10 INSURANCE PROBLEMS IN COMMERCIAL REAL ESTATE LEASES (AND HOW TO FIX THEM)

|

|

|

- Philomena Penelope Parsons

- 6 years ago

- Views:

Transcription

1 10 INSURANCE PROBLEMS IN COMMERCIAL REAL ESTATE LEASES (AND HOW TO FIX THEM) By Jay Radov, Pegasus Insurance Consulting, Inc. December 2009 A prospective tenant s commercial real estate lease is a major factor in determining that tenant s entire insurance program. A business cannot be properly insured unless the provisions in the executed lease are consistent with the commercial insurance policies of the tenant. Since the tenant s insurance policies are usually in force BEFORE the proposed lease is executed, the best way to protect the interests of the prospective tenant is to make sure that the proposed lease (a) is not inconsistent with the prospective tenant s existing insurance policies; (b) does not impose unnecessary financial costs, in terms of requiring more coverage or additional policies, upon the prospective tenant; and (c) does not expose the prospective tenant to additional potential liability which might be insurable only at an excessive cost or completely uninsurable. PROBLEM # 1: Commercial real estate leases frequently use language that is outdated, ambiguous and irrelevant. Ten (10) examples of such language include the following: 1. fire and extended coverage or extended coverage endorsement 2. full insurable value 3. public liability insurance 4. contractual liability insurance 5. additional named insured, named insured, or coinsured 6. cross liability endorsement 7. broad form comprehensive general liability endorsement 8. broad form property damage endorsement 9. commercial general liability policy with a combined single limit of $ 10. boiler and machinery insurance For example, some of the above language appears in these actual clauses of leases: a. At all times during the term, Tenant will carry and maintain fire and extended coverage insurance covering the Premises; Page 1 of 16

2 b. Tenant shall keep in full force and effect during the Term a policy of general accident and public liability insurance with respect to the Premises and the area adjacent to the Premises and the business operated by Tenant with a combined single limit for bodily injury, including death, to any person or persons, and for property damages, of not less than One Million Dollars ($1,000,000); and c. Tenant agrees to keep said premises insured to the extent of its full insurable value. These outdated phrases and clauses create significant issues. Many businesses insure their property on a replacement cost basis with an 80% coinsurance clause. This provision means that as long as the business maintains insurance on its property equal to at least 80% of the full replacement cost of such property at the time of loss, the insurance company (a) will not impose a penalty when the business files a valid property insurance claim and (b) will pay the claim (up to the policy s Limit of Insurance) on a replacement cost basis, without subtracting for depreciation. But what does its full insurable value (referred to above) mean? Does it mean: (1) that any coinsurance condition must be satisfied; (2) that actual cash value is not a permissible method of valuation; or (3) that the business must insure its property on a replacement cost basis with a 100% coinsurance condition? SOLUTION # 1: The current terminology for the 10 outdated, ambiguous and irrelevant terms found above is listed below: 1. basic causes of loss form; broad causes of loss form; or special causes of loss form 2. on a replacement cost basis and in an amount sufficient to satisfy the application of a % coinsurance condition 3. commercial general liability insurance 4. commercial general liability insurance 5. additional insured 6. included in commercial general liability insurance 7. commercial general liability insurance 8. commercial general liability insurance 9. commercial general liability policy with: (1) a general aggregate limit of $ ; (2) a products completed operations aggregate limit of $ ; Page 2 of 16

3 (3) subject to the general aggregate limit, a per person or per entity limit of $ for Tenant s personal and advertising injury liability; and (4) subject to the general aggregate limit or products completed operations aggregate limit (whichever is applicable), an each occurrence limit of $ for bodily injury and property damage liability and medical expenses. 10. equipment breakdown insurance PROBLEM # 2: Unilateral waivers of subrogation should be avoided by the Tenant. Black s Law Dictionary defines subrogation as the right of one who has paid an obligation which another should have paid to be indemnified by the other. Commercial liability and property insurance policies (except for workers compensation insurance policies and most claims made policies) permit policyholders to waive their rights of subrogation before a loss. The typical insurance policy provides that: If any person or organization to or for whom we [the insurance company] make payment under this Coverage Part [policy] has rights to recover damages from another, those rights are transferred to us [the insurance company] to the extent of our [the insurance company s] payment. That person or organization must do everything necessary to secure our rights and must do nothing after loss to impair them. But you [the policyholder] may waive your rights against another party in writing: 1. Prior to a loss... (emphasis added). See the language in Section I. and in Section 8. of Exhibit 1 attached hereto. In virtually every lease, Landlord requires Tenant to waive subrogation. Typical language states that All policies procured by Tenant shall contain an endorsement or clause containing an express waiver of any right of subrogation by the insurance company against Landlord. 1 This provision is a unilateral waiver of subrogation because the lease only requires that Tenant waive subrogation. Hypothetical # 1: Most leases require that Landlord maintain, repair and replace the roof. Suppose Landlord s employee negligently repairs the roof and after the next significant rain storm, water leaks from the roof and destroys $25,000 of Tenant s business personal property. Tenant files a claim with its insurance company, which pays the claim after Tenant satisfies the $500 deductible. Tenant s insurance company is prohibited from seeking the $24,500 (as reimbursement) from Landlord because Tenant waived its right of subrogation. 1 As noted previously on this page, workers compensation insurance policies are one exception in that they do not automatically permit the policyholder to waive its right of subrogation. Rather, such policyholder must ask its workers compensation insurance company for permission to waive subrogation. The decision whether or not to waive subrogation in workers compensation policies is thus up to the discretion of the workers compensation insurance company. Consequently, the waiver of subrogation clauses found in commercial leases should be modified to reflect this fact. Page 3 of 16

4 Hypothetical # 2: Suppose that Tenant s employee, while laying cable in the premises, negligently drills into the building s sprinkler system which results in $50,000 of water damage to the walls, ceiling and flooring of Tenant s premises. Landlord files a claim with its insurance company, which pays the claim after Landlord satisfies its $1,000 deductible. Landlord s insurance company then sues Tenant for indemnification of the $49,000 that Landlord s insurance company paid to Landlord. SOLUTION # 2A: Tenant should insist upon a mutual waiver of subrogation. If the lease had contained a mutual waiver of subrogation, then Landlord s insurance company would have been prevented from seeking indemnification from Tenant. (What is good for the goose is good for the gander.) A mutual waiver of subrogation requires both Landlord and Tenant to waive their rights of subrogation. A typical mutual waiver of subrogation might provide that: Landlord and Tenant each hereby waives subrogation and all of its rights of recovery against the other party and any other person or entity claiming subrogation or rights of recovery by, under, or through such other party. SOLUTION # 2B: If Tenant cannot get Landlord to agree to a mutual waiver of subrogation 2, then Tenant must purchase a Legal Liability Coverage Policy 3 a separate insurance policy, which obviously costs money to protect itself. Commercial general liability (CGL) insurance policies provide liability coverage to Tenants when they act negligently and cause property damage by FIRE to premises rented to them. But the CGL provides no coverage for non fire perils when Tenants negligently damage the premises rented to them. 4 The Legal Liability Coverage Policy, however, does provide such coverage. In Hypothetical #2, Tenant s employee negligently damaged the premises and the cause of loss was water not fire. If fire had been the result, Tenant s CGL would have provided coverage. But since water was the cause of loss, Tenant s CGL does not provide any insurance coverage. PROBLEM #3: Even if the lease contains a mutual waiver of subrogation, Tenant still faces potentially catastrophic liability. 2 In a minority of states, the law provides that generally in a landlord tenant relationship, the landlord s insurance company has no right of subrogation against the tenant, and thus automatically provides the desired landlord s waiver of subrogation. See Sutton v. Jondahl, 532 P.2d 478 (Okla. Ct. App 1975). That is not the law in Maryland. See Rausch v. Allstate Insurance Company, 388 Md. 690, 882 A.2d 801 (2005), attached hereto as Exhibit 2. For a list of the law in each state on this subject, see Exhibit 3 attached hereto. 3 This type of policy is attached hereto as Exhibit 4. 4 The CGL provides in relevant part that this insurance does not apply to: Property damage to property you own, rent or occupy, including any costs or expenses incurred by you... [but that exclusion does] not apply to damage by fire to premises while rented to you or temporarily occupied by you with permission of the owner. See the language in Section 2.j.(1) and at the end of Section 2.q. of Exhibit 5 attached hereto. Page 4 of 16

5 Hypothetical # 3: Suppose that Tenant occupies a suite in a multi story building and that Tenant s employee negligently causes a fire in Tenant s premises which then spreads to several other parts of the building. Suppose further that Tenant has $1,000,000 of liability insurance per occurrence; that Landlord has $10,000,000 of property insurance on the multi story building; that the actual damages to the building are $12,500,000; and that Landlord s insurance company has paid Landlord $10,000,000 (Landlord s Limit of Insurance) to repair and/or replace the damage. Because Landlord, in the lease, has waived its right of subrogation against Tenant, Landlord s insurance company is prohibited from suing Tenant for any of the $10,000,000 that it, the insurer, has paid to the Landlord. However, Landlord s actual damages are $12,500,000 or $2,500,000 more than it has collected from its insurance company, and Landlord then sends Tenant a demand letter (and ultimately sues Tenant) seeking indemnification for the $2,500,000 in damages over and above the $10,000,000 that Landlord has already collected. Nothing in the lease has prohibited Landlord from seeking recovery over and above the payment made by Landlord s insurance company. SOLUTION # 3: Tenant should include a (mutual) release of liability in the lease. An example of such language is the following: Landlord and Tenant hereby agree to release and hold harmless each other and any other person or entity claiming by, under, or through either or both of them, whether by way of subrogation or otherwise, from any and all liability, loss, claims, judgments, damages, costs, fees (including reasonable attorneys fees), expenses, or responsibility suffered by such party, whether or not covered by any insurance, even if such liability, loss, claims, judgments, damages, costs, fees (including reasonable attorneys fees), expenses, or responsibility shall have been caused by the recklessness or negligence of the other party or any person or entity for whom such party may be legally liable. Whether or not Tenant can successfully add the above language to the lease will largely depend upon the bargaining strength of each party. PROBLEM # 4: If Tenant is not successful in having a (mutual) release of liability added to the lease, then the indemnification provisions of the lease must be very carefully written to limit Tenant s liability. SOLUTION # 4: Four points need to be made regarding indemnification provisions in commercial real estate leases. If these four points are correctly addressed, then Tenant s indemnification of Landlord will successfully limit Tenant s potential liability. First, any indemnification provisions should be mutual and symmetrical. That is, Landlord should indemnify Tenant to the same extent that Tenant indemnifies Landlord. It is not the case that only Tenants (or their agents) can be negligent in ways that can impose liabilities, costs, damages and expenses upon Landlords for which Landlords would seek indemnification from Tenants. Landlords (or their agents) can also be negligent in ways that can impose liabilities, costs, damages and expenses upon Tenants for which Tenants would seek indemnification from Landlords. Page 5 of 16

6 Second, the indemnification language should be written so that Tenant only indemnifies Landlord for the negligent actions or omissions of (a) Tenant, (b) Tenant s employees acting within the scope of their employment, and (c) any other person (or entity) for which Tenant is legally liable. Leases frequently provide that Tenant shall indemnify and hold Landlord harmless from claims, damages and expenses caused not only by Tenant but also by Tenant s employees, agents, contractors, servants, lessees, or invitees. Here is a sample of such indemnification language: Tenant will indemnify Landlord and save it harmless from and against any and all claims, actions, damages, liabilities and expenses (including reasonable attorneys' fees) in connection with loss of life, personal injury and/or damage to property arising from or out of any occurrence in, upon or at the Premises, or the occupancy or use by Tenant of the Premises or any part thereof, to the extent occasioned wholly or in part, by act or omission of Tenant, its employees, its agents, contractors, servants, lessees, or invitees. Under the law, Tenants are liable for the actions of their employees when such actions are performed within the scope of their employment. The problem occurs with having Tenant indemnify Landlord for the actions of Tenant s agents, contractors, servants, lessees, or invitees. Under the legal concept of vicarious liability 5, Tenant might or might not actually be liable for the conduct of such persons or entities it depends upon the particular facts and circumstances of the case. However, because of this indemnification language in the lease, Tenant becomes (contractually) liable for the actions of these agents, contractors, servants, lessees, or invitees when, in fact, Tenant might not be liable for their negligence (in the absence of such indemnification language). The third point that needs to be made regarding indemnification provisions in commercial real estate leases is that Tenant should only indemnify Landlord when (a) Tenant or anybody for which Tenant is legally liable is negligent and (b) Landlord and anybody for which Landlord is legally liable is not negligent. Fourth, Tenant should both (1) limit the AMOUNT of the damages, costs, and expenses for which it indemnifies Landlord to Tenant s limits of liability under its commercial general liability (CGL) policy and (2) limit the TYPE of the damages, costs, and expenses for which it indemnifies Landlord to those which Tenant s CGL policy applies. An example will demonstrate the importance of Tenant limiting the AMOUNT of the damages, costs, and expenses for which it indemnifies Landlord in the lease. Let s refer back to the facts of Hypothetical # 3. Recall that Tenant had $1 million of liability insurance; that Landlord had $10 million of property insurance on the multi story building in which Tenant s premises were located; that the actual damages to the multi story building were $12.5 million; that Landlord s insurance company paid Landlord $10 million; that Landlord sought indemnification from Tenant for Landlord s unreimbursed $2.5 million; and that Tenant (despite having a mutual waiver of subrogation in the lease) faced $1.5 5 Vicarious liability arises from the common law doctrine of agency and holds one party liable for the actions of another party when the first party has the authority, ability, or duty to control the actions of the other party despite the fact that the first party has no active involvement in the activities of the other party. Page 6 of 16

7 million of uninsured, out of pocket expenses (namely, the $2.5 million in indemnification sought by Landlord minus the $1 million of insurance provided by Tenant s CGL policy). Now, however, using the same facts of Hypothetical # 3 but with a properly worded indemnification agreement that limits the amount of damages for which Landlord can seek indemnification from Tenant, Tenant s liability would be capped at $1,000,000, its limit of liability under its CGL, all of which would be paid by Tenant s CGL insurance company. The result is far better for Tenant!! A different example will demonstrate the importance of Tenant limiting the TYPE of the damages, costs, and expenses for which it indemnifies Landlord in the lease. 6 Hypothetical # 4: Shortly after 5:00 PM on Friday, after the Tenant, a manufacturer, ceases business for the week, two of its employees clean several of the large pieces of equipment on the factory floor. After cleaning the equipment, in a rush to begin the weekend, they accidentally spill several gallons of ammonia and various other chemicals outside. Shortly thereafter, local governmental authorities order the Landlord to test the groundwater for ammonia and these other chemicals and to remove and clean up any of these pollutants that have seeped into the groundwater. Landlord s cost to perform such tests and to remove and clean up such pollutants is $1,000,000. Landlord seeks indemnification from Tenant. 7 Unfortunately for Tenant, its CGL policy excludes coverage for this type of environmental claim. However, if Tenant had insisted upon a properly worded indemnification agreement that limits the type of damages for which Landlord can seek indemnification from Tenant, then Tenant would have had no liability since its liability would have been limited to those claims, damages, costs and expenses to which Tenant s commercial general liability policy applies! An example of indemnification provisions which satisfy these four points is attached hereto as Exhibit 6. PROBLEM # 5: In a commercial real estate lease, it is unusual for Tenant to require that Landlord maintain sufficient commercial property insurance on the premises and the building(s) of which the premises are a part. SOLUTION # 5: In the lease, Tenant should include language which requires that Landlord maintain sufficient commercial property insurance on the premises and the building(s) of which the premises are a part. An example of such language is attached hereto as Exhibit 7. 6 One might think that limiting the AMOUNT of the damages, costs and expenses is sufficient, but it is not. Suppose that the monetary cap is $1,000,000. If that indemnification expense is not covered by insurance, then the indemnitor faces a potential uninsured indemnification expense of $1,000,000. The indemnitor needs to make sure that this potential $1,000,000 indemnification expense is covered by its insurance. 7 If Landlord really expects Tenant to indemnify Landlord for environmental claims not covered by Tenant s commercial general liability policy, then Landlord should, in the lease, require Tenant to obtain an appropriate pollution liability policy. Tenant would then have the option of obtaining such policy or of refusing to obtain such policy. Once again, the bargaining power of Landlord and Tenant is key. One way to bridge the possible disagreement between Landlord and Tenant about limiting Tenant s liability in the indemnification provisions would be for Tenant to consider offering to obtain an excess and umbrella liability policy (or offering to increase the limits of its existing excess and umbrella liability policy). Page 7 of 16

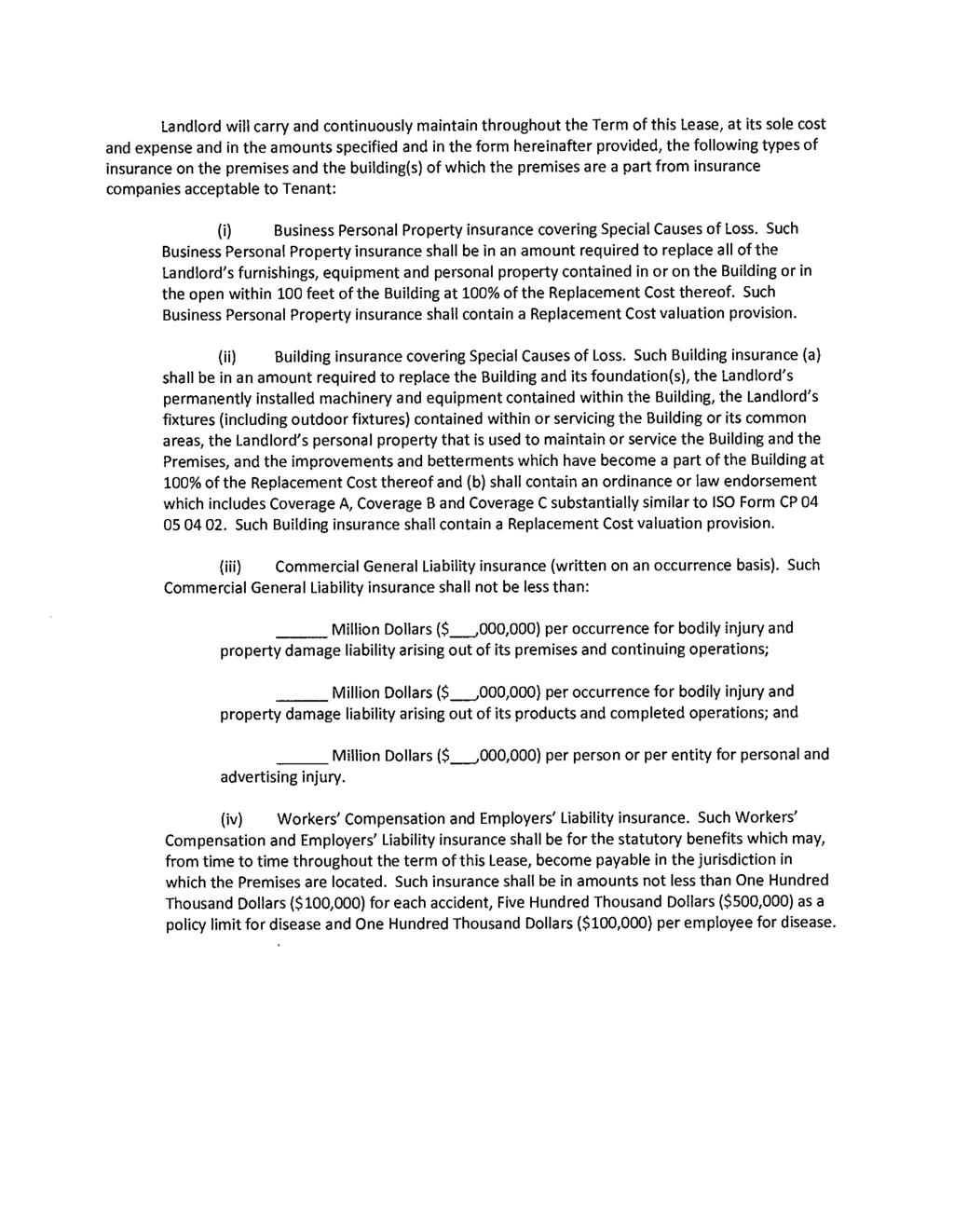

8 There are three reasons why Tenant should require Landlord to maintain such insurance. First, Tenant has a strong interest in making sure that if the premises and/or building(s) are damaged by a covered cause of loss, Landlord has enough insurance proceeds to completely repair and/or replace the premises and/or building(s). The last thing Tenant wants is for Landlord to terminate the lease because Landlord did not have enough insurance proceeds to repair and/or replace the premises (and/or the building(s) of which the premises are a part). Moreover, if Landlord does have sufficient insurance proceeds, Tenant wants Landlord to repair and/or replace the premises (and/or the building(s) of which the premises are a part) as quickly as possible because the longer it takes Landlord to repair or rebuild the premises and/or building(s), the more expensive it becomes for Tenant both in terms of Tenant s lost revenue and the additional expenses that Tenant must incur, whether or not Tenant must temporarily relocate. 8 Second, as Maryland s highest court explained in the Rausch decision (see Exhibit 2 attached hereto), when the lease contains language requiring Landlord to maintain sufficient property insurance, that is strong evidence that Landlord has waived subrogation against Tenant which, as noted above, prevents Landlord s insurance company from seeking reimbursement from Tenant for such insurance company s payment to Landlord. Thus, a provision in the lease requiring Landlord to maintain sufficient property insurance on the premises and/or building(s) is especially important when Landlord refuses to waive subrogation in the lease. Third, by requiring that Landlord maintain sufficient property insurance on the premises and/or building(s), Tenant reduces the probability (a) that Landlord will be underinsured in the event of a covered loss and (b) that Landlord will seek indemnification from Tenant because Landlord was underinsured. For example, recall again Hypothetical # 3 in which Landlord sought indemnification from Tenant for Landlord s unreimbursed $2.5 million and Tenant was faced with $1.5 million of uninsured, out of pocket expenses (equal to the $2.5 million in indemnification sought by Landlord minus the $1 million of insurance provided by Tenant s CGL policy). What if, because of language in the lease which had required Landlord to maintain sufficient property insurance, Landlord had maintained $13 million (rather than $10 million) of insurance on the multi story building? In that case, Landlord s property insurance company would have paid the entire $12.5 million of actual damages and Landlord would not have had any unreimbursed costs or expenses for which it could seek indemnification from Tenant. It is neither surprising nor unusual for Landlords of commercial real estate to be underinsured. Landlords are often underinsured for three reasons. First, the less insurance Landlords have, the less money Landlords pay for insurance (even though Landlords pass their insurance expenses on to their Tenants) 9. Second, to the extent that Landlords believe (or know) that they can successfully seek indemnification from their negligent Tenants who cause damage to the premises and/or building(s), Landlords have less incentive to insure their buildings at 100% of replacement cost. Third, as is 8 Tenant should have time element insurance coverage (business income, extra expense and extended business income) to minimize its financial impact from fire, and any other covered cause of loss, to the premises. 9 Of course, to the extent that Landlords have vacancies in their buildings, Landlords bear that insurance expense themselves. But it is true that the more expensive Landlords insurance is, the greater are the passthroughs to their Tenants and thus, comparatively speaking, the more expensive it becomes for prospective Tenants. Page 8 of 16

9 discussed below in PROBLEM # 9, the most common reason that Landlords are underinsured is because Landlords don t increase their insurance to accurately reflect the costs of the improvements and betterments made for Tenants which have become part of the building(s). PROBLEM # 6: Commercial real estate leases frequently contain Surrender of Premises provisions which impose unacceptable obligations upon Tenant. One common form of a Surrender of Premises provision reads as follows: At the expiration or earlier termination of this lease, Tenant shall peacefully surrender the premises to Landlord, in the same condition as the premises were upon the commencement of the term of this lease, ordinary wear and tear excepted. The problem with the above Surrender of Premises language is that Tenant now becomes obligated to maintain, repair and replace the premises from virtually any cause of loss such as fire, explosion, water, hurricane, burglary, etc. Hypothetical # 5: Suppose that lightning strikes the building in which the premises are located and that the premises suffer severe damage from fire caused by that lightning. Since this sample Surrender of Premises language requires Tenant to surrender the premises in the same condition as the premises were upon commencement of the term of [the] lease, ordinary wear and tear excepted, Tenant must repair and/or rebuild the premises. That is, in effect, what the above Surrender of Premises language says! Moreover, notice that the above sample Surrender of Premises language imposes these obligations upon Tenant even if Tenant were totally without fault as in the lightning strike example of Hypothetical # 5. SOLUTION # 6: Appropriate language must be added to the Surrender of Premises provision which eliminates these obligations from Tenant. Thus, the above sample Surrender of Premises premises should be altered to read as follows: (emphasis added) At the expiration or earlier termination of this lease, Tenant shall peacefully surrender the premises to Landlord, in the same condition as the premises were upon the commencement of the term of this lease, except for (a) ordinary wear and tear, (b) acts of God, (c) fire or (d) any other cause of loss. Tenant receives one additional, and important, benefit when the Surrender of Premises provision is amended to include an exception for fire [and any other cause of loss]. In the Rausch decision, Maryland s highest court ruled that whether a Landlord has waived subrogation against a Tenant for a fire caused by Tenant s negligence depends upon the intent and reasonable expectations of the parties as ascertained from the lease as a whole. The Maryland Court of Page 9 of 16

10 Appeals then noted that the existence of language excepting fire from Tenant s responsibility to return the premises in a good state and condition is indeed evidence that the parties had intended that Landlord waive subrogation against Tenant. Thus, Tenant can, essentially, get Landlord to waive subrogation against Tenant via the Surrender of Premises provision by making sure that the lease contains this additional language excepting fire [and any other cause of loss]. Of course, many Landlords realize this too. Thus, those Landlords which do not want to waive subrogation against Tenant and are aware of this issue will resist adding the fire [and any other cause of loss] language to the Surrender of Premises provision. Therefore, it is not uncommon to see commercial real estate leases (which of course are initially prepared by, or on behalf of, Landlords) completely omit the Surrender of Premises provision. PROBLEM # 7: Commercial real estate leases typically require that Tenant maintains (and, thus implicitly or explicitly, repairs or replaces) various parts of the premises. But Tenant cannot realistically properly insure these parts of the premises. Below is a typical maintenance provision in a commercial real estate lease: Tenant agrees that it will take good care (including repair and/or replacement) of the premises, fixtures, and appurtenances, including exterior doors and windows, window frames, meters, plumbing, heating and air conditioning equipment (including that on the exterior of the premises exclusively serving the premises) and keep the same in good order. Given the above typical maintenance provision, Tenant cannot properly insure the premises or its fixtures, exterior doors and windows, window frames, meters, plumbing, or heating and air conditioning equipment. Why not? The answer is because Tenant does not own any of these items which are (or have become) part of the building, and Tenant does not own the building. As indicated in the language in Section A.1.b. of Exhibit 8 attached hereto, Tenant can insure Tenant s business personal property. But none of the items listed in this typical maintenance provision are Tenant s business personal property. Rather, these items are (or have become) Landlord s building property. The problem is that Tenant has no insurable interest 10 in these building items, and thus no insurance company would pay a claim filed by Tenant for these items. 10 It is a fundamental tenet of insurance that in order to insure something, the person or entity seeking insurance must have an insurable interest in that something. Basically, an insurable interest is a financial interest. Owners of property have financial (or insurable) interests in their property. Lenders have financial (or insurable) interests in the property for which they lend money, at least to the extent to which they have provided such money. Contracts can also create financial (or insurable) interests. Thus, for example, a lessor can require that a lessee insure a particular property. Page 10 of 16

11 Could Tenant properly insure the fixtures, exterior doors and windows, window frames, meters, plumbing, and heating and air conditioning equipment of the premises which Tenant might like to do since the lease s typical maintenance provision requires Tenant to maintain, repair and replace such items? The answer is that it would be necessary to create an insurable interest by Tenant in these items. Creating this insurable interest could be done if Tenant paid for such items, because Tenant s use interest in fixtures, alterations, installations or additions which are (1) a part of the building occupied (but not owned) by Tenant and (2) paid for by Tenant would make such items Tenant s business personal property. (See PROBLEM #9 below for a discussion of the definition of Tenant s improvements and betterments.) However, this is not a realistic approach. 11 SOLUTION # 7A: Tenant can simply agree to maintain (and repair or replace) the premises and its fixtures, exterior doors and windows, window frames, meters, plumbing, and heating and air conditioning equipment without obtaining any insurance on such items. In that event, Tenant should ask Landlord what Landlord thinks it would cost Tenant to repair and/or replace each of such items. Tenant should then include in the lease a provision limiting Tenant s liability for repair and/or replacement of these items to a specific dollar amount. SOLUTION # 7B: It is very important to note that Landlord, in its property insurance policy on the premises and the building(s) of which the premises are a part, is already insuring the premises and its fixtures, exterior doors and windows, window frames, meters, plumbing, and heating and air conditioning equipment! 12 Realizing that fact, in the lease, Tenant could (a) agree to maintain the premises and its fixtures, exterior doors and windows, window frames, meters, plumbing, and heating and air conditioning equipment but (b) NOT to repair or replace any of such items. 13 The only exception to the preceding sentence might be that Tenant could agree to repair and/or replace the fixtures, exterior doors and windows, window frames, meters, plumbing, and heating and air conditioning equipment only if such repair or replacement becomes necessary due to a cause of loss for which insurance would not provide any coverage What Tenant (and Landlord) would agree that Tenant will pay for the premises fixtures, exterior doors and windows, window frames, meters, plumbing, and heating and air conditioning equipment so that Tenant could obtain insurance on such items? Moreover, as PROBLEM #10 below discusses, if a claim for any of these items occurs, Tenant might indeed have difficulty receiving the payment it anticipates from its insurance company for any such claim. The other way, of course, to create an insurable interest by Tenant in these items is for the lease to (contractually) require that Tenant insure the building. For obvious reasons, this is usually not a viable option. 12 This fact is yet another reason why Tenant should insist that the lease include language requiring Landlord to maintain sufficient commercial property insurance on the premises and the building(s) of which the premises are a part. See Solution # 5 above. 13 If Tenant covenants to maintain such items (and Tenant probably is also required by the lease to have an HVAC maintenance agreement with a contractor acceptable to Landlord) and Landlord has sufficient property insurance covering these items, then Landlord is protected. 14 One example in which insurance would not provide coverage is if an item (such as the HVAC system) needs to be repaired or replaced due to ordinary wear and tear. Page 11 of 16

12 Moreover, given the significant cost of repairing or replacing some of these items, Tenant should still include a provision in the lease limiting Tenant s liability for repair and/or replacement of these items to a specific dollar amount. PROBLEM # 8: Commercial real estate leases typically provide that Tenant s insurance company must give Landlord at least 30 days advance written notice before such insurance company cancels or non renews any of Tenant s commercial insurance policies. 15 This requirement is inconsistent with the language of (unendorsed) commercial insurance policies. Below is a sample provision concerning prior written notice of insurance found in leases: All of Tenant s insurance required by this lease shall contain a clause or endorsement prohibiting cancellation or failure to renew without the insurer first giving Landlord thirty (30) days prior written notice of such proposed action (no less than ten (10) days prior written notice for cancellation or failure to renew for nonpayment of premium). Commercial insurance policies provide that insurance companies will mail or deliver to the (first named) insured written notice of cancellation at least (a) 10 days before the effective date of cancellation in cases of nonpayment of premium and (b) 30 days before the effective date of cancellation if cancellation occurs for any other reason. See the language in Section A.2. of Exhibit 9 attached hereto. Moreover, in two circumstances, an insurance company will provide written notice to a person or entity other than the (first named) insured. First, an insurance company will provide written notification to a mortgageholder at least (a) 10 days before the effective date of cancellation in cases of nonpayment of premium; (b) 30 days before the effective date of cancellation if cancellation occurs for any other reason; and (c) 10 days before the expiration date of the policy if the insurance company elects not to renew the policy. See the language in Sections 2.f. and 2.g. of Exhibit 10 attached hereto. Second, an insurance company will give the same advance written notice to a loss payee whose interest as a creditor has been established by a written agreement; provided, however, that the insurance policy has been properly endorsed to include a lender s loss payable clause. 16 See the language in Sections D.1., D.3 and D.4. of Exhibit 11 attached hereto. 15 This 30 day requirement is frequently changed to 10 days for cancellation or non renewal due to Tenant s failure to pay the premium. 16 A lender s loss payable clause is a particular type of loss payable clause which gives the loss payee substantially greater rights than a loss payee receives from a typical loss payable clause. Page 12 of 16

13 Since Landlord is neither a mortgageholder nor a loss payee of Tenant, the standard (unendorsed) commercial insurance policy will not give any notice to Landlord of such insurance company s intent to cancel or non renew Tenant s insurance policy. 17 SOLUTION # 8: The provision in leases which requires Tenant s insurance company to provide prior written notice to Landlord before cancelling or non renewing Tenant s insurance policy should be either (a) amended to comply with the terms of insurance policies or (b) deleted. 18 If amended, the sample provision concerning prior written notice of insurance in leases could read as follows: All of Tenant s insurance required by this lease shall contain a clause or endorsement prohibiting cancellation or failure to renew without the insurer having provided Tenant with at least the number of days of prior written notice required by applicable state law. Tenant covenants and agrees to send any and all of such notices to Landlord within one business day after Tenant s receipt of each such notice. PROBLEM # 9: Commercial real estate leases frequently don t have specific provisions regarding tenant s improvements and betterments (TIB). This silence in leases regarding TIB can create a number of problems, the first of which is: Will Landlord or Tenant pay to insure the TIB? Commercial (property) insurance policies define TIB as the following kind of Business Personal Property : Your [the tenant s] use interest as tenant in improvements and betterments. Improvements and betterments are fixtures, alterations, installations or additions: (a) Made a part of the building or structure you [the tenant] occupy but do not own; and (b) You [the tenant] acquired or made at your expense but cannot legally remove See the language in Section A.1.b.(6) of Exhibit 13 attached hereto. 17 Until September 2009, the insurance industry s standard Certificate of Insurance that was used to provide proof of liability insurance (Acord 25) stated that: Should any of the above described policies be cancelled before the expiration date thereof, the issuing insurer will endeavor to mail days written notice to the certificate holder named to the left, but failure to do so shall impose no obligation or liability of any kind upon the insurer, its agents or representatives. Despite the fact that an insurance company will not provide notice of cancellation or non renewal of Tenant s insurance policy to Landlord, some insurance agents crossed out the words endeavor to when preparing these Certificates of Insurance. In September 2009, Acord revised Form 25 to eliminate this possibility. See the language regarding Cancellation at the bottom of Exhibit 12 attached hereto. 18 Deleting such provision will not have any impact upon either Tenant or Tenant s insurance company because the insurance policy still retains these advance written notice requirements. Moreover, the insurance law in each state mandates a specified number of days of prior written notice to the policyholder in the case of cancellation or non renewal, and these statutory provisions override any inconsistent contractual language. Page 13 of 16

14 Thus, Tenant can insure its TIB. Landlord can also insure TIB in Landlord s commercial property insurance policy as part of the Building. Moreover, even if the improvements and betterments were not paid for by Tenant, in which case such improvements and betterments are not defined as TIB, then Landlord can still insure these improvements and betterments as part of the Building. See the language in Section A.1.a. of Exhibit 14 attached hereto. Hypothetical # 6: Tenant signs a 10 year lease with Landlord. In order to get better financial terms in the lease, Tenant agrees to spend $250,000 on improvements and betterments to the premises. Because Tenant paid for these improvements and betterments, they satisfy the insurance policy s definition of TIB. If Landlord insures these TIB for $250,000, then Landlord would increase the amount of its Building insurance by that amount to reduce/eliminate the possibility that Landlord s insurance company might impose a coinsurance penalty upon Landlord if its property is subsequently damaged by a covered cause of loss, such as fire, leakage of water from the roof, wind, etc. 19 It is important to note that failure by landlords to include the value of TIB (as well as other additions, alterations, improvements and betterments made to Landlords buildings at their own expense which are not technically defined as TIB) in their business insurance policies is the most common reason that coinsurance penalties are imposed upon landlords in the United States. Alternatively, if Tenant insures these TIB for $250,000, then Tenant would increase the amount of its Business Personal Property insurance by that amount to reduce/eliminate the possibility that Tenant s insurance company might impose a coinsurance penalty upon Tenant if its property is subsequently damaged by a covered cause of loss, such as fire, leakage of water from the roof, wind, etc. 20 Landlord would then save money because it would not have to insure this $250,000 of TIB. 21 SOLUTION # 9: If Tenant agrees to pay for improvements and betterments to the premises, then the lease should specify (a) the dollar amount of these TIB and (b) whether Landlord or Tenant will insure these TIB. PROBLEM # 10: Commercial real estate leases frequently don t have specific provisions regarding tenant s improvements and betterments (TIB). This silence in leases regarding TIB can create additional problems, including the following: If Tenant is insuring the TIB and a covered cause of loss such as fire occurs, (a) what happens if the TIB are repaired or replaced and (b) what happens if Landlord terminates the lease because of the fire? 19 In this Hypothetical # 6, if Landlord insures the TIB, then Tenant can reduce the cost of its business insurance by using a specific endorsement, entitled Additional Property Not Covered, to exclude coverage for these $250,000 of TIB. 20 Tenant can reduce its cost of insuring these $250,000 of TIB by using another special endorsement, entitled Your Business Personal Property Separation of Coverage. This special endorsement allows Tenant to reclassify these TIB as Building (rather than Business Personal Property ); this reclassification saves Tenant money because it is cheaper to insure Building than Business Personal Property. 21 There is certainly no reason for both Landlord and Tenant to insure the same TIB for $250,000. Page 14 of 16

15 Hypothetical # 7: Tenant signs a 10 year lease with Landlord. In order to get better financial terms in the lease, Tenant agrees to spend $250,000 on improvements and betterments to the premises. Because Tenant paid for these improvements and betterments, they satisfy the insurance policy s definition of TIB. Throughout the term of the lease, Tenant has maintained $250,000 of insurance on the TIB. Five (5) years into the lease, a fire destroys the building which contains the premises. Now let s look at four different scenarios. Scenario # 1 assume that Tenant promptly replaces the TIB. In this case, per the Tenant s insurance policy, Tenant s insurance company will pay Tenant the replacement cost of the TIB. 22 See the language in Section 7.e.(1) of Exhibit 15 attached hereto. Scenario # 2 assume that Landlord rebuilds the premises (or the building containing the premises), which includes replacing the TIB. In this case, per the Tenant s insurance policy, Tenant s insurance company will pay Tenant nothing for the TIB since Tenant did not pay for the replacement of the TIB. See the language in Section 7.e.(3) of Exhibit 16 attached hereto. Scenario # 3 assume that Tenant replaces the TIB but not promptly. In this case, per the Tenant s insurance policy, Tenant s insurance company will pay Tenant $125,000, or one half of its $250,000 original cost of the TIB, because, at the time of the fire, one half of the lease term (or 5 years of the 10 year term of the lease), had elapsed since the TIB were originally installed. See the language in Section 7.e.(2) of Exhibit 17 attached hereto. Scenario # 4 assume that Landlord terminates the lease. In this case as in Scenario #3 per the Tenant s insurance policy, Tenant s insurance company will pay Tenant $125,000, or one half of its $250,000 original cost of the TIB, because, at the time of the fire, one half of the lease term had elapsed since the TIB were originally installed. 23 See the language in Section 7.e.(2) of Exhibit 17 attached hereto. Tenant might not be happy to receive only $125,000 in Scenario #3 or Scenario #4. Tenant might argue that it should receive $250,000 since (a) it paid $250,000 for the TIB five years ago and (b) it has consistently been paying insurance premiums for $250,000 of TIB for five years. Despite Tenant s possible objections, it is fair that Tenant receives only $125,000 in Scenario #3 or Scenario #4. It is fair because Tenant was insured on a worst case basis; thus, if the fire had destroyed the premises one day (rather than 5 years) after the TIB had been installed, Tenant would have received the entire $250,000 from its insurance company. 22 This result assumes that Tenant has chosen the replacement cost option. Alternatively, if Tenant has not chosen the replacement cost option, then Tenant would receive the actual cash value of the TIB, which equals replacement cost minus depreciation. Note that Tenant cannot promptly replace the TIB if Landlord does not promptly replace the remainder of the premises (or the building that contains the premises). Thus, Tenant would be wise add a provision in the lease requiring Landlord, after the loss, to promptly repair or replace the premises if Landlord decides not to terminate the lease. 23 To protect its investment in the TIB from cancellation of the lease by Landlord after a fire or other covered cause of loss, Tenant can, if it so desires, purchase another insurance policy. This other insurance policy is called a Leasehold Interest Coverage Policy and is attached hereto as Exhibit 18. Significantly, the Leasehold Interest Coverage Policy will provide coverage for Tenant s TIB if Landlord cancels the lease as a result of a fire or other covered cause of loss when the premises are damaged and also when the premises are not damaged but the building(s) which includes the premises is (are) damaged. Page 15 of 16

16 SOLUTION # 10: Before Tenant can make an informed business decision about whether to pay for, and whether to insure, its proposed improvements and betterments to the premises, Tenant must be told how its insurance policies would respond in a variety of scenarios. Only then can appropriate provisions regarding improvements and betterments be included in the lease provisions which will reduce uncertainty and will reflect the terms of the business transaction between Landlord and Tenant. Page 16 of 16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

INSURANCE AND INDEMNIFICATION MANUAL. Supplement to Policy 560 i

INSURANCE AND INDEMNIFICATION MANUAL Supplement to Policy 560 Table of Contents.1 INTRODUCTION... 1.2 EXHIBIT I INSURANCE AND INDEMNITY REQUIREMENTS FOR CONSTRUCTION AND SERVICE CONTRACTS... 1 2.1 INDEMNIFICATION/HOLD

INSURANCE AND INDEMNIFICATION MANUAL Supplement to Policy 560 Table of Contents.1 INTRODUCTION... 1.2 EXHIBIT I INSURANCE AND INDEMNITY REQUIREMENTS FOR CONSTRUCTION AND SERVICE CONTRACTS... 1 2.1 INDEMNIFICATION/HOLD

CAMBRIDGE PROPERTY & CASUALTY SPECIAL REPORT

CAMBRIDGE PROPERTY & CASUALTY SPECIAL REPORT DEFECTIVE TENANT LEASE PROVISIONS CAN DESTROY A TENANT S BUSINESS IN THE EVENT OF DAMAGE OR DESTRUCTION OF A LANDLORD S BUILDING This Special Report was written

CAMBRIDGE PROPERTY & CASUALTY SPECIAL REPORT DEFECTIVE TENANT LEASE PROVISIONS CAN DESTROY A TENANT S BUSINESS IN THE EVENT OF DAMAGE OR DESTRUCTION OF A LANDLORD S BUILDING This Special Report was written

Lease Agreement Between ANNE ARUNDEL COUNTY, MARYLAND and. Dated TABLE OF CONTENTS. Paragraph

Lease Agreement Between ANNE ARUNDEL COUNTY, MARYLAND and Dated TABLE OF CONTENTS Paragraph 1. Premises 2. Term 3. Rent 4. Assignment 5. Use of Leased Property 6. Permits 7. Tenant Improvements 8. Taxes

Lease Agreement Between ANNE ARUNDEL COUNTY, MARYLAND and Dated TABLE OF CONTENTS Paragraph 1. Premises 2. Term 3. Rent 4. Assignment 5. Use of Leased Property 6. Permits 7. Tenant Improvements 8. Taxes

Presenting a live 90-minute webinar with interactive Q&A. Today s faculty features: Scott D. Brooks, Partner, Cox Castle & Nicholson, San Francisco

Presenting a live 90-minute webinar with interactive Q&A Allocating Risk in Real Estate Leases: Contractual Indemnities, Additional Insured Endorsements, Subrogation Waivers Coordinating Lease Provisions

Presenting a live 90-minute webinar with interactive Q&A Allocating Risk in Real Estate Leases: Contractual Indemnities, Additional Insured Endorsements, Subrogation Waivers Coordinating Lease Provisions

YUCAIPA BUSINESS INCUBATOR CENTER LEASE AGREEMENT

YUCAIPA BUSINESS INCUBATOR CENTER LEASE AGREEMENT THIS YUCAIPA BUSINESS INCUBATOR CENTER LEASE AGREEMENT (this Agreement ) is dated as of the, 20 and is entered into by and between the CITY of YUCAIPA

YUCAIPA BUSINESS INCUBATOR CENTER LEASE AGREEMENT THIS YUCAIPA BUSINESS INCUBATOR CENTER LEASE AGREEMENT (this Agreement ) is dated as of the, 20 and is entered into by and between the CITY of YUCAIPA

APPENDIX B WASHINGTON SUBURBAN SANITARY COMMISSION PROCUREMENT OFFICE INSURANCE AND BONDING CONTRACT NO.

APPENDIX B WASHINGTON SUBURBAN SANITARY COMMISSION PROCUREMENT OFFICE INSURANCE AND BONDING CONTRACT NO. 1. INSURANCE REQUIREMENTS A. INSURANCE: The Contractor shall be required to maintain insurance for

APPENDIX B WASHINGTON SUBURBAN SANITARY COMMISSION PROCUREMENT OFFICE INSURANCE AND BONDING CONTRACT NO. 1. INSURANCE REQUIREMENTS A. INSURANCE: The Contractor shall be required to maintain insurance for

INSURANCE REQUIREMENTS FOR CONSTRUCTION PROJECTS Effective Date: April 23, 2018

INSURANCE REQUIREMENTS FOR CONSTRUCTION PROJECTS Effective Date: April 23, 2018 The contract documents for each construction project will identify the standard specifications to be used for that specific

INSURANCE REQUIREMENTS FOR CONSTRUCTION PROJECTS Effective Date: April 23, 2018 The contract documents for each construction project will identify the standard specifications to be used for that specific

The Role of the Certificate

Catherine Trischan, CPCU, CRM, CIC, ARM, AU, AAI, CRIS, MLIS The Role of the Certificate Informational Does it change the policy? Disclaimer language 1 Certificate Holder Expectations I will get an accurate

Catherine Trischan, CPCU, CRM, CIC, ARM, AU, AAI, CRIS, MLIS The Role of the Certificate Informational Does it change the policy? Disclaimer language 1 Certificate Holder Expectations I will get an accurate

TERREBONNE PARISH CONSOLIDATED GOVERNMENT INSURANCE REQUIREMENTS CONTRACTORS

TERREBONNE PARISH CONSOLIDATED GOVERNMENT INSURANCE REQUIREMENTS CONTRACTORS ARTICLE 5- Bonds and Insurance 5.1 PERFORMANCE AND OTHER BONDS: 5.1.1 CONTRACTOR shall furnish performance and payment Bonds,

TERREBONNE PARISH CONSOLIDATED GOVERNMENT INSURANCE REQUIREMENTS CONTRACTORS ARTICLE 5- Bonds and Insurance 5.1 PERFORMANCE AND OTHER BONDS: 5.1.1 CONTRACTOR shall furnish performance and payment Bonds,

REQUIRED AT PROPOSAL STAGE:

DATE: February 13, 2019 SUBJECT: ADDENDUM #1-2401 E. PACIFIC COAST HIGHWAY WILMINGTON, CA 90744 The Port of Los Angeles 2401 E. Pacific Coast Highway Wilmington, CA 90744 Request for Lease Proposals Exhibit

DATE: February 13, 2019 SUBJECT: ADDENDUM #1-2401 E. PACIFIC COAST HIGHWAY WILMINGTON, CA 90744 The Port of Los Angeles 2401 E. Pacific Coast Highway Wilmington, CA 90744 Request for Lease Proposals Exhibit

ICSC CANADIAN SHOPPING CENTRE LAW CONFERENCE APRIL 30, 2018 PLENARY SESSION INSURANCE 101 DEBORAH A. WATKINS. and BRIAN PARKER DAOUST VUKOVICH LLP

ICSC CANADIAN SHOPPING CENTRE LAW CONFERENCE APRIL 30, 2018 PLENARY SESSION INSURANCE 101 BY DEBORAH A. WATKINS and BRIAN PARKER OF DAOUST VUKOVICH LLP 20 Queen Street West, Suite 3000, Toronto, Ontario

ICSC CANADIAN SHOPPING CENTRE LAW CONFERENCE APRIL 30, 2018 PLENARY SESSION INSURANCE 101 BY DEBORAH A. WATKINS and BRIAN PARKER OF DAOUST VUKOVICH LLP 20 Queen Street West, Suite 3000, Toronto, Ontario

2010 INSURANCE MANUAL

2010 INSURANCE MANUAL All required insurance shall be in a form, amount, content and written by companies acceptable to the Georgia Department of Community Affairs (DCA). For identification purposes, all

2010 INSURANCE MANUAL All required insurance shall be in a form, amount, content and written by companies acceptable to the Georgia Department of Community Affairs (DCA). For identification purposes, all

Selected Insurance Issues in Commercial Real Estate Transactions Understanding the Nuances

Selected Insurance Issues in Commercial Real Estate Transactions Understanding the Nuances Richard A. Fineman, Esquire and Andrew H. Wagner, MBA What is Insurance? Insurance is the transfer of risk via

Selected Insurance Issues in Commercial Real Estate Transactions Understanding the Nuances Richard A. Fineman, Esquire and Andrew H. Wagner, MBA What is Insurance? Insurance is the transfer of risk via

5.0 TERREBONNE PARISH CONSOLIDATED GOVERNMENT, DEFINED.

ARTICLE 5 - Bonds and Insurance 5.0 TERREBONNE PARISH CONSOLIDATED GOVERNMENT, DEFINED. For the purposes of this Article, the terms Terrebonne Parish Consolidated Government, TPCG, and OWNER shall include,

ARTICLE 5 - Bonds and Insurance 5.0 TERREBONNE PARISH CONSOLIDATED GOVERNMENT, DEFINED. For the purposes of this Article, the terms Terrebonne Parish Consolidated Government, TPCG, and OWNER shall include,

ADM.21 INSURANCE AND INDEMNITY REQUIREMENTS FOR CONTRACTS

ADM.21 INSURANCE AND INDEMNITY REQUIREMENTS FOR CONTRACTS Washington Cities Insurance Authority PO Box 88030 Tukwila, WA 98138 (206) 575-6046 TABLE OF CONTENTS Insurance and Indemnity Requirements for

ADM.21 INSURANCE AND INDEMNITY REQUIREMENTS FOR CONTRACTS Washington Cities Insurance Authority PO Box 88030 Tukwila, WA 98138 (206) 575-6046 TABLE OF CONTENTS Insurance and Indemnity Requirements for

TRENTON AGRI PRODUCTS LLC INSURANCE & INDEMNIFICATION TERMS & CONDITIONS

TRENTON AGRI PRODUCTS LLC INSURANCE & INDEMNIFICATION TERMS & CONDITIONS These Insurance & Indemnification Terms & Conditions ( Terms ) are hereby incorporated in and made a part of each and every written

TRENTON AGRI PRODUCTS LLC INSURANCE & INDEMNIFICATION TERMS & CONDITIONS These Insurance & Indemnification Terms & Conditions ( Terms ) are hereby incorporated in and made a part of each and every written

LEASE AGREEMENT THE GREAT PLAINS BUSINESS DEVELOPMENT CENTER

LEASE AGREEMENT THE GREAT PLAINS BUSINESS DEVELOPMENT CENTER The Great Plains Technology Center (GPTC) welcomes you to The Great Plains Business Development Center (GPBDC). GPTC accepts into the Business

LEASE AGREEMENT THE GREAT PLAINS BUSINESS DEVELOPMENT CENTER The Great Plains Technology Center (GPTC) welcomes you to The Great Plains Business Development Center (GPBDC). GPTC accepts into the Business

SUBCONTRACT CONSTRUCTION AGREEMENT

SUBCONTRACT CONSTRUCTION AGREEMENT THIS SUBCONTRACT CONSTRUCTION AGREEMENT, made and executed this day of, 20, by and between SHERWOOD CONSTRUCTION, INC (hereinafter referred to as "Contractor"), and (hereinafter

SUBCONTRACT CONSTRUCTION AGREEMENT THIS SUBCONTRACT CONSTRUCTION AGREEMENT, made and executed this day of, 20, by and between SHERWOOD CONSTRUCTION, INC (hereinafter referred to as "Contractor"), and (hereinafter

PIERCE COUNTY AIRPORT THUN FIELD rd Avenue Ct. E Puyallup, WA (253)

") PIERCE COUNTY AIRPORT THUN FIELD 16915 103 rd Avenue Ct. E Puyallup, WA 98374 (253)798 7800 AIRCRAFT HANGAR / TIE DOWN AGREEMENT TENANT INFORMATION Name: Business Name: Address: City: State: Zip Code:

PIERCE COUNTY AIRPORT THUN FIELD 16915 103 rd Avenue Ct. E Puyallup, WA 98374 (253)798 7800 AIRCRAFT HANGAR / TIE DOWN AGREEMENT TENANT INFORMATION Name: Business Name: Address: City: State: Zip Code:

ADDENDUM TO STANDARD FORM OF AGREEMENT BETWEEN OWNER AND CONTRACTOR FOR A RESIDENTIAL OR SMALL COMMERCIAL PROJECT AIA DOCUMENT A

ADDENDUM TO STANDARD FORM OF AGREEMENT BETWEEN OWNER AND CONTRACTOR FOR A RESIDENTIAL OR SMALL COMMERCIAL PROJECT AIA DOCUMENT A105-2007 The following addendum modifies or supplements the standard form

ADDENDUM TO STANDARD FORM OF AGREEMENT BETWEEN OWNER AND CONTRACTOR FOR A RESIDENTIAL OR SMALL COMMERCIAL PROJECT AIA DOCUMENT A105-2007 The following addendum modifies or supplements the standard form

INDEPENDENT CONTRACTOR AGREEMENT

INDEPENDENT CONTRACTOR AGREEMENT WHEREAS Dixie Electric Membership Corporation (hereinafter DEMCO ) is a nonprofit electric membership cooperative authorized to do and doing business in the State of Louisiana;

INDEPENDENT CONTRACTOR AGREEMENT WHEREAS Dixie Electric Membership Corporation (hereinafter DEMCO ) is a nonprofit electric membership cooperative authorized to do and doing business in the State of Louisiana;

Lease Agreement between Napa Valley Community College District and Napa Valley Unified School District

Lease Agreement between Napa Valley Community College District and Napa Valley Unified School District This Agreement and Lease is entered into this 12th day of March 2015 between the Napa Valley Community

Lease Agreement between Napa Valley Community College District and Napa Valley Unified School District This Agreement and Lease is entered into this 12th day of March 2015 between the Napa Valley Community

CONTRACTUAL RISK TRANSFER SPONSORED BY

CONTRACTUAL RISK TRANSFER SPONSORED BY Slide 1 Contractual Risk Transfer November 8, 2013 Bruce Thomas, CIC, CPCU, CRIS Slide 2 Exposure Manager 5 Steps 5. Monitor account 4. Implement technique 3. Select

CONTRACTUAL RISK TRANSFER SPONSORED BY Slide 1 Contractual Risk Transfer November 8, 2013 Bruce Thomas, CIC, CPCU, CRIS Slide 2 Exposure Manager 5 Steps 5. Monitor account 4. Implement technique 3. Select

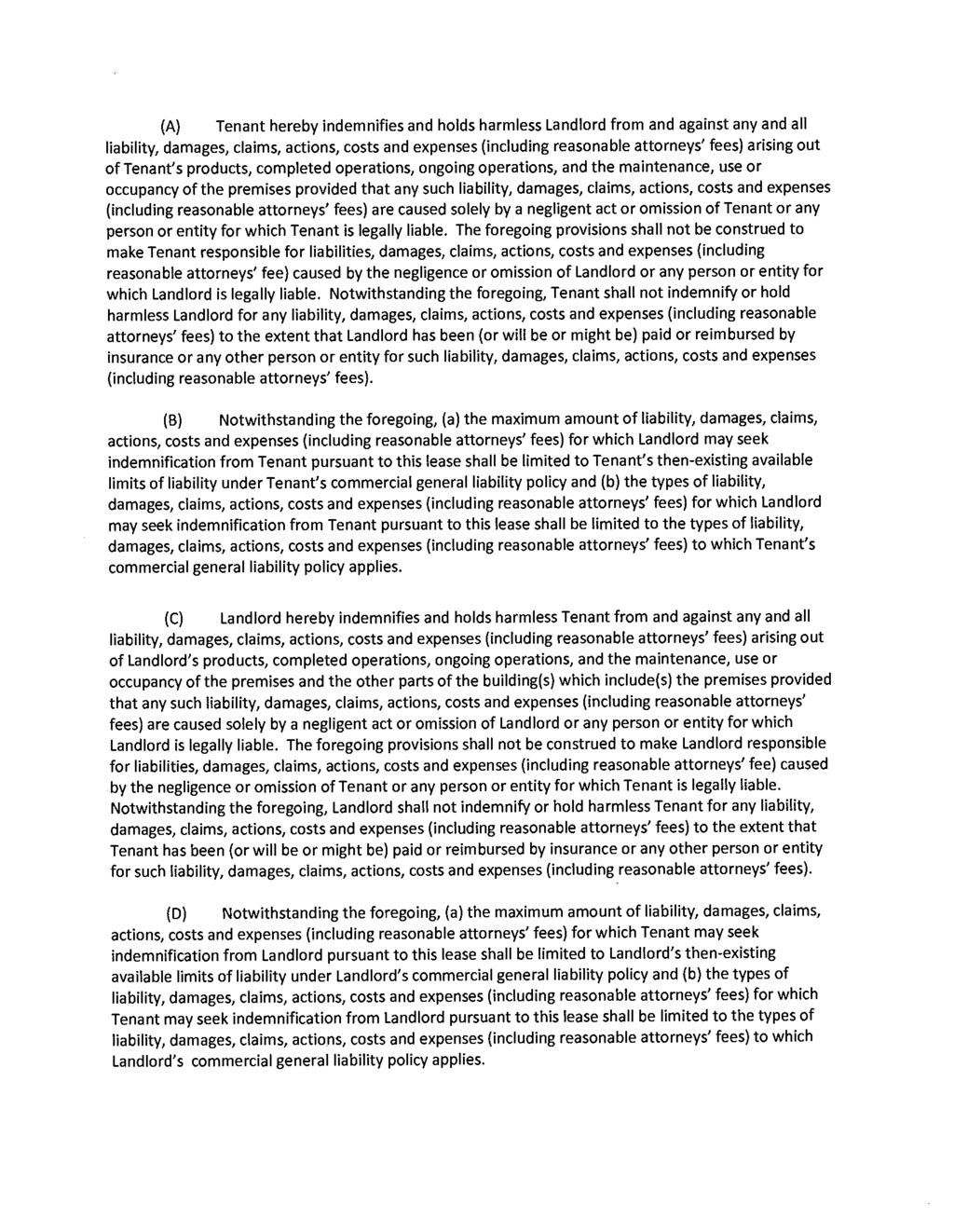

responsibility of Tenant and/or Construction Contractors or Construction Subcontractors to pay.

responsibility of Tenant and/or Construction Contractors or Construction Subcontractors to pay. (h) Primary Coverage. For claims arising out of or relating to work on the Specific Project, Tenant s insurance

responsibility of Tenant and/or Construction Contractors or Construction Subcontractors to pay. (h) Primary Coverage. For claims arising out of or relating to work on the Specific Project, Tenant s insurance

Insurance Applica on & Proposal

Business Insurance Property Owners Insurance Applica on & Proposal Intermediary Interim Cover. The Proposer Insured Name Business / Trading Name Are you registered for GST purposes? What is your ABN? Postal

Business Insurance Property Owners Insurance Applica on & Proposal Intermediary Interim Cover. The Proposer Insured Name Business / Trading Name Are you registered for GST purposes? What is your ABN? Postal

INSURANCE PROVISIONS AND CASUALTY LOSSES

Presented: 2017 Bernard O. Dow Leasing Institute Houston, Texas November 10, 2017 South Texas School of Law INSURANCE PROVISIONS AND CASUALTY LOSSES Aaron Johnston, Jr. Author contact information: Aaron

Presented: 2017 Bernard O. Dow Leasing Institute Houston, Texas November 10, 2017 South Texas School of Law INSURANCE PROVISIONS AND CASUALTY LOSSES Aaron Johnston, Jr. Author contact information: Aaron

EDUCATION AND ADVANCED EDUCATION (PUBLIC SCHOOL DISTRICTS AND PUBLIC POST SECONDARY INSTITUTIONS) OWNER INSURED CONSTRUCTION PROJECTS

OWNER INSURED CONSTRUCTION PROJECTS") EDUCATION AND ADVANCED EDUCATION (PUBLIC SCHOOL DISTRICTS AND PUBLIC POST SECONDARY INSTITUTIONS) OWNER INSURED CONSTRUCTION PROJECTS Indemnification and Insurance Clauses (to be included in Supplementary

EDUCATION AND ADVANCED EDUCATION (PUBLIC SCHOOL DISTRICTS AND PUBLIC POST SECONDARY INSTITUTIONS) OWNER INSURED CONSTRUCTION PROJECTS Indemnification and Insurance Clauses (to be included in Supplementary

The Laundromat Lease Trap By Larry Trapani President-Brooks Waterburn Corp.

The Laundromat Lease Trap By Larry Trapani President-Brooks Waterburn Corp. Our agency specializes in Laundromat Insurance. We protect over 1,000 Laundromats nationwide. A vast majority of those are leased

The Laundromat Lease Trap By Larry Trapani President-Brooks Waterburn Corp. Our agency specializes in Laundromat Insurance. We protect over 1,000 Laundromats nationwide. A vast majority of those are leased

Insurance Issues in Commercial Leasing Albert L. Sica, Esq.

Insurance Issues in Commercial Leasing by Albert L. Sica, Esq. The ALS Group Edison, New Jersey 177 178 Insurance Issues in Commercial Leasing Presented by: Albert L. Sica Managing Principal The ALS Group

Insurance Issues in Commercial Leasing by Albert L. Sica, Esq. The ALS Group Edison, New Jersey 177 178 Insurance Issues in Commercial Leasing Presented by: Albert L. Sica Managing Principal The ALS Group

MASTER PURCHASE AGREEMENT (For Sale of Non-Potable Fresh or Salt Water)

") MASTER PURCHASE AGREEMENT (For Sale of Non-Potable Fresh or Salt Water) THIS MASTER PURCHASE AGREEMENT (this Agreement ) is made and entered into this day of, 201 (the Effective Date ), by and between

MASTER PURCHASE AGREEMENT (For Sale of Non-Potable Fresh or Salt Water) THIS MASTER PURCHASE AGREEMENT (this Agreement ) is made and entered into this day of, 201 (the Effective Date ), by and between

AGREEMENT BY AND BETWEEN ROCKLIN UNIFIED SCHOOL DISTRICT AND ROCKLIN EDUCATIONAL EXCELLENCE FOUNDATION RECITALS

AGREEMENT BY AND BETWEEN ROCKLIN UNIFIED SCHOOL DISTRICT AND ROCKLIN EDUCATIONAL EXCELLENCE FOUNDATION This agreement ("Agreement") is made by and between Rocklin Unified School District, a public school

AGREEMENT BY AND BETWEEN ROCKLIN UNIFIED SCHOOL DISTRICT AND ROCKLIN EDUCATIONAL EXCELLENCE FOUNDATION This agreement ("Agreement") is made by and between Rocklin Unified School District, a public school

INDEMNITIES AND INSURANCE: ARE YOU COVERED?

INDEMNITIES AND INSURANCE: ARE YOU COVERED? ABA Section of Real Property, Trust & Estate Law Leasing Group Conference Call March 4, 2010 Jon F. ( Chip ) Leyens, Jr. (jleyens@steeglaw.com) Steeg Law Firm,

INDEMNITIES AND INSURANCE: ARE YOU COVERED? ABA Section of Real Property, Trust & Estate Law Leasing Group Conference Call March 4, 2010 Jon F. ( Chip ) Leyens, Jr. (jleyens@steeglaw.com) Steeg Law Firm,

MANUFACTURERS AND WHOLESALERS XTEND ENDORSEMENT

Page 1 of 7 CG D1 87 11 03 THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY. MANUFACTURERS AND WHOLESALERS XTEND ENDORSEMENT This endorsement modifies insurance provided under the following:

Page 1 of 7 CG D1 87 11 03 THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY. MANUFACTURERS AND WHOLESALERS XTEND ENDORSEMENT This endorsement modifies insurance provided under the following:

General Liability: Mind the (Potential) Gap. Gallagher Casualty Practice

Gap. Gallagher Casualty Practice") General Liability: Mind the (Potential) Gap Gallagher Casualty Practice JUNE 2016 The ISO general liability coverage form has changed many times over the years, but many of the terms have remained standard.

General Liability: Mind the (Potential) Gap Gallagher Casualty Practice JUNE 2016 The ISO general liability coverage form has changed many times over the years, but many of the terms have remained standard.

CASTAIC LAKE WATER AGENCY STANDARD CONTRACT RISK TRANSFER PROVISIONS, GENERAL CONDITIONS and REQUIRED INSURANCE for

CASTAIC LAKE WATER AGENCY STANDARD CONTRACT RISK TRANSFER PROVISIONS, GENERAL CONDITIONS and REQUIRED INSURANCE for SMALL CONSTRUCTION CONTRACT Typical CLWA services that would use Small Contracts with

CASTAIC LAKE WATER AGENCY STANDARD CONTRACT RISK TRANSFER PROVISIONS, GENERAL CONDITIONS and REQUIRED INSURANCE for SMALL CONSTRUCTION CONTRACT Typical CLWA services that would use Small Contracts with

Hinds Community College Facilities Use Agreement

Hinds Community College Facilities Use Agreement This agreement is made and entered into on, between Hinds Community College (HCC) and (Renter) having an address at for Renter s use of specific facilities

Hinds Community College Facilities Use Agreement This agreement is made and entered into on, between Hinds Community College (HCC) and (Renter) having an address at for Renter s use of specific facilities

DEMYSTIFYING INSURANCE

DEMYSTIFYING INSURANCE FOR COMMUNITY ORGANISATIONS Presented By Mark Fredericks & Brendon Durrant of Insurewest Pty Ltd General Advice Warning This advice does not take into account any of your particular

DEMYSTIFYING INSURANCE FOR COMMUNITY ORGANISATIONS Presented By Mark Fredericks & Brendon Durrant of Insurewest Pty Ltd General Advice Warning This advice does not take into account any of your particular

UNDERSTANDING WAIVERS OF SUBROGATION By Gary L. Wickert, Mohr & Anderson, S.C., Hartford, WI

UNDERSTANDING WAIVERS OF SUBROGATION By Gary L. Wickert, Mohr & Anderson, S.C., Hartford, WI Waivers of Subrogation are a necessary evil of underwriting, but their application and effect on subrogation

UNDERSTANDING WAIVERS OF SUBROGATION By Gary L. Wickert, Mohr & Anderson, S.C., Hartford, WI Waivers of Subrogation are a necessary evil of underwriting, but their application and effect on subrogation

IIAT Job Applicant Technical Test

Instructions How to use this test This test is designed to help member agents assess job applicants technical insurance knowledge. It is one of many tools that can be used to determine which candidate

Instructions How to use this test This test is designed to help member agents assess job applicants technical insurance knowledge. It is one of many tools that can be used to determine which candidate

GOLF COURSE FOOD AND BEVERAGE CONCESSION AGREEMENT

GOLF COURSE FOOD AND BEVERAGE CONCESSION AGREEMENT 1. Parties. This agreement is made and entered into between, Canyon Lake Chophouse, a South Dakota corporation, of 2720 Chapel Lane, Rapid City, SD 57702

GOLF COURSE FOOD AND BEVERAGE CONCESSION AGREEMENT 1. Parties. This agreement is made and entered into between, Canyon Lake Chophouse, a South Dakota corporation, of 2720 Chapel Lane, Rapid City, SD 57702

PROPERTY MANAGEMENT AGREEMENT

PROPERTY MANAGEMENT AGREEMENT Owner: Manager: Bridge Management LLC, 3077 Merriam Lane Kansas City, KS Property(ies): THIS PROPERTY MANAGEMENT AGREEMENT ( Agreement ) is made this day of _, 20 by and between

PROPERTY MANAGEMENT AGREEMENT Owner: Manager: Bridge Management LLC, 3077 Merriam Lane Kansas City, KS Property(ies): THIS PROPERTY MANAGEMENT AGREEMENT ( Agreement ) is made this day of _, 20 by and between

THE STATE OF TEXAS Landscape Maintenance and Use Agreement COUNTY OF TARRANT

THE STATE OF TEXAS Landscape Maintenance and Use Agreement COUNTY OF TARRANT THIS LANDSCAPE MAINTENANCE AND USE AGREEMENT (hereinafter referred to as "Agreement") is made and entered into on this day of,

THE STATE OF TEXAS Landscape Maintenance and Use Agreement COUNTY OF TARRANT THIS LANDSCAPE MAINTENANCE AND USE AGREEMENT (hereinafter referred to as "Agreement") is made and entered into on this day of,

Wednesday, October 24, :30 4:45 PM. Peer to Peer 1

Wednesday, October 24, 2018 3:30 4:45 PM Peer to Peer 1 Subject to Review by Risk Management : Earn Confidence in Your Ability to Review Insurance and Indemnity Provisions Abe Freeland Executive Vice President

Wednesday, October 24, 2018 3:30 4:45 PM Peer to Peer 1 Subject to Review by Risk Management : Earn Confidence in Your Ability to Review Insurance and Indemnity Provisions Abe Freeland Executive Vice President

Consumer General Collateral Mortgage Standard Charge Terms Land Registration Reform Act

Page 1 of 20 Consumer General Collateral Mortgage Standard Charge Terms Land Registration Reform Act Filed By: Canadian Imperial Bank of Commerce Filing Number: 200816 Filing Date: August 8, 2008 The following

Page 1 of 20 Consumer General Collateral Mortgage Standard Charge Terms Land Registration Reform Act Filed By: Canadian Imperial Bank of Commerce Filing Number: 200816 Filing Date: August 8, 2008 The following

Town of Highlands Board Approved as of May 17, 2012

TOWN OF HIGHLANDS INTERCONNECTION AGREEMENT FOR SMALL PHOTOVOLTAIC GENERATION FACILITY OF 10 kw OR LESS This PHOTOVOLTAIC INTERCONNECTION AGREEMENT FOR SMALL GENERATION 10 kw or less (the Agreement ),

TOWN OF HIGHLANDS INTERCONNECTION AGREEMENT FOR SMALL PHOTOVOLTAIC GENERATION FACILITY OF 10 kw OR LESS This PHOTOVOLTAIC INTERCONNECTION AGREEMENT FOR SMALL GENERATION 10 kw or less (the Agreement ),

Debbie Sines Crockett CHEFFY PASSIDOMO ATTORNEYS AT LAW Tampa & Naples, Florida

2017 Risk Management Conference Airport Council International North America Friday, January 13, 2017 Debbie Sines Crockett DSCrockett@NaplesLaw.com CHEFFY PASSIDOMO ATTORNEYS AT LAW Tampa & Naples, Florida

2017 Risk Management Conference Airport Council International North America Friday, January 13, 2017 Debbie Sines Crockett DSCrockett@NaplesLaw.com CHEFFY PASSIDOMO ATTORNEYS AT LAW Tampa & Naples, Florida

RICE UNIVERSITY SHORT FORM CONTRACT

RICE UNIVERSITY SHORT FORM CONTRACT This Rice University Short Form Contract (this Contract ) is entered into by and between WILLIAM MARSH RICE UNIVERSITY, a Texas non-profit corporation (the University

RICE UNIVERSITY SHORT FORM CONTRACT This Rice University Short Form Contract (this Contract ) is entered into by and between WILLIAM MARSH RICE UNIVERSITY, a Texas non-profit corporation (the University

This Rental Agreement is subject to the Terms and Conditions set forth on Appendix A

RENTAL SPACE AGREEMENT This Rental Agreement is subject to the Terms and Conditions set forth on Appendix A attached hereto which is incorporated by reference herein. Appendix A TERMS AND CONDITIONS 1.

RENTAL SPACE AGREEMENT This Rental Agreement is subject to the Terms and Conditions set forth on Appendix A attached hereto which is incorporated by reference herein. Appendix A TERMS AND CONDITIONS 1.

INDEMNITY AGREEMENTS. Benefits and Pitfalls. Clayton Hill Arthur J. Gallagher Risk Management Services Inc.

INDEMNITY AGREEMENTS Benefits and Pitfalls Clayton Hill Arthur J. Gallagher Risk Management Services Inc. What Is Indemnity? Indemnity is holding someone harmless for something. Two types of indemnity

INDEMNITY AGREEMENTS Benefits and Pitfalls Clayton Hill Arthur J. Gallagher Risk Management Services Inc. What Is Indemnity? Indemnity is holding someone harmless for something. Two types of indemnity

SERVICES LEASE AGREEMENT

SERVICES LEASE AGREEMENT This Services Lease Agreement ( Agreement ), which becomes effective upon all parties signing, is between Maryland Public Television ( MPT ), an agency of the State of Maryland

SERVICES LEASE AGREEMENT This Services Lease Agreement ( Agreement ), which becomes effective upon all parties signing, is between Maryland Public Television ( MPT ), an agency of the State of Maryland

BUILDERS RISK COVERAGE FORM

BUILDERS RISK COVERAGE FORM COMMERCIAL PROPERTY CP 00 20 06 07 Various provisions in this policy restrict coverage. Read the entire policy carefully to determine rights, duties and what is and is not covered.

BUILDERS RISK COVERAGE FORM COMMERCIAL PROPERTY CP 00 20 06 07 Various provisions in this policy restrict coverage. Read the entire policy carefully to determine rights, duties and what is and is not covered.

Allocating Risk in Real Estate Leases: Contractual Indemnities, Additional Insured Endorsements and Waivers of Subrogation

Presenting a live 90-minute webinar with interactive Q&A Allocating Risk in Real Estate Leases: Contractual Indemnities, Additional Insured Endorsements and Waivers of Subrogation Structuring Lease Provisions

Presenting a live 90-minute webinar with interactive Q&A Allocating Risk in Real Estate Leases: Contractual Indemnities, Additional Insured Endorsements and Waivers of Subrogation Structuring Lease Provisions

Lease Agreement Maintenance and Repair of the Playing Fields.

Lease Agreement This Lease is made this 24 th day of June, 2013, by and between the Brecksville- Broadview Heights Board of Education, ( Landlord ) with a notice address of 6638 Mill Road, Brecksville,

Lease Agreement This Lease is made this 24 th day of June, 2013, by and between the Brecksville- Broadview Heights Board of Education, ( Landlord ) with a notice address of 6638 Mill Road, Brecksville,

Consumer General Collateral Mortgage Standard Mortgage Terms

Consumer General Collateral Mortgage Standard Mortgage Terms Filed By: Canadian Imperial Bank of Commerce Filing Number: MT080113 Filing Date: August 1, 2008 The following set of standard mortgage terms

Consumer General Collateral Mortgage Standard Mortgage Terms Filed By: Canadian Imperial Bank of Commerce Filing Number: MT080113 Filing Date: August 1, 2008 The following set of standard mortgage terms

State of [INSERT STATE] County of [INSERT COUNTY] Facilities Use Agreement Between [INSERT COMPANY NAME] and [INSERT UNIVERSITY] for access to

![State of [INSERT STATE] County of [INSERT COUNTY] Facilities Use Agreement Between [INSERT COMPANY NAME] and [INSERT UNIVERSITY] for access to](/thumbs/77/74925145.jpg "State of [INSERT STATE] County of [INSERT COUNTY] Facilities Use Agreement Between [INSERT COMPANY NAME] and [INSERT UNIVERSITY] for access to") State of [INSERT STATE] County of [INSERT COUNTY] Facilities Use Agreement Between [INSERT COMPANY NAME] and [INSERT UNIVERSITY] for access to [INSERT BUILDING AND ROOM NUMBER] THIS FACTILITIES USE AGREEMENT

State of [INSERT STATE] County of [INSERT COUNTY] Facilities Use Agreement Between [INSERT COMPANY NAME] and [INSERT UNIVERSITY] for access to [INSERT BUILDING AND ROOM NUMBER] THIS FACTILITIES USE AGREEMENT

RESEARCH AGREEMENT University of Hawai i

RESEARCH AGREEMENT This Research Agreement ( Agreement ) is made and entered into this day of, ( Effective Date ), by and between the whose address is, Office of Research Services, 2440 Campus Road, Box

RESEARCH AGREEMENT This Research Agreement ( Agreement ) is made and entered into this day of, ( Effective Date ), by and between the whose address is, Office of Research Services, 2440 Campus Road, Box

ABA Film Services Ltd. Terms and Conditions of Hire

ABA Film Services Ltd Terms and Conditions of Hire 1 INTERPRETATION 1.1 In these conditions the following words have the following meanings: Contract means a contract which incorporates these conditions

ABA Film Services Ltd Terms and Conditions of Hire 1 INTERPRETATION 1.1 In these conditions the following words have the following meanings: Contract means a contract which incorporates these conditions

PROFESSIONAL SERVICES and NON-CONSTRUCTION CONRACTS

CASTAIC LAKE WATER AGENCY STANDARD CONTRACT RISK TRANSFER PROVISIONS, GENERAL CONDITIONS, REQUIRED INSURANCE and CALIFORNIA LABOR CODE REQUIREMENTS for PROFESSIONAL SERVICES and NON-CONSTRUCTION CONRACTS

CASTAIC LAKE WATER AGENCY STANDARD CONTRACT RISK TRANSFER PROVISIONS, GENERAL CONDITIONS, REQUIRED INSURANCE and CALIFORNIA LABOR CODE REQUIREMENTS for PROFESSIONAL SERVICES and NON-CONSTRUCTION CONRACTS

RULES AND REGULATIONS FOR ELECTRIC SERVICE. These Rules and Regulations, approved by the Florida Public Utilities Commission, constitute the Company's

GULF POWER COMPANY Section No. IV Original Sheet No. 4.3 RULES AND REGULATIONS FOR ELECTRIC SERVICE These Rules and Regulations, approved by the Florida Public Utilities Commission, constitute the Company's

GULF POWER COMPANY Section No. IV Original Sheet No. 4.3 RULES AND REGULATIONS FOR ELECTRIC SERVICE These Rules and Regulations, approved by the Florida Public Utilities Commission, constitute the Company's

Registration Number: Date: February 4, 2016

Filed By: Canadian Imperial Bank of Commerce 6213-2016/03 Page 1 of 17 Consumer General Collateral Mortgage Standard Mortgage Terms Registration Number: 161036262 Date: February 4, 2016 The following set

Filed By: Canadian Imperial Bank of Commerce 6213-2016/03 Page 1 of 17 Consumer General Collateral Mortgage Standard Mortgage Terms Registration Number: 161036262 Date: February 4, 2016 The following set

The following set of additional terms and conditions form part of Canadian Imperial Bank of Commerce. Contents

Page 1 of 23 Consumer General Collateral Mortgage Additional Terms and Conditions The following set of additional terms and conditions form part of Canadian Imperial Bank of Commerce. Contents 1. Definitions...

Page 1 of 23 Consumer General Collateral Mortgage Additional Terms and Conditions The following set of additional terms and conditions form part of Canadian Imperial Bank of Commerce. Contents 1. Definitions...

PROPERTY MANAGEMENT AGREEMENT

PROPERTY MANAGEMENT AGREEMENT This Property Management Agreement ( Agreement ) is made on / / between ( Owner ) and ( Agent ), who have agreed as follows: 1. DEFINITIONS Whenever the following capitalized

PROPERTY MANAGEMENT AGREEMENT This Property Management Agreement ( Agreement ) is made on / / between ( Owner ) and ( Agent ), who have agreed as follows: 1. DEFINITIONS Whenever the following capitalized

STANDARD MORTGAGE TERMS