NÁKLADY A CENY - COSTS AND PRICES

|

|

|

- Simon Barnett

- 5 years ago

- Views:

Transcription

1 Moderné vzdelávanie pre vedomostnú spoločnosť/ Projekt je spolufinancovaný zo zdrojov EÚ NÁKLADY A CENY - COSTS AND PRICES Stavebná fakulta Alena Tažiková

2 Táto publikácia vznikla za finančnej podpory z Európskeho sociálneho fondu v rámci Operačného programu Vzdelávanie. Prioritná os 1 Reforma vzdelávania a odbornej prípravy Opatrenie 1.2 Vysoké školy a výskum a vývoj ako motory rozvoja vedomostnej spoločnosti. Názov projektu: Balík doplnkov pre ďalšiu reformu vzdelávania na TUKE ITMS Názov : Náklady a ceny - Costs and prices Autor: Alena Tažiková Vydavateľ: Technická univerzita v Košiciach Rok: 2015 Vydanie: prvé Počet výtlačkov: 10 ks Rozsah: 114 strán Rukopis neprešiel jazykovou úpravou. Za odbornú a obsahovú stránku zodpovedá autor.

3 Introduction to the issue Learning objectives To understand the strategic importance of costs and prices in the corporate practice (with emphasis on the specifics of construction) To understand the peculiarities of construction (in analysis, planning, and setting costs and prices of construction processes). To master the basic principles, methods and practices as well as the importance of costs in pricing

4 Basic terms used in the calculations Investment process public procurement process of new and reconstruction of old construction work, participants of the investment process Construction works - a general term referring to any result of the installation and construction activity including built-in materials, products, intermediate products, machinery and equipment Construction structure built with construction works of the construction products, which is connects to ground firmly, or which requires a modification of surface (Building Law 50/1976 Zb.). This is a unit that performs a separate technical-economic or other social function and represents tangible investment assets.

5 Basic terms used in the calculations Construction - for valuation purposes - is a summary of building materials and components, works and supply of machinery, equipment and inventory, including their installation, implementation in continuous time and continuous place. Their result is the construction of a new tangible fixed assets (TFA), - change or renewal of an existing tangible fixed assets (reconstruction, modernization, expansion). This tangible fixed assets performs as a whole a separate techno-economic or other social function. building object result of building production, which has the character of tangible fixed assets and produces spatially coherent or at least technically a separate part of the building.

6 Basic terms used in the calculations Structure of construction work construction Construction section technological section Construction objects operational files Equipment boiler, etc. assembly E.g. air conditioning, elevators, etc. delivery E.g. machine line assembly assembly PSV delivery assembly delivery HSV Assembly works delivery Construction works

7 Basic terms used in the calculations Construction part is all construction objects of building which together ensure the required purpose and utility functions of building. Construction object - is the result of building production, creates spatially coherent, technical separate part of the building with a defined purpose and function. After realization it is the tangible fixed assets (DHM). Technological part - all operating units, sets of machinery and equipment, including their assemblies, which in total provide for the execution of technological processes. Operation set - summary of machinery, equipment and inventory, including their installation. It carries a separate technological process of underlying technology of production, or complete technological process and ancillary production is put into operation in continuous time and after realization is the tangible fixed assets.

8 Basic terms used in the calculations Price is the financial expression the value of goods and services Price = cost + profit price is not equal to the value if the offer = demand so regards the equilibrium Value of goods - is formed amount of work spent on the production of goods. The work includes the past work and lives work. Costs- value terms of all inputs in the production process. Costs represent a monetary valuation of production factors and the other purposefully incurred costs, which are associated with its activities. Costs incurred at the time of consumption. Expenses - means reduce the amount financial resources in the company. Not every expense is reflected as a cost and the contrary. Between costs and expenses exists factual and time differences. Expenses incurred at the time of payment.

9 Basic terms used in the calculations Calculating - a summary of the procedures and methods, which are identified and calculated the necessary means to achieve a specific economic target. The result of calculating is calculation. Calculation - means any calculation (simplified), used to calculate costs and prices on the calculation unit. Subject of calculations is performance, which were the cause of costs. Calculation unit - CU is a performance defined by unit of measure for which finding their own costs. CU must be defined by the type (structural component) and volume (e.g., number, weight, length, area). In terms of construction output may be CU whole object or the coherent part of construction work or construction, time unit of worker labour, and the time unit of the machine performance.

10 Costs Costs and economic benefits The costs are defined as the expending of economic resources on a performance, result of the activity, from which is expected economic effect. In other words: Effective consumption of production factors associated with the activity of the company, expressed in money. Cost carriers: Product Service, Department (Centre) Market segment Activity

11 Characteristics of costs The competition and lack of resources is forcing all construction companies to : increasing of economy increasing the efficiency Increased level of scope and quality of construction work at continuous pressure on the: Optimization and cost reduction

12 Ensuring efficiency = 1. Ratio monitoring performance to cost 2. Increasing the volume of output per unit cost Ensuring of economy = 1. Ensuring the same volume of performance at lower cost 2. Minimizing the cost of the activity of construction company

between the costs and expenses can be defined as : Costs = use of")

13 The difference between costs and expenses Differences (factual and time) between the costs and expenses can be defined as : Costs = use of funds for certain performances incurred at the moment of consumption Expenses = reduction of volume of funds incurred at the moment of the payment

14 Classification of costs - is needed for planning, record keeping and managing costs - Classification is a list of categories that structure the information in a particular area.

15 Classification of costs Classification of costs according to different points of view: 1. by cost types (Species the breakdown) 2. by items of calculation formula (calculation the breakdown) 3. by attributting to products and performance 4. by depending the cost of production volume

16 1. Species (economic) the breakdown Breakdown by economically homogeneous types of costs : material costs (material and energy consumption) services (external) Salaries and other personnel costs taxes and fees other operating expenses (including fines and penalties) depreciations and reserves. financial costs. Special costs (including shortages and losses) income taxes

17 A characteristic of the species breakdown of is the economic unity of the individual cost items, because they contain only one type of cost. Species classification divided costs in the form and amount as originally (initially) in the organization have originated.

18 Lack of species breakdowns Difficult breakdown for planning performance and follow costs difficulty records Lower visibility data Low interconnection on performances, and results of the organization The complexity of the economic analysis of costs

19 2. Classification of expenses by items of the calculation formula Costs are classified according to their relation to the productive process (construction activity) of the company The organization divides all activities under organization's performance (for individual constructions)

20 Cost clasification by calculation - costs are divided according to their relationship to the production process - it is used in the creation of prices of products General clasification of costs by type calculation formula: direct material direct labour Basic other direct costs Budgetary production overheads Costs BBC 1 till 4 constitutes inherent costs of production administrative overheads 1 till 5 constitutes own costs performance selling costs Additional Secondary 1 till 6 represents full costs of performance BC BC Profit (loss) 1 till 7 constitutes wholesale price

21 Calculation formula used in building production in Slovakia: Direct material (H) Direct labor (M) Cost of machinery and equipment(s) other direct costs(opn) Subcontracts (SUB) Direct processing costs Directs costs 6. production overheads(rv) Own production costs Indirect costs 7. administrative overheads(rs) Complete own costs 8. reasonable profit (Z) 9. business risk(pr) Total price Gross range

22 3. Costs classification by attributting to products and performance Direct costs costs that can be directly attributed to individual performance. They can be counted directly to the unit of production. Indirect costs costs that can not be directly attributed to individual performance, since they are executed in connection with various types of products, or for the whole of the production, or running of the business.

23 4. Cost clasification by depending the cost of production volume - change in volume production affects the development costs directly, variable costs - their absolute amount varies with changes in production volume, the degree of variability is different, therefore: 2 costs 1 proportional growth of production and rising costs in the same proportion Disproportional - cost does not develop in the same direction than production. There are: 2 progressive - cost growing faster than production - overtime, scrap, days of work 3 degressive- height of cost grows more slowly than the volume of performances technological fuel, repair TFA 4 regressive- cost is inversely proportional to the volume of production directly related to productivity, pay for downtime Volume of production

24 fixed costs by the changes in the volume of production within existing capacities, costs do not change 1 absolutely (new technological equipment, depreciations, wages, interest, rents, costs for lighting, heating) Profit Costs ko fixed costs Mž Mž variable costs 2 relatively (costs, which change by Costs jumping in some volume) 2 1 Volume of production Performances Mž margin gross profit % Ko critical point of costs, profit = 0

25 Classification and describing of construction production Law No. 18/1996 about prices When negotiating prices are binding on specification of the product: name, possibly numerical code of the Customs Tariff duties, unit of quantity, quality and delivery terms or other conditions ( 3) The importance for the calculating practice - ensure unambiguous definition calculation unit for which, we calculate cost. The uniform classification systems of the construction production are the basis of the information system in the construction. It is basic communication means between all participants of the investment process.

26 1. Final construction production: - Uniform classification of buildings JKSO - Classification of construction KS construction work, construction building, buildings object, assembly work, 2. Partial construction production: - Common procurement vocabulary CPV Classification of Products KP The Classification of building structures and works TSKP The Classification of works TSP The Classification construction output TPS Statistical Classification of Economic Activities -SK NACE rev.2

27 The Statistical Classification of Economic Activities in the European Community, commonly referred to as NACE, is a European industry standard classification system consisting of a 6 digit code. NACE is similar in function to the SIC and NAICS systems: Standard Industrial Classification North American Industry Classification System The first four digits of the code, which is the first four levels of the classification system, are the same in all European countries. The fifth digit might vary from country to country and further digits are sometimes placed by suppliers of databases.

28 A screenshot of NACE being used in a computer program

29 Industry classification Industry classification or industry taxonomy organizes companies into industrial groupings based on similar production processes, similar products, or similar behavior in financial markets. A wide variety of taxonomies is in use, sponsored by different organizations and based on different criteria.

30 Slovakia In Slovakia existed Slovak implementation called NACE Classification of Economic Activities (OKEČ- abbreviation), then (since 2003) under the name of the Statistical Classification of Economic Activities. Implementation force in Slovakia, since 2008, is called the Statistical Classification of Economic Activities, SK NACE Rev. 2 Use: For example NACE used catalog firms, that classify companies into categories.

31 The areas where the use of classification structures. Descriptions Pricing Calculation Specification Clasification Invoicing Indicators Realization Scheme of systems which build on classification of buildings.

32 PRICES, THEIR IMPORTANCE AND ROLE IN CONSTRUCTION BUSINESS Prices have an important role for several reasons, in the construction business. In particular, prices are tools to make a prof Their movement up or down, increase or decrease revenues in the construction company. The company may lose market share improperly determined prices, but with good pricing policy, on the contrary, this proportion increased. In terms of production cost, height price represents the lowe limit, should not be lower than its own production costs. Thus, the price becomes an important consideration when deciding of acceptance or rejection of the contract.

33 PRICES, THEIR IMPORTANCE AND ROLE IN CONSTRUCTION BUSINESS On the market, effect of competitors does not allow to companies exceed the upper limit of the price. The upper limit of price determined by the market and the effect of competition on the market. In construction, the role of price is to ensure the correct orientation and motivation of suppliers of construction works, as well as their customers investors.

34 PRICES, THEIR IMPORTANCE AND ROLE IN CONSTRUCTION BUSINESS Úspešnosť podnikania v stavebníctve závisí od mnohých faktorov. Úroveň zvládnutia všetkých činností a vplyvov, ktoré súvisia s podnikaním, sa nakoniec prejaví vo výške nákladov a cien realizovaných výkonov, a tým aj v konečnom efekte zisku. Pri úvahách o cenách vychádzame zo všeobecného poznatku, že cieľom každého podnikateľa je dosiahnuť zisk. To znamená byť úspešný pri realizácii svojich výkonov v takej miere, aby ceny, za ktoré predáva podnikateľ svoje stavebné výkony, resp. služby na trhu, boli vyššie ako ním vynaložené náklady. Preto platí vzťah : Price = Costs + Profit

35 PRICES, THEIR IMPORTANCE AND ROLE IN CONSTRUCTION BUSINESS Price = Costs + Profit Profit do not understand only as a reward for business, but also as a condition for further development. In particular, the company can affect the creation of profit: topicality of their business ideas and economic viability of their business ideas.

36 Analysis of the current situation in the pricing in the construction companies in Slovakia bids are processed in the pressure of time there is no analysis of the optimal design of technical and organizational procedure of construction realisation in pricing is applied the routine and the improvisation used calculation system based on a biased documents, that don t reflect actual conditions of construction company incorrectness of scheduling indirect costs bids are generated using a database of the average guide prices

37 Analysis of the current situation in the pricing in the construction companies in Slovakia The cost information is often inaccurate and it has an adverse impact on the competitiveness and profitability define the fixed and variable costs is not unambiguous clear pricing strategy is missing Price decision on the acceptance of a contract is often intuitive.

38 The basic objectives of pricing policy of the construction company When creating the tender prices, we take into account: amount of profit domination of the market positions, percentage of obtaining the contract in the tender, etc.

39 Contents : Processing bid in stages : The study, construction permit, realization of the construction The budget of the construction building: Definition, purpose, function Information for processing of the budget The structure of budgetary costs The methodology for establishing the budget

40 Costs clasification Calculation clasification of costs - costs are divided according to their relationship to the production process - this classification is used in the creation of product prices The general clasification of costs by type calculation formula: direct material direct labour other direct costs production overheads Basic 1 till 4 constitutes inherent costs of production Costs BC administrative overheads 1 till 5 constitutes own costs performance selling costs 1 till 6 represents full costs of performance Profit (loss) Construction 1 till 7 constitutes wholesale price Additional site costs Costs AC CSC

41 Calculation formula used in building production in Slovakia: Direct material (H) Direct labor (M) Cost of machinery and equipment (S) other direct costs(opn) Subcontracts (SUB) Direct processing costs Directs costs 6. production overheads (RV) Own production costs Indirect costs 7. administrative overheads (RS) Complete own costs 8. reasonable profit (Z) 9. business risk (PR) Total price Gross range

42 Investment process - Supply construction work Before the project preparation The study, construction intention, territorial proceedings Project preparation Building realization construction proceedings Building technology Preparation, realization and handover to use The production invoice Invoice, inventory of work carried out, declaratory Protocol The Updated the Contractual production production price cost of the cost of the contractor contractor The actual cost of construction work invoiced budgets Estimate prices, Conversion Planned investment costs control approxima te price Investor, contracting authority, offer Offer price contractor production contractual calculation agreement Contractor Costing draws up the between the shall prepare, contractor for its internal investor and paid by needs the contractor investor

43 PROCESSING PRICE OFFER IN PHASES Number Title phases of phases Valuation tools Output form Deviation of accuracy valuation I. Study -Budgetary indicators of construction objects (RUSO) -Gross design elements - The conversion price of the work - Preliminary calculation - Budget Summary % II. Documentati on for construction permit -Budgetary indicators of gross design elements -The indicative valuation tools (SON) -Individual calculation Itemized budget with bills 5-10 % of quantities by construction. parts - Valued inventory of works by the Classification TSP Realisation documentati on -The indicative valuation tools (SON) Individual calculation - Itemized budget with bills of quantities by construction parts - Production calculation - Valued inventory of works by the III.?? 0-5%?

44 Study The conversion of guide price of the building object is a preliminary price calculation, which shall be drawn up in the stage before project preparation and in the proje preparation work. it is part of the calculation of the total cost of construction drawn up using price indicators, which are traced from realized buildings It is a quick and easy way to identify the amount of price The calculation procedure: Step 1: Classifications of valued building object to the classification system JKSO, KS Step 2: Finding of relevant price indicator on the unit of measurement of building object Step 3: Calculation of the range of valued building object, which is expressed in appropriate units of measurement Step 4: Own calculation of the indicative price building object according to the formula: OCSO= Q x THU x kcu Step 5: (when using older data base) Update price level using statistical indices of price development in construction

45 OCSO = Q x THU x kcu THU- technical and economic indicator - price indicator Companies in which are published indicators: Technical and economic indicators Budgetary indicators Indicators budget prices - CENEKON Bratislava ÚEOS Commerce Bratislava UNIKA Bratislava Kcu- - Coefficient expressing the development of prices The coefficient expresses the difference in price levels between the period of which we have technical and economic indicator and the period for which we want to perform a valuation of the object. - to Coefficients broken down by Uniform classification of building objects - JKSO -from Coefficients broken down by Classification of buildings -KS

46 Documentation for architectural studies: 1. geometric plan (altimetry + plan metric) plus engineering networks and neighboring buildings 2. local regulations as a permissible density of construction, permissible height, etc photo documentation of plot 4. basic requirements for the house (building area, Converted space, number of floors, number and size of rooms, the requirements for rooms, bathroom, toilet, etc.). 5. A possible geological exploration on account of the resistance of soil

47 The budget of building construction Definition, purpose, function The budget of Building construction is a preliminary price calculation. Preliminary price calculation because of its treatment in the pre-realization phase of construction of building works Price calculation - the result of calculation will be price The result is contractual price on the basis of detailed - itemized description of the works. Conflict of view of the investor and contractor to price of the work Processor Investor Contractor The check budget The bidding budget Methodology of budgets is identical, but we do budgets of other documents and for other purposes

48 Investment process - Supply construction work Before the project preparation The study, construction intention, territorial proceedings Project preparation Building realization construction proceedings Building technology Preparation, realization and handover to use The production invoice Invoice, inventory of work carried out, declaratory Protocol The Updated the Contractual production production price cost of the cost of the contractor contractor The actual cost of construction work invoiced budgets estimate prices, Conversion Planned investment costs control approxima te price Investor, contracting authority, offer Offer price contractor production contractual calculation agreement Contractor Costing draws up the between the shall prepare, contractor for its internal investor and paid by needs the contractor investor

49 Documents on the budget process: Technical documentation-project documentation and technical report to project construction Technological descriptions-construction project of organizations affecting the fundamental relations on site, describing objects of site equipment, transportation distances, etc. valuation documents. Methods pricing: Indicative orientation prices by companies, (Cenekon Bratislava, Odis Žilina, UEOS Bratislava, RTS Trnava), Indicative valuation tools SON or Individual a calculated business prices Report and assessment - Required in public sector -processed by investor, base for contractor

50 The structure of budgetary costs The budgets are compiled separately for construction objekcts A. B. Basic Costs BC and operational files C. Additional AC Construction site costs CSC Another form of clasification depends on the selected sorting (resp. Documents)!

51 Basic Budgetary Costs BBC Basic Costs BC Main building production Earth works Foundations Vertical structures Horizontal structures Communications Surfacing, doors and windows, floors Pipe lines Other structures and work Basic Costs BC Affiliated building production Water proofing Coating coverings Thermal insulation... Basic Costs BC Assembly works Electrical installations Assembly indication devices...

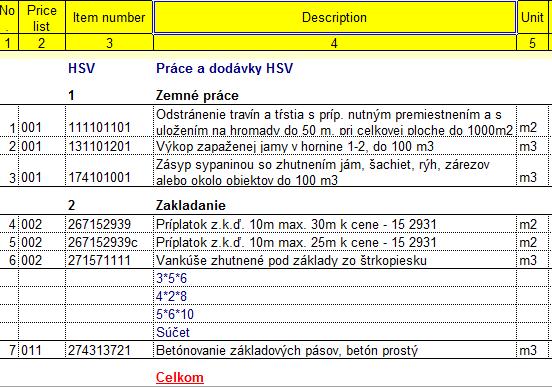

52 4. The methodology for establishing the budget The methodology for establishing the budget is not specified, in the process of free price formation, with the exception of procurement. The procedure for establishing the budget - according to the procedure of construction - according to the price lists of construction works Types of items in the budget - Items of construction works - Items of supplies (specifications) materials and equipment - So called R -Item that represent works and materials which are not classifiable according to the used classification (not included in the database)

53 4. The methodology for establishing the budget Each costing unit Budget item- is presented: - its numerical code, - description of the item, - the unit of measurement, - unit price, - acreage, - total cost of the item - the unit and the total weight.

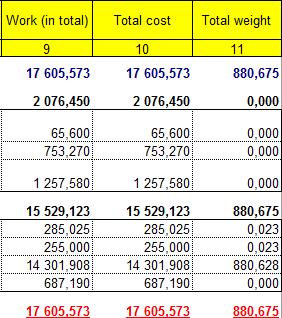

54 Usually layout of the forms in the construction budget : Summary sheet of construction Estimate cost Overview Estimate summary Cost estimate Bill of quantities

55 Estimate cost Overview

56 Estimate cost Overview

57 Estimate cost Overview (continue)

58 Estimate summary

59 Cost Estimate

60 Cost Estimate

61 Cost Estimate

62 Cost estimate - Bill of quantities

63 Cost estimate bill of quantities

64 Cost estimate bill of quantities

65 Costs clasification Calculation clasification of costs - costs are divided according to their relationship to the production process - this classification is used in the creation of product prices The general clasification of costs by type calculation formula: direct material direct labour other direct costs production overheads 1 till 4 constitutes inherent costs of production Basic Costs BC administrative overheads 1 till 5 constitutes own costs performance selling costs 1 till 6 represents full costs of performance Profit (loss) Secondary 1 till 7 constitutes wholesale price Additional BC C

66 Calculation formula used in building production in Slovakia: Direct material (H) Direct labor (M) Cost of machinery and equipment (S) other direct costs(opn) Subcontracts (SUB) Direct processing costs Directs costs 6. production overheads (RV) Own production costs Indirect costs 7. administrative overheads (RS) Complete own costs 8. reasonable profit (Z) 9. business risk (PR) Total price Gross range

67 The cost of direct materials (mass) M: 1. Identify the different types of materials The basic material Directly built material Other minor material Connecting material The material for re-use Formworks, scaffolds 2. Determine the quantities of the various materials The basic material technical standards of material consumption professional conversion Standard material consumption -according of indicative guide prices amount of material shall be increased about the losses in justified cases Other minor material lump sum The material for re-use the relative amount of the total price relative amount is calculated according to the expected number of materials, until the time of its full wear of

")

68 The cost of direct materials (mass) M: 1. Identify the different types of materials 2. Determine the quantities of the various materials 3. Determine the price of individual materials The price agreed with the supplier of the material Acquisition costs VAT (without VAT VAT payer) (with VAT no VAT payer)

69 The cost of direct wages W: - costs constitute wages of production workers and a crew of construction machinery and equipment 1. We must determine the optimal composition of the work crews with employment qualifications classification of individual members 2. We must Identify consumption time achievement standards professional conversion achievement standards referred to in the of indicative guide prices normatives of work time normatives of the technology of similar works 3. We must appreciate the time consumption rates of the tariff scale (rate the entrepreneur determines individually)

70 The cost of the operation construction machinery and equipment Machine hours (Mh) is a time machine operation hours, which includes its own for net operating performance, this is the time for which the machine is operating To the time machine hours is not included: time of working breaks the machine operator, shift maintenance, relocation and machine downtime, loss of time due to bad organization of work, breakdowns, weather, etc. The rate of the Machine hour is: Depreciation + repair + transfers + assembly + disassembly + fuel + electricity + clean. products time (Mh)

71 Other direct costs mandatory contributions health insurance, sickness insurance accident insurance, pension insurance and disability insurance, unemployment insurance, including the guarantee and reserve fund. transport costs, the in-site transport (mass transfer), or even offsite transport, if not included in the item M direct material.

72 Other direct costs depreciation of sets of steel formwork, scaffolding sets etc., if not been included in the cost of direct materials. and all other incurred costs, that are evaluated directly, financially and are not included in the other components of the calculation formula (e.g. agreed terms of pay for overtime, night, during public holidays and other premiums and discounts arising from individual buildings terms).

73 Profit and risk In the prices of construction works, in order to ensure their competitiveness, should be calculated the reasonable profit. At the present, in the indicative prices of construction works be counted profit of 10 20% from the processing costs, which are: the cost of direct labor, operating construction machinery, other direct costs, production overheads and administrative overheads.

74 Bill of quantities = blind budget : There is no way for the formation of the construction budget, without bill of quantities. Bill of quantities is a basic inventory of the work and materials required for the realization of the project. For each individual item of the budget must be determined its amount. Good project includes a detailed Bill of quantities. But the cheapest offer may comprise a plurality of uncertainty!

75 Bill of quantities (BQ) = blind budget : BQ - it is a separate document, in the public procurement BQ is a part of the tender documents. It is a mathematical documentation of the area calculation. The basic function is to describe the object so that both sides had the same idea about it. Individual area are supported by the project documentation. Complicated geometric shapes are divided into simpler and labeled as figures.

76 Bill of quantities (BQ) = blind budget : -It is necessary to observe the general conditions in selected sorting system -method of making bill of quantities -technical documents - information about what each item include and does not include (e.g. Formwork, Scaffolding, Specification...) -Losses

77 Bill of quantities (BQ) = blind budget : Unwritten principle of making of the Bill of quantities (BQ): The calculation is divided into simpler geometric shapes. Calculation figures include the phrase description. We maintain a uniform direction of the calculation procedure, for example from left to right and top to bottom. Always we write the calculation in the same order - area = length x width x height, different order is necessary to explain.

78 Calculation formulas used in the calculation of the individual unit prices of construction work Until 1990 prices were calculated with a uniform prescribed manner by mandatory of trade union calculation formulas, using a common normative base and prescribed overhead rates and profit Since 1991 under conditions of free pricing is not binding normative base, and also using trade and type calculation formula There is no obligation to use binding calculation formulas for the calculation of the individual unit prices of construction work.

79 Calculation formulas used in the calculation of the individual unit prices of construction work The trade union calculation formula: 1. Direct costs 2. Direct labour 3. Costs of machinery and equipment 4. Other direct costs Total direct costs 5. Production overheads 5.1 technological production overheads 5.2 general production overheads own costs performance 6. Správna réžia Full own costs performance 7. Subcontracts (SUB) 8. Profit (Loss) Type calculation formula: 1. Direct costs 2. Direct labour 3. Other direct costs 4. Production overheads 1 till 4 constitutes inherent costs of production 5. Administrative overheads 1 till 5 constitutes own costs performance 6. Selling costs 1 till 6 represents full own costs of performance 7. Profit (Loss) 1 till 7 constitutes wholesale price

80 Unit price calculation elements: Classification by type calculation formula Own costs OC Direct costs DC M M L ME Profit P Undirect costs UC ODC PO DPC M M AO P P The gross margin PCP AO PC P P Price without VAT M- costs of the direct material L- costs of the direct labour ME- costs of the machinery and equipment ODC- other direct costs PO- production overheads AO- administrative overheads P- profit PSN- Direct processing costs SNV- processing cost of production PC - processing costs GM - the gross margin VAT - Value Added Tax DPC = base for production overheads PO PCP = base for administrative overheads AO PC = base for profit P

81 Contents Indirect costs Budget of overhead costs Documentation for budgeting of overhead costs Standardization of overhead costs Fixed and variable overhead costs

82 Costs clasification Calculation clasification of costs - costs are divided according to their relationship to the production process - this classification is used in the creation of product prices The general clasification of costs by type calculation formula: direct material direct labour other direct costs production overheads Basic 1 till 4 constitutes inherent costs of production Costs BC administrative overheads 1 till 5 constitutes own costs performance selling costs 1 till 6 represents full costs of performance Profit (loss) Construction 1 till 7 constitutes wholesale price Additional site costs Costs AC CSC

83 Calculation formula used in building production in Slovakia: Direct material (H) Direct labor (M) Cost of machinery and equipment (S) Other direct costs(opn) Subcontracts (SUB) Direct processing costs Directs costs 6. production overheads (RV) Own production costs Indirect costs 7. administrative overheads (RS) Complete own costs 8. reasonable profit (Z) 9. business risk (PR) Total price Gross range

84 Overhead costs - They are the indirect costs - they are the most difficult part of the calculation of construction works - They do not count directly to the performance unit, but in the form of surcharges as % of budget base -they include the cost of site and the territorial impacts- it is standard -above standard contains Construction site costs CSC -They are provide for the construction

85 Overhead costs -they reflect the estimated costs of overheads -This is specifically the cost of the contractor -They are essential in the creation of the construction works

86 Production overheads - It includes the cost of construction, which can not be assigned to the item list of works - These are the costs associated with the operation and management of the construction - Calculation unit is the whole building, (or the building structure) Allocation base: - There is no fixed compulsory the allocation base. -It is a matter of the creator of the bid -Allocation base in Cenkros plus: - wages - machinery - Social and health insurance - ODC other direct costs

consumption of material related with the construction site (office supplies and aids, depreciation, etc..) costs for external services (telephone, site guarding, various rents.")

87 Production overheads Basic Costs BC They are the costs related to the operation and management of the construction eg.: construction site costs (site equipment and its removal, access roads, etc..) consumption of material related with the construction site (office supplies and aids, depreciation, etc..) costs for external services (telephone, site guarding, various rents...) labor costs a auxiliary operating staff, technical and administrative staff (masters, site manager, etc.). the cost of the concrete test, quality control... the consumption energy and water at the construction site.

88 Production overheads PO Costs related to the management activities and operation of the production process, which can not be established directly for the calculation of unit. They are calculated with so-called surcharge method - amount of overhead costs for the calculation unit is calculated by the percentage surcharge Established by use base of the direct costs of complex work PSN (direct labor + the cost of running machines + other direct costs) rv= RV / PSN x 100 (%) rv - percentage of production overheads RV - costs of the production overhead PSN - direct costs of complex work

89 Calculation of production overheads (PO) for the construction Wages Number of Eur/mount h Eur/year mounths bonus Utilization (%) Total Eur Site Manager % 4260 Foreman at a construction site % 5200 Technical and administrative staff % 5190 Office Supplies % 360 Auxiliary material % 360 Transport costs % 4200 OPERATING COSTS ENERGY Electric power 14kW % 1800 water l 68,88 826, % 526, % 300 Technical documents Project documentation PO= ,56 Eur

90 Calculate the rate of production overhead of the construction PO=(M+OPN)* s1 s1= PO / (L+ ODC) s1= / = 0,40 s1=0,4*100 = 40% Ldirect labor ODC- other direct costs s1rate of production overhead data from the budget direct labor + other direct costs

91 Administrative overheads outside of the construction site Costs related to the management and administration of the organization and general service activities which can not be established directly for the calculation unit, not fall within production overheads They are calculated with so-called surcharge method - amount of overhead costs for the calculation unit is calculated by the percentage surcharge Established by use base of the complex work cost of production SNV (direct labor + the cost of running machines + other direct costs + production overhead) Their height can be obtained from the accounts for the last financial year, either in whole or for individual centers or construction.

rs= RS / SNV x 100 (%) rs - percentage of the administrative overheads RS -costs of the administrative overheads SNV - complex work cost of")

92 Administrative overheads AO outside of the construction site Established by use base of the complex work cost of production SNV (direct labor + the cost of running machines + other direct costs + production overhead) rs= RS / SNV x 100 (%) rs - percentage of the administrative overheads RS -costs of the administrative overheads SNV - complex work cost of production

93 Calculation Výpočet správnej of administrative réžie overheads for the construction Wages Numbe r of Eur/moun th Eur/ye ar mounths bonus Utilization (%) Total Eur charwoman % 804 guard % 1200 Pomocný pracovník % 1206 Auxiliary worker % 1836 Office Supplies % 480 Maintenance of the company % 180 Transport costs % 1200 Advertising Costs % 100 Other cost (post,telefon...) % 1800 Auxiliary material % 360 Electric power % 660 gas % 1200 water % 300 OPERATING COSTS Eur ENERGY

94 Calculation of administrative overheads (AO) for the construction AO = (L+ODC+PO)* s2 S2 = Rs/ (M+OPN+Rv) S2 = / = 0,14 S2 = 0,14*100 = 14% L- direct labor ODC- other direct costs PO- production overhead S2 - rate of administrative overheads

95 Summary: Production and administrative overhead - They are calculated using markups, determined on the basis of previous period The base for calculation of the production overhead = direct costs without material costs The base for calculation of the administrative overhead = direct costs + production overhead without material costs

96 Outsourcing "outside" "resource" In business, outsourcing involves the contracting out of a business process to another party (compare business process outsourcing). The term "outsourcing" dates back to at least Outsourcing sometimes involves transferring employees and assets from one firm to another, but not always. Outsourcing is also the practice of handing over control of public services to for-profit corporations. - supporting activities, which providing core business for example facility management, information technology and financial accounting, vehicle fleet etc.

97 Outsourcing Outsourcing includes both foreign and domestic contracting, and sometimes includes offshoring (relocating a business function to another country). Financial savings from lower international labor rates can provide a major motivation for outsourcing/offshoring. Reasons for outsourcing Companies primarily outsource to reduce certain costs - such as peripheral or "noncore" business expenses, high taxes, high energy costs, excessive government regulation/mandates, production and/or labor costs. The incentive to outsource may be greater for U.S. companies due to unusually high corporate taxes and mandated benefits, like social security, Medicare, and safety protection

98 Outsourcing Outsourcing can offer greater budget flexibility and control. Outsourcing lets organizations pay for only the services they need, when they need them. It also reduces the need to hire and train specialized staff, brings in fresh engineering expertise, and reduces capital and operating expenses.

99 Insourcing The opposite of outsourcing, insourcing, entails bringing processes handled by third-party firms in-house, and is sometimes accomplished via vertical integration. Outsourcing has gone through many iterations and reinventions. Some outsourcing contracts have been partially or fully reversed, citing an inability to execute strategy, lost transparency & control, onerous contractual models, a lack of competition, recurring costs, hidden costs, and so on. Many companies are now moving to more tailored models where along with outsource vendor diversification, key parts of what was previously outsourced has been insourced.

100 Insourcing Insourcing has been identified as a means to ensure control, compliance and to gain competitive differentiation through vertical integration or the development of shared services [commonly called a 'center of excellence']. Insourcing at some level also tends to be leveraged to enable organizations to undergo significant transformational change.

, by means of internal (captive) or external")

101 Offshoring is the relocation, by a company, of a business process from one country to another typically an operational process, such as manufacturing, or supporting processes, such as accounting. Even state governments employ offshoring. More recently, offshoring has been associated primarily with the outsourcing of technical and administrative services supporting domestic and global operations from outside the home country ("offshore outsourcing"), by means of internal (captive) or external (outsourcing) delivery models.

102 Price decision making on the implementation of the construction contract Contractor Knowledge of the pricing The market environment Predictable and unpredictable factors Flexible and fast reacting Price decision making = difficult process Own production Subcontracting

103 Price decision making on the implementation of the construction contract The factors that affect the choice between own production or subcontracting? Own production subcontract price is higher than their own cost higher quality with own production available the unused own construction capacity company has own know-how can not be found enough reliable suppliers

104 Price decision making on the implementation of the construction contract The factors that affect the choice between own production or subcontracting? Subcontracting subcontract price is the lower than their own cost Subcontractor will ensure a higher quality of work capital of the company is fully exploited There is no experience with technology, materials, manufacturing etc.

105 Price decision making on the implementation of the construction contract? Subcontracting A business practice where main contractor hires additional individuals or companies called subcontractors to help complete a project. The main contractor is still in charge and must oversee hires to ensure project is executed and completed as specified in contract.

106 Price decision making on the implementation of the construction contract Subcontracting

is an international standards organization for the construction industry, best known for the FIDIC family of contract")

107 The International Federation of Consulting Engineers (commonly known as FIDIC, acronym for its French name Fédération Internationale Des Ingénieurs-Conseils) is an international standards organization for the construction industry, best known for the FIDIC family of contract templates.

108 The fact that the organisation has a French title bears testimony to its foundation in 1915 by three countries each wholly or partly francophone. The founding member countries of the FIDIC were Belgium, France and Switzerland. FIDIC, the International Federation of Consulting Engineers represents globally the consulting engineering industry. As such, the Federation promotes the business interest of firms supplying technology-based intellectual services for the built and natural environment. FIDIC acronym stands for the French version of the name - Fédération Internationale des Ingénieurs-Conseils.

109 FIDIC Vision Enabling the development of a sustainable world as the recognised global voice for the consulting engineering industry. FIDIC Mission To work closely with our stakeholders to improve the business climate in which we operate and enable our members to contribute to making the world a better place to live in, now and in the future.

110 FIDIC Values Quality Integrity Sustainability

111 Application of FIDIC conditions: Sample form of contract Agreement Bill of quantity BoQ Letter of Acceptance Conditions of particular Application General contract conditions Contract condition for... Payment schedule (Milestone plan) Sample advance payment guarantee Sample performance bond Subcontractor s list Time schedule Types of tenders: List of drawings a) open tendering, b) single stage, two stage selective tendering, c) negotiated tendering.

112 The formula for inflation index The formula accepted and approved for inclusion in the General Conditions of Contract for Construction Works (SAICE 2010), is based on the Haylett Formula for escalation, which has been adopted by the industry and it has been developed by the SAICE, Construction Industry Development Board (CIDB) and the South African Federation of Civil Engineering Contractors (SAFCEC). The expression utilized by the SAICE to calculate the Contract Price Adjustment Factor, fcpa, is presented in Equation 1.

113 Where: The formula x is the proportion of the contract value that is not subject to adjustment (i.e. the fixed portion), and unless stated otherwise in the contract the fixed proportion will be 0.10 or 10%. Thus the portion that will be subject to adjustment is 0.9 or 90% of the contract/claim value. a, b, c and d are the coefficients contained in the contract which are deemed, irrespective of the actual constituents of the work, to be representative of the proportionate value of labour, contractor s equipment, materials (excluding specialist materials which must be separately stipulated in the contract) and fuel respectively. The arithmetical sum of a, b, c and d must be equal to unity. Thus these coefficients are effectively weighting factors that account for the proportion of the labour, plant, material and fuel values of the construction works being carried out. L is the Labour Index, the value for which is taken as the Consumer Price Index for labour in the province where the work is to be carried out.

114 The formula P is the Plant Index, the value for which will be taken as the Producer Price Index for Civil Engineering Plant. M is the Materials Index, the value for which will be taken as the Civil Engineering Producer Price Index for materials. F is the Fuel Index, the value for which will be taken as the Producer Price Index for Diesel at wholesale level for the area where the contract is being carried out.

PA P E R S. HMS Belmonte. Aurecon, Lynnwood Bridge Office Park, 4 Daventry Street, Lynnwood Manor, 0081;

HMS Belmonte Aurecon, Lynnwood Bridge Office Park, 4 Daventry Street, Lynnwood Manor, 0081; E-mail halbelmonte@aurecongroup.com ABSTRACT Municipalities are under a legislative imperative to compile asset

HMS Belmonte Aurecon, Lynnwood Bridge Office Park, 4 Daventry Street, Lynnwood Manor, 0081; E-mail halbelmonte@aurecongroup.com ABSTRACT Municipalities are under a legislative imperative to compile asset

BPC6C Cost and Management Accounting. Unit : I to V

BPC6C Cost and Management Accounting Unit : I to V UNIT -1 FUNDAMENTALS OF COST ACCOUNTING Nature and scope of Cost Accounting, Distinction between cost and financial accounting, Cost sheet, tenders Characteristics

BPC6C Cost and Management Accounting Unit : I to V UNIT -1 FUNDAMENTALS OF COST ACCOUNTING Nature and scope of Cost Accounting, Distinction between cost and financial accounting, Cost sheet, tenders Characteristics

Attachment 17 RTD Pricing Conditions

Attachment 17 RTD Pricing Conditions 1. General conditions Incurred Costs may be claimed by the Concessionaire under this Agreement only to the extent such Incurred Costs have been incurred in compliance

Attachment 17 RTD Pricing Conditions 1. General conditions Incurred Costs may be claimed by the Concessionaire under this Agreement only to the extent such Incurred Costs have been incurred in compliance

COST ACCOUNTING STANDARD ON MATERIAL COST

CAS-6 (REVISED 2017) COST ACCOUNTING STANDARD ON MATERIAL COST The following is the COST ACCOUNTING STANDARD 6 (CAS 6) (Revised 2017) issued by the Council of The Institute of Cost Accountants of India

CAS-6 (REVISED 2017) COST ACCOUNTING STANDARD ON MATERIAL COST The following is the COST ACCOUNTING STANDARD 6 (CAS 6) (Revised 2017) issued by the Council of The Institute of Cost Accountants of India

TABLE OF CONTENTS PREFACE 0 GENERAL PROVISIONS 1 STAFF COSTS 2 OFFICE AND ADMINISTRATIVE EXPENDITURE 3 TRAVEL AND ACCOMMODATION COSTS

CATALOGUE OF ELIGIBLE COSTS Interreg V-A Euregio Meuse-Rhine Version 3 - December 2018 TABLE OF CONTENTS PREFACE 0 GENERAL PROVISIONS 0.1 LEGAL BASIS 0.2 ELIGIBLE COSTS 0.2.1 INTERNAL INVOICING 0.2.2 CASH

CATALOGUE OF ELIGIBLE COSTS Interreg V-A Euregio Meuse-Rhine Version 3 - December 2018 TABLE OF CONTENTS PREFACE 0 GENERAL PROVISIONS 0.1 LEGAL BASIS 0.2 ELIGIBLE COSTS 0.2.1 INTERNAL INVOICING 0.2.2 CASH

INTERMEDIATE EXAMINATION

INTERMEDIATE EXAMINATION GROUP II (SYLLABUS 2008) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2011 Paper-8 : COST AND MANAGEMENT ACCOUNTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin

INTERMEDIATE EXAMINATION GROUP II (SYLLABUS 2008) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2011 Paper-8 : COST AND MANAGEMENT ACCOUNTING Time Allowed : 3 Hours Full Marks : 100 The figures in the margin

Capital Area Council of Governments FY 2018 Cost Policy Statement and Cost Allocation Plan

Capital Area Council of Governments FY 2018 Cost Policy Statement and Cost Allocation Plan The Capital Area Council of Governments uses the cost allocation method prescribed in OMB Uniform Administrative

Capital Area Council of Governments FY 2018 Cost Policy Statement and Cost Allocation Plan The Capital Area Council of Governments uses the cost allocation method prescribed in OMB Uniform Administrative

Measuring performance

Measuring performance Business CoaCH series Importance of tracking performance How to measure performance Internal and external yardsticks Early warning system Business Coach series Is your business doing

Measuring performance Business CoaCH series Importance of tracking performance How to measure performance Internal and external yardsticks Early warning system Business Coach series Is your business doing

Cost of Construction Labor and Equipment

Cost of Construction Labor and Equipment Steps of Detailed Cost Estimate Review the bidding documents. Check for general conditions, specifications and drawings. If any discrepancies exist, record them

Cost of Construction Labor and Equipment Steps of Detailed Cost Estimate Review the bidding documents. Check for general conditions, specifications and drawings. If any discrepancies exist, record them

THE EAST AFRICAN COMMUNITY CUSTOMS UNION (RULES OF ORIGIN) RULES ANNEX III

RULES ANNEX III") THE EAST AFRICAN COMMUNITY CUSTOMS UNION (RULES OF ORIGIN) RULES ANNEX III THE EAST AFRICAN COMMUNITY CUSTOMS UNION (RULES OF ORIGIN) RULES TABLE OF CONTENTS RULE TITLE 1 Citation 2 Purpose of the Rules

THE EAST AFRICAN COMMUNITY CUSTOMS UNION (RULES OF ORIGIN) RULES ANNEX III THE EAST AFRICAN COMMUNITY CUSTOMS UNION (RULES OF ORIGIN) RULES TABLE OF CONTENTS RULE TITLE 1 Citation 2 Purpose of the Rules

Capital Area Council of Governments FY 2019 Cost Policy Statement and Cost Allocation Plan

Capital Area Council of Governments FY 2019 Cost Policy Statement and Cost Allocation Plan The Capital Area Council of Governments uses the cost allocation method prescribed in OMB Uniform Administrative

Capital Area Council of Governments FY 2019 Cost Policy Statement and Cost Allocation Plan The Capital Area Council of Governments uses the cost allocation method prescribed in OMB Uniform Administrative

CAS-3 : Overheads 1. Introduction

1 CAS-3 : Overheads 1. Introduction 2. Object In Cost Accounting the analysis and collection overheads, their allocation and apportionment to different cost centres and absorption to products or services

1 CAS-3 : Overheads 1. Introduction 2. Object In Cost Accounting the analysis and collection overheads, their allocation and apportionment to different cost centres and absorption to products or services

Comments: SNA 2008 (1993 Rev 1), from AEG member Robin Lynch, 28 April 2008

, from AEG member Robin Lynch, 28 April 2008") Comments: SNA 2008 (1993 Rev 1), from AEG member Robin Lynch, 28 April 2008 General comment The style is clear, but could give problems for a non-english speaking reader. The main barrier is the use of

Comments: SNA 2008 (1993 Rev 1), from AEG member Robin Lynch, 28 April 2008 General comment The style is clear, but could give problems for a non-english speaking reader. The main barrier is the use of

APPENDIX - A TECHNICAL SPECIFICATIONS. JEA Fleet Services Heavy Duty Maintenance and Repair

APPENDIX - A TECHNICAL SPECIFICATIONS JEA Fleet Services Heavy Duty Maintenance and Repair 1. GENERAL SCOPE OF WORK The purpose of this Invitation to Negotiate (the "ITN") is to evaluate and select a Respondent

APPENDIX - A TECHNICAL SPECIFICATIONS JEA Fleet Services Heavy Duty Maintenance and Repair 1. GENERAL SCOPE OF WORK The purpose of this Invitation to Negotiate (the "ITN") is to evaluate and select a Respondent

Financial Guidelines for Beneficiaries EDCTP Association October 2016

Financial Guidelines for Beneficiaries EDCTP Association October 2016 This document is prepared as a supplement to the Grant Agreement (GA), where majority of the information is extracted from. In the

Financial Guidelines for Beneficiaries EDCTP Association October 2016 This document is prepared as a supplement to the Grant Agreement (GA), where majority of the information is extracted from. In the

Supply and Use Tables for Macedonia. Prepared by: Lidija Kralevska Skopje, February 2016

Supply and Use Tables for Macedonia Prepared by: Lidija Kralevska Skopje, February 2016 Contents Introduction Data Sources Compilation of the Supply and Use Tables Supply and Use Tables as an integral

Supply and Use Tables for Macedonia Prepared by: Lidija Kralevska Skopje, February 2016 Contents Introduction Data Sources Compilation of the Supply and Use Tables Supply and Use Tables as an integral

Financial Procedures Pertaining to Contracts for Services, Work and Labour

Financial Procedures Pertaining to Contracts for Services, Work and Labour Accounting Notes Relating to the General Terms of Contract governing Contracts for Consulting Services, February 2007 These accounting

Financial Procedures Pertaining to Contracts for Services, Work and Labour Accounting Notes Relating to the General Terms of Contract governing Contracts for Consulting Services, February 2007 These accounting

Industry Financial Report

Industry Financial Report release date: June 214 Harrisburg-Lebanon-Carlisle, PA [23822] Plumbing, Heating, and Air-Conditioning Contractors Sector: Construction Sales Class: $1m - $2.49m Contents Income-Expense

Industry Financial Report release date: June 214 Harrisburg-Lebanon-Carlisle, PA [23822] Plumbing, Heating, and Air-Conditioning Contractors Sector: Construction Sales Class: $1m - $2.49m Contents Income-Expense

JBCC CONTRACT PRICE ADJUSTMENT PROVISIONS (CPAP)

") JBCC CONTRACT PRICE ADJUSTMENT PROVISIONS (CPAP) CPAP Indices Application Manual The CPAP indices are calculated and published by Stats SA and are licensed for distribution only on subscription from JBCC

JBCC CONTRACT PRICE ADJUSTMENT PROVISIONS (CPAP) CPAP Indices Application Manual The CPAP indices are calculated and published by Stats SA and are licensed for distribution only on subscription from JBCC

ACIS Administration Regulations 2000

ACIS Administration Regulations 2000 Statutory Rules 2000 No. 243 as amended made under the ACIS Administration Act 1999 This compilation was prepared on 4 May 2001 taking into account amendments up to

ACIS Administration Regulations 2000 Statutory Rules 2000 No. 243 as amended made under the ACIS Administration Act 1999 This compilation was prepared on 4 May 2001 taking into account amendments up to

Terms and conditions applicable to a sale offer

1. Acceptance of the offer and terms and conditions a. Acceptance of our offer necessarily invokes the unconditional and irrevocable acceptance of our terms and conditions. b. Save prior written agreement

1. Acceptance of the offer and terms and conditions a. Acceptance of our offer necessarily invokes the unconditional and irrevocable acceptance of our terms and conditions. b. Save prior written agreement

Answer to PTP_Intermediate_Syllabus 2008_Jun2015_Set 1

Paper 8: Cost & Management Accounting Time Allowed: 3 Hours Full Marks: 100 Question No 1 is Compulsory. Answers any five Questions from the rest. Working Notes should form part of the answer. Question.1

Paper 8: Cost & Management Accounting Time Allowed: 3 Hours Full Marks: 100 Question No 1 is Compulsory. Answers any five Questions from the rest. Working Notes should form part of the answer. Question.1

The Instantaneous Cost of Failure on Your Business

Abstract The Instantaneous Cost of Failure on Your Business The Instantaneous Cost and Failure on Your Business. When a failure incident occurs there is a consequential loss of profits and amassing of

Abstract The Instantaneous Cost of Failure on Your Business The Instantaneous Cost and Failure on Your Business. When a failure incident occurs there is a consequential loss of profits and amassing of

COST MANAGEMENT. discretionary costs, relevant and nonrelevant

C H A P T E R 7 COST MANAGEMENT I N T R O D U C T I O N This chapter introduces and describes various costs that exist in a business operation, including direct costs, indirect costs, controllable and

C H A P T E R 7 COST MANAGEMENT I N T R O D U C T I O N This chapter introduces and describes various costs that exist in a business operation, including direct costs, indirect costs, controllable and

Infor LN Project User Guide for Project Estimation

Infor LN Project User Guide for Project Estimation Copyright 2015 Infor Important Notices The material contained in this publication (including any supplementary information) constitutes and contains confidential

Infor LN Project User Guide for Project Estimation Copyright 2015 Infor Important Notices The material contained in this publication (including any supplementary information) constitutes and contains confidential

Total number of questions : 8 Total number of printed pages : 8

Roll No Time allowed : 3 hours : 1 : Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 8 NOTE : All working notes should be shown distinctly. PART A (Answer Question No.1

Roll No Time allowed : 3 hours : 1 : Maximum marks : 100 Total number of questions : 8 Total number of printed pages : 8 NOTE : All working notes should be shown distinctly. PART A (Answer Question No.1

ARCHITECT/ENGINEER CONTRACTS, FEE ESTIMATION, AND REQUESTS FOR PAYMENT

ARCHITECT/ENGINEER CONTRACTS, FEE ESTIMATION, AND REQUESTS FOR PAYMENT Overview Introduction This document supplements the Smithsonian Institution Office of Facilities Engineering & Operations Special

ARCHITECT/ENGINEER CONTRACTS, FEE ESTIMATION, AND REQUESTS FOR PAYMENT Overview Introduction This document supplements the Smithsonian Institution Office of Facilities Engineering & Operations Special

COSTING AND PROJECT EVALUATION USING NODOC

COSTING AND PROJECT EVALUATION USING NODOC Three types of Capital cost estimates 1- Preliminary (approximate) estimates 2- Authorization (Budgeting) estimates 3- Detailed (Quotation) estimates 1- Preliminary

COSTING AND PROJECT EVALUATION USING NODOC Three types of Capital cost estimates 1- Preliminary (approximate) estimates 2- Authorization (Budgeting) estimates 3- Detailed (Quotation) estimates 1- Preliminary

PLANNING SUPERVISOR'S APPOINTMENT

PLANNING SUPERVISOR'S APPOINTMENT PART 2 CONDITIONS OF ENGAGEMENT C 0 INTRODUCTION Co-ordination concerning the health and safety of workers should be organized for every of building or civil engineering

PLANNING SUPERVISOR'S APPOINTMENT PART 2 CONDITIONS OF ENGAGEMENT C 0 INTRODUCTION Co-ordination concerning the health and safety of workers should be organized for every of building or civil engineering

COST ACCOUNTING STANDARD ON MATERIAL COST

CAS- 6 (REVISED 2017) CAS-6 (REVISED 2017) COST ACCOUNTING STANDARD ON MATERIAL COST The following is the COST ACCOUNTING STANDARD 6 (CAS 6) (Revised 2017) issued by the Council of The Institute of Cost

CAS- 6 (REVISED 2017) CAS-6 (REVISED 2017) COST ACCOUNTING STANDARD ON MATERIAL COST The following is the COST ACCOUNTING STANDARD 6 (CAS 6) (Revised 2017) issued by the Council of The Institute of Cost

Discretionary Owner Earnings (%) Firms Analyzed

Firms Analyzed") Industry Financial Report release date: June 218 Harrisburg, PA Metro Area [23822] Plumbing, Heating, and Air-Conditioning Contractors Sector: Construction Sales Class: $1m - $2.49m Contents Income-Expense

Industry Financial Report release date: June 218 Harrisburg, PA Metro Area [23822] Plumbing, Heating, and Air-Conditioning Contractors Sector: Construction Sales Class: $1m - $2.49m Contents Income-Expense

Yellow cells denote information required to be entered. Grey cells denote no information should be entered.

A guide and toolkit on project budgeting and cost allocation This guide contains a budget template to help organisations calculate the full cost of a particular project or service, including an appropriate

A guide and toolkit on project budgeting and cost allocation This guide contains a budget template to help organisations calculate the full cost of a particular project or service, including an appropriate

Pricing for Services

Pricing for Services 1. Introduction This aid discusses costing and pricing of services to assure that each job earns a reasonable profit. The figures used in the tables and examples do not reflect what

Pricing for Services 1. Introduction This aid discusses costing and pricing of services to assure that each job earns a reasonable profit. The figures used in the tables and examples do not reflect what

ANNEX K GUIDELINES and CHECKLIST for assessing ACTION BUDGETs and SIMPLIFIED COST OPTIONS for Union financed GRANT CONTRACTS

ANNEX K GUIDELINES and CHECKLIST for assessing ACTION BUDGETs and SIMPLIFIED COST OPTIONS for Union financed GRANT CONTRACTS Introduction This document includes guidance and a checklist for the Contracting

ANNEX K GUIDELINES and CHECKLIST for assessing ACTION BUDGETs and SIMPLIFIED COST OPTIONS for Union financed GRANT CONTRACTS Introduction This document includes guidance and a checklist for the Contracting

Building and Construction

12 Building and Construction The number of planning permissions granted for new dwellings decreased from 17,491 to 10,380 between 2008 and 2009, a fall of 40.7%. The volume of production in building and

12 Building and Construction The number of planning permissions granted for new dwellings decreased from 17,491 to 10,380 between 2008 and 2009, a fall of 40.7%. The volume of production in building and

The BASICS of CONSTRUCTION ACCOUNTING Workshop GLOSSARY

The BASICS of CONSTRUCTION ACCOUNTING Workshop GLOSSARY From Financial Management & Accounting for the Construction Industry, CFMA. Accounts Payable Obligations to pay for goods and services that have

The BASICS of CONSTRUCTION ACCOUNTING Workshop GLOSSARY From Financial Management & Accounting for the Construction Industry, CFMA. Accounts Payable Obligations to pay for goods and services that have

100 Accounting Interview Questions and Answers

100 Accounting Interview Questions and Answers 1) Why did you select accounting as your profession? Well, I was quite good in accounting throughout but in my masters, when I got distinction I decided to

100 Accounting Interview Questions and Answers 1) Why did you select accounting as your profession? Well, I was quite good in accounting throughout but in my masters, when I got distinction I decided to

ACCOUNTING INTERVIEW QUESTIONS

www.globalcma.in Learning Platform for Cost Accountants (CMA) 1) Why did you select accounting as your profession? Well, I was quite good in accounting throughout but in my masters, when I got distinction

www.globalcma.in Learning Platform for Cost Accountants (CMA) 1) Why did you select accounting as your profession? Well, I was quite good in accounting throughout but in my masters, when I got distinction

Steve Ashley. Chair Service Delivery Working Group. Highways Term Maintenance Association

Steve Ashley Chair Service Delivery Working Group Highways Term Maintenance Association Agenda The HTMA Indexation for Highway Term Maintenance Contract Best Value from Constrained Budgets TUPE Best Practice

Steve Ashley Chair Service Delivery Working Group Highways Term Maintenance Association Agenda The HTMA Indexation for Highway Term Maintenance Contract Best Value from Constrained Budgets TUPE Best Practice

Chapter 8 Special Categories of Contracts

Sam Chapter 8 Special Categories of Contracts Section 1 Supplemental Policy and Procedure................................. 207 8.1.1 General......................................................... 207

Sam Chapter 8 Special Categories of Contracts Section 1 Supplemental Policy and Procedure................................. 207 8.1.1 General......................................................... 207

CS Executive Programme Module - I December Paper - 2 : Cost and Management Accounting

ISBN : 978-93-5034-747-8 Solved Scanner Appendix CS Executive Programme Module - I December - 2013 Paper - 2 : Cost and Management Accounting Chapter - 1 : Introduction to Cost and Management Accounting

ISBN : 978-93-5034-747-8 Solved Scanner Appendix CS Executive Programme Module - I December - 2013 Paper - 2 : Cost and Management Accounting Chapter - 1 : Introduction to Cost and Management Accounting

NATIONAL 5 Accounting

MADRAS COLLEGE FACULTY OF TECHNOLOGIES DEPARTMENT OF BUSINESS AND ENTERPRISE NATIONAL 5 Accounting Course Information Name: ACCOUNTING NATIONAL 5 COURSE AIMS AND STRUCTURE The course aims to enable learners

MADRAS COLLEGE FACULTY OF TECHNOLOGIES DEPARTMENT OF BUSINESS AND ENTERPRISE NATIONAL 5 Accounting Course Information Name: ACCOUNTING NATIONAL 5 COURSE AIMS AND STRUCTURE The course aims to enable learners

What does the Eurostat-OECD PPP Programme do? Why is GDP compared from the expenditure side? What are PPPs? Overview

What does the Eurostat-OECD PPP Programme do? 1. The purpose of the Eurostat-OECD PPP Programme is to compare on a regular and timely basis the GDPs of three groups of countries: EU Member States, OECD

What does the Eurostat-OECD PPP Programme do? 1. The purpose of the Eurostat-OECD PPP Programme is to compare on a regular and timely basis the GDPs of three groups of countries: EU Member States, OECD

Cost Accounting: A Managerial Emphasis, 16e, Global Edition (Horngren) Chapter 4 Job Costing

Chapter 4 Job Costing") Cost Accounting: A Managerial Emphasis, 16e, Global Edition (Horngren) Chapter 4 Job Costing 4.1 Objective 4.1 1) A cost is considered direct if it can be traced to a particular cost object in a cost effective

Cost Accounting: A Managerial Emphasis, 16e, Global Edition (Horngren) Chapter 4 Job Costing 4.1 Objective 4.1 1) A cost is considered direct if it can be traced to a particular cost object in a cost effective

TRADE AGREEMENT BETWEEN THE GOVERNMENT OF THE REPUBLIC OF ZIMBABWE AND THE GOVERNMENT OF THE REPUBLIC OF NAMIBIA

TRADE AGREEMENT BETWEEN THE GOVERNMENT OF THE REPUBLIC OF ZIMBABWE AND THE GOVERNMENT OF THE REPUBLIC OF NAMIBIA The Government of the Republic of Zimbabwe and the Government of the Republic of Namibia,

TRADE AGREEMENT BETWEEN THE GOVERNMENT OF THE REPUBLIC OF ZIMBABWE AND THE GOVERNMENT OF THE REPUBLIC OF NAMIBIA The Government of the Republic of Zimbabwe and the Government of the Republic of Namibia,

VAT reclaim Don t leave money on the table

VAT reclaim Don t leave money on the table Don t leave money on the table Infographic: You re leaving money on the table.......... 3 Introduction: Foreign VAT: The elusive savings opportunity... 4 The

VAT reclaim Don t leave money on the table Don t leave money on the table Infographic: You re leaving money on the table.......... 3 Introduction: Foreign VAT: The elusive savings opportunity... 4 The

[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Subsection GOVERNMENT OF INDIA MINISTRY OF CORPORATE AFFAIRS NOTIFICATION

[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Subsection (i)] GOVERNMENT OF INDIA MINISTRY OF CORPORATE AFFAIRS NOTIFICATION New Delhi, the August, 2017 G.S.R.. (E).- In

[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Subsection (i)] GOVERNMENT OF INDIA MINISTRY OF CORPORATE AFFAIRS NOTIFICATION New Delhi, the August, 2017 G.S.R.. (E).- In

Public Sector Wage System Act Zakon o sistemu plač v javnem sektorju (ZSPJS)

") National Assembly of the Republic of Slovenia No. 430-03/02-17/3 Ljubljana, 26 April 2002-06-29 At its session of 26 April 2002 the National Assembly adopted the Public Sector Wage System Act (the ZSPJS)

National Assembly of the Republic of Slovenia No. 430-03/02-17/3 Ljubljana, 26 April 2002-06-29 At its session of 26 April 2002 the National Assembly adopted the Public Sector Wage System Act (the ZSPJS)

THE CROATIAN PARLIAMENT ACT ON INVESTMENT PROMOTION AND DEVELOPMENT OF INVESTMENT CLIMATE I. GENERAL PROVISIONS. Scope and purpose of the Act

THE CROATIAN PARLIAMENT 2391 ACT ON INVESTMENT PROMOTION AND DEVELOPMENT OF INVESTMENT CLIMATE I. GENERAL PROVISIONS Scope and purpose of the Act Article 1 This Act shall regulate the promotion of investments

THE CROATIAN PARLIAMENT 2391 ACT ON INVESTMENT PROMOTION AND DEVELOPMENT OF INVESTMENT CLIMATE I. GENERAL PROVISIONS Scope and purpose of the Act Article 1 This Act shall regulate the promotion of investments

Terms & Conditions. NIES electronic gmbh Edisonstraße Frankfurt Germany HRB Page 1 of 6

Terms & Conditions 1 General 1.1 These terms and conditions are subject to the laws of the Federal Republic of Germany. All legal transactions underlie the following terms and conditions. In contracts

Terms & Conditions 1 General 1.1 These terms and conditions are subject to the laws of the Federal Republic of Germany. All legal transactions underlie the following terms and conditions. In contracts

Training on EU policies for Directors of the Region of Sicily. Brussels Office of the Region of Sicily Rue Belliard 12

Training on EU policies for Directors of the Region of Sicily Brussels Office of the Region of Sicily Rue Belliard 12 EU Budget CZ state budget Other public budgets Direct gains to contractors Transfers

Training on EU policies for Directors of the Region of Sicily Brussels Office of the Region of Sicily Rue Belliard 12 EU Budget CZ state budget Other public budgets Direct gains to contractors Transfers

Disclaimer: This resource package is for studying purposes only EDUCATIO N

Disclaimer: This resource package is for studying purposes only EDUCATIO N Chapter 9: Budgeting The Basic Framework of Budgeting Master budget - a summary of a company s plans in which specific targets

Disclaimer: This resource package is for studying purposes only EDUCATIO N Chapter 9: Budgeting The Basic Framework of Budgeting Master budget - a summary of a company s plans in which specific targets

Disclaimer: This resource package is for studying purposes only EDUCATIO N

Disclaimer: This resource package is for studying purposes only EDUCATIO N Chapter 1 Managerial accounting vs. financial accounting Qualities Financial Accounting Managerial Accounting Reports Externally

Disclaimer: This resource package is for studying purposes only EDUCATIO N Chapter 1 Managerial accounting vs. financial accounting Qualities Financial Accounting Managerial Accounting Reports Externally

Ran Gao 1, *, Beijin Ye 2 1 Department of Engineering Management, School of Civil Engineering of Northeast

[Type text] [Type text] [Type text] ISSN : 0974-7435 Volume 10 Issue 17 BioTechnology 2014 An Indian Journal FULL PAPER BTAIJ, 10(17), 2014 [9761-9766] Research on cost control management of civil engineering

[Type text] [Type text] [Type text] ISSN : 0974-7435 Volume 10 Issue 17 BioTechnology 2014 An Indian Journal FULL PAPER BTAIJ, 10(17), 2014 [9761-9766] Research on cost control management of civil engineering

Cambridge International General Certificate of Secondary Education 0452 Accounting November 2014 Principal Examiner Report for Teachers

ACCOUNTING Cambridge International General Certificate of Secondary Education Paper 0452/11 Paper 11 Key Messages Questions can be set on any section of the syllabus and a good knowledge of all sections

ACCOUNTING Cambridge International General Certificate of Secondary Education Paper 0452/11 Paper 11 Key Messages Questions can be set on any section of the syllabus and a good knowledge of all sections

Proposal Pricing Instructions Page 1 of 7 Supplier Proposal Adequacy Checklist Instructions

Proposal Pricing Instructions Page 1 of 7 Supplier Proposal Adequacy Checklist Instructions Unless a valid exemption applies, Cost or Pricing Data is required to support proposals exceeding $750,000. Contractors

Proposal Pricing Instructions Page 1 of 7 Supplier Proposal Adequacy Checklist Instructions Unless a valid exemption applies, Cost or Pricing Data is required to support proposals exceeding $750,000. Contractors

322 Roll No : 1 : Time allowed : 3 hours Maximum marks : 100

2/2013/CMA (N/S) Roll No : 1 : Time allowed : 3 hours Maximum marks : 100 Total number of questions : 6 Total number of printed pages : 7 NOTE : 1. Answer ALL Questions. 2. All working notes should be

2/2013/CMA (N/S) Roll No : 1 : Time allowed : 3 hours Maximum marks : 100 Total number of questions : 6 Total number of printed pages : 7 NOTE : 1. Answer ALL Questions. 2. All working notes should be

ACCA F2 FLASH NOTES. Describe a pie chart?

ACCA F2 FLASH NOTES Describe a pie chart? A pie chart is a circle that is divided into segments representing each type of observation. The size of each segment is proportional to the proportion of the

ACCA F2 FLASH NOTES Describe a pie chart? A pie chart is a circle that is divided into segments representing each type of observation. The size of each segment is proportional to the proportion of the

Fact Sheet 14 - Partnership Agreement

- Partnership Agreement Valid from Valid to Main changes Version 2 27.04.15 A previous version was available on the programme website but all projects must use this version. Core message: It is a regulatory

- Partnership Agreement Valid from Valid to Main changes Version 2 27.04.15 A previous version was available on the programme website but all projects must use this version. Core message: It is a regulatory

Institutional Sectors

[ 05 ] Institutional Sectors Paul McCarthy National Accounts Workshop Washington - DC, October 25-26, 2010 Institutional units An institutional unit is an economic entity capable, in its own right, of

[ 05 ] Institutional Sectors Paul McCarthy National Accounts Workshop Washington - DC, October 25-26, 2010 Institutional units An institutional unit is an economic entity capable, in its own right, of

CLASSIFICATION OF COST

Cost Accounting Standard 1 CLASSIFICATION OF COST Draft Developed by Technical Support and Practice Development Committee Institute of Cost and Managemet Accountants of Pakistan Implementation Status This