A Primer on Reading Monthly Financial Reports by The Finance Committee

|

|

|

- Maud Payne

- 5 years ago

- Views:

Transcription

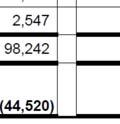

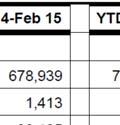

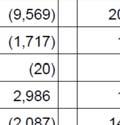

1 A Primer on Reading Monthly Financial Reports by The Finance Committee Every month our director of operations posts a set of financial reports on the church website. Here follows a brief description of the files to orient newcomers to church finances. The first thing to note when looking at files on the Budget and Financials page is the special coding system used for naming the files. Consider, for example, the file named fn td.pdf. fn td.pdf fn indicates a financial report year and month of report: February 2015 in this instance a two (or three) letter code indicating which report this is. See below for codes. A note on fiscal year terminology: everyone is used to the idea of a calendar year. A fiscal year is simply the 12 months over which an organization's budget operates. Fiscal years may start in any month of the year. First Parish's fiscal year begins July 1. When we talk about the 2015 fiscal year, also known as FY15, we are referring to income and spending between July 1, 2014, and June 30, A fiscal year is usually designated by the year in which it ends. We turn next to a description of each of these reports. At the left is the two or three letter code used in the file name as noted above. pls Monthly and Year to Date Income and Spending against Budget (Short Form) (Figure 1) This is a great report to start with as it gives a high level overview of income and spending at any point in time. Any report ending in the code pls is a monthly income and spending report. The "s" indicates this is a short form of this report. More on that below. This table reports income and spending by broad categories for the most recent month along with some other information. Let's take this report column by column using the February 2015 report as an example. That is the file fn pls.pdf and is shown below as Figure 1. The first column reports income and spending in February For example, $35,585 was collected in contribution income. (The numbers to the left of the descriptors, such as 3010, are accounting reference numbers you may ignore.) Similarly, $16,022 was spent on salaries for ministers. The second column reports year to date income and spending. Note that the column is titled "Jul 14 Feb 15." That is because the church's fiscal year began in July 2014, as noted above. We have received $678,939 in contribution income through February 2015 of the current fiscal year. The next column (titled "YTD Budg") indicates (based on historical patterns) what the year to date amount (income or spending) was expected to be. Overall income is slightly below expectations ($842,507 in actual income 1

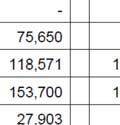

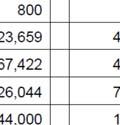

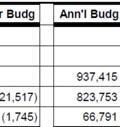

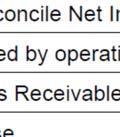

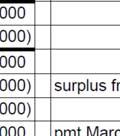

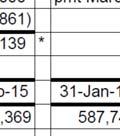

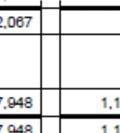

2 versus $896,642 budgeted expectations through February 2015). Similarly, expenses through February are below expected expenses over the same time period. The next column ("$ Over Budg") reports the difference between these two numbers. This column serves as an alert to budget watchers to possible spending or income variations that require attention. Mostly, entries in this column are not a concern: budget deviations typically occur and are usually explainable. The fifth column ("Ann'l Budg") is very important. This is the actual budget passed at the previous year s Annual Meeting and is the guide for all income and spending decisions. The final column ( Budg Rmng ) reports how much of the budget is unallocated as of the end of the current month. For income, this simply means how much income we expect to receive between now and the end of the fiscal year ($363,609 in this report) or how much spending can occur without going over budget ($450,433). The final row in the table shows net income, the difference between total income and total expenses. For February, we spent $44,520 more than we received in income. For the year to date (second column), we've received $87,181 more in income than we've spent. Given the monthly variation in pledge income, we can expect any individual month's net income to be positive or negative; but assuming we keep to the budget the net income will be close to zero ($357) by the end of the fiscal year. pl Monthly and Year to Date Income and Spending against Budget (Long Form) (Figure 2) This report is similar to the pls report described above except it provides information at a much more detailed level. So while the pls report shows information about contribution income, for example, this report breaks that income down into current and prior year pledge payments, non pledge contributions, and other categories. Similar detail is provided for other income and spending categories. This report also provides short notes from the business office to explain certain lines. This is mainly for the Treasurer and Standing Committee's benefit as they review these monthly reports. Figure 2 shows an excerpt from the pl report for February cf Cash Flow Report (Figure 3) The next report to turn to is the Cash Flow report (see Figure 3 below). Cash holdings are not literally cash but monies held in various savings and checking accounts that can be accessed immediately (i.e., we don't have to sell an asset to access the funds.) Recall in the pls report that net income (loss) in February 2015 was $44,520. In other words, we spent $44,520 more than we took in that month. This is not unusual; spending tends to be fairly constant across months, but income comes in at a less regular rate. We tend to get large bursts of income in July and December, for example; the former because many church members pay their entire pledge at or before the beginning of the fiscal year, and the latter as other church members pre pay their pledge before the end of the calendar year for tax purposes. The negative net income for February is reported in the Cash Flow report since spending in excess of income leads to a reduction in our cash holdings. In addition to the difference between income and spending in the pls sheet, there are other demands on our cash holdings. We hold cash not only for church operations but also for a variety of activities that aren't part of the annual operations budget. Think of these items as virtual savings accounts. For example, funds are collected from participants in retreats that aren't all spent at once. Those moneys are put in the bank for safekeeping and a careful record is kept of the amount and which group "owns" those funds. In February 2015, there was a reduction in the Retreats account of $321 as some retreatrelated spending took place for which funds had been set aside. Taking into account the various 2

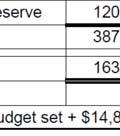

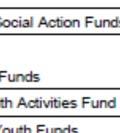

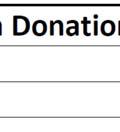

3 additions and withdrawals from these virtual savings accounts, our cash holdings fell by $42,722 in February and our cash at the end of the month equaled $550,369. cp Cash Position (Figure 4) This report (sample report for February 2015 in Figure 4 below) has two parts. The upper part of the report tracks available cash as of the end of the last completed fiscal year. The bottom part focuses on claims on the cash holdings of the church. We'll focus here on the latter. At the end of February 2015, cash on hand equaled $550,369 (the same as the end of month cash holdings in the Cash Flow report discussed above). As noted in the Cash Flow report, a number of church groups have claims on these cash holdings. These are grouped under the Mission and Special Program Funds and equaled $118,791 in the February 2015 report. There are other set asides from cash for various things as listed in the report. Finally, church policy requires a cash reserve equal to 10 percent of annual expenses be set aside for emergencies. After all these set asides, there is $163,190 in available cash. This is analogous to "Free Cash" in the town budget. bs Balance Sheet (Figure 5) This report shows the operating assets, liabilities, and equities of the church. Two excerpts from the February 2015 balance sheet report are shown in Figure 5: one from the assets section and the other from the liabilities section. Current assets include funds in checking and savings accounts (as noted in the Cash Position report). Fixed assets provide a valuation on our building and organ (note that these are not updated to market values). Valuing fixed assets makes sense for a private profit making corporation reporting to shareholders; for a church, the fixed asset value (and total asset value, for that matter) are not particularly relevant. Liabilities are reported after assets. Current liabilities include a number of useful details including a listing of all the special funds in the Cash Position report under Mission and Special Program Funds. Here you can get a breakdown of the Mission Funds ($66,326) and Special Programs ($52,464). td Trustees of Parish Donations Report (Figure 6) This report (see Figure 6) provides an overview of the value of investments overseen by the Trustees as well as funds provided to the Church for its operations in the current fiscal year $90,548 as of the end of February, $135,822 anticipated for the entire fiscal year. The Trustees provide an annual report with considerably more detail than is in these brief monthly updates. * * * * * We hope this overview is helpful in orienting you to the monthly financial reports posted to the web each month. If you have questions about any of the reports, please reach out to any member of the Finance Committee and we'll do our best to answer your questions or direct you to someone else who can. Please let us know if you find this primer useful. We also welcome suggestions for how we could improve it. This is all part of an ongoing effort to make First Parish finances more transparent and understandable to all church members. The Finance Committee April

4 Figure 1. Sample (Short) Income and Spending (pls) Report 4

")

5 Figure 2. Excerpt from Detailed Income and Spending (pl) Report 5

")

6 Figure 3. Sample Cash Flow (cf) Report 6

7 Figure 4. Sample Cash Position (cp) Report 7

")

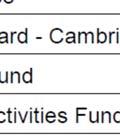

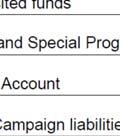

8 Figure 5. Excerpts from Balance Sheet (bs) Portion of Assets Section of Balance Sheet Portion of Liabilities Section of Balance Sheet 8

")

9 Figure 6. Sample Trustees of Parish Donations (td) Report 9

Treasurer s Half Yearly Financial Report. For. Total & Planned Giving General Review

General Review 8 Castle Street HighWycombe Bucks HP13 6RF 1494 527526 office@allsaintshighwycombe.org Treasurer s Half Yearly Financial Report For 215 www.allsaintshighwycombe.org For those of you who

General Review 8 Castle Street HighWycombe Bucks HP13 6RF 1494 527526 office@allsaintshighwycombe.org Treasurer s Half Yearly Financial Report For 215 www.allsaintshighwycombe.org For those of you who

Church Administration Matters

Church Administration Matters Greg Hickle Minnesota District Secretary/Treasurer Church Budgeting 101 Except that it has 6 letters many people seem to have the idea that BUDGET is a 4-letter word. Many

Church Administration Matters Greg Hickle Minnesota District Secretary/Treasurer Church Budgeting 101 Except that it has 6 letters many people seem to have the idea that BUDGET is a 4-letter word. Many

Chapter 9. Is the Filer a Public Charity or Private Foundation?

Chapter 9 Is the Filer a Public Charity or Private Foundation? All section 501(c)(3) nonprofits are either private foundations or nonprivate foundations. The term private foundation is a technical term

Chapter 9 Is the Filer a Public Charity or Private Foundation? All section 501(c)(3) nonprofits are either private foundations or nonprivate foundations. The term private foundation is a technical term

Debt of the Elderly and Near Elderly,

March 5, 2018 No. 443 Debt of the Elderly and Near Elderly, 1992 2016 By Craig Copeland, Ph.D., Employee Benefit Research Institute A T A G L A N C E Much of the attention to retirement preparedness focuses

March 5, 2018 No. 443 Debt of the Elderly and Near Elderly, 1992 2016 By Craig Copeland, Ph.D., Employee Benefit Research Institute A T A G L A N C E Much of the attention to retirement preparedness focuses

Hello I'm Professor Brian Bueche, welcome back. This is the final video in our trilogy on time value of money. Now maybe this trilogy hasn't been as

Hello I'm Professor Brian Bueche, welcome back. This is the final video in our trilogy on time value of money. Now maybe this trilogy hasn't been as entertaining as the Lord of the Rings trilogy. But it

Hello I'm Professor Brian Bueche, welcome back. This is the final video in our trilogy on time value of money. Now maybe this trilogy hasn't been as entertaining as the Lord of the Rings trilogy. But it

Gift Aid Guide. Introduction An Overview Declarations Donations Sponsored Events Annual Reminder...

Index Introduction......... 2 An Overview......... 2 Declarations......... 3 Donations......... 4 Sponsored Events........ 4 Annual Reminder........ 4 Gift Aid Small Donations Scheme...... 5 Record Keeping........

Index Introduction......... 2 An Overview......... 2 Declarations......... 3 Donations......... 4 Sponsored Events........ 4 Annual Reminder........ 4 Gift Aid Small Donations Scheme...... 5 Record Keeping........

IB Interview Guide: Case Study Exercises Three-Statement Modeling Case (30 Minutes)

") IB Interview Guide: Case Study Exercises Three-Statement Modeling Case (30 Minutes) Hello, and welcome to our first sample case study. This is a three-statement modeling case study and we're using this

IB Interview Guide: Case Study Exercises Three-Statement Modeling Case (30 Minutes) Hello, and welcome to our first sample case study. This is a three-statement modeling case study and we're using this

Basics of Financial Statement Analysis: Statements

Basics of Financial Statement Analysis: Statements The current presentation covers the first part of the basics of financial statement analysis. In this first part we will learn how to manipulate entire

Basics of Financial Statement Analysis: Statements The current presentation covers the first part of the basics of financial statement analysis. In this first part we will learn how to manipulate entire

Chapter 18: The Correlational Procedures

Introduction: In this chapter we are going to tackle about two kinds of relationship, positive relationship and negative relationship. Positive Relationship Let's say we have two values, votes and campaign

Introduction: In this chapter we are going to tackle about two kinds of relationship, positive relationship and negative relationship. Positive Relationship Let's say we have two values, votes and campaign

The role of a Gift Aid Secretary

Gift Aid Basics Gift Aid 2014 3 Role of Gift Aid Secretary Basics Operating a Scheme Update on other Gift Aid issues October 2014 St James House Any questions? The role of a Gift Aid Secretary 4 Encourage

Gift Aid Basics Gift Aid 2014 3 Role of Gift Aid Secretary Basics Operating a Scheme Update on other Gift Aid issues October 2014 St James House Any questions? The role of a Gift Aid Secretary 4 Encourage

Real Estate Private Equity Case Study 3 Opportunistic Pre-Sold Apartment Development: Waterfall Returns Schedule, Part 1: Tier 1 IRRs and Cash Flows

Real Estate Private Equity Case Study 3 Opportunistic Pre-Sold Apartment Development: Waterfall Returns Schedule, Part 1: Tier 1 IRRs and Cash Flows Welcome to the next lesson in this Real Estate Private

Real Estate Private Equity Case Study 3 Opportunistic Pre-Sold Apartment Development: Waterfall Returns Schedule, Part 1: Tier 1 IRRs and Cash Flows Welcome to the next lesson in this Real Estate Private

I S S U E B R I E F PUBLIC POLICY INSTITUTE PPI PRESIDENT BUSH S TAX PLAN: IMPACTS ON AGE AND INCOME GROUPS

PPI PUBLIC POLICY INSTITUTE PRESIDENT BUSH S TAX PLAN: IMPACTS ON AGE AND INCOME GROUPS I S S U E B R I E F Introduction President George W. Bush fulfilled a 2000 campaign promise by signing the $1.35

PPI PUBLIC POLICY INSTITUTE PRESIDENT BUSH S TAX PLAN: IMPACTS ON AGE AND INCOME GROUPS I S S U E B R I E F Introduction President George W. Bush fulfilled a 2000 campaign promise by signing the $1.35

THE METHODIST CHURCH STANDARD FORM OF ACCOUNTS. FOR THE YEAR ENDED 31 August 2012

THE METHODIST CHURCH STANDARD FORM OF ACCOUNTS CHURCH RECEIPTS AND PAYMENTS ACCOUNTS FOR THE YEAR ENDED 31 August 2012 Circuit Circuit no Registered Charity - Charity Registration number If not a registered

THE METHODIST CHURCH STANDARD FORM OF ACCOUNTS CHURCH RECEIPTS AND PAYMENTS ACCOUNTS FOR THE YEAR ENDED 31 August 2012 Circuit Circuit no Registered Charity - Charity Registration number If not a registered

Savings Services of Local Financial Institutions in Semi-Urban and Rural Thailand

Savings Services of Local Financial Institutions in Semi-Urban and Rural Thailand Robert Townsend Principal Investigator Joe Kaboski Research Associate March 1999 This report summarizes the savings services

Savings Services of Local Financial Institutions in Semi-Urban and Rural Thailand Robert Townsend Principal Investigator Joe Kaboski Research Associate March 1999 This report summarizes the savings services

Presenting and Understanding Financial Information

The best source of information and training on Aboriginal finance and management The Aboriginal Finance and Management Capacity Development Series Presenting and Understanding Financial Information 2 The

The best source of information and training on Aboriginal finance and management The Aboriginal Finance and Management Capacity Development Series Presenting and Understanding Financial Information 2 The

REPORT OF THE TREASURER OF THE BOARD OF TRUSTEES

REPORT OF THE TREASURER OF THE BOARD OF TRUSTEES To the One Hundred Thirty-eighth Council Of the Diocese of the Northeast and Mid-Atlantic Of the Reformed Episcopal Church Dear Brethren, The overall improvement

REPORT OF THE TREASURER OF THE BOARD OF TRUSTEES To the One Hundred Thirty-eighth Council Of the Diocese of the Northeast and Mid-Atlantic Of the Reformed Episcopal Church Dear Brethren, The overall improvement

Parish Financial Audit Guidelines

Parish Financial Audit Guidelines Version 1.0 Table of Contents Forward... 3 Introduction... 4 Guidelines... 5 Getting Started... 5 Verifying Income... 6 Verifying Disbursements... 7 Compensation and Taxes...

Parish Financial Audit Guidelines Version 1.0 Table of Contents Forward... 3 Introduction... 4 Guidelines... 5 Getting Started... 5 Verifying Income... 6 Verifying Disbursements... 7 Compensation and Taxes...

Policy on Restricted and Designated Funds

Policy on Restricted and Designated Funds The Right Reverend Scott B. Hayashi, Eleventh Bishop of Utah Policy Number: B004 Revision Number: 1 Approved by the Bishop and Diocesan Council: November 2009

Policy on Restricted and Designated Funds The Right Reverend Scott B. Hayashi, Eleventh Bishop of Utah Policy Number: B004 Revision Number: 1 Approved by the Bishop and Diocesan Council: November 2009

Q U I C K E N L O A N S G U I D E. Understanding Mortgage Rates

Q U I C K E N L O A N S G U I D E Understanding Mortgage Rates Home Loan U is a free educational series from Quicken Loans, created to help you make the most of your home, and home financing, at every

Q U I C K E N L O A N S G U I D E Understanding Mortgage Rates Home Loan U is a free educational series from Quicken Loans, created to help you make the most of your home, and home financing, at every

Potential Output in Denmark

43 Potential Output in Denmark Asger Lau Andersen and Morten Hedegaard Rasmussen, Economics 1 INTRODUCTION AND SUMMARY The concepts of potential output and output gap are among the most widely used concepts

43 Potential Output in Denmark Asger Lau Andersen and Morten Hedegaard Rasmussen, Economics 1 INTRODUCTION AND SUMMARY The concepts of potential output and output gap are among the most widely used concepts

YOUR FINANCIAL COMPARISON REPORT

Prepared on April 12th, 2009 INGCompareMe.com ALL RESULTS OK. You've compared yourself to other people like you. What's next? First, you can use this checklist and personalized report to help you keep

Prepared on April 12th, 2009 INGCompareMe.com ALL RESULTS OK. You've compared yourself to other people like you. What's next? First, you can use this checklist and personalized report to help you keep

Policy on Parish Financial Management

Policy on Parish Financial Management The Right Reverend Scott B. Hayashi, Eleventh Bishop of Utah Policy Number: P005 Revision Number: 1 Approved by the Bishop and Diocesan Council: May, 2010 PURPOSE

Policy on Parish Financial Management The Right Reverend Scott B. Hayashi, Eleventh Bishop of Utah Policy Number: P005 Revision Number: 1 Approved by the Bishop and Diocesan Council: May, 2010 PURPOSE

Numerical Descriptive Measures. Measures of Center: Mean and Median

Steve Sawin Statistics Numerical Descriptive Measures Having seen the shape of a distribution by looking at the histogram, the two most obvious questions to ask about the specific distribution is where

Steve Sawin Statistics Numerical Descriptive Measures Having seen the shape of a distribution by looking at the histogram, the two most obvious questions to ask about the specific distribution is where

RetirementWorks. The input can be made extremely simple and approximate, or it can be more detailed and accurate:

Retirement Income Amount RetirementWorks The RetirementWorks Retirement Income Amount calculator analyzes how much someone should withdraw from savings at or during retirement. It uses a needs-based approach,

Retirement Income Amount RetirementWorks The RetirementWorks Retirement Income Amount calculator analyzes how much someone should withdraw from savings at or during retirement. It uses a needs-based approach,

and NOT getting took Keeping the Books - PRC Leader Dev. Day

Keeping the books and NOT getting took 1 Signposts of a Financially Healthy Congregation (PC USA Stewardship Manual)» Understands that all giving, of ourselves as well as our financial resources, is in

Keeping the books and NOT getting took 1 Signposts of a Financially Healthy Congregation (PC USA Stewardship Manual)» Understands that all giving, of ourselves as well as our financial resources, is in

SSA TREASURER S REPORT PHILLIP C. UMPHRES FEBRUARY 2015

I. YEAR END RESULTS FOR 2014 SSA TREASURER S REPORT PHILLIP C. UMPHRES FEBRUARY 2015 Preliminary (unaudited) financial results for SSA Core Operations for 2014 are shown in Attachment A (Statement of Revenues

I. YEAR END RESULTS FOR 2014 SSA TREASURER S REPORT PHILLIP C. UMPHRES FEBRUARY 2015 Preliminary (unaudited) financial results for SSA Core Operations for 2014 are shown in Attachment A (Statement of Revenues

Brief: Potential Impacts of the FY House Budget on Federal R&D

Brief: Potential Impacts of the FY 2013 By Matt Hourihan Director, R&D Budget and Policy Program House Budget on Federal R&D KEY FINDINGS: Under some simple assumptions, the House budget could reduce total

Brief: Potential Impacts of the FY 2013 By Matt Hourihan Director, R&D Budget and Policy Program House Budget on Federal R&D KEY FINDINGS: Under some simple assumptions, the House budget could reduce total

4: Single Cash Flows and Equivalence

4.1 Single Cash Flows and Equivalence Basic Concepts 28 4: Single Cash Flows and Equivalence This chapter explains basic concepts of project economics by examining single cash flows. This means that each

4.1 Single Cash Flows and Equivalence Basic Concepts 28 4: Single Cash Flows and Equivalence This chapter explains basic concepts of project economics by examining single cash flows. This means that each

Webinar 1 - Financial Management

Webinar 1 - Financial Management PRESENTER: Welcome to the webinar on the core principles of financial management, presented by the US Department of Housing and Urban Development. Many of the ideas we

Webinar 1 - Financial Management PRESENTER: Welcome to the webinar on the core principles of financial management, presented by the US Department of Housing and Urban Development. Many of the ideas we

HOMEWORK 3 SOLUTION. a. Which of the forecasters A, B or the forward rate made the most accurate forecast?

HOMEWORK 3 SOLUTION Chapter 8 1. Assume that your company exports to Japan and earns yen revenues, thus forecasts of the Yen/$ rate are important. Suppose two forecasters issue their predictions for the

HOMEWORK 3 SOLUTION Chapter 8 1. Assume that your company exports to Japan and earns yen revenues, thus forecasts of the Yen/$ rate are important. Suppose two forecasters issue their predictions for the

Narrator: Welcome to financial management. To begin, let s work some problems related to corporate taxes.

MGT 325: Module 1 AVP Transcript Title: Tax Effects Slide 1 Title Slide Narrator: Welcome to financial management. To begin, let s work some problems related to corporate taxes. Slide 2 Title: Corporate

MGT 325: Module 1 AVP Transcript Title: Tax Effects Slide 1 Title Slide Narrator: Welcome to financial management. To begin, let s work some problems related to corporate taxes. Slide 2 Title: Corporate

MEDICARE ADVANTAGE PLAN ADMINISTRATIVE COST TRENDS: FIRST OVERALL PMPM COST GROWTH SINCE 2013

Transcript MEDICARE ADVANTAGE PLAN ADMINISTRATIVE COST TRENDS: FIRST OVERALL PMPM COST GROWTH SINCE 2013 September 28, 2017 Douglas B. Sherlock, CFA sherlock@sherlockco.com (215) 628-2289

Transcript MEDICARE ADVANTAGE PLAN ADMINISTRATIVE COST TRENDS: FIRST OVERALL PMPM COST GROWTH SINCE 2013 September 28, 2017 Douglas B. Sherlock, CFA sherlock@sherlockco.com (215) 628-2289

Your guide to putting funeral plans in place

Your guide to putting funeral plans in place Pre-arrange and pre-pay for your perfect goodbye Taking out a funeral plan is not only one of the most thoughtful and caring things you can do, it provides

Your guide to putting funeral plans in place Pre-arrange and pre-pay for your perfect goodbye Taking out a funeral plan is not only one of the most thoughtful and caring things you can do, it provides

Welcome to NCSSSA s webinar on Qualified versus Qualifying retirement plans.

Welcome to NCSSSA s webinar on Qualified versus Qualifying retirement plans. Just a bit of housekeeping before we get started--- Through Webex we can mute all participants so we don t hear all of your

Welcome to NCSSSA s webinar on Qualified versus Qualifying retirement plans. Just a bit of housekeeping before we get started--- Through Webex we can mute all participants so we don t hear all of your

HPM Module_6_Capital_Budgeting_Exercise

HPM Module_6_Capital_Budgeting_Exercise OK, class, welcome back. We are going to do our tutorial on the capital budgeting module. And we've got two worksheets that we're going to look at today. We have

HPM Module_6_Capital_Budgeting_Exercise OK, class, welcome back. We are going to do our tutorial on the capital budgeting module. And we've got two worksheets that we're going to look at today. We have

THE METHODIST CHURCH STANDARD FORM OF ACCOUNTS. FOR THE YEAR ENDED 31 August 2018

THE METHODIST CHURCH STANDARD FORM OF ACCOUNTS CHURCH RECEIPTS AND PAYMENTS ACCOUNTS FOR THE YEAR ENDED 31 August 2018 Circuit Circuit no Registered Charity - Charity Registration number If not a registered

THE METHODIST CHURCH STANDARD FORM OF ACCOUNTS CHURCH RECEIPTS AND PAYMENTS ACCOUNTS FOR THE YEAR ENDED 31 August 2018 Circuit Circuit no Registered Charity - Charity Registration number If not a registered

R02 Performance Measure and evaluation

R02 Performance Measure and evaluation Investment assessment is the final part of the advice process. There are several measures and can be split into three groups. Absolute returns Relative returns Risk

R02 Performance Measure and evaluation Investment assessment is the final part of the advice process. There are several measures and can be split into three groups. Absolute returns Relative returns Risk

PRODUCING BUDGETS AND ACQUITTAL REPORTS from MYOB and spreadsheets

Appendix 1 PRODUCING BUDGETS AND ACQUITTAL REPORTS from MYOB and spreadsheets Explanation of Budgeting and Acquitting This appendix outlines the process of preparing budgets and reports so that you can

Appendix 1 PRODUCING BUDGETS AND ACQUITTAL REPORTS from MYOB and spreadsheets Explanation of Budgeting and Acquitting This appendix outlines the process of preparing budgets and reports so that you can

The Cornell Retirement and Well-Being Study. Final Report 2000

The Cornell Retirement and Well-Being Study Final Report 2000 Phyllis Moen, Ph.D., Principal Investigator with William A. Erickson, M.S., Madhurima Agarwal, M.R.P., Vivian Fields, M.A., and Laurie Todd

The Cornell Retirement and Well-Being Study Final Report 2000 Phyllis Moen, Ph.D., Principal Investigator with William A. Erickson, M.S., Madhurima Agarwal, M.R.P., Vivian Fields, M.A., and Laurie Todd

Facilities Benchmarking Report

Pennsylvania Association of School Business Officials Facilities Benchmarking Report 20 5 (Based upon 20 3-4 data) c PASBO 2015 Rights Reserved Unauthorized copying strictly prohibited April 2015 PASBO

Pennsylvania Association of School Business Officials Facilities Benchmarking Report 20 5 (Based upon 20 3-4 data) c PASBO 2015 Rights Reserved Unauthorized copying strictly prohibited April 2015 PASBO

Retirement. Optimal Asset Allocation in Retirement: A Downside Risk Perspective. JUne W. Van Harlow, Ph.D., CFA Director of Research ABSTRACT

Putnam Institute JUne 2011 Optimal Asset Allocation in : A Downside Perspective W. Van Harlow, Ph.D., CFA Director of Research ABSTRACT Once an individual has retired, asset allocation becomes a critical

Putnam Institute JUne 2011 Optimal Asset Allocation in : A Downside Perspective W. Van Harlow, Ph.D., CFA Director of Research ABSTRACT Once an individual has retired, asset allocation becomes a critical

OCTOBER 1, 2007 RECORDED CALL TRANSCRIPT

ART TILDESLEY Good morning. This is Art Tildesley, Director of Investor Relations at Citigroup. I am here with Chuck Prince, our Chairman and Chief Executive Officer, and Gary Crittenden, our Chief Financial

ART TILDESLEY Good morning. This is Art Tildesley, Director of Investor Relations at Citigroup. I am here with Chuck Prince, our Chairman and Chief Executive Officer, and Gary Crittenden, our Chief Financial

FACTSHEET. Reserves Policies for Charities July What are charity reserves? Why have a Reserves Policy?

Reserves Policies for Charities July 2018 What are charity reserves? For the purposes of this document reserves can be understood as income which is available to the charity and which can be spent at the

Reserves Policies for Charities July 2018 What are charity reserves? For the purposes of this document reserves can be understood as income which is available to the charity and which can be spent at the

How Do You Calculate Cash Flow in Real Life for a Real Company?

How Do You Calculate Cash Flow in Real Life for a Real Company? Hello and welcome to our second lesson in our free tutorial series on how to calculate free cash flow and create a DCF analysis for Jazz

How Do You Calculate Cash Flow in Real Life for a Real Company? Hello and welcome to our second lesson in our free tutorial series on how to calculate free cash flow and create a DCF analysis for Jazz

Arranging and paying for a funeral in advance. Pre-arrange and pre-pay for your perfect goodbye

Arranging and paying for a funeral in advance Pre-arrange and pre-pay for your perfect goodbye Welcome Taking out a funeral plan is not only one of the most thoughtful and caring things you can do, it

Arranging and paying for a funeral in advance Pre-arrange and pre-pay for your perfect goodbye Welcome Taking out a funeral plan is not only one of the most thoughtful and caring things you can do, it

UCRP and GEP Quarterly Investment Risk Report

UCRP and GEP Quarterly Investment Risk Report Quarter ending June 2011 Committee on Investments/ Investment Advisory Group September 14, 2011 Contents UCRP Asset allocation history 5 17 What are the fund

UCRP and GEP Quarterly Investment Risk Report Quarter ending June 2011 Committee on Investments/ Investment Advisory Group September 14, 2011 Contents UCRP Asset allocation history 5 17 What are the fund

TDS Lite. TDS Lite is a simplified version of the official Young Life TDS program. For more detailed information consult Young Life s TDS handbook.

TDS Lite TDS stands for Taking Donors Seriously. It is the official fund-raising program for Young Life areas. Key Assessment Questions Who owns fundraising in the area? Is the vision and commitment for

TDS Lite TDS stands for Taking Donors Seriously. It is the official fund-raising program for Young Life areas. Key Assessment Questions Who owns fundraising in the area? Is the vision and commitment for

Budgeting and Accounting Perspectives

Excerpts from J.L. Chan (1998), The Bases of Accounting for Budgeting and Financial Reporting, in Handbook of Government Budgeting, edited by R.T. Meyers (Josey-Bass), pp. 357-380., 2005 DEGREES OF ACCRUAL

Excerpts from J.L. Chan (1998), The Bases of Accounting for Budgeting and Financial Reporting, in Handbook of Government Budgeting, edited by R.T. Meyers (Josey-Bass), pp. 357-380., 2005 DEGREES OF ACCRUAL

Notes on a California Perspective of the Dairy Margin Protection Program (DMPP)

") Notes on a California Perspective of the Dairy Margin Protection Program (DMPP) Leslie J. Butler Department of Agricultural & Resource Economics University of California-Davis If I were a California dairy

Notes on a California Perspective of the Dairy Margin Protection Program (DMPP) Leslie J. Butler Department of Agricultural & Resource Economics University of California-Davis If I were a California dairy

Auxiliary Periodic Report Instructions

Auxiliary Periodic Report Instructions Overview Auxiliary Periodic Reports provide Periodic projections of revenues, expenses, transfers-in and transfers-out. After Auxiliary Periodic Reports are prepared,

Auxiliary Periodic Report Instructions Overview Auxiliary Periodic Reports provide Periodic projections of revenues, expenses, transfers-in and transfers-out. After Auxiliary Periodic Reports are prepared,

USJE-PSAC. Local Treasurers Handbook

USJE-PSAC Local Treasurers Handbook 2018 1 Table of Contents INTRODUCTION... 3 DEFINITIONS - EXPENSES... 4 DEFINITIONS - REVENUES... 8 GENERAL... 9 BANK ACCOUNT(S)... 10 LOCAL BANK ACCOUNT INFORMATION...

USJE-PSAC Local Treasurers Handbook 2018 1 Table of Contents INTRODUCTION... 3 DEFINITIONS - EXPENSES... 4 DEFINITIONS - REVENUES... 8 GENERAL... 9 BANK ACCOUNT(S)... 10 LOCAL BANK ACCOUNT INFORMATION...

What Is Risk? (Part II)

") What Is Risk? (Part II) This essay was originally published in Muhlenkamp Memorandum Issue 28, October 1993. At that time, one of Ron s largest clients (a pension fund) was being told by a stock brokerage

What Is Risk? (Part II) This essay was originally published in Muhlenkamp Memorandum Issue 28, October 1993. At that time, one of Ron s largest clients (a pension fund) was being told by a stock brokerage

AN ANNUITY THAT PEOPLE MIGHT ACTUALLY BUY

July 2007, Number 7-10 AN ANNUITY THAT PEOPLE MIGHT ACTUALLY BUY By Anthony Webb, Guan Gong, and Wei Sun* Introduction Immediate annuities provide insurance against outliving one s wealth. Previous research

July 2007, Number 7-10 AN ANNUITY THAT PEOPLE MIGHT ACTUALLY BUY By Anthony Webb, Guan Gong, and Wei Sun* Introduction Immediate annuities provide insurance against outliving one s wealth. Previous research

Federal Home Loan Bank of Pittsburgh First Quarter 2018 Member Conference Call

Federal Home Loan Bank of Pittsburgh First Quarter 2018 Member Conference Call May 1, 2018 at 9 a.m. ET WINTHROP WATSON Good morning and thanks for attending our quarterly member call. I m joined by Kris

Federal Home Loan Bank of Pittsburgh First Quarter 2018 Member Conference Call May 1, 2018 at 9 a.m. ET WINTHROP WATSON Good morning and thanks for attending our quarterly member call. I m joined by Kris

There are several types of tax-favored retirement

Tax-Favored Retirement Plans Steve Rosenthal April 20, 2017 There are several types of tax-favored retirement plans. They differ mainly on the type of sponsor and the tax treatment of contributions and

Tax-Favored Retirement Plans Steve Rosenthal April 20, 2017 There are several types of tax-favored retirement plans. They differ mainly on the type of sponsor and the tax treatment of contributions and

Management Reports. June for PREPARED BY POWERED BY

Management Reports for June 217 PREPARED BY POWERED BY Contents 1. Management Reports Cashflow Forecast Actual vs Budget P&L Forecast Where Did Our Money Go? Net Worth 2. Understanding your Reports 3.

Management Reports for June 217 PREPARED BY POWERED BY Contents 1. Management Reports Cashflow Forecast Actual vs Budget P&L Forecast Where Did Our Money Go? Net Worth 2. Understanding your Reports 3.

Short Form Return of Organization Exempt From Income Tax

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Form 99-EZ Department of the Treasury Internal Revenue Service Short Form Return of Organization Exempt From Income Tax Under section 51(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private

Statistical commentary on preliminary locational and consolidated international banking statistics at end-june Monetary and Economic Department

Statistical commentary on preliminary locational and consolidated international banking statistics at end-june 2011 Monetary and Economic Department October 2011 Queries concerning this release should

Statistical commentary on preliminary locational and consolidated international banking statistics at end-june 2011 Monetary and Economic Department October 2011 Queries concerning this release should

Corridor District of the North Carolina Conference The United Methodist Church

Audit Information Corridor District of the North Carolina Conference Section 258.4(d) of the 2012 Book of Discipline makes it MANDATORY that every church finance committee shall make provision for an annual

Audit Information Corridor District of the North Carolina Conference Section 258.4(d) of the 2012 Book of Discipline makes it MANDATORY that every church finance committee shall make provision for an annual

Brainy's Trading News and BullCharts Tips Monthly e-newsletters

Brainy's Trading News and BullCharts Tips Monthly e-newsletters 24 Nov 2008 Special preview of Brainy's monthly articles This pdf file contains only the first page of each of the articles that are available

Brainy's Trading News and BullCharts Tips Monthly e-newsletters 24 Nov 2008 Special preview of Brainy's monthly articles This pdf file contains only the first page of each of the articles that are available

Arithmetic Sequences (Sequence Part 2) Supplemental Material Not Found in You Text

Supplemental Material Not Found in You Text") Math 34: Fall 015 Arithmetic Sequences (Sequence Part ) Supplemental Material Not Found in You Text Arithmetic Sequences Recall an Arithmetic Sequence is a sequence where the difference between any two

Math 34: Fall 015 Arithmetic Sequences (Sequence Part ) Supplemental Material Not Found in You Text Arithmetic Sequences Recall an Arithmetic Sequence is a sequence where the difference between any two

Diocesan Cashbook v3.1

Diocesan Cashbook v3.1 1. About the Diocesan Cashbook... 2 2. Cashbook Layout... 2 2.1 Main Menu...2 2.2 Transactions...3 2.3 Previous year...3 New for version 3.1: 2.4 Fees Summary...3 2.5 Balances...3

Diocesan Cashbook v3.1 1. About the Diocesan Cashbook... 2 2. Cashbook Layout... 2 2.1 Main Menu...2 2.2 Transactions...3 2.3 Previous year...3 New for version 3.1: 2.4 Fees Summary...3 2.5 Balances...3

HPM Module_1_Income_Statement_Analysis

HPM Module_1_Income_Statement_Analysis All right, class, we're going to do another tutorial. And this is going to be on the income statement financial analysis. And we have a problem here that we took

HPM Module_1_Income_Statement_Analysis All right, class, we're going to do another tutorial. And this is going to be on the income statement financial analysis. And we have a problem here that we took

2018 Report. July 2018

2018 Report July 2018 Foreword This year the FCA and FCA Practitioner Panel have, for the second time, carried out a joint survey of regulated firms to monitor the industry s perception of the FCA and

2018 Report July 2018 Foreword This year the FCA and FCA Practitioner Panel have, for the second time, carried out a joint survey of regulated firms to monitor the industry s perception of the FCA and

Individual Account Retirement Plans: An Analysis of the 2016 Survey of Consumer Finances

March 13, 2018 No. 445 Individual Account Retirement Plans: An Analysis of the 2016 Survey of Consumer Finances By Craig Copeland, Employee Benefit Research Institute A T A G L A N C E Individual account

March 13, 2018 No. 445 Individual Account Retirement Plans: An Analysis of the 2016 Survey of Consumer Finances By Craig Copeland, Employee Benefit Research Institute A T A G L A N C E Individual account

Parish Finance Statistics 2016

Parish Finance Statistics 2016 Research and Statistics unit Church House Great Smith Street London SW1P 3AZ Tel: 020 7898 1547 Published 2018 by Research and Statistics unit Copyright Research and Statistics

Parish Finance Statistics 2016 Research and Statistics unit Church House Great Smith Street London SW1P 3AZ Tel: 020 7898 1547 Published 2018 by Research and Statistics unit Copyright Research and Statistics

PRESENTATION. Mike Majors - Torchmark Corporation - VP of IR

1st Quarter 2017 Conference Call April 20, 2017 CORPORATE PARTICIPANTS Mike Majors Torchmark - VP of IR Gary Coleman Torchmark - Larry Hutchison Torchmark - Frank Svoboda Torchmark - Brian Mitchell Torchmark

1st Quarter 2017 Conference Call April 20, 2017 CORPORATE PARTICIPANTS Mike Majors Torchmark - VP of IR Gary Coleman Torchmark - Larry Hutchison Torchmark - Frank Svoboda Torchmark - Brian Mitchell Torchmark

401(k) Plan Asset Allocation, Account Balances, and Loan Activity in 1998

Plan Asset Allocation, Account Balances, and Loan Activity in 1998") February 2000 Jan. 401(k) Plan Asset Allocation, Account Balances, and Loan Activity in 1998 by Jack VanDerhei, Temple University; Sarah Holden, ICI; and Carol Quick, EBRI EBRI EMPLOYEE BENEFIT RESEARCH

February 2000 Jan. 401(k) Plan Asset Allocation, Account Balances, and Loan Activity in 1998 by Jack VanDerhei, Temple University; Sarah Holden, ICI; and Carol Quick, EBRI EBRI EMPLOYEE BENEFIT RESEARCH

AN ANNUITY THAT PEOPLE MIGHT ACTUALLY BUY

July 2007, Number 7-10 AN ANNUITY THAT PEOPLE MIGHT ACTUALLY BUY By Anthony Webb, Guan Gong, and Wei Sun* Introduction Immediate annuities provide insurance against outliving one s wealth. Previous research

July 2007, Number 7-10 AN ANNUITY THAT PEOPLE MIGHT ACTUALLY BUY By Anthony Webb, Guan Gong, and Wei Sun* Introduction Immediate annuities provide insurance against outliving one s wealth. Previous research

Annual Parish Assessment Worksheet

Parish Assessment Calendar: Annual Parish Assessment Worksheet 1. August 31, 2018: Accounting & Finance uses all General Ledger revenue and approved expense account balances for the 12 months ended June

Parish Assessment Calendar: Annual Parish Assessment Worksheet 1. August 31, 2018: Accounting & Finance uses all General Ledger revenue and approved expense account balances for the 12 months ended June

December 2018 Financial Report Summary

The Diocese of the West, The Orthodox Church in America Office of the Treasurer 1520 Green St San Francisco, CA 94123-5102 Web Site for links to prior month Monthly Reports: http://dowoca.org/reports_financial.html

The Diocese of the West, The Orthodox Church in America Office of the Treasurer 1520 Green St San Francisco, CA 94123-5102 Web Site for links to prior month Monthly Reports: http://dowoca.org/reports_financial.html

UTILITY RESERVE POLICY FINAL REPORT

To: Utility Rate Advisory Commission (URAC) From: Reserve Fund Subcommittee (L. Kristov, R. McCann, E. Roberts Musser) Re: Reserve Fund Policy Date: Feb. 20, 2019 UTILITY RESERVE POLICY FINAL REPORT The

To: Utility Rate Advisory Commission (URAC) From: Reserve Fund Subcommittee (L. Kristov, R. McCann, E. Roberts Musser) Re: Reserve Fund Policy Date: Feb. 20, 2019 UTILITY RESERVE POLICY FINAL REPORT The

On track. with The Wrigley Pension Plan

Issue 2 September 2013 On track with The Wrigley Pension Plan Pensions: a golden egg? There s a definite bird theme to this edition of On Track. If you want to add to your nest egg for retirement, we ll

Issue 2 September 2013 On track with The Wrigley Pension Plan Pensions: a golden egg? There s a definite bird theme to this edition of On Track. If you want to add to your nest egg for retirement, we ll

Balance Sheets» How Do I Use the Numbers?» Analyzing Financial Condition» Scenic Video

Balance Sheets» How Do I Use the Numbers?» Analyzing Financial Condition» Scenic Video www.navigatingaccounting.com/video/scenic-financial-leverage Scenic Video Transcript Financial Leverage Topics Intel

Balance Sheets» How Do I Use the Numbers?» Analyzing Financial Condition» Scenic Video www.navigatingaccounting.com/video/scenic-financial-leverage Scenic Video Transcript Financial Leverage Topics Intel

Supporting Asbury. Asbury. Transforming Lives... Retreat Center

Supporting Asbury Transforming Lives... Asbury Retreat Center Those who have experienced the spirit of Asbury... have a common thread that weaves their lives together. With this bond, comes the opportunity

Supporting Asbury Transforming Lives... Asbury Retreat Center Those who have experienced the spirit of Asbury... have a common thread that weaves their lives together. With this bond, comes the opportunity

AF4 Asset Classes Part 3: Shares

AF4 Asset Classes Part 3: Shares The milestones for this part are to understand: The main types of share. The difference between technical and fundamental analysis How to calculate and interpret Price/Earnings

AF4 Asset Classes Part 3: Shares The milestones for this part are to understand: The main types of share. The difference between technical and fundamental analysis How to calculate and interpret Price/Earnings

Real Estate Ownership by Non-Real Estate Firms: The Impact on Firm Returns

Real Estate Ownership by Non-Real Estate Firms: The Impact on Firm Returns Yongheng Deng and Joseph Gyourko 1 Zell/Lurie Real Estate Center at Wharton University of Pennsylvania Prepared for the Corporate

Real Estate Ownership by Non-Real Estate Firms: The Impact on Firm Returns Yongheng Deng and Joseph Gyourko 1 Zell/Lurie Real Estate Center at Wharton University of Pennsylvania Prepared for the Corporate

Unit 4 Budgeting, Variance Analysis, and Pricing

Unit 4 Budgeting, Variance Analysis, and Pricing Learning Objectives: After completing this unit, you should understand: The value of budgets in planning and control. The use and preparation of the four

Unit 4 Budgeting, Variance Analysis, and Pricing Learning Objectives: After completing this unit, you should understand: The value of budgets in planning and control. The use and preparation of the four

Draft Parish Financial Reporting Policy

The Diocese of the Midwest, OCA Draft Parish Financial Reporting Policy Effective Date: 01 January 2018 Revision Date: 10 August 2016 Page 1 of 6 NOTICE: This document is being distributed to the Diocese

The Diocese of the Midwest, OCA Draft Parish Financial Reporting Policy Effective Date: 01 January 2018 Revision Date: 10 August 2016 Page 1 of 6 NOTICE: This document is being distributed to the Diocese

9 Investing Questions You're Too Embarrassed to Ask

9 Investing Questions You're Too Embarrassed to Ask By Tim Lemke 26 April 2016 You can't build wealth through investing if you never get started. And sometimes, getting started is just a matter of overcoming

9 Investing Questions You're Too Embarrassed to Ask By Tim Lemke 26 April 2016 You can't build wealth through investing if you never get started. And sometimes, getting started is just a matter of overcoming

Canon 17 Business Methods in Church Affairs [Renumbered in 1997; Amended in 2000; Amended in 2002]

![Canon 17 Business Methods in Church Affairs [Renumbered in 1997; Amended in 2000; Amended in 2002]](/thumbs/84/90567506.jpg "Canon 17 Business Methods in Church Affairs [Renumbered in 1997; Amended in 2000; Amended in 2002]") Diocese of North Carolina Procedures for Audit Committee Revised for the 2014 audit year and forward until such time as Diocesan Council requests a change. Canon 17 Business Methods in Church Affairs [Renumbered

Diocese of North Carolina Procedures for Audit Committee Revised for the 2014 audit year and forward until such time as Diocesan Council requests a change. Canon 17 Business Methods in Church Affairs [Renumbered

Trends. o The take-up rate (the A T A. workers. Both the. of workers covered by percent. in Between cent to 56.5 percent.

April 2012 No o. 370 Employment-Based Health Benefits: Trends in Access and Coverage, 1997 20100 By Paul Fronstin, Ph.D., Employeee Benefit Research Institute A T A G L A N C E Since 2002 the percentage

April 2012 No o. 370 Employment-Based Health Benefits: Trends in Access and Coverage, 1997 20100 By Paul Fronstin, Ph.D., Employeee Benefit Research Institute A T A G L A N C E Since 2002 the percentage

Endowment funds at the Catholic Foundation can support things like:

HOW TO GIVE Making a Gift Why give to the Foundation? The Catholic Foundation of Maine offers donors several gifting opportunities to help them fulfill their charitable intentions. By creating a legacy

HOW TO GIVE Making a Gift Why give to the Foundation? The Catholic Foundation of Maine offers donors several gifting opportunities to help them fulfill their charitable intentions. By creating a legacy

The BrightScope/ICI Defined Contribution Plan Profile: A Close Look at ERISA 403(b) Plans, 2013

Plans, 2013") The BrightScope/ICI Defined Contribution Plan Profile: A Close Look at ERISA 403(b) Plans, 2013 MAY 2016 The BrightScope/ICI Defined Contribution Plan Profile: A Close Look at ERISA 403(b) Plans, 2013

The BrightScope/ICI Defined Contribution Plan Profile: A Close Look at ERISA 403(b) Plans, 2013 MAY 2016 The BrightScope/ICI Defined Contribution Plan Profile: A Close Look at ERISA 403(b) Plans, 2013

PowerPoint. to accompany. Chapter 11. Systematic Risk and the Equity Risk Premium

PowerPoint to accompany Chapter 11 Systematic Risk and the Equity Risk Premium 11.1 The Expected Return of a Portfolio While for large portfolios investors should expect to experience higher returns for

PowerPoint to accompany Chapter 11 Systematic Risk and the Equity Risk Premium 11.1 The Expected Return of a Portfolio While for large portfolios investors should expect to experience higher returns for

The Relationship Between Medical Utilization and Indemnity Claim Severity

NCCI RESEARCH BRIEF February 2011 by Tanya Restrepo and Harry Shuford The Relationship Between Medical Utilization and Indemnity Claim Severity Comparing the Factors Driving Medical and Indemnity Severity

NCCI RESEARCH BRIEF February 2011 by Tanya Restrepo and Harry Shuford The Relationship Between Medical Utilization and Indemnity Claim Severity Comparing the Factors Driving Medical and Indemnity Severity

The Church in Wales Membership and Finances

The Church in Wales Membership and Finances 2014 Welcome to the Church in Wales Membership and Finances report for 2014. This year s report is based upon a 94% return from Church in Wales parishes, and

The Church in Wales Membership and Finances 2014 Welcome to the Church in Wales Membership and Finances report for 2014. This year s report is based upon a 94% return from Church in Wales parishes, and

RetirementWorks. The input can be made extremely simple and approximate, or it can be more detailed and accurate:

Retirement Income Annuitization The RetirementWorks Retirement Income Annuitization calculator analyzes how much of a retiree s savings should be converted to a monthly annuity stream. It uses a needs-based

Retirement Income Annuitization The RetirementWorks Retirement Income Annuitization calculator analyzes how much of a retiree s savings should be converted to a monthly annuity stream. It uses a needs-based

Charitable Gift Annuities

Charitable Gift Annuities What is a Charitable Gift Annuity? A charitable gift annuity is a planned giving tool that allows the donor to make a gift while at the same time receiving a constant stream of

Charitable Gift Annuities What is a Charitable Gift Annuity? A charitable gift annuity is a planned giving tool that allows the donor to make a gift while at the same time receiving a constant stream of

15 LMR JULY Financing. by Robert P. Murphy, PhD

15 LMR JULY 2012 Equipment Financing with IBC PART I: The Base Case by Robert P. Murphy, PhD 16 LMR JULY 2012 Regular readers of the Lara-Murphy Report know that we are strong advocates of the Infinite

15 LMR JULY 2012 Equipment Financing with IBC PART I: The Base Case by Robert P. Murphy, PhD 16 LMR JULY 2012 Regular readers of the Lara-Murphy Report know that we are strong advocates of the Infinite

Understanding Your Personal Balance Sheet

Understanding Your Personal Balance Sheet A Personal Balance Sheet (PBS) is one of two basic financial statements that are vital to one's financial security. Along with the Personal Cash Flow Statement

Understanding Your Personal Balance Sheet A Personal Balance Sheet (PBS) is one of two basic financial statements that are vital to one's financial security. Along with the Personal Cash Flow Statement

DIGGING DEEPER INTO THE VOLATILITY ASPECTS OF AGRICULTURAL OPTIONS

R.J. O'BRIEN ESTABLISHED IN 1914 DIGGING DEEPER INTO THE VOLATILITY ASPECTS OF AGRICULTURAL OPTIONS This article is a part of a series published by R.J. O Brien & Associates Inc. on risk management topics

R.J. O'BRIEN ESTABLISHED IN 1914 DIGGING DEEPER INTO THE VOLATILITY ASPECTS OF AGRICULTURAL OPTIONS This article is a part of a series published by R.J. O Brien & Associates Inc. on risk management topics

With-profits summary. 1. Introduction. Aims of this summary

With-profits summary On 31 December 2015 business from other insurance company subsidiaries of Lloyds Banking Group was transferred into Clerical Medical Investment Group Limited, which contains the Clerical

With-profits summary On 31 December 2015 business from other insurance company subsidiaries of Lloyds Banking Group was transferred into Clerical Medical Investment Group Limited, which contains the Clerical

Unitarian Universalist Church of Arlington Board of Trustees Meeting Minutes September 18, 2018

UUCA Board Meeting Minutes September 18, 2018 Attendees Unitarian Universalist Church of Arlington Board of Trustees Meeting Minutes September 18, 2018 Board of Trustees: Ai Himes - Chair, Linda Battaglini,

UUCA Board Meeting Minutes September 18, 2018 Attendees Unitarian Universalist Church of Arlington Board of Trustees Meeting Minutes September 18, 2018 Board of Trustees: Ai Himes - Chair, Linda Battaglini,

This is How Do Managers Use Financial and Nonfinancial Performance Measures?, chapter 13 from the book Accounting for Managers (index.html) (v. 1.0).

(v. 1.0).") This is How Do Managers Use Financial and Nonfinancial Performance Measures?, chapter 13 from the book Accounting for Managers (index.html) (v. 1.0). This book is licensed under a Creative Commons by-nc-sa

This is How Do Managers Use Financial and Nonfinancial Performance Measures?, chapter 13 from the book Accounting for Managers (index.html) (v. 1.0). This book is licensed under a Creative Commons by-nc-sa

Charitable Giving Opportunities Under the New Tax Law

Charitable Giving Opportunities Under the New Tax Law November 12, 2018 by Robert Huebscher Kim Laughton is president of Schwab Charitable, a non-profit, donoradvised fund (DAF) provider established with

Charitable Giving Opportunities Under the New Tax Law November 12, 2018 by Robert Huebscher Kim Laughton is president of Schwab Charitable, a non-profit, donoradvised fund (DAF) provider established with

Church Contribution Getting Started Guide 2017 Icon Systems Inc.

Church Contribution Getting Started Guide IconCMO Church Software by Icon Systems Inc. Church Contribution Getting Started Guide All rights reserved. No parts of this work may be reproduced in any form

Church Contribution Getting Started Guide IconCMO Church Software by Icon Systems Inc. Church Contribution Getting Started Guide All rights reserved. No parts of this work may be reproduced in any form