Internal Control in Poland. Monika Kos Lima, 30 March 2016

|

|

|

- Arlene Ramsey

- 5 years ago

- Views:

Transcription

1 Internal Control in Poland Monika Kos Lima, 30 March 2016

2 Plan of the presentation Poland in numbers Factors of reforms Reference models Legal basic and definition Implementation and reporting Role of the CHU Challenges and benefits

3 Poland in numbers

4 Poland in numbers Central Europe Country, since 2004 European Union Member State Total area: 312,7 thousand kilometres square Population: 38,5 million people Poland Government Budget for 2016: State budget revenue 313,8 billion PLN State budget expenditure 368,5 billion PLN One of the safer country in the world to live (Global Peace Index for 2014)

; almost 3000 municipalities Total")

5 Poland in numbers Public administration: 19 ministries Central offices: agencies, funds, inspectorates, institutes, etc. 16 administration regions: 16 regional government offices 16 local government offices (self-government); almost 3000 municipalities Total 60,000 public sector entities

6 Factors of reforms

7 Background of the public management reform in the EU Countries Factors for the reform: accessions to the EU of 2004, 2007 and 2013 need for administrative reforms recognition of need to manage risk reduce budget deficit following the financial crisis tax payers claiming value for money

8 Managerial accountability direction across the EU Focus on compliance with rules and legal and/or administrative provisions (input oriented) Focus on the achievement of organisational objectives and efficient, economic and effective use of public money (output oriented)

Internal Audit (IA) Central Harmonisation")

9 Public Internal (Financial) Control European approach FMC PIFC IA CHU Public Internal Financial Control (PIFC) Financial Management and Control (FMC) Internal Audit (IA) Central Harmonisation Unit (CHU)

10 PIC - European framework for Internal Control in the Public Sector

11 COSO ERM model WHAT? GOVERNANCE COMPONENTS & ACTIVITIES WHO?

12 Public Internal Control Entire control system within the public finance sector and all institutions involved in controlling public funds (Treasury, SAI, etc)

13 Interconnection - 5 layers of defence Entity - wide Gov t - wide National Layer 1 Layer 2 Layer 3 Layer 4 Layer 5 Management Control system Internal Audit Centralised Budget Inspection State Audit Office National Parliament (Complaintdriven function to investigate cases of fraud and serious irregularity) Audit Committee/ Council CHU Source: based on European Commission, DG Budget

14 Legal basis and definition

15 Legal basis Key regulations included in the Public Finance Act were introduced in The PFA was updated 3 times (2005, 2006 and 2009) current came into force in January 2010 Standards issued by the Minister of Finance for the public finance sector

Decentralised IA Service")

16 Key actors The Polish CHU in the MoF for IC and IA Decentralised IC system (all entities) Audit Committees (ministries) Decentralised IA Service (selected)

17 Key roles Head of public entity ensures functioning of an adequate, efficient and effective management control in the organisation The minister, a commune foreman, a mayor, a chairman of the management board of the local government unit - ensures functioning of an adequate, efficient and effective management control in the supervised organisations Audit Committees (established in all ministries) - provide consulting services to the minister in the scope of ensuring adequate, efficient and effective management control Internal audit assurance provider and consultant Minister of Finance (CHU) develops and disseminates the law regulations, standards and guidelines, assess the system in practice and takes improvement actions. 17

.")

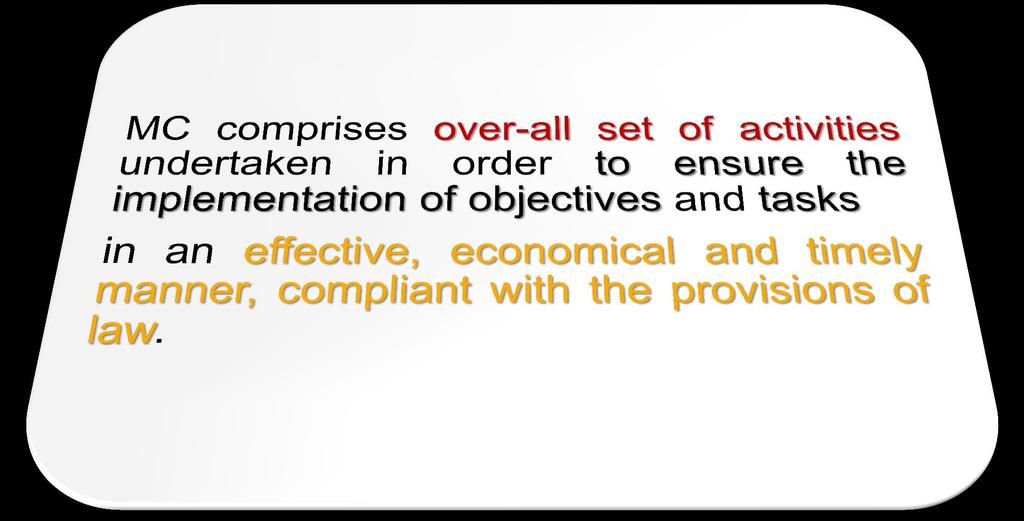

18 In Poland Internal Control = Management Control Internal Control in the Polish law is defined as Management Control (MC). Decentralised managerial accountability for stewardship of the organisation. MC is understood as general model of management binding in the public sector.

19 Definition

20 The MC objectives are to ensure in particular: risk management compliance with the provisions of law and internal procedures efficiency and effectivenes s of operation efficiency and effectivenes s of information flow observance and promotion of rules of ethical conduct protection of resources credibility of reports

21 What is (not) MC Management and control system based on international standards to make public organizations better managed, more transparent and accountable. MC is not additional bureaucracy, but motivation to check what is already in place, how it works and what should be improve. MC is continual improvement of the organisation.

22 Main characteristics of MC: the process integrated with the activity of the organisation, effected by people on all levels of the organisation, supports achieving objectives, provides reasonable assurance.

23 Key MC elements: principles procedures organization attitudes resources

24 Managerial accountability Managers of all levels public finance sector entities are taking responsibility for the performance of the organisation and system, and being accountable for its results.

25 Managerial accountability Important questions Did the organisation: follow the rules? achieve its objectives? meet expectations? provide information on its activities and achievements? face consequences for its actions?

26 Requirements for managerial accountability Authority for head of public entity to make decisions Managerial structure within the organisation and delegation of authority to individual managers Objectives set for each level of management, agreed resources, timescales, accountability arrangements, boundaries of the manager s responsibilities Good quality information Action taken when there is management failure

27 MA implementation and reporting

28 MC levels 1st level of the manage ment control 1st level of the manage ment control The head of the entity The Minister The Mayor The commune foreman The head of the entity 2nd level of the manage ment control

29 MC elements Management control standards Public Finance Act Obligatory for all entities Obligatory for appointed entities internal environment objectives and risk management control mechanisms Annual action plan Report on the execution of the action plan information and communication monitoring and evaluation Statement on the condition of the management control 29

30 MC - annual action plan Indicators of the level of achievement of the objective Planned values of indicators Objectives Reference to the strategic documents Tasks aimed at achievement of the objectives 30

31 Statement on MC conditions The statement is divided into three sections: Section one is the statement itself evaluation of the condition of the management control (levels A, B, C) Section two shall contain reservations in regard to the functioning of the management control Section three provides description of activities undertaken to enhance the management control The statement refers to the year preceding the year of submission of the statement The minister in charge of the branch may oblige the head of entity in the branch to submit a statement on the condition of management control covering the entity he/she is in charge of 31

32 Code of Ethics Anticorruption policy HR policies and practices Organisational structure MC in practice, examples Annual activity plan (indicators) Performance budgeting Risk mamagement Objectives & risk mgnt Approvals, reviews, Securing assets Segregation of duties Information Technology controls Ongoing supervision Management control statement Self-assessment Internal audit Report on annual activity plan execution Control & peer review Management Control STANDARDS STANDARDS IMPLEMENTATION Public Information Bulletin e-office Intranet meetings

33 Internal audit where it is? In Poland there are three types of public finance sector entities covered by internal audit: 1. entities specified directly in the PFA (for example the Chancellery of the Prime Minister, Chancellery of the President, ministries, central agencies, tax and customs chambers, etc.); 2. entities where the amount of incomes or costs declared in the financial plan exceeds PLN (included local government units); 3. the entities in which carrying out internal audit is optional (up to decision of the head of entity). 33

34 Structure of IA units Obligation of internal audit function against the PFA According to the threshold regulation According to decision of head of public organization (minister or Prime Minister) Total number of PFSO Number of PFSO, including: government sector Self-government sector self-government organizational units ND ND ND Based on information collected by the CHU in 2012

35 Internal audit key roles Providing assurance - independent and systematic assessment of the adequacy of existing systems and recommend improvements if necessary; Supporting the head of entity in achieving the objectives and tasks Independent consulting activities.

36 Internal audit since 2010 Internal audit shall be carried out by: or internal auditor employed in the entity external contractor (qualified as internal auditor). 36

37 Audit Committee - objectives Audit Committees were established in 2010 in all ministries. The objective of the Audit Committee is to advice the minister in charge of the branch in the scope of ensuring adequate, efficient and effective management control and efficient internal audit 37

38 Audit Committee key challenges How to support the minister to improve management system in the ministry and supervised entities? How to support improvement of internal audit quality in the ministry and supervised entities? 38

39 Audit Committee - tasks indicating material risks indicating material weaknesses in management control and proposing measures to improve it setting priorities for annual and strategic internal audit plans reviewing material internal audit results and monitoring the implementation thereof monitoring the effectiveness of the internal audit, including reviewing results of internal and external evaluations of the internal audit activity approving termination of employment and changing the pay and work conditions of the heads of internal audit teams 39

40 Audit Committee AC does not overlap an internal audit unit activity. AC does not carry out internal audit engagements. Advisory services delivering by the AC are not consulting services delivering by internal audit. AC advices are related to management control system and internal audit activity in the whole branch administered by the minister (including all entities supervised by the minister). The AC may suggest internal audit units to take particular actions. The AC strengthens the internal audit function. Internal audit unit supports AC. The AC usually bases on results of internal audit work. 40

41 Role of the CHU and activities taken

42 Central Harmonization Unit in Poland CHU PFSO

43 Key objectives of CHU

44 Key tasks of CHU Legislation and methodology concerning internal control (management control) and internal audit Establishing internal audit function, its promotion and protection Delivering internal auditors trainings and certification process Dissemination of law provisions and standards Assessment, monitoring and reporting on management control and internal audit in the public sector Cooperation and network, identification and promotion of good practice examples

45 Role of the CHU - maturity levels Improvement Strengthening Establishing

Basic law")

46 Main challenges Key actions Setting up MC (IC) and IA Awareness and accountability of the heads of public sector entities Understanding of internal audit role and responsibilities Building up certified/qualified cadre of internal auditors Platform for cooperation between internal and external audit/ internal audit and internal inspection Political influence (instability) Basic law regulations FMC & IA Standards and IA Manual Establishing IA function Seminars for heads of entities Trainings and national certification system for internal auditors Promotion and protection of internal audit function Assessments of FMC and IA (CHU on the spot) Analysis of information and reporting Common terminology for internal and external auditors 46

47 Main challenges Key actions Strengthening MC (IC) and IA FMC treated only as financial matters New definitions and IIA Standards Risk management approach Independence of IA Not sufficient number of certified internal auditors Risk management Manual Self-assessment guidelines (for IA and FMC) Trainings and pilots Many one-post (or part time) IA units IA profession opened for other certificates Quality and usefulness of results of IA work Political influence (instability) Outsourcing or own IAU in small public entities IA assessments (CHU) Analysis of information and reporting Coordinated internal audit 47

48 Cooperation The Treasury Services The Supreme Audit Office The Chancellery of the Prime Minister CHU Internal Auditors Associations The Ministry of Administrati on Independent experts

49 Main external assessors of MC SAI Chancellery of the Prime Minister CHU

50 Challenges and benefits of IC

51 Challenges on the strategic level: IC should be a part of public administration reform, including public finance management reform; Introduction of the legal provisions on IC should be properly coordinated with all other relevant laws. Development of IC is not only a role of the CHU and the Ministry of Finance; there should be close cooperation with other institutions involved in public reform process. The law is just a first not the final step in the reform, there should be a strategy for its implementation and maintaining.

52 Challenges on the coordination level Vision: Vision about the IC and its good communication is required. Control: Understanding that the IC is not a new type of control activities but a management system, involving all levels of management and staff. Monitoring by CHU: Not to focus on the existence of bureaucratic processes but promote a new management style based on planning, risk management and measuring achievements of objectives. Timetable: Assuring time and support to the head of entities for building new approach within entity.

53 Challenges on the operational level: Raising management awareness and professionalism by: providing seminars, conferences and training; introducing pilots programmes; sharing good practice examples. Creating management tools: standards, guidelines, methodology; professional internal audit service; tools for self-assessment, etc.

54 The sound IC should help public entities to: ensure optimum utilisation of resources, guide operations to achieve objectives, improve quality of the service and products, minimise deviations and risks of irregularities, establish responsibility and facilitate delegations, motivate employees, facilitate coordination and information flow between departments, increase efficiency, increase trust and improve image of the public sector.

55 Conclusion Implementation of PIA system is a circle Building up; IA cadre, Heads of PFSOs awareness Assessment/ verification Development Strategy/ CHU/ Legal act Implementation in the PFSOs Peer reviews/ evaluations by CHU EU Experts/ exchange of know how International best practices Regulations/ standards Seminars/ workshops Study visits

56 Conclusion: Developing IC is thus an iterative process that involves continually improving performance and governance, rather than introducing a new, extra system. The existing management system shall be structured, formalised and improved in accordance with identified needs and cost considerations. Internationally-recognised or national standards and frameworks offer common points of reference within trends in modern management and provide a comprehensive, structured approach to internal control.

57 Sources The presentation was based on: 1) the Polish regulations and experience 2) PIC framework developed by DG Budget 3) COSO model 4) international exchange of practice during events organised by: DG Budget PEMPAL Internal Audit Community of Practice and many other projects and initiatives.

58 QUESTIONS

59 Monika Kos 59

PIFC Public Internal Financial Control

PIFC Public Internal Financial Control Istanbul, February 2008 Robert de Koning European Commission DG BUDGET.B.3 10/11/2011 1 What is PIFC? Comprehensive concept and strategy to improve the quality of

PIFC Public Internal Financial Control Istanbul, February 2008 Robert de Koning European Commission DG BUDGET.B.3 10/11/2011 1 What is PIFC? Comprehensive concept and strategy to improve the quality of

SIGMA Support for Improvement in Governance and Management A joint initiative of the OECD and the European Union, principally financed by the EU

SIGMA Support for Improvement in Governance and Management A joint initiative of the OECD and the European Union, principally financed by the EU KOSOVO PUBLIC INTERNAL FINANCIAL CONTROL (PIFC) ASSESSMENT

SIGMA Support for Improvement in Governance and Management A joint initiative of the OECD and the European Union, principally financed by the EU KOSOVO PUBLIC INTERNAL FINANCIAL CONTROL (PIFC) ASSESSMENT

STRATEGY OF PUBLIC INTERNAL FINANCIAL CONTROL DEVELOPMENT IN THE REPUBLIC OF SERBIA FOR THE PERIOD OF

Ministry of Finance STRATEGY OF PUBLIC INTERNAL FINANCIAL CONTROL DEVELOPMENT IN THE REPUBLIC OF SERBIA FOR THE PERIOD OF 2017-2020 www.mfin.gov.rs REPUBLIC OF SERBIA MINISTRY OF FINANCE TABLE OF CONTENTS

Ministry of Finance STRATEGY OF PUBLIC INTERNAL FINANCIAL CONTROL DEVELOPMENT IN THE REPUBLIC OF SERBIA FOR THE PERIOD OF 2017-2020 www.mfin.gov.rs REPUBLIC OF SERBIA MINISTRY OF FINANCE TABLE OF CONTENTS

Project fiche IPA National programmes 2012/ Component I

Project fiche IPA National programmes 2012/ Component I 1. IDENTIFICATION Project Title Implementation of a modern Financial Management and Control system and Public Financial Inspection in Albania CRIS

Project fiche IPA National programmes 2012/ Component I 1. IDENTIFICATION Project Title Implementation of a modern Financial Management and Control system and Public Financial Inspection in Albania CRIS

BELARUS: NOTE on the REFORM of INTERNAL AUDIT

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized 70044 BELARUS: NOTE on the REFORM of INTERNAL AUDIT The government of Belarus requested

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized 70044 BELARUS: NOTE on the REFORM of INTERNAL AUDIT The government of Belarus requested

PRIORITIES ALBANIA MAY 2013

www.sigmaweb.org PRIORITIES ALBANIA MAY 2013 This document has been produced with the financial assistance of the European Union. The views expressed herein can in no way be taken to reflect the official

www.sigmaweb.org PRIORITIES ALBANIA MAY 2013 This document has been produced with the financial assistance of the European Union. The views expressed herein can in no way be taken to reflect the official

MANAGERIAL ACCOUNTABILITY AND RISK MANAGEMENT

MANAGERIAL ACCOUNTABILITY AND RISK MANAGEMENT concept and practical implementation Discussion paper I Introduction The objective of this discussion paper is to explain the concept of managerial accountability

MANAGERIAL ACCOUNTABILITY AND RISK MANAGEMENT concept and practical implementation Discussion paper I Introduction The objective of this discussion paper is to explain the concept of managerial accountability

Factors Affecting the Effectiveness of the Implementation of a Modern System of Financial Management and Control in Albania

Factors Affecting the Effectiveness of the Implementation of a Modern System of Financial Management and Control in Albania Abstract Ariana Konomi Eqrem Cabej University, Gjirokastra, Albania arianakonomi@yahoo.com

Factors Affecting the Effectiveness of the Implementation of a Modern System of Financial Management and Control in Albania Abstract Ariana Konomi Eqrem Cabej University, Gjirokastra, Albania arianakonomi@yahoo.com

It is currently the institution whose role consists of supporting the promotion of:

The supreme audit institution of Romania, the Court of Accounts, was initially set up in 1864 and operated until 1948. For the following 25 years financial control was initially the responsibility of the

The supreme audit institution of Romania, the Court of Accounts, was initially set up in 1864 and operated until 1948. For the following 25 years financial control was initially the responsibility of the

COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL. Towards robust quality management for European Statistics

EN EN EN EUROPEAN COMMISSION Brussels, 15.4.2011 COM(2011) 211 final COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL Towards robust quality management for European Statistics

EN EN EN EUROPEAN COMMISSION Brussels, 15.4.2011 COM(2011) 211 final COMMUNICATION FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL Towards robust quality management for European Statistics

PRIORITIES TURKEY MAY Authorised for publication by Karen Hill, Head of the SIGMA Programme

PRIORITIES TURKEY MAY 2014 Authorised for publication by Karen Hill, Head of the SIGMA Programme These priorities have been produced with the financial assistance of the European Union. They should not

PRIORITIES TURKEY MAY 2014 Authorised for publication by Karen Hill, Head of the SIGMA Programme These priorities have been produced with the financial assistance of the European Union. They should not

Managing the Transition to Internal Audit

Managing the Transition to Internal Audit PEMPAL workshop OECD/SIGMA, Noel Hepworth Yalta, Ukraine 26-28 May 2010 The transition to internal audit Transition plans often have the wrong order of priorities.

Managing the Transition to Internal Audit PEMPAL workshop OECD/SIGMA, Noel Hepworth Yalta, Ukraine 26-28 May 2010 The transition to internal audit Transition plans often have the wrong order of priorities.

THE IMPLEMENTATION OF INTERNAL CONTROL USING THE THREE LINES OF DEFENSE MODEL IN CONTROLLING CORRUPTION IN THE MINISTRY OF FINANCE OF INDONESIA

THE IMPLEMENTATION OF INTERNAL CONTROL USING THE THREE LINES OF DEFENSE MODEL IN CONTROLLING CORRUPTION IN THE MINISTRY OF FINANCE OF INDONESIA Nur Achmad, HaulaRosdiana, SafriNurmantu Faculty of Administrative

THE IMPLEMENTATION OF INTERNAL CONTROL USING THE THREE LINES OF DEFENSE MODEL IN CONTROLLING CORRUPTION IN THE MINISTRY OF FINANCE OF INDONESIA Nur Achmad, HaulaRosdiana, SafriNurmantu Faculty of Administrative

From spending to managing public funds

PERFORMANCE BUDGET, RESULTS - ORIENTED BUDGET From spending to managing public funds The Chancellery of the Prime Minister and the World Bank International Conference Performance-Based Budgeting: Lessons

PERFORMANCE BUDGET, RESULTS - ORIENTED BUDGET From spending to managing public funds The Chancellery of the Prime Minister and the World Bank International Conference Performance-Based Budgeting: Lessons

Screening report Serbia

[date] Screening report Serbia Chapter 32 Financial control Date of screening meetings: Explanatory meeting: 17 October 2013 Bilateral meeting: 26 November 2013 I. CHAPTER CONTENT This chapter contains

[date] Screening report Serbia Chapter 32 Financial control Date of screening meetings: Explanatory meeting: 17 October 2013 Bilateral meeting: 26 November 2013 I. CHAPTER CONTENT This chapter contains

Standard Summary Project Fiche IPA centralised programmes Project Fiche: 9

Standard Summary Project Fiche IPA centralised programmes Project Fiche: 9 1. Basic information 1.1 CRIS Number: 2009/021-170 1.2 Title: Strengthening the management and control systems for EU financial

Standard Summary Project Fiche IPA centralised programmes Project Fiche: 9 1. Basic information 1.1 CRIS Number: 2009/021-170 1.2 Title: Strengthening the management and control systems for EU financial

MONTENEGRO. Support to the Tax Administration INSTRUMENT FOR PRE-ACCESSION ASSISTANCE (IPA II) Action summary

Action summary") INSTRUMENT FOR PRE-ACCESSION ASSISTANCE (IPA II) 2014-2020 MONTENEGRO Support to the Tax Administration Action summary This Action aims to support Montenegro in the process of fulfilling the EU preaccession

INSTRUMENT FOR PRE-ACCESSION ASSISTANCE (IPA II) 2014-2020 MONTENEGRO Support to the Tax Administration Action summary This Action aims to support Montenegro in the process of fulfilling the EU preaccession

BERGRIVIER MUNICIPALITY. Risk Management Risk Appetite Framework

BERGRIVIER MUNICIPALITY Risk Management Risk Appetite Framework APRIL 2018 1 Document review and approval Revision history Version Author Date reviewed 1 2 3 4 5 This document has been reviewed by Version

BERGRIVIER MUNICIPALITY Risk Management Risk Appetite Framework APRIL 2018 1 Document review and approval Revision history Version Author Date reviewed 1 2 3 4 5 This document has been reviewed by Version

City Commission Policy 104 AUDIT POLICY. DEPARTMENT: City Auditor. DATE ADOPTED: April 22, DATE OF LAST REVISION: December 5, 2018

City Commission Policy 104 AUDIT POLICY DEPARTMENT: City Auditor DATE ADOPTED: April 22, 1987 DATE OF LAST REVISION: December 5, 2018 104.01 AUTHORITY: City Commission. 104.02 SCOPE AND APPLICABILITY:

City Commission Policy 104 AUDIT POLICY DEPARTMENT: City Auditor DATE ADOPTED: April 22, 1987 DATE OF LAST REVISION: December 5, 2018 104.01 AUTHORITY: City Commission. 104.02 SCOPE AND APPLICABILITY:

Guidance document on. management verifications to be carried out by Member States on operations co-financed by

Final version of 05/06/2008 COCOF 08/0020/04-EN Guidance document on management verifications to be carried out by Member States on operations co-financed by the Structural Funds and the Cohesion Fund

Final version of 05/06/2008 COCOF 08/0020/04-EN Guidance document on management verifications to be carried out by Member States on operations co-financed by the Structural Funds and the Cohesion Fund

Table of contents. Introduction Regulatory requirements... 3

COCOF 08/0020/02-EN DRAFT Guidance document on management verifications to be carried out by Member States on projects co-financed by the Structural Funds and the Cohesion Fund for the 2007 2013 programming

COCOF 08/0020/02-EN DRAFT Guidance document on management verifications to be carried out by Member States on projects co-financed by the Structural Funds and the Cohesion Fund for the 2007 2013 programming

Romanian Court of Accounts RISK MANAGEMENT 24 April 2012 Warsaw, Poland

Romanian Court of Accounts RISK MANAGEMENT 24 April 2012 Warsaw, Poland 1 INTOSAI GOV 9100 Guidelines for Internal Control Standards in Public Sector and INTOSAI GOV 9130 Further Information on Entity

Romanian Court of Accounts RISK MANAGEMENT 24 April 2012 Warsaw, Poland 1 INTOSAI GOV 9100 Guidelines for Internal Control Standards in Public Sector and INTOSAI GOV 9130 Further Information on Entity

COMMUNICATION TO THE COMMISSION MISSION CHARTER OF THE INTERNAL AUDIT SERVICE OF THE EUROPEAN COMMISSION

EUROPEAN COMMISSION Brussels, 30.6.2017 C(2017) 4435 final COMMUNICATION TO THE COMMISSION MISSION CHARTER OF THE INTERNAL AUDIT SERVICE OF THE EUROPEAN COMMISSION EN EN COMMUNICATION TO THE COMMISSION

EUROPEAN COMMISSION Brussels, 30.6.2017 C(2017) 4435 final COMMUNICATION TO THE COMMISSION MISSION CHARTER OF THE INTERNAL AUDIT SERVICE OF THE EUROPEAN COMMISSION EN EN COMMUNICATION TO THE COMMISSION

The development and current situation of ICPAC and the Accountancy profession in Cyprus. September 2017

The development and current situation of ICPAC and the Accountancy profession in Cyprus September 2017 Agenda 1. ICPAC in brief 2. Milestones in the Institute s / profession s development 3. Current position

The development and current situation of ICPAC and the Accountancy profession in Cyprus September 2017 Agenda 1. ICPAC in brief 2. Milestones in the Institute s / profession s development 3. Current position

Legal and Institutional Frameworks Supporting Accountability in Budgeting and Service Delivery Performance. Veronika Meszarits, Mostar, 4-6 Dec 2007

Legal and Institutional Frameworks Supporting Accountability in Budgeting and Service Delivery Performance Veronika Meszarits, Mostar, 4-6 Dec 2007 1 Supporting performance accountability Introduction

Legal and Institutional Frameworks Supporting Accountability in Budgeting and Service Delivery Performance Veronika Meszarits, Mostar, 4-6 Dec 2007 1 Supporting performance accountability Introduction

South East Europe (SEE) SEE Control Guidelines

SEE Control Guidelines") South East Europe (SEE) SEE Control Guidelines Version 1.4. Final version approved by the MC 10 th June 2009 1 st amendment to be approved by MC (2.0) 1 CONTENTS 1 Purpose and content of the SEE Control

South East Europe (SEE) SEE Control Guidelines Version 1.4. Final version approved by the MC 10 th June 2009 1 st amendment to be approved by MC (2.0) 1 CONTENTS 1 Purpose and content of the SEE Control

Guidance on a common methodology for the assessment of management and control systems in the Member States ( programming period)

") Final version of 12/09/2008 EUROPEAN COMMISSION DIRECTORATE-GENERAL MARITIME AFFAIRS AND FISHERIES EFFC/27/2008 Guidance on a common methodology for the assessment of management and control systems in

Final version of 12/09/2008 EUROPEAN COMMISSION DIRECTORATE-GENERAL MARITIME AFFAIRS AND FISHERIES EFFC/27/2008 Guidance on a common methodology for the assessment of management and control systems in

LAW ON BANKING AGENCY OF REPUBLIKA SRPSKA. Article 1

Translation by Banking Agency of Republika Srpska LAW ON BANKING AGENCY OF REPUBLIKA SRPSKA I. GENERAL PROVISIONS Article 1 This Law shall regulate the status, authority, organization, financing and operation

Translation by Banking Agency of Republika Srpska LAW ON BANKING AGENCY OF REPUBLIKA SRPSKA I. GENERAL PROVISIONS Article 1 This Law shall regulate the status, authority, organization, financing and operation

ANTI-FRAUD STRATEGY INTERREG IPA CBC PROGRAMMES BULGARIA SERBIA BULGARIA THE FORMER YUGOSLAV REPUBLIC OF MACEDONIA BULGARIA TURKEY

ANTI-FRAUD STRATEGY INTERREG IPA CBC PROGRAMMES 2014-2020 BULGARIA SERBIA BULGARIA THE FORMER YUGOSLAV REPUBLIC OF MACEDONIA BULGARIA TURKEY VERSION NOVEMBER 2016 1 TABLE OF CONTENTS PRINCIPLE 3 FOREWORD

ANTI-FRAUD STRATEGY INTERREG IPA CBC PROGRAMMES 2014-2020 BULGARIA SERBIA BULGARIA THE FORMER YUGOSLAV REPUBLIC OF MACEDONIA BULGARIA TURKEY VERSION NOVEMBER 2016 1 TABLE OF CONTENTS PRINCIPLE 3 FOREWORD

ANNEX ICELAND NATIONAL PROGRAMME IDENTIFICATION. Iceland CRIS decision number 2012/ Year 2012 EU contribution.

ANNEX ICELAND NATIONAL PROGRAMME 2012 1 IDENTIFICATION Beneficiary Iceland CRIS decision number 2012/023-648 Year 2012 EU contribution 11,997,400 EUR Implementing Authority European Commission Final date

ANNEX ICELAND NATIONAL PROGRAMME 2012 1 IDENTIFICATION Beneficiary Iceland CRIS decision number 2012/023-648 Year 2012 EU contribution 11,997,400 EUR Implementing Authority European Commission Final date

Internal audit Community of Practice

Internal audit Community of Practice Control model evolution in ex soviet countries Diana Grosu-Axenti Head of IA CoP Ruslana Rudnitka RIFIX expert Background of communist system No democracy: No real

Internal audit Community of Practice Control model evolution in ex soviet countries Diana Grosu-Axenti Head of IA CoP Ruslana Rudnitka RIFIX expert Background of communist system No democracy: No real

Background paper. The ECA s modified approach to the Statement of Assurance audits in Cohesion

Background paper The ECA s modified approach to the Statement of Assurance audits in Cohesion December 2017 1 In our 2018-2020 strategy the European Court of Auditors (ECA) decided to take a fresh look

Background paper The ECA s modified approach to the Statement of Assurance audits in Cohesion December 2017 1 In our 2018-2020 strategy the European Court of Auditors (ECA) decided to take a fresh look

Cross-cutting audit issues

6th MEETING of the High Level Expert Group on Monitoring Simplification for Beneficiaries of ESI Funds Cross-cutting audit issues 1. Although there have been some improvement in quality and professionalisation

6th MEETING of the High Level Expert Group on Monitoring Simplification for Beneficiaries of ESI Funds Cross-cutting audit issues 1. Although there have been some improvement in quality and professionalisation

Training on EU policies for Directors of the Region of Sicily. Brussels Office of the Region of Sicily Rue Belliard 12

Training on EU policies for Directors of the Region of Sicily Brussels Office of the Region of Sicily Rue Belliard 12 EU Budget CZ state budget Other public budgets Direct gains to contractors Transfers

Training on EU policies for Directors of the Region of Sicily Brussels Office of the Region of Sicily Rue Belliard 12 EU Budget CZ state budget Other public budgets Direct gains to contractors Transfers

COMMISSION DECISION. of on technical provisions necessary for the operation of the transition facility in the Republic of Croatia

EUROPEAN COMMISSION Brussels, 13.6.2013 C(2013) 3463 final COMMISSION DECISION of 13.6.2013 on technical provisions necessary for the operation of the transition facility in the Republic of Croatia EN

EUROPEAN COMMISSION Brussels, 13.6.2013 C(2013) 3463 final COMMISSION DECISION of 13.6.2013 on technical provisions necessary for the operation of the transition facility in the Republic of Croatia EN

Annex 1. Action Fiche for Solomon Islands

Annex 1 Action Fiche for Solomon Islands 1. IDENTIFICATION Title/Number FED/2012/023-802 Second Solomon Islands Technical Cooperation Facility (TCF II) Total cost EUR 1,157,000 Aid method / Method of implementation

Annex 1 Action Fiche for Solomon Islands 1. IDENTIFICATION Title/Number FED/2012/023-802 Second Solomon Islands Technical Cooperation Facility (TCF II) Total cost EUR 1,157,000 Aid method / Method of implementation

CYPRUS INVESTMENT FIRM CIF

CYPRUS INVESTMENT FIRM CIF The Applicable Legislation The Law governing the Cyprus Investment Firms (the CIF ) is the Law 144(I)/2007 as amended (the Law ). The Law has adopted a number of the EU Directives

CYPRUS INVESTMENT FIRM CIF The Applicable Legislation The Law governing the Cyprus Investment Firms (the CIF ) is the Law 144(I)/2007 as amended (the Law ). The Law has adopted a number of the EU Directives

SOLVENCY AND FINANCIAL CONDITION REPORT EUROLIFE LTD

SOLVENCY AND FINANCIAL CONDITION REPORT EUROLIFE LTD FOR THE YEAR ENDING 31 DECEMBER 2016 1 Table of Contents 1.Executive Summary... 5 1.1 Overview... 5 1.2 Business and performance... 5 1.3 System of

SOLVENCY AND FINANCIAL CONDITION REPORT EUROLIFE LTD FOR THE YEAR ENDING 31 DECEMBER 2016 1 Table of Contents 1.Executive Summary... 5 1.1 Overview... 5 1.2 Business and performance... 5 1.3 System of

Governance, and Legal and Institutional Arrangements

Governance, and Legal and Institutional Arrangements Based on Client Presentation October 2010 1 Outline Wider institutional structures Coordination challenges Accountability [For issues surrounding the

Governance, and Legal and Institutional Arrangements Based on Client Presentation October 2010 1 Outline Wider institutional structures Coordination challenges Accountability [For issues surrounding the

Guidance document on a common methodology for the assessment of management and control systems in the Member States ( programming period)

") EUROPEAN COMMISSION DG Regional Policy DG Employment, Social Affairs and Equal Opportunities Guidance document on a common methodology for the assessment of management and control systems in the Member

EUROPEAN COMMISSION DG Regional Policy DG Employment, Social Affairs and Equal Opportunities Guidance document on a common methodology for the assessment of management and control systems in the Member

Encl.: Report on the annual accounts of the Clean Sky Joint Undertaking for the financial year 2015 together with the Joint Undertaking's reply.

Council of the European Union Brussels, 17 November 2016 (OR. en) 14055/16 FIN 760 COVER NOTE From: date of receipt: 17 November 2016 To: Subject: Mr Klaus-Heiner LEHNE, President of the European Court

Council of the European Union Brussels, 17 November 2016 (OR. en) 14055/16 FIN 760 COVER NOTE From: date of receipt: 17 November 2016 To: Subject: Mr Klaus-Heiner LEHNE, President of the European Court

STANDARD TWINNING PROJECT FICHE

STANDARD TWINNING PROJECT FICHE 1. Basic Information 1.1 Publication reference Number: EuropeAid/ 136-263/IH/ACT/AL 1.2 Programme: IPA National programmes/component I (2013) 1.3 Twinning Number: AL 13

STANDARD TWINNING PROJECT FICHE 1. Basic Information 1.1 Publication reference Number: EuropeAid/ 136-263/IH/ACT/AL 1.2 Programme: IPA National programmes/component I (2013) 1.3 Twinning Number: AL 13

Republic of Kosovo. Public Financial Management Reform Action Plan (PFM RAP)

") Republic of Kosovo Public Financial Management Reform Action Plan (PFM RAP) November 2009 1 Table of Contents 1 INTRODUCTION...5 2. REFORM THEMES...6 2.1 CREDIBLE POLICY BASED BUDGET...6 2.2 TAX ADMINISTRATION...9

Republic of Kosovo Public Financial Management Reform Action Plan (PFM RAP) November 2009 1 Table of Contents 1 INTRODUCTION...5 2. REFORM THEMES...6 2.1 CREDIBLE POLICY BASED BUDGET...6 2.2 TAX ADMINISTRATION...9

BOSNIA AND HERZEGOVINA

INSTRUMENT FOR PRE-ACCESSION ASSISTANCE (IPA II) 2014-2020 BOSNIA AND HERZEGOVINA Improving Public Internal Financial Control (PIFC) Action summary The present Action is to be seen as a continuation of

INSTRUMENT FOR PRE-ACCESSION ASSISTANCE (IPA II) 2014-2020 BOSNIA AND HERZEGOVINA Improving Public Internal Financial Control (PIFC) Action summary The present Action is to be seen as a continuation of

1.5 Contracting Authority (EC) European Commission, EC Delegation, on behalf of the beneficiary

European Commission, EC Delegation, on behalf of the beneficiary") Project Fiche 1.2: Supporting the process of fiscal decentralization through strengthening the capacities for sound financial management and internal financial control on local and central level 1. Basic

Project Fiche 1.2: Supporting the process of fiscal decentralization through strengthening the capacities for sound financial management and internal financial control on local and central level 1. Basic

Appendix B - Treasury Management Policy 2019/20

Appendix B - Treasury Management Policy 2019/20 B.1 Definition The Council adopts the CIPFA definition of Treasury management as: The management of the organisation s investments and cash flows, its banking,

Appendix B - Treasury Management Policy 2019/20 B.1 Definition The Council adopts the CIPFA definition of Treasury management as: The management of the organisation s investments and cash flows, its banking,

Public Administration Reform Strategy a Framework Document for the Public Financial Management Reform

Public Financial Management Reform: Trends and Lessons Learned The Experience of Bosnia and Herzegovina Public Administration Reform Strategy a Framework Document for the Public Financial Management Reform

Public Financial Management Reform: Trends and Lessons Learned The Experience of Bosnia and Herzegovina Public Administration Reform Strategy a Framework Document for the Public Financial Management Reform

THE GREEK ANTI-FRAUD STRATEGY FOR STRUCTURAL ACTIONS - ACTION PLAN (update 2017)

") THE GREEK ANTI-FRAUD STRATEGY FOR STRUCTURAL - ACTION PLAN (update 2017) COMPETENT AUTHORITY TARGET GROUPS INDICATORS OF SUCCESS (/IN OBJECTIVE 1: Promote and establish an Ethical, Anti-Fraud Culture 1.1

THE GREEK ANTI-FRAUD STRATEGY FOR STRUCTURAL - ACTION PLAN (update 2017) COMPETENT AUTHORITY TARGET GROUPS INDICATORS OF SUCCESS (/IN OBJECTIVE 1: Promote and establish an Ethical, Anti-Fraud Culture 1.1

Declaration on Internal Controls

of the Declaration on Internal Controls Paris, 18. 09. 2008 Nataša Prah, Director 1 of the Introduction WHAT IS THE DECLARATION ON INTERNAL CONTROLS? WHO HAS TO PREPARE IT? WHEN IT SHOULD BE PREPARED?

of the Declaration on Internal Controls Paris, 18. 09. 2008 Nataša Prah, Director 1 of the Introduction WHAT IS THE DECLARATION ON INTERNAL CONTROLS? WHO HAS TO PREPARE IT? WHEN IT SHOULD BE PREPARED?

Code of audit practice 2010

The statutory responsibilities and powers of appointed auditors are set out in the Audit Commission Act 1998. In discharging these specific statutory responsibilities and powers, auditors are required

The statutory responsibilities and powers of appointed auditors are set out in the Audit Commission Act 1998. In discharging these specific statutory responsibilities and powers, auditors are required

Republika e Kosovës Republika Kosovo - Republic of Kosovo Kuvendi - Skupština - Assembly

Republika e Kosovës Republika Kosovo - Republic of Kosovo Kuvendi - Skupština - Assembly Law No. 06/L 032 ON ACCOUNTING, FINANCIAL REPORTING AND AUDITING Assembly of the Republic of Kosovo, Based on Article

Republika e Kosovës Republika Kosovo - Republic of Kosovo Kuvendi - Skupština - Assembly Law No. 06/L 032 ON ACCOUNTING, FINANCIAL REPORTING AND AUDITING Assembly of the Republic of Kosovo, Based on Article

Workshop on Enhancing Financial Inclusion in the COMESA Region through Enhancement of the Regulatory and Supervisory Framework

Workshop on Enhancing Financial Inclusion in the COMESA Region through Enhancement of the Regulatory and Supervisory Framework Presented By Sylvester Mutale Kabwe Senior Analyst Licensing and Enforcement

Workshop on Enhancing Financial Inclusion in the COMESA Region through Enhancement of the Regulatory and Supervisory Framework Presented By Sylvester Mutale Kabwe Senior Analyst Licensing and Enforcement

IMPLEMENTING THE STATUTORY AUDIT DIRECTIVE IN CROATIA

MINISTRY OF FINANCE IMPLEMENTING THE STATUTORY AUDIT DIRECTIVE IN CROATIA MSc Žana Pedić Head of the Financial System Directorate Directive 2006/43/EC of the European Parliament and of the Council of 17

MINISTRY OF FINANCE IMPLEMENTING THE STATUTORY AUDIT DIRECTIVE IN CROATIA MSc Žana Pedić Head of the Financial System Directorate Directive 2006/43/EC of the European Parliament and of the Council of 17

OECD GUIDELINES ON INSURER GOVERNANCE

OECD GUIDELINES ON INSURER GOVERNANCE Edition 2017 OECD Guidelines on Insurer Governance 2017 Edition FOREWORD Foreword As financial institutions whose business is the acceptance and management of risk,

OECD GUIDELINES ON INSURER GOVERNANCE Edition 2017 OECD Guidelines on Insurer Governance 2017 Edition FOREWORD Foreword As financial institutions whose business is the acceptance and management of risk,

Department of Enterprise, Trade & Employment

Department of Enterprise, Trade & Employment Circular No. ESF/PA/1-2001 31 July 2001 FINANCIAL MANAGEMENT AND CONTROL PROCEDURES FOR THE EUROPEAN SOCIAL FUND (ESF) 2000-2006 1. Background The purpose of

Department of Enterprise, Trade & Employment Circular No. ESF/PA/1-2001 31 July 2001 FINANCIAL MANAGEMENT AND CONTROL PROCEDURES FOR THE EUROPEAN SOCIAL FUND (ESF) 2000-2006 1. Background The purpose of

International Monetary Fund s Financial Sector Stability Assessment. Force Report

International Monetary Fund s Financial Sector Stability Assessment and Caribbean Financial Task Force Report Cherno Jallow,QC Director, Policy, Research and Statistics Meet The Regulator 16 March 2011

International Monetary Fund s Financial Sector Stability Assessment and Caribbean Financial Task Force Report Cherno Jallow,QC Director, Policy, Research and Statistics Meet The Regulator 16 March 2011

INTERREG - IPA CBC ROMANIA-SERBIA PROGRAMME

ANTI-FRAUD STRATEGY INTERREG - IPA CBC ROMANIA-SERBIA PROGRAMME VERSION 2016 1 TABLE OF CONTENTS PRINCIPLE 4 FOREWORD 4 LEGAL BASIS 4 DEFINITIONS 5 I. GENERAL CONSIDERATIONS 5 I.1. AIM 5 I.2. MISSION 6

ANTI-FRAUD STRATEGY INTERREG - IPA CBC ROMANIA-SERBIA PROGRAMME VERSION 2016 1 TABLE OF CONTENTS PRINCIPLE 4 FOREWORD 4 LEGAL BASIS 4 DEFINITIONS 5 I. GENERAL CONSIDERATIONS 5 I.1. AIM 5 I.2. MISSION 6

For the year ended 31 August 2016 for Buckinghamshire University Technical College

Audit management letter For the year ended 31 August 2016 for Buckinghamshire University Technical College Contents 1. Introduction 1 2. Overview 2 3. Independence 5 4. Audit scope and objectives 7 5.

Audit management letter For the year ended 31 August 2016 for Buckinghamshire University Technical College Contents 1. Introduction 1 2. Overview 2 3. Independence 5 4. Audit scope and objectives 7 5.

Assessment of Angolan Oil Sector - Final Report VOLUME 4c - Review of the Regulatory roles of State owned Oil Companies in Norway and Indonesia

Assessment of Angolan Oil Sector - Final Report VOLUME 4c - Review of the Regulatory roles of State owned Oil Companies in Norway and Indonesia This report contains 8 pages Contents 1 Introduction 1 1.1

Assessment of Angolan Oil Sector - Final Report VOLUME 4c - Review of the Regulatory roles of State owned Oil Companies in Norway and Indonesia This report contains 8 pages Contents 1 Introduction 1 1.1

Having regard to the Treaty establishing the European Atomic Energy Community, and in particular Articles 31 and 32 thereof,

L 219/42 COUNCIL DIRECTIVE 2014/87/EURATOM of 8 July 2014 amending Directive 2009/71/Euratom establishing a Community framework for the nuclear safety of nuclear installations THE COUNCIL OF THE EUROPEAN

L 219/42 COUNCIL DIRECTIVE 2014/87/EURATOM of 8 July 2014 amending Directive 2009/71/Euratom establishing a Community framework for the nuclear safety of nuclear installations THE COUNCIL OF THE EUROPEAN

Audit manual - general part

Audit manual - general part Audit manual - general part Helsinki 2015 National Audit Office Registry no. 23/01/2015 The National Audit Office of Finland (hereafter National Audit Office) is Finland's

Audit manual - general part Audit manual - general part Helsinki 2015 National Audit Office Registry no. 23/01/2015 The National Audit Office of Finland (hereafter National Audit Office) is Finland's

ANNEX. to the COMMISSION DECISION

EUROPEAN COMMISSION Brussels, 15.12.2017 C(2017) 8512 final ANNEX 1 ANNEX to the COMMISSION DECISION on the adoption of a financing decision for 2017 and 2018 for the pilot project "Pilot project - Rare

EUROPEAN COMMISSION Brussels, 15.12.2017 C(2017) 8512 final ANNEX 1 ANNEX to the COMMISSION DECISION on the adoption of a financing decision for 2017 and 2018 for the pilot project "Pilot project - Rare

European Commission Directorate General for Development and Cooperation - EuropeAid

European Commission Directorate General for Development and Cooperation - EuropeAid Practical guide to procedures for programme estimates (project approach) Version 4.0 December 2012 CONTENTS 1. INTRODUCTION...

European Commission Directorate General for Development and Cooperation - EuropeAid Practical guide to procedures for programme estimates (project approach) Version 4.0 December 2012 CONTENTS 1. INTRODUCTION...

The tasks of the Managing Authority under IPARD II. Multi-country workshop, 13 November 2015 Tirana

The tasks of the Managing Authority under IPARD II Multi-country workshop, 13 November 2015 Tirana 1 Whatsapp? Quick look Closer look Programme monitoring IPARD II monitoring committee Evaluation Reporting

The tasks of the Managing Authority under IPARD II Multi-country workshop, 13 November 2015 Tirana 1 Whatsapp? Quick look Closer look Programme monitoring IPARD II monitoring committee Evaluation Reporting

REPORT on the annual accounts of the European Medicines Agency for the financial year 2010, together with the Agency s replies (2011/C 366/06)

") 15.12.2011 Official Journal of the European Union C 366/27 REPORT on the annual accounts of the European Medicines Agency for the financial year 2010, together with the Agency s replies (2011/C 366/06)

15.12.2011 Official Journal of the European Union C 366/27 REPORT on the annual accounts of the European Medicines Agency for the financial year 2010, together with the Agency s replies (2011/C 366/06)

Strategic report. Corporate governance. Financial statements. Financial statements

Strategic report Corporate governance Financial statements 76 Statement of Directors responsibilities 77 Independent auditor s report to the members of Tesco PLC 85 Group income statement 86 Group statement

Strategic report Corporate governance Financial statements 76 Statement of Directors responsibilities 77 Independent auditor s report to the members of Tesco PLC 85 Group income statement 86 Group statement

COMMISSION OF THE EUROPEAN COMMUNITIES COMMUNICATION TO THE COMMISSION. Revision of the Internal Control Standards and Underlying Framework

COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 16 October 2007 SEC(2007)1341 EN COMMUNICATION TO THE COMMISSION Revision of the Internal Control Standards and Underlying Framework - Strengthening Control

COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 16 October 2007 SEC(2007)1341 EN COMMUNICATION TO THE COMMISSION Revision of the Internal Control Standards and Underlying Framework - Strengthening Control

ANNEX: IPA 2010 NATIONAL PROGRAMME PART II - BOSNIA AND HERZEGOVINA. at the latest by 31 December years from the final date for contracting.

EN EN EN ANNEX: IPA 2010 NATIONAL PROGRAMME PART II - BOSNIA AND HERZEGOVINA 1. IDENTIFICATION Beneficiary Bosnia and Herzegovina CRIS number 2010 / 022-674 Year 2010 Cost EUR 6 000 000 Implementing Authority

EN EN EN ANNEX: IPA 2010 NATIONAL PROGRAMME PART II - BOSNIA AND HERZEGOVINA 1. IDENTIFICATION Beneficiary Bosnia and Herzegovina CRIS number 2010 / 022-674 Year 2010 Cost EUR 6 000 000 Implementing Authority

Independent Auditor's Report To the General Shareholders Meeting and Supervisory Board of Alior Bank S.A.

This document is a free translation of the Polish original. Terminology current in Anglo-Saxon countries has been used where practicable for the purposes of this translation in order to aid understanding.

This document is a free translation of the Polish original. Terminology current in Anglo-Saxon countries has been used where practicable for the purposes of this translation in order to aid understanding.

1. BASIC INFORMATON 2. OBJECTIVE

1. BASIC INFORMATON 1.1 PROGRAMME ENP National Annual Action Program 2007 for Azerbaijan. 1.2 TWINNING NUMBER AZ10/ENP-PCA/FI/15 1.3 TITLE Assisting the Public Financial Control Service (PFCS) in improving

1. BASIC INFORMATON 1.1 PROGRAMME ENP National Annual Action Program 2007 for Azerbaijan. 1.2 TWINNING NUMBER AZ10/ENP-PCA/FI/15 1.3 TITLE Assisting the Public Financial Control Service (PFCS) in improving

Regional Policy in the Czech Republic in the Period Around Its Accession to the European Union

Regional Policy in the Czech Republic in the Period Around Its Accession to the European Union Vladimír Sodomka This study analyses critical issues of the preparation for using structural assistance in

Regional Policy in the Czech Republic in the Period Around Its Accession to the European Union Vladimír Sodomka This study analyses critical issues of the preparation for using structural assistance in

Having regard to the Treaty on the Functioning of the European Union, and in particular Article 291 thereof,

L 244/12 COMMISSION IMPLEMTING REGULATION (EU) No 897/2014 of 18 August 2014 laying down specific provisions for the implementation of cross-border cooperation programmes financed under Regulation (EU)

L 244/12 COMMISSION IMPLEMTING REGULATION (EU) No 897/2014 of 18 August 2014 laying down specific provisions for the implementation of cross-border cooperation programmes financed under Regulation (EU)

Program budgeting - the EU approach: from theory to practice

PEMPAL Plenary Meeting of Budget Community of Practice (BCOP) Program budgeting - the EU approach: from theory to practice Grzegorz Orawiec Slovenia 27-29 March 2012 1 Program budgeting like taxes 2 Questions

PEMPAL Plenary Meeting of Budget Community of Practice (BCOP) Program budgeting - the EU approach: from theory to practice Grzegorz Orawiec Slovenia 27-29 March 2012 1 Program budgeting like taxes 2 Questions

Independent Registered Auditor s Report

TRANSLATORS EXPLANATORY NOTE The English content of this report is a free translation of the registered auditor s report of the below-mentioned Polish Company. In Poland statutory accounts as well as the

TRANSLATORS EXPLANATORY NOTE The English content of this report is a free translation of the registered auditor s report of the below-mentioned Polish Company. In Poland statutory accounts as well as the

GENERAL RISK CONTROL AND MANAGEMENT POLICY

GENERAL RISK CONTROL AND MANAGEMENT POLICY OF SIEMENS GAMESA RENEWABLE ENERGY, S.A. (Text approved by resolution of the Board of Directors dated September 12, 2018) GENERAL RISK CONTROL AND MANAGEMENT

GENERAL RISK CONTROL AND MANAGEMENT POLICY OF SIEMENS GAMESA RENEWABLE ENERGY, S.A. (Text approved by resolution of the Board of Directors dated September 12, 2018) GENERAL RISK CONTROL AND MANAGEMENT

Corporate Governance Statement 1. Organisation and governing bodies of the group 2. General Meeting of Shareholders 2

Table of contents Corporate Governance Statement 1 Organisation and governing bodies of the group 2 General Meeting of Shareholders 2 Shareholders' Nomination Board 3 The Board of Directors 4 The Board

Table of contents Corporate Governance Statement 1 Organisation and governing bodies of the group 2 General Meeting of Shareholders 2 Shareholders' Nomination Board 3 The Board of Directors 4 The Board

(Non-legislative acts) REGULATIONS

REGULATIONS") 12.7.2012 Official Journal of the European Union L 181/1 II (Non-legislative acts) REGULATIONS COMMISSION REGULATION (EU) No 600/2012 of 21 June 2012 on the verification of greenhouse gas emission reports

12.7.2012 Official Journal of the European Union L 181/1 II (Non-legislative acts) REGULATIONS COMMISSION REGULATION (EU) No 600/2012 of 21 June 2012 on the verification of greenhouse gas emission reports

Greece The former Yugoslav Republic of Macedonia IPA Cross-Border Programme OVERALL CONTRACT. Document No. 12.1: OVERALL MA CONTRACT

Greece The former Yugoslav Republic of Macedonia IPA Cross-Border Programme 2007-2013 OVERALL CONTRACT No. : < > Document No. 12.1: OVERALL MA CONTRACT OVERALL CONTRACT No. In Athens, today, the

Greece The former Yugoslav Republic of Macedonia IPA Cross-Border Programme 2007-2013 OVERALL CONTRACT No. : < > Document No. 12.1: OVERALL MA CONTRACT OVERALL CONTRACT No. In Athens, today, the

PUBLIC SECTOR AUDITING

PUBLIC SECTOR AUDITING A. Institutional Framework for Public Sector Auditing 20. Effective scrutiny by the legislature through comprehensive, competent external audit underpinned by international standards

PUBLIC SECTOR AUDITING A. Institutional Framework for Public Sector Auditing 20. Effective scrutiny by the legislature through comprehensive, competent external audit underpinned by international standards

Work Programme 2007 Report 1/2007

Work Programme 2007 Report 1/2007 WORK PROGRAMME 2007 NORDIC ENERGY REGULATORS (NordREG) Nordic Energy Regulators 2007 Report 1/2007 NordREG c/o The Energy Markets Inspectorate P.O. Box 310 SE- 631 04

Work Programme 2007 Report 1/2007 WORK PROGRAMME 2007 NORDIC ENERGY REGULATORS (NordREG) Nordic Energy Regulators 2007 Report 1/2007 NordREG c/o The Energy Markets Inspectorate P.O. Box 310 SE- 631 04

VOLUME VIII: PROCEDURES MANUAL FOR PLANNING AND RESEARCH UNIT

REPUBLIC OF RWANDA RWANDA EDUCATION BOARD (REB) REB HEADQUARTERS BUILDING VOLUME VIII: PROCEDURES MANUAL FOR PLANNING AND RESEARCH UNIT This procedures manual for Planning and Research Unit is Volume VIII

REPUBLIC OF RWANDA RWANDA EDUCATION BOARD (REB) REB HEADQUARTERS BUILDING VOLUME VIII: PROCEDURES MANUAL FOR PLANNING AND RESEARCH UNIT This procedures manual for Planning and Research Unit is Volume VIII

Producing a National SAI report on EU financial management

Producing a National SAI report on EU financial management (Version: November 30, 2004) Executive summary The Working Group on National SAI reports on EU financial management (WG) strives to assist SAIs

Producing a National SAI report on EU financial management (Version: November 30, 2004) Executive summary The Working Group on National SAI reports on EU financial management (WG) strives to assist SAIs

IPA 2011 Annual programme Public Finance : /3

IPA 2011 Annual programme Public Finance : 14-2011/3 1. Basic information 1.1 CRIS number: 2011/022-939 1.2 Title: Public Finance 1.3 ELARG statistical code: 02.32 1.4 Location: Kosovo* Implementing arrangements

IPA 2011 Annual programme Public Finance : 14-2011/3 1. Basic information 1.1 CRIS number: 2011/022-939 1.2 Title: Public Finance 1.3 ELARG statistical code: 02.32 1.4 Location: Kosovo* Implementing arrangements

Audit & Compliance Guidance

Audit & Compliance Guidance Green Infrastructure Fund Guidance for Applicants September 2018 Disclaimer Applicants should be aware that as the Green Infrastructure Fund is a new programme, the guidance

Audit & Compliance Guidance Green Infrastructure Fund Guidance for Applicants September 2018 Disclaimer Applicants should be aware that as the Green Infrastructure Fund is a new programme, the guidance

LAW ON AUDIT ON I. GENERAL PROVISIONS. Article 1

LAW ON AUDIT ON INSTRUMENT FOR PRE-ACCESSION ASSISTANCE (IPA) I. GENERAL PROVISIONS Article 1 This Law shall regulate subject-matter of audit, organization and competences of Audit Authority and manner

LAW ON AUDIT ON INSTRUMENT FOR PRE-ACCESSION ASSISTANCE (IPA) I. GENERAL PROVISIONS Article 1 This Law shall regulate subject-matter of audit, organization and competences of Audit Authority and manner

General approach to UK PFM Very centralised control of financial policy Very decentralised operation of PFM

Centralised Policy Decentralised operation Study visit PEMPAL Treasury Community of Practice (TCOP) Implementing Accounting Reform in the UK Government London, United Kingdom From September 23 to 25, eleven

Centralised Policy Decentralised operation Study visit PEMPAL Treasury Community of Practice (TCOP) Implementing Accounting Reform in the UK Government London, United Kingdom From September 23 to 25, eleven

REPORT on the annual accounts of the European Medicines Agency for the financial year 2012, together with the Agency s replies (2013/C 365/21)

") C 365/150 Official Journal of the European Union 13.12.2013 REPORT on the annual accounts of the European Medicines Agency for the financial year 2012, together with the Agency s replies (2013/C 365/21)

C 365/150 Official Journal of the European Union 13.12.2013 REPORT on the annual accounts of the European Medicines Agency for the financial year 2012, together with the Agency s replies (2013/C 365/21)

IPA TWINNING NEWS NEAR SPECIAL

IPA TWINNING NEWS NEAR SPECIAL European IPA Twinning Projects Pipeline from July till December 2016 Project title ALBANIA IPA 2014 (Indirect management CFCU) - "Strengthening of capacities of the Consumer

IPA TWINNING NEWS NEAR SPECIAL European IPA Twinning Projects Pipeline from July till December 2016 Project title ALBANIA IPA 2014 (Indirect management CFCU) - "Strengthening of capacities of the Consumer

Translation of auditor s report originally issued in Polish. The Polish original should be referred to in matters of interpretation.

Translation of auditor s report originally issued in Polish. The Polish original should be referred to in matters of interpretation. INDEPENDENT AUDITOR S REPORT ON THE AUDIT OF THE ANNUAL FINANCIAL STATEMENTS

Translation of auditor s report originally issued in Polish. The Polish original should be referred to in matters of interpretation. INDEPENDENT AUDITOR S REPORT ON THE AUDIT OF THE ANNUAL FINANCIAL STATEMENTS

2 nd INDEPENDENT EXTERNAL EVALUATION of the EUROPEAN UNION AGENCY FOR FUNDAMENTAL RIGHTS (FRA)

") 2 nd INDEPENDENT EXTERNAL EVALUATION of the EUROPEAN UNION AGENCY FOR FUNDAMENTAL RIGHTS (FRA) TECHNICAL SPECIFICATIONS 15 July 2016 1 1) Title of the contract The title of the contract is 2nd External

2 nd INDEPENDENT EXTERNAL EVALUATION of the EUROPEAN UNION AGENCY FOR FUNDAMENTAL RIGHTS (FRA) TECHNICAL SPECIFICATIONS 15 July 2016 1 1) Title of the contract The title of the contract is 2nd External

CENTRAL FINANCE AND CONTRACTS UNIT (CFCU) POLAND MEMORANDUM OF UNDERSTANDING. Article 1 - Explanatory Statement

POLAND MEMORANDUM OF UNDERSTANDING. Article 1 - Explanatory Statement") CENTRAL FINANCE AND CONTRACTS UNIT (CFCU) POLAND MEMORANDUM OF UNDERSTANDING Article 1 - Explanatory Statement The Establishment of a Central Finance and Contracts Unit (CFCU) is to be seen against the

CENTRAL FINANCE AND CONTRACTS UNIT (CFCU) POLAND MEMORANDUM OF UNDERSTANDING Article 1 - Explanatory Statement The Establishment of a Central Finance and Contracts Unit (CFCU) is to be seen against the

1 July Guideline for Municipal Competency Levels: Chief Financial Officers

1 July 2007 Guideline for Municipal Competency Levels: Chief Financial Officers issued in terms of the Local Government: Municipal Finance Management Act, 2003 Introduction This guideline is one of a series

1 July 2007 Guideline for Municipal Competency Levels: Chief Financial Officers issued in terms of the Local Government: Municipal Finance Management Act, 2003 Introduction This guideline is one of a series

CITY OF JOHANNESBURG METROPOLITAN MUNICIPALITY GROUP RISK AND ASSURANCE SERVICES GROUP RISK MANAGEMENT POLICY

CITY OF JOHANNESBURG METROPOLITAN MUNICIPALITY Effective Date 1 July 2015 TABLE OF CONTENTS 1. POLICY STATEMENT... 3 2. POLICY CONTEXT... 4 3. PURPOSE... 5 4. POLICY SCOPE AND APPLICATION... 6 5. RISK

CITY OF JOHANNESBURG METROPOLITAN MUNICIPALITY Effective Date 1 July 2015 TABLE OF CONTENTS 1. POLICY STATEMENT... 3 2. POLICY CONTEXT... 4 3. PURPOSE... 5 4. POLICY SCOPE AND APPLICATION... 6 5. RISK

ANNUAL REPORT ON THE ACTIVITIES FUNDED BY THE 8TH, 9TH AND 10TH EUROPEAN DEVELOPMENT FUNDS (EDFs)

") 10.11.2011 Official Journal of the European Union 251 ANNUAL REPORT ON THE ACTIVITIES FUNDED BY THE 8TH, 9TH AND 10TH EUROPEAN DEVELOPMENT FUNDS (EDFs) (2011/C 326/02) 10.11.2011 Official Journal of the

10.11.2011 Official Journal of the European Union 251 ANNUAL REPORT ON THE ACTIVITIES FUNDED BY THE 8TH, 9TH AND 10TH EUROPEAN DEVELOPMENT FUNDS (EDFs) (2011/C 326/02) 10.11.2011 Official Journal of the

Evidence of compliance

Appendix 3 Expanded / additional governance requirements from the Chief Financial Officer statement reflected in the local Code of Corporate Governance 1. Core Principle: Focusing on the purpose of the

Appendix 3 Expanded / additional governance requirements from the Chief Financial Officer statement reflected in the local Code of Corporate Governance 1. Core Principle: Focusing on the purpose of the

PUBLIC ADMINISTRATION REFORM MONITORING PUBLIC FINANCE

PUBLIC ADMINISTRATION REFORM MONITORING PUBLIC FINANCE 2015 This document has been prepared under the Public Administration Reform Monitoring (PARM) project, implemented by TI BiH and CIN, with financial

PUBLIC ADMINISTRATION REFORM MONITORING PUBLIC FINANCE 2015 This document has been prepared under the Public Administration Reform Monitoring (PARM) project, implemented by TI BiH and CIN, with financial

TREASURY MANAGEMENT POLICY The Association s Treasury Management Policy will be operated by the following principles:

1.0 STATEMENT OF PRINCIPLES TREASURY MANAGEMENT POLICY 2017 The Association s Treasury Management Policy will be operated by the following principles: (i) (ii) (iii) The Association regards the successful

1.0 STATEMENT OF PRINCIPLES TREASURY MANAGEMENT POLICY 2017 The Association s Treasury Management Policy will be operated by the following principles: (i) (ii) (iii) The Association regards the successful

GOOD PRACTICES FOR GOVERNANCE OF PENSION SUPERVISORY AUTHORITIES

. GOOD PRACTICES FOR GOVERNANCE OF PENSION SUPERVISORY AUTHORITIES November 2013 GOOD PRACTICES FOR GOVERNANCE OF PENSION SUPERVISORY AUTHORITIES Introduction 1. Promoting good governance has been at the

. GOOD PRACTICES FOR GOVERNANCE OF PENSION SUPERVISORY AUTHORITIES November 2013 GOOD PRACTICES FOR GOVERNANCE OF PENSION SUPERVISORY AUTHORITIES Introduction 1. Promoting good governance has been at the

Document No: AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF MUNICIPALITY OF KAMENICA FOR THE YEAR ENDED 31 DECEMBER 2017

Document No: 22.29.1-2017-08 AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF MUNICIPALITY OF KAMENICA FOR THE YEAR ENDED 31 DECEMBER 2017 Prishtina, May 2018 The National Audit Office of the Republic

Document No: 22.29.1-2017-08 AUDIT REPORT ON THE ANNUAL FINANCIAL STATEMENTS OF MUNICIPALITY OF KAMENICA FOR THE YEAR ENDED 31 DECEMBER 2017 Prishtina, May 2018 The National Audit Office of the Republic

BANK OCHRONY ŚRODOWISKA S.A. LONG-FORM AUDITORS REPORT ON THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2016

LONG-FORM AUDITORS REPORT ON THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2016 I. GENERAL NOTES 1. Background Bank Ochrony Środowiska S.A. (hereinafter the Bank ) was incorporated on the basis

LONG-FORM AUDITORS REPORT ON THE FINANCIAL STATEMENTS FOR THE YEAR ENDED 31 DECEMBER 2016 I. GENERAL NOTES 1. Background Bank Ochrony Środowiska S.A. (hereinafter the Bank ) was incorporated on the basis