Changes in Ethics NASBA Regional Meetings Dr. Raymond Johnson, CPA- East John F. Dailey, Jr., CPA- West

|

|

|

- Mercy Wiggins

- 6 years ago

- Views:

Transcription

1 Changes in Ethics 2013 NASBA Regional Meetings Dr. Raymond Johnson, CPA- East John F. Dailey, Jr., CPA- West

2 Recent Changes in Ethics AICPA Ethics Codification Project Revision of ET 101-3, Non-attest Services Holding Out as a CPA Requests for Client Records Subordination of Judgment Partner Equivalents Client Affiliates

3 Changes in Ethics AICPA Ethics Codification Project

4 Project Objective Create user friendly, intuitively arranged Code Physically different Separate parts Part 1: Members in public practice Part 2: Members in business Part 3: All Other Members Revise without making significant changes to existing requirements and restrictions Clarity through better drafting conventions Substantive changes will follow due process

5 Project Objective Incorporate conceptual framework approach Incorporate threats and safeguards Conceptual framework only applies when no guidance in Code exists Cannot be used to override existing requirements Incorporate references to division s nonauthoritative guidance On-line Codification with enhanced functionality Pages/aicpa-ethics-codification-project.aspx

6 Your State s Code of Professional Conduct? Does it stand by itself? How does it mirror the AICPA Code of Professional Conduct? How much does it refer to the AICPA Code of Professional Conduct? Does it refer to the AICPA Code of Professional Conduct as of a given date?

7 State Board Awareness State Board Advisory Group Daniel Sweetwood (Exec Director, NE) Edith Steele (Former Exec Director, OK) Kent Bailey (Former Member, OR Board) Mark Crocker (Executive Director, TN Board) Rona Shor Cherno (Member, NY Board) Susan Harris (Exec Director, MS)

8 State Board Awareness The Codification Project provides an excellent opportunity for State Boards to review their regulations relative to the Code Does your Board make reference to the Code in its regulations? Some State Board s regulations may be out of date compared to the Code

Approval (First Q 2014) Release (TBD)")

9 Project Timing Currently in Phase Three which consists of: Exposed For Comment (April 15, 2013) Approval (First Q 2014) Release (TBD)

10 AICPA Ethics Codification Project Substantive Changes

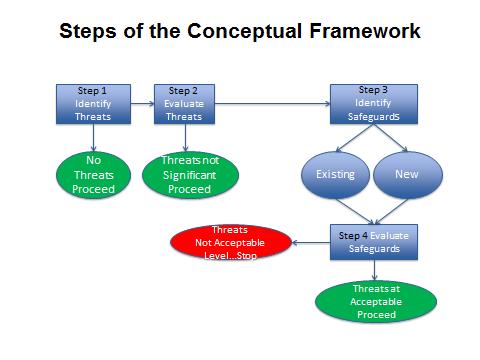

11 Incorporate Conceptual Frameworks Two New Frameworks Conceptual Framework for Members in the Practice of Public Accounting Conceptual Framework for Members in Business Applied when no guidance on a particular relationship or circumstance It is considered a violation of applicable rule if the member cannot demonstrate that safeguards were applied that eliminated or reduced significant threats to an acceptable level

12 What is a Conceptual Framework? When there is nothing on point in the Code Old Thinking o Relationship or circumstance must be permitted Revised Thinking o Apply the conceptual framework Requires professional judgment (risk based) Reasonable Third Party o For example, if the situation involves a staff person often an effective safeguard is: The staff's removal from the engagement Additional review of the staff s work

13

14 Substantive Changes Report AICPA has released a report entitled Proposed Substantive Changes AICPA Codification Project A copy is included in your materials

15 Mapping Document excerpt

16 Changes in Ethics Non-attest Services

17 Revisions to Nonattest Services Interpretation Period of Impairment Independence not impaired if member performed prohibited nonattest services during the period covered by the F/S if performed before entity became an attest client and certain other criteria are met Activities Related to Attest Services Clarified certain communications during an attest engagement are not nonattest services Management Responsibilities Replaced the term management functions General Activities section Management Responsibilities Incorporates guidance from IFAC IESBA Code Effective August 31, 2012

18 Revisions to Nonattest Services Interpretation Outside Scope of Attest Service: Financial Statement Preparation and Cash to Accrual Conversions Considered a nonattest service (i.e., outside scope of attest service) Must apply the general requirements Consistent with GAO Independence Standards Revisions to SSARS pending exposure Effective for engagements covering periods beginning on or after December 15, 2014

19 Revisions to Nonattest Services Interpretation Internal Audit Services Clarifies the impact performing ongoing and separate evaluations have on independence. o Ongoing evaluations would impair independence Direct user to the COSO Internal Control Integrated Framework Effective for engagements covering periods beginning on or after December 15, 2013

20 Changes in Ethics Holding Out as a CPA

21 Deletion of Holding Out Requirement Task force chaired by NASBA Chairman Gaylen Hansen, former PEEC member Delete holding out as CPA requirement from definitions of practice of public accounting and professional services Members should be held to the Code regardless if holding out as CPAs Definition of professional services broadened to provide examples of additional services

22 Deletion of Holding Out Requirement Practice of public accounting public practice Definition of public practice = professional services provided to client Effective May 30, 2013

23 Changes in Ethics Requests for Client Records

24 Response to Requests by Clients for Records Highlights State Boards may be more restrictive Unpaid fees from client Client provided records Must always return Member prepared records Must return if relate to completed/issued work product unless unpaid fees

25 Response to Requests by Clients for Records Member s Work Product Should provide unless unpaid fees or work product incomplete Member s Working Papers Property of member

26 Changes in Ethics Subordination of Judgment

27 Subordination of Judgment Provides guidance when member and supervisor have difference of opinion relating to application of professional standards, or applicable laws/regulations If member concludes supervisor s position results in material misrepresentation of fact or violation of laws, should discuss concerns with supervisor If difference of opinion not resolved, should discuss concerns with appropriate higher level(s) of management Consider documenting facts & discussions held Consider seeking legal guidance Consider continuing relationship with entity if no action taken

28 Subordination of Judgment Approved by PEEC at its May 2014 meeting Effective the last day of the month published in the Journal of Accountancy

29 Changes in Ethics Partner Equivalents

30 Partner Equivalents Capture members who act in a partner capacity with respect to attest engagements but are not partners Authority to bind firm with respect to attest engagement without partner approval Ultimate responsibility for attest engagement o Authority to issue or authorize others to issue an attest report without partner approval o Authority to sign or affix the firm s name to an attest report Only applies for purposes of Independence rule o Not to be used for ownership purposes

31 Partner Equivalents Subject to same independence rules as partners Effective for engagements covering periods beginning on or after December 15, 2014

32 Changes in Ethics Client Affiliates

33 Client Affiliates Provides guidance on which entities are affiliates of a client and subject to independence rules Certain exceptions apply Affiliates of a financial statement attest client include a: Entity that client can control Entity in which client has material direct financial interest and significant influence over entity Entity that controls client when client is material Entity with material direct financial interest in client and significant influence over client

34 Client Affiliates Affiliates of a financial statement attest client include a (cont d): Sister entity if client and sister entity material to parent Trustee of trust client Sponsor of benefit plan client Benefit plan sponsored by client Effective January 1, 2014

35 Why do changes in the AICPA Code of Professional Conduct Matter to State Boards of Accountancy?

36 Any Questions?

AICPA Code of Professional Conduct

AICPA Code of Professional Conduct Effective December 15, 2014. Updated for all Official Releases through December 31, 2017 Copyright 2017, American Institute of Certified Public Accountants, Inc. All

AICPA Code of Professional Conduct Effective December 15, 2014. Updated for all Official Releases through December 31, 2017 Copyright 2017, American Institute of Certified Public Accountants, Inc. All

AICPA Code of Professional Conduct

AICPA Code of Professional Conduct Effective December 15, 2014. Updated for all Official Releases through August 31, 2017 Copyright 2016, American Institute of Certified Public Accountants, Inc. All Rights

AICPA Code of Professional Conduct Effective December 15, 2014. Updated for all Official Releases through August 31, 2017 Copyright 2016, American Institute of Certified Public Accountants, Inc. All Rights

PEEC Agenda August 2018

PEEC Agenda August 2018 Task Force Name and Charge Information Technology and Cloud Services Recommend to PEEC any updates necessary to the nonattest services subtopic, including the Information Systems

PEEC Agenda August 2018 Task Force Name and Charge Information Technology and Cloud Services Recommend to PEEC any updates necessary to the nonattest services subtopic, including the Information Systems

The New Ethics Code: What Tax People Need to Know

SESSION E5 60TH ANNUAL MNCPA TAX CONFERENCE November 17-18, 2014 Minneapolis Convention Center ONLINE RESOURCES Session Handouts Most session handouts are available on the MNCPA website. To access: Go

SESSION E5 60TH ANNUAL MNCPA TAX CONFERENCE November 17-18, 2014 Minneapolis Convention Center ONLINE RESOURCES Session Handouts Most session handouts are available on the MNCPA website. To access: Go

AICPA Code of Professional Conduct. Effective December 15, 2014 (early implementation permitted).

.") AICPA Code of Professional Conduct Effective December 15, 2014 (early implementation permitted). Copyright 2014, American Institute of Certified Public Accountants, Inc. All Rights Reserved. This PDF created

AICPA Code of Professional Conduct Effective December 15, 2014 (early implementation permitted). Copyright 2014, American Institute of Certified Public Accountants, Inc. All Rights Reserved. This PDF created

PEEC Agenda January 2018

PEEC Agenda January 2018 Task Force Name and Charge Information Technology and Cloud Services Recommend to PEEC any updates necessary to the nonattest services subtopic, including the Information Systems

PEEC Agenda January 2018 Task Force Name and Charge Information Technology and Cloud Services Recommend to PEEC any updates necessary to the nonattest services subtopic, including the Information Systems

Not In Attendance: Janice Gray

AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS DIVISION OF PROFESSIONAL ETHICS PROFESSIONAL ETHICS EXECUTIVE COMMITTEE OPEN MEETING MINUTES FEBRUARY 4, 2016 NEW ORLEANS, LOUSIANNA The Professional

AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS DIVISION OF PROFESSIONAL ETHICS PROFESSIONAL ETHICS EXECUTIVE COMMITTEE OPEN MEETING MINUTES FEBRUARY 4, 2016 NEW ORLEANS, LOUSIANNA The Professional

SSARS No Update Part 2 Compilation and Review Standards

1 SSARS No. 21-23 Update Part 2 Compilation and Review Standards 7 Hours PDH Academy PO Box 449 Pewaukee, WI 53072 www.pdhacademy.com pdhacademy@gmail.com 888-564-9098 2 The purpose of this course is to

1 SSARS No. 21-23 Update Part 2 Compilation and Review Standards 7 Hours PDH Academy PO Box 449 Pewaukee, WI 53072 www.pdhacademy.com pdhacademy@gmail.com 888-564-9098 2 The purpose of this course is to

2017 CIRA PREPARATIONS, COMPILATIONS AND REVIEWS OVERVIEW FOR KNOWLEDGE COACH USERS

2017 CIRA PREPARATIONS, COMPILATIONS AND REVIEWS OVERVIEW FOR KNOWLEDGE COACH USERS PURPOSE This document is published for the purpose of communicating, to users of the toolset, updates and enhancements

2017 CIRA PREPARATIONS, COMPILATIONS AND REVIEWS OVERVIEW FOR KNOWLEDGE COACH USERS PURPOSE This document is published for the purpose of communicating, to users of the toolset, updates and enhancements

Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Module B Professional Ethics Auditors must approach their jobs with independence and skepticism. How do we instill

McGraw-Hill/Irwin Copyright 2013 by The McGraw-Hill Companies, Inc. All rights reserved. Module B Professional Ethics Auditors must approach their jobs with independence and skepticism. How do we instill

Article 5.--CODE OF PROFESSIONAL CONDUCT

Article 5.--CODE OF PROFESSIONAL CONDUCT Part I.--DEFINITIONS, INDEPENDENCE, INTEGRITY AND OBJECTIVITY, COMMISSIONS AND REFERRAL FEES, CONTINGENT FEES 74-5-2. Definitions. Each of the following terms,

Article 5.--CODE OF PROFESSIONAL CONDUCT Part I.--DEFINITIONS, INDEPENDENCE, INTEGRITY AND OBJECTIVITY, COMMISSIONS AND REFERRAL FEES, CONTINGENT FEES 74-5-2. Definitions. Each of the following terms,

October 16, Mail to:

Deloitte & Touche LLP 695 East Main Street Stamford, CT 06901-2150 75201-6778 USA Tel: +1 203 708 4000 Fax: +1 203 705 5455 www.deloitte.com Mr. Samuel L. Burke Chair, Professional Ethics Executive Committee

Deloitte & Touche LLP 695 East Main Street Stamford, CT 06901-2150 75201-6778 USA Tel: +1 203 708 4000 Fax: +1 203 705 5455 www.deloitte.com Mr. Samuel L. Burke Chair, Professional Ethics Executive Committee

EXPOSURE DRAFT AFFILIATE PROPOSED REVISED DEFINITION AICPA PROFESSIONAL ETHICS DIVISION. April 16, Comments are requested by May 18, 2015

EXPOSURE DRAFT AFFILIATE PROPOSED REVISED DEFINITION AICPA PROFESSIONAL ETHICS DIVISION April 16, 2015 Comments are requested by May 18, 2015 Prepared by the AICPA Professional Ethics Executive Committee

EXPOSURE DRAFT AFFILIATE PROPOSED REVISED DEFINITION AICPA PROFESSIONAL ETHICS DIVISION April 16, 2015 Comments are requested by May 18, 2015 Prepared by the AICPA Professional Ethics Executive Committee

Professional Ethics Executive Committee. Peer Review Board. November 3-4, 2016 Open Meeting Agenda Austin, TX

Professional Ethics Executive Committee Peer Review Board November 3-4, 2016 Open Meeting Agenda Austin, TX AICPA Professional Ethics Executive Committee Open Meeting Agenda November 3-4, 2016 Austin,

Professional Ethics Executive Committee Peer Review Board November 3-4, 2016 Open Meeting Agenda Austin, TX AICPA Professional Ethics Executive Committee Open Meeting Agenda November 3-4, 2016 Austin,

100.2 AR C 70does not apply when the accountant prepares financial statements to be

Checkpoint Contents Accounting, Audit & Corporate Finance Library Editorial Materials Accounting Services SSARS Preparation Engagements Chapter 1 Introduction and Background 100 Introduction 100 Introduction

Checkpoint Contents Accounting, Audit & Corporate Finance Library Editorial Materials Accounting Services SSARS Preparation Engagements Chapter 1 Introduction and Background 100 Introduction 100 Introduction

Not-for-Profit Conference A&A Update for NFPs

Not-for-Profit Conference A&A Update for NFPs James Schmutte July 24, 2014 This session focuses on recent and developing activities of the four standard setters (FASB, AICPA, OMB and GAO) that impact nonprofit

Not-for-Profit Conference A&A Update for NFPs James Schmutte July 24, 2014 This session focuses on recent and developing activities of the four standard setters (FASB, AICPA, OMB and GAO) that impact nonprofit

Update on Standards for Audits, Reviews, and Compilations

Update on Standards for Audits, Reviews, and Compilations Mike Glynn, CPA Senior Technical Manager AICPA Audit and Attest Standards Team mglynn@aicpa.org 1 1 DISCLAIMER Views expressed by AICPA employees

Update on Standards for Audits, Reviews, and Compilations Mike Glynn, CPA Senior Technical Manager AICPA Audit and Attest Standards Team mglynn@aicpa.org 1 1 DISCLAIMER Views expressed by AICPA employees

UPDATE: YELLOW BOOK EXPOSURE DRAFT James Dalkin NASACT Emerging Leaders Conference April 19, 2018

UPDATE: YELLOW BOOK EXPOSURE DRAFT 2017 James Dalkin NASACT Emerging Leaders Conference April 19, 2018 Session Objective Provide an update on proposed revisions in the 2017 Yellow Book Exposure Draft 2

UPDATE: YELLOW BOOK EXPOSURE DRAFT 2017 James Dalkin NASACT Emerging Leaders Conference April 19, 2018 Session Objective Provide an update on proposed revisions in the 2017 Yellow Book Exposure Draft 2

Update on the Developments in Government Auditing Standards

Update on the Developments in Government Auditing Standards Yellow Book Update Presentation to the AGA PDT July 22, 2018 Session Objective Provide an update on revisions to the 2018 Yellow Book 2 1 GAGAS

Update on the Developments in Government Auditing Standards Yellow Book Update Presentation to the AGA PDT July 22, 2018 Session Objective Provide an update on revisions to the 2018 Yellow Book 2 1 GAGAS

Book Governmental Title Accounting and Auditing Supplement No

Book Governmental Title Accounting and Auditing Supplement No. 1-2017 GOVERNMENTAL ACCOUNTING AND AUDITING SUPPLEMENT NO. 1-2017 Chapter 1 GOVERNMENTAL ACCOUNTING AND AUDITING SUPPLEMENT NO. 1-2017 INTRODUCTION

Book Governmental Title Accounting and Auditing Supplement No. 1-2017 GOVERNMENTAL ACCOUNTING AND AUDITING SUPPLEMENT NO. 1-2017 Chapter 1 GOVERNMENTAL ACCOUNTING AND AUDITING SUPPLEMENT NO. 1-2017 INTRODUCTION

May 5, Mr. Mike Glynn American Institute of Certified Public Accountants 1211 Avenue of the Americas New York, NY

Deloitte & Touche LLP Ten Westport Road PO Box 820 Wilton, CT 06897-0820 Tel: +1 203 761 3000 Fax: +1 203 834 2200 www.deloitte.com May 5, 2014 Mr. Mike Glynn American Institute of Certified Public Accountants

Deloitte & Touche LLP Ten Westport Road PO Box 820 Wilton, CT 06897-0820 Tel: +1 203 761 3000 Fax: +1 203 834 2200 www.deloitte.com May 5, 2014 Mr. Mike Glynn American Institute of Certified Public Accountants

Comments to be received by 1 August 2008

16 June 2008 To: Members of the Hong Kong Institute of CPAs All other interested parties INVITATION TO COMMENT ON IFAC S INTERNATIONAL ETHICS STANDARDS BOARD FOR ACCOUNTANTS (IESBA) RE EXPOSURE DRAFT ON

16 June 2008 To: Members of the Hong Kong Institute of CPAs All other interested parties INVITATION TO COMMENT ON IFAC S INTERNATIONAL ETHICS STANDARDS BOARD FOR ACCOUNTANTS (IESBA) RE EXPOSURE DRAFT ON

THE ETHICS INTERPRETATIONS AND ETHICS RULINGS CONTAINED IN THIS DOCUMENT ARE EFFECTIVE ON JANUARY 31, 2013

THE ETHICS INTERPRETATIONS AND ETHICS RULINGS CONTAINED IN THIS DOCUMENT ARE EFFECTIVE ON JANUARY 31, 2013 Ethics interpretations and rulings are promulgated by the executive committee of the Professional

THE ETHICS INTERPRETATIONS AND ETHICS RULINGS CONTAINED IN THIS DOCUMENT ARE EFFECTIVE ON JANUARY 31, 2013 Ethics interpretations and rulings are promulgated by the executive committee of the Professional

Preparation of Financial Statements

Preparation of Financial Statements 2133 AR-C Section 70 Preparation of Financial Statements Source: SSARS No. 21; SSARS No. 23. Effective for the preparation of financial statements for periods ending

Preparation of Financial Statements 2133 AR-C Section 70 Preparation of Financial Statements Source: SSARS No. 21; SSARS No. 23. Effective for the preparation of financial statements for periods ending

This section includes the AICPA Code of Professional Conduct. It has been updated for all Official Releases through April 2006.

This section includes the AICPA Code of Professional Conduct. It has been updated for all Official Releases through April 2006. Introduction Section 50 - Principles of Professional Conduct Section 90 -

This section includes the AICPA Code of Professional Conduct. It has been updated for all Official Releases through April 2006. Introduction Section 50 - Principles of Professional Conduct Section 90 -

APRIL 1, Prospective Financial Information

GUIDE APRIL 1, 2017 Prospective Financial Information GUIDE Prospective Financial Information 20974-349 Copyright 2017 by American Institute of Certified Public Accountants, Inc. New York, NY 10036-8775

GUIDE APRIL 1, 2017 Prospective Financial Information GUIDE Prospective Financial Information 20974-349 Copyright 2017 by American Institute of Certified Public Accountants, Inc. New York, NY 10036-8775

Proposed Revisions Pertaining to Safeguards in the Code Phase 2 and Related Conforming Amendments

Exposure Draft January 2017 Comments due: April 25, 2017 International Ethics Standards Board for Accountants Proposed Revisions Pertaining to Safeguards in the Code Phase 2 and Related Conforming Amendments

Exposure Draft January 2017 Comments due: April 25, 2017 International Ethics Standards Board for Accountants Proposed Revisions Pertaining to Safeguards in the Code Phase 2 and Related Conforming Amendments

Ms. Sucher noted that the Code contained provisions to address inadvertent violations of the Code but this was a different matter.

Drafting Conventions Report Back This agenda paper contains extracts from the minutes of the March 2008 CAG meeting related to the discussion of the drafting conventions project and describes how the Task

Drafting Conventions Report Back This agenda paper contains extracts from the minutes of the March 2008 CAG meeting related to the discussion of the drafting conventions project and describes how the Task

ISRS 4410 Compilation Engagements. Objective of Agenda Item 1. To receive an update on the IAASB project to revise ISRS 4410 Compilation Engagements.

Agenda Item 9 Meeting Location: Sofitel Warsaw Victoria, Warsaw, Poland Meeting Date: June 15-17, 2011 ISRS 4410 Compilation Engagements Objective of Agenda Item 1. To receive an update on the IAASB project

Agenda Item 9 Meeting Location: Sofitel Warsaw Victoria, Warsaw, Poland Meeting Date: June 15-17, 2011 ISRS 4410 Compilation Engagements Objective of Agenda Item 1. To receive an update on the IAASB project

New Standards for Accounting and Review Services (SSARS 21) CPE Edition. Distributed by The CPE Store. Steven C. Fustolo, CPA

CPE Edition. Distributed by The CPE Store. Steven C. Fustolo, CPA") New Standards for Accounting and Review Services (SSARS 21) Steven C. Fustolo, CPA CPE Edition Distributed by The CPE Store www.cpestore.com 1-800-910-2755 New Standards for Accounting and Review Services

New Standards for Accounting and Review Services (SSARS 21) Steven C. Fustolo, CPA CPE Edition Distributed by The CPE Store www.cpestore.com 1-800-910-2755 New Standards for Accounting and Review Services

Andrew Mintzer* Lawrence I. Shapiro James Smolinski Shelly Van Dyne

AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS DIVISION OF PROFESSIONAL ETHICS PROFESSIONAL ETHICS EXECUTIVE COMMITTEE OPEN MEETING MINUTES May 5 6, 2016 DURHAM, NC The Professional Ethics Executive

AMERICAN INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS DIVISION OF PROFESSIONAL ETHICS PROFESSIONAL ETHICS EXECUTIVE COMMITTEE OPEN MEETING MINUTES May 5 6, 2016 DURHAM, NC The Professional Ethics Executive

Proposed Interpretation of the AICPA Code of Professional Conduct

EXPOSURE DRAFT Proposed Interpretation of the AICPA Code of Professional Conduct Disclosing Client Information in Connection With a Quality Review (ET sec. 1.700.110) AICPA Professional Ethics Division

EXPOSURE DRAFT Proposed Interpretation of the AICPA Code of Professional Conduct Disclosing Client Information in Connection With a Quality Review (ET sec. 1.700.110) AICPA Professional Ethics Division

Basis for Conclusions: Code of Ethics for Professional Accountants

Basis for Conclusions: Code of Ethics for Professional Accountants Prepared by the Staff of the International Ethics Standards Board for Accountants July 2009 July 2009 BASIS FOR CONCLUSIONS This Basis

Basis for Conclusions: Code of Ethics for Professional Accountants Prepared by the Staff of the International Ethics Standards Board for Accountants July 2009 July 2009 BASIS FOR CONCLUSIONS This Basis

Compilation & Review Standards (Updated for SSARS 21)

") Compilation & Review Standards (Updated for SSARS 21) Authored by: David W. Holt, CPA, CFE www.holtcpe.com david@holtcpe.com 830-486-5222 COMPILATION & REVIEW STANDARDS This seminar has the following learning

Compilation & Review Standards (Updated for SSARS 21) Authored by: David W. Holt, CPA, CFE www.holtcpe.com david@holtcpe.com 830-486-5222 COMPILATION & REVIEW STANDARDS This seminar has the following learning

100 Background Information

Page 1 of 27 Checkpoint Contents Accounting, Audit & Corporate Finance Library Editorial Materials Accounting and Financial Statements (US GAAP) Cash, Tax, and Other Bases of Accounting Chapter 1 An Introduction

Page 1 of 27 Checkpoint Contents Accounting, Audit & Corporate Finance Library Editorial Materials Accounting and Financial Statements (US GAAP) Cash, Tax, and Other Bases of Accounting Chapter 1 An Introduction

Re: AICPA Professional Ethics Division, Proposed Revisions to the AICPA Code of Professional Conduct, Leases Interpretation (ET sec

January 19, 2018 Ms. Toni Lee-Andrews Director, AICPA Professional Ethics Division AICPA Professional Ethics Executive Committee 1211 Avenue of the Americas New York, NY 10036-8775 Re: AICPA Professional

January 19, 2018 Ms. Toni Lee-Andrews Director, AICPA Professional Ethics Division AICPA Professional Ethics Executive Committee 1211 Avenue of the Americas New York, NY 10036-8775 Re: AICPA Professional

American Institute of CPAs

Statement on Standards for Accounting and Review Services No. 21, Statements on Standards for Accounting and Review Services: Clarification and Recodification DISCLAIMER: This publication has not been

Statement on Standards for Accounting and Review Services No. 21, Statements on Standards for Accounting and Review Services: Clarification and Recodification DISCLAIMER: This publication has not been

ARSC Meeting April 6-7, Statements on Standards for Accounting and Review Standards

ARSC Meeting April 6-7, 2009 Agenda Item 2B Statements on Standards for Accounting and Review Standards Chapter 1 Framework and Objectives for Performing and Reporting on Compilation And Review Engagements

ARSC Meeting April 6-7, 2009 Agenda Item 2B Statements on Standards for Accounting and Review Standards Chapter 1 Framework and Objectives for Performing and Reporting on Compilation And Review Engagements

Welcome To. Cecil Patterson, Jr., CPA

Welcome To CIRA Compilation and Review Update - 2010 Cecil Patterson, Jr., CPA Patterson & Associates, P. A. Post Office Box 2229 Ponte Vedra Beach, FL 32004-2229 (904) 285-4489 Fax (904) 285-1805 pat@pattersoncpafirm.com

Welcome To CIRA Compilation and Review Update - 2010 Cecil Patterson, Jr., CPA Patterson & Associates, P. A. Post Office Box 2229 Ponte Vedra Beach, FL 32004-2229 (904) 285-4489 Fax (904) 285-1805 pat@pattersoncpafirm.com

Audit Engagement Letter a. [CPA Firm s Letterhead]

![Audit Engagement Letter a. [CPA Firm s Letterhead]](/thumbs/82/86656009.jpg "Audit Engagement Letter a. [CPA Firm s Letterhead]") 8 EBP 2/15 EBP-CL-1.1: Audit Engagement Letter a [CPA Firm s Letterhead] [Date] [Identify the body or individual(s) charged with governance.] and [Name of Management] b [Client s Name and Address] We are

8 EBP 2/15 EBP-CL-1.1: Audit Engagement Letter a [CPA Firm s Letterhead] [Date] [Identify the body or individual(s) charged with governance.] and [Name of Management] b [Client s Name and Address] We are

IFAC 2012 Report. Jim Sylph Executive Director Professional Standards & External Relations

IFAC 2012 Report Jim Sylph Executive Director Professional Standards & External Relations NASBA International Forum October 31-November 1, 2012 Orlando, Florida International Federation of Accountants

IFAC 2012 Report Jim Sylph Executive Director Professional Standards & External Relations NASBA International Forum October 31-November 1, 2012 Orlando, Florida International Federation of Accountants

Office of the Secretary Public Company Accounting Oversight Board 1666 K Street, NW Washington, DC

Office of the Secretary 1666 K Street, NW Washington, DC 20006-2803 RE: PCAOB Rulemaking Docket Matter No. 017-Concept Release Concerning Scope of Rule 3523, Tax Services for Persons in Financial Reporting

Office of the Secretary 1666 K Street, NW Washington, DC 20006-2803 RE: PCAOB Rulemaking Docket Matter No. 017-Concept Release Concerning Scope of Rule 3523, Tax Services for Persons in Financial Reporting

Not-for-Profit Accounting and Auditing Supplement No

Not-for-Profit Accounting and Auditing Supplement No. 1 2018 Chapter 1 Not-for-Profit Accounting and Auditing Supplement No. 1 2018 Introduction This update includes the more significant accounting and

Not-for-Profit Accounting and Auditing Supplement No. 1 2018 Chapter 1 Not-for-Profit Accounting and Auditing Supplement No. 1 2018 Introduction This update includes the more significant accounting and

2017 Annual Improvements to Accounting Standards for Private Enterprises

Basis for Conclusions 2017 Annual Improvements to Accounting Standards for Private Enterprises July 2017 CPA Canada Handbook Accounting, Part II Prepared by the staff of the Accounting Standards Board

Basis for Conclusions 2017 Annual Improvements to Accounting Standards for Private Enterprises July 2017 CPA Canada Handbook Accounting, Part II Prepared by the staff of the Accounting Standards Board

Yellow Book and Single Audit Update Bruce A. Nunnally, CPA, CGMA June 2016

Yellow Book and Single Audit Update Bruce A. Nunnally, CPA, CGMA June 2016 1 Yellow Book Introduction 2 GAS When Applicable FL Govt Audits Local governmental entities located in Florida are, in general,

Yellow Book and Single Audit Update Bruce A. Nunnally, CPA, CGMA June 2016 1 Yellow Book Introduction 2 GAS When Applicable FL Govt Audits Local governmental entities located in Florida are, in general,

Chapter Four. AICPA Code of Professional Conduct. McGraw-Hill/Irwin. Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter Four AICPA Code of Professional Conduct McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. Investigations of the Profession High profile frauds in the 1970s,

Chapter Four AICPA Code of Professional Conduct McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. Investigations of the Profession High profile frauds in the 1970s,

Auditing and Assurance Services, 15e (Arens) Chapter 2 The CPA Profession. Learning Objective 2-1

Chapter 2 The CPA Profession. Learning Objective 2-1") Auditing and Assurance Services, 15e (Arens) Chapter 2 The CPA Profession Learning Objective 2-1 1) The legal right to perform audits is granted to a CPA firm by regulation of: A) each state. B) the Financial

Auditing and Assurance Services, 15e (Arens) Chapter 2 The CPA Profession Learning Objective 2-1 1) The legal right to perform audits is granted to a CPA firm by regulation of: A) each state. B) the Financial

Mapping Table of Comparison Proposed Section 600, Provisions of Non-Assurance Services to an Audit Client

Agenda Item 2-H Mapping Table of Comparison Proposed Section 600, Provisions of Non-Assurance Services to an Audit Client 290.154 Firms have traditionally provided to their audit clients a range of non-assurance

Agenda Item 2-H Mapping Table of Comparison Proposed Section 600, Provisions of Non-Assurance Services to an Audit Client 290.154 Firms have traditionally provided to their audit clients a range of non-assurance

Tax Practitioner s Guide to Accounting and Reporting Issues (TPG)

") Tax Practitioner s Guide to Accounting and Reporting Issues (TPG) Rebecca Lee, CPA (Licensed in Alabama and South Carolina) and Kenneth Heaslip, CPA (Licensed in New Jersey) TAX PRACTITIONER S GUIDE TO

Tax Practitioner s Guide to Accounting and Reporting Issues (TPG) Rebecca Lee, CPA (Licensed in Alabama and South Carolina) and Kenneth Heaslip, CPA (Licensed in New Jersey) TAX PRACTITIONER S GUIDE TO

Omnibus Statement on Auditing Standards 2018 Cover Memo, Summary of Responses and Issues

ASB Meeting July 23-26, 2018 Omnibus Statement on Auditing Standards 2018 Cover Memo, Summary of Responses and Issues Agenda Item 5 Objective of Agenda Item To discuss comment letters received in response

ASB Meeting July 23-26, 2018 Omnibus Statement on Auditing Standards 2018 Cover Memo, Summary of Responses and Issues Agenda Item 5 Objective of Agenda Item To discuss comment letters received in response

Description of Concern

Numeric Citation Issue of Concern 0.000.000 Editorial Description of Concern Modernized the Preface especially to accommodate for members in business and part 3 members 0.100,.400.38 and many other places

Numeric Citation Issue of Concern 0.000.000 Editorial Description of Concern Modernized the Preface especially to accommodate for members in business and part 3 members 0.100,.400.38 and many other places

EXPOSURE DRAFT PROPOSED STATEMENT ON AUDITING STANDARDS THE AUDITOR S RESPONSIBILITIES RELATING TO OTHER INFORMATION INCLUDED IN ANNUAL REPORTS

EXPOSURE DRAFT PROPOSED STATEMENT ON AUDITING STANDARDS THE AUDITOR S RESPONSIBILITIES RELATING TO OTHER INFORMATION INCLUDED IN ANNUAL REPORTS (To supersede AU-C section 720, Other Information in Documents

EXPOSURE DRAFT PROPOSED STATEMENT ON AUDITING STANDARDS THE AUDITOR S RESPONSIBILITIES RELATING TO OTHER INFORMATION INCLUDED IN ANNUAL REPORTS (To supersede AU-C section 720, Other Information in Documents

2015 PREPARATIONS, COMPILATIONS AND REVIEWS TITLES OVERVIEW FOR KNOWLEDGE COACH USERS

2015 PREPARATIONS, COMPILATIONS AND REVIEWS TITLES OVERVIEW FOR KNOWLEDGE COACH USERS PURPOSE This document is published for the purpose of communicating, to users of the toolset, updates and enhancements

2015 PREPARATIONS, COMPILATIONS AND REVIEWS TITLES OVERVIEW FOR KNOWLEDGE COACH USERS PURPOSE This document is published for the purpose of communicating, to users of the toolset, updates and enhancements

Survey of Standard Setters Work Plans and Existing Standards

Survey of Standard Setters Work Plans and Existing Standards This paper outlines matters are on the work plans of selected IFAC member bodies or other ethical standard setters. It also outlines matters

Survey of Standard Setters Work Plans and Existing Standards This paper outlines matters are on the work plans of selected IFAC member bodies or other ethical standard setters. It also outlines matters

Update on 2007 Revision to the Yellow Book

Update on 2007 Revision to the Yellow Book AASHTO Administrative Subcommittee Conference on Internal/External Audit July 18, 2007 Gail Flister Vallieres 1 Session Objectives Explain the process being used

Update on 2007 Revision to the Yellow Book AASHTO Administrative Subcommittee Conference on Internal/External Audit July 18, 2007 Gail Flister Vallieres 1 Session Objectives Explain the process being used

2017 PREPARATION, COMPILATION, AND REVIEWS OF NOT-FOR-PROFIT ENTITIES TITLE OVERVIEW FOR KNOWLEDGE COACH USERS

2017 PREPARATIO, COMPILATIO, AD REVIEWS OF OT-FOR-PROFIT ETITIES TITLE OVERVIEW FOR KOWLEDGE COACH USERS PURPOSE This document is published for the purpose of communicating, to users of the toolset, updates

2017 PREPARATIO, COMPILATIO, AD REVIEWS OF OT-FOR-PROFIT ETITIES TITLE OVERVIEW FOR KOWLEDGE COACH USERS PURPOSE This document is published for the purpose of communicating, to users of the toolset, updates

ARSC Meeting August 20, 2013

ARSC Meeting August 20, 2013 Agenda Item 2C Summary of Comment Letters on Draft of the SSARSs, Review of Financial Statements and Review of Financial Statements Special Considerations Comment Letter No.

ARSC Meeting August 20, 2013 Agenda Item 2C Summary of Comment Letters on Draft of the SSARSs, Review of Financial Statements and Review of Financial Statements Special Considerations Comment Letter No.

GASB Today and Tomorrow

GASB Today and Tomorrow How Did We Get Here and How I Can Participate? Government Finance Officers Association of Texas Fall Conference San Antonio, Texas Kevin W. Smith November 14, 2014 Audit Tax Advisory

GASB Today and Tomorrow How Did We Get Here and How I Can Participate? Government Finance Officers Association of Texas Fall Conference San Antonio, Texas Kevin W. Smith November 14, 2014 Audit Tax Advisory

NEW YORK STATE SOCIETY OF CERTIFIED PUBLIC ACCOUNTANTS COMMENTS ON AICPA EXPOSURE DRAFT

January 27, 2006 Ms. Lisa A. Snyder Director Professional Ethics Division AICPA Harborside Financial Center 201 Plaza Three Jersey City, NJ 07311-3881 By email: lsnyder@aicpa.org In re: Exposure Draft

January 27, 2006 Ms. Lisa A. Snyder Director Professional Ethics Division AICPA Harborside Financial Center 201 Plaza Three Jersey City, NJ 07311-3881 By email: lsnyder@aicpa.org In re: Exposure Draft

Basis for Conclusions: IESBA Strategic and Operating Plan,

October 2007 Basis for Conclusions: IESBA Strategic and Operating Plan, 2008-2009 Prepared by the Staff of the International Ethics Standards Board for Accountants Basis for Conclusions IESBA Strategic

October 2007 Basis for Conclusions: IESBA Strategic and Operating Plan, 2008-2009 Prepared by the Staff of the International Ethics Standards Board for Accountants Basis for Conclusions IESBA Strategic

Non-Assurance Services Report Back

November 2014 CAG Discussion Agenda Item D-1 Non-Assurance Services Report Back Below are extracts from the draft minutes of the November 2014 CAG teleconference, 1 and an indication of how the Task Force

November 2014 CAG Discussion Agenda Item D-1 Non-Assurance Services Report Back Below are extracts from the draft minutes of the November 2014 CAG teleconference, 1 and an indication of how the Task Force

Re: Exposure Draft, AICPA Professional Ethics Division Proposed Revised AICPA Code of Professional Conduct, April 15, 2013

August 13, 2013 Lisa A. Snyder Director of the Professional Ethics Division AICPA 1211 Avenue of the Americas New York, NY 10036 By email: lsnyder@aicpa.org Dear Ms. Snyder: Re: Exposure Draft, AICPA Professional

August 13, 2013 Lisa A. Snyder Director of the Professional Ethics Division AICPA 1211 Avenue of the Americas New York, NY 10036 By email: lsnyder@aicpa.org Dear Ms. Snyder: Re: Exposure Draft, AICPA Professional

MANAGING RISK AND CLIENT EXPECTATIONS THROUGH ENGAGEMENT LETTERS AND OTHER MEANS

11/17/2015 MANAGING RISK AND CLIENT EXPECTATIONS THROUGH ENGAGEMENT LETTERS AND OTHER MEANS Michael J. Allen Carruthers & Roth, P.A. Direct Line: 336-478-1190 E-mail: mja@crlaw.com Michael J. Allen Managing

11/17/2015 MANAGING RISK AND CLIENT EXPECTATIONS THROUGH ENGAGEMENT LETTERS AND OTHER MEANS Michael J. Allen Carruthers & Roth, P.A. Direct Line: 336-478-1190 E-mail: mja@crlaw.com Michael J. Allen Managing

Responses to the specific questions outlined in the Guide for Respondents section of the Exposure Draft, are as follows:

Chartered Professional Accountants of Canada 277 Wellington Street West Toronto ON CANADA M5V 3H2 T. 416 977.3222 F. 416 977.8585 www.cpacanada.ca Comptables professionnels agréés du Canada 277, rue Wellington

Chartered Professional Accountants of Canada 277 Wellington Street West Toronto ON CANADA M5V 3H2 T. 416 977.3222 F. 416 977.8585 www.cpacanada.ca Comptables professionnels agréés du Canada 277, rue Wellington

STATE OF NEW MEXICO Office of the State Auditor

STATE OF NEW MEXICO Office of the State Auditor AUDIT DOCUMENTATION REVIEW GUIDE Revised November 2006 To be used for review of audits of the Fiscal year ended June 30, 2006 AGENCY UNDER REVIEW AGENCY

STATE OF NEW MEXICO Office of the State Auditor AUDIT DOCUMENTATION REVIEW GUIDE Revised November 2006 To be used for review of audits of the Fiscal year ended June 30, 2006 AGENCY UNDER REVIEW AGENCY

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS. PPC s Guide to Cash, Tax, and Other Bases of Accounting. Nineteenth Edition (August 2015)

") Route To: j Partners j Managers j Staff j File P.O. Box 115008 Carrollton, TX 75011-5008 Tel (972) 250-7750 (800) 431-9025 Fax (888) 216-1929 tax.thomsonreuters.com LIST OF SUBSTANTIVE CHANGES AND ADDITIONS

Route To: j Partners j Managers j Staff j File P.O. Box 115008 Carrollton, TX 75011-5008 Tel (972) 250-7750 (800) 431-9025 Fax (888) 216-1929 tax.thomsonreuters.com LIST OF SUBSTANTIVE CHANGES AND ADDITIONS

Re: Exposure Draft, Proposed Revisions Pertaining to Safeguards in the Code Phase 2 and Related Conforming Amendments

Deloitte Touche Tohmatsu Limited 30 Rockefeller Plaza New York, NY 10112-0015 USA April 26, 2017 Tel: +1 212 492 4000 Fax: +1 212 492 4001 www.deloitte.com Chair International Ethics Standards Board for

Deloitte Touche Tohmatsu Limited 30 Rockefeller Plaza New York, NY 10112-0015 USA April 26, 2017 Tel: +1 212 492 4000 Fax: +1 212 492 4001 www.deloitte.com Chair International Ethics Standards Board for

Framework for Performing and Reporting on Compilation and Review Engagements

Compilation and Review Engagements 2509 AR Section 60 Framework for Performing and Reporting on Compilation and Review Engagements Issue date, unless otherwise indicated: December 2009 Source: SSARS No.

Compilation and Review Engagements 2509 AR Section 60 Framework for Performing and Reporting on Compilation and Review Engagements Issue date, unless otherwise indicated: December 2009 Source: SSARS No.

IESBA Meeting (December 2018) Agenda Item. Alignment of Part 4B with ISAE 3000 (Revised) Proposed Revisions to the Code

Agenda Item. Alignment of Part 4B with ISAE 3000 (Revised) Proposed Revisions to the Code") Agenda Item 12-A Alignment of Part 4B with ISAE 3000 (Revised) Proposed Revisions to the Code Introduction 1. The purpose of this paper is to seek the views of the IESBA on the revisions that the Part

Agenda Item 12-A Alignment of Part 4B with ISAE 3000 (Revised) Proposed Revisions to the Code Introduction 1. The purpose of this paper is to seek the views of the IESBA on the revisions that the Part

Retired Exposure Draft Comments: Addendum 2

Retired Exposure Draft Comments: Addendum 2 Florida Institute of Certified Public Accountants: Is generally supportive, but would like to express a cautionary note that adding an additional category of

Retired Exposure Draft Comments: Addendum 2 Florida Institute of Certified Public Accountants: Is generally supportive, but would like to express a cautionary note that adding an additional category of

IFAC Ethics Committee Meeting Agenda Item 3-B September 2004 Helsinki, Finland

Definitions [Please note only definitions relating to independence are presented below] Financial aaudit client statementan entity in respect of which a firm conducts an financial statement audit engagement.

Definitions [Please note only definitions relating to independence are presented below] Financial aaudit client statementan entity in respect of which a firm conducts an financial statement audit engagement.

Proposed SSARSs Preparation of Financial Statements; Compilation Engagements; and Association With Financial Statements

ARSC Meeting May 20-22, 2014 Agenda Item 1 Proposed SSARSs Preparation of Financial Statements; Compilation Engagements; and Association With Financial Statements Objective of Agenda Item To discuss issues

ARSC Meeting May 20-22, 2014 Agenda Item 1 Proposed SSARSs Preparation of Financial Statements; Compilation Engagements; and Association With Financial Statements Objective of Agenda Item To discuss issues

Private Companies Practice Section. Avoid potholes. for a smooth ride to peer review. i Avoid potholes for a smooth ride to peer review

Private Companies Practice Section Avoid potholes for a smooth ride to peer review i Avoid potholes for a smooth ride to peer review Disclaimer: The contents of this publication do not necessarily reflect

Private Companies Practice Section Avoid potholes for a smooth ride to peer review i Avoid potholes for a smooth ride to peer review Disclaimer: The contents of this publication do not necessarily reflect

Statute Changes for Firm Mobility

Introduction This is the only course content available authorized by the VBOA to fulfill your Virginia-specific Ethics requirement. While you re waiting to get started, you can view the appendices online

Introduction This is the only course content available authorized by the VBOA to fulfill your Virginia-specific Ethics requirement. While you re waiting to get started, you can view the appendices online

Compliance Issues and Update /22/17

Compliance Update 2017 NC State Treasurer s NC and Review June 22, 2017 Compliance Audit Update 2017 Potential changes to the Yellow Book New standards for auditing and attestation Uniform Guidance (UG)

Compliance Update 2017 NC State Treasurer s NC and Review June 22, 2017 Compliance Audit Update 2017 Potential changes to the Yellow Book New standards for auditing and attestation Uniform Guidance (UG)

Jerry is an Assistant Director for the State of Tennessee, Comptroller of the Treasury, Division of Local Government Audit.

Jerry is an Assistant Director for the State of Tennessee, Comptroller of the Treasury, Division of Local Government Audit. The division has statutory responsibility for audits of approximately 1800 local

Jerry is an Assistant Director for the State of Tennessee, Comptroller of the Treasury, Division of Local Government Audit. The division has statutory responsibility for audits of approximately 1800 local

EXPOSURE DRAFT PROPOSED STATEMENTS ON AUDITING STANDARDS AUDITOR REPORTING. Forming an Opinion and Reporting on Financial Statements

EXPOSURE DRAFT PROPOSED STATEMENTS ON AUDITING STANDARDS AUDITOR REPORTING Forming an Opinion and Reporting on Financial Statements Communicating Key Audit Matters in the Independent Auditor s Report Modifications

EXPOSURE DRAFT PROPOSED STATEMENTS ON AUDITING STANDARDS AUDITOR REPORTING Forming an Opinion and Reporting on Financial Statements Communicating Key Audit Matters in the Independent Auditor s Report Modifications

Virginia Board of Accountancy Providing Volunteer Services as a Virginia CPA

Virginia Board of Accountancy Providing Volunteer Services as a Virginia CPA 2012 Copyright 2012 Virginia Society of Certified Public Accountants. All Rights Reserved. 24 Table of Contents Section Paragraph

Virginia Board of Accountancy Providing Volunteer Services as a Virginia CPA 2012 Copyright 2012 Virginia Society of Certified Public Accountants. All Rights Reserved. 24 Table of Contents Section Paragraph

Checkpoint - Accounting, Audit & Corporate Finance Library

Checkpoint - Accounting, Audit & Corporate Finance Library Accounting & Financial Statements Accounting and Auditing Disclosure Manual Accounting and Auditing Update Accounting and Reporting for Estates

Checkpoint - Accounting, Audit & Corporate Finance Library Accounting & Financial Statements Accounting and Auditing Disclosure Manual Accounting and Auditing Update Accounting and Reporting for Estates

ACCOUNTING AND AUDITING SUPPLEMENT NO

4 ACCOUNTING AND AUDITING SUPPLEMENT NO. 4-2016 INTRODUCTION This update includes the more significant accounting and auditing developments from October through November 2016. Included in this update

4 ACCOUNTING AND AUDITING SUPPLEMENT NO. 4-2016 INTRODUCTION This update includes the more significant accounting and auditing developments from October through November 2016. Included in this update

2018 PREPARATIONS, COMPILATIONS AND REVIEWS OF REAL ESTATE ENTITIES TITLES OVERVIEW FOR KNOWLEDGE COACH USERS

2018 PREPARATIONS, COMPILATIONS AND REVIEWS OF REAL ESTATE ENTITIES TITLES OVERVIEW FOR KNOWLEDGE COACH USERS PURPOSE This document is published for the purpose of communicating, to users of the toolset,

2018 PREPARATIONS, COMPILATIONS AND REVIEWS OF REAL ESTATE ENTITIES TITLES OVERVIEW FOR KNOWLEDGE COACH USERS PURPOSE This document is published for the purpose of communicating, to users of the toolset,

October 18, VIA Dear Chairman Burke:

October 18, 2017 Mr. Samuel L. Burke, Chair AICPA Professional Ethics Executive Committee American Institute of Certified Public Accountants, Inc. New York, NY 10036-8775 RE: Proposed Interpretation and

October 18, 2017 Mr. Samuel L. Burke, Chair AICPA Professional Ethics Executive Committee American Institute of Certified Public Accountants, Inc. New York, NY 10036-8775 RE: Proposed Interpretation and

Communicating Breaches of Independence Requirements

Agenda Item 2-I Communicating Breaches of Independence Requirements Purpose of the Discussion The key questions to be addressed during the session relate to: Whether the proposed statement of compliance

Agenda Item 2-I Communicating Breaches of Independence Requirements Purpose of the Discussion The key questions to be addressed during the session relate to: Whether the proposed statement of compliance

International Federation of Accountants 529 Fifth Avenue, 6th Floor New York, New York USA

International Federation of Accountants 529 Fifth Avenue, 6th Floor New York, New York 10017 USA This publication was published by the International Federation of Accountants (IFAC). Its mission is to

International Federation of Accountants 529 Fifth Avenue, 6th Floor New York, New York 10017 USA This publication was published by the International Federation of Accountants (IFAC). Its mission is to

2017 Update on Audit and Attest Standards (SASs and SSAEs)

") 2017 Update on Audit and Attest Standards (SASs and SSAEs) Mike Glynn, CPA, CGMA mike.glynn@aicpa-cima.com Speaker Biography Michael P. (Mike) Glynn is a Senior Technical Manager in the AICPA Audit and

2017 Update on Audit and Attest Standards (SASs and SSAEs) Mike Glynn, CPA, CGMA mike.glynn@aicpa-cima.com Speaker Biography Michael P. (Mike) Glynn is a Senior Technical Manager in the AICPA Audit and

545 Fifth Avenue, 14th Floor Tel: +1 (212) New York, New York Fax: +1 (212) Internet:

New York, New York Fax: +1 (212) Internet:") INTERNATIONAL FEDERATION OF ACCOUNTANTS 545 Fifth Avenue, 14th Floor Tel: +1 (212) 286-9344 New York, New York 10017 Fax: +1 (212) 856-9420 Internet: http://www.ifac.org Agenda Item 2 Board International

INTERNATIONAL FEDERATION OF ACCOUNTANTS 545 Fifth Avenue, 14th Floor Tel: +1 (212) 286-9344 New York, New York 10017 Fax: +1 (212) 856-9420 Internet: http://www.ifac.org Agenda Item 2 Board International

PwC Comment Letter on the Exposure Draft issued by the IESBA, July 2007

PricewaterhouseCoopers LLP 1 Embankment Place London WC2N 6RH Telephone +44 (0) 20 7583 5000 Facsimile +44 (0) 20 7822 4652 www.pwc.com/uk Senior Technical Manager International Ethics Standards Board

PricewaterhouseCoopers LLP 1 Embankment Place London WC2N 6RH Telephone +44 (0) 20 7583 5000 Facsimile +44 (0) 20 7822 4652 www.pwc.com/uk Senior Technical Manager International Ethics Standards Board

Audit, Review, Compilation, and Preparation of Financial Statements

Audit, Review, Compilation, and Preparation of Financial Statements DISCLAIMER: This publication has not been approved, disapproved or otherwise acted upon by any senior technical committees of, and does

Audit, Review, Compilation, and Preparation of Financial Statements DISCLAIMER: This publication has not been approved, disapproved or otherwise acted upon by any senior technical committees of, and does

Agenda Item 2A PROPOSED STATEMENT ON STANDARDS FOR ACCOUNTING AND REVIEW SERVICES REVIEW OF FINANCIAL STATEMENTS CONTENTS

ARSC Meeting August 21-23, 2012 Agenda Item 2A PROPOSED STATEMENT ON STANDARDS FOR ACCOUNTING AND REVIEW SERVICES REVIEW OF FINANCIAL STATEMENTS Introduction CONTENTS Prepared by: Mike Glynn (August 2012)

ARSC Meeting August 21-23, 2012 Agenda Item 2A PROPOSED STATEMENT ON STANDARDS FOR ACCOUNTING AND REVIEW SERVICES REVIEW OF FINANCIAL STATEMENTS Introduction CONTENTS Prepared by: Mike Glynn (August 2012)

Auditor Reporting Cover Letter and Issue Paper

ASB Meeting May 24-26, 2016 Agenda Item 3 Auditor Reporting Cover Letter and Issue Paper Objective To discuss certain elements of the auditor s report relating to ASB s convergence with the International

ASB Meeting May 24-26, 2016 Agenda Item 3 Auditor Reporting Cover Letter and Issue Paper Objective To discuss certain elements of the auditor s report relating to ASB s convergence with the International

EXPOSURE DRAFT PROPOSED STATEMENT ON AUDITING STANDARDS

EXPOSURE DRAFT PROPOSED STATEMENT ON AUDITING STANDARDS AN AUDIT OF INTERNAL CONTROL OVER FINANCIAL REPORTING THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL STATEMENTS (AICPA, Professional Standards, AU-C

EXPOSURE DRAFT PROPOSED STATEMENT ON AUDITING STANDARDS AN AUDIT OF INTERNAL CONTROL OVER FINANCIAL REPORTING THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL STATEMENTS (AICPA, Professional Standards, AU-C

TIC has reviewed the ED and is providing the following comments for your consideration. GENERAL COMMENTS

December 9, 2015 Susan M. Cosper, CPA Technical Director FASB 401 Merritt 7 PO Box 5116 Norwalk, CT 06856 5116 Re: September 24, 2015 Exposure Draft of a Proposed Accounting Standards Update (ASU), Notes

December 9, 2015 Susan M. Cosper, CPA Technical Director FASB 401 Merritt 7 PO Box 5116 Norwalk, CT 06856 5116 Re: September 24, 2015 Exposure Draft of a Proposed Accounting Standards Update (ASU), Notes

IAASB Main Agenda (September 2008) Page ISAs 800, 805 and 810 (Revised and Redrafted) Special Reports

Page ISAs 800, 805 and 810 (Revised and Redrafted) Special Reports") IAASB Main Agenda (September 2008) Page 2008 2325 Agenda Item 11 Committee: IAASB Meeting Location: Miami Meeting Date: September 15-19, 2008 ISAs 800, 805 and 810 (Revised and Redrafted) Special Reports

IAASB Main Agenda (September 2008) Page 2008 2325 Agenda Item 11 Committee: IAASB Meeting Location: Miami Meeting Date: September 15-19, 2008 ISAs 800, 805 and 810 (Revised and Redrafted) Special Reports

Auditor Independence Series Spotlight on Auditor Independence and You Presentation to: CPAacademy.org

Auditor Independence Series Spotlight on Auditor Independence and You Presentation to: CPAacademy.org Jay M. Bornstein, CPA Auditor Independence Consultant November 2, 2017 Spotlight - Independence and

Auditor Independence Series Spotlight on Auditor Independence and You Presentation to: CPAacademy.org Jay M. Bornstein, CPA Auditor Independence Consultant November 2, 2017 Spotlight - Independence and

Summary of July 2018 Content Updates

Summary of July 2018 Content Updates July 2018 Hello Future CPAs, With a new exam interface and significant test-taking improvements rolled out in April 2018, you can look forward to your next exam experience

Summary of July 2018 Content Updates July 2018 Hello Future CPAs, With a new exam interface and significant test-taking improvements rolled out in April 2018, you can look forward to your next exam experience

VIRGINIA CPA ETHICS 2016 REQUIRED COURSE

VIRGINIA CPA ETHICS 2016 REQUIRED COURSE Virginia CPA Ethics: 2016 Required Course CPE presentation developed by: Virginia Society of CPAs (VSCPA) Jim Cole, CPA Clare Levison, CPA Jim Shepherd, CPA Edited

VIRGINIA CPA ETHICS 2016 REQUIRED COURSE Virginia CPA Ethics: 2016 Required Course CPE presentation developed by: Virginia Society of CPAs (VSCPA) Jim Cole, CPA Clare Levison, CPA Jim Shepherd, CPA Edited

Independence provisions in the IESBA Code of Ethics that apply to audits of Public Interest Entities Draft for discussion

Independence provisions in the IESBA Code of Ethics that apply to audits of Public Interest Entities Draft for discussion 1 BACKGROUND Purpose This document has been prepared by the Board to isolate the

Independence provisions in the IESBA Code of Ethics that apply to audits of Public Interest Entities Draft for discussion 1 BACKGROUND Purpose This document has been prepared by the Board to isolate the

Governmental Finance Online Courses

Governmental Finance Online Courses Center for Continuing Education Carl Vinson Institute of Government Introductory Governmental Accounting Part I & Part II Intermediate Governmental Accounting These

Governmental Finance Online Courses Center for Continuing Education Carl Vinson Institute of Government Introductory Governmental Accounting Part I & Part II Intermediate Governmental Accounting These

LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC's Guide to Audits of Nonpublic Companies. Thirty third Edition (February 2015)

") Route To: Partners Managers Staff File LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC's Guide to Audits of Nonpublic Companies Thirty third Edition (February 2015) Highlights of this Edition The following

Route To: Partners Managers Staff File LIST OF SUBSTANTIVE CHANGES AND ADDITIONS PPC's Guide to Audits of Nonpublic Companies Thirty third Edition (February 2015) Highlights of this Edition The following

Minutes of the Meeting of the International Ethics Standards Board for Accountants Held on October 16-18, 2006 Sydney, Australia

Minutes of the Meeting of the International Ethics Standards Board for Accountants Held on October 16-18, 2006 Sydney, Australia Members Technical Advisors Present: Richard George (chair) Heather Briers

Minutes of the Meeting of the International Ethics Standards Board for Accountants Held on October 16-18, 2006 Sydney, Australia Members Technical Advisors Present: Richard George (chair) Heather Briers