Citigroup UBS Investment Bank JPMorgan

|

|

|

- Kevin Wilkins

- 5 years ago

- Views:

Transcription

1 NEW ISSUE-BOOK-ENTRY ONLY Ratings: See RATINGS herein In the opinion of Preston Gates & Ellis LLP, Bond Counsel, assuming compliance with certain covenants of the District, interest on the 2006A Bonds is excludable from gross income of the owners of the 2006A Bonds for federal income tax purposes under existing law. Interest on the 2006A Bonds is not an item of tax preference for purposes of either individual or corporate alternative minimum tax. Interest on the 2006A Bonds may be indirectly subject to corporate alternative minimum tax and certain other taxes imposed on certain corporations. See TAX MATTERS The 2006A Bonds herein for a discussion of the opinion of Bond Counsel. In the opinion of Bond Counsel, assuming compliance by the District with certain covenants, interest on the 2006B Bonds is excludable from the gross income of the owners of the 2006B Bonds for federal income tax purposes under existing law except with respect to any period during which a 2006B Bond is held by a substantial user of the facilities refinanced by the 2006B Bonds or a related person to such substantial user, within the meaning of Section 147 of the Code. Interest on the 2006B Bonds is an item of tax preference for purposes of computing the federal alternative minimum tax imposed on individuals and corporations. See TAX MATTERS The 2006B Bonds herein for a discussion of the opinion of Bond Counsel. Interest on the 2006Z Bonds is included in gross income for federal income tax purposes. Certain information regarding the federal income tax treatment of the 2006Z Bonds is set forth under TAX MATTERS The 2006Z Bonds. PUBLIC UTILITY DISTRICT NO. 2 OF GRANT COUNTY, WASHINGTON Wanapum Hydroelectric Development Revenue and Refunding Bonds, 2006 $71,395,000 SERIES A (Not Subject to AMT) Bonds Dated: Date of Delivery $18,190,000 SERIES B (Subject to AMT) $96,845,000 SERIES Z (Taxable) Due: January 1, as shown on the inside cover The Bonds are issuable only as fully registered bonds without coupons and, when issued, will be registered in the name of Cede & Co., as nominee of The Depository Trust Company ( DTC ), New York, New York. DTC will act as securities depository of the Bonds. Individual purchases will be made in book entry form only, in the principal amount of $5,000 and integral multiples thereof. Purchasers will not receive certificates representing their interest in the Bonds purchased. The fiscal agency of the State of Washington in New York, New York, currently The Bank of New York, has been appointed as the Paying Agent and Registrar for the Bonds. The Bank of New York Trust Company, N.A., Seattle, Washington, has been appointed as Trustee for the Bonds. Interest on the Bonds, first payable on July 1, 2007, and thereafter semiannually thereafter on January 1 and July 1 of each year, and principal of the Bonds are payable by the Paying Agent to DTC or its nominee, which is obligated to remit such principal and interest to its broker dealer Participants, which are obligated in turn to remit such principal and interest to the Beneficial Owners of the Bonds, as described in APPENDIX F BOOK-ENTRY SYSTEM. The Bonds are subject to optional and mandatory redemption prior to maturity. See DESCRIPTION OF THE BONDS. The Bonds are being issued by the District to finance improvements to the Wanapum Development and to refund certain outstanding bonds of the Wanapum Development. See PURPOSE AND APPLICATION OF BOND PROCEEDS. The Bonds are payable from and secured by a lien and charge on the Gross Revenues of the Wanapum Development, after payment of Operating Expenses, and on certain other money, funds and accounts of the Wanapum Development. The Bonds are issued on a parity with Parity Bonds outstanding in the principal amount of $283,600,000 (of which $28,275,000 are being refunded with proceeds of the Bonds) and any Future Parity Bonds. The District has covenanted not to issue any bonds with a lien senior to the Parity Bonds. See SECURITY FOR THE PARITY BONDS. Once certain bonds are retired, the District may consolidate the Priest Rapids and Wanapum Developments. See SECURITY FOR THE PARITY BONDS Potential Consolidation of Developments. Payment of the principal of and interest on the Bonds when due will be insured by a financial guaranty insurance policy to be issued by MBIA Insurance Corporation simultaneously with the delivery of the Bonds. See BOND INSURANCE. THE BONDS ARE SPECIAL LIMITED OBLIGATIONS OF THE DISTRICT AND ARE NOT OBLIGATIONS OF THE STATE OF WASHINGTON OR ANY POLITICAL SUBDIVISION THEREOF OTHER THAN THE DISTRICT, AND NEITHER THE FULL FAITH AND CREDIT OF THE DISTRICT NOR THE TAXING POWER OF THE DISTRICT IS PLEDGED TO THE PAYMENT THEREOF. The maturity schedules for the Bonds are set forth on the inside of this cover page. This cover page is not intended to be a summary of the terms of, or security for, the Bonds. Investors are advised to read the entire Official Statement to obtain information essential to the making of an informed investment decision. The Bonds are offered when, as and if issued and received by the Underwriters, subject to the approval of legality by Preston Gates & Ellis LLP, Seattle, Washington, Bond Counsel, and certain other conditions. Certain legal matters will be passed upon for the Underwriters by their counsel, Orrick, Herrington & Sutcliffe LLP, Seattle, Washington. The Bonds are expected to be delivered on or about December 13, 2006, through the facilities of DTC in New York, New York, by Fast Automated Securities Transfer. Citigroup UBS Investment Bank JPMorgan Dated: November 30, 2006

2 MATURITY SCHEDULE, INTEREST RATES, YIELDS AND CUSIP NUMBERS Maturity (January 1) Amount Interest Rate Initial Reoffering Yield $71,395, A Bonds (Not subject to AMT) CUSIP No. Maturity (January 1) Amount Interest Rate Initial Reoffering Price or Yield 2008 $ 530, % 3.60% TQ $ 2,010, % 3.70% TW , TR ,600, TX ,700, TS ,690, TY ,735, TT ,765, TZ ,815, TU ,620, * UA ,910, TV4 $2,335, % Term Bonds due January 1, 2020 at a yield of 3.97%* CUSIP No.** UB6 $2,570, % Term Bonds due January 1, 2022 at a yield of 4.04%* CUSIP No.** UC4 $2,835, % Term Bonds due January 1, 2024 at a yield of 4.07%* CUSIP No.** UD2 $3,125, % Term Bonds due January 1, 2026 at a yield of 4.09%* CUSIP No.** UE0 $11,435, % Term Bonds due January 1, 2032 at a yield of 4.10%* CUSIP No.** UF7 $12,440, % Term Bonds due January 1, 2037 at a yield of 4.13%* CUSIP No.** UG5 $19,560, % Term Bonds due January 1, 2043 at a yield of 4.20%* CUSIP No.** UH3 CUSIP No.** Maturity (January 1) Amount Interest Rate Initial Reoffering Yield $18,190, B Bonds (Subject to AMT) CUSIP No. Maturity (January 1) Amount Interest Rate Initial Reoffering Price or Yield 2009 $ 25, % 3.83% UJ $ 1,740, % 3.92% UP ,425, UK , UQ ,500, UL , UR ,575, UM , US ,645, UN0 $1,275, % Term Bonds due January 1, 2020 at a yield of 4.17%* CUSIP No.** UT7 $1,490, % Term Bonds due January 1, 2023 at a yield of 4.23%* CUSIP No.** UU4 $1,715, % Term Bonds due January 1, 2026 at a yield of 4.28%* CUSIP No.** UV2 $3,425, % Term Bonds due January 1, 2031 at a yield of 4.55% CUSIP No.** UW0 CUSIP No.** $96,845, Z Bonds (Taxable) $13,440, % Term Bonds due January 1, 2017 at a yield of 5.15% CUSIP No.** UX8 $53,275, % Term Bonds due January 1, 2037 at a yield of 5.33% CUSIP No.** UY6 $30,130, % Term Bonds due January 1, 2043 at a yield of 5.42% CUSIP No.** UZ3 * Priced to the par call date of January 1, ** The CUSIP numbers are included for convenience of the holders and potential holders of the Bonds. No assurance can be given that the CUSIP numbers for the Bonds will remain the same after the date of issuance and delivery of the Bonds.

3 No dealer, broker, salesperson, or any other person has been authorized by the District or the Underwriters to give any information or to make any representation, other than the information and representations contained herein, in connection with the offering of the Bonds and, if given or made, such information or representations must not be relied upon as having been authorized by any of the foregoing. This Official Statement does not constitute an offer to sell or solicitation of an offer to buy any of the Bonds in any jurisdiction in which it is unlawful to make such offer, solicitation or sale. The information set forth herein has been obtained from the District and other sources that are believed to be reliable, but it is not guaranteed as to accuracy or completeness and is not to be construed as a representation by the Underwriters. The information herein is subject to change without notice, and neither the delivery of this Official Statement nor any sale made hereunder shall, under any circumstances, create any implication that there has been no change in the affairs of the District since the date hereof. The Underwriters have provided the following sentence for inclusion in this Official Statement. The Underwriters have reviewed the information in this Official Statement in accordance with, and as part of, their responsibilities to investors under the federal securities laws as applied to the facts and circumstances of this transaction, but the Underwriters do not guarantee the accuracy or completeness of such information. In connection with the offering of the Bonds, the Underwriters may overallot or effect transactions which stabilize or maintain the market price of such Bonds at levels above that which might otherwise prevail in the open market. Such stabilizing, if commenced, may be discontinued at any time. The achievement of certain results or other expectations contained in forward-looking statements in this Official Statement involves known and unknown risks, uncertainties and other factors that may cause actual results, performance or achievements described to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. The District does not plan to issue any updates or revisions to those forward-looking statements if or when their expectations or events, conditions or circumstances on which such statements are based occur.

4 PUBLIC UTILITY DISTRICT NO. 2 OF GRANT COUNTY 30 C Street S.W. Ephrata, Washington (509) Commissioners Randall M. Allred... President Greg P. Hansen...Vice President Thomas W. Flint...Secretary Vera B. Claussen... Assistant Secretary William E. Bjork, Jr....Commissioner Senior Management Tim Culbertson... General Manager Joseph A. Lukas...Assistant General Manager Nickolai A. Gerde... Treasurer/Controller Ray A. Foianini...Attorney Leon W. Hoepner... Hydro Director Dawn M. Woodward... Hydro Director Stephen R. Brown... Director of Natural Resources William G. Dearing... Director of Power Management Jim A. Bunch... Director of Accounting, Finance and Strategic Planning Anthony J. Webb...Director of Customer Service Lawrence L. Jones... Director of Information Technology Michael V. Woywod...Director of Human Resources and Support Services Kim K Justice... Auditor Bond Counsel Preston Gates & Ellis LLP Seattle, Washington Bond Trustee The Bank of New York Trust Company, N.A. Seattle, Washington -i-

5 INTRODUCTION... 1 PURPOSE AND APPLICATION OF BOND PROCEEDS... 2 Purpose of the Bonds... 2 Application of the Bond Proceeds... 3 SECURITY FOR THE PARITY BONDS... 3 Pledge of Revenues... 3 Obligations of the Electric System... 4 Potential Consolidation of Developments... 4 Flow of Funds... 5 Limited Obligations... 5 Rate Covenants... 6 Reserve Account... 6 Supplemental Renewal and Contingency Fund... 8 Additional Parity Bonds... 8 Derivative Products... 8 Contingent Payment Obligations... 9 No Acceleration Upon Default... 9 Investment of Funds... 9 BOND INSURANCE... 9 The MBIA Insurance Corporation Insurance Policy... 9 MBIA Insurance Corporation Regulation Financial Strength Ratings of MBIA MBIA Financial Information Incorporation of Certain Documents by Reference DESCRIPTION OF THE BONDS General Terms Termination of Book-Entry Transfer System Transfer and Exchange Optional Redemption Mandatory Redemption Partial Redemption Notice of Redemption Open Market Purchases THE DISTRICT General The Priest Rapids Development Management and Administration District Employees and Retirement Plans and Other Post-Employment Benefits Insurance Strategic Planning Investments Hazardous Waste Issues Security Efforts at the District THE WANAPUM DEVELOPMENT Description Wanapum Development Output and Power Sales Contracts Coordination Agreements Transmission of Power from Wanapum Development TABLE OF CONTENTS Page Page Rehabilitation Program Estimated Capital and Financing Requirements Operating Results License Status Regulatory Proceedings Affecting the Developments Debt Service Requirements for Wanapum Development THE ELECTRIC SYSTEM...41 Retail Energy Sales and Customers Power Supply Management and Power Marketing Electric Rates The Electric System s Power Supply Telecommunications Borrowings of the District Electric System Operating Results Management s Discussion of Results Operating Results Capital Requirements ECONOMIC AND DEMOGRAPHIC INFORMATION...58 LITIGATION...61 INITIATIVE AND REFERENDUM...62 Current State Initative LIMITATIONS ON REMEDIES...62 TAX MATTERS...62 The 2006A Bonds The 2006B Bonds The 2006Z Bonds Pending Audit CERTAIN LEGAL MATTERS...67 UNDERWRITING...67 CONTINUING DISCLOSURE...67 Prior Compliance with Continuing Disclosure Undertakings RATINGS...70 INDEPENDENT ACCOUNTANTS...70 MISCELLANEOUS...70 APPENDIX A SUMMARY OF CERTAIN PROVISIONS OF THE PARITY BOND RESOLUTIONS APPENDIX B SUMMARY OF CERTAIN PROVISIONS OF THE POWER CONTRACTS APPENDIX C AUDITED FINANCIAL STATEMENTS OF THE WANAPUM DEVELOPMENT AND ELECTRIC SYSTEM AS OF DECEMBER 31, 2005 AND 2004 APPENDIX D DESCRIPTION OF MAJOR POWER PURCHASERS (CURRENT OBLIGATED PERSONS) APPENDIX E PROPOSED FORM OF OPINION OF BOND COUNSEL APPENDIX F BOOK-ENTRY SYSTEM APPENDIX G SPECIMEN FORM OF BOND INSURANCE POLICY -ii-

6 LIST OF TABLES Table 1 WANAPUM DEVELOPMENT HISTORICAL ENERGY PRODUCTION...26 Table 2 PARTICIPATION IN THE WANAPUM DEVELOPMENT OUTPUT...27 Table 3 WANAPUM DEVELOPMENT HISTORICAL ENERGY SALES...29 Table 4 WANAPUM DEVELOPMENT FORECAST RENEWAL AND REHABILITATION PROGRAMS EXPENDITURES...32 Table 5 WANAPUM DEVELOPMENT OPERATING RESULTS...34 Table 6 WANAPUM DEVELOPMENT TOTAL DEBT SERVICE REQUIREMENTS...40 Table 7 ELECTRIC SYSTEM 2005 RETAIL CUSTOMERS, ENERGY SALES AND REVENUES...41 Table 8 ELECTRIC SYSTEM LARGEST CUSTOMERS...42 Table 9 ELECTRIC SYSTEM RETAIL CUSTOMERS, ENERGY SALES, AND REVENUES...43 Table 10 ELECTRIC SYSTEM WHOLESALE ENERGY SALES...45 Table 11 ELECTRIC SYSTEM MONTHLY ELECTRIC BILLS COMPARISON...46 Table 12 ELECTRIC SYSTEM RECENT RETAIL RATE INCREASES...47 Table 13 GRANT COUNTY PUD SUMMARY OF OUTSTANDING LONG-TERM DEBT...53 Table 14 ELECTRIC SYSTEM HISTORICAL OPERATING RESULTS...54 Table 15 ELECTRIC SYSTEM HISTORICAL ENERGY REQUIREMENTS, RESOURCES AND POWER COSTS...56 Table 16 ELECTRIC SYSTEM PROJECTED CAPITAL IMPROVEMENTS PROGRAM Table 17 GRANT COUNTY SELECTED ECONOMIC INDICATORS...59 Table 18 GRANT COUNTY MAJOR TAXPAYERS...59 Table 19 GRANT COUNTY MAJOR EMPLOYERS...60 Table 20 GRANT COUNTY RESIDENT CIVILIAN LABOR FORCE AND EMPLOYMENT...60 Table 21 MOSES LAKE MSA (GRANT COUNTY) NONAGRICULTURAL WAGE AND SALARY EMPLOYMENT...61 Page -iii-

7 PUBLIC UTILITY DISTRICT NO. 2 OF GRANT COUNTY, WASHINGTON OFFICIAL STATEMENT RELATING TO $71,395,000 WANAPUM HYDROELECTRIC DEVELOPMENT REVENUE AND REFUNDING BONDS, 2006 SERIES A (NOT SUBJECT TO AMT) $18,190,000 WANAPUM HYDROELECTRIC DEVELOPMENT REVENUE REFUNDING BONDS, 2006 SERIES B (SUBJECT TO AMT) $96,845,000 WANAPUM HYDROELECTRIC DEVELOPMENT REVENUE AND REFUNDING BONDS, 2006 SERIES Z (TAXABLE) INTRODUCTION The purpose of this Official Statement, which includes the cover page and appendices, is to set forth information concerning Public Utility District No. 2 of Grant County, Washington (the District or Grant County PUD ), the District s Wanapum Hydroelectric Development (the Wanapum Development ), certain of the purchasers of the output of the Wanapum Development other than the District (the Power Purchasers ), the District s electric transmission, distribution, telecommunications, and generating system (the Electric System ), and the District s $71,395,000 aggregate principal amount of Wanapum Hydroelectric Development Revenue and Refunding Bonds, Series 2006A (the 2006A Bonds ), $18,190,000 aggregate principal amount of Wanapum Hydroelectric Development Revenue Refunding Bonds, Series 2006B (the 2006B Bonds ), and $96,845,000 aggregate principal amount of Wanapum Hydroelectric Development Revenue and Refunding Bonds, Series 2006Z (the 2006Z Bonds, and together with the 2006A Bonds and 2006B Bonds, the Bonds ). Capitalized terms used herein and not defined have the meanings ascribed thereto in APPENDIX A SUMMARY OF CERTAIN PROVISIONS OF THE PARITY BOND RESOLUTIONS. The Bonds are to be issued pursuant to Chapter 1 of the Laws of Washington, 1931, as amended and supplemented, constituting Title 54 of the Revised Code of Washington and Chs and of the Revised Code of Washington (collectively, the Enabling Act ). The Bonds are authorized by Resolution No of the District, adopted November 30, 2006 (the Bond Resolution ). The District has previously issued $28,965,000 principal amount of its Wanapum Hydroelectric Development Second Series Revenue Bonds, 1996A and B (the 1996 Bonds ), $18,547,000 principal amount of its Wanapum Hydroelectric Development Second Series Revenue Refunding Bonds, Series 1997A, B and E (the 1997A, B and E Bonds ), $8,690,000 principal amount of its Wanapum Hydroelectric Development Second Series Revenue Refunding Bonds, Series 1997C and D (the 1997C and D Bonds and together with the 1997A, B and E Bonds, the 1997 Bonds ), $31,620,000 principal amount of its Wanapum Hydroelectric Development Second Series Revenue Refunding Bonds, Series 1998A (the 1998 Bonds ), $17,837,000 principal amount of its Wanapum Hydroelectric Development Second Series Revenue Refunding Bonds, Series 1999A, B and C (the 1999A, B and C Bonds ), $18,750,000 principal amount of its Wanapum Hydroelectric Development Second Series Revenue Refunding Bonds, 1999 Series D (the 1999D Bonds and together with the 1999A, B and C Bonds, the 1999 Bonds ), $17,165,000 principal amount of its Wanapum Hydroelectric Development Second Series Revenue Refunding Bonds, Series 2001B and C (the 2001 Bonds ), $57,280,000 principal amount of its Wanapum Hydroelectric Development Second Series Revenue Bonds, Series 2003A, B and Z (the 2003 Bonds ), and $127,780,000 principal amount of its Wanapum Hydroelectric Development Revenue and Refunding Bonds, 2005A, B and Z (the 2005 Bonds ). The 1996 Bonds, 1997 Bonds, 1998 Bonds, 1999 Bonds, 2001 Bonds, 2003 Bonds and 2005 Bonds are referred to herein as the Outstanding

8 Parity Bonds, and the Outstanding Parity Bonds, the Bonds and any other bonds hereafter issued on a parity with such bonds are collectively referred to herein as the Parity Bonds. The Outstanding Parity Bonds are currently outstanding in the aggregate principal amount of $283,600,000. The pledges and covenants and other terms and provisions of the Bond Resolution are substantially the same as those of Resolution Nos. 7017, 7080, 7079, 7254, 7268, 7487, 7604, and 7777 authorizing the issuance of the Outstanding Parity Bonds (collectively with the Bond Resolution, the Bond Resolutions ). The Parity Bonds are secured by a lien and charge on the Gross Revenues, after payment of Operating Expenses, and on certain other money, funds and accounts of the Wanapum Development. See SECURITY FOR THE PARITY BONDS. Once the 1996 Bonds, 1997 Bonds, 1998 Bonds, 1999 Bonds and bonds of the Priest Rapids Development issued prior to 2000 are no longer Outstanding, the District may combine the Wanapum Development and the Priest Rapids Development into one system for financing and accounting purposes. In such event, the Parity Bonds and bonds issued to fund the Priest Rapids Development would be paid from revenues of the combined system. See SECURITY FOR THE PARITY BONDS Potential Consolidation of Developments. Purpose of the Bonds PURPOSE AND APPLICATION OF BOND PROCEEDS The Bonds are being issued to finance improvements at the Wanapum Development, refund certain outstanding bonds of the Wanapum Development, and pay costs of issuance of the Bonds. The net proceeds of the 2006B Bonds and 2006Z Bonds will be used to finance the portion of the costs of such improvements allocable to the use of the Wanapum Development output by the investor-owned utilities and other private purchasers and to refund certain outstanding bonds of the Wanapum Development, as described below. The bonds to be refunded with the proceeds of the Bonds are identified below (the Refunded Bonds ). Refunded Bonds Series Principal Amount Interest Rates Maturities Redemption Date 1996B $ 10,885, % /1/ % 1997A 2,620, /1/ B 4,720, /1/ C 1,840, , /1/ D 3,160, , /1/ A 5,050, /1/ A portion of the net proceeds from the sale of the Bonds will be deposited in the 2006 Refunding Account (the Refunding Account ) and used to purchase Escrow Obligations (as defined below) to be held by The Bank of New York Trust Company, N.A. (the Escrow Agent ) under an escrow agreement (the Escrow Agreement ), dated the date of delivery of the Bonds, between the District and the Escrow Agent. Funds will be irrevocably deposited in the Refunding Account and will be used to purchase direct, noncallable, obligations of the United States of America (the Escrow Obligations ). The Escrow Obligations will mature at such times and pay interest in such amounts so that, with other available funds held by the Escrow Agent under the Escrow Agreement, sufficient money will be available to pay the interest on the Refunded Bonds coming due on and prior to their respective redemption dates and to redeem and retire the Refunded Bonds on the respective redemption dates set forth above. Since all payments of principal of and interest on the Refunded Bonds will thereafter be provided for from money and securities on deposit with the Escrow Agent under the Escrow Agreement, the liens, pledges and covenants of the Refunded Bonds will terminate and be discharged and released. An independent verification shall be obtained from Causey Demgen & Moore Inc. stating that the Escrow Obligations held by the Escrow Agent and the interest to be earned thereon, together with any money held by the Price -2-

9 Escrow Agent, shall be sufficient to make all such interest payments on the Refunded Bonds to pay the principal of the Refunded Bonds on the dates fixed for redemption. The verification will also confirm the correctness of the mathematical computations supporting the conclusion of Bond Counsel that the 2006A Bonds and 2006B Bonds are not arbitrage bonds as defined by Section 148 of the Internal Revenue Code of 1986, as amended. Application of the Bond Proceeds The proceeds of the Bonds and other sources are funds are estimated to be applied as follows: Sources Series 2006A Series 2006B Series 2006Z Par Amount of Bonds... $ 71,395,000 $ 18,190,000 $ 96,845,000 Net Original Issue Premium/Discount... 5,078, , Z Bond Proceeds ,541 0 Bond Fund , ,190 31,876 Total... $ 76,655,888 $ 19,702,669 $ 96,876,876 Uses Series 2006A Series 2006B Series 2006Z Deposit to the Project Account... $ 67,300,000 $ 0 $ 93,702,000 Deposit to the Refunding Account... 8,476,530 19,504,881 1,454, Z Bond Proceeds to Series 2006B Refunding Account ,541 Underwriters Discount and Costs of Issuance (1) , ,788 1,231,062 Total... $ 76,655,888 $ 19,702,669 $ 96,876,876 (1) Includes premiums for bond insurance and reserve surety policy and other costs of issuance. Pledge of Revenues SECURITY FOR THE PARITY BONDS The Parity Bonds are special limited obligations of the District payable from and secured solely by a lien and charge on (i) Gross Revenues, which include all income, revenues, receipts and profits received by the District through the ownership and operation of the Wanapum Development, together with the proceeds received by the District from the sale, lease or other disposition of any properties, rights or facilities of the Wanapum Development and certain investment income, subject only to the prior payment of Operating Expenses, and (ii) the money and assets, if any, credited to the Bond Fund, the Project Account and the Supplemental Renewal and Contingency Fund (the Supplemental R&C Fund ), and the income therefrom. The items described above are pledged as security for the payment of the principal of, premium, if any, and interest on all Parity Bonds in accordance with the provisions of the Bond Resolutions. See APPENDIX A SUMMARY OF CERTAIN PROVISIONS OF THE PARITY BOND RESOLUTIONS for a description of the security for the Parity Bonds and Flow of Funds below for a description of the priority of payments from the Gross Revenues of the Wanapum Development. All Parity Bonds are equally and ratably payable and secured under the Bond Resolutions without priority, except as otherwise expressly provided or permitted in the Bond Resolutions and except as to municipal bond insurance which may be obtained by the District to insure the repayment of one or more series or maturities within a series. State law provides that the revenue obligations issued by a public utility district and interest thereon shall be a valid claim of the owner thereof only as against the special fund or funds provided for the payment of such obligations and the proportion or amount of the revenues pledged to such fund or funds, and that (i) such pledge of the revenues or other money or obligations shall be valid and binding from the time made, (ii) the revenues or other money or obligations so pledged and thereafter received by a public utility district shall immediately be subject to the lien of such pledge without any physical delivery or further act, and (iii) the lien of any such pledge shall be valid and binding as against any parties having claims of any kind in tort, contract or otherwise against a district irrespective -3-

10 of whether such parties have notice thereof. The Bonds are not secured by a mortgage, deed of trust, or security interest in the Wanapum Development or any of the physical plant and facilities thereof. Obligations of the Electric System The District s Electric System currently purchases 36.5% of the output of the Wanapum Development, and the remaining output is sold to nine utilities under the 1959 Power Sales Contracts, which expire on October 31, The Parity Bonds are payable indirectly from the revenues of the District s Electric System to the extent that the Electric System is required under the 1959 Power Sales Contracts to purchase 36.5% of the output of the Wanapum Development. See THE WANAPUM DEVELOPMENT Wanapum Development Output and Power Sales Contracts. So long as the 1959 Power Sales Contracts are in effect, the District has covenanted to establish, maintain and collect rates and charges for electric power and energy sold through the Electric System sufficient to pay the Electric System s obligations under the 1959 Power Sales Contracts. Once the 1959 Power Sales Contracts are no longer in effect, if any power and energy is produced or capable of being produced in any given fiscal year by the Wanapum Development, the District has covenanted (1) to pay to the Wanapum Development from the Electric System that portion of the annual costs of the Wanapum Development for such fiscal year, including without limitation for operating and maintenance expenses and debt service on the Parity Bonds, that is not otherwise paid or provided for from payments received by the Wanapum Development from the sale of power and energy and related products from the Wanapum Development to purchasers other than the District and (2) to establish, maintain and collect rates or charges for electric power and energy and related products sold through the Electric System sufficient to make any such payments to the Wanapum Development. For so long as the 1996 Bonds, 1997 Bonds and 1998 Bonds are Outstanding (which are expected to be retired by January 1, 2009), the District is obligated to pay from Electric System revenues or other legally available funds all amounts required to be paid under the Bond Resolutions, including debt service on the Parity Bonds, to the extent payment or provision for payment of such amounts is not otherwise made, and (ii) to establish, maintain and collect rates or charges for electric power and energy sold through the Electric System sufficient to pay all costs chargeable against the revenues of the Electric System and all amounts required to be paid under the Bond Resolutions to the extent payment or provision for payment of such amounts is not otherwise made. Once the 1996 Bonds, 1997 Bonds and 1998 Bonds are no longer Outstanding, the Electric System will not be obligated to pay any costs of the Wanapum Development for any fiscal year (i) if the Electric System does not receive power from the Development during such fiscal year and (ii) no power or energy is produced or capable of being produced by the Wanapum Development during such fiscal year. Payments made by the Electric System for its share of the Wanapum Development s output, currently 36.5%, and other costs of purchased power and energy from the Wanapum Development are operating expenses of the Electric System, and, therefore, are payable prior to debt service on the Electric System bonds. The obligation of the Electric System to pay for all other costs associated with the Wanapum Development are junior in rank to all other obligations of the Electric System. For a summary of outstanding debt of the District, see Table 13. The Electric System has substantially identical obligations with respect to the Priest Rapids Development and the bonds issued by the District payable from revenues of the Priest Rapids Development. Thus, any financial difficulties encountered by the Priest Rapids Development could indirectly affect the security provided by the Electric System with respect to the Parity Bonds. Potential Consolidation of Developments Once the 1996 Bonds, 1997 Bonds, 1998 Bonds and 1999 Bonds and the Priest Rapids Development bonds issued prior to 2000 are no longer Outstanding, the District may elect to combine the Wanapum Development and the Priest Rapids Development into a single system for accounting and financing purposes. The District may consider consolidating the Developments effective on or after November 1, 2009, when output of the Wanapum Development will be subject to the New Power Sales Contracts. In such event, the revenues of both Developments would be pledged and available to pay and secure debt service on the Bonds and any Future Parity Bonds, as well as bonds of the Priest Rapids Development, and the operation and maintenance expenses, capital costs and other obligations of -4-

11 both Developments would be payable from the revenues of both Developments. For a summary of currently outstanding debt of both Developments, see Table 13. Prior to consolidating the Developments, the District must obtain confirmation from each rating agency then rating the Parity Bonds that the consolidation will not adversely impact the then current rating(s) on the Parity Bonds. In addition, the District must obtain an opinion of bond counsel that the consolidation will not adversely affect the tax-exempt status of any Outstanding Parity Bonds. The District can give no assurance that such a consolidation would not have a material adverse effect on the security for the Bonds. Flow of Funds The District has covenanted that so long as any of the Parity Bonds are Outstanding and unpaid it will continue to pay into the Revenue Fund all Gross Revenues. Earnings on money in the Supplemental R&C Fund and the Bond Fund may be paid into such funds as provided by the Bond Resolutions. The Bond Resolutions create a charge and obligation against the Revenue Fund in an amount equal to the Coverage Requirement. The Coverage Requirement is defined as (a) 1.15 times the Annual Debt Service in a Fiscal Year plus (b) any amounts required to be deposited into the Reserve Account in a Fiscal Year less (c) amounts transferred to the Bond Fund from the Supplemental R&C Fund in excess of the Supplemental Fund Cap (currently $6,000,000) as of the end of the preceding Fiscal Year. So long as any Parity Bonds are Outstanding, the amounts in the Revenue Fund will be used only for the following purposes and in the following order of priority: (1) to pay or provide for Operating Expenses; (2) to make all payments required to be made into the Interest Account in the Bond Fund; (3) to make all payments required to be made into the Principal Account in the Bond Fund and to make all required payments into the Bond Retirement Account in the Bond Fund; (4) to make all payments required to be made into the Reserve Account in the Bond Fund; (5) to make all payments required to be made into the Supplemental R&C Fund (currently an amount in each month equal to.0125 of Annual Debt Service); and (6) to make all payments required to be made into any special fund or account created to pay or secure the payment of junior lien obligations of the Wanapum Development. After all of the above payments and credits have been made, amounts remaining in the Revenue Fund may be used for any other lawful purpose of the District relating to the Wanapum Development. If required by contract with the purchasers of power from the Wanapum Development, the District may rebate money in any fund except the Bond Fund to those purchasers. If the rebate is paid from the Supplemental R&C Fund, the District may again establish in the Supplemental R&C Fund an amount equal to the Supplemental Fund Cap (currently $6,000,000) from the proceeds of Parity Bonds, from Gross Revenues, or from any other sources. Any rebates may be paid to the Electric System on the same basis as to the other purchasers of power. Under the Bond Resolutions, the District is not permitted to issue additional bonds with a lien and charge upon Gross Revenues prior to the lien and charge of the Parity Bonds. Limited Obligations The Parity Bonds do not in any manner or to any extent constitute general obligations of the District or of the State of Washington, or any political subdivision of the State of Washington, or a charge upon any general fund or upon any money or other property of the District or of the State of Washington, or of any political subdivision of the State of Washington, not specifically pledged thereto by the Bond Resolutions. -5-

12 Rate Covenants The District has covenanted in the Bond Resolutions to establish, maintain and collect rates or charges in connection with the ownership and operation of the Wanapum Development that are fair and nondiscriminatory and adequate to provide Gross Revenues sufficient for the payment of the principal of and interest on all Outstanding Parity Bonds, all amounts which the District is obligated to set aside in the Bond Fund, the payment of all Operating Expenses of the Wanapum Development, and for the payment of any amounts that the District may now or hereafter become obligated to pay from Gross Revenues. The District has also covenanted to establish, maintain and collect rates or charges in connection with the ownership and operation of the Wanapum Development sufficient to provide Net Revenues in any Fiscal Year in an amount that is at least equal to (i) 1.15 times Annual Debt Service, plus (ii) any amounts required to be deposited into the Reserve Account, less (iii) amounts transferred to the Bond Fund from the Supplemental R&C Fund in excess of the Supplemental Fund Cap at the end of the preceding Fiscal Year, in addition to the amounts required to pay debt service on any junior lien obligations of the Wanapum Development. Retail electric rates and charges of the District are fixed by the Commission, free from the jurisdiction and control of the Washington Utilities and Transportation Commission and, in the opinion of the District, free from the jurisdiction and control of the Federal Energy Regulatory Commission ( FERC ). Wholesale electric rates and charges, however, are subject to certain regulations by FERC. See THE WANAPUM DEVELOPMENT Regulatory Proceedings Affecting the Developments Proceedings Related to Allocation of Output. Additionally, the Developments are owned and operated by the District under a long-term license from FERC. See THE WANAPUM DEVELOPMENT License Status. See THE ELECTRIC SYSTEM Electric Rates for a discussion of telecommunication rates. Reserve Account There is a single Reserve Account securing all Parity Bonds. The Bond Resolutions require that there be deposited into the Reserve Account in the Bond Fund for each series of Parity Bonds an amount equal to the maximum amount of interest due in any Fiscal Year on such series of Parity Bonds, calculated as of the date of issuance of such series (the Reserve Account Requirement ). Once the 1996 Bonds, 1997 Bonds, 1998 Bonds, and 1999 Bonds are no longer Outstanding, Reserve Account Requirement will mean, with respect to a series of Future Parity Bonds, an amount set forth in the resolution authorizing such bonds; provided, however, that so long as any 2001 Bonds are insured by Financial Security Assurance Inc. ( FSA ) or any 2005 Bonds are insured by Financial Guaranty Insurance Company ( Financial Guaranty ), the Reserve Account Requirement with respect to any Future Parity Bonds secured by the Reserve Account shall be an amount equal to the maximum amount of interest due in any Fiscal Year on such Future Parity Bonds. The Reserve Account Requirement may be funded either from Parity Bond proceeds or from Gross Revenues over a five-year period following the date of issuance, except that so long as the 2001 Bonds are insured by FSA or the 2005 Bonds are insured by Financial Guaranty, the Reserve Account Requirement must be fully funded on the date of issuance of any Parity Bonds. As an alternative, the District may fund all or a portion of the Reserve Account through the purchase of Qualified Insurance or a Qualified Letter of Credit. See Certain Definitions and Bond Fund in APPENDIX A SUMMARY OF CERTAIN PROVISIONS OF THE PARITY BOND RESOLUTIONS relating to the satisfaction of the Reserve Account Requirement through the deposit of a letter of credit or insurance policy. To meet the Reserve Account Requirement for the Outstanding Parity Bonds, the District has reserve account surety policies in the aggregate amount of $6,082, with Ambac Assurance Corporation ( Ambac Assurance ), surety policies in the aggregate amount of $893, with FSA, a surety policy in the amount of $2,647, with MBIA Insurance Corporation ( MBIA ), and a surety policy in the amount of $6,050, with Financial Guaranty. See Reserve Account Surety Bonds below. In addition, upon delivery of the Bonds, there will be on deposit in the Reserve Account a reserve surety policy with MBIA to satisfy the Reserve Account Requirement for the Bonds. For information about MBIA, see BOND INSURANCE MBIA Insurance Corporation. The valuation of the amount on deposit in the Reserve Account is required to be made by the Trustee on each December 31, and after certain withdrawals, and may be made on each June 30. Such valuation shall be at the -6-

13 market value thereof (including accrued interest) for obligations maturing more than six months from the valuation date or at par for obligations maturing within six months of the valuation date. The District has covenanted to make up any deficiency in the Interest Account, the Principal Account, and the Bond Retirement Account from the funds available in the Reserve Account. The District has covenanted to replenish such withdrawals from money in the Revenue Fund, Supplemental R&C Fund or the Project Account created for the Parity Bonds, in not more than six equal monthly installments. Reserve Account Surety for the Bonds Application has been made to the MBIA for a commitment to a issue surety bond (the Debt Service Reserve Fund Surety Bond ) in the amount of $10,066,601. The Debt Service Reserve Fund Surety Bond will provide that upon notice from the Registrar to the Insurer to the effect that insufficient amounts are on deposit in the Bond Fund to pay the principal of (at maturity or pursuant to mandatory redemption requirements) and interest on the Bonds, the Insurer will promptly deposit with the Registrar an amount sufficient to pay the principal of and interest on the Bonds or the available amount of the Debt Service Reserve Fund Surety Bond, whichever is less. Upon the later of: (i) three days after receipt by the Insurer of a Demand for Payment in the form attached to the Debt Service Reserve Fund Surety Bond, duly executed by the Registrar or (ii) the payment date of the Bonds as specified in the Demand for Payment presented by the Registrar to the Insurer, the Insurer will make a deposit of funds in an account with U.S. Bank National Association, in New York, New York, or its successor, sufficient for the payment to the Registrar, of amounts which are then due to the Registrar (as specified in the Demand for Payment) subject to the surety bond coverage. The available amount of the Debt Service Reserve Fund Surety Bond is the initial face amount of the Debt Service Reserve Fund Surety Bond less the amount of any previous deposits by the Insurer with the Registrar which have not been reimbursed by the District. The District and the Insurer will enter into a Financial Guaranty Agreement dated December 13, 2006 (the Agreement ). Pursuant to the Agreement, the District is required to reimburse the Insurer, within one year of any deposit, the amount of such deposit made by the Insurer with the Registrar under the Debt Service Reserve Fund Surety Bond. Such reimbursement shall be made only after payment of Operating Expenses and required deposits to the Bond Fund have been made. Under the terms of the Agreement, the District is required to reimburse the Insurer, with interest, until the face amount of the Debt Service Reserve Fund Surety Bond is reinstated before any deposit is made to the Revenue Fund. No optional redemption of Bonds may be made until the Insurer s Debt Service Reserve Fund Surety Bond is reinstated. The Debt Service Reserve Fund Surety Bond will be held by the Trustee in the Bond Fund and is provided as an alternative to the District depositing funds equal to the Debt Service Requirement for outstanding Bonds. The Debt Service Reserve Fund Surety Bond will be issued in the face amount equal to the Reserve Account Requirement and the premium therefor will be fully paid by the District at the time of delivery of the Bonds. Reserve Account Sureties for Outstanding Parity Bonds The surety bonds issued by Ambac Assurance, FSA and Financial Guaranty provide that upon the later of (i) one day after the receipt by the applicable surety of a demand for payment executed by the Paying Agent certifying that provision for the payment of principal of or interest on the Parity Bonds when due has not been made or (ii) the interest payment date specified in the demand for payment submitted to the applicable surety, the applicable surety will promptly deposit funds with the Paying Agent sufficient to enable the Paying Agent to make such payments due on the Parity Bonds, but in no event exceeding the policy limit of the surety bond so drawn on. Pursuant to the terms of the surety bonds, the policy limits of each are automatically reduced to the extent of each payment made by the applicable surety under the terms of the surety bonds, and the District is required to reimburse the applicable surety for any draws under the surety bonds with interest at a market rate. Upon such reimbursement, the surety bonds are reinstated to the extent of each reimbursement up to but not exceeding the applicable policy limits. The reimbursement obligation of the District under the surety bonds is subordinate to the District s obligations with respect to the Parity Bonds. -7-

14 In the event the amount on deposit in, or credited to, the Reserve Account exceeds the amount of the surety bonds, any draw on the surety bonds shall be made only after all the funds in the Reserve Account have been expended. In the event that the amount on deposit in, or credited to, the Reserve Account, in addition to the amount available under the surety bonds, includes amounts available under a letter of credit, insurance policy, surety bond or other such funding instrument, draws on the surety bonds and additional funding instruments shall be made on a pro rata basis to fund the insufficiency. The Bond Resolutions provide that the Reserve Account shall be replenished in the following priority: principal and interest on the surety bonds and on the additional funding instrument shall be paid from first-available Gross Revenues on a pro rata basis. The surety bonds do not insure against nonpayment caused by the insolvency or negligence of the Trustee or the Paying Agent. Ambac Assurance, FSA, MBIA and Financial Guaranty are subject to the informational requirements of the Exchange Act and in accordance therewith file reports, proxy statements and other information with the SEC. Certain SEC filings of Ambac Assurance are available on the company s website, (which is not incorporated herein by this reference). Certain SEC filings of FSA are available on the company s website, (which is not incorporated herein by this reference). Certain SEC filings of MBIA are available on the company s website, (which is not incorporated herein by this reference). Certain SEC filings of Financial Guaranty are available on the company s website, (which is not incorporated herein by this reference). Such reports, proxy statements and other information may also be inspected and copied at the SEC s Public Reference Room at 100 F Street, N.E., Washington, D.C See APPENDIX A SUMMARY OF CERTAIN PROVISIONS OF THE PARITY BOND RESOLUTION Bond Fund. Supplemental Renewal and Contingency Fund The Bond Resolutions provide that the Supplemental R&C Fund must be maintained at a balance not to exceed $6,000,000 or such greater amount as may be authorized by resolution of the Commission. Money in the Supplemental R&C Fund must be used to make up any deficiency in the Bond Fund and to the extent not required for such purpose may be applied to other specified purposes. See APPENDIX A SUMMARY OF CERTAIN PROVISIONS OF THE PARITY BOND RESOLUTIONS Supplemental Renewal and Contingency Fund. Additional Parity Bonds Under the Bond Resolutions, the District is not permitted to issue additional bonds with a lien and charge upon Gross Revenues prior to the lien and charge of the Parity Bonds. Additional Parity Bonds may be issued for any lawful purpose relating to the Wanapum Development upon the terms and conditions stated in the Bond Resolutions. Such conditions include the delivery of an opinion of a Professional Utility Consultant to the effect that the issuance of such Parity Bonds and the expenditure of the proceeds thereof will not result in a violation of the District s rate covenants; provided, however, that such report will not be required under certain circumstances once the 1996 Bonds, 1997 Bonds, 1998 Bonds, 1999 Bonds and 2001 Bonds are no longer Outstanding. See Rate Covenants above and Additional Parity Bonds in APPENDIX A SUMMARY OF CERTAIN PROVISIONS OF THE PARITY BOND RESOLUTIONS. The District may issue bonds, notes, warrants or other obligations having a lien and charge against the Gross Revenues of the Wanapum Development junior to the Parity Bonds upon the terms and conditions stated in the Bond Resolutions. Derivative Products Once the 1996 Bonds, 1997 Bonds, 1998 Bonds and 1999 Bonds are no longer Outstanding, to the extent permitted by state law, the District may enter into Derivative Products secured by a pledge and lien on Gross Revenues on a parity with the Bonds subject to the satisfaction of certain conditions precedent. A Derivative Product is a written contract between the District and a third party obligating the District to make District Payments (subject to certain conditions) on one or more scheduled and specified payment dates in exchange for a Reciprocal Payor s obligation to pay or cause to be paid Reciprocal Payments to the District on scheduled and specified payment dates. Derivative Products include agreements providing for an exchange of payments based on interest rates (known as interest rate swaps) or providing for ceilings or floors on such payments. For a definition of terms used in this paragraph and a -8-

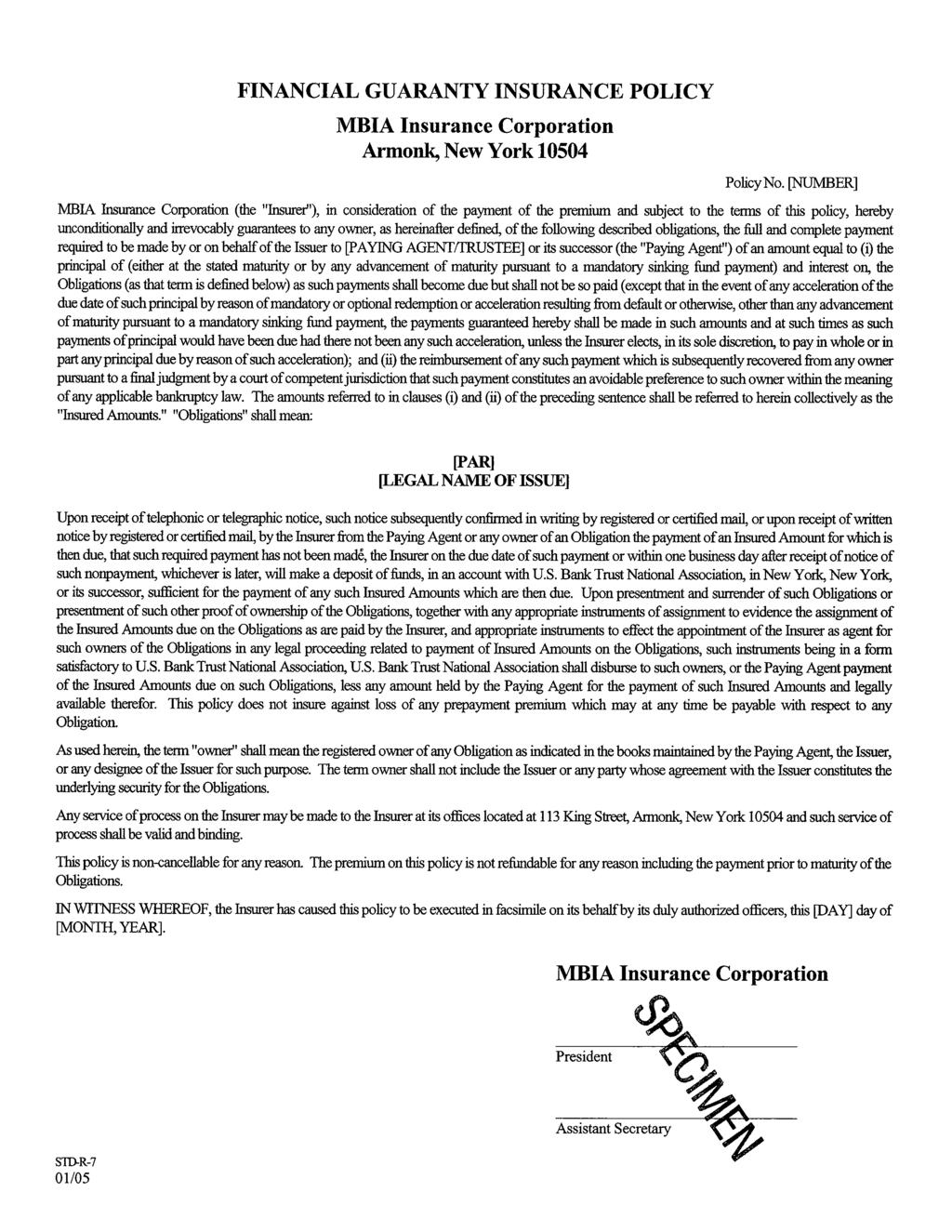

15 summary of the conditions precedent to the District s entering into a Derivative Product, see APPENDIX A SUMMARY OF CERTAIN PROVISIONS OF THE PARITY BOND RESOLUTIONS Derivative Products. Contingent Payment Obligations The District has entered into, and may in the future enter into, contracts and agreements in the course of its business that include an obligation on the part of the District to make payments or post collateral contingent upon the occurrence or nonoccurrence of certain future events, including events that are beyond the direct control of the District. These agreements may include interest rate swaps and other similar agreements, agreements with respect to the delivery of electric energy or other energy, letter of credit agreements and other financial and energy hedging transactions. Such contingent payments or posting of collateral may be conditioned upon the future credit ratings of the District and/or other parties, maintenance by the District of specified financial ratios, future changes in energy prices, and other factors. The amount of any such payments or posting of collateral can be substantial. Some such payments may be characterized as Operating Expenses, and thus may be payable from Gross Revenues prior to the payment of debt service on the Bonds. Other such payments may be payable on a parity with debt service on the Bonds, including any regularly scheduled payments with respect to Derivative Products. The District has entered into the Western Systems Power Pool Agreements that include such contingent payment obligations. The agreements include obligations on the part of the District to post collateral or a letter of credit contingent upon the occurrence or nonoccurrence of certain future events, such as future credit ratings below investment grade or defaults under power marketing contracts or indebtedness. See APPENDIX A SUMMARY OF CERTAIN PROVISIONS OF THE PARITY BOND RESOLUTIONS Derivative Products. No Acceleration Upon Default Upon the occurrence and continuance of an Event of Default under the Bond Resolutions, payment of the principal amount of the Parity Bonds is not subject to acceleration. The District thus would be liable only for principal and interest payments as they became due, and the Trustee or the Bondowners Trustee would be required to seek a separate judgment for each payment, if any, not made. Any such action for money damages would be subject to limitations on legal claims and remedies against public bodies under Washington law. Amounts recovered would be applied to unpaid installments of interest prior to being applied to unpaid principal and premium, if any, which had become due. The District has never defaulted in the payment of principal, premium or interest on any of its bonds. See APPENDIX A SUMMARY OF CERTAIN PROVISIONS OF THE PARITY BOND RESOLUTIONS Events Of Default, Trustee, Remedies. Investment of Funds Money in the Bond Fund and any construction funds and/or project accounts may be, and money in the Supplemental R&C Fund is required to be, invested in Permitted Investments as defined in the Bond Resolutions. Investments in the Bond Fund must mature or be retireable at the option of the owner prior to the date needed or prior to the maturity date of the final installment of principal of the Parity Bonds payable out of the Bond Fund. The MBIA Insurance Corporation Insurance Policy BOND INSURANCE The following information has been furnished by MBIA for use in this Official Statement. Reference is made to Appendix G for a specimen of MBIA's policy (the Policy ). MBIA does not accept any responsibility for the accuracy or completeness of this Official Statement or any information or disclosure contained herein, or omitted herefrom, other than with respect to the accuracy of the information regarding the Policy and MBIA set forth under the heading BOND INSURANCE. Additionally, MBIA makes no representation regarding the Bonds or the advisability of investing in the Bonds. The MBIA Policy unconditionally and irrevocably guarantees the full and complete payment required to be made by or on behalf of the District to the Paying Agent or its successor of an amount equal to (i) the principal of (either at the stated maturity or by an advancement of maturity pursuant to a mandatory sinking fund payment) and interest -9-

16 on, the Bonds as such payments shall become due but shall not be so paid (except that in the event of any acceleration of the due date of such principal by reason of mandatory or optional redemption or acceleration resulting from default or otherwise, other than any advancement of maturity pursuant to a mandatory sinking fund payment, the payments guaranteed by the MBIA Policy shall be made in such amounts and at such times as such payments of principal would have been due had there not been any such acceleration, unless MBIA elects in its sole discretion, to pay in whole or in part any principal due by reason of such acceleration); and (ii) the reimbursement of any such payment which is subsequently recovered from any Owner of the Bonds pursuant to a final judgment by a court of competent jurisdiction that such payment constitutes an avoidable preference to such Owner within the meaning of any applicable bankruptcy law (a Preference ). MBIA s Policy does not insure against loss of any prepayment premium which may at any time be payable with respect to any Bonds. MBIA's Policy does not, under any circumstance, insure against loss relating to: (i) optional or mandatory redemptions (other than mandatory sinking fund redemptions); (ii) any payments to be made on an accelerated basis; (iii) payments of the purchase price of Bonds upon tender by an owner thereof; or (iv) any Preference relating to (i) through (iii) above. MBIA's Policy also does not insure against nonpayment of principal of or interest on the Bonds resulting from the insolvency, negligence or any other act or omission of the Paying Agent or any other paying agent for the Bonds. Upon receipt of telephonic or telegraphic notice, such notice subsequently confirmed in writing by registered or certified mail, or upon receipt of written notice by registered or certified mail, by MBIA from the Paying Agent or any owner of a Bond the payment of an insured amount for which is then due, that such required payment has not been made, MBIA on the due date of such payment or within one business day after receipt of notice of such nonpayment, whichever is later, will make a deposit of funds, in an account with U.S. Bank Trust National Association, in New York, New York, or its successor, sufficient for the payment of any such insured amounts which are then due. Upon presentment and surrender of such Bonds or presentment of such other proof of ownership of the Bonds, together with any appropriate instruments of assignment to evidence the assignment of the insured amounts due on the Bonds as are paid by MBIA, and appropriate instruments to effect the appointment of MBIA as agent for such owners of the Bonds in any legal proceeding related to payment of insured amounts on the Bonds, such instruments being in a form satisfactory to U.S. Bank Trust National Association, U.S. Bank Trust National Association shall disburse to such owners or the Paying Agent payment of the insured amounts due on such Bonds, less any amount held by the Paying Agent for the payment of such insured amounts and legally available therefor. MBIA Insurance Corporation MBIA Insurance Corporation ( MBIA ) is the principal operating subsidiary of MBIA Inc., a New York Stock Exchange listed company (the Company ). The Company is not obligated to pay the debts of or claims against MBIA. MBIA is domiciled in the State of New York and licensed to do business in and subject to regulation under the laws of all 50 states, the District of Columbia, the Commonwealth of Puerto Rico, the Commonwealth of the Northern Mariana Islands, the Virgin Islands of the United States and the Territory of Guam. MBIA, either directly or through subsidiaries, is licensed to do business in the Republic of France, the United Kingdom and the Kingdom of Spain and is subject to regulation under the laws of those jurisdictions. The principal executive offices of MBIA are located at 113 King Street, Armonk, New York and the main telephone number at that address is (914) Regulation As a financial guaranty insurance company licensed to do business in the State of New York, MBIA is subject to the New York Insurance Law which, among other things, prescribes minimum capital requirements and contingency reserves against liabilities for MBIA, limits the classes and concentrations of investments that are made by MBIA and requires the approval of policy rates and forms that are employed by MBIA. State law also regulates the amount of both the aggregate and individual risks that may be insured by MBIA, the payment of dividends by MBIA, changes in control with respect to MBIA and transactions among MBIA and its affiliates. -10-

17 The Policy is not covered by the Property/Casualty Insurance Security Fund specified in Article 76 of the New York Insurance Law. Financial Strength Ratings of MBIA Moody's Investors Service, Inc. rates the financial strength of MBIA Aaa. Standard & Poor's, a division of The McGraw-Hill Companies, Inc., rates the financial strength of MBIA AAA. Fitch Ratings rates the financial strength of MBIA AAA. Each rating of MBIA should be evaluated independently. The ratings reflect the respective rating agency's current assessment of the creditworthiness of MBIA and its ability to pay claims on its policies of insurance. Any further explanation as to the significance of the above ratings may be obtained only from the applicable rating agency. The above ratings are not recommendations to buy, sell or hold the Bonds, and such ratings may be subject to revision or withdrawal at any time by the rating agencies. Any downward revision or withdrawal of any of the above ratings may have an adverse effect on the market price of the Bonds. MBIA does not guaranty the market price of the Bonds nor does it guaranty that the ratings on the Bonds will not be revised or withdrawn. MBIA Financial Information As of December 31, 2005, MBIA had admitted assets of $11.0 billion (audited), total liabilities of $7.2 billion (audited), and total capital and surplus of $3.8 billion (audited), each as determined in accordance with statutory accounting practices prescribed or permitted by insurance regulatory authorities. As of September 30, 2006, MBIA had admitted assets of $11.5 billion (unaudited), total liabilities of $7.0 billion (unaudited), and total capital and surplus of $4.4 billion (unaudited), each as determined in accordance with statutory accounting practices prescribed or permitted by insurance regulatory authorities. For further information concerning MBIA, see the consolidated financial statements of MBIA and its subsidiaries as of December 31, 2005 and December 31, 2004 and for each of the three years in the period ended December 31, 2005, prepared in accordance with generally accepted accounting principles, included in the Annual Report on Form 10-K of the Company for the year ended December 31, 2005 and the consolidated financial statements of MBIA and its subsidiaries as of September 30, 2006 and for the nine month periods ended September 30, 2006 and September 30, 2005 included in the Quarterly Report on Form 10-Q of the Company for the period ended September 30, 2006, which are hereby incorporated by reference into this Official Statement and shall be deemed to be a part hereof. Copies of the statutory financial statements filed by MBIA with the State of New York Insurance Department are available over the Internet at the Company s web site at (which is not incorporated herein by this reference) and at no cost, upon request to MBIA at its principal executive offices. Incorporation of Certain Documents by Reference The following documents filed by the Company with the Securities and Exchange Commission (the SEC ) are incorporated by reference into this Official Statement: (1) The Company s Annual Report on Form 10-K for the year ended December 31, 2005; and (2) The Company s Quarterly Report on Form 10-Q for the quarter ended September 30, Any documents, including any financial statements of MBIA and its subsidiaries that are included therein or attached as exhibits thereto, filed by the Company pursuant to Sections 13(a), 13(c), 14 or 15(d) of the Exchange Act after the date of the Company s most recent Quarterly Report on Form 10-Q or Annual Report on Form 10-K, and prior to the termination of the offering of the Bonds offered hereby shall be deemed to be incorporated by reference in this Official Statement and to be a part hereof from the respective dates of filing such documents. Any statement contained in a document incorporated or deemed to be incorporated by reference herein, or contained in this Official Statement, shall be deemed to be modified or superseded for purposes of this Official Statement to the -11-

18 extent that a statement contained herein or in any other subsequently filed document which also is or is deemed to be incorporated by reference herein modifies or supersedes such statement. Any such statement so modified or superseded shall not be deemed, except as so modified or superseded, to constitute a part of this Official Statement. The Company files annual, quarterly and special reports, information statements and other information with the SEC under File No Copies of the Company s SEC filings (including (1) the Company s Annual Report on Form 10-K for the year ended December 31, 2005, and (2) the Company s Quarterly Reports on Form 10-Q for the quarters ended March 31, 2006, June 30, 2006 and September 30, 2006 are available (i) over the Internet at the SEC s web site at (which is not incorporated herein by this reference); (ii) at the SEC s public reference room in Washington, D.C.; (iii) over the Internet at the Company s web site at (which is not incorporated herein by this reference); and (iv) at no cost, upon request to MBIA at its principal executive offices. General Terms DESCRIPTION OF THE BONDS The 2006A Bonds will be issued in the aggregate principal amount of $71,395,000 and will be dated the date of their delivery. The 2006A Bonds will bear interest at the rates per annum set forth on the inside cover page hereof, payable July 1, 2007, and semiannually thereafter on each January 1 and July 1, and will mature on January 1 in each year as set forth on the inside cover page hereof. The 2006A Bonds are not private activity bonds, and interest on the 2006A Bonds is not an item of tax preference for purposes of the federal alternative minimum tax imposed on individuals. See TAX MATTERS The 2006A Bonds. The 2006B Bonds will be issued in the aggregate principal amount of $18,190,000 and will be dated the date of their delivery. The 2006B Bonds will bear interest at the rates per annum set forth on the inside cover page hereof, payable July 1, 2007, and semiannually thereafter on each January 1 and July 1, and will mature on January 1 in each year as set forth on the inside cover page hereof. The 2006B Bonds are private activity bonds, and interest on the 2006B Bonds is a preference item for purposes of the federal alternative minimum tax imposed on individuals and corporations. See TAX MATTERS The 2006B Bonds. The 2006Z Bonds will be issued in the aggregate principal amount of $96,845,000 and will be dated the date of their delivery. The 2006Z Bonds will bear interest at the rates per annum set forth on the inside cover page hereof, payable July 1, 2007, and semiannually thereafter on each July 1 and January 1, and will mature on January 1 in each year as set forth on the inside cover page hereof. The District has taken no action to cause interest on the 2006Z Bonds to be excluded from gross income for purposes of federal income taxation. Certain information regarding the federal income tax treatment of the 2006Z Bonds is set forth under the heading TAX MATTERS The 2006Z Bonds. The Bonds will be issuable in registered form, in the denomination of $5,000 or any integral multiple thereof. Interest is calculated based on a 360-day year consisting of 12 months of 30 days each. The Bank of New York Trust Company, N.A., Seattle, Washington, has been appointed by the District as Trustee for the Bonds. Once the 1996 Bonds, 1997 Bonds, 1998 Bonds and the 1999 Bonds are no longer outstanding and as long as an Event of Default has not occurred, the District may require the Trustee to transfer the Bond Fund to the District and discharge the Trustee, in which case (i) a Trustee is not required to hold the Bond Fund and (ii) the District is not required to appoint a trustee for the Parity Bonds as long as an Event of Default has not occurred. The fiscal agency of the State of Washington in New York, New York, currently The Bank of New York, is the initial Registrar and Paying Agent for the Bonds. The Bonds will be issued in fully registered form initially in the name of Cede & Co., as registered owner and nominee of The Depository Trust Company, New York, New York ( DTC ). DTC will act as securities depository for the Bonds. Individual purchases may be made in book-entry form only as described below. Purchasers will not receive certificates representing their interest in the Bonds purchased. So long as Cede & Co. is the registered owner of the Bonds, as nominee of DTC, references herein to the registered owners or bondowners shall mean Cede & Co. and shall not mean the Beneficial Owners of the Bonds. In this Official Statement, the term -12-

19 Beneficial Owner shall mean the person for whom a DTC participant or indirect participant acquires an interest in the Bonds. So long as Cede & Co. is the registered owner of the Bonds, principal of and interest on the Bonds are payable by wire transfer by the Registrar to DTC, which in turn is obligated to remit such principal and interest to the DTC participants for subsequent disbursements to Beneficial Owners of the Bonds. See APPENDIX F BOOK- ENTRY SYSTEM. Termination of Book-Entry Transfer System If DTC or its successor resigns as the securities depository or if the District determines that it is no longer in the best interests of owners of beneficial interests in the Bonds to continue the system of book-entry transfers through DTC or its successor, the District will deliver at no cost to the beneficial owners of the Bonds or their nominees Bonds in registered certificate form, in the denomination of $5,000 or any integral multiple thereof. Thereafter, the principal of the Bonds will be payable upon due presentment and surrender thereof at the principal office of the Paying Agent. Interest on the Bonds will be payable by check or draft mailed on the interest payment date to the persons in whose names the Bonds are registered, at the address appearing upon the Bond Register on the 15 th day of the month prior to such interest payment date or, at the request of the owner of $1,000,000 or more in aggregate principal amount of Bonds, by wire transfer. Transfer and Exchange As long as DTC (or a successor or substitute depository) is not the registered owner of the Bonds, any Bond may be transferred at the principal office for such purpose of the Registrar by surrender of such Bond for cancellation, accompanied by a written instrument of transfer, in form satisfactory to the Registrar, duly executed by the registered owner in person or by his/her duly authorized attorney, and thereupon the District will issue and the Registrar will authenticate and deliver at the principal office of the Registrar (or send by registered or first class insured mail to the owner thereof at his expense), in the name of the transferee or transferees, a new Bond or Bonds of the same interest rate, aggregate principal amount and maturity, and on which interest accrues from the last interest payment date to which interest has been paid so that there shall result no gain or loss of interest as a result of such transfer, upon payment of any applicable tax or governmental charge. Optional Redemption 2006A Bonds The 2006A Bonds are subject to redemption prior to maturity, at the option of the District, in whole or in part, on January 1, 2017, or any date thereafter, at 100% of the principal amount thereof, plus accrued interest, if any, to the date of redemption. 2006B Bonds The 2006B Bonds are subject to redemption prior to maturity, at the option of the District, in whole or in part on January 1, 2017, or any date thereafter, at 100% of the principal amount thereof, plus accrued interest, if any, to the date of redemption. 2006Z Bonds The 2006Z Bonds are subject to optional redemption, in whole or in part, at any time prior to their maturity at the option of the District, at a redemption price equal to 100% of the principal amount thereof plus the Make-Whole Premium (as defined below), if any, plus the interest accrued to the date fixed for redemption. To the extent that any 2006ZBonds maturing in 2017, 2037 and 2043 are redeemed in part at the option of the District, the principal amount redeemed shall be applied to reduce each remaining mandatory sinking fund payment and the amount of the final payment at maturity with respect thereto pro-rata, rounded to the nearest $5,000 denomination. -13-

20 Make-Whole Premium means, with respect to any 2006Z Bond to be redeemed, an amount calculated by an Independent Banking Institution equal to the positive difference, if any, between: (i) The sum of the present values, calculated as of the redemption date of: (A) Each interest payment that, but for the redemption, would have been payable on the 2006Z Bond or portion thereof being redeemed on each regularly scheduled interest payment date occurring after the redemption date through the maturity date of such 2006Z Bond (excluding any accrued interest for the period prior to the redemption date); provided, that if the redemption date is not a regularly scheduled interest payment date with respect to such 2006Z Bond, the amount of the next regularly scheduled interest payment will be reduced by the amount of interest accrued on such 2006Z Bond to the redemption date; plus (B) The principal amount that, but for such redemption, would have been payable on the maturity date of the 2006Z Bond or portion thereof being redeemed; minus (ii) The principal amount of the 2006Z Bond or portion thereof being redeemed. The present values of the interest and principal payments referred to in clause (i) above shall be determined by discounting the amount of each such interest and principal payment from the date that each such payment would have been payable but for the redemption to the redemption date on a semiannual basis (assuming a 360-day year consisting of twelve 30-day months) at a discount rate equal to the Comparable Treasury Yield (as defined below), plus 15.0 basis points. Comparable Treasury Yield means the yield which represents the weekly average yield to maturity for the preceding week appearing in the most recently published statistical release designated H.15(519) Selected Interest Rates under the heading Treasury Constant Maturities, or any successor publication selected by the Independent Banking Institution that is published weekly by the Board of Governors of the Federal Reserve System and that establishes yields on actively traded U.S. Treasury securities adjusted to constant maturity, for the maturity corresponding to the remaining term to maturity of the 2006Z Bond being redeemed. The Comparable Treasury Yield shall be determined as of the third business day immediately preceding the applicable redemption date. If the H.15(519) statistical release sets forth a weekly average yield for U.S. Treasury securities that have a constant maturity that is within three months of the remaining term to maturity of the 2006Z Bond being redeemed, then the Comparable Treasury Yield shall be equal to such weekly average yield. In all other cases, the Comparable Treasury Yield shall be calculated by interpolation on a straight-line basis, between the weekly average yields on the U.S. Treasury securities that have a constant maturity (i) closest to and greater than the remaining term to maturity of the 2006Z Bond being redeemed; and (ii) closest to and less than the remaining term to maturity of the 2006Z Bond being redeemed. Any weekly average yields calculated by interpolation will be rounded to the nearest 1/100 th of 1%, with any figure of 1/200 th of 1% or above being rounded upward. If, and only if, weekly average yields for U.S. Treasury securities for the preceding week are not available in the H.15(519) statistical release or any successor publication, then the Comparable Treasury Yield shall be the rate of interest per annum equal to the semi-annual equivalent yield to maturity of the Comparable Treasury Issue (expressed as a percentage of its principal amount) equal to the Comparable Treasury Price (as defined below) as of the redemption date. Comparable Treasury Issue means the U.S. Treasury security selected by the Independent Banking Institution as having a maturity comparable to the remaining term to maturity of the 2006Z Bond being redeemed and that would be utilized in accordance with customary financial practice in pricing new issues of corporate debt securities of comparable maturity to the remaining term to maturity of the 2006Z Bond to be redeemed. Independent Banking Institution means an investment banking institution of national standing that is a primary U.S. government securities dealer in the City of New York (which may be one of the Underwriters) designated by the District. Comparable Treasury Price means, with respect to any redemption date for a particular 2006Z Bond, (1) the average of five Reference Treasury Dealer quotations for such redemption date, after excluding the highest and -14-

21 lowest such quotations, or (2) if the Independent Banking Institution is unable to obtain five such quotations, the average of the quotations that are obtained. Reference Treasury Dealer means a primary U.S. Government securities dealer in the United States appointed by the District and reasonably acceptable to the Independent Banking Institution (which may be one of the Underwriters). Mandatory Redemption The 2006A Bonds maturing on January 1, 2020 shall be redeemed prior to maturity at random (or paid at maturity), on January 1 in the years and amounts set forth below, by payment of the principal amount thereof, together with the interest accrued thereon to the date fixed for redemption. *Final maturity. Year Principal Amount 2019 $ 1,140, * 1,195,000 The 2006A Bonds maturing on January 1, 2022 shall be redeemed prior to maturity at random (or paid at maturity), on January 1 in the years and amounts set forth below, by payment of the principal amount thereof, together with the interest accrued thereon to the date fixed for redemption. *Final maturity. Year Principal Amount 2021 $ 1,255, * 1,315,000 The 2006A Bonds maturing on January 1, 2024 shall be redeemed prior to maturity at random (or paid at maturity), on January 1 in the years and amounts set forth below, by payment of the principal amount thereof, together with the interest accrued thereon to the date fixed for redemption. *Final maturity. Year Principal Amount 2023 $ 1,385, * 1,450,000 The 2006A Bonds maturing on January 1, 2026 shall be redeemed prior to maturity at random (or paid at maturity), on January 1 in the years and amounts set forth below, by payment of the principal amount thereof, together with the interest accrued thereon to the date fixed for redemption. *Final maturity. Year Principal Amount 2025 $ 1,525, * 1,600,

22 The 2006A Bonds maturing on January 1, 2032 shall be redeemed prior to maturity at random (or paid at maturity), on January 1 in the years and amounts set forth below, by payment of the principal amount thereof, together with the interest accrued thereon to the date fixed for redemption. *Final maturity. Year Principal Amount 2027 $ 1,680, ,765, ,855, ,945, ,045, * 2,145,000 The 2006A Bonds maturing on January 1, 2037 shall be redeemed prior to maturity at random (or paid at maturity), on January 1 in the years and amounts set forth below, by payment of the principal amount thereof, together with the interest accrued thereon to the date fixed for redemption. *Final maturity. Year Principal Amount 2033 $ 2,250, ,365, ,485, ,605, * 2,735,000 The 2006A Bonds maturing on January 1, 2043 shall be redeemed prior to maturity at random (or paid at maturity), on January 1 in the years and amounts set forth below, by payment of the principal amount thereof, together with the interest accrued thereon to the date fixed for redemption. *Final maturity. Year Principal Amount 2038 $ 2,875, ,020, ,170, ,330, ,495, * 3,670,000 The 2006B Bonds maturing on January 1, 2020 shall be redeemed prior to maturity at random (or paid at maturity), on January 1 in the years and amounts set forth below, by payment of the principal amount thereof, together with the interest accrued thereon to the date fixed for redemption. *Final maturity. Year Principal Amount 2018 $ 405, , * 445,