CP:

|

|

|

- Bernice Adams

- 5 years ago

- Views:

Transcription

1 Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: adengpustikaningsih@uny.ac.id

2 3 The Adjusting Process 2

3 After studying this chapter, you should be able to: 1. Describe the nature of the adjusting process. 2. Journalize entries for accounts requiring adjustment. 3. Summarize the adjustment process. 4. Prepare an adjusted trial balance. 3

4 3-1 Objective 1 Describe the nature of the adjusting process. 34

5 3-1 Under the accrual basis of accounting, revenues are reported in the income statement in the period in which they are earned. 5

6 3-1 The accounting concept that supports this approach to reporting of revenues is called the revenue recognition concept. 6

7 3-1 The accounting concept that supports reporting revenues and related expenses in the same period is called the matching concept, or matching principle. 7

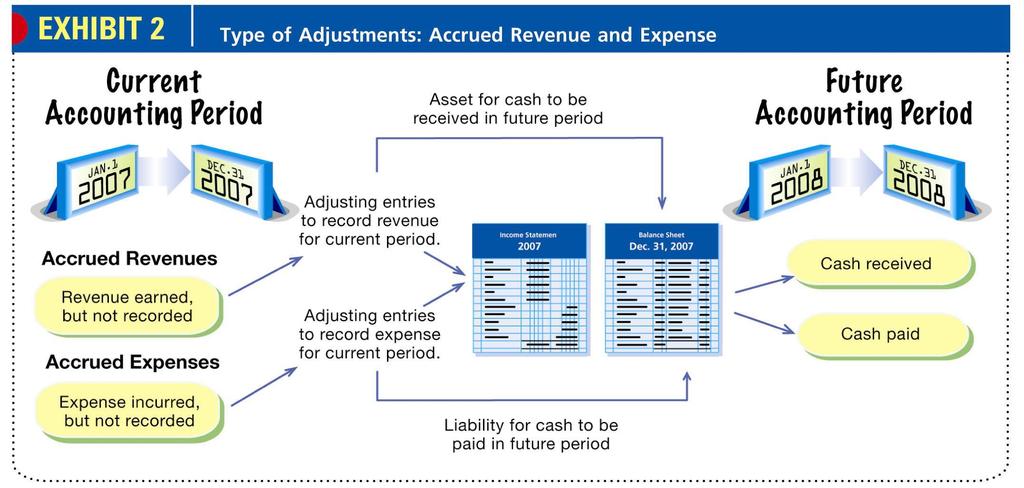

8 3-1 Under the cash basis of accounting, revenues and expenses are reported in the income statement in the period in which cash is received or paid. 8

9 3-1 The analysis and updating of accounts at the end of the period before the financial statements are prepared is called the adjusting process. 9

10 3-1 The journal entries that bring the accounts up to date at the end of the accounting period are called adjusting entries. 10

11 3-1 Example Exercise 3-1 Indicate with a Yes or No whether or not each of the following accounts normally requires an adjusting entry. a. Cash c. Wages Expense e. Accounts Receivable b. Prepaid Rent d. Office Equipment f. Unearned Rent Follow My Example 3-1 a. No c. Yes e. Yes b. Yes d. No f. Yes For Practice: PE 3-1A, PE 3-1B 10 11

12 Items That Need Adjusting 3-1 Prepaid expenses, sometimes referred to as deferred expenses, are items that have been initially recorded as assets but are expected to become expenses over time or through the normal operations of the business. 12

13 Items That Need Adjusting 3-1 Unearned revenues, sometimes referred to as deferred revenues, are items that have been initially recorded as liabilities but are expected to become revenues over time or through the normal operations of the business. 13

14 3-1 Insert Exhibit

15 Items That Need Adjusting 3-1 Accrued revenues, sometimes referred to as accrued assets (accrued means unpaid), are revenues that have been earned but have not been recorded in the accounts. 15

16 Items That Need Adjusting 3-1 Accrued expenses, sometimes referred to as accrued liabilities, are expenses that have been incurred but have not been recorded in the accounts. 16

17

18 3-1 Example Exercise 3-2 Classify the following items as (1) prepaid expense, (2) unearned revenue, (3) accrued expense, or (4) accrued revenue. a. Wages owed but not c. Fees received but not yet yet paid. earned. b. Supplies on hand. d. Fees earned but not yet received. Follow My Example 3-2 a. Accrued expense c. Unearned revenue b. Prepaid expense d. Accrued revenue For Practice: PE 3-2A, PE 3-2B 17 18

19 3-2 Objective 2 Journalize entries for accounts requiring adjustment. 19

20 Unadjusted Trial Balance for SolusiNet SolusiNet Adjusted Trial Balance December 31, 2007 Debit Balances Credit Balances Cash Accounts Receivable Supplies Prepaid Insurance Land Office Equipment Accumulated Depreciation-Equipment Accounts Payable Wages Payable Unearned Rent Cinta Cita, Capital Cinta Cita, Drawing Fees Earned Rent Revenue Wages Expense Rent Expense Depreciation Expense Utilities Expense Supplies Expense Insurance Expense Misscellaneous Expense

21 Adjusting Process for Prepaid Expenses SolusiNet Supplies account has a balance of Rp2,000,000 in the unadjusted trial balance. Some of these supplies have been used. On December 31, a count reveals that Rp760,000 of supplies are on hand. 21

22 3-2 Supplies (balance on trial balance) Rp2,000,000 Supplies on hand, December ,000 Supplies used Rp1,240,000 22

23 Dec. 31 Supplies Expense Supplies Supplies used (Rp2,000,000 Rp760,000) Bal. 2,000, ,000 Supplies Supplies Expense Dec. 31 1,240,000 Bal. 800,000 Dec. 31 1,240,000 2,040,

24 The debit balance of Rp2,400,000 in SolusiNet Prepaid Insurance account represents the December 1 prepayment of insurance for 12 months. 24

25 Insurance Expense Prepaid Insurance Insurance expired (Rp2,400,000/12). Prepaid Insurance 15 Insurance Expense 56 Bal. 2,400,000 Dec ,000 Dec ,000 2,200,

26 3-2 Example Exercise 3-3 The prepaid insurance account had a beginning balance of Rp6,400,000 and was debited for Rp3,600,000 of premiums paid during the year. Journalize the adjusting entry required at the end of the year assuming the amount of unexpired insurance related to future periods is Rp3,250,000. Follow My Example 3-3 Insurance Expense 6,750,000 Prepaid Insurance 6,750,000 Insurance expired (Rp6,400,000 + Rp3,600,000 Rp3,250,000). For Practice: PE 3-3A, PE 3-3B 25 26

27 On December 1, the tenant prepaid three months rent for use of an office building owned by SolusiNet. As of December 31, only Rp120,000 has been earned. 27

28 Unearned Rent Rent Revenue Rent earned (Rp360,000/3 months) Unearned Rent 23 Rent Revenue 42 Dec ,000 Bal. 360,000 Dec ,000 Bal. 240,

29 3-2 Example Exercise 3-4 The balance in the unearned fees account, before adjustment at the end of the year, is Rp44,900,000. Journalize the adjusting entry required if the amount of unearned fees at the end of the year is Rp22,300,000. Follow My Example 3-4 Unearned Fees 22,600,000 Fees Earned 22,600,000 Fees earned (Rp44,900,000 Rp22,300,000). For Practice: PE 3-4A, PE 3-4B 29 28

30 SolusiNet provided Rp500,000 in services during December for which the customer has not been billed. 30

31 Accounts Receivable Fees Earned Accrued fees (25 hrs. x Rp20,000) Accounts Receivable 12 Fees Earned 41 Bal. 2,220,000 Bal. 16,340,000 Dec ,000 Dec ,000 Bal. 2,720,000 Bal. 16,840,

32 3-2 Example Exercise 3-5 At the end of the current year, Rp13,680,000 of fees have been earned but have not been billed to clients. Journalize the adjusting entry to record the accrued fees. Follow My Example 3-5 Accounts Receivable 13,680,000 Fees Earned 13,680,000 Accrued fees. For Practice: PE 3-5A, PE 3-5B 31 32

33 At the end of December, accrued wages amounted to Rp250,000. Without this adjusting entry, Wages Expense is understated. 33

34 Wages Expense Wages Payable Accrued wages. Wages Payable 22 Wages Expense 51 Dec ,000 Bal. 4,275,000 Dec ,000 Bal. 4,525,

35 3-2 Wages Payable 22 Wages Expense 51 Dec ,000 Bal. 4,275,000 Dec ,000 Bal. 4,525,000 Closing entries will be discussed in a later chapter. For now, just be aware that Wages Expense is closed after financial statements are prepare and its balance rolled back to zero

36 3-2 The payment of January 10 wages totaling Rp1,275,000 is shown below. Jan. 10 Wages Expense Wages Payable Cash

37 3-2 Wages Payable 22 Wages Expense 51 Jan ,000 Dec ,000 Bal. 4,275,000 Dec ,000 Bal. 4,525,000 The liability is cancelled. Jan.10 1,025,000 An expense for wages of Rp1,025,000 is recorded in the new fiscal year

38 Example Exercise 3-6 PT Sumitama Daya pays weekly salaries of Rp12,500,000 on Friday for a five-day week ending on that day. Journalize the necessary adjusting entry at the end of the accounting period, assuming that the period ends on Thursday. Follow My Example 3-6 Salaries Expense 10,000,000 Salaries Payable 10,000,000 Accrued salaries (Rp12,500,000/5 x 4 days). For Practice: PE 3-6A, PE 3-6B

39 Physical resources that are owned and used by a business and are permanent or have a long life are called fixed assets, or plant assets. 39

40 3-2 As time passes, a fixed asset loses its ability to provide useful services. This decrease in usefulness is called depreciation. 40

41 3-2 Normal titles for fixed asset accounts and their related contra asset accounts are as follows: Fixed Asset Land Buildings Store Equipment Office Equipment Contra Asset None Land is not depreciated Accumulated Depreciation Buildings Accumulate Depreciation Store Equipment Accumulated Depreciation Office Equipment 41

42 SolusiNet estimates the depreciation on its office equipment to be Rp50,000 for the month of December. 42

43 Depreciation Expense Accum. Depreciation Office Equipment Depreciation of office equipment. Depreciation Expense Dec , Accum. Depr. Office Equip. 19 Dec ,

44 3-2 SolusiNet balance sheet would show the office equipment at cost, less the accumulated depreciation. Office equipment Rp1,800,000 Less accumulated depreciation 50,000 Rp1,750,000 Book value 44

45 3-2 Example Exercise 3-7 The estimated amount of depreciation on equipment for the current year is Rp4,250,000. Journalize the adjusting entry to record the depreciation. Follow My Example 3-7 Depreciation Expense 4,250,000 Accumulated Depreciation Equipment 4,250,000 Depreciation on equipment. For Practice: PE 3-7A, PE 3-7B 44 45

46 3-3 Objective 3 Summarize the adjustment process 46

47 Adjusting Entry SolusiNet 3-3 JOURNAL Post Date Description Ref Debit Credit Adjusting Entries Dec Supplies Expense Supplies Supplies used (Rp2,000,000 - Rp 760,000) 31 Insurance Expense Prepaid Insurance Insrance expired (Rp2,400,000/12 months) 31 Unearned Rent Rent Revenue Rent earned (Rp360,000/3months) 31 Accounts Receivable Fees Earned Accrued fees (25 hrs. Rp20,000) 31 Wages Expense Wages Payable Accrued wages. 31 Depreciation Expense Accum. Depr.-Office Equip Depreciation on office equip. 47

48 (In Rp000) 3-3 (Continued) Ledger with Adjusting Entries SolusiNet 47 48

49 (Continued) 3-3 Ledger with Adjusting Entries SolusiNet (In Rp000) 48 49

3-3 (In")

50 Ledger with Adjusting Entries SolusiNet (Continued) 3-3 (In Rp000) 49 50

3-3 (In")

51 Ledger with Adjusting Entries SolusiNet (Concluded) 3-3 (In Rp000) 51 50

52 Example Exercise 3-8 For the year ending December 31, 2008, Mega Medika mistakenly omitted adjusting entries for (1) Rp8,600,000 of unearned revenue that was earned, (2) earned revenue that was not billed of Rp12,500,000, and (3) accrued wages of Rp2,900,000. Indicate the combined effect of the errors on (a) revenues, (b) expenses, and (c) net income for Follow My Example 3-8 a. Revenues were understated by Rp21,100,000 (Rp8,600,000 + Rp12,500,000). b. Expenses were understated by Rp2,900,000. c. Net income was understated by Rp18,200,000 (Rp8,600,000 +Rp12,500,000 Rp2,900,000). For Practice: PE 3-8A, PE 3-8B

53 3-4 Objective 4 Prepare an adjusted trial balance. 53

54 3-4 The purpose of the adjusted trial balance is to verify the equality of the total debit balances and total credit balances before the financial statements are prepared. 54

55 3-4 SolusiNet Adjusted Trial Balance December 31, 2007 Debit Balances Credit Balances Cash Accounts Receivable Supplies Prepaid Insurance Land Office Equipment Accumulated Depreciation-Equipment Accounts Payable Wages Payable Unearned Rent Cinta Cita, Capital Cinta Cita, Drawing Fees Earned Rent Revenue Wages Expense Rent Expense Depreciation Expense Utilities Expense Supplies Expense Insurance Expense Misscellaneous Expense

56 Example Exercise 3-9 For each of the following errors, considered individually, indicate whether the error would cause the adjusted trial balance totals to be unequal. If the error would cause the adjusted trial balance total to be unequal, indicate whether the debit or credit total is higher and by how much. a. The adjustment for accrued fees of Rp5,340,000 was journalized as a debit to Accounts Payable for Rp5,340,000 and a credit to Fees Earned of Rp5,340,000. b. The adjustment for depreciation of Rp3,260,000 was journalized as a debit to Depreciation Expense for Rp3,620,000 and a credit to Accumulated Depreciation for Rp3,260,

57 3-4 Follow My Example 3-9 a. The totals are equal even though the debit should have been to Accounts Receivable instead of Accounts Payable. b. The totals are unequal. The debit total is higher by Rp360,000 (Rp3,620,000 Rp3,260,000). For Practice: PE 3-9A, PE 3-9B 57 56

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 1 2 6 Accounting for Merchandising

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 1 2 6 Accounting for Merchandising

Do you subscribe to any magazines? Most of us subscribe

C H A P T E R 3 The Adjusting Process AP Photo/Jeff Kravitz M A R V E L E N T E R T A I N M E N T, I N C. Do you subscribe to any magazines? Most of us subscribe to one or more magazines such as Cosmopolitan,

C H A P T E R 3 The Adjusting Process AP Photo/Jeff Kravitz M A R V E L E N T E R T A I N M E N T, I N C. Do you subscribe to any magazines? Most of us subscribe to one or more magazines such as Cosmopolitan,

Click to edit Master title style

1 Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 1 2 15 Bonds Payable and Investments

1 Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 1 2 15 Bonds Payable and Investments

Click to edit Master title style

1 Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 1 2 Income Taxes, 14 Unusual Income

1 Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 1 2 Income Taxes, 14 Unusual Income

Chapter 3 the Adjusting Process. Learning Objective 1 Describe the nature of the adjusting process.

1 Chapter 3 Adjusting Process Chapter 3 the Adjusting Process Learning Objective 1 Describe the nature of the adjusting process. Nature of the Adjusting Process General concept: revenues are earned when

1 Chapter 3 Adjusting Process Chapter 3 the Adjusting Process Learning Objective 1 Describe the nature of the adjusting process. Nature of the Adjusting Process General concept: revenues are earned when

Chapter 4 Question Review 1

Chapter 4 Question Review 1 Chapter 4 Questions Multiple Choice 1. The final step in the accounting cycle is to prepare: a. closing entries. b. financial statements. c. a post-closing trial balance. d.

Chapter 4 Question Review 1 Chapter 4 Questions Multiple Choice 1. The final step in the accounting cycle is to prepare: a. closing entries. b. financial statements. c. a post-closing trial balance. d.

The Accounting Cycle: Accruals and Deferrals

The Accounting Cycle: Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Adjusting Entries Adjusting entries are needed whenever revenue

The Accounting Cycle: Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin Copyright 2010 by The McGraw-Hill Companies, Inc. All rights reserved. Adjusting Entries Adjusting entries are needed whenever revenue

Click to edit Master title style

1 Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 1 2 Corporations: 13 Organization,

1 Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 1 2 Corporations: 13 Organization,

The Accounting Cycle Accruals and Deferrals

The Accounting Cycle Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J.

The Accounting Cycle Accruals and Deferrals Chapter 4 McGraw-Hill/Irwin PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J.

THE ACCOUNTING CYCLE: Accruals and Deferrals

Chapter 4 THE ACCOUNTING CYCLE: Accruals and Deferrals Presented by: Endra M. Sagoro Economic Faculty YSU endra_ms@uny.ac.id At the end of the period, we need to make adjusting entries to get the accounts

Chapter 4 THE ACCOUNTING CYCLE: Accruals and Deferrals Presented by: Endra M. Sagoro Economic Faculty YSU endra_ms@uny.ac.id At the end of the period, we need to make adjusting entries to get the accounts

Click to edit Master title style

1 Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 1 2 9 Receivables 2 3 After studying

1 Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 1 2 9 Receivables 2 3 After studying

PE 3 1A Page 131 Indicate with a Yes or No whether or not each of the following accounts normally requires an adjusted entry.

PE 3 1A Page 131 Indicate with a Yes or No whether or not each of the following accounts normally requires an adjusted entry. A. Accumulated Depreciation yes B. Albert Stucky, Drawings No C. Office equipment

PE 3 1A Page 131 Indicate with a Yes or No whether or not each of the following accounts normally requires an adjusted entry. A. Accumulated Depreciation yes B. Albert Stucky, Drawings No C. Office equipment

Chapter 3 The Adjusting Process

Instant download and all chapters Solution Manual Horngren s Financial Managerial Accounting 4th Edition Tracie L. Nobles, Brenda L. Mattison, Ella Mae Matsumura https://testbankdata.com/download/solution-manual-horngrens-financialmanagerial-accounting-4th-edition-tracie-l-nobles-brenda-l-mattison-ella-maematsumura/

Instant download and all chapters Solution Manual Horngren s Financial Managerial Accounting 4th Edition Tracie L. Nobles, Brenda L. Mattison, Ella Mae Matsumura https://testbankdata.com/download/solution-manual-horngrens-financialmanagerial-accounting-4th-edition-tracie-l-nobles-brenda-l-mattison-ella-maematsumura/

The Adjustment Process and Financial Statements Irwin/McGraw-Hill

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

Chapter 4 The Adjustment Process and Financial Statements Business Background: The Accounting Cycle Phase 1: During the Accounting Period. Start of the Accounting Period! Perform transaction analysis.!

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 20-1 20-2 PREVIEW OF CHAPTER 20 20-3

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 20-1 20-2 PREVIEW OF CHAPTER 20 20-3

Accounting Cycle Review Problem. Michelle Clark. Accounting 1110 Section 401. Fall 2014

Accounting Cycle Review Problem Michelle Clark Accounting 1110 Section 401 Fall 2014 General Journal DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Record Transactions, Adjusting Entries, Closing Entries

Accounting Cycle Review Problem Michelle Clark Accounting 1110 Section 401 Fall 2014 General Journal DATE ACCOUNT TITLES AND EXPLANATION DEBIT CREDIT Record Transactions, Adjusting Entries, Closing Entries

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 22-1 22-2 PREVIEW OF CHAPTER 22 22-3

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 22-1 22-2 PREVIEW OF CHAPTER 22 22-3

Accounting 1A Class Notes Chapter 3 The Adjusting Process

Source Documents General Journal General Ledger Trial Balance Adjusting Entries Difference between TRANSACTIONS and ADJUSTMENTS Transactions occur through-out the accounting cycle and normally involve

Source Documents General Journal General Ledger Trial Balance Adjusting Entries Difference between TRANSACTIONS and ADJUSTMENTS Transactions occur through-out the accounting cycle and normally involve

After studying this chapter, you should be able to: adjusted account balances.

4 Completing the Accounting Cycle 1 After studying this chapter, you should be able to: 1. Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance

4 Completing the Accounting Cycle 1 After studying this chapter, you should be able to: 1. Describe the flow of accounting information from the unadjusted trial balance into the adjusted trial balance

Chapter 4: Completing the Accounting Cycle

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

1 Chapter 4 Completing the Accounting cycle Chapter 4: Completing the Accounting Cycle Learning Objective 1 Describe the financial statements of a proprietorship and explain how they interrelate. Financial

Learning Outcomes. The Basic Accounting Cycle

Chapter 2: Review of the Accounting Process Part 3: Accounting Cycle with Emphasis on Year End Activities Intermediate Accounting 1 Dr. Chula King Learning Outcomes After completing this part, you should

Chapter 2: Review of the Accounting Process Part 3: Accounting Cycle with Emphasis on Year End Activities Intermediate Accounting 1 Dr. Chula King Learning Outcomes After completing this part, you should

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 5-1 5-2 PREVIEW OF CHAPTER 5 5-3

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 5-1 5-2 PREVIEW OF CHAPTER 5 5-3

Financial & Managerial Accounting 13th Edition Solutions Manual Warren

Financial & Managerial Accounting 13th Edition Solutions Manual Warren Completed downloadable package SOLUTIONS MANUAL for Financial & Managerial Accounting 13th Edition by Carl S Warren, James M Reeve,

Financial & Managerial Accounting 13th Edition Solutions Manual Warren Completed downloadable package SOLUTIONS MANUAL for Financial & Managerial Accounting 13th Edition by Carl S Warren, James M Reeve,

2014 Mar. 31 Balance 30, Adjusting 26 22,500 7, Mar. 31 Balance 3, Adjusting 26 1,800 1,800

Prob. 4 4A 1., 3., and 6. Cash Account No. 11 Mar. 31 12,000 Supplies Account No. 13 Mar. 31 30,000 31 Adjusting 26 22,500 7,500 Prepaid Insurance Account No. 14 Mar. 31 3,600 31 Adjusting 26 1,800 1,800

Prob. 4 4A 1., 3., and 6. Cash Account No. 11 Mar. 31 12,000 Supplies Account No. 13 Mar. 31 30,000 31 Adjusting 26 22,500 7,500 Prepaid Insurance Account No. 14 Mar. 31 3,600 31 Adjusting 26 1,800 1,800

Chapter 4: Completing the Accounting Cycle. Learning Objective 2 Prepare financial statements from adjusted account balances.

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

1 Chapter 4 Completing the Accounting Cycle Chapter 4: Completing the Accounting Cycle Learning Objective 2 Prepare financial statements from adjusted account balances. From chapter 3 NetSolutions Adjusted

CHAPTER 3 THE ADJUSTING PROCESS

1. a. Under cash-basis accounting, revenues are reported in the period in which cash is received and expenses are reported in the period in which cash is paid. b. Under accrual-basis accounting, revenues

1. a. Under cash-basis accounting, revenues are reported in the period in which cash is received and expenses are reported in the period in which cash is paid. b. Under accrual-basis accounting, revenues

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

Learning Objective. LO1 Prepare an income statement for a merchandising business organized as a corporation.

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

Learning Objective LO1 Prepare an income statement for a merchandising business organized as a corporation. Lesson 16-1 Uses of Financial Statements LO1 A corporation prepares an income statement and a

Chapter 4. The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio

Chapter 4 The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio The Accounting Cycle Accounting cycle process Records individual transactions Produces the four basic financial

Chapter 4 The Accounting Cycle Adjusting Entries Closing Process Net Profit Margin Ratio The Accounting Cycle Accounting cycle process Records individual transactions Produces the four basic financial

Week 3. Topic 3 Chapter 3. ACT102 Introduction to Accounting. Accounting for end of financial period adjustments 21/02/2018

ACT102 Introduction to Accounting Week 3 Accounting for end of financial period adjustments Topic 3 Chapter 3 2 RECAP Topic 2: Recording Business Transactions The accounting equation must always balance

ACT102 Introduction to Accounting Week 3 Accounting for end of financial period adjustments Topic 3 Chapter 3 2 RECAP Topic 2: Recording Business Transactions The accounting equation must always balance

SOLUTIONS Learning Goal 8

Learning Goal 8: Prepare Closing Entries S1 Learning Goal 8 Multiple Choice 1. d 2. a 3. b 4. d Because the dividends account is closed directly into the retained earnings account, not into income summary.

Learning Goal 8: Prepare Closing Entries S1 Learning Goal 8 Multiple Choice 1. d 2. a 3. b 4. d Because the dividends account is closed directly into the retained earnings account, not into income summary.

Acct 151A Week 7, Chap 6. Instructor: Michael Booth Cabrillo College

Acct 151A Week 7, Chap 6 Instructor: Michael Booth Cabrillo College McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Closing Entries and the Postclosing Trial Balance Closing Entries

Acct 151A Week 7, Chap 6 Instructor: Michael Booth Cabrillo College McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. Closing Entries and the Postclosing Trial Balance Closing Entries

Chapter 5 Accrual Adjustments and Financial Statement Preparation. Revenue recognition Matching expenses to revenues Expenses related to periods

Chapter 5 Accrual Adjustments and Financial Statement Preparation Revenue recognition Matching expenses to revenues Expenses related to periods 1 The Measurement of Income major function of accounting

Chapter 5 Accrual Adjustments and Financial Statement Preparation Revenue recognition Matching expenses to revenues Expenses related to periods 1 The Measurement of Income major function of accounting

Chapter 3. Learning Objectives. Distinguish accrual accounting from cash-basis accounting. Objective 1. The Adjusting Process

PowerPoint to accompany Chapter 3 The Adjusting Process Learning Objectives 1. Distinguish accrual accounting from cash-basis accounting. 2. Make adjusting entries at the end of the accounting period.

PowerPoint to accompany Chapter 3 The Adjusting Process Learning Objectives 1. Distinguish accrual accounting from cash-basis accounting. 2. Make adjusting entries at the end of the accounting period.

Chapter 17 Accounting for Accruals and Deferrals

Chapter 17 Accounting for Accruals and Deferrals o Understand Accrual and Deferrals o Accrued Expense o Accrued Revenue o Deferred Expense o Deferred Revenue 1 Accruals and Deferrals Accruals Expenses

Chapter 17 Accounting for Accruals and Deferrals o Understand Accrual and Deferrals o Accrued Expense o Accrued Revenue o Deferred Expense o Deferred Revenue 1 Accruals and Deferrals Accruals Expenses

REINFORCEMENT ACTIVITY 3, Part B, p. 715

REINFORCEMENT ACTIVITY 3, Part B, p. 715 10. Unadjusted Trial Balance December 31, 20X4 ACCOUNT TITLE DEBIT CREDIT Cash 25 0 0 1 40 Petty Cash 4 0 0 00 Accounts Receivable 15 7 8 9 20 Allowance for Uncollectible

REINFORCEMENT ACTIVITY 3, Part B, p. 715 10. Unadjusted Trial Balance December 31, 20X4 ACCOUNT TITLE DEBIT CREDIT Cash 25 0 0 1 40 Petty Cash 4 0 0 00 Accounts Receivable 15 7 8 9 20 Allowance for Uncollectible

Business Background Management is responsible for preparing...

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

Business Background Management is responsible for preparing... Financial Statements High Quality = Relevance + Reliability... Are useful to investors and creditors. Business Background Revenues are recorded

Adjustments, Financial Statements and the Quality of Earnings

Adjustments, Financial Statements and the Quality of Earnings Chapter 4 Accounting Cycle 4-2 1 Unadjusted Trial Balance Listing of all the balance sheet and income statement accounts, usually in financial

Adjustments, Financial Statements and the Quality of Earnings Chapter 4 Accounting Cycle 4-2 1 Unadjusted Trial Balance Listing of all the balance sheet and income statement accounts, usually in financial

Chapter 2 Analyzing Transactions

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

1 Chapter 2 Analyzing Transactions Chapter 2 Analyzing Transactions From Chapter 1: The Accounting Equation Assets = Liabilities + Owner's Equity Assets = Liabilities + Capital Drawing + Revenues - Expenses

Ch.4 The Accounting Cycle for a Service Business (cont )

") Ch.4 The Accounting Cycle for a Service Business (cont ) Adjusting entries using T-accounts Work with a Worksheet for a service business Prepare Financial Statements Journalizing and posting adjusting

Ch.4 The Accounting Cycle for a Service Business (cont ) Adjusting entries using T-accounts Work with a Worksheet for a service business Prepare Financial Statements Journalizing and posting adjusting

Cash. Laundry Equipment. Hilda Dinero, Capital Oct. 31 Clos. 1,000 Oct. 31 Bal. 18, Clos. 12, Bal. 30,200

1, 3, 6. Oct. 31 Bal. 1,450 Cash Laundry Supplies Oct. 31 Bal. 3,750 Oct. 31 Adj. 2,800 31 Adj. Bal. 950 Prepaid Insurance Oct. 31 Bal. 2,400 Oct. 31 Adj. 2,000 31 Adj. Bal. 400 Oct. 31 Bal. 54,500 Laundry

1, 3, 6. Oct. 31 Bal. 1,450 Cash Laundry Supplies Oct. 31 Bal. 3,750 Oct. 31 Adj. 2,800 31 Adj. Bal. 950 Prepaid Insurance Oct. 31 Bal. 2,400 Oct. 31 Adj. 2,000 31 Adj. Bal. 400 Oct. 31 Bal. 54,500 Laundry

CHAPTER 3. Adjusting the Accounts 6, 7 1 8, 9, 10, 11, 12, 13, 18, 19, , 18 6A 12, 13 14, 15

CHAPTER 3 Adjusting the Accounts ASSIGNMENT CLASSIFICATION TABLE Learning Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems *1. Explain the time period assumption. *2. Explain

CHAPTER 3 Adjusting the Accounts ASSIGNMENT CLASSIFICATION TABLE Learning Objectives Questions Brief Exercises Do It! Exercises A Problems B Problems *1. Explain the time period assumption. *2. Explain

Dec. 4: Paid $ 750 cash for office supplies. Date Accounts Debit Credit Dec. 4 Office Supplies 750 Cash 750

Requirement 1. Record each transaction in the journal. Explanations are not required. (Record debits first, then credits. Exclude explanations from journal entries.) 1: began operations by receiving $

Requirement 1. Record each transaction in the journal. Explanations are not required. (Record debits first, then credits. Exclude explanations from journal entries.) 1: began operations by receiving $

Fill-in-the-Blank Equations. Exercises

Chapter 3 The Adjusting Process Study Guide Solutions 1. Net book value Fill-in-the-Blank Equations 2. Depreciation expense 3. Supplies expense 4. Expense Exercises 1. Determine if each of the following

Chapter 3 The Adjusting Process Study Guide Solutions 1. Net book value Fill-in-the-Blank Equations 2. Depreciation expense 3. Supplies expense 4. Expense Exercises 1. Determine if each of the following

Adjusting the Accounts

HOSP 1860 (Financial Acct) Learning Centre Adjusting the Accounts Anytime we prepare financial statements or reach the end of an accounting period, there are account adjustments that need to be made to

HOSP 1860 (Financial Acct) Learning Centre Adjusting the Accounts Anytime we prepare financial statements or reach the end of an accounting period, there are account adjustments that need to be made to

MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 3)

") MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 3) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following statement shows the revenues and expenses of the

MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 3) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following statement shows the revenues and expenses of the

Some deferred items for which adjusting entries would be made include: Prepaid insurance Prepaid rent Office supplies Depreciation Unearned revenue

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

WWW.VUTUBE.EDU.PK Paper 1 MIDTERM EXAMINATION Spring 2009 FIN621- Financial Statement Analysis (Session - 1) Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the acronym for GAAP?

CHAPTER 3 THE ACCOUNTING INFORMATION SYSTEM. MULTIPLE CHOICE Conceptual. Test Bank Chapter 3

CHAPTER 3 THE ACCOUNTING INFORMATION SYSTEM MULTIPLE CHOICE Conceptual Answer No. Description d 1. Purpose of an accounting system. d 2. Criteria for recording events. c 3. Purpose of trial balance. b

CHAPTER 3 THE ACCOUNTING INFORMATION SYSTEM MULTIPLE CHOICE Conceptual Answer No. Description d 1. Purpose of an accounting system. d 2. Criteria for recording events. c 3. Purpose of trial balance. b

Adjusting the Accounts

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

3-1 Chapter 3 Adjusting the Accounts Learning Objectives After studying this chapter, you should be able to: 1. Explain the time period assumption. 2. Explain the accrual basis of accounting. 3. Explain

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty

Chapter 2 Review of the Accounting Process AACSB assurance of learning standards in accounting and business education require documentation of outcomes assessment. Although schools, departments, and faculty

Chapter 2 Review of the Accounting Process

True/False Questions 1. Owners' equity can be expressed as assets minus liabilities. True Learning Objective: 1 Level of Learning: 1 2. Debits increase asset accounts and decrease liability accounts. True

True/False Questions 1. Owners' equity can be expressed as assets minus liabilities. True Learning Objective: 1 Level of Learning: 1 2. Debits increase asset accounts and decrease liability accounts. True

PRINCIPLES OF FINANCIAL ACCOUNTING CANADIAN EDITION

WEYGANDT. KIO. KIMMEL. TRENHOLM. KINNEAR. BARLOW. ATKINS PRINCIPLES OF FINANCIAL ACCOUNTING CANADIAN EDITION Chapter 3 Adjusting the Accounts PART 1 Prepared by: Debbie Musil Kwantlen Polytechnic University

WEYGANDT. KIO. KIMMEL. TRENHOLM. KINNEAR. BARLOW. ATKINS PRINCIPLES OF FINANCIAL ACCOUNTING CANADIAN EDITION Chapter 3 Adjusting the Accounts PART 1 Prepared by: Debbie Musil Kwantlen Polytechnic University

ACCOUNTING 201. PRACTICE MIDTERM - (Covering Chapters 1-5)

") Problem - I Multiple Choice (20 points) ACCOUNTING 201 PRACTICE MIDTERM - (Covering Chapters 1-5) 1. A private organization which establishes broad accounting principles as well as specific accounting

Problem - I Multiple Choice (20 points) ACCOUNTING 201 PRACTICE MIDTERM - (Covering Chapters 1-5) 1. A private organization which establishes broad accounting principles as well as specific accounting

Ch.2 A Review of the Accounting Cycle

Ch.2 A Review of the Accounting Cycle 1. Basic steps in the accounting process (accounting cycle) 2. Analyze transactions and make and post journal entries 3. Make adjusting entries, produce financial

Ch.2 A Review of the Accounting Cycle 1. Basic steps in the accounting process (accounting cycle) 2. Analyze transactions and make and post journal entries 3. Make adjusting entries, produce financial

Chapter 5 Accrual Adjustments and Financial Statement Preparation. Revenue recognition Matching expenses to revenues Expenses related to periods

Chapter 5 Accrual Adjustments and Financial Statement Preparation Revenue recognition Matching expenses to revenues Expenses related to periods 1 The Measurement of Income major function of accounting

Chapter 5 Accrual Adjustments and Financial Statement Preparation Revenue recognition Matching expenses to revenues Expenses related to periods 1 The Measurement of Income major function of accounting

CHAPTER 3 Adjusting the Accounts

Solutions Manual Financial and Managerial Accounting, 2nd Edition Weygandt Kimmel Kieso Completed Instant download SOLUTIONS MANUAL for Financial and Managerial Accounting, 2nd Edition by Jerry J. Weygandt,

Solutions Manual Financial and Managerial Accounting, 2nd Edition Weygandt Kimmel Kieso Completed Instant download SOLUTIONS MANUAL for Financial and Managerial Accounting, 2nd Edition by Jerry J. Weygandt,

The Accounting Cycle. End of the Period C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM

The Accounting Cycle End of the Period E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information,

The Accounting Cycle End of the Period E DWIN R ENÁN MALDONADO C AT EDRÁTICO U PR R I O P I EDRAS S EG. S EM. 2 017-18 Textbook: Financial Accounting, Spiceland This presentation contains information,

Chapter 2 Review of the Accounting Process

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Chapter 2 Review of the Accounting Process QUESTIONS FOR REVIEW OF KEY TOPICS Question 2 1 External events involve an exchange transaction between the company and a separate economic entity. For every

Adjustments, Financial Statements, and the Quality of Earnings

Adjustments, Financial Statements, and the Quality of Earnings Chapter 4 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Understanding the Business Management is responsible for preparing... Financial

Adjustments, Financial Statements, and the Quality of Earnings Chapter 4 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Understanding the Business Management is responsible for preparing... Financial

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 11-1 11-2 PREVIEW OF CHAPTER 11 11-3

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 11-1 11-2 PREVIEW OF CHAPTER 11 11-3

4/9/2012. Accrual Accounting and Financial Statements. Learning Objectives (LO) LO 1 - Adjustments to the Accounts. Learning Objectives (LO)

LO 1 - Adjustments to the Accounts. Learning Objectives (LO)") Accrual Accounting and Financial s CHAPTER 4 Learning Objectives (LO) After studying this chapter, you should be able to 1. Understand the role of adjustments in accrual accounting 2. Make adjustments

Accrual Accounting and Financial s CHAPTER 4 Learning Objectives (LO) After studying this chapter, you should be able to 1. Understand the role of adjustments in accrual accounting 2. Make adjustments

Adjusting The Accounts

3 Adjusting The Accounts Learning Objectives 1 2 Explain the accrual basis of accounting and the reasons for adjusting entries. Prepare adjusting entries for deferrals. 3 Prepare adjusting entries for

3 Adjusting The Accounts Learning Objectives 1 2 Explain the accrual basis of accounting and the reasons for adjusting entries. Prepare adjusting entries for deferrals. 3 Prepare adjusting entries for

Chapter 2 Review of the Accounting Process

Intermediate Accounting 8th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-8th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Intermediate Accounting 8th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-8th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

PROBLEM 3-2B. (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense Prepaid Insurance...

J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense Prepaid Insurance...") PROBLEM 3-2B (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense... 722 190 Prepaid Insurance... ($2,280 X 1/12) 130 190 31 Supplies Expense... Supplies ($2,200 $)... 631 126 1,450 1,450

PROBLEM 3-2B (a) J1 Date Account Titles Ref. Debit Credit May 31 Insurance Expense... 722 190 Prepaid Insurance... ($2,280 X 1/12) 130 190 31 Supplies Expense... Supplies ($2,200 $)... 631 126 1,450 1,450

Chapter 2 Review of the Accounting Process

Intermediate Accounting 9th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-9th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Intermediate Accounting 9th Edition Spiceland Solutions Manual Full Download: http://testbanklive.com/download/intermediate-accounting-9th-edition-spiceland-solutions-manual/ Chapter 2 Review of the Accounting

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1 In this chapter of notes I ll provide a complete example of the accounting cycle. The order of the tasks to complete

Prof Albrecht s Notes Example of Complete Accounting Cycle Intermediate Accounting 1 In this chapter of notes I ll provide a complete example of the accounting cycle. The order of the tasks to complete

Enter account titles and their unadjusted balances in the Trial Balance columns Total the amounts

Process by which companies produce their financial statements Chapter 4 Copyright 2009 Prentice Hall. All rights reserved 2 Journalize Transaction Post to Accounts Adjust Accounts Prepare an accounting

Process by which companies produce their financial statements Chapter 4 Copyright 2009 Prentice Hall. All rights reserved 2 Journalize Transaction Post to Accounts Adjust Accounts Prepare an accounting

Unit five: Adjusting the accounts Accruals and Prepayments

Unit five: Adjusting the accounts Accruals and Prepayments اسم الطالب:... رقم الطالب:... الصف:... المدرسة:... الرقم التسلسلي Uploaded By: Ayman Ayyad (Danger3) Prepare by T. Abdul Jalil Alaiwi Uploaded

Unit five: Adjusting the accounts Accruals and Prepayments اسم الطالب:... رقم الطالب:... الصف:... المدرسة:... الرقم التسلسلي Uploaded By: Ayman Ayyad (Danger3) Prepare by T. Abdul Jalil Alaiwi Uploaded

Completing the accounting cycle

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd Learning Objectives 1. Understand all the steps in the complete

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd Learning Objectives 1. Understand all the steps in the complete

Completing the accounting cycle

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd THE COMPLETE ACCOUNTING CYCLE 1. Recognise and record transactions

Chapter 5 Completing the accounting cycle PowerPoint presentation by Anne Abraham University of Wollongong 2009 John Wiley & Sons Australia, Ltd THE COMPLETE ACCOUNTING CYCLE 1. Recognise and record transactions

1. Paid rent for the next three months. 2. Paid property taxes that have already been accrued. 3. Declared cash dividends on commonshares

02 Student: 1. Paid rent for the next three months. 2. Paid property taxes that have already been accrued. 3. Declared cash dividends on commonshares 4. Closed the income summary account, assuming there

02 Student: 1. Paid rent for the next three months. 2. Paid property taxes that have already been accrued. 3. Declared cash dividends on commonshares 4. Closed the income summary account, assuming there

Full file at CHAPTER 3

CHAPTER 3 Adjusting the Accounts ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Exercises A Problems B Problems *1. Explain the time period assumption. 1, 2 *2. Explain the

CHAPTER 3 Adjusting the Accounts ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Exercises A Problems B Problems *1. Explain the time period assumption. 1, 2 *2. Explain the

SOLUTIONS TO EXERCISES SET B

SOLUTIONS TO EXERCISES SET B EXERCISE 2-1B 1. False. An account is an accounting record of a specific asset, liability, or stockholders equity item. 2. True. 3. False. Each asset, liability, and stockholders

SOLUTIONS TO EXERCISES SET B EXERCISE 2-1B 1. False. An account is an accounting record of a specific asset, liability, or stockholders equity item. 2. True. 3. False. Each asset, liability, and stockholders

CHAPTER 3. The Adjusting Process. Chapter Overview

CHAPTER 3 The Adjusting Process Chapter Overview This chapter introduces the student to the adjusting process. Cash and accrual accounting are illustrated and differentiated. The accounting period concept,

CHAPTER 3 The Adjusting Process Chapter Overview This chapter introduces the student to the adjusting process. Cash and accrual accounting are illustrated and differentiated. The accounting period concept,

SOLUTIONS. Learning Goal 14

S1 Learning Goal 14 Multiple Choice 1. a 2. c The capital balance to use on the balance sheet is the final balance from the statement of owner s equity. The capital balance showing on the worksheet does

S1 Learning Goal 14 Multiple Choice 1. a 2. c The capital balance to use on the balance sheet is the final balance from the statement of owner s equity. The capital balance showing on the worksheet does

Financial Statements and Closing Entries for a Merchandising Business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

Ch.10 Financial Statements and Closing Entries for a Merchandising Business o Prepare financial statements for a merchandising business o Journalize adjusting and closing entries for a merchandising business

CHAPTER3. Adjusting the Accounts. Apago PDF Enhancer. Study Objectives. Feature Story WHAT WAS YOUR PROFIT?

CHAPTER3 Study Objectives After studying this chapter, you should be able to: [1] Explain the time period assumption. [2] Explain the accrual basis of accounting. [3] Explain the reasons for adjusting

CHAPTER3 Study Objectives After studying this chapter, you should be able to: [1] Explain the time period assumption. [2] Explain the accrual basis of accounting. [3] Explain the reasons for adjusting

CHAPTER 2 Solutions MEASUREMENT CONCEPTS: RECORDING BUSINESS TRANSACTIONS

CHAPTER 2 Solutions MEASUREMENT CONCEPTS: RECORDING BUSINESS TRANSACTIONS Discussion Questions DQ1. DQ2. DQ3. DQ4. DQ5. DQ6. DQ7. DQ8. All equipment needs normal repairs. These are considered an ongoing

CHAPTER 2 Solutions MEASUREMENT CONCEPTS: RECORDING BUSINESS TRANSACTIONS Discussion Questions DQ1. DQ2. DQ3. DQ4. DQ5. DQ6. DQ7. DQ8. All equipment needs normal repairs. These are considered an ongoing

Module 3 Exhibits and Key Terms. Table of Contents. 1 Principles of Accounting Adjustments for Financial Reporting

Table of Contents Exhibit 14: Cash basis and accrual basis of accounting compared... 2 Exhibit 15: Summary fiscal year ending by Month... 2 Exhibit 16: Two classes and four types of adjusting entries...

Table of Contents Exhibit 14: Cash basis and accrual basis of accounting compared... 2 Exhibit 15: Summary fiscal year ending by Month... 2 Exhibit 16: Two classes and four types of adjusting entries...

Chapter 9 Recording Adjusting and Closing Entries

Chapter 9 Recording Adjusting and Closing Entries Fiscal Period Length of time for which a business reports and summarizes financial information Concept: Accounting Period Cycle: reporting changes in financial

Chapter 9 Recording Adjusting and Closing Entries Fiscal Period Length of time for which a business reports and summarizes financial information Concept: Accounting Period Cycle: reporting changes in financial

Look at Chapter 2 of Horngren. Make sure that you understand and can describe the following:

Week 1 Revise the introduction to Financial Accounting from CMA100, Chapters 1 and 2, Horngren and then look at Week 1 s topic The Adjusting Process, Chapter 3. Look at Chapter 1 of Horngren. Make sure

Week 1 Revise the introduction to Financial Accounting from CMA100, Chapters 1 and 2, Horngren and then look at Week 1 s topic The Adjusting Process, Chapter 3. Look at Chapter 1 of Horngren. Make sure

Principles of Accounting II

Principles of Accounting II Lecture 1 Adjusting the Accounts Basic Accounting Equation What the business owns = What the business owes Assets = Liabilities (owed to creditors)+ Owners Equity (residual

Principles of Accounting II Lecture 1 Adjusting the Accounts Basic Accounting Equation What the business owns = What the business owes Assets = Liabilities (owed to creditors)+ Owners Equity (residual

TH E ACCO U NTI NG LEARNING OBJECTIVES. Needed: A Reliable Information System. After studying this chapter, you should be able to:

2760T_c03_066-129.qxd 11/4/08 9:31 PM Page 66 C H A P T E R 3 TH E ACCO U NTI NG I N F O R M ATI O N SYSTE M LEARNING OBJECTIVES After studying this chapter, you should be able to: 1 Understand basic accounting

2760T_c03_066-129.qxd 11/4/08 9:31 PM Page 66 C H A P T E R 3 TH E ACCO U NTI NG I N F O R M ATI O N SYSTE M LEARNING OBJECTIVES After studying this chapter, you should be able to: 1 Understand basic accounting

Horngren's Accounting,11e (Miller-Nobles) Chapter 3 The Adjusting Process. Learning Objective 3-1

Chapter 3 The Adjusting Process. Learning Objective 3-1") Horngren's Accounting 11th Edition Test Bank Miller-Nobles TEST BANK for Horngren's Accounting 11th Edition by Tracie L. Miller-Nobles, Brenda L. Mattison, Ella Mae Matsumura. All chapters instant download:

Horngren's Accounting 11th Edition Test Bank Miller-Nobles TEST BANK for Horngren's Accounting 11th Edition by Tracie L. Miller-Nobles, Brenda L. Mattison, Ella Mae Matsumura. All chapters instant download:

Chapter 4 Mechanics of Financial Information

BUS210 9.15.14 Chapter 4 Mechanics of Financial Information Before Class starts.(make sure your name is on all submissions) First Homework 14 Fall Emory Inc. Due 9/17 before class; No EXCEPTIONS Help Session

BUS210 9.15.14 Chapter 4 Mechanics of Financial Information Before Class starts.(make sure your name is on all submissions) First Homework 14 Fall Emory Inc. Due 9/17 before class; No EXCEPTIONS Help Session

REVIEW Which of the following would be classified as external users of financial statements?

REVIEW 1 1. The three forms of business entities are: a. Government, cooperatives, and philanthropic organizations b. Financing, investing, and operating c. Sole proprietorships, partnerships, and corporations

REVIEW 1 1. The three forms of business entities are: a. Government, cooperatives, and philanthropic organizations b. Financing, investing, and operating c. Sole proprietorships, partnerships, and corporations

Learning Objectives. LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet.

Learning Objectives LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet. Lesson 6-1 Consistent Reporting The accounting concept Consistent Reporting is applied

Learning Objectives LO1 Prepare the heading of a work sheet. LO2 Prepare the trial balance section of a work sheet. Lesson 6-1 Consistent Reporting The accounting concept Consistent Reporting is applied

CHAPTER3 Adjusting the Accounts

CHAPTER3 Adjusting the Accounts 3-1 3-2 Timing Issues Accountants divide the economic life of a business into artificial time periods (Time Period Assumption)...... Jan. Feb. Mar. Apr. Dec. Generally a

CHAPTER3 Adjusting the Accounts 3-1 3-2 Timing Issues Accountants divide the economic life of a business into artificial time periods (Time Period Assumption)...... Jan. Feb. Mar. Apr. Dec. Generally a

CP:

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 13-1 13-2 PREVIEW OF CHAPTER 13 13-3

Adeng Pustikaningsih, M.Si. Dosen Jurusan Pendidikan Akuntansi Fakultas Ekonomi Universitas Negeri Yogyakarta CP: 08 222 180 1695 Email : adengpustikaningsih@uny.ac.id 13-1 13-2 PREVIEW OF CHAPTER 13 13-3

Important Terminology

Important Terminology Recognition When we "recognize" a revenue or expense, it means that we record the amount in our general ledger and the amount is included in our income statement. Deferral When we

Important Terminology Recognition When we "recognize" a revenue or expense, it means that we record the amount in our general ledger and the amount is included in our income statement. Deferral When we

3. Balance sheet accounts are referred to as temporary accounts because their balances are always changing.

Chapter 02 Review of the Accounting Process True / False Questions 1. Owners' equity can be expressed as assets minus liabilities. True False 2. Debits increase asset accounts and decrease liability accounts.

Chapter 02 Review of the Accounting Process True / False Questions 1. Owners' equity can be expressed as assets minus liabilities. True False 2. Debits increase asset accounts and decrease liability accounts.

10. Describe an account and its use in recording transactions.

1MODULE learning objective Accounting in Business, Analyzing Transactions, and Preparing Journal 10. Describe an account and its use in recording transactions. 1. THE ACCOUNT AND ITS ANALYSIS An account

1MODULE learning objective Accounting in Business, Analyzing Transactions, and Preparing Journal 10. Describe an account and its use in recording transactions. 1. THE ACCOUNT AND ITS ANALYSIS An account

Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield. Slide 3-2

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

3-1 C H A P T E R 3 THE ACCOUNTING INFORMATION SYSTEM Intermediate Accounting IFRS Edition Kieso, Weygandt, and Warfield 3-2 Learning Objectives 1. Understand basic accounting terminology. 2. Explain double-entry

The General Journal and the General Ledger Instructor: Michael Booth

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

The General Journal and the General Ledger Instructor: Michael Booth

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

Week 5, Chap 4 The General Journal and the General Ledger Instructor: Michael Booth McGraw-Hill 2007 The McGraw-Hill Companies, Inc. All rights reserved. The General Journal and the General Ledger The

MANAGEMENT 2100Y - MIDTERM EXAM SPRING 2013

MANAGEMENT 2100Y - MIDTERM EXAM SPRING 2013 INSTRUCTOR: Steven Dyer STUDENT: INSTRUCTIONS: 1. Programmable calculators are not allowed in this exam. 2. Check that there are 15 pages (including the title

MANAGEMENT 2100Y - MIDTERM EXAM SPRING 2013 INSTRUCTOR: Steven Dyer STUDENT: INSTRUCTIONS: 1. Programmable calculators are not allowed in this exam. 2. Check that there are 15 pages (including the title

CHAPTER 4 EXERCISES: SET B. E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows.

CHAPTER 4 EXERCISES: SET B E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows. Complete the worksheet. LAMAR COMPANY Worksheet for the Month Ended June

CHAPTER 4 EXERCISES: SET B E4-1B The trial balance columns of the worksheet for Lamar Company at June 30, 2017, are as follows. Complete the worksheet. LAMAR COMPANY Worksheet for the Month Ended June

Commecs College Macro Plan ( )

") Commecs College Macro Plan (-) Subject: Accounting Class: XI Sections: AZIZ TABBA, BUKHARI Unit No. Start Date 1 Aug 01, End Date Aug 03, Number Of Periods Topic/Chapter Contents Objectives By the end

Commecs College Macro Plan (-) Subject: Accounting Class: XI Sections: AZIZ TABBA, BUKHARI Unit No. Start Date 1 Aug 01, End Date Aug 03, Number Of Periods Topic/Chapter Contents Objectives By the end

T Accounts Very useful to understand how the double-entry system works. They are the basic representations of the accounts and have three parts:

Recap from Week 2 Rules Of Double-entry Bookkeeping T Accounts Very useful to understand how the double-entry system works. They are the basic representations of the accounts and have three parts: Title

Recap from Week 2 Rules Of Double-entry Bookkeeping T Accounts Very useful to understand how the double-entry system works. They are the basic representations of the accounts and have three parts: Title