UNIVERZAL BANKA AD BELGRADE. Financial Statements for the Year Ended 31 December 2012 and

|

|

|

- Philomena Brown

- 5 years ago

- Views:

Transcription

1 Financial Statements for the Year Ended 31 December 2012 and This is an English translation on the Tel: , , Fax:

2 TABLE OF CONTENTS P a g e s INDEPENDENT 1-2 FINANCIAL STATEMENTS Income statement 3 Balance sheet 4 Cash flow statement 5-6 Statement of changes in equity 7 Notes to the financial statements 8-48

3 This is an on the To the shareholders of Univerzal Banka a.d. Belgrade Report on the Financial Statements We have audited the accompanying financial statements of Univerzal Banka a.d. Belgrade (the Bank), which comprise the balance sheet as at 31 December 2012, and the income statement, statement of changes in equity and cash flow statement for the year then ended, and a summary of significant accounting policies and other explanatory information. Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with the current accounting regulations in effect in the Republic of Serbia, regulations of the National Bank of Serbia governing financial reporting of banks and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error. Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the audit the risks of material misstatement of the financial statements, whether due to fraud or error. In making those presentation of the financial statements in order to design audit procedures that are appropriate in the control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

4 Report on the Financial Statements - continued Opinion In our opinion, the financial statements, in all material respects, give a true and fair view of the financial position of Univerzal Banka a.d. Belgrade as at 31 December 2012, and its financial performance and its cash flows for the year then ended in accordance with current accounting regulations in effect in the Republic of Serbia, accounting policies disclosed in the notes to the financial statements and regulations of the National Bank of Serbia governing financial reporting of banks. Emphasise of Matter 1) at the end of the year the Bank had a capital adequacy ratio of 9.55% that was less than was under its value that is contrary to the provisions of the Decision on the capital adequacy of banks, on the basis of which the Bank is required to have a minimum capital adequacy ratio of 12%. A fall in capital adequacy ratio was caused by worsening in major debtors operation, some of which went bankrupt, and in addition from 31 December 2011 the new regulations of the National Bank of Serbia were in effect in respect of capital calculation (Basel II Standards. The Bank has taken corrective action to reduce negative impacts, and in 2012 the shareholders paid subordinated loan in the amount of RSD 710,739 thousand. 2) ratio of total large exposures amounted to 509,50% exceeding the limit of 400% prescribed by the Decision on Risk Management. An indicator is the result of reduced capital, calculated in accordance with a Decision on the capital adequacy ratio, that figures as denominator in the large exposures calculation. As a result of the capital reduction, the indicator of large exposure to six group of related parties exceeded the prescribed limit whereby the bank's exposure to one body or group of related parties shall not exceed 25% of capital. National Bank of Serbia has given the Bank deadline till 30 September 2013 to harmonise capital adequacy indicator and indicator of exposure to one body or group of related parties, with prescribed ones. The financial statements are prepared on the assumption that the Bank is a going concern and aforementioned may put in doubt the validity of that principle. Measures taken by the management in overcoming the situation have been disclosed in Note 38. Our opinion is not qualified in respect of this matter. Belgrade, 13 March 2013 MOORE STEPHENS Managing Partner

5

6

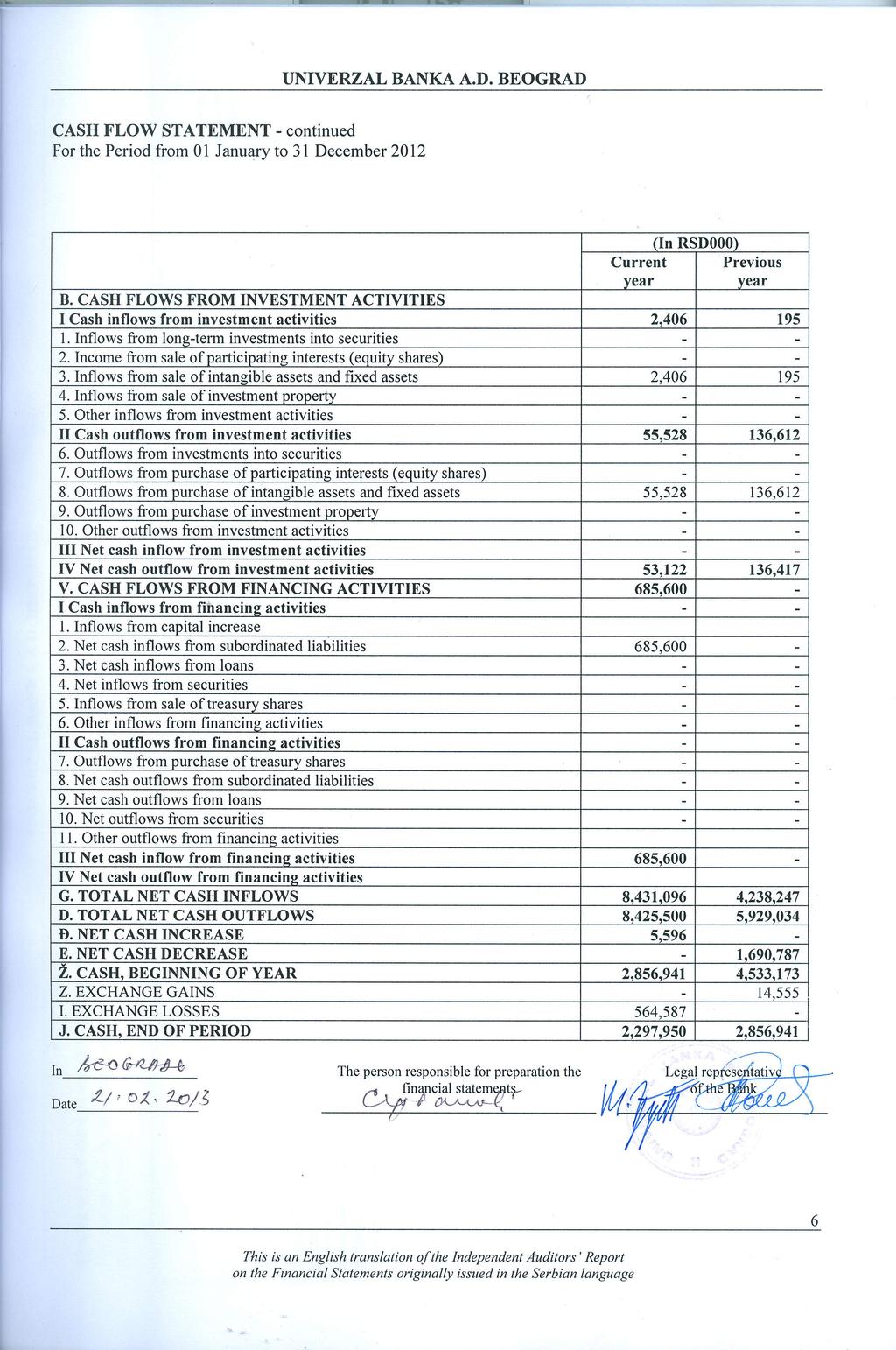

7 UNIVERZAL BANKA A.D. BEOGRAD CASH FLOW STATEMENT For the Period from 01 January to 31 December 2012 Item A. CASH FLOWS FROM OPERATING ACTIVITIES Current year (In RSD000) Previous year I Cash inflows from operating activities 3,457,730 4,238, Interest inflow 2,823,768 3,453, Inflow from fees and commissions 565, , Inflow from other operating income 67, , Inflow from dividends and participating interests II Cash outflows from operating activities 3,099,885 3,594, Outflow for interest 1,621,383 1,973, Outflow for fees and commissions 37,709 38, Outflow for gross salaries, benefits and other personnel expenses 644, , Outflow for taxes, contributions and other duties charged to income 156, , Outflow for other operating expenses 640, ,037 III Net cash inflow from operating activities prior to increase or decrease in placements and deposits 357, ,484 IV Net cash outflow from operating activities prior to increase or decrease in placements and deposits - - V Decrease in placements and increase in deposits 4,285, Decrease in loans and placements to banks and clients 4,159, Decrease in securities at fair value through Profit and Loss Statement, trading placements and short-term securities held to maturity 126, Increase in deposits from banks and clients - - VI Increase in placements and decrease in deposits 5,255,471 2,197, Increase in loans and placements to banks and clients - 1,114, Increase in securities at fair value through Profit and Loss Statement, trading placements and short-term securities held to maturity - 939, Decrease in deposits from banks and clients 5,255, ,878 VII Net cash inflow from operating activities before profit tax - - VIII Net cash outflow from operating activities before profit tax 612,266 1,554, Profit tax paid 14, Dividends paid 2 23 IX Net cash inflow from operating activities - - X Net cash outflow from operating activities 626,882 1,554,370 5 This is an English translation of the on the

8

9

10 FOR THE YEAR 2012 Beograd, 22 February 2013

11 1. CORPORATE INFORMATION Univerzal banka a.d. Beograd (hereinafter referred as to 'the Bank') was established in Until 1997 the Bank operated under the name Mesovita banka "Asi banka" a.d. Beograd. The Bank is registered for providing all types of banking services in the Republic of Serbia. The Bank is registered to provide a wide range of banking services associated with deposit, loan, cash, guarantees, foreign currency, foreign exchange, issue and deposit, clearing and settlement activities in accordance with the Law, activities of mediation in trade with securities, purchase and collection of receivables and other banking and financial activities in accordance with the Law on banks. The Bank's headquarter is in Belgrade, 29 Francuska St. The Bank's identification number is The Bank's tax identification number is As of 31 December 2012 the Bank had 448 employees (2011: 482 employees). The Bank comprises 13 branches and 48 sub-branches. 2. ACCOUNTING POLICIES 2.1. Basis of preparation and presentation of the financial statements The financial statements have been prepared in accordance with the accounting regulations in the Republic of Serbia. Financial statements for 2010 for all obligators shall be submitted within the timeframe and manner specified by the Law on Accounting and Auditing, the Law on Amending Accounting and Auditing Law and other legislation. Changes made in connection with the submission of financial statements and consolidating the status registers and the register of financial statements in one institution - the Agency, and public disclosure of financial statements on the Agency s website has been done to comply with the EU practice, and the EU Directive and Art. 47. and 48 IV of the EU. Banks, stock exchanges and broker dealers, insurance companies, pension funds and companies managing pension funds, companies managing investment funds submit financial statements on forms specific prescribed for that particular group Significant accounting judgments and estimates In the process of applying the Bank's accounting policies, management has used its judgments and made estimates in determining the amounts recognized in the financial statements. The most significant use of judgments and estimates are as follows: 9

12 1) Fair value of financial instruments In the Republic of Serbia does not exist sufficient market experience, stability and liquidity for the purchase and sale of loans and other financial assets and liabilities, and the official information is not readily available. Therefore, fair value may not be reliably determined in the absence of an active market, as required by IAS / IFRS. 2) Losses on impairment of loans The Bank s management considers the loans and placements as of financial reporting date in order to estimate whether it is necessary to recognize impairment losses in the income statement. Assessment of impairment of loans and other placements that are in terms of IAS / IFRS may be regarded as financial instruments, the Bank is determines individually for each placement, or financial instrument applying discounting method of expected future flows to their present value. The amount of loss determined by discounting, the Bank determines as the difference between the reported nominal value of assets and the net value of expected future cash flows. Determined loss (provision) the Bank records in its books against expenses. The amount of estimated reserve for potential losses from guarantees and other off-balance sheet items is recorded against income statement and discloses as a liability in the balance sheet. 3) Impairment of equity investments and other securities available for sale Securities available for sale (equity investments and other securities available for sale) are stated at cost less provision, or at market value, whichever is lower. Securities for which there is no active market are carried at recoverable value. The Bank considers equity investments and other securities available for sale impaired when there is a significant or prolonged decrease in the fair value of these assets below their cost or when there are other objective evidence of impairment. The Bank s management are weighed what is considered significant or prolonged decrease in the fair value. In addition, the Bank estimates other factors, such as oscillations in the stock market. 4) Deferred tax assets The Bank recognizes deferred tax assets arising from unused tax losses and transferable tax credits to the extent that it is probable that the level of expected future taxable profit will allow transferable unused tax credits and unused transferable tax losses are used. 5) Long-term employee benefits Liabilities and costs of long-term employee benefits are determined using discount rates The Bank makes provision for retirement benefits by discounting, using a discount rate that is equal to the interest rate on longterm foreign currency saving. For retirement benefits adequate provisions have been made. 10

13 The Bank does not have its own pension funds or options to pay employees in the form of shares and the identified obligations. For retirement benefits, the Bank has booked adequate provisions. 2.3 Summary of significant accounting policies The most important accounting policies used in preparation of the financial statements are as follows: (1) Foreign currency translation Foreign currency transactions are translated into dinars at the official exchange rate of the National Bank of Serbia, prevailing at the transaction date. Receivables and assets denominated in foreign currencies, at the balance sheet date, are translated into dinars at official middle exchange rate of the National Bank of Serbia prevailing at the balance sheet date. Exchange rate differences originating from foreign currency translation, as well as from translation of monetary assets and liabilities denominated in foreign currency, are taken to "Foreign exchange gains and losses" in the income statement. Contingencies and commitments denominated in foreign currency are translated into dinars at the official middle exchange rate of the National Bank of Serbia prevailing at the balance sheet date. (2) Financial instruments (i) Date of initial recognition Purchases or sales of financial assets that require delivery of assets within the time frame generally established by regulations or conventions in the market place are recognized on the trade date, i.e. the date that the Bank commits to receive or transfer the assets. (ii) Initial recognition of financial instruments The classification of financial instruments at initial recognition depends on the purpose for which the financial instruments were acquired and their characteristics. All financial instruments are measured at their fair value plus any directly attributable costs of acquisition or issue, except in the case of securities and other placements held for trading. (iii) Derivatives Derivatives are measured at fair value and recorded as assets when fair value is positive, or liabilities, if their fair value is negative. Changes in fair value of derivatives are recognized in the income statement. Derivatives embedded in other financial instruments are specifically identified and treated as separate derivatives and measured at fair value, if their economic characteristics and risks are not closely related to the economic 11

14 characteristics and risks of the parent contract and if the parent contract is not hold for trading and stated at fair value. (iv) Securities and other investments held for trading Securities and other investments held for trading comprise all financial instruments held for trading and derivatives that are recognized in the balance sheet at fair value. Changes in fair value are recognized in the income statement. Interest and dividend income from on these instruments are recognized in interest income and income from dividends in accordance with the defined contractual terms, or when the right to receive the dividend. If negative effects, or decrease in the value of securities available for sale (mostly stocks), do not represent a permanent impairment, but fluctuations from extraordinary circumstances which caused the fall in stock prices and consequently, impairment losses on impairment of securities available for sale are not transferred to the income statement, but are included within the balance sheet as a deduction from capital. (v) Financial liabilities held for trading The Bank has no financial liabilities held for trading. (vi) Financial assets or financial liabilities designated at fair value through income statement The management did not classify financial instruments, on initial recognition, into the category of the financial assets or liabilities recorded at fair value through profit or loss. (vii) Gains on first day When the transaction price in inactive market is different than the fair value based on other current market transactions in the same instrument or based on a valuation technique whose variables include only data from observable markets, the Bank immediately recognized a difference between the transaction price and fair value (gain on the first day) in the income statement. In cases where data not comparable to market information is used, the difference between the transaction price and the value determined using the model is recognized in the income statement when the input parameters become comparable with market information, or when the instrument is derecognised. (viii) Investments in securities held-to-maturity Securities held-to-maturity are those which carry fixed or determinable payments and have fixed maturities and which the Bank has the intention and ability to hold to maturity. After initial measurement, investments in securities held-to-maturity are measured at amortized cost which is calculated by taking into account any discount or premium on acquisition, less allowance for impairment. Fees which are part of the effective income from these instruments are accrued and recorded as deferrals in the income statement during the useful life of the instrument. 12

15 (ix) Securities acquired under repo transactions with the National Bank of Serbia The securities acquired by the Bank purchase from National Bank of Serbia, with a contractual obligation to their resell, on the basis of the Framework Agreement on the sale of securities with the obligation to purchase such securities, are measured at depreciated cost on the balance sheet date. (x) Due from banks and loans to customers Loans are stated at the balance sheet at the amount of approved loan, deducted by repaid principal and a provision that is based on an estimate of the value of particular risks identified for individual investments and risks for which experience shows that are contained in the portfolio. In assessing the risks the Bank s management is applying internally adopted methodology as disclosed in Note Provisions and Provisions for uncollectible receivables. In 2012 the Bank calculated the provision as the difference between the receivable of principal and interest showed in records and amount of receivable that can be collected, calculated as the present value of expected cash flows, discounted using the effective interest rate, in accordance with IAS 39-Financial Instruments: Recognition and Measurement. The Bank s management asses credit risk, or allowance for impairment losses on the basis of individual assessments of risky loans for 80% of credit portfolio and for 20% (less separate significant placements) in whole in accordance with specially determined Methodology. Expected cash flow is estimated by taking into account the regularity of the payment, the financial situation of the debtor and the quality of collateral. Thus calculated provision of balance sheet assets and provisions for losses on off-balance sheet items are booked as expenses of the Bank. Specific reserve for potential losses is estimated in accordance with regulations of the National Bank of Serbia. Loans, deposits and other exposure is classified in category A, B, V, G, and D, in accordance with the evaluation of collectability of loans and other investments, depending on the number of days the level of overdue payments are in arrears, the financial position of the client and the quality of collaterals. The difference amount of specific reserves for potential losses calculated in accordance with the National Bank of Serbia on the classification of balance sheet assets and off-balance and the amount of value adjustments of balance sheet assets and provisions for off-balance sheet items, calculated in accordance with the internal methodology is distinguished from retained earnings. Write-offs of uncollectible receivables is based on court decisions, settlement of interested parties or based on decisions of the Management Board. (xi) Determination of fair value The fair value of financial instruments traded in active markets at the balance sheet date is based on their quoted market price, without any deduction for transaction costs. 13

16 For all other financial instruments not listed in an active market, the fair value is determined using appropriate valuation techniques. Valuation techniques include net present value techniques, comparison to similar instruments for which market observable price exist and other relevant valuation models. (xii) Financial assets impairment The Bank assesses at each balance sheet date whether there is any objective evidence that a financial asset or a group of financial assets is impaired. A financial asset or a group of financial assets is deemed to be impaired if, and only if, there is objective evidence of impairment as a result of one or more events that has occurred after the initial recognition of the asset (an incurred "loss event") and that loss event (or events) has an impact on the estimated future cash flows of the financial asset or the group of financial assets that can be reliably estimated. Evidence of impairment may include indications that the borrower or a group of borrowers is experiencing significant financial difficulty, default or delinquency in interest or principal payments, the probability that they will enter bankruptcy or other financial reorganization and where observable data indicate that there is a measurable decrease in the estimated future cash flows, such as changes in arrears or economic conditions that correlate with defaults. Investments in securities held-to-maturity For held-to-maturity investments the Bank assesses individually whether there is objective evidence of impairment. If there is objective evidence that an impairment loss has been incurred, the amount of the loss is measured as the difference between the asset's carrying amount and the present value of estimated future cash flows. The carrying amount of the asset is reduced and the amount of the loss is recognized in the income statement. If, in a subsequent year, the amount of the estimated impairment loss decreases because of an event occurring after the impairment was recognized, any amounts formerly recognized is reduced and the effects are recognized in the income statement. Investment in shares and other available-for-sale investments For investment in shares and other available-for-sale investments, the Bank assesses at each balance sheet date whether there is objective evidence that an investment or a group of investments is impaired. In the case of other legal entities' equity investments classified as available-for-sale, objective evidence would include a significant or prolonged decline in the fair value of the investment below its cost. Where there is evidence of impairment, the cumulative loss-measured as the difference between the acquisition cost and the current fair values, less any impairment loss on that investment previously recognized in the income statement - is removed from equity and recognized in the income statement. Impairment losses on equity investments are not reversed through the income statement; increases in their fair value after impairment are recognized directly in equity. Allowance for impairment of investments in shares that are not listed on the active market and whose value cannot be determined with certainty, is measured as the difference between the asset's carrying amount and the present value of estimated future cash flows and recognized in the income statement and not reversed until termination of recognition. 14

17 In the case of debt instruments classified as available for sale, impairment is assessed on the same criteria as financial assets declared at amortized cost. If, in a subsequent year, the fair value of the debt instrument increases and if this growth can be related objectively to an event occurring after the impairment loss recognized in the income statement, the impairment loss is reversed in the income statement. (xiii) Renegotiated loans When possible, the Bank seeks to restructure loans rather than to take possession of collateral. This may involve extending the payment arrangements and the agreement of new loan conditions. Once the terms have been renegotiated, the loan is no longer considered past due. Management continuously reviews renegotiated loans to ensure that all criteria are met and that future payments are likely to occur. The loans continue to be subject to an individual or collective impairment assessment, calculated using the loan's original effective interest rate. (xiv) Offsetting financial assets and liabilities Financial assets and liabilities are offset and the net amount reported in the balance sheet if, and only if, there is a currently enforceable legal right to offset the recognized amounts and there is an intention to settle on a net basis, or to realize the asset and settle the liability simultaneously. (xv) Hedge accounting The Bank does not use hedge accounting. (3) Lease Consideration of whether a particular contract is lease or contains a lease element is based on the essence of the contract and requires an assessment of whether fulfilment of the contract depends on the use of a specific asset or group of assets and whether the contract involves the transfer of rights to use assets. The Bank does not have a contract that can be regarded as leasing contracts. (4) Recognition of income and expenses Revenue is recognized to the extent that it is probable that the economic benefits will flow to the Bank and the revenue can be measured. (i) Interest and similar interest and expense For all financial instruments measured at amortized cost and interest bearing financial instruments classified as available-for-sale financial instruments, interest income or expense is recorded using the effective interest rate. The calculation of the effective interest rate takes into account all contractual terms of the financial instrument. All receivables with a clear problem in the due collection, the accrued interest is transferred to the account suspended interest - off-balance sheet item. 15

18 Transfer and cancellation of accrued interest from income account to the account of suspended interest is done from the date of charges being filed on claims for payment, or from the date of making decision by the Executive Board on the transfer of accrued interest to the suspended interest account for receivables for which the competent department estimates that they may not collect within one year, although the receivable is not disputed. (ii) Fee and commission income The Bank earns fee and commission income from a diverse range of services it provides to its customers. Commission income may be classified into two categories: (iii) Fee for services provided at the appropriate time Fees received for rendering services during a specified period are deferred during this period. (iv) Fee income from certain performances Fees or components of fees that are linked to a certain performance are recognized after fulfilling the corresponding criteria. (v) Dividend income Dividend income is recognized when the bank's right to receive the payment is established. (vi) Rental income Rental income related to investment property and recognized evenly over the lease period and disclosed in the income statement within other operating income. (5) Cash and cash equivalents For purpose of the cash flows statement, "Cash and cash equivalents" include cash and balances on gyro and current accounts held with other banks and funds to the bank account and other funds. (6) Property and equipment Property and equipment are stated at cost, excluding daily maintenance expenses, less accumulated depreciation and accumulated allowance for impairment. The cost includes in addition to the purchase price all other costs such as (customs and import duties, nonrefundable taxes, transportation costs) Depreciation is calculated using the straight-line method to write down the cost of property and equipment to their residual value over their useful lives. The estimated useful lives are as follows: 16

19 Buildings Computer equipment Other equipment up to 77 years from 3 to 5 years from 6 to 14 years Changes in expected useful life of assets are considered as changes in accounting estimations. Any item of property and equipment is derecognized upon disposal or when no future economic benefits are expected from its use. Any gain or loss arising on termination of recognition of the asset (calculated as the difference between the net disposal proceeds and the carrying amount of the asset) is recognized in "Other operating income" or "Other operating expenses/revenues" in the income statement in the year the asset is derecognized. (7) Investment Property The bank holds a property as an investment with a view to rental income and / or increase the property value. The Bank applies the same accounting treatment for investment property as well as other property. (8) Intangible assets Intangible assets are declared at cost less accumulated amortization and accumulated impairment losses. The useful lives of intangible assets are assessed to be either finite or indefinite. Intangible assets with finite lives are amortized over the useful economic life. The amortization period and the amortization method for an intangible asset with a finite useful life are reviewed at least at each financial year-end. Changes in the expected useful life or the expected pattern of consumption of future economic benefits embodied in the asset are accounted for by changing the amortization period or method, as appropriate, and treated as changes in accounting estimates. The amortization expense on intangible assets with finite lives is recognized in the income statement in the "Other operating income". Amortization is calculated using the straight-line method to write down the cost of intangible assets to their residual values over their estimated useful lives as follows: Software licences from 3 to 5 years Other intangible assets from 3 to 5 years (9) Impairment of non-financial assets The Bank assesses at each reporting date if events or changes in circumstances indicate that the carrying value may be impaired, whether there is an indication that non-financial asset may be impaired. If any such indication exists, or when annual impairment testing for an asset is required, the Bank makes an estimate of the assets' recoverable amount. Where the carrying amount of an asset (or group of asset, cashgenerating units) exceeds its recoverable amount, the asset is considered impaired and is written down to its recoverable amount. 17

20 A previously recognized impairment loss is reversed only if there has been a change in the estimates used to determine the asset's recoverable amount since the last impairment loss was recognized. If that is the case, the carrying amount of the asset is increased to its recoverable amount. (10) Financial guarantees The Bank gives financial guarantees, consisting of payable and performance guarantees, letters of credit, acceptances and other warranties. Financial guarantees are initially recognized in the balance sheet at fair value, upon fee inflow from financial guarantee approval. Subsequent to initial recognition, the bank's liability under each guarantee is measured at the higher of the amortized premium and the best estimate of expenditure required to settle any financial obligation arising as a result of the guarantee. Any increase in the liability relating the financial guarantees is taken to the income statement in "Expenses in indirect placements write-off and provisions". The premium received is recognized in the income statement in "Fees and commission income" on a straight-line basis over the life of the guarantee. (11) Employees benefits Defined benefit plan The Bank's calculates and pays contributions for pension and health insurance and contributions for unemployment insurance at the rates prescribed by the law on the basis of the gross salaries. The contributions expenses are recognized in the income statement in the same period as appropriate salary expenses. The Bank has no further liabilities for contributions in this respect. Long-term benefits to employees In accordance with Labour Law there is a mandatory retirement indemnity equal to 3 gross monthly salaries, based on the average salary in the Republic of Serbia in the month prior to retirement. Expenses and liabilities for these plans are not provided by funds. Liabilities from the benefits and related expenses are recognized at future cash flows present value using actuarial valuation using the projected cost unit method. Actuarial gains and losses and expenses of previous services rendered are recognized in the income statement when incurred. (12) Provisions Provisions are recognized when the Bank has a present obligation (legal or constructive) as a result of a past event, and it is probable that an outflow of resources embodying economic benefits will be required to settle the obligation and a reliable estimate of the amount of the obligation can be made. 18

21 (13) Income tax Current tax Current tax assets and liabilities for the current and prior years are measured at the amount expected to be recovered from or paid to the taxation authorities. The tax rates and tax laws used to compute the amount are those that are enacted or substantively enacted by the balance sheet date. Current tax relating to items recognized directly in equity is also recognized in equity. Income tax represents the amount of tax calculated using tax rates of 10% on the profit before tax, after deduction of the effects of permanent differences that the prescribed tax rate reduce to an effective tax rate. The final amount of liabilities for income taxes is determined by applying the statutory income tax rate on the tax base, established in Tax statement. Law on Profit Tax of the Republic of Serbia does not allow any tax losses in the current period to be used to recover taxes paid in previous periods. However, losses of the items reported in the income tax can be used to reduce the tax base in future periods, but not more than five years. Deferred tax Deferred tax is provided on temporary differences at the balance sheet date between the tax bases of assets and liabilities and their carrying amounts for financial reporting purposes. Applicable tax rate on the balance sheet date or the tax rates that are after that date in effect are used to determine deferred income tax expense. Deferred tax liabilities are recognized for all taxable temporary differences. Deferred tax receivables are recognized for all deductible temporary differences and the effects of tax losses and tax credits, which can be used in future fiscal periods, to the extent of likelihood of transferred tax losses and credits can be utilized from taxable profit. Taxes and contributions independent of the results Taxes and contributions independent of the results include property taxes, taxes and contributions paid by employers, as well as other taxes and contributions in accordance with the republic, tax and general regulations. These taxes and contributions are included in other operating expenses. Funds managed on behalf of third parties Funds managed on behalf of third parties, managed by the Bank for a fee, are included in the balance sheet. Fair value The financial statements are prepared on a historical cost basis, including adjustments and provisions made to reduce assets to their recoverable amounts. 19

22 Policy of the Bank is to disclose information about the fair value of assets and liabilities for which published market information that is obtained on the basis of alternative valuation techniques and are readily significantly different from book value. As Management believes, amounts in the financial statements reflect the real value in the circumstances the most accurate and useful financial reporting in accordance with the Law on Accounting and Auditing of the Republic of Serbia and National Bank of Serbia regulations governing financial reporting of banks. (14) Comparative data Reclassification of comparative data was done, when it was necessary, for the purpose of reconciliation with the current year presentation. 20

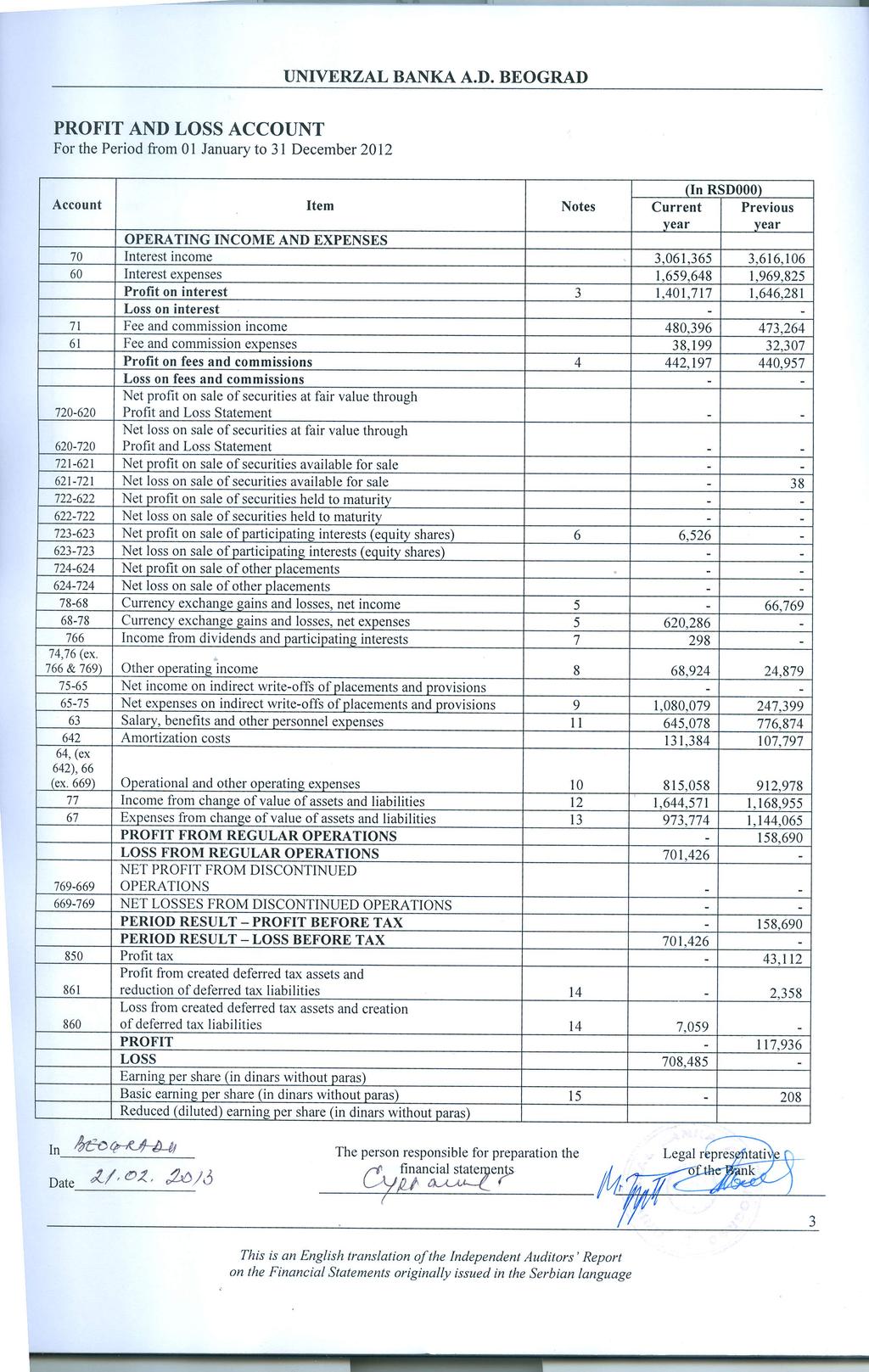

23 3. INTEREST INCOME AND EXPENSES Interest income 3,061,365 3,616,106 Other banks 35,737 38,207 National Bank of Serbia 55, ,843 Corporate 2,237,394 2,645,596 Public sector 64,535 79,469 Retail 268, ,636 Other customers 1, Private companies 30,921 34,439 Securties 367, ,604 Interest expenses 1,659,648 1,969,825 Other banks 246, ,757 Corporate 879,618 1,027,396 Public sector 30,073 26,603 Private companies 3,742 3,289 Retail sector 415, ,492 Foreign entities 2, Other customers 55,221 71,207 Securities Subordinated liabilities 26,625 - Net interest income 1,401,717 1,646,281 Interest income and expenses according to financial instruments classes: Interest income 3,061,365 3,616,106 Cash and short-term assets 12,059 55,278 Deposits with the National Bank of Serbia 43,151 36,995 Due from banks 35,737 38,207 Placements to customers 2,334,022 2,759,816 Securities held-to-maturity 367, ,175 Other-retail 268, ,635 Interest expenses 1,659,648 1,969,825 Deposits with other banks 246, ,757 Deposits to customers 971,675 1,128,495 Liabilities for subortinated loans 26,625 - Retail sector 415, ,281 Net interest income 1,401,717 1,646,281 21

24 4. FEE AND COMMISSION INCOME AND EXPENSES Fee and commission income 480, ,264 Domestic clearing and settlement 260, ,934 Foreign clearing and settlement 15,750 14,411 Sales and purchase of foreign currencies 1,253 1,819 Credit cards operations 37,687 29,946 Guarantees and other off-balance sheet items 80,761 96,514 Funds managed on behalf of third parties 41,971 40,096 Other fees and commissions 42,338 46,544 Fee and commission expenses 38,199 32,307 Domestic clearing and settlement 15,698 14,337 Foreign clearing and settlement 2,611 2,268 Sales and purchase of foreign currencies Fees and commissions for brokers 275 1,344 Other fees and commission 19,263 14,357 Net fee and commission income 442, ,957 Fee and commission income from sales and purchase of foreign currencies in 2012 were recorded on an account of exchange differences from foreign exchange transactions in the amount of RSD 12,073 thousand-fx losses and RSD 70,806 thousand-fx gains. 5. NET FOREIGN EXCHANGE GAINS / LOSSES Foreign exchange gains 2,545,169 4,027,426 Foreign exchange losses 3,165,455 3,960,657 Net foreign exchange gains/(losses) (620,286) 66,769 Net foreign exchange gains in 2011 were increased by the amount of revenues and expenses from sale and purchase of foreign currencies, which were in 2011 recorded on account of fee income such as: foreign exchange gains in RSD 64,602 thousand and foreign exchange losses in RSD 5,828 thousand. 22

25 6. NET PROFIT FROM SHARE SELLING Profit from selling of shares 6,526 - Profit from selling of shares 6, DIVIDENDS AND INVESTMENTS INCOME Total income from dividends and investments Income from dividends OTHER OPERATING INCOME Other operating income and refund of legal fees Gains from sales of fixed assets and received asset - - Reversals of allowances for impairment 1,790 5,334 Collected insurance premiums - 29 Rentals 59,644 3,565 Other income 7,174 15,691 Total other operating income 68,924 24, GAINS/LOSSES ON IMPAIRMENT AND PROVISIONS Releases of allowances for impairment losses: 2,288,072 2,787,687 On-balance sheet items 2,091,871 2,375,734 Off-balance sheet items 148, ,613 Income from collected suspended interest 44, ,340 Income from cancelation of unused retirement benefit provisions 3,242 - Losses on contingent liabilities 3,368,151 3,035,085 On-balance sheet items 3,257,053 2,739,753 Off-balance sheet items 109, ,179 Provision for retirement benefits - 1,790 Expenses from interest suspension 1,479 1,363 Loss on impairment and provisions, net 1,080, ,398 23

26 10. OPERATING AND OTHER EXPENSES Material costs 62,287 57,855 Production cots 354, ,027 Non-material costs 224, ,766 Tax duties 31,040 23,765 Contribution costs 103, ,982 Other 27,289 29,331 Losses on disposal of fixed and intangible assets Direct write off 3,292 86,631 Costs from sale of material values obtained by collection of receivables 6,729 - Subsequently determined interest expenses - enforced collection ,442 Total operating and other expenses 815, , COST OF SALARIES, FRINGE BENEFITS AND OTHER PERSONAL EXPENSES Net salaries 423, ,524 Tax payable 66,709 83,976 Contributions payable 101, ,520 Other staff costs 53,829 44,854 Total costs of salaries, fringe benefits and other personal expenses 645, , INCOME FROM CHANGES IN VALUE OF ASSETS AND LIABILITIES Income from changes in value of placements 1,616,497 1,168,949 Income from changes in value of other receivables 28,074 6 Total income from changes in value of assets and liabilities 1,644,571 1,168,955 24

27 13. EXPENSES FROM CHANGES IN VALUE OF ASSETS AND LIABILITIES Expenses from changes in value of placements 939,396 1,143,929 Expenses from changes in value of securities Expenses from changes in subordinated liabilities 34,323 - Total expenses from changes in value of assets and liabilities 973,774 1,144, INCOME TAX Deferred income tax relating to amounts recorded directly in the equity is as follows: Deferred tax benefit recorded in/against equity (7,059) 2,358 Total deferred tax benefit recorded in/against equity (7,059) 2, EARNINGS/(LOSS) PER SHARE Basic earnings per share are calculated as follows: annual net gains or losses, which can be attributed to the owners of the Bank's ordinary shares, is divided by weighted average number of ordinary shares that were in circulation during the period. In 2012 the loss incurred from ordinary course of business was amounted RSD 701,426 thousand. Loss per share amounted RSD 1,236. The following table shows information related to income and number of shares, which were used in the calculations of basic earnings per share: Net gains/(losses), which can be attributed to the owners of the Bank's ordinary shares (1,236) 208 Net gains/(losses, which can be attributed to the owners of the Bank's ordinary shares adjusted for the effects of convertible financial instruments (1,236)

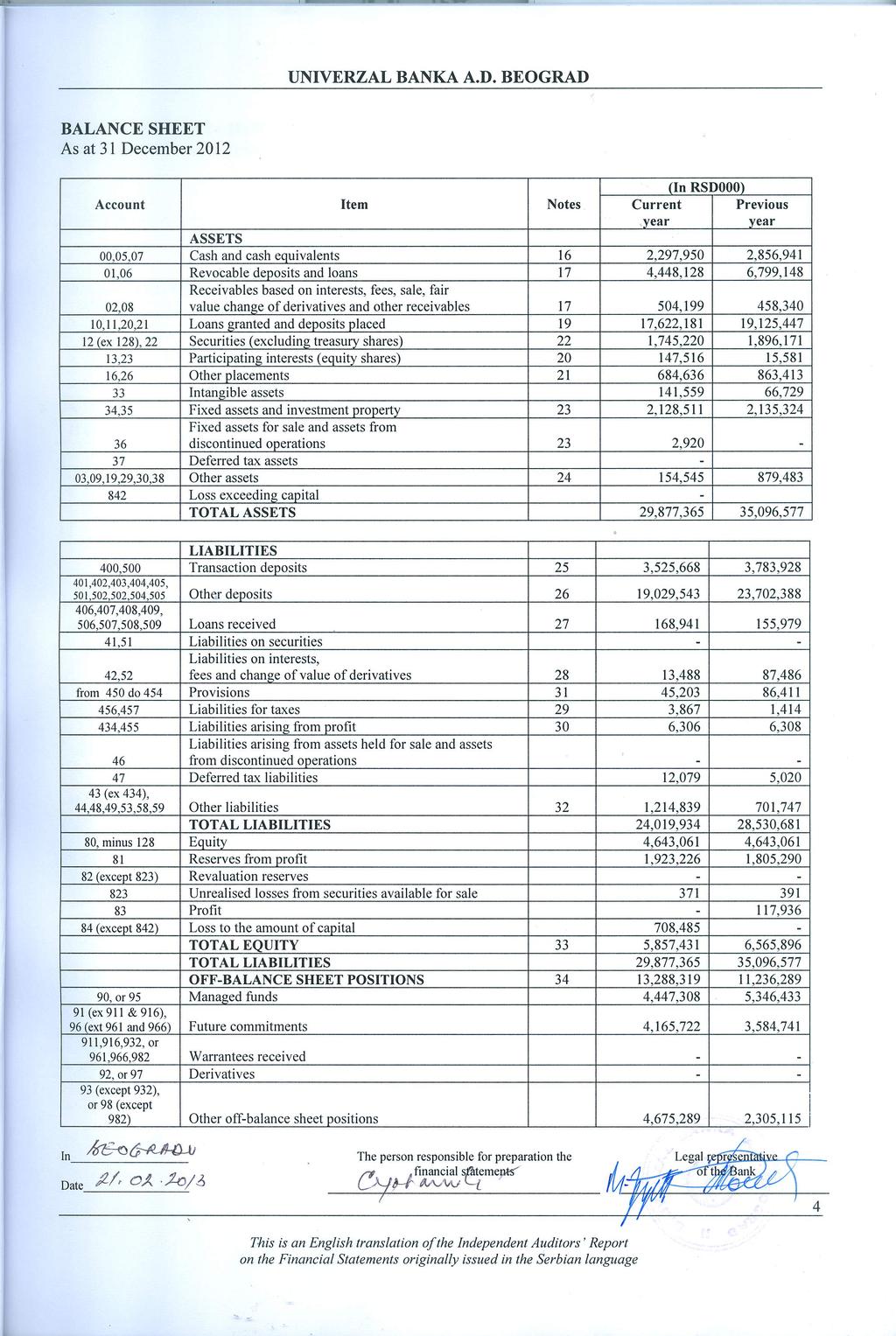

28 16. CASH AND CASH EQUIVALENTS In RSD 2,057,332 1,939,685 Gyro account 1,601,056 1,208,204 Petty cash 456, ,721 Bills - 205,760 In foreign currencies 240, ,256 Accounts with domestic banks 3,250 2,475 Accounts with foreign banks 120, ,054 Petty cash in foreign currencies 117, ,665 Cheques send to collection Less: Provision (247) - As of 31 December 2,297,950 2,856, CALLABLE DEPOSITS AND CREDITS In dinars - 2,924,297 Repo placements with the National Bank of Serbia - 2,504,297 Other cash assets - 420,000 In foreign currency 4,448,128 3,874,851 Obligatory reserve in foreign currency 4,448,128 3,874,373 Callable deposits Balance at 31 December 4,448,128 6,799,148 26

29 18. INTEREST, FEES AND COMMISSIONS RECEIVABLES In dinars 784, ,010 Other banks 6, National Bank of Serbia 1,687 2,773 Corporate 754, ,845 Public sector - 1,251 Retail sector 20,599 15,515 Other customers In foreign currency 24,423 14,712 Corporate 21,423 14,712 Allowance for impairment (301,270) (226,382) Balance at 31 December 504, , LOANS, ADVANCES AND DEPOSITS In dinars Shortterm Long-term Total Shortterm Longterm -Banking sector 242,286 28, , , ,000 -Corporate 14,325,159 3,773,154 18,098,313 14,642,990 3,434,213 18,077,203 -Retail 357,190 1,375,653 1,732, ,849 1,432,796 1,681,645 -Public sector 31,141 7,004 38,145 16,000-16,000 -Foreign entities Total in dinars 14,955,804 5,184,374 20,140,178 15,107,844 4,867,107 19,974,951 In foreign currency - Banking sector 35,117-35,117 1, ,046 - Corporate 480, , , ,662 - Foreign banks , ,026 Total in foreign currency 515, ,225 1,190,734-1,190,734 Total placements 15,471,029 5,184,374 20,655,403 16,298,578 4,867,107 21,165,685 Allowance for impairment: (3,033,222) (2,040,238) Balance at 31 December 17,622,181 19,125,447 Total 27

30 20. EQUITY INVESTMENT In dinars -banks 1,551 1,925 - corporate 142,929 10,393 Total in dinars 144,480 12,318 In foreign currency -banks 3,476 3,263 Allowances for impairment (440) - Balance at 31 December 147,516 15, OTHER LENDING In dinars 878, ,713 - Receivables for the amounts paid by the Bank on the basis of issued guarantees 466, ,723 -bought placements 383, ,999 - Other placements 27,598 17,991 In foreign currency 1,919, ,524 - Receivables for the amounts paid by the Bank on the basis of issued guarantees 142, ,228 - Other placements 49, ,296 Allowances for impairment (385,911) (251,824) Balance at 31 December 684, ,413 Factoring in the amount of RSD 383,999 thousand relates to PU Direkcija za izgradnju,urbanizam i stambene poslove Municipality Prokuplje in the amount of RSD thousand and Rudnik- fashion factory from Gornji Milanovac in the amount of RSD 100,141 thousand. 22. SECURITIES 28

31 In dinars Securities available for sale Securities held to maturity 1,026,023 1,618,954 Bills 426, ,830 Deviation from nominal value (9) (29) Allowances for impairment (48,309) (40,924) Total in dinars 1,404,065 1,896,171 In foreign currency Securities of RS held to maturity 341,155 - Net balance at 31 December 1,745,220 1,896, PROPERTY, PLANT, EQUIPMENT, INVESTMENT PROPERTY AND INTANGIBLE ASSETS Changes in fixed assets, investment property and intangible asset are: Land and buildings Total fixed assets Investment property Intangible assets Equipment Cost Opening balance 801, ,889 1,376,823 1,171, ,720 Aditions - 10,331 10,331 74,316 65,471 Transfers - 6,585 6, ,010 57,288 Disposals - sale - (4790) (4,790) - - Disposals - (14,522) (14,522) - - Other recording (666,010) (12,978) As of 31 December 801, ,493 1,374,427 1,245, ,501 Accumulated depreciation and impairment Opening balance 45, , ,771 2,237 41,991 Additions 10,425 68,084 78,509 14,631 42,732 Transfers - 3,292 3,292 - (4,818) Disposals - sale - (4170) (4170) - - Disposals - (13,530) (13,530) - - Other recording (2,963) As of 31 December 56, , ,872 16,867 76,942 Net book value 31 December , , ,555 1,228, , December , , ,050 1,169,274 66,729 The Bank has no buildings under mortgage in order to secure loan liabilities repayment. As of 31 December 2012 net present value was comprised mostly of computer and telecommunication equipment, office furniture and motor vehicles. In 2011 and 2012 the Bank received properties by collection of receivables, and the part amounting to RSD 1,245,825 thousand, was classified as investment property and rented. 29

32 In December 2011 the significant numbers of object were placed in the investment property, as follows: - Office Building of the Red Cross Nis - the value of RSD 117,271, area 1,073 m2, - Part of building of the Port of Belgrade, ground floor, and 1 st floor - value RSD 392,959, area 5,744 m2, - Office building of the Velefarm Vojvode Stepe 414/V value RSD 319,167, area 1,833 m2; - Office building Velefarm in Uzice Borići-value RSD 145,872, area 1,658 m2. In 2012 the following facilities were placed as investment properties: - Unit 105 in Shopping business center Kalča Nis in the amount of RSD 15,232, area 150 m2, - Store at Kralja Aleksandra 128 street Kragujevac in the amount of RSD 17,140, area 149 m2, - Production plant and land in Vitanovac Kraljevo in the amount of RSD 29,762, Total income from lease of the investment properties amounted to RSD 59,644 thousand. 24. OTHER ASSETS Receivables from employees 10,119 9,766 Receivables for corporate tax prepayment, except income tax Advances placed 8,633 54,060 Other receivables from business relationships 206, ,110 Stock 3,915 3,315 Tangibles received from collection of receivables 13, ,223 Other assets - income tax prepayment receivables 34,282 19,668 Accrued expenses for calculated interest: - in dinars 29,601 17,392 - in foreign currency Other accruals: - in dinars 7,662 10,208 Total other assets and accruals - 1,012,955 Allowance for impairment (159,036) (133,472) Balance at 31 December 154, ,483 30

33 25. TRANSACTION DEPOSITS In dinars 2,677,244 2,910,170 Banking sector 172, ,225 Public entities 146, ,897 Corporate 1,969,591 2,068,799 Public sector 14,094 20,142 Retail 373, ,710 Foreign entities 1, In foreign currency 848, ,758 Banking sector 126,360 64,115 Public entities 13,783 45,518 Corporate 503, ,850 Public sector 9 8 Retail 204, ,989 Foreign entities 21,125 27,278 Balance at 31 December 3,525,668 3,783, OTHER DEPOSITS Short -term Total Short -term Longterm Longterm Total In dinars 6,419, ,320 6,571,357 10,233, ,344 10,723,194 Banking sector 135, ,348 2,150,605-2,150,605 Public utilities 760, ,050 1,375,000 20,050 1,395,050 Corporate 4,927, ,063 5,078,430 6,376, ,259 6,645,878 Public sector 513, , , , ,200 Retail 82, ,177 88, ,461 Foreign entities In foreign currencies 6,515,476 5,942,710 12,458,186 10,319,658 2,659,536 12,979,194 Banking sector 456, , , ,825 Public utilities 1,133, ,992 1,718, ,706 1,460,287 1,836,993 Corporate 2,841,509 56,089 2,897,598 1,987,487 90,016 2,077,503 Retail 1,940,856 5,201,939 7,142,795 6,447,631 1,108,855 7,556,486 Foreign banks 113, , , ,089 Foreign entities 29,080 99, ,770 7, ,298 Balance at 31 December 12,934,513 6,095,030 19,029,543 20,553,508 3,148,880 23,702, BORROWINGS 31

34 In dinars 72, ,038 Liabilities for student loans 72, ,012 Other liabilities In foreign currency 96,780 4,941 Liabilities for undistributed collection 94,184 4,076 Liabilities for foreign payments 7, Balance at 31 December 168, , INTEREST, FEES AND COMMISSIONS PAYABLE Interest payables 13,367 87,354 Banking sector 170 4,615 Public utilities 1,118 19,210 Corporate 12,079 61,481 Public sector - 2,048 Fees payable Balance at 31 December 13,488 87, TAX DUTIES Tax on interest payable on individuals' savings accounts VAT duties 2, Taxes and contributions Balance at 31 December 3,867 1, LIABILITIES FROM PROFIT Dividends 6,306 6,308 Balance at 31 December 6,306 6, PROVISIONS 32

35 Provisions for losses on guaranties 26,472 62,805 Provisions for losses on acceptances 1, Provisions for post-employees benefits 17,685 23,580 Balance at 31 December 45,203 86, OTHER LIABILITIES AND DEFFERALS In dinars 798, ,948 Liabilities for subordinated loans 483,303 Liabilities to suppliers 55,543 27,300 Liabilities for student loans 88, ,652 Liabilities for deposits for incorporation 2,777 4,691 Other liabilities 21,025 19,199 Deferred interest liabilities 48,357 19,593 Deferred interest income 43,737 85,608 Deferred fee income 55,290 76,905 In foreign currency 415,874 89,799 Liabilities for subordinated loans 227,437 - Grants 32,198 13,236 Liabilities for collection from Kosovo and Metohia - 22 Other liabilities Deferred interest liabilities 42,766 9,201 Deferred interest on savings accounts 113,227 66,468 Balance at 31 December 1,214, ,747 Due to decreased capital adequacy in 2012 the bank received subordinated loans in the amount of RSD 710,740 thousand (EUR 6,250 thousand). 33. EQUITY 33

36 Share capital ordinary shares 3,404,886 3,404,886 Share premium 1,238,175 1,238,175 Statutory reserves un realized losses (371) (391) Reserves from retained earnings 1,923,226 1,669,515 Retained earnings - 117,936 Legal reserves - 135,775 Loss up to the value of capital (708,485) - Share capital Balance at 31 December 5,857,431 6,565,896 On 31 December 2012 authorized share comprised 567,481 ordinary shares with nominal value of RSD 6,000 (2011: 567,481 ordinary shares with a nominal value of RSD 6,000). Share repurchase No repurchased own shares incurred as at 31 December 2012 and Share premium Share premium comprises positive difference between achieved selling value of shares and their nominal value, as well as gains and losses on sales and repurchases of own shares. Revalorisation reserves Revalorisation reserves comprise of fair value change effects within financial instruments available for sale. Reserves from retained earnings Reserves from profit are formed in accordance with regulations for the estimated losses, reserves for general bank risks and other reserves from allocation of profit, in accordance with the law, statute and other Bank's Acts. Pursuant to Decision made by Shareholders Assembly in 2012, legal reserves in the amount of RSD 135,775 thousand were distributed to reserves from profit for potential losses. Loss to the level of capital Bank incurred a loss in the amount of RSD 708,485 thousand whereby the loss from ordinary course of business amounts RSD 701,426 thousand and loss of deferred tax liabilities amounts RSD 7,059 thousand. 34

37 34. OFF-BALANCE SHEET ITEMS Funds on behalf of third parties 4,447,308 5,346,433 Guarantees, other contingent liabilities and commitments 4,165,722 3,584,741 Other off-balance sheet items 4,675,289 2,305,115 Balance at 31 December 13,288,319 11,236,289 Funds managed on behalf of third parties Student loans 4,438,519 5,337,262 Short-term placements - agriculture 8,115 8,256 Long-term placements - Retail Balance at 31 December 4,447,308 5,346,433 Guarantees and other commitments and contingencies Guarantees, bills of guarantee and acceptances Issued payable guarantees for loan repayment 915, ,282 Issued other payable guarantees 2,276,616 1,699,752 Performance guarantees 973,350 1,004,398 Placed bills of guarantee and acceptances Total guarantees, bills of guarantee and acceptances 4,165,722 3,584,741 Other off-balance sheet items Revocable commitments 1,491, ,428 Guarantees received from foreign banks and other financial institutions 1,595, ,671 Suspended interest 1,541,124 1,082,353 Other 47,929 29,663 Balance at 31 December 4,675,289 2,305, RELATED PARTY TRANSACTIONS The Bank enters business relationships and arrangements with members of the Executive Board and other employees in its regular operations, based on usual market terms 35

38 36. FINANCIAL INSTRUMENTS FAIR VALUE Assets for which fair value approximates carrying value For liquid or financial assets and liabilities with short maturity (up to 12 months) it is assumed that the carrying values approximate to their fair values. This assumption is also relevant for demand deposits, savings accounts without specified maturity and financial instruments with variable interest rates. Fixed rate financial instruments The fair value of fixed rate financial assets and liabilities declared at amortized cost are estimated by comparing market interest rates when they were first recognized with current market rates for similar financial instruments. The estimated fair value of fixed interest bearing deposits is based on discounted cash flows using prevailing money-market interest rates for debts with similar credit risk and maturity. For quoted debt instruments the fair values are calculated based on quoted market prices. For those instruments issued where quoted market prices are not available, a discounted cash flow model based on a current interest rate yield curve appropriate for the remaining term to maturity is used. 37. RISK MANAGEMENT Introduction Risk is inherent in the Bank's activities but it is managed through a process of ongoing identification, measurement and monitoring subject to risk and other controls. This process of risk management is critical to the Bank's continuing profitability and each individual within the Bank is accountable for the risk exposures relating to his or her responsibilities. The Bank is exposed to credit risk, liquidity risk and market risk. It is also subject to operating risks. Risk management structure comprise the Board of Directors and the Executive Board, Audit Committee, Internal Audit, Solvency and risk management department, and other organizational units of the Bank in different stages of risk management processes, whose authority and responsibilities in risk management of the Bank, are defined by legal and regulatory provisions, as well as documents of the Bank.. Solvency and risk management department Solvency and risk management department in the organizational structure is a function of organizational separation of the two functions of the Bank and performing operational tasks on the one hand, and risk management processes related to the provision of such services, on the other side. Solvency and risk management department deals with all risks to which the Bank is exposed, paying particular attention primarily present risk or credit risk, liquidity risk, interest rate risk, currency risk and exposure. 36

39 Risk management by the Department of solvency and risk management involve the implementation of procedures to identify risks, measure, assess and monitor, control the compliance status of certain positions of the Bank to the applicable limits, reporting, organizational units and organs of governance and management of the Bank about it and propose measures to minimizing risk in Bank operations Risk management adequacy In accordance with the provisions of the Banking Law and its Implementing Regulations for the implementation of this Act the Bank has adopted policies and procedures and organizational structure, risk management tailored to the requirements stemming from regulations pertaining to the segment of risk management and enables the achievement of stated objectives and principles for risk management. In 2012 the Bank managed risk in accordance with the prudential requirements of regulatory authorities in accordance with internal regulations adopted for better risk management. Financial risk management is consistent with the size and organizational structure of the Bank, the scope of activities and type and complexity of tasks performed by the bank Risk management and reporting systems Monitoring and controlling risks is primarily based on the establishment of limits. These limits reflect the business strategy and market environment of the Bank, and the level of risk that the Bank is willing to accept. The Bank monitors and measures the capacity of the overall risk by taking into account the overall exposure to all types of risk. Board of Directors, Executive Committee, Audit Committee and the Department of Internal Audit quarterly presents a overall report on risk management that includes all the necessary information to evaluate and draw conclusions about the risks to which the Bank is exposed. Given their importance, are compiled monthly reports on credit, interest rate and liquidity risk, to be submitted to the competent authorities for consideration Credit risk Credit risk is the risk of adverse effects on the financial result and equity due to failure to fulfil obligations toward the Bank as a client. Identification of credit risk is performed at the stage of establishing initial contact the client with the Bank, in the process of forming a client file in the course of the Bank s placements. Credit risk measurement is done by: 1) calculating the values of certain indicators of financial condition of the client, whereas species using these indicators depends on the client and the specifics of his legal status, activities and other characteristics of the condition. 37

40 2) analyzing the data collected about the client and his current business of the client application, which must be correct, complete and updated to provide quality information on the financial condition and creditworthiness of the borrower. The assessment of credit risk is expressed categorization receivables and is subject to: - Provisions of the decision of the National Bank of Serbia s governing classification of balance sheet assets and off-balance bank accounts to reserves for potential losses, and - Approved the Bank s internal model for risk assessment in order to accounts for impairment of balance sheet assets and provisions for losses on off-balance sheet items. Solvency Division and Risk Management in 2012, conducted an analysis of current data supplied by clients, Sector placements and corporate sector for retail and on the basis of all quantitative and qualitative criteria, the categorization of loans in accordance with the said decision of the NBS and the Bank s internal model for risk assessment. Risk mitigation measures include establishing rules for the implementation of these measures, relating to taking, reduction, diversification, risk transfer and avoidance by the Bank identify, measure and evaluate. Risk mitigation is achieved by: - Consistent application of procedures of identifying, measuring and risk assessment by the competent organizational unit of the Bank and the Bank s bodies - Using an information system that provides information for timely and continuous analysis and monitoring changes status and structure, i.e. quality of the loan portfolio of the Bank. Credit risk monitoring is done as well at the individual client level, as at a total loan portfolio of the Bank level. Maximum exposure to credit risk without taking into account of any collateral and other credit enhancements 38

41 The following table shows the maximum exposure to credit risk for the components of the balance sheet including derivatives. The maximum exposure is shown gross, before the effect of mitigation through the use of master netting and collateral agreements Maximum net exposures Cash and cash equivalents (excluding petty cash) 1,724,127 2,226,495 Callable deposits and loans 4,448,128 6,799,148 Interest and fee receivables 504, ,340 Loans and other placements 17,622,181 19,125,447 Investments in securities held to maturity 1,745,220 1,896,171 Investments in shares and other securities available for sale 147,516 15,581 Total 26,191,371 30,521,182 Total financial guarantees 4,165,722 3,584,741 Total credit risk exposure 30,357,093 34,105,923 Collateral and other credit enhancements The amount and type of collateral depends on an assessment of the credit risk of each customer. The main types of collateral for commercial lending are mortgages over real estate, inventory, trade receivables and other movable and immovable property, co-debtor / guaranties of other body. The bank monitors the market value of collateral, requests additional collateral in accordance with the underlying agreement. It is in the Bank's policy to dispose of repossessed properties and hence reduce or repay the outstanding claim. Impairment assessment The main considerations for the impairment assessment of placement are: placement principal and mature interest are overdue, difficulties in cash flows of customers, credit rating downgrades, or infringement of the original terms of the contract. The Bank addresses impairment assessment in two areas: individually assessed allowances and collectively assessed allowances. In relation to impairment assessment, the international accounting standards have been used in order to assess balance sheet and off-balance sheet placements, i.e. to calculate allowance for impairment of balance sheet assets and provisions for losses on off-balance sheet items since 31 December

42 Solvency and risk management Sector assess the loans to legal entities under International Accounting Standards (IAS), in accordance with the financial ability and credit history of clients, i.e. in accordance with the reality of the collection of placement, or the reality of cash flows on these loans in the future. The assessment was made in accordance with the accounting policies of the Bank. This form of assessment was carried out in Department of operations for the retail loans to individuals in accordance with an accounting policy of the Bank for this type of placement, which placement adjusted book value in accordance with IAS. Individually assessed allowances In the process of placements assessment the Bank individually evaluated loans to customers that are 80% of the gross income covered by the portfolio. The Bank determines the allowances appropriate for each individually significant loan or placement. Items considered when determining allowance amounts include the sustainability of customer's business plan, its ability to improve performance once a financial difficulty has arisen, realizable value of collateral and its timing, the availability of other financial support, possibility to repay due receivables and the timing of expected cash flows. From 31 January 2011 the impairment losses were made at the end of each month. Off-balance sheet investments which relate to the same customers as well as individually assessed balance receivables, are value adjusted by the weighted average rates, by which the balance receivables from these customers are individually evaluated. Collectively assessed allowances Allowances are assessed collectively for losses on loans that are not individually significant (including credit cards, residential mortgages and unused consumer lending) and for individually significant loans where there is not yet objective evidence of individual impairment. Starting from 31 January 2011 allowances are evaluated at the end of each month with each portfolio receiving a separate review. Impairment of financial guarantees and letters of credit is estimated and provisions are made in the similar way as for the loans Liquidity Risk Liquidity risk is the risk of adverse effects on the financial result and equity due to the inability of the Bank to fulfil its due obligations. The liquidity of the Bank is it ability to timely meet liabilities when due, and it depends primarily on having liquid assets, from cash flow and ability of the Bank to provide funds in the market. In order to reduce or limit this risk, the Bank seeks to diversify its sources of funding, to manage the assets, i.e. liabilities, reviewing its liquidity and to monitor future cash flows and daily liquidity. This includes an assessment of expected cash flows and availability of high or low grade financial instruments. The Bank maintains a portfolio of highly marketable and diverse assets that can be easily liquidated in the event of an unforeseen interruption of cash flow. The Bank maintains a mandatory reserve in RSD and foreign currency, in accordance with the requirements of the National Bank of Serbia. 40

43 The Bank continuously measure and monitor the liquidity of the Bank indicators of the liquidity determined in accordance with the decision of the National Bank of Serbia governing liquidity risk management. Aforementioned ratio during the year was as follows: The coefficient of liquidity Average during period In addition to the above indicators, the Bank continuously measure and monitor the level of liquidity using internal methodologies through: - Monitoring the situation and change the structure of its balance sheet as of and for the period (based on average daily values) - Gap analysis (analysis of mismatch assets and liabilities, and inflows and outflows into time segments) - Indicators (ratios) liquidity - Analysis of stress scenarios (include analysis of changes to the state of liquidity of the Bank under the assumption of formation of extreme changes of key internal and external factors that affect the liquidity and implement the design changes in the assets of the Bank, the Bank in response to projected changes in its liabilities, i.e. by testing its ability to meet customer requirements when it comes to withdrawals: all transactions and deposits, deposits of the five largest corporate depositors, deposits by ten largest depositors) Interest rate risk Interest rate risk is the possibility of negative effects on the financial result and capital of the bank due to changes in interest rates, and the Bank is exposed to this risk based on items declared in the banking book. The basic method for measuring interest rate risk is based on the definition and grouping of assets and liabilities of the Bank in several time ( repricing ) intervals according to their maturity, which is the point of interest rate risk, coincides with the period remaining until: - Contractual maturities, the items with the agreed fixed interest rates, - Following the determination (or re-establish automatic updating) interest rates, items with contracted at variable interest rates. For every group of balance sheet items and each defined time ('repricing ) interval, weighted-average interest rates of assets and liabilities are calculated on a particular day and are compared to rates in previous periods of observation and interest rates on financial markets. The amount and structure of noninterest bearing assets and liabilities is also monitored, as well as the currency structure of interest and non-interest bearing items of balance sheet of the Bank. 41

44 Basic measure of interest rate risk is the interest sensitivity ratio (ratio gap) which is calculated as the ratio of interest-sensitive assets and interest-sensitive liabilities and reflects the willingness of banks to take a risk in terms of future movements in market interest rates, especially in periods of great fluctuations in market interest rates. The sensitivity of the Bank s financial results for the expected or projected changes in interest rates depends on the structure and maturity level of existing-contracted rates of interest-bearing assets and liabilities. Gap analysis allows the measurement and assessment of the sensitivity of calculating the net change in the projected financial results of changes in interest rates. - coefficient of interest sensitivity - participation of gap positions in interest rate sensitive assets - relationship of average weighted interest rate on interest bearing assets and the weighted average rate on interest bearing, liabilities increased by the projected annual increase in the Consumer Price Index - participation of the measured changes in net interest income in the projected changes in interest rates in net income from interest on current interest rates - ability to measure the sensitivity of financial results to changes in interest rates on assets and liabilities in different directions and different intensity Foreign currency risk Foreign currency risk is the risk of negative effects on financial results and equity due to exchange rate changes, and the Bank is exposed to him on the basis of items that are kept in the banking book and trading book. The function of managing foreign exchange risk, the Bank uses the limits prescribed by the National Bank of Serbia, as well as the limits adopted by the competent authorities of the Bank. Positions for each major currency are monitored daily to ensure that the values given position remain within established limits. 42

45 EUR ASSETS EUR USD Other currencies Total FC RSD Index EUR USD Index.USD Other Index. other Sub-balance Sub-balance Total 1 Cash and cash equivalents 155, , , ,618 2,057,332 2,297,950 2 Revocable deposits and loans 4,290, , ,448, ,448,128 3 Receivables for interest and fees 6, , , , , ,199 4 Placements - banks 1, , ,134 5 Placements - other financial sector Placements - corporate 311,604 8,160,895 10, , ,898,175 7,173,693 16,071,868 7 Retail placements 0 506, ,498 1,042,681 1,549,179 8 Securities for trade purposes 341, ,155 1,404,065 1,745,220 9 Equity investments 0 0 3, , , , Other placements 67,914 40,248 2, , , , Intangible assets , , Fixed assets ,128,511 2,128, Other assets and accruals 3,588 24, , , , Fixed assets held for sale ,920 2, Total assets 5,177,587 8,921, , ,674 54, ,775,657 15,100,708 29,877, Transaction deposits - banks , ,551 12,067 30, Transaction deposits - other FS 107, , , , Transaction deposits - corporate 466, , , ,963 2,147,534 2,662, Transaction deposits - retail 182, , , , , , Other deposits - banks 113, , , Other deposits other FS 536, ,856 1,485,700 2,023, Other deposits corporate 4,044, , , ,177,620 4,357,236 9,534, Other deposits - retails 7,209, , , ,274,090 83,323 7,357, Received loans 76, , , ,827 72, , Liabilities for securities Liabilities for interest and fees ,488 13, Provisions ,203 45, Tax duties ,867 3, Liabilities from profit ,306 6, Other liabilities and accruals 409, ,821 6, , ,146 1,214, Deferred tax liabilities ,079 12,079 Total liabilities 13,147,583 1,132, , , ,952,228 9,067,706 24,019, Share and other capital ,643,061 4,643, Reserves ,923,226 1,923, Accumulated profit , , Unrealised loss on AFS securities Total liability and equity 13,147,583 1,132, , , ,952,228 14,925,137 29,877,365 Net FC position as of 31 December -7,969,996 7,788, , ,674 11, , ,571 43

46 The Bank continually measures and monitors foreign currency risk through foreign currency indicators, and in the manner prescribed by the National Bank of Serbia. The bank determined the foreign exchange risk ratio of, for all working days of the month, as well as a monthly indicator of foreign exchange risk, for each month during the year. Foreign exchange risk is the ratio of total net open foreign currency position (which is a higher amount of total long open positions or the total short open position depending on which of the two absolute values greater), including the absolute value of net open positions in gold and other precious metals on the one hand, and the Bank s capital, on the other side. The following table presents the Bank s foreign exchange risk at 31 December 2012 the table includes assets and liabilities at their book values. EUR USD CHF GBP Other From that in From that in From that in From that No. Item From that in Total RSD RSD RSD in RSD Total Total Total Total RSD indexed Total indexed by indexed by indexed by indexed by by FC clause FC clause FC clause FC clause FC clause Net spot position Foreign currency assets Foreign currency liabilities Irrevocable guarantees, uncovered letters of credit and similar offbalance 1.3. sheet items on which the bank will have to pay, and it is possible that these funds will not be refunded Net forward 2. position Long position Short position Options Long position Short position Long open position Short open position 6. Net open FC position Equity Foreign currency indicator Country risk Country risk is defined as the risk the possibility of negative effects on financial results and equity of the Bank due to inability to collect receivables from the entity to which the Bank is exposed for reasons that are a consequence of political, economic or social conditions in the country of origin of that person. Identification of country risk is based on customer data given by the Bank headquartered outside the Republic of Serbia and the amount receivables from these clients. 44

47 Country risk is measured by determining the debtor countries belonging to a group of countries and country rating of the debtor who, according to the latest rating, the agency established for a particular country. Risk assessment can be organized on the basis of established land belonging to a group of debtor countries, and comparing the results of measurements rating debtor country with, at the time of the current assessment, rating values, which determine a country risk as zero, eligible or partially eligible Concentration risk The concentration risk directly or indirectly arises from the bank's exposure to the same or similar sources of risk, the same or similar type of risk. The identification of risk concentrations is based on information of clients, their mutual connection or connection with the Bank and the amount of receivables, as well as on other information. In this regards the group determination is made. The concentration risk is measured by: - Exposure to a single body or a group of related parties - Exposure to a person related with the Bank - Total exposure to persons related with the Bank - Sum of all large exposures, which in addition to the sum of large exposures to a single body or group of related parties includes the overall exposure to persons related with the Bank - Total group exposures with the same or similar risk factors on other bases, such as economic sectors, geographic regions, product types, instrument of collaterals - Relations exposure from the first four tips and equity, calculated in accordance with the decision on the capital adequacy, or participation of its exposure from the fifth tip in credit portfolio. Concentration risk assessment is done by comparing result of measuring risk exposure with applicable at the time of assessment exposure limits, and comparing result determines measured risk exposure as acceptable or unacceptable Investment risk Investment risk means the risk of investing in other legal entities and assets. Identification of investment risk is made based on data and information on investments in other legal entities, the Bank s investments in fixed assets and bank capital. Investment risk is measured by the Investment Bank s review of non-financial sector entities in the fixed assets of the Bank and data on the Bank s capital 45

48 Risk assessment is done by comparing the results of measurement of investment risk to the Bank, at the time of the applicable evaluation, investment limit, the result of comparison determines the measured risk of investment banks as an acceptable or unacceptable Operational risk Operational risk is the risk of negative effects on the financial result and equity due to failures by employees, inadequate procedures and processes in the Bank, inadequate management information and other systems in the Bank, and due to the occurrence of unexpected external events. The Bank can not expect to eliminate all operational risks, but the introduction of rigorous control framework and monitoring and responding to potential risks, the Bank is able to manage these risks. The long term objective of the Bank in operational risk management is to minimize its negative effects on the financial result and equity. Operational risk management includes effective segregation of duties, access, authorization and compliance procedures, staff training and monitoring process. Monitoring of operational risk involves recording the events that are operational risk and their association to a particular type of operational errors, business line to which an event affects, the class of products affected by the event, loss event brings with it the measures taken to avoid such events in the future Market Risk Market risks are risks of negative effects on the financial result and equity due to changes in the value of a portfolio of financial instruments due to changes in market variables such as interest rates, exchange rates, securities prices, commodity prices, and including interest rate, foreign exchange and other market risks. The Bank is not exposed to other market risks arising from positions held by the Bank s trading book. 38. CAPITAL MANAGEMENT The objectives of the Bank s capital management, which is a broader concept than the amount of capital shown in the balance sheet, are: to ensure compliance with the requirements of the National Bank of Serbia provide for the long-term going concern with the provision of return to shareholders and benefits for other parties, to ensure a strong capital base to support further development of its business. 46