Pearson LCCI Level 3 Certificate in Management Accounting (ASE3024)

|

|

|

- Patience Bailey

- 5 years ago

- Views:

Transcription

1 Pearson LCCI Level 3 Certificate in Management Accounting (ASE3024) Annual Qualification Review 2013/2014 For further information contact us: Tel. +44 (0) internationalenquiries@pearson.com

2 CONTENTS Introduction 2 Pass Rate Statistics 2 General Strengths and Weaknesses 3 Teaching Points by Syllabus Topic 4 Examples of Candidate Responses 10 1

3 INTRODUCTION The annual qualification review provides qualification specific support and guidance to centres. This information is designed to help teachers preparing to teach the subject and to help candidates preparing to take the examination. The reviews are published in September and take into account candidate performance, demonstrated in both on demand and series examinations, over the preceding 12 months. Global pass rates are published so you can measure the performance of your centre against these. The review identifies candidate strengths and weaknesses by syllabus topic area and provides examples of good and poorer candidate responses. It should therefore be read in conjunction with details of the structure and learning objectives contained within the syllabus for this qualification found on the website. The review also identifies any actual or proposed changes to the syllabus or question types together with their implications. PASS RATE STATISTICS The following statistics are based on the performance of candidates who took this qualification between 1 September 2013 and 31 August Global pass rate 39.1%* Grade distributions Pass 19.0% Credit 16.7% Distinction 3.5% * This figure excludes absences on the day of the exam 2

4 GENERAL STRENGTHS AND WEAKNESSES Strengths Students are becoming more familiar with the requirements of the syllabus Time management, which enables them to answer all the questions Weaknesses Not reading the questions fully, or re-checking their work Not showing all their workings this is a major issue (see later) Issues with the narrative elements of questions/syllabus Not showing an actual answer, but an extended formula (see exam paper examples) 3

5 TEACHING POINTS BY SYLLABUS TOPIC 1 Short-term cost behaviour 1.1 Define costs as variable, semi-variable, stepped or fixed 1.2 Separate costs into fixed and variable (Series 3) 1.3 Use the high low method (Series 2) 1.4 Calculate costs per period (Series 3) 1.5 Forecast costs using the high/low method (Series 2) 1.6 Explain the effect of time on cost behaviour Question 1a (Series 2) required students to break down costs (fixed and variable) and by function - it was reasonably well answered Question 1a (Series 3) required candidates to use the high-low method but with an index. Many candidates answered this poorly - they were either unable to use an index or misread the question. 2 Cost/volume/profit analysis 2.1 Calculate the contribution/sales ratio 2.2 Explain and calculate the break-even point (Series 2/3) 2.3 Explain and calculate the margin of safety 2.4 Apply CVP analysis (Series 2) 2.5 Construct charts (Series 3) 2.6 Read the B.E and MOS from a chart 2.7 Discuss the assumptions and limitations of CVP analysis (Series 2) Q1 b (Series 2) was answered well. However 1c and 1d were not well answered as candidates were unable to apply their knowledge of CVP analysis. With most papers the written part was poorly answered - many candidates repeating a model answer that was unrelated to the question. Q1 b and c (Series 3) required the candidate to calculate the contribution, break even and plot a profit volume chart. This was generally well done. However, a lot of candidates did not draw the chart on the graph paper provided and did not label their items correctly. Candidates should note that a graph is all about the presentation and the ability to be read by another person clearly. 4

6 3 Short-term decision-making This syllabus topic area is a compulsory topic area 3.1 Absorption and marginal costing terms 3.2 Absorption and marginal costing profit statements (Series 2) 3.3 Usefulness of absorption and marginal costing (Series 2) 3.4 Relevant costs and limitations (3.10) 3.5 Limiting factor analysis (3.6, 3.7 and 3.9) (Series 3) 3.8 Linear programming 3.11 Identify products or departments for closure 3.12 The limitations of short term decision making 3.13 Calculate a selling price for a product (3.13) Question 4 a, b & c (Series 2) required profit statements based on marginal and absorption costing. The same topic appeared in Series The majority of students found this question challenging. This area of work requires concentrated study and a good deal of exam practice. It is not an area that a student can rote learn or copy model answers. The written q (4d) was poorly answered. Q5 (Series 3) was a make or buy question. This also appeared in The answers in 2014 were an improvement on The written part (5b) was reasonably well answered. Make or buy is a topic area that hadn't been covered for some time until students should be prepared to expect questions from the whole of the syllabus area. (See additional comment on the next page) 4 Budgetary planning and control 4.1 Benefits, limitations and process 4.2 Budget planning and control 4.3 Principle budget factor (4.4) 4.4 Prepare a variety of budgets (4.5) (Series 2) 4.6 Flexible budgets (4.7 and 4.8) 4.9 Other approaches and behaviour 4.10 Behavioural aspects 5

7 A small question appeared in Series 2 (Q2d) - prepare a budgeted profit statement. This was well answered by the majority of candidates. This topic area did not appear in Series 2 or 3 (2013) apart from Q1 in Series 2 which had a question based on flexible budgets 5 Cash & working capital management 5.1 Explain liquidity and cash flow 5.2 Cash budgets (5.3) 5.4 Working capital requirements (5.6) (Series 2) 5.5 Working capital budgets (Series 2) 5.7 Reconcile profit and cash (budgets) 5.8 Interpret w/c ratios (5.9) (Series 3) 5.10 Calculate the w/c cycle (Series 2) Q2 a, b & c (Series 2) involved working capital management. Most candidates did well on parts a and b. Part c proved problematic. The first two parts asked for the information in days, whilst part c asked for the information in values ( 000). Many candidates didn't read this and tried to give an answer in days. This type of question has appeared in many series and is a prime area of the syllabus. Q4 (Series 3) asked for the working capital ratios and their meaning. Most candidates could calculate the ratios reasonably well but the majority of students failed to give a reasonable analysis of what the ratios actually meant. A similar question appeared in Series Candidates were also asked to refer to the financial statement provided in the question, but failed to do so. 6 Standard costing and variances This syllabus topic area did not feature in Series Explain the meaning of a standard cost 6.2 Calculate total sales, selling price and sales volume 6.3 Direct material variances 6.4 Define the standard hour 6.5 Direct labour variances 6.6 Fixed production overhead variances (6.7) 6.8 Reconcile budgeted and actual profits 6

8 6.9 Calculate standard or actual costs 6.10 Cost control 6.11 Interpret variances 6.12 Calculate production ratios 6.13 Explain the use of ex-ante and ex-post standards 6.14 Calculate and interpret planning/operational variances Q2 a & b (Series 3) featured the calculation of fixed overhead variances which was generally well answered. Part b required a reconciliation which was not well answered. 7 Long-term decision-making Once again a compulsory topic area 7.1 Difference between long term and short term decision making 7.2 Relevant and irrelevant costs 7.3 Capital appraisal techniques payback and ARR 7.4 DCF appraisal techniques (7.5 and 7.7) 7.6 NPV and IRR discounting methods (7.8 and 7.9) 7.10 Calculate discounted payback 7.11 Calculate a profitability index 7.12 Calculate a weighted average cost of capital 7.13 Apply risk analysis 7.14 Incorporate inflation in appraisal techniques 7.15 Interpret analysis The Series 2 question (5a) was well answered by most students except for the ARR, which required the calculation of the profit and the average investment value. This continues to give many candidates problems despite appearing in many papers. Part b required the calculation of a profitability index which caused quite a few students problems. Part c which was an unusual calculation was poorly answered by the majority of candidates, as was the written part (d) despite this appearing in one of last year's papers. Q3ai (Series 3) was poorly answered by many candidates who could not work out the net cash flow. Part 3a(iii) required a 'discounted' payback which many 7

9 candidates failed to provide. The written part (b) was poorly answered; showing a lack of understanding. 8 Performance evaluation This topic area did not feature in Series Explain why an enterprise may wish to decentralise 8.2 Define cost, profit and investment centres 8.3 Evaluate centres based on ROCE and RI 8.4 Contrast ROCE with RI 8.5 Calculate and interpret Profitability and use of Asset Ratios 8.6 The Balanced Scorecard not covered these series 8.7 Financial and non-financial performance measures - not covered these series 8.6 Explain why transfer pricing is necessary - not covered these series Calculate market and cost based transfer prices - not covered these series - Q5c (Series 2) asked students to explain what is meant by the terms residual income and return on capital employed. Many candidates showed the formulae for calculating these two items, which was not what was requested. Q5d requiring the calculations of these two items was reasonably well answered. Further guidance In order to improve their performance and secure the minimum pass mark in future examinations, candidates are advised to: Have a clear understanding of the elements of the eight syllabus topics through formal instruction provided by reputable teaching institutions; Learn the relevant managerial accounting concepts and terminologies in order to adequately attempt the narrative parts of questions; Practice past exam questions on a regular basis, under strict examination condition; Read the requirements of a question as these are designed to assist in answering the question; Plan the layout of an answer before beginning to carry out calculations; Show clear workings in questions that require calculations. 8

10 A major failing for many candidates (particularly the weaker students) is an in ability to show workings. A further cause for concern seems to be that a lot of students (who are presumably good at Maths) are entering long calculations into their mathematical calculators and then writing down the equation as the answer to the question. You will see examples of this in the section showing copies of actual student responses. Tutors and students should be aware of the rule that if an answer is correct (without workings) the examiner is duty bound to give it the required marks. However, if an answer is incorrect, without 'adequate' workings, the examiner is not required to determine how the candidate arrived at that answer in an attempt to award partial marks. Tutors and students should also be aware that the examiner is under no obligation to try and interpret the student's answer, nor complete any partial calculation. 9

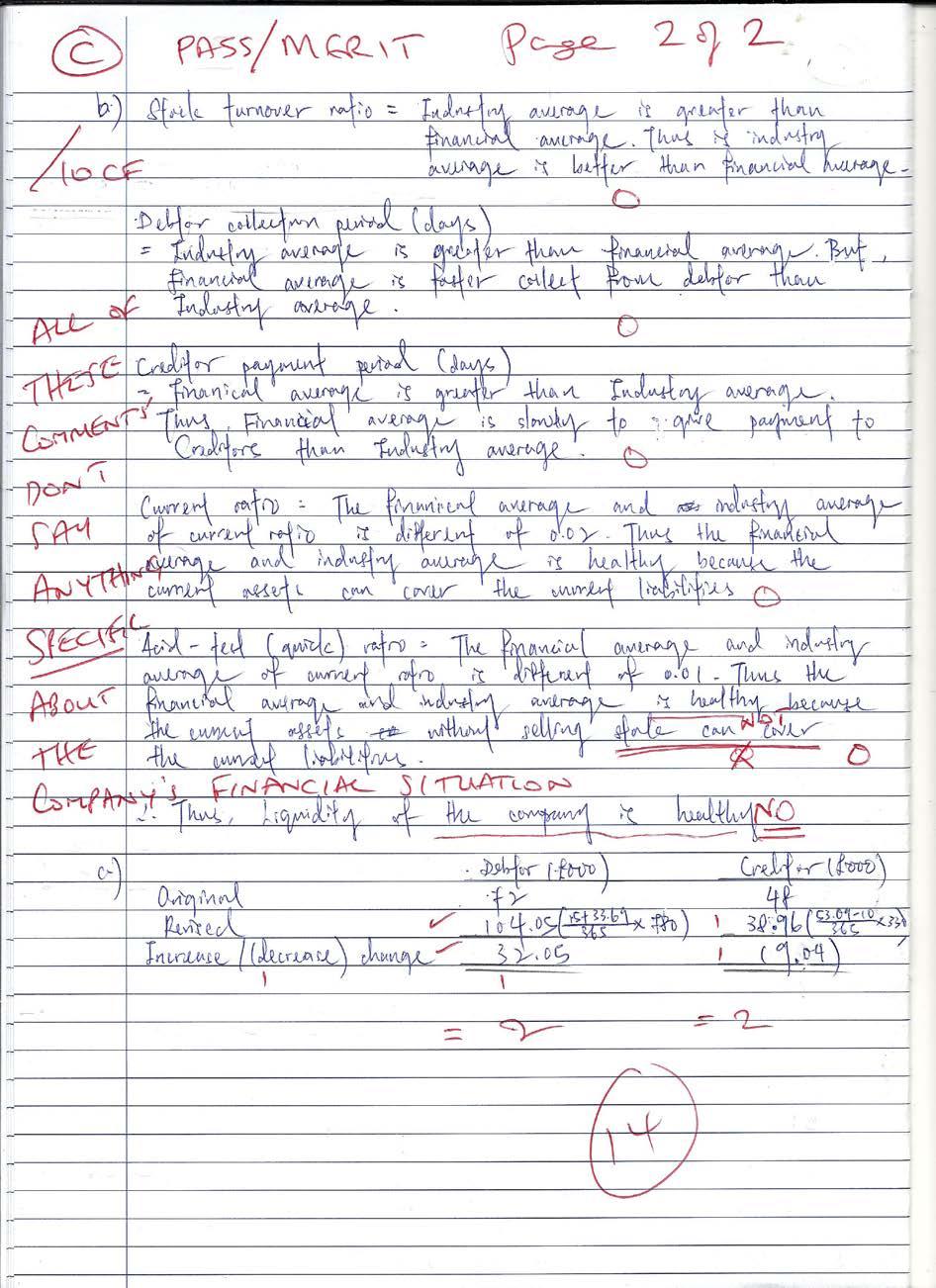

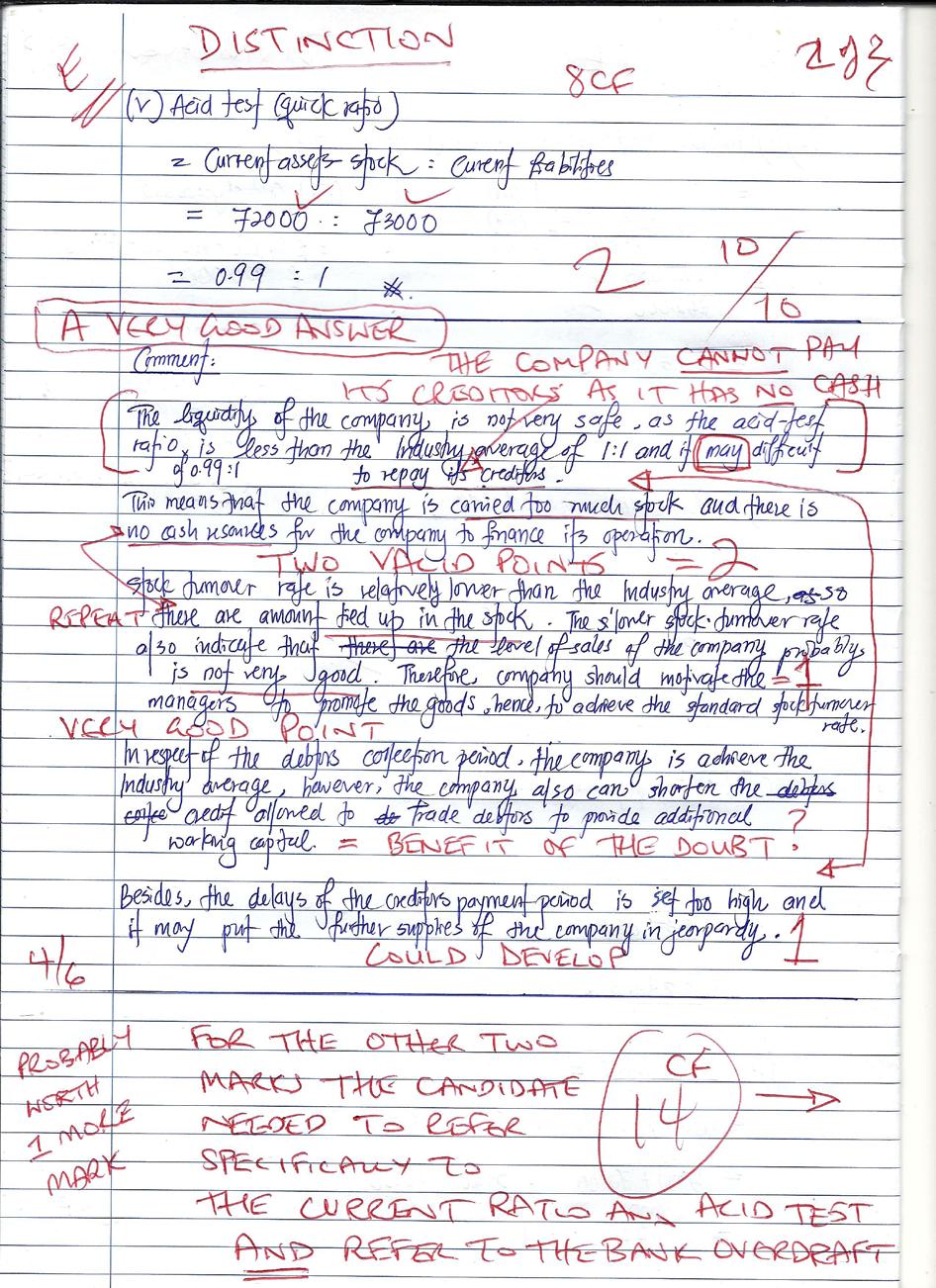

11 EXAMPLES OF CANDIDATE RESPONSES Based on Q4 series The following financial information has been extracted by Sing When for the financial year ending 30 th May 2014: 000 Sales 780 Purchases 330 Closing stock of finished goods 57 Debtors 72 Bank overdraft 25 Creditors 48 Further information: All of the sales and purchases were on credit. 1 year = 365 days. The opening stock of finished goods was 47,000. REQUIRED: (a) Calculate the following working capital ratios (to two decimal places): (i) finished goods stock turnover (number of times). (3 marks) (ii) debtor collection period (days). (2 marks) (iii) creditor payment period (days). (iv) current ratio. (v) acid test (quick) ratio. (1 mark) (2 marks) (2 marks) (b) Using the ratios calculated in (a), as well as the financial information provided, critically comment on the liquidity of the company, using the following industry averages as a basis for your answer: Ratio Stock turnover Debtor collection period (days) Creditor payment period (days) Industry average 10 times per year 35 days 35 days 10

12 Current ratio 1.75 : 1 Acid test (quick) ratio 1.0 : 1 (6 marks) (c) Calculate the change in value, in the relevant balance sheet item, resulting from each of the following, and indicate whether it is an increase or decrease: (i) an increase of 15 days in the period of credit granted to customers. (2 marks) (ii) a reduction of 10 days in the credit terms offered by suppliers. (2 marks) (Total 20 marks) 11

13 12

14 13

15 14

16 15

17 16

18 17

19 18

20 19

21 20

22 21

23 Pearson 190 High Holborn London WC1V 7BH Tel. +44 (0) Fax. +44 (0)

Pearson LCCI Level 3 Management Accounting (ASE3024)

") Pearson LCCI Level 3 Management Accounting (ASE3024) Annual Qualification Review 2014/2015 CONTENTS Introduction 2 Pass Rate Statistics 2 General Strengths and Weaknesses 3 Teaching Points by Syllabus

Pearson LCCI Level 3 Management Accounting (ASE3024) Annual Qualification Review 2014/2015 CONTENTS Introduction 2 Pass Rate Statistics 2 General Strengths and Weaknesses 3 Teaching Points by Syllabus

Pearson LCCI Level 3 Cost Accounting (ASE3017)

") Pearson LCCI Level 3 Cost Accounting (ASE3017) Annual Qualification Review 2013/2014 For further information contact us: Tel. +44 (0) 247 6518951 Email. internationalenquiries@pearson.com www.lcci.org.uk,

Pearson LCCI Level 3 Cost Accounting (ASE3017) Annual Qualification Review 2013/2014 For further information contact us: Tel. +44 (0) 247 6518951 Email. internationalenquiries@pearson.com www.lcci.org.uk,

Level 3 Management Accounting

Level 3 Management Accounting Syllabus Effective for examinations to be held after 1 January 2008 ASPE0483 >f0t@wjy9w2`4s3dpd# Vision Statement Our vision is to contribute to the achievements of learners

Level 3 Management Accounting Syllabus Effective for examinations to be held after 1 January 2008 ASPE0483 >f0t@wjy9w2`4s3dpd# Vision Statement Our vision is to contribute to the achievements of learners

Cost Accounting Level 3

Cost Accounting Level 3 Model Answers Series 4 2013 (ASE3017) For further information contact us: Tel. +44 (0) 247 6518951 Email. internationalenquiries@pearson.com www.lcci.org.uk, www.pearson.com/uk

Cost Accounting Level 3 Model Answers Series 4 2013 (ASE3017) For further information contact us: Tel. +44 (0) 247 6518951 Email. internationalenquiries@pearson.com www.lcci.org.uk, www.pearson.com/uk

Management Accounting Level 3

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 4 2011 (3024) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 4 2011 (3024) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

Level 3 Certificate in Accounting (IAS) Effective for examinations to be held after January 2008

Effective for examinations to be held after January 2008") LCCI International Qualifications Level 3 Certificate in Accounting (IAS) Syllabus Effective for examinations to be held after January 2008 For further information contact us: Tel. +44 (0) 8707 202909

LCCI International Qualifications Level 3 Certificate in Accounting (IAS) Syllabus Effective for examinations to be held after January 2008 For further information contact us: Tel. +44 (0) 8707 202909

Pearson LCCI Level 3 Certificate in Accounting

Pearson LCCI Level 3 Certificate in Accounting Model Answers Series 4 2013 (ASE3012) For further information contact us: Tel. +44 (0) 247 6518951 Email. internationalenquiries@pearson.com www.lcci.org.uk,

Pearson LCCI Level 3 Certificate in Accounting Model Answers Series 4 2013 (ASE3012) For further information contact us: Tel. +44 (0) 247 6518951 Email. internationalenquiries@pearson.com www.lcci.org.uk,

Unit 4: Elements of Managerial Accounting Syllabus Section Absorption (Total) costing

costing") www.xtremepapers.com Unit 4: Elements of Managerial Accounting Syllabus Section Absorption (Total) costing Learning Outcomes Suggested Teaching Activities Resources Online Resources Students will learn

www.xtremepapers.com Unit 4: Elements of Managerial Accounting Syllabus Section Absorption (Total) costing Learning Outcomes Suggested Teaching Activities Resources Online Resources Students will learn

Management Accounting

Management Accounting Level 3 Model Answers Series 3 2008 (Code 3023) 1 ASE 3023 2 06 1 3023/2/06 >f0t@w9w2`?[i]bkbw5k# Management Accounting Level 3 Series 3 2008 How to use this booklet Model Answers

Management Accounting Level 3 Model Answers Series 3 2008 (Code 3023) 1 ASE 3023 2 06 1 3023/2/06 >f0t@w9w2`?[i]bkbw5k# Management Accounting Level 3 Series 3 2008 How to use this booklet Model Answers

Management Accounting Level 3

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 2 2011 (3024) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 2 2011 (3024) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

Management Accounting Level 3

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 3 2010 (3024) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 3 2010 (3024) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

Annual Qualification Review

LCCI International Qualifications Level 2 Certificate in Business Calculations Annual Qualification Review 2011 For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com

LCCI International Qualifications Level 2 Certificate in Business Calculations Annual Qualification Review 2011 For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com

Management Accounting Level 3

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 4 2012 (3024) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 4 2012 (3024) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

Pearson LCCI Level 3 Certificate in Cost and Management Accounting (VRQ)

") Pearson LCCI Level 3 Certificate in Cost and Management Accounting (VRQ) (ASE20098) L3 SPECIFICATION Issue 2 First teaching from September 2015 Pearson LCCI Level 3 Certificate in Cost and Management

Pearson LCCI Level 3 Certificate in Cost and Management Accounting (VRQ) (ASE20098) L3 SPECIFICATION Issue 2 First teaching from September 2015 Pearson LCCI Level 3 Certificate in Cost and Management

Annual Qualification Review 2010

LCCI International Qualifications Level 2 Book-keeping & Accounts Annual Qualification Review 2010 For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

LCCI International Qualifications Level 2 Book-keeping & Accounts Annual Qualification Review 2010 For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

MANAGEMENT ACCOUNTING

Series 3 Examination 2008 MANAGEMENT ACCOUNTING Level 3 Monday 9 June Subject Code: 3023 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

Series 3 Examination 2008 MANAGEMENT ACCOUNTING Level 3 Monday 9 June Subject Code: 3023 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal marks. Write your

Management Accounting

Management Accounting Level 3 Model Answers Series 4 2007 (Code 3023) Vision Statement Our vision is to contribute to the achievements of learners around the world by providing integrated assessment and

Management Accounting Level 3 Model Answers Series 4 2007 (Code 3023) Vision Statement Our vision is to contribute to the achievements of learners around the world by providing integrated assessment and

Annual Qualification Review

LCCI International Qualifications Level 2 Certificate in Book-Keeping and Accounts Annual Qualification Review 2008 For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com

LCCI International Qualifications Level 2 Certificate in Book-Keeping and Accounts Annual Qualification Review 2008 For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com

Management Accounting

Management Accounting Course map This document outlines the course structure. ACCA: FMA-F2.x Management Accounting Introduction course orientation Lesson 1: Welcome Lesson 2: What, when and why? Lesson

Management Accounting Course map This document outlines the course structure. ACCA: FMA-F2.x Management Accounting Introduction course orientation Lesson 1: Welcome Lesson 2: What, when and why? Lesson

Level 2 Cost Accounting

Level 2 Cost Accounting Syllabus Effective for examinations to be held after 1 January 2008 ASPE0483 >f0t@wjy9w2`4s3dpd# Vision Statement Our vision is to contribute to the achievements of learners around

Level 2 Cost Accounting Syllabus Effective for examinations to be held after 1 January 2008 ASPE0483 >f0t@wjy9w2`4s3dpd# Vision Statement Our vision is to contribute to the achievements of learners around

CERTIFICATE IN MANAGEMENT ACCOUNTING

Series 2 Examination 2007 CERTIFICATE IN MANAGEMENT ACCOUNTING Level 3 Monday 2 April Subject Code: 3023 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal

Series 2 Examination 2007 CERTIFICATE IN MANAGEMENT ACCOUNTING Level 3 Monday 2 April Subject Code: 3023 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal

Paper P1 Performance Operations Post Exam Guide November 2014 Exam. General Comments

General Comments Performance on this paper was fairly poor, with the pass rate below the average for the 2010 syllabus. Many candidates scored very highly; however there were a large number of low-scoring

General Comments Performance on this paper was fairly poor, with the pass rate below the average for the 2010 syllabus. Many candidates scored very highly; however there were a large number of low-scoring

Management Accounting Level 3

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 4 2008 (3023) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

LCCI International Qualifications Management Accounting Level 3 Model Answers Series 4 2008 (3023) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk

Institute of Certified Bookkeepers

Institute of Certified Bookkeepers Level III Diploma in Costing and Budgeting Introduction: Financial Accounting is the reporting of financial information to users of Financial Statements both internal

Institute of Certified Bookkeepers Level III Diploma in Costing and Budgeting Introduction: Financial Accounting is the reporting of financial information to users of Financial Statements both internal

Cambridge International Advanced Subsidiary Level and Advanced Level 9706 Accounting November 2014 Principal Examiner Report for Teachers

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice 1 B 16 B 2 B 17 B 3 B 18 D 4 C 19 D 5 C 20 C 6 D 21 C 7 B 22 C 8 B 23

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice 1 B 16 B 2 B 17 B 3 B 18 D 4 C 19 D 5 C 20 C 6 D 21 C 7 B 22 C 8 B 23

Cambridge International Advanced Subsidiary Level and Advanced Level 9706 Accounting June 2014 Principal Examiner Report for Teachers

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 C 16 B 2 B 17 D 3 C 18 C 4 C 19 A 5 B 20 A 6 C 21

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 C 16 B 2 B 17 D 3 C 18 C 4 C 19 A 5 B 20 A 6 C 21

Management Accounting

Examiner s Report and Model Answers for Management Accounting THIRD LEVEL Series 4 (Code 3023) 2000 LCCI Examinations Board MH N T336 9 RNM >f2[ew2r@o2`0t1f3]e]2r2[1_# Management Accounting Third Level

Examiner s Report and Model Answers for Management Accounting THIRD LEVEL Series 4 (Code 3023) 2000 LCCI Examinations Board MH N T336 9 RNM >f2[ew2r@o2`0t1f3]e]2r2[1_# Management Accounting Third Level

Cambridge International Advanced Subsidiary Level and Advanced Level 9706 Accounting November 2011 Principal Examiner Report for Teachers

ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 B 16 C 2 D 17 A 3 C 18 C 4 B 19 D 5 A 20 A 6 A 21 B 7 B 22 C 8 A 23 C 9 D 24 B 10 C 25 D 11 B 26

ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 B 16 C 2 D 17 A 3 C 18 C 4 B 19 D 5 A 20 A 6 A 21 B 7 B 22 C 8 A 23 C 9 D 24 B 10 C 25 D 11 B 26

Pearson LCCI Certificate in Accounting (VRQ) Level 3 (ASE20104)

Level 3 (ASE20104)") Pearson LCCI Certificate in Accounting (VRQ) Level 3 (ASE20104) Examiners Report November 2016 1 LCCI Certificate in Accounting ASE20104 LCCI Qualifications LCCI qualifications come from Pearson, the world

Pearson LCCI Certificate in Accounting (VRQ) Level 3 (ASE20104) Examiners Report November 2016 1 LCCI Certificate in Accounting ASE20104 LCCI Qualifications LCCI qualifications come from Pearson, the world

Management Accounting

Management Accounting Course map This document outlines the course structure. Duration 10 weeks ACCA: FMA-F2.x Management Accounting Course orientation Start of course survey Lesson 1: Welcome Lesson 2:

Management Accounting Course map This document outlines the course structure. Duration 10 weeks ACCA: FMA-F2.x Management Accounting Course orientation Start of course survey Lesson 1: Welcome Lesson 2:

Management Accounting (F2/FMA) September 2015 to August 2016 (for CBE exams up to 22 September 2016)

September 2015 to August 2016 (for CBE exams up to 22 September 2016)") Management Accounting (F2/FMA) September 2015 to August 2016 (for CBE exams up to 22 September 2016) This syllabus and study guide are designed to help with teaching and learning and is intended to provide

Management Accounting (F2/FMA) September 2015 to August 2016 (for CBE exams up to 22 September 2016) This syllabus and study guide are designed to help with teaching and learning and is intended to provide

LCCI International Qualifications. Cost Accounting Level 3. Model Answers Series (3017)

") LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 3 2010 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 3 2010 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

Investment decisions. Guidance and teaching advice. Basic principles

88 Investment decisions 09 Guidance and teaching advice We wrote this chapter with the premise that non-accounting students need to develop skills in using investment appraisal information to support good

88 Investment decisions 09 Guidance and teaching advice We wrote this chapter with the premise that non-accounting students need to develop skills in using investment appraisal information to support good

9706 Accounting November 2008

Paper 9706/01 Multiple Choice 1 A 16 B 2 B 17 A 3 B 18 B 4 B 19 C 5 B 20 B 6 D 21 C 7 A 22 B 8 B 23 D 9 D 24 C 10 B 25 B 11 A 26 B 12 A 27 B 13 D 28 A 14 D 29 D 15 B 30 D General comments Many of the 7300

Paper 9706/01 Multiple Choice 1 A 16 B 2 B 17 A 3 B 18 B 4 B 19 C 5 B 20 B 6 D 21 C 7 A 22 B 8 B 23 D 9 D 24 C 10 B 25 B 11 A 26 B 12 A 27 B 13 D 28 A 14 D 29 D 15 B 30 D General comments Many of the 7300

(F2/FMA) December 2011

December 2011") Manage ment Accounting (F2/FMA) December 2011 This syllabus and study guide is designed to help with teaching and learning and is intended to provide detailed information on what could be assessed in any

Manage ment Accounting (F2/FMA) December 2011 This syllabus and study guide is designed to help with teaching and learning and is intended to provide detailed information on what could be assessed in any

Institute of Certified Bookkeepers

Making you count Institute of Certified Bookkeepers Level IV Module 1 Management Accounting Topic 1 - The Business Environment Explain the role and purpose of management accounting as a business activity.

Making you count Institute of Certified Bookkeepers Level IV Module 1 Management Accounting Topic 1 - The Business Environment Explain the role and purpose of management accounting as a business activity.

(F2/FMA) December 2011

December 2011") Manage ment Accounting (F2/FMA) December 2011 This syllabus and study guide is designed to help with teaching and learning and is intended to provide detailed information on what could be assessed in any

Manage ment Accounting (F2/FMA) December 2011 This syllabus and study guide is designed to help with teaching and learning and is intended to provide detailed information on what could be assessed in any

MARK SCHEME for the November 2004 question paper 9706 ACCOUNTING

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS GCE Advanced Level MARK SCHEME for the November 2004 question paper 9706 ACCOUNTING 9706/04 Paper 4 Problem Solving (Supplementary Topics), maximum raw

UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS GCE Advanced Level MARK SCHEME for the November 2004 question paper 9706 ACCOUNTING 9706/04 Paper 4 Problem Solving (Supplementary Topics), maximum raw

Cambridge International General Certificate of Secondary Education 0452 Accounting November 2012 Principal Examiner Report for Teachers

ACCOUNTING Cambridge International General Certificate of Secondary Education Paper 0452/11 Paper 1 Key Messages This question paper contained a mixture of multiple-choice, short-answer and structured

ACCOUNTING Cambridge International General Certificate of Secondary Education Paper 0452/11 Paper 1 Key Messages This question paper contained a mixture of multiple-choice, short-answer and structured

Management Accounting (MA)/FMA September 2018 to August 2019

/FMA September 2018 to August 2019") Management Accounting (MA)/FMA September 2018 to August 2019 Guide to structure of the syllabus and Study guide This syllabus and study guide are designed to help with teaching and learning and is intended

Management Accounting (MA)/FMA September 2018 to August 2019 Guide to structure of the syllabus and Study guide This syllabus and study guide are designed to help with teaching and learning and is intended

CERTIFICATE IN MANAGEMENT ACCOUNTING

Series 2 Examination 2007 CERTIFICATE IN MANAGEMENT ACCOUNTING Level 3 Tuesday 29 May Subject Code: 3623/M Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal

Series 2 Examination 2007 CERTIFICATE IN MANAGEMENT ACCOUNTING Level 3 Tuesday 29 May Subject Code: 3623/M Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer 5 questions. All questions carry equal

Cambridge International Advanced Subsidiary Level and Advanced Level 9706 Accounting June 2015 Principal Examiner Report for Teachers

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 D 16 A 2 C 17 A 3 D 18 B 4 B 19 A 5 D 20 D 6 A 21

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 D 16 A 2 C 17 A 3 D 18 B 4 B 19 A 5 D 20 D 6 A 21

Level 3 Certificate in Advanced Business Calculations

LCCI International Qualifications Level 3 Certificate in Advanced Business Calculations Syllabus Effective from 2001 For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com

LCCI International Qualifications Level 3 Certificate in Advanced Business Calculations Syllabus Effective from 2001 For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com

Cambridge International Advanced Subsidiary and Advanced Level 9706 Accounting June 2016 Principal Examiner Report for Teachers

ACCOUNTING Cambridge International Advanced Subsidiary and Advanced Level Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 D 16 C 2 A 17 A 3 C 18 B 4 D 19 B 5 B 20 A 6 C 21 C 7 C

ACCOUNTING Cambridge International Advanced Subsidiary and Advanced Level Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 D 16 C 2 A 17 A 3 C 18 B 4 D 19 B 5 B 20 A 6 C 21 C 7 C

SERIES 3 EXAMINATION 2001 MANAGEMENT ACCOUNTING THIRD LEVEL. (Code No: 3023) FRIDAY 15 JUNE

FRIDAY 15 JUNE") SERIES 3 EXAMINATION 2001 MANAGEMENT ACCOUNTING THIRD LEVEL (Code No: 3023) FRIDAY 15 JUNE Instructions to Candidates (e) (f) (g) The time allowed for this examination is 3 hours. Answer 5 questions. All

SERIES 3 EXAMINATION 2001 MANAGEMENT ACCOUNTING THIRD LEVEL (Code No: 3023) FRIDAY 15 JUNE Instructions to Candidates (e) (f) (g) The time allowed for this examination is 3 hours. Answer 5 questions. All

MANAGEMENT ACCOUNTING

SERIES 4 EXAMINATION 2004 MANAGEMENT ACCOUNTING LEVEL 3 (Code No: 3023) FRIDAY 19 NOVEMBER Instructions to Candidates (d) (e) (f) (g) The time allowed for this examination is 3 hours. Answer 5 questions.

SERIES 4 EXAMINATION 2004 MANAGEMENT ACCOUNTING LEVEL 3 (Code No: 3023) FRIDAY 19 NOVEMBER Instructions to Candidates (d) (e) (f) (g) The time allowed for this examination is 3 hours. Answer 5 questions.

AM Syllabus ( ): Accounting AM SYLLABUS ( ) ACCOUNTING AM 01 SYLLABUS

: Accounting AM SYLLABUS ( ) ACCOUNTING AM 01 SYLLABUS") AM SYLLABUS (2008-2013) ACCOUNTING AM 01 SYLLABUS 1 Accounting AM 01 Syllabus (Available in September) Paper I (3 hrs) + Paper II (3 hrs) Introduction The syllabus builds on the topics set for the SEC

AM SYLLABUS (2008-2013) ACCOUNTING AM 01 SYLLABUS 1 Accounting AM 01 Syllabus (Available in September) Paper I (3 hrs) + Paper II (3 hrs) Introduction The syllabus builds on the topics set for the SEC

Mark Scheme (Results) Series Pearson LCCI Level 3 COST ACCOUNTING (ASE3017)

Series Pearson LCCI Level 3 COST ACCOUNTING (ASE3017)") Mark Scheme (Results) Series 3 2014 Pearson LCCI Level 3 COST ACCOUNTING (ASE3017) LCCI International Qualifications LCCI International Qualifications are awarded by Pearson, the UK s largest awarding

Mark Scheme (Results) Series 3 2014 Pearson LCCI Level 3 COST ACCOUNTING (ASE3017) LCCI International Qualifications LCCI International Qualifications are awarded by Pearson, the UK s largest awarding

Intermediate Financial and Management Accounting

Intermediate Financial and Management Accounting Course map This document outlines the course structure. ACCA: FA2-MA2.X Intermediate Financial and Management Accounting Intermediate course orientation

Intermediate Financial and Management Accounting Course map This document outlines the course structure. ACCA: FA2-MA2.X Intermediate Financial and Management Accounting Intermediate course orientation

Cambridge International General Certificate of Secondary Education 0452 Accounting November 2014 Principal Examiner Report for Teachers

ACCOUNTING Cambridge International General Certificate of Secondary Education Paper 0452/11 Paper 11 Key Messages Questions can be set on any section of the syllabus and a good knowledge of all sections

ACCOUNTING Cambridge International General Certificate of Secondary Education Paper 0452/11 Paper 11 Key Messages Questions can be set on any section of the syllabus and a good knowledge of all sections

LCCI International Qualifications. Cost Accounting Level 3. Model Answers Series (3017)

") LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 2 2012 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

LCCI International Qualifications Cost Accounting Level 3 Model Answers Series 2 2012 (3017) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Cost

Pearson LCCI Level 3 Certificate in Advanced Business Calculations (ASE3003)

") Pearson LCCI Level 3 Certificate in Advanced Business Calculations (ASE3003) Specification First teaching from 2001 Issue 2 Edexcel, BTEC and LCCI qualifications Edexcel, BTEC and LCCI qualifications are

Pearson LCCI Level 3 Certificate in Advanced Business Calculations (ASE3003) Specification First teaching from 2001 Issue 2 Edexcel, BTEC and LCCI qualifications Edexcel, BTEC and LCCI qualifications are

Intermediate Management Accounting

Intermediate Management Accounting Course map This document outlines the course structure. Course orientation Lesson 1: Welcome Lesson 2: Getting your diploma Lesson 3: How do I study this course? Unit

Intermediate Management Accounting Course map This document outlines the course structure. Course orientation Lesson 1: Welcome Lesson 2: Getting your diploma Lesson 3: How do I study this course? Unit

Pearson LCCI Level 3 Certificate in Accounting (VRQ)

") Pearson LCCI Level 3 Certificate in Accounting (VRQ) (ASE3012X) L3 SPECIFICATION Issue 2 Pearson LCCI Level 3 Certificate in Accounting (VRQ) (ASE3012X) Specification Issue 2 Edexcel, BTEC and LCCI qualifications

Pearson LCCI Level 3 Certificate in Accounting (VRQ) (ASE3012X) L3 SPECIFICATION Issue 2 Pearson LCCI Level 3 Certificate in Accounting (VRQ) (ASE3012X) Specification Issue 2 Edexcel, BTEC and LCCI qualifications

Cost Accounting. Level 3. Model Answers. Series (Code 3016) 1 ASE /2/06

1 ASE /2/06") Cost Accounting Level 3 Model Answers Series 2 2006 (Code 3016) 1 ASE 3016 2 06 1 3016/2/06 >f0t@w9w2`?[6zbkbwgc# Cost Accounting Level 3 Series 2 2006 How to use this booklet Model Answers have been developed

Cost Accounting Level 3 Model Answers Series 2 2006 (Code 3016) 1 ASE 3016 2 06 1 3016/2/06 >f0t@w9w2`?[6zbkbwgc# Cost Accounting Level 3 Series 2 2006 How to use this booklet Model Answers have been developed

CERTIFICATE IN MANAGEMENT ACCOUNTING

Series 3 Examination 2010 CERTIFICATE IN MANAGEMENT ACCOUNTING Level 3 Tuesday 8 June Subject Code: 3024 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer all 5 questions. All questions carry equal

Series 3 Examination 2010 CERTIFICATE IN MANAGEMENT ACCOUNTING Level 3 Tuesday 8 June Subject Code: 3024 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer all 5 questions. All questions carry equal

Management Accounting

Management Accounting Level 3 Model Answers Series 4 2006 Singapore (Code 3723) Vision Statement Our vision is to contribute to the achievements of learners around the world by providing integrated assessment

Management Accounting Level 3 Model Answers Series 4 2006 Singapore (Code 3723) Vision Statement Our vision is to contribute to the achievements of learners around the world by providing integrated assessment

PAPER C01 Fundamentals of Management Accounting Acorn chapters

PAPER C01 Fundamentals of Management Accounting Acorn chapters 1 Classification of costs 2 The context of management accounting 3 Absorbing fixed production overhead 4 Absorption and marginal costing 5

PAPER C01 Fundamentals of Management Accounting Acorn chapters 1 Classification of costs 2 The context of management accounting 3 Absorbing fixed production overhead 4 Absorption and marginal costing 5

Pearson LCCI Level 4 Certificate in Management Accounting (VRQ)

") Pearson LCCI Level 4 Certificate in Management Accounting (VRQ) (ASE20102) L4 SPECIFICATION First teaching from January 2015 Pearson LCCI Level 4 Certificate in Management Accounting (VRQ) (ASE20102)

Pearson LCCI Level 4 Certificate in Management Accounting (VRQ) (ASE20102) L4 SPECIFICATION First teaching from January 2015 Pearson LCCI Level 4 Certificate in Management Accounting (VRQ) (ASE20102)

P1 Performance Operations September 2013 examination

Operational Level Paper P1 Performance Operations September 2013 examination Examiner s Answers Note: Some of the answers that follow are fuller and more comprehensive than would be expected from a well-prepared

Operational Level Paper P1 Performance Operations September 2013 examination Examiner s Answers Note: Some of the answers that follow are fuller and more comprehensive than would be expected from a well-prepared

ACCA F2 FLASH NOTES. Describe a pie chart?

ACCA F2 FLASH NOTES Describe a pie chart? A pie chart is a circle that is divided into segments representing each type of observation. The size of each segment is proportional to the proportion of the

ACCA F2 FLASH NOTES Describe a pie chart? A pie chart is a circle that is divided into segments representing each type of observation. The size of each segment is proportional to the proportion of the

ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA. Examiner's Report AA3 EXAMINATION - JULY 2015 (AA32) MANAGEMENT ACCOUNTING AND FINANCE

MANAGEMENT ACCOUNTING AND FINANCE") ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA Examiner's Report AA3 EXAMINATION - JULY 2015 (AA32) MANAGEMENT ACCOUNTING AND FINANCE OVERVIEW: This paper has three sections covering 100 marks, 1.

ASSOCIATION OF ACCOUNTING TECHNICIANS OF SRI LANKA Examiner's Report AA3 EXAMINATION - JULY 2015 (AA32) MANAGEMENT ACCOUNTING AND FINANCE OVERVIEW: This paper has three sections covering 100 marks, 1.

SERIES 4 EXAMINATION 2001 MANAGEMENT ACCOUNTING THIRD LEVEL. (Code No: 3023) TUESDAY 13 NOVEMBER

TUESDAY 13 NOVEMBER") SERIES 4 EXAMINATION 2001 MANAGEMENT ACCOUNTING THIRD LEVEL (Code No: 3023) TUESDAY 13 NOVEMBER Instructions to Candidates (d) (e) (f) (g) The time allowed for this examination is 3 hours. Answer 5 questions.

SERIES 4 EXAMINATION 2001 MANAGEMENT ACCOUNTING THIRD LEVEL (Code No: 3023) TUESDAY 13 NOVEMBER Instructions to Candidates (d) (e) (f) (g) The time allowed for this examination is 3 hours. Answer 5 questions.

FOREWORD... 1 ACCOUNTING... 2

FOREWORD... 1 ACCOUNTING... 2 GCE Advanced Level and GCE Advanced Subsidiary Level... 2 Paper 9706/01 Multiple Choice (Core)... 2 Paper 9706/02 Structured Questions... 3 Paper 9706/03 Multiple Choice (Extension)...

FOREWORD... 1 ACCOUNTING... 2 GCE Advanced Level and GCE Advanced Subsidiary Level... 2 Paper 9706/01 Multiple Choice (Core)... 2 Paper 9706/02 Structured Questions... 3 Paper 9706/03 Multiple Choice (Extension)...

RELATIONAL DIAGRAM OF MAIN CAPABILITIES

Syllabus MAIN CAPABILITIES APM (P5) On successful completion of this paper, candidates should be able to: A Explain the nature and purpose of cost and management accounting PM (F5) FM (F9) B Describe costs

Syllabus MAIN CAPABILITIES APM (P5) On successful completion of this paper, candidates should be able to: A Explain the nature and purpose of cost and management accounting PM (F5) FM (F9) B Describe costs

Cost Accounting. Level 3. Model Answers. Series (Code 3616) 1 ASE /2/06

1 ASE /2/06") Cost Accounting Level 3 Model Answers Series 2 2006 (Code 3616) 1 ASE 3016 2 06 3 3616/2/06 >f0t@w?h2`?[6zbk0j3d# Certificate in Cost Accounting Level 3 - Malaysia Series 2 2006 How to use this booklet

Cost Accounting Level 3 Model Answers Series 2 2006 (Code 3616) 1 ASE 3016 2 06 3 3616/2/06 >f0t@w?h2`?[6zbk0j3d# Certificate in Cost Accounting Level 3 - Malaysia Series 2 2006 How to use this booklet

9706 Accounting November 2007

www.xtremepapers.com ACCOUNTING Paper 9706/01 Multiple Choice Question Number Key Question Number Key 1 C 16 C 2 D 17 C 3 C 18 B 4 C 19 D 5 A 20 A 6 B 21 C 7 D 22 D 8 A 23 B 9 C 24 A 10 D 25 D 11 B 26

www.xtremepapers.com ACCOUNTING Paper 9706/01 Multiple Choice Question Number Key Question Number Key 1 C 16 C 2 D 17 C 3 C 18 B 4 C 19 D 5 A 20 A 6 B 21 C 7 D 22 D 8 A 23 B 9 C 24 A 10 D 25 D 11 B 26

Cambridge International Advanced Subsidiary Level and Advanced Level 9706 Accounting June 2012 Principal Examiner Report for Teachers

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING Paper 9706/11 Multiple Choice (Core) Question Number Key Question Number Key 1 A 16 A 2 B 17 C 3 D 18 A 4 D 19 C 5 B 20 B

Cambridge International Advanced Subsidiary Level and Advanced Level ACCOUNTING Paper 9706/11 Multiple Choice (Core) Question Number Key Question Number Key 1 A 16 A 2 B 17 C 3 D 18 A 4 D 19 C 5 B 20 B

Paper P1 Performance Operations Post Exam Guide November 2012 Exam. General Comments

General Comments This sitting produced a reasonably good pass rate although lower than in the last two main exam sittings. Performance varied considerably by section and from previous sittings. There were

General Comments This sitting produced a reasonably good pass rate although lower than in the last two main exam sittings. Performance varied considerably by section and from previous sittings. There were

SEC Syllabus (2020) Accounting

Accounting") SEC SYLLABUS (2020) ACCOUNTING SEC 01 SYLLABUS 1 Accounting SEC 01 Syllabus (not available in September) Paper 1 (2hrs) + Paper II (2 hrs) The aims of the syllabus are to enable students: 1. To understand

SEC SYLLABUS (2020) ACCOUNTING SEC 01 SYLLABUS 1 Accounting SEC 01 Syllabus (not available in September) Paper 1 (2hrs) + Paper II (2 hrs) The aims of the syllabus are to enable students: 1. To understand

PRINCIPLES OF ACCOUNTS

PRINCIPLES OF ACCOUNTS Paper 7110/11 Multiple Choice 11 Question Number Key Question Number Key 1 C 16 A 2 B 17 B 3 A 18 B 4 C 19 D 5 D 20 B 6 D 21 B 7 A 22 D 8 A 23 C 9 C 24 B 10 D 25 D 11 C 26 A 12 A

PRINCIPLES OF ACCOUNTS Paper 7110/11 Multiple Choice 11 Question Number Key Question Number Key 1 C 16 A 2 B 17 B 3 A 18 B 4 C 19 D 5 D 20 B 6 D 21 B 7 A 22 D 8 A 23 C 9 C 24 B 10 D 25 D 11 C 26 A 12 A

P1 Performance Evaluation

Management Accounting Pillar Managerial Level Paper P1 Management Accounting Performance Evaluation 24 November 2009 Tuesday Morning Session Instructions to candidates You are allowed three hours to answer

Management Accounting Pillar Managerial Level Paper P1 Management Accounting Performance Evaluation 24 November 2009 Tuesday Morning Session Instructions to candidates You are allowed three hours to answer

Cambridge International Advanced Subsidiary Level and Advanced Level 9706 Accounting June 2011 Principal Examiner Report for Teachers

ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice (Core) Question Number Key Question Number Key 1 D 16 C 2 D 17 C 3 C 18 C 4 B 19 B 5 D 20 D 6 A 21 C 7 D 22 B 8 A 23 D 9 A 24 A 10 C 25 A 11

ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice (Core) Question Number Key Question Number Key 1 D 16 C 2 D 17 C 3 C 18 C 4 B 19 B 5 D 20 D 6 A 21 C 7 D 22 B 8 A 23 D 9 A 24 A 10 C 25 A 11

LCCI International Qualifications. Accounting (IAS) Level 3. Model Answers Series (3902)

Level 3. Model Answers Series (3902)") LCCI International Qualifications Accounting (IAS) Level 3 Model Answers Series 2 2011 (3902) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Accounting

LCCI International Qualifications Accounting (IAS) Level 3 Model Answers Series 2 2011 (3902) For further information contact us: Tel. +44 (0) 8707 202909 Email. enquiries@ediplc.com www.lcci.org.uk Accounting

AM01 Syllabus (2019): Accounting AM SYLLABUS (2019) SYLLABUS

: Accounting AM SYLLABUS (2019) SYLLABUS") ACCOUNTING AM SYLLABUS (2019) AM01 SYLLABUS 1 Accounting AM01 Syllabus (Available in September) Paper I (3 hrs) + Paper II (3 hrs) Introduction The syllabus seeks to develop the students financial literacy,

ACCOUNTING AM SYLLABUS (2019) AM01 SYLLABUS 1 Accounting AM01 Syllabus (Available in September) Paper I (3 hrs) + Paper II (3 hrs) Introduction The syllabus seeks to develop the students financial literacy,

The Complete Course On Budgeting: Planning, Forecasting, What If Analysis And Reporting

The Complete Course On Budgeting: Planning, Forecasting, What If Analysis And Reporting SECTOR / ACCOUNTING AND FINANCE NON-TECHNICAL & CERTIFIED TRAINING COURSE The use of Excel as the toolbox of choice

The Complete Course On Budgeting: Planning, Forecasting, What If Analysis And Reporting SECTOR / ACCOUNTING AND FINANCE NON-TECHNICAL & CERTIFIED TRAINING COURSE The use of Excel as the toolbox of choice

PRINCIPLES OF ACCOUNTS

PRINCIPLES OF ACCOUNTS Paper 7110/11 Paper 11 Question Question Key Number Number Key 1 D 16 B 2 A 17 B 3 D 18 C 4 C 19 C 5 B 20 A 6 D 21 B 7 D 22 C 8 A 23 A 9 C 24 D 10 A 25 A 11 D 26 C 12 D 27 D 13 A

PRINCIPLES OF ACCOUNTS Paper 7110/11 Paper 11 Question Question Key Number Number Key 1 D 16 B 2 A 17 B 3 D 18 C 4 C 19 C 5 B 20 A 6 D 21 B 7 D 22 C 8 A 23 A 9 C 24 D 10 A 25 A 11 D 26 C 12 D 27 D 13 A

Accounting & Finance for Managers

Accounting & Finance for Managers SYLLABUS UNIT 1 INTRODUCTION TO FINANCIAL ACCOUNTING * Introduction to Accounting * Meaning * Evolution of Accounting * Importance of Accounting * Users of financial statements

Accounting & Finance for Managers SYLLABUS UNIT 1 INTRODUCTION TO FINANCIAL ACCOUNTING * Introduction to Accounting * Meaning * Evolution of Accounting * Importance of Accounting * Users of financial statements

Introduction Financial record keeping Income statements The balance sheet Further adjustments to the income statement 47

CONTENTS Introduction 1 01 Financial record keeping 3 Introduction 3 Single-entry bookkeeping 4 Double-entry bookkeeping 6 Balancing accounts 10 The trial balance 13 Daybooks and ledgers 15 Modern double-entry

CONTENTS Introduction 1 01 Financial record keeping 3 Introduction 3 Single-entry bookkeeping 4 Double-entry bookkeeping 6 Balancing accounts 10 The trial balance 13 Daybooks and ledgers 15 Modern double-entry

CARIBBEAN EXAMINATIONS COUNCIL

CARIBBEAN EXAMINATIONS COUNCIL REPORT ON CANDIDATES WORK IN THE CARIBBEAN SECONDARY EDUCATION CERTIFICATE JANUARY 2009 PRINCIPLES OF ACCOUNTS Copyright 2009 Caribbean Examinations Council St Michael Barbados

CARIBBEAN EXAMINATIONS COUNCIL REPORT ON CANDIDATES WORK IN THE CARIBBEAN SECONDARY EDUCATION CERTIFICATE JANUARY 2009 PRINCIPLES OF ACCOUNTS Copyright 2009 Caribbean Examinations Council St Michael Barbados

CERTIFICATE IN MANAGEMENT ACCOUNTING

Series 2 Examination 2011 CERTIFICATE IN MANAGEMENT ACCOUNTING Level 3 Tuesday 12 April Subject Code: 3024 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer all 5 questions. All questions carry

Series 2 Examination 2011 CERTIFICATE IN MANAGEMENT ACCOUNTING Level 3 Tuesday 12 April Subject Code: 3024 Time allowed: 3 hours INSTRUCTIONS FOR CANDIDATES Answer all 5 questions. All questions carry

Management Accounting

Management Accounting Level 3 Model Answers Series 4 2004 (Code 3023) ASP M 1697 >f0t@wjy2[2`6zpw4m # Vision Statement Our vision is to contribute to the achievements of learners around the world by providing

Management Accounting Level 3 Model Answers Series 4 2004 (Code 3023) ASP M 1697 >f0t@wjy2[2`6zpw4m # Vision Statement Our vision is to contribute to the achievements of learners around the world by providing

Cambridge International General Certificate of Secondary Education 0452 Accounting June 2014 Principal Examiner Report for Teachers

ACCOUNTING Cambridge International General Certificate of Secondary Education Paper 0452/11 Paper 11 Key Messages Question 1 consisted of ten multiple choice items covering topics across the whole syllabus.

ACCOUNTING Cambridge International General Certificate of Secondary Education Paper 0452/11 Paper 11 Key Messages Question 1 consisted of ten multiple choice items covering topics across the whole syllabus.

P1 Performance Operations Post Exam Guide May 2014 Exam. General Comments

General Comments Performance on this paper was reasonably good with the pass rate above average for the 2010 syllabus. Many candidates scored very highly and there were fewer marginal scripts. However

General Comments Performance on this paper was reasonably good with the pass rate above average for the 2010 syllabus. Many candidates scored very highly and there were fewer marginal scripts. However

Syllabus Cambridge International A & AS Level Accounting Syllabus code 9706 For examination in June and November 2011

www.xtremepapers.com Syllabus Cambridge International A & AS Level Accounting Syllabus code 9706 For examination in June and November 2011 Note for Exams Officers: Before making Final Entries, please check

www.xtremepapers.com Syllabus Cambridge International A & AS Level Accounting Syllabus code 9706 For examination in June and November 2011 Note for Exams Officers: Before making Final Entries, please check

Pearson LCCI Level 2 Certificate in Bookkeeping and Accounting (VRQ)

") L2 Pearson LCCI Level 2 Certificate in Bookkeeping and Accounting (VRQ) (ASE20093) SPECIFICATION Issue 3 First teaching from September 2015 Pearson LCCI Level 2 Certificate in Bookkeeping and Accounting

L2 Pearson LCCI Level 2 Certificate in Bookkeeping and Accounting (VRQ) (ASE20093) SPECIFICATION Issue 3 First teaching from September 2015 Pearson LCCI Level 2 Certificate in Bookkeeping and Accounting

Cambridge International Advanced Subsidiary Level and Advanced Level 9706 Accounting November 2013 Principal Examiner Report for Teachers

ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 D 16 D 2 C 17 B 3 C 18 B 4 B 19 A 5 C 20 B 6 B 21 C 7 C 22 D 8 C 23 D 9 C 24 C 10 A 25 B 11 A 26

ACCOUNTING www.xtremepapers.com Paper 9706/11 Multiple Choice Question Number Key Question Number Key 1 D 16 D 2 C 17 B 3 C 18 B 4 B 19 A 5 C 20 B 6 B 21 C 7 C 22 D 8 C 23 D 9 C 24 C 10 A 25 B 11 A 26

BCS Professional Certificate in Business Finance Syllabus Version 1.2 December 2016

BCS Professional Certificate in Business Finance Syllabus Version 1.2 December 2016 This professional certification is not regulated by the following United Kingdom Regulators - Ofqual, Qualification in

BCS Professional Certificate in Business Finance Syllabus Version 1.2 December 2016 This professional certification is not regulated by the following United Kingdom Regulators - Ofqual, Qualification in

Management Accounting Fundamentals (FMAF)

") POST EXM GUIE May 2001 Exam Management ccounting Fundamentals (FMF) IM publishes a Question and nswer booklet for each paper of the May 2001 exam which is essential reading for students and tutors. The

POST EXM GUIE May 2001 Exam Management ccounting Fundamentals (FMF) IM publishes a Question and nswer booklet for each paper of the May 2001 exam which is essential reading for students and tutors. The

PRINCIPLES OF ACCOUNTS

PRINCIPLES OF ACCOUNTS Paper 7110/11 Multiple Choice Question Question Key Number Number Key 1 D 16 C 2 C 17 A 3 C 18 C 4 B 19 C 5 D 20 D 6 A 21 C 7 A 22 A 8 D 23 D 9 C 24 B 10 C 25 B 11 A 26 A 12 B 27

PRINCIPLES OF ACCOUNTS Paper 7110/11 Multiple Choice Question Question Key Number Number Key 1 D 16 C 2 C 17 A 3 C 18 C 4 B 19 C 5 D 20 D 6 A 21 C 7 A 22 A 8 D 23 D 9 C 24 B 10 C 25 B 11 A 26 A 12 B 27

Paper P1 Performance Operations Post Exam Guide November 2011 Exam

General Comments Performance on this paper was better than in previous diets, mainly as a result of improved performance in Sections A and B. Candidates scored better on average in the multiple choice

General Comments Performance on this paper was better than in previous diets, mainly as a result of improved performance in Sections A and B. Candidates scored better on average in the multiple choice

P1 Performance Operations September 2014 examination

Operational Level Paper P1 Performance Operations September 2014 examination Examiner s Answers Note: Some of the answers that follow are fuller and more comprehensive than would be expected from a well-prepared

Operational Level Paper P1 Performance Operations September 2014 examination Examiner s Answers Note: Some of the answers that follow are fuller and more comprehensive than would be expected from a well-prepared

Paper P1 Management Accounting Performance Evaluation Post Exam Guide November 2008 Exam. General Comments

General Comments The overall result on this paper was reasonable and, while performance was well below the level seen in May 2008, there was a small improvement on the previous November sitting. gained

General Comments The overall result on this paper was reasonable and, while performance was well below the level seen in May 2008, there was a small improvement on the previous November sitting. gained

Pearson LCCI Level 4 Certificate in Financial Accounting (VRQ)

") Pearson LCCI Level 4 Certificate in Financial Accounting (VRQ) (ASE20101) L4 SPECIFICATION Issue 4 First teaching from September 2015 Edexcel, BTEC and LCCI qualifications Edexcel, BTEC and LCCI qualifications

Pearson LCCI Level 4 Certificate in Financial Accounting (VRQ) (ASE20101) L4 SPECIFICATION Issue 4 First teaching from September 2015 Edexcel, BTEC and LCCI qualifications Edexcel, BTEC and LCCI qualifications

School of Business & Enterprise. Module Code: ACCT08009 ACCOUNTING & FINANCE. Date: 19 June 2017 Time:

School of Business & Enterprise Paisley Campus Session 2016-17 Resit Paper Module Code: ACCT08009 ACCOUNTING & FINANCE Date: 19 June 2017 Time: 0900-1100 EXAM PAPER HAS TWO SECTIONS: A AND B Answer Questions

School of Business & Enterprise Paisley Campus Session 2016-17 Resit Paper Module Code: ACCT08009 ACCOUNTING & FINANCE Date: 19 June 2017 Time: 0900-1100 EXAM PAPER HAS TWO SECTIONS: A AND B Answer Questions

Financial Management (F9) June & December 2012

June & December 2012") Financial Management (F9) June & December 2012 This syllabus and study guide is designed to help with planning study and to provide detailed information on what could be assessed in any examination session.

Financial Management (F9) June & December 2012 This syllabus and study guide is designed to help with planning study and to provide detailed information on what could be assessed in any examination session.

Example Candidate Responses

Example Candidate Responses Cambridge O Level Principles of Accounts 7110 Cambridge Secondary 2 In order to help us develop the highest quality Curriculum Support resources, we are undertaking a continuous

Example Candidate Responses Cambridge O Level Principles of Accounts 7110 Cambridge Secondary 2 In order to help us develop the highest quality Curriculum Support resources, we are undertaking a continuous

C A R I B B E A N E X A M I N A T I O N S C O U N C I L REPORT ON CANDIDATES WORK IN THE CARIBBEAN ADVANCED PROFICIENCY EXAMINATION MAY/JUNE 2014

C A R I B B E A N E X A M I N A T I O N S C O U N C I L REPORT ON CANDIDATES WORK IN THE CARIBBEAN ADVANCED PROFICIENCY EXAMINATION MAY/JUNE 2014 ACCOUNTING Copyright 2014 Caribbean Examinations Council

C A R I B B E A N E X A M I N A T I O N S C O U N C I L REPORT ON CANDIDATES WORK IN THE CARIBBEAN ADVANCED PROFICIENCY EXAMINATION MAY/JUNE 2014 ACCOUNTING Copyright 2014 Caribbean Examinations Council

P1 Performance Operations November 2013 examination

Operational Level Paper P1 Performance Operations November 2013 examination Examiner s Answers Note: Some of the answers that follow are fuller and more comprehensive than would be expected from a well-prepared

Operational Level Paper P1 Performance Operations November 2013 examination Examiner s Answers Note: Some of the answers that follow are fuller and more comprehensive than would be expected from a well-prepared

PRINCIPLES OF ACCOUNTS

PRINCIPLES OF ACCOUNTS Paper 7110/11 Multiple Choice Question Number Key Question Number Key 1 C 16 C 2 D 17 A 3 D 18 B 4 B 19 B 5 A 20 A 6 D 21 D 7 D 22 A 8 C 23 D 9 A 24 A 10 B 25 D 11 A 26 C 12 A 27

PRINCIPLES OF ACCOUNTS Paper 7110/11 Multiple Choice Question Number Key Question Number Key 1 C 16 C 2 D 17 A 3 D 18 B 4 B 19 B 5 A 20 A 6 D 21 D 7 D 22 A 8 C 23 D 9 A 24 A 10 B 25 D 11 A 26 C 12 A 27