HENDERSON GROUP HOLDINGS ASSET MANAGEMENT LIMITED Pillar 3 Disclosures As at 31 December 2017

|

|

|

- Antonia Constance Booth

- 5 years ago

- Views:

Transcription

1 HENDERSON GROUP HOLDINGS ASSET MANAGEMENT LIMITED Pillar 3 Disclosures As at 31 December 2017 Page 1 of 18

2 1. Introduction Henderson Group Holdings Assets Management Limited ( HGHAML ) is subject to prudential oversight by the various regulators of the countries in which it operates. Its primary regulator is the Financial Conduct Authority ( FCA ) in the UK. The FCA is responsible for implementing and enforcing the European Union Capital Requirements Directive ( CRD ), a capital adequacy framework consisting of three pillars : Pillar 1 sets minimum capital requirements that firms must meet for credit, market and operational risk. These comprise: base capital resources requirements; credit risk and market risk capital requirements; and the fixed overhead requirement. Pillar 2 requires that firms undertake an overall assessment of their capital adequacy, taking into account all risks to which the firm is exposed and whether additional capital should be held to cover risks not adequately covered by Pillar 1 requirements. Pillar 3 complements Pillars 1 and 2 and improves market discipline by requiring firms to disclose information on their capital resources and requirements, risk exposures and their risk management framework. This document satisfies the Pillar 3 disclosure requirements as at 31 December HGHAML benefits from the FCA Capital Requirements Regulation derogation allowing it to carry forward the CRD III rules as at 31 December 2013 and the following disclosures are in accordance with the requirements of Chapter 11 of the Prudential Sourcebook for Banks, Building Societies and Investment Firms ( BIPRU ). 1.1 Janus Henderson Structure and the UK Group The ultimate parent company is Janus Henderson Group plc ( JHG ), a company incorporated in Jersey. JHG was formerly known as Henderson Group plc and changed its name following the merger of Henderson Group plc with Janus Capital Group, Inc. on 30 May HGHAML is an immediate subsidiary of JHG and is the parent financial holding company that heads the European Economic Area sub-group supervised by the FCA for prudential purposes. HGHAML is not required to prepare consolidated statutory financial statements. It does, however, prepare special purpose consolidated financial statements for regulatory purposes. At 31 December 2017 HGHAML had six legal subsidiaries registered with and regulated by the FCA. The regulatory consolidation for prudential purposes also includes Janus Capital International Limited as a result of the application of Article 134 of the Banking Consolidation Directive. The solo regulated firms are as follows: BIPRU Limited Licence Investment Firms ( LLIFs ); Henderson Global Investors Limited ( HGIL ); Gartmore Investment Limited ( GIL ) Henderson Investment Management Limited ( HIML ) (deregistered April 2018); AlphaGen Capital Limited ( ACL ); and Janus Capital International Limited ( JCIL ). Regulated firms not subject to CRD: Henderson Equity Partners Limited ( HEPL ); Henderson Investment Funds Limited ( HIFL ). Page 2 of 18

3 The Pillar 3 disclosures are applicable to the HGHAML s LLIFs. HIFL is an Alternative Investment Fund Manager ( AIFM ) and HEPL is supervised under IPRU (INV). Neither is subject to CRD and nor is Henderson Management SA ( HMSA ), a firm regulated in Luxembourg. A simplified group structure chart showing the position at 31 December 2017 is shown on the following page. Page 3 of 18

4 Page 4 of 18

5 1.2 Scope of Application The Pillar 3 disclosures set out in this document are made in accordance with the requirements contained within BIPRU Chapter 11. Specifically, it covers risk management objectives and policies; the processes for managing material risks; the structure and organisation of the risk management functions within the Group; the scope and nature of risk reporting and measurement systems; and the policies for mitigating risk. The risk management and control framework described in this document is at the HGHAML level. JHG operates a Group-wide risk management framework and the HGHAML framework is part of and is consistent with the JHG global framework. 1.3 Frequency of Disclosures These disclosures, which are approved by the HGHAML Board, are required to be made at least annually and, if appropriate, some disclosures will be made more frequently as a result of material updates to the firm s internal capital adequacy assessment. JHG and HGHAML have a financial year end reporting date of 31 December and disclosures are made as at 31 December as soon as is practicable after publication of the Annual Report and Accounts. Disclosures will be made at other dates if appropriate. 1.4 Verification, Media and Location These disclosures explain the basis of preparation of certain capital requirements and provide information about the management of specific risks. They do not constitute, in any form, audited financial statements and have been produced solely for the purposes of Pillar 3. They should not be relied on in making any investment decisions in relation to JHG (or any of the funds managed by JHG or any of its subsidiaries).these disclosures are published on the JHG Group s website ( within the Corporate Governance section on internal controls. 1.5 Governance Arrangements Details of JHG s approach to corporate governance and board of directors are contained within Item 10 of the 2017 Annual Report and Accounts on pages 125 to 135. The HGHAML Board is comprised of four directors, two of whom are Executive Directors (Richard Weil and Roger Thompson) and two of whom are Non-Executive Directors (Sarah Arkle and Angela Seymour-Jackson). Angela Seymour-Jackson is the Chair of the Board. All the directors of HGHAML other than Roger Thompson are also directors of JHG. The HGHAML Board is responsible for ensuring that the JHG strategy, risk appetite and key policies are suitable for the HGHAML Group and for adjusting how they are applied to the HGHAML Group should this be necessary. They are also responsible for overseeing the performance of the HGHAML Group against the approved strategy and risk appetite, overseeing its control framework and ensuring it remains aligned to the strategy and risk appetite (including in respect of capital and liquidity adequacy), overseeing its control framework and ensuring it remains aligned to the strategy and risk appetite, overseeing and approving key HGHAML regulatory interaction and approving key remuneration decisions in terms of policy and application where relevant to HGHAML. The HGHAML Board relies on the JHG Board Audit and Risk Committees for the safeguarding of the independence of and oversight of the Internal Audit, Risk and Compliance functions and has delegated executive management of the HGHAML Group to the Chief Executive Officer (Richard Weil). 2. Risk and Control Framework 2.1 Risk Management The HGHAML Board considers risk assessment and the existence of effective controls to be fundamental to achieving its corporate objectives within an acceptable risk and reward profile. The JHG Board Risk Committee has approved an Enterprise Risk Management Framework ( ERMF ) and the HGHAML Board has adopted this ERMF. The purpose of the ERMF is to ensure that risks arising Page 5 of 18

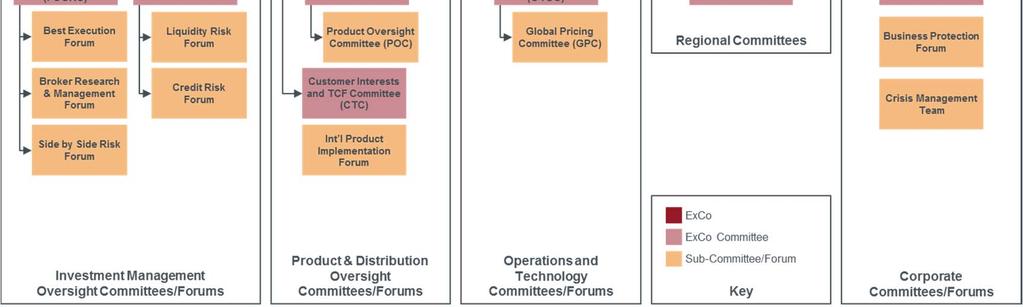

6 from the Group s business are properly identified, evaluated, managed, monitored and reported on in line with the Risk Appetite. The key components of the ERMF are: Roles and Responsibilities clear assignment of accountabilities and responsibilities for different aspects of risk management (see discussion of three lines of defence below) and delegated authorities; Risk strategy a structured approach to the identification, assessment and management of risk; Risk culture the desired behaviours that characterise and reflect the Group s core values and attitudes towards risk; Risk appetite the level of risk the Board is willing to accept in relation to each of the key risks the Group is exposed to (see discussion below); Risk governance framework; Risk policies and risk limits; Risk identification processes (including emerging risks); Risk measurement and monitoring processes and supporting tools and models; Risk management in accordance with risk appetite (including internal controls, management of any identified risk issues and processes for managing risk events) ; and Risk reporting to business and functional management, internal committees, boards and regulators. The HGHAML Group s framework utilises a three lines of defence approach to managing risk. The first line comprises the Chief Executive Officer and business management. Risk management is seen as an integral part of overall business processes and a robust framework of identification, evaluation, management and monitoring of risk exists. Each risk category in the risk appetite statement is assigned to a risk owner who is either a member of the Executive Committee ( ExCo ) or a senior manager who reports to an ExCo member. The risk owner is responsible for understanding the risk and for ensuring that the risk is appropriately and effectively managed in line with the Group s risk appetite. There are also a number of management committees chaired by risk owners consisting of senior managers in the first and second line functions and which provide a forum to assist the risk owner in managing and resolving risk issues. The high level features of the governance arrangements are illustrated in the chart on the following page. Page 6 of 18

7 Page 7 of 18

8 The second line comprises the independent Risk function and Compliance. Since February 2018 the second line Risk function has included an Enterprise Risk function, which is formed of three teams (Enterprise Risk Strategy, Enterprise Risk Business Partners and Business Continuity) who support the business in the delivery and embedding of a robust risk management framework, governance structure and control environment across the JHG Group. The Risk function also includes a first line Portfolio Risk and Analytics team who report to the Chief Investment Officer and a second line Investment Risk team who report to the Chief Risk Officer. The Portfolio Risk and Analytics team work with the portfolio managers to ensure that the risk characteristics, risk concentrations and stress scenarios for the portfolios for which they are responsible are fully understood. This first line team also own the primary risk models and risk dashboards and lead the engagement with the portfolio managers. The second line Investment Risk team is responsible for monitoring whether the risk exposures of funds and mandates are in line with what clients should expect. The third line of defence is provided by Internal Audit, which operates and reports independently of management to the JHG Audit Committee and is responsible for assessing the control design and overall effectiveness of controls and, where necessary, making recommendations for improvements and monitoring management action plans to implement such improvements. The reporting lines of the second line Risk, Compliance and Internal Audit functions are independent of line management, with the Chief Risk Officer reporting to the non-executive Chair of the JHG Board Risk Committee and the Global Head of Internal Audit reporting to the non-executive Chair of the JHG Board Audit Committee. The respective responsibilities of each of the three lines of defence are illustrated in the chart below. The Risk, Compliance and Internal Audit functions provide regular reports to each meeting of the JHG Risk Committee, the JHG Audit Committee and HGHAML Board. The regular reporting from Risk covers all risks included in the risk taxonomy and the JHG Risk Committee undertakes a deep dive into all risk categories on a cyclical basis. The deep dive papers are prepared by the first line risk owners in conjunction with Risk and presented by a combination of first and second line teams. The HGHAML Board considers the scope of the reporting framework gives it sufficient information upon which to assess the effectiveness of the HGHAML Group s system of internal controls and to assess the actual and potential risks facing the HGHAML Group. Page 8 of 18

9 The ASX Corporate Governance Principles apply to Janus Henderson Group plc as a result of its listing on the Australian Securities Exchange. They include the Principle that Companies should establish a sound risk management framework and periodically review the effectiveness of that framework. The associated ASX commentary states that it is the role of management to design and implement the risk management framework and to ensure that the entity operates within the risk appetite set by the JHG Board. It is the role of the JHG Board to set the risk appetite for the entity, to oversee its risk management and to satisfy itself that the framework is sound. The JHG Board is satisfied that JHG s global framework continues to be sound. This framework is applied consistently to the HGHAML Group. 2.2 Oversight of Internal Controls The JHG Board has overall responsibility for the global Group s system of internal controls. The system of internal controls is designed to manage, rather than eliminate, the risk of failure to achieve business objectives and can provide only reasonable, and not absolute, assurance against material loss. As part of the Risk and Control Self-Assessment process, line managers responsible for operating key processes assess the effectiveness and adequacy of controls operated to determine the level of residual risk which is then compared with risk tolerance. For any risks assessed as being outside of risk tolerance an issue and action plan are determined. If any such risk cannot be mitigated to within risk tolerance a risk acceptance is formally agreed by the Enterprise Risk function and approved by ExCo. The combination of the Risk Events, Issues and Actions report and Risk Dashboard reporting, which are submitted by the Chief Risk Officer to the JHG Board Risk Committee and HGHAML Board, provide effective reporting of both historical incidents and forward-looking assessments. The Risk Dashboard reports include a detailed metric driven assessment of the trends in key risk indicators against the risk limits outlined in the Risk Appetite Statement, and provide details of any risks which are outside of appetite and their associated management actions. These reports also highlight any material emerging risks. Additional assurance on the design and effectiveness of internal controls is provided by the Internal Audit function and the independent testing that they carry out during each year. Internal Audit provide quarterly reports to the JHG Audit Committee and HGHAML Board on key findings from their audits and on the status of management actions to address any weaknesses found as part of this testing. 2.3 Risk Appetite Statement (RAS) In pursuing its strategy, Janus Henderson Group has to accept, tolerate or be exposed to a certain level of risk. It is also necessary, however, for the Group to ensure that the amount of risk taken is within acceptable boundaries and that these are commensurate with its financial strength and consistent with its corporate strategy. Good risk management does not imply avoiding all risks at any cost; rather it implies making informed and coherent choices regarding the risks the Group wants to take in pursuit of its strategy and objectives. The Risk Appetite Statement (RAS) approved by the JHG Board sets out how much risk is acceptable to JHG in pursuing its strategy and objectives. The risk appetite framework comprises: Risk Taxonomy a clearly defined list of the key risks that the Group faces given its business model; Overarching Risk Appetite statements that describe qualitatively (on a scale from very low to high) how much risk JHG seeks to pursue; and Risk triggers and limits quantitative and qualitative boundaries that either trigger further management action when reached or constrain specific risk-taking activities, e.g. a limit on the permissible amount of seed investments. The HGHAML Board has approved its own risk appetite statement consistent with the JHG risk appetite and receives reports at each board meeting comparing HGHAML s risk exposures with its risk appetite. This report also highlights action plans for any risks that are outside appetite. Page 9 of 18

10 The JHG Board empowers management of the global Group to take on risk actively in order to achieve the JHG Group s objectives, but within the risk boundaries outlined in the RAS. Risks taken must be well understood and adequately measured to ensure that the risk exposure is appropriate for the returns anticipated both for each individual risk and, when aggregated, with all the other risks to which the global Group is exposed. Furthermore, the risks taken must be consistent with the JHG Group s obligations to stakeholders. The objective is to safeguard the JHG Group s and clients assets, and comply with client mandates and the terms of the funds prospectuses, whilst allowing sufficient operational freedom to seek a satisfactory return. In response to a risk, management is empowered to deal with the exposure in the most effective manner. One, or combinations, of the following responses are permitted: Transfer reduce the impact of the risk through various means of risk transfer such as insurance purchase, hedging or effective structuring of contracts Avoid some risks may be entirely avoided or eliminated through sale or divestment Mitigate address the causes of the risk and apply controls or other mitigating actions to reduce the impact and/or likelihood Accept accept the risk in knowledge of its nature and potential quantum, with communication to the relevant governing body as appropriate. Page 10 of 18

11 3. Risk Exposure Overview The HGHAML Group is exposed to a range of risks, which are categorised internally using an agreed risk taxonomy. The table below shows this taxonomy and how the internal taxonomy maps to the regulatory categories that are used for regulatory capital purposes and are the basis on which risks are represented in this Pillar 3 document. Regulatory Risk Categorisation HGHAML Risk Taxonomy Contractual Obligations (including breach of client mandates) Fiduciary/Conduct/TCF Compliance with Laws and Regulations (including mis-selling) Employment Practices External Reporting Disclosure Risk (inc. Corporate, Fund and Financial) Operational Risk Operational or administrative failure (including trading errors) Business Resiliency--Failure to safeguard and maintain operations Cyber Security / Data Breach Failure of/by a third party service provider Fraud and Unauthorized Activities Workplace safety Damage to physical assets Credit Risk Market Risk Liquidity Risk Interest Rate Risk Pension Obligation Risk Market (Seed Capital) Corporate Credit/Counterparty Foreign Currency Corporate Liquidity Interest Rate Pension Obligation Risk Strategy failure due to external Market Dynamics Failure to deliver strategy due to poor decision / execution Acquisition failure due to external factors Acquisition failure to deliver due to poor execution Client Concentration Business Risk Product / Market / Geography Concentration Regulatory Change Tax Change Political Change Concentration / Key Person Risk Attracting, Retaining and Developing Top Talent Market (AUM) Group Risk Group Risk Page 11 of 18

12 3.1 Operational Risk Operational risk is the risk that the HGHAML Group could sustain losses through inadequate or failed internal processes, people, systems and external events. Operational risk losses include the direct financial consequences of failures in operational processes and any compensation paid to clients, legal claim settlements and regulatory fines. In addition, significant operational failures could damage the reputation of companies in the HGHAML Group, resulting in lower sales to and higher redemptions by clients. This would result in lower fee income; these indirect financial impacts are considered part of business risk. The Group mitigates operational risks through design and implementation of strong processes and effective internal controls. Operational risk is inherent in the business and these internal control systems are designed to manage risks to the level of the HGHAML Board s risk appetite rather than eliminate the possibility of all losses due to operational risk. The operation and effectiveness of the controls is regularly assessed and confirmed through the work of the Group s second and third line functions: the Risk function, Compliance and Internal Audit. As part of regularly updating the HGHAML Group s Internal Capital Adequacy Assessment Process ( ICAAP ), the Risk function facilitates a series of business wide workshops to gather expert opinion on the key operational risks and to provide an assessment of the future frequency and potential impact of each risk through the development of key risk scenarios. Senior management are selected by the Risk function on the basis of their expertise in their relevant business area, knowledge of business process and controls and the specific risk categories under review. The workshops consider a combination of internal and external historical data to determine the severity and frequency of each key risk on both an average and worst case basis. The workshops also consider the internal control environment around each risk and any mitigating actions that would be brought to bear in the event of the risk crystallising. The outputs from the workshops are then statistically modelled to produce a 1 in 200 year capital impact estimate for the HGHAML Group, which is an estimate of the capital required to cover direct losses to HGHAML and any costs of compensating clients as a result of an operational incident. The model aggregates the risks and calculates an operational value at risk (OpVaR) figure for each key risk category. The model uses fat-tailed distributions to adequately allow for extreme events and also incorporates a degree of correlation between risks. The results of the modelling are analysed and challenged by Risk and Business unit managers before the HGHAML Board assesses how much capital it is appropriate for the firm to hold in respect of operational risks. 3.2 Credit Risk Credit risk is the risk of a debtor of HGHAML defaulting on the amounts due to HGHAML. This includes trade debtors and counterparties to hedging trades. The majority of the debtor balance relates to amounts owing by funds and clients in respect of fee income. Credit risk also arises in relation to cash deposits in the event that the bank with which the money has been deposited goes into default. There is also credit risk in respect of any amounts owing to entities in the HGHAML Group by JHG plc and any of its subsidiaries which are not part of the HGHAML Group. The HGHAML Group also makes seed investments in certain funds to assist with a fund s development and marketability. This results in the HGHAML Group having an exposure to equities, bonds and other securities not included in the trading book. The risk of losses from a decline in value of these investments is treated as credit risk for regulatory capital purposes because these exposures are not trading book investments. Tangible fixed assets are not considered to be a credit risk under the Group s internal risk taxonomy. There is, however, a credit risk requirement on these amounts for Pillar 1 purposes. Page 12 of 18

13 The JHG Group has an established Credit Risk Policy, to ensure that it transacts only with counterparties or places deposits with banks that are able to meet satisfactory credit rating and other requirements at levels that are consistent with the risk appetite approved by the JHG Group Board. Credit ratings are monitored daily by the Credit Risk team. Only counterparties or deposit taking banks approved by the Credit Risk Forum ( CRF ) are used. The CRF monitors exposures to counterparties against the limits it sets and makes senior management and the Board aware any credit concerns and actions taken to mitigate material credit risks. The CRF includes members from Risk, Compliance, Credit Analysis, Dealing, Legal and Derivative Operations functions and meets monthly. The risk of default on fee income debtors is considered to be low. HGHAML has many clients that have fees deducted directly from their assets via a trustee or alternatively are invoiced frequently with strict payment terms which significantly reduces credit risk on these receivables. The JHG and HGHAML Groups mitigate the risk of loss on the seed capital portfolio by setting limits for the aggregate seed portfolio and for any single seed investment and by hedging against risk where appropriate. New investments and divestments are approved by the Chief Executive Officer and Chief Financial Officer (executive directors), with full reporting to the ExCo and JHG Board on a monthly basis. HGHAML adopts the standardised approach to calculating Pillar 1 credit risk. Under this approach it uses ratings assigned by Fitch to assess the exposure classes for cash balances held with banks. Other exposures, such as trade debtors and accrued income, are treated as unrated. The internal quantification of credit risk (risk of loss on seed investments and risk of default on trade debtors and cash balances with banks) uses statistical modelling techniques. 3.3 Market Risk The HGHAML Group does not have a proprietary trading book. Market risk for regulatory capital purposes, therefore, comprises foreign currency risk resulting from the effect of movements in exchange rates on the Sterling value of certain assets and liabilities denominated in currencies other than Sterling. These are mainly foreign currency cash and trade debtor balances. Foreign currency cash balances are actively managed and kept at a working minimum. As a significant proportion of the HGHAML Group revenue is invoiced monthly foreign currency trade debtor balances are also kept to a minimum. HGHAML mitigates this risk through the effect of natural hedges i.e. holding financial assets and liabilities of equal value in the same currency; by limiting the net exposure to an individual currency; and by entering into hedging instruments such as forward foreign exchange contracts. 3.4 Business Risk Business risk is the risk that the revenues of the HGHAML Group decline and any offsetting reduction in costs is insufficient to offset the decline in revenues and, as a result, profitability is impaired. Business risk is driven by many factors, both industry-wide and specific to HGHAML, which could adversely impact assets under management and fee income. These factors include: A general decline in the levels of equity, fixed income and other markets. Poor relative investment performance of our funds, which directly reduces our assets under management and management fees and performance fees from these funds. This could also have an indirect impact if investors redeem their investments because of poor performance. Competitive pressure and market dynamics reducing fee levels and margins including through new entrants disrupting existing business models. Increased redemptions and/or reduced sales to clients as a result of a major operational risk event adversely affecting the Group s reputation. Reduced investor appetite (for whatever reason) for the types of funds / asset classes that we manage. Page 13 of 18

14 Loss of key individuals, which may have an adverse impact on investment performance and/or result in lower sales and higher redemptions in our funds. Political changes that may result in declines in market levels, reduced investor risk appetite, higher costs and/or higher tax rates. Regulatory changes that may result in lower fee margins, higher costs and/or make it more difficult to sell funds and/or carry out investment management activities in certain jurisdictions. Potential concentration in certain geographic regions, asset classes, client types and/or distribution partners that may increase the risk of low sales and/or high redemptions in certain circumstances. Adverse foreign exchange rate movements which reduce the HGHAML Group s revenues and/or increase its costs where these revenues or costs are denominated in currencies other than Sterling. Fiscal changes which may increase effective corporate tax rates. These risks are considered as part of the HGHAML Group s overall strategy and management of its business by ExCo and the HGHAML Board. Stress tests using severe but plausible scenarios of a number of business risks crystallising during the HGHAML Group s five year planning period are used to assess whether any of the business risks could be large enough to result in a net loss and, therefore, require additional capital resources to maintain capital adequacy. None of the stress tests resulted in a need to hold additional capital. 3.5 Exposures To Interest Rates On Positions Not Included In The Trading Book None of the firms within the HGHAML Group has a trading book. The HGHAML Group is exposed to interest rate movements on cash balances held on short term deposit with banking institutions in the ordinary course of business. The impact of interest rate movements is not material. 3.6 Pension Obligation Risk This is the risk to the HGHAML Group caused by its contractual or other liabilities to or with respect to the Henderson Defined Benefit pension schemes. These schemes are closed to new members and the HGHAML Group along with the Trustees of the scheme regularly monitor the position of the schemes to ensure that they are well funded. Independent actuaries provide the HGHAML Group with an assessment of the accounting surplus and a 1 in 200 year value at risk calculation. 3.7 Liquidity Risk Liquidity risk is the risk that the HGHAML Group may be unable to meet its payment obligations as they fall due. The HGHAML Group manages its liquidity on a daily basis within the Finance function to ensure that the HGHAML Group and regulated entities within the HGHAML Group each has sufficient cash and/or highly liquid assets available to meet their liabilities in both business as usual and stress circumstances. The HGHAML Group ensures that it has access to funds to cover all forecast commitments for at least the following 12 months. The HGHAML Group does not bear any liquidity risk associated with its clients funds and has no obligation to provide short term liquidity to its clients. 3.8 Group Risk Group risk is the risk posed to the HGHAML Group by JHG plc and any of its subsidiaries that are not part of the HGHAML Group. It includes: Credit risk on intercompany receivables; Operational risk from the possibility of failures of systems, processes or people in relation to activities delegated to these entities by the HGHAML Group (e.g. some investment management) or carried out on behalf of the HGHAML Group (e.g. shared IT systems); Key person dependencies; Reputational contagion risk; and Page 14 of 18

15 Liquidity risk if these entities draw down on liquidity facilities that are available to the entire JHG Group. These risks are monitored by the HGHAML Board. 4. Capital Adequacy 4.1 Capital Resources At 31 December 2017 and throughout the year, all of the LLIFs in the HGHAML Group complied with their individual capital requirements as set out by the Financial Conduct Authority. The table below summarises the total capital at HGHAML Group level as at 31 December Capital resources Group '000 Tier 1 Share capital 125 Share premium 847,063 Profit & loss and other reserves 229,857 Total tier 1 before deductions 1,077,045 Deductions from tier 1: Goodwill and intangibles (631,581) Retirement benefit assets (128,715) Material holdings (43) Total Tier 1 after deductions 316,706 Tier 2 Revaluation reserve 2,776 Other deductions from total capital - Own Funds 319,482 Tier 1 capital comprises of share capital, share premium, profit and loss and other reserves. Tier 2 capital is represented by revaluation reserves. 4.2 Capital Requirements The Pillar 1 variable capital requirement is calculated as the higher of: the base capital resources requirement; the sum of the credit and market risk capital requirements; and the fixed overhead requirement. A summary of the capital requirements is shown in the table below: Capital requirement '000 (a) Base Capital requirement n/a (b) Credit risk (see separate table) 65,436 (c) Market risk 11,242 (d) Sum of (b) and (c) 76,678 (e) Fixed overhead requirement 69,398 Total requirement - higher of (a), (d) and (e). 76,678 Page 15 of 18

16 The market risk for the Group relates to foreign exchange. The Pillar 1 credit risk capital requirement is calculated in accordance with the standardised approach. The components of the credit risk capital requirement are shown in the table below. Risk weighted exposure Requirement Credit risk requirement '000 '000 Institutions 46,315 3,705 Corporates 507,216 40,577 Collective investment undertakings 217,971 17,438 Items associated with particularly high risk 23,550 1,884 Other 22,897 1,832 Total credit risk and counterparty risk 817,949 65, ICAAP and Pillar 2 Capital Requirements The Internal Capital Adequacy Assessment Process ( ICAAP ) is the means by which the HGHAML Group assesses the level of capital (Pillar 2) that adequately supports all of the relevant current and future risks in its business. The methodology is designed to assess the amount of capital needed to meet unexpected losses at a confidence level of 99.5% on a 1 year time horizon. The ICAAP and the underlying methodology is updated and formally reviewed by the HGHAML Board on at least an annual basis or more frequently if necessary. Reports are prepared for ExCo and the HGHAML Board, giving an assessment of the amounts, types and distribution of capital resources that HGHAML considers appropriate for the nature and level of risks to which it is or might be exposed. Section 3.1 above details the approach to operational risk with the use of risk workshops and statistical modelling to generate capital required to be held under this category. Each other risk exposure is assessed using the most appropriate technique to determine how much capital is appropriate for that particular risk category. For those risks that would cause either reputational damage or reduce future revenue, rather than causing an immediate depletion of the HGHAML Group s capital surplus, assessment has been made through downside stress and scenario testing of the impact on HGHAML Group financial forecasts during its 5 year plan period. These scenarios are designed to cover severe but plausible circumstances. The ICAAP also considers the HGHAML s long term capital outlook, along with a downside scenario, a process which is incorporated into the annual budgeting process and reviewed by ExCo and the Board. In addition, it considers a wind-down analysis which looks at whether HGHAML would be required to hold additional capital over the period that it would take to wind down the HGHAML Group. 5. Remuneration The following disclosures are required under BIPRU and should be read in conjunction with the Janus Henderson Group Global Remuneration Policy Statement, which provides more information on the activities of our Compensation Committee and our remuneration principles and policies. This document is attached to the 2017 Annual Report on Form 10-K as Exhibit and is available at Decision-making process for determining the remuneration policy Janus Henderson Group plc was formed in 2017 through the merger of Henderson Group plc, and Janus Capital Inc. The newly formed group has established a Compensation Committee consisting of independent non-executive Directors of Janus Henderson Group plc. The Compensation Committee Page 16 of 18

17 met seven times during It is responsible for making recommendations to the JHG and HGHAML Board on the Group s remuneration plans, policies and practices and for determining, within agreed terms of reference, specific remuneration packages for the Executive Directors and other members of the JHG Group s Executive Committee. The Compensation Committee also maintains and periodically reviews a list of Code Staff to ensure that their remuneration structures are compliant with the FCA Remuneration Code. The Committee s Charter is available on the Group s website. 5.2 Code Staff criteria The HGHAML Group complies with the FCA Remuneration Code for BIPRU firms. Under the Pillar 3 disclosure requirements, the Compensation Committee must report annually on the remuneration policy and practice for employees termed Code Staff, including Material Risk Takers defined under the Regulatory Technical Standard. The list of individuals reviewed in determining those who are Code Staff and included in the Pillar 3 disclosure includes: 1. Executive Directors of Janus Henderson Group plc; 2. Non-Executive Directors of Janus Henderson Group plc; 3. Members of the Janus Henderson Group plc Executive Committee; 4. Employees in key control function roles within HGHAML Group; 5. Material Risk Takers within HGHAML Group; and 6. Employees who are remunerated at the same levels as Senior Management and Material Risk Takers identified above. 5.3 Link between pay and performance The main elements of fixed and variable remuneration are set out below. Fixed pay: principally comprised of salaries or fees. All Code Staff receive either a salary (for employees) or fees (for non-executive directors) which are commensurate with the incumbent s role, responsibilities and experience and with reference to competitive market rates within the industry. Fixed pay also includes pensions and benefits in kind which are provided in line with all other employees across the Group to enable employees to undertake their role by ensuring their wellbeing and security. Variable remuneration includes the following: Short Term Incentives: performance-related awards principally comprised of annual bonus awards. Non-executive directors do not receive variable performance-related pay. The funding frameworks are largely discretionary in nature under which annual incentive awards are delivered to participating staff. The frameworks take the form of indicative, but non-contractual, funding formulae based on relevant financial and non-financial metrics which are typically set as part of annual business planning and budgeting cycles. The primary short term incentive arrangement is called the Partnership Profit Pool (covering 96% of staff within the JHG Group) and is constructed as a profit share arrangement with the pool being initially set as a (discretionary) share of Pre-Incentive Operating Income (PIOI) between shareholders and employees. All Code Staff who are permanent employees are eligible to be considered for an annual bonus award each year, taking into account overall Group, team and individual performance against agreed objectives and Group values, including both financial and non-financial measures, risk performance and any other relevant factors. In determining individual awards for Code Staff who are fund managers, both quantitative and qualitative factors are used. Such factors include, among other things, consistent short-term and longterm relative Fund performance (i.e., one-, three-, and five-year performance), client support and investment team support through the sharing of ideas, leadership, development, mentoring, and team work. In addition a number of fund managers are also entitled to share in Performance Fees, further Page 17 of 18

18 enhancing the alignment with investors through the investment performance of the funds that they manage. In 2017 transitionary arrangements applied to the company s mandatory deferral policy, where legacy Company rules applied to the respective legacy populations. The mandatory deferral policy going forwards is as follows, 40% of aggregate short term variable incentives above an annual threshold of US$75,000/ 58,000 (or local equivalent) are deferred into Company shares and/or products, vesting in equal tranches over a three year period. The deferral rate increases to 50% and 60% in respect of variable remuneration above thresholds of US$750,000/ 582,000 and US$3,000,000/ 2,328,000 respectively. These new rules were applied to the Executive Committee and post-merger joiners in the 2017 performance year, and will apply to all employees going forward. For individuals who are designated as Code/Identified staff under both the FCA and AIFMD remuneration codes the deferral rates mandated by the AIFMD remuneration code, if higher, were applied irrespective of which set of standard deferral rules were used. The amount deferred in 2017 was: 11.0m in respect of Senior Management; 52.1m in respect of Other Code Staff. 5.4 Quantitative Remuneration Disclosures Janus Henderson Group is considered as a single business unit for the purposes of these disclosures. In respect of the 2017 performance year, 121 individuals have been identified as Code Staff, of whom 22 were classified as Senior Management (including 10 non-executive directors). The aggregate annual remuneration for these individuals is set out in the table below: Senior Management 000 s Other Code Staff 000 s Fixed remuneration 5,092 17,660 Variable remuneration 23, ,146 Total remuneration 28, ,807 Aggregate remuneration disclosed includes, in respect of the 2017 performance year: Annual base salaries paid during the year; Non-executive director fees received during the year; Employer paid contributions and the value of benefits in kind delivered during 2017; Short-term incentives awarded in respect of the year (prior to any mandatory deferral), comprising; discretionary annual bonus; other short term variable incentive awards (predominantly a share of Performance Fees); Long-term incentives awarded during the year, comprising the total amounts awarded under executive and employee share plans. Page 18 of 18

ICAAP Pillar 3 Disclosure

ICAAP Pillar 3 Disclosure This document is for professionals only Contents A1.1 Introduction 3 A1.2 Risk Framework 4 A1.3 Material Risks 6 A1.4 Capital Resources 8 A1.5 Capital Requirements 9 A1.6 ICAAP

ICAAP Pillar 3 Disclosure This document is for professionals only Contents A1.1 Introduction 3 A1.2 Risk Framework 4 A1.3 Material Risks 6 A1.4 Capital Resources 8 A1.5 Capital Requirements 9 A1.6 ICAAP

Ashmore Group plc Pillar 3 Disclosures as at 30 June 2018

Ashmore Group plc Pillar 3 Disclosures as at 30 June 2018 Table of Contents 1. OVERVIEW 3 1.1 BASIS OF DISCLOSURES 1.2 FREQUENCY OF DISCLOSURES 1.3 MEDIA AND LOCATION OF DISCLOSURES 2. CORPORATE GOVERNANCE

Ashmore Group plc Pillar 3 Disclosures as at 30 June 2018 Table of Contents 1. OVERVIEW 3 1.1 BASIS OF DISCLOSURES 1.2 FREQUENCY OF DISCLOSURES 1.3 MEDIA AND LOCATION OF DISCLOSURES 2. CORPORATE GOVERNANCE

Pillar 3 Disclosures. Invesco UK Limited

s Document Version: Version 1 Version Date: 30 July 2014 Table of Contents 1 Background 3 1.1 Basis of Disclosure 3 1.2 Frequency of Disclosure 4 1.3 Media and Location of Publication 4 2 Risk Management

s Document Version: Version 1 Version Date: 30 July 2014 Table of Contents 1 Background 3 1.1 Basis of Disclosure 3 1.2 Frequency of Disclosure 4 1.3 Media and Location of Publication 4 2 Risk Management

PILLAR 3 DISCLOSURES MERCER UK AUGUST 2016

PILLAR 3 DISCLOSURES MERCER UK AUGUST 2016 CONTENTS 1. Background... 1 1.1 Basis of Disclosures... 2 1.2 Frequency of Publication... 2 1.3 Verification... 2 1.4 Media & Location of Publication... 2 2.

PILLAR 3 DISCLOSURES MERCER UK AUGUST 2016 CONTENTS 1. Background... 1 1.1 Basis of Disclosures... 2 1.2 Frequency of Publication... 2 1.3 Verification... 2 1.4 Media & Location of Publication... 2 2.

Ashmore Group plc Pillar 3 Disclosures as at 30 June 2016

Ashmore Group plc Pillar 3 Disclosures as at 30 June 2016 Table of Contents 1. OVERVIEW 3 1.1 BASIS OF DISCLOSURES 1.2 FREQUENCY OF DISCLOSURES 1.3 MEDIA AND LOCATION OF DISCLOSURES 2. CAPITAL RESOURCES

Ashmore Group plc Pillar 3 Disclosures as at 30 June 2016 Table of Contents 1. OVERVIEW 3 1.1 BASIS OF DISCLOSURES 1.2 FREQUENCY OF DISCLOSURES 1.3 MEDIA AND LOCATION OF DISCLOSURES 2. CAPITAL RESOURCES

PILLAR 3 REGULATORY DISCLOSURES REPORT AS AT 30 NOVEMBER 2017 LEUCADIA INVESTMENT MANAGEMENT LIMITED

PILLAR 3 REGULATORY DISCLOSURES REPORT AS AT 30 NOVEMBER 2017 LEUCADIA INVESTMENT MANAGEMENT LIMITED CONTENTS 1 OVERVIEW AND BASIS OF PREPARATION OF THE PILLAR 3 DISCLOSURES... 1 1.1 Business Background...

PILLAR 3 REGULATORY DISCLOSURES REPORT AS AT 30 NOVEMBER 2017 LEUCADIA INVESTMENT MANAGEMENT LIMITED CONTENTS 1 OVERVIEW AND BASIS OF PREPARATION OF THE PILLAR 3 DISCLOSURES... 1 1.1 Business Background...

Ashmore Group plc Pillar 3 Disclosures as at 30 June 2015

Ashmore Group plc Pillar 3 Disclosures as at 30 June 2015 1.0 Overview The purpose of this document is to outline the Pillar 3 disclosures for the Ashmore Group (the Group). The disclosures on risk management

Ashmore Group plc Pillar 3 Disclosures as at 30 June 2015 1.0 Overview The purpose of this document is to outline the Pillar 3 disclosures for the Ashmore Group (the Group). The disclosures on risk management

T. Rowe Price International Ltd. Pillar 3 & Remuneration Code Disclosure. 31 December 2016

T. Rowe Price International Ltd Pillar 3 & Remuneration Code Disclosure 31 December 2016 Background: The Capital Requirements Directive ( CRD ) sets out the regulatory capital framework for Europe based

T. Rowe Price International Ltd Pillar 3 & Remuneration Code Disclosure 31 December 2016 Background: The Capital Requirements Directive ( CRD ) sets out the regulatory capital framework for Europe based

China International Capital Corporation (UK) Limited Pillar 3 Disclosure In respect of Financial Year Ended 31 December 2016

Limited Pillar 3 Disclosure In respect of Financial Year Ended 31 December 2016") Pillar 3 Disclosure December 2016 China International Capital Corporation (UK) Limited Pillar 3 Disclosure In respect of Financial Year Ended 31 December 2016 1. Overview Capital Requirements Regulation

Pillar 3 Disclosure December 2016 China International Capital Corporation (UK) Limited Pillar 3 Disclosure In respect of Financial Year Ended 31 December 2016 1. Overview Capital Requirements Regulation

Pillar 3 Regulatory Disclosure (UK)

") Pillar 3 Regulatory Disclosure (UK) As at 30 June 2017 Approved by the Board 12 December 2017 THE UK CAPITAL CONSOLIDATION REGULATED GROUP, INCLUDING: PRAEMIUM ADMINISTRATION LTD (FRN 463566) SMART INVESTMENT

Pillar 3 Regulatory Disclosure (UK) As at 30 June 2017 Approved by the Board 12 December 2017 THE UK CAPITAL CONSOLIDATION REGULATED GROUP, INCLUDING: PRAEMIUM ADMINISTRATION LTD (FRN 463566) SMART INVESTMENT

CBRE Clarion Securities UK Limited PILLAR 3 RISK DISCLOSURES April 2017

CBRE Clarion Securities UK Limited PILLAR 3 RISK DISCLOSURES April 2017 1. Introduction The Capital Requirements Directive (CRD) sets out regulatory capital adequacy standards and an associated supervisory

CBRE Clarion Securities UK Limited PILLAR 3 RISK DISCLOSURES April 2017 1. Introduction The Capital Requirements Directive (CRD) sets out regulatory capital adequacy standards and an associated supervisory

Neptune Investment Management Limited ( Neptune or the Company ) Pillar 3 Disclosures 2017

Pillar 3 Disclosures 2017") Neptune Investment Management Limited ( Neptune or the Company ) Pillar 3 Disclosures 2017 Approved by the Board of Neptune on 26 th June 2018-1 - Contents 1. Overview 2. Risk Management Objectives and

Neptune Investment Management Limited ( Neptune or the Company ) Pillar 3 Disclosures 2017 Approved by the Board of Neptune on 26 th June 2018-1 - Contents 1. Overview 2. Risk Management Objectives and

T. Rowe Price International Ltd. Pillar 3 & Remuneration Code Disclosure. 31 st December 2017

T. Rowe Price International Ltd Pillar 3 & Remuneration Code Disclosure 31 st December 2017 Background: The Capital Requirements Directive ( CRD ) sets out the regulatory capital framework for Europe based

T. Rowe Price International Ltd Pillar 3 & Remuneration Code Disclosure 31 st December 2017 Background: The Capital Requirements Directive ( CRD ) sets out the regulatory capital framework for Europe based

Pillar 3 Disclosure ICAP Europe Limited

Pillar 3 Disclosure 31 st March 2017 1. INTRODUCTION AND SCOPE The purpose of this report is to meet Pillar 3 requirements laid out by the European Banking Authority (EBA) in Part Eight of the Capital

Pillar 3 Disclosure 31 st March 2017 1. INTRODUCTION AND SCOPE The purpose of this report is to meet Pillar 3 requirements laid out by the European Banking Authority (EBA) in Part Eight of the Capital

Pillar 3 Disclosure November 2016

Pillar 3 Disclosure November 2016 1 1. Overview 1.1 Background This document comprises the Capital and Risk Management Pillar 3 disclosures as at 30 September 2016 for River and Mercantile Group PLC and

Pillar 3 Disclosure November 2016 1 1. Overview 1.1 Background This document comprises the Capital and Risk Management Pillar 3 disclosures as at 30 September 2016 for River and Mercantile Group PLC and

TD BANK INTERNATIONAL S.A.

TD BANK INTERNATIONAL S.A. Pillar 3 Disclosures Year Ended October 31, 2013 1 Contents 1. Overview... 3 1.1 Purpose...3 1.2 Frequency and Location...3 2. Governance and Risk Management Framework... 4 2.1

TD BANK INTERNATIONAL S.A. Pillar 3 Disclosures Year Ended October 31, 2013 1 Contents 1. Overview... 3 1.1 Purpose...3 1.2 Frequency and Location...3 2. Governance and Risk Management Framework... 4 2.1

Ingenious Capital Management Limited: Pillar III Disclosure

CONTENTS 1. Introduction 2. Risk Management 3. Capital Resources 4. Internal Capital Adequacy Assessment Process (ICAAP) 5. Remuneration Policy Disclosure 1. INTRODUCTION 1.1 Scope of Application Ingenious

CONTENTS 1. Introduction 2. Risk Management 3. Capital Resources 4. Internal Capital Adequacy Assessment Process (ICAAP) 5. Remuneration Policy Disclosure 1. INTRODUCTION 1.1 Scope of Application Ingenious

RSMR Portfolio Services Limited RSMR-PS Pillar 3 Disclosure

RSMR Portfolio Services Limited RSMR-PS Pillar 3 Disclosure 1 Introduction Firms are required under the Senior Management Arrangements, Systems and Controls (SYSC) manual of the Financial Conduct Authority

RSMR Portfolio Services Limited RSMR-PS Pillar 3 Disclosure 1 Introduction Firms are required under the Senior Management Arrangements, Systems and Controls (SYSC) manual of the Financial Conduct Authority

Schroders Pillar 3 disclosures as at 31 December 2015

Schroders Pillar 3 disclosures as at 31 December 2015 Contents Page Overview... 2 Regulatory framework... 3 Risk management framework... 4 Capital management and regulatory own funds... 7 Capital resource

Schroders Pillar 3 disclosures as at 31 December 2015 Contents Page Overview... 2 Regulatory framework... 3 Risk management framework... 4 Capital management and regulatory own funds... 7 Capital resource

Valu-Trac Investment Management Limited Pillar 3 Disclosure

Valu-Trac Investment Management Limited Pillar 3 Disclosure The Capital Requirements Directive (CRD) of the European Union created a revised regulatory capital framework across Europe governing how much

Valu-Trac Investment Management Limited Pillar 3 Disclosure The Capital Requirements Directive (CRD) of the European Union created a revised regulatory capital framework across Europe governing how much

Capital Requirements Directive Pillar 3 Disclosure. June 2017

Capital Requirements Directive Pillar 3 Disclosure June 2017 1. Background The purpose of this document is to outline the Pillar 3 disclosures for BlueBay Asset Management LLP ( LLP ). LLP is a subsidiary

Capital Requirements Directive Pillar 3 Disclosure June 2017 1. Background The purpose of this document is to outline the Pillar 3 disclosures for BlueBay Asset Management LLP ( LLP ). LLP is a subsidiary

Prudential Standard GOI 3 Risk Management and Internal Controls for Insurers

Prudential Standard GOI 3 Risk Management and Internal Controls for Insurers Objectives and Key Requirements of this Prudential Standard Effective risk management is fundamental to the prudent management

Prudential Standard GOI 3 Risk Management and Internal Controls for Insurers Objectives and Key Requirements of this Prudential Standard Effective risk management is fundamental to the prudent management

Pillar 1 sets out the minimum capital resource requirement firms are required to maintain to meet credit, market and operational risks

Gresham House Asset Management Limited Pillar 3 Disclosure 1 Introduction Firms are required under the Senior Management Arrangements, Systems and Controls (SYSC) manual of the Financial Conduct Authority

Gresham House Asset Management Limited Pillar 3 Disclosure 1 Introduction Firms are required under the Senior Management Arrangements, Systems and Controls (SYSC) manual of the Financial Conduct Authority

M&G Group Pillar 3 Disclosures

M&G Group Pillar 3 Disclosures As at 31 December 2016 Page 1 of 24 CONTENT 1 Overview 4 1.1 Introduction 4 1.2 M&G overview 4 1.3 Disclosure policy 5 1.4 Accounting consolidation 5 1.5 Prudential consolidation

M&G Group Pillar 3 Disclosures As at 31 December 2016 Page 1 of 24 CONTENT 1 Overview 4 1.1 Introduction 4 1.2 M&G overview 4 1.3 Disclosure policy 5 1.4 Accounting consolidation 5 1.5 Prudential consolidation

PIMCO Europe Ltd Pillar 3 Disclosure. As at 31 December 2015

Pillar 3 Disclosure As at 31 December 2015 1. Introduction PIMCO Europe Ltd ( PEL ) is a company incorporated under the laws of England and Wales on 24 April 1991, and authorized and regulated by the Financial

Pillar 3 Disclosure As at 31 December 2015 1. Introduction PIMCO Europe Ltd ( PEL ) is a company incorporated under the laws of England and Wales on 24 April 1991, and authorized and regulated by the Financial

Crown Agents Investment Management Limited. Pillar 3 Disclosures. December 2014

Crown Agents Investment Management Limited December 2014 Page 0 CONTENTS Introduction... 2 Corporate Governance... 3 Risk Appetite... 7 Capital Resource... 9 Capital Management... 10 Risk Categories...

Crown Agents Investment Management Limited December 2014 Page 0 CONTENTS Introduction... 2 Corporate Governance... 3 Risk Appetite... 7 Capital Resource... 9 Capital Management... 10 Risk Categories...

TESCO PERSONAL FINANCE GROUP LTD PILLAR 3 DISCLOSURES FOR THE YEAR ENDED 28 FEBRUARY 2017

PILLAR 3 DISCLOSURES FOR THE YEAR ENDED 28 FEBRUARY 2017 1 CONTENTS: 1. Introduction and Basel Framework 4 2. Disclosure Policy 5 2.1 Frequency of Disclosure 5 2.2 Verification and Medium 5 2.3 Use of

PILLAR 3 DISCLOSURES FOR THE YEAR ENDED 28 FEBRUARY 2017 1 CONTENTS: 1. Introduction and Basel Framework 4 2. Disclosure Policy 5 2.1 Frequency of Disclosure 5 2.2 Verification and Medium 5 2.3 Use of

Redburn (Europe) Limited Pillar 3 Disclosures

Limited Pillar 3 Disclosures") REDBURN PILLAR 3 DISCLOSURES 30 SEPTEMBER 2017 Important Notice On 20 September 2017, the FCA approved a variation in regulatory permissions requested by Redburn (Europe) Limited (the Company ), such that

REDBURN PILLAR 3 DISCLOSURES 30 SEPTEMBER 2017 Important Notice On 20 September 2017, the FCA approved a variation in regulatory permissions requested by Redburn (Europe) Limited (the Company ), such that

Pillar 3 As at 31st March 2011

Pillar 3 As at 31 st March 2011 Purpose of Disclosure This document sets out the Pillar 3 market disclosures for Threadneedle Asset Management Holdings an authorised and regulated limited license firm

Pillar 3 As at 31 st March 2011 Purpose of Disclosure This document sets out the Pillar 3 market disclosures for Threadneedle Asset Management Holdings an authorised and regulated limited license firm

Brewin Dolphin Holdings PLC

Brewin Dolphin Holdings PLC Pillar 3 Disclosures 2017 TABLE OF CONTENTS 1. Executive Summary... 3 2. Company Overview... 3 3. Regulatory Framework... 4 4. Scope of Application... 5 5. Frequency of Disclosure...

Brewin Dolphin Holdings PLC Pillar 3 Disclosures 2017 TABLE OF CONTENTS 1. Executive Summary... 3 2. Company Overview... 3 3. Regulatory Framework... 4 4. Scope of Application... 5 5. Frequency of Disclosure...

First State Investments (UK Holdings) Ltd

Ltd") First State Investments (UK Holdings) Ltd Pillar 3 disclosures For the year ended 30 June 2016 Contents 1. INTRODUCTION... 3 2. SCOPE OF APPLICATION... 4 2.1 Group structure... 4 2.2 FSI Corporate Structure...

First State Investments (UK Holdings) Ltd Pillar 3 disclosures For the year ended 30 June 2016 Contents 1. INTRODUCTION... 3 2. SCOPE OF APPLICATION... 4 2.1 Group structure... 4 2.2 FSI Corporate Structure...

FIDANTE PARTNERS EUROPE LIMITED. Pillar III Disclosure. 30 June 2017

FIDANTE PARTNERS EUROPE LIMITED Pillar III Disclosure 30 June 2017 Fidante Partners Europe LimitedPillar III Disclosure 30 June 2017 Fidante Partners Europe Limited ( Fidante Partners Europe or the Firm

FIDANTE PARTNERS EUROPE LIMITED Pillar III Disclosure 30 June 2017 Fidante Partners Europe LimitedPillar III Disclosure 30 June 2017 Fidante Partners Europe Limited ( Fidante Partners Europe or the Firm

Pillar 3 disclosures 3I GROUP PLC. As at 31 March 2018

Pillar 3 disclosures 3I GROUP PLC As at 31 March 2018 1. Overview The Capital Requirements Directive ( CRD ) and the Alternative Investment Fund Managers Directive ( AIFMD ) established a regulatory capital

Pillar 3 disclosures 3I GROUP PLC As at 31 March 2018 1. Overview The Capital Requirements Directive ( CRD ) and the Alternative Investment Fund Managers Directive ( AIFMD ) established a regulatory capital

Pillar 3 Disclosures. 31 December 2013

Pillar 3 Disclosures 31 December 2013 Contents 1. Overview... 3 1.1 Background... 3 1.2 Scope of application... 3 1.3 Basis and frequency of disclosures... 3 1.4 External audit... 3 2. Risk Management

Pillar 3 Disclosures 31 December 2013 Contents 1. Overview... 3 1.1 Background... 3 1.2 Scope of application... 3 1.3 Basis and frequency of disclosures... 3 1.4 External audit... 3 2. Risk Management

Pillar 3 Disclosures. Sterling ISA Managers Limited Year Ending 31 st December 2017

Pillar 3 Disclosures Sterling ISA Managers Limited Year Ending 31 st December 2017 1. Background and Scope 1.1 Background Sterling ISA Managers Limited (the Company) is supervised by the Financial Conduct

Pillar 3 Disclosures Sterling ISA Managers Limited Year Ending 31 st December 2017 1. Background and Scope 1.1 Background Sterling ISA Managers Limited (the Company) is supervised by the Financial Conduct

Neptune Investment Management Limited ( Neptune or the Company ) Pillar 3 Disclosures 2013

Pillar 3 Disclosures 2013") Neptune Investment Management Limited ( Neptune or the Company ) Pillar 3 Disclosures 2013 Approved by the Board of Neptune on 25 th April 2014-1 - Contents 1. Overview 2. Risk Management Objectives and

Neptune Investment Management Limited ( Neptune or the Company ) Pillar 3 Disclosures 2013 Approved by the Board of Neptune on 25 th April 2014-1 - Contents 1. Overview 2. Risk Management Objectives and

PILLAR 3 Disclosures

PILLAR 3 Disclosures Published April 2016 Contacts: Rajeev Adrian Sedjwick Joseph Chief Financial Officer Chief Risk Officer 0207 776 4006 0207 776 4014 Rajeev.adrian@bank-abc.com sedjwick.joseph@bankabc.com

PILLAR 3 Disclosures Published April 2016 Contacts: Rajeev Adrian Sedjwick Joseph Chief Financial Officer Chief Risk Officer 0207 776 4006 0207 776 4014 Rajeev.adrian@bank-abc.com sedjwick.joseph@bankabc.com

Capital & Risk Management Pillar 3 Disclosures

Capital & Risk Management Pillar 3 Disclosures 31st December 2017 Company Registration no. 06736473 Contents Introduction...3 Activities and Scope...3 Regulatory framework for disclosures...4 Basis and

Capital & Risk Management Pillar 3 Disclosures 31st December 2017 Company Registration no. 06736473 Contents Introduction...3 Activities and Scope...3 Regulatory framework for disclosures...4 Basis and

Pillar 3 Disclosures. GAIN Capital UK Limited

Pillar 3 Disclosures GAIN Capital UK Limited December 2015 Contents 1. Overview 3 2. Risk Management Objectives & Policies 5 3. Capital Resources 8 4. Principle Risks 11 Appendix 1: Disclosure Waivers

Pillar 3 Disclosures GAIN Capital UK Limited December 2015 Contents 1. Overview 3 2. Risk Management Objectives & Policies 5 3. Capital Resources 8 4. Principle Risks 11 Appendix 1: Disclosure Waivers

Pillar 3 Risk Disclosure Statement AS OF DECEMBER 2016

Pillar 3 Risk Disclosure Statement AS OF DECEMBER 2016 1 INTRODUCTION The Pillar 3 disclosures relate to Dimensional Fund Advisors Ltd. ( DFAL ), a 100% owned subsidiary of Dimensional Fund Advisors LP

Pillar 3 Risk Disclosure Statement AS OF DECEMBER 2016 1 INTRODUCTION The Pillar 3 disclosures relate to Dimensional Fund Advisors Ltd. ( DFAL ), a 100% owned subsidiary of Dimensional Fund Advisors LP

Pillar 3. Partners Group (UK) Ltd. As at 31/12/16

Ltd. As at 31/12/16") Pillar 3 Partners Group (UK) Ltd As at 31/12/16 1. Pillar 3 Disclosure 2. Executive Summary 3. Risk Management Objectives, Policies and Governance 4. Own Funds and Capital Adequacy 5. Remuneration 1. PILLAR

Pillar 3 Partners Group (UK) Ltd As at 31/12/16 1. Pillar 3 Disclosure 2. Executive Summary 3. Risk Management Objectives, Policies and Governance 4. Own Funds and Capital Adequacy 5. Remuneration 1. PILLAR

Merrill Lynch Equity S.àr.l. Pillar 3 Disclosures. As at December 31, 2012

Merrill Lynch Equity S.àr.l. Pillar 3 Disclosures As at December 31, 2012 1 2 Contents 1. Introduction 2. Capital Resources and Requirements 3. Risk Management Objectives and Policies 4. Further Detail

Merrill Lynch Equity S.àr.l. Pillar 3 Disclosures As at December 31, 2012 1 2 Contents 1. Introduction 2. Capital Resources and Requirements 3. Risk Management Objectives and Policies 4. Further Detail

BAILLIE GIFFORD. Governance, Risk Management and Capital Disclosures ( Pillar 3 ) June 2018

June 2018") BAILLIE GIFFORD Governance, Risk Management and Capital Disclosures ( Pillar 3 ) June 2018 Contents Introduction and Context 3 Purpose of Disclosures Scope Basis of Preparation Governance Arrangements

BAILLIE GIFFORD Governance, Risk Management and Capital Disclosures ( Pillar 3 ) June 2018 Contents Introduction and Context 3 Purpose of Disclosures Scope Basis of Preparation Governance Arrangements

Rynda Property Investors LLP (the Firm )

") Rynda Property Investors LLP (the Firm ) Disclosure Statement under Pillar III as at 30 th June 2018 Contents 1. Overview 2. Risk Management Objectives and Policies 3. Capital Resources 4. Capital Adequacy

Rynda Property Investors LLP (the Firm ) Disclosure Statement under Pillar III as at 30 th June 2018 Contents 1. Overview 2. Risk Management Objectives and Policies 3. Capital Resources 4. Capital Adequacy

Invesco UK Limited Pillar 3 Disclosure As at 31 December 2017

Invesco UK Limited Pillar 3 Disclosure As at 31 December 2017 Contents 1 Background... 3 1.1 Basis of Disclosure 3 1.2 Frequency of Disclosure 3 1.3 Media and Location of Publication 3 1.4 Scope of Application

Invesco UK Limited Pillar 3 Disclosure As at 31 December 2017 Contents 1 Background... 3 1.1 Basis of Disclosure 3 1.2 Frequency of Disclosure 3 1.3 Media and Location of Publication 3 1.4 Scope of Application

PILLAR 3 DISCLOSURE POLICY

PILLAR 3 DISCLOSURE POLICY Part 1. Overview of the Disclosure requirements 1.1 Introduction The European Union Capital Requirements Directive (EU CRD) was introduced in January 2007 to ensure consistent

PILLAR 3 DISCLOSURE POLICY Part 1. Overview of the Disclosure requirements 1.1 Introduction The European Union Capital Requirements Directive (EU CRD) was introduced in January 2007 to ensure consistent

PILLAR 3 DISCLOSURES. As at December avivainvestors.com

As at December 2014 avivainvestors.com Contents Abbreviations and glossary of terms 3 1. Introduction 4 1.1 Overview 4 1.1.1 Introduction 4 1.1.2 Basis of disclosures 4 1.1.3 Frequency of disclosures 4

As at December 2014 avivainvestors.com Contents Abbreviations and glossary of terms 3 1. Introduction 4 1.1 Overview 4 1.1.1 Introduction 4 1.1.2 Basis of disclosures 4 1.1.3 Frequency of disclosures 4

Tungsten Corporation plc Tungsten Bank plc. Pillar 3 Disclosures. 8 July / 20

Tungsten Corporation plc Tungsten Bank plc Pillar 3 Disclosures 8 July 2014 1 / 20 Table of Contents 1 Overview... 4 Introduction... 4 Basis and Frequency of Disclosures... 4 Published Information... 4

Tungsten Corporation plc Tungsten Bank plc Pillar 3 Disclosures 8 July 2014 1 / 20 Table of Contents 1 Overview... 4 Introduction... 4 Basis and Frequency of Disclosures... 4 Published Information... 4

GOLDENBURG GROUP LIMITED PILLAR III DISCLOSURES BASEL III

GOLDENBURG GROUP LIMITED PILLAR III DISCLOSURES BASEL III YEAR ENDED 31 DECEMBER 2014 May 2015 ACCORDING TO SECTION 4 (PAR. 32) OF THE CYPRUS SECURITIES AND EXCHANGE COMMISSION DIRECTIVE DI144-2014-14

GOLDENBURG GROUP LIMITED PILLAR III DISCLOSURES BASEL III YEAR ENDED 31 DECEMBER 2014 May 2015 ACCORDING TO SECTION 4 (PAR. 32) OF THE CYPRUS SECURITIES AND EXCHANGE COMMISSION DIRECTIVE DI144-2014-14

DARLINGTON BUILDING SOCIETY CAPITAL REQUIREMENTS DIRECTIVE

DARLINGTON BUILDING SOCIETY CAPITAL REQUIREMENTS DIRECTIVE PILLAR 3 DISCLOSURE DOCUMENT AS AT 31 st DECEMBER 2018 Contents 1 Introduction 2 Risk Management 3 Capital 4 Credit Risk (Mortgages) 5 Provisions

DARLINGTON BUILDING SOCIETY CAPITAL REQUIREMENTS DIRECTIVE PILLAR 3 DISCLOSURE DOCUMENT AS AT 31 st DECEMBER 2018 Contents 1 Introduction 2 Risk Management 3 Capital 4 Credit Risk (Mortgages) 5 Provisions

NUMIS SECURITIES LIMITED

NUMIS SECURITIES LIMITED Capital, Risk Management, Governance and Remuneration Disclosures 2016 (Pillar 3) 1 1 Overview 1.1 Introduction The following disclosures are prepared in accordance with the Capital

NUMIS SECURITIES LIMITED Capital, Risk Management, Governance and Remuneration Disclosures 2016 (Pillar 3) 1 1 Overview 1.1 Introduction The following disclosures are prepared in accordance with the Capital

BAILLIE GIFFORD. Governance, Risk Management and Capital Disclosures ( Pillar 3 ) June 2017

June 2017") BAILLIE GIFFORD Governance, Risk Management and Capital Disclosures ( Pillar 3 ) June 2017 Contents Introduction and Context 3 Purpose of Disclosures Scope Basis of Preparation Governance Arrangements

BAILLIE GIFFORD Governance, Risk Management and Capital Disclosures ( Pillar 3 ) June 2017 Contents Introduction and Context 3 Purpose of Disclosures Scope Basis of Preparation Governance Arrangements

Hermes Fund Managers Limited

Hermes Fund Managers Limited Pillar 3 Disclosures as at 31 December 2013 Issued in April 2014 by Hermes Investment Management Limited. Lloyds Chambers, 1 Portsoken Street, London, E1 8HZ. Registered No.

Hermes Fund Managers Limited Pillar 3 Disclosures as at 31 December 2013 Issued in April 2014 by Hermes Investment Management Limited. Lloyds Chambers, 1 Portsoken Street, London, E1 8HZ. Registered No.

Aberdeen Asset Management PLC

For professional investors and financial advisers only not for use by retail investors Aberdeen Asset Management PLC Pillar 3 Market Disclosure Statement 2016 Contents 1. Overview...4 1.1 Introduction...

For professional investors and financial advisers only not for use by retail investors Aberdeen Asset Management PLC Pillar 3 Market Disclosure Statement 2016 Contents 1. Overview...4 1.1 Introduction...

CAPITAL REQUIREMENTS DIRECTIVE Pillar 3 Disclosure Document 2015 (As at 28 th February 2015)

") CAPITAL REQUIREMENTS DIRECTIVE Pillar 3 Disclosure Document 2015 (As at 28 th February 2015) Contents 1. Introduction... 1 2. Risk management objectives and policies... 2 2.1 Principal risks and uncertainties...

CAPITAL REQUIREMENTS DIRECTIVE Pillar 3 Disclosure Document 2015 (As at 28 th February 2015) Contents 1. Introduction... 1 2. Risk management objectives and policies... 2 2.1 Principal risks and uncertainties...

Pillar 3 Disclosures

Pillar 3 Disclosures 31 December 2017 Contents 1. Introduction: Pillar 3... 2 2. BIPRU 11.5.1 - Risk management objectives and policies... 3 3. BIPRU 11.5.3 - Capital resources... 5 4. BIPRU 11.5.4 - Compliance

Pillar 3 Disclosures 31 December 2017 Contents 1. Introduction: Pillar 3... 2 2. BIPRU 11.5.1 - Risk management objectives and policies... 3 3. BIPRU 11.5.3 - Capital resources... 5 4. BIPRU 11.5.4 - Compliance

Capital Requirements Directive Pillar 3 Disclosures For the year ended 31 August 2017

Capital Requirements Directive Pillar 3 Disclosures For the year ended 31 August 2017 Contents INTRODUCTION... 2 RISK MANAGEMENT POLICIES AND OBJECTIVES... 3 BOARD & SUB-COMMITTEES... 3 THREE LINES OF

Capital Requirements Directive Pillar 3 Disclosures For the year ended 31 August 2017 Contents INTRODUCTION... 2 RISK MANAGEMENT POLICIES AND OBJECTIVES... 3 BOARD & SUB-COMMITTEES... 3 THREE LINES OF

SEI Investments (Europe) Limited Pillar 3 Disclosure

Limited Pillar 3 Disclosure") SEI Investments (Europe) Limited Pillar 3 Disclosure June 2018 Table of Contents 1. Overview 1.1. Introduction 1.2. Purpose of Pillar 3 1.3. Frequency of Disclosure 2. Structure of SEI 3. Capital Resources

SEI Investments (Europe) Limited Pillar 3 Disclosure June 2018 Table of Contents 1. Overview 1.1. Introduction 1.2. Purpose of Pillar 3 1.3. Frequency of Disclosure 2. Structure of SEI 3. Capital Resources

Pillar III Disclosures

GIB Capital Pillar III Disclosures Year ended 31 December 2017 Table of Contents 1. OVERVIEW... 3 2. SCOPE OF APPLICATION... 3 2.1 Pillar I Minimum capital requirements... 3 2.2 Pillar II Internal Capital

GIB Capital Pillar III Disclosures Year ended 31 December 2017 Table of Contents 1. OVERVIEW... 3 2. SCOPE OF APPLICATION... 3 2.1 Pillar I Minimum capital requirements... 3 2.2 Pillar II Internal Capital

MAINFIRST BANK AG. BASEL III Pillar 3 - Disclosures as at. 31 December 2014

MAINFIRST BANK AG BASEL III Pillar 3 - Disclosures as at 31 December 2014 BASEL III PILLAR 3 - DISCOSURES AS AT 31 DECEMBER 2014 1 INTRODUCTION GENERAL The main purpose of this document is to set out MainFirst

MAINFIRST BANK AG BASEL III Pillar 3 - Disclosures as at 31 December 2014 BASEL III PILLAR 3 - DISCOSURES AS AT 31 DECEMBER 2014 1 INTRODUCTION GENERAL The main purpose of this document is to set out MainFirst

King & Shaxson Group Pillar 3 Disclosures 2016

1. Introduction 1.1 Background The European Union Capital Requirements Directive ( CRD ) established a regulatory framework for capital adequacy across the European Union. CRD was replaced by the Capital

1. Introduction 1.1 Background The European Union Capital Requirements Directive ( CRD ) established a regulatory framework for capital adequacy across the European Union. CRD was replaced by the Capital

NUMIS SECURITIES LIMITED

NUMIS SECURITIES LIMITED Capital, Risk Management, Governance and Remuneration Disclosures 2014 (Pillar 3) 1 1 Overview 1.1 Introduction The following disclosures are prepared in accordance with the Capital

NUMIS SECURITIES LIMITED Capital, Risk Management, Governance and Remuneration Disclosures 2014 (Pillar 3) 1 1 Overview 1.1 Introduction The following disclosures are prepared in accordance with the Capital

CAPITAL REQUIREMENTS DIRECTIVE PILLAR 3 DISCLOSURE DOCUMENT 31 ST MARCH P a g e

CAPITAL REQUIREMENTS DIRECTIVE PILLAR 3 DISCLOSURE DOCUMENT 31 ST MARCH 2017 1 P a g e CONTENTS Page 1. Introduction 3 2. Risk Management Objectives and Policies 3-7 3. Capital Resources 7 4. Capital Adequacy

CAPITAL REQUIREMENTS DIRECTIVE PILLAR 3 DISCLOSURE DOCUMENT 31 ST MARCH 2017 1 P a g e CONTENTS Page 1. Introduction 3 2. Risk Management Objectives and Policies 3-7 3. Capital Resources 7 4. Capital Adequacy

Sainsbury s Bank plc. Pillar 3 Disclosures for the year ended 31 December 2008

Sainsbury s Bank plc Pillar 3 Disclosures for the year ended 2008 1 Overview 1.1 Background 1 1.2 Scope of Application 1 1.3 Frequency 1 1.4 Medium and Location for Publication 1 1.5 Verification 1 2 Risk

Sainsbury s Bank plc Pillar 3 Disclosures for the year ended 2008 1 Overview 1.1 Background 1 1.2 Scope of Application 1 1.3 Frequency 1 1.4 Medium and Location for Publication 1 1.5 Verification 1 2 Risk

Pillar 3 Disclosure and Policy. Stenham Asset Management (UK) Plc. ( The Firm )

Plc. ( The Firm )") Pillar 3 Disclosure and Policy Stenham Asset Management (UK) Plc. ( The Firm ) May 2017 The following information is provided pursuant to the Pillar 3 disclosure rules as laid out by the Financial Conduct

Pillar 3 Disclosure and Policy Stenham Asset Management (UK) Plc. ( The Firm ) May 2017 The following information is provided pursuant to the Pillar 3 disclosure rules as laid out by the Financial Conduct

PILLAR 3 DISCLOSURE 31ST December 2013

PILLAR 3 DISCLOSURE 31 ST December 2013 1 BIPRU 11 Pillar 3 disclosure Background The Capital Requirements Directive ( CRD ), which represents the European Union s implementation of the Basel II Accord,

PILLAR 3 DISCLOSURE 31 ST December 2013 1 BIPRU 11 Pillar 3 disclosure Background The Capital Requirements Directive ( CRD ), which represents the European Union s implementation of the Basel II Accord,

RISK PROFILE DISCLOSURE Pillar 3 Capital Requirements Directive

RISK PROFILE DISCLOSURE Pillar 3 Capital Requirements Directive Northern Trust Holdings Limited (incorporating Northern Trust Global Services Limited) June 2012 CONTENTS 1 Overview 1 2 Location and Frequency

RISK PROFILE DISCLOSURE Pillar 3 Capital Requirements Directive Northern Trust Holdings Limited (incorporating Northern Trust Global Services Limited) June 2012 CONTENTS 1 Overview 1 2 Location and Frequency

THE INVESTOR FOR SECURITIES COMPANY. PILLAR III DISCLOSURE As of 31 December 2017

THE INVESTOR FOR SECURITIES COMPANY PILLAR III DISCLOSURE As of 31 December 2017 Table of Contents 1. Scope of Application... 3 1.1. Basis of Disclosure... 4 1.2. Frequency of Disclosures... 4 1.3. Material

THE INVESTOR FOR SECURITIES COMPANY PILLAR III DISCLOSURE As of 31 December 2017 Table of Contents 1. Scope of Application... 3 1.1. Basis of Disclosure... 4 1.2. Frequency of Disclosures... 4 1.3. Material

Citadel Europe LLP. Pillar 3 disclosures for the year ended 31 December 2014

Section Index 1. Introduction: Pillar 3 2. BIPRU 11.5.1 Risk management framework and policies 3. BIPRU 11.5.3 Capital resources 4. BIPRU 11.5.4 Overall Pillar 2 rule 5. BIPRU 11.5.8 Credit risk 6. BIPRU

Section Index 1. Introduction: Pillar 3 2. BIPRU 11.5.1 Risk management framework and policies 3. BIPRU 11.5.3 Capital resources 4. BIPRU 11.5.4 Overall Pillar 2 rule 5. BIPRU 11.5.8 Credit risk 6. BIPRU

Contents 1 Overview Background Basis and frequency of disclosures Location and verification Scope

Contents 1 Overview...4 1.1 Background...4 1.2 Basis and frequency of disclosures...4 1.3 Location and verification...4 1.4 Scope...4 1.5 Changes to disclosure requirements...4 2 Risk management...5 2.1

Contents 1 Overview...4 1.1 Background...4 1.2 Basis and frequency of disclosures...4 1.3 Location and verification...4 1.4 Scope...4 1.5 Changes to disclosure requirements...4 2 Risk management...5 2.1

FCA Pillar 3 Disclosure

FCA Pillar 3 Disclosure Introduction Regulatory Context Evoia Capital LLP ( Evoia or the Firm ) is incorporated in the UK and authorised and regulated by the Financial Conduct Authority ( FCA ). As such,

FCA Pillar 3 Disclosure Introduction Regulatory Context Evoia Capital LLP ( Evoia or the Firm ) is incorporated in the UK and authorised and regulated by the Financial Conduct Authority ( FCA ). As such,

Pillar 3 Disclosure. Sumitomo Mitsui Trust Bank (Thai) Public Company Limited. March 31 st, Pillar 3 Disclosures 31 March 2018

Public Company Limited. March 31 st, Pillar 3 Disclosures 31 March 2018") Sumitomo Mitsui Trust Bank (Thai) Public Company Limited Pillar 3 Disclosure March 31 st, 2018 Sumitomo Mitsui Trust Bank (Thai) Public Company Limited 1 Contents 1. Scope of Application... 3 2. Capital...

Sumitomo Mitsui Trust Bank (Thai) Public Company Limited Pillar 3 Disclosure March 31 st, 2018 Sumitomo Mitsui Trust Bank (Thai) Public Company Limited 1 Contents 1. Scope of Application... 3 2. Capital...

MORGAN STANLEY SMITH BARNEY HOLDINGS (UK) LIMITED AS AT 31 DECEMBER 2013

LIMITED AS AT 31 DECEMBER 2013") MORGAN STANLEY SMITH BARNEY HOLDINGS (UK) LIMITED AS AT 31 DECEMBER 2013 Disclosure (UK) TABLE OF CONTENTS 1. BASEL II ACCORD... 2 2. BACKGROUND TO PILLAR 3 DISCLOSURES... 2 3. APPLICATION OF THE PILLAR

MORGAN STANLEY SMITH BARNEY HOLDINGS (UK) LIMITED AS AT 31 DECEMBER 2013 Disclosure (UK) TABLE OF CONTENTS 1. BASEL II ACCORD... 2 2. BACKGROUND TO PILLAR 3 DISCLOSURES... 2 3. APPLICATION OF THE PILLAR

DARLINGTON BUILDING SOCIETY CAPITAL REQUIREMENTS DIRECTIVE

DARLINGTON BUILDING SOCIETY CAPITAL REQUIREMENTS DIRECTIVE PILLAR 3 DISCLOSURE DOCUMENT AS AT 31 st DECEMBER 2016 CONTENTS Section Title 1 Introduction 2 Risk Management Objectives and Policies 3 Capital

DARLINGTON BUILDING SOCIETY CAPITAL REQUIREMENTS DIRECTIVE PILLAR 3 DISCLOSURE DOCUMENT AS AT 31 st DECEMBER 2016 CONTENTS Section Title 1 Introduction 2 Risk Management Objectives and Policies 3 Capital

Mizuho Securities UK Holdings Ltd Basel III Pillar 3 Disclosures 31 March 2015

Mizuho Securities UK Holdings Ltd Basel III Pillar 3 Disclosures 31 March 2015 Mizuho Securities UK Holdings Ltd Bracken House One Friday Street London EC4M 9JA Telephone +44 (0) 20 7236 1090 Mizuho Securities

Mizuho Securities UK Holdings Ltd Basel III Pillar 3 Disclosures 31 March 2015 Mizuho Securities UK Holdings Ltd Bracken House One Friday Street London EC4M 9JA Telephone +44 (0) 20 7236 1090 Mizuho Securities

PILLAR III DISCLOSURES

PILLAR III DISCLOSURES 6102 PILLAR III Disclosures - 6102 Page 1 of 21 TABLE OF CONTENT 1 SCOPE OF APPLICATION... 4 1.1 PILLAR I MINIMUM CAPITAL REQUIREMENTS... 4 1.2 PILLAR II INTERNAL CAPITAL ADEQUACY

PILLAR III DISCLOSURES 6102 PILLAR III Disclosures - 6102 Page 1 of 21 TABLE OF CONTENT 1 SCOPE OF APPLICATION... 4 1.1 PILLAR I MINIMUM CAPITAL REQUIREMENTS... 4 1.2 PILLAR II INTERNAL CAPITAL ADEQUACY

DARLINGTON BUILDING SOCIETY CAPITAL REQUIREMENTS DIRECTIVE