Monitoring and Evaluation of Budget Performance CPA John Kauta Partner, Ariska Associates March 31, 2017

|

|

|

- Daniela Hensley

- 6 years ago

- Views:

Transcription

1 Monitoring and Evaluation of Budget Performance CPA John Kauta Partner, Ariska Associates March 31, 2017

2 Outline Introduction Monitoring Budget Performance Evaluating Budget Performance Conclusion 2

3 Introduction

4 Definitions A government budget: shows government's proposed revenues and spending for a financial year that is often passed by the legislature, approved by the Head of State/President and presented by the Finance Minister to the nation. Could be a balanced budget (when government revenue and expenditure are equal), surplus budget (when anticipated revenues exceed expenditure) or a deficit budget (when anticipated expenditure is greater than revenues). Budget Performance: is measured to ascertain whether public entity or activity is achieving its objectives and if progress is being made toward attaining policy or organizational goals. is a quantifiable expression of the amount, cost, or result of activities that indicate how much, how well, and at what level, products or services are provided to clients/customers/the public during a given time period. 4

5 Why do we Measure Budget Performance? Promotes credibility and public confidence by reporting on the results of programs Helps formulate and justify budget requests Provides crucial information about public sector performance Provides a view over time on the status of a project, program, or policy Permits managers of public resources to identify and take action to correct weaknesses Focuses attention on achieving outcomes important to the public entity and its stakeholders Provides timely and frequent information to government and the public 5

6 Good budget performance measures Understandable - are clear, concise, and easy for a non-specialist to comprehend. Timely - have information available frequently enough to have value in making decisions. Comparable - have enough data to tell if performance is getting better, worse or staying about the same. Reliable - have data that is verifiable, free from bias, and an accurate representation of what it is intended to be. Cost effective - justify the time and effort to collect, record, display, and analyze the data given the measure s value. Another aspect of costeffectiveness is feasibility. Useful - help people doing the work understand what is happening with 6 their business process, and how to get better results for customers.

7 The PFM Cycle Planning /Policy Scrutiny and Audit Optimum utilization Budgeting Budget implementation. Accounting, recording and reporting 7

8 Key areas of Budget Performance that are Measured? Budget Realism: Is the budget realistic, and implemented as intended in a predictable manner? Comprehensive, Policy-based, budget: Does the budget capture all relevant fiscal transactions, and is the process, giving regard to government policy? Six core objectives of PFM system Accountability and Transparency : Are effective external financial accountability and transparency arrangements in place? Control : Is effective control and stewardship exercised in the use of public funds? Comprehensive fiscal risk oversight : Is oversight of fiscal risk arising from public enterprises and sub-national governments adequate? Information: Is adequate fiscal, revenue and expenditure information produced and disseminated to meet decision-making and management purposes? 8

9 Comparison between Monitoring and Evaluation Monitoring Evaluation Focus Continuous. Clarifies program objectives Periodic. Analyzes why intended results were or were not achieved Links activities and their resources to objectives Translates objectives into performance indicators and set targets Routinely collects data on these indicators, compares actual results with targets Reports progress to managers and alerts them to problems Time Focus Present Past - Future Main Question What needs to happen now to reach our goal? Attention Level Details Big Picture Assesses specific causal contributions of activities to results Examines implementation process Explores unintended results Provides lessons, highlights significant accomplishment or program potential, and offers recommendations for improvement Have we achieved our goal? 9

10 Monitoring Budget Performance

11 Definition of Monitoring Is a continuous process of collecting and analyzing information to compare how well a project, program or policy is performing against expected results Is a planned/systematic process of observation that closely follows a course of activities and compares what is happening with what is expected to happen Is the periodic collection and review of information on programme implementation, coverage and use for comparison with implementation plans. Allows for modifying original plans during implementation Identifies shortcomings before it is too late. Provides elements of analysis as to why progress fell short of 11 expectations

12 Types of Monitoring 1. Traditional/Implementation monitoring: This involves tracking inputs, activities (what actually took place) and outputs (the products or services produced) This approach focuses on monitoring how well a project, program or policy is being implemented Often used to assess compliance with work plans and budget 2. Results-based monitoring: the regular collection of information on how effectively is performing demonstrates whether a project, program, or policy is achieving its stated goals Focus is on outcomes and Impact 12

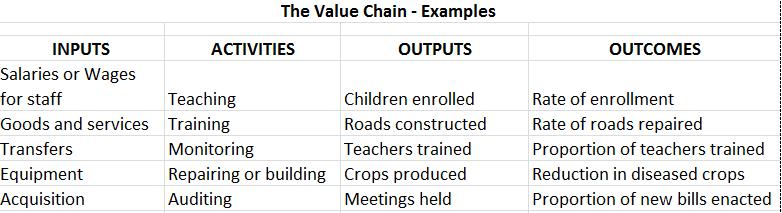

13 The results chain under Program Based Budgeting Inputs (Resources) Activities (Processes) Outputs Intermediate Outcomes High-level (Ultimate) Outcomes INPUTS are used in carrying out ACTIVITIES in order to produce OUTPUTS and thereby achieving OUTCOMES. 13

14 14

15 Example of Budget Performance Indicators Type of Indicator Definition Example Outcome - Effectiveness Indicator Degree to which the program objective is being met Increase in immunisation coverage Increased life expectancy % decrease in infant mortality Increased deliveries in health facilities Output Quantity Indicator Quantity of service provided No. of children immunised No. of births at health facilities Output - Equity Indicator Participation of target group Proportion of girls accessing reproductive health services % of people from poor households accessing the health facilities Output Quality Indicator Quality of the service provided Client satisfaction Proportion of health facilities accredited Output Efficiency Indicator Cost per unit of output Cost per vaccination Cost per medical doctor educated Activity Indicator Indicator of internal work processes Number of positions filled No of policy statements developed Input Indicator Measure of resources employed Number of doctors per patient 15

16 Evaluating Budget Performance

17 Definition of Evaluation A process that assesses an achievement against preset criteria. A systematic process to determine the extent to which service needs and results have been or are being achieved and analyse the reasons for any discrepancy. Attempts to measure service s relevance, efficiency and effectiveness. It measures whether and to what extent the program s inputs and services are improving the quality of people s lives. 17

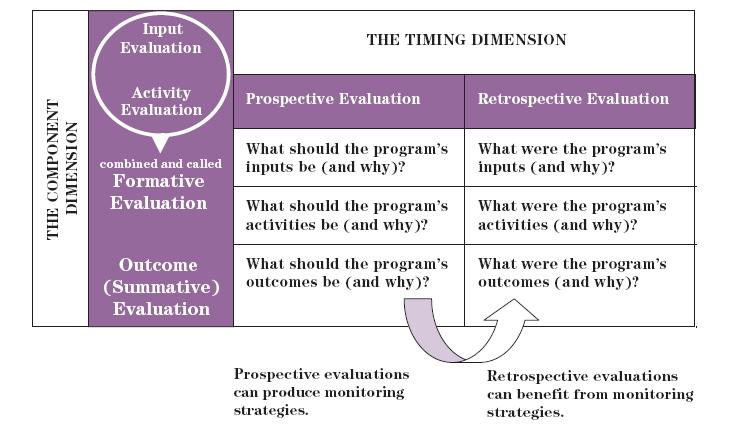

18 Types of Evaluations Retrospective Evaluation Often used when programs have been functioning for some time. Determines what actually happened (and why) Prospective Evaluations Conducted when a new program within a service is being introduced. Identifies ways to increase the impact of a program on clients; It identifies how to improve delivery mechanisms in order to be more effective. Determines what ought to happen (and why) 18

19 Evaluation Matrix 19

20 Conducting Evaluations Ongoing program evaluation End of program evaluation Impact evaluation Spot check evaluation Desk evaluation Internal evaluation (self evaluation) - in which people within a program sponsor, conduct and control the evaluation. External evaluation - in which someone from beyond the program acts as the evaluator and controls the evaluation. 20

21 Qualitative Evaluation Tools Unobtrusive seeing - involving an observer who is not seen by those who are observed; Participant observation - involving an observer who does not take part in an activity but is seen by the activity s participants. Interviewing - involving a more active role for the evaluator because she /he poses questions to the respondent, usually on a one-on-one basis Group-based data collection processes such as focus groups Content analysis - which involves reviewing documents and transcripts to identify patterns within the material 21

22 Evaluation Tools Surveys/questionnaires Registries Activity logs Administrative records Registration forms Case studies Attendance sheets Cost benefit analysis Cause-effect diagram 22

23 Conclusion

24 24 Conclusion Developing effective budget monitoring and evaluation systems requires welldefined formulation and implementation strategies for setting up performance indicators These strategies vary depending on a country s priority for measuring results and on the scope and pace of its performance management reform objectives Some countries have followed an incremental method for developing performance indicators, (for example, Canada, the United Kingdom, and Colombia), while others have taken big bang approach (for example, Mexico and the Republic of Korea) Either way there is need to continuously improve the quality and meaningfulness of the indicators to inform government processes Its important to note that Prospective evaluations can produce monitoring strategies. Also Monitoring strategies can inform retrospective evaluations.

25 Thank you

Illustrative IPSAS Entity Financial Statements Public Sector Entity (PSE) Year ended 31 December [January 2016]

![Illustrative IPSAS Entity Financial Statements Public Sector Entity (PSE) Year ended 31 December [January 2016]](/thumbs/94/120288745.jpg "Illustrative IPSAS Entity Financial Statements Public Sector Entity (PSE) Year ended 31 December [January 2016]") Illustrative IPSAS Entity Financial Statements Public Sector Entity (PSE) Year ended 31 December [January 2016] Introduction A cornerstone of accountability is fair and transparent reporting of transactions

Illustrative IPSAS Entity Financial Statements Public Sector Entity (PSE) Year ended 31 December [January 2016] Introduction A cornerstone of accountability is fair and transparent reporting of transactions

Toward Better Accountability Quality of Annual Reporting

Toward Better Accountability Quality of Annual Reporting Each year, our Annual Report addresses issues of accountability and initiatives to help improve accountability in government and across the broader

Toward Better Accountability Quality of Annual Reporting Each year, our Annual Report addresses issues of accountability and initiatives to help improve accountability in government and across the broader

Public Expenditure and Financial Accountability Baseline Report. Central Provincial Government

Public Expenditure and Financial Accountability Baseline Report Central Provincial Government 1 Table of Contents Summary Assessment... 4 (i) Integrated assessment of PFM performance... 4 (ii) Assessment

Public Expenditure and Financial Accountability Baseline Report Central Provincial Government 1 Table of Contents Summary Assessment... 4 (i) Integrated assessment of PFM performance... 4 (ii) Assessment

PLANNING and M&E for RESULTS

PLANNING and M&E for RESULTS Planning, Budgeting, Execution and Monitoring for Results Pillars of a Strong Public Financial Management Presented during the PAGBA 1 st Quarterly and Meeting THE ORIENTAL

PLANNING and M&E for RESULTS Planning, Budgeting, Execution and Monitoring for Results Pillars of a Strong Public Financial Management Presented during the PAGBA 1 st Quarterly and Meeting THE ORIENTAL

Illustrative IPSAS Entity Financial Statements Public Sector Entity (PSE) Year ended 31 December 2014

Year ended 31 December 2014") Illustrative IPSAS Entity Financial Statements Public Sector Entity (PSE) Year ended 31 December Issued April 2015 Introduction A cornerstone of accountability is fair and transparent reporting of transactions

Illustrative IPSAS Entity Financial Statements Public Sector Entity (PSE) Year ended 31 December Issued April 2015 Introduction A cornerstone of accountability is fair and transparent reporting of transactions

EUROPEAN PUBLIC SECTOR ACCOUNTING STANDARDS

EUROPEAN COMMISSION EUROSTAT Directorate C: National Accounts, Prices and Key Indicators Task Force EPSAS EPSAS WG 18/07 Luxembourg, 25 April 2018 EUROPEAN PUBLIC SECTOR ACCOUNTING STANDARDS CONCEPTUAL

EUROPEAN COMMISSION EUROSTAT Directorate C: National Accounts, Prices and Key Indicators Task Force EPSAS EPSAS WG 18/07 Luxembourg, 25 April 2018 EUROPEAN PUBLIC SECTOR ACCOUNTING STANDARDS CONCEPTUAL

Review Criteria. Robotics Program. Reviewer SCORE SUMMARY. Extent of Need 25 Goals Objectives and Milestones

Proposal Lead Agency: Proposal Title: Review Criteria [Additional Information]: Robotics Program Reviewer Reviewer: Signature: Date: SCORE SUMMARY Section Maximum Score Extent of Need 25 Goals Objectives

Proposal Lead Agency: Proposal Title: Review Criteria [Additional Information]: Robotics Program Reviewer Reviewer: Signature: Date: SCORE SUMMARY Section Maximum Score Extent of Need 25 Goals Objectives

PROJECT CYCLE MANAGEMENT & LOGICAL FRAMEWORK MATRIX TRAINING CYPRIOT CIVIL SOCIETY IN ACTION V INNOVATION AND CHANGES IN EDUCATION VI

PROJECT CYCLE MANAGEMENT & LOGICAL FRAMEWORK MATRIX TRAINING CYPRIOT CIVIL SOCIETY IN ACTION V INNOVATION AND CHANGES IN EDUCATION VI Objectives of the training Understand the definition of project and

PROJECT CYCLE MANAGEMENT & LOGICAL FRAMEWORK MATRIX TRAINING CYPRIOT CIVIL SOCIETY IN ACTION V INNOVATION AND CHANGES IN EDUCATION VI Objectives of the training Understand the definition of project and

INTOSAI Performance Audit Subcommittee

INTOSAI Performance Audit Subcommittee Selecting performance audit topics 1. Introduction This paper aims to assist Supreme Audit Institutions (SAIs) in selecting audit topics. As SAIs operate differently,

INTOSAI Performance Audit Subcommittee Selecting performance audit topics 1. Introduction This paper aims to assist Supreme Audit Institutions (SAIs) in selecting audit topics. As SAIs operate differently,

INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS GUIDELINE. Nepal Rastra Bank Bank Supervision Department. August 2012 (updated July 2013)

") INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS GUIDELINE Nepal Rastra Bank Bank Supervision Department August 2012 (updated July 2013) Table of Contents Page No. 1. Introduction 1 2. Internal Capital Adequacy

INTERNAL CAPITAL ADEQUACY ASSESSMENT PROCESS GUIDELINE Nepal Rastra Bank Bank Supervision Department August 2012 (updated July 2013) Table of Contents Page No. 1. Introduction 1 2. Internal Capital Adequacy

Allocation / Assessment

Strategic Resource Allocation / Assessment CSU Fullerton Larry Goldstein President, Campus Strategies September 23, 2008 Campus Strategies 1 Agenda Resource allocation through budgeting Various budgeting

Strategic Resource Allocation / Assessment CSU Fullerton Larry Goldstein President, Campus Strategies September 23, 2008 Campus Strategies 1 Agenda Resource allocation through budgeting Various budgeting

DESK REVIEW UNDP AFGHANISTAN OVERSIGHT OF THE MONITORING AGENT OF THE LAW AND ORDER TRUST FUND FOR AFGHANISTAN

UNITED NATIONS DEVELOPMENT PROGRAMME DESK REVIEW OF UNDP AFGHANISTAN OVERSIGHT OF THE MONITORING AGENT OF THE LAW AND ORDER TRUST FUND FOR AFGHANISTAN Report No. 1310 Issue Date: 9 October 2014 Table of

UNITED NATIONS DEVELOPMENT PROGRAMME DESK REVIEW OF UNDP AFGHANISTAN OVERSIGHT OF THE MONITORING AGENT OF THE LAW AND ORDER TRUST FUND FOR AFGHANISTAN Report No. 1310 Issue Date: 9 October 2014 Table of

Overview of ERM Assessment Viewpoints (June 2016) Overview

Overview") ERM assessment main category Culture & Governance Control & Capital Adequacy Profile & Measurement Application to Business Management Overview of ERM Assessment Viewpoints (June 2016) Overview Examine

ERM assessment main category Culture & Governance Control & Capital Adequacy Profile & Measurement Application to Business Management Overview of ERM Assessment Viewpoints (June 2016) Overview Examine

MANAGERIAL ACCOUNTABILITY AND RISK MANAGEMENT

MANAGERIAL ACCOUNTABILITY AND RISK MANAGEMENT concept and practical implementation Discussion paper I Introduction The objective of this discussion paper is to explain the concept of managerial accountability

MANAGERIAL ACCOUNTABILITY AND RISK MANAGEMENT concept and practical implementation Discussion paper I Introduction The objective of this discussion paper is to explain the concept of managerial accountability

Public Financial Management

UNITAR Mustofi Fellowship Hiroshima, Japan 18 22 February 2012! Index! Overview and Objectives! Limitations and Problems! Public Financial Systems! Financial Management System Boundaries! Framework! Government

UNITAR Mustofi Fellowship Hiroshima, Japan 18 22 February 2012! Index! Overview and Objectives! Limitations and Problems! Public Financial Systems! Financial Management System Boundaries! Framework! Government

Institutional Consulting Services Presentation

Institutional Consulting Services Presentation Investment Management Services Presented by: FA, Title ADDRESS CITY, STATE ZIP PHONE Table Of Contents Section 1 Introduction/Facts About Prudential Section

Institutional Consulting Services Presentation Investment Management Services Presented by: FA, Title ADDRESS CITY, STATE ZIP PHONE Table Of Contents Section 1 Introduction/Facts About Prudential Section

School Development Plan

SCHOOL FINANCIAL PROCEDURES MANUAL Chapter 12 School Development Plan September 2007 Chapter 12 School Development Plan Page 3 SCHOOL DEVELOPMENT PLAN 3 GENERAL 3 GUIDANCE 5 WHAT IS IN A SCHOOL DEVELOPMENT

SCHOOL FINANCIAL PROCEDURES MANUAL Chapter 12 School Development Plan September 2007 Chapter 12 School Development Plan Page 3 SCHOOL DEVELOPMENT PLAN 3 GENERAL 3 GUIDANCE 5 WHAT IS IN A SCHOOL DEVELOPMENT

TRAINING KIT MODULE 3. Introduction to Results-Based Budgeting

TRAINING KIT MODULE 3 Introduction to Results-Based Budgeting Summary Clarification of key RBB concepts RBB Context and Rationale Budgetary processes focused on development results Conclusion RBB and RBM:

TRAINING KIT MODULE 3 Introduction to Results-Based Budgeting Summary Clarification of key RBB concepts RBB Context and Rationale Budgetary processes focused on development results Conclusion RBB and RBM:

Conceptual Framework for General Purpose Financial Reporting by Public Sector Entities - IPSAS. Vladimír Zelenka

Conceptual Framework for General Purpose Financial Reporting by Public Sector Entities - IPSAS Vladimír Zelenka From PSC Studies to Conceptual Framework Conceptual issues of Public Sector Committee and

Conceptual Framework for General Purpose Financial Reporting by Public Sector Entities - IPSAS Vladimír Zelenka From PSC Studies to Conceptual Framework Conceptual issues of Public Sector Committee and

EPWP INCENTIVE GRANT MANUAL

EPWP Incentive Grant Manual 2009/10 EPWP INCENTIVE GRANT MANUAL FROM THE NATIONAL DEPARTMENT OF PUBLIC WORKS FOR THE IMPLEMENTATION OF THE EPWP INCENTIVE GRANT BY IMPLEMENTING PUBLIC BODIES Version 1 May

EPWP Incentive Grant Manual 2009/10 EPWP INCENTIVE GRANT MANUAL FROM THE NATIONAL DEPARTMENT OF PUBLIC WORKS FOR THE IMPLEMENTATION OF THE EPWP INCENTIVE GRANT BY IMPLEMENTING PUBLIC BODIES Version 1 May

OPPORTUNITIES FOR REFORM IN KENYA Progress and Challenges

OPPORTUNITIES FOR REFORM IN KENYA Progress and Challenges BY SAMUEL KIIRU NATIONAL TREASURY REPUBLIC OF KENYA Introduction The Constitution of Kenya 2010 provides a clear set of principles that spell out

OPPORTUNITIES FOR REFORM IN KENYA Progress and Challenges BY SAMUEL KIIRU NATIONAL TREASURY REPUBLIC OF KENYA Introduction The Constitution of Kenya 2010 provides a clear set of principles that spell out

FAQ: Estimating, Budgeting, and Controlling

Question 1: Why do project managers need to create a budget? Answer 1: The budget is designed to tell how much the total project should cost and when these costs will occur. This information is beneficial

Question 1: Why do project managers need to create a budget? Answer 1: The budget is designed to tell how much the total project should cost and when these costs will occur. This information is beneficial

Cross Border Co-operation between Bulgaria & Romania Multi-annual Programme Project Fiche for Programme Support

Cross Border Co-operation between Bulgaria & Romania Multi-annual Programme 2003 2006 2005 Project Fiche for Programme Support 1. Basic Information 1.1 CRIS Number: BG 2005/017-455.01;04 1.2 1.2 Title:

Cross Border Co-operation between Bulgaria & Romania Multi-annual Programme 2003 2006 2005 Project Fiche for Programme Support 1. Basic Information 1.1 CRIS Number: BG 2005/017-455.01;04 1.2 1.2 Title:

COMMISSION OF THE EUROPEAN COMMUNITIES. CORRIGENDUM : Ce document annule et remplace le COM(2008)334 final du Concerne la version EN.

334 final du Concerne la version EN.") EN EN EN COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 22.01.2009 COM(2008)334 final/2 CORRIGENDUM : Ce document annule et remplace le COM(2008)334 final du 3.6.2008. Concerne la version EN. COMMUNICATION

EN EN EN COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 22.01.2009 COM(2008)334 final/2 CORRIGENDUM : Ce document annule et remplace le COM(2008)334 final du 3.6.2008. Concerne la version EN. COMMUNICATION

Operating Budget Policies. Financial Reserve Policies (a.k.a. Fund Balance Policies) City of Sebastian, Florida Financial Policies.

City of Sebastian, Florida Financial Policies.") Operating Budget Policies Accounting Basis The General, Special Revenue, and Debt Service Funds shall be prepared on a modified accrual basis of accounting. Under the modified accrual basis of accounting,

Operating Budget Policies Accounting Basis The General, Special Revenue, and Debt Service Funds shall be prepared on a modified accrual basis of accounting. Under the modified accrual basis of accounting,

REPORT BY THE COMPTROLLER AND AUDITOR GENERAL HC 1698 SESSION MAY HM Treasury and Cabinet Office. Assurance for major projects

REPORT BY THE COMPTROLLER AND AUDITOR GENERAL HC 1698 SESSION 2010 2012 2 MAY 2012 HM Treasury and Cabinet Office Assurance for major projects 4 Key facts Assurance for major projects Key facts 205 projects

REPORT BY THE COMPTROLLER AND AUDITOR GENERAL HC 1698 SESSION 2010 2012 2 MAY 2012 HM Treasury and Cabinet Office Assurance for major projects 4 Key facts Assurance for major projects Key facts 205 projects

OSC Staff Notice Office of the Chief Accountant. Financial Reporting Bulletin

OSC Staff Notice 52-723 Office of the Chief Accountant Financial Reporting Bulletin November 2016 Table of Contents Introduction... 2 Executive Summary... 2 Disclosure Effectiveness... 4 Going Concern...

OSC Staff Notice 52-723 Office of the Chief Accountant Financial Reporting Bulletin November 2016 Table of Contents Introduction... 2 Executive Summary... 2 Disclosure Effectiveness... 4 Going Concern...

Final Audit Report. Audit of Financial Forecasting and Year-End Expenditures

Health Canada Santé Canada Final Audit Report Audit of Financial Forecasting and Year-End Expenditures September 2009 Table of Contents Executive Summary... ii Introduction... 1 Background... 1 Objectives...

Health Canada Santé Canada Final Audit Report Audit of Financial Forecasting and Year-End Expenditures September 2009 Table of Contents Executive Summary... ii Introduction... 1 Background... 1 Objectives...

The George Washington University Regulatory Studies Center

Public Interest Comment 1 on The Securities and Exchange Commission s Proposed Rule: Recordkeeping and Reporting Requirements for Security-Based Swap Dealers, Major Security-Based Swap Participants, and

Public Interest Comment 1 on The Securities and Exchange Commission s Proposed Rule: Recordkeeping and Reporting Requirements for Security-Based Swap Dealers, Major Security-Based Swap Participants, and

SPECIFIC TERMS OF REFERENCE. EU contribution to 2012 Federal PEFA assessment in Pakistan

SPECIFIC TERMS OF REFERENCE EU contribution to 2012 Federal PEFA assessment in Pakistan FWC BENEFICIARIES 2009 - LOT 11: Macro economy, Statistics and Public finance management DCI-ASIE/2011/277245/1 1

SPECIFIC TERMS OF REFERENCE EU contribution to 2012 Federal PEFA assessment in Pakistan FWC BENEFICIARIES 2009 - LOT 11: Macro economy, Statistics and Public finance management DCI-ASIE/2011/277245/1 1

Terms of Reference for the Mid-term Evaluation of the Implementation of UN-Habitat s Strategic Plan,

Terms of Reference for the Mid-term Evaluation of the Implementation of UN-Habitat s Strategic Plan, 2014-2019 I. Introduction and Mandate 1. The Governing Council (GC) of the United Nations Human Settlement

Terms of Reference for the Mid-term Evaluation of the Implementation of UN-Habitat s Strategic Plan, 2014-2019 I. Introduction and Mandate 1. The Governing Council (GC) of the United Nations Human Settlement

Performance Budgeting in Australia

ISSN 1608-7143 OECD Journal on Budgeting Volume 7 No. 3 OECD 2007 Chapter 1 Performance Budgeting in Australia by Lewis Hawke* This article describes how the principles of management for results have worked

ISSN 1608-7143 OECD Journal on Budgeting Volume 7 No. 3 OECD 2007 Chapter 1 Performance Budgeting in Australia by Lewis Hawke* This article describes how the principles of management for results have worked

Unit Standard : Apply the principles of budgeting within a municipality. Karel van der Molen

Unit Standard 116345: Apply the principles of budgeting within a municipality Karel van der Molen Group The full programme 1. Strategic Management; Budgeting Implementation & Performance Management 2.

Unit Standard 116345: Apply the principles of budgeting within a municipality Karel van der Molen Group The full programme 1. Strategic Management; Budgeting Implementation & Performance Management 2.

FINANCIAL PLANNING AND BUDGETING - CENTRAL GOVERNMENT AND DEPARTMENTS

42 FINANCIAL PLANNING AND BUDGETING - CENTRAL GOVERNMENT AND DEPARTMENTS. FINANCIAL PLANNING AND BUDGETING - CENTRAL GOVERNMENT AND DEPARTMENTS BACKGROUND.1 This Chapter describes the results of our government-wide

42 FINANCIAL PLANNING AND BUDGETING - CENTRAL GOVERNMENT AND DEPARTMENTS. FINANCIAL PLANNING AND BUDGETING - CENTRAL GOVERNMENT AND DEPARTMENTS BACKGROUND.1 This Chapter describes the results of our government-wide

Module 4. College of Development Communication

Module 4 Follows a systematic process that involves: Determining the needs and problems, Planning Implementing Evaluating It entails ensuring that the resources needed for all project activities are available

Module 4 Follows a systematic process that involves: Determining the needs and problems, Planning Implementing Evaluating It entails ensuring that the resources needed for all project activities are available

B.29[17d] Medium-term planning in government departments: Four-year plans

![B.29[17d] Medium-term planning in government departments: Four-year plans](/thumbs/77/76271875.jpg "B.29[17d] Medium-term planning in government departments: Four-year plans") B.29[17d] Medium-term planning in government departments: Four-year plans Photo acknowledgement: mychillybin.co.nz Phil Armitage B.29[17d] Medium-term planning in government departments: Four-year plans

B.29[17d] Medium-term planning in government departments: Four-year plans Photo acknowledgement: mychillybin.co.nz Phil Armitage B.29[17d] Medium-term planning in government departments: Four-year plans

REPORT 2015/115 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/115 Audit of the statistics subprogramme and related technical cooperation projects in the Economic Commission for Africa Overall results relating to effective management

INTERNAL AUDIT DIVISION REPORT 2015/115 Audit of the statistics subprogramme and related technical cooperation projects in the Economic Commission for Africa Overall results relating to effective management

MODUL E 5: PERFORMANCE BUDGE T ING

I NTR ODUCT ION MODUL E 5: PERFORMANCE BUDGE T ING 1. This paper provides an overview of how a performance orientation can be applied to the public financial management system through performance budgeting.

I NTR ODUCT ION MODUL E 5: PERFORMANCE BUDGE T ING 1. This paper provides an overview of how a performance orientation can be applied to the public financial management system through performance budgeting.

PROJECT PROPOSAL WRITING (A Tool for Resource Mobilization and Effective Attainment of Organization Objectives) OJI OGBUREKE, PhD November 2011

OJI OGBUREKE, PhD November 2011") PROJECT PROPOSAL WRITING (A Tool for Resource Mobilization and Effective Attainment of Organization Objectives) OJI OGBUREKE, PhD November 2011 OBJECTIVES OF THE PRESENTATION By the end of the presentation,

PROJECT PROPOSAL WRITING (A Tool for Resource Mobilization and Effective Attainment of Organization Objectives) OJI OGBUREKE, PhD November 2011 OBJECTIVES OF THE PRESENTATION By the end of the presentation,

NYISO Capital Budgeting Process. Draft 01/13/03

NYISO Capital Budgeting Process Draft 01/13/03 1 1.0 INTRODUCTION An effective, capital budgeting process is essential to ensure sound capital investment decisions. This report details a recommended approach

NYISO Capital Budgeting Process Draft 01/13/03 1 1.0 INTRODUCTION An effective, capital budgeting process is essential to ensure sound capital investment decisions. This report details a recommended approach

Transfer Payment Agency Accountability and Governance

MINISTRY OF COMMUNITY AND SOCIAL SERVICES Transfer Payment Agency Accountability and Governance The Ministry of Community and Social Services plans and arranges for a wide variety of social services throughout

MINISTRY OF COMMUNITY AND SOCIAL SERVICES Transfer Payment Agency Accountability and Governance The Ministry of Community and Social Services plans and arranges for a wide variety of social services throughout

June 10 th, 2015 / Ankara, Turkey

L O G I C A L F R A M E W O R K A P P R O A C H June 10 th, 2015 / Ankara, Turkey ANALYSIS PHASE 1. Problem Analysis 2. Stakeholder Analysis 3. Objective Analysis 4. Strategy Analysis PLANNING PHASE 1.

L O G I C A L F R A M E W O R K A P P R O A C H June 10 th, 2015 / Ankara, Turkey ANALYSIS PHASE 1. Problem Analysis 2. Stakeholder Analysis 3. Objective Analysis 4. Strategy Analysis PLANNING PHASE 1.

Paying providers to increase Value for Money: Is Pay for Performance the Answer? Review of OECD experience

Paying providers to increase Value for Money: Is Pay for Performance the Answer? Review of OECD experience Michael Borowitz OECD Health Division SBO Network on Health Expenditures 1 Productivity Challenge:

Paying providers to increase Value for Money: Is Pay for Performance the Answer? Review of OECD experience Michael Borowitz OECD Health Division SBO Network on Health Expenditures 1 Productivity Challenge:

BUDGETING FOR HEALTH: WHAT? WHY? HOW?

Community of Practice Health Systems Governance Platform Webinar, June 8 th 2017 BUDGETING FOR HEALTH: WHAT? WHY? HOW? Helene Barroy Sr Health Financing Specialist Department for Health Systems Governance

Community of Practice Health Systems Governance Platform Webinar, June 8 th 2017 BUDGETING FOR HEALTH: WHAT? WHY? HOW? Helene Barroy Sr Health Financing Specialist Department for Health Systems Governance

Joint Venture on Managing for Development Results

Joint Venture on Managing for Development Results Managing for Development Results - Draft Policy Brief - I. Introduction Managing for Development Results (MfDR) Draft Policy Brief 1 Managing for Development

Joint Venture on Managing for Development Results Managing for Development Results - Draft Policy Brief - I. Introduction Managing for Development Results (MfDR) Draft Policy Brief 1 Managing for Development

Risk Assessment Mitigation Phase Risk Mitigation Plan Lessons Learned (RAMP B) November 30, 2016

November 30, 2016") Risk Assessment Mitigation Phase Risk Mitigation Plan Lessons Learned (RAMP B) November 30, 2016 #310403 Risk Management Framework Consistent with the historic commitment of Southern California Gas Company

Risk Assessment Mitigation Phase Risk Mitigation Plan Lessons Learned (RAMP B) November 30, 2016 #310403 Risk Management Framework Consistent with the historic commitment of Southern California Gas Company

Public Financial Management and Pro-Poor Service Delivery

Public Financial Management and Pro-Poor Service Delivery National Budget and Poverty Reduction Workshop December 8, 2005 Rob Taliercio, Senior Country Economist World Bank Cambodia Country Office Policy

Public Financial Management and Pro-Poor Service Delivery National Budget and Poverty Reduction Workshop December 8, 2005 Rob Taliercio, Senior Country Economist World Bank Cambodia Country Office Policy

Introduction. The Assessment consists of: A checklist of best, good and leading practices A rating system to rank your company s current practices.

ESG / CSR / Sustainability Governance and Management Assessment By Coro Strandberg President, Strandberg Consulting www.corostrandberg.com September 2017 Introduction This ESG / CSR / Sustainability Governance

ESG / CSR / Sustainability Governance and Management Assessment By Coro Strandberg President, Strandberg Consulting www.corostrandberg.com September 2017 Introduction This ESG / CSR / Sustainability Governance

Child Budget in Bangladesh Report

Child Budget in Bangladesh Report Summary of the Child Budget in Bangladesh Report, June 2014 Introduction The report initiated by the Centre for Services and Information on Disability, and supported by

Child Budget in Bangladesh Report Summary of the Child Budget in Bangladesh Report, June 2014 Introduction The report initiated by the Centre for Services and Information on Disability, and supported by

Booklet C.2: Estimating future financial resource needs

Booklet C.2: Estimating future financial resource needs This booklet describes how managers can use cost information to estimate future financial resource needs. Often health sector budgets are based on

Booklet C.2: Estimating future financial resource needs This booklet describes how managers can use cost information to estimate future financial resource needs. Often health sector budgets are based on

Council of the European Union Brussels, 29 November 2016 (OR. en)

") Conseil UE Council of the European Union Brussels, 29 November 2016 (OR. en) PUBLIC 14814/16 LIMITE ECOFIN 1107 UEM 399 COVER NOTE From: To: Subject: General Secretariat of the Council Permanent Representatives

Conseil UE Council of the European Union Brussels, 29 November 2016 (OR. en) PUBLIC 14814/16 LIMITE ECOFIN 1107 UEM 399 COVER NOTE From: To: Subject: General Secretariat of the Council Permanent Representatives

Executive summary 20 September 2010

Study on the feasibility of alternative methods for improving and simplifying the collection of VAT through the means of modern technologies and/or financial intermediaries Executive summary 20 September

Study on the feasibility of alternative methods for improving and simplifying the collection of VAT through the means of modern technologies and/or financial intermediaries Executive summary 20 September

PROGRAM-FOR-RESULTS FINANCING INTERIM GUIDANCE NOTE TO STAFF: FIDUCIARY SYSTEMS ASSESSMENT. Operations Policy and Country Services

PROGRAM-FOR-RESULTS FINANCING INTERIM GUIDANCE NOTE TO STAFF: FIDUCIARY SYSTEMS ASSESSMENT These interim guidance notes are intended for internal use by Bank staff to provide a framework to conduct assessments

PROGRAM-FOR-RESULTS FINANCING INTERIM GUIDANCE NOTE TO STAFF: FIDUCIARY SYSTEMS ASSESSMENT These interim guidance notes are intended for internal use by Bank staff to provide a framework to conduct assessments

1. Introduction 1.1. BACKGROUND

INTRODUCTION 1. Introduction 1.1. BACKGROUND The G20 has had a long-standing commitment to promoting sustainable infrastructure development as a key mechanism for supporting economic growth, in both developed

INTRODUCTION 1. Introduction 1.1. BACKGROUND The G20 has had a long-standing commitment to promoting sustainable infrastructure development as a key mechanism for supporting economic growth, in both developed

INTERNATIONAL MONETARY FUND ECUADOR. Report on Observance of Standards and Codes (ROSC) Response of the Authorities.

Response of the Authorities.") INTERNATIONAL MONETARY FUND ECUADOR Report on Observance of Standards and Codes (ROSC) Response of the Authorities January --, 2003 I. Introduction...2 II. Comments (by section of the ROSC)...2 Executive

INTERNATIONAL MONETARY FUND ECUADOR Report on Observance of Standards and Codes (ROSC) Response of the Authorities January --, 2003 I. Introduction...2 II. Comments (by section of the ROSC)...2 Executive

REPORT 2015/174 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION REPORT 2015/174 Audit of management of selected subprogrammes and related capacity development projects in the United Nations Economic and Social Commission for Asia and the Pacific

INTERNAL AUDIT DIVISION REPORT 2015/174 Audit of management of selected subprogrammes and related capacity development projects in the United Nations Economic and Social Commission for Asia and the Pacific

Performance Based Budgeting in OECD Countries

Performance Based Budgeting in OECD Countries International Conference on Performance Budgeting Lessons for Poland Warsaw 7-9 November Teresa Curristine, Budgeting and Public Expenditures Division, Public

Performance Based Budgeting in OECD Countries International Conference on Performance Budgeting Lessons for Poland Warsaw 7-9 November Teresa Curristine, Budgeting and Public Expenditures Division, Public

Large Bank Supervision

EP-CBS O Comptroller of the Currency Administrator of National Banks Large Bank Supervision Comptroller s Handbook January 2010 EP Bank Supervision and Examination Process Large Bank Supervision Table

EP-CBS O Comptroller of the Currency Administrator of National Banks Large Bank Supervision Comptroller s Handbook January 2010 EP Bank Supervision and Examination Process Large Bank Supervision Table

Interest Rates and Monetary Policy

14 Interest Rates and Monetary Policy 14-1 Chapter Objectives How the equilibrium interest rate is determined in the market for money. The goals and tools of monetary policy. The federal funds rate and

14 Interest Rates and Monetary Policy 14-1 Chapter Objectives How the equilibrium interest rate is determined in the market for money. The goals and tools of monetary policy. The federal funds rate and

ContractCoach, LLC. A Jeff Hastings Agency, Inc. Company A-Coach

ContractCoach, LLC. www.contractcoach.com A Jeff Hastings Agency, Inc. Company 281-752-6565 844-4A-Coach 2 Budget Design Leads the Agency Toward the Vision Like anything else, you have to have a plan for

ContractCoach, LLC. www.contractcoach.com A Jeff Hastings Agency, Inc. Company 281-752-6565 844-4A-Coach 2 Budget Design Leads the Agency Toward the Vision Like anything else, you have to have a plan for

FINAL TEXT OF THE THREE REVISED INDICATORS FOR THE PERFORMANCE MEASUREMENT FRAMEWORK

FINAL TEXT OF THE THREE REVISED INDICATORS FOR THE PERFORMANCE MEASUREMENT FRAMEWORK PI-2 Composition of expenditure out-turn compared to original approved budget Where the composition of expenditure varies

FINAL TEXT OF THE THREE REVISED INDICATORS FOR THE PERFORMANCE MEASUREMENT FRAMEWORK PI-2 Composition of expenditure out-turn compared to original approved budget Where the composition of expenditure varies

Conceptual Framework (Revised) Issued June Conceptual Framework for Financial Reporting 2018

Issued June Conceptual Framework for Financial Reporting 2018") Conceptual Framework (Revised) Issued June 2018 Conceptual Framework for Financial Reporting 2018 COPYRIGHT Copyright 2018 Hong Kong Institute of Certified Public Accountants This Framework contains the

Conceptual Framework (Revised) Issued June 2018 Conceptual Framework for Financial Reporting 2018 COPYRIGHT Copyright 2018 Hong Kong Institute of Certified Public Accountants This Framework contains the

Performance Budgeting for Federal Agencies. A Framework. JOHN MERCER (link to John Mercer's Website) IN PARTNERSHIP WITH AMS MARCH 18, 2002

IN PARTNERSHIP WITH AMS MARCH 18, 2002") Performance Budgeting for Federal Agencies A Framework JOHN MERCER (link to John Mercer's Website) IN PARTNERSHIP WITH AMS MARCH 18, 2002 For additional information please contact us at: John Mercer: GPRA@john-mercer.com

Performance Budgeting for Federal Agencies A Framework JOHN MERCER (link to John Mercer's Website) IN PARTNERSHIP WITH AMS MARCH 18, 2002 For additional information please contact us at: John Mercer: GPRA@john-mercer.com

Performance Management in Whitehall. DSO Review Guidance

Performance Management in Whitehall DSO Review Guidance April 2008 Table of Contents 1 Introduction... 1 1.1 Aims of Guidance... 1 1.2 Departmental Strategic Objectives and Performance Management... 1

Performance Management in Whitehall DSO Review Guidance April 2008 Table of Contents 1 Introduction... 1 1.1 Aims of Guidance... 1 1.2 Departmental Strategic Objectives and Performance Management... 1

Business Auditing - Enterprise Risk Management. October, 2018

Business Auditing - Enterprise Risk Management October, 2018 Contents The present document is aimed to: 1 Give an overview of the Risk Management framework 2 Illustrate an ERM model Page 2 What is a risk?

Business Auditing - Enterprise Risk Management October, 2018 Contents The present document is aimed to: 1 Give an overview of the Risk Management framework 2 Illustrate an ERM model Page 2 What is a risk?

IFRS Conceptual Framework Conceptual Framework for Financial Reporting

March 2018 IFRS Conceptual Framework Conceptual Framework for Financial Reporting Conceptual Framework for Financial Reporting Conceptual Framework for Financial Reporting is issued by the International

March 2018 IFRS Conceptual Framework Conceptual Framework for Financial Reporting Conceptual Framework for Financial Reporting Conceptual Framework for Financial Reporting is issued by the International

Executive Board Annual Session Rome, May 2015 POLICY ISSUES ENTERPRISE RISK For approval MANAGEMENT POLICY WFP/EB.A/2015/5-B

Executive Board Annual Session Rome, 25 28 May 2015 POLICY ISSUES Agenda item 5 For approval ENTERPRISE RISK MANAGEMENT POLICY E Distribution: GENERAL WFP/EB.A/2015/5-B 10 April 2015 ORIGINAL: ENGLISH

Executive Board Annual Session Rome, 25 28 May 2015 POLICY ISSUES Agenda item 5 For approval ENTERPRISE RISK MANAGEMENT POLICY E Distribution: GENERAL WFP/EB.A/2015/5-B 10 April 2015 ORIGINAL: ENGLISH

T H E NA I RO B I C A L L TO A C T I O N F O R C L O S I N G T H E I M P L E M E N TA T I O N G A P I N H E A LT H P RO M O T I O N

T H E NA I RO B I C A L L TO A C T I O N F O R C L O S I N G T H E I M P L E M E N TA T I O N G A P I N H E A LT H P RO M O T I O N 1. INTRODUCTION PURPOSE The Nairobi Call to Action identifies key strategies

T H E NA I RO B I C A L L TO A C T I O N F O R C L O S I N G T H E I M P L E M E N TA T I O N G A P I N H E A LT H P RO M O T I O N 1. INTRODUCTION PURPOSE The Nairobi Call to Action identifies key strategies

Definition of Standard Costing

Standard Costing Cost control leads to cost reduction which is the objective of every firm that is in business. The essence of standard costing is to Set target of costs Try to achieve these targets Compare

Standard Costing Cost control leads to cost reduction which is the objective of every firm that is in business. The essence of standard costing is to Set target of costs Try to achieve these targets Compare

Quality Control & Compliance Initiative. This document is publicly available to any staff member on the following network path:

Quality Control & Compliance Initiative RISK ASSESSMENT Author: Phonovation Quality Control Group Gavin Carpenter Effective Date: 20 th Nov 2013 Revised: 20 th Jan 2015 Revised by: To: Pedro Quintas All

Quality Control & Compliance Initiative RISK ASSESSMENT Author: Phonovation Quality Control Group Gavin Carpenter Effective Date: 20 th Nov 2013 Revised: 20 th Jan 2015 Revised by: To: Pedro Quintas All

THE ROLE OF PUBLIC DEBT MANAGERS IN CONTINGENT LIABILITY MANAGEMENT

Session 5: The five steps of contingent liability management THE ROLE OF PUBLIC DEBT MANAGERS IN CONTINGENT LIABILITY MANAGEMENT Lerzan ÜLGENTÜRK lerzan.ulgenturk@hazine.gov.tr Turkish Treasury Pretoria,

Session 5: The five steps of contingent liability management THE ROLE OF PUBLIC DEBT MANAGERS IN CONTINGENT LIABILITY MANAGEMENT Lerzan ÜLGENTÜRK lerzan.ulgenturk@hazine.gov.tr Turkish Treasury Pretoria,

AT KAARVAN CRAFTS FOUNDATION INSTITUTES - BAHAWALPUR & GUJRANWALA

IMPACT EVALUATION STUDY PSDF s Funded Skills For Employability 16, (April 16 - June 16) AT KAARVAN CRAFTS FOUNDATION INSTITUTES - BAHAWALPUR & GUJRANWALA INTRODUCTION The Monitoring, Evaluation and Research

IMPACT EVALUATION STUDY PSDF s Funded Skills For Employability 16, (April 16 - June 16) AT KAARVAN CRAFTS FOUNDATION INSTITUTES - BAHAWALPUR & GUJRANWALA INTRODUCTION The Monitoring, Evaluation and Research

WHO reform: programmes and priority setting

WHO REFORM: MEETING OF MEMBER STATES ON PROGRAMMES AND PRIORITY SETTING Document 1 27 28 February 2012 20 February 2012 WHO reform: programmes and priority setting Programmes and priority setting in WHO

WHO REFORM: MEETING OF MEMBER STATES ON PROGRAMMES AND PRIORITY SETTING Document 1 27 28 February 2012 20 February 2012 WHO reform: programmes and priority setting Programmes and priority setting in WHO

An overview of the South African macroeconomic. environment

An overview of the South African macroeconomic environment 1 Study instruction Study Study guide: study unit 1 Study unit outcomes Once you have worked through this study unit, you should be able to give

An overview of the South African macroeconomic environment 1 Study instruction Study Study guide: study unit 1 Study unit outcomes Once you have worked through this study unit, you should be able to give

Managing the costs of clinical negligence in trusts

Report by the Comptroller and Auditor General Department of Health Managing the costs of clinical negligence in trusts HC 305 SESSION 2017 2019 7 SEPTEMBER 2017 Managing the costs of clinical negligence

Report by the Comptroller and Auditor General Department of Health Managing the costs of clinical negligence in trusts HC 305 SESSION 2017 2019 7 SEPTEMBER 2017 Managing the costs of clinical negligence

Performance Measurement of Supreme Audit Institutions in 4 Anglo-Saxon Countries: Leading by Example

Performance Measurement of Supreme Audit Institutions in 4 Anglo-Saxon Countries: Leading by Example Nobuo AZUMA* Director, Study Division, Board of Audit I. Introduction In Japan, performance measurement

Performance Measurement of Supreme Audit Institutions in 4 Anglo-Saxon Countries: Leading by Example Nobuo AZUMA* Director, Study Division, Board of Audit I. Introduction In Japan, performance measurement

SUMMARY PROGRAM IMPACT ASSESSMENT. I. Introduction

Local Government Finance and Fiscal Decentralization Reform Program, SP1 (RRP PHI 44253) SUMMARY PROGRAM IMPACT ASSESSMENT I. Introduction 1. This program s impact assessment (PIA) supports the Local Government

Local Government Finance and Fiscal Decentralization Reform Program, SP1 (RRP PHI 44253) SUMMARY PROGRAM IMPACT ASSESSMENT I. Introduction 1. This program s impact assessment (PIA) supports the Local Government

Managing Project Risk DHY

Managing Project Risk DHY01 0407 Copyright ESI International April 2007 All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or

Managing Project Risk DHY01 0407 Copyright ESI International April 2007 All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or

READING 5.1 SHARPENING A BUDGET ADVOCACY OBJECTIVE

READING 5.1 SHARPENING A BUDGET ADVOCACY OBJECTIVE The five elements of an advocacy strategy are as follows: 1. Strategic Analysis 2. Advocacy Objective 3. Stakeholder Analysis 4. Advocacy Message (Development

READING 5.1 SHARPENING A BUDGET ADVOCACY OBJECTIVE The five elements of an advocacy strategy are as follows: 1. Strategic Analysis 2. Advocacy Objective 3. Stakeholder Analysis 4. Advocacy Message (Development

Scientific Council Forty-sixth Session 07/12/2009. KEY PERFORMANCE INDICATORS (KPIs) FOR THE AGENCY

FOR THE AGENCY") Forty-sixth Session 07/12/2009 Lyon, 27 29 January 2010 Princess Takamatsu Hall KEY PERFORMANCE INDICATORS (KPIs) FOR THE AGENCY What are Key Performance Indicators (KPIs)? 1. KPIs represent a set of measures

Forty-sixth Session 07/12/2009 Lyon, 27 29 January 2010 Princess Takamatsu Hall KEY PERFORMANCE INDICATORS (KPIs) FOR THE AGENCY What are Key Performance Indicators (KPIs)? 1. KPIs represent a set of measures

CAPACITY DEVELOPMENT WORKSHOP AIDE MEMOIRE AUDITING FOR SOCIAL CHANGE

6 th Global Forum on Reinventing Government Towards Participatory and Transparent Governance 24 27 May 2005, Seoul, Republic of Korea CAPACITY DEVELOPMENT WORKSHOP AIDE MEMOIRE AUDITING FOR SOCIAL CHANGE

6 th Global Forum on Reinventing Government Towards Participatory and Transparent Governance 24 27 May 2005, Seoul, Republic of Korea CAPACITY DEVELOPMENT WORKSHOP AIDE MEMOIRE AUDITING FOR SOCIAL CHANGE

Endorsement of the Amendments to IAS 19 Employee benefits. Introduction, background and conclusions

EUROPEAN COMMISSION Internal Market and Services DG FREE MOVEMENT OF CAPITAL, COMPANY LAW AND CORPORATE GOVERNANCE Accounting Brussels, December 2011 MARKT F3 (2011) Endorsement of the Amendments to IAS

EUROPEAN COMMISSION Internal Market and Services DG FREE MOVEMENT OF CAPITAL, COMPANY LAW AND CORPORATE GOVERNANCE Accounting Brussels, December 2011 MARKT F3 (2011) Endorsement of the Amendments to IAS

Basic Introduction to Project Cycle. Management Using the. Logical Framework Approach

Basic Introduction to Project Cycle Management Using the Logical Framework Approach Developed and Presented by: Umhlaba Development Services Umhlaba Development Services Noswal Hall, Braamfontein, Johannesburg,

Basic Introduction to Project Cycle Management Using the Logical Framework Approach Developed and Presented by: Umhlaba Development Services Umhlaba Development Services Noswal Hall, Braamfontein, Johannesburg,

Ministry of Health / Ministry of Finance Toolkit

Ministry of Health / Ministry of Finance Toolkit December 11, 2014 Montreux, Switzerland Abt Associates Inc. In collaboration with: Broad Branch Associates Development Alternatives Inc. (DAI) Futures Institute

Ministry of Health / Ministry of Finance Toolkit December 11, 2014 Montreux, Switzerland Abt Associates Inc. In collaboration with: Broad Branch Associates Development Alternatives Inc. (DAI) Futures Institute

Guidance document on a common methodology for the assessment of management and control systems in the Member States ( programming period)

") EUROPEAN COMMISSION DG Regional Policy DG Employment, Social Affairs and Equal Opportunities Guidance document on a common methodology for the assessment of management and control systems in the Member

EUROPEAN COMMISSION DG Regional Policy DG Employment, Social Affairs and Equal Opportunities Guidance document on a common methodology for the assessment of management and control systems in the Member

Terms of Reference (ToR)

") Terms of Reference (ToR) Mid -Term Evaluations of the Two Programmes: UNDP Support to Deepening Democracy and Accountable Governance in Rwanda (DDAG) and Promoting Access to Justice, Human Rights and Peace

Terms of Reference (ToR) Mid -Term Evaluations of the Two Programmes: UNDP Support to Deepening Democracy and Accountable Governance in Rwanda (DDAG) and Promoting Access to Justice, Human Rights and Peace

Japanese ODA Loan. Ex-ante Evaluation

Japanese ODA Loan Ex-ante Evaluation 1. Name of the Program Country: The Islamic Republic of Pakistan Project: Energy Sector Reform Program Loan Agreement Signed: June 4, 2014 Loan Amount: 5,000 million

Japanese ODA Loan Ex-ante Evaluation 1. Name of the Program Country: The Islamic Republic of Pakistan Project: Energy Sector Reform Program Loan Agreement Signed: June 4, 2014 Loan Amount: 5,000 million

Program Performance Review

Program Performance Review Facilities Maintenance Division of the Public Works and Transportation Department July 21, 2006 Report No. 06-18 Office of the County Auditor Evan A. Lukic, CPA County Auditor

Program Performance Review Facilities Maintenance Division of the Public Works and Transportation Department July 21, 2006 Report No. 06-18 Office of the County Auditor Evan A. Lukic, CPA County Auditor

Performance Audits. Chapter 1 Use and Application of GAGAS. entities, organizations, programs, activities, and functions.

Performance Audits 1.25 Performance audits are defined as engagements that provide assurance or conclusions based on an evaluation of sufficient, appropriate evidence against stated criteria, such as specific

Performance Audits 1.25 Performance audits are defined as engagements that provide assurance or conclusions based on an evaluation of sufficient, appropriate evidence against stated criteria, such as specific

Improving the quality of policymaking and government spending: A review of budgetary and regulatory instruments and the perspective of OECD countries

Improving the quality of policymaking and government spending: A review of budgetary and regulatory instruments and the perspective of OECD countries Luiz De Mello Deputy Director Public Governance & Territorial

Improving the quality of policymaking and government spending: A review of budgetary and regulatory instruments and the perspective of OECD countries Luiz De Mello Deputy Director Public Governance & Territorial

PRINCE2 Sample Papers

PRINCE2 Sample Papers The Official PRINCE2 Accreditor Sample Examination Papers Terms of use Please note that by downloading and/or using this document, you agree to comply with the terms of use outlined

PRINCE2 Sample Papers The Official PRINCE2 Accreditor Sample Examination Papers Terms of use Please note that by downloading and/or using this document, you agree to comply with the terms of use outlined

Improving the efficiency and transparency of the UNFCCC budget process

United Nations FCCC/SBI/2016/INF.14 Distr.: General 27 September 2016 English only Subsidiary Body for Implementation Forty-fifth session Marrakech, 7 14 November 2016 Item 17(c) of the provisional agenda

United Nations FCCC/SBI/2016/INF.14 Distr.: General 27 September 2016 English only Subsidiary Body for Implementation Forty-fifth session Marrakech, 7 14 November 2016 Item 17(c) of the provisional agenda

Japanese ODA Loan. Ex-Ante Evaluation

Japanese ODA Loan Ex-Ante Evaluation 1. Name of the Project Country: The Democratic Socialist Republic of Sri Lanka Project: Development Policy Loan (Private Sector Development, Governance Improvement,

Japanese ODA Loan Ex-Ante Evaluation 1. Name of the Project Country: The Democratic Socialist Republic of Sri Lanka Project: Development Policy Loan (Private Sector Development, Governance Improvement,

IMPROVING BUDGET TRANSPARENCY IN SOUTH AFRICA

IMPROVING BUDGET TRANSPARENCY IN SOUTH AFRICA FISCAL TRANSPARENCY AND ACCOUNTABILITY MEETING - MOSCOW, RUSSIA Presented by: Dr Kay Brown Chief Director, Expenditure Planning 29 May 2014 Presentation outline

IMPROVING BUDGET TRANSPARENCY IN SOUTH AFRICA FISCAL TRANSPARENCY AND ACCOUNTABILITY MEETING - MOSCOW, RUSSIA Presented by: Dr Kay Brown Chief Director, Expenditure Planning 29 May 2014 Presentation outline

Topics 1 PFM Best Practice for DSM Revenues 2. 3 Comprehensiveness & Transparency 4 Policy-based Budgeting 5 External Scrutiny

PFM Issues for DSM Funds R. Hackett- PFM Advisor, PFTAC/IMF 1 Topics 1 PFM Best Practice for DSM Revenues 2 What can we learn from PEFA assessments? 3 Comprehensiveness & Transparency 4 Policy-based Budgeting

PFM Issues for DSM Funds R. Hackett- PFM Advisor, PFTAC/IMF 1 Topics 1 PFM Best Practice for DSM Revenues 2 What can we learn from PEFA assessments? 3 Comprehensiveness & Transparency 4 Policy-based Budgeting

Risk Management Plan for the <Project Name> Prepared by: Title: Address: Phone: Last revised:

for the Prepared by: Title: Address: Phone: E-mail: Last revised: Document Information Project Name: Prepared By: Title: Reviewed By: Document Version No: Document Version Date: Review Date:

for the Prepared by: Title: Address: Phone: E-mail: Last revised: Document Information Project Name: Prepared By: Title: Reviewed By: Document Version No: Document Version Date: Review Date:

The Financial Reporter

Article from: The Financial Reporter December 2004 Issue 59 Rethinking Embedded Value: The Stochastic Modeling Revolution Carol A. Marler and Vincent Y. Tsang Carol A. Marler, FSA, MAAA, currently lives

Article from: The Financial Reporter December 2004 Issue 59 Rethinking Embedded Value: The Stochastic Modeling Revolution Carol A. Marler and Vincent Y. Tsang Carol A. Marler, FSA, MAAA, currently lives

Managing for Results Fiscal Year 2000 Performance Measures

Performance Audit Report Managing for Results Fiscal Year 2000 Performance Measures University System of Maryland University of Maryland, College Park August 2001 This report and any related follow-up

Performance Audit Report Managing for Results Fiscal Year 2000 Performance Measures University System of Maryland University of Maryland, College Park August 2001 This report and any related follow-up

Appendix B: Glossary of Project Management Terms

Appendix B: Glossary of Project Management Terms Assumption - There may be external circumstances or events that must occur for the project to be successful (or that should happen to increase your chances

Appendix B: Glossary of Project Management Terms Assumption - There may be external circumstances or events that must occur for the project to be successful (or that should happen to increase your chances

How To Make Your Financial Plan CPA Strong

How To Make Your Financial Plan CPA Strong 11457B-302_CFF Revised CPA Brochure-PS.indd 1 Why Work With a CPA Financial Planner? Because the person who does your financial planning must also underst the

How To Make Your Financial Plan CPA Strong 11457B-302_CFF Revised CPA Brochure-PS.indd 1 Why Work With a CPA Financial Planner? Because the person who does your financial planning must also underst the