- Forming an audit opinion - Communication of Key Audit Matters

|

|

|

- Melvin Warner

- 5 years ago

- Views:

Transcription

1 - Forming an audit opinion - Communication of Key Audit Matters Presented by FCPA SAID ABEID Uphold public interest

2 Presentation outline 1. Introductory examples 2. Why change is important 3. Key benefits according to IAASB 4. What is new? 5. Key concepts 6. Forms of modified opinions 7. ISAs affected 8. Discussion on what is in the horizon?

3 Introductory examples Audit report in 1990 Audit report in 2010 Audit report in 2015 Audit report in 2016

4 The IAASB has responded to calls from investors and others that it is in the Public interest for an auditor to provide greater transparency about the audit that was performed. Increasing the communicative value of the auditor s report is critical to the perceived value of the financial statement audit Dan Montgomery, former IAASB Deputy Chair and Chair of the Auditor reporting project Source: IAASB press release dated 15 Jan 2015

5 Why is the change important Audit report is a key deliverable addressing the output of the audit process. Financial statements users need more informative report Auditors to provide more relevant information to users

6 Why is the change important (continued) Enhanced reporting will influence the value of the financial statement audit Increase transparency in the reporting It will ensure continued relevance of the auditing profession.

7 Key benefits according to IAASB Increased informational value of the auditor s report. Enhanced communications between investors and the auditor, Enhanced communication between the auditor and those charged with governance

8 Key benefits according to IAASB (continued) Increased attention by management to the disclosures in the financial statements to which reference is made in the auditor s report Renewed focus of the auditor on matters to be communicated in the auditor s report, which could indirectly result in an increase in professional skepticism.

9 What is new? Dichotomy - between listed and non listed entities. Mandatory for audits of financial statements of listed entities, voluntarily application allowed for entities other than listed entities. New KAM section - to communicate key audit matters (KAM). KAM are those matters that, in the auditor s judgment, were of most significance in the audit of the current period financial statements.

10 What is new? contd. Name of engagement Partner - Disclosure of the name of the engagement partner. Other changes for all entities see next slide.

11 What is new? contd. Changes affecting all entities:- a) Report layout b) Going concern c) Auditor s independence d) Auditor s responsibilities

12 Report layout Opinion section required to be presented first. Basis for Opinion section comes second Typical layout Title and addressee Report of audit of the financial statements Opinion Basis for opinion Key Audit Matters

13 Report layout (cont d) Other information Responsibility of the directors for the financial statements Auditor s responsibility for the for the audit of the financial statements Report on other legal and regulatory requirements Engagement partner name and number Signature Place where registered Date Note: Exemption to this format only if regulation prescribes otherwise

14 Going concern ISA 570 Enhanced auditor reporting on going concern Includes more description of the respective responsibilities of management and the auditor for going concern A separate section when a material uncertainty exists and is adequately disclosed, under the heading Material Uncertainty Related to Going Concern

15 Going concern ISA 570 (continued) New requirement to challenge adequacy of disclosures, in view of the applicable financial reporting framework when events or conditions are identified that may cast significant doubt on an entity s ability to continue as a going concern

16 Auditor s independence Affirmative statement about the auditor s independence and fulfillment of relevant ethical responsibilities, with disclosure of the jurisdiction of origin of those requirements or reference to the International Ethics Standards Board for Accountants Code of Ethics for Professional Accountants.

17 Auditor s responsibilities Enhanced description of the auditor s responsibilities and key features of an audit. Certain components of the description of the auditor s responsibilities may be presented in an appendix to the auditor s report or, where law, regulation or national auditing standards expressly permit, by reference in the auditor s report to a website of an appropriate authority.

18 Key concepts to note a)pervasive b)key Audit Matters (KAM) c) Emphasis of matter d)adverse opinion e)disclaimer of opinion

19 Pervasive Pervasive effect are those that in the auditors judgement: Are not confined to specific elements, accounts or items of the financial statements; If so confined, represent or could represent a substantial proportion of the financial statements; or In relation to disclosures, are fundamental to users understanding of the financial statements

20 Pervasive cont. Pervasiveness is a matter that confuses many new auditors as, it is a matter that requires professional judgment. In this case the judgment is whether the matter is isolated to specific components of the financial statements, or whether the matter pervades many elements of the financial statements, rendering them unreliable as a whole.

21 Pervasive cont. The bottom line is that if the auditor believes that the financial statements may be relied upon in some part for decision making then the matter is material and not pervasive. If, however, they believe the financial statements should not be relied upon at all for making decisions then the matter is pervasive.

22 Emphasis of matter EOM is rarely dealt with satisfactorily by some auditors. This is mainly because some auditors believe that EOM is linked to modifications of the opinion. This is not the case: EOM and modified opinions are separate matters. EOM A paragraph included in the auditor s report that refers to a matter appropriately presented or disclosed in the financial statements that, in the auditor s judgment, is of such importance that it is fundamental to users understanding of the financial statements.

23 Form of a modified audit opinion a)circumstances leading to modified opinion b)qualified opinion c) Adverse opinion d)disclaimer of opinion e)decision matrix

24 Circumstances leading to modification The auditor shall modify the opinion in the auditor s report when: The auditor concludes that, based on the audit evidence obtained, the financial statements as a whole are not free from material misstatement; or The auditor is unable to obtain sufficient appropriate audit evidence to conclude that the financial statements as a whole are free from material misstatement.

25 Decision matrix Nature of matter Auditors judgement on pervasiveness Financial statements are materially misstated Material but not pervasive Qualified opinion Material and pervasive Adverse opinion Inability to obtain sufficient appropriate audit evidence Qualified opinion Disclaimer of opinion

26 Qualified opinion The auditor shall express a qualified opinion when: The auditor, having obtained sufficient appropriate audit evidence, concludes that misstatements, individually or in the aggregate, are material, but not pervasive, to the financial statements; or The auditor is unable to obtain sufficient appropriate audit evidence on which to base the opinion, but the auditor concludes that the possible effects on the financial statements of undetected misstatements, if any, could be material but not pervasive.

27 Adverse The auditor shall express an adverse opinion when the auditor, having obtained sufficient appropriate audit evidence, concludes that misstatements, individually or in the aggregate, are both material and pervasive to the financial statements.

28 Disclaimer The auditor shall disclaim an opinion when the auditor is unable to obtain sufficient appropriate audit evidence on which to base the opinion, and the auditor concludes that the possible effects on the financial statements of undetected misstatements, if any, could be both material and pervasive. The auditor shall disclaim an opinion when, in extremely rare circumstances involving multiple uncertainties, the auditor concludes that, notwithstanding having obtained sufficient appropriate audit evidence regarding each of the individual uncertainties, it is not possible to form an opinion on the financial statements due to the potential interaction of the uncertainties and their possible cumulative effect on the financial statements.

29 Which ISAs are changing? Contd. Forming an opinion and reporting on financial statements (ISA 700 Revised) Modified audit report (ISA 705 Revised) Emphasis of matter and other matters (ISA 706 Revised) Going concern (ISA 570 revised) Key Audit Matters (ISA 701 Revised) Auditors responsibility on other information (ISA 720 Revised) Other considerations: Communication with those charged with Governance (ISA 260) Other ISAs changed for conformity.

30 ISA 700 Revised Objectives of an auditor are: i. To form an opinion on the financial statements based on an evaluation of the conclusions drawn from the audit evidence obtained; and ii. To express clearly that opinion through writing. The auditor shall form an opinion on whether the financial statements are prepared, in all material respect, in accordance with the applicable financial reporting framework.

31 ISA 700 contd. (Forming an opinion) In order to form that opinion, the auditor shall conclude as to whether the auditor has obtained reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error. That conclusion shall take into account: i. The auditor conclusion in accordance with ISA 330, whether sufficient appropriate evidence has been obtained ii. The auditors conclusion in accordance with ISA 450 whether uncorrected misstatements are material, individually or in aggregate; and iii. The financial statements have been presented in all material respect in accordance with the requirements of the applicable framework

32 ISA 700 contd. (Format of an audit report) Title (clearly indicate it is the report of the independent auditor) Addressee (The auditors report shall be addressed as appropriate) Auditors opinion Basis of opinion (state the audit was conducted in accordance with ISAs, Refer to section in the audit report that describes the auditors responsibilities, include a statement that the auditor is independent of the entity, state whether audit evidence was sufficient and appropriate) Going concern (to report in accordance with ISA 570) Key Audit Matters (for listed entities and certain regulated entities, proposed ISA 701) Other information (to report in accordance with ISA 720) Responsibilities for the financial statements

33 ISA 700 contd. (Format of an audit report (contd) Auditors responsibilities for the financial statements Other reporting responsibilities Name of engagement (required for listed companies in rare circumstances such disclosure is reasonably expected to lead to a significant security threat) Auditors address Date of the auditors report

34 ISA 705 revised Objectives of the auditor is to express an appropriately modified opinion on the financial statements that is necessary when: i. The auditor concludes, based on audit evidence, that the financial statements as a whole are not free from material misstatements; or ii. The auditor is unable to obtain sufficient appropriate audit evidence to conclude that the financial statements as a whole are free from material misstatement

35 ISA Emphasis of Matter The objective of the auditor, having formed an opinion on the financial statements, is to draw users attention, when in the auditor s judgment it is necessary to do so, by way of clear additional communication in the auditor s report, to: i. A matter, although appropriately presented or disclosed in the financial statements, that is of such importance that it is fundamental to users understanding of the financial statements; or ii. As appropriate, any other matter that is relevant to users understanding of the audit, the auditor s responsibilities or the auditor s report.

36 ISA 706 Examples of circumstances requiring emphasis of matter an uncertainty relating to the future outcome of exceptional litigation or regulatory action. A new accounting standard (for example, a new International Financial Reporting Standard) that is not yet effective but is expected to have a material effect on the financial statements A major catastrophe that has had, or continues to have, a significant effect on the entity s financial position. A significant subsequent event that occurs between the date of the financial statements and the date of the auditor s report.

37 ISA 720 Other matters paragraph Other matter paragraphs are used to refer to matters that have not been disclosed in the financial statements that the auditor believes are significant to user understanding. One usage of these paragraphs is where the auditor concludes that there is a material inconsistency between the audited financial statements and the other (unaudited) information contained within the annual report and accounts, as required by ISA 720, The Auditor s Responsibilities Relating to Other Information in Documents Containing Audited Financial Statements.

38 ISA 701 Key Audit Matters Key audit matters - Those matters that, in the auditor s professional judgment, were of most significance in the audit of the financial statements of the current period. KAM are selected from matters communicated with those charged with governance(tcwg). (ISA 260)

39 KAM is not: A substitute for disclosures in the financial statements A substitute for the auditor to express a modified opinion A substitute for reporting any matters relating to going concern, A seperate opinion on an individual matter

40 ISA 701 Determining Key Audit Matters The auditor shall determine which of the matters communicated with those charged with governance are the key audit matters. In making this determination, the auditor shall take into account areas of significant auditor attention in performing the audit, including: Areas identified as significant risks in accordance with ISA 315 (Revised) Areas in which the auditor encountered significant difficulty during the audit, including with respect to obtaining sufficient appropriate audit evidence. Circumstances that required significant modification of the auditor s planned approach to the audit, including as a result of the identification of a significant deficiency in internal control.

41 ISA 701 Communication of Key Audit Matters The auditor shall communicate the key audit matters determined in accordance with paragraph 8 in a separate section of the auditor s report under the heading Key Audit Matters. NB- the descriptions of KAM should be clear, concise, understandable and entity-specific

42 KAM relates to Significant complex matters disclosed in the financial statements e,g Valuation of goodwill and other long term assets, Valuation of financial instruments, Difficult or unique aspects of revenue recognition, Accounting for significant acquisitions,

43 SURVEY IN UK, done by UK Financial reporting Council In a survey of more than 150 auditor report, it was found the top five KAMs most reported in UK were, Impairment of assets, Tax, Goodwill impairment Management override of controls, Fraud in revenue recognition,

44 Is a KAM a form of qualification?? Stakeholders are used to the binary pass/ fail opinion. With KAM reporting, the stakeholders might perceive it as a piecemeal qualification on matters determined to be KAMs. The description of auditors procedures contained in the KAM section of the auditors report might be misunderstood without proper context

45 OTHER CONCERNS ON KAM Will KAMs make the auditors report as the primary source of red flags such as going concern How will KAMs be interpreted by stakeholders and the market? Would it trigger a negative reponse? Will stakeholders perceive matters highlighted as KAMs as areas where manangement and TCWG failed to discharge their responsibilities properly,

46 WAY FORWARD ON KAM Convey important message to stakeholders that KAMs, are not avenue for the auditor to express qualification on matters highlighted, KAMs are addressed in the context of the audit of the financial statements as a whole, and the auditor does not provide a separate opinion on these matters FINALY, stakeholders education is critical, through ICPAK, authorities/ regulators (SASRA), etc,

47 THANK YOU, ANY QUESTIONS?

48 48

49 Any questions??

50 50

51 51

52 52

53 53

54 54

Reporting- The New Auditor s Report Presentation by: CPA Stephen Obock Associate Director, KPMG March 2018

Reporting- The New Auditor s Report Presentation by: CPA Stephen Obock Associate Director, KPMG sobock@kpmg.co.ke March 2018 Uphold public interest Agenda Why the changes? Key Audit Matters (KAM) - (ISA

Reporting- The New Auditor s Report Presentation by: CPA Stephen Obock Associate Director, KPMG sobock@kpmg.co.ke March 2018 Uphold public interest Agenda Why the changes? Key Audit Matters (KAM) - (ISA

Audit Opinion Session-02. November

Audit Opinion Session-02 November - - 2018 Audit Opinion After concluding the field work the auditor forms an opinion on whether the financial statements are prepared, in all material respects, in accordance

Audit Opinion Session-02 November - - 2018 Audit Opinion After concluding the field work the auditor forms an opinion on whether the financial statements are prepared, in all material respects, in accordance

Enhanced auditor s reporting

Enhanced auditor s reporting Assurance Special edition January 2016 A new foundation in auditor s reporting In January 2015, the International Auditing and Assurance Standards Board (IAASB) issued its

Enhanced auditor s reporting Assurance Special edition January 2016 A new foundation in auditor s reporting In January 2015, the International Auditing and Assurance Standards Board (IAASB) issued its

AUDITOR REPORTING: FREQUENTLY ASKED QUESTIONS

QUESTIONS AND ANSWERS November 2016 AUDITOR REPORTING: FREQUENTLY ASKED QUESTIONS This publication has been prepared by the Auditor Reporting Implementation Working Group (ARIWG). It does not constitute

QUESTIONS AND ANSWERS November 2016 AUDITOR REPORTING: FREQUENTLY ASKED QUESTIONS This publication has been prepared by the Auditor Reporting Implementation Working Group (ARIWG). It does not constitute

IAASB Main Agenda (September 2016) Draft Auditor Reporting: Frequently Asked Questions

Draft Auditor Reporting: Frequently Asked Questions") Agenda Item 7-B Draft Auditor Reporting: Frequently Asked Questions This publication has been prepared by the Auditor Reporting Implementation Working Group. It does not constitute an authoritative pronouncement

Agenda Item 7-B Draft Auditor Reporting: Frequently Asked Questions This publication has been prepared by the Auditor Reporting Implementation Working Group. It does not constitute an authoritative pronouncement

Processes, Controls and Audit [AA34] Supplementary for Chapter 08. Audit Reporting

![Processes, Controls and Audit [AA34] Supplementary for Chapter 08. Audit Reporting](/thumbs/84/89340608.jpg "Processes, Controls and Audit [AA34] Supplementary for Chapter 08. Audit Reporting") [AA34] Supplementary for Chapter 08 Audit Reporting This supplementary to the Study Text will be tested from January 2019 Examination. The printed chapter in the book will not be applicable from January

[AA34] Supplementary for Chapter 08 Audit Reporting This supplementary to the Study Text will be tested from January 2019 Examination. The printed chapter in the book will not be applicable from January

Mark-up Copy (showing changes from September 2004)

") IAASB Main Agenda (December 2004) Page 2004 2299 Agenda Item 8-B International Auditing and Assurance Standards Board Mark-up Copy (showing changes from September 2004) Proposed Final Pronouncements on

IAASB Main Agenda (December 2004) Page 2004 2299 Agenda Item 8-B International Auditing and Assurance Standards Board Mark-up Copy (showing changes from September 2004) Proposed Final Pronouncements on

WK Update for Auditors and Audit Committees

WK Update for Auditors and Audit Committees A brief round-up of the proposed changes to auditor reporting Sweeping changes to the auditor s report, already published internationally, are expected to be

WK Update for Auditors and Audit Committees A brief round-up of the proposed changes to auditor reporting Sweeping changes to the auditor s report, already published internationally, are expected to be

The Independent Auditor s Report on a Complete Set of General Purpose Financial Statements

International Auditing and ISA 700 (Revised) December 2004 Assurance Standards Board International Standards on Auditing (ISA) 700 (Revised) The Independent Auditor s Report on a Complete Set of General

International Auditing and ISA 700 (Revised) December 2004 Assurance Standards Board International Standards on Auditing (ISA) 700 (Revised) The Independent Auditor s Report on a Complete Set of General

IAASB Main Agenda (April 2013) Agenda Item. Auditor Reporting Illustrative Auditors Reports

Agenda Item. Auditor Reporting Illustrative Auditors Reports") Agenda Item 2-A A. Illustrations of an Unmodified ( Clean ) Auditor s Report 1 Illustration 1 Listed Entity Required to Communicate Key Audit Matters For purposes of this illustrative auditor s report,

Agenda Item 2-A A. Illustrations of an Unmodified ( Clean ) Auditor s Report 1 Illustration 1 Listed Entity Required to Communicate Key Audit Matters For purposes of this illustrative auditor s report,

International Standard on Auditing (UK) 700 (Revised June 2016)

700 (Revised June 2016)") Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 700 (Revised June 2016) Forming an Opinion and Reporting on Financial Statements The FRC s mission

Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 700 (Revised June 2016) Forming an Opinion and Reporting on Financial Statements The FRC s mission

Auditor Reporting Cover Letter and Issues Paper

ASB Meeting May 15-18, 2017 Agenda Item 3 Auditor Reporting Cover Letter and Issues Paper Objective To consider discussion drafts of proposed revisions to AU-C section 705, Modifications to the Opinion

ASB Meeting May 15-18, 2017 Agenda Item 3 Auditor Reporting Cover Letter and Issues Paper Objective To consider discussion drafts of proposed revisions to AU-C section 705, Modifications to the Opinion

Click to edit Master title style. Changes to Independent Auditors Report

Click to edit Master title style Changes to Independent Auditors Report Scope Case for a new auditors report IAASB effort to develop new auditors report Areas to improve in auditors report Key changes

Click to edit Master title style Changes to Independent Auditors Report Scope Case for a new auditors report IAASB effort to develop new auditors report Areas to improve in auditors report Key changes

Audit Reporting Standards (SAs)

") Audit Reporting Standards (SAs) Seminar on Practical Aspects relating to Standards on Auditing (SAs) at WIRC of Institute of Chartered Accountants of India Seminar on 7 th January, 2017 CA Bipeen G. Mundade

Audit Reporting Standards (SAs) Seminar on Practical Aspects relating to Standards on Auditing (SAs) at WIRC of Institute of Chartered Accountants of India Seminar on 7 th January, 2017 CA Bipeen G. Mundade

New and Revised Auditing Standards Presentation by: CPA Stephen Obock Associate Director, KPMG 30 May 2017

New and Revised Auditing Standards Presentation by: CPA Stephen Obock Associate Director, KPMG 30 May 2017 Uphold public interest Presentation agenda Overview of new changes ISA 700 Forming Audit Opinion

New and Revised Auditing Standards Presentation by: CPA Stephen Obock Associate Director, KPMG 30 May 2017 Uphold public interest Presentation agenda Overview of new changes ISA 700 Forming Audit Opinion

Reporting on Audited Financial Statements: Proposed New and Revised International Standards on Auditing (ISAs)

") IFAC Board Exposure Draft July 2013 Comments due: November 22, 2013 International Standards on Auditing Reporting on Audited Financial Statements: Proposed New and Revised International Standards on Auditing

IFAC Board Exposure Draft July 2013 Comments due: November 22, 2013 International Standards on Auditing Reporting on Audited Financial Statements: Proposed New and Revised International Standards on Auditing

Forming an Opinion and Reporting on Financial Statements

ISA 700 (Revised) Issued April 2015; updated July 2018 International Standard on Auditing Forming an Opinion and Reporting on Financial Statements INTERNATIONAL STANDARD ON AUDITING 700 (REVISED) FORMING

ISA 700 (Revised) Issued April 2015; updated July 2018 International Standard on Auditing Forming an Opinion and Reporting on Financial Statements INTERNATIONAL STANDARD ON AUDITING 700 (REVISED) FORMING

Modifications to the Opinion in the Independent Auditor s Report

SINGAPORE STANDARD ON AUDITING SSA 705 (Revised) Modifications to the Opinion in the Independent Auditor s Report SSA 705 was issued in January 2010. The Companies (Amendment) Act 2014 gave rise to conforming

SINGAPORE STANDARD ON AUDITING SSA 705 (Revised) Modifications to the Opinion in the Independent Auditor s Report SSA 705 was issued in January 2010. The Companies (Amendment) Act 2014 gave rise to conforming

Forming an Opinion and Reporting on Financial Statements

HKSA 700 (Revised) Issued August 2015; revised January 2016, August 2016, June 2017 Effective for audits of financial statements for periods ending on or after 15 December 2016 Hong Kong Standard on Auditing

HKSA 700 (Revised) Issued August 2015; revised January 2016, August 2016, June 2017 Effective for audits of financial statements for periods ending on or after 15 December 2016 Hong Kong Standard on Auditing

Auditor Reporting. Agenda

Auditor Reporting Dan Montgomery, IAASB Deputy Chair and Auditor Reporting TF Chair Bruce Winter, IAASB Member and ISA 700 Drafting Team Chair IAASB Consultative Advisory Group April 8 9, 2013 Page 1 Agenda

Auditor Reporting Dan Montgomery, IAASB Deputy Chair and Auditor Reporting TF Chair Bruce Winter, IAASB Member and ISA 700 Drafting Team Chair IAASB Consultative Advisory Group April 8 9, 2013 Page 1 Agenda

Forming an Opinion and Reporting on Financial Statements

SINGAPORE STANDARD ON AUDITING SSA 700 (Revised) Forming an Opinion and Reporting on Financial Statements SSA 700, Forming an Opinion and Reporting on Financial Statements superseded SSA 700, The Independent

SINGAPORE STANDARD ON AUDITING SSA 700 (Revised) Forming an Opinion and Reporting on Financial Statements SSA 700, Forming an Opinion and Reporting on Financial Statements superseded SSA 700, The Independent

Forming an Opinion and Reporting on Financial Statements

SINGAPORE STANDARD ON AUDITING SSA 700 (Revised) Forming an Opinion and Reporting on Financial Statements SSA 700, Forming an Opinion and Reporting on Financial Statements superseded SSA 700, The Independent

SINGAPORE STANDARD ON AUDITING SSA 700 (Revised) Forming an Opinion and Reporting on Financial Statements SSA 700, Forming an Opinion and Reporting on Financial Statements superseded SSA 700, The Independent

New Auditor Reporting Standards

New Auditor Reporting Standards June 2015 These standards have not been approved by the AASB and are provided to readers of the Invitation to Comment for reference purposes only. Table of Contents CAS

New Auditor Reporting Standards June 2015 These standards have not been approved by the AASB and are provided to readers of the Invitation to Comment for reference purposes only. Table of Contents CAS

International Standards on Auditing (ISAs) Updates By: Neema Kiure Mssusa. 20 August 2016 Dar es Salaam

Updates By: Neema Kiure Mssusa. 20 August 2016 Dar es Salaam") International Standards on Auditing (ISAs) Updates By: Neema Kiure Mssusa 20 August 2016 Dar es Salaam Agenda ISA 700 (Revised), Forming an Opinion and Reporting on Financial Statements New ISA 701, Communicating

International Standards on Auditing (ISAs) Updates By: Neema Kiure Mssusa 20 August 2016 Dar es Salaam Agenda ISA 700 (Revised), Forming an Opinion and Reporting on Financial Statements New ISA 701, Communicating

The New Auditor s Report: A Comparison between the ISAs and the US PCAOB Reproposal

The New Auditor s Report: A Comparison between the ISAs and the US PCAOB Reproposal May 2016 This publication has been prepared by the Auditor Reporting Implementation Working Group. It does not constitute

The New Auditor s Report: A Comparison between the ISAs and the US PCAOB Reproposal May 2016 This publication has been prepared by the Auditor Reporting Implementation Working Group. It does not constitute

PROPOSED INTERNATIONAL STANDARD ON AUDITING 705 (REVISED) MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT

MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT") Agenda Item 4-C PROPOSED INTERNATIONAL STANDARD ON AUDITING 705 (REVISED) MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT (Effective for audits of financial statements for periods [beginning/ending

Agenda Item 4-C PROPOSED INTERNATIONAL STANDARD ON AUDITING 705 (REVISED) MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT (Effective for audits of financial statements for periods [beginning/ending

International Standard on Auditing (Ireland) 705 Modifications to the Opinion in the Independent Auditor s Report

705 Modifications to the Opinion in the Independent Auditor s Report") International Standard on Auditing (Ireland) 705 Modifications to the Opinion in the Independent Auditor s Report MISSION To contribute to Ireland having a strong regulatory environment in which to do

International Standard on Auditing (Ireland) 705 Modifications to the Opinion in the Independent Auditor s Report MISSION To contribute to Ireland having a strong regulatory environment in which to do

ISA (NZ) 700 Issued 10/15 Compiled 11/18

700 Issued 10/15 Compiled 11/18") ISA (NZ) 700 Issued 10/15 Compiled 11/18 INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 700 (REVISED) Forming an Opinion and Reporting on Financial Statements (ISA (NZ) 700 (Revised)) This Standard was

ISA (NZ) 700 Issued 10/15 Compiled 11/18 INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 700 (REVISED) Forming an Opinion and Reporting on Financial Statements (ISA (NZ) 700 (Revised)) This Standard was

INTERNATIONAL STANDARD ON AUDITING 700 FORMING AN OPINION AND REPORTING ON FINANCIAL STATEMENTS CONTENTS

INTERNATIONAL STANDARD ON 700 FORMING AN OPINION AND REPORTING ON FINANCIAL STATEMENTS (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Introduction

INTERNATIONAL STANDARD ON 700 FORMING AN OPINION AND REPORTING ON FINANCIAL STATEMENTS (Effective for audits of financial statements for periods beginning on or after December 15, 2009) CONTENTS Introduction

Adoption of new auditor s reports

Adoption of new auditor s reports AASB and PCAOB approve new standards July 2017 What you need to know The Auditing and Assurance Standards Board (AASB) approved a package of standards, effective in 2018,

Adoption of new auditor s reports AASB and PCAOB approve new standards July 2017 What you need to know The Auditing and Assurance Standards Board (AASB) approved a package of standards, effective in 2018,

This Standard has been issued as a result of International Standard on Auditing 705 being revised.

INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 705 (REVISED) Modifications to the Opinion in the Independent Auditor s Report (ISA (NZ) 705 (Revised)) This Standard was issued on 1 October 2015 by the

INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 705 (REVISED) Modifications to the Opinion in the Independent Auditor s Report (ISA (NZ) 705 (Revised)) This Standard was issued on 1 October 2015 by the

REQUEST FOR COMMENTS

EXPOSURE DRAFT Reporting on Audited Financial Statements Proposed New and Revised Singapore Standards on Auditing (SSAs) and Related Conforming Amendments May 2015 REQUEST FOR COMMENTS This Exposure Draft

EXPOSURE DRAFT Reporting on Audited Financial Statements Proposed New and Revised Singapore Standards on Auditing (SSAs) and Related Conforming Amendments May 2015 REQUEST FOR COMMENTS This Exposure Draft

International Standard on Auditing (UK) 705 (Revised June 2016)

705 (Revised June 2016)") Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 705 (Revised June 2016) Modifi cations to the Opinion in the Independent Auditor s Report The

Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 705 (Revised June 2016) Modifi cations to the Opinion in the Independent Auditor s Report The

PHILIPPINE STANDARD ON AUDITING 705 (REVISED) MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT

MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT") PHILIPPINE STANDARD ON AUDITING 705 (REVISED) MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT (Effective for audits of financial statements for periods ending on or after December 15,

PHILIPPINE STANDARD ON AUDITING 705 (REVISED) MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT (Effective for audits of financial statements for periods ending on or after December 15,

ISA 705, Modifications to the Opinion in the Independent Auditor s Report

International Auditing and Assurance Standards Board ISA 705 (Revised and Redrafted) October 2008 Revised and Redrafted International Standard on Auditing ISA 705, Modifications to the Opinion in the Independent

International Auditing and Assurance Standards Board ISA 705 (Revised and Redrafted) October 2008 Revised and Redrafted International Standard on Auditing ISA 705, Modifications to the Opinion in the Independent

SUMMARY COMPARISON BETWEEN THE IAASB AND THE US PCAOB STANDARDS

The New Auditor s Report July 2017 SUMMARY COMPARISON BETWEEN THE IAASB AND THE US PCAOB STANDARDS This publication has been prepared by the Auditor Reporting Implementation Working Group. It does not

The New Auditor s Report July 2017 SUMMARY COMPARISON BETWEEN THE IAASB AND THE US PCAOB STANDARDS This publication has been prepared by the Auditor Reporting Implementation Working Group. It does not

Forming an Opinion and Reporting on Financial Statements: Auditing Interpretations of Section 700

Forming an Opinion and Reporting on Financial Statements 817 AU-C Section 9700 Forming an Opinion and Reporting on Financial Statements: Auditing Interpretations of Section 700 1. Reporting on Financial

Forming an Opinion and Reporting on Financial Statements 817 AU-C Section 9700 Forming an Opinion and Reporting on Financial Statements: Auditing Interpretations of Section 700 1. Reporting on Financial

Please refer to Annexure 1 for some examples of Key Audit Matters (KAM) for illustrative purposes.

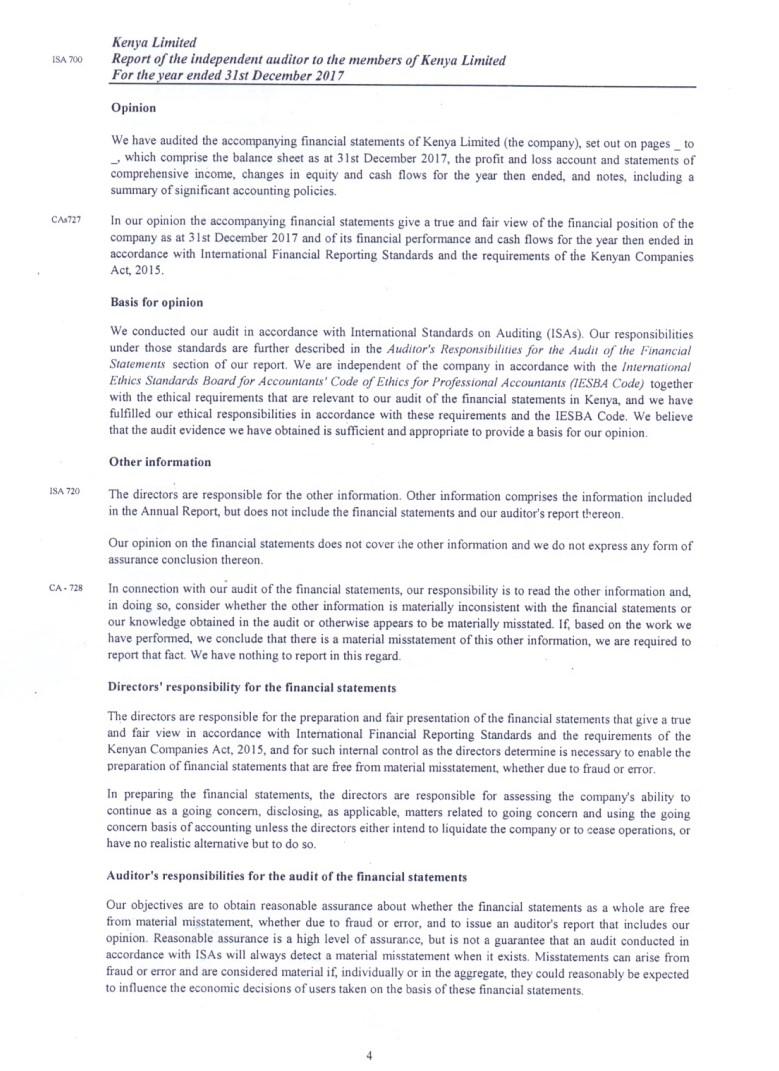

for illustrative purposes.") Independent Auditor s Report To the Shareholders of ABC Life Insurance Company Limited Report on the Audit of the Financial Statements Opinion We have audited the financial statements of ABC Life Insurance

Independent Auditor s Report To the Shareholders of ABC Life Insurance Company Limited Report on the Audit of the Financial Statements Opinion We have audited the financial statements of ABC Life Insurance

SRI LANKA AUDITING STANDARD 705 MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT CONTENTS

SRI LANKA AUDITING STANDARD 705 MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT (Effective for audits of financial statements for periods beginning on or after 01 January 2014) CONTENTS

SRI LANKA AUDITING STANDARD 705 MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT (Effective for audits of financial statements for periods beginning on or after 01 January 2014) CONTENTS

Introduction Scope of this SA 1. This Standard on Auditing (SA) deals with the auditor s responsibility to form an opinion on the financial statements

deals with the auditor s responsibility to form an opinion on the financial statements") Standard on Auditing (SA) 700 (Revised), Forming an Opinion and Reporting on Financial Statements Introduction Contents Scope of this SA... 1 4 Effective Date... 5 Objectives... 6 Definitions... 7 9 Requirements

Standard on Auditing (SA) 700 (Revised), Forming an Opinion and Reporting on Financial Statements Introduction Contents Scope of this SA... 1 4 Effective Date... 5 Objectives... 6 Definitions... 7 9 Requirements

NEW AND REVISED AUDITOR REPORTING

NEW AND REVISED AUDITOR REPORTING INTRODUCTION The IRBA Board adopts the IAASB's new and revised Auditor Reporting Standards and related conforming amendments. The changes to the auditor s report was primarily

NEW AND REVISED AUDITOR REPORTING INTRODUCTION The IRBA Board adopts the IAASB's new and revised Auditor Reporting Standards and related conforming amendments. The changes to the auditor s report was primarily

Auditing and Assurance Standards Council

Auditing and Assurance Standards Council Philippine Standard on Auditing (PSA) 700 (Revised) THE INDEPENDENT AUDITOR S REPORT ON A COMPLETE SET OF GENERAL PURPOSE FINANCIAL STATEMENTS Conforming Amendments

Auditing and Assurance Standards Council Philippine Standard on Auditing (PSA) 700 (Revised) THE INDEPENDENT AUDITOR S REPORT ON A COMPLETE SET OF GENERAL PURPOSE FINANCIAL STATEMENTS Conforming Amendments

AG ISA (NZ) 705 (REVISED) THE AUDITOR-GENERAL S STATEMENT ON MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT.

705 (REVISED) THE AUDITOR-GENERAL S STATEMENT ON MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT.") AG ISA (NZ) 705 (REVISED) THE AUDITOR-GENERAL S STATEMENT ON MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT Contents Page Introduction 3-4901 Scope of this Statement 3-4901 Application

AG ISA (NZ) 705 (REVISED) THE AUDITOR-GENERAL S STATEMENT ON MODIFICATIONS TO THE OPINION IN THE INDEPENDENT AUDITOR S REPORT Contents Page Introduction 3-4901 Scope of this Statement 3-4901 Application

Regional Conference of Northern Indian Regional Council of the ICAI

Regional Conference of Northern Indian Regional Council of the ICAI At: Hotel The Park, New Delhi C.A. Sanjay Vasudeva Vice Chairman AASB, Vice Chairman DAAB Presentation Overview : SA 700 (R); 705 (R);

Regional Conference of Northern Indian Regional Council of the ICAI At: Hotel The Park, New Delhi C.A. Sanjay Vasudeva Vice Chairman AASB, Vice Chairman DAAB Presentation Overview : SA 700 (R); 705 (R);

The Independent Auditor s Report on Other Historical Financial Information. The Independent Auditor s Report on Summary Audited Financial Statements

International Auditing and Assurance Standards Board Exposure Draft June 2005 Comments are requested by October 31, 2005 Proposed International Standard on Auditing 701 The Independent Auditor s Report

International Auditing and Assurance Standards Board Exposure Draft June 2005 Comments are requested by October 31, 2005 Proposed International Standard on Auditing 701 The Independent Auditor s Report

ISA 210, Agreeing the Terms of Audit Engagements. Conforming Amendments to Other ISAs. ISA 210 (Redrafted)

") International Auditing and Assurance Standards Board ISA 210 (Redrafted) March 2009 Redrafted International Standard on Auditing ISA 210, Agreeing the Terms of Audit Engagements Conforming Amendments to

International Auditing and Assurance Standards Board ISA 210 (Redrafted) March 2009 Redrafted International Standard on Auditing ISA 210, Agreeing the Terms of Audit Engagements Conforming Amendments to

Standard on Auditing (SA) 705 (Revised), Modifications to the Opinion in the Independent. Auditor s Report

705 (Revised), Modifications to the Opinion in the Independent. Auditor s Report") Introduction Standard on Auditing (SA) 705 (Revised), Modifications to the Opinion in the Independent Auditor s Report Contents Paragraphs Scope of this SA... 1 Types of Modified Opinions... 2 Effective

Introduction Standard on Auditing (SA) 705 (Revised), Modifications to the Opinion in the Independent Auditor s Report Contents Paragraphs Scope of this SA... 1 Types of Modified Opinions... 2 Effective

International Standard on Auditing (Ireland) 805 Special Considerations Audits of Single Financial Statements and Specific Elements, Accounts or

805 Special Considerations Audits of Single Financial Statements and Specific Elements, Accounts or") International Standard on Auditing (Ireland) 805 Special Considerations Audits of Single Financial Statements and Specific Elements, Accounts or Items of a Financial Statement MISSION To contribute to

International Standard on Auditing (Ireland) 805 Special Considerations Audits of Single Financial Statements and Specific Elements, Accounts or Items of a Financial Statement MISSION To contribute to

Forming an Opinion and Reporting on Financial Statements

ISA 700 March 2009 International Standard on Auditing Forming an Opinion and Reporting on Financial Statements INTERNATIONAL STANDARD ON AUDITING 700 Forming an Opinion and Reporting on Financial Statements

ISA 700 March 2009 International Standard on Auditing Forming an Opinion and Reporting on Financial Statements INTERNATIONAL STANDARD ON AUDITING 700 Forming an Opinion and Reporting on Financial Statements

Revised format of Audit Reports SA 700, 705 & 706

Revised format of Audit Reports SA 700, 705 & 706 Disclaimers 2 These are my personal views and cannot be construed to be the views of WIRC or M P Chitale & Co. No representations or warranties are made

Revised format of Audit Reports SA 700, 705 & 706 Disclaimers 2 These are my personal views and cannot be construed to be the views of WIRC or M P Chitale & Co. No representations or warranties are made

ISA 700 Issues and Drafting Team Recommendations

IAASB Main Agenda (June 2014) Agenda Item 2-A ISA 700 Issues and Drafting Team Recommendations Summary of the IAASB s Discussions at Its March 2014 Meeting Statement of Independence and Other Relevant

IAASB Main Agenda (June 2014) Agenda Item 2-A ISA 700 Issues and Drafting Team Recommendations Summary of the IAASB s Discussions at Its March 2014 Meeting Statement of Independence and Other Relevant

International Standard on Auditing (ISA )

") Final Pronouncement January 2016 International Standard on Auditing (ISA ) ISA 805 (Revised), Special Considerations Audits of Single Financial Statements and Specific Elements, Accounts or Items of a

Final Pronouncement January 2016 International Standard on Auditing (ISA ) ISA 805 (Revised), Special Considerations Audits of Single Financial Statements and Specific Elements, Accounts or Items of a

International Standard on Auditing (Ireland) 706 Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Independent Auditor s Report

706 Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Independent Auditor s Report") International Standard on Auditing (Ireland) 706 Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Independent Auditor s Report MISSION To contribute to Ireland having a strong regulatory

International Standard on Auditing (Ireland) 706 Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Independent Auditor s Report MISSION To contribute to Ireland having a strong regulatory

Report on the Observance of Standards & Codes (ROSC) Accounting & Auditing (A&A)

Accounting & Auditing (A&A)") Public Disclosure Authorized Public Disclosure Authorized Report on the Observance of Standards & Codes (ROSC) Accounting & Auditing (A&A) Public Disclosure Authorized Module A - Accounting & Auditing

Public Disclosure Authorized Public Disclosure Authorized Report on the Observance of Standards & Codes (ROSC) Accounting & Auditing (A&A) Public Disclosure Authorized Module A - Accounting & Auditing

IAASB Main Agenda (June 2013) Agenda Item

Agenda Item") Agenda Item 2-G Proposed International Standard on Auditing (ISA) 700 (Revised) Forming an Opinion and Reporting on Financial Statements (Effective for audits of financial statements for periods beginning

Agenda Item 2-G Proposed International Standard on Auditing (ISA) 700 (Revised) Forming an Opinion and Reporting on Financial Statements (Effective for audits of financial statements for periods beginning

Chapter 5 THE AUDIT REPORT

Chapter 5 THE AUDIT REPORT 23 1. Introduction Now we begin to look at the audit report. For many people, this is the only purpose of an audit and it s one of the few parts of the financial statements they

Chapter 5 THE AUDIT REPORT 23 1. Introduction Now we begin to look at the audit report. For many people, this is the only purpose of an audit and it s one of the few parts of the financial statements they

International Standard on Auditing

ISA 805 (Revised) May 2016 International Standard on Auditing ISA 805 (Revised), Special Considerations Audits of Single Financial Statements and Specific Elements, Accounts or Items of a Financial Statement

ISA 805 (Revised) May 2016 International Standard on Auditing ISA 805 (Revised), Special Considerations Audits of Single Financial Statements and Specific Elements, Accounts or Items of a Financial Statement

ISA 810 (Revised), Engagements to Report on Summary Financial Statements

, Engagements to Report on Summary Financial Statements") Final Pronouncement March 2016 International Standard on Auditing (ISA) ISA 810 (Revised), Engagements to Report on Summary Financial Statements This document was developed and approved by the International

Final Pronouncement March 2016 International Standard on Auditing (ISA) ISA 810 (Revised), Engagements to Report on Summary Financial Statements This document was developed and approved by the International

International Standard on Auditing (UK) 706 (Revised June 2016)

706 (Revised June 2016)") Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 706 (Revised June 2016) Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Independent

Standard Audit and Assurance Financial Reporting Council June 2016 International Standard on Auditing (UK) 706 (Revised June 2016) Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Independent

INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS OF KENYA. Credibility. Professionalism. AccountAbility

INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS OF KENYA Credibility. Professionalism. AccountAbility Auditor s Report FCPA FCPA John Kabiru Kabiru EXTERNAL AUDITORS, REGULATORS, AND OTHER EXTERNAL BODIES External

INSTITUTE OF CERTIFIED PUBLIC ACCOUNTANTS OF KENYA Credibility. Professionalism. AccountAbility Auditor s Report FCPA FCPA John Kabiru Kabiru EXTERNAL AUDITORS, REGULATORS, AND OTHER EXTERNAL BODIES External

Requiring the Opinion section to be presented first in the auditor s report, followed by the Basis for Opinion section.

Deloitte & Touche LLP 695 E. Main Street Stamford, CT 06901-2150 Tel: +1 203 761 3000 Fax: +1 203 761 3013 www.deloitte.com May 21, 2018 Ms. Sherry Hazel American Institute of Certified Public Accountants

Deloitte & Touche LLP 695 E. Main Street Stamford, CT 06901-2150 Tel: +1 203 761 3000 Fax: +1 203 761 3013 www.deloitte.com May 21, 2018 Ms. Sherry Hazel American Institute of Certified Public Accountants

INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 706 (REVISED)

706 (REVISED)") INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 706 (REVISED) Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Independent Auditor s Report ISA (NZ) 706 (Revised) This Standard was issued

INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 706 (REVISED) Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Independent Auditor s Report ISA (NZ) 706 (Revised) This Standard was issued

INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 805 (REVISED)

805 (REVISED)") INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 805 (REVISED) Special Considerations Audits of Single Financial Statements and Specific Elements, Accounts or Items of a Financial Statement (ISA (NZ) 805

INTERNATIONAL STANDARD ON AUDITING (NEW ZEALAND) 805 (REVISED) Special Considerations Audits of Single Financial Statements and Specific Elements, Accounts or Items of a Financial Statement (ISA (NZ) 805

Proposed International Standard on Auditing (ISA) 701 Communicating Key Audit Matters in the Independent Auditor s Report

701 Communicating Key Audit Matters in the Independent Auditor s Report") Updated Agenda Item 2-C Proposed International Standard on Auditing (ISA) 701 Communicating Key Audit Matters in the Independent Auditor s Report Introduction Effective for audits of financial statements

Updated Agenda Item 2-C Proposed International Standard on Auditing (ISA) 701 Communicating Key Audit Matters in the Independent Auditor s Report Introduction Effective for audits of financial statements

Changes to auditor reporting standards in Canada: What to expect

Audit Changes to auditor reporting standards in Canada: What to expect April 2018 Insert brand illustration into frame Contents Section Page Overview 03 Enhanced auditor s report 04 How will this impact

Audit Changes to auditor reporting standards in Canada: What to expect April 2018 Insert brand illustration into frame Contents Section Page Overview 03 Enhanced auditor s report 04 How will this impact

Update on Auditing and Assurance Standards

Professional Development Course Update on Auditing and Assurance Standards COPYRIGHT Chartered Professional Accountants of British Columbia All rights reserved. No part of this publication/course material

Professional Development Course Update on Auditing and Assurance Standards COPYRIGHT Chartered Professional Accountants of British Columbia All rights reserved. No part of this publication/course material

Proposed Statement on Auditing Standards Auditor reporting and Proposed Amendments Addressing disclosures in the audit of financial statements

Ernst & Young LLP 5 Times Square New York, NY 10036 Tel: +1 212 773 3000 ey.com Ms. Sherry Hazel American Institute of Certified Public Accountants 1211 Avenue of the Americas New York, NY 10036-8775 15

Ernst & Young LLP 5 Times Square New York, NY 10036 Tel: +1 212 773 3000 ey.com Ms. Sherry Hazel American Institute of Certified Public Accountants 1211 Avenue of the Americas New York, NY 10036-8775 15

Beyond auditor's report

Beyond auditor's report Example description Extract from KPMG Audit Plc, report to Rolls-Royce Holdings plc shareholders for the year ended 31 December 2013 The measurement of revenue and profit in the

Beyond auditor's report Example description Extract from KPMG Audit Plc, report to Rolls-Royce Holdings plc shareholders for the year ended 31 December 2013 The measurement of revenue and profit in the

ISA 706 (Revised), Emphasis of Matter Paragraphs and Other Matter(s) Paragraphs in the Independent Auditor s Report

, Emphasis of Matter Paragraphs and Other Matter(s) Paragraphs in the Independent Auditor s Report") International Auditing and Assurance Standards Board Exposure Draft July 2007 Comments are requested by November 30, 2007 Proposed Revised and Redrafted International Standard on Auditing ISA 706 (Revised),

International Auditing and Assurance Standards Board Exposure Draft July 2007 Comments are requested by November 30, 2007 Proposed Revised and Redrafted International Standard on Auditing ISA 706 (Revised),

Implementation Guide to Standard on Auditing (SA) 701, Communicating Key Audit Matters in the Independent Auditor s Report

701, Communicating Key Audit Matters in the Independent Auditor s Report") Implementation Guide to Standard on Auditing (SA) 701, Communicating Key Audit Matters in the Independent Auditor s Report The Institute of Chartered Accountants of India (Set up by an Act of Parliament)

Implementation Guide to Standard on Auditing (SA) 701, Communicating Key Audit Matters in the Independent Auditor s Report The Institute of Chartered Accountants of India (Set up by an Act of Parliament)

Illustrative Reports

Proposed SAAPS 3 (Revised 2015) August 2015 Comments due: 19 October 2015 Proposed South African Auditing Practice Statement (SAAPS) 3 (Revised 2015) Illustrative Reports WARNING TO READERS: The content

Proposed SAAPS 3 (Revised 2015) August 2015 Comments due: 19 October 2015 Proposed South African Auditing Practice Statement (SAAPS) 3 (Revised 2015) Illustrative Reports WARNING TO READERS: The content

International Standard on Auditing (UK and Ireland) 705

705") Standard Audit and Assurance Financial Reporting Council October 2012 International Standard on Auditing (UK and Ireland) 705 Modifications to the opinion in the independant auditor s report The FRC is

Standard Audit and Assurance Financial Reporting Council October 2012 International Standard on Auditing (UK and Ireland) 705 Modifications to the opinion in the independant auditor s report The FRC is

Auditing and Assurance Standards Council

Auditing and Assurance Standards Council Philippine Standard on Review Engagements 2410 REVIEW OF INTERIM FINANCIAL INFORMATION PERFORMED BY THE INDEPENDENT AUDITOR OF THE ENTITY Conforming Amendments

Auditing and Assurance Standards Council Philippine Standard on Review Engagements 2410 REVIEW OF INTERIM FINANCIAL INFORMATION PERFORMED BY THE INDEPENDENT AUDITOR OF THE ENTITY Conforming Amendments

Documentation requirements under Standards on Auditing (SAs)

") Documentation requirements under Standards on Auditing (SAs) Presented By C.A. Abhijit Sanzgiri Standards on Auditing Ensures information in FS is of high quality & acceptable worldwide Formulated by AASB

Documentation requirements under Standards on Auditing (SAs) Presented By C.A. Abhijit Sanzgiri Standards on Auditing Ensures information in FS is of high quality & acceptable worldwide Formulated by AASB

Proposed International Standard on Auditing. Review of Interim Financial Information Performed by the Auditor of the Entity.

IFAC International Auditing and Assurance Standards Board June 2003 Exposure Draft Response Due Date September 30, 2003 Proposed International Standard on Auditing Review of Interim Financial Information

IFAC International Auditing and Assurance Standards Board June 2003 Exposure Draft Response Due Date September 30, 2003 Proposed International Standard on Auditing Review of Interim Financial Information

International Standard on Auditing (Ireland) 800 Special Considerations Audits of Financial Statements Prepared in Accordance with Special Purpose

800 Special Considerations Audits of Financial Statements Prepared in Accordance with Special Purpose") International Standard on Auditing (Ireland) 800 Special Considerations Audits of Financial Statements Prepared in Accordance with Special Purpose Frameworks MISSION To contribute to Ireland having a strong

International Standard on Auditing (Ireland) 800 Special Considerations Audits of Financial Statements Prepared in Accordance with Special Purpose Frameworks MISSION To contribute to Ireland having a strong

The Auditor s Responsibilities Relating to Other Information

Final Pronouncement April 2015 International Standard on Auditing (ISA ) 720 (Revised) The Auditor s Responsibilities Relating to Other Information and Related Conforming Amendments This document was developed

Final Pronouncement April 2015 International Standard on Auditing (ISA ) 720 (Revised) The Auditor s Responsibilities Relating to Other Information and Related Conforming Amendments This document was developed

IAASB Main Agenda (May 2006) Page Agenda Item PROPOSED CONFORMING AMENDMENTS

Page Agenda Item PROPOSED CONFORMING AMENDMENTS") IAASB Main Agenda (May 2006) Page 2006 957 Agenda Item 7-E PROPOSED CONFORMING AMENDMENTS [Note: Only further changes to the conforming amendments previously exposed, or new conforming amendments, are

IAASB Main Agenda (May 2006) Page 2006 957 Agenda Item 7-E PROPOSED CONFORMING AMENDMENTS [Note: Only further changes to the conforming amendments previously exposed, or new conforming amendments, are

(Effective for audits of financial statements for periods [beginning/ending on or after December 15, 2009date]) CONTENTS [MARKED FROM EXTANT ISA 706]

![(Effective for audits of financial statements for periods [beginning/ending on or after December 15, 2009date]) CONTENTS [MARKED FROM EXTANT ISA 706]](/thumbs/80/81038580.jpg "(Effective for audits of financial statements for periods [beginning/ending on or after December 15, 2009date]) CONTENTS [MARKED FROM EXTANT ISA 706]") PROPOSED INTERNATIONAL STANDARD ON AUDITING 706 (REVISED) EMPHASIS OF MATTER PARAGRAPHS AND OTHER MATTER PARAGRAPHS IN THE (Effective for audits of financial statements for periods [beginning/ending on

PROPOSED INTERNATIONAL STANDARD ON AUDITING 706 (REVISED) EMPHASIS OF MATTER PARAGRAPHS AND OTHER MATTER PARAGRAPHS IN THE (Effective for audits of financial statements for periods [beginning/ending on

Going Concern. SSA 570, Going Concern superseded SSA 570 of the same title in September 2009.

SINGAPORE STANDARD ON AUDITING SSA 570 (Revised) Going Concern SSA 570, Going Concern superseded SSA 570 of the same title in September 2009. This SSA is revised in July 2015. SSA 720 (Revised), The Auditor

SINGAPORE STANDARD ON AUDITING SSA 570 (Revised) Going Concern SSA 570, Going Concern superseded SSA 570 of the same title in September 2009. This SSA is revised in July 2015. SSA 720 (Revised), The Auditor

Report on the Financial Statements (ISA 700 (Revised) Report)

Report)") Report on the Financial Statements (ISA 700 (Revised) Report) Circumstances Audit of a complete set of financial statements of a medical scheme prepared in accordance with International Financial Reporting

Report on the Financial Statements (ISA 700 (Revised) Report) Circumstances Audit of a complete set of financial statements of a medical scheme prepared in accordance with International Financial Reporting

STANDARD FOR AUDITS OF SMALL ENTITIES

STANDARD FOR AUDITS OF SMALL ENTITIES DRAFT JUNE 4 TH 2015 Contents Preface... 1 1 General Principles and Responsibilities... 2 1.1 Overall Objectives...2 1.2 Supervision and quality control...2 1.3 Performing

STANDARD FOR AUDITS OF SMALL ENTITIES DRAFT JUNE 4 TH 2015 Contents Preface... 1 1 General Principles and Responsibilities... 2 1.1 Overall Objectives...2 1.2 Supervision and quality control...2 1.3 Performing

The Auditor s Report on Financial Statements

Issued December 2007 International Standard on Auditing The Auditor s Report on Financial Statements The Malaysian Institute Of Certified Public Accountants (Institut Akauntan Awam Bertauliah Malaysia)

Issued December 2007 International Standard on Auditing The Auditor s Report on Financial Statements The Malaysian Institute Of Certified Public Accountants (Institut Akauntan Awam Bertauliah Malaysia)

Navigating the Auditor Reporting Journey

Navigating the Auditor Reporting Journey Navigating the Auditor Reporting Journey As Canada continues its commitment to adopting international standards on auditing, of particular significance are new

Navigating the Auditor Reporting Journey Navigating the Auditor Reporting Journey As Canada continues its commitment to adopting international standards on auditing, of particular significance are new

ISA 700, The Independent Auditor s Report on General Purpose Financial Statements

International Auditing and Assurance Standards Board Exposure Draft July 2007 Comments are requested by November 30, 2007 Proposed Redrafted International Standard on Auditing ISA 700, The Independent

International Auditing and Assurance Standards Board Exposure Draft July 2007 Comments are requested by November 30, 2007 Proposed Redrafted International Standard on Auditing ISA 700, The Independent

International Standard on Auditing (UK) 800 (Revised)

800 (Revised)") Standard Audit and Assurance Financial Reporting Council October 2016 International Standard on Auditing (UK) 800 (Revised) Special Considerations Audits of Financial Statements prepared in accordance

Standard Audit and Assurance Financial Reporting Council October 2016 International Standard on Auditing (UK) 800 (Revised) Special Considerations Audits of Financial Statements prepared in accordance

Report TO THE MEMBERS OF LIONGOLD CORP LTD

on the Audit of the Financial Statements Qualified Opinion We have audited the accompanying consolidated financial statements of LionGold Corp Ltd and its subsidiaries (collectively referred to as the

on the Audit of the Financial Statements Qualified Opinion We have audited the accompanying consolidated financial statements of LionGold Corp Ltd and its subsidiaries (collectively referred to as the

Edition Volume II

International Auditing and Assurance Standards Board Handbook of International Quality Control, Auditing, Review, Other Assurance, and Related Services Pronouncements 2016 2017 Edition Volume II The structures

International Auditing and Assurance Standards Board Handbook of International Quality Control, Auditing, Review, Other Assurance, and Related Services Pronouncements 2016 2017 Edition Volume II The structures

Addressing Disclosures in the Audit of Financial Statements

Exposure Draft Disclosures/2014 25 June 2014 Proposed Changes to the International Standards on Auditing (ISAs) Addressing Disclosures in the Audit of Financial Statements Issued for Comment Response Due

Exposure Draft Disclosures/2014 25 June 2014 Proposed Changes to the International Standards on Auditing (ISAs) Addressing Disclosures in the Audit of Financial Statements Issued for Comment Response Due

SRI LANKA AUDITING STANDARD 700 THE AUDITOR S REPORT ON FINANCIAL STATEMENTS CONTENTS

SRI LANKA AUDITING STANDARD 700 THE AUDITOR S REPORT ON FINANCIAL STATEMENTS (Effective for all the audits carried out on or after..) CONTENTS Paragraph Introduction 1-4 Basic Elements of the Auditor s

SRI LANKA AUDITING STANDARD 700 THE AUDITOR S REPORT ON FINANCIAL STATEMENTS (Effective for all the audits carried out on or after..) CONTENTS Paragraph Introduction 1-4 Basic Elements of the Auditor s

Audit of Financial Statements Prepared in Accordance with the Small and Medium-sized Entity Financial Reporting Standard

PN 900 (Revised) Issued September 2014; revised August 2016 Effective for a Qualifying Entity's financial statements which cover a period ending on or after 15 December 2016 Practice Note 900 (Revised)

PN 900 (Revised) Issued September 2014; revised August 2016 Effective for a Qualifying Entity's financial statements which cover a period ending on or after 15 December 2016 Practice Note 900 (Revised)

2 November Dear Ms. Healy,

30 Rockefeller Plaza New York, NY 10112-0015 United States of America www.deloitte.com 2 November 2015 Kathleen Healy Technical Director International Auditing and Assurance Standards Board International

30 Rockefeller Plaza New York, NY 10112-0015 United States of America www.deloitte.com 2 November 2015 Kathleen Healy Technical Director International Auditing and Assurance Standards Board International

Auditor Reporting Cover Letter and Issue Paper

ASB Meeting May 24-26, 2016 Agenda Item 3 Auditor Reporting Cover Letter and Issue Paper Objective To discuss certain elements of the auditor s report relating to ASB s convergence with the International

ASB Meeting May 24-26, 2016 Agenda Item 3 Auditor Reporting Cover Letter and Issue Paper Objective To discuss certain elements of the auditor s report relating to ASB s convergence with the International

Our responses to each of the question made in the Request for Comments document are included in the Appendix to this letter.

November 22, 2013 Ref.: SEC/210/2013 - DN International Auditing and Assurance Standards Board (IAASB) 529 Fifth Avenue, 6th Floor New York, New York, 10017 USA Dear Sirs, We, the (Institute of Independent

November 22, 2013 Ref.: SEC/210/2013 - DN International Auditing and Assurance Standards Board (IAASB) 529 Fifth Avenue, 6th Floor New York, New York, 10017 USA Dear Sirs, We, the (Institute of Independent

AG ISA (NZ) 706 (Revised) Emphasis of matter paragraphs and other matter paragraphs

706 (Revised) Emphasis of matter paragraphs and other matter paragraphs") AG ISA (NZ) 706 (Revised) Emphasis of matter paragraphs and other matter paragraphs AG ISA (NZ) 706 (REVISED) THE AUDITOR-GENERAL S STATEMENT ON EMPHASIS OF MATTER PARAGRAPHS AND OTHER MATTER PARAGRAPHS

AG ISA (NZ) 706 (Revised) Emphasis of matter paragraphs and other matter paragraphs AG ISA (NZ) 706 (REVISED) THE AUDITOR-GENERAL S STATEMENT ON EMPHASIS OF MATTER PARAGRAPHS AND OTHER MATTER PARAGRAPHS

SRI LANKA AUDITING STANDARD 706 EMPHASIS OF MATTER PARAGRAPHS AND OTHER MATTER PARAGRAPHS IN THE INDEPENDENT AUDITOR S REPORT CONTENTS

SRI LANKA AUDITING STANDARD 706 EMPHASIS OF MATTER PARAGRAPHS AND OTHER MATTER PARAGRAPHS IN THE INDEPENDENT AUDITOR S REPORT (Effective for audits of financial statements for periods beginning on or after

SRI LANKA AUDITING STANDARD 706 EMPHASIS OF MATTER PARAGRAPHS AND OTHER MATTER PARAGRAPHS IN THE INDEPENDENT AUDITOR S REPORT (Effective for audits of financial statements for periods beginning on or after

TOPIC 50: AUDIT REPORTING. AUDIT REPORTING (ISA 700 Forming an Opinion and Reporting on Financial Statements)

") TOPIC 50: AUDIT REPORTING AUDIT REPORTING (ISA 700 Forming an Opinion and Reporting on Financial Statements) A company s auditors must report their opinions to the shareholders/members on two primary matters:

TOPIC 50: AUDIT REPORTING AUDIT REPORTING (ISA 700 Forming an Opinion and Reporting on Financial Statements) A company s auditors must report their opinions to the shareholders/members on two primary matters:

IAASB Main Agenda (March 2005) Page Agenda Item [MARK-UP COPY]

![IAASB Main Agenda (March 2005) Page Agenda Item [MARK-UP COPY]](/thumbs/82/85470903.jpg "IAASB Main Agenda (March 2005) Page Agenda Item [MARK-UP COPY]") IAASB Main Agenda (March 2005) Page 2005 623 Agenda Item 14-B [MARK-UP COPY] REVIEW OF INTERIM FINANCIAL INFORMATION PERFORMED BY THE AUDITOR OF THE ENTITY CONTENTS Paragraphs Introduction... 1 5 General

IAASB Main Agenda (March 2005) Page 2005 623 Agenda Item 14-B [MARK-UP COPY] REVIEW OF INTERIM FINANCIAL INFORMATION PERFORMED BY THE AUDITOR OF THE ENTITY CONTENTS Paragraphs Introduction... 1 5 General

2016 INTERNATIONAL OVERVIEW FOR KNOWLEDGE COACH USERS

2016 INTERNATIONAL OVERVIEW FOR KNOWLEDGE COACH USERS PURPOSE This document is published for the purpose communicating, to users the toolset, updates and enhancements included in the current version. This

2016 INTERNATIONAL OVERVIEW FOR KNOWLEDGE COACH USERS PURPOSE This document is published for the purpose communicating, to users the toolset, updates and enhancements included in the current version. This

PHILIPPINE STANDARD ON AUDITING 810 ENGAGEMENTS TO REPORT ON SUMMARY FINANCIAL STATEMENTS CONTENTS

Introduction PHILIPPINE STANDARD ON AUDITING 810 ENGAGEMENTS TO REPORT ON SUMMARY FINANCIAL STATEMENTS (Effective for engagements for periods beginning on or after December 15, 2009) CONTENTS Paragraph

Introduction PHILIPPINE STANDARD ON AUDITING 810 ENGAGEMENTS TO REPORT ON SUMMARY FINANCIAL STATEMENTS (Effective for engagements for periods beginning on or after December 15, 2009) CONTENTS Paragraph