Achieving Value-based Care in Rural Populations through Provider-Sponsored Health Plans. February 11, 2014

|

|

|

- Grace Taylor

- 5 years ago

- Views:

Transcription

1 Achieving Value-based Care in Rural Populations through Provider-Sponsored Health Plans February 11,

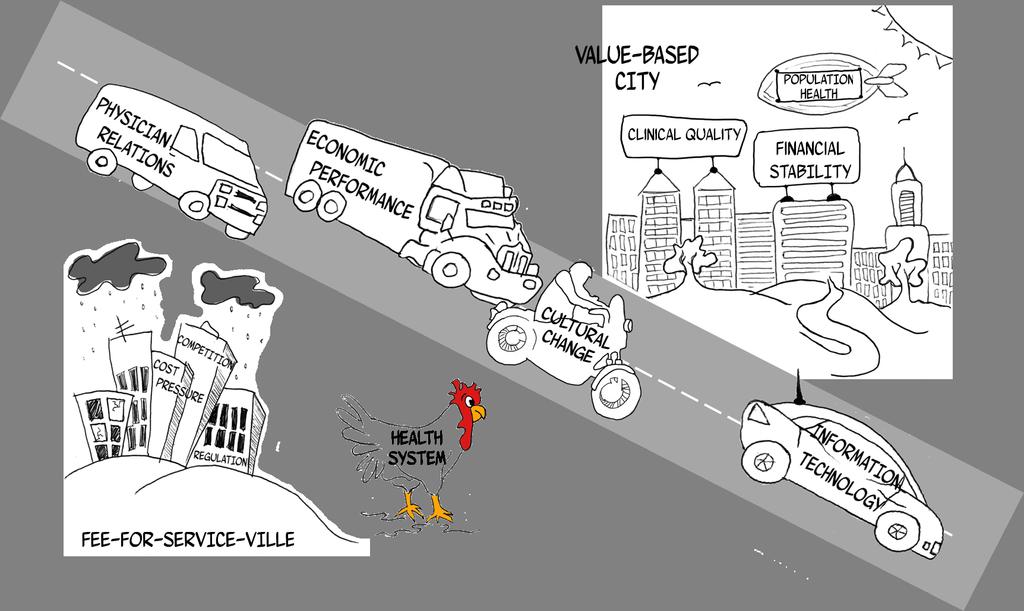

2 Value-Based Care is No Joke 2

3 What is Value-Based or Accountable Care? Value- Based Care = (Access + Quality = Outcomes ) Cost Financial Opportunity & Incentive Alignment FEE FOR SERVICE P4P SHARED SAVINGS BUNDLED PAYMENTS SHARED RISK CAPITATION FULL RISK PROVIDER- SPONSORED PLAN License & Regulatory Compliance Marketing and Sales Administration Analytics Clinical Integration Care Management Network Management

4 Why Value-based Care Makes Sense Timing the Move To Risk Greater mission Health of Population Align incentives for bending the cost curve Protect enhance market share Cost and Utilization X Early move to risk X Late move to risk Provider Risk time Economic Advantage to Provider Not as risky as it seems Payer cost Fixed costs Variable costs Provider Risk Fixed costs Variable costs Payer cost Government-Based Commercial 4

5 Higher Quality and Lower Cost Tied to Coordination and Compliance Longitudinal Experience Of Ambulatory Medicare Beneficiaries Assigned To Extended Hospital Medical Staffs (EHMSs) $6,000 42% $5,000 41% 40% $4,000 39% $3,000 38% $2,000 37% 36% $1,000 35% $- Highest High Middling Low Lowest 34% Spending per Member Quality Index Source: Elliott S. Fisher, Douglas O. Staiger, Julie P.W. Bynum and Daniel J. Gottlieb, (published online December 5, 2006; /hlthaff.26.1.w44). Health Affairs, 26, no.1 (2007):w44-w57. Creating Accountable Care Organizations: The Extended Hospital Medical Staff. Note: Quality Index on graph is average of Quality measures from Exhibit. All four quality compliance measures, essentially delivery of recommended test or care) were averaged to one number. 5

6 Predictions and Perspectives Massive Shift in Payment Models 100% Likelihood of Hospitals Gaining Payer Capabilities in the Next 5 Years* (N=192) Percent of Respondents 60 90% 80% 70% 47% 20% % 78% 50% 40% 30% 20% 10% 22% 53% 80% Very likely % Fee-for-Service P4p / Full Risk Bearing / ACO < >500 Bed Count 1 - Not likely at all Mean Source: Oliver Wyman Source: L.E.K. interviews and the L.E.K. Strategic Hospital Priorities Study

7 What We Are Seeing in the Market Model Trends Clinically Integrated Networks ACO s and Full Risk contracts Major momentum in many/most markets Drivers different by market type Some cross-system collaborations Some IPA/Physician lead models, but mostly hospital / system supported Commercial and Medicare ~50/50 Latest Batch of MSSP about to be released to applicants Data reporting/sharing often still problematic Seeing selected expansion of full-risk contracts some provider inspired Medicaid risk contracts in some states Source: Leavitt Partners Center for Accountable Care Intelligence, 2013 Provider- Sponsored Plans Bundled Payments PCMH Some marquis growth (Sutter, NSLIJ) and smaller players (CHOMP, Florida Hospital, solutions ABCO says 1 in 5 systems to be payers by 2018 Still limited in total application Still focused around cardio, ortho and birth episodes/procedures Illinois Bone and Joint - Leader ~5000 accredited sites New growth has slowed Funding from commercial payers may be focused elsewhere Source: Leavitt Partners Center for Accountable Care Intelligence, CHS Oppenheimer presentation 12/13. 7

8 What is Different This Time Around Then First round in 1980s and 1990s Some successes, but many failures Challenges Lack of expertise Wrong people in charge Bad deals from the outset Lack of data Data Affordable Care Act Expertise Technology Now Cost Pressures creating imperative Macro at the country level Micro at the provider lever Consumer Driven Healthcare 8

9 Doing Nothing Does Not Mean that Nothing Will Change Rate pressure Rate freezes Changes in payment methodology Pricing transparency Lower complexity care Utilization pressure Shift towards outpatient and observation Reduced ER visits Market pressure Shifting referrals to competitor Shift to lower cost diagnostic options High % of charges contracts are no guarantees of revenue Utilization Rates Status Quo Risk Arrangement Operating Margin Operating Margin What s a Win? Status Quo time Risk Arrangement -15% +2% Market Share time 9

10 Setting a Plan Physician Alignment Market Position Payor Readiness Organization & Leadership OPTIONS DESCRIPTION MDs in leadership; Strong PCPs Emerging PCP alignment; No PHO Little PCP connection Dominant market leader Market leaders, but competition Not market leader Dominant payers in risk contracting Payers with limited risk contracting experience Adversarial relationships Strong executive alignment Consensus-based leadership Divided leadership FULL RISK Percentage of premium for all services Certain services may be carved out (e.g., mental health, pharmacy) Owned and tightly contracted SNFs Loose affiliations with SNF,LTC,HC No management or ownership Care Continuum All on common platform Most on EMR, limited connectivity Limited EMR, no connectivity Health IT Strong balance sheet, growing revenue Strong balance sheet; flat revenue Weak balance sheet; shrinking revenue Financial Position Current experience in risk management Past experience in risk Little or no risk experience Expertise SHARED RISK Shared risk arrangement with payers based upon agreed upon budget Could be a percentage of premium or a set amount (e.g., 50 / 50 sharing) Premium is reset based on medical expenses Typically up and down-side risk Hospitals Business Line Specialists Primary Care Commercial Medicaid Medicare P4P Clinical Integration Bundled Payments Shared Savings Shared Risk Full Risk Health Plan More Likely CORRIDORS SHARED SAVINGS Upper and lower limits of risk sharing Beyond the corridor, the health plan takes the risk Can do a corridor with full risk or shared Budgeted dollars Upside only Premium is reset based on medical expenses 10

11 Evaluate Readiness Least Influence Greatest Influence Market Intrinsic Value Prop Market Competitive Org Capacity Physician Alignment Collaboration Culture Care Continuum Technology MSA Market Population Primary Care Value-based Competitors MD-Hospital Collaboration Hospital Private MD Relations PCP Specialty Relations Service Distribution EMR Population Density of MSA Specialist PCP Control Financial Position and Strength Economic Alignment System-ness VNA & SNF HIE Analytics MSA Payer Mix Hospital Market Share Differentiable Service Lines Claims-Based Performance Data Clinical Alignment Referral Management PCMH Portal Population Trends Payer MD Reimburseme nt Cross- Continuum Services Urgency for Change Forums Disease Mgt Pop. Health MSA Utilization Rates Payer Relations Executive Alignment P4P Experience Care Coordination Patient Registry Bandwidth Pharmacy Patient Attribution 11

Physician recruitment may be an issue Specialists less available Fewer commercially insured")

12 Rural Situation Generally more mission driven mentality and collaborative environment as patients & providers = friends and neighbors Fewer specialists, more mid-levels Less healthy patients 40 percent of rural adults are obese 44% of year olds smoke Fewer resources (providers and patients) Physician recruitment may be an issue Specialists less available Fewer commercially insured Physician compensation may be higher 12

13 Value-Based Care: Why and How in a Rural Setting Value-Based model increases incentive alignment and care coordination Clinically Integrated: Can begin contracting Clinically Integrated: Delivering results Progression to new models Greater coordination higher quality lower costs More health dials to turn (e.g. benefit design) more impact on patients Use market power and shared goals to drive participation Providers Payers Employers Clinical Integration as Foundation Establish Structure & Network Clinical Integration Program Delivery System Improvement Accountability: Financial Management Information Technology Population Management: ACO; Bundled Payments; Value-Based Care Regional CIN or micro ACO across systems CO-OP Full risk or ACO for specific population (e.g. duals, diabetics, etc.) Health Plan 13

14 Getting to a Provider-Sponsored Plan First question do you need to go all the way to the end of the spectrum Second question - Medicare Advantage, Medicaid, Commercial Third question market reaction and opportunity Fourth question who will perform which functions SERVICE System Partner Elig & Cap Mgmt?? Invoice Management Group/Broker?? UM Precert & Concurrent/DC?? Care Management?? Claims/Audit/ Recoup/Check?? In/Outbound Customer Service?? Data Integration Trading partners?? Financial Statement?? Analytics?? Provider Relations?? Pay for Performance Support?? 14

15 Provider-Sponsored Plan: Could be Evolutionary Provider- Sponsored Health Plan Full Risk Shared Risk without Corridors Increased risk and reward Complete behavior change Form Clinically Integrated Network Agreed upon care models Metrics Define total of care Beginnings of mid-shift Shared Risk with Corridors Limited upside and downside Increased behavior change 15

16 Starting with Employees Just a starting point Need to follow VERY quickly with bigger move 16

:w44-w57, January 2007.")

17 Advantages of Rural Settings Physician loyalty Market power relative to payors Employer relationships Culture Competitive picture (sometimes) Percent of Physicians Practicing at One Hospital Overall Rural Fisher, E. S., and others. Creating accountable care organizations: the extended hospital medical staff. Health Affairs. 26(1):w44-w57, January Source: Medscape Family Medicine Compensation Report

18 Clinically Integrated Network: QHS FEE FOR SERVICE P4P SHARED SAVINGS BUNDLED PAYMENTS SHARED RISK CAPITATION FULL RISK PROVIDER- SPONSORED PLAN Rural, Urban and Suburban participants 7 health systems 28 Hospitals Medical School of Wisconsin 4,000 physicians Clinical integration as prelude to valuebased care Care Management Direct employer contracting Employee-based health plan Client since

19 Provider-Sponsored Plan: Hamilton FEE FOR SERVICE P4P SHARED SAVINGS BUNDLED PAYMENTS SHARED RISK CAPITATION FULL RISK PROVIDER- SPONSORED PLAN Dominant payer in Dalton, GA, <150,000 people Commercial provider-sponsored health plan (Alliant) with 30,000 lives Operating since late 1990s Profitable for 10 of last 11 years Jointly owned by hospital and physicians Also support clinical integration with IPA Anchored by single hospital system Plan likely to expand to additional systems Client since

20 Provider-Sponsored Plan: Driscoll Children s FEE FOR SERVICE P4P SHARED SAVINGS BUNDLED PAYMENTS SHARED RISK CAPITATION FULL RISK PROVIDER- SPONSORED PLAN Medicaid health plan with more than 110,000 lives Dominant Plan in Service Area 70% Plan revenues now exceed hospital revenues Plan is the largest feeder to the hospital Ongoing quality improvement programs Largest Valence client by revenue Client since 2002 Initiative Cadena de Madres Program Maternal Fetal Medicine Specialist Healthy Smiles Results 8% reduction in Premature Birth 17% reduction in birth resulting in NICU stay 18% reduction in Dental OR cases Client since

21 Rural Challenges Scale and resources Cash reserves Human capital Technology Sufficient continuum of care facilities and providers to manage lives vs. specific episodes Access to existing programs due to size of populations (e.g. IL ACE Medicaid program requires 5,000 lives) Geography of patients may impact care management programs (e.g. transportation to care settings) Actuarial accuracy and risk adjustment with smaller patient populations Culture willingness to change 21

22 Questions? Phil Kamp CEO, Valence Health 22

31 Flavors of Risk: Effectively Making the Transition to Value- Based Care. November 2013

31 Flavors of Risk: Effectively Making the Transition to Value- Based Care November 2013 1 Objectives Understand the Bigger Picture Define the Flavors of Risk Understand Key Capabilities, Benefits, & Challenges

31 Flavors of Risk: Effectively Making the Transition to Value- Based Care November 2013 1 Objectives Understand the Bigger Picture Define the Flavors of Risk Understand Key Capabilities, Benefits, & Challenges

Provider-Sponsored Health Plans for ACOs

Provider-Sponsored Health Plans for ACOs Phil Kamp, CEO November 5, 2013 Change is Coming Or is Here in Some Cases Massive Shift in Payment Models Likelihood of Hospitals Gaining Payer Capabilities in

Provider-Sponsored Health Plans for ACOs Phil Kamp, CEO November 5, 2013 Change is Coming Or is Here in Some Cases Massive Shift in Payment Models Likelihood of Hospitals Gaining Payer Capabilities in

Is a Provider Sponsored Health Plan Right for You?

Is a Provider Sponsored Health Plan Right for You? Ten Steps to a Provider- Sponsored Health Plan March 20, 2014 Objectives Identify contributing factors leading to a shift in value based care Understand

Is a Provider Sponsored Health Plan Right for You? Ten Steps to a Provider- Sponsored Health Plan March 20, 2014 Objectives Identify contributing factors leading to a shift in value based care Understand

Gulf Coast and LA HFMA Payer Summit Value-based contracts same healthcare business?

Gulf Coast and LA HFMA Payer Summit Value-based contracts same healthcare business? Richard R. Vath, MD FMOLHS SVP/Chief Clinical Transformation Officer President Health Leaders Network and Medicare ACO

Gulf Coast and LA HFMA Payer Summit Value-based contracts same healthcare business? Richard R. Vath, MD FMOLHS SVP/Chief Clinical Transformation Officer President Health Leaders Network and Medicare ACO

Approved Models to Align Incentives between Hospitals and their Physicians

Approved Models to Align Incentives between Hospitals and their Physicians Agenda I. Alignment Model Overview II. Co-Management III. Clinically Integrated Networks CIN Definition & Overview Network Development

Approved Models to Align Incentives between Hospitals and their Physicians Agenda I. Alignment Model Overview II. Co-Management III. Clinically Integrated Networks CIN Definition & Overview Network Development

THE $10,000 QUESTION: TACKLING THE COMPLEXITIES OF VALUE-BASED PHYSICIAN COMPENSATION

THE $10,000 QUESTION: TACKLING THE COMPLEXITIES OF VALUE-BASED PHYSICIAN COMPENSATION HFMA First Illinois Chapter August 12, 2014 Stu Schaff Manager, DGA Partners Agenda > Background & Context > Measures

THE $10,000 QUESTION: TACKLING THE COMPLEXITIES OF VALUE-BASED PHYSICIAN COMPENSATION HFMA First Illinois Chapter August 12, 2014 Stu Schaff Manager, DGA Partners Agenda > Background & Context > Measures

10/17/2014 Risk-Based Payment Methodologies A National Perspective Art Jones, MD. AccountableCareInstitute.com

10/17/2014 Risk-Based Payment Methodologies A National Perspective Art Jones, MD FQHCs Bridge the Gap in Care Bridge Built and Maintained by FFS Dollars 2 CMMI View of FFS Medicine 3 Accountability High

10/17/2014 Risk-Based Payment Methodologies A National Perspective Art Jones, MD FQHCs Bridge the Gap in Care Bridge Built and Maintained by FFS Dollars 2 CMMI View of FFS Medicine 3 Accountability High

Using Analytics To Transform Your ACO

Using Analytics To Transform Your ACO How to Develop Effective Cost Reduction Strategies Presented July 2016 Agenda and Presenter External Forces and Market Response Critical Success Factors Analytics

Using Analytics To Transform Your ACO How to Develop Effective Cost Reduction Strategies Presented July 2016 Agenda and Presenter External Forces and Market Response Critical Success Factors Analytics

Session 115IF, Provider Risk-Sharing Arrangements in Medicaid. Presenters: Puneet Budhiraja, ASA, MAAA Michael Minor Sudha Shenoy, FSA, MAAA, CERA

Session 115IF, Provider Risk-Sharing Arrangements in Medicaid Presenters: Puneet Budhiraja, ASA, MAAA Michael Minor Sudha Shenoy, FSA, MAAA, CERA SOA Antitrust Disclaimer SOA Presentation Disclaimer 2018

Session 115IF, Provider Risk-Sharing Arrangements in Medicaid Presenters: Puneet Budhiraja, ASA, MAAA Michael Minor Sudha Shenoy, FSA, MAAA, CERA SOA Antitrust Disclaimer SOA Presentation Disclaimer 2018

How are the State, Managed Medicaid Organizations and Providers Preparing for Medicaid Value-Based Payments?

How are the State, Managed Medicaid Organizations and Providers Preparing for Medicaid Value-Based Payments? 1:10 PM 2:10 PM Steering Toward Success: Achieving Value in Whole Person Care September 25 and

How are the State, Managed Medicaid Organizations and Providers Preparing for Medicaid Value-Based Payments? 1:10 PM 2:10 PM Steering Toward Success: Achieving Value in Whole Person Care September 25 and

Provider-Sponsored Health Plans: The Ultimate Value-Based Healthcare Plan

Provider-Sponsored Health Plans: The Ultimate Value-Based Healthcare Plan Competition among healthcare providers and pressure to lower costs has never been higher. There also has been a tsunami of value-based

Provider-Sponsored Health Plans: The Ultimate Value-Based Healthcare Plan Competition among healthcare providers and pressure to lower costs has never been higher. There also has been a tsunami of value-based

Population-Based Healthcare: Structural Models and Options

Population-Based Healthcare: Structural Models and Options George Choriatis, Esq. Rivkin Radler LLP Presented at: Annual Fall Meeting New York State Bar Association Health Law Section Albany, New York

Population-Based Healthcare: Structural Models and Options George Choriatis, Esq. Rivkin Radler LLP Presented at: Annual Fall Meeting New York State Bar Association Health Law Section Albany, New York

11/16/2015. Valence Health Solutions To Support. Vision. 20 years of Serving ~100 Hospital & Health System Clients Nationally.

Valence Health Solutions To Support Prepared for First Illinois HFMA Optimize risk contracts Analyze and improve in-network utilization Improve quality November 2015 2015 Valence Health. All rights reserved.

Valence Health Solutions To Support Prepared for First Illinois HFMA Optimize risk contracts Analyze and improve in-network utilization Improve quality November 2015 2015 Valence Health. All rights reserved.

Value Based Payment 101

Value Based Payment 101 NewYork Presbyterian & NewYork-Presbyterian Queens PPS Network Education Primary Care Providers 02.13.2018 Outline Value Based Payment (VBP) 1. Introductions & Welcome 2. National

Value Based Payment 101 NewYork Presbyterian & NewYork-Presbyterian Queens PPS Network Education Primary Care Providers 02.13.2018 Outline Value Based Payment (VBP) 1. Introductions & Welcome 2. National

FUNDS FLOW METHODOLOGY FOR RISK-BASED CONTRACTS

CENTER FOR INDUSTRY TRANSFORMATION MAY 2015 FUNDS FLOW METHODOLOGY FOR RISK-BASED CONTRACTS Authors Amy Bibby Partner, DHG Healthcare amy.bibby@dhgllp.com Matthew Fadel Manager, DHG Healthcare matt.fadel@dhgllp.com

CENTER FOR INDUSTRY TRANSFORMATION MAY 2015 FUNDS FLOW METHODOLOGY FOR RISK-BASED CONTRACTS Authors Amy Bibby Partner, DHG Healthcare amy.bibby@dhgllp.com Matthew Fadel Manager, DHG Healthcare matt.fadel@dhgllp.com

Aetna s value based payment models aim to pay for value delivered, not services rendered

Aetna s value based payment models aim to pay for value delivered, not services rendered Aetna currently has 22% of spend running through contracts with a value based component. Value Based Contracting

Aetna s value based payment models aim to pay for value delivered, not services rendered Aetna currently has 22% of spend running through contracts with a value based component. Value Based Contracting

PATH TOWARD PAYMENTS THAT REWARD VALUE

PATH TOWARD PAYMENTS THAT REWARD VALUE David Muhlestein, PhD JD Chief Research Officer Leavitt Partners @DavidMuhlestein December 18, 2017 1 PRESENTATION OVERVIEW 1. Current Trends 2. Are ACOs Delivering

PATH TOWARD PAYMENTS THAT REWARD VALUE David Muhlestein, PhD JD Chief Research Officer Leavitt Partners @DavidMuhlestein December 18, 2017 1 PRESENTATION OVERVIEW 1. Current Trends 2. Are ACOs Delivering

Session 75 OF, Advantages & Challenges for Provider Led Health Plans. Moderator: LuCretia Leola Hydell, ASA, MAAA

Session 75 OF, Advantages & Challenges for Provider Led Health Plans Moderator: LuCretia Leola Hydell, ASA, MAAA Presenters: Jerry Clark, MD, FACP Josh Martin Mark Rishell SOA Antitrust Disclaimer SOA

Session 75 OF, Advantages & Challenges for Provider Led Health Plans Moderator: LuCretia Leola Hydell, ASA, MAAA Presenters: Jerry Clark, MD, FACP Josh Martin Mark Rishell SOA Antitrust Disclaimer SOA

Health Care Reform in the United States

Health Care Reform in the United States 4 Corners MGMA Conference April 2014 Karl Rebay, MBA, FHFMA Director, Health Care Consulting 1 The material appearing in this presentation is for informational purposes

Health Care Reform in the United States 4 Corners MGMA Conference April 2014 Karl Rebay, MBA, FHFMA Director, Health Care Consulting 1 The material appearing in this presentation is for informational purposes

Society of Professors of Child and Adolescent Psychiatry. Michael Jellinek, M.D. May 9, 2013

Society of Professors of Child and Adolescent Psychiatry Michael Jellinek, M.D. May 9, 2013 Health Care Reform: Drivers Extend Coverage (Social justice and efficiency) Cost (versus public acceptance, politics)

Society of Professors of Child and Adolescent Psychiatry Michael Jellinek, M.D. May 9, 2013 Health Care Reform: Drivers Extend Coverage (Social justice and efficiency) Cost (versus public acceptance, politics)

Clinically Integrated Networks and Population Health The next chapter in healthcare

Clinically Integrated Networks and Population Health The next chapter in healthcare M A T T H E W M A T U S I A K, D H S C, F R I P H ( UK) M T ( A S C P ) Health System Challenges While the Uninsured

Clinically Integrated Networks and Population Health The next chapter in healthcare M A T T H E W M A T U S I A K, D H S C, F R I P H ( UK) M T ( A S C P ) Health System Challenges While the Uninsured

Robert Resnik MD MBA

Robert Resnik MD MBA Movement from FFS to Value Based Value Based Spectrum P4P Clinical Integration Shared Savings Bundled Payments Shared Risk Capitation Global Full Risk Partial Risk ACO vs. Clinically

Robert Resnik MD MBA Movement from FFS to Value Based Value Based Spectrum P4P Clinical Integration Shared Savings Bundled Payments Shared Risk Capitation Global Full Risk Partial Risk ACO vs. Clinically

How Bundled Payments Create Value in New Product Designs Cognizant

How Bundled Payments Create Value in New Product Designs 1 About Cognizant 2 This Will Not Take Long. 3 What is a Health Insurance Product? 4 Understanding Product Design Commercial Insurance One specific

How Bundled Payments Create Value in New Product Designs 1 About Cognizant 2 This Will Not Take Long. 3 What is a Health Insurance Product? 4 Understanding Product Design Commercial Insurance One specific

An Introduction to Value Based Care. Evan Richards Product Leader Value Based Care Solutions May 2016

An Introduction to Value Based Care Evan Richards Product Leader Value Based Care Solutions May 2016 2016 General Electric Company All rights reserved. This does not constitute a representation or warranty

An Introduction to Value Based Care Evan Richards Product Leader Value Based Care Solutions May 2016 2016 General Electric Company All rights reserved. This does not constitute a representation or warranty

Lehigh Valley Health Network

Lehigh Valley Health Network Journey to Accountable Care November 19, 2014 Powered by Populytics Lehigh Valley Health Network Fast Facts In Allentown/Bethlehem area, north of Philadelphia Recognized by

Lehigh Valley Health Network Journey to Accountable Care November 19, 2014 Powered by Populytics Lehigh Valley Health Network Fast Facts In Allentown/Bethlehem area, north of Philadelphia Recognized by

Presentation to the IOM Committee on Core Metrics Tom Williams, Dr PH, President & CEO, IHA January 7, 2014, Irvine, California

Presentation to the IOM Committee on Core Metrics Tom Williams, Dr PH, President & CEO, IHA January 7, 2014, Irvine, California Organization: California multi-sector healthcare leadership group Mission:

Presentation to the IOM Committee on Core Metrics Tom Williams, Dr PH, President & CEO, IHA January 7, 2014, Irvine, California Organization: California multi-sector healthcare leadership group Mission:

CLINICALLY INTEGRATED REGIONAL CONSORTIA

CLINICALLY INTEGRATED REGIONAL CONSORTIA How Providers Are Coming Together in New Partnership Models and Implications for Payors Fall Managed Care Forum November 13, 2014 The Chartis Group, LLC The Proliferation

CLINICALLY INTEGRATED REGIONAL CONSORTIA How Providers Are Coming Together in New Partnership Models and Implications for Payors Fall Managed Care Forum November 13, 2014 The Chartis Group, LLC The Proliferation

The Emergence of Value-Based Care: Present and Future Tense

The Emergence of Value-Based Care: Present and Future Tense Erik Johnson, Vice President for Value-Based Care May 2016 What Is Value-Based Care? While the concept of value-based care has existed for years,

The Emergence of Value-Based Care: Present and Future Tense Erik Johnson, Vice President for Value-Based Care May 2016 What Is Value-Based Care? While the concept of value-based care has existed for years,

THE FAST AND THE FURIOUS REVENUE CYCLE (A.K.A.) THE REVENUE CYCLE OF THE FUTURE

THE REVENUE CYCLE OF THE FUTURE") THE FAST AND THE FURIOUS REVENUE CYCLE - 3.0 (A.K.A.) THE REVENUE CYCLE OF THE FUTURE INDUSTRY ANALYSIS 82% of people say price is the most important factor when making a healthcare purchasing decision*

THE FAST AND THE FURIOUS REVENUE CYCLE - 3.0 (A.K.A.) THE REVENUE CYCLE OF THE FUTURE INDUSTRY ANALYSIS 82% of people say price is the most important factor when making a healthcare purchasing decision*

Risky Business: Crystal Run Health Plans. Michelle A. Koury, MD Jonathan Nasser, MD Crystal Run Healthcare

Risky Business: Crystal Run Health Plans Michelle A. Koury, MD Jonathan Nasser, MD Crystal Run Healthcare About Crystal Run Healthcare Physician owned MSG in NY State, founded 1996 >350 providers, >30

Risky Business: Crystal Run Health Plans Michelle A. Koury, MD Jonathan Nasser, MD Crystal Run Healthcare About Crystal Run Healthcare Physician owned MSG in NY State, founded 1996 >350 providers, >30

New Opportunities, With ACA & QHI Support

New Opportunities, With ACA & QHI Support Philip Gaziano, MD April 5 th, 2012 ACA & QHI Introductions: QHI (an IT and Data company) Physician Owned and Run, and Founded in 2003 Owners and leaders Include:

New Opportunities, With ACA & QHI Support Philip Gaziano, MD April 5 th, 2012 ACA & QHI Introductions: QHI (an IT and Data company) Physician Owned and Run, and Founded in 2003 Owners and leaders Include:

The Case For Value ACA to MACRA to MIPS

The Case For Value ACA to MACRA to MIPS 2016-2019 Robert E Nesse M.D. Professor of Family Medicine Mayo Medical School Senior Director of Health Care Policy and Payment Reform nesse.robert@mayo.edu What

The Case For Value ACA to MACRA to MIPS 2016-2019 Robert E Nesse M.D. Professor of Family Medicine Mayo Medical School Senior Director of Health Care Policy and Payment Reform nesse.robert@mayo.edu What

Future Healthcare Payment Models An Overview

Future Healthcare Payment Models An Overview Carter Dredge THERE IS A CRITICAL NEED TO TRANSFORM HEALTHCARE DELIVERY & PAYMENT 2 Significant Variation in Population Utilization Spine Surgeries per 1,000

Future Healthcare Payment Models An Overview Carter Dredge THERE IS A CRITICAL NEED TO TRANSFORM HEALTHCARE DELIVERY & PAYMENT 2 Significant Variation in Population Utilization Spine Surgeries per 1,000

Embracing the Future of Care Delivery: What have we learned?

Embracing the Future of Care Delivery: What have we learned? Robert Nesse, M.D. Senior Advisor for Healthcare Policy and Payment Reform CEO, Mayo Clinic Health System 2010-2015 2014 MFMER slide-1 Fundamental

Embracing the Future of Care Delivery: What have we learned? Robert Nesse, M.D. Senior Advisor for Healthcare Policy and Payment Reform CEO, Mayo Clinic Health System 2010-2015 2014 MFMER slide-1 Fundamental

Q SPECIAL TOPIC REPORT: PROVIDER-OWNED HEALTH PLANS

THE ACADEMY LUMERIS STRATEGIC TRACKING SURVEY Q3 2018 SPECIAL TOPIC REPORT: PROVIDER-OWNED HEALTH PLANS SEPTEMBER 2018 PROVIDER-OWNED HEALTH PLANS INTRODUCTION As health systems increasingly participate

THE ACADEMY LUMERIS STRATEGIC TRACKING SURVEY Q3 2018 SPECIAL TOPIC REPORT: PROVIDER-OWNED HEALTH PLANS SEPTEMBER 2018 PROVIDER-OWNED HEALTH PLANS INTRODUCTION As health systems increasingly participate

9/23/2016. Our Services. Transitioning from Fee-for-Service to Value-based Reimbursement. Key Trends and Strategies for Rural Health Providers

Transitioning from Fee-for-Service to Value-based Reimbursement Key Trends and Strategies for Rural Health Providers Paul MacLellan, CEO >> Health care consulting company >> Wholly owned subsidiary of

Transitioning from Fee-for-Service to Value-based Reimbursement Key Trends and Strategies for Rural Health Providers Paul MacLellan, CEO >> Health care consulting company >> Wholly owned subsidiary of

partnering with payers? key lessons to keep in mind

REPRINT January 2014 Bill Eggbeer Kevin Sears Kenneth Homer healthcare financial management association hfma.org partnering with payers? key lessons to keep in mind As providers enter into risk-sharing

REPRINT January 2014 Bill Eggbeer Kevin Sears Kenneth Homer healthcare financial management association hfma.org partnering with payers? key lessons to keep in mind As providers enter into risk-sharing

Payment Reform in Support of Population Health Management

Payment Reform in Support of Population Health Management Aligning Forces for Quality Employers - Providers Summit October 25, 2011 Charles Chodroff, MD, MBA, FACP Senior Vice President, Chief Clinical

Payment Reform in Support of Population Health Management Aligning Forces for Quality Employers - Providers Summit October 25, 2011 Charles Chodroff, MD, MBA, FACP Senior Vice President, Chief Clinical

MANAGEMENT S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS FOR ASCENSION

MANAGEMENT S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS FOR ASCENSION As of and for the six months ended December 31, 2014 and 2013 The following information should be read

MANAGEMENT S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS FOR ASCENSION As of and for the six months ended December 31, 2014 and 2013 The following information should be read

developing a CIN for strategic value

REPRINT July 2014 Daniel Grauman John Harris Idette Elizondo Sean Looby healthcare financial management association hfma.org developing a CIN for strategic value Having a clinically integrated network

REPRINT July 2014 Daniel Grauman John Harris Idette Elizondo Sean Looby healthcare financial management association hfma.org developing a CIN for strategic value Having a clinically integrated network

COVERED CALIFORNIA: THE GOOD, THE BAD & THE UNDEFINED FOR CHILDREN WITH SPECIAL HEALTH CARE NEEDS

1 COVERED CALIFORNIA: THE GOOD, THE BAD & THE UNDEFINED FOR CHILDREN WITH SPECIAL HEALTH CARE NEEDS Ann-Louise Kuhns President & CEO California Children s Hospital Association Health Care Reform: The Basics

1 COVERED CALIFORNIA: THE GOOD, THE BAD & THE UNDEFINED FOR CHILDREN WITH SPECIAL HEALTH CARE NEEDS Ann-Louise Kuhns President & CEO California Children s Hospital Association Health Care Reform: The Basics

Risk Adjusted Episodes as Benchmarks for ACOs: A Society of Actuaries Sponsored Study

Risk Adjusted Episodes as Benchmarks for ACOs: A Society of Actuaries Sponsored Study Presented by Bill O Brien, FSA, MAAA Consulting Actuary Milliman Houston, TX (832) 878-4078 Preconference I Agenda

Risk Adjusted Episodes as Benchmarks for ACOs: A Society of Actuaries Sponsored Study Presented by Bill O Brien, FSA, MAAA Consulting Actuary Milliman Houston, TX (832) 878-4078 Preconference I Agenda

P r e p a r i n g f o r G l o b a l P a y m e n t : W h a t Yo u S h o u l d B e D o i n g N o w

P r e p a r i n g f o r G l o b a l P a y m e n t : W h a t Yo u S h o u l d B e D o i n g N o w Peter R. Epp, CPA Managing Director May 9, 2013 O V E R V I E W Commonwealth s Payment Reform Overview and

P r e p a r i n g f o r G l o b a l P a y m e n t : W h a t Yo u S h o u l d B e D o i n g N o w Peter R. Epp, CPA Managing Director May 9, 2013 O V E R V I E W Commonwealth s Payment Reform Overview and

The Health Management Academy Strategic Survey Q1 2019: Defining Risk. March 2019

The Health Management Academy Strategic Survey Q1 2019: Defining Risk March 2019 1 Defining Risk In 2019, the U.S. healthcare market is poised to continue its march towards value-based care. In the context

The Health Management Academy Strategic Survey Q1 2019: Defining Risk March 2019 1 Defining Risk In 2019, the U.S. healthcare market is poised to continue its march towards value-based care. In the context

The Road to Value. Aric R. Sharp, MHA, CMPE, FACHE Vice President Accountable Care UnityPoint Health February 3, 2017

The Road to Value Aric R. Sharp, MHA, CMPE, FACHE Vice President Accountable Care UnityPoint Health February 3, 2017 1,500 Physicians UnityPoint Clinic 17 hospitals + 15 rural network hospitals 35,000

The Road to Value Aric R. Sharp, MHA, CMPE, FACHE Vice President Accountable Care UnityPoint Health February 3, 2017 1,500 Physicians UnityPoint Clinic 17 hospitals + 15 rural network hospitals 35,000

A Practical Discussion of Value and Quality Based Payments What Do I Do Now?

Emerging Challenges in Primary Care: 2016 A Practical Discussion of Value and Quality Based Payments What Do I Do Now? Modified from AHLA Physicians and Hospitals Law Institute 2016 Faculty Ellie Bane

Emerging Challenges in Primary Care: 2016 A Practical Discussion of Value and Quality Based Payments What Do I Do Now? Modified from AHLA Physicians and Hospitals Law Institute 2016 Faculty Ellie Bane

Learning Community Integrated Health Care for Older Adults

Learning Community Integrated Health Care for Older Adults Aligning with New Payors for Integrated Services: Emerging provisions in contracting for integrated care services presented by: Adam J. Falcone,

Learning Community Integrated Health Care for Older Adults Aligning with New Payors for Integrated Services: Emerging provisions in contracting for integrated care services presented by: Adam J. Falcone,

Is There a Role for the Orthopaedic Surgeon in ACOs?

Is There a Role for the Orthopaedic Surgeon in ACOs? Michael R. Redler, MD Head Team Physician Sacred Heart University Visiting Assistant Clinical Professor University of Virginia Orthopaedic Consultant

Is There a Role for the Orthopaedic Surgeon in ACOs? Michael R. Redler, MD Head Team Physician Sacred Heart University Visiting Assistant Clinical Professor University of Virginia Orthopaedic Consultant

Evaluating the Fair Market Value of Pay for Performance

April 2014 healthcare financial management FEATURE STORY Jen Johnson Alexandra Higgins Evaluating the Fair Market Value of Pay for Performance 1 AT A GLANCE When assessing a pay-for-performance arrangement,

April 2014 healthcare financial management FEATURE STORY Jen Johnson Alexandra Higgins Evaluating the Fair Market Value of Pay for Performance 1 AT A GLANCE When assessing a pay-for-performance arrangement,

Transitioning Into a Successful Risk-Based ACO

Transitioning Into a Successful Risk-Based ACO Part 2: How to prepare for risk June 19, 2018 1pm EST PRESENTERS John Schmitt, Ph.D., FASHCRM Managing Director Reliance Consulting Group Chuck Newton Sr.

Transitioning Into a Successful Risk-Based ACO Part 2: How to prepare for risk June 19, 2018 1pm EST PRESENTERS John Schmitt, Ph.D., FASHCRM Managing Director Reliance Consulting Group Chuck Newton Sr.

Moving to Value with a Population Health Services Organization

Moving to Value with a Population Health Services Organization Lumeris Authors: Jeff Smith Senior Vice President Head of US Markets Jay Shah Senior Vice President Lumeris Advisory Services Page 2 AN INDUSTRY

Moving to Value with a Population Health Services Organization Lumeris Authors: Jeff Smith Senior Vice President Head of US Markets Jay Shah Senior Vice President Lumeris Advisory Services Page 2 AN INDUSTRY

Eight Indispensable Financial Considerations of Shifting from Volume to Value Reimbursement

Eight Indispensable Financial Considerations of Shifting from Volume to Value Reimbursement September 25-26, 2017 Max Reiboldt, CPA President CEO Learning Objectives This session will provide you with

Eight Indispensable Financial Considerations of Shifting from Volume to Value Reimbursement September 25-26, 2017 Max Reiboldt, CPA President CEO Learning Objectives This session will provide you with

Advancing Risk Capability in 2015: Medicare Shared Savings Program and ACO Investment Model. March 23, 2015 // 12:00 P.M. 1:00 P.M.

Advancing Risk Capability in 2015: Medicare Shared Savings Program and ACO Investment Model March 23, 2015 // 12:00 P.M. 1:00 P.M. EST CENTER FOR INDUSTRY TRANSFORMATION The DHG Healthcare Center for Industry

Advancing Risk Capability in 2015: Medicare Shared Savings Program and ACO Investment Model March 23, 2015 // 12:00 P.M. 1:00 P.M. EST CENTER FOR INDUSTRY TRANSFORMATION The DHG Healthcare Center for Industry

Minnesota Medical Association: Background and Opportunities. House Health & Human Services Finance Committee February 8, 2011

1 Minnesota Medical Association: Background and Opportunities House Health & Human Services Finance Committee February 8, 2011 2 Objectives Overview of the MMA Quick Facts about MN Physicians Shared Goals

1 Minnesota Medical Association: Background and Opportunities House Health & Human Services Finance Committee February 8, 2011 2 Objectives Overview of the MMA Quick Facts about MN Physicians Shared Goals

Best Practices Value-Based Bundled Programs

Best Practices Value-Based Bundled Programs From Strategy through Execution June 27, 2017 Value-based payments end-to-end impacts Strategy and governance Care delivery innovation and collaboration Unit

Best Practices Value-Based Bundled Programs From Strategy through Execution June 27, 2017 Value-based payments end-to-end impacts Strategy and governance Care delivery innovation and collaboration Unit

Healthcare Reform and Its Impact on the Care Delivery System

Healthcare Reform and Its Impact on the Care Delivery System Agenda 1) The Era of Healthcare Reform 2) Healthcare Reform and Post-Acute Care 3) Succeeding in the Reform Era: Managing the Continuum of Health

Healthcare Reform and Its Impact on the Care Delivery System Agenda 1) The Era of Healthcare Reform 2) Healthcare Reform and Post-Acute Care 3) Succeeding in the Reform Era: Managing the Continuum of Health

Preconference IV: Analysis of the Proposed ACO Regulations

Preconference IV: Analysis of the Proposed ACO Regulations Keith Wilson, M.D., F.A.C.O.G. Chairman of the Board California Association of Physician Groups Agenda Introduction & Welcome Need for Change

Preconference IV: Analysis of the Proposed ACO Regulations Keith Wilson, M.D., F.A.C.O.G. Chairman of the Board California Association of Physician Groups Agenda Introduction & Welcome Need for Change

Improving health care affordability Helping health plans bend the cost curve

Improving health care affordability Helping health plans bend the cost curve What s at stake? After years of escalating costs, US health care has become unaffordable for many. Industry stakeholders, including

Improving health care affordability Helping health plans bend the cost curve What s at stake? After years of escalating costs, US health care has become unaffordable for many. Industry stakeholders, including

Fee for Service: Paying for Volume, Not Value

Payment Reform 1 Fee for Service: Paying for Volume, Not Value Most healthcare services are reimbursed with a fee-for-service model. Pay regardless of quality, outcomes Pay for every test and procedure

Payment Reform 1 Fee for Service: Paying for Volume, Not Value Most healthcare services are reimbursed with a fee-for-service model. Pay regardless of quality, outcomes Pay for every test and procedure

evaluating the fair market value of pay for performance

REPRINT April 2014 Jen Johnson Alexandra Higgins healthcare financial management association hfma.org evaluating the fair market value of pay for performance A critical test for determining whether a pay-for-performance

REPRINT April 2014 Jen Johnson Alexandra Higgins healthcare financial management association hfma.org evaluating the fair market value of pay for performance A critical test for determining whether a pay-for-performance

Narrow, Tailored, Tiered and High Performance Networks: An Emerging Trend

Narrow, Tailored, Tiered and High Performance Networks: An Emerging Trend Bill Eggbeer, Managing Director, and Dudley Morris, Senior Advisor, BDC Advisors, LLC Executive Summary A recent BDC survey of

Narrow, Tailored, Tiered and High Performance Networks: An Emerging Trend Bill Eggbeer, Managing Director, and Dudley Morris, Senior Advisor, BDC Advisors, LLC Executive Summary A recent BDC survey of

Risk Contracting: What to Know About Stop Loss Insurance KATHRYN A BOWEN, EXECUTIVE VICE-PRESIDENT OCTOBER 27, 2016

Risk Contracting: What to Know About Stop Loss Insurance KATHRYN A BOWEN, EXECUTIVE VICE-PRESIDENT OCTOBER 27, 2016 Provider Stop Loss Insurance Premiums Program Structure Losses within Retention What

Risk Contracting: What to Know About Stop Loss Insurance KATHRYN A BOWEN, EXECUTIVE VICE-PRESIDENT OCTOBER 27, 2016 Provider Stop Loss Insurance Premiums Program Structure Losses within Retention What

10 Best Practices For Payer Contracting: A Roadmap for Successful Negotiations

10 Best Practices For Payer Contracting: A Roadmap for Successful Negotiations Steve Selbst Healthcents, Inc. Speaker Disclosures Steve Selbst is employed by a business firm that provides services related

10 Best Practices For Payer Contracting: A Roadmap for Successful Negotiations Steve Selbst Healthcents, Inc. Speaker Disclosures Steve Selbst is employed by a business firm that provides services related

10 Best Practices For Payer Contracting:

10 Best Practices For Payer Contracting: A Roadmap for Successful Negotiations Steve Selbst Healthcents, Inc. 2016 NHIA Annual Conference & Exposition 1 Speaker Disclosures Steve Selbst is employed by

10 Best Practices For Payer Contracting: A Roadmap for Successful Negotiations Steve Selbst Healthcents, Inc. 2016 NHIA Annual Conference & Exposition 1 Speaker Disclosures Steve Selbst is employed by

FMV Considerations for Bundled Payment Arrangements

FMV Considerations for Bundled Payment Arrangements Matthew J. Milliron, MBA HealthCare Appraisers, Inc. Becker s CEO + CFO Roundtable November 8, 2016 Today s Roadmap Healthcare Transactions Refresh Bundled

FMV Considerations for Bundled Payment Arrangements Matthew J. Milliron, MBA HealthCare Appraisers, Inc. Becker s CEO + CFO Roundtable November 8, 2016 Today s Roadmap Healthcare Transactions Refresh Bundled

MACRAnomics. Patient-Level Economics and Strategic Implications for Providers. Presented to: NW Ohio HFMA October 20, 2016

MACRAnomics Patient-Level Economics and Strategic Implications for Providers Presented to: NW Ohio HFMA October 20, 2016 Property of HealthScape Advisors Strictly Confidential 2 MACRAnomics: Objectives

MACRAnomics Patient-Level Economics and Strategic Implications for Providers Presented to: NW Ohio HFMA October 20, 2016 Property of HealthScape Advisors Strictly Confidential 2 MACRAnomics: Objectives

Predictive Analytics and Technology Session

Predictive Analytics and Technology Session Eric Widen, CEO HBI Solutions Population Health Colloquium March 28 th, 2017 HBI Solutions Session Agenda Introductions and Overview Eric Widen Session 1: Michael

Predictive Analytics and Technology Session Eric Widen, CEO HBI Solutions Population Health Colloquium March 28 th, 2017 HBI Solutions Session Agenda Introductions and Overview Eric Widen Session 1: Michael

Aligning health plans and providers: Working together to control costs

Aligning health plans and providers: Working together to control costs US health care costs continue to rise more rapidly than is sustainable. Health care spending was $3.2 trillion in 2015, a 5.3% increase

Aligning health plans and providers: Working together to control costs US health care costs continue to rise more rapidly than is sustainable. Health care spending was $3.2 trillion in 2015, a 5.3% increase

Market Access Strategy and Planning: Succeeding in the Age of Value-based Reimbursement

Market Access Strategy and Planning: Succeeding in the Age of -based Reimbursement Presented by: Michael J. Lacey, Senior Director, Strategic Consulting (Life Sciences) Date: March 01, 2017 Truven Health

Market Access Strategy and Planning: Succeeding in the Age of -based Reimbursement Presented by: Michael J. Lacey, Senior Director, Strategic Consulting (Life Sciences) Date: March 01, 2017 Truven Health

Figure 1: Original APM Framework

Contents Overview... 2 This Year s APM Measurement Effort... 3 Scope... 3 Data Source... 4 The LAN Survey... 4 The Blue Cross Blue Shield Association Survey... 8 The America s Health Insurance Plans Survey...

Contents Overview... 2 This Year s APM Measurement Effort... 3 Scope... 3 Data Source... 4 The LAN Survey... 4 The Blue Cross Blue Shield Association Survey... 8 The America s Health Insurance Plans Survey...

Lessons Learned from the Financial Front Lines of Population Health Management

Lessons Learned from the Financial Front Lines of Population Health Management Presenters Deborah Bloomfield, PhD, CPA Central Markets CFO for Catholic Health Partners and CFO for Mercy Health Charles

Lessons Learned from the Financial Front Lines of Population Health Management Presenters Deborah Bloomfield, PhD, CPA Central Markets CFO for Catholic Health Partners and CFO for Mercy Health Charles

What s Next for MSSP ACOs? The Case for Moving to Medicare Risk

What s Next for MSSP ACOs? The Case for Moving to Medicare Risk Picking Your Path on a Journey Towards Value-Based Care Participants in one of Medicare s boldest attempts to overhaul how doctors and physicians

What s Next for MSSP ACOs? The Case for Moving to Medicare Risk Picking Your Path on a Journey Towards Value-Based Care Participants in one of Medicare s boldest attempts to overhaul how doctors and physicians

Non-Profit Health Care Investor Conference. SSM Health Care May 22, 2014

Non-Profit Health Care Investor Conference SSM Health Care May 22, 2014 Disclaimer The statements made by representatives of SSM Health Care that are not historical facts are forward-looking statements.

Non-Profit Health Care Investor Conference SSM Health Care May 22, 2014 Disclaimer The statements made by representatives of SSM Health Care that are not historical facts are forward-looking statements.

Coverage Expansion [Sections 310, 323, 324, 341, 342, 343, 344, and 1701]

![Coverage Expansion [Sections 310, 323, 324, 341, 342, 343, 344, and 1701]](/thumbs/87/96500790.jpg "Coverage Expansion [Sections 310, 323, 324, 341, 342, 343, 344, and 1701]") Summary of the U.S. House of Representatives Health Reform Bill October 2009 The following summarizes the major hospital and health system provisions included in the U.S. House of Representatives health

Summary of the U.S. House of Representatives Health Reform Bill October 2009 The following summarizes the major hospital and health system provisions included in the U.S. House of Representatives health

PREPARING FOR THE NEXT GENERATION OF MANAGED CARE CONTRACTING

PREPARING FOR THE NEXT GENERATION OF MANAGED CARE CONTRACTING Nanci Robertson, RN BSN President - Robertson Consulting, Inc. Doral Jacobsen, MBA FACMPE CEO - Prosper Beyond, Inc. DORAL JACOBSEN AND NANCI

PREPARING FOR THE NEXT GENERATION OF MANAGED CARE CONTRACTING Nanci Robertson, RN BSN President - Robertson Consulting, Inc. Doral Jacobsen, MBA FACMPE CEO - Prosper Beyond, Inc. DORAL JACOBSEN AND NANCI

EXECUTIVE SUMMARY ENROLLMENT GROWS YET MARGINS DROP FOR OHIO S HEALTH INSURING CORPORATIONS. 970,000 Ohioans remained uninsured in 2014.

OHA exists to collaborate with member hospitals and health systems to ensure a healthy Ohio. February 2016 EXECUTIVE SUMMARY ENROLLMENT GROWS YET MARGINS DROP FOR OHIO S HEALTH INSURING CORPORATIONS In

OHA exists to collaborate with member hospitals and health systems to ensure a healthy Ohio. February 2016 EXECUTIVE SUMMARY ENROLLMENT GROWS YET MARGINS DROP FOR OHIO S HEALTH INSURING CORPORATIONS In

DHCFP. Provider Payment: Trends and Methods in the Massachusetts Health Care System

DHCFP Provider Payment: Trends and Methods in the Massachusetts Health Care System Prepared by Allison Barrett and Timothy Lake, Mathematica Policy Research, Inc. February 2010 Deval L. Patrick, Governor

DHCFP Provider Payment: Trends and Methods in the Massachusetts Health Care System Prepared by Allison Barrett and Timothy Lake, Mathematica Policy Research, Inc. February 2010 Deval L. Patrick, Governor

Sutter Medical Network

Sutter Medical Network Sutter Care Pattern Analyzer making the case for affordability Fifth National Pay for Performance Summit March 9, 2010 Michael van Duren, M.D., CMO Sutter Physician Services Colleen

Sutter Medical Network Sutter Care Pattern Analyzer making the case for affordability Fifth National Pay for Performance Summit March 9, 2010 Michael van Duren, M.D., CMO Sutter Physician Services Colleen

State of Georgia Department of Community Health

State of Georgia Department of Community Health Medicaid and PeachCare for Kids Design Strategy Report EXECUTIVE SUMMARY January 23, 2012 Recognizing that this is a critical time for Georgia to carefully

State of Georgia Department of Community Health Medicaid and PeachCare for Kids Design Strategy Report EXECUTIVE SUMMARY January 23, 2012 Recognizing that this is a critical time for Georgia to carefully

Charity Care and Your Organization: Compliance Considerations that Shed Light on the Topic

Charity Care and Your Organization: Compliance Considerations that Shed Light on the Topic HCCA Audio Conference February 15, 2006 David Orbuch, EVP Corporate Responsibility and Community Relations Nancy

Charity Care and Your Organization: Compliance Considerations that Shed Light on the Topic HCCA Audio Conference February 15, 2006 David Orbuch, EVP Corporate Responsibility and Community Relations Nancy

Presentation by Kevin Stone Senior Consultant and Principal Helms & Company Concord NH

Presentation by Kevin Stone Senior Consultant and Principal Helms & Company Concord NH Medicaid is Largest Payer- covers 1/3 of entire population Vt. funded Medicaid Expansion program pre- ACA (VHAP; Catamount)

Presentation by Kevin Stone Senior Consultant and Principal Helms & Company Concord NH Medicaid is Largest Payer- covers 1/3 of entire population Vt. funded Medicaid Expansion program pre- ACA (VHAP; Catamount)

CPI Antitrust Chronicle July 2012 (1)

") CPI Antitrust Chronicle July 2012 (1) Health Care Reform, Provider Affiliations, and Antitrust Risks Lona Fowdur & John M. Gale Economists Incorporated www.competitionpolicyinternational.com Competition

CPI Antitrust Chronicle July 2012 (1) Health Care Reform, Provider Affiliations, and Antitrust Risks Lona Fowdur & John M. Gale Economists Incorporated www.competitionpolicyinternational.com Competition

C - Suite Transformation Management Training: Finance and Operations Overview. May 17, 2017

C - Suite Transformation Management Training: Finance and Operations Overview Presented by: Peter R. Epp, CPA May 17, 2017 Overview Summary of Value Based Payment (VBP) Initiatives Underlying VBP Payment

C - Suite Transformation Management Training: Finance and Operations Overview Presented by: Peter R. Epp, CPA May 17, 2017 Overview Summary of Value Based Payment (VBP) Initiatives Underlying VBP Payment

Assessing ACO Performance

Assessing ACO Performance David V. Axene, FSA, FCA, CERA, MAAA As more health plans utilize Accountable Care Organizations (i.e., ACOs) as part of their network operations, ACO performance assessment is

Assessing ACO Performance David V. Axene, FSA, FCA, CERA, MAAA As more health plans utilize Accountable Care Organizations (i.e., ACOs) as part of their network operations, ACO performance assessment is

Impact of ACOs on Care Coordination

Impact of ACOs on Care Coordination Presented by: Michelle L. Templin Vice President Legislative Affairs and Business Development MHA ACO Network March 2, 2017 Agenda Agenda Key Regulatory Drivers Accountable

Impact of ACOs on Care Coordination Presented by: Michelle L. Templin Vice President Legislative Affairs and Business Development MHA ACO Network March 2, 2017 Agenda Agenda Key Regulatory Drivers Accountable

Configuration of Network and Financial Management Systems to Support Multiple Value Based Reimbursement Models

Configuration of Network and Financial Management Systems to Support Multiple Value Based Reimbursement Models Kristina Rollings Product Director, Emerging Solutions March 24, 2014 Agenda 1. State of the

Configuration of Network and Financial Management Systems to Support Multiple Value Based Reimbursement Models Kristina Rollings Product Director, Emerging Solutions March 24, 2014 Agenda 1. State of the

MGMA BUSINESS PLAN COMPETITION. Team 2

MGMA BUSINESS PLAN COMPETITION Team 2 IDS HOSPITAL, LAREDO, TX (Team 2) Executive Summary Integrated Delivery Systems (IDS) is a 200 bed, medium-sized comprehensive service provider hospital in Laredo,

MGMA BUSINESS PLAN COMPETITION Team 2 IDS HOSPITAL, LAREDO, TX (Team 2) Executive Summary Integrated Delivery Systems (IDS) is a 200 bed, medium-sized comprehensive service provider hospital in Laredo,

Health Plan Design Options August 23, 2012

Health Plan Design Options August 23, 2012 Leslie Schneider Bill Danish 2012/2013 Employer Focus Managing costs while maintaining a benefits package that Supports organizational attraction and retention

Health Plan Design Options August 23, 2012 Leslie Schneider Bill Danish 2012/2013 Employer Focus Managing costs while maintaining a benefits package that Supports organizational attraction and retention

Health Action Council. Community Health Data: Improving Employer Investment in Overall Employee Health

Health Action Council Health Data: Improving Employer Investment in Overall Employee Health Health Data: Improving Employer Investment in Overall Employee Health. UnitedHealthcare White Paper Employers

Health Action Council Health Data: Improving Employer Investment in Overall Employee Health Health Data: Improving Employer Investment in Overall Employee Health. UnitedHealthcare White Paper Employers

Growth and Success of Accountable Care Organizations (ACOs) in the US from Dennis Horrigan June 2016

in the US from Dennis Horrigan June 2016") Growth and Success of Accountable Care Organizations (ACOs) in the US from 2010-2016 Dennis Horrigan June 2016 Introducing Dennis Horrigan Dennis R. Horrigan President and Chief Executive Officer Catholic

Growth and Success of Accountable Care Organizations (ACOs) in the US from 2010-2016 Dennis Horrigan June 2016 Introducing Dennis Horrigan Dennis R. Horrigan President and Chief Executive Officer Catholic

Point of View: Medicare Profitability in a Reform Market

Point of View: Profitability in a Reform Market Bill Eggbeer, Managing Director, & Krista Bowers, Director, BDC Advisors, LLC Introduction Overall, accounts for approximately 20% of the total domestic

Point of View: Profitability in a Reform Market Bill Eggbeer, Managing Director, & Krista Bowers, Director, BDC Advisors, LLC Introduction Overall, accounts for approximately 20% of the total domestic

THE FUTURE OF HEALTHCARE: TRENDS THAT WILL AFFECT YOUR PROFESSIONAL AND PERSONAL LIFE

THE FUTURE OF HEALTHCARE: TRENDS THAT WILL AFFECT YOUR PROFESSIONAL AND PERSONAL LIFE Dr. Keith Hornberger, BSRT, MBA, DHA, FACHE 1 The Future Direction of Healthcare Healthcare Reform will catalyze a

THE FUTURE OF HEALTHCARE: TRENDS THAT WILL AFFECT YOUR PROFESSIONAL AND PERSONAL LIFE Dr. Keith Hornberger, BSRT, MBA, DHA, FACHE 1 The Future Direction of Healthcare Healthcare Reform will catalyze a

Health Care in Maine: An Overview

Legislative Policy Forum on Health Care February 4 th, 2011 Health Care in Maine: An Overview Wendy J. Wolf, MD, MPH President & CEO Maine Health Access Foundation www.mehaf.org Health Forum Sponsor: The

Legislative Policy Forum on Health Care February 4 th, 2011 Health Care in Maine: An Overview Wendy J. Wolf, MD, MPH President & CEO Maine Health Access Foundation www.mehaf.org Health Forum Sponsor: The

Journey To Value: The State of Value-Based Reimbursement

White Paper Journey To Value: The State of Value-Based Reimbursement Second in a series of national research studies on healthcare s transition from volume to value, conducted by ORC International and

White Paper Journey To Value: The State of Value-Based Reimbursement Second in a series of national research studies on healthcare s transition from volume to value, conducted by ORC International and

Healthcare Financial Management Association Certification Program. Module I: The Business of Health Care Learner s Guide

Healthcare Financial Management Association Certification Program Module I: The Business of Health Care Learner s Guide For examination period beginning June 2015 1 Course 1 - The Big Picture Learning

Healthcare Financial Management Association Certification Program Module I: The Business of Health Care Learner s Guide For examination period beginning June 2015 1 Course 1 - The Big Picture Learning

37 th Annual J.P. Morgan Healthcare Conference January 9, 2019

37 th Annual J.P. Morgan Healthcare Conference January 9, 2019 1 Disclaimer Statement This presentation contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933,

37 th Annual J.P. Morgan Healthcare Conference January 9, 2019 1 Disclaimer Statement This presentation contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933,

A Path to Accountable Care Organizations: How Do We Get From There to Here? Financial Considerations for Accountable

A Path to Accountable Care Organizations: How Do We Get From There to Here? Financial Considerations for Accountable Care Entity Engagement Presented by Milliman, Inc. San Francisco, CA susan.pantely@milliman.com

A Path to Accountable Care Organizations: How Do We Get From There to Here? Financial Considerations for Accountable Care Entity Engagement Presented by Milliman, Inc. San Francisco, CA susan.pantely@milliman.com

Integrated Health Partnerships Demonstration

INFORMATION BRIEF Research Department Minnesota House of Representatives 600 State Office Building St. Paul, MN 55155 Randall Chun, Legislative Analyst 651-296-8639 December 2017 Integrated Health Partnerships

INFORMATION BRIEF Research Department Minnesota House of Representatives 600 State Office Building St. Paul, MN 55155 Randall Chun, Legislative Analyst 651-296-8639 December 2017 Integrated Health Partnerships

Succeeding with APMs: Structuring Relationships Between Payers and Providers

Succeeding with APMs: Structuring Relationships Between Payers and Providers OCTOBER 30, 2017 Crystal Gateway Marriott Hotel Arlington, VA Enhance your Summit experience with Log in at: glsr.it/lansummit

Succeeding with APMs: Structuring Relationships Between Payers and Providers OCTOBER 30, 2017 Crystal Gateway Marriott Hotel Arlington, VA Enhance your Summit experience with Log in at: glsr.it/lansummit

How ACO s Can Impact Contracting A Real World Example. Mike Medel Pharm D, MBA Banner Health

How ACO s Can Impact Contracting A Real World Example Mike Medel Pharm D, MBA Banner Health Agenda Banner Pharmacy Services Introduction Accountable Care Organization Summary Basic Constructs of ACO Partnership

How ACO s Can Impact Contracting A Real World Example Mike Medel Pharm D, MBA Banner Health Agenda Banner Pharmacy Services Introduction Accountable Care Organization Summary Basic Constructs of ACO Partnership