Chapter 1. Accounting for Engineers. Eng. Osama Aljarrah, MBA Hashemite University

|

|

|

- Maria Allison

- 6 years ago

- Views:

Transcription

1 Chapter 1 Accounting for Engineers Eng. Osama Aljarrah, MBA Hashemite University osamaiemba@gmail.com

2 Intended learning outcomes Introduction to accounting Financial Accounting versus Management Accounting Introduction in Financial Accounting Introduction in Management Accounting Cost accounting in manufacturing companies Inventories in manufacturing companies Budgeting Use cost accounting for decision making

3 Objective of accounting To provide information Economic useful for decision maker

4 Introduction to accounting Accounting Financial Accounting Management Accounting

5 Financial Accounting Objectives 1- Economic resources & obligations on these resources (قائمة الميزانية) Balance Sheet (األصول) Economic resources Assets Obligations Liability and owner equity (االلتزامات وحقوق الملكية)

6 Financial Accounting Objectives 2- Earning Generation Power (قائمة الدخل) Income statement (اإليرادات) Revenues (تكلفة البضاعة المباعة) - Cost of Goods Sold (الربح اإلجمالي) Gross Profit (المصاريف األخرى) - Other Expenses (الربح الصافي) Net Profit

7 Financial Accounting Objectives 3- Cash sources and uses Cash flow statement Cash in Cash out

8 Financial Statement Balance Sheet: (At any moment of time) 1- Assets األصول 2- Liabilities االلتزامات 3- Owner Equity حقوق الملكية

9 Balance Sheet 1- Assets: 1-1 Current Assets (Converted to cash before one year) Cash and Cash Equivalent Accounts Receivables Inventory Prepaid Expenses

10 Financial Statement Balance Sheet Assets (continue..) 1-2 Long terms assets (Normally don t convert to cash within one year) Property, plant, and equipment Intangible assets (Goodwill, Trade name)

11 Balance Sheet 2- Liabilities 2-1 Current Liabilities (Paid within one year) Accounts Payable Accrued Payroll Tax Payable Advanced payments Others

12 Balance Sheet Liabilities (Continue ) 2-2 Long terms liabilities (Normally paid after one year) Long terms notes payable Long terms debt

13 Balance Sheet 3- Owner Equity 3-1 Capital 3-2 Reserves 3-3 Common stock 3-4 Retained Earnings

14 Balance Sheet Assets = Liabilities + Owner Equity

15 Financial statement Income statement (Profit and Loss statement) (within specific period) Sales - Cost of Goods Sold Gross Profit - Operating Expenses Operating Income - Non Operating gains and losses Net Income

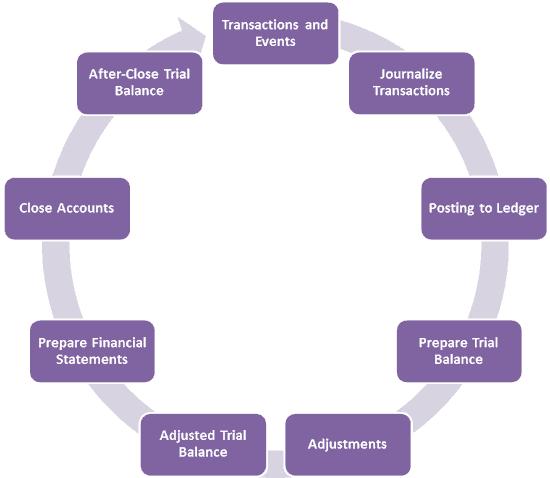

16 Accounting cycle

17 Accounting Cycle Each financial event affects two accounts. Nature of accounts: 1- Assets: Debit 2- Liabilities: Credit 3- Owner Equity: Credit 4- Sales: Credit 5- Cost of goods sold: Debit 6- Expenses: Debit

18 Accounting Cycle Each account increases by it s nature and decreases by the opposite of it s nature. Examples: 1- Increase cash increase assets debit 2- Decrease payables decrease liability debit 3- Increase sales credit 4- Increase expense debit

19

20 Accounting Cycle - Exercise Example 1.1- Open new trading company: You have 5000 JOD and you borrow 5000 JOD. You deposited these in a new bank account: Dr/ Cr/ Cr/

21 Accounting Cycle - Exercise Example 1.2- Purchasing goods for resale: You purchased 10 smart phones for resale by credit for 30 days. Purchase price is 500 JOD/ unit: Dr/ Cr/

22 Accounting Cycle - Exercise Example 1.3- Selling Goods to customers in credit You sold 5 smart phones in credit for 15 days. Selling price 600 JOD / unit: Dr/ Cr/ Dr/ Cr/

23 Accounting Cycle - Exercise Example 1.4- Collect cash from customer You collected from the customer 3000 JOD: Dr/ Cr/

24 Accounting Cycle - Exercise Example 1.5- Vendor Payment You paid to vendor 5000 JOD Dr/ Cr/

25 Accounting Cycle - Exercise Example 1.6- Period Expenses: You paid electrical invoice for 100 JOD by cash: Dr/ Cr/

26 Accounting Cycle - Exercise Example 1.7- Period expenses You paid 500 JOD by cash for office rent: Dr/ Cr/

27 Accounting Cycle - Exercise Example 1.8- Payroll calculation You calculated payroll expense of 500 JOD at the end of the year but not paid at the current year Dr/ Cr/

28 Accounting Cycle Exercise Example 1.9- Year End Closing Only previous transaction occurred during the year. You decided to retain all of the profit to next year operations Dr/ Cr/

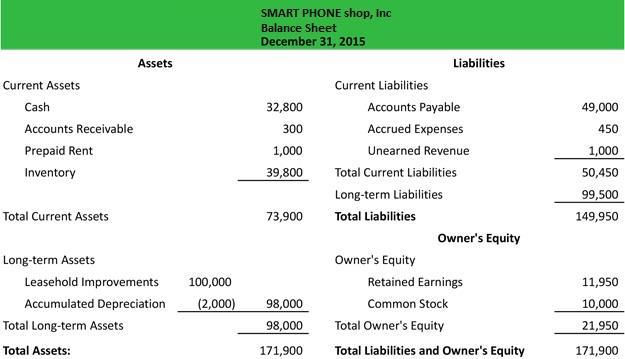

29 Accounting Cycle - Exercise Prepare balance sheet. Prepare income statement. Prepare cash flow statement

30 Financial Ratios Make comparisons through: 1- Single Company 2- Other companies in the same industry 3- Management Expectations

31 Short term Liquidity Current Ratio = Current Assets Current Liabilities Quick Ratio = Current Assets -Inventory Current Liabilities Cash Ratio = Cash + Cash Equivalents Current Liabilities

32 Short term liquidity - Exercise For example company, calculate: 1- Current ratio 2- Quick ratio 3- Cash ratio

33 Inventory Ratios Inventory Turnover Ratio = Cost of Goods Sold Average Inventory Days of Sales in Inventory = 365 Inventory Turnover

34 Inventory Ratios - Exercise For example company, calculate: 1- Inventory turnover ratio 2- Days of sales in inventory

35 Receivables Ratios Accounts Receivable Turnover Ratio = Sales Average Accounts Receivable Days of Sales in Receivables = 365 Receivables Turnover

36 Receivable Ratios - Exercise For example company, calculate: 1- Accounts receivable turnover ratio 2- Days of sales in receivable

37 Solvency Ratios Financial Leverage Ratio = Total Assets Owner Equity Total Debt to Total Assets = Total liabilities Total Assets

38 Solvency Ratios - Exercise For example company, calculate: 1- Financial leverage ratio 2- Total debt to total assets

39 Return on Investment Return on Invested Net Income Capital = Average Invested Capital Return on Assets = Net Income Total Assets

40 Return on Investment - Exercise For example company, calculate: 1- Return on Invested capital 2- ROA

41 Profitability Ratio Gross Profit Margin = Sales Cost of Goods Sold Sales

42 Profitability ratio - Exercise For example company, calculate: Gross Profit Margin

43 Objectives of Management Accounting Product Costing (for income determination and inventory valuation.) Performance evaluation: (Compare actual figures with estimated figures; Cost Control.) Short term decision (make or buy, pricing, cost volume profit analysis.) Long term decision (Capital budgeting system.)

44 Classification of costs Fixed Costs: Total amount costs does not change with a change in production. Cost per unit decrease as production increase. Variable Costs: Total costs increases as production increases. Cost per unit will remain unchanged. (at relevant range of production) Mixed Costs Semi-variable: utilizations, salesperson Semi-fixed: some machines

45 Product costs versus Period costs Product costs (Inventoriable costs) Without it the product could not be made Period costs Not involved in the production of the product

46 Product costs Direct materials Direct labor Manufacturing overheads: Includes: Indirect labor Indirect materials

47 Grouping of Product Costs Prime Costs Conversion Costs Includes: Direct Labor Overheads

48 Exercise Cost Fixed or variable? Product or period cost? DM, DL, or OH Conversion Costs? Packaging materials Production manager Screws Labor Office building Factory Cafeteria Overtime QC R&D

49 Other Cost Classification Opportunity Costs: Income lost by not using alternatives Carrying Costs: Costs incurred by carrying inventory Sunk Costs: Costs incurred and cannot be recovered Committed Costs: Not be spent but committed to be spent Discretionary Costs: May or may not be spent at the decision of the manager Marginal Costs: Costs necessary to produce one more unit

50 Types of Pharmaceutical Inventories 1- Raw materials inventory (مخزون مواد أولية) 2- Packaging materials inventory (مخزون مواد تعبئة وتغليف ( 3- Work in process inventory (مخزون بضاعة تحت التصنيع ) 4- Finished products inventory (مخزون مواد جاهزة)

51 Types of inventories Raw materials Direct labor- Bulk Overheads- Bulk Work in process FP

52 Types of inventory Raw materials inventory Beginning Inventory + Purchasing - Used in production = Ending Inventory

53 Types of inventory Work in process inventory Beginning Inventory { + Direct materials Direct Labor Factory Overheads - Cost of Goods Manufactured = Ending Inventory

54 Types of inventory Finished products inventory Beginning Inventory + Cost of goods manufactured - Cost of goods sold = Ending Inventory

55 Product Costs Finished Product Cost Direct Materials Direct Labor Manufacturing Overheads Formula Route Depend on the method of allocation

56 Direct materials Bulk: 1101, Pharmadol 5 mg Tablets Qty: 1tablet Bulk Pharmadol 5 mg Tablets RAC001 Paracetamol RIN001 Filler Qty: 0.5 Qty: 0.5 Unit Cost = 20 JOD Unit Cost = 1 JOD

57 Direct labor Opr. No. Operation Run time (hr) Next Labor hour rate (JOD) 10 Dispensing Mixing Compression

58 Overhead Annual expected manufacturing of FP:1101 = 2000 pcs Annual expected electricity expenses = 5000 JOD Annual expected depreciation expenses = JOD Annual sales forecast for Bulk:1101 = 100 pcs Annual marketing expenses for Bulk:1101=500 JOD

59 Calculate unit cost of Bulk:1101

Marketing and Distribution Services and")

60 Life-Cycle Costing 1- Upstream Costs (before production) R&D, Quality Development 2- Manufacturing Costs Materials, Labor, OH 3- Downstream Costs (after production) Marketing and Distribution Services and warranties

61 Budgeting Planning versus Budgeting: Planning is essentially the process of determining answers to : 1- Who? 2- What? 3- When? 4- Where? 5- How? Questions of business operations

62 Types of planning Strategic Planning Tactical Planning Operational Planning Time Frame Long Term (more than five years) Medium (One to five years) Short (One week to one year) Focus Strategies, objectives and goals of the company Implement specific parts of the strategic plan Day-to-day operations Done by Top Management Upper and Middle managers Lower Level of Management Examples Vision, Mission, Capital budgeting Budgeting MPS, MRP, and Capacity Planning

63 Budgeting Budgeting: the process of creating a formal plan and translating goals into a quantitative format.

64 Budgeting Advantages Help in Strategic Planning Provides Motivation Provides frame of reference evaluation For communications between different departments

65 Master budget A summarized set of budgeted financial statements (sometimes called pro forma financial statements), including budgeted income statement, budgeted balance sheet, and budgeted cash flow.

66 Budgeted Income Statement (Operating Budget) Sales budget Based on sales forecast First budget to be prepared Most difficult to produce

67 Operating Budget Production budget Based on: 1- Sales Budget 2- Production Capacity 3- Inventory Objectives Provide information for: 1- Direct Materials Budget 2- Direct Labor Budget 3- OH Budget

68 Operating Budget Cost of Goods Sold Budget Beginning Inventory + Expected Budgeted Production - Desired Ending Inventory = Budgeted Cost of Goods Sold

69 Operating Budget Other Budgets: R&D Budget Selling and Marketing Budget Admin. and general Expense Budget Other Revenues and Expenses Budget

70 Capital Budget The budget of long-term capital expenditures Only expenditure that are to be made in the budget year will be included in the master budget

71 Cash Budget Called Working Capital Budget Last budget created Tracks the inflows and outflows of a month-by-month (possibly week-by-week or day-by-day basis)

72 Static Budget versus Flexible Budget Static budget is prepared for only one level of sales Static budget not used for control and evaluation purposes

73 Static Budget versus Flexible Budget Flexible budget includes what the budget should be for different levels of sales To prepare flexible budget the company needs to use standard cost system The difference between actual amount and flexible budget is called flexible budget variance Flexible budget variances is used for control and performance evaluation

74 Exercise (Flexible Budget) Level of sales 100,000 90, ,000 Sales ( $ 9 per unit) 900,000 Variable costs ($ 5 per unit) (500,000) Contribution Margin 400,000 Fixed Costs (380,000) Operating Income 20,000

75 Other types of Budgeting Zero-Based Budgeting Life Cycle Budgeting Activity Based Budgeting Kaizen Budgeting Continuous Budgeting Project Budgeting

76 Budget Reports 1- Establish the budget 2- Measure the actual performance 3- Analyze and compare actual with budget 4- Investigate unexpected variances 5- Devise and implement corrective actions 6- Review and revise the standards

77 Exercise (Operation Budget) Budgeted amounts: 1- DM: $5 per Kg = $10 per unit 2- DL: $6 per unit = $24 per unit 3- VOH: $3 per hr = $12 per unit 4- FOH: $ Selling price = $100 per unit 6- Expected sales: 1000 units 7- Variable selling expenses = $2 per unit 8- Fixed S&A = $5000

78 Exercise (Operation Budget) 7- Inventory Balances: Beginning Balance FG per unit DM 1000 $5 per Kg Target Balance 300 units 1200 $5 per Kg 8- Assume no WIP inventories

79 Exercise (Operation Budget) Prepare Operation Budget (Net Income Budget). What is purchase budget of DM? Expected Net Income = $39000

80 Successful Budgeting Starts with the company s short term and long term plans Must have support of management at all levels People should believe in budgeting Must be flexible

81 Make or Buy Decisions Relevant Costs: Costs differ among alternatives (incremental costs) (Variable costs and avoidable fixed costs) Highest purchase price = relevant costs

82 Special order decision Operating at less than full capacity: Avoidable Costs Operating at full capacity: Unit selling price

83 Pricing Short Term Price: Minimum price must be higher than unit variable costs. Long Term Price: Minimum price must be higher than all unit costs.

84 Cost Volume-Profit Analysis Unit Contribution Margin = Unit Selling Price Unit Variable Costs Breakeven Point in units = Total Fixed Costs Unit Contribution Margin

MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47

Time: 60 min Marks: 47") MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Which of the following product cost is Included

MID TERM EXAMINATION Spring 2010 MGT402- Cost and Management Accounting (Session - 2) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Which of the following product cost is Included

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material. Chapter 10: Static and Flexible Budgets

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material Chapter 10: Static and Flexible Budgets Budget: formalized financial plan for operations of an organization for a specified

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material Chapter 10: Static and Flexible Budgets Budget: formalized financial plan for operations of an organization for a specified

MGT402 - COST & MANAGEMENT ACCOUNTING

MGT402 - COST & MANAGEMENT ACCOUNTING Lesson No. TOPICS Page No. 1 Cost Classification and Cost Behavior 1 2 Important Terminologies 11 3 Financial Statements 15 4 Financial Statements (Continued)....

MGT402 - COST & MANAGEMENT ACCOUNTING Lesson No. TOPICS Page No. 1 Cost Classification and Cost Behavior 1 2 Important Terminologies 11 3 Financial Statements 15 4 Financial Statements (Continued)....

B.COM II ADVANCED AND COST ACCOUNTING

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

FINALTERM EXAMINATION Spring 2010 MGT402- Cost & Management Accounting (Session - 4) Solved by Mehreen Humayun vuzs Team.

Solved by Mehreen Humayun vuzs Team.") FINALTERM EXAMINATION Spring 2010 MGT402- Cost & Management Accounting (Session - 4) Solved by Mehreen Humayun vuzs Team Time: 90 min Marks: 69 Question No: 1 ( Marks: 1 ) - Please choose one Cost of finished

FINALTERM EXAMINATION Spring 2010 MGT402- Cost & Management Accounting (Session - 4) Solved by Mehreen Humayun vuzs Team Time: 90 min Marks: 69 Question No: 1 ( Marks: 1 ) - Please choose one Cost of finished

Financial Statements, Forecasts, and Planning Chapter 6

C H A P T E R 6 Financial Statements, Forecasts, and Planning Chapter 6 Chapter Objectives Identify the elements of the balance sheet. Identify the elements of the income statement. Discuss the cash flow

C H A P T E R 6 Financial Statements, Forecasts, and Planning Chapter 6 Chapter Objectives Identify the elements of the balance sheet. Identify the elements of the income statement. Discuss the cash flow

Budgeting planning. Breakers, Inc. is preparing budgets for the quarter ending June 30. Budgeted sales for the next five months are:

Budgeting planning We use budgets as a target that we hope or expect to achieve. These are financial and non-financial in nature, but typically offer some quantitative measure We will begin by talking

Budgeting planning We use budgets as a target that we hope or expect to achieve. These are financial and non-financial in nature, but typically offer some quantitative measure We will begin by talking

2018 LAST MINUTE CPA EXAM NOTES

2018 LAST MINUTE CPA EXAM NOTES Page intentionally left blank 2018 LAST MINUTE CPA EXAM NOTES BEC (Volume 1) Copyright 2018 by Glomont LLC. First edition Notice of Rights. All rights reserved. No part

2018 LAST MINUTE CPA EXAM NOTES Page intentionally left blank 2018 LAST MINUTE CPA EXAM NOTES BEC (Volume 1) Copyright 2018 by Glomont LLC. First edition Notice of Rights. All rights reserved. No part

Analysing cost and revenues

Osborne Books Tutor Zone Analysing cost and revenues Chapter activities answers Osborne Books Limited, 2013 2 a n a l y s i n g c o s t s a n d r e v e n u e s t u t o r z o n e 1 An introduction to cost

Osborne Books Tutor Zone Analysing cost and revenues Chapter activities answers Osborne Books Limited, 2013 2 a n a l y s i n g c o s t s a n d r e v e n u e s t u t o r z o n e 1 An introduction to cost

REVIEW FOR FINAL EXAM, ACCT-2302 (SAC)

") 1. Types of Cost Classification REVIEW FOR FINAL EXAM, ACCT-2302 (SAC) CHAPTER 16 a. By Behavior: (1) Variable Cost - constant per unit, changes proportionally with volume. (2) Fixed Cost - fixed in total

1. Types of Cost Classification REVIEW FOR FINAL EXAM, ACCT-2302 (SAC) CHAPTER 16 a. By Behavior: (1) Variable Cost - constant per unit, changes proportionally with volume. (2) Fixed Cost - fixed in total

MIDTERM EXAMINATION Spring 2009 MGT402- Cost & Management Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one D Corporation uses process costing to calculate the cost of manufacturing

MIDTERM EXAMINATION Spring 2009 MGT402- Cost & Management Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one D Corporation uses process costing to calculate the cost of manufacturing

ALL IN ONE MGT 402 MIDTERM PAPERS MORE THAN ( 10 )

") ALL IN ONE MGT 402 MIDTERM PAPERS MORE THAN ( 10 ) MIDTERM EXAMINATION MGT402- Cost & Management Accounting Question No: 1 ( Marks: 1 ) - Please choose one D Corporation uses process costing to calculate

ALL IN ONE MGT 402 MIDTERM PAPERS MORE THAN ( 10 ) MIDTERM EXAMINATION MGT402- Cost & Management Accounting Question No: 1 ( Marks: 1 ) - Please choose one D Corporation uses process costing to calculate

Exercise E21-1 page 932. (a) Factory Labor 103,000 Factory Wages Payable 90,000 Employer Payroll Taxes Payable 9,000

Factory Labor 103,000 Factory Wages Payable 90,000 Employer Payroll Taxes Payable 9,000") Exercise E21-1 (a) Factory Labor 103,000 Factory Wages Payable 90,000 Employer Payroll Taxes Payable 9,000 Employer Fringe Benefits Payable 4,000 (b) Work in Process Inventory 92,700 Manufacturing Overhead

Exercise E21-1 (a) Factory Labor 103,000 Factory Wages Payable 90,000 Employer Payroll Taxes Payable 9,000 Employer Fringe Benefits Payable 4,000 (b) Work in Process Inventory 92,700 Manufacturing Overhead

'.fc 1. Chapter 1 Elements of Financial Statements 2. Chapter 2 Understanding the Accounting Cycle 40. Questions 23. Second Accounting Cycle 50

Boston Burr Ridge, IL Dubuque, IA Madison, Wl New York San Francisco St. Louis Bangkok Bogota Caracas Kuala Lumpur Lisbon London Madrid Mexico City Milan Montreal New Delhi Santiago Seoul Singapore Sydney

Boston Burr Ridge, IL Dubuque, IA Madison, Wl New York San Francisco St. Louis Bangkok Bogota Caracas Kuala Lumpur Lisbon London Madrid Mexico City Milan Montreal New Delhi Santiago Seoul Singapore Sydney

5_MGT402_Spring_2010_Final_Term_Solved_paper

5_MGT402_Spring_2010_Final_Term_Solved_paper http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one BDH produced 30,500 units of Kisty (a product). Each unit of Kisty takes two units

5_MGT402_Spring_2010_Final_Term_Solved_paper http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one BDH produced 30,500 units of Kisty (a product). Each unit of Kisty takes two units

Sales budget, direct labor budget, production budget, cost of goods sold budget

FINALTERM EXAMINATION Fall 2008 MGT402- Cost & Management Accounting (Session - 1) Marks: 80 Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the correct order of preparation for

FINALTERM EXAMINATION Fall 2008 MGT402- Cost & Management Accounting (Session - 1) Marks: 80 Question No: 1 ( Marks: 1 ) - Please choose one Which of the following is the correct order of preparation for

MIDTERM EXAMINATION Spring 2010 MGT101- Financial Accounting (Session - 6)

") MIDTERM EXAMINATION Spring 2010 MGT101- Financial Accounting (Session - 6) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Double entry accounting system includes: Accrual accounting

MIDTERM EXAMINATION Spring 2010 MGT101- Financial Accounting (Session - 6) Time: 60 min Marks: 47 Question No: 1 ( Marks: 1 ) - Please choose one Double entry accounting system includes: Accrual accounting

Introduction to CMA Part Section A External Financial Reporting Decisions... 2 A.1. Financial Statements... 2

CMA Part 1 Introduction to CMA Part 1... 1 Section A External Financial Reporting Decisions... 2 A.1. Financial Statements... 2 Users of Financial Information 2 The Financial Statements 3 Differences Between

CMA Part 1 Introduction to CMA Part 1... 1 Section A External Financial Reporting Decisions... 2 A.1. Financial Statements... 2 Users of Financial Information 2 The Financial Statements 3 Differences Between

Answer to PTP_Intermediate_Syllabus 2008_Jun2015_Set 1

Paper 8: Cost & Management Accounting Time Allowed: 3 Hours Full Marks: 100 Question No 1 is Compulsory. Answers any five Questions from the rest. Working Notes should form part of the answer. Question.1

Paper 8: Cost & Management Accounting Time Allowed: 3 Hours Full Marks: 100 Question No 1 is Compulsory. Answers any five Questions from the rest. Working Notes should form part of the answer. Question.1

Index. Cambridge University Press Short Introduction to Accounting Richard Barker Index More information

accountants, roles, 4 5 accounting applications, 11 12 approaches, 8 9 building blocks, 64 coverage, 9 divisiveness of, 3 foundations of, 11, 65 83 importance of, 1 3 incompleteness, 7 knowledge of, 1

accountants, roles, 4 5 accounting applications, 11 12 approaches, 8 9 building blocks, 64 coverage, 9 divisiveness of, 3 foundations of, 11, 65 83 importance of, 1 3 incompleteness, 7 knowledge of, 1

Account = the form used to record additions and deductions for each individual asset, liability, owner s equity, revenue, and expense.

A Accelerated depreciation method = a depreciation method that provides for high depreciation expense in the first year of use an asset and a gradually declining expense thereafter. Account = the form

A Accelerated depreciation method = a depreciation method that provides for high depreciation expense in the first year of use an asset and a gradually declining expense thereafter. Account = the form

Illustrative Example Xander Barkley s XYX Company manufactures a single product. The standard cost card for one unit is as follows:

Appendix 11A General Ledger Entries to Record Variances 11A-1 General Ledger Entries to Record Variances Although standard costs and variances can be computed and used by management without being formally

Appendix 11A General Ledger Entries to Record Variances 11A-1 General Ledger Entries to Record Variances Although standard costs and variances can be computed and used by management without being formally

MGT402 Cost & Management Accounting. Composed By Faheem Saqib MIDTERM EXAMINATION. Spring MGT402- Cost & Management Accounting (Session - 1)

") MGT402 Cost & Management Accounting Composed By Faheem Saqib 14 Midterm Papers 3 of 2010 & 11 of 2009 For more Help Rep At Faheem_saqib2003@yahoo.com Faheem.saqib2003@gmail.com 0334-6034849 MIDTERM EXAMINATION

MGT402 Cost & Management Accounting Composed By Faheem Saqib 14 Midterm Papers 3 of 2010 & 11 of 2009 For more Help Rep At Faheem_saqib2003@yahoo.com Faheem.saqib2003@gmail.com 0334-6034849 MIDTERM EXAMINATION

FINALTERM EXAMINATION Fall 2009 MGT402- Cost & Management Accounting (Session - 3) Ref No: 1232793 Time: 120 min : 84 Student Info ExamDate: 2/22/2010 12:00:00 AM For Teacher's Use Only Q 1 2 3 4 5 6 7

FINALTERM EXAMINATION Fall 2009 MGT402- Cost & Management Accounting (Session - 3) Ref No: 1232793 Time: 120 min : 84 Student Info ExamDate: 2/22/2010 12:00:00 AM For Teacher's Use Only Q 1 2 3 4 5 6 7

Suggested layouts for financial statements in National 5 and Higher Accounting courses

Suggested layouts for financial statements in National 5 and Higher Accounting courses The following suggested layouts may be used when presenting financial statements in the Accounting courses for National

Suggested layouts for financial statements in National 5 and Higher Accounting courses The following suggested layouts may be used when presenting financial statements in the Accounting courses for National

Index COPYRIGHTED MATERIAL

A ABC (activity-based costing). See also costs; peanut butter costing allocating indirect costs, 77 78 allocations to cost pools, 79 analyzing cost activities, 78 79 applying to bottlenecks, 353 applying

A ABC (activity-based costing). See also costs; peanut butter costing allocating indirect costs, 77 78 allocations to cost pools, 79 analyzing cost activities, 78 79 applying to bottlenecks, 353 applying

Chapter 4. Funds-Flow Analysis and Forecasting. Overview of the Lecture. September The Statement of Cash Flows. Pro Forma Financial Statements

Chapter 4 Funds-Flow Analysis and Forecasting September 2004 Overview of the Lecture The Statement of Cash Flows Pro Forma Financial Statements 2 The Statement of Cash Flows The statement of cash flows

Chapter 4 Funds-Flow Analysis and Forecasting September 2004 Overview of the Lecture The Statement of Cash Flows Pro Forma Financial Statements 2 The Statement of Cash Flows The statement of cash flows

Disclaimer: This resource package is for studying purposes only EDUCATIO N

Disclaimer: This resource package is for studying purposes only EDUCATIO N Chapter 1 Managerial accounting vs. financial accounting Qualities Financial Accounting Managerial Accounting Reports Externally

Disclaimer: This resource package is for studying purposes only EDUCATIO N Chapter 1 Managerial accounting vs. financial accounting Qualities Financial Accounting Managerial Accounting Reports Externally

FINALTERM EXAMINATION Fall 2009 MGT402- Cost & Management Accounting (Session - 3) Ref No: Time: 120 min Marks: Total

Ref No: Time: 120 min Marks: Total") Student Info FINALTERM EXAMINATION Fall 2009 MGT402- Cost & Management Accounting (Session - 3) Ref No: 1232793 Time: 120 min Marks: 84 ExamDate: 2/22/2010 12:00:00 AM For Teacher's Use Only Q No. 1 2

Student Info FINALTERM EXAMINATION Fall 2009 MGT402- Cost & Management Accounting (Session - 3) Ref No: 1232793 Time: 120 min Marks: 84 ExamDate: 2/22/2010 12:00:00 AM For Teacher's Use Only Q No. 1 2

FINALTERM EXAMINATION. Spring MGT402- Cost & Management Accounting (Session - 2)

") FINALTERM EXAMINATION Spring 2009 MGT402- Cost & Management Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one All of the following indicate the problems in traditional budget EXCEPT:

FINALTERM EXAMINATION Spring 2009 MGT402- Cost & Management Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one All of the following indicate the problems in traditional budget EXCEPT:

SUGGESTED ANSWERS SPRING 2015 EXAMINATIONS 1 of 7 FUNDAMENTALS OF COST & MANAGEMENT ACCOUNTING SEMESTER-2

SUGGESTED ANSWERS SPRING 2015 EXAMINATIONS 1 of 7 Q. 2 (a) The Role of the Management Accountant: The management accountant plays a critical role in providing information to management to assist in planning,

SUGGESTED ANSWERS SPRING 2015 EXAMINATIONS 1 of 7 Q. 2 (a) The Role of the Management Accountant: The management accountant plays a critical role in providing information to management to assist in planning,

FINALTERM EXAMINATION Spring 2009 MGT402- Cost & Management Accounting (Session - 3) Question No: 1 ( Marks: 1 ) - Please choose one All of the following are a part of Planning Process EXCEPT: Identifying

FINALTERM EXAMINATION Spring 2009 MGT402- Cost & Management Accounting (Session - 3) Question No: 1 ( Marks: 1 ) - Please choose one All of the following are a part of Planning Process EXCEPT: Identifying

MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4)

") MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4) Time: 60 min Marks: 50 Asslam O Alikum FIN621- Financial Statement Analysis 2009 (Session 4) solved by Afaaq n Shani Bhai

MIDTERM EXAMINATION Fall 2009 FIN621- Financial Statement Analysis (Session - 4) Time: 60 min Marks: 50 Asslam O Alikum FIN621- Financial Statement Analysis 2009 (Session 4) solved by Afaaq n Shani Bhai

Answer to MTP_Intermediate_Syllabus 2012_Jun2017_Set 1 Paper 8- Cost Accounting & Financial Management

Paper 8- Cost Accounting & Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-8: Cost Accounting & Financial

Paper 8- Cost Accounting & Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-8: Cost Accounting & Financial

Chapter 10 Static and Flexible Budgets

Cost Management Measuring, Monitoring, and Motivating Performance Chapter 10 Static and Flexible Budgets Prepared by Gail Kaciuba Midwestern State University Eldenburg & Wolcott s Cost Management, 1e Slide

Cost Management Measuring, Monitoring, and Motivating Performance Chapter 10 Static and Flexible Budgets Prepared by Gail Kaciuba Midwestern State University Eldenburg & Wolcott s Cost Management, 1e Slide

B.COM II ADVANCED AND COST ACCOUNTING

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

The workings under the heading of Additional Working are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.net

CBSE Quick Revision Notes and Chapter Summary Class-12 Accountancy Part B Accounting Ratios

Book Recommended: ULTIMATE BOOK OF ACCOUNTANCY (By Dr. Vinod Kumar, Vishvas Publications) Warning: This is copyrighted content of Dr. Vinod Kumar. Not to be reproduced in any form, anywhere else. Introduction

Book Recommended: ULTIMATE BOOK OF ACCOUNTANCY (By Dr. Vinod Kumar, Vishvas Publications) Warning: This is copyrighted content of Dr. Vinod Kumar. Not to be reproduced in any form, anywhere else. Introduction

Planning and Control. Control involves the steps taken by management that attempt to ensure the objectives are attained.

Profit Planning Planning and Control Planning -- involves developing objectives and preparing various budgets to achieve these objectives. Control involves the steps taken by management that attempt to

Profit Planning Planning and Control Planning -- involves developing objectives and preparing various budgets to achieve these objectives. Control involves the steps taken by management that attempt to

Online Course Manual By Craig Pence. Module 7

Online Course Manual By Craig Pence Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled

Online Course Manual By Craig Pence Copyright Notice. Each module of the course manual may be viewed online, saved to disk, or printed (each is composed of 10 to 15 printed pages of text) by students enrolled

Prepared and solved by Cyberian www,vuaskari.com

Franchise rights, goodwill and patents are the examples of: Liquid assets Tangible assets Intangible assets Current assets Any expense that gives benefit for a period of less than twelve months is called.

Franchise rights, goodwill and patents are the examples of: Liquid assets Tangible assets Intangible assets Current assets Any expense that gives benefit for a period of less than twelve months is called.

Answer to MTP_Intermediate_Syl2016_June2017_Set 1 Paper 10- Cost & Management Accounting and Financial Management

Paper 10- Cost & Management Accounting and Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-10: Cost & Management

Paper 10- Cost & Management Accounting and Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-10: Cost & Management

MGT402 Subjective Material

MGT402 Subjective Material Question No: 49 ( Marks: 3 ) A company is considering publishing a limited edition book bound in special leather. It has in stock the leather bought some years ago for Rs. 1,000.

MGT402 Subjective Material Question No: 49 ( Marks: 3 ) A company is considering publishing a limited edition book bound in special leather. It has in stock the leather bought some years ago for Rs. 1,000.

Solution to Cost Paper of CA IPCC COST MAY Solution to Question 1 (a) 10% = Avg. No. of workers on roll = 500

10% = Avg. No. of workers on roll = 500") Solution to Cost Paper of CA IPCC COST MAY 2017 Solution to Question 1 (a) Average no. of workers on roll during the year No.of replacements 1. Labour turnover rate under replacement method = x 100 Average

Solution to Cost Paper of CA IPCC COST MAY 2017 Solution to Question 1 (a) Average no. of workers on roll during the year No.of replacements 1. Labour turnover rate under replacement method = x 100 Average

Analysing cost and revenues

Osborne Books Tutor Zone Analysing cost and revenues Chapter activities Osborne Books Limited, 2013 2 a n a l y s i n g c o s t s a n d r e v e n u e s t u t o r z o n e 1 An introduction to cost accounting

Osborne Books Tutor Zone Analysing cost and revenues Chapter activities Osborne Books Limited, 2013 2 a n a l y s i n g c o s t s a n d r e v e n u e s t u t o r z o n e 1 An introduction to cost accounting

MGT402 Short Notes Lecture 23 to 45 By

MGT402 Short Notes Lecture 23 to 45 By http://vustudents.ning.com Lec # 23 PROCESS COSTING SYSTEM (Opening balance of work in process) Two methods of cost allocation (1) The weighted average (or averaging)

MGT402 Short Notes Lecture 23 to 45 By http://vustudents.ning.com Lec # 23 PROCESS COSTING SYSTEM (Opening balance of work in process) Two methods of cost allocation (1) The weighted average (or averaging)

FINALTERM EXAMINATION Fall 2009 MGT402- Cost & Management Accounting (Session - 3) Solved by vuzs Team Mehreen Humayun

Solved by vuzs Team Mehreen Humayun") FINALTERM EXAMINATION Fall 2009 MGT402- Cost & Management Accounting (Session - 3) Solved by vuzs Team Mehreen Humayun www.vuzs.net Question No: 1 ( Marks: 1 ) - Please choose one All of the following

FINALTERM EXAMINATION Fall 2009 MGT402- Cost & Management Accounting (Session - 3) Solved by vuzs Team Mehreen Humayun www.vuzs.net Question No: 1 ( Marks: 1 ) - Please choose one All of the following

FOR MORE PAPERS LOGON TO

MGT402 - Cost & Management Accounting Question No: 1 ( Marks: 1 ) - Please choose one Opportunity cost is the best example of: Sunk Cost Standard Cost Relevant Cost Irrelevant Cost Question No: 2 ( Marks:

MGT402 - Cost & Management Accounting Question No: 1 ( Marks: 1 ) - Please choose one Opportunity cost is the best example of: Sunk Cost Standard Cost Relevant Cost Irrelevant Cost Question No: 2 ( Marks:

MTP_ Inter _Syllabus 2016_ Dec 2017_Set 2 Paper 10 Cost & Management Accounting and Financial Management

Paper 10 Cost & Management Accounting and Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 10 Cost & Management

Paper 10 Cost & Management Accounting and Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 10 Cost & Management

Answer to MTP_Intermediate_Syl2016_June2017_Set 1 Paper 8- Cost Accounting

Paper 8 Cost Accounting Page 1 Page 1 Paper8: Cost Accounting Full Marks: 100 Time allowed: 3 hours Section A Answer the following questions: 1. Choose the correct answer from the given four alternatives:

Paper 8 Cost Accounting Page 1 Page 1 Paper8: Cost Accounting Full Marks: 100 Time allowed: 3 hours Section A Answer the following questions: 1. Choose the correct answer from the given four alternatives:

SUGGESTED SOLUTION IPCC NOVEMBER 2018 EXAM. Test Code -

SUGGESTED SOLUTION IPCC NOVEMBER 2018 EXAM COSTING Test Code - BRANCH - (MUMBAI-2 (DB) (Date : 01.07.2018) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

SUGGESTED SOLUTION IPCC NOVEMBER 2018 EXAM COSTING Test Code - BRANCH - (MUMBAI-2 (DB) (Date : 01.07.2018) Head Office : Shraddha, 3 rd Floor, Near Chinai College, Andheri (E), Mumbai 69. Tel : (022) 26836666

C521 CHAPTER 13 & REVIEW FOR MIDTERM FINANCIAL ACCOUNTING EXAM

1 C521 CHAPTER 13 & REVIEW FOR MIDTERM FINANCIAL ACCOUNTING EXAM What have we done in the course? On a chapter by chapter basis, we primarily have examined specific transactions and the effect on financial

1 C521 CHAPTER 13 & REVIEW FOR MIDTERM FINANCIAL ACCOUNTING EXAM What have we done in the course? On a chapter by chapter basis, we primarily have examined specific transactions and the effect on financial

ACC406 Tip Sheet. Direct Labour (DL): labour that is directly attributable to the goods and service that are being produced by a firm.

: labour that is directly attributable to the goods and service that are being produced by a firm.") ACC406 Tip Sheet Definitions Direct Cost: a cost that can be easily allocated to a certain object. Variable Cost (VC): a cost that changes in direct relation to output (output increases VC increases) Fixed

ACC406 Tip Sheet Definitions Direct Cost: a cost that can be easily allocated to a certain object. Variable Cost (VC): a cost that changes in direct relation to output (output increases VC increases) Fixed

MTP_Intermediate_Syl2016_June2017_Set 1 Paper 10- Cost & Management Accounting and Financial Management

Paper 10- Cost & Management Accounting and Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-10: Cost & Management

Paper 10- Cost & Management Accounting and Financial Management Academics Department, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper-10: Cost & Management

Question No: 5 ( Marks: 1 ) - Please choose one Which of the following manufacturers is most likely to use a job order cost accounting system?

- Please choose one Which of the following manufacturers is most likely to use a job order cost accounting system?") MGT402 Latest Solved MCQs From Current Papers 2010 By http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one If Selling price per unit Rs. 15.00; Direct Materials cost per unit Rs.

MGT402 Latest Solved MCQs From Current Papers 2010 By http://vustudents.ning.com Question No: 1 ( Marks: 1 ) - Please choose one If Selling price per unit Rs. 15.00; Direct Materials cost per unit Rs.

Rocco Sabino MBA, CPA

Rocco Sabino MBA, CPA Rocco.Sabino@Stonybrook.edu Agenda: I. Understanding Financial Information Ø Financial Statements q Income Statement It s all about earning income How does Human Resource (HR) affect

Rocco Sabino MBA, CPA Rocco.Sabino@Stonybrook.edu Agenda: I. Understanding Financial Information Ø Financial Statements q Income Statement It s all about earning income How does Human Resource (HR) affect

Budgets and Budgetary Control. By: CA Kapileshwar Bhalla

Budgets and Budgetary Control By: CA Kapileshwar Bhalla Learning Objectives Understand the objectives and importance of budgeting and budgetary control Understand the Advantages and disadvantages of budgetary

Budgets and Budgetary Control By: CA Kapileshwar Bhalla Learning Objectives Understand the objectives and importance of budgeting and budgetary control Understand the Advantages and disadvantages of budgetary

Accountants Guidebook

Accountants Guidebook 3 rd Edition Steven M. Bragg Chapter 1 The Role of the Accountant... 1 Learning Objectives... 1 Introduction... 1 The Accountancy Concept... 1 Financial and Managerial Accounting...

Accountants Guidebook 3 rd Edition Steven M. Bragg Chapter 1 The Role of the Accountant... 1 Learning Objectives... 1 Introduction... 1 The Accountancy Concept... 1 Financial and Managerial Accounting...

BUDGET- CONCEPTS AND METHODOLOGIES

Budgeting Concepts and Methodologies Application & Awareness 1 BUDGET- CONCEPTS AND METHODOLOGIES WWW.CMAEXAMSTUDY.COM WWW.IMANET.ORG 2 Agenda Introduction of 3FOLD Budget Budgeting Role, Process and Approaches

Budgeting Concepts and Methodologies Application & Awareness 1 BUDGET- CONCEPTS AND METHODOLOGIES WWW.CMAEXAMSTUDY.COM WWW.IMANET.ORG 2 Agenda Introduction of 3FOLD Budget Budgeting Role, Process and Approaches

Fundamental Financial and Manageria Accounting Concepts

Fundamental Financial and Manageria Accounting Concepts 1-; *Th

Fundamental Financial and Manageria Accounting Concepts 1-; *Th

Accounting Definitions. Definitions

Accounting Definitions Definitions What s Here Introduction Definitions Introduction This training contains definitions of common accounting terms. If you come across accounting or financial terms with

Accounting Definitions Definitions What s Here Introduction Definitions Introduction This training contains definitions of common accounting terms. If you come across accounting or financial terms with

Manufacturing Accounts

All questions copyright of Cambridge International Examinations 1 Manufacturing Accounts All questions copyright of Cambridge International Examinations 2 2 1 The following balances were extracted from

All questions copyright of Cambridge International Examinations 1 Manufacturing Accounts All questions copyright of Cambridge International Examinations 2 2 1 The following balances were extracted from

BATCH All Batches. DATE: MAXIMUM MARKS: 100 TIMING: 3 Hours. PAPER 3 : Cost Accounting

BATCH All Batches DATE: 25.09.2017 MAXIMUM MARKS: 100 TIMING: 3 Hours PAPER 3 : Cost Accounting Q. No. 1 is compulsory. Wherever necessary suitable assumptions should be made by the candidates. Working

BATCH All Batches DATE: 25.09.2017 MAXIMUM MARKS: 100 TIMING: 3 Hours PAPER 3 : Cost Accounting Q. No. 1 is compulsory. Wherever necessary suitable assumptions should be made by the candidates. Working

Interpretation of Financial Statements

Interpretation of Financial Statements Steven M. Bragg Chapter 1 Overview of the Financial Statements... 1 Learning Objectives... 1 Introduction... 1 The General Ledger... 1 The Accrual Basis of Accounting...

Interpretation of Financial Statements Steven M. Bragg Chapter 1 Overview of the Financial Statements... 1 Learning Objectives... 1 Introduction... 1 The General Ledger... 1 The Accrual Basis of Accounting...

FORENSIC ACCOUNTING VERSION

FORENSIC ACCOUNTING VERSION Fraudulent or incorrect transactions are presented below. Your job as a forensic accountant is to correct the financial statements and determine how income and total assets

FORENSIC ACCOUNTING VERSION Fraudulent or incorrect transactions are presented below. Your job as a forensic accountant is to correct the financial statements and determine how income and total assets

Plz Remember Me in ur Prayers.

Assalam-0-Alaikum Cost & Management Accounting (MGT402) Final term papers Solved by SilentLips Ghulam Abbas Zahid MC090402571 MBA 3 rd (Management) Cell # +92-300-687 6387 +92-345-873 2201 E-mail silentlips687@hotmail.com

Assalam-0-Alaikum Cost & Management Accounting (MGT402) Final term papers Solved by SilentLips Ghulam Abbas Zahid MC090402571 MBA 3 rd (Management) Cell # +92-300-687 6387 +92-345-873 2201 E-mail silentlips687@hotmail.com

Question Paper Management Accounting (MB161) : October 2004

: October 2004") Question Paper Management Accounting (MB161) : October 2004 Answer all questions. Marks are indicated against each question. 1. A Balance Sheet account, which has significant overlap between Managerial

Question Paper Management Accounting (MB161) : October 2004 Answer all questions. Marks are indicated against each question. 1. A Balance Sheet account, which has significant overlap between Managerial

STANDARD COSTS AND VARIANCE ANALYSIS

STANDARD COSTS AND VARIANCE ANALYSIS Key Terms and Concepts to Know Static or Planning Budgets Used for planning purposes Prepared at the beginning of the period Based on one projected level of activity

STANDARD COSTS AND VARIANCE ANALYSIS Key Terms and Concepts to Know Static or Planning Budgets Used for planning purposes Prepared at the beginning of the period Based on one projected level of activity

COPYRIGHT PAGE. Published by: Flat World Knowledge, Inc th St NW Washington, DC 20036

COPYRIGHT PAGE Published by: Flat World Knowledge, Inc. 1111 19 th St NW Washington, DC 20036 2016 by Flat World Knowledge, Inc. All rights reserved. Your use of this work is subject to the License Agreement

COPYRIGHT PAGE Published by: Flat World Knowledge, Inc. 1111 19 th St NW Washington, DC 20036 2016 by Flat World Knowledge, Inc. All rights reserved. Your use of this work is subject to the License Agreement

PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART-I: COST ACCOUNTING QUESTIONS

Material PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART-I: COST ACCOUNTING QUESTIONS 1. Ananya Ltd. produces a product Exe using a raw material Dee. To produce one unit of Exe, 2 kg of Dee is required.

Material PAPER 3: COST ACCOUNTING AND FINANCIAL MANAGEMENT PART-I: COST ACCOUNTING QUESTIONS 1. Ananya Ltd. produces a product Exe using a raw material Dee. To produce one unit of Exe, 2 kg of Dee is required.

Chapter 8. Recording Adjusting and Closing Entries

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

Chapter 8 Recording Adjusting and Closing Entries Adjusting Entries Adjusting Entries - journal entries recorded to update general ledger accounts at the end of a fiscal period (Supplies & Prepaid Insurance).

Product Cost. Direct Material s. Vari able Cost. Fixed Cost

Problem 2-19 1 Vari able Fixed Direct Material s Product Direct Labour Mfg. Overh ead Period (sellin g and admin) Opport unity Name of the Staci's current salary, $3,800 per month... X X Building rent,

Problem 2-19 1 Vari able Fixed Direct Material s Product Direct Labour Mfg. Overh ead Period (sellin g and admin) Opport unity Name of the Staci's current salary, $3,800 per month... X X Building rent,

PTP_Intermediate_Syllabus 2008_Jun2015_Set 3

Paper 8: Cost & Management Accounting Time Allowed: 3 Hours Full Marks: 100 Question No 1 is Compulsory. Answers any five Questions from the rest. Working Notes should form part of the answer. Question.1

Paper 8: Cost & Management Accounting Time Allowed: 3 Hours Full Marks: 100 Question No 1 is Compulsory. Answers any five Questions from the rest. Working Notes should form part of the answer. Question.1

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material Chapter 11 & 13. Chapter 11: Standard Costs and Variance Analysis

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material Chapter 11 & 13 Chapter 11: Standard Costs and Variance Analysis Variance Analysis: calculating variances and investigating

AFM481 - Advanced Cost Accounting Professor Grant Russell Final Exam Material Chapter 11 & 13 Chapter 11: Standard Costs and Variance Analysis Variance Analysis: calculating variances and investigating

Small Business Management MGMT5601 Topic 9: Financing the Small Firm (2) Cash & Profit

Cash & Profit") Small Business Management MGMT5601 Topic 9: Financing the Small Firm (2) Cash & Profit Professor Tim Mazzarol UWA Business School SBM MGMT5601 UWA Business School MBA Program tim.mazzarol@uwa.edu.au Learning

Small Business Management MGMT5601 Topic 9: Financing the Small Firm (2) Cash & Profit Professor Tim Mazzarol UWA Business School SBM MGMT5601 UWA Business School MBA Program tim.mazzarol@uwa.edu.au Learning

Appendix. IPCC Gr. I (Solution of May ) Paper - 3A : Cost Accounting

Paper - 3A : Cost Accounting") Solved Scanner Appendix IPCC Gr. I (Solution of May - 2015 ) Paper - 3A : Cost Accounting Chapter - 1: Basic Concepts 2015 - May [5] (a) Sunk Cost: Sunk costs are historical costs incurred in the past

Solved Scanner Appendix IPCC Gr. I (Solution of May - 2015 ) Paper - 3A : Cost Accounting Chapter - 1: Basic Concepts 2015 - May [5] (a) Sunk Cost: Sunk costs are historical costs incurred in the past

BPC6C Cost and Management Accounting. Unit : I to V

BPC6C Cost and Management Accounting Unit : I to V UNIT -1 FUNDAMENTALS OF COST ACCOUNTING Nature and scope of Cost Accounting, Distinction between cost and financial accounting, Cost sheet, tenders Characteristics

BPC6C Cost and Management Accounting Unit : I to V UNIT -1 FUNDAMENTALS OF COST ACCOUNTING Nature and scope of Cost Accounting, Distinction between cost and financial accounting, Cost sheet, tenders Characteristics

CLASSIFICATION OF COST

Cost Accounting Standard 1 CLASSIFICATION OF COST Draft Developed by Technical Support and Practice Development Committee Institute of Cost and Managemet Accountants of Pakistan Implementation Status This

Cost Accounting Standard 1 CLASSIFICATION OF COST Draft Developed by Technical Support and Practice Development Committee Institute of Cost and Managemet Accountants of Pakistan Implementation Status This

Suggested Answer_Syl12_Dec2014_Paper_8 INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2012)

") INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2014 Paper-8: COST ACCOUNTING AND FINANCIAL MANAGEMENT Time Allowed : 3 Hours Full Marks : 100 The figures in the

INTERMEDIATE EXAMINATION GROUP I (SYLLABUS 2012) SUGGESTED ANSWERS TO QUESTIONS DECEMBER 2014 Paper-8: COST ACCOUNTING AND FINANCIAL MANAGEMENT Time Allowed : 3 Hours Full Marks : 100 The figures in the

Gurukripa s Guideline Answers to Nov 2016 Exam Questions CA Inter (IPC) Cost Accounting & Financial Management Working Notes should form part of the answers. Question No.1 is compulsory (4 5 20 Marks).

Gurukripa s Guideline Answers to Nov 2016 Exam Questions CA Inter (IPC) Cost Accounting & Financial Management Working Notes should form part of the answers. Question No.1 is compulsory (4 5 20 Marks).

2. State any four tools and techniques of management accounting.

SUBJECT : MANAGEMENT ACCOUNTING SUB CODE : CM616S SUB HANDLING : Dr. F.ANDREWS CLASS: III B.COM 1. Define management Accounting. 2. State any four tools and techniques of management accounting. 3. What

SUBJECT : MANAGEMENT ACCOUNTING SUB CODE : CM616S SUB HANDLING : Dr. F.ANDREWS CLASS: III B.COM 1. Define management Accounting. 2. State any four tools and techniques of management accounting. 3. What

MBP1133 Managerial Accounting Prepared by Dr Khairul Anuar

1 MBP1133 Managerial Accounting Prepared by Dr Khairul Anuar L9 Master Budgeting www.notes638.wordpress.com 2 Learning Objective 1 Understand why organizations budget and the processes they use to create

1 MBP1133 Managerial Accounting Prepared by Dr Khairul Anuar L9 Master Budgeting www.notes638.wordpress.com 2 Learning Objective 1 Understand why organizations budget and the processes they use to create

Standard Costing and Variance Analysis

Standard Costing and Variance Analysis Standard Costing Standard cost is predetermined cost agreed earlier under specific working conditions. Standard costing is a technique which establishes predetermined

Standard Costing and Variance Analysis Standard Costing Standard cost is predetermined cost agreed earlier under specific working conditions. Standard costing is a technique which establishes predetermined

Accounting For Decision Making

Accounting For Decision Making Topic 7 Costing products and services Goals for this session Explain why managers need estimates of the costs of both responsibility centres and products; Describe the basic

Accounting For Decision Making Topic 7 Costing products and services Goals for this session Explain why managers need estimates of the costs of both responsibility centres and products; Describe the basic

2013 Accounting. Intermediate 2 Solutions. Finalised Marking Instructions

2013 Accounting Intermediate 2 Solutions Finalised Marking Instructions Scottish Qualifications Authority 2013 The information in this publication may be reproduced to support SQA qualifications only on

2013 Accounting Intermediate 2 Solutions Finalised Marking Instructions Scottish Qualifications Authority 2013 The information in this publication may be reproduced to support SQA qualifications only on

ACG 3024 Accounting for Non-Financial Majors Homework Portfolio (This is an individual assignment)

") ACG 3024 Accounting for Non-Financial Majors Homework Portfolio (This is an individual assignment) Make sure you complete the homework portfolio version assigned to you from your sign-in on the Florida

ACG 3024 Accounting for Non-Financial Majors Homework Portfolio (This is an individual assignment) Make sure you complete the homework portfolio version assigned to you from your sign-in on the Florida

ACCT 101 Statement of Cash Flows Lecture Notes Chapter 12 Prof. Johnson. The statement of cash flows is a required component of financial statements.

ACCT 101 Statement of Cash Flows Lecture Notes Chapter 12 Prof. Johnson The statement of cash flows is a required component of financial statements. BASICS OF CASH FLOW REPORTING Purpose of the Statement

ACCT 101 Statement of Cash Flows Lecture Notes Chapter 12 Prof. Johnson The statement of cash flows is a required component of financial statements. BASICS OF CASH FLOW REPORTING Purpose of the Statement

Understanding Where You Stand

SMALL BUSINESS Access to Opportunity Understanding Where You Stand A Simple Guide to Your Company s Financial Statements Reading Your Statements Balance Sheets Income Statements Ratios Cash Flow Statements

SMALL BUSINESS Access to Opportunity Understanding Where You Stand A Simple Guide to Your Company s Financial Statements Reading Your Statements Balance Sheets Income Statements Ratios Cash Flow Statements

Chapter 12 - Reporting and Analyzing Cash Flows. Chapter Outline

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

I. Basics of Cash Flow Reporting A. Purpose of the Statement of Cash Flows To report cash receipts (inflows) and cash payments (outflows) during a period. This report classifies cash flows into operating,

Paper 8- Cost Accounting

Paper 8- Cost Accounting Dos, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 8- Cost Accounting Full Marks : 100 Time allowed: 3 hours Section A Question

Paper 8- Cost Accounting Dos, The Institute of Cost Accountants of India (Statutory Body under an Act of Parliament) Page 1 Paper 8- Cost Accounting Full Marks : 100 Time allowed: 3 hours Section A Question

MARGINAL COSTING. Calculate (a) P/V ratio, (b) Total fixed cost, and (c) Sales required to earn a Profit of 12,00,000.

P/V ratio, (b) Total fixed cost, and (c) Sales required to earn a Profit of 12,00,000.") MARGINAL COSTING Question 1Arnav Ltd. manufacture and sales its product R-9. The following figures have been collected from cost records of last year for the product R-9: Elements of Cost Variable Cost

MARGINAL COSTING Question 1Arnav Ltd. manufacture and sales its product R-9. The following figures have been collected from cost records of last year for the product R-9: Elements of Cost Variable Cost

Code No. : Sub. Code : R 3 BA 52/ B 3 BA 52

(8 pages) Reg. No. :... Sub. Code : R 3 BA 52/ B 3 BA 52 B.B.A. (CBCS) DEGREE EXAMINATION, NOVEMBER 2014. Fifth Semester Business Administration Main MANAGEMENT ACCOUNTING (For those who joined in July

(8 pages) Reg. No. :... Sub. Code : R 3 BA 52/ B 3 BA 52 B.B.A. (CBCS) DEGREE EXAMINATION, NOVEMBER 2014. Fifth Semester Business Administration Main MANAGEMENT ACCOUNTING (For those who joined in July

Principles of Managerial Accounting

GALILEO, University System of Georgia GALILEO Open Learning Materials Business Administration, Management, and Economics Open Textbooks Business Administration, Management, and Economics Spring 2019 Principles

GALILEO, University System of Georgia GALILEO Open Learning Materials Business Administration, Management, and Economics Open Textbooks Business Administration, Management, and Economics Spring 2019 Principles

7 Solved Mid Term Papers of MGT402 BY.

7 Solved Mid Term Papers of MGT402 BY http://vustudents.ning.com Spring 2009 MGT402- Cost & Management Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one D Corporation uses process

7 Solved Mid Term Papers of MGT402 BY http://vustudents.ning.com Spring 2009 MGT402- Cost & Management Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one D Corporation uses process

Understanding Financial Data

May 22-25, 2016 Los Angeles Convention Center Los Angeles, California Understanding Presented by Brenda M. Clarke, CPA/ABV/CFF, CVA FM25 5/24/2016 2:30 PM - 3:30 PM The handouts and presentations attached

May 22-25, 2016 Los Angeles Convention Center Los Angeles, California Understanding Presented by Brenda M. Clarke, CPA/ABV/CFF, CVA FM25 5/24/2016 2:30 PM - 3:30 PM The handouts and presentations attached

MGT101 FINANCIAL ACCOUNTING SOLVED QUIZZES 3 LESSON 1 30

MGT101 FINANCIAL ACCOUNTING SOLVED QUIZZES 3 LESSON 1 30 Wages paid to laborers working in the manufacturing department is treated as an expense of: Cost of goods sold Administrative expense Selling expense

MGT101 FINANCIAL ACCOUNTING SOLVED QUIZZES 3 LESSON 1 30 Wages paid to laborers working in the manufacturing department is treated as an expense of: Cost of goods sold Administrative expense Selling expense

FMA. Management Accounting. OpenTuition.com ACCA FIA. March/June 2016 exams. Free resources for accountancy students

OpenTuition.com Free resources for accountancy students March/June 2016 exams ACCA FIA F2 FMA Management Accounting Please spread the word about OpenTuition, so that all ACCA students can benefit. ONLY

OpenTuition.com Free resources for accountancy students March/June 2016 exams ACCA FIA F2 FMA Management Accounting Please spread the word about OpenTuition, so that all ACCA students can benefit. ONLY

MGT402 Cost & Management Accounting Golden File. For: Final Term Exam Preparation

MGT402 Cost & Management Accounting Golden File For: Final Term Exam Preparation princesajjadali@gmail.com princetanveerahmed@gmail.com 03337567657 Remember us in your prayers Quality of our File: All

MGT402 Cost & Management Accounting Golden File For: Final Term Exam Preparation princesajjadali@gmail.com princetanveerahmed@gmail.com 03337567657 Remember us in your prayers Quality of our File: All

MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2)

") MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one Particulars Rs. Opening written down value of machine 1,00,000 Cost of new machine

MIDTERM EXAMINATION Fall 2009 MGT101- Financial Accounting (Session - 2) Question No: 1 ( Marks: 1 ) - Please choose one Particulars Rs. Opening written down value of machine 1,00,000 Cost of new machine

BUSINESS FINANCE. Financial Statement Analysis. 1. Introduction to Financial Analysis. Copyright 2004 by Larry C. Holland

BUSINESS FINANCE Financial Statement Analysis 1. Introduction to Financial Analysis Slide 1 Welcome to the study of business finance. The major topic in this module is Financial Statement Analysis. And

BUSINESS FINANCE Financial Statement Analysis 1. Introduction to Financial Analysis Slide 1 Welcome to the study of business finance. The major topic in this module is Financial Statement Analysis. And

Tiill now you have learnt about the financial

Cash Flow Statement 6 LEARNING OBJECTIVES After studying this chapter, you will be able to : state the purpose and preparation of statement of cash flow statement; distinguish between operating activities,

Cash Flow Statement 6 LEARNING OBJECTIVES After studying this chapter, you will be able to : state the purpose and preparation of statement of cash flow statement; distinguish between operating activities,