The PPACA's Summary of Benefits and Coverage: What Do the Final Rules Mean for Insurers and Self- Funded Employers?

|

|

|

- Felicity Craig

- 5 years ago

- Views:

Transcription

1 The PPACA's Summary of Benefits and Coverage: What Do the Final Rules Mean for Insurers and Self- Funded Employers? This roundtable discussion is brought to you by the Health Plan Affinity Group (HP AG) of the Payors, Plans, and Managed Care (PPMC) Practice Group March 30, :00-1:00 pm Eastern Presenter: Martin L. Mitchell, Jr., Esquire State Policy Department America s Health Insurance Plans, Washington, DC, mmitchell@ahip.org Moderator: Kirk J. Nahra, Esquire Partner Wiley Rein LLP, Washington, DC knahra@wileyrein.com 1

2 Overview of Roundtable Discussion PHSA Section 2715 History and Setting NAIC Subgroup & its Proposal Final Rule (Released February 9 th ) Applicability date Required format and content Who must produce the SBC When must it be delivered How can an SBC be delivered Coverage Examples Penalties for non-compliance Questions 2

3 PHSA Section 2715 (a) IN GENERAL. - Not later than 12 months after the date of enactment of the Patient Protection and Affordable Care Act, the Secretary shall develop standards for use by a group health plan and a health insurance issuer offering group or individual health insurance coverage, in compiling and providing to applicants, enrollees, and policyholders or certificate holders a summary of benefits and coverage explanation that accurately describes the benefits and coverage under the applicable plan or coverage. In developing such standards, the Secretary shall consult with the NAIC, a working group composed of representatives of health insurance-related consumer advocacy organizations, health insurance issuers, health care professionals, patient advocates including those representing individuals with limited English proficiency, and other qualified individuals. 3

4 NAIC Subgroup & Its Proposal Work began summer of 2010 NAIC led work group - 23 state regulators; 3 federal; 9 consumers; 4 carriers; AMA; URAC Coverage Team led by Commissioner T. Miller (OR) Definition Team led by Superintendent M. Kofman (ME) Self-funded business never addressed by NAIC Innovative products not addressed by NAIC Operations & implementation issues not addressed by NAIC Consumer testing conducted on late drafts of SBC 4

5 NAIC Subgroup & Its Proposal (Con t) Final NAIC transmittal letter July 7, _transmittal_letter.pdf The SBC Template The Carrier Instructions Individual instructions 14 pages _inst_ind.pdf Group Instructions 15 pages _inst_grp.pdf 5

6

7

8

9

10

11

12 HHS, DOL, Treasury NPRM (Released 7/22/2011) The Departments are appreciative of the detailed and valuable work the NAIC and its working group has performed in developing recommended standards and materials including the NAIC's extensive efforts to involve numerous stakeholder groups in that process Accordingly, as noted, the Departments are appending to the document accompanying these proposed regulations the NAIC's SBC work product for public comment &AgencyId=8&DocumentType=1 12

13 HHS, DOL, Treasury Final Rule (Released 2/9/2012) Per the HHS Press Release: People in the market for health insurance will soon have clear, understandable and straightforward information on what health plans will cover, what limitations or conditions will apply, and what they will pay for services thanks to the Affordable Care Act Federal Register Volume 77, Number 30 (Tuesday, February 14, 2012) Pages cid=25818&agencyid=8&documenttype=2 13

14 Applicability Date Rule establishes 6 month extension for implementation New Date September 23, 2012 For group coverage disclosures (employer based) Through open enrollment sessions - First day of enrollment on or after 9/23/2012 Through enrollments made other than through open enrollment sessions (including special enrollees and newly eligible enrollees) First day of the first plan year beginning on or after 9/23/2012 For individual or non-group disclosures (self-purchasers) September 23,

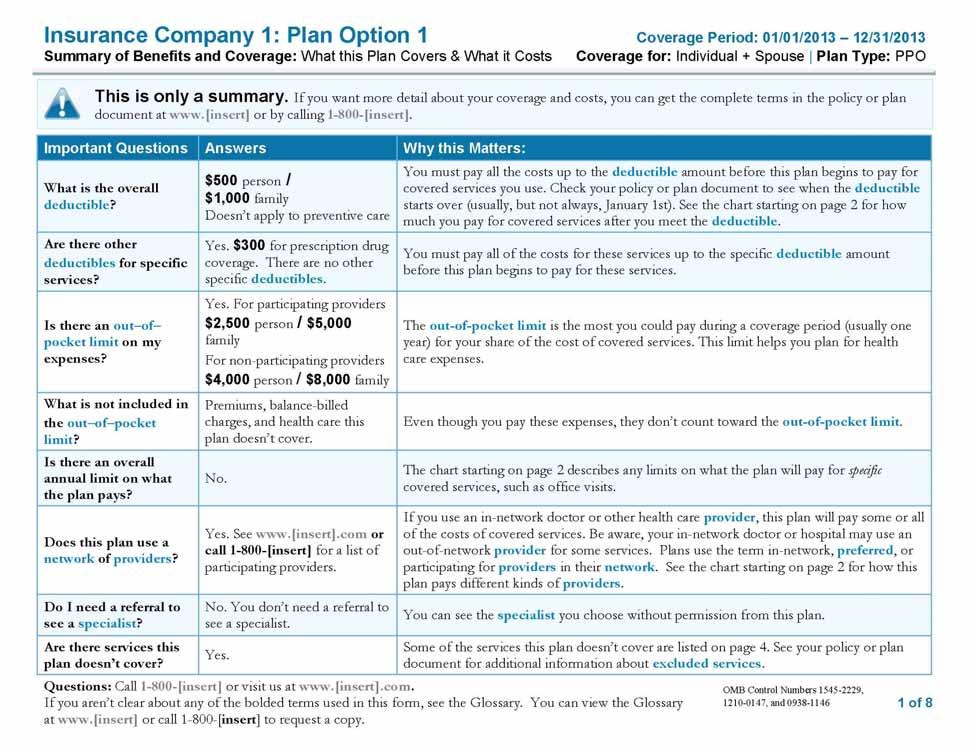

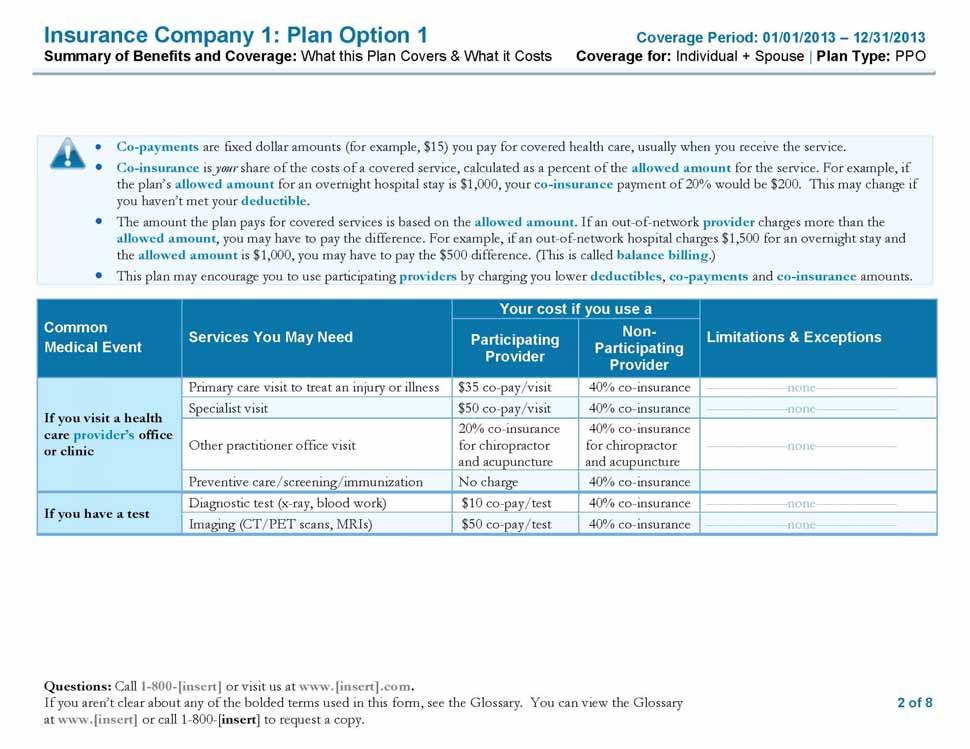

15 Required Format and Content At least 12-point font typeface No more than 4 pages in length (now 2-sided) Terminology must be understandable to average enrollee In a culturally and linguistically appropriate manner Generally following claims & appeals standards Standard insurance and medical terms ( Glossary ) Description of the coverage, including cost sharing of EHBs Exceptions, reductions, and limitations of the coverage Renewability and continuation of coverage provisions 15

16 Required Format and Content (con t) Coverage Examples Statement the SBC is only a summary, not policy language Contact Information for questions or to obtain a free SBC Information about any utilized provider networks Information about any utilized drug formularies Contact information on how to obtain the policy or plan docs 16

17 Final SBC Template and Carrier Instructions Final rule adopted, with one major modification, the SBC Template and carrier instructions proposed by NAIC Template designed to provide comparable comparisons To assist consumers in the selection of coverage To educate consumers about coverage before obtaining care Final rule adopted NAIC approach calling for strict compliance with instructions and template form Link to group instructions: Link to non-group instructions: 17

18 Final Rule SBC Template 18

19

20

21

22

23

24

25

26

27 Evolution on Concept of Template Strict Compliance Industry Concerns dating from early NAIC calls Ability of template to accommodate current & innovative products Ability of carriers to present information in compliance with strict requirements laid down by the instructions Ability for carriers to present other important information Modification in Final Rule Modifications in post-rule sub-regulatory guidance 27

28 Who Must Produce the SBC Individual Coverage Health insurance carriers to shoppers, policy holders, and to certain beneficiaries HHS Portal deemer provision Concerns with Coverage Examples, and production responsibilities Insured Group Coverage Health insurance carriers to employers shopping for coverage Joint responsibility for insurer and plan administrator to eligible/enrolled participants and to certain beneficiaries Self-funded Group Coverage Health plan administrator to eligible/enrolled participants and to certain beneficiaries 28

29 When Must an SBC be Delivered Individual Coverage New sales as soon as practical on receiving an application, no later than 7 business days thereafter; if SBC changes, at fulfillment Renewals by application delivery along with application materials Auto renewals 30 days prior to renewal date Group Coverage New sales- to group applicant as soon as practical on receiving an application, no later than 7 business days thereafter; to enrollees with application packages, or upon opening of enrollment window Renewals by application delivery along with renewal packages Auto renewals 30 days prior to new plan or policy year Special/Late Enrollees within 90 days of enrollment 29

30 When Must an SBC be Delivered (con t) Upon Request - soon as practicable, or w/i 7 business days, w/o cost - request can be made by beneficiary Special Rule on Duplicate Deliveries to Participants/Benes Special Group Rule on Deliveries compliant delivery by either carrier or plan is sufficient delivery for both entities Individual Coverage Deemer compliance with HHS Portal filing requirements will be deemed to satisfy the requirements to provide an SBC to any individual or dependent with respect to a request for an SBC prior to application for coverage. No deemer available with regard to subsequent requirements 30

31 How Can an SBC be Delivered Individual Coverage by mail, by e:mail upon agreement of the individual, by internet posting, again with the agreement of the individual, and by any other method that can reasonably be expected to provide actual notice subject to certain communications and posting requirements Group Coverage (where coverage not in place) electronic delivery permitted subject to certain communications and posting requirements Group Coverage (where coverage already in place) electronic delivery permitted under 29 CFR b-1 31

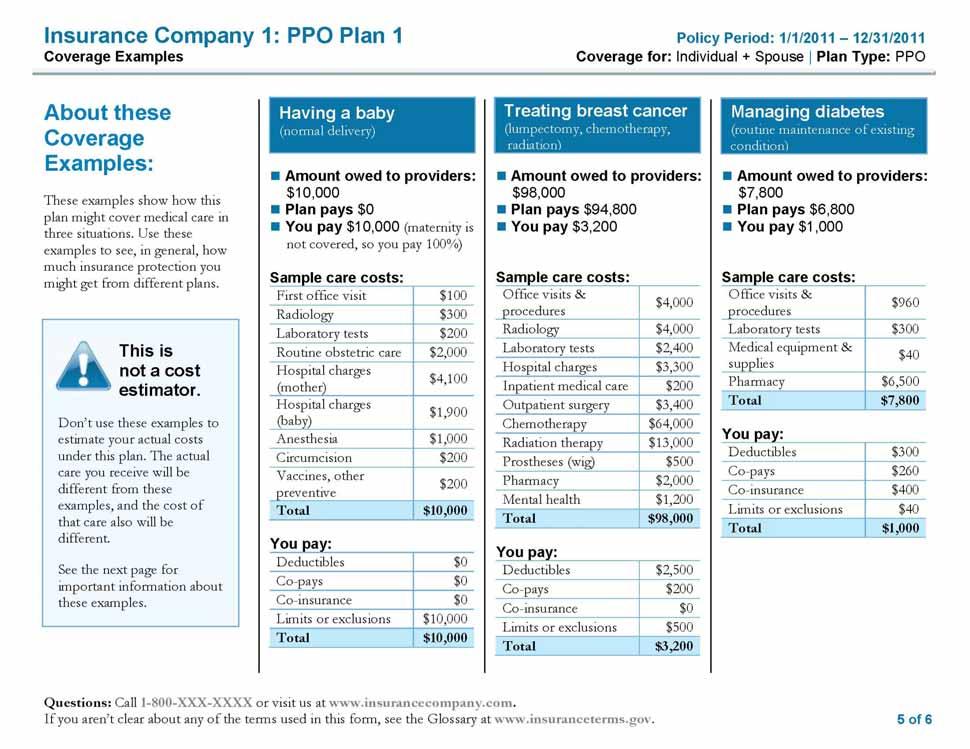

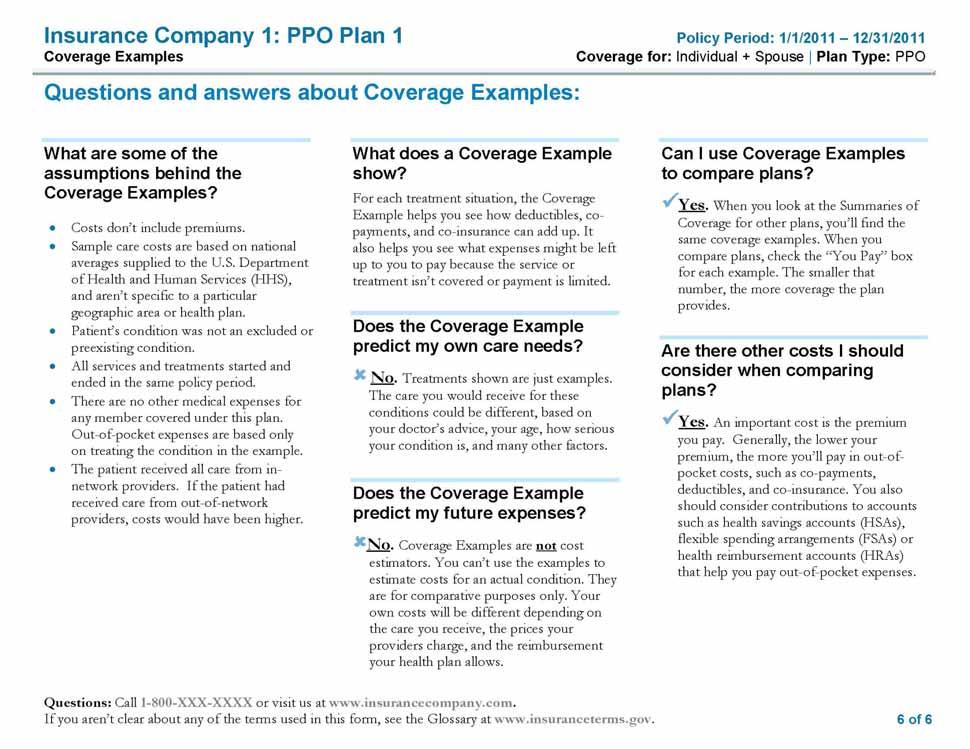

32 Coverage Examples 32

33 DEVELOPMENT OF STANDARD DEFINITIONS The Glossary IN GENERAL. The Secretary shall, by regulation, provide for the development of standards for the definitions of terms used in health insurance coverage, including the insurance- related terms and the medical terms premium, deductible, co-insurance, co-payment, out-of-pocket limit, preferred provider, non-preferred provider, out-of-network copayments, UCR (usual, customary and reasonable) fees, excluded services, grievance and appeals hospitalization, hospital outpatient care, emergency room care, physician services, prescription drug coverage, durable medical equipment, home health care, skilled nursing care, rehabilitation services, hospice services, emergency medical transportation 33

34

35

36

37

38 Penalties for Non-Compliance State Enforcement Under PHSA section 2723, a State has the discretion to enforce the provisions against health insurance issuers in the first instance. State enforcement may include imposition of state penalties Federal Enforcement (basic) If states fail to substantially enforce SBC provisions, the PHSA penalty - $100 per day per affected individual and IRS Code excise tax - $100 per day per affected individual may be imposed Federal Enforcement (enhanced) PHSA Section 2715 (f) also establishes a new $1,000 per day penalty for willful violations 38

39 APPENDIX 39

40 FAQs About ACA Implementation (Part VIII) Q2: What is the Departments' basic approach to implementation of the SBC requirement during the first year of applicability? The Departments' basic approach to ACA implementation is: "[to work] together with employers, issuers, States, providers and other stakeholders to help them come into compliance with the new law and [to work] with families and individuals to help them understand the new law and benefit from it, as intended. Compliance assistance is a high priority for the Departments. Our approach to implementation is and will continue to be marked by an emphasis on assisting (rather than imposing penalties on) plans, issuers and others that are working diligently and in good faith to understand and come into compliance with the new law. 40

41 FAQs About ACA Implementation (Part VIII) (Con t) Q3: Are plans and issuers required to provide a separate SBC for each coverage tier (e.g., self-only coverage, employee-plus-one coverage, family coverage) within a benefit package? No, plans and issuers may combine information for different coverage tiers in one SBC, provided the appearance is understandable. In such circumstances, the coverage examples should be completed using the cost sharing (e.g., deductible and out-of-pocket limits) for the self-only coverage tier (also sometimes referred to as the individual coverage tier). In addition, the coverage examples should note this assumption. 41

42 News Release Health Reform to Require Insurers to Use Plain Language in Describing Health Plan Benefits, Coverage People in the market for health insurance will soon have clear, understandable and straightforward information on what health plans will cover, what limitations or conditions will apply, and what they will pay for services thanks to the Affordable Care Act the health reform law according to final regulations published today. The marketing materials that insurers use can sometimes make it difficult for consumers to understand exactly what they are buying. The new rules, published jointly by the Departments of Health and Human Services, Labor and Treasury, require health insurers and group health plans to provide concise and comprehensible information about health plan benefits and coverage to the millions of Americans with private health coverage. The new rules will also make it easier for people and employers to directly compare one plan to another. All consumers, for the first time, will really be able to clearly comprehend the sometimes confusing language insurance plans often use in marketing, said HHS Secretary Kathleen Sebelius. This will give them a new edge in deciding which plan will best suit their needs and those of their families or employees. Under the rule announced today, health insurers must provide consumers with clear, consistent and comparable summary information about their health plan benefits and coverage. The new explanations, which will be available beginning, or soon after, September 23, 2012 will be a critical resource for the roughly 150 million Americans with private health insurance today. Specifically, these rules will ensure consumers have access to two key documents that will help them understand and evaluate their health insurance choices: A short, easy-to-understand Summary of Benefits and Coverage ( or SBC ); and A uniform glossary of terms commonly used in health insurance coverage, such as deductible and co-payment. All health plans and insurers will provide an SBC to shoppers and enrollees at important points in the enrollment process, such as upon application and at renewal. A key feature of the SBC is a new, standardized plan comparison tool called coverage examples, similar to the Nutrition Facts label required for packaged foods. The coverage examples will illustrate sample medical situations and describe how much coverage the plan would provide in an event such as having a baby (normal delivery) or managing Type II diabetes (routine maintenance, well-controlled) These examples will help consumers understand and compare what they would have to pay under each plan they are considering. Today s rules finalize the proposed rules issued in August Input was received from such stakeholders as the National Association of Insurance Commissioners (NAIC) and a working group composed of health insurance-related consumer advocacy organizations, health insurers, health care professionals, patient advocates including those representing people with limited English proficiency, and others. The final rules aim to ensure strong consumer information while minimizing paperwork and cost. 42

43 Q2: What is the Departments' basic approach to implementation of the SBC requirement during the first year of applicability? The Departments' basic approach to ACA implementation, as stated in a previous FAQ (see is: "[to work] together with employers, issuers, States, providers and other stakeholders to help them come into compliance with the new law and [to work] with families and individuals to help them understand the new law and benefit from it, as intended. Compliance assistance is a high priority for the Departments. Our approach to implementation is and will continue to be marked by an emphasis on assisting (rather than imposing penalties on) plans, issuers and others that are working diligently and in good faith to understand and come into compliance with the new law. This approach includes, where appropriate, transition provisions, grace periods, safe harbors, and other policies to ensure that the new provisions take effect smoothly, minimizing any disruption to existing plans and practices." In addition to the general approach to implementation, in the instructions for completing the SBC, we stated: "To the extent a plan's terms do not reasonably correspond to these instructions, the template should be completed in a manner that is as consistent with the instructions as possible, while still accurately reflecting the plan's terms. This may occur, for example, if a plan provides a different structure for provider network tiers or drug tiers than is represented in the SBC template and these instructions, if a plan provides different benefits based on facility type (such as hospital inpatient versus non-hospital inpatient), in a case where a plan is denoting the effects of a related health flexible spending arrangement or a health reimbursement arrangement, or if a plan provides different cost sharing based on participation in a wellness program." Consistent with this guidance, during this first year of applicability, the Departments will not impose penalties on plans and issuers that are working diligently and in good faith to provide the required SBC content in an appearance that is consistent with the final regulations. The Departments intend to work with stakeholders over time to achieve maximum uniformity for consumers and certainty for the regulated community. 43

44 Additional Links NAIC Consumer Information (B) Subgroup: HHS Regulations and Guidance: DOL PPACA: NPRM: d=25258&agencyid=8&documenttype=1 FAQs: 44

45 Q&A 45

46 The PPACA's Summary of Benefits and Coverage: What do the Final Rules Mean for Insurers and Self-Funded Employers? 2012 is published by the American Health Lawyers Association. All rights reserved. No part of this publication may be reproduced in any form except by prior written permission from the publisher. Printed in the United States of America. Any views or advice offered in this publication are those of its authors and should not be construed as the position of the American Health Lawyers Association. This publication is designed to provide accurate and authoritative information in regard to the subject matter covered. It is provided with the understanding that the publisher is not engaged in rendering legal or other professional services. If legal advice or other expert assistance is required, the services of a competent professional person should be sought from a declaration of the American Bar Association. 46

Summary of Benefits and Coverage and Uniform Glossary

Summary of Benefits and Coverage and Uniform Glossary Final Regulation from Pre-Publication version at http://www.dol.gov/ebsa/pdf/sbcfinalreg.pdf Federal Register version set to be published February

Summary of Benefits and Coverage and Uniform Glossary Final Regulation from Pre-Publication version at http://www.dol.gov/ebsa/pdf/sbcfinalreg.pdf Federal Register version set to be published February

Self-Compliance Tool for Part 7 of ERISA: Affordable Care Act Provisions

Self-Compliance Tool for Part 7 of ERISA: Affordable Care Act Provisions INTRODUCTION While this self-compliance tool does not necessarily cover all the specifics of these laws, it is intended to assist

Self-Compliance Tool for Part 7 of ERISA: Affordable Care Act Provisions INTRODUCTION While this self-compliance tool does not necessarily cover all the specifics of these laws, it is intended to assist

Summary of Benefits and Coverage and Uniform Glossary. AGENCIES: Internal Revenue Service, Department of the Treasury; Employee Benefits

DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Parts 54 and 602 TD 9575 RIN 1545-BJ94 DEPARTMENT OF LABOR Employee Benefits Security Administration 29 CFR Part 2590 RIN 1210-AB52 DEPARTMENT

DEPARTMENT OF THE TREASURY Internal Revenue Service 26 CFR Parts 54 and 602 TD 9575 RIN 1545-BJ94 DEPARTMENT OF LABOR Employee Benefits Security Administration 29 CFR Part 2590 RIN 1210-AB52 DEPARTMENT

ERISA Compliance: It s not an option, it s the law.

COMPLIANCE CORNER Q2 2012 ERISA Compliance: It s not an option, it s the law. Preparing for Medical Loss Ratio (MLR) and Summary of Benefits and Coverage (SBC) requirements? Medical Loss Ratio (MLR)...Is

COMPLIANCE CORNER Q2 2012 ERISA Compliance: It s not an option, it s the law. Preparing for Medical Loss Ratio (MLR) and Summary of Benefits and Coverage (SBC) requirements? Medical Loss Ratio (MLR)...Is

An Employers Guide to The Summary of Benefits and Coverage (SBC)

") SBC Employer Guide If you have questions at any time, contact your Sales Account Executive. An Employers Guide to The Summary of Benefits and Coverage (SBC) Overview Make sure you comply! Willful failure

SBC Employer Guide If you have questions at any time, contact your Sales Account Executive. An Employers Guide to The Summary of Benefits and Coverage (SBC) Overview Make sure you comply! Willful failure

What Employers Need to Know About the Health Reform Rules for Summaries of Benefits and Coverage

What Employers Need to Know About the Health Reform Rules for Summaries of Benefits and Coverage April 10, 2012 Presented by: Jeffrey R. Capwell James P. McElligott, Jr. Felicia L. Mitchell www.mcguirewoods.com

What Employers Need to Know About the Health Reform Rules for Summaries of Benefits and Coverage April 10, 2012 Presented by: Jeffrey R. Capwell James P. McElligott, Jr. Felicia L. Mitchell www.mcguirewoods.com

HEALTH CARE REFORM: EMPLOYER ACTION OVERVIEW

CORPORATE BENEFITS COMPLIANCE WHITE PAPER HEALTH CARE REFORM: EMPLOYER ACTION OVERVIEW MARCH 23, 2010 EMPLOYER ACTION REQUIRED NOTES Nursing Mothers Employers must provide a reasonable break time for non-exempt

CORPORATE BENEFITS COMPLIANCE WHITE PAPER HEALTH CARE REFORM: EMPLOYER ACTION OVERVIEW MARCH 23, 2010 EMPLOYER ACTION REQUIRED NOTES Nursing Mothers Employers must provide a reasonable break time for non-exempt

Health Care Reform. Employer Action Overview

Health Care Reform Page 2 of 10 Health Care Reform Immediatemmediate Employer Action Required Notes Nursing Mothers Employers must provide a reasonable break time for employees who are nursing mothers

Health Care Reform Page 2 of 10 Health Care Reform Immediatemmediate Employer Action Required Notes Nursing Mothers Employers must provide a reasonable break time for employees who are nursing mothers

4/13/16. Provided by: Zywave W. Innovation Drive, Suite 300 Milwaukee, WI

4/13/16 Provided by: Zywave 10100 W. Innovation Drive, Suite 300 Milwaukee, WI 53226 Email: marketing@zywave.com Design 2015 Zywave, Inc. All rights reserved. Table of Contents Introduction... 3 Plan Design

4/13/16 Provided by: Zywave 10100 W. Innovation Drive, Suite 300 Milwaukee, WI 53226 Email: marketing@zywave.com Design 2015 Zywave, Inc. All rights reserved. Table of Contents Introduction... 3 Plan Design

Employer Mandate: Employer Action Overview

HEALTH CARE REFORM Employer Mandate: Page 2 of 11 Immediatemmediate Employer Action Required Notes Nursing Mothers Employers must provide a reasonable break time for non-exempt employees who are nursing

HEALTH CARE REFORM Employer Mandate: Page 2 of 11 Immediatemmediate Employer Action Required Notes Nursing Mothers Employers must provide a reasonable break time for non-exempt employees who are nursing

1/5/16. Provided by: The Lank Group Winterthur Close Kennesaw, GA Tel: Design 2015 Zywave, Inc. All rights reserved.

1/5/16 Provided by: The Lank Group 2971 Winterthur Close Kennesaw, GA 30144 Tel: 770-683-6423 Design 2015 Zywave, Inc. All rights reserved. Table of Contents Introduction... 3 Plan Design and Coverage

1/5/16 Provided by: The Lank Group 2971 Winterthur Close Kennesaw, GA 30144 Tel: 770-683-6423 Design 2015 Zywave, Inc. All rights reserved. Table of Contents Introduction... 3 Plan Design and Coverage

4/13/16. Provided by: KRA Agency Partners, Inc. 99 Cherry Hill Road, Suite 200 Parsippany, NJ Tel:

4/13/16 Provided by: KRA Agency Partners, Inc 99 Cherry Hill Road, Suite 200 Parsippany, NJ 07054 Tel: 973-588-1800 Design 2015 Zywave, Inc. All rights reserved. Table of Contents Introduction...3 Plan

4/13/16 Provided by: KRA Agency Partners, Inc 99 Cherry Hill Road, Suite 200 Parsippany, NJ 07054 Tel: 973-588-1800 Design 2015 Zywave, Inc. All rights reserved. Table of Contents Introduction...3 Plan

2018 Compliance Checklist

Provided by Hodge, Hart & Schleifer 2018 Compliance Checklist The Affordable Care Act (ACA) has made a number of significant changes to group health plans since the law was enacted in 2010. Many of these

Provided by Hodge, Hart & Schleifer 2018 Compliance Checklist The Affordable Care Act (ACA) has made a number of significant changes to group health plans since the law was enacted in 2010. Many of these

The ACA: Health Plans Overview

The ACA: Health Plans Overview Agenda What is the legal status of the ACA? Which plans must comply? Reforms currently in place 2013 compliance deadlines 2014 compliance deadlines 2015 compliance deadlines

The ACA: Health Plans Overview Agenda What is the legal status of the ACA? Which plans must comply? Reforms currently in place 2013 compliance deadlines 2014 compliance deadlines 2015 compliance deadlines

TITLE I QUALITY, AFFORDABLE HEALTH CARE FOR ALL AMERICANS Subtitle A Immediate Improvements in Health Care Coverage for All Americans

H. R. 3590 12 Sec. 10502. Infrastructure to Expand Access to Care. Sec. 10503. Community Health Centers and the National Health Service Corps Fund. Sec. 10504. Demonstration project to provide access to

H. R. 3590 12 Sec. 10502. Infrastructure to Expand Access to Care. Sec. 10503. Community Health Centers and the National Health Service Corps Fund. Sec. 10504. Demonstration project to provide access to

ERISA: Title I, Part 7

ERISA: Title I, Part 7 U.S. Department of Labor Employee Benefits Security Administration Office of Health Plan Standards and Compliance Assistance Laws Contained in Part 7 of ERISA Health Insurance Portability

ERISA: Title I, Part 7 U.S. Department of Labor Employee Benefits Security Administration Office of Health Plan Standards and Compliance Assistance Laws Contained in Part 7 of ERISA Health Insurance Portability

Health Care Reform Toolkit Large Employers

Health Care Reform Toolkit Large Employers Table of Contents Introduction... 3 Plan Design and Coverage Issues: 2014 and Beyond... 4 Employer Obligations... 11 Notice and Disclosure Requirements... 19

Health Care Reform Toolkit Large Employers Table of Contents Introduction... 3 Plan Design and Coverage Issues: 2014 and Beyond... 4 Employer Obligations... 11 Notice and Disclosure Requirements... 19

PPACA and Health Care Reform. A Chronological Guide to Changes and Provisions Affecting Employee Benefits Plans and HR Administration

PPACA and Health Care Reform A Chronological Guide to Changes and Provisions Affecting Employee Benefits Plans and HR Administration AS OF 8/27/2013 Provisions Organized by Effective Date The Affordable

PPACA and Health Care Reform A Chronological Guide to Changes and Provisions Affecting Employee Benefits Plans and HR Administration AS OF 8/27/2013 Provisions Organized by Effective Date The Affordable

AMERICAN HEALTH BENEFIT EXCHANGE MODEL ACT

Draft: 11/15/10 A new model As adopted by the Exchanges (B) Subgroup, Nov. 15, 2010 Underlining and overstrikes show changes from the previous Nov. 11 draft. Comments are being requested on this draft

Draft: 11/15/10 A new model As adopted by the Exchanges (B) Subgroup, Nov. 15, 2010 Underlining and overstrikes show changes from the previous Nov. 11 draft. Comments are being requested on this draft

EXPERT UPDATE. Compliance Headlines from Henderson Brothers:.

EXPERT UPDATE Compliance Headlines from Henderson Brothers:. Health Care Reform Timeline Health Care Reform Timeline This Henderson Brothers Summary provides a timeline of the of key reform provisions

EXPERT UPDATE Compliance Headlines from Henderson Brothers:. Health Care Reform Timeline Health Care Reform Timeline This Henderson Brothers Summary provides a timeline of the of key reform provisions

MVP Insurance Agency October 2013 Newsletter - Your Health Care Reform Partner

MVP Insurance October 2013 Newsletter - Your Health Care Reform Partner Are you in compliance with health care reform regulations? We can help you stay on top of health care reform to avoid penalties from

MVP Insurance October 2013 Newsletter - Your Health Care Reform Partner Are you in compliance with health care reform regulations? We can help you stay on top of health care reform to avoid penalties from

ERISA Litigation Update for Health Plans

ERISA Litigation Update for Health Plans This roundtable discussion is brought to you by the Payors, Plans, and Managed Care (PPMC) Practice Group. May 17, 2013 12:00-1:15 pm Eastern Presenter Patrick

ERISA Litigation Update for Health Plans This roundtable discussion is brought to you by the Payors, Plans, and Managed Care (PPMC) Practice Group. May 17, 2013 12:00-1:15 pm Eastern Presenter Patrick

Except for the upon request requirement, the date by which the SBC needs to be provided is actually driven by the enrollment method.

informed on reform KEEPING YOU UP-TO-DATE ON THE PPACA Web Meeting Q&A Summary This Q&A overview summarizes the question and answer session that followed Cigna's September 22, 2011 health care reform webinar,

informed on reform KEEPING YOU UP-TO-DATE ON THE PPACA Web Meeting Q&A Summary This Q&A overview summarizes the question and answer session that followed Cigna's September 22, 2011 health care reform webinar,

MCHO Informational Series

MCHO Informational Series Glossary of Health Insurance & Medical Terminology How to use this glossary This glossary has many commonly used terms, but isn t a full list. These glossary terms and definitions

MCHO Informational Series Glossary of Health Insurance & Medical Terminology How to use this glossary This glossary has many commonly used terms, but isn t a full list. These glossary terms and definitions

Healthcare Reform Timeline

Healthcare Reform Timeline Provisions That Will Impact Individuals & Employers August 2012 No one sees the direct results of the Patient Protection and Affordable Care Act (PPACA) like the health insurance

Healthcare Reform Timeline Provisions That Will Impact Individuals & Employers August 2012 No one sees the direct results of the Patient Protection and Affordable Care Act (PPACA) like the health insurance

Health Care Reform Update

Health Care Reform Update Issue 9a-2013 March 21, 2013 Compliance Checklist for Determining Grandfathered Status The Affordable Care Act (ACA) contains many provisions that affect the health coverage you

Health Care Reform Update Issue 9a-2013 March 21, 2013 Compliance Checklist for Determining Grandfathered Status The Affordable Care Act (ACA) contains many provisions that affect the health coverage you

Final Benefit and Payment Parameters Regulations Have Wide Ranging Implications Cost-Sharing Limits

» 3/19/15 2015-03 Regulatory Roundup: Flex Credit/Cash-in-Lieu Potential Impact on Plan Affordability and New Guidance on Cost- Sharing Limits, Reinsurance, Essential Health Benefits, and More Flex Credits

» 3/19/15 2015-03 Regulatory Roundup: Flex Credit/Cash-in-Lieu Potential Impact on Plan Affordability and New Guidance on Cost- Sharing Limits, Reinsurance, Essential Health Benefits, and More Flex Credits

Summary of Benefits and Coverage Distribution Instructions

Summary of Benefits and Coverage Distribution Instructions Federal law requires you, as an employer, to provide your employees with a Summary of Benefits and Coverage (SBC) at certain times. You can read

Summary of Benefits and Coverage Distribution Instructions Federal law requires you, as an employer, to provide your employees with a Summary of Benefits and Coverage (SBC) at certain times. You can read

NFIB v. Kathleen Sebelius and its Impact on Employers: Healthcare Reform Revisited

July 5, 2012 NFIB v. Kathleen Sebelius and its Impact on Employers: Healthcare Reform Revisited The Patient Protection and Affordable Care Act (the Affordable Care Act ) imposes new requirements on individuals

July 5, 2012 NFIB v. Kathleen Sebelius and its Impact on Employers: Healthcare Reform Revisited The Patient Protection and Affordable Care Act (the Affordable Care Act ) imposes new requirements on individuals

Phase II CORE 260 Eligibility and Benefits (270/271) Data Content Rule Appendix 6.2 Glossary of Terms version March 2011

Data Content Rule Appendix 6.2 Glossary of Terms version March 2011") Phase II CORE 260 Eligibility and Benefits (270/271) Data Content Rule Appendix 6.2 Glossary of Terms CAQH 2008-2011. All rights reserved. 1 Table of Contents 1 Introduction... 3 2 Rules vs. Glossary Terms...

Phase II CORE 260 Eligibility and Benefits (270/271) Data Content Rule Appendix 6.2 Glossary of Terms CAQH 2008-2011. All rights reserved. 1 Table of Contents 1 Introduction... 3 2 Rules vs. Glossary Terms...

Enacted in March 2010 Makes significant ifi changes to health care system Implemented over several years

Health Care Reform: Top Employer Questions October 2013 Nancy Johnson Tommy Morris Agency LLC Introduction Health Care Reform Affordable Care Act Enacted in March 2010 Makes significant ifi changes to

Health Care Reform: Top Employer Questions October 2013 Nancy Johnson Tommy Morris Agency LLC Introduction Health Care Reform Affordable Care Act Enacted in March 2010 Makes significant ifi changes to

Title 24-A: MAINE INSURANCE CODE

Maine Revised Statutes Title 24-A: MAINE INSURANCE CODE Chapter 56-A: HEALTH PLAN IMPROVEMENT ACT 4303. PLAN REQUIREMENTS A carrier offering or renewing a health plan in this State must meet the following

Maine Revised Statutes Title 24-A: MAINE INSURANCE CODE Chapter 56-A: HEALTH PLAN IMPROVEMENT ACT 4303. PLAN REQUIREMENTS A carrier offering or renewing a health plan in this State must meet the following

New Developments in 501(r) Compliance

Compliance") New Developments in 501(r) Compliance This roundtable discussion is brought to you by the Tax and Finance Practice Group. Monday February 27, 2012 12:00 1:00 pm Eastern Presenters: Keith Hearle, MBA Founder

New Developments in 501(r) Compliance This roundtable discussion is brought to you by the Tax and Finance Practice Group. Monday February 27, 2012 12:00 1:00 pm Eastern Presenters: Keith Hearle, MBA Founder

ERISA GUIDELINES. Who must abide by ERISA?

ERISA GUIDELINES The Employee Retirement Income Security Act (ERISA) of 1974 establishes minimum standards for retirement, health, and other welfare benefit plans, including life insurance, disability

ERISA GUIDELINES The Employee Retirement Income Security Act (ERISA) of 1974 establishes minimum standards for retirement, health, and other welfare benefit plans, including life insurance, disability

Navigating the Legal Issues in Wellness Programs Sponsored by the Payors,, Plans, and Managed Care Practice Group

Navigating the Legal Issues in Wellness Programs Sponsored by the Payors,, Plans, and Managed Care Practice Group September 8, 2010 12:00 1:00 pm Eastern Presenter: Heidi E. Garwood Senior Legal Counsel,

Navigating the Legal Issues in Wellness Programs Sponsored by the Payors,, Plans, and Managed Care Practice Group September 8, 2010 12:00 1:00 pm Eastern Presenter: Heidi E. Garwood Senior Legal Counsel,

An Employer s Guide to Health Care Reform

An Employer s Guide to Health Care Reform Background On March 23, 2010, President Obama signed into law the Patient Protection and Affordable Care Act (PPACA). Less than a week later, Congress passed the

An Employer s Guide to Health Care Reform Background On March 23, 2010, President Obama signed into law the Patient Protection and Affordable Care Act (PPACA). Less than a week later, Congress passed the

Introduction Notice and Disclosure Requirements Plan Design and Coverage Issues: Prior to

8/22/13 Table of Contents Introduction... 3 Notice and Disclosure Requirements... 4 Plan Design and Coverage Issues: Prior to 2014... 10 Plan Design and Coverage Issues: 2014 and Beyond... 12 Wellness

8/22/13 Table of Contents Introduction... 3 Notice and Disclosure Requirements... 4 Plan Design and Coverage Issues: Prior to 2014... 10 Plan Design and Coverage Issues: 2014 and Beyond... 12 Wellness

Health Care Reform Path to Compliance

Internal Claims Review and External Review of Appeals processes must be in place (only applies to non-grandfathered plans) One thing s certain, change is constant as employers and employees navigate ate

Internal Claims Review and External Review of Appeals processes must be in place (only applies to non-grandfathered plans) One thing s certain, change is constant as employers and employees navigate ate

2016 Open Enrollment Checklist

To prepare for open enrollment, group health plan sponsors should be aware of the legal changes affecting the design and administration of their plans for plan years beginning on or after Jan. 1, 2016.

To prepare for open enrollment, group health plan sponsors should be aware of the legal changes affecting the design and administration of their plans for plan years beginning on or after Jan. 1, 2016.

Mental Health Parity and Addiction Equity Act FAQs

Mental Health Parity and Addiction Equity Act FAQs This document contains the Frequently Asked Questions and responses (FAQs) concerning implementation of the Paul Wellstone and Pete Domenici Mental Health

Mental Health Parity and Addiction Equity Act FAQs This document contains the Frequently Asked Questions and responses (FAQs) concerning implementation of the Paul Wellstone and Pete Domenici Mental Health

A SUMMARY OF MEDICARE PARTS A, B, C, & D

A SUMMARY OF MEDICARE PARTS A, B, C, & D PROVIDED BY: RETIRED INDIANA PUBLIC EMPLOYEES ASSOCIATION RIPEA AUTHOR: JAMES BENGE, RIPEA INSURANCE CONSULTANT 1 M E D I C A R E A Summary of Parts A, B, C, &

A SUMMARY OF MEDICARE PARTS A, B, C, & D PROVIDED BY: RETIRED INDIANA PUBLIC EMPLOYEES ASSOCIATION RIPEA AUTHOR: JAMES BENGE, RIPEA INSURANCE CONSULTANT 1 M E D I C A R E A Summary of Parts A, B, C, &

HealtH Care reform 2012 and beyond

HealtH Care reform 2012 and beyond A guide to the major provisions of health care reform legislation affecting employers in 2012 and 2013 and a timeline of the reforms to be introduced through 2018. Employers

HealtH Care reform 2012 and beyond A guide to the major provisions of health care reform legislation affecting employers in 2012 and 2013 and a timeline of the reforms to be introduced through 2018. Employers

Summary of Benefits and Coverage (SBC) & Uniform Glossary A Supplement to the Insurance & Benefits Information Guide

& Uniform Glossary A Supplement to the Insurance & Benefits Information Guide") 2017-2018 Summary of Benefits and Coverage (SBC) & Uniform Glossary A Supplement to the 2017-2018 Insurance & Benefits Information Guide Nassau County School Board 1201 Atlantic Avenue Fernandina Beach,

2017-2018 Summary of Benefits and Coverage (SBC) & Uniform Glossary A Supplement to the 2017-2018 Insurance & Benefits Information Guide Nassau County School Board 1201 Atlantic Avenue Fernandina Beach,

December 12, 2012 OVERVIEW OF THE TRANSITIONAL REINSURANCE PROGRAM

December 12, 2012 On November 30, 2012, the Department of Health and Human Services ( HHS ) released for public inspection proposed regulations ( New Proposed Regulations ) setting forth guidance with

December 12, 2012 On November 30, 2012, the Department of Health and Human Services ( HHS ) released for public inspection proposed regulations ( New Proposed Regulations ) setting forth guidance with

The Affordable Care Act and the Essential Health Benefits Package

October 24, 2011 The Affordable Care Act and the Essential Health Benefits Package A. Background Under the Affordable Care Act (the ACA or the Act ), and starting in 2014, certain low to moderate income

October 24, 2011 The Affordable Care Act and the Essential Health Benefits Package A. Background Under the Affordable Care Act (the ACA or the Act ), and starting in 2014, certain low to moderate income

Hardee s Q4 Franchise System Call. Health Care Reform Update November 5, 2013

Hardee s Q4 Franchise System Call Health Care Reform Update November 5, 2013 Key Elements of Health Care Reform for Employers Change in tax treatment for over-age 2010 dependent coverage Early retiree

Hardee s Q4 Franchise System Call Health Care Reform Update November 5, 2013 Key Elements of Health Care Reform for Employers Change in tax treatment for over-age 2010 dependent coverage Early retiree

BENEFITS REQUIREMENTS

Client Name: No. of Employees: Note: This list is for use by employers with 50 or more employees. Plan Year: BENEFITS REQUIREMENTS Employer Payment Plans Prohibited. Ensure that an employer payment plan

Client Name: No. of Employees: Note: This list is for use by employers with 50 or more employees. Plan Year: BENEFITS REQUIREMENTS Employer Payment Plans Prohibited. Ensure that an employer payment plan

Participant Handout Presented by

Healthcare Reform PPACA Continues... What Do You Do Now? Participant Handout Presented by HCR ICCCFO October 2012 Healthcare Reform PPACA Continues... What Do You Do Now? 2012 Gallagher Benefits Services,

Healthcare Reform PPACA Continues... What Do You Do Now? Participant Handout Presented by HCR ICCCFO October 2012 Healthcare Reform PPACA Continues... What Do You Do Now? 2012 Gallagher Benefits Services,

Issue Eighty-One February 2014

Issue Eighty-One February 2014 February 10, 2014 The Departments of Labor (DOL), Health and Human Services (HHS) and Treasury (collectively called the Departments) recently released a set of Frequently

Issue Eighty-One February 2014 February 10, 2014 The Departments of Labor (DOL), Health and Human Services (HHS) and Treasury (collectively called the Departments) recently released a set of Frequently

2016 Compliance Checklist

Brought to you by Risk Management Advisors, Inc. 2016 Compliance Checklist The Affordable Care Act (ACA) has made a number of significant changes to group health plans since the law was enacted over four

Brought to you by Risk Management Advisors, Inc. 2016 Compliance Checklist The Affordable Care Act (ACA) has made a number of significant changes to group health plans since the law was enacted over four

Glossary of Terms. Adjudication: The way a health plan decides how much it will pay for certain expenses.

Page 1 Glossary of Terms Adjudication: The way a health plan decides how much it will pay for certain expenses. Affordable Care Act (ACA): The comprehensive health care reform law enacted in March 2010.

Page 1 Glossary of Terms Adjudication: The way a health plan decides how much it will pay for certain expenses. Affordable Care Act (ACA): The comprehensive health care reform law enacted in March 2010.

Health Care Reform Compliance: An Employer Perspective

Health Care Reform Compliance: An Employer Perspective L& E Breakfast Briefing February 20, 2014 Houston, Texas Presented by: Andrea Bailey Powers 205.244.3809 apowers@bakerdonelson.com Select ACA Provisions

Health Care Reform Compliance: An Employer Perspective L& E Breakfast Briefing February 20, 2014 Houston, Texas Presented by: Andrea Bailey Powers 205.244.3809 apowers@bakerdonelson.com Select ACA Provisions

Guide to Participant Notices

Guide to Participant s What What Groups Description Who When Distributed Annually Group health plan sponsors must provide a Medicare-eligible notice of creditable or non-creditable employees who are prescription

Guide to Participant s What What Groups Description Who When Distributed Annually Group health plan sponsors must provide a Medicare-eligible notice of creditable or non-creditable employees who are prescription

This is only a summary. Important Questions $500 $1,000 $500 $1,000. Why this Matters: $50 $4,850 $9,700 $2,000 $4, of 10

This is only a summary. Important Questions Answers $500 $1,000 $500 $1,000 Why this Matters: $50 $4,850 $9,700 $2,000 $4,000 1 of 10 Common Medical Event Services You May Need In-network Out-of-network

This is only a summary. Important Questions Answers $500 $1,000 $500 $1,000 Why this Matters: $50 $4,850 $9,700 $2,000 $4,000 1 of 10 Common Medical Event Services You May Need In-network Out-of-network

Implementing the Affordable Care Act: Countdown to Employer Requirements

Implementing the Affordable Care Act: Countdown to Employer Requirements What you need to know about being in compliance American Health Care Association August 6, 2013 The Patient Protection and Affordable

Implementing the Affordable Care Act: Countdown to Employer Requirements What you need to know about being in compliance American Health Care Association August 6, 2013 The Patient Protection and Affordable

DRAFT Premium Adjustment Percentage

Washington Health Benefit Exchange Comments: Proposed Federal Rule Patient Protection and Affordable Care Act; HHS Notice of Benefit and Payment Parameters for 2020 The Washington State Health Benefit

Washington Health Benefit Exchange Comments: Proposed Federal Rule Patient Protection and Affordable Care Act; HHS Notice of Benefit and Payment Parameters for 2020 The Washington State Health Benefit

The Affordable Care Act (ACA) What are the Financial Impacts to your Business? Presented For: Dallas CPA Society May 8 th, 2013

What are the Financial Impacts to your Business? Presented For: Dallas CPA Society May 8 th, 2013") The Affordable Care Act (ACA) What are the Financial Impacts to your Business? Presented For: Dallas CPA Society May 8 th, 2013 Employer Questions Is the transitional reinsurance fee tax deductible? What

The Affordable Care Act (ACA) What are the Financial Impacts to your Business? Presented For: Dallas CPA Society May 8 th, 2013 Employer Questions Is the transitional reinsurance fee tax deductible? What

H E A L T H C A R E R E F O R M T I M E L I N E

H E A L T H C A R E R E F O R M T I M E L I N E On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into law. The ACA makes sweeping changes to the U.S.

H E A L T H C A R E R E F O R M T I M E L I N E On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into law. The ACA makes sweeping changes to the U.S.

Important information about the Summary of Benefits and Coverage

l Important information about the Summary of Benefits and Coverage Enclosed is/are your Summary of Benefits and Coverage (SBC) document(s) for your Aetna medical coverage(s). The SBC is a requirement of

l Important information about the Summary of Benefits and Coverage Enclosed is/are your Summary of Benefits and Coverage (SBC) document(s) for your Aetna medical coverage(s). The SBC is a requirement of

Glossary of Health Coverage and Medical Terms x

Glossary of Health Coverage and Medical Terms x x x This glossary defines many commonly used terms, but isn t a full list. These glossary terms and definitions are intended to be educational and may be

Glossary of Health Coverage and Medical Terms x x x This glossary defines many commonly used terms, but isn t a full list. These glossary terms and definitions are intended to be educational and may be

United States Department of Labor Employee Benefits Security Administration Technical Release No

Page 1 of 5 United States Department of Labor Employee Benefits Security Administration Technical Release No. 2013-02 Guidance on the Notice to Employees of Coverage Options under Fair Labor Standards

Page 1 of 5 United States Department of Labor Employee Benefits Security Administration Technical Release No. 2013-02 Guidance on the Notice to Employees of Coverage Options under Fair Labor Standards

Important Effective Dates for Employers and Health Plans

Brought to you by Hipskind Seyfarth Risk Solutions Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act

Brought to you by Hipskind Seyfarth Risk Solutions Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act

Medical Loss Ratio. Institute for Health Plan Counsel May 8, Presenters:

Medical Loss Ratio Institute for Health Plan Counsel May 8, 2013 Presenters: Melissa J. Hulke, CPA, ABV, CFF Navigant, Phoenix, AZ melissa.hulke@navigant.com Scott O. Jones, FSA, MAAA Milliman, Seattle,

Medical Loss Ratio Institute for Health Plan Counsel May 8, 2013 Presenters: Melissa J. Hulke, CPA, ABV, CFF Navigant, Phoenix, AZ melissa.hulke@navigant.com Scott O. Jones, FSA, MAAA Milliman, Seattle,

Affordable Care Act employee notification deadline October 1, 2013

Affordable Care Act employee notification deadline October 1, 2013 HCANJ members are reminded that the Affordable Care Act requires all employers to provide a notice of health coverage options to employees

Affordable Care Act employee notification deadline October 1, 2013 HCANJ members are reminded that the Affordable Care Act requires all employers to provide a notice of health coverage options to employees

CANCER LEADERSHIP COUNCIL

CANCER LEADERSHIP COUNCIL A PATIENT-CENTERED FORUM OF NATIONAL ADVOCACY ORGANIZATIONS ADDRESSING PUBLIC POLICY ISSUES IN CANCER December 26, 2012 Via Electronic Filing http://www.regulations.gov The Honorable

CANCER LEADERSHIP COUNCIL A PATIENT-CENTERED FORUM OF NATIONAL ADVOCACY ORGANIZATIONS ADDRESSING PUBLIC POLICY ISSUES IN CANCER December 26, 2012 Via Electronic Filing http://www.regulations.gov The Honorable

Some of the services this plan doesn t cover are listed on page 5. See your policy Yes plan doesn t cover?

Summary of Benefits and Coverage: What this Plan Covers & What it Costs Coverage for: Individual Plan Type: Network This is only a summary. If you want more detail about your coverage and costs, you can

Summary of Benefits and Coverage: What this Plan Covers & What it Costs Coverage for: Individual Plan Type: Network This is only a summary. If you want more detail about your coverage and costs, you can

ACA Violations Penalties and Excise Taxes

Provided by Propel Insurance ACA Violations Penalties and Excise Taxes The Affordable Care Act (ACA) includes numerous reforms for group health plans and creates new compliance obligations for employers

Provided by Propel Insurance ACA Violations Penalties and Excise Taxes The Affordable Care Act (ACA) includes numerous reforms for group health plans and creates new compliance obligations for employers

Schools Insurance Group

Contra C t C Costa t C County t Schools Insurance Group p Presented by: Debra DeSpain Senior Account Manager February 8, 2013 Mandate Overview Individual Mandate Full-Time Employees Employer Shared Responsibility

Contra C t C Costa t C County t Schools Insurance Group p Presented by: Debra DeSpain Senior Account Manager February 8, 2013 Mandate Overview Individual Mandate Full-Time Employees Employer Shared Responsibility

Affordable Care Act Guidance on Employers Shared Responsibility & Coverage Waiting Period

Affordable Care Act Guidance on Employers Shared Responsibility & Coverage Waiting Period September 12, 2012 The Internal Revenue Service ( IRS ) and the Departments of the Treasury, Labor ( DOL ), and

Affordable Care Act Guidance on Employers Shared Responsibility & Coverage Waiting Period September 12, 2012 The Internal Revenue Service ( IRS ) and the Departments of the Treasury, Labor ( DOL ), and

Health Care Reform at-a-glance

Health Care Reform at-a-glance August 2015 Table of Contents Employer mandate...3 Individual mandate...3 Health plan provisions applying to both grandfathered and non-grandfathered employer plans...4 Health

Health Care Reform at-a-glance August 2015 Table of Contents Employer mandate...3 Individual mandate...3 Health plan provisions applying to both grandfathered and non-grandfathered employer plans...4 Health

Health Care Reform: Legislative Brief Important Effective Dates for Employers and Health Plans

Health Care Reform: Legislative Brief Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into

Health Care Reform: Legislative Brief Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into

Looking for a Life Vest?

Looking for a Life Vest? November 20 th, 2014 @thomasharte Agenda: Looking for a Life Vest? Health Care Reform: What s new with ACA?? Provisions Already in Effect Preparing for Health Care Reform Primary

Looking for a Life Vest? November 20 th, 2014 @thomasharte Agenda: Looking for a Life Vest? Health Care Reform: What s new with ACA?? Provisions Already in Effect Preparing for Health Care Reform Primary

The Patient Protection and Affordable Care Act. An In-Depth Analysis of Provisions Directly or Indirectly Affecting Group Health Plans

The Patient Protection and Affordable Care Act An In-Depth Analysis of Provisions Directly or Indirectly Affecting Group Health Plans Table of Contents Section 1 Insurance Plan Provisions Prohibition on

The Patient Protection and Affordable Care Act An In-Depth Analysis of Provisions Directly or Indirectly Affecting Group Health Plans Table of Contents Section 1 Insurance Plan Provisions Prohibition on

GLOSSARY OF KEY AFFORDABLE CARE ACT AND COMMON HEALTH PLAN TERMS

GLOSSARY OF KEY AFFORDABLE CARE ACT AND COMMON HEALTH PLAN TERMS Note: in the event of any conflict between this glossary and your plan document/summary plan description (SPD) or policy/certificate, the

GLOSSARY OF KEY AFFORDABLE CARE ACT AND COMMON HEALTH PLAN TERMS Note: in the event of any conflict between this glossary and your plan document/summary plan description (SPD) or policy/certificate, the

March 15, Center for Consumer Information and Insurance Oversight Centers for Medicare & Medicaid Services Department of Health & Human Services

1015 15 th Street, N.W., Suite 950 Washington, DC 20005 Tel. 202.204.7508 Fax 202.204.7517 www.communityplans.net March 15, 2013 Center for Consumer Information and Insurance Oversight Centers for Medicare

1015 15 th Street, N.W., Suite 950 Washington, DC 20005 Tel. 202.204.7508 Fax 202.204.7517 www.communityplans.net March 15, 2013 Center for Consumer Information and Insurance Oversight Centers for Medicare

Provision Description Effective Date(s)

") Patient Protection and Affordable Care Act, Pub. L. No. 111-148 ( PPACA ) Health Care and Education Reconciliation Act of 2010, Pub. L. No. 111-152 ( Recon. ) Provisions Imposing New Requirements on Penalties

Patient Protection and Affordable Care Act, Pub. L. No. 111-148 ( PPACA ) Health Care and Education Reconciliation Act of 2010, Pub. L. No. 111-152 ( Recon. ) Provisions Imposing New Requirements on Penalties

5GBenefits, LLC Your Health Care Reform Partner

5GBenefits, LLC Your Health Care Reform Partner Are you in compliance with health care reform regulations? We can help you stay on top of health care reform in order to avoid penalties from legislative

5GBenefits, LLC Your Health Care Reform Partner Are you in compliance with health care reform regulations? We can help you stay on top of health care reform in order to avoid penalties from legislative

Health Care Reform: Be Prepared for 2014

Health Care Reform: Be Prepared for 2014 Your Health Care Reform Team: Moderator Eboni Britt POMCO Group Marketing Manager Co-presenter Jessica Marabella POMCO Group Account Manager Co-presenter Amy Zell

Health Care Reform: Be Prepared for 2014 Your Health Care Reform Team: Moderator Eboni Britt POMCO Group Marketing Manager Co-presenter Jessica Marabella POMCO Group Account Manager Co-presenter Amy Zell

Evidence of Coverage. Stanford Health Care Advantage - Platinum (HMO) January 1 - December 31, 2016

January 1 - December 31, 2016") Evidence of Coverage Stanford Health Care Advantage - Platinum (HMO) January 1 - December 31, 2016 January 1 December 31, 2016 Evidence of Coverage: Your Medicare Health Benefits and Services and Prescription

Evidence of Coverage Stanford Health Care Advantage - Platinum (HMO) January 1 - December 31, 2016 January 1 December 31, 2016 Evidence of Coverage: Your Medicare Health Benefits and Services and Prescription

Implementation of the ACA: Essential Health Benefits

Implementation of the ACA: Essential Health Benefits 2013 Disability Policy Seminar April 15, 2012 Theresa T. Morgan Powers Pyles Sutter & Verville, P.C. Theresa.Morgan@ppsv.com 202-466-6550 Outline! Essential

Implementation of the ACA: Essential Health Benefits 2013 Disability Policy Seminar April 15, 2012 Theresa T. Morgan Powers Pyles Sutter & Verville, P.C. Theresa.Morgan@ppsv.com 202-466-6550 Outline! Essential

Health Care Reform Group Medicare Advantage. John F. DiLorenzo Michael A. DiLorenzo

Health Care Reform Group Medicare Advantage October 3, 2012 John F. DiLorenzo Michael A. DiLorenzo 42400 Garfield Road, Clinton Township 48038 503 South Saginaw, Flint 48502 www.miplanners.com 1.800.MPI.9235

Health Care Reform Group Medicare Advantage October 3, 2012 John F. DiLorenzo Michael A. DiLorenzo 42400 Garfield Road, Clinton Township 48038 503 South Saginaw, Flint 48502 www.miplanners.com 1.800.MPI.9235

Summary of the Impact of Health Care Reform on Employers

Summary of the Impact of Health Care Reform on Employers How to Use this Summary This summary identifies the main provisions of the Patient Protection and Affordable Care Act (Act), as amended by the Health

Summary of the Impact of Health Care Reform on Employers How to Use this Summary This summary identifies the main provisions of the Patient Protection and Affordable Care Act (Act), as amended by the Health

Child Health Advocates Guide to Essential Health Benefits

Child Health Advocates Guide to Essential Health Benefits One of the Affordable Care Act s important features for health insurance consumers is the establishment of a package of essential health benefits

Child Health Advocates Guide to Essential Health Benefits One of the Affordable Care Act s important features for health insurance consumers is the establishment of a package of essential health benefits

Health Care Reform and Religious Organizations

Health Care Reform and Religious Organizations cliftonlarsonallen.com Circular 230 To ensure compliance imposed by IRS Circular 230, any U. S. federal tax advice contained in this presentation is not intended

Health Care Reform and Religious Organizations cliftonlarsonallen.com Circular 230 To ensure compliance imposed by IRS Circular 230, any U. S. federal tax advice contained in this presentation is not intended

Patient Protection and Affordable Care Act; Exchange Functions: Standards for

DEPARTMENT OF HEALTH AND HUMAN SERVICES 45 CFR Part 155 [CMS-9955-P] RIN 0938-AR75 Patient Protection and Affordable Care Act; Exchange Functions: Standards for Navigators and Non-Navigator Assistance

DEPARTMENT OF HEALTH AND HUMAN SERVICES 45 CFR Part 155 [CMS-9955-P] RIN 0938-AR75 Patient Protection and Affordable Care Act; Exchange Functions: Standards for Navigators and Non-Navigator Assistance

Checkup on Health Insurance Choices

Page 1 of 17 Checkup on Health Insurance Choices Today, there are more types of health insurance, and more choices, than ever before. The information presented here will help you choose a plan that is

Page 1 of 17 Checkup on Health Insurance Choices Today, there are more types of health insurance, and more choices, than ever before. The information presented here will help you choose a plan that is

AFFORDABLE CARE ACT LARGE EMPLOYER HEALTH REFORM CHECKLIST. Edition: August 2015

AFFORDABLE CARE ACT Employers that offer health care coverage to employees are responsible for complying with many of the provisions of the Affordable Care Act (ACA). Most health reform changes apply regardless

AFFORDABLE CARE ACT Employers that offer health care coverage to employees are responsible for complying with many of the provisions of the Affordable Care Act (ACA). Most health reform changes apply regardless

Affordable Care Act: What Employers Need to Know to be in Compliance in 2014

Affordable Care Act: What Employers Need to Know to be in Compliance in 2014 October 2013 Stacy H. Barrow sbarrow@proskauer.com 1 Agenda Initial Observations Compliance Calendar Checklist: Important dates,

Affordable Care Act: What Employers Need to Know to be in Compliance in 2014 October 2013 Stacy H. Barrow sbarrow@proskauer.com 1 Agenda Initial Observations Compliance Calendar Checklist: Important dates,

Healthcare Reform Handbook

Last revised: December 5, 2012 Healthcare Reform Handbook Keeping you compliant 2012 & beyond Table of Contents Overview, Individual Mandate, & Exchanges Information. 2 Women s Preventive Care (2012)..

Last revised: December 5, 2012 Healthcare Reform Handbook Keeping you compliant 2012 & beyond Table of Contents Overview, Individual Mandate, & Exchanges Information. 2 Women s Preventive Care (2012)..

ACA Provisions Summary. Self Funded Group Health Plans

ACA Provisions Summary Self Funded Group Health Plans January 2013 Table of Contents Introduction... 1 Compliance with State Law... 1 Grandfathered Health Plans... 2 Prohibition Against Preexisting Condition

ACA Provisions Summary Self Funded Group Health Plans January 2013 Table of Contents Introduction... 1 Compliance with State Law... 1 Grandfathered Health Plans... 2 Prohibition Against Preexisting Condition

Comments on Certain Preventive Services Under the Affordable Care Act, CMS-9968-ANPRM

June 18, 2012 Secretary Kathleen Sebelius US Department of Health and Human Services 200 Independence Avenue, SW Washington, DC 20201 Re: Comments on Certain Preventive Services Under the Affordable Care

June 18, 2012 Secretary Kathleen Sebelius US Department of Health and Human Services 200 Independence Avenue, SW Washington, DC 20201 Re: Comments on Certain Preventive Services Under the Affordable Care

Health Care Reform Timeline Last Updated: March 12, 2014

Health Care Reform Timeline Last Updated: March 12, 2014 On March 23, 2010, President Obama signed into law the Patient Protection and Affordable Care Act ( PPACA or ACA or Health Care Reform ). Health

Health Care Reform Timeline Last Updated: March 12, 2014 On March 23, 2010, President Obama signed into law the Patient Protection and Affordable Care Act ( PPACA or ACA or Health Care Reform ). Health

Anne Wilde. Grandfathered Health Plans. Planning for PPACA: New Appeals Rules 2014 Employer Decisions October 27, 2011

Planning for PPACA: Grandfathered Health Plans New Appeals Rules 2014 Employer Decisions October 27, 2011 Anne Wilde The HR & Benefits Advisor PLLC anne@thehrandbenefitsadvisor.com 208.424.8704 Ben Conley

Planning for PPACA: Grandfathered Health Plans New Appeals Rules 2014 Employer Decisions October 27, 2011 Anne Wilde The HR & Benefits Advisor PLLC anne@thehrandbenefitsadvisor.com 208.424.8704 Ben Conley

LOCAL. HONEST. INDEPENDENT.

LOCAL. HONEST. INDEPENDENT. WHAT SMALL BUSINESSES NEED TO KNOW ABOUT HEALTH CARE REFORM The information that matters most to your business and employees Health care reform changes health insurance The

LOCAL. HONEST. INDEPENDENT. WHAT SMALL BUSINESSES NEED TO KNOW ABOUT HEALTH CARE REFORM The information that matters most to your business and employees Health care reform changes health insurance The

ESSENTIAL HEALTH BENEFITS BULLETIN Center for Consumer Information and Insurance Oversight December 16, 2011

ESSENTIAL HEALTH BENEFITS BULLETIN Center for Consumer Information and Insurance Oversight December 16, 2011 Contents ESSENTIAL HEALTH BENEFITS BULLETIN... 1 Purpose... 1 Defining Essential Health Benefits...

ESSENTIAL HEALTH BENEFITS BULLETIN Center for Consumer Information and Insurance Oversight December 16, 2011 Contents ESSENTIAL HEALTH BENEFITS BULLETIN... 1 Purpose... 1 Defining Essential Health Benefits...

Health Care Reform: What It Means for Employers and the Health Plans They Sponsor APRIL 22, 2010

Health Care Reform: What It Means for Employers and the Health Plans They Sponsor APRIL 22, 2010 Moderator and Panelists Andrea O Brien Meredith Horton Thora Johnson Greg Ossi Martha Jo Wagner 22 Agenda

Health Care Reform: What It Means for Employers and the Health Plans They Sponsor APRIL 22, 2010 Moderator and Panelists Andrea O Brien Meredith Horton Thora Johnson Greg Ossi Martha Jo Wagner 22 Agenda

No. What is not included in the out of pocket limit? Even though you pay these expenses, they don t count toward the out-of-pocket limit.

This is only a summary. If you want more detail about your coverage and costs, you can get the complete terms in the plan s summary plan description at www.psbenefitstrust.com or by calling (206) 441-7574,

This is only a summary. If you want more detail about your coverage and costs, you can get the complete terms in the plan s summary plan description at www.psbenefitstrust.com or by calling (206) 441-7574,

Important Questions Answers Why this Matters:

Summary of Benefits and Coverage: What this Plan Covers & What it Costs Coverage for: Individual Plan Type: Premium Plan This is only a summary. If you want more detail about your coverage and costs, you

Summary of Benefits and Coverage: What this Plan Covers & What it Costs Coverage for: Individual Plan Type: Premium Plan This is only a summary. If you want more detail about your coverage and costs, you

COORDINATION OF BENEFITS STUDY

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp COORDINATION OF BENEFITS

This document is made available electronically by the Minnesota Legislative Reference Library as part of an ongoing digital archiving project. http://www.leg.state.mn.us/lrl/lrl.asp COORDINATION OF BENEFITS

Health Insurance Glossary of Terms

1 Health Insurance Glossary of Terms On March 23, 2010, President Obama signed the Patient Protection and Affordable Care Act (PPACA) into law. When making decisions about health coverage, consumers should

1 Health Insurance Glossary of Terms On March 23, 2010, President Obama signed the Patient Protection and Affordable Care Act (PPACA) into law. When making decisions about health coverage, consumers should