Audit based on the agreement for the project financed from funds allocated by the World Bank

|

|

|

- Alberta Leonard

- 5 years ago

- Views:

Transcription

1 Document No: AUDIT REPORT ON SPECIAL PURPOSE FINANCIAL STATEMENTS FOR THE PROJECT IMPROVEMENT OF THE KOSOVO EDUCATION SYSTEM FOR THE PERIOD to Audit based on the agreement for the project financed from funds allocated by the World Bank Prishtina, September 2018

2 The National Audit Office of the Republic of Kosovo is the highest institution of economic and financial control which, according to the Constitution and domestic laws, enjoys functional, financial and operational independence. The National Audit Office undertakes regularity and performance audits and is accountable to the Assembly of Kosovo. Our Mission is through quality audits strengthen accountability in public administration for an effective, efficient and economic use of national resources. We perform audits in line with internationally recognized public sector auditing standards and good European practices. The reports of the National Audit Office directly promote accountability of public institutions as they provide a base for holding managers of individual budget organisations to account. We are thus building confidence in the spending of public funds and playing an active role in securing taxpayers and other stakeholders interests in enhancing public accountability. The Auditor General has decided on the audit opinion on the Annual Financial Report for the project Improvement of the Kosovo Education System, in consultation with the Assistant Auditor General, Emine Fazliu, who supervised the audit. The report issued is a result of the audit carried out by Ariana Berisha-Rexhëbeqaj (Team Leader) and Natyra Kasumaj (team member) under the management of the Head of Audit Department (Florim Beqiri). NATIONAL AUDIT OFFICE-St. Musine Kokollari, No. 87, Prishtina 10000, Kosova Tel: +381(0) /

3 ZYRA KOMBËTARE E AUDITIMIT - NACIONALNA KANCELARIJA REVIZIJE - NATIONAL AUDIT OFFICE TABLE OF CONTENTS Executive Summary Audit Scope and Methodology Special Purpose Annual Financial Statements and the audit opinion... 6 Annex I: Explanation of the different types of opinion applied by the NAO... 8 Annex II: Special purpose financial statements of the project for

4 ZYRA KOMBËTARE E AUDITIMIT - NACIONALNA KANCELARIJA REVIZIJE - NATIONAL AUDIT OFFICE Executive Summary Introduction This report summarises key issues arising from our audit of the 2017 Annual Financial Statements for special purpose for the project Improvement of the Kosovo Education System, for the period to , which determines the Opinion given by the Auditor General. The examination of special purpose Financial Statements for the audited period was undertaken in accordance with the International Standards on Supreme Audit Institutions (ISSAIs). Our approach included such tests and procedures as we deemed necessary to arrive at an opinion on the financial report. Our audit focus has been on: The Annual Financial Report Financial Management and Control Issues related to procurement and the process of payments The level of work undertaken by the National Audit Office to complete the audit for the audited period has been determined depending on expenditures incurred for this period. The National Audit Office acknowledges the Senior Management and the Staff of the Ministry of Education Science and Technology for cooperation during the audit process. Opinion of the Auditor General Unmodified Opinion with emphasis of matter The Annual Financial Statements for Special Purpose present a true and fair view in all material aspects. Emphasis of matter We would like to draw your attention to the fact that the AFS have been prepared based on the cash basis of accounting. For more, please refer to Section 2.1 of this report. Annex I explains the different types of Opinions applied by the National Audit Office. 4

5 ZYRA KOMBËTARE E AUDITIMIT - NACIONALNA KANCELARIJA REVIZIJE - NATIONAL AUDIT OFFICE 1 Audit Scope and Methodology Introduction The National Audit (NAO) is responsible for carrying out a Regularity Audit which involves the examination and evaluation of the financial report and other financial records, and expression of opinion on: Whether special purpose financial statements give a true and fair view of the accounts and financial affairs for the audited period; Whether foreign funds have been used in compliance with conditions of respective financing agreements; Whether the data, financial systems, and transactions comply with applicable laws and regulations for funds allocated by the World Bank; Whether financial statements comply with the requirements of the agreement between the Republic of Kosovo represented by the Minister of Finance and the International Development Association 1 ; The appropriateness of internal controls and internal audit functions; and All matters arising from or relating to the audit. Audit methodology was focused on examination of financial data and transactions, including the supporting documentation. We have determined the level of detailed tests needed to provide evidence that support the opinion of the AG. Audit findings should not be considered as a comprehensive overview of all weaknesses that may exist, or of all improvements that can be done in operated systems and procedures. In the report shall be presented findings that are part of the opinion on the financial statements. While findings related to the financial management aspect, internal control functioning, and compliance issues will be summarised in the management letter. 1 IDA- Loan number-5726-xk- Financed by the World Bank 5

6 ZYRA KOMBËTARE E AUDITIMIT - NACIONALNA KANCELARIJA REVIZIJE - NATIONAL AUDIT OFFICE 2 Special Purpose Annual Financial Statements and the audit opinion Introduction Our audit of the Special Purpose Annual Financial Statements considers compliance with the reporting requirements according to the agreement, and the quality and accuracy of information presented in the financial statements. 2.1 Audit Opinion Unmodified Opinion with Emphasis of Matter We have audited the Special Purpose Financial Statements of the project financed by the World Bank Improvement of the Kosovo Education System for the period to , which includes a summary of sources of funds and expenditures incurred, statement of applications for withdrawal of funds and disclosures. In our opinion, audited the Special Purpose Financial Statements of the project Improvement of the Kosovo Education System for the period to present a true and fair view in all material respects in accordance with reporting requirements under the agreement between parties, by adhering to principles of cash based accounting. Basis for the opinion Our audit was conducted in accordance with International Standards of Supreme Audit Institutions (ISSAIs). Our responsibilities under those standards are further described in the Auditor s Responsibilities for the Audit of the Financial Statements section of our report. We believe that audit evidence obtained is sufficient and appropriate to provide a basis for the opinion. Emphasis of Matter Basis for accounting We draw your attention to the section 3, clause 2 of the AFS, which explains the basis for accounting. Annual Financial Statements are prepared under cash based accounting in order to assist the Ministry meet the requirements of the World Bank. As a result of this, these AFS may not be suitable for another purpose. Our opinion is not modified in this regard. Responsibility of Management and Persons Charged with Governance The management of the Ministry of Education, Science and Technology as project implementer is responsible for true and fair preparation of the special purpose financial statements, according to the agreement signed between the Republic of Kosovo represented by the Minister of Finance and 6

7 ZYRA KOMBËTARE E AUDITIMIT - NACIONALNA KANCELARIJA REVIZIJE - NATIONAL AUDIT OFFICE the International Development Association. This information is comprised of the Statement of Funds and Their Use, and the Statement of Withdrawal of Funds. Auditor General s Responsibility for the Audit Our responsibility is to express an opinion on the special purpose financial statements based on the audit carried out. We conducted our audit in accordance with ISSAIs. These standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance that financial statements are free from material misstatements. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with ISSAIs will detect any material misstatement that might exist. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could influence the decisions taken on the basis of this financial report. The audit involves performing procedures to obtain evidence about the financial records and disclosures in the special purpose financial statements. The procedures selected depend on the auditor s judgment, including the assessment of the risks of material misstatement in the financial report, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the preparation of special purpose financial statements by the Ministry, in order to design audit procedures that are appropriate for entity s circumstances, but not for the purpose of expressing an opinion on the effectiveness of entity s internal control. The audit also includes evaluation of the appropriateness of accounting policies used and the reasonableness of accounting estimates made by Management, as well as evaluation of the presentation of the financial report. 7

8 ZYRA KOMBËTARE E AUDITIMIT - NACIONALNA KANCELARIJA REVIZIJE - NATIONAL AUDIT OFFICE Annex I: Explanation of the different types of opinion applied by the NAO (extract from ISSAI 200) Form of opinion 147. The auditor should express an unmodified opinion if it is concluded that the financial statements are prepared, in all material respects, in accordance with the applicable financial framework. If the auditor concludes that, based on the audit evidence obtained, the financial statements as a whole are not free from material misstatement, or is unable to obtain sufficient appropriate audit evidence to conclude that the financial statements as a whole are free from material misstatement, the auditor should modify the opinion in the auditor s report in accordance with the section on Determining the type of modification to the auditor s opinion If financial statements prepared in accordance with the requirements of a fair presentation framework do not achieve fair presentation, the auditor should discuss the matter with the management and, depending on the requirements of the applicable financial reporting framework and how the matter is resolved, determine whether it is necessary to modify the audit opinion. Modifications to the opinion in the auditor s report 151. The auditor should modify the opinion in the auditor's report if it is concluded that, based on the audit evidence obtained, the financial statements as a whole are not free from material misstatement, or if the auditor was unable to obtain sufficient appropriate audit evidence to conclude that the financial statements as a whole are free from material misstatement. Auditors may issue three types of modified opinions: a qualified opinion, an adverse opinion and a disclaimer of opinion. 8

9 ZYRA KOMBËTARE E AUDITIMIT - NACIONALNA KANCELARIJA REVIZIJE - NATIONAL AUDIT OFFICE Determining the type of modification to the auditor s opinion 152. The decision regarding which type of modified opinion is appropriate depends upon: The nature of the matter giving rise to the modification that is, whether the financial statements are materially misstated or, in the event that it was impossible to obtain sufficient appropriate audit evidence, may be materially misstated; and The auditor s judgment about the pervasiveness of the effects or possible effects of the matter on the financial statements The auditor should express a qualified opinion if: (1) having obtained sufficient appropriate audit evidence, the auditor concludes that misstatements, individually or in the aggregate, are material, but not pervasive, to the financial statements; or (2) the auditor was unable to obtain sufficient appropriate audit evidence on which to base an opinion, but concludes that the effects on the financial statements of any undetected misstatements could be material but not pervasive The auditor should express an adverse opinion if, having obtained sufficient appropriate audit evidence, the auditor concludes that misstatements, individually or in the aggregate, are both material and pervasive to the financial statements The auditor should disclaim an opinion if, having been unable to obtain sufficient appropriate audit evidence on which to base the opinion, the auditor concludes that the effects on the financial statements of any undetected misstatements could be both material and pervasive. If, after accepting the engagement, the auditor becomes aware that management has imposed a limitation on the audit scope that the auditor considers likely to result in the need to express a qualified opinion or to disclaim an opinion on the financial statements, the auditor should request that management remove the limitation If expressing a modified audit opinion, the auditor should also modify the heading to correspond with the type of opinion expressed. ISSAI provides additional guidance on the specific language to use when expressing a modified opinion and describing the auditor s responsibility. It also includes illustrative examples of reports. Emphasis of Matter paragraphs and Other Matters paragraphs in the auditor s report 157. If the auditor considers it necessary to draw users attention to a matter presented or disclosed in the financial statements that is of such importance that it is fundamental to their understanding of the financial statements, but there is sufficient appropriate evidence that the matter is not materially misstated in the financial statements, the auditor should include an Emphasis of Matter paragraph in the auditor s report. Emphasis of Matter paragraphs should only refer to information presented or disclosed in the financial statements. 9

10 ZYRA KOMBËTARE E AUDITIMIT - NACIONALNA KANCELARIJA REVIZIJE - NATIONAL AUDIT OFFICE 158. An Emphasis of Matter paragraph should: be included immediately after the opinion; use the Heading Emphasis of Matter or another appropriate heading; include a clear reference to the matter being emphasised and indicate where the relevant disclosures that fully describe the matter can be found in the financial statements; and indicate that the auditor s opinion is not modified in respect of the matter emphasised If the auditor considers it necessary to communicate a matter, other than those that are presented or disclosed in the financial statements, which, in the auditor s judgement, is relevant to users understanding of the audit, the auditor s responsibilities or the auditor s report, and provided this is not prohibited by law or regulation, this should be done in a paragraph with the heading Other Matter, or another appropriate heading. This paragraph should appear immediately after the opinion and any Emphasis of Matter paragraph. 10

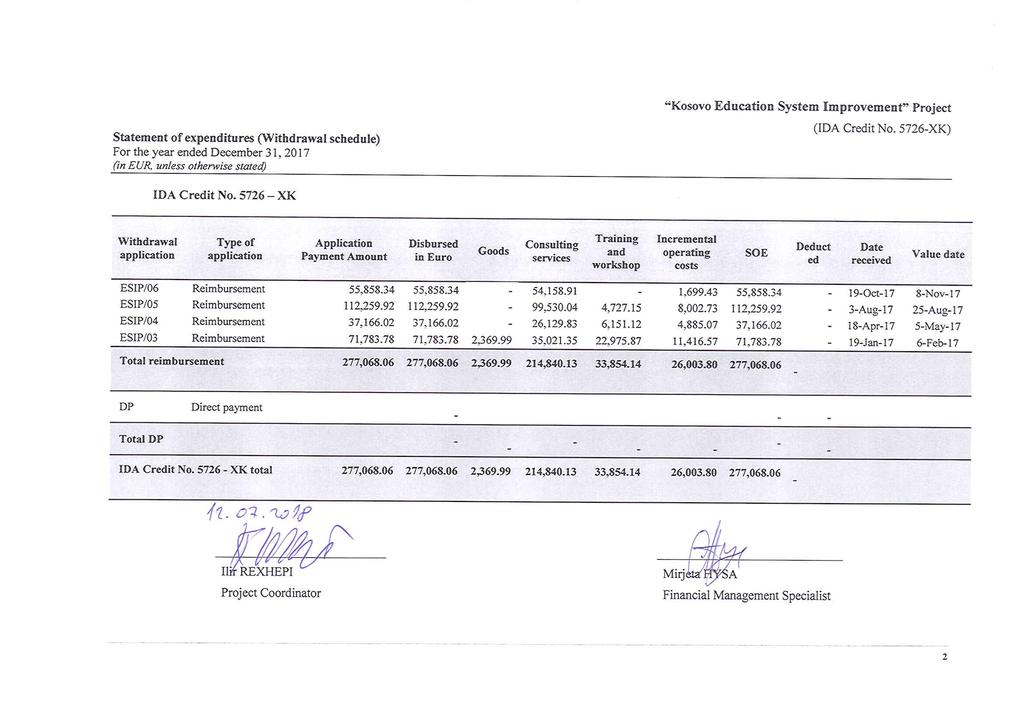

11 ZYRA KOMBËTARE E AUDITIMIT - NACIONALNA KANCELARIJA REVIZIJE - NATIONAL AUDIT OFFICE Annex II: Special purpose financial statements of the project for

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

Audit based on the agreement for the project financed from funds allocated by the World Bank

Public Disclosure Authorized Public Disclosure Authorized Document No: 21.10.7-2017-08 Public Disclosure Authorized AUDIT REPORT ON SPECIAL PURPOSE FINANCIAL STATEMENTS FOR THE PROJECT KOSOVO AGRICULTURE

Public Disclosure Authorized Public Disclosure Authorized Document No: 21.10.7-2017-08 Public Disclosure Authorized AUDIT REPORT ON SPECIAL PURPOSE FINANCIAL STATEMENTS FOR THE PROJECT KOSOVO AGRICULTURE

AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF THE CIVIL AVIATION AUTHORITY FOR THE YEAR ENDED 31 DECEMBER 2017

REPUBLIKA E KOSOVËS / REPUBLIKA KOSOVA / REPUBLIC OF KOSOVA ZYRA KOMBËTARE E AUDITIMIT NACIONALNA KANCELARIJA REVIZIJE NATIONAL AUDIT OFFICE Document No: 24.29.1-2017-08 AUDIT REPORT ON THE ANNUAL FINANCIAL

REPUBLIKA E KOSOVËS / REPUBLIKA KOSOVA / REPUBLIC OF KOSOVA ZYRA KOMBËTARE E AUDITIMIT NACIONALNA KANCELARIJA REVIZIJE NATIONAL AUDIT OFFICE Document No: 24.29.1-2017-08 AUDIT REPORT ON THE ANNUAL FINANCIAL

REPUBLIC OF KOSOVA OFFICE OF THE AUDITOR GENERAL

REPUBLIC OF KOSOVA Document No: 24.17.1-2013-08 AUDIT REPORT ON THE FINANCIAL STATEMENTS OF THE KOSOVO JUDICIAL INSTITUTE FOR THE YEAR ENDED 31 DECEMBER 2013 Prishtina, June 2014 The Office of the Auditor

REPUBLIC OF KOSOVA Document No: 24.17.1-2013-08 AUDIT REPORT ON THE FINANCIAL STATEMENTS OF THE KOSOVO JUDICIAL INSTITUTE FOR THE YEAR ENDED 31 DECEMBER 2013 Prishtina, June 2014 The Office of the Auditor

AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF THE MINSITRY OF COMMUNITIES AND RETURN FOR THE YEAR ENDED 31 DECEMBER 2017

Document No: 21.14.1-2017-08 AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF THE MINSITRY OF COMMUNITIES AND RETURN FOR THE YEAR ENDED 31 DECEMBER 2017 Prishtina, June 2018 The National Audit Office

Document No: 21.14.1-2017-08 AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF THE MINSITRY OF COMMUNITIES AND RETURN FOR THE YEAR ENDED 31 DECEMBER 2017 Prishtina, June 2018 The National Audit Office

AUDIT REPORT ON THE ANNUAL FINANCIAL REPORT OF THE MINISTRY OF TRADE AND INDUSTRY FOR THE YEAR ENDED 31 DECEMBER 2016

REPUBLIKA E KOSOVËS / REPUBLIKA KOSOVA / REPUBLIC OF KOSOVA ZYRA KOMBËTARE E AUDITIMIT NACIONALNA KANCELARIJA REVIZIJE NATIONAL AUDIT OFFICE Document no: 21.2.1-2016-08 AUDIT REPORT ON THE ANNUAL FINANCIAL

REPUBLIKA E KOSOVËS / REPUBLIKA KOSOVA / REPUBLIC OF KOSOVA ZYRA KOMBËTARE E AUDITIMIT NACIONALNA KANCELARIJA REVIZIJE NATIONAL AUDIT OFFICE Document no: 21.2.1-2016-08 AUDIT REPORT ON THE ANNUAL FINANCIAL

AUDIT REPORT ON THE ANNUAL FINANCIAL REPORT OF THE MUNICIPALITY OF VITIA FOR THE YEAR ENDED 31 DECEMBER 2016

REPUBLIKA E KOSOVËS / REPUBLIKA KOSOVA / REPUBLIC OF KOSOVA ZYRA KOMBËTARE E AUDITIMIT NACIONALNA KANCELARIJA REVIZIJE NATIONAL AUDIT OFFICE Document No: 22.22.1-2016-08 AUDIT REPORT ON THE ANNUAL FINANCIAL

REPUBLIKA E KOSOVËS / REPUBLIKA KOSOVA / REPUBLIC OF KOSOVA ZYRA KOMBËTARE E AUDITIMIT NACIONALNA KANCELARIJA REVIZIJE NATIONAL AUDIT OFFICE Document No: 22.22.1-2016-08 AUDIT REPORT ON THE ANNUAL FINANCIAL

AUDIT REPORT ON THE ANNUAL FINANCIAL REPORT OF THE MINISTRY OF LABOUR AND SOCIAL WELFARE FOR THE YEAR ENDED 31 DECEMBER 2016

REPUBLIKA E KOSOVËS / REPUBLIKA KOSOVA / REPUBLIC OF KOSOVA ZYRA KOMBËTARE E AUDITIMIT NACIONALNA KANCELARIJA REVIZIJE NATIONAL AUDIT OFFICE Document No: 21.7.1-2016-08 AUDIT REPORT ON THE ANNUAL FINANCIAL

REPUBLIKA E KOSOVËS / REPUBLIKA KOSOVA / REPUBLIC OF KOSOVA ZYRA KOMBËTARE E AUDITIMIT NACIONALNA KANCELARIJA REVIZIJE NATIONAL AUDIT OFFICE Document No: 21.7.1-2016-08 AUDIT REPORT ON THE ANNUAL FINANCIAL

AUDIT REPORT ON THE ANNUAL FINANCIAL REPORT OF PRIZREN MUNICIPALITY FOR THE YEAR ENDED 31 DECEMBER 2016

REPUBLIKA E KOSOVËS / REPUBLIKA KOSOVA / REPUBLIC OF KOSOVA ZYRA KOMBËTARE E AUDITIMIT NACIONALNA KANCELARIJA REVIZIJE NATIONAL AUDIT OFFICE Document No: 22.14.1-2016-08 AUDIT REPORT ON THE ANNUAL FINANCIAL

REPUBLIKA E KOSOVËS / REPUBLIKA KOSOVA / REPUBLIC OF KOSOVA ZYRA KOMBËTARE E AUDITIMIT NACIONALNA KANCELARIJA REVIZIJE NATIONAL AUDIT OFFICE Document No: 22.14.1-2016-08 AUDIT REPORT ON THE ANNUAL FINANCIAL

Document No: AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF MUNICIPALITY OF KAMENICA FOR THE YEAR ENDED 31 DECEMBER 2017

Document No: 22.29.1-2017-08 AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF MUNICIPALITY OF KAMENICA FOR THE YEAR ENDED 31 DECEMBER 2017 Prishtina, May 2018 The National Audit Office of the Republic

Document No: 22.29.1-2017-08 AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF MUNICIPALITY OF KAMENICA FOR THE YEAR ENDED 31 DECEMBER 2017 Prishtina, May 2018 The National Audit Office of the Republic

Audit Opinion Session-02. November

Audit Opinion Session-02 November - - 2018 Audit Opinion After concluding the field work the auditor forms an opinion on whether the financial statements are prepared, in all material respects, in accordance

Audit Opinion Session-02 November - - 2018 Audit Opinion After concluding the field work the auditor forms an opinion on whether the financial statements are prepared, in all material respects, in accordance

AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF THE MINISTRY OF AGRICULTURE, FORESTRY AND RURAL DEVELOPMENT FOR THE YEAR ENDED 31 DECEMBER 2017

Document No: 21.10.1-2017-08 AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF THE MINISTRY OF AGRICULTURE, FORESTRY AND RURAL DEVELOPMENT FOR THE YEAR ENDED 31 DECEMBER 2017 Prishtina, Jun 2018 The National

Document No: 21.10.1-2017-08 AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF THE MINISTRY OF AGRICULTURE, FORESTRY AND RURAL DEVELOPMENT FOR THE YEAR ENDED 31 DECEMBER 2017 Prishtina, Jun 2018 The National

Document No: AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF BUS STATION J.S.C PRISHTINA FOR THE YEAR ENDED 31 DECEMBER 2017

Document No: 23.14.1-2017-08 AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF BUS STATION J.S.C PRISHTINA FOR THE YEAR ENDED 31 DECEMBER 2017 Prishtina, July 2018 The National Audit Office of the Republic

Document No: 23.14.1-2017-08 AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF BUS STATION J.S.C PRISHTINA FOR THE YEAR ENDED 31 DECEMBER 2017 Prishtina, July 2018 The National Audit Office of the Republic

Initial Audit Engagements Opening Balances

International Auditing and Assurance Standards Board ISA 510 April 2009 International Standard on Auditing Initial Audit Engagements Opening Balances International Auditing and Assurance Standards Board

International Auditing and Assurance Standards Board ISA 510 April 2009 International Standard on Auditing Initial Audit Engagements Opening Balances International Auditing and Assurance Standards Board

STANDARD FOR AUDITS OF SMALL ENTITIES

STANDARD FOR AUDITS OF SMALL ENTITIES DRAFT JUNE 4 TH 2015 Contents Preface... 1 1 General Principles and Responsibilities... 2 1.1 Overall Objectives...2 1.2 Supervision and quality control...2 1.3 Performing

STANDARD FOR AUDITS OF SMALL ENTITIES DRAFT JUNE 4 TH 2015 Contents Preface... 1 1 General Principles and Responsibilities... 2 1.1 Overall Objectives...2 1.2 Supervision and quality control...2 1.3 Performing

Initial Audit Engagements Opening Balances

SINGAPORE STANDARD ON AUDITING SSA 510 Initial Audit Engagements Opening Balances This SSA 510 supersedes the SSA 510 Initial Audit Engagements Opening Balances in January 2010. Auditors are required to

SINGAPORE STANDARD ON AUDITING SSA 510 Initial Audit Engagements Opening Balances This SSA 510 supersedes the SSA 510 Initial Audit Engagements Opening Balances in January 2010. Auditors are required to

SRI LANKA AUDITING STANDARD 510 INITIAL AUDIT ENGAGEMENTS OPENING BALANCES CONTENTS

SRI LANKA AUDITING STANDARD 510 INITIAL AUDIT ENGAGEMENTS OPENING BALANCES (Effective for audits of financial statements for periods beginning on or after 01 January 2014) CONTENTS Paragraph Introduction

SRI LANKA AUDITING STANDARD 510 INITIAL AUDIT ENGAGEMENTS OPENING BALANCES (Effective for audits of financial statements for periods beginning on or after 01 January 2014) CONTENTS Paragraph Introduction

INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 510 INITIAL AUDIT ENGAGEMENTS OPENING BALANCES

510 INITIAL AUDIT ENGAGEMENTS OPENING BALANCES") INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 510 INITIAL AUDIT ENGAGEMENTS OPENING BALANCES (Effective for audits of financial statements for periods ending on or after 15 December 2010) CONTENTS

INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 510 INITIAL AUDIT ENGAGEMENTS OPENING BALANCES (Effective for audits of financial statements for periods ending on or after 15 December 2010) CONTENTS

AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF THE MINISTRY OF CULTURE, YOUTH AND SPORTS FOR THE YEAR ENDED 31 DECEMBER 2017

Document No: 25.5.1-2017-08 AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF THE MINISTRY OF CULTURE, YOUTH AND SPORTS FOR THE YEAR ENDED 31 DECEMBER 2017 Prishtina, June 2018 The National Audit Office

Document No: 25.5.1-2017-08 AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF THE MINISTRY OF CULTURE, YOUTH AND SPORTS FOR THE YEAR ENDED 31 DECEMBER 2017 Prishtina, June 2018 The National Audit Office

Report on the Observance of Standards & Codes (ROSC) Accounting & Auditing (A&A)

Accounting & Auditing (A&A)") Public Disclosure Authorized Public Disclosure Authorized Report on the Observance of Standards & Codes (ROSC) Accounting & Auditing (A&A) Public Disclosure Authorized Module A - Accounting & Auditing

Public Disclosure Authorized Public Disclosure Authorized Report on the Observance of Standards & Codes (ROSC) Accounting & Auditing (A&A) Public Disclosure Authorized Module A - Accounting & Auditing

INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 710 COMPARATIVE INFORMATION CORRESPONDING FIGURES AND COMPARATIVE FINANCIAL STATEMENTS

710 COMPARATIVE INFORMATION CORRESPONDING FIGURES AND COMPARATIVE FINANCIAL STATEMENTS") INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 710 COMPARATIVE INFORMATION CORRESPONDING FIGURES AND COMPARATIVE FINANCIAL STATEMENTS Introduction (Effective for audits of financial statements for

INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 710 COMPARATIVE INFORMATION CORRESPONDING FIGURES AND COMPARATIVE FINANCIAL STATEMENTS Introduction (Effective for audits of financial statements for

Auditors Report Booklet

Auditors Report Booklet Table of Illustrations Unmodified Opinion Illustration 1 Illustration 2 Illustration 3 Illustration 4 Illustration 5 Illustration 6 Illustration 7 Illustration 8 Companies with

Auditors Report Booklet Table of Illustrations Unmodified Opinion Illustration 1 Illustration 2 Illustration 3 Illustration 4 Illustration 5 Illustration 6 Illustration 7 Illustration 8 Companies with

Document No: AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF THE MINISTRY OF INFRASTRUCTURE FOR THE YEAR ENDED 31 DECEMBER 2017

Document No: 21.8.1-2017-08 AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF THE MINISTRY OF INFRASTRUCTURE FOR THE YEAR ENDED 31 DECEMBER 2017 Prishtina, June 2018 The National Audit Office of the Republic

Document No: 21.8.1-2017-08 AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF THE MINISTRY OF INFRASTRUCTURE FOR THE YEAR ENDED 31 DECEMBER 2017 Prishtina, June 2018 The National Audit Office of the Republic

ANNUAL AUDIT REPORT. Prishtina, August 2018

ANNUAL AUDIT REPORT 2017 Prishtina, August 2018 ANNUAL AUDIT REPORT - 2017 Table of Content List of Abbreviations... 3 Foreword of the Auditor General... 4 Introduction... 6 Executive Summary... 7 Part

ANNUAL AUDIT REPORT 2017 Prishtina, August 2018 ANNUAL AUDIT REPORT - 2017 Table of Content List of Abbreviations... 3 Foreword of the Auditor General... 4 Introduction... 6 Executive Summary... 7 Part

Audit of Financial Statements Prepared in Accordance with the Small and Medium-sized Entity Financial Reporting Standard

PN 900 (Revised) Issued September 2014; revised August 2016 Effective for a Qualifying Entity's financial statements which cover a period ending on or after 15 December 2016 Practice Note 900 (Revised)

PN 900 (Revised) Issued September 2014; revised August 2016 Effective for a Qualifying Entity's financial statements which cover a period ending on or after 15 December 2016 Practice Note 900 (Revised)

Circular on Reporting to Grantees of the Quality Education Fund

Circular on Reporting to Grantees of the Quality Education Fund This Circular is intended to be used as general guidance for practising members of the Hong Kong Institute of Certified Public Accountants

Circular on Reporting to Grantees of the Quality Education Fund This Circular is intended to be used as general guidance for practising members of the Hong Kong Institute of Certified Public Accountants

International Standard on Auditing (Ireland) 705 Modifications to the Opinion in the Independent Auditor s Report

705 Modifications to the Opinion in the Independent Auditor s Report") International Standard on Auditing (Ireland) 705 Modifications to the Opinion in the Independent Auditor s Report MISSION To contribute to Ireland having a strong regulatory environment in which to do

International Standard on Auditing (Ireland) 705 Modifications to the Opinion in the Independent Auditor s Report MISSION To contribute to Ireland having a strong regulatory environment in which to do

SRI LANKA AUDITING STANDARD 705 MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT CONTENTS

SRI LANKA AUDITING STANDARD 705 MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT (Effective for audits of financial statements for periods beginning on or after 01 January 2014) CONTENTS

SRI LANKA AUDITING STANDARD 705 MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT (Effective for audits of financial statements for periods beginning on or after 01 January 2014) CONTENTS

Fundamental Principles of Financial Auditing

ISSAI 200 Endorsement Version ISSAI 200 Fundamental Principles of Financial Auditing The International Standards of Supreme Audit Institutions, ISSAI, are issued by the International Organization of Supreme

ISSAI 200 Endorsement Version ISSAI 200 Fundamental Principles of Financial Auditing The International Standards of Supreme Audit Institutions, ISSAI, are issued by the International Organization of Supreme

ISA 705, Modifications to the Opinion in the Independent Auditor s Report

International Auditing and Assurance Standards Board ISA 705 (Revised and Redrafted) October 2008 Revised and Redrafted International Standard on Auditing ISA 705, Modifications to the Opinion in the Independent

International Auditing and Assurance Standards Board ISA 705 (Revised and Redrafted) October 2008 Revised and Redrafted International Standard on Auditing ISA 705, Modifications to the Opinion in the Independent

SRI LANKA AUDITING STANDARD 706 EMPHASIS OF MATTER PARAGRAPHS AND OTHER MATTER PARAGRAPHS IN THE INDEPENDENT AUDITOR S REPORT CONTENTS

SRI LANKA AUDITING STANDARD 706 EMPHASIS OF MATTER PARAGRAPHS AND OTHER MATTER PARAGRAPHS IN THE INDEPENDENT AUDITOR S REPORT (Effective for audits of financial statements for periods beginning on or after

SRI LANKA AUDITING STANDARD 706 EMPHASIS OF MATTER PARAGRAPHS AND OTHER MATTER PARAGRAPHS IN THE INDEPENDENT AUDITOR S REPORT (Effective for audits of financial statements for periods beginning on or after

International Standard on Auditing (Ireland) 805 Special Considerations Audits of Single Financial Statements and Specific Elements, Accounts or

805 Special Considerations Audits of Single Financial Statements and Specific Elements, Accounts or") International Standard on Auditing (Ireland) 805 Special Considerations Audits of Single Financial Statements and Specific Elements, Accounts or Items of a Financial Statement MISSION To contribute to

International Standard on Auditing (Ireland) 805 Special Considerations Audits of Single Financial Statements and Specific Elements, Accounts or Items of a Financial Statement MISSION To contribute to

PHILIPPINE STANDARD ON AUDITING 705 (REVISED) MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT

MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT") PHILIPPINE STANDARD ON AUDITING 705 (REVISED) MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT (Effective for audits of financial statements for periods ending on or after December 15,

PHILIPPINE STANDARD ON AUDITING 705 (REVISED) MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT (Effective for audits of financial statements for periods ending on or after December 15,

Initial Audit Engagements Opening Balances

SINGAPORE STANDARD SSA 510 ON AUDITING Initial Audit Engagements Opening Balances SSA 510, Initial Audit Engagements Opening Balances superseded SSA 510, Initial Engagements Opening Balances in January

SINGAPORE STANDARD SSA 510 ON AUDITING Initial Audit Engagements Opening Balances SSA 510, Initial Audit Engagements Opening Balances superseded SSA 510, Initial Engagements Opening Balances in January

ISA 805, Special Considerations Audits of Single Financial Statements and Specific Elements, Accounts or Items of a Financial Statement

International Auditing and Assurance Standards Board ISA 805 (Revised and Redrafted) March 2009 Revised and Redrafted International Standard on Auditing ISA 805, Special Considerations Audits of Single

International Auditing and Assurance Standards Board ISA 805 (Revised and Redrafted) March 2009 Revised and Redrafted International Standard on Auditing ISA 805, Special Considerations Audits of Single

IPCC November AUDIT Test Code 8059 Branch (MULTIPLE) (Date : ) All questions are compulsory. Question 1(6 marks)

(Date : ) All questions are compulsory. Question 1(6 marks)") IPCC November 07 AUDIT Test Code 8059 Branch (MULTIPLE) (Date : 6.07.07) (50 Marks) Note: All questions are compulsory. Question (6 marks) This is a case of external confirmation. covered by SA 505 External

IPCC November 07 AUDIT Test Code 8059 Branch (MULTIPLE) (Date : 6.07.07) (50 Marks) Note: All questions are compulsory. Question (6 marks) This is a case of external confirmation. covered by SA 505 External

INDEPENDENT AUDITORS REPORT ON CONSOLIDATED FINANCIAL STATEMENTS

INDEPENDENT AUDITORS REPORT ON CONSOLIDATED STATEMENTS TO THE MEMBERS OF TATA STEEL LIMITED Report on the Consolidated Ind AS Financial Statements We have audited the accompanying consolidated Ind AS financial

INDEPENDENT AUDITORS REPORT ON CONSOLIDATED STATEMENTS TO THE MEMBERS OF TATA STEEL LIMITED Report on the Consolidated Ind AS Financial Statements We have audited the accompanying consolidated Ind AS financial

Processes, Controls and Audit [AA34] Supplementary for Chapter 08. Audit Reporting

![Processes, Controls and Audit [AA34] Supplementary for Chapter 08. Audit Reporting](/thumbs/84/89340608.jpg "Processes, Controls and Audit [AA34] Supplementary for Chapter 08. Audit Reporting") [AA34] Supplementary for Chapter 08 Audit Reporting This supplementary to the Study Text will be tested from January 2019 Examination. The printed chapter in the book will not be applicable from January

[AA34] Supplementary for Chapter 08 Audit Reporting This supplementary to the Study Text will be tested from January 2019 Examination. The printed chapter in the book will not be applicable from January

External and internal auditing in Estonia

External and internal auditing in Estonia Gert Schultz Auditor at Financial Audit Department National Audit Office of Estonia 7.02.2013 Themes: 1. Overall framework of auditing in Estonia 2. Public sector

External and internal auditing in Estonia Gert Schultz Auditor at Financial Audit Department National Audit Office of Estonia 7.02.2013 Themes: 1. Overall framework of auditing in Estonia 2. Public sector

TERMS OF REFERENCE FOR AUDITS OF NIM/NGO PROJECTS

United Nations Development Programme Office of Audit and Investigations Annex I TERMS OF REFERENCE FOR AUDITS OF NIM/NGO PROJECTS 2014 02 November 2014 TABLE OF CONTENTS Page INTRODUCTION... 3 A. Background...

United Nations Development Programme Office of Audit and Investigations Annex I TERMS OF REFERENCE FOR AUDITS OF NIM/NGO PROJECTS 2014 02 November 2014 TABLE OF CONTENTS Page INTRODUCTION... 3 A. Background...

International Standard on Auditing (Ireland) 706 Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Independent Auditor s Report

706 Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Independent Auditor s Report") International Standard on Auditing (Ireland) 706 Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Independent Auditor s Report MISSION To contribute to Ireland having a strong regulatory

International Standard on Auditing (Ireland) 706 Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Independent Auditor s Report MISSION To contribute to Ireland having a strong regulatory

NOTES ON STANDARDS OF AUDITING [APPLICABLE FOR MAY 2016 & ONWARDS] BY A. AMOGH

![NOTES ON STANDARDS OF AUDITING [APPLICABLE FOR MAY 2016 & ONWARDS] BY A. AMOGH](/thumbs/74/70331585.jpg "NOTES ON STANDARDS OF AUDITING [APPLICABLE FOR MAY 2016 & ONWARDS] BY A. AMOGH") NOTES ON STANDARDS OF AUDITING [APPLICABLE FOR MAY 2016 & ONWARDS] BY A. AMOGH +91 9666460051. Amogh Ashtaputre @amoghashtaputre Amogh Ashtaputre Amogh Ashtaputre THIS BOOK CONTAINS 2 PARTS: I. PART A-

NOTES ON STANDARDS OF AUDITING [APPLICABLE FOR MAY 2016 & ONWARDS] BY A. AMOGH +91 9666460051. Amogh Ashtaputre @amoghashtaputre Amogh Ashtaputre Amogh Ashtaputre THIS BOOK CONTAINS 2 PARTS: I. PART A-

Comparative Information Corresponding Figures and Comparative Financial Statements

SINGAPORE STANDARD SSA 710 ON AUDITING Comparative Information Corresponding Figures and Comparative Financial Statements This SSA 710 Comparative Information Corresponding Figures and Comparative Financial

SINGAPORE STANDARD SSA 710 ON AUDITING Comparative Information Corresponding Figures and Comparative Financial Statements This SSA 710 Comparative Information Corresponding Figures and Comparative Financial

Standard on Auditing (SA) 705 (Revised), Modifications to the Opinion in the Independent. Auditor s Report

705 (Revised), Modifications to the Opinion in the Independent. Auditor s Report") Introduction Standard on Auditing (SA) 705 (Revised), Modifications to the Opinion in the Independent Auditor s Report Contents Paragraphs Scope of this SA... 1 Types of Modified Opinions... 2 Effective

Introduction Standard on Auditing (SA) 705 (Revised), Modifications to the Opinion in the Independent Auditor s Report Contents Paragraphs Scope of this SA... 1 Types of Modified Opinions... 2 Effective

AG ISA (NZ) 705 (REVISED) THE AUDITOR-GENERAL S STATEMENT ON MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT.

705 (REVISED) THE AUDITOR-GENERAL S STATEMENT ON MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT.") AG ISA (NZ) 705 (REVISED) THE AUDITOR-GENERAL S STATEMENT ON MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT Contents Page Introduction 3-4901 Scope of this Statement 3-4901 Application

AG ISA (NZ) 705 (REVISED) THE AUDITOR-GENERAL S STATEMENT ON MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT Contents Page Introduction 3-4901 Scope of this Statement 3-4901 Application

INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 510

510") Issued 07/11 Compiled 0711/13 INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 510 Initial Audit Engagements Opening Balances (ISA (NZ) 510) This compilation was prepared in JulyNovember 2013 and incorporates

Issued 07/11 Compiled 0711/13 INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 510 Initial Audit Engagements Opening Balances (ISA (NZ) 510) This compilation was prepared in JulyNovember 2013 and incorporates

Rural Renewable Energy Agency (RREA) Financial Audit Report. for the period from 1 March 2016 to 30 June Project ID: P

Financial Audit Report. for the period from 1 March 2016 to 30 June Project ID: P") Public Disclosure Authorized Public Disclosure Authorized Rural Renewable Energy Agency (RREA) Financial Audit Report for the period from 1 March 2016 to 30 June 2017 Public Disclosure Authorized Liberia

Public Disclosure Authorized Public Disclosure Authorized Rural Renewable Energy Agency (RREA) Financial Audit Report for the period from 1 March 2016 to 30 June 2017 Public Disclosure Authorized Liberia

Appendix Illustrative Auditor s Reports for Program-Specific Audits

NOTE: The illustrative reports included here represent a sampling of the guidance included in chapter 14 of the AICPA's Audit Guide, Government Auditing Standards and Single Audits (GAS-SA Guide). Purchase

NOTE: The illustrative reports included here represent a sampling of the guidance included in chapter 14 of the AICPA's Audit Guide, Government Auditing Standards and Single Audits (GAS-SA Guide). Purchase

Reporting on Audited Financial Statements: Proposed New and Revised International Standards on Auditing (ISAs)

") IFAC Board Exposure Draft July 2013 Comments due: November 22, 2013 International Standards on Auditing Reporting on Audited Financial Statements: Proposed New and Revised International Standards on Auditing

IFAC Board Exposure Draft July 2013 Comments due: November 22, 2013 International Standards on Auditing Reporting on Audited Financial Statements: Proposed New and Revised International Standards on Auditing

(Effective for all audits relating to accounting periods beginning on or after April 1, )

") SA 706 EMPHASIS OF MATTER PARAGRAPHS AND OTHER MATTER PARAGRAPHS IN THE INDEPENDENT AUDITOR S REPORT (Effective for all audits relating to accounting periods beginning on or after April 1, 2011 1 ) Contents

SA 706 EMPHASIS OF MATTER PARAGRAPHS AND OTHER MATTER PARAGRAPHS IN THE INDEPENDENT AUDITOR S REPORT (Effective for all audits relating to accounting periods beginning on or after April 1, 2011 1 ) Contents

(Effective for all audits relating to accounting periods beginning on or after April 1, 2011)

") SA 805 SPECIAL CONSIDERATIONS AUDITS OF SINGLE FINANCIAL STATEMENTS AND SPECIFIC ELEMENTS, ACCOUNTS OR ITEMS OF A FINANCIAL STATEMENT (Effective for all audits relating to accounting periods beginning

SA 805 SPECIAL CONSIDERATIONS AUDITS OF SINGLE FINANCIAL STATEMENTS AND SPECIFIC ELEMENTS, ACCOUNTS OR ITEMS OF A FINANCIAL STATEMENT (Effective for all audits relating to accounting periods beginning

Emphasis-of-Matter Paragraphs and Other-Matter Paragraphs in the Independent Auditor s Report

Emphasis-of-Matter Paragraphs and Other-Matter Paragraphs 865 AU-C Section 706 Emphasis-of-Matter Paragraphs and Other-Matter Paragraphs in the Independent Auditor s Report Source: SAS No. 122. Effective

Emphasis-of-Matter Paragraphs and Other-Matter Paragraphs 865 AU-C Section 706 Emphasis-of-Matter Paragraphs and Other-Matter Paragraphs in the Independent Auditor s Report Source: SAS No. 122. Effective

New and Revised Auditing Standards Presentation by: CPA Stephen Obock Associate Director, KPMG 30 May 2017

New and Revised Auditing Standards Presentation by: CPA Stephen Obock Associate Director, KPMG 30 May 2017 Uphold public interest Presentation agenda Overview of new changes ISA 700 Forming Audit Opinion

New and Revised Auditing Standards Presentation by: CPA Stephen Obock Associate Director, KPMG 30 May 2017 Uphold public interest Presentation agenda Overview of new changes ISA 700 Forming Audit Opinion

Revised format of Audit Reports SA 700, 705 & 706

Revised format of Audit Reports SA 700, 705 & 706 Disclaimers 2 These are my personal views and cannot be construed to be the views of WIRC or M P Chitale & Co. No representations or warranties are made

Revised format of Audit Reports SA 700, 705 & 706 Disclaimers 2 These are my personal views and cannot be construed to be the views of WIRC or M P Chitale & Co. No representations or warranties are made

TECHNICAL RELEASE TECH09/13 AAF ASSURANCE REVIEW ENGAGEMENTS ON HISTORICAL FINANCIAL STATEMENTS

TECHNICAL RELEASE TECH09/13 AAF ASSURANCE REVIEW ENGAGEMENTS ON HISTORICAL FINANCIAL STATEMENTS ABOUT ICAEW ICAEW is a professional membership organisation, supporting over 140,000 chartered accountants

TECHNICAL RELEASE TECH09/13 AAF ASSURANCE REVIEW ENGAGEMENTS ON HISTORICAL FINANCIAL STATEMENTS ABOUT ICAEW ICAEW is a professional membership organisation, supporting over 140,000 chartered accountants

PROPOSED INTERNATIONAL STANDARD ON AUDITING 705 (REVISED) MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT

MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT") Agenda Item 4-C PROPOSED INTERNATIONAL STANDARD ON AUDITING 705 (REVISED) MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT (Effective for audits of financial statements for periods [beginning/ending

Agenda Item 4-C PROPOSED INTERNATIONAL STANDARD ON AUDITING 705 (REVISED) MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT (Effective for audits of financial statements for periods [beginning/ending

Corporate Overview Statutory Reports Financial Statements Independent Auditor s Report

Independent Auditor s Report To the Members of The Indian Hotels Company Limited Report on the Audit of Consolidated Ind AS Financial Statements We have audited the accompanying consolidated Ind AS financial

Independent Auditor s Report To the Members of The Indian Hotels Company Limited Report on the Audit of Consolidated Ind AS Financial Statements We have audited the accompanying consolidated Ind AS financial

Document No: AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF MUNICIPALITY OF PRIZREN FOR THE YEAR ENDED 31 DECEMBER 2017

Document No: 22.14.1-2017-08 AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF MUNICIPALITY OF PRIZREN FOR THE YEAR ENDED 31 DECEMBER 2017 Prishtina, June 2018 The National Audit Office of the Republic

Document No: 22.14.1-2017-08 AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF MUNICIPALITY OF PRIZREN FOR THE YEAR ENDED 31 DECEMBER 2017 Prishtina, June 2018 The National Audit Office of the Republic

Appendix Amendments to Various Sections in SAS No. 122, Statements on Auditing Standards: Clarification and Recodification, as Amended

ASB Meeting July 17-20, 2017 (marked) Agenda Item 3D1F Appendix Amendments to Various Sections in SAS No. 122, Statements on Auditing Standards: Clarification and Recodification, as Amended (Boldface italics

ASB Meeting July 17-20, 2017 (marked) Agenda Item 3D1F Appendix Amendments to Various Sections in SAS No. 122, Statements on Auditing Standards: Clarification and Recodification, as Amended (Boldface italics

Initial Audit Engagements Opening Balances

ISA 510 Issued November 2009; updated June 2018 International Standard on Auditing Initial Audit Engagements Opening Balances INTERNATIONAL STANDARD ON AUDITING 510 INITIAL AUDIT ENGAGEMENTS OPENING BALANCES

ISA 510 Issued November 2009; updated June 2018 International Standard on Auditing Initial Audit Engagements Opening Balances INTERNATIONAL STANDARD ON AUDITING 510 INITIAL AUDIT ENGAGEMENTS OPENING BALANCES

Refresher : Standards on Auditing

Refresher : Standards on Auditing M P Vijay Kumar FCA 1 M P Vijay Kumar FCA INSURANCE!! The views expressed are those of the presenter and, therefore, do not necessarily represent the views of either the

Refresher : Standards on Auditing M P Vijay Kumar FCA 1 M P Vijay Kumar FCA INSURANCE!! The views expressed are those of the presenter and, therefore, do not necessarily represent the views of either the

Audit communication and reporting

Audit communication and reporting Report of the Auditor-General to Parliament or the Provincial Legislature on the financial statements and performance information Content Report on the financial statements

Audit communication and reporting Report of the Auditor-General to Parliament or the Provincial Legislature on the financial statements and performance information Content Report on the financial statements

A Guide to Understanding National and County Audit Report

A Guide to Understanding National and County Audit Report Published by: Parliamentary Initiatives Network With funding from International Budget Partnership IBP INTERNATIONAL BUDGET PARTNERSHIP Open Budget.

A Guide to Understanding National and County Audit Report Published by: Parliamentary Initiatives Network With funding from International Budget Partnership IBP INTERNATIONAL BUDGET PARTNERSHIP Open Budget.

ISA 210, Agreeing the Terms of Audit Engagements. Conforming Amendments to Other ISAs. ISA 210 (Redrafted)

") International Auditing and Assurance Standards Board ISA 210 (Redrafted) March 2009 Redrafted International Standard on Auditing ISA 210, Agreeing the Terms of Audit Engagements Conforming Amendments to

International Auditing and Assurance Standards Board ISA 210 (Redrafted) March 2009 Redrafted International Standard on Auditing ISA 210, Agreeing the Terms of Audit Engagements Conforming Amendments to

PHILIPPINE STANDARD ON AUDITING 805

PHILIPPINE STANDARD ON AUDITING 805 SPECIAL CONSIDERATIONS AUDITS OF SINGLE FINANCIAL STATEMENTS AND SPECIFIC ELEMENTS, ACCOUNTS OR ITEMS OF A FINANCIAL STATEMENT Introduction (Effective for audits for

PHILIPPINE STANDARD ON AUDITING 805 SPECIAL CONSIDERATIONS AUDITS OF SINGLE FINANCIAL STATEMENTS AND SPECIFIC ELEMENTS, ACCOUNTS OR ITEMS OF A FINANCIAL STATEMENT Introduction (Effective for audits for

The Independent Auditor s Report on a Complete Set of General Purpose Financial Statements

International Auditing and ISA 700 (Revised) December 2004 Assurance Standards Board International Standards on Auditing (ISA) 700 (Revised) The Independent Auditor s Report on a Complete Set of General

International Auditing and ISA 700 (Revised) December 2004 Assurance Standards Board International Standards on Auditing (ISA) 700 (Revised) The Independent Auditor s Report on a Complete Set of General

Zyra e Ministrit / Kancelarija Ministra / Cabinet of the Minister. Ministers Heads of Budget Organisations Officials of Budget Organizations

DATË/A: PËR/ZA/TO: NGA/OD/FROM: Republika e Kosovës Republika Kosova - Republic of Kosovo Qeveria - Vlada - Government Ministria e Financave Ministarstvo za Finansije Ministry of Finance Zyra e Ministrit

DATË/A: PËR/ZA/TO: NGA/OD/FROM: Republika e Kosovës Republika Kosova - Republic of Kosovo Qeveria - Vlada - Government Ministria e Financave Ministarstvo za Finansije Ministry of Finance Zyra e Ministrit

PREPARING AN AUDIT REPORT FOR A GROUP COMBINED AUDIT REPORT FOR THE GROUP AND PARENT COMPANY September 2018

ICAEW AUDIT AND ASSURANCE FACULTY HELPSHEET PREPARING AN AUDIT REPORT FOR A GROUP COMBINED AUDIT REPORT FOR THE GROUP AND PARENT COMPANY September 2018 This helpsheet was last updated in September 2018

ICAEW AUDIT AND ASSURANCE FACULTY HELPSHEET PREPARING AN AUDIT REPORT FOR A GROUP COMBINED AUDIT REPORT FOR THE GROUP AND PARENT COMPANY September 2018 This helpsheet was last updated in September 2018

SOCIJALDEMOKRATIJA. Campaign Financial Disclosure Report with Independent Auditors Report thereon. Local Elections 03 October November 2013

Campaign Financial Disclosure Report with Independent Auditors Report thereon Local Elections 03 October 013 0 November 013 Table of Contents: Independent Auditors report..... 3 Statement of financial

Campaign Financial Disclosure Report with Independent Auditors Report thereon Local Elections 03 October 013 0 November 013 Table of Contents: Independent Auditors report..... 3 Statement of financial

TOPIC 50: AUDIT REPORTING. AUDIT REPORTING (ISA 700 Forming an Opinion and Reporting on Financial Statements)

") TOPIC 50: AUDIT REPORTING AUDIT REPORTING (ISA 700 Forming an Opinion and Reporting on Financial Statements) A company s auditors must report their opinions to the shareholders/members on two primary matters:

TOPIC 50: AUDIT REPORTING AUDIT REPORTING (ISA 700 Forming an Opinion and Reporting on Financial Statements) A company s auditors must report their opinions to the shareholders/members on two primary matters:

INTERNATIONAL STANDARD ON AUDITING 700 FORMING AN OPINION AND REPORTING ON FINANCIAL STATEMENTS CONTENTS

INTERNATIONAL STANDARD ON 700 FORMING AN OPINION AND REPORTING ON FINANCIAL STATEMENTS (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Introduction

INTERNATIONAL STANDARD ON 700 FORMING AN OPINION AND REPORTING ON FINANCIAL STATEMENTS (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Introduction

Comparative Information- Corresponding Figures and Comparative Financial Statements

ISA 710 (Redrafted) Issued March 2009 International Standard on Auditing Comparative Information- Corresponding Figures and Comparative Financial Statements The Malaysian Institute of Certified Public

ISA 710 (Redrafted) Issued March 2009 International Standard on Auditing Comparative Information- Corresponding Figures and Comparative Financial Statements The Malaysian Institute of Certified Public

COVER LETTER The Head: Financial Surveillance Department South African Reserve Bank PO Box 3125 Pretoria Dear Sir,

COVER LETTER The Head: Financial Surveillance Department South African Reserve Bank PO Box 3125 Pretoria 0001 Dear Sir, INDEPENDENT [AUDITOR S/AUDITORS [ use the plural form when more than one firm is

COVER LETTER The Head: Financial Surveillance Department South African Reserve Bank PO Box 3125 Pretoria 0001 Dear Sir, INDEPENDENT [AUDITOR S/AUDITORS [ use the plural form when more than one firm is

Engagements on Attorneys Trust Accounts

Revised Guide March 2017 Revised Guide for Registered Auditors Engagements on Attorneys Trust Accounts Independent Regulatory Board for Auditors PO Box 8237, Greenstone, 1616 Johannesburg This Revised

Revised Guide March 2017 Revised Guide for Registered Auditors Engagements on Attorneys Trust Accounts Independent Regulatory Board for Auditors PO Box 8237, Greenstone, 1616 Johannesburg This Revised

SPECIAL CONSIDERATIONS - AUDITS OF SINGLE FINANCIAL STATEMENTS AND SPECIFIC ELEMENTS, ACCOUNTS OR ITEMS OF A FINANCIAL STATEMENT

SRI LANKA STANDARD 805 SPECIAL CONSIDERATIONS - AUDITS OF SINGLE FINANCIAL STATEMENTS AND SPECIFIC ELEMENTS, ACCOUNTS OR ITEMS OF A FINANCIAL STATEMENT (Effective for audits for periods beginning on or

SRI LANKA STANDARD 805 SPECIAL CONSIDERATIONS - AUDITS OF SINGLE FINANCIAL STATEMENTS AND SPECIFIC ELEMENTS, ACCOUNTS OR ITEMS OF A FINANCIAL STATEMENT (Effective for audits for periods beginning on or

Modifications to the Opinion in the Independent Auditor s Report

SINGAPORE STANDARD ON AUDITING SSA 705 (Revised) Modifications to the Opinion in the Independent Auditor s Report SSA 705 was issued in January 2010. The Companies (Amendment) Act 2014 gave rise to conforming

SINGAPORE STANDARD ON AUDITING SSA 705 (Revised) Modifications to the Opinion in the Independent Auditor s Report SSA 705 was issued in January 2010. The Companies (Amendment) Act 2014 gave rise to conforming

Practice Note 10: Audit of financial statements of public sector bodies in the United Kingdom

Practice Note 10: Audit of financial statements of public sector bodies in the United Kingdom This Practice Note replaces Practice Note 10: Audit of Financial Statements of Public Sector Bodies in the

Practice Note 10: Audit of financial statements of public sector bodies in the United Kingdom This Practice Note replaces Practice Note 10: Audit of Financial Statements of Public Sector Bodies in the

Chapter 17. Auditors Reports. McGraw-Hill/Irwin. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter 17 Auditors Reports McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Audit Report Providing an independent and expert opinion on the fairness of financial

Chapter 17 Auditors Reports McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. Audit Report Providing an independent and expert opinion on the fairness of financial

International Standard on Auditing (UK) 705 (Revised June 2016)

705 (Revised June 2016)") Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 705 (Revised June 2016) Modifi cations to the Opinion in the Independent Auditor s Report The

Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 705 (Revised June 2016) Modifi cations to the Opinion in the Independent Auditor s Report The

Background paper. The ECA s modified approach to the Statement of Assurance audits in Cohesion

Background paper The ECA s modified approach to the Statement of Assurance audits in Cohesion December 2017 1 In our 2018-2020 strategy the European Court of Auditors (ECA) decided to take a fresh look

Background paper The ECA s modified approach to the Statement of Assurance audits in Cohesion December 2017 1 In our 2018-2020 strategy the European Court of Auditors (ECA) decided to take a fresh look

Independent Auditor s Report

Independent Auditor s Report To the Members of Bharat Forge Limited Report on the Consolidated Ind AS Financial Statements We have audited the accompanying consolidated Ind AS financial statements of Bharat

Independent Auditor s Report To the Members of Bharat Forge Limited Report on the Consolidated Ind AS Financial Statements We have audited the accompanying consolidated Ind AS financial statements of Bharat

International Standard on Auditing (UK and Ireland) 705

705") Standard Audit and Assurance Financial Reporting Council October 2012 International Standard on Auditing (UK and Ireland) 705 Modifications to the opinion in the independant auditor s report The FRC is

Standard Audit and Assurance Financial Reporting Council October 2012 International Standard on Auditing (UK and Ireland) 705 Modifications to the opinion in the independant auditor s report The FRC is

Audit of Financial Statements Prepared in Accordance with the Small and Medium-sized Entity Financial Reporting Standard

PN 900 (Revised) Issued December 2006; revised June 2010 Effective for audits of financial statements for periods beginning before 15 December 2009 Practice Note 900 (Revised) Audit of Financial Statements

PN 900 (Revised) Issued December 2006; revised June 2010 Effective for audits of financial statements for periods beginning before 15 December 2009 Practice Note 900 (Revised) Audit of Financial Statements

This Standard has been issued as a result of International Standard on Auditing 705 being revised.

INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 705 (REVISED) Modifications to the Opinion in the Independent Auditor s Report (ISA (NZ) 705 (Revised)) This Standard was issued on 1 October 2015 by the

INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 705 (REVISED) Modifications to the Opinion in the Independent Auditor s Report (ISA (NZ) 705 (Revised)) This Standard was issued on 1 October 2015 by the

AAPG 1 is previously RPG 13. No changes have been made to the original approved text other than as mentioned below:

February 2018 (Previously RPG 13 March 2017) Audit and Assurance Practice Guide 1 Auditors report on financial statements prepared in accordance with the Malaysian Financial Reporting Standards (MFRS)

February 2018 (Previously RPG 13 March 2017) Audit and Assurance Practice Guide 1 Auditors report on financial statements prepared in accordance with the Malaysian Financial Reporting Standards (MFRS)

Objective and General

(Revised)* Issued October 2006 Effective for audits of financial statements for periods beginning on or after 15 December 2005 and where auditor s reports are dated on or after 31 December 2006* Hong Kong

(Revised)* Issued October 2006 Effective for audits of financial statements for periods beginning on or after 15 December 2005 and where auditor s reports are dated on or after 31 December 2006* Hong Kong

Opening Balances Initial Audit Engagements, Including Reaudit Engagements

Opening Balances Initial Audit Engagements 479 AU-C Section 510 Opening Balances Initial Audit Engagements, Including Reaudit Engagements Source: SAS No. 122. Effective for audits of financial statements

Opening Balances Initial Audit Engagements 479 AU-C Section 510 Opening Balances Initial Audit Engagements, Including Reaudit Engagements Source: SAS No. 122. Effective for audits of financial statements

External Audit. April 2012

External Audit April 2012 Audit Definition Ex post review of the books of account, financial statements, records of transactions & financial systems Examines the adequacy of accounting systems & procedures,

External Audit April 2012 Audit Definition Ex post review of the books of account, financial statements, records of transactions & financial systems Examines the adequacy of accounting systems & procedures,

International Standard on Auditing (Ireland) 800 Special Considerations Audits of Financial Statements Prepared in Accordance with Special Purpose

800 Special Considerations Audits of Financial Statements Prepared in Accordance with Special Purpose") International Standard on Auditing (Ireland) 800 Special Considerations Audits of Financial Statements Prepared in Accordance with Special Purpose Frameworks MISSION To contribute to Ireland having a strong

International Standard on Auditing (Ireland) 800 Special Considerations Audits of Financial Statements Prepared in Accordance with Special Purpose Frameworks MISSION To contribute to Ireland having a strong

Appendix Illustrative Auditor s Reports Under Government Auditing Standards

NOTE: The illustrative reports included here represent a sampling of the report examples included in chapter 4 of the AICPA's Audit Guide, Government Auditing Standards and Single Audits (GAS-SA Guide).

NOTE: The illustrative reports included here represent a sampling of the report examples included in chapter 4 of the AICPA's Audit Guide, Government Auditing Standards and Single Audits (GAS-SA Guide).

Audit Engagement Letter a. [CPA Firm s Letterhead]

![Audit Engagement Letter a. [CPA Firm s Letterhead]](/thumbs/82/86656009.jpg "Audit Engagement Letter a. [CPA Firm s Letterhead]") 8 EBP 2/15 EBP-CL-1.1: Audit Engagement Letter a [CPA Firm s Letterhead] [Date] [Identify the body or individual(s) charged with governance.] and [Name of Management] b [Client s Name and Address] We are

8 EBP 2/15 EBP-CL-1.1: Audit Engagement Letter a [CPA Firm s Letterhead] [Date] [Identify the body or individual(s) charged with governance.] and [Name of Management] b [Client s Name and Address] We are

International Standard on Auditing (UK) 700 (Revised June 2016)

700 (Revised June 2016)") Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 700 (Revised June 2016) Forming an Opinion and Reporting on Financial Statements The FRC s mission

Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 700 (Revised June 2016) Forming an Opinion and Reporting on Financial Statements The FRC s mission

Our responsibility is to express an opinion on these financial statements based on our audit.

INDEPENDENT AUDITOR S REPORT TO THE MEMBERS OF PUNARVASU FINANCIAL SERVICES PRIVATE LIMITED (Formerly Known as PUNARVASU HOLDING AND TRADING COMPANY PRIVATE LIMITED) Report on the Financial Statements

INDEPENDENT AUDITOR S REPORT TO THE MEMBERS OF PUNARVASU FINANCIAL SERVICES PRIVATE LIMITED (Formerly Known as PUNARVASU HOLDING AND TRADING COMPANY PRIVATE LIMITED) Report on the Financial Statements

Samostalna Liberalna Stranka Campaign Financial Disclosure Report with Independent Auditors Report thereon

Campaign Financial Disclosure Report with Independent Auditors Report thereon Extraordinary national elections 28 May 2014 06 June 2014 Table of Contents: Independent Auditors report..... 3 Statement of

Campaign Financial Disclosure Report with Independent Auditors Report thereon Extraordinary national elections 28 May 2014 06 June 2014 Table of Contents: Independent Auditors report..... 3 Statement of

RURAL ELECTRIFICATION CORPORATION LIMITED

Independent Auditors Report To, The Members, Rural Electrification Corporation Limited New Delhi Report on the Consolidated Financial Statements We have audited the accompanying consolidated financial

Independent Auditors Report To, The Members, Rural Electrification Corporation Limited New Delhi Report on the Consolidated Financial Statements We have audited the accompanying consolidated financial

Appendix Illustrative Auditor's Reports Under Government Auditing Standards

NOTE: The illustrative reports included here represent a sampling of the report examples included in chapter 4 of the AICPA's Audit Guide, Government Auditing Standards and Single Audits (GAS-SA Guide).

NOTE: The illustrative reports included here represent a sampling of the report examples included in chapter 4 of the AICPA's Audit Guide, Government Auditing Standards and Single Audits (GAS-SA Guide).

Opinion on Receipts, Expenditure, Investment of Moneys and the Acquisition and Disposal of Assets by Statutory Boards

AUDIT GUIDANCE STATEMENT AGS 9 Opinion on Receipts, Expenditure, Investment of Moneys and the Acquisition and Disposal of Assets by Statutory Boards This Audit Guidance Statement was approved by the Council

AUDIT GUIDANCE STATEMENT AGS 9 Opinion on Receipts, Expenditure, Investment of Moneys and the Acquisition and Disposal of Assets by Statutory Boards This Audit Guidance Statement was approved by the Council

Reporting- The New Auditor s Report Presentation by: CPA Stephen Obock Associate Director, KPMG March 2018

Reporting- The New Auditor s Report Presentation by: CPA Stephen Obock Associate Director, KPMG sobock@kpmg.co.ke March 2018 Uphold public interest Agenda Why the changes? Key Audit Matters (KAM) - (ISA

Reporting- The New Auditor s Report Presentation by: CPA Stephen Obock Associate Director, KPMG sobock@kpmg.co.ke March 2018 Uphold public interest Agenda Why the changes? Key Audit Matters (KAM) - (ISA

International Standard on Auditing (UK) 706 (Revised June 2016)

706 (Revised June 2016)") Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 706 (Revised June 2016) Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Independent

Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 706 (Revised June 2016) Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Independent

March 4, 2015 To the Board Members of the Housing Finance Authority of Pinellas County and Kathryn Driver, Executive Director We are pleased to

March 4, 2015 To the Board Members of the Housing Finance Authority of Pinellas County and Kathryn Driver, Executive Director We are pleased to confirm our understanding of the services we are to provide

March 4, 2015 To the Board Members of the Housing Finance Authority of Pinellas County and Kathryn Driver, Executive Director We are pleased to confirm our understanding of the services we are to provide

PUBLIC PROCUREMENT LEGISLATION IN KOSOVO

1 PUBLIC PROCUREMENT LEGISLATION IN KOSOVO Consists of: a ) Law on Public Procurement No. 04/L-042 - LPP No. 04/L-042 is approved by the Parliament of Kosovo on August 29 th, 2011, whereas has entered

1 PUBLIC PROCUREMENT LEGISLATION IN KOSOVO Consists of: a ) Law on Public Procurement No. 04/L-042 - LPP No. 04/L-042 is approved by the Parliament of Kosovo on August 29 th, 2011, whereas has entered