White Paper. Basel III Liquidity Risk. Perspectives on the implementation challenges facing banks

|

|

|

- Nickolas Washington

- 6 years ago

- Views:

Transcription

1 White Paper Basel III Liquidity Risk Perspectives on the implementation challenges facing banks

2 Contents New Liquidity Risk Management Regime... 1 Implementation Challenges of Basel III Liquidity Risk Ratios... 1 SAS Liquidity Risk Management Framework... 3 Liquidity Data Enrichment...3 Liquidity Portfolio Manager...4 Designing Basel III Based LCR...5 Creating and Running LCR Analysis...6 Conclusion... 8 About SAS Asset and Liability Management... 8 About the Author This white paper was written by Sumit Mathur, Global Product Manager for SAS Asset and Liability Management and SAS Capital Planning and Management at SAS.

3 1 New Liquidity Risk Management Regime Basel III liquidity risk guidelines are uncharted territory for most middle-tier and large banks. The complexity of their operations in multiple currencies and legal entities spread across various geographical locations pose a significant implementation challenge. The new paradigm for liquidity covers both longterm, structural funding and immediate or short-term liquidity. The new regulatory guidelines reflect the lessons learned from the financial crisis and are driving banks to plan and manage liquidity based on very stringent quantitative and qualitative standards. The guidelines concerning medium- to long-term funding require banks to calculate a net stable funding ratio (NSFR) i.e., the available amount of stable funding relative to the amount of required stable funding over a one-year horizon and ensure that it is greater than 100 percent on an ongoing basis. Banks must also fund long-term assets with reliable sources of funds that have an effective (residual) maturity greater than one year. To comply with this regulation, banks need to classify their equity, liabilities and assets with an effective maturity of greater than one year, at an individual account or position level into either available stable funding or required stable funding based on their liquidity attributes and stability under stressed conditions. The guidelines for short-term liquidity require banks to demonstrate that they can meet all the payment obligations that may arise during a period of continued stress lasting for 30 days or longer. To fulfill this regulation, banks must calculate a liquidity coverage ratio (LCR). Accordingly, banks must always maintain a buffer in the form of highly liquid assets sufficient to withstand the cash outflow during this period. This arrangement is basically to make sure that a bank gets a sufficient window of time i.e., 30 days to address the causal factors to create lasting normalcy as an alternative to being forced into bankruptcy. The LCR must be greater than 100 percent and must be measured and reported to the regulators as the simple average of daily observations over the previous quarter. Other equally important aspects of the Basel III regulation aimed at creating a sound liquidity management infrastructure require banks to: Manage liquidity of significant currencies. This involves monitoring the LCR ratio in each significant currency, which requires the calculation of foreign currency LCR ratios. It also involves examining a bank s ability to transfer a liquidity surplus in one currency to mitigate a liquidity deficit in another currency during a stress period. Transfer pricing involving liquidity credits and charges to provide an incentive or disincentive for business units based on the liquidity impact of each new transaction. Monitor the diversification of the funding base or, in other words, examine funding concentrations. This requires banks to monitor proportions of liabilities in each significant currency, product type and counterparties relative to the total liabilities on the balance sheet. Put in place an appropriate liquidity limits management system to monitor and control liquidity risk, as well as have an action plan for resolving limit breaches. Create a formal contingency funding plan that should lay out orderly liquidation of securities and funding activities that will be carried out in the event of a liquidity stress. Implementation Challenges of Basel III Liquidity Risk Ratios The existing liquidity management systems in most banks primarily comprise: Cash management units responsible for tactical liquidity, such as for intra-day or overnight funding and manages daily payment and settlement in a variety of accounts that a bank has with other banks, clearing corporations or the central bank (for example, real-time gross settlement). Asset and liability management unit in the treasury department performing cash forecasts arrived at from all future contractual and behavioral cash inflows and outflows, and summing up the observations in a liquidity mismatch report. This framework for tuning cash inflows and outflows has worked so far to manage end-of-day cash balances in various nostro accounts and to manage liquidity in an orderly market. However, this approach has an operational focus and, as a result, management of liquidity risk is ignored. Prior to Basel III liquidity risk norms, most banks were required to submit simple monthly or biweekly liquidity mismatch reports to the regulators. The liquidity risk analysis was typically done at a fairly high level (or a pool level), and it used to involve simple assumptions regarding the behavior of assets and liabilities. There was limited assessment of the impact of contingent or off-balance-sheet positions, such as derivatives and guarantees on a bank s liquidity. It is already known that liquidity risk was a major problem for banks that relied excessively on wholesale unsecured funding and had large derivative operations. The new Basel III regime for liquidity risk has increased the scope of liquidity management by asking banks to identify potential liquidity impacts from all the contingent sources.

4 2 Another change implied in the Basel III regime is for banks to do a detailed liquidity profiling of assets and liabilities, which requires delving into an individual position or account s attributes. The rules ask for a priori classification of each account into a predefined liquidity class that will be assigned a specific liquidity treatment downstream. This classification process is rules-driven and takes into account the fundamental characteristics, such as low credit and market risk, and market characteristics, such as bid-ask spread, active and sizable market and so on. Basel III has for the first time therefore addressed liquidity risk as a consequential risk resulting from problems with poor credit quality and market volatility. The integration of liquidity risk with credit risk and market risk poses implementation challenges, especially for middle-tier and large banks where risk systems are not as well integrated with each other. For example, assessing the impact of derivative collateral on liquidity requires the middle office (which is in charge of market risk) to provide this assessment to the liquidity risk team so that it can be factored into the LCR computations. In addition to calculating the net payable or receivable on derivatives, the middle office also needs to run a more comprehensive assessment that takes into account the following scenarios that will lead to increased liquidity requirements: Activation of downgrade triggers (1-notch to 3-notch) embedded in securities financial transactions and derivatives. Potential valuation changes in posted collateral. Market valuation changes on derivatives. Most banks lack integration of market risk and liquidity risk systems, so the current infrastructure leads to errors stemming from manual work. In addition, working with high-level assumptions can often be inaccurate. Basel III liquidity risk compliance will produce big benefits for banks in the form of better management of collateral portfolios and integration of stress testing derivatives portfolio activity with liquidity management processes. However, given the inadequacy of the liquidity management infrastructure and its connections with other risk applications, the implementation definitely poses a huge systems challenge for banks. For example, at any given point in time, a treasurer should be able to obtain a consolidated collateral report across different products, currencies, businesses and regional hubs. Such information, if available promptly, has a lot of value for liquidity management since it can ease the pressure on money market teams to raise costly short terms from market. Traditional liquidity systems have not needed to assess liquidity characteristics of the hold-to-maturity portfolio. Until the financial crisis, it was believed possible to use most of such securities in a repo transaction and roll over the contract to create permanent funding. During the crisis, however, it was proved by flight-to-quality that nothing other than sovereign bonds serve as good collateral for repos. This has raised the bar for securities that can be used in a repo transaction. It is practically impossible now to repo assets with high market volatility or less credit quality without steep haircuts. Market behavior during the crisis made it clear that only extremely liquid assets are good for generating cash during an acute liquidity crisis; therefore, the Basel III regulations require banks to create a liquidity buffer comprising extremely high liquid assets, classified based on a number of properties e.g., issuer type, credit risk weight, under independent control of liquidity management function, etc. Banks now must assess each and every security individually in this classification process. Therefore, it is not surprising that a supervisory guidance paper published by BCBS in January 2014 suggests methods such as liquidity scoring by using a number of key metrics and devising a liquidity threshold for assigning a security to the liquidity buffer. The LCR norms tend to calibrate the liquidity buffer for a 30-day stress period. At the same time, banks are also advised to do a more conservative internal assessment, thereby testing to what extent a buffer may be needed for a stress duration longer than 30 days. Some banks also have demanded liquidity monitoring for a shorter period, anywhere from one to 29 days. Indeed, liquidity measurement systems need to be flexible and should be able to adapt to any buffer calibration window or multiple windows. This is not a trivial task it requires a complete reassessment that takes into account collateral flows and maturing transactions that happen in a broader or narrower time window. The main challenge is that some of the liquidity risk applications that middle-tier and large banks support continue to work as black boxes that do not allow possibilities for user-defined configurations and custom risk analysis. There are a host of other challenges that are more technical and system-oriented. The span of operations of middle-tier and large banks invariably involves multiple currencies and entities. Such banks are required to do consolidated reporting in their base or jurisdictional currency for their home regulator and in local reporting for each legal entity to the respective host regulator as well. The LCR norms for the classification of

5 3 securities into liquidity buffer, application of haircuts and reporting rules, though broadly guided by BCBS, are jurisdiction-specific. Therefore, banks have to deploy liquidity systems to cover legal entities in various jurisdictions. They need the flexibility to not only adapt to the local jurisdiction rules, but also enable a consolidated view of liquidity that combines the liquidity risk of all entities across currencies, monitors risks and reports this consolidated liquidity situation. Above all, transparency in different liquidity calculations (e.g., calculation of unencumbrance accounting for collateralization, marking-to-market, contractual cash flow computation, haircut assignments, aggregation of data and mapping results to the right place in the reporting template) and the flexibility to configure different stress scenarios and re-run liquidity calculations to assess the impact are critical aspects of a good liquidity risk solution. Provided a liquidity risk solution addresses these aspects, liquidity analysts can easily use it to perform their everyday activities. Another important requirement of a good system is the ability to trace results back to the portfolio data and clearly bring out any information on the model used in the computations. This is called data lineage, and it allows risk analysts to work back from output to the source system data, as well as trace each aggregation to the drill-down to a view comprising individual exposures. The entire data processing flow from portfolio data and liquidity classifications up to the liquidity ratio calculation should be open to allow for regulatory and internal risk auditing of the calculations. With most traditional systems, this can be quite a challenge for IT departments and business users alike. That s because most of the existing applications work like reporting solutions that provide a regulatory template or just a view of the results. However, such applications take away a lot of important possibilities that could help an analyst diagnose and repair a liquidity problem. In the next section of this paper, we will provide some insights on the liquidity risk management framework offered as part of SAS Asset and Liability Management for addressing the business and technical challenges we have discussed. SAS Liquidity Risk Management Framework The liquidity risk management framework provides an end-to-end analytical and technical infrastructure that addresses the needs of modern-day liquidity risk management. Together with other applications e.g., SAS Credit Risk for Banking and SAS Market Risk for Banking the liquidity risk framework also provides an integrated risk management platform for banks that want consistent enterprisewide implementation of different risks on a same platform. The liquidity risk infrastructure includes a risk data warehouse, a liquidity-specific data mart, analytical computations for Basel III ratios, and liquidity risk integrated with a dedicated reporting warehouse. The architecture supports multi-entity implementation for a global bank, including support for different analysis configurations and jurisdiction-specific business rules. The span of LCR computations is intended to break up a complex process into individual data processing steps and enable analysts to get maximum insights from the output of each step. The following sections will describe the data process flow as well as the functional and technical capabilities for accommodating the LCR process. Liquidity Data Enrichment Various provisions of Basel III liquidity LCR and NSFR norms are prebuilt into the liquidity data enrichment process that checks every individual asset and liability position and its liquidity attributes to determine its appropriate liquidity class. There are more than 60 different liquidity classifications built into a standard process, which can also be customized to include a greater number of classifications as needed based on a bank s portfolio. The system also has the flexibility to bypass this classification step if a bank chooses to provide liquidity classification as an input feed. The enrichment process includes classification logic based on Basel III. There are rules for various types of assets, liabilities, derivatives and off-balance-sheet exposures, including margining and collateralization. For example, analysts can perform appropriate checks to see if positions in a particular security can be included in the liquidity buffer over the next 30 days; if so, whether it should belong to Level 1, Level 2A or Level 2B Basel III classification; and to what extent, based on the unencumbered holdings. This multitier logic is fairly dataintensive and is arrived at by simultaneously looking into the pledged holdings across all the trading counterparties, the right to re-hypothecate a security, the nature of the security, including its issuer type, date of maturity, etc. Another example is where deposit accounts need to be examined for classification as stable or less stable based on the presence of a deposit insurance, and also examining other operational characteristics, such as the account type, deposit withdrawal option with the depositor and the denomination currency.

6 4 Liquidity Portfolio Manager The liquidity data enrichment step is followed by creating an LCR group structure that basically groups or segments processed data into LCR specific sub-portfolios and maps them in an LCR tree structure as provided in Basel III. In other words, it is the pooling of financial accounts and instruments belonging to the same liquidity class into one sub-portfolio so that it meets with consistent regulatory treatment. The process enables a liquidity analyst to view the enriched liquidity portfolio right in the application interface to check the classification accuracy and then create liquidity sub-portfolios. For example, a liquidity analyst may want to group positions classified as Stable Deposits from any region ABC together in a sub-portfolio for analysis compared with Stable Deposits from region XYZ, because they may have different behavioral characteristics. Even though they may have the same liquidity classification, the bank may want to assign different run-off treatments based on what may be specific to the individual regions. Likewise, analysts can quickly and interactively create as many sub-portfolios and save them in the system for subsequent analysis. Figure 1 shows a liquidity risk interface where an analyst has created the relevant sub-portfolios for analysis. Figure 2 shows that the analyst has opened a high-quality liquid asset (HQLA) portfolio to view a list of high-quality bonds with filters corresponding to its classification applied. This portfolio can be quickly exported to Microsoft Excel for further analysis, saved and shared with the rest of the team members. The system also allows an analyst to import a portfolio from Excel and use it directly in any analysis. This option is for banks that want a quick data load and analyze option. Figure 1: Portfolio manager. Figure 2: Portfolio view.

7 5 Figure 3: Basel III LCR group structure and node properties (LCR factor assignment). Designing Basel III Based LCR The liquidity application provides a value-added workflow for creating a Basel III LCR and NSFR grouping structure, as shown in Figure 3. The liquidity group structure enables the creation of nodes that are based on Basel III definitions, such as HQLA, Level 1 assets, Level 2A assets and Level 2B assets, etc., for further analysis. The unique aspect of the liquidity group structure is that it offers flexibility in defining different categories, assigning an LCR factor to that category based on Basel III or a bank s internal requirement, and then mapping sub-portfolios to the category. The LCR factor applied to a node in the group is applied to all the portfolios that are mapped with this node. Through this feature, liquidity analysts can create one or more LCR and NSFR grouping schemes applicable to one or more entities. More than one group can be opened via the interface for editing and comparison with each other. This enables an analyst at global headquarters to oversee the LCR configurations for a host country right beside the consolidated LCR, as shown in Figure 4.

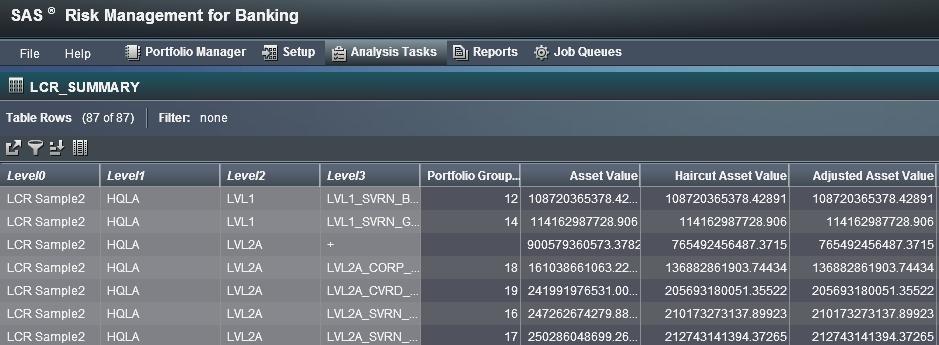

8 6 Figure 4: Creating and comparing two LCR groups. Creating and Running LCR Analysis With traditional liquidity risk solutions, an analyst sometimes cannot even create and run LCR analysis with custom specifications, which leads to some dependence on the IT department. Figure 5 shows how this problem can be solved by empowering an analyst to quickly create and run LCR analysis after completing all the workflow steps. A liquidity analyst can view the LCR USA Consolidated portfolio group and Basel III LCR (0-30 Day) time grid inputs. All the objects that are selected with an analysis task can be created and modified, depending on the need of the analysis. For example, the LCR measurement time horizon can be made more conservative to 0-45 Days, and the LCR group can be changed from LCR USA Consolidated (the consolidated entity) to LCR Germany (the host country). As you can see, implementation of the SAS liquidity risk solution is flexible and gives the liquidity manager a lot of control over creating, running and re-running an analysis under the same or different stress scenarios. Once the analysis is triggered and successfully completed, users have an option to verify the results data sets, as shown in Figure 6. The mark-to-market value and the haircut applied can be viewed at different levels at which data is post-processed. An example of this is each node of the HQLA comprising break-up between Level 1, Level 2A and Level 2B, and then within Level 1, for example, central bank reserves, securities issued by sovereigns, etc. The LCR calculation comprising the numerator (HQLA) and the denominator (total net cash outflow) is also shown in the results. Once the results are verified, the analyst can generate specific Basel III LCR templates (based on BCBS 2013 QIS monitoring standards) and obtain a full Excel-based report that can be analyzed and submitted to the regulator. An analyst may also choose to generate the LCR Excel template for any of the past dates. In this case, the system will fetch the data from the reporting warehouse called a SAS Risk Reporting Repository and produce the desired historical reports.

9 7 Figure 5: Creating and running an LCR analysis. Figure 5: Creating and running an LCR analysis.

10 8 Conclusion The new liquidity risk regulations pose tremendous implementation challenges for banks. Owing to the increasingly complex nature of the regulation, banks need more flexible and comprehensive systems to help them comply with the regulation and, at the same time, help improve the risk management processes. The SAS liquidity risk management framework enables banks to establish the right infrastructure using prebuilt advanced analytics and reporting capabilities for Basel III liquidity risk LCR and NSFR norms and beyond. This, in turn, enables treasurers to get complete control over their bank s liquidity situation. About SAS Asset and Liability Management SAS Asset and Liability Management enables banks to manage interest rate risk, liquidity risk and funds transfer pricing from a single platform. The solution comes with out-of-the-box reporting templates for liquidity risk and interest rate risk, as well as analytical capabilities that support fixed-income analytics suited for a range of risk management activities.

11 To contact your local SAS office, please visit: sas.com/offices SAS and all other SAS Institute Inc. product or service names are registered trademarks or trademarks of SAS Institute Inc. in the USA and other countries. indicates USA registration. Other brand and product names are trademarks of their respective companies. Copyright 2014, SAS Institute Inc. All rights reserved _S

The Use of IFRS for Prudential and Regulatory Purposes

REPARIS A REGIONAL PROGRAM The Use of IFRS for Prudential and Regulatory Purposes Liquidity Risk Management THE ROAD TO EUROPE: PROGRAM OF ACCOUNTING REFORM AND INSTITUTIONAL STRENGTHENING (REPARIS) !

REPARIS A REGIONAL PROGRAM The Use of IFRS for Prudential and Regulatory Purposes Liquidity Risk Management THE ROAD TO EUROPE: PROGRAM OF ACCOUNTING REFORM AND INSTITUTIONAL STRENGTHENING (REPARIS) !

White Paper. Liquidity Optimization: Going a Step Beyond Basel III Compliance

White Paper Liquidity Optimization: Going a Step Beyond Basel III Compliance Contents SAS: Delivering the Keys to Liquidity Optimization... 2 A Comprehensive Solution...2 Forward-Looking Insight...2 High

White Paper Liquidity Optimization: Going a Step Beyond Basel III Compliance Contents SAS: Delivering the Keys to Liquidity Optimization... 2 A Comprehensive Solution...2 Forward-Looking Insight...2 High

Basel III: The Liquidity Coverage Ratio and Liquidity Risk Monitoring Tools

P2.T7. Operational & Integrated Risk Management Basel III: The Liquidity Coverage Ratio and Liquidity Risk Monitoring Tools Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com

P2.T7. Operational & Integrated Risk Management Basel III: The Liquidity Coverage Ratio and Liquidity Risk Monitoring Tools Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com

LIQUIDITY MANAGEMENT UNDER BASEL III & KEY CHALLENGES FACED IN THE IMPLEMENTATION OF BASEL III

LIQUIDITY MANAGEMENT UNDER BASEL III & KEY CHALLENGES FACED IN THE IMPLEMENTATION OF BASEL III SUMMARY Basel III is a comprehensive set of reform BASEL III, which was introduced in January 2013, measures

LIQUIDITY MANAGEMENT UNDER BASEL III & KEY CHALLENGES FACED IN THE IMPLEMENTATION OF BASEL III SUMMARY Basel III is a comprehensive set of reform BASEL III, which was introduced in January 2013, measures

2017 Seminar for Senior Bank Supervisors from Emerging Economies. Implementation of Basel III Liquidity Requirements in Emerging Markets

2017 Seminar for Senior Bank Supervisors from Emerging Economies Implementation of Basel III Liquidity Requirements in Emerging Markets Christopher Wilson Monetary and Capital Markets Department International

2017 Seminar for Senior Bank Supervisors from Emerging Economies Implementation of Basel III Liquidity Requirements in Emerging Markets Christopher Wilson Monetary and Capital Markets Department International

Strengthening the resilience of the banking sector: the Basel proposal for an international framework for liquidity risk

Strengthening the resilience of the banking sector: the Basel proposal for an international framework for liquidity risk Money Market Contact Group Frankfurt, 10 February 2010 Outline I Background II III

Strengthening the resilience of the banking sector: the Basel proposal for an international framework for liquidity risk Money Market Contact Group Frankfurt, 10 February 2010 Outline I Background II III

Guidance Note: Stress Testing Credit Unions with Assets Greater than $500 million. May Ce document est également disponible en français.

Guidance Note: Stress Testing Credit Unions with Assets Greater than $500 million May 2017 Ce document est également disponible en français. Applicability This Guidance Note is for use by all credit unions

Guidance Note: Stress Testing Credit Unions with Assets Greater than $500 million May 2017 Ce document est également disponible en français. Applicability This Guidance Note is for use by all credit unions

Liquidity Risk Management. Thomas Schmale, Solution Management Analytical Banking, SAP AG, 29 th May 2014

Liquidity Risk Management Thomas Schmale, Solution Management Analytical Banking, SAP AG, 29 th May 2014 Agenda Introduction Regulatory challenges in Liquidity Risk Management Further derived challenges

Liquidity Risk Management Thomas Schmale, Solution Management Analytical Banking, SAP AG, 29 th May 2014 Agenda Introduction Regulatory challenges in Liquidity Risk Management Further derived challenges

Learn the Fundamentals of Managing Liquidity Under U.S. Basel III

Learn the Fundamentals of Managing Liquidity Under U.S. Basel III Originally presented as a part of a Moody s Analytics recorded webinar on May 1, 2014 Agenda» Key Aspects of the Planned U.S. Basel III

Learn the Fundamentals of Managing Liquidity Under U.S. Basel III Originally presented as a part of a Moody s Analytics recorded webinar on May 1, 2014 Agenda» Key Aspects of the Planned U.S. Basel III

Liquidity Coverage Ratio Disclosures

Liquidity Coverage Ratio Disclosures June 30, 2018 TABLE OF CONTENTS Introduction................................................................................... Liquidity Management...........................................................................

Liquidity Coverage Ratio Disclosures June 30, 2018 TABLE OF CONTENTS Introduction................................................................................... Liquidity Management...........................................................................

Appendix B: HQLA Guide Consultation Paper No Basel III: Liquidity Management

Appendix B: HQLA Guide Consultation Paper No.3 2017 Basel III: Liquidity Management [Draft] Guide on the calculation and reporting of HQLA Issued: 26 April 2017 Contents Contents Overview... 3 Consultation...

Appendix B: HQLA Guide Consultation Paper No.3 2017 Basel III: Liquidity Management [Draft] Guide on the calculation and reporting of HQLA Issued: 26 April 2017 Contents Contents Overview... 3 Consultation...

Liquidity Coverage Ratio Disclosure. Bank AlBilad Liquidity Coverage Ratio Disclosure Dec 31, 2015

Bank AlBilad Liquidity Coverage Ratio Disclosure Dec 31, 2015 1 I. LIQUIDITY COVERAGE RATIO (LCR): QUANTITATIVE DISCLOSURE Date: 31 Dec 2015 LCR Common Disclosure Template (In SR 000`s) Total UNWEIGHTED

Bank AlBilad Liquidity Coverage Ratio Disclosure Dec 31, 2015 1 I. LIQUIDITY COVERAGE RATIO (LCR): QUANTITATIVE DISCLOSURE Date: 31 Dec 2015 LCR Common Disclosure Template (In SR 000`s) Total UNWEIGHTED

Liquidity Regulation in the UK & Europe Impact on International Banks and Broker-Dealers

S T R I C T L Y P R I V A T E A N D C O N F I D E N T I A L 7 th July, 2010 Liquidity Regulation in the UK & Europe Impact on International Banks and Broker-Dealers Derek Paine - Compliance Manager (Speaker)

S T R I C T L Y P R I V A T E A N D C O N F I D E N T I A L 7 th July, 2010 Liquidity Regulation in the UK & Europe Impact on International Banks and Broker-Dealers Derek Paine - Compliance Manager (Speaker)

Project Editor, Yale Program on Financial Stability (YPFS), Yale School of Management

, Yale School of Management") yale program on financial stability case study 2014-1b-v1 november 1, 2014 Basel III B: 1 Basel III Overview Christian M. McNamara 2 Michael Wedow 3 Andrew Metrick 4 Abstract In the wake of the financial

yale program on financial stability case study 2014-1b-v1 november 1, 2014 Basel III B: 1 Basel III Overview Christian M. McNamara 2 Michael Wedow 3 Andrew Metrick 4 Abstract In the wake of the financial

Basel Committee on Banking Supervision. Liquidity coverage ratio disclosure standards

Basel Committee on Banking Supervision Liquidity coverage ratio disclosure standards January 2014 This publication is available on the BIS website (www.bis.org). Bank for International Settlements 2014.

Basel Committee on Banking Supervision Liquidity coverage ratio disclosure standards January 2014 This publication is available on the BIS website (www.bis.org). Bank for International Settlements 2014.

Overview of the Net Stable Funding Ratio

Overview of the Net Stable Funding Ratio Presentation to the Canadian Fixed Income Forum January 23, 2018 Brian Rumas, Director, Capital Division Robert Belanger, Senior Analyst, Capital Division Agenda

Overview of the Net Stable Funding Ratio Presentation to the Canadian Fixed Income Forum January 23, 2018 Brian Rumas, Director, Capital Division Robert Belanger, Senior Analyst, Capital Division Agenda

DB USA Corporation U.S. LIQUIDITY COVERAGE RATIO DISCLOSURES

DB USA Corporation U.S. LIQUIDITY COVERAGE RATIO DISCLOSURES For the quarter ended 1 Table of Contents The Liquidity Coverage Ratio (LCR)... 3 U.S. Disclosure Requirements... 3 U.S. Qualitative Disclosures...

DB USA Corporation U.S. LIQUIDITY COVERAGE RATIO DISCLOSURES For the quarter ended 1 Table of Contents The Liquidity Coverage Ratio (LCR)... 3 U.S. Disclosure Requirements... 3 U.S. Qualitative Disclosures...

Liquidity Coverage Ratio Disclosures Report. For the Quarterly Period Ended September 30, 2017

Liquidity Coverage Ratio Disclosures Report For the Quarterly Period Ended September 30, 2017 U.S. LCR DISCLOSURES REPORT For the quarterly period ended September 30, 2017 Table of Contents Page 1 Morgan

Liquidity Coverage Ratio Disclosures Report For the Quarterly Period Ended September 30, 2017 U.S. LCR DISCLOSURES REPORT For the quarterly period ended September 30, 2017 Table of Contents Page 1 Morgan

BNP Paribas USA, Inc. Liquidity Coverage Ratio Disclosure

BNP Paribas USA, Inc. Liquidity Coverage Ratio Disclosure Table of Contents Introduction & IHC Overview 1 Liquidity Coverage Ratio Overview 2 LCR Overview 2 LCR Quantitative Disclosure 2 High Quality Liquid

BNP Paribas USA, Inc. Liquidity Coverage Ratio Disclosure Table of Contents Introduction & IHC Overview 1 Liquidity Coverage Ratio Overview 2 LCR Overview 2 LCR Quantitative Disclosure 2 High Quality Liquid

Liquidity Coverage Ratio Disclosure For the Quarterly Period Ended March 31, 2018 THE BANK OF NEW YORK MELLON CORPORATION

Liquidity Coverage Ratio Disclosure For the Quarterly Period Ended March 31, 2018 THE BANK OF NEW YORK MELLON CORPORATION Table of Contents Introduction... 2... 3 Quarterly Variance in the LCR... 3 Drivers

Liquidity Coverage Ratio Disclosure For the Quarterly Period Ended March 31, 2018 THE BANK OF NEW YORK MELLON CORPORATION Table of Contents Introduction... 2... 3 Quarterly Variance in the LCR... 3 Drivers

TABLE 2: CAPITAL STRUCTURE - December 31, 2015

Frequency : Quarterly Location : Quarterly Financial Statement TABLE 2: CAPITAL STRUCTURE - December 31, 2015 Balance sheet - Step 1 (Table 2(b)) All figures are in SAR '000 Assets Balance sheet in Published

Frequency : Quarterly Location : Quarterly Financial Statement TABLE 2: CAPITAL STRUCTURE - December 31, 2015 Balance sheet - Step 1 (Table 2(b)) All figures are in SAR '000 Assets Balance sheet in Published

Wells Fargo & Company. Liquidity Coverage Ratio Disclosure

Wells Fargo & Company Liquidity Coverage Ratio Disclosure For the quarter ended September 30, 2017 1 Table of Contents Introduction... 3 Executive Summary... 3 Company Overview... 4 LCR Rule Overview...

Wells Fargo & Company Liquidity Coverage Ratio Disclosure For the quarter ended September 30, 2017 1 Table of Contents Introduction... 3 Executive Summary... 3 Company Overview... 4 LCR Rule Overview...

Liquidity Coverage Ratio Disclosure. For the quarter ended September 2018

Liquidity Coverage Ratio Disclosure For the quarter ended September 2018 Liquidity Coverage Ratio ("LCR") and the Disclosure Template The Monetary Authority of Singapore ( MAS ) had designated Citibank

Liquidity Coverage Ratio Disclosure For the quarter ended September 2018 Liquidity Coverage Ratio ("LCR") and the Disclosure Template The Monetary Authority of Singapore ( MAS ) had designated Citibank

Wells Fargo & Company. Liquidity Coverage Ratio Disclosure

Wells Fargo & Company Liquidity Coverage Ratio Disclosure For the quarter ended September 30, 2018 1 Table of Contents Introduction... 3 Executive Summary... 3 Company Overview... 4 LCR Rule Overview...

Wells Fargo & Company Liquidity Coverage Ratio Disclosure For the quarter ended September 30, 2018 1 Table of Contents Introduction... 3 Executive Summary... 3 Company Overview... 4 LCR Rule Overview...

Liquidity Coverage Ratio Disclosures Report. For the Quarterly Period Ended March 31, 2018

Liquidity Coverage Ratio Disclosures Report For the Quarterly Period Ended March 31, 2018 LCR DISCLOSURES REPORT For the quarterly period ended March 31, 2018 Table of Contents Page 1 Morgan Stanley 1

Liquidity Coverage Ratio Disclosures Report For the Quarterly Period Ended March 31, 2018 LCR DISCLOSURES REPORT For the quarterly period ended March 31, 2018 Table of Contents Page 1 Morgan Stanley 1

Liquidity Coverage Ratio Disclosure For the Quarterly Period Ended September 30, 2017

Liquidity Coverage Ratio Disclosure For the Quarterly Period Ended September 30, 2017 THE BANK OF NEW YORK MELLON CORPORATION Table of Contents Introduction... 2... 3 Quarterly Variance in the LCR... 3

Liquidity Coverage Ratio Disclosure For the Quarterly Period Ended September 30, 2017 THE BANK OF NEW YORK MELLON CORPORATION Table of Contents Introduction... 2... 3 Quarterly Variance in the LCR... 3

Guideline. Liquidity Adequacy Requirements (LAR) Chapter 5 Liquidity Monitoring Tools Date: May 2014

Chapter 5 Liquidity Monitoring Tools Date: May 2014") Guideline Subject: Liquidity Adequacy Requirements (LAR) Chapter 5 Date: May 2014 Subsection 485(1) and 949(1) of the Bank Act (BA), subsection 473(1) of the Trust and Loan Companies Act (TLCA) and subsection

Guideline Subject: Liquidity Adequacy Requirements (LAR) Chapter 5 Date: May 2014 Subsection 485(1) and 949(1) of the Bank Act (BA), subsection 473(1) of the Trust and Loan Companies Act (TLCA) and subsection

Demystifying the New Liquidity Requirements

Your State Association Presents Demystifying the New Liquidity Requirements Program Materials Use this document to follow along with the live webinar presentation. Please test your system before the broadcast.

Your State Association Presents Demystifying the New Liquidity Requirements Program Materials Use this document to follow along with the live webinar presentation. Please test your system before the broadcast.

Policy Guideline of the Bank of Thailand Re: Liquidity Risk Management of Financial Institutions

Policy Guideline of the Bank of Thailand Re: Liquidity Risk Management of Financial Institutions 28 January 2010 Prepared by: Risk Management Policy Office Prudential Policy Department Financial Institution

Policy Guideline of the Bank of Thailand Re: Liquidity Risk Management of Financial Institutions 28 January 2010 Prepared by: Risk Management Policy Office Prudential Policy Department Financial Institution

Appendix 3 In this appendix underlining indicates proposed new text and striking through indicates deleted text. The DFSA Rulebook

Appendix 3 In this appendix underlining indicates proposed new text and striking through indicates deleted text. The DFSA Rulebook Prudential Investment, Insurance Intermediation and Banking Module (PIB)

Appendix 3 In this appendix underlining indicates proposed new text and striking through indicates deleted text. The DFSA Rulebook Prudential Investment, Insurance Intermediation and Banking Module (PIB)

Decision on liquidity risk management. General provisions Article 1

Pursuant to Article 101, paragraph (2), item (1) of the Credit Institutions Act (Official Gazette 159/2013), and Article 43, paragraph (2), item (9) of the Act on the Croatian National Bank (Official Gazette

Pursuant to Article 101, paragraph (2), item (1) of the Credit Institutions Act (Official Gazette 159/2013), and Article 43, paragraph (2), item (9) of the Act on the Croatian National Bank (Official Gazette

REGULATORY GUIDELINE Liquidity Risk Management Principles TABLE OF CONTENTS. I. Introduction II. Purpose and Scope III. Principles...

REGULATORY GUIDELINE Liquidity Risk Management Principles SYSTEM COMMUNICATION NUMBER Guideline 2015-02 ISSUE DATE June 2015 TABLE OF CONTENTS I. Introduction... 1 II. Purpose and Scope... 1 III. Principles...

REGULATORY GUIDELINE Liquidity Risk Management Principles SYSTEM COMMUNICATION NUMBER Guideline 2015-02 ISSUE DATE June 2015 TABLE OF CONTENTS I. Introduction... 1 II. Purpose and Scope... 1 III. Principles...

Pillar 3 U.S. Liquidity Coverage Ratio (LCR) Disclosures. For the quarter ended September 30, 2017

Disclosures. For the quarter ended September 30, 2017") Pillar 3 U.S. Liquidity Coverage Ratio (LCR) Disclosures For the quarter ended September 30, 2017 Bank of America Pillar 3 U.S. Liquidity Coverage Ratio Disclosures TABLE OF CONTENTS DISCLOSURE MAP...

Pillar 3 U.S. Liquidity Coverage Ratio (LCR) Disclosures For the quarter ended September 30, 2017 Bank of America Pillar 3 U.S. Liquidity Coverage Ratio Disclosures TABLE OF CONTENTS DISCLOSURE MAP...

Regulatory Practice Letter December 2013 RPL 13-20

Regulatory Practice Letter December 2013 RPL 13-20 Basel III Liquidity Coverage Ratio Proposal of U.S. Bank Regulators Executive Summary The Federal Reserve Board (Federal Reserve), the Office of the Comptroller

Regulatory Practice Letter December 2013 RPL 13-20 Basel III Liquidity Coverage Ratio Proposal of U.S. Bank Regulators Executive Summary The Federal Reserve Board (Federal Reserve), the Office of the Comptroller

COMMUNIQUE. Page 1 of 13

COMMUNIQUE 16-COM-001 Feb. 1, 2016 Release of Liquidity Risk Management Guiding Principles The Credit Union Prudential Supervisors Association (CUPSA) has released guiding principles for Liquidity Risk

COMMUNIQUE 16-COM-001 Feb. 1, 2016 Release of Liquidity Risk Management Guiding Principles The Credit Union Prudential Supervisors Association (CUPSA) has released guiding principles for Liquidity Risk

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure. For the quarterly period ended December 31, 2017

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure For the quarterly period ended December 31, 2017 0 Table of Contents 1. Overview..... 2 2. Liquidity Coverage Ratio Template... 3 3. LCR

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure For the quarterly period ended December 31, 2017 0 Table of Contents 1. Overview..... 2 2. Liquidity Coverage Ratio Template... 3 3. LCR

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure. For the quarterly period ended September 30, 2017

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure For the quarterly period ended September 30, 2017 1 Table of Contents 1. Overview... 3 2. Liquidity Coverage Ratio Template... 4 3. LCR Drivers

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure For the quarterly period ended September 30, 2017 1 Table of Contents 1. Overview... 3 2. Liquidity Coverage Ratio Template... 4 3. LCR Drivers

Pillar 3 Disclosures. Liquidity Coverage Ratio ( LCR ) For the quarter ended 31 March 2016

For the quarter ended 31 March 2016") Pillar 3 Disclosures Liquidity Coverage Ratio ( LCR ) For the quarter ended 31 March 016 DBS Group Holdings Ltd Incorporated in the Republic of Singapore Company Registration Number: 19990115M The following

Pillar 3 Disclosures Liquidity Coverage Ratio ( LCR ) For the quarter ended 31 March 016 DBS Group Holdings Ltd Incorporated in the Republic of Singapore Company Registration Number: 19990115M The following

12. LIQUIDITY RISK LIQUIDITY RISK MANAGEMENT AND ASSESSMENT MANAGEMENT MODEL

12. LIQUIDITY RISK 12.1. LIQUIDITY RISK MANAGEMENT AND ASSESSMENT LIQUIDITY MANAGEMENT The BCP Group liquidity management is globally accompanied and the supervision is coordinated at a consolidated level

12. LIQUIDITY RISK 12.1. LIQUIDITY RISK MANAGEMENT AND ASSESSMENT LIQUIDITY MANAGEMENT The BCP Group liquidity management is globally accompanied and the supervision is coordinated at a consolidated level

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure. For the quarterly period ended March 31, 2018

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure For the quarterly period ended March 31, 2018 0 Table of Contents 1. Overview..... 2 2. Liquidity Coverage Ratio Template... 3 3. LCR Drivers.

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure For the quarterly period ended March 31, 2018 0 Table of Contents 1. Overview..... 2 2. Liquidity Coverage Ratio Template... 3 3. LCR Drivers.

DWS USA Corporation. U.S. Liquidity Coverage Ratio Disclosures. For the quarter ended December 31, 2018

DWS USA Corporation U.S. Liquidity Coverage Ratio Disclosures For the quarter ended December 31, 2018 1 Table of Contents The Liquidity Coverage Ratio (LCR) 3 U.S. Disclosure Requirements 4 U.S. Qualitative

DWS USA Corporation U.S. Liquidity Coverage Ratio Disclosures For the quarter ended December 31, 2018 1 Table of Contents The Liquidity Coverage Ratio (LCR) 3 U.S. Disclosure Requirements 4 U.S. Qualitative

Northern Trust Corporation Liquidity Coverage Ratio Public Disclosure

Northern Trust Corporation Liquidity Coverage Ratio Public Disclosure For the quarterly period ended June 30, 2018 1 Northern Trust Corporation Liquidity Coverage Ratio Public Disclosure For the quarterly

Northern Trust Corporation Liquidity Coverage Ratio Public Disclosure For the quarterly period ended June 30, 2018 1 Northern Trust Corporation Liquidity Coverage Ratio Public Disclosure For the quarterly

Liquidity Coverage Ratio Disclosure. For the quarter ended June 2018

Liquidity Coverage Ratio Disclosure For the quarter ended June 2018 Liquidity Coverage Ratio ("LCR") and the Disclosure Template The Monetary Authority of Singapore ( MAS ) had designated Citibank Singapore

Liquidity Coverage Ratio Disclosure For the quarter ended June 2018 Liquidity Coverage Ratio ("LCR") and the Disclosure Template The Monetary Authority of Singapore ( MAS ) had designated Citibank Singapore

Basel II to Basel III The Way forward

White Paper Basel II to Basel III The Way forward - Rohit VM, Sudarsan Kumar, Jitendra Kumar Abstract Basel III guidelines are the response of BCBS (Basel Committee on Banking Supervision) to the 2008

White Paper Basel II to Basel III The Way forward - Rohit VM, Sudarsan Kumar, Jitendra Kumar Abstract Basel III guidelines are the response of BCBS (Basel Committee on Banking Supervision) to the 2008

LIQUIDITY ADEQUACY GUIDELINE. January 2015

LIQUIDITY ADEQUACY GUIDELINE January 2015 Liquidity Adequacy Guideline 1 Table of contents Table of Contents Abbreviations... ii Introduction... iv Scope of application... v Chapter 1. Overview... 1 1.1

LIQUIDITY ADEQUACY GUIDELINE January 2015 Liquidity Adequacy Guideline 1 Table of contents Table of Contents Abbreviations... ii Introduction... iv Scope of application... v Chapter 1. Overview... 1 1.1

LIQUIDITY ADEQUACY GUIDELINE. January 2016

LIQUIDITY ADEQUACY GUIDELINE January 2016 Liquidity Adequacy Guideline 1 Table of contents TABLE OF CONTENTS Abbreviations... ii Introduction... iv Scope of application... v Chapter 1. Overview... 1 1.1

LIQUIDITY ADEQUACY GUIDELINE January 2016 Liquidity Adequacy Guideline 1 Table of contents TABLE OF CONTENTS Abbreviations... ii Introduction... iv Scope of application... v Chapter 1. Overview... 1 1.1

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure. For the quarterly period ended December 31, 2018

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure For the quarterly period ended December 31, 2018 Table of Contents 1. Overview..... 2 2. Liquidity Coverage Ratio Template... 3 3. Main Drivers

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure For the quarterly period ended December 31, 2018 Table of Contents 1. Overview..... 2 2. Liquidity Coverage Ratio Template... 3 3. Main Drivers

Guidance to completing the LCR module of Form LCR

Guidance to completing the LCR module of Form LCR LIQUIDITY COVERAGE RATIO GUIDANCE Introduction The Liquidity Coverage Ratio ( LCR ) promotes the short-term resilience of the liquidity risk profile of

Guidance to completing the LCR module of Form LCR LIQUIDITY COVERAGE RATIO GUIDANCE Introduction The Liquidity Coverage Ratio ( LCR ) promotes the short-term resilience of the liquidity risk profile of

Managing liquidity risk in a changed and global world

Managing liquidity risk in a changed and global world September 15 th, 2010 PwC Agenda 1) Introduction to Liquidity Risk and Monetary Policy 2) Liquidity Risk from a supranational regulatory perspective

Managing liquidity risk in a changed and global world September 15 th, 2010 PwC Agenda 1) Introduction to Liquidity Risk and Monetary Policy 2) Liquidity Risk from a supranational regulatory perspective

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure. For the quarterly period ended June 30, 2018

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure For the quarterly period ended June 30, 2018 Table of Contents 1. Overview..... 2 2. Liquidity Coverage Ratio Template... 3 3. Main Drivers

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure For the quarterly period ended June 30, 2018 Table of Contents 1. Overview..... 2 2. Liquidity Coverage Ratio Template... 3 3. Main Drivers

Liquidity Risk Management After the Crisis WHITE PAPER

Liquidity Risk Management After the Crisis WHITE PAPER Table of Contents Introduction... 1 New Regulations for Liquidity Risk... 2 Components of Liquidity Risk... 4 Modeling Cash Flows for Liquidity Risk...

Liquidity Risk Management After the Crisis WHITE PAPER Table of Contents Introduction... 1 New Regulations for Liquidity Risk... 2 Components of Liquidity Risk... 4 Modeling Cash Flows for Liquidity Risk...

Information on Capital Structure, Liquidity Coverage and Leverage Ratios as per Basel-III Framework as at June 30, 2016

Information on Capital Structure, Liquidity Coverage and Leverage Ratios as per Basel-III Framework as at June 30, 2016 Table of Contents Capital Structure Statement of Financial Position - Step 1 ( Table

Information on Capital Structure, Liquidity Coverage and Leverage Ratios as per Basel-III Framework as at June 30, 2016 Table of Contents Capital Structure Statement of Financial Position - Step 1 ( Table

2016 Seminar for Senior Bank Supervisors from Emerging Economies. Implementation of Basel III Liquidity Requirements in Emerging Markets

2016 Seminar for Senior Bank Supervisors from Emerging Economies Implementation of Basel III Liquidity Requirements in Emerging Markets Christopher Wilson Monetary and Capital Markets Department International

2016 Seminar for Senior Bank Supervisors from Emerging Economies Implementation of Basel III Liquidity Requirements in Emerging Markets Christopher Wilson Monetary and Capital Markets Department International

Samba Financial Group Basel III - Pillar 3 Disclosure Report. September 2017 PUBLIC

Basel III - Pillar 3 Disclosure Report September 2017 Basel III - Pillar 3 Disclosure Report as at September 30, 2017 Page 1 of 12 Table of contents Capital Structure Page Statement of financial position

Basel III - Pillar 3 Disclosure Report September 2017 Basel III - Pillar 3 Disclosure Report as at September 30, 2017 Page 1 of 12 Table of contents Capital Structure Page Statement of financial position

Liquidity Coverage Ratio Public Disclosure

Liquidity Coverage Ratio Public Disclosure For the Quarter Ended December 31, 2018 Table of Contents INTRODUCTION 1 LIQUIDITY COVERAGE RATIO 1 PRIMARY DRIVERS OF THE LCR 1 U.S. LCR QUANTITATIVE DISCLOSURE

Liquidity Coverage Ratio Public Disclosure For the Quarter Ended December 31, 2018 Table of Contents INTRODUCTION 1 LIQUIDITY COVERAGE RATIO 1 PRIMARY DRIVERS OF THE LCR 1 U.S. LCR QUANTITATIVE DISCLOSURE

Implementing the new liquidity risk management frameworks the lessons learned

Implementing the new liquidity risk management frameworks the lessons learned September 15 th, 2010 PwC Agenda 1) Linking liquidity management and liquidity risk management 2) Setting strategic objectives

Implementing the new liquidity risk management frameworks the lessons learned September 15 th, 2010 PwC Agenda 1) Linking liquidity management and liquidity risk management 2) Setting strategic objectives

BC Liquidity Coverage Ratio Reporting Guide

BC Liquidity Coverage Ratio Reporting Guide J une 2017 BC C r ed i t Un i on s www.fic.gov.bc.ca Table of Contents Contents 1. INTRODUCTION... 2 1.1 Background... 2 1.2 Objectives... 2 2. LCR REPORTING...

BC Liquidity Coverage Ratio Reporting Guide J une 2017 BC C r ed i t Un i on s www.fic.gov.bc.ca Table of Contents Contents 1. INTRODUCTION... 2 1.1 Background... 2 1.2 Objectives... 2 2. LCR REPORTING...

Liquidity Coverage Ratio ( LCR ) For the quarter ended 31 Mar 2017

For the quarter ended 31 Mar 2017") Liquidity Coverage Ratio ( LCR ) For the quarter ended 31 Mar 017 DBS Group Holdings Ltd Incorporated in the Republic of Singapore Company Registration Number: 19990115M The following disclosures for the

Liquidity Coverage Ratio ( LCR ) For the quarter ended 31 Mar 017 DBS Group Holdings Ltd Incorporated in the Republic of Singapore Company Registration Number: 19990115M The following disclosures for the

CENTRAL BANK OF THE RUSSIAN FEDERATION (BANK OF RUSSIA) 30 May 2014 No. 421-P. Moscow REGULATION

30 May 2014 No. 421-P. Moscow REGULATION") CENTRAL BANK OF THE RUSSIAN FEDERATION (BANK OF RUSSIA) 30 May 2014 No. 421-P Moscow REGULATION On the Calculation of the Liquidity Coverage Ratio ( Basel III ) List of Amending Documents (as amended by

CENTRAL BANK OF THE RUSSIAN FEDERATION (BANK OF RUSSIA) 30 May 2014 No. 421-P Moscow REGULATION On the Calculation of the Liquidity Coverage Ratio ( Basel III ) List of Amending Documents (as amended by

Additional Liquidity Monitoring Metrics

Additional Liquidity Monitoring Metrics Implementation factors and data management Jacek Rzeźnik Market and Liquidity Risk Reporting and Analytics The opinion and views expressed herein are those of the

Additional Liquidity Monitoring Metrics Implementation factors and data management Jacek Rzeźnik Market and Liquidity Risk Reporting and Analytics The opinion and views expressed herein are those of the

Guideline. Liquidity Adequacy Requirements (LAR) Chapter 1 Overview Date: February 2018

Chapter 1 Overview Date: February 2018") Guideline Subject: Liquidity Adequacy Requirements (LAR) Chapter 1 Date: February 2018 Subsection 485(1) and 949(1) of the Bank Act (BA), subsection 473(1) of the Trust and Loan Companies Act (TLCA) and

Guideline Subject: Liquidity Adequacy Requirements (LAR) Chapter 1 Date: February 2018 Subsection 485(1) and 949(1) of the Bank Act (BA), subsection 473(1) of the Trust and Loan Companies Act (TLCA) and

Regions Financial Corporation. Liquidity Coverage Ratio Disclosure

Regions Financial Corporation Liquidity Coverage Ratio Disclosure As of and for the quarter ended December 31, 2018 Table of Contents Introduction 3 Main Drivers of LCR 3 High Quality Liquid Assets 4 Net

Regions Financial Corporation Liquidity Coverage Ratio Disclosure As of and for the quarter ended December 31, 2018 Table of Contents Introduction 3 Main Drivers of LCR 3 High Quality Liquid Assets 4 Net

African Bank Holdings Limited and African Bank Limited

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 7 3. Supplementary

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 7 3. Supplementary

Regulatory Capital Pillar 3 Disclosures

Regulatory Capital Pillar 3 Disclosures June 30, 2015 Table of Contents Background 1 Overview 1 Corporate Governance 1 Internal Capital Adequacy Assessment Process 2 Capital Demand 3 Capital Supply 3 Capital

Regulatory Capital Pillar 3 Disclosures June 30, 2015 Table of Contents Background 1 Overview 1 Corporate Governance 1 Internal Capital Adequacy Assessment Process 2 Capital Demand 3 Capital Supply 3 Capital

African Bank Holdings Limited and African Bank Limited

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 7 3. Supplementary

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 7 3. Supplementary

CENTRAL BANK OF THE BAHAMAS

CENTRAL BANK OF THE BAHAMAS I M P L E M E N T I N G B A S E L I II: L I Q U I D I T Y C O V E R A G E R A T I O ( L C R ) & N E T S TA B L E F U N D I N G R A T I O ( N S F R ) DISCUSSION PAPER 24 th December,

CENTRAL BANK OF THE BAHAMAS I M P L E M E N T I N G B A S E L I II: L I Q U I D I T Y C O V E R A G E R A T I O ( L C R ) & N E T S TA B L E F U N D I N G R A T I O ( N S F R ) DISCUSSION PAPER 24 th December,

Realize Tomorrow. Liquidity Coverage Ratio (LCR) Disclosure Report

Disclosure Report") Realize Tomorrow Liquidity Coverage Ratio (LCR) Disclosure Report March 2017 Content Introduction:... 2 I. Liquidity Governance... 2 II. Funding Strategy... 2 III. Liquidity Framework & Liquidity Risk

Realize Tomorrow Liquidity Coverage Ratio (LCR) Disclosure Report March 2017 Content Introduction:... 2 I. Liquidity Governance... 2 II. Funding Strategy... 2 III. Liquidity Framework & Liquidity Risk

Decision on liquidity risk management. General provisions Article 1

Pursuant to Article 101, paragraph (2), item (1) of the Credit Institutions Act (Official Gazette 159/2013, 19/2015 and 102/2015), and Article 43, paragraph (2), item (9) of the Act on the Croatian National

Pursuant to Article 101, paragraph (2), item (1) of the Credit Institutions Act (Official Gazette 159/2013, 19/2015 and 102/2015), and Article 43, paragraph (2), item (9) of the Act on the Croatian National

Guideline. Liquidity Adequacy Requirements (LAR) Chapter 2 Liquidity Coverage Ratio Date: June 2017

Chapter 2 Liquidity Coverage Ratio Date: June 2017") Guideline Subject: Liquidity Adequacy Requirements (LAR) Chapter 2 Date: June 2017 Subsection 485(1) and 949(1) of the Bank Act (BA), subsection 473(1) of the Trust and Loan Companies Act (TLCA) and subsection

Guideline Subject: Liquidity Adequacy Requirements (LAR) Chapter 2 Date: June 2017 Subsection 485(1) and 949(1) of the Bank Act (BA), subsection 473(1) of the Trust and Loan Companies Act (TLCA) and subsection

African Bank Holdings Limited and African Bank Limited

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 9 3. Supplementary

African Bank Holdings Limited and African Bank Limited Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 CONTENTS 1. Executive summary... 3 2. Basis of compilation... 9 3. Supplementary

Draft Guideline. Liquidity Adequacy Requirements (LAR) Chapter 2 Liquidity Coverage Ratio Date: June 2017February 2019

Chapter 2 Liquidity Coverage Ratio Date: June 2017February 2019") Draft Guideline Subject: Liquidity Adequacy Requirements (LAR) Chapter 2 Date: June 2017February 2019 Subsection 485(1) and 949(1) of the Bank Act (BA), subsection 473(1) of the Trust and Loan Companies

Draft Guideline Subject: Liquidity Adequacy Requirements (LAR) Chapter 2 Date: June 2017February 2019 Subsection 485(1) and 949(1) of the Bank Act (BA), subsection 473(1) of the Trust and Loan Companies

The BBA is pleased to respond to this consultation on the net stable funding ratio. Please find below are comments on the key issues in the paper.

BBA response to BCBS 271: Basel III: The Net Stable Funding Ratio Introduction The British Bankers Association ( BBA ) is the leading association for UK banking and financial services for the UK banking

BBA response to BCBS 271: Basel III: The Net Stable Funding Ratio Introduction The British Bankers Association ( BBA ) is the leading association for UK banking and financial services for the UK banking

Tailored to Small Markets: Implementation of Basel III Liquidity Requirements

Tailored to Small Markets: Implementation of Basel III Liquidity Requirements Christopher h Wilson Financial Supervision and Regulation Division Monetary and Capital Markets Department October 2015 Outline

Tailored to Small Markets: Implementation of Basel III Liquidity Requirements Christopher h Wilson Financial Supervision and Regulation Division Monetary and Capital Markets Department October 2015 Outline

Guidance on Liquidity Risk Management

2017 CONTENTS 1. Introduction... 3 2. Minimum Liquidity and Reporting Requirements... 5 3. Additional Liquidity Monitoring... 7 4. Liquidity Management Policy ( LMP )... 8 5. Fundamental principles for

2017 CONTENTS 1. Introduction... 3 2. Minimum Liquidity and Reporting Requirements... 5 3. Additional Liquidity Monitoring... 7 4. Liquidity Management Policy ( LMP )... 8 5. Fundamental principles for

ECB Guide to the internal liquidity adequacy assessment process (ILAAP)

") ECB Guide to the internal liquidity adequacy assessment process (ILAAP) March 2018 Contents 1 Introduction 2 1.1 Purpose 3 1.2 Scope and proportionality 3 2 Principles 5 Principle 1 The management body

ECB Guide to the internal liquidity adequacy assessment process (ILAAP) March 2018 Contents 1 Introduction 2 1.1 Purpose 3 1.2 Scope and proportionality 3 2 Principles 5 Principle 1 The management body

Collateralized Banking

Collateralized Banking A Post-Crisis Reality Dr. Matthias Degen Senior Manager, KPMG AG ETH Risk Day 2014 Zurich, 12 September 2014 Definition Collateralized Banking Totality of aspects and processes relating

Collateralized Banking A Post-Crisis Reality Dr. Matthias Degen Senior Manager, KPMG AG ETH Risk Day 2014 Zurich, 12 September 2014 Definition Collateralized Banking Totality of aspects and processes relating

Table 1: LCR Three Months Ended Average Weighted Amount (millions)

") Executive Summary The Board of Governors of the Federal Reserve System (the Federal Reserve ) requires public disclosure of the liquidity coverage ratio (the LCR ) by depository institution holding companies

Executive Summary The Board of Governors of the Federal Reserve System (the Federal Reserve ) requires public disclosure of the liquidity coverage ratio (the LCR ) by depository institution holding companies

Liquidity Risk in Albania

ISSN 2286-4822, www.euacademic.org IMPACT FACTOR: 0.485 (GIF) DRJI VALUE: 5.9 (B+) Liquidity Risk in Albania ANJEZA BEJA Faculty of Economy University of Tirana, Tirana Albania Abstract: Interbank markets

ISSN 2286-4822, www.euacademic.org IMPACT FACTOR: 0.485 (GIF) DRJI VALUE: 5.9 (B+) Liquidity Risk in Albania ANJEZA BEJA Faculty of Economy University of Tirana, Tirana Albania Abstract: Interbank markets

Basel III Liquidity Options

Basel III Liquidity Options FRDP 2011-02 May 28, 2011 In this ACFS Discussion Paper, Professor Kevin Davis examines the new Basel Liquidity Requirements announced at the end of 2010, focusing primarily

Basel III Liquidity Options FRDP 2011-02 May 28, 2011 In this ACFS Discussion Paper, Professor Kevin Davis examines the new Basel Liquidity Requirements announced at the end of 2010, focusing primarily

Amex Bank of Canada. Basel III Pillar III Disclosures December 31, AXP Internal Page 1 of 15

December 31, 2013 AXP Internal Page 1 of 15 Table of Contents 1 Scope of application 3 2 Capital structure and adequacy 4 3 Credit risk management 6 4 Asset liability management 11 Structural interest

December 31, 2013 AXP Internal Page 1 of 15 Table of Contents 1 Scope of application 3 2 Capital structure and adequacy 4 3 Credit risk management 6 4 Asset liability management 11 Structural interest

(Text with EEA relevance)

") L 271/10 COMMISSION DELEGATED REGULATION (EU) 2018/1620 of 13 July 2018 amending Delegated Regulation (EU) 2015/61 to supplement Regulation (EU) No 575/2013 of the European Parliament and the Council with

L 271/10 COMMISSION DELEGATED REGULATION (EU) 2018/1620 of 13 July 2018 amending Delegated Regulation (EU) 2015/61 to supplement Regulation (EU) No 575/2013 of the European Parliament and the Council with

Samba Financial Group Basel III - Pillar 3 Disclosure Report. September 2018 PUBLIC

Basel III - Pillar 3 Disclosure Report September 2018 Basel III - Pillar 3 Disclosure Report as at September 30, 2018 Page 1 of 6 Table of Contents Liquidity Page LIQ1 - Liquidity coverage ratio ( LCR

Basel III - Pillar 3 Disclosure Report September 2018 Basel III - Pillar 3 Disclosure Report as at September 30, 2018 Page 1 of 6 Table of Contents Liquidity Page LIQ1 - Liquidity coverage ratio ( LCR

SEPTEMBER 2016 BC Credit Unions

Net Cumulative Cash Flow Reporting Guide SEPTEMBER 2016 BC Credit Unions www.fic.gov.bc.ca Table of Contents 1 INTRODUCTION... 1 1.1 Background... 1 1.2 Objectives... 2 2 NCCF REPORTING... 2 3 ASSUMPTIONS...

Net Cumulative Cash Flow Reporting Guide SEPTEMBER 2016 BC Credit Unions www.fic.gov.bc.ca Table of Contents 1 INTRODUCTION... 1 1.1 Background... 1 1.2 Objectives... 2 2 NCCF REPORTING... 2 3 ASSUMPTIONS...

TABLE 2: CAPITAL STRUCTURE - June 30, 2018

TABLE 2: CAPITAL STRUCTURE - June 30, 2018 Balance sheet - Step 1 (Table 2(b)) All figures are in SAR '000 Assets Balance sheet in Published financial statements Adjustment of banking associates / other

TABLE 2: CAPITAL STRUCTURE - June 30, 2018 Balance sheet - Step 1 (Table 2(b)) All figures are in SAR '000 Assets Balance sheet in Published financial statements Adjustment of banking associates / other

LIQUIDITY RISK MANAGEMENT MODULE

LIQUIDITY RISK MANAGEMENT MODULE MODULE: LM (Liquidity Risk Management) Table of Contents Date Last Changed LM-A Introduction LM A.1 Purpose 08/2018 LM A.2 Module History 08/2018 LM-1 Governance of Liquidity

LIQUIDITY RISK MANAGEMENT MODULE MODULE: LM (Liquidity Risk Management) Table of Contents Date Last Changed LM-A Introduction LM A.1 Purpose 08/2018 LM A.2 Module History 08/2018 LM-1 Governance of Liquidity

Guidance to completing the NSFR module of Form LCR and LMR

Guidance to completing the NSFR module of Form LCR and LMR 1 Net Stable Funding Ratio (NSFR) The Net Stable Funding Ratio has been developed to ensure a stable funding profile in relation to the characteristics

Guidance to completing the NSFR module of Form LCR and LMR 1 Net Stable Funding Ratio (NSFR) The Net Stable Funding Ratio has been developed to ensure a stable funding profile in relation to the characteristics

BASEL III: LIQUIDITY STANDARDS

BASEL III: LIQUIDITY STANDARDS Issued under BPRD circular # 08 dated June 23, 2016 BANKING POLICY & REGULATIONS DEPARTMENT STATE BANK OF PAKISTAN This page is left blank intentionally BPRD circular # 08

BASEL III: LIQUIDITY STANDARDS Issued under BPRD circular # 08 dated June 23, 2016 BANKING POLICY & REGULATIONS DEPARTMENT STATE BANK OF PAKISTAN This page is left blank intentionally BPRD circular # 08

Lombard Odier Group Pillar 3 Disclosures at 30 June 2018

Lombard Odier Group Pillar 3 Disclosures at 30 June 2018 Contents Introduction 5 Consolidation scope 5 Composition of capital 7 Risk-weighted assets and minimum capital requirements 9 Market Risks 10

Lombard Odier Group Pillar 3 Disclosures at 30 June 2018 Contents Introduction 5 Consolidation scope 5 Composition of capital 7 Risk-weighted assets and minimum capital requirements 9 Market Risks 10

The Bank of East Asia, Limited 東亞銀行有限公司. Banking Disclosure Statement

Banking Disclosure Statement For the period ended 30 September 2018 Table of contents Introduction... 1 Template KM1: Key prudential ratios... 2 Template OV1: Overview of RWA... 3 Template LR2: Leverage

Banking Disclosure Statement For the period ended 30 September 2018 Table of contents Introduction... 1 Template KM1: Key prudential ratios... 2 Template OV1: Overview of RWA... 3 Template LR2: Leverage

Regulatory Notice 15-33

Regulatory Notice 15-33 Liquidity Risk Guidance on Liquidity Risk Management Practices Executive Summary Effective liquidity management is a critical control function at brokerdealers and across firms

Regulatory Notice 15-33 Liquidity Risk Guidance on Liquidity Risk Management Practices Executive Summary Effective liquidity management is a critical control function at brokerdealers and across firms

Oracle Financial Services Liquidity Risk Management

Oracle Financial Services Liquidity Risk Management Analytics User Guide Oracle Financial Services Liquidity Risk Management Analytics User Guide, Copyright 2017, Oracle and/or its affiliates. All rights

Oracle Financial Services Liquidity Risk Management Analytics User Guide Oracle Financial Services Liquidity Risk Management Analytics User Guide, Copyright 2017, Oracle and/or its affiliates. All rights

DRAFT ANNEX XXV REPORTING ON LIQUIDITY (PART 2 OUTFLOWS)

") DRAFT ANNEX XXV REPORTING ON LIQUIDITY (PART 2 OUTFLOWS) 1. Outflows 1.1. General remarks 1. This is a summary template which contains information about liquidity outflows measured over the next 30 days,

DRAFT ANNEX XXV REPORTING ON LIQUIDITY (PART 2 OUTFLOWS) 1. Outflows 1.1. General remarks 1. This is a summary template which contains information about liquidity outflows measured over the next 30 days,

Regulatory Capital Pillar 3 Disclosures

Regulatory Capital Pillar 3 Disclosures June 30, 2014 Table of Contents Background 1 Overview 1 Corporate Governance 1 Internal Capital Adequacy Assessment Process 2 Capital Demand 3 Capital Supply 3 Capital

Regulatory Capital Pillar 3 Disclosures June 30, 2014 Table of Contents Background 1 Overview 1 Corporate Governance 1 Internal Capital Adequacy Assessment Process 2 Capital Demand 3 Capital Supply 3 Capital

4. Regulatory capital adequacy

4. Regulatory capital adequacy R 000 29 Feb Composition of qualifying regulatory capital Ordinary share capital (1) 5 649 020 5 649 020 Accumulated profit 8 772 714 7 772 004 14 421 734 13 421 024 Regulatory

4. Regulatory capital adequacy R 000 29 Feb Composition of qualifying regulatory capital Ordinary share capital (1) 5 649 020 5 649 020 Accumulated profit 8 772 714 7 772 004 14 421 734 13 421 024 Regulatory

Managing Liquidity Risk with RiskAuthority & RiskConfidence : US Basel 3 Liquidity Coverage Ratio and Beyond

Managing Liquidity Risk with RiskAuthority & RiskConfidence : US Basel 3 Liquidity Coverage Ratio and Beyond Olivier Brucker Senior Director, Sales Management Yannick Fessler Senior Director, ALM Product

Managing Liquidity Risk with RiskAuthority & RiskConfidence : US Basel 3 Liquidity Coverage Ratio and Beyond Olivier Brucker Senior Director, Sales Management Yannick Fessler Senior Director, ALM Product

Guideline on Liquidity Risk Management

BOM/BSD 4/January 2000 BANK OF MAURITIUS Guideline on Liquidity Risk Management January 2000 Revised October 2009 Revised August 2010 Revised October 2017 Table of Contents INTRODUCTION... 1 Authority...

BOM/BSD 4/January 2000 BANK OF MAURITIUS Guideline on Liquidity Risk Management January 2000 Revised October 2009 Revised August 2010 Revised October 2017 Table of Contents INTRODUCTION... 1 Authority...

Basel III Pillar III DISCLOSURES REPORT

Basel III Pillar III DISCLOSURES REPORT Pillar III Disclosures Report December 31st 2016 ARESBANK PILAR III DISCLOSURES (December 31 st, 2016) TABLE OF CONTENTS 1. INTRODUCTION... 3 2. INTERNAL GOVERNANCE

Basel III Pillar III DISCLOSURES REPORT Pillar III Disclosures Report December 31st 2016 ARESBANK PILAR III DISCLOSURES (December 31 st, 2016) TABLE OF CONTENTS 1. INTRODUCTION... 3 2. INTERNAL GOVERNANCE

Regulatory Capital Pillar 3 Disclosures

Regulatory Capital Pillar 3 Disclosures December 31, 2016 Table of Contents Background 1 Overview 1 Corporate Governance 1 Internal Capital Adequacy Assessment Process 2 Capital Demand 3 Capital Supply

Regulatory Capital Pillar 3 Disclosures December 31, 2016 Table of Contents Background 1 Overview 1 Corporate Governance 1 Internal Capital Adequacy Assessment Process 2 Capital Demand 3 Capital Supply

African Bank Holdings Limited and African Bank Limited. Annual Public Pillar III Disclosures

African Bank Holdings Limited and African Bank Limited Annual Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 as at 30 September 2016 1 African Bank Holdings Limited and African

African Bank Holdings Limited and African Bank Limited Annual Public Pillar III Disclosures in terms of the Banks Act, Regulation 43 as at 30 September 2016 1 African Bank Holdings Limited and African

The Federal Reserve s proposed rule for enhanced prudential standards: what it means to insurers and what they should do now

The Federal Reserve s proposed rule for enhanced prudential standards: what it means to insurers and what they should do now On June 3, 2016, the Federal Reserve Board of Governors (FRB) released a notice

The Federal Reserve s proposed rule for enhanced prudential standards: what it means to insurers and what they should do now On June 3, 2016, the Federal Reserve Board of Governors (FRB) released a notice