Piecing Together Financial Puzzles tm. Copyright 2014 Forensic Accounting Services, LLC All Rights Reserved

|

|

|

- Alaina Boone

- 5 years ago

- Views:

Transcription

1

2 Physician s Computer Company PCC 2014 Users Conference Safeguarding Your Practice's Fiscal Health (from undetected fraud scheme) Burlington, Vermont Wednesday, July 16, 2014

Startedfifth book - Employee Theft and")

3 Stephen Pedneault, CPA/CFF, CFE Founder of Forensic Accounting Services, LLC 26 years of fraud experience Investigated embezzlements and fraud ranging from a few thousand to over $6 million Frequent speaker and writer Adjunct Professor of Forensic Accounting, UConn MSA Program and Manchester Community College Member of AICPA, CSCPA, ACFE, NACVA Author of four books, Fraud 101; Anatomy of a Fraud Investigation; Preventing and Detecting Employee Theft and Embezzlement; and Forensic Accounting/Fraud Investigation for Non-Experts, 3rd. (Wiley) Startedfifth book - Employee Theft and Embezzlement Within A Medical Practice (MGMA)

4 Session Objective Medical practices continue to get victimized by someone working within the practice. Due to the volume and complexities of medical billing, schemes are frequently perpetrated within billing and collections, well concealed from detection within the volume of transactions.

5 Session Objective A scheme could go undetected for years, and amount to tens and hundreds of thousands. In this session we will focus the discussions on employee embezzlement schemes, and identify practical measures every practice can implement to minimize their risk of loss due to the dishonest actions of an employee.

6 Session Outline Headlines Outsider Threats Insider Threats Your Practice s Environment

7

8

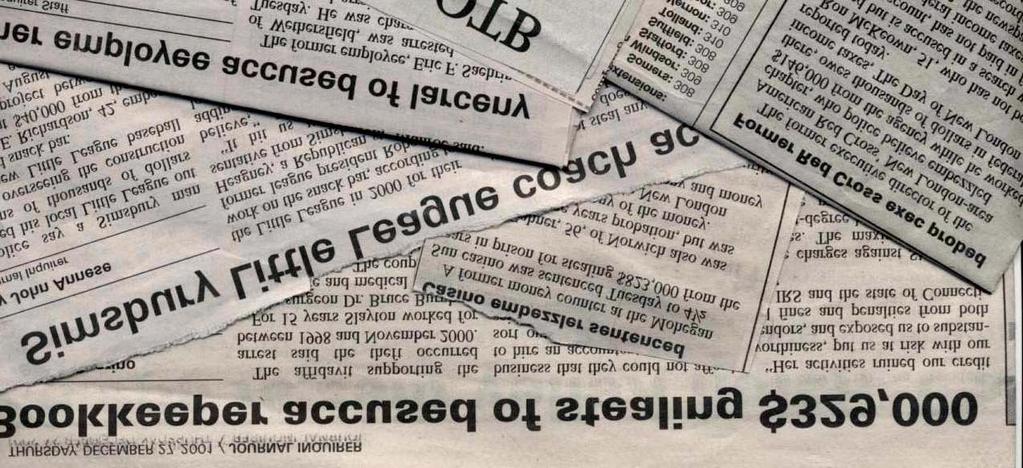

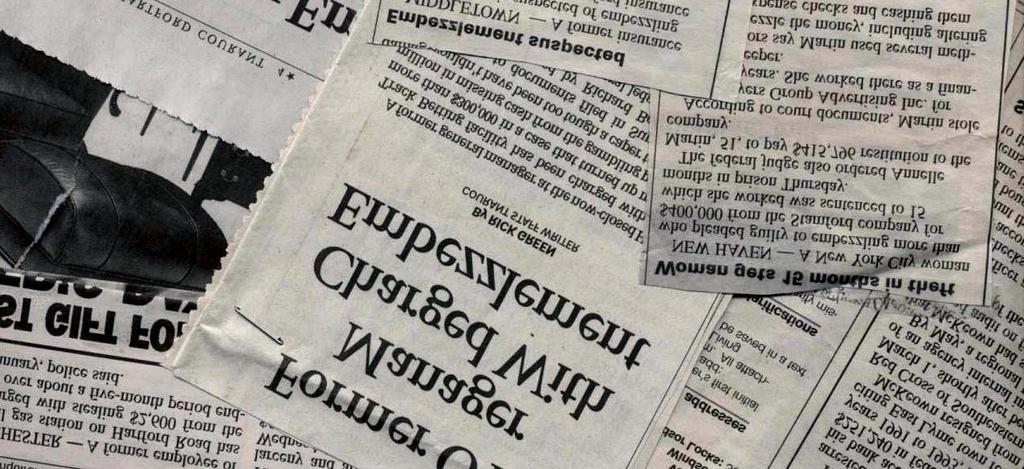

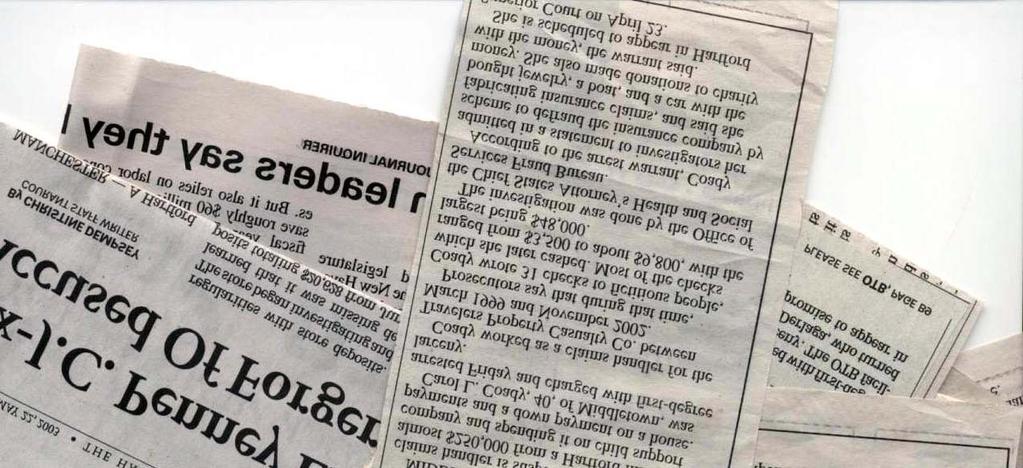

9 How many cases of employee embezzlement ever appear in the media? 1 in 9cases and there is one in the media pretty much every day!

10 Session Outline Headlines Outsider Threats Insider Threats Your Practice s Environment

11 Outsider Threats Patient Identity Theft Insurance Fraud Patient Credit Card Theft Bank Account Theft Product Theft Vendor Schemes System Access

12 Vendors Thefts againstyour practices Returns? Credits? Overpayments?

13 Protecting Patient Information

14 See The Difference? Which one would you prefer to find in your practice?

15 Your Environment? What would I have access to in your office when no one was around?

16 Hopefully NotYour Environment

17 Even Your Shredding

18 Session Outline Headlines Outsider Threats Insider Threats Your Practice s Environment

19 Insider Threats Embezzlement Schemes Theft of Supplies Theft of Patient Information Billing Schemes System Access

20 What wasthe most common form of theft from a medical practice?

21 What has becomethe most common form of theft from a medical practice?

22 The Fraud Triangle Financial Pressure A Recipe for Embezzlement Opportunity Rationalization

23 Embezzlement Concerns Insurance Payments Patient Payments Patient Refunds Credit Card System Cash Disbursements Employee Reimbursements Payroll

24 3 Step Approach to Fraud: I. Prevent fraudfrom occurring II. Detect itas soon as possible III. Obtain adequateinsurance coverage - employee dishonesty or employee crime.

25 Session Outline Headlines Outsider Threats Insider Threats Your Practice s Environment

26 Effective Internal Controls Expectations Adherence Consequences

27 Embezzlement Theft Concealment Conversion

28 3 Step Approach to Fraud: I. Prevent fraudfrom occurring II. Detect itas soon as possible III. Obtain adequateinsurance coverage - employee dishonesty or employee crime.

29 Fraud Approach Triangle Prevention Detection Insurance

30 What can you do? Financial Pressure Opportunity Rationalization to the extent you can

31 Employees respect what you inspect and monitor.

32 Trust is notan internal control. Trust with verification.

33 Screen all new hires, especially individuals who will handle your money and finances Contact listed references Call all previous employers (would they re-hire the person?) Criminal check CREDIT CHECK (with their authorization)

34 Know Your Employees! What Else? What s going on in their lives? Where do they spend their nights and weekends? Living extravagantly? Never taking any vacation time? Facebook IT Manager

35 What To Look For To Determine If Someone Is Embezzling Funds Unusual Employee Behavior Unreconciled Accounts Missing Documents Unexplained Differences Unusual Behavior

36 In any medical practice where does the process start? Scheduling

37 Scheduling

38 Revenue Cycle Charges Collections Adjustments Aging

39 Revenue Cycle Charges Collections Adjustments Aging

40 Revenue Cycle Scheduling Arriving

41 Revenue Cycle Patient Seen Charting

42 Revenue Cycle Co-Payments Collected Billing Completed

43 Revenue Cycle Billing Submitted Payments Received

44 Revenue Cycle Payments/Adjustments Posted Bank Deposit

45 Revenue Cycle Patient Statements A/R Follow-up

46 Revenue Cycle Posting to Accounting System Reconciling Collections

47 Possible Scenarios Charges are captured completely and accurately in the billing system Posted as payment Adjusted Off Still on the Aging

48 Know Your Patients! What Else? Reconcile charges with schedules Account for No Shows, Missed Appointments and Walk-ins Gross Fee Schedule is Fixed Employees cannot override

49 Cash Receipts Who collects payments? Who makes the deposits? Who reconciles the receipts, deposits and postings?

50 Reconciling Payments $ Received $ Deposited $ Posted

51 Co-Pays and Patient Payments Collection Points Satellite Offices, Retail Products Any add-on charges?

52 Create Expectations $5.00 off your next visit if we fail to issue you a receipt

53 Every practice should have two prominently posted signs We expect your payment at the time of your visit

54 The sign we never see Expect a receipt for any payment you make today

55

56

57

58

59 Revenue Cycle Charges Collections Adjustments Aging

60 Co-Pays and Patient Payments Where are your collection points? Satellite offices? Retail sales? Non-billing receipts?

61 Processing Payments Lockbox? Who has access -payments and posting? Receipt books used? Pre-numbered, three-part?

62 Conversion of Checks

63 Remote Deposit Capture

64 Today s Deposit Method

65

66 High Tech Piecing Together Financial Puzzlestm

67 Credit Card Payments Who has accessto process credit card payments? Who reviews the credit card activity? How is your patient s credit card information protected?

68 Merchant Statement

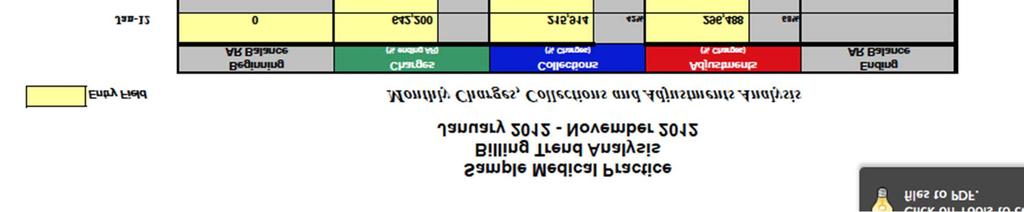

69 Revenue Cycle Charges Collections Adjustments Aging

70 Posting Adjustments Who has access -payments and posting? Adjustments Tracked and monitored? By reason, and by month?

71 Revenue Cycle Charges Collections Adjustments Aging

72 How do you find fraud or embezzlement within the billing cycle? Reviewing and reconciling Random audits Monthly trending

73 Excel Monthly Roll Trends S a m p le M e d ic a l P ra c tic e A c c o u n ts R e c e iv a b le A n a l y s is J a n u a r y D e c e m b e r S a m p le P ra c tic e M on th ly A /R R oll A n alysis B e g i n n i n g A R B a la n c e C h a rg e s (% e n d i n g A R ) C o l le c ti o n s (% C h a rg e s) A d j u s tm e n ts (% C h a r g e s) E n d i n g A R B a la n c e J a n F e b , % 1, % 2, % 1 1 0,3 8 0 M a r , , % 1 4, % 1 6, % 2 0 8,0 8 2 A p r , , % 4 3, % 5 7, % 2 2 2,8 0 1 M a y , , % 4 3, % 4 9, % 2 2 0,1 5 6 J u n , , % 8 0, % 1 0 2, % 1 6 1,1 8 4 J u l , , % 2 9, % 4 5, % 1 9 2,8 1 8 A u g , , % 3 1, % 3 0, % 2 7 0,9 1 2 S e p , , % 6 1, % 1 3 0, % 1 8 5,7 9 0 O c t , , % 6 3, % 8 0, % 1 8 5,6 6 6 N o v , , % 2 9, % 3 8, % 2 3 8,6 4 3 D e c , , % 8 6, % 9 2, % 2 2 9,5 2 2 J a n -0 1 # D IV /0! 0 F e b -0 1 # D IV /0! 0 M a r -0 1 # D IV /0! 0 A p r -0 1 # D IV /0! 0 M a y -0 1 # D IV /0! 0 Y T D A v e r a g e 4 4, % 2 0 2, ,8 6 4 # D IV /0! 5 8, % N u m b e r o f M o n t h s R e p o r t e d ,0 0 0 C h a r g e s, C o l l e c t i o n s & A d j u s t m e n t s 1 5 0,0 0 0 C h a rg e s 1 0 0,0 0 0 A d j u s tm e n ts 5 0,0 0 0 C o l le c ti o n s 0 J a n -0 0 F e b -0 0 M a r-0 0 A p r-0 0 M a y -0 0 J u n -0 0 J u l-0 0 A u g -0 0 S e p -0 0 O c t-0 0 N o v -0 0 D e c -0 0 J a n -0 1 F e b -0 1 M a r-0 1 A p r-0 1 M a y -0 1

74 Excel Monthly Aging Trends Sam p le M ed ical P rac tice Acc o u n ts Re ce iva b le A na l ysis F o r t he Pe ri o d Ju l y, Ju l y, Sa m p le P ra c tice A ging Trend A nalysis O ve r 120 T o ta l C u rre n t Da ys Da ys Da ys Da ys A/ R J u l y 1,485, % 506, % 330,438 7 % 240,076 5 % 1,859, % 4,423,040 A u g us t 1,285, % 549, % 322,611 8 % 229,110 6 % 1,511, % 3,897,754 Se p te m be r 1,285, % 550, % 423, % 263,352 6 % 1,588, % 4,111,799 O c t obe r 1,555, % 565, % 418,187 9 % 239,625 5 % 1,665, % 4,444,653 N ove m be r 1,284, % 591, % 464, % 333,284 8 % 1,504, % 4,179,126 De ce m be r 1,150, % 502, % 421, % 446, % 1,653, % 4,173, Ja n u a ry 1,563, % 383,470 8 % 357,905 8 % 344,882 7 % 2,016, % 4,666,100 F e b rua ry 1,402, % 596, % 226,219 5 % 322,946 7 % 2,225, % 4,773,713 M a rc h 1,412, % 554, % 357,108 7 % 199,631 4 % 2,251, % 4,775,538 Ap ri l 1,399, % 421,674 9 % 309,634 7 % 262,745 6 % 2,298, % 4,692,315 M a y 1,370, % 441, % 233,778 5 % 240,806 5 % 2,275, % 4,561,406 J u ne 1,351, % 453, % 253,774 6 % 187,375 4 % 2,325, % 4,571,615 J u l y 1,441, % 619, % 276,644 6 % 200,190 4 % 2,251, % 4,790,288 YTD A v e r a g e 1, 38 3, ,154 1, 9 5 5, , , A g in g T r e n d A n a ly s is Cu r re n t O v e r Ju ly A u g u s t Se p te m b e r O c to b e r No v e m b e r De c e m b e r Ja n u a ry Fe b ru a r y M a rc h A p ril M a y Ju n e Ju ly

75 How is Medical Billing Like An EKG?

76

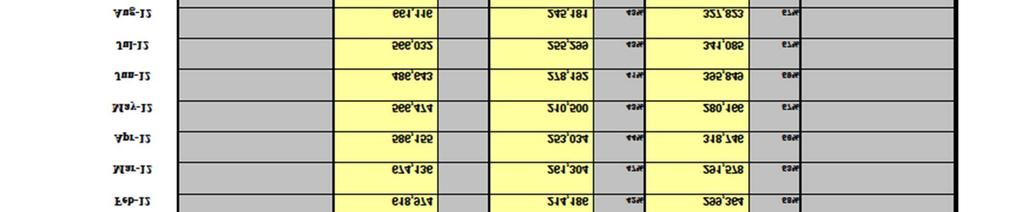

77 Entry Field Sample Medical Practice Billing Trend Analysis January November 2012 Monthly Charges, Collections and Adjustments Analysis Beginning Charges Collections Adjustments Ending AR Balance (% ending AR) (% Charges) (% Charges) AR Balance Jan , ,914 42% 296,488 58% Feb , ,186 42% 299,364 58% Mar , ,304 47% 291,578 53% Apr , ,034 44% 318,746 56% May , ,500 43% 280,166 57% Jun , ,192 41% 395,849 59% Jul , ,299 43% 341,085 57% Aug , ,181 43% 327,823 57% Sep , ,828 41% 347,236 59% Oct , ,809 44% 324,167 56% Nov , ,216 41% 254,313 59% Dec , ,597 40% 291,086 60% Jan , ,668 48% 240,000 52% Feb , ,217 51% 239,137 49% Mar , ,188 48% 296,887 52% Apr , ,409 46% 284,083 54% May ,695 88,824 42% 121,492 58% YTD Average 162,966 43% Jan-May To be entered manually 393, ,301 57% 700,000 Charges, Collections & Adjustments 650, ,000 Charges 550, , , , , , , , , ,000 50,000 0 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13

78 Entry Field Sample Medical Practice Billing Trend Analysis January November 2012 Monthly Charges, Collections and Adjustments Analysis Beginning Charges Collections Adjustments Ending AR Balance (% ending AR) (% Charges) (% Charges) AR Balance Jan , ,914 42% 296,488 58% Feb , ,186 42% 299,364 58% Mar , ,304 47% 291,578 53% Apr , ,034 44% 318,746 56% May , ,500 43% 280,166 57% Jun , ,192 41% 395,849 59% Jul , ,299 43% 341,085 57% Aug , ,181 43% 327,823 57% Sep , ,828 41% 347,236 59% Oct , ,809 44% 324,167 56% Nov , ,216 41% 254,313 59% Dec , ,597 40% 291,086 60% Jan , ,668 48% 240,000 52% Feb , ,217 51% 239,137 49% Mar , ,188 48% 296,887 52% Apr , ,409 46% 284,083 54% May ,695 88,824 42% 121,492 58% YTD Average 162,966 43% 393, ,301 57% Jan-May To be entered manually 700, , , , , , , , , ,000 Charges, Collections & Adjustments Charges Monthly charges are trending downward. Why? 200, , ,000 50,000 0 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13

79 Entry Field Sample Medical Practice Billing Trend Analysis January November 2012 Monthly Charges, Collections and Adjustments Analysis Beginning Charges Collections Adjustments Ending AR Balance (% ending AR) (% Charges) (% Charges) AR Balance Jan , ,914 42% 296,488 58% Feb , ,186 42% 299,364 58% Mar , ,304 47% 291,578 53% Apr , ,034 44% 318,746 56% May , ,500 43% 280,166 57% Jun , ,192 41% 395,849 59% Jul , ,299 43% 341,085 57% Aug , ,181 43% 327,823 57% Sep , ,828 41% 347,236 59% Oct , ,809 44% 324,167 56% Nov , ,216 41% 254,313 59% Dec , ,597 40% 291,086 60% Jan , ,668 48% 240,000 52% Feb , ,217 51% 239,137 49% Mar , ,188 48% 296,887 52% Apr , ,409 46% 284,083 54% May ,695 88,824 42% 121,492 58% YTD Average 162,966 43% 393, ,301 57% Jan-May To be entered manually 700, , , , , , , , , , , , ,000 Charges, Collections & Adjustments Charges Nice, direct relationship between Collections and Adjustments. 50,000 0 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13

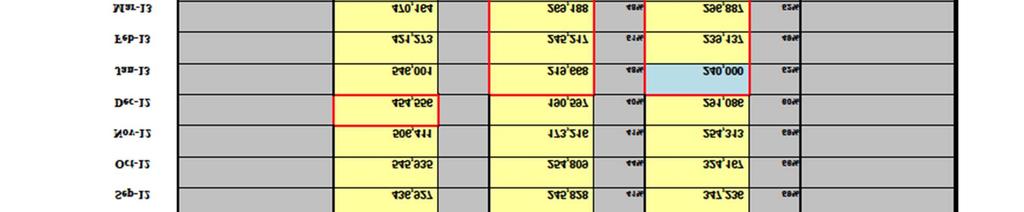

80 Entry Field Sample Medical Practice Billing Trend Analysis January November 2012 Monthly Charges, Collections and Adjustments Analysis Beginning Charges Collections Adjustments Ending AR Balance (% ending AR) (% Charges) (% Charges) AR Balance Jan , ,914 42% 296,488 58% Feb , ,186 42% 299,364 58% Mar , ,304 47% 291,578 53% Apr , ,034 44% 318,746 56% May , ,500 43% 280,166 57% Jun , ,192 41% 395,849 59% Jul , ,299 43% 341,085 57% Aug , ,181 43% 327,823 57% Sep , ,828 41% 347,236 59% Oct , ,809 44% 324,167 56% Nov , ,216 41% 254,313 59% Dec , ,597 40% 291,086 60% Jan , ,668 48% 240,000 52% Feb , ,217 51% 239,137 49% Mar , ,188 48% 296,887 52% Apr , ,409 46% 284,083 54% May ,695 88,824 42% 121,492 58% YTD Average 162,966 43% 393, ,301 57% Jan-May To be entered manually 700, , , , , , , , , , , , ,000 Charges, Collections & Adjustments Charges Adjustments spiked in December, but not Collections. Why? 50,000 0 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13

81 Entry Field Sample Medical Practice Billing Trend Analysis January November 2012 Monthly Charges, Collections and Adjustments Analysis Beginning Charges Collections Adjustments Ending AR Balance (% ending AR) (% Charges) (% Charges) AR Balance Jan , ,914 42% 296,488 58% Feb , ,186 42% 299,364 58% Mar , ,304 47% 291,578 53% Apr , ,034 44% 318,746 56% May , ,500 43% 280,166 57% Jun , ,192 41% 395,849 59% Jul , ,299 43% 341,085 57% Aug , ,181 43% 327,823 57% Sep , ,828 41% 347,236 59% Oct , ,809 44% 324,167 56% Nov , ,216 41% 254,313 59% Dec , ,597 40% 291,086 60% Jan , ,668 48% 240,000 52% Feb , ,217 51% 239,137 49% Mar , ,188 48% 296,887 52% Apr , ,409 46% 284,083 54% May ,695 88,824 42% 121,492 58% YTD Average 162,966 43% 393, ,301 57% Jan-May To be entered manually 700, , , , , , , , , , , , ,000 Charges, Collections & Adjustments Charges Adjustments down, yet Collections going upward. Why? 50,000 0 Jan-12 Feb-12 Mar-12 Apr-12 May-12 Jun-12 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13

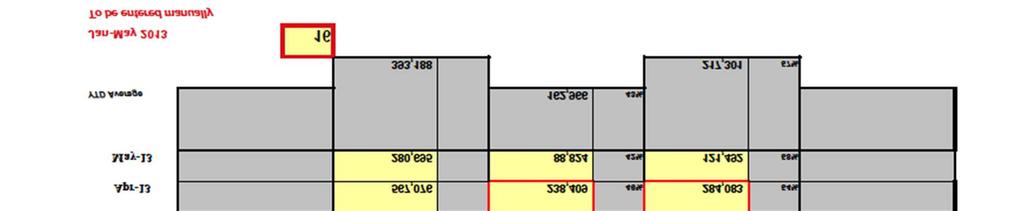

82 Samp le Medica l P rac tice Acc o u n ts Receivab le A na lysis Ja n ua ry Decembe r Samp le P rac tice Monthly A/R Roll Analysis Begin ning A R Ba la nce C ha rges (% ending AR) C o llectio ns (% C ha rges) Adjus tme n ts (% C ha rges) E nding A R Ba la nce Jan Feb , % 1,104 30% 2,541 70% 110,380 Mar , ,471 62% 14,651 48% 16,118 52% 208,082 Apr , ,906 52% 43,686 43% 57,500 57% 222,801 M ay ,801 90,688 41% 43,449 47% 49,884 53% 220,156 Jun , ,101 77% 80,802 44% 102,271 56% 161,184 Jul , ,044 56% 29,795 40% 45,615 60% 192,818 Aug , ,463 52% 31,619 51% 30,750 49% 270,912 Sep , ,351 57% 61,019 32% 130,454 68% 185,790 Oct , ,535 78% 63,861 44% 80,798 56% 185,666 Nov , ,304 51% 29,476 43% 38,851 57% 238,643 Dec , ,620 74% 86,350 48% 92,391 52% 229,522 Jan-01 #DIV/0! 0 Feb-01 #DIV/0! 0 Mar-01 #DIV/0! 0 Apr-01 #DIV/0! 0 M ay-01 #DIV/0! 0 YTD A v e ra g e 44,165 43% 202, ,864 #DIV/0! 58,834 57% N u m b e r o f M o n th s R e p o rte d ,000 C h a rg e s, C o lle c tio n s & A d ju s tm e n ts 150,000 C ha rges 100,000 Adjus tme n ts 50,000 C o llectio ns 0 Jan-00 Feb-00 M ar-00 A pr-00 May-00 Jun-00 Jul-00 A ug-00 Sep-00 Oct-00 Nov-00 Dec-00 Jan-01 Feb-01 M ar-01 Apr-01 M ay-01

83 Samp le Medica l P rac tice Acco u n ts Receivab le A na lysis Jan ua r y Decembe r Samp le P ractice Monthly A/R Roll Analysis Begin ning A R Ba la nce C ha rges (% ending AR) C o llec tio ns (% C ha rges) Adjus tme n ts (% C ha rges) E nding A R Ba la nce Jan Feb , % 1,104 30% 2,541 70% 110,380 Mar , ,471 62% 14,651 48% 16,118 52% 208,082 Apr , ,906 52% 43,686 43% 57,500 57% 222,801 May ,801 90,688 41% 43,449 47% 49,884 53% 220,156 Jun , ,101 77% 80,802 44% 102,271 56% 161,184 Jul , ,044 56% 29,795 40% 45,615 60% 192,818 Aug , ,463 52% 31,619 51% 30,750 49% 270,912 Sep , ,351 57% 61,019 32% 130,454 68% 185,790 Oct , ,535 78% 63,861 44% 80,798 56% 185,666 Nov , ,304 51% 29,476 43% 38,851 57% 238,643 Dec , ,620 74% 86,350 48% 92,391 52% 229,522 Jan-01 #DIV /0! 0 Feb-01 #DIV /0! 0 Mar-01 #DIV /0! 0 Apr-01 #DIV /0! 0 May-01 #DIV /0! 0 YTD A v e ra g e 44,165 43% 202, ,864 #DIV /0! 58,834 57% N u m b e r o f M o n th s R e p o r te d ,000 C h a rg e s, C o lle c tio n s & A d ju s tm e n ts 150, ,000 C ha rges Adjus tme n ts Why did Adjustments spike but not Collections? 50,000 C o llectio ns 0 Jan-00 Feb-00 Mar-00 A pr-00 M ay-00 Jun-00 Jul-00 A ug-00 S ep-00 Oct-00 Nov-00 Dec-00 Jan-01 Feb-01 M ar-01 Apr-01 M ay-01

84 Sample Medical Practice Billing Analysis September September 2010 Fields for entry Aging Trend Analysis Over 120 Total Current Days Days Days Days A/R Jul-12 1,484,209 42% 495,012 14% 385,571 11% 194,705 5% 1,006,263 28% 3,565,760 Aug-12 1,837,462 54% 603,254 18% 250,428 7% 338,230 10% 376,326 11% 3,405,700 Sep-12 1,489,441 41% 963,246 27% 311,945 9% 193,210 5% 650,313 18% 3,608,155 Oct-12 1,459,773 38% 538,716 14% 756,766 20% 245,845 6% 805,766 21% 3,806,866 Nov-12 1,404,324 34% 714,720 17% 390,927 10% 663,007 16% 932,664 23% 4,105,642 Dec-12 1,523,656 36% 613,620 14% 455,550 11% 243,791 6% 1,439,285 34% 4,275,902 Jan-13 1,551,543 37% 428,460 10% 355,634 8% 400,725 10% 1,458,885 35% 4,195,247 Feb-13 1,348,229 33% 544,551 13% 249,850 6% 296,801 7% 1,673,079 41% 4,112,510 Mar-13 1,981,272 42% 576,913 12% 343,493 7% 154,448 3% 1,658,040 35% 4,714,166 Apr-13 1,576,355 32% 1,123,422 23% 348,644 7% 276,204 6% 1,589,595 32% 4,914,220 May-13 1,742,115 34% 673,517 13% 800,677 16% 313,612 6% 1,625,254 32% 5,155,175 Jun-13 1,485,659 31% 785,963 17% 421,585 9% 419,863 9% 1,638,526 34% 4,751,596 Jul-13 1,685,742 36% 596,852 13% 489,653 10% 348,562 7% 1,574,886 34% 4,695,695 YTD Average 1,582,291 38% 427,748 10% 1,263,760 29% Number of Months in Analysis 13 To be entered manually 666,019 16% 314,539 7% 4,254,356 6,000,000 Accounts Receivable Aging Trend Analysis 5,000,000 4,000,000 Current 3,000, ,000, ,000,000 Over Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13

85 Sample Medical Practice Billing Analysis September September 2010 Fields for entry Aging Trend Analysis Over 120 Total Current Days Days Days Days A/R Jul-12 1,484,209 42% 495,012 14% 385,571 11% 194,705 5% 1,006,263 28% 3,565,760 Aug-12 1,837,462 54% 603,254 18% 250,428 7% 338,230 10% 376,326 11% 3,405,700 Sep-12 1,489,441 41% 963,246 27% 311,945 9% 193,210 5% 650,313 18% 3,608,155 Oct-12 1,459,773 38% 538,716 14% 756,766 20% 245,845 6% 805,766 21% 3,806,866 Nov-12 1,404,324 34% 714,720 17% 390,927 10% 663,007 16% 932,664 23% 4,105,642 Dec-12 1,523,656 36% 613,620 14% 455,550 11% 243,791 6% 1,439,285 34% 4,275,902 Jan-13 1,551,543 37% 428,460 10% 355,634 8% 400,725 10% 1,458,885 35% 4,195,247 Feb-13 1,348,229 33% 544,551 13% 249,850 6% 296,801 7% 1,673,079 41% 4,112,510 Mar-13 1,981,272 42% 576,913 12% 343,493 7% 154,448 3% 1,658,040 35% 4,714,166 Apr-13 1,576,355 32% 1,123,422 23% 348,644 7% 276,204 6% 1,589,595 32% 4,914,220 May-13 1,742,115 34% 673,517 13% 800,677 16% 313,612 6% 1,625,254 32% 5,155,175 Jun-13 1,485,659 31% 785,963 17% 421,585 9% 419,863 9% 1,638,526 34% 4,751,596 Jul-13 1,685,742 36% 596,852 13% 489,653 10% 348,562 7% 1,574,886 34% 4,695,695 YTD Average 1,582,291 38% 427,748 10% 1,263,760 29% Number of Months in Analysis 13 To be entered manually 666,019 16% 314,539 7% 4,254,356 6,000,000 5,000,000 4,000,000 3,000,000 2,000,000 1,000,000 Accounts Receivable Aging Trend Analysis Current Over 120 Aging is getting bigger and bigger over time. Why? 0 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13

86 Sample Medical Practice Billing Analysis September September 2010 Fields for entry Aging Trend Analysis Over 120 Total Current Days Days Days Days A/R Jul-12 1,484,209 42% 495,012 14% 385,571 11% 194,705 5% 1,006,263 28% 3,565,760 Aug-12 1,837,462 54% 603,254 18% 250,428 7% 338,230 10% 376,326 11% 3,405,700 Sep-12 1,489,441 41% 963,246 27% 311,945 9% 193,210 5% 650,313 18% 3,608,155 Oct-12 1,459,773 38% 538,716 14% 756,766 20% 245,845 6% 805,766 21% 3,806,866 Nov-12 1,404,324 34% 714,720 17% 390,927 10% 663,007 16% 932,664 23% 4,105,642 Dec-12 1,523,656 36% 613,620 14% 455,550 11% 243,791 6% 1,439,285 34% 4,275,902 Jan-13 1,551,543 37% 428,460 10% 355,634 8% 400,725 10% 1,458,885 35% 4,195,247 Feb-13 1,348,229 33% 544,551 13% 249,850 6% 296,801 7% 1,673,079 41% 4,112,510 Mar-13 1,981,272 42% 576,913 12% 343,493 7% 154,448 3% 1,658,040 35% 4,714,166 Apr-13 1,576,355 32% 1,123,422 23% 348,644 7% 276,204 6% 1,589,595 32% 4,914,220 May-13 1,742,115 34% 673,517 13% 800,677 16% 313,612 6% 1,625,254 32% 5,155,175 Jun-13 1,485,659 31% 785,963 17% 421,585 9% 419,863 9% 1,638,526 34% 4,751,596 Jul-13 1,685,742 36% 596,852 13% 489,653 10% 348,562 7% 1,574,886 34% 4,695,695 YTD Average 1,582,291 38% 427,748 10% 1,263,760 29% Number of Months in Analysis 13 To be entered manually 666,019 16% 314,539 7% 4,254,356 6,000,000 5,000,000 4,000,000 3,000,000 2,000,000 Accounts Receivable Aging Trend Analysis Current Nice monthly trend for the most recent (current) receivables. 1,000,000 Over Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13

87 Sample Medical Practice Billing Analysis September September 2010 Fields for entry Aging Trend Analysis Over 120 Total Current Days Days Days Days A/R Jul-12 1,484,209 42% 495,012 14% 385,571 11% 194,705 5% 1,006,263 28% 3,565,760 Aug-12 1,837,462 54% 603,254 18% 250,428 7% 338,230 10% 376,326 11% 3,405,700 Sep-12 1,489,441 41% 963,246 27% 311,945 9% 193,210 5% 650,313 18% 3,608,155 Oct-12 1,459,773 38% 538,716 14% 756,766 20% 245,845 6% 805,766 21% 3,806,866 Nov-12 1,404,324 34% 714,720 17% 390,927 10% 663,007 16% 932,664 23% 4,105,642 Dec-12 1,523,656 36% 613,620 14% 455,550 11% 243,791 6% 1,439,285 34% 4,275,902 Jan-13 1,551,543 37% 428,460 10% 355,634 8% 400,725 10% 1,458,885 35% 4,195,247 Feb-13 1,348,229 33% 544,551 13% 249,850 6% 296,801 7% 1,673,079 41% 4,112,510 Mar-13 1,981,272 42% 576,913 12% 343,493 7% 154,448 3% 1,658,040 35% 4,714,166 Apr-13 1,576,355 32% 1,123,422 23% 348,644 7% 276,204 6% 1,589,595 32% 4,914,220 May-13 1,742,115 34% 673,517 13% 800,677 16% 313,612 6% 1,625,254 32% 5,155,175 Jun-13 1,485,659 31% 785,963 17% 421,585 9% 419,863 9% 1,638,526 34% 4,751,596 Jul-13 1,685,742 36% 596,852 13% 489,653 10% 348,562 7% 1,574,886 34% 4,695,695 YTD Average 1,582,291 38% 427,748 10% 1,263,760 29% Number of Months in Analysis 13 To be entered manually 666,019 16% 314,539 7% 4,254,356 6,000,000 5,000,000 4,000,000 3,000,000 2,000,000 1,000,000 Accounts Receivable Aging Trend Analysis Current Over 120 Good distribution of the receivables, with the most recent the largest portion. 0 Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13

88 Sample Medical Practice Billing Analysis September September 2010 Fields for entry Aging Trend Analysis Over 120 Total Current Days Days Days Days A/R Jul-12 1,484,209 42% 495,012 14% 385,571 11% 194,705 5% 1,006,263 28% 3,565,760 Aug-12 1,837,462 54% 603,254 18% 250,428 7% 338,230 10% 376,326 11% 3,405,700 Sep-12 1,489,441 41% 963,246 27% 311,945 9% 193,210 5% 650,313 18% 3,608,155 Oct-12 1,459,773 38% 538,716 14% 756,766 20% 245,845 6% 805,766 21% 3,806,866 Nov-12 1,404,324 34% 714,720 17% 390,927 10% 663,007 16% 932,664 23% 4,105,642 Dec-12 1,523,656 36% 613,620 14% 455,550 11% 243,791 6% 1,439,285 34% 4,275,902 Jan-13 1,551,543 37% 428,460 10% 355,634 8% 400,725 10% 1,458,885 35% 4,195,247 Feb-13 1,348,229 33% 544,551 13% 249,850 6% 296,801 7% 1,673,079 41% 4,112,510 Mar-13 1,981,272 42% 576,913 12% 343,493 7% 154,448 3% 1,658,040 35% 4,714,166 Apr-13 1,576,355 32% 1,123,422 23% 348,644 7% 276,204 6% 1,589,595 32% 4,914,220 May-13 1,742,115 34% 673,517 13% 800,677 16% 313,612 6% 1,625,254 32% 5,155,175 Jun-13 1,485,659 31% 785,963 17% 421,585 9% 419,863 9% 1,638,526 34% 4,751,596 Jul-13 1,685,742 36% 596,852 13% 489,653 10% 348,562 7% 1,574,886 34% 4,695,695 YTD Average 1,582,291 38% 427,748 10% 1,263,760 29% Number of Months in Analysis 13 To be entered manually 666,019 16% 314,539 7% 4,254,356 Accounts Receivable Aging Trend Analysis 6,000,000 5,000,000 4,000,000 Current 3,000, ,000, ,000,000 Over Jul-12 Aug-12 Sep-12 Oct-12 Nov-12 Dec-12 Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Oldest unpaid accounts are becoming large portion of the receivables. Why?

89 Weekly Summary Flash Reports Cash (Bank) Balances / Lines of Credit Balances Receivables: Insurance / Private / Credit Balances Charges, Collections, Adjustments Major Payables (Bills Due)

Accounts Receivable credit balances Upcoming Payroll Supporting reports from")

90 Management Reports Monthly Summary Cash Balances Line of credit balances Accounts Receivable Aging Charges, Collections, Adjustments Major Unpaid Payables (Bills Due) Accounts Receivable credit balances Upcoming Payroll Supporting reports from billing system

91 Key Financial Indicators Cash Balances & Lines of Credit Accounts Receivables / Aging Charges Collections

92 3 Step Approach to Fraud: I. Prevent fraudfrom occurring II. Detect itas soon as possible III. Obtain adequateinsurance coverage - employee dishonesty or employee crime.

93 Patient Refunds Who prepares the requests? What is required to support each refund request? Who reviews the refunds? What account are refunds paid?

94 Product Sales & Cosmetic Procedures (Dermatology, Veins, Hair Removal ) What controls can be implemented for these retail areas?

95 Supplies For patients use only? Tracked? Access restricted to those authorized How are these safeguarded?

96 On-Line Banking? What are the controls? Where will you find the evidence?

97 On-Line Banking? How about now?

98 On-Line Banking? How about now?

99 Cash Disbursements Who writes the checks? Who signs the checks? Who reviews the bank statement? How secure is your check information?

100 Employee Expense Reimbursements What are your policies? Do you require original supporting receipts? Who reviews it? How can you be fooled?

101 CompensationStructure How do your employees get paid? How do your physicians and other providers get paid?

102 Payroll Who handles your payroll processing? Who reviews it? Who is on your payroll? Net versus Gross

103 Time Tracking How are employees paid? How do you track their days and time worked? Where are the weaknesses?

104 Fixed Assets Business use only? Tracked and monitored? What s on the hard drives?

105 In Summary: Know your employees Evaluate vulnerabilities to outsiders Evaluate vulnerabilities to employees Consider having an outside review of your internal controls and procedures Remain vigilant!

106

107 Fraud-Related Writing: Coming Early 20?? Preventing/Detecting Employee Theft and Embezzlement within a Medical Practice MGMA

108 Piecing Together Financial Puzzles Stephen Pedneault, CPA/CFF, CFE Forensic Accounting Services, LLC 2389 Main Street Glastonbury, CT Piecing Together Financial Puzzlestm

109 Physician s Computer Company PCC 2014 Users Conference Safeguarding Your Practice's Fiscal Health (from undetected fraud scheme) Questions / Discussion forensic accounting services, LLC 2389 main street glastonbury, ct (860) steve@fasman.com stephen a. pedneault

Business & Financial Services December 2017

Business & Financial Services December 217 Completed Procurement Transactions by Month 2 4 175 15 125 1 75 5 2 1 Business Days to Complete 25 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 217 Procurement

Business & Financial Services December 217 Completed Procurement Transactions by Month 2 4 175 15 125 1 75 5 2 1 Business Days to Complete 25 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 217 Procurement

XML Publisher Balance Sheet Vision Operations (USA) Feb-02

Feb-02") Page:1 Apr-01 May-01 Jun-01 Jul-01 ASSETS Current Assets Cash and Short Term Investments 15,862,304 51,998,607 9,198,226 Accounts Receivable - Net of Allowance 2,560,786

Page:1 Apr-01 May-01 Jun-01 Jul-01 ASSETS Current Assets Cash and Short Term Investments 15,862,304 51,998,607 9,198,226 Accounts Receivable - Net of Allowance 2,560,786

Management Reports. June for PREPARED BY POWERED BY

Management Reports for June 217 PREPARED BY POWERED BY Contents 1. Management Reports Cashflow Forecast Actual vs Budget P&L Forecast Where Did Our Money Go? Net Worth 2. Understanding your Reports 3.

Management Reports for June 217 PREPARED BY POWERED BY Contents 1. Management Reports Cashflow Forecast Actual vs Budget P&L Forecast Where Did Our Money Go? Net Worth 2. Understanding your Reports 3.

CORPORATE PERFORMANCE DASHBOARD. August 2010

Quality care for you, with you CORPORATE PERFORMANCE DASHBOARD August 21 Approved by the Board of Directors on 3 th September 21 1 CONTENT: Page Introduction 3 Targets: 1 st OP Appointment 4 Diagnostic

Quality care for you, with you CORPORATE PERFORMANCE DASHBOARD August 21 Approved by the Board of Directors on 3 th September 21 1 CONTENT: Page Introduction 3 Targets: 1 st OP Appointment 4 Diagnostic

Factor Leave Accruals. Accruing Vacation and Sick Leave

Factor Leave Accruals Accruing Vacation and Sick Leave Factor Leave Accruals As part of the transition of non-exempt employees to biweekly pay, the UC Office of the President also requires standardization

Factor Leave Accruals Accruing Vacation and Sick Leave Factor Leave Accruals As part of the transition of non-exempt employees to biweekly pay, the UC Office of the President also requires standardization

QUARTERLY FINANCIAL REPORT June 30, 2017

California Independent System Operator QUARTERLY FINANCIAL REPORT June 30, 2017 250 Outcropping Way Folsom, CA 95630 (916) 351-4000 CALIFORNIA INDEPENDENT SYSTEM OPERATOR CORPORATION QUARTERLY FINANCIAL

California Independent System Operator QUARTERLY FINANCIAL REPORT June 30, 2017 250 Outcropping Way Folsom, CA 95630 (916) 351-4000 CALIFORNIA INDEPENDENT SYSTEM OPERATOR CORPORATION QUARTERLY FINANCIAL

FOR RELEASE: MONDAY, MARCH 21 AT 4 PM

Interviews with 1,012 adult Americans conducted by telephone by Opinion Research Corporation on March 18-20, 2011. The margin of sampling error for results based on the total sample is plus or minus 3

Interviews with 1,012 adult Americans conducted by telephone by Opinion Research Corporation on March 18-20, 2011. The margin of sampling error for results based on the total sample is plus or minus 3

Understanding Benchmarking for Healthcare Organizations

Understanding Benchmarking for Healthcare Organizations Melissa M. Meeker, CPA MSA, Accounting, Franklin University Tina R. Wright, CPA, CHBC BSBA, Accounting, The Ohio State University Benchmarking Basics

Understanding Benchmarking for Healthcare Organizations Melissa M. Meeker, CPA MSA, Accounting, Franklin University Tina R. Wright, CPA, CHBC BSBA, Accounting, The Ohio State University Benchmarking Basics

Financial Statements. Kit Carson County Health Service District. October 2018

Financial Statements Kit Carson County Health Service District Kit Carson County Health Service District Rooted in excellence. Growing in trust. FINANCIAL STATEMENT SUMMARY Income Statement Summary Kit

Financial Statements Kit Carson County Health Service District Kit Carson County Health Service District Rooted in excellence. Growing in trust. FINANCIAL STATEMENT SUMMARY Income Statement Summary Kit

QUARTERLY FINANCIAL REPORT December 31, 2017

California Independent System Operator QUARTERLY FINANCIAL REPORT December 31, 2017 Preliminary and Unaudited 250 Outcropping Way Folsom, CA 95630 (916) 351-4000 CALIFORNIA INDEPENDENT SYSTEM OPERATOR

California Independent System Operator QUARTERLY FINANCIAL REPORT December 31, 2017 Preliminary and Unaudited 250 Outcropping Way Folsom, CA 95630 (916) 351-4000 CALIFORNIA INDEPENDENT SYSTEM OPERATOR

Current Employment Statistics

Current Employment Statistics October 2017 If you have any questions or seek additional information, please contact: Vermont Department of Labor Economic and Labor Market Information Division 802-828-4202

Current Employment Statistics October 2017 If you have any questions or seek additional information, please contact: Vermont Department of Labor Economic and Labor Market Information Division 802-828-4202

Membership Report November 2018

Membership Report November 2018 Agenda Financial Commentary 2018 Budget/Actual Net Income Actual/Budget Variance Total Managed Assets On- & Off-Balance Sheet Liquidity Commentary Historical Member Overnight

Membership Report November 2018 Agenda Financial Commentary 2018 Budget/Actual Net Income Actual/Budget Variance Total Managed Assets On- & Off-Balance Sheet Liquidity Commentary Historical Member Overnight

Mechanics of Cash Flow Forecasting

Texas Association Of State Senior College & University Business Officers July 13, 2015 Mechanics of Cash Flow Forecasting Susan K. Anderson, CEO Anderson Financial Management, L.L.C. 130 Pecan Creek Drive

Texas Association Of State Senior College & University Business Officers July 13, 2015 Mechanics of Cash Flow Forecasting Susan K. Anderson, CEO Anderson Financial Management, L.L.C. 130 Pecan Creek Drive

QUARTERLY FINANCIAL REPORT March 31, 2018

California Independent System Operator QUARTERLY FINANCIAL REPORT March 31, 2018 250 Outcropping Way Folsom, CA 95630 (916) 351-4000 CALIFORNIA INDEPENDENT SYSTEM OPERATOR CORPORATION QUARTERLY FINANCIAL

California Independent System Operator QUARTERLY FINANCIAL REPORT March 31, 2018 250 Outcropping Way Folsom, CA 95630 (916) 351-4000 CALIFORNIA INDEPENDENT SYSTEM OPERATOR CORPORATION QUARTERLY FINANCIAL

Paul D. Vanchiere, MBA

Paul D. Vanchiere, MBA Theft-Proof Your Practice PEDIATRIC MANAGEMENT INSTITUTE Disclosures Pediatric Management Institute Consulting services for Pediatric Practices PhysicianIntelligence.com Business

Paul D. Vanchiere, MBA Theft-Proof Your Practice PEDIATRIC MANAGEMENT INSTITUTE Disclosures Pediatric Management Institute Consulting services for Pediatric Practices PhysicianIntelligence.com Business

Review of Registered Charites Compliance Rates with Annual Reporting Requirements 2016

Review of Registered Charites Compliance Rates with Annual Reporting Requirements 2016 October 2017 The Charities Regulator, in accordance with the provisions of section 14 of the Charities Act 2009, carried

Review of Registered Charites Compliance Rates with Annual Reporting Requirements 2016 October 2017 The Charities Regulator, in accordance with the provisions of section 14 of the Charities Act 2009, carried

To Receive CPE Credit

Fraud Prevention Strategies for Financial Institutions: A Forensic Accountant s Top 20 List Presenter Photo Angela Morelock Partner amorelock@bkd.com 417.865.8701 August 15, 2013 To Receive CPE Credit

Fraud Prevention Strategies for Financial Institutions: A Forensic Accountant s Top 20 List Presenter Photo Angela Morelock Partner amorelock@bkd.com 417.865.8701 August 15, 2013 To Receive CPE Credit

Credit Suisse Swiss Pension Fund Index Q3 2015

Credit Suisse Swiss Pension Fund Index Q3 2015 YTD 2015: 1.47% Q3 2015: 1.31% Return on the Credit Suisse Pension Fund Index continues to fall, despite good July performance Annualized returns fall, while

Credit Suisse Swiss Pension Fund Index Q3 2015 YTD 2015: 1.47% Q3 2015: 1.31% Return on the Credit Suisse Pension Fund Index continues to fall, despite good July performance Annualized returns fall, while

Current Employment Statistics

Current Employment Statistics December 2017 If you have any questions or seek additional information, please contact: Vermont Department of Labor Economic and Labor Market Information Division 802-828-4202

Current Employment Statistics December 2017 If you have any questions or seek additional information, please contact: Vermont Department of Labor Economic and Labor Market Information Division 802-828-4202

QUESTION 2. QUESTION 3 Which one of the following is most indicative of a flexible short-term financial policy?

QUESTION 1 Compute the cash cycle based on the following information: Average Collection Period = 47 Accounts Payable Period = 40 Average Age of Inventory = 55 QUESTION 2 Jan 41,700 July 39,182 Feb 18,921

QUESTION 1 Compute the cash cycle based on the following information: Average Collection Period = 47 Accounts Payable Period = 40 Average Age of Inventory = 55 QUESTION 2 Jan 41,700 July 39,182 Feb 18,921

HIPIOWA - IOWA COMPREHENSIVE HEALTH ASSOCIATION Unaudited Balance Sheet As of July 31

Unaudited Balance Sheet As of July 31 Total Enrollment: 407 Assets: Cash $ 9,541,661 $ 1,237,950 Invested Cash 781,689 8,630,624 Premiums Receivable 16,445 299,134 Prepaid 32,930 34,403 Assessments Receivable

Unaudited Balance Sheet As of July 31 Total Enrollment: 407 Assets: Cash $ 9,541,661 $ 1,237,950 Invested Cash 781,689 8,630,624 Premiums Receivable 16,445 299,134 Prepaid 32,930 34,403 Assessments Receivable

Spheria Australian Smaller Companies Fund

29-Jun-18 $ 2.7686 $ 2.7603 $ 2.7520 28-Jun-18 $ 2.7764 $ 2.7681 $ 2.7598 27-Jun-18 $ 2.7804 $ 2.7721 $ 2.7638 26-Jun-18 $ 2.7857 $ 2.7774 $ 2.7690 25-Jun-18 $ 2.7931 $ 2.7848 $ 2.7764 22-Jun-18 $ 2.7771

29-Jun-18 $ 2.7686 $ 2.7603 $ 2.7520 28-Jun-18 $ 2.7764 $ 2.7681 $ 2.7598 27-Jun-18 $ 2.7804 $ 2.7721 $ 2.7638 26-Jun-18 $ 2.7857 $ 2.7774 $ 2.7690 25-Jun-18 $ 2.7931 $ 2.7848 $ 2.7764 22-Jun-18 $ 2.7771

HIPIOWA - IOWA COMPREHENSIVE HEALTH ASSOCIATION Unaudited Balance Sheet As of January 31

Unaudited Balance Sheet As of January 31 Total Enrollment: 371 Assets: Cash $ 1,408,868 $ 1,375,117 Invested Cash 4,664,286 4,136,167 Premiums Receivable 94,152 91,261 Prepaid 32,270 33,421 Assessments

Unaudited Balance Sheet As of January 31 Total Enrollment: 371 Assets: Cash $ 1,408,868 $ 1,375,117 Invested Cash 4,664,286 4,136,167 Premiums Receivable 94,152 91,261 Prepaid 32,270 33,421 Assessments

Employers Compliance with the Health Insurance Act ANNUAL REPORT. Bermuda. Health Council

Employers Compliance with the Health Insurance Act 1970 2016 ANNUAL REPORT Bermuda ea Health Council Employers Compliance with the Health Insurance Act 1970 2016 Annual Report Contact us: If you would

Employers Compliance with the Health Insurance Act 1970 2016 ANNUAL REPORT Bermuda ea Health Council Employers Compliance with the Health Insurance Act 1970 2016 Annual Report Contact us: If you would

2009 Reassessment As Impacted by Senate Bill 711

Saint Louis County 2009 Reassessment As Impacted by Senate Bill 711 Impacts of SB711 on the 2009 Reassessment Plan The County must notify property owners of changes in the projected tax liability resulting

Saint Louis County 2009 Reassessment As Impacted by Senate Bill 711 Impacts of SB711 on the 2009 Reassessment Plan The County must notify property owners of changes in the projected tax liability resulting

Fiscal Year 2018 Project 1 Annual Budget

Fiscal Year 2018 Project 1 Annual Budget Table of Contents Table Page Summary 3 Summary of Costs Table 1 4 Treasury Related Expenses Table 2 5 Summary of Full Time Equivalent Table 3 6 Positions Cost-to-Cash

Fiscal Year 2018 Project 1 Annual Budget Table of Contents Table Page Summary 3 Summary of Costs Table 1 4 Treasury Related Expenses Table 2 5 Summary of Full Time Equivalent Table 3 6 Positions Cost-to-Cash

Organization. 4 Health Texas Senior Centers. VP, Internal Audit Team of 11 Auditors

Organization Regional Non-Profit Acute Care Hospital System 26 Owned/Operated/Ventured/Affiliated Hospitals 21 Joint Ventured Ambulatory Surgical Centers 41 Satellite Outpatient Facilities 136 Health Texas

Organization Regional Non-Profit Acute Care Hospital System 26 Owned/Operated/Ventured/Affiliated Hospitals 21 Joint Ventured Ambulatory Surgical Centers 41 Satellite Outpatient Facilities 136 Health Texas

Financial & Business Highlights For the Year Ended June 30, 2017

Financial & Business Highlights For the Year Ended June, 17 17 16 15 14 13 12 Profit and Loss Account Operating Revenue 858 590 648 415 172 174 Investment gains net 5 162 909 825 322 516 Other 262 146

Financial & Business Highlights For the Year Ended June, 17 17 16 15 14 13 12 Profit and Loss Account Operating Revenue 858 590 648 415 172 174 Investment gains net 5 162 909 825 322 516 Other 262 146

HUD NSP-1 Reporting Apr 2010 Grantee Report - New Mexico State Program

HUD NSP-1 Reporting Apr 2010 Grantee Report - State Program State Program NSP-1 Grant Amount is $19,600,000 $9,355,381 (47.7%) has been committed $4,010,874 (20.5%) has been expended Grant Number HUD Region

HUD NSP-1 Reporting Apr 2010 Grantee Report - State Program State Program NSP-1 Grant Amount is $19,600,000 $9,355,381 (47.7%) has been committed $4,010,874 (20.5%) has been expended Grant Number HUD Region

Asset Manager Performance Comparison

Cape Peninsula University of Technology Retirement Fund August 2017 DISCLAIMER AND WARNINGS: Towers Watson (Pty) Ltd, a Willis Towers Watson company, is an authorised financial services provider. Although

Cape Peninsula University of Technology Retirement Fund August 2017 DISCLAIMER AND WARNINGS: Towers Watson (Pty) Ltd, a Willis Towers Watson company, is an authorised financial services provider. Although

Asset Manager Performance Comparison

Cape Peninsula University of Technology Retirement Fund September 2017 DISCLAIMER AND WARNINGS: Towers Watson (Pty) Ltd, a Willis Towers Watson company, is an authorised financial services provider. Although

Cape Peninsula University of Technology Retirement Fund September 2017 DISCLAIMER AND WARNINGS: Towers Watson (Pty) Ltd, a Willis Towers Watson company, is an authorised financial services provider. Although

Quarterly Performance Report

w e a l t h Quarterly Performance Report Client Name Executive Summary REVENUE Revenue (Last quarter $381,226) Positive trend upwards. PROFITABILITY Profitability Ratio 9.83% (Last quarter 30%) Negative

w e a l t h Quarterly Performance Report Client Name Executive Summary REVENUE Revenue (Last quarter $381,226) Positive trend upwards. PROFITABILITY Profitability Ratio 9.83% (Last quarter 30%) Negative

Membership Report September 2018

Membership Report September 2018 Agenda Financial Commentary 2018 Budget/Actual Net Income Actual/Budget Variance Total Managed Assets On- & Off-Balance Sheet Liquidity Commentary Historical Member Overnight

Membership Report September 2018 Agenda Financial Commentary 2018 Budget/Actual Net Income Actual/Budget Variance Total Managed Assets On- & Off-Balance Sheet Liquidity Commentary Historical Member Overnight

WESTWOOD LUTHERAN CHURCH Summary Financial Statement YEAR TO DATE - February 28, Over(Under) Budget WECC Fund Actual Budget

Budget WECC Fund Actual Budget") WESTWOOD LUTHERAN CHURCH Summary Financial Statement YEAR TO DATE - February 28, 2018 General Fund Actual A B C D E F WECC Fund Actual Revenue Revenue - Faith Giving 1 $ 213 $ 234 $ (22) - Tuition $ 226

WESTWOOD LUTHERAN CHURCH Summary Financial Statement YEAR TO DATE - February 28, 2018 General Fund Actual A B C D E F WECC Fund Actual Revenue Revenue - Faith Giving 1 $ 213 $ 234 $ (22) - Tuition $ 226

TERMS OF REFERENCE FOR THE INVESTMENT COMMITTEE

I. PURPOSE The purpose of the Investment Committee (the Committee ) is to recommend to the Board the investment policy, including the asset mix policy and the appropriate benchmark for both ICBC and any

I. PURPOSE The purpose of the Investment Committee (the Committee ) is to recommend to the Board the investment policy, including the asset mix policy and the appropriate benchmark for both ICBC and any

Healthy Michigan Plan signing, September 2013

Healthy Michigan Plan signing, September 2013 Richard Hirth, Ph.D. Professor & Chair Department of Health Management & Policy National Significance of Michigan Medicaid Expansion Model for compromise as

Healthy Michigan Plan signing, September 2013 Richard Hirth, Ph.D. Professor & Chair Department of Health Management & Policy National Significance of Michigan Medicaid Expansion Model for compromise as

IMPROVING THE FINANCIAL HEALTH OF YOUR PRACTICE. D e b b i e R i c c i a n d D o n n a R u s s o

IMPROVING THE FINANCIAL HEALTH OF YOUR PRACTICE D e b b i e R i c c i a n d D o n n a R u s s o Please silence or turn off all electronic devices at this time. THANK YOU Agenda Key Performance Indicators

IMPROVING THE FINANCIAL HEALTH OF YOUR PRACTICE D e b b i e R i c c i a n d D o n n a R u s s o Please silence or turn off all electronic devices at this time. THANK YOU Agenda Key Performance Indicators

LOUISVILLE GAS AND ELECTRIC COMPANY Gas Rates 2018 Monthly Billing Adjustments

2018 Monthly Billing Adjustments GAS LINE TRACKER CHARGES GAS LINE TRACKER CHARGES DSM (2) PER MONTH PER METER PER MONTH PER CCF TAX CUTS AND JOBS ACT $ Per CCF Firm Trans. SURCREDIT ($ per ccf) (3) GAS

2018 Monthly Billing Adjustments GAS LINE TRACKER CHARGES GAS LINE TRACKER CHARGES DSM (2) PER MONTH PER METER PER MONTH PER CCF TAX CUTS AND JOBS ACT $ Per CCF Firm Trans. SURCREDIT ($ per ccf) (3) GAS

Common stock prices 1. New York Stock Exchange indexes (Dec. 31,1965=50)2. Transportation. Utility 3. Finance

2. Transportation. Utility 3. Finance") Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis 000 97 98 99 I90 9 9 9 9 9 9 97 98 99 970 97 97 ""..".'..'.."... 97 97 97 97 977 978 979 980 98 98 98 98 98 98 987 988

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis 000 97 98 99 I90 9 9 9 9 9 9 97 98 99 970 97 97 ""..".'..'.."... 97 97 97 97 977 978 979 980 98 98 98 98 98 98 987 988

NR614: Foundations of Health Care Economics, Accounting and Financial Management

NR614: Foundations of Health Care Economics, Accounting and Financial Management WEEK 7: Budgeting SLIDE 1: Week 7: Week Seven Sample Problem: Budgeting... There is one sample problem provided in week

NR614: Foundations of Health Care Economics, Accounting and Financial Management WEEK 7: Budgeting SLIDE 1: Week 7: Week Seven Sample Problem: Budgeting... There is one sample problem provided in week

Division of Bond Finance Interest Rate Calculations. Revenue Estimating Conference Interest Rates Used for Appropriations, including PECO Bond Rates

Division of Bond Finance Interest Rate Calculations Revenue Estimating Conference Interest Rates Used for Appropriations, including PECO Bond Rates November 16, 2018 Division of Bond Finance Calculation

Division of Bond Finance Interest Rate Calculations Revenue Estimating Conference Interest Rates Used for Appropriations, including PECO Bond Rates November 16, 2018 Division of Bond Finance Calculation

INCREASING INVESTIGATOR EFFICIENCY USING NETWORK ANALYTICS

INCREASING INVESTIGATOR EFFICIENCY USING NETWORK ANALYTICS ACFE ANNUAL CONFERENCE ORLANDO, FL JUNE 20, 2012 DAN BARTA CPA, CFE DAVID STEWART CAMS Fraud & Financial Crimes Practice TOPICS INCREASING INVESTIGATOR

INCREASING INVESTIGATOR EFFICIENCY USING NETWORK ANALYTICS ACFE ANNUAL CONFERENCE ORLANDO, FL JUNE 20, 2012 DAN BARTA CPA, CFE DAVID STEWART CAMS Fraud & Financial Crimes Practice TOPICS INCREASING INVESTIGATOR

The Financial Reporting Checklists Every Firm should be Doing

The Financial Reporting Checklists Every Firm should be Doing Presented by Rebecca Kelley, CPA Maggie Kennedy, CPA FM34 4/5/2017 3:00 PM - 4:15 PM The handouts and presentations attached are copyright

The Financial Reporting Checklists Every Firm should be Doing Presented by Rebecca Kelley, CPA Maggie Kennedy, CPA FM34 4/5/2017 3:00 PM - 4:15 PM The handouts and presentations attached are copyright

ICO Market Report December December Unlock your Crypto Potential. 1 P a g e

December 2018 Unlock your Crypto Potential 1 P a g e Contents DISCLAIMER 3 ICO MARKET STATS (DECEMBER 18) 4 HARD CAP/SOFT CAP INFO 5 NOVEMBER VS DECEMBER STATISTICS 6 TOP 5 ICOS (DECEMBER 18) 7 AMOUNT

December 2018 Unlock your Crypto Potential 1 P a g e Contents DISCLAIMER 3 ICO MARKET STATS (DECEMBER 18) 4 HARD CAP/SOFT CAP INFO 5 NOVEMBER VS DECEMBER STATISTICS 6 TOP 5 ICOS (DECEMBER 18) 7 AMOUNT

11 May Report.xls Office of Budget & Fiscal Planning

Education and General Fund Actual Revenues and s by Month MTD YTD Change Revenue Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Per 14 Total over FY06 Enrollment Fees $ 8,211 $ 219 $ 41,952 ($ 818) $

Education and General Fund Actual Revenues and s by Month MTD YTD Change Revenue Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Per 14 Total over FY06 Enrollment Fees $ 8,211 $ 219 $ 41,952 ($ 818) $

Voya Indexed Universal Life-Protector

calculation examples Values as of 07/28/2018 Voya ed Universal Life-Protector Issued by Security Life of Denver Insurance Company Required training! VFA Registered Representatives must review the Required

calculation examples Values as of 07/28/2018 Voya ed Universal Life-Protector Issued by Security Life of Denver Insurance Company Required training! VFA Registered Representatives must review the Required

Exchange Rate Requirements

C APPENDIX Foreign Currency Financial Reporting from Euro to Yen to Yuan: A Guide to Fundamental Concepts and Practical Applications By Robert Rowanc Copyright 2011 by SAS Institute, Inc. Exchange Rate

C APPENDIX Foreign Currency Financial Reporting from Euro to Yen to Yuan: A Guide to Fundamental Concepts and Practical Applications By Robert Rowanc Copyright 2011 by SAS Institute, Inc. Exchange Rate

REAL EARNINGS DECEMBER 2018

Transmission of material in this release is embargoed until 8:30 a.m. (EST), Friday, January 11, 2019 USDL-19-0019 Technical Information: (202) 691-6555 cesinfo@bls.gov www.bls.gov/ces Media Contact: (202)

Transmission of material in this release is embargoed until 8:30 a.m. (EST), Friday, January 11, 2019 USDL-19-0019 Technical Information: (202) 691-6555 cesinfo@bls.gov www.bls.gov/ces Media Contact: (202)

Isle Of Wight half year business confidence report

half year business confidence report half year report contents new company registrations closed companies (dissolved) net company growth uk company share director age director gender naming trends sic

half year business confidence report half year report contents new company registrations closed companies (dissolved) net company growth uk company share director age director gender naming trends sic

Employee Dishonesty Lessons Learned: Internal Controls

Employee Dishonesty Lessons Learned: Internal Controls Presented by: Doug Roossien, CRM, CFE Business Protection Risk Management CUNA Mutual Group CUNA Mutual Group Proprietary Reproduction, Adaptation

Employee Dishonesty Lessons Learned: Internal Controls Presented by: Doug Roossien, CRM, CFE Business Protection Risk Management CUNA Mutual Group CUNA Mutual Group Proprietary Reproduction, Adaptation

Financial Exploitation Investigations Protocols for APS. State Perspective: PA s Aging Population

Financial Exploitation Investigations Protocols for APS National Adult Protective Services Association Conference 2013 Denise Getgen, RN, Pennsylvania Department of Aging Linda Mill, CFE, Temple University

Financial Exploitation Investigations Protocols for APS National Adult Protective Services Association Conference 2013 Denise Getgen, RN, Pennsylvania Department of Aging Linda Mill, CFE, Temple University

Credit Suisse Swiss Pension Fund Index Q2 2017

Credit Suisse Swiss Pension Fund Index Q2 217 YTD 217: 3.94% Q2 217: 1.15% Positive second quarter, with slowdown in June Significant positive contribution from Swiss equities in reporting quarter Sharp

Credit Suisse Swiss Pension Fund Index Q2 217 YTD 217: 3.94% Q2 217: 1.15% Positive second quarter, with slowdown in June Significant positive contribution from Swiss equities in reporting quarter Sharp

9/15/2017. RSA ESS vs Harris School Solutions ESS

RSA Reporting NextGen RSA ESS vs Harris School Solutions ESS RSA ESS Employer Self Service a portal that will be used by districts to submit RSA enrollment and contribution files as well as make online

RSA Reporting NextGen RSA ESS vs Harris School Solutions ESS RSA ESS Employer Self Service a portal that will be used by districts to submit RSA enrollment and contribution files as well as make online

Using Computers to Adapt to Changing Markets

Using Computers to Adapt to Changing Markets By Dr. Robert C. Smithson Anava Capital Management LLC Cupertino, CA 408-918-9333 Please Note: Individual companies shown or discussed in this presentation

Using Computers to Adapt to Changing Markets By Dr. Robert C. Smithson Anava Capital Management LLC Cupertino, CA 408-918-9333 Please Note: Individual companies shown or discussed in this presentation

Second Quarter 2016 Earnings Presentation. July 29, 2016

Second Quarter 2016 Earnings Presentation July 29, 2016 Agenda Strategic Review Financial Review Questions and Answers Edward Tilly Chief Executive Officer Alan Dean Executive Vice President, CFO and Treasurer

Second Quarter 2016 Earnings Presentation July 29, 2016 Agenda Strategic Review Financial Review Questions and Answers Edward Tilly Chief Executive Officer Alan Dean Executive Vice President, CFO and Treasurer

Balance Sheet - Consolidated August 31, 2018

1 ASSETS Current Assets - Funds Total Operating Total KVFD Reserve Total Restricted Total Capital Reserve Total Snow Removal Reserve Total COP Reserve Fund Total Current Assets - Funds Current Assets -

1 ASSETS Current Assets - Funds Total Operating Total KVFD Reserve Total Restricted Total Capital Reserve Total Snow Removal Reserve Total COP Reserve Fund Total Current Assets - Funds Current Assets -

Beginning Date: January 2016 End Date: June Managers in Zephyr: Benchmark: Morningstar Short-Term Bond

Beginning Date: January 2016 End Date: June 2018 Managers in Zephyr: Benchmark: Manager Performance January 2016 - June 2018 (Single Computation) 11200 11000 10800 10600 10400 10200 10000 9800 Dec 2015

Beginning Date: January 2016 End Date: June 2018 Managers in Zephyr: Benchmark: Manager Performance January 2016 - June 2018 (Single Computation) 11200 11000 10800 10600 10400 10200 10000 9800 Dec 2015

SURVEY OF BUSINESSES INFLATION EXPECTATIONS JULY 2018 RESEARCH SERVICES DEPARTMENT RESEARCH AND ECONOMIC PROGRAMMING DIVISION

SURVEY OF BUSINESSES INFLATION EXPECTATIONS JULY 2018 RESEARCH SERVICES DEPARTMENT RESEARCH AND ECONOMIC PROGRAMMING DIVISION Jul-15 Nov-15 Jan-16 Mar-16 Jul-16 Nov-16 Jan-17 Jan-18 Annual point to point

SURVEY OF BUSINESSES INFLATION EXPECTATIONS JULY 2018 RESEARCH SERVICES DEPARTMENT RESEARCH AND ECONOMIC PROGRAMMING DIVISION Jul-15 Nov-15 Jan-16 Mar-16 Jul-16 Nov-16 Jan-17 Jan-18 Annual point to point

Questions to Consider When You Implement Oracle Assets

Questions to Consider When You Implement Oracle Assets Cindy Cline Cline Consulting and Training Solutions, LLC During the implementation of Oracle Assets, several issues will arise and numerous decisions

Questions to Consider When You Implement Oracle Assets Cindy Cline Cline Consulting and Training Solutions, LLC During the implementation of Oracle Assets, several issues will arise and numerous decisions

Foundations of Investing

www.edwardjones.com Member SIPC Foundations of Investing 1 5 HOW CAN I STAY ON TRACK? 4 HOW DO I GET THERE? 1 WHERE AM I TODAY? MY FINANCIAL NEEDS 3 CAN I GET THERE? 2 WHERE WOULD I LIKE TO BE? 2 Develop

www.edwardjones.com Member SIPC Foundations of Investing 1 5 HOW CAN I STAY ON TRACK? 4 HOW DO I GET THERE? 1 WHERE AM I TODAY? MY FINANCIAL NEEDS 3 CAN I GET THERE? 2 WHERE WOULD I LIKE TO BE? 2 Develop

SURVEY OF BUSINESSES INFLATION EXPECTATIONS JULY 2017 RESEARCH SERVICES DEPARTMENT RESEARCH AND ECONOMIC PROGRAMMING DIVISION

SURVEY OF BUSINESSES INFLATION EXPECTATIONS JULY 217 RESEARCH SERVICES DEPARTMENT RESEARCH AND ECONOMIC PROGRAMMING DIVISION The Statistical Institute of Jamaica (STATIN) undertakes surveys of businesses

SURVEY OF BUSINESSES INFLATION EXPECTATIONS JULY 217 RESEARCH SERVICES DEPARTMENT RESEARCH AND ECONOMIC PROGRAMMING DIVISION The Statistical Institute of Jamaica (STATIN) undertakes surveys of businesses

Its Not About If, Its About When! Learning how to protect your organization.

Learning how to protect your organization. Presentation Overview Summary off FFraud S d St Statistics ti ti Definitions of Fraud How and Why Fraud Happens Fraud Prevention and Deterrence Steps to Reducing

Learning how to protect your organization. Presentation Overview Summary off FFraud S d St Statistics ti ti Definitions of Fraud How and Why Fraud Happens Fraud Prevention and Deterrence Steps to Reducing

Effective Revenue Cycles Are No Accident

Effective Revenue Cycles Are No Accident Physician Leadership Institute March 7,2015 Jerrie K. Weith, MBA, FHFMA, CMPE, CMOM Learning Objectives Characteristics of Best Performers Efficient Encounters

Effective Revenue Cycles Are No Accident Physician Leadership Institute March 7,2015 Jerrie K. Weith, MBA, FHFMA, CMPE, CMOM Learning Objectives Characteristics of Best Performers Efficient Encounters

What do they investigate

What is Forensic Accounting & What do they investigate Presented by: Doug Cash MBA, CFE, CFI, CFCI Manager Forensic Accounting & Investigative Services Specialization i What is Forensic Accounting? What

What is Forensic Accounting & What do they investigate Presented by: Doug Cash MBA, CFE, CFI, CFCI Manager Forensic Accounting & Investigative Services Specialization i What is Forensic Accounting? What

Beginning Date: January 2016 End Date: September Managers in Zephyr: Benchmark: Morningstar Short-Term Bond

Beginning Date: January 2016 End Date: September 2018 Managers in Zephyr: Benchmark: Manager Performance January 2016 - September 2018 (Single Computation) 11400 - Yorktown Funds 11200 11000 10800 10600

Beginning Date: January 2016 End Date: September 2018 Managers in Zephyr: Benchmark: Manager Performance January 2016 - September 2018 (Single Computation) 11400 - Yorktown Funds 11200 11000 10800 10600

Economic Activity Index ( GDB-EAI ) For the month of May 2013 G O V E R N M E N T D E V E L O P M E N T B A N K F O R P U E R T O R I C O

For the month of May 2013 G O V E R N M E N T D E V E L O P M E N T B A N K F O R P U E R T O R I C O") Economic Activity Index ( GDB-EAI ) For the month of May 2013 General Commentary May 2013 GDB-EAI for the month of May registered a 3.4% year-over-year ( YOY ) reduction May 2013 EAI was 126.7, a 3.4%

Economic Activity Index ( GDB-EAI ) For the month of May 2013 General Commentary May 2013 GDB-EAI for the month of May registered a 3.4% year-over-year ( YOY ) reduction May 2013 EAI was 126.7, a 3.4%

Credit Suisse Swiss Pension Fund Index Q1 2017

Credit Suisse Swiss Pension Fund Index Q1 217 YTD 217: 2.76% Q1 217: 2.76% Credit Suisse Pension Fund Index starts year at all-time high Allocation to foreign equities at all-time high; allocation to Swiss

Credit Suisse Swiss Pension Fund Index Q1 217 YTD 217: 2.76% Q1 217: 2.76% Credit Suisse Pension Fund Index starts year at all-time high Allocation to foreign equities at all-time high; allocation to Swiss

Survey of Businesses Inflation Expectations. September 2018 RESEARCH SERVICES DEPARTMENT RESEARCH AND ECONOMIC PROGRAMMING DIVISION

Survey of Businesses Inflation Expectations September 2018 RESEARCH SERVICES DEPARTMENT RESEARCH AND ECONOMIC PROGRAMMING DIVISION The Statistical Institute of Jamaica (STATIN) undertakes surveys of businesses

Survey of Businesses Inflation Expectations September 2018 RESEARCH SERVICES DEPARTMENT RESEARCH AND ECONOMIC PROGRAMMING DIVISION The Statistical Institute of Jamaica (STATIN) undertakes surveys of businesses

Arkansas Works Overview. Work And Community Engagement Requirement

1 Arkansas Works Overview Work And Community Engagement Requirement Arkansas Works Populations & Work and Community Engagement Requirement 2 Arkansas Works enrollees will fall into three categories for

1 Arkansas Works Overview Work And Community Engagement Requirement Arkansas Works Populations & Work and Community Engagement Requirement 2 Arkansas Works enrollees will fall into three categories for

Big Walnut Local School District

Big Walnut Local School District Monthly Financial Report for the month ended September 30, 2013 Prepared By: Felicia Drummey Treasurer BIG WALNUT LOCAL SCHOOL DISTRICT SUMMARY OF YEAR TO DATE FINANCIAL

Big Walnut Local School District Monthly Financial Report for the month ended September 30, 2013 Prepared By: Felicia Drummey Treasurer BIG WALNUT LOCAL SCHOOL DISTRICT SUMMARY OF YEAR TO DATE FINANCIAL

Survey of Businesses Inflation Expectations. December 2018 RESEARCH SERVICES DEPARTMENT RESEARCH AND ECONOMIC PROGRAMMING DIVISION

Survey of Businesses Inflation Expectations December 2018 RESEARCH SERVICES DEPARTMENT RESEARCH AND ECONOMIC PROGRAMMING DIVISION The Statistical Institute of Jamaica (STATIN) undertakes surveys of businesses

Survey of Businesses Inflation Expectations December 2018 RESEARCH SERVICES DEPARTMENT RESEARCH AND ECONOMIC PROGRAMMING DIVISION The Statistical Institute of Jamaica (STATIN) undertakes surveys of businesses

EFFECTIVE REVENUE CYCLE MANAGEMENT IN YOUR NETWORK

EFFECTIVE REVENUE CYCLE MANAGEMENT IN YOUR NETWORK 1 INTRODUCTION Revenue Cycle Management has become an even more complex issue with declining reimbursements, implementation of Electronic Health Records,

EFFECTIVE REVENUE CYCLE MANAGEMENT IN YOUR NETWORK 1 INTRODUCTION Revenue Cycle Management has become an even more complex issue with declining reimbursements, implementation of Electronic Health Records,

Describe Fraud in the Context of Financial

Misappropriation of Assets and Fraudulent Financial Reporting Loscalzo s September 24, 2014 2012 Template for PowerPoint Slides A SmartPros Ltd. Company www.loscalzo.com (732) 741 1600 1 CPE Instructions

Misappropriation of Assets and Fraudulent Financial Reporting Loscalzo s September 24, 2014 2012 Template for PowerPoint Slides A SmartPros Ltd. Company www.loscalzo.com (732) 741 1600 1 CPE Instructions

FOR RELEASE: MONDAY, JANUARY 11 AT NOON

Interviews with 1,021 adult Americans, including 955 registered voters, conducted by telephone by Opinion Research Corporation on January 8-10,. The margin of sampling error for results based on the total

Interviews with 1,021 adult Americans, including 955 registered voters, conducted by telephone by Opinion Research Corporation on January 8-10,. The margin of sampling error for results based on the total

General Fund Revenue

Millions Percent of Kathy Steinert, Director of Fiscal Services Phone: 541.923.8927 145 SE Salmon Ave Redmond, OR 97756 kathy.steinert@redmond.k12.or.us Date: May 23, 2014 To: Redmond School District Board

Millions Percent of Kathy Steinert, Director of Fiscal Services Phone: 541.923.8927 145 SE Salmon Ave Redmond, OR 97756 kathy.steinert@redmond.k12.or.us Date: May 23, 2014 To: Redmond School District Board

Status of the Unemployment Trust Fund and Related Issues. Commission on Unemployment Compensation. Ellen Marie Hess, Commissioner.

Status of the Unemployment Trust Fund and Related Issues Commission on Unemployment Compensation August 8, 2018 Ellen Marie Hess, Commissioner 2 Trust Fund Data Standard Forecast (Millions of Dollars)

Status of the Unemployment Trust Fund and Related Issues Commission on Unemployment Compensation August 8, 2018 Ellen Marie Hess, Commissioner 2 Trust Fund Data Standard Forecast (Millions of Dollars)

BANK OF GUYANA. BANKING SYSTEM STATISTICAL ABSTRACT Website:

BANK OF GUYANA BANKING SYSTEM STATISTICAL ABSTRACT Website: www.bankofguyana.org.gy RESEARCH DEPARTMENT November 2010 STATISTICAL ABSTRACT TABLES CONTENTS 1. MONETARY AUTHORITY 1.1 Bank of Guyana: Assets

BANK OF GUYANA BANKING SYSTEM STATISTICAL ABSTRACT Website: www.bankofguyana.org.gy RESEARCH DEPARTMENT November 2010 STATISTICAL ABSTRACT TABLES CONTENTS 1. MONETARY AUTHORITY 1.1 Bank of Guyana: Assets

ADDENDUM NO. 4 REQUEST FOR PROPOSAL NO. R BANKING AND MERCHANT SERVICES FOR HIGHER EDUCATION

Attention to Proposers: This constitutes Addendum No. 4 to the referenced Request for Proposals (RFP), and consists of: This eight (8) page cover letter, which provides responses to questions raised by

Attention to Proposers: This constitutes Addendum No. 4 to the referenced Request for Proposals (RFP), and consists of: This eight (8) page cover letter, which provides responses to questions raised by

Full file at CHAPTER 3

CHAPTER 3 Adjusting the Accounts ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Exercises A Problems B Problems *1. Explain the time period assumption. 1, 2 *2. Explain the

CHAPTER 3 Adjusting the Accounts ASSIGNMENT CLASSIFICATION TABLE Study Objectives Questions Brief Exercises Exercises A Problems B Problems *1. Explain the time period assumption. 1, 2 *2. Explain the

EMBARGOED FOR RELEASE: Thursday, March 19 at 6:00 a.m. ET

Interviews with 1,009 adult Americans conducted by telephone by ORC International on March 13-15, 2015. The margin of sampling error for results based on the total sample is plus or minus 3 percentage

Interviews with 1,009 adult Americans conducted by telephone by ORC International on March 13-15, 2015. The margin of sampling error for results based on the total sample is plus or minus 3 percentage

Big Walnut Local School District

Big Walnut Local School District Monthly Financial Report for the month ended September 30, 2012 Prepared By: Felicia Drummey Treasurer BIG WALNUT LOCAL SCHOOL DISTRICT SUMMARY OF YEAR-TO-DATE FINANCIAL

Big Walnut Local School District Monthly Financial Report for the month ended September 30, 2012 Prepared By: Felicia Drummey Treasurer BIG WALNUT LOCAL SCHOOL DISTRICT SUMMARY OF YEAR-TO-DATE FINANCIAL

Financial Year End Procedures 2012/13

1. Introduction The University's financial year ends on the 31st July. Each year the Finance Office must publish a set of audited accounts for the whole University which give a true and fair view of the

1. Introduction The University's financial year ends on the 31st July. Each year the Finance Office must publish a set of audited accounts for the whole University which give a true and fair view of the

NH Community Behavioral Health Association Workforce Challenges and Opportunities

NH Community Behavioral Health Association Workforce Challenges and Opportunities January 10, 2018 Prepared by Patrick Miller, Founder and Principal Pero Consulting Group, LLC 1 Topics of Discussion 1.

NH Community Behavioral Health Association Workforce Challenges and Opportunities January 10, 2018 Prepared by Patrick Miller, Founder and Principal Pero Consulting Group, LLC 1 Topics of Discussion 1.

Fraud & Forensic Accounting Update for CPAs

Fraud & Forensic Accounting Update for CPAs Presented by: Brett A. Johnson CPA/CFF, CFE, CFI Forensic Accounting Manager Background Eide Bailly LLP Top 25 CPA firm in the nation (Est. 1917) More than 49,000

Fraud & Forensic Accounting Update for CPAs Presented by: Brett A. Johnson CPA/CFF, CFE, CFI Forensic Accounting Manager Background Eide Bailly LLP Top 25 CPA firm in the nation (Est. 1917) More than 49,000

Inflation Education. September Spear Street, Suite 950 San Francisco, CA Phone:

Inflation Education September 2014 150 Spear Street, Suite 950 San Francisco, CA 94105 Phone: 866-627-6984 DISCLAIMER The charts in this presentation are for illustrative purposes only. Individual clients

Inflation Education September 2014 150 Spear Street, Suite 950 San Francisco, CA 94105 Phone: 866-627-6984 DISCLAIMER The charts in this presentation are for illustrative purposes only. Individual clients

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention Michigan Municipal Treasurers Association June 16, 2017 Scott Sternhagen, CPA Manager Ryan Ritchay, CPA, CFE Senior Accountant

Reduce Your Risk: Understanding Internal Controls and Fraud Risks and Prevention Michigan Municipal Treasurers Association June 16, 2017 Scott Sternhagen, CPA Manager Ryan Ritchay, CPA, CFE Senior Accountant

Second Quarter 2013 Earnings Presentation. August 2, 2013

Second Quarter 2013 Earnings Presentation August 2, 2013 Agenda Strategic Review Financial Review Questions and Answers Edward Tilly Chief Executive Officer Alan Dean Executive Vice President, CFO and

Second Quarter 2013 Earnings Presentation August 2, 2013 Agenda Strategic Review Financial Review Questions and Answers Edward Tilly Chief Executive Officer Alan Dean Executive Vice President, CFO and

R o l l i n g F o r e c a s t i n g :

R o l l i n g F o r e c a s t i n g : A S t r a t e g y f o r E f f e c t i v e F i n a n c i a l M a n a g e m e n t Debra Miller Vice President Client Success January 22, 2016 Discussion Topics Overview

R o l l i n g F o r e c a s t i n g : A S t r a t e g y f o r E f f e c t i v e F i n a n c i a l M a n a g e m e n t Debra Miller Vice President Client Success January 22, 2016 Discussion Topics Overview

REAL EARNINGS AUGUST 2018

Transmission of material in this release is embargoed until 8:30 a.m. (EDT), Thursday, September 13, 2018 USDL-18-1454 Technical Information: (202) 691-6555 cesinfo@bls.gov www.bls.gov/ces Media Contact:

Transmission of material in this release is embargoed until 8:30 a.m. (EDT), Thursday, September 13, 2018 USDL-18-1454 Technical Information: (202) 691-6555 cesinfo@bls.gov www.bls.gov/ces Media Contact:

22 June To the Chair and Members of the AUDIT COMMITTEE ANNUAL PAYROLL OVERPAYMENTS UPDATE REPORT 2015/2016

22 June 2016 To the Chair and Members of the AUDIT COMMITTEE ANNUAL PAYROLL OVERPAYMENTS UPDATE REPORT 2015/2016 EXECUTIVE SUMMARY 1. This report provides the Audit Committee with an annual update on progress

22 June 2016 To the Chair and Members of the AUDIT COMMITTEE ANNUAL PAYROLL OVERPAYMENTS UPDATE REPORT 2015/2016 EXECUTIVE SUMMARY 1. This report provides the Audit Committee with an annual update on progress

ESTABLISHING A CASH FLOW MODEL

Government Finance Officers Association of Texas Fall Conference 2017 ESTABLISHING A CASH FLOW MODEL EMILY A. UPSHAW, CPA VALLEY VIEW CONSULTING, LLC Objectives: Understand the importance of developing

Government Finance Officers Association of Texas Fall Conference 2017 ESTABLISHING A CASH FLOW MODEL EMILY A. UPSHAW, CPA VALLEY VIEW CONSULTING, LLC Objectives: Understand the importance of developing

PAYROLL STANDARDIZATION. Transitioning from Monthly to Biweekly Pay on January 1, 2019

PAYROLL STANDARDIZATION Transitioning from Monthly to Biweekly Pay on January 1, 2019 Why? There are several reason why the University decided to standardize their payroll processes: System Security Administrative

PAYROLL STANDARDIZATION Transitioning from Monthly to Biweekly Pay on January 1, 2019 Why? There are several reason why the University decided to standardize their payroll processes: System Security Administrative

World Meteorological Organization Working together in weather, climate and water

WMO World Meteorological Organization Working together in weather, climate and water Existing Flood Management Guidance Materials, Databases and Training Materials Joachim Saalmüller WMO Sectretariat Commission

WMO World Meteorological Organization Working together in weather, climate and water Existing Flood Management Guidance Materials, Databases and Training Materials Joachim Saalmüller WMO Sectretariat Commission

REAL EARNINGS JUNE 2018

Transmission of material in this release is embargoed until 8:30 a.m. (EDT), Thursday, July 12, 2018 USDL-18-1144 Technical Information: (202) 691-6555 cesinfo@bls.gov www.bls.gov/ces Media Contact: (202)

Transmission of material in this release is embargoed until 8:30 a.m. (EDT), Thursday, July 12, 2018 USDL-18-1144 Technical Information: (202) 691-6555 cesinfo@bls.gov www.bls.gov/ces Media Contact: (202)

BANK OF GUYANA. BANKING SYSTEM STATISTICAL ABSTRACT Website:

BANK OF GUYANA BANKING SYSTEM STATISTICAL ABSTRACT Website: www.bankofguyana.org.gy RESEARCH DEPARTMENT March 2010 STATISTICAL ABSTRACT TABLES CONTENTS 1. MONETARY AUTHORITY 1.1 Bank of Guyana: Assets

BANK OF GUYANA BANKING SYSTEM STATISTICAL ABSTRACT Website: www.bankofguyana.org.gy RESEARCH DEPARTMENT March 2010 STATISTICAL ABSTRACT TABLES CONTENTS 1. MONETARY AUTHORITY 1.1 Bank of Guyana: Assets

2nd Quarter 2018 Webcast

2nd Quarter 2018 Webcast Classic Large Cap Value Equity Presented by James J. Clarke Director of Fundamental Research & Portfolio Manager This material may not be reproduced or used in any form or medium

2nd Quarter 2018 Webcast Classic Large Cap Value Equity Presented by James J. Clarke Director of Fundamental Research & Portfolio Manager This material may not be reproduced or used in any form or medium

University System of Georgia s 2016 Georgia Summit Fraud in Higher Education

University System of Georgia s 2016 Georgia Summit Fraud in Higher Education How to Protect your Institutions! September 14 2016 Jeff Fucito, CPA Aleisa Howell, CPA Jon Schultz, CPA Augusta Marriott at

University System of Georgia s 2016 Georgia Summit Fraud in Higher Education How to Protect your Institutions! September 14 2016 Jeff Fucito, CPA Aleisa Howell, CPA Jon Schultz, CPA Augusta Marriott at

Section 6621 of the Internal Revenue Code establishes the interest rates on

Part 1 Section 6621.--Determination of Rate of Interest 26 CFR 301.6621-1: Interest rate. Rev. Rul. -32 Section 6621 of the Internal Revenue Code establishes the interest rates on overpayments and underpayments

Part 1 Section 6621.--Determination of Rate of Interest 26 CFR 301.6621-1: Interest rate. Rev. Rul. -32 Section 6621 of the Internal Revenue Code establishes the interest rates on overpayments and underpayments

Cost Estimation of a Manufacturing Company

Cost Estimation of a Manufacturing Company Name: Business: Date: Economics of One Unit: Manufacturing Company (Only complete if you are making a product, such as a bracelet or beauty product) Economics

Cost Estimation of a Manufacturing Company Name: Business: Date: Economics of One Unit: Manufacturing Company (Only complete if you are making a product, such as a bracelet or beauty product) Economics

Raymond James The 35 th Annual Institutional Investors Conference

Raymond James The 35 th Annual Institutional Investors Conference Edward Tilly, CEO March 4, 2014 1 Forward-Looking Statements This presentation may contain forward-looking statements, within the meaning

Raymond James The 35 th Annual Institutional Investors Conference Edward Tilly, CEO March 4, 2014 1 Forward-Looking Statements This presentation may contain forward-looking statements, within the meaning