June 29, Ms. Mary Jo Kunkle Executive Secretary Michigan Public Service Commission 6545 Mercantile Way, P.O. Box Lansing, MI 48909

|

|

|

- Vincent Russell

- 5 years ago

- Views:

Transcription

487-2070 FAX (517) 374-6304 www.millercanfield.")

1 Founded in 1852 by Sidney Davy Miller SHERRI A. WELLMAN TEL (517) FAX (517) Miller, Canfield, Paddock and Stone, P.L.C. One Michigan Avenue, Suite 900 Lansing, Michigan TEL (517) FAX (517) June 29, 2010 MICHIGAN: Ann Arbor Detroit Grand Rapids Kalamazoo Lansing Saginaw Troy FLORIDA: Naples ILLINOIS: Chicago NEW YORK: New York OHIO: Cincinnati CANADA: Toronto Windsor CHINA: Shanghai MEXICO: Monterrey POLAND: Gdynia Warsaw Wrocław Ms. Mary Jo Kunkle Executive Secretary Michigan Public Service Commission 6545 Mercantile Way, P.O. Box Lansing, MI Re: SEMCO Energy Gas Company 2011 Rate Case MPSC Case No. U Dear Ms. Kunkle: Attached for electronic filing are SEMCO Energy Gas Company s Application, Draft Notice of Hearing, and supporting Direct Testimony, Exhibits and Workpapers of George A. Schreiber, Bruce H. Fairchild, James VanSickle, John R. Alger, Marc A. Simone, Mark A. Moses, Paul R. Carpenter, Paul H. Raab, Steven W. Warsinske, and Timothy J. Lubbers, as well as Part II of the MPSC filing requirements. In accordance with MPSC filing requirements, electronic files on CDs and Part III have been transmitted to the Commission staff and will be made available to all parties upon request. Should you have any questions, please advise. Very truly yours, Miller, Canfield, Paddock and Stone, P.L.C. Enclosure cc: Thomas Connelly, SEMCO SAW/tmb 18,112,013.2\ /29/10 9:40 AM By: Sherri A. Wellman

2 S T A T E O F M I C H I G A N BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION * * * * In the matter of the application of ) SEMCO ENERGY GAS COMPANY ) Case No. U to combine its MPSC Division and Battle Creek Division rates and for authority to redesign and increase its rates, on a combined basis, for the sale and transportation of natural gas and for other relief. ) ) ) ) ) APPLICATION Now comes SEMCO ENERGY GAS COMPANY ( SEMCO Gas or the Company ), a division of SEMCO Energy, Inc., and hereby requests authority from the Michigan Public Service Commission (the MPSC or the Commission ) to (i) combine its MPSC Division and Battle Creek Division base and depreciation rates, (ii) increase rates, on a combined basis, for the sale, transportation and distribution of natural gas, (iii) redesign the way in which the Company charges its customers for natural gas service, (iv) implement an Infrastructure Replacement Program for unprotected metallic mains and related cost recovery mechanism, (v) recover in rates the discounts associated with special transportation contracts pursuant to MCL 460.6a(5), and (vi) obtain other related approvals and relief. I. INTRODUCTION 1. SEMCO Gas is a division of SEMCO Energy, Inc., with its principal offices located at 1411 Third Street, Suite A, Port Huron, Michigan. The Company is engaged as a

3 public utility in the business of selling, transmitting, and distributing natural gas to the public in service areas throughout the State of Michigan. 2. The Company currently serves customers in two divisions. SEMCO Gas s Battle Creek Division, which became subject to the Commission s jurisdiction pursuant to its June 26, 2007 Order issued in Case No. U-14882, is defined as including the environs of the City of Battle Creek and several adjacent municipalities, the City of Springfield and the Townships of Assyris, Athens, Baltimore, Battle Creek, Bedford, Convis, Emmett, Johnstown, Leroy, Newton and Pennfield. The Company s MPSC Division is comprised of various non-contiguous areas in Michigan, including areas in and around Port Huron, Richmond, Chesterfield, Sandusky, Romeo, Albion, Niles, Three Rivers, Holland, St. Ignace, Newberry, Engadine, Manistique, Negaunee, Houghton and Ontonagon. On a combined division basis, SEMCO Gas serves approximately 285,000 residential, commercial and industrial customers, with residential customers comprising approximately 91% of the Company's customer base. 3. SEMCO Gas s retail natural gas business is subject to the jurisdiction of the Commission pursuant to 1909 PA 300, as amended, MCL et seq.; 1919 PA 419, as amended, MCL et seq.; and 1939 PA 3, as amended, MCL et seq. Pursuant to these statutory provisions, the Commission has jurisdiction to regulate the Company s retail natural gas sales, transportation and distribution rates in its Battle Creek and MPSC Divisions. This includes jurisdiction over the ways in which such rates are designed to provide the Company with a fair opportunity to recover the costs of providing service to its customers. 4. SEMCO Gas s last MPSC Division base rate case was Case No. U That case was concluded by a Commission Order dated January 9, The revised base rates established in that case were established based on an adjusted test year ending December 31, 2

4 2007, and an authorized rate of return on common equity of 11.00%. SEMCO Gas s base rates for its Battle Creek Division were adopted in Case No. U The Company also recovers its booked cost of gas sold for both its MPSC and Battle Creek Divisions pursuant to its Gas Cost Recovery ( GCR ) clauses authorized by the Commission pursuant to 1982 PA 304, MCL 460.6h et seq. 5. This Application is accompanied and supported by the written testimony, exhibits and workpapers of 10 witnesses. The Company s presentation in this case was prepared in accordance with the Rate Case Filing Requirements established by the Commission s Orders dated December 23, 2008, and February 20, 2009, issued in Case No. U II. COMBINATION OF DIVISION RATES 6. SEMCO Gas seeks authority to combine its MPSC Division and Battle Creek Division rates into one set of common base rates, one GCR clause, and one tariff book. The Company represents that the proposed combination will promote operating efficiencies and reduce the number of GCR and other annual filings before the Commission. 7. The base rate increase proposed in this case is based on the cost of service of serving customers in the combined divisions. 8. SEMCO Gas also seeks to combine the now separate depreciation rates for the MPSC Division and the Battle Creek Division as approved in Case No. U-15778, by using an average deprecation rate for each asset type as the rate to be applied to these asset types on a combined basis. SEMCO Gas seeks approval of these new depreciation rates. 1 The rates adopted in Case No. U reflect the rates established by the Battle Creek City Commission on February 15,

5 III. REQUESTED BASE RATE INCREASE 9. (i) Because the costs of providing service to the Company's customers have increased, and (ii) due, in large part, to a substantial and continuing decline in per customer natural gas usage resulting from the recession and conservation, the Company s existing retail base rates for natural gas services are unreasonably low and inadequate, and SEMCO Gas has not been earning its authorized return on common equity. In fact, in 2009, SEMCO Gas earned 7.69% and 5.32% rates of return for its MPSC Division and Battle Creek Division respectively, as compared to an MPSC-authorized return on equity for the MPSC Division of 11.00%. 10. This rate filing presents data for a historical year ended December 31, 2009, as required by the Commission Orders in Case No. U SEMCO Gas proposes, however, that rates be established based upon a test year ending December 31, 2011, adjusted for known and measurable changes in the costs of providing service to customers. Use of this adjusted test year data allows the revised base rates established in this case to more closely reflect conditions that will likely exist at and after the time the revised base rates set by the final order in this case are placed in effect. 11. Several factors have, and are expected to continue to have, a significant impact upon the Company s costs of providing service to its customers, rendering existing base rates unreasonably low and inadequate and precluding the Company from earning a reasonable return on its investments used and useful in providing service to customers. The most significant factor contributing to the Company s revenue shortfall, as discussed in greater detail in Section IV herein and the testimony accompanying this Application, is declining per customer use of natural gas, including the effects of the recent recession and reduced usage of natural gas now encouraged by State-mandated conservation and energy efficiency programs. Among other things, SEMCO Gas s existing base rates do not reflect recent increases in (i) inflation, (ii) 4

6 operations and maintenance ( O&M ) expenses (including the Service Valve Replacement Program), and (iii) necessary capital investments. The level of capital investment (such as replacement of aging unprotected metallic mains) and O&M expenses necessary to maintain, strengthen, and expand the existing natural gas transportation and distribution system and to assure safe and reliable service to customers have increased significantly beyond the levels currently reflected in the Company s base rates. These and other factors, as described in more detail in the supporting testimony and exhibits, necessitate an increase in SEMCO Gas s current retail natural gas rates. 12. Unless timely rate relief is granted by the Commission, the Company will experience a revenue deficiency of $19,847,589 in This 2011 test year revenue deficiency represents the results of a complete examination of the relevant items of investment, expense, and revenues for the determination of just and reasonable retail natural gas rates for SEMCO Gas s customers. 13. SEMCO Gas proposes that retail natural gas rates be established that reflect an overall rate of return on total rate base of 7.50% and a rate of return on common equity of 11.00%. The capital structure ratios used are based upon the Company s actual capital structure as of December 31, SEMCO Gas represents that, without taking into account the rate design changes proposed by the Company, the proposed rate increase of not less that $19,847,589 annually is required in order for the Company to maintain an adequate, reliable, and safe natural gas transportation and distribution system and to allow SEMCO Gas a reasonable opportunity to earn the return to which the Company is entitled by law. 5

7 IV. PROPOSED IMPROVEMENTS IN RATE DESIGN 15. Reflecting an industry-wide trend as well as local economic conditions, a sharp and continued decline in per customer natural gas use continues to be a major cause for the Company s revenue shortfall and inadequate earnings over the last several years. Actual use per customer is substantially below levels used to establish rates in Case No. U-14893, 2 and this difference between the Company s actual experience and the assumptions used to establish the Company s base rates has adversely affected the Company s collection of revenues through its volumetric distribution rates. In sum, the Company s existing rate design, which provides for the recovery of fixed costs through a combination of fixed charges and volumetric distribution rates based on estimates of customer natural gas use, effectively precludes the Company from earning sufficient revenues to cover the cost of providing service to customers, including a reasonable return on its investments used and useful in providing such service. Under current conditions, the logic of continuing to collect the Company's fixed costs this way is questionable, especially when there are simple ways to sever the recovery of fixed costs from usage. 16. In this case, the Company is proposing that the Commission adopt a different rate design for SEMCO Gas base rates, on a pilot program basis, including: (i) a single fixed monthly charge applied to residential and commercial customers whose usage exceeds a specified level per year and for all transportation customers, thereby replacing the existing combined fixed monthly customer charge and the volume-based distribution charge; or (ii), alternatively, establishing rates for all customers using appropriate rate effective year billing determinants. 2 This is also true regarding the rates established for the Battle Creek Division as initially established in February 2005 by the Battle Creek City Commission which were later adopted by the MPSC in its June 26, 2007 order issued in Case No. U

8 17. The Company is also proposing that the Commission permit SEMCO Gas to collect certain capital costs associated with the accelerated replacement of certain unprotected and bare metallic mains. In view of the Company s (i) relatively small size, (ii) its already substantial capital spending program, and (iii) the non-revenue producing nature of these needed projects, it would be an appropriate exercise of ratemaking discretion for the Commission to authorize the Company to collect the capital-related costs on this project before they are placed in rate base. V. SPECIAL CONTRACTS 18. Section 6a(5) of 2008 PA 286, MCL 460.6a(5) provides as follows: The commission shall, if requested by a gas utility, establish load retention transportation rate schedules or approve gas transportation contracts as required for the purpose of retaining industrial or commercial customers whose individual annual transportation volumes exceed 500,000 decatherms on the gas utility s system. The commission shall approve these rate schedules or approve transportation contracts entered into by the utility in good faith if the industrial or commercial customer has the installed capability to use an alternative fuel or otherwise has a viable alternative to receiving natural gas transportation service from the utility, the customer can obtain the alternative fuel or gas transportation from an alternative source at a price which would cause them to cease using the gas utility s system, and the customer, as a result of their use of the system and receipt of transportation service, makes a significant contribution to the utility s fixed costs. The commission shall adopt accounting and rate-making policies to ensure that the discounts associated with the transportation rate schedules and contracts are recovered by the gas utility through charges applicable to other customers if the incremental costs related to the discounts are no greater than the costs that would be passed on to those customers as the result of a loss of the industrial or commercial customer s contribution to a utility s fixed costs. 19. Pursuant to MCL 460.6a(5) SEMCO Gas is seeking approval of 5 special gas transportation contracts entered into in good faith with industrial customers for the purpose of retaining their load, and for which, as demonstrated in the testimony and exhibits supporting this 7

9 application, the Company is seeking to recover the discounts associated with the contracts through rates charged to its other customers as the discounts are not greater than the costs that would be passed onto the other customers as the result of the loss of the industrial customers contribution to SEMCO Gas s fixed costs. VI. OTHER RELIEF 20. The Company is proposing, among other things, to (i) replace defectively designed service valves on an accelerated basis (known as the Service Valve Replacement Program) to ensure public safety and system reliability, (ii) adopt heat value, or therm-based, billing for all classes of customers, (iii) combine the current Balancing Charge and Capacity Demand Charge into a single Balancing and Demand Charge, (iv) revise its general rules, and (v) revise or implement charges for certain services. This other relief sought by SEMCO Gas is more fully described in the accompanying testimony and exhibits. The relief more fully described in the testimony and exhibits is an integral part of this Application and should be considered as if specifically requested in this Application. VII. SELF-IMPLEMENTATION 21. In accordance with MCL 460.6a(1), if the Commission has not acted on the Company s application within 180 days after the filing is determined to be complete, SEMCO Gas intends to implement for service rendered on and after January 1, 2011, up to the amount of the proposed annual rate request at equal percentage increases applied to all rates. The accompanying testimony and exhibits support an alternative proposal for self-implementation that reflects the fact that current Battle Creek Division and MPSC Division base rates are 8

10 different. This alternative proposal is equitable and should be approved by the Commission for implementation. VIII. REQUEST FOR RELIEF 22. SEMCO Gas s presently-effective retail rates for the sale, transportation and distribution of natural gas are now, and in the future will continue to be, unjust and unreasonable. Such rates are not sufficient to permit the Company to recoup the costs of providing service to its customers, including a reasonable return on investments used and useful in providing such service, to which SEMCO Gas is entitled by law. SEMCO Gas s retail natural gas rates are, and are expected to remain, so low as to deprive it of a reasonable return on its property and to amount to confiscation of the Company s property contrary to SEMCO Gas s rights under the Constitution of the United States and the Constitution and laws of the State of Michigan. The inadequacy of these natural gas rates reduced the Company s revenues and overall rate of return below a proper and reasonable level, and it is unjust and unreasonable to require SEMCO Gas to render natural gas service to its customers at such rates. WHEREFORE, SEMCO Energy Gas Company requests the Commission to: A. Issue and publish its Notice of Hearing setting an early hearing date; B. Combine MPSC Division and Battle Creek Division rates, including the terms and conditions of service to customers; C. Find and determine that existing rates and charges are unreasonably low and inadequate and should be increased to protect the constitutional rights of the Company to earn a reasonable and non-confiscatory return; 9

11 D. Authorize the Company to adjust its existing rates and charges so as to produce additional revenue of not less that $19,847,589 annually, without taking into account the rate design changes proposed by the Company. E. Redesign rates as requested in this Application and addressed in the supporting testimony and exhibits; F. Authorize all other changes and suggestions made and supported in the Company s testimony and exhibits; and G. Grant such other further relief as may be lawful and proper. Respectfully submitted, SEMCO ENERGY GAS COMPANY Dated: June 29, 2010 By: One of its Attorneys Harvey J. Messing (P23309) Sherri A. Wellman (P38989) Paul M. Collins (P69719) MILLER, CANFIELD, PADDOCK AND STONE, P.L.C. One Michigan Avenue, Suite 900 Lansing, Michigan ,049,021.1\ Peter F. Clark (P69185) SEMCO Energy Gas Company 1411 Third Street, Suite A P.O. Box 5004 Port Huron, MI

12

13 STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION NOTICE OF HEARING FOR THE CUSTOMERS OF SEMCO ENERGY GAS COMPANY CASE NO. U SEMCO Energy Gas Company may combine its MPSC Division and Battle Creek Division and may increase its retail natural gas rates for sales and transportation service on a combined basis by $19,847,589 annually, or 18.19%, if the Michigan Public Service Commission approves it requests. A TYPICAL RESIDENTIAL CUSTOMER IN THE MPSC DIVISION WHO USES 100 DTH OF NATURAL GAS PER YEAR MAY SEE AN ANNUAL INCREASE OF $82.69, OR ABOUT 29.9%, IF THE REQUESTED RATE RELIEF IS GRANTED. A TYPICAL RESIDENTIAL CUSTOMER IN THE BATTLE CREEK DIVISION WHO USES 100 DTH OF NATURAL GAS PER YEAR MAY SEE AN ANNUAL INCREASE OF $48.51, OR ABOUT 15.6%, IF THE REQUESTED RATE RELIEF IS GRANTED. The information below describes how a person may participate in this case. You may call or write SEMCO Energy Gas Company, 1411 Third Street, Suite A, Port Huron, Michigan 48060, (800) for a free copy of its application. Any person may review the application at the offices of SEMCO Gas. The first public hearing in this matter will be held: DATE/TIME: BEFORE: LOCATION: PARTICIPATION:, 2010, at.m. This hearing will be a prehearing conference to set future hearing dates and decide other procedural matters. Administrative Law Judge. Michigan Public Service Commission 6545 Mercantile Way, Suite 7 Lansing, Michigan Any interested person may attend and participate.

14 The hearing site is accessible, including handicapped parking. Persons needing any accommodation to participate should contact the Commission s Executive Secretary at (517) in advance to request mobility, visual, hearing or other assistance. The Michigan Public Service Commission (Commission) will hold a public hearing to consider the June 29, 2010 application of SEMCO Energy Gas Company (SEMCO Gas), which seeks Commission approval, among other things, to (i) combine its MPSC and Battle Creek Divisions, (ii) increase revenues for the sale, transportation and distribution of natural gas, (iii) redesign the way in which SEMCO Gas charges its customers for natural gas service, (iv) implement an Infrastructure Replacement Program for unprotected metallic mains and related cost recovery mechanism, and (v) recover in rates the discounts associated with special transportation contracts pursuant to MCL 460.6a(5). SEMCO Gas states that based on a 2011 test year it has a jurisdictional revenue deficiency of $19,847,589, or 18.19%. All documents filed in this case shall be submitted electronically through the Commission s E-Dockets Website at: michigan.gov/mpscedockets. Requirements and instructions for filing can be found in the User Manual on the E-Dockets help page. Documents may also be submitted, in Word or PDF format, as an attachment to an sent to mpscedockets@michigan.gov. If you require assistance prior to e-filing, contact Commission staff at (517) or by at mpscedockets@michigan.gov. Any person wishing to intervene and become a party to the case shall electronically file a petition to intervene with this Commission by, (Interested person may elect to file using the traditional paper format.) The proof of service shall indicate service upon SEMCO Gas s attorney, Sherri A. Wellman, Miller, Canfield, Paddock & Stone, P.L.C., One Michigan Avenue, Suite 900, Lansing, Michigan Any person wishing to make a statement of position without becoming a party to the case may participate by filing an appearance. To file an appearance, the individual must attend the hearing and advise the presiding administrative law judge of his/her wish to make a statement of position. All information submitted to the Commission in this matter will become public information: available on the Michigan Public Service Commission s Web site, and subject to disclosure. Requests for adjournment must be made pursuant to the Commission s Rules of Practice and Procedure R and R Requests for further information on adjournment should be directed to (517) A copy of SEMCO Gas s request may be reviewed on its website at or on the Commission s Web site at michigan.gov/mpscedockets, and at the office of SEMCO Energy Gas Company, 1411 Third Street, Suite A, Port Huron, Michigan. For more information on how to participate in a case, you may contact the Commission at the above address or by telephone at (517)

15 Jurisdiction is pursuant to 1909 PA 300, as amended, MCL et seq.; 1919 PA 419, as amended MCL et seq.; 1939 PA 3, as amended, MCL et seq.; 1982 PA 304, as amended, MCL 460.6h et seq.; 1969 PA 306, as amended, MCL et seq.; and the Commission s Rules of Practice and Procedure, as amended, 1999 AC, R et seq., \

16

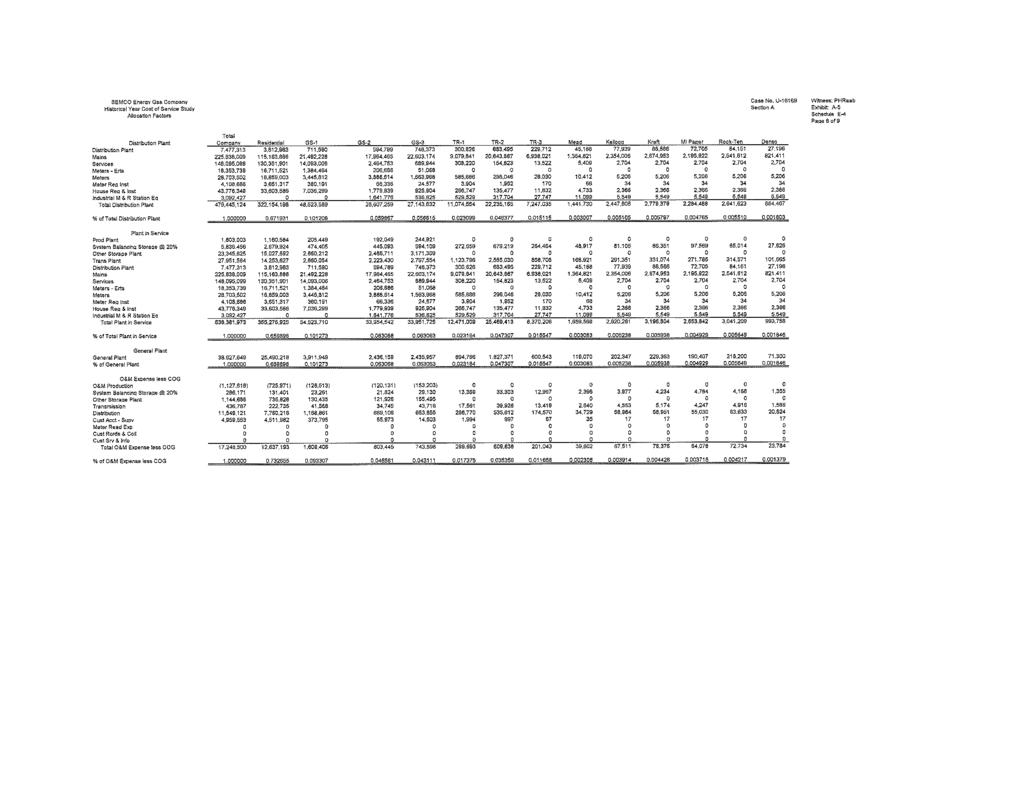

17 SEMCO Energy Gas Company Rate Case No. U Exhibit Summary Exhibit No. Section A Schedule No. Witness A-1 Revenue Deficiency Revenue Deficiency A-1 BHF for Year Ended December 31, 2009 Computation of Revenue Multiplier A-2 BHF for Year Ended December 31, 2009 Comparative Earnings Schedule A-3 BHF A-2 Rate Base Average Rate Base & Capital B-1 BHF Rate Base - Average Net Plant B-2 BHF Rate Base - Balance Sheet Working Capital B-3 BHF A-3 Adjusted Net Operating Income Adjusted Net Operating Income C-1 BHF Net Operating Income C-2 BHF Tax Effect of Interest C-3 BHF Synchronization Adjusment JDITC Adjustment C-4 BHF Advertising Classification C-5 JAV Non-Utility Expenditures C-6 JAV A-4 Rate of Return Overall Rate of Return Summary D-1 BHF Long Term Debt Cost D-2 BHF Cost of Short-term Debt D-3 BHF Preferred Stock Cost D-4 BHF Cost of Common Equity D-5 BHF Financial Metrics - Financial Basis D-6 BHF Financial Metrics - Rate Making Basis D-7 BHF A-5 Summary of Historical Year Revenues E-1 JAV Historical Year Customers and Volumes E-2 JAV Historical Year Operating Revenues E-3 JAV Historical Cost of Service Study E-4 PHR A-6 Rate Design Affiliated Company Transactions Corporate Structure of the Affiliated Group F-1 SWW Summary of Costs Billed To and From F-2 SWW Affiliated Companies Affiliated Companies Rate of Return F-3 SWW on Common Equity Consolidating Balance Sheets F-4 SWW Consolidating Income Statement F-5 SWW

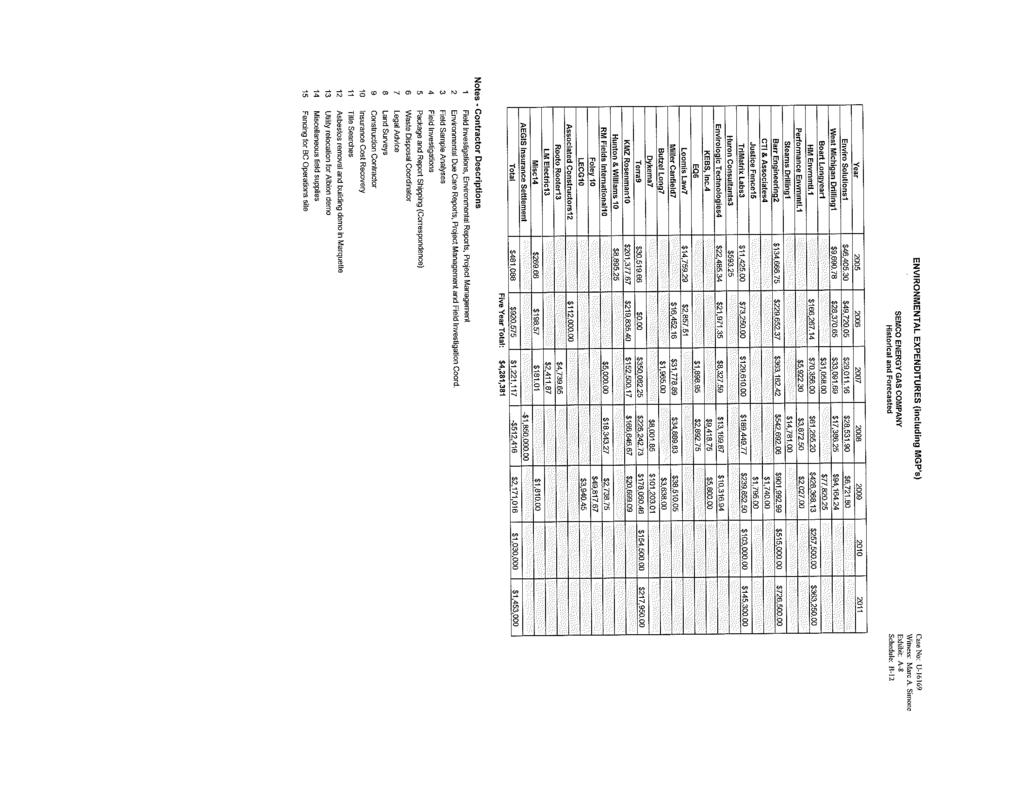

18 SEMCO Energy Gas Company Rate Case No. U Exhibit Summary Exhibit No. Section B Schedule No. Witness A-7 Revenue Revenue Deficiency A-1 BHF Comparison of Revenue Deficiency between the A-2 BHF Historical Period and 2011 Test Year Reconciliation of Revenue Deficiency A-3 BHF for the 2011 Test Year to the Historical Period A-8 Rate Base Rate Base for the 2011 Test Year B-1 BHF Utility Plant for the 2011 Test Year B-2 BHF Accumulated Depreciation B-3 BHF Balance Sheet Working Capital B-4 BHF Cost of Gas B-5 JAV Gas Stored Underground B-6 JAV Short Term Energy Outlook B-7 PRC Historical & Proposed Plant Additions B-8 MAS Infrastructure Replacement Program B-9 MAS Service Valve Replacement Program B-10 MAS Service Valve Compaint B-11 MAS Environmental Expenditures B-12 MAS A-9 Adjusted Net Operating Income Net Operating Income Adjustments C-1 BHF Computation of Revenue Multiplier C-2 BHF for the 2011 Test Year Revenues C-3 BHF Cost of Gas Sold C-4 BHF Other Operations & Maintenance Expense C-5 MAM Depreciation & Amortization Expense C-6 BHF Taxes Other than Income C-7 MAM Michigan Business Tax C-8 SWW Federal Income Taxes C-9 BHF Interest Syncronization C-10 BHF Operating Income Adjustments C-11 BHF LAUF and Company Use C-12 JAV Amortization of Pension and Other Post-Retirement C-13 SWW Benefit Expenses

19 SEMCO Energy Gas Company Rate Case No. U Exhibit Summary A-10 Rate of Return Overall Rate of Return Summary D-1 BHF Cost of Long Term Debt D-2 BHF Cost of Short Term Debt D-3 BHF Cost of Preferred Stock D-4 BHF Cost of Common Equity D-5 BHF Credit Ratings D-6 BHF Recent Utility Bond Issuances D-7 MAM Financial Metrics D-8 BHF Capital Structure D-9 BHF DCF Model - Dividend Yield D-10 BHF DCF Model - Earnings Growth D-11 BHF DCF Model - Sustainable Growth D-12 BHF DCF Model - Other Growth Rates D-13 BHF Capital Asset Pricing Model D-14 BHF Risk Premium Method D-15 BHF Comparable Earnings Method D-16 BHF IRP Capital Charge Rate D-17 BHF A-11 Rate Design Summary of Proposed Rate Increase E-1 PHR Test Year Volumes, Customers and Adjustments E-2 JAV Reduced Volumes Due to Energy Optimization E-3 JRA Calculation of Pro Forma and Proposed Revenues E-4 PHR Comparison of Current and Proposed Rates E-5 PHR Cost of Service Study E-6 PHR Summary of Proposed Tariff Sheet Changes E-7 JAV Proposed Tariff Sheets E-8 JAV Alternative Definitions of Normal Weather E-9 PHR Usage Level Rate Desighns E-10 PHR A-12 Self-Implementation of Rate Increase F-1 JRA Weather Normalized Residential Use per Customer F-2 GAS Not Used F-3 Special Contract F-4 TLJ Special Contract F-5 TLJ Special Contract F-6 TLJ Special Contract F-7 TLJ Map F-8 TLJ Special Contract F-9 TLJ Map F-10 TLJ Special Contract Summary F-11 TLJ

20 STATE OF MICHIGAN BEFORE THE MICHIGAN PUBLIC SERVICE COMMISSION ***** In the matter of the application of ) Case No. U SEMCO ENERGY GAS COMPANY to combine its ) MPSC Division and Battle Creek Division rates and ) for authority to redesign and increase its rates, on a ) combined basis, for the sale and transportation of ) natural gas and for other relief. ) DIRECT TESTIMONY AND EXHIBIT OF GEORGE A. SCHREIBER, JR. ON BEHALF OF SEMCO ENERGY GAS COMPANY 1

21 Direct Testimony of George A. Schreiber, Jr. On Behalf of SEMCO Energy Gas Company Introduction Q. Please state your name, title, current employer, and business address. A. My name is George A. Schreiber, Jr. I am President and Chief Executive Officer of Continental Energy Systems LLC ( Continental ) and serve on Continental s Board of Managers. Continental is headquartered in Troy, Michigan. In addition, I am President and Chief Executive Officer of SEMCO Energy, Inc. ( SEMCO ). I also serve on SEMCO s Board of Directors, as Chairman. SEMCO is headquartered at 1411 Third Street, Suite A, Port Huron, Michigan Q. Please describe the ownership of SEMCO. A. In 2007, after a series of transactions, SEMCO became a wholly-owned indirect subsidiary of Continental. Continental is controlled by affiliates of Lindsay Goldberg LLC. Lindsay Goldberg LLC is a private equity investment fund based in New York and currently has approximately $10 billion of capital under management. Q. On whose behalf are you testifying in this proceeding? In responding, please describe those entities. A. I am testifying on behalf of SEMCO Energy Gas Company. SEMCO Energy Gas Company is a division of SEMCO. SEMCO Energy Gas Company has two divisions known as the MPSC Division and Battle Creek Division. Those divisions provide retail natural gas service to approximately 285,000 customers in service areas located in the Upper and Lower peninsulas of Michigan. The retail natural gas distribution and transportation businesses of both the MPSC Division and Battle Creek Division are subject to the regulatory jurisdiction of the Michigan Public Service Commission (the MPSC or the Commission ). For convenience, and also because it is proposed in this proceeding to combine the MPSC Division and Battle Creek Division rates, I refer to both divisions as SEMCO Gas or the Company in this testimony. 2

22 Direct Testimony of George A. Schreiber, Jr. On Behalf of SEMCO Energy Gas Company Q. Please describe your educational background. A. I received both my Bachelor of Science (1970) and Masters of Business Administration (1971) degrees from Arizona State University. Arizona State University is located in Tempe, Arizona. Q. Please describe your professional experience prior to joining SEMCO. A. Before joining SEMCO in April 2004, I spent most of my career as an investment banker with various firms based in New York. As an investment banker, I was a financial advisor to regulated, investor-owned public utilities. Among other things, I provided financial advice relating to capital structures, credit quality and rating agency perspectives, asset acquisitions and dispositions, mergers and other business combinations, and financing plans. I also was involved, in various roles, in numerous transactions in both the domestic and international capital markets. Immediately prior to joining SEMCO, I was Chairman of the Global Energy Group of Credit Suisse First Boston. At other points in my career, I was President of Pinnacle West Capital Corporation and Manager of Regulatory Affairs at Arizona Public Service Company. A copy of my current resume is attached to this testimony as Attachment 1. Q. Have you previously testified in any regulatory proceedings before the MPSC or other state or federal regulatory agencies? A. I have not previously testified before the Commission. I have provided expert testimony before regulatory agencies in ten other states as well as before the Federal Energy Regulatory Commission and a federal bankruptcy court. Role, Purpose, and Topics Addressed Q. What is your role in this proceeding? A. I am the Company s chief policy witness, which means that, with substantial input from others, I set the overall direction for this filing. That included making various policy choices, 3

23 Direct Testimony of George A. Schreiber, Jr. On Behalf of SEMCO Energy Gas Company identified in this testimony. Witnesses did their work on this filing based on those choices, consistent with exercising their own professional judgment. Q. What is the purpose of your testimony in this proceeding? A. The purpose of my testimony is three-fold. First, I summarize the Company s proposals, so that the Commission will have, in one place, the essential elements of what SEMCO Gas is asking the Commission to do. Other witnesses provide additional detailed information the Commission should find useful in evaluating those proposals. Second, I identify the other witnesses appearing on behalf of SEMCO Gas in this proceeding and describe, in general terms, the topics they address in the case. In a sense, that testimony is a roadmap to this filing. Finally, I discuss what I believe are key issues or policy decisions raised by this filing. I detail the Company s proposals on these subjects, set the proposals in context, and explain the Company s overall thinking to the Commission. Again, other witnesses in the case also testify on these topics. Q. What specific topics do you address in your testimony? A. I discuss the following topics in my testimony: A summary of SEMCO Gas s proposals, including the base rate relief requested by the Company based on the combination of MPSC Division and Battle Creek Division rates. SEMCO Gas s rate design proposal for collecting the Company s revenue requirement, on a pilot program basis. The Company s primary proposal is to use a single fixed monthly charge rate design for collecting revenue from residential and commercial customers whose usage exceeds a specified therm level per year and for all transportation service customers. Alternatively, rates should be established for all customers using appropriate rate effective year billing determinants. Who is sponsoring prefiled direct testimony on behalf of the Company and on what topics. 4

24 Direct Testimony of George A. Schreiber, Jr. On Behalf of SEMCO Energy Gas Company The recommended return on equity (the ROE ) the Commission should allow SEMCO Gas a fair opportunity to earn during the period when revised base rates will be in effect. Q. Please identify the exhibits which you are sponsoring in this case. A. In addition to the exhibit summarizing my credentials, I am sponsoring the following: 5 Exhibit A-12 Schedule F-2 Weather Normalized Residential Use per Customer Q. Was this exhibit prepared by you or under your direction? A. Yes. Summary of SEMCO Gas Proposals Q. Please summarize SEMCO Gas s proposals in this proceeding. A. SEMCO Gas respectfully proposes, based on my testimony and the testimony of the other witnesses for the Company, that the Commission: Authorize the combination of the Company s MPSC Division and Battle Creek Division into one division with one set of common base rates, one Gas Cost Recovery ( GCR ) clause and one tariff book with the terms and conditions of service for all of the Company s Michigan customers. Authorize an overall annual base rate increase of $19.8 million (or approximately 5.3% on a total bill basis) in combined MPSC and Battle Creek Division rates for SEMCO Gas on the basis of a test year ending December 31, 2011, adjusted for known and measurable changes in the costs of providing service to customers. Absent issuance of a Commission order, the Company plans to self-implement rates for service rendered on or after January 1, 2011, up to the amount of the proposed request at equal percentage increases applied to all rates. The Company is also proposing, however, an alternative proposal for selfimplementation. This alternative proposal reflects the fact that current MPSC and Battle Creek Division base rates are different, making implementation of an across-the-board equal percentage self-implemented rate increase problematic. 5

25 Direct Testimony of George A. Schreiber, Jr. On Behalf of SEMCO Energy Gas Company Approve, on a three-year pilot program basis, a single fixed monthly charge rate design for residential customers whose usage is greater than 900 therms per year, all commercial customers (formerly rate class GS-1) whose usage is greater than 1,750 therms per year, and all for transportation service customers. These single fixed monthly charges would replace the combination of a fixed monthly charge and a volumetric-based distribution charge now used to collect the fixed costs of service from these customers. To accommodate concerns about the impact of such a rate design on lower-usage customers, for residential customers whose usage is below 900 therms per year and commercial (formerly rate class GS-1) customers whose usage is below 1,750 therms per year, the Company is proposing to maintain the traditional combination of a monthly customer charge and usage-based distribution charge. As an alternative, if the Commission does not elect to approve the proposed single fixed monthly charge rate design as proposed and a traditional rate design is used in which some portion of the Company s fixed costs are to be collected volumetrically, set the billing determinant for residential rates based on a use per customer of 899 therms per year and the billing determinant for the GS-1 commercial rate at 1,767 therms per year. Approve the Infrastructure Replacement Program for unprotected metallic main replacement and recovery of the associated costs. Approve the Company s Service Valve Replacement Program and recovery of the associated costs. Allow the Company a fair opportunity to earn a return on equity of 11.0%. Approve the use of therms as the basis of billing all customer classes. Approve all of the proposed adjustments and tariff changes sponsored by the Company s witnesses. Witnesses for SEMCO Gas in this Proceeding; Subjects Addressed 6

26 Direct Testimony of George A. Schreiber, Jr. On Behalf of SEMCO Energy Gas Company Q. What witnesses are appearing on behalf of SEMCO Gas in this proceeding and what is the subject-matter of their prefiled testimony? A. The following witnesses are sponsoring prefiled testimony on behalf of SEMCO Gas on the topics I describe: Bruce H. Fairchild Dr. Fairchild is sponsoring testimony and exhibits that constitute the schedules required by the Commission s standardized rate case filing requirements for both the historical and the forecast test years. He also sponsors the Company s requested rate of return and the Company s cost of debt and capital structure. James A. Van Sickle Mr. Van Sickle is sponsoring testimony and exhibits on the Company s Lost and Unaccounted for Gas, Company Use Gas, Gas in Storage, various adjustments to operating expenses, test year customer data, and various proposed tariff changes. John R. Alger Mr. Alger is sponsoring testimony and exhibits on the combination of the MPSC Division and Battle Creek Division, the Company s proposal to combine the current Balancing Charge and Capacity Demand Charge, the use of therms (or heat value) as the basis for billing all customer classes, the Company s self implementation of revised base rates, the ratemaking mechanics of the Infrastructure Replacement Program, and certain sales and transportation volume adjustments arising from the Company s Energy Optimization program and related legislative mandates to reduce gas usage by SEMCO Gas customers. Marc A. Simone Mr. Simone is sponsoring testimony and exhibits in support of SEMCO Gas s projected capital expenditures for 2010 and He also discusses the need for the Infrastructure Replacement Program for unprotected metallic mains. He also supports the Company s Service Valve Replacement Program and the Company s expenditures for environmental compliance. 7

27 Direct Testimony of George A. Schreiber, Jr. On Behalf of SEMCO Energy Gas Company Mark A. Moses Mr. Moses is sponsoring testimony and exhibits in support of the methodology used by the Company to forecast Operations and Maintenance expense, Property and Other Tax expense, and Other Gas Revenues. Paul R. Carpenter Dr. Carpenter is sponsoring testimony and exhibits in support of the forecasted price of natural gas in The price of gas is the basis for a number of revenue requirement items, given how those items are currently recovered in SEMCO Gas s base rates. Paul H. Raab Mr. Raab is sponsoring testimony and exhibits on the Company s proposed rate design, the Company s revenue and sales and transportation volume forecast, and weather normalization. He also sponsors the Company s cost of service study. Steven W. Warsinske Mr. Warsinske is sponsoring testimony and exhibits on intracompany transactions and allocations, the implementation of new depreciation rates approved in Case No. U and a proposal to combine those new depreciation rates into a single set of depreciation rates for the combined MPSC and Battle Creek Divisions, the recovery of the amortization of pension and post-retirement costs, and income and other taxes, including the Michigan Business Tax. Timothy J. Lubbers Mr. Lubbers is sponsoring testimony supporting the continuation of Special Transportation Agreements for certain customers and the recovery in base rates of the discounts in such contracts. Proposal to Combine the MPSC Division and Battle Creek Division Rates Q. Please describe the Company s proposal to combine MPSC and Battle Creek Division rates into a single set of rates and terms and conditions of service. A. The Company currently has two divisions that provide natural gas service to customers in various areas throughout Michigan. Rates and terms and conditions of service to customers in both divisions are regulated by the MPSC, though service to customers in the Battle 8

28 Direct Testimony of George A. Schreiber, Jr. On Behalf of SEMCO Energy Gas Company Creek Division was once regulated by the City Commission of Battle Creek. As a result of this now-ended separation in regulatory authority, the divisions currently have separate rates, tariffs and other terms and conditions of service. In June 2007, the MPSC assumed jurisdiction over the Battle Creek Division in Case No. U Now that the Commission has jurisdiction over both divisions, the Company is proposing to combine the rates, tariffs and other terms and conditions of service for these divisions into a single set of rates, tariffs and other terms and conditions of service. As such, the base rates proposed in this proceeding are based on the cost of service to all of the Company s Michigan customers, as if the historical divisional structure did not exist. Q. What is the thinking behind this change? A. The fact that there are different rates, tariffs and terms and conditions of service for customers in each division currently leads to confusion on the part of customers. Combining rate and terms and conditions of service should end this confusion. The Company believes that combining the existing separate sets of rates is appropriate and that a single set of rates will be better understood and accepted by customers. Mr. Alger discusses this in more detail in his testimony. Proposed Base Rate Revenue Increase Q. Please summarize SEMCO Gas s proposed annual base revenue increase. A. SEMCO Gas is requesting an annual base revenue increase of $19,847,589 for the combined MPSC and Battle Creek Divisions at the 11.0% authorized return on equity sponsored by Dr. Fairchild. This proposed annual revenue increase is based on a projected test year ending December 31, The Company s future revenues are expected to be negatively impacted due to a continued reduction in use per customer, as discussed by Mr. Raab, as well as further reductions in usage expected as a result of the State-mandated energy optimization programs and customer losses. Unless current base rates are adjusted, 9

29 Direct Testimony of George A. Schreiber, Jr. On Behalf of SEMCO Energy Gas Company the Company will not have a fair opportunity to recoup its costs of providing service to customers, including a reasonable return on its investments. Q. When did SEMCO Gas last increase its base rates? A. SEMCO Gas last filed a general rate case for its MPSC Division in May In its January 9, 2007 order, the MPSC approved a settlement agreement that, among other things, provided for an estimated annual revenue increase of $12.6 million based on a test year ending December 31, In February 2005, the Battle Creek Division was granted an annual revenue increase of $3.55 million by the Battle Creek City Commission. No base rate increase has been granted to the Battle Creek Division since the Commission assumed jurisdiction over the Battle Creek Division in June Since those cases, various factors have resulted in the need for the revenue increase requested in this proceeding, including the continued decline in use per customer as a result of the recession and conservation and increases in operations and maintenance expenses due to inflation and other factors, as discussed by Mr. Moses in his testimony. Q. Does SEMCO Gas plan to self-implement the proposed revenue increase? A. Yes, as permitted by Section 6a(1) of Public Act 286 of 2008, SEMCO Gas plans to selfimplement rates up to the amount of the proposed revenue increase request for service rendered on or after January 1, The Company has filed tariffs based on the statutory requirement that the proposed annual rate request be applied through equal percentage increases across all base rates. The Company is requesting, however, that the Commission approve an alternative methodology for self-implementation of the proposed revenue increase that reflects the fact that current MPSC Division and Battle Creek Division rates are different. For example, the monthly service charge and distribution charges are different in each division, and the Battle Creek Division rates currently include an additional monthly charge for certain costs that were included in cost of gas when this division operated under 10

30 Direct Testimony of George A. Schreiber, Jr. On Behalf of SEMCO Energy Gas Company the jurisdiction of the City Commission of Battle Creek but which are now included in base rates under the Commission s rules. Applying equal percentage increases to such different rates would result in further confusion on the part of customers as well as result in a situation in which certain customer classes would be over-charged and due a refund while others would be under-charged once final rates are determined in this proceeding. For these reasons, the Company is proposing to self-implement the rate changes in the alternative manner more fully described in Mr. Alger s testimony. Proposed Single Monthly Fixed Charge Rate Design; Pilot Program Q. Please discuss the Company s rate design proposal. A. SEMCO Gas proposes that the Commission authorize the Company to collect the revenue requirement assigned to certain customer classes through a single fixed monthly charge. This single fixed charge methodology would apply to residential customers whose usage is greater than 900 therms per year, all commercial customers (rate class GS-1) whose usage is greater than 1,750 therms per year, and all transportation service customers. These single fixed charges would replace the combination of a fixed monthly charge and a volumetric-based distribution charge now used to collect revenues from these customers. For residential customers whose usage is below 900 therms per year and commercial (rate class GS-1) customers whose usage is below 1,750 therms per year, the Company is proposing to maintain the traditional combination of a monthly charge and usage based distribution charge. I will refer to this aspect of the Company s proposal as the "usage level exception." In my view, while I am persuaded that it makes sense to collect a utility s fixed costs of providing service in a fixed monthly charge, this usage level exception addresses a common concern that lower usage customers will object to paying for service on a fixed charge basis. Q. Would this be a pilot program, subject to later Commission evaluation? 11

31 Direct Testimony of George A. Schreiber, Jr. On Behalf of SEMCO Energy Gas Company A. Yes. In this case, the Company is proposing that the Commission adopt the proposed rate design, including the usage level exception element of the proposal, for SEMCO Gas base rates, on a pilot program basis. The Company proposes to conduct such a pilot program over a period of three years and report to the Commission periodically and at the end of three years on its experience with this rate design. Q. What if the Commission exercises its discretion to maintain the current rate design? A. I recognize that the Commission may prefer to maintain the current two-part rate design. As an alternative, if the Commission elects to keep the current rate design, SEMCO Gas is proposing the Commission set base rates for all customers using appropriate billing determinants. Let me illustrate, using residential and small commercial customers as an example. In my view, the Commission should (1) conclude that, under normal weather conditions, the effects of volatile gas prices and ongoing conservation on consumption will cause residential and small commercial customers to use 899 and 1,767 therms of gas, respectively, on average, each year, and (2) order base rates to be set with those expected levels of usage as the billing determinants. Mr. Raab testifies on various aspects of these recommended usage figures as well as the consumption estimates to be used for all other classes of customers in his testimony. Q. Is the single fixed monthly charge rate design with the usage level exception designed to separate the recovery of fixed costs from usage? A. Yes. Adopting the single fixed monthly charge proposal would sever the Company s collection of fixed costs of service from the level of customer gas usage. That, in turn, would align Company and customer interests when it comes to the conservation of natural gas. I would call it a pro-conservation rate design. Such a rate design also would align Commission rate design policy and the legislative policy mandating the implementation of energy optimization programs by natural gas utilities in the State of Michigan. 12

32 Direct Testimony of George A. Schreiber, Jr. On Behalf of SEMCO Energy Gas Company Q. Describe in more detail how SEMCO Gas proposes to collect its base rate revenue from its customers. A. SEMCO Gas is requesting a rate design that separates the revenues needed to cover the cost of service from the volumetric consumption of most, but not all, of its customers. Except for residential customers whose annual usage is less that 900 therms and small commercial customers whose annual usage is less than 1,750 therms, the method that the Company is proposing is a singled fixed charge, paid by customers monthly, that recovers all the fixed costs of providing service to them. These fixed costs include preparing and transmitting customer bills, interacting with customers over the telephone and in-person (such as on service calls), maintaining meters, regulators, service lines, and recovering the Company s capital costs (including cost of the investments in facilities used to serve customers and an appropriate return on those investments) in sum, everything needed for a customer to receive natural gas from the Company s system for use in a home or business and for the Company to interact with that customer about his or her natural gas service. Q. How much are the proposed single fixed monthly charges? A. SEMCO Gas is proposing a fixed monthly charge of $29.94 for residential customers (Residential A), $63.19 for small commercial (GS-1A) customers, $ for GS-2 customers, $ for GS-3 customers, $1, for TR-1 customers, $8, for TR-2 customers and $31, for TR-3 customers. Q. How do these proposed charges compare to current charges paid by residential customers? A. For residential customers, the $29.94 monthly charge would replace the monthly customer charge (currently $10.00 for MPSC Division customers and $11.00 for Battle Creek Division customers) and the monthly distribution charge (currently $ per Mcf of usage for the MPSC Division and $ per Dth of usage for the Battle Creek Division). The new single 13

33 Direct Testimony of George A. Schreiber, Jr. On Behalf of SEMCO Energy Gas Company fixed monthly charges include all of the costs associated with serving these customers that were formerly collected through these two charges. The proposed single fixed monthly charges include the base rate increase proposed in this filing. To the extent the Commission alters SEMCO Gas s requested base rate increase, the proposed single fixed monthly charges would be altered accordingly. In discussing this topic, I am putting aside any separate surcharges and other similar amounts the Commission has authorized the Company to collect. Q. What rates is the Company proposing for those residential and commercial customers that would not be billed via single fixed monthly charges? A. For those residential customers whose usage does not exceed 900 therms per year (Residential B), the Company is proposing a monthly charge of $13.03 and a distribution charge of $ per therm. For those commercial customers whose usage does not exceed 1,750 therms per year (GS-1B), the Company is proposing a monthly charge of $23.24 and a distribution charge of $ per therm. Q. In your view, what are the primary reasons for adopting a single fixed monthly charge rate design for many of the Company s customers? A. The primary reasons for adopting a single fixed charge rate design are to: 1. Align Company and customer interests with respect to conservation, in this case by harmonizing a State of Michigan policy to encourage conservation through energy optimization programs with Commission-sponsored ratemaking policies that will give SEMCO Gas a fair opportunity to recover the costs of service, including the cost of capital. 2. Levelize SEMCO Gas s collection of its costs, by eliminating most volumebased distribution charges that are highest in the winter heating season when customers consume the most natural gas and therefore experience the highest bills. 14

34 Direct Testimony of George A. Schreiber, Jr. On Behalf of SEMCO Energy Gas Company Address, other than by implementing the proposed adjusted billing determinants, the effect of a substantial and continuing decline in use per customer on SEMCO Gas s collection of its revenue requirement. 4. Provide customers with a bill that is easier to understand, because volumetric recovery of SEMCO Gas s revenue requirement (the distribution charge) will be eliminated for most customer classes. 5. Clarify for most customers, on the face of their bills, the fact that SEMCO Gas makes no additional money on the gas cost commodity portion of a customer s bill. 6. Employ a rate design that reflects sound economic and ratemaking principles, as discussed by Mr. Raab, because fixed costs are collected through fixed charges, and for other reasons that are addressed at length in his testimony. Q. Why is SEMCO Gas proposing a set of fixed monthly charges for most customers? A. I believe that a single fixed monthly charge for most customers is the best overall rate design this time, primarily because: 1. A single fixed monthly charge should be easy for customers to understand. On its face, the customer s bill would clearly differentiate the costs of SEMCO Gas s providing service from the cost of the natural gas consumed by the customer. In that sense, the proposed bill makes it clearer that the Company does not profit on the gas commodity portion of the bill, since all of the Company s costs (including its return on investments in rate base) would be collected in a single fixed monthly charge. Under SEMCO Gas s current rate design, because revenue collection varies with the volumetric distribution rate, the Company collects more revenue to cover fixed costs when customers use more gas and less revenue to cover fixed costs when customers use less gas. So, it is understandable, given how they are charged, that 15

35 Direct Testimony of George A. Schreiber, Jr. On Behalf of SEMCO Energy Gas Company some customers find it difficult to believe that the Company is not profiting on the gas they consume. 2. Fixed monthly charges are familiar to, and accepted by, customers. It should be kept in mind that customers are already familiar with many forms of fixed charge bills, such as bills for internet service and cellular phone usage. 3. A single fixed monthly charge is a simpler, lower-cost method to achieve the same pro-conservation public policy objectives that other decoupling mechanisms are designed to address, in terms of regulatory oversight, accounting complexity, and billing system information technology changes. 4. Customers would no longer over-pay for the cost of Company-provided gas delivery services in colder-than-normal winters and under-pay for those services in warmer-than-normal winters. By definition, since there is a volumetric component in the Company s current rate design in the form of the distribution charge, the collection of SEMCO Gas s base rate revenue requirement is affected by the weather, making the Company a seasonal, weather-dependent business. Because of the resulting effects on revenue collection, and putting aside other factors affecting usage, the Company over-collects its revenue requirement in colder-than-normal periods and under-collects its revenue requirement in warmer-than-normal periods. Under the Company s preferred proposed rate design, the volumetric component is eliminated for most customers, thus taking weather "out of the equation" from the perspectives of both customers and the Company. 5. Volatility in customer bills will be reduced since a larger portion of the total bill would be fixed each month and would not be dependent on changes in weather or usage patterns. That said, as Mr. Raab confirms, customers would still receive an appropriate price signal, based on their consumption of natural gas, because they 16

36 Direct Testimony of George A. Schreiber, Jr. On Behalf of SEMCO Energy Gas Company would be charged in the gas cost commodity, or GCR, portion of their bill for their actual gas usage. Q. Why does SEMCO Gas believe that single fixed monthly charges are fair for customers? A. Let me add my perspective to what Mr. Raab says in his testimony. The elements that comprise the cost to provide service are essentially the same for all of the customers in each class, irrespective of the volume of gas those customers consume. For example, the cost to prepare and transmit a bill does not vary with usage in various customer groups. Similarly, all customer classes are provided the safety-related services by the Company, such as leak surveys and emergency response to potential leaks on customer premises, and the costs of these services do not vary with usage. SEMCO Gas s current rate design collects approximately 63% of these charges volumetrically from all customers, effectively allowing lower-usage customers to pay less than their full cost of service. Mr. Raab discusses this subject in detail. Q. Does a single fixed monthly charge disadvantage low-income residential customers? A. No. As mentioned earlier, within each class, the cost to serve these customers is essentially the same. A single fixed charge eliminates subsidies between different customers within each class regardless of socio-economic factors. In truth, most customers will not see much of a change in their overall bills, since the single fixed monthly charge is a replacement for both the monthly charge and the volumetric distribution charge. The small group of highusage customers should favor this change; it will eliminate what is, in effect, an intra-class subsidy provided to lower-usage customers. Q. Discuss the impact of the usage option rate design on lower-usage residential and small commercial customers. A. Again, Mr. Raab discusses this topic in his testimony. These groups of customers might consider themselves to be disadvantaged by a change to a single fixed monthly charge 17

37 Direct Testimony of George A. Schreiber, Jr. On Behalf of SEMCO Energy Gas Company method for recovering the Company s fixed costs of providing service. To address this perception, the Company proposes to maintain the traditional rate design for such customers (a fixed monthly service charge and a variable distribution charge). Under this approach, these lower-usage customers will continue to pay based on their level of consumption, thereby avoiding any perceived "over-charging" based on their lower usage compared to other customers within their class. Q. What customer response does the Company expect from a changeover to a single fixed monthly charge rate design for most of its customers? A. None; I do not expect a significant negative reaction from customers. Many customers are accustomed to fixed charges for other services and have frequently demonstrated a preference for this sort of fixed charge. Examples of monthly fixed charge services now paid by residential customers include: basic local telephone (including access taxes), mobile telephone, cable service, home alarm monitoring services, internet access, automobile leases, and apartment rent. SEMCO Gas is proposing a $29.94 per month fixed charge for certain residential customers. That proposed charge is comparable in concept to some of the examples given here and on a par with, or substantially below, the fixed charges customers pay for other services. In fact, in my experience, people are surprised to learn that the cost of the service the Company provides is so low, generally because they mistakenly believe that SEMCO Gas keeps the gas cost or GCR revenues it collects as profits as opposed to what the Company actually does, which is use that money to pay various producers for the gas customers use. Also, commonsense tells me that customers are likely to prefer a charge that reduces the amount they will pay during the months when their bills are the highest (i.e., during heating season), rather than a volumetric charge that effectively adds to the highest 18

38 Direct Testimony of George A. Schreiber, Jr. On Behalf of SEMCO Energy Gas Company bills they experience. Given customer acceptance of fixed charges, I do not expect a significant negative customer response from those customers who would be impacted by the proposed change. Q. Do you have anything to add on the subject of your expectations about the customer response to the Company s proposed single fixed monthly charges for most customers? A. Yes, I should add that the Company would propose to educate customers about the new single fixed charge rate design, if the Commission were to adopt it. There would be opportunities to do so at the time of approval, in materials included in each affected customer s monthly bill. It also is important to make it unattractive, financially through the use of re-connection charges, for customers to avoid the monthly single fixed charges by disconnecting and re-connecting service. Q. Do SEMCO Gas customers voluntarily participate in a budget bill program? A. Yes, as of April 30, 2010, approximately 44,000 SEMCO Gas residential customers participated in budget billing (which is a levelized payment plan for the entire bill for gas service). This number of customers represents about 17% of all current residential customers. Q. Does the Company believe that this participation in a levelized payment option indicates that customers are receptive to single fixed monthly charges? A. Yes. As an optional program, budget billing requires customers to make the effort to contact the Company and request to what is, in effect, levelized billing for their entire bill. In my opinion, the fact that about 17% of all residential customers took it upon themselves to make this choice indicates that customers are not adverse to the concept of single fixed monthly charges. Q. What does the next series of questions and answers in your testimony address? 19

39 Direct Testimony of George A. Schreiber, Jr. On Behalf of SEMCO Energy Gas Company A. The next series of questions and answers addresses common criticisms of the proposed single fixed monthly charge rate design. Q. Does SEMCO Gas believe that single fixed monthly charges are a disincentive to conservation? A. No. Even after changing over completely to a single fixed monthly charge, approximately 72% of the average total residential customer bill would still vary with usage and thus provide a sufficient incentive for conservation. The GCR or commodity portion of the bill is volumetric, and thus this percentage grows in winter months, when residential customers typically consume more gas when they heat their homes during Michigan s cold winters. As noted, this high percentage portion of the customer bill will continue to rise and fall with volumetric use, which is what a customer is trying to affect by conserving. In my view, having a bill that is 72% (or more in colder months) tied to consumption is such a significant component of the bill that conservation efforts will not be impacted by the comparatively minor percentage change that results from shifting the volumetric recovery of the Company s costs to a single fixed monthly charge, as proposed. Q. How does a fixed monthly service charge affect SEMCO Gas s perspective with respect to conservation and energy efficiency? A. The collection of the Company s revenue requirement from most customer classes through a single fixed monthly charge rate design aligns Company and customer interests with respect to conservation and energy efficiency. As noted earlier in my testimony, aligning Company and customer interests is especially important when the State of Michigan requires all utilities to offer energy optimization programs to all classes of customers. To me, state policy should be consistent if a state is encouraging conservation by legislative mandate, utility rate design should reflect that public policy. 20

40 Direct Testimony of George A. Schreiber, Jr. On Behalf of SEMCO Energy Gas Company Q. Does a single fixed monthly charge guarantee that the Company will earn its Commissionauthorized rate of return? A. No. The proposed single fixed charge, pro-conservation rate design does not guarantee that SEMCO Gas will recover its costs and earn its Commission-authorized return on equity. This is because there are other factors that affect the Company s ability to recoup its costs and earn its authorized return on equity. For example, increases in operations and maintenance costs resulting from increases in general inflation will affect the Company s financial performance. The state of the economy in Michigan and the absence of, or minimal, customer growth is another risk factor. SEMCO Gas continues to make expenditures for system improvements, main and service extensions and replacements, new vehicles and work equipment, and all of the other goods and services necessary or useful in providing safe, efficient, and reliable natural gas service to customers. Inflation tends to drive many of these costs higher each year. Q. Is the Company s rate design proposal, to implement single fixed monthly charges for most customers, dependent on either gas prices being more volatile or higher than in the past or a continuing pattern of declining per customer use? A. No. The proposed single fixed monthly charge rate design makes sense, whether gas prices are higher and more volatile, or not, and irrespective of whether use per customer continues to decline. If natural gas prices trend higher and exhibit volatility as they have in the past, or (2) use per customer continues to decline, customers will not be harmed by the proposed single fixed monthly charge rate design. In fact, SEMCO Gas would be harmed, in the sense that it had given up additional revenues that would be produced when a volumetric charge was applied to higher-than-expected consumption levels. Q. If the Commission does not approve the Company s preferred rate design, what is SEMCO Gas s rate design proposal? 21

41 Direct Testimony of George A. Schreiber, Jr. On Behalf of SEMCO Energy Gas Company A. SEMCO Gas s other rate design proposal is to maintain the traditional two-part rate design for all customer classes using appropriate billing determinants. That is the way in which the last MPSC Division rate increase was resolved. Q. What is a billing determinant? A. A billing determinant is, in this context, the assumed level of weather-normalized usage by an average customer in the rate class. This figure is used to determine what rate would be sufficient to collect the revenue requirement, or costs of providing service, allocated to the customer class in the cost-of-service study sponsored by Mr. Raab. I think of this as determining the rate per unit of consumption, in this case in therms, times an assumed level of consumption, with the assumed consumption level serving as the billing determinant. Q. Why is selecting the right billing determinants important? A. If the assumed level of usage, or billing determinant, for a particular customer class is too high, a volumetric distribution rate will not produce the revenue allocated to the customer class and the utility will not recoup its costs of providing service. Similarly, if the billing determinant is too low, too much revenue will be collected from the customer class by the utility. Q. Why is selecting the right billing determinant so important now? A. Because, as depicted on Exhibit A-12, Schedule F-2, weather-normalized customer usage at SEMCO Gas has been declining, consistent with trends elsewhere in the country (as Mr. Raab points out in his testimony). The Commission should explicitly take this declining usage pattern into account in setting SEMCO Gas s revised base rates if the Company s preferred rate design is not approved. To me, there is a commonsense set of reasons for this decline in per customer usage. (Mr. Raab also discusses these reasons at length in his testimony.) Energy equipment and appliance efficiency has improved, partly as a result of changed 22

42 Direct Testimony of George A. Schreiber, Jr. On Behalf of SEMCO Energy Gas Company governmental standards. Consumers simply cannot buy the kinds of inefficient equipment and appliances that used to be available in the market. Similarly, new and rehabilitated homes and buildings have more insulation and more efficient windows and doors; they are constructed to have tighter thermal envelopes. In addition, the Michigan legislature enacted and the Governor signed Public Act 286 of 2008, which requires all utilities to implement energy optimization programs that will support the conservation of natural gas and thus, in my view, reinforce the declining usage trend. As discussed by Mr. Raab, higher natural gas prices also have prompted customers to conserve gas, including by dialing back their thermostats, closing off unused rooms, and using supplemental energy sources. Where such a pattern of declining use per customer exists, SEMCO Gas s revised base rates will not collect enough revenue to cover the cost of service during the rate effective period, unless the Commission ensures that the correct billing determinants are used to calculate those rates or severs rates from volumetric usage as proposed in this filing. Q. Please discuss the residential use per customer experienced by SEMCO Gas. A. In 2009, weather-normalized residential per customer usage for SEMCO Gas s customers was 94.1 Dekatherms ( Dth ). This is down from an average per customer usage of Dth per residential customer in 2005, or an average annual decline of approximately 2.3%. Q. What billing determinants does SEMCO Gas propose to use to calculate revised base rates if the Commission does not approve the usage level option? A. For residential customers, SEMCO Gas has proposed to use a billing determinant of 899 therms per year. While I highlight this proposed billing determinant in discussing this topic, billing determinants for all rate classes have been adjusted using the methodology discussed by Mr. Raab. Q. Are there additional factors that could effect this usage level? 23

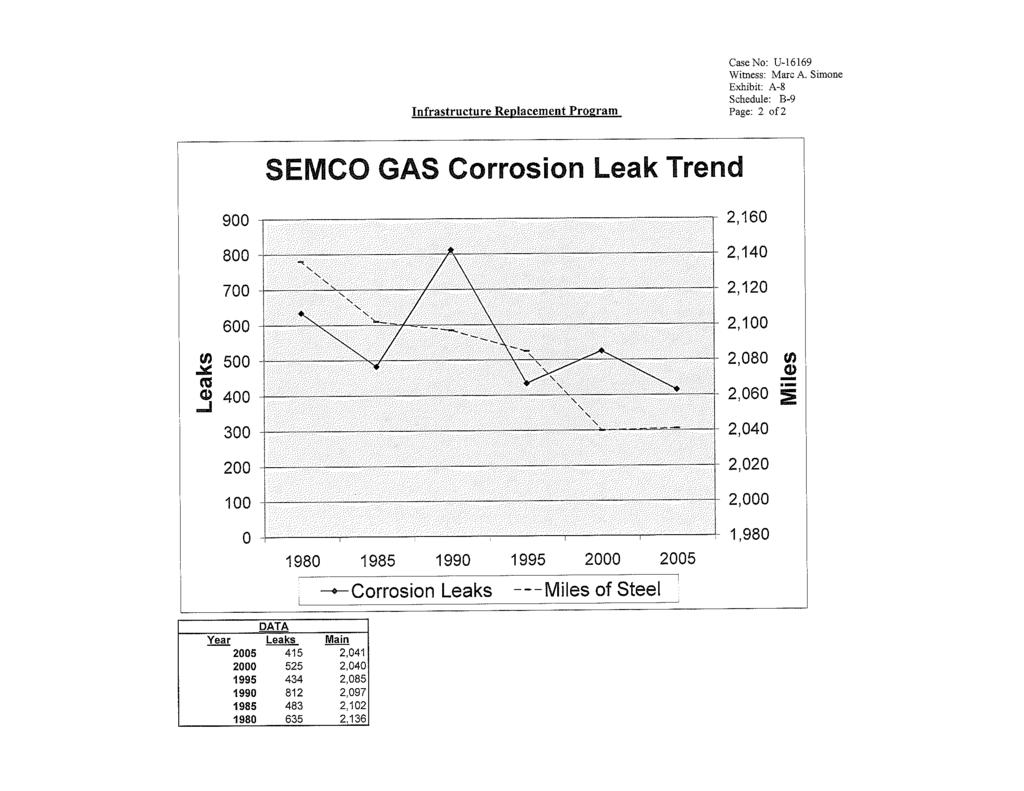

43 Direct Testimony of George A. Schreiber, Jr. On Behalf of SEMCO Energy Gas Company A. Yes, as discussed by Mr. Raab, there are two factors that could effect the future billing determinant proposed in this case. The normal weather estimates that indicate that future weather could be warmer than even the 15-year normal weather would indicate and price elasticity impact or repression adjustment could reduce residential use per customer to approximately 821 therms for the forecasted test year which supports the use of a billing determinant at such level.special Transportation Contracts Q. Please explain the special transportation agreements that SEMCO Gas has entered into. A. As discussed in more detail by Mr. Lubbers, SEMCO Gas has entered into special transportation agreements with certain of its large volume transportation customers. Most of these customers are located in the Company s Battle Creek Division, and the current contracts provide for a discounted transportation rate relative to a traditional cost of service based rate. Q. What is SEMCO Gas proposing with respect to such discounted transportation rate? A. Mr. Lubbers supports the Company s position that the contracts meet the requirements prescribed by the Michigan legislature and that the discounts in the special transportation contracts should be recovered from the Company s other customers. Infra-structure Replacement Program Q. Please discuss the Company s proposal for an Infrastructure Replacement Program. A. The Company is proposing an Infrastructure Replacement Program ( IRP ) to support the accelerated replacement of unprotected metallic mains in service in the SEMCO Gas 21 system. As described in detail in Mr. Simone s testimony, the 25-year program proposed by the Company is intended to speed up the replacement of about 13 miles of unprotected steel and cast iron pipe per year. The program is intended to add to the miles of unprotected metallic pipe that are routinely replaced by the Company each year in conjunction with public improvement projects. A substantial benefit associated with this 24

44 Direct Testimony of George A. Schreiber, Jr. On Behalf of SEMCO Energy Gas Company program is the reduction in leaks that would result from these non-revenue producing improvements. The program costs are offset by leak-related savings. Q. Please describe the ratemaking proposal for this program. A. The Company is proposing that the capital-related costs (including return on investment, depreciation expense and property taxes) for the approximate annual $4 million investment in unprotected and bare steel be surcharged to the Company s customers on an annual basis. When subsequent rate cases are filed and the IRP capital investments are included in rate base, the portion of the surcharge associated with the capital-related costs of those capital investments will cease. Mr. Simone explains how the surcharge is calculated and administered throughout the IRP in his testimony. Dr. Fairchild discusses the capital-related costs for the program in his testimony, and Mr. Alger discusses the annual surcharge mechanism in his testimony. Service Valve Replacement Program Q. Please discuss the Company s Service Valve Replacement Program. A. As described in more detail in Mr. Simone s testimony, it is necessary for the Company to remove and replace approximately 40,000 service line riser valves purchased and installed in the 1980 s and 1990 s. SEMCO Gas has experienced some failures of these valves and is proposing to replace all of these valves by 2015, with the objective of eliminating the risks to employees, customers, and the public from these facilities. The Company is requesting the Commission approve the recovery of the costs associated with the Service Valve Replacement Program. Q. How much does the Company expect to expend for the replacement of the service valves? A. Mr. Simone s testimony supports the Company s forecast of additional operation and maintenance expenses of approximately $2.0 million per year for the period 2011 through 2015 for the Service Valve Replacement Program. 25

45 Direct Testimony of George A. Schreiber, Jr. On Behalf of SEMCO Energy Gas Company Q. Is there anything else you wish to say about this valve replacement program? A. Yes. A lawsuit has been filed seeking recovery of the costs of the valve replacement program and other damages. To the extent that the Company is successful, by settlement or in trying the case, SEMCO Gas proposes to defer the proceeds from this lawsuit, net of legal fees and costs, so that the Commission can credit this sum to base rates at the next appropriate opportunity. Requested Rate of Return Q. Has the financial condition of SEMCO Gas improved since its last rate case? A. Yes. In 2004, SEMCO was rated below investment grade by major bond rating agencies and its financial position was precarious. In connection with SEMCO's acquisition by Continental in 2007, $100 million in additional equity was invested in the Company, which strengthened its balance sheet considerably. In April 2010, both Moody's and Standard & Poor's assigned investment grade ratings to SEMCO and its newly-issued senior debt. Q. What steps has SEMCO recently taken to ensure that it will continue to maintain a sound financial condition? A. Since 2007, the interest rate on SEMCO's debt has been variable, adjusting with changes in major short-term borrowing benchmarks. While this has been beneficial because of government actions keeping interest rates low to stimulate economic activity, I do not expect low interest rates to continue indefinitely. To lock in what appeared to be a favorable interest rate, SEMCO refinanced in April 2010 the majority of its variable rate debt, which was scheduled to mature in November 2014, and replaced it with $300 million in senior notes maturing in April 2020 that bear a fixed interest rate of 5.15%. Of course, another action being taken to maintain SEMCO's financial integrity is filing this case. Base rates should not lag rising costs and the necessary investments made to improve the SEMCO Gas system. In addition, the proposed single fixed monthly charge 26