This presentation should only be read along with the text of Ind AS. The views expressed are those of the presenter and, therefore, do not

Winds of Change in AS M P Vijay Kumar FCA, ACMA, FCS INSURANCE!! This presentation should only be read along with the text of Ind AS. The views expressed are those of the presenter and, therefore, do not

RBI defers the effective date for implementation of Ind AS for banks to 1 April 2019

29 Regulatory updates 30 RBI defers the effective date for implementation of Ind AS for banks to 1 April 2019 On 5 April 2018, the Reserve Bank of India (RBI) through its press release deferred the implementation

29 Regulatory updates 30 RBI defers the effective date for implementation of Ind AS for banks to 1 April 2019 On 5 April 2018, the Reserve Bank of India (RBI) through its press release deferred the implementation

Accounting for revenue is changing, are you ready?

1 Accounting for revenue is changing, are you ready? This article aims to: Highlight the key changes that Indian companies can expect on application of Ind AS 115, Revenue from Contracts with Customers.

1 Accounting for revenue is changing, are you ready? This article aims to: Highlight the key changes that Indian companies can expect on application of Ind AS 115, Revenue from Contracts with Customers.

- Ind AS Implication on MAT - Recent Ind AS Updates

Indian Accounting Standards (Ind AS) WIRC Study Group Meeting - 20 May 2017 - Ind AS Implication on MAT - Recent Ind AS Updates CA Santosh Maller and CA Jugal Joshi 20 May 2017 MAT Thank Impact you Due

Indian Accounting Standards (Ind AS) WIRC Study Group Meeting - 20 May 2017 - Ind AS Implication on MAT - Recent Ind AS Updates CA Santosh Maller and CA Jugal Joshi 20 May 2017 MAT Thank Impact you Due

Global vision backed by local knowledge. IND AS - APPLICATION, ANALYSIS & MAT Financial Year ended 31 March 2017 THE POWER OF BEING UNDERSTOOD

Global vision backed by local knowledge IND AS - APPLICATION, ANALYSIS & MAT Financial Year ended 31 March 2017 THE POWER OF BEING UNDERSTOOD IN INDIA India (comprising of Astute Consulting Group and affiliates)

Global vision backed by local knowledge IND AS - APPLICATION, ANALYSIS & MAT Financial Year ended 31 March 2017 THE POWER OF BEING UNDERSTOOD IN INDIA India (comprising of Astute Consulting Group and affiliates)

FINANCIAL INSTRUMENTS

FINANCIAL INSTRUMENTS Financial Instruments While the EBC notes many similarities between the accounting standards of financial instruments under IFRS and J-GAAP, there is one area where further alignment

FINANCIAL INSTRUMENTS Financial Instruments While the EBC notes many similarities between the accounting standards of financial instruments under IFRS and J-GAAP, there is one area where further alignment

Diploma in IFRS. Units with Learning Outcomes and Assessment Criteria

Diploma in IFRS Units with Learning Outcomes and Assessment Criteria Unit 1-IASB and regulatory framework Understand the need and role of the regulatory system Describe the impact of globalization Describe

Diploma in IFRS Units with Learning Outcomes and Assessment Criteria Unit 1-IASB and regulatory framework Understand the need and role of the regulatory system Describe the impact of globalization Describe

Contents. Financial instruments the complete standard. Fundamental changes call for careful planning. 1. Overview Complete IFRS 9

Financial instruments the complete standard Contents Fundamental changes call for careful planning 1. Overview Complete IFRS 9 2. Classification and measurement Facts 3. Classification and measurement

Financial instruments the complete standard Contents Fundamental changes call for careful planning 1. Overview Complete IFRS 9 2. Classification and measurement Facts 3. Classification and measurement

Are You IFRS Ready? Frank Brod Corporate Vice President, Finance & Administration Chief Accounting Officer Microsoft Corporation

Are You IFRS Ready? Frank Brod Corporate Vice President, Finance & Administration Chief Accounting Officer Microsoft Corporation Agenda IFRS Overview FASB and IASB Convergence Activity Memorandum of Understanding

Are You IFRS Ready? Frank Brod Corporate Vice President, Finance & Administration Chief Accounting Officer Microsoft Corporation Agenda IFRS Overview FASB and IASB Convergence Activity Memorandum of Understanding

Wrestling with the First-Time Adoption of IFRS. PwC

Wrestling with the First-Time Adoption of IFRS PwC First time adoption Session outline Exemptions and IFRS 1 General principles Will replace SIC-8 Application Requires To the first IFRS financial statements

Wrestling with the First-Time Adoption of IFRS PwC First time adoption Session outline Exemptions and IFRS 1 General principles Will replace SIC-8 Application Requires To the first IFRS financial statements

IFRS 1 First-time Adoption of International. Standards*

Wrestling with First-time Adoption of IFRS IFRS 1 First-time Adoption of International Financial Reporting Standards* Session Objective and Key Take aways Session Objective: The objective of this session

Wrestling with First-time Adoption of IFRS IFRS 1 First-time Adoption of International Financial Reporting Standards* Session Objective and Key Take aways Session Objective: The objective of this session

Impact of Ind AS adoption on Industry Applying it in simple way

Impact of Ind AS adoption on Industry Applying it in simple way CA Rakesh Agarwal Alumni - Harvard Business School Vice President Finance, Compliance and Accounts Centers of Excellence (CoE) Reliance Industries

Impact of Ind AS adoption on Industry Applying it in simple way CA Rakesh Agarwal Alumni - Harvard Business School Vice President Finance, Compliance and Accounts Centers of Excellence (CoE) Reliance Industries

Are you Ready for the biggest Accounting Reform in India? [ Converged IFRS ]

![Are you Ready for the biggest Accounting Reform in India? [ Converged IFRS ]](/thumbs/74/70304882.jpg "Are you Ready for the biggest Accounting Reform in India? [ Converged IFRS ]") Are you Ready for the biggest Accounting Reform in India? [ Converged IFRS ] Applicability of Ind AS (India s convergence with International Financial Reporting Standards) On February 16, 2015, the Ministry

Are you Ready for the biggest Accounting Reform in India? [ Converged IFRS ] Applicability of Ind AS (India s convergence with International Financial Reporting Standards) On February 16, 2015, the Ministry

PwC IFRS. The Complex Issues Banks Face* 8 June *connectedthinking

PwC IFRS The Complex Issues Banks Face* *connectedthinking Background Why is IFRS an issue? PSAK is converging with IFRS Growing need for one international set of accounting standards due to mergers &

PwC IFRS The Complex Issues Banks Face* *connectedthinking Background Why is IFRS an issue? PSAK is converging with IFRS Growing need for one international set of accounting standards due to mergers &

IFRS Compliant CGIAR Reporting Guidelines

Approved by the System Management Board at its 8 th meeting, 11-12 December 2017 (Decision Ref SMB/M8/DP8) Contents 1. Introduction & forewords on International Financial Reporting Standards (IFRS)...

Approved by the System Management Board at its 8 th meeting, 11-12 December 2017 (Decision Ref SMB/M8/DP8) Contents 1. Introduction & forewords on International Financial Reporting Standards (IFRS)...

2015 Amendments to the IFRS for SMEs

May 2015 International Financial Reporting Standard (IFRS ) for Small and Medium-sized Entities (SMEs) 2015 Amendments to the IFRS for SMEs 2015 Amendments to the International Financial Reporting Standard

May 2015 International Financial Reporting Standard (IFRS ) for Small and Medium-sized Entities (SMEs) 2015 Amendments to the IFRS for SMEs 2015 Amendments to the International Financial Reporting Standard

ILLUSTRATIVE FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2018

ILLUSTRATIVE FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2018 NEW ZEALAND EQUIVALENTS TO INTERNATIONAL FINANCIAL REPORTING STANDARDS Tier 1 For-Profit Reporters 2 A Layout (New Zealand) Group Ltd Annual

ILLUSTRATIVE FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2018 NEW ZEALAND EQUIVALENTS TO INTERNATIONAL FINANCIAL REPORTING STANDARDS Tier 1 For-Profit Reporters 2 A Layout (New Zealand) Group Ltd Annual

INDIAN ACCOUNTING STANDARDS

Index 1- Brief Summary of Introduction of Ind-AS 2- Applicability of INDIAN ACCOUNTING STANDARDS () 3- List of with objective and scope BRIEF SUMMARY OF INTRODUCTION OF IND-AS Indian Accounting Standards

Index 1- Brief Summary of Introduction of Ind-AS 2- Applicability of INDIAN ACCOUNTING STANDARDS () 3- List of with objective and scope BRIEF SUMMARY OF INTRODUCTION OF IND-AS Indian Accounting Standards

Comparative statement on Indian GAAP and IFRS

Comparative statement on Indian GAAP and IFRS (As on 1 January 2010) 2010 edition Contents i ii 6 Basic standards 7 First-time adoption 7 Small and medium sized entities (SMEs)/Small and medium sized companies

Comparative statement on Indian GAAP and IFRS (As on 1 January 2010) 2010 edition Contents i ii 6 Basic standards 7 First-time adoption 7 Small and medium sized entities (SMEs)/Small and medium sized companies

SUPPLEMENT FOR COMPANY ACCOUNTS AND AUDITING PRACTICES (Relevant for students appearing in June, 2016 Examination)

") EXECUTIVE PROGRAMME SUPPLEMENT FOR COMPANY ACCOUNTS AND AUDITING PRACTICES (Relevant for students appearing in June, 2016 Examination) MODULE 2 - PAPER 5 Disclaimer- This document has been prepared purely

EXECUTIVE PROGRAMME SUPPLEMENT FOR COMPANY ACCOUNTS AND AUDITING PRACTICES (Relevant for students appearing in June, 2016 Examination) MODULE 2 - PAPER 5 Disclaimer- This document has been prepared purely

Indian Accounting Standards (Ind AS) AT A GLANCE

AT A GLANCE") Indian Accounting Standards (Ind AS) AT A GLANCE Indian Accounting Standards (Ind AS) An Introduction The Hon'ble Finance Minister in the presentation of the Union Budget for 2014-15, proposed the adoption

Indian Accounting Standards (Ind AS) AT A GLANCE Indian Accounting Standards (Ind AS) An Introduction The Hon'ble Finance Minister in the presentation of the Union Budget for 2014-15, proposed the adoption

IASB update: Progress and Plans

Agenda paper 2.1 International Financial Reporting Standards IASB update: Progress and Plans November 2014 The views expressed in this presentation are those of the presenter, not necessarily those of

Agenda paper 2.1 International Financial Reporting Standards IASB update: Progress and Plans November 2014 The views expressed in this presentation are those of the presenter, not necessarily those of

CIMA Managerial Level Paper F2 FINANCIAL MANAGEMENT (REVISION SUMMARIES)

") CIMA Managerial Level Paper F2 FINANCIAL MANAGEMENT (REVISION SUMMARIES) Chapter Title Page number 1 The regulatory framework 3 2 What is a group 9 3 Group accounts the statement of financial position

CIMA Managerial Level Paper F2 FINANCIAL MANAGEMENT (REVISION SUMMARIES) Chapter Title Page number 1 The regulatory framework 3 2 What is a group 9 3 Group accounts the statement of financial position

ILLUSTRATIVE FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2017 INTERNATIONAL FINANCIAL REPORTING STANDARDS

ILLUSTRATIVE FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2017 INTERNATIONAL FINANCIAL REPORTING STANDARDS 2 A Layout (International) Group Ltd Annual report and financial statements For the year ended

ILLUSTRATIVE FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2017 INTERNATIONAL FINANCIAL REPORTING STANDARDS 2 A Layout (International) Group Ltd Annual report and financial statements For the year ended

Tier 2 For-Profit Reporters

ILLUSTRATIVE FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2017 NEW ZEALAND EQUIVALENTS TO INTERNATIONAL FINANCIAL REPORTING STANDARDS REDUCED DISCLOSURE REGIME Tier 2 For-Profit Reporters RDR Layout (New

ILLUSTRATIVE FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2017 NEW ZEALAND EQUIVALENTS TO INTERNATIONAL FINANCIAL REPORTING STANDARDS REDUCED DISCLOSURE REGIME Tier 2 For-Profit Reporters RDR Layout (New

Voices on Reporting. 20 May 2015

20 May 2015 Welcome Series of knowledge sharing calls Covering current and emerging reporting issues Scheduled towards the end of each month Look out for our Accounting and Auditing Update, IFRS Notes

20 May 2015 Welcome Series of knowledge sharing calls Covering current and emerging reporting issues Scheduled towards the end of each month Look out for our Accounting and Auditing Update, IFRS Notes

Voices on Reporting. 18 February 2015

18 February 2015 Welcome Series of knowledge sharing calls Covering current and emerging reporting issues Scheduled towards the end of each month Look out for our Accounting and Auditing Update, IFRS Notes

18 February 2015 Welcome Series of knowledge sharing calls Covering current and emerging reporting issues Scheduled towards the end of each month Look out for our Accounting and Auditing Update, IFRS Notes

Ind AS Transition Facilitation Group (ITFG) Clarification Bulletin 7

Clarification Bulletin 7") Ind AS Transition Facilitation Group (ITFG) Clarification Bulletin 7 Ind AS Transition Facilitation Group (ITFG) of Ind AS (IFRS) Implementation Committee has been constituted for providing clarifications

Ind AS Transition Facilitation Group (ITFG) Clarification Bulletin 7 Ind AS Transition Facilitation Group (ITFG) of Ind AS (IFRS) Implementation Committee has been constituted for providing clarifications

SUMMARY OF IASB WORK PLAN AS AT 23 AUGUST 2018

SUMMARY OF IASB WORK PLAN AS AT 23 AUGUST 2018 Page Standard-setting and Related Projects... 3 Management Commentary... 3 Rate-regulated Activities... 3 Research Projects... 4 Dynamic Risk Management...

SUMMARY OF IASB WORK PLAN AS AT 23 AUGUST 2018 Page Standard-setting and Related Projects... 3 Management Commentary... 3 Rate-regulated Activities... 3 Research Projects... 4 Dynamic Risk Management...

Applying IFRS for IFRS 14 Regulatory Deferral Accounts

Applying IFRS IFRS 14 Regulatory Deferral Accounts Applying IFRS for IFRS 14 Regulatory Deferral Accounts November 2014 Contents In this issue: 1. Introduction... 3 1.1 Key features of IFRS 14... 3 1.2

Applying IFRS IFRS 14 Regulatory Deferral Accounts Applying IFRS for IFRS 14 Regulatory Deferral Accounts November 2014 Contents In this issue: 1. Introduction... 3 1.1 Key features of IFRS 14... 3 1.2

IASB Projects A pocketbook guide. As at 31 March 2013

IASB Projects A pocketbook guide As at 31 March 2013 In this edition... Introduction... 2 Timeline for major IFRS projects... 3 Financial instruments classification and measurement (proposed limited scope

IASB Projects A pocketbook guide As at 31 March 2013 In this edition... Introduction... 2 Timeline for major IFRS projects... 3 Financial instruments classification and measurement (proposed limited scope

IFRS Consultancy Services. IFRS convergence for unlisted companies in KSA

IFRS Consultancy Services IFRS convergence for unlisted companies in KSA contents 01 IFRS- Road map 02 Key differences between SOCPA and IFRS in certain critical areas 03 Convergence process 04 Our Approach

IFRS Consultancy Services IFRS convergence for unlisted companies in KSA contents 01 IFRS- Road map 02 Key differences between SOCPA and IFRS in certain critical areas 03 Convergence process 04 Our Approach

IND AS CONVERGED WITH IFRS

Volume 5, Issue 1 (January, 2016) Online ISSN-2277-1166 Published by: Abhinav Publication Abhinav National Monthly Refereed Journal of Research in IND AS CONVERGED WITH IFRS Hiral Desai Assistance Professor,

Volume 5, Issue 1 (January, 2016) Online ISSN-2277-1166 Published by: Abhinav Publication Abhinav National Monthly Refereed Journal of Research in IND AS CONVERGED WITH IFRS Hiral Desai Assistance Professor,

Voices on Reporting. 4 October KPMG.com/in

Voices on Reporting 4 October 2017 KPMG.com/in 2017 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative

Voices on Reporting 4 October 2017 KPMG.com/in 2017 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative

FRS 102 PROFESSIONAL SERVICES. The main new Irish GAAP standard

FRS 102 PROFESSIONAL SERVICES The main new Irish GAAP standard November 2014 2 PROFESSIONAL SERVICES PROFESSIONAL SERVICES 3 The long awaited replacement for Irish GAAP has finally arrived in the form

FRS 102 PROFESSIONAL SERVICES The main new Irish GAAP standard November 2014 2 PROFESSIONAL SERVICES PROFESSIONAL SERVICES 3 The long awaited replacement for Irish GAAP has finally arrived in the form

Moving towards.. future Indian GAAP

Moving towards.. future Indian GAAP Comparison of Exposure Drafts issued by the ICAI and IFRS issued by the IASB Convergence Series June 2010 PwC Introduction Recently, the Institute of Chartered Accountants

Moving towards.. future Indian GAAP Comparison of Exposure Drafts issued by the ICAI and IFRS issued by the IASB Convergence Series June 2010 PwC Introduction Recently, the Institute of Chartered Accountants

About the authors I-5 Chapter-heads I-7. u Clarification regarding Applicability of New Schedule VI Format 1

Contents About the authors I-5 Chapter-heads I-7 1 ACCOUNTING FOR CORPORATE RESTRUCTURING u Clarification regarding Applicability of New Schedule VI Format 1 SECTION I - AMALGAMATION AND EXTERNAL RECONSTRUCTION

Contents About the authors I-5 Chapter-heads I-7 1 ACCOUNTING FOR CORPORATE RESTRUCTURING u Clarification regarding Applicability of New Schedule VI Format 1 SECTION I - AMALGAMATION AND EXTERNAL RECONSTRUCTION

Ind AS impact. Financial statements to undergo changes, but no major rating or criteria changes foreseen since fundamentals remain the same

Ind AS impact Financial statements to undergo changes, but no major rating or criteria changes foreseen since fundamentals remain the same August 2016 Table of contents Executive summary... 3 Background...

Ind AS impact Financial statements to undergo changes, but no major rating or criteria changes foreseen since fundamentals remain the same August 2016 Table of contents Executive summary... 3 Background...

IASB Update to IAASB. Mary Tokar, Board Member. IFRS Foundation. December 2016

IFRS Foundation IASB Update to IAASB Mary Tokar, Board Member December 2016 The views expressed in this presentation are those of the presenter, not necessarily those of the International Accounting Standards

IFRS Foundation IASB Update to IAASB Mary Tokar, Board Member December 2016 The views expressed in this presentation are those of the presenter, not necessarily those of the International Accounting Standards

The basics December 2011

versus The basics December 2011!@# Table of contents Introduction... 2 Financial statement presentation... 4 Interim financial reporting... 6 Consolidation, joint venture accounting and equity method

versus The basics December 2011!@# Table of contents Introduction... 2 Financial statement presentation... 4 Interim financial reporting... 6 Consolidation, joint venture accounting and equity method

PwC ReportingPerspectives

Special Edition: March 2015 Ind AS: India s accounting standards converged with IFRS are here! p4 /An in-depth analysis: Examining the implications p7 /What is changing from current Indian GAAP? p8 / Ind

Special Edition: March 2015 Ind AS: India s accounting standards converged with IFRS are here! p4 /An in-depth analysis: Examining the implications p7 /What is changing from current Indian GAAP? p8 / Ind

IFRS. B V Subramaniam FCMA A CONCEPTUAL ANALYSIS

IFRS 1 A CONCEPTUAL ANALYSIS INTRODUCTION International Financial Reporting Standards (IFRS) are the world-wide accounting standards which consists of 1) Standards (IFRS statements & IAS standards) 2)

IFRS 1 A CONCEPTUAL ANALYSIS INTRODUCTION International Financial Reporting Standards (IFRS) are the world-wide accounting standards which consists of 1) Standards (IFRS statements & IAS standards) 2)

SUMMARY OF IASB WORK PLAN AS AT 7 NOVEMBER 2018

SUMMARY OF IASB WORK PLAN AS AT 7 NOVEMBER 2018 Page Standard-setting and Related Projects... 3 Management Commentary... 3 Rate-regulated Activities... 4 Research Projects... 5 Business Combinations under

SUMMARY OF IASB WORK PLAN AS AT 7 NOVEMBER 2018 Page Standard-setting and Related Projects... 3 Management Commentary... 3 Rate-regulated Activities... 4 Research Projects... 5 Business Combinations under

Ind AS Transition Challenges & Key takeaways

Ind AS Transition Dolphy D Souza 2 September 2017 Page 1 Ind AS Implementation: A Giant Leap Step in the right direction Substantial improvement in accounting Financial instruments Business combinations

Ind AS Transition Dolphy D Souza 2 September 2017 Page 1 Ind AS Implementation: A Giant Leap Step in the right direction Substantial improvement in accounting Financial instruments Business combinations

IFRS for SMEs IFRS Foundation-World Bank

International Financial Reporting Standards 1 IFRS for SMEs IFRS Foundation-World Bank 26 27 May 2011 Kiev, Ukraine Copyright 2010 IFRS Foundation. All rights reserved. The IFRS for SMEs 2 Topic 1.2 Overview

International Financial Reporting Standards 1 IFRS for SMEs IFRS Foundation-World Bank 26 27 May 2011 Kiev, Ukraine Copyright 2010 IFRS Foundation. All rights reserved. The IFRS for SMEs 2 Topic 1.2 Overview

Recent developments in AS/ IFRS and IND AS Global and India.

Bombay Chartered Accountants Society Recent developments in AS/ IFRS and IND AS Global and India. Presented by: CA P.R.Ramesh December 07, 2011 Contents Amendments to Existing Standards 2 New Pronouncements

Bombay Chartered Accountants Society Recent developments in AS/ IFRS and IND AS Global and India. Presented by: CA P.R.Ramesh December 07, 2011 Contents Amendments to Existing Standards 2 New Pronouncements

Ind AS: Practical perspectives

Ind AS: Practical perspectives Year-end update Issue 3/217 Analysis of published results of Indian listed for the year ended 31 March 217 August 217 KPMG.com/in Table of contents Foreword Introduction

Ind AS: Practical perspectives Year-end update Issue 3/217 Analysis of published results of Indian listed for the year ended 31 March 217 August 217 KPMG.com/in Table of contents Foreword Introduction

IFRS for Boards Boards and Audit Committees Sang Sang--Kiet Ly Kiet Ly A d u i d t dit Par tner Victoria, BC March 1, 2011

IFRS for Boards and Audit Committees Sang-Kiet Ly Audit Partner Victoria, BC March 1, 2011 IFRS The Basics Canada s transition to IFRS Who is affected publicly accountable enterprises To be adopted by

IFRS for Boards and Audit Committees Sang-Kiet Ly Audit Partner Victoria, BC March 1, 2011 IFRS The Basics Canada s transition to IFRS Who is affected publicly accountable enterprises To be adopted by

Wrestling with the First-Time Adoption of IFRS. PwC

Wrestling with the First-Time Adoption of IFRS PwC First time adoption Session outline Exemptions and Preparation of the first IFRS financial statements IFRS 1 General principles Replaces SIC-8 Application

Wrestling with the First-Time Adoption of IFRS PwC First time adoption Session outline Exemptions and Preparation of the first IFRS financial statements IFRS 1 General principles Replaces SIC-8 Application

GN(A) 33 (Issued 2015) Guidance Note on Accounting for Derivative Contracts

33 (Issued 2015) Guidance Note on Accounting for Derivative Contracts") Introduction GN(A) 33 (Issued 2015) Guidance Note on Accounting for Derivative Contracts 1. In the year 2007, the Institute of Chartered Accountants of India (ICAI), issued Accounting Standard (AS) 30,

Introduction GN(A) 33 (Issued 2015) Guidance Note on Accounting for Derivative Contracts 1. In the year 2007, the Institute of Chartered Accountants of India (ICAI), issued Accounting Standard (AS) 30,

Why Global Accounting Standards Are Needed Investors seek investment opportunities all over the world. Companies seek capital at the lowest price anyw

IFRS Convergence Will Enhance Shareholder Value Paul Pacter Director, Deloitte IFRS Global Office ACCA Annual Conference Hong Kong, 23 June 2007 1 Agenda for this Session Why global accounting standards

IFRS Convergence Will Enhance Shareholder Value Paul Pacter Director, Deloitte IFRS Global Office ACCA Annual Conference Hong Kong, 23 June 2007 1 Agenda for this Session Why global accounting standards

Quarterly technical updates. April 2017

Agenda 1 Opening Remarks 2 Regulatory updates 3 Ind AS 4 Q & A 2 1. Opening Remarks 3 2. Regulatory updates 4 Integrated reporting in India SEBI reporting requirement for top 500 companies (by market cap.)

Agenda 1 Opening Remarks 2 Regulatory updates 3 Ind AS 4 Q & A 2 1. Opening Remarks 3 2. Regulatory updates 4 Integrated reporting in India SEBI reporting requirement for top 500 companies (by market cap.)

igaap 2005 in your pocket

igaap 2005 in your pocket A summary of international financial reporting from a UK perspective July 2005 Contents Deloitte guidance 1 Abbreviations used in this publication 2 Current international standards

igaap 2005 in your pocket A summary of international financial reporting from a UK perspective July 2005 Contents Deloitte guidance 1 Abbreviations used in this publication 2 Current international standards

Intergovernmental Working Group of Experts on International Standards of Accounting and Reporting (ISAR)

") Intergovernmental Working Group of Experts on International Standards of Accounting and Reporting (ISAR) 31st SESSION 15-17 October 2014 Room XVIII, Palais des Nations, Geneva Friday, 17 October 2014 Afternoon

Intergovernmental Working Group of Experts on International Standards of Accounting and Reporting (ISAR) 31st SESSION 15-17 October 2014 Room XVIII, Palais des Nations, Geneva Friday, 17 October 2014 Afternoon

Workshop on IND AS Property, plant & equipment WIRC of the ICAI April 23, 2016

Workshop on IND AS Property, plant & equipment WIRC of the ICAI April 23, 2016 Contents Background and Scope Definition Recognition & Measurement On initial recognition Accounting policy for subsequent

Workshop on IND AS Property, plant & equipment WIRC of the ICAI April 23, 2016 Contents Background and Scope Definition Recognition & Measurement On initial recognition Accounting policy for subsequent

GAPCO UGANDA LIMITED. GAPCO Uganda Limited

1 GAPCO Uganda Limited 2 GAPCO UGANDA LIMITED Independent Auditors Report TO THE MEMBERS OF GAPCO UGANDA LIMITED Report on the Financial Statements We have audited the accompanying financial statements

1 GAPCO Uganda Limited 2 GAPCO UGANDA LIMITED Independent Auditors Report TO THE MEMBERS OF GAPCO UGANDA LIMITED Report on the Financial Statements We have audited the accompanying financial statements

Use of Full IFRSs Around the World

Use of IFRSs Worldwide, First-time time Adoption of IFRSs, and IFRS Resources Paul Pacter Deloitte IFRS Global Office Deloitte Taiwan IFRS Seminar Taipei 9 December 2008 1 1. Use of International Financial

Use of IFRSs Worldwide, First-time time Adoption of IFRSs, and IFRS Resources Paul Pacter Deloitte IFRS Global Office Deloitte Taiwan IFRS Seminar Taipei 9 December 2008 1 1. Use of International Financial

Stay informed. Visit IFRS pocket guide 2012

Stay informed. Visit www.pwcinform.com IFRS pocket guide 2012 Introduction Introduction This pocket guide provides a summary of the recognition and measurement requirements of International Financial Reporting

Stay informed. Visit www.pwcinform.com IFRS pocket guide 2012 Introduction Introduction This pocket guide provides a summary of the recognition and measurement requirements of International Financial Reporting

Ernst & Young IFRS Core Tools April IFRS Update. of standards and interpretations in issue at 31 March 2012

Ernst & Young IFRS Core Tools April 2012 IFRS Update of standards and interpretations in issue at 31 March 2012 Contents Introduction 2 Section 1: New pronouncements issued as at 31 March 2012 4 Table

Ernst & Young IFRS Core Tools April 2012 IFRS Update of standards and interpretations in issue at 31 March 2012 Contents Introduction 2 Section 1: New pronouncements issued as at 31 March 2012 4 Table

ACCOUNTING AND AUDITING UPDATE

ACCOUNTING AND AUDITING UPDATE August 2015 In this edition Impact of the new revenue standard on the real estate sector p1 Pushdown accounting: A new basis of accounting in separate financial statements

ACCOUNTING AND AUDITING UPDATE August 2015 In this edition Impact of the new revenue standard on the real estate sector p1 Pushdown accounting: A new basis of accounting in separate financial statements