PPD September 6, PPD-023(R)

|

|

|

- Bathsheba Wilkerson

- 6 years ago

- Views:

Transcription

1 DEFENSE CONTRACT AUDIT AGENCY DEPARTMENT OF DEFENSE 8725 JOHN J. KINGMAN ROAD, SUITE 2135 FORT BELVOIR, VA IN REPLY REFER TO PPD September 6, PPD-023(R) MEMORANDUM FOR REGIONAL DIRECTORS, DCAA DIRECTOR, FIELD DETACHMENT, DCAA HEADS OF PRINCIPAL STAFF ELEMENTS, HQ, DCAA SUBJECT: Audit Guidance on Revised Policy and Procedures for Sampling Low-Risk Incurred Cost Proposals SUMMARY To ensure that our limited audit resources are applied to the areas and audits of highest risk, the policy for evaluating and reporting on low-risk annual incurred cost proposals is being revised (Enclosure 1). For the purposes of satisfying the audit requirements at FAR (a)(12), (b)(2), and (b)(2)(i), Defense Procurement and Acquisition Policy (DPAP) authorized a Class Deviation DCAA Policy and Procedure for Sampling Low-Risk Incurred Cost Proposals, dated July 24, 2012, (Enclosure 2). This deviation allows the Department of Defense contracting officers to continue to rely on either a DCAA audit report or a DCAA memorandum to satisfy the audit requirements in FAR. The revised policy and its implementation have been coordinated with Defense Contract Management Agency (DCMA). POLICY For in-process assignments where detailed audit steps have been started, auditors should complete the assignment as it was planned. For all other assignments, the auditor should follow the revised policy for sampling adequate low-risk incurred cost proposals described in Enclosure 1. In summary, all adequate incurred cost proposals under $250 million auditable dollar value (ADV) will be assessed for high or low risk using the Risk Assessment Checklist (Enclosure 3). All high-risk proposals will be audited and low-risk proposals will be sampled using the percentages identified in Enclosure 1. Under the revised policy, DCAA will no longer perform desk reviews. Those proposals not selected for audit will be dispositioned by a memorandum to the contracting officer (Enclosure 4). In addition, a mandatory audit of proposals will be performed every three years on proposals between $100 million and $250 million ADV. The criteria for assessing the risk of a proposal includes prior incurred cost audit experience, any audit leads or other significant risk identified, as well as the significance of prior questioned costs. Auditors must use their professional judgment when determining that a specific proposal can be placed in the low-risk pool for sampling. Auditors must consider their knowledge of the contractor, the results of adequacy reviews, and other audit activity performed since completion of the last incurred cost audit (e.g., reported business system deficiencies,

2 September 6, 2012 PPD PPD-023(R) SUBJECT: Audit Guidance on Revised Policy and Procedures for Sampling Low-Risk Incurred Cost Proposals establishment of provisional billing rates, voucher processing procedures, real-time testing of direct costs, forward pricing audits, etc.) to determine if there are any risks that would warrant the contractor to be classified as high risk and an audit be performed, especially when significant time has elapsed since the performance of the last incurred cost audit. Corporate, shared services and Intermediate Home Office (IHO) proposals will not be included in the low-risk sampling process. Corporate/IHO/shared services and segments should coordinate during the adequacy review and risk assessment process to determine if a corporate or home office audit is needed. Coordination efforts should be documented and maintained in the working papers at both Corporate/IHO and segments. As with the previous desk review process, the revised incurred cost sampling policy does not apply to nonprofit organizations and educational institutions. The revised policy also will not apply to 100% non-dod contractors at this time. Non-DoD agencies are interested in this process but are waiting to see the guidance before deciding whether to adopt the sampling process. We expect that it will be several months before the non-dod agencies reach a decision on whether to rely on this sampling process. Auditors are reminded that the primary objective of the initiative is to redirect audit effort to completion of high-risk and sampled incurred cost audits, beginning with the earlier year proposals first (i.e., oldest to newest). Therefore, to ensure the new policy does not adversely impact on-going audit effort, FAOs should coordinate with the contracting officer and time phase the issuance of the memorandums for proposals not selected for audit. To facilitate the implementation of the revised policy, we have included an implementation plan developed with the assistance of the Regions (Enclosure 5). Once high-risk and sampled audits have been identified, FAOs should develop a plan to prioritize completion of the audits to support the Agency s goal of being current by the end of FY Policy is in the process of updating CAM Chapters 6 and 10 to reflect the revised guidance. In addition, the low-risk sampling policy and procedures have been updated since issuance of the DPAP class deviation to remove the plan to not apply sampling to low-risk proposals $1M or less received prior to October 1, 2011 (Enclosure 1). SAMPLING GUIDANCE FAOs should perform risk determinations on all adequate final indirect rate proposals up to $250 million in ADV, focusing on the oldest proposals. DMIS Version 5.3 released in June 2012 allows FAOs to enter a risk code of high or low and a risk reason code for incurred cost proposals up to the $250 million threshold. 2

3 September 6, 2012 PPD PPD-023(R) SUBJECT: Audit Guidance on Revised Policy and Procedures for Sampling Low-Risk Incurred Cost Proposals Operations will provide each region and Field Detachment (FD) with lists of incurred cost assignments (activity code 10100) where the FAOs have received adequate proposals and determined them to be low risk. The lists may include assignments with ADV of $15M or less coded as high risk with a reason of mandatory third year audit, since the mandatory third year audit will now only apply to contractor proposals exceeding $100 million. The lists will not include assignments identified as corporate or home office submissions (corporate audit status code = C). The lists will identify proposals coded as direct costs only (Inc Cost Contractor Type = D) to facilitate coordination between FD offices and the cognizant office. Assignments for direct costs should not be included in the sample universes. The assignments on the lists provided to the regions will be coded in the sample universe field (i.e., LR4Q12) to indicate they have been included in a universe. The regions must review the lists and notify HQ-OWD of any assignments that should not be part of the universe. The assignment should be removed from the universe if, for example, the audit is already in process and detailed audit steps have been started; the submission is for a corporate or home office but not coded as such in DMIS; or all the contracts are non-dod. HQ-OWD will clear the sample universe field for those assignments in DMIS. Although these assignments will be removed from the current universe, they will appear again in the next universe unless the in-process audit is completed, or the corporate audit status field is revised. Regions should select a region-wide audit sample using EZ-Quant random number generator and apply the appropriate sampling rate for each universe strata described in Enclosure 1. The number of sample items should be rounded up. For example, if the universe consists of 169 incurred cost proposals with ADV of $1 to $15 million (5% sample rate), resulting in a sample of 8.45 items, the region should randomly select nine proposals for audit using EZ Quant to generate random numbers. The regions must return the lists to HQ-OWD annotating the Sample Code column with X for do not include in sample universe or Y for selected for audit. Using this data, Operations will either clear the sample universe field or enter the data identifying whether the proposal was selected for audit or not. Regions should document their sample selection process and file the documentation in Livelink under a folder named Incurred Cost Low-Risk Sample Selection with subfolders for each sample. Once the region completes the review of the sample universes and selects the samples, it should notify the FAOs to time phase (Enclosure 5) the closure of the low-risk proposals not selected using the procedures in Enclosure 1. Operations is currently working on an application, similar to the Overdue Incurred Cost Submission Letter Tool, which can be used to generate draft memorandums. We anticipate that this application will be available by September 30,

4 September 6, 2012 PPD PPD-023(R) SUBJECT: Audit Guidance on Revised Policy and Procedures for Sampling Low-Risk Incurred Cost Proposals CONCLUDING REMARKS Headquarters hosted a teleconference with the Incurred Cost RAMs on August 14, 2012 to address implementation of this guidance. Headquarters is planning to have a teleconference with all of the impacted FAO managers prior to the end of September to address questions and assess progress on implementation. In addition, please see the Frequently Asked Questions for additional information (Enclosure 6). FAOs with questions regarding this memorandum should contact their regional offices. Regional personnel should direct any questions regarding the sampling process to Workload Analysis Division at (703) , or by at dcaa-owd@dcaa.mil. Regional personnel with any questions regarding the policy should contact Policy Programs Division at (703) or via at dcaa-ppd@dcaa.mil. Enclosures: 6 1. Policy and Procedures for Low-Risk Sampling 2. DPAP Class Deviation 3. Risk Assessment Checklist 4. Memorandum to the ACO 5. Incurred Cost Sampling Implementation Plan 6. Frequently Asked Questions /Signed/ John C. Shire Deputy Assistant Director Policy and Plans DISTRIBUTION: E 4

5 DCAA Policy and Procedures for Sampling Low-Risk Incurred Cost Proposals POLICY All incurred cost proposals should be evaluated upon receipt for adequacy, in accordance with FAR , using the DCAA Incurred Cost Proposal Adequacy checklist. If the incurred cost proposal is not adequate and the deficiencies cannot be remedied with minor effort, the proposal will be returned to the contractor with written instructions on required corrective actions, in accordance with CAM Chapter 6. All adequate annual incurred cost proposals exceeding $250 million in auditable dollar value (ADV) will be audited. All other incurred cost proposals received and determined to be adequate will be assessed for risk. All adequate high-risk proposals will be audited. CRITERIA FOR CLASSIFICATION OF PROPOSALS TO HIGH-RISK AND LOW- RISK POOLS For all proposals with $250 million or less in ADV, FAOs should classify risk as high or low for all adequate incurred cost proposals on hand where an audit (field work) has not been started, using the criteria specified below: Low Risk Proposal Criteria We have prior incurred cost audit experience (i.e., an incurred cost audit has been performed). No significant audit leads (including assist audits, corporate, intermediate home office or service center) or no other significant risk has been identified. For example: o any known business system deficiencies that would have a significant impact on the final indirect rate proposal for this FY; o significant risk identified by the contracting officer; o significant changes in the contractor organization or operations (e.g., significant increase in ADV); or o other significant risk identified by the audit team. No prior significant total exception dollar reported in the last year audited. Significant exception dollars are defined by strata in the table below: Low-Risk Adequate Proposals by Auditable Dollar Value (ADV) Amount of Previous Exception Dollars (including Corporate, Intermediate Home Office, etc) Classified as Significant $1M or less $15,000 $1M to $15 Million $25,000 $15M to $50 Million $55,000 $50 Million to $250 Million $100,000 August 2012 Enclosure 1 Page 1 of 3

6 LOW-RISK SAMPLING PERCENTAGES DCAA Policy and Procedures for Sampling Low-Risk Incurred Cost Proposals Low-risk proposals will be selected for audit using sampling techniques based on the guidance below. An adequacy evaluation must be performed prior to designating a proposal as low risk. No other audit procedures will be applied to the remaining low-risk proposals not selected for audit. Low-Risk Adequate Proposals by Auditable Dollar Value (ADV) Low-Risk Sampling Percentages $1M or less 1% $1M to $50 Million 5% $50 Million to $100 Million 10% $100 Million to $250 Million* 20% Greater than $250 Million 100% * A mandatory incurred cost audit will be performed once every three years for all proposals greater than $100 million up to $250 million. If a contractor does not have a proposal selected for audit in the 20 percent sample in a three-year cycle, the FAO shall select a proposal for audit the third year after the last audit. This selection is in addition to those incurred cost proposals selected for audit in the 20 percent sample for any given Government fiscal year. CLOSURE METHODS TO BE USED FOR PROPOSAL CONSIDERED LOW-RISK NOT SELECTED FOR AUDIT The following procedures will be performed on the proposals in the low-risk pool that were not selected in the sample for audit: Issue a Memorandum for Contracting Officer, including the key steps performed from the adequacy checklist (Enclosure 4). Low-risk proposals not selected in the sample for audit should be closed with disposition code N Assignment completed but no formal report issued as of the date of the memorandum to the contracting officer. The proposal ADV should be reported in the Dollars Examined Gross field on the disposition tab in DMIS to ensure that we maintain visibility of the dollars associated with assignments closed without audit. Calculate the dollars examined using the same procedures as if an audit were performed. See page A-15 of the DMIS Users Guide for detailed procedures for calculating ADV. Costs questioned and total exception dollars will be reported as zero. The Audit, Desk Review, or No Audit field entry will be N = No Audit and the Audit Determined/Negotiated field entry will be N = Negotiated. August 2012 Enclosure 1 Page 2 of 3

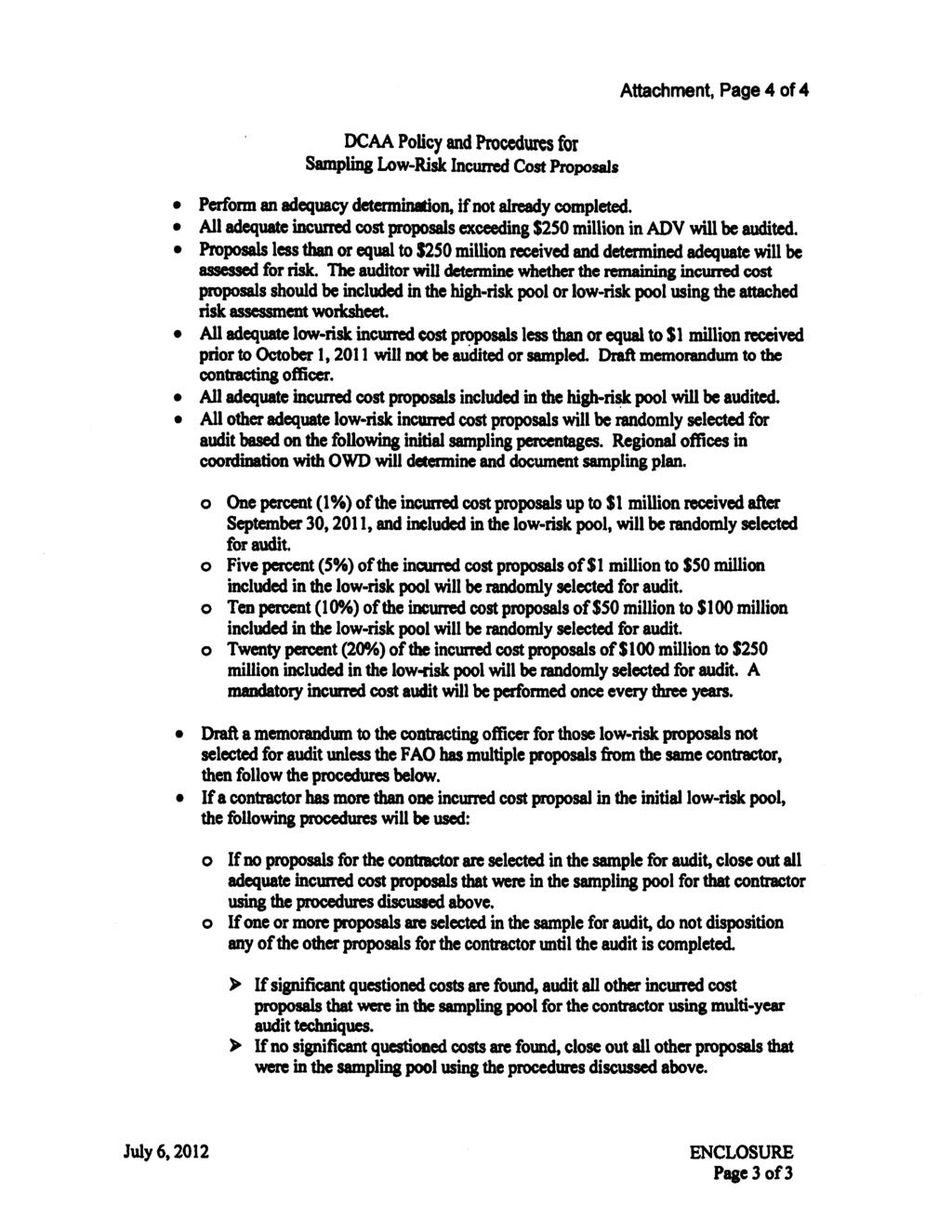

7 DCAA Policy and Procedures for Sampling Low-Risk Incurred Cost Proposals PROCEDURES Upon receipt of this guidance, the FAO should identify all incurred cost proposals on hand for which the audit has not started. Perform an adequacy determination, if not already completed. All adequate incurred cost proposals exceeding $250 million in ADV will be audited. Proposals less than or equal to $250 million received and determined adequate will be assessed for risk. The auditor will determine whether the remaining incurred cost proposals should be included in the high-risk pool or low-risk pool using the risk assessment worksheet (Enclosure 3). All adequate incurred cost proposals included in the high-risk pool will be audited. All adequate low-risk incurred cost proposals will be randomly selected for audit based on the following sampling percentages. Regional offices in coordination with OWD will determine and document sampling plan. o One percent (1%) of the incurred cost proposals up to $1 million o Five percent (5%) of the incurred cost proposals of $1 million to $50 million included in the low-risk pool will be randomly selected for audit. o Ten percent (10%) of the incurred cost proposals of $50 million to $100 million included in the low-risk pool will be randomly selected for audit. o Twenty percent (20%) of the incurred cost proposals of $100 million to $250 million included in the low-risk pool will be randomly selected for audit. A mandatory incurred cost audit will be performed once every three years. Draft a memorandum to the contracting officer for those low-risk proposals not selected for audit unless the FAO has multiple proposals from the same contractor, then follow the procedures below. If a contractor has more than one incurred cost proposal in the initial low-risk pool, the following procedures will be used: o If no proposals for the contractor are selected in the sample for audit, close out all adequate incurred cost proposals that were in the sampling pool for that contractor using the procedures discussed above. o If one or more proposals are selected in the sample for audit, do not disposition any of the other proposals for the contractor until the audit is completed. If significant questioned costs are found, audit all other incurred cost proposals that were in the sampling pool for the contractor using multi-year audit techniques. If no significant questioned costs are found, close out all other proposals that were in the sampling pool using the procedures discussed above. August 2012 Enclosure 1 Page 3 of 3

8

9

10

11

12

13 DEFENSE CONTRACT AUDIT AGENCY RISK DETERMINATION FOR CONTRACTOR YEARS WITH LESS THAN $250M IN ADV Version No. 1.4 August 2012 CONTRACTOR CFY LAST CFY AUDITED AUDIT REPORT NO. DATE CONTRACTOR S PROPOSAL RECEIVED IF THIS IS A REIMBURSABLE CONTRACTOR, DO WE HAVE AN AUDIT REQUEST? YES NO (If not, obtain request before further processing) FOR CONTRACTORS WITH $100 MILLION TO $250 MILLION IN ADV, WERE ADEQUACY DETERMINATION LETTERS USED TO CLOSE TWO PRIOR CFYs (i.e., IS THIS THE THIRD UNAUDITED YEAR)? (A YES response indicates proposal must be audited regardless of initial risk). YES NO AMOUNT OF ADV (000) (per incurred cost submission) (The audit team must use their professional judgment, combined with their knowledge of the contractor and the results of the adequacy and other reviews, to determine if there are any risks that would warrant the contractor to be classified as high risk and an audit be performed.) CRITERIA YES NO 1. Are there audit leads (including assist audits, corporate, intermediate home office or service center) or other significant risks identified? For example: any known business system deficiencies that have a significant impact on the incurred cost proposals for this fiscal year; significant risks identified by the contracting officer; significant changes in the contractor organization or operations (e.g., significant increase in ADV); or other significant risk identified by the audit team. Auditors should contact contracting officers to ascertain any known concerns that may impact this assignment. Document discussions (ACO name, phone number, and date contacted.) 2. We have no incurred cost audit experience with the contractor. 3. Are there significant total exception dollars (as described below) in the last completed incurred cost audit? See guidelines below for determining significance of exception dollars. Amount of Exception Dollars: $ With a yes response to ANY of these questions, place proposal in the high-risk pool. 31-a Enclosure 3 Page 1 of 2

14 Low-Risk Adequate Proposals by Auditable Dollar Value (ADV) Amount of Previous Total Exception Dollars Classified as Significant, including Corporate and Intermediate Home Office $1M or less $15,000 $1M to $15 Million $25,000 $15M to $50 Million $55,000 $50 Million to $250 Million $100,000 ASSIGNED TO: LOW-RISK POOL HIGH-RISK POOL SUPERVISORY REVIEW: (Supervisor s Signature and Date) 31-a Enclosure 3 Page 2 of 2

15 MEMORANDUM FOR CONTRACTING OFFICER SUBJECT: Fiscal Year (FY) 20[XX] Adequate Incurred Cost Proposal for [Contractor Name, Address][Contractor primary cage code] We received [Contractor Name] s ([Contractor Acronym]) FY 20[XX] incurred cost proposal dated [enter date of proposal] on [enter date proposal received]. Based on the results of our adequacy evaluation, we consider the [Contractor Acronym] s FY 20[XX] incurred cost proposal adequate in accordance with the requirements in FAR Our adequacy evaluation did not disclose any significant audit leads and during our initial coordination with your office you disclosed no concerns that would require an audit. Our adequacy evaluation included a mathematical verification and a determination that [Contractor Acronym] s proposal was certified by its top management officials that it does not include unallowable costs (see Enclosure 1). Based on the adequacy evaluation and an overall assessment of low risk, we placed the [Contractor Acronym] s FY 20[XX] incurred cost proposal in our sampling pool; it was not selected for audit. The contractor s proposed final annual indirect cost rates for the fiscal year ended [insert contractor s fiscal year] are as follows: Proposed Allocation Base Cost Center Amount Description Proposed Rate [Note: If this is related to corporate/home office proposal, please replace the indirect rate schedule with the appropriate corporate/home office schedule.] We discussed the results of our adequacy evaluation with [Name and Title of Contractor s Representative] on [Date]. The contracting officers may use their authority under FAR to determine the [Contractor Acronym] FY 20[XX] final indirect cost rates. In addition, we recommend that the contracting officer require [Contractor Acronym] to adjust its interim billings on all affected contracts to reflect the settled direct and indirect costs and update its schedule of cumulative direct and indirect costs claimed and billed. Please contact [Auditor s Name], Auditor, at [ and Phone Number], if you have questions concerning this memorandum or if you require additional information. Enclosure: Certificate of Final Indirect Costs cc: [Contractor Name] s ([Contractor Acronym] [FAO Manager Name] Branch Manager [FAO Name] Enclosure 4 Page 1 of 1

16 Milestones Plan Low-Risk Incurred Cost Proposal Initiative Regional/FAO Actions and Implementation Date Steps Implementation Plan Completion Date 1 Complete adequacy review and risk determinations for all in house proposals from oldest to newest so that low-risk proposals can be included in sampling universes quarterly. See steps below for the dates that sample universes will be created. 2 OWD will send the first low-risk proposal sample universe to the Regions (Excel Spreadsheet). The assignments in the first universe will be coded LR4Q12 in the sample universe field. This first universe will be limited to adequate proposals less than or equal to $15M. 3 Regions will: Review (i.e., scrub) the universe for proposals that should not be sampled (e.g., corporate and IHO proposals not properly coded in DMIS, 100% non-dod, and audits already in process). Then select a sample on a region-wide basis using the applicable percentage from the P&P for each universe strata (the number of sample items should be rounded up). Update the Excel Spreadsheet (annotating the Sample Code column with X for do not include in sample universe or Y for selected for audit). Submit the updated Excel Spreadsheet to OWD. Notify FAO which proposals are selected for audit and which will be closed without audit. 4 Using the information provided by the Regions, OWD will update the sample universe and selected for audit fields in DMIS. 5 For proposals not selected for audit, FAO should issue a memo to ACO and disposition the assignment in DMIS. Time phase the memos, working from oldest to newest CFYs, so that ACOs are not inundated with too many memos at once. 6 OWD will send the second low-risk proposal sample universe to the Regions (Excel Spreadsheet). The assignments in the second universe will be coded LR1Q13 in the sample universe field. This second universe will be limited to adequate proposals less than or equal to $100M. January 31, 2013 August 15, 2012 September 12, 2012 September 14, 2012 August 24, 2012 March 31, 2013 November 16, Regions will repeat the actions from the bullets in 3 above. December 14, Using the information provided by the Regions, OWD will update December 21, 2012 the sample universe and selected for audit fields in DMIS. 9 For proposals not selected for audit, FAO should issue a memo to ACO and disposition the assignment in DMIS. Time phase the memos, working from oldest to newest CFYs, so that ACOs are not inundated with too many memos at once. January 1, 2013 June 30, 2013 Enclosure 5 Page 1 of 2

17 Milestones Plan Low-Risk Incurred Cost Proposal Initiative Regional/FAO Actions and Implementation Date 10 The process outlined above will be repeated with the third lowrisk proposal sample universe (Excel Spreadsheet). The assignments in the third universe will be coded LR2Q13 in the sample universe field. This third universe will consist of all adequacy proposals less than or equal to $250M. At this point, the number of memos issued to ACO should be reduced to a level where they can be incorporated with the remaining memos from the prior quarter s sample. February 15, 2013 It is imperative that auditors remember the primary objective of the initiative is to redirect audit effort to completion of high-risk and sampled incurred cost audits, beginning with the earlier year proposals first (i.e., oldest to newest). Therefore, to ensure the new policy does not adversely impact on-going audit effort, FAOs should time phase issuance of memorandums to contracting officers for proposals not selected for audit. Scrubbing the HQ-OWD Initial Universe: If in doubt about whether a particular assignment should be excluded from the universe (e.g., corporate and IHO proposals not properly coded in DMIS, 100% non-dod, and audits already in-process), update the Excel Spreadsheet Sample Code column with an X. Although these assignments will be removed from the current universe, they will appear again in the next universe unless the in-process audit is completed, or the corporate audit status field is revised. Filing of Supporting Documentation: Regions should document their universe review and sample selection process and file the documentation in Livelink under a folder named Incurred Cost Low-Risk Sample Selection with subfolders for each sample. Coordination with DCMA: FAOs should coordinate with their respective ACOs to ensure that their time phasing of memos is appropriate and adjust, based on their resources and those of the ACO. Memos to ACOs: Once the number of memos to be issued has been reduced significantly, the expectation will be that all memos will be issued before the start of the next sampling process. Enclosure 5 Page 2 of 2

18 FREQUENTLY ASKED QUESTIONS Sampling Low-Risk Incurred Cost Proposal Question 1: Will the agency continue performing desk reviews of low-risk incurred costs proposals with less than $15M in ADV? Answer: No. The new sampling initiative for low-risk incurred cost proposals replaces the prior policy related to performing desk reviews. For in-process desk reviews where procedures have been substantially started or completed, auditors should complete the assignment as it was planned. Under the new policy, there is no longer a mandatory third-year audit requirement for proposals with less than $15M in ADV. Question 2: If we have five years in inventory for a contractor that we have not audited previously, can we audit first year s proposal, and if no costs are questioned, place the remaining unaudited years in the low-risk pool for sampling? Answer: Yes. Auditors should complete the adequacy review and risk determination for all years proposals and input high risk for all years in DMIS. On the remaining years, risk determinations should be reassessed after the 1st year s audit is completed. However, auditors should consider whether multiyear auditing may be appropriate based on their professional judgment. Question 3: Will we still issue rate agreement letters and cumulative allowable cost worksheets for low-risk proposals not selected for audit? Answer: No. If the low-risk proposal is not selected for audit, the auditor should issue a memorandum to the contracting officer using the proforma memorandum (Enclosure 4). Contracting officers will use their authority under the FAR to establish final indirect cost rates for the contractor fiscal year and provide a copy of the rate agreement letter to the audit office. Once the contracting officer has established the final rates, auditors will continue to follow the guidance in CAM and complete CACWS within 60 days of settlement of the indirect rates. Question 4: Has the guidance changed for adjusting ADV based on subcontract cost? Answer: No. Auditors should calculate initial ADV in accordance with current guidance. If the subcontract costs are being audited by another DCAA office, the ADV should be excluded at the prime level. Auditors should use professional judgment when assessing risk considering the materiality of the subcontract costs. Coordination between the prime auditors and the lower-tier auditors is required early in the process and should be documented and maintained in the assignment folder at both locations. Question 5: Will incurred cost proposals that include non-dod contracts be eligible for the lowrisk sampling initiative? Answer: Yes. During the adequacy review and risk determination process, auditors should make every effort to determine if non-dod agencies will be participating in order to calculate the appropriate ADV. However, if the auditor is unable to verify, at the time of the high/low-risk Enclosure 6 Page 1 of 3

19 determination, that a non-dod agency will participate in the audit (e.g., funding is uncertain), auditors should include the non-dod contract costs in the total ADV calculation for risk assessment purposes. However, proposals that are 100% non-dod will not be included in the low-risk sampling process at this time. Question 6: What if the contracting officer establishes final indirect cost rates for a proposal not selected for audit and we find significant indirect questioned costs in the next year audit. Should we go back and audit the earlier year? Answer: No. A signed rate agreement letter is a legally binding document that is incorporated into the contract and, generally, cannot be changed without consent of both the Government and the contractor, except for rare circumstances such as fraud or mutual mistake. Auditors should communicate and share with the ACO any significant indirect questioned costs that impact prior audited years, so that the ACO can attempt to negotiate with the contractor. Question 7: What if we find significant direct costs questioned and the contracting officer has already established the final indirect cost rates for a proposal not selected for audit? Should we go back and audit the earlier year contract costs? Answer: Yes, provided the contract has not already been closed. The contracting officer may recover unallowable direct contract costs any time before final payment is made on the contract, in accordance with FAR (g) for cost reimbursable contracts, and FAR (f) for Time and Material contracts. Auditors should coordinate with the contracting officer in these situations. Question 8: Can we rely on audits performed prior to 2008 in making risk classification decisions? Quality Assurance reviews have indicated that some of our audit work prior to 2008 may not have met GAGAS standards. Answer: Yes, generally we can rely on prior audit results (e.g., incurred cost, and real-time testing) in making risk classification decisions (e.g., questioned costs in prior years), unless the specific audit we are relying on was found to be performed in non-compliance with GAGAS. However, if auditors are relying on the audit effort to support their opinion in the current audit, the auditor should ensure that the audit was performed in accordance with GAGAS. Question 9: I am working at Field Detachment and have only direct cost audits; the indirect cost rate proposal is under the cognizance of another DCAA office. Do I have to follow this process if I audit only the direct cost portion of the proposal? Answer: The cognizant FAO responsible for auditing the indirect cost rate proposal will perform a single adequacy review and risk determination covering the total direct and indirect ADV, in coordination with the FD office. If the proposal is low risk and not selected for audit, the cognizant FAO assignment will be dispositioned with the memorandum to the contracting officer (copy to FD). FD will disposition their assignment with a memorandum to the contracting officer. Enclosure 6 Page 2 of 3

20 Question 10: Are corporate, shared services and home office proposals subject to the low-risk sampling initiative? Answer: No. Corporate, shared services and home office proposals will not be included in the low-risk sampling process. Corporate/home offices and segments should coordinate early in the process to determine if a corporate or home office audit is necessary. If, after coordination, the segment s proposal is high risk or sampled, the corporate/home office should perform the necessary audit procedures to cover the significant high-risk cost area(s) based on the coordination with segment(s). Auditors should use professional judgment, considering the materiality of the allocated costs when assessing risk. If the corporate/home office audit is not required, auditors should disposition the assignment with a memorandum to the contracting officer. All coordination efforts should be documented and maintained in the permanent file at both the Corporate/Intermediate Home Office and segment locations. Question 11: Are subcontract proposals subject to the low-risk sampling initiative? Answer: Yes. The low-risk sampling initiative applies to both prime contractor and subcontractor proposals. Prime contract auditors will determine the need for assist audits in accordance with current agency procedures. Subcontract auditors will follow the initiative policies and procedures, including performance of high/low-risk determinations for sampling purposes. If the subcontractor s proposal is not selected for audit, subcontract auditors should disposition the assignment with a memorandum to the contracting officer (cc: applicable prime contract or higher-tier subcontract auditors). Both prime contract auditors and subcontract auditors are reminded to coordinate early in the risk assessment process to identify any known risk that may impact the need for an audit. Question 12: Should I classify the FY 2010 proposal as low risk when the last incurred cost audit performed was back in FY 2002? Answer: It depends. In assessing the risk of any proposal, auditors must consider whether there are any audit leads or other significant risks identified. This may include the auditor s assessment of whether the contractor s business and organizational structure (including personnel and accounting operations), for the intervening years, has been relatively stable and consistent. When the last incurred cost audit performed is not recent, this assessment is especially important. If in your professional judgment, based on your adequacy review and other contractor information, you conclude the FY 2010 contractor operations are significantly different from the FY 2002 contractor operations, then you should classify the proposal as high risk. One example would be a material increase in ADV. If the contractor s ADV significantly increased from FY 2002 to FY 2010, we should classify the proposal as high risk. However, if in your professional judgment and building on your knowledge obtained through performance of other audit effort (e.g., provisional billing rates, public voucher processing, real-time testing of direct costs, forward pricing audits, etc.), the contractor s business and organizational structure has been relatively stable and consistent, and no audit leads or other significant risk is identified; you should classify the FY 2010 proposal as low risk. Enclosure 6 Page 3 of 3

MEMORANDUM FOR REGIONAL DIRECTORS, DCAA DIRECTOR, FIELD DETACHMENT, DCAA. SUBJECT: Audit Guidance on the Impact of the Pension Protection Act of 2006

DEFENSE CONTRACT AUDIT AGENCY DEPARTMENT OF DEFENSE 8725 JOHN J. KINGMAN ROAD, SUITE 2135 FORT BELVOIR, VA 22060-6219 IN REPLY REFER TO PAC 730.3.B.08/2007-01 MEMORANDUM FOR REGIONAL DIRECTORS, DCAA DIRECTOR,

DEFENSE CONTRACT AUDIT AGENCY DEPARTMENT OF DEFENSE 8725 JOHN J. KINGMAN ROAD, SUITE 2135 FORT BELVOIR, VA 22060-6219 IN REPLY REFER TO PAC 730.3.B.08/2007-01 MEMORANDUM FOR REGIONAL DIRECTORS, DCAA DIRECTOR,

CONTRACT ADMINISTRATION AND AUDIT SERVICES

CHAPTER 3042 CONTRACT ADMINISTRATION AND AUDIT SERVICES Subchapter 3042.002 Interagency agreements. Subchapter 3042.1 Contract Audit Services 3042.102 Assignment of contract audit services. 3042.170 Contract

CHAPTER 3042 CONTRACT ADMINISTRATION AND AUDIT SERVICES Subchapter 3042.002 Interagency agreements. Subchapter 3042.1 Contract Audit Services 3042.102 Assignment of contract audit services. 3042.170 Contract

PSP A/ August 26, PSP-020(R)

") DEFENSE CONTRACT AUDIT AGENCY DEPARTMENT OF DEFENSE 8725 JOHN J. KINGMAN ROAD, SUITE 2135 FORT BELVOIR, VA 22060-6219 IN REPLY REFER TO PSP 730.5.1.A/2013-009 August 26, 2013 13-PSP-020(R) MEMORANDUM FOR

DEFENSE CONTRACT AUDIT AGENCY DEPARTMENT OF DEFENSE 8725 JOHN J. KINGMAN ROAD, SUITE 2135 FORT BELVOIR, VA 22060-6219 IN REPLY REFER TO PSP 730.5.1.A/2013-009 August 26, 2013 13-PSP-020(R) MEMORANDUM FOR

DCMA Manual Terminations. Implements: DCMA-INST 2501, Contract Maintenance, August 15, October 10, 2014

DCMA Manual 2501-06 Terminations Office of Primary Responsibility Contract Maintenance Effective: October 2, 2018 Releasability: Cleared for public release Implements: DCMA-INST 2501, Contract Maintenance,

DCMA Manual 2501-06 Terminations Office of Primary Responsibility Contract Maintenance Effective: October 2, 2018 Releasability: Cleared for public release Implements: DCMA-INST 2501, Contract Maintenance,

Overview of the Defense Contract Audit Agency American Society of Military Comptrollers

Overview of the Defense Contract Audit Agency American Society of Military Comptrollers Ms. Anita Bales Director Page 1 Presentation Outline DCAA Mission and Impact DCAA Organization Pre-Award - Forward

Overview of the Defense Contract Audit Agency American Society of Military Comptrollers Ms. Anita Bales Director Page 1 Presentation Outline DCAA Mission and Impact DCAA Organization Pre-Award - Forward

PAC B.01/ August 7, PAC-013(R) MEMORANDUM FOR REGIONAL DIRECTORS, DCAA HEADS OF PRINCIPAL STAFF ELEMENTS, HQ, DCAA

MEMORANDUM FOR REGIONAL DIRECTORS, DCAA HEADS OF PRINCIPAL STAFF ELEMENTS, HQ, DCAA") DEFENSE CONTRACT AUDIT AGENCY DEPARTMENT OF DEFENSE 8725 JOHN J. KINGMAN ROAD, SUITE 2135 FORT BELVOIR, VA 22060-6219 IN REPLY REFER TO PAC 730.3.B.01/2013-02 August 7, 2014 MEMORANDUM FOR REGIONAL DIRECTORS,

DEFENSE CONTRACT AUDIT AGENCY DEPARTMENT OF DEFENSE 8725 JOHN J. KINGMAN ROAD, SUITE 2135 FORT BELVOIR, VA 22060-6219 IN REPLY REFER TO PAC 730.3.B.01/2013-02 August 7, 2014 MEMORANDUM FOR REGIONAL DIRECTORS,

Monitoring Subcontracts

Monitoring Subcontracts The views expressed in this presentation are DCAA's views and not necessarily the views of other DoD organizations Page 1 Subcontracts What should a contractor know about subcontracting:

Monitoring Subcontracts The views expressed in this presentation are DCAA's views and not necessarily the views of other DoD organizations Page 1 Subcontracts What should a contractor know about subcontracting:

Activity Code Compliance Audit CAS 403 Version 6.23, dated March 2018 B-1 Planning Considerations

Activity Code 19403 Compliance Audit CAS 403 B-1 Planning Considerations Type of Service - Attestation Examination Engagement Audit Specific Independence Determination Members of the audit team and internal

Activity Code 19403 Compliance Audit CAS 403 B-1 Planning Considerations Type of Service - Attestation Examination Engagement Audit Specific Independence Determination Members of the audit team and internal

IMMEDIATE POLICY CHANGE

DEPARTMENT OF DEFENSE Defense Contract Management Agency IMMEDIATE POLICY CHANGE Pricing and Negotiation Contracts Directorate DCMA-INST 120 (IPC-1) OPR: DCMA-AQ March 22, 2016 1. POLICY. This Immediate

DEPARTMENT OF DEFENSE Defense Contract Management Agency IMMEDIATE POLICY CHANGE Pricing and Negotiation Contracts Directorate DCMA-INST 120 (IPC-1) OPR: DCMA-AQ March 22, 2016 1. POLICY. This Immediate

Keys to Submitting an Adequate Incurred Cost Proposal

Keys to Submitting an Adequate Incurred Cost Proposal Presented By: Kiran Pinto, Senior Manager, Watkins Meegan Keith Romanowski, Compliance Director, WJ Technologies March 20, 2013 Agenda Who Needs to

Keys to Submitting an Adequate Incurred Cost Proposal Presented By: Kiran Pinto, Senior Manager, Watkins Meegan Keith Romanowski, Compliance Director, WJ Technologies March 20, 2013 Agenda Who Needs to

Master Document Audit Program. Activity Code Compliance Audit CAS 414 Version 5.20, dated March 2018 B-1 Planning Considerations

Activity Code 19414 Compliance Audit CAS 414 Version 5.20, dated March 2018 B-1 Planning Considerations Type of Service - Attestation Examination Engagement Audit Specific Independence Determination Members

Activity Code 19414 Compliance Audit CAS 414 Version 5.20, dated March 2018 B-1 Planning Considerations Type of Service - Attestation Examination Engagement Audit Specific Independence Determination Members

fersight Wort ßfr-&ö -ös-- /^on Office of the Inspector General Department of Defense

'?. i fersight Wort QUALITY CONTROL REVIEW OF KPMG PEAT MARWICK LLP AND THE DEFENSE CONTRACT AUDIT AGENCY MIDWEST RESEARCH INSTITUTE FISCAL YEAR ENDED JANUARY 31, 1997 Report Number PO 98-6-018 September

'?. i fersight Wort QUALITY CONTROL REVIEW OF KPMG PEAT MARWICK LLP AND THE DEFENSE CONTRACT AUDIT AGENCY MIDWEST RESEARCH INSTITUTE FISCAL YEAR ENDED JANUARY 31, 1997 Report Number PO 98-6-018 September

Virginia Department of Transportation Indirect Cost Rate Submission and Review Process Effective January 1, 2019

Virginia Department of Transportation Indirect Cost Rate Submission and Review Process Effective January 1, 2019 1. Policy, Regulation and Guidance a) In order to ensure that consultant costs reimbursed

Virginia Department of Transportation Indirect Cost Rate Submission and Review Process Effective January 1, 2019 1. Policy, Regulation and Guidance a) In order to ensure that consultant costs reimbursed

References: CAM Section 2 - General Audit Guidance for Termination of Negotiated Contracts

References: CAM 12-200 Section 2 - General Audit Guidance for Termination of Negotiated Contracts CAM 12-400 Section 4 - Auditing Terminations of Cost-Type Contracts Audit Program 17100 Termination, Cost

References: CAM 12-200 Section 2 - General Audit Guidance for Termination of Negotiated Contracts CAM 12-400 Section 4 - Auditing Terminations of Cost-Type Contracts Audit Program 17100 Termination, Cost

Click to edit Master title style

Click to edit Master title style Click to edit Master text styles Second level Click Indirect to edit Rate Master Cycle title style Factors that Drive Your Indirect Rates and Impact Click to edit Your

Click to edit Master title style Click to edit Master text styles Second level Click Indirect to edit Rate Master Cycle title style Factors that Drive Your Indirect Rates and Impact Click to edit Your

Falsification of Documents. Next Slide

Falsification of Documents Table of Contents Risk Assessment Research and Planning Risk Assessment Review of Permanent File Risk Assessment Initial Review of Proposal Document Risk Assessment Discussion

Falsification of Documents Table of Contents Risk Assessment Research and Planning Risk Assessment Review of Permanent File Risk Assessment Initial Review of Proposal Document Risk Assessment Discussion

DEPARTMENT OF DEFENSE Defense Contract Management Agency INSTRUCTION. Estimating System Review

DEPARTMENT OF DEFENSE Defense Contract Management Agency INSTRUCTION Estimating System Review Contracts Directorate DCMA-INST 133 OPR: DCMA-AQ Validated Current, September 8, 2014 1. PURPOSE. This Instruction:

DEPARTMENT OF DEFENSE Defense Contract Management Agency INSTRUCTION Estimating System Review Contracts Directorate DCMA-INST 133 OPR: DCMA-AQ Validated Current, September 8, 2014 1. PURPOSE. This Instruction:

Master Document Master Document. Compensation. Version 6.16, dated March 2018 B-1 Planning Considerations

Activity Code 19415 Version 6.16, dated March 2018 B-1 Planning Considerations Compliance Audit CAS 415 Deferred Compensation Type of Service - Attestation Examination Engagement Audit Specific Independence

Activity Code 19415 Version 6.16, dated March 2018 B-1 Planning Considerations Compliance Audit CAS 415 Deferred Compensation Type of Service - Attestation Examination Engagement Audit Specific Independence

DEPARTMENT OF DEFENSE Defense Contract Management Agency INSTRUCTION. Termination for Convenience

DEPARTMENT OF DEFENSE Defense Contract Management Agency INSTRUCTION Termination for Convenience Contracts Directorate DCMA-INST 101 OPR: DCMA-AQ SUMMARY OF CHANGES. This revision adds references and text

DEPARTMENT OF DEFENSE Defense Contract Management Agency INSTRUCTION Termination for Convenience Contracts Directorate DCMA-INST 101 OPR: DCMA-AQ SUMMARY OF CHANGES. This revision adds references and text

Report Documentation Page

Report Documentation Page Report Date 28Mar2002 Report Type N/A Dates Covered (from... to) - Title and Subtitle Audit Oversight: Report on Quality Control Review of KPMG, LLP and Defense Contract Audit

Report Documentation Page Report Date 28Mar2002 Report Type N/A Dates Covered (from... to) - Title and Subtitle Audit Oversight: Report on Quality Control Review of KPMG, LLP and Defense Contract Audit

Contract Closeout for Cost Type Contracts

Contract Closeout for Cost Type Contracts Breakout Session #: E16 Johanna P. Akinfenwa, MSA, Contracts Team Chief, DCMA Jennifer Quinones, CPA, MSA, Deputy Assistant Director, Policy and Plans, DCAA Cassandra

Contract Closeout for Cost Type Contracts Breakout Session #: E16 Johanna P. Akinfenwa, MSA, Contracts Team Chief, DCMA Jennifer Quinones, CPA, MSA, Deputy Assistant Director, Policy and Plans, DCAA Cassandra

SUBPART CONTRACT PRICING (Revised November 24, 2008)

") SUBPART 215.4--CONTRACT PRICING (Revised November 24, 2008) 215.402 Pricing policy. Follow the procedures at PGI 215.402 when conducting cost or price analysis, particularly with regard to acquisitions

SUBPART 215.4--CONTRACT PRICING (Revised November 24, 2008) 215.402 Pricing policy. Follow the procedures at PGI 215.402 when conducting cost or price analysis, particularly with regard to acquisitions

Incurred Cost Submissions

Incurred Cost Submissions Further information is available in the Information for Contractors Manual under Enclosure 6 The views expressed in this presentation are DCAA's views and not necessarily the

Incurred Cost Submissions Further information is available in the Information for Contractors Manual under Enclosure 6 The views expressed in this presentation are DCAA's views and not necessarily the

Subcontract Pricing Deficiencies. Next Slide

Subcontract Pricing Deficiencies Table of Contents Risk Assessment Research and Planning Risk Assessment Review of Contract and Price Negotiation Memorandum (PNM) Risk Assessment Overrun/Underrun Analysis

Subcontract Pricing Deficiencies Table of Contents Risk Assessment Research and Planning Risk Assessment Review of Contract and Price Negotiation Memorandum (PNM) Risk Assessment Overrun/Underrun Analysis

DEFENSE CONTRACT AUDIT AGENCY 8725 JOHN J. KINGMAN ROAD, SUITE 2135 FORT BELVOIR, VA PPS June 26, 2012 INFORMATION FOR CONTRACTORS

DEFENSE CONTRACT AUDIT AGENCY 8725 JOHN J. KINGMAN ROAD, SUITE 2135 FORT BELVOIR, VA 22060-6219 PPS June 26, 2012 DCAA MANUAL NO. 7641.90 INFORMATION FOR CONTRACTORS 1. PURPOSE. This manual supersedes

DEFENSE CONTRACT AUDIT AGENCY 8725 JOHN J. KINGMAN ROAD, SUITE 2135 FORT BELVOIR, VA 22060-6219 PPS June 26, 2012 DCAA MANUAL NO. 7641.90 INFORMATION FOR CONTRACTORS 1. PURPOSE. This manual supersedes

DEPARTMENT OF DEFENSE Defense Contract Management Agency INSTRUCTION. Consent to Subcontract

DEPARTMENT OF DEFENSE Defense Contract Management Agency INSTRUCTION Consent to Subcontract Contracts Directorate DCMA-INST 143 OPR: DCMA-AQCF 1. PURPOSE. This Instruction: a. Cancels DCMA Instruction

DEPARTMENT OF DEFENSE Defense Contract Management Agency INSTRUCTION Consent to Subcontract Contracts Directorate DCMA-INST 143 OPR: DCMA-AQCF 1. PURPOSE. This Instruction: a. Cancels DCMA Instruction

Item No. Adequacy Consideration Adequate Notes

References: CAM 12-200 Section 2 - General Audit Guidance for Termination of Negotiated Contracts CAM 12-300 Section 3 - Auditing Terminations of Fixed-Price Contracts Audit Program 17100 Termination,

References: CAM 12-200 Section 2 - General Audit Guidance for Termination of Negotiated Contracts CAM 12-300 Section 3 - Auditing Terminations of Fixed-Price Contracts Audit Program 17100 Termination,

Item No. Adequacy Consideration Adequate Notes

References: CAM 12-200 Section 2 - General Audit Guidance for Termination of Negotiated Contracts CAM 12-300 Section 3 - Auditing Terminations of Fixed-Price Contracts Audit Program 17100 Termination,

References: CAM 12-200 Section 2 - General Audit Guidance for Termination of Negotiated Contracts CAM 12-300 Section 3 - Auditing Terminations of Fixed-Price Contracts Audit Program 17100 Termination,

DEPARTMENT OF DEFENSE Defense Contract Management Agency INSTRUCTION. Disallowance of Costs

DEPARTMENT OF DEFENSE Defense Contract Management Agency INSTRUCTION Disallowance of Costs Contracts Directorate DCMA-INST 128 OPR: DCMA-AQ 1. PURPOSE. This Instruction: a. Revises DCMA Instruction (DCMA-INST)

DEPARTMENT OF DEFENSE Defense Contract Management Agency INSTRUCTION Disallowance of Costs Contracts Directorate DCMA-INST 128 OPR: DCMA-AQ 1. PURPOSE. This Instruction: a. Revises DCMA Instruction (DCMA-INST)

Master Document Audit Program. Corporate and Home Office Shell. Version 3.10, dated March 2018 B-1 Planning Considerations

Activity Code 10100 Version 3.10, dated March 2018 B-1 Planning Considerations Incurred Cost Audit of Corporate and Home Office Shell Type of Service - Attestation Examination Engagement Audit Specific

Activity Code 10100 Version 3.10, dated March 2018 B-1 Planning Considerations Incurred Cost Audit of Corporate and Home Office Shell Type of Service - Attestation Examination Engagement Audit Specific

Office of the Inspector General «la.»««'«" Department of Defense

ffi QUALITY CONTROL REVIEW OF KPMG PEAT MARWICK LLP AND THE DEFENSE CONTRACT AUDIT AGENCY THE AEROSPACE CORPORATION FISCAL YEAR ENDED SEPTEMBER 30, 1995 Report Number PO 98-6-007 March 6, 1998 Office of

ffi QUALITY CONTROL REVIEW OF KPMG PEAT MARWICK LLP AND THE DEFENSE CONTRACT AUDIT AGENCY THE AEROSPACE CORPORATION FISCAL YEAR ENDED SEPTEMBER 30, 1995 Report Number PO 98-6-007 March 6, 1998 Office of

Contractor Purchasing System Review (CPSR) Guidebook. October 2, 2017 DEPARTMENT OF DEFENSE (DOD) DEFENSE CONTRACT MANAGEMENT AGENCY (DCMA)

Guidebook. October 2, 2017 DEPARTMENT OF DEFENSE (DOD) DEFENSE CONTRACT MANAGEMENT AGENCY (DCMA)") DEPARTMENT OF DEFENSE (DOD) Contractor Purchasing System Review (CPSR) Guidebook October 2, 2017 DEFENSE CONTRACT MANAGEMENT AGENCY (DCMA) This revision supersedes all previous versions. Table of Contents

DEPARTMENT OF DEFENSE (DOD) Contractor Purchasing System Review (CPSR) Guidebook October 2, 2017 DEFENSE CONTRACT MANAGEMENT AGENCY (DCMA) This revision supersedes all previous versions. Table of Contents

Master Document Audit Program. Activity Code Compliance Audit CAS 409 Version 5.22, dated March 2018 B-1 Planning Considerations

Activity Code 19409 Compliance Audit CAS 409 B-1 Planning Considerations Type of Service - Attestation Examination Engagement Audit Specific Independence Determination Members of the audit team and internal

Activity Code 19409 Compliance Audit CAS 409 B-1 Planning Considerations Type of Service - Attestation Examination Engagement Audit Specific Independence Determination Members of the audit team and internal

Accounting System Requirements

Accounting System Requirements Further information is available in the Information for Contractors Manual under Enclosure 2 The views expressed in this presentation are DCAA's views and not necessarily

Accounting System Requirements Further information is available in the Information for Contractors Manual under Enclosure 2 The views expressed in this presentation are DCAA's views and not necessarily

July 16, Audit Oversight

July 16, 2004 Audit Oversight Quality Control Review of PricewaterhouseCoopers, LLP and the Defense Contract Audit Agency Office of Management and Budget Circular A-133 Audit Report of the Institute for

July 16, 2004 Audit Oversight Quality Control Review of PricewaterhouseCoopers, LLP and the Defense Contract Audit Agency Office of Management and Budget Circular A-133 Audit Report of the Institute for

Contractor Purchasing System Review (CPSR) Guidebook. October 25, 2016 DEPARTMENT OF DEFENSE (DOD) DEFENSE CONTRACT MANAGEMENT AGENCY (DCMA)

Guidebook. October 25, 2016 DEPARTMENT OF DEFENSE (DOD) DEFENSE CONTRACT MANAGEMENT AGENCY (DCMA)") DEPARTMENT OF DEFENSE (DOD) Contractor Purchasing System Review (CPSR) Guidebook October 25, 2016 DEFENSE CONTRACT MANAGEMENT AGENCY (DCMA) This revision supersedes all previous versions. Table of Contents

DEPARTMENT OF DEFENSE (DOD) Contractor Purchasing System Review (CPSR) Guidebook October 25, 2016 DEFENSE CONTRACT MANAGEMENT AGENCY (DCMA) This revision supersedes all previous versions. Table of Contents

versight eport Office of the Inspector General Department of Defense

versight eport REPORT ON QUALITY CONTROL REVIEW OF ARTHUR ANDERSEN, LLP, FOR OMB CIRCULAR NO. A-133 AUDIT REPORT OF THE HENRY M. JACKSON FOUNDATION FOR THE ADVANCEMENT OF MILITARY MEDICINE, FISCAL YEAR

versight eport REPORT ON QUALITY CONTROL REVIEW OF ARTHUR ANDERSEN, LLP, FOR OMB CIRCULAR NO. A-133 AUDIT REPORT OF THE HENRY M. JACKSON FOUNDATION FOR THE ADVANCEMENT OF MILITARY MEDICINE, FISCAL YEAR

Defective Pricing Selective Disclosure. Next Slide

Defective Pricing Selective Disclosure Table of Contents Risk Assessment Research and Planning Risk Assessment Review of Pricing Action Information Preliminary Analytical Procedures Meeting with Contractor

Defective Pricing Selective Disclosure Table of Contents Risk Assessment Research and Planning Risk Assessment Review of Pricing Action Information Preliminary Analytical Procedures Meeting with Contractor

(We have reported on several of the CWC hearings and reports before. To find those stories, type CWC in the search window on the website.

On July 26, 2010, the Commission on Wartime Contracting in Iraq and Afghanistan (CWC) held a hearing entitled Subcontracting: Who s Minding the Store to address concerns about the subcontracting process

On July 26, 2010, the Commission on Wartime Contracting in Iraq and Afghanistan (CWC) held a hearing entitled Subcontracting: Who s Minding the Store to address concerns about the subcontracting process

ONR Guidance for Indirect Cost Rate Proposals for Non-Profits with less than $10M Federal Funding of Direct Costs in a Fiscal Year

ONR Guidance for Indirect Cost Rate Proposals for Non-Profits with less than $10M Funding of Direct Costs in a Fiscal Year A non-profit organization will submit an indirect cost rate proposal primarily

ONR Guidance for Indirect Cost Rate Proposals for Non-Profits with less than $10M Funding of Direct Costs in a Fiscal Year A non-profit organization will submit an indirect cost rate proposal primarily

VSRA Contract Compliance Seminar August 23, 2011

VSRA Contract Compliance Seminar August 23, 2011 Topics Overview What s new? Defense Federal Acquisition Regulation Supplement; Business Systems Definition and Administration (DFARS Case 2009-D038) Reporting

VSRA Contract Compliance Seminar August 23, 2011 Topics Overview What s new? Defense Federal Acquisition Regulation Supplement; Business Systems Definition and Administration (DFARS Case 2009-D038) Reporting

Cost Estimating and Truthful Cost or Pricing Data Requirements

Cost Estimating and Truthful Cost or Pricing Data Requirements Steven M. Masiello Jeremiah J. McIntyre Agenda Cost Estimating FAR cost estimating DFARS cost estimating system rule Government Proposal Analysis

Cost Estimating and Truthful Cost or Pricing Data Requirements Steven M. Masiello Jeremiah J. McIntyre Agenda Cost Estimating FAR cost estimating DFARS cost estimating system rule Government Proposal Analysis

Defense Contract Audit Agency

FY 2002 Amended Budget Submission Defense Contract Audit Agency (DCAA) June 2001 DCAA - 1 Operation and Maintenance, Defense-Wide Summary: (Dollars in Thousands) FY 2000 Price Program FY 2001 Price Program

FY 2002 Amended Budget Submission Defense Contract Audit Agency (DCAA) June 2001 DCAA - 1 Operation and Maintenance, Defense-Wide Summary: (Dollars in Thousands) FY 2000 Price Program FY 2001 Price Program

DEPARTMENT OF DEFENSE Defense Contract Management Agency INSTRUCTION. Voluntary Refunds

DEPARTMENT OF DEFENSE Defense Contract Management Agency INSTRUCTION Voluntary Refunds Contracts Directorate DCMA-INST 113 DCMA-AQC 1. PURPOSE. This Instruction: a. Reissues DCMA Instruction (DCMA-INST)

DEPARTMENT OF DEFENSE Defense Contract Management Agency INSTRUCTION Voluntary Refunds Contracts Directorate DCMA-INST 113 DCMA-AQC 1. PURPOSE. This Instruction: a. Reissues DCMA Instruction (DCMA-INST)

Master Document Audit Program. Version 4.21, dated March 2018 B-1 Planning Considerations

Activity Code 17200 B-1 Planning Considerations Claim Audit, Other Type of Service - Attestation Examination Engagement Audit Specific Independence Determination Members of the audit team and internal

Activity Code 17200 B-1 Planning Considerations Claim Audit, Other Type of Service - Attestation Examination Engagement Audit Specific Independence Determination Members of the audit team and internal

Master Document Audit Program. Defense Security Cooperation Agency (DSCA) Version No. 4.21, dated March 2018 B-1 Planning Considerations

Version No. 4.21, dated March 2018 B-1 Planning Considerations") Activity Code 17900 Defense Security Cooperation Agency (DSCA) Version No. 4.21, dated March 2018 B-1 Planning Considerations Type of Service - Attestation Examination Engagement Audit Specific Independence

Activity Code 17900 Defense Security Cooperation Agency (DSCA) Version No. 4.21, dated March 2018 B-1 Planning Considerations Type of Service - Attestation Examination Engagement Audit Specific Independence

Master Document Audit Program (APCPR-CSSR) Version 4.5, dated May 2014 B-1 Planning Considerations

Version 4.5, dated May 2014 B-1 Planning Considerations") Activity Code 17850 B-1 Planning Considerations CPRs, C/SSRs, and CFSRs Audit Specific Independence Determination Members of the audit team and internal specialists consulting on this audit must complete

Activity Code 17850 B-1 Planning Considerations CPRs, C/SSRs, and CFSRs Audit Specific Independence Determination Members of the audit team and internal specialists consulting on this audit must complete

Government Contracts Pricing Strategies and Rate Structures

Government Contracts Pricing Strategies and Rate Structures Presented By: Brandon Smith bsmith@anglincpa.com Jon Levin jlevin@maynardcooper.com Provisional Billing Rates Provisional, Target, Budget, Billing,

Government Contracts Pricing Strategies and Rate Structures Presented By: Brandon Smith bsmith@anglincpa.com Jon Levin jlevin@maynardcooper.com Provisional Billing Rates Provisional, Target, Budget, Billing,

Current Issues in Contractor Incurred Cost Submissions and Government Audits

Current Issues in Contractor Incurred Cost Submissions and Government Audits Breakout Session #: C03 Presented by: Stephen H. Bishop, Accounting Director at CGS Administrators, LLC Steven Masiello, McKenna

Current Issues in Contractor Incurred Cost Submissions and Government Audits Breakout Session #: C03 Presented by: Stephen H. Bishop, Accounting Director at CGS Administrators, LLC Steven Masiello, McKenna

UACES Subrecipient Monitoring Policy Statement

UACES Subrecipient Monitoring Policy Statement UACES monitors the financial and programmatic performance of Subrecipients, and evaluates their capacity to effectively manage a Subaward. The university

UACES Subrecipient Monitoring Policy Statement UACES monitors the financial and programmatic performance of Subrecipients, and evaluates their capacity to effectively manage a Subaward. The university

Contractor Purchasing System Review (CPSR) Guidebook

Guidebook") DEPARTMENT OF DEFENSE (DOD) Contractor Purchasing System Review (CPSR) Guidebook April 7, 2016 DEFENSE CONTRACT MANAGEMENT AGENCY (DCMA) This revision supersedes all previous versions. Table of Contents

DEPARTMENT OF DEFENSE (DOD) Contractor Purchasing System Review (CPSR) Guidebook April 7, 2016 DEFENSE CONTRACT MANAGEMENT AGENCY (DCMA) This revision supersedes all previous versions. Table of Contents

Introduction to the Cost Accounting Standards Mike Mardesich & Brad Tress April 25, 2017

Introduction to the Cost Accounting Standards Mike Mardesich & Brad Tress April 25, 2017 The Fundamentals of Government Contracting Webinar Series 1 Your Presenters Mike Mardesich Dixon Hughes Goodman

Introduction to the Cost Accounting Standards Mike Mardesich & Brad Tress April 25, 2017 The Fundamentals of Government Contracting Webinar Series 1 Your Presenters Mike Mardesich Dixon Hughes Goodman

Master Document Audit Program

Activity Code 19413 CAS 413.50(c)(12) Segment Closing Adjustments Version 2.22, dated March 2018 B-1 Planning Considerations Type of Service - Attestation Examination Engagement Audit Specific Independence

Activity Code 19413 CAS 413.50(c)(12) Segment Closing Adjustments Version 2.22, dated March 2018 B-1 Planning Considerations Type of Service - Attestation Examination Engagement Audit Specific Independence

Master Document Audit Program

Activity Code 19500 Cost Impact Statement (Price Adjustment) Version 4.23, dated December 2017 B-1 Planning Considerations Type of Service - Attestation Examination Engagement Audit Specific Independence

Activity Code 19500 Cost Impact Statement (Price Adjustment) Version 4.23, dated December 2017 B-1 Planning Considerations Type of Service - Attestation Examination Engagement Audit Specific Independence

The Fundamentals of Government Contracting Webinar Series

An Introduction to the Incurred Cost Submission Part II: Preparation and Adequacy Review March 24 th, 2016 The Fundamentals of Government Contracting Webinar Series 1 Your Presenters David King Dixon Hughes

An Introduction to the Incurred Cost Submission Part II: Preparation and Adequacy Review March 24 th, 2016 The Fundamentals of Government Contracting Webinar Series 1 Your Presenters David King Dixon Hughes

Indirect Rates for Cost Plus Contracting Jenny W Clark. Jenny Clark

Indirect Rates for Cost Plus Contracting Jenny W Clark Jenny Clark jwclark@solvability.com Jenny W Clark The Oprah of Federal Contracting Solvability, Inc. www.solvability.com Phone 256-882-6276 E-mail

Indirect Rates for Cost Plus Contracting Jenny W Clark Jenny Clark jwclark@solvability.com Jenny W Clark The Oprah of Federal Contracting Solvability, Inc. www.solvability.com Phone 256-882-6276 E-mail

TERMS OF REFERENCE (TOR) FOR AUDITS OF UN-WOMEN NGO, GOV T, IGO AND GRANT PROJECTS

FOR AUDITS OF UN-WOMEN NGO, GOV T, IGO AND GRANT PROJECTS") TERMS OF REFERENCE (TOR) FOR AUDITS OF UN-WOMEN NGO, GOV T, IGO AND GRANT PROJECTS TABLE OF CONTENTS Introduction... 3 A. Background... 7 B. Project Management... 7 C. Consultations with concerned parties...

TERMS OF REFERENCE (TOR) FOR AUDITS OF UN-WOMEN NGO, GOV T, IGO AND GRANT PROJECTS TABLE OF CONTENTS Introduction... 3 A. Background... 7 B. Project Management... 7 C. Consultations with concerned parties...

Adequacy of Proposals for. Global Supply Chain

Adequacy of Proposals for Global Supply Chain 1 Adequacy of Proposals Objectives This resource document covers the following: An overview of the proposal process, including applicable FAR (Federal Acquisition

Adequacy of Proposals for Global Supply Chain 1 Adequacy of Proposals Objectives This resource document covers the following: An overview of the proposal process, including applicable FAR (Federal Acquisition

TERMS OF REFERENCE FOR AUDITS OF NIM/NGO PROJECTS

United Nations Development Programme Office of Audit and Investigations Annex I TERMS OF REFERENCE FOR AUDITS OF NIM/NGO PROJECTS 2014 02 November 2014 TABLE OF CONTENTS Page INTRODUCTION... 3 A. Background...

United Nations Development Programme Office of Audit and Investigations Annex I TERMS OF REFERENCE FOR AUDITS OF NIM/NGO PROJECTS 2014 02 November 2014 TABLE OF CONTENTS Page INTRODUCTION... 3 A. Background...

STUDENT GUIDE. CON 170 Fundamentals of Cost & Price Analysis. Unit 3, Lesson 2 Contract Financing

STUDENT GUIDE CON 170 Fundamentals of Cost & Price Analysis Unit 3, Lesson 2 Contract Financing October 2017 CON170, Unit 3 Lesson 2 Contract Financing - Page 1 STUDENT PREPARATION Required Student Preparation

STUDENT GUIDE CON 170 Fundamentals of Cost & Price Analysis Unit 3, Lesson 2 Contract Financing October 2017 CON170, Unit 3 Lesson 2 Contract Financing - Page 1 STUDENT PREPARATION Required Student Preparation

Final Indirect Cost Rate Proposals: Auditor Focus Areas, Trends and Best Practices

Final Indirect Cost Rate Proposals: Auditor Focus Areas, Trends and Best Practices Steven M. Masiello K. Tyler Thomas February 14, 2017 Agenda Regulatory Requirements DCAA Audit Environment Recent Developments

Final Indirect Cost Rate Proposals: Auditor Focus Areas, Trends and Best Practices Steven M. Masiello K. Tyler Thomas February 14, 2017 Agenda Regulatory Requirements DCAA Audit Environment Recent Developments

Defense Affordability Expensive Contracting Policies

Defense Affordability Expensive Contracting Policies Eleanor Spector, VP Contracts, Navy Postgraduate School, 5/16/12 2010 Fluor. All Rights Reserved. Report Documentation Page Form Approved OMB No. 0704-0188

Defense Affordability Expensive Contracting Policies Eleanor Spector, VP Contracts, Navy Postgraduate School, 5/16/12 2010 Fluor. All Rights Reserved. Report Documentation Page Form Approved OMB No. 0704-0188

COST ACCOUNTING STANDARDS NOTICES AND CERTIFICATION

COST ACCOUNTING STANDARDS NOTICES AND CERTIFICATION Introduction The Prime Contract under which this solicitation is issued requires that APL determine the applicability of Cost Accounting Standards Board

COST ACCOUNTING STANDARDS NOTICES AND CERTIFICATION Introduction The Prime Contract under which this solicitation is issued requires that APL determine the applicability of Cost Accounting Standards Board

DCMA MANUAL Contract Debts

DCMA MANUAL 2501-10 Contract Debts Office of Primary Responsibility: Contract Maintenance Capability Effective: April 13, 2018 Releasability: Cleared for public release New Issuance Implements: DCMA-INST

DCMA MANUAL 2501-10 Contract Debts Office of Primary Responsibility: Contract Maintenance Capability Effective: April 13, 2018 Releasability: Cleared for public release New Issuance Implements: DCMA-INST

GCS 224 Surviving DCAA Audits with GCS Premier. Presented by: Nicole Mitchell, Aronson & Company

GCS 224 Surviving DCAA Audits with GCS Premier Presented by: Nicole Mitchell, Aronson & Company Agenda Government Contract Audits and the Role of DCAA and DCMA Basic Attributes of a Government Approved

GCS 224 Surviving DCAA Audits with GCS Premier Presented by: Nicole Mitchell, Aronson & Company Agenda Government Contract Audits and the Role of DCAA and DCMA Basic Attributes of a Government Approved

Chapter 12. Auditing Contract Termination Delay Disruption and Other Price Adjustment Proposals or Claims

Chapter 12 Auditing Contract Termination Delay Disruption and Other Price Adjustment Proposals or Claims Table of Contents 12-000 Auditing Contract Termination, Delay/Disruption, and Other Price Adjustment

Chapter 12 Auditing Contract Termination Delay Disruption and Other Price Adjustment Proposals or Claims Table of Contents 12-000 Auditing Contract Termination, Delay/Disruption, and Other Price Adjustment

International Cost Estimating & Analysis Association. Supplier Cost/Price Analyses June 20, 2013

International Cost Estimating & Analysis Association Supplier Cost/Price Analyses June 20, 2013 David Eck and Todd W. Bishop Dixon Hughes Goodman LLP Government Contract Consulting Services Group Agenda

International Cost Estimating & Analysis Association Supplier Cost/Price Analyses June 20, 2013 David Eck and Todd W. Bishop Dixon Hughes Goodman LLP Government Contract Consulting Services Group Agenda

Proposal Pricing Instructions Page 1 of 7 Supplier Proposal Adequacy Checklist Instructions

Proposal Pricing Instructions Page 1 of 7 Supplier Proposal Adequacy Checklist Instructions Unless a valid exemption applies, Cost or Pricing Data is required to support proposals exceeding $750,000. Contractors

Proposal Pricing Instructions Page 1 of 7 Supplier Proposal Adequacy Checklist Instructions Unless a valid exemption applies, Cost or Pricing Data is required to support proposals exceeding $750,000. Contractors

Contract Closeout Update. Ms. Anita Bales, DCAA Mr. Timothy Callahan, DCMA Ms. Rebecca Beck, DFAS

Contract Closeout Update Ms. Anita Bales, DCAA Mr. Timothy Callahan, DCMA Ms. Rebecca Beck, DFAS Overview Contract Life Cycle Industry Common Barriers Glide Paths Agency Material Weakness Contract Closeout

Contract Closeout Update Ms. Anita Bales, DCAA Mr. Timothy Callahan, DCMA Ms. Rebecca Beck, DFAS Overview Contract Life Cycle Industry Common Barriers Glide Paths Agency Material Weakness Contract Closeout

Chapter 37 Joint Ventures and Teaming Arrangements

Chapter 37 Joint Ventures and Teaming Arrangements Authoritative Sources Cost Accounting Standards FAR Subpart 9.6 Contractor Team Arrangements FASB ASC 323 Investments - Equity Method and Joint Ventures

Chapter 37 Joint Ventures and Teaming Arrangements Authoritative Sources Cost Accounting Standards FAR Subpart 9.6 Contractor Team Arrangements FASB ASC 323 Investments - Equity Method and Joint Ventures

PROCEDURAL GUIDE. Procedures for Financial Reporting at the Department of Defense Education Activity

Department of Defense Education Activity PROCEDURAL GUIDE NUMBER 14-PGRMD-024 DATE October 3, 2014 RESOURCE MANAGEMENT DIVISION SUBJECT: Procedures for Financial Reporting at the Department of Defense

Department of Defense Education Activity PROCEDURAL GUIDE NUMBER 14-PGRMD-024 DATE October 3, 2014 RESOURCE MANAGEMENT DIVISION SUBJECT: Procedures for Financial Reporting at the Department of Defense

COST ACCOUNTING STANDARDS BOARD DISCLOSURE STATEMENT REQUIRED BY PUBLIC LAW EDUCATIONAL INSTITUTIONS

INDEX GENERAL INSTRUCTIONS--Continuation Sheet.............. (i) COVER SHEET AND CERTIFICATION................... C-1 PART I General Information.................. I-1 Part II Part III Part IV Direct Costs......................

INDEX GENERAL INSTRUCTIONS--Continuation Sheet.............. (i) COVER SHEET AND CERTIFICATION................... C-1 PART I General Information.................. I-1 Part II Part III Part IV Direct Costs......................

2 CFR 215 (A-110) or 2 CFR 230 (A-122) Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards.

or 2 CFR 230 (A-122) Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards.") Significant Changes for Selected Items of Cost Office of Management and Budget Guidance PART 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS Item of

Significant Changes for Selected Items of Cost Office of Management and Budget Guidance PART 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS Item of

National Association of Community Health Centers FOM / IT

National Association of Community Health Centers FOM / IT FINANCIAL POLICY CONSIDERATIONS IN PREPARATION FOR HRSA SITE VISITS OCTOBER 29, 2017 David Fields BKD,LLP Partner Catherine Gilpin BKD, LLP Senior

National Association of Community Health Centers FOM / IT FINANCIAL POLICY CONSIDERATIONS IN PREPARATION FOR HRSA SITE VISITS OCTOBER 29, 2017 David Fields BKD,LLP Partner Catherine Gilpin BKD, LLP Senior

What Government Contractors Should Know:

What Government Contractors Should Know: 10 Regulatory Compliance and DCAA Guidance Updates to be Aware of Now and Heading into 2017 Craig Stetson, Managing Director, Capital Edge Consulting, Inc. Introduction

What Government Contractors Should Know: 10 Regulatory Compliance and DCAA Guidance Updates to be Aware of Now and Heading into 2017 Craig Stetson, Managing Director, Capital Edge Consulting, Inc. Introduction

Industry Trends from the Trenches

Industry Trends from the Trenches Presented by CohnReznick s Government Contracting Industry Practice Christine Williamson, Partner and Kristen Soles, Partner PLEASE READ This presentation has been prepared

Industry Trends from the Trenches Presented by CohnReznick s Government Contracting Industry Practice Christine Williamson, Partner and Kristen Soles, Partner PLEASE READ This presentation has been prepared

Contract Closeout Update. Mr. Kenneth Saccoccia, DCAA Mr. James Russell, DCMA Ms. Pamela Franceschi, DFAS

Contract Closeout Update Mr. Kenneth Saccoccia, DCAA Mr. James Russell, DCMA Ms. Pamela Franceschi, DFAS Overview Contract Life Cycle Common Barriers Status of Incurred Cost Audits Agency Material Weakness

Contract Closeout Update Mr. Kenneth Saccoccia, DCAA Mr. James Russell, DCMA Ms. Pamela Franceschi, DFAS Overview Contract Life Cycle Common Barriers Status of Incurred Cost Audits Agency Material Weakness

MG-3 - Supplier Cost Price Analyses Best Practices for Evaluating Supplier Proposals and Quotes

International Cost Estimating & Analysis Association - Supplier Cost / Price Analyses June 10-13, 2014 Presented By: David Eck, CPA Director Mike Mardesich, CPA Manager Dixon Hughes Goodman Government

International Cost Estimating & Analysis Association - Supplier Cost / Price Analyses June 10-13, 2014 Presented By: David Eck, CPA Director Mike Mardesich, CPA Manager Dixon Hughes Goodman Government

UNCLASSIFIED. ACC-Warren Industry Engagement Session #2 27 January Certified Cost or Pricing Data. Chief, Pricing Division

ACC-Warren Industry Engagement g Session #2 27 January 2015 Certified Cost or Pricing Data Rich Kulczycki Chief, Pricing Division Agile Proficient Trusted UNCLASSIFIED Certified Cost or Pricing Data: Agenda

ACC-Warren Industry Engagement g Session #2 27 January 2015 Certified Cost or Pricing Data Rich Kulczycki Chief, Pricing Division Agile Proficient Trusted UNCLASSIFIED Certified Cost or Pricing Data: Agenda

(Revised June 29, 2012) MATERIAL MANAGEMENT AND ACCOUNTING SYSTEM (MAY 2011)

MATERIAL MANAGEMENT AND ACCOUNTING SYSTEM (MAY 2011)") (Revised June 29, 2012) 252.242-7000 Reserved. 252.242-7001 Reserved. 252.242-7002 Reserved. 252.242-7003 Reserved. 252.242-7004 Material Management and Accounting System. As prescribed in 242.7204, use

(Revised June 29, 2012) 252.242-7000 Reserved. 252.242-7001 Reserved. 252.242-7002 Reserved. 252.242-7003 Reserved. 252.242-7004 Material Management and Accounting System. As prescribed in 242.7204, use

Master Document Audit Program. Version 6.21, dated March 2018 B-1 Planning Considerations

Activity Code 17200 B-1 Planning Considerations Claim Audit, Delay Disruption Type of Service - Attestation Examination Engagement Audit Specific Independence Determination Members of the audit team and

Activity Code 17200 B-1 Planning Considerations Claim Audit, Delay Disruption Type of Service - Attestation Examination Engagement Audit Specific Independence Determination Members of the audit team and

DEPARTMENT OF DEFENSE Defense Contract Management Agency INSTRUCTION. Forward Pricing Rates

DEPARTMENT OF DEFENSE Defense Contract Management Agency INSTRUCTION Forward Pricing Rates Contracts Directorate DCMA-INST 130 CPR: DCMA-AQ 1. PURPOSE. This Instruction: a. Revises and reissues DCMA Instruction

DEPARTMENT OF DEFENSE Defense Contract Management Agency INSTRUCTION Forward Pricing Rates Contracts Directorate DCMA-INST 130 CPR: DCMA-AQ 1. PURPOSE. This Instruction: a. Revises and reissues DCMA Instruction

STATEMENT OF WORK FOR RECIPIENT CONTRACTED AUDIT OF USAID RESOURCES MANAGED BY THE WEST AFRICAN HEALTH ORGANIZATION (WAHO)

") STATEMENT OF WORK FOR RECIPIENT CONTRACTED AUDIT OF USAID RESOURCES MANAGED BY THE WEST AFRICAN HEALTH ORGANIZATION (WAHO) AUDIT OF USAID RESOURCES MANAGED BY WEST AFRICAN HEALTH ORGANIZATION UNDER THE

STATEMENT OF WORK FOR RECIPIENT CONTRACTED AUDIT OF USAID RESOURCES MANAGED BY THE WEST AFRICAN HEALTH ORGANIZATION (WAHO) AUDIT OF USAID RESOURCES MANAGED BY WEST AFRICAN HEALTH ORGANIZATION UNDER THE

Current Issues in Government Contract Accounting

Current Issues in Government Contract Accounting Jim Thomas, Partner David Eastwood, Senior Manager PricewaterhouseCoopers LLP Tysons Corner, VA Agenda Page 1 Revenue Recognition Update 1 2 Current Environment

Current Issues in Government Contract Accounting Jim Thomas, Partner David Eastwood, Senior Manager PricewaterhouseCoopers LLP Tysons Corner, VA Agenda Page 1 Revenue Recognition Update 1 2 Current Environment

University of Alaska Statewide System

FOR CASB DS-2 Effective 8/17/95 INDEX GENERAL INSTRUCTIONS -- Continuation Sheet...(ii) COVER SHEET AND CERTIFICATION... C-1 PART I PART II PART III PART IV PART V PART VI PART VII General Information...I-1

FOR CASB DS-2 Effective 8/17/95 INDEX GENERAL INSTRUCTIONS -- Continuation Sheet...(ii) COVER SHEET AND CERTIFICATION... C-1 PART I PART II PART III PART IV PART V PART VI PART VII General Information...I-1

Peer Review Recommendations, Lessons Learned

Peer Review s, Lessons Learned Pricing Feedback Weapon System, Production Lot Buy (Sole Source) Recommended that the team (preparing to negotiate the undefinitized contract action) coordinate with DCMA