BERKELEY RESEARCH GROUP. Executive Summary

|

|

|

- Bartholomew McDowell

- 6 years ago

- Views:

Transcription

1

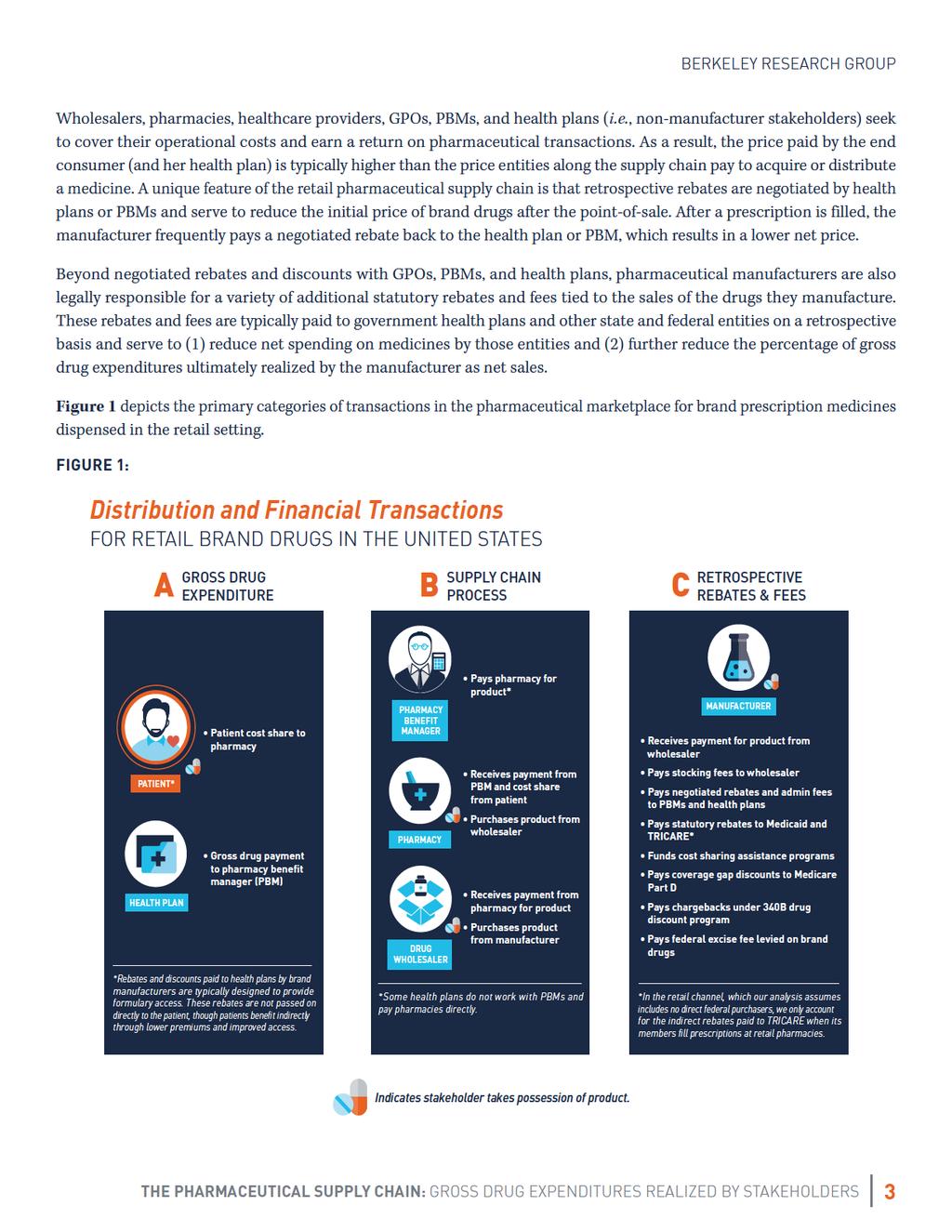

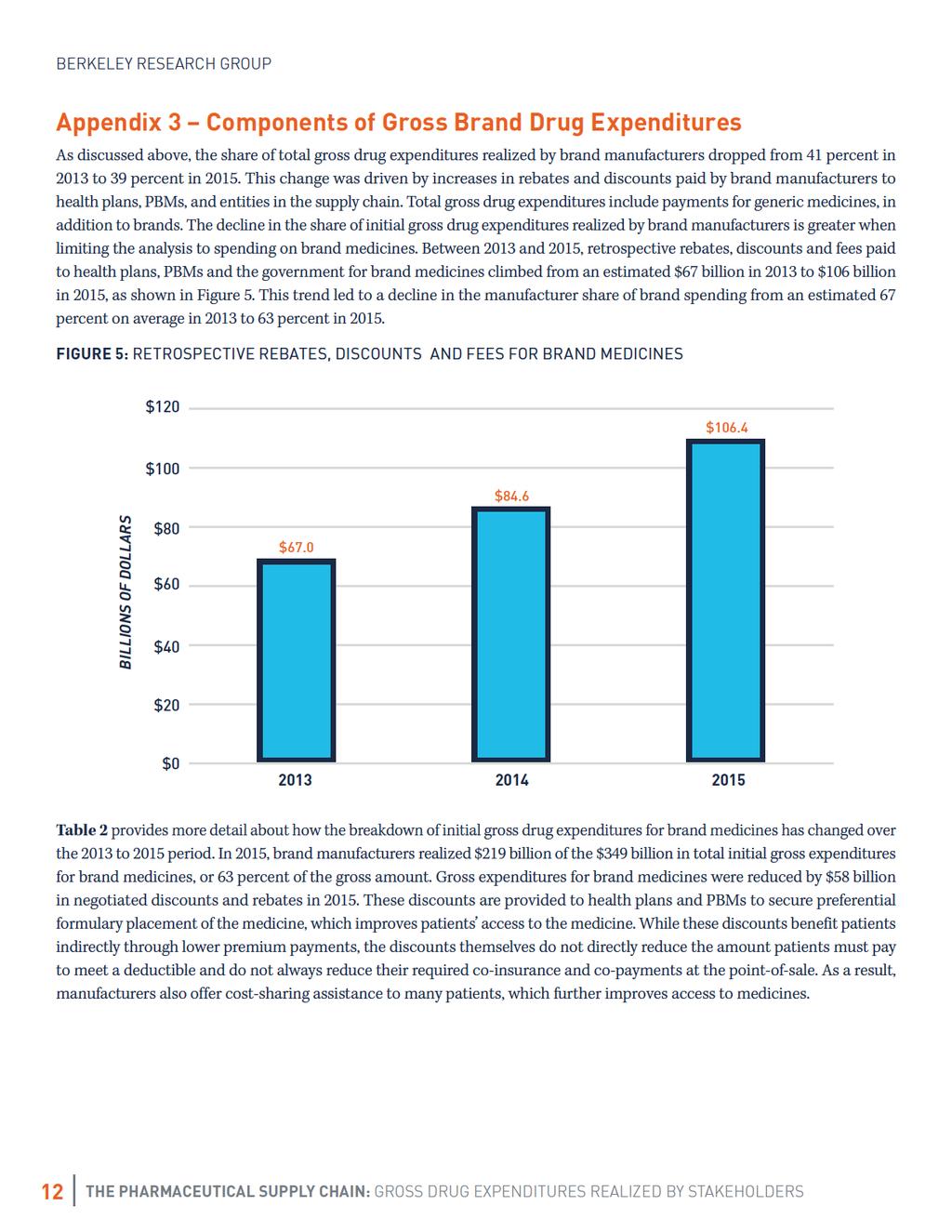

2 Executive Summary Within the U.S. healthcare system, the flow of dollars in the pharmaceutical marketplace is a complex process involving a variety of stakeholders and myriad rebates, discounts, and fees some of which are paid after a prescription drug is dispensed to the patient. Commonly reported figures for pharmaceutical spending fail to capture these retrospective rebates and discounts, which lower final net spending for payers and the healthcare system. Pharmaceutical spending estimates that omit rebates and discounts do not fully reflect the underlying competitive dynamics of the pharmaceutical sector and provide a misleading impression of drug spending. In recent years, news of rising list prices and increased patient cost sharing has triggered calls for greater visibility into the pharmaceutical distribution and payment process. Against this backdrop, the market has experienced enhanced competition, especially in certain therapeutic areas, resulting in higher rebates from manufacturers to payers in exchange for patient access to medications. The goal of this paper is to bring clarity to the drug distribution and payment process and to estimate the share of spending realized by manufacturers and other entities along the supply chain. For purposes of this paper, we begin the analysis with initial gross drug expenditures, which we define as the sum of payments for prescription drugs made by patients and their health plans at the point of sale (e.g., pharmacy, outpatient hospital) prior to any rebate, discount, or fee provided by manufacturers. By using this starting point, the analysis makes it possible to measure prescription drug spending by consumers, health plans, government payers, and employers, and the portion thereof realized by manufacturer and non-manufacturer stakeholders. Our analysis indicates that brand manufacturers realize 39 percent of initial gross drug expenditures. Of the remainder, 42 percent is realized by non-manufacturer entities, including amounts realized by participants in the supply chain (22 percent) and transferred by manufacturers to other stakeholders through retrospective rebates, discounts, and fees (20 percent). After deducting price concessions that lower the cost of medicines to payers and patients, the actual, final cost of medicines is significantly less than initial gross drug expenditures. We define these final costs to payers as net drug expenditures, which we estimate totaled $469 billion in Brand manufacturers realized $219 billion of this amount in 2015, or less than half of net spending on prescription drugs (47 percent). We also observe that rebates and discounts have grown as a share of gross drug expenditures over time. As a result, the share of gross drug expenditures realized by brand manufacturers has declined ( from 41 percent in 2013 to 39 percent in 2015), while the share realized by non-manufacturer entities has increased. This trend in increased retrospective rebates and discounts paid by brand manufacturers has largely offset increases to drug list prices, and reflects the increasingly competitive marketplace for brand drugs. 1

3 Background and Introduction Estimates of U.S. prescription drug spend have historically been available from a variety of private institutions as well as the U.S. government. Notable among these are IMS Health, Symphony Health Solutions ( f/k/a Wolters Kluwer Health), and Kaiser Family Foundation. Additionally, Centers for Medicare & Medicaid Services (CMS) publishes historical and forecasted spending on prescription drugs in the U.S. through the National Healthcare Expenditure (NHE) Data. Estimates of prescription drug spend vary depending on the starting point and assumptions relied on by the reporting source. (i.e., do they measure payments to pharmacies at the time a medicine is dispensed or payments by pharmacies to acquire drugs? Do they measure gross drug spend or spend that is net of rebates and other discounts provided by manufacturers?) One of the most widely cited data sources is IMS National Sales Perspective (NSP), which measures invoice prices paid by pharmacies and other providers to acquire the product those entities dispense to patients. While reporting based on invoice prices is relevant in some contexts, the competitive structure of the U.S. pharmaceutical market makes invoice prices an incomplete picture of gross spend by the end consumer (patients and their insurers) and an overstatement of payments realized by the manufacturer. Focusing on invoice prices also ignores important rebates, discounts, and other price concessions offered by drug manufacturers that lower the cost of medicines to the purchaser. 1 As described in greater detail in Appendix 2, invoice sales account for most of the discounts offered by generic manufacturers but do not account for off-invoice rebates and fees paid primarily by brand manufacturers. This paper addresses these issues by estimating total initial gross drug expenditures made by patients and insurers at the point of sale, apportioning the share of those payments realized by different stakeholders, and arriving at the net amount actually realized by manufacturers. Overview of the Pharmaceutical Marketplace The flow of dollars in the pharmaceutical marketplace is complex. In addition to multiple stakeholders that participate in the distribution of and payment for medicines, manufacturers face a blended marketplace with public and private payers and varied regulatory requirements depending on the payer (e.g., commercial insurer versus Medicaid), sales channel (e.g., 340B hospital versus retail pharmacy), and provider type (e.g., private clinician versus Veterans Administration hospital). However, the purchase price of a prescription drug can ultimately be distilled into three types of transactions: initial gross expenditures on prescription drugs made by patients and their health plans (both public and private), payments and discounts along the supply chain, and retrospective rebates and fees paid by manufacturers. 2 Much like any consumer good, prescription drugs have an end buyer, in this case patients and their health plans. Also similar to most consumer goods, patients and their health plans do not buy drugs directly from the manufacturer. Rather, there is a multi-step supply chain comprised of wholesalers, pharmacies, and others where each entity plays a role in bringing medicines from manufacturer to patient. Wholesalers purchase directly from the manufacturer, and in turn sell drugs to the pharmacies or healthcare providers that dispense them to patients. Although pharmacy benefit managers (PBMs) do not take physical possession of drugs, in many cases they aggregate the buying power of health plans and employer groups by negotiating discounted purchase prices with retail pharmacies, purchasing drugs at discounted prices for delivery by mail, and separately securing rebates on brand pharmaceuticals from manufacturers. For nonretail drugs, healthcare providers who administer drugs in the office or hospital typically purchase from a wholesaler and realize price concessions at the time of purchase through membership in a group purchasing organization (GPO) rather than through retrospective rebates and discounts. 1 To address the omission of rebates, discounts, and other price concessions, IMS began publishing estimates of net drug spending in For additional background on the payment for and distribution of pharmaceuticals, see the Academy of Managed Care Pharmacy Guide to Pharmaceutical Payment Methods (available at: 2

4

5

6

7

8 Defined Terms Brand Drug: Innovator drug with no marketed generic equivalent, the manufacturer of which typically negotiates rebates and discounts with commercial payers for formulary placement and other forms of market access for retail drugs, and negotiates purchase discounts with providers for market access for non-retail drugs. Generic Drug: Any drug with at least one generic equivalent, the manufacturer of which typically negotiates purchase discounts and rebates with retail and non-retail providers to ensure stocking and dispensing of the drug. Initial Gross Drug Expenditure: Initial point-of-sale payment by a payer and patient for a drug prior to accounting for any negotiated rebates, discounts, or fees. Does not include dispensing fees or claims administration fees. Net Drug Expenditure: Net amount paid by a payer and patient for a drug after accounting for any negotiated rebates, discounts, or fees. Non-retail Setting: Healthcare provider locations where drugs are dispensed or administered directly to patients (e.g., inpatient and outpatient hospitals, physician offices, Veterans Administration facilities). Market Access: Set of mechanisms through which payers and PBMs structure patient access to medicines, such as formulary tiers, copays, step therapy, prior authorization, etc. Retail Setting: Chain, independent, long-term care, and mail order pharmacies, in addition to food stores with pharmacies. Supply Chain: Stakeholders involved in bringing medicines from manufacturer to patient, including wholesalers, pharmacies, and healthcare provider locations. 7

9 Appendix 1 Methodology and Data Sources Considered The analysis presented in this paper encompasses all prescription drug sales in the U.S. in addition to a variety of rebates and fees, many of which are proprietary to the parties involved. As a result, there is no single source to rely on for this analysis. Our analysis uses Wholesale Acquisition Cost (WAC) sales and invoice sales data from IMS Health s National Sales Perspectives (NSP) as a baseline for the estimation of gross drug expenditures. The analysis relies on secondary research to estimate the portion of gross drug expenditures realized by manufacturers and supply chain stakeholders, as well as amounts paid by manufacturers through retrospective rebates, discounts, and fees. To calculate gross drug expenditures, we rely on third-party data sources to convert WAC sales into an estimate of initial gross drug expenditures paid by patients and their health plans to pharmacies and other providers. We calculate gross drug expenditures separately for brand and generic drugs within the retail and non-retail channels to account for differences in payer reimbursement schemes within these four categories. For the retail channel, reimbursement is often determined based on WAC or Average Wholesale Price (AWP). Contracts between health plans and PBMs that are based on WAC or AWP incorporate negotiated adjustments that differ dramatically for brands versus generics. For the non-retail channel, reimbursement is more often determined based on Average Sales Price (ASP), hospital submitted charges, or bundled payment arrangements. When reimbursement is based on ASP, as is the case under Medicare Part B, a percentage is added to ASP. The purchase discounts provided to non-retail providers by brand and generic manufacturers are reflected within ASP. In addition to calculating on-invoice discounts, we also calculate prompt-pay discounts, stocking fees, and other margin realized by wholesalers, as well as the many off-invoice discounts, rebates, and fees paid by manufacturers to health plans, PBMs, patients, and the government. We estimate these payments based on secondary research where exact numbers are not publicly available. This analysis is developed separately for the retail and non-retail channels, as well as for brand and generic drugs, in order to identify key differences in the supply chain for each. We exclude additional fees and costs in the pharmaceutical supply chain, such as dispensing fees paid to pharmacies, manufacturer payments to specialty pharmacies, and claims administration fees paid to PBMs by health plans and employer groups. These are fees for a service and not adjustments to initial gross drug expenditures (i.e., the fee is not calculated as a percentage of the gross drug expenditure but rather is usually a flat dollar amount for the service performed). This analysis also does not take into account operating expenses (e.g., sales, marketing, and general administrative expenses) of manufacturers or supply chain stakeholders that further reduce margins and realized net revenue. To calculate gross drug expenditures and amounts realized by each participant, we rely on secondary research from sources listed in Table 1. There are inherent limitations with the data sources we use in this analysis, particularly those that attempt to estimate metrics based on proprietary information. For instance, the Pharmacy Benefit Management Institute (PBMI) offers useful survey data on typical pharmacy discounts off of AWP negotiated by employers and/or their PBMs. Though this data does not represent the entire universe of commercial health plans, we assume that the average discounts reported serve as a reasonable estimate of average discounts across the market. We make a similar assumption on wholesaler margin, referencing financial data from the three largest wholesalers (McKesson, Cardinal, and AmerisourceBergen) to estimate margins realized by the wholesaler industry at large. Though a precise calculation is not possible with such a high-level analysis, our methodology results in a reasonable estimate of the amounts realized by stakeholders in the pharmaceutical supply chain. 8

10 TABLE 1: SOURCES CONSIDERED CATEGORY COMPONENT SOURCES Gross Drug Expenditures Supply Chain Discounts Gross Drug Expenditures Pharmacy/ Provider Margin Wholesaler Margin GPO Fees IMS WAC Sales Data for (2015 projected based on prior years) IMS NPA Data, (2015 projected based on prior years) Pharmacy Benefit Management Institute, Prescription Drug Benefit Cost and Plan Design Report Pharmacy Benefit Management Institute, Prescription Drug Benefit Cost and Plan Design Report CMS ASP Drug Pricing Files MagellanRx Management, Medical Pharmacy Trend Report: 2015, Sixth Edition Medical Group Management Association, MGMA Cost Survey: 2014 Report Based on 2013 Data: Key Findings Summary Report Becker s Hospital Review, 50 Things to Know About the Hospital Industry, July 23, 2013 McKesson, Becoming a Long-Term Care Pharmacy: Opportunities and Important Considerations PharMerica, 2015 Annual Report Omnicare, 2014 Annual Report Medicaid Covered Outpatient Prescription Drug Reimbursement Information by State, Quarter Ending June 2016 IMS NSP Sales Data for McKesson, 2015 Annual Report Cardinal, 2015 Annual Report AmerisourceBergen, 2015 Annual Report Morningstar, Healthcare Observer, April 2014 Barron s, Prescription for Success, June 16, 2012 Congressional Budget Office, Prescription Drug Pricing in the Private Sector, January 2007 Government Accountability Office, Group Purchasing Organizations: Funding Structure Has Potential Implications for Medicare Costs, October 2014 Healthcare Supply Chain Association, Frequently Asked Questions 9

11 CATEGORY COMPONENT SOURCES 340B Program Income Federal Supply Schedule Discounts 340B Prime Vendor Apexus disclosure on sales at 340B price IMS NSP Sales and WAC Data for Statutory Rebates & Fees Medicaid Rebates MACPAC, Medicaid Spending for Prescription Drugs, January 2016 MACPAC, Medicaid Gross Spending and Rebates for Drugs by Delivery System & Medicaid Gross Spending for Drugs by Delivery System and Brand or Generic Status, FY 2015 Excise Fee IRS, Annual Fee on Branded Prescription Drug Manufacturers and Importers TRICARE Rebates Medical Expenditure Panel Survey (MEPS) data Defense Department, Civilian Health and Medical Program of the Uniformed Services (CHAMPUS)/TRICARE: Inclusion of TRICARE Retail Pharmacy Program in Federal Procurement of Pharmaceuticals, October 15, 2010 Market Access Rebates and Discounts Medicare Part D Coverage Gap Discounts Patient Cost Sharing Assistance Negotiated Health Plan and PBM Rebates CMS, Coverage Gap Discount Data Spreadsheets Bloomberg, That Drug Coupon Isn t Really Clipping Costs, December 23, Annual Report of the Boards of Trustees of the Federal Hospital Insurance and Federal Supplementary Medical Insurance Trust Funds 2016 Annual Report of the Boards of Trustees of the Federal Hospital Insurance and Federal Supplementary Medical Insurance Trust Funds Visante, The Return on Investment (ROI) on PBM Services, November 2016 Quintiles IMS Institute, Estimate of Medicare Part D Costs After Accounting for Manufacturer Rebates, October

12 Appendix 2 Invoice Pricing as a Measure of Drug Expenditures As described above, relying on invoice prices as a measure of drug expenditures does not account for the amounts actually paid by patients and their health plans at the point of sale. Notably, initial gross drug expenditures for generic drugs are significantly higher than the price at which retail and mail order pharmacies acquire generic drugs. This is not the case for brand drugs, on which pharmacies tend to earn small margins, meaning that pharmacies are typically paid an amount that does not significantly exceed their acquisition cost. As a result of this dynamic, relying on invoice sales data overstates actual spending on brands, and understates spending on generics relative to brands. Similarly, invoice prices do not account for retrospective rebates and fees that lower the net amount actually realized by manufacturers. For generics, nearly all discounting is in the form of purchase discounts or rebates offered directly to pharmacies and wholesalers in an effort to secure shelf space at the retail or mail order pharmacy. For brands, however, the majority of discounting occurs off-invoice after the pharmacy s initial purchase in the form of rebates negotiated with health plans and PBMs and through statutory rebates and fees provided to government programs, many of which are only paid by brand manufacturers. While generic manufacturers realize the vast majority of invoice payments made by wholesalers and pharmacies when they acquire product, brand manufacturers transfer much of the invoice payments to other stakeholders through rebates, patient cost-sharing assistance, and other fees that are paid after the initial sale to wholesalers and pharmacies. 11

13

14 TABLE 2: INITIAL GROSS BRAND DRUG EXPENDITURES BY COMPONENT, GROSS BRAND DRUG EXPENDITURES BY COMPONENT (IN BILLIONS) TYPE OF COMPONENT COMPONENT Initial Gross Drug Expenditures 1 $264.9 $306.3 $349.1 Statutory Rebates and Fees Medicaid Drug Rebate Program 2 $19.1 $23.0 $28.3 Part D Coverage Gap Discounts TRICARE Rebates & Federal Supply Schedule Discounts $4.2 $5.1 $5.8 $3.5 $4.6 $4.7 Excise Fee 3 $2.8 $3.0 $3.0 Market Access Rebates and Discounts Negotiated Health Plan and PBM Rebates and Fees 4 $33.2 $43.5 $57.7 Patient Cost Sharing Assistance $4.2 $5.4 $6.9 Pharmacy/Provider Margin 5 $17.5 $18.5 $20.4 Supply Chain Entities Wholesaler Margin 6 $2.3 $2.7 $3.1 GPO Administrative Fees $0.6 $0.6 $0.7 Net Amount Realized by Brand Manufacturer ($) $177.5 $199.9 $218.6 Net Amount Realized by Brand Manufacturer (%) 67.0% 65.3% 62.6% [1] Components may not sum to total due to rounding. [2] Component includes statutory rebates, supplemental rebates negotiated by states and managed care plans, and 340B margin. [3] Component represents annual fee paid by brand manufacturers as stipulated in the Affordable Care Act (ACA). [4] Component includes the portion of gross drug expenditures that may be retained by health plans and PBMs through their role in the pharmaceutical payment process. This may not be inclusive of all health plan or PBM revenue streams (e.g., claims administration fees, utilization management service fees, etc.). [5] Component represents the difference between what a pharmacy or non-retail provider is paid for the drugs it dispenses and the price at which those drugs were acquired. Includes rebates paid by manufacturers to long-term care pharmacies. [6] Component represents the difference between what a drug wholesaler is paid by pharmacies for drugs and what the wholesaler paid to acquire those drugs from the manufacturer, inclusive of prompt-pay discounts and stocking fees. 13

Marc Claussen, Chiesi USA, Director, Market Access. Donna White, Chiesi USA, Sr. Director, Contracting and Compliance

Marc Claussen, Chiesi USA, Director, Market Access Donna White, Chiesi USA, Sr. Director, Contracting and Compliance The views/observations expressed in this presentation are the personal views/observations

Marc Claussen, Chiesi USA, Director, Market Access Donna White, Chiesi USA, Sr. Director, Contracting and Compliance The views/observations expressed in this presentation are the personal views/observations

Federal Spending on Brand Pharmaceuticals. April 2011

Federal Spending on Brand Pharmaceuticals April 2011 Summary Avalere Health estimates that manufacturers of brand-name prescription drugs will receive about $777 billion in revenues from the sales of outpatient

Federal Spending on Brand Pharmaceuticals April 2011 Summary Avalere Health estimates that manufacturers of brand-name prescription drugs will receive about $777 billion in revenues from the sales of outpatient

Overview of Coverage of Drugs Under the Medicaid Medical Benefit

Overview of Coverage of Drugs Under the Medicaid Medical Benefit June 4, 2008 Amanda Bartelme Avalere Health LLC Avalere Health LLC The intersection of business strategy and public policy Medical vs. Pharmacy

Overview of Coverage of Drugs Under the Medicaid Medical Benefit June 4, 2008 Amanda Bartelme Avalere Health LLC Avalere Health LLC The intersection of business strategy and public policy Medical vs. Pharmacy

Savings Generated by New York s Medicaid Pharmacy Reform

Savings Generated by New York s Medicaid Pharmacy Reform Sponsored by: Pharmaceutical Care Management Association Prepared by: Special Needs Consulting Services, Inc. October 2012 Table of Contents I.

Savings Generated by New York s Medicaid Pharmacy Reform Sponsored by: Pharmaceutical Care Management Association Prepared by: Special Needs Consulting Services, Inc. October 2012 Table of Contents I.

Medicaid Prescription Drug Payment Reform

Medicaid Prescription Drug Payment Reform Spring 2006 NCSL Health Chairs Meeting John M. Coster, Ph.D., R.Ph. June 10, 2006 1 Community Retail Pharmacy In 2005, there were approximately 56,000 community

Medicaid Prescription Drug Payment Reform Spring 2006 NCSL Health Chairs Meeting John M. Coster, Ph.D., R.Ph. June 10, 2006 1 Community Retail Pharmacy In 2005, there were approximately 56,000 community

Estimate of Medicare Part D Costs After Accounting for Manufacturer Rebates

October 2016 Estimate of Medicare Part D Costs After Accounting for Manufacturer Rebates A Study of Original Branded Products in the U.S. $ Introduction The cost of medicines in the U.S. has been the subject

October 2016 Estimate of Medicare Part D Costs After Accounting for Manufacturer Rebates A Study of Original Branded Products in the U.S. $ Introduction The cost of medicines in the U.S. has been the subject

KEEPING PRESCRIPTION DRUGS AFFORDABLE: The Value of Pharmacy Benefit Managers (PBMs)

") The Texas Association of Health Plans Representing health insurers, health maintenance organizations, and other related health care entities operating in Texas. KEEPING PRESCRIPTION DRUGS AFFORDABLE: The

The Texas Association of Health Plans Representing health insurers, health maintenance organizations, and other related health care entities operating in Texas. KEEPING PRESCRIPTION DRUGS AFFORDABLE: The

CBI 4th Reimbursement and Contracting Conference: Key Challenges Related to Specialty Drug Pricing and Contracting

CBI 4th Reimbursement and Contracting Conference: Key Challenges Related to Specialty Drug Pricing and Contracting Avalere Health An Inovalon Company February 28, 2017 Growth in Drug Costs Relative to

CBI 4th Reimbursement and Contracting Conference: Key Challenges Related to Specialty Drug Pricing and Contracting Avalere Health An Inovalon Company February 28, 2017 Growth in Drug Costs Relative to

Delivering Value for All Health Care Stakeholders. Larry Merlo President & Chief Executive Officer

Delivering Value for All Health Care Stakeholders Larry Merlo President & Chief Executive Officer Agenda Our Value Proposition Has Never Been Stronger We See Compelling Opportunities in a Robust Health

Delivering Value for All Health Care Stakeholders Larry Merlo President & Chief Executive Officer Agenda Our Value Proposition Has Never Been Stronger We See Compelling Opportunities in a Robust Health

Prescription Drugs Spending Distribution and Cost Drivers. Steve Kappel January 25, 2007

Prescription Drugs Spending Distribution and Cost Drivers Steve Kappel January 25, 2007 Introduction Why Focus on Drugs? Compared to other health care spending: Even faster annual growth Higher reliance

Prescription Drugs Spending Distribution and Cost Drivers Steve Kappel January 25, 2007 Introduction Why Focus on Drugs? Compared to other health care spending: Even faster annual growth Higher reliance

CWAG Prescription Drug Pricing Webinar

CWAG Prescription Drug Pricing Webinar January 9, 2018 Kipp Snider, J.D. Vice President, State Policy Pharmaceutical Research & Manufacturers of America (PhRMA) Medicines Are Expected to Account for a

CWAG Prescription Drug Pricing Webinar January 9, 2018 Kipp Snider, J.D. Vice President, State Policy Pharmaceutical Research & Manufacturers of America (PhRMA) Medicines Are Expected to Account for a

The Declining Value of Payer Access: Defining and improving Rebate Efficiency in the current healthcare landscape

The Declining Value of Payer Access: Defining and improving Rebate Efficiency in the current healthcare landscape Lucas Greenwalt, Senior Principal Amundsen Consulting Prepared for: CBI Gross to Net Boot

The Declining Value of Payer Access: Defining and improving Rebate Efficiency in the current healthcare landscape Lucas Greenwalt, Senior Principal Amundsen Consulting Prepared for: CBI Gross to Net Boot

Pharmacy Program Management: Pitfalls, Challenges, and Best Practices About Solid Benefit Guidance specialty 60,000,000 covered member lives INSIDER

Pharmacy Program Management: Pitfalls, Challenges, and Best Practices October 2, 2017 This presentation contains proprietary information and is not to be reproduced or further distributed without permission

Pharmacy Program Management: Pitfalls, Challenges, and Best Practices October 2, 2017 This presentation contains proprietary information and is not to be reproduced or further distributed without permission

Understanding Pharmacy Benefit Management Services

Understanding Pharmacy Benefit Management Services Peter Cullen VP, Business Development and Strategic Initiatives March 12, 2014 Innovation Session Overview and Learning Objectives Session Overview: Provide

Understanding Pharmacy Benefit Management Services Peter Cullen VP, Business Development and Strategic Initiatives March 12, 2014 Innovation Session Overview and Learning Objectives Session Overview: Provide

Medicaid Program; Covered Outpatient Drugs; Proposed Rule (CMS-2345-P) NHIA Summary

NHIA Summary") Medicaid Program; Covered Outpatient Drugs; Proposed Rule (CMS-2345-P) NHIA Summary The Centers for Medicare & Medicaid Services (CMS) on February 2, 2012 published in the Federal Register a proposed rule

Medicaid Program; Covered Outpatient Drugs; Proposed Rule (CMS-2345-P) NHIA Summary The Centers for Medicare & Medicaid Services (CMS) on February 2, 2012 published in the Federal Register a proposed rule

Re: CMS 2238 FC (Final Rule: Medicaid Program; Prescription Drugs)

") January 2, 2008 Reference No.: FASC08001 Kerry Weems Acting Administrator, Centers for Medicare and Medicaid Services Department of Health and Human Services Room 445-G Hubert H. Humphrey Building 200

January 2, 2008 Reference No.: FASC08001 Kerry Weems Acting Administrator, Centers for Medicare and Medicaid Services Department of Health and Human Services Room 445-G Hubert H. Humphrey Building 200

Insightsfeature. Managing Specialty Drug Spend Under the Medical Benefit. Innovations and Automation for More Effective Management.

Insightsfeature Managing Specialty Drug Spend Under the Medical Benefit Innovations and Automation for More Effective Management March 30, 2017 The Less-Visible Part of Specialty Spend By most estimates,

Insightsfeature Managing Specialty Drug Spend Under the Medical Benefit Innovations and Automation for More Effective Management March 30, 2017 The Less-Visible Part of Specialty Spend By most estimates,

Modeling Price Increases and the Effects on Customer Segments

Modeling Price Increases and the Effects on Customer Segments CBI Medicaid Congress May 9, 2017 Jennifer English Director, Pricing, Contracting and Govt Programs, Insmed, Inc. Disclaimer The opinions and

Modeling Price Increases and the Effects on Customer Segments CBI Medicaid Congress May 9, 2017 Jennifer English Director, Pricing, Contracting and Govt Programs, Insmed, Inc. Disclaimer The opinions and

Glossary of Terms (Terms are listed in Alphabetical Order)

") Glossary of Terms (Terms are listed in Alphabetical Order) Access Access refers to the availability and location of pharmacies that participate in the network that serves your pharmacy benefit plan. Acute

Glossary of Terms (Terms are listed in Alphabetical Order) Access Access refers to the availability and location of pharmacies that participate in the network that serves your pharmacy benefit plan. Acute

Workers Compensation Board Pharmacy Benefit Plan

1.0 Introduction Workers Compensation Board Pharmacy Benefit Plan Options for pharmaceutical care have greatly expanded over the past several years. New pharmaceuticals and pharmaceutical treatment modalities

1.0 Introduction Workers Compensation Board Pharmacy Benefit Plan Options for pharmaceutical care have greatly expanded over the past several years. New pharmaceuticals and pharmaceutical treatment modalities

Prescription Drug Rebates and Part D Drug Costs

Prescription Drug Rebates and Part D Drug Costs Analysis of historical Medicare Part D drug prices and manufacturer rebates Prepared for: America s Health Insurance Plans Prepared by: Nicholas J. Johnson,

Prescription Drug Rebates and Part D Drug Costs Analysis of historical Medicare Part D drug prices and manufacturer rebates Prepared for: America s Health Insurance Plans Prepared by: Nicholas J. Johnson,

340B Drug Program Compliance: Focus on Disproportionate Hospitals

340B Drug Program Compliance: Focus on Disproportionate Hospitals Part II: 340B Drug Program Compliance: Pharmacy Operations and the DSH January 29, 2014 1 Faculty Stephen J. Weiser, JD, LLM Director 312-403-4284

340B Drug Program Compliance: Focus on Disproportionate Hospitals Part II: 340B Drug Program Compliance: Pharmacy Operations and the DSH January 29, 2014 1 Faculty Stephen J. Weiser, JD, LLM Director 312-403-4284

DIR fees are knocking down pharmacy profits

16 America s PHARMACIST November 2016 DIR fees are knocking down pharmacy profits by Bruce A. Semingson, Pharmacist In 2016, retail pharmacy will pay between $360 million and $2.16 billion in direct and

16 America s PHARMACIST November 2016 DIR fees are knocking down pharmacy profits by Bruce A. Semingson, Pharmacist In 2016, retail pharmacy will pay between $360 million and $2.16 billion in direct and

Pharmacy Billing and Reimbursement

FSHP Disclosure Pharmacy Billing and Tara L McNulty RPhT, CPhT I, Tara McNulty, do not have a vested interest in or affiliation with any corporate organization offering financial support or grant monies

FSHP Disclosure Pharmacy Billing and Tara L McNulty RPhT, CPhT I, Tara McNulty, do not have a vested interest in or affiliation with any corporate organization offering financial support or grant monies

Testimony of Mark Merritt. Pharmaceutical Care Management Association

Testimony of Mark Merritt Pharmaceutical Care Management Association Before the UNITED STATES SENATE COMMITTEE ON HEALTH, EDUCATION, LABOR, AND PENSIONS The Cost of Prescription Drugs: How the Drug Delivery

Testimony of Mark Merritt Pharmaceutical Care Management Association Before the UNITED STATES SENATE COMMITTEE ON HEALTH, EDUCATION, LABOR, AND PENSIONS The Cost of Prescription Drugs: How the Drug Delivery

Recent Developments In U.S. Pharmaceutical Pricing: The Case Example Of The Proposed Medicare Part B Experiment

Recent Developments In U.S. Pharmaceutical Pricing: The Case Example Of The Proposed Medicare Part B Experiment Presentation by Susan Dentzer President and CEO, NEHI (Network for Excellence in Health Innovation)

Recent Developments In U.S. Pharmaceutical Pricing: The Case Example Of The Proposed Medicare Part B Experiment Presentation by Susan Dentzer President and CEO, NEHI (Network for Excellence in Health Innovation)

The U.S. Healthcare System: How Pharmacy Benefit Managers Impact Prescription Drug Use. Presented by Daniel Tomaszewski Pharmd, PhD

The U.S. Healthcare System: How Pharmacy Benefit Managers Impact Prescription Drug Use Presented by Daniel Tomaszewski Pharmd, PhD 1 Medical Vs. Pharmacy Coverage Medical Insurance Managed by an Insurance

The U.S. Healthcare System: How Pharmacy Benefit Managers Impact Prescription Drug Use Presented by Daniel Tomaszewski Pharmd, PhD 1 Medical Vs. Pharmacy Coverage Medical Insurance Managed by an Insurance

Covered Outpatient Drugs Federal Final Rule. Medical Assistance (MA) Program Fee-for-Service (FFS) Pharmacy Reimbursement

Program Fee-for-Service (FFS) Pharmacy Reimbursement") Covered Outpatient Drugs Federal Final Rule Medical Assistance (MA) Program Fee-for-Service (FFS) Pharmacy Reimbursement 1 Background On February 1, 2016, the Centers for Medicare and Medicaid Services

Covered Outpatient Drugs Federal Final Rule Medical Assistance (MA) Program Fee-for-Service (FFS) Pharmacy Reimbursement 1 Background On February 1, 2016, the Centers for Medicare and Medicaid Services

Common Managed Care Terms & Definitions

Contact Us: Email: info@emedbiz.com Phone: 561-430-2090 Fax: 561-430-2091 Website: www.emedbiz.com Common Managed Care Terms & Definitions Balance billing: The practice of billing a patient for the amount

Contact Us: Email: info@emedbiz.com Phone: 561-430-2090 Fax: 561-430-2091 Website: www.emedbiz.com Common Managed Care Terms & Definitions Balance billing: The practice of billing a patient for the amount

REGULATORY ISSUES IMPACTING SUPPLY CHAIN

REGULATORY ISSUES IMPACTING SUPPLY CHAIN Michael Nachman Associate General Counsel John W. Jones, Jr. Partner Allan A. Thoen Partner April 27, 2017 2017 In House Counsel Conference Presenters: John W.

REGULATORY ISSUES IMPACTING SUPPLY CHAIN Michael Nachman Associate General Counsel John W. Jones, Jr. Partner Allan A. Thoen Partner April 27, 2017 2017 In House Counsel Conference Presenters: John W.

SAVINGS GENERATED BY PHARMACY BENEFIT MANAGERS IN THE MEDICARE PART D PROGRAM

February 6, 2014 GLENN GIESE KELLY BACKES SAVINGS GENERATED BY PHARMACY BENEFIT MANAGERS IN THE MEDICARE PART D PROGRAM June 26, 2017 GLENN GIESE RANDALL FITZPATRICK KEVIN MEYER CONTENTS Findings... 1

February 6, 2014 GLENN GIESE KELLY BACKES SAVINGS GENERATED BY PHARMACY BENEFIT MANAGERS IN THE MEDICARE PART D PROGRAM June 26, 2017 GLENN GIESE RANDALL FITZPATRICK KEVIN MEYER CONTENTS Findings... 1

Growth in an Evolving Health Care Market

Driving Enterprise Growth in an Evolving Health Care Market Larry Merlo President & Chief Executive Officer Agenda Our Compelling Value Proposition Evolving Health Care Market Creates Opportunities Strategic

Driving Enterprise Growth in an Evolving Health Care Market Larry Merlo President & Chief Executive Officer Agenda Our Compelling Value Proposition Evolving Health Care Market Creates Opportunities Strategic

An Overview of the Medicare Part D Prescription Drug Benefit

October 2018 Fact Sheet An Overview of the Medicare Part D Prescription Drug Benefit Medicare Part D is a voluntary outpatient prescription drug benefit for people with Medicare, provided through private

October 2018 Fact Sheet An Overview of the Medicare Part D Prescription Drug Benefit Medicare Part D is a voluntary outpatient prescription drug benefit for people with Medicare, provided through private

NCPA Summary of CMS Medicaid Covered Outpatient Drugs AMP Final Rule Prepared January NCPA Advocacy at Work

NCPA Summary of CMS Medicaid Covered Outpatient Drugs AMP Final Rule Prepared January 2016 The Centers for Medicare & Medicaid Services (CMS) recently issued a 658-page, oftendelayed, final rule on the

NCPA Summary of CMS Medicaid Covered Outpatient Drugs AMP Final Rule Prepared January 2016 The Centers for Medicare & Medicaid Services (CMS) recently issued a 658-page, oftendelayed, final rule on the

Rx Watchdog Report Comparative Measures of Price Change for Prescription Drugs and Other Goods

Rx Watchdog Report Comparative Measures of Price Change for Prescription Drugs and Other Goods Stephen W. Schondelmeyer PRIME Institute, University of Minnesota Leigh Purvis AARP Public Policy Institute

Rx Watchdog Report Comparative Measures of Price Change for Prescription Drugs and Other Goods Stephen W. Schondelmeyer PRIME Institute, University of Minnesota Leigh Purvis AARP Public Policy Institute

MEASURING THE IMPACT OF POINT OF SALE REBATES IN COLORADO S COMMERCIAL MARKET

MEASURING THE IMPACT OF POINT OF SALE REBATES IN COLORADO S COMMERCIAL MARKET FEBRUARY 2019 Anna Bunger, FSA, MAAA Jason Gomberg, FSA, MAAA Jason Petroske, FSA, MAAA Sharing Pharmacy May Lower Patient

MEASURING THE IMPACT OF POINT OF SALE REBATES IN COLORADO S COMMERCIAL MARKET FEBRUARY 2019 Anna Bunger, FSA, MAAA Jason Gomberg, FSA, MAAA Jason Petroske, FSA, MAAA Sharing Pharmacy May Lower Patient

How the Federal Government Can Help States Address Rising Prescription Drug Costs

A PUBLICATION OF THE NATIONAL ACADEMY FOR STATE HEALTH POLICY February 2018 How the Federal Government Can Help States Address Rising Prescription Drug Costs Supported by The Commonwealth Fund Introduction

A PUBLICATION OF THE NATIONAL ACADEMY FOR STATE HEALTH POLICY February 2018 How the Federal Government Can Help States Address Rising Prescription Drug Costs Supported by The Commonwealth Fund Introduction

Survey Analysis of January 2014 CMS Medicare Part D Proposed Rule

Survey Analysis of January 2014 CMS Medicare Part D Proposed Rule Prepared for: Pharmaceutical Care Management Association Prepared by: Stephen J. Kaczmarek, FSA, MAAA Principal and Consulting Actuary

Survey Analysis of January 2014 CMS Medicare Part D Proposed Rule Prepared for: Pharmaceutical Care Management Association Prepared by: Stephen J. Kaczmarek, FSA, MAAA Principal and Consulting Actuary

CRS Report for Congress Received through the CRS Web

CRS Report for Congress Received through the CRS Web Order Code RS20295 August 9, 1999 Outpatient Prescription Drugs: Acquisition and Reimbursement Policies Under Selected Federal Programs Heidi G. Yacker

CRS Report for Congress Received through the CRS Web Order Code RS20295 August 9, 1999 Outpatient Prescription Drugs: Acquisition and Reimbursement Policies Under Selected Federal Programs Heidi G. Yacker

GERALD (JERRY) LEWANDOWSKI. BERKELEY RESEARCH GROUP, LLC 1800 M Street NW, Second Floor Washington, DC 20036

LEWANDOWSKI. BERKELEY RESEARCH GROUP, LLC 1800 M Street NW, Second Floor Washington, DC 20036") Curriculum Vitae GERALD (JERRY) LEWANDOWSKI BERKELEY RESEARCH GROUP, LLC 1800 M Street NW, Second Floor Washington, DC 20036 Direct: 202.480.2643 Mobile: 202.258.2669 jlewandowski@thinkbrg.com Jerry Lewandowski

Curriculum Vitae GERALD (JERRY) LEWANDOWSKI BERKELEY RESEARCH GROUP, LLC 1800 M Street NW, Second Floor Washington, DC 20036 Direct: 202.480.2643 Mobile: 202.258.2669 jlewandowski@thinkbrg.com Jerry Lewandowski

Pharmaceutical Management Community Plans 2018

Pharmaceutical Management Community Plans 2018 Customer Service: (888) 327-0671 TTY: 711 Pharmacy Administration: (810) 244-1660 Introduction Pharmaceutical management promotes the use of the most clinically

Pharmaceutical Management Community Plans 2018 Customer Service: (888) 327-0671 TTY: 711 Pharmacy Administration: (810) 244-1660 Introduction Pharmaceutical management promotes the use of the most clinically

Table of Contents. I. Executive Summary and Introduction..2 A. Overview.2 B. Key Findings...2 C. Summary of Approach...5

Table of Contents I. Executive Summary and Introduction..2 A. Overview.2 B. Key Findings...2 C. Summary of Approach......5 II. III. Detailed Data Analyses Findings...6 A. Louisiana Rankings on Key Metrics....6

Table of Contents I. Executive Summary and Introduction..2 A. Overview.2 B. Key Findings...2 C. Summary of Approach......5 II. III. Detailed Data Analyses Findings...6 A. Louisiana Rankings on Key Metrics....6

Establish fair elmbursements

Needed PBM (Pharmacy BeneFit Manager] ReForms - for patients NOW O j.imit purpose nd scope Require price transparency Establish fair elmbursements PBMs started as third party admintsbalors simply chargingan

Needed PBM (Pharmacy BeneFit Manager] ReForms - for patients NOW O j.imit purpose nd scope Require price transparency Establish fair elmbursements PBMs started as third party admintsbalors simply chargingan

Pharmacy Benefit Managers Overview

Pharmacy Benefit Managers Overview A Presentation to the House Health Innovation Subcommittee Mary Alice Nye, Ph.D. Health and Human Services Staff Director, OPPAGA December 6, 2017 Pharmacy Benefit Managers

Pharmacy Benefit Managers Overview A Presentation to the House Health Innovation Subcommittee Mary Alice Nye, Ph.D. Health and Human Services Staff Director, OPPAGA December 6, 2017 Pharmacy Benefit Managers

State of New Jersey. State Health Benefits Program. Plan Year 2019 Rate Renewal Recommendation Report. State Employee Group

State of New Jersey State Health Benefits Program Plan Year 2019 Rate Renewal Recommendation Report State Employee Group September 2018 Table of Contents Subject Page Executive Summary 3 Plan Year 2019

State of New Jersey State Health Benefits Program Plan Year 2019 Rate Renewal Recommendation Report State Employee Group September 2018 Table of Contents Subject Page Executive Summary 3 Plan Year 2019

Appendix I: Data Sources and Analyses. Appendix II: Pharmacy Benefit Management Tools

Appendix I: Data Sources and Analyses This brief includes findings from analyses of the Centers for Medicare & Medicaid Services (CMS) State Drug Utilization Data 1 and CMS 64 reports for federal fiscal

Appendix I: Data Sources and Analyses This brief includes findings from analyses of the Centers for Medicare & Medicaid Services (CMS) State Drug Utilization Data 1 and CMS 64 reports for federal fiscal

340B Drug Pricing Program

340B Drug Pricing Program Mary Stepanyan, PharmD Candidate 2018 University of Southern California, School of Pharmacy Pro Pharma Pharmaceutical Consultants Under the preceptorship of Dr. Craig Stern WHY

340B Drug Pricing Program Mary Stepanyan, PharmD Candidate 2018 University of Southern California, School of Pharmacy Pro Pharma Pharmaceutical Consultants Under the preceptorship of Dr. Craig Stern WHY

NCPDP Electronic Prescribing Standards

NCPDP Electronic Prescribing Standards May 2014 1 What is NCPDP? An ANSI-accredited standards development organization. Provides a forum and marketplace for a diverse membership focused on health care

NCPDP Electronic Prescribing Standards May 2014 1 What is NCPDP? An ANSI-accredited standards development organization. Provides a forum and marketplace for a diverse membership focused on health care

AMCP Guide to Pharmaceutical Payment Methods

AMCP Guide to Pharmaceutical Payment Methods EXECUTIVE EDITION AMCP Task Force on Drug Payment Methodologies October 2007 This AMCP Guide to Pharmaceutical Payment Methods was created by the Editor-in-Chief

AMCP Guide to Pharmaceutical Payment Methods EXECUTIVE EDITION AMCP Task Force on Drug Payment Methodologies October 2007 This AMCP Guide to Pharmaceutical Payment Methods was created by the Editor-in-Chief

We applied the following methodology and assumptions changes to our original estimates:

333 Clay Street Suite 4330 Houston, TX 77002 USA Tel +1 713 658 8451 Fax +1 713 658 9656 April 1, 2013 milliman.com Ms. Barbara Maxwell Deputy Director Texas Association of Health Plans 1001 Congress Avenue,

333 Clay Street Suite 4330 Houston, TX 77002 USA Tel +1 713 658 8451 Fax +1 713 658 9656 April 1, 2013 milliman.com Ms. Barbara Maxwell Deputy Director Texas Association of Health Plans 1001 Congress Avenue,

Health Benefits Briefing

Health Benefits Briefing Teacher Retirement System of Texas December 7, 2016 Copyright 2015 GRS All rights reserved. TRS-Care Health Care Program For Retired Public School Employees and Their Dependents

Health Benefits Briefing Teacher Retirement System of Texas December 7, 2016 Copyright 2015 GRS All rights reserved. TRS-Care Health Care Program For Retired Public School Employees and Their Dependents

Optum. Actuarial Toolbox Proven, sophisticated and market-leading actuarial models for health plans and benefits consultants

Optum Actuarial Toolbox Proven, sophisticated and market-leading actuarial models for health plans and benefits consultants In recent years, the health care landscape has shifted tremendously, prompting

Optum Actuarial Toolbox Proven, sophisticated and market-leading actuarial models for health plans and benefits consultants In recent years, the health care landscape has shifted tremendously, prompting

The 2018 Economic Report on U.S. Pharmacies and Pharmacy Benefit Managers

The 2018 Economic Report on U.S. Pharmacies and Pharmacy Benefit Managers Adam J. Fein, Ph.D. Drug Channels Institute February 2018 Full report available at http://drugch.nl/pharmacy COPYRIGHT Copyright

The 2018 Economic Report on U.S. Pharmacies and Pharmacy Benefit Managers Adam J. Fein, Ph.D. Drug Channels Institute February 2018 Full report available at http://drugch.nl/pharmacy COPYRIGHT Copyright

HEATHER I. BATES Managing Director, BRG Health Analytics. BERKELEY RESEARCH GROUP, LLC 1800 M Street NW, 2 nd Floor Washington, DC 20036

Curriculum Vitae HEATHER I. BATES Managing Director, BRG Health Analytics BERKELEY RESEARCH GROUP, LLC 1800 M Street NW, 2 nd Floor Washington, DC 20036 Direct: 202.480.2660 Cell: 202.641.1035 hbates@thinkbrg.com

Curriculum Vitae HEATHER I. BATES Managing Director, BRG Health Analytics BERKELEY RESEARCH GROUP, LLC 1800 M Street NW, 2 nd Floor Washington, DC 20036 Direct: 202.480.2660 Cell: 202.641.1035 hbates@thinkbrg.com

Pharmacy Benefit Managers (PBMs)

") Pharmacy Benefit Managers (PBMs) Reducing Costs and Improving Quality Lauren Rowley, VP State Affairs National Conference of State Legislatures May 18, 2018 Overview What is the problem? What is a PBM?

Pharmacy Benefit Managers (PBMs) Reducing Costs and Improving Quality Lauren Rowley, VP State Affairs National Conference of State Legislatures May 18, 2018 Overview What is the problem? What is a PBM?

August 11, Submitted electronically via Regulations.gov

August 11, 2017 Submitted electronically via Regulations.gov Centers for Medicare & Medicaid Services Department of Health and Human Services Attention: CMS-1678-P PO Box 8013 Baltimore, MD 21244-1850

August 11, 2017 Submitted electronically via Regulations.gov Centers for Medicare & Medicaid Services Department of Health and Human Services Attention: CMS-1678-P PO Box 8013 Baltimore, MD 21244-1850

The Florida Legislature

The Florida Legislature OFFICE OF PROGRAM POLICY ANALYSIS AND GOVERNMENT ACCOUNTABILITY RESEARCH MEMORANDUM Feasibility of Consolidating Statewide Pharmaceutical Services Summary As directed by Ch. 2009-15,

The Florida Legislature OFFICE OF PROGRAM POLICY ANALYSIS AND GOVERNMENT ACCOUNTABILITY RESEARCH MEMORANDUM Feasibility of Consolidating Statewide Pharmaceutical Services Summary As directed by Ch. 2009-15,

Understanding Patient Access in Health Insurance Exchanges. August 2014 avalerehealth.net

Understanding Patient Access in Health Insurance Exchanges August 2014 avalerehealth.net Agenda Exchange Basics and Patient Protections Formulary Coverage Cost-Sharing Transparency 2 Exchange Basics and

Understanding Patient Access in Health Insurance Exchanges August 2014 avalerehealth.net Agenda Exchange Basics and Patient Protections Formulary Coverage Cost-Sharing Transparency 2 Exchange Basics and

November 2017 Follow the Dollar

November 2017 Follow the Dollar Understanding How the Pharmaceutical Distribution and Payment System Shapes the Prices of Brand Medicines Table of Contents Introduction 1 From the Factory to the Pharmacy

November 2017 Follow the Dollar Understanding How the Pharmaceutical Distribution and Payment System Shapes the Prices of Brand Medicines Table of Contents Introduction 1 From the Factory to the Pharmacy

Payer Channel Forecasting and Analysis. Patrick J. Park, PharmD, MBA Director, Business Decision Support Daiichi Sankyo, Inc.

Payer Channel Forecasting and Analysis Patrick J. Park, PharmD, MBA Director, Business Decision Support Daiichi Sankyo, Inc. Disclaimer The views and opinions expressed in this presentation are those of

Payer Channel Forecasting and Analysis Patrick J. Park, PharmD, MBA Director, Business Decision Support Daiichi Sankyo, Inc. Disclaimer The views and opinions expressed in this presentation are those of

Follow the Dollar / Understanding Drug Prices and Beneficiary Costs Under Medicare Part D

Follow the Dollar / Understanding Drug Prices and Beneficiary Costs Under Medicare Part D Prepared for: The National Pharmaceutical Council Prepared by: Avalere Health LLC Lindy Hinman John Richardson

Follow the Dollar / Understanding Drug Prices and Beneficiary Costs Under Medicare Part D Prepared for: The National Pharmaceutical Council Prepared by: Avalere Health LLC Lindy Hinman John Richardson

2009 UBS Healthcare Services Conference

2009 UBS Healthcare Services Conference February 10, 2009 John H. Hammergren Chairman and Chief Executive Officer Safe Harbor Clause Some of the information in this presentation may constitute forwardlooking

2009 UBS Healthcare Services Conference February 10, 2009 John H. Hammergren Chairman and Chief Executive Officer Safe Harbor Clause Some of the information in this presentation may constitute forwardlooking

TouchScript Medication Management System. Financial Impact Analysis on Pharmacy Risk Pools

TouchScript Medication Management System Financial Impact Analysis on Pharmacy Risk Pools October 2000 Table of Contents Introduction 3 Executive Summary.. 4-5 Quantitative Analysis 6-10 TouchScript Impact

TouchScript Medication Management System Financial Impact Analysis on Pharmacy Risk Pools October 2000 Table of Contents Introduction 3 Executive Summary.. 4-5 Quantitative Analysis 6-10 TouchScript Impact

WorldatWork You and Your PBM: Improving Discounts, Fees and Rebates, and Beyond. Kristin Begley, Pharm.D. Principal

WorldatWork You and Your PBM: Improving Discounts, Fees and Rebates, and Beyond Kristin Begley, Pharm.D. Principal Presentation Overview The future of drug trend Prescription drug management levers: Contracting

WorldatWork You and Your PBM: Improving Discounts, Fees and Rebates, and Beyond Kristin Begley, Pharm.D. Principal Presentation Overview The future of drug trend Prescription drug management levers: Contracting

Pharmaceutical Management Commercial Plans

Pharmaceutical Management Commercial Plans 2015 Toll Free Contact Number: (888) 327-0671 Medical Management: (810) 733-9711 Visit our website at: MclarenHealthPlan.org Introduction Pharmaceutical Management

Pharmaceutical Management Commercial Plans 2015 Toll Free Contact Number: (888) 327-0671 Medical Management: (810) 733-9711 Visit our website at: MclarenHealthPlan.org Introduction Pharmaceutical Management

Texas Vendor Drug Program. Pharmacy Provider Procedure Manual Pricing & Reimbursement. Effective Date. March 2018

Texas Vendor Drug Program Pharmacy Provider Procedure Manual Pricing & Reimbursement Effective Date March 2018 The Pharmacy Provider Procedure Manual (PPPM) is available online at txvendordrug.com/about/policy/manual.

Texas Vendor Drug Program Pharmacy Provider Procedure Manual Pricing & Reimbursement Effective Date March 2018 The Pharmacy Provider Procedure Manual (PPPM) is available online at txvendordrug.com/about/policy/manual.

MELINTA THERAPEUTICS, INC. (Exact name of registrant specified in its charter)

") 3 3 UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, DC 20549 FORM 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

3 3 UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, DC 20549 FORM 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

340B Program Risk: A Perspective for Pharmaceutical Manufacturers

CiiTA Monograph Series 340B Program Risk: A Perspective for Pharmaceutical Manufacturers EXECUTIVE SUMMARY The number of ineligible prescriptions purchased through the PHS 340B Drug Discount Program represents

CiiTA Monograph Series 340B Program Risk: A Perspective for Pharmaceutical Manufacturers EXECUTIVE SUMMARY The number of ineligible prescriptions purchased through the PHS 340B Drug Discount Program represents

How the Blueprint Policy Statement to Lower Drug Costs and Reduce Out-of- Pocket Costs May Affect Employers

How the Blueprint Policy Statement to Lower Drug Costs and Reduce Out-of- Pocket Costs May Affect Employers Presented by: Lorie Maring Phone: (404) 240-4225 Email: lmaring@ AGENDA Provide an overview of

How the Blueprint Policy Statement to Lower Drug Costs and Reduce Out-of- Pocket Costs May Affect Employers Presented by: Lorie Maring Phone: (404) 240-4225 Email: lmaring@ AGENDA Provide an overview of

Access, Quality & Transparency: The Forgotten Issues in the Healthcare Debate Presented at WCIF Benefits Summit April 19, 2017

Access, Quality & Transparency: The Forgotten Issues in the Healthcare Debate Presented at WCIF Benefits Summit April 19, 2017 What s happened? What s next? The ACA remains the Law of the Land for now!

Access, Quality & Transparency: The Forgotten Issues in the Healthcare Debate Presented at WCIF Benefits Summit April 19, 2017 What s happened? What s next? The ACA remains the Law of the Land for now!

2013 Milliman Medical Index

2013 Milliman Medical Index $22,030 MILLIMAN MEDICAL INDEX 2013 $22,261 ANNUAL COST OF ATTENDING AN IN-STATE PUBLIC COLLEGE $9,144 COMBINED EMPLOYEE CONTRIBUTION $3,600 EMPLOYEE OUT-OF-POCKET $5,544 EMPLOYEE

2013 Milliman Medical Index $22,030 MILLIMAN MEDICAL INDEX 2013 $22,261 ANNUAL COST OF ATTENDING AN IN-STATE PUBLIC COLLEGE $9,144 COMBINED EMPLOYEE CONTRIBUTION $3,600 EMPLOYEE OUT-OF-POCKET $5,544 EMPLOYEE

Public and Private Payer Responses to Pharmaceutical Pricing in the United States

Public and Private Payer Responses to Pharmaceutical Pricing in the United States James C. Robinson Leonard D. Schaeffer Professor of Health Economics Director, Berkeley Center for Health Technology University

Public and Private Payer Responses to Pharmaceutical Pricing in the United States James C. Robinson Leonard D. Schaeffer Professor of Health Economics Director, Berkeley Center for Health Technology University

The 340B drug discount program was created in 1992

Proposed Rule Changes for 340B Programs: Overview and Impact Anthony Zappa, PharmD, MBA Specialty Healthcare Benefits Council The 340B drug discount program was created in 1992 as a means for certain nonprofit

Proposed Rule Changes for 340B Programs: Overview and Impact Anthony Zappa, PharmD, MBA Specialty Healthcare Benefits Council The 340B drug discount program was created in 1992 as a means for certain nonprofit

MEDICARE PLAN PAYMENT GROUP

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services 7500 Security Boulevard Baltimore, Maryland 21244-1850 MEDICARE PLAN PAYMENT GROUP Date: June 23, 2017 To: From: All Part

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services 7500 Security Boulevard Baltimore, Maryland 21244-1850 MEDICARE PLAN PAYMENT GROUP Date: June 23, 2017 To: From: All Part

Amgen GLOBAL CORPORATE COMPLIANCE POLICY

1. Scope Applicable to all Amgen Inc. and subsidiary or affiliated company staff members, consultants, contract workers, secondees and temporary staff worldwide ( Covered Persons ). Consultants, contract

1. Scope Applicable to all Amgen Inc. and subsidiary or affiliated company staff members, consultants, contract workers, secondees and temporary staff worldwide ( Covered Persons ). Consultants, contract

Pharmaceutical Summit on Business and Compliance Issues in Managed Markets

Pharmaceutical Summit on Business and Compliance Issues in Managed Markets TRACK A: 340B PROGRAM CONSIDERATIONS A Panel Discussion By: Agenda Panel Introductions Overview of 340B Program Compliance Considerations

Pharmaceutical Summit on Business and Compliance Issues in Managed Markets TRACK A: 340B PROGRAM CONSIDERATIONS A Panel Discussion By: Agenda Panel Introductions Overview of 340B Program Compliance Considerations

Drug Costs Driven By Rebates

Drug Costs Driven By Rebates OVER $100 BILLION IN PRICE CUTS GO DIRECTLY TO INSURERS, NOT PATIENTS Robert Goldberg, PhD VICE PRESIDENT, CENTER FOR MEDICINE IN THE PUBLIC INTEREST RGOLDBERG@CMPI.ORG Most

Drug Costs Driven By Rebates OVER $100 BILLION IN PRICE CUTS GO DIRECTLY TO INSURERS, NOT PATIENTS Robert Goldberg, PhD VICE PRESIDENT, CENTER FOR MEDICINE IN THE PUBLIC INTEREST RGOLDBERG@CMPI.ORG Most

Health Plan Approach to Operationalizing a Specialty Drug Management Program

Health Plan Approach to Operationalizing a Specialty Drug Management Program Mesfin Tegenu, MS, RPh Abstract BACKGROUND: Expenditures related to specialty drugs consume a significant percentage of available

Health Plan Approach to Operationalizing a Specialty Drug Management Program Mesfin Tegenu, MS, RPh Abstract BACKGROUND: Expenditures related to specialty drugs consume a significant percentage of available

UNDERSTANDING YOUR HEALTH INSURANCE CHOICES

UNDERSTANDING YOUR HEALTH INSURANCE CHOICES This booklet will provide you with a general overview of health insurance plan types, common terminology and factors to consider when choosing health insurance.

UNDERSTANDING YOUR HEALTH INSURANCE CHOICES This booklet will provide you with a general overview of health insurance plan types, common terminology and factors to consider when choosing health insurance.

THIRD PARTY REIMBURSEMENT OF COVERED ENTITIES: MANUFACTURERS PERSPECTIVE

THIRD PARTY REIMBURSEMENT OF COVERED ENTITIES: MANUFACTURERS PERSPECTIVE Donna Lee Yesner Morgan Lewis and Bockius Phone : 202.739.5887 Email: dyesner@morganlewis.com www.morganlewis.com BACKGROUND In

THIRD PARTY REIMBURSEMENT OF COVERED ENTITIES: MANUFACTURERS PERSPECTIVE Donna Lee Yesner Morgan Lewis and Bockius Phone : 202.739.5887 Email: dyesner@morganlewis.com www.morganlewis.com BACKGROUND In

Life Sciences Accounting and Financial Reporting Update Interpretive Guidance on Revenue Recognition Under ASC 605

Life Sciences Accounting and Financial Reporting Update Interpretive Guidance on Revenue Recognition Under ASC 605 March 2017 Revenue Recognition Introduction Many transactions in the life sciences industry

Life Sciences Accounting and Financial Reporting Update Interpretive Guidance on Revenue Recognition Under ASC 605 March 2017 Revenue Recognition Introduction Many transactions in the life sciences industry

Moving From PBM to PBA Model

Moving From PBM to PBA Model Lindsey Imada, PharmD Candidate 2016 Midwestern University, Chicago College of Pharmacy Pro Pharma Pharmaceutical Consultants, Inc. Under the preceptorship of Dr. Craig Stern

Moving From PBM to PBA Model Lindsey Imada, PharmD Candidate 2016 Midwestern University, Chicago College of Pharmacy Pro Pharma Pharmaceutical Consultants, Inc. Under the preceptorship of Dr. Craig Stern

CRS Report for Congress Received through the CRS Web

CRS Report for Congress Received through the CRS Web Order Code RS22059 February 18, 2005 The Pros and Cons of Allowing the Federal Government to Negotiate Prescription Drug Prices Summary Jim Hahn Analyst

CRS Report for Congress Received through the CRS Web Order Code RS22059 February 18, 2005 The Pros and Cons of Allowing the Federal Government to Negotiate Prescription Drug Prices Summary Jim Hahn Analyst

Inside: Critical information about your company s prescription drug benefit.

Inside: Critical information about your company s prescription drug benefit. Questions Company Benefits Managers Must Ask Their PBM It pays to make an informed decision harmacy Benefit Managers, often

Inside: Critical information about your company s prescription drug benefit. Questions Company Benefits Managers Must Ask Their PBM It pays to make an informed decision harmacy Benefit Managers, often

Pharmacy Benefit Management in Oncology

Pharmacy Benefit Management in Oncology October 28 th, 2015 Business Health Care Group Protecting the Future of Oncology Care: A Community Conversation Brent Eberle RPh MBA Chief Pharmacy Officer, Navitus

Pharmacy Benefit Management in Oncology October 28 th, 2015 Business Health Care Group Protecting the Future of Oncology Care: A Community Conversation Brent Eberle RPh MBA Chief Pharmacy Officer, Navitus

Medicare Congress: Fee for Service Trends: A Look at Medicare Part B

Medicare Congress: Fee for Service Trends: A Look at Medicare Part B November 1, 2005 Lauren Geyer Barnes Avalere Health LLC Avalere Health LLC The intersection of business strategy and public policy Three

Medicare Congress: Fee for Service Trends: A Look at Medicare Part B November 1, 2005 Lauren Geyer Barnes Avalere Health LLC Avalere Health LLC The intersection of business strategy and public policy Three

Annual Notice of Changes for 2019

Preferred Gold with Part D (HMO-POS) offered by MVP Health Plan, Inc. Annual Notice of Changes for 2019 You are currently enrolled as a member of Preferred Gold with Part D. Next year, there will be some

Preferred Gold with Part D (HMO-POS) offered by MVP Health Plan, Inc. Annual Notice of Changes for 2019 You are currently enrolled as a member of Preferred Gold with Part D. Next year, there will be some

Unique PBM Capabilities

Gaining Lives With Our Unique PBM Capabilities Jon Roberts Executive Vice President & President, CVS/caremark Agenda Performance Highlights Pharmacy Trends and Cost Management Programs Well Positioned

Gaining Lives With Our Unique PBM Capabilities Jon Roberts Executive Vice President & President, CVS/caremark Agenda Performance Highlights Pharmacy Trends and Cost Management Programs Well Positioned

Public Employees Benefits Program Legislative Session Bill Tracking Updated: 3/27/2017

Public Employees Benefits Program Legislative Session Bill Tracking Updated: 3/27/2017 Bill Number & Description Impact to PEBP & Bill Status AB249 (BDR 38-858) Requires the State Plan for Medicaid and

Public Employees Benefits Program Legislative Session Bill Tracking Updated: 3/27/2017 Bill Number & Description Impact to PEBP & Bill Status AB249 (BDR 38-858) Requires the State Plan for Medicaid and

Thank you for downloading this patient assistance document from NeedyMeds. We hope this program will help you get the medicine you need.

Thank you for downloading this patient assistance document from NeedyMeds. We hope this program will help you get the medicine you need. Did you know that NeedyMeds has thousands of other free resources?

Thank you for downloading this patient assistance document from NeedyMeds. We hope this program will help you get the medicine you need. Did you know that NeedyMeds has thousands of other free resources?

REPORT OF THE COUNCIL ON MEDICAL SERVICE. (J. Leonard Lichtenfeld, MD, Chair)

") REPORT OF THE COUNCIL ON MEDICAL SERVICE CMS Report -A-0 Subject: Presented by: Referred to: Appropriate Hospital Charges David O. Barbe, MD, Chair Reference Committee G (J. Leonard Lichtenfeld, MD, Chair)

REPORT OF THE COUNCIL ON MEDICAL SERVICE CMS Report -A-0 Subject: Presented by: Referred to: Appropriate Hospital Charges David O. Barbe, MD, Chair Reference Committee G (J. Leonard Lichtenfeld, MD, Chair)

TITLE IX REVENUE PROVISIONS Subtitle A Revenue Offset Provisions

H. R. 3590 729 Advisory Panel for the purpose of examining and advising the Secretary and Congress on workforce issues related to personal care attendant workers, including with respect to the adequacy

H. R. 3590 729 Advisory Panel for the purpose of examining and advising the Secretary and Congress on workforce issues related to personal care attendant workers, including with respect to the adequacy

Healthcare Options for Veterans

Healthcare Options for Veterans January 2017 (This information was copied from Unit 3 of Module 4 in the 2017 WIPA Training Manual) Introduction The U.S. Department of Defense (DoD) and the Department

Healthcare Options for Veterans January 2017 (This information was copied from Unit 3 of Module 4 in the 2017 WIPA Training Manual) Introduction The U.S. Department of Defense (DoD) and the Department

Glossary. Last Reviewed 11/10/14

Glossary ACCC ACA ACS AHFS AHRQ AMA APC Association of Community Cancer Centers Affordable Care Act American Cancer Society American Hospital Formulary Service Agency for Healthcare Research and Quality

Glossary ACCC ACA ACS AHFS AHRQ AMA APC Association of Community Cancer Centers Affordable Care Act American Cancer Society American Hospital Formulary Service Agency for Healthcare Research and Quality

A Payor and Provider s Perspective on Drug Pricing. Sharon Levine, MD Executive Vice President, The Permanente Federation

A Payor and Provider s Perspective on Drug Pricing Sharon Levine, MD Executive Vice President, The Permanente Federation National Academies of Sciences, Engineering and Medicine Stakeholder Meeting on

A Payor and Provider s Perspective on Drug Pricing Sharon Levine, MD Executive Vice President, The Permanente Federation National Academies of Sciences, Engineering and Medicine Stakeholder Meeting on

Calculating Accurate Metrics for the Actuarial Cost Model. Introduction. William Bednar, FSA, FCA, MAAA

Calculating Accurate Metrics for the Actuarial Cost Model William Bednar, FSA, FCA, MAAA Introduction Calculating metrics for an actuarial model sounds simple enough (just sum up the data!), but if proper

Calculating Accurate Metrics for the Actuarial Cost Model William Bednar, FSA, FCA, MAAA Introduction Calculating metrics for an actuarial model sounds simple enough (just sum up the data!), but if proper

Annual Notice of Changes for 2019

Gold PPO with Part D (PPO) offered by MVP Health Plan, Inc. Annual Notice of Changes for 2019 You are currently enrolled as a member of Gold PPO with Part D. Next year, there will be some changes to the

Gold PPO with Part D (PPO) offered by MVP Health Plan, Inc. Annual Notice of Changes for 2019 You are currently enrolled as a member of Gold PPO with Part D. Next year, there will be some changes to the

1/16/2014. David Pointer President, SolutionsRx

David Pointer President, SolutionsRx 417.679.2203 david@pointerlaw.com 1 340B Program Overview Physician-Administered Drugs Contract Pharmacies 340B Compliance Expanding 340B Utilization 2 Federally mandated

David Pointer President, SolutionsRx 417.679.2203 david@pointerlaw.com 1 340B Program Overview Physician-Administered Drugs Contract Pharmacies 340B Compliance Expanding 340B Utilization 2 Federally mandated

Fourth Quarter 2016 Earnings Conference Call

Fourth Quarter 2016 Earnings Conference Call Larry Merlo President & Chief Executive Officer Dave Denton Executive Vice President & Chief Financial Officer February 9, 2017 Revised 2/9 Forward-looking

Fourth Quarter 2016 Earnings Conference Call Larry Merlo President & Chief Executive Officer Dave Denton Executive Vice President & Chief Financial Officer February 9, 2017 Revised 2/9 Forward-looking

Implement a definition of negotiated price to include all pharmacy price concessions.

NCPA Analysis of Medicare Part D Pharmacy DIR Fee Reform Policy Proposal and Other Policies Impacting Community Pharmacies in the CMS Proposed Rule, Modernizing Part D and Medicare Advantage to Lower Drug

NCPA Analysis of Medicare Part D Pharmacy DIR Fee Reform Policy Proposal and Other Policies Impacting Community Pharmacies in the CMS Proposed Rule, Modernizing Part D and Medicare Advantage to Lower Drug