Methodology for Takaful & Retakaful Firms

|

|

|

- Rodney Morrison

- 6 years ago

- Views:

Transcription

1 Methodology for Takaful & Retakaful Firms By: Sobia Maqbool Senior Manager JCR-VIS Credit Rating Company Limited Singapore, November 25, 2008

2 Takaful Market Global Takaful market estimated at $ 4 billion visà-vis insurance premium of $ 3.7 trillion. As Shari a scholars are increasingly looking to utilize Takaful capacity, there exists an intrinsic demand for growth. Insurance penetration in most of the Muslim countries still considerably low compared to economies like USA, UK, France, Singapore, etc.

3 Pakistan Takaful Market Estimated at under $ 1 billion with insurance penetration being considerably low at under 1% of GDP. Number of industry participants: Rating Distribution 38 JCR-VIS universe of ratings includes almost 70% of the insurance universe. Takaful has only started to take root in Pakistan. JCR-VIS rates the entire universe of Takaful operators in Pakistan. Rating Universe

4 Industry Participants General/Life Insurance Companies ACE Insurance Ltd. Alpha Insurance Co. Ltd Asia Insurance Co. Ltd. Askari Gen. Insurance Co. Ltd. Capital Insurance Co. Ltd. Central Insurance Co. Ltd. Century Insurance Co. Ltd. East West Insurance Co. Ltd East West Life Assurance Co. Ltd EFU General Insurance Ltd. EFU Life Assurance Ltd Excel Insurance Co. Ltd. National Insurance Co. Ltd. New Jubilee General Insurance Co. Ltd New Jubilee Life Insurance Co. Ltd PICIC Insurance Ltd. Premier Insurance Co. of Pakistan Ltd. Reliance Insurance Co. Ltd. Saudi Pak Insurance Co. Ltd. Security General Insurance Co. Ltd. Silver Star Insurance Co. Ltd The Co-operative Insurance Society of Pakistan Ltd The Crescent Star Insurance Co. of Pakistan Ltd. The Pakistan General Insurance Co. Ltd The Universal Insurance Co. Ltd. UBL Insurers Ltd. Back

5 Rating Universe General/Family Takaful Dawood Family Takaful Co. Ltd. Pak Kuwait General Takaful Co. Ltd. Pak Qatar General Takaful Co. Ltd. Pak Qatar Family Takaful Co. Ltd. Takaful Pakistan Limited Back

6 Rating Distribution A+ 4% AA- 4% AA 8% AA+ 4% C 4% BB+ 8% BBB- 8% BBB 8% A 16% BBB+ 4% A- 32% Back

7 Definition of Ratings Insurer Financial Strength (IFS) rating is an assessment of a company s capacity to meet its contractual obligations that mainly constitute claims on insurance policies. For Takaful companies, the key philosophy remains same in so far as the capacity to meet policy holder obligations is concerned.

8 Ratings of Takaful Operators Level of risk borne by a Takaful operator: function of type of business underwritten. Takaful rating entails evaluation of: Management & controls Liquidity Capitalization Earnings and Franchise Value Reinsurance arrangements External environment

9 Key Rating Drivers Management & Controls Competency & skills of management team. When viewed as modarib or wakeel, the integrity of managers can have implications for franchise, viability & sustainability. Supervision by Shari a Board & Board of Directors Governance related concerns. Heightened principal-agent challenges if the Takaful operator does not suffer the negative consequences of poor underwriting.

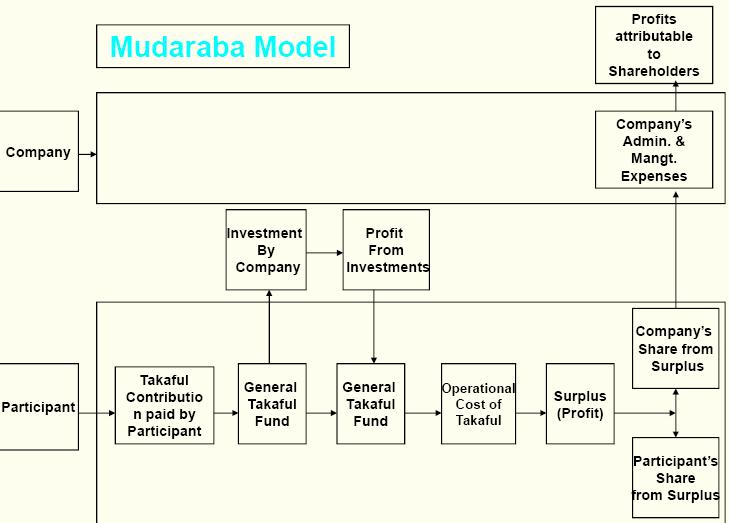

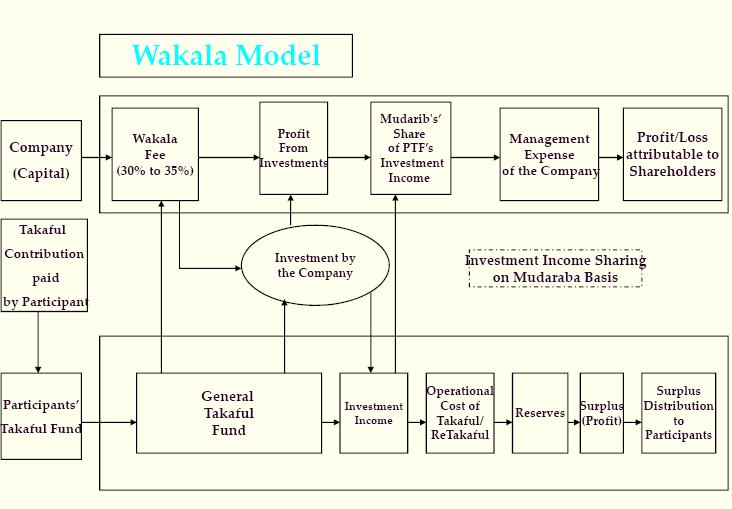

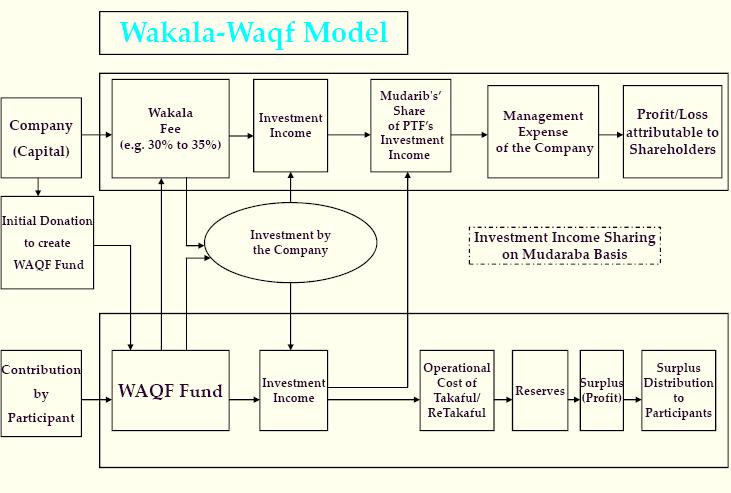

10 Key Rating Drivers Primary distinction between Ta awuni & Waqf Model. Within this, there can be two conceptual frameworks: Modarabah Wakala Wakala Waqf Model a hybrid of the above two.

11

12

13

14 Key Rating Factors Type of business model The model adopted by Takaful operators defines the relationship between the shareholders fund (SHF) and the participants fund (PTF). Claims paying ability, as reflected in financial strength ratings, are impacted by the degree of commitment of management to sound underwriting practices and prudent investment management.

15 Key Rating Factors Legal separation of PTF/SHF Legal separation makes it necessary to conduct tiered analysis. Adequacy of contributions relative to the volatility and level of claims. Firm wide assessment of capitalization on account of legal recourse to the SHF in the form of Qard-e-Hasanah. Shareholders liability limited to the extent of capital contributed. Calculation of deficit undertaken from a cashflow perspective rather than an accounting loss.

16 Nature of Relationship Legal separation of PTF/SHF Having accounted for the business model: SHF with greater financial strength than PTF will serve to enhance the capitalization assessment on firm-wide basis. PTF is ring-fenced and weak financial strength of the SHF will not reduce the claims paying ability of the PTF. Criterion for leverage ratios: A dollar of capital supporting more than three dollars of premium written denotes high operating leverage. Technical reserves exceeding three times capital indicates high financial leverage.

17 Key Rating Factors Priority of Claims Relative priority of claim of Qard-e-Hasanah offered by the SHF vis-à-vis other obligations, is also an important rating factor. Qard-e-Hasanah not explicitly subordinated to the interests of policyholders in some countries like Malaysia. In Pakistan, however, this is not the case as the company is only required to pay Qard-e- Hasanah from underwriting surplus.

18 Key Rating Factors Surplus distribution Surplus generated within the PTF is shared with the participants, which may prevent capital formation. Policy with respect to creation of surplus equalization reserve is considered important in terms of future assessment of claims paying ability. A more rigid structure may result in a greater need to call for capital from the SHF: Extent of ring-fencing amongst various product lines. Degree to which surplus from one may be used to off-set the losses on others.

19 Key Rating Factors Liquidity Liquidity position will need to be analyzed both from the perspective of the Takaful fund itself as well as the company as a whole. Two sources of liquidity. Operating cash flows (including re-insurance arrangements) & investment portfolio. Limited spectrum of investible assets while a young sukuk market may render over-exposure to equities. Analyze concentration in terms of exposure, credit worthiness of counterparties and any impairment in the portfolio.

20 Key Rating Factors Re-Takaful There are over 250 Takaful companies in the world today, yet there are fewer re-takaful operators. Scarcity of suitable (Islamic-compliant) reinsurers exposes a company to concentration related risks Regulations & Shari a scholars in Pakistan however allow takaful operators to seek retakaful support from conventional re-insurers. Strength of re-insurance arrangements would be evaluated on a case by case basis.

21 Key Rating Factors Earnings Profitability: function of underwriting and investment strategy Results from underwriting operations affected by: Choice of business segment Geographical outreach Diversification of underwritten risks Primary profitability analysis conducted at the PTF level while a supplementary analysis also undertaken for the SHF. Level of Wakala fees is expected to enable the PTF to generate surplus over the long term while also allowing the operator to cover its costs. The investment management function may be based on either of Wakala or modaraba concept, with varying degrees of implications in terms of incentive for improving returns for the operator.

22 Takaful Ratings Future Challenges Development & harmonization of regulatory framework. Ability to extend outreach and diversify underlying risks. Creation of strongly capitalized global re- Takaful operators. Introduction of Management Quality Ratings Akin to Islamic banks where management is considered as modarib, JCR-VIS appreciates the role of managers in a takaful firm. Undertaking the first Management Quality Rating for Takaful operators.

23 Thank You Sobia Maqbool JCR-VIS Credit Rating Company Limited

JCR-VIS Credit Rating Company Limited. Affiliate of Japan Credit Rating Agency, Ltd.

Rating Agencies Methodologies for Takaful and Re-Takaful Firms By Sobia Maqbool Senior Manager JCR-VIS Credit Rating Company Limited Singapore, November 25, 2008 Honorable speakers, distinguished ladies

Rating Agencies Methodologies for Takaful and Re-Takaful Firms By Sobia Maqbool Senior Manager JCR-VIS Credit Rating Company Limited Singapore, November 25, 2008 Honorable speakers, distinguished ladies

The development of Takaful is

JCR-VIS GENERAL TAKAFUL Rating Methodology Akin to conventional insurance, an Insurer Financial Strength (IFS) rating is an assessment of a company s capacity to meet its contractual obligations that mainly

JCR-VIS GENERAL TAKAFUL Rating Methodology Akin to conventional insurance, an Insurer Financial Strength (IFS) rating is an assessment of a company s capacity to meet its contractual obligations that mainly

FAMILY TAKAFUL. (Shariah compliant life insurance) Assessment of Business Risk Financial Risk. Presenter: Amara Gondal

Assessment of Business Risk Financial Risk. Presenter: Amara Gondal") FAMILY TAKAFUL (Shariah compliant life insurance) Assessment of Business Risk Financial Risk Presenter: Amara Gondal Contents: SCOPE IFS Rating Takaful Structure Why need a modified rating approach Key

FAMILY TAKAFUL (Shariah compliant life insurance) Assessment of Business Risk Financial Risk Presenter: Amara Gondal Contents: SCOPE IFS Rating Takaful Structure Why need a modified rating approach Key

TRUST. TRANSPARENCY. INDEPENDENCE. Takaful Rating Methodology

TRUST. TRANSPARENCY. INDEPENDENCE Takaful Rating Methodology TAKAFUL RATING METHODOLOGY Preamble Shari a (Islamic Laws) may be termed as a rule of law, which fundamentally covers all practical and spiritual

TRUST. TRANSPARENCY. INDEPENDENCE Takaful Rating Methodology TAKAFUL RATING METHODOLOGY Preamble Shari a (Islamic Laws) may be termed as a rule of law, which fundamentally covers all practical and spiritual

ANALYSIS OF NON-LIFE INSURANCE COMPANIES IN PAKISTAN FOR THE YEAR ENDED 31 st DECEMBER 2017

ANALYSIS OF NONLIFE INSURANCE COMPANIES IN PAKISTAN FOR THE YEAR ENDED 31 st DECEMBER 2017 CONTENTS Introduction Gross Premium Retention Ratio Loss Ratio Commission Ratio Expense Ratio Investment Ratio

ANALYSIS OF NONLIFE INSURANCE COMPANIES IN PAKISTAN FOR THE YEAR ENDED 31 st DECEMBER 2017 CONTENTS Introduction Gross Premium Retention Ratio Loss Ratio Commission Ratio Expense Ratio Investment Ratio

General Insurance Sector Update

General Insurance Sector Update October 2017 Insurance Sector Overview Gross Premium Written No.of players CY16 (PKR mln) Rated PACRA Rated JCR Dual Rated Large (>5%) 4 46,209 4 2 2 Medium(2-5%) 12 22,179

General Insurance Sector Update October 2017 Insurance Sector Overview Gross Premium Written No.of players CY16 (PKR mln) Rated PACRA Rated JCR Dual Rated Large (>5%) 4 46,209 4 2 2 Medium(2-5%) 12 22,179

6 th Global Conference of Actuaries 18-19, February, 2004, New Delhi

6 th Global Conference of Actuaries 18-19, February, 2004, New Delhi Takaful An Alternate Insurance Model By Abdul Rahim Abdul Wahab, FSA abdul.rahim@pk.ey.com (Subject Code 05 - Subject Group: General

6 th Global Conference of Actuaries 18-19, February, 2004, New Delhi Takaful An Alternate Insurance Model By Abdul Rahim Abdul Wahab, FSA abdul.rahim@pk.ey.com (Subject Code 05 - Subject Group: General

The primary objective of ratings in the life insurance sector is to provide an independent assessment

JCR-VIS LIFE INSURANCE FAMILY TAKAFUL Rating Methodology The primary objective of ratings in the life insurance sector is to provide an independent assessment of the company s ability to pay promised benefits

JCR-VIS LIFE INSURANCE FAMILY TAKAFUL Rating Methodology The primary objective of ratings in the life insurance sector is to provide an independent assessment of the company s ability to pay promised benefits

Annexure 4: List of Financial Institutions

Annexure 4: List of Financial Institutions Annex 4.1: List of Scheduled and Microfinance Banks Operating in Pakistan As on 30 th June 2007 As on 30 th June 2008 Public Sector Commercial Banks Public Sector

Annexure 4: List of Financial Institutions Annex 4.1: List of Scheduled and Microfinance Banks Operating in Pakistan As on 30 th June 2007 As on 30 th June 2008 Public Sector Commercial Banks Public Sector

GIFF and IFN Asia Forum Mandarin Oriental Hotel-October 27 th 2010

GIFF and IFN Asia Forum Mandarin Oriental Hotel-October 27 th 2010 Risk Management and Disclosure in Takaful Practices Dawood Y Taylor Senior Regional Executive-Takaful, Middle East Prudential Corporation

GIFF and IFN Asia Forum Mandarin Oriental Hotel-October 27 th 2010 Risk Management and Disclosure in Takaful Practices Dawood Y Taylor Senior Regional Executive-Takaful, Middle East Prudential Corporation

WINDOW TAKAFUL OPERATIONS

WINDOW TAKAFUL OPERATIONS PARTICIPANT TAKAFUL FUND POLICIES 1. SHORT TITLE - These shall be called Participant Takaful Fund Policies 2. DEFINITIONS- Following are the definitions of the terminologies used

WINDOW TAKAFUL OPERATIONS PARTICIPANT TAKAFUL FUND POLICIES 1. SHORT TITLE - These shall be called Participant Takaful Fund Policies 2. DEFINITIONS- Following are the definitions of the terminologies used

Annexure I - Balance Sheet and Profit & Loss Statement of Banks. Dec-12

Annexures Annexure I - Balance Sheet and Profit & Loss Statement of Banks BALANCE SHEET PKR million ASSETS Cash & Balances With Treasury Banks 805,672 840,233 723,664 909,429 1,184,521 Balances With Other

Annexures Annexure I - Balance Sheet and Profit & Loss Statement of Banks BALANCE SHEET PKR million ASSETS Cash & Balances With Treasury Banks 805,672 840,233 723,664 909,429 1,184,521 Balances With Other

Takaful. Azeem Pirani Head of Marketing & Alternate Distribution Pak-Qatar Family Takaful. July. 13 th, 2007 M.A.J.U. Karachi.

Takaful Azeem Pirani Head of Marketing & Alternate Distribution Pak-Qatar Family Takaful July. 13 th, 2007 M.A.J.U. Karachi 13th July 2007 1 Agenda Takaful A product and an ideology History of Takaful

Takaful Azeem Pirani Head of Marketing & Alternate Distribution Pak-Qatar Family Takaful July. 13 th, 2007 M.A.J.U. Karachi 13th July 2007 1 Agenda Takaful A product and an ideology History of Takaful

A Review of the Development of GCC Takaful Rating Fundamentals and Catalysts for Growth Over the Next Decade

10 th Anniversary The A Review of the Development of GCC Takaful Rating Fundamentals and Catalysts for Growth Over the Next Decade Mahesh Mistry Director - Analytics A.M. Best Europe Rating Services Ltd

10 th Anniversary The A Review of the Development of GCC Takaful Rating Fundamentals and Catalysts for Growth Over the Next Decade Mahesh Mistry Director - Analytics A.M. Best Europe Rating Services Ltd

Rating Takaful (Shari a Compliant) Companies

Companies") BEST S METHODOLOGY AND CRITERIA Rating Takaful (Shari a Compliant) Companies October 13, 2017 Mahesh Mistry: +44 20-7-397-0325 Mahesh.Mistry@ambest.com Salman Siddiqui: +44 20 7 397 0331 Salman.Siddiqui@ambest.com

BEST S METHODOLOGY AND CRITERIA Rating Takaful (Shari a Compliant) Companies October 13, 2017 Mahesh Mistry: +44 20-7-397-0325 Mahesh.Mistry@ambest.com Salman Siddiqui: +44 20 7 397 0331 Salman.Siddiqui@ambest.com

13th Global Conference of Actuaries 2011

13th Global Conference of Actuaries 2011 Emerging Risks Daring Solutions Azim Mithani Chief Executive Officer Prudential BSN Takaful Berhad Malaysia February 20 22, 2011 1 Market Opportunity 2 Understanding

13th Global Conference of Actuaries 2011 Emerging Risks Daring Solutions Azim Mithani Chief Executive Officer Prudential BSN Takaful Berhad Malaysia February 20 22, 2011 1 Market Opportunity 2 Understanding

Pak-Qatar Family Takaful Limited

Rating Report RATING REPORT REPORT DATE: June 30, 2017 RATING ANALYSTS: Muniba Khan muniba.khan@jcrvis.com.pk RATING DETAILS Latest Rating Previous Rating Rating Category Long-term Long-term Entity A A

Rating Report RATING REPORT REPORT DATE: June 30, 2017 RATING ANALYSTS: Muniba Khan muniba.khan@jcrvis.com.pk RATING DETAILS Latest Rating Previous Rating Rating Category Long-term Long-term Entity A A

Takaful and Poverty Alleviation. 8 th International Microinsurance Conference Dar es Salaam, Tanzania 8 November 2012

Takaful and Poverty Alleviation 8 th International Microinsurance Conference Dar es Salaam, Tanzania 8 November 2012 Overview of presentation Why is conventional insurance not allowed? Takaful principles

Takaful and Poverty Alleviation 8 th International Microinsurance Conference Dar es Salaam, Tanzania 8 November 2012 Overview of presentation Why is conventional insurance not allowed? Takaful principles

A.M. Best s TAKAFUL REVIEW 2012 EDITION

A.M. Best s TAKAFUL REVIEW 2012 EDITION Contents 2 FOREWORD By Vasilis Katsipis, General Manager, Market Development MENA, South & Central Asia 4 METHODOLOGY: RATING TAKAFUL (SHARI A COMPLIANT) INSURANCE

A.M. Best s TAKAFUL REVIEW 2012 EDITION Contents 2 FOREWORD By Vasilis Katsipis, General Manager, Market Development MENA, South & Central Asia 4 METHODOLOGY: RATING TAKAFUL (SHARI A COMPLIANT) INSURANCE

Takaful: Concepts and Practical Issues

Takaful: Concepts and Practical Issues Singapore Actuarial Society Inaugural General Insurance Conference 06-07 May 2009, Singapore Hussain Ahmad, FCAS Consulting Actuary Towers Perrin Agenda What is takaful

Takaful: Concepts and Practical Issues Singapore Actuarial Society Inaugural General Insurance Conference 06-07 May 2009, Singapore Hussain Ahmad, FCAS Consulting Actuary Towers Perrin Agenda What is takaful

Dawood Family Takaful Limited

Powered by TCPDF (www.tcpdf.org) The Pakistan Credit Rating Agency Limited Rating Report Report Contents 1. Rating Analysis 2. Financial Information 3. Rating Scale 4. Regulatory and Supplementary Disclosure

Powered by TCPDF (www.tcpdf.org) The Pakistan Credit Rating Agency Limited Rating Report Report Contents 1. Rating Analysis 2. Financial Information 3. Rating Scale 4. Regulatory and Supplementary Disclosure

Takaful and Retakaful Challenges and Opportunities for Actuaries

Life Conference and Exhibition 2011 Safder Jaffer and Lindsay Unwin (Milliman) Takaful and Retakaful Challenges and Opportunities for Actuaries 22 November 2011 2010 The Actuarial Profession www.actuaries.org.uk

Life Conference and Exhibition 2011 Safder Jaffer and Lindsay Unwin (Milliman) Takaful and Retakaful Challenges and Opportunities for Actuaries 22 November 2011 2010 The Actuarial Profession www.actuaries.org.uk

AL MADINA INSURANCE COMPANY SAOG

1 AL MADINA INSURANCE COMPANY SAOG UNAUDITED CONDENSED INTERIM STATEMENT OF FINANCIAL POSITION AS AT 31 MARCH Note Shareholders fund Participants fund General takaful Family takaful Total participants

1 AL MADINA INSURANCE COMPANY SAOG UNAUDITED CONDENSED INTERIM STATEMENT OF FINANCIAL POSITION AS AT 31 MARCH Note Shareholders fund Participants fund General takaful Family takaful Total participants

AL MADINA INSURANCE COMPANY SAOG UNAUDITED CONDENSED INTERIM STATEMENT OF FINANCIAL POSITION AS AT 30 JUNE Participants fund. Total participants

AL MADINA INSURANCE COMPANY SAOG 2 UNAUDITED CONDENSED INTERIM STATEMENT OF FINANCIAL POSITION AS AT 30 JUNE Note Shareholders General takaful Participants fund Family takaful Total participants fund Grand

AL MADINA INSURANCE COMPANY SAOG 2 UNAUDITED CONDENSED INTERIM STATEMENT OF FINANCIAL POSITION AS AT 30 JUNE Note Shareholders General takaful Participants fund Family takaful Total participants fund Grand

The Successful Development of a Dual Islamic Finance and Takaful System in Malaysia - Takaful Zainal Abidin Mohd. Kassim, FIA

The Successful Development of a Dual Islamic Finance and Takaful System in Malaysia - Takaful Zainal Abidin Mohd. Kassim, FIA 23rd Pacific Insurance Conference Kuala Lumpur October 2007 Introduction The

The Successful Development of a Dual Islamic Finance and Takaful System in Malaysia - Takaful Zainal Abidin Mohd. Kassim, FIA 23rd Pacific Insurance Conference Kuala Lumpur October 2007 Introduction The

Conceptual. Objectives of Parties. Unique Challenges

13th Global Conference of Actuaries 2011 Emerging Risks Daring Solutions Debo Ajayi, FSA, FCIA, MAAA Managing Director & Actuary Milliman LLC UAE February 20 22, 2011 Conceptual Objectives of Parties Models

13th Global Conference of Actuaries 2011 Emerging Risks Daring Solutions Debo Ajayi, FSA, FCIA, MAAA Managing Director & Actuary Milliman LLC UAE February 20 22, 2011 Conceptual Objectives of Parties Models

RBC for Takaful Differences from Conventional, Impact and Opportunities. Charlene Lee Senior Actuary Munich Re Retakaful

RBC for Takaful Differences from Conventional, Impact and Opportunities Charlene Lee Senior Actuary Munich Re Retakaful Agenda Typical Takaful Models in Malaysia Solvency Requirements in Malaysia Evolution

RBC for Takaful Differences from Conventional, Impact and Opportunities Charlene Lee Senior Actuary Munich Re Retakaful Agenda Typical Takaful Models in Malaysia Solvency Requirements in Malaysia Evolution

Al Khaleej Takaful Group Q.S.C. CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED FINANCIAL STATEMENTS 31 December 2012 INDEPENDENT AUDITORS' REPORT TO THE SHAREHOLDERS OF AL KHALEEJ TAKAFUL GROUP Q.S.C. We have audited the accompanying consolidated financial statements

CONSOLIDATED FINANCIAL STATEMENTS 31 December 2012 INDEPENDENT AUDITORS' REPORT TO THE SHAREHOLDERS OF AL KHALEEJ TAKAFUL GROUP Q.S.C. We have audited the accompanying consolidated financial statements

RBC and Economic Capital: The Malaysian Experience

building value together 19 th September 2012 RBC and Economic Capital: The Malaysian Experience Farzana Ismail, FIA Principal www.actuarialpartners.com Agenda Introduction to economic capital RBC: The

building value together 19 th September 2012 RBC and Economic Capital: The Malaysian Experience Farzana Ismail, FIA Principal www.actuarialpartners.com Agenda Introduction to economic capital RBC: The

ISLAMIC INSURANCE: TAKAFUL

ISLAMIC INSURANCE: TAKAFUL A majority of Shari'a scholars find conventional insurance inadmissible in the Islamic framework. They have several objections against conventional insurance because it practiced

ISLAMIC INSURANCE: TAKAFUL A majority of Shari'a scholars find conventional insurance inadmissible in the Islamic framework. They have several objections against conventional insurance because it practiced

A.M. BEST METHODOLOGY

A.M. BEST METHODOLOGY December 2, 2011 Contents Principles of Takaful...1 Takaful Models & Structures...2 Main Characteristics of Takaful Companies....3 Analysing a Takaful Company...4 Appendix 1 Sample

A.M. BEST METHODOLOGY December 2, 2011 Contents Principles of Takaful...1 Takaful Models & Structures...2 Main Characteristics of Takaful Companies....3 Analysing a Takaful Company...4 Appendix 1 Sample

Zeti Akhtar Aziz: Islamic finance a global growth opportunity amidst a challenging environment

Zeti Akhtar Aziz: Islamic finance a global growth opportunity amidst a challenging environment Keynote address by Dr Zeti Akhtar Aziz, Governor of the Central Bank of Malaysia, at the State Street Islamic

Zeti Akhtar Aziz: Islamic finance a global growth opportunity amidst a challenging environment Keynote address by Dr Zeti Akhtar Aziz, Governor of the Central Bank of Malaysia, at the State Street Islamic

ISSUES SURROUNDING MANAGEMENT OF TAKAFUL SURPLUS. Sutan Emir Hidayat Senior Lecturer, Islamic Finance University College of Bahrain

ISSUES SURROUNDING MANAGEMENT OF TAKAFUL SURPLUS Sutan Emir Hidayat Senior Lecturer, Islamic Finance University College of Bahrain 1 OBJECTIVES OF THE PRESENTATION To explain the differences in the treatment

ISSUES SURROUNDING MANAGEMENT OF TAKAFUL SURPLUS Sutan Emir Hidayat Senior Lecturer, Islamic Finance University College of Bahrain 1 OBJECTIVES OF THE PRESENTATION To explain the differences in the treatment

Revisiting the Fundamentals

Islamic Financial Services Group trends and future direction Noor Ur Rahman Abid International Islamic Financial Market Board Meeting 4 February 2008 Revisiting the Fundamentals Investment avenues in conventional

Islamic Financial Services Group trends and future direction Noor Ur Rahman Abid International Islamic Financial Market Board Meeting 4 February 2008 Revisiting the Fundamentals Investment avenues in conventional

The DFSA is the independent financial services regulator for the DIFC

Address by Paul M Koster - Chief Executive Dubai Financial Services Authority (DFSA) at the World Takaful Conference Dusit Hotel, Dubai 14 April 2009 ====================================== The title I

Address by Paul M Koster - Chief Executive Dubai Financial Services Authority (DFSA) at the World Takaful Conference Dusit Hotel, Dubai 14 April 2009 ====================================== The title I

Presentation to Bancassurance Conference Takaful Products

Presentation to Bancassurance Conference Takaful Products Johan Potgieter 13 May 2013 Aon Hewitt (Actuarial) / QED Actuaries & Consultants (Pty) Ltd 0 Contents Overview Islamic Law Principles Models of

Presentation to Bancassurance Conference Takaful Products Johan Potgieter 13 May 2013 Aon Hewitt (Actuarial) / QED Actuaries & Consultants (Pty) Ltd 0 Contents Overview Islamic Law Principles Models of

Takaful & Re-Takaful Introducing Size, growth and regional trends of takaful

Sudan Saudi Arabia Bahrain Malaysia Total United Arad Emirates Indonesia Other countries 85% Chapter 16 Figure 98: Sigma 0% 5% 10% 15% 20% 25% 30% 35% 40% 2007 2015 Takaful & Re-Takaful Gross Takaful contributions

Sudan Saudi Arabia Bahrain Malaysia Total United Arad Emirates Indonesia Other countries 85% Chapter 16 Figure 98: Sigma 0% 5% 10% 15% 20% 25% 30% 35% 40% 2007 2015 Takaful & Re-Takaful Gross Takaful contributions

EXPLORING GROWTH OF TAKAFUL MARKET IN PAKISTAN. Muhammad Kashif Siddiqee, ACA Joint Director - SECP

EXPLORING GROWTH OF TAKAFUL MARKET IN PAKISTAN Muhammad Kashif Siddiqee, ACA Joint Director - SECP 1 2 THE NEED FOR INSURANCE All humans and/or Organizations inevitably are exposed to various types of

EXPLORING GROWTH OF TAKAFUL MARKET IN PAKISTAN Muhammad Kashif Siddiqee, ACA Joint Director - SECP 1 2 THE NEED FOR INSURANCE All humans and/or Organizations inevitably are exposed to various types of

Takaful Accounting. By Omer Morshed September 3, 2003 DISCLAIMER:

By Omer Morshed September 3, 2003 DISCLAIMER: This document is provided for informational purposes only, and the information herein is subject to change without notice. Please report any errors herein

By Omer Morshed September 3, 2003 DISCLAIMER: This document is provided for informational purposes only, and the information herein is subject to change without notice. Please report any errors herein

Seminar on Islamic Finance. Challenges in Developing Islamic Financial Services in Europe. 11 November 2009, Rome, Italy.

Seminar on Islamic Finance Challenges in Developing Islamic Financial Services in Europe 11 November 2009, Rome, Italy Speech by Professor Rifaat Ahmed Abdel Karim Secretary-General Islamic Financial Services

Seminar on Islamic Finance Challenges in Developing Islamic Financial Services in Europe 11 November 2009, Rome, Italy Speech by Professor Rifaat Ahmed Abdel Karim Secretary-General Islamic Financial Services

Can Islamic Finance Promotes Sustainable Development and Inclusive Growth?

Can Islamic Finance Promotes Sustainable Development and Inclusive Growth? Dr. Azmi Omar Director General Islamic Research and Training Institute http://www.irti.org Presentation Outline o Value Proposition

Can Islamic Finance Promotes Sustainable Development and Inclusive Growth? Dr. Azmi Omar Director General Islamic Research and Training Institute http://www.irti.org Presentation Outline o Value Proposition

ypt Briefings May years, with itself in 1978, 1984). worth noting Islamic penetration

. worth noting Islamic penetration") The Dynamics of Takaful Markets of the Middle East and Malaysia: Similar Models, Different Approaches, Contrasting Fortunes A.M. Best Introduction The concept of Sharia compliant insurance has gained significant

The Dynamics of Takaful Markets of the Middle East and Malaysia: Similar Models, Different Approaches, Contrasting Fortunes A.M. Best Introduction The concept of Sharia compliant insurance has gained significant

Reliance Insurance Company Limited (RICL)

") RATING REPORT REPORT DATE: January 7, 2019 RATING ANALYSTS: Narendar Shankar Lal narendar.shankar@jcrvis.com.pk RATING DETAILS Latest Rating Previous Rating Rating Category Long-term Long-term IFS A A

RATING REPORT REPORT DATE: January 7, 2019 RATING ANALYSTS: Narendar Shankar Lal narendar.shankar@jcrvis.com.pk RATING DETAILS Latest Rating Previous Rating Rating Category Long-term Long-term IFS A A

The Future of Islamic Wealth Management in Malaysia and the OIC World: Challenges and Opportunities Iqbal Khan

The Future of Islamic Wealth Management in Malaysia and the OIC World: Challenges and Opportunities Iqbal Khan Twitter: @IqbalKhanCEO BNP Paribas - INCEIF Centre of Islamic Wealth Management Inaugural

The Future of Islamic Wealth Management in Malaysia and the OIC World: Challenges and Opportunities Iqbal Khan Twitter: @IqbalKhanCEO BNP Paribas - INCEIF Centre of Islamic Wealth Management Inaugural

Islamic Finance Achievements and Prospects

Islamic Finance Achievements and Prospects Emeritus Professor Rodney Wilson Toronto University lecture, 30 th October 2014 The Second Annual Conference of Islamic Economics & Islamic Finance Venue: Chestnut

Islamic Finance Achievements and Prospects Emeritus Professor Rodney Wilson Toronto University lecture, 30 th October 2014 The Second Annual Conference of Islamic Economics & Islamic Finance Venue: Chestnut

Investor Presentation. June 2018

Investor Presentation June 2018 Contents Bank Muscat Introduction Operating environment Bank Muscat business - Overview Financial Performance Annexure Note: The financial information is updated as of 30

Investor Presentation June 2018 Contents Bank Muscat Introduction Operating environment Bank Muscat business - Overview Financial Performance Annexure Note: The financial information is updated as of 30

Disclosure Prudential Disclosure Report. 12/31/2017 Derayah Financial

Derayah - Pillar III Disclosure -2017 Prudential Disclosure Report 12/31/2017 Derayah Financial Table of Contents 1. OVERVIEW... 2 2. CAPITAL STRUCTURE... 2 2.1. Disclosure on Capital Base... 3 3. CAPITAL

Derayah - Pillar III Disclosure -2017 Prudential Disclosure Report 12/31/2017 Derayah Financial Table of Contents 1. OVERVIEW... 2 2. CAPITAL STRUCTURE... 2 2.1. Disclosure on Capital Base... 3 3. CAPITAL

Managing Performance in a Recovery The World Takaful Report 2010

report Managing Performance in a Recovery The World Takaful Report 2010 THE WORLD TAKAFUL REPORT 2010: Managing performance in a recovery Dear Insurance Industry Leader, It is with great pleasure that

report Managing Performance in a Recovery The World Takaful Report 2010 THE WORLD TAKAFUL REPORT 2010: Managing performance in a recovery Dear Insurance Industry Leader, It is with great pleasure that

IFN Oman Forum, Mar 7 th 2017

Fundamental & Essence of Takaful Tabrez Farooquee Head of Bancatakaful & Marketing Takaful Oman Insurance SAOG 92876789 IFN Oman Forum, Mar 7 th 2017 Agenda Introduction & Evolution of Takaful Takaful

Fundamental & Essence of Takaful Tabrez Farooquee Head of Bancatakaful & Marketing Takaful Oman Insurance SAOG 92876789 IFN Oman Forum, Mar 7 th 2017 Agenda Introduction & Evolution of Takaful Takaful

Key Statistics of Global Islamic Finance Industry

Treasury Markets Association Workshop on Islamic Finance 18 August 2008 Perspectives on Development of Islamic Finance in Hong Kong Mr. Edmond Lau Executive Director (Monetary Management) Hong Kong Monetary

Treasury Markets Association Workshop on Islamic Finance 18 August 2008 Perspectives on Development of Islamic Finance in Hong Kong Mr. Edmond Lau Executive Director (Monetary Management) Hong Kong Monetary

Islamic Financial Services Board (IFSB)

") Islamic Financial Services Board (IFSB) Mutual Insurance and Takāful in a Changing World 12-13 November 2012 27-28 Zulhijjah 1433 Ceylan Intercontinental Hotel Istanbul, Turkey www.ifsb.org AGENDA About

Islamic Financial Services Board (IFSB) Mutual Insurance and Takāful in a Changing World 12-13 November 2012 27-28 Zulhijjah 1433 Ceylan Intercontinental Hotel Istanbul, Turkey www.ifsb.org AGENDA About

Credit ratings provide an opinion on a company s ability and willingness to meet

JCR-VIS RATING THE ISSUE Rating Criteria Credit ratings provide an opinion on a company s ability and willingness to meet its obligations on time. JCR-VIS Credit Rating Company Limited assigns credit ratings

JCR-VIS RATING THE ISSUE Rating Criteria Credit ratings provide an opinion on a company s ability and willingness to meet its obligations on time. JCR-VIS Credit Rating Company Limited assigns credit ratings

Family Takaful Agents' Certification. Summary of the Syllabus

Family Takaful Agents' Certification Summary of the Syllabus Institute of Financial Markets of Pakistan 2016 OBJECTIVE OF THE EXAMINATION The objective of this course is to equip the trainee with the knowledge

Family Takaful Agents' Certification Summary of the Syllabus Institute of Financial Markets of Pakistan 2016 OBJECTIVE OF THE EXAMINATION The objective of this course is to equip the trainee with the knowledge

Insurance Business Rules 2006 (PINS)

") () Version No. 9 Effective: 1 July 2011 Includes amendments made by Captive Insurance Business (Consequential Amendments) Rules 2011 QFCRA Rules 2011-2 Insurance Mediation Business (Consequential Amendments)

() Version No. 9 Effective: 1 July 2011 Includes amendments made by Captive Insurance Business (Consequential Amendments) Rules 2011 QFCRA Rules 2011-2 Insurance Mediation Business (Consequential Amendments)

CAPITAL ADEQUACY MODULE

CAPITAL ADEQUACY MODULE Table of Contents CA-A Date Last Changed Introduction CA-A.1 Purpose 01/2011 CA-A.2 Module History 04/2014 CA-B Scope of Application CA-B.1 Bahraini Licensee and Overseas Licensee

CAPITAL ADEQUACY MODULE Table of Contents CA-A Date Last Changed Introduction CA-A.1 Purpose 01/2011 CA-A.2 Module History 04/2014 CA-B Scope of Application CA-B.1 Bahraini Licensee and Overseas Licensee

HABIB INSURANCE COMPANY LIMITED (HICL)

") HABIB INSURANCE COMPANY LIMITED (HICL) IFS RATING REPORT NEW [DEC-17] PREVIOUS [JUNE-17] Insurer Financial Strength (IFS) Rating A+ A+ Outlook Positive Positive Profile & Ownership Habib Insurance Company

HABIB INSURANCE COMPANY LIMITED (HICL) IFS RATING REPORT NEW [DEC-17] PREVIOUS [JUNE-17] Insurer Financial Strength (IFS) Rating A+ A+ Outlook Positive Positive Profile & Ownership Habib Insurance Company

Pillar 3 Disclosure Statement

ALJAZIRA CAPITAL COMPANY (A Closed Saudi Joint Stock Company) Pillar 3 Disclosure Statement As at 31 December 2015 1 TABLE OF CONTENTS 1. INTRODUCTION... 3 2. CAPITAL STRUCTURE... 3 3. CAPITAL ADEQUACY...

ALJAZIRA CAPITAL COMPANY (A Closed Saudi Joint Stock Company) Pillar 3 Disclosure Statement As at 31 December 2015 1 TABLE OF CONTENTS 1. INTRODUCTION... 3 2. CAPITAL STRUCTURE... 3 3. CAPITAL ADEQUACY...

Islamic Finance: Coming of Age. 10/29/13 GAB Annual Islamic Finance Conference

Islamic Finance: Coming of Age 1 Islamic Finance Sector in Kenya 1. A Sector View 2. A Company View 2 Sector View 3 Company View 4 The Takaful Concept What is it? How does it work? How is it different

Islamic Finance: Coming of Age 1 Islamic Finance Sector in Kenya 1. A Sector View 2. A Company View 2 Sector View 3 Company View 4 The Takaful Concept What is it? How does it work? How is it different

TAKAFUL CONFERENCE ON ISLAMIC INVESTMENT MANAGEMENT 12 FEBRUARY 2008, DUBAI. KEYNOTE ADDRESS Dr. Nasser Saidi Chief Economist, DIFCA

TAKAFUL CONFERENCE ON ISLAMIC INVESTMENT MANAGEMENT 12 FEBRUARY 2008, DUBAI KEYNOTE ADDRESS Dr. Nasser Saidi Chief Economist, DIFCA It is indeed a pleasure and an honour for me to address participants

TAKAFUL CONFERENCE ON ISLAMIC INVESTMENT MANAGEMENT 12 FEBRUARY 2008, DUBAI KEYNOTE ADDRESS Dr. Nasser Saidi Chief Economist, DIFCA It is indeed a pleasure and an honour for me to address participants

Introduction & Historical Background How to sell Takaful Products? Recent Developments Bancatakful What is Banca & Why?

November 9 th - 10 th, 2015 Takaful is a fast growing concept of Islamic Insurance and it is not only the Shari ah Compliant risk covering product rather its feature of potential return gives it a competitive

November 9 th - 10 th, 2015 Takaful is a fast growing concept of Islamic Insurance and it is not only the Shari ah Compliant risk covering product rather its feature of potential return gives it a competitive

Meezan Bank Limited (MBL)

") Rating Report RATING REPORT Meezan Bank Limited (MBL) REPORT DATE: June 29, 2017 RATING ANALYSTS: Osman Rahi, Osman.rahi@jcrvis.com.pk Talha Iqbal Chhangolia Talha.iqbal@jcrvis.com.pk RATING DETAILS Latest

Rating Report RATING REPORT Meezan Bank Limited (MBL) REPORT DATE: June 29, 2017 RATING ANALYSTS: Osman Rahi, Osman.rahi@jcrvis.com.pk Talha Iqbal Chhangolia Talha.iqbal@jcrvis.com.pk RATING DETAILS Latest

GENERAL INSURANCE RATING METHODOLOGY. Presented by: CREDIT RATING AGENCY OF

GENERAL INSURANCE RATING METHODOLOGY Presented by: CREDIT RATING AGENCY OF BANGLADESH LIMITED 1 RATING PROCESS FLOW Rating Frame Work Analysis and Evaluation Rating Committee Meeting Final Rating 2 2 Rating

GENERAL INSURANCE RATING METHODOLOGY Presented by: CREDIT RATING AGENCY OF BANGLADESH LIMITED 1 RATING PROCESS FLOW Rating Frame Work Analysis and Evaluation Rating Committee Meeting Final Rating 2 2 Rating

Islamic Finance Rules (IFR)

") Islamic Finance Rules (IFR) IFR VER02.150617 TABLE OF CONTENTS The contents of this module are divided into the following chapters, sections and appendices: 1. INTRODUCTION... 1 2. ISLAMIC FINANCE... 2

Islamic Finance Rules (IFR) IFR VER02.150617 TABLE OF CONTENTS The contents of this module are divided into the following chapters, sections and appendices: 1. INTRODUCTION... 1 2. ISLAMIC FINANCE... 2

Jubilee Life Insurance Company Limited

Rating Report RATING REPORT REPORT DATE: June 04, 2018 RATING ANALYSTS: Maimoon Rasheed maimoon@jcrvis.com.pk M. Daniyal daniyal.kamran@jcrvis.com.pk Jubilee Life Insurance Company Limited RATING DETAILS

Rating Report RATING REPORT REPORT DATE: June 04, 2018 RATING ANALYSTS: Maimoon Rasheed maimoon@jcrvis.com.pk M. Daniyal daniyal.kamran@jcrvis.com.pk Jubilee Life Insurance Company Limited RATING DETAILS

Building an Effective Islamic Financial System

Building an Effective Islamic Financial System Dr. Shamshad Akhtar Governor, State Bank of Pakistan Global Islamic Financial Forum Governor s: Financial Regulators Forum in Islamic Finance Kuala Lumpur,

Building an Effective Islamic Financial System Dr. Shamshad Akhtar Governor, State Bank of Pakistan Global Islamic Financial Forum Governor s: Financial Regulators Forum in Islamic Finance Kuala Lumpur,

GOVERNMENT NOTICE No.. published on THE INSURANCE ACT (CAP.394) REGULATIONS. (Made under section 167) PART I PRELIMINARY

REGULATIONS. (Made under section 167) PART I PRELIMINARY") GOVERNMENT NOTICE No.. published on THE INSURANCE ACT (CAP.394) REGULATIONS (Made under section 167) THE INSURANCE (TAKAFUL) REGULATIONS, 2014 PART I PRELIMINARY Citation 1. These Regulations may be cited

GOVERNMENT NOTICE No.. published on THE INSURANCE ACT (CAP.394) REGULATIONS (Made under section 167) THE INSURANCE (TAKAFUL) REGULATIONS, 2014 PART I PRELIMINARY Citation 1. These Regulations may be cited

Company Information Saifuddin N. Zoomkawala Managing & Chief Executive Hasanali Abdullah s Rafique R. Bhimjee Abdul Rehman Haji Habib Muneer R. Bhimje

Defining excellence since 1932 Report (Un-Audited) First Quarter Company Information Saifuddin N. Zoomkawala Managing & Chief Executive Hasanali Abdullah s Rafique R. Bhimjee Abdul Rehman Haji Habib Muneer

Defining excellence since 1932 Report (Un-Audited) First Quarter Company Information Saifuddin N. Zoomkawala Managing & Chief Executive Hasanali Abdullah s Rafique R. Bhimjee Abdul Rehman Haji Habib Muneer

SECTOR ASSESSMENT (SUMMARY): FINANCE 1

: FINANCE 1") Country Partnership Strategy: Pakistan, 2015 2019 SECTOR ASSESSMENT (SUMMARY): FINANCE 1 1. Sector Performance, Issues and Opportunities 1. Financial sector participants. Pakistan s financial sector is

Country Partnership Strategy: Pakistan, 2015 2019 SECTOR ASSESSMENT (SUMMARY): FINANCE 1 1. Sector Performance, Issues and Opportunities 1. Financial sector participants. Pakistan s financial sector is

Advanced Diploma in Insurance

THE CHARTERED INSURANCE INSTITUTE 590 Advanced Diploma in Insurance Unit 590 Principles of Takaful October 2015 examination Instructions Three hours are allowed for this paper. Do not begin writing until

THE CHARTERED INSURANCE INSTITUTE 590 Advanced Diploma in Insurance Unit 590 Principles of Takaful October 2015 examination Instructions Three hours are allowed for this paper. Do not begin writing until

Takaful Business Challenges and Opportunities

Life Insurance Conference 2012 Takaful Business Challenges and Opportunities 9 November 2012 Amara Sanctuary Resort Sentosa, Singapore By: Hans De Cuyper Chief Executive Officer Etiqa Insurance & Takaful

Life Insurance Conference 2012 Takaful Business Challenges and Opportunities 9 November 2012 Amara Sanctuary Resort Sentosa, Singapore By: Hans De Cuyper Chief Executive Officer Etiqa Insurance & Takaful

MOBILIZING ISLAMIC FINANCE FOR INFRASTRUCTURE PUBLIC- PRIVATE PARTNERSHIPS

MOBILIZING ISLAMIC FINANCE FOR INFRASTRUCTURE PUBLIC- PRIVATE PARTNERSHIPS REPORT 2017 OVERVIEW M uslims constitute a vast majority of the population in emerging market and developing economies (EMDE)

MOBILIZING ISLAMIC FINANCE FOR INFRASTRUCTURE PUBLIC- PRIVATE PARTNERSHIPS REPORT 2017 OVERVIEW M uslims constitute a vast majority of the population in emerging market and developing economies (EMDE)

Reliance Bank Limited. Pillar 3 Disclosures

Version 1.2 Contents 1 Introduction... 2 2 Capital Resources... 2 3 Approach to Assessing Adequacy of Internal Capital... 2 4 Credit Risk and Dilution Risk... 3 4.1 Standardised Approach to Credit Risk...

Version 1.2 Contents 1 Introduction... 2 2 Capital Resources... 2 3 Approach to Assessing Adequacy of Internal Capital... 2 4 Credit Risk and Dilution Risk... 3 4.1 Standardised Approach to Credit Risk...

HALF YEARLY REPORT. June 30, 2016

HALF YEARLY REPORT HALF YEARLY REPORT JUNE 30, Certified True Copy Najam Ul Hassan Janjua Company Secretary www.jubileelife.com Table of Contents 1 Profile Vision, Mission & Core Values 2 Our Company Company

HALF YEARLY REPORT HALF YEARLY REPORT JUNE 30, Certified True Copy Najam Ul Hassan Janjua Company Secretary www.jubileelife.com Table of Contents 1 Profile Vision, Mission & Core Values 2 Our Company Company

Reviving the Cooperative Spirit through Takaful. Hassan Scott Odierno, FSA Actuarial Partners (Malaysia) 15 October 2014

15 October 2014") Reviving the Cooperative Spirit through Takaful Hassan Scott Odierno, FSA Actuarial Partners (Malaysia) 15 October 2014 1 The cooperative spirit is members helping each other to succeed Discretionary and

Reviving the Cooperative Spirit through Takaful Hassan Scott Odierno, FSA Actuarial Partners (Malaysia) 15 October 2014 1 The cooperative spirit is members helping each other to succeed Discretionary and

ISLAMIC FINANCIAL SERVICES BOARD. and INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS

Issues paper ISLAMIC FINANCIAL SERVICES BOARD and INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS ISSUES IN REGULATION AND SUPERVISION OF TAKAFUL (ISLAMIC INSURANCE) August 2006 THE JOINT WORKING GROUP:

Issues paper ISLAMIC FINANCIAL SERVICES BOARD and INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS ISSUES IN REGULATION AND SUPERVISION OF TAKAFUL (ISLAMIC INSURANCE) August 2006 THE JOINT WORKING GROUP:

Tax Briefing No 78. This content is more than 5 years old. Where still relevant it has been incorporated. into a Tax and Duty Manual

Revenue Commissioners Tax Briefing No 78 2009 Islamic Finance Introduction Islamic finance covers any financing arrangement that is compliant with the principles of Shari'a law. Specifically, there are

Revenue Commissioners Tax Briefing No 78 2009 Islamic Finance Introduction Islamic finance covers any financing arrangement that is compliant with the principles of Shari'a law. Specifically, there are

Zeti Akhtar Aziz: Metamorphosis into an international islamic banking and financial hub

Zeti Akhtar Aziz: Metamorphosis into an international islamic banking and financial hub Special address by Dr Zeti Akhtar Aziz, Governor of the Central Bank of Malaysia, at the ASLI s World Islamic Economic

Zeti Akhtar Aziz: Metamorphosis into an international islamic banking and financial hub Special address by Dr Zeti Akhtar Aziz, Governor of the Central Bank of Malaysia, at the ASLI s World Islamic Economic

BANK ALJAZIRA (A Saudi Joint Stock Company)

") BANK ALJAZIRA UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS FOR THE SIX MONTHS PERIOD ENDED 30 JUNE 2014 INTERIM CONSOLIDATED STATEMENT OF FINANCIAL POSITION Note 30 June 2014 31 December

BANK ALJAZIRA UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS FOR THE SIX MONTHS PERIOD ENDED 30 JUNE 2014 INTERIM CONSOLIDATED STATEMENT OF FINANCIAL POSITION Note 30 June 2014 31 December

INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS

Principles No. 3.4 INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS PRINCIPLES ON GROUP-WIDE SUPERVISION OCTOBER 2008 This document has been prepared by the Financial Conglomerates Subcommittee (renamed

Principles No. 3.4 INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS PRINCIPLES ON GROUP-WIDE SUPERVISION OCTOBER 2008 This document has been prepared by the Financial Conglomerates Subcommittee (renamed

BANK ALJAZIRA (A Saudi Joint Stock Company)

") BANK ALJAZIRA UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS FOR THE NINE MONTHS ENDED 30 SEPTEMBER AND REVIEW REPORT INTERIM CONSOLIDATED STATEMENT OF FINANCIAL POSITION Notes 31 December

BANK ALJAZIRA UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS FOR THE NINE MONTHS ENDED 30 SEPTEMBER AND REVIEW REPORT INTERIM CONSOLIDATED STATEMENT OF FINANCIAL POSITION Notes 31 December

Islamic Arab Insurance Co. (Salama) PJSC and its subsidiaries. Condensed consolidated interim financial statements

PJSC and its subsidiaries. Condensed consolidated interim financial statements") Islamic Arab Insurance Co. (Salama) PJSC and its subsidiaries Condensed consolidated interim financial statements for the nine-month period ended 30 September 2018 Condensed consolidated interim financial

Islamic Arab Insurance Co. (Salama) PJSC and its subsidiaries Condensed consolidated interim financial statements for the nine-month period ended 30 September 2018 Condensed consolidated interim financial

Takaful : defining ethical insurance. Zainal Abidin Mohd. Kassim Partner Mercer

Takaful : defining ethical insurance Zainal Abidin Mohd. Kassim Partner Mercer Presentation contents Takaful a primer Shariah Laws governing trade and business Takaful in practice Shariah compliant investments

Takaful : defining ethical insurance Zainal Abidin Mohd. Kassim Partner Mercer Presentation contents Takaful a primer Shariah Laws governing trade and business Takaful in practice Shariah compliant investments

Islamic finance in Bermuda Bermuda: Islamic finance hub in the western hemisphere

www.pwc.com/bermuda Islamic finance in Bermuda Bermuda: Islamic finance hub in the western hemisphere Contents Page 1. Bermuda: Islamic finance hub in the western hemisphere 2 2. Why Bermuda 3 3. Retakaful

www.pwc.com/bermuda Islamic finance in Bermuda Bermuda: Islamic finance hub in the western hemisphere Contents Page 1. Bermuda: Islamic finance hub in the western hemisphere 2 2. Why Bermuda 3 3. Retakaful

Takaful articles. Introduction. Susan Dingwall Partner, Norton Rose, Ffion Griffiths Associate, Norton Rose, United KIngdom.

Takaful articles Susan Dingwall Partner, Norton Rose, United Kingdom Ffion Griffiths Associate, Norton Rose, United KIngdom Number 7: November 2006 The United Kingdom: Regulatory approach to Takaful Introduction

Takaful articles Susan Dingwall Partner, Norton Rose, United Kingdom Ffion Griffiths Associate, Norton Rose, United KIngdom Number 7: November 2006 The United Kingdom: Regulatory approach to Takaful Introduction

Our Journey. The journey begins. Creation of All Rajhi Trading & Exchange Corporation. Conversion of Al Rajhi to a joint Stock Exchange Company

Introduction Founded in 1957, Al Rajhi Bank ( Al Rajhi or ARB ) is one of the largest Islamic banks globally. With assets of USD 59 billion plus, equity of over USD 8 billion and a team of 7,5 employees,

Introduction Founded in 1957, Al Rajhi Bank ( Al Rajhi or ARB ) is one of the largest Islamic banks globally. With assets of USD 59 billion plus, equity of over USD 8 billion and a team of 7,5 employees,

HISAAR SAVINGS PLAN. Consumer Banking. Committed to People

HISAAR SAVINGS PLAN Consumer Banking Committed to People HISAAR - meaning Fort and Fence is exactly what this new takaful plan from Jubilee Life Insurance - Window Takaful Operations in partnership with

HISAAR SAVINGS PLAN Consumer Banking Committed to People HISAAR - meaning Fort and Fence is exactly what this new takaful plan from Jubilee Life Insurance - Window Takaful Operations in partnership with

BANKING CONVENTIONAL. Overview

CONVENTIONAL BANKING Overview Is the Bank s Board spending enough time and resources on making sure the Bank is developing the desired culture and is it strong enough to be sustainable for the long run?

CONVENTIONAL BANKING Overview Is the Bank s Board spending enough time and resources on making sure the Bank is developing the desired culture and is it strong enough to be sustainable for the long run?

Islamic Insurance revisited

Islamic Insurance revisited September 2011 Economic Research & Consulting Published by: Swiss Reinsurance Company Ltd 28th Floor Mevara Keck Seng 203 Jalan Bukit Bintang 55100 Kuala Lumpur Malaysia Telephone

Islamic Insurance revisited September 2011 Economic Research & Consulting Published by: Swiss Reinsurance Company Ltd 28th Floor Mevara Keck Seng 203 Jalan Bukit Bintang 55100 Kuala Lumpur Malaysia Telephone

Islamic International Rating Agency 1

AN INTRODUCTION: Islamic International Rating Agency ( IIRA ) Islamic International Rating Agency 1 What is credit rating? A credit rating is an independent and objective OPINION on the ability and willingness

AN INTRODUCTION: Islamic International Rating Agency ( IIRA ) Islamic International Rating Agency 1 What is credit rating? A credit rating is an independent and objective OPINION on the ability and willingness

August 3, Presentation on Takaful Investments Dr. Omar Clark Fisher, PhD Takaful 8/11/2009 1

August 3, 2009 Presentation on Takaful Investments Dr. Omar Clark Fisher, PhD Takaful 8/11/2009 1 Agenda Investment Objectives & Asset Classes permitted under Shariah Examples of Islamic Assets available

August 3, 2009 Presentation on Takaful Investments Dr. Omar Clark Fisher, PhD Takaful 8/11/2009 1 Agenda Investment Objectives & Asset Classes permitted under Shariah Examples of Islamic Assets available

Swiss Re s new sigma study explores the growth of insurance in emerging markets and the prospects for Islamic insurance

Media release ab Swiss Re s new sigma study explores the growth of insurance in emerging markets and the prospects for Islamic insurance Contact: Patrizia Baur, Zurich Telephone +41 43 285 3153 Clarence

Media release ab Swiss Re s new sigma study explores the growth of insurance in emerging markets and the prospects for Islamic insurance Contact: Patrizia Baur, Zurich Telephone +41 43 285 3153 Clarence

In collaboration with

In collaboration with 7th Annual 16 & 17 April 2012, Dusit Thani Dubai, UAE Dear Insurance Industry Leader, It is with great pleasure that we present to you the 5th annual edition of the World Takaful

In collaboration with 7th Annual 16 & 17 April 2012, Dusit Thani Dubai, UAE Dear Insurance Industry Leader, It is with great pleasure that we present to you the 5th annual edition of the World Takaful

The Co-operative Insurance Society of Pakistan Limited

Rating Report RATING REPORT REPORT DATE: December 19, 2017 RATING ANALYSTS: Maimoon Rasheed maimoon@jcrvis.com.pk M. Daniyal daniyal.kamran@jcrvis.com.pk RATING DETAILS Latest Rating Previous Rating Rating

Rating Report RATING REPORT REPORT DATE: December 19, 2017 RATING ANALYSTS: Maimoon Rasheed maimoon@jcrvis.com.pk M. Daniyal daniyal.kamran@jcrvis.com.pk RATING DETAILS Latest Rating Previous Rating Rating

Tax Treatment of Islamic Financial Transactions

Tax Treatment of Islamic Financial Transactions This document should be read in conjunction with Part 8A Taxes Consolidation Act 1997 Document created November 2018. 1 Table of Contents 1 Introduction

Tax Treatment of Islamic Financial Transactions This document should be read in conjunction with Part 8A Taxes Consolidation Act 1997 Document created November 2018. 1 Table of Contents 1 Introduction

PILLAR 3 REPORT FOR THE FINANCIAL YEAR ENDED 31 MARCH 2017

PILLAR 3 REPORT FOR THE FINANCIAL YEAR ENDED 31 MARCH 2017 Overview Bank Negara Malaysia's ("BNM") guidelines on capital adequacy require Alliance Islamic Bank Berhad ("the Bank") to maintain an adequate

PILLAR 3 REPORT FOR THE FINANCIAL YEAR ENDED 31 MARCH 2017 Overview Bank Negara Malaysia's ("BNM") guidelines on capital adequacy require Alliance Islamic Bank Berhad ("the Bank") to maintain an adequate

building value together 26 April 2013 Takaful in Africa Hassan Scott Odierno, FSA Lome

building value together 26 April 2013 Takaful in Africa Hassan Scott Odierno, FSA Lome www.actuarialpartners.com Takaful in Africa 2 Extent of religion in insurance Religious buildings and property can

building value together 26 April 2013 Takaful in Africa Hassan Scott Odierno, FSA Lome www.actuarialpartners.com Takaful in Africa 2 Extent of religion in insurance Religious buildings and property can

Takaful. Dr. Muhammad Imran Usmani. SECP Takaful Conference March 14, 2007

Takaful Dr. Muhammad Imran Usmani SECP Takaful Conference March 14, 2007 Presentation Outline Conventional Insurance How Qimar & Riba exist in Conventional Insurance Definition of Takaful Mudarabah Model

Takaful Dr. Muhammad Imran Usmani SECP Takaful Conference March 14, 2007 Presentation Outline Conventional Insurance How Qimar & Riba exist in Conventional Insurance Definition of Takaful Mudarabah Model

QUARTERLY REPORT Quarter Ended September 30, 2018 (Un-Audited)

") 36 Years of Quality Service QUARTERLY REPORT Quarter Ended September 30, 2018 (UnAudited) SERVING RELIABLY 19812017 Reliance Insurance Company Limited Window Takaful Contents 02 03 04 06 08 09 10 11 13

36 Years of Quality Service QUARTERLY REPORT Quarter Ended September 30, 2018 (UnAudited) SERVING RELIABLY 19812017 Reliance Insurance Company Limited Window Takaful Contents 02 03 04 06 08 09 10 11 13

The Evolution of Islamic Finance

The Evolution of Islamic Finance Islamic finance lexicon/1 Ijara: leasing transaction where the purchase of the leased equipment at the end of the rental period is optional Mudaraba: form of financial

The Evolution of Islamic Finance Islamic finance lexicon/1 Ijara: leasing transaction where the purchase of the leased equipment at the end of the rental period is optional Mudaraba: form of financial

SYARIKAT TAKAFUL MALAYSIA KELUARGA BERHAD (formerly known as Syarikat Takaful Malaysia Berhad)

") 1 Basis of Preparation The unaudited interim financial statements have been prepared in accordance with MFRS 134: Interim Financial Reporting issued by the Malaysian Accounting Standards Board ( MASB ),

1 Basis of Preparation The unaudited interim financial statements have been prepared in accordance with MFRS 134: Interim Financial Reporting issued by the Malaysian Accounting Standards Board ( MASB ),