Garage and Garage Keepers Claim Handling. James W. Marshall III, Esquire Michael W. Taylor, Esquire

|

|

|

- Alfred Richards

- 6 years ago

- Views:

Transcription

1 Garage and Garage Keepers Claim Handling James W. Marshall III, Esquire Michael W. Taylor, Esquire

2 Introduction to Garage Owner s Insurance Businesses involved in selling, servicing, repairing, storing, or parking automobiles Potential liability is extraordinarily broad: automobile accident involving a vehicle owned by the insured business or a customer wrongful repossession of a vehicle premises liability claims Due to these exposure risks associated with garage-related businesses, the insurance industry developed garage owners insurance.

3

4 GARAGE COVERAGE FORM SECTION I COVERED AUTO

5 What is a Covered Auto? Indicated by Symbols Example:

6 Covered Auto under symbol 27? Mountaineerville Car Sales & Symbol 27: Dec page lists 2004 Nissan Altima as a covered auto; this car gets damaged: Covered auto Same dec page. Does not list 2006 Ford Escape; this car gets damaged: not a covered auto Trailer attached to a truck or other vehicle that is described in the Dec page maybe a covered auto, depending upon jurisdiction

7 Covered Auto under symbol 28? Mountaineerville Wrecking Services& Symbol 28: Insured leases a its tow truck: Covered Auto

8 Covered Auto under symbol 29? Mountaineerville Wrecking Services& Symbol 29: Insured leases a its tow truck: Not a Covered Auto Employee using tow truck that he personally owns to tow a vehicle to the shop: Covered

9 Covered Auto under symbol 30? Head down to Mountaineerville Service Station Customer leaves his car on lot to get service next day: Covered Customer leaves his golf cart on the lot to get service next day: Covered auto Customer leaves his helicopter on lot to get service: Not a covered auto Employee parks his car on lot while he works; not to get any service: Not a covered auto Employee leaves his car on the lot that is there to get service: Covered auto

10 Covered Auto under symbol 31? Mountaineerville Car Sales & Symbol 31: Dec page lists 2004 Nissan Altima as a covered auto; this car gets damaged: Covered auto Same dec page. Does not list 2006 Ford Escape; this car gets damaged: not a covered auto Similar to Symbol 27, but symbol 31 is restrictive to physical damage coverages

11 NOT A COVERED AUTO NOW WHAT? If you find that the vehicle involved was not a covered auto THERE STILL MAY BE COVERAGE!!! Different than BAP. Regardless of whether vehicle is a covered auto, you MUST look at section II to truly determine coverage

12 GARAGE COVERAGE FORM SECTION II LIABILITY COVERAGE This is the insuring agreement Where you find out what constitutes a covered damage and covered accident

13 Definition of Accident under the policy: "Accident" includes continuous or repeated exposure to the same conditions resulting in "bodily injury" or "property damage".

14 Was there an accident: Two boys trespassing on the insured property started a vehicle left for repair at the insured s garage facility. One of the trespassing boys was injured. The insurer argued that there was no accident because the trespassing boy was not injured as a result of a continuous or repeated exposure. Holding: Accident. Court found that the definition of accident is not limited to just continuous or repeated exposure to the same conditions. The definition states includes which is not a limiting phrase.

15 Other examples Accident or no Accident: Substituting gasoline for kerosene, resulting in a house fire off-site: Accident Employees suing Owner for miscalculations in sales commissions owed: Accident. Intentional overcharging fees in connection with registration and titling for the purchase of the automobile: Not an Accident Manager of a repair facility assaulted a customer: Not an Accident Tampering with the vehicle s odometer: Not an accident

16 Accident in Mountaineerville: We are at the Mountaineerville Towing Company: Big Taylor Swift concert in Mountaineerville. Many dignitaries, including the Vice-President and Secretary of State arrive and park in a fire lane, with Taylor Swift s personal car. Police arrive and contact Mountaineerville Towing Company to tow these cars from the fire lane. Mountaineerville Towing arrives and does so. Mountaineerville Towing does an excellent job and there is no damage. Afterwards these dignitaries unite and sue Mountaineerville Towing under a theory of conversion and trespass. Is this an accident under the policy? No. Because the act of conversion and trespass were intentional acts and there was no damage to the vehicles, the Court found this was not an accident under the policy.

17 Bodily Injury and Property Damage "Bodily injury" means bodily injury, sickness or disease sustained by a person including death re sulting from any of these. Property damage" means damage to or loss of use of tangible property.

18 REMINDER Just because a covered auto is NOT involved, does not mean there is no coverage.

19 Garage Operation -- Other than Covered Auto Policy Excerpt: 1. Garage Operation -- Other than Covered Auto b. This insurance applies to "bodily injury" and "property damage" only if:» (2) The "bodily injury" or "property damage" occurs during the policy period;

20 Example - Garage Operation -- Other than Covered Auto Mountaineerville Auto Sales: In 2006, Sally purchases a vehicle from Mountaineerville Auto Sales. The vehicle she purchases is not a covered auto under the garage policy purchased insured through Farmers. The vehicle she purchased was in a prior accident, but this was not disclosed to her at the time of the accident. After the purchase of the vehicle, Mountaineerville Auto Sales decides to take their insurance needs elsewhere. In 2008, Sally learns that her vehicle was involved in an accident and sues Mountaineerville Auto Sales for mental anguish. Mountaineerville Auto Sales makes a claim to Farmers because the vehicle was purchased during that policy period. Does this claim fall within the policy that was in effect in 2006? No. Sally s damage aka her mental anguish occurred outside the policy period, so the policy was not applicable.

21 Garage Operation -- Covered Auto Policy Excerpt 2. Garage Operation -- Covered Auto Does not have a similar policy limitation!!

22 Example - Garage Operation -- Covered Auto Same fact pattern, but change one fact (change in bold and underlined) Mountaineerville Auto Sales: In 2006, Sally purchases a vehicle from Mountaineerville Auto Sales. The vehicle she purchases is a covered auto under the garage policy purchased insured through Farmers. The vehicle she purchased was in a prior accident, but this was not disclosed to her at the time of the accident. After the purchase of the vehicle, Mountaineerville Auto Sales decides to take their insurance needs elsewhere. In 2008, Sally learns that her vehicle was involved in an accident and sues Mountaineerville Auto Sales for mental anguish. Mountaineerville Auto Sales makes a claim to Farmers because the vehicle was purchased during that policy period. Does this claim fall within the policy that was in effect in 2006? Yes. Damages to Covered Auto will be paid even if occur outside the policy period

23 One More Example - Garage Operation -- Covered Auto Fact Pattern: A dealership sold a vehicle in 2001 that was involved in an accident in The person involved in the accident sued the dealership under a theory that the seatbelt in the vehicle was defective. At the time of the sale, the vehicle was a covered auto. The dealership submitted the claim to its insurer under a policy that was effective for the year Court: The policy is effective because, even though the damage occurred outside the policy period, this was a covered auto and the policy did not have any time limitations. The Court went further and stated If an insurer wishes to restrict coverage for incidents or circumstances which occurred during the policy period, it is free to expressly say so.

24 Garage Operations: What is it? Policy definition: "Garage operations" means the ownership, main tenance or use of locations for garage business and that portion of the roads or other accesses that adjoin these locations. "Garage operations" includes the ownership, maintenance or use of the "autos" indicated in Section I of this coverage form as covered "autos". "Garage operations" also in clude all operations necessary or incidental to a garage business.

25 Examples of Garage Operations: A dealership loaned a vehicle to a customer while the customer's vehicle was being repaired. While driving the loaner vehicle, the customer was involved in an accident causing multiple deaths and injuries: Garage Operation. A business-related dispute between a management corporation which operated car dealerships and a rival executive group. Allegations included unlawful retaliation for a report of sexual harassment. Policy had an additional endorsement that included employment claims, if arising out of garage operations : Garage Operation. After an accident in which an employee of the insured car dealer hit a motorcycle rider, while the employee was operating the car on behalf of the car dealership, the underlying plaintiff sued the dealership for negligent supervision: Garage Operation. A car detailing business would pick up cars that needed detailing and drive the cars back to the shop to get detailed. Upon returning a car from being detailed, the car rear-ended another vehicle: Garage Operation A hotel guest suffered injuries after being struck by a luggage cart being pushed across the hotel lobby by a valet parker: Garage Operation.

26 Examples of No Garage Operation The insured picked up a customer's car for repairs. The owner of the repair facility used this car to ram his estranged wife's vehicle: Not a garage operation A dealership forcibly repossessed a vehicle it had sold by shooting the owner of the vehicle being reposed. Not a garage operation. The plaintiff was a passenger in a vehicle that had a temporary dealer's license plate, given to the owner of the vehicle by an auto dealer. A claim was made against the auto dealer s garage policy: Not a garage operation. The insured owned and operated a service station. He also sold reloaded shotgun shells from the garage storefront. The underlying plaintiff was injured while using the insured's reloaded shells: Not a garage operation

27 Mountaineerville Auto Repair Shop Example 1 Fact Pattern An accident occurred as an employee of Mountaineerville Auto Repair shop was delivering a vehicle back to the customer following repairs and service. This was the custom of the Mountaineerville Auto Repair shop and was agreed to by the customer. Garage operation? Yes. Returning the car to the customer in this manner was acceptable custom and agreement and therefore, was necessary and incidental to the operation of the station.

28 Mountaineerville Auto Repair Shop Example 2 Fact Pattern Customer drops off a vehicle to Mountaineerville Auto Repair shop for a routine oil change. After the routine oil change, the customer returns to the vehicle, but while pulling out onto the road, he notices that his tire is flat. Owner of Mountaineerville Auto Repair shop decides that he will put air in the tire at no charge. He drives the car into the garage to have an employee put air in the tire. When he does so, he accidently hits the back wall of the garage damaging the vehicle. Garage operation? Yes. The accident here was a natural consequence of the operation of a service station. Court under similar circumstances stated: It is patently unreasonable to expect that a service station owner would not help a customer [with his] vehicle [that] the owner has just serviced. That the owner renders the aid voluntarily, to obtain or maintain good will, and for no extra charge, does not remove the act from the range of coverage.

29 Mountaineerville Auto Repair Shop Example 3 Fact Pattern Mountaineerville Auto Repair Shop owned a vehicle that it used to pick up automobile parts for the business. The owner allowed his son to use this particular vehicle for personal matters. The son had permission to use the vehicle to go hunting and then take the vehicle home after work. On the day of the accident, the son drove the vehicle to a local bar after the end of the work day. He and a female companion left the bar and were traveling to his house at the time of the accident. Garage operation? No. Under a similar factual scenario Court held that "[t]here is not a faint hint of use of the [vehicle] for garage operations under the circumstances herein."

30 One Wrinkle to what is a Garage Operation: Certain courts have found coverage when the accident involved only a covered auto, but not a garage operation. Why? Definition of Garage Operations in the policy states, in part, Garage operations includes the ownership, maintenance, or use of the auto indicated in section 1 of this coverage form as a covered auto, Courts in California, Virginia, Colorado, Florida, and West Virginia have accepted this argument. Courts in Delaware, Idaho, Michigan, New Hampshire, Pennsylvania, Connecticut, Hawaii and Kansas have expressly rejected this argument.

31 Who is an insured for accidents involving Covered Auto: Policy Excerpt: (1) You for any covered "auto".

32 Who is an insured for accidents involving Covered Auto: Policy Excerpt (continued): (2) Anyone else while using with your per mission a covered "auto" you own, hire or borrow except: (a) The owner or anyone else from whom you hire or borrow a covered "auto". This exception does not apply if the covered "auto" is a "trailer" connected to a covered "auto" you own. (b) Your "employee" if the covered "auto" is owned by that "employee" or a member of his or her household. (c) Someone using a covered "auto" while he or she is working in a busi ness of selling, servicing or repairing "autos" unless that business is your "garage operations". (d) Your customers. However, if a customer of yours: (i) Has no other available insurance (whether primary, excess or con tingent), they are an "insured" but only up to the compulsory or financial responsibility law limits where the covered "auto" is principally garaged. (ii) Has other available insurance (whether primary, excess or contingent) less than the compulsory or financial responsibility law limits where the cov ered "auto" is principally garaged, they are an "insured" only for the amount by which the compulsory or financial responsibility law limits exceed the limit of their other insurance. (e) A partner (if you are a partnership) or a member (if you are a limited liability company) for a covered "auto" owned by him or her or a member of his or her household.

33 Permissive Users: Courts have looked at this issue very broadly Example: A customer goes onto the car lot and obtains initial permission to test drive the vehicle, but was instructed to return it that day. The customer does not return it and in fact never returned the vehicle. Sixteen days later, the customer was in a car accident involving the vehicle he got from the lot. Court found that under the policy, the customer was still a permissive user because he had initial permission. Therefore, he was an insured under the garage policy. Courts have looked at this issue very narrowly: Example: Employee worked as a car salesman for the employer. Employee was granted permission to take a car home for the night and to return it to the employer the next day. The employee was not authorized to use the car for any other purpose or to drive the car anywhere else. The employee took the car out of town to a party and was involved in a car accident. No coverage because he was outside the scope of his permission to use the car

34 Who is an insured for accidents involving Covered Auto: Policy Excerpt (continued): (3) Anyone liable for the conduct of an "in sured" described above but only to the extent of that liability. (4) Your "employee" while using a covered "auto" you do not own, hire or borrow in your business or your personal affairs.

35 Who is an insured for accidents involving Non-Covered Auto: Policy Excerpt: (1) You. (2) Your partners (if you are a partnership), members (if you are a limited liability company), "employees", directors or shareholders but only while acting within the scope of their duties.

36 Employees within the Scope of Their Duties Examples: A salesman in Hilton Head, SC attending an annual meeting was within the scope of his duties when he was driving from the hotel to a restaurant on a Saturday evening A used car salesman drove a used car primarily for the purpose of familiarizing himself with its operation in order to better represent the car to a prospective customer, although he joined with such purpose his personal business of going home for lunch, and was involved in a collision on his way home An employee returning a customer auto and when he got to the customer s house, the customer asked the employee to drive him and a friend to his friend s car. On the way to the friend s car, the employee and passengers were in an accident.

37 Employees Not within the Scope of Their Duties Example: an employee of a used car dealer driving an automobile belonging to the dealer on a purely private business was involved in an accident and left the damaged automobile standing on the street;

38 Mountaineerville Example - Covered Auto 1 Is this person an insured: Mountaineerville Auto Sales loans a used car to a family for a weekend test drive. Mountaineerville Auto Sales did not place any restrictions on its use. A friend of the family was using the automobile and was in an accident. Insured under the policy? Yes, likely will be determined to be a permissive use.

39 Mountaineerville Example - Covered Auto 2 Is this person an insured: Mountaineerville Auto Sales employee takes a car home for a weekend test drive to potentially purchase the vehicle. Over the weekend, the employee gets in an accident. Insured under the policy? Yes, but not because he was an employee, but as a permissive user

40 Mountaineerville Example - Covered Auto 3 Is this person an insured: Same car salesman, only this time he is riding along with a potential customer on a test drive. A warning light comes on in the vehicle and the potential customer pulls over so the car salesman can look at the vehicle. When the car salesman gets out of the vehicle, the potential customer speeds away, causing injury to the salesman. Is the potential customer an insured? Depends on the jurisdiction. The fact pattern this is based off of, the Court found not an insured. However, in a jurisdiction that has a broad definition of permissive user, the potential customer/thief may be considered an insured.

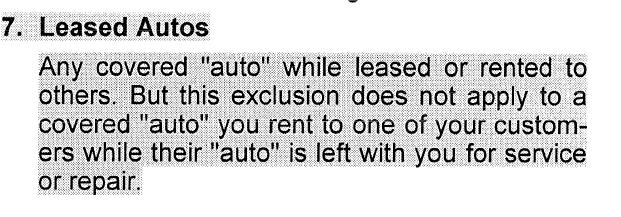

41 Mountaineerville Example - Non-Covered Auto 1 Is he an insured? At Mountaineerville Service Station. Employee returning a non-covered auto to the customer. On his way, he notices that the gas tank is low and decides to refuel the vehicle. When pulling into the gas station, he hit a pedestrian. A claim is made under Mountaineerville Service Station s garage policy. Is the employee an Insured? Yes. Acting within the scope of his duties.

42 Mountaineerville Example - Non-Covered Auto 2 Is he an insured? At Mountaineerville Auto Sales. Employee, was involved in an accident while returning from driving a customer s automobile which had been previously repaired by the sales agency. The salesman had no authority to road-test any automobile. Insured? No. Acted outside the scope of his authority

43 Coverage Limits: Per Accident vs. Aggregate Limit Garage Operations -- Other Than Covered Autos Typically the most we will pay for the sum of all damages involving garage operations other than auto is the Aggregate Limit of Insurance Garage Operations Other Than Covered "Autos" for Liability Coverage shown in the Declarations. Example: $100,000 Aggregate limit for 12 month period. Each claim for an other than covered auto will reduce the $100,000 by the amount paid out for the claim.

44 Coverage Limits: Per Accident vs. Aggregate Limit Garage Operations -- Covered Autos Typically the most we will pay for the total of all damages and covered pollution cost or expense combined, resulting from any one accident involving a covered auto is the Each Accident Limit of Insurance Garage Operations Covered Autos for Liability Coverage shown in the Declarations. This is similar to an auto policy where will pay $20,000 per person or total of $40,000 per accident. Limits found on Declarations page.

45 Exclusions Section II liability coverage Section III garage keepers coverage Section II and Section III are separate because Section II liability coverage has an exclusion for property in the insured s care, custody, or control. Section III covers this specific exclusion.

46 Section II liability coverage exclusions Expected or intended injuries Exception

47

48 Section II liability exclusion Leased auto Exception

49

50 Section II liability exclusion Pollution Exclusion Applicable to garage operations other than covered autos

51

52 Section II liability exclusion Work performed

53

54 Section II liability exclusion Loss of Use

55

56 Section II liability exclusion Products Recall

57

58 Distinguishing Garagekeepers Coverage Provides bailment-related liability coverage for the insured Provides third-party liability coverage for the insured Despite the care, custody or control exclusion, a garage policy insured may have liability coverage in bailment situations but only if garagekeepers coverage has been purchased Garagekeepers provides protection under different legal principles which result in increased risk. This generally translates into a higher premium commensurate with the greater risk

59 Covered Auto Versus Customer s Auto We will pay all sums the "insured" legally must pay as damages for "loss" to a "customer's auto" or "customer's auto" equipment left in the "insured's" care while the "insured" is attending, servicing, repairing, parking or storing it in your "garage operations". Customer s Auto is defined as: "Customer's auto" means a land motor vehicle, "trailer" or semitrailer lawfully within your posses sion for service, repair, storage or safe keeping, with or without the vehicle owner's knowledge or consent. A "customer's auto" also includes any such vehicle left in your care by your "employees" and members of their households, who pay for services performed.

60 Hypothetical: Safekeeping Customer leased a vehicle from dealer with option to purchase and the end of the contract period Dispute arises over the purchase price at the end of the contract term and the dealer reposes the vehicle under the protest of the customer Customer sues dealer and dealer seeks indemnification and a defense under his Garagekeepers insurance. Does coverage apply? Is the customer s vehicle being stored for safekeeping?

61 There Must Be an Underlying Loss Loss is defined as direct and accidental loss or damage. For garagekeepers coverage only, Loss is expanded to includes any resulting loss of use.

62 Narrow View of loss: Dodgeland of Columbia, Inc. v. Federated Mutual Insurance Co. The vehicles were to be modified to include scrolling advertising billboards. Dodgeland delivered the vehicles, after they had been sold to the customers, to a separate company to make those modifications, but the separate company went out of business and never completed the work. The court determined that the vehicles were not covered autos under the garagekeepers coverage section of Dodgeland s policy, but also found that the policy did not cover the type of loss allegedly suffered. The court held that [t]he loss suffered in this case was economic in nature and not the result of any direct or accidental harm to the vehicles and, thus, narrowed the definition of loss to preclude economic loss.

63 Broad View of Loss: In Universal Collision Center, Inc. v. Travelers Indemnity Co. of Connecticut, Inc., Florida Accident occurred and Vehicle was transferred for storage pending litigation. After the transfer, the key evidence which was the vehicle's right wheel assembly was lost. Florida determined the definition of loss was broad so as cover both the loss of automotive property and loss of use of such property as evidence in civil action, whether the loss is borne from a negligent or intentional act. Loss broadly defined to include the loss of intangible property which is the negligence claim in pending litigation.

64 Garage operations requirement in garagekeepers section Consistent with the requirement within the liability portion of the garage policy, i.e., whether the underlying accident involved covered autos or not, it must have resulted from garage operations. Lambert v. Northwestern National Insurance Co. Idaho Insured owned a repair shop specializing in four-wheel drive vehicles. Insured takes vehicle for lengthy test drive after repairs are performed and an accident occurs. Insured took his wife, a friend, the friend's wife and their friend's baby on the test drive. Insured and his friend also took hunting rifles to do some road hunting. The court rejected the insured s contention that he was entitled to garagekeepers coverage and found the policy generally limited to uses within the reasonable, objectively determined scope of the garage operations and found that such coverage should not be extended to include personal uses which are in no way germane to the attending, servicing, repairing, parking or storage of the vehicle.

65 Three types of Coverage Comprehensive Coverage From any cause except: (1) The "customer's auto's" collision with another object; or (2) The "customer's auto's" overturn. Specified Causes Of Loss Coverage Caused by: (1) Fire, lightning or explosion; (2) Theft; or (3) Mischief or vandalism. Collision Coverage Caused by: (1) The "customer's auto's" collision with another object; or (2) The "customer's auto's" overturn.

66 Limits 1. Regardless of the number of "customer's autos", "insureds", premiums paid, claims made or "suits" brought, the most we will pay for each "loss" at each location is the Garagekeepers Coverage Limit of Insurance shown in the Declarations for that location. Prior to the application of this limit, the damages for "loss" that would otherwise be payable will be reduced by the applicable deductibles for "loss" caused by: a. Collision; or b. With respect to Garagekeepers Coverage Comprehensive or Specified Causes Of Loss Coverage: (1) Theft or mischief or vandalism; or (2) All perils. 2. The maximum deductible stated in the Declara tions for Garagekeepers Coverage Compre hensive or Specified Causes Of Loss Cover age is the most that will be deducted for all "loss" in any one event caused by: a. Theft or mischief or vandalism; or b. All perils. 3. Sometimes to settle a claim or "suit", we may pay all or any part of the deductible. If this happens you must reimburse us for the de ductible or that portion of the deductible that we paid.

67 Section III Garage Keepers Coverage Exclusions Contractual Obligations

68

69 Section III Garage Keepers Coverage Exclusions Theft caused by you

70

71 Section III Garage Keepers Coverage Exclusions Defective parts or materials

72

73 Section III Garage Keepers Coverage Exclusions Faulty work

74

75 Section III Garage Keepers Coverage Exclusions Tape decks or other sound reproducing equipment unless permanently installed in customers auto

76

77 Section III Garage Keepers Coverage Exclusions Sound receiving equipment not permanently installed Radar detector War

78 Physical Damage Coverage No reference to indemnity for legally obligated damages No reference to any type of duty to defend or settle States that the insurer will pay for loss to a covered auto or its equipment where coverage applies

79 Loss under Physical Damage Section Requires loss to a covered auto Analysis is the same as garage liability

80 Types of Coverage Comprehensive Coverage From any cause except: (1) The covered "auto's" collision with another object; or (2) The covered "auto's" overturn. Specified Causes Of Loss Coverage Caused by: (1) Fire, lightning or explosion; (2) Theft; (3) Windstorm, hail or earthquake; (4) Flood; (5) Mischief or vandalism; or (6) The sinking, burning, collision or derailment of any conveyance transporting the covered "auto". c. Collision Coverage Caused by: (1) The covered "auto's" collision with another object; or (2) The covered "auto's" overturn.

81 Theft Coverage v. False Pretense Exclusion 4. False Pretense We will not pay for "loss" to a covered "auto" caused by or resulting from: a. Someone causing you to voluntarily part with it by trick or scheme or under false pre tenses; or b. Your acquiring an "auto" from a seller who did not have legal title. Liggans R.V. Center v. John Deere Insurance Co. Alabama Purported customers received permission to drive a motor home to a local mechanic for inspection, and left a Chevrolet Blazer with the insured. The customers never returned and it was discovered that the Blazer had actually been stolen from Georgia. The insured R.V. dealer had physical damage coverage that included theft but the policy precluded coverage for loss resulting from false pretense. In comparing the theft coverage with the false pretense exclusion, and based on the particular facts of this case, the court concluded that the loss of the motor home was attributable to trickery and not theft as an ordinary person would understand that undefined term within the policy.

82 Hypothetical: Coverage for Theft Dealer obtains new inventory to place on the lot. While in transition to be delivered to the dealership in Mountaineerville, a 2009 Camaro was stolen, completely dismantled, stripped and carried away except for the frame. The dealer did not have possession, does coverage still exist? Theft coverage has been extended to include situations in which the theft occurred while the vehicle was outside the possession of the insured. However, the theft must be of the covered auto (or its equipment) rather than any lost proceeds from a sale.

83 Coverage Limits C. Limits Of Insurance 1. The most we will pay for "loss" to any one cov ered "auto" is the lesser of: a. The actual cash value of the damaged or stolen property as of the time of "loss"; or b. The cost of repairing or replacing the dam aged or stolen property with other property of like kind and quality.

84 Coverage Limits 2. $1,000 is the most we will pay for "loss" in any one "accident" to all electronic equipment that reproduces, receives or transmits audio, visual or data signals which, at the time of "loss", is: A. Permanently installed in or upon the cov ered "auto" in a housing, opening or other location that is not normally used by the "auto" manufacturer for the installation of such equipment; B. Removable from a permanently installed housing unit as described in Paragraph 2.a. above; or C. An integral part of such equipment.

85 Coverage Limits 3. An adjustment for depreciation and physical condition will be made in determining actual cash value in the event of a total "loss". 4. If a repair or replacement results in better than like kind or quality, we will not pay for the amount of the betterment.

86 Coverage Limits 5. The following provisions also apply: a. Regardless of the number of covered "autos" involved in the "loss", the most we will pay for all "loss" at any one location is the amount shown in the Declarations for that location. Regardless of the number of covered "autos" involved in the "loss", the most we will pay for all "loss" in transit is the amount shown in the Declarations for "loss" in transit. b. Quarterly Or Monthly Reporting Premium Basis If, on the date of your last report, the actual value of the covered "autos" at the "loss" location exceeds what you last reported, when a "loss" occurs we will pay only a percentage of what we would otherwise be obligated to pay. We will determine this percentage by dividing your total reported value for the involved location by the total actual value at the "loss" location on the date of your last report. If the first report due is delinquent on the date of "loss", the most we will pay will not exceed 75 percent of the Limit of Insurance shown in the Declarations for the applicable location. c. Non-reporting Premium Basis If, when "loss" occurs, the total value of your covered "autos" exceeds the Limit of Insurance shown in the Declarations, we will pay only a percentage of what we would otherwise be obligated to pay. We will determine this percentage by dividing the Limit of Insurance by the total actual value at the "loss" location at the time the "loss" occurred.

87

Garage Basics. Training for Agents

Garage Basics Training for Agents Garage Basics Training for Agents Learner Guide Garage Basics Training for Agents Designed 01/2013 Last Revision Date 02/13/2013 2013 Western Heritage Insurance Company

Garage Basics Training for Agents Garage Basics Training for Agents Learner Guide Garage Basics Training for Agents Designed 01/2013 Last Revision Date 02/13/2013 2013 Western Heritage Insurance Company

Garage Basics. Training for Agents

Garage Basics Training for Agents Garage Basics Training for Agents Learner Guide Garage Basics Training for Agents Designed 01/2013 Last Revision Date 02/2017 Nationwide and the Nationwide N and Eagle

Garage Basics Training for Agents Garage Basics Training for Agents Learner Guide Garage Basics Training for Agents Designed 01/2013 Last Revision Date 02/2017 Nationwide and the Nationwide N and Eagle

GARAGE INSURANCE: The Basics How to make garage risks a part of your agency portfolio.

GARAGE INSURANCE: The Basics How to make garage risks a part of your agency portfolio. By Jim Krotki, CPCU An often overlooked source of commercial insurance prospects is garage business. Some agents are

GARAGE INSURANCE: The Basics How to make garage risks a part of your agency portfolio. By Jim Krotki, CPCU An often overlooked source of commercial insurance prospects is garage business. Some agents are

CA Policy Comparisons

CA 00 01 Policy Comparisons CA 00 01 10 01 Form # CA 00 01 03 06 October 2001 Form Date March 2006 Occurrence Policy Type Occurrence Various provisions in this policy restrict coverage. Read the entire

CA 00 01 Policy Comparisons CA 00 01 10 01 Form # CA 00 01 03 06 October 2001 Form Date March 2006 Occurrence Policy Type Occurrence Various provisions in this policy restrict coverage. Read the entire

Commercial Auto Coverage

10 Commercial Auto Coverage LEARNING OBJECTIVES Upon the completion of this chapter, you will be able to: 1. Identify the role of the Commercial Auto Coverage Part 2. Recognize the usage of the Business

10 Commercial Auto Coverage LEARNING OBJECTIVES Upon the completion of this chapter, you will be able to: 1. Identify the role of the Commercial Auto Coverage Part 2. Recognize the usage of the Business

TRUCKERS ENDORSEMENT

POLICY NUMBER: COMMERCIAL AUTO THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY. TRUCKERS ENDORSEMENT This endorsement modifies insurance provided under the following: BUSINESS AUTO COVERAGE

POLICY NUMBER: COMMERCIAL AUTO THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY. TRUCKERS ENDORSEMENT This endorsement modifies insurance provided under the following: BUSINESS AUTO COVERAGE

CHANGES IN THE GARAGE COVERAGE FORM

THIS ENDORSEMENT RESTRICTS YOUR POLICY. PLEASE READ IT CAREFULLY. CHANGES IN THE GARAGE COVERAGE FORM This endorsement modifies the insurance provided under the following: GARAGE COVERAGE FORM I. CHANGES

THIS ENDORSEMENT RESTRICTS YOUR POLICY. PLEASE READ IT CAREFULLY. CHANGES IN THE GARAGE COVERAGE FORM This endorsement modifies the insurance provided under the following: GARAGE COVERAGE FORM I. CHANGES

Automobile Insurers Bureau

Automobile Insurers Bureau Massachusetts Automobile Insurance Policy Please read your policy. Part of the policy is a page marked Coverage Selections. It shows the types and amounts of coverage you have

Automobile Insurers Bureau Massachusetts Automobile Insurance Policy Please read your policy. Part of the policy is a page marked Coverage Selections. It shows the types and amounts of coverage you have

Chapter 1: The Business Auto Coverage Form... 1 ISO Rules...1 The Declarations Form...2

Table of Contents Chapter 1: The Business Auto Coverage Form... 1 ISO Rules...1 The Declarations Form...2 Chapter 2: Covered Auto Designations... 5 Coverage Symbols...5 Owned Autos Acquired after Policy

Table of Contents Chapter 1: The Business Auto Coverage Form... 1 ISO Rules...1 The Declarations Form...2 Chapter 2: Covered Auto Designations... 5 Coverage Symbols...5 Owned Autos Acquired after Policy

Massachusetts Automobile Insurance Policy

Massachusetts Automobile Policy 121209 121206-161428 PRA00001215231 0000001 0345001 121206_161814 0 1 I 1 25 68 35 25 Please read your policy. Part of the policy is a page marked Coverage Selections. It

Massachusetts Automobile Policy 121209 121206-161428 PRA00001215231 0000001 0345001 121206_161814 0 1 I 1 25 68 35 25 Please read your policy. Part of the policy is a page marked Coverage Selections. It

AUTOMOBILE LIABILITY & PHYSICAL DAMAGE COVERAGE AGREEMENT

AUTOMOBILE LIABILITY & PHYSICAL DAMAGE COVERAGE AGREEMENT PART A GENERAL I. The TASB Risk Management Fund (Fund) provides coverage as outlined in this Automobile Liability & Physical Damage Coverage Agreement.

AUTOMOBILE LIABILITY & PHYSICAL DAMAGE COVERAGE AGREEMENT PART A GENERAL I. The TASB Risk Management Fund (Fund) provides coverage as outlined in this Automobile Liability & Physical Damage Coverage Agreement.

Self-Insured Coverage Document Auto Physical Damage

Self-Insured Coverage Document Auto Physical Damage 2012 WCIA Auto Physical Damage Coverage Document Page 2 Washington Cities Insurance Authority Self-Insured Coverage Document Auto Physical Damage APDCov2012

Self-Insured Coverage Document Auto Physical Damage 2012 WCIA Auto Physical Damage Coverage Document Page 2 Washington Cities Insurance Authority Self-Insured Coverage Document Auto Physical Damage APDCov2012

TABLE OF CONTENTS. SECTION A THIRD PARTY LIABILITY 8 Insured persons 8 Insuring Agreements 8 Exclusions 9 Additional Agreements 10 Your Agreements 10

TABLE OF CONTENTS INTRODUCTION 1 PART 1 - GENERAL DEFINITIONS 2 PART 2 AUTOMOBILES TO WHICH THIS POLICY APPLIES 3 PART 3 - GENERAL PROVISIONS AND EXCLUSIONS 6 PART 4 COVERAGES 8 Page SECTION A THIRD PARTY

TABLE OF CONTENTS INTRODUCTION 1 PART 1 - GENERAL DEFINITIONS 2 PART 2 AUTOMOBILES TO WHICH THIS POLICY APPLIES 3 PART 3 - GENERAL PROVISIONS AND EXCLUSIONS 6 PART 4 COVERAGES 8 Page SECTION A THIRD PARTY

Commercial Business Automobile Coverage Section Policy wording

The terms and conditions of the Entertainment Policy Jacket and the following terms and conditions all apply to this Coverage Section. I. WHAT IS COVERED The Covered Auto Designation Symbols stated in

The terms and conditions of the Entertainment Policy Jacket and the following terms and conditions all apply to this Coverage Section. I. WHAT IS COVERED The Covered Auto Designation Symbols stated in

Ontario Application for Automobile Insurance Garage Form (OAF 4)

") New policy Replacing Policy No. Ontario Application for Automobile Insurance Garage Form (OAF 4) Language Preferred English French Policy No. Assigned Insurance Company Broker/Agent Item Application Building

New policy Replacing Policy No. Ontario Application for Automobile Insurance Garage Form (OAF 4) Language Preferred English French Policy No. Assigned Insurance Company Broker/Agent Item Application Building

MASSACHUSETTS ENDORSEMENT -M-0108-S Personal Vehicle Sharing Exclusion

MASSACHUSETTS ENDORSEMENT -M--S Personal Vehicle Sharing Exclusion We will not pay any claim for injury or property damage under the policy, while your auto is being used in a personal vehicle sharing

MASSACHUSETTS ENDORSEMENT -M--S Personal Vehicle Sharing Exclusion We will not pay any claim for injury or property damage under the policy, while your auto is being used in a personal vehicle sharing

AUTOMOBILE LIABILITY & PHYSICAL DAMAGE COVERAGE AGREEMENT PART A GENERAL

AUTOMOBILE LIABILITY & PHYSICAL DAMAGE COVERAGE AGREEMENT PART A GENERAL I. The TASB Risk Management Fund (Fund) provides coverage as outlined in this Automobile Liability & Physical Damage Coverage Agreement.

AUTOMOBILE LIABILITY & PHYSICAL DAMAGE COVERAGE AGREEMENT PART A GENERAL I. The TASB Risk Management Fund (Fund) provides coverage as outlined in this Automobile Liability & Physical Damage Coverage Agreement.

MASSACHUSETTS AUTOMOBILE INSURERS BUREAU AUTOMOBILE INSURANCE POLICY

AUTOMOBILE INSURERS BUREAU MASSACHUSETTS AUTOMOBILE INSURANCE POLICY PLEASE READ YOUR POLICY. Part of the policy is a page marked Coverage Selections. It shows the types and amounts of coverage you have

AUTOMOBILE INSURERS BUREAU MASSACHUSETTS AUTOMOBILE INSURANCE POLICY PLEASE READ YOUR POLICY. Part of the policy is a page marked Coverage Selections. It shows the types and amounts of coverage you have

Massachusetts Automobile Insurance Policy. Amica Mutual Insurance Company

Massachusetts Automobile Insurance Policy Amica Mutual Insurance Company Corporate One Hundred Amica Way, Lincoln, RI 02865-1156 Office Mail: PO Box 6008, Providence, RI 02940-6008 Toll Free: 1-800-242-6422

Massachusetts Automobile Insurance Policy Amica Mutual Insurance Company Corporate One Hundred Amica Way, Lincoln, RI 02865-1156 Office Mail: PO Box 6008, Providence, RI 02940-6008 Toll Free: 1-800-242-6422

Saskatchewan Extension Automobile Policy

THIS POLICY CONTAINS A PARTIAL PAYMENT OF LOSS CLAUSE INTRODUCTION On the understanding that the information you have given us in your application for this policy is correct, we provide the insurance described

THIS POLICY CONTAINS A PARTIAL PAYMENT OF LOSS CLAUSE INTRODUCTION On the understanding that the information you have given us in your application for this policy is correct, we provide the insurance described

BCAA Optional Car Insurance Policy

BCAA Optional Car Insurance Policy Effective : November 23, 2017 INTRODUCING YOUR POLICY INDEX SECTION 1 GENERAL PROVISIONS 4 1.1 Insuring agreement 4 1.1.1 Where and when you are covered 4 1.1.2 Conditions

BCAA Optional Car Insurance Policy Effective : November 23, 2017 INTRODUCING YOUR POLICY INDEX SECTION 1 GENERAL PROVISIONS 4 1.1 Insuring agreement 4 1.1.1 Where and when you are covered 4 1.1.2 Conditions

Strickland General Agency of LA, Inc.

Strickland General Agency of LA, Inc. 201 Evans Rd., Suite 212 * Harahan, LA 70123 504-738-8352 * Fax: 504-738-8359 www.sgainla.com Professional Insurance Wholesaler LOUISIANA GARAGE DEALER / NON - DEALER

Strickland General Agency of LA, Inc. 201 Evans Rd., Suite 212 * Harahan, LA 70123 504-738-8352 * Fax: 504-738-8359 www.sgainla.com Professional Insurance Wholesaler LOUISIANA GARAGE DEALER / NON - DEALER

Aviation Insurance. Chapter Objectives. Introduction to Aviation Insurance. Licensing Manual Aviation Insurance. Aircraft Hull Policies

Chapter Objectives Understand the various aviation coverages. Study the aircraft hull coverages and understand the methods of providing coverages and the application of deductibles. Understand the methods

Chapter Objectives Understand the various aviation coverages. Study the aircraft hull coverages and understand the methods of providing coverages and the application of deductibles. Understand the methods

Pacific Specialty Insurance Company California Non-Franchised Auto Dealer Program Manual Underwriting Guidelines

Underwriting Guidelines This program is designed for California non-franchised used car dealerships only. All risks must meet the following requirements: a) 90% or more of auto sales must be from private

Underwriting Guidelines This program is designed for California non-franchised used car dealerships only. All risks must meet the following requirements: a) 90% or more of auto sales must be from private

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY. AMENDMENT OF POLICY PROVISIONS NEW HAMPSHIRE

PERSONAL AUTO PP 01 76 01 11 THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY. AMENDMENT OF POLICY PROVISIONS NEW HAMPSHIRE This endorsement amends your policy to make it the equivalent of

PERSONAL AUTO PP 01 76 01 11 THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY. AMENDMENT OF POLICY PROVISIONS NEW HAMPSHIRE This endorsement amends your policy to make it the equivalent of

Auto Dealers Application

Auto Dealers Application APPLICANT INFORMATION Proposed Policy Term: From: To: Address: Phone: Contact Location Address: 1. Home Phone: 2. Web Address: 3. Form of Business: Individual Partnership Corporation

Auto Dealers Application APPLICANT INFORMATION Proposed Policy Term: From: To: Address: Phone: Contact Location Address: 1. Home Phone: 2. Web Address: 3. Form of Business: Individual Partnership Corporation

Massachusetts Automobile Insurance Policy

Massachusetts Automobile Insurance Policy Please read your policy. As you read the policy, check the Coverage Selections Page to make sure it shows exactly what you intended to buy. If there is any question,

Massachusetts Automobile Insurance Policy Please read your policy. As you read the policy, check the Coverage Selections Page to make sure it shows exactly what you intended to buy. If there is any question,

BUSINESS AUTO DECLARATIONS

AMERICAN ALTERNATIVE INSURANCE CORPORATION Administration Office: 555 College Road East, Princeton, NJ 08543-5241 800.305.4954 Statutory Office: 2711 Centerville Road, Suite 400 Wilmington, DE 19805 (a

AMERICAN ALTERNATIVE INSURANCE CORPORATION Administration Office: 555 College Road East, Princeton, NJ 08543-5241 800.305.4954 Statutory Office: 2711 Centerville Road, Suite 400 Wilmington, DE 19805 (a

QUÉBEC AUTOMOBILE INSURANCE POLICY FORM (Q.P.F.) No. 4 Garage Form

No. 4 Garage Form") QUÉBEC AUTOMOBILE INSURANCE POLICY FORM (Q.P.F.) No. 4 Garage Form Q.P.F. No. 4 1 April 1 st, 2018 TABLE OF CONTENTS INTRODUCTION... 5 1. DOCUMENTS INCLUDED IN INSURANCE CONTRACT... 5 2. OBLIGATION TO

QUÉBEC AUTOMOBILE INSURANCE POLICY FORM (Q.P.F.) No. 4 Garage Form Q.P.F. No. 4 1 April 1 st, 2018 TABLE OF CONTENTS INTRODUCTION... 5 1. DOCUMENTS INCLUDED IN INSURANCE CONTRACT... 5 2. OBLIGATION TO

Strickland General Agency, Inc.

Strickland General Agency, Inc. P. O. Box 4084 * Duluth, GA 30096 678-259-3700 * 800-825-5742 * Fax: 678-259-3701 www.sgainga.com Professional Insurance Wholesaler ALABAMA GARAGE DEALER / NON - DEALER

Strickland General Agency, Inc. P. O. Box 4084 * Duluth, GA 30096 678-259-3700 * 800-825-5742 * Fax: 678-259-3701 www.sgainga.com Professional Insurance Wholesaler ALABAMA GARAGE DEALER / NON - DEALER

Personal Auto Insurance

Chapter Objectives Learn the eligibility requirements Learn the definitions in an auto policy Know the different parts of the policy and their exclusions. There are usually questions on the state exam

Chapter Objectives Learn the eligibility requirements Learn the definitions in an auto policy Know the different parts of the policy and their exclusions. There are usually questions on the state exam

INFORMATION NOTICE AUTO POLICY SUMMARY AND RELATED DISCLOSURES

INFORMATION NOTICE AUTO POLICY SUMMARY AND RELATED DISCLOSURES THIS INFORMATIVE OOKLET, CONTAINING: a) Information notice, including policy summary and related disclosures, and b) Glossary, SHALL E AVAILALE

INFORMATION NOTICE AUTO POLICY SUMMARY AND RELATED DISCLOSURES THIS INFORMATIVE OOKLET, CONTAINING: a) Information notice, including policy summary and related disclosures, and b) Glossary, SHALL E AVAILALE

PREMISES LIABILITY ENDORSEMENT For Use With Rental Dwelling Policy - DH (01-97) For Use With Rental Dwelling Policy - DH (01-97)

For Use With Rental Dwelling Policy - DH (01-97)") PREMISES LIABILITY ENDORSEMENT For Use With Rental Dwelling Policy - DH 25-05 (01-97) For Use With Rental Dwelling Policy - DH 25-06 (01-97) In consideration of payment of premium and subject to all terms

PREMISES LIABILITY ENDORSEMENT For Use With Rental Dwelling Policy - DH 25-05 (01-97) For Use With Rental Dwelling Policy - DH 25-06 (01-97) In consideration of payment of premium and subject to all terms

CAR INSURANCE VISIT IBC.CA ALL ABOUT AUTO INSURANCE

CAR INSURANCE VISIT IBC.CA ALL ABOUT AUTO INSURANCE TABLE OF CONTENTS DO I REALLY NEED AUTO INSURANCE? 3 BUYING AUTO INSURANCE 4 Who is insured?...4 If you are borrowing a car...4 If you are lending a

CAR INSURANCE VISIT IBC.CA ALL ABOUT AUTO INSURANCE TABLE OF CONTENTS DO I REALLY NEED AUTO INSURANCE? 3 BUYING AUTO INSURANCE 4 Who is insured?...4 If you are borrowing a car...4 If you are lending a

EXPLANATORY MEMORANDUM STATE OF MASSACHUSETTS AIG PRIVATE CLIENT GROUP PERSONAL AUTOMOBILE PROGRAM AMERICAN INTERNATIONAL INSURANCE COMPANY

EXPLANATORY MEMORANDUM STATE OF MASSACHUSETTS AIG PRIVATE CLIENT GROUP PERSONAL AUTOMOBILE PROGRAM AMERICAN INTERNATIONAL INSURANCE COMPANY AIG Private Client Group (PCG) offers personal lines products

EXPLANATORY MEMORANDUM STATE OF MASSACHUSETTS AIG PRIVATE CLIENT GROUP PERSONAL AUTOMOBILE PROGRAM AMERICAN INTERNATIONAL INSURANCE COMPANY AIG Private Client Group (PCG) offers personal lines products

How to Handle a Car Accident

How to Handle a Car Accident Heselmeyer Zinda, PLLC Attorneys at Law Heselmeyer Zinda, PLLC Copyright 2010 All Rights Reserved Contact Information: Principal Office 108 E. Bagdad, Ste. 300 Round Rock,

How to Handle a Car Accident Heselmeyer Zinda, PLLC Attorneys at Law Heselmeyer Zinda, PLLC Copyright 2010 All Rights Reserved Contact Information: Principal Office 108 E. Bagdad, Ste. 300 Round Rock,

A CONSUMER S GUIDE TO MANUFACTURED HOMEOWNERS INSURANCE

A CONSUMER S GUIDE TO MANUFACTURED HOMEOWNERS INSURANCE INTRODUCTION Manufactured-homeowners insurance policies available in North Carolina may be used to provide coverage for your manufactured home, personal

A CONSUMER S GUIDE TO MANUFACTURED HOMEOWNERS INSURANCE INTRODUCTION Manufactured-homeowners insurance policies available in North Carolina may be used to provide coverage for your manufactured home, personal

Ontario Automobile Policy

Ontario Automobile Policy (OAP 1) Owner s Policy Approved by the Superintendent of Financial Services for use as the standard Owner s Policy on or after September 01, 2010. This Booklet includes several

Ontario Automobile Policy (OAP 1) Owner s Policy Approved by the Superintendent of Financial Services for use as the standard Owner s Policy on or after September 01, 2010. This Booklet includes several

Used Auto and Motorhome Dealer Application

Used Auto and Motorhome Dealer Application COLUMBIA INSURANCE COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL INDEMNITY COMPANY OF MID-AMERICA NATIONAL INDEMNITY COMPANY

Used Auto and Motorhome Dealer Application COLUMBIA INSURANCE COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL INDEMNITY COMPANY OF MID-AMERICA NATIONAL INDEMNITY COMPANY

GENERAL INFORMATION. (b) Have you ever been cancelled or non-renewed for this kind of insurance? Yes No If yes, explain

Have you ever been cancelled or non-renewed for this kind of insurance? Yes No If yes, explain") Trailer Dealer Application COLUMBIA INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL LIABILITY & FIRE INSURANCE COMPANY NATIONAL INDEMNITY COMPANY OF THE SOUTH

Trailer Dealer Application COLUMBIA INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL LIABILITY & FIRE INSURANCE COMPANY NATIONAL INDEMNITY COMPANY OF THE SOUTH

Lesson 3 Medical Payments

Lesson 3 Medical Payments Lesson 3 Med Pay Intro p1 (PA) Medical Payments is an optional coverage that your clients are not typically required by state law to purchase when buying their Personal Auto Policy.

Lesson 3 Medical Payments Lesson 3 Med Pay Intro p1 (PA) Medical Payments is an optional coverage that your clients are not typically required by state law to purchase when buying their Personal Auto Policy.

Ready to rent? Terms and Conditions. Florida

Ready to rent? Terms and Conditions. Florida Sixt rent a car - Rental Agreement, Terms & Conditions 1. Definitions. Agreement means the Terms and Conditions on this page and the provisions found on the

Ready to rent? Terms and Conditions. Florida Sixt rent a car - Rental Agreement, Terms & Conditions 1. Definitions. Agreement means the Terms and Conditions on this page and the provisions found on the

Home Auto Business Agricultural Good to know. Auto Pak. Policy booklet /2013. Saskatchewan

Home Auto Business Agricultural Good to know Auto Pak Policy booklet www.sgicanada.ca 1169-2 01/2013 Saskatchewan If You Have an Accident 1. You should take any action needed to save lives. Have someone

Home Auto Business Agricultural Good to know Auto Pak Policy booklet www.sgicanada.ca 1169-2 01/2013 Saskatchewan If You Have an Accident 1. You should take any action needed to save lives. Have someone

SUMMARY. Right to sue; In the course of employment (reasonably incidental activity test); Words and phrases (while in the employment).

; Words and phrases (while in the employment).") SUMMARY DECISION NO. 1410/98 Lessing v. Krolyk Right to sue; In the course of employment (reasonably incidental activity test); Words and phrases (while in the employment). The plaintiff in a court action

SUMMARY DECISION NO. 1410/98 Lessing v. Krolyk Right to sue; In the course of employment (reasonably incidental activity test); Words and phrases (while in the employment). The plaintiff in a court action

GENERAL INFORMATION. (b) Have you ever been cancelled or non-renewed for this kind of insurance? Yes No If yes, explain

Have you ever been cancelled or non-renewed for this kind of insurance? Yes No If yes, explain") Trailer Dealer Application COLUMBIA INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL LIABILITY & FIRE INSURANCE COMPANY NATIONAL INDEMNITY COMPANY OF THE SOUTH

Trailer Dealer Application COLUMBIA INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL LIABILITY & FIRE INSURANCE COMPANY NATIONAL INDEMNITY COMPANY OF THE SOUTH

Special Car Insurance Conditions Limited comprehensive

01. WHO ARE INSURED? The insurance applies to all people listed below. These people are referred to as you in the conditions set out below. The person taking out this insurance. The person who uses the

01. WHO ARE INSURED? The insurance applies to all people listed below. These people are referred to as you in the conditions set out below. The person taking out this insurance. The person who uses the

Automobile Service Operations Application

Automobile Service Operations Application COLUMBIA INSURANCE COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL INDEMNITY COMPANY OF MID-AMERICA NATIONAL INDEMNITY COMPANY

Automobile Service Operations Application COLUMBIA INSURANCE COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL INDEMNITY COMPANY OF MID-AMERICA NATIONAL INDEMNITY COMPANY

Automobile Service Operations Application

Automobile Service Operations Application COLUMBIA INSURANCE COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL INDEMNITY COMPANY OF MID-AMERICA NATIONAL INDEMNITY COMPANY

Automobile Service Operations Application COLUMBIA INSURANCE COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL INDEMNITY COMPANY OF MID-AMERICA NATIONAL INDEMNITY COMPANY

M.S.P.F. No. 4 - MANITOBA STANDARD GARAGE AUTOMOBILE POLICY (Owner's Form)

") M.S.P.F. No. 4 - MANITOBA STANDARD GARAGE AUTOMOBILE POLICY (Owner's Form) INSURING AGREEMENTS In consideration of the payment of the premium specified and of the statements contained in the application

M.S.P.F. No. 4 - MANITOBA STANDARD GARAGE AUTOMOBILE POLICY (Owner's Form) INSURING AGREEMENTS In consideration of the payment of the premium specified and of the statements contained in the application

Policy No. Assigned Insurance Company (Herinafter called the insurer) New Replacing Policy No Preferred Language English French

New Replacing Policy No Preferred Language English French") NEW BRUNSWICK STANDARD GARAGE AUTOMOBILE APPLICATION (N.B.A.F. No. 4) Policy No. Assigned Insurance Company (Herinafter called the insurer) New Replacing Policy No Preferred Language English French Company

NEW BRUNSWICK STANDARD GARAGE AUTOMOBILE APPLICATION (N.B.A.F. No. 4) Policy No. Assigned Insurance Company (Herinafter called the insurer) New Replacing Policy No Preferred Language English French Company

GARAGE PROTECTOR PLUS ENDORSEMENT

COMMERCIAL MULTI-LINE CF-2025 (Ed. 11-12) THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY. This endorsement modifies insurance provided under the following: BUILDING AND PERSONAL PROPERTY

COMMERCIAL MULTI-LINE CF-2025 (Ed. 11-12) THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY. This endorsement modifies insurance provided under the following: BUILDING AND PERSONAL PROPERTY

Used Auto and Motorhome Dealer Application

Used Auto and Motorhome Dealer Application COLUMBIA INSURANCE COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL INDEMNITY COMPANY OF MID-AMERICA NATIONAL INDEMNITY COMPANY

Used Auto and Motorhome Dealer Application COLUMBIA INSURANCE COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL INDEMNITY COMPANY OF MID-AMERICA NATIONAL INDEMNITY COMPANY

Automobile Service Operations Application

Automobile Service Operations Application COLUMBIA INSURANCE COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL INDEMNITY COMPANY OF MID-AMERICA NATIONAL INDEMNITY COMPANY

Automobile Service Operations Application COLUMBIA INSURANCE COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL INDEMNITY COMPANY OF MID-AMERICA NATIONAL INDEMNITY COMPANY

MASSACHUSETTS PRIVATE PASSENGER AUTOMOBILE INSURANCE MANUAL

The filing of a financial responsibility certificate of insurance as the result of a conviction of a motor vehicle violation requires the following premium adjustments to be added to the otherwise applicable

The filing of a financial responsibility certificate of insurance as the result of a conviction of a motor vehicle violation requires the following premium adjustments to be added to the otherwise applicable

GARAGE AND AUTO DEALERS APPLICATION

GARAGE AND AUTO DEALERS APPLICATION Proposed Effective Date: Producer: Name Proposed Expiration Date: Address Phone # Applicant Name and Mailing Address: Contact & Email: Individual Partnership Corporation

GARAGE AND AUTO DEALERS APPLICATION Proposed Effective Date: Producer: Name Proposed Expiration Date: Address Phone # Applicant Name and Mailing Address: Contact & Email: Individual Partnership Corporation

Used Auto and Motorhome Dealer Application

Used Auto and Motorhome Dealer Application COLUMBIA INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL LIABILITY & FIRE INSURANCE COMPANY NATIONAL INDEMNITY

Used Auto and Motorhome Dealer Application COLUMBIA INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL LIABILITY & FIRE INSURANCE COMPANY NATIONAL INDEMNITY

Personal Auto Policy

ATLANTA,GEORGIA Personal Auto Policy Omni Insurance Company PENNSYLVANIA Form 0837 Pennsylvania (11/08) LIMITED TORT ALTERNATIVE INFORMATION NOTICE Each person who elects the limited tort alternative remains

ATLANTA,GEORGIA Personal Auto Policy Omni Insurance Company PENNSYLVANIA Form 0837 Pennsylvania (11/08) LIMITED TORT ALTERNATIVE INFORMATION NOTICE Each person who elects the limited tort alternative remains

Coverage Selections Page This is a description of your coverage. Please retain for your records.

GOVERNMENT EMPLOYEES INSURANCE COMPANY PO BOX 9015, Woodbury, NY 11797-9015 Date Issued: April 3, 2014 Tel: Fax: Coverage Selections Page This is a description of your coverage. Please retain for your

GOVERNMENT EMPLOYEES INSURANCE COMPANY PO BOX 9015, Woodbury, NY 11797-9015 Date Issued: April 3, 2014 Tel: Fax: Coverage Selections Page This is a description of your coverage. Please retain for your

North Carolina Personal Automobile Policy

North Carolina Personal Automobile Policy We know how important it is for you to stay on the move. 500 W 5th Street Winston-Salem NC 27102-3199 Integon General Insurance Corporation New South Insurance

North Carolina Personal Automobile Policy We know how important it is for you to stay on the move. 500 W 5th Street Winston-Salem NC 27102-3199 Integon General Insurance Corporation New South Insurance

GENERAL INFORMATION. Lift Kit (suspension) Installation/Sales

Installation/Sales") Automobile Service Operations Application COLUMBIA INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL LIABILITY & FIRE INSURANCE COMPANY NATIONAL INDEMNITY COMPANY

Automobile Service Operations Application COLUMBIA INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL LIABILITY & FIRE INSURANCE COMPANY NATIONAL INDEMNITY COMPANY

made simple Landlords Package Policy Insurance What s inside:

Landlords Package Policy Insurance made simple What s inside: How to read a Landlords Package Policy Declarations Understanding Landlords Package Policy Insurance Coverages Deductibles Coverage limits

Landlords Package Policy Insurance made simple What s inside: How to read a Landlords Package Policy Declarations Understanding Landlords Package Policy Insurance Coverages Deductibles Coverage limits

BUSINESS AUTO COVERAGE FORM

CA 00 01 10 13 BUSINESS AUTO COVERAGE FORM Various provisions in this policy restrict coverage. Read the entire policy carefully to determine rights, duties and what is and is not covered. Throughout this

CA 00 01 10 13 BUSINESS AUTO COVERAGE FORM Various provisions in this policy restrict coverage. Read the entire policy carefully to determine rights, duties and what is and is not covered. Throughout this

HO-3 Special Standard Homeowners Structure = Open, Contents = Broad

DP-1 Basic Named Peril Fire, Lightning Explosion -- Extended : Wind Hail Aircraft Riot Volcano Internal Explosion Smoke WHARVES DP-2 Broad Named Peril WHARVES + BBBICEGOLF Ice, Burglary, Collapse, DP-3

DP-1 Basic Named Peril Fire, Lightning Explosion -- Extended : Wind Hail Aircraft Riot Volcano Internal Explosion Smoke WHARVES DP-2 Broad Named Peril WHARVES + BBBICEGOLF Ice, Burglary, Collapse, DP-3

CLASSIC LIMITED. Private Passenger Automobile Insurance Policy

CLASSIC LIMITED Private Passenger Automobile Insurance Policy READ YOUR POLICY CAREFULLY Issued by: Western General Insurance Company Calabasas, California IMPORTANT THIS POLICY COVERS DRIVERS AND VEHICLES

CLASSIC LIMITED Private Passenger Automobile Insurance Policy READ YOUR POLICY CAREFULLY Issued by: Western General Insurance Company Calabasas, California IMPORTANT THIS POLICY COVERS DRIVERS AND VEHICLES

PERSONAL AUTO POLICY

PERSONAL AUTO PP 00 01 01 05 PERSONAL AUTO POLICY AGREEMENT In return for payment of the premium and subject to all the terms of this policy, we agree with you as follows: DEFINITIONS A. Throughout this

PERSONAL AUTO PP 00 01 01 05 PERSONAL AUTO POLICY AGREEMENT In return for payment of the premium and subject to all the terms of this policy, we agree with you as follows: DEFINITIONS A. Throughout this

Landlords Package Policy Insurance. made simple

Landlords Package Policy Insurance made simple What s inside: How to read a Landlords Package Policy Declarations Understanding Landlords Package Policy Insurance Coverages Deductibles Coverage limits

Landlords Package Policy Insurance made simple What s inside: How to read a Landlords Package Policy Declarations Understanding Landlords Package Policy Insurance Coverages Deductibles Coverage limits

MASSACHUSETTS - PERSONAL INJURY PROTECTION COVERAGE

**THIS ENDORSEMENT CHANGES YOUR POLICY. PLEASE READ IT CAREFULLY** MASSACHUSETTS - PERSONAL INJURY PROTECTION COVERAGE This endorsement changes certain parts of your Auto Policy. Every coverage, exclusion,

**THIS ENDORSEMENT CHANGES YOUR POLICY. PLEASE READ IT CAREFULLY** MASSACHUSETTS - PERSONAL INJURY PROTECTION COVERAGE This endorsement changes certain parts of your Auto Policy. Every coverage, exclusion,

Business and Personal Finance Unit 4 Chapter Glencoe/McGraw-Hill

0 Chapter 13 Home and Motor Vehicle Insurance What You ll Learn Section 13.1 Identify types of risks and risk management methods. Explain how an insurance program can help manage risks. Describe the importance

0 Chapter 13 Home and Motor Vehicle Insurance What You ll Learn Section 13.1 Identify types of risks and risk management methods. Explain how an insurance program can help manage risks. Describe the importance

GENERAL INFORMATION. Camper Trailers (pull type)

") Motorcycle & Recreational Vehicle Dealers Garage Application (Motorhomes not included) COLUMBIA INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL LIABILITY

Motorcycle & Recreational Vehicle Dealers Garage Application (Motorhomes not included) COLUMBIA INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL LIABILITY

Chapter 22 Auto insurance

Chapter 22 Auto insurance QUESTION one ( Multiple choice) 1- Which of the following statements about the liability limits of the PAP is (are) true? I- The policy is written with split limits of liability

Chapter 22 Auto insurance QUESTION one ( Multiple choice) 1- Which of the following statements about the liability limits of the PAP is (are) true? I- The policy is written with split limits of liability

LIQUOR LIABILITY COVERAGE FORM

UTICA FIRST INSURANCE COMPANY CONSTITUTED IN OHIO AS UTICA FIRST INSURANCE COMPANY (MUTUAL) Home Office - 5981 Airport Road, Oriskany, NY 13424 Mail Address - P.O. Box 851, Utica, NY 13503.0851 This endorsement

UTICA FIRST INSURANCE COMPANY CONSTITUTED IN OHIO AS UTICA FIRST INSURANCE COMPANY (MUTUAL) Home Office - 5981 Airport Road, Oriskany, NY 13424 Mail Address - P.O. Box 851, Utica, NY 13503.0851 This endorsement

GARAGE APPLICATION. Other Organization, including a Corporation (Please Describe)

") GARAGE APPLICATION Name of Agent: General Information Effective Date: FEIN # : 1. Your Name Phone No. (dba) 2. Mailing Address 3. Your Web site address 4. Location #1 Address 5. Location #2 Address Is

GARAGE APPLICATION Name of Agent: General Information Effective Date: FEIN # : 1. Your Name Phone No. (dba) 2. Mailing Address 3. Your Web site address 4. Location #1 Address 5. Location #2 Address Is

GARAGE AND AUTO DEALERS APPLICATION

GARAGE AND AUTO DEALERS APPLICATION Proposed Effective Date: Producer: Name Proposed Expiration Date: Address Phone # Applicant Name and Mailing Address: Contact & Email: Individual Partnership Corporation

GARAGE AND AUTO DEALERS APPLICATION Proposed Effective Date: Producer: Name Proposed Expiration Date: Address Phone # Applicant Name and Mailing Address: Contact & Email: Individual Partnership Corporation

LIABILITY COVERAGE SECTION PRINCIPAL LIABILITY AND MEDICAL PAYMENTS COVERAGES

ML-9 Ed. 1/87 LIABILITY COVERAGE SECTION PRINCIPAL LIABILITY AND MEDICAL PAYMENTS COVERAGES Coverage L-Personal Liability We pay, up to our limit of liability, all sums for which any insured is legally

ML-9 Ed. 1/87 LIABILITY COVERAGE SECTION PRINCIPAL LIABILITY AND MEDICAL PAYMENTS COVERAGES Coverage L-Personal Liability We pay, up to our limit of liability, all sums for which any insured is legally

Budget UK Rental Agreement

Budget UK Rental Agreement Please find below an example of the UK rental agreement terms and conditions. 1. Rental Period The conditions of this Agreement apply to any vehicles, including replacement vehicles,

Budget UK Rental Agreement Please find below an example of the UK rental agreement terms and conditions. 1. Rental Period The conditions of this Agreement apply to any vehicles, including replacement vehicles,

North Carolina Business Auto Policy

North Carolina Business Auto Policy PERSONAL COMMERCIAL MOTORCYCLE RV HOMEOWNERS FLOOD HEALTH & LIFE 10954 (05/16) 5630 University Parkway PO Box 3199 Winston-Salem NC 27102-3199 Integon National Insurance

North Carolina Business Auto Policy PERSONAL COMMERCIAL MOTORCYCLE RV HOMEOWNERS FLOOD HEALTH & LIFE 10954 (05/16) 5630 University Parkway PO Box 3199 Winston-Salem NC 27102-3199 Integon National Insurance

Location #2 Address DBA: Address:

GENERAL INFORMATION : : Mailing State, Zip Web Years in business? Years of related experience? Agency: Producer: Phone: Type of Legal entity: Corporation Partnership Individual Limited Liability Corp.

GENERAL INFORMATION : : Mailing State, Zip Web Years in business? Years of related experience? Agency: Producer: Phone: Type of Legal entity: Corporation Partnership Individual Limited Liability Corp.

ATLANTA, GEORGIA. Personal Auto Policy. Omni Insurance Company PENNSYLVANIA. Form 1037 Pennsylvania (06/10)

") ATLANTA, GEORGIA Personal Auto Policy Omni Insurance Company PENNSYLVANIA Form 1037 Pennsylvania (06/10) LIMITED TORT ALTERNATIVE INFORMATION NOTICE Each person who elects the limited tort alternative

ATLANTA, GEORGIA Personal Auto Policy Omni Insurance Company PENNSYLVANIA Form 1037 Pennsylvania (06/10) LIMITED TORT ALTERNATIVE INFORMATION NOTICE Each person who elects the limited tort alternative

Used Auto and Motorhome Dealer Application

Used Auto and Motorhome Dealer Application COLUMBIA INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL LIABILITY & FIRE INSURANCE COMPANY NATIONAL INDEMNITY

Used Auto and Motorhome Dealer Application COLUMBIA INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL LIABILITY & FIRE INSURANCE COMPANY NATIONAL INDEMNITY

Questions About This Publication

Questions About This Publication For assistance with shipments, billing or other customer service matters, please call our Customer Service Department at: 1-631-350-2100 To obtain a copy of this book,

Questions About This Publication For assistance with shipments, billing or other customer service matters, please call our Customer Service Department at: 1-631-350-2100 To obtain a copy of this book,

LIABILITY COVERAGE SECTION-FARM

ML-10 Ed. 1/87 LIABILITY COVERAGE SECTION-FARM DEFINITIONS-The following additional definitions apply to the Liability Coverage Section. 1. Farming means the ownership, maintenance or use of premises for

ML-10 Ed. 1/87 LIABILITY COVERAGE SECTION-FARM DEFINITIONS-The following additional definitions apply to the Liability Coverage Section. 1. Farming means the ownership, maintenance or use of premises for

Montpelier Village Club, Inc. Vehicle Storage Application

Montpelier Village Club, Inc. Vehicle Storage Application Montpelier Village Club, Inc. Phone (407) 352-0385 Leeann@bonomgmt.com Vehicle : Boat, Boat Trailer, Trailer, Motor Home, Truck, RV, Car & any

Montpelier Village Club, Inc. Vehicle Storage Application Montpelier Village Club, Inc. Phone (407) 352-0385 Leeann@bonomgmt.com Vehicle : Boat, Boat Trailer, Trailer, Motor Home, Truck, RV, Car & any

Lesson 3 - Golf Carts

Lesson 3 - Golf Carts Lesson 3 Introduction p1 (PM) Golf carts are another type of recreational vehicle that clients may own, rent or borrow. In addition to being used for golf, motorized golf carts are

Lesson 3 - Golf Carts Lesson 3 Introduction p1 (PM) Golf carts are another type of recreational vehicle that clients may own, rent or borrow. In addition to being used for golf, motorized golf carts are

Drive ago LLC Member Agreement

Drive ago LLC Member Agreement The following Agreement are hereby agreed to between Drive ago LLC, a Delaware Limited Liability Company ( ago ), and the Member whose name and address is set forth on the

Drive ago LLC Member Agreement The following Agreement are hereby agreed to between Drive ago LLC, a Delaware Limited Liability Company ( ago ), and the Member whose name and address is set forth on the

Your Guide to Cars, Insurance and Identity Theft

Ignition Your Guide to Cars, Insurance and Identity Theft Each step toward independence comes with questions about finances that may affect your future. We ve got you covered; this booklet can answer some

Ignition Your Guide to Cars, Insurance and Identity Theft Each step toward independence comes with questions about finances that may affect your future. We ve got you covered; this booklet can answer some

ARKANSAS PERSONAL INJURY PROTECTION

POLICY NUMBER: THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY. ARKANSAS PERSONAL INJURY PROTECTION This endorsement modifies insurance provided under the following: BUSINESS AUTO COVERAGE

POLICY NUMBER: THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY. ARKANSAS PERSONAL INJURY PROTECTION This endorsement modifies insurance provided under the following: BUSINESS AUTO COVERAGE

Lesson 2 Liability Coverage

Lesson 2 Liability Coverage Intro p1 (PA) Lesson 2 Liability Coverage The first coverage section of the Personal Auto Policy is Part A - Liability Coverage. In this section we will determine whether or

Lesson 2 Liability Coverage Intro p1 (PA) Lesson 2 Liability Coverage The first coverage section of the Personal Auto Policy is Part A - Liability Coverage. In this section we will determine whether or

AAA Member Package Endorsement

The Commerce Insurance Company 211 Main Street, Webster, MA 01570 AAA Member Package Endorsement The additional benefits and enhancements provided by this endorsement are available only to policies issued

The Commerce Insurance Company 211 Main Street, Webster, MA 01570 AAA Member Package Endorsement The additional benefits and enhancements provided by this endorsement are available only to policies issued

Automobile Service Operations Application

Automobile Service Operations Application COLUMBIA INSURANCE COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL INDEMNITY COMPANY OF MID-AMERICA NATIONAL INDEMNITY COMPANY

Automobile Service Operations Application COLUMBIA INSURANCE COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL INDEMNITY COMPANY OF MID-AMERICA NATIONAL INDEMNITY COMPANY

2016 Massachusetts Automobile Insurance Policy. Memorandum of Changes

2016 Massachusetts Automobile Insurance Policy Memorandum of Changes This edition of the policy incorporates the provisions of the Massachusetts Mandatory Endorsement M-0099-S (Ed. 9-11), and, in addition,

2016 Massachusetts Automobile Insurance Policy Memorandum of Changes This edition of the policy incorporates the provisions of the Massachusetts Mandatory Endorsement M-0099-S (Ed. 9-11), and, in addition,

GENERAL INFORMATION. Lift Kit (suspension) Installation/Sales

Installation/Sales") Automobile Service s Application COLUMBIA INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL LIABILITY & FIRE INSURANCE COMPANY NATIONAL INDEMNITY COMPANY OF

Automobile Service s Application COLUMBIA INSURANCE COMPANY NATIONAL INDEMNITY COMPANY NATIONAL FIRE & MARINE INSURANCE COMPANY NATIONAL LIABILITY & FIRE INSURANCE COMPANY NATIONAL INDEMNITY COMPANY OF

Premium Dollars in Private Passenger Market

E ru Q Q 0\ Premium Dollars in Private Passenger Market - 2009 Over $11.9 billion in direct written premiums (3 rd largest market in the U.S.) More than 600/0 of the Florida market written by 10 insurers

E ru Q Q 0\ Premium Dollars in Private Passenger Market - 2009 Over $11.9 billion in direct written premiums (3 rd largest market in the U.S.) More than 600/0 of the Florida market written by 10 insurers

Program Manager: TRADERS INSURANCE CONNECTION, INC Troost, Kansas City, MO 64131

ARKANSAS PERSONAL AUTO POLICY SPECIAL POLICY FORM FOR PERSONS WHO DO NOT OWN AN AUTOMOBILE The coverage provided by this policy varies from a policy provided to a person who owns an automobile. Please

ARKANSAS PERSONAL AUTO POLICY SPECIAL POLICY FORM FOR PERSONS WHO DO NOT OWN AN AUTOMOBILE The coverage provided by this policy varies from a policy provided to a person who owns an automobile. Please

MOTOR CARRIER COVERAGE FORM

MOTOR CARRIER COVERAGE FORM COMMERCIAL AUTO CA 00 20 10 13 Various provisions in this policy restrict coverage. Read the entire policy carefully to determine rights, duties and what is and is not covered.

MOTOR CARRIER COVERAGE FORM COMMERCIAL AUTO CA 00 20 10 13 Various provisions in this policy restrict coverage. Read the entire policy carefully to determine rights, duties and what is and is not covered.

LOUISIANA DEPARTMENT OF INSURANCE. Consumer s Guide to. Auto. Auto Insurance. James J. Donelon, Commissioner of Insurance

LOUISIANA DEPARTMENT OF INSURANCE Consumer s Guide to Auto Auto Insurance Insurance James J. Donelon, Commissioner of Insurance A message from Commissioner of Insurance Jim Donelon Some of us spend up

LOUISIANA DEPARTMENT OF INSURANCE Consumer s Guide to Auto Auto Insurance Insurance James J. Donelon, Commissioner of Insurance A message from Commissioner of Insurance Jim Donelon Some of us spend up

Lesson 4 Uninsured/Underinsured Motorists

Lesson 4 Uninsured/Underinsured Motorists Lesson 4 UM/UIM Intro p1 (PA) The next mini-policy of the Personal Auto Policy that we will study is Uninsured/Underinsured Motorists Coverage (UM/UIM). This coverage