Designing Privacy Policies and Identifying Privacy Risks for Financial Institutions. June 2016

|

|

|

- Gwen Shields

- 6 years ago

- Views:

Transcription

1 Designing Privacy Policies and Identifying Privacy Risks for Financial Institutions June 2016

2 Program Overview Regulatory Environment Who Needs a Privacy Program and Common Questions Components of a Comprehensive Privacy Program Tailoring, Implementing and Monitoring Your Privacy Program Understanding Contractual Liabilities Key Takeaways from OCIE s September 15, 2015 Risk Alert Recent SEC Enforcement Actions 2

3 Key Statutes And Regulations Federal Laws Title V of the Gramm-Leach-Bliley Act of 1999 Regulation S-P FTC Privacy of Consumer Financial Information Rule ( FTC Privacy Rule ) FTC Standards for Safeguarding Customer Information ( FTC Safeguards Rule ) Regulation S-AM Regulation S-ID FTC Act Section 5 State Laws Massachusetts Standards for the Protection of Personal Information 201 CMR 17, et. Seq. California Online Privacy Protection Act ( CalOPPA ) 3

4 Basis For Liability FTC Act Section 5 SEC/FTC Enforcement Actions Litigation State AG Enforcement Actions 4

5 Who Needs a Privacy Program? In General: Any financial institution that obtains nonpublic personal information from its customers needs a privacy program. Consumer means an individual who obtains or has obtained a financial product or service from you that is to be used primarily for personal, family, or household purposes, or that individual s legal representative. Customer means a consumer who has a customer relationship with you. Nonpublic personal information means (i) personally identifiable financial information; and (ii) any list, description, or other grouping of consumers (and publicly available information pertaining to them) that is derived using any personally identifiable financial information that is not publicly available information. Personally identifiable financial information means any information: (i) a consumer provides to you to obtain a financial product or service from you; (ii) about a consumer resulting from any transaction involving a financial product or service between you and a consumer; or (iii) You otherwise obtain about a consumer in connection with providing a financial product or service to that consumer. 5

6 Who Needs a Privacy Program? Common Questions I am a registered investment adviser ( RIA ) to registered investment companies that have individual, natural person investors. Regulation S-P applies to the adviser and to the funds. The adviser on its own behalf (and on behalf of the funds) needs a privacy program. I am a RIA, but the registered investment companies I manage only have institutional investors. Reg. S-P and the FTC Privacy Rules do not apply to information relating to institutional investors or pension funds. The RIA and the funds do not need a privacy program. I am a RIA and private fund manager. My clients (for purposes of Form ADV) are the private funds I manage. High net worth individuals invest in those funds. The FTC Privacy Rules are broad enough to encompass private funds and Reg. S-P applies to the adviser. Both need a privacy program. I am a RIA, but the individual investors in the funds I manage are non-u.s. persons. I conduct activities only through non-u.s. offices and branches. Reg. S-P explicitly applies. The adviser needs a privacy program. I am an investment adviser, and I manage individual investors money. I am not registered with the SEC. The FTC Privacy Rules are broad enough to encompass non-registered advisers. The adviser needs a privacy program. 6

7 Components of a Privacy Program Privacy Programs have a number of components, including a: Privacy Notice Regulation S-P and the FTC Privacy Rule Written Information Security Program Regulation S-P and the FTC Privacy Rule Regulation S-AM Notice Regulation S-AM Red Flags Program Regulation S-ID Online Privacy Policy California Online Privacy Protection Act ( CalOPPA ) Incident Response Plan SEC Guidance; SEC Cybersecurity Examination Initiative; SEC Enforcement Order Whether a given entity needs all, or only some, of the listed components depends on that entity s specific business practices. 7

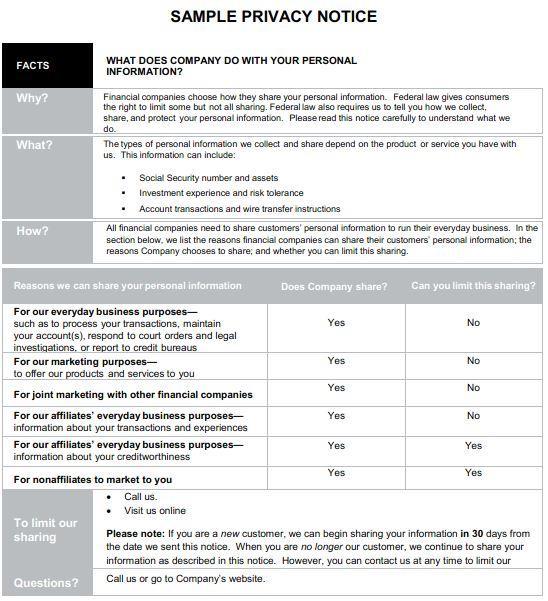

8 Privacy Notice Generally (Reg. S-P / FTC Privacy Rule) Regulation S-P and the FTC Privacy Rule require financial institutions to provide customers with initial and annual privacy notices with respect to their sharing of nonpublic personal information with affiliates and unaffiliated third parties. When the financial institution shares consumer information in certain ways, these notices also must provide a reasonable opportunity for the consumer to opt out of having the consumer s information shared. 8

9 Privacy Notice Who needs to provide one? (Reg. S-P / FTC Privacy Rule) Financial institutions are required to provide customers with initial and annual privacy notices with respect to their sharing of nonpublic personal information with affiliates and unaffiliated third parties. Financial institution means any institution the business of which is engaging in activities that are financial in nature or incidental to such financial activities as described in section 4(k) of the Bank Holding Company Act of 1956 (12 U.S.C. 1843(k)). Under the FTC Privacy Rule, it means a business significantly engaged in financial activities under section 4(k) of the Bank Holding Company Act. Consumer means an individual who obtains or has obtained a financial product or service from you that is to be used primarily for personal, family, or household purposes, or that individual s legal representative. Customer means a consumer who has a customer relationship with you. Customer relationship means a continuing relationship between a consumer and you under which you provide one or more financial products or services to the consumer that are to be used primarily for personal, family, or household purposes. Nonpublic personal information means (i) personally identifiable financial information; and (ii) any list, description, or other grouping of consumers (and publicly available information pertaining to them) that is derived using any personally identifiable financial information that is not publicly available information. Personally identifiable financial information means any information: (i) a consumer provides to you to obtain a financial product or service from you; (ii) about a consumer resulting from any transaction involving a financial product or service between you and a consumer; or (iii) You otherwise obtain about a consumer in connection with providing a financial product or service to that consumer. 9

10 Privacy Notice Timing and Content (Reg. S-P / FTC Privacy Rule) A notice and opt-out form must be provided at the time a customer relationship is formed, and then annually thereafter SEC/FTC take the view that you violate Reg. S-P by sharing information before disclosure and opportunity to opt-out. The SEC/FTC have not been aggressive about enforcing this, yet. 10

11 11

12 Privacy Notice A Key Practice Point (Reg. S-P / FTC Privacy Rule) Financial institutions must abide by the policies set out in the privacy notices they deliver. 12

13 Written Information Security Program ( WISP ) (Reg. S-P / FTC Safeguards Rule) Reg. S-P and the FTC Safeguards Rule also require financial institutions to adopt policies and procedures that address administrative, technical, and physical safeguards for the protection of customer records and information. The policies and procedures must be reasonably designed to: Insure the security and confidentiality of customer records and information; Protect against any anticipated threats or hazards to the security or integrity of customer records and information; and Protect against unauthorized access to or use of customer records or information that could result in substantial harm or inconvenience to any customer. What does this mean and how do you do it? Many U.S. firms look to the Massachusetts Standards for the Protection of Personal Information (the Massachusetts Standards ) for guidance. Require administrative, physical and technical safeguards. 13

14 Written Information Security Program ( WISP ) Massachusetts Standards: Administrative Safeguards Designated employee to maintain information security program; At least annual review of Program; Monitoring security Program Identify and assess reasonably foreseeable internal and external risks; Develop security policies for employees that account for which employees have access to information Employee training and employee disciplinary procedures Third Party Service Provider Verification 14

15 Written Information Security Program ( WISP ) Massachusetts Standards: Technical Safeguards Numerous technical requirements including: Secure user IDs and other identifiers; Secure access control measures; Encryption of both (1) laptops, and (2) other portable devices; System monitoring; Firewall protection; Up-to-date patches and virus definitions; and Education and training Conduct gap analysis inventory all current I.T. procedures and identify any deficiencies 15

16 Regulation S-AM Notices: Generally Adopted by the SEC in 2010 Applies to brokers, dealers, investment companies, registered investment advisers, and registered transfer agents ( S-AM Institutions ) Governs the ability of S-AM Institutions to use certain consumer information obtained from their affiliates to make marketing solicitations Regulation S-AM applies only when an S-AM entity uses information obtained from an affiliate, unlike Regulation S-P, which governs information sharing 16

17 Regulation S-AM Notices: Requirements An S-AM Institution may not use eligibility information about a consumer received from an affiliate to make marketing solicitations to customers unless: The consumer has received notice; The consumer has a reasonable chance to opt-out; and The consumer did not opt out A marketing solicitation is any communication made to a consumer based on eligibility information that is intended to encourage the consumer to buy a product or use a service offered by the marketer 17

18 Regulation S-AM Notices: Exceptions There are six exceptions to Regulation S-AM for persons that receive eligibility information from an affiliate: To make a marketing solicitation to a consumer with whom the person has a pre-existing business relationship; To facilitate communications to an individual for whose benefit the person provides employee benefit or other services pursuant to a contract with an employer related to and arising out of the current employment relationship or status of the individual as a participant or beneficiary of an employee benefit plan; To perform services on behalf of an affiliate (subject to certain exceptions); In response to a communication about its product and services initiated by the consumer; In response to solicitations authorized or requested by the consumer; or If compliance would conflict with applicable provisions of state insurance laws pertaining to unfair discrimination. Generally, the preexisting business relationship is the most useful. 18

19 Regulation S-AM Notices: Exceptions An S-AM Institution will not need to comply with Regulation S-AM in connection with making solicitations to consumers with whom the institution has a preexisting business relationship, which is defined as a relationship based on: A financial contract in force at the time the marketing A financial transaction (including an active account) within 18 months preceding the date of the marketing; An inquiry or application by the consumer regarding a product or service during the three months preceding the date the marketing solicitation. For example, if a consumer has an account with an adviser and also deposit at an affiliated bank, the adviser may use eligibility information obtained from the bank to market additional products or services to the consumer without having to provide notice or an opportunity to opt-out. 19

20 Regulation S-AM: Notice and Opt-Out Requirements If Regulation S-AM applies, an S-AM Institution must send customers an initial notice that is clear, conspicuous and concise The notice must disclose: A list of the affiliates or types of affiliates whose use of eligibility information is covered by the Notice; A general description of the types of eligibility information that may be used; That the consumer may elect to limit the use of eligibility information to make marketing solicitations to the consumer; That the consumer s election will apply for a specified period of time stated in the Notice and, if applicable, that the consumer will be allowed to renew the election once that period expires; If the Notice is provided to consumers who may have previously opted out, such as if a Notice is provided to consumers annually, that the consumer who has chosen to limit solicitations does not need to act again until the consumer receives a renewal notice; and A reasonable and simple method for the consumer to opt out. 20

21 Regulation S-AM Notices: Delivery Regulation S-AM permits an S-AM Institution to combine Regulation S- AM notices with Regulation S-P notices. This would probably be most useful where the institution plans to send annual Regulation S-AM notices. 21

22 Red Flags Rule: Overview (Regulation S-ID) Regulation S-ID (the Red Flags Rule ) requires financial institutions and creditors to: Establish a written, board approved Identity Theft Program; Identify red flags of identity theft any pattern, practice, or specific activity that indicates the possible existence of identity theft ; Detect red flags ; Prevent and mitigate identity theft; Update the Identity Theft Program; and Administer the Program. Guidelines suggest oversight of the Program by the board of directors, an appropriate committee of the board, or a designated employee at the level of senior management. 22

23 Red Flags Rule: Triggers (Regulation S-ID) Financial Institution is a bank, credit union, or any other person that holds a transaction account Transaction Account is generally considered a deposit or account on which the depositor or account holder is permitted to make withdrawals for the purpose of making payments to third parties. Creditor is defined broadly as any entity or person who regularly arranges for, extends, renews or continues credit Interpreted expansively; includes any situation in which services or goods are provided prior to receipt of full payment Creditor may include lenders such as banks, brokers, finance companies, auto dealers, mortgage brokers, utility companies, telecommunications companies, and professional services providers Covered Account is an account primarily for personal, family, or household purposes that is designed to permit multiple payments or transactions to third parties; or any other account for which there is a reasonably foreseeable risk to customers or to the safety and soundness of the financial institution or creditor from identity theft 23

24 Red Flags Rule: Identifying Red Flags (Regulation S-ID) Analyze and inventory all past data security threats Industry alerts, customer notifications or concerns, presentation of suspicious documents, unusual account activity, etc. should all be considered red flags of identity theft Analyze and inventory past responses to such incidents Have remedial technical measures been implemented? Were past notification procedures effective? Were accounts monitored? Create matrix of all sources of personal information, and how that information is maintained Assess vulnerabilities: How long is information stored, how is it stored, who has access to the information, is more sensitive information stored in a secure environment? Analyze threats to current maintenance and overview procedures 24

25 Red Flags Rule: Prevention and Mitigation (Regulation S-ID) Prepare incident response protocol Incident response should dependent on type of threat, incident, information involved, etc. Match response to type of threat/risk/sensitive information Monitor account for unusual activity, contact customer, change passwords, shut down account, notify law enforcement, etc. Rule does not mandate specific technical requirements Document all incidents, responses, and outcomes. Administer and update program accordingly 25

26 Online Privacy Policy (California Online Privacy Protection Act) Companies that use websites to engage with their customers need to have an online privacy policy Policies should be drafted in accordance with the California Online Privacy Protection Act Online privacy policies explain: The categories of personal information collected about users via the website The categories of third parties with whom that information is shared Any opportunities that consumers may have to opt out of that information sharing Whether the website employs data collection technologies, such as cookies or other tracking technologies How the company s website responds to do not track signals it receives from browsers Whether other parties may collect personal information about a website user when the collection is done over time and across different websites 26

27 Incident Response Plan An incident response plan details, in writing, a concrete plan for what a company will do if it faces a suspected or actual data breach or cyberattack. The plan should, at a minimum: Identify the company s most vulnerable data; Assign responsibility for each element of the response plan and provide 24-hour contact information for all personnel and back-up personnel; Explain how to determine whether an incident is actually a breach and whether and how it should be escalated; Indicate that data should be preserved so that a forensic investigation can be conducted; Identify who will keep logs and records of all information relating to the incident; and Include procedures for notifying law enforcement and criteria for whether customers or third-parties need to be notified. Incident response plans should be tested Personnel need to be trained and know how to respond to a data breach or cyber-attack. 27

28 Tailoring Your Program: Data Flows How is personal data obtained, directly or indirectly? Where is the data held? How long is data kept? How is data used? Who has access to data? Employees Affiliates Third Parties: vendors, service providers What data is shared with business partners? 28

29 Implementing Your Program Firms must actually implement the policies and procedures they adopt. Firms should conduct periodic assessments, create a strategy designed to prevent, detect and respond to cybersecurity threats, and Implement the strategy through written policies and procedures and training that provide guidance to officers and employees concerning applicable threats and measures to prevent, detect and respond to such threats, and that monitor compliance with cybersecurity policies and procedures. SEC IM Guidance Update, Cybersecurity Update, April 2015 [P]ublic reports have identified cybersecurity breaches related to weaknesses in basic controls. As a result, examiners will gather information on cybersecurity-related controls and will also test to assess implementation of certain firm controls. OCIE 2015 Cybersecurity Examination Initiative, September 2015 R.T. Jones failed to adopt any written policies and procedures reasonably designed to safeguard its clients PII as required by the Safeguards Rule. To mitigate against any future risk of cyber threats, R.T. Jones has appointed an information security manager to oversee data security and protection of PII, and adopted and implemented a written information security policy as a remedial effort. SEC Order, R.T. Jones Capital Equities Management, Inc., September 22,

30 Testing and Monitoring Your Program Firms should continually monitor their vulnerabilities and conduct regular evaluations to ensure their policies and procedures are working. Create a strategy that is designed to prevent, detect and respond to cybersecurity threats. Routine testing of strategies could also enhance the effectiveness of any strategy. SEC IM Guidance Update, Cybersecurity Update, April 2015 Examiners also may assess whether firms are periodically evaluating cybersecurity risks and whether their controls and risk assessment processes are tailored to their business. OCIE 2015 Cybersecurity Examination Initiative, September 2015 R.T. Jones failed to adopt any written policies and procedures reasonably designed to safeguard its clients PII as required by the Safeguards Rule. R.T. Jones s procedures for protecting its clients information did not include, for example: conducting periodic risk assessments... SEC Order, R.T. Jones Capital Equities Management, Inc., September 22,

31 The Downstream Effects of Reg. S-P / FTC Privacy Rules: Step I If you, as a financial institution, receive nonpublic personal information from a nonaffiliated financial institution under an exception to the notice and opt out requirements, your disclosure is limited. You essentially step into the shoes of the disclosing entity, and must limit your sharing the same way the disclosing entity does. Familiarize Yourself with Your Current Agreements If you receive nonpublic personal information from other financial institutions you may be contractually required to protect it in very specific ways. 31

32 The Downstream Effects of Reg. S-P / FTC Privacy Rules: Step II You may also share nonpublic personal information with non-financial institutions, such as vendors and third-party service providers Raises liability issues for you (the disclosing entity) because you are obligated to ensure down-stream protection of nonpublic personal information Consider that service providers and third party vendors may not be subject to the relevant laws 32

33 Dealing with Third-Party Vendors / Service Providers Conduct due diligence with regard to vendor selection Hold service providers to the same legal standard Require service providers to provide notice of security breaches Supervise and monitor service providers compliance 33

34 Model Provisions: Contracts with Third-Party Vendors / Service Providers Maintain confidentiality and comply with applicable law "Confidential Information" shall include, but not be limited to, any or all of the following: (a) the names, addresses, telephone, facsimile numbers, financial data, addresses, and any other "Non- Public Personal Information" as that term is used in the Gramm- Leach-Bliley Act of 1999 (the "Act"), regarding Bank's, its operating subsidiaries, or its affiliates' customers, or prospective customers... Consider that service provider may not be subject to the relevant laws Service provider may have different security standards 34

35 Holding Service Provider to Same Legal Standard Contractor acknowledges that (1) Bank is subject to the consumer and customer privacy provisions of the Gramm Leach Bliley Act and Federal regulations that implement the Act (the "Regulation"); (2) the Confidential Information covered by this Agreement may include Non-Public Personal Information as defined in the Regulation; and (3) that Bank has certain obligations to protect the Confidential Information from unauthorized disclosure to third parties. Contractor understands that Contractor's willingness and ability to cooperate with and assist Bank in this regard is a material factor in Bank's willingness to enter into this Agreement, and such other agreements as Bank may enter into, or have entered into, with Contractor, through which agreements Confidential Information will be released from Bank to Contractor Contractor acknowledges receipt from Bank of a copy of the Gramm-Leach- Bliley Act and acknowledges that it has access to all applicable rules and regulations promulgated thereunder, and warrants that its procedures with regard to preventing release of Confidential Information are such as to be fully compliant with the Regulation as if Contractor were fully subject to the Regulation to the same extent as Bank 35

36 Establishing Security Standards for Data Recipients Specifically, and not by way of limitation, Contractor shall: (1) maintain Confidential Information of Bank in physical and electronically secure media and facilities, subject to commercially reasonable security procedures; (2) not use, nor permit its employees, agents, subcontractors or affiliates to use, such Confidential Information for any purpose whatsoever except strictly in connection with performance of its contractual duties to Bank; (3) neither use, nor permit use of, such data for any sales or marketing purposes; (4) make and enforce policies and procedures in hiring, training, supervision and monitoring of its staff, agents and subcontractors in proper handling and protection of Confidential Information, including, at a minimum and not by way of limitation, written agreements for confidentiality to be signed personally by all such parties, training, and provision for disciplinary action where appropriate; and (5) not copy, nor permit copying of, the Confidential Information, in any manner, or in any medium, whatsoever, and return all such data immediately upon completion of the task for which it was received, or with Bank's prior written approval, certify destruction of such data in writing 36

37 Addressing Security Breaches Notice of Security Breach. If a party to this Agreement becomes aware of any actual or suspected loss of, unauthorized access to, or unauthorized use or disclosure of any Confidential Information of the other party, including any Personal Information covered by this Agreement, such party promptly shall, at its expense: (a) notify the other party in writing; (b) investigate the circumstances relating to such actual or suspected loss or unauthorized access, use or disclosure; (c) take commercially reasonable steps to mitigate the effects of such loss or unauthorized access, use or disclosure and to prevent any reoccurrence; (d) provide to the Owner such information regarding such loss or unauthorized access, use or disclosure as is reasonably required for the Owner to evaluate the likely consequences and any regulatory or legal requirements arising out of such loss or unauthorized access, use or disclosure; and (e) cooperate with the Owner to further comply with all relevant laws, rules and regulations 37

38 OCIE s September 15, 2015 Risk Alert: Key Takeaways Unlike OCIE s 2014 Cybersecurity Examination Initiative, OCIE s 2015 Cybersecurity Examination Initiative will focus on whether firms are actually implementing the policies and procedures they have adopted The staff s document reviews and questions were designed to discern basic distinctions among the level of preparedness of the examined firms. The staff conducted limited testing of the accuracy of the responses and the extent to which firms policies and procedures were implemented. The examinations did not include reviews of technical sufficiency of the firms programs. OCIE s Cybersecurity Examination Sweep Summary February 2015 OCIE is issuing this Risk Alert to provide additional information on the areas of focus for OCIE s second round of cybersecurity examinations, which will involve more testing to assess implementation of firm procedures and controls. OCIE s 2015 Cybersecurity Examination Initiative September

39 OCIE s September 15, 2015 Risk Alert: Key Takeaways OCIE has indicated that in its 2015 Cybersecurity Examination Initiative, it will drill-down on the specific technical controls firms have in place to protect customer information. Firms may be particularly at risk of a data breach from a failure to implement basic controls to prevent unauthorized access to systems or information, such as multifactor authentication or updating access rights based on personnel or system changes. OCIE s 2015 Cybersecurity Examination Initiative September 2015 Examiners may review how firms control access to various systems and data via management of user credentials, authentication and authorization methods. This may include a review of controls associated with remote access, customer logins, passwords, firm protocols to address customer login problems, network segmentation, and tiered access. OCIE s 2015 Cybersecurity Examination Initiative September 2015 OCIE may request firms policies and procedures relating to Patch management practices, including those regarding the prompt installation of critical patches and the documentation evidencing such actions. OCIE s 2015 Cybersecurity Examination Initiative September

40 OCIE s September 15, 2015 Risk Alert: Key Takeaways OCIE s 2015 Cybersecurity Examination Initiative Risk Alert demonstrates an increased focus on Vendor Management OCIE s 2015 Cybersecurity Examination Initiative September 2015 Some of the largest data breaches over the last few years may have resulted from the hacking of third party vendor platforms. As a result, examiners may focus on firm practices and controls related to vendor management, such as due diligence with regard to vendor selection, monitoring and oversight of vendors, and contract terms. Examiners may assess how vendor relationships are considered as part of the firm s ongoing risk assessment process as well as how the firm determines the appropriate level of due diligence to conduct on a vendor. OCIE s 2015 Cybersecurity Examination Initiative September 2015 This focus on vendor management is particularly interesting due to the following findings reported by OCIE in February 2015: The vast majority of examined firms conduct periodic risk assessments, on a firm-wide basis, to identify cybersecurity threats, vulnerabilities and potential business consequences. Fewer firms apply these requirements to their vendors. A majority of broker-dealers (84%) and a third of the advisers (32%) require cybersecurity risk assessments of vendors with access to their firms networks. OCIE s Cybersecurity Examination Sweep Summary February

41 In the Matter of R.T. Jones Capital Equities Management, Inc. (September 22, 2015) SEC released an Order regarding a settlement with R. T. Jones in connection with its alleged violation of Rule 30(a) of Regulation S-P (the Safeguards Rule ). Alleged Facts: For approximately 4 years, R. T. Jones an SEC-registered investment adviser with 8,400 client accounts and $480 million in assets under management stored sensitive personally identifiable information ( PII ) of clients and other persons on its third party-hosted web server. R.T. Jones did not adopt written policies and procedures regarding the security and confidentiality of that information and the protection of that information from anticipated threats or unauthorized access. In July 2013, the firm s web server was hacked and the PII over more than 100,000 individuals, including thousands of R.T. Jones s clients, was left vulnerable to theft. R.T Jones retained more than one cybersecurity consulting firm to confirm and assess the attack. Neither could confirm whether the PII stored on the server had been accessed or compromised. R.T. Jones notified the affected individuals and provided free identity monitoring. At the time of the Order, there was no indication that any client has suffered actual financial harm as a result of the breach. SEC Findings: R.T. Jones failed to adopt any written policies and procedures reasonably designed to safeguard its clients PII as required by the Safeguards Rule. R. T. Jones s policies and procedures did not include, for example: Conducting periodic risk assessments; Employing a firewall to protect the web server containing client PII; Establishing procedures to respond to a cybersecurity incident; or Encrypting client PII. 41

42 In the Matter of Craig Scott Capital, LLC (April 12, 2016) SEC released an Order regarding a $100K settlement with Craig Scott Capital, LLC ( CSC ), which arose out of CSC s alleged violation of Rule 30(a) of Regulation S-P (the Safeguards Rule ). Alleged Facts: From January 2012-June 2014, the staff at Craig Scott Capital-an SEC-registered broker-dealer-used addresses other than those with the firm s domain name to electronically receive more than 4,000 faxes from customers and other third parties. The Faxes routinely included sensitive customer records and information, such as customer names, addresses, Social Security numbers, bank and brokerage account numbers, copies of drivers licenses and passports and other customer financial information. Some employees, including the firm s principles, used non-firm accounts for firm business. In addition, many of the written policies and procedures were not implemented in practice. 42

43 In the Matter of Craig Scott Capital, LLC (April 12, 2016) SEC Findings Included the Following: While CSC had adopted written policies and procedures, which included a section directly addressing the Safeguards Rule, the Staff concluded and charged that the existing policies were not reasonably designed to protect customer records and information and indicated that they were not tailored to the actual practices at the firm. The policy stated that the Designated Supervisor was responsible for ensuring compliance with the policy, but did not identify the Designated Supervisor. Though CSC used an efax System, the policy did not address either the efax System or how to handle the customer records and information contained in efaxes. As a result, none of the efaxes received by the non-firm addresses were maintained and preserved by CSC. The policy contained blanks to be filled in later, such as, [The Firm] has adopted procedures to protect customer information, including the following [methods]. 43

44 In the Matter of Morgan Stanley Smith Barney LLC (June 8, 2016) SEC released an Order regarding a $1M settlement with Morgan Stanley Smith Barney ( Morgan Stanley ) and an agreement that Morgan Stanley would cease and desist from committing or causing any violations and any future violations of Rule 30(a) of Regulation S-P (the Safeguards Rule ). Alleged Facts: From at least August 2001 through December 2014, Morgan Stanley stored PII of individuals to whom Morgan Stanley provided brokerage and investment advisory services on two of the firm s applications: the Business Information System ( BIS ) Portal and the Fixed Income Division Select ( FID Select ) Portal. Galen Marsh (then a Morgan Stanley employee) misappropriated data regarding ~730K customer accounts, associated with ~330K different households by accessing the portals between 2011 and The data included PII, such as customers full names, phone numbers, street addresses, account numbers, account balances and securities holdings. Between December 15, 2014 and February 3, 2015, portions of the stolen data were posted for sale on at least three Internet sites. Morgan Stanley discovered the breach through one of its routine Internet sweeps on December 27, 2014 and identified Marsh as the likely source of the breach. Marsh admitted to storing the data on his personal server and a subsequent forensic analysis of the server showed a third party likely hacked into it and copied the customer data that Marsh had downloaded from the Portals. 44

45 In the Matter of Morgan Stanley Smith Barney LLC (June 8, 2016) SEC Findings Included the Following: Morgan Stanley violated the Safeguards Rule because its policies and procedures were not reasonably designed to meet the requirements of the Safeguards Rule and failed to include: Reasonably designed and operating authorization modules for the Portals that restricted employee access to only the confidential customer data to which such employees had a legitimate business need; Auditing and/or testing of the effectiveness of such authorization modules; and Monitoring and analysis of employee access to and use of the Portals. 45

46 What Will the SEC Really Want to Know in an Examination of Asset Managers, Investment Advisers, Custodian Banks, or Broker Dealers? 1. Do you truly understand your firm s cybersecurity infrastructure? 2. Have you enacted policies and internal procedures specifically tailored to your risks? 3. Can you prove - - with documents - - that you adhere to and enforce your own policies? 4. Can you detect - - in real time - - any unlawful access to your firm s data networks? 5. Are you actively monitoring and minimizing the risks associated with your third party vendors and service providers? 46

47 Thank You For further information, visit our website at dechert.com or contact any of today s presenters. Dechert practices as a limited liability partnership or limited liability company other than in Dublin and Hong Kong.

NATIONAL RECOVERY AGENCY COMPLIANCE INFORMATION GRAMM-LEACH-BLILEY SAFEGUARD RULE

NATIONAL RECOVERY AGENCY COMPLIANCE INFORMATION GRAMM-LEACH-BLILEY SAFEGUARD RULE As many of you know, Gramm-Leach-Bliley requires "financial institutions" to establish and implement a Safeguard Rule Compliance

NATIONAL RECOVERY AGENCY COMPLIANCE INFORMATION GRAMM-LEACH-BLILEY SAFEGUARD RULE As many of you know, Gramm-Leach-Bliley requires "financial institutions" to establish and implement a Safeguard Rule Compliance

Identity Theft Prevention Program Lake Forest College Revision 1.0

Identity Theft Prevention Program Lake Forest College Revision 1.0 This document supersedes all previous identity theft prevention program documents. Approved and Adopted by: The Board of Directors Date:

Identity Theft Prevention Program Lake Forest College Revision 1.0 This document supersedes all previous identity theft prevention program documents. Approved and Adopted by: The Board of Directors Date:

SUMMARY: The Federal Trade Commission ( FTC or Commission ) requests public

requests public") [Billing Code: 6750-01S] FEDERAL TRADE COMMISSION 16 CFR Part 314 RIN 3084-AB35 Standards for Safeguarding Customer Information AGENCY: Federal Trade Commission. ACTION: Request for public comment. SUMMARY:

[Billing Code: 6750-01S] FEDERAL TRADE COMMISSION 16 CFR Part 314 RIN 3084-AB35 Standards for Safeguarding Customer Information AGENCY: Federal Trade Commission. ACTION: Request for public comment. SUMMARY:

H 7789 S T A T E O F R H O D E I S L A N D

======== LC001 ======== 01 -- H S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 01 A N A C T RELATING TO INSURANCE - INSURANCE DATA SECURITY ACT Introduced By: Representatives

======== LC001 ======== 01 -- H S T A T E O F R H O D E I S L A N D IN GENERAL ASSEMBLY JANUARY SESSION, A.D. 01 A N A C T RELATING TO INSURANCE - INSURANCE DATA SECURITY ACT Introduced By: Representatives

Privacy and Data Breach Protection Modular application form

Instructions The Hiscox Technology, Privacy and Cyber Portfolio Policy may be purchased on an a-la-carte basis. Some organizations may require coverage for their technology errors and omissions, while

Instructions The Hiscox Technology, Privacy and Cyber Portfolio Policy may be purchased on an a-la-carte basis. Some organizations may require coverage for their technology errors and omissions, while

Compliance With the Red Flags Rules

For Audio Participation, Please Call 1.866.281.4322, *1382742* Attorney Advertising Prior results do not guarantee a similar outcome Models used are not clients but may be representative of clients 321

For Audio Participation, Please Call 1.866.281.4322, *1382742* Attorney Advertising Prior results do not guarantee a similar outcome Models used are not clients but may be representative of clients 321

Cyber, Data Risk and Media Insurance Application form

Instructions The Hiscox Technology, Privacy and Cyber Portfolio Policy may be purchased on an a-la-carte basis. Some organizations may require coverage for their technology errors and omissions, while

Instructions The Hiscox Technology, Privacy and Cyber Portfolio Policy may be purchased on an a-la-carte basis. Some organizations may require coverage for their technology errors and omissions, while

Cybersecurity, Privacy and Communications Webinar: Financial Privacy Primer

Cybersecurity, Privacy and Communications Webinar: Financial Privacy Primer March 23, 2017 Heather Zachary, Partner Nicole Ewart, Senior Associate Attorney Advertising Speakers Heather Zachary, Partner

Cybersecurity, Privacy and Communications Webinar: Financial Privacy Primer March 23, 2017 Heather Zachary, Partner Nicole Ewart, Senior Associate Attorney Advertising Speakers Heather Zachary, Partner

Attachment to Identity Theft Prevention Service Provider Attestation

Attachment to Identity Theft Prevention Service Provider Attestation Identify Theft Prevention Policy Effective January 1, 2011 Identity Theft is a crime in which an individual wrongfully obtains and uses

Attachment to Identity Theft Prevention Service Provider Attestation Identify Theft Prevention Policy Effective January 1, 2011 Identity Theft is a crime in which an individual wrongfully obtains and uses

South Carolina General Assembly 122nd Session,

South Carolina General Assembly 122nd Session, 2017-2018 R184, H4655 STATUS INFORMATION General Bill Sponsors: Reps. Sandifer and Spires Document Path: l:\council\bills\nbd\11202cz18.docx Companion/Similar

South Carolina General Assembly 122nd Session, 2017-2018 R184, H4655 STATUS INFORMATION General Bill Sponsors: Reps. Sandifer and Spires Document Path: l:\council\bills\nbd\11202cz18.docx Companion/Similar

Cybersecurity Privacy and Network Security and Risk Mitigation

Ask the Experts at fi360 2016 Cybersecurity Privacy and Network Security and Risk Mitigation Gary Sutherland, NAPLIA CEO Brian Edelman, Financial Computer Inc. CEO Paul Smith, AIF NAPLIA SVP SEC s 1st

Ask the Experts at fi360 2016 Cybersecurity Privacy and Network Security and Risk Mitigation Gary Sutherland, NAPLIA CEO Brian Edelman, Financial Computer Inc. CEO Paul Smith, AIF NAPLIA SVP SEC s 1st

IDENTITY THEFT DETECTION POLICY

IDENTITY THEFT DETECTION POLICY PC 6.9 Date of Last Update: May 05, 2009 Approved By: President's Cabinet Responsible Office: Business and Finance POLICY STATEMENT Grand Valley State University (GVSU)

IDENTITY THEFT DETECTION POLICY PC 6.9 Date of Last Update: May 05, 2009 Approved By: President's Cabinet Responsible Office: Business and Finance POLICY STATEMENT Grand Valley State University (GVSU)

A Step By Step Guide To Dealership Compliance Team One research and Training /Summit Group

A Step By Step Guide To Dealership Compliance 2008 Team One research and Training /Summit Group As you probably already know, 2008 has brought the automobile dealer a whole new set of compliance issues

A Step By Step Guide To Dealership Compliance 2008 Team One research and Training /Summit Group As you probably already know, 2008 has brought the automobile dealer a whole new set of compliance issues

WEB ACCESS AGREEMENT

WEB ACCESS AGREEMENT This Web Access Agreement (the Agreement ) is entered into on, 200, by and between Specialized Loan Servicing LLC, a Delaware limited liability company, with principal offices at 8742

WEB ACCESS AGREEMENT This Web Access Agreement (the Agreement ) is entered into on, 200, by and between Specialized Loan Servicing LLC, a Delaware limited liability company, with principal offices at 8742

NEW CYBER RULES FOR NEW YORK-BASED BANKING, INSURANCE AND FINANCIAL SERVICE FIRMS HAVE FAR-REACHING EFFECTS

REGULATORY LAW ALERT JUNE 2017 NEW CYBER RULES FOR NEW YORK-BASED BANKING, INSURANCE AND FINANCIAL SERVICE FIRMS HAVE FAR-REACHING EFFECTS OVERVIEW In potentially the most significant state-level expansion

REGULATORY LAW ALERT JUNE 2017 NEW CYBER RULES FOR NEW YORK-BASED BANKING, INSURANCE AND FINANCIAL SERVICE FIRMS HAVE FAR-REACHING EFFECTS OVERVIEW In potentially the most significant state-level expansion

Financial Industry Developments

2016 INVESTMENT MANAGEMENT CONFERENCE Financial Industry Developments Nicholas S. Hodge, Partner, Boston Michael W. McGrath, Partner, Boston Copyright 2016 by K&L Gates LLP. All rights reserved. Hedge

2016 INVESTMENT MANAGEMENT CONFERENCE Financial Industry Developments Nicholas S. Hodge, Partner, Boston Michael W. McGrath, Partner, Boston Copyright 2016 by K&L Gates LLP. All rights reserved. Hedge

Record Management & Retention Policy

POLICY TYPE: Corporate Divisional EFFECTIVE DATE: INITIAL APPROVAL DATE: NEXT REVIEW DATE: POLICY NUMBER: May 15, 2010 May - 2010 March 2015 REVISION APPROVAL DATE: 5/10, 3/11, 5/12, 9/13, 4/14, 11/14

POLICY TYPE: Corporate Divisional EFFECTIVE DATE: INITIAL APPROVAL DATE: NEXT REVIEW DATE: POLICY NUMBER: May 15, 2010 May - 2010 March 2015 REVISION APPROVAL DATE: 5/10, 3/11, 5/12, 9/13, 4/14, 11/14

AUDIT AND FINANCE COMMITTEE Wednesday, June 17, 2009

Item: AF: A-1 AUDIT AND FINANCE COMMITTEE Wednesday, June 17, 2009 SUBJECT: REQUEST FOR APPROVAL OF FLORIDA ATLANTIC UNIVERSITY S IDENTITY THEFT PREVENTION PROGRAM. PROPOSED COMMITTEE ACTION Recommend

Item: AF: A-1 AUDIT AND FINANCE COMMITTEE Wednesday, June 17, 2009 SUBJECT: REQUEST FOR APPROVAL OF FLORIDA ATLANTIC UNIVERSITY S IDENTITY THEFT PREVENTION PROGRAM. PROPOSED COMMITTEE ACTION Recommend

University of Connecticut IDENTITY THEFT PREVENTION PROGRAM

University of Connecticut IDENTITY THEFT PREVENTION PROGRAM I. BACKGROUND II. III. IV. PURPOSE AND SCOPE DEFINITIONS IDENTIFICATION & DETECTION OF RED FLAGS V. APPROPRIATELY RESPONDING WHEN RED FLAGS ARE

University of Connecticut IDENTITY THEFT PREVENTION PROGRAM I. BACKGROUND II. III. IV. PURPOSE AND SCOPE DEFINITIONS IDENTIFICATION & DETECTION OF RED FLAGS V. APPROPRIATELY RESPONDING WHEN RED FLAGS ARE

LICENSE AGREEMENT. Security Software Solutions

LICENSE AGREEMENT Security Software Solutions VERIS ACTIVE ID SERVICES AGREEMENT between Timothy J. Rollins DBA Security Software Solutions, having an office at 5215 Sabino Canyon Road and 4340 N Camino

LICENSE AGREEMENT Security Software Solutions VERIS ACTIVE ID SERVICES AGREEMENT between Timothy J. Rollins DBA Security Software Solutions, having an office at 5215 Sabino Canyon Road and 4340 N Camino

AS PASSED BY HOUSE AND SENATE H Page 1 of 37 H.764. An act relating to data brokers and consumer protection

2018 Page 1 of 37 H.764 An act relating to data brokers and consumer protection It is hereby enacted by the General Assembly of the State of Vermont: Sec. 1. FINDINGS AND INTENT (a) The General Assembly

2018 Page 1 of 37 H.764 An act relating to data brokers and consumer protection It is hereby enacted by the General Assembly of the State of Vermont: Sec. 1. FINDINGS AND INTENT (a) The General Assembly

DAWSON PUBLIC POWER DISTRICT 300 South Washington Street P. O. Box Lexington, Nebraska Tel. No.- 308/324/2386 Fax No.

DAWSON PUBLIC POWER DISTRICT 300 South Washington Street P. O. Box 777 - Lexington, Nebraska - 68850 Tel. No.- 308/324/2386 Fax No.-308/324/2907 CUSTOMER POLICY IDENTITY THEFT PREVENTION I. OBJECTIVE Page

DAWSON PUBLIC POWER DISTRICT 300 South Washington Street P. O. Box 777 - Lexington, Nebraska - 68850 Tel. No.- 308/324/2386 Fax No.-308/324/2907 CUSTOMER POLICY IDENTITY THEFT PREVENTION I. OBJECTIVE Page

Polson/ Ronan Ambulance Service Identity Theft Prevention Program

Purpose Polson/ Ronan Ambulance is committed to providing all aspects of our service and conducting our business operations in compliance with all applicable laws and regulations. This policy sets forth

Purpose Polson/ Ronan Ambulance is committed to providing all aspects of our service and conducting our business operations in compliance with all applicable laws and regulations. This policy sets forth

NEW YORK STATE DEPARTMENT OF FINANCIAL SERVICES PROPOSED 23 NYCRR 500 CYBERSECURITY REQUIREMENTS FOR FINANCIAL SERVICES COMPANIES

NEW YORK STATE DEPARTMENT OF FINANCIAL SERVICES PROPOSED 23 NYCRR 500 CYBERSECURITY REQUIREMENTS FOR FINANCIAL SERVICES COMPANIES I, Maria T. Vullo, Superintendent of Financial Services, pursuant to the

NEW YORK STATE DEPARTMENT OF FINANCIAL SERVICES PROPOSED 23 NYCRR 500 CYBERSECURITY REQUIREMENTS FOR FINANCIAL SERVICES COMPANIES I, Maria T. Vullo, Superintendent of Financial Services, pursuant to the

FREQUENTLY ASKED QUESTIONS REGARDING 23 NYCRR PART 500

FREQUENTLY ASKED QUESTIONS REGARDING 23 NYCRR PART 500 Effective March 1, 2017, the Superintendent of Financial Services promulgated 23 NYCRR Part 500, a regulation establishing cybersecurity requirements

FREQUENTLY ASKED QUESTIONS REGARDING 23 NYCRR PART 500 Effective March 1, 2017, the Superintendent of Financial Services promulgated 23 NYCRR Part 500, a regulation establishing cybersecurity requirements

Driven. FTC Red Flags and Address Discrepancy Rules: Protecting Against Identity Theft L50 L50

Driven NADA Management series L50 A Dealer Guide to THE FTC Red Flags and Address Discrepancy Rules: Protecting Against Identity Theft L50 The National Automobile Dealers Association (NADA) has prepared

Driven NADA Management series L50 A Dealer Guide to THE FTC Red Flags and Address Discrepancy Rules: Protecting Against Identity Theft L50 The National Automobile Dealers Association (NADA) has prepared

Cybersecurity Threats: What Retirement Plan Sponsors and Fiduciaries Need to Know and Do

ARTICLE Cybersecurity Threats: What Retirement Plan Sponsors and Fiduciaries Need to Know and Do By Gene Griggs and Saad Gul This article analyzes cybersecurity issues for retirement plans. Introduction

ARTICLE Cybersecurity Threats: What Retirement Plan Sponsors and Fiduciaries Need to Know and Do By Gene Griggs and Saad Gul This article analyzes cybersecurity issues for retirement plans. Introduction

NEW FTC RED FLAG REQUIREMENTS AS APPLICABLE TO CREDITORS AND COVERED ACCOUNTS

NLBMDA STAFF ANALYSIS NEW FTC RED FLAG REQUIREMENTS AS APPLICABLE TO CREDITORS AND COVERED ACCOUNTS SUMMARY The new Red Flag rule, finalized in November 2007, goes into effect on November 1, 2008. The

NLBMDA STAFF ANALYSIS NEW FTC RED FLAG REQUIREMENTS AS APPLICABLE TO CREDITORS AND COVERED ACCOUNTS SUMMARY The new Red Flag rule, finalized in November 2007, goes into effect on November 1, 2008. The

PRIVACY OF CONSUMER FINANCIAL INFORMATION NEW FINAL RULES. By Russell J. Bruemmer and Franca E. Harris *

PRIVACY OF CONSUMER FINANCIAL INFORMATION NEW FINAL RULES By Russell J. Bruemmer and Franca E. Harris * The Federal Trade Commission ("FTC") published its rule on Privacy of Consumer Financial Information

PRIVACY OF CONSUMER FINANCIAL INFORMATION NEW FINAL RULES By Russell J. Bruemmer and Franca E. Harris * The Federal Trade Commission ("FTC") published its rule on Privacy of Consumer Financial Information

TITLE II ADMINISTRATIVE REGULATIONS IDENTITY THEFT PREVENTION PROGRAM

TITLE II ADMINISTRATIVE REGULATIONS CHAPTER 30 IDENTITY THEFT PREVENTION PROGRAM 30.01 Program The Town of Flower Mound, Texas, as a utility provider ( Utility ), has developed an Identity Theft Prevention

TITLE II ADMINISTRATIVE REGULATIONS CHAPTER 30 IDENTITY THEFT PREVENTION PROGRAM 30.01 Program The Town of Flower Mound, Texas, as a utility provider ( Utility ), has developed an Identity Theft Prevention

VIII 6.1. VIII. Privacy FCRA. Fair Credit Reporting Act 1. Introduction. Structure and Overview of Examination Modules.

Fair Credit Reporting Act 1 Introduction The Fair Credit Reporting Act (FCRA) (15 USC 1681-1681u) became effective on April 25, 1971. The FCRA is a part of a group of acts contained in the Federal Consumer

Fair Credit Reporting Act 1 Introduction The Fair Credit Reporting Act (FCRA) (15 USC 1681-1681u) became effective on April 25, 1971. The FCRA is a part of a group of acts contained in the Federal Consumer

MEMORANDUM. Background

MEMORANDUM TO: FROM: Governmental Pension Plans Ice Miller (Mary Beth Braitman and Tom Walsh) DATE: September 23, 2001 RE: Analysis of the Duties Imposed by Title V of the Gramm-Leach-Bliley Act on Public

MEMORANDUM TO: FROM: Governmental Pension Plans Ice Miller (Mary Beth Braitman and Tom Walsh) DATE: September 23, 2001 RE: Analysis of the Duties Imposed by Title V of the Gramm-Leach-Bliley Act on Public

16 C.F.R AND APPENDIX A (GLB REGULATIONS)

") 16 C.F.R. 313.1-313.18 AND APPENDIX A (GLB REGULATIONS) 313.1 Purpose and scope. (a) Purpose. This part governs the treatment of nonpublic personal information about consumers by the financial institutions

16 C.F.R. 313.1-313.18 AND APPENDIX A (GLB REGULATIONS) 313.1 Purpose and scope. (a) Purpose. This part governs the treatment of nonpublic personal information about consumers by the financial institutions

NEVADA SYSTEM OF HIGHER EDUCATION PROCEDURES AND GUIDELINES MANUAL CHAPTER 13 IDENTITY THEFT PREVENTION PROGRAM (RED FLAG RULES)

") NEVADA SYSTEM OF HIGHER EDUCATION PROCEDURES AND GUIDELINES MANUAL CHAPTER 13 IDENTITY THEFT PREVENTION PROGRAM (RED FLAG RULES) Section 1. NSHE... 2 Section 2. UNR... 4 Section 3. WNC... 8 Chapter 13,

NEVADA SYSTEM OF HIGHER EDUCATION PROCEDURES AND GUIDELINES MANUAL CHAPTER 13 IDENTITY THEFT PREVENTION PROGRAM (RED FLAG RULES) Section 1. NSHE... 2 Section 2. UNR... 4 Section 3. WNC... 8 Chapter 13,

Minnesota State Colleges and Universities Identity Theft Prevention Program

Effective 3-18-09 Identity Theft Prevention Program 1 This is the Minnesota State Colleges and Universities Identity Theft Prevention Program, including more detailed guidelines. The initial Program was

Effective 3-18-09 Identity Theft Prevention Program 1 This is the Minnesota State Colleges and Universities Identity Theft Prevention Program, including more detailed guidelines. The initial Program was

AIMS COMMUNITY COLLEGE PROCEDURE IDENTITY THEFT PREVENTION - RED FLAG PROCEDURE

3-950A AIMS COMMUNITY COLLEGE PROCEDURE IDENTITY THEFT PREVENTION - RED FLAG PROCEDURE HISTORY In response to the growing threat of identity theft, the United States Congress passed the Fair and Accurate

3-950A AIMS COMMUNITY COLLEGE PROCEDURE IDENTITY THEFT PREVENTION - RED FLAG PROCEDURE HISTORY In response to the growing threat of identity theft, the United States Congress passed the Fair and Accurate

Georgia Health Information Network, Inc. Georgia ConnectedCare Policies

Georgia Health Information Network, Inc. Georgia ConnectedCare Policies Version History Effective Date: August 28, 2013 Revision Date: August 2014 Originating Work Unit: Health Information Technology Health

Georgia Health Information Network, Inc. Georgia ConnectedCare Policies Version History Effective Date: August 28, 2013 Revision Date: August 2014 Originating Work Unit: Health Information Technology Health

HIPAA Information. Who does HIPAA apply to? What are Sync.com s responsibilities? What is a Business Associate?

HIPAA Information Who does HIPAA apply to? HIPAA applies to all Covered Entities (entities that collect, access, use and/or disclose Protected Health Data (PHI) and are subject to HIPAA regulations). What

HIPAA Information Who does HIPAA apply to? HIPAA applies to all Covered Entities (entities that collect, access, use and/or disclose Protected Health Data (PHI) and are subject to HIPAA regulations). What

Christopher Newport University. Policy: Red Flag Identity Theft Identification and Prevention Program Policy Number: 3030

Christopher Newport University Policy: Red Flag Identity Theft Identification and Prevention Program Policy Number: 3030 Executive Oversight: Executive Vice President Contact Office: Comptroller s Office

Christopher Newport University Policy: Red Flag Identity Theft Identification and Prevention Program Policy Number: 3030 Executive Oversight: Executive Vice President Contact Office: Comptroller s Office

Georgia Power Valdosta Federal credit union Privacy Policy

Georgia Power Valdosta Federal credit union Privacy Policy Review/Revision Date: October 20,2016 Approval Date: February 26, 2001 Approved by: Board of Directors General Policy Statement: The Georgia Power

Georgia Power Valdosta Federal credit union Privacy Policy Review/Revision Date: October 20,2016 Approval Date: February 26, 2001 Approved by: Board of Directors General Policy Statement: The Georgia Power

Cyber Risk Proposal Form

Cyber Risk Proposal Form Company or trading name Address Postcode Country Telephone Email Website Date business established Number of employees Do you have a Chief Privacy Officer (or Chief Information

Cyber Risk Proposal Form Company or trading name Address Postcode Country Telephone Email Website Date business established Number of employees Do you have a Chief Privacy Officer (or Chief Information

ARE YOU HIP WITH HIPAA?

ARE YOU HIP WITH HIPAA? Scott C. Thompson 214.651.5075 scott.thompson@haynesboone.com February 11, 2016 HIPAA SECURITY WHY SHOULD I CARE? Health plan fined $1.2 million for HIPAA breach. Health plan fined

ARE YOU HIP WITH HIPAA? Scott C. Thompson 214.651.5075 scott.thompson@haynesboone.com February 11, 2016 HIPAA SECURITY WHY SHOULD I CARE? Health plan fined $1.2 million for HIPAA breach. Health plan fined

Bank Secrecy Act Examination Procedures. Sections 313, 314, and 319(b) of the USA PATRIOT Act (31 CFR , , , 103.

of the USA PATRIOT Act (31 CFR , , , 103.") Bank Secrecy Act Examination Procedures Sections 313, 314, and 319(b) of the USA PATRIOT Act (31 CFR 103.100, 103.110, 103.177, 103.185) Table of Contents Correspondent Accounts for Foreign Shell Banks

Bank Secrecy Act Examination Procedures Sections 313, 314, and 319(b) of the USA PATRIOT Act (31 CFR 103.100, 103.110, 103.177, 103.185) Table of Contents Correspondent Accounts for Foreign Shell Banks

THE PRIVACY PROVISIONS OF THE GRAMM-LEACH-BLILEY ACT AND THEIR IMPACT ON INSURANCE AGENTS & BROKERS PREPARED BY THE OFFICE OF THE GENERAL COUNSEL

THE PRIVACY PROVISIONS OF THE GRAMM-LEACH-BLILEY ACT AND THEIR IMPACT ON INSURANCE AGENTS & BROKERS This memorandum is not intended to provide specific advice about individual legal, business or other

THE PRIVACY PROVISIONS OF THE GRAMM-LEACH-BLILEY ACT AND THEIR IMPACT ON INSURANCE AGENTS & BROKERS This memorandum is not intended to provide specific advice about individual legal, business or other

Privacy for Customer Contact Personnel Privacy for Customer Contact Personnel

Privacy for Customer Contact Personnel 12/2015 American Bankers Association Page 1 Menu Course Introduction Overview of Privacy Related Laws Privacy and the GLBA Benefits of Information Sharing Course

Privacy for Customer Contact Personnel 12/2015 American Bankers Association Page 1 Menu Course Introduction Overview of Privacy Related Laws Privacy and the GLBA Benefits of Information Sharing Course

Claims Made Basis. Underwritten by Underwriters at Lloyd s, London

APPLICATION for: NetGuard Plus Claims Made Basis. Underwritten by Underwriters at Lloyd s, London tice: The Policy for which this Application is made applies only to Claims made against any of the Insureds

APPLICATION for: NetGuard Plus Claims Made Basis. Underwritten by Underwriters at Lloyd s, London tice: The Policy for which this Application is made applies only to Claims made against any of the Insureds

Jack Byrne Ford & Mercury Identity Theft Program (ITPP)

") Jack Byrne Ford & Mercury Identity Theft Program (ITPP) PART ONE BACKGROUND 1. Effective Date All affected employees of Jack Byrne Ford & Mercury ( Dealership ) must comply with the terms of this policy

Jack Byrne Ford & Mercury Identity Theft Program (ITPP) PART ONE BACKGROUND 1. Effective Date All affected employees of Jack Byrne Ford & Mercury ( Dealership ) must comply with the terms of this policy

MEMORANDUM. Health Care Information Privacy The HIPAA Regulations What Has Changed and What You Need to Know

1801 California Street Suite 4900 Denver, CO 80202 303-830-1776 Facsimile 303-894-9239 MEMORANDUM To: Adam Finkel, Assistant Director, Government Relations, NCRA From: Mel Gates Date: December 23, 2013

1801 California Street Suite 4900 Denver, CO 80202 303-830-1776 Facsimile 303-894-9239 MEMORANDUM To: Adam Finkel, Assistant Director, Government Relations, NCRA From: Mel Gates Date: December 23, 2013

UNIVERSITY OF DENVER POLICY MANUAL IDENTITY THEFT PREVENTION

UNIVERSITY OF DENVER POLICY MANUAL IDENTITY THEFT PREVENTION Responsible Department: Provost and Business and Financial Affairs Recommended By: Provost, VC Business and Financial Affairs Approved By: Chancellor

UNIVERSITY OF DENVER POLICY MANUAL IDENTITY THEFT PREVENTION Responsible Department: Provost and Business and Financial Affairs Recommended By: Provost, VC Business and Financial Affairs Approved By: Chancellor

EXHIBIT A IDENTITY THEFT PREVENTION PROGRAM

EXHIBIT A IDENTITY THEFT PREVENTION PROGRAM I. ADOPTION Michigan State University Identity Theft Prevention Program The Board of Trustees of Michigan State University adopted this Identity Theft Prevention

EXHIBIT A IDENTITY THEFT PREVENTION PROGRAM I. ADOPTION Michigan State University Identity Theft Prevention Program The Board of Trustees of Michigan State University adopted this Identity Theft Prevention

Washington Association of Sewer and Water Districts (WASWD) IDENTITY THEFT PREVENTION PROGRAM

IDENTITY THEFT PREVENTION PROGRAM") IDENTITY THEFT PREVENTION PROGRAM Note: This sample identity theft prevention program is for informational purposes only. It may not be suitable for your district depending on its size, complexity and

IDENTITY THEFT PREVENTION PROGRAM Note: This sample identity theft prevention program is for informational purposes only. It may not be suitable for your district depending on its size, complexity and

Five Key Steps to Developing an nformation Security Program

Five Key Steps to Developing an nformation Security Program Driving Business Advantage Five Key Steps to Developing an Information Security Program by Gabriel M. Helmer Foley Hoag ebook Contents Introduction...

Five Key Steps to Developing an nformation Security Program Driving Business Advantage Five Key Steps to Developing an Information Security Program by Gabriel M. Helmer Foley Hoag ebook Contents Introduction...

Identity Theft Prevention. Red Flags. Training Program

Identity Theft Prevention Red Flags Training Program 1 Red Flags Training Program Adoption Amendment passed in 2003 to the Fair Credit Reporting Act called The Fair and Accurate Credit Transactions Act

Identity Theft Prevention Red Flags Training Program 1 Red Flags Training Program Adoption Amendment passed in 2003 to the Fair Credit Reporting Act called The Fair and Accurate Credit Transactions Act

Illinois Eastern Community Colleges. Frontier Community College Lincoln Trail College Olney Central College Wabash Valley College

Illinois Eastern Community Colleges Frontier Community College Lincoln Trail College Olney Central College Wabash Valley College Identity Theft Prevention Program Approved by the Cabinet: February 4, 2015

Illinois Eastern Community Colleges Frontier Community College Lincoln Trail College Olney Central College Wabash Valley College Identity Theft Prevention Program Approved by the Cabinet: February 4, 2015

Cyber Risks & Insurance

Cyber Risks & Insurance Bob Klobe Asst. Vice President & Cyber Security Subject Matter Expert Chubb Specialty Insurance Legal Disclaimer The views, information and content expressed herein are those of

Cyber Risks & Insurance Bob Klobe Asst. Vice President & Cyber Security Subject Matter Expert Chubb Specialty Insurance Legal Disclaimer The views, information and content expressed herein are those of

INFORMATION AND CYBER SECURITY POLICY V1.1

Future Generali 1 INFORMATION AND CYBER SECURITY V1.1 Future Generali 2 Revision History Revision / Version No. 1.0 1.1 Rollout Date Location of change 14-07- 2017 Mumbai 25.04.20 18 Thane Changed by Original

Future Generali 1 INFORMATION AND CYBER SECURITY V1.1 Future Generali 2 Revision History Revision / Version No. 1.0 1.1 Rollout Date Location of change 14-07- 2017 Mumbai 25.04.20 18 Thane Changed by Original

Implementing the Obligations of the Gramm-Leach-Bliley Act The NAIC Model for State Privacy Regulation

Implementing the Obligations of the Gramm-Leach-Bliley Act The NAIC Model for State Privacy Regulation This memorandum provides an analysis of the provisions of the National Association of Insurance Commissioners

Implementing the Obligations of the Gramm-Leach-Bliley Act The NAIC Model for State Privacy Regulation This memorandum provides an analysis of the provisions of the National Association of Insurance Commissioners

MEMORANDUM OF UNDERSTANDING for DATA SHARING BETWEEN DISTRICT AND SCCOE

MEMORANDUM OF UNDERSTANDING Pg. 1 of 3 DATA SHARING BETWEEN DISTRICT AND SCCOE MEMORANDUM OF UNDERSTANDING for DATA SHARING BETWEEN DISTRICT AND SCCOE This Memorandum of Understanding (MOU) is entered

MEMORANDUM OF UNDERSTANDING Pg. 1 of 3 DATA SHARING BETWEEN DISTRICT AND SCCOE MEMORANDUM OF UNDERSTANDING for DATA SHARING BETWEEN DISTRICT AND SCCOE This Memorandum of Understanding (MOU) is entered

Middlebury Institute of International Studies Identity Theft Prevention Program

Middlebury Institute of International Studies Identity Theft Prevention Program I. PROGRAM ADOPTION Middlebury Institute of International Studies, hereafter referred to as the Institute, has developed

Middlebury Institute of International Studies Identity Theft Prevention Program I. PROGRAM ADOPTION Middlebury Institute of International Studies, hereafter referred to as the Institute, has developed

Fitchburg State College Identity Theft Prevention Program updated 11/17/09

Fitchburg State College Identity Theft Prevention Program updated 11/17/09 Program Adoption Purpose Definitions Fitchburg State College (College) developed this Identity Theft Prevention Program to detect,

Fitchburg State College Identity Theft Prevention Program updated 11/17/09 Program Adoption Purpose Definitions Fitchburg State College (College) developed this Identity Theft Prevention Program to detect,

APPLICATION FOR DATA BREACH AND PRIVACY LIABILITY, DATA BREACH LOSS TO INSURED AND ELECTRONIC MEDIA LIABILITY INSURANCE

Deerfield Insurance Company Evanston Insurance Company Essex Insurance Company Markel American Insurance Company Markel Insurance Company Associated International Insurance Company DataBreach SM APPLICATION

Deerfield Insurance Company Evanston Insurance Company Essex Insurance Company Markel American Insurance Company Markel Insurance Company Associated International Insurance Company DataBreach SM APPLICATION

Identity Theft Prevention Program

Identity Theft Prevention Program In December 2008 the VSC Board of Trustees recognized that some activities of the VSC are subject to the provisions of the Fair and Accurate Credit Transactions Act (FACT

Identity Theft Prevention Program In December 2008 the VSC Board of Trustees recognized that some activities of the VSC are subject to the provisions of the Fair and Accurate Credit Transactions Act (FACT

University Data Policies

BACKGROUND Data are valuable institutional assets of Washington State University. Data policies are needed to ensure that these resources are carefully managed, maintained, protected, and used appropriately.

BACKGROUND Data are valuable institutional assets of Washington State University. Data policies are needed to ensure that these resources are carefully managed, maintained, protected, and used appropriately.

University of Cincinnati FACTA Red Flag Identity Theft Prevention Program

FACTA Red Flag Identity Theft Prevention Program FACTA Red Flag Policy Program, page 1 of 6 Contents Overview 3 Definition of Terms 3 Covered Accounts..3 List of Red Flags 3 Suspicious Documents...4 Suspicious

FACTA Red Flag Identity Theft Prevention Program FACTA Red Flag Policy Program, page 1 of 6 Contents Overview 3 Definition of Terms 3 Covered Accounts..3 List of Red Flags 3 Suspicious Documents...4 Suspicious

Cyber ERM Proposal Form

Cyber ERM Proposal Form This document allows Chubb to gather the needed information to assess the risks related to the information systems of the prospective insured. Please note that completing this proposal

Cyber ERM Proposal Form This document allows Chubb to gather the needed information to assess the risks related to the information systems of the prospective insured. Please note that completing this proposal

Information Security and Third-Party Service Provider Agreements

The Iowa State Bar Association s ecommerce & Intellectual Property Law Sections presents 2016 Intellectual Property Law & ecommerce Seminar Information Security and Third-Party Service Provider Agreements

The Iowa State Bar Association s ecommerce & Intellectual Property Law Sections presents 2016 Intellectual Property Law & ecommerce Seminar Information Security and Third-Party Service Provider Agreements

The Federal Identity Theft Red Flag Rules and North Carolina Local Health Departments

Health Law bulletin number 89 november 2008 The Federal Identity Theft Red Flag Rules and North Carolina Local Health Departments Jill Moore In November 2007, several federal agencies jointly issued a

Health Law bulletin number 89 november 2008 The Federal Identity Theft Red Flag Rules and North Carolina Local Health Departments Jill Moore In November 2007, several federal agencies jointly issued a

MEDIATECH INSURANCE APPLICATION THIS APPLICATION IS FOR A CLAIMS MADE POLICY PLEASE INDICATE WHICH COVERAGES ARE REQUIRED Technology and Professional

THIS APPLICATION IS FOR A CLAIMS MADE POLICY PLEASE INDICATE WHICH COVERAGES ARE REQUIRED Technology and Professional Services: $100,000 $250,000 $500,000 $1,000,000 $2,000,000 Other:$ Technology Product

THIS APPLICATION IS FOR A CLAIMS MADE POLICY PLEASE INDICATE WHICH COVERAGES ARE REQUIRED Technology and Professional Services: $100,000 $250,000 $500,000 $1,000,000 $2,000,000 Other:$ Technology Product

SEC PROPOSES AMENDMENTS TO REGULATION S-P TO SAFEGUARD CUSTOMER PRIVACY

CLIENT MEMORANDUM SEC PROPOSES AMENDMENTS TO REGULATION S-P TO SAFEGUARD CUSTOMER PRIVACY On March 4, 2008, the Securities and Exchange Commission ( SEC ) proposed for comment amendments to Regulation

CLIENT MEMORANDUM SEC PROPOSES AMENDMENTS TO REGULATION S-P TO SAFEGUARD CUSTOMER PRIVACY On March 4, 2008, the Securities and Exchange Commission ( SEC ) proposed for comment amendments to Regulation

Federal Reserve Bank of Dallas

ll K Federal Reserve Bank of Dallas 2200 N. PEARL ST. DALLAS, TX 75201-2272 October 31, 2003 Notice 03-63 TO: The Chief Executive Officer of each financial institution and others concerned in the Eleventh

ll K Federal Reserve Bank of Dallas 2200 N. PEARL ST. DALLAS, TX 75201-2272 October 31, 2003 Notice 03-63 TO: The Chief Executive Officer of each financial institution and others concerned in the Eleventh

INTEGRITY TRUST COMPANY ALTERNATIVE INVESTMENT CUSTODY AGREEMENT

INTEGRITY TRUST COMPANY ALTERNATIVE INVESTMENT CUSTODY AGREEMENT This Alternative Investment Custody Agreement ("Agreement") is entered into as of the day of, 20 by and among: (i) (ii) Firm Name (the "Advisor")

INTEGRITY TRUST COMPANY ALTERNATIVE INVESTMENT CUSTODY AGREEMENT This Alternative Investment Custody Agreement ("Agreement") is entered into as of the day of, 20 by and among: (i) (ii) Firm Name (the "Advisor")

THE GRAMM-LEACH-BLILEY ACT FOR INDEPENDENT SCHOOLS

THE GRAMM-LEACH-BLILEY ACT FOR INDEPENDENT SCHOOLS Timothy Tobin, Partner Michael Epshteyn, Associate Of Hogan Lovells US LLP February 2014 Introduction The federal Gramm-Leach-Bliley Act ( GLBA ) 1 regulates

THE GRAMM-LEACH-BLILEY ACT FOR INDEPENDENT SCHOOLS Timothy Tobin, Partner Michael Epshteyn, Associate Of Hogan Lovells US LLP February 2014 Introduction The federal Gramm-Leach-Bliley Act ( GLBA ) 1 regulates

CBSA PRIVACY POLICY. Canadian Business Strategy Association Page 1

CBSA PRIVACY POLICY The CBSA Privacy Policy is a statement of principles and policies regarding the protection of personal information provided by the Canadian Business Strategy Association. The objective

CBSA PRIVACY POLICY The CBSA Privacy Policy is a statement of principles and policies regarding the protection of personal information provided by the Canadian Business Strategy Association. The objective

Data Security Addendum for inclusion in the Contract between George Mason University (the University ) and the Selected Firm/Vendor

and the Selected Firm/Vendor") Data Security Addendum for inclusion in the Contract between George Mason University (the University ) and the Selected Firm/Vendor This Addendum is applicable only in those situations where the Selected

Data Security Addendum for inclusion in the Contract between George Mason University (the University ) and the Selected Firm/Vendor This Addendum is applicable only in those situations where the Selected

CITY OF ISSAQUAH. Identity Theft Prevention Program

Attachment A CITY OF ISSAQUAH Identity Theft Prevention Program Effective beginning May 1, 2009 Page 1 of 6 I. PROGRAM ADOPTION The City of Issaquah ( Utility ) developed this Identity Theft Prevention

Attachment A CITY OF ISSAQUAH Identity Theft Prevention Program Effective beginning May 1, 2009 Page 1 of 6 I. PROGRAM ADOPTION The City of Issaquah ( Utility ) developed this Identity Theft Prevention

Chapter 3. Identifying Red Flags. 3:1 Overview

Chapter 3 Identifying Red Flags 3:1 Overview 3:1.1 Identity Theft 3:1.2 Red Flag 3:2 Conducting an Initial Risk Assessment 3:2.1 Practical Considerations 3:2.2 Risk Factors to Consider 3:2.3 Other Sources

Chapter 3 Identifying Red Flags 3:1 Overview 3:1.1 Identity Theft 3:1.2 Red Flag 3:2 Conducting an Initial Risk Assessment 3:2.1 Practical Considerations 3:2.2 Risk Factors to Consider 3:2.3 Other Sources

UNITED STATES OF AMERICA DEPARTMENT OF THE TREASURY FINANCIAL CRIMES ENFORCEMENT NETWORK

UNITED STATES OF AMERICA DEPARTMENT OF THE TREASURY FINANCIAL CRIMES ENFORCEMENT NETWORK IN THE MATTER OF: ) ) ) Number 2018-03 UBS Financial Services Inc. ) Weehawken, NJ ) ASSESSMENT OF CIVIL MONEY PENALTY

UNITED STATES OF AMERICA DEPARTMENT OF THE TREASURY FINANCIAL CRIMES ENFORCEMENT NETWORK IN THE MATTER OF: ) ) ) Number 2018-03 UBS Financial Services Inc. ) Weehawken, NJ ) ASSESSMENT OF CIVIL MONEY PENALTY

Testimony. Submitted for the Record. American Bankers Association. Financial Institutions and Consumer Credit Subcommittee

Testimony Submitted for the Record from the American Bankers Association for the Financial Institutions and Consumer Credit Subcommittee of the Committee on Financial Services United States House of Representatives

Testimony Submitted for the Record from the American Bankers Association for the Financial Institutions and Consumer Credit Subcommittee of the Committee on Financial Services United States House of Representatives

ELECTRONIC SIGNATURE REQUIREMENTS FOR LENDERS

ELECTRONIC SIGNATURE REQUIREMENTS FOR LENDERS June 2015 Purpose The Electronic Signatures in Global and National Commerce (ESIGN) Act (15 U.S.C. 7001-7006), enacted in 2000, permits, but does not require,

ELECTRONIC SIGNATURE REQUIREMENTS FOR LENDERS June 2015 Purpose The Electronic Signatures in Global and National Commerce (ESIGN) Act (15 U.S.C. 7001-7006), enacted in 2000, permits, but does not require,

Identity Theft Prevention Program

ILLINOIS EASTERN COMMUNITY COLLEGES 0 Identity Theft Prevention Program Our mission is to deliver exceptional education and services to improve the lives of our students and to strengthen our communities.

ILLINOIS EASTERN COMMUNITY COLLEGES 0 Identity Theft Prevention Program Our mission is to deliver exceptional education and services to improve the lives of our students and to strengthen our communities.

CLIENT UPDATE SEC AND CFTC ISSUE FINAL RULES ON IDENTITY THEFT PROTECTION

CLIENT UPDATE SEC AND CFTC ISSUE FINAL RULES ON IDENTITY THEFT PROTECTION WASHINGTON, DC Satish M. Kini smkini@debevoise.com Kenneth J. Berman kjberman@debevoise.com Renee M. Cipro* rmcipro@debevoise.com

CLIENT UPDATE SEC AND CFTC ISSUE FINAL RULES ON IDENTITY THEFT PROTECTION WASHINGTON, DC Satish M. Kini smkini@debevoise.com Kenneth J. Berman kjberman@debevoise.com Renee M. Cipro* rmcipro@debevoise.com

HIPAA vs. GDPR vs. NYDFS - the New Compliance Frontier. March 22, 2018

1 HIPAA vs. GDPR vs. NYDFS - the New Compliance Frontier March 22, 2018 2 Today s Panel: Kimberly Holmes - Moderator - Vice President, Health Care, Cyber Liability & Emerging Risks, TDC Specialty Underwriters,

1 HIPAA vs. GDPR vs. NYDFS - the New Compliance Frontier March 22, 2018 2 Today s Panel: Kimberly Holmes - Moderator - Vice President, Health Care, Cyber Liability & Emerging Risks, TDC Specialty Underwriters,

Anti-Money Laundering and Terrorist Financing Prevention Compliance Program Creation Guide

Anti-Money Laundering and Terrorist Financing Prevention Compliance Program Creation Guide Compliance Program Creation Guide January 2015 1 Compliance Program Creation Guide January 2015 2 Insert Business

Anti-Money Laundering and Terrorist Financing Prevention Compliance Program Creation Guide Compliance Program Creation Guide January 2015 1 Compliance Program Creation Guide January 2015 2 Insert Business

Title Insurance and Settlement Company Best Practices

ALTA Best Practices Framework: Title Insurance and Settlement Company Best Practices Page 1 of 8 ALTA Best Practices Framework The ALTA Best Practices Framework has been developed to assist lenders in

ALTA Best Practices Framework: Title Insurance and Settlement Company Best Practices Page 1 of 8 ALTA Best Practices Framework The ALTA Best Practices Framework has been developed to assist lenders in

THE COOPER UNION FOR THE ADVANCEMENT OF SCIENCE AND ART. February 24, 2010

I. Introduction THE COOPER UNION FOR THE ADVANCEMENT OF SCIENCE AND ART RED FLAGS IDENTITY THEFT PREVENTION PROGRAM A. Purpose February 24, 2010 The Cooper Union for the Advancement of Science and Art

I. Introduction THE COOPER UNION FOR THE ADVANCEMENT OF SCIENCE AND ART RED FLAGS IDENTITY THEFT PREVENTION PROGRAM A. Purpose February 24, 2010 The Cooper Union for the Advancement of Science and Art

APPLICATION for: TechGuard Liability Insurance Claims Made Basis. Underwritten by Underwriters at Lloyd s, London

APPLICATION for: TechGuard Liability Insurance Claims Made Basis. Underwritten by Underwriters at Lloyd s, London SECTION I. GENERAL INFORMATION 1. Name of Applicant: Physical Address: (as it should appear