SAMPLE CONDO RESERVE STUDY for fiscal year 2012

|

|

|

- Cory Wilkerson

- 6 years ago

- Views:

Transcription

780-7943")

1 SAMPLE CONDO RESERVE STUDY for fiscal year 2012 RDA REPORT - UPDATED RESERVE ANALYSIS FOR FISCAL YEAR 2012 RESERVE DATA ANALYSIS, INC MPLS (612) TOLL FREE (866) UPDATE INCLUDING ON-SITE REVIEW, REPORT VERSION 002

616-4817 - TOLL FREE: (866) 780-7943 - FAX: (866) 484-7943 Email: info@rdamidwest.")

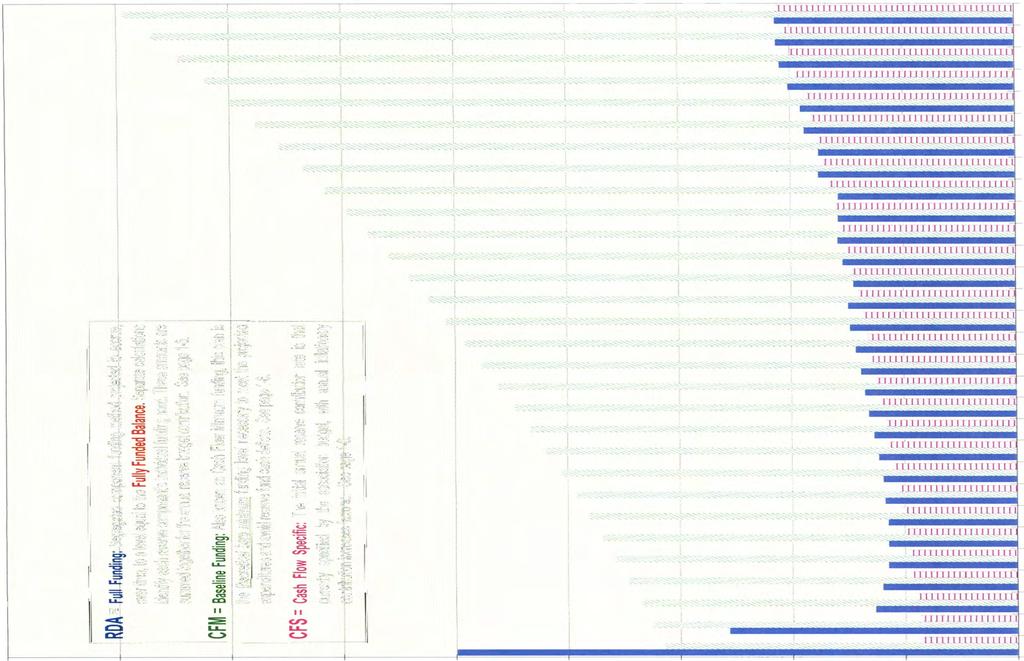

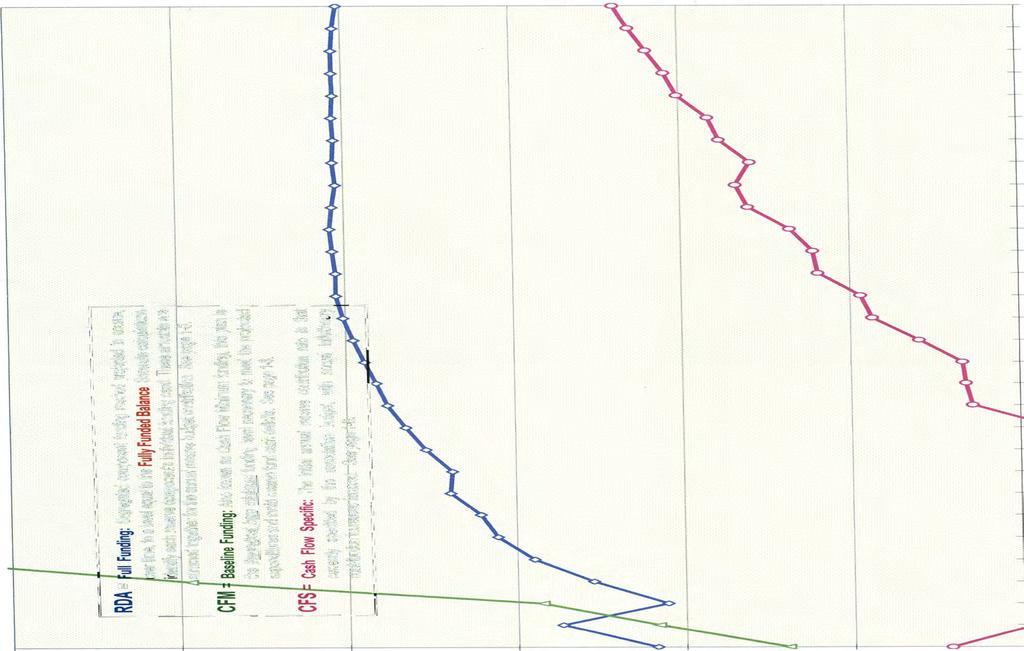

2 RESERVE DATA ANALYSIS, INC. December 30, 2011 Ms. Association Manager, CMCA, AMS SAMPLE Condo Association c/o Professional Management Company 123 Anystreet City, Minnesota ZIP Dear Ms. Manager: Osborne Road Northeast - Minneapolis, Minnesota MPLS (612) TOLL FREE: (866) FAX: (866) info@rdamidwest.com Enclosed is the completed Updated reserve study RDA REPORT, Version 002, for the fiscal year beginning January 1, This report compares three different primary funding plans, each of which is restricted to 3.25% annual contribution increases in order to provide for an equitable distribution of reserve funding expenses among current and future owners: Full Funding (Segregated Component Funding, RDA), Baseline Funding (Cash Flow Minimum, CFM) and Cash Flow Specific (2012 budgeted funding rate, CFS). Summarized here, each method is more fully explained beginning on page 1-5 of this report. CURRENT FUNDING (CFS): This analysis simply projects the likely outcome of your current funding rate based solely upon the expenditures scheduled in the report, assuming future 3.25% annual contribution increases beginning January 1, Pages 2-3 and 2-15 provide a summary and 30 year projections. The projections illustrate the inadequacy of the current funding rate ($ per unit, monthly); rendering cash deficits no later than 2013 with a peak projected shortfall of $380, by 2014 ($5, average per unit). FULL FUNDING (RDA Method): The goal of this funding plan is to gradually accumulate, by 2027, reserve savings directly proportionate to the total accrued depreciation for all components funded by reserves in this report. Pages 2-1 and 2-13 provide a summary and 30 year projections. With a 3.25% annual contribution increase restriction, the 2012 monthly contribution to reserves required under this method is $ average per unit per month (though it declines to $ by fiscal year 2017). This initial amount is $ average per unit per month above the current rate. Though considered the most conservative of official funding strategies, we find no practical or statutory need to fund to this high level. BASELINE FUNDING (CFM method): The goal of this funding plan is simply to maintain a positive reserve fund cash balance, avoiding deficits, while increasing contributions 3.25% annually. Pages 2-2 and 2-14 provide a summary and 30 year projections. The 2012 monthly contribution to reserves required under this method is $ average per unit per month (Beyond 2013, this contribution amount becomes overly aggressive). This plan projects to be sufficient to meet the expenditures scheduled in the analysis, fulfilling the mandates of state statute and the association's governing documents while providing an equitable distribution of financial burden between current and future owners. This is $ average per unit per month above the current rate. The four graphs following page 2-15 illustrate the projected performance of these three plans over a 30 year period. Directed Cash Flow Modeling - Example Incremental Underfunding Recovery Scenario: In addition to the comparative analysis outlined above we have prepared a Directed Cash Flow modeling spreadsheet which you will find at the end of the financial summaries section. The example funding scenario presented here is not limited to 3.25% annual increases. However, it does provide for reserve underfunding recovery while reducing the larger immediate initial contribution otherwise required for conventional Baseline Funding, detailed above. Rather than $ per unit monthly contributions in 2013, this schedule calls for 113.5% increases in 2013 and 2014: requiring funding of $ per unit monthly for fiscal 2013; $ per unit monthly for fiscal 2014; 80% DECREASE to $98.22 in 2015; and 3.25% annual increases thereafter. Special Note: The client s current reserve balance and contribution rate are insufficient to meet the $659, in expenditures which are scheduled for 2013 and Most of these components are already deferred and have exceeded their useful lives. It is our recommendation that the client consider obtaining a 10 year loan from a commercial bank of in the amount of at least $650, for Further, if a loan is desireable, we recommend the client consider adding $80, for the replacement of the old boilers with a new mid or high efficiency system. In either case, the client s current contribution of $ Per Unit Monthly, if increased 3.25% annualy for inflation, would project to be adequate for the ongoing maintenance of the components contained in the study, as well as for repayment of the loan.

3 We are providing you an electronic version of the DCF spreadsheet, with interest estimating formulae, which you may use to test unlimited alternative funding scenarios, perhaps even including any planned future special assessments or loan payment schedules. The spreadsheet includes several columns used to document the means of funding each component's expense. It is designed as an aid to note the association's funding policy for each component. Reserve funding policies must fulfill both statutory and governing document requirements. Also, specific disclosures regarding reserves and other funding means are required of all common interest communities by Minnesota Statute 515B Detailed funding policies will help the association satisfy Annual Report and Resale Disclosure requirements, and manage owner expectations. Where any uncertainties exists, we urge the association obtain a legal review and written opinion of the legitimacy of the funding policies, as stipulated or permitted under your Declaration and Minnesota statutes. As these are legal questions, we highly recommend use of an experienced real property attorney specializing in association law. We advise you to then prepare a document similar to our newly redesigned sample Funding Matrix to facilitate distribution of information required in your annual report and resale deisclosure certificates. Should the association adopt a reserve funding plan such as the Full Funding, Baseline or example Directed Cash Flow model we have presented, you might consider including a statement in your Resale Disclosure Certificates, such as: "The association has commissioned a professional Reserve Study which meets or exceeds the National Study Standards of The Community Associations Institute, Alexandria, VA ( the Association of Professional Reserve Analysts ( and the American Institute of Certified Public Accountants. The analysis was performed by a Professional Reserve Analyst from Reserve Data Analysis, Inc. The findings indicate the current reserve funding plan, which includes annual contribution increases, is sufficient to meet the association's long term maintenance and replacement obligations as detailed in the study. The reserve study report is available for review upon request from the association." Your RDA REPORT is presented in five parts: Part 1 User Guide: Includes a Table of Contents and offers an easy-to-understand introduction to reserve budgeting and terminology along with a guide to your reserve analysis study. Part 2 Financial Summaries: Includes a Reserve Component Funding Summary, Funding Plan Summaries & Projections, a Distribution of Accumulated Reserves report, a Fund Status Report, color charts, an Annual Expenditure Schedule (lists future expenses in future costs) and copies of the Directed Cash Flow funding scenario we prepared for your consideration. Part 3 Detail Reports: Includes detailed information for each component included in your report together with a detail report index. Part 4 Photos: Includes color photos collected during our on-site inventory or review of the property. Part 5 Appendix: Includes various supplementary information: a copy of the Minnesota Common Interest Ownership Act, a sample maintenance matrix, a reserve study update worksheet and a Minnesota Resale Disclosure Certificate form. We hope that you find our report format both informative and useful. Our services include a meeting with the board to discuss the results of the study, and to review the report and the revision process. Please call to schedule this meeting with your board. Our services also include one free revision for the fiscal year 2012 report after your review and consideration of this initial draft (within 180 days please). Each of the 93 component detail reports should be reviewed. These reports are found on pages 2-24 through An index is found on pages & Please also review the report parameters (interest yield, tax rate on earnings) on summary pages 2-1 thru 2-3. Note any desired revisions on these pages and forward them to us. Please be advised the Directed Cash Flow Modeling Spreadsheet is an auxiliary tool prepared and supplied for your use and does not supply sufficient data for purposes of revising your RDA Report. Please note any revisions on their respective Component Detail Report pages (noted above). When your revised report is prepared we will export your adjusted data and prepare a corresponding new spreadsheet for your continued use. All of us at RDA have enjoyed serving you and providing SAMPLE Condominium Association with the most detailed, comprehensive and useful reserve analysis study available. I wish you the greatest success in maintaining and enhancing property values in your community. Thank you, Jonathan Pettersen, RS

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

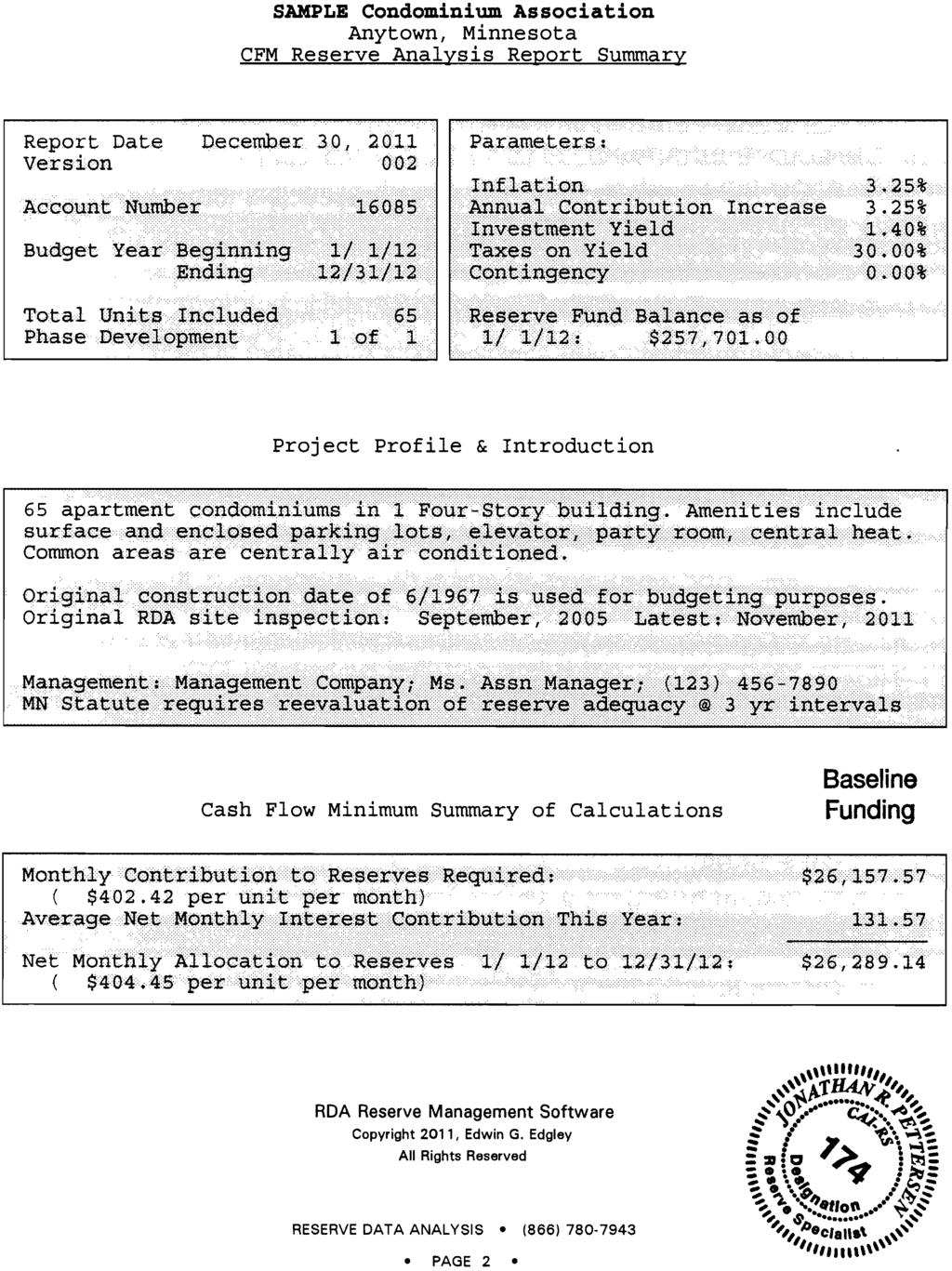

22 RESERVE COMPONENT FUNDING SUMMARY REPORT Sample Condos Minneapolis, Minnesota 65 units Based upon the reserve study prepared for the fiscal year beginning January 1, 2012 the Reserve Component Assessment plan is not sufficient to meet the expenditures projected for the next 30 years. *Based on 3.25% Annual Reserve Contribution Increases. SEE DISCLOSURES BELOW First Year of Projected Cash Deficit Amount of Shortfall Average Cost Per Unit 2013 $17, $ Year of Peak Projected Cash Deficit Amount of Shortfall Average Cost Per Unit 2014 $380, $5, Note: Becaus assessments vary by unit, the assessment applicable to a specific unit must accompany this document when included as part of a resale disclosure. BUDGETED FY 2012 RESERVE COMPONENT ASSESSMENT: Annual Amount Annual Per Unit (Average) Monthly Per Unit (Average) $84, $1, $ Note: Because assessments vary by unit, the assessment applicable to a specific unit must accompany this document when included as part of a resale disclosure. RESERVE FUND STATUS CALCULATED AS OF JANUARY 1, 2012: A) *Fully Funded Balance (total accrued depreciation) for Reserve Components $1,104, B) Reserve Fund Beginning Balance: (funded depreciation liability) $257, C) Percent (of depreciation) Funded. Line B divided by line A. 23% D) Total unfunded depreciation liability. Line A minus line B. $846, E) Average owner's unfunded depreciation liability. Line D divided by # of units. $13, *Fully Funded Balance: Effective Age of Component Estimated Useful Life X Current Replacement Cost, summed for all components. The following issues, if not disclosed, would cause a distortion of the association's condition: *Our analysis indicates that annual reserve contribution increases of 113.5% will be required for 2013 and Essentially, a need exists for Special Assessments or Alternative Funding (Such as a Commercial Bank Loan or municipal HIA assistance) to meet the expenditures estimated to be required through See the example DCF Underfunding Recovery spreadsheet included with this report. Jonathan R. Pettersen December 30, 2011 Reserve Data Analysis, Inc. Signature credentials Date NOTE: The financial representations set forth in this summary are based on information provided by the association (in part) and the best estimates of the preparer at the time the summary was prepared. The estimates are subject to change. A copy of the full reserve study report is available for review from the association upon request.

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50 Page 1 of A B C D E F G H I J K L M N O P Q R S T U V W X Y Z AA AB AC AD AE AF AG AH AI AJ AK AL AM AN AO AP AQ AR AS AT Means by Which Funding is Provided SAMPLE Condominium Assn Report 002 DCF Underfunding Recovery Example Report Date: 12/30/11 Funding to be included Funding by other Expense Special Expense charged to Reserve Funding Reserve Funding to Version Basis: 002 Funding to accrue in in annual Operating means: Specified Assessed among all benefited unit(s) when assessed only to begin when remaining Cost Inflation: 3.25% Reserve Budget. Budget. below. units when incurred. incurred. benefited unit(s). life is 30 years or less. EXPENDITURE DETAIL Asset Placed in Useful Adjust Remain Description ID Service Life +/- Life X Asphalt Drives - Chipcoating / $1, $1, $1, $1, $2, $2, X Asphalt Drives - Repairs / $4, $9, X Asphalt Drives - Replace / $17, $32, X Block Wall - Outdoor Parking Perim / $69, X Concrete - Front Entry / $20, X Garage Floor - Concrete Sealer / $18, $25, $35, Maintenance, repair & replacement is direct unit owner responsibility.? EXCLUDED Garage Floor - Concrete Replacement Excluded / $0.00 X Grate - Garage Floor Drain / $2, X Rear Parking - Concrete Sealer / $35, $49, $68, X Rear Parking - Concrete, Replace / $143, X Rear Parking - Seam Sealer / $32, X Steps - Concrete, Outdoor Parking / $2, X Roof Deck - Wood, Rooftop / $29, $56, X Roofs - Ballasted EPDM, East / $29, $52, X Roofs - Unballasted EPDM, West/Ctr / $81, X Caulk - Exterior doors & windows / $19, $26, $36, X Paint - Block Wall, Exterior Pkg / $4, $6, $8, X Paint - Ceiling & Floor, Stair Well / $6, $8, X Paint - Ceiling, Interior / $7, $10, X Paint - Garage / $8, $11, $15, X Paint - Outdoor Parking Stalls / $2, $3, $3, $4, $5, $6, X Paint - Railing, Interior, Wrought / $2, $4, X Paint - Railing, Parking, HVAC / $ $ $ $ $ $ $ $ $ $ X Paint - Railing, Parking, Wood / $ $ $ $ $ $ $ $ $ $ X Paint - Railing, Parking, Wrought / $ $ $ $ $ $ $ $ $ $ X Paint - Walls, Interior / $6, $8, $9, $11, $14, X Paint - Walls, Stairwells / $6, $9, $12, X Lighting - Entry/Lobby / $7, X Lighting - Exterior / $4, $8, X Lighting - Garage / $7, X Lighting - Hallways 1, 2, 3 & / $34, X Lighting - Laundry Room / $ X Lighting - Rear Entry Hallways / $2, X Carpet - Hallways / $33, $43, $56, $73, X Carpet - Hallways, Rear Entries / $3, $3, $5, $6, X Counter Tops - Laminate, Laundry / $ $ X Floor Cover - Eng. Wood, Lobby / $4, $6, X Floor Cover - Tile, Front Entry / $13, X Floor Cover - Tile, Laundry Room / $10, X Floor Cover - Tile, Rear Entries / $1, $3, X Furniture - Entry/Lobby / $10, $13, $18, $23, X Plumbing Fixtures / $2, $6, X Wall Cover - Dec. Wood Trim, Halls / $29, X Wall Cover - Tile, Laundry / $14, X Wallpaper - Halls, painted / $36, $56, X Wallpaper - Laundry, painted / $2, $4, $6, X Wallpaper - Lobby/Entry / $51, $75, X **Tank - Underground Fuel Storage** / $31, X Access - Entrance, Access Phone / $8, $12, X Boiler - Refurbish, Industrial / $34, X Elevator - Compliance & Refurbish / $160, X Hot Water - Domestic, Bulk Tank / $6, $10, X Hot Water - Domestic, Heater / $23, $52, X HVAC - A/C Condensing Units / $7, $10, $15, X HVAC - Carrier A/C / $22, X HVAC - Expansion Tanks / $3,500.47

51 Page 2 of A B C D E F G H I J K L M N O P Q R S T U V W X Y Z AA AB AC AD AE AF AG AH AI AJ AK AL AM AN AO AP AQ AR AS AT SAMPLE Condominium Assn Report Means by Which Funding is Provided 002 DCF Underfunding Recovery Example Report Date: 12/30/11 Funding to be included Funding by other Expense Special Expense charged to Reserve Funding Reserve Funding to Version Basis: 002 Funding to accrue in in annual Operating means: Specified Assessed among all benefited unit(s) when assessed only to begin when remaining Cost Inflation: 3.25% Reserve Budget. Budget. below. units when incurred. incurred. benefited unit(s). life is 30 years or less. EXPENDITURE DETAIL Asset Placed in Useful Adjust Remain Description ID Service Life +/- Life Maintenance, repair & replacement is direct unit owner responsibility. X HVAC - Heaters: Hydronic, Garage / $5, $10, X HVAC - Shell & Tube Heat Exchanger / $10, X Pump Replacements - Centrifugal / $9, $13, $20, X Brick - Front Entry Landscape / $ $1, $1, X Brick - Front Entry Limestone Cap / $10, X Door - Overhead, High Traffic / $8, $10, $13, $18, X Doors - Interior, Metal / $13, X Doors - Interior, Wood / $38, X Downspouts / $7, $14, X Fire Extinguisher Cabinets / $5, X Fire Protection - Control Panel / $26, $49, X Furniture - Patio / $8, $12, $17, X Railing - Wood, Interior / $ $ $ X Railing - Wood, Outdoor Parking / $2, X Railing - Wrought Iron, Exterior / $2, X Railing - Wrought Iron, Stairwells / $33, X Mailboxes - Wall Clusters / $6, X Signs - Metal, Stairwell Floor #'s / $2, X Signs - Metal, Unit Numbers / $10, X Sky Lights / $12, X Windows & Doors - Storefront, Entry / $14,739.22??? X Windows - Replacement, Condo Units / $286, Sell? X Windows - Replacement, Party Room / $2, Sell? X Paint - Ceiling, Party Room / $ $1, Sell? X Paint - Walls, Party Room / $ $ $ $1, $1, Sell? X Lighting - Party Room / $2, $4, Sell? X Appliances - Party Room Cooktop / $ $1, Sell? X Cabinets - Base & Wall, Party Room / $5, $12, Sell? X Carpet - Party Room / $2, $2, $3, $4, Sell? X Counter Tops - Cultured, Party Room / $ $ Sell? X Counter Tops - Laminate, Party Room / $1, $3, Sell? X Floor Cover - Eng. Wood, Party Room / $4, $7, Sell? X Floor Cover - Tile, Party Restroom / $ $1, Sell? X Wall Cover - Tile, Party Room / $2, Sell? X Window Covering - Mini Blinds, Party Room / $ $1, Sell? X HVAC - Sleeve Unit Air Conditioner, Party Room / $1, $1, $2, Sell? X Doors - Party Room / $ Specific disclosures regarding reserves and other funding means are required by Minnesota Statute 515B Detailed funding policies and distribution of a funding matrix will help the association satisfy disclosure requirements and manage owner expectations. Reserve funding policies must satisfy both statutory and governing document requirements. To ensure the validity of your policies, if uncertainty exists, we recommend the client obtain verification from a real estate attorney specializing in community association law. A written legal opinion is preferred. A formal reserve funding policy resolution can then be drafted, adopted by the board and permanently preserved, together with the legal opinion. Fiscal Year Beginning January 1: >> BEGINNING RESERVE BALANCE $257, $101, $75, $5, $46, $116, $162, $146, $226, $89, $154, $204, $293, $283, $268, $319, $389, $392, $473, $465, $509, $629, $655, $574, $675, $704, $845, $904, $1,008, $1,129, Yr Total Expenditures Expenditures Projected for Fiscal Year (detailed above) $240, $206, $453, $35, $9, $36, $101, $8, $227, $28, $47, $11, $114, $122, $60, $45, $116, $42, $135, $88, $17, $115, $226, $49, $127, $21, $108, $69, $58, $60, $2,989, Funding Status as of Fiscal Year Start Date $16, $104, $377, $30, $36, $80, $61, $137, $1, $60, $106, $192, $179, $160, $207, $273, $273, $350, $338, $377, $491, $513, $428, $524, $548, $683, $736, $834, $949, $1,069, Member Contributions Member Contributions Projected for Reserves $84, $84, $179, $383, $76, $79, $81, $84, $87, $89, $92, $95, $98, $102, $105, $108, $112, $116, $119, $123, $127, $131, $136, $140, $145, $149, $154, $159, $165, $170, $175, $3,879, Total Net Interest Earnings Net Projected Interest Earnings Contribution to Reserves (1.4% yield minus 30% tax) $ $ $20.96 $ $ $1, $ $1, $ $ $1, $2, $2, $2, $2, $3, $3, $3, $3, $4, $5, $5, $4, $5, $5, $7, $7, $8, $10, $11, $108, % Fiscal Year Projected ENDING RESERVE BALANCE $101, $75, $5, $46, $116, $162, $146, $226, $89, $154, $204, $293, $283, $268, $319, $389, $392, $473, $465, $509, $629, $655, $574, $675, $704, $845, $904, $1,008, $1,129, $1,256, Accrued 12/31/41 Depreciation $2,585, Depreciation Funded 12/31/41 Average per unit monthly contribution $ $ $ $ $98.22 $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ % Member Contribution Dollar Amount Increase/Decrease from previous year -$0.64 $ $ $ $3.19 $3.30 $3.40 $3.51 $3.63 $3.75 $3.87 $3.99 $4.12 $4.26 $4.40 $4.54 $4.69 $4.84 $5.00 $5.16 $5.33 $5.50 $5.68 $5.86 $6.05 $6.25 $6.45 $6.66 $6.88 $7.10 Member Contribution Percentage Increase/Decrease from previous year -0.59% % % % 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% Accrued Depreciation 1/1/ $1,104, Average Per Unit Total Annual Reserve Assessment $1, $1, $2, $5, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $2, $2, $2, $2, $2, $2, $2, $2, $2, $2, Depreciation Funded 1/1/2012 Increase/Decrease from previous year $7.70 $1, $3, $4, $38.31 $39.55 $40.84 $42.16 $43.54 $44.95 $46.41 $47.92 $49.48 $51.08 $52.75 $54.46 $56.23 $58.06 $59.94 $61.89 $63.90 $65.98 $68.12 $70.34 $72.62 $74.98 $77.42 $79.94 $82.54 $ % CRITICAL YEAR 80% DECREASE Spending thru 2014: $899, Contributions thru 2014: $646,538.63

52 $1,400, $1,200, $1,000, $800, Sample Condo Assn Report Reserve Analysis for Fiscal Year 2012 EXAMPLE Incremental Underfunding Recovery Scenario Directed Cash Flow (DCF) Modeling Excel Spreadsheet Projected Depreciation Funded 12/31/2041: 49% Depreciation Funded 1/1/2012: 23% $600, $400, $200, $ Expenditures $240, $206, $453, $35, $9, $36, $101, $8, $227, $28, $47, $11, $114, $122, $60, $45, $116, $42, $135, $88, $17, $115, $226, $49, $127, $21, $108, $69, $58, $60, Contributions $84, $179, $383, $76, $79, $81, $84, $87, $89, $92, $95, $98, $102, $105, $108, $112, $116, $119, $123, $127, $131, $136, $140, $145, $149, $154, $159, $165, $170, $175, Interest Earnings $ $ $20.96 $ $ $1, $ $1, $ $ $1, $2, $2, $2, $2, $3, $3, $3, $3, $4, $5, $5, $4, $5, $5, $7, $7, $8, $10, $11, Year End Balance $101, $75, $5, $46, $116, $162, $146, $226, $89, $154, $204, $293, $283, $268, $319, $389, $392, $473, $465, $509, $629, $655, $574, $675, $704, $845, $904, $1,008,144. $1,129,846. $1,256,213. Monthly Per Unit Contribution $ $ $ $98.22 $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ Monthly Change From Previous Year -$0.64 $ $ $ $3.19 $3.30 $3.40 $3.51 $3.63 $3.75 $3.87 $3.99 $4.12 $4.26 $4.40 $4.54 $4.69 $4.84 $5.00 $5.16 $5.33 $5.50 $5.68 $5.86 $6.05 $6.25 $6.45 $6.66 $6.88 $7.10 Expenditures Contributions Interest Earnings Year End Balance Monthly Per Unit Contribution Monthly Change From Previous Year

53 A B C D E F G H I J K L M N O P Q R S T U V W X Y Z AA AB AC AD AE AF AG AH AI AJ AK AL AM AN AO AP AQ AR AS AT Means by Which Funding is Provided Sample Condo Assn 002 DCF Underfunding Recovery Example Report Date: 12/30/11 Funding to be included Funding by other Expense Special Expense charged to Reserve Funding Reserve Funding to Version Basis: 002 Funding to accrue in in annual Operating means: Specified Assessed among all benefited unit(s) when assessed only to begin when remaining Cost Inflation: 3.25% Reserve Budget. Budget. below. units when incurred. incurred. benefited unit(s). life is 30 years or less. EXPENDITURE DETAIL Asset Placed in Useful Adjust Remain Description ID Service Life +/- Life X Asphalt Drives - Chipcoating / $1, $1, $1, $1, $2, $2, X Asphalt Drives - Repairs / $4, $9, X Asphalt Drives - Replace / $17, $32, X Block Wall - Outdoor Parking Perim / $69, X Concrete - Front Entry / $20, X Garage Floor - Concrete Sealer / $18, $25, $35, Maintenance, repair & replacement is direct unit owner responsibility.? EXCLUDED Garage Floor - Concrete Replacement Excluded / $0.00 X Grate - Garage Floor Drain / $2, X Rear Parking - Concrete Sealer / $35, $49, $68, X Rear Parking - Concrete, Replace / $143, X Rear Parking - Seam Sealer / $32, X Steps - Concrete, Outdoor Parking / $2, X Roof Deck - Wood, Rooftop / $29, $56, X Roofs - Ballasted EPDM, East / $29, $52, X Roofs - Unballasted EPDM, West/Ctr / $81, X Caulk - Exterior doors & windows / $19, $26, $36, X Paint - Block Wall, Exterior Pkg / $4, $6, $8, X Paint - Ceiling & Floor, Stair Well / $6, $8, X Paint - Ceiling, Interior / $7, $10, X Paint - Garage / $8, $11, $15, X Paint - Outdoor Parking Stalls / $2, $3, $3, $4, $5, $6, X Paint - Railing, Interior, Wrought / $2, $4, X Paint - Railing, Parking, HVAC / $ $ $ $ $ $ $ $ $ $ X Paint - Railing, Parking, Wood / $ $ $ $ $ $ $ $ $ $ X Paint - Railing, Parking, Wrought / $ $ $ $ $ $ $ $ $ $ X Paint - Walls, Interior / $6, $8, $9, $11, $14, X Paint - Walls, Stairwells / $6, $9, $12, X Lighting - Entry/Lobby / $7, X Lighting - Exterior / $4, $8, X Lighting - Garage / $7, X Lighting - Hallways 1, 2, 3 & / $34, X Lighting - Laundry Room / $ X Lighting - Rear Entry Hallways / $2, X Carpet - Hallways / $33, $43, $56, $73, X Carpet - Hallways, Rear Entries / $3, $3, $5, $6, X Counter Tops - Laminate, Laundry / $ $ X Floor Cover - Eng. Wood, Lobby / $4, $6, X Floor Cover - Tile, Front Entry / $13, X Floor Cover - Tile, Laundry Room / $10, X Floor Cover - Tile, Rear Entries / $1, $3, X Furniture - Entry/Lobby / $10, $13, $18, $23, X Plumbing Fixtures / $2, $6, X Wall Cover - Dec. Wood Trim, Halls / $29, X Wall Cover - Tile, Laundry / $14, X Wallpaper - Halls, painted / $36, $56, X Wallpaper - Laundry, painted / $2, $4, $6, X Wallpaper - Lobby/Entry / $51, $75, X **Tank - Underground Fuel Storage** / $31, X Access - Entrance, Access Phone / $8, $12, X Boiler - Refurbish, Industrial / $34, X Elevator - Compliance & Refurbish / $160, X Hot Water - Domestic, Bulk Tank / $6, $10, X Hot Water - Domestic, Heater / $23, $52, X HVAC - A/C Condensing Units / $7, $10, $15, X HVAC - Carrier A/C / $22, X HVAC - Expansion Tanks / $3, X HVAC - Heaters: Hydronic, Garage / $5, $10, X HVAC - Shell & Tube Heat Exchanger / $10, X Pump Replacements - Centrifugal / $9, $13, $20,345.92

54 A B C D E F G H I J K L M N O P Q R S T U V W X Y Z AA AB AC AD AE AF AG AH AI AJ AK AL AM AN AO AP AQ AR AS AT Sample Condo Assn Means by Which Funding is Provided 002 DCF Underfunding Recovery Example Report Date: 12/30/11 Funding to be included Funding by other Expense Special Expense charged to Reserve Funding Reserve Funding to Version Basis: 002 Funding to accrue in in annual Operating means: Specified Assessed among all benefited unit(s) when assessed only to begin when remaining Cost Inflation: 3.25% Reserve Budget. Budget. below. units when incurred. incurred. benefited unit(s). life is 30 years or less. EXPENDITURE DETAIL Asset Placed in Useful Adjust Remain Description ID Service Life +/- Life Maintenance, repair & replacement is direct unit owner responsibility. X Brick - Front Entry Landscape / $ $1, $1, X Brick - Front Entry Limestone Cap / $10, X Door - Overhead, High Traffic / $8, $10, $13, $18, X Doors - Interior, Metal / $13, X Doors - Interior, Wood / $38, X Downspouts / $7, $14, X Fire Extinguisher Cabinets / $5, X Fire Protection - Control Panel / $26, $49, X Furniture - Patio / $8, $12, $17, X Railing - Wood, Interior / $ $ $ X Railing - Wood, Outdoor Parking / $2, X Railing - Wrought Iron, Exterior / $2, X Railing - Wrought Iron, Stairwells / $33, X Mailboxes - Wall Clusters / $6, X Signs - Metal, Stairwell Floor #'s / $2, X Signs - Metal, Unit Numbers / $10, X Sky Lights / $12, X Windows & Doors - Storefront, Entry / $14,739.22??? X Windows - Replacement, Condo Units / $286, Sell? X Windows - Replacement, Party Room / $2, Sell? X Paint - Ceiling, Party Room / $ $1, Sell? X Paint - Walls, Party Room / $ $ $ $1, $1, Sell? X Lighting - Party Room / $2, $4, Sell? X Appliances - Party Room Cooktop / $ $1, Sell? X Cabinets - Base & Wall, Party Room / $5, $12, Sell? X Carpet - Party Room / $2, $2, $3, $4, Sell? X Counter Tops - Cultured, Party Room / $ $ Sell? X Counter Tops - Laminate, Party Room / $1, $3, Sell? X Floor Cover - Eng. Wood, Party Room / $4, $7, Sell? X Floor Cover - Tile, Party Restroom / $ $1, Sell? X Wall Cover - Tile, Party Room / $2, Sell? X Window Covering - Mini Blinds, Party Room / $ $1, Sell? X HVAC - Sleeve Unit Air Conditioner, Party Room / $1, $1, $2, Sell? X Doors - Party Room / $ X Loan Payments Jan years $89, $89, $89, $89, $89, $89, $89, $89, $89, $89, Specific disclosures regarding reserves and other funding means are required by Minnesota Statute 515B Detailed funding policies and distribution of a funding matrix will help the association satisfy disclosure requirements and manage owner expectations. Reserve funding policies must satisfy both statutory and governing document requirements. To ensure the validity of your policies, if uncertainty exists, we recommend the client obtain verification from a real estate attorney specializing in community association law. A written legal opinion is preferred. A formal reserve funding policy resolution can then be drafted, adopted by the board and permanently preserved, together with the legal opinion. Fiscal Year Beginning January 1: >> BEGINNING RESERVE BALANCE $257, $101, $1,181, $717, $673, $658, $618, $514, $505, $278, $253, $211, $298, $286, $268, $316, $383, $383, $461, $450, $490, $606, $628, $543, $641, $665, $802, $856, $955, $1,072, Yr Total Expenditures Expenditures Projected for Fiscal Year (detailed above) $240, $295, $542, $124, $98, $125, $190, $97, $316, $117, $136, $11, $114, $122, $60, $45, $116, $42, $135, $88, $17, $115, $226, $49, $127, $21, $108, $69, $58, $60, $3,879, Funding Status as of Fiscal Year Start Date $16, $456, $639, $593, $575, $533, $427, $416, $188, $161, $116, $200, $184, $163, $207, $270, $267, $341, $325, $361, $472, $490, $402, $494, $514, $644, $693, $786, $896, $1,011, Member Contributions Member Contributions Projected for Reserves $84, $84, $70, $72, $74, $77, $79, $82, $84, $87, $90, $93, $96, $99, $102, $106, $109, $113, $116, $120, $124, $128, $132, $137, $141, $146, $150, $155, $160, $166, $171, $3,375, Total Net Interest Earnings Net Projected Interest Earnings Contribution to Reserves (1.4% yield minus 30% tax) $ $4, $6, $6, $5, $5, $4, $4, $2, $1, $1, $2, $2, $2, $2, $3, $3, $3, $3, $4, $5, $5, $4, $5, $5, $6, $7, $8, $9, $10, $139, % Loan Proceeds $650, Fiscal Year Projected ENDING RESERVE BALANCE $101, $1,181, $717, $673, $658, $618, $514, $505, $278, $253, $211, $298, $286, $268, $316, $383, $383, $461, $450, $490, $606, $628, $543, $641, $665, $802, $856, $955, $1,072, $1,193, Accrued 12/31/41 Depreciation $2,585, Depreciation Funded 12/31/41 Average per unit monthly contribution $ $ $89.74 $92.66 $95.67 $98.78 $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ % Member Contribution Dollar Amount Increase/Decrease from previous year -$0.64 -$18.00 $2.92 $3.01 $3.11 $3.21 $3.31 $3.42 $3.53 $3.65 $3.77 $3.89 $4.02 $4.15 $4.28 $4.42 $4.56 $4.71 $4.87 $5.02 $5.19 $5.36 $5.53 $5.71 $5.89 $6.09 $6.28 $6.49 $6.70 $6.92 Member Contribution Percentage Increase/Decrease from previous year -0.59% % 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% Accrued Depreciation 1/1/ $1,104, Average Per Unit Total Annual Reserve Assessment $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $2, $2, $2, $2, $2, $2, $2, $2, $2, Depreciation Funded 1/1/2012 Increase/Decrease from previous year $7.70 $ $35.00 $36.14 $37.31 $38.52 $39.78 $41.07 $42.40 $43.78 $45.21 $46.67 $48.19 $49.76 $51.37 $53.04 $54.77 $56.55 $58.39 $60.28 $62.24 $64.27 $66.35 $68.51 $70.74 $73.04 $75.41 $77.86 $80.39 $ % CRITICAL YEAR Spending thru 2014: $1,077, Contributions thru 2014: $226,315.00

55 $1,200, $1,000, $800, $600, SAMPLE Condo Association Reserve Analysis for Fiscal Year 2012 EXAMPLE Scenario Including LOAN Payment Schedule Directed Cash Flow (DCF) Modeling Excel Spreadsheet Projected Depreciation Funded 12/31/2041: 46% Depreciation Funded 1/1/2012: 23% $400, $200, $ Expenditures $240, $295, $542, $124, $98, $125, $190, $97, $316, $117, $136, $11, $114, $122, $60, $45, $116, $42, $135, $88, $17, $115, $226, $49, $127, $21, $108, $69, $58, $60, Contributions $84, $70, $72, $74, $77, $79, $82, $84, $87, $90, $93, $96, $99, $102, $106, $109, $113, $116, $120, $124, $128, $132, $137, $141, $146, $150, $155, $160, $166, $171, Interest Earnings $ $4, $6, $6, $5, $5, $4, $4, $2, $1, $1, $2, $2, $2, $2, $3, $3, $3, $3, $4, $5, $5, $4, $5, $5, $6, $7, $8, $9, $10, Year End Balance $101, $1,181,055. $717, $673, $658, $618, $514, $505, $278, $253, $211, $298, $286, $268, $316, $383, $383, $461, $450, $490, $606, $628, $543, $641, $665, $802, $856, $955, $1,072,384. $1,193,596. Monthly Per Unit Contribution $ $89.74 $92.66 $95.67 $98.78 $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ Monthly Change From Previous Year -$0.64 -$18.00 $2.92 $3.01 $3.11 $3.21 $3.31 $3.42 $3.53 $3.65 $3.77 $3.89 $4.02 $4.15 $4.28 $4.42 $4.56 $4.71 $4.87 $5.02 $5.19 $5.36 $5.53 $5.71 $5.89 $6.09 $6.28 $6.49 $6.70 $6.92 Expenditures Contributions Interest Earnings Year End Balance Monthly Per Unit Contribution Monthly Change From Previous Year

56 Page 1 of A B C D E F G H I J K L M N O P Q R S T U V W X Y Z AA AB AC AD AE AF AG AH AI AJ AK AL AM AN AO AP AQ AR AS AT ALTERNATE DCF UNDERFUNDING RECOVERY EXAMPLE - EXCLUDING UNIT WINDOWS Maintenance, repair & replacement is direct unit owner responsibility. Funding to be included in annual Operating Budget. Funding by other means: Specified below. Means by Which Funding is Provided Expense Special Assessed among all units when incurred. Expense charged to benefited unit(s) when incurred. Reserve Funding assessed only to benefited unit(s). Reserve Funding to begin when remaining life is 30 years or less. Sample Condominium Alternate DCF Underfunding Recovery Example Report Date: 12/30/11 Version Basis: 002 DCF - EXCLUDING WINDOWS Cost Inflation: 3.25% EXPENDITURE DETAIL Asset Placed in Useful Adjust Remain Description ID Service Life +/- Life X Asphalt Drives - Chipcoating / $1, $1, $1, $1, $2, $2, X Asphalt Drives - Repairs / $4, $9, X Asphalt Drives - Replace / $17, $32, X Block Wall - Outdoor Parking Perim / $69, X Concrete - Front Entry / $20, X Garage Floor - Concrete Sealer / $18, $25, $35, Funding to accrue in Reserve Budget.? EXCLUDED Garage Floor - Concrete Replacement Excluded / $0.00 X Grate - Garage Floor Drain / $2, X Rear Parking - Concrete Sealer / $35, $49, $68, X Rear Parking - Concrete, Replace / $143, X Rear Parking - Seam Sealer / $32, X Steps - Concrete, Outdoor Parking / $2, X Roof Deck - Wood, Rooftop / $29, $56, X Roofs - Ballasted EPDM, East / $29, $52, X Roofs - Unballasted EPDM, West/Ctr / $81, X Caulk - Exterior doors & windows / $19, $26, $36, X Paint - Block Wall, Exterior Pkg / $4, $6, $8, X Paint - Ceiling & Floor, Stair Well / $6, $8, X Paint - Ceiling, Interior / $7, $10, X Paint - Garage / $8, $11, $15, X Paint - Outdoor Parking Stalls / $2, $3, $3, $4, $5, $6, X Paint - Railing, Interior, Wrought / $2, $4, X Paint - Railing, Parking, HVAC / $ $ $ $ $ $ $ $ $ $ X Paint - Railing, Parking, Wood / $ $ $ $ $ $ $ $ $ $ X Paint - Railing, Parking, Wrought / $ $ $ $ $ $ $ $ $ $ X Paint - Walls, Interior / $6, $8, $9, $11, $14, X Paint - Walls, Stairwells / $6, $9, $12, X Lighting - Entry/Lobby / $7, X Lighting - Exterior / $4, $8, X Lighting - Garage / $7, X Lighting - Hallways 1, 2, 3 & / $34, X Lighting - Laundry Room / $ X Lighting - Rear Entry Hallways / $2, X Carpet - Hallways / $33, $43, $56, $73, X Carpet - Hallways, Rear Entries / $3, $3, $5, $6, X Counter Tops - Laminate, Laundry / $ $ X Floor Cover - Eng. Wood, Lobby / $4, $6, X Floor Cover - Tile, Front Entry / $13, X Floor Cover - Tile, Laundry Room / $10, X Floor Cover - Tile, Rear Entries / $1, $3, X Furniture - Entry/Lobby / $10, $13, $18, $23, X Plumbing Fixtures / $2, $6, X Wall Cover - Dec. Wood Trim, Halls / $29, X Wall Cover - Tile, Laundry / $14, X Wallpaper - Halls, painted / $36, $56, X Wallpaper - Laundry, painted / $2, $4, $6, X Wallpaper - Lobby/Entry / $51, $75, X **Tank - Underground Fuel Storage** / $31, X Access - Entrance, Access Phone / $8, $12, X Boiler - Refurbish, Industrial / $34, X Elevator - Compliance & Refurbish / $160,016.00

57 Page 2 of 2 A B C D E F G H I J K L M N O P Q R S T U V W X Y Z AA AB AC AD AE AF AG AH AI AJ AK AL AM AN AO AP AQ AR AS AT Means by Which Funding is Provided Sample Condominium Alternate DCF Underfunding Recovery Example Report Date: 12/30/11 Funding to be included Expense Special Expense charged to Reserve Funding Reserve Funding to Version Basis: 002 DCF - EXCLUDING WINDOWS Funding by other Funding to accrue in in annual Operating Assessed among all benefited unit(s) when assessed only to begin when remaining Cost Inflation: 3.25% means: Specified below. Reserve Budget. Budget. units when incurred. incurred. benefited unit(s). life is 30 years or less. EXPENDITURE DETAIL Asset Placed in Useful Adjust Remain Description ID Service Life +/- Life Maintenance, repair & replacement is direct unit owner responsibility. X Hot Water - Domestic, Bulk Tank / $6, $10, X Hot Water - Domestic, Heater / $23, $52, X HVAC - A/C Condensing Units / $7, $10, $15, X HVAC - Carrier A/C / $22, X HVAC - Expansion Tanks / $3, X HVAC - Heaters: Hydronic, Garage / $5, $10, X HVAC - Shell & Tube Heat Exchanger / $10, X Pump Replacements - Centrifugal / $9, $13, $20, X Brick - Front Entry Landscape / $ $1, $1, X Brick - Front Entry Limestone Cap / $10, X Door - Overhead, High Traffic / $8, $10, $13, $18, X Doors - Interior, Metal / $13, X Doors - Interior, Wood / $38, X Downspouts / $7, $14, X Fire Extinguisher Cabinets / $5, X Fire Protection - Control Panel / $26, $49, X Furniture - Patio / $8, $12, $17, X Railing - Wood, Interior / $ $ $ X Railing - Wood, Outdoor Parking / $2, X Railing - Wrought Iron, Exterior / $2, X Railing - Wrought Iron, Stairwells / $33, X Mailboxes - Wall Clusters / $6, X Signs - Metal, Stairwell Floor #'s / $2, X Signs - Metal, Unit Numbers / $10, X Sky Lights / $12, X Windows & Doors - Storefront, Entry / $14,739.22??? EXCLUDED Windows - Replacement, Condo Units / $0.00 Sell? X Windows - Replacement, Party Room / $2, Sell? X Paint - Ceiling, Party Room / $ $1, Sell? X Paint - Walls, Party Room / $ $ $ $1, $1, Sell? X Lighting - Party Room / $2, $4, Sell? X Appliances - Party Room Cooktop / $ $1, Sell? X Cabinets - Base & Wall, Party Room / $5, $12, Sell? X Carpet - Party Room / $2, $2, $3, $4, Sell? X Counter Tops - Cultured, Party Room / $ $ Sell? X Counter Tops - Laminate, Party Room / $1, $3, Sell? X Floor Cover - Eng. Wood, Party Room / $4, $7, Sell? X Floor Cover - Tile, Party Restroom / $ $1, Sell? X Wall Cover - Tile, Party Room / $2, Sell? X Window Covering - Mini Blinds, Party Room / $ $1, Sell? X HVAC - Sleeve Unit Air Conditioner, Party Room / $1, $1, $2, Sell? X Doors - Party Room / $ Specific disclosures regarding reserves and other funding means are required by Minnesota Statute 515B Detailed funding policies and distribution of a funding matrix will help the association satisfy disclosure requirements and manage owner expectations. Reserve funding policies must satisfy both statutory and governing document requirements. To ensure the validity of your policies, if uncertainty exists, we recommend the client obtain verification from a real estate attorney specializing in community association law. A written legal opinion is preferred. A formal reserve funding policy resolution can then be drafted, adopted by the board and permanently preserved, together with the legal opinion. Fiscal Year Beginning January 1: >> BEGINNING RESERVE BALANCE $257, $101, $10, $1, $44, $117, $166, $152, $235, $100, $168, $221, $314, $307, $295, $349, $423, $430, $515, $511, $559, $683, $714, $637, $744, $778, $924, $988, $1,098, $1,226, Yr Total Expenditures Expenditures Projected for Fiscal Year (detailed above) $240, $206, $166, $35, $9, $36, $101, $8, $227, $28, $47, $11, $114, $122, $60, $45, $116, $42, $135, $88, $17, $115, $226, $49, $127, $21, $108, $69, $58, $60, $2,702, Funding Status as of Fiscal Year Start Date $16, $104, $155, $34, $35, $81, $64, $143, $7, $71, $121, $209, $199, $184, $234, $304, $307, $388, $379, $423, $541, $568, $487, $588, $617, $756, $815, $918, $1,039, $1,165, Member Contributions Member Contributions Projected for Reserves $84, $84, $115, $157, $78, $81, $84, $86, $89, $92, $95, $98, $101, $105, $108, $112, $115, $119, $123, $127, $131, $135, $140, $144, $149, $154, $159, $164, $169, $175, $181, $3,685, Total Net Interest Earnings Net Projected Interest Earnings Contribution to Reserves (1.4% yield minus 30% tax) $ $42.93 $7.19 $ $ $1, $ $1, $ $1, $1, $2, $2, $2, $2, $3, $3, $4, $4, $4, $5, $6, $5, $6, $6, $8, $8, $9, $10, $12, $118, % Fiscal Year Projected ENDING RESERVE BALANCE $101, $10, $1, $44, $117, $166, $152, $235, $100, $168, $221, $314, $307, $295, $349, $423, $430, $515, $511, $559, $683, $714, $637, $744, $778, $924, $988, $1,098, $1,226, $1,358, Accrued 12/31/41 Depreciation $2,585, Depreciation Funded 12/31/41 Average per unit monthly contribution $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ % Member Contribution Dollar Amount Increase/Decrease from previous year -$0.64 $39.87 $ $ $3.29 $3.39 $3.50 $3.62 $3.73 $3.86 $3.98 $4.11 $4.24 $4.38 $4.52 $4.67 $4.82 $4.98 $5.14 $5.31 $5.48 $5.66 $5.84 $6.03 $6.23 $6.43 $6.64 $6.86 $7.08 $7.31 Member Contribution Percentage Increase/Decrease from previous year -0.59% 37.00% 37.00% % 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% 3.25% Accrued Depreciation 1/1/ $1,104, Average Per Unit Total Annual Reserve Assessment $1, $1, $1, $2, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $1, $2, $2, $2, $2, $2, $2, $2, $2, $2, $2, $2, Depreciation Funded 1/1/2012 Increase/Decrease from previous year $7.70 $ $ $1, $39.43 $40.72 $42.04 $43.40 $44.82 $46.27 $47.78 $49.33 $50.93 $52.59 $54.30 $56.06 $57.88 $59.76 $61.71 $63.71 $65.78 $67.92 $70.13 $72.41 $74.76 $77.19 $79.70 $82.29 $84.96 $ % CRITICAL YEAR 50% DECREASE Spending thru 2014: $613, Contributions thru 2014: $356,909.48

58 $1,400, $1,200, $1,000, $800, $600, Sample Condominium Association Reserve Analysis for Fiscal Year 2012 EXAMPLE Incremental Underfunding Recovery Scenario Directed Cash Flow (DCF) Modeling Excel Spreadsheet Projected Depreciation Funded 12/31/2041: 53% Depreciation Funded 1/1/2012: 23% $400, $200, $ Expenditures $240, $206, $166, $35, $9, $36, $101, $8, $227, $28, $47, $11, $114, $122, $60, $45, $116, $42, $135, $88, $17, $115, $226, $49, $127, $21, $108, $69, $58, $60, Contributions $84, $115, $157, $78, $81, $84, $86, $89, $92, $95, $98, $101, $105, $108, $112, $115, $119, $123, $127, $131, $135, $140, $144, $149, $154, $159, $164, $169, $175, $181, Interest Earnings $ $42.93 $7.19 $ $ $1, $ $1, $ $1, $1, $2, $2, $2, $2, $3, $3, $4, $4, $4, $5, $6, $5, $6, $6, $8, $8, $9, $10, $12, Year End Balance $101, $10, $1, $44, $117, $166, $152, $235, $100, $168, $221, $314, $307, $295, $349, $423, $430, $515, $511, $559, $683, $714, $637, $744, $778, $924, $988, $1,098,388. $1,226,007. $1,358,511. Monthly Per Unit Contribution $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ Monthly Change From Previous Year -$0.64 $39.87 $ $ $3.29 $3.39 $3.50 $3.62 $3.73 $3.86 $3.98 $4.11 $4.24 $4.38 $4.52 $4.67 $4.82 $4.98 $5.14 $5.31 $5.48 $5.66 $5.84 $6.03 $6.23 $6.43 $6.64 $6.86 $7.08 $7.31 Expenditures Contributions Interest Earnings Year End Balance Monthly Per Unit Contribution Monthly Change From Previous Year

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

100

101

102

103

104

105

106

107

108

109

110

111

112

113

114

115

116

117

118

119

120

121

122

123

124

125

126

127

128

129

130

131

132

133

134

135

136

137

138

139

140

141

142

143

144

145

146

147

148

149

150

151

152

153

154

155

156

157 Sample Condo site pics 1 / 13 IMG_6568.JPG IMG_6569.JPG IMG_6570.JPG IMG_6571.JPG IMG_6572.JPG IMG_6573.JPG IMG_6574.JPG IMG_6575.JPG IMG_6576.JPG IMG_6577.JPG IMG_6578.JPG IMG_6579.JPG

158 Sample Condo site pics 2 / 13 IMG_6580.JPG IMG_6581.JPG IMG_6582.JPG IMG_6583.JPG IMG_6584.JPG IMG_6585.JPG IMG_6586.JPG IMG_6587.JPG IMG_6588.JPG IMG_6589.JPG IMG_6590.JPG IMG_6591.JPG

159 Sample Condo site pics 3 / 13 IMG_6592.JPG IMG_6593.JPG IMG_6594.JPG IMG_6595.JPG IMG_6596.JPG IMG_6597.JPG IMG_6598.JPG IMG_6599.JPG IMG_6600.JPG IMG_6601.JPG IMG_6602.JPG IMG_6603.JPG

160 Sample Condo site pics 4 / 13 IMG_6604.JPG IMG_6605.JPG IMG_6609.JPG IMG_6610.JPG IMG_6611.JPG IMG_6612.JPG IMG_6613.JPG IMG_6614.JPG IMG_6615.JPG IMG_6616.JPG IMG_6617.JPG IMG_6618.JPG

161 Sample Condo site pics 5 / 13 IMG_6619.JPG IMG_6620.JPG IMG_6621.JPG IMG_6622.JPG IMG_6623.JPG IMG_6624.JPG IMG_6625.JPG IMG_6626.JPG IMG_6627.JPG IMG_6628.JPG IMG_6629.JPG IMG_6630.JPG

162 Sample Condo site pics 6 / 13 IMG_6631.JPG IMG_6632.JPG IMG_6633.JPG IMG_6634.JPG IMG_6635.JPG IMG_6636.JPG IMG_6637.JPG IMG_6638.JPG IMG_6639.JPG IMG_6640.JPG IMG_6641.JPG IMG_6642.JPG

163 Sample Condo site pics 7 / 13 IMG_6643.JPG IMG_6644.JPG IMG_6645.JPG IMG_6646.JPG IMG_6647.JPG IMG_6648.JPG IMG_6649.JPG IMG_6650.JPG IMG_6651.JPG IMG_6652.JPG IMG_6653.JPG IMG_6654.JPG

164 Sample Condo site pics 8 / 13 IMG_6655.JPG IMG_6656.JPG IMG_6657.JPG IMG_6658.JPG IMG_6659.JPG IMG_6660.JPG IMG_6661.JPG IMG_6662.JPG IMG_6663.JPG IMG_6664.JPG IMG_6665.JPG IMG_6666.JPG

165 Sample Condo site pics 9 / 13 IMG_6667.JPG IMG_6668.JPG IMG_6669.JPG IMG_6670.JPG IMG_6671.JPG IMG_6672.JPG IMG_6673.JPG IMG_6674.JPG IMG_6675.JPG IMG_6676.JPG IMG_6677.JPG IMG_6678.JPG

166 Sample Condo site pics 10 / 13 IMG_6679.JPG IMG_6680.JPG IMG_6681.JPG IMG_6682.JPG IMG_6683.JPG IMG_6684.JPG IMG_6685.JPG IMG_6686.JPG IMG_6687.JPG IMG_6688.JPG IMG_6689.JPG IMG_6690.JPG

167 Sample Condo site pics 11 / 13 IMG_6691.JPG IMG_6692.JPG IMG_6693.JPG IMG_6694.JPG IMG_6695.JPG IMG_6696.JPG IMG_6697.JPG IMG_6698.JPG IMG_6699.JPG IMG_6700.JPG IMG_6701.JPG IMG_6702.JPG

168 Sample Condo site pics 12 / 13 IMG_6703.JPG IMG_6704.JPG IMG_6705.JPG IMG_6706.JPG IMG_6707.JPG IMG_6708.JPG IMG_6709.JPG IMG_6710.JPG IMG_6711.JPG IMG_6712.JPG IMG_6713.JPG IMG_6714.JPG

169 Sample Condo site pics 13 / 13 IMG_6715.JPG IMG_6716.JPG IMG_6717.JPG IMG_6718.JPG IMG_6719.JPG IMG_6720.JPG IMG_6721.JPG IMG_6722.JPG IMG_6723.JPG IMG_6724.JPG

170

171

172 RESERVE DATA ANALYSIS, INC Osborne Road Northeast - Minneapolis, Minnesota MPLS (612) TOLL FREE: (866) FAX: (866) info@rdamidwest.com On May 27, 2011 Minnesota Statutes 2010, section 515B was amended to read: 515B REPLACEMENT RESERVES. (a) The association shall include in its annual budgets replacement reserves projected by the board to be adequate, together with past and future contributions to replacement reserves, to fund the replacement of those components of the common interest community which the association is obligated to replace, by reason of ordinary wear and tear or obsolescence, subject to the following: (1) The amount annually budgeted for replacement reserves shall be adequate, together with past and future contributions to replacement reserves, to replace the components as determined based upon the estimated remaining useful life of each component; provided that portions of replacement reserves need not be segregated for the replacement of specific components. (2) Unless otherwise required by the declaration, annual budgets need not include reserves for the replacement of (i) components that [have] a remaining useful life of more than 30 years, or (ii) components whose replacement will be funded by assessments authorized under section 515B (e)(1), or approved in compliance with clause (5). (3) The association shall keep the replacement reserves in an account or accounts separate from the association's operating funds, and shall not use or borrow from the replacement reserves to fund the association's operating expenses, provided that this restriction shall not affect the association's authority to pledge the replacement reserves as security for a loan to the association. (4) The association shall reevaluate the adequacy of its budgeted replacement reserves at least every third year after the recording of the declaration creating the common interest community. (5) Unless otherwise required by the declaration, after the termination of the period of declarant control, and subject to approval (i) by the board and (ii) by unit owners, other than declarant or its affiliates, of units to which 51 percent of the votes in the association are allocated, the association need not annually assess for replacement reserves to replace those components whose replacement is planned to be paid for by special assessments, if the declaration authorizes special assessments, or by assessments levied under section 515B (e)(2). The approval provided for in the preceding sentence shall be effective for no more than the association's current and three following fiscal years, subject to modification or renewal by the same approval standards. (6) Unless otherwise required by the declaration, subsection (a) shall not apply to a common interest community which is restricted to nonresidential use. (b) Unless the declaration provides otherwise, any surplus funds that the association has remaining after payment of or provision for common expenses and reserves shall be (i) credited to the unit owners to reduce their future common expense assessments or (ii) credited to reserves, or any combination thereof, as determined by the board of directors. (c) This section applies to common interest communities only for their fiscal years commencing on or after January 1, 2012.

173

174

175

176

177

178

179

180

181

182

183

184

185

186

187

188

189

190

191

192

193

194

195

196

197

198

199

200

201

202

203

204

205

206

207

208

209

210

211

212

213

214

215

216

217

218

219

220

221

222

223

224

225

226

227

228

229

230

231

232

233

234

235

236

237

238

239

240

241

242

243

244

245

246

247

248

249

250

251

252

253

254

255

256

257

258

259

260

261

262

263

264

265

266

267 Reserve Data Analysis Example Association Maintenance Responsibility and Funding Matrix Component Description Level of Service - Maintain; Repair; Replace. 1 2 Reserve Funding to Funding to begin when accrue in remaining Reserve life 30 years Budget. or less. Means by Which Funding is Provided 3 Reserve Funding assessed only to unit(s) benefited. 4 5 Expense Expense Special charged to Assessed benefited among all owner(s) at units when time cost incurred. incurred. 6 Maintenance, repair & replacement is direct homeowner's responsibility. 7 OTHER: Specify Below Roofs: composite shingles, architectural grade, 30 year warranty. Repair X Replace X Siding: standard grade Dutch Lap vinyl Repair X Replace X Soffit & Fascia: prefinished metal. Repair X Replace X Gutters & Downspouts - Standard Quantity common to all units. Repair X Replace X Gutters & Downspouts - Non-Standard extra guttering; added by unit Repair X owner. Replace X Common area sidewalks Repair X Replace X Unit Sidewalks Repair X Replace X Unit Stoops Repair X Replace X Unit Patios Repair X Replace X Unit Decks & Railings Paint/Stain X Repair X Replace X Unit Windows Repair X Replace 50% 50% Unit Doors Paint X Repair X Replace X Unit Exterior Lighting Repair X Replace X Garage Aprons Repair X Replace X Overhead Garage Doors Paint X Repair X Replace X Garage Door Openers All X Concrete Curbs & Gutters Repair X Replacement scheduled to coincide with street 40 years. Replace X Driveways - Asphalt Annual Clean, X crack seal, minor repairs Sealcoat replaces lost aggregate fines & binders. Sealcoat X Midlife failures provides for replacement of failed base and subsoil. Midlife X Failures Replace X Streets Annual X Cleaning, crack seal, minor repairs Chipcoat provides new wear surface and UV protection. Chipcoat X Midlife failures provides for replacement of failed base and subsoil. Overlays & reconstruction scheduled to Alternate at 20 year intervals. Midlife Failures X Overlay X Reconstruct X Continued on next page 8 Funding to be included in annual Operating Budget.

268 Continued from previous page Means by Which Funding is Provided Component Description Level of Service - Maintain; Repair; Replace. 1 2 Reserve Funding to Funding to begin when accrue in remaining Reserve life 30 years Budget. or less. 3 Reserve Funding assessed only to unit(s) benefited. 4 5 Expense Expense Special charged to Assessed benefited among all owner(s) at units when time cost incurred. incurred. 6 Maintenance, repair & replacement is direct homeowner's responsibility. 7 OTHER: Specify Below 8 Funding to be included in annual Operating Budget. Entrance - Wrought Iron, Gates All X Mailboxes: Cluster Box Units Repair USPS Replace X Street, traffic & directional signs Repair X Replace X Monument Signs Repair X Replace X Keystone Retaining Walls Repair X Replace X Landscape: periodic refurbishment, rock beds, tree trimming, etc. Refurbish X Shrubs & Trees Replace X Irrigation System: Replace X Backflows inspected annually; repair/replace as-needed or minimum 5 year interval per state law. Total system replacement unbudgeted; individual zones or areas may be Controller Backflow Valve X replaced upon failure. Special assessment will be required if total system Repairs X replacement becomes necessary or desirable. Replace X Sanitary Sewer Lateral Lines to homes All X Water lines from valve to structure All X Water Mains; sanitary sewer; storm sewer lines, catch basins, etc. All If assessed City TV Inspect all sewer lines before street reconstruction. Inspection X Streetlights All Utility Co. Boat Slips: All X Main Dock Repair X Replace X Reserve Study Update with On-site Review, 3 year intervals. Update X 1) These expenses are budgeted to accrue in the association's replacement reserve account and are included in the annual assessment. 2) These expenses are not currently budgeted in reserves but are to be added when the estimated remaining life falls within 30 years. 3) These expenses are budgeted to accrue in replacement reserves. However, their reserve contributions are assessed only to the benefited unit(s). 4) These expenses are to be special assessed, if the declaration allows special assessments, against all owners at the time the expense is incurred. The board and at least 51% of unit owners must approve exclusion from reserve funding at least every 3 years. NOTE: Declaration may limit implementing Special Assessments. 5) These expenses are to be assessed only against benefited owners at the time the expense is incurred. Unless the declaration requires otherwise, Limited Common Elements may be excluded [5115B.3-115(e)(1)] from reserve funding simply by policy. For so-called benefit assessments [515B.3-115(e)(2)], both the board and at least 51% of unit owners must approve exclusion from reserve funding at least every 3 years. 6) The administrative and financial obligations are the homeowners direct and individual responsibility, subject to community standards. 7) These expenses are funded by the entity or means noted. 8) These expenses are to be included in the association's annual operating budget for the year in which they occur. Note: Funding obligations and options are subject to the association's declaration as well as statutory stipulations. Minnesota Statute was amended in 2010 & B Replacement Reserves. While the Amendment retains the basic standard for 'adequate' replacement reserves, it stipulates the basis on which reserves must be determined, but stops short of requiring a professional Reserve Study. It requires replacement reserves be kept separate from operating funds, and expressly prohibits the use of, or borrowing from, replacement reserves to fund the association's operating expenses. The association must reevaluate the adequacy of its replacement reserves at least every third year after the recording of the declaration. Reserve funding is optional for Limited Common Elements and components with a remaining estimated useful life greater than 30 years. The Amendment includes a flexibility provision whereby, unless otherwise provided by the declaration, after the termination of the period of declarant control the association may fund certain replacement costs through special assessments (if the Declaration provides for special assessments) or other assessments rather than annual assessments; provided that such a plan is approved by the board and by 51% of unit owners-- excluding the declarant or its affiliates. The vote must be reaffirmed at 3 year intervals, per 515B (a)(5).

269 COMMON INTEREST COMMUNITY RESALE DISCLOSURE CERTIFICATE Name of Common Interest Community: Name of Association: Address of Association: Unit Number(s) (include principal unit and any garage, storage, or other auxiliary units): Common elements licensed under Minnesota Statutes, subsection 515B.2-109(e): The following information is furnished by the association named above according to Minnesota Statutes, section 515B There is no right of first refusal or other restraint on the free alienability of the above unit(s) contained in the declaration, bylaws, rules and regulations, or any amendment to them, except as follows: 2. The following periodic installments of common expense assessments and special assessments are payable with respect to the above unit(s): a. Annual assessment installments: $ Due: b. Special assessment installments: $ Due: c. Unpaid assessments, fines, or other charges: (1) Annual $ (2) Special $ (3) Fines $ (4) Other Charges $ d. The association has/has not (strike one) approved a plan for levying certain common expense assessments against fewer than all the units according to Minnesota Statutes, subsection 515B.3-115(e). If a plan is approved, a description of the plan is attached to this certificate. 3. In addition to the amounts due under paragraph 2, the following additional fees or charges other than assessments are payable by unit owners (include late payment charges, user fees, etc.): 4. There are no extraordinary expenditures approved by the association, and not yet assessed, for the current and two succeeding fiscal years, except as follows: page 1 of 4

270 5. The association is obligated to replace the following components of the common interest community: The association has the following amounts in its reserves for replacement of those components: The replacement of the following components is funded by assessments levied only against the unit or units served by the component, pursuant to Minnesota Statutes subsection 515B.3-115(e) (1) or (2). 6. The following documents are furnished with this certificate according to statute: a. The most recent regularly prepared balance sheet and income and expense statement of the association. b. The current budget of the association. 7. There are no unsatisfied judgments against the association, except as follows (identify creditor and amount): 8. There are no pending lawsuits to which the association is a party, except as follows (identify and summarize status): 9. Description of insurance coverages: a. The association provides the following insurance coverage for the benefit of unit owners: (Reference may be made to applicable sections of the declaration or bylaws; however, any additional coverages should be described in this space) b. The following described fixtures, decorating items, or construction items within the unit referred to in Minnesota Statutes, subsection 515B.3-113(b), are insured by the association (check as applicable): Ceiling or wall finishing materials Finished Flooring Cabinetry page 2 of 4

271 Finished millwork Electrical, heating, ventilating and air conditioning equipment or plumbing fixtures serving a single unit Built-in appliances Improvements and betterments as originally constructed Additional improvements and betterments installed by unit owners 10. The board of directors of the association has not notified the unit owner -- (i) that any alterations or improvements to the unit or to the limited common elements assigned to it violate any provision of the declaration; or (ii) that the unit is in violation of any governmental statute, ordinance, code, or regulation, --except as follows: 11. The remaining term of any leasehold estate affecting the common interest community and the premises governing any extension or renewal of it are as follows: 12. This Resale Disclosure Certificate is given in connection with the resale of a unit by a unit owner who is not a declarant and who, therefore, is not liable for express warranties under Minnesota Statutes, section 515B or implied warranties under Minnesota Statutes, section 515B The conveyance of this unit may, however, result in a transfer of pre-existing warranties made by a declarant under the referenced statutes, subject to the terms of Minnesota Statutes, sections 515B and 515B In addition to the above, the following matters affecting the occupancy or use of the unit, or the unit owner's obligations with respect to the unit, are deemed material: I hereby certify that the foregoing information and statements are true and correct as of (Date) By: Title: (Association representative) Address: Phone Number: page 3 of 4

272 RECEIPT [Of Common Interest Community Resale Disclosure Documents] In addition to the foregoing information furnished by the association, the unit owner is obligated to furnish to the purchaser before execution of any purchase agreement for a unit or otherwise before conveyance, copies of the following documents relating to the association or to the master association (as applicable): the declaration (other than any common interest community plat), articles of incorporation, bylaws, rules and regulations (if any), and any amendments to these documents. Receipt of the foregoing documents, and the resale disclosure certificate, is acknowledged by the undersigned buyer(s). Dated: (Buyer) Dated: (Buyer) page 4 of 4

273 XYZ Homeowners Association RDA (SAMPLE) POLICY ON RESERVES Adopted: xx/xx/xxxx Definitions: The determination of whether an expense should be labeled an operational expense, a reserve expense, or excluded altogether from a budget is sometimes subjective. Since this classification may have a major impact on the financial plans of the association, subjective determinations should be minimized. Therefore, for purposes of this policy: "Operational Expenses" and "Operating Budget Items" shall be defined as expenses, which are identified by the Board of Directors, as occurring on an annual or greater frequency, no matter the size of the expense, and are considered by the Board to be effectively budgeted for on an annual basis. They are characterized as being reasonably predictable both in terms of frequency and cost. Operational expenses normally include all minor expenses which would not otherwise adversely affect an operational budget from one year to the next. "Reserve Expenses" and "Reserve Budget Items" shall be defined as expenses, which are identified by the Board of Directors, as major expenses which occur other than annually and which are budgeted for in advance in order to provide the necessary funds in time for their occurrence. Reserve expenses are generally reasonably predictable both in terms of frequency and cost. However, they may include significant components which have an indeterminable but potential liability to the development and which may be demonstrated as a likely occurrence. They are expenses, which when incurred, would have a significant effect on the smooth operation of the budgetary process from one year to the next, were they not reserved for in advance. Reserve budgets for associations normally do not include repairs or replacements of assets which are deemed to have an estimated useful life equal to or exceeding the estimated useful life of the facility or development itself, or exceeding the legal life of the development as defined in an association's governing documents. Also excluded are insignificant expenses which may be covered either by an operating or reserve contingency, or otherwise in a general maintenance fund. Costs which are caused by acts of God, accidents or other occurrences which are more properly insured for, rather than reserved for, are also normally excluded. Section I: As soon as possible after construction of the initial phase of the project, the Association shall cause a Reserve Study to be completed incorporating all aspects of the existing development. The study, and written report, must meet or exceed the National Reserve Study Standards of the Community Associations Institute (CAI) of Alexandria, Virginia ( and be performed by a qualified person with experience in conducting such studies. The Reserve Study preparer shall abide by the CAI Code of Ethics for Reserve Specialists (whether credentialed or not) and shall certify full compliance with all these aforementioned requirements. Section II: The Board of Directors for the association shall review the completed reserve study for content and take all necessary precautions to assure that the analysis is as complete and accurate as possible, and that the analysis accurately reflects the goals, policies and procedures set forth and practiced by the Association. Section III: The Board of Directors shall adopt a reserve funding plan calculated to avoid special assessments and to assure that the Association will accrue adequate reserves on a cumulative basis to meet its obligations in maintaining the development in a good state of repair, in accordance with its own policies, and in accordance with the requirements set forth by the Association's governing documents and applicable statutes. In adopting a funding plan, the Board of Directors shall act in good faith, in a manner believed to be in the best interest of the present and future membership, and with such care as an ordinarily prudent and reasonable person in like position would use under similar circumstances. Section IV: All reserve funds shall be segregated from other association monies and shall be invested only in accounts or instruments fully guaranteed against any loss of principal and accrued interest earnings. Expenditures of reserve funds for items contained in the reserve schedule are subject to prior approval by a vote (simple majority) of the Board of Directors. Expenditures of reserve funds for items NOT funded in the reserve schedule must first be approved by either a unanimous vote of the Board of Directors or by a vote (simple majority) of the entire membership. Reserve funds may only be used for capital expenditures, except in the case of disbursements related to dissolution of the corporate entity. Section V: The Board of Directors shall review the reserve study and adopted funding plan at least annually, and shall consider and implement any necessary adjustments to the reserve budget as a result of that review. At least once every three years the Board of Directors shall cause an updated analysis of the reserve study to be conducted incorporating all new and/or changed aspects of the development. This update must be performed in full compliance with Section I, above, and shall meet the level of service "Update with Site Visit" as defined by the National Reserve Study Standards. Revised November, 2005 COPYRIGHT RESERVE DATA ANALYSIS MIDWEST TOLL FREE (866)

274 RESERVE UPDATE WORKSHEET page 1 of 2 NAME OF ASSOCIATION DATE REPRESENTATIVE TELEPHONE PART 1 PROJECTED RESERVE BALANCE Please estimate the reserve balance at the beginning of the fiscal year for which this report is being prepared. CURRENT RESERVE BALANCE: / / 1 MONTHLY CONTRIBUTION TO RESERVES: NUMBER OF MONTHS TO END OF CURRENT FISCAL YEAR: REMAINING CONTRIBUTIONS (Line 2 x Line 3): ANTICIPATED EXPENDITURES (List IN PART 3): PROJECTED RESERVE BALANCE (Line 1 + Line 4 - Line 5): PART 2 RESERVE EXPENDITURES SINCE LAST STUDY Please provide the following information for reserve expenditures completed since the last RDA reserve study. Or make appropriate notations on past RDA reserve study and mail copy to us. COMPLETION QUANTITY/ RDA ASSET # DESCRIPTION DATE UNITS COST

275 PART 3 ANTICIPATED RESERVE EXPENDITURES Please indicate any anticipated reserve expenditures to be completed this fiscal year. RDA ASSET # DESCRIPTION COMPLETION QUANTITY/ DATE UNITS COST PART 4 ADDITIONAL CHANGES, ADDITIONS OR COMMENTS Please indicate any additional changes, report additions or comments. Please return Update Worksheet and any additional information to: RESERVE DATA ANALYSIS - MIDWEST Phone: (612) (866) Osborne Road NE Fax: (763) (866) Minneapolis, MN info@rdamidwest.com Thank you! page 2 of 2

616-4817 - TOLL FREE: (866) 780-7943 - FAX: (866) 484-7943 Email: info@rdamidwest.")

276 RESERVE DATA ANALYSIS - MIDWEST Osborne Road Northeast - Minneapolis, Minnesota MPLS (612) TOLL FREE: (866) FAX: (866) info@rdamidwest.com Protect Your Association Finances Volunteer boards of directors of condominiums, cooperatives, and homeowners' associations often perform a number of functions vital to the successful self-governance of the association: fostering community harmony, maintaining common areas and establishing and enforcing rules. The ability of the association to perform these functions depends upon its success as a business. One of the most important business functions of the board is to oversee the association's financial well-being. Here are several proven practices that will help protect association finances. Before implementing the following suggestions, however, always check your governing documents and state statutes. 1 Conduct An Annual Audit, Review Or Compilation. A certified public accountant (CPA), selected by the association board, should conduct an annual analysis of the association's finances. The accountant should have access to original books and records. All personnel, contractors, and volunteers should cooperate fully during the course of the analysis. The association board may request one of three levels of service from the accountant: compilation, review or audit. In a compilation, the accountant presents the association's financial statements in a manner consistent with generally accepted accounting principles. A compilation involves little analysis and no confirmation of balances. Often, the accountant will prepare the yearend adjustments, such as accounts payable or income tax accruals. In a review, the accountant investigates record-keeping practices and accounting policies and analyzes the statements. The accountant prepares disclosures on unusual items or trends that may require explanation. In an audit, the accountant performs a more thorough analysis, which may include confirming bank balances, making physical inspections, and tracing transactions to invoices and evidence of payments. Although an audit is a more comprehensive examination of an association's financial statements, it is not an analysis of the board's policy decisions or its use of resources. After the analysis is completed, the accountant expresses an opinion based on the results of the audit tests and examinations. The opinion is independent of the association and management. Before deciding which method to use, check association documents and state statutes. A full audit may be required. And always consider conducting a review or audit when a major change is made in the way the association handles its finances (e.g., transition from developer to owner control or a change in management) 2 Ask For A Management Letter. Ask your accountant for a management letter. In this letter, the accountant reports any weaknesses in the association's financial systems, as well as issues concerning internal control, income tax, reserves, and document compliance. The cost of the report is minor compared to the consequences of an inadequately scrutinized financial system. After the accountant has written the management letter, he or she should review it with the board 3 Reconcile Statements Quarterly. The board should review bank statements or passbooks for all cash accounts at least every three months. The board must see that bank statements are reconciled in a timely fashion. If the treasurer reconciles the bank statements, then the board should designate another person to review the reconciliation. If the reconciliations are done by a manager, management agent, or bookkeeping service, the treasurer of the board should carefully evaluate the system, its internal controls, and the reconciliations and calculations. 4 Request Monthly or Quarterly Financial Statements. The accountant should submit a financial report to the board at least every three months. The report should include a balance sheet, profit and loss statement, and a comparison of the budget to actual expenditures. The financial statements should show activity for both the operating and reserve funds. The financial statements may be prepared on either a cash, accrual, or modified cash basis. The accrual method is effective for most associations because it matches revenues to expenses incurred more accurately Regardless of the accounting method used by the association, the board should monitor an aged list of accounts receivable (delinquencies) and accounts payable (unpaid hills) The financial report should he accompanied by an explanation of any significant variances, such as significant cash surpluses, shortages, excessive accounts payable or receivable, or major budget overruns The board should investigate any excessive variance and ask questions if the financial statements are not produced 15 to 30 days after the close of the period The board should closely review the income statement, compare it with the budget, and question any major difference. 5 Exclusive Board Control of Reserve Transactions. The board must have full and separate control over the association's reserve account(s), including the signatory control of bank accounts. All transactions made by board designees should be reported and verified in writing. These transactions should he approved by the board, and that