Christian Leadership Alliance May 2, :00 a.m.

|

|

|

- Corey Stevenson

- 5 years ago

- Views:

Transcription

1 Christian Leadership Alliance May 2, :00 a.m.

2 Presenters Mark Jones VP & Senior Banking Consultant ECCU Caryn Ryan Managing Member Missionwell LLC

3 Clear performance expectations Optimize around constraints Actualize long term plans Inputs Budget Actions Results Meaning Learning Coordinate the team s activities Control over processes

4 Benefits Cements business planning Aligns teams and units around goals Measurement of results against a standard can drive performance Creates a dialogue and solutions around constraints Integrates with financial reporting Drawbacks Ties company to one year look Too much effort for benefit Goals are either too easy or unrealistically difficult; gamesmanship to spend it all Doesn t accommodate changes in the business May feel off plan in some years, thus demotivating Focus on short term results at the expense of value drivers Internally focused

5 Activity based budgeting Zero based budgeting Rolling budgets/rolling forecasts Flexible budgets Risk weighted budgeting Targets through benchmarking Statistical forecasting techniques Aligning budgets for impact

6 Concerns >> High overhead Low objectivity Unclear program costs Irregular revenue Budget Inputs relevance vary a lot High seasonality Overstated revenue Rapid growth LT plan delivery Activity-based budgeting x x x x Zero-based budgeting x x x Rolling budgets/rolling forecasts x x x Flexible budgets x x Risk-weighted budgeting x x Targets through benchmarking Statistical forecasting techniques Aligning budgets for impact x x x x x

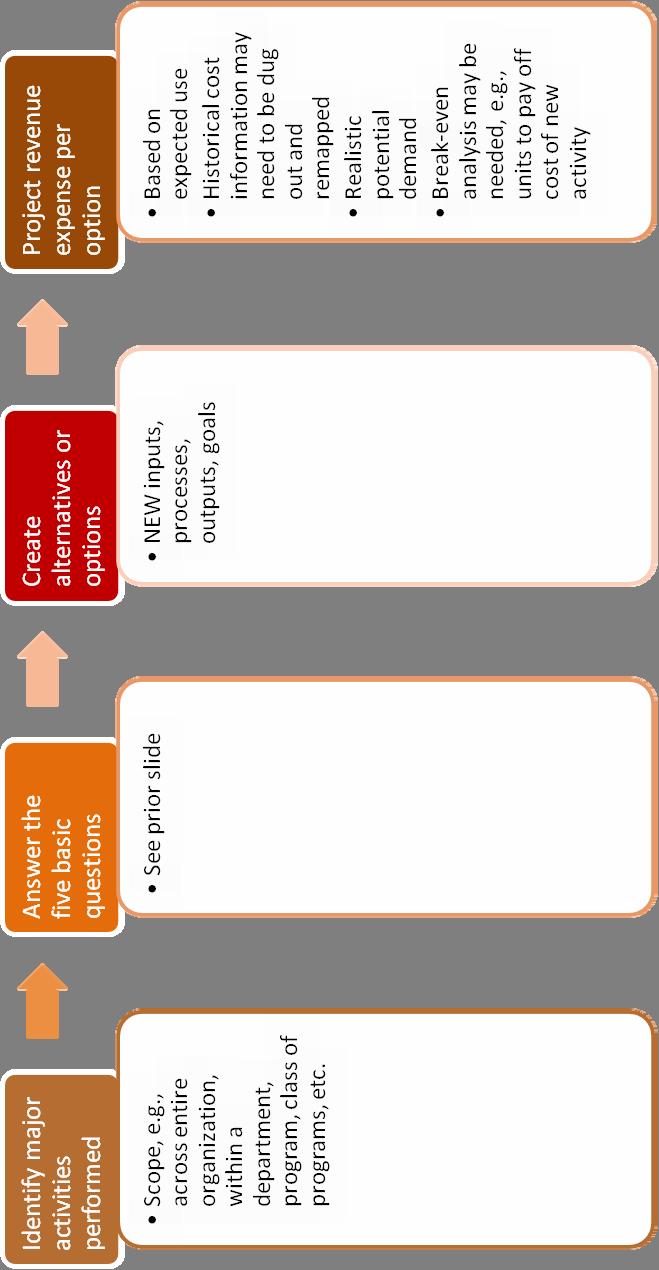

7 Based on activity based costing: Approach to overhead allocation enhancing accuracy of costs Applicable when overhead is a significant portion of costs and products or services differ greatly in volume or complexity Two step process: Defining activities and their cost drivers Benefit: More accurate cost of services/products Multiple cost pools vs. one (traditional) Improved control over overhead as managers see connections to cost drivers Improved pricing of services/products and decisions over manufacturing Drawback: Time consuming (use only as needed)

8 You need to determine profitability of grants: Grantors may ask for ABB You need to determine whether programs are recovering their costs. You want to benchmark your costs and need a standard methodology. You are stuck trying to determine where to focus cost reductions or activity increases.

9 What if scenarios used to test/optimize budget cases

10 Traditional budgeting is incremental. With ZBB, an activity, program, or position must make the cut off for investment each year. Introduced by Peter Drucker in the 1960s. It s andated for certain governmental units at times. Benefits: Ties use of resources to today s goals. Every year is new. Challenges the status quo > Fresh ideas and innovation Drawbacks: Challenging status quo can be uncomfortable. Time intensive. May work best to use on select activities rather than across the board Use when: Assumptions or circumstances have changed and a new approach is required. Generally not useful for grants (justified by funding).

11 1. Should the activity, program, or position be continued, or might other activities be higher priority? 2. Should the manner it s performed change? 3. If so, how, when, and by whom? 4. How much should be spent on the activity or program? 5. Is change doable?

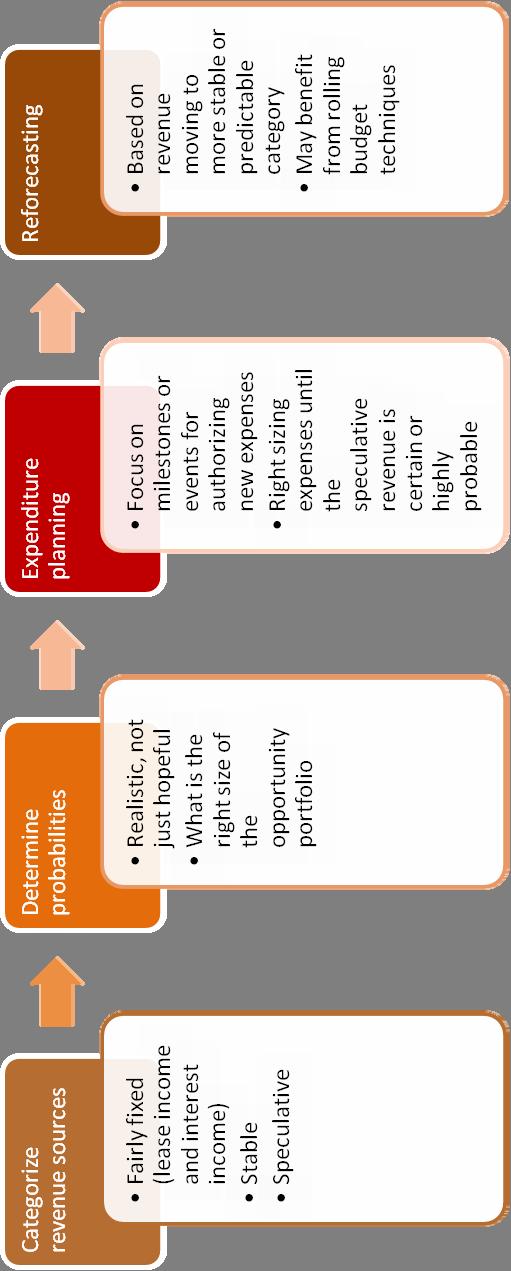

12

13 Abandon Change existing effort: Outsource, automate, simplify, improve, redirect Leave as is

14 Traditional budget has static time frame of next fiscal year. Rolling, or continuous, budget adds a period (month or quarter, typically) as the current budget expires. Example: Budgeting horizon is 18 months. A new quarter is added to the end of the period as every quarter completes. Advantages: Better reflection of actual results than a static budget Organization focus is always out to the budget horizon (which requires more planning) Multi year rolling budget alerts you faster when you re off long term plan Avoids coasting if objectives are met early Disadvantages: More resource intensive Generally early budget assumptions are not revised, which can make early periods irrelevant. If early periods are revised (rolling forecast), it makes accountability (and aligning rewards) more difficult Generally cannot be as much of a participative budgeting process

15 Use when: You need to identify and adjust to trouble spots beyond the budget horizon, e.g., liquidity as a seasonal issue. Timing of revenue (month to month or quarterto quarter) is more difficult to plan, though you re confident it will eventually happen. You want staff to focus on the pipeline of opportunities and cycle time to convert.

16 Efficient implementation typically requires automated budget tools.

17 Traditional: Static budget looking at one scenario Flexible: Multiple scenarios, each with its own revenue and expenses: Initiated in manufacturing industry to handle variable costs Useful for non profits that may have different program capacities depending on contributions or other fundraising Split costs into those that vary with the program size (variable) and those that do not (fixed) Example based on units: Church school budgets for 80, 90, or 100 students per year. Enrollment closes after budget is prepared, allowing choice of which budget applies. Example based on fundraising (conditional): Budget with and without major gift or grant, e.g., change in program scope. One is base and one is conditional.

18 Advantages: Multiple cases prepared, organization poised to move between cases and take necessary cost actions Disadvantages: Accountability if there is a degree of control over what is flexing. If lose important grant, should organization be accountable? Use when: Not clear what demand for services will take place Not clear which grants will be received, impacting size or existence of certain programs

19 Use when not all sources of revenue will come to pass. Use flexible budgets if there are only a few significant scenarios; use risk weighted budgeting if many irons in the fire. Controlling cost of uncertain revenues is critical.

20 Activity $ Amount % Likelihood Grant Grant Grant Grant Subtotal grants Risk weighted 289

21

22 What are benchmarks? Any aspect of operations, financial or non financial, can be benchmarked. Benchmarks may be internal (program to program) or external (comparable or out of the box ). Easiest (and not very useful due to comparability issues): Form 990 data, Charity Navigator How are they used in budgeting? Expenses: See ABC/B, benchmark the cost driver Revenue: Benchmark the value driver

23 A key question for non profits is how to evaluate and forecast returns for different aspects of development: Channels (direct mail, special events, major giving, web, radio, etc.) Within categories, campaigns or positions may be compared.

24 Can also prepare by development representative

25 Need a track record or some history as baseline Performance goals may be one year or multiyear: Tie to long term planning objectives Incorporate transparently into budget: May budget 80 percent of goal Align variable compensation, contract renewals, other rewards, and incentives to percent achievement of the goals: Variable pay may start above 100% (budget or selffunded)

26

27 Simple regression techniques: Exponential growth Linear (least squares) Use Excel (and common sense) Multiple regression Non linear regression Fuzzy logic Don t worry, we aren t going here!

28 Month Actual revenue Forecast Month FY Tot GROWTH: Exponential growth trend think compound interest" Last 12 months Last 6 months FORECAST: Linear growth continue a straight line Last 12 months Last 6 months

29 Plot the data Learn to use R2 and other statistical techniques for validity Correlation is NOT causality

30 Every long term plan is achieved a day at a time. Budget is a slice of your long term plan. Annual goals build to long term goals. Or, they do not! Budget Long term goals

31 Occurs when each layer of the pyramid further articulates and describes the preceding layers, beginning at the top

32

Program dollars Staff FTEs Tactics in budget")

33 Strategic goals Strategic priorities Strategies (includes those crossing budget year) Program dollars Staff FTEs Tactics in budget year

34 Determine what techniques best fit your circumstances: Culture Resources available Pressing issue you want to solve Consider the extra effort of advanced budgeting: Need to go beyond financial system for data (e.g., donor data base) Budgeting software to allow greater frequency Get senior leadership buy in to approach ahead: Unless its just analytical or simple forecasting (e.g., regression)

35 For more resources, visit

36

From Cost to Value: Reframe How You Measure Travel. The Link Between Business Strategy and Travel Cost- Savings. How to Manage Hidden Travel Costs

The days of quick wins and sweeping savings in travel management are probably over. If you've not already been through multiple cost-saving initiatives, you're the exception rather than the rule. So when

The days of quick wins and sweeping savings in travel management are probably over. If you've not already been through multiple cost-saving initiatives, you're the exception rather than the rule. So when

explain why organisations use budgeting and how budgetary systems fit within the performance hierarchy

Budgeting Outcome By the end of this session you should be able to: explain why organisations use budgeting and how budgetary systems fit within the performance hierarchy describe the factors which influence

Budgeting Outcome By the end of this session you should be able to: explain why organisations use budgeting and how budgetary systems fit within the performance hierarchy describe the factors which influence

Control: Actual results can be compared against the budget and action is taken as appropriate.

Understanding Budgeting Budgeting is a key aspect of management accounting and particularly impacts on the areas of planning, control and performance management. A budget is a quantitative plan prepared

Understanding Budgeting Budgeting is a key aspect of management accounting and particularly impacts on the areas of planning, control and performance management. A budget is a quantitative plan prepared

Impact of changes to the Paper P3, Business Analysis and Paper P5, Advanced Performance Management syllabuses from June 2011

RELEVANT TO ACCA QUALIFICATION PAPERS P3 AND P5 Impact of changes to the Paper P3, Business Analysis and Paper P5, Advanced Performance Management syllabuses from June 2011 This article explains the rationale

RELEVANT TO ACCA QUALIFICATION PAPERS P3 AND P5 Impact of changes to the Paper P3, Business Analysis and Paper P5, Advanced Performance Management syllabuses from June 2011 This article explains the rationale

FRx FORECASTER FRx SOFTWARE CORPORATION

FRx FORECASTER FRx SOFTWARE CORPORATION Photo: PhotoDisc FRx Forecaster It s about control. Today s dynamic business environment requires flexible budget development and fast, easy revision capabilities.

FRx FORECASTER FRx SOFTWARE CORPORATION Photo: PhotoDisc FRx Forecaster It s about control. Today s dynamic business environment requires flexible budget development and fast, easy revision capabilities.

BUDGETING FOR SUCCESS Thursday, November 1, Presented by : Dr Brian Hankerson Hankerson Consulting Group

BUDGETING FOR SUCCESS Thursday, November 1, 2018 Presented by : Dr Brian Hankerson Hankerson Consulting Group WORKSHOP OBJECTIVES Many institutions in our sector struggle to achieve enrollment growth and

BUDGETING FOR SUCCESS Thursday, November 1, 2018 Presented by : Dr Brian Hankerson Hankerson Consulting Group WORKSHOP OBJECTIVES Many institutions in our sector struggle to achieve enrollment growth and

Running Your Business for Growth

Accenture Insurance Running Your Business for Growth Could Your Operating Model Be Standing in the Way? 1 95 percent of senior executives are not certain their companies have the right operating model

Accenture Insurance Running Your Business for Growth Could Your Operating Model Be Standing in the Way? 1 95 percent of senior executives are not certain their companies have the right operating model

Survey Rolling forecasting anno 2018

Survey Rolling forecasting anno 2018 Executive summary, April 2018 Patrick Tullemans Finext The survey reflects on the status of Rolling Forecasting in the Netherlands as per April 2018 Key question: Does

Survey Rolling forecasting anno 2018 Executive summary, April 2018 Patrick Tullemans Finext The survey reflects on the status of Rolling Forecasting in the Netherlands as per April 2018 Key question: Does

BUSINESS AND FINANCIAL AFFAIRS DIVISION BUDGET OFFICE

Six-Year Planning: Initiative Summary Title: Implement More Effective and Efficient Budget Tools Initiative description, including statement of purpose and anticipated outcomes: The purpose of this initiative

Six-Year Planning: Initiative Summary Title: Implement More Effective and Efficient Budget Tools Initiative description, including statement of purpose and anticipated outcomes: The purpose of this initiative

SIZING UP ZERO- BASED BUDGETING. A closer look at a promising alternative to traditional fiscal planning

SIZING UP ZERO- BASED BUDGETING A closer look at a promising alternative to traditional fiscal planning A closer look at a promising alternative to traditional fiscal planning: SIZING UP ZERO-BASED BUDGETING

SIZING UP ZERO- BASED BUDGETING A closer look at a promising alternative to traditional fiscal planning A closer look at a promising alternative to traditional fiscal planning: SIZING UP ZERO-BASED BUDGETING

Budgeting for Small Schools

Budgeting for Small Schools College Business Management Institute July 2017 Presented by Lisa Marie McCauley, Ed.D, CPA Senior Vice President for Finance Middle States Commission on Higher Education Chief

Budgeting for Small Schools College Business Management Institute July 2017 Presented by Lisa Marie McCauley, Ed.D, CPA Senior Vice President for Finance Middle States Commission on Higher Education Chief

Lessons from two case-studies: How to Build Accurate and models

Lessons from two case-studies: How to Build Accurate and Decision-Focused @RISK models Palisade Risk Conference New Orleans, LA Nov, 2014 Huybert Groenendaal, PhD, MBA Managing Partner EpiX Analytics Two

Lessons from two case-studies: How to Build Accurate and Decision-Focused @RISK models Palisade Risk Conference New Orleans, LA Nov, 2014 Huybert Groenendaal, PhD, MBA Managing Partner EpiX Analytics Two

Transforming the Insurance Enterprise through Adaptive Systems. An Oracle White Paper December 2009

Transforming the Insurance Enterprise through Adaptive Systems An Oracle White Paper December 2009 Transforming the Insurance Enterprise through Adaptive Systems By Chuck Johnston TRANSFORMATION: BUSINESS

Transforming the Insurance Enterprise through Adaptive Systems An Oracle White Paper December 2009 Transforming the Insurance Enterprise through Adaptive Systems By Chuck Johnston TRANSFORMATION: BUSINESS

UNIVERSITY OF TOLEDO INTERNAL AUDIT DEPARTMENT DEVELOP BUDGETS

The following control objectives provide a basis for strengthening your control environment for the process of developing budgets. When you select an objective, you will access a list of the associated

The following control objectives provide a basis for strengthening your control environment for the process of developing budgets. When you select an objective, you will access a list of the associated

Chapter 9 Activity-Based Costing

Chapter 9 Activity-Based Costing SUMMARY This chapter deals with the allocation of indirect costs to products. Product cost information helps managers make numerous decisions, such as pricing, keeping

Chapter 9 Activity-Based Costing SUMMARY This chapter deals with the allocation of indirect costs to products. Product cost information helps managers make numerous decisions, such as pricing, keeping

Upstream and downstream costs are often interdependent: eg. R+D and customer service.

CHAPTER 14. PERIOD COST APPLICATION Support department cost allocation is treated separately in part because most period costs are excluded from inventoriable costs by accounting standards. But prices

CHAPTER 14. PERIOD COST APPLICATION Support department cost allocation is treated separately in part because most period costs are excluded from inventoriable costs by accounting standards. But prices

Effective Corporate Budgeting

Effective Corporate Budgeting in 8 Easy Steps This ebook will offer 8 easy and easy and proven steps for improving your corporate budgeting and planning process. You will see that by making a few small

Effective Corporate Budgeting in 8 Easy Steps This ebook will offer 8 easy and easy and proven steps for improving your corporate budgeting and planning process. You will see that by making a few small

The value of a stand-alone rating engine

WHITE PAPER The value of a stand-alone rating engine As more carriers move from legacy policy administration systems (PAS) to newer technologies, critical choices must be made: Do they choose an all-in-one

WHITE PAPER The value of a stand-alone rating engine As more carriers move from legacy policy administration systems (PAS) to newer technologies, critical choices must be made: Do they choose an all-in-one

Board for Actuarial Standards

MEMORANDUM To: From: Board for Actuarial Standards Chaucer Actuarial Date: 20 November 2009 Subject: Chaucer Response to BAS Consultation Paper: Insurance TAS Introduction This

MEMORANDUM To: From: Board for Actuarial Standards Chaucer Actuarial Date: 20 November 2009 Subject: Chaucer Response to BAS Consultation Paper: Insurance TAS Introduction This

Strategic Budgeting Workgroup April 4, 2007

Strategic Budgeting Workgroup April 4, 2007 Recap goals Agenda Planned sequence of meetings Today s s objectives 1 1 Recap: Producing flexibility Mandate internal reallocations in units Eliminate or reduce

Strategic Budgeting Workgroup April 4, 2007 Recap goals Agenda Planned sequence of meetings Today s s objectives 1 1 Recap: Producing flexibility Mandate internal reallocations in units Eliminate or reduce

Cabinet Committee on State Sector Reform and Expenditure Control STAGE 2 OF TRANSFORMING NEW ZEALAND S REVENUE SYSTEM

Cabinet Committee on State Sector Reform and Expenditure Control In Confidence Office of the Minister of Revenue STAGE 2 OF TRANSFORMING NEW ZEALAND S REVENUE SYSTEM Proposal 1. This paper provides an

Cabinet Committee on State Sector Reform and Expenditure Control In Confidence Office of the Minister of Revenue STAGE 2 OF TRANSFORMING NEW ZEALAND S REVENUE SYSTEM Proposal 1. This paper provides an

True Program Costs: Program Budgets and Allocations

True Program Costs: Program Budgets and Allocations While the long-term goal for nonprofits is not to return profits to shareholders, we all know that nonprofits are business entities that need to maintain

True Program Costs: Program Budgets and Allocations While the long-term goal for nonprofits is not to return profits to shareholders, we all know that nonprofits are business entities that need to maintain

Article from. Risks and Rewards. February 2017 Issue 69

Article from Risks and Rewards February 2017 Issue 69 Strategic Asset Allocation in Asia: Optimizing Across Portfolios By Michael Chan, Fred Ngan, Thomas Tang and Jack Law Note: This is an excerpt of a

Article from Risks and Rewards February 2017 Issue 69 Strategic Asset Allocation in Asia: Optimizing Across Portfolios By Michael Chan, Fred Ngan, Thomas Tang and Jack Law Note: This is an excerpt of a

Brief Contents. Preface xv Acknowledgements xix

Brief Contents Preface xv Acknowledgements xix PART ONE Foundations of Management Accounting 1 Chapter 1 Why Management Accounting Matters 3 Chapter 2 Cost Concepts and Classifications 27 Chapter 3 Cost

Brief Contents Preface xv Acknowledgements xix PART ONE Foundations of Management Accounting 1 Chapter 1 Why Management Accounting Matters 3 Chapter 2 Cost Concepts and Classifications 27 Chapter 3 Cost

Straight-Through Processing: What Does This Mean to Treasury?

Straight-Through Processing: What Does This Mean to Treasury? Mike Gallanis Treasury Strategies Inc. Partner Al Briand The Bank of New York Mellon Head of Product Management Treasury Services Division

Straight-Through Processing: What Does This Mean to Treasury? Mike Gallanis Treasury Strategies Inc. Partner Al Briand The Bank of New York Mellon Head of Product Management Treasury Services Division

Building a Strong Organizational Financial Plan. Michigan Association of United Ways Annual Meeting

Building a Strong Organizational Financial Plan Michigan Association of United Ways Annual Meeting 7/8/2015 Agenda 1. Financial Planning The chicken or the Egg? 2. Mission Based Budgeting 3. The Expense

Building a Strong Organizational Financial Plan Michigan Association of United Ways Annual Meeting 7/8/2015 Agenda 1. Financial Planning The chicken or the Egg? 2. Mission Based Budgeting 3. The Expense

Risk averse. Patient.

Risk averse. Patient. Opportunistic. For discretionary use by investment professionals. Litman Gregory Portfolio Strategies at a Glance We employ tactical asset allocation by identifying undervalued asset

Risk averse. Patient. Opportunistic. For discretionary use by investment professionals. Litman Gregory Portfolio Strategies at a Glance We employ tactical asset allocation by identifying undervalued asset

The Complete Course On Budgeting: Planning, Forecasting, What If Analysis And Reporting

The Complete Course On Budgeting: Planning, Forecasting, What If Analysis And Reporting SECTOR / ACCOUNTING AND FINANCE NON-TECHNICAL & CERTIFIED TRAINING COURSE The use of Excel as the toolbox of choice

The Complete Course On Budgeting: Planning, Forecasting, What If Analysis And Reporting SECTOR / ACCOUNTING AND FINANCE NON-TECHNICAL & CERTIFIED TRAINING COURSE The use of Excel as the toolbox of choice

RACC CRA. Certified Research Administrator. Download Full Version :

RACC CRA Certified Research Administrator Download Full Version : http://killexams.com/pass4sure/exam-detail/cra Successful budget process relies greatly upon effective communications. Strong communication

RACC CRA Certified Research Administrator Download Full Version : http://killexams.com/pass4sure/exam-detail/cra Successful budget process relies greatly upon effective communications. Strong communication

MODULE 4 PLANNING AND CONTROL

MODULE 4 PLANNING AND CONTROL OUTLINES The purpose of budgetary control system Alternative approaches to budgeting, including incremental budgeting, Zero-based budgeting, Activity-based budgeting, rolling

MODULE 4 PLANNING AND CONTROL OUTLINES The purpose of budgetary control system Alternative approaches to budgeting, including incremental budgeting, Zero-based budgeting, Activity-based budgeting, rolling

2. Identify four factors of management intention in regard to the cash flow budget.

Answer on Question #54480, Economics / Other 1. What are the two types of information available to complete the budget? Describe the benefits and disadvantages of them and give an example of each. 2. Identify

Answer on Question #54480, Economics / Other 1. What are the two types of information available to complete the budget? Describe the benefits and disadvantages of them and give an example of each. 2. Identify

Retired Executives: e Untapped Resource for Tackling Tough Business Challenges

A REPORT FROM EXECBRAINTRUST.COM Retired Executives: e Untapped Resource for Tackling Tough Business Challenges Copyright 2012 ExecBrainTrust All rights reserved The Conundrum Around the country, in every

A REPORT FROM EXECBRAINTRUST.COM Retired Executives: e Untapped Resource for Tackling Tough Business Challenges Copyright 2012 ExecBrainTrust All rights reserved The Conundrum Around the country, in every

Jacob: What data do we use? Do we compile paid loss triangles for a line of business?

PROJECT TEMPLATES FOR REGRESSION ANALYSIS APPLIED TO LOSS RESERVING BACKGROUND ON PAID LOSS TRIANGLES (The attached PDF file has better formatting.) {The paid loss triangle helps you! distinguish between

PROJECT TEMPLATES FOR REGRESSION ANALYSIS APPLIED TO LOSS RESERVING BACKGROUND ON PAID LOSS TRIANGLES (The attached PDF file has better formatting.) {The paid loss triangle helps you! distinguish between

Introduction. I hope you find it helpful. Do get in touch if you have any other questions, or want to give Vestd a try. Thanks,

Introduction There are so many great reasons to set up a company share scheme. Distributing equity is a fantastic motivator for your team, and helps underpin a strong company culture. The problem is that

Introduction There are so many great reasons to set up a company share scheme. Distributing equity is a fantastic motivator for your team, and helps underpin a strong company culture. The problem is that

Mapping the Member Journey

THE ONLY ALL-DIGITAL, ALL-BUSINESS RESOURCE FOR CREDIT UNIONS THE CFO ISSUE APRIL 2018 VOLUME 13 ISSUE 4 Mapping the Member Journey ROB VANASCO ALSO IN THIS ISSUE: Rising Rates End of 2018 May Put Credit

THE ONLY ALL-DIGITAL, ALL-BUSINESS RESOURCE FOR CREDIT UNIONS THE CFO ISSUE APRIL 2018 VOLUME 13 ISSUE 4 Mapping the Member Journey ROB VANASCO ALSO IN THIS ISSUE: Rising Rates End of 2018 May Put Credit

VENTURE ANALYSIS WORKBOOK

VENTURE ANALYSIS WORKBOOK ANALYSIS SECTION VERSION 1.2 Copyright (1990, 2000) Michael S. Lanham Eugene B. Lieb Customer Decision Support, Inc. P.O. Box 998 Chadds Ford, PA 19317 (610) 793-3520 genelieb@lieb.com

VENTURE ANALYSIS WORKBOOK ANALYSIS SECTION VERSION 1.2 Copyright (1990, 2000) Michael S. Lanham Eugene B. Lieb Customer Decision Support, Inc. P.O. Box 998 Chadds Ford, PA 19317 (610) 793-3520 genelieb@lieb.com

INVESTMENT APPROACH & PHILOSOPHY

INVESTMENT APPROACH & PHILOSOPHY INVESTMENT APPROACH & PHILOSOPHY - Equities 2. Invest regularly 1. Invest early 3. Stay Invested Research: We receive in-depth research on companies and the macro environment

INVESTMENT APPROACH & PHILOSOPHY INVESTMENT APPROACH & PHILOSOPHY - Equities 2. Invest regularly 1. Invest early 3. Stay Invested Research: We receive in-depth research on companies and the macro environment

Nonprofit Budgeting Part 2: Building Better Budgets

Nonprofit Budgeting Part 2: Building Better Budgets CompassPoint Nonprofit Services 500 12 th Street Suite 320 Oakland, CA 94607 ph 510-318-3755 fax 415-541-7708 web: www.compasspoint.org e-mail: workshops@compasspoint.org

Nonprofit Budgeting Part 2: Building Better Budgets CompassPoint Nonprofit Services 500 12 th Street Suite 320 Oakland, CA 94607 ph 510-318-3755 fax 415-541-7708 web: www.compasspoint.org e-mail: workshops@compasspoint.org

BPC Upgrade to v10. Technical upgrade service from BPS or BPC to BPC v10. Method360 EPM Practice 2012

BPC Upgrade to v10 Technical upgrade service from BPS or BPC to BPC v10 Method360 EPM Practice 2012 Method360 technical BPC upgrade service Content 1. Method360 BPC technical upgrade service: 2. Upgrade

BPC Upgrade to v10 Technical upgrade service from BPS or BPC to BPC v10 Method360 EPM Practice 2012 Method360 technical BPC upgrade service Content 1. Method360 BPC technical upgrade service: 2. Upgrade

Seeing financing in a new light

Seeing financing in a new light Managing capital budgets is no easy task. Every department seems to have a unique opportunity they want to pursue or a pressing problem that has to be solved. Opportunities

Seeing financing in a new light Managing capital budgets is no easy task. Every department seems to have a unique opportunity they want to pursue or a pressing problem that has to be solved. Opportunities

2. Criteria for a Good Profitability Target

Setting Profitability Targets by Colin Priest BEc FIAA 1. Introduction This paper discusses the effectiveness of some common profitability target measures. In particular I have attempted to create a model

Setting Profitability Targets by Colin Priest BEc FIAA 1. Introduction This paper discusses the effectiveness of some common profitability target measures. In particular I have attempted to create a model

DRAFT August 2, Overview of OSU New Education and General (or Shared Responsibility) Budget Model Academic Colleges Focus

Budget Model Academic Colleges Focus") Overview of OSU New Education and General (or Shared Responsibility) Budget Model Academic Colleges Focus OSU-Corvallis is implementing a new budget model with the FY18 E&G budget. The model was used to

Overview of OSU New Education and General (or Shared Responsibility) Budget Model Academic Colleges Focus OSU-Corvallis is implementing a new budget model with the FY18 E&G budget. The model was used to

Transparency case study. Assessment of adequacy and portfolio optimization through time. THE ARCHITECTS OF CAPITAL

Transparency case study Assessment of adequacy and portfolio optimization through time. THE ARCHITECTS OF CAPITAL Transparency is a fundamental regulatory requirement as well as an ethical driver for highly

Transparency case study Assessment of adequacy and portfolio optimization through time. THE ARCHITECTS OF CAPITAL Transparency is a fundamental regulatory requirement as well as an ethical driver for highly

INVESTMENT FUNDS. Your guide to getting started. Registered charity number

INVESTMENT FUNDS Your guide to getting started Registered charity number 268369 CONTENTS Introduction 3 Balancing risk and reward 4 Get to grips with asset allocation 6 Make the management decision 8 Go

INVESTMENT FUNDS Your guide to getting started Registered charity number 268369 CONTENTS Introduction 3 Balancing risk and reward 4 Get to grips with asset allocation 6 Make the management decision 8 Go

Microsoft Forecaster. FRx Software Corporation - a Microsoft subsidiary

Microsoft Forecaster FRx Software Corporation - a Microsoft subsidiary Make your budget meaningful The very words budgeting and planning remind accounting professionals of long, exhausting hours spent

Microsoft Forecaster FRx Software Corporation - a Microsoft subsidiary Make your budget meaningful The very words budgeting and planning remind accounting professionals of long, exhausting hours spent

2014 EY US life insuranceannuity

2014 EY US life insuranceannuity outlook Market summary Evolving external forces and improved internal operating fundamentals confront the US life insurance-annuity market at the onset of 2014. Given the

2014 EY US life insuranceannuity outlook Market summary Evolving external forces and improved internal operating fundamentals confront the US life insurance-annuity market at the onset of 2014. Given the

Strategic Budgeting: 10 Critical Policy Decisions

Strategic Budgeting: 10 Critical Policy Decisions Facilitator Andrew Laws Managing Director Huron Consulting Group Panelists Melissa Johnson Director of Budget and Fiscal Planning Purdue University Chad

Strategic Budgeting: 10 Critical Policy Decisions Facilitator Andrew Laws Managing Director Huron Consulting Group Panelists Melissa Johnson Director of Budget and Fiscal Planning Purdue University Chad

Deans and Chairs Retreat

Deans and Chairs Retreat 1. Finance Update 2. Rationalizing Our Financial Landscape Vice Chancellor John Wilton February 2013 Finance Update As you all know, the environment has changed State support declined

Deans and Chairs Retreat 1. Finance Update 2. Rationalizing Our Financial Landscape Vice Chancellor John Wilton February 2013 Finance Update As you all know, the environment has changed State support declined

COPYRIGHTED MATERIAL. The first known hedge fund was created by Alfred Winslow Jones in Introduction CHAPTER 1 DEFINITION OF HEDGE FUND

CHAPTER 1 Introduction The first known hedge fund was created by Alfred Winslow Jones in 1949. His fund should look familiar to today s hedge fund participants. The fund was organized as a limited partnership

CHAPTER 1 Introduction The first known hedge fund was created by Alfred Winslow Jones in 1949. His fund should look familiar to today s hedge fund participants. The fund was organized as a limited partnership

VOLATILITY EFFECTS AND VIRTUAL ASSETS: HOW TO PRICE AND HEDGE AN ENERGY PORTFOLIO

VOLATILITY EFFECTS AND VIRTUAL ASSETS: HOW TO PRICE AND HEDGE AN ENERGY PORTFOLIO GME Workshop on FINANCIAL MARKETS IMPACT ON ENERGY PRICES Responsabile Pricing and Structuring Edison Trading Rome, 4 December

VOLATILITY EFFECTS AND VIRTUAL ASSETS: HOW TO PRICE AND HEDGE AN ENERGY PORTFOLIO GME Workshop on FINANCIAL MARKETS IMPACT ON ENERGY PRICES Responsabile Pricing and Structuring Edison Trading Rome, 4 December

We recommend AGAINST investing R$ 35 million in the V:House multifamily development (303 pre-sold units) in São Paulo

in São Paulo") Executive Summary We recommend AGAINST investing R$ 35 million in the V:House multifamily development (303 pre-sold units) in São Paulo Although we achieve a 26% IRR in the Base Case, we earn above the

Executive Summary We recommend AGAINST investing R$ 35 million in the V:House multifamily development (303 pre-sold units) in São Paulo Although we achieve a 26% IRR in the Base Case, we earn above the

Investment outsourcing options for your pension plan

Fiduciary solutions for CORPORATE PENSION PLANS Investment outsourcing options for your pension plan INVESTED. TOGETHER. Managing complexity Managing a pension plan is not getting any easier. Rapid-fire

Fiduciary solutions for CORPORATE PENSION PLANS Investment outsourcing options for your pension plan INVESTED. TOGETHER. Managing complexity Managing a pension plan is not getting any easier. Rapid-fire

Helping clients accumulate a little more with life insurance

Indexed universal life insurance Helping clients accumulate a little more with life insurance Sales guide Indexed universal life (IUL) insurance offers a great story to clients. It begins by helping them

Indexed universal life insurance Helping clients accumulate a little more with life insurance Sales guide Indexed universal life (IUL) insurance offers a great story to clients. It begins by helping them

A G E N D A Revised WORKSHOP BUDGET MEETING OF THE PARK RIDGE CITY COUNCIL CITY HALL COUNCIL CHAMBERS 505 BUTLER PLACE PARK RIDGE, IL

CITY OF PARK RIDGE 505 BUTLER PLACE PARK RIDGE, IL 60068 TEL: 847/ 318-5200 FAX: 847/ 318-5300 TDD: 847/ 318-5252 URL: http://www.parkridge.us A G E N D A Revised WORKSHOP BUDGET MEETING OF THE PARK RIDGE

CITY OF PARK RIDGE 505 BUTLER PLACE PARK RIDGE, IL 60068 TEL: 847/ 318-5200 FAX: 847/ 318-5300 TDD: 847/ 318-5252 URL: http://www.parkridge.us A G E N D A Revised WORKSHOP BUDGET MEETING OF THE PARK RIDGE

Expected Return Methodologies in Morningstar Direct Asset Allocation

Expected Return Methodologies in Morningstar Direct Asset Allocation I. Introduction to expected return II. The short version III. Detailed methodologies 1. Building Blocks methodology i. Methodology ii.

Expected Return Methodologies in Morningstar Direct Asset Allocation I. Introduction to expected return II. The short version III. Detailed methodologies 1. Building Blocks methodology i. Methodology ii.

Climb to Profits WITH AN OPTIONS LADDER

Climb to Profits WITH AN OPTIONS LADDER We believe what matters most is the level of income your portfolio produces... Lattco uses many different factors and criteria to analyze, filter, and identify stocks

Climb to Profits WITH AN OPTIONS LADDER We believe what matters most is the level of income your portfolio produces... Lattco uses many different factors and criteria to analyze, filter, and identify stocks

THE CASH INVESTMENT POLICY STATEMENT DEVELOPING, DOCUMENTING AND MAINTAINING A CASH MANAGEMENT PLAN

THE CASH INVESTMENT POLICY STATEMENT DEVELOPING, DOCUMENTING AND MAINTAINING A CASH MANAGEMENT PLAN [2] THE CASH INVESTMENT POLICY STATEMENT The Cash Investment Policy Statement (IPS) The face of the cash

THE CASH INVESTMENT POLICY STATEMENT DEVELOPING, DOCUMENTING AND MAINTAINING A CASH MANAGEMENT PLAN [2] THE CASH INVESTMENT POLICY STATEMENT The Cash Investment Policy Statement (IPS) The face of the cash

A Priority System for Allocating an O&M Budget

A Priority System for Allocating an O&M Budget Elsie Myers Martin Lee Merkhofer Lee Merkhofer Consulting This paper describes a priority system developed for Northern States Power to allocate its annual

A Priority System for Allocating an O&M Budget Elsie Myers Martin Lee Merkhofer Lee Merkhofer Consulting This paper describes a priority system developed for Northern States Power to allocate its annual

MANAGING YOUR BUSINESS S CASH FLOW. Managing Your Business s Cash Flow. David Oetken, MBA CPM

MANAGING YOUR BUSINESS S CASH FLOW Managing Your Business s Cash Flow David Oetken, MBA CPM 1 2 Being a successful entrepreneur takes a unique mix of skills and practices. You need to generate exciting

MANAGING YOUR BUSINESS S CASH FLOW Managing Your Business s Cash Flow David Oetken, MBA CPM 1 2 Being a successful entrepreneur takes a unique mix of skills and practices. You need to generate exciting

Central Connecticut State University Integrated Budget Model. Pilot Department Overview and Training Session

Central Connecticut State University Integrated Budget Model Pilot Department Overview and Training Session Welcome and Introductions CCSU Budget Current As Is Process Zero-Based Budgeting in Practice

Central Connecticut State University Integrated Budget Model Pilot Department Overview and Training Session Welcome and Introductions CCSU Budget Current As Is Process Zero-Based Budgeting in Practice

Formalizing a Debt Management Strategy

Public Disclosure Authorized 69929 Tomas I. Magnusson, World Bank December 2005 Formalizing a Debt Management Strategy Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Public Disclosure Authorized 69929 Tomas I. Magnusson, World Bank December 2005 Formalizing a Debt Management Strategy Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

First Quarter 2015 Earnings. May 11, 2015

First Quarter 2015 Earnings May 11, 2015 1 Forward-Looking Statements Some of the statements made in this presentation are forward-looking and are made pursuant to the safe harbor provision of the Private

First Quarter 2015 Earnings May 11, 2015 1 Forward-Looking Statements Some of the statements made in this presentation are forward-looking and are made pursuant to the safe harbor provision of the Private

Financial Instruments Credit Losses How to Calculate CECL in Excel Monday, June 11, 2018

Financial Instruments Credit Losses How to Calculate CECL in Excel Monday, June 11, 2018 Presented by: Ryan Abdoo, CPA, CGMA Industry Technical Leader Plante Moran Chris Ritter, CPA Partner Plante Moran

Financial Instruments Credit Losses How to Calculate CECL in Excel Monday, June 11, 2018 Presented by: Ryan Abdoo, CPA, CGMA Industry Technical Leader Plante Moran Chris Ritter, CPA Partner Plante Moran

PART 1 Financial Planning, Performance and Control

PART 1 Financial Planning, Performance and Control Section A. Planning, Budgeting and Forecasting (30% - Levels A, B, and C) Section A, Planning, Budgeting and Forecasting, represents 30% of the exam,

PART 1 Financial Planning, Performance and Control Section A. Planning, Budgeting and Forecasting (30% - Levels A, B, and C) Section A, Planning, Budgeting and Forecasting, represents 30% of the exam,

Better decision making under uncertain conditions using Monte Carlo Simulation

IBM Software Business Analytics IBM SPSS Statistics Better decision making under uncertain conditions using Monte Carlo Simulation Monte Carlo simulation and risk analysis techniques in IBM SPSS Statistics

IBM Software Business Analytics IBM SPSS Statistics Better decision making under uncertain conditions using Monte Carlo Simulation Monte Carlo simulation and risk analysis techniques in IBM SPSS Statistics

Financial Performance and Development Impact Evidence from Research in Ghana and Uganda

Financial Performance and Development Impact Evidence from Research in Ghana and Uganda Ph.D. Candidate Frankfurt, 20th July 2012 UMM - PhD- v1 _ 14Jul2012 -JF.pptx The Ph.D. research is driven by several

Financial Performance and Development Impact Evidence from Research in Ghana and Uganda Ph.D. Candidate Frankfurt, 20th July 2012 UMM - PhD- v1 _ 14Jul2012 -JF.pptx The Ph.D. research is driven by several

INVESTMENT FUNDS. Your guide to getting started. Registered charity number

INVESTMENT FUNDS Your guide to getting started Registered charity number 268369 CONTENTS Introduction 3 Balancing risk and reward 4 Get to grips with asset allocation 6 Make the management decision 8 Go

INVESTMENT FUNDS Your guide to getting started Registered charity number 268369 CONTENTS Introduction 3 Balancing risk and reward 4 Get to grips with asset allocation 6 Make the management decision 8 Go

Traditional vs. Annual Opportunity Approaches

January 2015 High-growth biotech companies can benefit greatly from alternative methods for right-sizing employee stock option grants, but no method is free from potential drawbacks. Compensation professionals

January 2015 High-growth biotech companies can benefit greatly from alternative methods for right-sizing employee stock option grants, but no method is free from potential drawbacks. Compensation professionals

Allstate Agency Value Index 2011 Year Review

Allstate Agency Value Index Year Review In there were many active topics of discussion in the Allstate Community. Agency Terminations, Mergers and Acquisitions, Esurance along with the hottest of all topics:

Allstate Agency Value Index Year Review In there were many active topics of discussion in the Allstate Community. Agency Terminations, Mergers and Acquisitions, Esurance along with the hottest of all topics:

Modern Budgeting for Profit Planning & Control

Modern Budgeting for Profit Planning & Control Course Description The course is intended for business professionals engaged in budgeting, financial planning, forecasting, profit planning, and control.

Modern Budgeting for Profit Planning & Control Course Description The course is intended for business professionals engaged in budgeting, financial planning, forecasting, profit planning, and control.

THE LA RETIREMENT FUND (The Fund) INVESTMENT POLICY STATEMENT SUMMARY

INVESTMENT POLICY STATEMENT SUMMARY") THE LA RETIREMENT FUND (The Fund) INVESTMENT POLICY STATEMENT SUMMARY Last updated April 2017 1. INTRODUCTION This Investment Policy Statement ( IPS ) is a formal statement of the main principles underlying

THE LA RETIREMENT FUND (The Fund) INVESTMENT POLICY STATEMENT SUMMARY Last updated April 2017 1. INTRODUCTION This Investment Policy Statement ( IPS ) is a formal statement of the main principles underlying

CHAPTER 6: PLANNING. Multiple Choice Questions

Multiple Choice Questions CHAPTER 6: PLANNING 1. Current research suggests that an organization s is critical to the successful implementation of its strategic plans. a. complexity b. human capital c.

Multiple Choice Questions CHAPTER 6: PLANNING 1. Current research suggests that an organization s is critical to the successful implementation of its strategic plans. a. complexity b. human capital c.

Fundamentals of Cash Forecasting

Fundamentals of Cash Forecasting May 29, 2013 Presented To Presented By Mike Gallanis Partner 2013 Treasury Strategies, Inc. All rights reserved. Cash Forecasting Defined Cash forecasting defined: the

Fundamentals of Cash Forecasting May 29, 2013 Presented To Presented By Mike Gallanis Partner 2013 Treasury Strategies, Inc. All rights reserved. Cash Forecasting Defined Cash forecasting defined: the

Public Financial Management

UNITAR Mustofi Fellowship Hiroshima, Japan 18 22 February 2012! Index! Overview and Objectives! Limitations and Problems! Public Financial Systems! Financial Management System Boundaries! Framework! Government

UNITAR Mustofi Fellowship Hiroshima, Japan 18 22 February 2012! Index! Overview and Objectives! Limitations and Problems! Public Financial Systems! Financial Management System Boundaries! Framework! Government

ANYTIME ANYPLACE ANYWHERE

ANYTIME ANYPLACE ANYWHERE Who are we? What do we do? Imagine: A business service with no physical boundaries, no time constraints. Your TCW business can be performed in an office, in your business, at

ANYTIME ANYPLACE ANYWHERE Who are we? What do we do? Imagine: A business service with no physical boundaries, no time constraints. Your TCW business can be performed in an office, in your business, at

UNTHSC. Annual Budget Development Process Fiscal Year 2019 Guidelines & Instructions - Spring 2018

UNTHSC Annual Budget Development Process Fiscal Year 2019 Guidelines & Instructions - Spring 2018 INTRODUCTION: The budgeting process at the University of North Texas Health Science Center (UNTHSC) assigns

UNTHSC Annual Budget Development Process Fiscal Year 2019 Guidelines & Instructions - Spring 2018 INTRODUCTION: The budgeting process at the University of North Texas Health Science Center (UNTHSC) assigns

Cloud Accounting For Charities. Coping with the challenges of SORP

Cloud Accounting For Charities Coping with the challenges of SORP Introduction Cloud accounting has progressed from basic SME solutions to more advanced software for larger and more complex multi-entity

Cloud Accounting For Charities Coping with the challenges of SORP Introduction Cloud accounting has progressed from basic SME solutions to more advanced software for larger and more complex multi-entity

MANAGING YOUR EO BUDGET BEFORE IT MANAGES YOU. Brian Yacker, JD/CPA Stacey Bergman, CPA

MANAGING YOUR EO BUDGET BEFORE IT MANAGES YOU Brian Yacker, JD/CPA Stacey Bergman, CPA August 18, 2015 1. WHAT IS A BUDGET? DEFINITION Strategic organizational plan Based on facts, events in progress &

MANAGING YOUR EO BUDGET BEFORE IT MANAGES YOU Brian Yacker, JD/CPA Stacey Bergman, CPA August 18, 2015 1. WHAT IS A BUDGET? DEFINITION Strategic organizational plan Based on facts, events in progress &

Coronado Unified School District

Coronado Unified School District Workshop Outcomes / Objectives Understand how Board Policy 3050 guides financial decision-making that align with Board fiduciary responsibilities while prioritizing student

Coronado Unified School District Workshop Outcomes / Objectives Understand how Board Policy 3050 guides financial decision-making that align with Board fiduciary responsibilities while prioritizing student

Chapter 7: Investment Decision Rules

Chapter 7: Investment Decision Rules -1 Chapter 7: Investment Decision Rules Note: Read the chapter then look at the following. Fundamental question: What criteria should firms use when deciding which

Chapter 7: Investment Decision Rules -1 Chapter 7: Investment Decision Rules Note: Read the chapter then look at the following. Fundamental question: What criteria should firms use when deciding which

FINANCIAL MODELING IN EXCEL

Title Heading Here FINANCIAL MODELING IN EXCEL Become productive and creative in Microsoft Excel 1 Contents Excel Essentials 2 Advanced Excel 3 Data Analysis and Dashboard Reporting 4 Advanced Data Analysis

Title Heading Here FINANCIAL MODELING IN EXCEL Become productive and creative in Microsoft Excel 1 Contents Excel Essentials 2 Advanced Excel 3 Data Analysis and Dashboard Reporting 4 Advanced Data Analysis

ACCA Paper F5 Performance Management

ACCA Paper F5 Performance Management Mock Exam Question Paper Time allowed 3 hours 15 minutes This paper is divided into three sections Section A Section B Section C ALL FIFTEEN questions are compulsory

ACCA Paper F5 Performance Management Mock Exam Question Paper Time allowed 3 hours 15 minutes This paper is divided into three sections Section A Section B Section C ALL FIFTEEN questions are compulsory

Exit Baby Boomers, Enter a New Generation of Owners

February 2016 Exit Baby Boomers, Enter a New Generation of Owners By Timothy J. Iszler, CPA, and Larry A. Mackowiak, CPA Audit Tax Advisory Risk Performance Over the next 10 years, tremendous value will

February 2016 Exit Baby Boomers, Enter a New Generation of Owners By Timothy J. Iszler, CPA, and Larry A. Mackowiak, CPA Audit Tax Advisory Risk Performance Over the next 10 years, tremendous value will

Our original CHAOS Report in 1994 started with the paragraph, In 1986, Alfred Spector, president of Transarc Corporation,

CHAOS RepORt: 21 ST ANNIVERSARY EDITION Our original CHAOS Report in 1994 started with the paragraph, In 1986, Alfred Spector, president of Transarc Corporation, co-authored a paper comparing bridge building

CHAOS RepORt: 21 ST ANNIVERSARY EDITION Our original CHAOS Report in 1994 started with the paragraph, In 1986, Alfred Spector, president of Transarc Corporation, co-authored a paper comparing bridge building

Financial Reporting. University Senate January 22, 2016

Financial Reporting University Senate January 22, 2016 J. Michael Gower Executive Vice President for Finance & Administration and University Treasurer Financial Statements vs. University Budget The annual

Financial Reporting University Senate January 22, 2016 J. Michael Gower Executive Vice President for Finance & Administration and University Treasurer Financial Statements vs. University Budget The annual

Comprehensive plan services with an eye toward tomorrow

Comprehensive plan services with an eye toward tomorrow Schwab Retirement Plan Services, Inc. Always put the client first. No matter what. Charles Schwab Our culture of service At Schwab Retirement Plan

Comprehensive plan services with an eye toward tomorrow Schwab Retirement Plan Services, Inc. Always put the client first. No matter what. Charles Schwab Our culture of service At Schwab Retirement Plan

Budgeting, Forecasting and the Planning Process

Budgeting, Forecasting and the Planning Process Budgeting, Forecasting and the Planning Process Course Objective Develop strategic thinking, understand and participate in the strategic management process;

Budgeting, Forecasting and the Planning Process Budgeting, Forecasting and the Planning Process Course Objective Develop strategic thinking, understand and participate in the strategic management process;

profitable solutions for nonprofits

Winter 2013 profitable solutions for nonprofits The Financial Side of the Nonprofit Industry IN THIS ISSUE 2 Getting a Handle on the Flow of Cash 3 Maintaining the 501(c)(3) Status 6 Newsbits 8 KSM Not-for-Profit

Winter 2013 profitable solutions for nonprofits The Financial Side of the Nonprofit Industry IN THIS ISSUE 2 Getting a Handle on the Flow of Cash 3 Maintaining the 501(c)(3) Status 6 Newsbits 8 KSM Not-for-Profit

Interest rates in the United States and in most developed

committee report: charitable giving By Roger D. Silk Evaluating the Risks Challenges and opportunities resulting from the current low interest rate environment Interest rates in the United States and in

committee report: charitable giving By Roger D. Silk Evaluating the Risks Challenges and opportunities resulting from the current low interest rate environment Interest rates in the United States and in

Form 990: A Powerful Tool. Kim Hunwardsen, Partner Deb N elson, Senior Manager

Form 990: A Powerful Tool Kim Hunwardsen, Partner Deb N elson, Senior Manager Agenda W hy does the Form 990 matter? W ho is looking at the Form 990 and why? How can the Form 990 serve as a marketing tool?

Form 990: A Powerful Tool Kim Hunwardsen, Partner Deb N elson, Senior Manager Agenda W hy does the Form 990 matter? W ho is looking at the Form 990 and why? How can the Form 990 serve as a marketing tool?

_CH01 7/31/2000 4:39 PM Page 1 PART ONE BUDGETING AND FORECASTING OVERVIEW

01.66878_CH01 7/31/2000 4:39 PM Page 1 PART ONE BUDGETING AND FORECASTING OVERVIEW 01.66878_CH01 7/31/2000 4:39 PM Page 2 01.66878_CH01 7/31/2000 4:39 PM Page 3 CHAPTER 1 BUDGETING TODAY: OVERVIEW AND

01.66878_CH01 7/31/2000 4:39 PM Page 1 PART ONE BUDGETING AND FORECASTING OVERVIEW 01.66878_CH01 7/31/2000 4:39 PM Page 2 01.66878_CH01 7/31/2000 4:39 PM Page 3 CHAPTER 1 BUDGETING TODAY: OVERVIEW AND

A History of Shaping Financial Success THE QUICK GUIDE TO FINANCIAL SUCCESS

A History of Shaping Financial Success THE QUICK GUIDE TO FINANCIAL SUCCESS Success is No Accident. It is hard work, perseverance, learning, studying, sacrifice and most of all, love of what you are doing.

A History of Shaping Financial Success THE QUICK GUIDE TO FINANCIAL SUCCESS Success is No Accident. It is hard work, perseverance, learning, studying, sacrifice and most of all, love of what you are doing.

Measuring Impact. Impact Evaluation Methods for Policymakers. Sebastian Martinez. The World Bank

Impact Evaluation Measuring Impact Impact Evaluation Methods for Policymakers Sebastian Martinez The World Bank Note: slides by Sebastian Martinez. The content of this presentation reflects the views of

Impact Evaluation Measuring Impact Impact Evaluation Methods for Policymakers Sebastian Martinez The World Bank Note: slides by Sebastian Martinez. The content of this presentation reflects the views of

Voya Target Retirement Fund Series

Voya Target Retirement Fund Series The Target Date Choice to Help Keep Retirement Goals on Track Holistic Retirement Solution Sophisticated Glide Path Design Open Architecture Approach Blend of Active

Voya Target Retirement Fund Series The Target Date Choice to Help Keep Retirement Goals on Track Holistic Retirement Solution Sophisticated Glide Path Design Open Architecture Approach Blend of Active

GREAT REASONS TO MAKE ALLIANCE FINANCING GROUP YOUR MAIN CHOICE FOR LEASING

GREAT REASONS TO MAKE ALLIANCE FINANCING GROUP YOUR MAIN CHOICE FOR LEASING Alliance Financing Group is active North America wide in providing innovative financing solutions to all types of businesses.

GREAT REASONS TO MAKE ALLIANCE FINANCING GROUP YOUR MAIN CHOICE FOR LEASING Alliance Financing Group is active North America wide in providing innovative financing solutions to all types of businesses.

Math of Finance Exponential & Power Functions

The Right Stuff: Appropriate Mathematics for All Students Promoting the use of materials that engage students in meaningful activities that promote the effective use of technology to support mathematics,

The Right Stuff: Appropriate Mathematics for All Students Promoting the use of materials that engage students in meaningful activities that promote the effective use of technology to support mathematics,

Nonprofit Financial Statements. What Every Executive Director Must Know

Nonprofit Financial Statements What Every Executive Director Must Know Today s Lesson Plan 1. Introductions 2. Financial Reporting Overview 3. 4 Financial Reports every Executive Director Must Know 4.

Nonprofit Financial Statements What Every Executive Director Must Know Today s Lesson Plan 1. Introductions 2. Financial Reporting Overview 3. 4 Financial Reports every Executive Director Must Know 4.

Hers Institute Budgeting. This Session Will Include a Discussion of:

Hers Institute 2016 Budgeting This Session Will Include a Discussion of: The Purpose of the Budgeting Process Budget Types Approaches to Budgeting The Budget Process Why do we participate in the budget

Hers Institute 2016 Budgeting This Session Will Include a Discussion of: The Purpose of the Budgeting Process Budget Types Approaches to Budgeting The Budget Process Why do we participate in the budget

Empowering the customer journey in retail banking

Empowering the customer journey in retail banking Introducing: Rob Parker Australia and New Zealand Banking Group (ANZ) Stephanie Leroy Experian Name: Stephanie Leroy Role: Director Originations products

Empowering the customer journey in retail banking Introducing: Rob Parker Australia and New Zealand Banking Group (ANZ) Stephanie Leroy Experian Name: Stephanie Leroy Role: Director Originations products

ASSET MANAGEMENT. Why Cidel? Our risk approach.

ASSET MANAGEMENT GLOBAL Why Cidel? Our risk approach. At Cidel, our primary focus is managing risk to ensure each client s assets are protected. Our proactive risk approach ensures that as risks change

ASSET MANAGEMENT GLOBAL Why Cidel? Our risk approach. At Cidel, our primary focus is managing risk to ensure each client s assets are protected. Our proactive risk approach ensures that as risks change