Programmatic and Fiscal Accountability Administrative Overview Ryan White Part B

|

|

|

- Brett Hall

- 5 years ago

- Views:

Transcription

1 Programmatic and Fiscal Accountability Administrative Overview Ryan White Part B June 6, 2011 Frances Hodge Project Officer Southern Services Branch Health Resources and Services Administration Department of Health and Human Services

2 Reporting Requirements and Conditions of Award Definitions of terms Why are they important? How are they used? How should they be completed? How are they submitted?

3 Definitions Conditions of Award : Conditions of Award (COA) is the term generally used to describe the entire universe of documents and expectations outline for grantees in the Notice of Grant Award (NGA) under the heading Terms and Conditions.

4 Definitions Terms and Conditions Include: Grant Specific Terms Program Terms and Reporting Requirements

5 Definitions (continued) Reporting Requirements: Reporting requirements are specific documents grantees are required to submit to HRSA in order to document program planning, operations and outcomes. Specific reporting requirements are listed in the Notice of Grant Award.

6 Definitions (continued) Reporting Requirements and Conditions Include: Federal Financial Reports (FFR) Annual Progress Reports Match Expenditure Reports Program Terms Report

7 Reporting Requirements and Conditions of Award Why Are They Important? They are the documents that the federal government uses to assess the progress of funded programs. They help determine the degree to which legislative mandates are met. They become are part of a program s history.

8 How Are They Used Reporting Requirements and Conditions are used in the following ways: Document program operations both fiscal and programmatic. Support planning and program development activities and Assess program success by HRSA and other federal agencies.

9 How Should They Be Completed Grantees are provided copies of the Reporting Requirement and Condition of Award forms along with the instructions in the Electronic Handbook (EHB). We will not cover each of the Reporting Requirements or COAs listed in the NGA but will cover the Program Terms Report and the FFR in detail.

10 Program Terms Report Purpose: Serves as a instrument to provide an overview of the program through individual reports on planned allocations, the annual work plan and an itemized budget. The Program Terms Report also includes a list of funded providers and a document that certifies the amount all contracts administered by the grantee.

11 Program Terms Report Components: Part B & MAI Planned Allocation Table FY 2011 Implementation Plan Consolidated List of Contractors (CLC) Contract Review Certification (CRC) Revised SF 424A and Budget Narrative

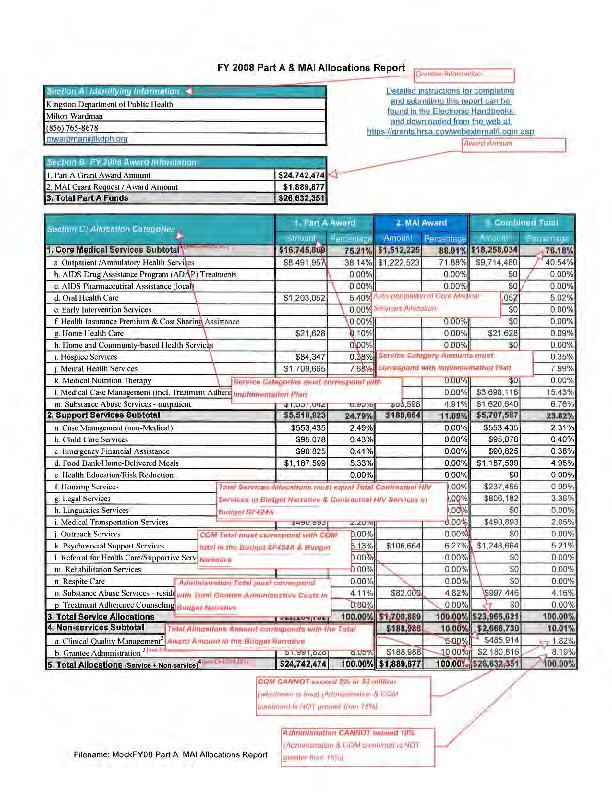

12 Allocations Table Purpose: Serves as a monitoring tool to track and monitor the use of Ryan White funds. The Allocations Report identifies: Categories of services that are being delivered Changes in the type of services being provided over time Trends in the amount of funds being used to deliver these services

13 Allocations Table (continued) An Allocations Table: Outlines the dollar amounts allocated for the RW program for the current fiscal year, including MAI amounts Accounts for prioritized funding set by the planning council/planning body with regard to the 75/25 rule and needs within EMA/TGA Accounts for administrative dollars and QM (where applicable)

14

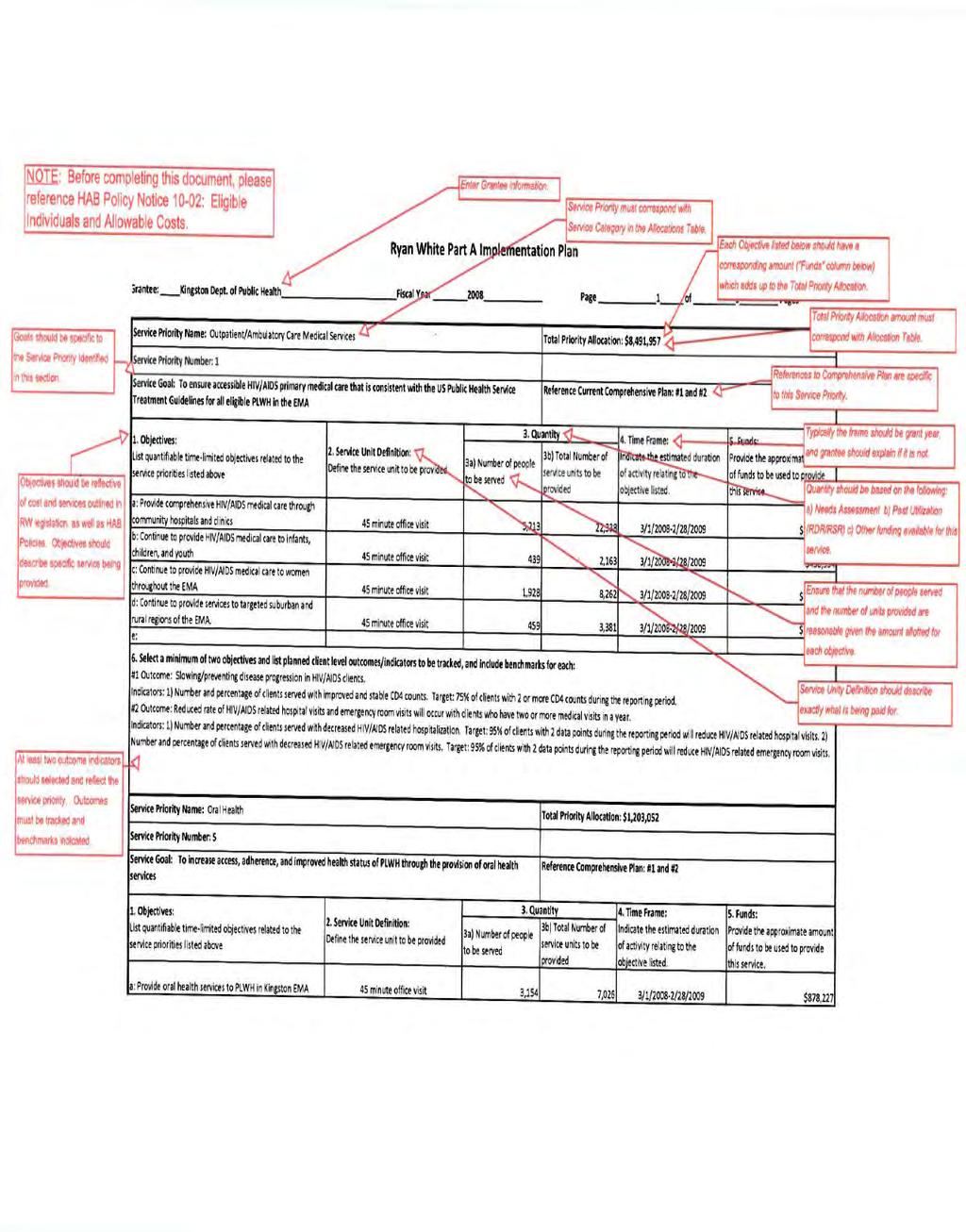

15 Implementation Plan Purpose: Serves as a monitoring tool to verify: Service priority Goals Objectives Unit of service Number of Clients to be served Total priority allocation planned for the grant year Note: Plan should include all service categories and priorities established and reflected in the planned Allocations Report

16 Implementation Plan An implementation plan should include: Objective(s): list objective that are required to implement a new or continue an existing service Service Unit Definition: provide the name and definition of the unit of service provided Quantity: provide the number of people to be served and service unit. Time Frame: indicate the estimated duration of the activity relating to the objectives Funds: provide the amount allocated for each service Outcomes: Select a minimum of two objective and list outcomes/indicators to be tracked

17

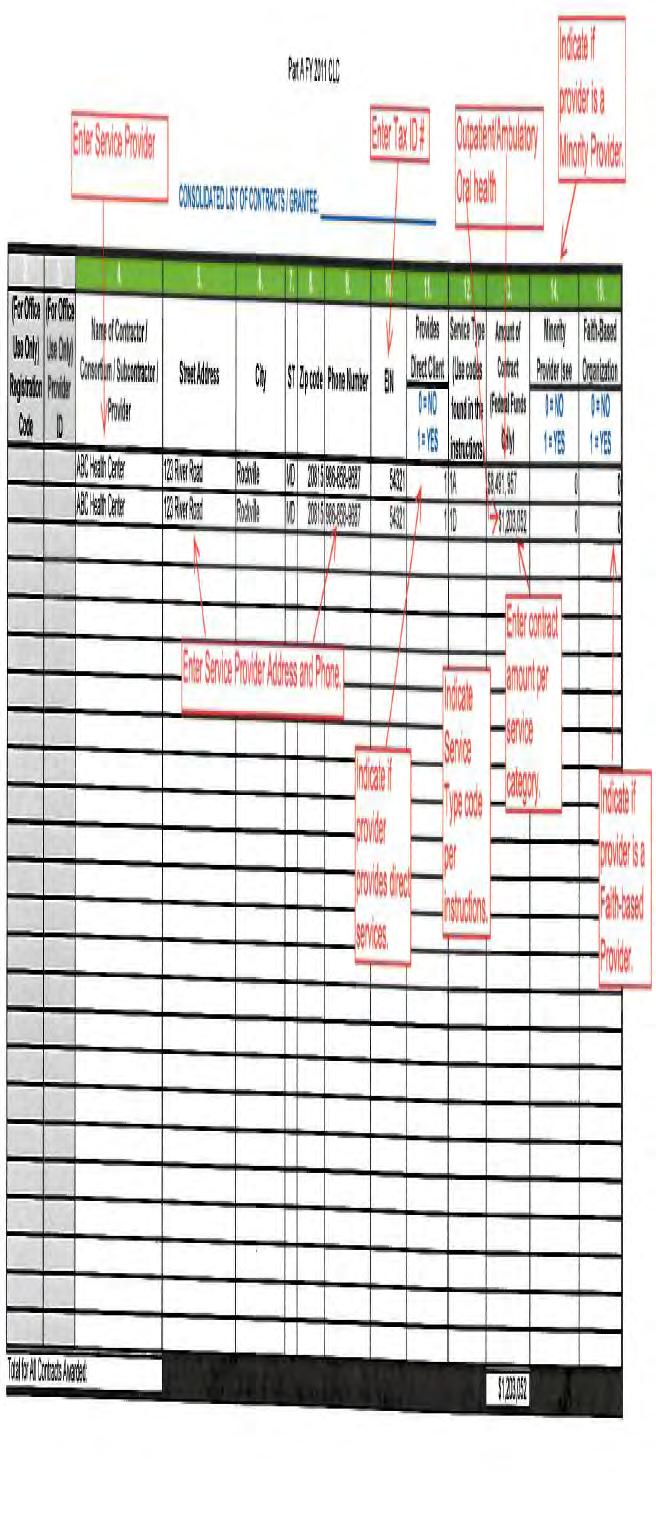

18 Consolidated List of Contracts Purpose: Serves as a monitoring tool to identify ALL Part B and MAI service providers receiving funds for the current grant year.

19 Consolidated List of Contracts For each service provider input: Identifying Information Tax Payer Identification # (EIN) Service Provider Code Contract Amount Minority Provider Status

20

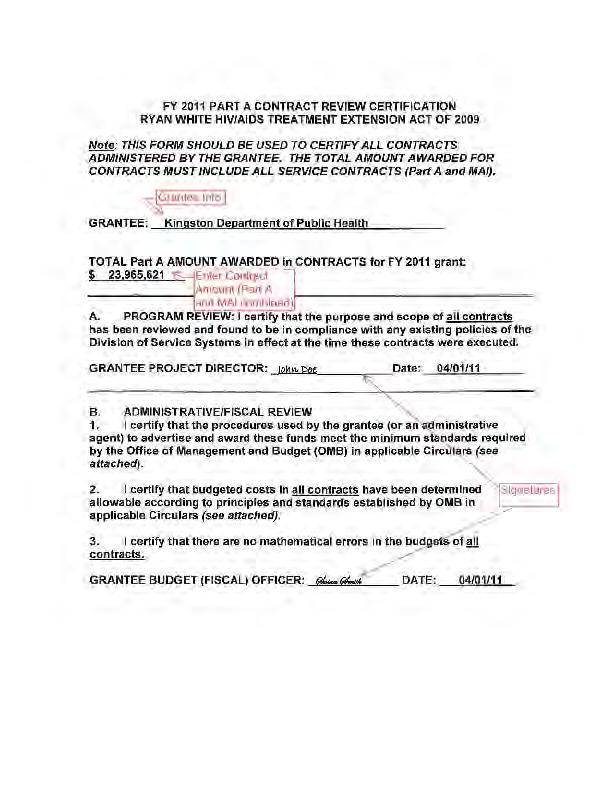

21 Contract Review Certification Purpose: Serves as a monitoring tool to certify all contracts administered by the grantee for the current grant year and comply with OMB circulars and other Ryan White requirements.

22 Contract Review Certification Denotes the total grant amount awarded in contracts for the current fiscal year Certifies that the procedures used by the grantee (or an administrative agent) to advertise and award funds meet the minimum standards required by the Office of Management and Budget (OMB) in applicable Circulars Certifies the budgeted costs in all contracts have been determined allowable according to principles and standards established by OMB in applicable Circulars Certifies that there are no mathematical errors in the budgets of all contracts

23

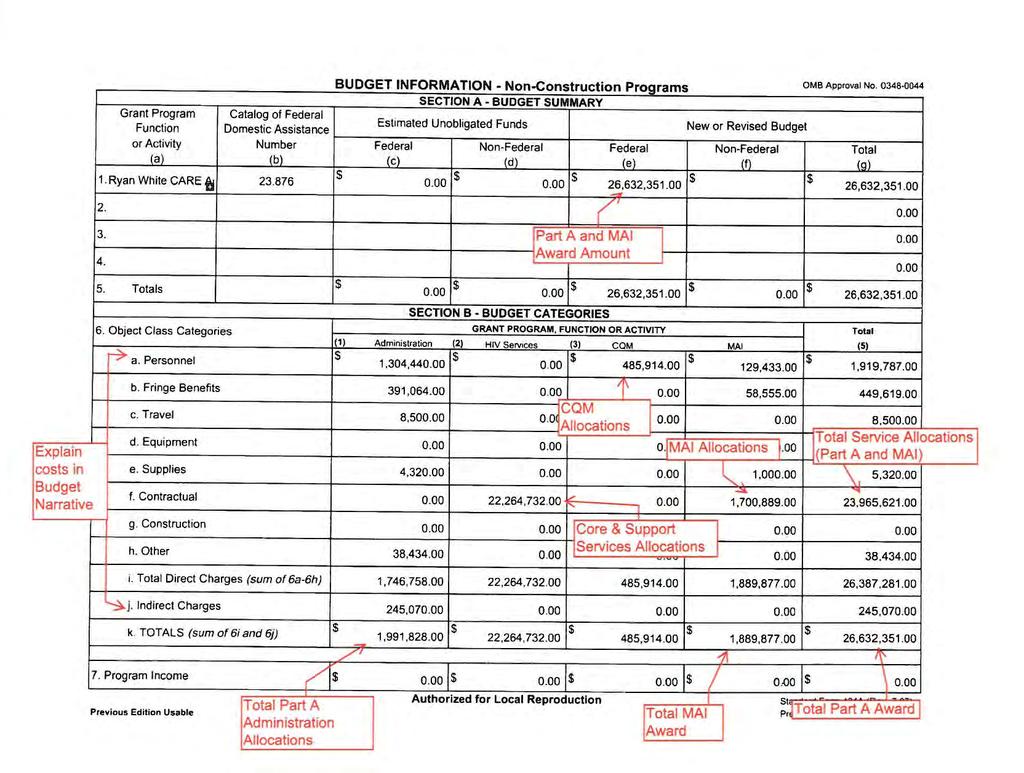

24 SF-424A This form must be revised and submitted with the Final Part A Program Budget to reflect budget allocations based on the actual amount of funds awarded to the state with respect to the following:

25 SF-424A Administration HIV Services including MAI funds Clinical Quality Management ADAP

26

27 Budget A program budget must be submitted for each Part B award. It must be based on: Priorities established by the State Reflect the amount of all Part B funds awarded Reflect costs in accordance with legislative and programmatic requirements.

28 Budget The budget must reflect administrative caps: Grantee Administration: up to 10% Program Evaluation: up to 5% Clinical Quality Management: up to 5% of the total award or $3 million dollars, which ever is less

29 Budget Narrative Descriptive information used to explain and justify the amounts budgeted within each program budget category. It must include specific information about: Who? What? Where? When? Why?

30 Budget Narrative A budget narrative is required for: Grantee Administration Grantee Quality Management ADAP Planning and Evaluation

31 Federal Financial Report The Federal Financial Report (FFR) SF-425 is used to report financial data and to verify amounts available for carry over requests The FFR should be completed by an authorized fiscal official

32 Part B Mid-Year Progress Report Purpose: The Part B Mid-Year Progress Report (Progress Report) is used to inform program officials of progress made in the administration of Part B programs; identify accomplishments and challenges in meeting planned goals and objectives The Progress Report highlights successes and challenges Identifies technical assistance needs

33 Part B Progress Report The Part B Progress Report includes the following components: Part B Implementation Plan Early Identification of Individuals with HIV/AIDS (EIIHA) Update Narrative Report for Part B program Challenges and technical assistance

34 Part B Progress Report Part B Implementation Plan Update should reflect progress made for each funded program area: Goals, objectives, service unit definitions, number of people served, number of service units provided and the total amount of 2011 funds expended should be included States receiving Emerging Community (EC) funding should include a separate EC section providing the required data.

35 Early Identification Of Individuals with HIV/AIDS The EIIHA Update should include and update on the following as of September 30, 2011: Total number of individuals tested Total number of individuals informed of their status Total number identified as HIV positive and informed of their status Total number identified as HIV positive, informed and referred to care Total number identified as HIV positive and not informed

36 Part B Progress Report Total number identified as HIV negative and informed of their status Total number of identified as HIV negative and not informed of their status The narrative should provide an update on: New services added or deleted in 2011 New access points created to provide Part B services Contract monitoring activities

37 Part B Progress Report Deficit Reduction Act (DRA) Accomplishments The Progress Report must also include total year-to-date expenditures for the following categories: Part B Base and MAI funds ADAP Earmark and Supplemental (if applicable) EC

38 Part B Progress Report Challenges and Technical Assistance This section of the Progress Report should identify challenges experienced during the reporting period with focus on the following: Impact of State budget reductions or Part B service delivery Efforts to avoid or eliminate ADAP waiting lists and other service limitation

39 Part B Progress Report Efforts to identify and bring into care individual who are unaware of their HIV status Administrative structure of Part B program to include key staff vacancies, lack of qualified personnel, geographic challenges related to Consortia distribution Financial management systems Contract monitoring including program, fiscal, clinical quality assurance and evaluation mechanisms Impact of client level data Statewide data issues related to collection of client level data

40 Final Progress Report The Final Progress Report (Final Report) enables the grantee to document progress made in reaching the goals, objectives and outcomes for program areas submitted in the FY 2011 Grant Application, resubmitted as a Reporting Requirement and updated in the Mid-Year Progress Report.

41 Final Report The Part B Final Report is completed by updating the components of the Mid-Year Report. The components include: Implementation Plan EIIHA Update Narrative Report Contract monitoring activities Accomplishments

42 Part B Final Progress Report The FY 2011 Final Report must also include the following data: Accomplishments for MAI funded Outreach and Education services reported in the Excel workbook in relation to the specific communities that were served including strategies used to achieve outcomes Challenges and lessons learned A discussion of any significant change to planned service objectives, budgeted amounts and/or planned outcomes

43 Part B Final Progress Report Other Final Report Requirements Match Requirement Grantees must include the following: The dollar amount of the FY 2011 Match requirement Activities, personnel and other budget categories supported through the use of matching funds The dollar amount of the ADAP Supplemental and documentation of the States contribution

44 Certification of Aggregate Administrative Cost The Certification of Aggregate Administrative Costs: Should reflect the actual amount expended on administrative costs by first line entities The statement must identify and certify the amount of funds not to exceed 10% in the aggregate used for administrative expenditures The amount of expenditures as a percentage of the amount of funds available and must be signed by the financial official responsible for Part B funds

45 Quality Management Activities The Final Report must: Provide information on the clinical quality assurance/quality management activities undertaken in FY 2011 discussing current and planned activities Include a list of services for which quality measures are being monitored and a discussion of how quality findings from these measures have been used to inform funding decisions

46 FY 2011 WICY Report The FY 2011 WICY Report documents that grantees have expended the minimum amount of funds required for services to women, infants, children and youth Specific instructions are provided

47 Technical Assistance Grantees must describe any specific HRSA sponsored or other technical assistance activity received during the reporting period including: The purpose of the technical assistance The outcome of the technical assistance

48 Contact Information Frances Hodge Project Officer, Southern Services Branch Telephone:

49 Administrative Overview Ryan White Part A & Part B Grantees Division of Financial Integrity (DFI) June 6 & June 13, 2011 Presented by Department of Health and Human Services Health Resources and Services Administration Office of Federal Assistance Management Division of Financial Integrity

50 Division of Financial Integrity (DFI) Presenters: Sandy Seaton, DFI, Acting Director Sherry Angwafo, Team Leader, Financial Analysis Wayne Bulls, Financial Analysis Team Bob Noethe, Financial Analysis Team

51 Division of Financial Integrity DFI. What do we do?

52 Division of Financial Integrity DFI serves as HRSA s focal point for reviewing HRSA grantee s financial integrity. Three major DFI Functions: Performing Financial Assessments (Pre award) In depth Reviews (Post award) Resolving A-133 Audit Findings (Post award)

53 Division of Financial Integrity (DFI) Financial Assessments (FAs) Presented by Wayne Bulls

54 Division of Financial Integrity (DFI) What is a Financial Assessment? A financial assessment is a pre-award review of an organization s financial condition to determine their suitability to manage and account for federal funds. Based on the FA, DFI provides funding (competitive and non competitiv recommendations to HRSA grant funding decision makers.

55 Division of Financial Integrity (DFI) When are Financial Assessments done? A Financial Assessment is done for new HRSA Grantees Financial Assessment are done once a year For the 2010 Calendar Year DFI prepared over 2,800 Financial Assessments!

56 Division of Financial Integrity (DFI) What is the Goal of a FAs? To Make a funding Recommendation to HRSA grant decision makers. DFI funding recommendations to HRSA grant decision makers should be updated annually for all grantees both new and existing; competitive and budget year funding.

57 Division of Financial Integrity (DFI) How are Financial Assessments Performed? DFI reviews five major areas: DUNS (CCR) Alerts (Excluded Parties, DFI Watch List, etc.) A-133 Audit Financial Statements/IRS 990 Form Other Financial Information (internet searches, press releases, etc.)

58 Division of Financial Integrity (DFI) Third Party Reimbursements What is a DUNS and why is it important? Any organization that does business with the Federal Government, including grantees, is required to have an active registration with the CCR (Central Contractor Registration) using their DUNS number. The CCR requires re-registration every year to remain in active status.

59 Division of Financial Integrity (DFI) DFI s Recommendations The following are the possible funding recommendations to HRSA grant funding decision makers: Fund without conditions or restrictions. This recommendation is used when the grantee s financial position is good. Fund with conditions or restrictions. For organizations that have had previous challenges managing federal funds this recommendation is used. Fund without restrictions or conditions; DFI will closely monitor. DFI closely monitors some organizations that have negative net assets or have financial results that have declined the past few years.

60 Division of Financial Integrity (DFI) The following are the possible recommendations (continued): Deferral of recommendation. DFI was unable to assess the grantee s financial position due to lack of information such as audits or financial statements. Also, if there is no valid DUNS number the organization will receive this recommendation until a valid DUNS number is obtained. Do Not Fund. Organizations that are bankrupt or has had significant allegations of fraud, misuse or abuse of funds will most likely receive this recommendation.

61 Division of Financial Integrity (DFI) In Depth Reviews by Sherry Angwafo

62 Division of Financial Integrity (DFI) In Depth Reviews: At Risk Grantees Potentially At Risk Grantees (PII)

63 Division of Financial Integrity (DFI) What is an At Risk Grantees? At Risk Grantees are grantees with reported financial issues such as: OIG Hotline Complaints Potential Misuse of grant funds (embezzlement, drawing downs) In adequate financial management system (no internal controls, accounting system, inadequate timekeeping)

64 Division of Financial Integrity (DFI) Potentially At Risk Grantees (PII) Potentially At Risk Grantees are grantees whose financial position is negative or trending negative. HRSA has established Program Integrity Initiative (PII) work group to mine for grantees with potential financial issues not yet discovered.

65 Division of Financial Integrity (DFI) How does DFI identify Potentially At Risk Grantees? Through HHS Program Integrity Initiative (PII), HRSA has set up a data mining work group. This work group uses attributes financial markers from the Federal Audit Clearinghouse (FAC) along with HRSA s internal database to select grantees that may be in financial trouble or heading in that direction. Once identify, HRSA may assist the grantee with technical assistance (TA) or a site visit.

66 Division of Financial Integrity (DFI) A-133 Audit What to Expect? By Sandy Seaton

67 What is an A-133 Audit? OMB Circular A-133 Audits are required for non-federal entities that expend $500,000 or more of federal award funds in their fiscal year. Auditors publish an opinion on financial statements and federal programs: Unqualified means that the auditor does not qualify his opinion that the financial statements and programs accurately reflect the financial position or expenditures reported. Qualified means that the auditor qualifies his opinion that the financial statements and programs accurately reflect the financial position or expenditures reported. Adverse means that the auditor does not agree that the financial statements and programs accurately reflect the financial position or expenditures reported. Disclaimer means that the auditor cannot form an opinion on the financial statements or federal programs due to missing or incomplete data or documents.

68 Division of Financial Integrity (DFI) What is an A133 audit? An A-133 audit sets forth standards for obtaining consistency and uniformity among Federal agencies for the audit of non-federal entities expending Federal awards. OMB Circular A Financial Statement Audit (OMB Circular A (b) Internal Controls (OMB Circular A (c) Compliance Audit (Federal Programs) (OMB Circular A (d)

69 Division of Financial Integrity (DFI) What are some of the A133 requirements? (OMB Circular A (a) Shall be conducted in accordance with GAGAS Shall cover the entire operations Shall cover the financial statements and schedule of expenditures of federal awards (SEFA) The financial statements and SEFA shall be for the same fiscal year

70 Division of Financial Integrity (DFI) Financial Statement (FS) Audit (OMB Circular A (b) Auditor shall determine if FS are presented fairly in accordance with Generally Accepted Accounting Principles (GAAP) Auditor shall determine if the SEFA is presented fairly in relationship to the auditees financial statements

71 Division of Financial Integrity (DFI) What should be prepared for the FS review? Prepare financial statements (OMB Circular A (a) Prepare a SEFA for the same period covered by grantees financial statements (OMB Circular A (b)

72 Division of Financial Integrity (DFI) Internal Controls (IC) (OMB Circular A (C) Auditor shall perform procedures to obtain an understanding of IC over federal programs Auditor shall obtain sufficient understanding over IC to plan the audit

73 Division of Financial Integrity (DFI) What is the most important item to prepare for the IC review? As part of a adequate Financial Management System (45 CFR 74.21), a grantee should have written policies and procedures to assist the auditors in gaining an understanding of internal controls of applicable compliance requirements. Written policies and procedures are the auditors roadmap to how you comply with the various compliance requirements applicable to your major federal programs.

74 Division of Financial Integrity (DFI) Compliance Audit OMB Circular A (d) Auditor shall determine if the auditee has compiled with laws, regulations, and grant terms and conditions that may have a direct and material effect on each major programs. The principle compliance requirements for most Federal program are included in the compliance supplement Compliance testing shall include tests of transactions (transaction testing)

75 Division of Financial Integrity (DFI) What should prepared for the Compliance review? (OMB Circular.300) For compliance testing, the most important activity, the grantee must have supporting documentation available for the auditor to review. Supporting documentation includes, but not limited to, invoices, vouchers, checks, agreements, contractors, consultant work product, timesheets, paystubs, procuring files, etc. Other financial documents general ledger, chart of accounts, Federal Financial Reporting, grant agreements, etc.

76 Division of Financial Integrity (DFI) Other A133 Audit Grantee Responsibility Audit Finding Follow up (OMB Circular A (a)) Summary Schedule of prior audit findings (OMB Circular A (b)) The auditee shall prepare a summary schedule of prior audit findings Corrective Action Plan (CAP) (OMB Circular A (c)) At completion of audit, the auditee shall prepare a CAP to address each audit findings Report submission (OMB Circular A ) Data collection form and reporting package

77 A-133 Audit If a grantee has good Federal Financial Management Systems in place and has followed the Federal Cost Principles then the A-133 audit should go well.

78 Contact Information Health Resources and Services Administration U.S. Department of Health and Human Services 5600 Fishers Lane Rockville, MD

Programmatic and Fiscal Accountability Administrative Overview Ryan White Part A

Programmatic and Fiscal Accountability Administrative Overview Ryan White Part A June 13, 2011 Frances Hodge Project Officer Southern Services Branch Health Resources and Services Administration Department

Programmatic and Fiscal Accountability Administrative Overview Ryan White Part A June 13, 2011 Frances Hodge Project Officer Southern Services Branch Health Resources and Services Administration Department

Ryan White Part B Reporting Requirements- Ryan White Part B Administrative Reverse Site Visit Meeting June 18, 2013

Ryan White Part B Reporting Requirements- Ryan White Part B Administrative Reverse Site Visit Meeting June 18, 2013 Terri` Richards, MPH U.S. Department of Health and Human Services (HHS) Health Resources

Ryan White Part B Reporting Requirements- Ryan White Part B Administrative Reverse Site Visit Meeting June 18, 2013 Terri` Richards, MPH U.S. Department of Health and Human Services (HHS) Health Resources

HIV/AIDS Bureau, Division of Service Systems Monitoring Standards for Ryan White Part A and B Grantees: Part A Fiscal Monitoring Standards

HIV/AIDS Bureau, Division of Service Systems Monitoring s for Ryan White Part A and B Grantees: Part A Fiscal Monitoring s Table of Contents Section A: Limitation on Uses of Part A funding Section B: Unallowable

HIV/AIDS Bureau, Division of Service Systems Monitoring s for Ryan White Part A and B Grantees: Part A Fiscal Monitoring s Table of Contents Section A: Limitation on Uses of Part A funding Section B: Unallowable

HIV/AIDS Bureau, Division of Metropolitan HIV/AIDS Programs National Monitoring Standards for Ryan White Part A Grantees: Fiscal Part A

HIV/AIDS Bureau, Division of Metropolitan HIV/AIDS Programs National Monitoring Standards for Ryan White Part A Grantees: Fiscal Part A Table of Contents Section A: Limitation on Uses of Part A funding

HIV/AIDS Bureau, Division of Metropolitan HIV/AIDS Programs National Monitoring Standards for Ryan White Part A Grantees: Fiscal Part A Table of Contents Section A: Limitation on Uses of Part A funding

FEDERAL GRANTS MANAGEMENT FOR HEALTH CENTERS

FEDERAL GRANTS MANAGEMENT FOR HEALTH CENTERS MISSION: ACHIEVEMENT Operational Excellence Alabama Primary Health Care Association October 5, 2017 Presenter: Adrienne Hurtt Introduction Adrienne Hurtt, CEO

FEDERAL GRANTS MANAGEMENT FOR HEALTH CENTERS MISSION: ACHIEVEMENT Operational Excellence Alabama Primary Health Care Association October 5, 2017 Presenter: Adrienne Hurtt Introduction Adrienne Hurtt, CEO

National Association of Community Health Centers FOM / IT

National Association of Community Health Centers FOM / IT FINANCIAL POLICY CONSIDERATIONS IN PREPARATION FOR HRSA SITE VISITS OCTOBER 29, 2017 David Fields BKD,LLP Partner Catherine Gilpin BKD, LLP Senior

National Association of Community Health Centers FOM / IT FINANCIAL POLICY CONSIDERATIONS IN PREPARATION FOR HRSA SITE VISITS OCTOBER 29, 2017 David Fields BKD,LLP Partner Catherine Gilpin BKD, LLP Senior

SuperCircular and Budget and Accounting PIN

SuperCircular and Budget and Accounting PIN Presented by: Gil Bernhard, CPA October 31, 2015 HMA Overview New Federal Grants Management Requirements OMB SuperCircular Budget and Accounting PIN 2 New Federal

SuperCircular and Budget and Accounting PIN Presented by: Gil Bernhard, CPA October 31, 2015 HMA Overview New Federal Grants Management Requirements OMB SuperCircular Budget and Accounting PIN 2 New Federal

Updated 07/07/2018 ID 19, Page 1 of 6

Requirement: Frequency: Due Date: Purpose Financial Management Requirements 2 C.F.R., part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards; The U.S.

Requirement: Frequency: Due Date: Purpose Financial Management Requirements 2 C.F.R., part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards; The U.S.

SINGLE AUDIT UPDATE. Presented By Joel Knopp, CPA

SINGLE AUDIT UPDATE Presented By Joel Knopp, CPA Session Covers Uniform Guidance Circular Components Single Audit Changes Auditee and Auditor Impact Scope of Audit under Uniform Guidance Florida Single

SINGLE AUDIT UPDATE Presented By Joel Knopp, CPA Session Covers Uniform Guidance Circular Components Single Audit Changes Auditee and Auditor Impact Scope of Audit under Uniform Guidance Florida Single

FEDERAL SINGLE AUDIT

FEDERAL SINGLE AUDIT Uniform Guidance: Lessons learned post-implementation and continuing developments Presented by: Gil Bernhard, CPA Learning Objectives To summarize the changes created by Uniform Guidance

FEDERAL SINGLE AUDIT Uniform Guidance: Lessons learned post-implementation and continuing developments Presented by: Gil Bernhard, CPA Learning Objectives To summarize the changes created by Uniform Guidance

10/30/2015 OBJECTIVES. CPAs & ADVISORS. Present an overview of the Super Circular. Contents of the Super Circular. Discuss Administrative Requirements

CPAs & ADVISORS experience direction // 2 CFR 200 UNIFORM GRANT GUIDANCE Presented by Andy Richards, CPA, Partner October 30, 2015 OBJECTIVES Present an overview of the Super Circular Contents of the Super

CPAs & ADVISORS experience direction // 2 CFR 200 UNIFORM GRANT GUIDANCE Presented by Andy Richards, CPA, Partner October 30, 2015 OBJECTIVES Present an overview of the Super Circular Contents of the Super

Audits: Reports and Resolutions

Audits: Reports and Resolutions Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, requirements Designed for governing DOL-ETA cost direct principles, recipients administrative and their

Audits: Reports and Resolutions Uniform Guidance vs. OMB Circulars Prior to the Uniform Guidance, requirements Designed for governing DOL-ETA cost direct principles, recipients administrative and their

Section 5000 Visits, Reviews and Audits

Section 5000 Visits, Reviews and Audits Table of Contents 5100 Visit Prior to Approval 5200 90-day Technical Assistance Visit 5300 Administrative Reviews 5310 Frequency and Scope 5320 Entrance Conference

Section 5000 Visits, Reviews and Audits Table of Contents 5100 Visit Prior to Approval 5200 90-day Technical Assistance Visit 5300 Administrative Reviews 5310 Frequency and Scope 5320 Entrance Conference

Section 5000 Visits, Reviews and Audits

Section 5000 Visits, Reviews and Audits Table of Contents 5100 Visit Prior to Approval 5200 Administrative Reviews 5210 Frequency and Scope 5220 Entrance Conference 5230 Meal Service Observation 5240 Review

Section 5000 Visits, Reviews and Audits Table of Contents 5100 Visit Prior to Approval 5200 Administrative Reviews 5210 Frequency and Scope 5220 Entrance Conference 5230 Meal Service Observation 5240 Review

Section 5000 Visits, Reviews and Audits

Section 5000 Visits, Reviews and Audits Table of Contents 5100 Visit Prior to Approval 5200 Administrative Reviews 5210 Frequency and Scope 5220 Entrance Conference 5230 Review of Records 5240 Exit Conference

Section 5000 Visits, Reviews and Audits Table of Contents 5100 Visit Prior to Approval 5200 Administrative Reviews 5210 Frequency and Scope 5220 Entrance Conference 5230 Review of Records 5240 Exit Conference

Harris County Hospital District and Affiliates, a Component Unit of Harris County, Texas

Harris County Hospital District and Affiliates, a Component Unit of Harris County, Texas Reports on Federal and State Award Programs for the Year Ended February 28, 2011 HARRIS COUNTY HOSPITAL DISTRICT

Harris County Hospital District and Affiliates, a Component Unit of Harris County, Texas Reports on Federal and State Award Programs for the Year Ended February 28, 2011 HARRIS COUNTY HOSPITAL DISTRICT

EARLY LEARNING COALITION OF NORTHWEST FLORIDA, INC. Financial Statements and Independent Auditor's Report. June 30, 2010 and 2009

EARLY LEARNING COALITION OF NORTHWEST FLORIDA, INC. Financial Statements and Independent Auditor's Report June 30, 2010 and 2009 EARLY LEARNING COALITION OF NORTHWEST FLORIDA, INC. Financial Statements

EARLY LEARNING COALITION OF NORTHWEST FLORIDA, INC. Financial Statements and Independent Auditor's Report June 30, 2010 and 2009 EARLY LEARNING COALITION OF NORTHWEST FLORIDA, INC. Financial Statements

versight eport Office of the Inspector General Department of Defense

versight eport REPORT ON QUALITY CONTROL REVIEW OF ARTHUR ANDERSEN, LLP, FOR OMB CIRCULAR NO. A-133 AUDIT REPORT OF THE HENRY M. JACKSON FOUNDATION FOR THE ADVANCEMENT OF MILITARY MEDICINE, FISCAL YEAR

versight eport REPORT ON QUALITY CONTROL REVIEW OF ARTHUR ANDERSEN, LLP, FOR OMB CIRCULAR NO. A-133 AUDIT REPORT OF THE HENRY M. JACKSON FOUNDATION FOR THE ADVANCEMENT OF MILITARY MEDICINE, FISCAL YEAR

Federal Financial Report (FFR) Overview for HRSA Grantees

Overview for HRSA Grantees") Health Resources and Services Administration (HRSA) Federal Financial Report (FFR) Overview for HRSA Grantees Presented To: HRSA Grantees 289 1 of 13 FFR Overview Agenda Purpose and Goals Federal Financial

Health Resources and Services Administration (HRSA) Federal Financial Report (FFR) Overview for HRSA Grantees Presented To: HRSA Grantees 289 1 of 13 FFR Overview Agenda Purpose and Goals Federal Financial

Subgrantee Monitoring and Risk Assessment Principles. Brian Sass, OVC

Subgrantee Monitoring and Risk Assessment Principles Brian Sass, OVC Objectives I. Become familiar with the rules and regulations requiring the monitoring of VOCA Victim Assistance subawards II. III. IV.

Subgrantee Monitoring and Risk Assessment Principles Brian Sass, OVC Objectives I. Become familiar with the rules and regulations requiring the monitoring of VOCA Victim Assistance subawards II. III. IV.

ATTACHMENT D Fiscal Rules FY 2014

ATTACHMENT D Fiscal Rules FY 2014 The, HIV/AIDS Services Division (Grantee) expects that all Part A contracted providers will expend 100% of their award in accordance with all federal, local, and BPHC

ATTACHMENT D Fiscal Rules FY 2014 The, HIV/AIDS Services Division (Grantee) expects that all Part A contracted providers will expend 100% of their award in accordance with all federal, local, and BPHC

Community Development Block Grant - Disaster Recovery (CDBG-DR)

") U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT Community Development Block Grant - Disaster Recovery (CDBG-DR) P.L. 115-56 Financial Management and Grant Compliance Certification for States and s subject

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT Community Development Block Grant - Disaster Recovery (CDBG-DR) P.L. 115-56 Financial Management and Grant Compliance Certification for States and s subject

Uniform Guidance for Federal Awards Key Changes and Lessons

Uniform Guidance for Federal Awards Key Changes and Lessons Learned Kinman Tong, Senior Manager Moss Adams LLP 1 PRESENTER Kinman Tong, Senior Manager Kinman has been in public accounting since 2003. He

Uniform Guidance for Federal Awards Key Changes and Lessons Learned Kinman Tong, Senior Manager Moss Adams LLP 1 PRESENTER Kinman Tong, Senior Manager Kinman has been in public accounting since 2003. He

HOPE HOUSE DAY CARE CENTER, INC. FINANCIAL STATEMENTS

HOPE HOUSE DAY CARE CENTER, INC. FINANCIAL STATEMENTS June 30, 2016 (with Comparative Totals for 2015) TABLE OF CONTENTS INDEPENDENT AUDITOR S REPORT 1 FINANCIAL STATEMENTS Statement of Financial Position

HOPE HOUSE DAY CARE CENTER, INC. FINANCIAL STATEMENTS June 30, 2016 (with Comparative Totals for 2015) TABLE OF CONTENTS INDEPENDENT AUDITOR S REPORT 1 FINANCIAL STATEMENTS Statement of Financial Position

National Association of State Auditors, Comptrollers and Treasurers

National Association of State Auditors, Comptrollers and Treasurers EXECUTIVE COMMITTEE OFFICERS President MARTIN J. BENISON Comptroller Massachusetts First Vice President JAMES B. LEWIS State Treasurer

National Association of State Auditors, Comptrollers and Treasurers EXECUTIVE COMMITTEE OFFICERS President MARTIN J. BENISON Comptroller Massachusetts First Vice President JAMES B. LEWIS State Treasurer

HAMILTON SOUTHEASTERN SCHOOLS REQUEST FOR PROPOSAL OF AUDIT SERVICES

HAMILTON SOUTHEASTERN SCHOOLS REQUEST FOR PROPOSAL OF AUDIT SERVICES PURPOSE OF THE REQUEST FOR PROPOSAL ( RFP ) The purpose of this RFP is to select a vendor that can satisfy the Hamilton Southeastern

HAMILTON SOUTHEASTERN SCHOOLS REQUEST FOR PROPOSAL OF AUDIT SERVICES PURPOSE OF THE REQUEST FOR PROPOSAL ( RFP ) The purpose of this RFP is to select a vendor that can satisfy the Hamilton Southeastern

U.S. Department of Housing and Urban Development Office of Housing Counseling

U.S. Department of Housing and Urban Development Office of Housing Counseling Facilitated by Booth Management Consulting 7230 Lee Deforest Drive, Suite 202 Columbia, MD 21046 Best Practices & Lessons Learned,

U.S. Department of Housing and Urban Development Office of Housing Counseling Facilitated by Booth Management Consulting 7230 Lee Deforest Drive, Suite 202 Columbia, MD 21046 Best Practices & Lessons Learned,

Uniform Guidance Overview

Compliance Auditing Update NC Local Government Auditing, Reporting and Review June 14, 2016 Uniform Guidance Overview Course Objectives-Uniform Administrative Requirements, Cost Principles, and Audit Requirements

Compliance Auditing Update NC Local Government Auditing, Reporting and Review June 14, 2016 Uniform Guidance Overview Course Objectives-Uniform Administrative Requirements, Cost Principles, and Audit Requirements

2018 Single Audit Update

2018 Single Audit Update July 24, 2018 Webinar Presented in association with Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Governmental Audit Quality Rehmann 2 Outline Components of a Single

2018 Single Audit Update July 24, 2018 Webinar Presented in association with Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Governmental Audit Quality Rehmann 2 Outline Components of a Single

Planning for your Financial Audit with Booth Management. August 5, 2015

Planning for your Financial Audit with Booth Management August 5, 2015 1 Facilitators & Speakers Facilitator: Phyllis Ford, Division Director, Office of Oversight & Accountability, HUD Speakers: Robin

Planning for your Financial Audit with Booth Management August 5, 2015 1 Facilitators & Speakers Facilitator: Phyllis Ford, Division Director, Office of Oversight & Accountability, HUD Speakers: Robin

Booth Management Consulting, LLC. Facilitated by Lee Deforest Drive, Suite 202, Columbia, MD 21046

U.S. Department of Housing and Urban Development Office of Housing Counseling Best Practices/Lessons Learned LHCAs June 19, 2015 12:00 PM Eastern Standard Time Facilitated by Booth Management Consulting,

U.S. Department of Housing and Urban Development Office of Housing Counseling Best Practices/Lessons Learned LHCAs June 19, 2015 12:00 PM Eastern Standard Time Facilitated by Booth Management Consulting,

July 16, Audit Oversight

July 16, 2004 Audit Oversight Quality Control Review of PricewaterhouseCoopers, LLP and the Defense Contract Audit Agency Office of Management and Budget Circular A-133 Audit Report of the Institute for

July 16, 2004 Audit Oversight Quality Control Review of PricewaterhouseCoopers, LLP and the Defense Contract Audit Agency Office of Management and Budget Circular A-133 Audit Report of the Institute for

Financial Management for AmeriCorps Grants

1 Financial Management for AmeriCorps Grants Session Objectives 2 Review The Following Key Elements for Managing an AmeriCorps Grant: Common Audit Findings Regulation and Requirements Financial Management

1 Financial Management for AmeriCorps Grants Session Objectives 2 Review The Following Key Elements for Managing an AmeriCorps Grant: Common Audit Findings Regulation and Requirements Financial Management

The Priority Setting and Resource Allocation Process: Planning Council Training

The Priority Setting and Resource Allocation Process: Planning Council Training March 25, 2010 Broward County HIV Health Services Planning Council Presentation Outline PSRA Process PSRA Principles & Criteria

The Priority Setting and Resource Allocation Process: Planning Council Training March 25, 2010 Broward County HIV Health Services Planning Council Presentation Outline PSRA Process PSRA Principles & Criteria

2 CFR 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR. Kirsten Rigg

2 CFR 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS Kirsten Rigg WYDOT Internal Review 307-777-4252 kirsten.rigg@wyo.gov TRAINING OBJECTIVES Background

2 CFR 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS Kirsten Rigg WYDOT Internal Review 307-777-4252 kirsten.rigg@wyo.gov TRAINING OBJECTIVES Background

HRSA/HAB Site Visits: Top Findings

Ryan White HIV/AIDS Program Fiscal Health Series Systems to Sustainability TM HRSA/HAB Site Visits: Top Findings INTRODUCTION Sound fiscal management is critical for organizations to improve access to

Ryan White HIV/AIDS Program Fiscal Health Series Systems to Sustainability TM HRSA/HAB Site Visits: Top Findings INTRODUCTION Sound fiscal management is critical for organizations to improve access to

COMMUNITY DEVELOPMENT BLOCK GRANT (CDBG) SUBRECIPIENT WORKSHOP FY October 2014 Santa Ana, CA

SUBRECIPIENT WORKSHOP FY October 2014 Santa Ana, CA") COMMUNITY DEVELOPMENT BLOCK GRANT (CDBG) SUBRECIPIENT WORKSHOP FY 215-216 October 214 Santa Ana, CA CDBG SUBRECIPIENT TRAINING Overview of CDBG Anticipated Timeline Key Considerations Grant Requirements

COMMUNITY DEVELOPMENT BLOCK GRANT (CDBG) SUBRECIPIENT WORKSHOP FY 215-216 October 214 Santa Ana, CA CDBG SUBRECIPIENT TRAINING Overview of CDBG Anticipated Timeline Key Considerations Grant Requirements

FFRs, Carryovers & UOBs

FFRs, Carryovers & UOBs Brad Barney Branch Chief OFAM/DGMO/HRHB Michael Goldrosen Division Director Division of State HIV/AIDS Program June 14 th, 2017 HAB DSHAP Mission To provide leadership and support

FFRs, Carryovers & UOBs Brad Barney Branch Chief OFAM/DGMO/HRHB Michael Goldrosen Division Director Division of State HIV/AIDS Program June 14 th, 2017 HAB DSHAP Mission To provide leadership and support

OMB CIRCULAR A-133 REPORT ON FEDERAL FINANCIAL ASSISTANCE PROGRAMS

OMB CIRCULAR A-133 REPORT ON FEDERAL FINANCIAL ASSISTANCE PROGRAMS Virgin Islands Port Authority (a component unit of the Government of the United States Virgin Islands) Report of Independent Auditors

OMB CIRCULAR A-133 REPORT ON FEDERAL FINANCIAL ASSISTANCE PROGRAMS Virgin Islands Port Authority (a component unit of the Government of the United States Virgin Islands) Report of Independent Auditors

Report Documentation Page

Report Documentation Page Report Date 08 Nov 2002 Report Type N/A Dates Covered (from... to) - Title and Subtitle Oversight: Summary of Quality Control Review of Office of Management and Budget Circular

Report Documentation Page Report Date 08 Nov 2002 Report Type N/A Dates Covered (from... to) - Title and Subtitle Oversight: Summary of Quality Control Review of Office of Management and Budget Circular

WYOMING PRIMARY CARE ASSOCIATION, INC.

FINANCIAL AND COMPLIANCE REPORT MARCH 31, 2015 CONTENTS INDEPENDENT AUDITOR S REPORT 1 and 2 FINANCIAL STATEMENTS Statement of cash receipts and disbursements 3 Notes to financial statement 4-6 SUPPLEMENTARY

FINANCIAL AND COMPLIANCE REPORT MARCH 31, 2015 CONTENTS INDEPENDENT AUDITOR S REPORT 1 and 2 FINANCIAL STATEMENTS Statement of cash receipts and disbursements 3 Notes to financial statement 4-6 SUPPLEMENTARY

UNIFIED GOVERNMENT OF WYANDOTTE COUNTY / KANSAS CITY, KANSAS

OMB CIRCULAR A-133, SINGLE AUDIT REPORT YEAR ENDED DECEMBER 31, 2010 WITH INDEPENDENT AUDITORS REPORT OMB CIRCULAR A-133, SINGLE AUDIT REPORT YEAR ENDED DECEMBER 31, 2010 WITH INDEPENDENT AUDITORS REPORT

OMB CIRCULAR A-133, SINGLE AUDIT REPORT YEAR ENDED DECEMBER 31, 2010 WITH INDEPENDENT AUDITORS REPORT OMB CIRCULAR A-133, SINGLE AUDIT REPORT YEAR ENDED DECEMBER 31, 2010 WITH INDEPENDENT AUDITORS REPORT

Exhibit B A3 Budget Detail and Payment Provisions. Part I General Fiscal Provisions

Budget Detail and Payment Provisions Part I General Fiscal Provisions Section 1 General Fiscal Provisions A. Fiscal Provisions For services satisfactorily rendered, and upon receipt and approval of documentation

Budget Detail and Payment Provisions Part I General Fiscal Provisions Section 1 General Fiscal Provisions A. Fiscal Provisions For services satisfactorily rendered, and upon receipt and approval of documentation

Washington State Auditor s Office. Financial Statements and Federal Single Audit Report. Skagit County

Washington State Auditor s Office Financial Statements and Federal Single Audit Report Skagit County Audit Period January 1, 2009 through December 31, 2009 Report No. 1004270 Issue Date September 27, 2010

Washington State Auditor s Office Financial Statements and Federal Single Audit Report Skagit County Audit Period January 1, 2009 through December 31, 2009 Report No. 1004270 Issue Date September 27, 2010

PART 6 - INTERNAL CONTROL

PART 6 - INTERNAL CONTROL INTRODUCTION The A-102 Common Rule and OMB Circular A-110 (2 CFR part 215) require that non-federal entities receiving Federal awards (i.e., auditee management) establish and

PART 6 - INTERNAL CONTROL INTRODUCTION The A-102 Common Rule and OMB Circular A-110 (2 CFR part 215) require that non-federal entities receiving Federal awards (i.e., auditee management) establish and

CHILD CARE INFORMATION SERVICES (CCIS) Audit Guidelines. Fiscal Year

Audit Guidelines. Fiscal Year") COMMONWEALTH OF PENNSYLVANIA DEPARTMENT OF HUMAN SERVICES CHILD CARE INFORMATION SERVICES (CCIS) Audit Guidelines Fiscal Year 2016-17 1 CHILD CARE INFORMATION SERVICES (CCIS) Audit Guidelines Introduction

COMMONWEALTH OF PENNSYLVANIA DEPARTMENT OF HUMAN SERVICES CHILD CARE INFORMATION SERVICES (CCIS) Audit Guidelines Fiscal Year 2016-17 1 CHILD CARE INFORMATION SERVICES (CCIS) Audit Guidelines Introduction

February 17, Office of Management and Budget Office of Federal Financial Management th St. NW. Washington, DC 20500

Main Office 7501 Wisconsin Ave. Suite 1100W Bethesda, MD 20814 301.347.0400 Tel 301.347.0459 Fax February 17, 2015 Office of Management and Budget Office of Federal Financial Management 175 17th St. NW.

Main Office 7501 Wisconsin Ave. Suite 1100W Bethesda, MD 20814 301.347.0400 Tel 301.347.0459 Fax February 17, 2015 Office of Management and Budget Office of Federal Financial Management 175 17th St. NW.

Florida MIECHV Initiative Provider Fiscal Policy Manual

2018 Florida MIECHV Initiative Provider Fiscal Policy Manual Florida MIECHV Initiative This project is supported by the Health Resources and Services Administration (HRSA) of the U.S. Department of Health

2018 Florida MIECHV Initiative Provider Fiscal Policy Manual Florida MIECHV Initiative This project is supported by the Health Resources and Services Administration (HRSA) of the U.S. Department of Health

March 4, 2015 To the Board Members of the Housing Finance Authority of Pinellas County and Kathryn Driver, Executive Director We are pleased to

March 4, 2015 To the Board Members of the Housing Finance Authority of Pinellas County and Kathryn Driver, Executive Director We are pleased to confirm our understanding of the services we are to provide

March 4, 2015 To the Board Members of the Housing Finance Authority of Pinellas County and Kathryn Driver, Executive Director We are pleased to confirm our understanding of the services we are to provide

STATE OF OHIO DEPARTMENT OF MENTAL HEALTH AND ADDICTION SERVICES OFFICE OF FINANCIAL MANAGEMENT REPORT OF SUBRECIPIENT MONITORING ONSITE VISIT OF THE

STATE OF OHIO DEPARTMENT OF MENTAL HEALTH AND ADDICTION SERVICES OFFICE OF FINANCIAL MANAGEMENT REPORT OF SUBRECIPIENT MONITORING ONSITE VISIT OF THE MENTAL HEALTH & RECOVERY SERVICES BOARD OF SENECA,

STATE OF OHIO DEPARTMENT OF MENTAL HEALTH AND ADDICTION SERVICES OFFICE OF FINANCIAL MANAGEMENT REPORT OF SUBRECIPIENT MONITORING ONSITE VISIT OF THE MENTAL HEALTH & RECOVERY SERVICES BOARD OF SENECA,

Subrecipient monitoring responsibilities are shared among the following:

SUBRECIPIENT MONITORING PURPOSE The OMB Uniform Guidance, 2 CFR Part 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS section 200.331 requires prime recipients

SUBRECIPIENT MONITORING PURPOSE The OMB Uniform Guidance, 2 CFR Part 200 UNIFORM ADMINISTRATIVE REQUIREMENTS, COST PRINCIPLES, AND AUDIT REQUIREMENTS FOR FEDERAL AWARDS section 200.331 requires prime recipients

No new accounting policies were adopted and the application of existing policies was not changed during 2016.

CliftonLarsonAllen LLP CLAconnect.com Board of Directors UNAVCO, Inc. Boulder, Colorado We have audited the financial statements of UNAVCO, Inc. as of and for the year ended December 31, 2016, and have

CliftonLarsonAllen LLP CLAconnect.com Board of Directors UNAVCO, Inc. Boulder, Colorado We have audited the financial statements of UNAVCO, Inc. as of and for the year ended December 31, 2016, and have

2017 Single Audit Update

2017 Single Audit Update July 25, 2017 Webinar Presented in association with Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Governmental Audit Quality Rehmann 2 Outline Components of a Single

2017 Single Audit Update July 25, 2017 Webinar Presented in association with Presented by: Stephen W. Blann, CPA, CGFM, CGMA Director of Governmental Audit Quality Rehmann 2 Outline Components of a Single

ACT14 Are You Ready for the New Federal Uniform Grant Guidance?

APRIL 13-16, 2016 ACT14 Are You Ready for the New Federal Uniform Grant Guidance? THESE MATERIALS HAVE BEEN PREPARED BY Vicenti, Lloyd & Stutzman, LLP THEY HAVE NOT BEEN REVIEWED BY STATE CASBO FOR APPROVAL,

APRIL 13-16, 2016 ACT14 Are You Ready for the New Federal Uniform Grant Guidance? THESE MATERIALS HAVE BEEN PREPARED BY Vicenti, Lloyd & Stutzman, LLP THEY HAVE NOT BEEN REVIEWED BY STATE CASBO FOR APPROVAL,

U. S. DEPARTMENT OF HEALTH AND HUMAN SERVICES CENTERS FOR DISEASE CONTROL AND PREVENTION Federal Authorization:

APRIL 2015 93.945 93.757 State Project/Program: STATE PUBLIC HEALTH ACTIONS TO PREVENT AND CONTROL DIABETES, HEART DISEASE, OBESITY AND ASSOCIATED RISK FACTORS AND PROMOTE SCHOOL HEALTH STATE PUBLIC HEALTH

APRIL 2015 93.945 93.757 State Project/Program: STATE PUBLIC HEALTH ACTIONS TO PREVENT AND CONTROL DIABETES, HEART DISEASE, OBESITY AND ASSOCIATED RISK FACTORS AND PROMOTE SCHOOL HEALTH STATE PUBLIC HEALTH

Community Development Block Grant (CDBG) Disaster Mitigation for Public Housing Authorities. Our Staff

Disaster Mitigation for Public Housing Authorities. Our Staff") Community Development Block Grant (CDBG) Disaster Mitigation for Public Housing Authorities Implementation Workshop April 14, 2008 / Miami Grant administration workshop sponsored by Department of Community

Community Development Block Grant (CDBG) Disaster Mitigation for Public Housing Authorities Implementation Workshop April 14, 2008 / Miami Grant administration workshop sponsored by Department of Community

AMENDMENT TO DELEGATE AGENCY GRANT AGREEMENT (ARRA)

") Contract #/ P.O. #/ Release #: Amendment No. Vendor Code#: Maximum Compensation (Amount of Recovery Act Funds): $ Maximum Compensation (Amount of Non Recovery Act Funds): $ Fund # (Recovery Act Funds):

Contract #/ P.O. #/ Release #: Amendment No. Vendor Code#: Maximum Compensation (Amount of Recovery Act Funds): $ Maximum Compensation (Amount of Non Recovery Act Funds): $ Fund # (Recovery Act Funds):

Uniform Guidance: Key Points of the UNC Implementation - Getting to the Real Impacts of 2 CFR Part 200

Uniform Guidance: Key Points of the UNC Implementation - Getting to the Real Impacts of 2 CFR Part 200 Sharon Brooks Director of Award Management Services and Cash Management Robin Cyr Associate Vice Chancellor

Uniform Guidance: Key Points of the UNC Implementation - Getting to the Real Impacts of 2 CFR Part 200 Sharon Brooks Director of Award Management Services and Cash Management Robin Cyr Associate Vice Chancellor

AID ATLANTA, INCORPORATED. FINANCIAL STATEMENTS YEARS ENDED DECEMBER 31, 2017 AND 2016 and SUPPLEMENTARY INFORMATION. with INDEPENDENT AUDITORS REPORT

FINANCIAL STATEMENTS YEARS ENDED DECEMBER 31, 2017 AND 2016 and SUPPLEMENTARY INFORMATION with INDEPENDENT AUDITORS REPORT TABLE OF CONTENTS PAGE INDEPENDENT AUDITORS REPORT 3-4 STATEMENT OF FINANCIAL

FINANCIAL STATEMENTS YEARS ENDED DECEMBER 31, 2017 AND 2016 and SUPPLEMENTARY INFORMATION with INDEPENDENT AUDITORS REPORT TABLE OF CONTENTS PAGE INDEPENDENT AUDITORS REPORT 3-4 STATEMENT OF FINANCIAL

U.S. Department of Housing and Urban Development Office of Housing Counseling

U.S. Department of Housing and Urban Development Office of Housing Counseling Facilitated by Booth Management Consulting 7230 Lee Deforest Drive, Suite 202 Columbia, MD 21046 Preparing a Budget October

U.S. Department of Housing and Urban Development Office of Housing Counseling Facilitated by Booth Management Consulting 7230 Lee Deforest Drive, Suite 202 Columbia, MD 21046 Preparing a Budget October

Webinar 1 - Financial Management

Webinar 1 - Financial Management PRESENTER: Welcome to the webinar on the core principles of financial management, presented by the US Department of Housing and Urban Development. Many of the ideas we

Webinar 1 - Financial Management PRESENTER: Welcome to the webinar on the core principles of financial management, presented by the US Department of Housing and Urban Development. Many of the ideas we

EMERGENCY FINANCIAL ASSISTANCE

I. DEFINITION OF SERICE EMERGENCY FINANCIAL ASSISTANCE Emergency Financial Assistance is the provision of short-term payments to agencies or establishment of voucher programs to assist with emergency expenses

I. DEFINITION OF SERICE EMERGENCY FINANCIAL ASSISTANCE Emergency Financial Assistance is the provision of short-term payments to agencies or establishment of voucher programs to assist with emergency expenses

Independent Auditors. Consolidated Audit Guide for Audits of HUD Programs. August 1997

Handbook 2000.04 REV-2 U.S. Department of Housing and Urban Development Office of Inspector General Independent Auditors August 1997 Consolidated Audit Guide for Audits of HUD Programs GA: Distribution:

Handbook 2000.04 REV-2 U.S. Department of Housing and Urban Development Office of Inspector General Independent Auditors August 1997 Consolidated Audit Guide for Audits of HUD Programs GA: Distribution:

Lee County, Illinois Dixon, Illinois. Report on Federal Awards Year Ended November 30, 2016

Dixon, Illinois Report on Federal Awards Year Ended November 30, 2016 Year Ended November 30, 2016 Table of Contents Independent Auditor s Report on Internal Control over Financial Reporting and on Compliance

Dixon, Illinois Report on Federal Awards Year Ended November 30, 2016 Year Ended November 30, 2016 Table of Contents Independent Auditor s Report on Internal Control over Financial Reporting and on Compliance

General Accounting Policies & Procedures

General Accounting Policies & Procedures POLICY NO.: MB-10012 ORIGINAL ISSUE DATE: October 1, 2015 ORIGINATOR: Chief Financial Officer SUBJECT: FISCAL CONTROL & ACCOUNTABILITY PROCEDURES I. PURPOSE AND

General Accounting Policies & Procedures POLICY NO.: MB-10012 ORIGINAL ISSUE DATE: October 1, 2015 ORIGINATOR: Chief Financial Officer SUBJECT: FISCAL CONTROL & ACCOUNTABILITY PROCEDURES I. PURPOSE AND

Report Documentation Page

Report Documentation Page Report Date 28Mar2002 Report Type N/A Dates Covered (from... to) - Title and Subtitle Audit Oversight: Report on Quality Control Review of KPMG, LLP and Defense Contract Audit

Report Documentation Page Report Date 28Mar2002 Report Type N/A Dates Covered (from... to) - Title and Subtitle Audit Oversight: Report on Quality Control Review of KPMG, LLP and Defense Contract Audit

B STATE ton Street CITY OF. January 1, 2014 FILED 06/13/2016

B46436 STATE BOARD OF ACCOUNTS 302 West Washingt ton Street Room E418 INDIANAPOLIS, INDIANA 46204-2769 SUPPLEMENTALL COMPLIANCE REPORT OF CITY OF LOGANSPORT CASS COUNTY, INDIANA January 1, 2014 to December

B46436 STATE BOARD OF ACCOUNTS 302 West Washingt ton Street Room E418 INDIANAPOLIS, INDIANA 46204-2769 SUPPLEMENTALL COMPLIANCE REPORT OF CITY OF LOGANSPORT CASS COUNTY, INDIANA January 1, 2014 to December

STANDARD ADMINISTRATIVE PROCEDURE

STANDARD ADMINISTRATIVE PROCEDURE 15.01.01.M1.03 Cost-Sharing Procedures Approved October 6, 1997 Revised May 9, 1999 Revised October 2, 2001 Revised October 21, 2009 Revised January 11, 2013 Next scheduled

STANDARD ADMINISTRATIVE PROCEDURE 15.01.01.M1.03 Cost-Sharing Procedures Approved October 6, 1997 Revised May 9, 1999 Revised October 2, 2001 Revised October 21, 2009 Revised January 11, 2013 Next scheduled

8/2/2011. Dealing with Audit Findings August 3, Mary Pockl & Mike Zeno. Webinar Control Panel

Webinar Control Panel Raise your hand to ask a question Only enabled if you have entered your Audio Pin! Enter Your Audio Pin Enter questions & comments here 1 Dealing with Audit Findings August 3, 2011

Webinar Control Panel Raise your hand to ask a question Only enabled if you have entered your Audio Pin! Enter Your Audio Pin Enter questions & comments here 1 Dealing with Audit Findings August 3, 2011

LATEST DEVELOPMENTS CHANGES IN A 133. OMB Uniform Grant Guidance 7/13/2015 STEVEN L. BLAKE, CPA, CFE, CICA, CGMA PRESENTED BY

CHANGES IN A 133 PRESENTED BY STEVEN L. BLAKE, CPA, CFE, CICA, CGMA LATEST DEVELOPMENTS The OMB published in the Federal Register the document, Uniform Administrative Requirements, Cost Principles, and

CHANGES IN A 133 PRESENTED BY STEVEN L. BLAKE, CPA, CFE, CICA, CGMA LATEST DEVELOPMENTS The OMB published in the Federal Register the document, Uniform Administrative Requirements, Cost Principles, and

21 st Century Community Learning Centers Program. Monitoring Document Fiduciary Responsibilities

21 st Century Community Learning Centers Program Monitoring Document Fiduciary Responsibilities Frances Aubuchon Budget Analyst 2 faubuchon@doe.k12.ga.us (404) 657-7144 August 24, 2010 GaDOE Strategic

21 st Century Community Learning Centers Program Monitoring Document Fiduciary Responsibilities Frances Aubuchon Budget Analyst 2 faubuchon@doe.k12.ga.us (404) 657-7144 August 24, 2010 GaDOE Strategic

Management Representation Letter (PHA) PROJECT S LETTERHEAD

PROJECT S LETTERHEAD") Management Representation Letter (PHA) PROJECT S LETTERHEAD DATE CPA FIRM S NAME AND ADDRESS This representation letter is provided in connection with your audit(s) of the financial statements of PHA Name

Management Representation Letter (PHA) PROJECT S LETTERHEAD DATE CPA FIRM S NAME AND ADDRESS This representation letter is provided in connection with your audit(s) of the financial statements of PHA Name

CRE. Expanding & Implementing. Ryan White HIV/AIDS Program Core Medical Providers. EIGHT ESSENTIAL ACTIONS for A GUIDE DEVELOPED FOR

EIGHT ESSENTIAL ACTIONS for Expanding & Implementing Contracting With MEDICAID & Marketplace Insurance Plans A GUIDE DEVELOPED FOR Ryan White HIV/AIDS Program Core Medical Providers By National Technical

EIGHT ESSENTIAL ACTIONS for Expanding & Implementing Contracting With MEDICAID & Marketplace Insurance Plans A GUIDE DEVELOPED FOR Ryan White HIV/AIDS Program Core Medical Providers By National Technical

March 23, /1/2018 WASHINGTON STATE UNIVERSITY. Subcontracting. Overview. Recording date of this workshop is

Subcontracting Presented by: Derek Brown, ORSO Anke Moore, SPS Lucas Sanchez, ORSO Ty Simanson, IPN March 2018 Recording date of this workshop is March 23, 2018 Some of the rules and procedures discussed

Subcontracting Presented by: Derek Brown, ORSO Anke Moore, SPS Lucas Sanchez, ORSO Ty Simanson, IPN March 2018 Recording date of this workshop is March 23, 2018 Some of the rules and procedures discussed

SIGAR. Department of State s Afghanistan Justice Sector Support Program II: Audit of Costs Incurred by Pacific Architects and Engineers, Inc.

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 15-69 Financial Audit Department of State s Afghanistan Justice Sector Support Program II: Audit of Costs Incurred by Pacific Architects

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 15-69 Financial Audit Department of State s Afghanistan Justice Sector Support Program II: Audit of Costs Incurred by Pacific Architects

PREVENTIVE HEALTH AND SERVICES BLOCK GRANT U. S. DEPARTMENT OF HEALTH AND HUMAN SERVICES 130A-223; 15A NCAC 16A

APRIL 2014 93.991 PREVENTIVE HEALTH AND HEALTH SERVICES BLOCK GRANT State Project/Program: PREVENTIVE HEALTH AND SERVICES BLOCK GRANT U. S. DEPARTMENT OF HEALTH AND HUMAN SERVICES Federal Authorization:

APRIL 2014 93.991 PREVENTIVE HEALTH AND HEALTH SERVICES BLOCK GRANT State Project/Program: PREVENTIVE HEALTH AND SERVICES BLOCK GRANT U. S. DEPARTMENT OF HEALTH AND HUMAN SERVICES Federal Authorization:

Provider Audit Guidelines

Washington County Behavioral Health and Developmental Services 100 W. Beau Street, Suite 302 Washington, PA 15301 724.228.6832 Provider Audit Guidelines Effective for all audits submitted for Fiscal Years

Washington County Behavioral Health and Developmental Services 100 W. Beau Street, Suite 302 Washington, PA 15301 724.228.6832 Provider Audit Guidelines Effective for all audits submitted for Fiscal Years

2) Budgetary Comparison Schedule - General Fund and All Major Special Revenue Funds

Budgetary Comparison Schedule - General Fund and All Major Special Revenue Funds") Herbein + Company, Inc. 2763 Century Boulevard Reading, PA 19610 P: 610.378.1175 F: 610.378.0999 www.herbein.com March 22, 2018 Board of Directors Oley Valley School District 17 Jefferson Street Oley,

Herbein + Company, Inc. 2763 Century Boulevard Reading, PA 19610 P: 610.378.1175 F: 610.378.0999 www.herbein.com March 22, 2018 Board of Directors Oley Valley School District 17 Jefferson Street Oley,

EARLY LEARNING COALITION OF NORTHWEST FLORIDA, INC. Financial Statements and Independent Auditor's Report. June 30, 2011 and 2010

EARLY LEARNING COALITION OF NORTHWEST FLORIDA, INC. Financial Statements and Independent Auditor's Report June 30, 2011 and 2010 EARLY LEARNING COALITION OF NORTHWEST FLORIDA, INC. Financial Statements

EARLY LEARNING COALITION OF NORTHWEST FLORIDA, INC. Financial Statements and Independent Auditor's Report June 30, 2011 and 2010 EARLY LEARNING COALITION OF NORTHWEST FLORIDA, INC. Financial Statements

A.R. BANCROFT COMMUNITY DEVELOPMENT CORPORATION HUD PROJECT NO.: 000-EH EH EH EH EH-055

A.R. BANCROFT COMMUNITY DEVELOPMENT CORPORATION HUD PROJECT NO.: 000-EH-020 000-EH-052 000-EH-053 000-EH-054 000-EH-055 FINANCIAL REPORT FOR HUD (IN ACCORDANCE WITH THE UNIFORM GUIDANCE) JUNE 30, 2016

A.R. BANCROFT COMMUNITY DEVELOPMENT CORPORATION HUD PROJECT NO.: 000-EH-020 000-EH-052 000-EH-053 000-EH-054 000-EH-055 FINANCIAL REPORT FOR HUD (IN ACCORDANCE WITH THE UNIFORM GUIDANCE) JUNE 30, 2016

Core Principles of Financial Management. Webinar 1

Core Principles of Financial Management Webinar 1 1 Who Is Our Primary Audience? Our primary audience is grantees and subrecipients of five Multifamily Housing grant programs: Assisted Living Conversion

Core Principles of Financial Management Webinar 1 1 Who Is Our Primary Audience? Our primary audience is grantees and subrecipients of five Multifamily Housing grant programs: Assisted Living Conversion

CHAPTER 11: FINANCIAL MANAGEMENT

CHAPTER 11: FINANCIAL MANAGEMENT CHAPTER PURPOSE & CONTENTS This chapter provides an overview of all of the requirements applicable to the financial management of the CDBG Program. Administrative and planning

CHAPTER 11: FINANCIAL MANAGEMENT CHAPTER PURPOSE & CONTENTS This chapter provides an overview of all of the requirements applicable to the financial management of the CDBG Program. Administrative and planning

Data Collection Form for Reporting on

INTERNET REPORT ID: 383869 VERSION: FORM SF-SAC (8-6-008) PART Data Collection Form for Reporting on AUDITS OF STATES, LOCAL GOVERNMENTS, AND NON-PROFIT ORGANIZATIONS for Fiscal Year Ending Dates in 008,

INTERNET REPORT ID: 383869 VERSION: FORM SF-SAC (8-6-008) PART Data Collection Form for Reporting on AUDITS OF STATES, LOCAL GOVERNMENTS, AND NON-PROFIT ORGANIZATIONS for Fiscal Year Ending Dates in 008,

Department of Children and Youth Services. Fiscal Management Training Workshop Kennedy King College. Auditing

Department of Children and Youth Services Fiscal Management Training Workshop Kennedy King College Auditing March 17 and 18, 2008 1 Audits Unit: Purpose and Objectives To conduct annual program and fiscal

Department of Children and Youth Services Fiscal Management Training Workshop Kennedy King College Auditing March 17 and 18, 2008 1 Audits Unit: Purpose and Objectives To conduct annual program and fiscal

CONTRA COSTA PUBLIC HEALTH AIDS PROGRAM 597 Center Avenue, Suite 200 Martinez, California

WILLIAM B. WALKER, M.D. HEALTH SERVICES DIRECTOR WENDEL BRUNNER, M.D. PUBLIC HEALTH DIRECTOR CONTRA COSTA PUBLIC HEALTH AIDS PROGRAM 597 Center Avenue, Suite 200 Martinez, California 94553-4675 PH 925

WILLIAM B. WALKER, M.D. HEALTH SERVICES DIRECTOR WENDEL BRUNNER, M.D. PUBLIC HEALTH DIRECTOR CONTRA COSTA PUBLIC HEALTH AIDS PROGRAM 597 Center Avenue, Suite 200 Martinez, California 94553-4675 PH 925

SIGAR SEPTEMBER. Special Inspector General for Afghanistan Reconstruction. SIGAR Financial Audit. SIGAR FA/SPECS Project

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 18-68 Financial Audit USAID s Strengthening Political Entities and Civil Society Program: Audit of Costs Incurred by the National Democratic

SIGAR Special Inspector General for Afghanistan Reconstruction SIGAR 18-68 Financial Audit USAID s Strengthening Political Entities and Civil Society Program: Audit of Costs Incurred by the National Democratic

Guard Your Investment in Valuable Contracts

Guard Your Investment in Valuable Contracts 1 PRESENTERS Mark Steranka Partner Moss Adams Consulting Robert Gutierrez, CPA, JD Manager Moss Adams Consulting 2 AGENDA Why Audit Contracts Federal Contracts

Guard Your Investment in Valuable Contracts 1 PRESENTERS Mark Steranka Partner Moss Adams Consulting Robert Gutierrez, CPA, JD Manager Moss Adams Consulting 2 AGENDA Why Audit Contracts Federal Contracts

Compliance Risk Areas for Health Centers: A Financial Perspective. Marcie H. Zakheim Partner

Compliance Risk Areas for Health Centers: A Financial Perspective Marcie H. Zakheim Partner DISCLAIMER This training has been prepared by the attorneys of Feldesman Tucker Leifer Fidell LLP. The opinions

Compliance Risk Areas for Health Centers: A Financial Perspective Marcie H. Zakheim Partner DISCLAIMER This training has been prepared by the attorneys of Feldesman Tucker Leifer Fidell LLP. The opinions

Alabama s Ryan White Part B Program Eligibility Standard

PURPOSE This document establishes guidelines to determine eligibility of persons seeking services through Ryan White Part B and the State s AIDS Drug Assistance Program (ADAP). This policy is binding to

PURPOSE This document establishes guidelines to determine eligibility of persons seeking services through Ryan White Part B and the State s AIDS Drug Assistance Program (ADAP). This policy is binding to

Yellow Book and Single Audit Update Bruce A. Nunnally, CPA, CGMA June 2016

Yellow Book and Single Audit Update Bruce A. Nunnally, CPA, CGMA June 2016 1 Yellow Book Introduction 2 GAS When Applicable FL Govt Audits Local governmental entities located in Florida are, in general,

Yellow Book and Single Audit Update Bruce A. Nunnally, CPA, CGMA June 2016 1 Yellow Book Introduction 2 GAS When Applicable FL Govt Audits Local governmental entities located in Florida are, in general,

Uniform Guidance. Diane E. Edelstein, CPA. Sources

Uniform Guidance August 29, 2016 Central KY Chapter of AGA Diane E. Edelstein, CPA Diane is a partner at Maher Duessel, a regional firm in Pennsylvania. Diane has over 25 years of experience with auditing

Uniform Guidance August 29, 2016 Central KY Chapter of AGA Diane E. Edelstein, CPA Diane is a partner at Maher Duessel, a regional firm in Pennsylvania. Diane has over 25 years of experience with auditing

Intro to Single Audit/Uniform Guidance Presented by: Andrew D. Kehl, CPA, Audit Manager Nicole M. Yuengel, Audit Senior

Intro to Single Audit/Uniform Guidance Presented by: Andrew D. Kehl, CPA, Audit Manager Nicole M. Yuengel, Audit Senior 1 Agenda What is the Single Audit Act / Uniform Guidance? Who is Subject to a Single

Intro to Single Audit/Uniform Guidance Presented by: Andrew D. Kehl, CPA, Audit Manager Nicole M. Yuengel, Audit Senior 1 Agenda What is the Single Audit Act / Uniform Guidance? Who is Subject to a Single

STATEMENT OF QUALIFICATIONS

STATEMENT OF QUALIFICATIONS workforceconnections is an Equal Opportunity Employer/Program Auxiliary aids and services available upon request for individuals with disabilities from workforceconnections

STATEMENT OF QUALIFICATIONS workforceconnections is an Equal Opportunity Employer/Program Auxiliary aids and services available upon request for individuals with disabilities from workforceconnections

NOT-FOR-PROFIT INSIDER

NOT-FOR-PROFIT INSIDER VOLUME 10 :: ISSUE 1 In This Issue: Procurement Standards Under The OMB s New Guidelines For Administrative Requirements Six IRS Requirements For Donor Receipts To Ensure A Charitable

NOT-FOR-PROFIT INSIDER VOLUME 10 :: ISSUE 1 In This Issue: Procurement Standards Under The OMB s New Guidelines For Administrative Requirements Six IRS Requirements For Donor Receipts To Ensure A Charitable

TEXOMA AREA PARATRANSIT SYSTEM, INC. AUDITED FINANCIAL STATEMENTS Year Ended September 30, 2014

TEXOMA AREA PARATRANSIT SYSTEM, INC. AUDITED FINANCIAL STATEMENTS Year Ended September 30, 2014 TABLE OF CONTENTS September 30, 2014 PAGE INDEPENDENT AUDITOR S REPORT... 1 STATEMENT OF NET POSITION...

TEXOMA AREA PARATRANSIT SYSTEM, INC. AUDITED FINANCIAL STATEMENTS Year Ended September 30, 2014 TABLE OF CONTENTS September 30, 2014 PAGE INDEPENDENT AUDITOR S REPORT... 1 STATEMENT OF NET POSITION...

Effective Strategies for Assessing, Collecting, and Monitoring Client Charges HRSA HIV/AIDS Bureau All Grantee Meeting Session 217, November 27, 2012

Effective Strategies for Assessing, Collecting, and Monitoring Client Charges HRSA HIV/AIDS Bureau All Grantee Meeting Session 217, November 27, 2012 Julia Hidalgo, ScD, MSW, MPH Positive Outcomes, Inc.

Effective Strategies for Assessing, Collecting, and Monitoring Client Charges HRSA HIV/AIDS Bureau All Grantee Meeting Session 217, November 27, 2012 Julia Hidalgo, ScD, MSW, MPH Positive Outcomes, Inc.

NATIONAL WIC ASSOCIATION

FINANCIAL REPORT December 31, 2017 and 2016 C O N T E N T S PAGE INDEPENDENT AUDITOR'S REPORT...l and 2 FINANCIAL STATEMENTS Statements of Financial Position... 3 and 4 Statements of Activities... 5 and

FINANCIAL REPORT December 31, 2017 and 2016 C O N T E N T S PAGE INDEPENDENT AUDITOR'S REPORT...l and 2 FINANCIAL STATEMENTS Statements of Financial Position... 3 and 4 Statements of Activities... 5 and

La Familia Medical Center

Accountants Reports and Financial Statements June 30, 2009 and 2008 June 30, 2009 and 2008 Contents Independent Accountants Report... 1 Financial Statements Balance Sheets... 3 Statements of Operations...

Accountants Reports and Financial Statements June 30, 2009 and 2008 June 30, 2009 and 2008 Contents Independent Accountants Report... 1 Financial Statements Balance Sheets... 3 Statements of Operations...

REQUEST FOR PROPOSALS

REQUEST FOR PROPOSALS FOR AUDIT SERVICES FOR THE COLQUITT COUNTY BOARD OF COMMISSIONERS COLQUITT COUNTY, GEORGIA June 6, 2017 TABLE OF CONTENTS 1. 0 INTRODUCTION 1.1 Purpose for Request for Proposal (RFP)

REQUEST FOR PROPOSALS FOR AUDIT SERVICES FOR THE COLQUITT COUNTY BOARD OF COMMISSIONERS COLQUITT COUNTY, GEORGIA June 6, 2017 TABLE OF CONTENTS 1. 0 INTRODUCTION 1.1 Purpose for Request for Proposal (RFP)

RWHAP Parts C and D Frequently Asked Questions April 2016 Division of Community HIV/AIDS Programs Program Income/Maintenance of Effort

RWHAP Parts C and D Frequently Asked Questions April 2016 Division of Community HIV/AIDS Programs Program Income/Maintenance of Effort The following are responses to frequently asked questions (FAQs) presented

RWHAP Parts C and D Frequently Asked Questions April 2016 Division of Community HIV/AIDS Programs Program Income/Maintenance of Effort The following are responses to frequently asked questions (FAQs) presented