MISSISSIPPI DEPARTMENT OF EDUCATION

|

|

|

- Dylan Lane

- 5 years ago

- Views:

Transcription

359-3294")

1 MISSISSIPPI DEPARTMENT OF EDUCATION Local Education Agency Federal Indirect Cost Proposal March 2016 Office of School Financial Services P. O. Box 771 Jackson, MS (601)

2 Table of Contents Certification and Request for Authorized Indirect Cost Rate: General Information... 3 Indirect Cost Proposals... 4 Audit Requirements... 5 Type of Plan and Rate: Restricted & Unrestricted... 6 Definitions... 7 &11 Guide for Schedule A 8-9 Schedule A 10 Subawards/Subcontracts Limitations on the Recover of Indirect Costs Period for Which Rates are applicable Application of Rate Additional Information Development of the Indirect Cost Proposal Submitting the Indirect Cost Proposal Certification and Request for Authorized Indirect Cost Rate Carry Forward Computations Indirect Cost Matrix Glossary Applying the Indirect Cost Rates Limitations Time Sheet

3 Certification and Request for Authorized Indirect Cost Rate General Information The U. S. Office of Management and Budget (OMB), Omni Circular (CFR) Title 2 Part 200, sets forth the cost principles and standards for determining the allowable costs of federally-funded grants administered by state and local governments. The objectives of the circular are: 1. Establish uniform standards of allow ability. All federal agencies agree to recognize that central service costs will benefit grant programs as allowable costs of those programs. 2. Establish uniform standards of allocation. All federal agencies accept the method of allocation agreed to by the cognizant federal agency. Costs are allocated to the benefitting departments regardless of the funding source or the ability of that source to pay. 3. Identify the full cost of federal programs. By identifying, accumulating, and allocating all allowable direct and indirect costs to the program for which the cost was incurred, the exact cost of all federal programs may be determined. 4. Ensure federal programs bear their fair share of costs. Only by identifying and allocating all direct and indirect costs within a central service cost allocation plan will localities be reimbursed for the total cost of federal programs. 5. Simplify intergovernmental relations. Under (CFR) Title 2 Part 200 concept of the cognizant agency, one agency with one group of reviewers approves a cost plan. All other agencies accept the plan. Thus, uniform methods of allocation and allow ability are applied to all federal grants. 6. Encourages consistency of treatment. Grantee organizations are encouraged to process all grant applications through a central office that is also aware of the basis of which an indirect cost rate was developed to minimize inconsistent treatment. Applications for grants usually involve a request for reimbursement of both direct and indirect costs. (CFR) Title 2 Part 200 contains provisions for determining indirect cost rates for grantees and sub-grantees of federal grants. Local educational agencies (LEAs) are not required to develop an indirect cost proposal; however, if they fail to do so, they will not be allowed to recover any indirect costs related to federal grants. To recover any indirect costs for the administration of federal grants, a LEA must have an approved indirect cost rate. 3

4 Indirect Cost Proposals The advantage of an indirect cost proposal and rate is that it is a simplified means for determining a fair share of indirect costs for federal grants which are acceptable to federal grantor agencies. The Mississippi Department of Education (MDE) has, in cooperation with the U. S. Department of Education, developed an indirect cost plan to be used by local education agencies in Mississippi. The MDE has been delegated the authority by the U. S. Department of Education to review indirect cost proposals and to approve indirect cost rates for local education agencies. An indirect cost rate is a means of determining in a reasonable manner the percentage of allowable general administrative expense that each federal grant should bear. Generally, an indirect cost rate is the ratio of total indirect costs to total direct costs, based on the LEA s actual expenditures, exclusive of any extraordinary or distorting expenditures such as capital outlay and major subcontracts. Expenditures for the second preceding fiscal year are to be used when completing the Indirect Cost Proposals for a given fiscal year. For example, expenditures for FY will be used to complete the Indirect Cost Proposals for FY (CFR) Title 2 Part 200 requires that all expenditures of an LEA be included in the preparation of an indirect cost plan. These costs are derived from the general fund, the special revenue funds, and any other applicable funds for the administration of the district. Financial data from the Superintendent s Annual Report to the State Department of Education will be used in preparing the indirect cost rate. Use expenditures from the second preceding fiscal year, i.e., use expenditures for when filing application for indirect cost rates for fiscal year All applications must balance with this source of financial data and be traceable to the accounts and books of record supporting these reports. To assure that all costs are considered in the computation of the rates, the LEAs indirect cost rate application must be reconciled and cross-referenced to the LEAs financial statement (Superintendent s Annual Report to the State Department of Education.) Mississippi LEA s use the Fixed with Carry-Forward rate for indirect costs. MDE submits the proposed LEA Plan to the U. S. Department of Education for their approval. LEA indirect cost proposals must be submitted annually to the MDE for approval of new rates. Generally, records and documentation supporting the indirect cost allocation plan must be retained for a period of five years after the last day of the fiscal year to which the proposal applies or until audited, whichever occurs sooner. If audit exceptions have been noted, records must be retained until those exceptions have been resolved. 4

5 Audit Requirements 1. General Statement The classification of expenditures must be in conformance with Handbook II (Financial Accounting for Local and State School Systems 1990). Failure to comply with the classification of expenditures as required may result in Single Audit questioned costs related to indirect cost recovery. Note: Handbook II is for sale by the Superintendent of Documents, U. S. Government Printing Office, Washington, DC Additional Documentation - Indirect Costs Certain districts Superintendent s office costs can be classified as indirect. Detail records are required and should be kept on file to support this survey and document the indirect costs attributed to function 2320 (Executive Admin Services). Failure to provide adequate documentation may result in Single Audit questioned costs related to indirect cost recovery. Given compliance with item number one above, all expenditures recorded in functions 2500 (Business Admin Services) and 2800 (Central Services) do not require additional documentation in support of classification as indirect costs. 2A. Certain costs associated with the Superintendent s office will be included as indirect cost if the following requirements are met: 1. A District s month s 1-9 Average Daily Attendance is 2,500 or less 2. The Superintendent completes a time sheet the first week of each quarter, which shall be signed by the Superintendent and the President of the Local School Board, indicating the percentage of time spent in allowable indirect functions. See page 24 for recommended time sheet. For the FY17 school year, a total of seven (7) districts provided additional documentation in support of certain costs being classified as indirect. The districts are as follows: (1) 0900-Chickasaw County School District, (2) Forrest County School District, (3) 5131-Union Public School District, (4) Poplarville School District (5) 5711-North Pike School District, (6) 6600-Stone County School District, and (7) 7613-Western Line School District. 3. Additional Documentation - Excluded Costs Schedules or other records should be maintained that document the reporting of all expenditures recorded as excluded costs. Failure to document that all excluded type costs have been reflected accurately may result in Single Audit comments relative to indirect cost calculation. 5

6 Type of Plan and Rate: Restricted and Unrestricted The following Indirect Cost Plan will be submitted to the U. S. Department of Education for approval. Restricted The Restricted Indirect Cost Rate is for use with grants subject to the supplement but not supplant legislative restrictions. 1. Restricted rates apply to grants that are made under federal programs with supplement and in no case supplant requirements. This means that the funds are for support in addition to state and local funding. Such amounts are intended to supplement, but in no way replace, local funds. Most of the federal grants that the LEA obtains through the MDE are of the restricted type. 2. Restricted grants include only indirect cost of administrative and fixed charges as defined below. Unrestricted Unrestricted rates apply to grants not subject to the supplement but not supplant legislative restriction. 1. Indirect Costs - The unallowed portion of Executive Admin Services and the direct portion of operation and maintenance of plant are classified as an indirect cost when calculating an unrestricted rate. All other costs are classified the same as with the restricted rate calculations. 2. Direct Costs, Disallowed Costs, and Excluded Costs are also classified the same as with the restricted rate calculations. Exceptions to the above are costs related to unallowable Restricted indirect employees, such as the chief executive officer of the recipient, or the chief executive officer of the recipient s components. These costs are treated as direct when computing the Restricted Rate. Definitions 1. Indirect Costs - Those costs of a general nature which benefit the district as a whole. These expenditures are for direction and control of system-wide activities and not those confined to one project, program or phase of operation. 6

7 As prescribed by (CFR) Title 2 Part 200, indirect costs are costs meeting the following criteria: a. Incurred for a common or joint purpose benefitting more than one cost objective b. Not readily assignable to the cost objectives specifically benefitted Administrative indirect costs consist of the salaries and expenses for people who are engaged in administrative activities from which the entire LEA benefits. Those activities that are limited to one school, subject, or phase of operation, are not indirect costs. General Management Costs: Generally, salaries and expenses for budgeting, payroll, personnel, purchasing, and employee relations are examples of services which typically benefit several activities and programs for which costs may be attributed by means of an indirect cost proposal. In theory, all costs can be charged directly. However, practical limitation and consideration of efficiency in accounting preclude such an approach. Salaries and expenses related to the direction and supervision of such functions as instruction, guidance, attendance, transportation, community services, and student services are not indirect costs. The costs of these functions are considered as direct costs. For example: the business manager, accounting manager, and accounting section are included as administrative indirect costs but the director of transportation would be classified as a direct cost. 2. Direct Costs - a direct cost is one that is incurred specifically for one activity and can be identified specifically with that activity. These costs may be charged directly to grants, contracts, or to other programs against which costs are finally lodged. 3. Disallowed Costs (CFR) Title 2 Part 200 classified certain items of cost as disallowed which means that the federal funds cannot be used for these purposes. These are costs directly attributable to governance. These include expenditures for the Board of Education and Executive Admin Services. For formula computational purposes, these costs are combined with direct cost. 4. Excluded Costs - Certain items of costs are classified in (CFR) Title 2 Part 200 as extraordinary or distorting expenditures and are excluded from the computation of the indirect cost rate. Excluded costs in this category include capital outlay, debt service, payments to other LEAs, internal funds, food service food supplies and equipment, and judgments, fines and damages. For formula computational purposes, debt service, payments to other LEAs, repayments to state agency and transfers are excluded by leaving these functions off the application. To exclude property, and cost of food used, use the OMIT column of Schedule A which is used for balancing purposes only. 7

8 5. Net Costs - Those direct costs of School Food Services that are to be included in the indirect cost plan. To arrive at Net Cost, deduct from Total Food Service Cost the following expenditure categories: Purchased Food Used, Donated Commodities Used, and Equipment Capitalized (these expenditures are totaled under the OMIT column of the application). Schedule A By using the five columns on Schedule A (omit, unallowed, indirect, direct and total), all figures from the Superintendent s Annual Report can be entered and balanced with each line of that report as well as with the total of that report. Enter the amounts from the Total Expenditures column of Schedule A then distribute to the other columns as applicable. The OMIT Column 1. Omit object 700, property, under all functions. 2. Omit function 5000, Facilities Acquisition and Construction except District-level management, if any, which would be eligible for indirect cost column. 3. Omit food service objects 641, 642, 643 and Omit judgments, fines and penalties, if any. The Unallowed Costs Column 1. Function 2310, Board of Education 2. Function 2320, Executive Administrative Services. The Indirect Costs Column 1. Those expenditures under function 2320, Executive Administrative Services, which are documented to benefit the entire LEA, are not included in unallowed costs, and are eligible by definition as indirect costs. Only districts with less than 2,500 ADA may be eligible (see page 5). 2. Function 2500, Business Admin Services 3. Function 2800 or that portion that fits indirect costs by definition. That portion of this function that is a direct cost should go in the Direct Costs Column. The Direct Costs Column 1. Function 1000, Instruction (except 700, Property). 2. Function 2100, Student Services (except 700, Property). 3. Function 2210, Improvement of Instructional Services 4. Function 2220, Educational Media Services 5. Function 2290, Other Support Instr Services 6. Function 2330, Special Area Admin Services 8

9 7. Function 2400, School Admin Services 8. Function 2600, Operation & Maintenance of Plant 9. Function 2700, Pupil Transportation 10. Function 3100, Food Service Operations (except cost of food used) 11. Function 3200, Enterprise Operations 12. Function 3300, Community Service 13. Function 3900, Other Non-instructional Services Types of Rates: Beginning this year, we were advised by USOE, to use the Fixed with Carry-forward. The Fixed with Carry-forward rates will be based on an estimate of a future period s costs using the second preceding year s financial statements. These rates will not be subject to revision and should be applied to all eligible expenditures for the fiscal year for which they were approved. However, differences between the estimated indirect cost and actual indirect costs will be carried forward in calculating the second preceding year. For the first two initial years there will not be a carry-forward. 9

10 MISSISSIPPI DEPARTMENT OF EDUCATION INDIRECT COST RATE APPLICATION SCHEDULE A DISTRICT NUMBER AND NAME 1 OMIT 2 UNALLOWED COST 3 INDIRECT COST 1000 Instruction xxxxxxxxxxxxx xxxxxxxxxxxxx 2100 Student Services xxxxxxxxxxxxx xxxxxxxxxxxxx 2210 Imp of Instructional Services xxxxxxxxxxxxx xxxxxxxxxxxxx 2220 Educational Media Services xxxxxxxxxxxxx xxxxxxxxxxxxx 2290 Other Support Instr Services xxxxxxxxxxxxx xxxxxxxxxxxxx 4 DIRECT COST 2310 Board of Education xxxxxxxxxxxxx xxxxxxxxxxxxx 2320 Executive Admin Services 2330 Special Area Admin Services xxxxxxxxxxxxx xxxxxxxxxxxxx 2400 School Admin Services xxxxxxxxxxxxx xxxxxxxxxxxxx 2500 Business Admin Services xxxxxxxxxxxxx xxxxxxxxxxxxx 2600 Operation & Maintenance of Plant xxxxxxxxxxxxx xxxxxxxxxxxxx 2700 Pupil Transportation xxxxxxxxxxxxx xxxxxxxxxxxxx 2800 Central Services xxxxxxxxxxxxx xxxxxxxxxxxxx 3100 Food Service Operations xxxxxxxxxxxxx xxxxxxxxxxxxx 3200 Enterprise Operations xxxxxxxxxxxxx xxxxxxxxxxxxx 3300 Community Service Operations xxxxxxxxxxxxx xxxxxxxxxxxxx 3900 Other Non-instructional Services xxxxxxxxxxxxx xxxxxxxxxxxxx 5000 Facility Acquisition & Const xxxxxxxxxxxxx xxxxxxxxxxxxx xxxxxxxxxxxxx 5 TOTAL ALL FUNDS TOTAL: SIGNATURE, SUPERINTENDENT 10

11 Definitions Other cost which are not indirect costs include, but are not limited to, all expenditures for the school board, contributions and donations, bad debts, contingencies, debt services and interest, stipends, capital outlay, entertainment, fines, and penalties. Except for School Districts whose ADA is less than 2,500, the superintendent, the superintendent s secretary, and expenses related directly to the operation of the superintendent s immediate offices, specifically, are not included in indirect costs and are considered, for rate computation purposes, to be disallowed costs. An individual principal, a principal s secretary, and the expenses related to the operation of these immediate offices are not included in indirect costs but are considered to be direct costs for rate computation purposes. Fixed charges classified as indirect costs are limited to those amounts which are associated with administrative indirect costs. The fixed charges can be viewed as appended to those administrative functions, and the classification rules are the same as those applied to salaries. These expenditures are exclusively identified as: a. Employee retirement b. Social Security c. Pension fund payments d. Premium expenditures for: (1) Employee insurance (2) Liability insurance e. Unemployment and workers compensation, and f. All similar costs normally considered being employee fringe benefits. No other items of expenditure of the fixed kind are to be classified as indirect fixed charges. NOTE: Identified fringe benefits are only those related to allowable Restricted indirect staff (with the following exceptions). Terminal Leave and Worker s Compensation Costs In May 1995, the Office of Management and Budget revised Circular A-87. The following fringe benefit costs under the circumstances described below, must be treated as indirect. Terminal leave. These are payments to separating employees for unused leave. If costs are charged upon payment of the unused leave, they must be treated as indirect (CFR) Title 2 Part If costs are charged annually as they are accrued, they may be charged based on the assignment of the employees they are related to (CFR) Title 2 Part

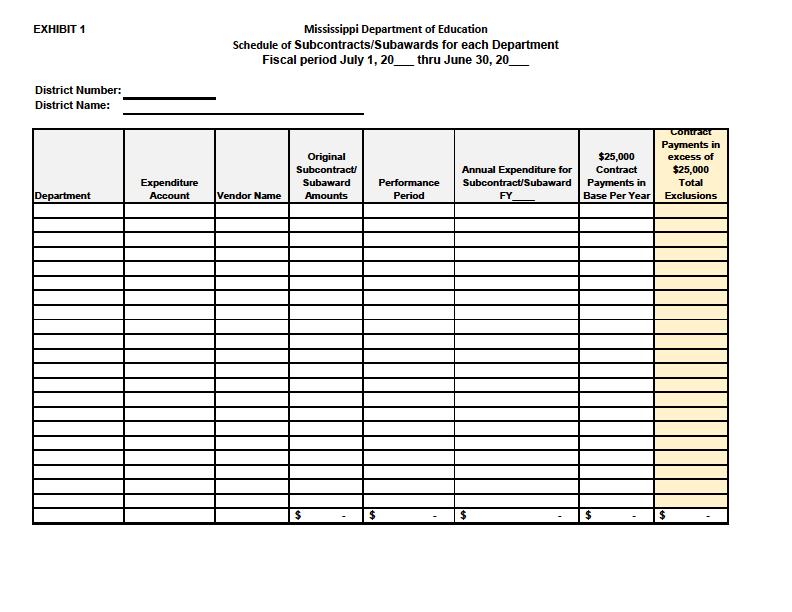

12 Worker s Compensation. These costs are indirect if they are charged upon payment to the employees. They may follow the salaries if costs charged are based on premiums paid. Compensation Fringe Benefits Unused leave: Per 2 CFR Part Compensation-Fringe Benefits (3)(i) when a governmental unit uses the cash basis of accounting (or modified cash), the cost of leave is recognized in the period that the leave is taken and paid for. Payments for unused leave when an employee retires or terminates employment are allowable as indirect costs in the year of payment. Pension Plan Costs: Per 2 CFR Part Compensation-Fringe Benefits (6)(i)(ii) Pension plans financed on a pay as you go basis are allowable; however, the costs are limited to using an actuarial cost method recognized by GAAP are allowable for a fiscal year as long as the costs are funded for that year within six months after the end of that year. Any pension costs funded after the six month period are allowable in the year funded. Sub-awards: Sub-award-an award made by a recipient to an eligible sub-recipient. The term includes financial assistance provided by any legal agreement (including contracts) but does not include the procurement of goods and services. The Mississippi Department of Education interprets sub-awards to also mean sub-grants. The Mississippi Department of Education provided for adjustments, if any, to be made where the activity is un-allowed or limited based on USDE definitions provided in the Cost Allocation Guide for State and Local Governments, September 2009 edition. Sub-awards generally include sub-grants and subcontracts. Major sub-awards do not incur (or benefit from) indirect costs to the same degree as other activities. The generally accepted definition of a major sub-award is one that exceeds $25,000 in expenditures per year. ED s policy on sub-award treatment applies on a yearly basis. Grantees must exclude the amount of sub-award costs exceeding $25,000 per sub-award, per year. As such, the indirect cost rate will be applied only to the first $25,000 of each sub-award, each year For the FY15 school year, the Mississippi Department of Education, is not reporting any sub-award activity by its school districts. Should sub-awards or sub-grant activity be reported by a recipient, the following schedule will be utilized to document all sub-award activity. 12

13 13

14 Limitations on the recovery of indirect costs Three major limitations affect how much indirect costs may be recovered. limitations are: These 1. The rate negotiated with MDE is the maximum allowable indirect cost rate. Indirect Costs rates from zero to the maximum rate may be approved for a program or project by a MDE program administrator. Federal law or grant conditions may limit the amount of indirect costs or the indirect cost rate. For example, if the LEA has a restricted rate of 5 percent and the law allows only a three percent rate of recovery, then the LEA can recover only indirect costs equal to three percent of the direct costs. Grant terms and conditions may also exist on some grants that prohibit any recovery of indirect cost. 2. Recovery of indirect costs on grants is subject to the availability of funds. Most restricted grants are allocated to the state as a block grant in which each LEA is entitled to a maximum grant amount. The total direct costs plus indirect costs cannot exceed the maximum entitlement. 3. Indirect costs are recovered only to the extent of direct costs incurred. The indirect cost rate is applied to the direct cost amount expended, not to the grant award. Period for which rates are applicable An indirect cost rate certification issued by the MDE is established for a specific state fiscal year. The rate is valid from July 1 through June 30 of the applicable fiscal year of approval. To recover indirect costs, the LEA applies the indirect cost rate in effect for a given fiscal year to the grant expenditures during that fiscal year. Indirect cost rates approval for fiscal year apply to all disbursements made within that fiscal year that are eligible for earning indirect cost, including any disbursements made on project balances that are brought forward. Application of Predetermined Rate If indirect cost collections are below $1,000 annually and the district makes a request, the State Department of Education will consider setting a predetermined rate for that district in an effort to reduce the amount of paperwork and record keeping involved in calculating an indirect cost rate. For FY17, the districts requesting the predetermined rate are as follows: (1) Coahoma County AHS and (2) Forrest County AHS. The annual costs collections for each school district are reviewed for compliance with the $1,000 annual limitation before rates are issued to the school districts. Effective with the FY17 school year, the Mississippi Department of Education will have one new charter school starting operation: (1) Smilow Prep-Charter. The Mississippi Department of Education has been advised by USOE to use either the pre-determined rate or to use the rate of the district in which the charter school resides when calculating the restricted and unrestricted indirect cost rates for charter schools. 14

15 Application of rate Once the proposal has been approved by the MDE the district may elect to: 1. Apply the approved and applicable rate to all projects 2. Apply the approved an applicable rate only to specific eligible projects. The rate may be applied at the maximum rate or less than the maximum rate. If the rate applied is less than the maximum rate, then it is not necessary that the reduced rate be applied uniformly to all projects. However, a district may not average the indirect cost charges to projects; that is, if the approved rate was six percent, charge one project at three percent and another project at nine percent for an average of six percent. In the application process, the district must be consistent with the development of the rate. For example, if depreciation cost cannot be included in the base when applying the rate. This same principle applies to all elements of the indirect cost rate developed. Additional Information 1. All employee benefits including Workers Compensation (W/C) and Unemployment Compensation must be charged to the same function as salaries. For those districts that do not charge Workers Compensation to the same function as salary, it will be necessary to prorate the total W/C cost into the ratio of direct, indirect, and disallowed salaries. Only that portion relating to indirect salaries will be allowed as indirect. 2. Judgments, fines, interest, and penalties should be entered under the omit column, not as indirect, and considered as reconciling items. Development of the Indirect Cost Proposal As noted above, the proposal is based on total expenditures of all General Fund and Special Revenue Funds and must be traceable to those accounts of record that report these amounts. The other two governmental funds, Debt Service and Capital Projects Funds, are excluded as well as Expendable Trust Funds. There is no logic in including them because all of the expenditures of these funds would be removed in the calculations to arrive at direct costs. A reconciliation to total LEA s expenditures should be completed on Schedule A as part of the LEA rate determination. Schedule A is a Special Expenditure report, combining General Fund and Special Revenue Funds. Note that certain costs are to be excluded, namely property, debt service, payments to other LEAs, transfers and cost of food and food processing supplies (Cost of Food Used). 15

16 Description of Fund Classification, Function Codes, and Object Codes can be found in the glossary section of this plan. Submitting the Indirect Cost Proposal Return one copy of the completed application and time sheet (if applicable) signed by the appropriate individuals to: Mississippi Department of Education Office of School Financial Services P. O. Box 771 Jackson, MS After approval a copy of the approved plan will be returned to the superintendent of local educational agency with an assigned rate. 16

17 Indirect Cost Rate District: District Number The information contained herein has been prepared by the Mississippi Department of Education and conforms to the criteria in the U. S. Office of Management and Budget (OMB), Omni Circular (CFR) Title 2 Part 200 (see page 3). The information used in determining the indirect rate was taken from the attached form submitted by your district. All data on this form are referenced to the Superintendent s Annual Report to the Department of Education for fiscal year and are in conformance with the Mississippi Accounting Chart of Accounts. Restricted Rate % Unrestricted Rate % COMPUTATION OF INDIRECT COST Restricted: (Carry-forward* + B) divided by (A + C) = % + / + = % (Carry-forward) (B) (A) (C) (Restricted Rate) Unrestricted: (B + E + Carry-forward*) divided by (A + C - E) = % + _ + / + - = % (B) (E) (Carry-forward) (A) (C) (E) (Restricted Rate) A = Unallowed Cost (from Indirect Cost Application) B = Indirect Costs (from Indirect Cost Application) C = Direct Cost (from Indirect Cost Application) E = Unallowed Portion of Executive Admin Services + Direct Portion of Operation & Maint of Plant * Carry-forward - Initial Years have no carry-forward (First Even Year & First Odd Year) APPROVED: 17

18 Kimberly C. McCurley, Director Office of School Financial Services Date Approved INDIRECT COST RATES - CARRY FORWARD COMPUTATIONS District: District Number RESTRICTED RATE: Initial Year - FY XX % (a) Projected Cost based on Second Preceding Year: Fixed Rate - B divided by (A+C) A + C...FY XX... B (Indirect) Per Calculation...FY XX... Carry-Forward Total... (b) Actual Costs: A + C (unallowed + direct) FY XX... B (Indirect) Per Calculation... FY XX... Carry- Forward Total... (c) Carry-Forward Computations: RECOVERED Fixed Rate times Actual A + C X... 18

19 SHOULD HAVE RECOVERED Actual Indirect Cost for FY XX... Under-recovery Carry-Forward OR Over-recovery Carry-Forward INDIRECT COST RATES - CARRY FORWARD COMPUTATIONS District: Number District UNRESTRICTED RATE: INITIAL YEAR - FY XX % (a) Projected Cost based on Second Preceding Year: Fixed Rate - (B + E) divided by (A + C - E) A + C - E...FY XX... B + E Per Calculation...FY XX... Carry-Forward Total... (b) Actual Costs: A + C - F... B + E Per Calculation... FY XX... Carry-Forward Total... (c) Carry-Forward Computations: RECOVERED Fixed Rate times Actual A + C - E 19

20 X...FY XX... SHOULD HAVE RECOVERED Actual Indirect Cost for FY XX... Under-recovery Carry-Forward OR Over-recovery Carry-Forward Indirect Cost Matrix The following matrix classifies expenditures by category and is provided as a guide in preparing indirect cost proposals. The matrix identifies by function and object when expenditures are appropriate for classification in a specific category. Description of the Function CATEGORIES and Object Codes can be found in the glossary section Direct/ of this plan. Disallowed Indirect Excluded Costs Costs Costs General Fund: Current: Function 1000 Instruction Yes No No 2100 Student Services Yes No No 2210 Imp of Instructional Services Yes No No 2220 Educational Media Services Yes No No 2290 Other Support Instr Services Yes No No 2310 Board of Education Yes No No 2320 Executive Admin Services Yes Yes* No 2330 Special Area Admin Serv Yes No No 2440 School Admin Services Yes No No 2500 Business Admin Services No Yes No 2600 Oper & Maintenance of Plant Yes No No 2700 Pupil Transportation Yes No No 2800 Central Services No Yes No 3200 Enterprise Operations Yes No No 3300 Community Service Operations Yes No No 3900 Other Noninstructional Services Yes No No Capital Outlay: Function 5000 Facility Acquisition & Constr No No Yes Object 0700 Property No No Yes 20

21 Special Revenue Funds: Food Services: Function 3100 Food Service Operations Yes No Yes * Districts with month s 1-9 ADA of 2,500 or less shall maintain documentation to explain the classification of expenditures as indirect for these functions. # All functions may contain excluded costs, i.e., capital outlay. Identify all excluded costs by function and maintain documentation for Reporting on Schedule A. Glossary Fund Classifications 1. General Fund. The fund used to account for all financial resources, except those required to be accounted for in another fund. 2. Special Revenue Funds. A fund used to account for the proceeds of specific revenue sources (other than expendable trusts or major capital projects) that are legally restricted to expenditure for specified purposes. 3. Capital Projects Funds. A fund created to account for financial resources to be used for the acquisition or construction of major capital facilities (other than those financed by proprietary funds and trust funds). 4. Debt Service Funds. A fund established to account for the accumulation of resources for and the payment of, general long-term debt principal and interest. Sometimes referred to as a sinking fund. CODE DESCRIPTION 1000 Instruction - Instruction includes the activities dealing directly with the interaction between teachers and students. Teaching may be provided for students in a school classroom, in another location such as a home or hospital, and in other learning situations such as those involving co-curricular activities. It may also be provided through some other approved medium such as television, radio, telephone and correspondence. Included here are the activities of aides or classroom assistants of any type (clerks, graders, teaching machines, etc.) which assist in the instructional process. If proration of expenditures is not possible for department chairpersons who also teach, include department chairpersons who also teach in instruction. Full-time department chairpersons expenditures should be included only in Student Services - Activities designed to assess and improve the well-being of students and to supplement the teaching process. 21

22 2210 Improvement of Instructional Services - Activities primarily for assisting instructional staff in planning, developing and evaluating the process of providing learning experiences for students. These activities include curriculum development, techniques of instruction, child development and understanding, staff training, etc. CODE DESCRIPTION 2220 Educational Media Services - Activities concerned with the use of all teaching and learning resources, including hardware and content materials. Educational media are defined as any devices, content materials, methods or experiences used for teaching and learning purposes. These include printed and nonprinted sensory materials Other Support Services - Instructional Staff - Services supporting the instructional staff not classified elsewhere in the 2200 series Board of Education Services - Activities of the elected or appointed body which has been created according to state law and vested with responsibilities for educational activities in a given administrative unit Executive Administration Services - Activities associated with the overall general administration of or executive responsibility for the entire LEA Special Area Administration Services - Activities concerned with are wide supervisory responsibility. This function could include the activities of the chief business official and directors of district wide instructional programs that have administrative responsibilities. It also would include such general administrative activities as federal programs coordinators. When two or more service areas are directed by the same individual, the services of that individual may be charged to this function or prorated between the service areas concerned Support Services - School Administration - Activities concerned with overall administrative responsibility for a school Support Services - Business - Activities concerned with paying, transporting, exchanging and maintaining goods and services for the LEA. Included are the fiscal and internal services necessary for operating the LEA. The chief business official and the activities of the chief business official are included here. 22

23 2600 Operation & Maintenance of Plant Services - Activities concerned with keeping the physical plant open, comfortable and safe for use, and keeping the grounds, buildings and equipment in effective working condition and state of repair. These include the activities of maintaining safety in buildings, on the grounds and in the vicinity of schools Student Transportation Services (Pupil Transportation) - Activities concerned with conveying students to and from school, as provided by state and federal law. This includes trips between home and school, and trips to school activities. CODE DESCRIPTION 2800 Support Services -Central - Activities, other than general administration, which support each of the other instructional and supporting services program. These activities include planning, research, development, evaluation, information, staff and data processing services Food Service Operations - Activities concerned with providing food to students and staff in a school or LEA. This service are includes preparing and serving regular and incidental meals, lunches or snacks in connection with school activities and food delivery Enterprise Operations - Activities that are financed and operated in a manner similar to private business enterprises where the stated intent is that the costs are financed or recovered primarily through user charges. Food services should not be charged here but rather to function One example could be the LEA bookstore Community Services Operations - Activities concerned with providing community services to students, staff or other community participants. Examples of this function would be the operation of a community swimming pool, a recreation program for the elderly, a child care center for working mothers, etc Other Non-instructional Services - Activities concerned with noninstructional services not described above Facilities Acquisition and Construction Services - Activities concerned with acquiring land and buildings; remodeling buildings; constructing buildings and additions to buildings; initially installing or extending service systems and other built-in equipment; and improving sites. Object This dimension is used to describe the service or commodity obtained as the result of a specific expenditure. Following are definitions of the selected object classes 23

24 CODE DESCRIPTION 600 Supplies - Amounts paid for items that are consumed, worn out, or deteriorated through use or items that lose their identity through fabrication or incorporation into different or more complex units or substances. 700 Property - Expenditures for acquiring fixed assets, including land or existing buildings, improvements of grounds, initial equipment, additional equipment, and replacement of equipment. 820 Judgments and Claims Against the LEA - Expenditures from current funds for all judgments and claims (except as indicated below) against the LEA that are not covered by liability insurance, but are of a type that might have been covered by insurance. Judgments and claims against the LEA resulting from failure to pay bills or debt service are recorded under the appropriate expenditure accounts as though the bills or debt service had been paid when due. Applying the Indirect Cost Rates The indirect cost plan will establish maximum, Fixed with Carry-Forward rates for a fiscal year. Amounts claimed for indirect costs are not subject to adjustment based on a new rate determined by actual expenditures at the close of the fiscal year. Once the plan has been developed and maximum rates approved by the Mississippi Department of Education, the district may elect to: 1. Apply the approved and applicable rate across the board to all eligible projects. 2. Apply the approved and applicable rate only to specific eligible projects. The rate may be applied at the maximum rate or less than the maximum rate. If the rate applied is less than the maximum rate then it is not necessary that the reduced rate be applied uniformly to all projects. However, a district may not average the indirect cost charges to projects, i.e., charge one project at 3% and another project at 9% for an average of 6%. The indirect cost rate is necessary in order to compute the indirect costs dollar amount. For example, on a fixed grant with a restricting clause in the enabling act (Chapter 1) the applicable rate would be the restricted rate. Given the following: Fixed Grant Amount $105,000.00, Restricted Rate 4.25%, Project Capital Outlay $1, Calculation: Fixed Grant Amount $105, Less: Project Capital Outlay 1, Net available for both direct and indirect costs $103,

25 Divide the amount available for both direct and indirect costs ($103,500.00) by (100% of direct cost plus 4.25% indirect cost) = $99, (the amount of direct cost.) Subtract the direct cost ($99,280.58) from the amount available for both direct and indirect costs ($103,500.00) and you have the dollar amount for indirect costs ($4,219.42). Proof: $99, X.0425 = $4, Applying the Indirect Cost Rates (continued) Project Budget: Fixed Grant Amount $105, Direct costs $ 99, (Salaries, supplies, etc.) Indirect costs 4, Capital Outlay 1, Fixed Grant Amount $105, Should the program be an add on such as School Food Service rather than a fixed grant amount as in Chapter 1, the formula would be: (TOTAL FOOD SERVICE COSTS) - (COST OF FOOD USED) X (UNRESTRICTED RATE) = INDIRECT COST DOLLAR AMOUNT Example: Total Cost of Food Service $395, Less: Cost of Food & Food Processing Supplies* 217, $178, Unrestricted Rate (19.80%).1980 Indirect Cost Dollar Amount $ 35, *This includes purchased food, donated commodities, capitalized equipment, indirect cost paid, and repayments to the State Agency. 25

26 Limitations 1. Federal law may limit the amount of indirect costs which may be recovered, i. e., the maximum indirect costs allowable by law for a particular program, may be less than the amount allowable under (CFR) Title 2 Part Recovery of Indirect Costs is subject to availability of funds. If a combination of direct and indirect costs exceeds funds available, then the district will not be able to recover the total costs of the project or program. 3. Indirect Cost may be recovered only to the extent that Direct Costs were incurred. The indirect cost rate is applied to the amount expended, not the total grant award. 4. Indirect Cost rates approved for a fiscal year apply to all disbursements made within that fiscal year that are eligible for earning indirect cost, including any disbursements made on project balances that are brought forward. It is essential that districts classify expenditures uniformly and consistently. Generally, records and documents supporting the indirect cost rate application must be retained for a period of five (5) years after the last day of the fiscal year to which they apply or until audited, whichever is sooner. If audit exceptions have been noted, records must be retained until those exceptions have been resolved. 26

27 DISTRICT DISTRICT NO. Local Education Agencies Direct and Indirect Functions Breakdown of Superintendent s time according to performance of Direct and Indirect Functions Period covered by report (month/day/year): through I. Direct Activities: Hours Day 1 Hours Day 2 Hours Day 3 Hours Day 4 Hours Day 5 Total Hours 1. General Administration 2. Direct Instruction 3. Instructional Support 4. Pupil related services, e.g., health, transportation, non-instructional student support, school food service 5. Operation and Maintenance of Plant 6. Community service 7. Other (Identify ) TOTAL HOURS DIRECT ACTIVITIES II. Indirect Activities Hours Day 1 Hours Day 2 Hours Day 3 Hours Day 4 Hours Day 5 Total Hours 8. Payroll 9. Purchasing 10. Inventory 11. Accounting 12. Financial Reports 13. Personnel Relations 14. Other (Identify ) TOTAL HOURS INDIRECT ACTIVITIES TOTAL HOURS DIRECT ACTIVITIES TOTAL HOURS INDIRECT ACTIVITIES GRAND TOTAL HOURS % OF DIRECT ACTIVITIES (DIRECT/TOTAL) % OF INDIRECT ACTIVITIES (INDIRECT/TOTAL) Signature of School Superintendent Date I certify that the above information related to the Superintendent s time is true and correct to the best of my understanding and is based on first-hand knowledge of time spent as reported. Signature of School Board President 27 Date

Allowable Uses of Funds and Adherence to Cost Circulars

Procedure: Policy: Number: Restricted and Unrestricted Indirect Cost Rates Allowable Uses of Funds and Adherence to Cost Circulars GP0800.4 ( ) Complete Revision Supersedes: Page: ( ) Partial Revision

Procedure: Policy: Number: Restricted and Unrestricted Indirect Cost Rates Allowable Uses of Funds and Adherence to Cost Circulars GP0800.4 ( ) Complete Revision Supersedes: Page: ( ) Partial Revision

Indirect Cost Allocation Plan For Local Education Agencies

Indirect Cost Allocation Plan For Local Education Agencies Wyoming Department of Education 2300 Capitol Avenue Cheyenne, WY 82002 Finance Division (307) 7777675 Effective: July 1, 2016 The Wyoming Department

Indirect Cost Allocation Plan For Local Education Agencies Wyoming Department of Education 2300 Capitol Avenue Cheyenne, WY 82002 Finance Division (307) 7777675 Effective: July 1, 2016 The Wyoming Department

Local Education Agency Indirect Cost Application

Local Education Agency Indirect Cost Application Introduction The Delaware Department of Education (DDOE) has, in cooperation with the United States Department of Education (USDOE) developed an indirect

Local Education Agency Indirect Cost Application Introduction The Delaware Department of Education (DDOE) has, in cooperation with the United States Department of Education (USDOE) developed an indirect

CHAPTER 13 FINANCIAL ACCOUNTING AND REPORTING SECTION 1 COST ALLOCATION STANDARDS

Minnesota Department of Education Chapter 13 Financial Accounting and Reporting CHAPTER 13 FINANCIAL ACCOUNTING AND REPORTING Introduction SECTION 1 COST ALLOCATION STANDARDS The purpose of this chapter

Minnesota Department of Education Chapter 13 Financial Accounting and Reporting CHAPTER 13 FINANCIAL ACCOUNTING AND REPORTING Introduction SECTION 1 COST ALLOCATION STANDARDS The purpose of this chapter

INDIRECT COSTS. A Direct Explanation. July 18, What Federal Regulations Govern?

INDIRECT COSTS A Direct Explanation July 18, 2017 What Federal Regulations Govern? Office of Management and Budget (OMB) Uniform Administrative Requirements, Cost Principles, and Audit Requirements for

INDIRECT COSTS A Direct Explanation July 18, 2017 What Federal Regulations Govern? Office of Management and Budget (OMB) Uniform Administrative Requirements, Cost Principles, and Audit Requirements for

INDIRECT COSTS. Yes, there are several different types of indirect cost rates. Examples include:

What federal regulations govern indirect costs for LEAs? Indirect costs for LEAs have historically been governed by OMB Circular A-87. OMB Circular A- 87, along with many other OMB circulars has been replaced

What federal regulations govern indirect costs for LEAs? Indirect costs for LEAs have historically been governed by OMB Circular A-87. OMB Circular A- 87, along with many other OMB circulars has been replaced

FINANCIAL MANAGEMENT FOR GEORGIA LOCAL UNITS OF ADMINISTRATION

FINANCIAL MANAGEMENT FOR GEORGIA LOCAL UNITS OF ADMINISTRATION Issued Effective Section Title: 10/30/91 7/1/92 II Financial Reporting Revision No. Revised Chapter Title: 1 March 2017 INTRODUCTION II-9

FINANCIAL MANAGEMENT FOR GEORGIA LOCAL UNITS OF ADMINISTRATION Issued Effective Section Title: 10/30/91 7/1/92 II Financial Reporting Revision No. Revised Chapter Title: 1 March 2017 INTRODUCTION II-9

SEQUOIA UNION HIGH SCHOOL DISTRICT COUNTY OF SAN MATEO REDWOOD CITY, CALIFORNIA AUDIT REPORT JUNE 30, 2013

SEQUOIA UNION HIGH SCHOOL DISTRICT COUNTY OF SAN MATEO REDWOOD CITY, CALIFORNIA AUDIT REPORT JUNE 30, 2013 CHAVAN &ASSOCIATES, LLP CERTIFIED PUBLIC ACCOUNTANTS 1475 SARATOGA AVE., SUITE 180 SAN JOSE, CA

SEQUOIA UNION HIGH SCHOOL DISTRICT COUNTY OF SAN MATEO REDWOOD CITY, CALIFORNIA AUDIT REPORT JUNE 30, 2013 CHAVAN &ASSOCIATES, LLP CERTIFIED PUBLIC ACCOUNTANTS 1475 SARATOGA AVE., SUITE 180 SAN JOSE, CA

BURLINGAME SCHOOL DISTRICT COUNTY OF SAN MATEO REDWOOD CITY, CALIFORNIA AUDIT REPORT JUNE 30, 2017

BURLINGAME SCHOOL DISTRICT COUNTY OF SAN MATEO REDWOOD CITY, CALIFORNIA AUDIT REPORT JUNE 30, 2017 CHAVAN & ASSOCIATES, LLP CERTIFIED PUBLIC ACCOUNTANTS 1475 SARATOGA AVE., SUITE 180 SAN JOSE, CA 95129

BURLINGAME SCHOOL DISTRICT COUNTY OF SAN MATEO REDWOOD CITY, CALIFORNIA AUDIT REPORT JUNE 30, 2017 CHAVAN & ASSOCIATES, LLP CERTIFIED PUBLIC ACCOUNTANTS 1475 SARATOGA AVE., SUITE 180 SAN JOSE, CA 95129

Jackson County Board of Education

Jackson County Board of Education Financial Statements Year Ended June 30, 2018 Sylva, North Carolina Members of the Board of Education Ali Laird-Large, Chairperson Elizabeth Cooper, Vice Chairperson Abigail

Jackson County Board of Education Financial Statements Year Ended June 30, 2018 Sylva, North Carolina Members of the Board of Education Ali Laird-Large, Chairperson Elizabeth Cooper, Vice Chairperson Abigail

Indirect costs are those costs incurred for a common or joint purpose. benefiting more than one cost objective and not readily assignable to the cost

NATURE OF INDIRECT COST Indirect costs are those costs incurred for a common or joint purpose benefiting more than one cost objective and not readily assignable to the cost objectives specifically benefited.

NATURE OF INDIRECT COST Indirect costs are those costs incurred for a common or joint purpose benefiting more than one cost objective and not readily assignable to the cost objectives specifically benefited.

SEQUOIA UNION HIGH SCHOOL DISTRICT COUNTY OF SAN MATEO REDWOOD CITY, CALIFORNIA AUDIT REPORT JUNE 30, 2015

SEQUOIA UNION HIGH SCHOOL DISTRICT COUNTY OF SAN MATEO REDWOOD CITY, CALIFORNIA AUDIT REPORT JUNE 30, 2015 CHAVAN & ASSOCIATES, LLP CERTIFIED PUBLIC ACCOUNTANTS 1475 SARATOGA AVE., SUITE 180 SAN JOSE,

SEQUOIA UNION HIGH SCHOOL DISTRICT COUNTY OF SAN MATEO REDWOOD CITY, CALIFORNIA AUDIT REPORT JUNE 30, 2015 CHAVAN & ASSOCIATES, LLP CERTIFIED PUBLIC ACCOUNTANTS 1475 SARATOGA AVE., SUITE 180 SAN JOSE,

PARADISE UNIFIED SCHOOL DISTRICT. County of Butte Paradise, California

County of Butte Paradise, California FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION WITH INDEPENDENT AUDITORS REPORTS TABLE OF CONTENTS Page Number FINANCIAL SECTION Independent Auditors Report 1 Required

County of Butte Paradise, California FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION WITH INDEPENDENT AUDITORS REPORTS TABLE OF CONTENTS Page Number FINANCIAL SECTION Independent Auditors Report 1 Required

WHITE & ASSOCIATES, PSC CERTIFIED PUBLIC ACCOUNTANTS 1407 Lexington Road Richmond, Kentucky Phone (859) Fax (859)

Fax (859)") ESTILL COUNTY SCHOOL DISTRICT AUDITED FINANCIAL STATEMENTS AND SUPPLEMENTAL SCHEDULES For the year ended June 30, 2012 Prepared by: WHITE & ASSOCIATES, PSC CERTIFIED PUBLIC ACCOUNTANTS 1407 Lexington Road

ESTILL COUNTY SCHOOL DISTRICT AUDITED FINANCIAL STATEMENTS AND SUPPLEMENTAL SCHEDULES For the year ended June 30, 2012 Prepared by: WHITE & ASSOCIATES, PSC CERTIFIED PUBLIC ACCOUNTANTS 1407 Lexington Road

WHITE & ASSOCIATES, PSC CERTIFIED PUBLIC ACCOUNTANTS 1407 Lexington Road Richmond, Kentucky Phone (859) Fax (859)

Fax (859)") ESTILL COUNTY SCHOOL DISTRICT AUDITED FINANCIAL STATEMENTS AND SUPPLEMENTAL SCHEDULES For the year ended June 30, 2013 Prepared by: WHITE & ASSOCIATES, PSC CERTIFIED PUBLIC ACCOUNTANTS 1407 Lexington Road

ESTILL COUNTY SCHOOL DISTRICT AUDITED FINANCIAL STATEMENTS AND SUPPLEMENTAL SCHEDULES For the year ended June 30, 2013 Prepared by: WHITE & ASSOCIATES, PSC CERTIFIED PUBLIC ACCOUNTANTS 1407 Lexington Road

CAJON VALLEY UNION SCHOOL DISTRICT COUNTY OF SAN DIEGO EL CAJON, CALIFORNIA AUDIT REPORT JUNE 30, 2015

COUNTY OF SAN DIEGO EL CAJON, CALIFORNIA AUDIT REPORT JUNE 30, 2015 Wilkinson Hadley King & Co. LLP CPA's and Advisors 218 W. Douglas Ave El Cajon, CA 92020 Introductory Section Cajon Valley Union School

COUNTY OF SAN DIEGO EL CAJON, CALIFORNIA AUDIT REPORT JUNE 30, 2015 Wilkinson Hadley King & Co. LLP CPA's and Advisors 218 W. Douglas Ave El Cajon, CA 92020 Introductory Section Cajon Valley Union School

Weslaco Independent School District. Board of Trustees

Weslaco Independent School District August 31, 2014 Board of Trustees David L. Fuentes Erasmo López Óscar Caballero Adrián González Andrew González Isidoro Nieto Dr. Richard Rivera President Vice-President

Weslaco Independent School District August 31, 2014 Board of Trustees David L. Fuentes Erasmo López Óscar Caballero Adrián González Andrew González Isidoro Nieto Dr. Richard Rivera President Vice-President

Financial Statements Regulatory Basis And Reports Required by Uniform Guidance June 30, 2017 Putnam City Independent School District No.

Financial Statements Regulatory Basis And Reports Required by Uniform Guidance June 30, 2017 Putnam City Independent School District No. 1 Table of Contents June 30, 2017 Independent Auditor s Report...

Financial Statements Regulatory Basis And Reports Required by Uniform Guidance June 30, 2017 Putnam City Independent School District No. 1 Table of Contents June 30, 2017 Independent Auditor s Report...

COMPREHENSIVE ANNUAL FINANCIAL REPORT FISCAL YEAR ENDED JUNE 3D, 2011

FOUNDATION ACADEMY CHARTER SCHOOL COMPREHENSIVE ANNUAL FINANCIAL REPORT FISCAL YEAR ENDED JUNE 3D, 2011 FOUNDATION ACADEMY CHARTER SCHOOL Foundation Academy Charter School Board of Trustees Trenton, New

FOUNDATION ACADEMY CHARTER SCHOOL COMPREHENSIVE ANNUAL FINANCIAL REPORT FISCAL YEAR ENDED JUNE 3D, 2011 FOUNDATION ACADEMY CHARTER SCHOOL Foundation Academy Charter School Board of Trustees Trenton, New

ESPARTO UNIFIED SCHOOL DISTRICT COUNTY OF YOLO ESPARTO, CALIFORNIA FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR'S REPORT JUNE 30, 2014

COUNTY OF YOLO ESPARTO, CALIFORNIA FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR'S REPORT JUNE 30, 2014 TABLE OF CONTENTS PAGE INDEPENDENT AUDITOR'S REPORT 1 MANAGEMENT S DISCUSSION AND ANALYSIS 3 BASIC

COUNTY OF YOLO ESPARTO, CALIFORNIA FINANCIAL STATEMENTS WITH INDEPENDENT AUDITOR'S REPORT JUNE 30, 2014 TABLE OF CONTENTS PAGE INDEPENDENT AUDITOR'S REPORT 1 MANAGEMENT S DISCUSSION AND ANALYSIS 3 BASIC

SCHOOL DISTRICT OF HARTFORD JT #1

AUDITED FINANCIAL STATEMENTS JUNE 30, 2014 TABLE OF CONTENTS Independent Auditor s Report... 4-5 Basic Financial Statements Page Statement of Net Position... 7 Statement of Activities... 8 Balance Sheet

AUDITED FINANCIAL STATEMENTS JUNE 30, 2014 TABLE OF CONTENTS Independent Auditor s Report... 4-5 Basic Financial Statements Page Statement of Net Position... 7 Statement of Activities... 8 Balance Sheet

COUNTY OF SAN MATEO SUPERINTENDENT OF SCHOOLS COUNTY SCHOOL SERVICE FUND AUDIT REPORT JUNE 30, 2016 * * *

COUNTY OF SAN MATEO SUPERINTENDENT OF SCHOOLS AUDIT REPORT JUNE 30, 2016 * * * TABLE OF CONTENTS JUNE 30, 2016 TITLE PAGE FINANCIAL SECTION: Independent Auditors Report... 1-3 Management s Discussion and

COUNTY OF SAN MATEO SUPERINTENDENT OF SCHOOLS AUDIT REPORT JUNE 30, 2016 * * * TABLE OF CONTENTS JUNE 30, 2016 TITLE PAGE FINANCIAL SECTION: Independent Auditors Report... 1-3 Management s Discussion and

SPARTANBURG COUNTY SCHOOL DISTRICT FIVE DUNCAN, SOUTH CAROLINA FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION

DUNCAN, SOUTH CAROLINA FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION FOR THE FISCAL YEAR ENDED JUNE 30, 2014 FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION FOR THE FISCAL YEAR ENDED JUNE 30,

DUNCAN, SOUTH CAROLINA FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION FOR THE FISCAL YEAR ENDED JUNE 30, 2014 FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION FOR THE FISCAL YEAR ENDED JUNE 30,

CENTRAL UNION HIGH SCHOOL DISTRICT COUNTY OF IMPERIAL EL CENTRO, CALIFORNIA AUDIT REPORT JUNE 30, 2018

COUNTY OF IMPERIAL EL CENTRO, CALIFORNIA AUDIT REPORT JUNE 30, 2018 Introductory Section Central Union High School District Audit Report For The Year Ended June 30, 2018 TABLE OF CONTENTS Page Exhibit/Table

COUNTY OF IMPERIAL EL CENTRO, CALIFORNIA AUDIT REPORT JUNE 30, 2018 Introductory Section Central Union High School District Audit Report For The Year Ended June 30, 2018 TABLE OF CONTENTS Page Exhibit/Table

Middlesex School District Financial Statements For The Year Ended June 30, 2015

Middlesex School District Financial Statements Middlesex School District Table of Contents Page Number -- Independent Auditors Report 3-5 -- Management Discussion and Analysis 6 EXHIBIT I District -Wide

Middlesex School District Financial Statements Middlesex School District Table of Contents Page Number -- Independent Auditors Report 3-5 -- Management Discussion and Analysis 6 EXHIBIT I District -Wide

MILLBRAE SCHOOL DISTRICT COUNTY OF SAN MATEO MILLBRAE, CALIFORNIA AUDIT REPORT. June 30, 2016

MILLBRAE SCHOOL DISTRICT COUNTY OF SAN MATEO MILLBRAE, CALIFORNIA AUDIT REPORT June 30, 2016 CHAVAN & ASSOCIATES, LLP CERTIFIED PUBLIC ACCOUNTANTS 1475 SARATOGA AVE., SUITE 180 SAN JOSE, CA 95129 This

MILLBRAE SCHOOL DISTRICT COUNTY OF SAN MATEO MILLBRAE, CALIFORNIA AUDIT REPORT June 30, 2016 CHAVAN & ASSOCIATES, LLP CERTIFIED PUBLIC ACCOUNTANTS 1475 SARATOGA AVE., SUITE 180 SAN JOSE, CA 95129 This

EAST TROY COMMUNITY SCHOOL DISTRICT

EAST TROY COMMUNITY SCHOOL DISTRICT AUDITED FINANCIAL STATEMENTS JUNE 30, 2015 James R. Frechette CERTIFIED PUBLIC ACCOUNTANT June 30, 2015 TABLE OF CONTENTS Page Independent Auditor s Report 1-2 Basic

EAST TROY COMMUNITY SCHOOL DISTRICT AUDITED FINANCIAL STATEMENTS JUNE 30, 2015 James R. Frechette CERTIFIED PUBLIC ACCOUNTANT June 30, 2015 TABLE OF CONTENTS Page Independent Auditor s Report 1-2 Basic

CENTRAL UNION HIGH SCHOOL DISTRICT COUNTY OF IMPERIAL EL CENTRO, CALIFORNIA AUDIT REPORT JUNE 30, 2016

COUNTY OF IMPERIAL EL CENTRO, CALIFORNIA AUDIT REPORT JUNE 30, 2016 Wilkinson Hadley King & Co. LLP CPA's and Advisors 218 W. Douglas Ave. El Cajon, California Introductory Section Central Union High School

COUNTY OF IMPERIAL EL CENTRO, CALIFORNIA AUDIT REPORT JUNE 30, 2016 Wilkinson Hadley King & Co. LLP CPA's and Advisors 218 W. Douglas Ave. El Cajon, California Introductory Section Central Union High School

SONOMA VALLEY UNIFIED SCHOOL DISTRICT COUNTY OF SONOMA SONOMA, CALIFORNIA AUDIT REPORT. June 30, 2016

SONOMA VALLEY UNIFIED SCHOOL DISTRICT COUNTY OF SONOMA SONOMA, CALIFORNIA AUDIT REPORT June 30, 2016 CHAVAN & ASSOCIATES, LLP CERTIFIED PUBLIC ACCOUNTANTS 1475 SARATOGA AVE., SUITE 180 SAN JOSE, CA 95129

SONOMA VALLEY UNIFIED SCHOOL DISTRICT COUNTY OF SONOMA SONOMA, CALIFORNIA AUDIT REPORT June 30, 2016 CHAVAN & ASSOCIATES, LLP CERTIFIED PUBLIC ACCOUNTANTS 1475 SARATOGA AVE., SUITE 180 SAN JOSE, CA 95129

MILLBRAE SCHOOL DISTRICT COUNTY OF SAN MATEO MILLBRAE, CALIFORNIA AUDIT REPORT. June 30, 2013

MILLBRAE SCHOOL DISTRICT COUNTY OF SAN MATEO MILLBRAE, CALIFORNIA AUDIT REPORT June 30, 2013 CHAVAN &ASSOCIATES, LLP CERTIFIED PUBLIC ACCOUNTANTS 1475 SARATOGA AVE., SUITE 180 SAN JOSE, CA 95129 This Page

MILLBRAE SCHOOL DISTRICT COUNTY OF SAN MATEO MILLBRAE, CALIFORNIA AUDIT REPORT June 30, 2013 CHAVAN &ASSOCIATES, LLP CERTIFIED PUBLIC ACCOUNTANTS 1475 SARATOGA AVE., SUITE 180 SAN JOSE, CA 95129 This Page

San Dieguito Union High School District

San Dieguito Union High School District INFORMATION REGARDING BOARD AGENDA ITEM TO: BOARD OF TRUSTEES DATE OF REPORT: January 4, 2016 BOARD MEETING DATE: January 14, 2016 PREPARED BY: SUBMITTED BY: SUBJECT:

San Dieguito Union High School District INFORMATION REGARDING BOARD AGENDA ITEM TO: BOARD OF TRUSTEES DATE OF REPORT: January 4, 2016 BOARD MEETING DATE: January 14, 2016 PREPARED BY: SUBMITTED BY: SUBJECT:

TATUM INDEPENDENT SCHOOL DISTRICT

TATUM INDEPENDENT SCHOOL DISTRICT ANNUAL FINANCIAL REPORT FOR THE YEAR ENDED AUGUST 31, 2017 Tatum Independent School District Annual Financial Report For The Year Ended August 31, 2017 TABLE OF CONTENTS

TATUM INDEPENDENT SCHOOL DISTRICT ANNUAL FINANCIAL REPORT FOR THE YEAR ENDED AUGUST 31, 2017 Tatum Independent School District Annual Financial Report For The Year Ended August 31, 2017 TABLE OF CONTENTS

GUILDERLAND CENTRAL SCHOOL DISTRICT AUDITED FINANCIAL STATEMENTS AND SUPPLEMENTAL SCHEDULES JUNE 30, 2015

AUDITED FINANCIAL STATEMENTS AND SUPPLEMENTAL SCHEDULES JUNE 30, 2015 C O N T E N T S PAGE INDEPENDENT AUDITORS REPORT... 1 2 MANAGEMENT S DISCUSSION AND ANALYSIS... 3 11 BASIC FINANCIAL STATEMENTS Statement

AUDITED FINANCIAL STATEMENTS AND SUPPLEMENTAL SCHEDULES JUNE 30, 2015 C O N T E N T S PAGE INDEPENDENT AUDITORS REPORT... 1 2 MANAGEMENT S DISCUSSION AND ANALYSIS... 3 11 BASIC FINANCIAL STATEMENTS Statement

Middlesex School District Financial Statements For The Year Ended June 30, 2011

Middlesex School District Financial Statements Middlesex School District Table of Contents Page Number -- Independent Auditors Report 3-4 -- Management Discussion and Analysis 5 EXHIBIT I Statement of

Middlesex School District Financial Statements Middlesex School District Table of Contents Page Number -- Independent Auditors Report 3-4 -- Management Discussion and Analysis 5 EXHIBIT I Statement of

CITY OF BUFORD BOARD OF EDUCATION

CITY OF BUFORD BOARD OF EDUCATION A COMPONENT UNIT OF THE CITY OF BUFORD GWINNETT COUNTY, GEORGIA ANNUAL FINANCIAL REPORT (Including Independent Auditor s Report) FOR THE FISCAL YEAR ENDED JUNE 30, 2017

CITY OF BUFORD BOARD OF EDUCATION A COMPONENT UNIT OF THE CITY OF BUFORD GWINNETT COUNTY, GEORGIA ANNUAL FINANCIAL REPORT (Including Independent Auditor s Report) FOR THE FISCAL YEAR ENDED JUNE 30, 2017

IROQUOIS CENTRAL SCHQQ:L DISTRICT ELMA, NEW YORK

AUDITED BASIC FINANCIAL STATEMENTS IROQUOIS CENTRAL SCHQQ:L DISTRICT ELMA, NEW YORK JUNE 30, 2016 TABLE OF CONTENTS SECTION A FINANCIAL SECTION Independent Auditor's Report Management's Discussion and

AUDITED BASIC FINANCIAL STATEMENTS IROQUOIS CENTRAL SCHQQ:L DISTRICT ELMA, NEW YORK JUNE 30, 2016 TABLE OF CONTENTS SECTION A FINANCIAL SECTION Independent Auditor's Report Management's Discussion and

MILLBRAE SCHOOL DISTRICT COUNTY OF SAN MATEO MILLBRAE, CALIFORNIA AUDIT REPORT. June 30, 2014

MILLBRAE SCHOOL DISTRICT COUNTY OF SAN MATEO MILLBRAE, CALIFORNIA AUDIT REPORT June 30, 2014 CHAVAN & ASSOCIATES, LLP CERTIFIED PUBLIC ACCOUNTANTS 1475 SARATOGA AVE., SUITE 180 SAN JOSE, CA 95129 Received

MILLBRAE SCHOOL DISTRICT COUNTY OF SAN MATEO MILLBRAE, CALIFORNIA AUDIT REPORT June 30, 2014 CHAVAN & ASSOCIATES, LLP CERTIFIED PUBLIC ACCOUNTANTS 1475 SARATOGA AVE., SUITE 180 SAN JOSE, CA 95129 Received

CENTRAL UNION HIGH SCHOOL DISTRICT COUNTY OF IMPERIAL EL CENTRO, CALIFORNIA AUDIT REPORT (REVISED) JUNE 30, 2014

JUNE 30, 2014") COUNTY OF IMPERIAL EL CENTRO, CALIFORNIA AUDIT REPORT (REVISED) JUNE 30, 2014 Wilkinson Hadley King & Co. LLP CPA's and Advisors 218 W. Douglas Ave. El Cajon, California Introductory Section Central Union

COUNTY OF IMPERIAL EL CENTRO, CALIFORNIA AUDIT REPORT (REVISED) JUNE 30, 2014 Wilkinson Hadley King & Co. LLP CPA's and Advisors 218 W. Douglas Ave. El Cajon, California Introductory Section Central Union

AMADOR COUNTY UNIFIED SCHOOL DISTRICT. FINANCIAL STATEMENTS June 30, 2018

FINANCIAL STATEMENTS June 30, 2018 FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION For the Year Ended June 30, 2018 CONTENTS INDEPENDENT AUDITOR'S REPORT... 1 MANAGEMENT'S DISCUSSION AND ANALYSIS...

FINANCIAL STATEMENTS June 30, 2018 FINANCIAL STATEMENTS WITH SUPPLEMENTARY INFORMATION For the Year Ended June 30, 2018 CONTENTS INDEPENDENT AUDITOR'S REPORT... 1 MANAGEMENT'S DISCUSSION AND ANALYSIS...

COTATI-ROHNERT PARK UNIFIED SCHOOL DISTRICT COUNTY OF SONOMA ROHNERT PARK, CALIFORNIA

COTATI-ROHNERT PARK UNIFIED SCHOOL DISTRICT COUNTY OF SONOMA ROHNERT PARK, CALIFORNIA AUDIT REPORT JUNE 30, 2016 CHAVAN & ASSOCIATES, LLP CERTIFIED PUBLIC ACCOUNTANTS 1475 SARATOGA AVE., SUITE 180 SAN

COTATI-ROHNERT PARK UNIFIED SCHOOL DISTRICT COUNTY OF SONOMA ROHNERT PARK, CALIFORNIA AUDIT REPORT JUNE 30, 2016 CHAVAN & ASSOCIATES, LLP CERTIFIED PUBLIC ACCOUNTANTS 1475 SARATOGA AVE., SUITE 180 SAN

ARK-TEX COUNCIL OF GOVERNMENTS REPORT ON AUDIT OF FINANCIAL STATEMENTS AND SUPPLEMENTAL INFORMATION

ARK-TEX COUNCIL OF GOVERNMENTS REPORT ON AUDIT OF FINANCIAL STATEMENTS AND SUPPLEMENTAL INFORMATION FOR THE YEAR ENDED SEPTEMBER 30, 2014 ARK-TEX COUNCIL OF GOVERNMENTS TABLE OF CONTENTS SEPTEMBER 30,

ARK-TEX COUNCIL OF GOVERNMENTS REPORT ON AUDIT OF FINANCIAL STATEMENTS AND SUPPLEMENTAL INFORMATION FOR THE YEAR ENDED SEPTEMBER 30, 2014 ARK-TEX COUNCIL OF GOVERNMENTS TABLE OF CONTENTS SEPTEMBER 30,

WHITE & ASSOCIATES, PSC CERTIFIED PUBLIC ACCOUNTANTS 1407 Lexington Road Richmond, Kentucky Phone (859) Fax (859)

Fax (859)") MENIFEE COUNTY SCHOOL DISTRICT AUDITED FINANCIAL STATEMENTS AND SUPPLEMENTAL SCHEDULES For the year ended June 30, 2012 Prepared by: WHITE & ASSOCIATES, PSC CERTIFIED PUBLIC ACCOUNTANTS 1407 Lexington

MENIFEE COUNTY SCHOOL DISTRICT AUDITED FINANCIAL STATEMENTS AND SUPPLEMENTAL SCHEDULES For the year ended June 30, 2012 Prepared by: WHITE & ASSOCIATES, PSC CERTIFIED PUBLIC ACCOUNTANTS 1407 Lexington

CENTRAL UNION HIGH SCHOOL DISTRICT COUNTY OF IMPERIAL EL CENTRO, CALIFORNIA AUDIT REPORT JUNE 30, 2017

COUNTY OF IMPERIAL EL CENTRO, CALIFORNIA AUDIT REPORT JUNE 30, 2017 Wilkinson Hadley King & Co. LLP CPA's and Advisors 218 W. Douglas Ave. El Cajon, California Introductory Section Central Union High School

COUNTY OF IMPERIAL EL CENTRO, CALIFORNIA AUDIT REPORT JUNE 30, 2017 Wilkinson Hadley King & Co. LLP CPA's and Advisors 218 W. Douglas Ave. El Cajon, California Introductory Section Central Union High School

FINANCIAL MANAGEMENT FOR GEORGIA LOCAL UNITS OF ADMINISTRATION

FINANCIAL MANAGEMENT FOR GEORGIA LOCAL UNITS OF ADMINISTRATION Date Issued Effective Date Section Title: October 1992 October 1992 II Financial Reporting Revision No. Date Revised Chapter Title: 3 March

FINANCIAL MANAGEMENT FOR GEORGIA LOCAL UNITS OF ADMINISTRATION Date Issued Effective Date Section Title: October 1992 October 1992 II Financial Reporting Revision No. Date Revised Chapter Title: 3 March

GUILDERLAND CENTRAL SCHOOL DISTRICT AUDITED FINANCIAL STATEMENTS AND SUPPLEMENTAL SCHEDULES JUNE 30, 2017

AUDITED FINANCIAL STATEMENTS AND SUPPLEMENTAL SCHEDULES JUNE 30, 2017 C O N T E N T S PAGE INDEPENDENT AUDITORS REPORT... 1 2 MANAGEMENT S DISCUSSION AND ANALYSIS... 3 11 BASIC FINANCIAL STATEMENTS Statement

AUDITED FINANCIAL STATEMENTS AND SUPPLEMENTAL SCHEDULES JUNE 30, 2017 C O N T E N T S PAGE INDEPENDENT AUDITORS REPORT... 1 2 MANAGEMENT S DISCUSSION AND ANALYSIS... 3 11 BASIC FINANCIAL STATEMENTS Statement

Fort Sam Houston Independent School District Annual Financial and Compliance Report

Fort Sam Houston Independent School District Annual Financial and Compliance Report Year Ended August 31, 2015 Annual Financial Report Year Ended August 31, 2015 Table of Contents Page Exhibit INTRODUCTORY

Fort Sam Houston Independent School District Annual Financial and Compliance Report Year Ended August 31, 2015 Annual Financial Report Year Ended August 31, 2015 Table of Contents Page Exhibit INTRODUCTORY

GENERAL INSTRUCTIONS--Continuation Sheet... COVER SHEET AND CERTIFICATION... C-1. PART I General Information... I-1. Indirect Costs...

Revision Number 1 Effective Date June 30, 2006 INDEX GENERAL INSTRUCTIONS--Continuation Sheet.............. (i) COVER SHEET AND CERTIFICATION................... C-1 PART I General Information..................

Revision Number 1 Effective Date June 30, 2006 INDEX GENERAL INSTRUCTIONS--Continuation Sheet.............. (i) COVER SHEET AND CERTIFICATION................... C-1 PART I General Information..................

AUDITED FINANCIAL STATEMENTS - REGULATORY BASIS AND REPORTS OF INDEPENDENT AUDITOR BUTNER SCHOOL DISTRICT NO. I-15, SEMINOLE COUNTY, OKLAHOMA

AUDITED FINANCIAL STATEMENTS - REGULATORY BASIS AND REPORTS OF INDEPENDENT AUDITOR BUTNER SCHOOL DISTRICT NO. I-15, SEMINOLE COUNTY, OKLAHOMA JUNE 30, 2016 INDEPENDENT SCHOOL DISTRICT NO. I-15 SEMINOLE

AUDITED FINANCIAL STATEMENTS - REGULATORY BASIS AND REPORTS OF INDEPENDENT AUDITOR BUTNER SCHOOL DISTRICT NO. I-15, SEMINOLE COUNTY, OKLAHOMA JUNE 30, 2016 INDEPENDENT SCHOOL DISTRICT NO. I-15 SEMINOLE

GLENN COUNTY OFFICE OF EDUCATION AUDIT REPORT

GLENN COUNTY OFFICE OF EDUCATION AUDIT REPORT For the Fiscal Year Ended June 30, 2010 AUDIT REPORT For the Fiscal Year Ended June 30, 2010 Table of Contents FINANCIAL SECTION Page Independent Auditor s

GLENN COUNTY OFFICE OF EDUCATION AUDIT REPORT For the Fiscal Year Ended June 30, 2010 AUDIT REPORT For the Fiscal Year Ended June 30, 2010 Table of Contents FINANCIAL SECTION Page Independent Auditor s

PARKVIEW SCHOOL DISTRICT FINANCIAL STATEMENTS. Including Independent Auditor s Report. As of and for the year ended June 30, 2017

PARKVIEW SCHOOL DISTRICT FINANCIAL STATEMENTS Including Independent Auditor s Report As of and for the year ended June 30, 2017 Johnson Block and Company, Inc. Certified Public Accountants 2500 Business

PARKVIEW SCHOOL DISTRICT FINANCIAL STATEMENTS Including Independent Auditor s Report As of and for the year ended June 30, 2017 Johnson Block and Company, Inc. Certified Public Accountants 2500 Business

AUDITED FINANCIAL STATEMENTS - REGULATORY BASIS AND REPORTS OF INDEPENDENT AUDITOR QUINTON SCHOOL DISTRICT NO. I-17, PITTSBURG COUNTY, OKLAHOMA

AUDITED FINANCIAL STATEMENTS - REGULATORY BASIS AND REPORTS OF INDEPENDENT AUDITOR QUINTON SCHOOL DISTRICT NO. I-17, PITTSBURG COUNTY, OKLAHOMA JUNE 30, 2016 INDEPENDENT SCHOOL DISTRICT NO. I-17 PITTSBURG

AUDITED FINANCIAL STATEMENTS - REGULATORY BASIS AND REPORTS OF INDEPENDENT AUDITOR QUINTON SCHOOL DISTRICT NO. I-17, PITTSBURG COUNTY, OKLAHOMA JUNE 30, 2016 INDEPENDENT SCHOOL DISTRICT NO. I-17 PITTSBURG

STATE OF NEW MEXICO ARTESIA PUBLIC SCHOOLS. ANNUAL FINANCIAL REPORT June 30, 2010

ANNUAL FINANCIAL REPORT June 30, 2010 De'Aun Willoughby CPA, PC Certified Public Accountant Melrose, New Mexico Table of Contents Official Roster 6 Independent Auditor's Report. 7-8 Basic Financial Statements

ANNUAL FINANCIAL REPORT June 30, 2010 De'Aun Willoughby CPA, PC Certified Public Accountant Melrose, New Mexico Table of Contents Official Roster 6 Independent Auditor's Report. 7-8 Basic Financial Statements

CLINTON COMMUNITY SCHOOL DISTRICT

CLINTON COMMUNITY SCHOOL DISTRICT AUDITED FINANCIAL STATEMENTS JUNE 30, 2015 James R. Frechette CERTIFIED PUBLIC ACCOUNTANT June 30, 2015 TABLE OF CONTENTS Independent Auditor s Report 1-2 Basic Financial

CLINTON COMMUNITY SCHOOL DISTRICT AUDITED FINANCIAL STATEMENTS JUNE 30, 2015 James R. Frechette CERTIFIED PUBLIC ACCOUNTANT June 30, 2015 TABLE OF CONTENTS Independent Auditor s Report 1-2 Basic Financial

SCHOOL DISTRICT OF AMERY Amery, Wisconsin FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION YEAR ENDED JUNE 30, 2018

FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION YEAR ENDED TABLE OF CONTENTS YEAR ENDED FINANCIAL SECTION INDEPENDENT AUDITORS' REPORT 1 REQUIRED SUPPLEMENTARY INFORMATION Management's Discussion and

FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION YEAR ENDED TABLE OF CONTENTS YEAR ENDED FINANCIAL SECTION INDEPENDENT AUDITORS' REPORT 1 REQUIRED SUPPLEMENTARY INFORMATION Management's Discussion and

LEXINGTON CITY SCHOOLS, NORTH CAROLINA. Financial Statements June 30, 2017

LEXINGTON CITY SCHOOLS, NORTH CAROLINA Financial Statements Board of Education Members John Burke, Chair Robert Curlee, Vice Chair Hector Padial Brian Lancaster Angela McDuffie Sam Lem Scott Biesecker

LEXINGTON CITY SCHOOLS, NORTH CAROLINA Financial Statements Board of Education Members John Burke, Chair Robert Curlee, Vice Chair Hector Padial Brian Lancaster Angela McDuffie Sam Lem Scott Biesecker

VESTAVIA HILLS CITY BOARD OF EDUCATION BASIC FINANCIAL STATEMENTS SEPTEMBER 30, 2015

BASIC FINANCIAL STATEMENTS SEPTEMBER 30, 2015 TABLE OF CONTENTS Page Independent Auditors' Report 3 Management's Discussion and Analysis 5 Basic Financial Statements: Government-Wide Financial Statements:

BASIC FINANCIAL STATEMENTS SEPTEMBER 30, 2015 TABLE OF CONTENTS Page Independent Auditors' Report 3 Management's Discussion and Analysis 5 Basic Financial Statements: Government-Wide Financial Statements:

FRANKFORT INDEPENDENT SCHOOL DISTRICT AUDIT REPORT JUNE 30, 2015

FRANKFORT INDEPENDENT SCHOOL DISTRICT AUDIT REPORT JUNE 30, 2015 TABLE OF CONTENTS Independent Auditor s Report 1-3 Management Discussion and Analysis 4-10 Basic Financial Statements: Government-Wide Financial

FRANKFORT INDEPENDENT SCHOOL DISTRICT AUDIT REPORT JUNE 30, 2015 TABLE OF CONTENTS Independent Auditor s Report 1-3 Management Discussion and Analysis 4-10 Basic Financial Statements: Government-Wide Financial

MONTGOMERY COUNTY SCHOOL DISTRICT

BASIC FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION YEAR ENDED JUNE 30, 2015 WITH REPORT OF INDEPENDENT AUDITORS TABLE OF CONTENTS Independent Auditor's Report Management's Discussion and Analysis

BASIC FINANCIAL STATEMENTS AND SUPPLEMENTARY INFORMATION YEAR ENDED JUNE 30, 2015 WITH REPORT OF INDEPENDENT AUDITORS TABLE OF CONTENTS Independent Auditor's Report Management's Discussion and Analysis

ARK-TEX COUNCIL OF GOVERNMENTS REPORT ON AUDIT OF FINANCIAL STATEMENTS AND SUPPLEMENTAL INFORMATION

ARK-TEX COUNCIL OF GOVERNMENTS REPORT ON AUDIT OF FINANCIAL STATEMENTS AND SUPPLEMENTAL INFORMATION FOR THE YEAR ENDED SEPTEMBER 30, 2013 ARK-TEX COUNCIL OF GOVERNMENTS TABLE OF CONTENTS SEPTEMBER 30,

ARK-TEX COUNCIL OF GOVERNMENTS REPORT ON AUDIT OF FINANCIAL STATEMENTS AND SUPPLEMENTAL INFORMATION FOR THE YEAR ENDED SEPTEMBER 30, 2013 ARK-TEX COUNCIL OF GOVERNMENTS TABLE OF CONTENTS SEPTEMBER 30,

Financial statements and report of independent certified public accountants State of Hawaii, Department of Education June 30, 2002

Financial statements and report of independent certified public accountants, C O N T E N T S I. INTRODUCTION 1 II. FINANCIAL SECTION Report of Independent Certified Public Accountants 3 Management s Discussion

Financial statements and report of independent certified public accountants, C O N T E N T S I. INTRODUCTION 1 II. FINANCIAL SECTION Report of Independent Certified Public Accountants 3 Management s Discussion

GAYLORD COMMUNITY SCHOOLS GAYLORD, MICHIGAN FINANCIAL STATEMENTS JUNE 30, 2015

GAYLORD, MICHIGAN FINANCIAL STATEMENTS JUNE 30, 2015 TABLE OF CONTENTS Independent Auditor's Report 1-3 Management's Discussion and Analysis 4-12 Basic Financial Statements District-wide Financial Statements

GAYLORD, MICHIGAN FINANCIAL STATEMENTS JUNE 30, 2015 TABLE OF CONTENTS Independent Auditor's Report 1-3 Management's Discussion and Analysis 4-12 Basic Financial Statements District-wide Financial Statements

CITY OF TRION BOARD OF EDUCATION CHATTOOGA COUNTY, GEORGIA

CITY OF TRION BOARD OF EDUCATION CHATTOOGA COUNTY, GEORGIA ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED JUNE 30, 2014 (Including Independent Auditor's Reports) CITY OF TRION BOARD OF EDUCATION - CHATTOOGA

CITY OF TRION BOARD OF EDUCATION CHATTOOGA COUNTY, GEORGIA ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED JUNE 30, 2014 (Including Independent Auditor's Reports) CITY OF TRION BOARD OF EDUCATION - CHATTOOGA

CITY OF BUFORD BOARD OF EDUCATION

A COMPONENT UNIT OF THE CITY OF BUFORD, GEORGIA ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED JUNE 30, 2015 A COMPONENT UNIT OF THE CITY OF BUFORD, GEORGIA ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR

A COMPONENT UNIT OF THE CITY OF BUFORD, GEORGIA ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED JUNE 30, 2015 A COMPONENT UNIT OF THE CITY OF BUFORD, GEORGIA ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR

FALLBROOK UNION HIGH SCHOOL DISTRICT ANNUAL FINANCIAL REPORT JUNE 30, 2017

FALLBROOK UNION HIGH SCHOOL DISTRICT ANNUAL FINANCIAL REPORT TABLE OF CONTENTS FINANCIAL SECTION Independent Auditor's Report 2 Management's Discussion and Analysis 5 Basic Financial Statements Government-Wide

FALLBROOK UNION HIGH SCHOOL DISTRICT ANNUAL FINANCIAL REPORT TABLE OF CONTENTS FINANCIAL SECTION Independent Auditor's Report 2 Management's Discussion and Analysis 5 Basic Financial Statements Government-Wide

CITY OF BUFORD BOARD OF EDUCATION

ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED JUNE 30, 2013 ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED JUNE 30, 2013 TABLE OF CONTENTS FINANCIAL SECTION Independent Auditor s Report... 1-3 Basic

ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED JUNE 30, 2013 ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED JUNE 30, 2013 TABLE OF CONTENTS FINANCIAL SECTION Independent Auditor s Report... 1-3 Basic

GAYLORD COMMUNITY SCHOOLS GAYLORD, MICHIGAN FINANCIAL STATEMENTS JUNE 30, 2016

GAYLORD, MICHIGAN FINANCIAL STATEMENTS JUNE 30, 2016 TABLE OF CONTENTS Independent Auditor's Report 1-3 Management's Discussion and Analysis 4-11 Basic Financial Statements District-wide Financial Statements

GAYLORD, MICHIGAN FINANCIAL STATEMENTS JUNE 30, 2016 TABLE OF CONTENTS Independent Auditor's Report 1-3 Management's Discussion and Analysis 4-11 Basic Financial Statements District-wide Financial Statements

MORGAN COUNTY BOARD OF EDUCATION MADISON, GEORGIA

MORGAN COUNTY BOARD OF EDUCATION MADISON, GEORGIA ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED JUNE 30, 2017 (Including Independent Auditor's Reports) - TABLE OF CONTENTS - Page SECTION I FINANCIAL

MORGAN COUNTY BOARD OF EDUCATION MADISON, GEORGIA ANNUAL FINANCIAL REPORT FOR THE FISCAL YEAR ENDED JUNE 30, 2017 (Including Independent Auditor's Reports) - TABLE OF CONTENTS - Page SECTION I FINANCIAL

BRADLEY BEACH SCHOOL DISTRICT. Bradley Beach, New Jersey County of Monmouth COMPREHENSIVE ANNUAL FINANCIAL REPORT FOR FISCAL YEAR ENDED JUNE 30, 2017

BRADLEY BEACH SCHOOL DISTRICT Bradley Beach, New Jersey County of Monmouth COMPREHENSIVE ANNUAL FINANCIAL REPORT FOR FISCAL YEAR ENDED JUNE 30, 2017 COMPREHENSIVE ANNUAL FINANCIAL REPORT OF THE BRADLEY

BRADLEY BEACH SCHOOL DISTRICT Bradley Beach, New Jersey County of Monmouth COMPREHENSIVE ANNUAL FINANCIAL REPORT FOR FISCAL YEAR ENDED JUNE 30, 2017 COMPREHENSIVE ANNUAL FINANCIAL REPORT OF THE BRADLEY

PRIVATE SCHOOLS FOR STUDENTS WITH DISABILITIES NARRATIVE EXPLANATION OF THE CHART OF ACCOUNTS

PRIVATE SCHOOLS FOR STUDENTS WITH DISABILITIES NARRATIVE EXPLANATION OF THE CHART OF ACCOUNTS FORWARD This handbook describes the coding of accounts in New Jersey Approved Private Schools for Students

PRIVATE SCHOOLS FOR STUDENTS WITH DISABILITIES NARRATIVE EXPLANATION OF THE CHART OF ACCOUNTS FORWARD This handbook describes the coding of accounts in New Jersey Approved Private Schools for Students

BRAWLEY ELEMENTARY SCHOOL DISTRICT COUNTY OF IMPERIAL BRAWLEY, CALIFORNIA ANNUAL FINANCIAL REPORT JUNE 30, 2016

COUNTY OF IMPERIAL BRAWLEY, CALIFORNIA ANNUAL FINANCIAL REPORT JUNE 30, 2016 Wilkinson Hadley King & Co. LLP CPA's and Advisors 218 W. Douglas Ave El Cajon, CA 92020 Introductory Section Brawley Elementary

COUNTY OF IMPERIAL BRAWLEY, CALIFORNIA ANNUAL FINANCIAL REPORT JUNE 30, 2016 Wilkinson Hadley King & Co. LLP CPA's and Advisors 218 W. Douglas Ave El Cajon, CA 92020 Introductory Section Brawley Elementary