Reserving in Non-Life Insurance Company. April 21 st, 2012

|

|

|

- Luke White

- 6 years ago

- Views:

Transcription

1 Reserving in Non-Life Insurance Company April 21 st, 2012

2 Agenda Reserving Seminar a Types of Reserve b Principles and Method of Reserving c Financial Impact of Reserving & Key Ratio 236 d Reserving Trends in India 2

3 Slide Need to add pramod's slides , 4/19/2012

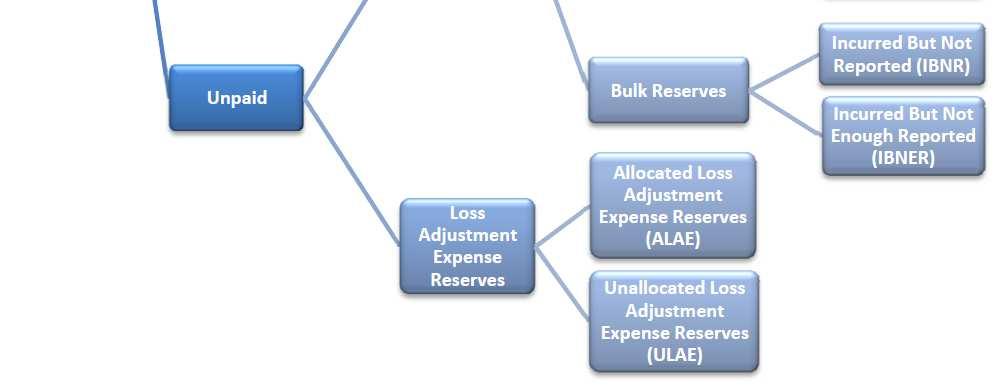

4 Types of Reserve in General Insurance

5 Typical cash-flow of a General Insurer Policyholder pays premium 1 Shareholders funds Commission paid to agent Company puts premium into unearned premium reserve Company earns premium over term of policy Full premium now earned Company pays claims or creates loss reserves to pay unsettled claims Company pays other business expenses 2 Company pays taxes and fees 3 Underwriting profit or loss Notes 1. The excess of assets over liabilities. 2. Overhead costs rent, salaries, etc. 3. Federal, state, local taxes, licenses, and fees. 4. Includes interest, dividends, rents, and realized capital gains. 5. Costs of operating the company s investment program. 6. If underwriting loss exceeds investment gain, there will be a net operating loss. Premium reserves produce 4 Loss reserves produce 6 Shareholders funds produce Investment income Investment income Investment income Net operating income (or loss) Total Investment income Net investment gain (or loss) Investment expenses 5 Dividends to stakeholders Additions to shareholders surplus to support future growth 4

6 Types of Reserve Unearned Premium Reserve UPR Case Estimates / Reserve Incurred but not reported IBNR Incurred but not enough reported IBNER Premium Deficiency Reserve PDR Catastrophe Reserve Cat Reserve 5

7 Life Cycle of a Claim Reserve 6 Accident Date Report Date Event: Status: Accident occurs Pure IBNR Accident reported Claims In Transit 6

8 Life Cycle of a Claim Reserve 7 Recorded Date Accident entered `1,000 Formula Reserve Formula Reserve Individual reserve established as `10,000 Case Reserve 7

9 Life Cycle of a Claim Reserve 8 Estimate revised `25,000 Case Reserve Settlement agreed `30,000 Case Reserve Development on known claims 8

10 Life Cycle of a Claim Reserve 9 Payment sent `30,000 Draft clears ` 0 Case Reserve Claim Closed Complications. Claim re-opens `10,00 Case Reserve Re-opened Claims Reserve 9

11 Life Cycle of a Claim Reserve 10 Settlement agreed `10,000 Case Reserve Payment sent `10,000 Draft clears ` 0 Case Reserve Claim Closed 10

12 11 Graphical Representation Claims cycle

13 Principles and Method of Reserving

14 Principles Actuarially Sound Based on estimates From reasonable assumptions Using appropriate methods Inherent Uncertainty A range can be actuarially sound True value know only after all claims are settled Purpose of Reserving Relative likelihood of estimates Reporting context Financial Management Pricing 13

15 Methods of Reserving - UPR Uniform Earning Pattern 1/365 th Method 1/24 th Method 1/8 th Method Marine Insurance Specific Cargo Policies Open policies & Open Covers Uneven Earning Pattern Extended Warranty EAR / CAR 14

16 UPR calculation for EAR / CAR Policy Characteristics Generally more than One year Policy Term Exposure is steadily increasing More commonly used = 1/365 th Method Important to Understand the risk Exposure 15

17 16 Example of different UPR methodology

18 Method of Reserving IBNR / IBNER Data Considerations Homogeneity Credibility Trade-Off between above Few Definitions Loss Development Triangles Loss development factor Other data sources / Proxies 17

19 Understanding Triangles Cumulative Paid Losses ($000 Omitted) Accident Development Stage in Months Year ,780 6,671 8,156 9,205 9,990 10, ,212 7,541 9,351 10,639 11, ,901 8,864 10,987 12, ,708 10,268 12, ,093 11, ,962 18

20 Loss Development Factor Evaluation Interval in Months Accident 72 to Year Ultimate ??? Sample Calculation for Accident Year 2002: 12-to-24 Months = 7,541 / 4,212 From the end of the accident year (at 12 months) to the end of the following year (at 24 months), paid losses for 2002 grew 79%. During the next year (from 24 to 36 months), paid losses experienced an additional 24% growth (or development) and so forth. 19

21 Estimating Ultimate Loss & IBNR/IBNER Cumulative Paid Losses ($000 Omitted) Accident Cumulative Accident Year Paid as of Year End Year ,780 6,671 8,156 9,205 9,990 10, ,212 7,541 9,351 10,639 11, ,901 8,864 10,987 12, ,708 10,268 12, ,093 11, ,962 IBNR/IBNER = Ultimate Losses Paid Claims Case Reserve 20

22 Estimating Ultimate Loss & IBNR/IBNER Ultimate Losses Minus Paid Losses Minus Case Reserves Ultimate Losses Minus Reported Losses Unpaid Losses Minus Case Reserves 21

23 Different Methods for Estimating IBNR Different Methods Paid / Incurred Claims Triangles Average Cost per claims B-F Evaluation of Different Methods Which estimate is right? Which is best estimate? Application of underlying assumption Stochastic 22

24 Method of Reserving - PDR Is sum total of expected net claim costs, related expenses and maintenance costs Exceeding the related premium carried forward to the subsequent accounting periods as reserve for unexpired risk. 23

25 Method of Reserving - PDR Grouping of Products / LoBs Have the same risk characteristics Asset backing the technical reserves are available for each other 24

26 Financial Impact of Reserving & Key Ratios

27 Key Performance Measure LossRatio = NetIncurredLoss NetEarned Pr emium ExpenseRatio = Expenses Commission NetWritten Pr emium SolvencyRatio = ShareholdersFund NetEarned Pr emium CombinedRa tio = LossRatio + ExpenseRatio 26

28 Ratio Pyramid ROE Combined 100% - X Operating Ratio 1 Solvency Ratio Combined Ratio - Investment Income Ratio Expense Ratio + Loss Ratio Commission & Brokerage Expense Ratio Other Acquisition General Expense Ratio Ratio Tax Incurred Ratio 27 27

29 Reserving Trends in India

30 Trends Provision as percentage of NEP has gone up to 72% from 65% in case of public sector companies. For Private sector, provision as percentage of NEP has gone down to 58% in FYE 2010 as compared to 66% in FY2006. Given that the premium rates have witnessed reduction in the range of 20% - 90%, the above trends makes us believe the relaxations in the reserving strength To Under reserve is to under-price the risk Warren Buffett 29

31 Latest Comparative Line of Business Private Sector But One All Significant Private Sector Public Sector Dec-2011 Mar-2011 Mar-2010 Dec-2011 Mar-2011 Mar-2010 Dec-2011 Mar-2011 Mar-2010 Aviation 7% 10% 15% 12% 8% 2% 32% 24% 23% Engineering 30% 29% 24% 12% 12% 8% 8% 9% 10% Fire 20% 18% 18% 8% 7% 6% 9% 12% 11% Health Insurance 70% 92% 89% 70% 83% 72% 56% 48% 49% Liabilities 119% 136% 90% 108% 129% 88% 22% 26% 19% Marine Cargo 27% 29% 30% 19% 17% 18% 11% 12% 9% Marine Hull 59% 69% 52% 8% 8% 5% 7% 12% 14% Motor 54% 43% 38% 61% 48% 43% 9% 8% 6% Others 74% 74% 69% 43% 36% 31% 18% 26% 24% Workmen Compensation 35% 48% 57% 35% 48% 57% Not Given Not Given Not Given Grand Total 52% 45% 41% 52% 43% 36% 11% 12% 10% 30

32 Any Questions

Basic Track I CLRS September 2009 Chicago, IL

Basic Track I 2009 CLRS September 2009 Chicago, IL Introduction to Loss 2 Reserving CAS Statement of Principles Definitions Principles Considerations Basic Reserving Techniques Paid Loss Development Method

Basic Track I 2009 CLRS September 2009 Chicago, IL Introduction to Loss 2 Reserving CAS Statement of Principles Definitions Principles Considerations Basic Reserving Techniques Paid Loss Development Method

Introduction to Casualty Actuarial Science

Introduction to Casualty Actuarial Science Executive Director Email: ken@theinfiniteactuary.com 1 Casualty Actuarial Science Two major areas are measuring 1. Written Premium Risk Pricing 2. Earned Premium

Introduction to Casualty Actuarial Science Executive Director Email: ken@theinfiniteactuary.com 1 Casualty Actuarial Science Two major areas are measuring 1. Written Premium Risk Pricing 2. Earned Premium

Introduction to Casualty Actuarial Science

Introduction to Casualty Actuarial Science Director of Property & Casualty Email: ken@theinfiniteactuary.com 1 Casualty Actuarial Science Two major areas are measuring 1. Written Premium Risk Pricing 2.

Introduction to Casualty Actuarial Science Director of Property & Casualty Email: ken@theinfiniteactuary.com 1 Casualty Actuarial Science Two major areas are measuring 1. Written Premium Risk Pricing 2.

Disclosures - IFFCO TOKIO General Insurance Co. Ltd. for the period 1st April - 31st December, 2017 S.No. Form No Description

Disclosures - IFFCO TOKIO General Insurance Co. Ltd. for the period 1st April - 31st December, 2017 S.No. Form No Description 1 NL-1-B-RA Revenue Account 2 NL-2-B-PL Profit & Loss Account 3 NL-3-B-BS Balance

Disclosures - IFFCO TOKIO General Insurance Co. Ltd. for the period 1st April - 31st December, 2017 S.No. Form No Description 1 NL-1-B-RA Revenue Account 2 NL-2-B-PL Profit & Loss Account 3 NL-3-B-BS Balance

Disclosures -NON LIFE INSURANCE COMPANIES

Disclosures -NON LIFE INSURANCE COMPANIES Sr No Form No Description 1 NL-1-B-RA Revenue Account 2 NL-2-B-PL Profit & Loss Account 3 NL-3-B-BS Balance Sheet 4 NL-4-PREMIUM SCHEDULE Premium 5 NL-5-CLAIMS

Disclosures -NON LIFE INSURANCE COMPANIES Sr No Form No Description 1 NL-1-B-RA Revenue Account 2 NL-2-B-PL Profit & Loss Account 3 NL-3-B-BS Balance Sheet 4 NL-4-PREMIUM SCHEDULE Premium 5 NL-5-CLAIMS

RELIANCE GENERAL INSURANCE COMPANY LIMITED - NON- LIFE INSURANCE COMPANIES

Disclosures - NON- LIFE INSURANCE COMPANIES S.No. Form No Description 1 NL-1-B-RA Revenue Account 2 NL-2-B-PL Profit & Loss Account 3 NL-3-B-BS Balance Sheet 4 NL-4-PREMIUM SCHEDULE Premium 5 NL-5-CLAIMS

Disclosures - NON- LIFE INSURANCE COMPANIES S.No. Form No Description 1 NL-1-B-RA Revenue Account 2 NL-2-B-PL Profit & Loss Account 3 NL-3-B-BS Balance Sheet 4 NL-4-PREMIUM SCHEDULE Premium 5 NL-5-CLAIMS

IFRS 4 / IND AS 104 As applicable to General Insurance Companies

TATA AIG GENERAL INSURANCE COMPANY LTD IFRS 4 / IND AS 104 As applicable to General Insurance Companies MIRANJIT MUKHERJEE 1 1-1 - AGENDA 1. Background of IFRS 4 2. Background of IND AS 104 3. What is

TATA AIG GENERAL INSURANCE COMPANY LTD IFRS 4 / IND AS 104 As applicable to General Insurance Companies MIRANJIT MUKHERJEE 1 1-1 - AGENDA 1. Background of IFRS 4 2. Background of IND AS 104 3. What is

It is the actuary s responsibility to ensure the accuracy of the unpaid claims and loss ratio analysis exhibit and accompanying electronic filing.

INSTRUCTIONS FOR THE UNPAID CLAIMS AND LOSS RATIO ANALYSIS EXHIBIT The Unpaid Claims and Loss Ratio Analysis Exhibits (see Appendix II) are constructed to allow the presentation and collection of industry

INSTRUCTIONS FOR THE UNPAID CLAIMS AND LOSS RATIO ANALYSIS EXHIBIT The Unpaid Claims and Loss Ratio Analysis Exhibits (see Appendix II) are constructed to allow the presentation and collection of industry

A company authorised under the Insurance Law to carry out general (or non life) insurance business.

insurance business.") International comparison of insurance taxation Cambodia General insurance overview Definition Definition of property and casualty insurance company A company authorised under the Insurance Law to carry

International comparison of insurance taxation Cambodia General insurance overview Definition Definition of property and casualty insurance company A company authorised under the Insurance Law to carry

IASB Educational Session Non-Life Claims Liability

IASB Educational Session Non-Life Claims Liability Presented by the January 19, 2005 Sam Gutterman and Martin White Agenda Background The claims process Components of claims liability and basic approach

IASB Educational Session Non-Life Claims Liability Presented by the January 19, 2005 Sam Gutterman and Martin White Agenda Background The claims process Components of claims liability and basic approach

Year Ended March 31, 2011

FORM NL-1-B-RA Name of the Insurer: TATA AIG GENERAL INSURANCE COMPANY LIMITED IRDA Registration No. 108, dated January 22, 2001 REVENUE ACCOUNT FOR THE YEAR ENDED MARCH 31, 2011 Particulars Schedule Year

FORM NL-1-B-RA Name of the Insurer: TATA AIG GENERAL INSURANCE COMPANY LIMITED IRDA Registration No. 108, dated January 22, 2001 REVENUE ACCOUNT FOR THE YEAR ENDED MARCH 31, 2011 Particulars Schedule Year

Basic Reserving: Estimating the Liability for Unpaid Claims

Basic Reserving: Estimating the Liability for Unpaid Claims September 15, 2014 Derek Freihaut, FCAS, MAAA John Wade, ACAS, MAAA Pinnacle Actuarial Resources, Inc. Loss Reserve What is a loss reserve? Amount

Basic Reserving: Estimating the Liability for Unpaid Claims September 15, 2014 Derek Freihaut, FCAS, MAAA John Wade, ACAS, MAAA Pinnacle Actuarial Resources, Inc. Loss Reserve What is a loss reserve? Amount

Understanding of Financial Statement of General Insurance

Understanding of Financial Statement of General Insurance August 4, 2018 CA Rakesh Rathi Indian General Insurance Industry Overview 15 th largest market - 0.83% of global non-life premium; Low penetration,

Understanding of Financial Statement of General Insurance August 4, 2018 CA Rakesh Rathi Indian General Insurance Industry Overview 15 th largest market - 0.83% of global non-life premium; Low penetration,

TWIN CITY FIRE INSURANCE COMPANY ASSETS

ASSETS Current Year Prior Year 1 2 3 4 Net Admitted Nonadmitted Assets Net Assets Assets (Cols. 1-2) Admitted Assets 1. Bonds (Schedule D)......595,649,174...0...595,649,174...592,035,687 2. Stocks (Schedule

ASSETS Current Year Prior Year 1 2 3 4 Net Admitted Nonadmitted Assets Net Assets Assets (Cols. 1-2) Admitted Assets 1. Bonds (Schedule D)......595,649,174...0...595,649,174...592,035,687 2. Stocks (Schedule

Non-Life Insurance in Latin America 2009 Casualty Loss Reserve Seminar

Non-Life Insurance in Latin America 2009 Casualty Loss Reserve Seminar Scott Kurban, FCAS, MAAA September 14, 2009 1 Regional Perspective - State of the Market Relevant Insurance Markets (By Population

Non-Life Insurance in Latin America 2009 Casualty Loss Reserve Seminar Scott Kurban, FCAS, MAAA September 14, 2009 1 Regional Perspective - State of the Market Relevant Insurance Markets (By Population

Revised Educational Note. Premium Liabilities. Committee on Property and Casualty Insurance Financial Reporting. March 2015.

Revised Educational Note Premium Liabilities Committee on Property and Casualty Insurance Financial Reporting March 2015 Document 215017 Ce document est disponible en français 2015 Canadian Institute of

Revised Educational Note Premium Liabilities Committee on Property and Casualty Insurance Financial Reporting March 2015 Document 215017 Ce document est disponible en français 2015 Canadian Institute of

Solvency Assessment and Management: Steering Committee. Position Paper 6 1 (v 1)

") Solvency Assessment and Management: Steering Committee Position Paper 6 1 (v 1) Interim Measures relating to Technical Provisions and Capital Requirements for Short-term Insurers 1 Discussion Document

Solvency Assessment and Management: Steering Committee Position Paper 6 1 (v 1) Interim Measures relating to Technical Provisions and Capital Requirements for Short-term Insurers 1 Discussion Document

Technical Provisions in Reinsurance: The Actuarial Perspective

Technical Provisions in Reinsurance: The Actuarial Perspective IAIS Reinsurance Subcommittee Copenhagen May 30, 2002 Presented by Dr. Hans Peter Boller, Converium Ltd (Switzerland) on behalf of the International

Technical Provisions in Reinsurance: The Actuarial Perspective IAIS Reinsurance Subcommittee Copenhagen May 30, 2002 Presented by Dr. Hans Peter Boller, Converium Ltd (Switzerland) on behalf of the International

Cambodia. A company authorised under the Insurance Law to carry out general (or non-life) insurance business.

insurance business.") Cambodia International Comparison of Insurance * May 2009 Cambodia General Insurance Definition Definition of property and casualty insurance company A company authorised under the Insurance Law to carry

Cambodia International Comparison of Insurance * May 2009 Cambodia General Insurance Definition Definition of property and casualty insurance company A company authorised under the Insurance Law to carry

9M2019 Performance Review

9M2019 Performance Review Agenda Company Strategy Financial Performance Industry Overview Agenda Company Strategy Financial Performance Industry Overview Strategy: Market leadership + Profitable growth

9M2019 Performance Review Agenda Company Strategy Financial Performance Industry Overview Agenda Company Strategy Financial Performance Industry Overview Strategy: Market leadership + Profitable growth

PERIODIC DISCLOSURES FORM NL-1-A-REVENUE ACCOUNT TATA AIG GENERAL INSURANCE COMPANY LIMITED IRDAI Registration No. 108, dated January 22, 2001

FORM NL-1-A-REVENUE ACCOUNT IRDAI Registration No. 18, dated January 22, 21 1 Premium earned (Net) NL-4- Premium Schedule 2 Profit/ Loss on sale/redemption of Investments Schedule REVENUE ACCOUNT FOR THE

FORM NL-1-A-REVENUE ACCOUNT IRDAI Registration No. 18, dated January 22, 21 1 Premium earned (Net) NL-4- Premium Schedule 2 Profit/ Loss on sale/redemption of Investments Schedule REVENUE ACCOUNT FOR THE

New Accounting Framework in Insurance Industry

New Accounting Framework in Insurance Industry R.C. Guria < E X E C U T I V E S U M M A R Y > With the opening of the insurance sector in India to the private and global giants the entire scenario of the

New Accounting Framework in Insurance Industry R.C. Guria < E X E C U T I V E S U M M A R Y > With the opening of the insurance sector in India to the private and global giants the entire scenario of the

An insurance company s investments in the stocks and bonds of its parents, subsidiaries and affiliates.

The Market Information Group Affiliated Investments An insurance company s investments in the stocks and bonds of its parents, subsidiaries and affiliates. BCAR Best s Capital Adequacy Ratio - A financial

The Market Information Group Affiliated Investments An insurance company s investments in the stocks and bonds of its parents, subsidiaries and affiliates. BCAR Best s Capital Adequacy Ratio - A financial

SCHEDULE P: MEMORIZE ME!!!

SCHEDULE P: MEMORIZE ME!!! NOTE: This skips all the prior years row calculation stuff, since it is covered pretty well by TIA (and I m sure any other manual). What are the cross-checks performed by the

SCHEDULE P: MEMORIZE ME!!! NOTE: This skips all the prior years row calculation stuff, since it is covered pretty well by TIA (and I m sure any other manual). What are the cross-checks performed by the

authorised under the Insurance Ordinance to carry on insurance business other than long-term (Life) insurance business.

insurance business.") International comparison of insurance taxation General insurance overview Definition Definition of property and casualty insurance company A company authorised under the Insurance Companies Ordinance to

International comparison of insurance taxation General insurance overview Definition Definition of property and casualty insurance company A company authorised under the Insurance Companies Ordinance to

Patrik. I really like the Cape Cod method. The math is simple and you don t have to think too hard.

Opening Thoughts I really like the Cape Cod method. The math is simple and you don t have to think too hard. Outline I. Reinsurance Loss Reserving Problems Problem 1: Claim report lags to reinsurers are

Opening Thoughts I really like the Cape Cod method. The math is simple and you don t have to think too hard. Outline I. Reinsurance Loss Reserving Problems Problem 1: Claim report lags to reinsurers are

ARGENTINA International Comparison of Insurance Taxation January 2005

International Comparison of Insurance International Comparison of Insurance Argentina General Insurance 1 Definition Definition of property and casualty insurance company Property and Casualty Insurance

International Comparison of Insurance International Comparison of Insurance Argentina General Insurance 1 Definition Definition of property and casualty insurance company Property and Casualty Insurance

University of California, Los Angeles Bruin Actuarial Society Information Session. Property & Casualty Actuarial Careers

University of California, Los Angeles Bruin Actuarial Society Information Session Property & Casualty Actuarial Careers November 14, 2017 Adam Adam Hirsch, Hirsch, FCAS, FCAS, MAAA MAAA Oliver Wyman Oliver

University of California, Los Angeles Bruin Actuarial Society Information Session Property & Casualty Actuarial Careers November 14, 2017 Adam Adam Hirsch, Hirsch, FCAS, FCAS, MAAA MAAA Oliver Wyman Oliver

Exam-Style Questions Relevant to the New Casualty Actuarial Society Exam 5B G. Stolyarov II, ARe, AIS Spring 2011

Exam-Style Questions Relevant to the New CAS Exam 5B - G. Stolyarov II 1 Exam-Style Questions Relevant to the New Casualty Actuarial Society Exam 5B G. Stolyarov II, ARe, AIS Spring 2011 Published under

Exam-Style Questions Relevant to the New CAS Exam 5B - G. Stolyarov II 1 Exam-Style Questions Relevant to the New Casualty Actuarial Society Exam 5B G. Stolyarov II, ARe, AIS Spring 2011 Published under

Argentina. Property and casualty insurance companies are those that insure the assets of the insured party.

Argentina International Comparison of Insurance * May 2009 Argentina General Insurance Definition Accounting Definition of property and casualty insurance company Commercial Accounts/Tax and Regulatory

Argentina International Comparison of Insurance * May 2009 Argentina General Insurance Definition Accounting Definition of property and casualty insurance company Commercial Accounts/Tax and Regulatory

Fire Marine Miscellaneous Total Fire Marine Miscellaneous Total 3,37,441 23,19,275 2,14,17,685 2,40,74,401 2,67,675 22,58,259 1,81,45,741 2,06,71,675

FORM NL-1-B-RA Name of the Insurer: TATA AIG GENERAL INSURANCE COMPANY IRDA Registration No. 108, dated January 22, 2001 REVENUE ACCOUNT FOR THE YEAR ENDED Particulars Schedule For the YEAR ENDED For the

FORM NL-1-B-RA Name of the Insurer: TATA AIG GENERAL INSURANCE COMPANY IRDA Registration No. 108, dated January 22, 2001 REVENUE ACCOUNT FOR THE YEAR ENDED Particulars Schedule For the YEAR ENDED For the

International comparison of insurance taxation. General insurance overview. Philippines. Definition of property and casualty insurance company

International comparison of insurance taxation Philippines General insurance overview Definition Definition of property and casualty insurance company Commercial accounts/ tax and regulatory returns Basis

International comparison of insurance taxation Philippines General insurance overview Definition Definition of property and casualty insurance company Commercial accounts/ tax and regulatory returns Basis

Basic non-life insurance and reserve methods

King Saud University College of Science Department of Mathematics Basic non-life insurance and reserve methods Student Name: Abdullah bin Ibrahim Al-Atar Student ID#: 434100610 Company Name: Al-Tawuniya

King Saud University College of Science Department of Mathematics Basic non-life insurance and reserve methods Student Name: Abdullah bin Ibrahim Al-Atar Student ID#: 434100610 Company Name: Al-Tawuniya

Second Revision Educational Note. Premium Liabilities. Committee on Property and Casualty Insurance Financial Reporting. July 2016.

Second Revision Educational Note Premium Liabilities Committee on Property and Casualty Insurance Financial Reporting July 2016 Document 216076 Ce document est disponible en français 2016 Canadian Institute

Second Revision Educational Note Premium Liabilities Committee on Property and Casualty Insurance Financial Reporting July 2016 Document 216076 Ce document est disponible en français 2016 Canadian Institute

Corporate Presentation

Corporate Presentation Agenda Industry Overview Operating Performance Financial Performance 2 Agenda Industry Overview Operating Performance Financial Performance 3 Industry has witnessed steady growth

Corporate Presentation Agenda Industry Overview Operating Performance Financial Performance 2 Agenda Industry Overview Operating Performance Financial Performance 3 Industry has witnessed steady growth

General Insurance Accounting

General Insurance Accounting PG JOSHI Though the basic accounting principles are same for accounting of general insurance business, due to very peculiar nature of general insurance business, there are

General Insurance Accounting PG JOSHI Though the basic accounting principles are same for accounting of general insurance business, due to very peculiar nature of general insurance business, there are

CAA Guideline for the Determination of A Proper Unexpired Risk Reserve

Contents CAA Guideline for the Determination of A Proper Unexpired Risk Reserve A. Purpose... 2 B. Scope... 2 C. Definitions... 2 D. Model Components... 5 D.1. Unearned Premium Reserve Component... 5 D.2.

Contents CAA Guideline for the Determination of A Proper Unexpired Risk Reserve A. Purpose... 2 B. Scope... 2 C. Definitions... 2 D. Model Components... 5 D.1. Unearned Premium Reserve Component... 5 D.2.

S I N G A P O R E. International Comparison of Insurance Taxation October 2007

S I N G A P O R E International Comparison of Insurance International Comparison of Insurance Singapore General Insurance 1 Definition Definition of property and casualty insurance company (Please note

S I N G A P O R E International Comparison of Insurance International Comparison of Insurance Singapore General Insurance 1 Definition Definition of property and casualty insurance company (Please note

Disclosures - IFFCO TOKIO General Insurance Co. Ltd. for the period 1st April - 30th September, 2017 S.No. Form No Description

Disclosures IFFCO TOKIO General Insurance Co. Ltd. for the period 1st April 30th September, 2017 S.No. Form No Description 1 NL1BRA Revenue Account 2 NL2BPL Profit & Loss Account 3 NL3BBS Balance Sheet

Disclosures IFFCO TOKIO General Insurance Co. Ltd. for the period 1st April 30th September, 2017 S.No. Form No Description 1 NL1BRA Revenue Account 2 NL2BPL Profit & Loss Account 3 NL3BBS Balance Sheet

General Insurance Industry in India

General Insurance Industry in India 2009 Casualty Loss Reserve Seminar September 14, 2009 Anita Sathe FCAS, FSA, MAAA ansathe@deloitte.com Contents History State of the market Removal of tariffs Key lines

General Insurance Industry in India 2009 Casualty Loss Reserve Seminar September 14, 2009 Anita Sathe FCAS, FSA, MAAA ansathe@deloitte.com Contents History State of the market Removal of tariffs Key lines

Premium Liabilities. Prepared by Melissa Yan BSc, FIAA

Prepared by Melissa Yan BSc, FIAA Presented to the Institute of Actuaries of Australia XVth General Insurance Seminar 16-19 October 2005 This paper has been prepared for the Institute of Actuaries of Australia

Prepared by Melissa Yan BSc, FIAA Presented to the Institute of Actuaries of Australia XVth General Insurance Seminar 16-19 October 2005 This paper has been prepared for the Institute of Actuaries of Australia

ANNUAL FINANCIAL REPORT. 31 December Assetinsure Pty Limited ABN

ANNUAL FINANCIAL REPORT 31 December Assetinsure Pty Limited ABN 65 066 463 803 ABN 65 066 463 803 Contents Directors report 1 Auditor s independence declaration 5 Statement of profit or loss and other

ANNUAL FINANCIAL REPORT 31 December Assetinsure Pty Limited ABN 65 066 463 803 ABN 65 066 463 803 Contents Directors report 1 Auditor s independence declaration 5 Statement of profit or loss and other

GIIRR Model Solutions Fall 2015

GIIRR Model Solutions Fall 2015 1. Learning Objectives: 1. The candidate will understand the key considerations for general insurance actuarial analysis. Learning Outcomes: (1k) Estimate written, earned

GIIRR Model Solutions Fall 2015 1. Learning Objectives: 1. The candidate will understand the key considerations for general insurance actuarial analysis. Learning Outcomes: (1k) Estimate written, earned

Q1 FY2019 Performance Review. July 17, 2018

Q1 FY2019 Performance Review July 17, 2018 Agenda Company Strategy Financial Performance Industry Overview 2 Agenda Company Strategy Financial Performance Industry Overview 3 Strategy: Market leadership

Q1 FY2019 Performance Review July 17, 2018 Agenda Company Strategy Financial Performance Industry Overview 2 Agenda Company Strategy Financial Performance Industry Overview 3 Strategy: Market leadership

authorised under the Insurance Act to carry out general (or non life) insurance business.

insurance business.") International comparison of insurance taxation Singapore General insurance overview Definition Definition of property and casualty insurance company Commercial accounts/ tax and regulatory returns Basis

International comparison of insurance taxation Singapore General insurance overview Definition Definition of property and casualty insurance company Commercial accounts/ tax and regulatory returns Basis

Prudential Standard FSM 2

Prudential Standard FSM 2 Valuation of Assets, Liabilities and Eligible Own Funds Objectives and Key Requirements of this Prudential Standard This Standard sets out the principles and requirements microinsurers

Prudential Standard FSM 2 Valuation of Assets, Liabilities and Eligible Own Funds Objectives and Key Requirements of this Prudential Standard This Standard sets out the principles and requirements microinsurers

FY 2018 Q3 Financial Results Presentation. Mumbai, 12 th February 2018

FY 2018 Q3 Financial Results Presentation Mumbai, 12 th February 2018 1 Agenda Market Review Strategic Overview Financial Performance 2 Market Review 3 Reinsurance Industry - Role Reinsurance is the foundation

FY 2018 Q3 Financial Results Presentation Mumbai, 12 th February 2018 1 Agenda Market Review Strategic Overview Financial Performance 2 Market Review 3 Reinsurance Industry - Role Reinsurance is the foundation

RELIANCE GENERAL INSURANCE COMPANY LIMITED - NON- LIFE INSURANCE COMPANIES

Disclosures - NON- LIFE INSURANCE COMPANIES S.No. Form No Description 1 NL-1-B-RA Revenue Account 2 NL-2-B-PL Profit & Loss Account 3 NL-3-B-BS Balance Sheet 4 NL-4-PREMIUM SCHEDULE Premium 5 NL-5-CLAIMS

Disclosures - NON- LIFE INSURANCE COMPANIES S.No. Form No Description 1 NL-1-B-RA Revenue Account 2 NL-2-B-PL Profit & Loss Account 3 NL-3-B-BS Balance Sheet 4 NL-4-PREMIUM SCHEDULE Premium 5 NL-5-CLAIMS

Prudential Standard FSI 4.3

Prudential Standard FSI 4.3 Non-life Underwriting Risk Capital Requirement Objectives and Key Requirements of this Prudential Standard This Standard sets out the details for calculating the capital requirement

Prudential Standard FSI 4.3 Non-life Underwriting Risk Capital Requirement Objectives and Key Requirements of this Prudential Standard This Standard sets out the details for calculating the capital requirement

(Legislative Supplement No. 16) THE INSURANCE ACT

THE INSURANCE ACT") CO SPECIAL ISSUE 127 Kenya Gazette Supplement No. 34 24th March, 2017 LEGAL NOTICE No. 37 (Legislative Supplement No. 16) THE INSURANCE ACT (Cap. 487) IN EXERCISE of the powers conferred by section 3A

CO SPECIAL ISSUE 127 Kenya Gazette Supplement No. 34 24th March, 2017 LEGAL NOTICE No. 37 (Legislative Supplement No. 16) THE INSURANCE ACT (Cap. 487) IN EXERCISE of the powers conferred by section 3A

COMBINED ANNUAL STATEMENT FOR THE YEAR ENDED DECEMBER 31, 2017 OF THE CONDITION AND AFFAIRS OF THE

*00000000* PROPERTY AND CASUALTY COMPANIES - ASSOCIATION EDITION COMBINED ANNUAL STATEMENT FOR THE YEAR ENDED DECEMBER, 0 OF THE CONDITION AND AFFAIRS OF THE AMERICAN INTERNATIONAL GROUP, INC. its affiliated

*00000000* PROPERTY AND CASUALTY COMPANIES - ASSOCIATION EDITION COMBINED ANNUAL STATEMENT FOR THE YEAR ENDED DECEMBER, 0 OF THE CONDITION AND AFFAIRS OF THE AMERICAN INTERNATIONAL GROUP, INC. its affiliated

FBD HOLDINGS PLC 4 TH I N T E R I M R E S U L T S A U G U S T

1 FBD HOLDINGS PLC 2 0 1 7 I N T E R I M R E S U L T S A U G U S T 4 TH 2 Forward looking statements This presentation contains certain forward-looking statements. Actual results may differ materially

1 FBD HOLDINGS PLC 2 0 1 7 I N T E R I M R E S U L T S A U G U S T 4 TH 2 Forward looking statements This presentation contains certain forward-looking statements. Actual results may differ materially

DOHA INSURANCE COMPANY Q.S.C. FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT FOR THE YEAR ENDED DECEMBER 31, 2013

FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT FOR THE YEAR ENDED DECEMBER 31, 2013 FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT INDEX Page Independent auditor s report -- Statement of

FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT FOR THE YEAR ENDED DECEMBER 31, 2013 FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT INDEX Page Independent auditor s report -- Statement of

National specific template Log NS.07 business model analysis non-life

National specific template Log NS.07 business model analysis non-life General Comments This Annex contains additional instructions and comments in relation to the national specific template NS.07. The

National specific template Log NS.07 business model analysis non-life General Comments This Annex contains additional instructions and comments in relation to the national specific template NS.07. The

FY2018 Performance Review. April 25, 2018

FY2018 Performance Review April 25, 2018 Agenda Company Strategy Financial Performance Industry Overview 2 Agenda Company Strategy Financial Performance Industry Overview 3 Strategy: Market leadership

FY2018 Performance Review April 25, 2018 Agenda Company Strategy Financial Performance Industry Overview 2 Agenda Company Strategy Financial Performance Industry Overview 3 Strategy: Market leadership

CAPITAL ADEQUACY MODULE

CAPITAL ADEQUACY MODULE Table of Contents CA-A Date Last Changed Introduction CA-A.1 Purpose 01/2011 CA-A.2 Module History 04/2014 CA-B Scope of Application CA-B.1 Bahraini Licensee and Overseas Licensee

CAPITAL ADEQUACY MODULE Table of Contents CA-A Date Last Changed Introduction CA-A.1 Purpose 01/2011 CA-A.2 Module History 04/2014 CA-B Scope of Application CA-B.1 Bahraini Licensee and Overseas Licensee

International Comparison of Insurance Taxation March Peru Subtitled (continued) International Comparison of Insurance Taxation October 2007

International Comparison of Insurance Taxation October 2007") International Comparison of Insurance March 2007 Peru Subtitled (continued) PERU International Comparison of Insurance International Comparison of Insurance Peru General Insurance 1 Definition According

International Comparison of Insurance March 2007 Peru Subtitled (continued) PERU International Comparison of Insurance International Comparison of Insurance Peru General Insurance 1 Definition According

Best Estimate Technical Provisions

Solvency II - QIS5 Non-Life Technical Provisions 15 September 2010 Dimitris Dimitriou 1 Best Estimate Technical Provisions 1 Agenda 1. Segmentation 2. Future Premiums 3. Valuation Techniques 4. Simplifications

Solvency II - QIS5 Non-Life Technical Provisions 15 September 2010 Dimitris Dimitriou 1 Best Estimate Technical Provisions 1 Agenda 1. Segmentation 2. Future Premiums 3. Valuation Techniques 4. Simplifications

GI IRR Model Solutions Spring 2015

GI IRR Model Solutions Spring 2015 1. Learning Objectives: 1. The candidate will understand the key considerations for general insurance actuarial analysis. Learning Outcomes: (1l) Adjust historical earned

GI IRR Model Solutions Spring 2015 1. Learning Objectives: 1. The candidate will understand the key considerations for general insurance actuarial analysis. Learning Outcomes: (1l) Adjust historical earned

Doha Insurance Company Q.S.C. INTERIM CONDENSED FINANCIAL STATEMENTS

Doha Insurance Company Q.S.C. INTERIM CONDENSED FINANCIAL STATEMENTS 30 JUNE 2010 Doha Insurance Company Q.S.C. INTERIM CONDENSED STATEMENT OF INCOME Six Months Period Ended 30 June 2010 Six Months Period

Doha Insurance Company Q.S.C. INTERIM CONDENSED FINANCIAL STATEMENTS 30 JUNE 2010 Doha Insurance Company Q.S.C. INTERIM CONDENSED STATEMENT OF INCOME Six Months Period Ended 30 June 2010 Six Months Period

London Market Pricing Framework

London Market Pricing Framework Hannes van Rensburg, Watson Wyatt Ryan Warren, Watson Wyatt GIRO 2009 - Edinburgh 8 October 2009 1 London Market Pricing Framework What we will cover Pricing framework Overview

London Market Pricing Framework Hannes van Rensburg, Watson Wyatt Ryan Warren, Watson Wyatt GIRO 2009 - Edinburgh 8 October 2009 1 London Market Pricing Framework What we will cover Pricing framework Overview

COMBINED ANNUAL STATEMENT FOR THE YEAR ENDED DECEMBER 31, 2016 OF THE CONDITION AND AFFAIRS OF THE

*00000000* PROPERTY AND CASUALTY COMPANIES - ASSOCIATION EDITION COMBINED ANNUAL STATEMENT FOR THE YEAR ENDED DECEMBER, 0 OF THE CONDITION AND AFFAIRS OF THE AMERICAN INTERNATIONAL GROUP, INC. its affiliated

*00000000* PROPERTY AND CASUALTY COMPANIES - ASSOCIATION EDITION COMBINED ANNUAL STATEMENT FOR THE YEAR ENDED DECEMBER, 0 OF THE CONDITION AND AFFAIRS OF THE AMERICAN INTERNATIONAL GROUP, INC. its affiliated

IMIA Working Group Paper 73 (11) Reserving - how to reserve an Engineering portfolio with its specific characteristics

Reserving - how to reserve an Engineering portfolio with its specific characteristics") IMIA Conference 2011 Amsterdam IMIA Working Group Paper 73 (11) - how to reserve an Engineering portfolio with its specific characteristics September 2011 Working Group Contributors 28.05.2009 2 Jürg Buff

IMIA Conference 2011 Amsterdam IMIA Working Group Paper 73 (11) - how to reserve an Engineering portfolio with its specific characteristics September 2011 Working Group Contributors 28.05.2009 2 Jürg Buff

Exploring the Fundamental Insurance Equation

Exploring the Fundamental Insurance Equation PATRICK STAPLETON, FCAS PRICING MANAGER ALLSTATE INSURANCE COMPANY PSTAP@ALLSTATE.COM CAS RPM March 2016 CAS Antitrust Notice The Casualty Actuarial Society

Exploring the Fundamental Insurance Equation PATRICK STAPLETON, FCAS PRICING MANAGER ALLSTATE INSURANCE COMPANY PSTAP@ALLSTATE.COM CAS RPM March 2016 CAS Antitrust Notice The Casualty Actuarial Society

UNITED STATES International Comparison of Insurance Taxation January 2005

International Comparison of Insurance International Comparison of Insurance United States General Insurance 1 Definition Definition of property and casualty insurance company A company to which insurance

International Comparison of Insurance International Comparison of Insurance United States General Insurance 1 Definition Definition of property and casualty insurance company A company to which insurance

Metropolitan Group Property and Casualty Insurance Company ASSETS

ASSETS Current Year Prior Year 1 2 3 4 Net Admitted Nonadmitted Assets Net Assets Assets (Cols. 1-2) Admitted Assets 1. Bonds (Schedule D)......351,261,854...0...351,261,854...369,773,387 2. Stocks (Schedule

ASSETS Current Year Prior Year 1 2 3 4 Net Admitted Nonadmitted Assets Net Assets Assets (Cols. 1-2) Admitted Assets 1. Bonds (Schedule D)......351,261,854...0...351,261,854...369,773,387 2. Stocks (Schedule

METLIFE, AMERICAN INTERNATIONAL GROUP AND ARAB NATIONAL BANK COOPERATIVE INSURANCE COMPANY (A SAUDI JOINT STOCK COMPANY)

") METLIFE, AMERICAN INTERNATIONAL GROUP AND ARAB NATIONAL BANK COOPERATIVE INSURANCE COMPANY (A SAUDI JOINT STOCK COMPANY) FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT 31 DECEMBER 2016 FINANCIAL

METLIFE, AMERICAN INTERNATIONAL GROUP AND ARAB NATIONAL BANK COOPERATIVE INSURANCE COMPANY (A SAUDI JOINT STOCK COMPANY) FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT 31 DECEMBER 2016 FINANCIAL

Solvency Assessment and Management. Non-Life Underwriting Risk Data Request 2012 User Manual

Solvency Assessment and Management Non-Life Underwriting Risk Data Request 2012 User Manual 03 October 2012 C O N T A C T D E T A I L S Physical Address: Riverwalk Office Park, Block B 41 Matroosberg Road

Solvency Assessment and Management Non-Life Underwriting Risk Data Request 2012 User Manual 03 October 2012 C O N T A C T D E T A I L S Physical Address: Riverwalk Office Park, Block B 41 Matroosberg Road

MINISTRY OF FINANCE OF THE REPUBLIC OF INDONESIA INDONESIA CAPITAL MARKET AND FINANCIAL INSTITUTIONS SUPERVISORY AGENCY COPY OF

Unofficial Translation MINISTRY OF FINANCE OF THE REPUBLIC OF INDONESIA COPY OF REGULATION OF THE CHAIRPERSON OF INDONESIA CAPITAL MARKET AND FINANCIAL INSTITUTIONS NUMBER: PER-09/BL/2012 CONCERNING THE

Unofficial Translation MINISTRY OF FINANCE OF THE REPUBLIC OF INDONESIA COPY OF REGULATION OF THE CHAIRPERSON OF INDONESIA CAPITAL MARKET AND FINANCIAL INSTITUTIONS NUMBER: PER-09/BL/2012 CONCERNING THE

PartnerRe Ltd Loss Development Triangles

2014 Loss Development Triangles Loss Development Triangle Cautionary Language The information in this financial supplement is for informational purposes only and is current only as of its stated date,

2014 Loss Development Triangles Loss Development Triangle Cautionary Language The information in this financial supplement is for informational purposes only and is current only as of its stated date,

Internal model outputs (Non-life) Log Instructions for templates IM IM and MO MO )NL.IMS.01-NL.IMS.

Log Instructions for templates IM IM and MO MO )NL.IMS.01-NL.IMS.") Draft for consultation as part of CP31/16, available at: www.bankofengland.co.uk/pra/pages/publications/cp/2016/cp3116.aspx In these draft instructions, deleted text is struck through and new text is underlined.

Draft for consultation as part of CP31/16, available at: www.bankofengland.co.uk/pra/pages/publications/cp/2016/cp3116.aspx In these draft instructions, deleted text is struck through and new text is underlined.

RELIANCE GENERAL INSURANCE COMPANY LIMITED Disclosures - NON- LIFE INSURANCE COMPANIES. S.No. Form No Description

Disclosures - NON- LIFE INSURANCE COMPANIES S.No. Form No Description 1 NL-1-B-RA Revenue Account 2 NL-2-B-PL Profit & Loss Account 3 NL-3-B-BS Balance Sheet 4 NL-4-PREMIUM SCHEDULE Premium 5 NL-5-CLAIMS

Disclosures - NON- LIFE INSURANCE COMPANIES S.No. Form No Description 1 NL-1-B-RA Revenue Account 2 NL-2-B-PL Profit & Loss Account 3 NL-3-B-BS Balance Sheet 4 NL-4-PREMIUM SCHEDULE Premium 5 NL-5-CLAIMS

Justification for, and Implications of, Regulators Suggesting Particular Reserving Techniques

Justification for, and Implications of, Regulators Suggesting Particular Reserving Techniques William J. Collins, ACAS Abstract Motivation. Prior to 30 th June 2013, Kenya s Insurance Regulatory Authority

Justification for, and Implications of, Regulators Suggesting Particular Reserving Techniques William J. Collins, ACAS Abstract Motivation. Prior to 30 th June 2013, Kenya s Insurance Regulatory Authority

IFRS 17 for non-life insurers

Ergebnisbericht des Ausschusses Rechnungslegung und Regulierung (Report on findings of the Accounting and Regulation Committee) IFRS 17 for non-life insurers Cologne, 17 August 2018 1 Preamble The Accounting

Ergebnisbericht des Ausschusses Rechnungslegung und Regulierung (Report on findings of the Accounting and Regulation Committee) IFRS 17 for non-life insurers Cologne, 17 August 2018 1 Preamble The Accounting

FY2006 Financial Results and Our Business Strategy

Code: 8754 http://www.nipponkoa.co.jp/ FY2006 Financial Results and Our Business Strategy May 2007 NIPPONKOA Insurance Co., Ltd. 1 Part I Toward Restoration of Consumers Confidence Outline of Events 3

Code: 8754 http://www.nipponkoa.co.jp/ FY2006 Financial Results and Our Business Strategy May 2007 NIPPONKOA Insurance Co., Ltd. 1 Part I Toward Restoration of Consumers Confidence Outline of Events 3

COMBINED ANNUAL STATEMENT FOR THE YEAR ENDED DECEMBER 31, 2016 OF THE CONDITION AND AFFAIRS OF THE

PROPERTY AND CASUALTY COMPANIES - ASSOCIATION EDITION COMBINED ANNUAL STATEMENT FOR THE YEAR ENDED DECEMBER, 0 OF THE CONDITION AND AFFAIRS OF THE Zurich American Insurance Company Affiliates its affiliated

PROPERTY AND CASUALTY COMPANIES - ASSOCIATION EDITION COMBINED ANNUAL STATEMENT FOR THE YEAR ENDED DECEMBER, 0 OF THE CONDITION AND AFFAIRS OF THE Zurich American Insurance Company Affiliates its affiliated

International Comparison of Insurance Taxation October 2007

International Comparison of Insurance International Comparison of Insurance Japan General Insurance 1 Definition Definition of property and casualty insurance company A company which is licensed by the

International Comparison of Insurance International Comparison of Insurance Japan General Insurance 1 Definition Definition of property and casualty insurance company A company which is licensed by the

Asia Insurance (Philippines) Corporation. Financial Statements As at and for the years ended December 31, 2012 and 2011

Corporation. Financial Statements As at and for the years ended December 31, 2012 and 2011") Asia Insurance (Philippines) Corporation Financial Statements As at and for the years ended December 31, 2012 and 2011 Asia Insurance (Philippines) Corporation Statements of Financial Position December

Asia Insurance (Philippines) Corporation Financial Statements As at and for the years ended December 31, 2012 and 2011 Asia Insurance (Philippines) Corporation Statements of Financial Position December

Financial Statements of. FACILITY ASSOCIATION RESIDUAL MARKET SEGMENT and UNINSURED AUTOMOBILE FUNDS

Financial Statements of FACILITY ASSOCIATION RESIDUAL MARKET SEGMENT and Table of Contents October 31, 2017 Independent Auditor s Report 1 Appointed Actuary s Report 3 Statement of Financial Position 4

Financial Statements of FACILITY ASSOCIATION RESIDUAL MARKET SEGMENT and Table of Contents October 31, 2017 Independent Auditor s Report 1 Appointed Actuary s Report 3 Statement of Financial Position 4

The term general insurance business is defined in the Insurance Act, 1995.

International comparison of insurance taxation Papua New Guinea General insurance overview Definition Definition of property and casualty insurance company Commercial accounts/ tax and regulatory returns

International comparison of insurance taxation Papua New Guinea General insurance overview Definition Definition of property and casualty insurance company Commercial accounts/ tax and regulatory returns

AAA REINSURANCE LIMITED FINANCIAL STATEMENTS FOR THE YEARS ENDED DECEMBER 31, 2016 AND 2015

FINANCIAL STATEMENTS (AND INDEPENDENT AUDITORS REPORT THEREON) FOR THE YEARS ENDED DECEMBER 31, 2016 AND 2015 FINANCIAL STATEMENTS AS AT DECEMBER 31, 2016 AND 2015 CONTENTS Independent Auditors Report....

FINANCIAL STATEMENTS (AND INDEPENDENT AUDITORS REPORT THEREON) FOR THE YEARS ENDED DECEMBER 31, 2016 AND 2015 FINANCIAL STATEMENTS AS AT DECEMBER 31, 2016 AND 2015 CONTENTS Independent Auditors Report....

Financial Report For the year ended 31 December 2012 ANNUAL REPORT 2012

Financial Report For the year ended 31 December ANNUAL REPORT 31 Statement of Comprehensive Income RACQ Group Note 3 Insurance claims expense 2(a) (399,895) (600,348) Outwards reinsurance premium expense

Financial Report For the year ended 31 December ANNUAL REPORT 31 Statement of Comprehensive Income RACQ Group Note 3 Insurance claims expense 2(a) (399,895) (600,348) Outwards reinsurance premium expense

Annexure-II Disclosures - NON- LIFE INSURANCE COMPANIES Form No Description Annually Halfyearly Quarterly Mode of Disclosure

S.No. Annexure-II Disclosures - NON- LIFE INSURANCE COMPANIES Form No Description Annually Halfyearly Quarterly Mode of Disclosure 1 NL-1-B-RA Revenue Account P 2 NL-2-B-PL Profit & Loss Account ** **

S.No. Annexure-II Disclosures - NON- LIFE INSURANCE COMPANIES Form No Description Annually Halfyearly Quarterly Mode of Disclosure 1 NL-1-B-RA Revenue Account P 2 NL-2-B-PL Profit & Loss Account ** **

Allianz Saudi Fransi Cooperative Insurance Company (A Saudi Joint Stock Company) AUDITED FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS AUDIT REPORT

AUDITED FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS AUDIT REPORT") Allianz Saudi Fransi Cooperative Insurance Company (A Saudi Joint Stock Company) AUDITED FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS AUDIT REPORT FOR THE YEAR ENDED 31 DECEMBER INDEX PAGES INDEPENDENT

Allianz Saudi Fransi Cooperative Insurance Company (A Saudi Joint Stock Company) AUDITED FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS AUDIT REPORT FOR THE YEAR ENDED 31 DECEMBER INDEX PAGES INDEPENDENT

IFRS Seminar for Regulators Accounting and Regulatory Issues Insurance Sector

REPARIS A REGIONAL PROGRAM IFRS Seminar for Regulators Accounting and Regulatory Issues Insurance Sector Session 2: Implications for regulators of IFRS4 Phase I versus Phase II Teddy Nyahasha May 31, 2011

REPARIS A REGIONAL PROGRAM IFRS Seminar for Regulators Accounting and Regulatory Issues Insurance Sector Session 2: Implications for regulators of IFRS4 Phase I versus Phase II Teddy Nyahasha May 31, 2011

POLAND International Comparison of Insurance Taxation January 2005

International Comparison of Insurance International Comparison of Insurance Poland General Insurance 1 Definition Definition of property and casualty insurance company An entity carrying out property and

International Comparison of Insurance International Comparison of Insurance Poland General Insurance 1 Definition Definition of property and casualty insurance company An entity carrying out property and

COMBINED ANNUAL STATEMENT

PROPERTY AND CASUALTY COMPANIES ASSOCIATION EDITION COMBINED ANNUAL STATEMENT FOR THE YEAR ENDING December, 06 OF THE CONDITION AND AFFAIRS OF THE ZENITH INSURANCE COMPANY AND ITS AFFILIATED PROPERTY AND

PROPERTY AND CASUALTY COMPANIES ASSOCIATION EDITION COMBINED ANNUAL STATEMENT FOR THE YEAR ENDING December, 06 OF THE CONDITION AND AFFAIRS OF THE ZENITH INSURANCE COMPANY AND ITS AFFILIATED PROPERTY AND

authorised under the Malaysian Insurance Act to carry out all insurance business

International comparison of insurance taxation Malaysia General insurance overview Definition Definition of property and casualty insurance company Commercial accounts/ tax and regulatory returns Basis

International comparison of insurance taxation Malaysia General insurance overview Definition Definition of property and casualty insurance company Commercial accounts/ tax and regulatory returns Basis

Financial Statements of FACILITY ASSOCIATION ONTARIO RISK SHARING POOL

Financial Statements of FACILITY ASSOCIATION Table of Contents October 31, 2017 Independent Auditor s Report 1 Appointed Actuary s Report 3 Statement of Financial Position 4 Statement of Operations 5 Statement

Financial Statements of FACILITY ASSOCIATION Table of Contents October 31, 2017 Independent Auditor s Report 1 Appointed Actuary s Report 3 Statement of Financial Position 4 Statement of Operations 5 Statement

Bajaj Allianz General Insurance Company Limited

Bajaj Allianz General Insurance Company Limited Fifth Annual Report 2004-2005 BAJAJ ALLIANZ GENERAL INSURANCE COMPANY LIMITED Message from the CEO 4. During the year, we issued over 2 million policies

Bajaj Allianz General Insurance Company Limited Fifth Annual Report 2004-2005 BAJAJ ALLIANZ GENERAL INSURANCE COMPANY LIMITED Message from the CEO 4. During the year, we issued over 2 million policies

Jamaica International Insurance Company Limited. Financial Statements 31 December 2004

Jamaica International Insurance Company Limited Financial Statements Index Actuary s Report Page Auditors Report to the Members Financial Statements Balance sheet 1 2 Profit and loss account 3 Statement

Jamaica International Insurance Company Limited Financial Statements Index Actuary s Report Page Auditors Report to the Members Financial Statements Balance sheet 1 2 Profit and loss account 3 Statement

Arab Misr Insurance Group An Egyptian Joint Stock Company Notes to the Financial Statements For the year ended June 30, 2005

Arab Misr Insurance Group An Egyptian Joint Stock Company Notes to the Financial Statements For the year ended June 30, 2005 1- Company background Arab Misr Insurance Group was established under the name

Arab Misr Insurance Group An Egyptian Joint Stock Company Notes to the Financial Statements For the year ended June 30, 2005 1- Company background Arab Misr Insurance Group was established under the name

INSTITUTE OF ACTUARIES OF INDIA

INSTITUTE OF ACTUARIES OF INDIA ACTUARIAL PRACTICE STANDARD (APS) 21 APPOINTED ACTUARY AND GENERAL INSURANCE BUSINESS Classification: Practice Standard Legislation or Authority: 1. The Insurance Act 1938

INSTITUTE OF ACTUARIES OF INDIA ACTUARIAL PRACTICE STANDARD (APS) 21 APPOINTED ACTUARY AND GENERAL INSURANCE BUSINESS Classification: Practice Standard Legislation or Authority: 1. The Insurance Act 1938

CHARTIS INSURANCE NEW ZEALAND LIMITED

INTERIM FINANCIAL STATEMENTS FOR THE SIX MONTHS ENDED 31 MAY 2012 STATEMENT OF COMPREHENSIVE INCOME (UNAUDITED) FOR THE SIX MONTHS ENDED 31 MAY 2012 31 May 31 May 2012 2011 Note Premium Revenue 70,183

INTERIM FINANCIAL STATEMENTS FOR THE SIX MONTHS ENDED 31 MAY 2012 STATEMENT OF COMPREHENSIVE INCOME (UNAUDITED) FOR THE SIX MONTHS ENDED 31 MAY 2012 31 May 31 May 2012 2011 Note Premium Revenue 70,183

Consolidated Hallmark Insurance Plc Interim Financial Statements Period Ended 31 March 2018

Consolidated Hallmark Insurance Plc Interim Financial Statements Period Ended 31 March 2018 1 FINANCIAL STATEMENTS PERIOD ENDED 31 MARCH 2018 INDEX Statement of Accounting Policies Statement of Financial

Consolidated Hallmark Insurance Plc Interim Financial Statements Period Ended 31 March 2018 1 FINANCIAL STATEMENTS PERIOD ENDED 31 MARCH 2018 INDEX Statement of Accounting Policies Statement of Financial

Statistical Modeling Techniques for Reserve Ranges: A Simulation Approach

Statistical Modeling Techniques for Reserve Ranges: A Simulation Approach by Chandu C. Patel, FCAS, MAAA KPMG Peat Marwick LLP Alfred Raws III, ACAS, FSA, MAAA KPMG Peat Marwick LLP STATISTICAL MODELING

Statistical Modeling Techniques for Reserve Ranges: A Simulation Approach by Chandu C. Patel, FCAS, MAAA KPMG Peat Marwick LLP Alfred Raws III, ACAS, FSA, MAAA KPMG Peat Marwick LLP STATISTICAL MODELING

REGULATION ON CALCULATION AND RETENTION OF TECHNICAL AND MATHEMATICAL PROVISIONS FOR LIFE AND NON-LIFE INSURERS. Article 1 Scope and Purpose

Based on Article 35, Paragraph 1, Subparagraph 1.1 of the Law No. 03/L209 on the Central Bank of the Republic of Kosovo (Official Gazette of the Republic of Kosovo, No. 77/16 August 2010) and Article 4,

Based on Article 35, Paragraph 1, Subparagraph 1.1 of the Law No. 03/L209 on the Central Bank of the Republic of Kosovo (Official Gazette of the Republic of Kosovo, No. 77/16 August 2010) and Article 4,

Institute of Actuaries of India. May 2010 EXAMINATION. Subject ST3 General Insurance Specialist Technical. Indicative Solution

Institute of Actuaries of India May 2010 EXAMINATION Subject ST3 General Insurance Specialist Technical Indicative Solution 1). i) The two main types of proportional reinsurance are quota share and surplus

Institute of Actuaries of India May 2010 EXAMINATION Subject ST3 General Insurance Specialist Technical Indicative Solution 1). i) The two main types of proportional reinsurance are quota share and surplus

FBD HOLDINGS PLC. 27 th F U L L Y E A R R E S U L T S F E B R U A R Y

1 FBD HOLDINGS PLC 2 0 1 7 F U L L Y E A R R E S U L T S F E B R U A R Y 27 th 2 Forward looking statements This presentation contains certain forward-looking statements. Actual results may differ materially

1 FBD HOLDINGS PLC 2 0 1 7 F U L L Y E A R R E S U L T S F E B R U A R Y 27 th 2 Forward looking statements This presentation contains certain forward-looking statements. Actual results may differ materially

SOCIETY OF ACTUARIES Introduction to Ratemaking & Reserving Exam GIIRR MORNING SESSION. Date: Wednesday, October 30, 2013 Time: 8:30 a.m. 11:45 a.m.

SOCIETY OF ACTUARIES Exam GIIRR MORNING SESSION Date: Wednesday, October 30, 2013 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 100 points.

SOCIETY OF ACTUARIES Exam GIIRR MORNING SESSION Date: Wednesday, October 30, 2013 Time: 8:30 a.m. 11:45 a.m. INSTRUCTIONS TO CANDIDATES General Instructions 1. This examination has a total of 100 points.