MOSCOW HALAL BUSINESS FORUM All-Russia Exhibition Centre June 2013 Moscow

|

|

|

- Byron Brown

- 6 years ago

- Views:

Transcription

1 MOSCOW HALAL BUSINESS FORUM All-Russia Exhibition Centre June 2013 Moscow Talk on Takaful 13 June 2013 Alberto G Brugnoni - ASSAIF

2 CONTENTS OF THE TALK INTRODUCTION The meaning of Takaful Shariah perspective Takaful and conventional THE CONTRACTS AND THE ACTUAL PRACTICE Contractual relationships Business forms and models THE PRESENT STATE OF THE TAKAFUL INDUSTRY An appraisal of the market Where to source information, major world events REGULATORY ISSUES Regulatory bodies and standards Some regulatory and accounting challenges 2

3 INTRODUCTION The Meaning of Takaful and a General Definition The Shariah Basis of Takaful The Shariah Perspective on Conventional Insurance From the Shariah Perspective the Key Issue is Gharar Some Additional Reflections on Conventional Insurance The Islamisation of Insurance: Tackling gharar with tabarru Insurance and Takaful: a Comparison 3

4 THE MEANING OF TAKAFUL & A GENERAL DEFINITION Takaful means a scheme based on brotherhood, solidarity and mutual assistance which provides for mutual financial aid and assistance to the participants in case of need whereby the participants mutually agree to contribute for that purpose (Laws of Malaysia, Act 312, Takaful Act 1984 Part 1 Preliminary) A strategy of risk mitigation by way of a collective risk taking that distributes risks and harms to large numbers of participants. This mitigates the otherwise very damaging harm that can be caused to a person if the risk is to be borne individually. The purpose of Takaful is not profit, but to uphold the principle of bear you one another's burden (dr Engku Rabiah Adawiah Engku Ali & Hassan Scott Odierno). Hence, Takaful embraces the following elements of cooperation, shared responsibility and mutual protection: policyholders cooperate among themselves for their common good every policyholder pays his subscription to help those who need assistance losses are divided and liabilities spread according to the community pooling system uncertainty is eliminated concerning subscription and compensation it does not derive advantage at the cost of others 4

5 THE SHARIAH BASIS OF TAKAFUL The world Takaful التكافل is the masdar of the 6 th form the Arabic root-verb kafala with the meaning of cooperation, shared responsibility and mutual protection. The Shariah basis of which, can be deduced from the Qur an, Hadith and a legal maxim (qa idah fiqhiyyah): Cooperation: Help one another in virtue and piety (al-birr wa al-taqwa), but do not help one another in sin and transgression (Qur an,5:2). And God will always help his servant for as long as he helps others (Ahmad bin Hanbal and Abu Daud) Shared responsibility: The place of relationships and feelings of people with faith, between each other, is just like the body; when one of its parts is afflicted with pain, then the rest of the body will be affected (al-bukhari and Muslim). And One Believer and another Believer are like a building, whereby every part in it strengthens the other part (Imam al-bukhari and Imam Muslim) Mutual protection: By my life (which is in God s power), nobody will enter Paradise if he does not protect his neighbour who is in distress (Ahmad bin Hanbal) The concept is also grounded in Islamic mu amalat, observing the rules and regulations of Islamic law. Muslim jurists acknowledge that the basis of shared responsibility in the system of aqila (payment of blood money or diyyah) laid the foundation of mutual insurance Finally, the legal maxim al-darar yuzal (damage or harm is removed) entails that once any damage is caused or occurred, efforts must be made to remove it 5

6 THE SHARIAH PERSPECTIVE ON INSURANCE Despite having the same noble objective of providing protection and coverage to the policy holders, conventional insurance suffers from fundamental problems in its modus operandi, mainly due to the occurrence of the Shariah non-compliant elements of gharar (uncertainty, deceit, risk, hazard), ribà (interest, usury) and maysir (gambling) The consensus of the fuqaha on the three key non-compliant elements is general and unchallenged. For ex.: 1972 fatwa by National Council for Islamic Religious Affairs of Malaysia that life insurance is not lawful as it contains gharar, riba and maysir in 1985, the Council of the Islamic Fiqh Academy under the auspices of the OIC in its resolution n 9(9/2) resolved that the commercial insurance contract with a fixed periodical premium contains major elements of gharar which void the contract and therefore is prohibited Ribà: its occurrence in conventional insurance is through the investment of the premia payments in ribà-based financial instruments Maysir: its element in conventional insurance is attributed to the act of purchasing the policy with the hope of getting more in term of compensation if any of the perils were to occur GHARAR 6

7 THE SHARIAH PERSPECTIVE ON GHARAR The existence of gharar may deny the contracting party/ies from equal bargaining power, resulting in the inability to make informed decisions as they do not adequately understand the attributes or consequences of the contract. This is the reason why gharar is prohibited under Islamic Law The Qur anic reference is: O ye who believe! eat not up your property among yourselves in vanities (batil): but let there be amongst you traffic and trade by mutual goodwill nor kill (or destroy) yourselves: for verily Allah hath been to you Most Merciful (4:29) Vanities (batil) is interpreted as all illegal and defective elements in contracts including those involving uncertainty Trade by mutual goodwill is reinforced by the requirement imposed by jurists for a formal offer and acceptance (indicating consent and eliminating mistakes, fraud, etc.) by the contracting parties in order to have a valid contract Hence: under Islamic legal principles, the subject matter of any exchange contract (e.g. sale) must be certain, i.e.: specific identification of the subject matter and its attributes and the certainty of its existence and deliverability in order to meet the obligation under the contract 7

8 THE SHARIAH PERSPECTIVE ON GHARAR In a sale contract the subject matter includes the assets (goods) and the consideration (price). In conventional insurance the main contract between the parties is an exchange (sale) contract where the goods are the policies (indemnity or protection) and the price is the premium From a Shariah perspective the problem in this sale transaction is the subject matter of the sale. Policy and premium (the subject matters) are not certain because the actual value or amounts of both are tied or conditional to the occurrence of uncertain events (the perils and hazard) The actual amount of coverage payable under the policy depends on the occurrence, timing, extent and type of peril or hazard, which are not known until the actual occurrence of the event Similarly, the total amount of premium payable is also uncertain because it depends on when the peril occurs In such a contract, the insurance company is aiming at making profits from the uncertainties inherent in the contract, making it illegal from the Shariah point-of-view Note that the prohibition of gharar does not strictly apply to charitable (gratuitous) and unilateral contracts where no counter-values are expected in return. Thus, its existence in these contracts does not render them void or voidable 8

9 SOME ADDITIONAL REFLECTIONS ON INSURANCE 1. Risk-transfer against risk-sharing. Conventional insurance is based on profit-motive and is owned by shareholders of the insurer company. Takaful itself is non-profit and is owned by policyholders. The insurer is now called the operator and receives a fair compensation 2. In conventional insurance, insurer s profits include underwriting surplus. Essentially, its profit comprises underwriting surplus plus investment income. The distribution of profits or surplus is a managerial and as a result there is a conflict of interest between the shareholders and the policyholders. In case Takaful the operator,, has no claims in underwriting surplus. Further, it is the Takaful contract, not the management of the operator company that specifies in advance how and when profit will be distributed 3. In conventional insurance, the sources of laws and regulations are set by state and are man-made. In Takaful, the laws and regulations are based on divine revelations 4. In case of dissolution of the conventional insurer, reserves and excess/surplus belong to the shareholders. In case of dissolution of the Takaful operator however, they could be returned to participants, or donated to charity. Most scholars would prefer the latter course of action 5. The Islamic insurance company has an additional obligation of annual payment of zakat 6. Even with cooperative insurance there are issues with Shariah compliant investments, shareholders surplus participation and shareholders governance 9

10 The Islamisation of Insurance: Tackling gharar with tabarru As we have seen, Islam is not against the concept of insurance itself. In fact, the concept of mitigation of risks by adopting the law of large numbers was widely used in Islam and especially in the practice of al- aqilah In my view, insurance against hazard can be modified in a manner which would bring it closer to the Islamic principle by means of a contract of donation with a condition of compensation (dr Yusuf al-qardawi, The Lawful and the Prohibited in Islam, 276) From the above quote, it is clear that the most essential modification is to substitute the contract of sale and purchase of the policy that give rise to the gharar issue with a contract of donation (tabarru ) with a condition of compensation Tabarru : contract of gratuity/charity, i.e. to relinquish a portion from the contribution as a donation for fulfilling obligation of mutual help, used to pay claims submitted by eligible claimants. Tabarru changes the nature of the insurance policy from an exchange contract (mu awadat), which is bilateral in nature, to a charitable contract, which is unilateral in nature This allows the existence of gharar to be tolerated, the logic being those paying the tabarru contributions are not aiming to profit from the uncertainty 10

11 INSURANCE AND TAKAFUL: A COMPARISON Contract Responsibility of participants/ policyholders Liability of the operator/ insurer Access to capital by operator/insurer Investment of Funds Takaful A combination of tabarru (donation) and wakalah or mudharabah contracts Make contributions to the scheme Mutually guarantee each other Acts as the administrator of the scheme and pays the benefits from the funds In the event of deficiency in the funds will provide qardh hasan to rectify the deficiency Share capital but not debt Funds invested in Shariah-compliant instruments only Insurance An exchange contract (sale and purchase) between insurer and insured Pay premium to the insurer Liable to pay the insurance benefits as promised from its assets (insurance funds and shareholder s funds) Share capital, debt, subordinated debt No restriction but use of prudential reasons 11

12 THE CONTRACTS AND THE ACTUAL PRACTICE Framing Takaful: Building Blocks Contractual Relationship Amongst the Participants Contractual Relationship The Participants & the Operator Five Possible Contracts: Three in Use and Two Not Adopted Two Takaful Business Forms First Takaful Business Form: Not-for-Profit: The Pure Cooperative Model Second Takaful Business Form: Commercial Mudharabah: The Mudharabah Pure Model The Mudharabah Modified Model Second Takaful Business Form: Commercial Wakalah: The Wakalah Model Second Takaful Business Form: Commercial Hybrid: The Hybrid Wakalah and Mudharabah Model 12

13 FRAMING TAKAFUL: BUILDING BLOCKS A Takaful scheme essentially involves two main parties: a group of participants (policyholders in conventional insurance) and the Takaful operator. An important principle for all profit-based models is the segregation between the participants contributions (participants Takaful fund) and the capital contribution of the Takaful operator representing the paid-capital of the company (shareholders fund) provided to develop the business The main sources of income for the Takaful operator are: (i) income from the investment of the shareholders fund; (ii) wakalah fees in accordance with agency arrangement of wakalah for underwriting operations, and/or (iii) share of income from investing the participants Takaful funds (on the basis of pre-agreed ratios according to mudarabah) The net underwriting surplus belongs, at least in principle, to the participants (AAOIFI Shariah Standards n 26 (5/5) 2007) an AAOIFI announcement in May 2011 indicated that performance fees to the operator could be paid out of surplus though the beneficiaries can only be the management and not shareholders Takaful is the Islamic counterpart of conventional insurance, and exists in both life (or family ) and general forms. It is based on concepts of mutual solidarity, and a typical Takaful undertaking will consist of a two-tier structure that is a hybrid of a mutual and a commercial form of company (Islamic Financial Services Board IFSB and International Association of Insurance Supervisors IAIS) 13

14 FRAMING TAKAFUL: BUILDING BLOCKS Islamic insurance is an agreement between persons who are exposed to risks to protect themselves against harms arising from the risks by paying contributions on the basis of commitment to donate (iltizam bi l-tabarru ) following from that, the insurance fund is established and it is treated as a separate legal entity (shakhsiyyah i tibariyyah) which has independent financial liability the fund will cover the compensation against harms that befall any of the participants due to the occurrence of the insured risks in accordance with the terms of the policy (Accounting & Auditing Organization for Islamic Financial Institutions, Shariah Standard 26 (2) of 2007) Islamic insurance is a system through which the participants donate part or all of their contributions which are used to pay claims for damages suffered by some of the participants the company s role is restricted to managing the insurance operations and investing the insurance contributions (AAOIFI - Financial Accounting Standard n 12, Appendix E) 14

15 CONTRACTUAL RELATIONSHIP PARTICIPANTS The participants are insuring themselves: the tabarru (donation) contract is the pillar in the Takaful scheme that allows the gharar element to be tolerated without affecting the validity of the contract. The donation can be either in the form of outright gift (hiba) or endowment (wafq) Note that if the participants also intend to invest some of their money as their savings then their governing contract is a musharakah Takaful participants Mutual indemnity Tabarru (donation) Mutual indemnity Takaful fund 15

16 CONTRACTUAL RELATIONSHIPS THE PARTICIPANTS & THE OPERATOR Note that there is no insurer-insured relationship between the participants and the Takaful operator. The Takaful operator is engaged by the participants as a group to manage the Takaful scheme for them. That s all. The operator is expected to: manage the underwriting of Takaful contributions and payments of claims manage the investment portfolio. The logic is to invest any available funds before and after payment of claims and other expenses to allow them to grow Depending on the type of underlying contract (mudharabah, wakalah, hybrid), the operator may receive a fee and/or a share of the investment profit as a reward for its activities Takaful participants Investments Donations Takaful fund jointly owned by the participants Manage Takaful operator Islamic finance contracts: mudharabah, wakalah, hybrid, others Pay Claims 16

17 FIVE POSSIBLE CONTRACTS: THREE IN USE AND TWO NOT ADOPTED Mudharabah: once the money has been contributed by the participants into the Takaful fund on the basis of tabarru the money belongs to them collectively. Hence, they act as rabb almal and appoint the Takaful operator to be their manager by way of mudharabah contract. Hence, the operator becomes the mudharib. Rules of mudharabah (profit sharing and loss bearing) apply Wakalah: the participants as a group appoint and authorize the Takaful operator (hence, they act as principal) to manage the Takaful fund (hence, it becomes the wakeel) for both insurance as well as investment activities. Rules of wakalah (remuneration with a fee) apply Hybrid: the contract of mudharabah is used for investment purposes of the fund, whilst the contract of wakalah for insurance activities of the fund ISLAMIC CONTRACTS NOT ADOPTED ju alah: similar to wakalah but with a commission/reward system tied to the performance wadi ah yad damanah: the participants deposit the fund to be safe-kept (wadi ah) by the operator. Profits from the investments belong to it (it may give some of them as hibah to the participants) but it bears the risks on any losses as well as any claims or expenses incurred. In addition, any net underwriting surplus, belongs to the Takaful participants 17

18 TWO TAKAFUL BUSINESS FORMS There is no single best form or model that exists for Takaful. The Shariah scholars worldwide concur on fundamental components that characterize a Takaful scheme, yet in their fatwas operational differences are tolerated as long as they do not contradict essential Islam religious tenets. This gives Takaful an unparalleled resiliency in adapting to local Shariah requirements For instance, in models and forms the Shariah scholars have expressed differences in opinions relating to charging of expenses (marketing v. administration) and also the fee structure, etc. Two business forms and three commercial models (based on the three contracts in use) are nowadays employed by the Takaful industry 18

19 FIRST TAKAFUL BUSINESS FORM: NOT-FOR-PROFIT Operations and profits are completely self contained Regardless of the formal legal structure, the business is run on a purely mutual and cooperative basis for the participants in the Takaful scheme. There are no shareholders in the commercial sense The participants (founders and promoters) pay their contribution as 100% tabarru and do not intend to receive any commercial return arising from the business Any surplus may be distributed for charitable purposes. Non-profit models include social governmental owned enterprises and programmes as well as endowment-like trusts operated on a non-profit basis There is little room for entrepreneurial spirit here and there are significant difficulties in raising capital 19

20 THE PURE COOPERATIVE MODEL PARTICIPANTS/ POLICYHOLDERS Contributions Takaful fund Policy benefits Investment Profits Participant Account (personal) Investment Profits Participant Special Account (common) Underwriting Surplus Operator Actual Management Expenses 20

21 SECOND TAKAFUL BUSINESS FORM: COMMERCIAL MUDHARABAH Two versions were developed: the pure mudharabah: whereas the participants are entitled to receive any distributable surplus generated from the underwriting operations and a share of the income from their funds invested by the operator. The operator expects to receive a return on its investment in the Takaful business through sharing in the profit in the income from investing the participants funds note that the tabarru element still exists, the mudharabah being just a side activity to optimize the use of the funds until claims are made or other expenses incurred the modified mudharabah which included the sharing of underwriting surplus note that the underwritings surplus should not in principle be shared with the operator because they are not mudharabah profits but residue of the Takaful fund which belongs to the participants together as a group the crux of the criticism centers around the definition of mudharabah profit, i.e. whether the net underwriting surplus can be treated as such mudharabah is defined as a surplus above the original capital. However, in this situation there is no such a surplus because of the reduction due to claims and expenses. What remains is the net underwriting surplus, which is lower than the original mudharabah capital even after the addition of any profit generated from the investment activities nonetheless, in the conventional insurance understanding this is considered as net underwriting surplus and treated as profit. 21

22 THE MUDHARABAH PURE MODEL PARTICIPANTS/ POLICYHOLDERS (100 - X)% Shareholders Fund/ Contributions Operator Claims Shariah compliant Investments = Mudharabah profits Takaful Fund - owned by the participants Reinsurance/ Retakaful Reserves Expenses investments and management Underwriting expenses Underwriting surplus Qardh Hasan x% Surplus 100% 22

23 THE MUDHARABAH MODIFIED MODEL PARTICIPANTS/ POLICYHOLDERS Management Expenses Contributions Claims Shareholders Fund/ Shariah compliant Investments Takaful Fund - owned by the participants Reinsurance/ Retakaful Operator Reserves Qard Hasan Underwriting expenses Investment Profits Underwriting surplus Surplus/(Deficit) X% of Surplus 100% - X% of Surplus 23

24 SECOND TAKAFUL BUSINESS FORM: COMMERCIAL WAKALAH Participants appoint and authorize the operator to be their agent to manage the Takaful fund. Generally, this is for both insurance as well as investment activities It should be noted that even in this model the issue on how to treat the net underwriting surplus remain as some operators claim a portion of it on the basis of performance fee. The argument being that good management in the underwriting, assessment of risks and claim management has contributed to the availability of the surplus. This has lead to the existence of a modified wakalah model along the lines of the modified mudharabah note that prior consent of the participants must be obtained before any payment of performance fees from the net underwriting surplus 24

25 THE WAKALAH MODEL PARTICIPANTS/ POLICYHOLDERS Management Expenses Contributions Wakalah Fee Shareholders Fund/ Claims Operator Shariah compliant Investments Takaful fund - owned by the participants Reinsurance/ Retakaful Reserves Qard Hasan Underwriting expenses Investment Profits Underwriting Surplus Surplus/(Deficit) 100% of Surplus 25

26 SECOND TAKAFUL BUSINESS FORM: COMMERCIAL HYBRID Some operators use a combination of mudarabah and wakalah with the latter being the predominant contract: wakalah for insurance activities : underwriting of contributions, risk assessment, claim management. Wakalah conditions apply mudharabah for investment management activities. Mudharabah conditions apply As for underwriting surpluses, the operator may: for family Takaful distribute them back to the participants for general Takaful use it as a rebate or NCD / NCB in favor of the participants when renewing their policy; keep it in the Takaful fund; distribute it back to the participants or other charities as agreed in the policy 26

27 THE HYBRID WAKALAH AND MUDHARABAH MODEL PARTICIPANTS/ POLICYHOLDERS Management Expenses Contributions Wakalah Fee Claims Shareholders Fund/ Operator Shariah compliant Investments Takaful Fund owned by the participants Reinsurance/ Retakaful Reserves Qardh Hasan Underwriting expenses Investment Profits Underwriting Surplus X% of Investment Profits 100% - X% of Investment Profits Surplus/(Deficit) 100% of Surplus 27

28 28

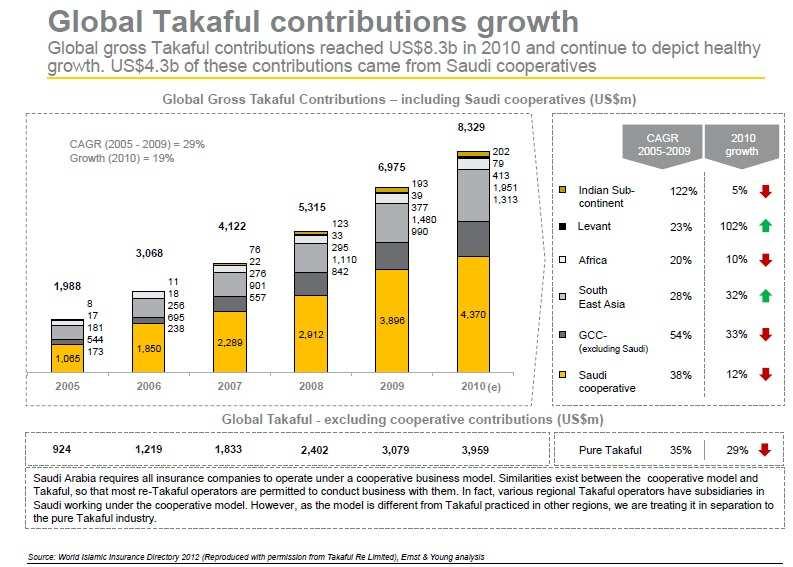

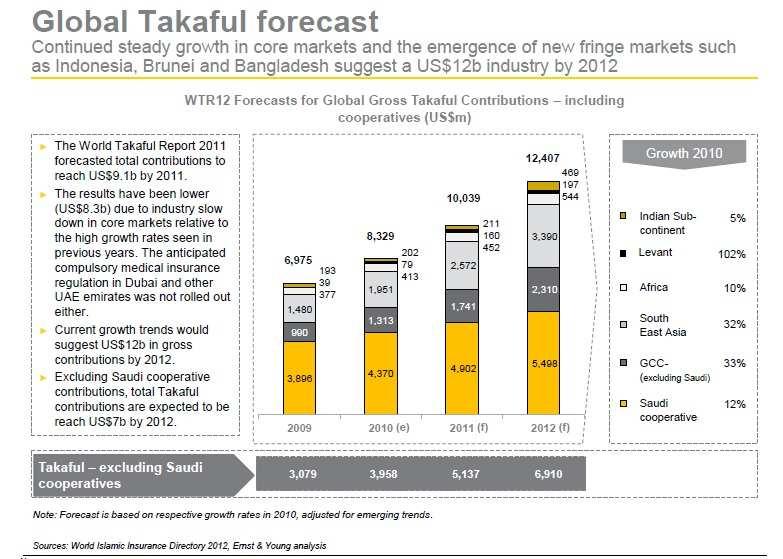

29 THE PRESENT STATE OF THE TAKAFUL INDUSTRY Global Takaful Contributions Growth Global Takaful Forecast Potential Takaful Markets Major World Annual Industry Events 29

30 30

31 31

32 32

33 MAJOR WORLD ANNUAL INDUSTRY EVENTS The World Takaful Summit (WTC), held in Dubai each April since 2006 ( The International Takaful Summit (ITS), held in London each July since 2007 ( The Middle East Takaful Forum (METF), held in Bahrain in October from 2012 The World Takaful Conference: Asia Leaders Summit, held in Kuala Lumpur each June 33

34 REGULATORY ISSUES Regulatory Bodies and Standards Some Regulatory and Accounting Challenges 34

35 REGULATORY BODIES AND STANDARDS Two bodies set the Islamic finance industry standards including Takaful: Bahrain-based AAOIFI (Accounting and Auditing Organization for Islamic Financial Institutions): Kuala Lumpur-based IFSB (Islamic Financial Services Board): Standards are issued by: IFSB & IAIS (International Association Of Insurance Supervisors), Issues In Regulation and Supervision of Takaful (Islamic Insurance), August 2006 IFSB, Guiding Principles on Governance for Takaful (Islamic Insurance) Undertakings, Dec 2009 IFSB, Standard n Solvency Requirements for Takaful (Islamic Insurance) Undertakings, Dec 2010 AAOIFI, General Presentation and Disclosure in the Financial Statements of Islamic Insurance Companies AAOIFI, Disclosure of Bases for Determining and Allocating Surplus or Deficit in Islamic Insurance Companies. AAOIFI, Provisions and Reserves in Islamic Insurance Companies AAOIFI, Contributions in Islamic Insurance Companies AAOIFI, Shariah Standards on Islamic Insurance and Islamic Reinsurance 35

36 SOME REGULATORY AND ACCOUNTING CHALLENGES Segregation of the shareholders fund and the participant s fund raises issues for solvency, accounting purposes and risk management: Solvency II will explicitly look at the capital of a company and estimate reserve requirements based on a best-estimate plus risk margin basis. However, within a Takaful business, although the best-estimate reserves will be retained within the participant s funds, any working capital required to cover the risk margin will be within the shareholders fund. This causes complications if trying to model the Takaful entity using a risk based capital approach IFSB solvency standard require the company as a whole to be solvent. This is on the ground that through a mandatory or constructive obligation of payments of qard al-hasan, the operators eventually become subject to a similar risk level, as of a conventional insurance company. Furthermore the policyholders fund also needs to become solvent. A balance between the two is probably amongst the most important regulatory challenges that regulators are facing note that Shariah scholars throughout the world are discouraging the increasing use of qard al-hasan 36

37 SOME REGULATORY AND ACCOUNTING CHALLENGES IFRS 4 (insurance contracts) Phase II. Under IFRS, Takaful businesses publish their accounts at a combined corporate entity level, with the participants fund and shareholders fund combined. This leads to questions of transparency: how will potential shareholders be able to assess the results of the company? How to compare the performance of Takaful businesses with conventional insurance. note that the AAIOFI standards show the accounts for the two funds separately Risk Management is complicated by the fact that the operator is managing the risks on behalf of the participants. An operator cannot generally look to participants funds to meet risks that are its alone, though as a matter of commercial reality the operator fund are standing behind the participants' risk fund, because of regulatory requirements for qard al-hasan Governance issues arise because of the unique relationship between an operator and the participants. Good governance mechanisms are essential to address these issues. AAOIFI s and IFSB s governance and Shariah governance standards provide guidance. Formal representation of participants (as in Sudan) may be beneficial 37

38 SOME REGULATORY AND ACCOUNTING CHALLENGES Shariah compliance. A Takaful business has two regulators : the state regulator, who ensures that policyholders are protected and the Shariah Board, who ensure that the Takaful business is operating in an Islamically appropriate manner note that regulators are not necessarily formally tasked with supervising Shariah compliance in Takaful companies. However, from the point of view of stakeholders, Shariah non-compliance is a serious matter and potentially damaging to the sector. Hence, regulators may reasonably be expected to require a company to have a proper governance framework for Shariah compliance, even if the regulator does not have explicit responsibility for supervising Shariah compliance 38

PRINCIPLES OF TAKAFUL

PRINCIPLES OF TAKAFUL PRESENTED BY: IIU PRINCIPLES OF TAKAFUL Introduction to Takaful Comparison between conventional and Islamic Insurance Main elements of Takaful Insurance Types of Takaful contracts

PRINCIPLES OF TAKAFUL PRESENTED BY: IIU PRINCIPLES OF TAKAFUL Introduction to Takaful Comparison between conventional and Islamic Insurance Main elements of Takaful Insurance Types of Takaful contracts

ISLAMIC INSURANCE: TAKAFUL

ISLAMIC INSURANCE: TAKAFUL A majority of Shari'a scholars find conventional insurance inadmissible in the Islamic framework. They have several objections against conventional insurance because it practiced

ISLAMIC INSURANCE: TAKAFUL A majority of Shari'a scholars find conventional insurance inadmissible in the Islamic framework. They have several objections against conventional insurance because it practiced

Islamic Insurance: An Alternative to Conventional Insurance

Islamic Insurance: An Alternative to Conventional Insurance Muamar Dahnoun & Dr. Basil Alqudwa Al-Huda University 1902 Baker Rd, Houston, TX 77094 Abstract The significance and importance of Takaful in

Islamic Insurance: An Alternative to Conventional Insurance Muamar Dahnoun & Dr. Basil Alqudwa Al-Huda University 1902 Baker Rd, Houston, TX 77094 Abstract The significance and importance of Takaful in

Takaful: Concepts and Practical Issues

Takaful: Concepts and Practical Issues Singapore Actuarial Society Inaugural General Insurance Conference 06-07 May 2009, Singapore Hussain Ahmad, FCAS Consulting Actuary Towers Perrin Agenda What is takaful

Takaful: Concepts and Practical Issues Singapore Actuarial Society Inaugural General Insurance Conference 06-07 May 2009, Singapore Hussain Ahmad, FCAS Consulting Actuary Towers Perrin Agenda What is takaful

TITLE OF THE PAPER: IS ISLAMIC INSURANCE AN ALTERNATIVE TO CONVENTIONAL INSURANCE? AUTHORS SHEILA NU NU HTAY 1

TITLE OF THE PAPER: IS ISLAMIC INSURANCE AN ALTERNATIVE TO CONVENTIONAL INSURANCE? AUTHORS SHEILA NU NU HTAY 1 sheila@iium.edu.my SYED AHMED SALMAN 2 salmaniium@gmail.com Contact details SYED AHMED SALMAN

TITLE OF THE PAPER: IS ISLAMIC INSURANCE AN ALTERNATIVE TO CONVENTIONAL INSURANCE? AUTHORS SHEILA NU NU HTAY 1 sheila@iium.edu.my SYED AHMED SALMAN 2 salmaniium@gmail.com Contact details SYED AHMED SALMAN

Business Operation Model with Sharia Concerns and Proposed Resolution for Takaful

Humanity & Social Sciences Journal 12 (1): 01-06, 2017 ISSN 1818-4960 IDOSI Publications, 2017 DOI: 10.5829/idosi.hssj.2017.01.06 Business Operation Model with Sharia Concerns and Proposed Resolution for

Humanity & Social Sciences Journal 12 (1): 01-06, 2017 ISSN 1818-4960 IDOSI Publications, 2017 DOI: 10.5829/idosi.hssj.2017.01.06 Business Operation Model with Sharia Concerns and Proposed Resolution for

GIFF and IFN Asia Forum Mandarin Oriental Hotel-October 27 th 2010

GIFF and IFN Asia Forum Mandarin Oriental Hotel-October 27 th 2010 Risk Management and Disclosure in Takaful Practices Dawood Y Taylor Senior Regional Executive-Takaful, Middle East Prudential Corporation

GIFF and IFN Asia Forum Mandarin Oriental Hotel-October 27 th 2010 Risk Management and Disclosure in Takaful Practices Dawood Y Taylor Senior Regional Executive-Takaful, Middle East Prudential Corporation

IFN Oman Forum, Mar 7 th 2017

Fundamental & Essence of Takaful Tabrez Farooquee Head of Bancatakaful & Marketing Takaful Oman Insurance SAOG 92876789 IFN Oman Forum, Mar 7 th 2017 Agenda Introduction & Evolution of Takaful Takaful

Fundamental & Essence of Takaful Tabrez Farooquee Head of Bancatakaful & Marketing Takaful Oman Insurance SAOG 92876789 IFN Oman Forum, Mar 7 th 2017 Agenda Introduction & Evolution of Takaful Takaful

The Successful Development of a Dual Islamic Finance and Takaful System in Malaysia - Takaful Zainal Abidin Mohd. Kassim, FIA

The Successful Development of a Dual Islamic Finance and Takaful System in Malaysia - Takaful Zainal Abidin Mohd. Kassim, FIA 23rd Pacific Insurance Conference Kuala Lumpur October 2007 Introduction The

The Successful Development of a Dual Islamic Finance and Takaful System in Malaysia - Takaful Zainal Abidin Mohd. Kassim, FIA 23rd Pacific Insurance Conference Kuala Lumpur October 2007 Introduction The

Takaful and Retakaful Challenges and Opportunities for Actuaries

Life Conference and Exhibition 2011 Safder Jaffer and Lindsay Unwin (Milliman) Takaful and Retakaful Challenges and Opportunities for Actuaries 22 November 2011 2010 The Actuarial Profession www.actuaries.org.uk

Life Conference and Exhibition 2011 Safder Jaffer and Lindsay Unwin (Milliman) Takaful and Retakaful Challenges and Opportunities for Actuaries 22 November 2011 2010 The Actuarial Profession www.actuaries.org.uk

Chapter 8: Takaful. Chapter Objectives. Students must be able to: Understand the Sources of Islamic Law. Understand the Concept of Takaful

Chapter 8 Takaful Chapter Objectives Students must be able to: Understand the Sources of Islamic Law Understand the Concept of Takaful Define and Relate to the 3 Principles of Syariah Relating to a Contract

Chapter 8 Takaful Chapter Objectives Students must be able to: Understand the Sources of Islamic Law Understand the Concept of Takaful Define and Relate to the 3 Principles of Syariah Relating to a Contract

Islamic Financial Services Board (IFSB)

") Islamic Financial Services Board (IFSB) Mutual Insurance and Takāful in a Changing World 12-13 November 2012 27-28 Zulhijjah 1433 Ceylan Intercontinental Hotel Istanbul, Turkey www.ifsb.org AGENDA About

Islamic Financial Services Board (IFSB) Mutual Insurance and Takāful in a Changing World 12-13 November 2012 27-28 Zulhijjah 1433 Ceylan Intercontinental Hotel Istanbul, Turkey www.ifsb.org AGENDA About

building value together 26 April 2013 Takaful in Africa Hassan Scott Odierno, FSA Lome

building value together 26 April 2013 Takaful in Africa Hassan Scott Odierno, FSA Lome www.actuarialpartners.com Takaful in Africa 2 Extent of religion in insurance Religious buildings and property can

building value together 26 April 2013 Takaful in Africa Hassan Scott Odierno, FSA Lome www.actuarialpartners.com Takaful in Africa 2 Extent of religion in insurance Religious buildings and property can

Takaful and Poverty Alleviation. 8 th International Microinsurance Conference Dar es Salaam, Tanzania 8 November 2012

Takaful and Poverty Alleviation 8 th International Microinsurance Conference Dar es Salaam, Tanzania 8 November 2012 Overview of presentation Why is conventional insurance not allowed? Takaful principles

Takaful and Poverty Alleviation 8 th International Microinsurance Conference Dar es Salaam, Tanzania 8 November 2012 Overview of presentation Why is conventional insurance not allowed? Takaful principles

Takaful : defining ethical insurance. Zainal Abidin Mohd. Kassim Partner Mercer

Takaful : defining ethical insurance Zainal Abidin Mohd. Kassim Partner Mercer Presentation contents Takaful a primer Shariah Laws governing trade and business Takaful in practice Shariah compliant investments

Takaful : defining ethical insurance Zainal Abidin Mohd. Kassim Partner Mercer Presentation contents Takaful a primer Shariah Laws governing trade and business Takaful in practice Shariah compliant investments

Takaful. Dr. Muhammad Imran Usmani. SECP Takaful Conference March 14, 2007

Takaful Dr. Muhammad Imran Usmani SECP Takaful Conference March 14, 2007 Presentation Outline Conventional Insurance How Qimar & Riba exist in Conventional Insurance Definition of Takaful Mudarabah Model

Takaful Dr. Muhammad Imran Usmani SECP Takaful Conference March 14, 2007 Presentation Outline Conventional Insurance How Qimar & Riba exist in Conventional Insurance Definition of Takaful Mudarabah Model

2 ND TAKAFUL SUMMIT JUMEIRAH CARLTON TOWER, LONDON 15 th & 16 th JULY 2008

2 ND TAKAFUL SUMMIT JUMEIRAH CARLTON TOWER, LONDON 15 th & 16 th JULY 2008 THE INSURANCE : HALAL/HARAM CONUNDRUM By: DATO MOHD FADZLI YUSOF Director/Principal Consultant, Malaysia DATO MOHD FADZLI YUSOF

2 ND TAKAFUL SUMMIT JUMEIRAH CARLTON TOWER, LONDON 15 th & 16 th JULY 2008 THE INSURANCE : HALAL/HARAM CONUNDRUM By: DATO MOHD FADZLI YUSOF Director/Principal Consultant, Malaysia DATO MOHD FADZLI YUSOF

International Conference on Innovation Challenges in Multidisciplinary Research & Practice, December 2013, Kuala Lumpur, Malaysia.

RETAKAFUL (ISLAMIC REINSURANCE): HISTORICAL, SHARI AH AND OPERATIONAL PERSPECTIVES Sheila Nu Nu Htay, Mustapha Hamat, Wan Zamri Wan Ismail and 1 Syed Ahmed Salman International Islamic University Malaysia,

RETAKAFUL (ISLAMIC REINSURANCE): HISTORICAL, SHARI AH AND OPERATIONAL PERSPECTIVES Sheila Nu Nu Htay, Mustapha Hamat, Wan Zamri Wan Ismail and 1 Syed Ahmed Salman International Islamic University Malaysia,

6 th Global Conference of Actuaries 18-19, February, 2004, New Delhi

6 th Global Conference of Actuaries 18-19, February, 2004, New Delhi Takaful An Alternate Insurance Model By Abdul Rahim Abdul Wahab, FSA abdul.rahim@pk.ey.com (Subject Code 05 - Subject Group: General

6 th Global Conference of Actuaries 18-19, February, 2004, New Delhi Takaful An Alternate Insurance Model By Abdul Rahim Abdul Wahab, FSA abdul.rahim@pk.ey.com (Subject Code 05 - Subject Group: General

Cooperatives. Perfect alignment of shareholders and consumers interest as they are one and the same entity. Theoretically this should result in;

www.mercer.com Cooperatives Autonomous association of persons united voluntarily to meet their common economic, social & cultural needs and aspirations through a jointly owned democratically controlled

www.mercer.com Cooperatives Autonomous association of persons united voluntarily to meet their common economic, social & cultural needs and aspirations through a jointly owned democratically controlled

Islamic Banking, Takaful and Al Rahnu LCA4562 DR. ZULKIFLI HASAN

Islamic Banking, Takaful and Al Rahnu LCA4562 DR. ZULKIFLI HASAN Contents Insurance Takaful HISTORICAL BACKGROUND OF WESTERN CONCEPT OF INSURANCE 1. Ottoman Empire- First introduce western concept of insurance-

Islamic Banking, Takaful and Al Rahnu LCA4562 DR. ZULKIFLI HASAN Contents Insurance Takaful HISTORICAL BACKGROUND OF WESTERN CONCEPT OF INSURANCE 1. Ottoman Empire- First introduce western concept of insurance-

In the Name of God. Takaful and Microtakaful: Islamic Instruments for protecting poor And Vulnerable Groups. Sadegh Bakhtiari

In the Name of God Takaful and Microtakaful: Islamic Instruments for protecting poor And Vulnerable Groups Sadegh Bakhtiari Professor of Economics, Islamic Azad University, Khorasgan, Isfahan, Iran The

In the Name of God Takaful and Microtakaful: Islamic Instruments for protecting poor And Vulnerable Groups Sadegh Bakhtiari Professor of Economics, Islamic Azad University, Khorasgan, Isfahan, Iran The

Help ye one another in righteousness and piety, but help ye not one another in sin and rancour. (The Holy Quran 5.3)

") CONCEPT OF ISLAMIC INSURANCE (TAKAFUL) AND REFORMS REQUIRED IN INSURANCE LAW. INTRODUCTION : Islamic Insurance (Takaful) is an alternative form of conventional insurance based on the concept of trusteeship

CONCEPT OF ISLAMIC INSURANCE (TAKAFUL) AND REFORMS REQUIRED IN INSURANCE LAW. INTRODUCTION : Islamic Insurance (Takaful) is an alternative form of conventional insurance based on the concept of trusteeship

13th Global Conference of Actuaries 2011

13th Global Conference of Actuaries 2011 Emerging Risks Daring Solutions Azim Mithani Chief Executive Officer Prudential BSN Takaful Berhad Malaysia February 20 22, 2011 1 Market Opportunity 2 Understanding

13th Global Conference of Actuaries 2011 Emerging Risks Daring Solutions Azim Mithani Chief Executive Officer Prudential BSN Takaful Berhad Malaysia February 20 22, 2011 1 Market Opportunity 2 Understanding

Takaful Accounting. By Omer Morshed September 3, 2003 DISCLAIMER:

By Omer Morshed September 3, 2003 DISCLAIMER: This document is provided for informational purposes only, and the information herein is subject to change without notice. Please report any errors herein

By Omer Morshed September 3, 2003 DISCLAIMER: This document is provided for informational purposes only, and the information herein is subject to change without notice. Please report any errors herein

ISLAMIC FINANCIAL SERVICES BOARD. and INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS

Issues paper ISLAMIC FINANCIAL SERVICES BOARD and INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS ISSUES IN REGULATION AND SUPERVISION OF TAKAFUL (ISLAMIC INSURANCE) August 2006 THE JOINT WORKING GROUP:

Issues paper ISLAMIC FINANCIAL SERVICES BOARD and INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS ISSUES IN REGULATION AND SUPERVISION OF TAKAFUL (ISLAMIC INSURANCE) August 2006 THE JOINT WORKING GROUP:

ISSUES SURROUNDING MANAGEMENT OF TAKAFUL SURPLUS. Sutan Emir Hidayat Senior Lecturer, Islamic Finance University College of Bahrain

ISSUES SURROUNDING MANAGEMENT OF TAKAFUL SURPLUS Sutan Emir Hidayat Senior Lecturer, Islamic Finance University College of Bahrain 1 OBJECTIVES OF THE PRESENTATION To explain the differences in the treatment

ISSUES SURROUNDING MANAGEMENT OF TAKAFUL SURPLUS Sutan Emir Hidayat Senior Lecturer, Islamic Finance University College of Bahrain 1 OBJECTIVES OF THE PRESENTATION To explain the differences in the treatment

Advanced Diploma in Insurance

590 Advanced Diploma in Insurance Unit 590 Principles of Takaful October 2018 Examination Guide SPECIAL NOTICES Candidates entered for the April 2019 examination should study this examination guide carefully

590 Advanced Diploma in Insurance Unit 590 Principles of Takaful October 2018 Examination Guide SPECIAL NOTICES Candidates entered for the April 2019 examination should study this examination guide carefully

Presentation to Bancassurance Conference Takaful Products

Presentation to Bancassurance Conference Takaful Products Johan Potgieter 13 May 2013 Aon Hewitt (Actuarial) / QED Actuaries & Consultants (Pty) Ltd 0 Contents Overview Islamic Law Principles Models of

Presentation to Bancassurance Conference Takaful Products Johan Potgieter 13 May 2013 Aon Hewitt (Actuarial) / QED Actuaries & Consultants (Pty) Ltd 0 Contents Overview Islamic Law Principles Models of

GOVERNMENT NOTICE No.. published on THE INSURANCE ACT (CAP.394) REGULATIONS. (Made under section 167) PART I PRELIMINARY

REGULATIONS. (Made under section 167) PART I PRELIMINARY") GOVERNMENT NOTICE No.. published on THE INSURANCE ACT (CAP.394) REGULATIONS (Made under section 167) THE INSURANCE (TAKAFUL) REGULATIONS, 2014 PART I PRELIMINARY Citation 1. These Regulations may be cited

GOVERNMENT NOTICE No.. published on THE INSURANCE ACT (CAP.394) REGULATIONS (Made under section 167) THE INSURANCE (TAKAFUL) REGULATIONS, 2014 PART I PRELIMINARY Citation 1. These Regulations may be cited

ESSENTIAL CONTRACTS IN TAKAFUL

ESSENTIAL CONTRACTS IN TAKAFUL PREPARED BY: HAJI MOHAMAD HELMI HAJI AHMAD Restricted 1 THEORY OF CONTRACT IN HISTORY OF SHARIAH Contract in Shariah include both bilateral and unilateral A contract is also

ESSENTIAL CONTRACTS IN TAKAFUL PREPARED BY: HAJI MOHAMAD HELMI HAJI AHMAD Restricted 1 THEORY OF CONTRACT IN HISTORY OF SHARIAH Contract in Shariah include both bilateral and unilateral A contract is also

Seminar on Islamic Finance. Challenges in Developing Islamic Financial Services in Europe. 11 November 2009, Rome, Italy.

Seminar on Islamic Finance Challenges in Developing Islamic Financial Services in Europe 11 November 2009, Rome, Italy Speech by Professor Rifaat Ahmed Abdel Karim Secretary-General Islamic Financial Services

Seminar on Islamic Finance Challenges in Developing Islamic Financial Services in Europe 11 November 2009, Rome, Italy Speech by Professor Rifaat Ahmed Abdel Karim Secretary-General Islamic Financial Services

MANUAL MONETARY AND FINANCIAL STATISTICS MANUAL AND COMPILATION GUIDE

MANUAL MONETARY AND FINANCIAL STATISTICS MANUAL AND COMPILATION GUIDE 2015 2016 I N T E R N A T I O N A L M O N E T A R Y F U N D ANNEX 1 Islamic 4.3 Financial Institutions and Instruments 4.256 This annex

MANUAL MONETARY AND FINANCIAL STATISTICS MANUAL AND COMPILATION GUIDE 2015 2016 I N T E R N A T I O N A L M O N E T A R Y F U N D ANNEX 1 Islamic 4.3 Financial Institutions and Instruments 4.256 This annex

Shariah Governance and Regulatory Aspects of Takaful

1 Shariah Governance and Regulatory Aspects of Takaful Introduction Kazi Md. Mortuza Ali Chief Consultant to the Board Prime Islami Life Insurance Ltd Every takaful scheme is and intended to be a legally

1 Shariah Governance and Regulatory Aspects of Takaful Introduction Kazi Md. Mortuza Ali Chief Consultant to the Board Prime Islami Life Insurance Ltd Every takaful scheme is and intended to be a legally

Takaful & IFRS on insurance contracts. MASB Islamic Finance Master Class 21 November 2013

Takaful & IFRS on insurance contracts MASB Islamic Finance Master Class 21 November 2013 2 COMPETITION LAW CAUTION The participants in this event and the MASB shall not enter into any discussion, activity

Takaful & IFRS on insurance contracts MASB Islamic Finance Master Class 21 November 2013 2 COMPETITION LAW CAUTION The participants in this event and the MASB shall not enter into any discussion, activity

Retakaful (Islamic Reinsurance): Historical, Shari ah and Operational Perspectives

: Historical, Shari ah and Operational Perspectives") World Applied Sciences Journal 30 (Innovation Challenges in Multidiciplinary Research & Practice): 185-190, 2014 ISSN 1818-4952 IDOSI Publications, 2014 DOI: 10.5829/idosi.wasj.2014.30.icmrp.24 Retakaful

World Applied Sciences Journal 30 (Innovation Challenges in Multidiciplinary Research & Practice): 185-190, 2014 ISSN 1818-4952 IDOSI Publications, 2014 DOI: 10.5829/idosi.wasj.2014.30.icmrp.24 Retakaful

Shariah Guidelines for Sukuk. Mufti Ismail Ebrahim Shariah Advisor Malta, October 2014

Shariah Guidelines for Sukuk Mufti Ismail Ebrahim Shariah Advisor Malta, October 2014 0 Outline of Presentation Page Credentials Mufti Ismail Ebrahim [2] Islamic Financial Services Products Mufti Ismail

Shariah Guidelines for Sukuk Mufti Ismail Ebrahim Shariah Advisor Malta, October 2014 0 Outline of Presentation Page Credentials Mufti Ismail Ebrahim [2] Islamic Financial Services Products Mufti Ismail

How it works for you?

N SECURITIES AND EXCHANGE COMMISSION OF PAKISTAN INSURANCE DIVISION Investor Education Guide Series 2010 TAKAFUL THE ISLAMIC INSURANCE How it works for you? s DISCLAIMER This is a general guide book developed

N SECURITIES AND EXCHANGE COMMISSION OF PAKISTAN INSURANCE DIVISION Investor Education Guide Series 2010 TAKAFUL THE ISLAMIC INSURANCE How it works for you? s DISCLAIMER This is a general guide book developed

UNDERWRITING AND MANAGING RISKS IN TAKAFUL

UNDERWRITING AND MANAGING RISKS IN TAKAFUL Azman Mohd Noor International Islamic University Malaysia, Seminar on Insurance and Risk in Asia Pacific Kyoto International Community House 24 September 2010

UNDERWRITING AND MANAGING RISKS IN TAKAFUL Azman Mohd Noor International Islamic University Malaysia, Seminar on Insurance and Risk in Asia Pacific Kyoto International Community House 24 September 2010

JCR-VIS Credit Rating Company Limited. Affiliate of Japan Credit Rating Agency, Ltd.

Rating Agencies Methodologies for Takaful and Re-Takaful Firms By Sobia Maqbool Senior Manager JCR-VIS Credit Rating Company Limited Singapore, November 25, 2008 Honorable speakers, distinguished ladies

Rating Agencies Methodologies for Takaful and Re-Takaful Firms By Sobia Maqbool Senior Manager JCR-VIS Credit Rating Company Limited Singapore, November 25, 2008 Honorable speakers, distinguished ladies

SUSTAINABLE DEVELOPMENT THROUGH THE ISLAMIC INSURANCE SYSTEM IN SUDAN. Fatima A. Galal 1 Zuriah A. Rahman 2 Mohamed Azam M.

SUSTAINABLE DEVELOPMENT THROUGH THE ISLAMIC INSURANCE SYSTEM IN SUDAN Fatima A. Galal 1 Zuriah A. Rahman 2 Mohamed Azam M. Adil 3 ABSTRACT Several Islamic insurance and solidarity companies have been established

SUSTAINABLE DEVELOPMENT THROUGH THE ISLAMIC INSURANCE SYSTEM IN SUDAN Fatima A. Galal 1 Zuriah A. Rahman 2 Mohamed Azam M. Adil 3 ABSTRACT Several Islamic insurance and solidarity companies have been established

Takaful and Micro-Insurance 1. Tsuneo Katayama Professor Tokyo Denki University

Takaful and Micro-Insurance 1 Tsuneo Katayama Professor Tokyo Denki University 1. What is Takaful? Takaful (Islamic insurance) may be defined as a system through which the participants donate part or all

Takaful and Micro-Insurance 1 Tsuneo Katayama Professor Tokyo Denki University 1. What is Takaful? Takaful (Islamic insurance) may be defined as a system through which the participants donate part or all

Zeti Akhtar Aziz: Islamic finance a global growth opportunity amidst a challenging environment

Zeti Akhtar Aziz: Islamic finance a global growth opportunity amidst a challenging environment Keynote address by Dr Zeti Akhtar Aziz, Governor of the Central Bank of Malaysia, at the State Street Islamic

Zeti Akhtar Aziz: Islamic finance a global growth opportunity amidst a challenging environment Keynote address by Dr Zeti Akhtar Aziz, Governor of the Central Bank of Malaysia, at the State Street Islamic

Factors Driving the Islamic Insurance System in Pakistan, a Social Perspective Approach

Journal of Social Economics Vol. 1, No. 2, 2014, 72-77 Factors Driving the Islamic Insurance System in Pakistan, a Social Perspective Approach Sania Khalid 1, Mobeen Ur Rehman 2 Abstract The aim of this

Journal of Social Economics Vol. 1, No. 2, 2014, 72-77 Factors Driving the Islamic Insurance System in Pakistan, a Social Perspective Approach Sania Khalid 1, Mobeen Ur Rehman 2 Abstract The aim of this

Revisiting Takaful Insurance: A Survey on Functions and Dominant Models

Afro Eurasian Studies, Vol. 2, Issues 1&2, Spring & Fall 2013, 231-253 Revisiting Takaful Insurance: A Survey on Functions and Dominant Models Hashem Abdullah AlNemer* Abstract Takaful is a growing and

Afro Eurasian Studies, Vol. 2, Issues 1&2, Spring & Fall 2013, 231-253 Revisiting Takaful Insurance: A Survey on Functions and Dominant Models Hashem Abdullah AlNemer* Abstract Takaful is a growing and

Rating Takaful (Shari a Compliant) Companies

Companies") BEST S METHODOLOGY AND CRITERIA Rating Takaful (Shari a Compliant) Companies October 13, 2017 Mahesh Mistry: +44 20-7-397-0325 Mahesh.Mistry@ambest.com Salman Siddiqui: +44 20 7 397 0331 Salman.Siddiqui@ambest.com

BEST S METHODOLOGY AND CRITERIA Rating Takaful (Shari a Compliant) Companies October 13, 2017 Mahesh Mistry: +44 20-7-397-0325 Mahesh.Mistry@ambest.com Salman Siddiqui: +44 20 7 397 0331 Salman.Siddiqui@ambest.com

CHEVALIER & SCIALES LUXEMBOURG: A HUB FOR ISLAMIC FINANCE

CHEVALIER & SCIALES LUXEMBOURG: A HUB FOR ISLAMIC FINANCE client memorandum banking & finance summary Well established as a world leader in the investment funds industry (second only to the USA), Luxembourg

CHEVALIER & SCIALES LUXEMBOURG: A HUB FOR ISLAMIC FINANCE client memorandum banking & finance summary Well established as a world leader in the investment funds industry (second only to the USA), Luxembourg

Advanced Diploma in Insurance

THE CHARTERED INSURANCE INSTITUTE 590 Advanced Diploma in Insurance Unit 590 Principles of Takaful April 2017 examination Instructions Three hours are allowed for this paper. Do not begin writing until

THE CHARTERED INSURANCE INSTITUTE 590 Advanced Diploma in Insurance Unit 590 Principles of Takaful April 2017 examination Instructions Three hours are allowed for this paper. Do not begin writing until

The Third Annual Conference of Islamic Economics & Islamic Finance. Venue: Chestnut Conference Center Date: October 29 th, 2016

The Third Annual Conference of Islamic Economics & Islamic Finance Venue: Chestnut Conference Center Date: October 29 th, 2016 Organized by: ECO-ENA, Inc., Canada Presenter Ahmad Wais Popalyar VP Business

The Third Annual Conference of Islamic Economics & Islamic Finance Venue: Chestnut Conference Center Date: October 29 th, 2016 Organized by: ECO-ENA, Inc., Canada Presenter Ahmad Wais Popalyar VP Business

MAGISTERARBEIT. Titel der Magisterarbeit. Takaful and its Business Models. Verfasserin. Birgit Bisani. angestrebter akademischer Grad

MAGISTERARBEIT Titel der Magisterarbeit Takaful and its Business Models Verfasserin Birgit Bisani angestrebter akademischer Grad Magistra der Sozial- und Wirtschaftswissenschaften (Mag. rer. soc. oec.)

MAGISTERARBEIT Titel der Magisterarbeit Takaful and its Business Models Verfasserin Birgit Bisani angestrebter akademischer Grad Magistra der Sozial- und Wirtschaftswissenschaften (Mag. rer. soc. oec.)

Islamic Insurance revisited

Islamic Insurance revisited September 2011 Economic Research & Consulting Published by: Swiss Reinsurance Company Ltd 28th Floor Mevara Keck Seng 203 Jalan Bukit Bintang 55100 Kuala Lumpur Malaysia Telephone

Islamic Insurance revisited September 2011 Economic Research & Consulting Published by: Swiss Reinsurance Company Ltd 28th Floor Mevara Keck Seng 203 Jalan Bukit Bintang 55100 Kuala Lumpur Malaysia Telephone

MUDARABAH Mudarabah: Investment Financing How does Mudarabah work as an Islamic mode of financing? A Mudarabah agreement creates a partnership business whereby an investing partner (rab al maal) brings

MUDARABAH Mudarabah: Investment Financing How does Mudarabah work as an Islamic mode of financing? A Mudarabah agreement creates a partnership business whereby an investing partner (rab al maal) brings

Glossary of Islamic Capital Market Terms

Glossary of Islamic Capital Market Terms Terms Definition Bai` Bithaman Ajil (BBA) Bai` al-`inah Bai` al-istijrar A contract that refers to the sale and purchase transaction for the financing of assets

Glossary of Islamic Capital Market Terms Terms Definition Bai` Bithaman Ajil (BBA) Bai` al-`inah Bai` al-istijrar A contract that refers to the sale and purchase transaction for the financing of assets

Takaful & Re-Takaful Introducing Size, growth and regional trends of takaful

Sudan Saudi Arabia Bahrain Malaysia Total United Arad Emirates Indonesia Other countries 85% Chapter 16 Figure 98: Sigma 0% 5% 10% 15% 20% 25% 30% 35% 40% 2007 2015 Takaful & Re-Takaful Gross Takaful contributions

Sudan Saudi Arabia Bahrain Malaysia Total United Arad Emirates Indonesia Other countries 85% Chapter 16 Figure 98: Sigma 0% 5% 10% 15% 20% 25% 30% 35% 40% 2007 2015 Takaful & Re-Takaful Gross Takaful contributions

Advanced Diploma in Insurance

THE CHARTERED INSURANCE INSTITUTE 590 Advanced Diploma in Insurance Unit 590 Principles of Takaful October 2017 examination Instructions Three hours are allowed for this paper. Do not begin writing until

THE CHARTERED INSURANCE INSTITUTE 590 Advanced Diploma in Insurance Unit 590 Principles of Takaful October 2017 examination Instructions Three hours are allowed for this paper. Do not begin writing until

Certified Takaful Professional Module II (Takaful & Risk Mitigation tools in Islamic Finance) CTP: 405: Takaful Models, Type & Structures

CTP: 405: Takaful Models, Type & Structures") Certified Takaful Professional Module II (Takaful & Risk Mitigation tools in Islamic Finance) CTP: 405: Takaful Models, Type & Structures TAKAFUL (ISLAMIC INSURANCE) Takaful is an Islamic alternative to

Certified Takaful Professional Module II (Takaful & Risk Mitigation tools in Islamic Finance) CTP: 405: Takaful Models, Type & Structures TAKAFUL (ISLAMIC INSURANCE) Takaful is an Islamic alternative to

CAPTIVE INSURANCE FROM AN ISLAMIC VIEWPOINT: AN ANALYSIS

CAPTIVE INSURANCE FROM AN ISLAMIC VIEWPOINT: AN ANALYSIS Hazmi Dahlan a, ψ,,norazua Mohd Marzuki b, Nurulasyikin Muda a, Siti Rahmah Man a, Nor Diyana Mohd Noor a, Norhaliza Mohd Sani a, Suzanna Musman

CAPTIVE INSURANCE FROM AN ISLAMIC VIEWPOINT: AN ANALYSIS Hazmi Dahlan a, ψ,,norazua Mohd Marzuki b, Nurulasyikin Muda a, Siti Rahmah Man a, Nor Diyana Mohd Noor a, Norhaliza Mohd Sani a, Suzanna Musman

Sharing and Transferring Risks in Retakāful and Conventional Reinsurance: A Critical Analysis

JKAU: Islamic Econ., Vol. 28 No. 2, pp: 111-146 (July 2015) DOI: 10.4197 / Islec. 28-2.4 Sharing and Transferring Risks in Retakāful and Conventional Reinsurance: A Critical Analysis Abu Umar Faruq Ahmad,

JKAU: Islamic Econ., Vol. 28 No. 2, pp: 111-146 (July 2015) DOI: 10.4197 / Islec. 28-2.4 Sharing and Transferring Risks in Retakāful and Conventional Reinsurance: A Critical Analysis Abu Umar Faruq Ahmad,

Mohd Bahroddin Bin Badri Researcher at ISRA Deputy Chairman of Shari ah Committee, Citibank Malaysia

Charging Fee for Guarantee in the Islamic Credit Guarantee Scheme by Credit Guarantee Corporation Malaysia Berhad: An Analysis from the Shari ah Perspective. Mohd Bahroddin Bin Badri Researcher at ISRA

Charging Fee for Guarantee in the Islamic Credit Guarantee Scheme by Credit Guarantee Corporation Malaysia Berhad: An Analysis from the Shari ah Perspective. Mohd Bahroddin Bin Badri Researcher at ISRA

Board of Directors Report

Board of Directors Report We are pleased to present Unicorn Investment Bank B.S.C. (c)'s report for our first financial period of operations from May 5th to December 31st, 2004. This period has seen Unicorn

Board of Directors Report We are pleased to present Unicorn Investment Bank B.S.C. (c)'s report for our first financial period of operations from May 5th to December 31st, 2004. This period has seen Unicorn

AN EMPIRICAL STUDY OF TAKAFUL PARTICIPANT S PERCEPTION OF THE DISTRIBUTION OF THE UNDERWRITING SURPLUS AND ITS IMPACT ON PARTICIPANTS BEHAVIOUR

International Journal of Economics, Commerce and Management United Kingdom Vol. III, Issue 4, April 2015 http://ijecm.co.uk/ ISSN 2348 0386 AN EMPIRICAL STUDY OF TAKAFUL PARTICIPANT S PERCEPTION OF THE

International Journal of Economics, Commerce and Management United Kingdom Vol. III, Issue 4, April 2015 http://ijecm.co.uk/ ISSN 2348 0386 AN EMPIRICAL STUDY OF TAKAFUL PARTICIPANT S PERCEPTION OF THE

Tatagroprombank. Talk on Islamic Finance. Kazan -17 June Alberto G. Brugnoni - ASSAIF

Tatagroprombank Talk on Islamic Finance Kazan -17 June 2013 Alberto G. Brugnoni - ASSAIF CONTENTS OF THE TALK WHAT IS ISLAMIC FINANCE ISLAMIC MODES OF FINANCE AVAILABLE TO SMEs ISLAMIC TRADE FINANCE ISLAMIC

Tatagroprombank Talk on Islamic Finance Kazan -17 June 2013 Alberto G. Brugnoni - ASSAIF CONTENTS OF THE TALK WHAT IS ISLAMIC FINANCE ISLAMIC MODES OF FINANCE AVAILABLE TO SMEs ISLAMIC TRADE FINANCE ISLAMIC

Syed Ahmed Salman * I J A B E R, Vol. 12, No. 4, (2014):

:") I J A B E R, Vol. 12, No. 4, (2014): 1079-1088 Syed Ahmed Salman * Abstract: Takaful industry is one of the fastest growing financial institutions and its rapid growth is impressive. It has been widely

I J A B E R, Vol. 12, No. 4, (2014): 1079-1088 Syed Ahmed Salman * Abstract: Takaful industry is one of the fastest growing financial institutions and its rapid growth is impressive. It has been widely

HISAAR SAVINGS PLAN. Consumer Banking. Committed to People

HISAAR SAVINGS PLAN Consumer Banking Committed to People HISAAR - meaning Fort and Fence is exactly what this new takaful plan from Jubilee Life Insurance - Window Takaful Operations in partnership with

HISAAR SAVINGS PLAN Consumer Banking Committed to People HISAAR - meaning Fort and Fence is exactly what this new takaful plan from Jubilee Life Insurance - Window Takaful Operations in partnership with

GE20803 DEPOSIT & FINANCING OPERATION OF ISLAMIC BANKING

GE20803 DEPOSIT & FINANCING OPERATION OF ISLAMIC BANKING DEPOSIT MOBILIZATION BY ISLAMIC BANKS Updated version 21st October 2015 BY DR. HANUDIN AMIN LABUAN FACULTY OF INTERNATIONAL FINANCE UNIVERSITI MALAYSIA

GE20803 DEPOSIT & FINANCING OPERATION OF ISLAMIC BANKING DEPOSIT MOBILIZATION BY ISLAMIC BANKS Updated version 21st October 2015 BY DR. HANUDIN AMIN LABUAN FACULTY OF INTERNATIONAL FINANCE UNIVERSITI MALAYSIA

Chapter 3. Islamic Finance and Investment- An Overview. outlining Shariah principles, features of the investment, key components of Shariah

Chapter 3 Islamic Finance and Investment- An Overview Introduction This chapter gives an overview about the concept of Shariah Finance by outlining Shariah principles, features of the investment, key components

Chapter 3 Islamic Finance and Investment- An Overview Introduction This chapter gives an overview about the concept of Shariah Finance by outlining Shariah principles, features of the investment, key components

Takaful. Azeem Pirani Head of Marketing & Alternate Distribution Pak-Qatar Family Takaful. July. 13 th, 2007 M.A.J.U. Karachi.

Takaful Azeem Pirani Head of Marketing & Alternate Distribution Pak-Qatar Family Takaful July. 13 th, 2007 M.A.J.U. Karachi 13th July 2007 1 Agenda Takaful A product and an ideology History of Takaful

Takaful Azeem Pirani Head of Marketing & Alternate Distribution Pak-Qatar Family Takaful July. 13 th, 2007 M.A.J.U. Karachi 13th July 2007 1 Agenda Takaful A product and an ideology History of Takaful

Advanced Diploma in Insurance

THE CHARTERED INSURANCE INSTITUTE 590 Advanced Diploma in Insurance Unit 590 Principles of Takaful April 2015 examination Instructions Three hours are allowed for this paper. Do not begin writing until

THE CHARTERED INSURANCE INSTITUTE 590 Advanced Diploma in Insurance Unit 590 Principles of Takaful April 2015 examination Instructions Three hours are allowed for this paper. Do not begin writing until

Profit-sharing investment accounts in Islamic banks: Regulatory problems and possible solutions

Original Article Profit-sharing investment accounts in Islamic banks: Regulatory problems and possible solutions Simon Archer is Visiting Professor at the ICMA Centre, Henley Business School, University

Original Article Profit-sharing investment accounts in Islamic banks: Regulatory problems and possible solutions Simon Archer is Visiting Professor at the ICMA Centre, Henley Business School, University

The Role for Takaful Companies

building value together 22 June 2012 The Role for Takaful Companies Hassan Scott Odierno, FSA Kuala Lumpur www.actuarialpartners.com Takaful is more than just Muslim insurance Takaful is a hybrid with

building value together 22 June 2012 The Role for Takaful Companies Hassan Scott Odierno, FSA Kuala Lumpur www.actuarialpartners.com Takaful is more than just Muslim insurance Takaful is a hybrid with

Takaful and Mutual Insurance

Takaful and Mutual Insurance Business Challenges in Mutual Insurance and Takaful Serap Gonulal November 13, 2012 The four pillars of Takaful Takaful Regulatory and legal framework Transparency and consumer

Takaful and Mutual Insurance Business Challenges in Mutual Insurance and Takaful Serap Gonulal November 13, 2012 The four pillars of Takaful Takaful Regulatory and legal framework Transparency and consumer

Takafu( and~etakafuf. 'Ach"anced Princyles andpractices. Munich Re IBFIM TOBIAS FRENZ YOUNES SOUALHI. Second:Edition. Published by.

BFI Munich RE. Takafu( and~etakafuf 'Ach"anced Princyles andpractices TOBIAS FRENZ YOUNES SOUALHI Second:Edition IBFIM Published by Kuala Lumpur 2010 Munich Re Published by IBFIM 063075-W) 3rd Floor, Dataran

BFI Munich RE. Takafu( and~etakafuf 'Ach"anced Princyles andpractices TOBIAS FRENZ YOUNES SOUALHI Second:Edition IBFIM Published by Kuala Lumpur 2010 Munich Re Published by IBFIM 063075-W) 3rd Floor, Dataran

Islamic Finance More Than Window Dressing?

Islamic Finance More Than Window Dressing? This article considers the most common structures employed in Islamic finance and deals with some of the criticisms surrounding its practice. Introduction Islamic

Islamic Finance More Than Window Dressing? This article considers the most common structures employed in Islamic finance and deals with some of the criticisms surrounding its practice. Introduction Islamic

Risk Participation Risk Management

Risk Participation Risk Management Islamic Insurance 3,000 years ago, Phoenician sea merchants formed trade communities. Each community member agreed to contribute a portion of his profit to compensate

Risk Participation Risk Management Islamic Insurance 3,000 years ago, Phoenician sea merchants formed trade communities. Each community member agreed to contribute a portion of his profit to compensate

FAMILY TAKAFUL. Savings PLUS. Jubilee Life Insurance Company Limited-Window Takaful Operations

FAMILY TAKAFUL Savings PLUS Takaful Plan Jubilee Life Insurance Company Limited-Window Takaful Operations As you climb up the success ladder and move on from successfully achieving one milestone after

FAMILY TAKAFUL Savings PLUS Takaful Plan Jubilee Life Insurance Company Limited-Window Takaful Operations As you climb up the success ladder and move on from successfully achieving one milestone after

ISLAMIC HEDGING MECHANISM: EMERGING TREND

ISLAMIC HEDGING MECHANISM: EMERGING TREND Dr. Mohd Daud Bakar President/CEO International Institute of Islamic Finance (IIIF) Inc. mdaud@iiif-inc.com www.iiif-inc.com Shariah Perspective on Economics of

ISLAMIC HEDGING MECHANISM: EMERGING TREND Dr. Mohd Daud Bakar President/CEO International Institute of Islamic Finance (IIIF) Inc. mdaud@iiif-inc.com www.iiif-inc.com Shariah Perspective on Economics of

BANKING CONVENTIONAL. Overview

CONVENTIONAL BANKING Overview Is the Bank s Board spending enough time and resources on making sure the Bank is developing the desired culture and is it strong enough to be sustainable for the long run?

CONVENTIONAL BANKING Overview Is the Bank s Board spending enough time and resources on making sure the Bank is developing the desired culture and is it strong enough to be sustainable for the long run?

Advanced Diploma in Insurance

THE CHARTERED INSURANCE INSTITUTE 590 Advanced Diploma in Insurance Unit 590 Principles of Takaful October 2015 examination Instructions Three hours are allowed for this paper. Do not begin writing until

THE CHARTERED INSURANCE INSTITUTE 590 Advanced Diploma in Insurance Unit 590 Principles of Takaful October 2015 examination Instructions Three hours are allowed for this paper. Do not begin writing until

TAKAFUL AT A CROSSROADS

TAKAFUL AT A CROSSROADS The recent growth of the takaful model is impressive, says Zainal Abidin Mohd Kassim but this is in danger of being restricted by a general lack of understanding of the product

TAKAFUL AT A CROSSROADS The recent growth of the takaful model is impressive, says Zainal Abidin Mohd Kassim but this is in danger of being restricted by a general lack of understanding of the product

CAPITAL ADEQUACY MODULE

CAPITAL ADEQUACY MODULE Table of Contents CA-A Date Last Changed Introduction CA-A.1 Purpose 01/2011 CA-A.2 Module History 04/2014 CA-B Scope of Application CA-B.1 Bahraini Licensee and Overseas Licensee

CAPITAL ADEQUACY MODULE Table of Contents CA-A Date Last Changed Introduction CA-A.1 Purpose 01/2011 CA-A.2 Module History 04/2014 CA-B Scope of Application CA-B.1 Bahraini Licensee and Overseas Licensee

IFRS 4 Phase I and II:

building value together 19 th September 2012 IFRS 4 Phase I and II: The issues for takaful, implications for the Mudharabah and Wakala Model Zainal Abidin Mohd Kassim, FIA Senior Partner www.actuarialpartners.com

building value together 19 th September 2012 IFRS 4 Phase I and II: The issues for takaful, implications for the Mudharabah and Wakala Model Zainal Abidin Mohd Kassim, FIA Senior Partner www.actuarialpartners.com

IFSB GLOSSARY. No Term Definition

IFSB GLOSSARY 1 2 Acquisition Cost Alpha (α) (Islamic Banking) 3 Aqd 4 Asset Liability Management 5 Bayʻ al-dayn 6 Bayʻ al- Īnah 7 Bayʻ al-istijrār 8 Brokerage 9 10 11 Captive Cedant Ceding Commission

IFSB GLOSSARY 1 2 Acquisition Cost Alpha (α) (Islamic Banking) 3 Aqd 4 Asset Liability Management 5 Bayʻ al-dayn 6 Bayʻ al- Īnah 7 Bayʻ al-istijrār 8 Brokerage 9 10 11 Captive Cedant Ceding Commission

RBC and Economic Capital: The Malaysian Experience

building value together 19 th September 2012 RBC and Economic Capital: The Malaysian Experience Farzana Ismail, FIA Principal www.actuarialpartners.com Agenda Introduction to economic capital RBC: The

building value together 19 th September 2012 RBC and Economic Capital: The Malaysian Experience Farzana Ismail, FIA Principal www.actuarialpartners.com Agenda Introduction to economic capital RBC: The

Islamic Banking, Takaful and Al Rahnu LCA4562 DR. ZULKIFLI HASAN

Islamic Banking, Takaful and Al Rahnu LCA4562 DR. ZULKIFLI HASAN Contents Legal requirements Takaful products Legal and syariah issues Legal Position S 4 of the TA- takaful operators only 1. Company 2.

Islamic Banking, Takaful and Al Rahnu LCA4562 DR. ZULKIFLI HASAN Contents Legal requirements Takaful products Legal and syariah issues Legal Position S 4 of the TA- takaful operators only 1. Company 2.

Takaful. Mohammad Khan Head of Islamic Finance in PwC. Mohammad Khan

Takaful Mohammad Khan Mohammad Khan Head of Islamic Finance in PwC Partner in PwC Actuarial Services Head of general insurance personal and commercial lines at PwC Member of PwC s Global Islamic Finance

Takaful Mohammad Khan Mohammad Khan Head of Islamic Finance in PwC Partner in PwC Actuarial Services Head of general insurance personal and commercial lines at PwC Member of PwC s Global Islamic Finance

Reviving the Cooperative Spirit through Takaful. Hassan Scott Odierno, FSA Actuarial Partners (Malaysia) 15 October 2014

15 October 2014") Reviving the Cooperative Spirit through Takaful Hassan Scott Odierno, FSA Actuarial Partners (Malaysia) 15 October 2014 1 The cooperative spirit is members helping each other to succeed Discretionary and

Reviving the Cooperative Spirit through Takaful Hassan Scott Odierno, FSA Actuarial Partners (Malaysia) 15 October 2014 1 The cooperative spirit is members helping each other to succeed Discretionary and

CURRENT ACCOUNT (WADI A/QARD) DEPOSIT

DEPOSIT") DEPOSIT PRODUCTS Mobilization of funds from depositors/savers to borrowers/investors is an important task of a financial intermediary in the economy. Financial intermediaries attempt to achieve this goal

DEPOSIT PRODUCTS Mobilization of funds from depositors/savers to borrowers/investors is an important task of a financial intermediary in the economy. Financial intermediaries attempt to achieve this goal

Takaful articles. Introduction. Susan Dingwall Partner, Norton Rose, Ffion Griffiths Associate, Norton Rose, United KIngdom.

Takaful articles Susan Dingwall Partner, Norton Rose, United Kingdom Ffion Griffiths Associate, Norton Rose, United KIngdom Number 7: November 2006 The United Kingdom: Regulatory approach to Takaful Introduction

Takaful articles Susan Dingwall Partner, Norton Rose, United Kingdom Ffion Griffiths Associate, Norton Rose, United KIngdom Number 7: November 2006 The United Kingdom: Regulatory approach to Takaful Introduction

SHARIAH PRONOUNCEMENT

SHARIAH PRONOUNCEMENT In the name of Allah, the Most Gracious, the Most Merciful All praise is due to Allah, the Cherisher of the world, and peace and blessing upon The Prophet of Allah, on his family

SHARIAH PRONOUNCEMENT In the name of Allah, the Most Gracious, the Most Merciful All praise is due to Allah, the Cherisher of the world, and peace and blessing upon The Prophet of Allah, on his family

The Commercialisation of Modern Islamic Insurance Providers: A Study of Takaful Business Frameworks in Malaysia

The Commercialisation of Modern Islamic Insurance Providers: A Study of Takaful Business Frameworks in Malaysia Kamaruzaman Noordin 1*, Mohd. Rizal Muwazir @Mukhazir 1 Azian Madun 1 1 Department of Shariah

The Commercialisation of Modern Islamic Insurance Providers: A Study of Takaful Business Frameworks in Malaysia Kamaruzaman Noordin 1*, Mohd. Rizal Muwazir @Mukhazir 1 Azian Madun 1 1 Department of Shariah

Islamic Finance: Coming of Age. 10/29/13 GAB Annual Islamic Finance Conference

Islamic Finance: Coming of Age 1 Islamic Finance Sector in Kenya 1. A Sector View 2. A Company View 2 Sector View 3 Company View 4 The Takaful Concept What is it? How does it work? How is it different

Islamic Finance: Coming of Age 1 Islamic Finance Sector in Kenya 1. A Sector View 2. A Company View 2 Sector View 3 Company View 4 The Takaful Concept What is it? How does it work? How is it different

INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS

Principles No. 3.4 INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS PRINCIPLES ON GROUP-WIDE SUPERVISION OCTOBER 2008 This document has been prepared by the Financial Conglomerates Subcommittee (renamed

Principles No. 3.4 INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS PRINCIPLES ON GROUP-WIDE SUPERVISION OCTOBER 2008 This document has been prepared by the Financial Conglomerates Subcommittee (renamed

TRUST. TRANSPARENCY. INDEPENDENCE. Takaful Rating Methodology

TRUST. TRANSPARENCY. INDEPENDENCE Takaful Rating Methodology TAKAFUL RATING METHODOLOGY Preamble Shari a (Islamic Laws) may be termed as a rule of law, which fundamentally covers all practical and spiritual

TRUST. TRANSPARENCY. INDEPENDENCE Takaful Rating Methodology TAKAFUL RATING METHODOLOGY Preamble Shari a (Islamic Laws) may be termed as a rule of law, which fundamentally covers all practical and spiritual

Islamic Arab Insurance Co. (Salama) PJSC and its subsidiaries Directors report and consolidated financial statements for the year ended 31 December

PJSC and its subsidiaries Directors report and consolidated financial statements for the year ended 31 December") Islamic Arab Insurance Co. (Salama) PJSC and its subsidiaries Directors report and consolidated financial statements for the year ended 31 December 2017 Directors report and consolidated financial statements

Islamic Arab Insurance Co. (Salama) PJSC and its subsidiaries Directors report and consolidated financial statements for the year ended 31 December 2017 Directors report and consolidated financial statements

44. Takaful Coverage for Islamic Financing

S H A R I A H R E S O L U T I O N S I N I S L A M I C F I N A N C E 67 Basis of the Ruling The aforesaid SAC s resolution has considered the following: i. Among the basic elements of the proposed model

S H A R I A H R E S O L U T I O N S I N I S L A M I C F I N A N C E 67 Basis of the Ruling The aforesaid SAC s resolution has considered the following: i. Among the basic elements of the proposed model

INSURANCE SOLVENCY SUPERVISION, EUROPEAN REGULATION AND TAKAFUL PRODUCTS

INSURANCE SOLVENCY SUPERVISION, EUROPEAN REGULATION AND TAKAFUL PRODUCTS ALBERTO DREASSI* Abstract This paper investigates the application of global solvency supervisory principles and the European Solvency

INSURANCE SOLVENCY SUPERVISION, EUROPEAN REGULATION AND TAKAFUL PRODUCTS ALBERTO DREASSI* Abstract This paper investigates the application of global solvency supervisory principles and the European Solvency

Methodology for Takaful & Retakaful Firms

Methodology for Takaful & Retakaful Firms By: Sobia Maqbool Senior Manager JCR-VIS Credit Rating Company Limited Singapore, November 25, 2008 Takaful Market Global Takaful market estimated at $ 4 billion

Methodology for Takaful & Retakaful Firms By: Sobia Maqbool Senior Manager JCR-VIS Credit Rating Company Limited Singapore, November 25, 2008 Takaful Market Global Takaful market estimated at $ 4 billion

Advanced Diploma in Insurance

THE CHARTERED INSURANCE INSTITUTE 590 Advanced Diploma in Insurance Unit 590 Principles of Takaful October 2013 examination Instructions Three hours are allowed for this paper. Do not begin writing until

THE CHARTERED INSURANCE INSTITUTE 590 Advanced Diploma in Insurance Unit 590 Principles of Takaful October 2013 examination Instructions Three hours are allowed for this paper. Do not begin writing until

INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS

INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS ISSUES PAPER ON GROUP-WIDE SOLVENCY ASSESSMENT AND SUPERVISION 5 MARCH 2009 This document was prepared jointly by the Solvency and Actuarial Issues Subcommittee

INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS ISSUES PAPER ON GROUP-WIDE SOLVENCY ASSESSMENT AND SUPERVISION 5 MARCH 2009 This document was prepared jointly by the Solvency and Actuarial Issues Subcommittee

Legal Documentation. Islamic Finance Seminar. Abdul Jabbar, Dato Dr Nik Norzrul Thani & Megat Hizaini Hassan Tuesday, 13 September 2005

Islamic Finance Seminar Legal Documentation Abdul Jabbar, Dato Dr Nik Norzrul Thani & Megat Hizaini Hassan Tuesday, 13 September 2005 1 Principles In Drafting Documentation 1.Experience of Drafting Conventional

Islamic Finance Seminar Legal Documentation Abdul Jabbar, Dato Dr Nik Norzrul Thani & Megat Hizaini Hassan Tuesday, 13 September 2005 1 Principles In Drafting Documentation 1.Experience of Drafting Conventional